Comparative Value Chain and Economic Analysis of...

55

119 IV. Comparative Value Chain and Economic Analysis of the Leather Shoe Sector (Sheepskin Loafers) in Ethiopia, Tanzania, Zambia, China and Vietnam 47 47 Although no leather casual or fashion shoes are manufactured in Zambia (only leather workboots and children‘s school shoes are manufactured in Zambia – all are cowhide), Zambian leather and leather products sectoral information is included in this chapter.

Transcript of Comparative Value Chain and Economic Analysis of...

119

IV. Comparative Value Chain and Economic

Analysis of the Leather Shoe Sector (Sheepskin

Loafers) in Ethiopia, Tanzania, Zambia, China

and Vietnam47

47

Although no leather casual or fashion shoes are manufactured in Zambia (only leather workboots and

children‘s school shoes are manufactured in Zambia – all are cowhide), Zambian leather and leather

products sectoral information is included in this chapter.

120

IV.1. Leather Products Analysis: Objectives

The purpose of the leather products analysis is to assess the current competitiveness of

the subsector. To do this, a typical product (sheepskin leather loafer) is analyzed in the

following manner:

Examine important issues and trends in the world leather products market;

Review the structures of the Ethiopian, Tanzanian, Zambian, Chinese and

Vietnamese leather goods markets;

Assess the key features, strengths and weaknesses of the existing supply chains

for leather products in Ethiopia, Tanzania, Zambia, China and Vietnam;

Assess the overall economic efficiency of domestic leather products production in

relation to world prices (based primarily on prices in China, a leading exporter of

leather shoes) using alternative cost projection scenarios to establish current and

medium term competitiveness;

Taking the economic efficiency result as a starting point, analyze the leather

products (loafers) value chain to identify key strengths, weaknesses and

opportunities or needs for investment, expansion or contraction to maintain and

increase leather products productivity and competitiveness at the business

strategy and business process level; and

Provide possible policy options and recommendations to help stimulate growth

and improve competitiveness in the sector.

IV.2. Product Selection Method

Following a review of the first product screening in which 40 products were selected for

consideration for the value chain analysis and feasibility study, the World Bank (WB)

and Global Development Solutions (GDS)/HQ teams immediately agreed on seven out of

the ten products needed for the analysis. The seven products selected by the teams were

as follows:

1. Apparel:

a. Polo shirt; and

b. Underwear

2. Agribusiness:

a. Milk; and

b. Wheat milling

3. Leather:

a. High-end sheepskin loafers

4. Wood:

121

a. Windows/French windows and frames

5. Metal:

a. Padlocks.

To finalize the selection of the remaining products from the wood, metal and leather

sectors, based on the Africa Competitiveness: Phase 1.1 - Preliminary Product Screening

in Ethiopia report (July 2010), the WB and GDS/HQ teams chose six products as

potential candidates to be included in the list of the final ten products to be the target

products for the value chain analysis and feasibility study. The six products included the

following:

1. Wood products:

a. Wooden doors; and

b. Wooden chairs (not upholstered).

2. Leather products:

a. Leather golf gloves; and

b. Sports footwear of leather.

3. Metal products:

a. Metal doors, window-frame (security window frame); and

b. Aluminum doors and windows.

In order to screen the final six products, a product screening survey was developed which

revolved around six factors:

1. Whether these products are currently produced by companies with less than

50 employees;

2. If companies identified in #1 above can be set up with less than US$100,000

in investment capital;

3. The minimum level of skills and know-how required to produce the products;

4. Whether the products produced by the companies in #1 are being exported;

5. Whether products produced by companies in #1 are consolidated by brokers

or other intermediaries for exports; and

6. Whether companies identified in #1 can readily access raw material inputs in

the market to produce the products.

These questions were posed to the wood, metal and leather sector associations in both

China and Vietnam. Following interviews with sector associations, additional interviews

were conducted at the firm level to identify specifically the level of investments and

minimum level of technical skills required for an entrepreneur or existing SMEs to set up

a production operation. These questions were posed to existing operators in China and

Vietnam to identify whether:

122

Barriers to market entry, particularly from a financial and skills

requirement, were sufficiently low to allow entrepreneurs and SMEs in

Ethiopia to easily establish operations; and

These products are currently being produced by SMEs in China and

Vietnam, and are effectively being sold in local and export markets.

The product screening survey identified the following products as viable candidates to be

targeted for the value chain and feasibility analysis.

1. Wood product:

a. Wooden chairs (soft wood); and

b. Wooden door (semi-solid).

Although French windows and their frames made of wood had originally been

preselected for analysis, a decision was made to opt to analyze both wooden

chairs and wooden doors. This decision stemmed from the fact that French

windows require glass thus introducing an outside factor that could influence

the manufacturing of the final product. Wooden doors (without glass) and

wooden chairs (without upholstery) are more representative of wood

processing exclusively.

2. Leather products: Leather golf gloves or sports glove of comparable structure

and weight.

3. Metal products: Both the pre-selected products (security window frame; and

aluminum doors and windows) were screened out of the selection due to

various factors including high initial investment requirements. As a result,

further analyses of products identified during the preliminary product

screening were conducted. Interviews with metal sector associations and

enterprises currently operating in China and Vietnam, as well as interviews

with existing operators in the fabricated metal products sector in Ethiopia

identified crown corks (bottle caps) as a viable candidate to be targeted for

value chain analysis. Crown corks currently are produced in four of the five

countries, but Ethiopia continues to import substantial volumes of this product,

including imports from China. As a result, crown corks have been chosen as

the final fabricated metal product to be the focus of a value chain analysis in

all target countries.

123

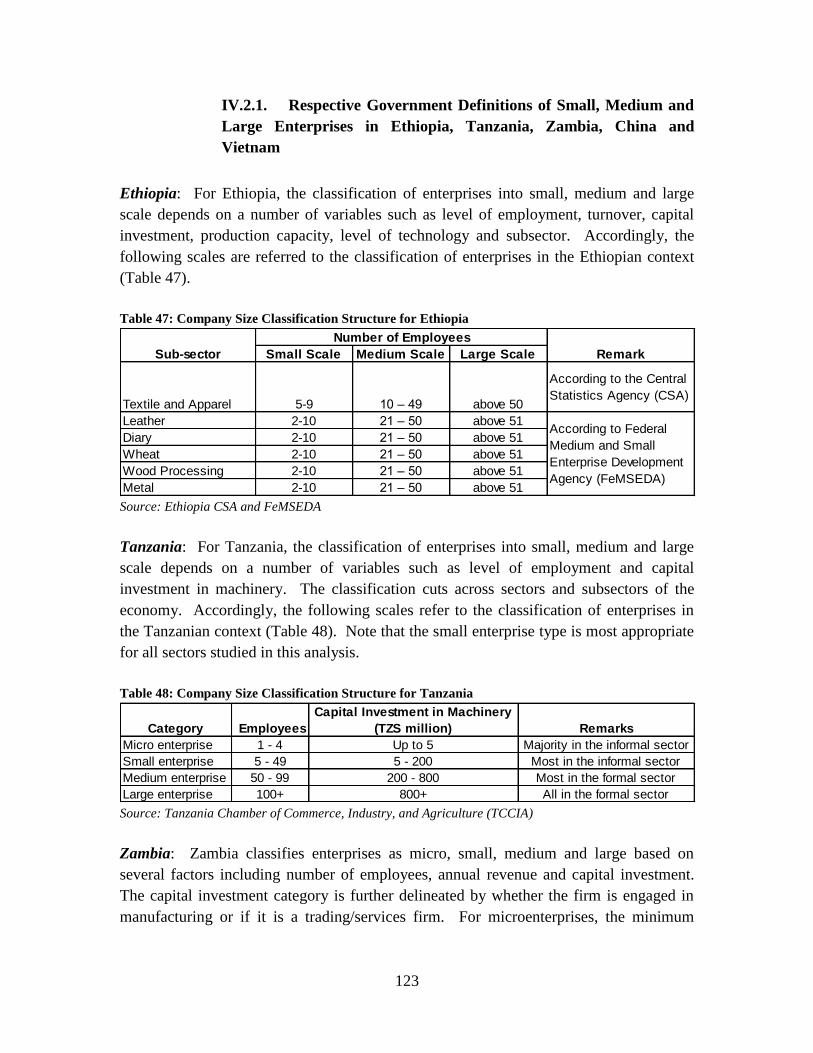

IV.2.1. Respective Government Definitions of Small, Medium and

Large Enterprises in Ethiopia, Tanzania, Zambia, China and

Vietnam

Ethiopia: For Ethiopia, the classification of enterprises into small, medium and large

scale depends on a number of variables such as level of employment, turnover, capital

investment, production capacity, level of technology and subsector. Accordingly, the

following scales are referred to the classification of enterprises in the Ethiopian context

(Table 47).

Table 47: Company Size Classification Structure for Ethiopia

Small Scale Medium Scale Large Scale

Textile and Apparel 5-9 10 – 49 above 50

According to the Central

Statistics Agency (CSA)

Leather 2-10 21 – 50 above 51

Diary 2-10 21 – 50 above 51

Wheat 2-10 21 – 50 above 51

Wood Processing 2-10 21 – 50 above 51

Metal 2-10 21 – 50 above 51

According to Federal

Medium and Small

Enterprise Development

Agency (FeMSEDA)

Sub-sector Remark

Number of Employees

Source: Ethiopia CSA and FeMSEDA

Tanzania: For Tanzania, the classification of enterprises into small, medium and large

scale depends on a number of variables such as level of employment and capital

investment in machinery. The classification cuts across sectors and subsectors of the

economy. Accordingly, the following scales refer to the classification of enterprises in

the Tanzanian context (Table 48). Note that the small enterprise type is most appropriate

for all sectors studied in this analysis.

Table 48: Company Size Classification Structure for Tanzania

Category Employees

Capital Investment in Machinery

(TZS million) Remarks

Micro enterprise 1 - 4 Up to 5 Majority in the informal sector

Small enterprise 5 - 49 5 - 200 Most in the informal sector

Medium enterprise 50 - 99 200 - 800 Most in the formal sector

Large enterprise 100+ 800+ All in the formal sector Source: Tanzania Chamber of Commerce, Industry, and Agriculture (TCCIA)

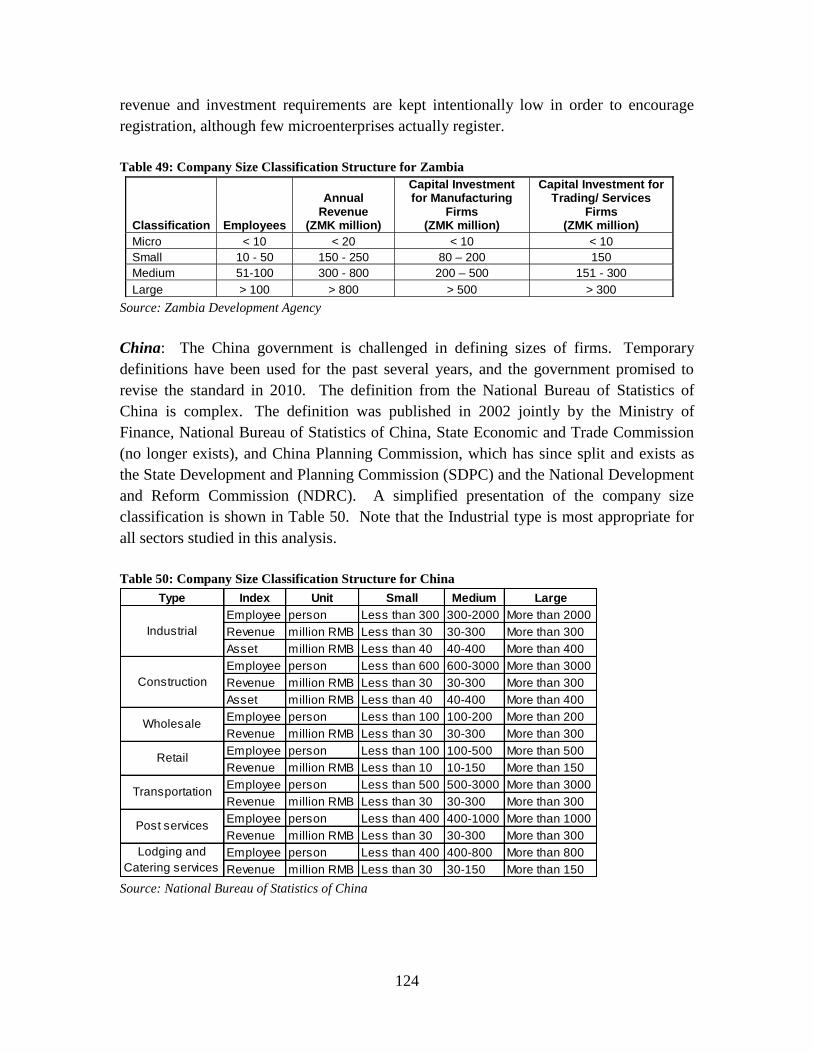

Zambia: Zambia classifies enterprises as micro, small, medium and large based on

several factors including number of employees, annual revenue and capital investment.

The capital investment category is further delineated by whether the firm is engaged in

manufacturing or if it is a trading/services firm. For microenterprises, the minimum

124

revenue and investment requirements are kept intentionally low in order to encourage

registration, although few microenterprises actually register.

Table 49: Company Size Classification Structure for Zambia

Classification Employees

Annual Revenue

(ZMK million)

Capital Investment for Manufacturing

Firms (ZMK million)

Capital Investment for Trading/ Services

Firms (ZMK million)

Micro < 10 < 20 < 10 < 10

Small 10 - 50 150 - 250 80 – 200 150

Medium 51-100 300 - 800 200 – 500 151 - 300

Large > 100 > 800 > 500 > 300

Source: Zambia Development Agency

China: The China government is challenged in defining sizes of firms. Temporary

definitions have been used for the past several years, and the government promised to

revise the standard in 2010. The definition from the National Bureau of Statistics of

China is complex. The definition was published in 2002 jointly by the Ministry of

Finance, National Bureau of Statistics of China, State Economic and Trade Commission

(no longer exists), and China Planning Commission, which has since split and exists as

the State Development and Planning Commission (SDPC) and the National Development

and Reform Commission (NDRC). A simplified presentation of the company size

classification is shown in Table 50. Note that the Industrial type is most appropriate for

all sectors studied in this analysis.

Table 50: Company Size Classification Structure for China

Type Index Unit Small Medium Large

Employee person Less than 300 300-2000 More than 2000

Revenue million RMB Less than 30 30-300 More than 300

Asset million RMB Less than 40 40-400 More than 400

Employee person Less than 600 600-3000 More than 3000

Revenue million RMB Less than 30 30-300 More than 300

Asset million RMB Less than 40 40-400 More than 400

Employee person Less than 100 100-200 More than 200

Revenue million RMB Less than 30 30-300 More than 300

Employee person Less than 100 100-500 More than 500

Revenue million RMB Less than 10 10-150 More than 150

Employee person Less than 500 500-3000 More than 3000

Revenue million RMB Less than 30 30-300 More than 300

Employee person Less than 400 400-1000 More than 1000

Revenue million RMB Less than 30 30-300 More than 300

Employee person Less than 400 400-800 More than 800

Revenue million RMB Less than 30 30-150 More than 150

Lodging and

Catering services

Industrial

Construction

Wholesale

Retail

Transportation

Post services

Source: National Bureau of Statistics of China

125

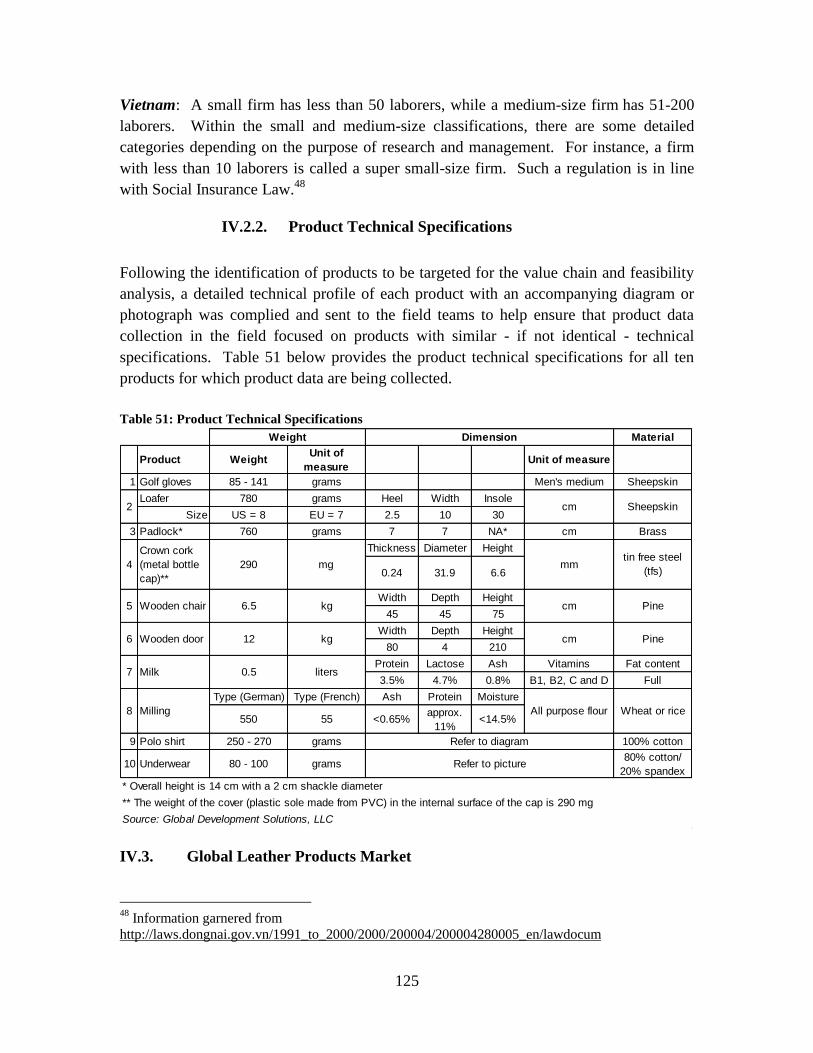

Vietnam: A small firm has less than 50 laborers, while a medium-size firm has 51-200

laborers. Within the small and medium-size classifications, there are some detailed

categories depending on the purpose of research and management. For instance, a firm

with less than 10 laborers is called a super small-size firm. Such a regulation is in line

with Social Insurance Law.48

IV.2.2. Product Technical Specifications

Following the identification of products to be targeted for the value chain and feasibility

analysis, a detailed technical profile of each product with an accompanying diagram or

photograph was complied and sent to the field teams to help ensure that product data

collection in the field focused on products with similar - if not identical - technical

specifications. Table 51 below provides the product technical specifications for all ten

products for which product data are being collected.

Table 51: Product Technical Specifications

Material

Product WeightUnit of

measureUnit of measure

1 Golf gloves 85 - 141 grams Men's medium Sheepskin

Loafer 780 grams Heel Width Insole

Size US = 8 EU = 7 2.5 10 30

3 Padlock* 760 grams 7 7 NA* cm Brass

Thickness Diameter Height

0.24 31.9 6.6

Width Depth Height

45 45 75

Width Depth Height

80 4 210

Protein Lactose Ash Vitamins Fat content

3.5% 4.7% 0.8% B1, B2, C and D Full

Type (German) Type (French) Ash Protein Moisture

550 55 <0.65%approx.

11%<14.5%

9 Polo shirt 250 - 270 grams 100% cotton

10 Underwear 80 - 100 grams80% cotton/

20% spandex

* Overall height is 14 cm with a 2 cm shackle diameter

** The weight of the cover (plastic sole made from PVC) in the internal surface of the cap is 290 mg

Source: Global Development Solutions, LLC

Pine

Wheat or rice

Dimension

All purpose flour

cm

Refer to diagram

Weight

cm

mm

cm

tin free steel

(tfs)

Sheepskin

Pine

mg

kg

kg

liters

Refer to picture

Crown cork

(metal bottle

cap)**

Wooden chair

Wooden door

Milk

Milling

290

6.5

12

0.5

2

4

5

6

7

8

IV.3. Global Leather Products Market

48

Information garnered from

http://laws.dongnai.gov.vn/1991_to_2000/2000/200004/200004280005_en/lawdocum

126

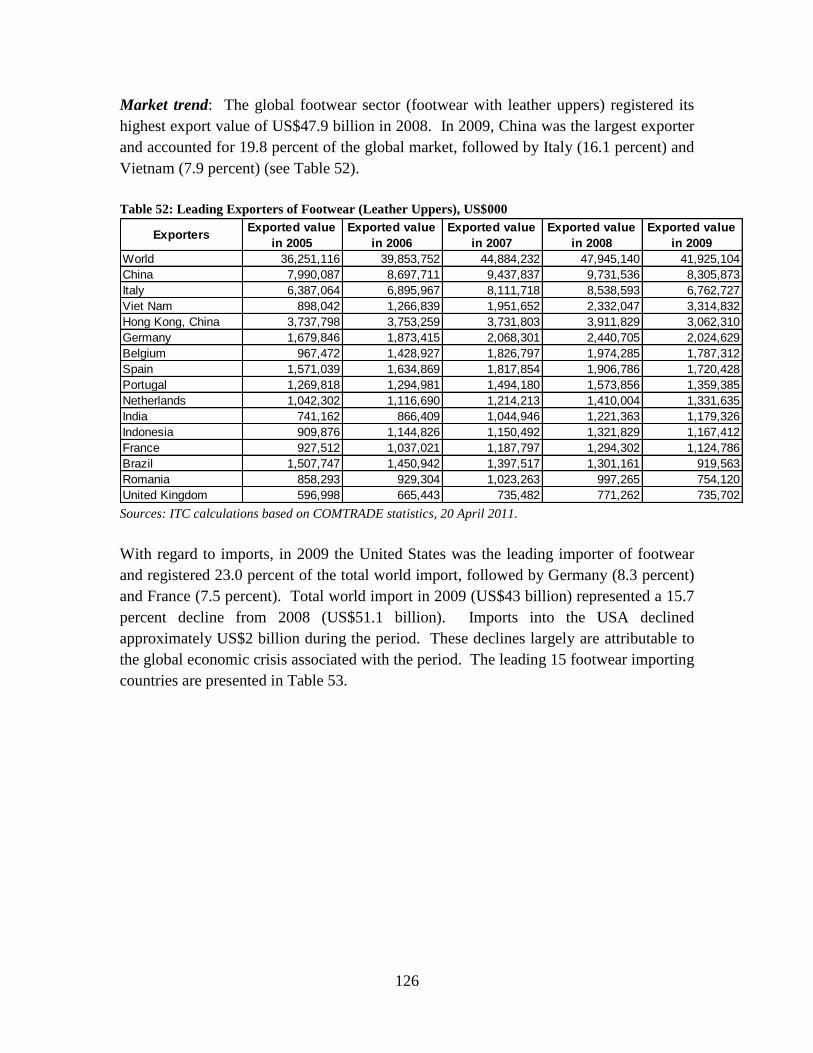

Market trend: The global footwear sector (footwear with leather uppers) registered its

highest export value of US$47.9 billion in 2008. In 2009, China was the largest exporter

and accounted for 19.8 percent of the global market, followed by Italy (16.1 percent) and

Vietnam (7.9 percent) (see Table 52).

Table 52: Leading Exporters of Footwear (Leather Uppers), US$000

ExportersExported value

in 2005

Exported value

in 2006

Exported value

in 2007

Exported value

in 2008

Exported value

in 2009

World 36,251,116 39,853,752 44,884,232 47,945,140 41,925,104

China 7,990,087 8,697,711 9,437,837 9,731,536 8,305,873

Italy 6,387,064 6,895,967 8,111,718 8,538,593 6,762,727

Viet Nam 898,042 1,266,839 1,951,652 2,332,047 3,314,832

Hong Kong, China 3,737,798 3,753,259 3,731,803 3,911,829 3,062,310

Germany 1,679,846 1,873,415 2,068,301 2,440,705 2,024,629

Belgium 967,472 1,428,927 1,826,797 1,974,285 1,787,312

Spain 1,571,039 1,634,869 1,817,854 1,906,786 1,720,428

Portugal 1,269,818 1,294,981 1,494,180 1,573,856 1,359,385

Netherlands 1,042,302 1,116,690 1,214,213 1,410,004 1,331,635

India 741,162 866,409 1,044,946 1,221,363 1,179,326

Indonesia 909,876 1,144,826 1,150,492 1,321,829 1,167,412

France 927,512 1,037,021 1,187,797 1,294,302 1,124,786

Brazil 1,507,747 1,450,942 1,397,517 1,301,161 919,563

Romania 858,293 929,304 1,023,263 997,265 754,120

United Kingdom 596,998 665,443 735,482 771,262 735,702 Sources: ITC calculations based on COMTRADE statistics, 20 April 2011.

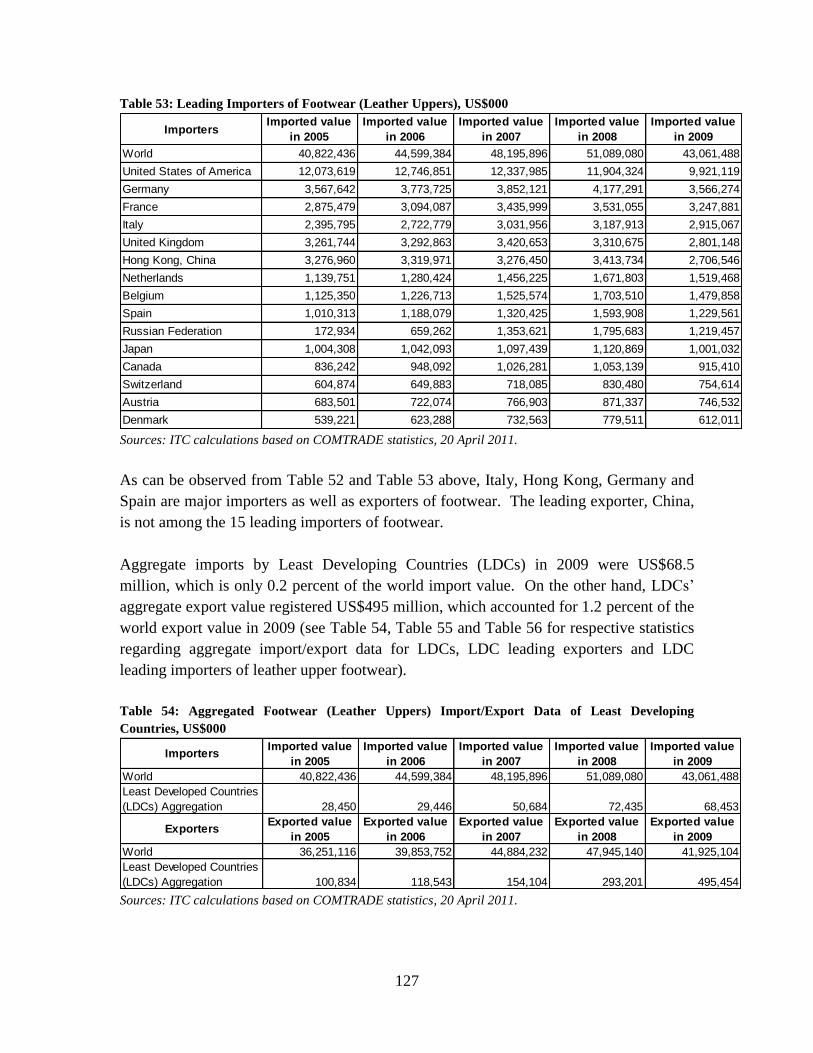

With regard to imports, in 2009 the United States was the leading importer of footwear

and registered 23.0 percent of the total world import, followed by Germany (8.3 percent)

and France (7.5 percent). Total world import in 2009 (US$43 billion) represented a 15.7

percent decline from 2008 (US$51.1 billion). Imports into the USA declined

approximately US$2 billion during the period. These declines largely are attributable to

the global economic crisis associated with the period. The leading 15 footwear importing

countries are presented in Table 53.

127

Table 53: Leading Importers of Footwear (Leather Uppers), US$000

ImportersImported value

in 2005

Imported value

in 2006

Imported value

in 2007

Imported value

in 2008

Imported value

in 2009

World 40,822,436 44,599,384 48,195,896 51,089,080 43,061,488

United States of America 12,073,619 12,746,851 12,337,985 11,904,324 9,921,119

Germany 3,567,642 3,773,725 3,852,121 4,177,291 3,566,274

France 2,875,479 3,094,087 3,435,999 3,531,055 3,247,881

Italy 2,395,795 2,722,779 3,031,956 3,187,913 2,915,067

United Kingdom 3,261,744 3,292,863 3,420,653 3,310,675 2,801,148

Hong Kong, China 3,276,960 3,319,971 3,276,450 3,413,734 2,706,546

Netherlands 1,139,751 1,280,424 1,456,225 1,671,803 1,519,468

Belgium 1,125,350 1,226,713 1,525,574 1,703,510 1,479,858

Spain 1,010,313 1,188,079 1,320,425 1,593,908 1,229,561

Russian Federation 172,934 659,262 1,353,621 1,795,683 1,219,457

Japan 1,004,308 1,042,093 1,097,439 1,120,869 1,001,032

Canada 836,242 948,092 1,026,281 1,053,139 915,410

Switzerland 604,874 649,883 718,085 830,480 754,614

Austria 683,501 722,074 766,903 871,337 746,532

Denmark 539,221 623,288 732,563 779,511 612,011 Sources: ITC calculations based on COMTRADE statistics, 20 April 2011.

As can be observed from Table 52 and Table 53 above, Italy, Hong Kong, Germany and

Spain are major importers as well as exporters of footwear. The leading exporter, China,

is not among the 15 leading importers of footwear.

Aggregate imports by Least Developing Countries (LDCs) in 2009 were US$68.5

million, which is only 0.2 percent of the world import value. On the other hand, LDCs‘

aggregate export value registered US$495 million, which accounted for 1.2 percent of the

world export value in 2009 (see Table 54, Table 55 and Table 56 for respective statistics

regarding aggregate import/export data for LDCs, LDC leading exporters and LDC

leading importers of leather upper footwear).

Table 54: Aggregated Footwear (Leather Uppers) Import/Export Data of Least Developing

Countries, US$000

ImportersImported value

in 2005

Imported value

in 2006

Imported value

in 2007

Imported value

in 2008

Imported value

in 2009

World 40,822,436 44,599,384 48,195,896 51,089,080 43,061,488

Least Developed Countries

(LDCs) Aggregation 28,450 29,446 50,684 72,435 68,453

ExportersExported value

in 2005

Exported value

in 2006

Exported value

in 2007

Exported value

in 2008

Exported value

in 2009

World 36,251,116 39,853,752 44,884,232 47,945,140 41,925,104

Least Developed Countries

(LDCs) Aggregation 100,834 118,543 154,104 293,201 495,454 Sources: ITC calculations based on COMTRADE statistics, 20 April 2011.

128

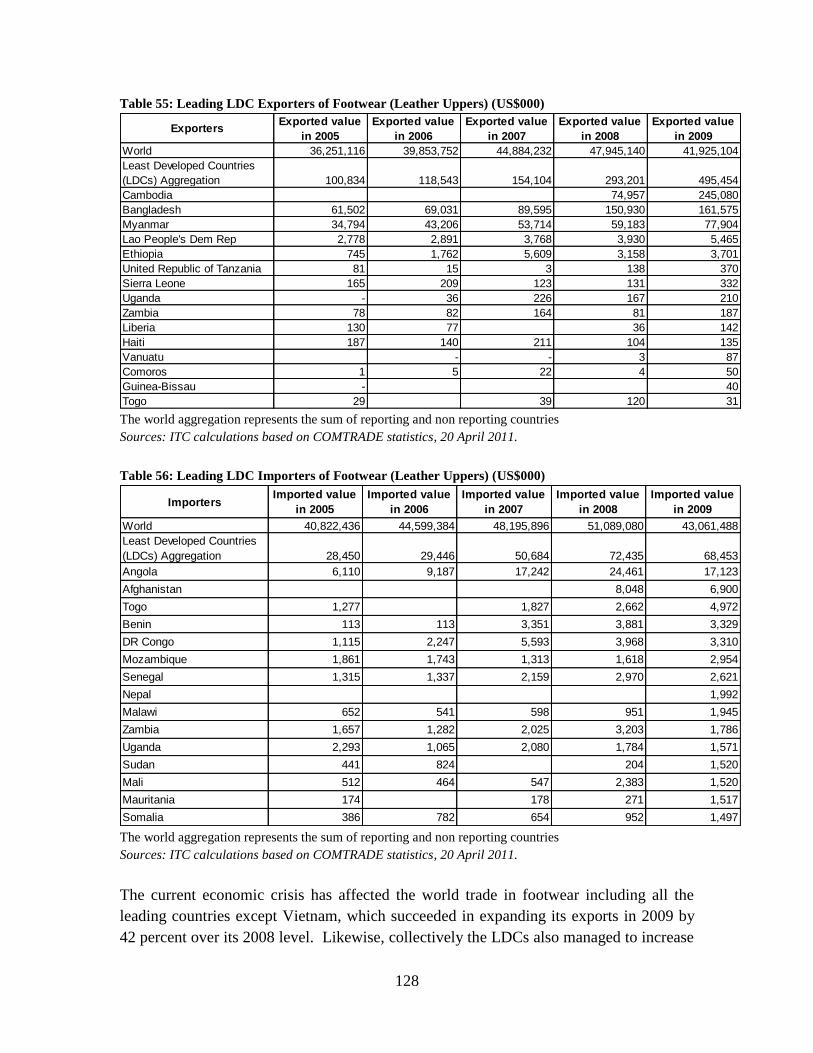

Table 55: Leading LDC Exporters of Footwear (Leather Uppers) (US$000)

ExportersExported value

in 2005

Exported value

in 2006

Exported value

in 2007

Exported value

in 2008

Exported value

in 2009

World 36,251,116 39,853,752 44,884,232 47,945,140 41,925,104

Least Developed Countries

(LDCs) Aggregation 100,834 118,543 154,104 293,201 495,454

Cambodia 74,957 245,080

Bangladesh 61,502 69,031 89,595 150,930 161,575

Myanmar 34,794 43,206 53,714 59,183 77,904

Lao People's Dem Rep 2,778 2,891 3,768 3,930 5,465

Ethiopia 745 1,762 5,609 3,158 3,701

United Republic of Tanzania 81 15 3 138 370

Sierra Leone 165 209 123 131 332

Uganda - 36 226 167 210

Zambia 78 82 164 81 187

Liberia 130 77 36 142

Haiti 187 140 211 104 135

Vanuatu - - 3 87

Comoros 1 5 22 4 50

Guinea-Bissau - 40

Togo 29 39 120 31 The world aggregation represents the sum of reporting and non reporting countries

Sources: ITC calculations based on COMTRADE statistics, 20 April 2011.

Table 56: Leading LDC Importers of Footwear (Leather Uppers) (US$000)

ImportersImported value

in 2005

Imported value

in 2006

Imported value

in 2007

Imported value

in 2008

Imported value

in 2009

World 40,822,436 44,599,384 48,195,896 51,089,080 43,061,488

Least Developed Countries

(LDCs) Aggregation 28,450 29,446 50,684 72,435 68,453

Angola 6,110 9,187 17,242 24,461 17,123

Afghanistan 8,048 6,900

Togo 1,277 1,827 2,662 4,972

Benin 113 113 3,351 3,881 3,329

DR Congo 1,115 2,247 5,593 3,968 3,310

Mozambique 1,861 1,743 1,313 1,618 2,954

Senegal 1,315 1,337 2,159 2,970 2,621

Nepal 1,992

Malawi 652 541 598 951 1,945

Zambia 1,657 1,282 2,025 3,203 1,786

Uganda 2,293 1,065 2,080 1,784 1,571

Sudan 441 824 204 1,520

Mali 512 464 547 2,383 1,520

Mauritania 174 178 271 1,517

Somalia 386 782 654 952 1,497 The world aggregation represents the sum of reporting and non reporting countries

Sources: ITC calculations based on COMTRADE statistics, 20 April 2011.

The current economic crisis has affected the world trade in footwear including all the

leading countries except Vietnam, which succeeded in expanding its exports in 2009 by

42 percent over its 2008 level. Likewise, collectively the LDCs also managed to increase

129

their exports by 69 percent over 2008 despite the global recession.

Industry and Consumer Trend: The footwear industry is increasing product value by

enhancing product functionality (e.g., making products water resistant, increasing

durability and improving comfort). Manufacturers have had to make changes to respond

quickly to fashion changes as well as become more resource efficient (e.g., minimizing

cutting wastes and using technologies that are more productive).

Notwithstanding the above, footwear is a consumer good for which consumption level

depends on population and its corresponding purchasing power. Consumption is closely

correlated with the income of people, which can be represented by per capita GDP of a

country.

Supply and Demand: As per the study conducted by United Nations Industrial

Development Organization (UNIDO),49

the lowest footwear consumption is in Africa

with 0.5 pairs/person/year, and the highest is in the USA with 7.1 pairs/person/year.

According to a conservative forecast, world shoe consumption is expected to increase to

2.5 pairs/person/year by year 2015, bringing the total world consumption to 17.2 billion

pairs, which is an increase of 4 billion pairs compared to the 2009 consumption level.

Important to note is that 55 percent of finished genuine leather produced globally is used

for footwear. According to the study by UNIDO, there is an anticipated shortage of

rawhide and skin, which suggests that there may be a shortfall of 2.4 billion pairs in the

world market by 2015. It is therefore anticipated that the scarcity of genuine leather will

result in significant price increases of finished leather goods, including leather shoes.

IV.4. Comparative Sector Profile: Leather Products Sector

Key Indicators: In Ethiopia, it is estimated that 1,000 small, eight medium-size, and six

large firms operate in the leather products sector. Approximately 5,000 people are

employed by the small firms, 800 by medium-size and 1,800 by large firms. Of the

approximately 7,600 employees working in the sector, 56 percent are male.

In Tanzania, an estimated eleven firms operate in the footwear (7) and leather products

(4) sector and employ an estimated 1,000 people, of which approximately 58 percent are

male.50

The bulk of employment (700-800 people) and export revenue (100 percent)

from the footwear sector in Tanzania is generated by two large firms that produce non-

49

Development Trends in the World Leather Products Trade, UNIDO, 2009 50

Data for Tanzania does not include micro/small enterprises employing less than 10 people. Data for such

firms, such as small workshops, repair shops, etc, are not available – an estimated 95 percent of all

manufacturing firms belong in this unrecorded category of firms.

130

leather footwear such as plastic slippers, shoes, etc. Only an estimated five small firms

produce leather footwear in Tanzania.51

In Zambia there are eight companies operating in the leather products sector, of which six

produce leather shoes.52

Three of these six companies are classified as small, two

medium-sizes and one large. Seventy-five percent of the employees are male.

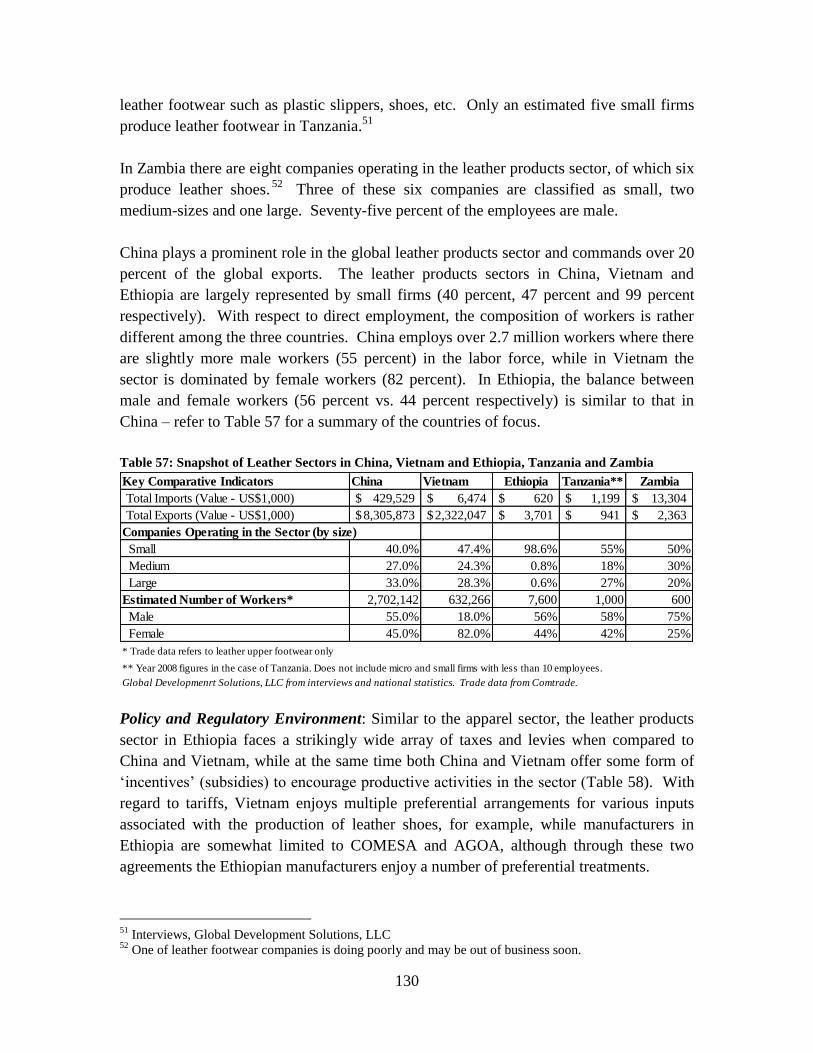

China plays a prominent role in the global leather products sector and commands over 20

percent of the global exports. The leather products sectors in China, Vietnam and

Ethiopia are largely represented by small firms (40 percent, 47 percent and 99 percent

respectively). With respect to direct employment, the composition of workers is rather

different among the three countries. China employs over 2.7 million workers where there

are slightly more male workers (55 percent) in the labor force, while in Vietnam the

sector is dominated by female workers (82 percent). In Ethiopia, the balance between

male and female workers (56 percent vs. 44 percent respectively) is similar to that in

China – refer to Table 57 for a summary of the countries of focus.

Table 57: Snapshot of Leather Sectors in China, Vietnam and Ethiopia, Tanzania and Zambia

Key Comparative Indicators China Vietnam Ethiopia Tanzania** Zambia

Total Imports (Value - US$1,000) 429,529$ 6,474$ 620$ 1,199$ 13,304$

Total Exports (Value - US$1,000) 8,305,873$ 2,322,047$ 3,701$ 941$ 2,363$

Companies Operating in the Sector (by size)

Small 40.0% 47.4% 98.6% 55% 50%

Medium 27.0% 24.3% 0.8% 18% 30%

Large 33.0% 28.3% 0.6% 27% 20%

Estimated Number of Workers* 2,702,142 632,266 7,600 1,000 600

Male 55.0% 18.0% 56% 58% 75%

Female 45.0% 82.0% 44% 42% 25%

* Trade data refers to leather upper footwear only

** Year 2008 figures in the case of Tanzania. Does not include micro and small firms with less than 10 employees.

Global Developmenrt Solutions, LLC from interviews and national statistics. Trade data from Comtrade.

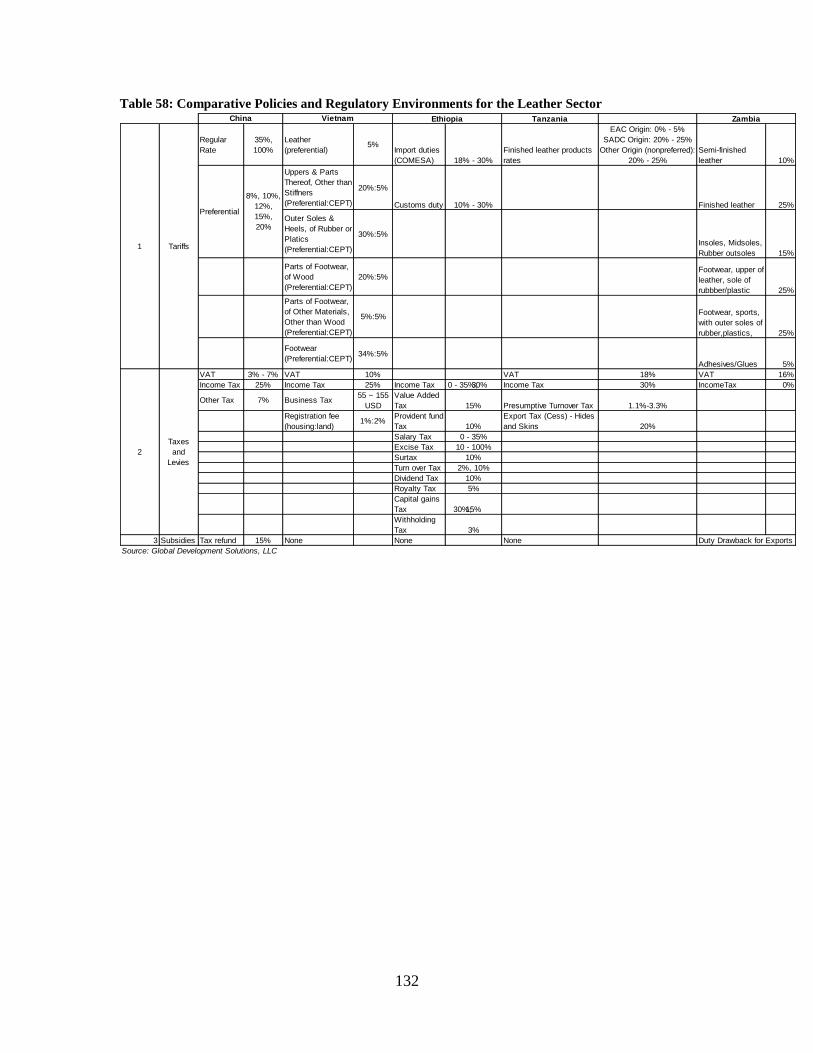

Policy and Regulatory Environment: Similar to the apparel sector, the leather products

sector in Ethiopia faces a strikingly wide array of taxes and levies when compared to

China and Vietnam, while at the same time both China and Vietnam offer some form of

‗incentives‘ (subsidies) to encourage productive activities in the sector (Table 58). With

regard to tariffs, Vietnam enjoys multiple preferential arrangements for various inputs

associated with the production of leather shoes, for example, while manufacturers in

Ethiopia are somewhat limited to COMESA and AGOA, although through these two

agreements the Ethiopian manufacturers enjoy a number of preferential treatments.

51

Interviews, Global Development Solutions, LLC 52

One of leather footwear companies is doing poorly and may be out of business soon.

131

In Tanzania, manufacturers of leather footwear and other leather products face a policy

and regulatory environment similar to most other sectors where support is limited to few

policies related to either waiving of duties and/or value added tax or providing refunds

for these taxes to exporting companies. In terms of trade policy, there is an export tax

(cess) of 20 percent on hides and skins exports from Tanzania. Similar to the export ban

on logs, however, according to interviews in the sector, the regulations are poorly

enforced and illegal export of hides and skins is pervasive. According to the managers of

some tanneries in the country, the export tax depressed hides and skins prices in the short

term (until 2006), but prices picked up soon after with the only difference that most of the

international trade in hides and skins now is through unofficial channels (largely via

Kenya).

Companies operating in the Zambia leather sector are granted zero-rated income tax. The

government encourages the export of processed leather by banning the export of

unprocessed raw hides and, further to this, wet blue exports to China are duty free.

According to a recent report by the International Trade Centre, among the non-traditional

exports (NTE), government has recognized the leather and leather products sector as a

means of increasing economic diversification and growth. Incentives such as reduced

corporate tax of 15 percent (instead of the standard 35 percent), and exemptions on duty

and sales tax on imports and machinery are offered to exporters of non-traditional

products with net foreign exchange earnings.53

The range of taxes and levies in the respective countries is provided in the table below.

53

Promoting Regional Trade in Leather and Leather Products; International Trade Centre, July 2010.

132

Table 58: Comparative Policies and Regulatory Environments for the Leather Sector Tanzania

Regular

Rate

35%,

100%

Leather

(preferential)5%

Import duties

(COMESA) 18% - 30%

Finished leather products

rates

EAC Origin: 0% - 5%

SADC Origin: 20% - 25%

Other Origin (nonpreferred):

20% - 25%

Semi-finished

leather 10%

Uppers & Parts

Thereof, Other than

Stiffners

(Preferential:CEPT)

20%:5%

Customs duty 10% - 30% Finished leather 25%

Outer Soles &

Heels, of Rubber or

Platics

(Preferential:CEPT)

30%:5%Insoles, Midsoles,

Rubber outsoles 15%

Parts of Footwear,

of Wood

(Preferential:CEPT)

20%:5%Footwear, upper of

leather, sole of

rubbber/plastic 25%

Parts of Footwear,

of Other Materials,

Other than Wood

(Preferential:CEPT)

5%:5%Footwear, sports,

with outer soles of

rubber,plastics, 25%

Footwear

(Preferential:CEPT)34%:5%

Adhesives/Glues 5%

VAT 3% - 7% VAT 10% VAT 18% VAT 16%

Income Tax 25% Income Tax 25% Income Tax 0 - 35%;30% Income Tax 30% IncomeTax 0%

Other Tax 7% Business Tax55 ~ 155

USD

Value Added

Tax 15% Presumptive Turnover Tax 1.1%-3.3%

Registration fee

(housing:land)1%:2%

Provident fund

Tax 10%

Export Tax (Cess) - Hides

and Skins 20%

Salary Tax 0 - 35%

Excise Tax 10 - 100%

Surtax 10%

Turn over Tax 2%, 10%

Dividend Tax 10%

Royalty Tax 5%

Capital gains

Tax 30%;15%

Withholding

Tax 3%

3 Subsidies Tax refund 15% None None None

Source: Global Development Solutions, LLC

Duty Drawback for Exports

1 Tariffs

China Vietnam

Preferential

8%, 10%,

12%,

15%,

20%

Ethiopia Zambia

2

Taxes

and

Levies

133

IV.5. Sector Profiles for the Leather Products Sector in Ethiopia, Tanzania,

Zambia, China, and Vietnam

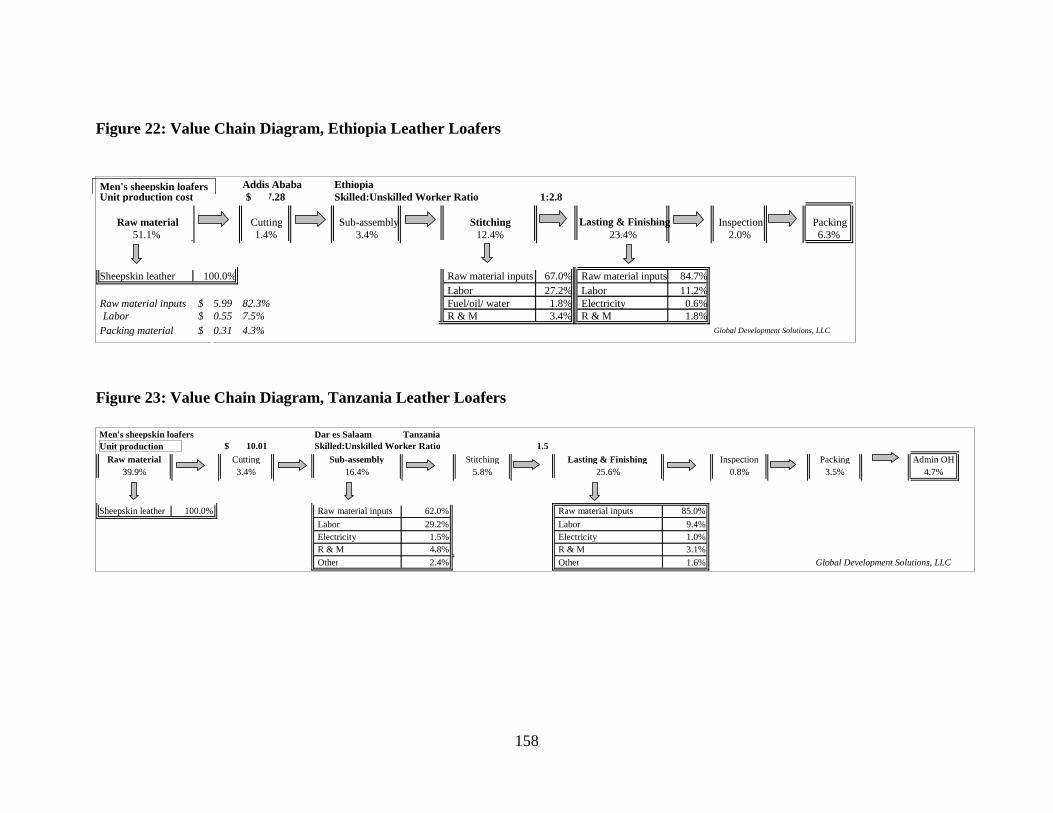

IV.5.1. Sector Profile: Leather and Leather Footwear in Ethiopia

The Ethiopian leather footwear and leather products sector accounted for 7.0 percent of

the country‘s industrial production in 2009/10. In the fiscal year 2009/2010 ending in

June 2010, the entire leather industry exported a total of US$56.5 million, which

comprised 2.8 percent of the country‘s total exports for the year.54

Key leather products

for the year were footwear, leather garments and leather goods. Major export

destinations were Italy, Germany, USA, Canada and Kenya.

From 2008 to 2009, as shown in Table 59 below, footwear experienced a significant

increase in both production volume (208 percent) and production value (more than a

fourfold increase). The dramatic rise in production from 2008 to 2009 reflects a direct

government intervention to help stimulate production in the sector through regular

meetings with the private sector, and the introduction in 2008 of a 150 percent tax on

exports on raw skins and hides, wet blue and pickled (see section IV.5.1.1 Supply Chain

and Institution Support Structure: Leather Products - Ethiopia below). In addition, the

increase reflects the entry of new manufacturers in the leather shoe industry, and a shift in

local consumer preference away from less expensive and low quality shoes from China to

a more durable locally manufactured leather shoe.

54

Ethiopia Ministry of Trade and Industry

134

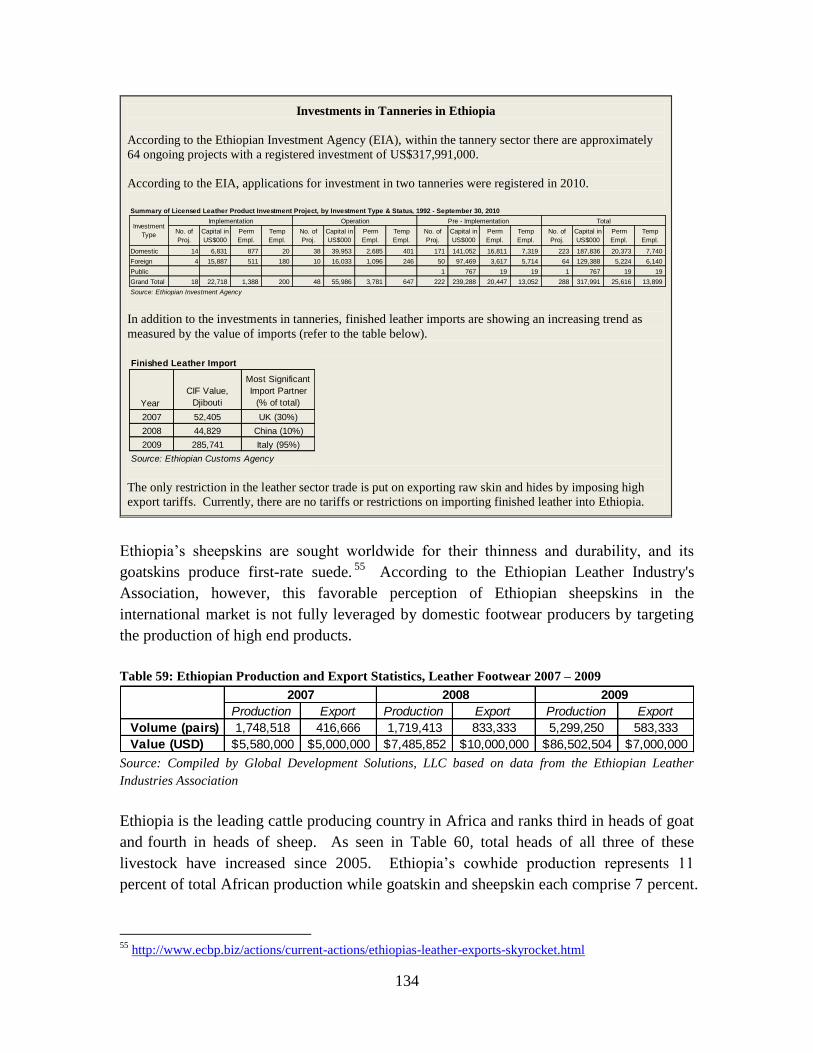

Investments in Tanneries in Ethiopia

According to the Ethiopian Investment Agency (EIA), within the tannery sector there are approximately

64 ongoing projects with a registered investment of US$317,991,000.

According to the EIA, applications for investment in two tanneries were registered in 2010.

In addition to the investments in tanneries, finished leather imports are showing an increasing trend as

measured by the value of imports (refer to the table below).

The only restriction in the leather sector trade is put on exporting raw skin and hides by imposing high

export tariffs. Currently, there are no tariffs or restrictions on importing finished leather into Ethiopia.

Summary of Licensed Leather Product Investment Project, by Investment Type & Status, 1992 - September 30, 2010

No. of

Proj.

Capital in

US$000

Perm

Empl.

Temp

Empl.

No. of

Proj.

Capital in

US$000

Perm

Empl.

Temp

Empl.

No. of

Proj.

Capital in

US$000

Perm

Empl.

Temp

Empl.

No. of

Proj.

Capital in

US$000

Perm

Empl.

Temp

Empl.

Domestic 14 6,831 877 20 38 39,953 2,685 401 171 141,052 16,811 7,319 223 187,836 20,373 7,740

Foreign 4 15,887 511 180 10 16,033 1,096 246 50 97,469 3,617 5,714 64 129,388 5,224 6,140

Public 1 767 19 19 1 767 19 19

Grand Total 18 22,718 1,388 200 48 55,986 3,781 647 222 239,288 20,447 13,052 288 317,991 25,616 13,899

Source: Ethiopian Investment Agency

Implementation Operation Pre - Implementation TotalInvestment

Type

Finished Leather Import

Year

CIF Value,

Djibouti

Most Significant

Import Partner

(% of total)

2007 52,405 UK (30%)

2008 44,829 China (10%)

2009 285,741 Italy (95%)

Source: Ethiopian Customs Agency

Ethiopia‘s sheepskins are sought worldwide for their thinness and durability, and its

goatskins produce first-rate suede.55

According to the Ethiopian Leather Industry's

Association, however, this favorable perception of Ethiopian sheepskins in the

international market is not fully leveraged by domestic footwear producers by targeting

the production of high end products.

Table 59: Ethiopian Production and Export Statistics, Leather Footwear 2007 – 2009

Production Export Production Export Production Export

Volume (pairs) 1,748,518 416,666 1,719,413 833,333 5,299,250 583,333

Value (USD) 5,580,000$ 5,000,000$ 7,485,852$ 10,000,000$ 86,502,504$ 7,000,000$

2007 2008 2009

Source: Compiled by Global Development Solutions, LLC based on data from the Ethiopian Leather

Industries Association

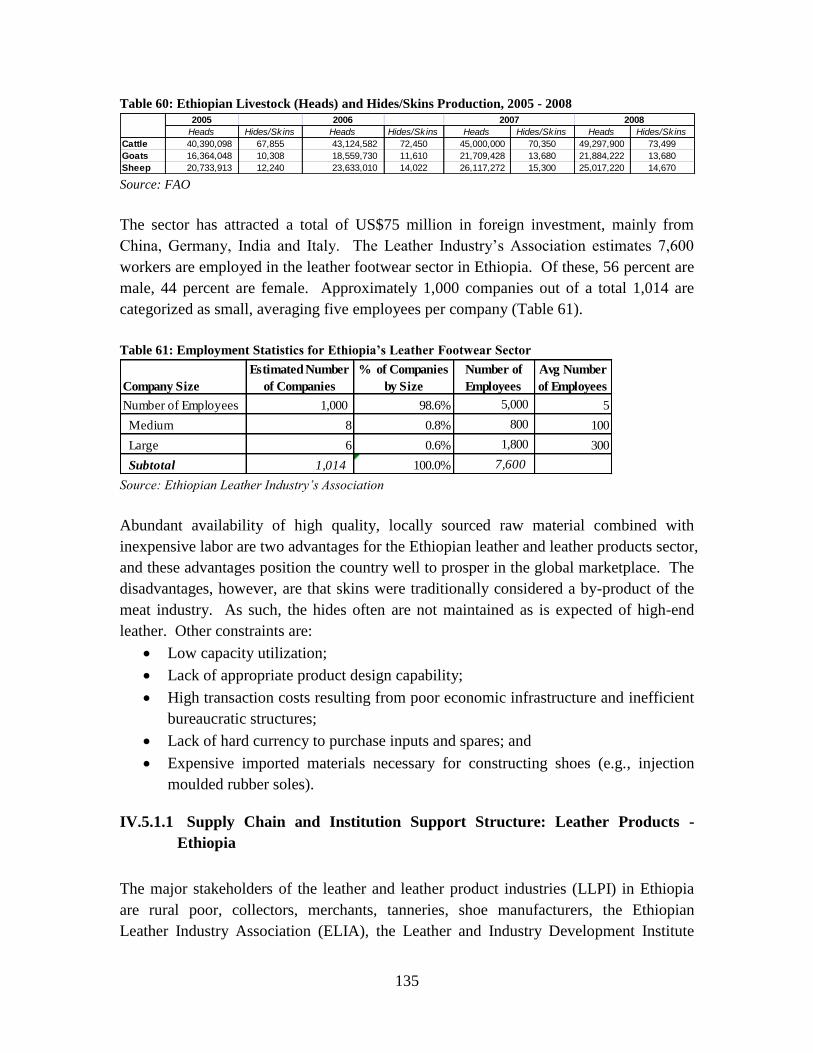

Ethiopia is the leading cattle producing country in Africa and ranks third in heads of goat

and fourth in heads of sheep. As seen in Table 60, total heads of all three of these

livestock have increased since 2005. Ethiopia‘s cowhide production represents 11

percent of total African production while goatskin and sheepskin each comprise 7 percent.

55

http://www.ecbp.biz/actions/current-actions/ethiopias-leather-exports-skyrocket.html

135

Table 60: Ethiopian Livestock (Heads) and Hides/Skins Production, 2005 - 2008

2005 2006

Heads Hides/Skins Heads Hides/Skins Heads Hides/Skins Heads Hides/Skins

Cattle 40,390,098 67,855 43,124,582 72,450 45,000,000 70,350 49,297,900 73,499

Goats 16,364,048 10,308 18,559,730 11,610 21,709,428 13,680 21,884,222 13,680

Sheep 20,733,913 12,240 23,633,010 14,022 26,117,272 15,300 25,017,220 14,670

2007 2008

Source: FAO

The sector has attracted a total of US$75 million in foreign investment, mainly from

China, Germany, India and Italy. The Leather Industry‘s Association estimates 7,600

workers are employed in the leather footwear sector in Ethiopia. Of these, 56 percent are

male, 44 percent are female. Approximately 1,000 companies out of a total 1,014 are

categorized as small, averaging five employees per company (Table 61).

Table 61: Employment Statistics for Ethiopia’s Leather Footwear Sector

Company Size

Estimated Number

of Companies

% of Companies

by Size

Number of

Employees

Avg Number

of Employees

Number of Employees 1,000 98.6% 5,000 5

Medium 8 0.8% 800 100

Large 6 0.6% 1,800 300

Subtotal 1,014 100.0% 7,600 Source: Ethiopian Leather Industry’s Association

Abundant availability of high quality, locally sourced raw material combined with

inexpensive labor are two advantages for the Ethiopian leather and leather products sector,

and these advantages position the country well to prosper in the global marketplace. The

disadvantages, however, are that skins were traditionally considered a by-product of the

meat industry. As such, the hides often are not maintained as is expected of high-end

leather. Other constraints are:

Low capacity utilization;

Lack of appropriate product design capability;

High transaction costs resulting from poor economic infrastructure and inefficient

bureaucratic structures;

Lack of hard currency to purchase inputs and spares; and

Expensive imported materials necessary for constructing shoes (e.g., injection

moulded rubber soles).

IV.5.1.1 Supply Chain and Institution Support Structure: Leather Products -

Ethiopia

The major stakeholders of the leather and leather product industries (LLPI) in Ethiopia

are rural poor, collectors, merchants, tanneries, shoe manufacturers, the Ethiopian

Leather Industry Association (ELIA), the Leather and Industry Development Institute

136

(LIDI), the Ethiopian Chamber of Commerce (ECC), the Quality and Standards

Authority of Ethiopia (QSAE), the Ministry of Trade and Industry (MoTI), the Ethiopian

Revenue and Customs Authority (ERCA) (formerly known as the Ethiopian Customs and

Inland Revenue Authority) and the Ministry of Agriculture and Rural Development.

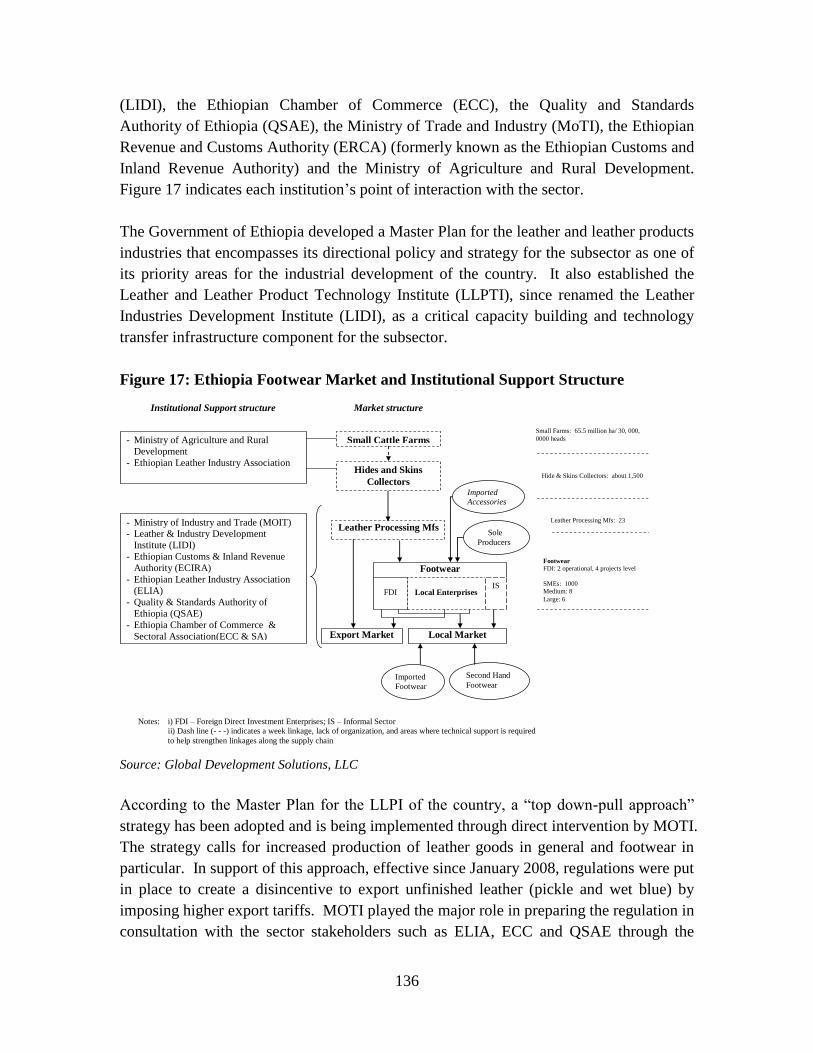

Figure 17 indicates each institution‘s point of interaction with the sector.

The Government of Ethiopia developed a Master Plan for the leather and leather products

industries that encompasses its directional policy and strategy for the subsector as one of

its priority areas for the industrial development of the country. It also established the

Leather and Leather Product Technology Institute (LLPTI), since renamed the Leather

Industries Development Institute (LIDI), as a critical capacity building and technology

transfer infrastructure component for the subsector.

Figure 17: Ethiopia Footwear Market and Institutional Support Structure Ethiopia Footwear Market and Institutional Support Structure

Market structure Institutional Support structure

Small Cattle Farms - Ministry of Agriculture and Rural

Development

- Ethiopian Leather Industry Association

Hides and Skins

Collectors

Leather Processing Mfs

Footwear

FDI

Export Market Local Market

- Ministry of Industry and Trade (MOIT) - Leather & Industry Development

Institute (LIDI)

- Ethiopian Customs & Inland Revenue

Authority (ECIRA)

- Ethiopian Leather Industry Association

(ELIA)

- Quality & Standards Authority of

Ethiopia (QSAE)

- Ethiopia Chamber of Commerce &

Sectoral Association(ECC & SA)

- SA

Notes: i) FDI – Foreign Direct Investment Enterprises; IS – Informal Sector

ii) Dash line (- - -) indicates a week linkage, lack of organization, and areas where technical support is required

to help strengthen linkages along the supply chain

Second Hand

Footwear Imported

Footwear

Imported

Accessories

Local Enterprises

Small Farms: 65.5 million ha/ 30, 000,

0000 heads

Hide & Skins Collectors: about 1,500

Leather Processing Mfs: 23

Footwear

FDI: 2 operational, 4 projects level

SMEs: 1000

Medium: 8

Large: 6

IS

Sole

Producers

Source: Global Development Solutions, LLC

According to the Master Plan for the LLPI of the country, a ―top down-pull approach‖

strategy has been adopted and is being implemented through direct intervention by MOTI.

The strategy calls for increased production of leather goods in general and footwear in

particular. In support of this approach, effective since January 2008, regulations were put

in place to create a disincentive to export unfinished leather (pickle and wet blue) by

imposing higher export tariffs. MOTI played the major role in preparing the regulation in

consultation with the sector stakeholders such as ELIA, ECC and QSAE through the

137

Public-Private Partnership dialogue. Now the ECIRA is implementing the regulation by

imposing the set taxation on unfinished leather products per the rates given in the

regulation.

The implementation of the policy has encouraged tanneries to strengthen and expand

their finishing sections thereby increasing the production of crust and finished leather for

export as well as for local production of finished leather goods. Shoe manufacturers

therefore are increasing their exports, which now have now attained a volume of above

3,000 pairs per day.

The MoARD currently is engaged in the task of improving the quality of skins and hides

by supporting smallholder farmers in overcoming the prevailing problem they have with

ectoparasites (ekek) and other diseases.

The QSAE recently completed a study to establish a skins and hides grading system for

the subsector so as to enable setting of prices based on the quality of skins and hides. It

also controls the quality of imported input materials for leather processing and

manufacturing of shoes.

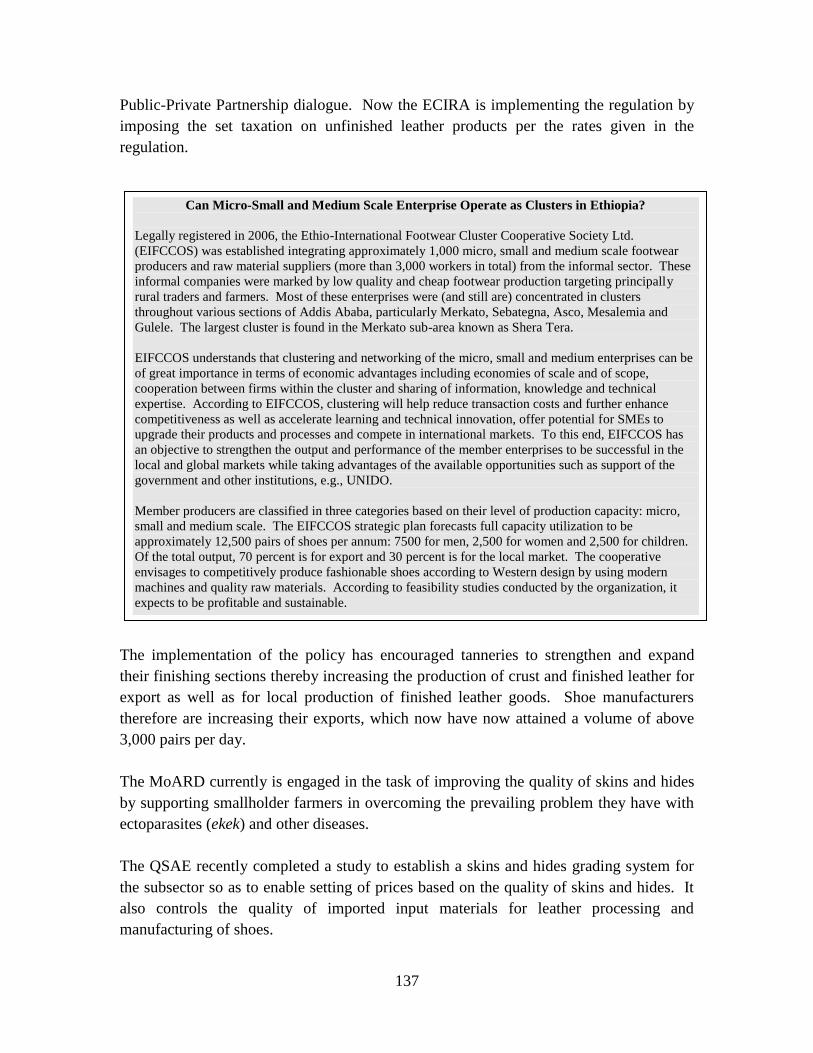

Can Micro-Small and Medium Scale Enterprise Operate as Clusters in Ethiopia?

Legally registered in 2006, the Ethio-International Footwear Cluster Cooperative Society Ltd.

(EIFCCOS) was established integrating approximately 1,000 micro, small and medium scale footwear

producers and raw material suppliers (more than 3,000 workers in total) from the informal sector. These

informal companies were marked by low quality and cheap footwear production targeting principally

rural traders and farmers. Most of these enterprises were (and still are) concentrated in clusters

throughout various sections of Addis Ababa, particularly Merkato, Sebategna, Asco, Mesalemia and

Gulele. The largest cluster is found in the Merkato sub-area known as Shera Tera.

EIFCCOS understands that clustering and networking of the micro, small and medium enterprises can be

of great importance in terms of economic advantages including economies of scale and of scope,

cooperation between firms within the cluster and sharing of information, knowledge and technical

expertise. According to EIFCCOS, clustering will help reduce transaction costs and further enhance

competitiveness as well as accelerate learning and technical innovation, offer potential for SMEs to

upgrade their products and processes and compete in international markets. To this end, EIFCCOS has

an objective to strengthen the output and performance of the member enterprises to be successful in the

local and global markets while taking advantages of the available opportunities such as support of the

government and other institutions, e.g., UNIDO.

Member producers are classified in three categories based on their level of production capacity: micro,

small and medium scale. The EIFCCOS strategic plan forecasts full capacity utilization to be

approximately 12,500 pairs of shoes per annum: 7500 for men, 2,500 for women and 2,500 for children.

Of the total output, 70 percent is for export and 30 percent is for the local market. The cooperative

envisages to competitively produce fashionable shoes according to Western design by using modern

machines and quality raw materials. According to feasibility studies conducted by the organization, it

expects to be profitable and sustainable.

138

IV.5.2. Sector Profile: Leather and Leather Footwear in Tanzania

Tanzanian annual industrial production surveys cover only ‗large industrial

establishments operating in mainland Tanzania‘56

– the term ‗large‘ as used in industrial

production surveys is a terminology used to highlight the fact that micro enterprises

(employing less than 10 people) are not covered by these surveys. Based on the Business

Survey 2007/08, there were 25,000 manufacturing enterprises with permanent premises

operating in Tanzania, and 97 percent of them were micro/small scale manufactures with

less than 10 workers. 57

The distribution of such enterprises across sectors, the number of

employees and other indicators are not known and are not covered in this sector profile.

This sector profile covers only firms employing 10 or more people, officially recorded as

‗industrial enterprises/manufacturing establishments‘ under national statistics.

Tanzanian leather products and leather footwear manufacturing is extremely limited. In

2008, the country had two operational tanneries out of six. The estimated annual leather

processing capacity in Tanzania is roughly 40 million square feet, only 9 percent of

which is utilized.58

In terms of leather products‘ manufacturers (of saddlery, harness,

belts, bags, etc.), there are an estimated four firms making such products in Tanzania.59

In terms of leather footwear producers, only five firms are estimated to make such

products.60

The industrial survey undertaken in 2008 does not distinguish leather

footwear firm employment from employment in footwear in general, and precise figures

of employment in the leather footwear sector are not available. According to interviews

with leather and other footwear firms in the country, not more than 200 workers are

employed in the leather footwear sector in Tanzania (excluding micro/small enterprises

employing less than 10 people). Of these, 58 percent are male and 42 percent are female

(see Table 62 below).61

56

Annual Survey of Industrial Production 2008, Tanzania Ministry of Industry, Trade, and Marketing. 57

National Bureau of Statistics, Tanzania 58

International Trade Center. 59

Note that shoe makers and other leather product makers make a variety of leather products

interchangeably, depending on orders. Micro/small firms employing less than ten people not included. 60

Ibid. 61

Average based on reported breakdown from Industrial Survey 2008, aggregate item ‗manufacture of

textiles, wearing apparel and leather products.‘

139

Table 62: Employment Statistics, Tanzanian Leather Footwear Sector

Company Size

Estimated Number of

Companies

% of Companies by

Size

Number of

Employees

Average Employees

per Company

Small 5 100% 150 - 200 10 - 45

Medium 0 0% - -

Large 0 0% - -

Subtotal 5 100% 150 -200

Informal 0 0

Formal 5 100%

State-owned enterprise 0 0%

Source: Interviews, Global Development Solutions, LLC

Note: Does not include micro/small firms employiong less than 10 employees

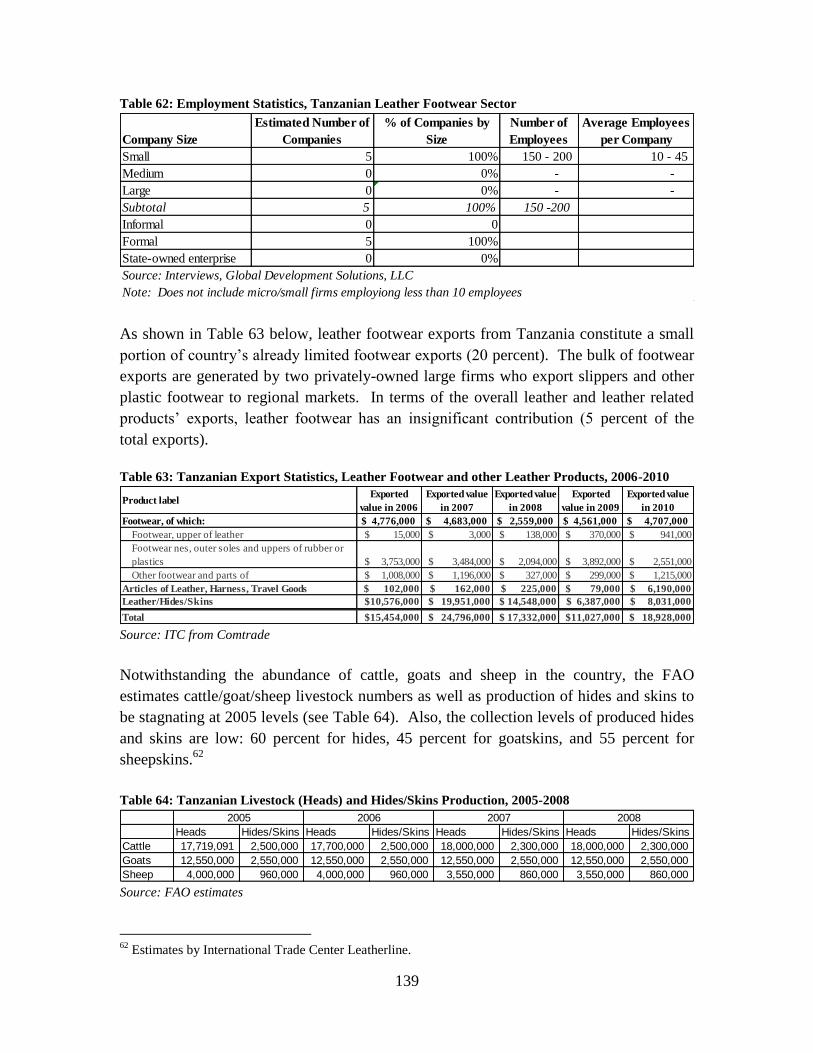

As shown in Table 63 below, leather footwear exports from Tanzania constitute a small

portion of country‘s already limited footwear exports (20 percent). The bulk of footwear

exports are generated by two privately-owned large firms who export slippers and other

plastic footwear to regional markets. In terms of the overall leather and leather related

products‘ exports, leather footwear has an insignificant contribution (5 percent of the

total exports).

Table 63: Tanzanian Export Statistics, Leather Footwear and other Leather Products, 2006-2010

Product labelExported

value in 2006

Exported value

in 2007

Exported value

in 2008

Exported

value in 2009

Exported value

in 2010

Footwear, of which: $ 4,776,000 $ 4,683,000 $ 2,559,000 $ 4,561,000 $ 4,707,000

Footwear, upper of leather $ 15,000 $ 3,000 $ 138,000 $ 370,000 $ 941,000

Footwear nes, outer soles and uppers of rubber or

plastics $ 3,753,000 $ 3,484,000 $ 2,094,000 $ 3,892,000 $ 2,551,000

Other footwear and parts of $ 1,008,000 $ 1,196,000 $ 327,000 $ 299,000 $ 1,215,000

Articles of Leather, Harness, Travel Goods $ 102,000 $ 162,000 $ 225,000 $ 79,000 $ 6,190,000

Leather/Hides/Skins $10,576,000 $ 19,951,000 $ 14,548,000 $ 6,387,000 $ 8,031,000

Total $15,454,000 $ 24,796,000 $ 17,332,000 $11,027,000 $ 18,928,000 Source: ITC from Comtrade

Notwithstanding the abundance of cattle, goats and sheep in the country, the FAO

estimates cattle/goat/sheep livestock numbers as well as production of hides and skins to

be stagnating at 2005 levels (see Table 64). Also, the collection levels of produced hides

and skins are low: 60 percent for hides, 45 percent for goatskins, and 55 percent for

sheepskins.62

Table 64: Tanzanian Livestock (Heads) and Hides/Skins Production, 2005-2008

Heads Hides/Skins Heads Hides/Skins Heads Hides/Skins Heads Hides/Skins

Cattle 17,719,091 2,500,000 17,700,000 2,500,000 18,000,000 2,300,000 18,000,000 2,300,000

Goats 12,550,000 2,550,000 12,550,000 2,550,000 12,550,000 2,550,000 12,550,000 2,550,000

Sheep 4,000,000 960,000 4,000,000 960,000 3,550,000 860,000 3,550,000 860,000

2005 2006 2007 2008

Source: FAO estimates

62

Estimates by International Trade Center Leatherline.

140

In the current environment, the leather products and footwear sector faces a range of

challenges:

Insufficient supply of quality of hides/skins/leather due to a combination of

factors:

o Poor flaying methods (99 percent by hand)63

;

o Major/most tanneries not operational;

o Higher quality hides/skins available/produced locally are exported

informally to avoid export taxes.

Lack of appropriate product design capability;

Poor enforcement of trade regulations and rules, especially in terms of flow of

informal trade in Asian footwear/leather products; and

Relatively high manufacturing wages.

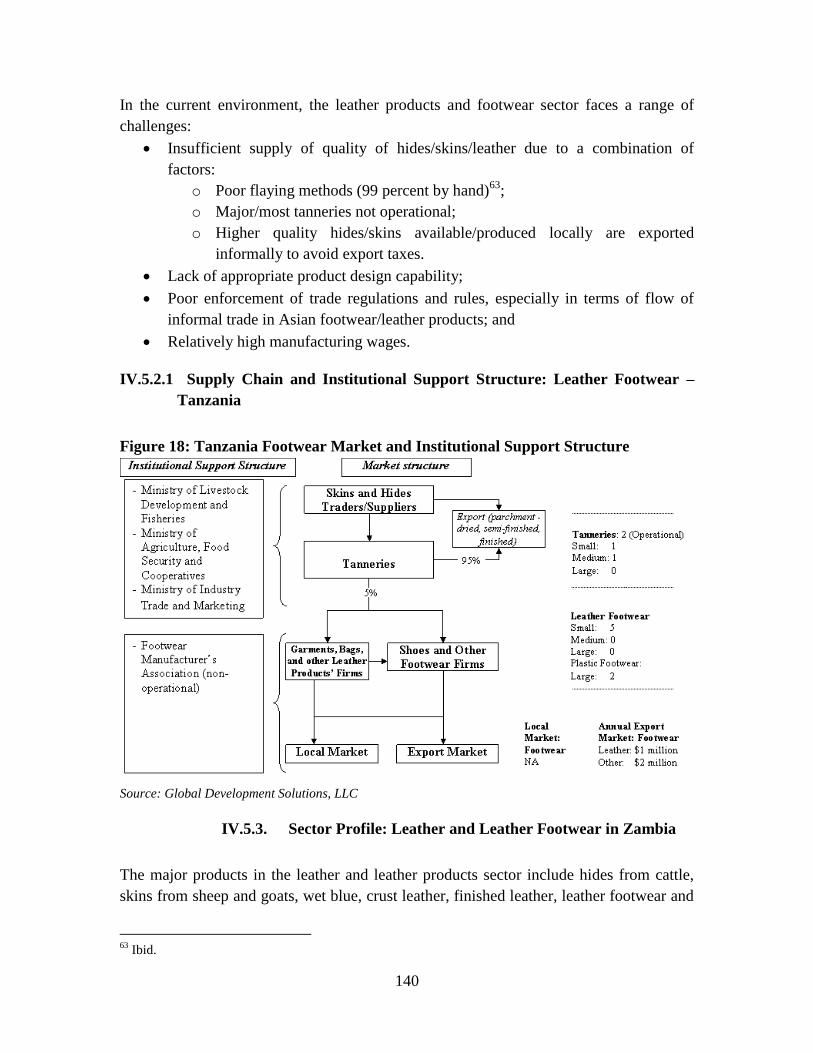

IV.5.2.1 Supply Chain and Institutional Support Structure: Leather Footwear –

Tanzania

Figure 18: Tanzania Footwear Market and Institutional Support Structure

Source: Global Development Solutions, LLC

IV.5.3. Sector Profile: Leather and Leather Footwear in Zambia

The major products in the leather and leather products sector include hides from cattle,

skins from sheep and goats, wet blue, crust leather, finished leather, leather footwear and

63

Ibid.

141

leather goods. Other sources of hides and skins include wildlife, game ranching and

crocodile farming.

The development of the processed leather industry in Zambia is strongly based on

availability of quality hides and skins, which are by-products of the meat industry. Hides

and skins are found throughout the country, and their availability depends on the

efficiency of collection and access to markets by traders, farmers and abattoir operators.

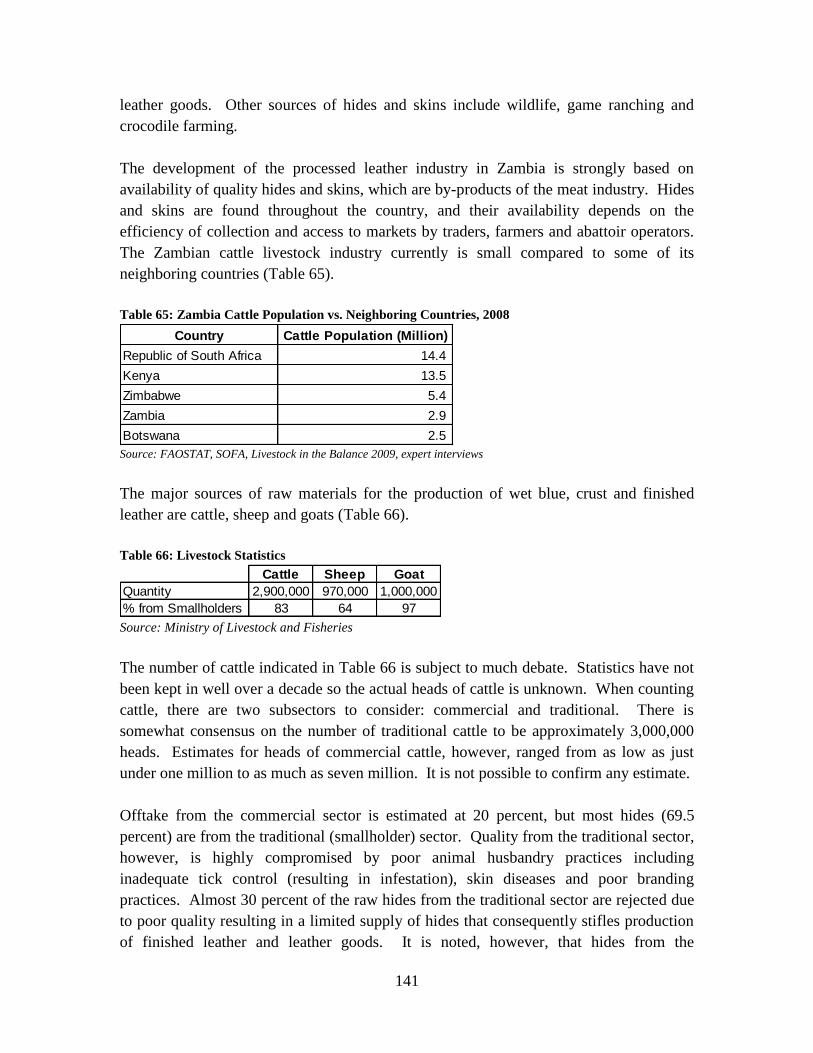

The Zambian cattle livestock industry currently is small compared to some of its

neighboring countries (Table 65).

Table 65: Zambia Cattle Population vs. Neighboring Countries, 2008

Country Cattle Population (Million)

Republic of South Africa 14.4

Kenya 13.5

Zimbabwe 5.4

Zambia 2.9

Botswana 2.5 Source: FAOSTAT, SOFA, Livestock in the Balance 2009, expert interviews

The major sources of raw materials for the production of wet blue, crust and finished

leather are cattle, sheep and goats (Table 66).

Table 66: Livestock Statistics

Cattle Sheep Goat

Quantity 2,900,000 970,000 1,000,000

% from Smallholders 83 64 97 Source: Ministry of Livestock and Fisheries

The number of cattle indicated in Table 66 is subject to much debate. Statistics have not

been kept in well over a decade so the actual heads of cattle is unknown. When counting

cattle, there are two subsectors to consider: commercial and traditional. There is

somewhat consensus on the number of traditional cattle to be approximately 3,000,000

heads. Estimates for heads of commercial cattle, however, ranged from as low as just

under one million to as much as seven million. It is not possible to confirm any estimate.

Offtake from the commercial sector is estimated at 20 percent, but most hides (69.5

percent) are from the traditional (smallholder) sector. Quality from the traditional sector,

however, is highly compromised by poor animal husbandry practices including

inadequate tick control (resulting in infestation), skin diseases and poor branding

practices. Almost 30 percent of the raw hides from the traditional sector are rejected due

to poor quality resulting in a limited supply of hides that consequently stifles production

of finished leather and leather goods. It is noted, however, that hides from the

142

commercial sector are usually of good quality. The Leather Industry Association of

Zambia (LIAZ) in collaboration with Zambia Bureau of Standards (ZABS) in 2004 has

since developed a standards and grading system for raw hides and skins for use by

abattoirs, traders and tanneries.64

Supplier awareness of quality standards for hides has

resulted in reduced rejection rates at the leather factories. However, supply of raw hides

remains a problem.

The Tanning Subsector

The tanning subsector is a major component of the leather industry; there were five

tanneries employing approximately 1,500 workers as of 2010. Capacity utilization of the

five tanneries in the country is reported to be between 50 percent and 65 percent. This is

a reflection of inadequate supply of good quality raw hides from the smallholder farming

system and slaughter facilities.

Footwear and Leather Goods Manufacturing Subsector

The footwear and leather goods manufacturing subsector utilizes mainly local finished

leather and imported components such as soles and midsoles. The industry specializes in

manufacturing footwear, particularly industrial safety boots, military boots, school shoes

and sandals. Leather fashion/casual shoes are not produced in Zambia. The leather

goods that are manufactured include handbags, table mats, wine holders, conference

folders, purses, belts and footballs.

The total official production of footwear is given in Table 67. Official manufactured

footwear data primarily excludes the microenterprises whose profiles are not documented

due to the informal nature of their operations.

Table 67: Zambia Total Footwear Production

2007 2008 2009

All Footwear 1,573,832 1,204,294 964,270

Leather Footwear 1,056,791 808,655 647,484

Total Production Volume (pairs)

Source: Central Statistical Office (Zambia)

The footwear subsector is relatively small and its products are targeted at domestic and

regional markets. The domestic market comprises mainly schools, manufacturing and

mining sectors; not fashion. The main footwear products produced include safety

boots/shoes, schools shoes and gum (non-leather) boots. The leather industry exports a

number of products (Table 68).

64

International Trade Center (ITC) Report, Supply Survey on the Leather Industry in Zambia, 2010.

143

Table 68: Share of export market by category of leather product, 2005-2009

Type of Leather

Product Exported

Cumulative Value

2005-2009 (US$)

Average Annual

Value (US$) Ranking

Crocodile Skins 15,138,390 3,027,678 1

Footwear 10,354,761 2,070,952 2

Wet blue 10,261,022 2,052,204 3

Finished Leather 445,990 891,198 4

Trophies 239,983 47,996 5

Total 36,440,146 8,090,029

Total may not sum due to rounding.

Source: Supply Survey on the Leather Industry in Zambia (2010)

Although small quantities of crocodile skins were exported, their value (37 percent) was

the largest, followed by footwear (26 percent), wet blue (25 percent), finished leather (11

percent) and wildlife hides/skins or trophies (1 percent).65

Considering the capacity

utilization of tanneries and leather goods manufacturing companies and the relatively

small quantities of crocodile skins produced, this suggests that Zambia has potential to

increase exports from crocodile skins, wet blue and footwear exports.

Table 69: Zambia Footwear Exports

Total Exports 2007 2008 2009

All Footwear

Volume (pairs) 340,912 134,024 148,148

Value (ZMK) 7,405,987,602 8,543,705,920 11,745,002,497

Value (USD) 1,853,962 2,344,944 2,362,965

Leather Footwear

Volume (pairs) 5,592 2,874 8,087

Value (ZMK) 1,189,862,111 728,725,042 1,098,679,307

Value (USD) 298,863 192,540 219,032

Main Destination Congo DR., Malawi, Singapore, Ukraine, Belgium

Source: Central Statistical Office (Zambia)

Recent and Current Import Trends

The Zambian footwear manufacturing subsector is small and does not produce fashion

shoes; all are imported. There is also a gap in meeting demand for protective boots and

shoes and these are imported in large quantities.

65

International Trade Center (ITC) report: Supply Survey on the Leather Industry in Zambia, 2010.

144

There is currently huge informal cross border importation of leather goods and an influx

of second hand leather products into the country. There is also a shift from low to high

quality leather products with rising household incomes. The imported footwear statistics

are given in Table 70.

Table 70: Zambia Footwear Imports

Total Imports 2007 2008 2009

All Footwear

Volume (pairs) 1,048,132 1,220,552 841,949

Value (ZMK) 58,850,012,401 55,584,127,546 66,837,864,517

Value (USD) 13,537,611 15,076,780 13,303,567

Leather Footwear

Volume (pairs) 79,601 99,339 59,526

Value (ZMK) 7,555,264,671 11,853,701,587 9,073,866,285

Value (USD) 1,903,527 3,232,011 1,820,152

Main Source of Imports China, Dubai, South Africa, Hong Kong, Europe Source: Central Statistical Office (Zambia)

Import of Hides and Skins

Tanneries imported hides, skins and finished leather from 2005-2009 in order to meet the

deficit in raw material supply from traders and abattoirs. There was critical short supply

of hides from 2004-2006 and this was attributed to the high level of smuggling outside

the country by traders seeking better prices. The shortage compelled tanneries and

manufacturers to import hides, wet blue and finished leather.

Sector Employment: The leather footwear sector employs at most 2,000 workers if all

informal microenterprises are included. Seventy-five percent of the workers are male

(Table 71).

Table 71: Employment Statistics for Zambia’s Leather Footwear Sector

Company Size

All

Footwear

Leather

Footwear

Sheepskin

Loafers

Avg No. of

employees/firm

Small 3 3 0 30

Medium 2 2 0 90

Large 3 1 0 100

Subtotal 8 6 0

Est. no. of workers employed by the sector1

2,000

% Male 75

% Female 251This is an approximation if all informal, microenterprises are considered.

Source: Global Development Solutions, LLC

Challenges in the Sector

145

The footwear and leather goods subsector currently is facing many challenges. The main

challenges are given as:

The use of old and obsolete machines;

The lack of design expertise and supporting technologies to produce fashionable

products;

Skills shortages;

Poor supply of quality raw hides;

The high costs of finance;

High costs of production inputs;

High import tariffs on inputs (25 percent on finished leather and 15 - 25 percent

on midsoles and outsoles);

High volatility of the local currency against major foreign currencies; and

High volume of second hand shoe imports due to the lack of import restrictions

and tariffs equal to that of raw materials for shoe manufacturing (25 percent).

Other challenges include the global economic downturn of 2008-2009 that made the

entire production sector decline. During the economic downturn, market access by

exporters of wet blue, finished leather and leather goods declined significantly due to low

demand for these products on the international market.

146

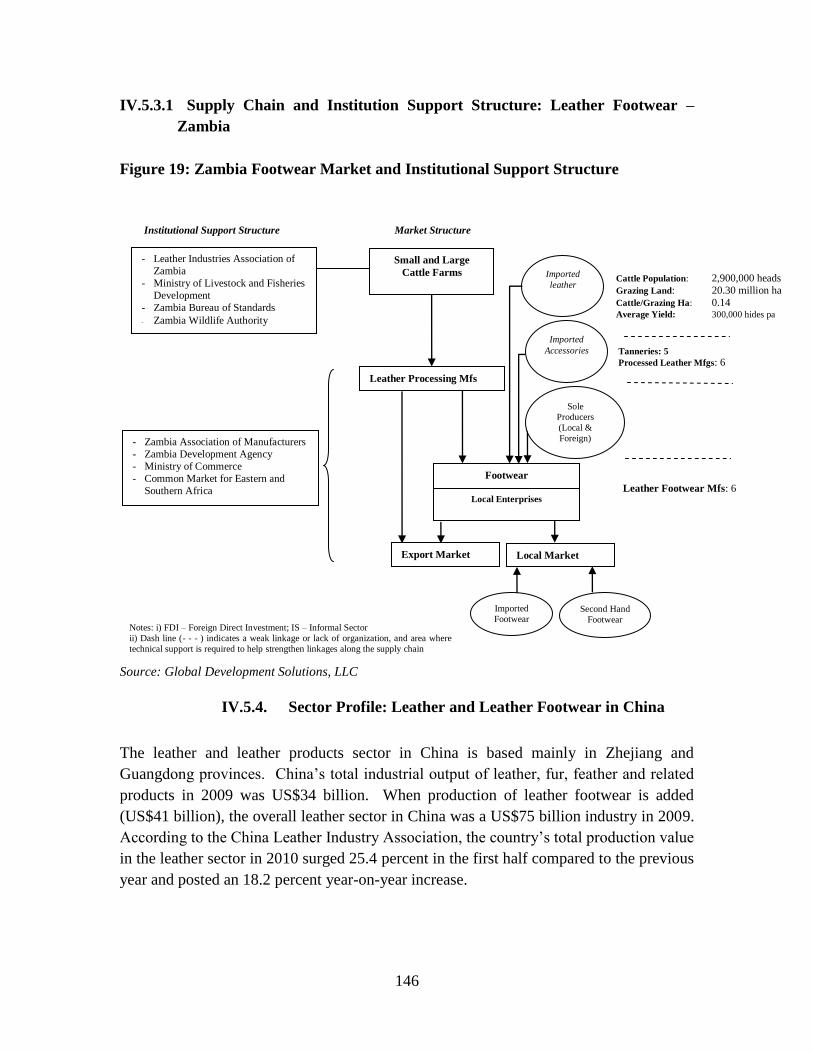

IV.5.3.1 Supply Chain and Institution Support Structure: Leather Footwear –

Zambia

Figure 19: Zambia Footwear Market and Institutional Support Structure

Tanneries: 5

Processed Leather Mfgs: 6

- Leather Industries Association of

Zambia

- Ministry of Livestock and Fisheries

Development

- Zambia Bureau of Standards

- Zambia Wildlife Authority

- Zambia Association of Manufacturers

- Zambia Development Agency

- Ministry of Commerce

- Common Market for Eastern and

Southern Africa

-

Institutional Support Structure Market Structure

Small and Large

Cattle Farms

Leather Footwear Mfs: 6

Notes: i) FDI – Foreign Direct Investment; IS – Informal Sector

ii) Dash line (- - - ) indicates a weak linkage or lack of organization, and area where

technical support is required to help strengthen linkages along the supply chain

Leather Processing Mfs

Imported

leather

Imported

Accessories

Sole

Producers

(Local &

Foreign)

Cattle Population: 2,900,000 heads

Grazing Land: 20.30 million ha

Cattle/Grazing Ha: 0.14 Average Yield: 300,000 hides pa

Export Market Local Market

Local Enterprises

Footwear

Second Hand

Footwear

Imported

Footwear

Source: Global Development Solutions, LLC

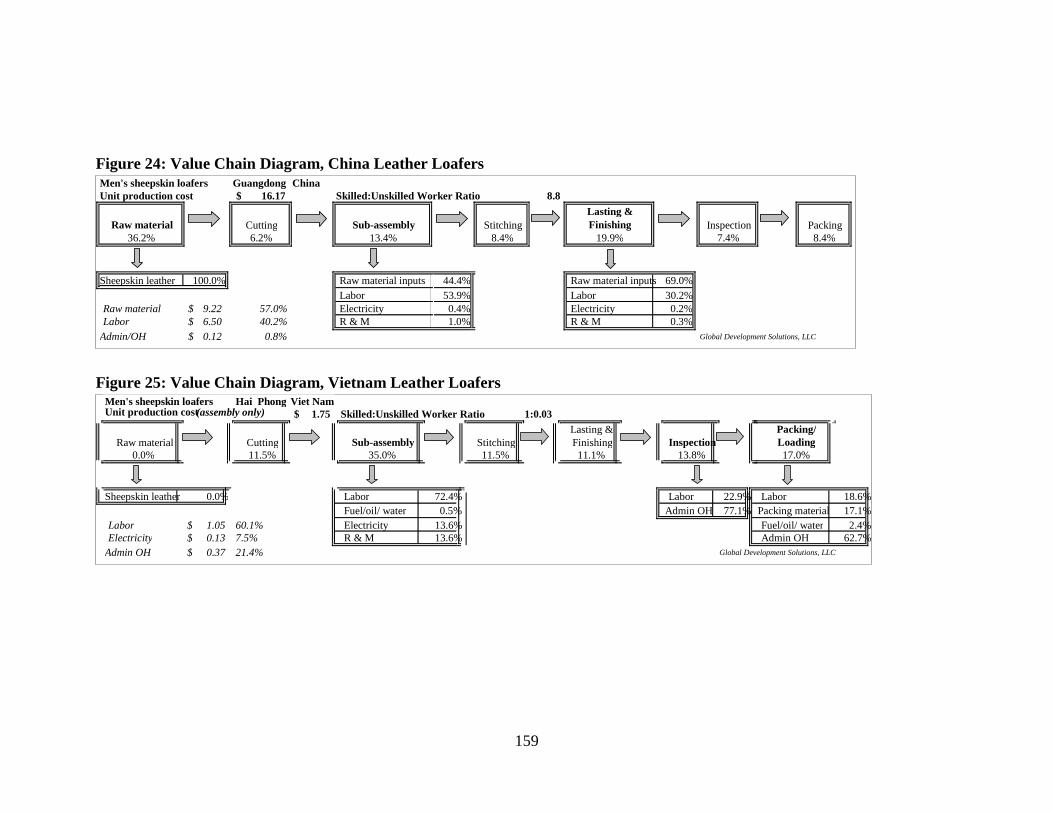

IV.5.4. Sector Profile: Leather and Leather Footwear in China

The leather and leather products sector in China is based mainly in Zhejiang and

Guangdong provinces. China‘s total industrial output of leather, fur, feather and related

products in 2009 was US$34 billion. When production of leather footwear is added

(US$41 billion), the overall leather sector in China was a US$75 billion industry in 2009.

According to the China Leather Industry Association, the country‘s total production value

in the leather sector in 2010 surged 25.4 percent in the first half compared to the previous

year and posted an 18.2 percent year-on-year increase.

147

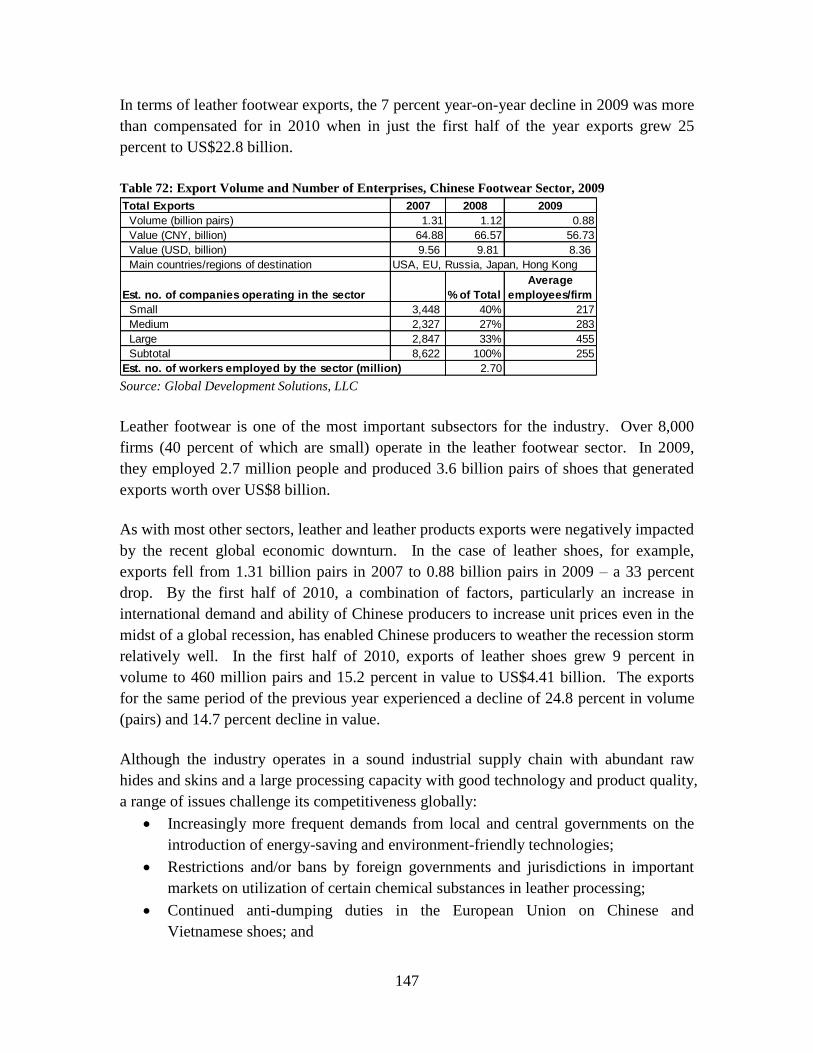

In terms of leather footwear exports, the 7 percent year-on-year decline in 2009 was more

than compensated for in 2010 when in just the first half of the year exports grew 25

percent to US$22.8 billion.

Table 72: Export Volume and Number of Enterprises, Chinese Footwear Sector, 2009

Total Exports 2007 2008 2009

Volume (billion pairs) 1.31 1.12 0.88

Value (CNY, billion) 64.88 66.57 56.73

Value (USD, billion) 9.56 9.81 8.36

Main countries/regions of destination USA, EU, Russia, Japan, Hong Kong

Est. no. of companies operating in the sector % of Total

Average

employees/firm

Small 3,448 40% 217

Medium 2,327 27% 283

Large 2,847 33% 455

Subtotal 8,622 100% 255

Est. no. of workers employed by the sector (million) 2.70 Source: Global Development Solutions, LLC

Leather footwear is one of the most important subsectors for the industry. Over 8,000

firms (40 percent of which are small) operate in the leather footwear sector. In 2009,

they employed 2.7 million people and produced 3.6 billion pairs of shoes that generated

exports worth over US$8 billion.

As with most other sectors, leather and leather products exports were negatively impacted

by the recent global economic downturn. In the case of leather shoes, for example,

exports fell from 1.31 billion pairs in 2007 to 0.88 billion pairs in 2009 – a 33 percent

drop. By the first half of 2010, a combination of factors, particularly an increase in

international demand and ability of Chinese producers to increase unit prices even in the

midst of a global recession, has enabled Chinese producers to weather the recession storm

relatively well. In the first half of 2010, exports of leather shoes grew 9 percent in

volume to 460 million pairs and 15.2 percent in value to US$4.41 billion. The exports

for the same period of the previous year experienced a decline of 24.8 percent in volume

(pairs) and 14.7 percent decline in value.

Although the industry operates in a sound industrial supply chain with abundant raw

hides and skins and a large processing capacity with good technology and product quality,

a range of issues challenge its competitiveness globally:

Increasingly more frequent demands from local and central governments on the

introduction of energy-saving and environment-friendly technologies;

Restrictions and/or bans by foreign governments and jurisdictions in important

markets on utilization of certain chemical substances in leather processing;

Continued anti-dumping duties in the European Union on Chinese and

Vietnamese shoes; and

148

Increasing labor costs and high labor turnover rates.

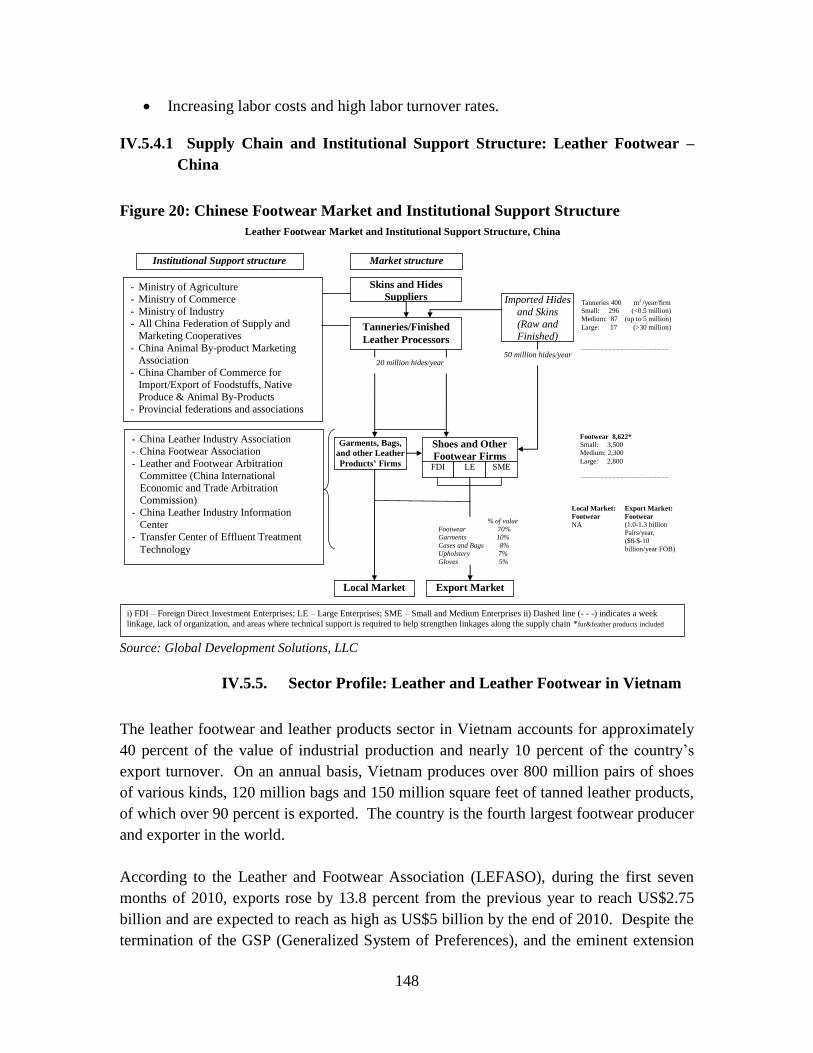

IV.5.4.1 Supply Chain and Institutional Support Structure: Leather Footwear –

China

Figure 20: Chinese Footwear Market and Institutional Support Structure

Market structure Institutional Support structure

- Ministry of Agriculture

- Ministry of Commerce

- Ministry of Industry

- All China Federation of Supply and

Marketing Cooperatives

- China Animal By-product Marketing

Association

- China Chamber of Commerce for

Import/Export of Foodstuffs, Native

Produce & Animal By-Products

- Provincial federations and associations

- China Leather Industry Association

- China Footwear Association

- Leather and Footwear Arbitration

Committee (China International

Economic and Trade Arbitration

Commission)

- China Leather Industry Information

Center

- Transfer Center of Effluent Treatment

Technology

i) FDI – Foreign Direct Investment Enterprises; LE – Large Enterprises; SME – Small and Medium Enterprises ii) Dashed line (- - -) indicates a week

linkage, lack of organization, and areas where technical support is required to help strengthen linkages along the supply chain *fur&feather products included

Skins and Hides

Suppliers

Tanneries/Finished

Leather Processors

Imported Hides

and Skins

(Raw and

Finished)

Garments, Bags,

and other Leather

Products’ Firms

Shoes and Other

Footwear Firms FDI LE SME

Local Market Export Market

Tanneries 400 m2 /year/firm Small: 296 (<0.5 million)

Medium: 87 (up to 5 million)

Large: 17 (>30 million)

Footwear 8,622*

Small: 3,500

Medium: 2,300

Large: 2,800

Export Market:

Footwear

(1.0-1.3 billion

Pairs/year,

($8-$-10

billion/year FOB)

Local Market:

Footwear

NA

50 million hides/year 20 million hides/year

% of value

Footwear 70%

Garments 10%

Cases and Bags 8%

Upholstery 7%

Gloves 5%

Leather Footwear Market and Institutional Support Structure, China

Source: Global Development Solutions, LLC

IV.5.5. Sector Profile: Leather and Leather Footwear in Vietnam

The leather footwear and leather products sector in Vietnam accounts for approximately

40 percent of the value of industrial production and nearly 10 percent of the country‘s

export turnover. On an annual basis, Vietnam produces over 800 million pairs of shoes

of various kinds, 120 million bags and 150 million square feet of tanned leather products,

of which over 90 percent is exported. The country is the fourth largest footwear producer

and exporter in the world.

According to the Leather and Footwear Association (LEFASO), during the first seven

months of 2010, exports rose by 13.8 percent from the previous year to reach US$2.75

billion and are expected to reach as high as US$5 billion by the end of 2010. Despite the

termination of the GSP (Generalized System of Preferences), and the eminent extension

149

of the anti-dumping duties on Vietnamese leather-capped shoes until 2011 by the EU,

currently the European market is Vietnam‘s biggest buyer with nearly 50 percent of the

country‘s total export turnover followed by the US (25 percent) and Japan (3 percent).

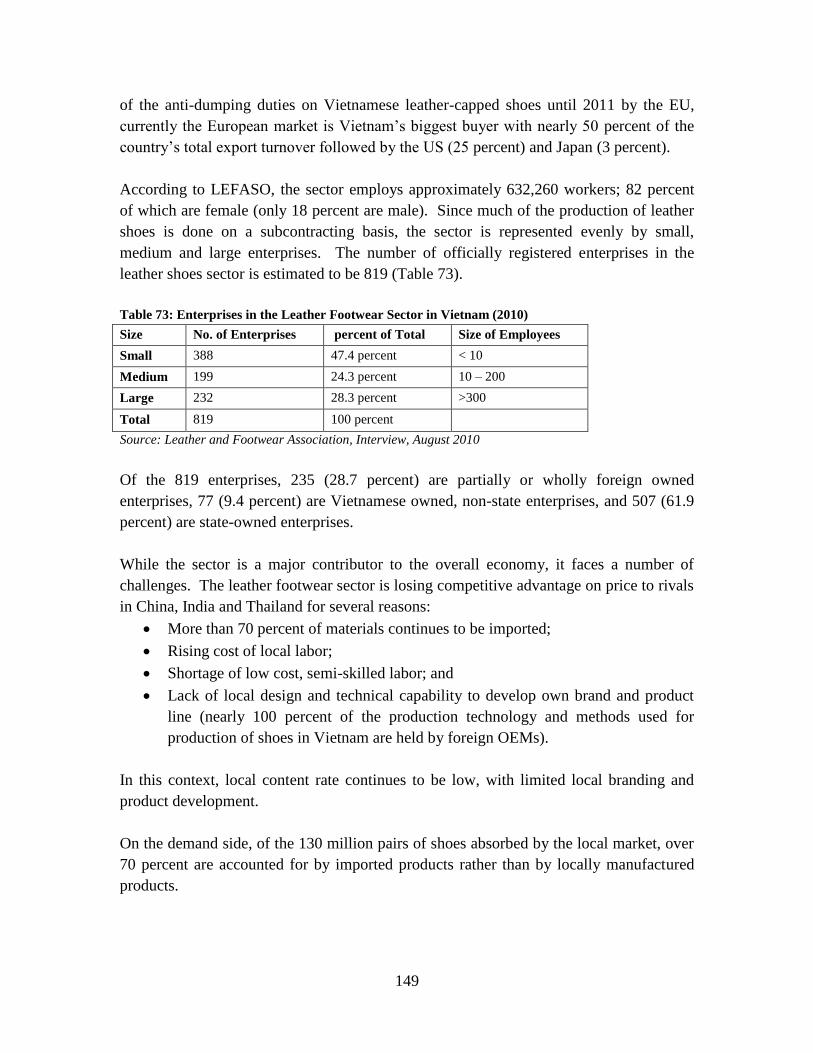

According to LEFASO, the sector employs approximately 632,260 workers; 82 percent

of which are female (only 18 percent are male). Since much of the production of leather

shoes is done on a subcontracting basis, the sector is represented evenly by small,

medium and large enterprises. The number of officially registered enterprises in the

leather shoes sector is estimated to be 819 (Table 73).

Table 73: Enterprises in the Leather Footwear Sector in Vietnam (2010)

Size No. of Enterprises percent of Total Size of Employees

Small 388 47.4 percent < 10

Medium 199 24.3 percent 10 – 200

Large 232 28.3 percent >300

Total 819 100 percent

Source: Leather and Footwear Association, Interview, August 2010

Of the 819 enterprises, 235 (28.7 percent) are partially or wholly foreign owned

enterprises, 77 (9.4 percent) are Vietnamese owned, non-state enterprises, and 507 (61.9

percent) are state-owned enterprises.

While the sector is a major contributor to the overall economy, it faces a number of

challenges. The leather footwear sector is losing competitive advantage on price to rivals

in China, India and Thailand for several reasons:

More than 70 percent of materials continues to be imported;

Rising cost of local labor;

Shortage of low cost, semi-skilled labor; and

Lack of local design and technical capability to develop own brand and product

line (nearly 100 percent of the production technology and methods used for

production of shoes in Vietnam are held by foreign OEMs).

In this context, local content rate continues to be low, with limited local branding and

product development.

On the demand side, of the 130 million pairs of shoes absorbed by the local market, over

70 percent are accounted for by imported products rather than by locally manufactured

products.

150

IV.5.5.1 Supply Chain and Institution Support Structure: Leather Footwear –

Vietnam

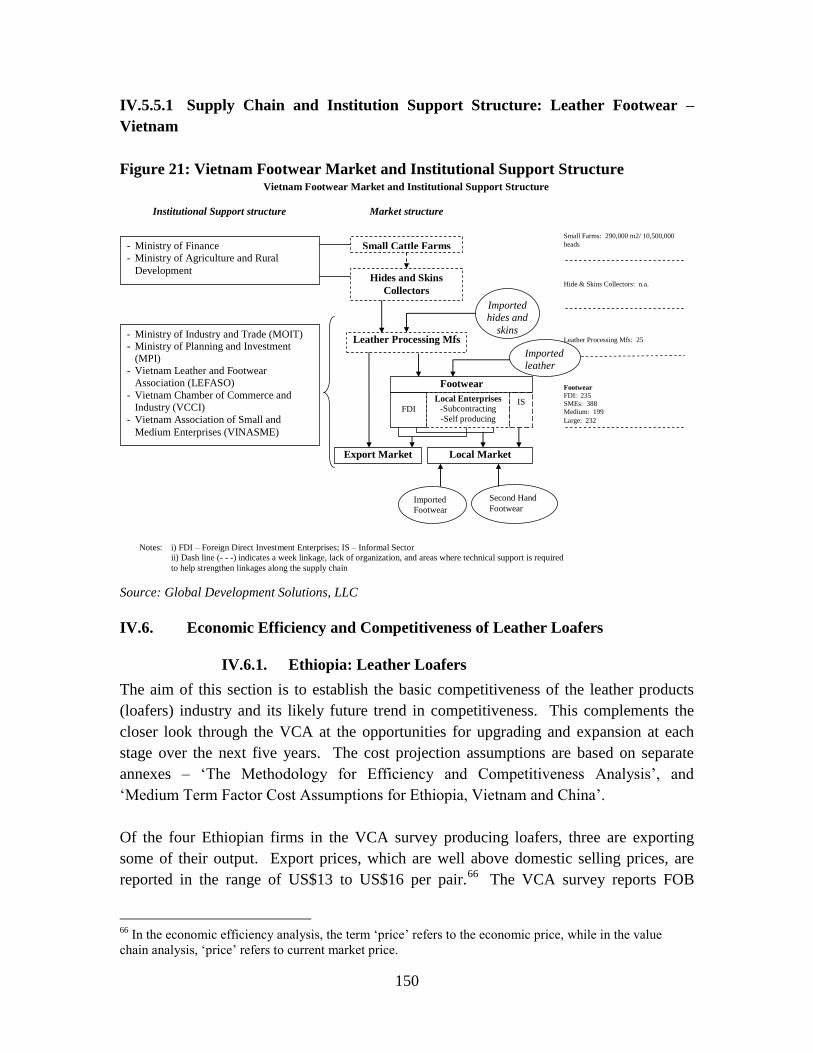

Figure 21: Vietnam Footwear Market and Institutional Support Structure Vietnam Footwear Market and Institutional Support Structure

Market structure Institutional Support structure

Small Cattle Farms - Ministry of Finance

- Ministry of Agriculture and Rural

Development Hides and Skins

Collectors

Leather Processing Mfs

Imported

hides and

skins

Footwear

FDI

Export Market Local Market

- Ministry of Industry and Trade (MOIT) - Ministry of Planning and Investment

(MPI)

- Vietnam Leather and Footwear

Association (LEFASO)

- Vietnam Chamber of Commerce and

Industry (VCCI)

- Vietnam Association of Small and

Medium Enterprises (VINASME)

Notes: i) FDI – Foreign Direct Investment Enterprises; IS – Informal Sector

ii) Dash line (- - -) indicates a week linkage, lack of organization, and areas where technical support is required

to help strengthen linkages along the supply chain

Second Hand

Footwear Imported

Footwear

Imported

leather

Local Enterprises

-Subcontracting

-Self producing

Small Farms: 290,000 m2/ 10,500,000

heads

Hide & Skins Collectors: n.a.

Leather Processing Mfs: 25

Footwear

FDI: 235

SMEs: 388

Medium: 199

Large: 232

IS

Source: Global Development Solutions, LLC

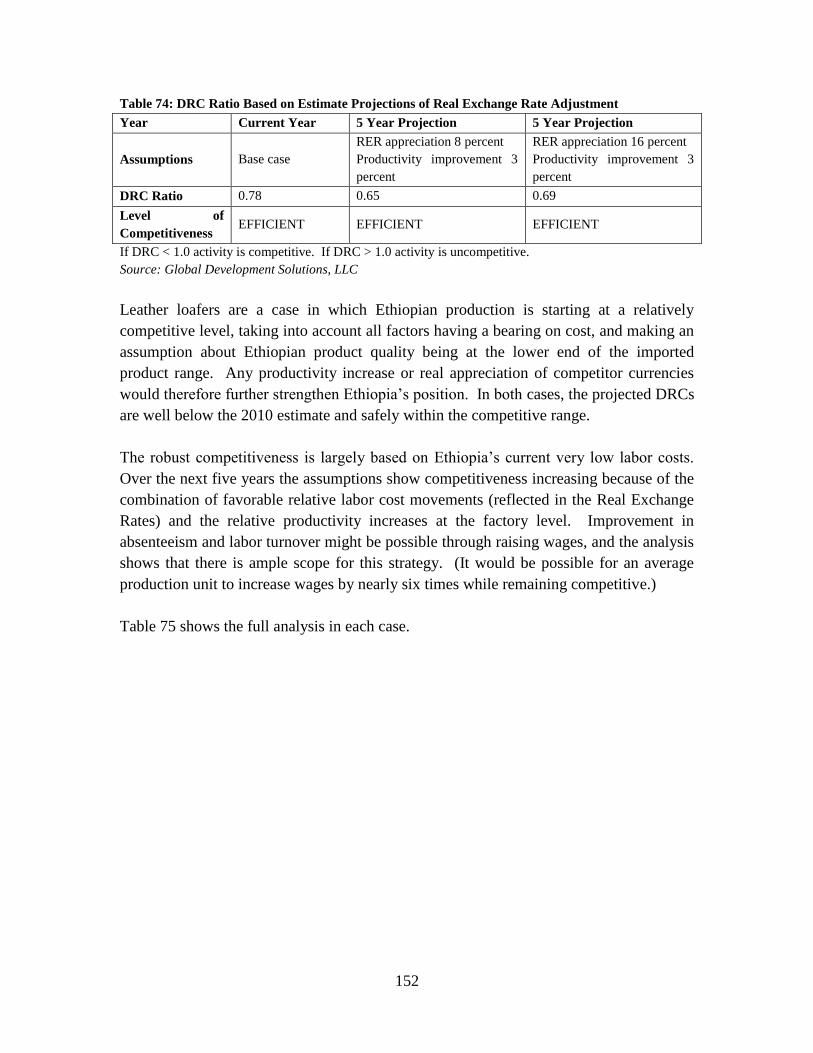

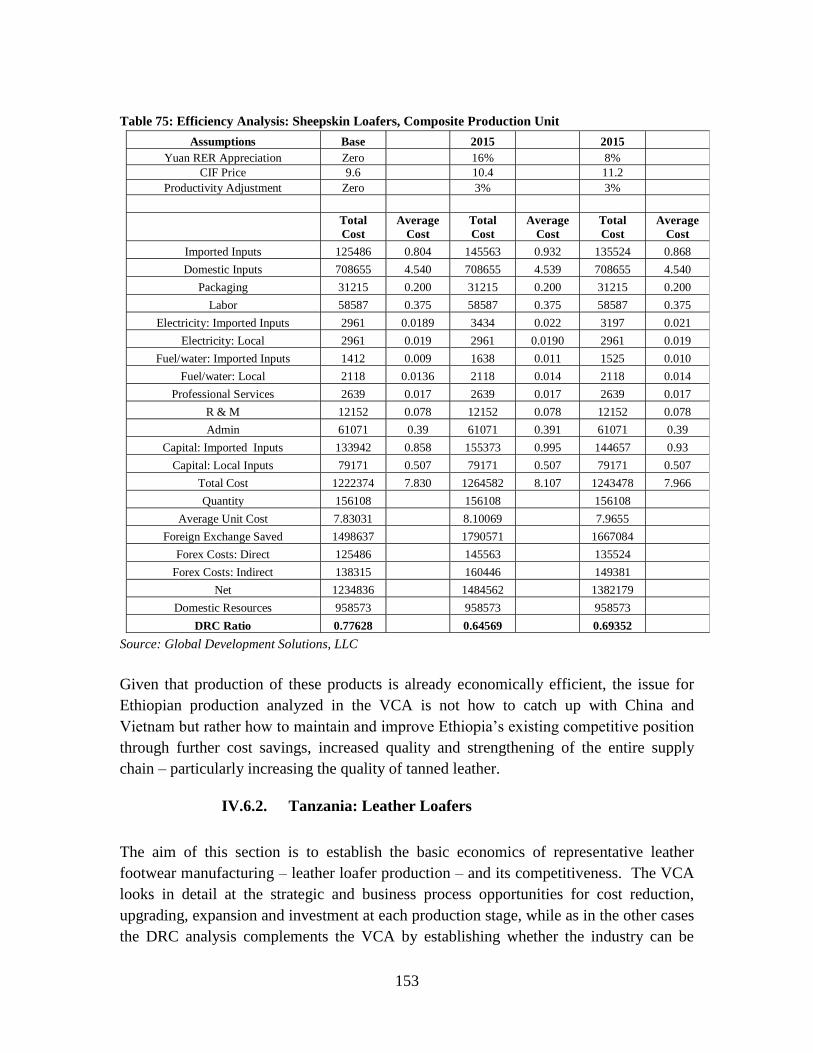

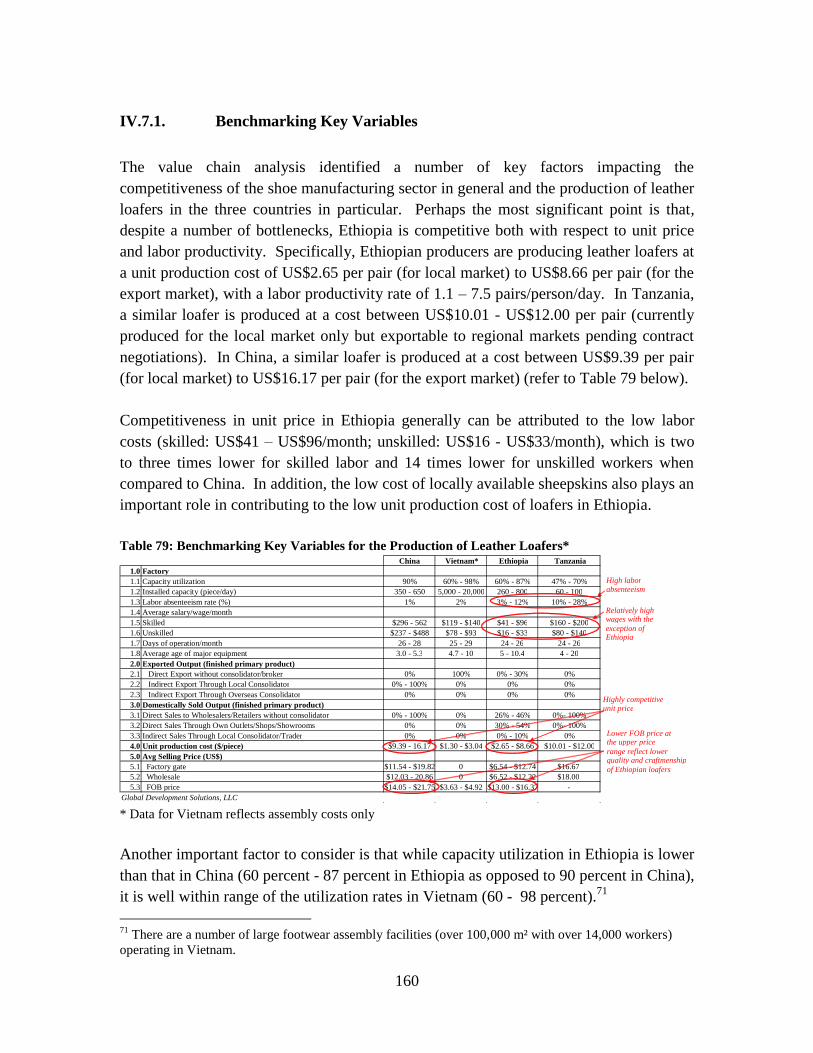

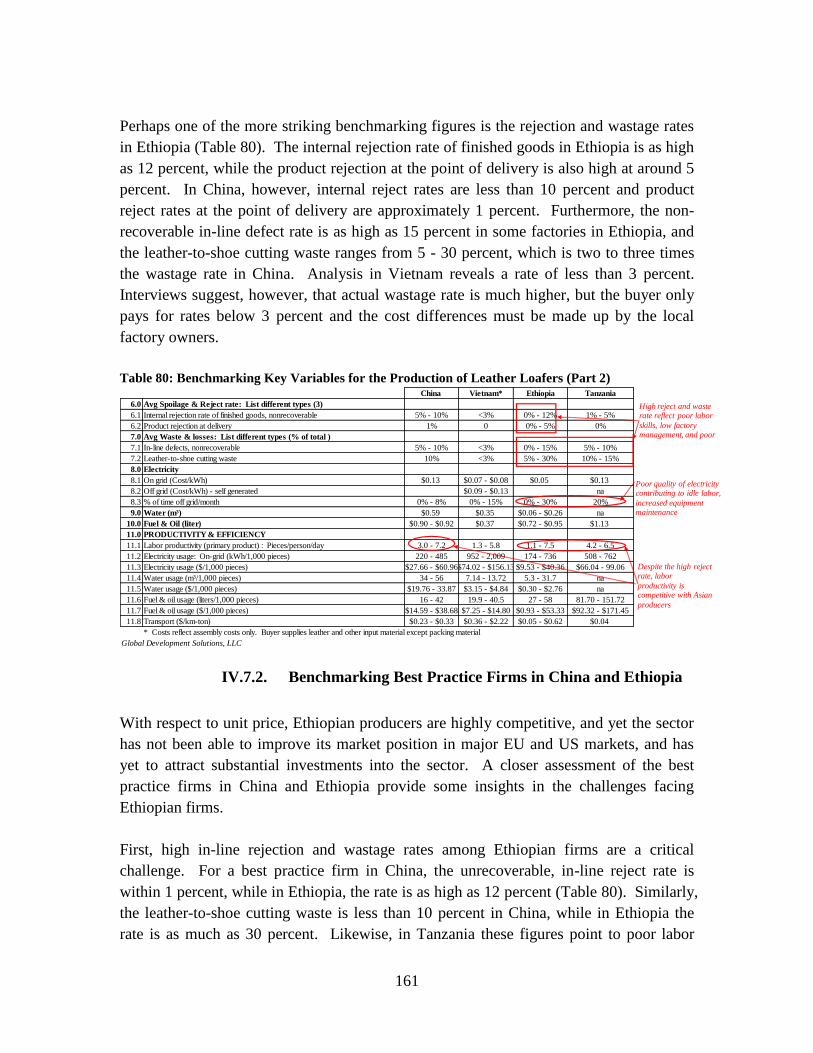

IV.6. Economic Efficiency and Competitiveness of Leather Loafers

IV.6.1. Ethiopia: Leather Loafers

The aim of this section is to establish the basic competitiveness of the leather products

(loafers) industry and its likely future trend in competitiveness. This complements the

closer look through the VCA at the opportunities for upgrading and expansion at each

stage over the next five years. The cost projection assumptions are based on separate

annexes – ‗The Methodology for Efficiency and Competitiveness Analysis‘, and

‗Medium Term Factor Cost Assumptions for Ethiopia, Vietnam and China‘.

Of the four Ethiopian firms in the VCA survey producing loafers, three are exporting

some of their output. Export prices, which are well above domestic selling prices, are

reported in the range of US$13 to US$16 per pair.66

The VCA survey reports FOB

66

In the economic efficiency analysis, the term ‗price‘ refers to the economic price, while in the value

chain analysis, ‗price‘ refers to current market price.

151

export prices for firms in China in the range US$9.60 to US$20 per pair. Ethiopian

prices are within this range but there are some quality differences with Chinese goods

because imports into Ethiopia tend to be high end fashion loafers that are not directly

comparable with Ethiopian goods.

To obtain an indication of the current and future competitiveness of Ethiopian producers,

a composite production unit was created by taking a weighted average of the cost

structure of the four representative firms in the VCA survey. Economic production costs

are derived according to the following procedures.

An annual capital charge is obtained by multiplying the estimated replacement

cost of assets by a capital recovery factor (ten-year asset life, 12 percent interest

rate);

All import tariffs on imported inputs and indirect taxes (VAT) are deducted where

these can be identified; and

Costs (capital cost, electricity, water/fuel, administration) that do not apply

specifically to the production of the primary output (loafers) are allocated on the

basis of the reported share of loafers in total output.

The resulting average economic cost of loafers for the composite firm is US$7.80/pair.

This is sufficiently low to allow local production to be currently profitable. The weighted

average price reported by firms is US$8.80/pair and, as noted, export prices are well

above this average cost.

To compare domestic cost with international competition, the average production cost is

compared with the bottom end of the range of Chinese FOB prices on the assumption that

these goods operate in the same quality segment of the market as Ethiopian exports.

Ethiopian average economic cost in the composite firm is well below the minimum

Chinese FOB price of US$9.60/pair and as a result the Domestic Resource Cost (DRC)

ratio is 0.78 thus indicating significant current competitiveness.