Composite Returns and Nonresident Withholding for Pass...

36

WHO TO CONTACT DURING THE LIVE EVENT For Additional Registrations: -Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1) For Assistance During the Live Program: -On the web, use the chat box at the bottom left of the screen If you get disconnected during the program, you can simply log in using your original instructions and PIN. IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved for 2 CPE credit hours. To earn credit you must: • Participate in the program on your own computer connection (no sharing) – if you need to register additional people, please call customer service at 1-800-926-7926 ext.1 (or 404-881-1141 ext. 1). Strafford accepts American Express, Visa, MasterCard, Discover. • Listen on-line via your computer speakers. • Respond to five prompts during the program plus a single verification code. • To earn full credit, you must remain connected for the entire program. Composite Returns and Nonresident Withholding for Pass-Through Entities: Navigating the Multistate Complexities TUESDAY, MAY 1, 2018, 1:00-2:50 pm Eastern FOR LIVE PROGRAM ONLY

Transcript of Composite Returns and Nonresident Withholding for Pass...

WHO TO CONTACT DURING THE LIVE EVENT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 ext.1 (or 404-881-1141 ext. 1).

Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

Composite Returns and Nonresident Withholding for

Pass-Through Entities: Navigating the Multistate Complexities

TUESDAY, MAY 1, 2018, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

FOR LIVE PROGRAM ONLY

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Composite Returns and Nonresident Withholding for Pass-Through Entities

May 1, 2018

William Brown

Brown Winick

(515) 242-2412

Jeff Weinkle, CPA

State & Local Tax Manager

Aprio LLP

(770) 353-3071

4

Business Tax Preparation Landscape

• Major shift over the past 30 years in the types of business tax returns prepared, because of:

– Federal tax reform in the 1980’s that inverted the relative corporate and individual tax rates

– General Utilities repeal

– “Check the box” entity classification rules

– Change in Subchapter S eligibility rules

– Emergence of limited liability companies in 1990’s

– Growth of robust computer tax preparation software and ability to easily prepare multistate returns with numerous owners

5

What are the stakes?

• Audit adjustments on entity returns affect tax liabilities of owners

• Impact on tax preparers

• Effect of new partnership audit rules

• States hungering for more tax dollars, particularly from out of state businesses

6

Constraints on State Taxation of Multistate Businesses

• Due Process Clause of the 14th Amendment

– Source of apportionment requirements

• Commerce Clause of U.S. Constitution

– “Dormant” commerce clause

• P.L. 86-272

– Applies to sales of goods only

– Not as broad an exemption as commonly viewed

7

Case History

• National Bellas Hess, Inc. v. Department of Revenue 385 U.S. 753 (1967)

• Complete Auto Transit, Inc. v. Brady 430 U.S. 274 (1977)

• Moorman Mfg. Co. v. Bair (1978)

• Quill Corp. v. North Dakota 504 U.S. 298 (1992)

• Wisconsin Department of Revenue v. William Wrigley, Jr. (1992)

8

State of South Dakota v. Wayfair

• Response to dicta from justices in U.S. Supreme Court regarding Quill decision

• 2016 South Dakota statute

• Declaratory judgment action by state

• Summary judgment motion by Wayfair

• State appeal to South Dakota Supreme Court

• Certiorari to U.S. Supreme Court granted; case argued on April 17, 2018

9

Why Wayfair?

• Justice Kennedy dicta in Direct Marketing Association v. Brohl (2015)

• Justice Thomas dicta in Comptroller v. Wynne (2015)

• Judge Gorsuch dicta in 10th Circuit decision in Direct Marketing Association v. Brohl (2016)

10

Nexus

• Physical presence – National Bellas Hess; Quill

• Agency nexus – Scripto, Tyler Pipe

• Affiliate nexus – SFA Folio Connections; Borders Online

• Click through nexus – Amazon

• Economic nexus – MBNA; Capital One

• Licensing nexus – Geoffrey; KFC

11

Allocation and Apportionment

• Allocation – principally regarding real estate income, personal services income or investment income of residents

• Apportionment – all other types of income

13

Apportionment

• Three factor – sales, property, payroll

• Single factor – sales only

• Modified three factor – double weighting of sales

• Special apportionment approaches for specific businesses, particularly transportation and utility businesses

14

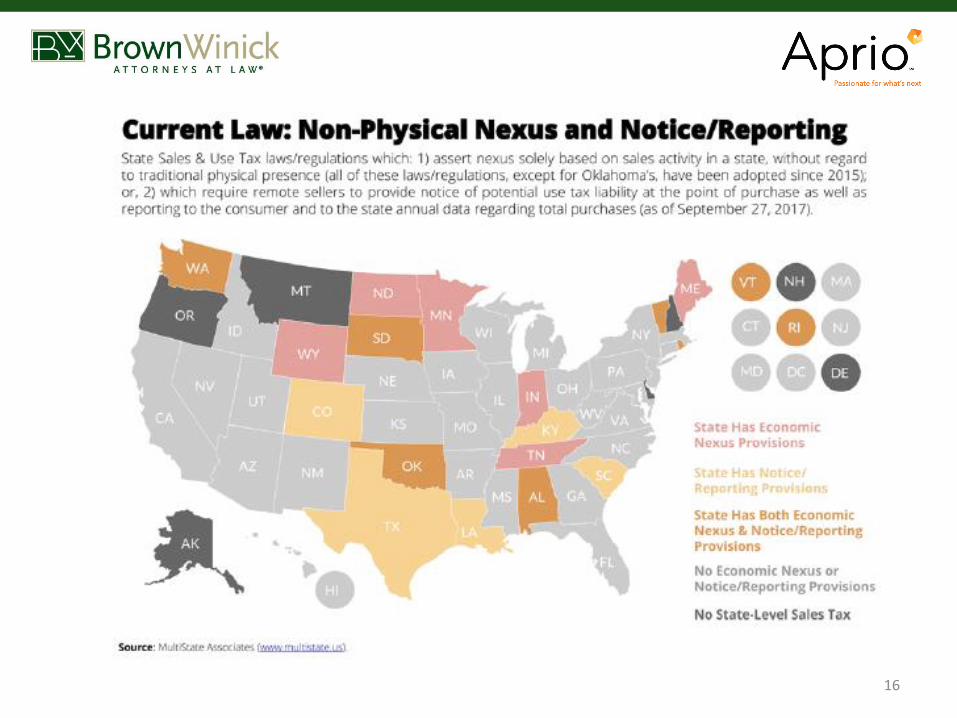

Methods of Enforcement

• Alternative taxes

– Franchise taxes

– Gross receipts taxes

• Nonrecognition of pass-through status; required C corporation treatment

• Withholding requirements

• Loss of qualification to do business in state and to access court system

15

16

17

18

Withholding

• Income base for withholding

– Pass through income

– Distributions

• Withholding rate

• Alternatives to withholding

– Submission to jurisdiction of state and agreement to file nonresident return

– Composite state filing by business on behalf of nonresident owners

– Estimated tax payment requirements19

Nonresident Withholding

• 33 states require withholding on certain nonresident partners

• Applicability & rates depend on type of owner

• How do states define “nonresident” for individual persons and business entities?

• Basis of Tax:– Distributive share of apportioned/allocated state income

– Actual distributions

• Owner files state return to claim payments against tax/obtain refunds

20

Withholding Exemptions/Opt-Out

• Rules may vary between partnerships and S-corporations

• Possible exemptions:– De minimis threshold

– Exemption Forms or Affidavits: owner consents to state taxation

– Participation in Composite/Group tax return

– Exempt entities, investment/publicly traded partnerships, etc.

21

Common Withholding Problems

• Withholding may not be reflective of ultimate tax liability– Issues with multi-tiered entities

– Net Operating Losses

• Owner may have to make separate estimated tax payments if withheld amount is insufficient to cover liability

• As partnership enters new states, distribution/guaranteed payment agreements with owners may need to be modified

22

Composite Returns

• Single group return filing on behalf of nonresident owners

• Eliminates need for owner to file separate state return

• Administrative convenience vs. lower tax liability

• Calculation of tax:– Typically computed by multiplying owner’s share of income

apportioned/allocated to state by the highest marginal tax rate

– Some states provide alternative calculation options

• Which entities can file?– State approval may be required

– Minimum number of participants may be required23

Composite Returns

• Which owners can participate? Typical requirements may include:– Nonresident for entire tax

– Does not maintain permanent place of abode in state

– The owner’s only source of state income comes from this pass-through entity (or other PTEs where composite returns are filed)

– Same tax year as PTE or other owners

• What about disregarded entities?

24

Mechanics - Required Information from Owners

• Entity type – how is the owner taxed?

• Is the owner a resident/nonresident of each state?

• Does the owner have a withholding exemption?

• Is the owner eligible to participate in the composite return?

• If eligible, does the owner choose to participate in the composite return?

• Has partnership/S-corporation collected the appropriate forms/affidavits?

• Annual election memo to owners strongly recommended

26

Example: Owner Memo LanguageGeorgia requires partnerships to withhold state income taxes on its nonresident members’ distributable shares of income

unless the member participates in the composite tax return or files a withholding exemption affidavit (see attached Form

NRW-Exemption). Members who do not participate in the composite return may be required to file a separate Georgia

tax return.

• 1. Are you a resident of Georgia during 2017?

Yes _____ No _____

• 2a. If you are a nonresident, are you eligible to participate in the composite tax return filing?

Yes _____ No _____

• 2b. If eligible, will you participate in the composite tax return filing?

Yes _____ No _____

• 2c. If participating in the Georgia composite return, do you have any other sources of taxable Georgia income?

Yes _____ No _____

• 2d. If participating in the Georgia composite return, please indicate your federal tax filing status and number of

dependents:

_____ Single _____ Married filing jointly _____ Married filing separately

_____ Number of dependents

• 3. If you are a nonresident who is not electing to participate in the composite return, have you requested a

withholding exemption by completing Form NRW-Exemption?

Yes _____ No _____

27

Challenges for Pass-through Entities

• Record keeping– Owners’ elections

– Calculating estimates and preparing returns

• Estimated payments – May need separate payments if withholding for some partners and

filing composite for others

• Coordinating scheduled distributions with state estimate/return payment requirements

• Mitigating risk

28

Mechanics - Withholding

• Election Timing– When should elections be collected from owners?

– Duration of elections: annual, biannual, or perpetual

– CA waiver request requires state approval

• Estimated Payments

• Information Reporting to State

• Inclusion of elections with partnership/S-corporation tax return

29

Mechanics - Composite Filing

• Entity election - may need approval prior to filing

• Partner elections – generally binding for the tax year– When can owners still file separate state returns?

• Some states require elections or consent forms from owners, tax power of attorney

30

Issues Concerning Sales of Partnership Interest

• How is gain taxed for state purposes?

• Withholding/composite considerations for multi-tiered partnerships

• Special rules regarding specific allocation vs. apportionment of gain

• Potential issues when partnership holds real estate

• Common mistake – distributing entire proceeds before state tax considerations examined/paid

31

Issues Unique to S-corporations

• Distributions must be equitable

• How to approach states that do not conform to federal S-election:– Potential opportunities

– Consider tax rates, taxes paid deductions/credits, costs of compliance

• Multiple instances of income, capital/net worth, and/or minimum taxes

32

Issues Unique to S-corporations

• Limitations on resident state credits for taxes paid to other states– Criticare Inc and Marina Shakour Haber v. Director, NJ Tax Court Docket

No. 008253-2013

• Sales of S-Corporation stock– Historically treated as intangible but some states may have special

rules

– NY Advisory Opinion TSB-A-15(5)I

33

Election/Planning Strategies

• Owners must evaluate their own tax situation– Composite tax at highest marginal rates vs. graduated rates

– Forego standard deductions, personal exemptions

• Re-evaluate for 2018 due to tax reform changes

• States that do not follow pass-through treatment – Owners may still benefit from tax paid by entity in certain states

– Planning in states that require separate S-elections and QSSS elections

– H. Alan Rosenberg v. Commissioner, GA Tax Tribunal No. 1414626

34

Election/Planning Strategies

• Loss years– States may not allow carryforwards on composite returns, no carryback

option

• Statute of Limitations risks for owners– Nexus/sourcing issues on other sources of income

– Residency/domicile issues

35

Composite Returns and Nonresident Withholding for Pass-Through Entities

Questions?

William Brown

Brown Winick

(515) 242-2412

Jeff Weinkle, CPA

State & Local Tax Manager

Aprio LLP

(770) 353-3071

36