Compass Group PLC Internal Controls...

146

Compass Group PLC Internal Controls Manual Version 2.0 October 2007

Transcript of Compass Group PLC Internal Controls...

Compass Group PLC Internal Controls Manual Version 2.0 October 2007

How to use this manual

This manual is organised by process and aims to cover the core internal controls and relevant to Compass Group companies as clearly as possible. It also identifies which of those core internal controls are relevant at each level of the business – Unit; Country; Operating Company and Group.

As an example each chapter is organised in a common format: Section contents indicates the sub-processes within each business process. Control objectives are defined within the Application of controls & use of manual section - A3. Control objectives are in italics text and are numbered x.x.x

Application of controls provides guidance on scope of responsibility for the application of controls at each level of the business (See section A4) Internal controls are defined within the Application of controls & use of manual section – A3. They are numbered x.x.x.x

Compass Group has made significant progress in improving corporate governance. This includes the introduction of Group Accounting Policies and Approvals Manuals, establishing a Major Risk Assessment process, introducing a Group statement of Business Principles, embedding a Group Internal Audit team and setting up the ‘Speak Up’ whistle blowing hot line across the Group.

An additional key building block, which will be of substantial benefit to the Group, is the introduction of this Internal Controls Manual, setting out the Group’s expectations of a minimum set of key controls that each and every business across the Group should operate. All relevant control objectives in each section should be addressed by Group businesses and good reasons should be given for any non- compliance.

To assist you in linking these generic internal controls minimum standards to your own particular business a Control Self Assessment (CSA) tool has been developed. You can use this to validate your degree of compliance and highlight any areas for corrective action.

I commend this Manual to you.

By its nature, it cannot cover every situation. It does, however, provide a minimum standard of internal control for each and every Compass Group business.

If you require more guidance or greater clarity, please feel free to contact any of the Contacts listed in the front of this manual.

As a Group, we are passionate about what we do. Effective internal controls strengthen our position in the market place and make us less vulnerable to potential internal weaknesses that could adversely affect deliverance of our corporate objectives and damage our reputation.

Andrew Martin Group Finance Director Oct 2007

Contacts Group Finance Director Andrew Martin Telephone number +44 (0)1932 573028 Group Financial Controller John Franke Telephone number +44 (0)1932 573013 Email address [email protected] Group Treasurer Justin Besley Telephone number +44 (0)1932 573022 Email address [email protected] Group Tax Manager David Brassington Telephone number +44 (0)1932 573014 Email address [email protected] Peter Frans European Tax and Treasury Manager Telephone number +31 20 4307 178 Email address [email protected] Group Director of Internal Audit Trevor Gelnar Telephone number +44 (0)1932 573158 Email address [email protected] Director of Risk Management – UK & Ireland Bernhard Mallette Telephone number +44 (0)121 457 5753 Email address [email protected]

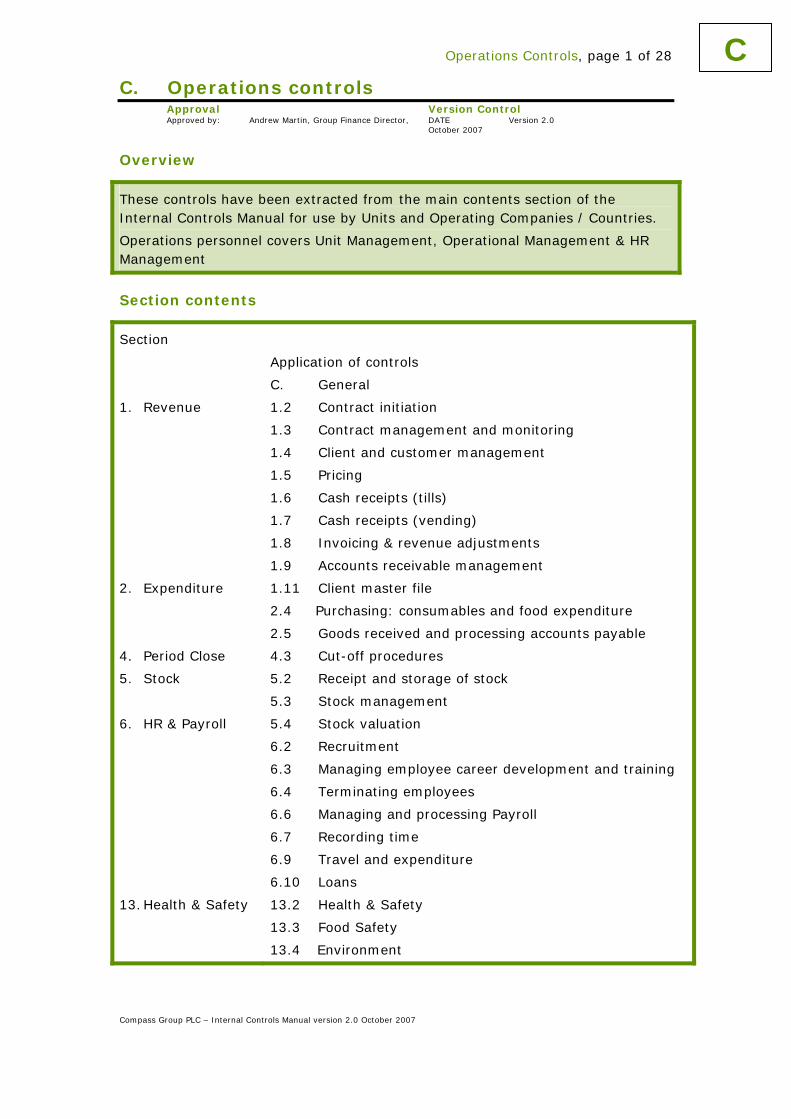

Contents

A Application of Controls & Use of Manual

B Internal Controls

Section

1 Revenue

2 Expenditure

3 Fixed Assets

4 Financial Closing & Reporting

5 Stock

6 HR & Payroll

7 Intra-Group

8 Treasury

9 Taxation

10 General Computer Controls

11 Legal & Statutory Requirements

12 Insurance & Security

13 Safety Health and Environment

C Operations Controls

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

A. Application of Controls & Use of Manual Approval Version control Approved by: Andrew Martin, Group Finance Director, October 2007, Version 2.0

Contents

A.1 Purpose of this manual 1 A.2 Scope 1 A.3 Definitions of key terms 1 A.4 Application of controls 2 A.5 Implementation guidance 4 A.6 Confidentiality 5

A.1 Purpose of this manual

Compass Group is always focusing on improving corporate governance throughout its business. The purpose of this manual is to provide Group-wide guidance on the minimum standard of internal control that should be applied across Group companies. It has been prepared with meeting the following objectives in mind:

to be a single reference source on a minimum set of key controls that should operate in all Compass Group businesses.

to enable all Compass Group businesses to implement a minimum standard of internal control in accordance with Group expectations by indicating the Control Objectives that must be addressed in all businesses where they are relevant.

A.2 Scope

This manual covers the key controls in business processes applicable to Compass Group Operating Companies as well as selected support / oversight functions. Where applicable the manual refers to other Group manuals / policies and procedures such as the Group Accounting Policies and Procedures Manual and the Group Approvals Manual to provide a more complete set of guidelines when implementing business controls.

A.3 Definitions of key terms

A.3.1 Internal control and control objectives*

Control objectives

Control Objectives are responses to business objectives. They are management directives which need to be met in order to effectively address risks to the achievement of the entity’s business objectives.

Throughout this manual the Control Objectives are highlighted in italics.

Internal control

An internal control is a “process, effected by an entity’s board of directors, management and other personnel, designed to provide reasonable assurance regarding the achievement of business objectives”, including:

Compass Group PLC – Internal Controls Manual version 2.0, October 2007 1

A. Application of Controls & Use of manual, Page 2 of 5

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

• effectiveness and efficiency of operations. • preparation of reliable published financial statements. • compliance with applicable laws and regulations.

* The above definitions of internal controls and control objectives have been taken from the Committee Of Sponsoring Organisations of the Treadway Commission (COSO).

A.3.2 Compass corporate structure

Group

The Group Head Office function.

Operating Company / Country

Operating Companies are also known as sector brands. These are our client facing companies, for example, Eurest (Business and Industry), Chartwells (Education) and Medirest, (Healthcare).

A ‘Country’ will hold individual Operating Companies.

Unit

Specific location / outlet / restaurant within a contract where a Compass Group Operating Company provides (agreed with / determined by the client / partner) food and other services to its customers.

Support functions

Collection of support functions serving a variety of businesses for example financial shared services.

A.4 Application of controls

A.4.1 General

This Internal Controls Manual documents a minimum expected set of key controls within business processes and, as such, internal controls within individual sections (and subsections) may only apply to parts of a business or to single or multiple levels of a business. For example revenue is split into subsections including management of contracts, which may be managed at an Operating Company or Country level and cash controls which are more likely to sit at a Unit level.

A Unit, Operating Company / Country or Group may also all need to apply the same control – for example controls around HR – recruitment- may apply to all levels of the business.

An appropriate level of management at each business area should determine which sections of the manual, and as such which controls, apply to that particular business area.

A. Application of Controls & Use of manual, Page 3 of 5

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

In particular, every Finance Director, Managing Director and Operational Director has the responsibility to determine which Control Objectives are relevant to his / her business and in doing so to be able to identify, for every such Control Objective:

i. Where all the internal controls addressing that objective are performed;

ii. Who performs that control;

iii. When that control is performed; and

iv. How the performance of that control is documented or evidenced.

A.4.2 Application principles

As Compass Group as a whole has a complex organisational structure, this manual has been produced with a varied audience in mind and the requirement that it will be applied across all levels of the Group.

When considering which controls are relevant to a particular business area and how these relevant controls can be applied by a business area, consideration should be given to whether the process is one that is relevant to that business area. As an obvious illustration, for example treasury controls would not apply to the HR function.

Once the processes relevant to that business area have been determined, the sections of that process relevant to the business area should be determined by reviewing the “Application of Controls” table at the front of each process (chapter).

Once the relevant sections have been determined, the control objectives within the section should be reviewed. It is expected that each control objective will be relevant to all such business areas. Business areas that believe control objectives are not relevant to them should be prepared to justify and document their reasons for that belief.

For each control objective, the business areas should identify the set of controls that achieve that control objective. The controls listed under that control objective in the section are designed to be the most likely set of control that will meet that control objective, but are not always going to be the right set for every business area.

If any of the sets of controls determined to be required by the business area to achieve that control objective are not in place and operating, they should be implemented.

Consequently every business area will be able to demonstrate the set of controls it has in place to achieve each control objective within each relevant section of each process (chapter) that is relevant to it.

Further, to assist in the ease of application of this manual to Units, those internal controls applicable to Units occurring throughout the manual have been reproduced together in Section C of the Manual.

A.4.3 Factors to consider when applying controls

A. Application of Controls & Use of manual, Page 4 of 5

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

Consideration should be given to the following factors when determining the exact controls which should be applied for any particular business area:

- Local legal requirements

- Existing Group manuals / policies and procedure guidance such as the Group Accounting Policies and Procedures Manual, Group Approvals Manual.

- Business area specific applicability (for example different exact controls may be required in a vending business area versus an education business area).

- Implementation issues (for example segregation of duties may not be possible if a business does not have a sufficient number of individuals in a business). However, mitigating / other controls that meet the control objective must be implemented if a control cannot be actually implemented as designed.

- Cost versus benefit considerations. As with the previous factor mitigating / other controls that meet the control objective should be considered and implemented if a control cannot be implemented on the basis of excess cost.

These factors in the application of controls should be considered on a case by case basis.

A.4.4 Control principles

The purpose of this manual is to provide group-wide guidance on implementing a minimum level of internal controls to allow Compass Group to continually improve the level of internal control within the Group. Some of the key principles to consider when implementing controls and answering the questions “what are the objectives of the controls” and “how can we satisfy these objectives?”, are:

- Who performs the control? Is this the appropriate individual? Is this person adequately qualified / trained?

- Are duties appropriately segregated? Is one person performing all activities within a process and does this create a situation where an error may not be detected or fraud could potentially occur?

- Is there a process in place to monitor whether actions / transactions are performed or processed as expected?

- Do guidance / timetables / checklists exist to ensure required actions are completed? Is their completeness appropriately documented?

- Are controls adequate and appropriate, do they meet the controls objective and are they ‘sensible’?

- Is evidence of review and approval of controls documented, ie are reconciliations signed off by reviewer?

A.5 Implementation guidance

A. Application of Controls & Use of manual, Page 5 of 5

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

Each business should undertake an assessment of their ability to comply with A.4 above using the Group’s Control Self Assessment (CSA) tool.

Where enhancements are required to internal controls to meet minimum expected standards, these should be implemented as soon as possible.

If guidance on relevance, application or implementation is required, or if notification of inability to comply in the timeframe needs to be made, John Franke, Group Financial Controller should be notified.

A.6 Confidentiality

This manual is available through the Finance section of the Group’s intranet, Mercury. It has been prepared exclusively for Compass Group and should not be made available outside the Group without written permission from Group Finance, Chertsey.

B. Internal Controls

Section

1. Revenue 1.1 General

1.2 Contract initiation

1.3 Contract management and monitoring

1.4 Client and customer management

1.5 Pricing

1.6 Cash receipts (tills)

1.7 Cash receipts (vending)

1.8 Invoicing and revenue adjustments

1.9 Accounts receivable management

1.10 Revenue recognition

1.11 Client master file

2. Expenditure 2.1 General

2.2 Selection and evaluation of suppliers

2.3 Purchasing: overhead and capital expenditure

2.4 Purchasing: consumables and food expenditure

2.5 Goods received and processing accounts payable

2.6 Processing payments

2.7 Maintaining product / supplier master file

2.8 Purchasing discounts

3. Fixed Assets 3.1 General

3.2 Acquisition of fixed assets

3.3 Use & maintenance of fixed assets

3.4 Disposals

3.5 Recording of fixed assets & managing of fixed assets

register

3.6 Depreciation and amortisation

3.7 Fixed asset security

3.8 Leased assets

3.9 Intangible assets and goodwill

4. Financial Closing & Reporting

4.1 General

4.2 Defining the financial closing and reporting process

4.3 Performing the accounting period close

4.4 Consolidation

4.5 Disclosure and financial statement review and

preparation

4.6 Budgeting and forecasts

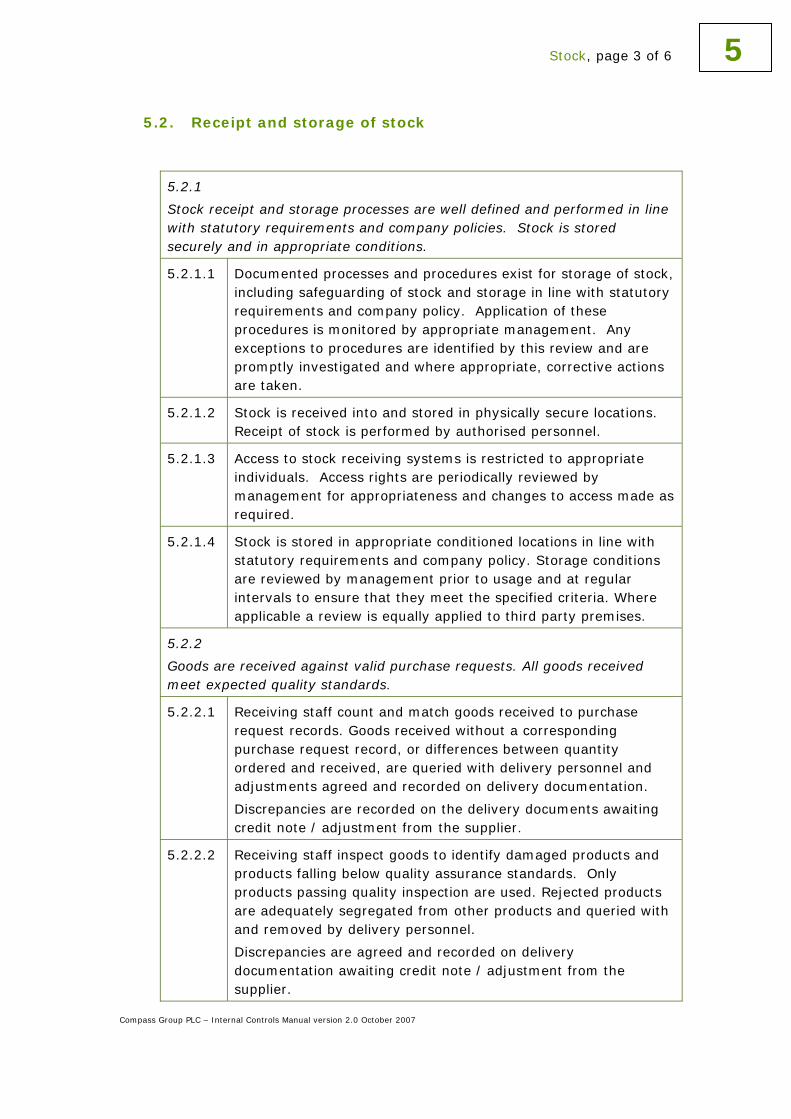

5. Stock 5.1 General

5.2 Receipt and storage of stock

5.3 Stock management

5.4 Stock valuation

6. HR & Payroll 6.1 General

6.2 Recruitment

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

B. Internal controls, page 2 of 3

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

6.3 Managing employee career development and training

6.4 Terminating employees

6.5 Managing employee information and payroll

masterfile

6.6 Managing and processing payroll

6.7 Recording time

6.8 Accounting and reporting

6.9 Travel and expenditure

6.10 Loans

6.11 Security of data

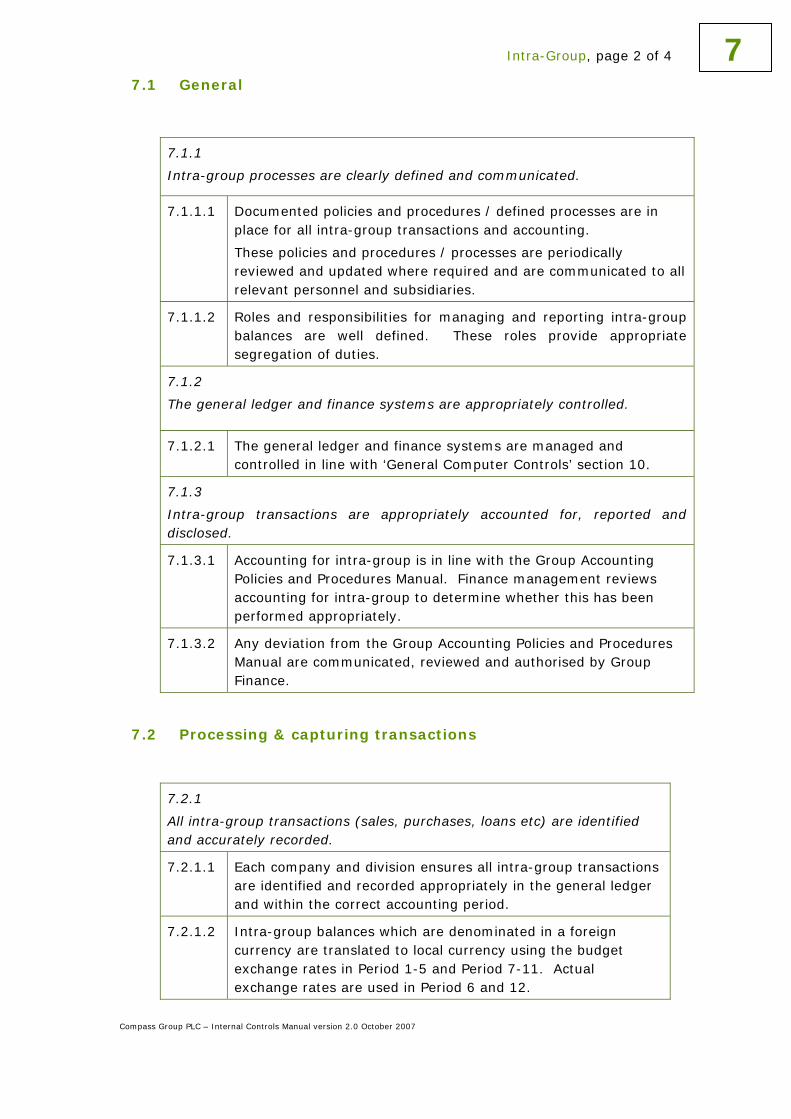

7. Intra-Group 7.1 General

7.2 Processing & capturing transactions

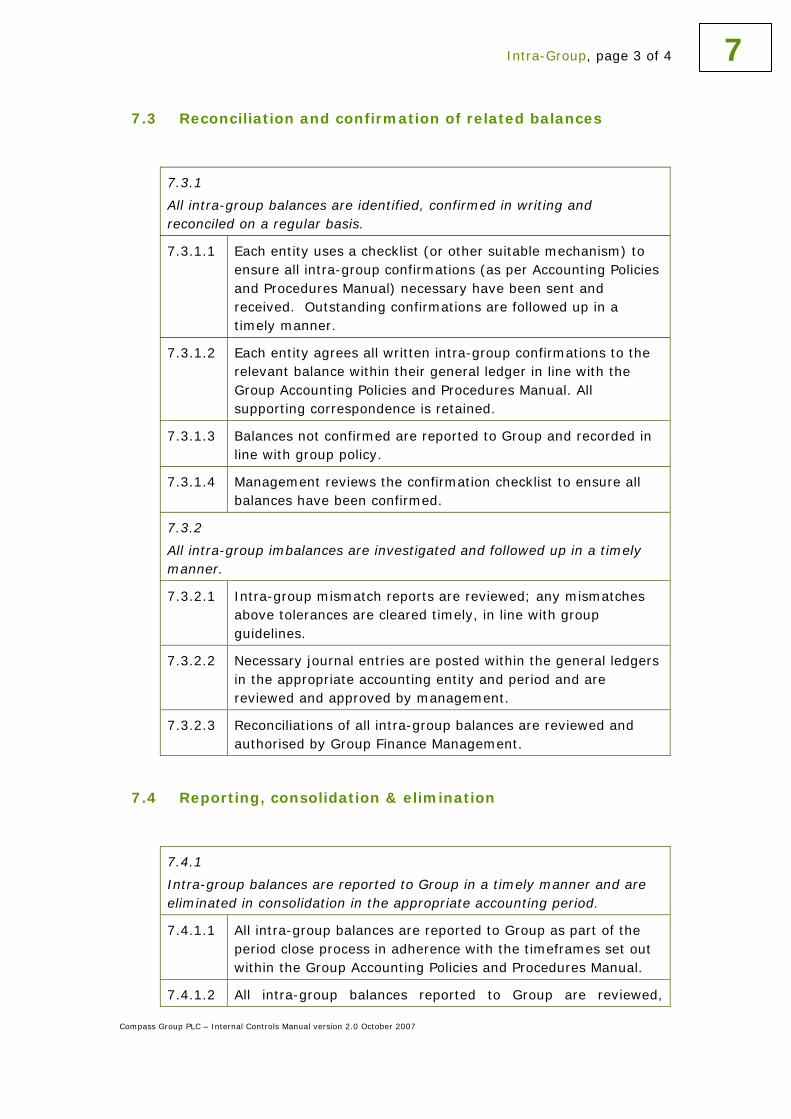

7.3 Reconciliation and confirmation of related balances

7.4 Reporting, consolidation & elimination

7.5 Intra-group pricing

7.6 Intra-group settlements

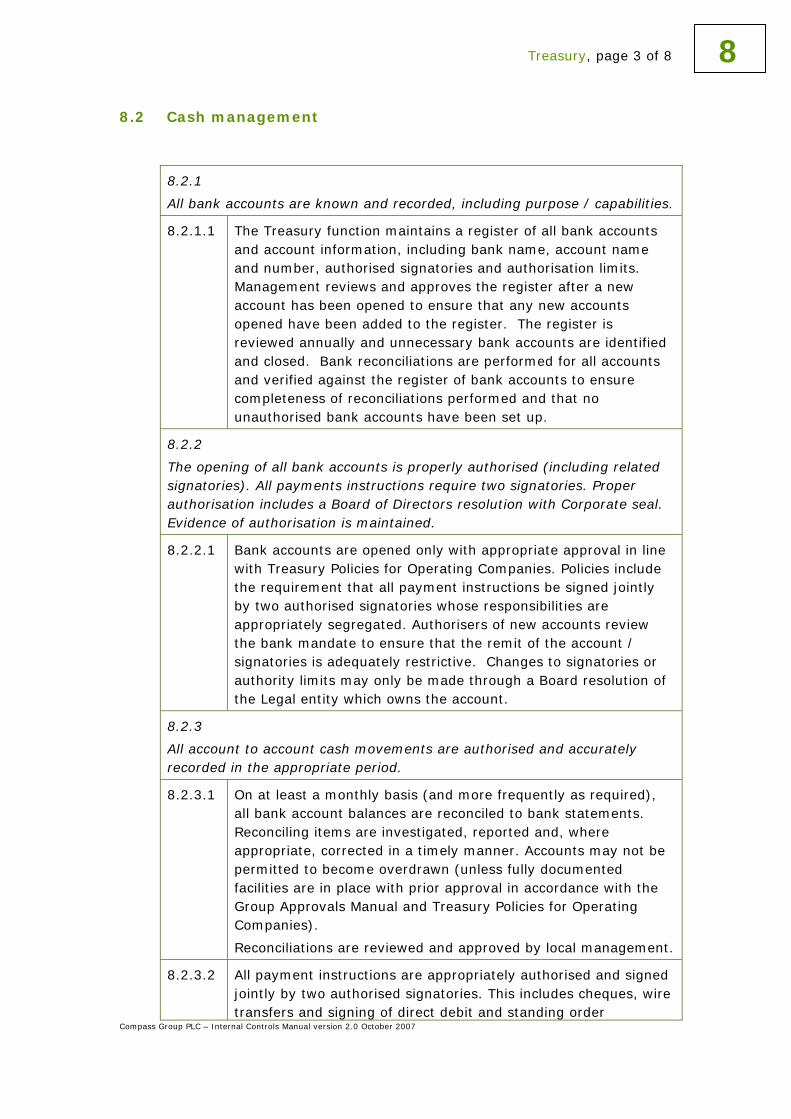

8. Treasury 8.1 General

8.2 Cash management

8.3 Borrowing

8.4 Investment

8.5 Derivatives

8.6 Dividends

9. Taxation 9.1 General

9.2 Business and regulatory environment

9.3 Tax reporting and compliance

10. General Computer Controls

10.1 General

10.2 Information resource strategy and planning

10.3 Application systems implementation and

maintenance

10.4 Information systems operations

10.5 Relationships with outsourced suppliers

10.6 Information security

10.7 Business continuity planning

10.8 Database implementation and support

10.9 Network Support

10.10 Systems software support

10.11 Hardware support

11. Legal & Statutory Requirements

11.1 General

11.2 Legal services

11.3 Claims and liquidation

11.4 Directors’ duties

11.5 Trading licences

11.6 Intellectual property

11.7 Contract bonds, letters of credit and parental

B. Internal controls, page 3 of 3

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

guarantee

12. Insurance & Security

12.1 Physical security of premises

12.2 Insurance

13. Safety Health and Environment

13.1 General

13.2 Health & safety

13.3 Food safety

13.4 Environment

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1. Revenue Approval Version control Approved by: Andrew Martin, Group Finance Director

DATE October 2007

Version 2.0

Section contents

Application of controls 1

1.1 General 2

1.2 Contract initiation 3

1.3 Contract management and monitoring 5

1.4 Client and customer management 6

1.5 Pricing 6

1.6 Cash receipts (tills) 7

1.7 Cash receipts (vending) 8

1.8 Invoicing & revenue adjustments 9

1.9 Accounts receivable management 10

1.10 Revenue recognition 12

1.11 Client master file 12

Application of controls

Company

level

Application of controls

Group Group personnel should perform controls within section 1.1 and 1.2.

Group should provide guidance on the operation of these controls.

Operating Companies / Countries

All relevant controls within sections 1.1 to 1.11 should be applied by Operating Companies / Countries. Operating Companies / Countries should provide guidance to Units on the operation of these controls.

Units Unit personnel should perform all relevant controls within sections 1.1 to 1.11.

1 Revenue, page 2 of 13

1.1 General

1.1.1

Revenue processes are clearly defined and communicated.

1.1.1.1 Documented policies and procedures / defined processes are in place for revenue functions. These include:

• Revenue recognition

• Contract initiation and management

• Bid/tendering process

• Client and customer management

• Pricing

• Cash collection and invoicing

• Till and vending cash monitoring and reporting

• Accounts receivable processing and monitoring

• Client master file maintenance

These policies and procedures / defined processes are reviewed and updated where required and at least annually and are communicated to all relevant personnel.

1.1.1.2 Roles and responsibilities within the accounts receivable, sales teams and trading units are well defined. These roles provide appropriate segregation of duties within all revenue and related functions.

1.1.2

Revenue and accounts receivable IT systems are appropriately controlled.

1.1.2.1 Revenue and accounts receivable IT systems are managed and controlled in line with ‘General Computer Controls’ section 10.

1.1.3

Revenue is properly accounted for.

1.1.3.1 Accounting for revenue is performed in line with the Group Accounting Policies and Procedures Manual. Finance management reviews accounting for revenue transactions at least annually to determine whether this has been performed appropriately.

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1 Revenue, page 3 of 13

1.2 Contract initiation

1.2.1

Policies and procedures exist surrounding the initiation and execution of tenders / bids and contracts.

1.2.1.1 Policies and procedures are in place outlining the principles and evaluation criteria to be followed when initiating and executing tenders / bids and sales contracts. These are reviewed and updated on a regular basis by management. Any changes are appropriately communicated to all relevant staff. These authorisation procedures are in line with Group Approvals Manual.

1.2.2

Potential bids / tenders and or contracts are evaluated prior to execution.

1.2.2.1 Potential clients are evaluated by management and legal using risk management and due diligence procedures prior to the bid / tendering process and / or contract execution (where appropriate). Review procedures are performed and recorded in writing to ensure appropriate expertise and resources exist to meet business needs, conflicts of interest are not present and potential contracts are in line with strategy.

1.2.2.2 Any noted exceptions to local policy or strategy identified during preparation of bids / tenders and / or contracts are evaluated by management and legal to determine whether to proceed. Appropriate additional approval is obtained where necessary.

1.2.3

Credit worthiness is evaluated prior to bid / tender submission or contract execution and is performed in line with credit policy.

1.2.3.1 A clear policy is in place that outlines processes to be performed in relation to credit checks. Credit checks are performed and documented prior to execution of a bid / tender or a client contract in accordance with policy. Compliance with this policy is monitored by management.

1.2.4

Bid / tender documentation and sales contracts are appropriately used to define all necessary terms and conditions.

1.2.4.1 Standard client contract terms and conditions exist. A policy is in place to define the use of these standard terms and conditions, where it is acceptable to deviate from these, and what steps should be taken (including appropriate approvals) when deviating from standard terms and conditions. Management monitors compliance with this policy. Non-standard contract terms and conditions are approved by appropriate levels of management and legal, in line with local policy.

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1 Revenue, page 4 of 13

1.2.5

All terms and conditions issued to clients are accepted in writing and evidence retained.

1.2.5.1 Contracts are accepted and agreed in writing by both management and the client to demonstrate agreement with terms and conditions prior to contract execution. All documentation of acceptance and any other related bid/tender and contract information is retained in a central location.

1.2.6

Sales staff commission paid is reflective of approved contract terms and conditions.

1.2.6.1 Checks, performed by independent personnel, are in place to ensure sales staff commission is only paid subsequent to formally approved sales contracts and other necessary documentation.

1.2.7

Sales contract prices and terms are set-up within finance systems accurately and on a timely basis.

1.2.7.1 Approved sales contracts are reviewed by finance management to determine the proper accounting treatment for revenue recognition prior to system input.

1.2.7.2 Approved sales contracts are appropriately recorded within financial systems to ensure future invoices generated reflect agreed contract terms and prices, and actual to budget revenue can be monitored accurately. Data input is independently reviewed for accuracy.

1.2.8

Defined policies and procedures / processes exist for the handover and ‘mobilisation’ of contracts.

1.2.8.1 Documented policies and procedures / defined processes are in place for handover of contracts to operational management / teams for ‘mobilisation’.

These include handover of key information including copies of contracts, bid / tender documents, meeting notes information regarding special requirements and guidance on any staff to be taken on and assets to be recorded.

Notes

Process and controls mentioned in this section also apply to re-bidding for contracts.

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1 Revenue, page 5 of 13

1.3 Contract management and monitoring

1.3.1

All contracts are effectively managed and monitored for compliance to agreed contract terms and conditions.

1.3.1.1 A member of the operations team is assigned to each contract entered into to ensure the client is managed effectively and appropriate services provided. Contracts are also reviewed and monitored on a regular basis against performance / services actually provided. Any issues are reported to management and resolved.

1.3.1.2 Actual revenue and margins from each contract are monitored against the contract budget on a regular basis. Variances are identified, investigated and appropriate action taken if necessary.

Any sales staff commission is reviewed and appropriate action taken in line with local policy if expected revenue targets are not being met. Changes to commissions are authorised by management.

1.3.1.3 Total contract risk is reviewed by management routinely to ensure the contract base is in line with expected and sustainable margins. Contracts are discussed, reviewed by management and exited if required.

1.3.2

Existing contracts are monitored to identify contracts up for renewal or re-bid.

1.3.2.1 At the end of the initial contractual period a formal review is undertaken to identify whether the contract requires renewal / re-bid and appropriate action is taken if necessary.

1.3.2.2 Contracts that are run on a rolling basis are regularly reviewed and appropriate action taken if not financially viable to retain.

1.3.3

Renewed contract terms and conditions are appropriately reviewed and authorised.

1.3.3.1 Changes made to existing contracts are subject to the evaluation and approval processes as outlined within local policy including appropriate legal and senior management review.

1.3.3.2 Updated contracts are authorised in writing by management and the customer to demonstrate acceptance of the updated terms and conditions. All documentation of acceptance is retained.

1.3.4

The status of expired contracts is changed to closed in all relevant systems

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1 Revenue, page 6 of 13

timely.

1.3.4.1 The status of all expired contracts is changed to closed within the financial systems on a timely basis.

Notes

1.3.3.1 includes the review for appropriateness of one-off incentives to re-tender contracts currently held.

1.4 Client and customer management

1.4.1

Customer / client service programmes are in place and satisfaction is monitored on a regular basis.

1.4.1.1 Policies and procedures / defined processes are in place to monitor client service and satisfaction. An escalation process is defined within these policies.

1.4.1.2 A customer / client service programme exists for all clients and is reviewed and updated on a regular basis. The programme is distributed to all customer service employees and client managers. Any changes to the programme or processes are communicated on a timely basis.

1.4.1.3 Customer / client satisfaction is measured and monitored on a regular basis and results communicated to relevant management and staff. Any follow up action required is performed on a timely basis.

1.4.1.4 Invoices queried by clients are followed up and discussed with clients where appropriate. Any necessary invoice or general ledger adjustments are made appropriately, if required. (See ‘Invoicing and Revenue Adjustments’ section).

1.5 Pricing

1.5.1

Sales reflect approved prices.

1.5.1.1 Sales are priced in line with contracts and defined pricing structures approved by Operating Company / Unit management. Price lists / menus are reviewed on a regular basis and any changes or amendments are appropriately authorised by management. Pricing on all invoices and transactions is independently checked by invoice periodically.

1.5.1.2 Any changes or amendments to prices are communicated to all necessary staff to ensure sales are reflective of new prices.

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1 Revenue, page 7 of 13

1.5.1.3 Any changes or amendments to prices are input into relevant systems accurately and on a timely basis.

1.5.1.4 Any price overrides at the transaction level are approved by the appropriate level of management prior to sale and recorded appropriately.

1.5.1.5 Management reviews recorded sales and gross margins and compares to budget regularly to identify any price discrepancies or unusual items. Any significant variances are investigated and resolved on a timely basis.

Notes

1.5.1.5 Target could be a simplified weekly P&L for each unit to react quickly to any deviation

1.6 Cash receipts (tills)

1.6.1

Only authorised employees enter sales transactions. Point of Sale (POS) terminal access is appropriately restricted.

1.6.1.1 POS procedures have been developed and distributed to all trading outlets. Compliance with policies is monitored.

1.6.1.2 All POS terminals are physically protected either by employee unique ID or by lock and key.

1.6.1.3 All POS terminals are closed and emptied at least once a day.

1.6.2

In Unit sales are appropriately captured, recorded and reconciled for completeness.

1.6.2.1 All customer sales (cash and card), including any related vouchers, are recorded using a POS terminal/cash register.

1.6.2.2 Total daily takings (cash and card) are reconciled to POS terminal / register. Any variances are investigated and resolved and the reconciliation of cash is independently reviewed.

1.6.2.3 Sales recorded by Units in returns to Operating Companies / finance centres are reconciled to POS records and bank records to ensure all sales are recorded. Any variances are investigated and cleared.

1.6.2.4 Unit bank statements are reconciled to the general ledger regularly. (See Treasury Section)

1.6.2.5 Sales are reconciled to goods purchased and any reconciling items

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1 Revenue, page 8 of 13

are investigated and cleared as appropriate. Management reviews and approves reconciliations.

1.6.3

Daily cash takings are appropriately safeguarded and banked.

1.6.3.1 Appropriate safety and security measures are in place to ensure staff members are not in danger and cash is secure.

1.6.3.2 Cash is banked regularly and cash takings not banked are held securely. Only authorised employees have access to safes or other secure locations.

1.6.4

In unit sales are reported on a timely basis.

1.6.4.1 All POS transactions are reported accurately to the finance centre in line with reporting timetables.

1.6.4.2 Transactions at, before or after period end are reviewed to ensure they are recorded in the correct accounting period.

1.6.4.3 The cut-off policy for cash is applied consistently in all reporting to finance centres in accordance with Group timetables.

1.6.5

Cashless system balances are appropriately reconciled.

1.6.5.1 Reconciliations of cashless sales (individual customer cards / balances) to the overall net balance held at the unit are performed at least once a month. Variances identified are investigated and action taken if necessary.

1.7 Cash receipts (vending)

1.7.1

Assets (both cash and stocks) within vending machines are safeguarded.

1.7.1.1 All vending machines, stock and cash are physically safeguarded through locks. Access to vending machine contents is restricted to authorised personnel.

1.7.2

Cash is received for all sales made through vending machines, cash and sales are recorded appropriately and timely.

1.7.2.1 Defined procedures exist for collecting and safely securing and banking cash from vending machines. These procedures are communicated to all relevant personnel. Management monitors compliance with these procedures.

1.7.2.2 Sales from vending machines and cash collected are recorded on a timely basis and in line with the Group Accounting Policies &

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1 Revenue, page 9 of 13

Procedures Manual.

1.7.2.3 Cash collected and banked is reconciled to vending machine ‘counter’ sales figures reported and value of stock consumed. Any variances are investigated and cleared.

1.7.2.4 Cut-off procedures are applied in line with Group Accounting Policies & Procedures.

1.7.2.5 Vending gross margins are periodically reviewed to determine whether appropriate sales / costs / cash receipts have been recorded and pricing within machines is appropriate. Any discrepancies are investigated and resolved on a timely basis.

1.8 Invoicing & revenue adjustments

1.8.1

All services provided are invoiced accurately in line with contracts and are recorded in the general ledger appropriately.

1.8.1.1 Invoices including contractually entitled discounts applied are automatically priced by the system based on approved contract terms and prices within the client master file (including management fees if relevant). Access to perform manual overrides of prices at the stage of invoice creation is restricted and any changes required to invoice amounts are authorised by management prior to issue. Sample checks of invoice prices are performed against contracts.

1.8.1.2 The calculation and application of tax amounts on invoices is automatically performed by relevant systems whose programming is regularly checked by tax professionals to ensure appropriate operation. Systems are maintained in line with ‘General Computer Controls’ section 10.

1.8.1.3 Where appropriate management fees are separately recorded on sales invoices in line with contract terms and conditions. Changes or amendments are appropriately authorised by management and the client.

1.8.1.4 The system automatically posts all invoiced amounts to the proper accounts in the general ledger.

1.8.2

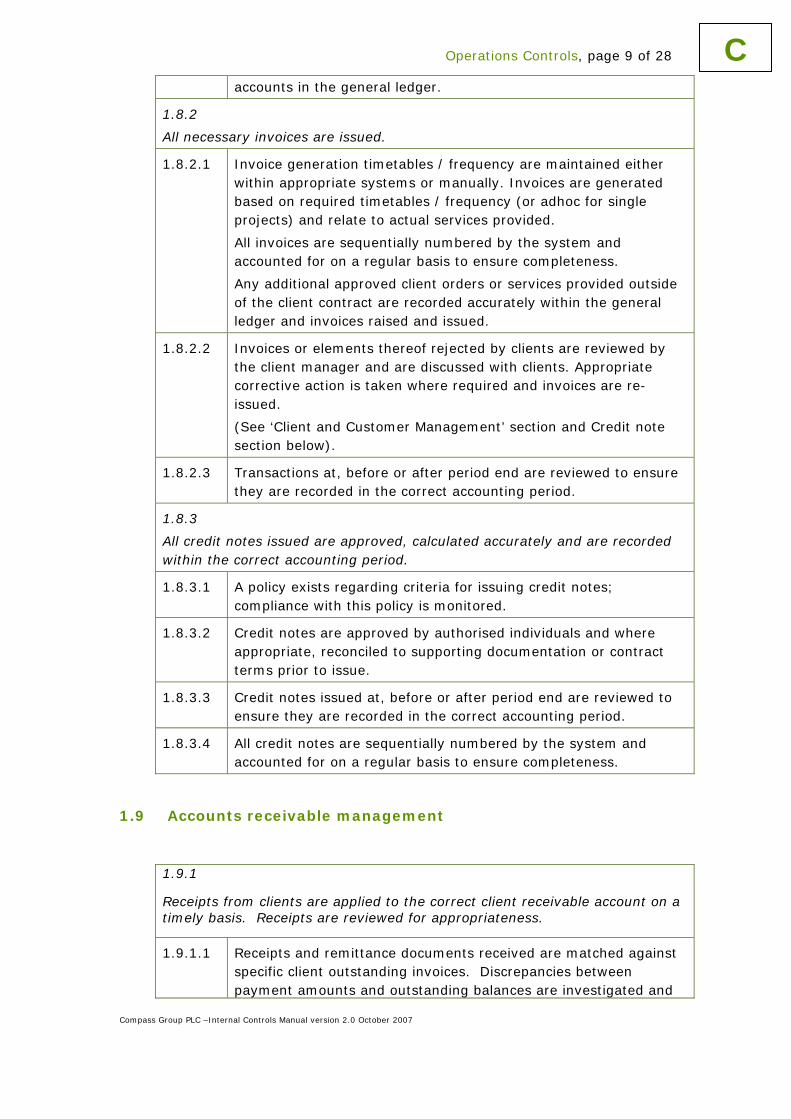

All necessary invoices are issued.

1.8.2.1 Invoice generation timetables / frequency are maintained either within appropriate systems or manually. Invoices are generated based on required timetables / frequency (or adhoc for single projects) and relate to actual services provided.

All invoices are sequentially numbered by the system and accounted for on a regular basis to ensure completeness.

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1 Revenue, page 10 of 13

Any additional approved client orders or services provided outside of the client contract are recorded accurately within the general ledger and invoices raised and issued.

1.8.2.2 Invoices or elements thereof rejected by clients are reviewed by the client manager and are discussed with clients. Appropriate corrective action is taken where required and invoices are re-issued.

(See ‘Client and Customer Management’ section and Credit note section below).

1.8.2.3 Transactions at, before or after period end are reviewed to ensure they are recorded in the correct accounting period.

1.8.3

All credit notes issued are approved, calculated accurately and are recorded within the correct accounting period.

1.8.3.1 A policy exists regarding criteria for issuing credit notes; compliance with this policy is monitored.

1.8.3.2 Credit notes are approved by authorised individuals and where appropriate, reconciled to supporting documentation or contract terms prior to issue.

1.8.3.3 Credit notes issued at, before or after period end are reviewed to ensure they are recorded in the correct accounting period.

1.8.3.4 All credit notes are sequentially numbered by the system and accounted for on a regular basis to ensure completeness.

1.9 Accounts receivable management

1.9.1

Receipts from clients are applied to the correct client receivable account on a timely basis. Receipts are reviewed for appropriateness.

1.9.1.1 Receipts and remittance documents received are matched against specific client outstanding invoices. Discrepancies between payment amounts and outstanding balances are investigated and resolved in a timely manner.

1.9.1.2 Receipts that are not immediately applied to a client account are recorded (in an unapplied receipts account if applicable). The unapplied receipts account is reconciled on a monthly basis and unapplied receipts are investigated and cleared in a timely manner.

1.9.1.3 Deductions taken by clients are properly authorised. All unauthorised deductions are investigated and resolved in a timely manner.

1.9.2

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1 Revenue, page 11 of 13

Sales related accounts are regularly reconciled and analysed to ensure the general ledger captures all relevant financial information. Any reconciling items or exceptions are investigated and cleared on a timely basis.

1.9.2.1 The accounts receivable sub-ledger is reconciled to the general ledger on at least a monthly basis. Reconciling items are investigated and resolved on a timely basis. Management reviews and approves reconciliations.

1.9.2.2 Accrued and deferred revenue balances are reconciled and analysed on a routine basis to ensure appropriate accounting treatment is adhered to in line with Group Accounting Policies and Procedures Manual. Management reviews and approves reconciliations.

1.9.3

Recoverability of accounts receivable is reviewed on a regular basis and additional collection procedures applied if necessary.

1.9.3.1 Documented procedures exist and are applied to monitor and collect overdue debts (includes legal measures to be taken where necessary). This policy is communicated to all relevant personnel.

1.9.3.2 Management regularly reviews aged accounts receivable analysis, and client accounts that are regularly overdue to determine appropriate follow-up actions. Any balances requiring follow-up are identified and acted upon on a timely basis.

1.9.4

Reserves/provisions are established for doubtful/bad debts in accordance with local policy.

1.9.4.1 Accounts receivable for which collectability is deemed doubtful are provided for in line with local policy, applying guidance through Group Accounting Policies and Procedures Manual. Bad debts are written off in a timely manner following proper authorisation.

1.9.4.2 On a periodic basis, management compares the provision for doubtful accounts balance to the results of their review of the accounts receivable ageing. Adjustments to provisions for doubtful accounts are appropriately approved and recorded on a timely basis.

1.9.5

In Unit credit sales are only performed in line with defined policy.

1.9.5.1 Policies and procedures exist regarding credit sales in Units including when these can be performed and appropriate authorisation required for these sales.

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1 Revenue, page 12 of 13

1.10 Revenue recognition

1.10.1

Revenue is recognised in accordance with the Group Accounting Policies and Procedures Manual.

1.10.1.1 All revenue is recognised in line with the Group Accounting Policies and Procedures Manual. Financial Management periodically monitors compliance with these policies.

1.10.1.2 All client contracts/agreements clearly define relevant sales terms. Management monitors compliance with these sales terms.

1.10.1.3 Invoices raised and revenue recorded are reviewed at, before and after accounting period ends to ensure they are recorded within the correct period.

1.10.1.4 Management performs budget to actual and prior year reviews for sales related accounts (sales, cost of sales, accounts receivable, inventory) each period end. Any significant unusual relationships are investigated and any required corrections made in a timely manner.

1.10.1.5 Sales related taxes are calculated based on client data within the client master file.

Notes

See also section 1.10 regarding accounts receivables and provisions for bad and doubtful debts.

1.11 Client master file

1.11.1

Access to the client master file is appropriately restricted and maintenance access is segregated from transaction processing.

1.11.1.1 The ability to view and modify the client master file is restricted to only necessary and authorised personnel. These personnel do not have the ability to enter sales credit notes and / or accounting transactions.

1.11.1.2 Access rights are reviewed periodically by management, and access rights withdrawn where required.

1.11.2

All changes to the client master file are valid, approved and accurately input in a timely manner.

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

1 Revenue, page 13 of 13

1.11.2.1 Changes to the client master file are approved by management and documentation supporting the change exists and is retained. All changes are made accurately and on a timely basis.

1.11.2.2 Change reports for the client master file are periodically reviewed against supporting documentation to ensure changes made are appropriate.

1.11.3

The client master file is reviewed by management.

1.11.3.1 Data within the client master file is regularly reviewed by management for accuracy and appropriateness. This includes review of client credit terms and discounts to highlight any non-standard terms. Any non-standard terms identified are investigated and resolved.

Compass Group PLC – Internal Controls Manual - version 2.0 October 2007

2 Expenditure, page 1 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2. Expenditure Approval Version control Approved by: Andrew Martin, Group Finance Director

DATE October 2007

Version 2.0

Section contents

Application of controls 1 2.1 General 2 2.2 Selection and evaluation of suppliers 3 2.3 Purchasing: overhead and capital expenditure 5 2.4 Purchasing: consumables and food expenditure 6 2.5 Goods received and processing accounts payable 7 2.6 Processing payments 10 2.7 Maintaining product / supplier master file 12 2.8 Purchasing discounts 13

Application of controls guidance

Company level Application of controls

Group All controls are applied by Group expenditure functions, excluding 2.4 and 2.6.

Group should provide guidance on the operation of these controls.

Operating Companies / Countries

All controls are applied by Operating Companies / Countries, excluding 2.4 and 2.8.

Operating Companies / Countries should provide guidance on the operation of these controls to Units.

Units Unit personnel should perform all relevant controls, excluding 2.6 to 2.8.

Expenditure, page 2 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2

2.1. General

2.1.1

Expenditure processes are clearly defined and communicated. Processes cover all types of expenditure from cost of sales, to general expenses (administration, professional fees, marketing, outsourcing contracts) and capital expenditure.

2.1.1.1 Documented policies and procedures / defined processes are in place for the expenditure functions. These include:

• Supplier selection and evaluation procedures

• Purchase approval process (including approval limits)

• Recording of accounts payable

• Payment initiation and authorisation procedures

• Accounting for accruals and pre-payments

• Procedures for recognising purchasing discounts

• Credit note and adjustment authorisation procedures

These policies and procedures / processes are periodically reviewed and updated where required and are communicated to all relevant personnel.

2.1.1.2 Roles and responsibilities within the expenditure functions are well defined. These roles allow appropriate segregation of duties within the purchasing, goods receipt, accounts payable, payment authorisation and supplier management functions.

2.1.2.

Expenditure related systems are appropriately controlled.

2.1.2.1 Expenditure related systems are managed and controlled in line with ‘General Computer Controls’ section 10.

2.1.3.

Expenditure and purchasing income is appropriately accounted for.

2.1.3.1 Accounting for expenditure and purchasing income is performed in line with the Group Accounting Policies & Procedures Manual. Finance management reviews accounting for expenditure and purchasing income to determine whether this has been performed appropriately.

Expenditure, page 3 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2

2.2. Selection and evaluation of suppliers

2.2.1

Processes for selecting all suppliers are well defined and performed in line with company policies. Suppliers are selected in accordance with defined and approved selection criteria.

2.2.1.1 Supplier selection decisions are reviewed and approved by management to determine whether the selection steps completed are appropriate and in line with applicable policies and procedures.

2.2.1.2 The purchasing function approves and performs due diligence of all new suppliers, including supplier product quality and financial stability and appropriate ethical background checks. Due diligence is consistently performed in line with documented and approved criteria. Only suppliers who meet the criteria are selected and approved.

2.2.1.3 Expenditure policies and procedures contain adequate guidelines for selection of suppliers, including tendering processes, approved suppliers and, where applicable, use of local or unauthorised suppliers. Guidelines provide direction, either financially or by reference to expenditure type, as to which type of selection process is appropriate.

2.2.1.4 Documented policies and procedures exist in relation to tendering. These include approval of contract specifications, supplier bidding processes and procedures, tender receipt and opening procedures, selection and evaluation criteria and selection approval.

Application of these procedures is monitored by appropriate purchasing management. Any deviations from procedures require specific management approval.

2.2.2

Supply / service contracts are held with all suppliers and are appropriately authorised and entered into at arms length.

2.2.2.1 Master supply / service contracts are held for all suppliers. All contracts are documented and readily available.

2.2.2.2 All supply / service contracts are reviewed and formally approved by management prior to execution and in accordance with the Group Approvals Manual. Where applicable, contracts contain standard terms and conditions and service level agreements.

Proper authorisation (signatures) is present on all contracts.

Expenditure, page 4 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2 2.2.2.3 Any variations to existing supply / service contracts are approved

in accordance with Group Approvals Manual. This includes processes used in assessing potential liabilities related to the contract terms and conditions.

2.2.2.4 Purchasing management follows appropriate procedures to ensure that supply / service contracts are with “arms-length” entities and without apparent or actual conflicts of interest or ownership. Further reputable business practices are applied when selecting suppliers.

2.2.2.5 Supplier entertainment is declared and appropriately recorded in accordance with policies and procedures. This is reviewed by management and appropriate action taken where necessary.

2.2.3

Lists of approved products and suppliers exist and are communicated to the relevant businesses. Non-compliance with the list is appropriately monitored and investigated.

2.2.3.1 List of approved products and suppliers exist and are communicated to the relevant businesses. Only approved additions and amendments to the list are processed. Access to amend the list is restricted to authorised individuals.

Where a manual list is maintained, responsibility for communicating updates is allocated to specific individuals.

2.2.3.2 Systems are in place to monitor the use of unapproved products and suppliers. Volumes purchased are compared to those anticipated and supplier lists are regularly reviewed for unusual items. Unexpected use of unapproved products or suppliers is investigated and appropriate action taken.

2.2.3.3 Defined policies and procedures exist in relation to terminating contracts / supplier accounts. These include processes for removing suppliers from the approved supplier list, de-activating supplier accounts within the master file and appropriate reconciliation of supplier accounts to identify any outstanding receivables (e.g. rebates, credit notes).

Application of these procedures is monitored by appropriate purchasing and accounting personnel. Any deviations from procedures require specific management approval.

2.2.4

Supplier and distributor performance against contracts is monitored to ensure quality and service levels are appropriate.

2.2.4.1 Open lines of communication exist between purchasing and operations to feedback comments on supplier performance. Purchasing monitors service levels against agreements and initiates corrective action if performance does not meet expected standards.

Expenditure, page 5 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2 2.2.4.2 Contingency plans are in place to protect the business from non-

performance by key suppliers. Where possible, for instance, purchasing has agreements with alternative suppliers for each product or service.

2.2.5

The purchasing function ensures the retention of contract documentation is in line with company policy and local statutory requirements.

2.2.5.1 A record retention policy is in place that meets appropriate statutory requirements, including retention of contracts and any other relevant documentation.

Copies of all supply / service contracts and other relevant documentation are appropriately stored in line with the level of access required and the confidentiality of the contents. The purchasing function holds copies of all relevant supply / service agreements to serve as source documents against future orders and issue resolution (i.e. payment terms, prices, discounts). Significant agreements, such as those with strategic partners, are held on a central database and maintained by central purchasing.

2.3. Purchasing: overhead and capital expenditure

2.3.1

All purchases relating to overhead and capital expenditure are valid and appropriately authorised.

2.3.1.1 Criteria for making purchases are clearly defined within the purchasing policies and procedures and communicated by management.

2.3.1.2 All capital expenditure requests are reviewed and approved prior to initiating the purchase order.

Purchase requests for overhead related expenditure are reviewed against the approved budget. Specific management approval is required for non-budgeted amounts and for amounts which exceed the budget allocation from the original authorising body.

A purchase authorisation list is maintained specifying the amounts up to which individuals are authorised to approve purchases. Purchases requiring specific approvals, such as capital items, are clearly defined. Purchases are authorised in accordance with the limits specified. These limits are consistent with the Group Approvals Manual.

2.3.1.3 Purchase orders, raised as appropriate, are reviewed and approved by management prior to mailing to the supplier.

Expenditure, page 6 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2 2.3.1.4 Procurement cards used for overhead and personal expenses

have set limits and restricted purchase categories. Procurement cards are approved by specific individuals to ensure that card users are appropriate.

Appropriate management periodically reviews / authorises purchases made through procurement cards to ensure that purchases are valid and reasonable. Any unusual or significant items are investigated.

2.3.1.5 On at least a monthly basis (and more frequently as required), appropriate management performs a review of actual expenditure to budget and a sales margin review. Any unusual purchasing activity is investigated, and where necessary corrected, in a timely manner.

Where possible, individuals responsible for reviewing actual expenditure to budget and margin reviews are independent of the functions responsible for initiating and approving purchases. Access to raise purchase orders is periodically reviewed for appropriateness and changes made where necessary.

Notes

Control 2.3.1.2

Prior to approval Section 3 Fixed Assets should be followed for purchases of a capital nature.

2.4. Purchasing: consumables and food expenditure

2.4.1

All purchases of consumables and food stocks are valid and appropriately authorised. A record of purchases made is retained.

2.4.1.1 Criteria for making purchases are clearly defined within the purchasing policies and procedures and communicated by management. All purchase requests should be recorded on an order sheet or appropriate alternative prior to order approval.

2.4.1.2 Purchase requests are reviewed and approved by an appropriate level of management prior to initiating a purchase. Management check that all purchases are approved products and from authorised suppliers.

All purchases should be made inside budget or authorised limits where appropriate. Higher level authority is required for all purchases that exceed budget or authorised limits and for non approved products.

2.4.1.3 Additional levels of approval are required for purchases from

Expenditure, page 7 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2 unauthorised suppliers. Approval limits are contained within purchasing policies and procedures, including specific limits for cash purchases.

2.4.1.4 Procurement cards used for consumables and food expenditure have set limits and restricted purchase categories. Procurement cards are approved by specific individuals to ensure that card users are appropriate.

Appropriate management periodically reviews / authorises purchases made through procurement cards to ensure that purchases are valid and reasonable. Any unusual or significant items are investigated.

2.4.1.5 On at least a monthly basis (and more frequently as required), appropriate management performs a review of actual expenditure to budget and a sales margin review. Any unusual purchasing activity is investigated, and where necessary corrected, in a timely manner.

Individuals responsible for reviewing actual expenditure to budget and performing margin analysis are independent of the functions responsible for initiating and approving purchases. Where segregation cannot be maintained, additional monitoring of expenditure, such as review by higher level management, is in place.

2.5. Goods received and processing accounts payable

2.5.1

All amounts posted to accounts payable represent valid goods or services received

2.5.1.1 Goods received are matched with the original order documentation raised / purchase orders (where applicable) and delivery notes to confirm that the quantity of goods ordered agree to the quantity received. Appropriate action is taken for variances identified.

Delivery notes not matched to goods received (or other appropriate supporting documentation for services received) are investigated with the supplier concerned and resolved.

2.5.1.2 Goods received and delivery documents are agreed to invoice to confirm appropriate quantities received (and ordered as per 2.5.1.1) and appropriate prices are charged on invoices. Appropriate action is taken for variances identified.

Expenditure, page 8 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2 2.5.1.3 Unmatched invoices (for example invoices for services) require

specific management approval prior to being processed. Any unauthorised, unmatched invoices are reviewed and appropriate action taken.

2.5.1.4 Credit requests are consistently raised to reflect actual orders received when receipts do not match purchase orders; including overages, shortages and substitutions. Appropriate management monitors credit notes received against credit requests. Credit notes outstanding for long periods are investigated with the supplier.

2.5.1.5 Where applicable, invoices that cannot be matched by the system to an existing product or supplier code are placed on hold. Specific management approval is required to release these invoices.

Guidelines for the treatment of invoices on hold are contained within policies and procedures, including appropriate use of one-time product / supplier accounts and appropriate use of new product / supplier accounts. The application of these procedures and the use of one-time product / supplier accounts are monitored by appropriate management.

2.5.1.6 Access to create one-time product and supplier accounts is restricted to authorised individuals. Use of one time product or supplier accounts is restricted and appropriate authorisation is required for use of these accounts. One time product and supplier accounts are periodically reviewed for usage and any repeat usage is highlighted and appropriate action taken.

2.5.1.7 Prices included on invoices are checked (either manually or electronically) against an approved price list (or contract price) prior to authorisation.

2.5.2

Amounts posted to accounts payable are recorded in the proper accounting period.

2.5.2.1 Supplier invoices, goods received and credit notes received at, before, or after the end of the accounting period are scrutinised and / reconciled to ensure complete and consistent recording in the appropriate accounting period.

2.5.2.2 Cost centre / unit management compares actual expenditure versus budget and margins for reasonableness and to ensure that expenditure is charged to the correct cost centre / unit code. Any significant variances are investigated and appropriate action taken.

2.5.2.3 Statements received from key suppliers are reconciled periodically to the supplier accounts in the accounts payable sub-ledger. All significant differences are investigated and resolved in a timely manner.

Expenditure, page 9 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2 2.5.2.4 The general ledger accounts payable balance is reconciled to the

accounts payable sub-ledger on a monthly basis and reviewed by appropriate management. All reconciling items are reviewed and corrected in a timely manner.

2.5.3

All credit notes and other adjustments to accounts payable are valid, approved and recorded in the appropriate period.

2.5.3.1 Management reviews and approves credit notes, adjustments and non-systematic debits (e.g., originating from sources other than a payments journal) prior to posting to accounts payable. Credit notes are matched to the credit note request, and where applicable pick-up notes, to ensure that credit received is accurate.

2.5.3.2 A periodic review of non-systematic debit balances is performed by appropriate personnel. Journals to clear debit balances require approval from appropriate management prior to posting.

2.5.4

All costs recorded in the period are properly classified in the appropriate financial statement account (i.e. Pre-payments, Accruals, Accounts Payables) based on payment date and the nature of the underlying expense.

2.5.4.1 Outstanding commitments, including goods receipt notes and unposted invoices, are reviewed at month end and accrued as appropriate.

2.5.4.2 On at least a monthly basis (and more frequently as required), reconciliations of prepaid expense and accrued expense accounts are performed and reviewed by management for accuracy.

2.5.5

Appropriate segregation of duties exists between the recording, approval and reconciliation functions related to accounts payable.

2.5.5.1 Individuals responsible for performing the physical receiving of goods do not have access to record goods received or invoices. A periodic review of user access rights is performed for appropriateness, and any necessary changes to access rights are performed on a timely basis.

2.5.5.2 Individuals responsible for reconciling accounts payable sub-ledgers to supplier statements are independent of the purchasing, recording, receiving and payment functions. A periodic review of user access rights is performed for appropriateness, and any necessary changes to access rights are performed on a timely basis.

Expenditure, page 10 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2 2.5.5.3 Purchase initiation, recording and approval functions are

adequately segregated from payment initiation, payment and approval functions. A periodic review of user access rights is performed for appropriateness, and any necessary changes to access rights are performed on a timely basis.

Notes

Adequate and appropriate justification should be provided if controls 2.5.1.1, 2.5.1.2 and 2.5.1.3 are not in place.

2.6. Processing payments

2.6.1

All payments are valid, authorised, paid to appropriate suppliers and recorded in the appropriate period.

2.6.1.1 Payment processes are well defined and performed in line with company policies. Processes include electronic and manual payment methods, unusual transactions and special payments. Management ensure processes are being performed appropriately.

2.6.1.2 The accounts payable system automatically identifies approved / matched invoices that are due for payment and creates a ‘payment run’ file. Where systems do not perform the above function invoices are manually reviewed to determine whether they are due for payment and a payment list of invoices is created.

2.6.1.3 Payments are made only against approved processed invoices.

Invoices and supporting documentation are marked appropriately and filed once payment is made to prevent reuse.

2.6.1.4 Payments are made on a timely basis and take advantage of any prompt payment discounts where beneficial.

2.6.1.5 Specific approval is required for special payments (as defined with Group Approvals Manual), unusual transactions and payments that exceed established limits, for example early payment requests.

2.6.1.6 Appropriate management reviews a listing of supplier payments prior to release. Any significant or unusual payments are reviewed against supporting documentation and for appropriate authorisation.

Expenditure, page 11 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2 2.6.1.7 Reviews are performed and appropriate approvals obtained for

suppliers requiring pre-payments. Pre-payments are recorded against the specific suppliers concerned.

2.6.1.8 Direct debits and other standing orders are reviewed at least annually. Mandates which are no longer required are promptly cancelled and investigations into potential over-payments are performed where appropriate. Any amendments to mandates are formally approved in accordance with Group Approvals Manual.

2.6.1.9 An aged creditors listing is periodically produced and reviewed by management. Any unusual items or old outstanding items are investigated and resolved.

2.6.2

Adequate control is maintained over payment related assets.

2.6.2.1 Cheques and other methods of payment are sequentially pre-numbered; the sequence of processed items is accounted for and the spoiled cheques are voided to prevent reuse and filed for subsequent inspection.

2.6.2.2 Cash and cheque stock is held securely and is accessible only to specifically authorised personnel.

2.6.2.3 Petty cash vouchers are issued for all cash taken for purchases. Vouchers are held in the safe until receipts are received, vouchers are reconciled to the actual purchase cost and any additional payments / re-payments are made.

All cash purchases are supported by receipts. Any exceptions require specific management approval.

2.6.2.4 Authorisation levels for signing cheques and executing electronic funds transfers are documented within local policies and are specified within bank mandates.

Individuals who sign cheques and execute electronic fund transfers are authorised to do so.

Management periodically reviews returned paid cheques for unauthorised signatures, alterations, and/ or endorsements.

(See Treasury section for further payment controls).

2.6.2.5 Total approved payment balance created within applicable banking systems is agreed to any bank confirmations received and variances are discussed with the bank and appropriate actions taken where necessary.

2.6.3

Appropriate segregation of duties exists between the recording, approval and reconciliation process related to payments.

2.6.3.1 Individuals responsible for the payment creation function are independent of payment approvals.

Expenditure, page 12 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2 2.6.3.2 Individuals responsible for the reconciliation of accounts payable

information to supplier statements are independent of the payment creation and approval functions. A periodic review of user access rights is performed for appropriateness, and any necessary changes to access rights are performed on a timely basis.

2.7. Maintaining product / supplier master file

2.7.1

All changes to product / supplier master file are valid, complete and accurately input in a timely manner. Product / supplier master file data remains accurate and access to the master files is restricted to authorised personnel.

2.7.1.1 Requests to change the product / supplier master file are documented on standard forms accompanied by appropriate supporting documentation (for example contracts, letters from suppliers requesting changes to bank details or address).

All change requests are reviewed for validity and authorised by appropriate individuals.

2.7.1.2 Changes to the product / supplier master file are reported and compared to authorised source documents to ensure that they were input accurately.

2.7.1.3 Requests to change the product / supplier master file are logged; the log is reviewed to ensure that all requested changes are processed on a timely basis.

2.7.1.4 Edit-change reports for the supplier master file are periodically reviewed and changes to the supplier master file are agreed to supporting documents. Any unusual / unsupported items are investigated and appropriate action taken. Review of edit-change reports is appropriately segregated and performed by an individual without access to the supplier master file.

2.7.1.5 The product and supplier master file are reviewed periodically by management for accuracy and appropriateness. Review of the supplier master file includes a review of payment terms to highlight supplier terms that do not conform to the expected payment terms documented within company policy.

Any duplicate or unused accounts (i.e. any accounts not used for a period specified by management) are de-activated or removed.

2.7.1.6 Management periodically reviews access reports to the product / supplier master file to ensure it is limited to authorised individuals. Access is password protected and passwords expire.

Expenditure, page 13 of 13

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

2 2.7.1.7 Adequate segregation of duties is maintained between supplier

master file maintenance and supplier selection, approval and management functions. A periodic review of user access rights is performed for appropriateness, and any necessary changes to access rights are performed on a timely basis.

2.7.1.8 Individuals responsible for supplier master file maintenance do not have access to purchasing functions. A periodic review of user access rights is performed for appropriateness, and any necessary changes to access rights are performed on a timely basis.

2.8. Purchasing discounts

2.8.1

Purchasing discounts are accounted for in line with the Group Accounting Policies Manual.

2.8.1.1 Purchasing discounts are accounted for in accordance with Group Accounting Policies and Procedures Manual. Appropriate management reviews the recording of purchasing discounts to ensure consistency with these policies and procedures.

2.8.1.2 Appropriate intra company entries are made in both party's accounts for purchasing discounts collected from a central buying function. Procedures for recording; reconciliation and elimination of balances are performed in line with the Group Accounting Policies and Procedures Manual.

2.8.1.3 Management reviews whether all expected purchase discounts are received. Any purchase discounts not received are communicated and followed up with the relevant supplier.

2.8.1.4 Management should review the movements in purchasing discounts by understanding the cause of change.

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

3. Fixed Assets Approval Version control Approved by: Andrew Martin, Group Finance Director

DATE October 2007

Version 2.0

Section contents

Application of controls 1 3.1 General 2 3.2 Acquisition of fixed assets 3 3.3 Use & maintenance of fixed assets 3 3.4 Disposals 4 3.5 Recording of fixed assets & managing of fixed asset register 4 3.6 Depreciation and amortisation 5 3.7 Fixed asset security 6 3.8 Leased assets 6 3.9 Intangible assets and goodwill 7

Application of controls

Company level Application of controls

Group All controls are applied by appropriate Group personnel.

Group should provide guidance on the operation of these controls.

Operating Companies / Countries

All controls should be applied by appropriate Operating Companies / Countries.

Operating Companies / Countries should provide guidance to units on the operation of these controls.

Units Unit personnel should perform section 3.7

Fixed Assets, page 2 of 7

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

3

3.1 General

3.1.1

Fixed asset processes are clearly defined and communicated.

3.1.1.1 Documented policies and procedures / defined processes are in place for the management of fixed assets these include:

• Acquisitions

• Use and maintenance of assets

• Disposals

• Asset specific policies and procedures for

o Physical assets

o Investments

o Intangibles

o Goodwill

o Leases

These policies and procedures / processes are periodically reviewed and updated where required and are communicated to all relevant personnel.

3.1.1.2 Roles and responsibilities for managing fixed assets are well defined. These roles provide appropriate segregation of duties.

3.1.2

Fixed asset management systems are appropriately controlled.

3.1.2.1 Fixed asset management systems are managed and controlled in line with ‘General Computer Controls’ section 10.

3.1.3

Fixed assets are appropriately accounted for.

3.1.3.1 Accounting for fixed assets is in line with the Group Accounting Policies and Procedures Manual. Finance management reviews accounting for fixed assets to determine whether this has been performed appropriately.

Fixed Assets, page 3 of 7

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

3

3.2 Acquisition of fixed assets

3.2.1

Capital expenditure is valid and approved.

3.2.1.1 Appropriate analysis of any capital expenditure is performed including pre-acquisition due diligence and analysis of all associated costs. Legal, accounting, treasury, human resource and tax departments, as applicable to the acquisition, are involved in the due diligence process.

Capital expenditure requests are reviewed against any supporting documentation, business cases or due diligence, assessed for appropriateness and authorised in line with Group Approvals Manual.

3.2.1.2 Capital expenditure invoices are approved in line with the Group Authorities Manual. Invoices are reviewed against initial authorisation of spend and any other appropriate supporting documentation prior to approval. Accruals are only raised for items that are received but not yet invoiced.

3.2.1.3 Management compares actual spending versus approved expenditure requests for reasonableness. Any unusual items are promptly reviewed and resolved as required.

3.2.1.4 Management monitors compliance with all significant policies concerning fixed assets. All exceptions to fixed asset policies and procedures noted are raised to the appropriate level within the Operating Company / Division or Group and pursued to proper resolution.

3.2.1.5 Where applicable, work in progress balances are reconciled to appropriate supporting documentation and unusual items are properly resolved. Processes are in place to transfer assets out of work in progress on completion in a timely manner.

3.3 Use & maintenance of fixed assets

3.3.1

Records of fixed asset maintenance requirements and activities are accurately retained.

3.3.1.1 Where applicable asset maintenance schedules are prepared, updated and monitored by management. Activity per the asset maintenance schedule is reviewed against the asset maintenance

Fixed Assets, page 4 of 7

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

3 history regularly to determine whether required maintenance has been performed.

3.3.1.2 Where applicable asset usage and maintenance requirements are periodically reviewed and updated to determine whether these requirements have changed.

3.4 Disposals

3.4.1

Disposals are appropriately authorised.

3.4.1.1 Disposals are made following a thorough review of options, and assessment of impact on results, cash flow and Return on Capital Employed (ROCE) of the business. The outcome of this review is assessed and the disposal decision is approved by appropriate management as defined by the Group Approvals Manual. A disposal form should be completed promptly and sent to appropriate personnel in the fixed asset function.

3.4.2

Profit or loss on disposal is appropriately calculated and the disposal is appropriately recorded.

3.4.2.1 Gains and losses are calculated and accounted for in accordance with Group Accounting Policies and Procedures Manual. Calculation and accounting is independently verified prior to being recorded.

3.5 Recording of fixed assets & managing of fixed asset register

3.5.1

All fixed assets are appropriately and accurately recorded. All changes to the fixed asset register are valid.

3.5.1.1 A fixed asset register is maintained & periodically reviewed for accuracy and reasonableness by management.

3.5.1.2 Changes made to the fixed asset register are approved by management. Changes made are checked against source documentation for accuracy.

3.5.1.3 The fixed asset register is reconciled to the General Ledger on a monthly basis. Reconciling items are investigated and corrected.

Fixed Assets, page 5 of 7

Compass Group PLC – Internal Controls Manual version 2.0 October 2007

3 Reconciliations are independently reviewed by management.

3.5.1.4 Individuals with access to amend the fixed asset register are independent of the purchasing functions. This access is periodically reviewed by management for appropriateness.

3.5.1.5 Fixed asset counts (from both register to asset and asset to register) are carried out periodically on significant / moveable assets and reconciled to the fixed asset register and any discrepancies are investigated and corrected.

3.5.1.6 Any unused fixed assets identified by management are reviewed on the fixed asset register and their value written down accordingly.

3.5.1.7 Ownership of fixed assets is identified when entering a site i.e. whether these belong to Compass or to the client. This is agreed in writing with the client and appropriate entries made to the general ledger and fixed asset register.

3.6 Depreciation and amortisation

3.6.1

Depreciation and amortisation charges are valid and accurate.

3.6.1.1 Depreciation and amortisation lives are periodically reviewed to determine whether they are appropriate and in line with Group Accounting Policies and Procedures Manual.

3.6.1.2 Depreciation and amortisation charges and calculation methods are periodically reviewed by management to ensure that they are reasonable and in accordance with the Group Accounting Policies and Procedures Manual. Overall charges are subject to an independently performed reconciliation monthly.

3.6.2