Compensation Consultants: Whom do they serve? Evidence ......3 consultant will serve whoever has the...

51

* We are appreciative of the helpful comments from Daewoung Choi (discussant), Brandon Cline, Steve Ferris, and Ralph Walkling. We would also like to thank the seminar and conference participants at the University of Missouri and the 2018 Eastern Finance Association’s (EFA) annual meeting for their helpful suggestions. Compensation Consultants: Whom do they serve? Evidence from Consultant Changes * January 11, 2019 Ryan Chacon Department of Finance University of Missouri Columbia, MO 65211 (619) 781-7948 [email protected] Rachel E. Gordon Department of Finance Towson University Towson, MD 21252 (410) 704-3019 [email protected] Adam S. Yore Department of Finance University of Missouri Columbia, MO 65211 (573) 884-1446 [email protected] Abstract: We use compensation consultant turnover to investigate optimal or excessive CEO compensation recommendations by consultants. Prior literature contends that consultants issue outsized pay recommendations in order to achieve repeat business; we present evidence suggesting their interests are, instead, aligned with shareholders’ desire to appropriately pay the CEO. We find that boards are more likely to dismiss their consultant when CEO pay is abnormally large. These pay-related switches are associated with a decrease in CEO compensation the following year and are concentrated at firms with stronger corporate governance. Lastly, directors representing shareholders’ interests are rewarded with higher votes in annual elections. JEL Classification: G30, G34, J33, M52 Keywords: compensation consultants, executive compensation, director elections, corporate governance

Transcript of Compensation Consultants: Whom do they serve? Evidence ......3 consultant will serve whoever has the...

* We are appreciative of the helpful comments from Daewoung Choi (discussant), Brandon Cline, Steve Ferris, and Ralph Walkling. We would

also like to thank the seminar and conference participants at the University of Missouri and the 2018 Eastern Finance Association’s (EFA) annual meeting for their helpful suggestions.

Compensation Consultants: Whom do they serve?

Evidence from Consultant Changes*

January 11, 2019

Ryan Chacon

Department of Finance

University of Missouri

Columbia, MO 65211

(619) 781-7948

Rachel E. Gordon

Department of Finance

Towson University

Towson, MD 21252

(410) 704-3019

Adam S. Yore

Department of Finance

University of Missouri

Columbia, MO 65211

(573) 884-1446

Abstract: We use compensation consultant turnover to investigate optimal or excessive CEO

compensation recommendations by consultants. Prior literature contends that consultants issue

outsized pay recommendations in order to achieve repeat business; we present evidence suggesting

their interests are, instead, aligned with shareholders’ desire to appropriately pay the CEO. We

find that boards are more likely to dismiss their consultant when CEO pay is abnormally large.

These pay-related switches are associated with a decrease in CEO compensation the following

year and are concentrated at firms with stronger corporate governance. Lastly, directors

representing shareholders’ interests are rewarded with higher votes in annual elections.

JEL Classification: G30, G34, J33, M52

Keywords: compensation consultants, executive compensation, director elections, corporate governance

1

“What consultant is ever going to get another assignment if he says you should pay your CEO

down in the fourth quartile? It isn’t that the people are evil or anything, it’s just that the nature of

the situation produces a result that is not consistent with how representatives of owners should

behave.”

- Warren Buffet, Berkshire Hathaway Annual Meeting, May 2017

1. Introduction

Approximately 90% of large public firms in the United States routinely retain

compensation consultants to provide guidance in setting executive pay packages.1 These

consultants provide services such as supplying proprietary data on the compensation of other firms,

selecting a list of peers to benchmark pay, and guiding the compensation committee through

compliance with regulatory and tax related issues. Perhaps most importantly, they offer

recommendations about formulating appropriate compensation contracts for top management.

Research shows that the size and structure of CEO compensation packages significantly affect firm

performance (Mehran, 1995; Core, Holthausen and Larker, 1999) and, in particular, excessive

CEO compensation is associated with the destruction of shareholder wealth (Bebchuck, Cremers,

and Peyer, 2011). It is, therefore, important to understand whether the usage of compensation

consultants actually benefits shareholders or is simply an extension of management’s power in an

effort to garner excess pay.

In this paper, we explore whether the use of compensation consultants serves shareholders’

interests or, alternatively, provides a mechanism by which management can earn compensation

rents. To that end, we examine instances when the board decides to change consultants where these

motivations should be most evident. We then study the subsequent impact on CEO compensation

to assess the question of whom consultants serve. The consultant industry has frequently been the

target of criticism by regulators, business leaders, and academics for the potential conflicts of

1 In our sample, the percentage of firms in the S&P 900 using consultants increased almost monotonically from 86.9% in 2006 to 94.5% in 2014.

2

interest that exist. These conflicts of interest are most apparent when consultants are dismissed and

new ones are hired.

As the lead-in Buffet quote suggests, many of these critics argue that rent-seeking

managers shop consultants, hiring those recommending the most lucrative pay packages. The

conflicts of interest facing the industry are broadly classified into two groups by the literature:

cross-selling and repeat business (Murphy and Sandino, 2010). Cross-selling is defined as the

conflict consultants face when they provide other services, such as benefits administration, to the

firm unrelated to compensation consulting. Some consultants may fear that they are less likely to

be rehired by the firm (i.e., earn repeat business) if they do not recommend outsized pay packages

to top management. However, the implicit assumption underlying this argument is that managers,

who desire excessive compensation, control the retention or dismissal of the consultant.

In current practice, the board of directors is ultimately responsible for approving CEO pay.

Furthermore, while management occasionally retains their own compensation consultants or

influences who is chosen, our data suggests that it is the board contracting with the compensation

advisor at nearly 90% of firms.2 Thus, we present the alternative argument that the repeat business

motivation may not be a conflict, but rather an incentive. If the board acts in the best interest of

the shareholders, and they hold the power to retain or dismiss compensation consultants, then the

consultants would be incentivized to suggest a pay package best aligned with shareholders.

To understand whom the consultants serve, we develop two competing hypotheses: the

Managerial Power hypothesis and the Shareholder Power hypothesis. A profit maximizing

2 It is typically clear in the firm proxy statement as to which party is responsible for retaining the consultant. For example: :

“In determining executive compensation for fiscal 2008, the Compensation Committee engaged F.W. Cook as its independent consultant.

This selection was made directly by the Compensation Committee. F.W. Cook provides no other compensation or benefit consulting services to ADC.” (ADC Tele communications DEF-14A filing, fiscal year 2008)

“In connection with the Company’s March 2011 annual compensation review meeting, management retained Compensia, Inc. to conduct

an independent review of the 2010 compensation peer group and the 2010 compensation peer group….” (Expedia DEF-14A filing, fiscal

year 2011)

3

consultant will serve whoever has the power to award them repeat business. Under the Managerial

Power hypothesis, compensation consultants are incentivized to suggest higher than optimal CEO

pay in order to achieve repeat business. In contrast, under the Shareholder Power hypothesis,

consultants serve the shareholders, by way of their representatives on the board, and are

incentivized to suggest optimal levels of CEO pay.

To test these hypotheses, we use a direct, easily observable ex-post measure of whether the

consultant achieved repeat business or not – consultant turnover. Such turnover is incredibly

common as over one in five firms decide to change consultants each year. This event provides

insight into two sub-questions. First, what motivates firms to change their compensation

consultant? Second, what impact does a change in consultant have on future pay

recommendations? The Managerial Power hypothesis suggests that consultants are evaluated (and

retained) based on their ability to justify or camouflage excessive pay to minimize social outrage

costs. If unhappy with current compensation, management can advocate for dismissing the existing

consultant and appoint a new advisor who would be more likely to recommend higher salaries.

The Shareholder Power hypothesis predicts that consultants are evaluated (and retained) based on

their ability to recommend optimal pay levels. A new consultant is expected to be more successful

at recommending optimal pay levels.

Naturally, the moderating factor between these two hypotheses is the capability of top

management to influence the board’s choice of consultants. We explore the influence of corporate

governance on managerial versus shareholder power in this context. Prior research suggests certain

factors that affect shareholders’ power relative to management. Specifically, shareholder power

increases when there is a higher percentage of board independence, a lower percentage of board

members hand-picked by the CEO, the CEO and chairman of the board are separate roles, and

4

when the CEO has shorter tenure. For brevity, we refer to these qualities as measures of strong

governance. We hypothesize that results consistent with the Managerial Power (Shareholder

Power) will be concentrated in firms with weak (strong) governance.

Using a sample of 6,230 firm-year observations of S&P 500 and S&P 400 (collectively

S&P 900) firms that employ a compensation consultant from 2006 to 2014, we present four

primary findings that address these questions. First, we find that firms are more likely to switch

compensation consultants following excessive levels of CEO pay. More specifically, boards

dismiss their consultant when abnormal compensation is positive, but there is no consultant change

following negative abnormal compensation. Second, this effect is most pervasive under strong

governance using commonly employed measures of board monitoring quality. Interestingly, we

find that changes in consultants are insensitive to CEO pay when board monitoring is weak.

However, they are positively related to pay when the board is actively monitoring the CEO.

Third, a change in compensation consultant is associated with subsequent declines in CEO

pay. Again, the effect is only present for CEOs with positive abnormal compensation. The results

from our primary tests are economically meaningful. CEO pay falls by $195,000 following a

consultant change for CEOs identified as previously overpaid. There is no identifiable effect for

CEOs that are arguably underpaid. Finally, our results indicate that shareholders reward the board

of directors for upholding their best interests. By examining over 20,000 individual director

elections, we find that the board of directors receives higher vote totals following a consultant

change when the CEO is overpaid. The effect is stronger for those directors serving on the

compensation committee. This finding suggests that the heightened shareholder support at the

ballot box is a result of the consultant change. Overall, our results are most consistent with the

Shareholder Power hypothesis.

5

One concern over these results is that the decision to dismiss a compensation consultant is

a choice variable with its own observable and unobservable determinants. Consequently, the

change in compensation consultants may be an endogenous decision by the firm leading to a self-

selection bias in the data. That is, firms switching consultants and those retaining consultants are

not randomly assigned. We address this endogeneity concern using a two-stage Heckman

treatment effects model where we achieve identification by using industry-by-industry time-series

variation in the number of consulting options available in the marketplace as a source of locally

exogenous variation. This test explicitly leverages the variation induced by the 2010 SEC

regulation that caused multiservice consulting firms to spinoff their pay advisory services, thereby

exogenously increasing the number of options in the market. The results are robust in this setting

and do not appear to be driven by self-selection bias. There is little evidence suggested by these

tests that unobserved heterogeneity drives the changes in pay, while we continue to find that

consultant changes are associated with declines in outsized CEO pay packages following the

advisor’s turnover.

Our research contributes to the growing compensation consultant literature in several ways.

First, while most studies have focused on the problem of cross-selling conflicts, this paper

addresses and reframes the repeat business conflict of interest, on which there is only a nascent

literature (Murphy and Sandino, 2010). We are the first, to our knowledge, to examine the

determinants of consultant switching behavior for large U.S. public companies in this context.3

We provide empirical support that consultants are incentivized by their ability to recommend

optimal pay. Second, our evidence adds to the larger debate regarding whether or not compensation

3 Goh and Gupta (2010) examine consultant switching in a sample of 350 United Kingdom firms from 2002 to 2008 and find that a consultant switch increases CEO pay. This finding is contrary to the primary results in this paper but explainable by a different country, time period, sample

size, and empirical method.

6

consultants face conflicts of interests that are detrimental to shareholders. To date, most of the

literature presents mixed results either finding support for conflicts of interest (Goh and Gupta,

2010; Cho, Hyun, and Sin, 2015; Chu, Faase, and Rau, 2017) or finding no significant evidence

for such conflicts (Cadman, Carter, and Hillegeist, 2010; Murphy and Sandino, 2010; Armstrong,

Ittner, and Larcker, 2012).4 Our paper suggests that such conflicts might be mitigated under the

right governance structure. Lastly, this study contributes to how boards can design optimal CEO

compensation contracts. Understanding the role and incentives of consultants in setting executive

pay levels allows shareholders and regulators to better monitor firm compensation practices.

2. Literature Review and Hypothesis Development

In this section we discuss the existing literature on compensation consultants, the potential

conflicts of interest inherent when retaining these consultants, and the rules issued by securities

regulators meant to curtail abuses. Building upon prior research, we develop two testable

hypotheses that guide our econometric analysis in order to shed light on the motivations for

employing compensation consultants.

2.1 Literature review and regulatory action

As evident by the volume of scholarship on the topic,5 designing an optimal compensation

contract that incentivizes top management to work in shareholders’ interest is challenging. It is not

surprising that around 90 percent of firms in the S&P 900 hire a consultant for expert assistance

with this process (Murphy and Sandino, 2010; Armstrong et al. 2012; Chu et al., 2017). Engaging

a consultant provides the board access to proprietary data on CEO pay at public and private peer

firms and may offer legal cover should a pay package ever be challenged in a court of law.

4 Murphy and Sandino (2010) find evidence for the cross selling conflict of interest and no result for the repeat business conflict of interest. 5 See Aggarwal (2007) and Murphy (2013) for excellent reviews on the subject.

7

However, many firm compensation committees simply follow the consultant’s recommendations

(Bebchuk and Fried, 2004). Doing so effectively hands shareholders’ delegated control rights on

CEO pay over to the compensation consultant. If managers influence which advisor is hired, then

there is the potential for conflicts of interest and self-dealing.

Prior evidence suggests that consultants face conflicts of interest when providing their

advisory services (Murphy, 1999; Bebchuk and Fried, 2003, 2004; Waxman, 2007). A stylized

fact in the compensation consultant literature is that firms using compensation consultants have

considerably higher total and equity-based pay than firms that do not retain consultants (Conyon,

Peck, and Sadler, 2009). Murphy and Sandino (2010) suggest two primary ways a compensation

consultant’s objectivity may be compromised: the lack of independence due to the other services

that the compensation consultant offers to the firm (i.e., cross-selling), and the incentive to

recommend higher than optimal pay to increase the likelihood of repeat business.

A typical regulatory response to perceived abuses in CEO pay is mandated disclosure,

under the assumption that sunlight is the best disinfectant (Murphy, 2013). In the last ten years,

the Securities and Exchange Commission (SEC) has issued a series of new regulations specifically

targeting the pay advisory industry. On August 11, 2006, the SEC issued Release 33-8732, which

modified the required disclosures under the Securities Exchange Acts of 1933 and 1934

(commonly known as the “Securities Acts”), effective November 7, 2006. This new rule mandated

that publicly traded U.S. corporations identify and describe the role of all consultants who provide

advice on executive compensation.6

On December 16, 2009, the SEC specifically targeted cross-selling conflicts for

compensation consultants with Release 33-9089.7 Effective February 28, 2010, if a firm hires a

6 https://www.sec.gov/rules/final/2006/33-8732a.pdf 7 https://www.sec.gov/rules/final/2009/33-9089.pdf

8

compensation consultant and the consultant provides other services to the firm in excess of

$120,000, the firm is required to disclose both the fees charged for compensation consulting and

the fees charged for other services. The 2009 rule caused a structural break in the compensation

consultant industry. Many of the largest “multi-service” consultants spun off their compensation

divisions to avoid the fee disclosure requirement.8 Firms could then continue to work with the

parent company and disclose fees, switch to the newly created spin off, or switch to a different

consultant altogether. Most recently, on June 20, 2012, the SEC amended Item 407(e)(3)9 in

Regulation S-K to again specifically address conflicts of interest. This rule, effective September

25, 2012, was part of the Dodd-Frank Act implementation and requires an assessment by the

compensation committee of the level of independence of the compensation consultants hired.

Following the 2006 disclosure requirements, several studies have examined the role and

conflicts of interest that compensation consultants may face using the new data created by these

regulations (Murphy and Sandino, 2010; Armstrong et al., 2012; Cho et al., 2015; Chu et al., 2017).

Examining concerns over cross-selling, Murphy and Sandino (2010) study both U.S. and Canadian

firms and find that consultants also offering non-pay advisory services provide higher pay

recommendations.10 In other work, Chu et al. (2017) focus on firms that switched to the newly

created spinoff consultants resultant from the 2009 SEC regulation. CEOs at these firms were paid

significantly more than those who stayed with the multi-service consultant or switched to a

different consultant. They interpret this result as evidence that firms who switched to newly created

spinoffs were the firms that were most affected by the cross-selling conflict of interest.

8 Notable spinoffs include: Towers Watson spun off Pay Governance. Aon Hewitt spun off Meridian. Mercer Human Resources spun off

Compensation Advisory Partners. 9 https://www.sec.gov/rules/final/2011/33-9330-secg.htm 10 Cadman et al. (2010) also test for the cross-selling conflict of interest but do not find a relation between CEO pay and potential conflicts of

interest of the compensation consultant.

9

The repeat business conflict of interest, however, has garnered much less attention in the

literature. Murphy and Sandino (2010) were the first to look at this conflict by examining whether

the consultants are hired by management or the compensation committee. However, they find no

evidence of the repeat business conflict of interest. Two notable studies, Goh and Gupta (2010)

and Cho et al. (2015), follow up their work. Similar to our paper, Goh and Gupta (2010) study 350

firms in the United Kingdom from 2002 to 2008. They show that firms who switch consultants in

a given year are paid more than matched firms that do not switch consultants, suggesting that

powerful managers have co-opted compensation consultants. However, a generalization to

domestic firms is uncertain given the differences in firm characteristics and governance regimes

between U.S. and U.K. listed companies. Cho et al. (2015) examine a small subset of firms that

report fees following the 2009 rule and show a positive relation between level of fees and CEO

pay levels. Both of these studies provide some limited evidence for the use of consultants to

support excessive pay packages and interpret the findings as evidence of a repeat business conflict.

Overall, the extant evidence on repeat business is incomplete and little work has been done on why

U.S. firms choose to switch compensation consultants, suggesting the need for more research.

2.2 Managerial power and shareholder hypotheses

We develop two competing hypotheses that shed light on our research question about the

motivations for engaging with a new compensation consultant. A profit maximizing consultant

firm will serve whoever has the power to retain them in order to earn repeat business (Murphy and

Sandino, 2010). Given the potentially negative implications to the firm of an overcompensated

CEO or a poorly designed pay package (Bebchuck et al., 2011), it is important to understand

whether management or shareholders hold the power to retain or dismiss a given compensation

consultant. If management has the power to retain the consultant, then the consultant will be

10

incentivized to reward management by advocating for higher than optimal pay. We label this

conflict of interest the Managerial Power hypothesis and it is similar to the repeat business conflict

of interest as put forth in Murphy and Sandino (2010).

The retention of a compensation consultant is a clear indication of whether they were

successful in obtaining repeat business from the firm hiring them. Examining pay prior to this

decision should be informative as to the motivations for such a change. Specifically, under the

Managerial Power hypothesis, we expect to find that firms change consultants following low

levels of CEO pay and retain those consultants when pay is high. The problem should be

particularly perverse at companies where the CEO is powerful and corporate governance is weak.

If management actively shops for consultants to earn compensation rents, then examining

the CEO’s pay package following the change should also be revealing. If there is a consultant

change and the Managerial Power hypothesis holds, we expect that the new consultant would be

more apt to reward managers with excessive pay. Therefore, in this case, CEO pay should rise

following the hiring of a new pay advisor. Further, we would expect that shareholders will express

disapproval with the compensation committee for allowing such opportunism. The Managerial

Power hypothesis predicts that changes in consultants should be associated with lower vote totals

for the compensation committee members when they go up for election at the annual meeting.

Managerial Power Hypothesis: Firms change compensation consultants following periods

where the CEO earns low abnormal pay and retain consultants when pay is abnormally

high. Following a change in consultants, CEO abnormal pay should increase in response.

Shareholders will withhold “for” votes in director elections for the compensation

committee members following a consultant switch.

If, however, shareholders ultimately hold the power through their representatives on the

board, then the consultant will be incentivized to serve the shareholders and recommend optimal

CEO pay levels. In this case, the repeat business motive is not a conflict of interest, but rather a

11

mechanism through which the consultant is incentivized to serve the shareholders. The board will

dismiss consultants that recommend overly generous compensation. We present this alternative

motivation to the Managerial Power hypothesis and label it the Shareholder Power hypothesis.

In this view, we expect to find that firms change consultants following their inability to

recommend the appropriate compensation contract. Finding such evidence would suggest that

consultants are evaluated and retained based on their ability to recommend optimal pay levels and

failure to do so means they did not achieve repeat business. As in the first hypothesis, the

Shareholder Power hypothesis might also suggest a change in consultants following periods of

abnormally low CEO pay, albeit for different reasons. For example, firms desire to retain high

quality CEOs and remuneration is a primary talent retention mechanism (Bizjak, Lemmon, and

Naveen, 2008). Thus, abnormally frugal compensation contracts may also be costly to shareholders

if they cause a high quality CEO to take a position elsewhere. The net effect depends upon the

relative costs of possibly losing a talented CEO balanced against the savings from limiting pay-

related agency problems.

Therefore, if a consultant change occurs following low levels of CEO pay, we cannot

distinguish between these two hypotheses. If, however, the change in consultants occurs after

excessive pay (i.e., positive abnormal compensation), this is consistent with the Shareholder

Power, but not the Managerial Power, hypothesis. Results in support of the Shareholder Power

hypothesis should be focused in firms with strong corporate governance where the board represents

the shareholder and is less apt to be influenced by management when choosing a pay advisor.

Under the Shareholder Power hypothesis, if there is a change, the new consultant would

be more successful at recommending optimal CEO pay. Therefore, following excessive pay,

consultant changes should result in declining CEO pay. Furthermore, under this hypothesis,

12

shareholders should be pleased with the compensation committee for choosing a better pay advisor

to design the CEO’s contract and will accordingly express that support with higher vote totals.

Shareholder Power Hypothesis: Firms change compensation consultants following periods

where the CEO earns high abnormal pay. Following a change in consultants, CEO

abnormal pay should decrease in response. Shareholders will award more “for” votes in

director elections for the compensation committee members following a consultant switch.

3. Sample Selection, Research Design, and Descriptive Statistics

In this section we discuss our sample selection and the structure of our primary empirical

tests to examine our testable hypotheses. We also present descriptive statistics on our sample firms

and the compensation consultant industry, as employed by major U.S. companies.

3.1 Sample selection

Our initial sample includes all firms listed in the Execucomp database as members of either

the S&P 500 Large Cap or S&P 400 Midcap (referred to as the S&P 900) indices for any duration

between 2006 and 2014. We collect data on compensation consultants by hand from DEF-14A

proxy statements found on the SEC’s Electronic Data Gathering, Analysis, and Retrieval

(EDGAR) system. The start of the sample period (2006) coincides with the first year that firms

were required to disclose detailed information regarding their compensation consultant. To assess

whether or not there was a change in consultant when there is no proxy in the previous year, we

count a change if the current consultant is different from the consultant listed in the last proxy

statement available. Therefore, we drop firm-years in which the firm does not file a proxy

statement. After these initial screens, we have 8,700 firm-year observations.

We remove firms from the sample that never hire a consultant during our period of study.

Based on previous literature, firms that never hire a compensation consultant appear to be

systematically different from those who hire consultants (Murphy and Sandino, 2017; Armstrong

et al., 2012); in particular, CEOs in these firms are paid consistently less than those who hire

13

consultants. Further, the focus of this study is on consultant switching and our hypotheses only

speak to companies engaging with consultants. This filter eliminates about 3% of the firm-years,

reducing our sample to 8,390 firm-year observations. If a firm hires a consultant in at least one

year during the sample, they are retained for all years.11

Next, we obtain firm characteristics, stock returns, CEO compensation, and corporate

governance variables from Compustat, CRSP, Execucomp, and ISS (RiskMetrics/IRRC),

respectively. All variables are defined in Appendix A. Our final sample is the intersection of all

S&P 900 firms that hire a consultant in at least one year and have non-missing data from each

database. After all data screens, we have a final sample of 6,230 firm-year observations

representing 989 unique firms. All regression estimations are for the 2007-2014 sample period.

3.2 Research design

3.2.1 Consultant switches

The most direct ex-post measure of whether a compensation consultant achieved repeat

business is whether they were retained for the next year. We exploit this setting to examine the

determinants of a firm changing consultants. We believe looking at these changes provides the

clearest signal of the firm’s and consultant’s motivations. While it is possible that a consultant

could resign, we believe the majority of the consultant changes are initiated by the sample firm.

Our key variable of interest is the change in consultant. It is an indicator variable that

equals one if the consultant retained in year t is different from the one retained in the prior year. A

consultant change also includes a situation when firms have no consultant in the prior year to

retaining one or vice versa.12 One concern may be that this situation is different from firing a

11 We do retain non-switchers so as not to bias our sample. That is, firms that retain a compensation consultant, but never switch, also remain in the

sample throughout the entire time. 12 This includes if a firm has two consultants in year t-1 and 1 consultant in year t (or vice versa). This type of change occurs in 8% of our sample.

Our primary results are robust to the exclusion of these cases of consultant changes.

14

current consultant and hiring a new one. The motivation, however, in our context is similar: firms

may hire a consultant because they wish to justify excessive pay (Managerial Power) or they may

do so to achieve optimal pay levels (Shareholder Power). Conversely, when firms stop using any

consultant, a similar intuition applies. Firms may decide not to retain a new one because the firm

is dissatisfied with the consultant’s ability to advocate generous CEO pay (Managerial Power) or

the consultant’s ability to recommend optimal CEO pay (Shareholder Power).

3.2.2 Econometric framework

To test our competing Managerial Power and Shareholder Power hypotheses, we propose

two primary empirical tests. The first test examines the determinants of changing consultants. We

run a Probit regression model of the following form:

𝐶ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝐶𝑜𝑛𝑠𝑢𝑙𝑡𝑎𝑛𝑡𝑡

= 𝛼 + 𝛽1𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙 𝑃𝑎𝑦𝑡−1 + 𝛽2𝐹𝑖𝑟𝑚 𝐶ℎ𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑡−1

+ 𝛽3𝐺𝑜𝑣𝑒𝑟𝑛𝑎𝑛𝑐𝑒 𝐶ℎ𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑡−1 + 𝛽4𝐶𝑜𝑛𝑠𝑢𝑙𝑡𝑎𝑛𝑡 𝐶ℎ𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑡−1

+ 𝑌𝑒𝑎𝑟 𝐹𝐸 + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦 𝐹𝐸 + 𝜀

(1)

where the dependent variable is an indicator variable that takes the value of one when the firm has

changed consultants from the previous year and zero otherwise. Firm Characteristics include the

natural logarithm of total assets, the market-to-book ratio, return on assets (ROA), institutional

ownership, number of analysts, annual stock returns, and the debt-to-asset ratio. Governance

Characteristics include CEO age, CEO tenure, CEO turnover, a dual class firm indicator, board

size, the percentage of board independence, the percentage of outside board members considered

busy, a CEO/Chairman duality indicator, a classified board indicator, the percentage of the outside

board members co-opted by the CEO, and an indicator for whether the firm engaged in M&A

activity. Consultant characteristics include an indicator for whether the consultant is an industry

specialist, an indicator for whether they are multi-service consultants, and an indicator for if the

15

firm retains more than one consultant. All variables are constructed as of the fiscal year prior to

the consultant change. We use year and industry fixed effects to absorb any time or industry

invariant unobserved heterogeneity. Throughout all tests, standard errors are clustered at the firm

level (Rogers, 1993) to account for serial dependence in the error term (Petersen, 2009).

The key variable in this analysis relates to abnormal CEO pay prior to the consultant switch

(Abnormal Payi,t-1). Specifically, we are concerned with whether or not the CEO received above

or below optimal pay levels. The optimal level of CEO pay, however, is inherently unobservable.

To address this challenge, we calculate abnormal pay following Yermack (2006) by assuming that

the appropriate level of CEO pay is a function of firm size, time on the job, shareholder wealth

creation, industry, and year. Abnormal pay is, therefore, the residual from a calendar year cross-

sectional regression explaining CEO pay, where the independent variables in the regression are

the log of sales, CEO tenure, abnormal stock returns, and industry fixed effects.

𝑇𝑜𝑡𝑎𝑙 𝐶𝑜𝑚𝑝𝑒𝑛𝑠𝑎𝑡𝑖𝑜𝑛𝑖,𝑡

= 𝛼 + 𝛽1ln (𝑆𝑎𝑙𝑒𝑠)𝑡 + 𝛽2𝐶𝐸𝑂 𝑇𝑒𝑛𝑢𝑟𝑒𝑡 + 𝛽3𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙 𝑆𝑡𝑜𝑐𝑘 𝑅𝑒𝑡𝑢𝑟𝑛𝑡

+ 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦 𝐹𝐸 + 𝜀

(2)

Abnormal Pay = Actual Total Compensation - Predicted Total Compensation (3)

where Salesi,t is net sales in millions for firm i at time t, and CEO Tenurei,t is the total number of

years the current CEO has served in that role at the company. Abnormal Stock Returni,t is the net

of market model cumulative abnormal stock returns for the fiscal year, where a value greater than

zero reflects a CEO that is paid higher than predicted.13 Appendix A defines all variables.

Regressing the change of a compensation consultant on Abnormal Payt-1 is informative in

distinguishing between the Managerial Power and the Shareholder Power hypotheses. A negative

13 Our results are robust to the use of industry-adjusted pay. We take the CEO total pay (TDC1 in EXECUCOMP) and subtract the average of the FF48 industry of all firm-years within the EXECUCOMP database. A value greater than zero reflects a CEO who is paid above the industry average

for that year. See Table 10.

16

coefficient would imply that firms are more likely to change consultants following low levels of

abnormal CEO pay. We note that this may be consistent with both hypotheses, depending on the

relative costs of pay-related agency problems verses the potential loss of good talent. Conversely,

a positive coefficient would imply that high abnormal CEO pay leads to the dismissal of their

compensation consultant. This may lend some support for the Shareholder Power hypothesis,

depending on the relative costs of pay-related agency problems verses the potential loss of good

talent. However, such evidence would be against the Managerial Power hypothesis.

We also run regressions where we split the abnormal pay variable based on positive and

negative values of abnormal pay. This separation focuses on the primary case of interest: when

abnormal pay values are high (e.g., the CEO received excessive compensation). Accordingly, we

create two variables, Positive Abnormal Payt-1 and Negative Abnormal Payt-1. Our testable

hypotheses have differing predictions for these two variables. Positive Abnormal Payt-1 is equal to

Abnormal Payt-1 when it is greater than zero and zero otherwise. Under the Managerial Power

hypothesis, Positive Abnormal Pay should take a negative coefficient, but it should load positively

under the Shareholder Power hypothesis. Negative Abnormal Payt-1 is equal to Abnormal Payt-1

when it is negative and zero otherwise. When regressing the consultant change indicator on this

variable, the Managerial Power hypothesis would predict a negative coefficient, but the sign is

ambiguous under the Shareholder Power hypothesis.

To further distinguish between the competing hypotheses, we focus on four corporate

governance variables from prior literature to distinguish between the Shareholder Power and

Managerial Power hypotheses: board independence, co-opted boards, CEO/chairman duality, and

CEO tenure. When the board is comprised of independent directors without compromising ties to

management, they are more likely they are to look out for shareholders (Weisbach, 1988; Dahya

17

and McConnell, 2007; Cai, Xu, and Yang, 2017). With respect to co-opted boards, Coles et al.

(2014) argue that directors appointed under a given CEO’s tenure feel beholden to that executive

for their board seat. Similar to the predictions regarding independence, the fewer board members

co-opted by the CEO (i.e., the CEO’s tenure exceeds that of the director’s), the more likely the

board represents shareholders. If the CEO is not the chairman of the board, the CEO has less direct

influence over board decisions (Jensen, 1993). Shorter tenured CEOs arguably have less power

than longer serving, possibly entrenched, managers (Berger, Ofek, and Yermack, 1997). Boards

that do not operate under such imperialistic CEOs are also more likely to represent the

shareholders. We suggest that corporate governance is stronger and the quality monitoring in the

pay setting process is better in the following subsets of firms: those with more independent boards,

fewer directors co-opted by the CEO, those where the CEO is not the chairman, and those where

the CEO has a shorter tenure.

We estimate the same regression in equation (1), but with sample splits on the four

governance variables. We split the sample in the following ways: on the median level of board

independence, on whether 50% of the board is co-opted by the CEO, on whether the CEO is the

chairman of the board, and on the median of CEO tenure.

Results consistent with the Managerial Power hypothesis should be concentrated in firm-

years that have weak governance (i.e., when managerial power is stronger). Similarly, results

consistent with the Shareholder Power hypothesis should be concentrated in firm-years that have

strong governance (i.e., when shareholders have more power).

Next, we examine the actual impact on CEO pay after a consultant switch has occurred.

We estimate an OLS regression of the following form:

18

∆𝑇𝑜𝑡𝑎𝑙 𝑃𝑎𝑦𝑡,𝑡−1

= 𝛼 + 𝛽1∆𝐶𝑜𝑛𝑠𝑢𝑙𝑡𝑎𝑛𝑡𝑡,𝑡−1 + 𝛽2𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙 𝑃𝑎𝑦𝑡−1

+ 𝛽3∆𝐶𝑜𝑛𝑠𝑢𝑙𝑡𝑎𝑛𝑡𝑡,𝑡−1 ∗ 𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙 𝑃𝑎𝑦𝑡−1

+ 𝛽4∆𝐹𝑖𝑟𝑚 𝐶ℎ𝑎𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑡,𝑡−1 + 𝛽5∆𝐺𝑜𝑣𝑒𝑟𝑛𝑎𝑛𝑐𝑒 𝑉𝑎𝑟𝑖𝑎𝑏𝑙𝑒𝑠𝑡,𝑡−1

+ 𝛽6𝛥𝐶𝑜𝑛𝑠𝑢𝑙𝑡𝑎𝑛𝑡 𝑉𝑎𝑟𝑖𝑎𝑏𝑙𝑒𝑠𝑡,𝑡−1 + 𝑌𝑒𝑎𝑟 𝐹𝐸 + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦 𝐹𝐸 + 𝜀

(4)

where the dependent variable is the change in total CEO pay from year t-1 to year t. Changes in

firm characteristics and governance variables are used where appropriate as well as a control for

prior M&A deal-making. We control for both the change and the level of firm size and consultant

characteristics as these models. We apply a similar approach to the previous regressions by

bifurcating abnormal pay into its positive and negative components. We use industry and year

fixed effects to absorb any time or industry invariant unobserved heterogeneity. Standard errors

are clustered at the firm level.

The primary variable of interest is the interaction between the change in consultant and

abnormal pay. For robustness, we use three specifications of this interaction for the abnormal pay

variable. First, we use the continuous abnormal pay variable. Second, we use an indicator variable

that equals one when abnormal pay is greater than zero. Third, we use an indicator that equals one

when the abnormal pay variable is greater than the within-sample median.

Next, we examine the effect of changing consultants on subsequent director votes. We test

whether there is a relation between the proportions of “for” votes for the board of directors

following the change of consultant. A favorable shareholder reaction to a change in compensation

consultant would manifest in a greater proportion of “for” votes for the board member, consistent

with the Shareholder Power hypothesis. If, however, the shareholders are unhappy with the change

of consultant, we would expect to see fewer “for” votes in the following election, consistent with

the Managerial Power hypothesis. We estimate the following model to test these hypotheses:

19

∆𝐷𝑖𝑟𝑒𝑐𝑡𝑜𝑟𝑉𝑜𝑡𝑒𝑠𝑡+1,𝑡

= 𝛼 + 𝛽1∆𝐶𝑜𝑛𝑠𝑢𝑙𝑡𝑎𝑛𝑡𝑡,𝑡−1 + 𝛽2𝐶𝑜𝑚𝑝𝐶𝑜𝑚𝑚𝑖𝑡𝑡𝑒𝑒+ 𝛽3∆𝐶𝑜𝑛𝑠𝑢𝑙𝑡𝑎𝑛𝑡𝑡,𝑡−1 ∗ 𝐶𝑜𝑚𝑝𝐶𝑜𝑚𝑚𝑖𝑡𝑡𝑒𝑒+ 𝛽4∆𝐹𝑖𝑟𝑚 𝐶ℎ𝑎𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑡,𝑡−1 + 𝐵5∆𝐺𝑜𝑣𝑒𝑟𝑛𝑎𝑛𝑐𝑒𝑡,𝑡−1 + 𝑌𝑒𝑎𝑟 𝐹𝐸+ 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦 𝐹𝐸 + 𝜀

(5)

where ∆𝐷𝑖𝑟𝑒𝑐𝑡𝑜𝑟𝑉𝑜𝑡𝑒𝑠𝑡+1,𝑡 is the change in the percentage of “for” votes for directors the year

following a consultant change, 𝐶𝑜𝑚𝑝𝐶𝑜𝑚𝑚𝑖𝑡𝑡𝑒𝑒 is an indicator which takes the value of 1 when

the board member is on the compensation committee.

[Table 1]

3.3 Descriptive Statistics

Table 1 presents descriptive statistics for the compensation consultant data by year. Panel

A shows how many firms in our sample change consultants in a given year. Strikingly, firms

change compensation consultants quite often, approximately 21% of firms per year on average.

The temporal distribution of the change in consultant exhibits some considerable variation. Of

particular note is the spike in consultant switching in 2009 and 2010. This spike is largely driven

by the consultant industry spin-offs documented in Chu et al. (2017). To avoid having to disclose

fee information following the 2009 SEC regulation, many of the largest, previously multi-service,

consultants chose to spin off their compensation consultant divisions. Firms could then continue

to work with the parent company and potentially disclose fees, switch to the newly created spin

off, or switch to a different consultant altogether. Although this regulation encouraged consultant

switching by providing additional options, firms were not forced to switch consultants. As

documented in Chu et al. (2017), many firms chose to stay with the parent company as their

consultant. Therefore, the choice to switch during these years is still relevant to our study.

Panel A of Table 1 also presents the breakdown of which party engages the consultant and

how many consultants each firm retains. The board or compensation committee (management) is

20

stated as the engaging party 89% (8%) of the time. The engaging party is unclear in 3% of the

cases. Approximately 9% of all firm-years retain two or more consultants (most of which retain

only two). Divided firms, firms where both the board and the management hire separate

consultants, make up about 6% of the sample.

Panel B of Table 1 presents details on firms that switch consultants. We classify consultants

along several dimensions. We classify firms by whether they have high market share or low market

share. A consultant has high market share if the consultant has greater than five percent market

share within our sample and low market share otherwise. Following Chu et al. (2017), we classify

whether the firm is a multiservice consultant or a single service consultant. Multiservice

consultants are larger firms offering a variety of other services to the firm. These services tend to

be more lucrative to the consultant than compensation consulting; thus, these consultants have

typically been the target of the aforementioned cross-selling conflict of interest.

Lastly, we classify a consultant as an industry specialist or generalist based on the

concentration of industries of the consultant’s clients. If the difference in size between the

consultant’s largest industry and second largest industry is greater than one standard deviation (of

all industries) then the consultant is classified as an industry specialist. According to this measure,

the following consultants are determined to be industry specialists: Frederic W Cook, Mercer,

Pearl Meyer, Compensia, Hay Group, Steven Hall & Partners, and FPL Advisors. Overall, more

firms in our sample tend to use a consultant with high market share, a consultant that only provides

compensation consulting, and one that is a generalist.

Further, we split our sample into two distinct time periods. The 2007 to 2010 time period

represents the start of when firms must disclose compensation consultants and also contains

significant other regulation affecting the consultant industry. The second sample is from 2011 to

21

2014 and is a sample with fewer confounding events present. The largest shift in consultant

characteristics that occurs between the two samples is the use of multiservice consultants or single

service consultants. In the 2007 to 2010 sample, 48.38% of firms use multiservice consultants.

Comparatively, in the 2011-2014 period, that percentage decreased to 22.39%. This drop is largely

a function of the large multiservice consultants spinning off their single service consulting firms.

We next examine consultant’s characteristics when firms switch. Perhaps unsurprisingly,

most firms switch laterally within the same type of consultant: from high market share to high

market share (and low market share to low market share) and from multiservice to multiservice

and single service to single service consultants. While there is a significant subset of firms that

switch across categories, it appears that most firms have a type of consultant they prefer. Potential

reasons for this include board preferences, firm size and complexity, and industry specialization.14

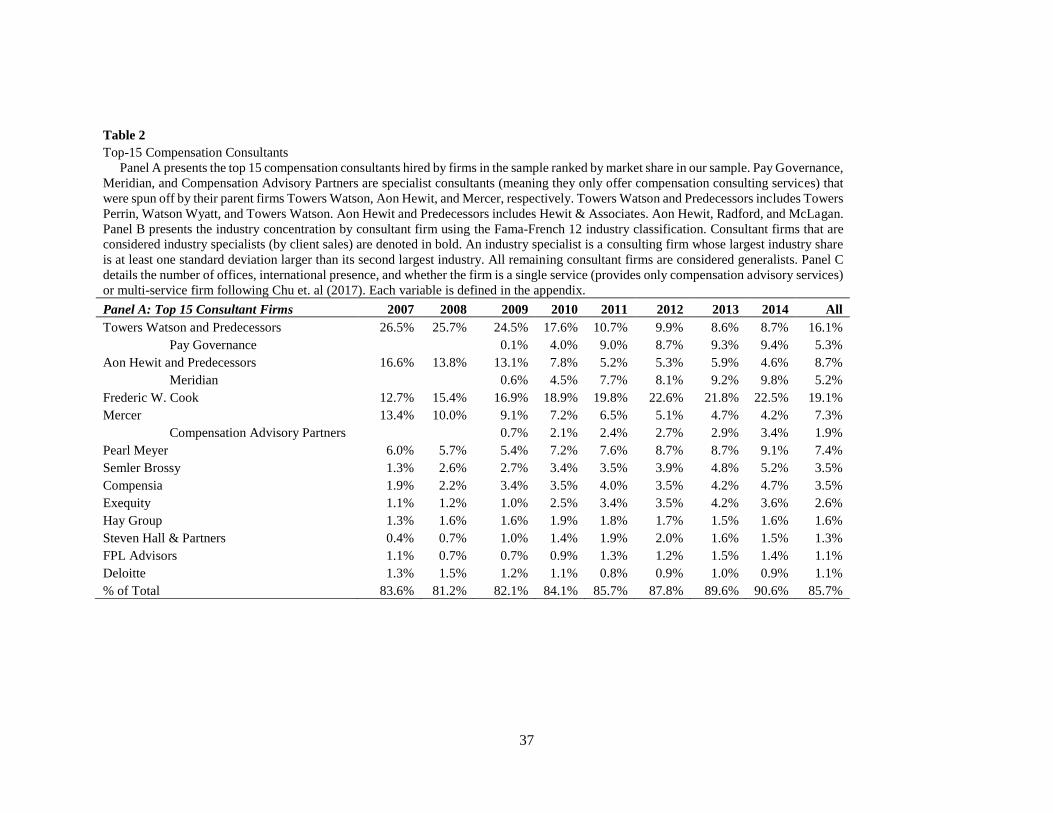

[Table 2]

Table 2, Panel A presents the top 15 consultant firms and their respective market shares.

As noted in the literature, several consultants hold a considerable portion of the market share, even

with the 2009 and 2010 SEC regulations’ impact. For example, Towers Watson in 2009 spun off

Pay Governance and many of their current clients chose to switch to Pay Governance (Towers

Watson shrunk from 26.5% in 2009 to 11.7% in 2011 and Pay Governance grew to 9.0% in 2011).

By 2014, Towers Watson had retained only 8.7% of the market share and Pay Governance retained

9.4%. As of 2014, Frederic W. Cook has the greatest market share at 22.5%. Frederic W. Cook

was the largest “specialist” consultant (meaning they offered no cross-selling services) leading up

14 While consultant tenure would also be interesting to examine, we are precluded from calculating consultant tenure because firms only began

consistently reporting consultant names in 2006.

22

to the 2009 SEC rule, and as the multi-service consultants spun off portions of their businesses,

Frederic W. Cook enjoyed a lasting increase in market share from 16.9% in 2009 to 18.9% in 2010.

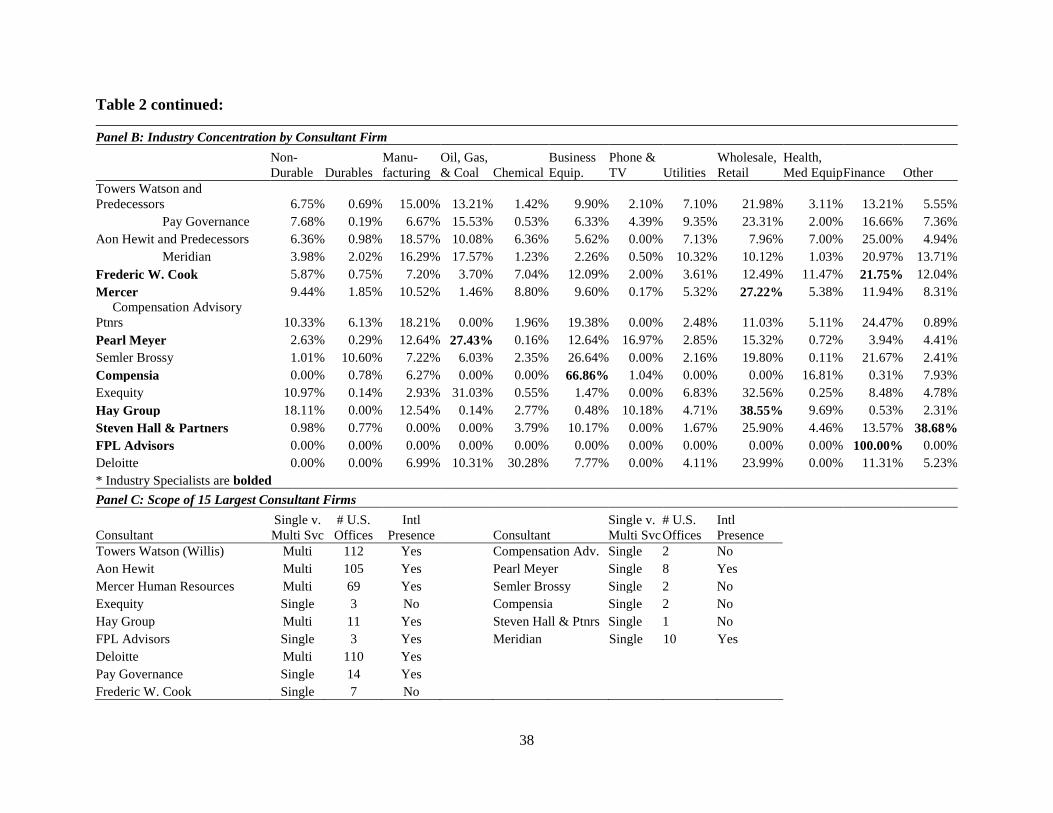

Panel B of Table 2 describes the industry concentration by consultant. Industry

specialization is likely a factor firms consider when selecting consultants and it appears at least

some consultants do specialize in a particular industry. For example, 66.86% of Compensia’s

clients are in the business equipment industry representing a specialization while FPL Advisors

exclusively consults for financials (all of them are REITs). Towers Watson is an example of a

“generalist,” having clients across a broad spectrum of industries. Panel C of Table 2 examines the

scope of the top 15 consultants. There is considerable variation in consultant size. Towers Watson

(Willis) is the largest multiservice consultancy with 112 US offices and a large international

presence. Many of the single service consultants have one to three US offices and limited or no

international presence.

[Table 3]

Table 3 presents firm, compensation, and board characteristics for the companies in the

sample. Of particular interest are the abnormal and industry-adjusted pay variables. Mechanically,

abnormal pay is on average near zero (our sample cuts create some deviation) with the median

being slightly negative. The industry-adjusted total pay has a positive average and median (with

the first quartile being slightly positive), suggesting that the average CEO in our sample is paid

higher than the industry average. This univariate statistic is natural as our sample is for S&P 900

firms and the industry average calculation is for all firms in EXECUCOMP, including the CEOs

at firms listed in the S&P 600 Small Cap index that tend to be paid less. Our results are robust to

the use of within sample industry-adjusted pay. Other firm characteristics and board characteristics

23

are in-line with previous literature (Faulkender and Yang, 2010; Cai, Kini, and Williams, 2016).

To mitigate the influence of outliers, all variables are winsorized at the 1% and 99% level.

4. Results

4.1 Why do firms switch compensation consultants?

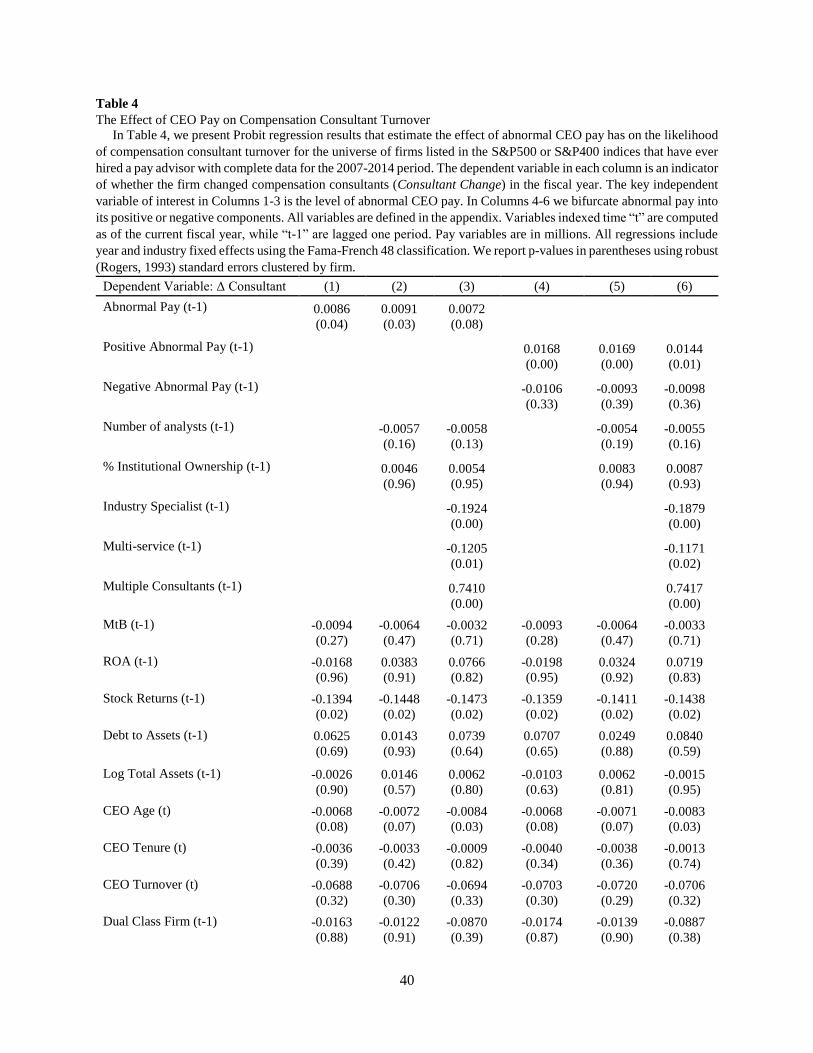

Table 4 presents results of the Probit regressions examining the determinants of consultant

switching. Columns 1 to 3 use the abnormal pay variable as the primary variable of interest and

columns 4 to 6 split abnormal pay into its positive and negative components. The columns differ

in the additional variables included that relate to other influences on whether the firm changes

consultants. In columns 1 to 3, the coefficients on abnormal pay are all positive and statistically

significant, indicating that higher abnormal CEO pay increases the likelihood that the firm changes

compensation consultants. For example, the marginal effect for column 3 is 0.0019 meaning that

an increase of one standard deviation in abnormal pay leads to a 4% increase in the likelihood of

changing consultants. Given that the unconditional probability of changing consultants is 20.8%,

this effect is economically relevant.

It is unclear, at this point, whether this finding is driven by CEOs who are under- or over-

paid. For example, a positive and significant loading would be consistent with the argument that

the firm likely changes consultants following excessive pay or retains consultants when pay is

abnormally low. To more directly address our hypotheses, we turn to columns 4 to 6 of Table 4.

These regressions indicate clearly that the effect is driven by the positive side of abnormal pay.

That is, firms are more likely to switch consultants following excessive CEO pay. The coefficient

on positive abnormal pay is consistently larger and more statistically significant than the abnormal

pay variable in columns 1 to 3. The marginal effect for column 6 signifies a 6.1% increase in the

likelihood of changing compensation consultants with a one standard deviation increase in the

24

CEO’s excessive pay in the prior year. Furthermore, the coefficient on the negative component of

abnormal pay is never statistically significant. Overall, the results on CEO pay are consistent with

the Shareholder Power hypothesis; it appears that firms are more likely to change consultants

following excessive levels of pay.

Focusing on control variables that are statistically significant in specifications, there are

three interesting results. In all specifications, the prior year stock return loads negatively and

significantly, suggesting that firms are more likely to change consultants following poor firm

performance. Firms are also more likely to change their consultant when the CEO is younger and

the CEO is not the chairman of the board. The last two results indicate a higher likelihood of

consultant turnover when the manager is less powerful. We find no evidence that consulting

switches are driven by merger activity.

It is plausible that variables omitted from our specifications may influence the firm’s

decision to provide the CEO with abnormal pay for a given period and any subsequent

compensation changes. As a further test, we re-estimate models (3) and (6) of Table 4 using firm

and year fixed effects to control for some of these possible firm-specific omitted variables. The

results are similar. The coefficient for abnormal compensation remains positive 0.0133 (p-value

0.05). When split, the coefficient on positive abnormal pay is 0.0181 (p-value 0.04) and remains

statistically insignificant for negative abnormal pay (unreported). Collectively, evidence from

Table 4 appears consistent with Shareholder Power and against the Managerial Power hypothesis.

4.2 Determinants: Governance Splits

Next, we rerun the tests using the governance splits between firms with strong versus weak

governance in Table 5. Given that the result in Table 4 is consistent with the Shareholder Power

hypothesis, we expect the positive and significant coefficient for abnormal pay (or positive

25

abnormal pay) to be concentrated in firms with strong governance. Panel A of Table 5 reports

results of regressions using the traditional abnormal pay variable and Panel B reports regressions

using the abnormal pay variable split on its positive and negative components.

Columns 1 and 2 of Panel A present results for the sample split on the median of board

independence. The coefficient on abnormal pay is positive and significant at the 5% level when

the board has a greater level of independence. When the board is below the median level of

independence, the coefficient is close to zero and insignificant (0.0004 coefficient with a 0.95 p-

value). Columns 3 and 4 of Panel A present results for the sample split on whether the board is co-

opted by the CEO. Similar to the sample split on independence, the coefficient on abnormal pay

for the subsample where the board is not co-opted by the CEO is positive and significant at the

10% level. The coefficient in the subsample with a co-opted board is statistically insignificant.

Columns 5 and 6 of Panel A present results for the sample split on whether the CEO is the chairman

of the board. The coefficient on abnormal pay does not appear to be significantly different based

on this sample split. Lastly, when the CEO has a tenure below the median, the coefficient on

abnormal pay is positive and significant at the 5% level and close to zero and insignificant when

the CEO has had a long tenure.

When we split abnormal pay into its positive and negative components and run the

governance splits, the results are even stronger (Table 5, Panel B). For all four governance splits,

in the strong governance sample, the positive component of abnormal pay is positive and

significant. The coefficients are not statistically significant in any of the four governance splits

that we identify as having weak governance. Additionally, the negative component of abnormal

pay is not significant in any specification.

26

Together, the results in Table 5 present consistent support for the Shareholder Power

hypothesis and against the Managerial Power hypothesis. On each sample split, the positive result

is stronger when shareholders have more power and insignificant when the manager is likely to

have more power. Combined with previous results, evidence supports the Shareholder Power

hypothesis. Firms are more likely to change their consultant when the CEO is paid excessively,

their board is attentive, and shareholders have the power to act. The evidence supports the

interpretation that consultants are evaluated on their ability to recommend optimal pay levels.

4.3 Regressions of the change in consultant on change in CEO pay

After examining the determinants of the choice to change consultants, we examine what

happens to the level of CEO pay following the consultant switch in Table 6. Column 1 uses the

continuous abnormal pay variable. Column 2 uses an indicator variable that takes the value of one

when abnormal pay is positive, zero otherwise. Column 3 uses an indicator variable that takes the

value of one if the abnormal pay is greater than the median abnormal pay in the sample. Lastly,

column 4 uses the previous split of abnormal pay into positive and negative values. The primary

variable of interest in each specification is the interaction coefficient between a change in

consultant and the abnormal pay variable. For columns 2 and 3 that use an indicator variable, the

interaction can be interpreted as the impact of switching consultants on the change in CEO pay

when the CEO has previously been overpaid. For the specifications using the continuous variables

(columns 1 and 4), the interaction reveals whether the effect of changing consultants on the change

in CEO pay depends on the level of abnormal CEO pay.

In all four specifications, the interaction variable is negative and statistically significant.

This significance implies that when the CEO is overpaid and the firm switches consultants, the

subsequent year’s CEO pay decreases. In terms of economic magnitude, for every million dollars

27

of abnormal CEO pay in the previous year, the CEO’s total compensation the following year

decreases by approximately $445,000. However, when the firm changes compensation consultants

following periods of excessive pay, the CEO’s total compensation reduces by another $135,500.

Together, this represents a total decrease in pay for the CEO of $580,500. Focusing on strictly

excessive abnormal pay, the consultant change reduces CEO compensation by an additional

$195,000 (column 4). This evidence is consistent with the Shareholder Power hypothesis and

against the Managerial Power hypothesis. When the compensation consultant changes,

particularly when the CEO has been overpaid, it results in a decrease in CEO pay.

There are two additional important findings. First, the coefficient on the change in

consultant is not significantly different from zero when the CEO is underpaid. Second, when the

interaction is removed, the coefficient on change in consultant is not significantly different from

zero (untabulated). Both of these are informative findings. The effect of changing consultant on

subsequent CEO pay appears to be driven primarily by when the CEO is excessively paid. While

the Shareholder Power hypothesis predicts that any deviation from optimal pay would trigger a

consultant switch and subsequent correction, it is logical to assume this effect is more prevalent

when the CEO is paid excessively than underpaid. It is not often that shareholders complain that

their CEO is underpaid, however, the opposite is a persistent occurrence. Additionally, these

results are inconsistent with the Managerial Power hypothesis. Under the Managerial Power

hypothesis, we expect that a consultant change would have the greatest impact on CEO pay when

the CEO was previously underpaid. However, we find no such relation.

The estimates on our control variables are omitted to conserve space, but they are in line

with prior research. Higher stock returns are associated with increases in CEO pay, as are changes

in firm size (Gabaix and Landier, 2008). Consistent with Grinstein and Hribar (2004) and Fich,

28

Starks, and Yore (2014), corporate deal-making is also associated with increases in CEO pay.

Increases in leverage conversely lead to declines in pay (Gilson and Vetsuypens, 1993; John and

John, 1993).

Overall, the results from Table 6 lend support for the Shareholder Power hypothesis.

Regardless of the specification, the interactions between the change in consultant and the abnormal

pay variables are negative and significant. This finding implies that when a firm changes its

compensation consultant following excess CEO pay, CEO pay declines in the subsequent year.

4.4 Endogeneity Concerns

One concern is that the change in consultant is subject to a potential self-selection bias.

Specifically, the change in consultant is a choice variable; the firm chooses whether to change its

current consultant. As such, firms changing consultants are not randomly assigned. If there is some

omitted variable that impacts both the choice to change consultants and the change in pay (the

dependent variable in equation 2) then the OLS estimates will be biased and inconsistent.

To address this concern, we employ a standard Heckman two stage treatment effects model.

In the first stage, we run a Probit regression modeling the choice to change consultants. Next, we

calculate the Inverse Mills Ratio from this regression and add it as a control variable in equation

two. The loading on the Inverse Mills Ratio and its impact on the coefficients can determine the

extent of the self-selection bias and its impact on the key results. Importantly, while the system is

technically identified by the nonlinearity of the first stage Probit model under the assumption of

bivariate normality, it is highly recommended to use an instrument in the first stage that is omitted

from the second stage regression to ensure proper identification (Li and Prabhala, 2007).

29

We use the number of compensation consulting firms available per industry in t-1 as our

instrument to identify the system.15 For the instrument to be valid, it must satisfy both the relevance

and exclusion conditions. First, the instrument must meaningfully influence the board’s choice to

change consultants. The relevance condition is testable by examining the statistical significance of

the coefficient in the first stage regression. Second, the instrument must not have a relation with

the dependent variable in the second stage regression (i.e., change in CEO pay) except through its

influence on the choice to change consultants. This exclusion condition is not testable and must be

supported through economic reasoning.

We contend that the number of options in the compensation consulting market, specifically

within a given industry, is likely to impact whether a firm changes its consultant, but is unlikely to

affect the following year’s change in CEO pay. When more compensation consultants are active

in the market, firms have a greater choice, which should increase the likelihood of a given firm

changing compensation consultants. Conversely, if the number of consultants decreases, the

number of choices decreases; therefore, the firm would be less likely to change its compensation

consultant that year. In particular, our instrument takes advantage of the 2010 SEC regulation (i.e.,

Release 33-9089) that caused many consultants to spinoff new advisory firms. Although our

instrument identifies all year-to-year and within industry changes, this regulation increased the

size of the consulting marketplace and our instrument exploits this exogenous variation.

Regardless of whether the number of consulting firms increases or decreases for a given year, it is

not clear how the number of advisors would influence the internal deliberations of the CEO’s

compensation at any given individual firm in the subsequent year.

15 We define industry using one-digit SIC codes. We count a consultant firm as being available in the industry if they

have any clients in that specific industry for a given year. We then sum the number of distinct consultants in a given

industry each year to obtain our instrument.

30

In Table 7, we report the first stage Probit regression with the instrument included. The

vector of independent variables is the same as those used in Table 4, but the estimates are omitted

to conserve space. Columns 1 and 2 use the abnormal pay variable with and without fixed effects.

Columns 3 and 4 use the abnormal pay split between positive and negative values with and without

fixed effects. Regardless of the specification, results are consistent. Both the abnormal pay variable

and positive abnormal pay variable continue to load positively and significantly. In fact, in all

specifications, the magnitude and significance are larger than in Table 4 without the instrument

included. Moreover, the instrument loads positively and is statistically significant at the 1% level

in all specifications, indicating the instrument satisfies the relevance condition. Our estimates

suggest that, as the number of available consulting options increase within the firm’s industry,

firms are more likely to change consultants. The marginal effects at sample means suggest that

increasing the number of consultant options in a given industry by one standard deviation increases

the likelihood of changing consultants by 2.2 percentage points to 23%

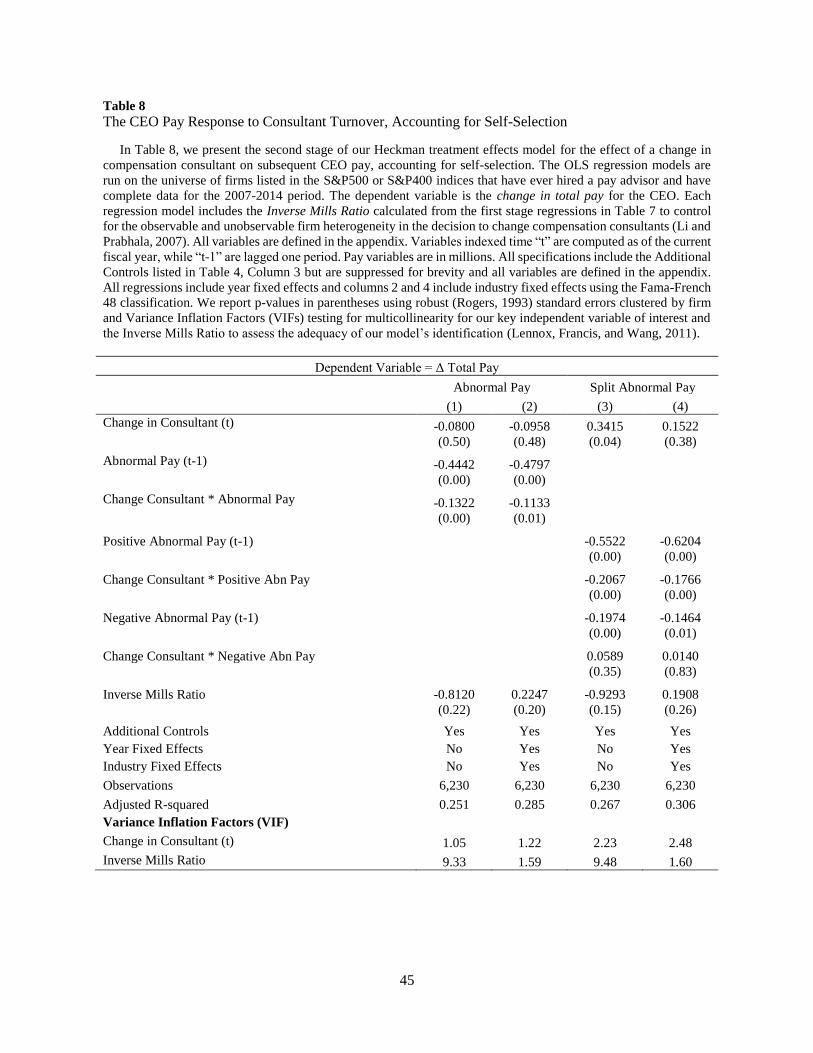

Table 8 presents the results of the second stage OLS regression with the Inverse Mills Ratio

from the first stage added as a control variable. Columns 1 and 2 present results using the abnormal

pay with and without fixed effects. Columns 3 and 4 present results using the abnormal pay split

between the positive and negative variables with and without fixed effects. In all specifications,

our primary results retain their sign and significance. Following a change in consultants, CEO pay

falls, particularly when they were overpaid in the prior year.

Further, we note that the Inverse Mills Ratio is statistically insignificant in all

specifications, implying that self-selection bias is not a major concern in our regressions. When

the exclusion condition is not met, the second stage model may suffer from multicollinearity issues

because the Inverse Mills Ratio is correlated with second stage variables (Lennox, Francis, and

31

Wang, 2011). High multicollinearity can inflate the standard errors, but may also indicate that the

model is not correctly specified. We report the variance inflation factors (VIF) for our endogenous

variable (consultant change) and our Inverse Mills Ratio in Table 8. All VIFs are below the

accepted critical value of 10, indicating that multicollinearity is not an issue in our specifications

(Greene, 2008).

4.5 Impact on Votes for Directors

Finally, we observe how shareholders react to a consultant change when they use their

“voice” in the director elections for the members of the compensation committee. Specifically, we

examine the number of “for” votes the committee member receives in the year following a

compensation consultant change. Provided the consultant change helps align the CEO’s incentives

and is in the shareholders’ best interests for the firm, then more shareholders should show support

for directors in the year following the change and vote “for” a given director. Conversely, if the

compensation consultant change is primarily motivated by management looking to obtain excess

pay, then shareholders show their displeasure by withholding “for” votes for directors.

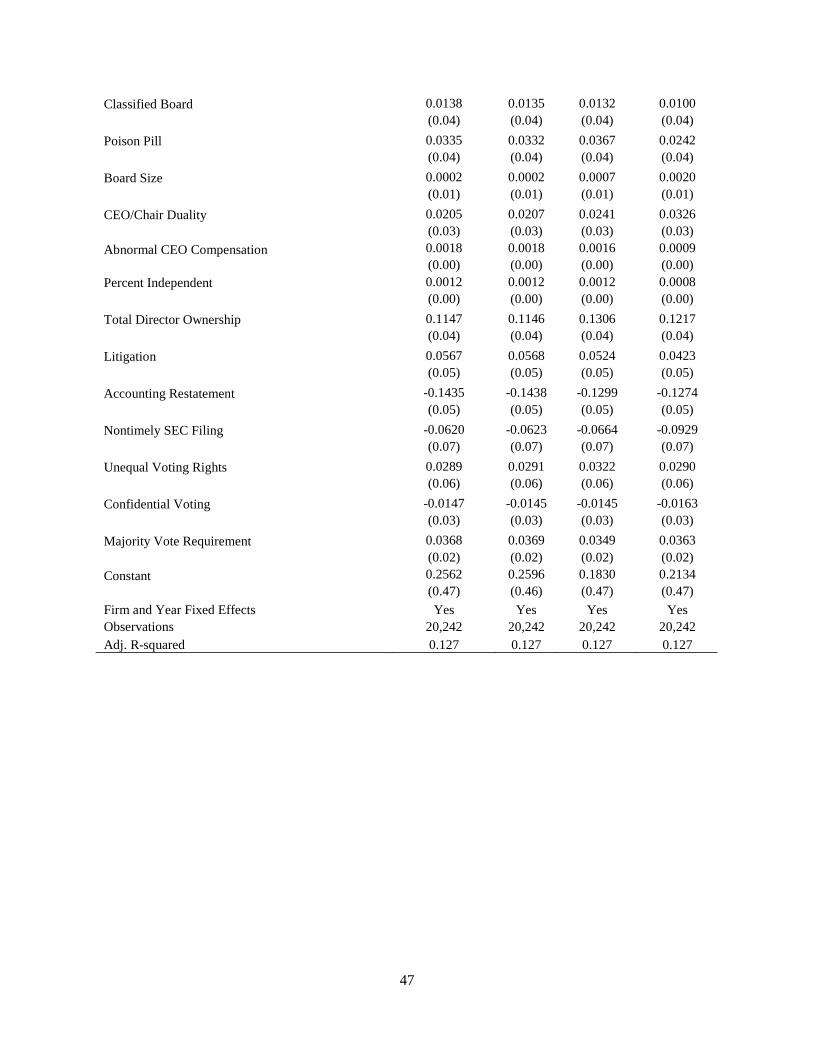

Using a sample of 20,242 director votes from the ISS Voting Analytics database, we

regress whether there was an increase in the percent of ‘for’ votes a director receives from the

previous year on whether there was a change in compensation consultants in the previous year.

We utilize additional control variables following the models outlined in Cai, Garner, and Walkling

(2003) and Field, Souther, and Yore (2018). Results are tabulated in Table 9. All specifications

include meeting clustered standard errors with firm and year fixed effects. As members of the

compensation committee tend to play a more significant role in CEO compensation, we focus on

the effect for directors on the compensation committee in column 2. The results show that in the

32

year following a change in compensation consultants, directors on the compensation committee

receive an additional 0.48% increase in votes.

Further, we explore shareholders’ reactions to a compensation consultant change when the

CEO was previously overpaid (column 3) or if there was a consultant change and that results in a

subsequent a decrease in CEO abnormal pay (column 4). In both of these instances, shareholders

reward the directors for changing consultants due to excessive pay with more “for” votes. For

example, directors receive a 5.3% increase in the percent of “for” votes when the CEO was

previously overpaid and the firm changes consultants. Overall, there appears some evidence that

there is a direct effect on directors when the company decides to change compensation consultants.

Particularly for members of the compensation committee and when the CEO is excessively paid,

these directors appear to garner more shareholder approval, further supporting our Shareholder

Power hypothesis.

4.6 Robustness

For robustness, we explore two main areas of concern: our main measure of abnormal pay

and the effect of regulation on the consulting industry. The main measure we use throughout our

estimations is abnormal pay. For robustness, we use an industry-adjusted CEO pay measure to

replace our abnormal CEO pay variables in all specifications (untabulated). In all specifications,

the results are quantitatively and statistically similar to our earlier findings. When CEOs receive

compensation higher than their industry peers, it leads to a greater likelihood that the firm changes

compensation consultants, supporting the Shareholder Power hypothesis (coefficient of 0.0095,

p-value = 0.02). Further, when the CEO is excessively paid compared to the industry and the firm

changes consultants, the CEO receives a subsequent reduction in compensation (coefficient of -

0.086, p-value = 0.00).

33

As noted, the significant regulation in 2009 created a shift in the compensation consultant

industry due to the mandatory disclosure of fees if a firm received additional services in excess of

$120,000 from their compensation consultant. This regulation created a number of consultant spin-

offs, which caused a spike in the percentage of firms that switched compensation consultants in

the 2009-2010 period (11-18% higher changes than the average). We examine the robustness of

our results by re-estimating the regressions only from 2011 to 2014 to avoid the shift in the

consultant industry after the 2009 regulation as well as year by year. Our results are quantitatively

similar and statistically significant. The coefficient for abnormal pay for the 2011-2014 period is

0.0133 (p-value = 0.05) (unreported), indicating a positive relationship between excessive CEO

pay and a firm changing compensation consultants. These results further support the Shareholder

Power hypothesis.

5. Conclusions

Compensation consultants face the repeat business incentive, whereby they wish to

continue providing services in future years. Whether this incentive creates a conflict of interest

depends on whom the consultants serve. If the consultant serves management’s desire to earn

excess pay, the repeat business incentive is in fact a conflict of interest. If, however, the consultant

serves the shareholders, the repeat business is a mechanism by which the incentives of the

consultant and those of the shareholders are aligned to recommend the best possible pay package

for the CEO. We argue that the consultant will serve whomever has the power to retain them for

future business. In this paper, we test two competing hypotheses to shed light on which party has

this power: the Managerial Power hypothesis and the Shareholder Power hypothesis. To test these

hypotheses, we utilize a unique event that speaks directly to whether the consultant earned repeat

business: consultant switching.

34

Under the Managerial Power hypothesis, consultants are evaluated (and retained) based

on their ability to recommend excessive CEO pay. In contrast, if the Shareholder Power hypothesis

holds, consultants should be evaluated (and retained) based on their ability to recommend optimal

levels of CEO pay. In this instance, a new consultant would be one who could be more successful

at recommending optimal pay levels.

We find strong and robust support for the Shareholder Power hypothesis and little support

for the Managerial Power hypothesis. Firms tend to change consultants following excessive levels

of CEO pay. When the CEO has been paid excessively, a consultant switch is associated with a

decrease in CEO pay in the following year. This finding is robust to endogeneity concerns and

different proxies for optimal levels of CEO pay. In addition, we find evidence that directors benefit

from a change in compensation consultants by receiving more shareholder support in their votes

further supporting the Shareholder Power hypothesis. Overall, our results suggest that the

considerable criticism of the compensation consultant industry may be overstated.

35

References

Aggarwal, R. K., 2007. Executive Compensation and Incentives, Handbook of Empirical Corporate Finance

Volume 2, pp. 498-534.

Armstrong, C.S., Ittner, C.D. and Larcker, D.F., 2012. Corporate governance, compensation consultants, and

CEO pay levels. Review of Accounting Studies, 17(2), pp.322-351.

Bebchuk, L.A. and Fried, J.M., 2003. Executive compensation as an agency problem. Journal of Economic Perspectives, 17(3), pp.71-92.

Bebchuk, L. and Fried, J., 2004. Pay without performance (Vol. 29). Cambridge, MA: Harvard University Press.

Bebchuk, L.A., Cremers, K.M. and Peyer, U.C., 2011. The CEO pay slice. Journal of Financial Economics,

102(1), pp.199-221.

Berger, P.G., Ofek, E. and Yermack, D.L., 1997. Managerial entrenchment and capital structure decisions. The

Journal of Finance, 52(4), pp.1411-1438.

Bizjak, J.M., Lemmon, M.L. and Naveen, L., 2008. Does the use of peer groups contribute to higher pay and

less efficient compensation?. Journal of Financial Economics, 90(2), pp.152-168.

Cadman, B., Carter, M.E. and Hillegeist, S., 2010. The incentives of compensation consultants and CEO pay.

Journal of Accounting and Economics, 49(3), pp.263-280.

Cai, C., Kini, O. and Williams, R., 2016. Do compensation consultants have distinct styles?. Available at SSRN:

https://ssrn.com/abstract=2724072

Cai, J., Garner, J.L. and Walkling, R.A., 2009. Electing directors. The Journal of Finance, 64(5), pp.2389-2421.

Cai, Ye and Xu, Jin and Yang, Jun, Paying by Donating: Corporate Donations Affiliated with Independent

Directors (August 15, 2017). Kelley School of Business Research Paper No. 16-51. Available at SSRN: