Compliance In A New Regulatory Environment Nothing herein should be construed as legal advice or as...

50

Compliance In A New Regulatory Environment Nothing herein should be construed as legal advice or as a legal opinion for any particular situation. Information is provided for general guidance and should not be substituted for formal legal advice from an experienced securities attorney. Joel H. Sauer Principal Consultant ACA Compliance Group [email protected] m October 20, 2009

-

Upload

branden-washington -

Category

Documents

-

view

217 -

download

0

Transcript of Compliance In A New Regulatory Environment Nothing herein should be construed as legal advice or as...

Compliance In A New Regulatory Environment

Nothing herein should be construed as legal advice or as a legal opinion for any particular situation. Information is provided for general guidance and should not be substituted for formal legal advice from an experienced securities attorney.

Joel H. SauerPrincipal ConsultantACA Compliance [email protected]

October 20, 2009

2

Table of Contents

• SEC Examinations

• Custody and Safekeeping of Assets

• Portfolio Mandate Compliance

• Marketing, Advertising and Investor Relations

• Best Execution and Soft Dollars

• Private Fund Regulation

• IA-BD Harmonization

• Questions

SEC Examinations

4

Re-Energized SEC Staff

“A strong and reinvigorated SEC will be on the beat like never before to catch wrongdoers.”

– Mary Schapiro, SEC Chairman

Source: Practicing Law Institute's "SEC Speaks in 2009" Program, Washington, DC, February 6, 2009.

5

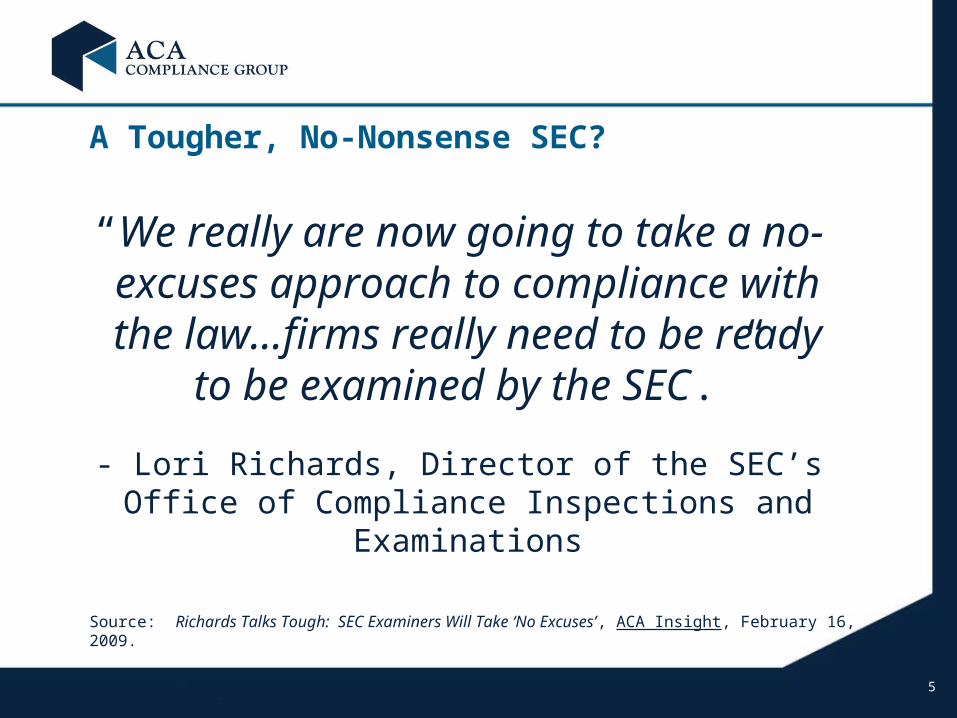

A Tougher, No-Nonsense SEC?

“We really are now going to take a no-excuses approach to

compliance with the law…firms really need to be ready to be

examined by the SEC.”

- Lori Richards, Director of the SEC’s Office of Compliance Inspections and

ExaminationsSource: Richards Talks Tough: SEC Examiners Will Take ‘No Excuses’, ACA Insight, February 16, 2009.

6

Better, faster, tougher enforcement

“The focus, as I said, is on being more strategic, swift, smart and successful in our job—protecting

the investor.”

- Robert Khuzami, SEC Director of Enforcement, before the Senate Banking, Housing and Urban Affairs Subcommittee

Source: Testimony of Mr. Robert Khuzami, “Hearing: Strengthening the S.E.C.’s Vital Enforcement Responsibilities” (May 7, 2009).

7

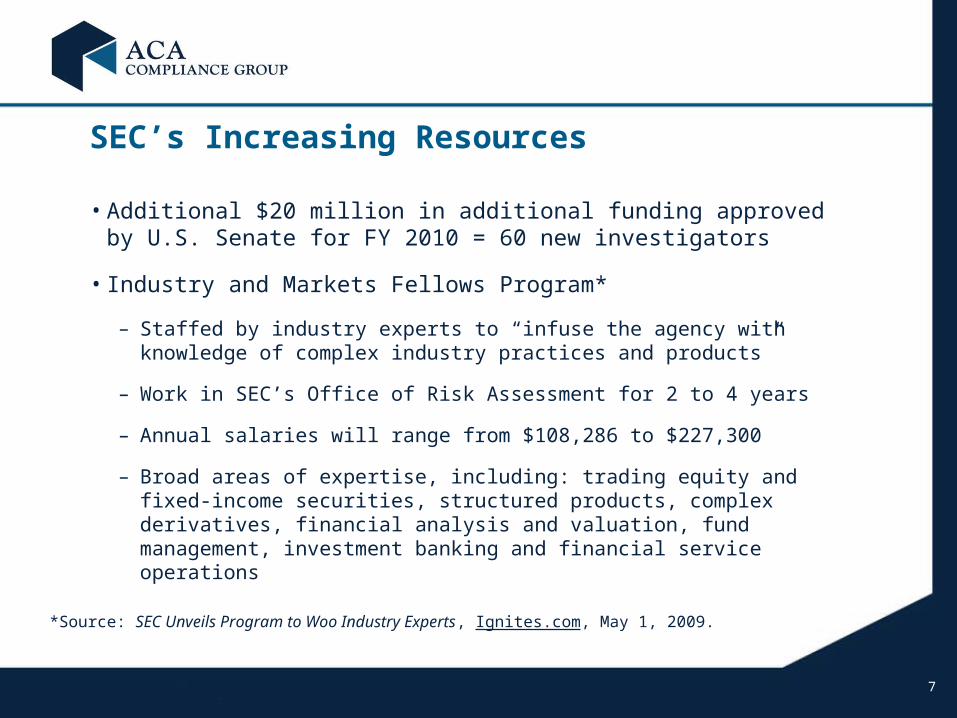

SEC’s Increasing Resources

• Additional $20 million in additional funding approved by U.S. Senate for FY 2010 = 60 new investigators

• Industry and Markets Fellows Program*

– Staffed by industry experts to “infuse the agency with knowledge of complex industry practices and products”

– Work in SEC’s Office of Risk Assessment for 2 to 4 years

– Annual salaries will range from $108,286 to $227,300

– Broad areas of expertise, including: trading equity and fixed-income securities, structured products, complex derivatives, financial analysis and valuation, fund management, investment banking and financial service operations

*Source: SEC Unveils Program to Woo Industry Experts, Ignites.com, May 1, 2009.

8

Production of Records: SEC Expectations

• OCIE working with the SEC’s Division of Enforcement to create a policy about when examiners will refer a delay in production or lack of cooperation to SEC enforcement attorneys

• “Examiners will be less tolerant of delays in the production of information and documents…I want examiners to have a clear sense of when they should refer matters to the Division of Enforcement staff when production of documents has not been timely and when we feel that firms have not been fully cooperative with examiners during the examination process.”

– Lori Richards, Director of the SEC’s Office of Compliance Inspections and Examinations

Source: Richards Talks Tough: SEC Examiners Will Take ‘No Excuses’, ACA Insight, February 16, 2009.

9

Recent SEC Examination Developments

•Interesting developments related to SEC inspections that have commenced within the past few months:

Surprise examinations are back!

Email requests span up to 2 years with no “keyword” qualifiers

Requests for all versions of particular documents during a review period (e.g., Form ADV, II, Compliance Manual, advertisements)

Questions about compliance budgets and potential cost cutting initiatives

10

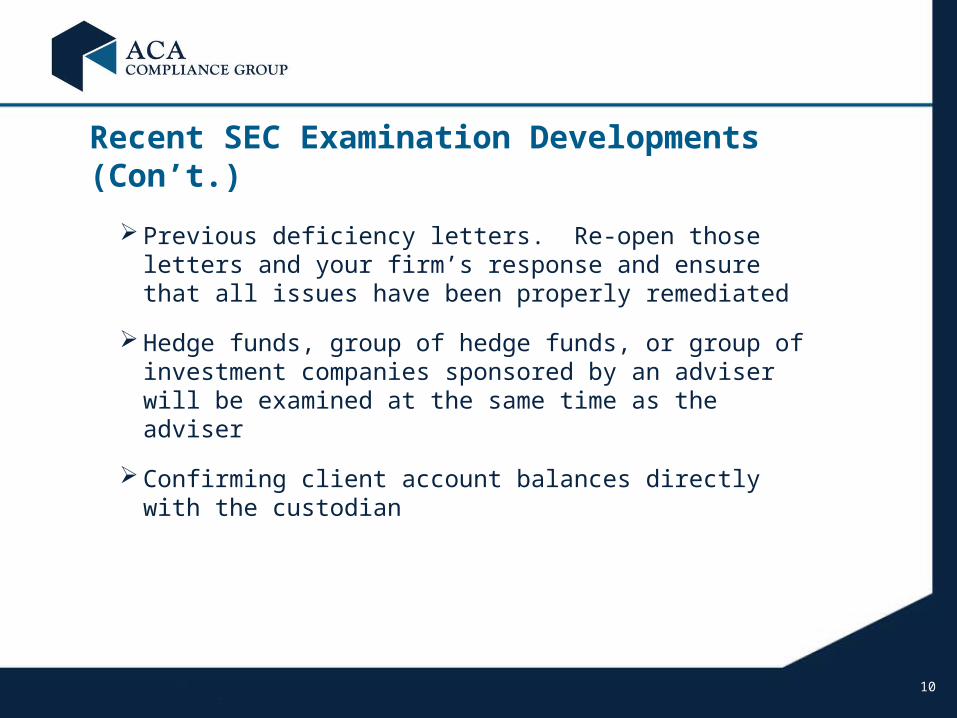

Recent SEC Examination Developments (Con’t.)

Previous deficiency letters. Re-open those letters and your firm’s response and ensure that all issues have been properly remediated

Hedge funds, group of hedge funds, or group of investment companies sponsored by an adviser will be examined at the same time as the adviser

Confirming client account balances directly with the custodian

11

Other New SEC Exam Initiatives

– More sweep exams formulated by specialized groups within the SEC;

– SEC internal hotline for examiners to call in the event officials at a firm become uncooperative or attempt to derail an inspection;

– A new staff category (“Senior Special Examiner”) to interview personnel in highly technical areas;

– A more holistic approach with better integration of the investment adviser and broker-dealer examination groups; and

– A periodic review of the SEC’s own internal policies and procedures.

12

Restructuring and Focus of Enforcement Division

- Streamlined formal order process

- Formation of five specialized units within the Enforcement Division

Asset Management, Structured Products, Municipal Securities and Public Pensions, Foreign Corrupt Practices, and Market Abuse

- Increased scrutiny of tolling agreements

- Elimination of branch chiefs

- Creation of an Office of Market Intelligence

13

Recent Exam Priorities

• Custody of client assets

• Personal trading by advisory staff (especially trades in private funds managed by the adviser)

• Valuation and liquidity issues

• Portfolio risk monitoring

• Disparate treatment of investors

• Sales of structured products by broker-dealers and advisers

• Controls and processes at recently merged or acquired firms, both advisers and broker-dealers

• Money market funds

• Short selling and compliance with Regulation SHO

Custody and Safekeeping of Client Assets

15

Custody and Safekeeping of Fund Assets

Current Custody Rule under Advisers Act

• Qualified Custodian

• Notice to Clients

• Quarterly Account Statements to Clients

• Private Fund Exception to Reporting

– GAAP audit requirement

– Distributed within 120 days to all investors/shareholders (180 for fund-of-funds)

– Unqualified opinion

16

SEC Director on Custody Focus

“Examiners are going to be out in force looking at your controls over custody…

Don’t wait for us to do it. Do it now…We will want to tie the firm’s records and the firm’s account statements to customers

back up to independent custodian … so we will be spending an enormous amount of time really confirming the existence of

client and customer assets.”

– Lori Richards, OCIE DirectorSource: Richards Talks Tough: SEC Examiners Will Take ‘No Excuses’ and SEC Sweeps on Custody, ACA Insight, February 16, 2009.

17

Simply “Verify”

“…to a greater extent, examinations of advisers and broker-dealers include a verification of the assets held…I like to say that our philosophy here isn’t so much Ronald Reagan’s ‘trust but

verify,’ but simply ‘verify.’”

Source: Lori Richards, Director, SEC’s Office of Compliance Inspections and Examinations,Strengthening Examination Oversight: Changes to Regulatory Examinations, June 17, 2009 at http://www.sec.gov/news/speech/2009/spch061709lar.htm.

18

Proposed Changes to Custody Rule (May 2009)

• Major proposed changes:

– Surprise audit by independent accountant for any adviser with custody, even if only because of ability to deduct fees; private funds also subject to surprise audit

– Written opinion from independent accountant regarding adviser’s internal controls related to custody

– Disclose the name of independent accountant conducting surprise audit (for hedge funds, the accountant conducting the GAAP financial audit) on Form ADV Part 1

– If custodian is adviser or affiliate, independent accountant must be PCAOB-registered and internal control report required (SAS 70, Level II)

19

SEC Focus on Auditor Relationships

• SEC examiners have asked advisers to sign an authorization requesting work papers from their Fund’s auditor

• SEC staff requesting meetings/discussions with a fund’s auditor with respect to various issues (e.g., clawbacks related to Madoff lawsuits)

• What due diligence did the adviser perform on the auditor for its funds? What documentation was maintained?

• Is the auditor registered with the PCAOB?

• Do the auditor or its personnel have any investments in the funds or with the adviser?

• Does the adviser or the auditor send audited financial statements and K-1s to investors?

20

Additional Custody Considerations

• SEC staff “down-the-chain” custody requests – contacting clients and investors to verify account balances (FoF – capital account balances, cash flows and all holdings of the fund)

• Liquidation audits – can a manager forgo a final audit due to expense considerations?

• “Due inquiry” requirement – what about clients that do not want to get “copies” of account statements (e.g., foreign clients)?

• Exception from qualified custodian requirement for certain privately offered securities – bank debt, trade claims and other investments subject to this provision?

Portfolio Mandate Compliance

22

SEC Focus on Portfolio Mandate Compliance

“Advisers simply cannot tell investors they are going to do one thing with their funds and

then not follow through on those promises.”

- Linda Chatman Thomsen, former Director of the SEC’s Enforcement Division, July 30,

2008Source: SEC Charges Mutual Fund Manager for Violating Socially Responsible Investment Restrictions, SEC Press Release No. 2008-157, July 30, 2008.

23

Recent Portfolio Mandate Case Studies

• In the Matter of Hennessee Group LLC and Charles J. Gradante, Advisers Act Release No. 2871, April 22, 2009

– In the course of soliciting clients, Hennessee Group…made numerous representations concerning the quality and rigor of its due diligence process for evaluating hedge funds.

• New York Law School v. Ascot Partners, L.P., J. Ezra Merkin and BDO Seidman LLP, December 16, 2008.

– “…neither the Offering Memorandum nor any other offering material used in soliciting investment in Ascot ever disclosed that virtually all of Ascot’s assets were invested with Madoff, BMIC or other Madoff controlled entities.”

• In the Matter of Pax World Management Corp., Advisers Act Release No. 2761, July 30, 2008.

– Sanctioned for not following stated social screens

– Note: no harm alleged

24

It’s More Than Just the PPM and IMA…

• Private Offering Memorandum (PPM)

• Investment Management Agreement (IMA)

• Flipbooks

• Due Diligence Questionnaires

• Responses to RFPs

• One-on-One Presentations

• Annual Client or Investor Meeting Materials

• Verbal Representations

Advertising, Marketing and Investor Relations

26

Regulatory Focus on Advertising and Performance and Investor Relations

• Are the materials accurate and truthful?

• Performance track records

• Composite construction

• Assets under management

• Pay-to-play and client/investor solicitation arrangements

• Selective disclosure

• Increasing use of social media (Facebook, LinkedIn, Twitter)

27

SEC Focus on Performance Claims

“Given the conflicts of interest in this area — the fact that advisory fees may be pegged on performance, the marketing significance of

performance claims, and the simple fact that there is a natural disinclination to deliver bad news to clients — this is an area where CCOs and compliance personnel will want to focus

their attention.”

– Lori Richards, Director of the SEC’s Office of Compliance Inspections and Examinations

Source: Compliance in Today’s Environment: Step Up to the Challenge, Speech by SEC Staff, March 12, 2009.

28

Pay-to-Play

• New York AG (Cuomo) investigation

• Morris/Loglisci Indictment

• Individual State Laws

• SEC Rule Proposal – Political Contributions by Investment Advisers (Aug. 3, 2009)

– Prohibit adviser from providing advisory services for compensation to a government client for 2 years after the adviser/employees made contributions to elected officials or candidates

29

Selective Disclosure

• Are those in pooled vehicles (private funds or mutual funds) treated equally with regard to the disclosure of important information about the fund?

• In the Matter of Evergreen Investment Management Company, LLC and Evergreen Investment Services, Inc., Advisers Act Release No. 2888, June 8, 2009.

– “talking points…intended to be shared with any Ultra Fund shareholder or registered representative who made an incoming call to any of the Evergreen Distributor’s wholesalers to discuss the Fund’s recent NAV decreases.”

– “Evergreen Adviser willfully violated Section 204A of the Advisers Act…Evergreen Adviser disclosed material, non-public information about the Ultra Fund to an affiliate…”

30

Regulatory Focus on Electronic Communications

• Emails and instant messages

• Internet websites

• Social networking sites (MySpace, Facebook, LinkedIn)

• Wikipedia

• You Tube

• Blogs

• Chat Rooms

31

Asset Managers and Social Networking Sites

• TIAA-CREF has gone where other asset management firms fear to tread and launched a Facebook page. New York-based TIAA-CREF is using Facebook to communicate with its 3.6 million clients.

• Accomplished with input from the firm’s compliance, legal and technology divisions.

Source: TIAA-CREF, Vanguard Launch Facebook Pages, Ignites.com, May 29, 2009.

32

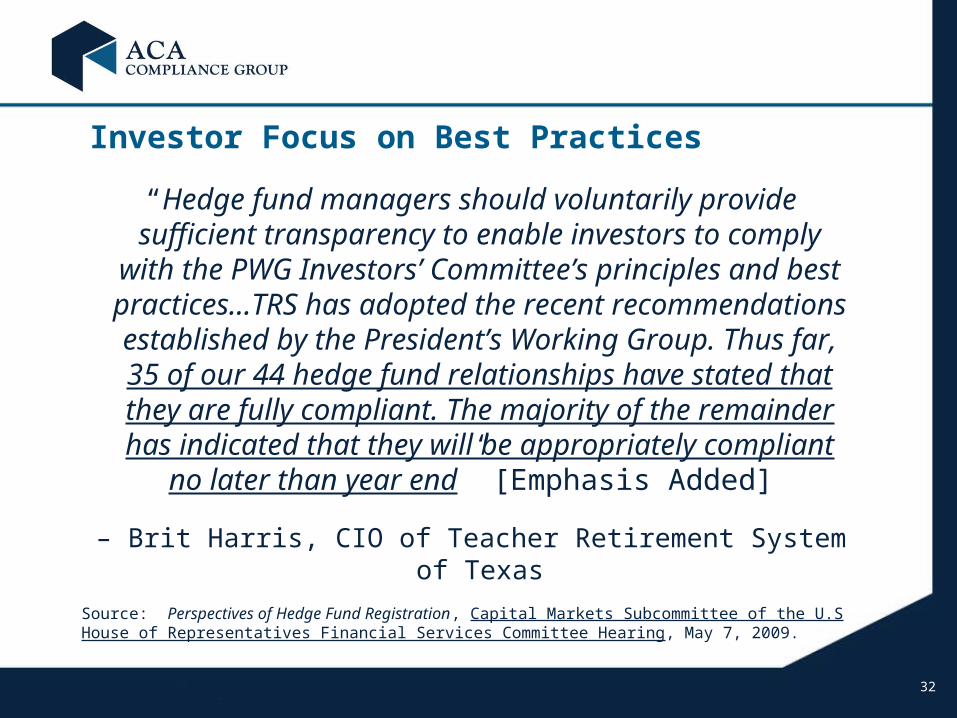

Investor Focus on Best Practices

“Hedge fund managers should voluntarily provide sufficient transparency to enable investors to comply with the PWG Investors’ Committee’s

principles and best practices…TRS has adopted the recent recommendations established by the

President’s Working Group. Thus far, 35 of our 44 hedge fund relationships have stated that they are fully compliant. The majority of the remainder has indicated that they will be appropriately compliant

no later than year end” [Emphasis Added]

– Brit Harris, CIO of Teacher Retirement System of Texas

Source: Perspectives of Hedge Fund Registration, Capital Markets Subcommittee of the U.S House of Representatives Financial Services Committee Hearing, May 7, 2009.

33

SEC Deficiency Letter on Specific Recommendations

“The examination revealed that Page 8 of the Annual Investor Meeting Presentation

contained a list of investments representing a cross section of the types of deals undertaken by XYZ. The methodology used to select such

investments does not appear to have been done using objective non-performance based criteria. Accordingly, XYZ should cease from advertising

in this manner going forward and re-issue a corrected presentation to current investors and inform the staff of the steps it intends to take

with respect to this matter” [Emphasis Added].

34

Eight Questions You Should Always Ask!(A Common Sense Checklist)

• Is it the whole truth?

• Will your audience understand what you are saying?

• Is the presentation misleading?

• Can you back it up?

• Have you checked the facts?

• Have you made promises you can’t keep?

• Are charts and graphs clearly labeled?

• Has the compliance team reviewed and approved the final version?

Best Execution and Soft Dollars

36

Best Execution

•What does best execution mean for:

– Fund of funds managers?

– Private equity/venture capital managers?

•Functions of best execution committee

37

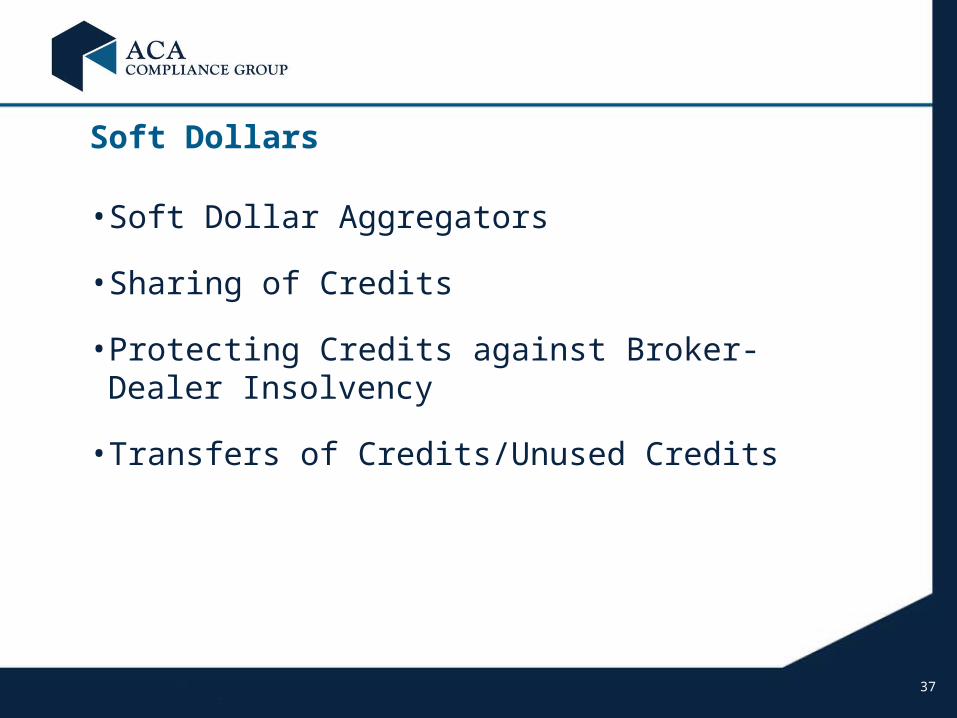

Soft Dollars

•Soft Dollar Aggregators

•Sharing of Credits

•Protecting Credits against Broker-Dealer Insolvency

•Transfers of Credits/Unused Credits

Private Fund Regulation

39

Private Fund Regulation

• Hedge fund manager registration is near certain

• Informational data collection on funds (e.g., assets under management)

• The Private Fund Investment Advisers Registration Act of 2009 would require the SEC to collect information on:

– Assets under management

– Leverage (including off-balance-sheet leverage)

– Counterparty credit risk exposures

– Trading and investment positions

– Trading practices

– Any other information determined necessary after consultation with the Fed

40

Private Fund Regulation

• Provides an exemption for advisers to venture capital funds, but not private equity

• Timeframe – Congressional action likely before year-end with SEC implementation in mid-late 2010

• Potential impact on other advisers:

– Elimination of “private adviser” exemption

– Extension of reporting requirements

Investment Adviser – Broker-Dealer Harmonization

42

Finding, Redefining and Refining the Fiduciary

A fiduciary duty has two parts:

– Duty of Loyalty = Duty to put your clients’ interests before your own and to disclose all conflicts of interest.

– Duty of Care = Duty to devote reasonable care and diligence to handling your clients’ business.

The current debate is primarily about the Duty of LoyaltyDuty of Loyalty.

43

Finding, Redefining and Refining the Fiduciary

“Historically, broker-dealers that simply effected transactions as directed by their clients generally would not be fiduciaries and had duties focusing on the transaction service they provided. As broker-dealers increasingly provide advice to their clients, the higher standards and fiduciary duties of advisers should also be applied to these broker-dealers.”

- SEC Commissioner Luis Aquilar - January 10, 2009 speech to the North American Securities Administrators Association

44

Finding, Redefining and Refining the Fiduciary

“Rather than perpetuating an obsolete regulatory regime, SIFMA recommends the adoption of a ‘universal standard of care’ that avoids the use of labels that tend to confuse the investing public, and expresses, in plain English, the fundamental principles of fair dealing that individual investors can expect from all of their financial services providers.”

- SIFMA President Timothy Ryan, Jr. - March 10, 2009testimony before the Senate Banking Committee

45

Finding, Redefining and Refining the Fiduciary

Expose or Eliminate? – Areas of Potential Impact

– Principal and agency cross trades – Will Rule 206(3)-3T become permanent or will its application be broadened or narrowed for different situations?

– Sale of proprietary products and services – What additional disclosures will be required for brokers selling proprietary products and services? Will some proprietary sales be restricted or prohibited?

– Suitability – Will brokers (and advisers) be required to recommend the “most” suitable product or service?

– Commission levels – Will broker-dealers create additional commission levels for different levels of service? Will broker-dealers be required or pushed to adopt level compensation policies?

– Fee-based vs. Transaction-based – Will brokers (and advisers) be required to assess whether fee-based or transaction based services are more appropriate for their clients?

– Research – NASD Rule 2711 could be a model for implementing a general broker-dealer or universal fiduciary duty.

46

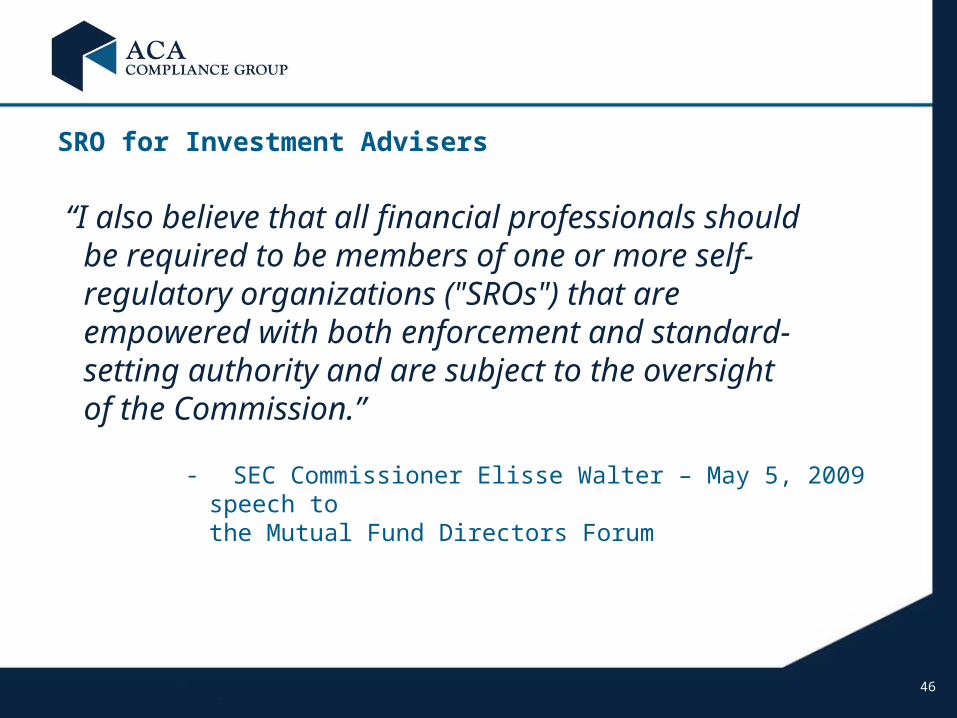

SRO for Investment Advisers

“I also believe that all financial professionals should be required to be members of one or more self-regulatory organizations ("SROs") that are empowered with both enforcement and standard-setting authority and are subject to the oversight of the Commission.”

- SEC Commissioner Elisse Walter – May 5, 2009 speech to the Mutual Fund Directors Forum

47

SRO for Investment Advisers – Continued Opposition

“There is no existing adviser membership organization that polices conduct. In short, it would be outsourcing a regulatory obligation rather than building on an existing structure. I personally believe that the SEC should not outsource its mission. It is the only entity with experience overseeing investment advisers, an industry governed by the Advisers Act, which is based on a principles-based regime. By contrast, broker-dealer SROs primarily regulate through the use of very detailed, specific sets of rules and are not well versed in the oversight of principles-based regulation.”

- SEC Commissioner Luis Aquilar – May 7, 2009 speech to the Investment Advisers Association

48

Investor Protection Act of 2009

• Applies Advisers Act fiduciary duty to broker-dealers providing investment advice to retail customers

• Requires the SEC to adopt rules defining this fiduciary duty (to retail customers) to require broker-dealers and investment advisers to act in the best interest of the customer without regard to their own financial or other interests

• Defines “retail customer” as an individual who

– Receives personalized investment advice from the broker-dealer

– Uses such advice primarily for personal, family, or household purposes

49

Investor Protection Act of 2009

• Requires the SEC to facilitate the provision of simple and clear disclosures to investors regarding the terms of their relationships with broker-dealers and investment advisers

• Requires the SEC to examine conflicts of interest and compensation schemes for financial intermediaries and empowers the agency to adopt rules regulating these areas

• Requires harmonization of enforcement options and remedies

• Permits the SEC to collect fees from investment advisers to cover the costs of the examination program – fees may be based on multiple measures of “risk” of the adviser

Questions

![[PROJECT ADDRESS]€¦ · Web view · 2017-11-21word "shall." Unless the context ... instrument or other document herein shall be construed as referring ... The rights conferred](https://static.fdocuments.in/doc/165x107/5ac8f1017f8b9a5d718d190f/project-address-web-view2017-11-21word-shall-unless-the-context-instrument.jpg)