COMPENSATION PAYMENTS; COMMERCIAL … PAYMENTS; COMMERCIAL CONTRACTS; AND THE I.T.A.A ... subject...

32

COMPENSATION PAYMENTS; COMMERCIAL CONTRACTS; AND THE I.T.A.A. 1936: THE GORDIAN KNOT REVISITED By GARRY A. MUIR* 1 INTRODUCTION In maintaining the distinction between capital and income first instituted by legislation nearly two centuries ago, the courts have occasionally faced intractable problems where pragmatism has necessarily triumphed over anal- ysis. Sir Owen Dixon's famous Sun Newspapers] test for distinguishing between revenue and capital outgoings is one example, where in reality a number of unweighted considerations were suggested, with but vague illus- trations for their application. The proper manner of apportioning outgoings, and the role of purpose and intention, are others. Yet a fourth, and the subject of this paper is the characterisation of receipts derived from the sale or loss of intangible rights. Although less frequently considered than is the case with the other exam- ples given above, the assessability of compensation payments still remains (as recent Supreme Court of Victoria and Federal Court of Australia deci- sions illustrate)2 a "hard case" category, where recitation of broad criteria is the judicial norm. The judgments of both Courts in Merv Brown Pty Ltd v Federal Commissioner of Taxation suffer no pretension of transmuting relatively formless inquiry into principle, but they do illustrate the difficul- ties which the existence of a number of diverse tests can cause. In fact Merv Brown was a relatively simple case, but it does provide a practical spring- board for a detailed study of the relevant principles. Merv Brown Pty Ltd, the taxpayer and appellant, was a clothing whole- saler, whose stock in trade consisted both of locally manufacturecl and imported goods. The latter were admitted into Australia under "impo.rt quota entitlements" held by the taxpayer. These in turn entitled the holder to a lower rate of duty on the imported goods covered by the quota. In 1980 45070 of gross sales of $22 million was attributable to imported clothing. The quotas were allocated by the Federal Government according to certain "classes" of clothing and subject to its approval, transferable. As a result of a governmental review of the quota rules in 1980, the tax- payer rationalised its business by selling those of its quotas which related to unprofitable lines, and acquiring by purchase others which would increase imports of profitable items. In the fiscal year ended 30 June 1981, the tax- payer realised $1,698,740 from the sale of quotas; although it appeared that total sales and purchases of quotas did not exceed 3070 of the taxpayer's total quota entitlement. Between 1980 and 1983, and partly as a consequence of its rationalisation, total'sales more than doubled to $47 million. *LLB (Hons) (Auckland); BCL (Oxon); Lecturer-in-Law; Australian National University. 1 Sun Newspapers Ltd v Federal Commissioner of Taxation (1938) 61 CLR 337, 363. 2 Merv Brown Pty Ltd v Federal Commissioner of Taxation [1984] ATe 4,394; (1985] ATC 4,080.

Transcript of COMPENSATION PAYMENTS; COMMERCIAL … PAYMENTS; COMMERCIAL CONTRACTS; AND THE I.T.A.A ... subject...

COMPENSATION PAYMENTS; COMMERCIAL CONTRACTS;AND THE I.T.A.A. 1936: THE GORDIAN KNOT REVISITED

By GARRY A. MUIR*

1 INTRODUCTION

In maintaining the distinction between capital and income first institutedby legislation nearly two centuries ago, the courts have occasionally facedintractable problems where pragmatism has necessarily triumphed over analysis. Sir Owen Dixon's famous Sun Newspapers] test for distinguishingbetween revenue and capital outgoings is one example, where in reality anumber of unweighted considerations were suggested, with but vague illustrations for their application. The proper manner of apportioning outgoings,and the role of purpose and intention, are others. Yet a fourth, and thesubject of this paper is the characterisation of receipts derived from the saleor loss of intangible rights.

Although less frequently considered than is the case with the other examples given above, the assessability of compensation payments still remains(as recent Supreme Court of Victoria and Federal Court of Australia decisions illustrate)2 a "hard case" category, where recitation of broad criteriais the judicial norm. The judgments of both Courts in Merv Brown Pty Ltdv Federal Commissioner of Taxation suffer no pretension of transmutingrelatively formless inquiry into principle, but they do illustrate the difficulties which the existence of a number of diverse tests can cause. In fact MervBrown was a relatively simple case, but it does provide a practical springboard for a detailed study of the relevant principles.

Merv Brown Pty Ltd, the taxpayer and appellant, was a clothing wholesaler, whose stock in trade consisted both of locally manufacturecl andimported goods. The latter were admitted into Australia under "impo.rt quotaentitlements" held by the taxpayer. These in turn entitled the holder to a lowerrate of duty on the imported goods covered by the quota. In 1980 45070 ofgross sales of $22 million was attributable to imported clothing. The quotaswere allocated by the Federal Government according to certain "classes" ofclothing and subject to its approval, transferable.

As a result of a governmental review of the quota rules in 1980, the taxpayer rationalised its business by selling those of its quotas which relatedto unprofitable lines, and acquiring by purchase others which would increaseimports of profitable items. In the fiscal year ended 30 June 1981, the taxpayer realised $1,698,740 from the sale of quotas; although it appeared thattotal sales and purchases of quotas did not exceed 3070 of the taxpayer's totalquota entitlement. Between 1980 and 1983, and partly as a consequence ofits rationalisation, total'sales more than doubled to $47 million.

*LLB (Hons) (Auckland); BCL (Oxon); Lecturer-in-Law; Australian National University.1 Sun Newspapers Ltd v Federal Commissioner of Taxation (1938) 61 CLR 337, 363.2 Merv Brown Pty Ltd v Federal Commissioner of Taxation [1984] ATe 4,394; (1985] ATC

4,080.

304 Federal Law Review [VOLUME 15

In allowing the appeal from the Commissioner's determination, and holdingthe receipts to be of a capital nature, Kaye J relied primarily on the testformulated by Lord Cave LC in British Insulated & Helsby Cables Ltd vAtherton;3 which is as follows:

... when an expenditure is made, not only once and for all, but with a viewto bringing into existence an asset or an advantage for the enduring benefit ofa trade, I think that there is very good reason (in the absence of special circumstances leading to an opposite conclusion) for treating such an expenditure asproperty attributable not to revenue but to capital.

However from his -'~review of the authorities" Kaye J concluded it was alsonecessary to consider other additional matters, which could include "thenature of the business and the use made of the commodity ... in question."4 On the facts of the instant case "foremost among those matters" isthe fact that the taxpayers business did not include speculating inimportquotas. 5 Nor was it in the ordinary course of its business. For these reasonsit was held the receipts by Merv Brown Pty Ltd from the sale of its quotaswere capital items. On appeal to the Federal Court, Bowen CJ and LockhartJ held (Jenkinson J dissenting) in response to the Commissioner's argumentthat the sales of the entitlements were brought about by exigencies occurring in the ordinary course of business, that the taxpayer was not in thebusiness of dealing in such entitlements. This was so even if the transactionshad no effect upon the fundamental structure of the business. The significanceof these findings will be discussed further below.6

2 INCOME/CAPITAL DICHOTOMY

It is submitted that the reasoning of the Supreme Court in Merv Brown PtyLtd v Federal Commissioner of Taxation employs a number of tests, themselves vague in character, to a problem divorced from their intended application. It is necessary in order to understand how this has occurred to examine some basic taxation principles. In demarcating between capital andincome, the existence of certain categories of tests has become tolerably clear.The first category is "source" based; that is to say the identification of thesource of· the receipt is usually sufficient to characterise it as income. Onecan identify two such "sources"; income from property:: and income frompersonal exertion,8 although it may be correct to say that whenever the legis-

3 [1926] AC 205, 213-214.4 Supra n2, 4,405.S Idem.6 Below 333.7 Eg Dividends; rents; interest. The so called "tree-fruit" metaphor is apposite to this type

of receipt: Eisney v Macomber (1919) US 189, 206; The term "source" is obviously used in itssecondary sense as meaning the activity or corpus which produces the income.

8 Providing the services have been rendered to the payer, or the taxpayer is in an employment relationship with the payer: turner y Cuxson (1888) 2 TC 422; Dixon v Federal Commissioner of Taxation (1952) 86 CLR 541, esp 554 per Dixon & Williams JJ. The point has beenmuch confused subsequently, first by statutory language (eg Herbert v Quade [1902] 2 KB 631;Duncan's Executors v Farmer (1909) 5 TC 417); secondly by confusion with the relevant testfor distinguishing "testimonial" payments from a person to whom services had been renderedetc (eg Cooper v Blakiston [1907] 2 KB 688; [1909] AC 106); and finally by failure to identifyclearly the source of payment; (eg Seymour v Reed [1927] AC 554; Moorhouse v Dooland [1955]1 Ch 284).

1985] Compensation Payments; 305

lature brings to tax a type of activity not previously exigible, this ex faciecreates another, albeit narrow, "source" of income.9

The second category catches receipts which may derive from diversesources, but which have the incidence of recurrence. In the SunNewspapers10 case Dixon J suggested that "recurrence is not a test, it is nomore than a consideration the weight of which depends upon the nature ofthe expenditure", but like all general statements it is subject to heavy qualification. First, it was an utterance made in the context of an expenditure,and the courts have found it even more difficult to draw a reasoned linebetween capital and revenue expenditure, than they have between capital andincome receipts. Secondly, recurrence is the one factor which most determines whether the sale of property is or is not in the course of a businessand thus (if it is otherwise a capital item) exigible. Where in fact the taxpayerhas bought and sold an item without expending any other time, energy, ormoney upon it, it may indeed be the only test. 11 In such circumstances it canseen how appropriate is the style of inquiry suggested by Kaye J in MervBrown Pty Ltd; that is, is this sale in the ordinary course of a business [ofbuying and selling similar items with sufficient regularity to constitute incomeand not a capital receipt].

Exactly the same distinction underlines the Cave test in British Insulated& Helsby Cables Ltd v Atherton 12 since something bought and sold once,or which has been of an enduring benefit, will not form the subject matterof a business.

Such an analysis is exceedingly simplistic, 'but it does not necessarily diminish the importance of recurrence as a test. Other factors are sometimes saidto be relevant to ascertaining the existence of a business. 13 For example asubject matter which is usually the subject of trade, or is not usually purchased for private consumption, or for income yield, is likely to suggest abusiness of selling such items, but again repetition is necessary. Converselythose items which are not normally the subject of trade are unlikely per seto involve a presumption of business if sold; but if several are sold theweaker is the presumption of private use. Similarly other so-called 'badgesof business"14 such as the length of period of ownership, or the circum-

9 Eg ss 25A(1); 26AAA; 26(f). CfRW Parsons, "The Meaning of Income and the Structureof Income Tax Assessment Act" (1978) XIII Taxation in Australia 379.

JO Sun Newspapers v Federal Commissioner of Taxation (1938) 62 CLR 337, 362.11 See eg London Australian Investment Co Ltd v Federal Commissioner of Taxation (1977)

138 CLR 106, 130 per Jacobs J, and 117 per Gibbs J; Rutlege v Inland Revenue Commis~ioners (1929) 14 TC 490. The other controlling factor appears to be the necessity for "a purJose, intention or expectation of resale"; and as indicated by Jacobs J at 130 the two factors)f frequency and intention are interrelated. The difficulty however in placing too great an=~mphasison the latter is that the normal legal attitude in revenue law is not to regard intention15 determinative of whether a sum is capital or income. CfRe Duty on Estate ofIncorporated::ouncil of Law Reporting for England and Wales (1888) 22 QBD 279, 293 per Coleridge CJ;JrijJiths v JP Harrison (Watford) Ltd. [1936] AC 1.

12 [1926] AC 205, 213 per Cave LC.13 See generally, United Kingdom Royal Commission on Taxation of Profits and Income,

:md 9474, para 116; Fergusson v Federal Commissioner of Taxation (1979) 26 ALR 307; Blinson, Pinson on Revenue Law (14th ed, 1981) 14-20; PG Whiteman & DC Milne, Whitemanrnd Wheatcroft on Income Tax (2nd ed, 1976) 246-265.

14 Cmd 9474, ibid; Whiteman & Milne, ibid 255.

306 Federal Law Review [VOLUME 15

stances responsible for the realisation, are qualified and perhaps even renderednugatory by the frequency. of similar transactions, since the inference ofprivate use they raise is rebutted.

Sometimes one transaction may be said to amount to a business; but thecircumstances in which this is so do not contradict the importance of recurrence. The first example is the one-off transaction, which because it is presumed it will continue is said to be a transaction in the course of a business. 15 The other is the purchase of an item on which a great deal of work I

is done before it is resold. It may be correct linguistically to characterise thetaxpayer as-carrying on a business of modifying such items during the periodin which he is doing so, but in reality where the taxpayer himself does thework the final sale represents not so much income from a business, as incomefrom personal exertion. 16

In terms of the result in the Merv Brown case, the fact that the taxpayerdid not carryon the business of dealing in import quota entitlements wasprobably correct on the facts. But the receipts from their sale while notincome on a recurrence test, were not thereby prevented from characterisation as income on other tests.

The third category of inquiry is "intentionr' based. According to the generallaw definition of income, a receipt from the sale, otherwise than in the courseof business, of property bought with the sole l7 intention of resale at a profit I

will be assessable as an adventure in the nature of trade. IS How far this principle remains part of Australian jurisprudence after the enactment of s 26(a) I

in 1936 is unclear. More pertinent to the Merv Brown decision is the fourth I

(and according to my analysis penultimate) category which embraces a "compensation" test. 19 The concept briefly stated is that where money is derived I

in lieu of an expected receipt, the character which that latter receipt would I

have had, had it been made, will be ascribed to the compensation received I

in lieu of it. The final category, and one conjectural in its existence and I

application is "an ordingary course of business" test, which brings to tax sums i

not otherwise included under any of the above four categories. 20

15 Rutledge v Inland Revenue C.:ommissioners (1929) 14 TC 490; Fairway Estates Pty Ltd VI

Federal Commissioner of Taxation (1970) 1 ATR 726; Clark v Follet (1973) 48 TC 677; John~

stan v Heath (1970) 46 TC 463; Western Gold Mines No Liability v Commissioner of Taxationfor Western Australia (1938) 1 AITR 248, 250.

16 This conclusion is not possible in the United Kingdom because there is no general cas(catching income from personal exertion, therefore such activity must be characterised as a business. The relationship between income from personal exertion in its common usage and no's6(1) sense,. and the mere realisation of an asset, has not yet been considered.

17 See eg Inland Revenue Commissioners v Fraser (1942) 24 TC 498; 502-503; Rutledge'Inland Revenue Commissioners (1929) 14 TC 490; Edwards v Bairstow [1956] AC 14; cfBlocke.,v Federal Commissioner of Taxation (1923) 31 CLR 503, 508 per Issacs J.

18 In both Investment & Merchant Finance Co Ltd v Federal Commissioner of Taxatiot(1971) 125 CLR 249, and Federal Commissioner of Taxation v Whitfords Beach Pty Ltd (198239 ALR 521 it was held that s 25 should be applied before 26(a) [now 25A(1)]. This would appeato reincorporate the learning on adventures in the nature of trade back into Australian revenulaw.

19 See Generally, KW Ryan, Manual of the Law of Income Tax in Australia (5th ed, 198106-115; RI Barrett, Principles of Income Tax (2nd ed, 1981) 77-82; AP Molloy, Income Ta(1976) Chpt 6; Pinson, supra n13, 32-34; Whiteman & Milne, supra n13, 335-345.

20 Discussed below 330 et seq.

1985] Compensation Payments; 307

3 THE COMPENSATION TEST

A Preliminary principles

The word "compensation" can be used in a number of possible contexts.First a money payment may compensate the recipient in the sense of makinggood a deficiency in relation to an agreed norm or standard. Gratuities paidto a waiter may compensate for a nominal wage. Secondly a sum may compensate in the sense of counterbalancing on unwanted imposition; for example"danger money" paid in addition to normal wages .to compensate for risksor unpleasantness attendant on performing some required task. Thirdly,compensation may refer in a very general way to the quid pro quo onepartly receives for a consensual adjustment of his rights; for example forrelinquishing property rights. Of course one would not usually employ theterm "compensation" to characterise any of the above receipts; colloquiallyand legally that term is employed in a fourth manner, where an adjustmentof property or other rights· occur either non-consensually; for example bycompulsory acquisition, destruction or loss; or on the deprivation of anopportunity to earn. All four classes of compensation may however beexigible.

If the receipt is compensation in the sense of making good a deficiencyin relation to an agreed norm, or counterbalancing an unwanted imposition,then whether or not it is income according to ordinary concepts will dependprimarily upon whether it is recieved as a reward for an income producingactivity.21 Where by contrast the receipt is in respect of a detraction of preexisting rights, surrendered consensually or otherwise; whether it is incomeaccording to ordinary concepts will depend upon properly characterising thenature of the rights relinquished. It is of course possible to characterise allrights as intangible assets so that their loss is a loss of capital, but this hasnever been accepted as a universal proposition.22

Where the rights relate to tangible property, there is a presumption thata receipt compensating for the loss of those rights will be paid on capitalaccount, unless the property is trading stock of the taxpayer. 23 Where theloss is a detraction from pre-existing rights to (or as) intangible property,such as choses in action, intellectual property, and transferable licences orconcessions; then again unless the taxpayer is in the business of trading insuch property, any loss will be presumed on capital account. Merv BrownPty Ltd v Federal Commissioner of Taxation falls within this class and willbe discussed further below.

The position becomes much less clear where the right lost does not relateto any recognised legal property; for example relinquishing a right to trade

21 See eg Hayes v Federal Commissioner of Taxation (1956) 96 CLR 47; Scott v Federal Commissioner of Taxation (1966) 10 AITR 367.

22· This crucial distinction between the abstract concept of a "right" in the air so to speak,~nd the "thing" to which the right relates, is often lost sight of. A right is always to have, touse, to do, something; or not to be interfered with in something. But to characterise "the right"1S capital by reference to nomenclature is fallacious; many "rights" have no capital attributesNhatsoever.

23 California Copper Syndicate (Limited & Reduced) v Harris (1904) 5 TC 159, 165-166;Western Gold Mines No Liability v Commissioner of Taxes for Western Australia (1938) 59:LR 729, 735, 737. And see Taylor v Good (1974) 49 TC 277; Simmons v Inland Revenue Comnissioners [1980] STC 350.

308 Federal Law Review [VOLUME 15

either geographically or temporally or the right to hold a certain office. Insuch cases the critical question is whether the receipt is in respect of the rightlost, or in respect of the profits or gains which the retention of that rightwould have enabled the taxpayer to receive.

Two other preliminary points can be made concerning compensationreceipts. First by their very nature they are unlikely to be received in theordinary course of business. Thus the use of an "ordinary course of business"test is plainly inappropriate to determine exclusively the exigibility of suchreceipts. Second, the application of the compensation test to insurance receiptsexpressly indemnifying for loss of trading stock24 or loss of profits25 is wellsettled. Although many of the relevant decisions rather obfuscate the reasonfor including these sums in the assessable income, Lord Cave LC in Commissioners of Inland Revenue v Newcastle Breweries26 clearly suggests it tobe on the basis that although the event producing the revenue was not contemplated, the taxpayer has nonetheless been placed in the position he wouldhave been in had he sold, (rather than lost) his stock. This makes good sense,otherwise traders would have a fiscal incentive to destroy rather than to selltheir wares. There is however the question as to which provisions bring suchreceipts for lost trading stock to tax. It appears that they will not be includedunder s36,27 but will be under s25 (as are all other exigible compensationreceipts) and must also be included in the calculation under s28(1). Wherethe trading stock is however only temporarily sterilised, for example certainclasses of goods placed under a moritorium on sale pending some outcome,the stock should be regarded as still on land at the close of the income year.

B Compensation payments prima facie capital receipts

(1) General ruleSubject to one caveat (relating to trading stock), money received from the

disposition of a tangible, or an intangible but inherently transmissible right,will prima facie be a capital receipt. Although many items of property, suchas machinery or a patent, have no commercial value (save as scrap) separatefrom their ability to contribute to the production of income, nonetheless thesignal notion that property, other than property the subject of trade, shouldbe exonerated from impost, automatically characterises a receipt from thesale of such property as capital. This result would be rationalised in legaltheory by the fact that the sale was of fixed not circulating capital;28 orbecause part of the income earning structure had been sold;29 or perhaps

24 Eg Gliksten v Green [1929] AC 381; and see s 26(j).2S Eg King v British Columbia Fir & Cedar Lumber Co Ltd [1932] AC 441; and see s 26 (j).26 (1926) 12 TC 927 at 953; and see Waterloo Main Colliery Co Ltd v Inland Revenue Com-

missioners (1947) TC 235; Ensign Shipping Co Ltd v Inland Revenue Commissioners (1928)!12 TC 1169.

27 Federal Commissioner of Taxation v Wade (1951) 84 CLR 105.28 Eg John Smith & Son v Moore [1921] 2 AC 13, 19-20; Davies v Shell Co of China Ltd l

(1951) 32 TC 133 but cf Commissioner of Taxes v Nchanga Consolidated Copper Mines [1964]:AC 948, 962 per Lord Radcliffe.

29 Eg Van den Bergh'S Ltd v Clark (1935) AC 431; discussed below 317. But cf Sun News~

papers Ltd v Federal Commissioner of Taxation (1938) 41 CLR 337, 359 et seq per Dixon J.

1985] Compensation Payments; 309

because something which was for the enduring benefit of the trade30 hasbeen realised.

(2) Exception: Quantification otherwise than by reference to a lump sum

Where property other than trading stock is sold, the method by which thesale price is determined is generally irrelevant. Thus a sum quantified by reference to expected profits will not change the character of the receipt, 31providing a quantifiable lump sum is expressed as the consideration for thesale. If, as may occasionally happen, the consideration is expressed otherthan as a valuation of the property sold (however arrived at), but rather bysome other criteria, for instance the use to which the property will be put,then the receipt will be characterised as income, and taxed. 32 It is not at allclear whether this is because it takes on the character of income frompropertY,33 or because of the recurrent nature of the receipts. Similarly theright to an annual payment without reference to a lump sum payable grantedin exchange for property is regarded as an annuity and exigible,34 presumably on the basis that it is of a recurrent nature.

Although these principles appear tolerably correct, it must be admittedthat their application has been unsettled by the law relating to the taxationof royalties. First in relation to those receipts, the courts have often failedto distinguish between the situation where rights are granted which (to utilisean overworked metaphor), represent fruit generated from a tree left essentially intact, and rights which by their exercise, diminish the corpus of the

30 Eg British Insulated & Helsby Cables Ltd v Atherton [1926] AC 205, 213 per Cave LC.Adopted Sun Newspapers Ltd v Federal Commissioner of Taxation (1938) 41 CLR 337, 355per Latham CJ.

31 Eg Glenboig Union Fire Co Ltd v Inland Revenue Commissioners (1922) 22 TC 427, 464;Inland Revenue Commissioners v Ramsey (1935) 20 TC 79; Commissioner of Taxes v E [1942]NZLR 115. Cf Egerton- Warburton v Federal Commissioner of Taxation (1934) 51 CLR 568.

32 Commissioner of Inland Revenue v Hogarth (1940) 23 TC 491. See also Orchard Wine& Supply Co v Laynes (1952) 33 TC 97; Lamport & Holt Line Ltd v Langwell (1958) 38 TC193; United Steel Companies Ltd v Cullington (No 1) (1939) 23 TC 71. Where the paymentis expressed to be a sum equal to profits over a number of years it appears to be capital if itis not quantifiable until the period is completed: Ledgard's case ibid; but the distinction betweenthis and sums equal to annual profits over a number of years which are income, appears tobe a matter of fine distinction: Dott v Brown [1936] 1 All ER 543, 550. Where the paymentis not expressed as a sum equal to profits, but rather a per centage of the profits themselves,it is to be regarded as income. Likewise where even though expressed as a sum equal to profitsover a number of years the term is a long one. Ramsay's case ibid, but for the reference tothe capital sum would have fallen into the last category; sed quaere the capital sum or partthereof not there being payable at the time of each return, it should have been disregarded asirrelevant. It is submitted that the distinction between Legard and Hogarth is too fine to beuseful, and that as a matter of substance the courts should disregard the language of the partiesand hold that any annual payments made without reference to a capital sum certain shouldbe regarded as income.

33 Cf Egerton-Warburton v Federal Commissioner of Taxation (1934) 51 CLR 568, 579.34 Commissioners of Inland Revenue v Hogarth (1940) 23 TC 491. And see Jones v Inlandevenue Commissions (1919) 7 TC 310. Cfs 262 concerning the assessability of periodic payents, which in an earlier form was unsuccessfully invoked in Californian Oil Products (Iniq) Ltd v Federal Commissoner of Taxation (1934) 52 CLR 28.

310 Federal Law Review [VOLUME 15

grantor. 35 The former, such as the right to playa piece of music, demonstrably represent income from property, and one susceptible to a definitionof royalties which requires payments conterminous with the exercise of a rightgranted. But where the royalty relates to, for example, a profit aprendre,where property removed is quantified on a per ton (or similar basis), the courtshave rather adroitly avoided the conclusion that the receipt is of a capitalnature by characterising the property disposed of as a right to enter andremove, rather than as a sale. 36 This has the consequence that the "right" I

falls within the common definition of "royalty" in section 26(1) and is therebyexigible. In effect this "rights" analysis hides the fact that the receipt in sucha case would normally 'be capital according to the principles outlined above;an unhappy formula which has disturbed not a few judges. 37

(3) Exception: Rights relin;quished but not transferred

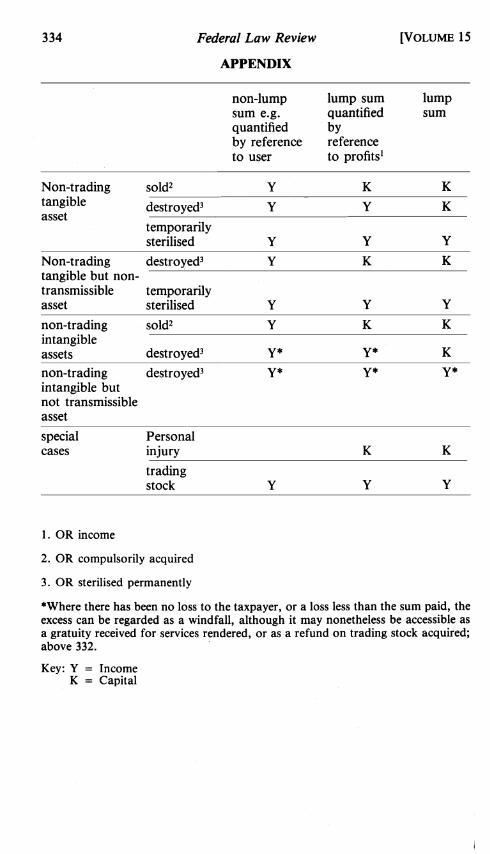

Where property or a proprietary right other than trading stock is sold,the sum is according to the above principles prima facie capital. However,where such an inherently transmissible right is not sold, but is destroyed orneutralised, then different rules may apply. A preliminary but crucial distinction must be made between a temporary and a permanent deprivation I

of property; and its importance becomes apparent in the following hypotheses I

using trading stock as an example:

1. Hypothesis: Stock is sold.Conclusion: receipt is assessable.

2. Hypothesis: Stock is destroyed, compulsorily acquired (etc.).Conclusion: receipt is assessable for reasons advanced previously.

3. Hypothesis: Stock is temporarily impounded or similar.Conclusion: the goods have not actually been disposed of consensually :or non-consensually, so there is no analogy with their sale in the course:of trade. Whether the receipt is assessable depends upon whether itrepresents:(a) loss of profits suffered during the period of retention (an excess i

demand market or at least market equilibrium being assumed);38

35 It is submitted that where the corpus remains relatively intact after use, then a sum received I

for that use will also be revenue, whether in a lump sum or not. An example would be a nonexclusive licence: cf. Inland Revenue Commissioner v Longharns Green & Co. (1932) 17 T.C.,272. Where the use depletes the corpus, or substantially lessens its value, then the sum receivedImay be either a royalty or a sale price. It will be a royalty if payment is quantified by reference'to user: cf. McCauley v Federal Commissioner of Taxation {1955) 92 C.L.R. 630. Informationand non-patented information causes problems of characterisation however because it does notlfit easily into a property analysis. The only qualification to the above analysis is that true annual'payments, that is recurrent payments quantified without reference to a lump sum, will tun~

what otherwise might be a capital receipt into revenue: see generally Murray v ICI Ltd [1967~1

2 All ER 980.36 Eg McCauley v Federal Commissioner of Taxation (1944) 69 CLR 235.37 Ibid per Rich J; Moriaty v Evans Medical Supplies Ltd [1957] 3 All ER 718.38 If there was an excess supply market, the taxpayer would find it difficult to prove tha

sterilisation resulted in a loss of profits; for problems with collateral sales in excess supply market~

see Re Vic Mills [1913] 1 Ch 465; cf Charter v SuI/ivan [1957] 2 QB 117. See also Waterlo(Main Colliery Co Ltd v Inland Revenue Commissioners (1947) 29 TC 235; Ensign Shippin~

Co Ltd v Inland Revenue Commissioners (1928) 12 TC 1169.

1985] Compensation Payments; 311

(b) other loss suffered, for example to goodwill, out-of-pocket expensessuch as rectifying damage to the goods; damages paid to third partiesfor breach of contract;

(c) an amount which does. not compensate inasmuch as no loss has beensuffered, or has been suffered to a lesser extent than the sum received;and which therefore represents a "windfall" to the recipient.

A similar analysis would also apply to the deprivation et cetera of a capitalitem, although a number of qualifications would need to be introduced. Thus,on the first and second hypotheses, the conclusion would be capital, unlessas previously outlined, the receipt is not a lump sum (however quantifiedor payable), but rather varies according to some other criteria, such as theuse made of the article. 39

If the above model is accepted, the next difficulty is to allocate the sum,or the parts of the sum, received to the proper category. Obviously if themoney is received expressly on account of one type of loss, then providingthe sum does not over-compensate for that loss (so that the excess does notfall within the third clause of the third hypothesis), intention should bedeterminative. Even without such direction regard could be had to the methodof quantification to ascertain or infer intention. Although the correctnessof this was emphatically denied by Gavan Duffy CJ and Dixon J in California Oil Products Ltd v Federal Commissioner of Taxation,40 it is submitted for reasons developed below41 that it makes good sense when one isattempting to ascertain intention to do so..

Where a global sum is received on account of both capital and revenueloss, it appears that the proper course is to make up losses on capital accountfirst before those on revenue account. 42 However, it is presumed such a rulewill only operate where the parties have not otherwise indicated (for exampleby the method of quantification) that it should be displaced. 43 Where therule does apply, it will operate in an obvious manner where for example bothcapital and trading stock losses occur. But it is less certain where there hasbeen a retention of capital items only. If trading stock is retained therewill be a presumption that the receipt is revenue, since the item of stock wouldprobably have been sold during the period of retention. This will certainlybe so where there is an excess demand for the product, since the owner has

39 Above 309. Where the capital asset is destroyed, the compensation may include a sum forprofits lost during the period of restoration: London & Thames Haven Oil Wharves Ltd v Attwooll [1967] 2 All ER 124.

40 (1934) 52 CLR 28, 41.41 Below 329.42 McLaurin v Federal Commissioner of Taxation (1961) 104 CLR 381,391; Allsop v Federal

Commissioner of Taxation (1965) 113 CLR 341. Watson v Samson Bros. (1959) 38 TC 346.As a matter of fairness it appears proper that if a dissection was to be made of a global sumcredit should first be given against property lost, and then against loss of profits, otherwise thetaxpayer is in a worse position than he would have been but for the event causing the loss;ie he is taxed on assumed realisation, but is not thereby adequately compensated for the expenseof re-establishing the profit earning structure. But to the extent the taxpayer can claim fulldepreciation on the capital loss, the exact apportionment would be a matter of indifference tohim: s 59. And see further: G Lehmann, "The Common Law, Tax Law and MathematicalCulture" (1984) ALJ 649. Different considerations may apply where tangible assets do not requirereconstruction before revenue activities recommence.

43 McLaurin v Federal Commissioner of Taxation, ibid.

312 Federal Law Review [VOLUME 15

lost a sale.44 Where this is not so the receipt is more difficult to characterise.If it is brought to tax at all, it is submitted it will only be through the application of some miscellaneous category of test such as receipts "in the ordinary I

course of business". 45 But for reasons developed below it is submitted sucha category (if it exists) must only be used as an inclusionary, and not as anexclusionary test.

Where the retention is of a capital asset, the only capital loss which willbe required to be off-set is loss to goodwill,46 and this if it exists will bedifficult to prove. It may be that a third category of loss, that is, sums received '1

as recompense for out-of-pocket expenses, should as a matter of presumedintention, be accounted for prior to setting off against revenue loss, or even I

possibly capital loss. 47 Whether these sums will be exigible will depend uponthe application of section 260).48 ,

The approach of the courts to receipts derived as compensation for rights ;not consensually relinquished has, however, been rather less structured. Thereare two leading authorities which illustrate the different types of difficultywhich can arise. The first, Burmah Steamship Co v Commissioners ofInland I

Revenue49 concerns the temporary retention of a capital asset.The appellant was part owner of a motor vessel which it had placed in I

the hands of a repairer for an overhaul. There was a penalty clause in the ~

contract for the late completion which in the circumstances of the case wasinvoked. The damages recovered were calculated by reference to the estimatedprofit which would have been earned by the vessel had it been trading duringthe period when the repairs ought to have been completed. The claim was I

compromised and under the terms of the settlement the owners received a I

global sum of £3,000. This amount was held to be an income receipt, paid I

in respect of a restriction of trading opportunities, rather than the deprivation of a capital asset. This it is submitted was correct, although a fortuitous i

conclusio'n given the nature of the inquiry. The deprivation of a capital assetis the event giving rise to the loss; but it is not in itself a loss. The inquiry I

then should not have been between retention of an asset and loss of profits, I

but rather "given the retention, what are the character of the losses suffered?" I

Although Lord President Clyde's question "was the 'hole' in the capital asset, I

44 Supra n37. The normal rule in assessing damages in contract law is that in an excess i

demand market damages are only minimal if the purchaser fails to complete because the vendoris limited in potential sales by the availability of products rather than purchasers. But in the:context of sterilisation or loss, the emphasis is different, because the product is not available I

for sale to a collateral purchaser and the vendor has truly lost the opportunity of sale.45 Discussed below 330.46 Below 326.47 It would not be unreasonable, as a matter of interpretation, to assume that the parties in

tended to compensate first for actual expenses incurred, before expectation loss (loss of profit).To offset against capital before actual incidental loss, where depreciation was available, mightldeprive the taxpayer of the full benefit of the receipt.

48 And in particular whether they are "as· insurance or indemnity": Allsop v Federal Commissioner oj Taxation (1965) 113 CLR 341; and see s.72(2). It is submitted that in the absencfof statutory provisions, a refund is not exigible, regardless of whether the payment was deduct·ible, because it would be out of sympathy with the principles that there is no "matching" 01deductions to income under the Act, and that the character of an outgoing does not affect iHcharacter when received: see Allsop, 350; H R Sinclair v Federal Commissioner oj Taxation (1966114 CLR 537 should be regarded as per incuriam on this point.

49 (1930) 16 TC 67.

1985] Compensation Payments; 313

or was it in the profit" is somewhat more colourful, .it is less likely to leadto the right result.

Lord Sands (dissenting) produced a much keener analysis than the majority,but like it he also made the same error. 50 This was a case he suggested,where the injury was not deprivation of the use of an existing seaworthy shipcapable of earning freight, but the non-production of a seaworthy ship capable of earning freight. In the first situation the payment is really analogousto hire (the second hypothesis); in the second it is for damages for want ofsuch a vessel (the third hypothesis). One can see, however, that this is a distinction without a difference. Merely because the facts fall within the thirdhypothesis does not as Lord Sands assumed characterise them as capital.Again the mistake is to think the retention of the vessel is a loss, rather thanthe cause of it. It is still necessary to inquire what monetary loss the damagescompensate for.

The second authority is Glenboig Union Fireclay Co Ltd v Commissioners of Inland Revenue. 51 The appellants were in the business of manufacturing fireclay goods and were also sellers of raw fireclay. They also leasedcertain fireclay fields over part of which ran the Caledonian Railway. TheRailway owned the land, the appellant had a lease of mineral rights underit. The Railway commenced an action to restrain the mining of fireclay undertheir track on the ground that it was not a mineral. The House of Lordseventually decided against the Railway. The latter then exercised its statutorypowers to require part of the fireclay to be left unworked in return for theirpaying compensation to the Glenboig company.

This decision is a difficult one, because the real issue in the case was entirelyoverlooked. The facts here clearly fell within the second hypothesis. If thefireclay was trading stock then the case was on all fours with the NewcastleBreweries52 decision. What would be permanently sterilised would be circulating not fixed capital, and as the acquisition by the Railway would betantamount to a sale, it would be the "purchaser's" property that was sterilised; a matter of indifference to the "vendor". If the fireclay was a capitalasset the sum received would be capital, although it was quantified by reference to lost profits. 53

Although the court refused to accept that there was any relationshipbetween the method of quantification and the character of the receipt, this

50 That is to regard the circumstances as fairly admitting of the possibility of capital loss.The analogy which Lord Sands found most compelling was that if the £3000 paid was said tobe an abatement of the cost of repairs, "it would have been very difficult for the revenue tomaintain that the £3000 was anything else but a capital savings". It is submitted that this isa non-sequitur. If the ship had been damaged by accident, the measure of damages in tort forinjury to a profit-earning chattel includes a sum for loss of profits which is taxable: Halsbury'sLaws of England (3d) 35 para 1073; And see Inland Revenue Commissioners v West (1950)31 TC 402; Liesboch Dredger v S~ Edison [1933] AC 449; London & Thames Haven Oil WharvesLtd v Attwood [1967] 2 All ER 124. If the abatement was for late repair the income questionwould not arise because a savings is not income: British Mexican Petroleum Co Ltd v Jackson(1932) 16 T.C. 570; Tennant v Smith [1892] AC 150. But see Crabb v Blue Star Line Ltd (1961)39 TC 482.

51 (1920) 12·TC 427. cf Waterloo Main Colliery Co Ltd v Inland Revenue Commissioners(1947) 29 TC 35.

52 (1920) 12 T.C. 927.53 Above 309.

314 Federal Law Review [VOLUME 15

was a case where that inquiry was irrelevant. While intention may determinewhether a sum is on account of a capital or revenue loss when a global sumis received and both types of loss have been suffered;54 this was a situationwhere probably only one type of loss had been suffered and the issue wasto identify the character of the event which caused the loss. If as a questionof law the fireclay in its unsevered state was trading stock it would inexorablyfollow that the receipt was on revenue account.

Their Lordships glossed over this question in holding the sum to be capi-tal receipt. Lord Buckmaster said:

... the sum of money is the sum paid to prevent the fireclay company obtaining the full benefit of the capital value of that part of the mines which they wereprevented from working.... [T]he capital asset of the company has been sterilised and destroyed . . . .55

Likewise Lord Wrenbury:

... the right to work the area ... was part of the capital asset consisting ofthe right to work the whole area demised. Had the! abandonment extended tothe whole area, all subsequent profit ... would ... have been impossible, butit would be impossible to contend that the compensation would be other thancapital. It was the price paid for sterilising the asset from which otherwise profitmight have been obtained. What is true of the whole must be equally true ofpart. 56

It is not sufficient to paint with such broad strokes. If a shopkeeper sellshis business (to use a close analogy), he is relinquishing certain capital rights;perhaps as in Glenboig his lease and his 'right to work'; but any trading stockincluded in the sale will need to be accounted for. 57 Similarly with regardto the fireclay, if, as a matter of law, it was trading stock.

C Rights not inherently tra,nsmissible

Rights which fall into this category include contractual rights where vicarious performance is not possible, and such "esoteric" rights as the 'right towork' and 'the right to trade'. They differ from transmissible rights or propertyin that if the holder of the right agrees to forego it, the promisee does notthereby acquire the right. It is true that atrader promising,to restrict his rightto trade, or to relinquish an advantageous trading contract, may indirectlycause the promisee to enlarge his trade, but this is not a direct or positivegain· in the sense that something is given and taken.58 The promise willusually have to enjoy the competition benefits in common with all othersin the market and may indeed be unable to capitalise on the market enlarge-

54 Eg destruction or sterilisation of tangible or transferable intangible property used in theproduction of income; or capital loss eg to goodwill existing dehors the loss of non-transferableright. See below, 329.

55 (1920) 12 TC 427, 463.56 Ibid 465.57 S 36 ITAA 1936.58 So that there is an abandonment, but no sale or disposition which would involve a property

analysis. This dichotomy between direct and indirect gains has caused the High Court somedifficulty on a number of occasions; see eg Hallstrom Pty Ltd v Federal Commissioner of Taxation(1946) 72 CLR 634; Dickerson v Federal Commissioner of Taxation (1958) 98 CLR 460.

1985] Compensation Payments; 315

ment caused by the partial withdrawal of the promisor. Contrast, however,the sale or compulsory .acquisition of a transmissible right. The transfereecan enjoy this to the exclusion of all others, even if as in Glenboig he choosesmerely to sterilise it.

The issue for taxation purposes is whether this distinction is important.When a recognised transmissible property right is sold or compulsorilyacquired the receipt is capital, even though the item may have little instrinsicvalue apart from its ability to contribute towards the production of profits,and even though it may also be quantified by reference to anticipatedprofits. 59 This 'exonerating' effect which also extends by analogy to thereceipt of compensation for property destroyed may be the product eitherof its character as proprietary simpliciter, or of it having a marketable (capital) value. To adopt the second of these rationes would give rise to few difficulties since it so obviously excludes non-transmissible rights. However, the factthat a capital item may be compulsorily acquired or destroyed which theowner had no intention of selling, tends to suggest the former. The mattercan be tested this way. The destruction of certain non-trading property, forexample a building, is the loss of a capital item, even though the buildingwas held under a settlement which prevented its transmission or sale. Therefore in respect of some property at least it is true that transmissibility is notessential to allow this 'exonerating' effect. Compare however the "loss" ofa non-transmissible intangible right, where the law has no coherentproprietary theory. 60 In this case it appears that marketability may be anecessarY,61 although by no means sufficient,62 attribute to attractproprietary consequences where the circumstances relate to the appropriation of commercial opportunity. 63 But in other contexts, for example theprotection of private information, private enjoyment, or reputation, theconcept of property which allows appropriate relief does not require transmissibility rather than an investment of effort,64 or an exclusiveness of

59 Above 309.60 See generally: DF Libling, "The Concept of Property: Property in Intangibles" (1978) 94

LQR 103; R Sackville & M Neave, Property Law: Cases & Materials (3rd ed, 1981) 1-52. Industrial Property is a concept which can be distinguished but need not be discussed. The legalmonopoly rights under a Patent, Registered Trademark, or Registered Design can not be destroyedor sterilised without legal justification. For goodwill below 326.

61 See eg Exchange Telegraph Co Ltd v Gregory & Co {l896] 1 QB 147, 152-153; TheExchange Telegraph Co Ltd v Howard (1906) 22 TLR 375; Exchange Telegraph Co v CentralNews Ltd [1897] 2 Ch 48,53; Henderson v Radio Corporation Pty Ltd (1960) 60 SR (NSW)576; Samuelson v Producers Distributing Co Ltd [1932] 1 Ch 201, 209; Federal Commissionerof Taxation v United Aircraft Corporation (1943) 68 CLR 525, 547-548.

62 In some cases the courts refuse to recognise the existence of a 'proprietary' right despiteits marketability: see eg Victoria Park Racing and Recreation Grounds Co Ltd v Taylor (1937)58 CLR 479; Federal Commissioner of Taxation v United Aircraft Corporation (1943) 68 CLR525, 534 per Latham CJ (diss).

63 Supra n61; Vokes Ltd v Evans (1931) 49 RPC 140; and see Dr Barnado's Homes v Barnardo Amalgamated Industries Ltd (1949)66 RPC 103; and British Legion v British LegionClub (Street) Ltd (1931) 48 RPC 555, both of which Libling Supra n60 argues are explicableon the investment of effort criteria, 114.

64 See Libling, ibid 114-119; Morris v Ashbee (1868) LR 7 Eq 34; Hamilton, "PropertyAccording to Locke" (1932) 41 Yale LJ 864. In addition the 'right' generated must not be a"social good"; that is a benefit inherently capable of joint consumption: see eg Huntley & Palmerv The Reading Biscuit Co Ltd (1893) 10 RPC 277. But cf Sports and General Press AgencyLtd v "Our Dogs" Publishing Co Ltd [1917] 2 KB 125; Victoria Park Racing and RecreationGrounds Co Ltd v Taylor & Others (1937) 58 CLR 479.

316 Federal Law Review [VOLUME 15

knowledge communicated in circumstances of confidence.6s Indeed it maybe that one of the latter concepts must always be present, and that marketability is in the circumstances of some cases, by the nature of the loss claimed,merely an additional element.

Obviously an inquiry into the definition of property is to be avoided ifpossible, as so often with such problems there is not one answer but several,each depending upon the context in which the answer is asked and the natureof the premises assumed. For example property or proprietary right has beenheld for the purposes of the Stamp Duties Act 1920 (NSW) not to includeinformation,66 whereas in other contexts courts have been prepared toaccord to information at least some of the incidents normally incumbent inproperty. Beyond indicating the consequences that follow from a 'property'or 'not property' conclusion there is no necessary reason in the assessabilityof compensation context for preferring one to the other. And it would bewrong to construe the Act as expressing a policy bias in favour of capitalor income.67

It is submitted that the proper, and less confusing approach, is a functional one; namely should a right (which would have no value if it providedno opportunity for profit) nonetheless support a presumption that compensation for its loss relates to its 'capital' value rather than the lost opportunityfor profit?

The argument in favour of a property characterisation runs as follows:the issue is the character of the receipt in the hands of the recipient, not thenature of the advantage in the payer's hands; the recipient is in no differentposition personally than had he been able to sell the right and had in factdone so, since in both examples it is lost to him. The weakness in this typeof analysis is that it assumes the presence of the very attribute which distinguishes non-transmissible" rights, namely that they cannot be sold. Nor is thisa mere exercise in knocking down carefully erected straw arguments. An"examination of the leading authorities will expose a paucity of any morecogent arguments in favour of a property character.

In the absence of such explanation, it is submitted that the way is openfor the courts to re-examine the issues involved in this category of cases. Sincewhat the writer regards as the true issue is res integra, the tentative opiriionis advanced (and assumed in the following discussion), that a non-marketableintangible right, being valuable only because it creates the opportunity forprofit-making, causes an income loss if it is destroyed. Further, to regardthe loss as capital is to adopt a property analysis which is patently too wide,as being capable of explaining every adjustment of an obligatory orproprietary nature.

Assuming·then that such rights are not in this context property, then thetypes of loss which the relinquishment of the right gives rise must approximate to those clauses listed above under the hypothesis of a temporary reten-

65 EgSeager v Copydex Ltd [1967] 1 WLR 923; Duchess of Argyll v Duke of Argyll [1967]Ch 302; Prince Albert v Strange (1849) 1 H & T 1.

66 JV (Crows Nest) Pty Ltd v Commissioner of Stamp Duties (NSW) [1985] ATC 4198; cfFederal Commissioner of Taxation v United Aircraft Corporation (1943) 68 CLR 525.

67 See eg Tennant v Smith [1892] AC 150, 154 per Lord Halsbury LC; Cape Brandy Syndicate v IRC [1921] 1 KB 64, 71; cf Coultness Iron Co v Black (1881) 6 App Cas 315.

1985] Compensation Payments,· 317

tion of a capital asset. The task would then be to allocate the receipt amongthe three classes. Unless there is a loss of goodwill, the sum can not be oncapital account as there is otherwise no capital loss. Goodwill is of coursea transmissible right, but unlike other such rights it may be deletoriouslyaffected by the extinction of non-transmissible rights. 68 Again where thereare different classes of loss suffered and the sum is sufficient to compensatefor only part of the loss, it is necessary to develop rules for allocation. I havealready suggested that in the absence of express or implied direction, capitalfirst then revenue appears the proper order. Where out-of-pocket expenseshave been incurred it may be that an intention should be presumed that theybe set-off before expectation losses (revenue), or perhaps even goodwill(capital) loss.

(1) Compensation for contractual rights

The leading decision is Van den Berghs Ltd v Clark. 69 The taxpayer wasa manufacturer of margarine. It entered into an agreement with a rival Dutchcompany to share profits and losses at an agreed rate. There were a numberof amendments and extensions to the original agreement, but it remainedessentially a classic producer cartel. Unfortunately a dispute arose which theparties were unable to resolve. They agreed to rescind the agreements, andthe Dutch company agreed to pay their English counterpart £450,000 "asdamages" without specifying the cause of action in respect of which they werepaid.

Lord MacMillan delivered the principal judgment. He asked the question'what did the rights given up represent?' The possibility that they representedpotential profits was considered unlikely since the agreements did more thanentitle them to share profits, nor was the method of quantification to beregarded as determinative. But in his opinion at least two criteria indicateda capital receipt. First they were contracts nor normally entered in the ordinarycourse of business; and secondly:

[H]ere the agreements related to the whole structure of the appellant's profitmaking apparatus. They regulated the appellant's activities, defined what theymight and what they might not do, and affected the whole conduct of their business .... I have difficulty in seeing how ... money received for the cancellation of so fundamental an. organisation of a trader's activities can be regardedas an income . . . receipt. 70

There are a number of difficulties with this "whole structure of business"approach. Certainly in order to fulfill the agreement certain structural changeshad to be made by the appellant and no doubt as a consequence of its cancellation those changes would need to be removed. But while they relatedto the agreement, they were not part of the bargained for consideration. Each

68 For a discussion of goodwill, below 326.69 (1935) 19 TC 390; cf the decision in In/and Revenue Commissioners v Northfleet Coal and

Ballast Co Ltd (1927) 12 TC 1102 which accords more with the analysis suggested by the writer;see also Greyhound Racing Association (Liverpool) Ltd v Cooper (1936) 20 TC 373; Shadholjv Salmon Estate (Kingsbury) Ltd (1943) 25 TC 52; Renfrew Town Council v In/and RevenueCommissioners (1934) 19 TC 13.

70 Ibid 431-432.

318 Federal Law Review [VOLUME 15

party no doubt made the changes in its 0 erations as it saw fit. It would havedoubtless made those changes even if the ontract had, contrary to Lord MacMillan's interpretation, expressly been a agreement to share profits, and ifthe damages had expressly been paid in espect of lost profits. If the moneywas paid here as damages for the costs he appellant incurred in returningto his normal operations they would ha e been reliance damages, althoughthere must be a presumption against their 0 being, since expectation damagesare the normal rule. 71 And secondly, be I ause it is difficult to see how therewas any reliance loss at all arising from the breach, since Van den BerghsLtd would inevitably have run into the cost of re-establishment when theagreements ended.

There is one other problem with Lord MacMillan's argument. If the moneypaid by the Dutch company ,had been paid as damages for breach of contract it would have been expectation damages; that is sufficient compensation to put the innocent party in the position he would have been in had thecontract been performed. But had the contract been fully performed theinnocent party would have had ,an accumulation of profits but no existingcontract, which would of course have by then expired. In other words thecontract itself has no value in assessing damages.

The notion that the "whole structure" must be affected is so obviously anattempt to draw parallels with the principle in British Insulated & HelsbyCables Ltd v Atherton72 and the so-called tree/fruit metaphor. But neitheris apposite here. The Atherton notion of something being for the enduringbenefit of trade is appropriate for discriminating between fixed and circulating capital, either in relation to expenditure or receipt. The tree/fruitmetaphor is of peculiar application to income from property, and it wouldbe a very strange tree indeed on the Van den Berghs facts. Once all the fruitwas picked the tree would disappear; the tree has no value apart from itsfruit; the tree is ajictionalejuris in that it is conjured in and out of existenceaccording to the agreement or actions of the parties.

If one accepts the writer's thesis that a receipt for the relinquishment ofa non-transmissible right should be analysed in terms of the classes of lossenumerated under the third hypothesis, there is no magic in the fact thatthe contract compromised affects the whole structure of the taxpayer's business, or that it is relatively minor. The cancellation is the event causing loss;the issue is to identify the (monetary) loss caused by the event. By definitionsuch contracts cannot be the subject of trade, and therefore the loss of evenseveral does not suggest that the taxpayer would otherwise have sold themand have had to bring the receipts to tax.

In uncritically introducing property notions, and also a test more properlyused for determining between fixed and circulating capital, Lord MacMillan'sjudgment forms the apex of an inverted pyramid, upon which most subsequent judgments balance precariously. A number were cited by Kaye J inMerv Brown Pty Ltd v Federal Commissioner of Taxation. 73 John Smith& Son v Moore74 concerned the purchase of contractual rights, and it was

71 Robinson v Harman (1848) 1 Ex 850.72 (1926] AC 205.73 [1984] ATC 4,394, 4,402.74 [1921] 2 AC 13.

1985] Compensation Payments; 319

rightly concluded that since the appellant was not in the business of dealingin such cpntracts, the sum was on capital account. But this was not a compensation case.

Short Bros Ltd v Inland Revenue Commissioners75 is a much more inconclusive case. The appellants had received an order to build two steamers,but the contracts were later cancelled and £100,000 was received as compensation. They were taxed as to "profits arising from any trade or business".At the initial hearing the appellants argued that this was not compensationfor loss of profits, but for the loss of the right to carryon their trade. TheCommissioners disagreed. 76 Rowlatt J on appeal to King's Bench, thoughtthe payment was neither for loss of profits nor for not being able to carryon their business, nor for a capital loss, but taxable simply because it wasa receipt in the ordinary course of an ongoing business. 77 In the Court ofAppeal the argument was· not as to whether it was capital or income, butwhether it was in the course of business to receive money in respect of cancelled contracts. 78 Thus, it would appear that counsel for the taxpayer hadaccepted the finding of the Commissioners as to income, but were arguingthat the receipt did not comply with the terms of the statute which requiredthat it arisefrom the business, not outside it. The Court of Appeal concludedit did comply. If this decision had been heard in Australia where tax is leviedon income received, and not (as in in England) onprofit, it would have beenmuch easier for Rowlatt J to accept that the money was received in lieu ofincome. One of the reasons why in Short Bros some of the Judges werereluctant to characterise it as received in lieu of profits was because there wasno guarantee profits would have been made. 79 That difficulty does not arisein this jurisdiction.

Kelsall Parsons & Co v Inland Revenue Commissioners80 concerned a firmof agents who held a number of (non-transmissible) agency contracts. Thecourt reached the right conclusion for (it is submitted) the wrong reason infinding a sum received as compensation for the cancellation of one of itsagency agreements assessable. The reasons given in judgment were that thecancelled agreement was not something which was of an enduring nature;nor did it relate to the whole structure of the business. 81 The subsequentdecisions in Wideburgh v Domville82 and Inland Revenue Commissioners vFleming & Co (Machinery) Ltd83 are open to identical criticism. Barr,

75 (1927) 12 TC 955.76 Ibid 964.77 Ibid 968-969.78 Ibid 972, per Lord Hanworth MR; 944 per Sargant LJ; 975 per Lawrence LJ.79 Cf ibid 974.80 [1938] SC 238. See also Elson v James G Johnston Ltd (1965) 42 TC 544; Anglo-french

Exploration Co Ltd v Clayson [1956] 1 All ER81 Eg ibid 246; 248. It is submitted the better basis of decision would have been that, the con

tracts being neither tangible nor transmissible, a proprietary analysis was completely inapposite:above 000.

82 [1956] 1 WLR 312.83 (1951) 33 TC 57. See also Bush, Beach and Gent Ltd v Read (1939) 22 TC 519; Black

burn v Close Brothers Ltd (1960) 39 TC 164. In Fleming Lord President Cooper suggested thatthe fact that the cancellation left him free to devote his energies to replacing the contract tendedtowards an income characterisation. It is submitted that this point is rather neutral. The problemis discussed more fully below 324 et seq.

320 Federal Law Review [VOLUME 15

Crombie & Com Ltd v Inland Revenue CommissionersM and Fleming v Bellow Machine Co Ltd85 were decisions on all fours with Van den BerghsLt(]86 yet only in the former was it found that the cancelled contract formeda substantial part of the taxpayer's business.

Two Australian cases which in contrast are much more sympathetic to theanalysis suggested by the writer are Commissioner of Taxes (NSW) vMeeksK' and Heavy Minerals Pty Ltd v Federal Commissioner of Taxation88

In the former decision a mining company in New South Wales entered intoa contract of sale with an English company in respect of 120,000 tons ofBroken Hill slime concentrates. Payments of £63,000 were made in advanceunder the contract, but the purchases defaulted on further advances and nodelivery was made. The parties agreed to cancel the contract and the £63,000already received was settled against any claims the vendor might have. GiffithsCJ observed:89

[D]amages received as compensation for non-performance of a business contract stand on the same footing as the profits for the loss of which the damagesare paid. It cannot therefore make any difference in principle whether the moneyis actually earned as a profit, ascertained by deducting expenses from receipts,or paid as compensation for the loss of the opportunity of earning that profit,or, in the latter case whether the amount of compensation is assessed by a juryor by mutual agreement.

Windeyer J in Heavy Minerals (a similar case) expressly approved this passage; and in response to the appellant's argument that the receipt was fora loss of "capital structure" described this and similar phrases "as used tobeg the question". 90

A cautionary note should be sounded against uncritically applying testsformulated for distinguishing between revenue and capital expenditure toan income inquiry. Not only is the deductibility of an outgoing irrelevantto its character in the hands of the recipient, but likewise while (for example) an outgoing which meets a continuous demand may be deductible,91 areceipt is not thereby capital because it is non-recurrent or unusual. Aninsurance payment for a loss of trading stock through fire would be exigiblenotwithstanding its unsual features. The fact that the compensation test hasno application to expenditures (as does in contrast the recurrence, enduringbenefit, or (perhaps) the tree/fruit tests) should indicate the dangers involvedin assuming a relationship between income and revenue.

There is a final difficulty. If the cancellation is made as a result of the payer's financial circumstances, for example where to perform the contract wouldresult in greater loss to him than the payment of compensation to the taxpayer, the taxpayer may well be able to recover a sum in excess of his own

84 [1945] SC 271.85 [1965] 1 WLR 873.86 (1935) 19 TC 390. See also John Mills Production Ltd v Matthias (1967) 44 TC 441. Cf

comments in Strick v Regent Oil Co Ltd [1966] AC 295, 318-319; 344-345.87 (1915) 19 CLR 568.88 (1966) 115 CLR 512.'89 Supra n86, 580.90 Supra n87, 517; cf Commissioner of Taxes v Nchanga Consolidated Copper Mines Ltd

[1964] AC 948, 959 per Lord Radcliffe.91 See eg Sun Newspapers Ltd v Federal Commissioner of Taxation (1938) 61 CLR 337,362.

1985] Compensation Payments; 321

loss from cancellation, because theoretically he can "hold out" against cancellation and extract any sum from the payee which is less than the cost tothe payee of continuing the contract. This will be particularly so where thetaxpayer can mitigate his loss by obtaining a substitute contract and substituteprofits. In such circumstances it could be said that the taxpayer has reallymade a windfall profit, providing that he would not have had both contractsif there had been no cancellation, (in which case he really has lost his profits),and providing that the sum received does not exceed the profits he wouldhave otherwise made.

To take an obvious example,. the labour of one man is a finite resource.If he contracts to paint a house for $100, and the owner of the house thenfinds that he can get someone else to do the same job for $50, the first paintercan probably demand and receive any sum up to $50 as compensation forbreaking the contract, because that would still result in a gain to the houseowner. If the expected profit from the job for our painter was only $20, anyexcess is in reality a windfall profit. If the housepainter quickly finds a substitute job which gives him a $20 profit, then in reality the whole sum receivedas compensation from the first contract is a windfall. Of course the ownerof the first house might prefer to break the contract, by excluding the taxpayer from his property. In the circumstances described the damages he wouldhave to pay to the taxpayer would only be nominal. That would not be sohowever if the taxpayer had been able to do both jobs at once, because thenhe would truly have lost the profits from the first.

Two points can be made from this analysis. First, if one accepts the concept of the windfall profit, there appears to be a symmetry between theassessable component of the payment, the expectation profits, and the liabilityof the payer, had he broken the contract instead of compromised it, to payexpectation damages. And secondly, the compensation test must be qualified,because the mere circumstance that the money has been paid in lieu of profitsexpected, need not of itself give the receipt an income character.

(2) Compensation for >Rights to Trade

The leading authorities on the assessibility of receipts derived for thevoluntary restriction on the right to trade or to work are Dickenson v FederalCommissioner of TaxationCIl and Higgs v Olivier. 93 In Dickenson the appellant was a retailer of petrol. He agreed:(i) to lease his premises to a wholesaler of petrol, and to take back a

sub-lease;(ii) to sell only the products of that wholesaler for ten years;(iii) not to operate any other petrol outlet in the area save those selling the

wholesaler's brand.The promisor received £4,000, but the money was said to be paid in respect

of the third promise only. The majority, however, held that viewing thesubstance of the agreement as a whole the sum was received in return forboth the second and third promise; an agreed rental being payable in respect

92 (1958) 98 CLR 460. Cf Thompson v Magnesium Elektron Ltd (1944) 26 TC 1; Hibbell vCommissioners of Inland Revenue.

I 93 [1952] 1 Ch 311.

322 Federal Law Review [VOLUME 15

of the first. 94 But assume for argument that it had only been for the lastpromise. There are two ways to approach its characterisation. First, aproprietary analysis might be applied, or secondly, the court might adoptthe style of inquiry suggested by the writer; that is to ask 'what losses has :the payee incurred?' A subjective inquiry would probably have indicated on I

the facts in Dickenson that the payee had no intention of opening anotherstation nearby, nor that he had suffered any loss of profits as a result of theagreement, rather it was the wholesaler who was protecting his profits bymaking the tie. This result would appear to place the £4,000 in the third classunder the last hypothesis above, so that it would only be taxable if miscellaneous receipts in the course of business are caught. 95

As discussed in relation to the cancellation of contracts, such an approach I

is predicated on the assumption that the right surrendered cannot be regarded I

as property, since that would suggest a capital receipt simpliciter. 96 Thereason against a property analysis in respect of cancelled contracts was saidto be that on ordinary contractual principles the contract itself was notregarded as having any intrinsic value. That obviously will not apply to thesurrender of a non-transmissible but non-contractual right of the type nowunder discussion, but it is suggested that there are two other reasons for nottreating such rights as proprietary. First, it introduces a concept of almostunlimited application, since any agreement requires an adjustment of "rights" I

held by the contractors. As a matter of principle if one is giving up a right(which because it is a "right" is capital on a property analysis) when arestriction on trade is accepted, why can one not be giving up a right to tradewhen, for example, trading stock is compulsorily acquired? Secondly as ageneral principle requiring qualification it introduces confusing distinctions :such as whether the promise is positive or negative in substance or form.

Dickenson must always be read in the light of the complicating factor thatthe taxpayer suffered no discernable material or monetary loss. On the basis ;that the money was received solely for the promise not to operate other outlets ;save those selling the wholesaler's brand the court regarded the sum as capital I

either because there was no loss of profits flowing from the· agreement, or 'because the promise was positive in imposing no restriction. If, as the majority'preferred, the sum was also receivea for the promise to buy only the wholesaler's brand for ten years, Taylor J. as judge 'illone97 and Webb and I

McTiernan J on appeal regarded the sum as income, either because it was:an ordinary incidence of carrying on such a business to receive such sums,97 I

or because it was paid for conducting the business, or employing its assets \in a certain way. 98 If, however, there had been a significant loss of profits:resulting from the agreement there is a suggestion that all three judges wouldhave regarded the sum as capita1. 99 If a non-proprietary analysis was;adopted the conclusion would of course be the other way.

94 Supra n92, 474 per Dixon CJ; 482 per Webb J; 487 per Williams J; 490 per Kitto J. Pe,contra 477 per McTiernan J.

95 Below 330 ct. Evans v Wheatley (1958) 38 TC 216; Strick v Regent Oil Co Ltd [1966:AC 29, 325 per Lord Reid.

96 Above 315.97 Supra n92, 477 per McTiernan J.98 Ibid 469 per Taylor J; 487 per Webb J.99 Ibid 477-478 per McTiernan J; 487 per Webb J.

1985] Compensation Payments; 323

Of the majority, it appears from the tenor of their judgments that theywould have reached the same conclusions whether there had been an effecton profits or not. Kitto J applied a rights analysis,l°O and regarded therestriction as a substantial and enduring detraction from pre-existing rights.Dixon J 101 also regarded it as significant that the business would have to berestored at the end of the ten years; but this consideration as it appearedin the Van den Bergh-s decision has been criticised above. In any event heconcluded even if it did represent in part compensation for loss of futureprofits, the sum paid amounted to a capitalisation of that element. 102 Butif this is accepted, it is difficult to see what scope the compensation principlecan have at all. Williams J preferred to equate a capital character with a lumpsum payment, and income with recurring payments,103 although it is suggested this is simply an exanlple of using one test to the exclusion of all others.

Higgs v Olivier concerned an actor who agreed in consideration of thepayment of £15,000 not to act in, or produce, or direct any film anywherein the world for a period of eighteen months, except at the request of thepayer. The English Court of Appeal held they were bound by the findingof the Special Commissioners that the sum received was not a profit or gainarising or accruing "from" his profession or vocation as an Clctor, andtherefore was not caught by the relevant Case and Schedule of the UnitedKingdom Income Tax Act 1918. 104 The principal judgment of Evershed MRthen, like that of Rowlatt J in Short Bros, must be cited very carefully, sincethe question of capital or income was not directly addressed.

However, it is possible to ascertain what the character of the receipt wouldhave been had the case been heard in Australia. There are at least three reasons why Olivier may have accepted this sum. First, he may have estimatedthat his expected earnings from films over the specified period to be £15,000.The compensation for that loss should be regarded as income. lOS Secondly,he may have had little or no intention of acting (etc.) in films over that period,but he may have 'held out' for the large sum knowing that the payer stoodto lose a larger amount if he did not pay it. This type of receipt does notrelate to any income producing activity, nor in any meaningful way to thesurrender of any right or property, so unless there is some miscellaneous testfor catching it, like the £4,000 in Dickenson it will escape tax. Thirdly, Oliviermay have enjoyed acting, and even if he was not intending to earn £15,000in the ensuing eighteen months, nonetheless he would not have relinquishedhis chance to act for less than that sum. Although this type of "idiosyncratic"valuation is unlikely to occur in a commercial contract, nonetheless it does

100 Ibid 492.101 Ibid 475.102 Ibid 474.103 Ibid 483.104 Schedule D, Case II; s 108. Cf an employee who receives a sum purportedly as a restricted

covenant, but where in order to be assessable the character must be much more of a remunerative one: Beak v Robson [1943] AC 352. The type of analysis applied in the text to Higgs v

livier could equally be applied to Murray v ICI Ltd (1967) 2 All ER 980; and Vaughan-NeilInland Revenue Commissioners (1979) 3 All ER 481.105 Because a "rights" analysis is artificial where the contract can not be performed vicari

usly (and can not therefore be sold); and any "right to work" has no basis of valuation apartrom profits expected from it: above 000; cf Commissioner of Taxes (Vic) v Phillips (1936) 55LR 144, 156.

324 Federal Law Review [VOLUME 15

not differ from the second reason above. The enjoyment of acting providesthe motive for 'holding out', whereas in the second category it is merely avaricewhich does so; but unless one falls into the fallacy of a rights/propertyanalysis, the two situations are very similar.

D Some Qualifications

(1) The Complete Cessation of Business

Californian Oil Products Ltd (In Liquidation) v Federal Commissionerof Taxation 106 introduces another complication into the above analysis. Thedecision stands for the supposed principle that where the receipt is in respectof a complete cessation of business, then the payment will per se be of acapital nature. 107 The taxpayer received £70,000 payable in ten six-monthlyrests in respect of the cancellation of an exclusive ag~ncy agreement, andfor a restrictive covenant on the future activities of the former agent. Theagency was the sole business of the taxpayer, and after the cancellation ofthe agreement it went into liquidation.