Competitiveness of Battery Energy Storage in the Future ...

140

1 Competitiveness of Battery Energy Storage in the Future Belgian Capacity Market Master thesis submitted to Delft University of Technology in partial fulfilment of the requirements for the degree of MASTER OF SCIENCE in Engineering and Policy Analysis Faculty of Technology, Policy and Management by Theodorus Johannes Albertus (Duco) Slooff Student number: 4295749 To be defended in public on November 26, 2019 Graduation committee Chair and first supervisor: Dr.ir. L.J. de Vries, Energy and Industry Second supervisor: Dr. M.E. Warnier, Systems Engineering External Supervisor: Ir. J.J. Hettema, Eneco

Transcript of Competitiveness of Battery Energy Storage in the Future ...

1

Competitiveness of Battery Energy

Storage in the Future Belgian Capacity

Market

Master thesis submitted to Delft University of Technology

in partial fulfilment of the requirements for the degree of

MASTER OF SCIENCE

in

Engineering and Policy Analysis

Faculty of Technology, Policy and Management

by

Theodorus Johannes Albertus (Duco) Slooff

Student number: 4295749

To be defended in public on November 26, 2019

Graduation committee

Chair and first supervisor: Dr.ir. L.J. de Vries, Energy and Industry

Second supervisor: Dr. M.E. Warnier, Systems Engineering

External Supervisor: Ir. J.J. Hettema, Eneco

2

3

Acknowledgements Throughout the writing of this master thesis, I have received support during various stages. I

express my sincere thanks to my academic supervisors Laurens de Vries and Martijn Warnier, for

their constructive feedback. I would also like to thank my external supervisor Jesse Hettema for

his guidance during my internship at Eneco. Furthermore, Jeroen and Paul from Eneco for the

discussions that have led to interesting insights.

Duco Slooff

Delft, 2019

4

Executive Summary

As the world is transitioning from conventional to renewable energy sources,

governments and energy utilities face the challenge to match the supply profile of these

intermittent sources to the energy demand. Energy storage is being considered as one of

the potential solutions to cope with the variability of renewables.

Belgium is not only challenged by the transition to renewable energy but must also deal

with the total nuclear power phase-out by 2025. The country significantly depends on the

seven nuclear power plants since they account for more than half of the national

electricity production (depending on the availability of the reactors). The Belgian TSO

Elia has investigated the urgency of adequacy and flexible electricity sources and

proposed a Capacity Remuneration Mechanism (CRM), which should encourage

investments in generation capacity to maintain the security of supply in Belgium. All

awarded capacity providers of the competitive auction receive financial compensation

for the availability of their generation capacity in the Belgian energy market.

Eneco is one of the largest utility companies in the Belgian electricity market for

consumers and provides clean energy through their wind and solar farms. However,

Eneco has no flexible generation capacity in Belgium, which makes the company more

sensitive to high electricity prices because of the abundant supply of solar and wind

energy. Electrical Energy Storage (EES) can reduce the risk of financial losses during high

electricity prices and can be seen as an additional income-generating asset next to

Eneco’s existing wind and solar assets in Belgium. Therefore, Eneco considers

participating in the Belgian capacity auction with EES capacity. As a result, this leads to

the following main research question:

What is the competitiveness of electrical energy storage in the future Belgian capacity

market?

5

The competitiveness of EES is assessed based on the constructed competitiveness

evaluation model. The model considers the long-term capacity remuneration, possible

costs related to the capacity market, storage costs, and revenue derived in the electricity

market. A capacity provider is considered as competitive if the expected costs are smaller

than the expected revenue from being in the capacity market. The net present value

(NPV) approach is chosen to investigate the economic competitiveness of EES. The

storage costs, intraday market income, payback obligation, and FCR income are modelled

for the photo years 2020, 2025 and 2030.

The most suitable storage technology for participating in the Belgian CRM auction, and

considered in this research, is Li-ion Battery Energy Storage (BES). This technology has

favourable characteristics such as short response time, high power and energy density,

high round-trip efficiency and low costs. Competing storage technologies are Large-scale

Pumped Hydroelectric Energy Storage (PHES) and Compressed Air Energy Storage

(CAES), however, both are not suitable in Belgium due to geographical restrictions.

The Battery Energy Storage System (BESS) will be deployed in the Frequency

Containment Reserve (FCR) market and intraday market because of the largest revenue

potential. FCR price is not expected to rise in the future and more likely to fall because of

the increase of flexible generation capacity and the further integration of European

ancillary service markets. Three FCR price scenarios are taken into consideration for

calculating the FCR income. The FCR price will be equal to today’s average FCR price

(€ 79.000/MW/year), the FCR price will be equal to the minimum FCR price scenario

observed since July 2019 (€ 51.000/MW/year) and the FCR price will be equal to the

halved today’s average FCR price (€ 39.000/MW/year). The expected intraday market

income is assessed by the software tool Linny-R which applies the optimization technique

linear programming based on the rolling horizon approach. The expected intraday

market income varies from € 16.000/MW/year in 2021 to € 19.000/MW/year from

2030.

6

BESS operating only in the intraday market is not expected to be competitive because of

the relatively high required capacity remuneration above € 100/kW/year. Auction

clearing prices in other European CRMs are below € 50/kW/year.

BES does not need capacity remuneration from 2025 onwards with today’s average FCR

price. However, it is not very likely that the FCR price stays the same in the future, as

described above. More realistic is 35% capacity price reduction from the average FCR

price scenario of € 79.000/MW/year to the minimum FCR price scenario of

€ 51.000 /MW/year. BES might be competitive in this scenario with a relatively high de-

rating factor and no payback obligation of the CRM. In the halved today’s average FCR

price scenario, BES will not be competitive in 2025 given the relatively high required

capacity remuneration of minimum capacity remuneration of at least € 69/kW/year. BES

might be competitive in 2030 with the halved today’s average FCR price since the

required capacity remuneration is at least € 21/kW/year. However, the capacity market

might be already saturated with capacity providers bidding near zero in the auctions.

Decisive parameters for competitiveness are the reference price, strike price and the de-

rating factor.

The results of this research are not convincing to regard BES as a competitive technology

in the upcoming Belgium capacity market. Revenue stacking by combining the FCR and

intraday market income would increase the competitiveness of BES and is necessary.

Further research should focus on deployment strategies of BESS in different markets and

FCR price developments.

7

Contents

Acknowledgements 3

Executive Summary 4

Contents 7

List of Figures 11

List of Tables 13

1. Introduction 15

1.1 Problem statement 15

1.2 Research objective 17

1.3 Outline 18

2. Literature review 19

2.1 Capacity Remuneration Mechanism 19

2.2 Central buyer mechanism based on reliability options 22

2.2.1 Reliability options mechanisms in Europe 22

2.3 Electrical Energy Storage (EES) 23

2.3.1 Presence of EES on European capacity markets 24

2.4 Competitiveness 26

2.5 Knowledge gap 27

3. Research questions and approach 30

3.1 Research questions 30

3.2 Research approach 31

3.3 Methods 33

3.3.1 Net Present Value 33

3.3.2 Linny-R 34

4. System description 36

4.1 Characteristics of the Belgian CRM 36

4.1.1 Description 37

4.1.1.1 Market reference price and strike price 38

4.1.1.2 Availability requirements and availability penalties 41

4.1.1.3 Clearing algorithm 42

4.1.1.4 Demand curve and price caps 43

4.1.1.5 T-1 reserved volume 43

8

4.1.1.6 Minimum participation threshold 43

4.1.1.7 De-rating factors 44

4.1.1.8 Investment levels 46

4.1.2 Conclusions 47

4.2 Appropriate EES technologies 48

4.2.1. Common BES projects 50

4.3 Opportunities in the electricity markets 51

4.3.1 Wholesale electricity market 51

4.3.1.1 Description 51

4.3.1.2 Analysis 53

4.3.2 Ancillary services 54

4.3.2.1 Description 54

4.3.2.1.1 Frequency Containment Reserve 56

4.3.2.1.2 Automatic Frequency Restoration Reserve 57

4.3.2.1.3 Manual Frequency Restoration Reserves 57

4.3.2.2 Analysis 58

4.4 Price developments 61

4.4.1 Intraday market 61

4.4.1.1 Relation between day-ahead and intraday market price 62

4.4.2 FCR 64

5. Model description 65

5.1 Conceptual model 65

5.2 BESS setup 66

5.2.1 Dimensioning 66

5.2.1.1 Intraday market 66

5.2.1.2 FCR market 67

5.2.1 Costs and technical parameters 68

5.3 Intraday market income modelling 69

5.3.1 Description 69

5.3.1.1 Roll and look-ahead period 70

5.4 FCR income modelling 71

5.4.1 Charging costs 73

5.5 CRM contract length 74

9

5.6 Scenarios 77

5.6.1 CRM design scenarios 77

5.6.2 Intraday market price scenarios 78

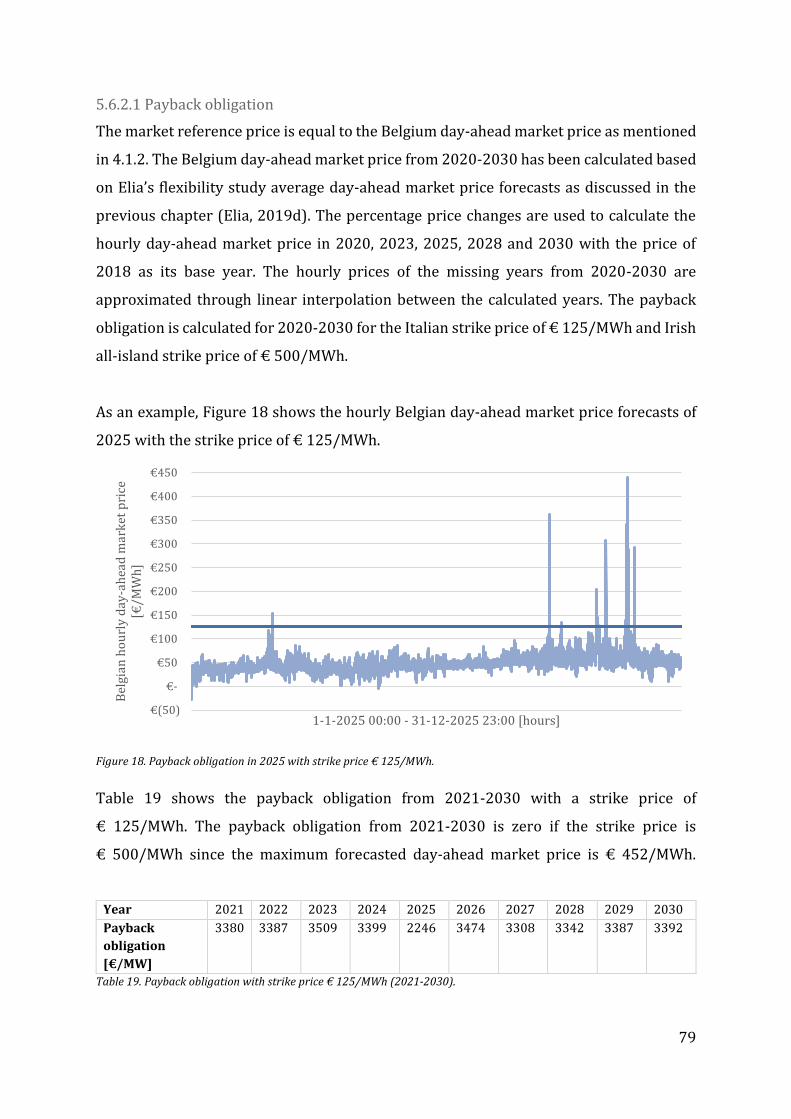

5.6.2.1 Payback obligation 79

5.6.3 FCR price scenarios 80

5.7 Experiment design 81

6 Verification and validation 83

6.1 Verification 83

6.2 Input validation 85

6.3 Model validation 86

7. Results 87

7.2 Competitiveness in the intraday market 88

7.2.1 Doubling the depth of storage 89

7.2.2 Conclusions 90

7.3 Competitiveness in the FCR market 91

7.3.1 Average FCR price scenario 91

7.3.2 Minimum FCR price scenario 92

7.3.3 50% Average FCR price scenario 93

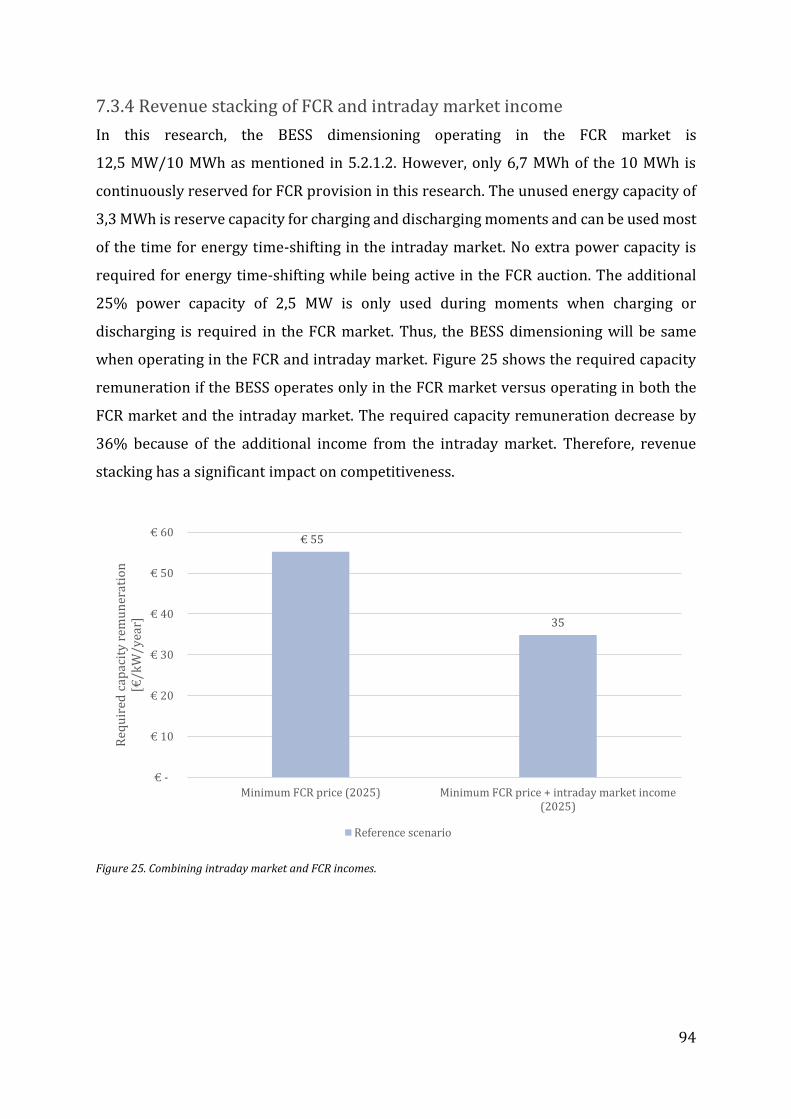

7.3.4 Revenue stacking of FCR and intraday market income 94

7.4 Conclusions 95

8 Discussion 96

8.1 Results 96

8.1.1 Intraday market income 96

8.1.2 Payback obligation 97

8.1.3 FCR income 98

8.2 Limitations 99

8.2.1 Data 99

8.2.2 Method 99

8.2.2.1 Net Present Value 99

8.2.2.2 Linny-R 100

8.2.3 Model and analysis 100

8.3 De-rating factor methodology 101

8.3.1 Belgian methodology 101

10

8.3.2 BES operation strategies 103

8.3.3 UK methodology 105

8.3.4 Conclusions 106

9 Conclusions 107

9.1 Answers to the sub-questions 107

9.2 Answer to the main research question 110

9.3 Policy recommendations 111

9.4 Recommendations for further research 112

10 Reflection 113

10.1 Scientific relevance 113

10.2 Societal relevance 114

10.3 Link to the EPA programme 114

11 References 115

12. Appendices 133

12.1 Full cycle definition 133

12.2 Intraday market 134

12.2.1 Input prices 134

12.2.2 Income build year 2020 135

12.2.3 Income build year 2025 135

12.2.4 Income build year 2030 136

12.3 FCR market 137

12.3.1 Cycles and energy delivery on FCR market 137

12.3.2 Price scenarios 140

11

List of Figures

Figure 1. Price duration curve of the EPEX SPOT day-ahead market price 2013-2018

(Elyxis, 2019). ................................................................................................................................................ 19

Figure 2. Taxonomy of the capacity mechanism models (European Commission, 2015).

............................................................................................................................................................................. 21

Figure 3. Rolling horizon approach (Lu, Ying, & Chen, 2016). ................................................... 35

Figure 4. Belgian CRM timeline until the first capacity auction (Elia, 2019i)....................... 36

Figure 5. Application of reliability options (Vázquez, Rivier, & Pérez-Arriaga, 2002). .... 38

Figure 6. Price development of Li-ion battery pack price outlook till 2030

(BloombergNEF, 2019a). .......................................................................................................................... 49

Figure 7. Sorted (high-low) difference in Belgian intraday and day-ahead prices of

consecutive hours for a half year between December 4, 2018, and June 4, 2019. (Eneco,

personal information, June 26, 2019). ................................................................................................. 53

Figure 8. Sorted (high-low) difference in Belgian intraday and day-ahead prices of

consecutive hours for a half year between December 4, 2018, and June 4, 2019, < 100

hours. (Eneco, personal information, June 26, 2019). ................................................................... 53

Figure 9. Average day-ahead market price forecasts in Belgium 2020-2030 under

different CO2 and technologies. .............................................................................................................. 62

Figure 10. Hourly VWAP Belgium intraday and day-ahead market prices March 2019. . 62

Figure 11. Hourly VWAP Belgium intraday and day-ahead market prices (per month)

January 2014 - July 2019. .......................................................................................................................... 63

Figure 12. Competitiveness evaluation model. ................................................................................ 65

Figure 15. Linny-R model for calculating the intraday market income. ................................. 69

Figure 17. Marginal capacity price in Belgium on the regional platform between July 1,

2019 – September 29, 2019 (Regelleistung, n.d. -b). ..................................................................... 71

Figure 18. Continental Europe synchronous area frequency 3-3-2018 00:00 - 4-3-2018

0:00 (RTE, 2019). ......................................................................................................................................... 72

Figure 19. Intraday market income (2026) by operating different number of cycles. ..... 75

Figure 20. Aggregated intraday market income for different BES lifetime (years). .......... 76

Figure 16. Payback obligation in 2025 with strike price € 125/MWh. ................................... 79

Figure 21. Verification of Linny-R model of 2026. .......................................................................... 83

Figure 22. Required capacity remuneration, given the day-ahead market income in the

reference scenario and in the optimistic scenario (2020, 2025, 2030). ................................. 88

Figure 23. Breakdown of the EBIDTA for 2020, 2025 and 2030. .............................................. 90

Figure 24. Required capacity remuneration, given the average FCR price in the reference

and optimistic scenario (2020, 2025, 2030). .................................................................................... 91

Figure 25. Required capacity remuneration, given the minimum FCR price in the

reference and optimistic scenario (2020, 2025, 2030). ................................................................ 92

Figure 26. Required capacity remuneration given 50% of the average FCR price in the

reference and optimistic scenario (2020, 2025, 2030). ................................................................ 93

Figure 27. Combining intraday market and FCR incomes. .......................................................... 94

12

Figure 28. Process overview of the methodology for determining the de-rating factors of

the Belgian CRM (based on Elia, 2019e). ......................................................................................... 101

Figure 29. Alternative contributions of BES to shortage periods (Based on Dent, Wilson

Zachary, 2017). .......................................................................................................................................... 104

Figure 14. Cycling process (Thirugnanam, Saini., & Kumar, 2012). ..................................... 133

13

List of Tables

Table 1. Auction results of battery storage in Irish all-island and United Kingdom

(EirGrid., & SONI, 2018; EirGrid., & SONI, 2019a; EirGrid., & SONI, 2019b; National Grid,

2018a; National Grid, 2018b; National Grid, 2019)........................................................................ 24

Table 2. Current state of scientific knowledge on the relevant subjects for evaluating the

competitiveness of EES in the future Belgian capacity market. ................................................. 29

Table 3. Set of BESS constraints and description (Hu., Chen., & Bak-Jensen, 2010). ......... 34

Table 4. Elements determining the functioning of the CRM (Elia, 2019i). ............................ 37

Table 5. Possible outcomes reliability options (Vázquez, Rivier, & Pérez-Arriaga, 2002).

............................................................................................................................................................................. 39

Table 6: Mentioned strike prices in Italy and Irish all-island CRM (European

Commission, 2018; EirGrid, & SONI, 2019). ...................................................................................... 40

Table 7. SLA categories for energy-constrained capacity providers. Adapted from Elia

(2019k). ........................................................................................................................................................... 41

Table 8. United Kingdom and Irish all-island De-rating factors T-4 capacity auction

(deliver year 2022/23) and Poland de-rating factors capacity auction (delivery year

2021-2022, 2022-2023, 2023-2024) (Rozporządzenie Minstra Energii; 2018; EirGrid., &

SONI, 2019; National Grid, 2018c). ....................................................................................................... 45

Table 9. Investment levels of European CRMs (CREG, 2019). .................................................... 46

Table 10. Specification of the three EPEX SPOT Belgium market segments (EPEX SPOT,

n.d. -e). .............................................................................................................................................................. 52

Table 11. Overview of the (future) ancillary services (Elia, 2017a; Elia 2018d; Elia,

2019b). ............................................................................................................................................................. 55

Table 12. Technical characteristics ancillary services (Elia, 2017a; Elia, 2018a; Elia,

2019b; Elia, 2019c). .................................................................................................................................... 58

Table 13. Average price of selected bids for the ancillary services between January 2019

– week 31 August 2019 (Elia, n.d. –c). ................................................................................................. 60

Table 14. BESS setups taken initially into consideration. ............................................................ 67

Table 15. Li-ion BESS costs parameters and values (IRENA, 2017; Eneco, personal

information, May 21, 2019; Eneco, personal information, August 2, 2019; XE, 2019;

Statbel, 2019; KBC, 2018). ........................................................................................................................ 68

Table 16. Investment levels of European CRMs (CREG, 2019). ................................................. 74

Table 17. Reference scenario and experiments for calculating the required capacity

remuneration. ................................................................................................................................................ 77

Table 18. Average day-ahead market price 2018 predictions for 2020, 2023, 2025, 2028,

2030 including percentage change. ...................................................................................................... 78

Table 19. Payback obligation with strike price € 125/MWh (2021-2030). .......................... 79

Table 20. Year description of scenarios 2020, 2025 and 2030. ................................................. 81

Table 21. Experiments for BESS (10 MW/10 MWh) operating in the intraday market. .. 81

Table 22. Experiments for BESS (12,5 MW/10 MWh) operating in the FCR market. ....... 82

14

Table 23. Experiments for BESS (12,5 MW/10 MWh) operating in both the intraday and

FCR market. .................................................................................................................................................... 82

Table 24. Published (approximated) project costs by developers compared to IRENA’s

estimated storage costs (Infigen, 2018; Enel, 2019; Endesa, 2017; IRENA, 2017). ........... 85

Table 25. Income differences in the intraday market and the FCR market (2020, 2025,

2030). ................................................................................................................................................................ 95

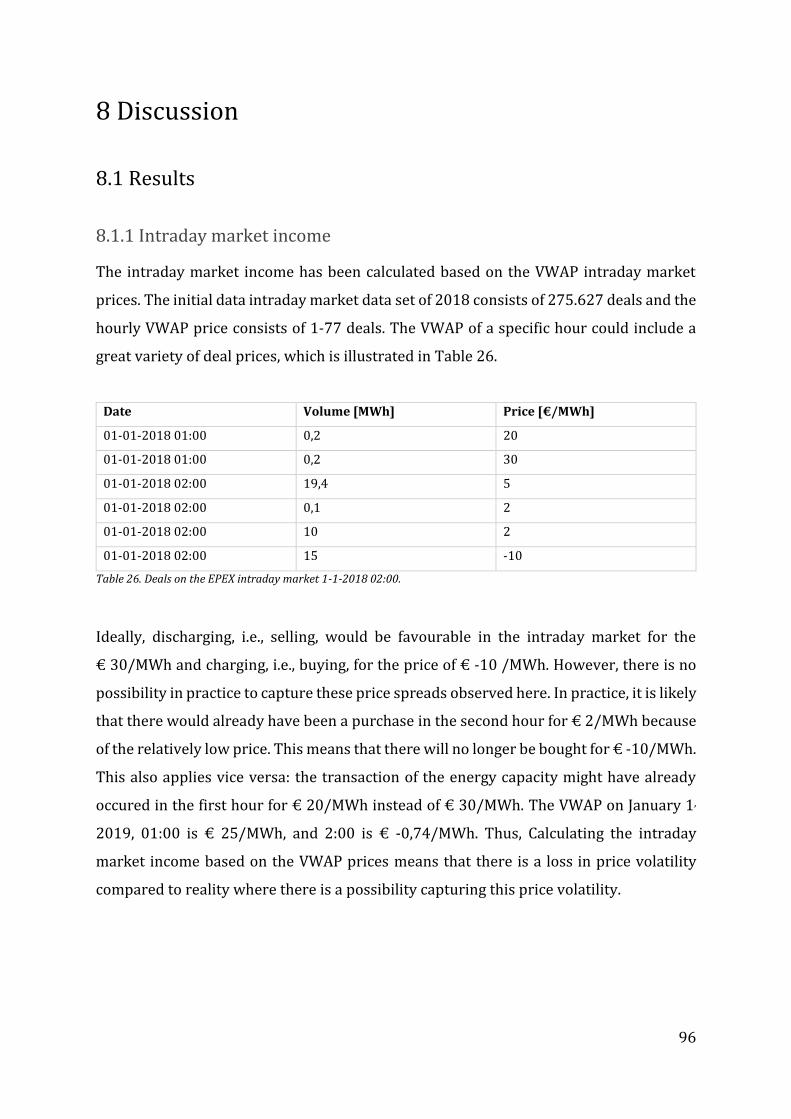

Table 26. Deals on the EPEX intraday market 1-1-2018 02:00. ................................................ 96

Table 27. Influence of the payback obligation on the required capacity remuneration. . 97

15

1. Introduction

1.1 Problem statement

The worldwide energy consumption should drastically change the coming decennia to

avoid dangerous climate change. In 2015, 175 parties signed the Paris Agreement to keep

the global temperature rise this century below 2 degrees Celsius, aiming for 1,5 degrees

Celsius (UNFCCC, 2015). In the same year, all the United Nations Member States adopted

the Sustainable Development Goals to provide affordable and clean energy for everyone

by 2030 (United Nations, 2015). Every country in the world faces the major challenge of

reducing greenhouse gas emissions.

Renewable energy sources, such as wind and solar energy, offer great opportunities to

make the energy supply more sustainable. However, the energy production of these

sources strongly depends on weather conditions. Besides, the energy consumption varies

per part of the day but also per season. The difference between the supply profile and the

energy demand is considered as a major challenge for governments, utility companies,

and transmission system operators (TSOs). Energy storage is considered as one of the

major components of the solution to deal with the variable nature of wind and solar

energy. By way of illustration, the world demand for battery storage is estimated to reach

2800 gigawatt-hours (GWh) in 2040 – corresponding to storing around half of 2019’s

global renewable energy production in a day (World Bank, 2019).

The transition to a low-carbon society with higher penetration levels of variable

renewables is not the only challenge for Belgium. On January 31, 2003, the Belgian

parliament approved the bill for the nuclear power phase-out, implying shutting down all

seven nuclear power plants. No new nuclear power plants will be built for industrial

electricity production (Belgisch Staatsblad, 2003). In the end, no electricity is generated

from nuclear energy in 2025. Belgium significantly depends on nuclear energy, as nuclear

power plants produce more than half of Belgium’s total electricity production in 2017.

Nuclear represented 34% of Belgium’s electricity production in 2018 because of

unavailability of nuclear multiple power plants, which led to a greater import of

electricity from abroad (Elia, 2019a).

16

The Belgian minister of Energy has commissioned the Belgian TSO Elia to investigate the

urgency of adequacy and flexible electricity sources to ensure the security of supply in

the period 2017-2027. Elia cannot guarantee that the current energy-only market,

combined with a strategic reserve mechanism, can ensure sufficient investments in

generation capacity to maintain the security of supply in Belgium (Elia, 2016a). The

proposed measure is a Capacity Remuneration Mechanism (CRM) based on reliability

options and should succeed the strategic reserve mechanism (Belgische Kamer van

volksvertegenwoordigers, 2019a).

The objective of the prospective Belgian CRM is to ensure a certain level of security of

supply at the lowest possible cost. Capacity providers are remunerated in auctions for

the availability of their capacity per megawatt (MW) in the energy market (Belgische

Kamer van volksvertegenwoordigers, 2019a). On April 4, 2019, the Belgian federal

parliament approved the bill for the adaption of the Belgian electricity act that allows the

introduction of a CRM to encourage investments in capacity (Belgische Kamer van

volksvertegenwoordigers, 2019a). According to Elia’s recent adequacy and flexibility

study, the new capacity required is 3,9 GW from 2025 to guarantee the security of supply

after a full nuclear power phase-out. The assumption takes into account the limited

options during the winter months because of planned coal exits of neighbouring countries

and in particular Germany (Elia, 2019d). There will be one auction four years ahead of

each delivery year and one auction a year ahead of each delivery year securing the

capacity required (Belgische Kamer van volksvertegenwoordigers, 2019a). The first

auction should take place in October 2021 to ensure sufficient capacity from November

2025 (Elia, 2019d).

The capacity auctions do not exclude any form of capacity because of the technological

neutrality requirement imposed by the European Commission. Each capacity provider

who can contribute to the security of supply can participate in the auction. Possible

candidates are power plants, demand response, storage, and renewable sources

(Belgische Kamer van volksvertegenwoordigers, 2019b). In the light of the world’s

energy transition to a sustainable energy future is whether storage is competitive with

(existing) conventional plants in the Belgian capacity auction.

17

1.2 Research objective

Eneco is one of the largest utility companies in the Belgian electricity market for

consumers (VREG, 2019). In 2019, Eneco has a substantial generation capacity of on- and

offshore wind energy and solar energy (resp. 436 MW, 178 MW, 78 MW) in Belgium but

no flexible capacity (Eneco, n.d. –a, Eneco, n.d. –b, Eneco, n.d. –c). This implies Eneco is

more sensitive to high electricity prices when the sun does not shine, and the wind does

not blow (Eneco, personal communication, April 25, 2019). Electrical Energy Storage

(EES) can reduce the risk of financial losses during high electricity prices and aligns

Eneco’s mission (‘everyone’s sustainable energy’) better than conventional power plants

(Eneco, 2019). Also, EES can be seen as an additional income-generating asset next to

Eneco’s existing wind and solar assets in Belgium. Therefore, Eneco considers

participating in the Belgian capacity auction with EES capacity.

The research objective is to evaluate the competitiveness of EES installed by Eneco in the

future Belgian capacity market. The long-term capacity remuneration, possible costs

related to the capacity market, storage costs, and revenue derived in the electricity

market are integrated into one analysis.

18

1.3 Outline

This research is structured as follows:

● Chapter 2 includes the literature review. The literature review explains the

scientific problem regarding EES in the future Belgian capacity market. This

section discusses the core concepts and the formulation of the academic

knowledge gap;

● Chapter 3 involves the main research question, sub-questions and the research

approach including the methods used;

● Chapter 4 entails the system description, discusses the characteristics of the

Belgian CRM and explorers appropriate EES technologies. Subsequently, the

chapter discovers opportunities in the Belgian electricity market and discusses

price developments in the electricity market;

● Chapter 5 includes the model description including the conceptual model, BESS

dimensiong, intraday market and FCR income modelling and the scenarios;

● Chapter 6 discusses verification and validation;

● Chapter 7 presents the results including the required capacity remuneration;

● Chapter 8 discusses the results and the limitations of this research;

● Chapter 9 presents the conclusions, policy recommendations and

recommendations for further research;

● Chapter 10 entails the reflection on the scientific relevance, societal relevance and

the link to the EPA programme;

● Chapter 11 includes the references;

● Chapter 12 involves the appendices;

19

2. Literature review

The core concepts of the research will be discussed and defined in this chapter.

Eventually, the knowledge gap in existing research will be addressed.

2.1 Capacity Remuneration Mechanism

The ideal situation would be to have an electricity market which ensures the security of

supply for the lowest consumer prices. Generation capacity investments might lead to

more competitive market results and maintain the reliability of the electrical grid.

However, power generation companies have to deal with demand uncertainty and

competition. Besides, investments are to a large extent sunk costs, and generators have

to make the investment decision at the right time (Genc, 2012). The investment in

generation capacity is profitable if the expected revenue during production hours are at

least equal to the investment costs (Mulder, 2017). The revenue of peak generation assets

significantly depends on the frequency, height, and duration of price spikes (De Vries,

2007). Figure 1 shows the price duration curve of the hourly day-ahead market price on

the Belgian EPEX SPOT exchange between 2013-2018 (Elyxis, 2019).

Figure 1. Price duration curve of the EPEX SPOT day-ahead market price 2013-2018 (Elyxis, 2019).

0

100

200

300

400

500

600

700

Be

lgia

n d

ay

-ah

ae

d m

ark

et

pri

ce [

€/

MW

h]

Duration [% of the time]

20

According to the underlying day-ahead market prices of the price duration curve, the

price rises only about 3% of the time above 100 euros per megawatt-hour (MWh). Small

differences in the occurrence of price spikes greatly affect the steepness of the price

duration curve and thus the expected profitability of generation capacity investments (De

Vries, 2007). Peak plants should recover their investment costs from these price spikes

(Cepeda & Finon, 2011). However, peak prices are subject to the political debate because

the introduction of price caps should protect consumers from prices higher than their

value of lost load (de Vries, Correljé, & Knops, 2017). The situation where the revenue

from the energy markets is insufficient for a generation asset to cover its capital and

operating expenses is called the ‘missing money’ problem (Newbery, 2016).

If the market provides insufficient generation capacity to meet the demand without

government intervention, the solution involves the introduction of additional

mechanisms to ensure the security of supply (Batlle & Pérez-Arriaga, 2008). This

situation applies to Belgium, where the energy-only market cannot provide proper

investments incentives to ensure the security of supply after 2025 (Elia, 2019d). The

European Directive 2003/54/EC has been implemented which provide designations for

transmission and distribution system operators for direct interventions in the electricity

market (Finon & Pignon, 2008). This development brings the introduction of capacity

(remuneration) mechanisms (CRM) into the spotlight. The objective of all capacity

mechanisms is to introduce incentives for utility companies to provide sufficient

generation capacity, even in the situation of imperfect information or concerns regarding

risk. Besides, it should stimulate to maximise utility companies’ generation output during

shortages in the electricity market (de Vries, Correljé, & Knops, 2017). Capacity

mechanisms differ from one another in structure and implementation. All mechanisms

each have their effects in the electricity market, and each country’s implementation is

unique (Meulman & Méray, 2012).

21

The capacity mechanisms can be divided into five types according to the European

Commission (2015). The first classification is based on whether the mechanism is

volume-based or price-based. Price-based means the TSO sets the price, and the volume

depends on the willingness of investors. The opposite of price-based is volume-based

where the TSO sets the volume, and market forces determine the price. Market-wide

capacity mechanisms reward all forms of capacity, whereas targeted capacity

mechanisms only reward a subset (Hancher, de Hauteclocque, & Sadowska, 2015). The

volume-based capacity mechanisms can be divided into the following subgroups;

targeted and market-wide. All five types of capacity mechanisms are presented in Figure

2. The type of capacity remuneration mechanism in the Belgian bill, and therefore

relevant in this research, is the (market-wide) central buyer capacity mechanism based

on reliability options, which is the red block in the figure below. The mechanism will be

explained in 2.2.

Figure 2. Taxonomy of the capacity mechanism models (European Commission, 2015).

22

2.2 Central buyer mechanism based on reliability options

Reliability contracts should provide capacity providers with better incentives for being

active in the energy market during scarcity (De Vries, 2007). The central buyer

mechanism based on reliability options has been first introduced by Pérez-Arriaga

(1999) and further elaborated by Vázquez, Rivier, & Pérez-Arriaga (2002). It is often

called in literature reliability contracts, reliability options mechanism and energy call

options auction (Bidwell, 2005; Vázquez, Rivier, & Pérez-Arriaga, 2002; De Vries, 2007;

Vázquez, Batlle, Rivier, & Pérez-Arriaga, 2003; Bezerra et al., 2006; Bezerra, Barroso, &

Pereira, 2011).

The regulatory authority of the energy market, e.g., the TSO, prescribes the market to

purchase reliability contracts, which represents the desired volume of capacity. The

reliability contracts are procured in a competitive auction and are composed of a financial

call option and a penalty for non-delivery of the auction item. The capacity providers

receive a fixed remuneration for the awarded capacity in the auction. The call option of

reliability contract entails that the contracted capacity provider should pay the positive

difference between a reference price, e.g., electricity market price, and a predetermined

strike price during the contracted period in return (often called the ‘payback obligation’).

Capacity providers are penalized if they do not meet the delivery obligation. An elaborate

explanation of the Belgian reliability options mechanism will be discussed in 4.1.

2.2.1 Reliability options mechanisms in Europe

Reliability options schemes have been approved by the European Commission in the

United Kingdom (only Northern Ireland), Ireland and Italy in 2017 and 2018 (European

Commission, n.d.). The electricity market on the island of Ireland, which refers to the

Republic of Ireland and Northern Ireland, is managed and regulated collectively by the

TSOs of the Republic of Ireland (‘EirGrid’) and Northern Ireland (‘SONI’) (European

Commission, 2017a). The jointly CRM of Ireland and Northern Ireland1 is hereafter

referred to as Irish all-island CRM.

1The Irish all-island electricity market operates as a single market under the same market wholesale electricity market arrangement Integrated Single Electricity Market (I-SEM) and capacity is reimbursed through one CRM.

23

2.3 Electrical Energy Storage (EES)

Electrical Energy Storage (EES) refers to the process of transforming electrical energy

from the electricity distribution network into any form allowing temporary storage and

transforming back to electrical energy when needed. The process makes it possible to

store electricity during periods of low demand and supplying energy to the grid during

periods of high demand or shortages (Chen, Cong, Yang, Tan, & Ding, 2009).

The characteristics of EES differ from conventional and non-conventional power plants,

such as gas-fired generation assets and wind turbines. A major feature of EES is the short

response time compared to non-conventional and conventional power plants. As an

example, the response times of gas generation assets are between 4-45 minutes in hot

starts (4-250 minutes in cold starts) and the response times of coal generation assets are

between 100-300 minutes in hot starts (450-900 minutes in cold starts) (Gonzalez-

Salazar, Kirsten, & Prchlik, 2018). In contrast, the response time of chemical storage, such

as Li-ion batteries, is a few milliseconds (Evans, Strezov, & Evans, 2012). The short

response time makes EES suitable for applications which require this feature, such as

ancillary services.

EES technologies differ primarily in efficiency, response time, lifetime, energy and power

capacity, and discharge time (Poullikkas, 2013). The storage characteristics of new

installations improve over time as research on material science continues, and capital

costs are coming down (Dvorkin et al., 2017).

The most common EES application in the world is (electric) energy time-shifting and

accounts for 85% of the total EES applications (US DOE, 2017). Energy time-shifting

involves buying and storing of (electric) energy when demand and energy prices are low

and selling and releasing the energy when demand and energy prices are high (Energy

Storage Association, n.d.-a). The objective is to find the most economically favourable

buying and selling moments. Other applications are electric supply capacity (4%), black

start (4%) and renewables capacity firming (3%) (US DOE, 2017).

24

2.3.1 Presence of EES on European capacity markets

Reliability options schemes are approved by the European Commission for the Irish all-

island CRM and Italian CRM, as mentioned in 2.2.1. EES has not been successful in the

Irish-island T-1 auctions (auction one year ahead the deliver year) in December 2017 and

2018, but has been successful in the T-4 auction (auction four years ahead the delivery

year) in May 2019 (EirGrid., & SONI, 2018; EirGrid., & SONI, 2019a; EirGrid., & SONI,

2019b). The auction clearing price, the awarded de-rated battery capacity2 in the CRM

auction and the share of battery capacity of the total de-rated capacity for the Irish all-

island capacity auctions are presented in Table 1. According to the Italian authority, the

first capacity auction should take place before end of 2019, so there are no results yet

(Terna 2019; Askanews, 2019).

CRM Type Date Deliver year Auction

clearing price

[€/kW/year]

Awarded de-

rated battery

capacity [MW]

Share of total

de-rated

capacity [%] Irish all-

island T-4 May. 2019 2022/23 46,15 81 1,1 T-1 Dec. 2018 2019/20 40,65 0 0 T-1 Dec. 2018 2018/19 41,80 0 0

United

Kingdom T-1 Jun. 2019 2019/20 0,87 (£ 0,77) 23 0,6 T-4 Feb. 2018 2021/22 9,52 (£ 8,40) 158 0,3 T-1 Feb. 2018 2018/19 6,80 (£ 6,00) 113 1,9

Table 1. Auction results of battery storage in Irish all-island and United Kingdom (EirGrid., & SONI, 2018; EirGrid., & SONI, 2019a; EirGrid., & SONI, 2019b; National Grid, 2018a; National Grid, 2018b; National Grid, 2019).

2 The de-rated capacity awarded in the CRM auction, which is the contributing to generation adequacy, is equal to the awarded nominal capacity times the relevant de-rating factor for the capacity provider (see 4.1.1.7).

25

The CRM in the United Kingdom differs from the upcoming Belgian CRM and existing Irish

all-island and Italian CRM because it not based on reliability options, which implies

United Kingdom’s CRM does not include the payback obligation for capacity providers.

However, a lot of battery storage participate in United Kingdom’s capacity auctions and

therefore relevant to take into account. Battery storage projects have broken through in

the United Kingdom and awarded since the T-4 capacity auction for 2021-2022 in

December 2016 (National Grid, 2016). Full details of awarded battery capacity for

T-1 auction on June 2019, T-4 auction and T-1 auction in February 2018 are presented in

Table 1.

Remarkable is the significant difference in auction clearing price between the Irish all-

island and United Kingdom’s capacity auctions, and especially the latest T-1 auction in

the United Kingdom with a clearing price near zero. This can be explained by the fact that

T-1 auction is a ‘top-up’ auction of the main T-4 auction to meet the additional capacity

demand of that particular deliver year. Therefore, less capacity is procured in the T-1

auction compared to the T-4 auction of the delivery year 2019-2020, respectively 3,7 GW

versus 46 GW (National Grid, 2015; National Grid, 2019). The clearing price near zero can

be explained by the large supply of (cheap) capacity. 9,4 GW entered the latest T-1

capacity auction, including 198 MW of battery storage, and only 38% was awarded. One

new battery project and five existing battery projects are awarded, which in total

accounted for only 0,6% of the total capacity. The big winners in this specific auction are,

mostly existing, Combined Cycle Gas Turbine (CCGT), Open Cycle Gas Turbine (OCGT) and

Combined Heat and Power (CHP) which accounts in total over 40% of the awarded

capacity. The supply curve of the auction clearly shows a lot of capacity providers are

willing to bid close to zero (National Grid, 2019). The example of the United Kingdom

underlines the fierce competition in the capacity auction between technologies and new

and existing assets.

26

2.4 Competitiveness

The conceptual term competitiveness has multiple meanings and depends upon context.

Here, it is in the context of the economic feasibility of EES participating in the future

central buyer mechanism based on reliability options in Belgium.

In theory, any capacity provider can be successful by bidding € 0/kW/year in the capacity

auction, assuming that he meets all conditions of the CRM. However, an economically

rational capacity provider would participate in the CRM if his expected costs are smaller

than his expected revenue from being active in the capacity market. From the perspective

of this research, the costs consist of the storage costs and possible costs arising from

participating in the CRM, i.e., payback obligations and penalties. The expected revenue

consists of the revenue derived in the electricity market and the capacity remuneration.

Thus, the competitiveness of EES in the future Belgian capacity market can be expressed

by the following inequality:

𝐶𝑠𝑡𝑜𝑟𝑎𝑔𝑒 + 𝐶𝑐𝑟𝑚 < 𝑅𝑚𝑎𝑟𝑘𝑒𝑡 + 𝑅𝑐𝑟𝑚

As mentioned in 2.2, the missing money problem occurs if the revenue from the energy

markets is insufficient for a generation unit to cover its capital expenses and operating

expenses. Given the occurrence of the ‘missing money’ problem, the inequality above

implies the capacity remuneration 𝑅𝑐𝑟𝑚 a capacity provider requires should be greater

than the missing money (i.e., the revenue derived in the electricity market minus the

storage costs 𝐶𝑠𝑡𝑜𝑟𝑎𝑔𝑒 and the possible costs arising from participating in the mechanism

𝐶𝑐𝑟𝑚.) Otherwise, there’s no economic incentive to participate in the market. This

inequality is expressed by the equation below:

𝐶𝑠𝑡𝑜𝑟𝑎𝑔𝑒 + 𝐶𝑐𝑟𝑚 − 𝑅𝑚𝑎𝑟𝑘𝑒𝑡 < 𝑅𝑐𝑟𝑚

The four cost and revenue components will be defined in the system description.

27

2.5 Knowledge gap

As mentioned in 2.2, much is known about capacity remuneration mechanisms in general

and in particular the central buyer mechanism based on reliability options. However, no

scientific research has been conducted on the performance of EES on a capacity market.

Over the past several years, a lot of research has been done on the role of utility-scale EES

and identifying suitable technologies, given the increasing presence of Renewable Energy

Sources (RES) (Ferreira, Garde, Fulli, Kling, & Lopes, 2013; Soloveichik, 2011; Dunn,

Kamath & Tarascon, 2011; Ibrahim, Ilinca, & Perron, 2008; Divya, & Østergaard, 2009).

The literature review showed that the most appropriate choice for an EES technology

highly depends on the application. It is nearly impossible to give one simple,

straightforward answer. Research has demonstrated that EES could contribute to the

security of supply by, for example, lowering peak demand (Zhou, Mancarella, & Mutale,

2015). Methodologies have been introduced to quantify the contribution of an EES unit

to the security of supply and estimate its capacity value, i.e., the quantification of the EES

unit’s effect on the system reliability (Zhou, Mancarella, & Mutale, 2015; Sioshansi,

Madaeni, & Denholm, 2013; Konstantelos, & Strbac, 2018; Evans, Tindemans, & Angeli,

2019). However, scientific research lacks on the contribution of EES in capacity auctions

and related market-specific rules.

The Belgian Commission for Electricity and Gas Regulation (CREG) and the Belgian

federal government service FOD Economy carried out the most recent research of the

possibilities of EES on specifically the Belgian electricity market in 2015 (CREG, 2015;

FOD Economie, 2015). At that time, Pumped Hydroelectric Energy Storage (PHES) had

the highest maturity in the study by FOD economy because of its high efficiency and high

energy density, which makes it suitable for balancing energy supply and demand across

the electric grid. Both studies explicitly mentioned that technology costs of storage could

fall substantially in the coming years due to technological advances and economies of

scale. Therefore, the results should be interpreted with caution because the findings are

based on technology cost data from more than five years ago and are a poor indication of

the economic feasibility of EES.

28

Two papers by Bezerra et al. (2006) and Bezerra, Barroso, & Pereira (2011) describe

bidding strategies for capacity providers participating in Brazilian reliability options. The

research focusses on calculating the optimal strike price bid, and option premium bid to

maximise the capacity provider’s revenue, given a desired risk-adjusted rate of return.

However, the described stochastic optimisation in the papers is less accurate for the

European central buyer mechanism based on reliability options. First, the Brazilian

reliability options mechanism differs from the European reliability options mechanism

because both the premium fee and the strike price should be proposed by the capacity

providers in the Brazilian auction. Second, the expected market revenue is calculated

using Monte Carlo simulation for different hydrological scenarios (Bezerra, Barroso, &

Pereira, 2011). The Brazilian power system is hydro-based, so the hydrological

conditions influence the market reference price (Bezerra et al., 2006). However, they are

less relevant in Europe since the European power system is not hydro-based. Besides, the

calculation in the research for the expected premium fee per year assumes that a fraction

of the hours per year the market reference price exceeds the strike price (Bezerra et al.,

2006; Bezerra, Barroso, & Pereira, 2011). Estimates can be made more accurate by

calculating the payback obligation based on market reference price forecasts.

Last, the variable market revenue (or losses) are calculated by subtracting the

operational costs from the strike price (Bezerra et al., 2006; Bezerra, Barroso, & Pereira,

2011). This implies the strike price is the highest price the capacity provider can receive

in the market. This does not have to be true since it might be possible the market

reference price is not related to the market where the capacity provider is active. For

example, the market reference price could be the day-ahead market price, and the

capacity provider receives revenue from ancillary services. The ancillary service market

prices are relatively higher compared to day-ahead market prices (Regelleistung, n.d -a.;

EPEX SPOT, n.d. -a). This means the capacity provider can earn more than the strike price

imposed by the TSO if the reference price is based on the day-ahead market price.

29

Based on outdated costs of EES technologies, lack of specific focus on the European

reliability options mechanism and the role of storage, no conclusion can be drawn as to

whether EES is competitive in the future Belgian capacity market. The findings of this

study for Belgium could help capacity providers in different countries whether they

should participate in an auction of a central buyer mechanism based on reliability

options.

Table 2 presents the current state of scientific knowledge on the relevant subjects for

evaluating the competitiveness of EES in the future Belgian capacity market.

Subject Scientific knowledge

None - little – sufficient – much

References

Central buyer mechanism based

on reliability options

Sufficient Bidwell (2005), Vázquez, Rivier, &

Pérez-Arriaga (2002), De Vries (2007),

Vázquez, Batlle, Rivier, & Pérez-

Arriaga (2003), Bezerra et al. (2006),

Bezerra, Barroso, & Pereira (2011)

Role of EES and increasing

(intermittent) RES capacity

Much Ferreira, Garde, Full, Kling, & Lopes

(2013), Soloveichik, (2011), Dunn,

Kamath, & Tarascon, (2011), Ibrahim,

Ilinca, & Perron (2008), Divya, &

Østergaard (2009)

Contribution of EES to the

security of supply

Sufficient Zhou, Mancarella, & Mutale (2015), Konstantelos, & Strbac (2018), Evans,

Tindemans, & Angeli (2019),

Sioshansi, Madaeni, & Denholm,

(2013)

Competitiveness (in central

buyer mechanism based on

reliability options)

Little Vázquez, Rivier, & Pérez-Arriaga

(2002) Bezerra et al., (2006), Bezerra,

Barroso, & Pereira (2011)

Market rules for EES

participating in capacity

auctions

None

Table 2. Current state of scientific knowledge on the relevant subjects for evaluating the competitiveness of EES in the

future Belgian capacity market.

30

3. Research questions and approach

3.1 Research questions

Based on the identified knowledge gap and research objective, the main research

question of the research can be formulated as follows:

What is the competitiveness of electrical energy storage in the future Belgian

capacity market?

And the following sub-questions need to be answered to answer the main research

question:

1. What are the characteristics of the Belgian Capacity Remuneration Mechanism?

2. Which EES technologies fit the characteristics of the Belgian capacity market best?

3. What is the revenue derived from the wholesale electricity market and the

potential payback obligation of the capacity remuneration mechanism?

4. What is the revenue derived from ancillary services?

5. What is the remuneration required for EES in Belgian capacity remuneration

mechanism auction?

31

3.2 Research approach

The research objective is to evaluate the competitiveness of EES in the future Belgian

capacity market by providing a systemic view of the problem. The first two sub-questions

of this study are qualitative in nature, and the last three sub-questions are quantitative in

nature. The relevant methodology to fulfil the objective of this study and answer the

research questions is mixed methods research. Mixed methods refer to the integration, or

‘mixing’ of both qualitative and quantitative data in one study. The idea behind the

methodology is that the combination of qualitative and quantitative approach leads to a

better understanding of the research problem than only one of the two approaches is

applied (Creswell, 2014). The relevant research approaches and research methods used

in this study will be discussed per sub-question.

What are the characteristics of the Belgian Capacity Remuneration Mechanism?

The question results in an overview of the Belgian CRM characteristics. The

characteristics will be identified through literature review and desk research. Literature

can help to understand the general functioning of CRMs. Desk research includes research

reports, consultation documents, and Belgian and European laws and legislations from

actors such as the CREG, Elia, the Belgian government and the European Commission.

Which EES technologies fit the characteristics of the Belgian capacity market best?

The most suitable EES technology in the future Belgian capacity market, and taken into

consideration in this research will be treated with the above question. Literature review

and desk research are suitable methods for identifying appropriate EES technologies in

the Belgian capacity market. Literature is relevant for comparing the characteristics of

the different EES technologies. Desk research includes studies on storage costs of energy

research agencies and reports on the suitability of specific technologies in Belgium.

32

What is the revenue derived from the wholesale electricity market and the

potential payback obligation of the capacity remuneration mechanism?

First, the wholesale electricity market with the greatest economic potential for the

considered EES technology from the previous sub-question will be determined.

Subsequently, the potential revenue and payback obligation are calculated under

different CRM design and price scenarios. The relevant research methods are desk

research for creating electricity market and payback obligation scenarios. The expected

intraday market income is assessed by the software tool Linny-R which applies the

optimization technique linear programming. Historical wholesale electricity market

prices obtained via Eneco will be used as input of the optimization model. The scenarios

will be further discussed in the 5.6 and Linny-R in 3.3.2.

What is the revenue derived from ancillary services?

Similar to the previous sub-question, the ancillary service with the greatest economic

potential for the considered EES technology will be determined. The potential revenue

will be calculated again under different CRM design and price scenarios. The appropriate

research method is desk research for creating ancillary service price scenarios, and Excel

will be used for analysing historical FCR prices and making relevant calculations.

Historical FCR prices are obtained from the ancillary services auction platform

Regelleistung.

What is the remuneration required for EES in Belgian capacity remuneration

mechanism auction?

Eventually, the required capacity remuneration will be calculated and based on the

revenue from the wholesale market or ancillary services, storage costs and the payback

obligation. The required capacity remuneration will be determined by Excel-based

financial modelling, using the Net Present Value (NPV), which will be further explained

in 3.3.1.

33

3.3 Methods

3.3.1 Net Present Value

Financial modelling is a meaningful methodology for decision-makers to offer business

solutions (Ho, & Lee, 2004). The financial modelling method Net Present Value (NPV) is

chosen to investigate the economic competitiveness of BES. The method is the most

commonly used for evaluating investments. The NPV is the sum of the cash inflows and

outflows discounted to the present values (Arnaboldi, Azzone, & Giorgino, 2014).

The formula of the NPV in this research is presented below. The income and costs are

calculated at each point in time 𝑡 over timespan 𝑁 and discounted at the discount rate 𝑟𝑟

(Belderbos, Delarue, & D'haeseleer, 2016). The cash flows taken into consideration in this

research include the earnings before interest, taxes, depreciation, and amortisation

(EBITDA) and the corporate tax. Thus, income revenue derived in the electricity market

𝑅𝑚𝑎𝑟𝑘𝑒𝑡, the capacity remuneration 𝑅𝑐𝑟𝑚, operations and maintenance (O&M) costs for

BES 𝐶𝑜&𝑚 and possible costs arising from participating in the CRM 𝐶𝑐𝑟𝑚. The capital

expenses (CAPEX) 𝐼0 are not discounted to today’s values in this research. The size of the

storage project in this research can be realized within a year. The total capital expenses

(CAPEX) of the EES system will be made at the beginning of the project (𝑡 = 0) and there

is no debt financing required. Therefore, CAPEX are not discounted (Arnaboldi, Azzone,

& Giorgino, 2014). A positive NPV will result in a net profit which means the investment

is acceptable. On the other hand, a negative NPV will result in a net loss, and the

investment should be rejected (Arnaboldi, Azzone, & Giorgino, 2014).

𝑁𝑃𝑉 = − 𝐼0 + ∑𝑅𝑚𝑎𝑟𝑘𝑒𝑡 + 𝑅𝑐𝑟𝑚 − 𝐶𝑜&𝑚 − 𝐶𝑐𝑟𝑚 − 𝐶𝑡𝑎𝑥

(1 + 𝑟𝑟)𝑡

𝑁

𝑡=1

The required capacity remuneration can be derived by complying with the condition that

the NPV should be greater than 0.

34

3.3.2 Linny-R

The expected wholesale market income is assessed by the software tool Linny-R which

applies the optimization technique linear programming. Linear programming involves

the minimising or maximising a linear objective function given certain equality and

equality constraints (Karloff, 2008). The program, developed by Dr. P.W.G. Bots,

determine the most appropriate operation schedule of BES in order to maximize profit

(Henriques, & Stikkelman, 2017). Thus, it calculates the optimal moments of buying and

selling electricity in the wholesale market. The objective function is shown below and is

subject to a set of constraints shown in Table 3.

max ∑ 𝑃𝑡 ∗ 𝐼𝐷𝑡

𝑇

𝑡=1

Constraints Description

𝑇 Planning horizon

𝑃𝑡>0 Charging power 𝑃 at hour 𝑡

𝑃𝑡<0 Discharging power 𝑃 at hour 𝑡

𝐸𝑡+1 = 𝐸𝑡 + η ∗ 𝑃𝑡 ∗ ℎ Energy capacity stored expressed for charging (𝑃𝑡>0) at hour 𝑡 and roundtrip

efficiency η

𝐸𝑡+1 = 𝐸𝑡 + 𝑃𝑡 ∗ ℎ Energy capacity stored expressed for discharging (𝑃𝑡<0) at hour 𝑡

𝐼𝐷𝑡 Wholesale market price at hour 𝑡

−𝑃𝑚𝑎𝑥 ≤ 𝑃𝑡 ≤ 𝑃𝑚𝑎𝑥 Charge-discharge power capacity at hour 𝑡 should be less than the maximum

power capacity of the BESS

0 ≤ 𝐸𝑡 ≤ 𝐸𝑚𝑎𝑥 Charge-discharge energy capacity at hour 𝑡 should be less than the maximum

energy capacity of the BESS

Table 3. Set of BESS constraints and description (Hu, Chen., & Bak-Jensen, 2010).

The optimisation of the charge-discharge decisions, and so the prediction of the

wholesale market income, in Linny-R is based on the rolling horizon approach (Bots,

2017). The approach uses currently known information and short-term forecasts which

has a higher level of reliability to solve the optimisation problem while retaining the

effectiveness of the calculation (Lu, Ying, & Chen, 2016). The rolling horizon approach is

commonly used for scheduling problems dealing with uncertainty such as inventory

control and traffic forecasts (Silvente, Kopanos, Dua, & Papageorgiou, 2018; Lu, Ying, &

Chen, 2016).

35

The rolling horizon approach is shown in Figure 3. The total planning horizon 𝑇 is split

up into 𝑁 stages where each stage 𝑛 contains 𝑚 intervals (where 𝑚 ≥ 1). Each stage 𝑛

consists of a roll period 𝑙, which represents reliable (short-term) forecasts and a look-

ahead period 𝑚 − 𝑙 which represents less reliable (medium-term) forecasts. The model

computes successive stages the roll period 𝑙 while taken into account the entire stage 𝑛.

Thereafter, the stage 𝑛 moves forward by 𝑙 time steps until stage 𝑛 + 1, both forecasts

will be updated and the procedure is done for all 𝑁 stages. It should be taken into

consideration that longer optimisation periods, and in particular longer the look-ahead

periods, which consists of medium-forecasts, decrease the reliability of the overall

prediction (Lu, Ying, & Chen, 2016).

Figure 3. Rolling horizon approach (Lu, Ying, & Chen, 2016).

36

4. System description

This chapter will first describe the characteristics of the Belgian CRM based on what is

known is so far. Thereafter the appropriate EES technologies on the Belgian capacity

market will be discussed. Lastly, the chapter describes the Belgian wholesale electricity

market and ancillary services and focusses on relevant market developments.

4.1 Characteristics of the Belgian CRM

The Belgian bill regarding the CRM has been adopted on April 4, 2019 (Belgische Kamer

van volksvertegenwoordigers, 2019a). The Belgian CRM should comply with the

European Union state aid rules, and the European Commission is expected to approve the

mechanism in June 2020. The prequalification period starts June 2021, and the first

auction (T-4) is planned in October 2021 to ensure sufficient capacity from November

2025 (Elia, 2019i; Elia, 2019d). Figure 4 presents the timeline until the first capacity

auction of the Belgian CRM. It can be concluded from the timeline that the final CRM

market rules and auction parameters will be published after writing this research.

Therefore, this section describes first the characteristics of the Belgian CRM from what is

known from the bill and reports from Elia meetings. It focusses on the most important

parameters within the scope of this research for determining the competitiveness of EES.

Subsequently, assumptions will be made for these parameters based on proposals from

CRM Task Force (stakeholder) meetings organized by Elia, CRM design notes and

parameters from European Commission approved CRMs in the United Kingdom, Ireland,

Italy and Poland (Elia, 2019h; European Commission, n.d.).

Figure 4. Belgian CRM timeline until the first capacity auction (Elia, 2019i).

37

4.1.1 Description

The capacity auction of the CRM is a competitive process in which capacity providers offer

a price for the provision of capacity. Capable capacity providers are existing and future

electricity generators, storage facilities, demand-side response and foreign capacity

(Belgische Kamer van volksvertegenwoordigers, 2019a). Two auctions will be organized

by Elia for each capacity delivery period: one auction four years ahead of each delivery

year (T-4 auction) and one auction a year ahead of each delivery year (T-1 auction). Elia

is responsible for the annual determination of the capacity required and the auction

parameters for the T-4 and the T-1 auctions, whereas the CREG monitors the CRM. The

volume report consists of the calculations of the total capacity required and the number

of hours during which the capacity will be used for the sake of adequacy to ensure the

security of supply. The parameter report includes the demand curve, price limit(s),

market reference price, strike price, and de-rating factors.

Table 4 provides an overview of the most important elements of the CRM that determines

the functioning. All the features will be described shortly.

Product design Auction design Economic parameters

demand curve

Volume assessment

Market reference price Clearing algorithm Demand curve (y-axis) Demand curve (x-axis)

Strike price Price/bid caps T-1 reserved volume

Availability requirements De-rating factors

Availability penalties Investment levels

Minimum participation

threshold

Table 4. Elements determining the functioning of the CRM (Elia, 2019i).

38

4.1.1.1 Market reference price and strike price

The CRM proposed in Belgium is based on reliability options. A reliability option is a call

option and refers to the contract that includes the obligation of the capacity provider to

pay the option buyer the positive difference between of the market reference price 𝑝 and

the strike price 𝑠 for the capacity sold under the contract. In return, the capacity provider

receives a fixed premium fee. The conditions mentioned above apply during the contract

period of the call option and are independent whether the capacity provider is trading

electricity in the spot market. The purchaser of the reliability option, which is the TSO

Elia, pays the market reference price 𝑝 and receive the difference between 𝑝 − 𝑠 if 𝑝 >

𝑠. This means if 𝑝 > 𝑠, the net payment is 𝑠 and the maximum price for the purchaser is

capped at the strike price 𝑠. The reliability option allows buying at 𝑝, but when 𝑠 > 𝑝

the purchaser will buy rationally at the market reference price 𝑝. Capacity providers limit

the highest possible price from 𝑝 to 𝑠 by selling reliability options. In other words,

capacity providers change their fluctuating revenue to a fixed revenue, and therefore

reducing their income risk. Choosing for reliability options might be interesting for

capacity providers dealing with fluctuating revenue, e.g., peak plants. As mentioned

above, the payback obligation when 𝑝 > 𝑠 is independent whether the capacity provider

is trading electricity on the spot market. If the capacity provider cannot deliver the

demand required while not trading on the energy market, the payback obligation with

the reliability option is (𝑝 − 𝑠) (Vázquez, Rivier, & Pérez-Arriaga, 2002).

Figure 5 shows the development of the market reference price (here spot price) over time

and the imposed strike price. 𝑠 > 𝑝 is true in 𝑡1 and 𝑡5, whereas 𝑝 > 𝑠 is true in 𝑡2, 𝑡3

and 𝑡4. 𝑡3 Illustrates the period where the capacity provider fails to deliver the contracted

capacity (Vázquez, Rivier, & Pérez-Arriaga, 2002).

Figure 5. Application of reliability options (Vázquez, Rivier, & Pérez-Arriaga, 2002).

39

The different outcomes of the reliability mechanism for the buyer of capacity and the

capacity provider are indicated in Table 5.

Time T1 T2 T3 T4 T5

Demand pays (€/MWh) 𝑝 𝑝 − (𝑝 − 𝑠) = 𝑠 𝑠 𝑠 𝑝 Capacity provider receives (€/MWh)

Excluding reliability option 𝑝 𝑝 𝑝 𝑝

Capacity provider receives (€/MWh)

Including reliability option 𝑝 𝑝 − (𝑝 − 𝑠) = 𝑠 −(𝑝 − 𝑠) − 𝑝𝑒𝑛 𝑠 𝑝

Table 5. Possible outcomes reliability options (Vázquez, Rivier, & Pérez-Arriaga, 2002).

Reliability options should limit windfall profits and increase the availability incentive

during moments of (imminent) scarcity. Imminent scarcity moments and moments when

the market reference price 𝑝 exceeds the strike price 𝑠 are highly correlated. This

provides an incentive for capacity providers to be active in the energy market during

moments of (imminent) scarcity (Elia, 2019f).

The equation below describes the payback obligation to the TSO if the market reference

price exceeds the strike price. The payback obligation is equal to the market reference

price minus the strike price (𝑝 − 𝑠) times the number of hours 𝑡 to which 𝑝 > 𝑠 is true.

(Vázquez, Rivier, & Pérez-Arriaga, 2002).

𝐶𝑐𝑟𝑚 = ∫ (𝑝 − 𝑠) ∗ 𝐶 𝑑𝑡𝑝>𝑠

(8)

𝐶𝑐𝑟𝑚 Costs arising from participating in the CRM [€/𝑦𝑒𝑎𝑟];

𝑝 Market reference price [€/𝑀𝑊ℎ];

𝑠 Strike price [€/𝑀𝑊ℎ];

𝐶 Obligated capacity, i.e., installed capacity times the corresponding de-rating factor [𝑀𝑊].

40

According to Elia’s proposal for the Belgian CRM, the market reference price ‘represents

a continuous and relevant energy (spot) price signal (€/MWh) of the Belgian power

market revenue, and capturing moments relevant for the security of supply’ (Elia, 2019f,

p. 4). The Belgian day-ahead market price has been proposed as the market reference

price because of its liquidity. The price signal is closely related to the (near) scarcity

moments, and all technologies can react to the price. No alternatives have been proposed

during the CRM Task Force stakeholder meetings organised by Elia. Therefore, the

Belgian day-ahead market price will be considered as the market reference price in this

research (Elia, 2019g; Elia, 2019f).

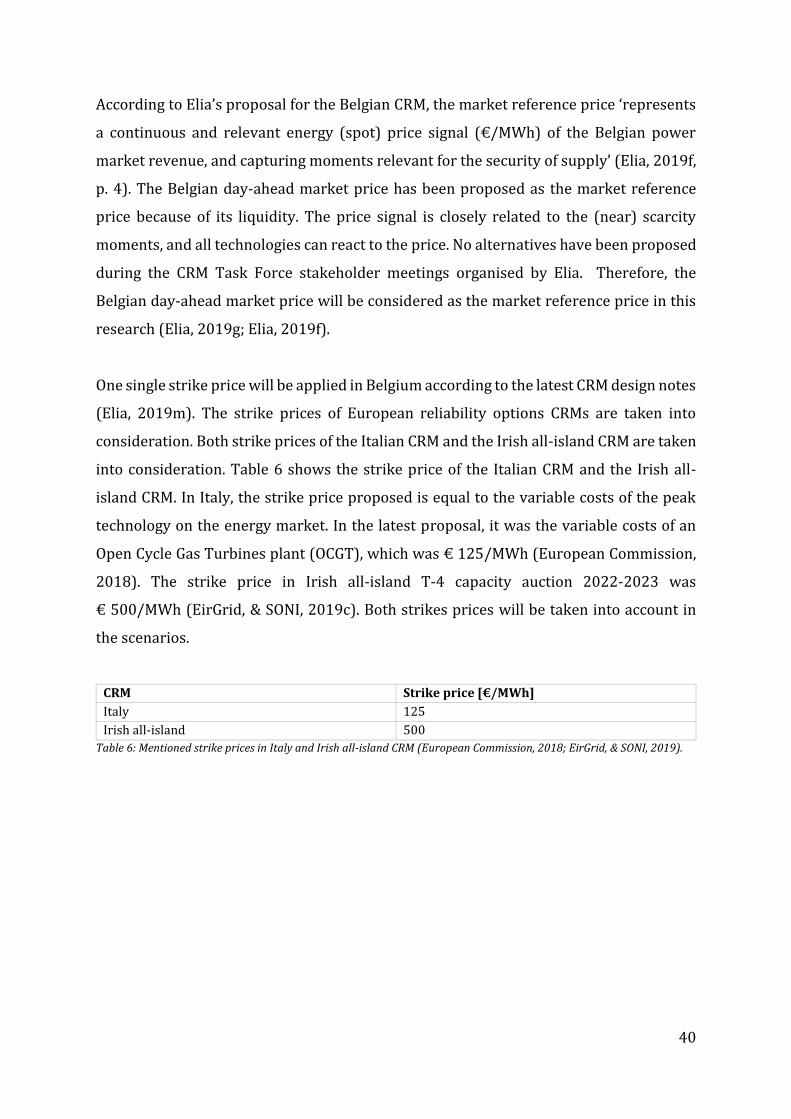

One single strike price will be applied in Belgium according to the latest CRM design notes

(Elia, 2019m). The strike prices of European reliability options CRMs are taken into

consideration. Both strike prices of the Italian CRM and the Irish all-island CRM are taken

into consideration. Table 6 shows the strike price of the Italian CRM and the Irish all-

island CRM. In Italy, the strike price proposed is equal to the variable costs of the peak

technology on the energy market. In the latest proposal, it was the variable costs of an

Open Cycle Gas Turbines plant (OCGT), which was € 125/MWh (European Commission,

2018). The strike price in Irish all-island T-4 capacity auction 2022-2023 was

€ 500/MWh (EirGrid, & SONI, 2019c). Both strikes prices will be taken into account in

the scenarios.

CRM Strike price [€/MWh]

Italy 125

Irish all-island 500

Table 6: Mentioned strike prices in Italy and Irish all-island CRM (European Commission, 2018; EirGrid, & SONI, 2019).

41

4.1.1.2 Availability requirements and availability penalties

All awarded capacity providers in the CRM auction contribute to the adequacy in Belgium.

Elia monitors the availability of each capacity provider during ‘adequacy relevant

moments’ in the contracted period. The Availability Monitoring Trigger (AMT) to identity

these adequacy relevant moments, i.e., AMT moments, is the Belgian day-ahead market

price. The availability monitoring of the contracted capacity providers is triggered if the

Belgian day-ahead market price exceeds a yearly defined AMT price. Every hour the

availability monitoring is triggered is called an AMT hour, and consecutive AMT hours is

called an AMT moment (Elia, 2019k).

Storage, aggregation of demand response and emergency assets capacity providers are

energy-constrained, so situations occur in which the AMT moment lasts longer than the

capacity provider’s (energy) reservoir constraint. Therefore, their contribution towards

adequacy is determined in a Service Level Agreement (SLA). The SLA is based on the

capacity’s energy constraint, i.e., maximum storage depth. The capacity provider should

provide according to the SLA their capacity until the energy reservoir of its asset is

exhausted. Hereafter, there is no delivery obligation for the capacity provider anymore

for that day since the limit is one activation per day. Table 7 shows the different SLA

categories for energy-energy constrained capacity providers and corresponding energy

delivery duration. As an example, if the storage depth of an asset is one hour, e.g., EES

power and energy capacity dimensioning is 10 MW/10 MWh, it should deliver only

during one AMT hour per day the (contracted) obligated capacity (Elia, 2019k).

Category Duration [hour] Limit [activation/day]

SLA #1 1

1

SLA #2 2

SLA #3 3

SLA #4 4

SLA #5 8

SLA #6 ∞

Table 7. SLA categories for energy-constrained capacity providers. Adapted from Elia (2019k).

42

Differences between the capacity provider’s available capacity and the obligated capacity,

i.e., missing capacity, could occur because of planned or forced outages (Elia, 2019k).

Capacity providers should cover the additional capacity required in a secondary market.

Elected bids from capacity providers could be (partly) transferred to other prequalified

capacity providers of the capacity auction with excess capacity of the capacity auctions

for a certain period and price. Capacity providers are penalized if they cannot cover the

missing capacity in the secondary market (Elia, 2019j).

The secondary market is considered as a liquid market. It is assumed in this research that

the capacity required to meet the contracted availability requirement is always met by

capacity from the secondary market. Besides, the Belgian CRM does not exclude any form

of capacity in the auctions because of the European Commission’s technological

neutrality requirement. EES is even mentioned as an example in Elia’s CRM presentation

(Elia, 2019i). Therefore, the availability requirement to participate in the capacity

auctions will be most likely no issue for EES. Last, the expected high penalties provide a

financial incentive to comply with the capacity delivery obligation. Therefore, payback

obligation in terms of penalties is not taken into consideration.

4.1.1.3 Clearing algorithm

The capacity remuneration is a yearly fixed premium in euro per MW. The pricing

depends on the type of CRM design. In the pay-as-bid design, the capacity provider

receives the accepted bid price in the auction whereas in the pay-as-clear design all

capacity providers receive the same market-clearing price (Harbordm & Pagnozzi, 2014).

The pay-as-bid design will be applied to the first two CRM auctions, i.e., the T-4 auction

in 2021 and 2022, and the pay-as-clear design will be applied in both T-1 and T-4

subsequent CRM auctions.

43

4.1.1.4 Demand curve and price caps

The demand curve describes the volume, i.e., capacity, to be contracted as a function of

the price per MW per year. The curve is often defined by three points, each representing

the willingness to pay for a certain level of security of supply. One point on the curve

corresponds to the minimum capacity which should be contracted at a certain price cap,

i.e., maximum price bid. The second point represents the price and capacity required to

ensure the desired security of supply level. The last point represents the maximum

capacity which could be contracted at zero euro per MW. Elia computes the capacity

required each year based on different scenarios and sensitives. No further details have

been published yet regarding the demand curve (Elia, 2019l).

4.1.1.5 T-1 reserved volume

The volume required for the T-4 auction is based on the desired security of supply level.

The T-1 auction is used for the refinement of capacity supply and demand. The minimum

reserved volume is at least equal to the capacity that has, on average less than 200

operating hours per year to cover the total peak capacity (Belgische Kamer van

volksvertegenwoordigers, 2019a).

4.1.1.6 Minimum participation threshold

The minimum capacity participation threshold, after applying de-rating factors, under

which capacity providers cannot participate in the prequalification process and

therefore, in the capacity auction (Belgische Kamer van volksvertegenwoordigers,

2019a).

44

4.1.1.7 De-rating factors

The CRM should contract the capacity to provide a secure energy supply. However,

generation units, demand response providers and storage facilities are assumed not

always to be able to continuously deliver 100% of their of generation capacity due to

malfunctions, lack of energy capacity, maintenance or weather conditions. In the Belgian