Comparative Matrix Of Corporate Governance Codes Relevant To...

379

Comparative Matrix Of Corporate Governance Codes Relevant To The European Union And Its Member States ANNEX V By Holly J. Gregory ©2002, Weil, Gotshal & Manges LLP

Transcript of Comparative Matrix Of Corporate Governance Codes Relevant To...

Comparative Matrix Of Corporate GovernanceCodes Relevant To The European Union AndIts Member States

ANNEX V

By Holly J. Gregory©2002, Weil, Gotshal & Manges LLP

Holly J. GregoryPartner

Weil, Gotshal & Manges LLPemail: [email protected]

Ms. Gregory specializes incorporate governance as a

field of legal practice.

©2002 Weil, Gotshal & Manges LLP

Corporate Governance Defined

Corporate Governance refers to that blend of law, regulation, and appropriate voluntary private-sector practiceswhich enables the corporation to attract financial and human capital, perform efficiently, and thereby perpetuateitself by generating long-term economic value for its shareholders, while respecting the interests of stakeholders andsociety as a whole.

Ira M. MillsteinSenior Partner, Weil, Gotshal & Manges LLPand noted authority on corporate governance

Weil, Gotshal & Manges LLP: Founded in 1931, Weil, Gotshal & Manges LLP is one of the world’slargest and most highly regarded full-service law firms, with over 875 attorneys in 12 offices worldwide.The Firm’s Corporate Governance Practice spans virtually all offices and departments -- including Corpo-rate, Trade Practices & Regulatory Law, Business & Securities Litigation, Business Finance &Restructuring and Tax. The Practice encompasses ongoing representation and counseling of boards, di-rectors, trustees, board committees, management, institutional investors and investment funds.Frequently, WG&M is called on to counsel on issues of board transition, CEO succession, crisis man-agement, and strategic decision-making; oversight of financial management and financial controls;investigations and employee-related matters; board composition, structure, process, and evaluation; boardindependence and accountability mechanisms; audit committee functions; board/CEO and investor rela-tions; director and trustee responsibilities and business judgment requirements, including use of specialcommittees; stock option-based incentive compensation plans; proxy rule compliance; and, tax and SECdisclosure requirements. In addition to corporate governance counseling, WG&M provides a full range oflegal services, including representation in the various forms of litigation involving shareholders.

EUROPEAN OFFICES: Brussels: 81 Avenue Louise, Box 9-10, B-1050, Belgium * Budapest: Bank Center, Granite Tower, H-1944, Hungary *Frankfurt: Main Tower, Box 19, 31st. Floor, Neue Mainzer Strasse 52-58, 60311, Germany * London: One South Place, EC2M 2WG, United Kingdom *Paris (affiliation): Derains & Assocíes, 167 Bis, Avenue, Victor-Hugo 75116, France * Prague: Charles Bridge Center, Krizovnicke Nam. 1, 110 00, CzechRepublic * Warsaw: Warsaw Financial Center, ul. Emilii Plater 53, 00-113, Poland

COMPARISON OF CORPORATE GOVERNANCE CODES

EUROPEAN UNION

TABLE OF CONTENTS

Page Page

i

OVERVIEW............................................................................................................................1

1. Definition of Corporate Governance...................................................................................11

2. The Mission of the Board of Directors................................................................................21

3. The Role of Stakeholders...................................................................................................31

4. Board Job Description .......................................................................................................41

5. Board Membership Criteria................................................................................................51

6. Selecting, Inviting and Orienting New Directors.................................................................61

7. Separation of Chairman and CEO ......................................................................................71

8. Lead Director ....................................................................................................................81

9. Board Size.........................................................................................................................91

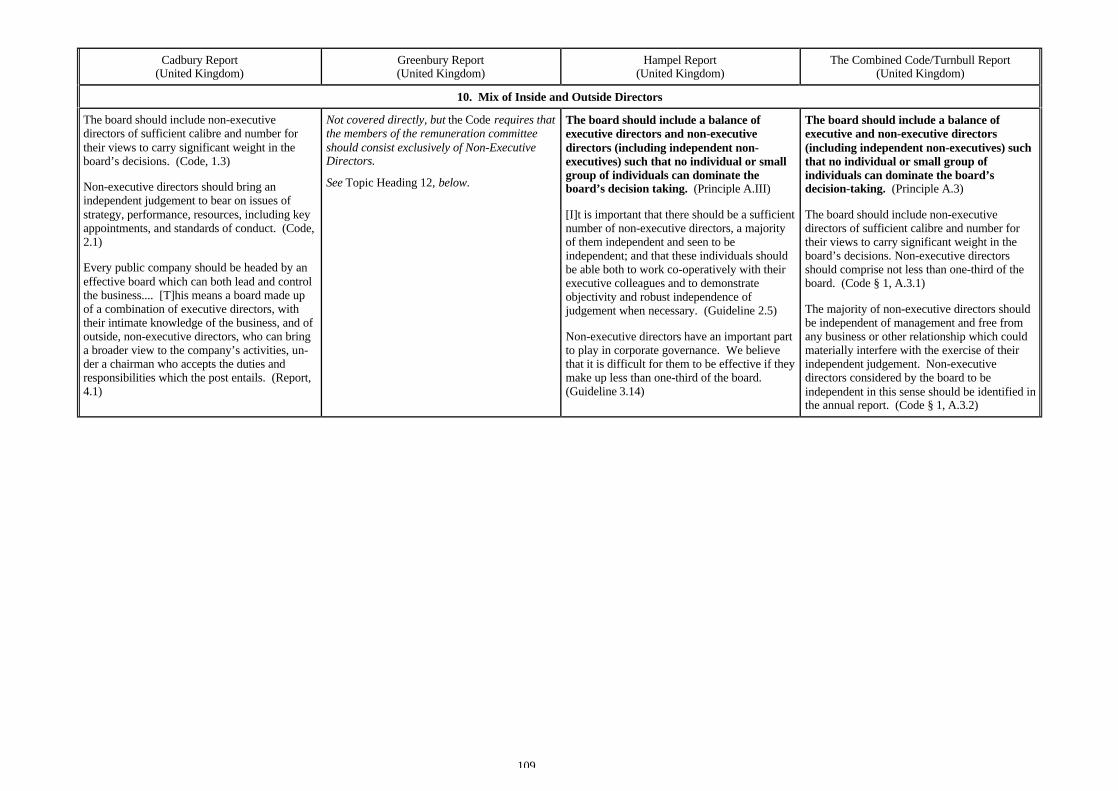

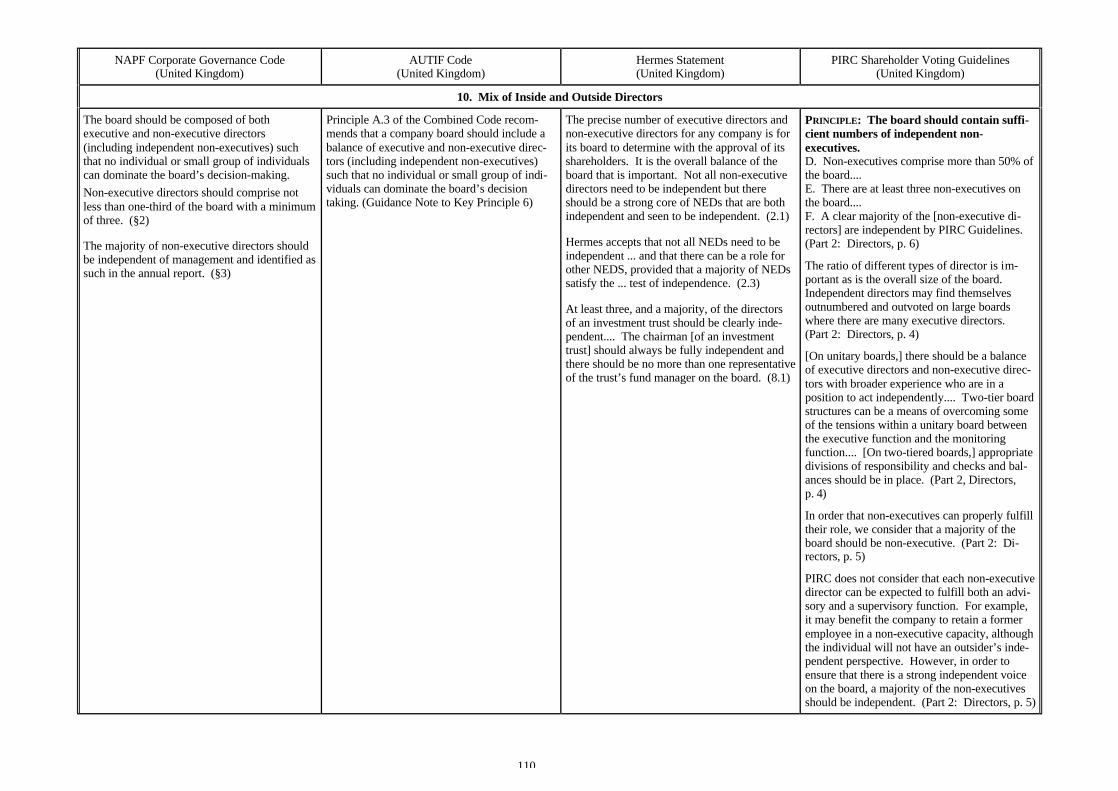

10. Mix of Inside and Outside Directors ...............................................................................101

11. Definition of “Independence”.........................................................................................111

12. Conflicts of Interest .......................................................................................................121

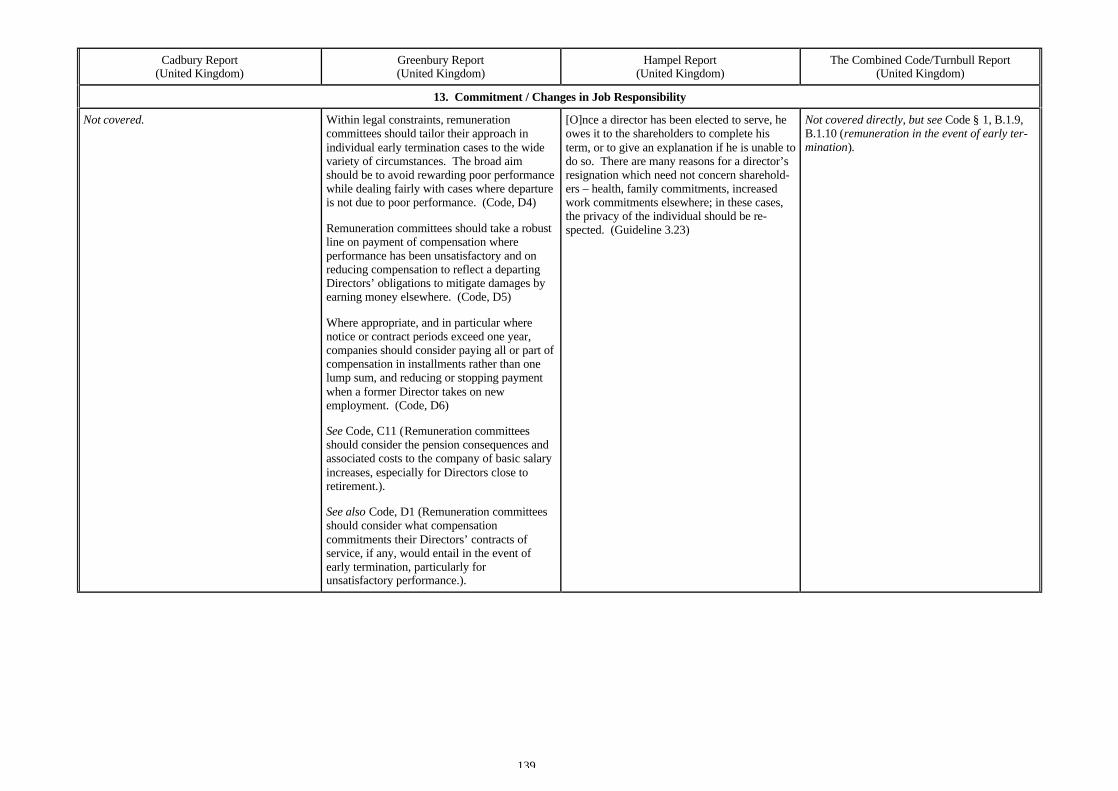

13. Commitment / Changes in Job Responsibility.................................................................131

14. Election Term / Term Limits / Mandatory Retirement .....................................................141

15. Evaluating Board Performance.......................................................................................151

16. Board Compensation Review.........................................................................................161

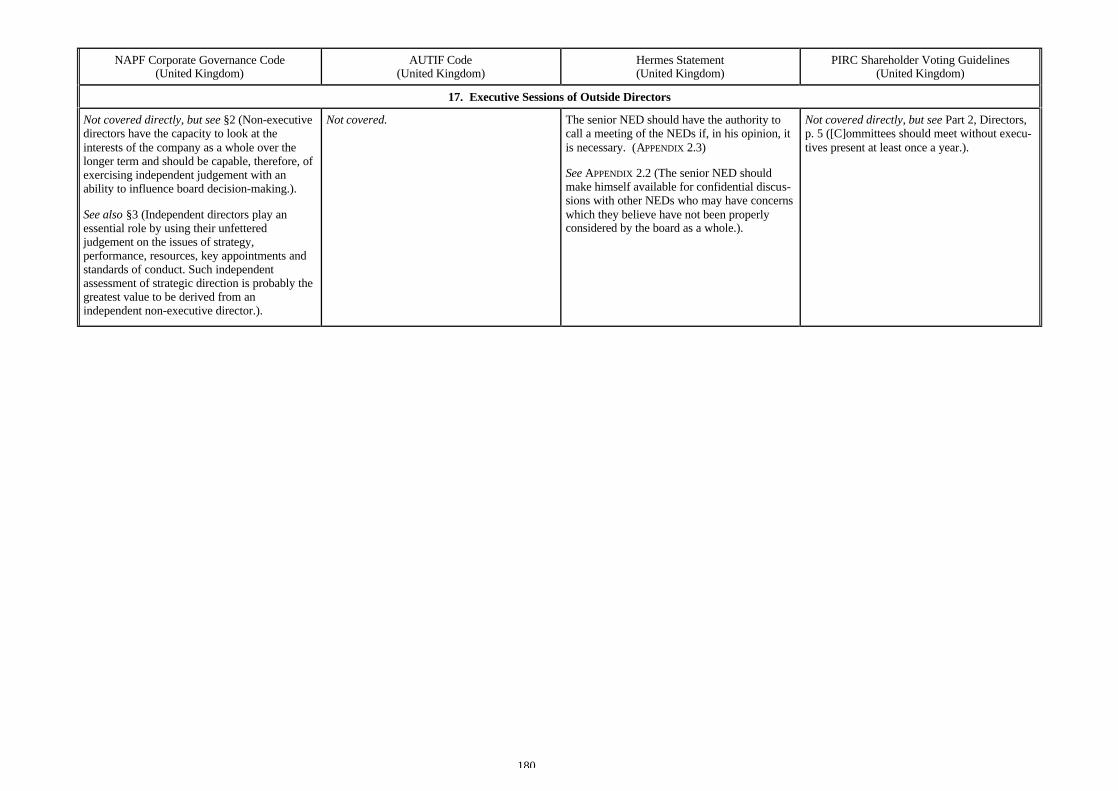

17. Executive Sessions of Outside Directors.........................................................................171

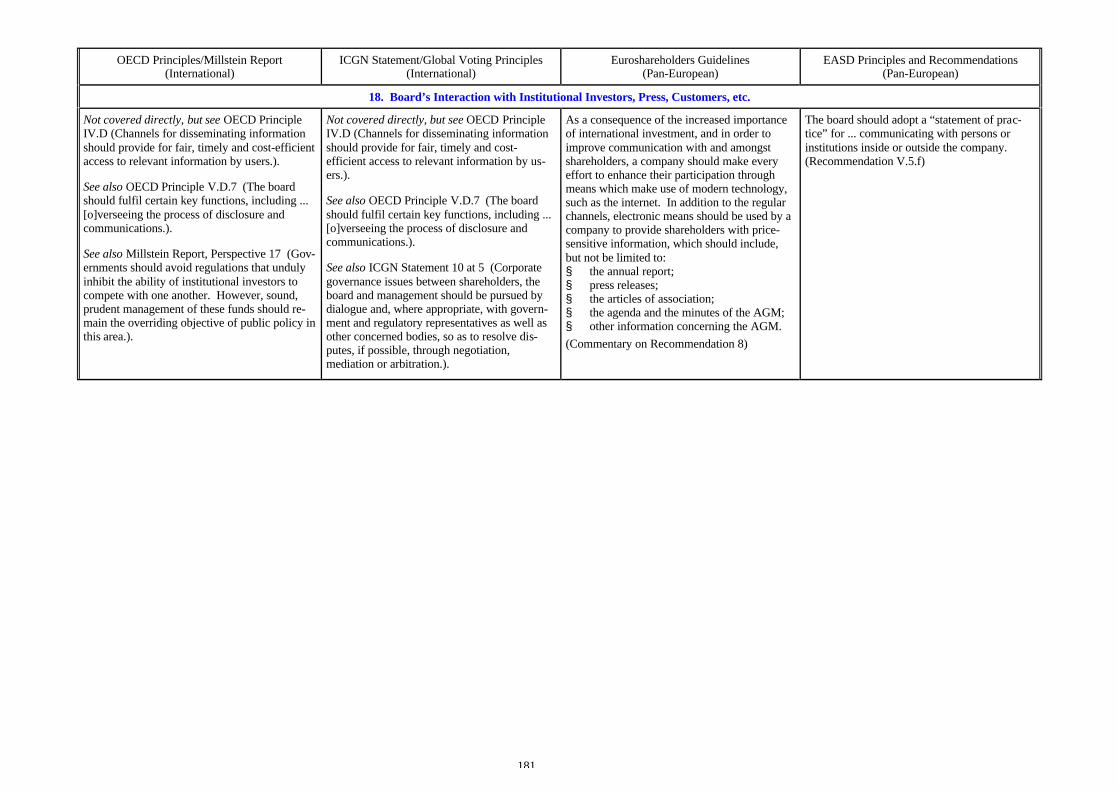

18. Board’s Interaction with Institutional Investors, Press, Customers, etc. ............................ 181

19. Attendance of Non-Directors at Board Meetings / Board Access to SeniorManagement .........................................................................................................191

20. Board Meetings and Agenda .......................................................................................... 201

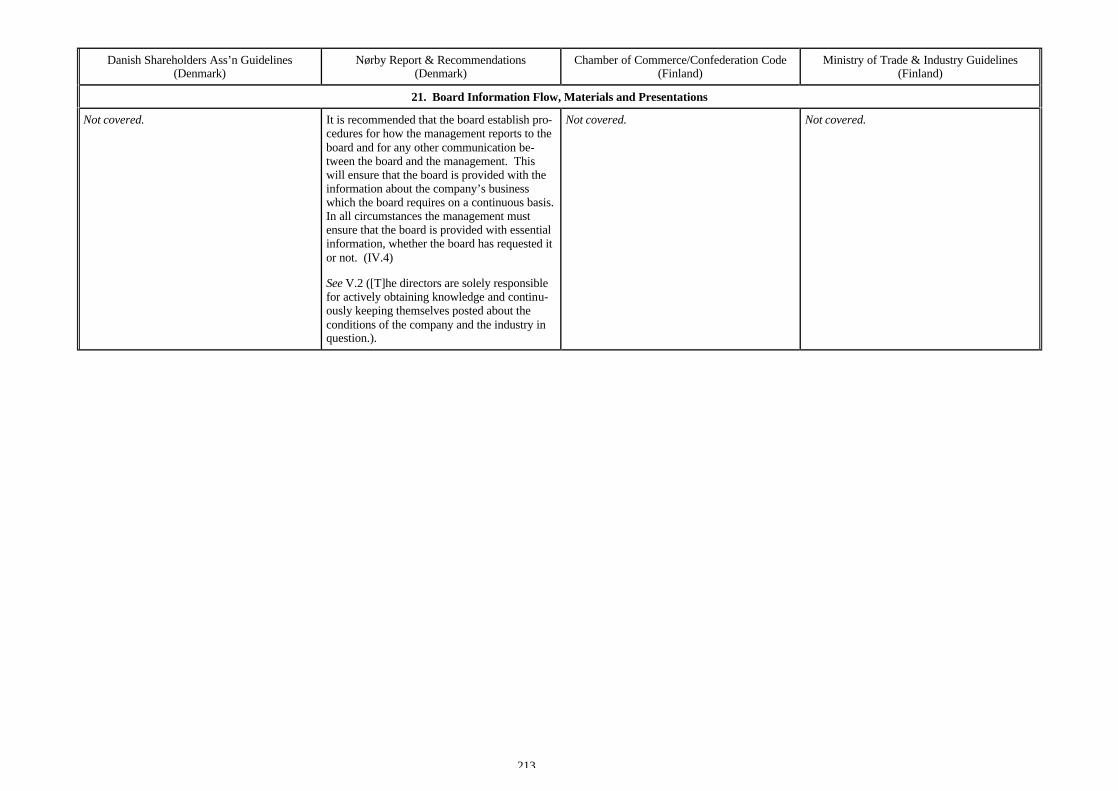

21. Board Information Flow, Materials and Presentations..................................................... 211

22. Number, Structure and Independence of Committees...................................................... 221

23. Committee Meeting Frequency, Length and Agenda ...................................................... 231

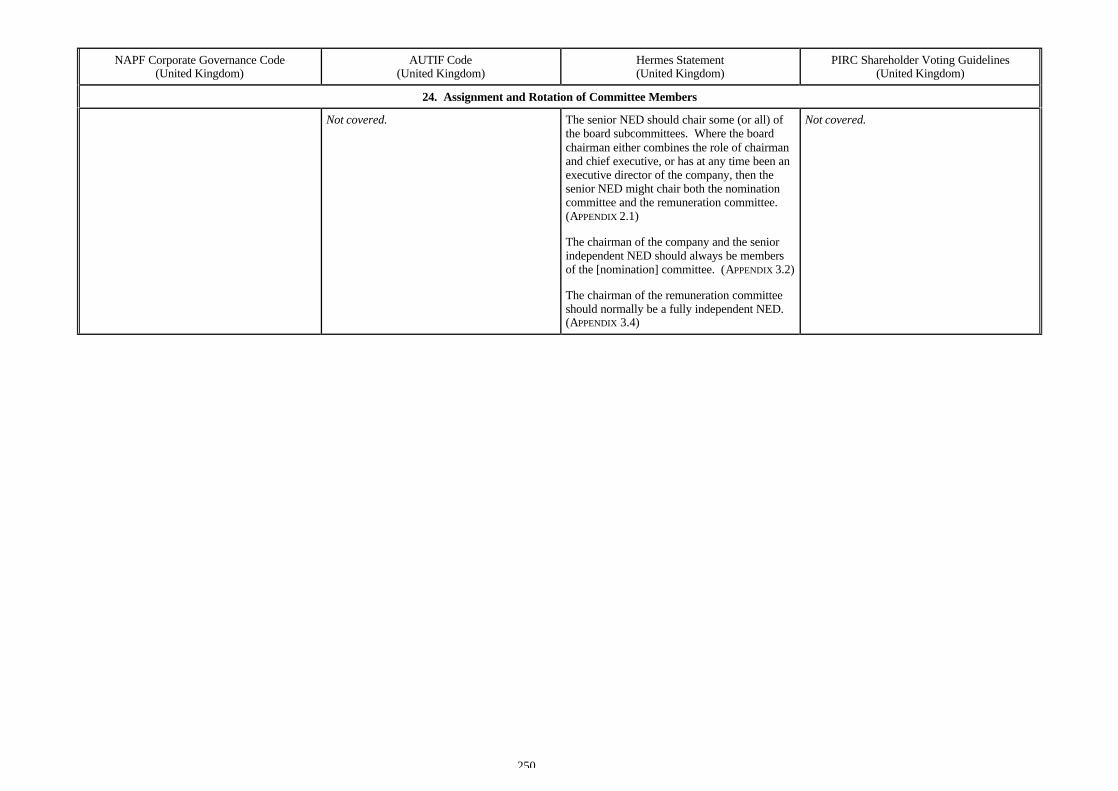

24. Assignment and Rotation of Committee Members .......................................................... 241

25. Formal Evaluation of the Chief Executive Officer .......................................................... 251

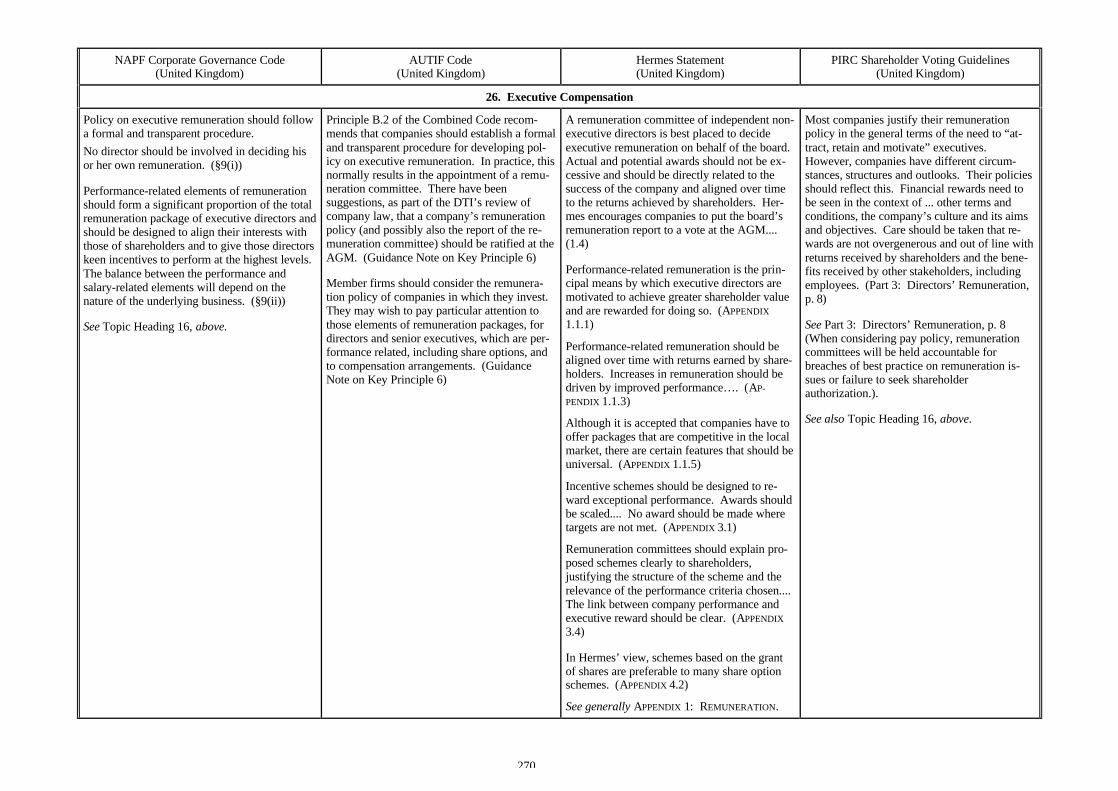

26. Executive Compensation ............................................................................................... 261

27. Succession Planning / Management Development .......................................................... 271

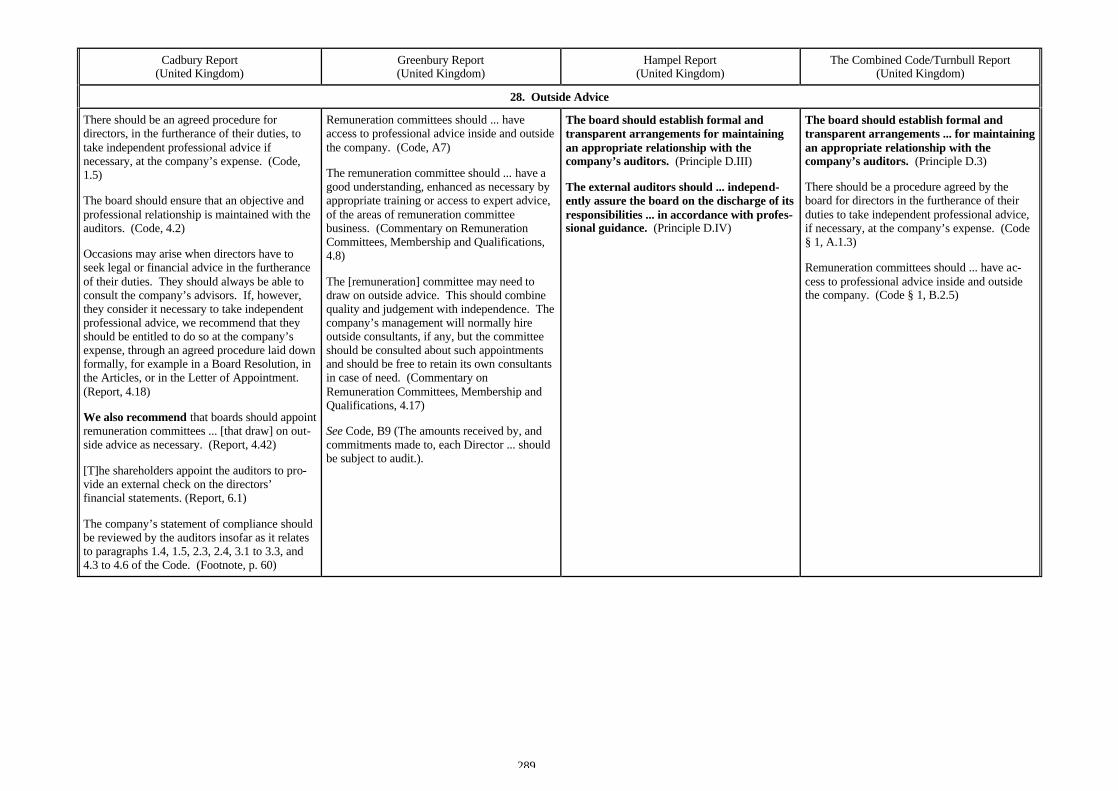

28. Outside Advice ............................................................................................................. 281

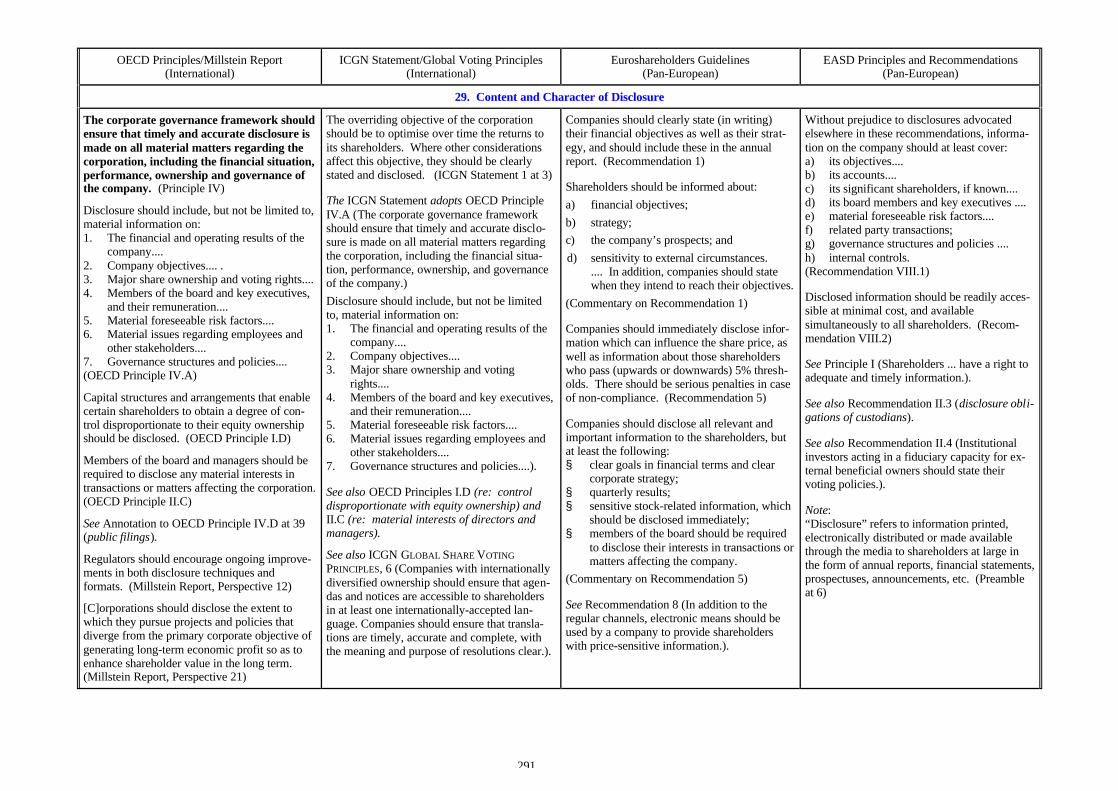

29. Content and Character of Disclosure .............................................................................. 291

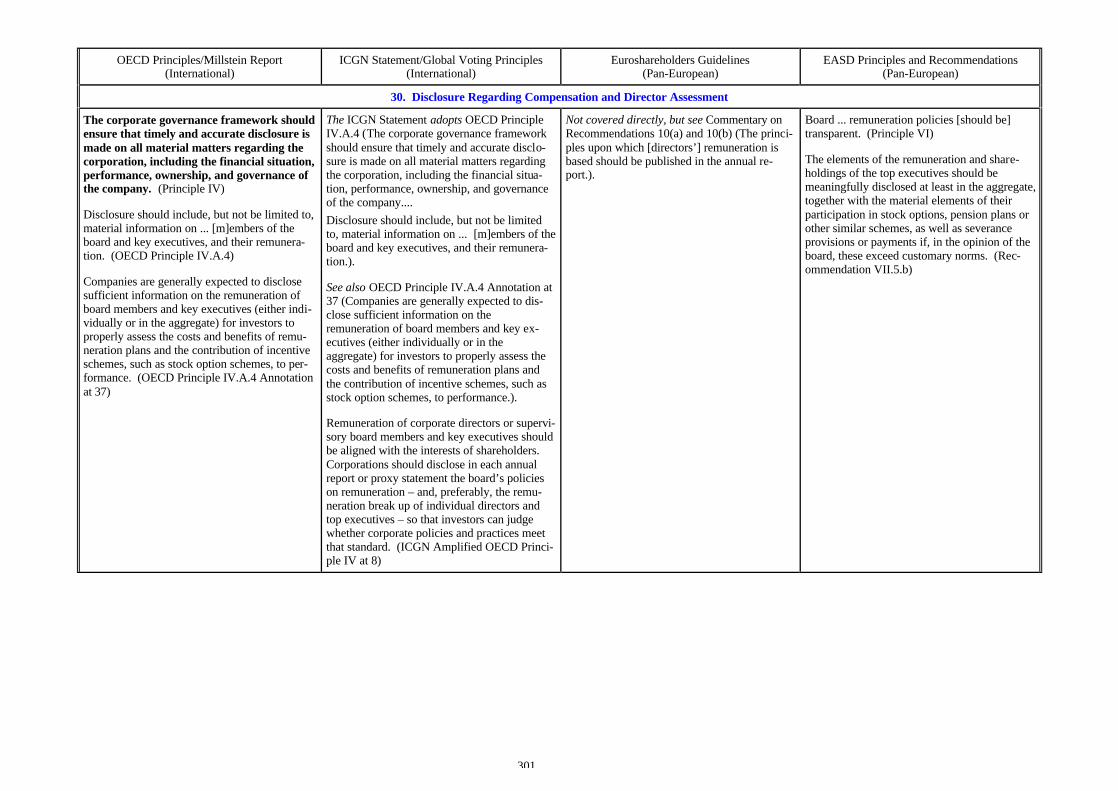

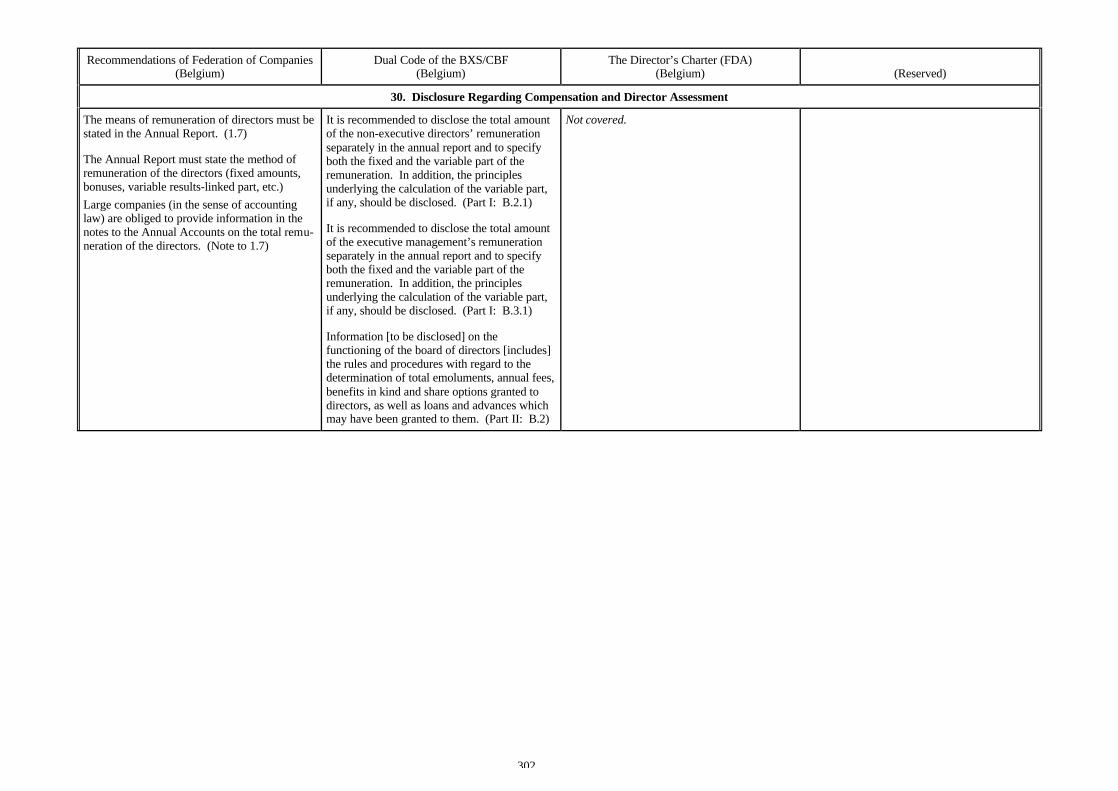

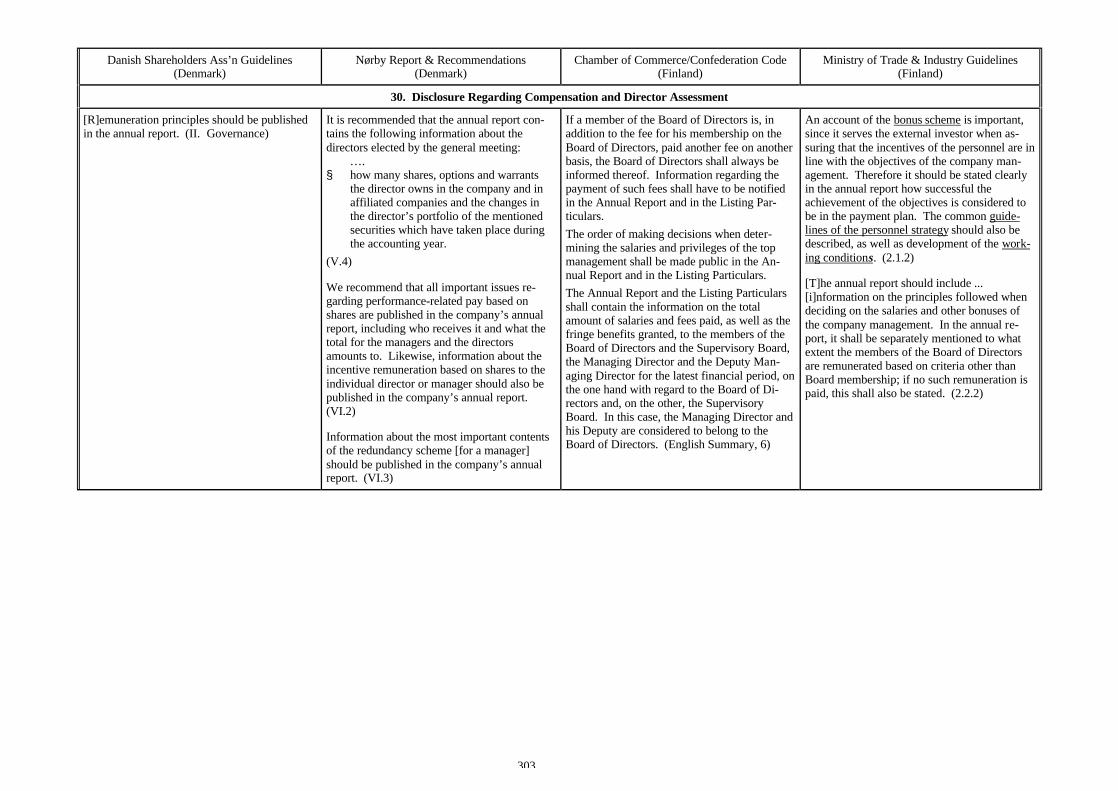

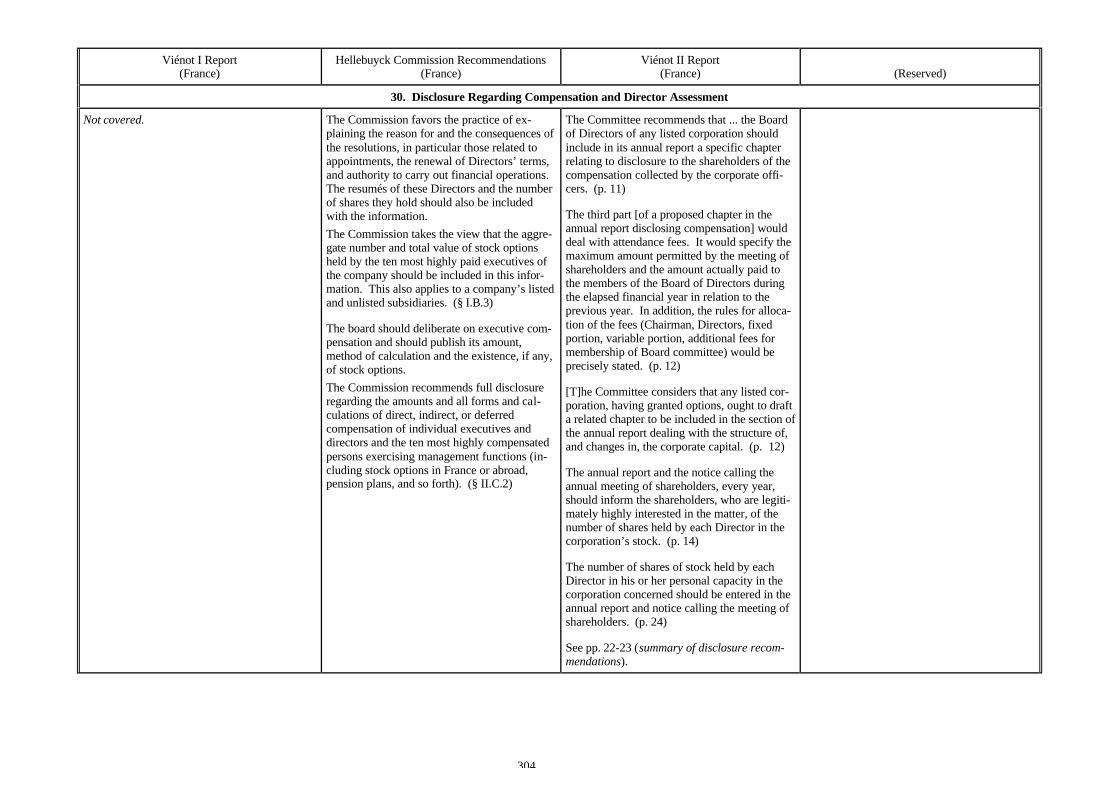

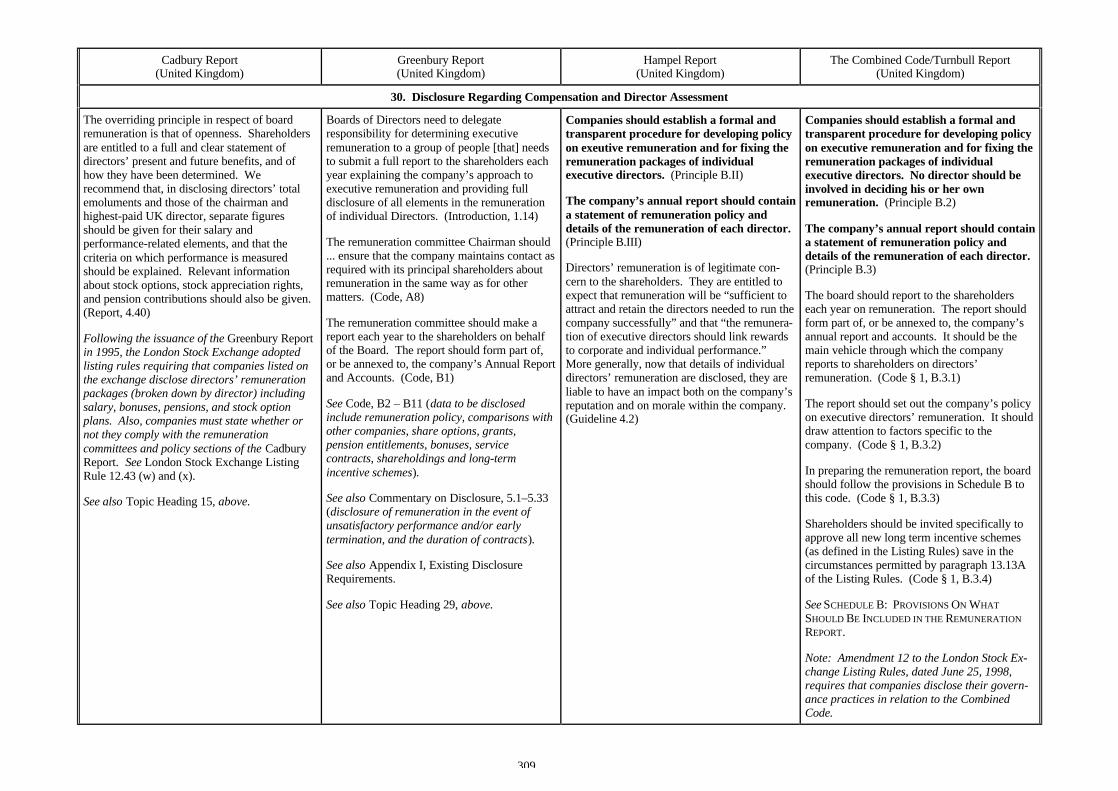

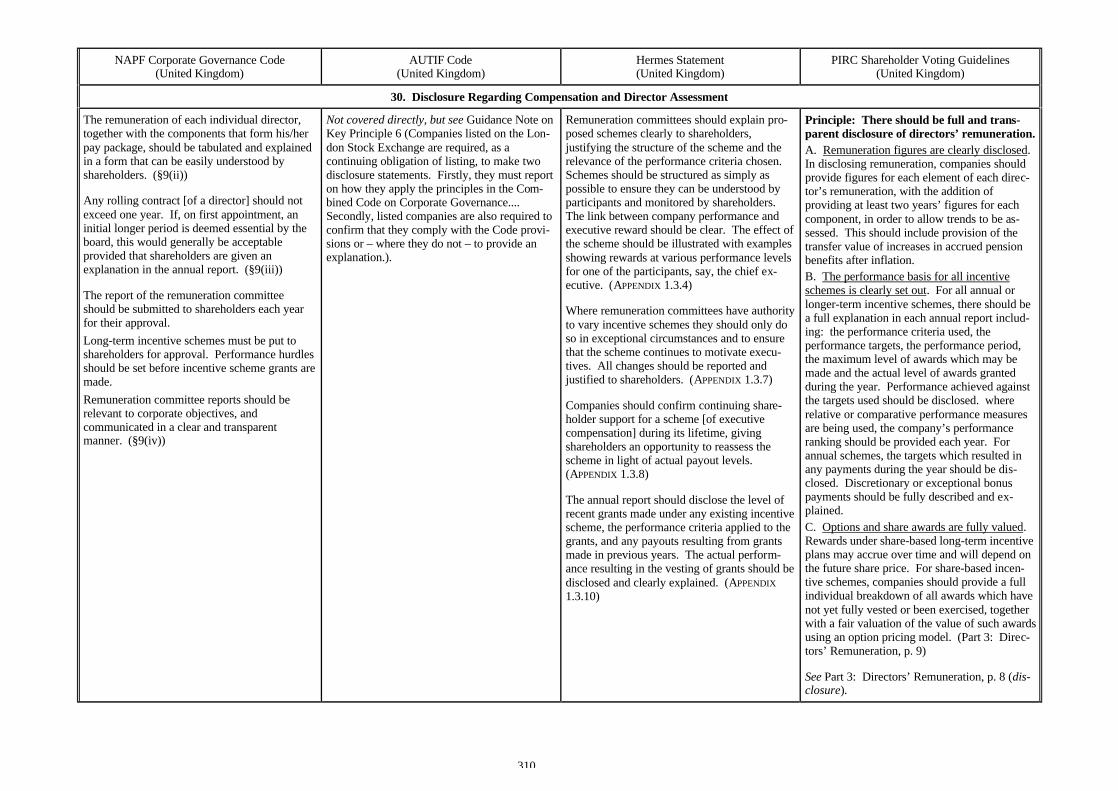

30. Disclosure Regarding Compensation and Director Assessment ....................................... 301

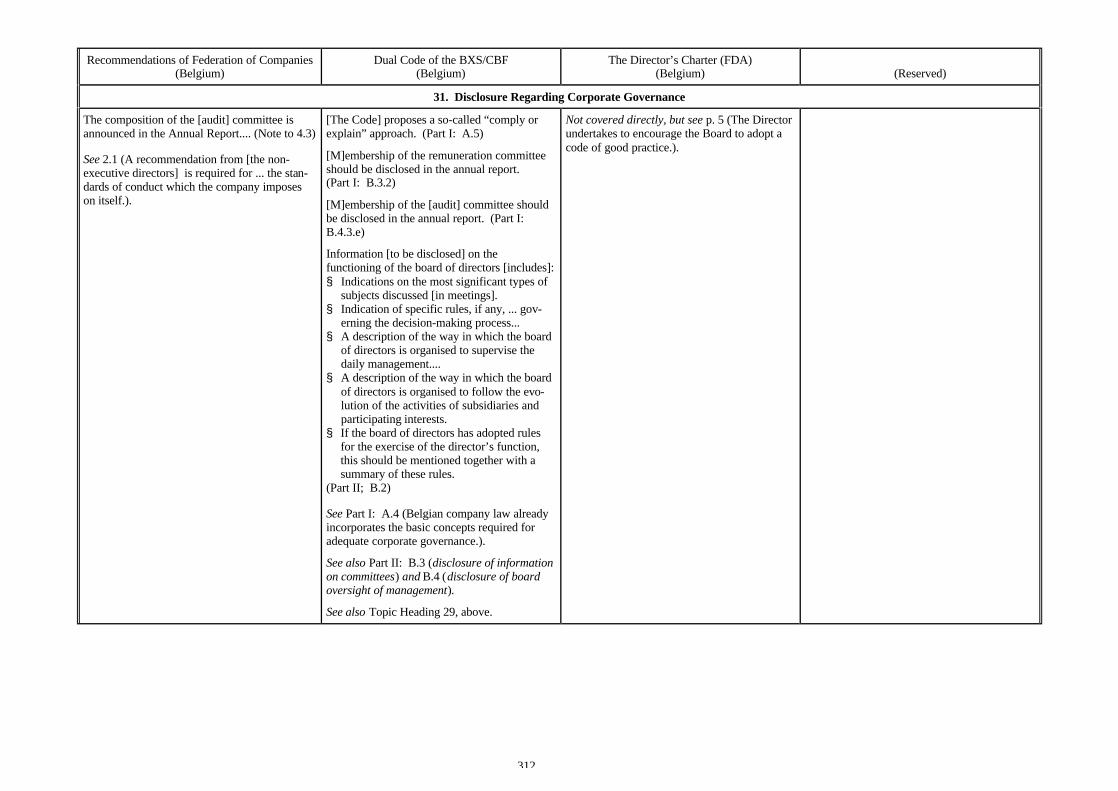

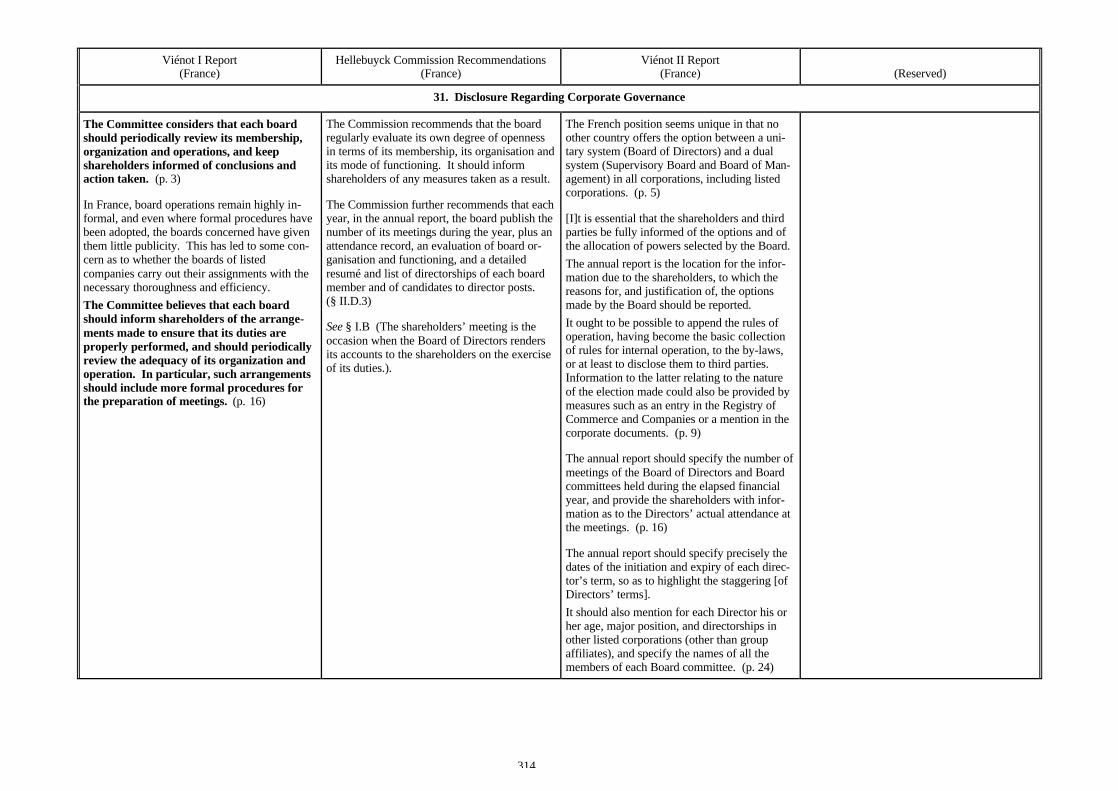

31. Disclosure Regarding Corporate Governance ................................................................. 311

32. Accuracy of Disclosure / Internal Control Systems / Liability ......................................... 321

33. Shareholder Voting Practices (Cumulative & Confidential Voting, Broker Non-Votes,One Share/One Vote)............................................................................................ 331

34. Shareholder Voting Powers ........................................................................................... 341

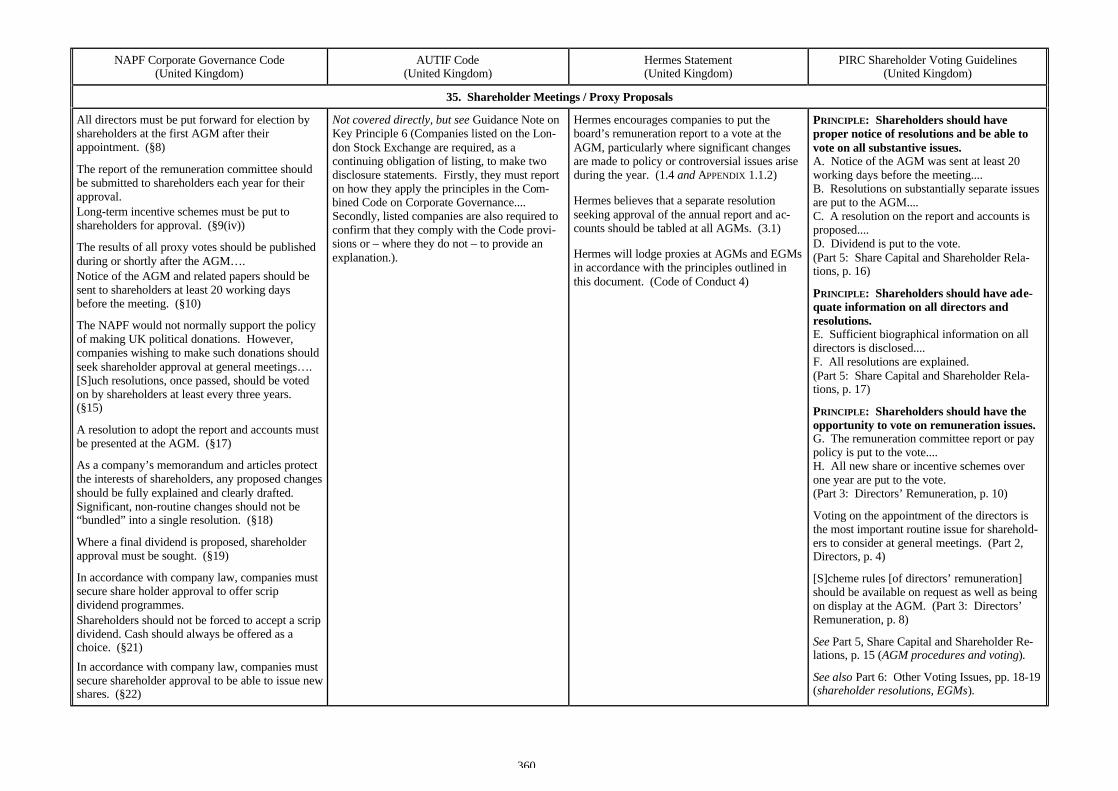

35. Shareholder Meetings / Proxy Proposals ........................................................................ 351

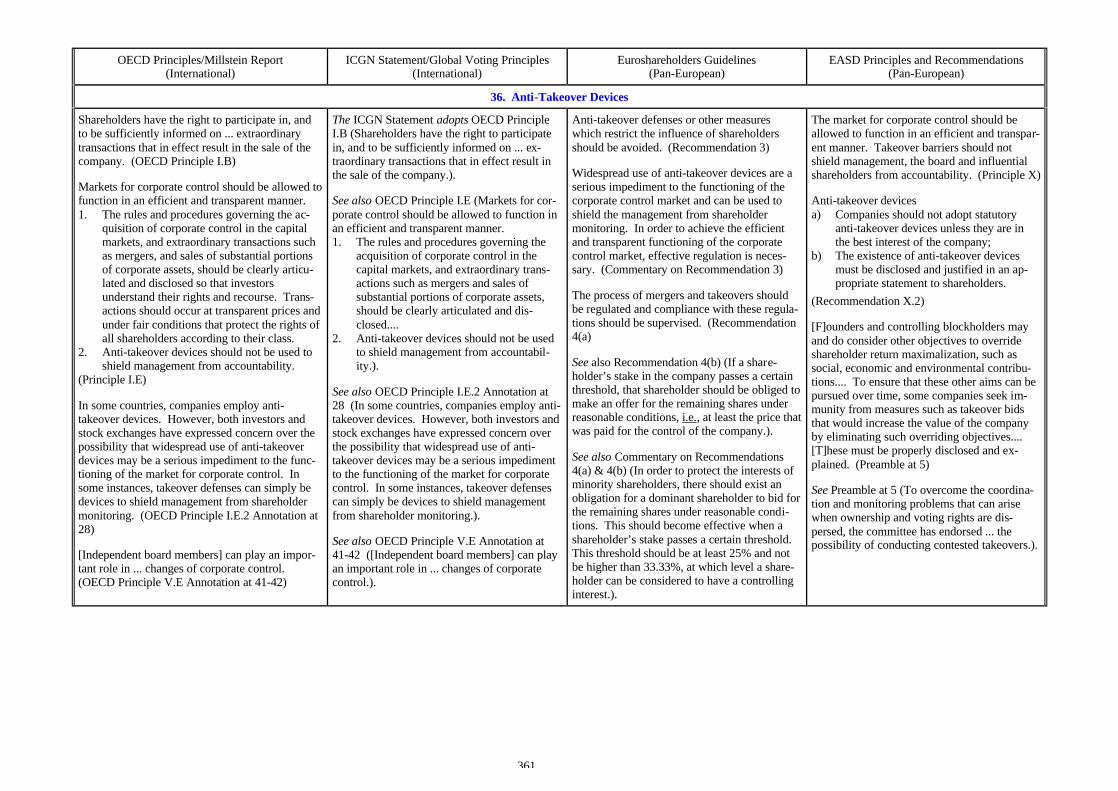

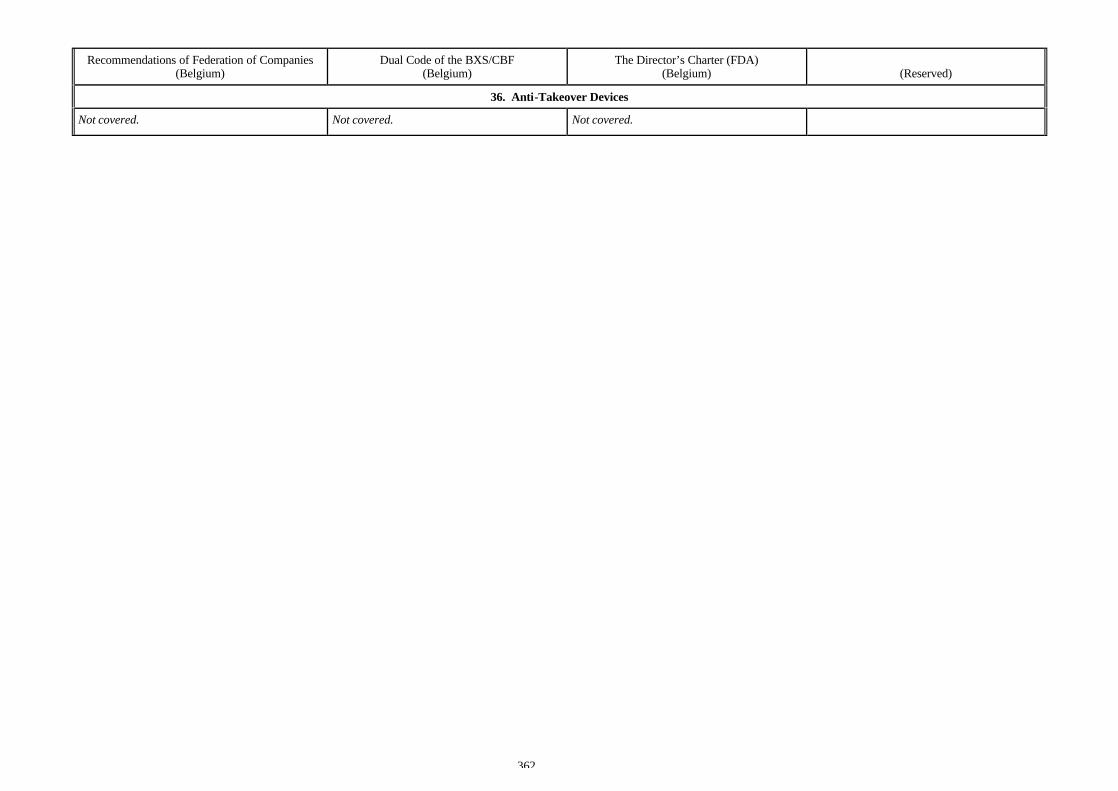

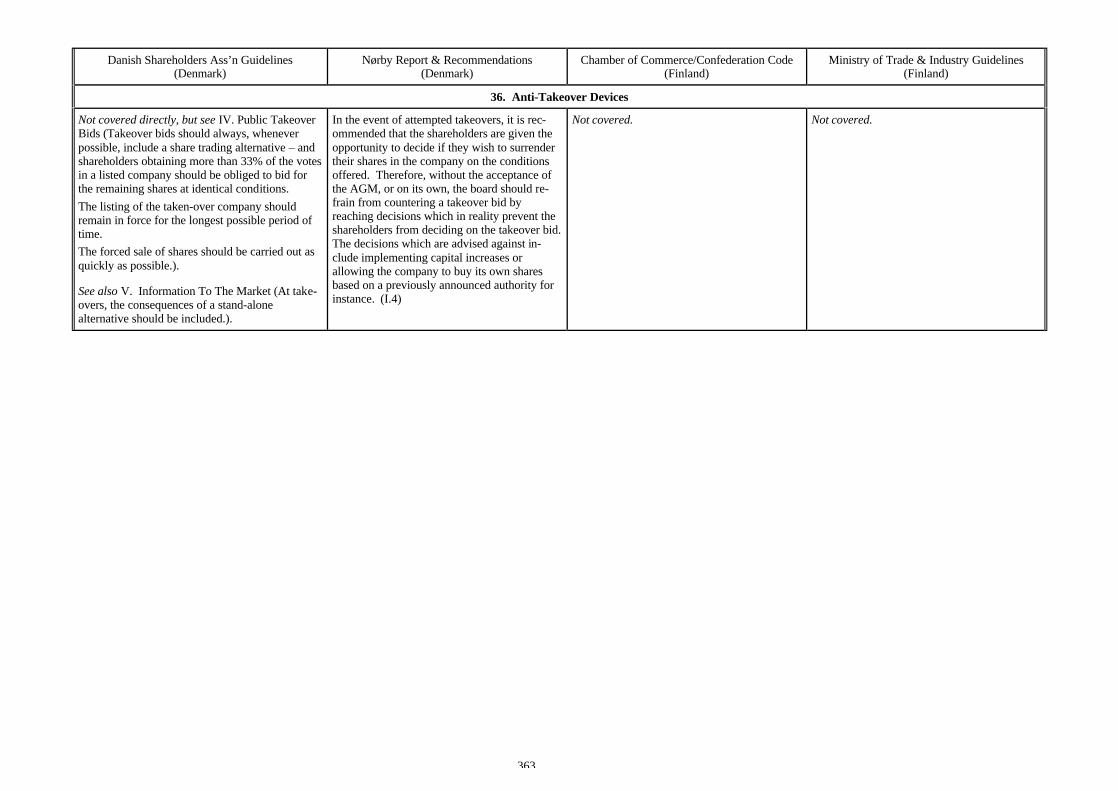

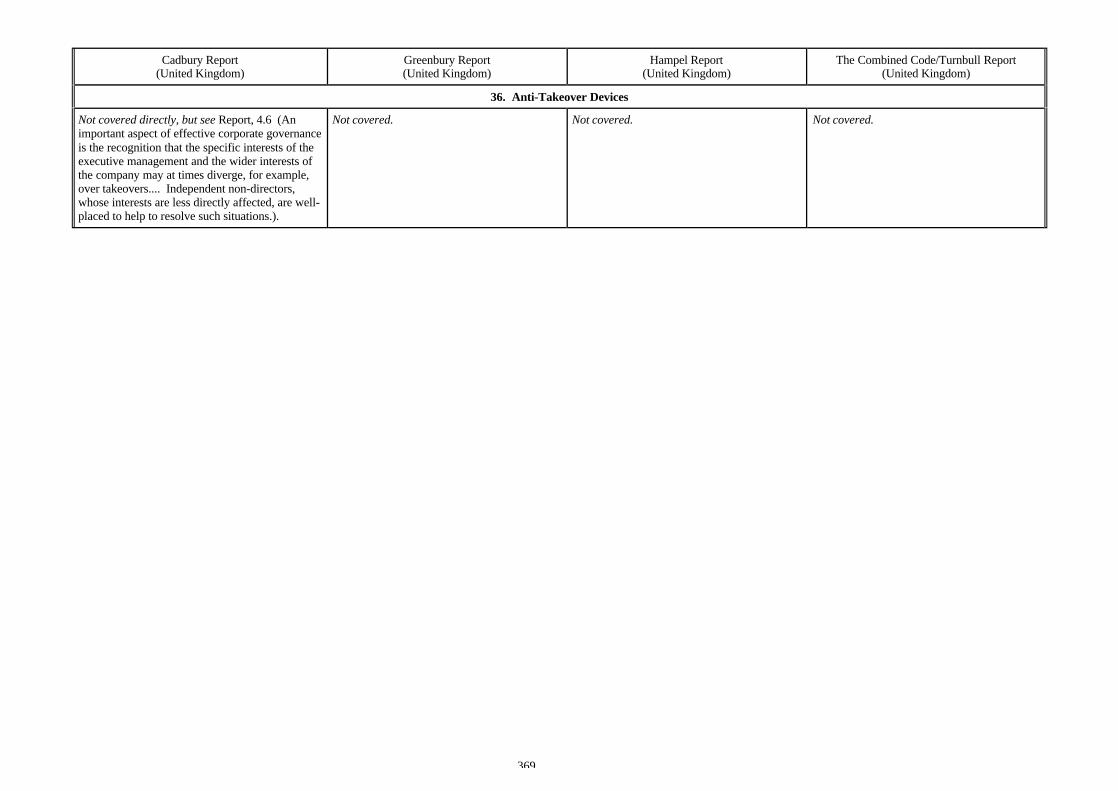

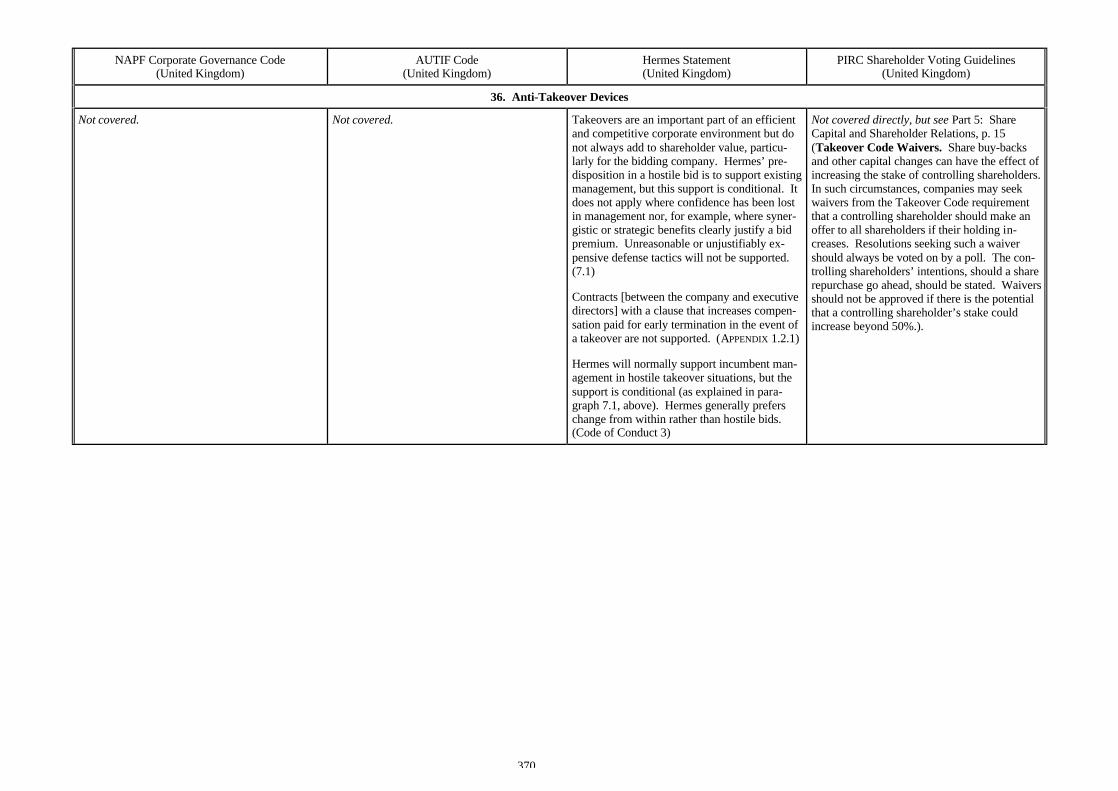

36. Anti-Takeover Devices.................................................................................................. 361

APPENDIX Partial Listing of Corporate Governance Guidelines and Codes of BestPractice Throughout the World........................................................................... APP-1

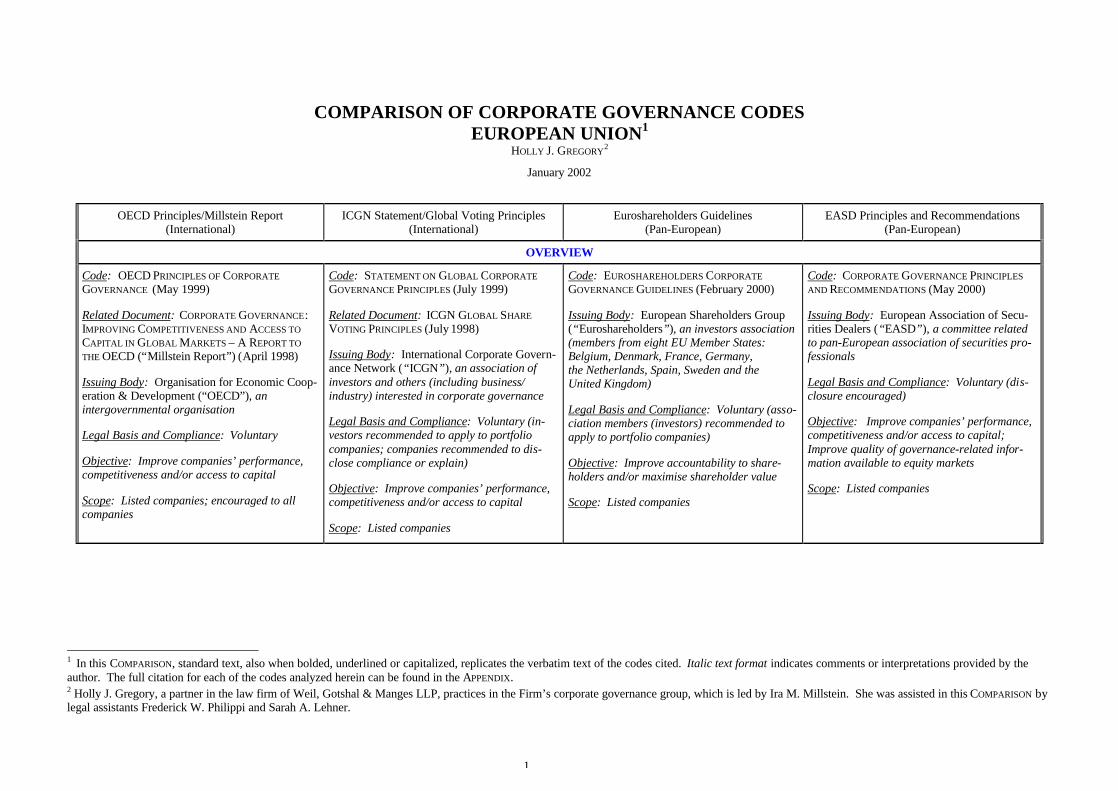

1

COMPARISON OF CORPORATE GOVERNANCE CODESEUROPEAN UNION1

HOLLY J. GREGORY2

January 2002

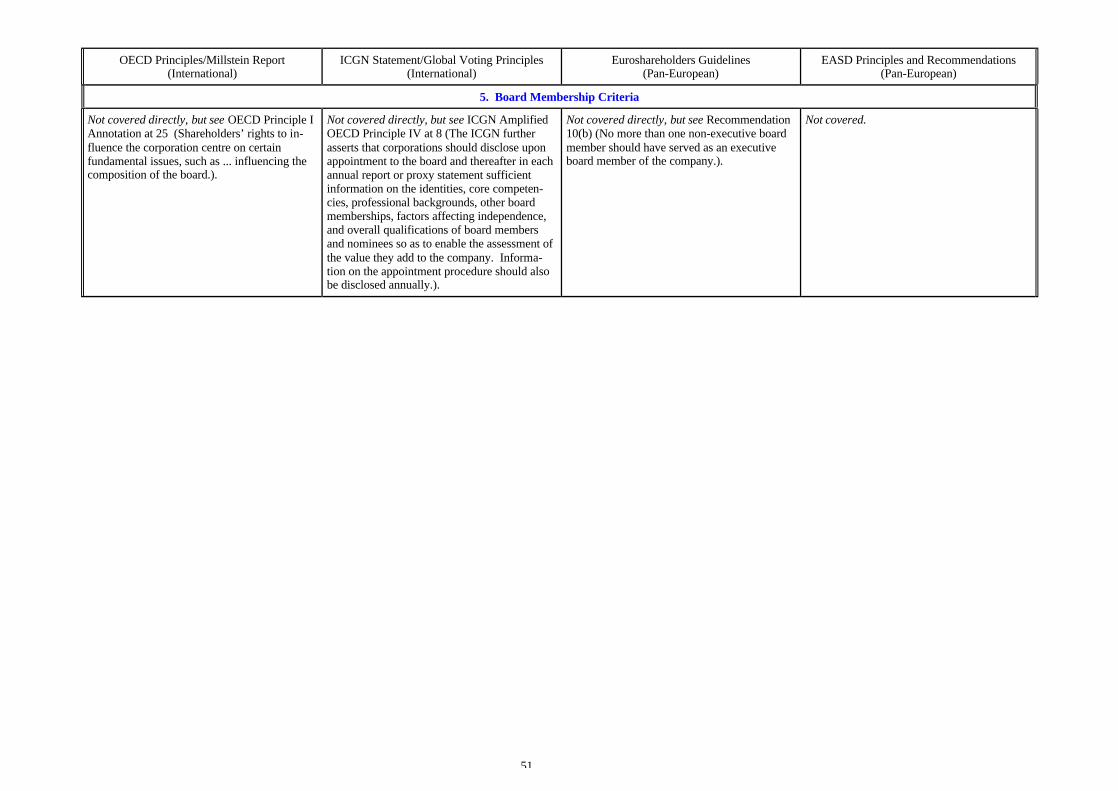

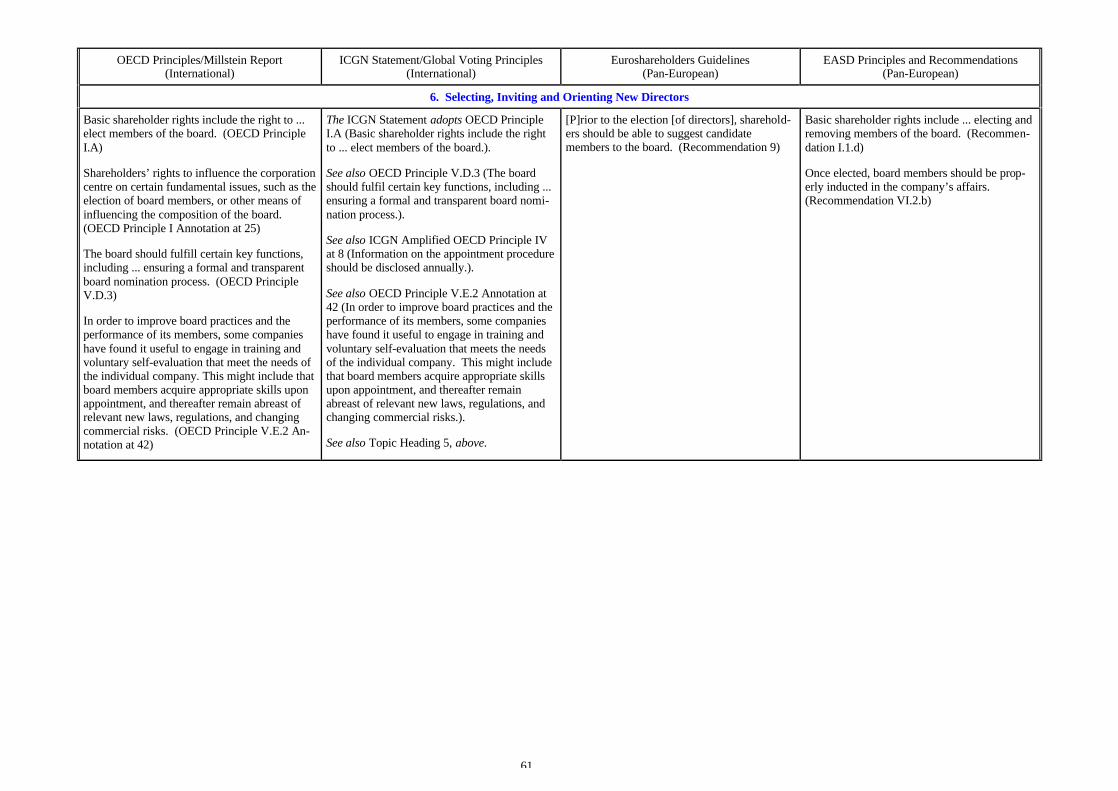

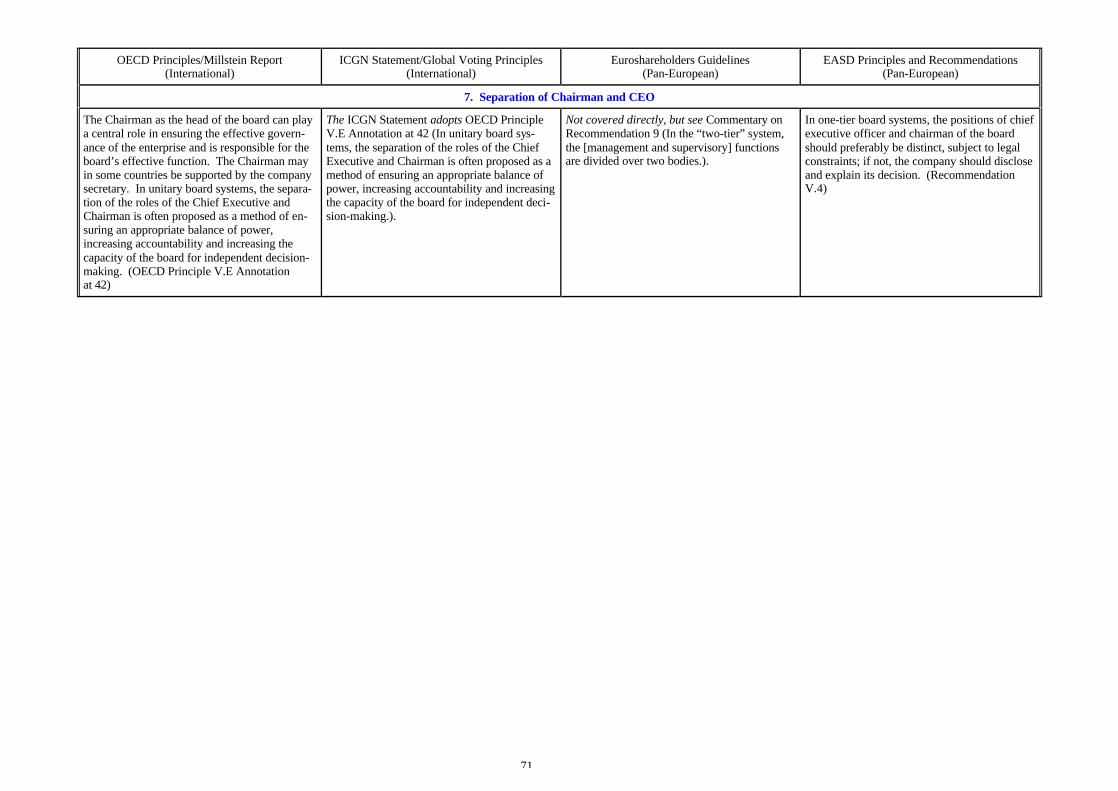

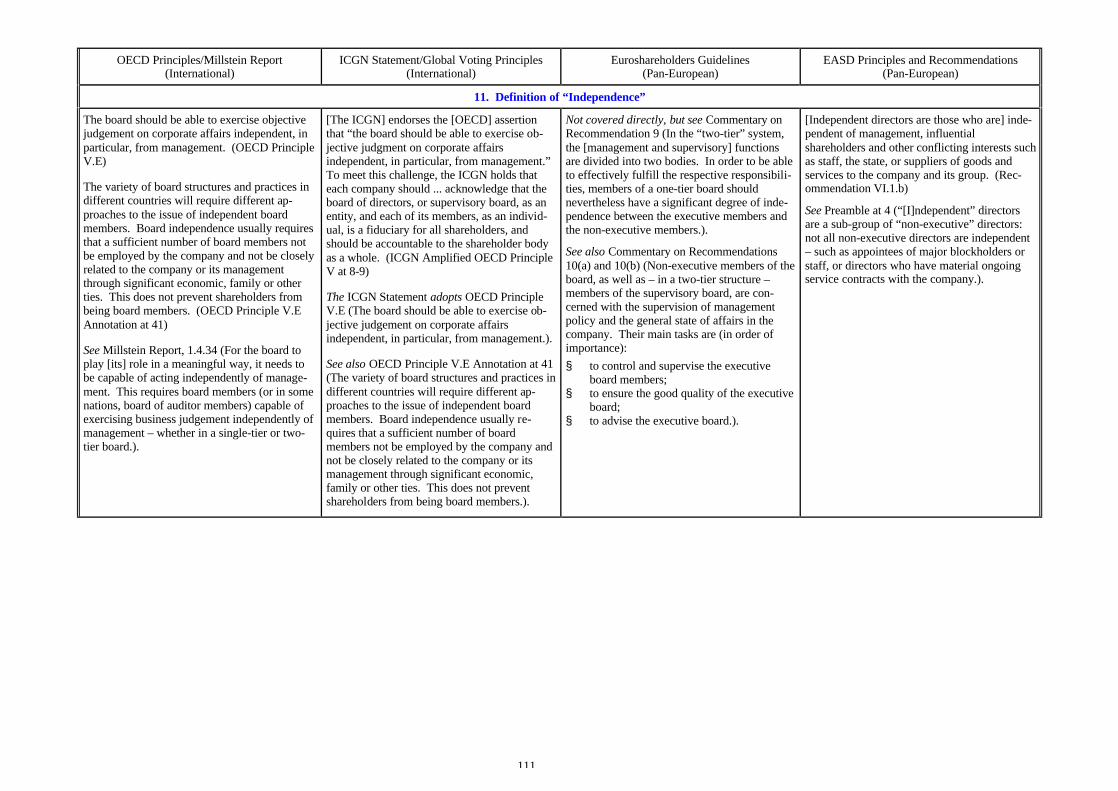

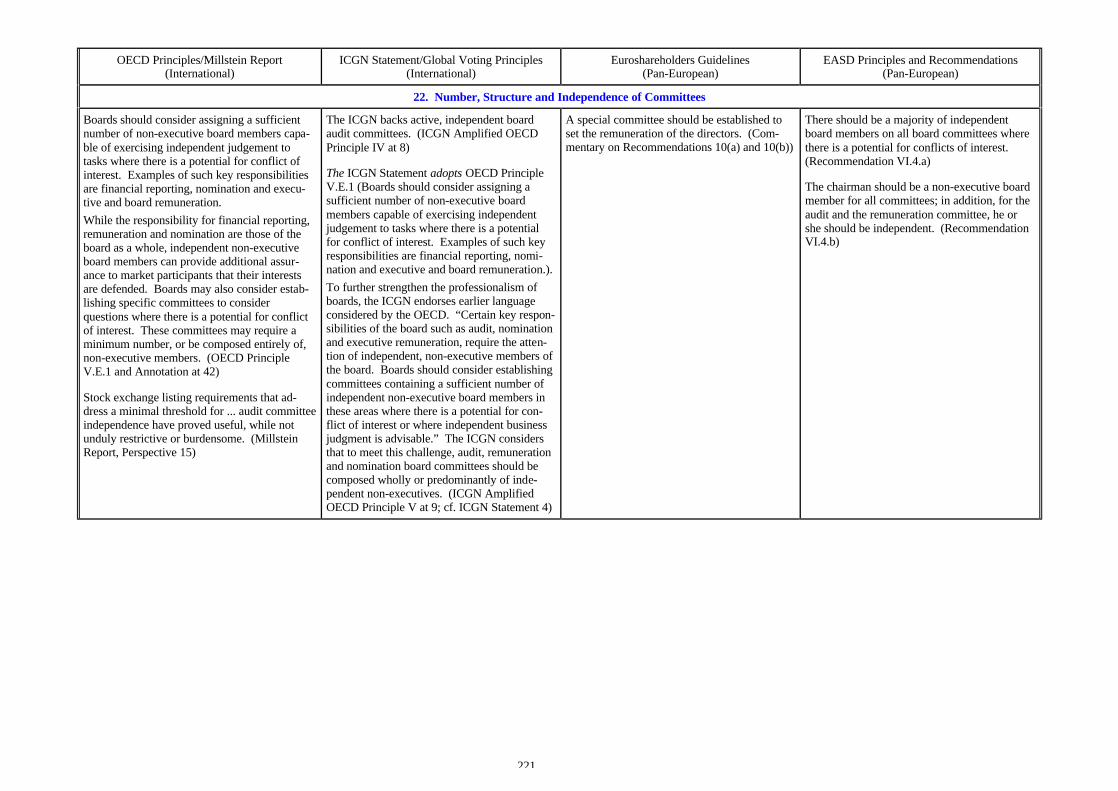

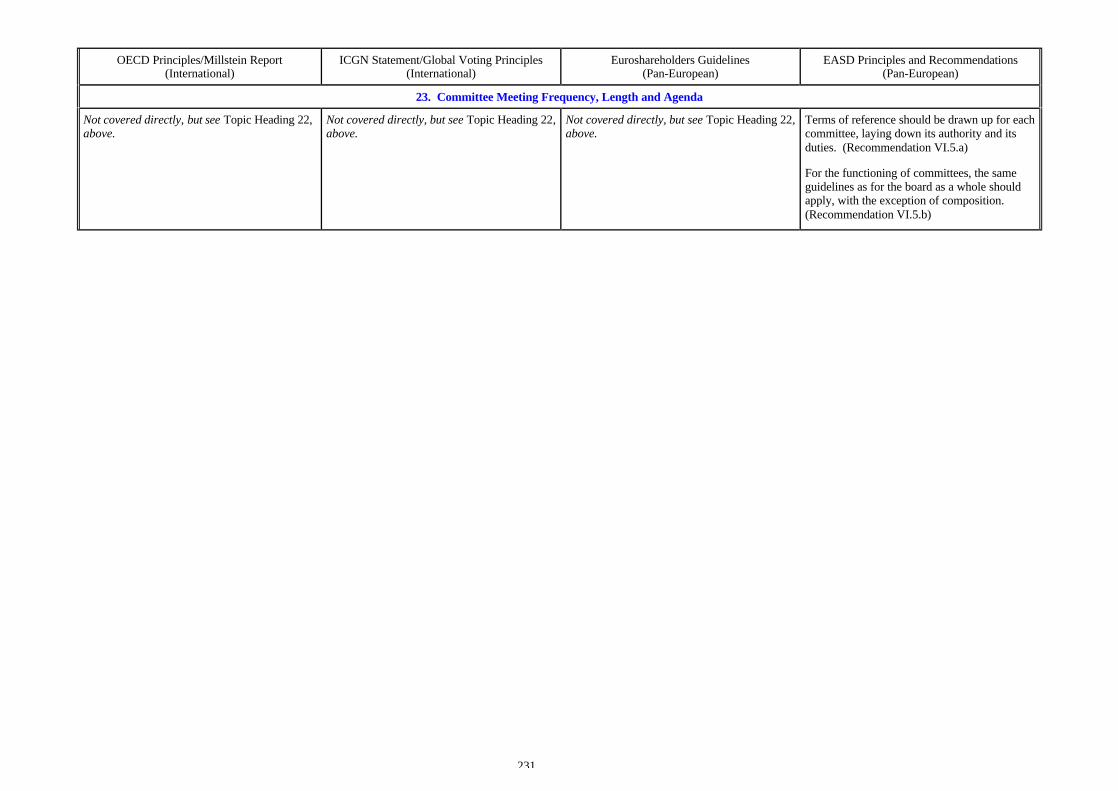

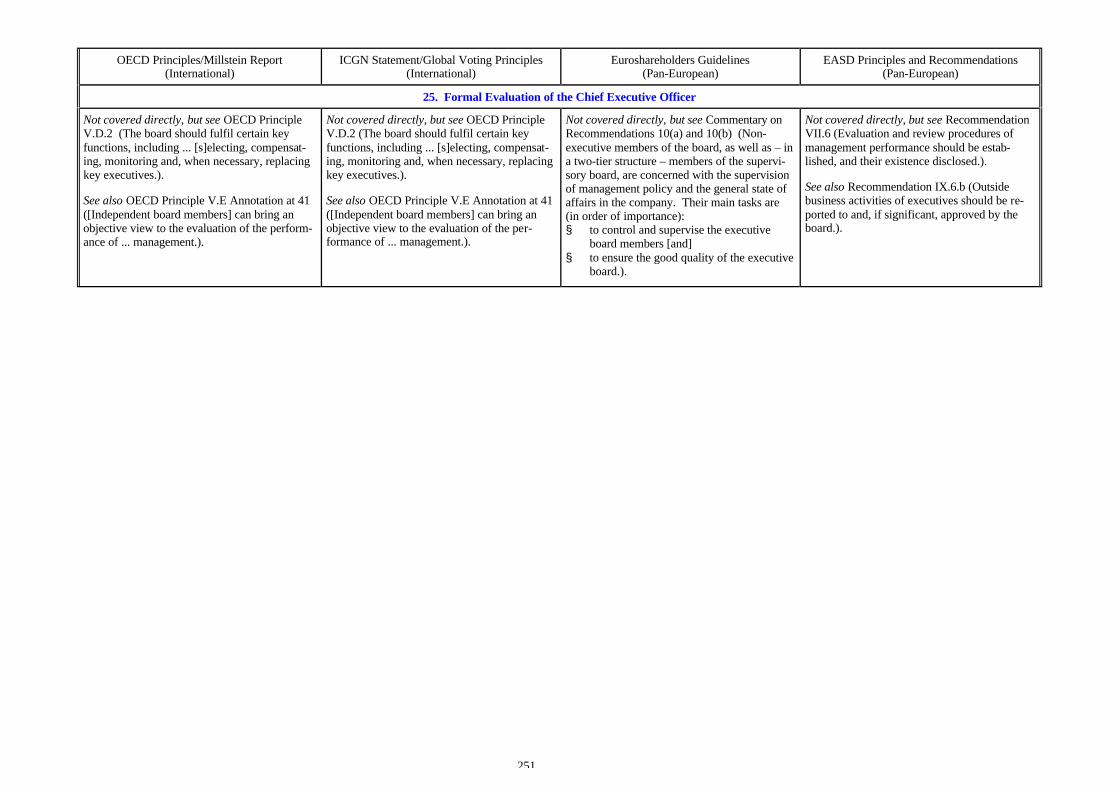

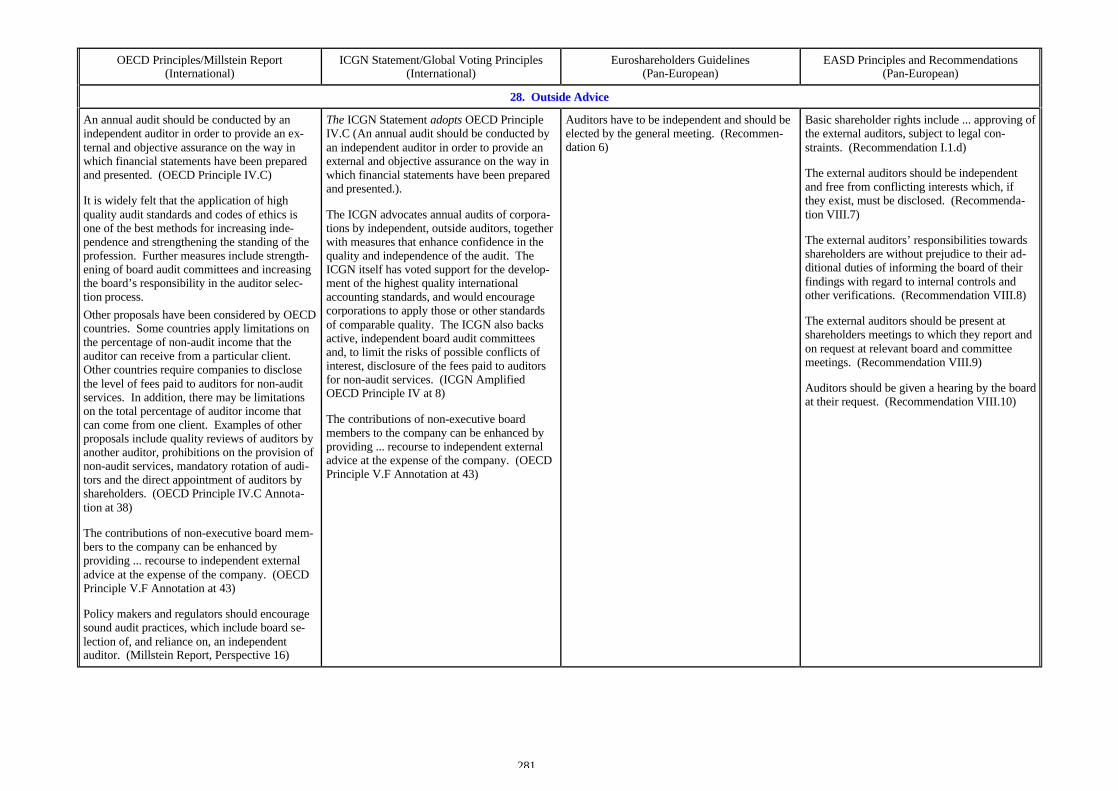

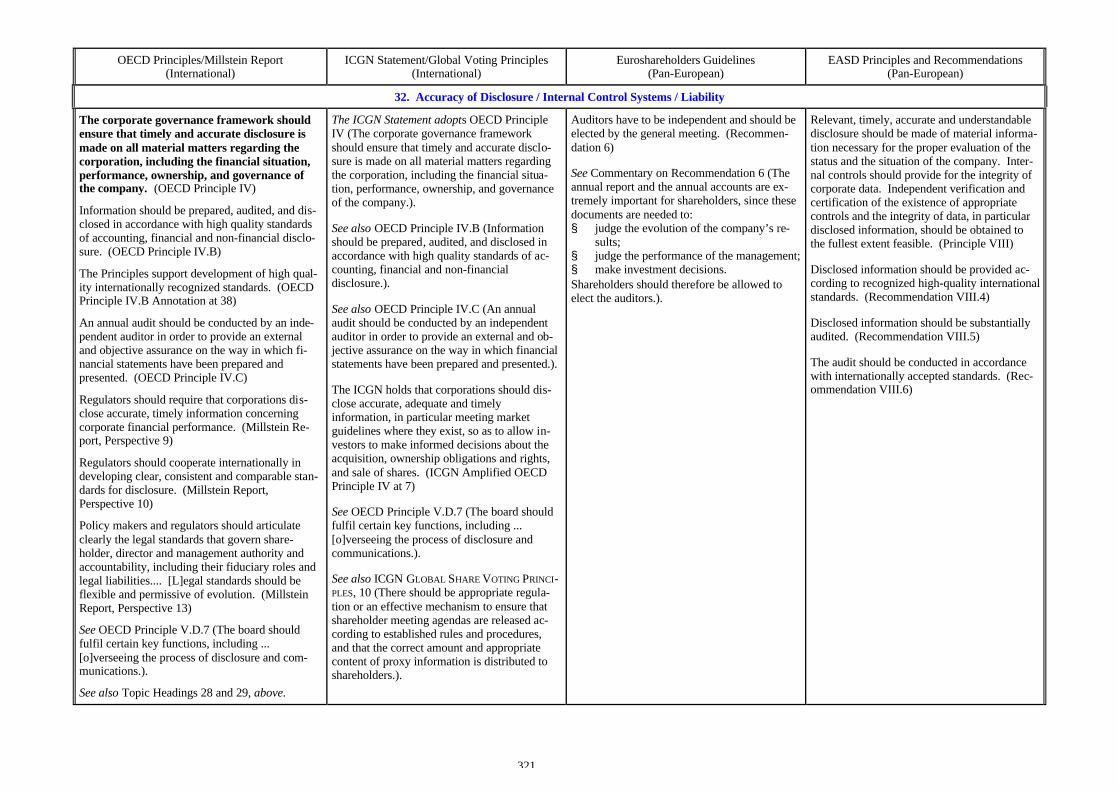

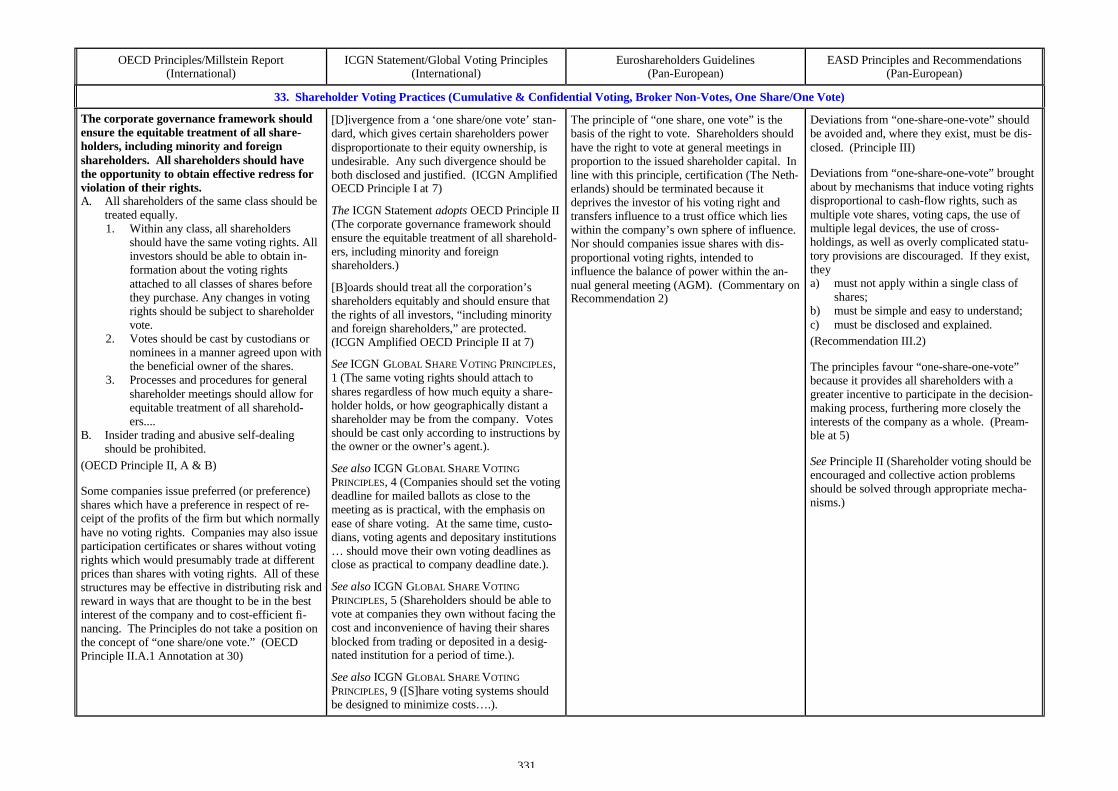

OECD Principles/Millstein Report(International)

ICGN Statement/Global Voting Principles(International)

Euroshareholders Guidelines(Pan-European)

EASD Principles and Recommendations(Pan-European)

OVERVIEW

Code: OECD PRINCIPLES OF CORPORATEGOVERNANCE (May 1999)

Related Document: CORPORATE GOVERNANCE:IMPROVING COMPETITIVENESS AND ACCESS TOCAPITAL IN GLOBAL MARKETS – A REPORT TOTHE OECD (“Millstein Report”) (April 1998)

Issuing Body: Organisation for Economic Coop-eration & Development (“OECD”), anintergovernmental organisation

Legal Basis and Compliance: Voluntary

Objective: Improve companies’ performance,competitiveness and/or access to capital

Scope: Listed companies; encouraged to allcompanies

Code: STATEMENT ON GLOBAL CORPORATEGOVERNANCE PRINCIPLES (July 1999)

Related Document: ICGN GLOBAL SHAREVOTING PRINCIPLES (July 1998)

Issuing Body: International Corporate Govern-ance Network (“ICGN”), an association ofinvestors and others (including business/industry) interested in corporate governance

Legal Basis and Compliance: Voluntary (in-vestors recommended to apply to portfoliocompanies; companies recommended to dis-close compliance or explain)

Objective: Improve companies’ performance,competitiveness and/or access to capital

Scope: Listed companies

Code: EUROSHAREHOLDERS CORPORATEGOVERNANCE GUIDELINES (February 2000)

Issuing Body: European Shareholders Group(“Euroshareholders”), an investors association(members from eight EU Member States:Belgium, Denmark, France, Germany,the Netherlands, Spain, Sweden and theUnited Kingdom)

Legal Basis and Compliance: Voluntary (asso-ciation members (investors) recommended toapply to portfolio companies)

Objective: Improve accountability to share-holders and/or maximise shareholder value

Scope: Listed companies

Code: CORPORATE GOVERNANCE PRINCIPLESAND RECOMMENDATIONS (May 2000)

Issuing Body: European Association of Secu-rities Dealers (“EASD”), a committee relatedto pan-European association of securities pro-fessionals

Legal Basis and Compliance: Voluntary (dis-closure encouraged)

Objective: Improve companies’ performance,competitiveness and/or access to capital;Improve quality of governance-related infor-mation available to equity markets

Scope: Listed companies

1 In this COMPARISON, standard text, also when bolded, underlined or capitalized, replicates the verbatim text of the codes cited. Italic text format indicates comments or interpretations provided by theauthor. The full citation for each of the codes analyzed herein can be found in the APPENDIX.2 Holly J. Gregory, a partner in the law firm of Weil, Gotshal & Manges LLP, practices in the Firm’s corporate governance group, which is led by Ira M. Millstein. She was assisted in this COMPARISON bylegal assistants Frederick W. Philippi and Sarah A. Lehner.

2

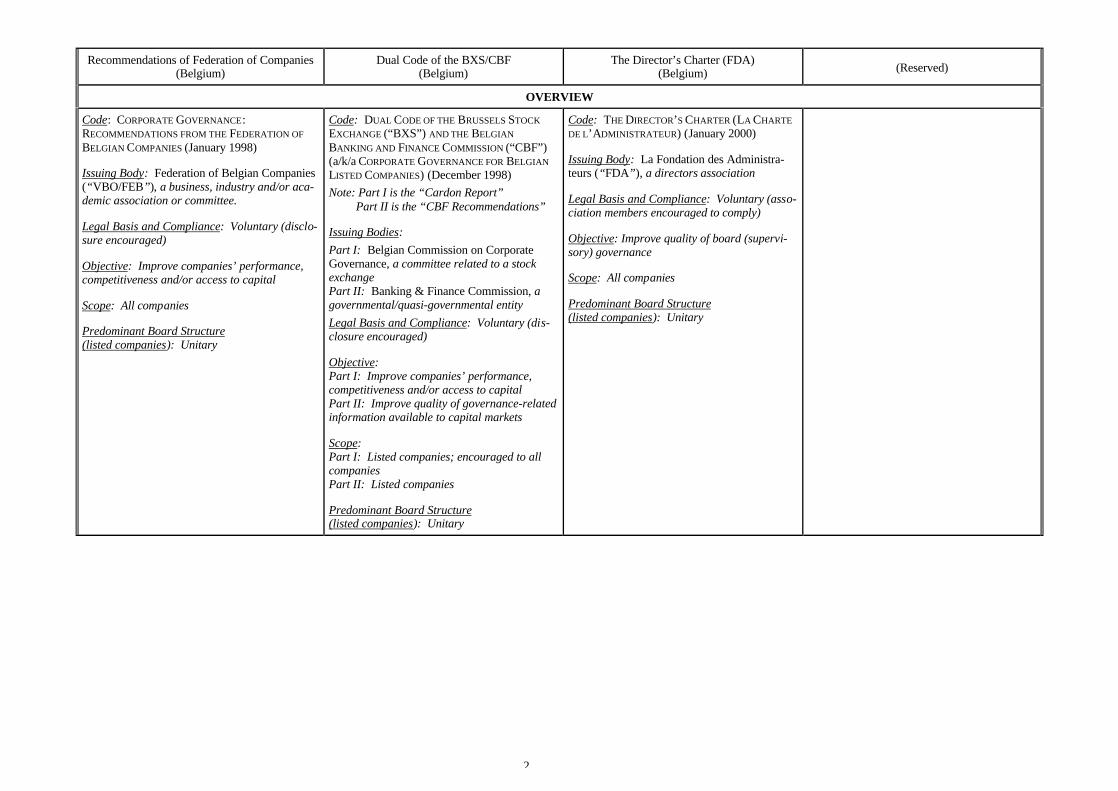

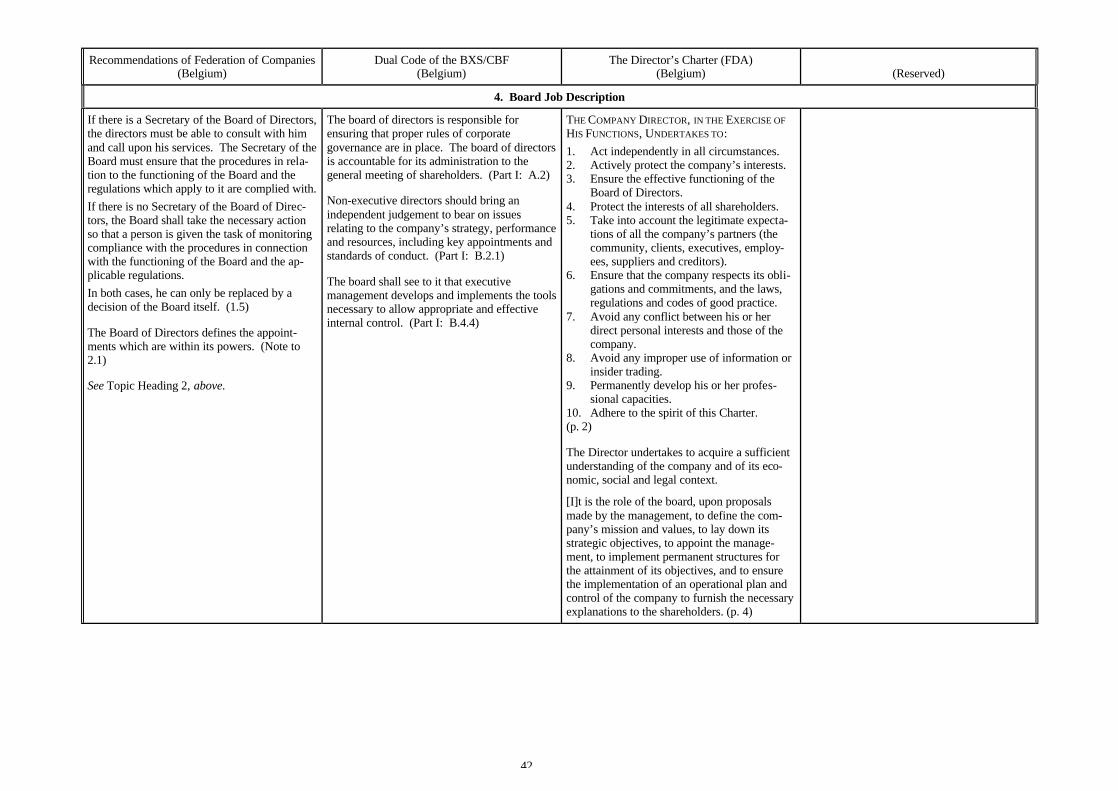

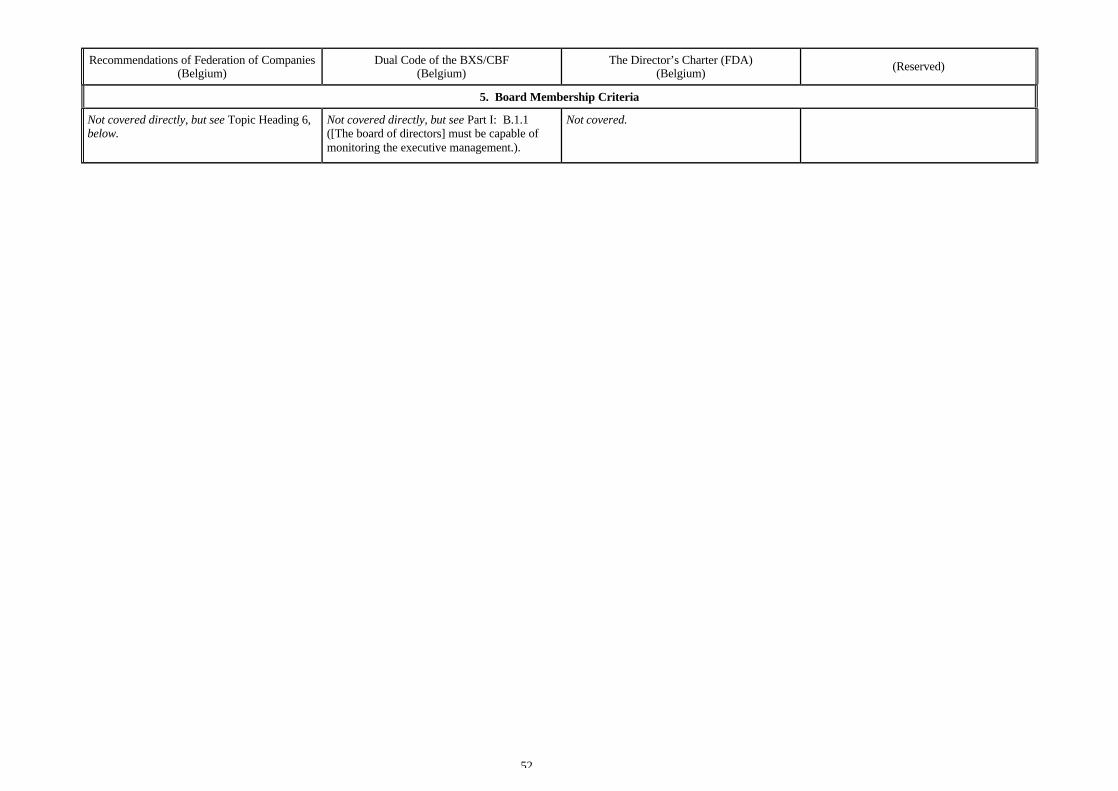

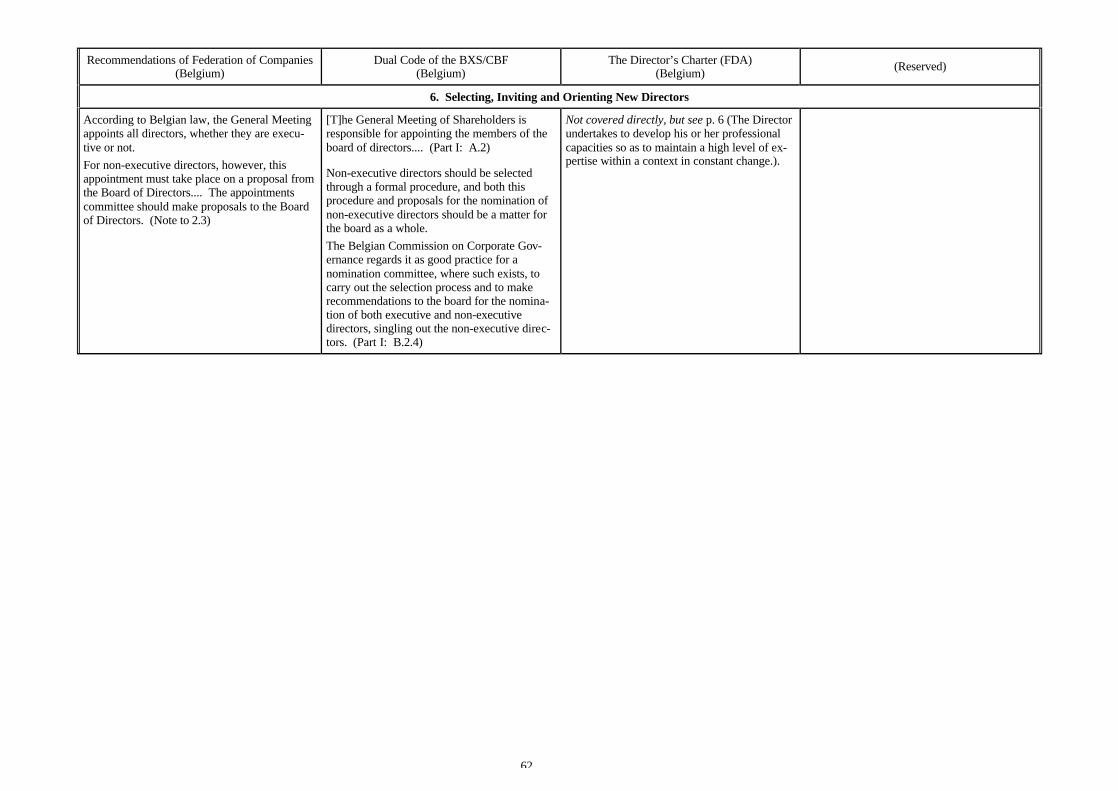

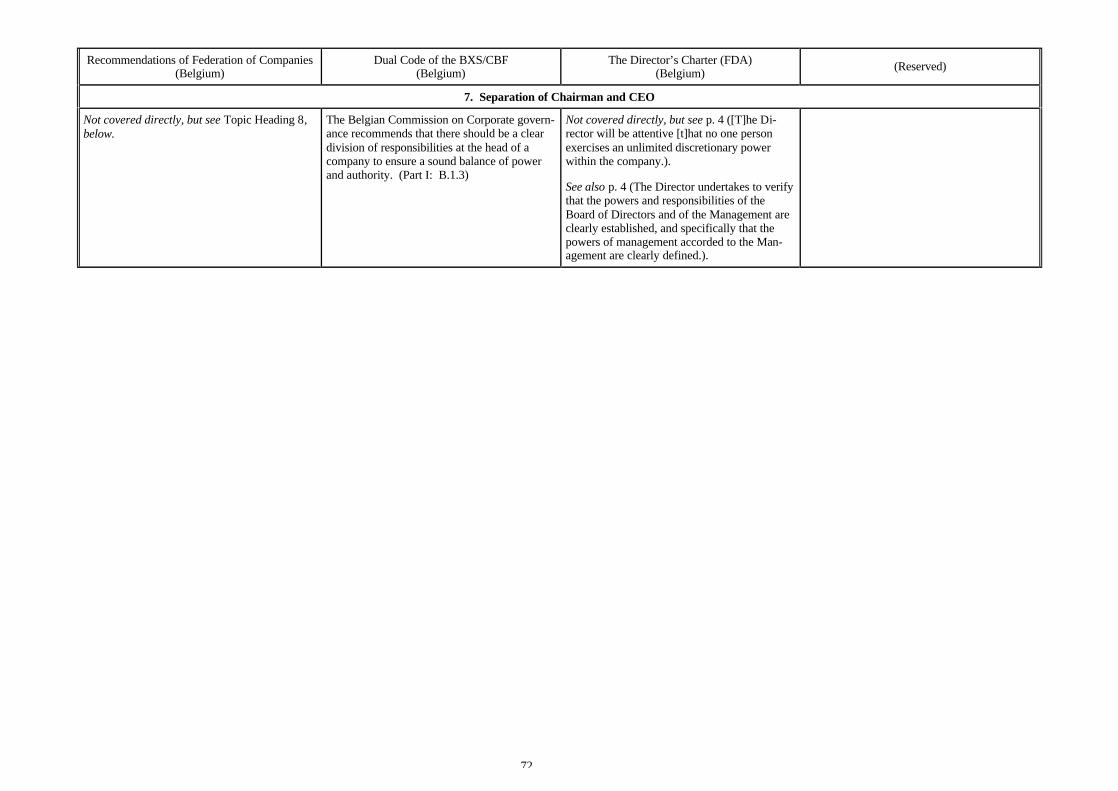

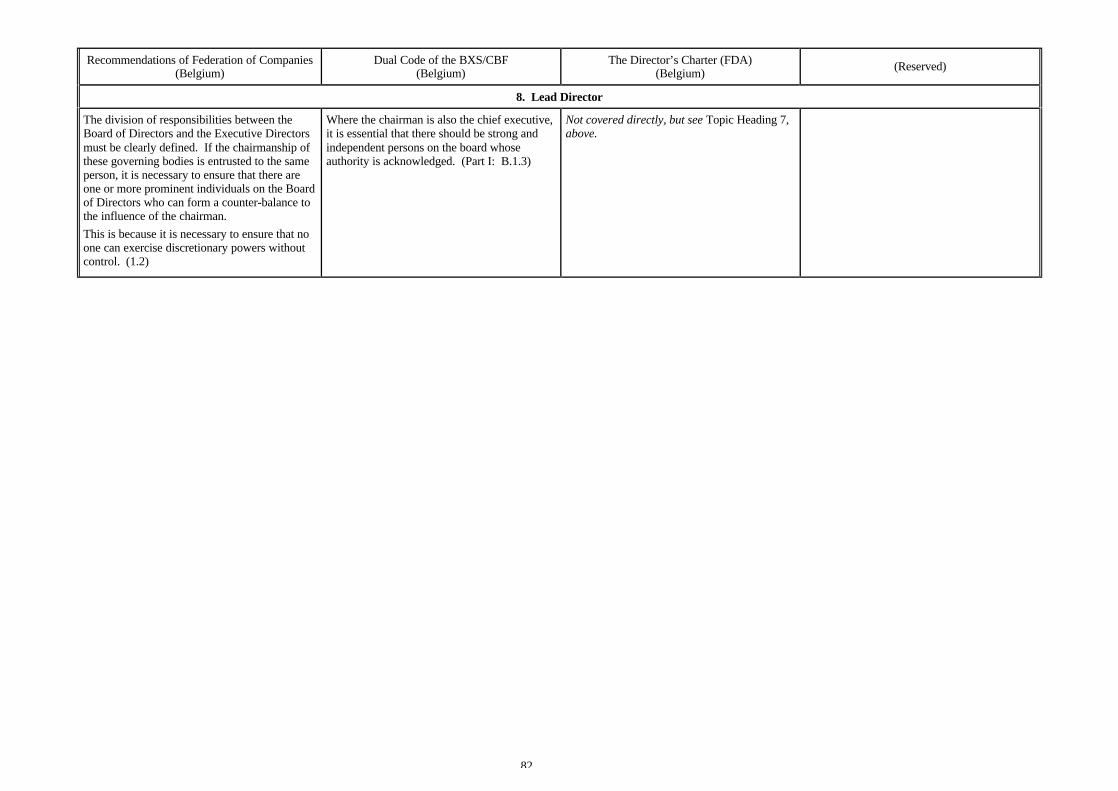

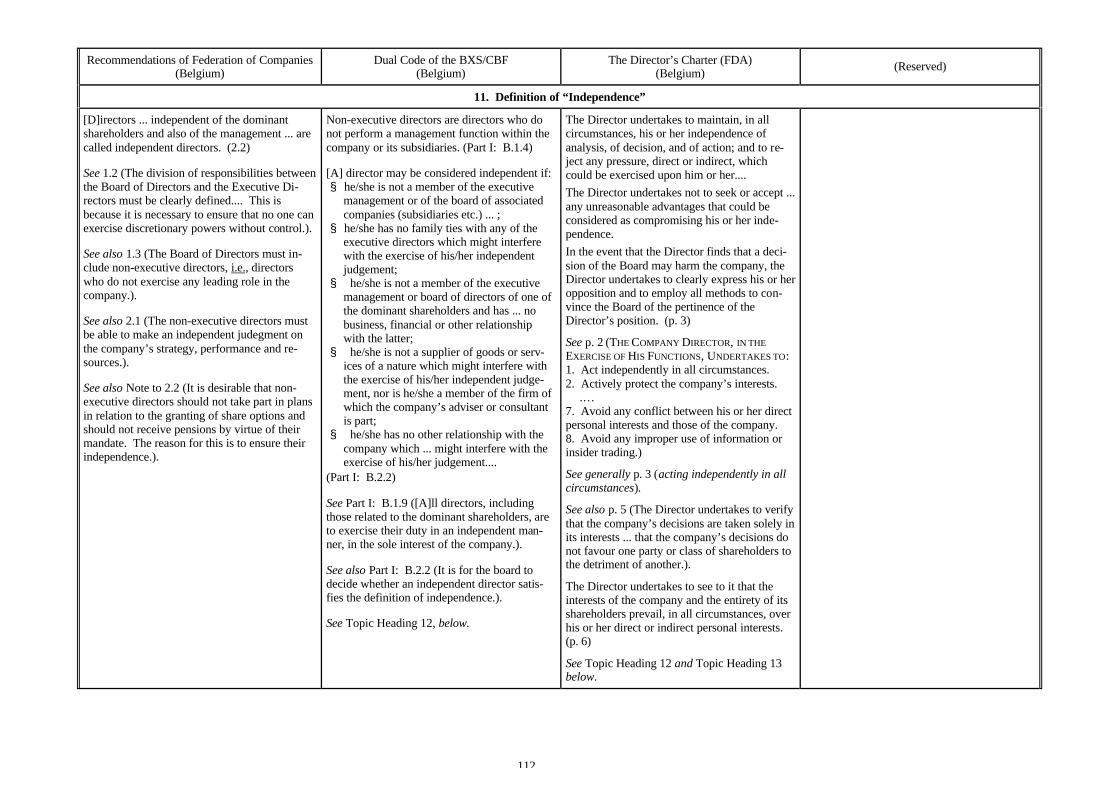

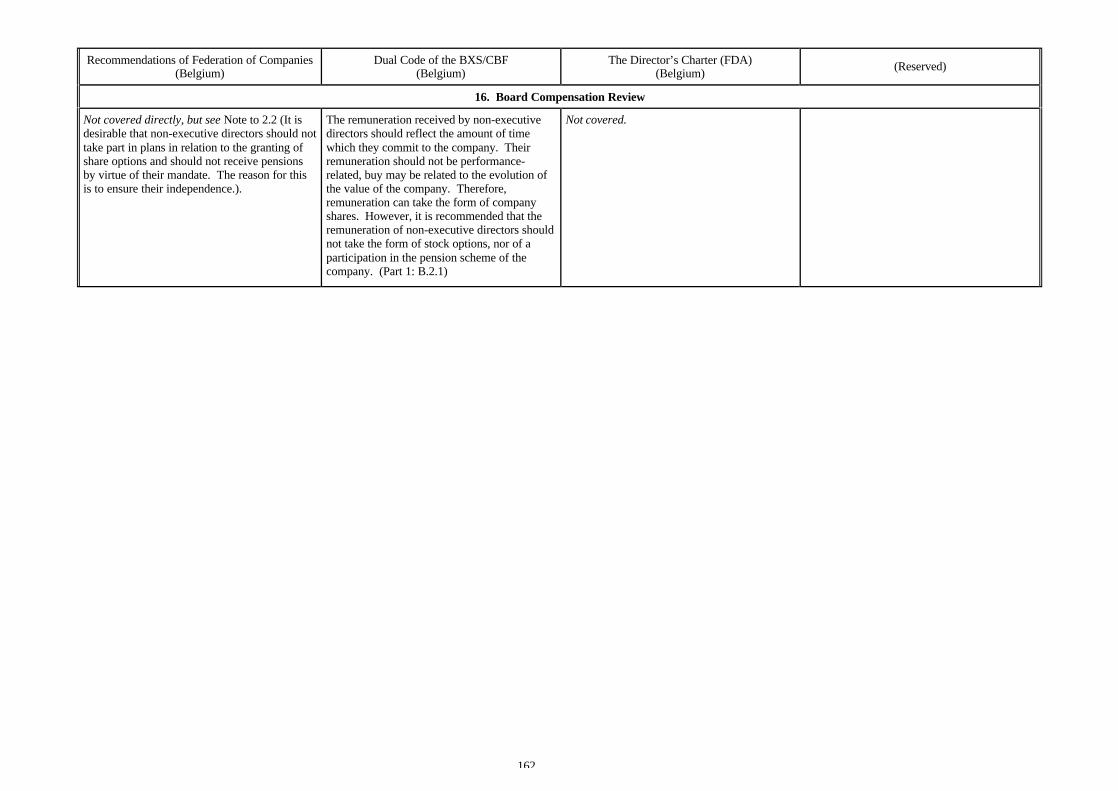

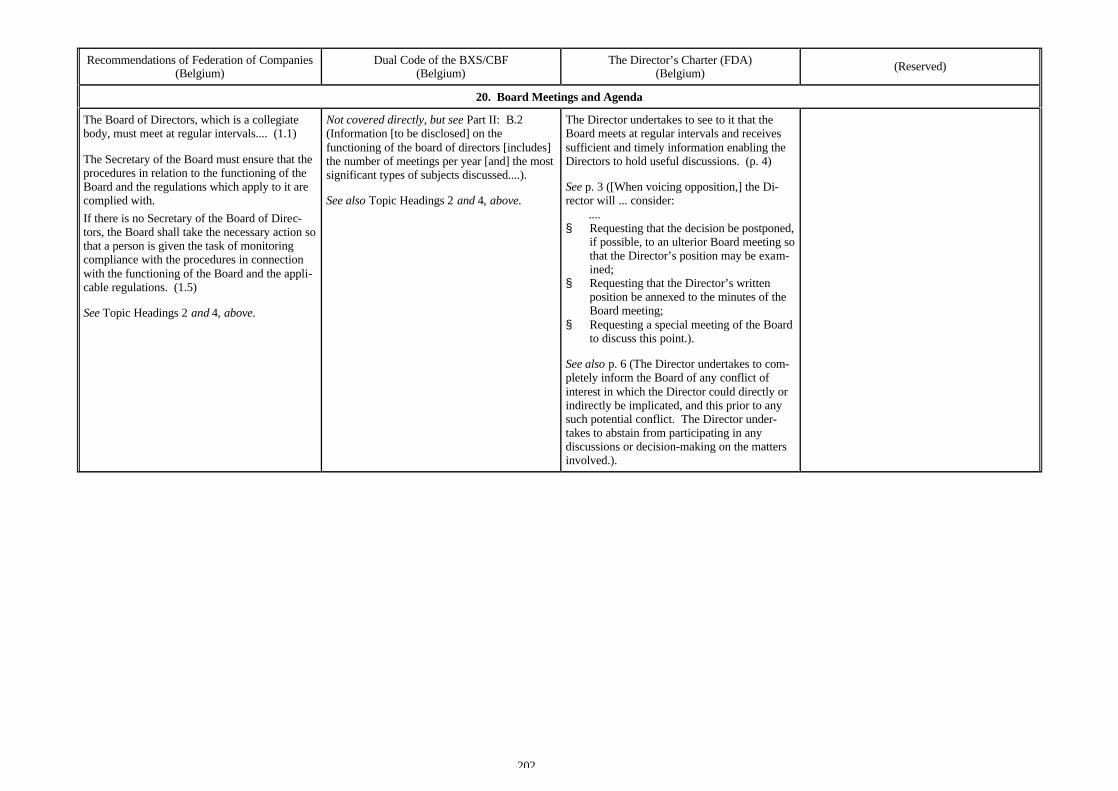

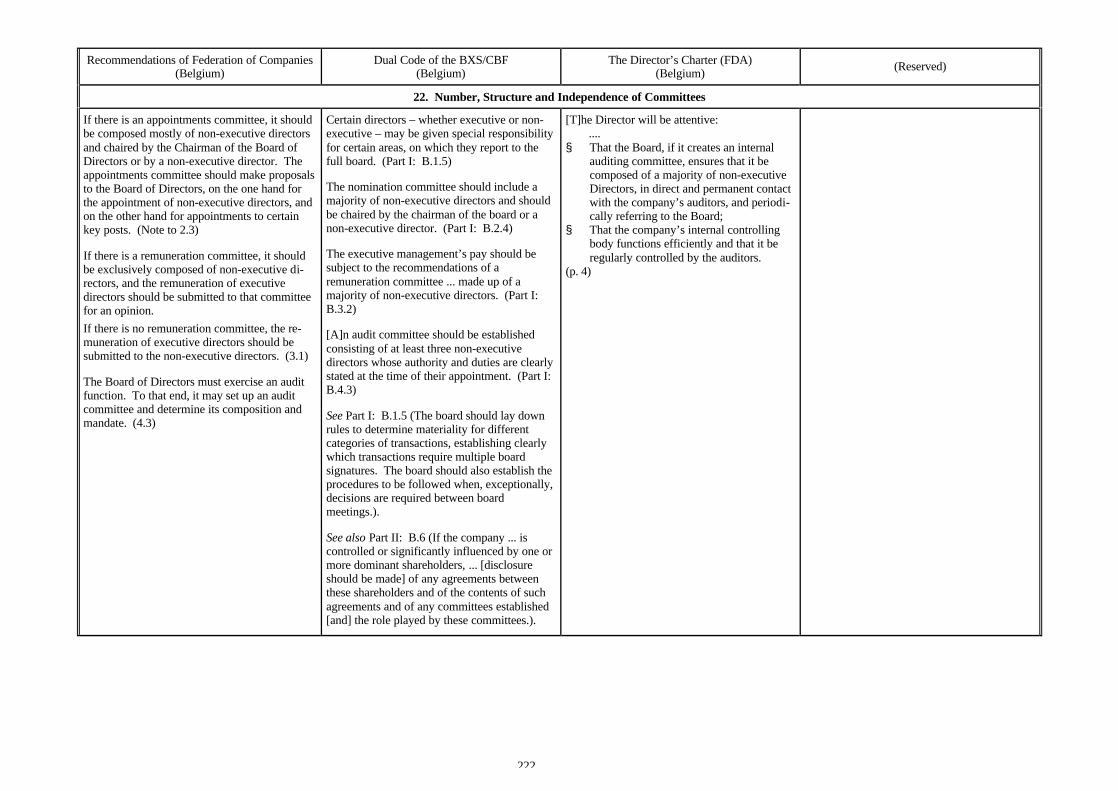

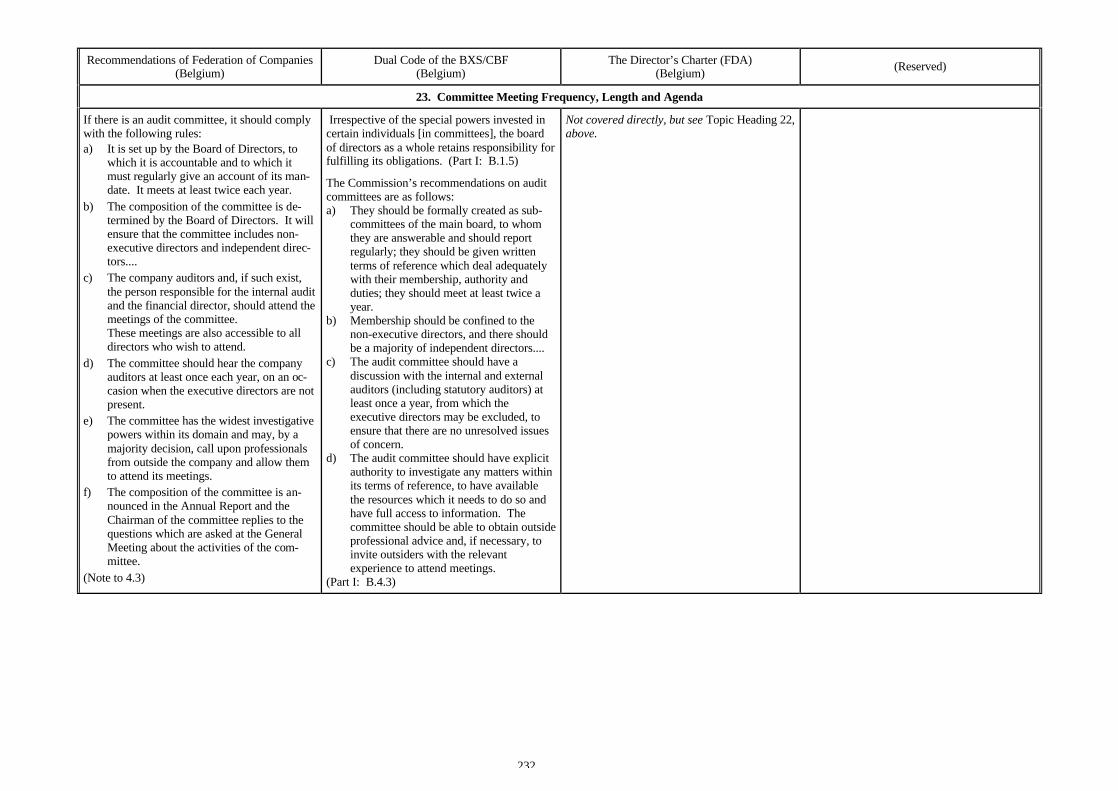

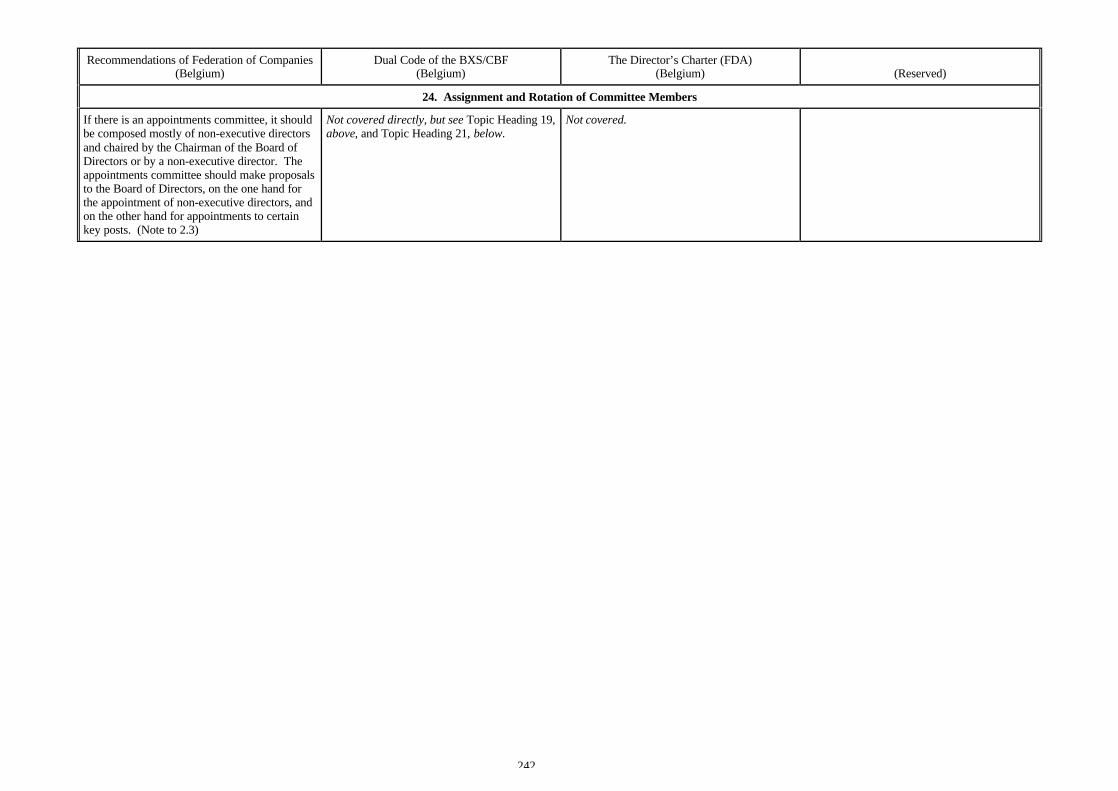

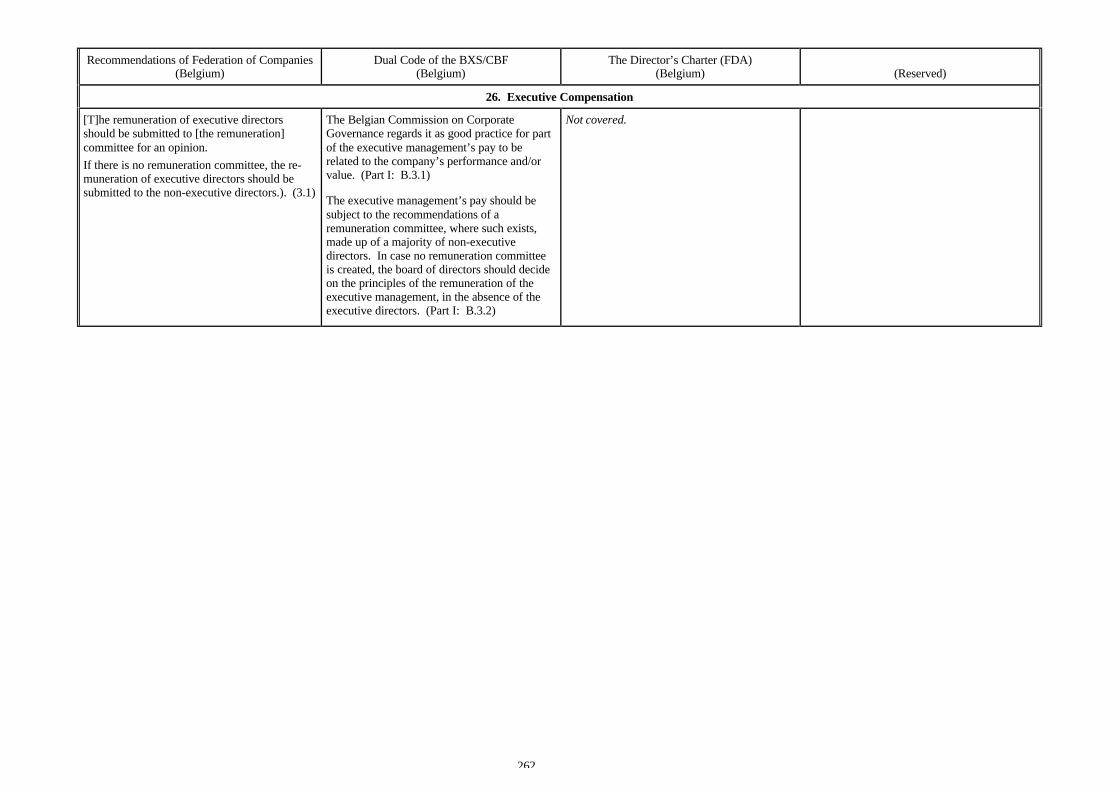

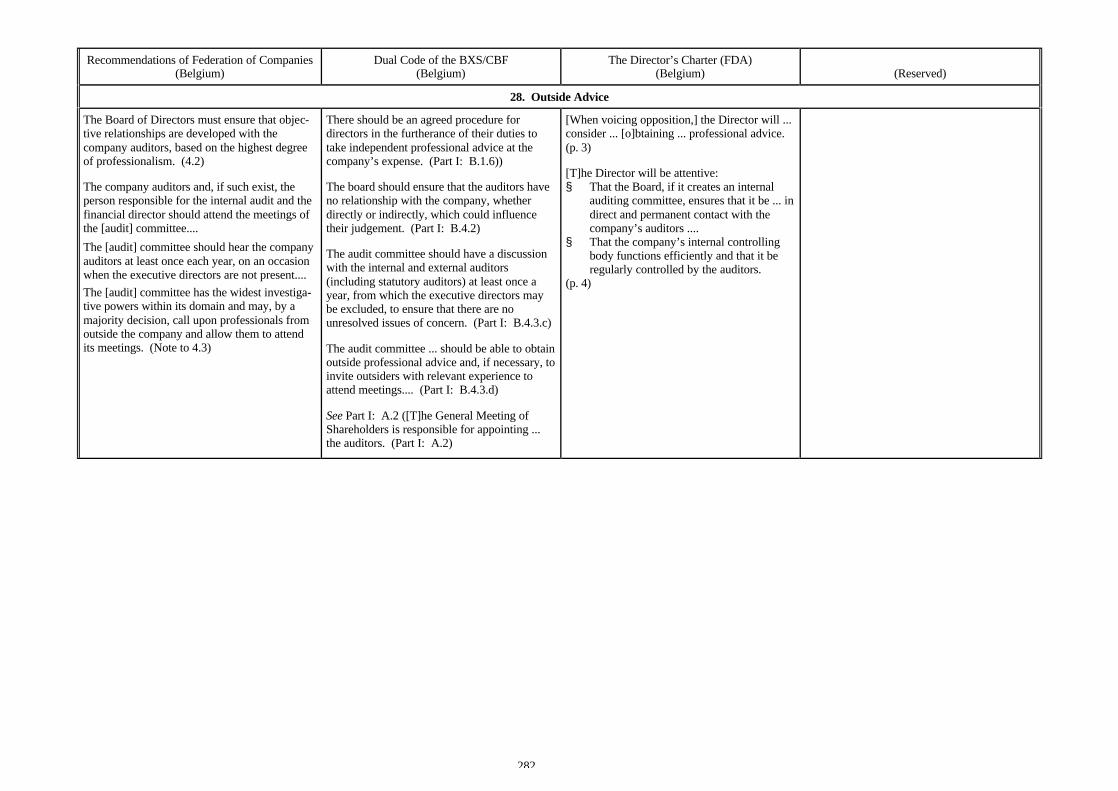

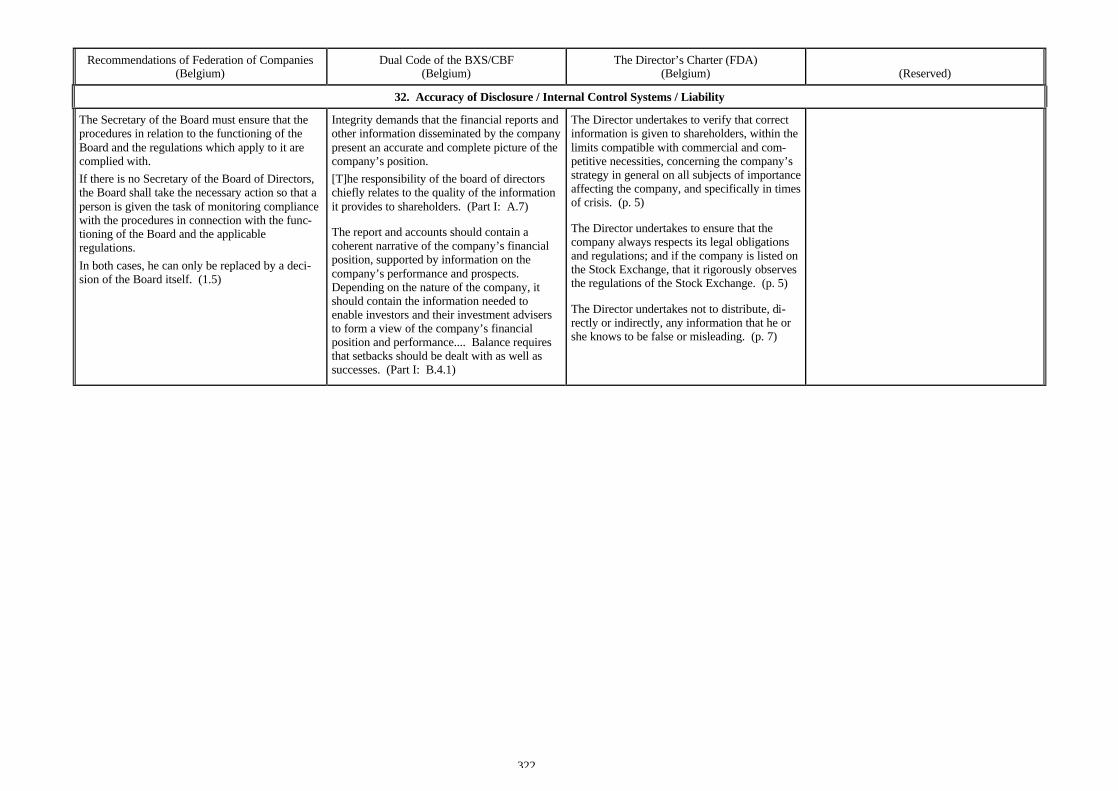

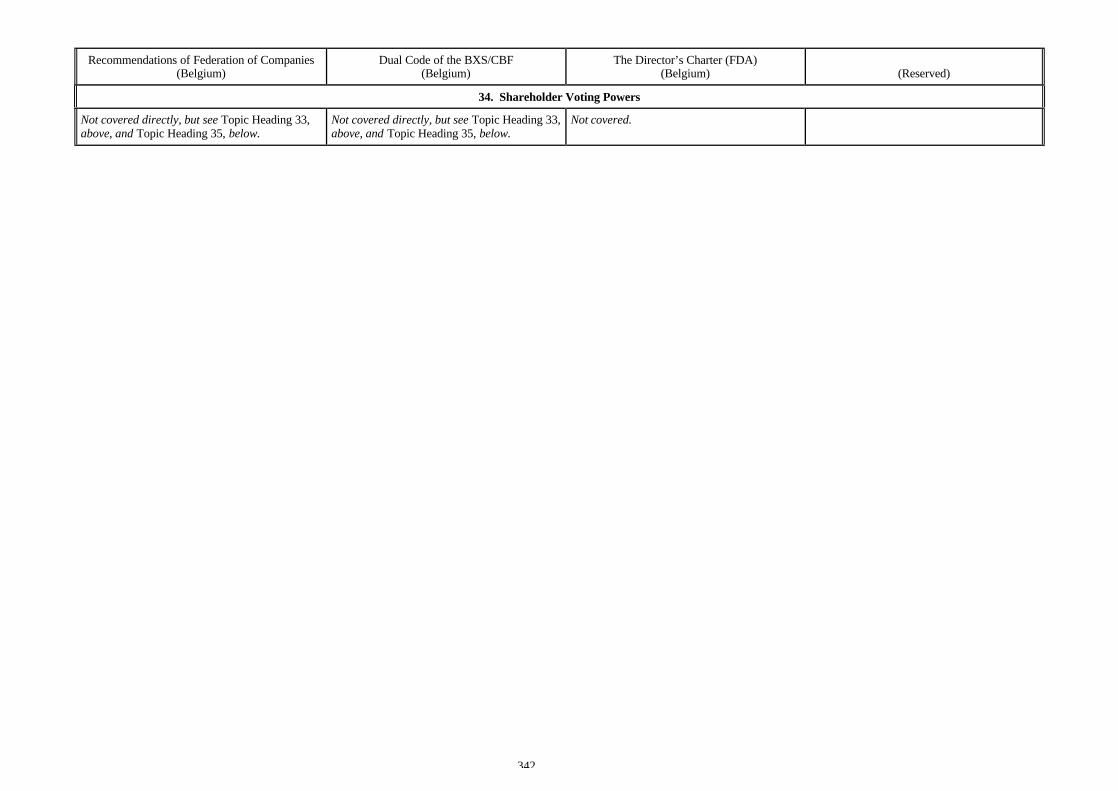

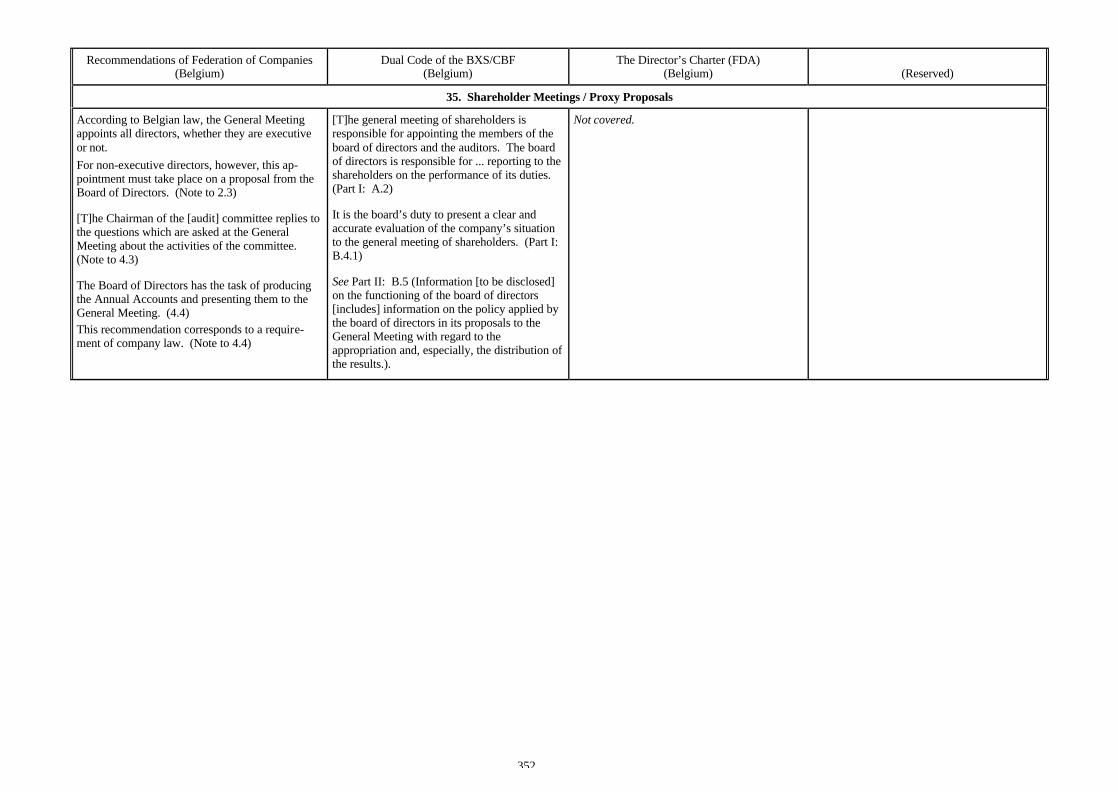

Recommendations of Federation of Companies(Belgium)

Dual Code of the BXS/CBF(Belgium)

The Director’s Charter (FDA)(Belgium) (Reserved)

OVERVIEW

Code: CORPORATE GOVERNANCE:RECOMMENDATIONS FROM THE FEDERATION OFBELGIAN COMPANIES (January 1998)

Issuing Body: Federation of Belgian Companies(“VBO/FEB”), a business, industry and/or aca-demic association or committee.

Legal Basis and Compliance: Voluntary (disclo-sure encouraged)

Objective: Improve companies’ performance,competitiveness and/or access to capital

Scope: All companies

Predominant Board Structure(listed companies): Unitary

Code: DUAL CODE OF THE BRUSSELS STOCKEXCHANGE (“BXS”) AND THE BELGIANBANKING AND FINANCE COMMISSION (“CBF”)(a/k/a CORPORATE GOVERNANCE FOR BELGIANLISTED COMPANIES) (December 1998)Note: Part I is the “Cardon Report” Part II is the “CBF Recommendations”

Issuing Bodies:Part I: Belgian Commission on CorporateGovernance, a committee related to a stockexchangePart II: Banking & Finance Commission, agovernmental/quasi-governmental entityLegal Basis and Compliance: Voluntary (dis-closure encouraged)

Objective:Part I: Improve companies’ performance,competitiveness and/or access to capitalPart II: Improve quality of governance-relatedinformation available to capital markets

Scope:Part I: Listed companies; encouraged to allcompaniesPart II: Listed companies

Predominant Board Structure(listed companies): Unitary

Code: THE DIRECTOR’S CHARTER (LA CHARTEDE L’ADMINISTRATEUR) (January 2000)

Issuing Body: La Fondation des Administra-teurs (“FDA”), a directors association

Legal Basis and Compliance: Voluntary (asso-ciation members encouraged to comply)

Objective: Improve quality of board (supervi-sory) governance

Scope: All companies

Predominant Board Structure(listed companies): Unitary

3

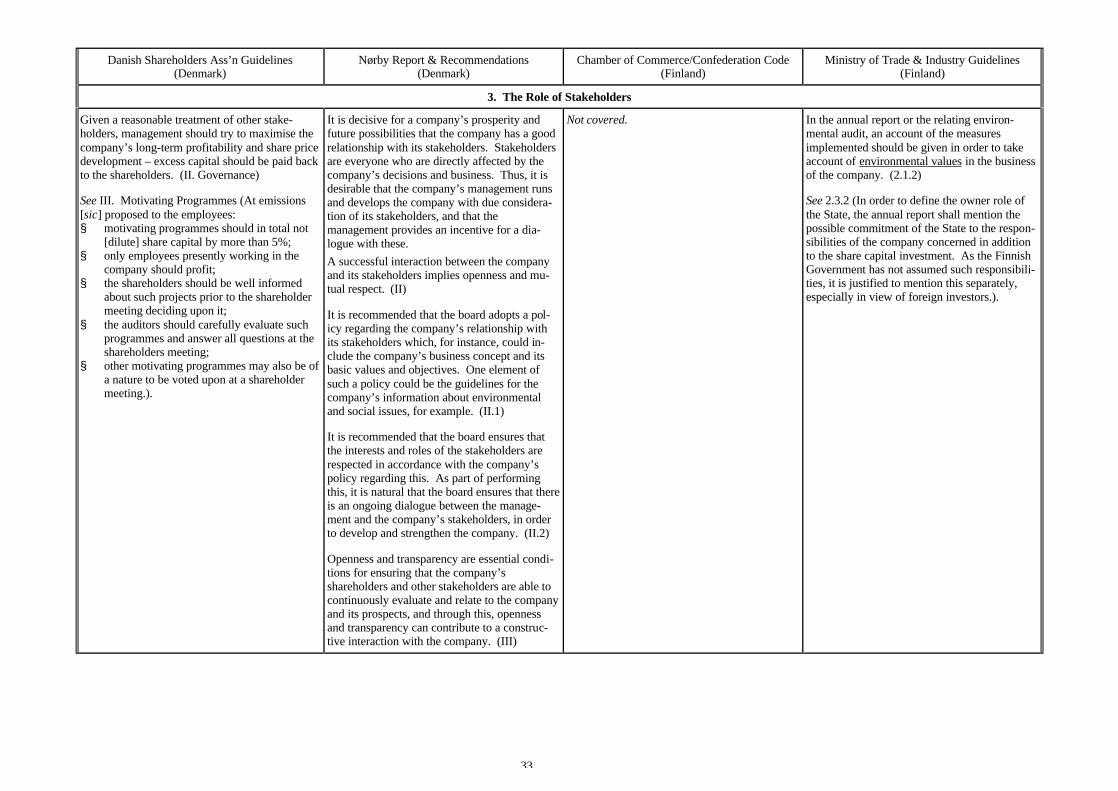

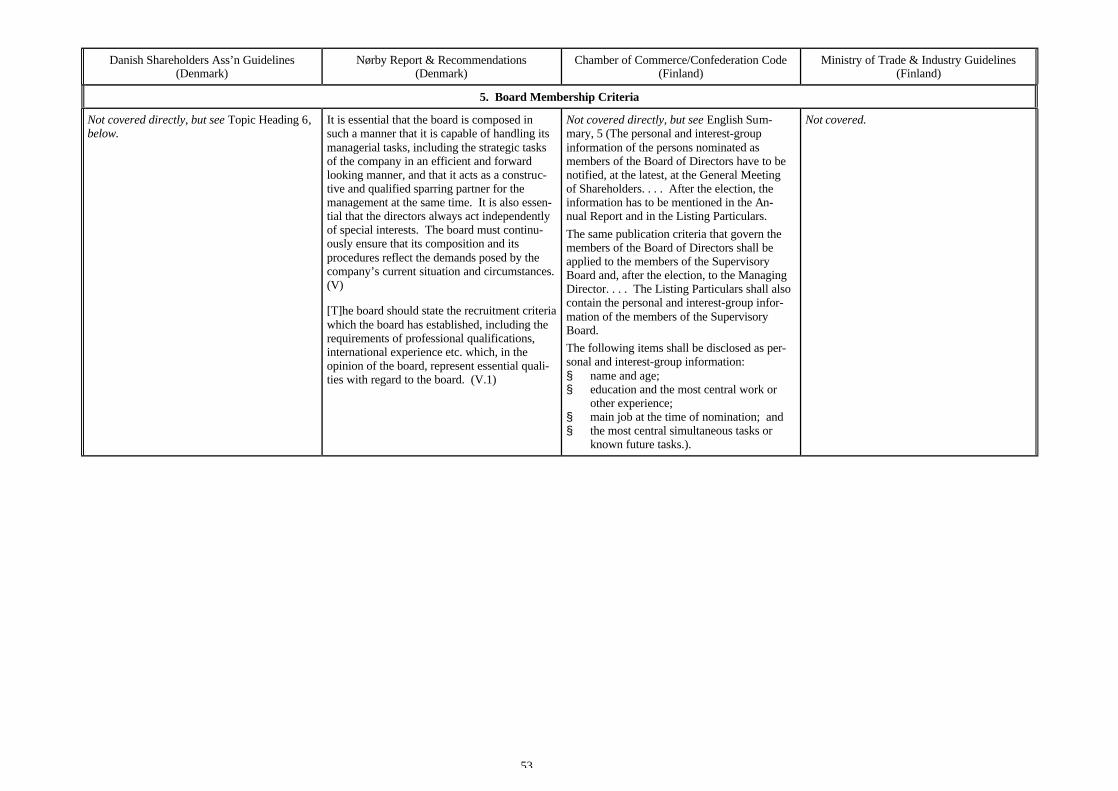

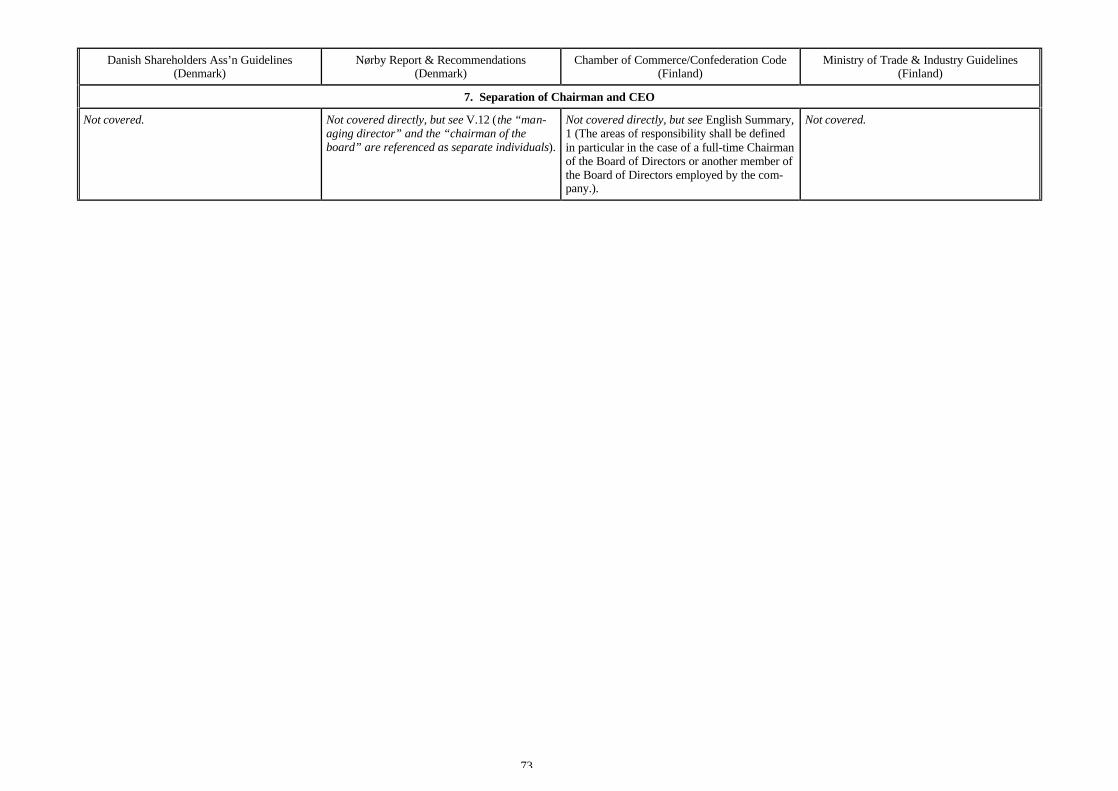

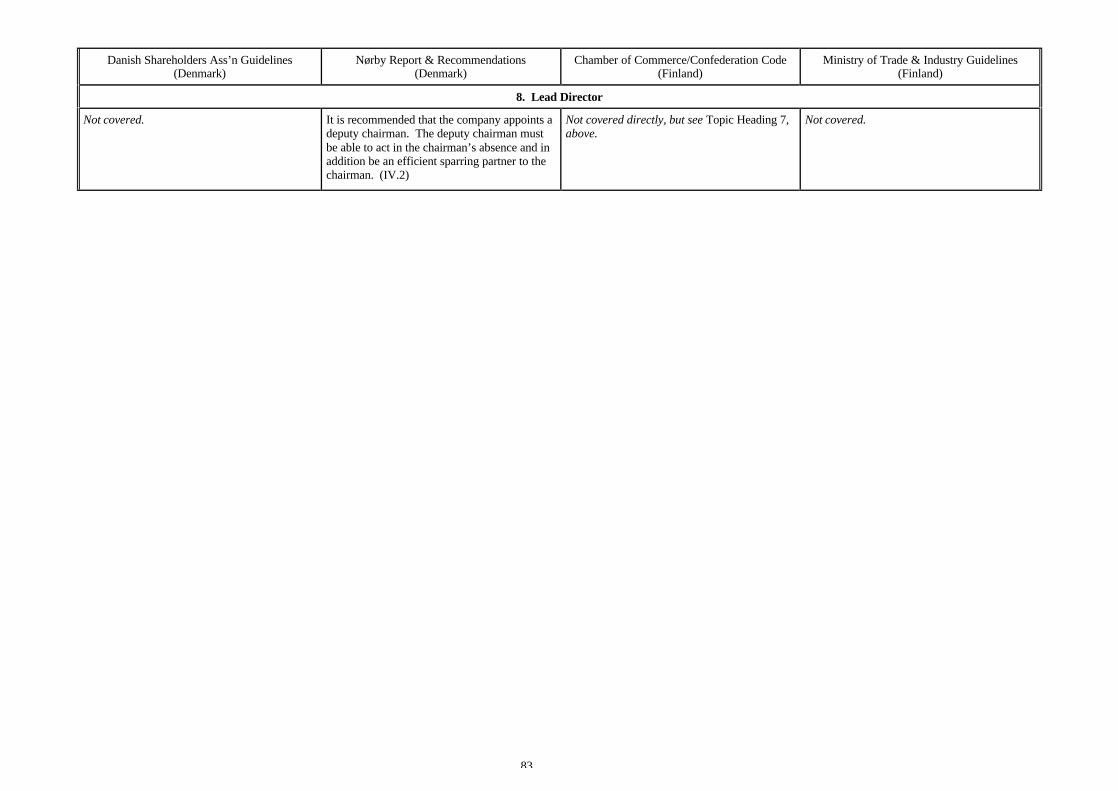

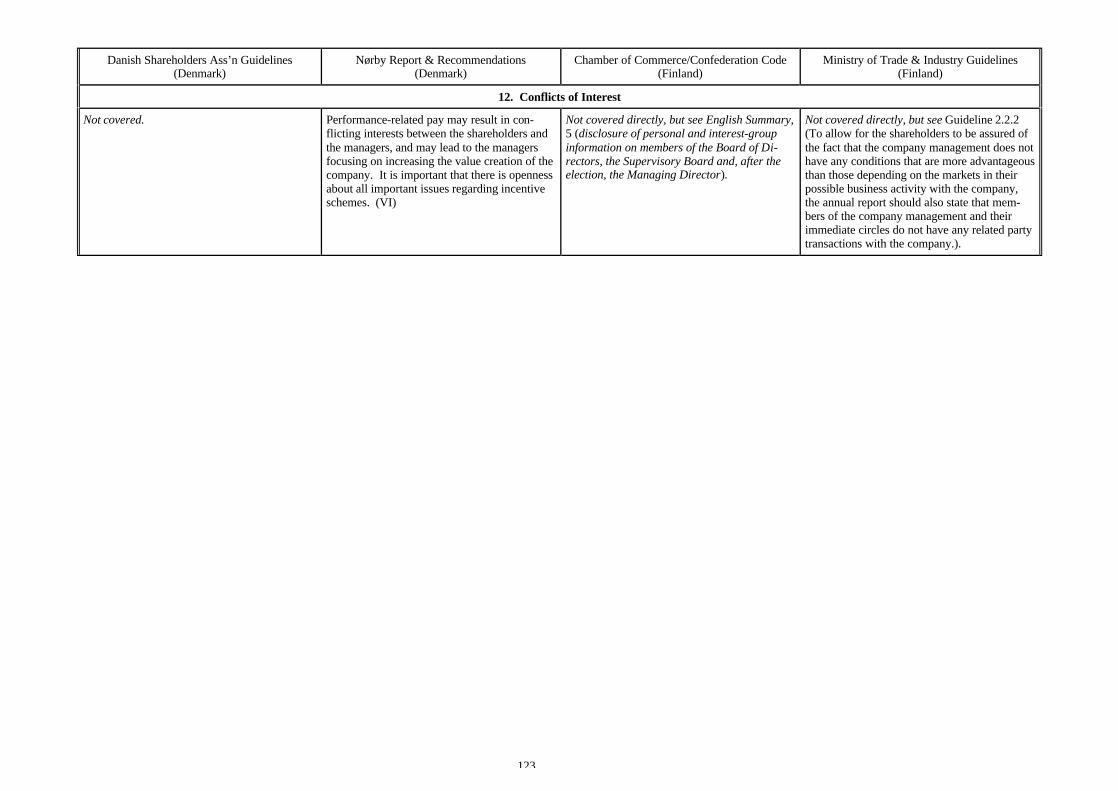

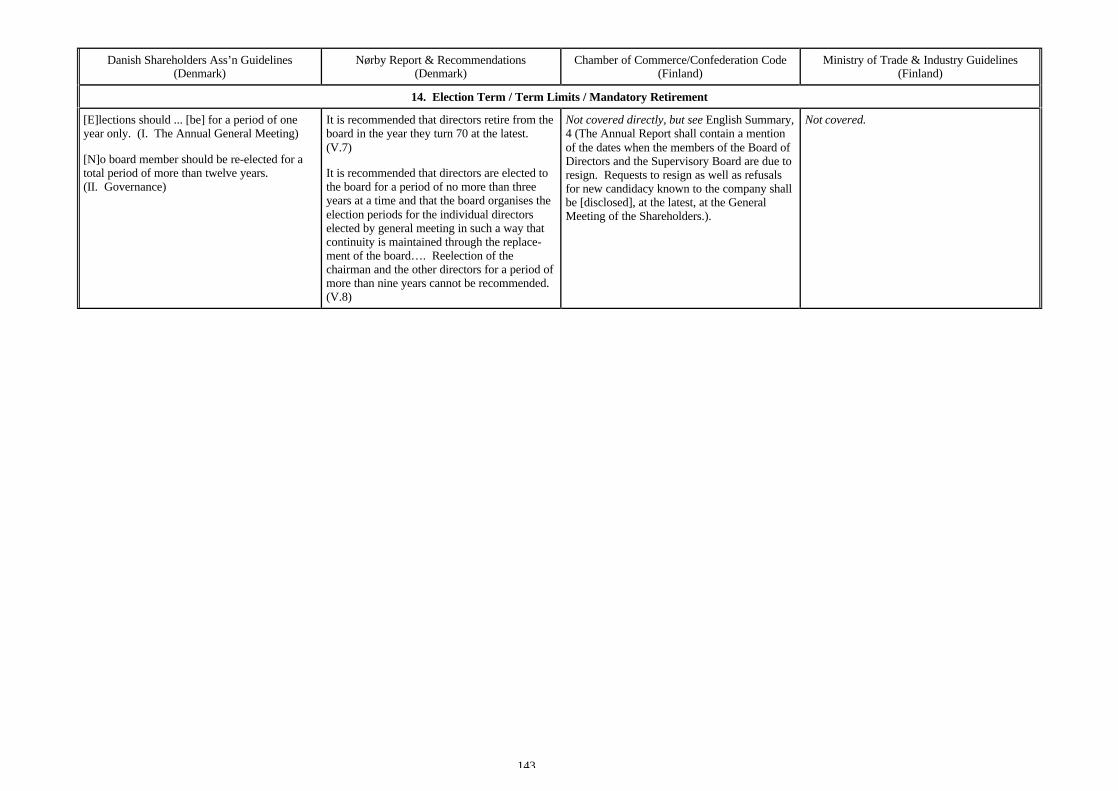

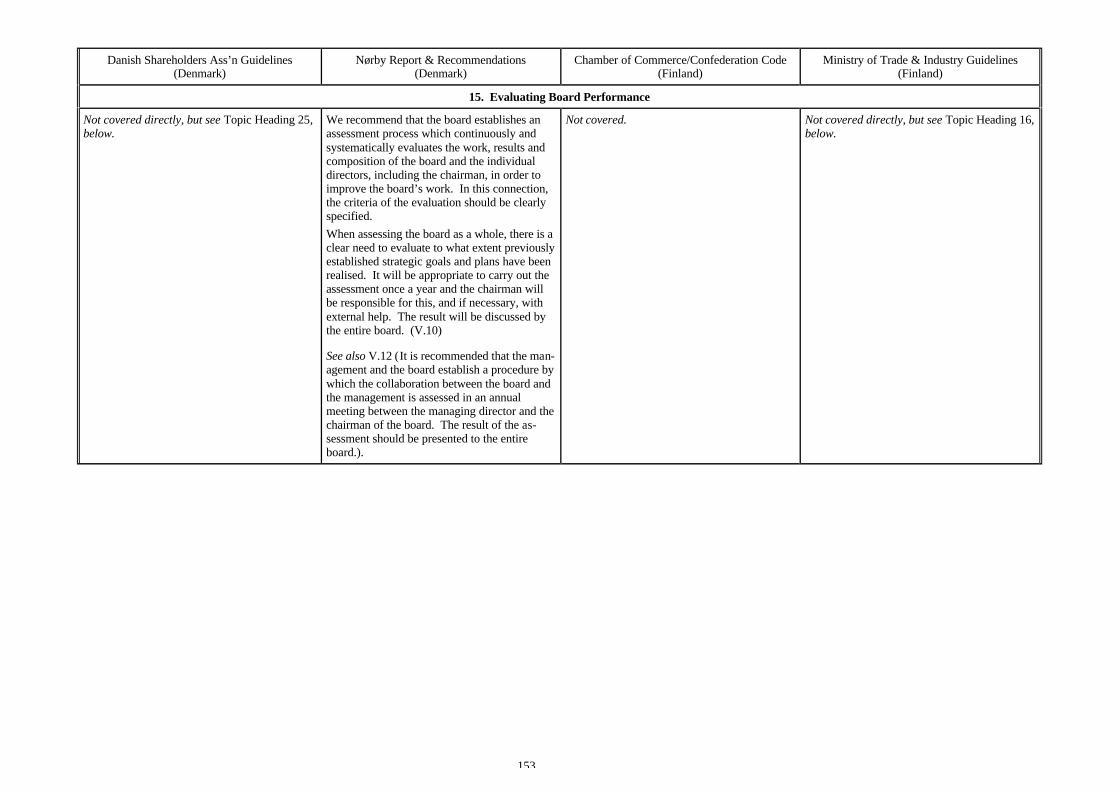

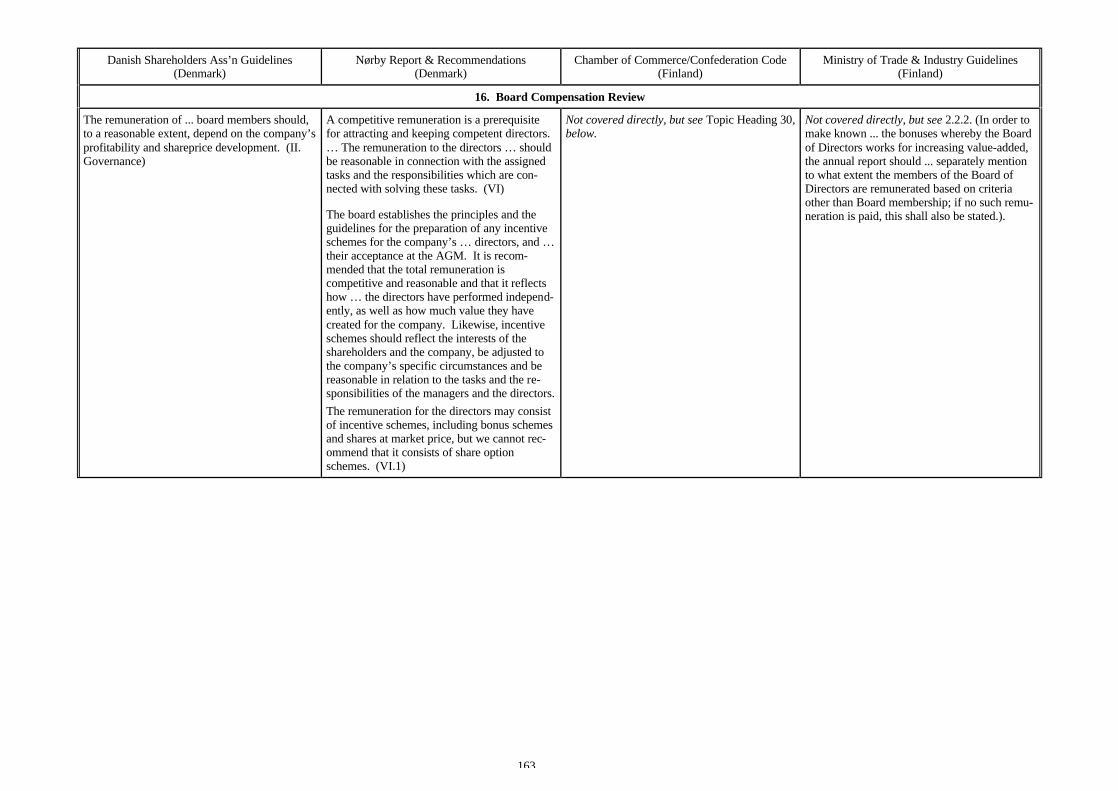

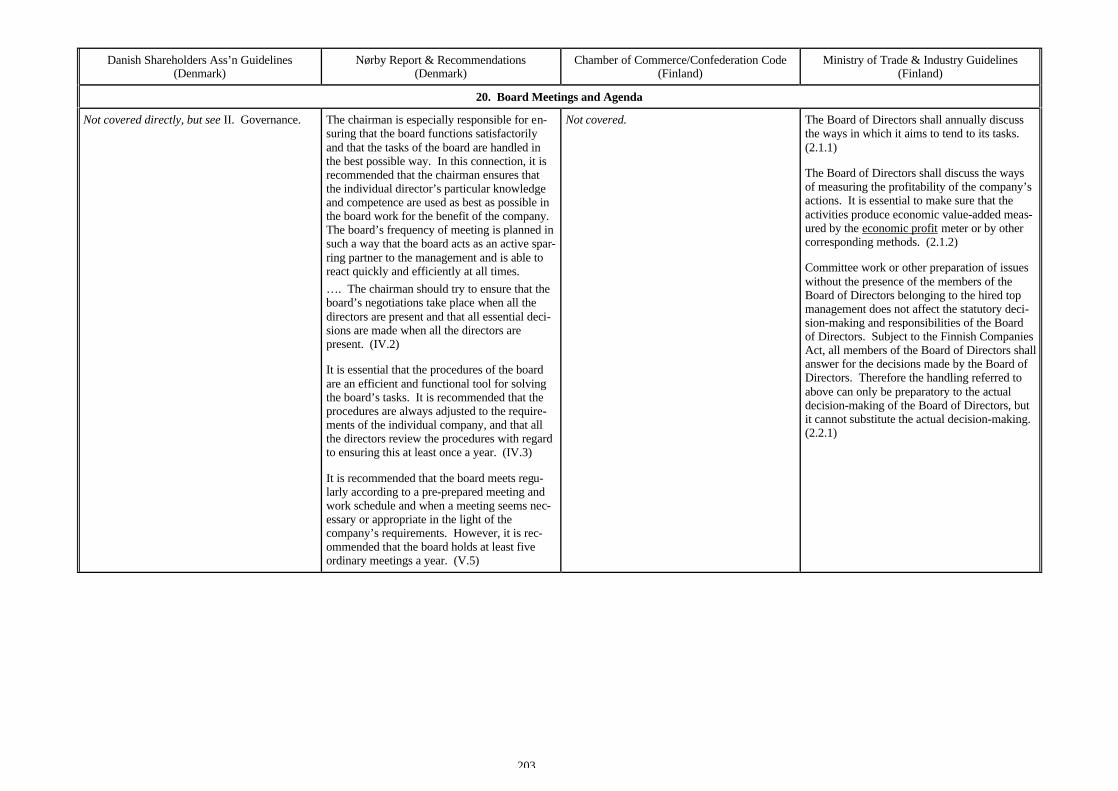

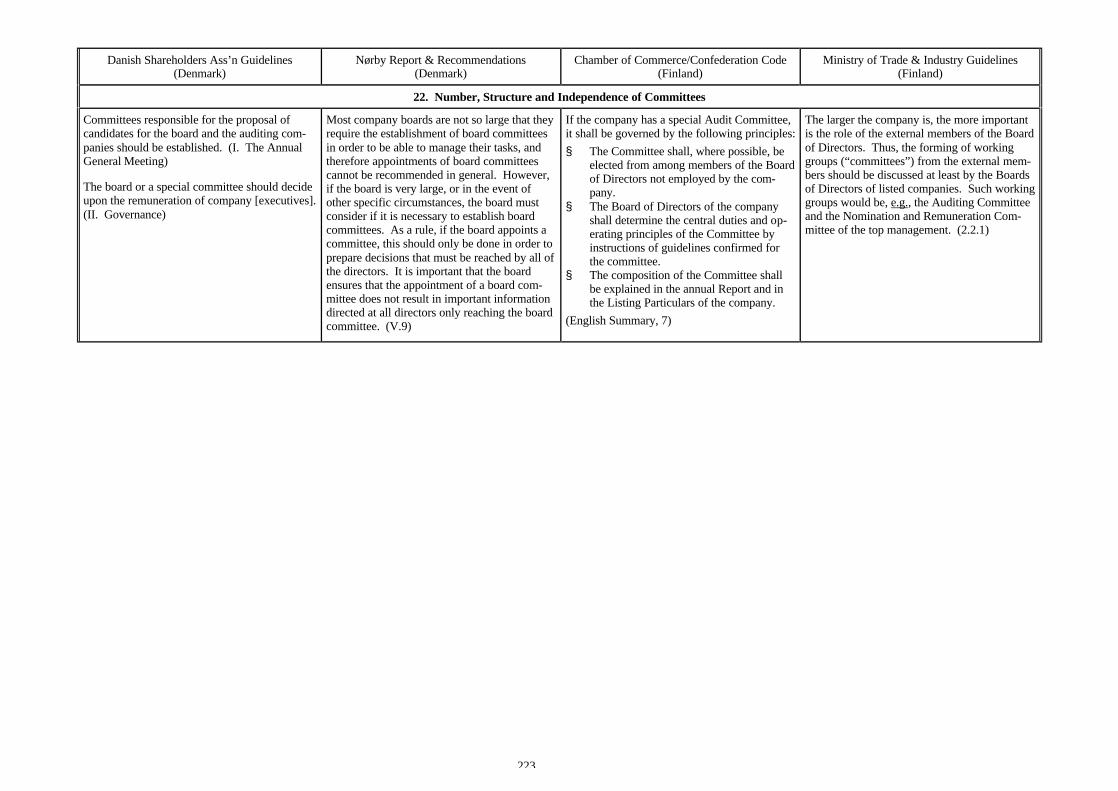

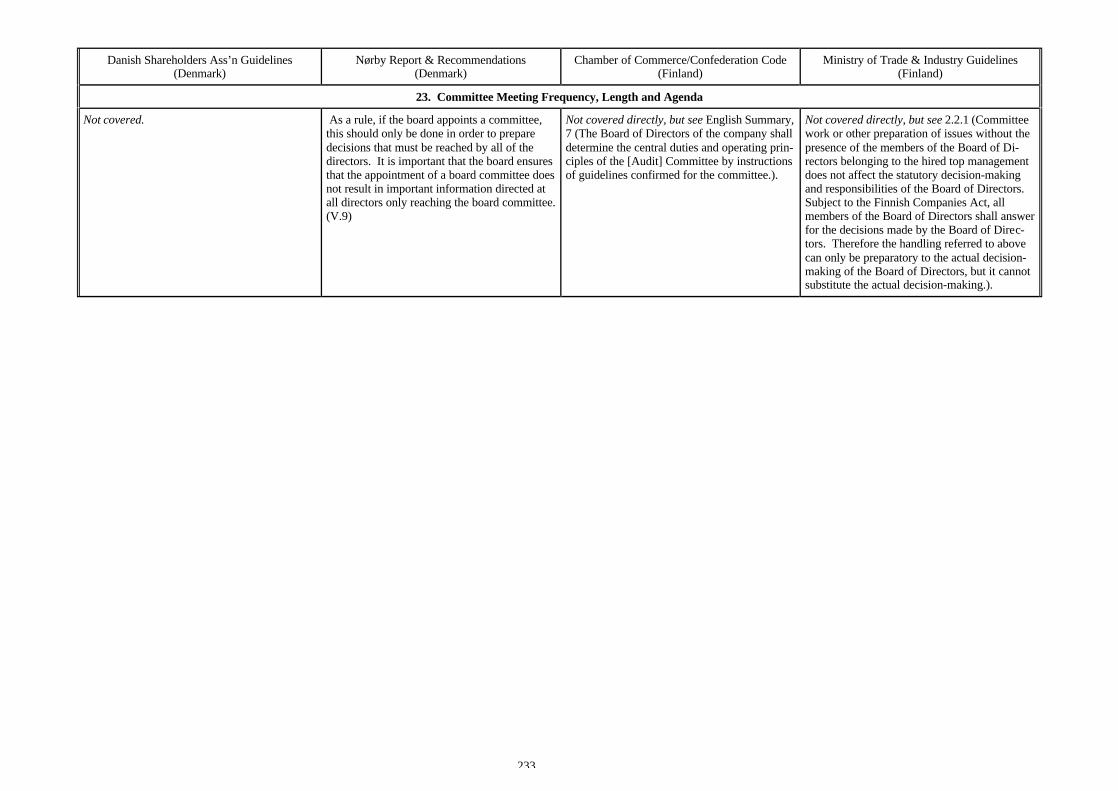

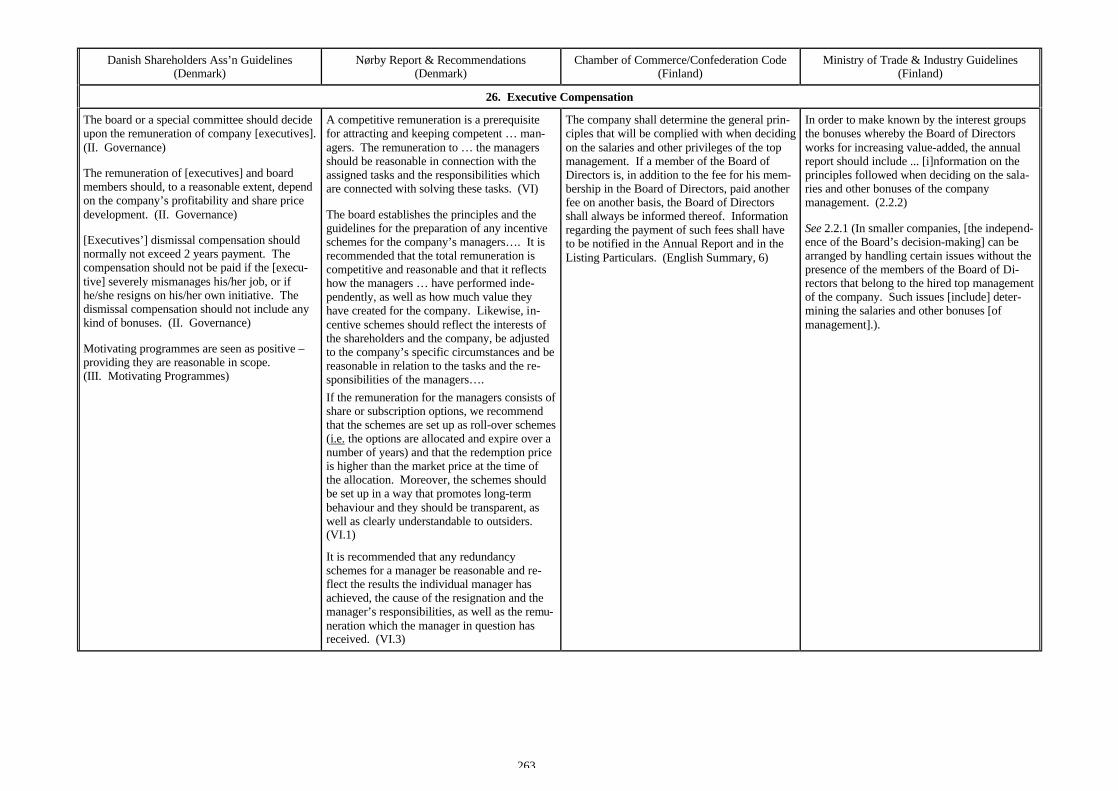

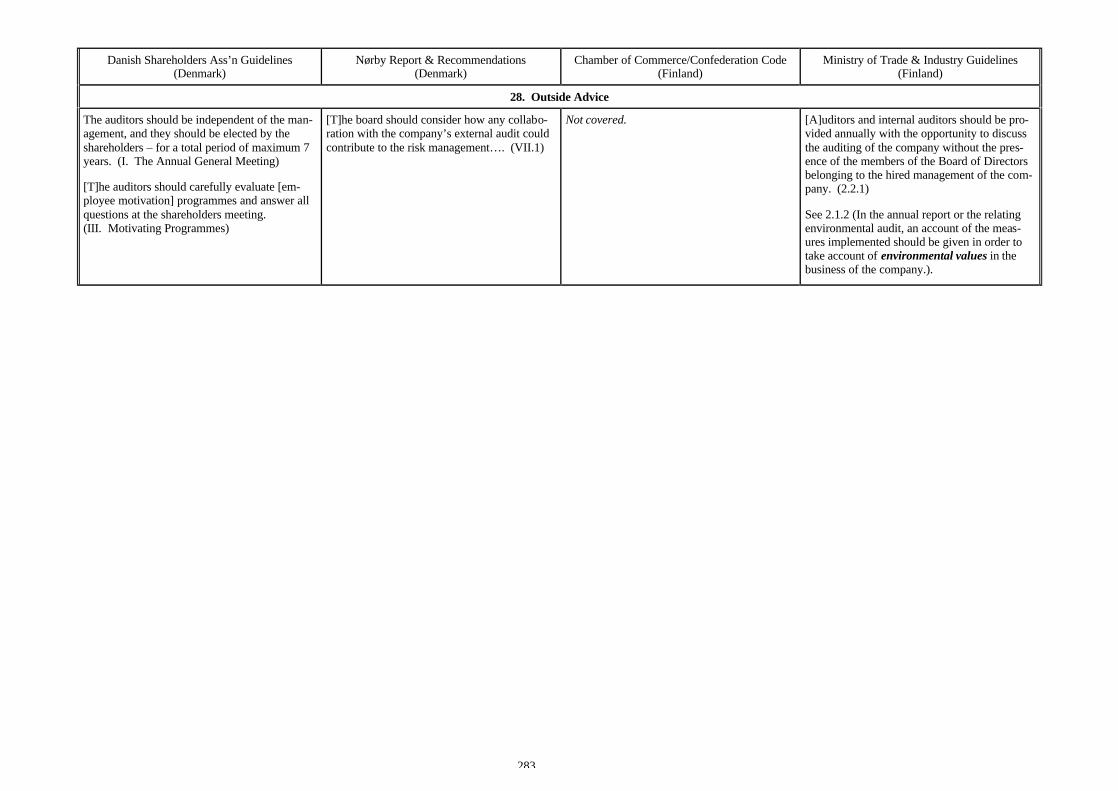

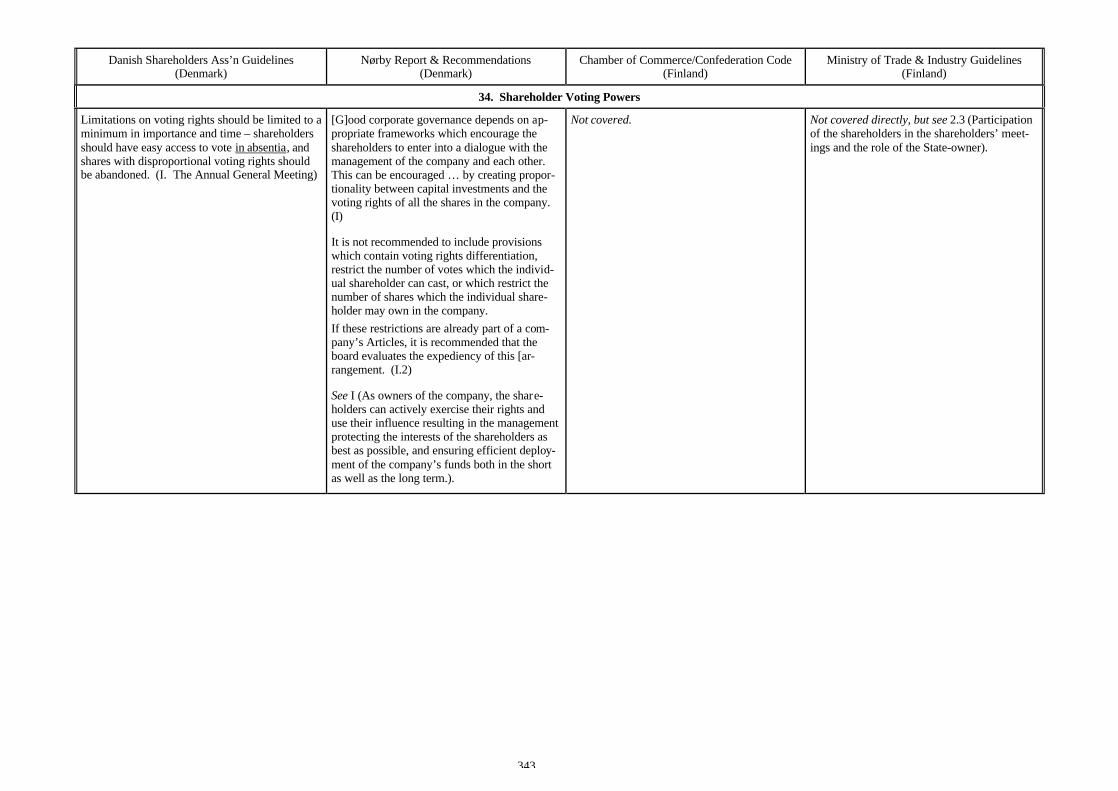

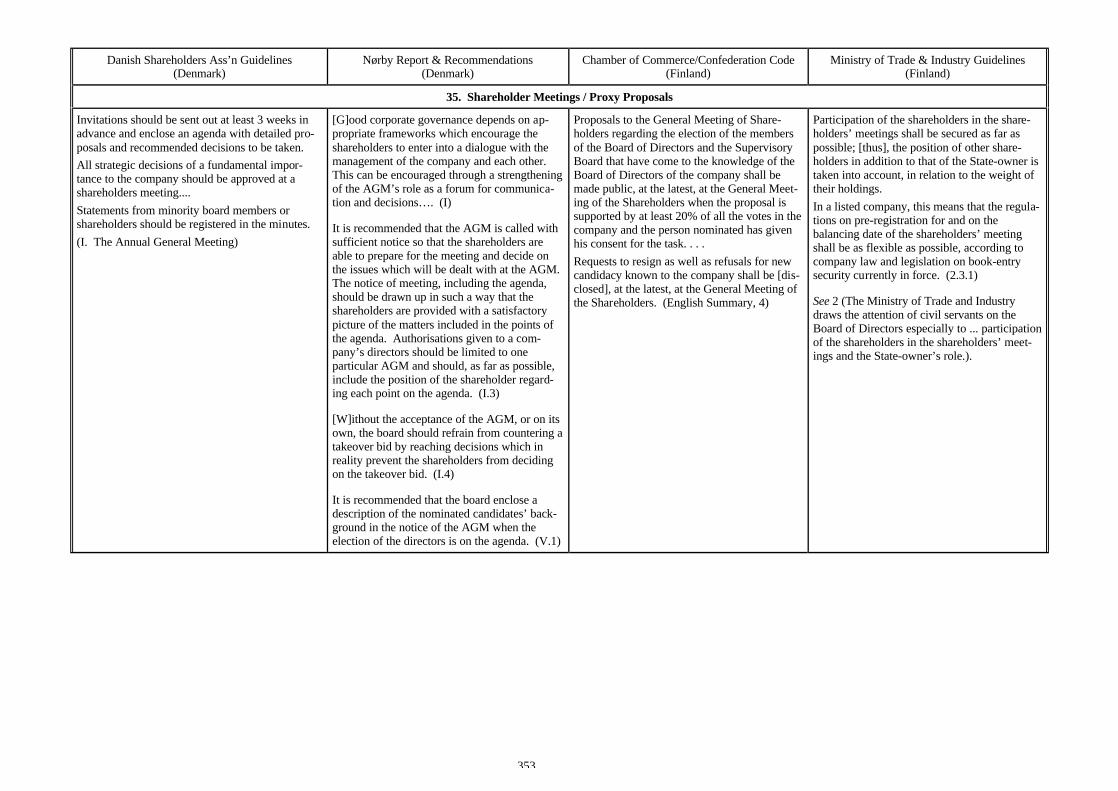

Danish Shareholders Ass’n Guidelines(Denmark)

Nørby Report & Recommendations(Denmark)

Chamber of Commerce/Confederation Code(Finland)

Ministry of Trade & Industry Guidelines(Finland)

OVERVIEW

Code: GUIDELINES ON GOOD MANAGEMENT OF ALISTED COMPANY (February 2000)

Issuing Body: The Danish Shareholders Asso-ciation, an investors association

Legal Basis and Compliance: Voluntary (disclo-sure encouraged)

Objective: Improve accountability to sharehold-ers and/or maximise shareholder value

Scope: Listed companies

Predominant Board Structure(listed companies): Two-tier

Code: RECOMMENDATIONS FOR GOODCORPORATE GOVERNANCE IN DENMARK(December 2001)

Issuing Body: The Nørby Commission, acommittee (commission) organized by govern-ment

Legal Basis and Compliance: Voluntary (dis-closure encouraged)

Objective: Improve companies’ performance,competitiveness and/or access to capital

Scope: Listed companies; encouraged to allcompanies

Predominant Board Structure(listed companies): Two-tier

Code: CORPORATE GOVERNANCE CODE FORPUBLIC LIMITED COMPANIES (February 1997).Note: This Code is available in English only insummary form.

Issuing Bodies: The Central Chamber ofCommerce and the Confederation of FinnishIndustry and Employers, a business, industryand/or academic association or committee

Legal Basis and Compliance: Voluntary (dis-closure encouraged)

Objective: Improve the quality of board (su-pervisory) governance

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

Code: HANDLING CORPORATE GOVERNANCEISSUES IN STATE-OWNED COMPANIES ANDASSOCIATED COMPANIES (November 2000)

Issuing Body: Finland Ministry of Trade andIndustry, a governmental/quasi-governmentalentity

Legal Basis and Compliance: Voluntary (dis-closure encouraged)

Objective: Improve companies’ performance,competitiveness and/or access to capital

Scope: Listed companies and other privatisedcompanies

Predominant Board Structure(listed companies): Unitary

4

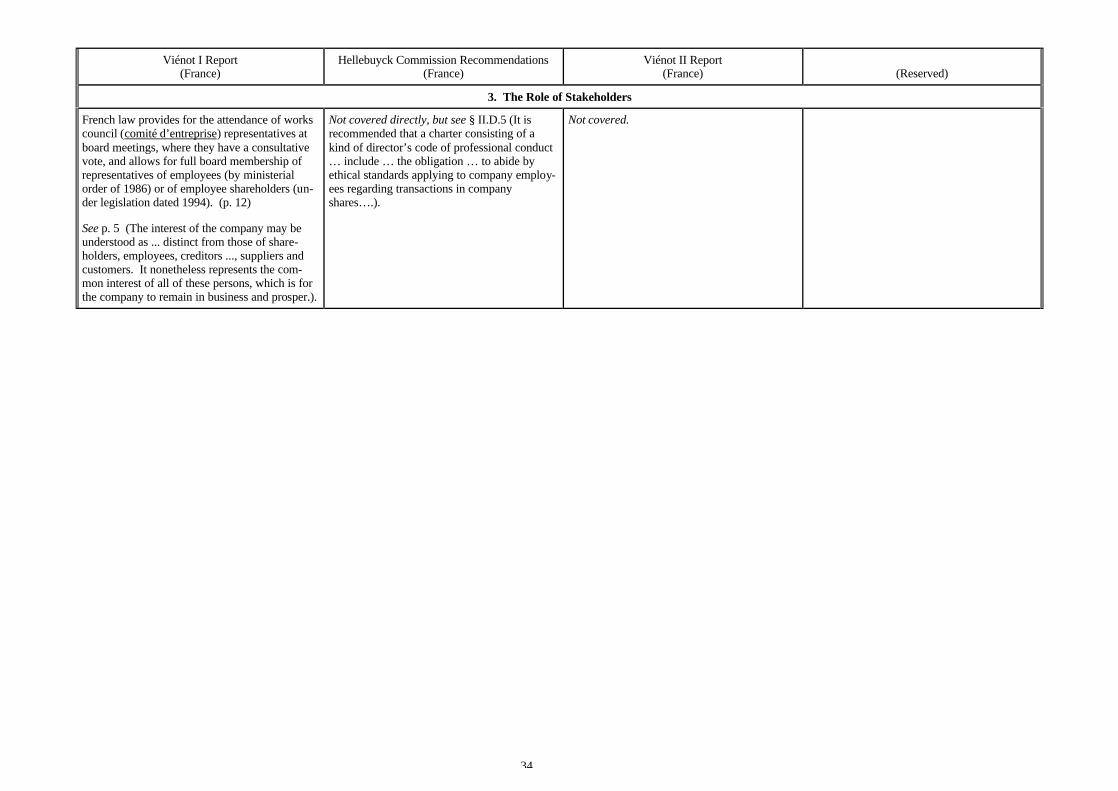

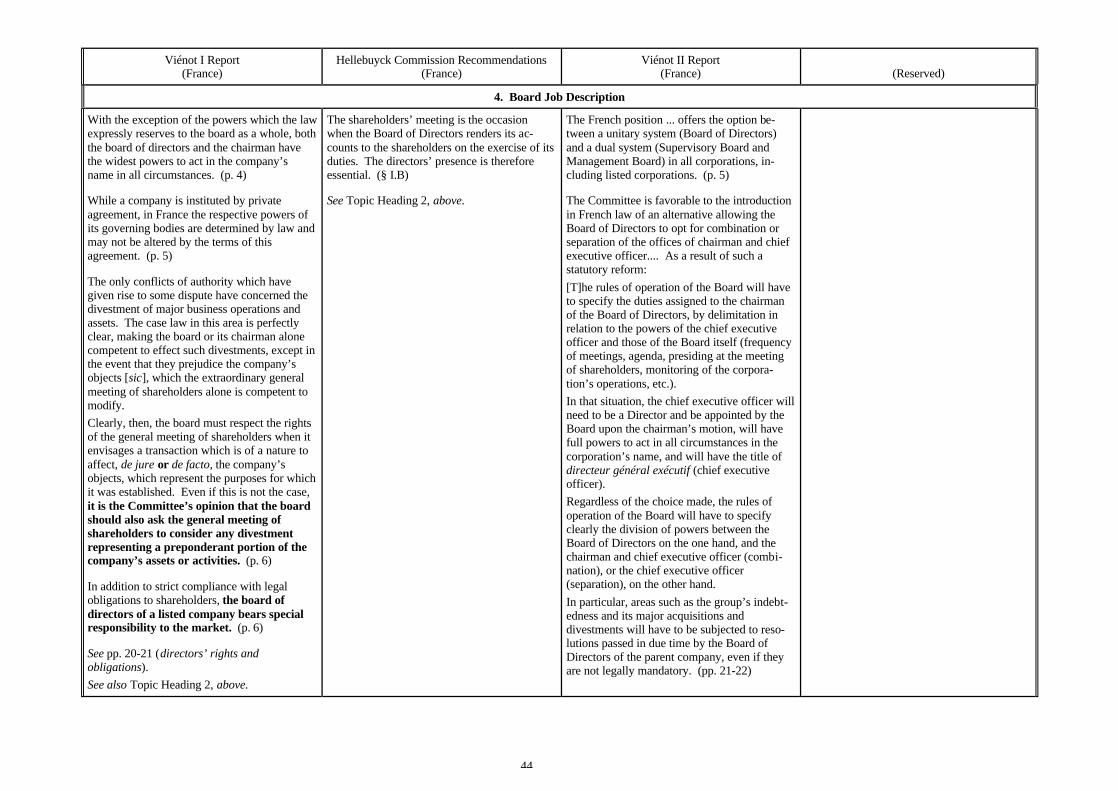

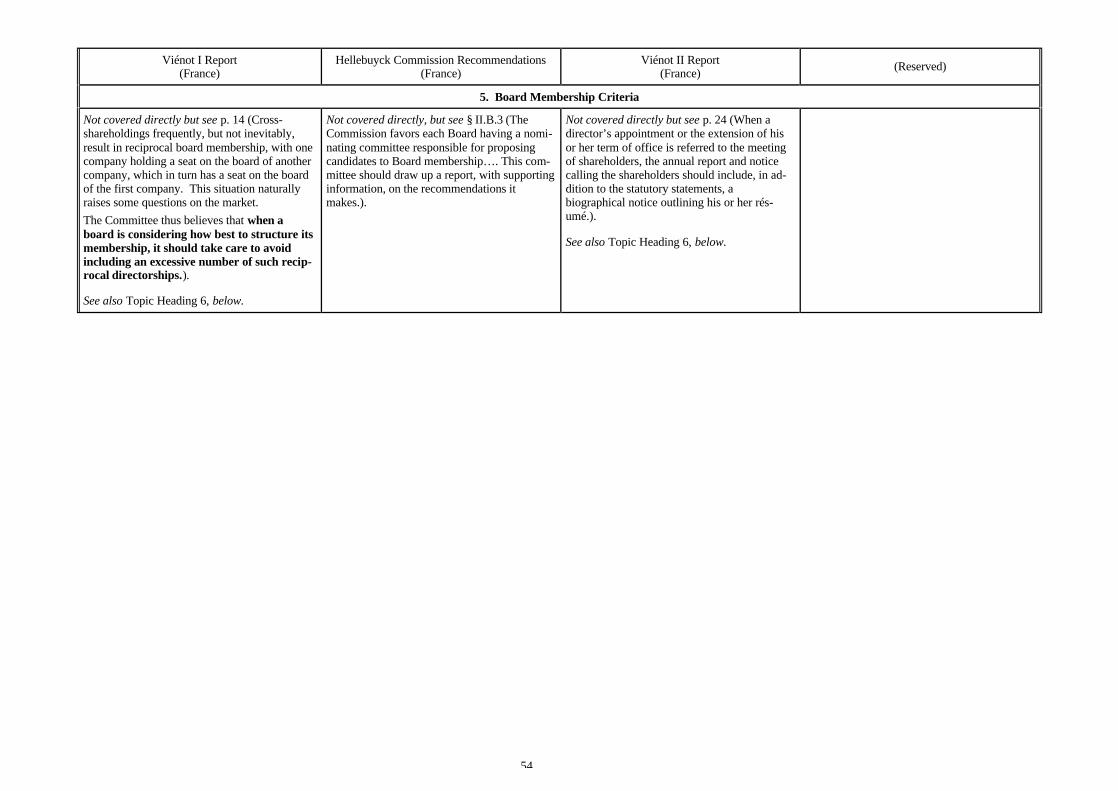

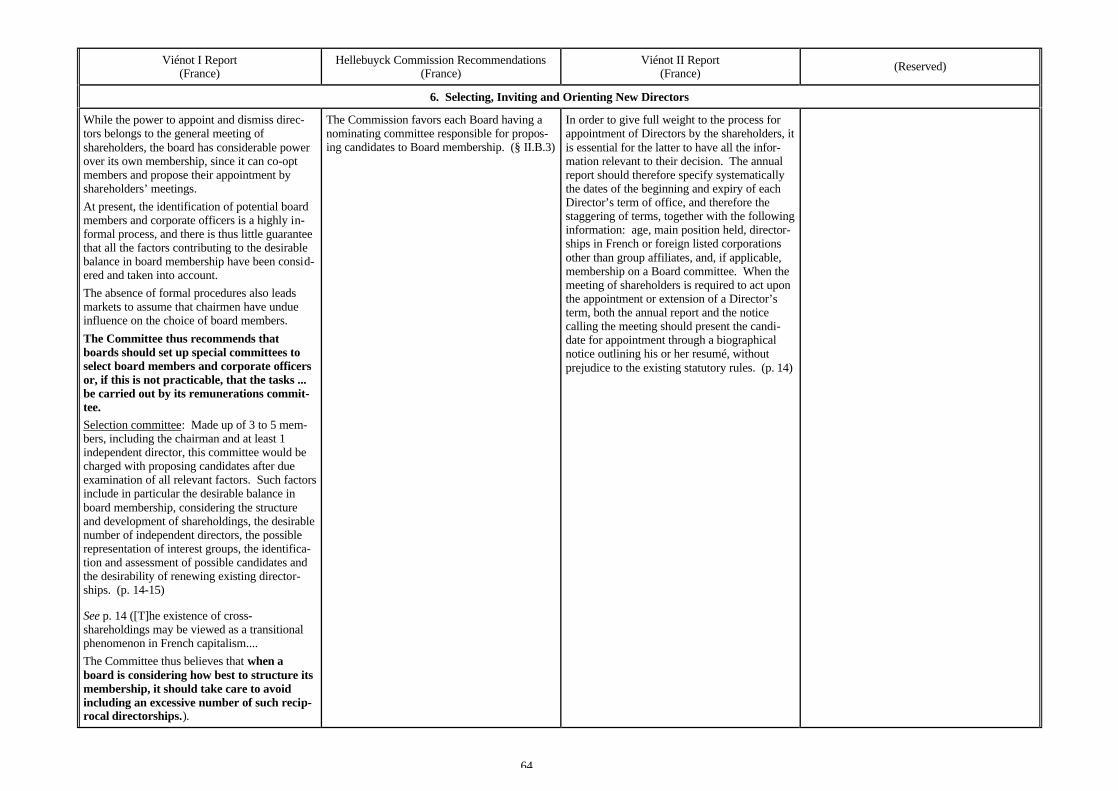

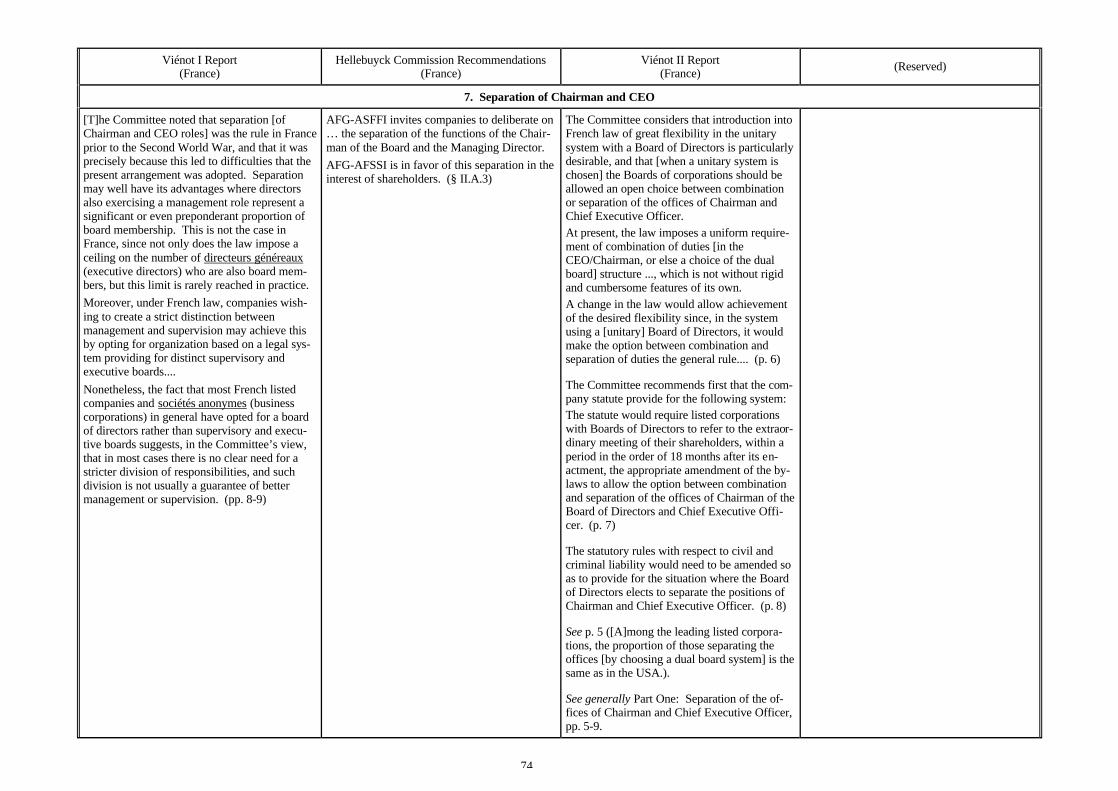

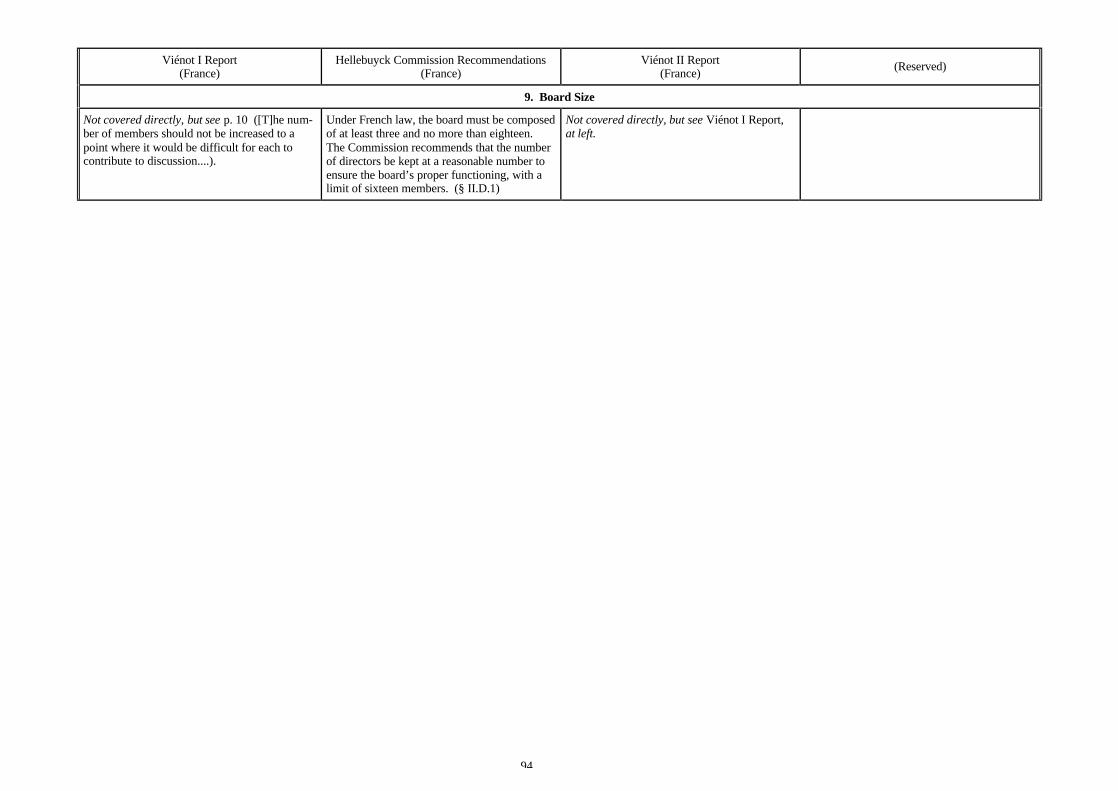

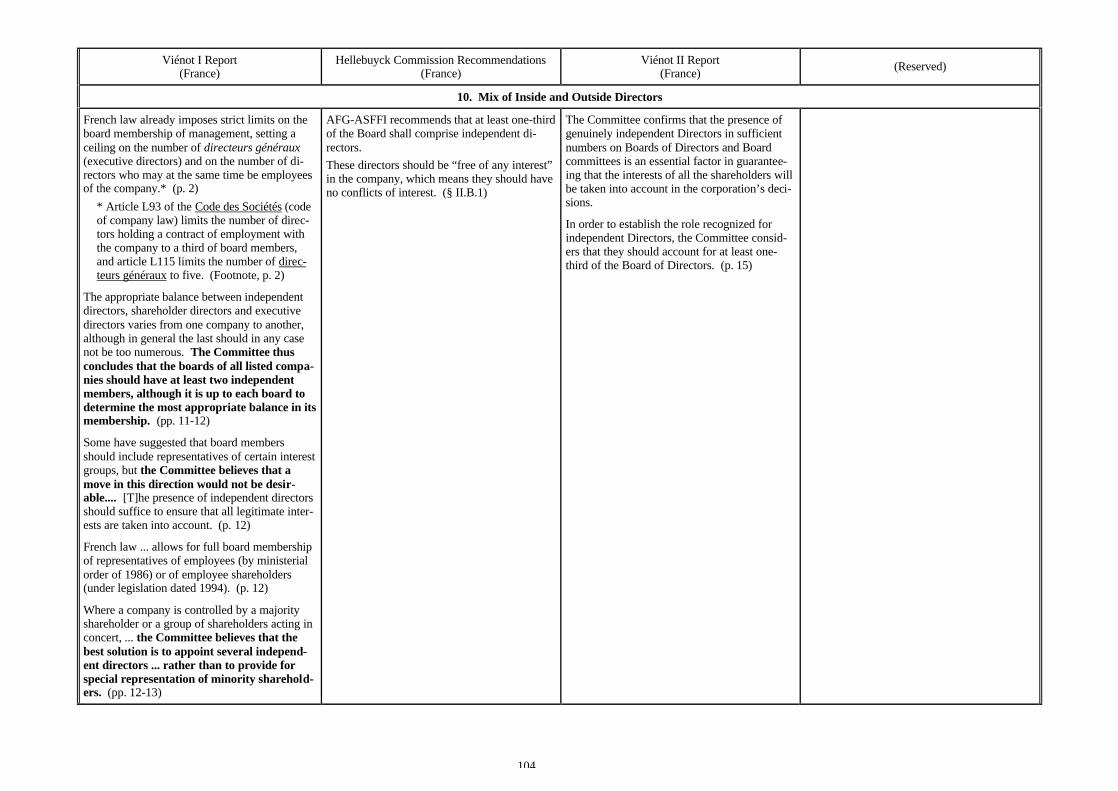

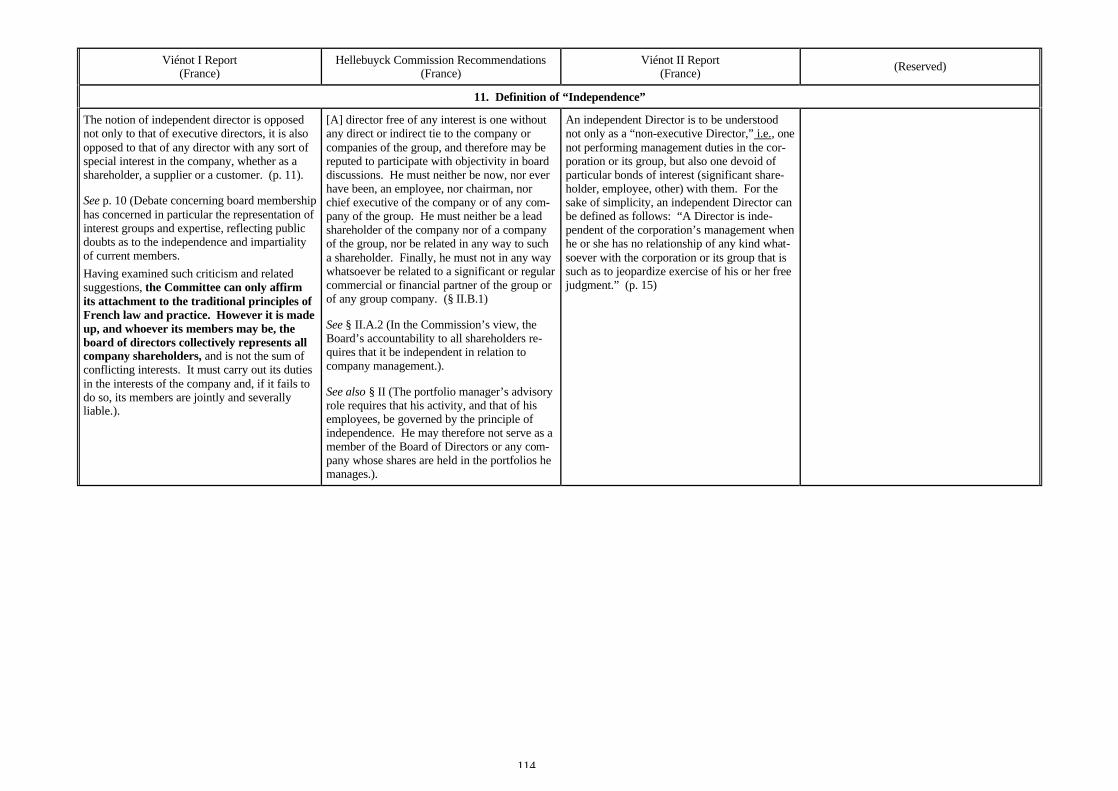

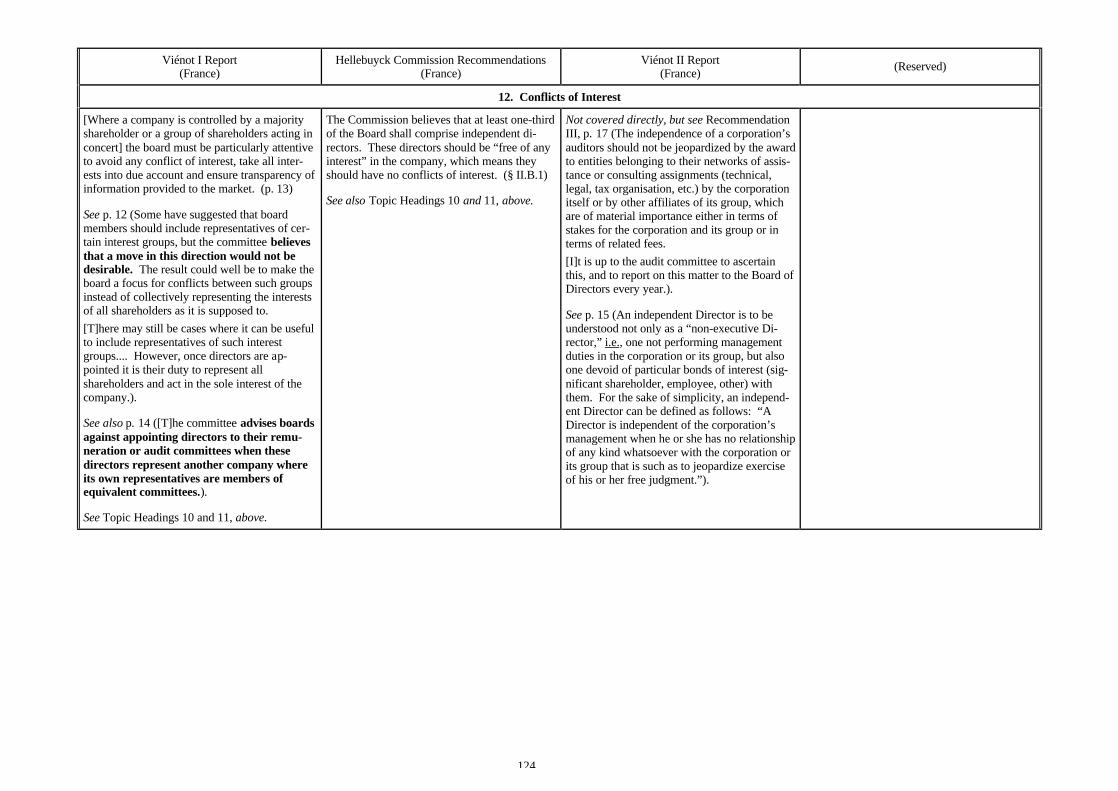

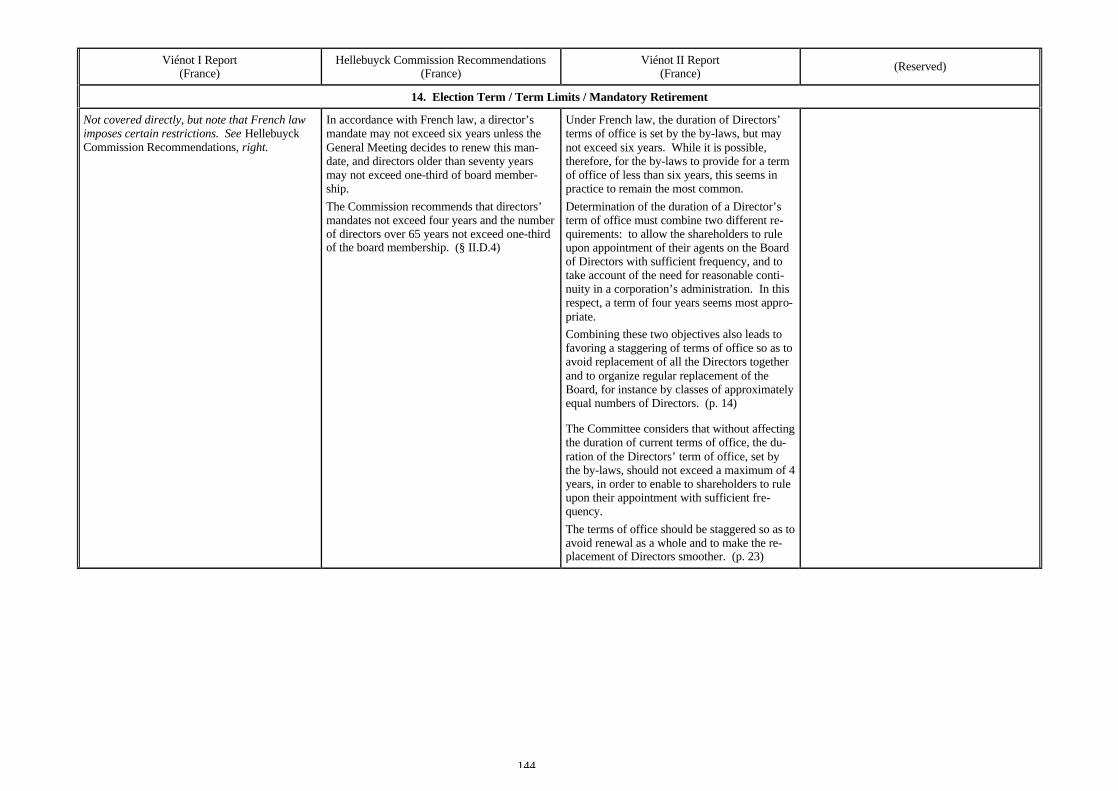

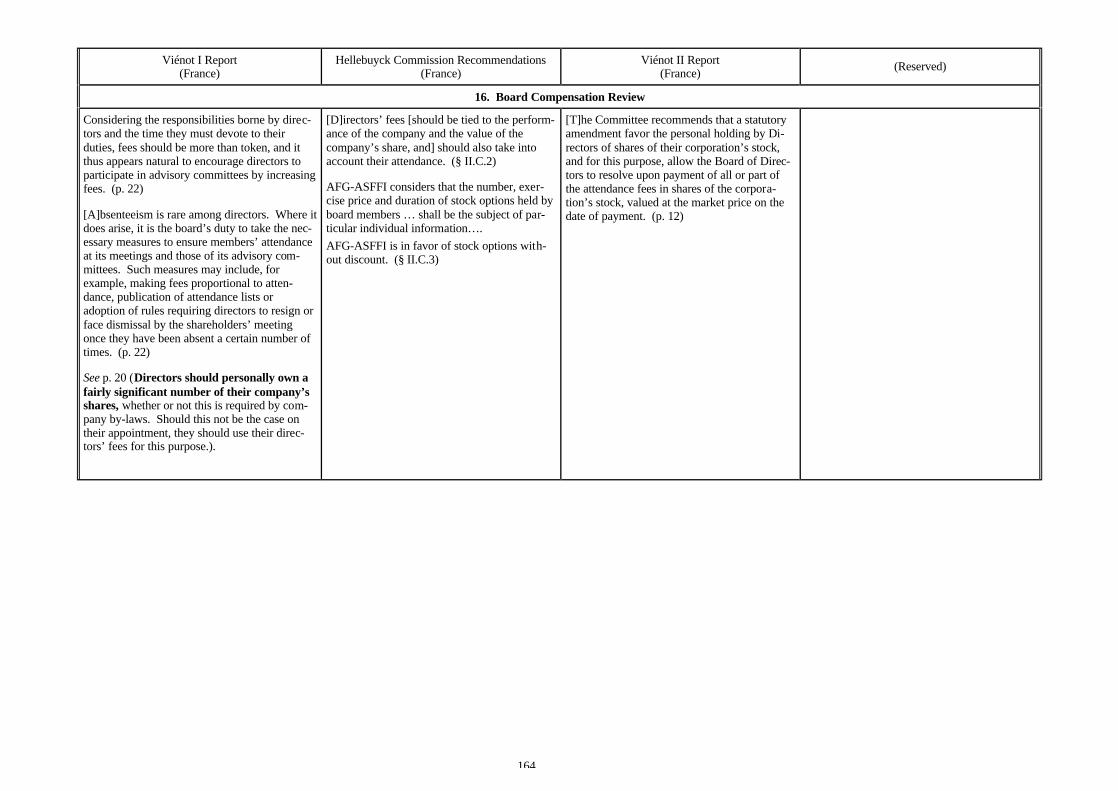

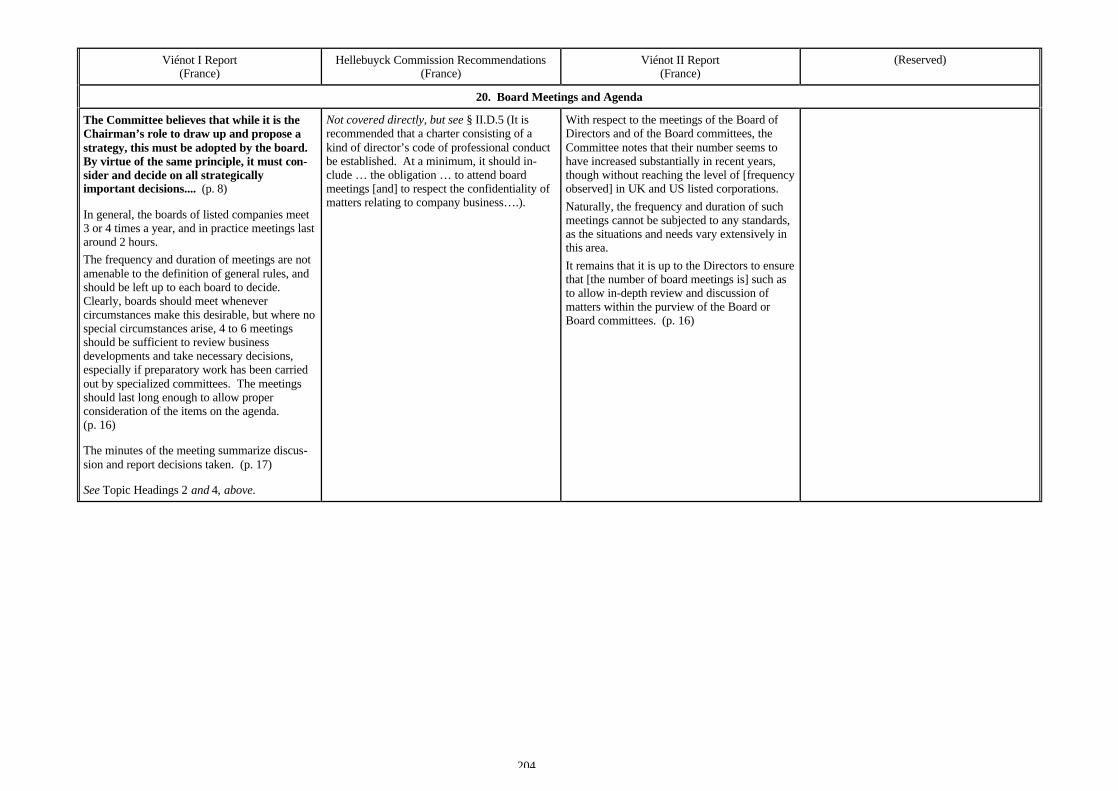

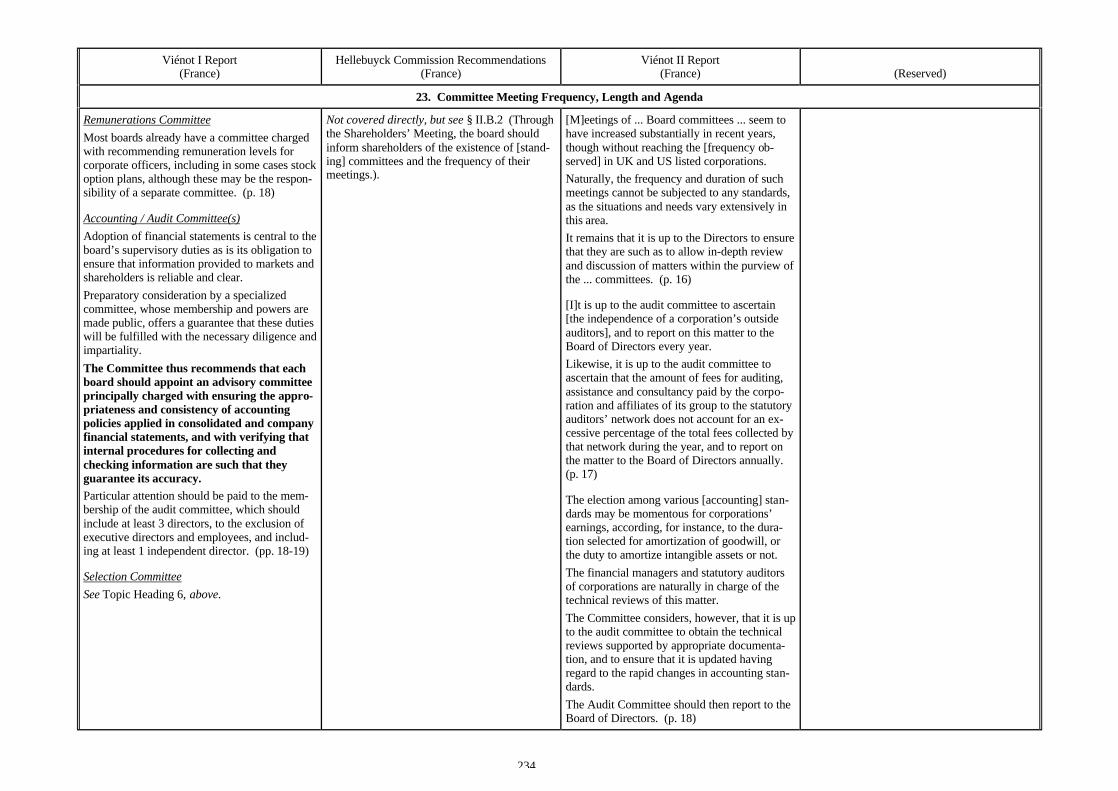

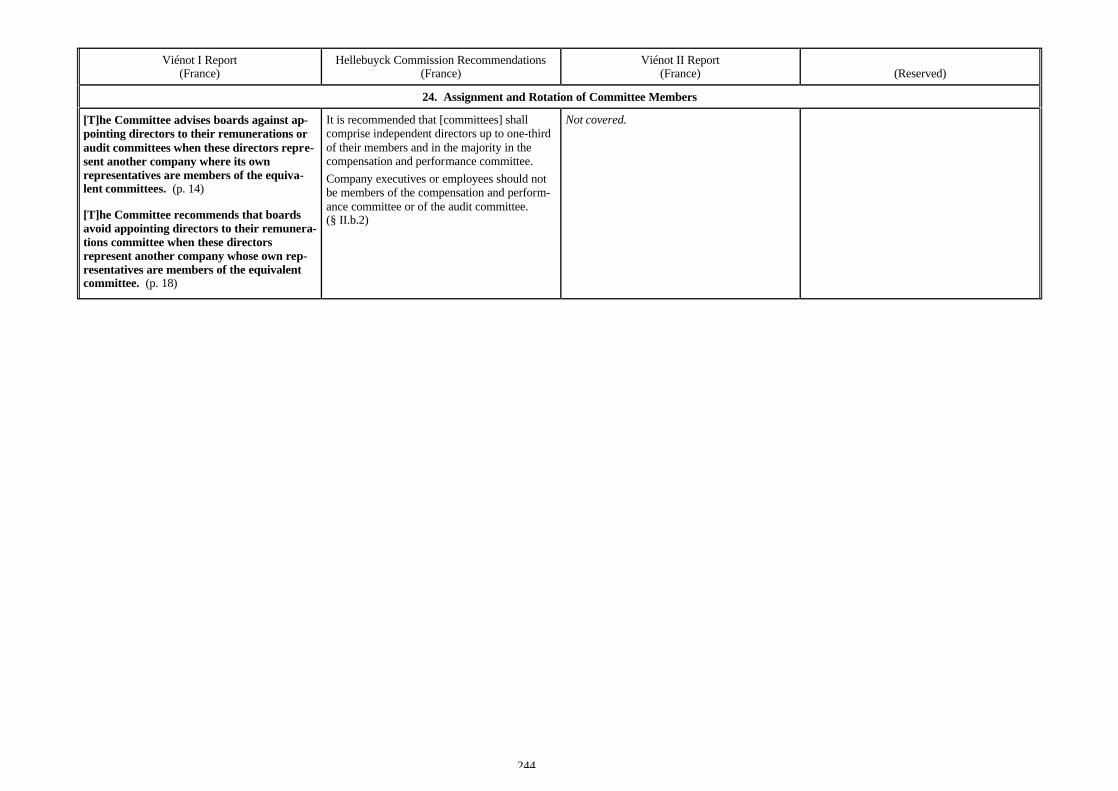

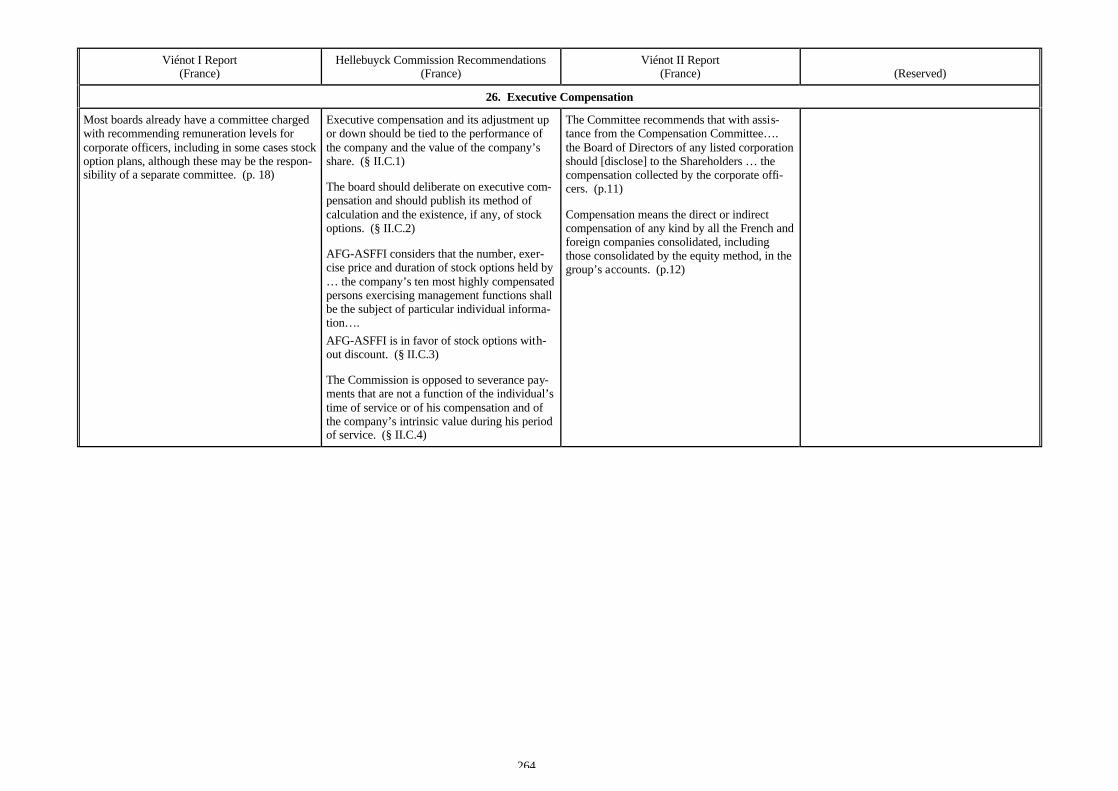

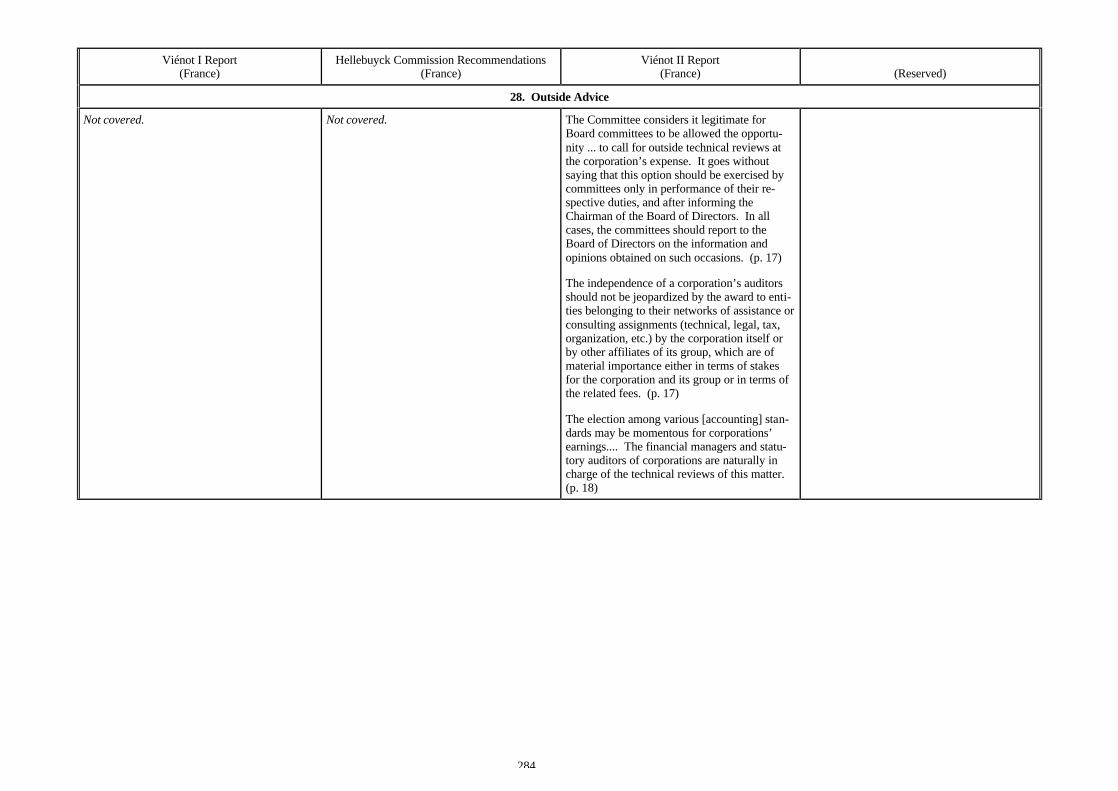

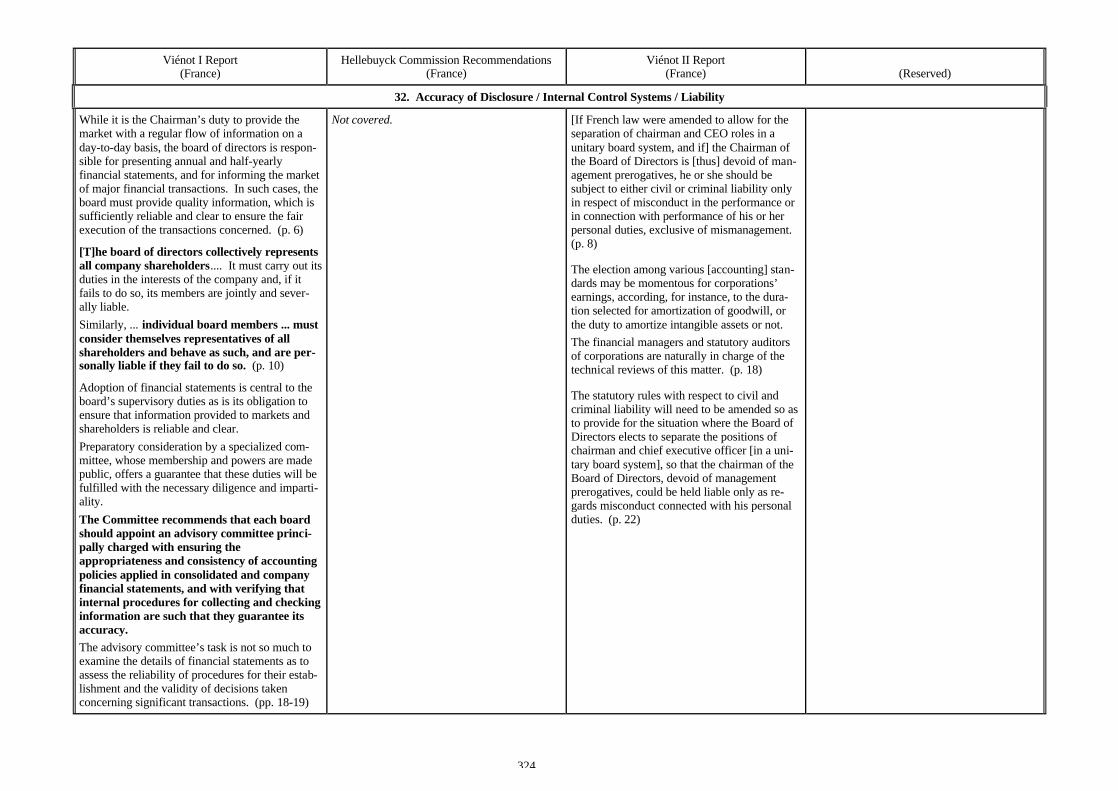

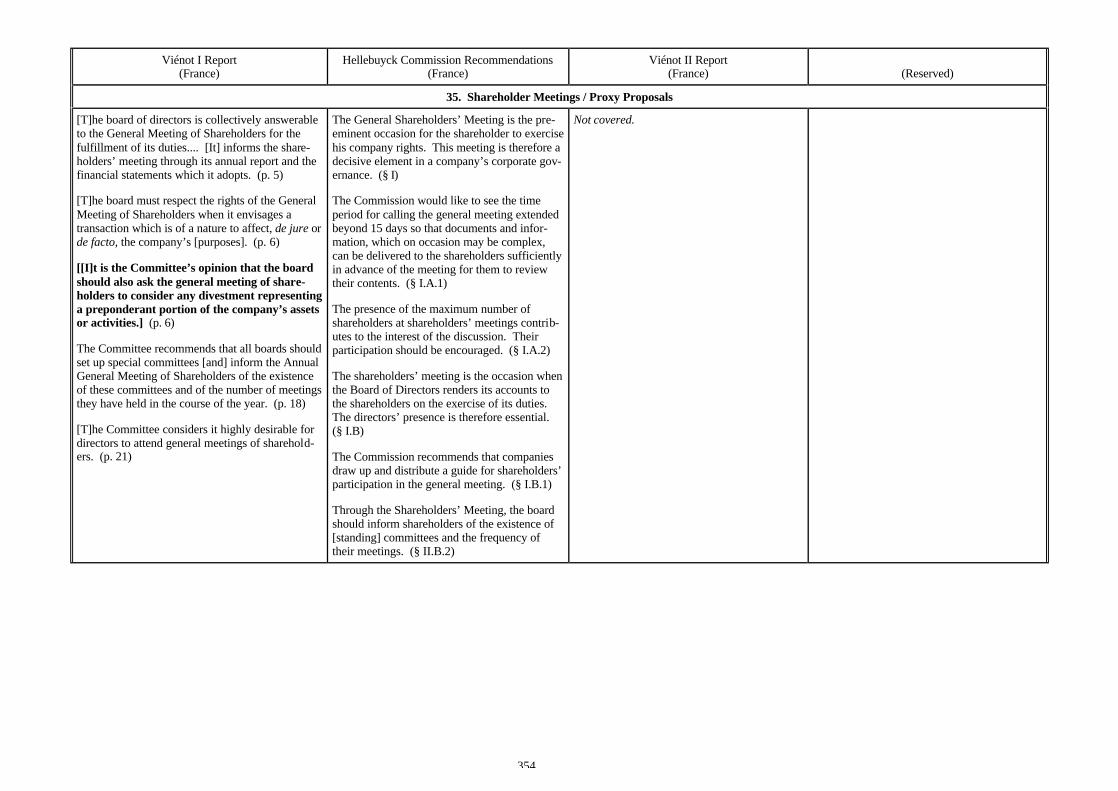

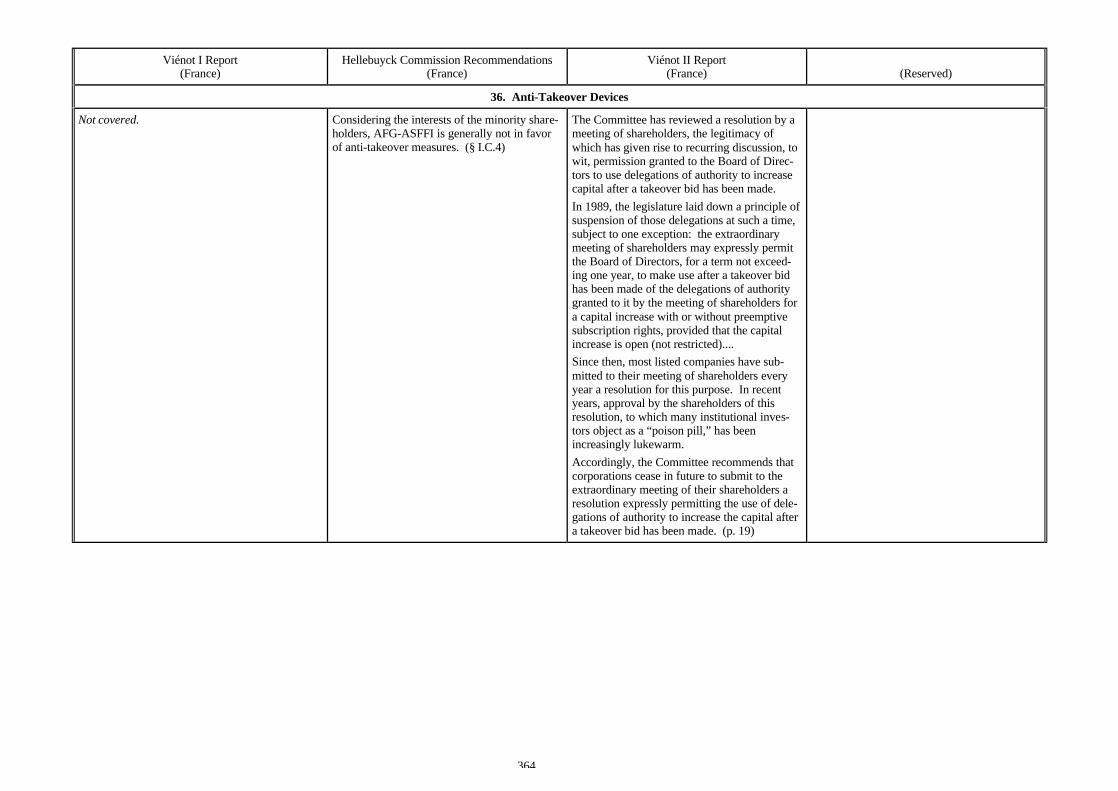

Viénot I Report(France)

Hellebuyck Commission Recommendations(France)

Viénot II Report(France) (Reserved)

OVERVIEW

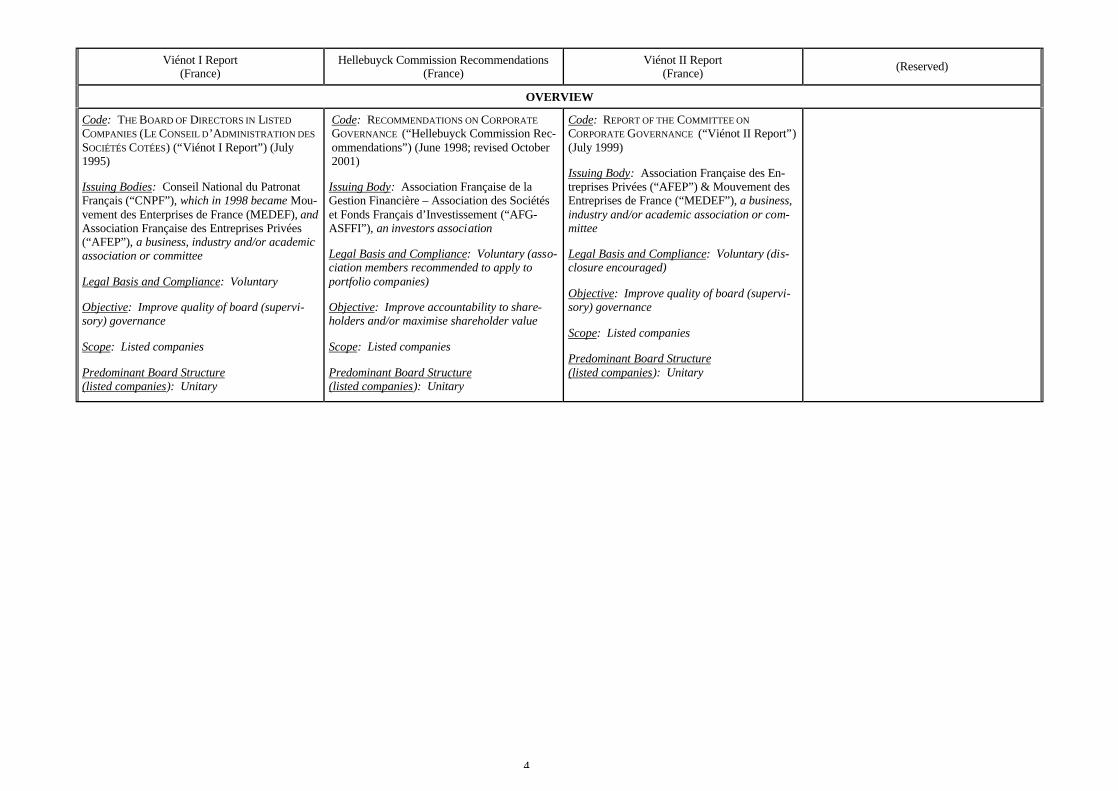

Code: THE BOARD OF DIRECTORS IN LISTEDCOMPANIES (LE CONSEIL D’ADMINISTRATION DESSOCIÉTÉS COTÉES) (“Viénot I Report”) (July1995)

Issuing Bodies: Conseil National du PatronatFrançais (“CNPF”), which in 1998 became Mou-vement des Enterprises de France (MEDEF), andAssociation Française des Entreprises Privées(“AFEP”), a business, industry and/or academicassociation or committee

Legal Basis and Compliance: Voluntary

Objective: Improve quality of board (supervi-sory) governance

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

Code: RECOMMENDATIONS ON CORPORATEGOVERNANCE (“Hellebuyck Commission Rec-ommendations”) (June 1998; revised October2001)

Issuing Body: Association Française de laGestion Financière – Association des Sociétéset Fonds Français d’Investissement (“AFG-ASFFI”), an investors association

Legal Basis and Compliance: Voluntary (asso-ciation members recommended to apply toportfolio companies)

Objective: Improve accountability to share-holders and/or maximise shareholder value

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

Code: REPORT OF THE COMMITTEE ONCORPORATE GOVERNANCE (“Viénot II Report”)(July 1999)

Issuing Body: Association Française des En-treprises Privées (“AFEP”) & Mouvement desEntreprises de France (“MEDEF”), a business,industry and/or academic association or com-mittee

Legal Basis and Compliance: Voluntary (dis-closure encouraged)

Objective: Improve quality of board (supervi-sory) governance

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

5

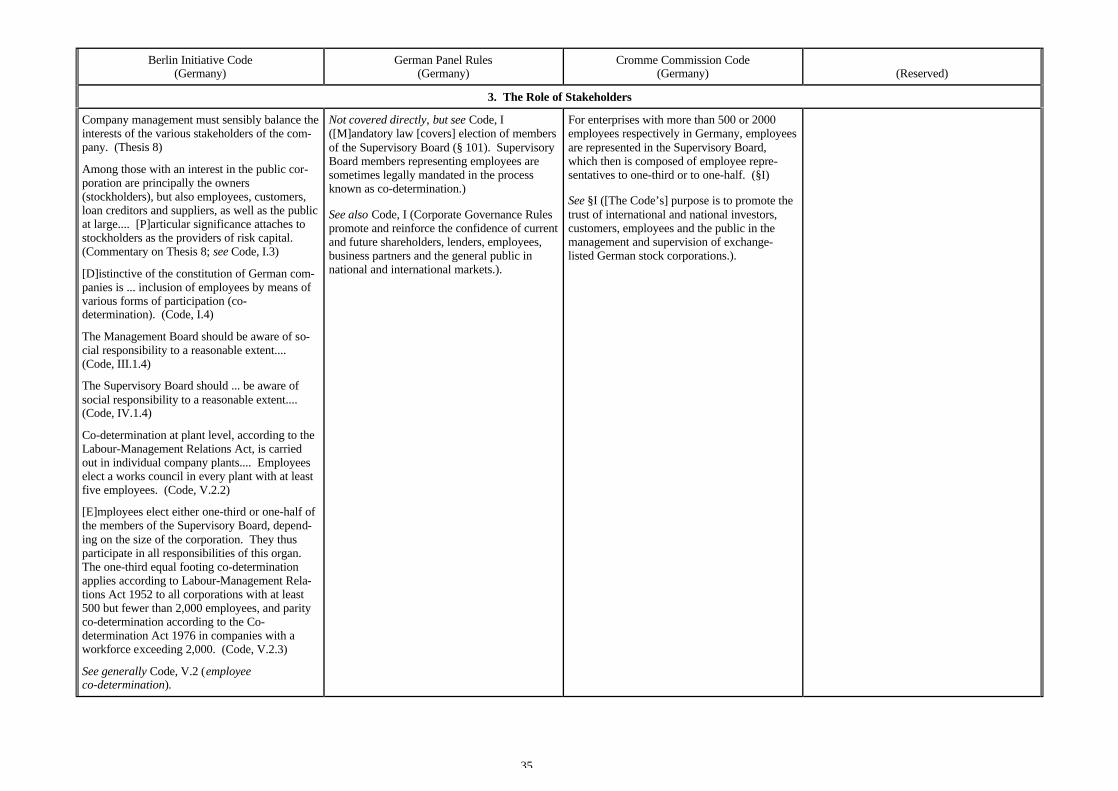

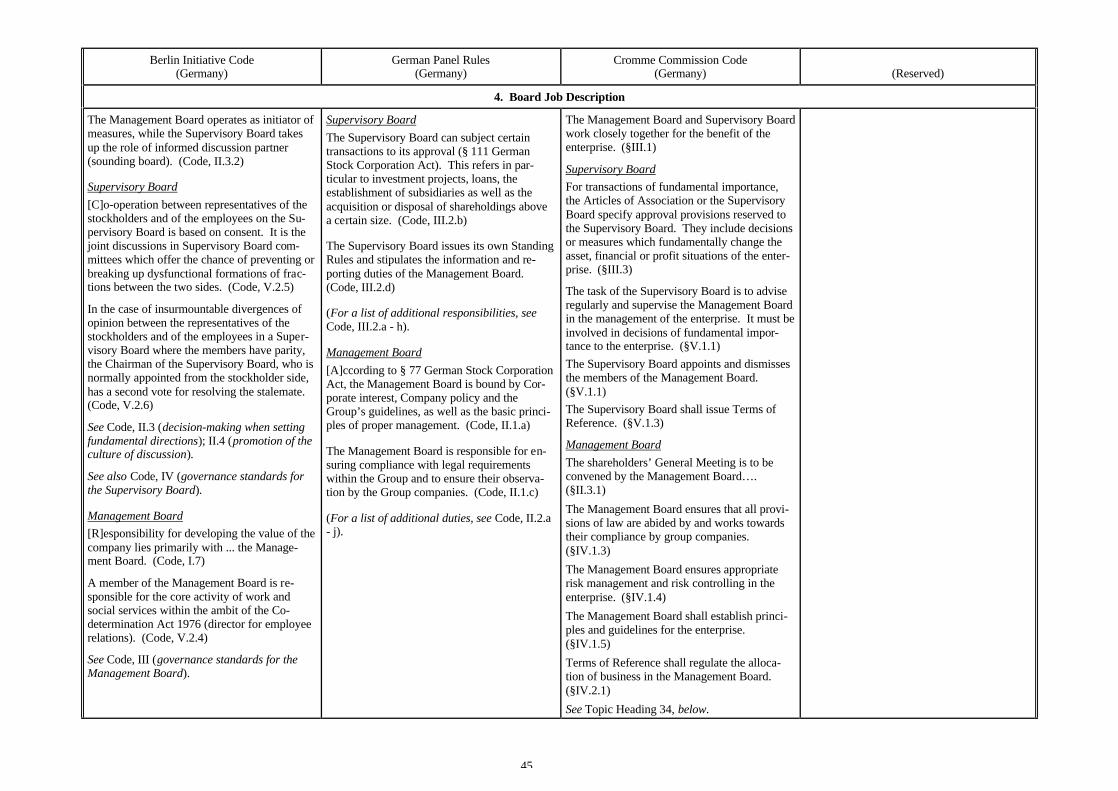

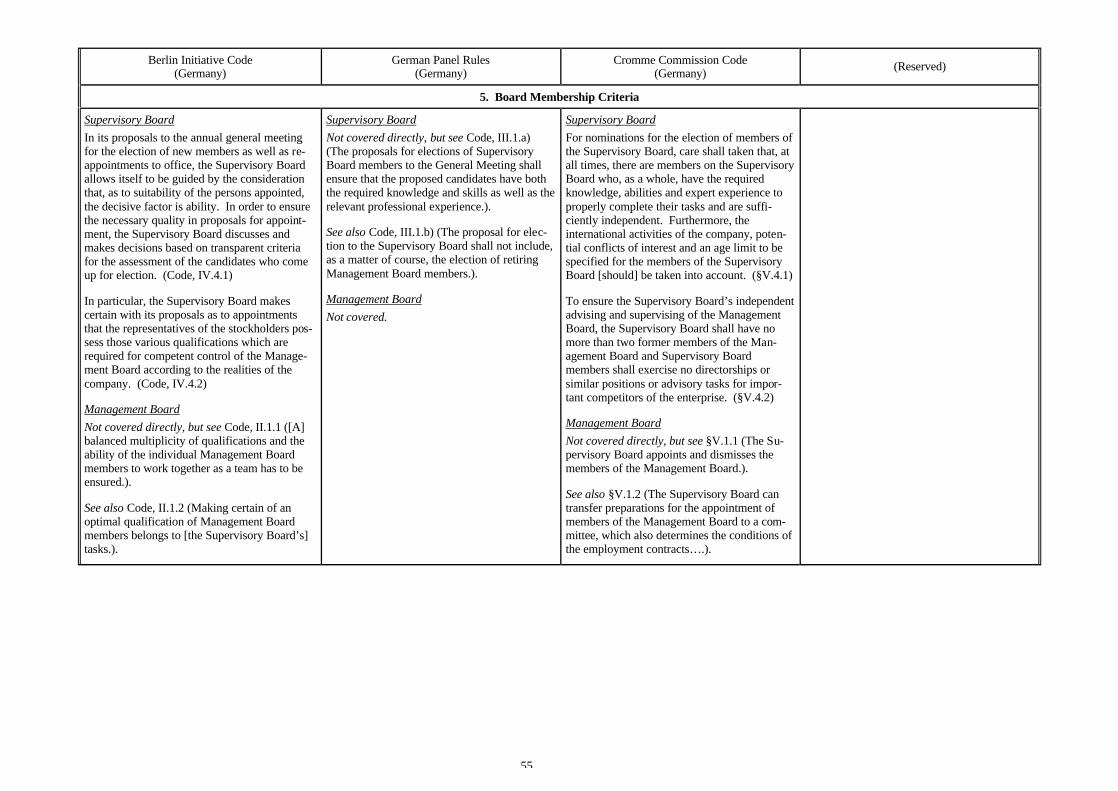

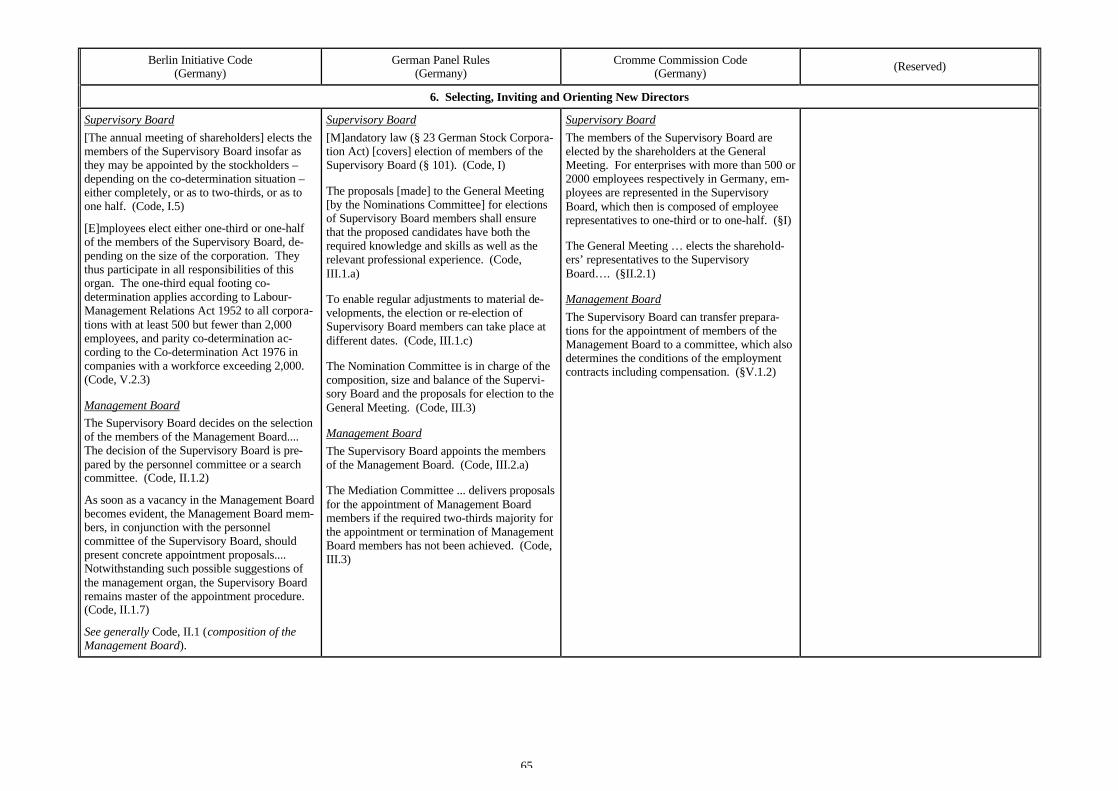

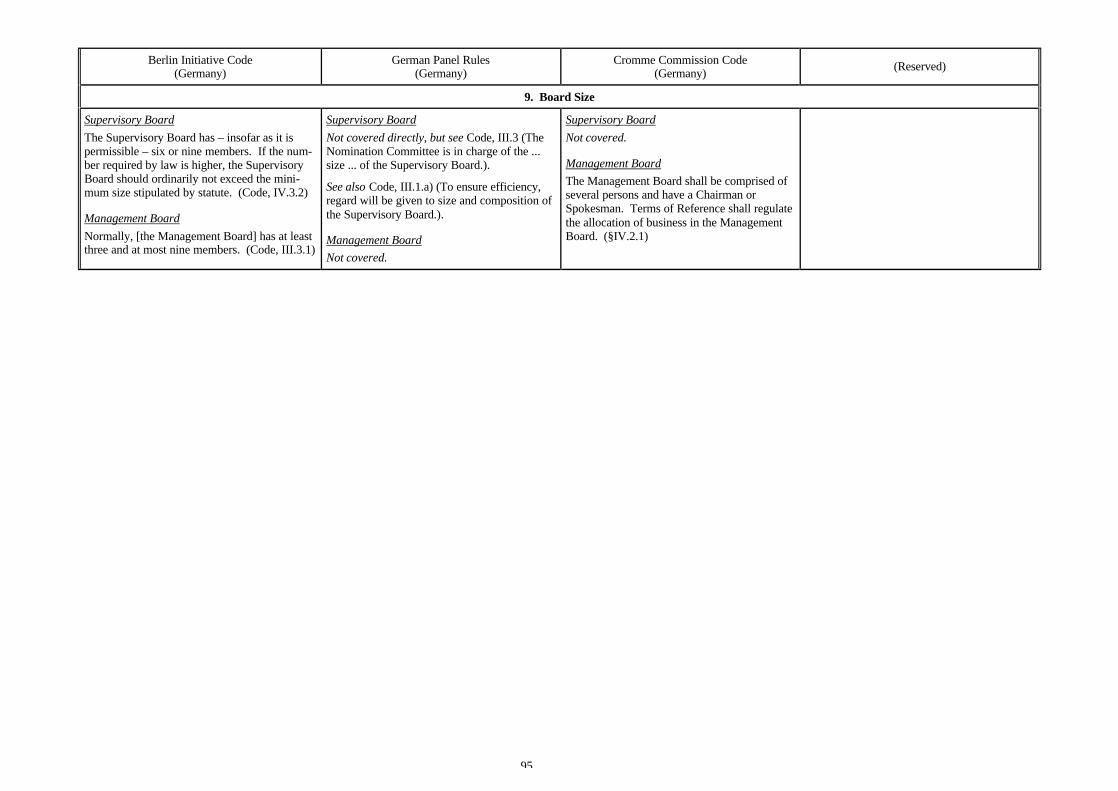

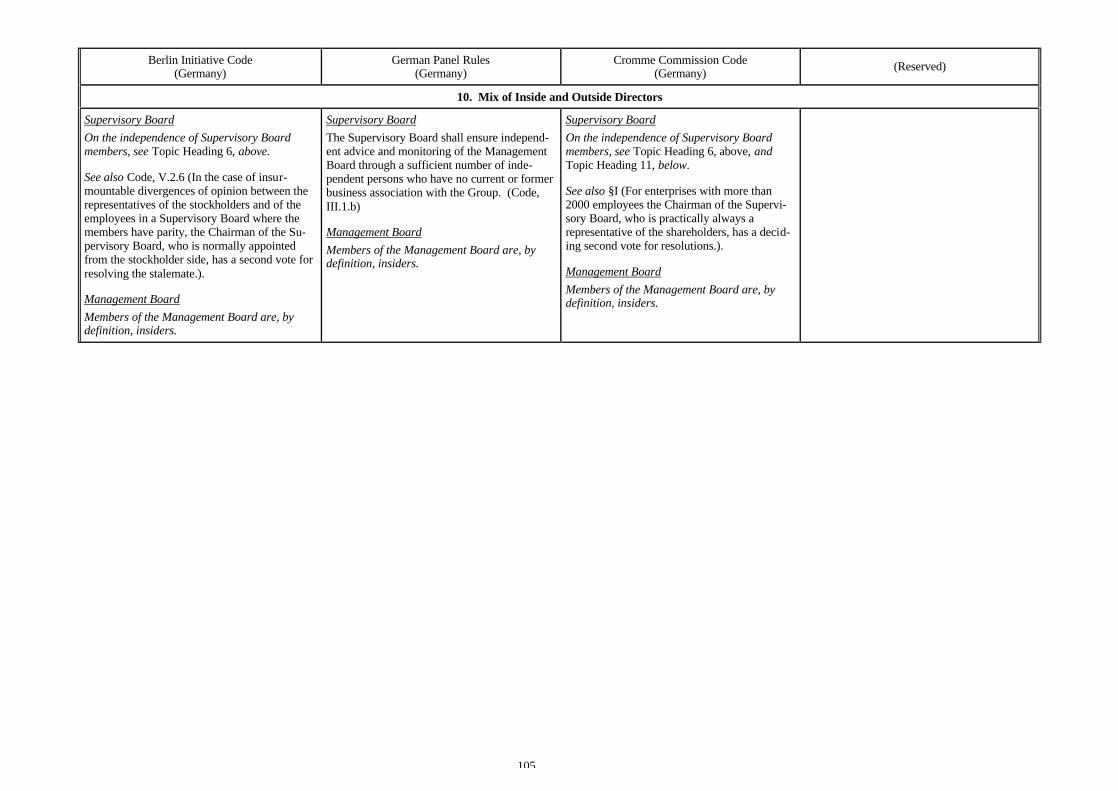

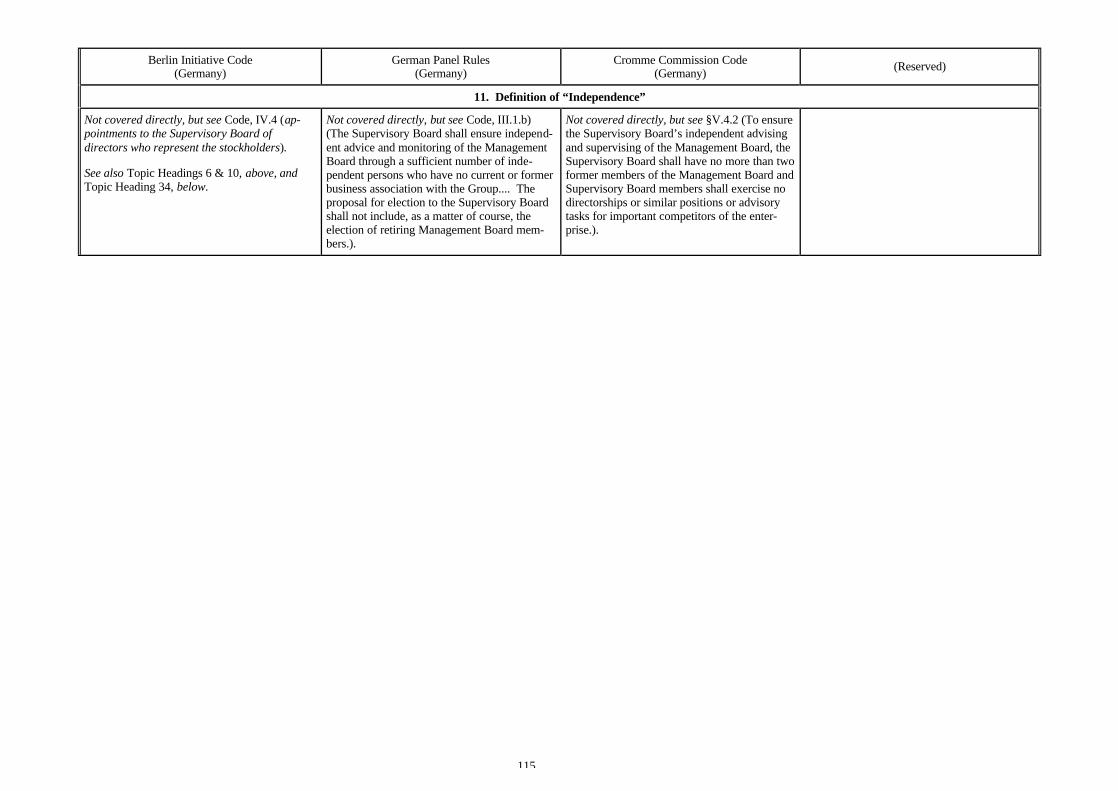

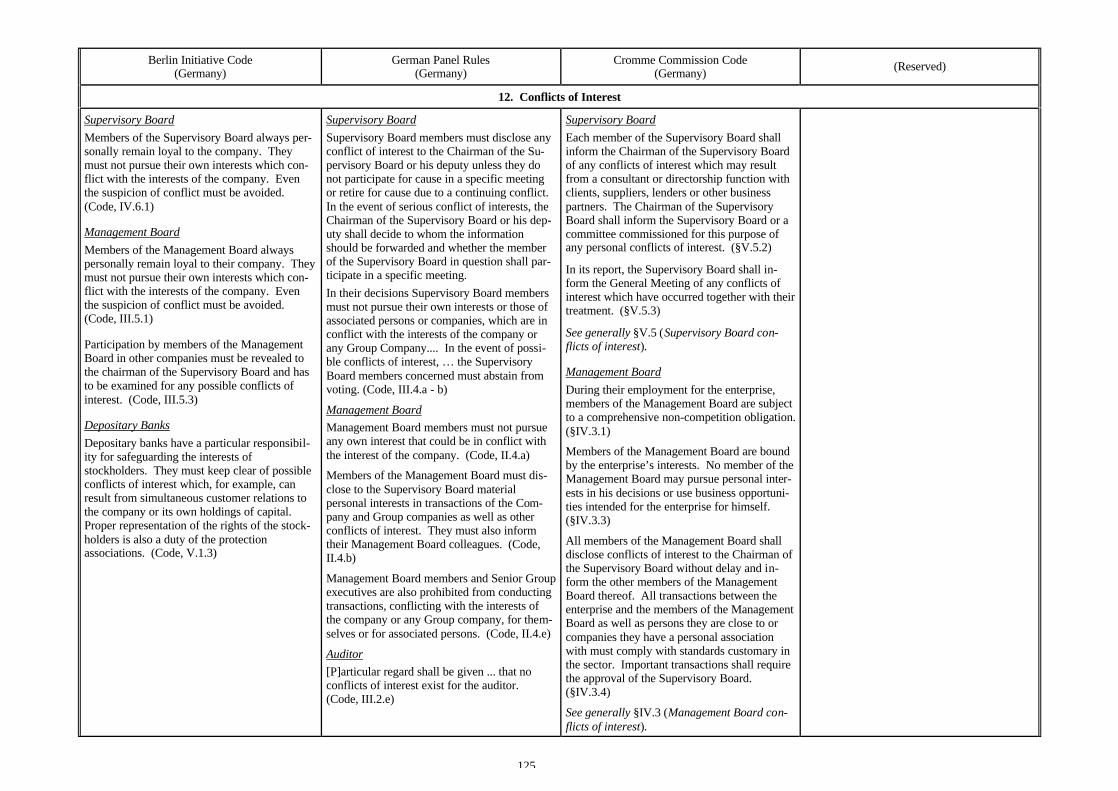

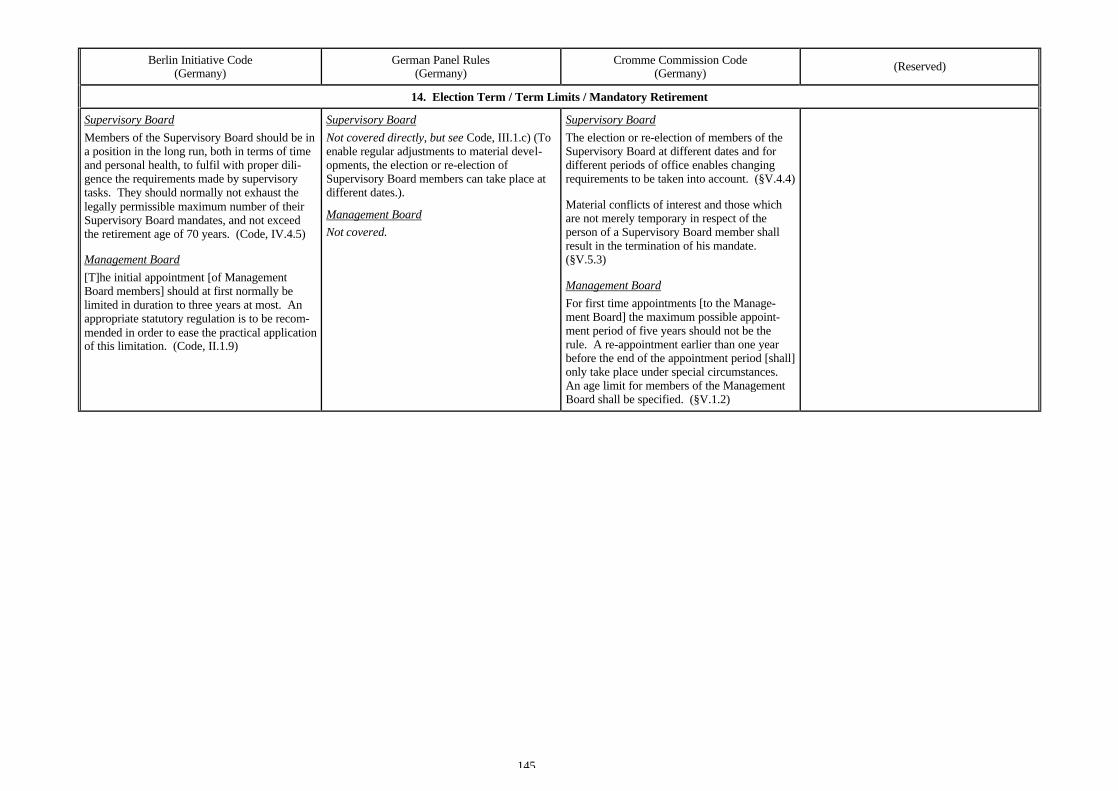

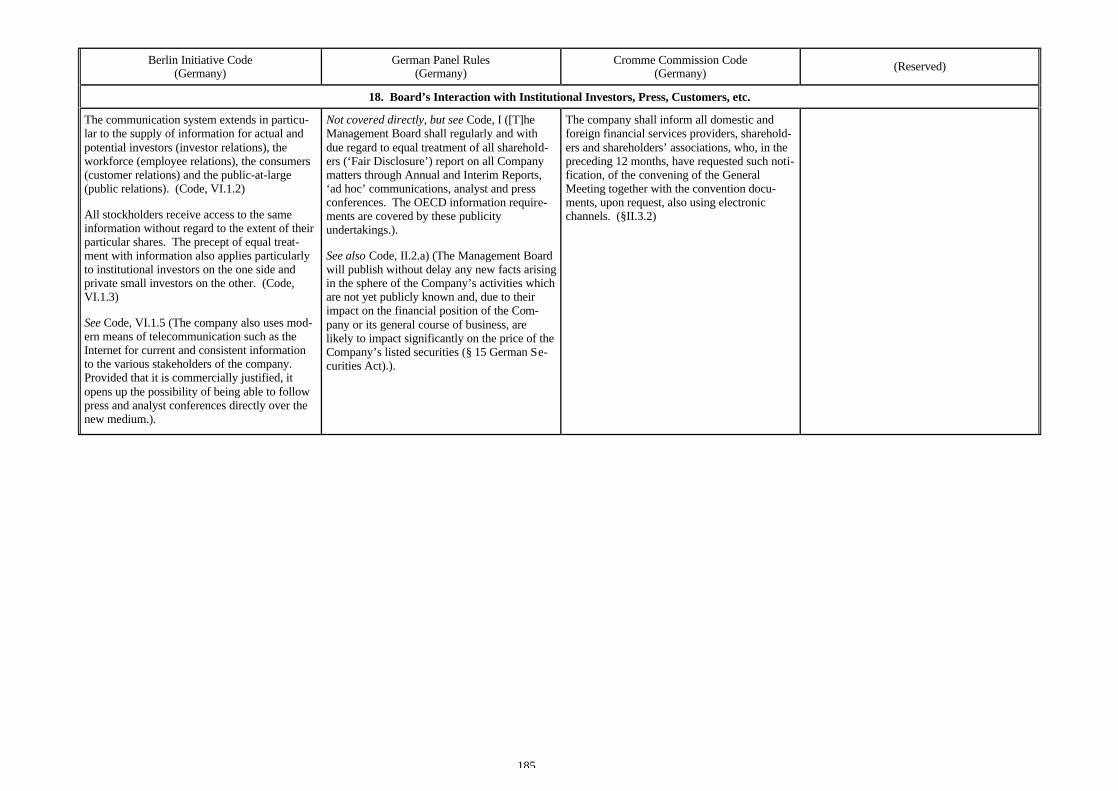

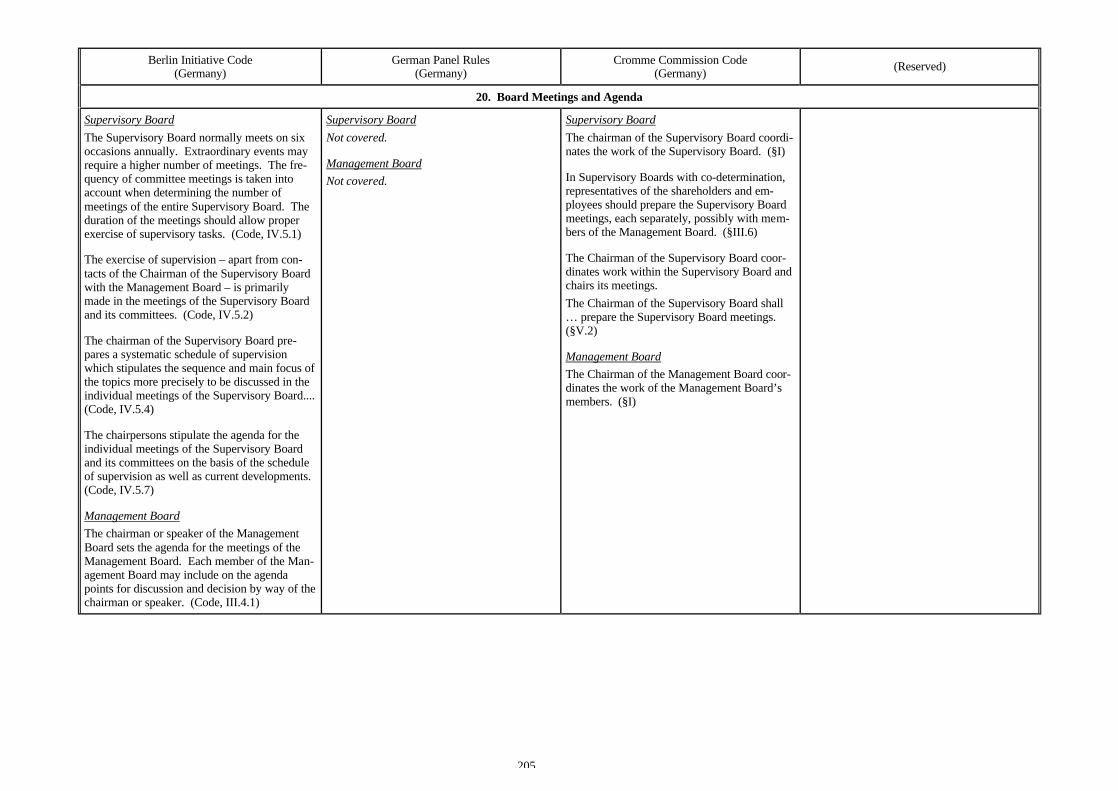

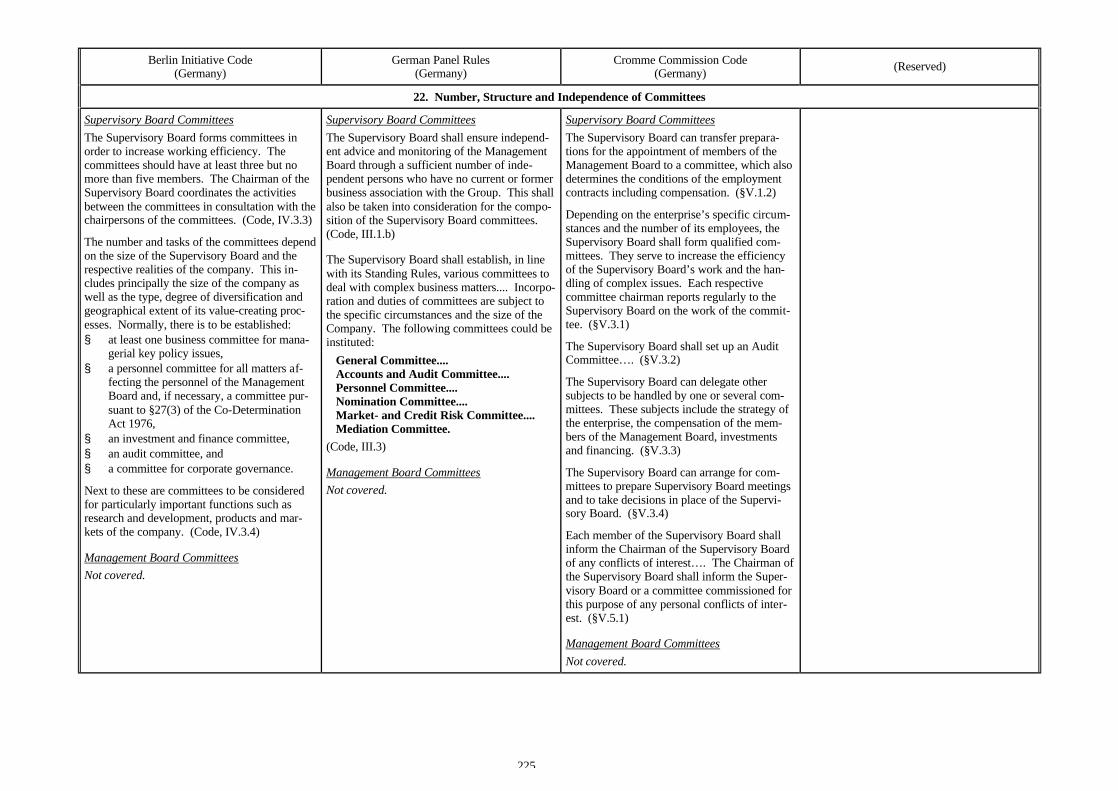

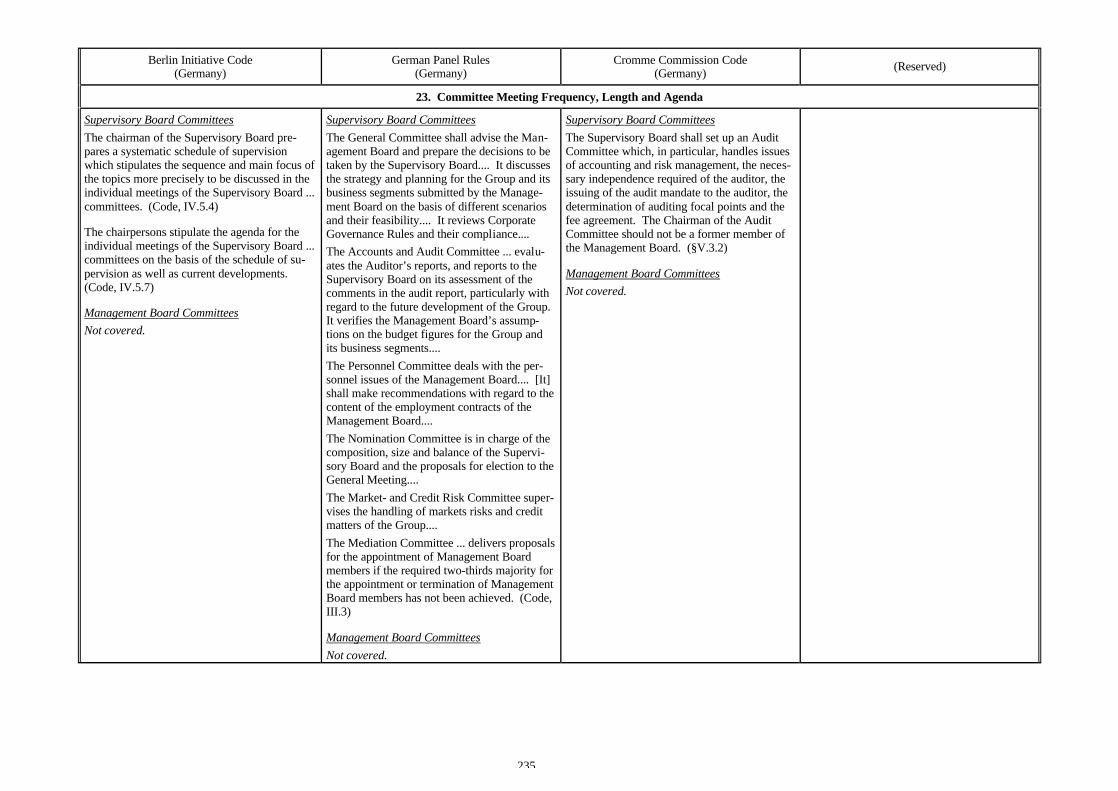

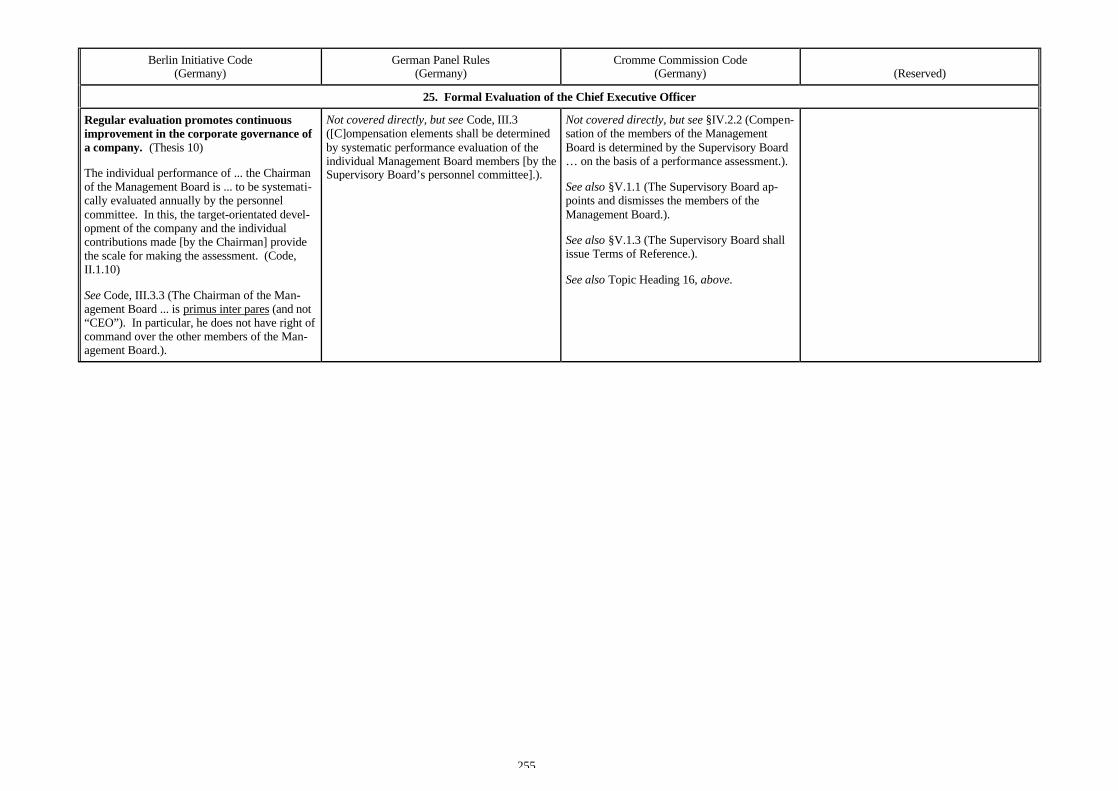

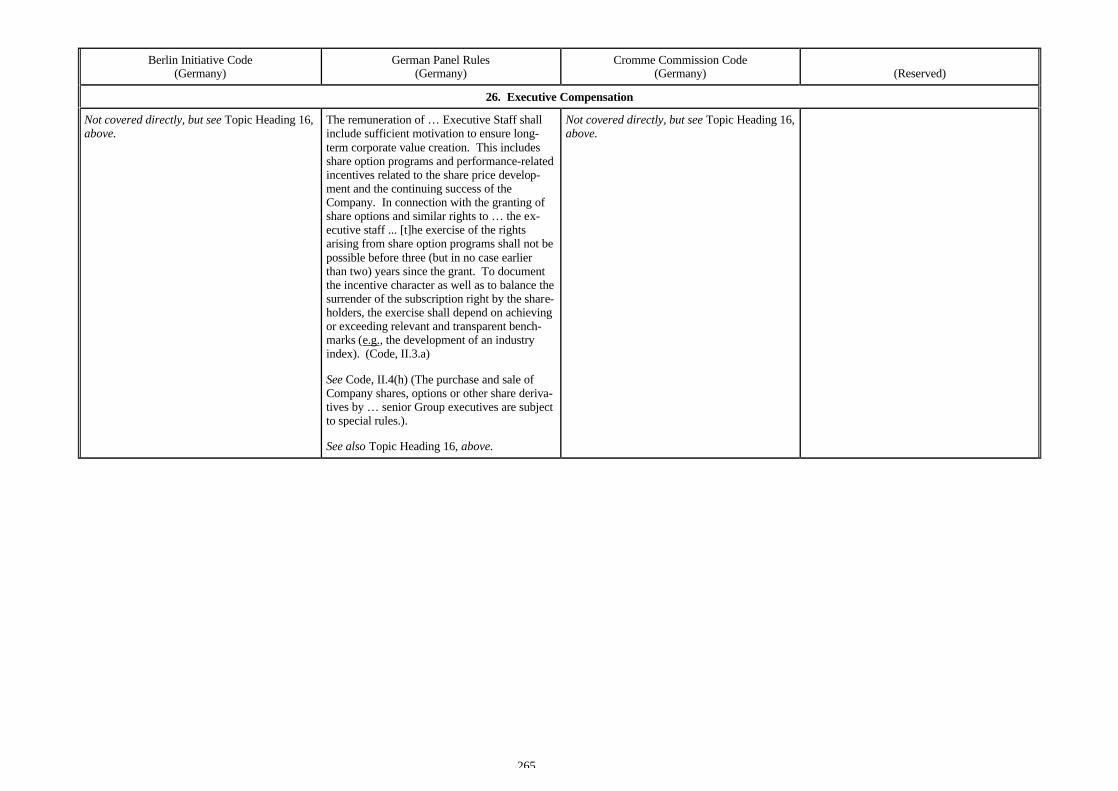

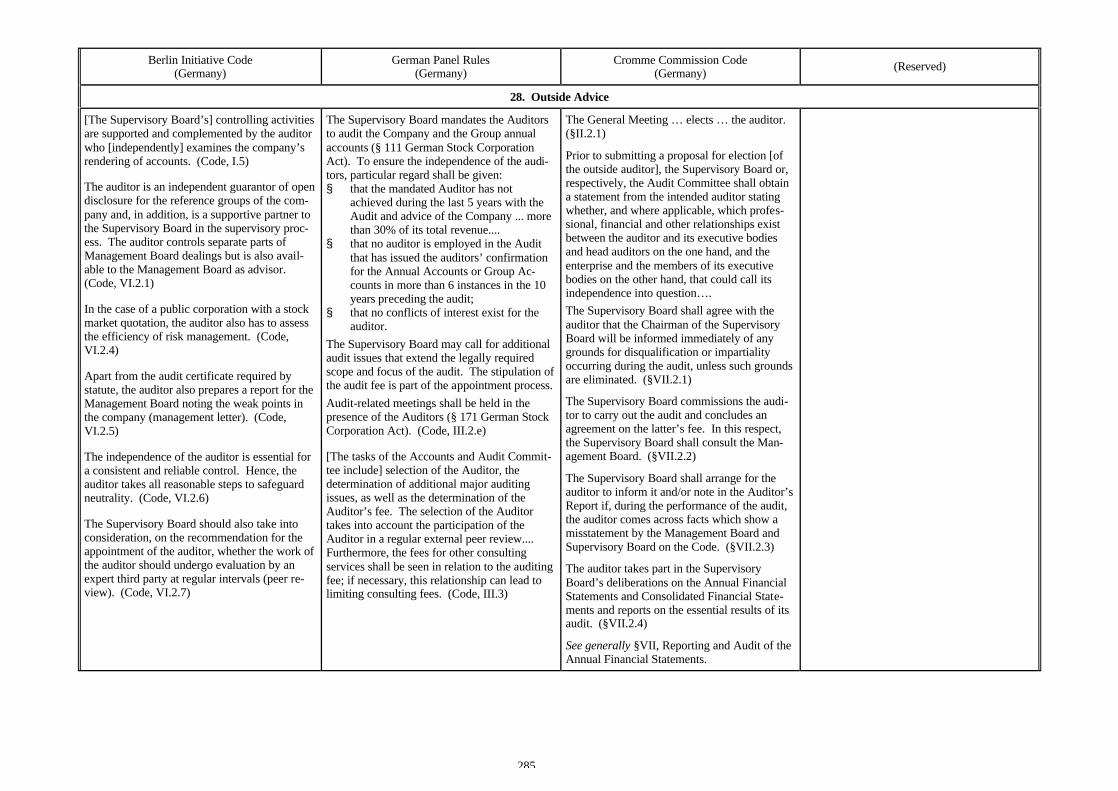

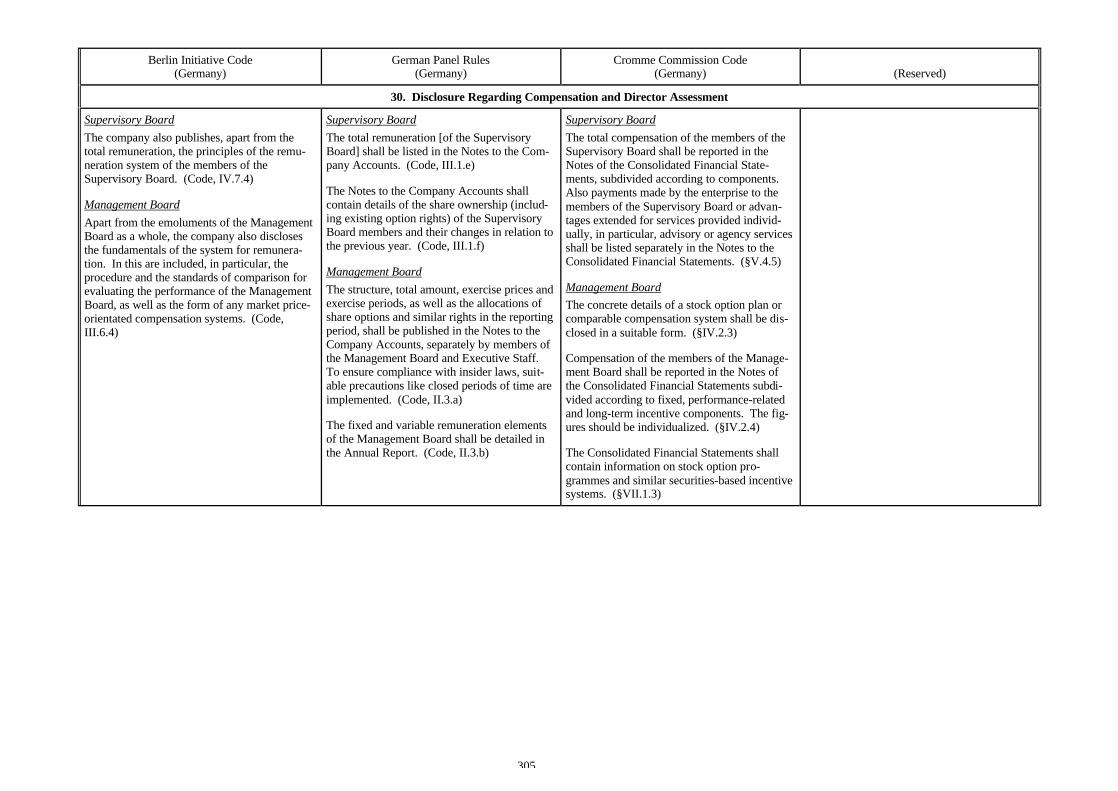

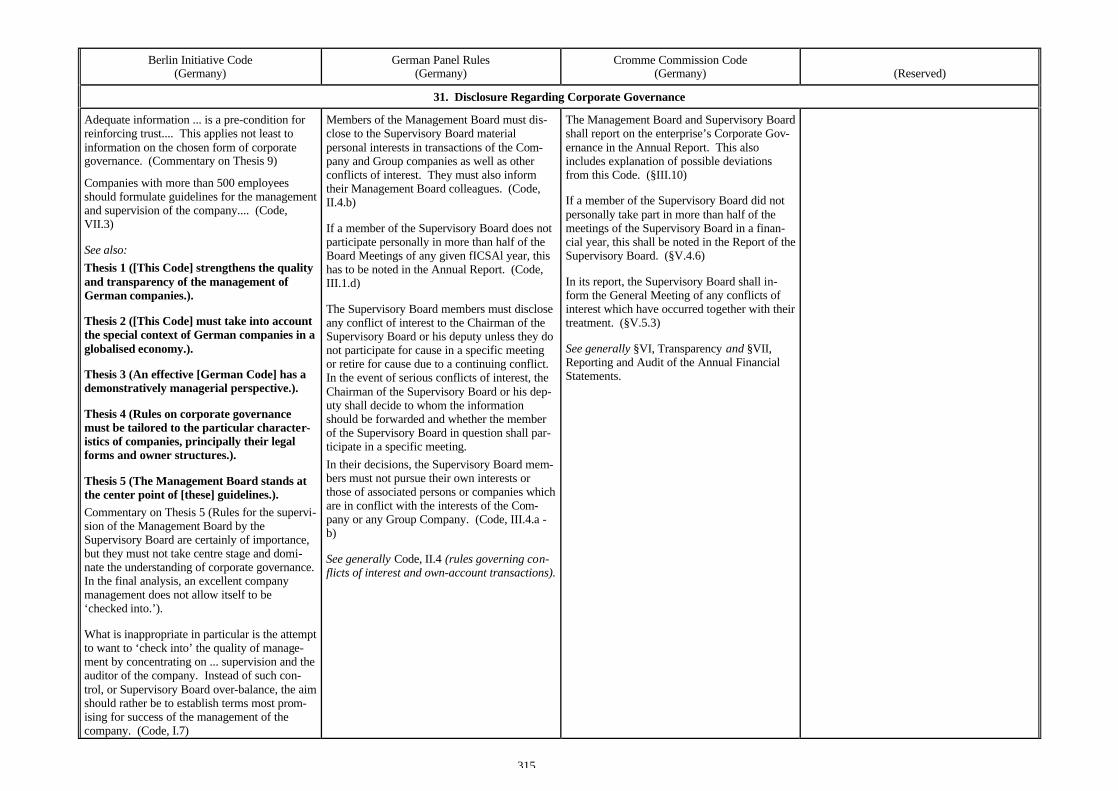

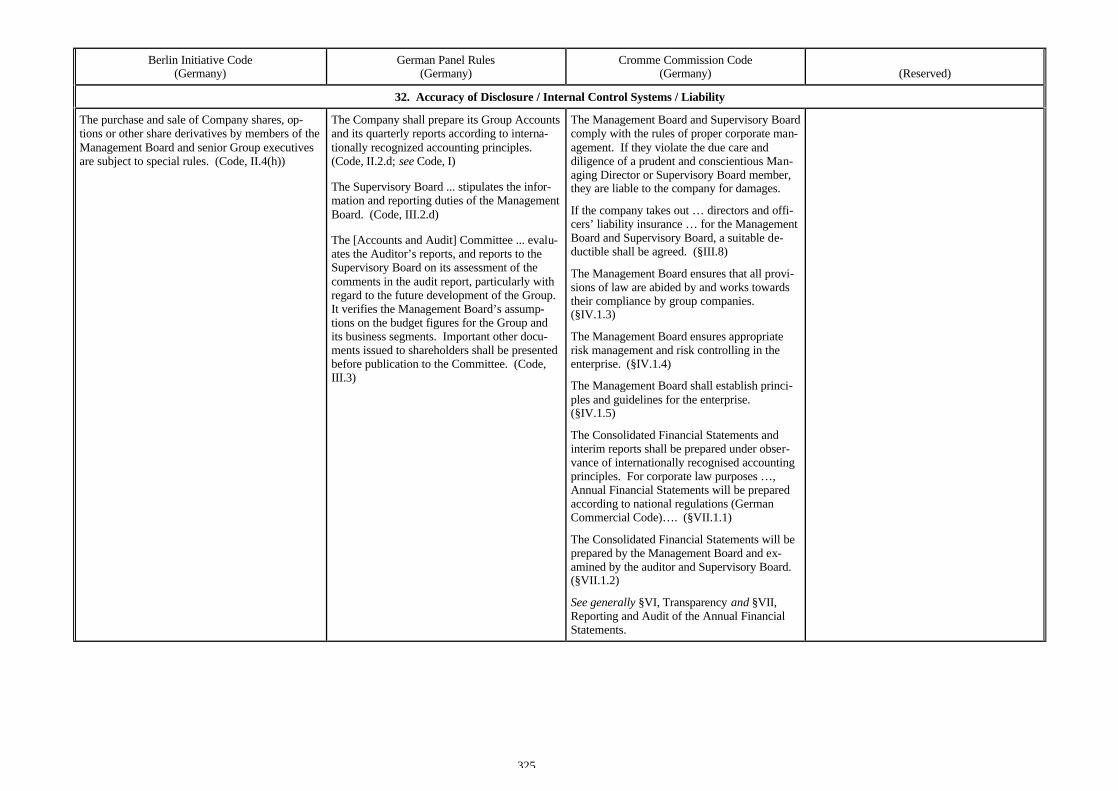

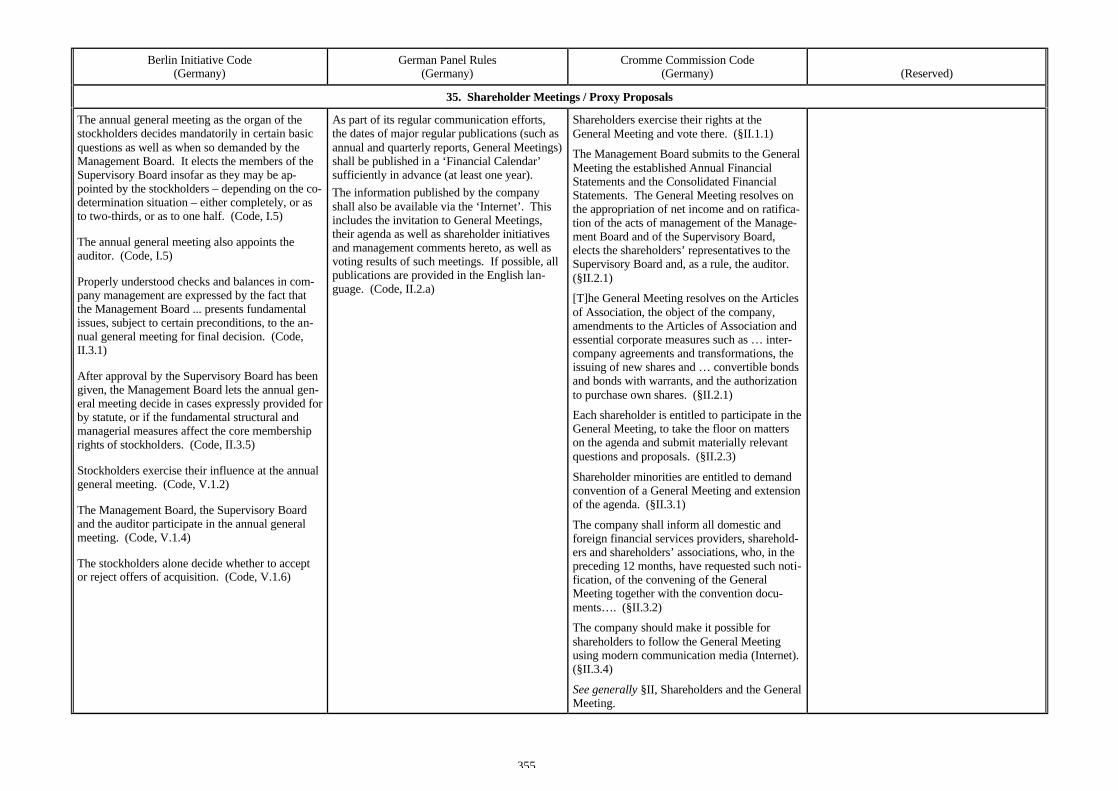

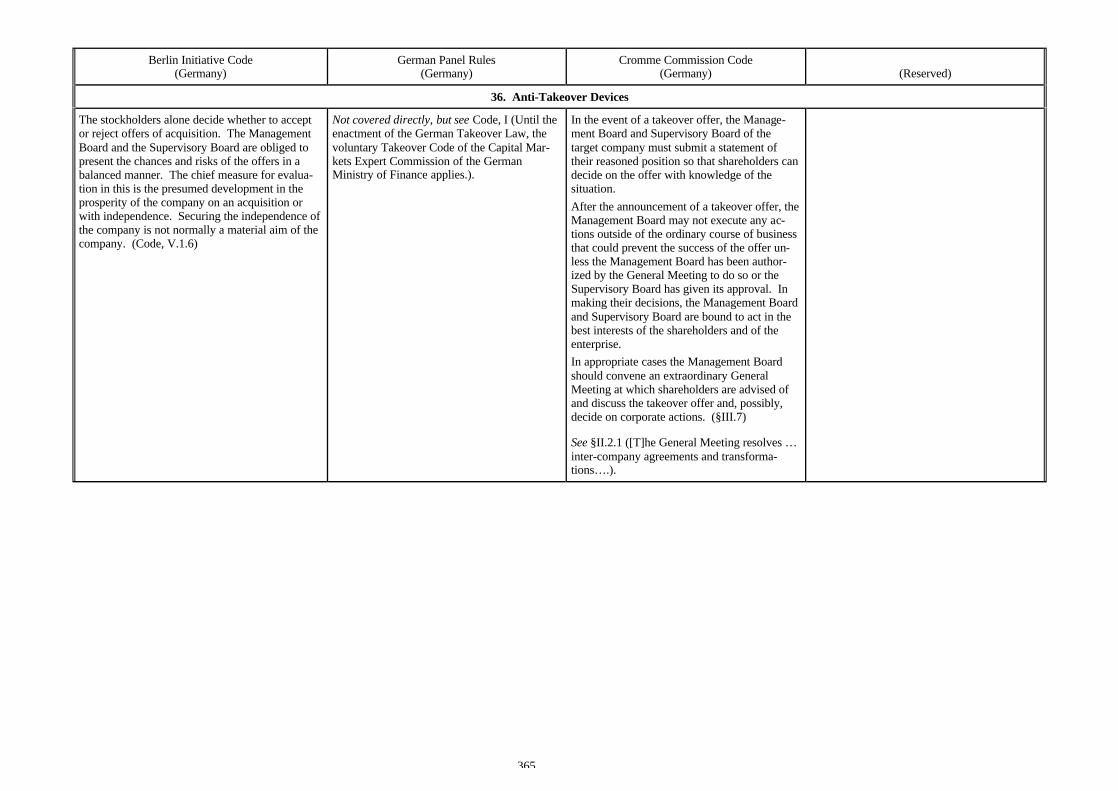

Berlin Initiative Code(Germany)

German Panel Rules(Germany)

Cromme Commission Code(Germany) (Reserved)

OVERVIEW

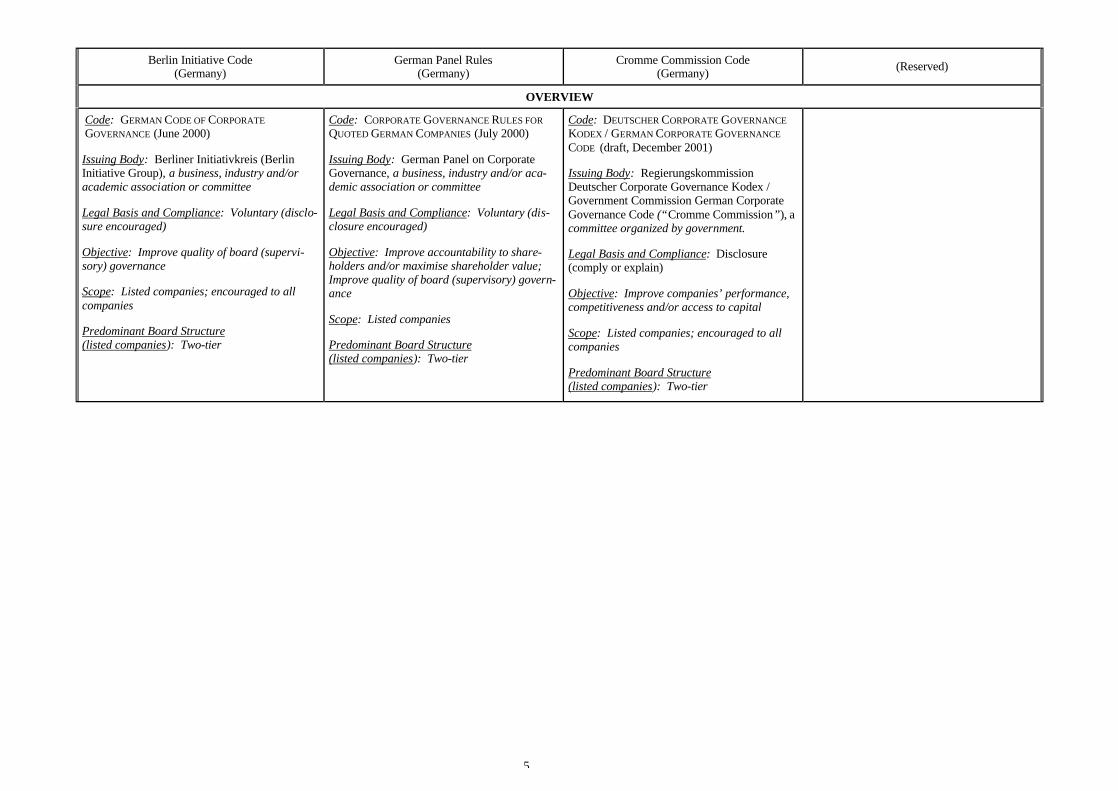

Code: GERMAN CODE OF CORPORATEGOVERNANCE (June 2000)

Issuing Body: Berliner Initiativkreis (BerlinInitiative Group), a business, industry and/oracademic association or committee

Legal Basis and Compliance: Voluntary (disclo-sure encouraged)

Objective: Improve quality of board (supervi-sory) governance

Scope: Listed companies; encouraged to allcompanies

Predominant Board Structure(listed companies): Two-tier

Code: CORPORATE GOVERNANCE RULES FORQUOTED GERMAN COMPANIES (July 2000)

Issuing Body: German Panel on CorporateGovernance, a business, industry and/or aca-demic association or committee

Legal Basis and Compliance: Voluntary (dis-closure encouraged)

Objective: Improve accountability to share-holders and/or maximise shareholder value;Improve quality of board (supervisory) govern-ance

Scope: Listed companies

Predominant Board Structure(listed companies): Two-tier

Code: DEUTSCHER CORPORATE GOVERNANCEKODEX / GERMAN CORPORATE GOVERNANCECODE (draft, December 2001)

Issuing Body: RegierungskommissionDeutscher Corporate Governance Kodex /Government Commission German CorporateGovernance Code (“Cromme Commission”), acommittee organized by government.

Legal Basis and Compliance: Disclosure(comply or explain)

Objective: Improve companies’ performance,competitiveness and/or access to capital

Scope: Listed companies; encouraged to allcompanies

Predominant Board Structure(listed companies): Two-tier

6

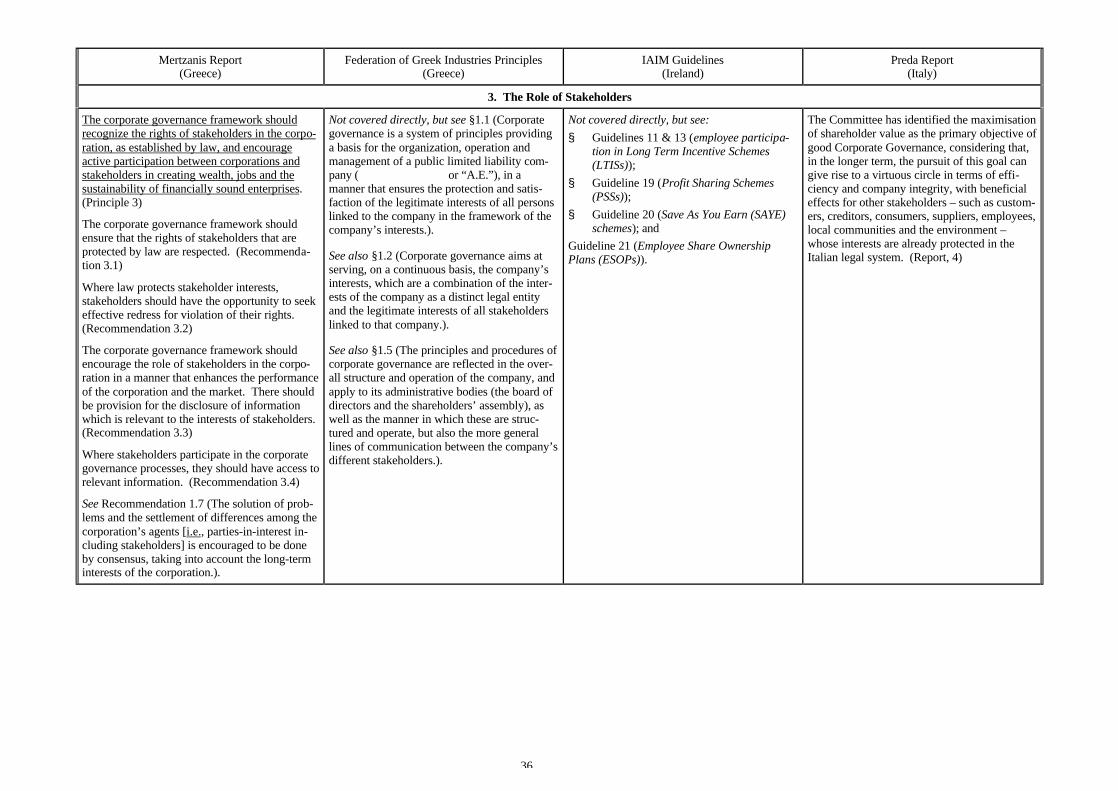

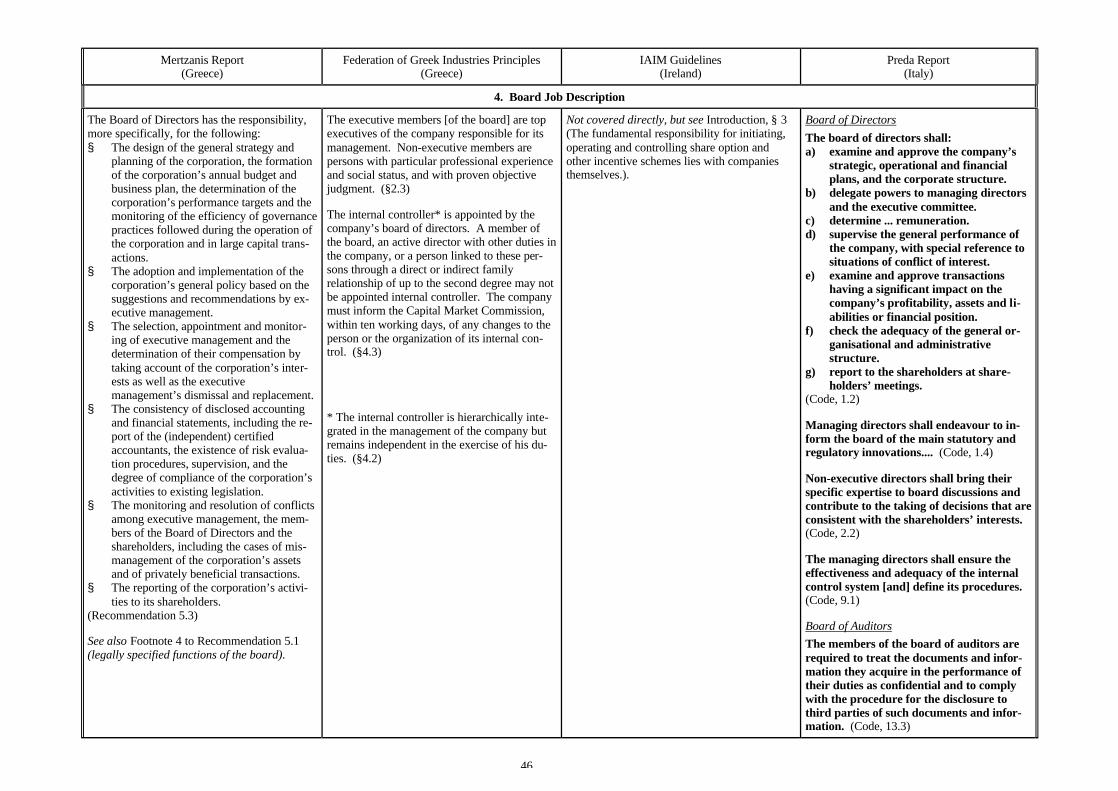

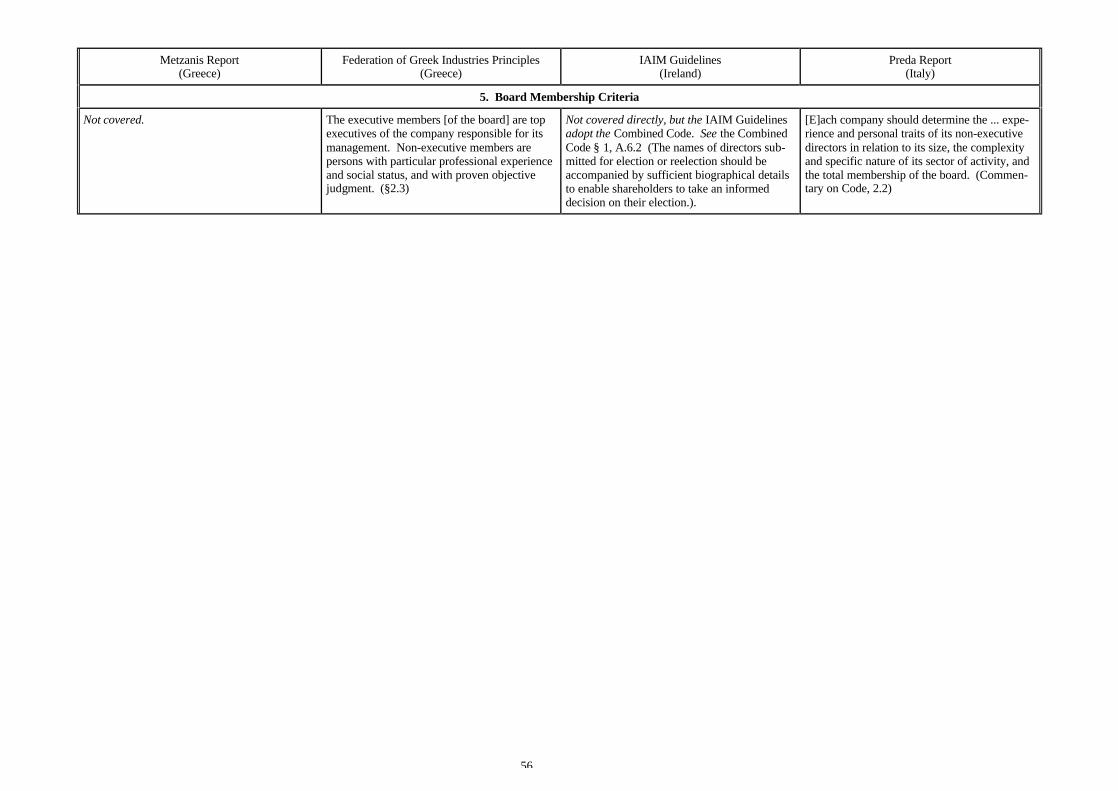

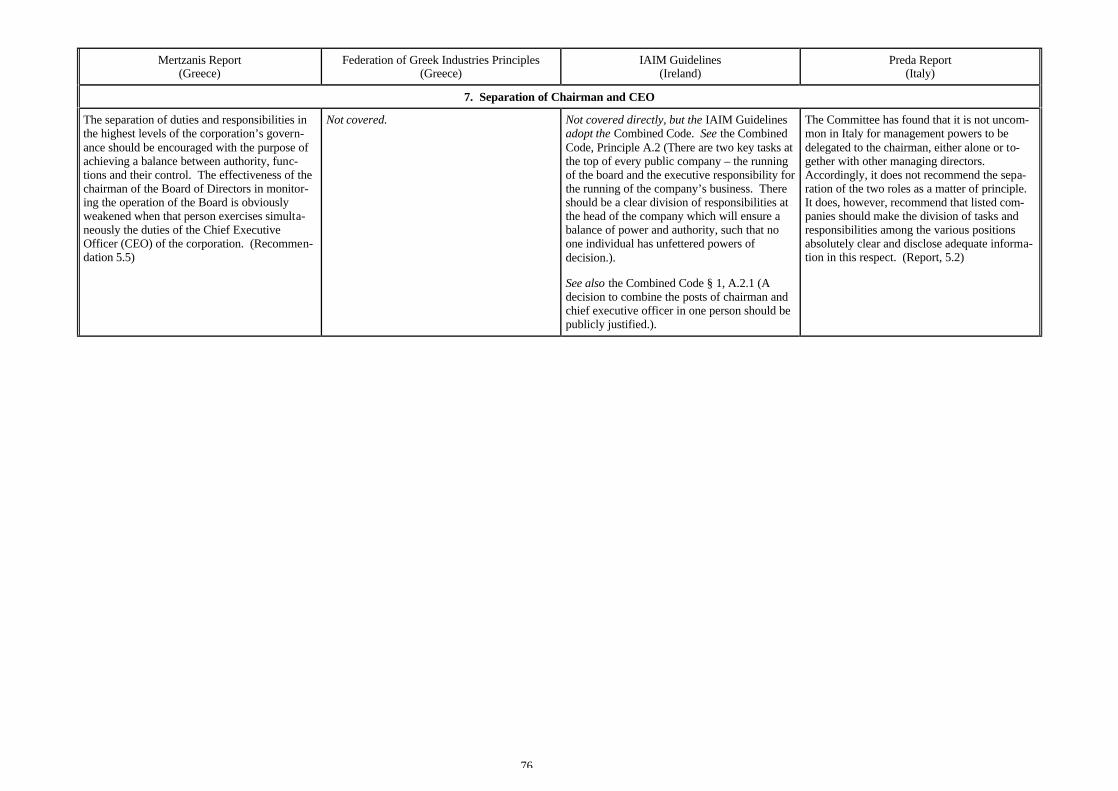

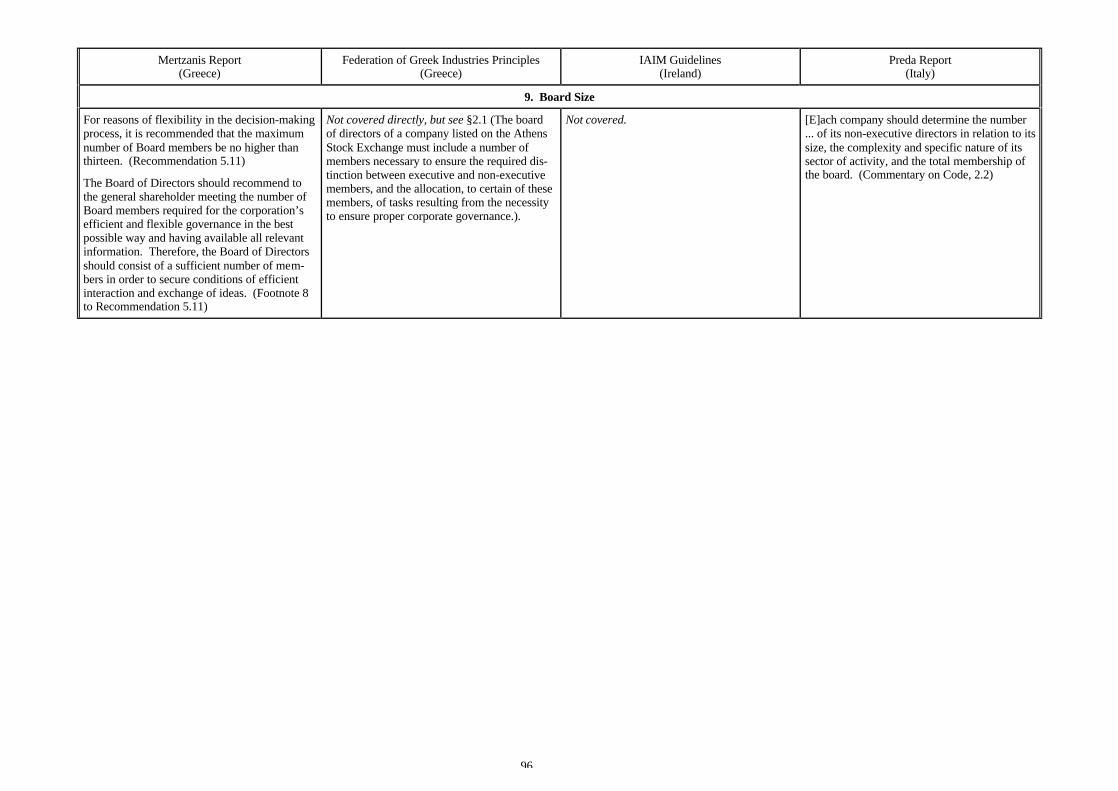

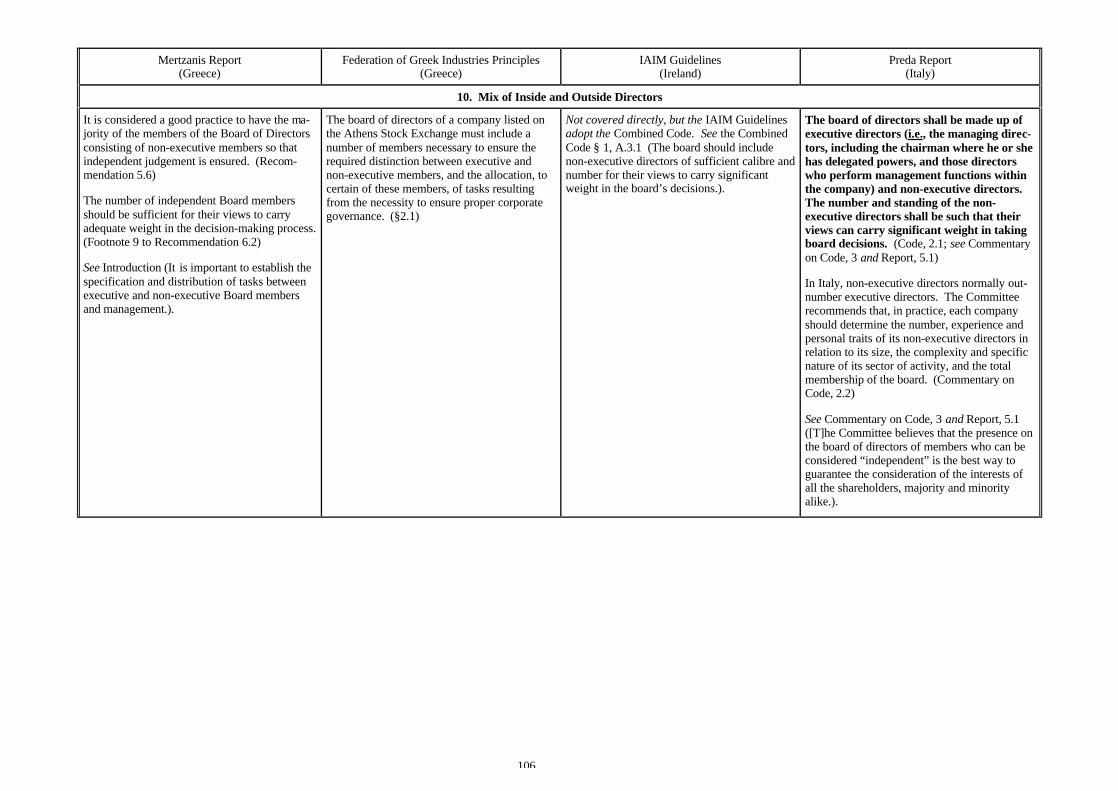

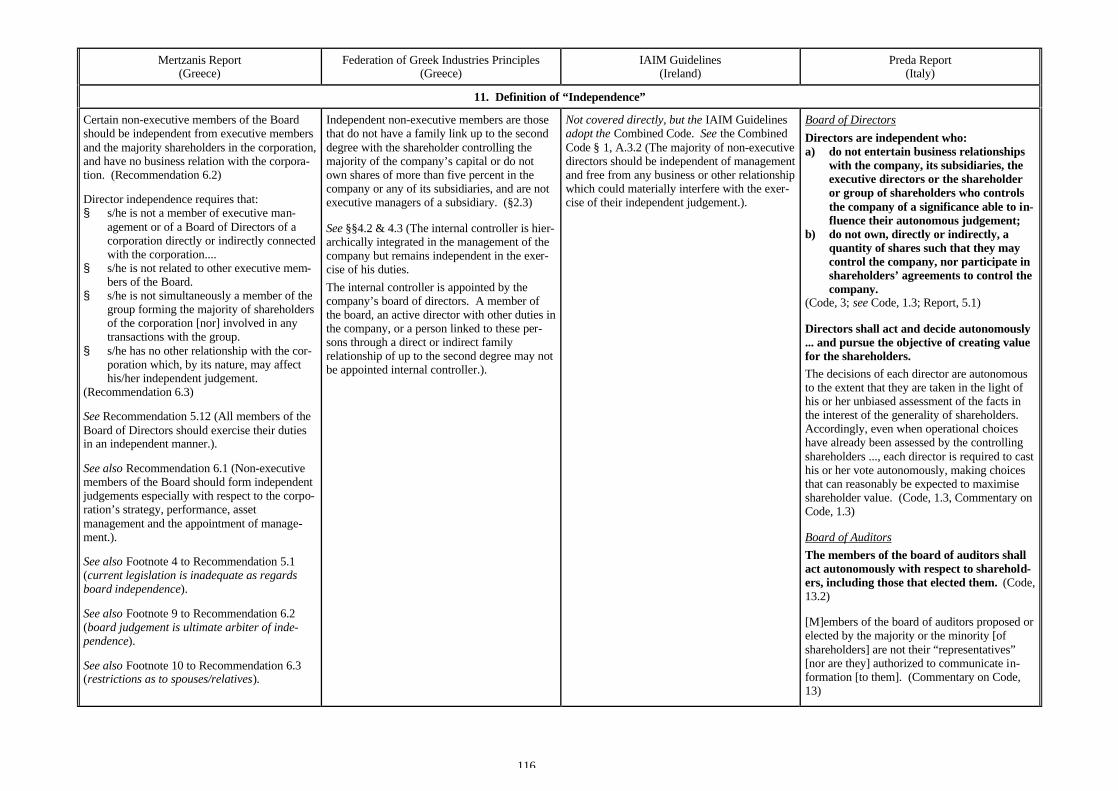

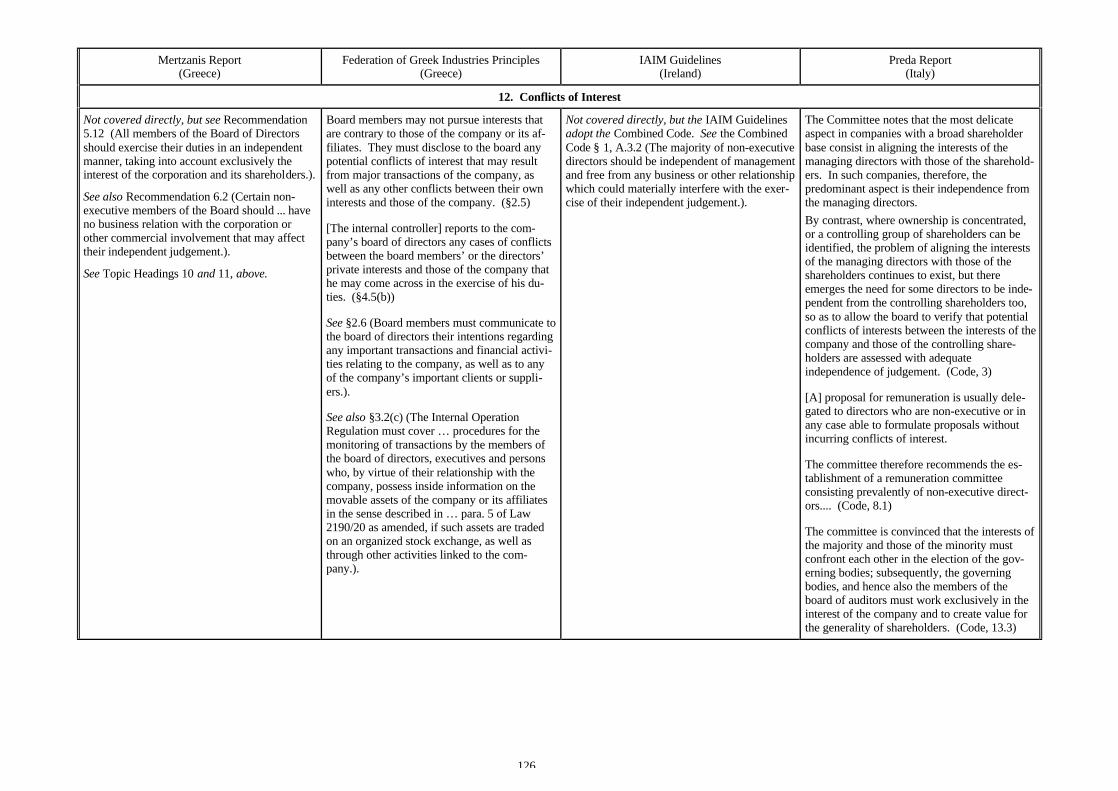

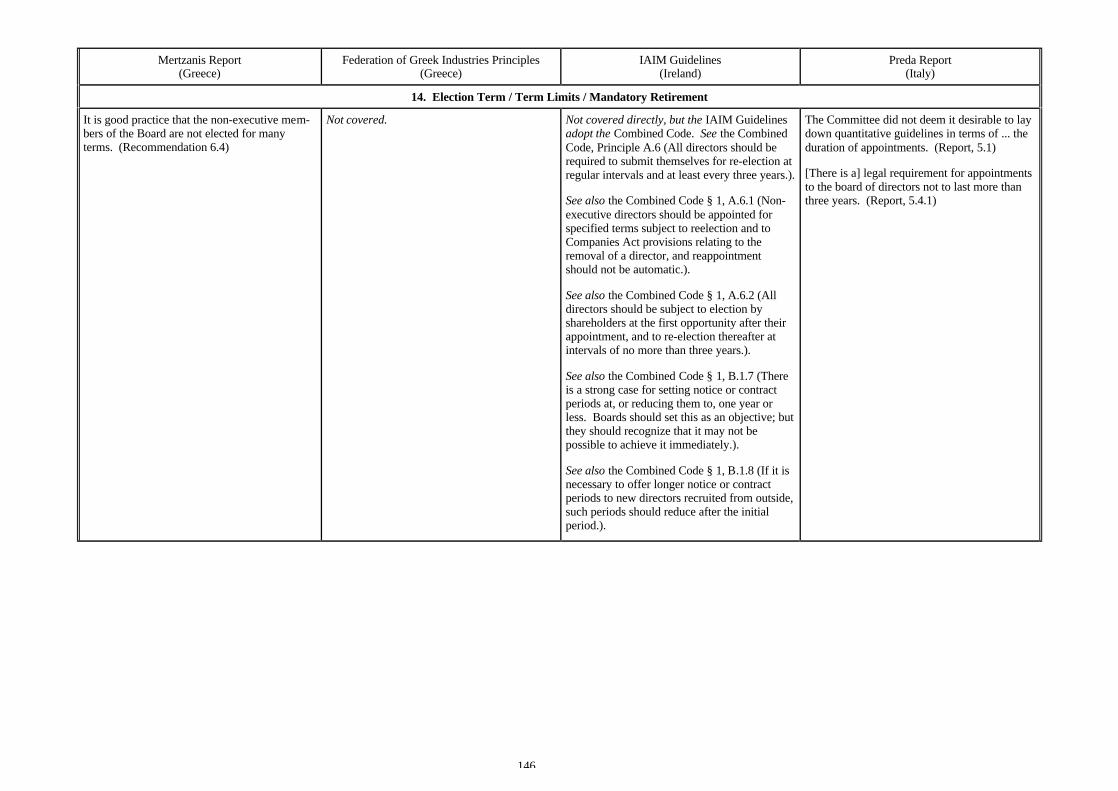

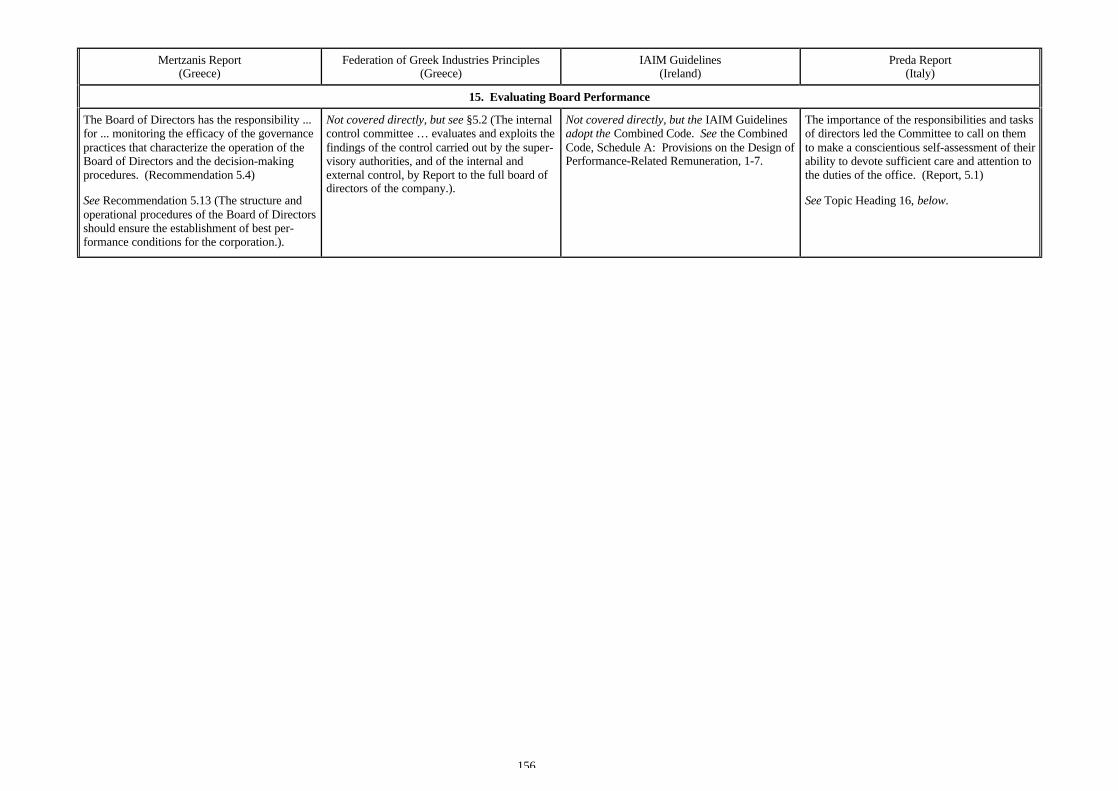

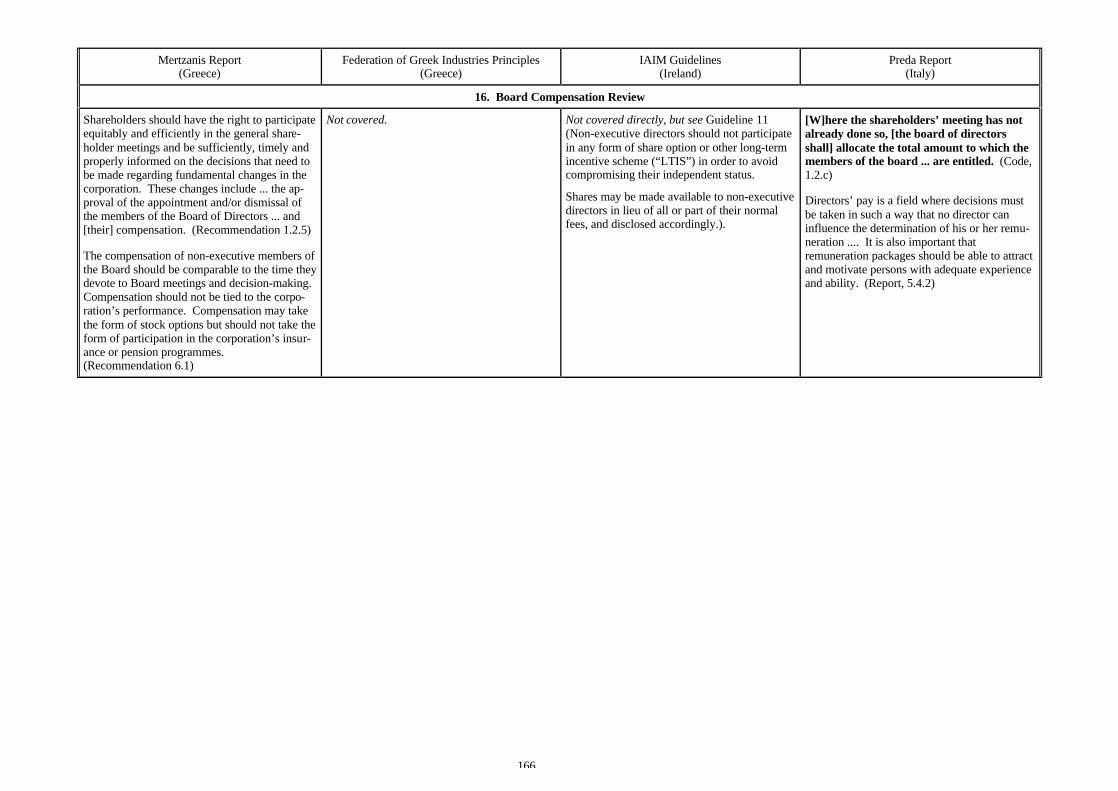

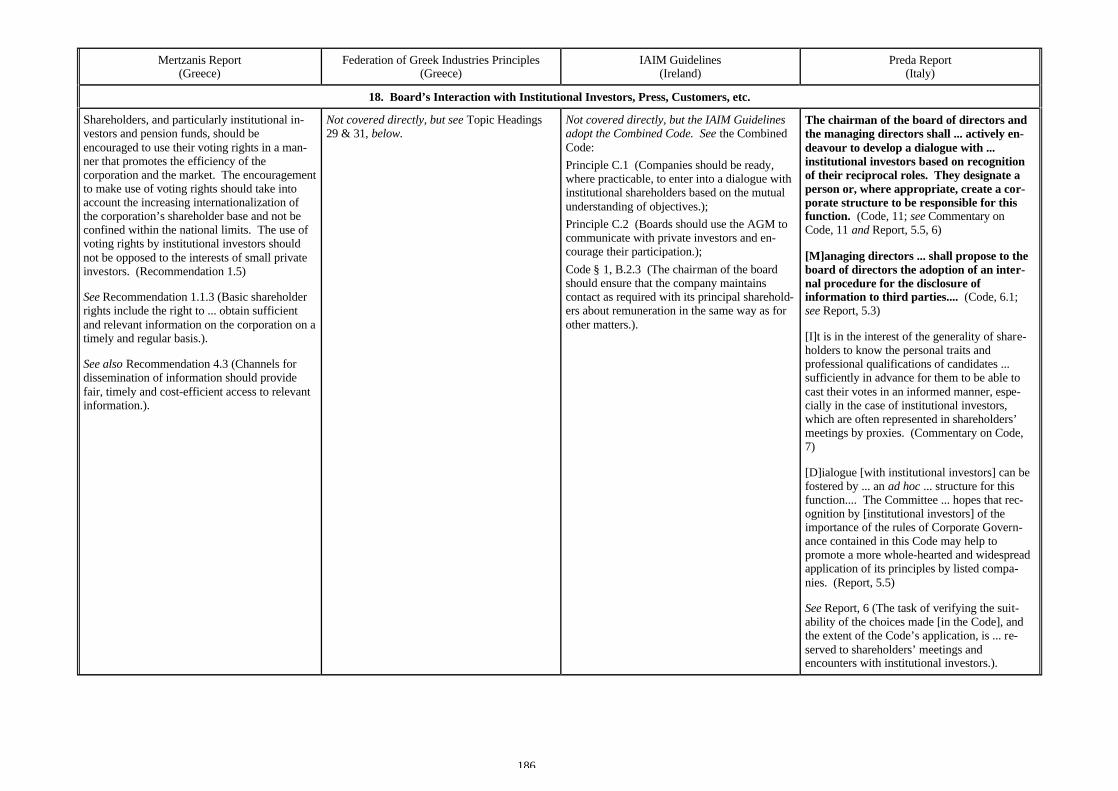

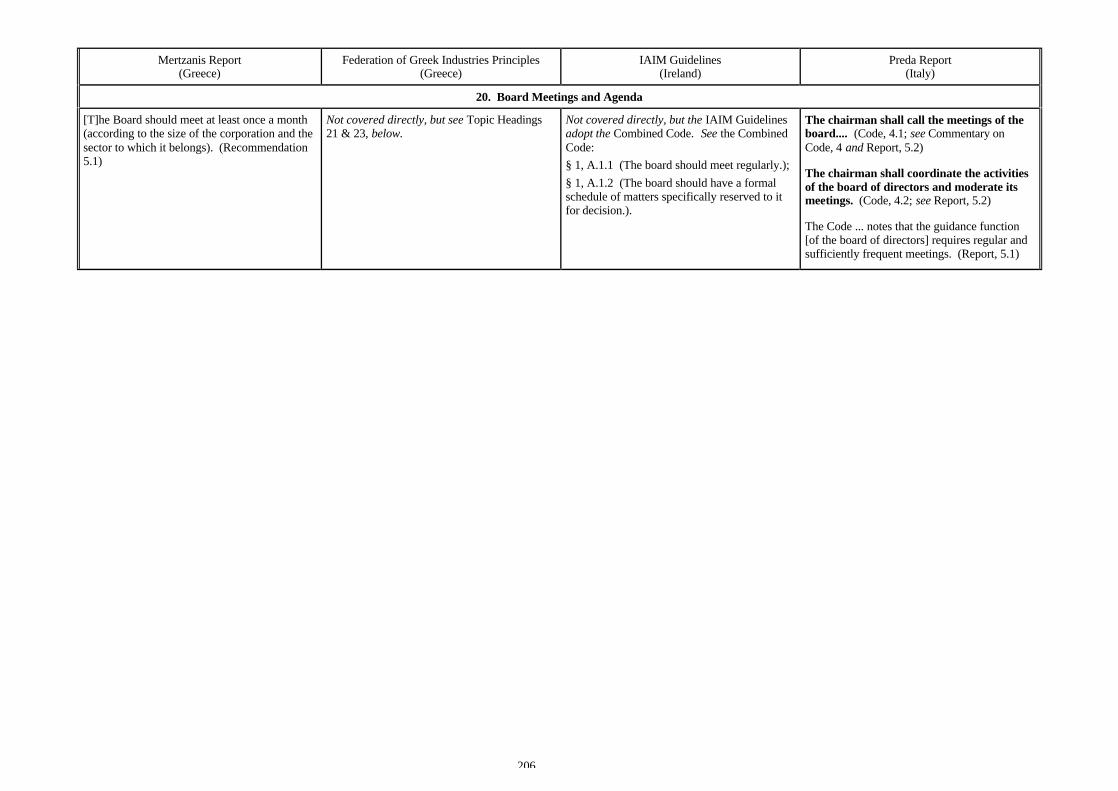

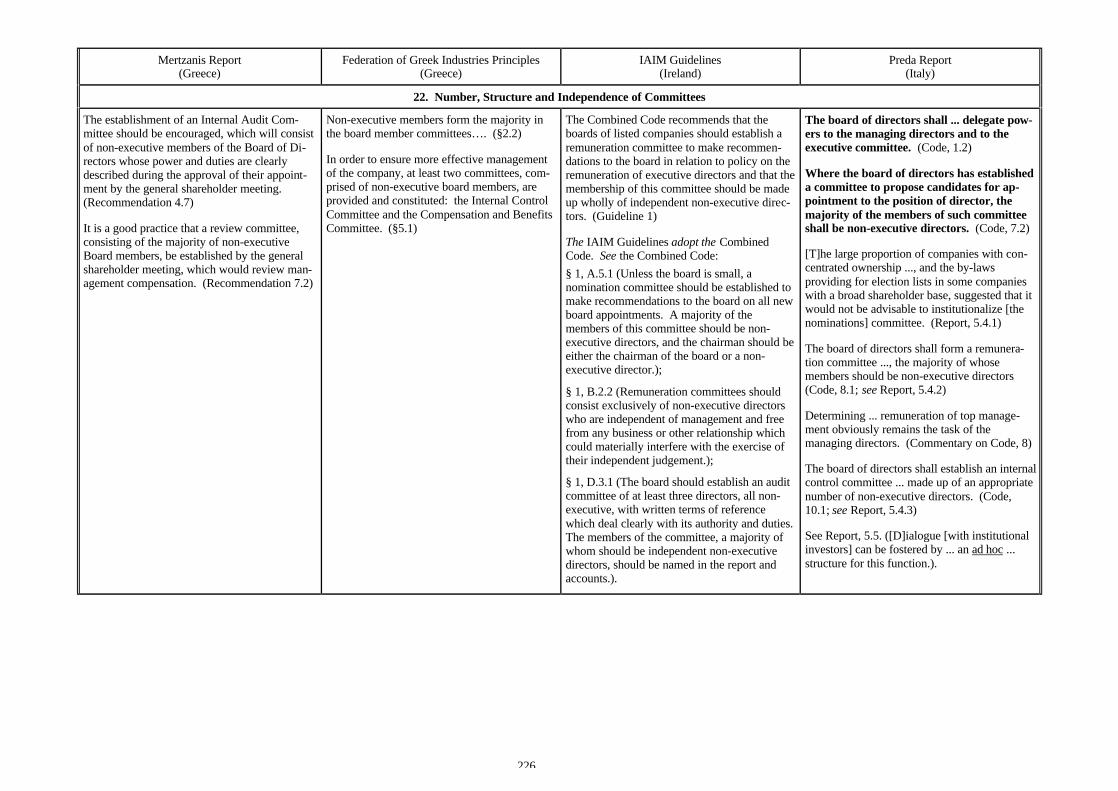

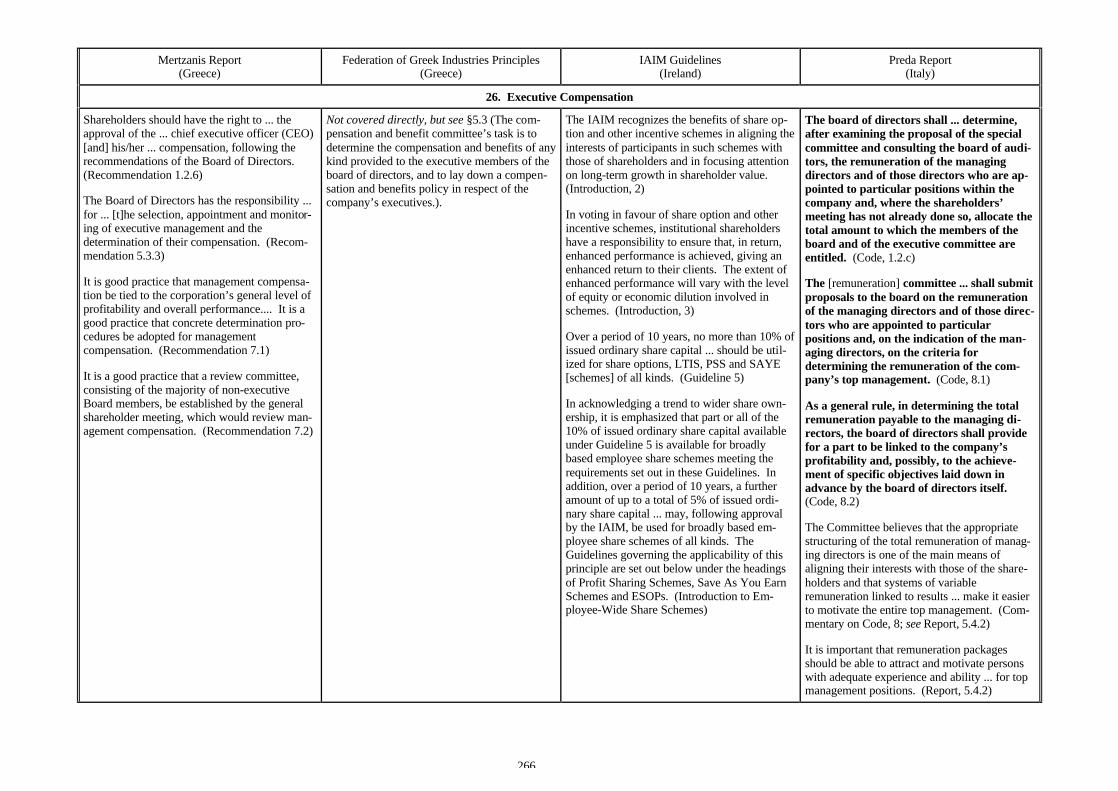

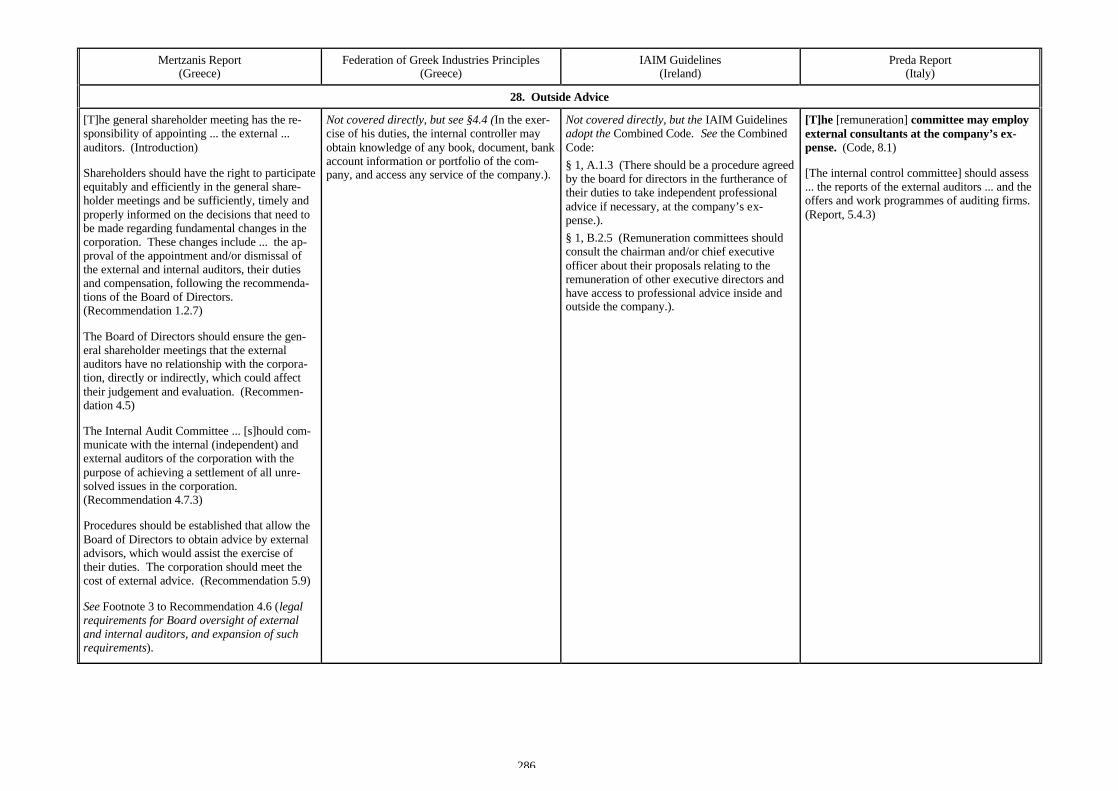

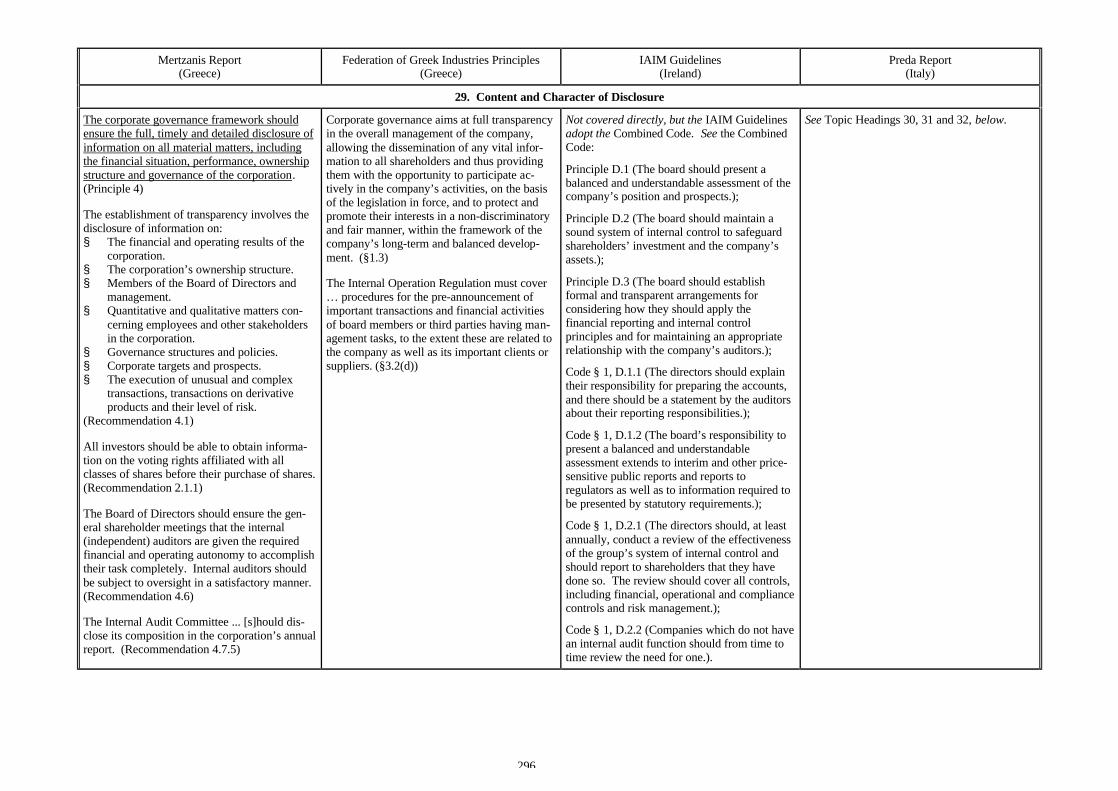

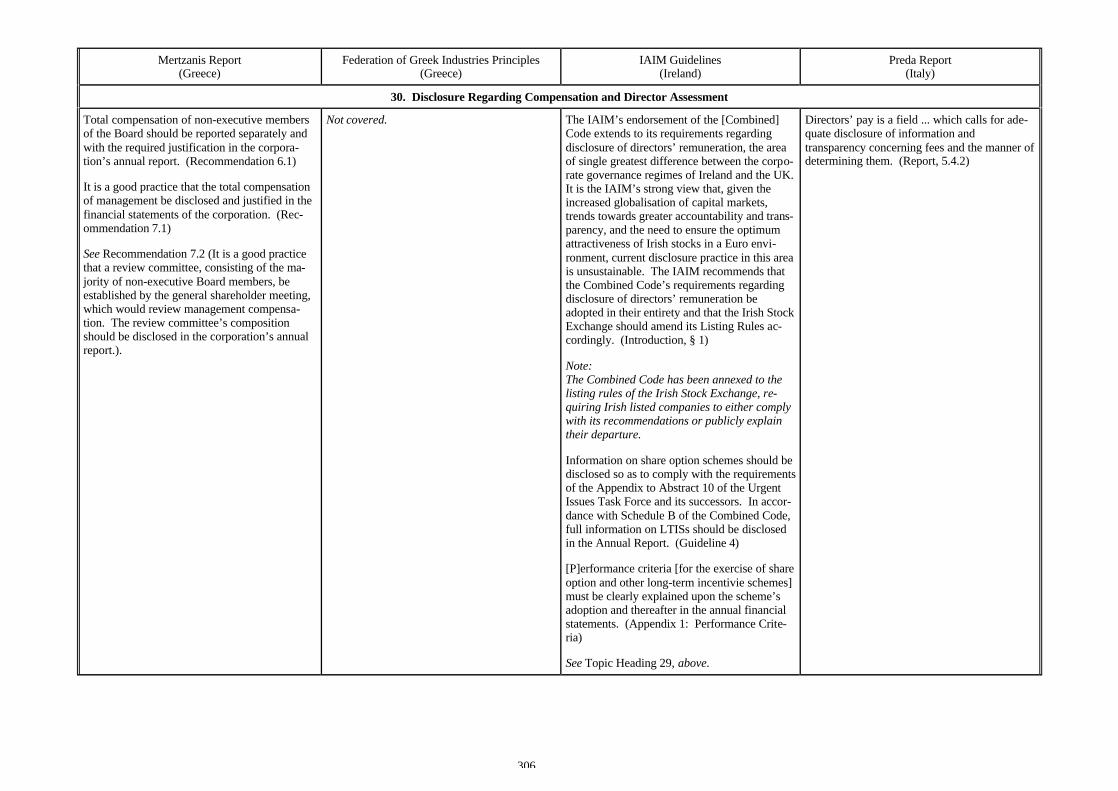

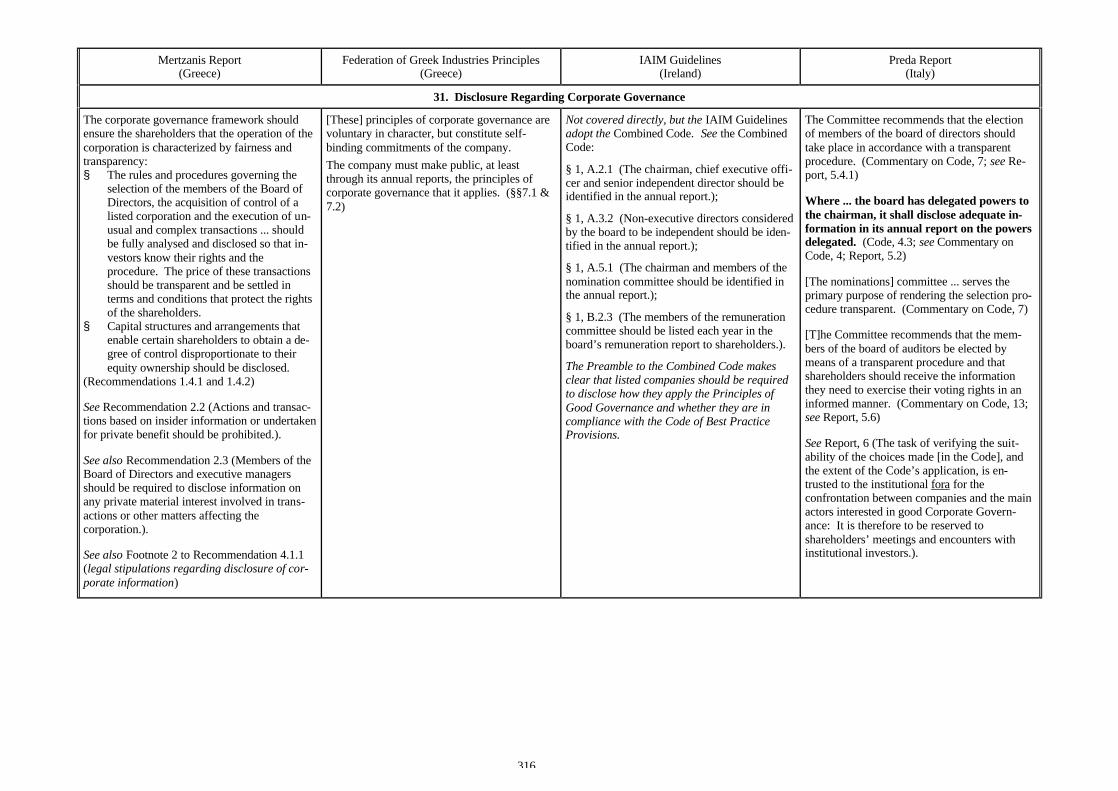

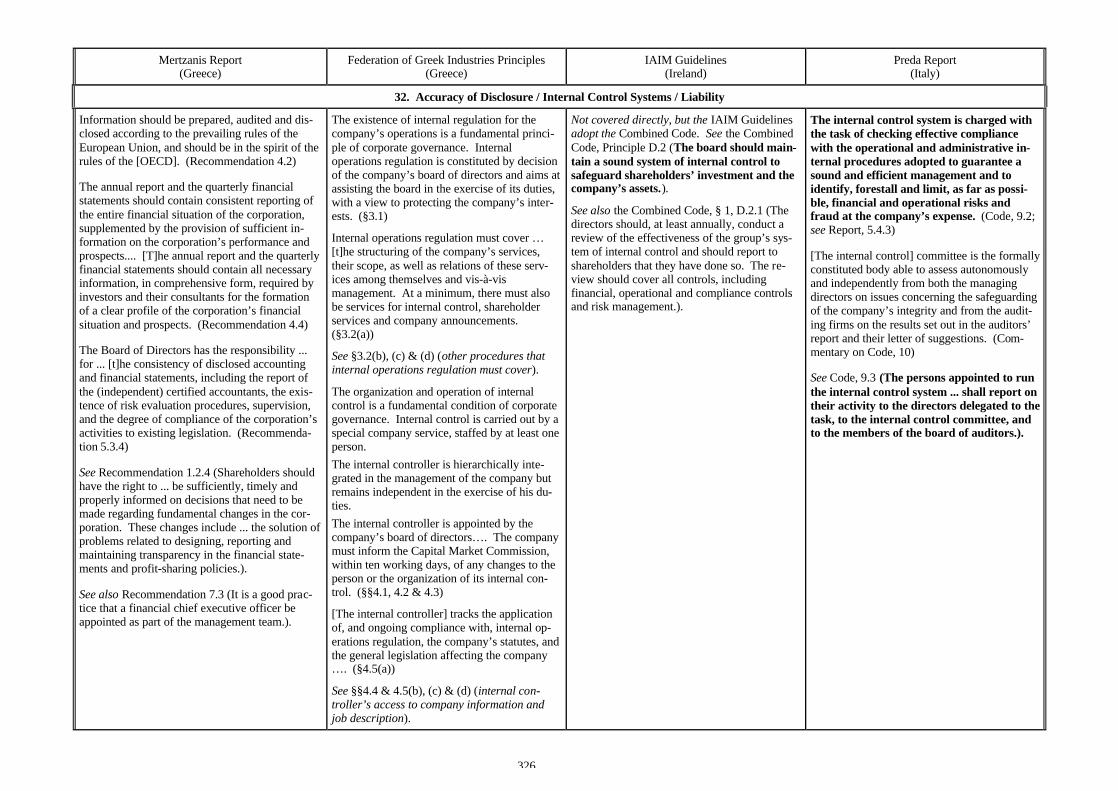

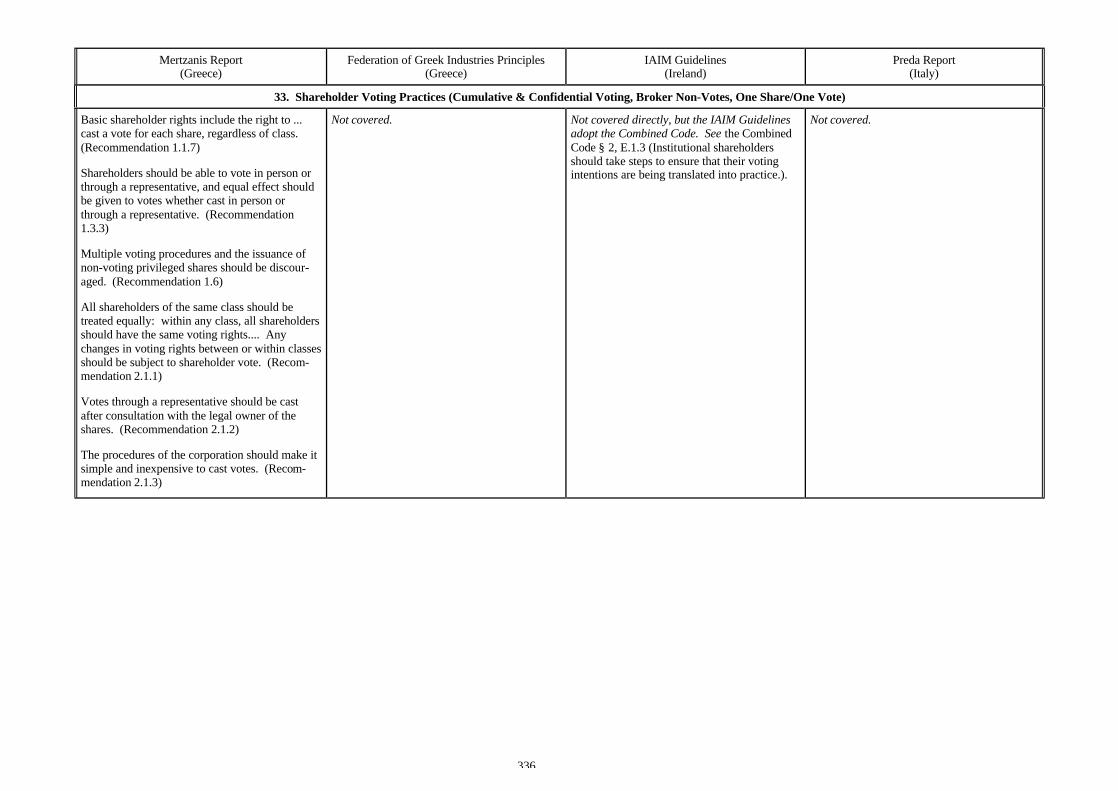

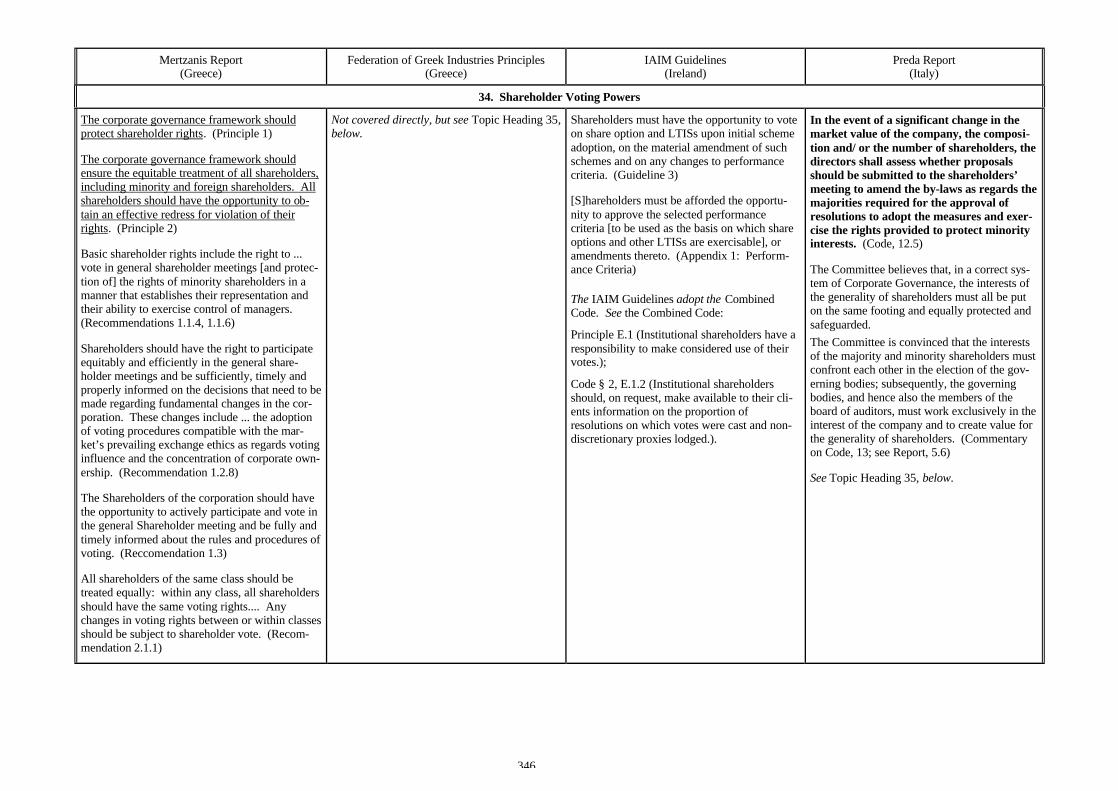

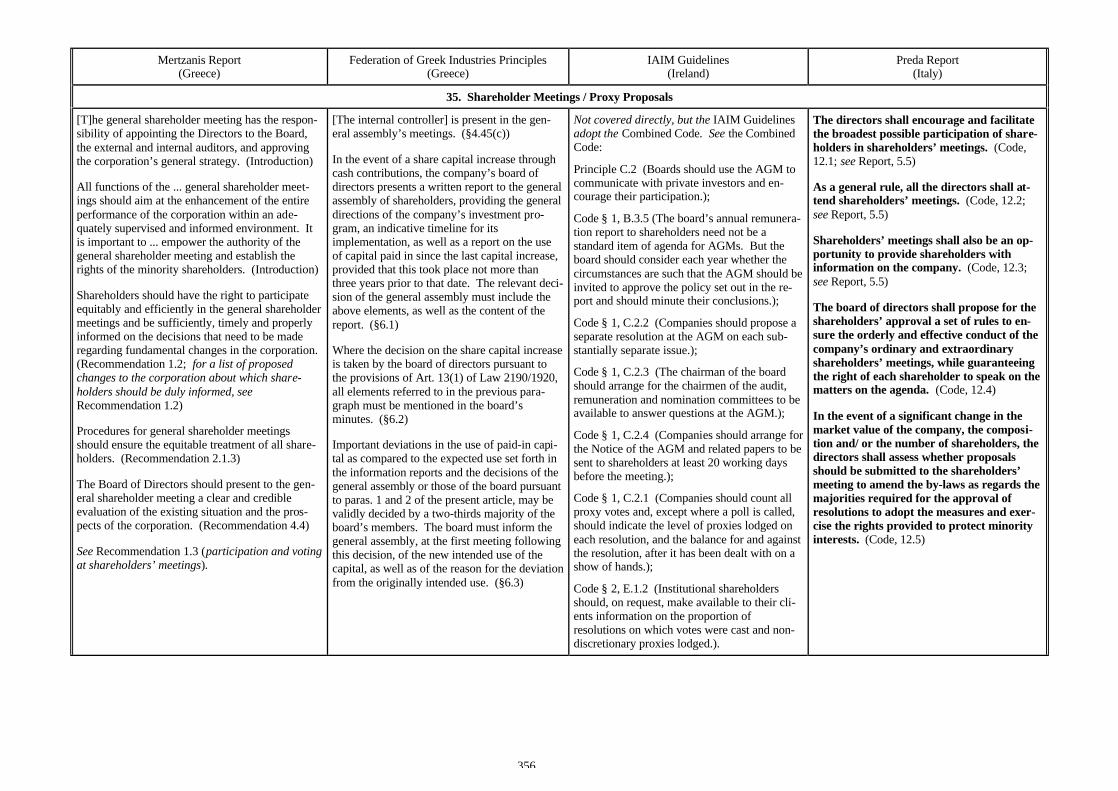

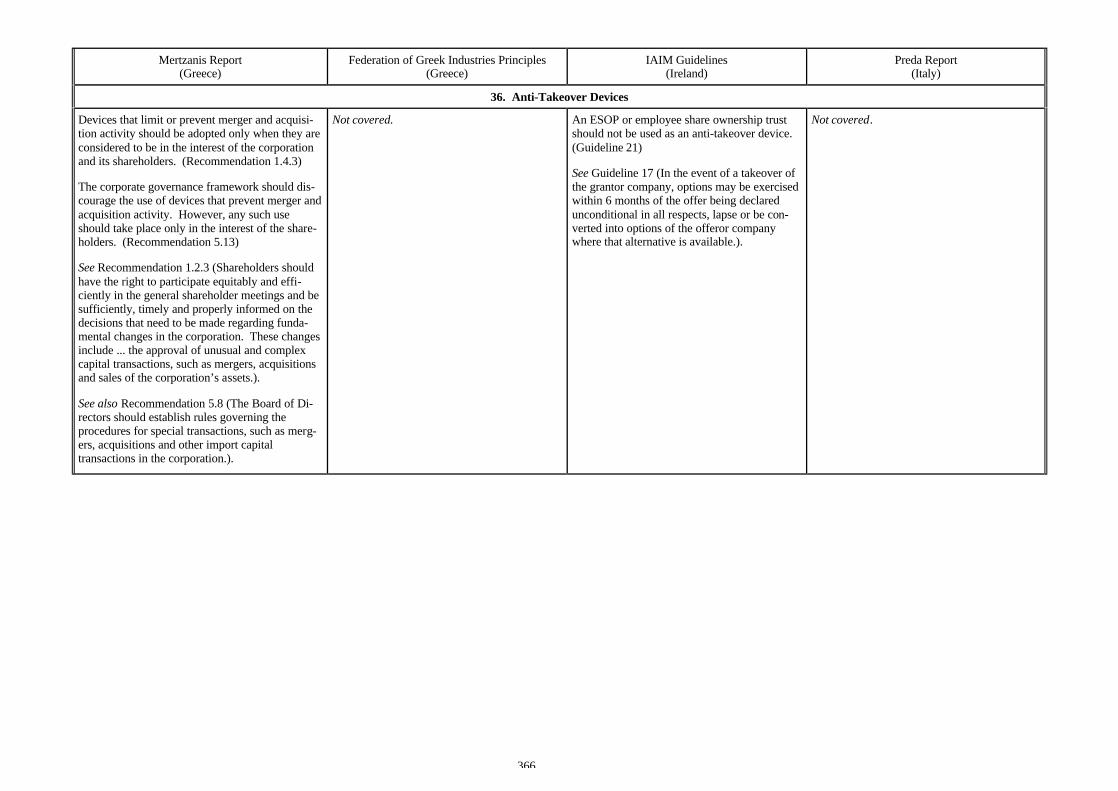

Mertzanis Report(Greece)

Federation of Greek Industries Principles(Greece)

IAIM Guidelines(Ireland)

Preda Report(Italy)

OVERVIEW

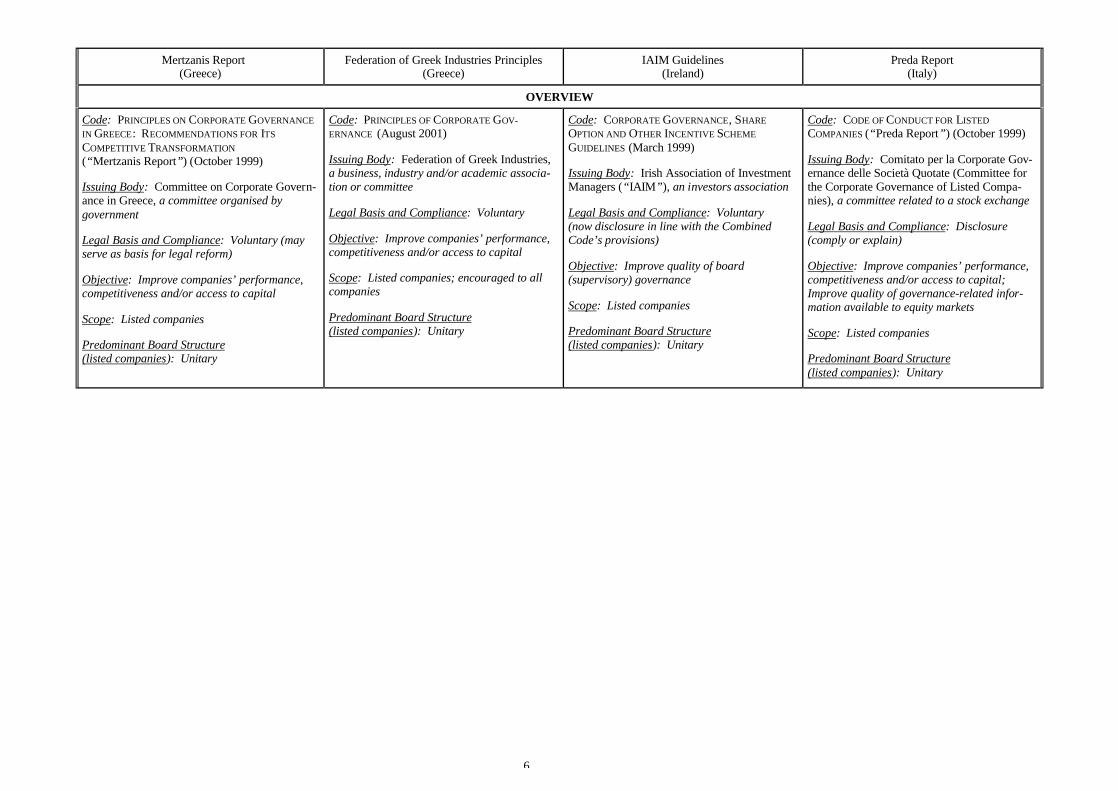

Code: PRINCIPLES ON CORPORATE GOVERNANCEIN GREECE: RECOMMENDATIONS FOR ITSCOMPETITIVE TRANSFORMATION(“Mertzanis Report”) (October 1999)

Issuing Body: Committee on Corporate Govern-ance in Greece, a committee organised bygovernment

Legal Basis and Compliance: Voluntary (mayserve as basis for legal reform)

Objective: Improve companies’ performance,competitiveness and/or access to capital

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

Code: PRINCIPLES OF CORPORATE GOV-ERNANCE (August 2001)

Issuing Body: Federation of Greek Industries,a business, industry and/or academic associa-tion or committee

Legal Basis and Compliance: Voluntary

Objective: Improve companies’ performance,competitiveness and/or access to capital

Scope: Listed companies; encouraged to allcompanies

Predominant Board Structure(listed companies): Unitary

Code: CORPORATE GOVERNANCE, SHAREOPTION AND OTHER INCENTIVE SCHEMEGUIDELINES (March 1999)

Issuing Body: Irish Association of InvestmentManagers (“IAIM”), an investors association

Legal Basis and Compliance: Voluntary(now disclosure in line with the CombinedCode’s provisions)

Objective: Improve quality of board(supervisory) governance

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

Code: CODE OF CONDUCT FOR LISTEDCOMPANIES (“Preda Report”) (October 1999)

Issuing Body: Comitato per la Corporate Gov-ernance delle Società Quotate (Committee forthe Corporate Governance of Listed Compa-nies), a committee related to a stock exchange

Legal Basis and Compliance: Disclosure(comply or explain)

Objective: Improve companies’ performance,competitiveness and/or access to capital;Improve quality of governance-related infor-mation available to equity markets

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

7

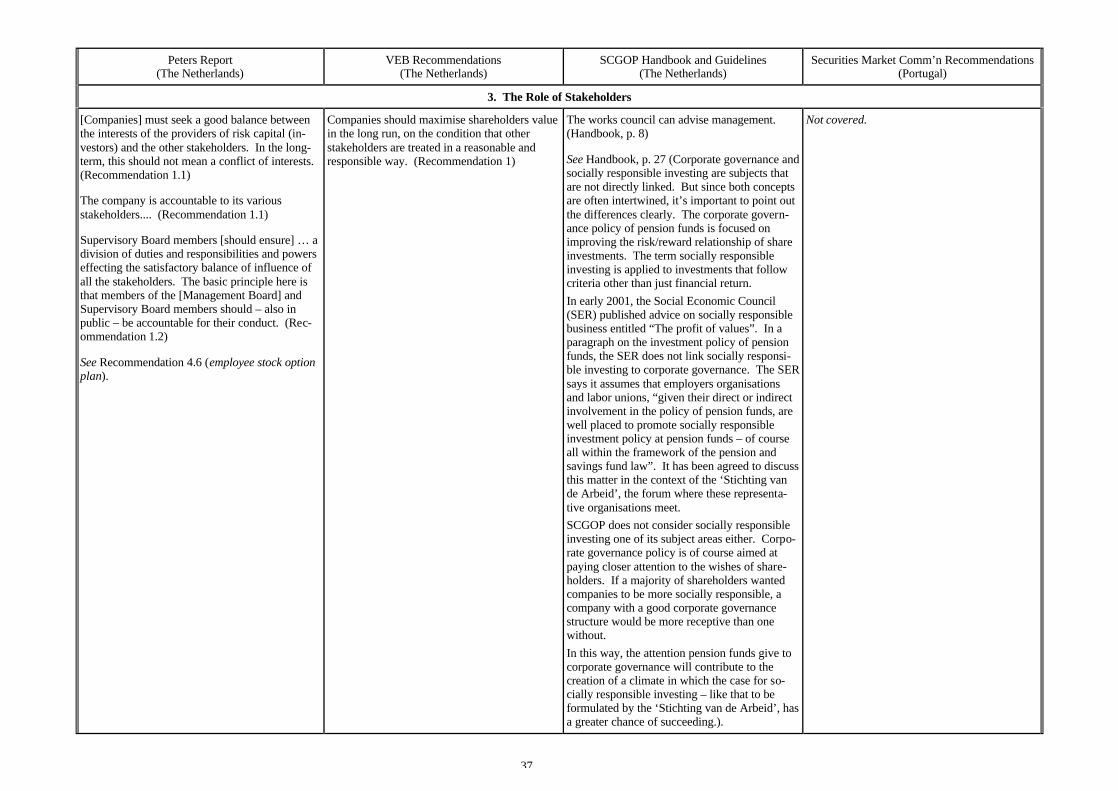

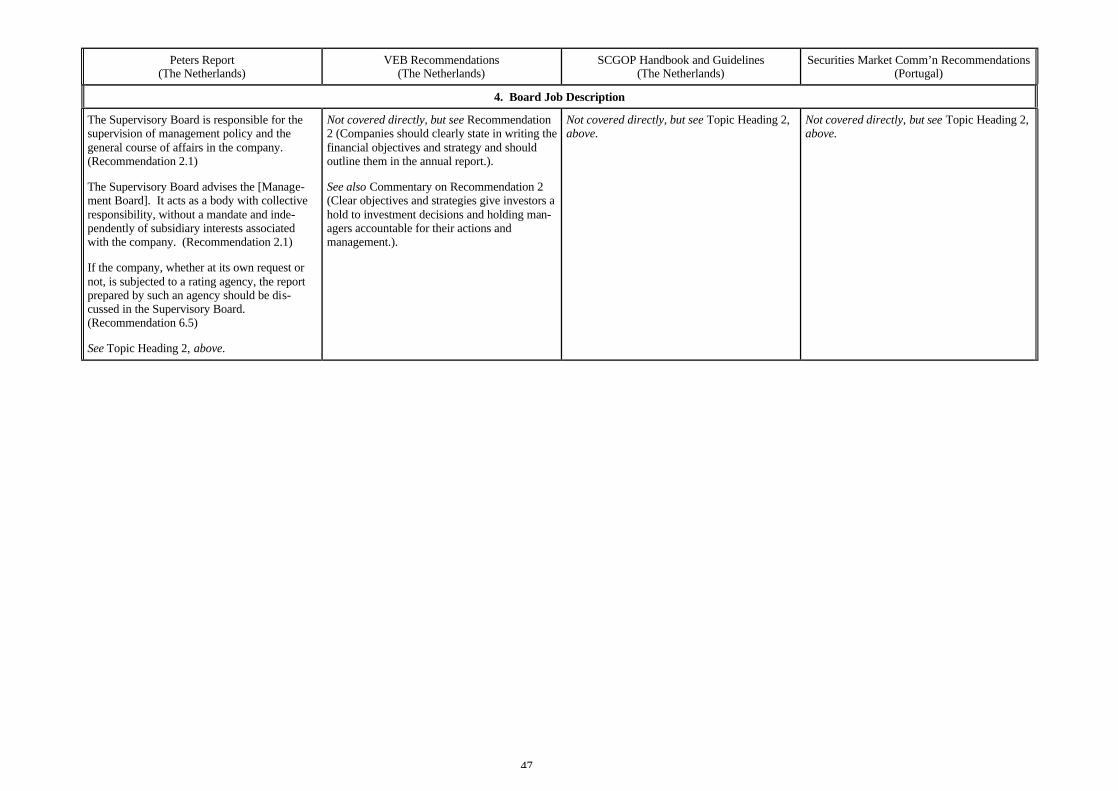

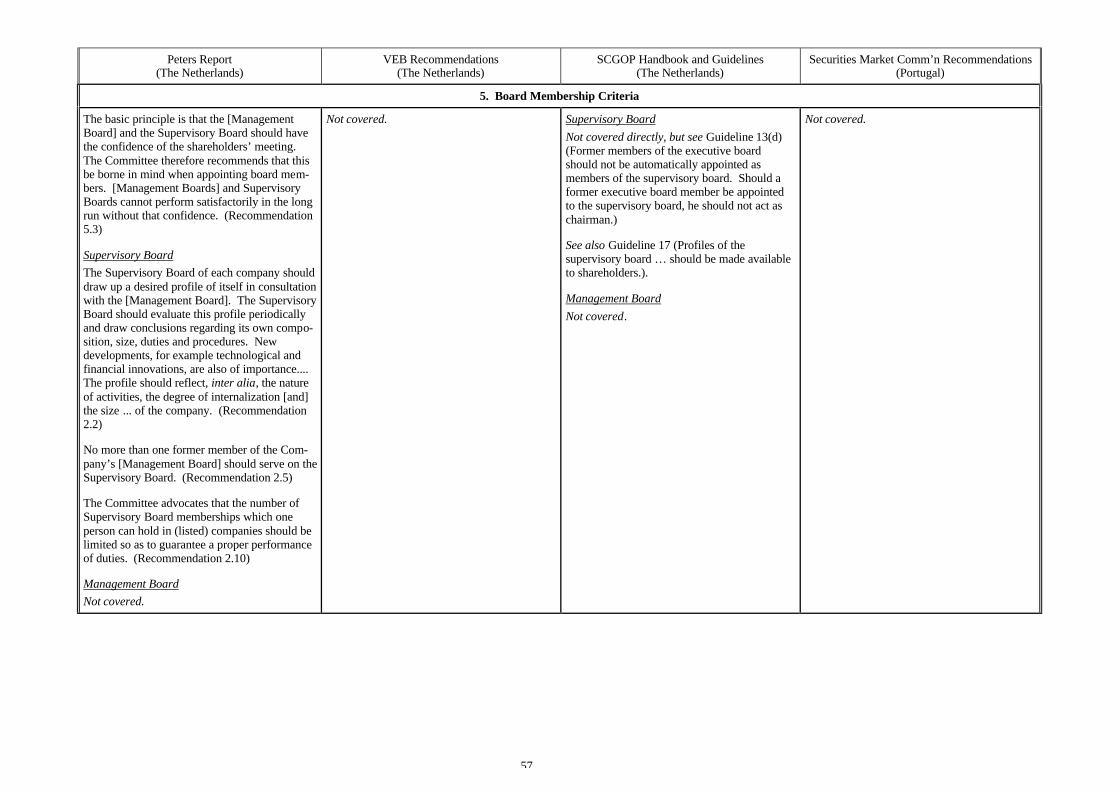

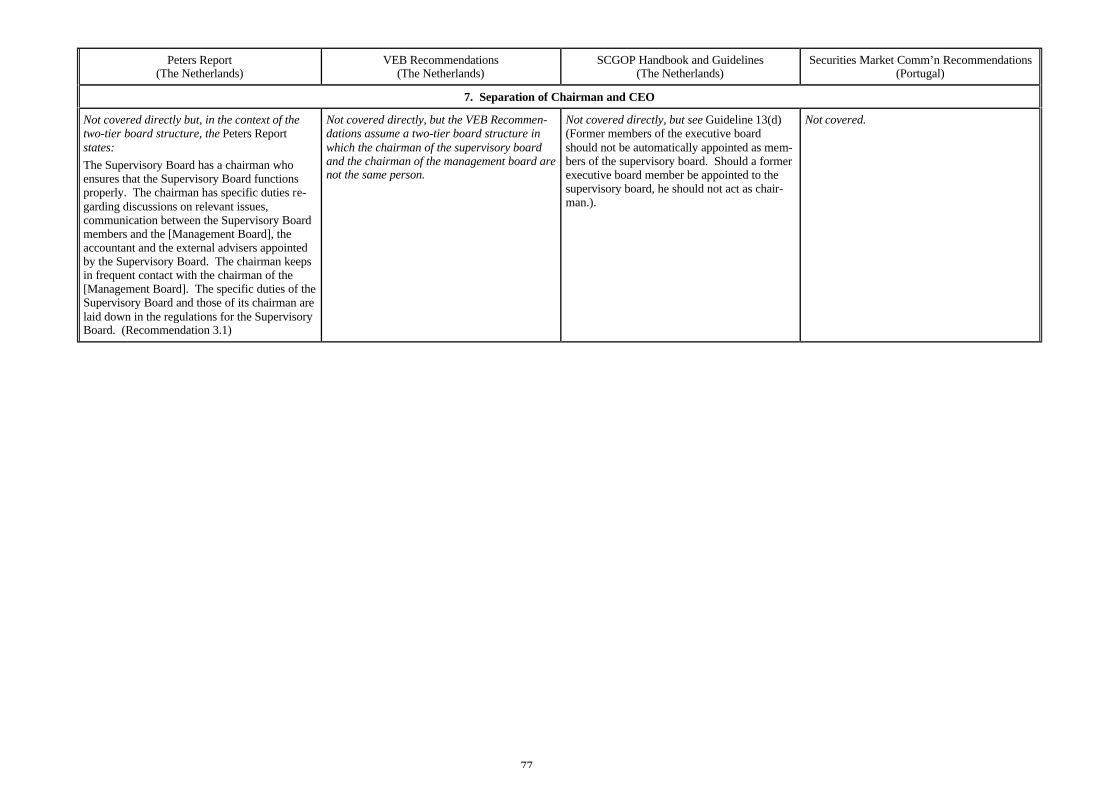

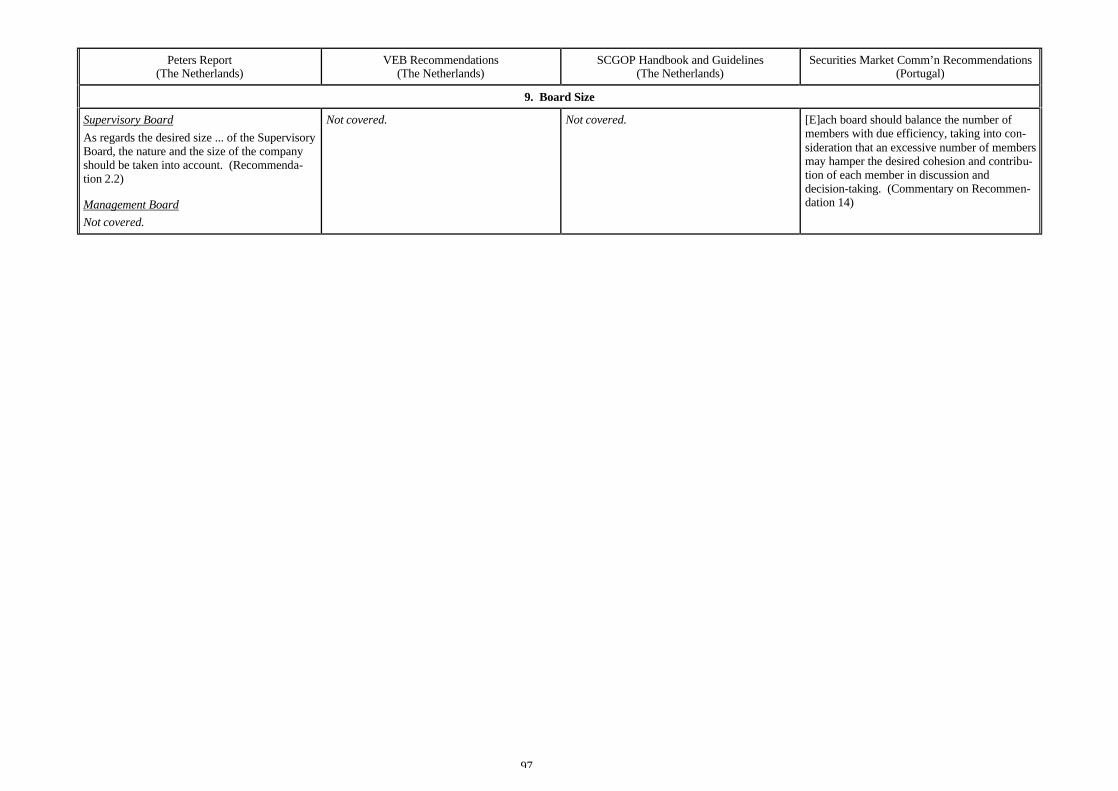

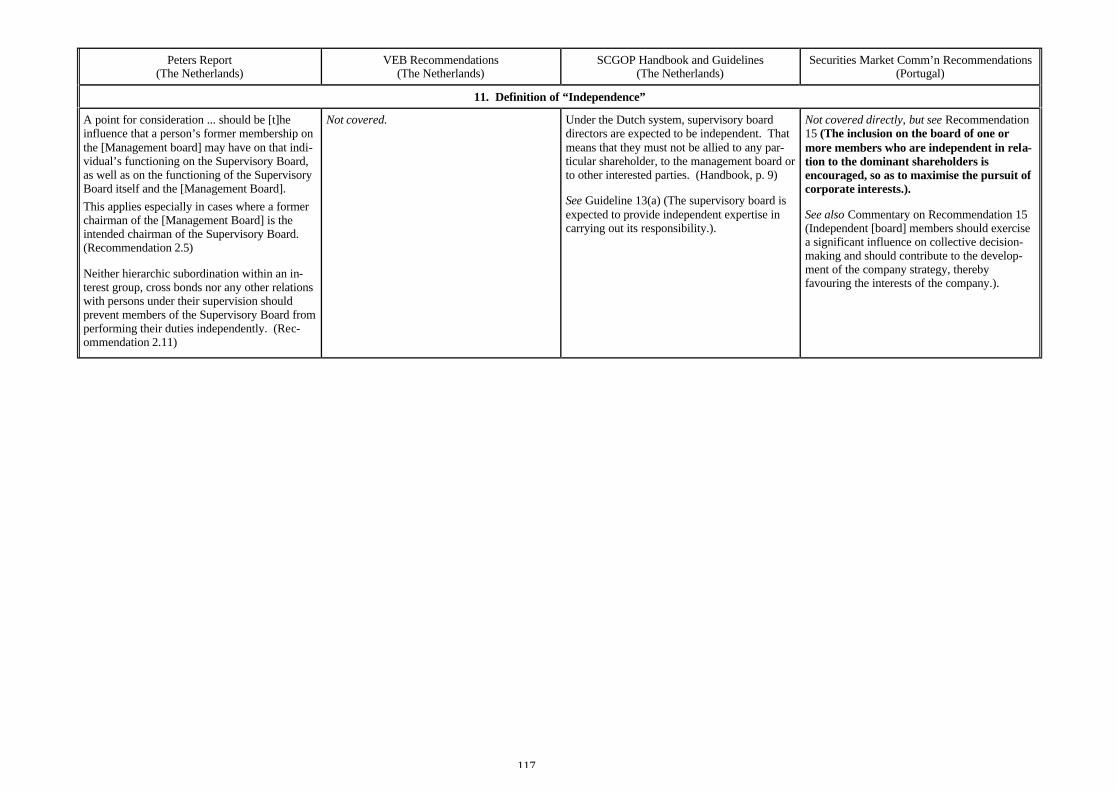

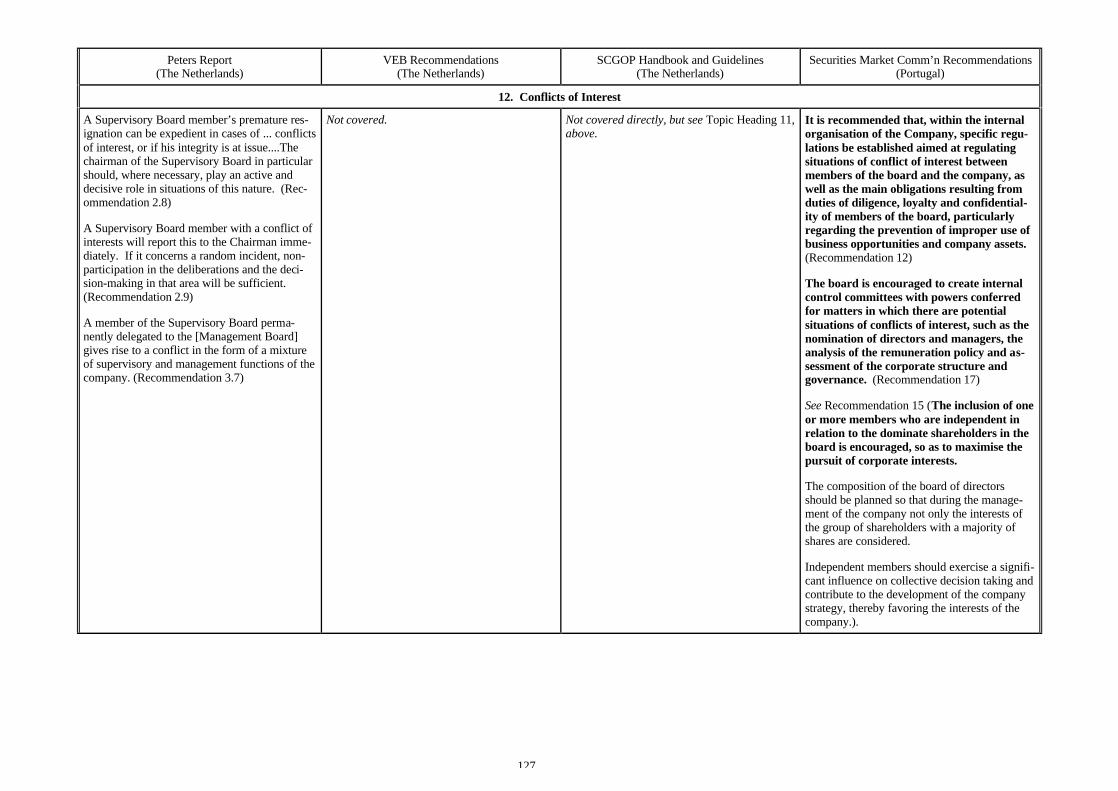

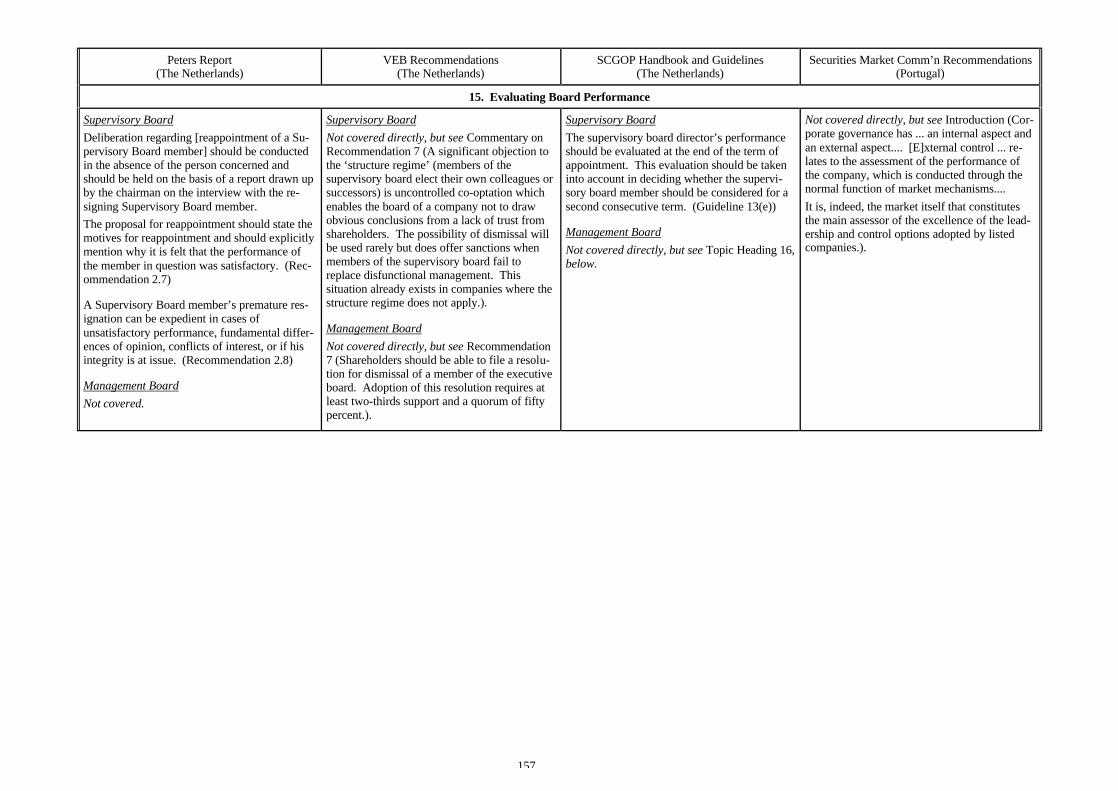

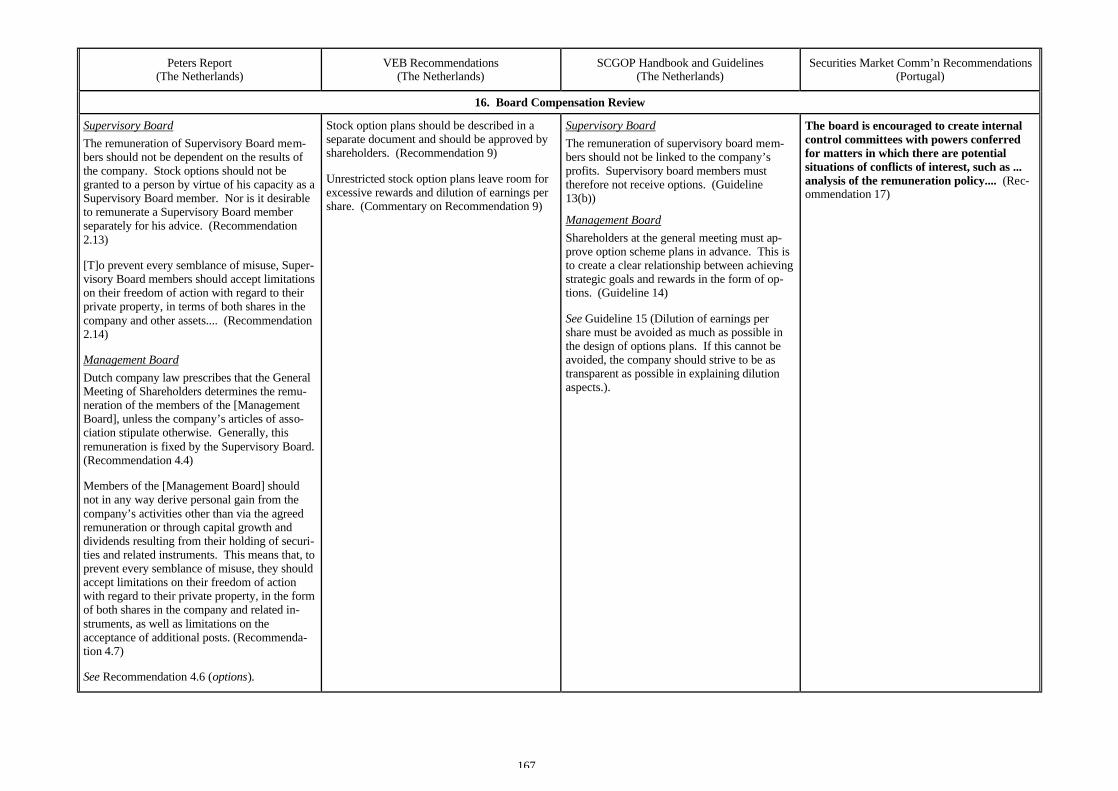

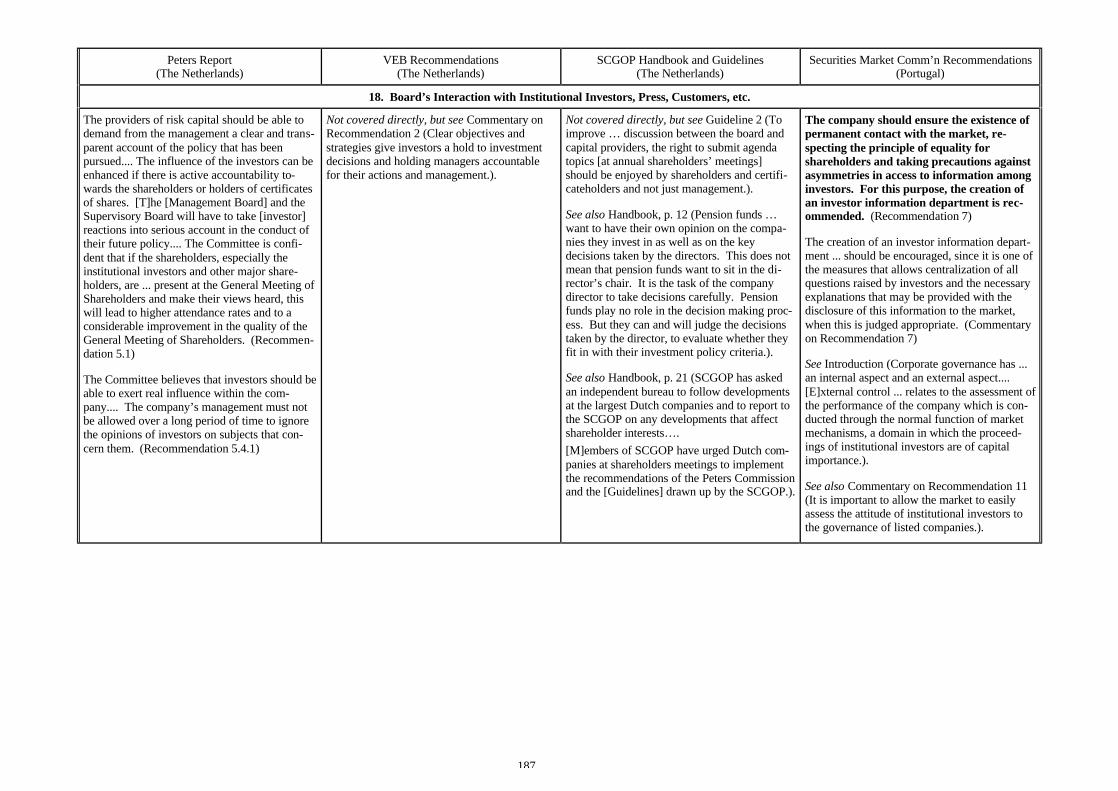

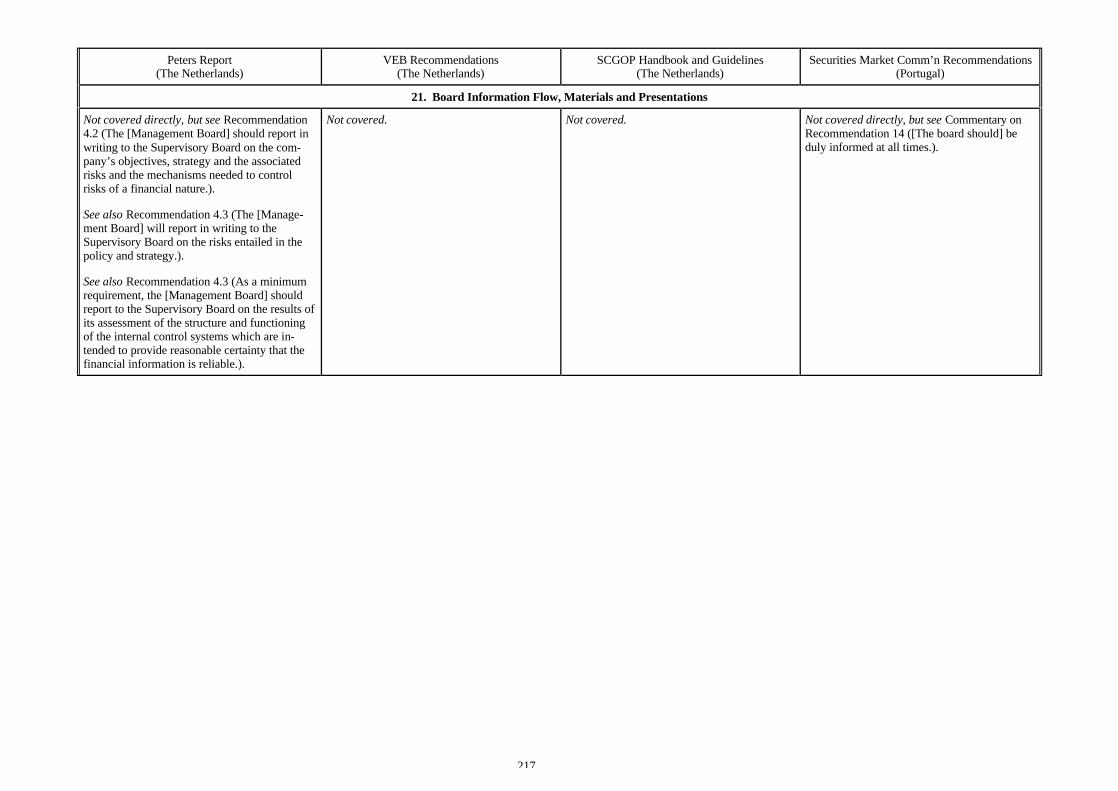

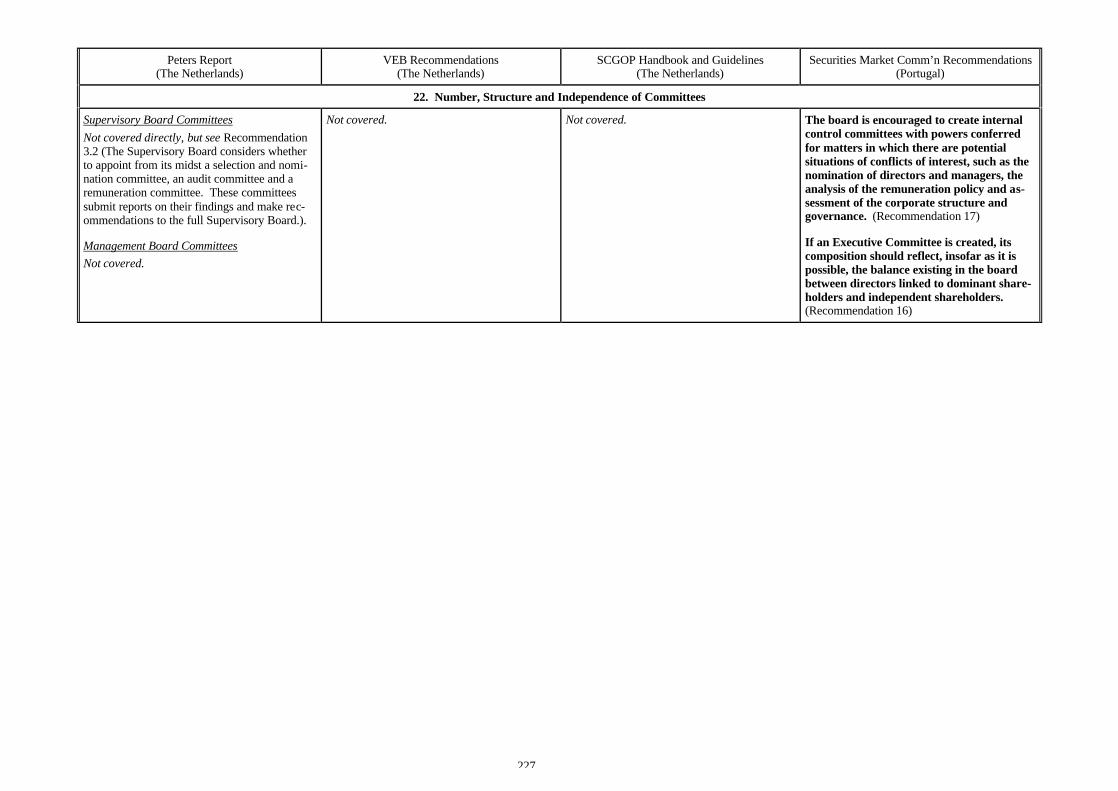

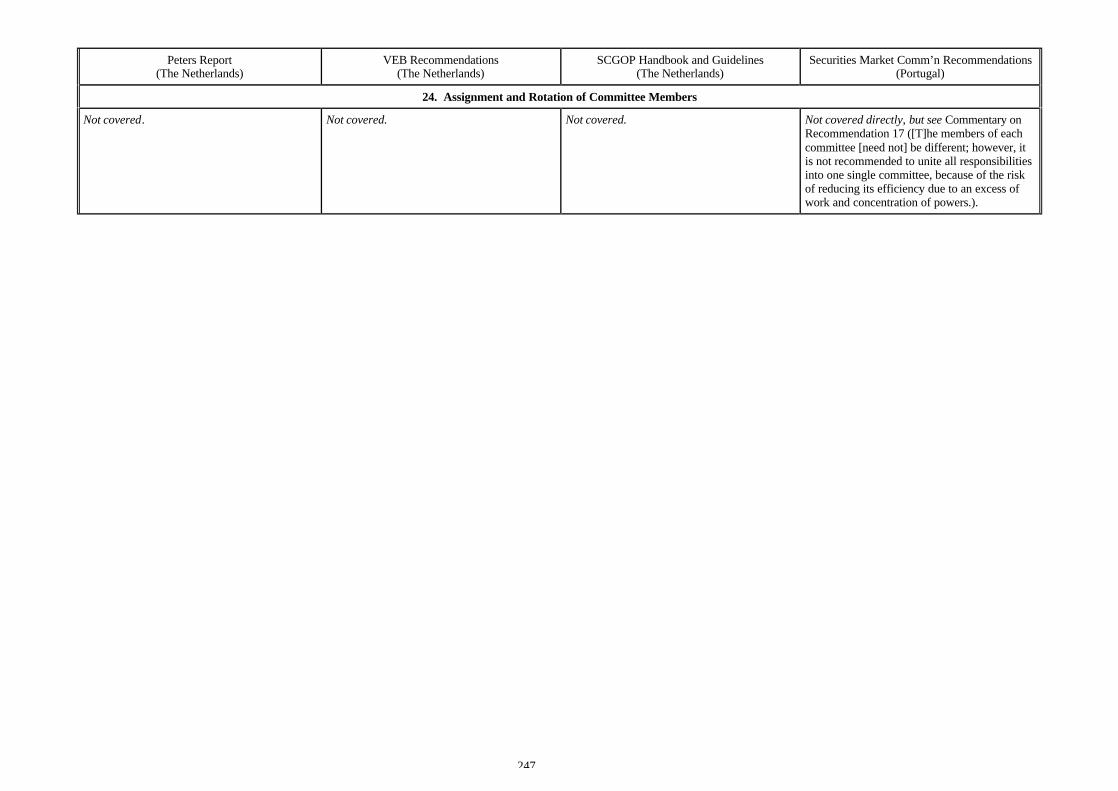

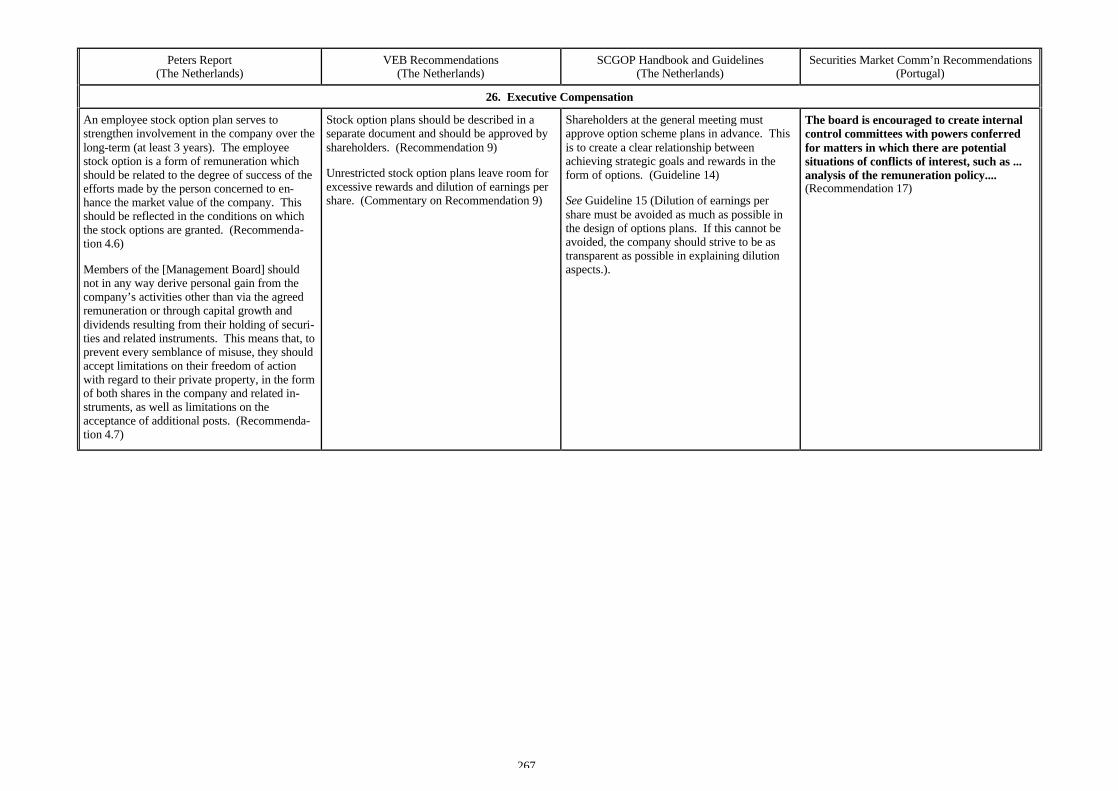

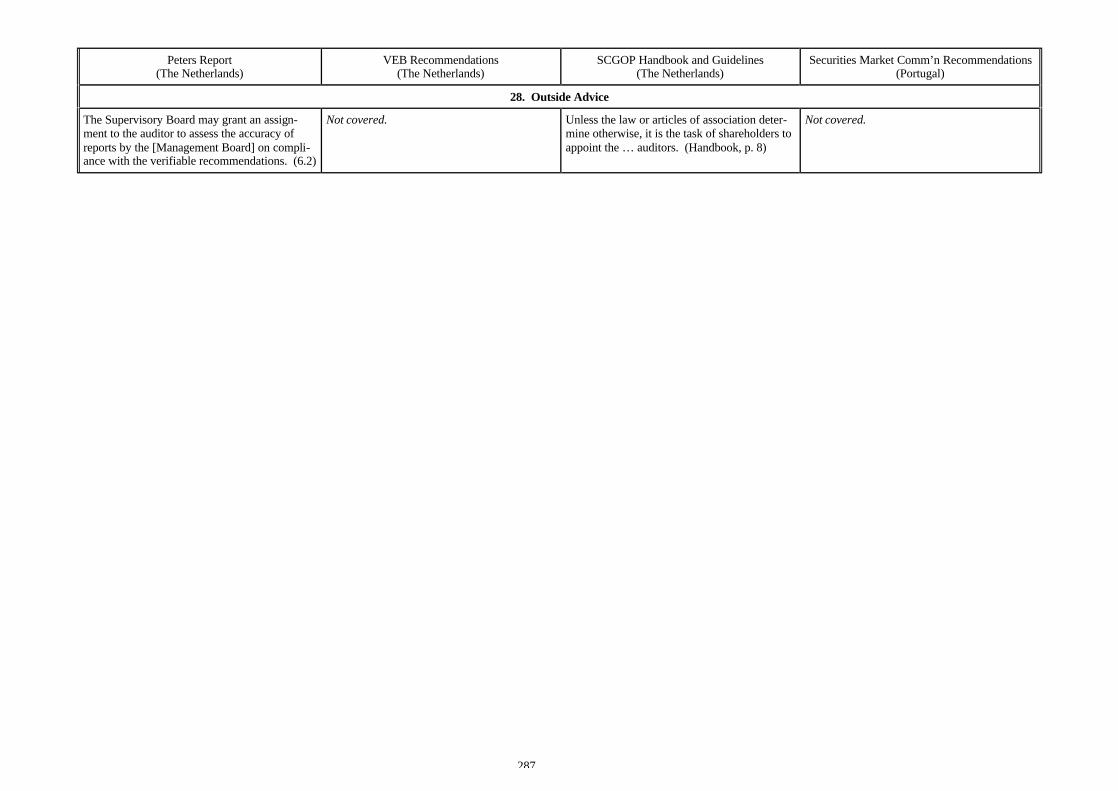

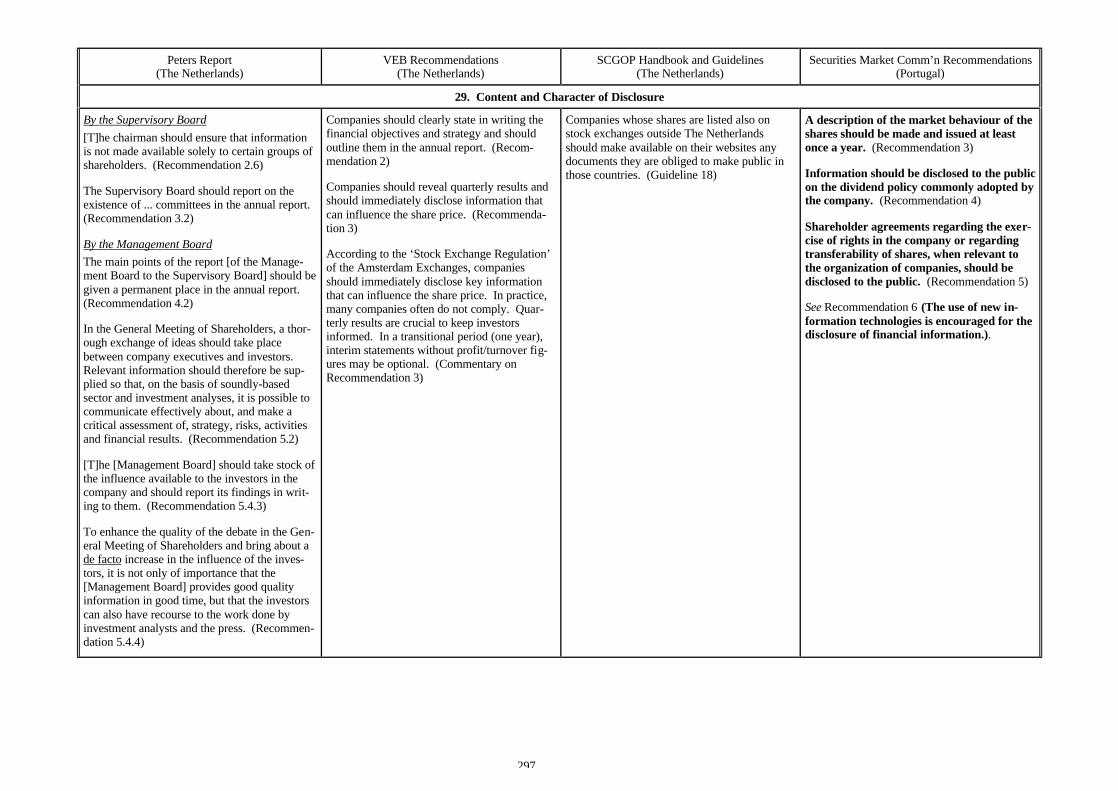

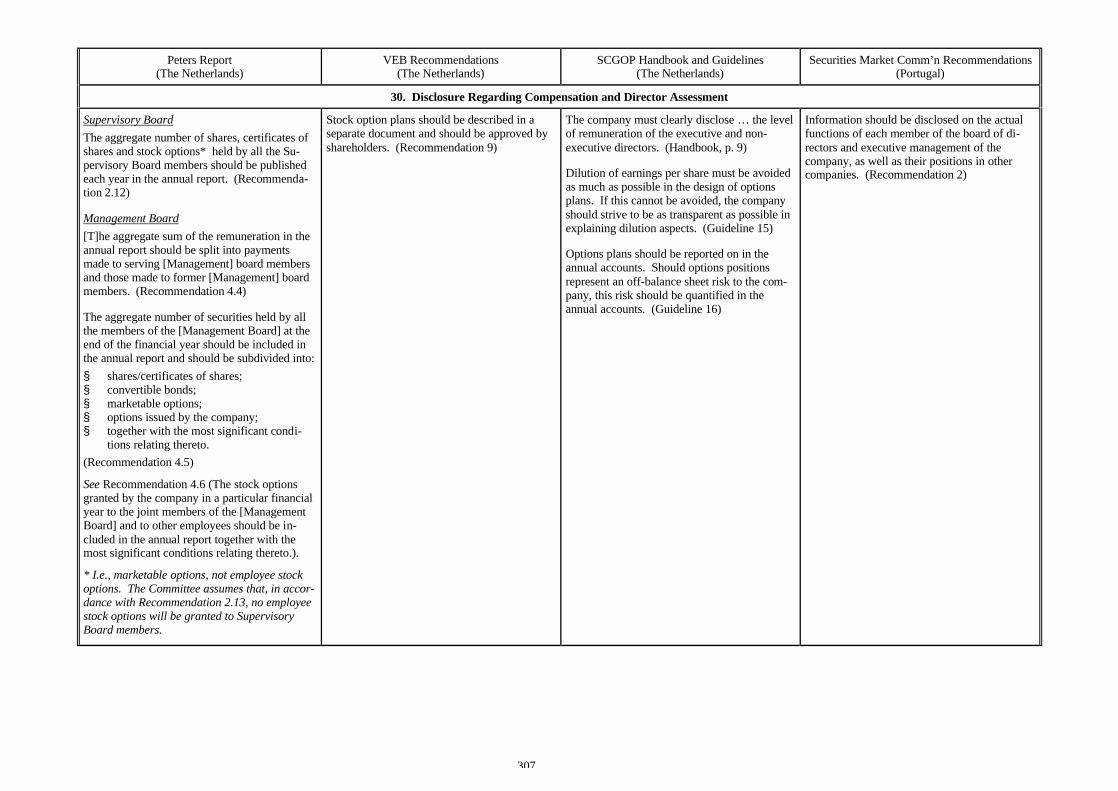

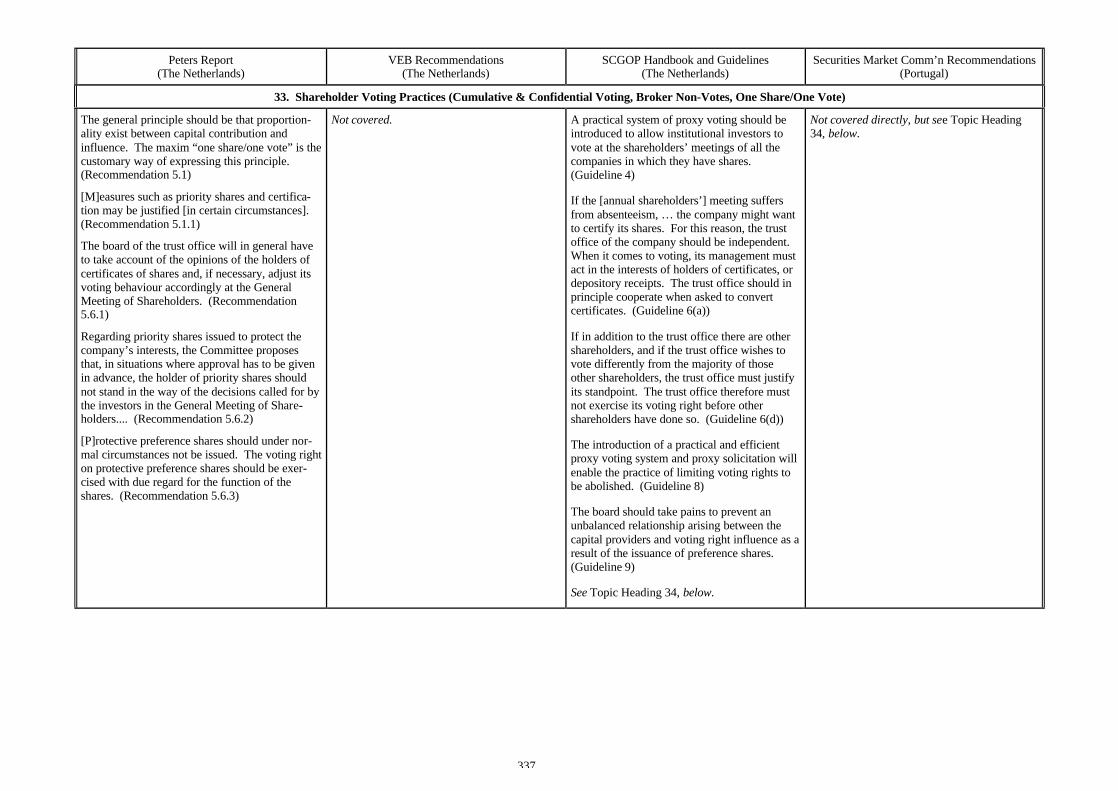

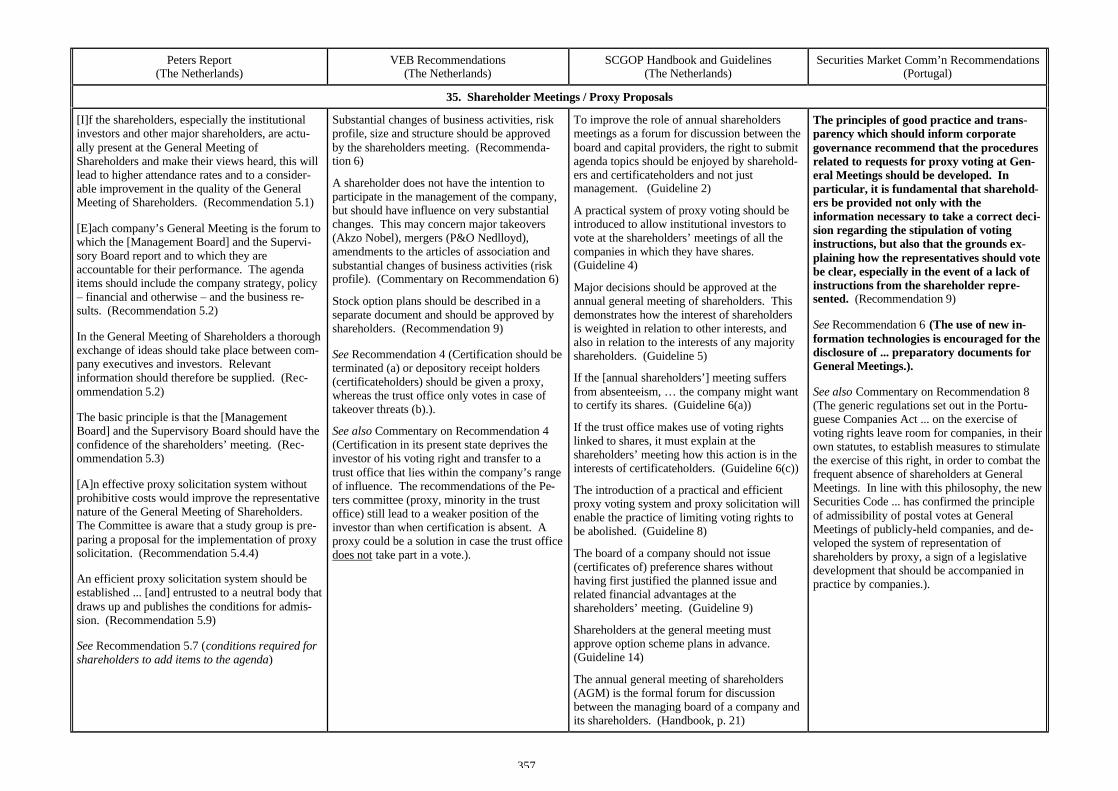

Peters Report(The Netherlands)

VEB Recommendations(The Netherlands)

SCGOP Handbook and Guidelines(The Netherlands)

Securities Market Comm’n Recommendations(Portugal)

OVERVIEW

Code: FORTY RECOMMENDATIONS ON COR-PORATE GOVERNANCE IN THE NETHERLANDS(“Peters Report”) (June 1997)

Issuing Body: Secretariat Committee on Corpo-rate Governance, a committee related to a stockexchange and a business, industry and/or aca-demic association

Legal Basis and Compliance: Voluntary (disclo-sure encouraged)

Objective: Improve quality of board(supervisory) governance

Scope: Listed companies

Predominant Board Structure(listed companies): Two-tier

Code: TEN RECOMMENDATIONS ON CORPORATEGOVERNANCE IN THE NETHERLANDS (1997)

Issuing Body: Vereniging van Effectenbezit-ters (“VEB”), an investors association

Legal Basis and Compliance: Voluntary (asso-ciation members recommended to apply toportfolio companies)

Objective: Improve accountability to share-holders and/or maximise shareholder value

Scope: Listed companies

Predominant Board Structure(listed companies): Two-tier

Code: CORPORATE GOVERNANCE HANDBOOKOF THE SCGOP (August 2001)

Issuing Body: Stichting Corporate GovernanceOnderzoek voor Pensioenfondsen (“SCGOP”)(Foundation for Corporate Governance Re-search for Pension Funds), an investorsassociation

Legal Basis and Compliance: Voluntary (dis-closure encouraged)

Objective: Improve accountability to share-holders and/or maximise shareholder value

Scope: Listed companies

Predominant Board Structure(listed companies): Two-tier

Code: RECOMMENDATIONS ON CORPORATEGOVERNANCE (November 1999)

Issuing Body: Comissão do Mercado deValores Mobiliáros (“CMVM”) (PortugueseSecurities Market Commission), agovernmental/quasi-governmental entity

Legal Basis and Compliance: Voluntary (dis-closure encouraged)

Objective: Improve companies’ performance,competitiveness and/or access to capital

Scope: Listed companies; encouraged to allcompanies

Predominant Board Structure(listed companies): Unitary

8

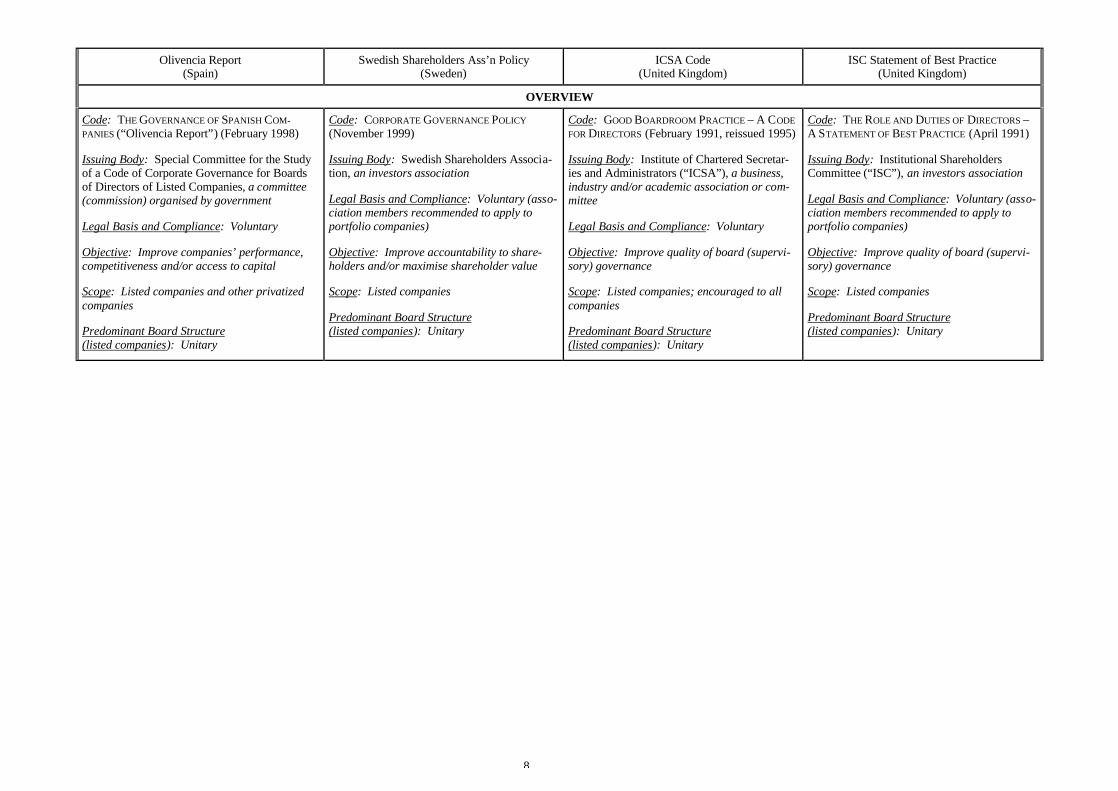

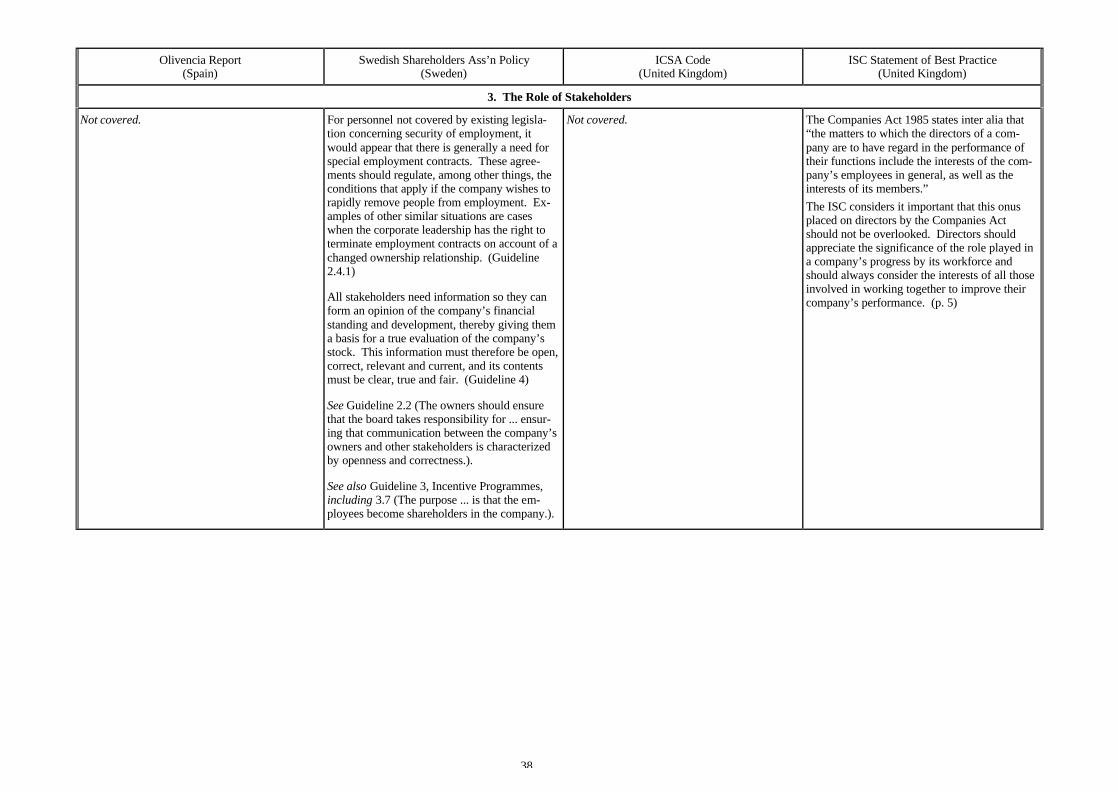

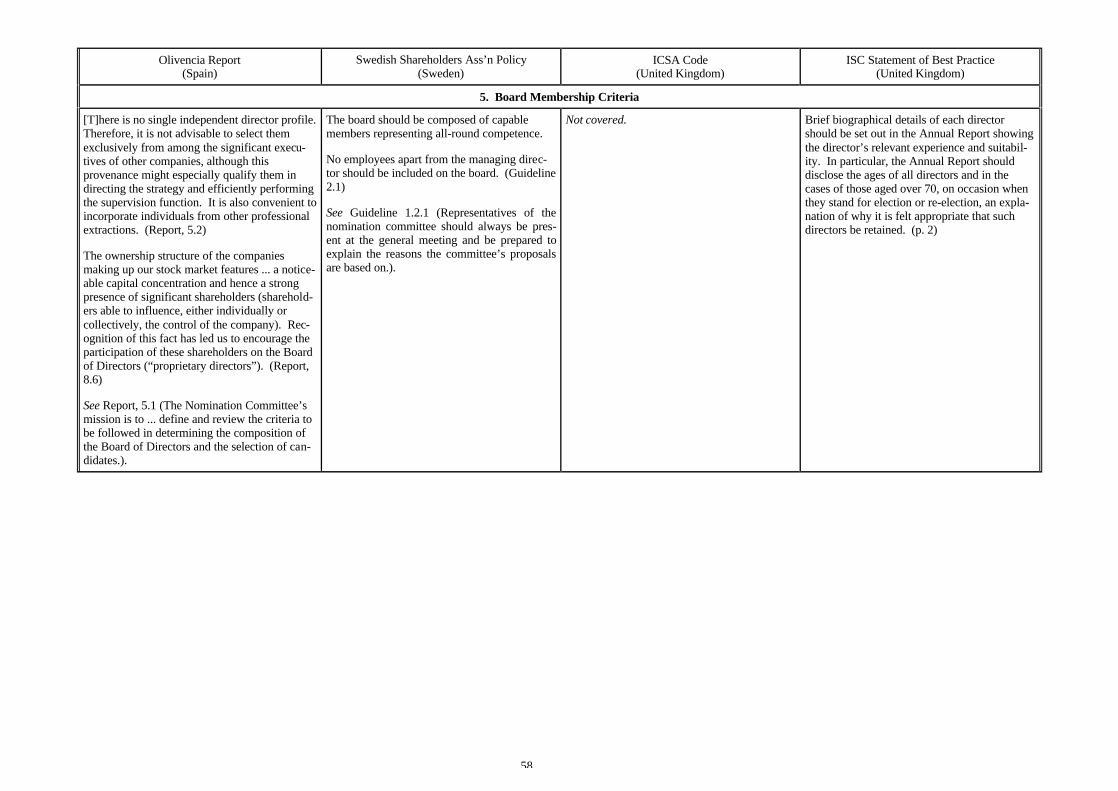

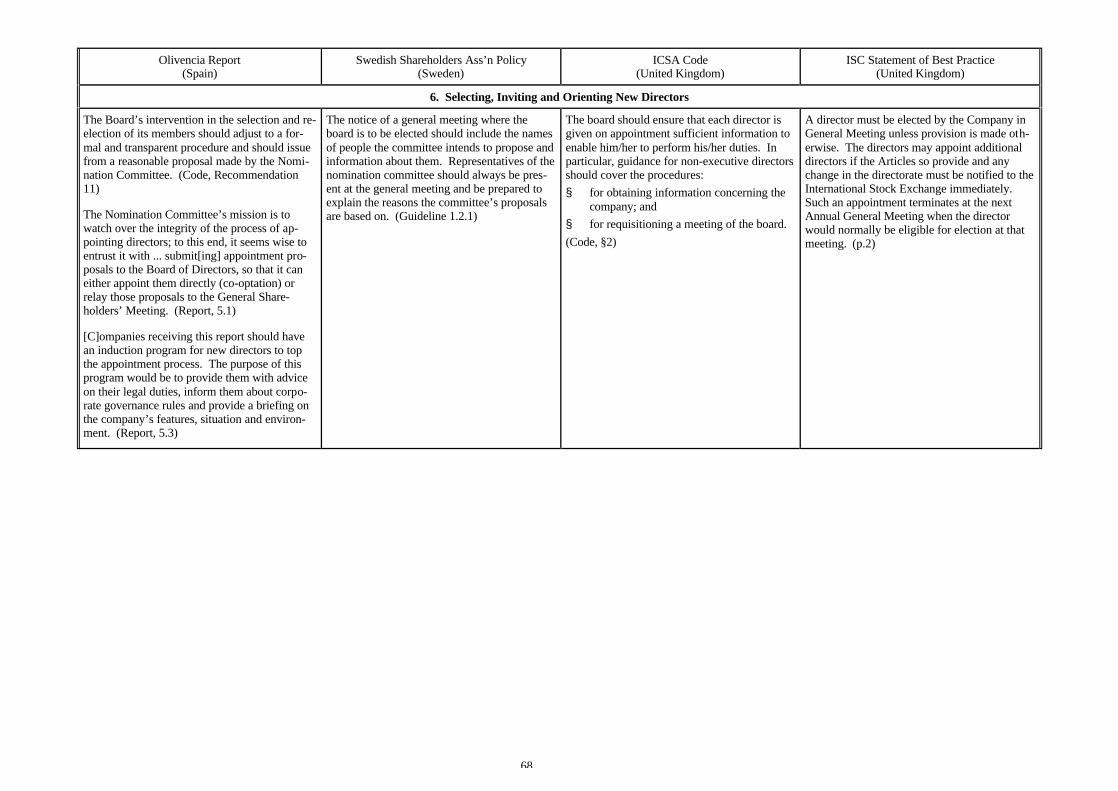

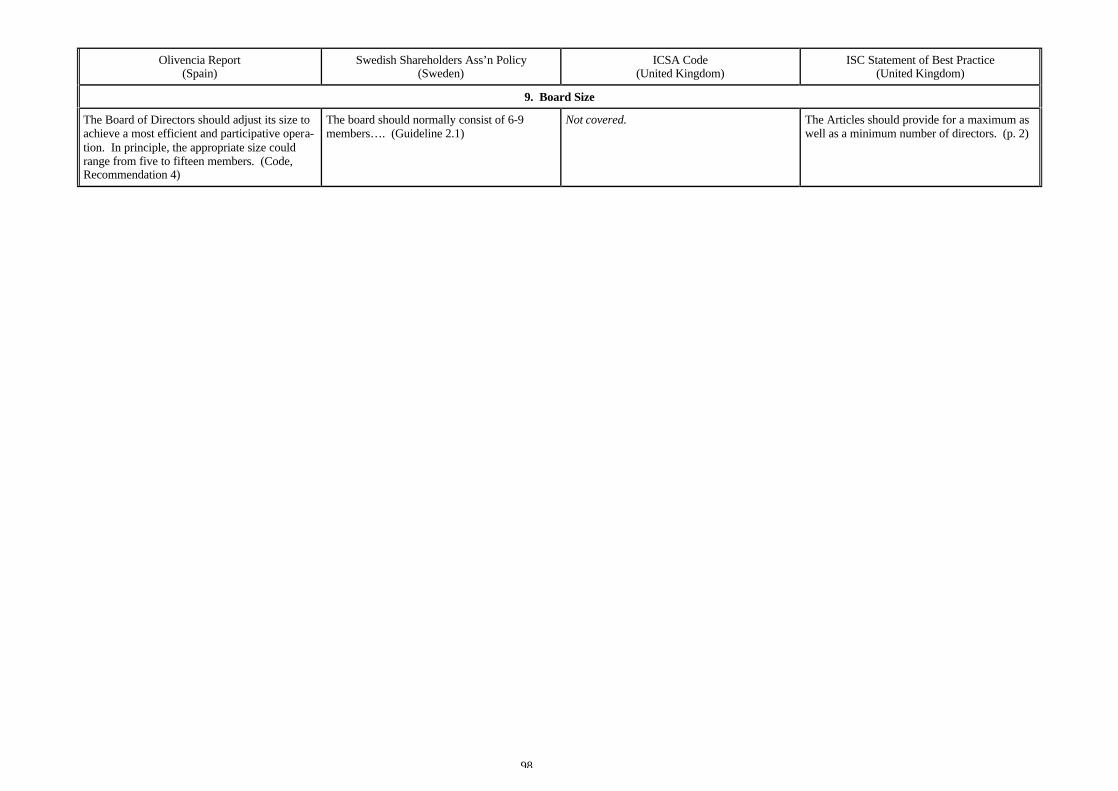

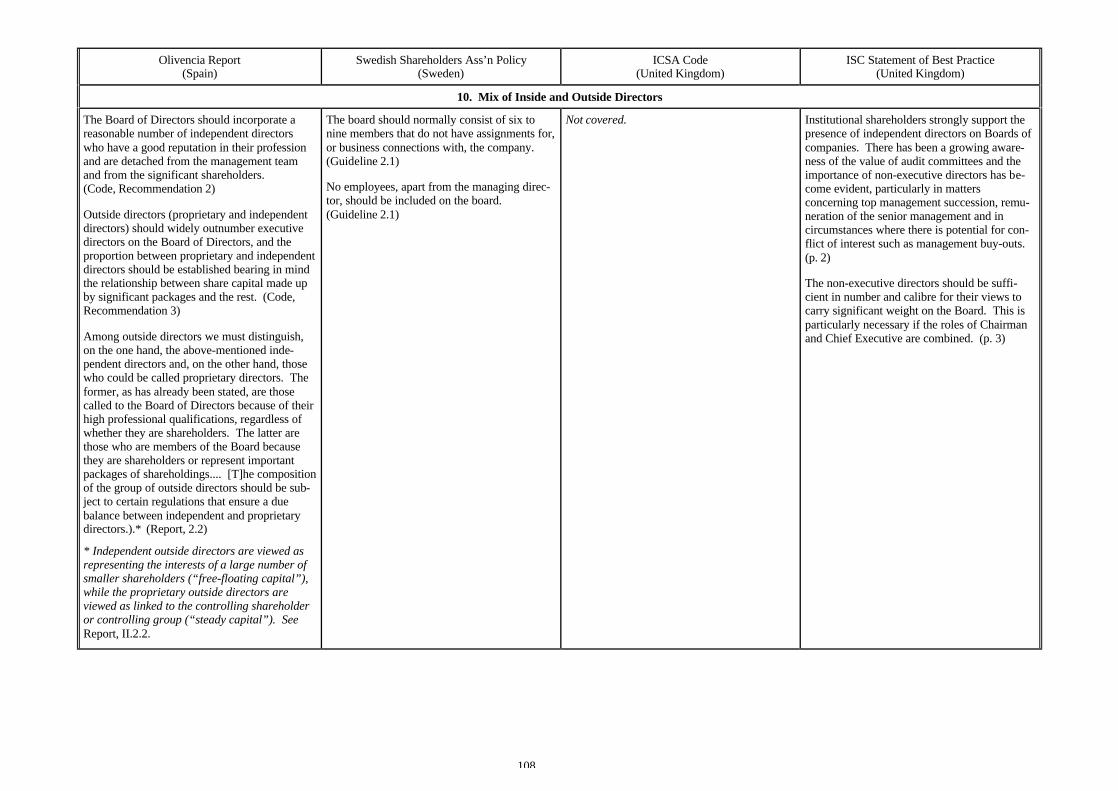

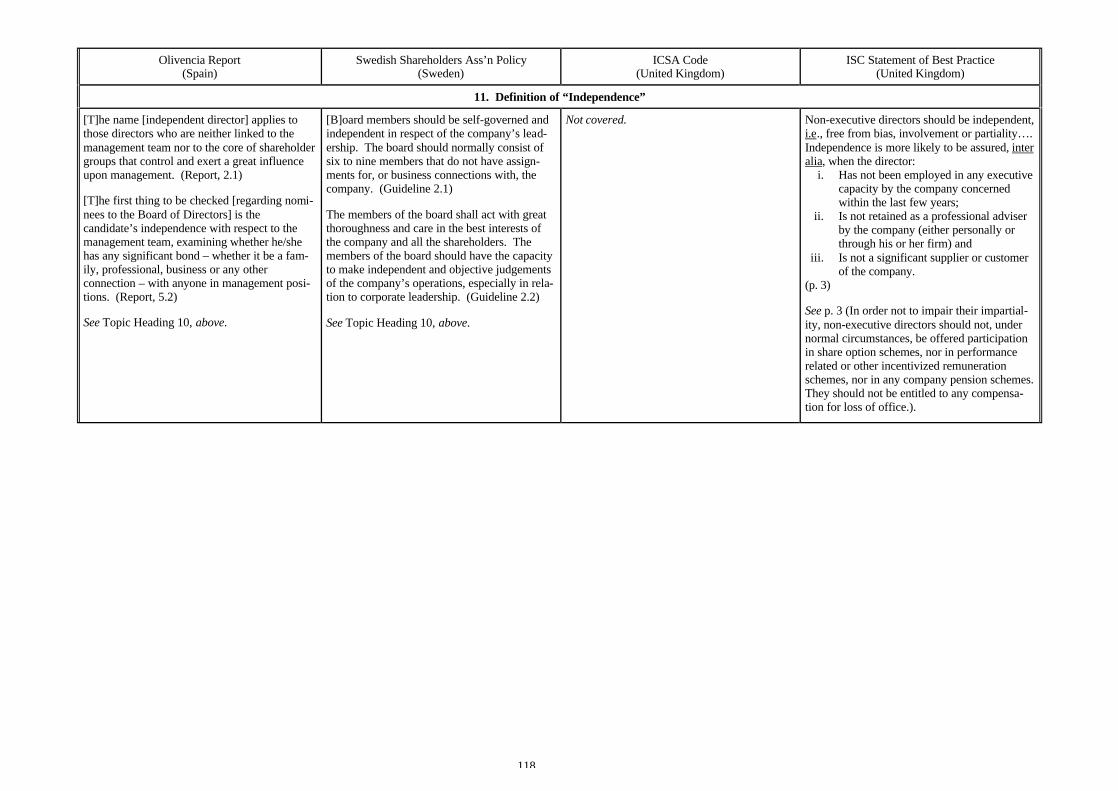

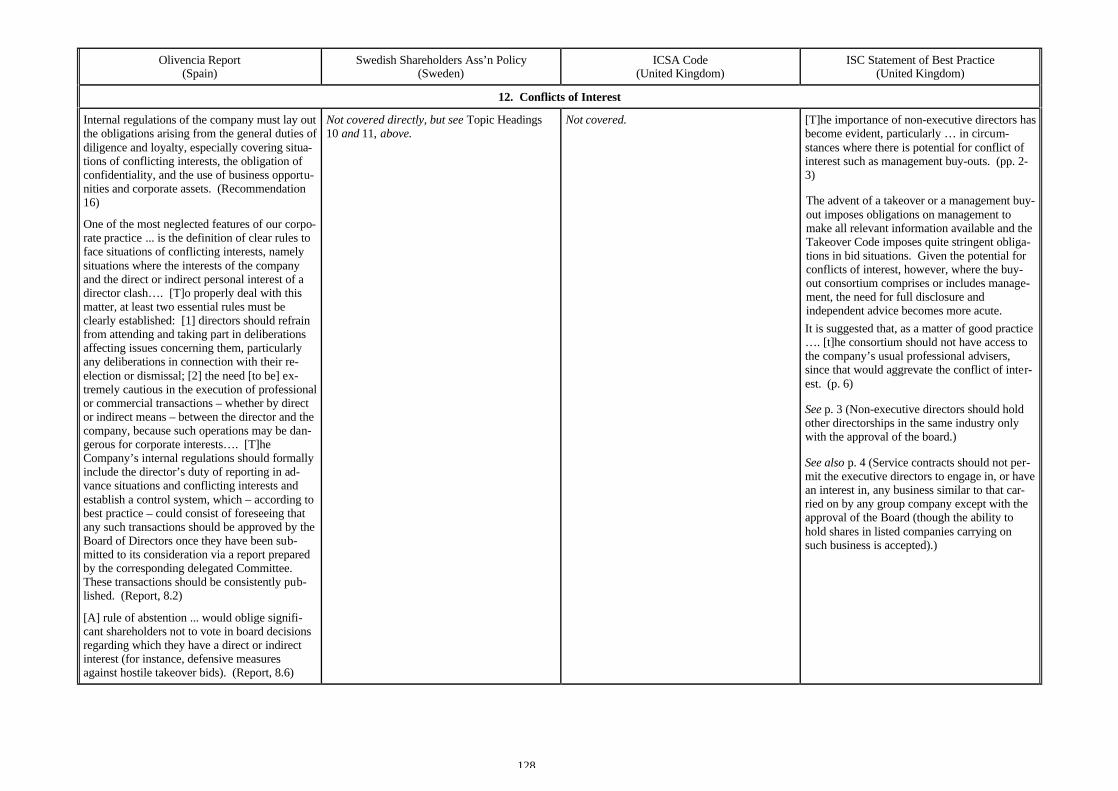

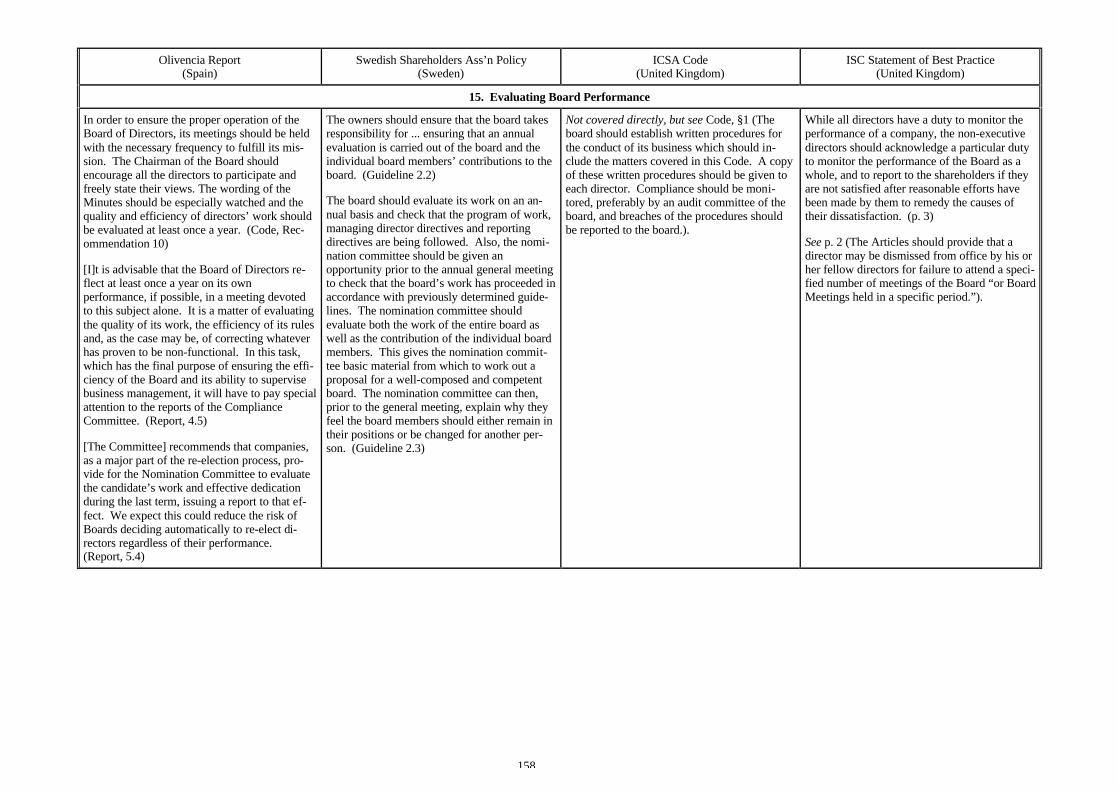

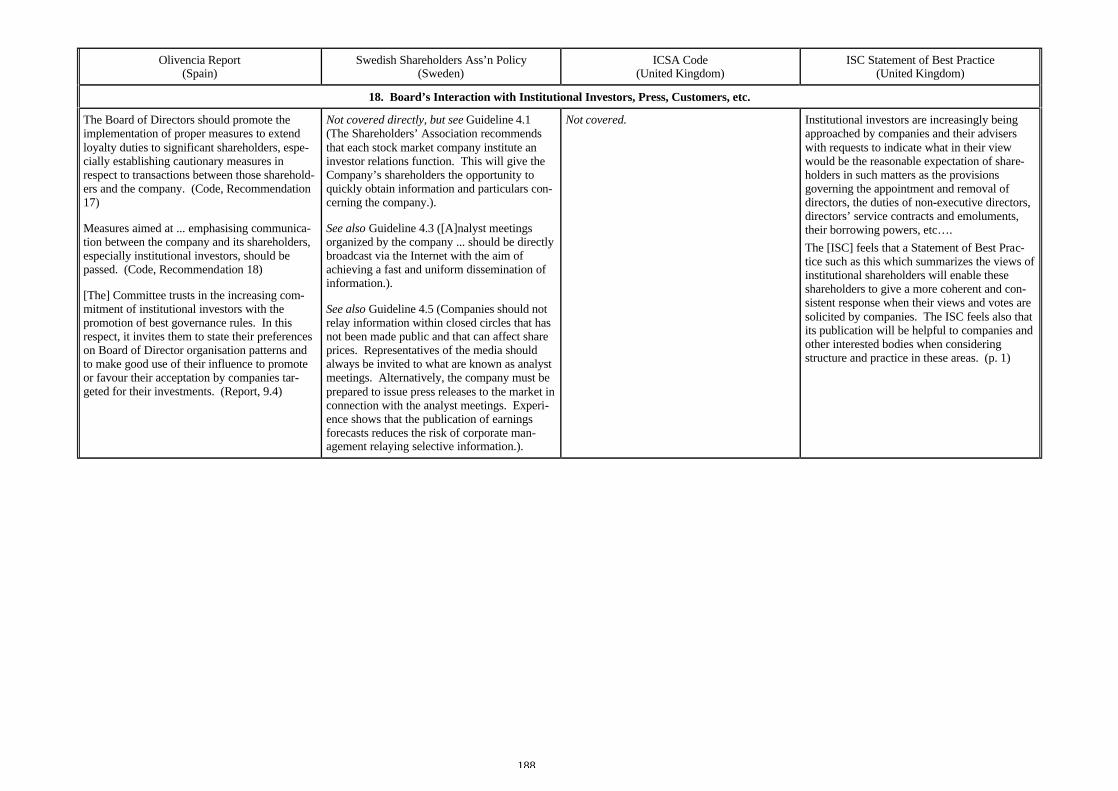

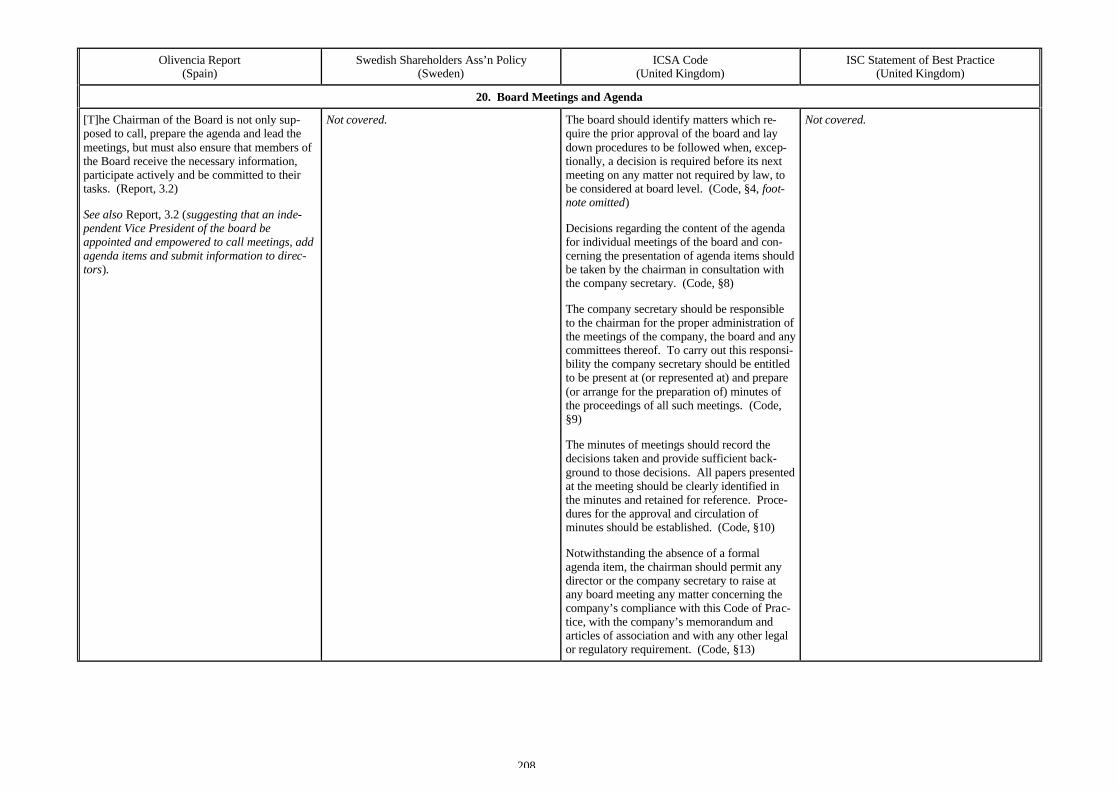

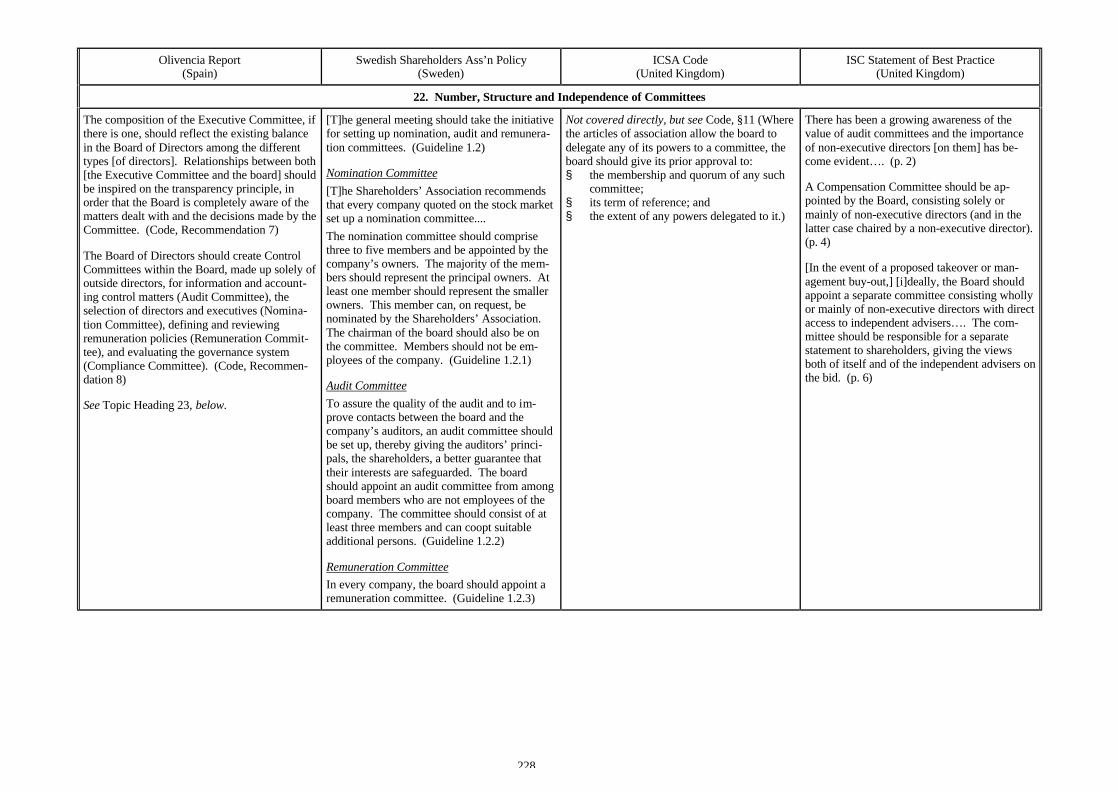

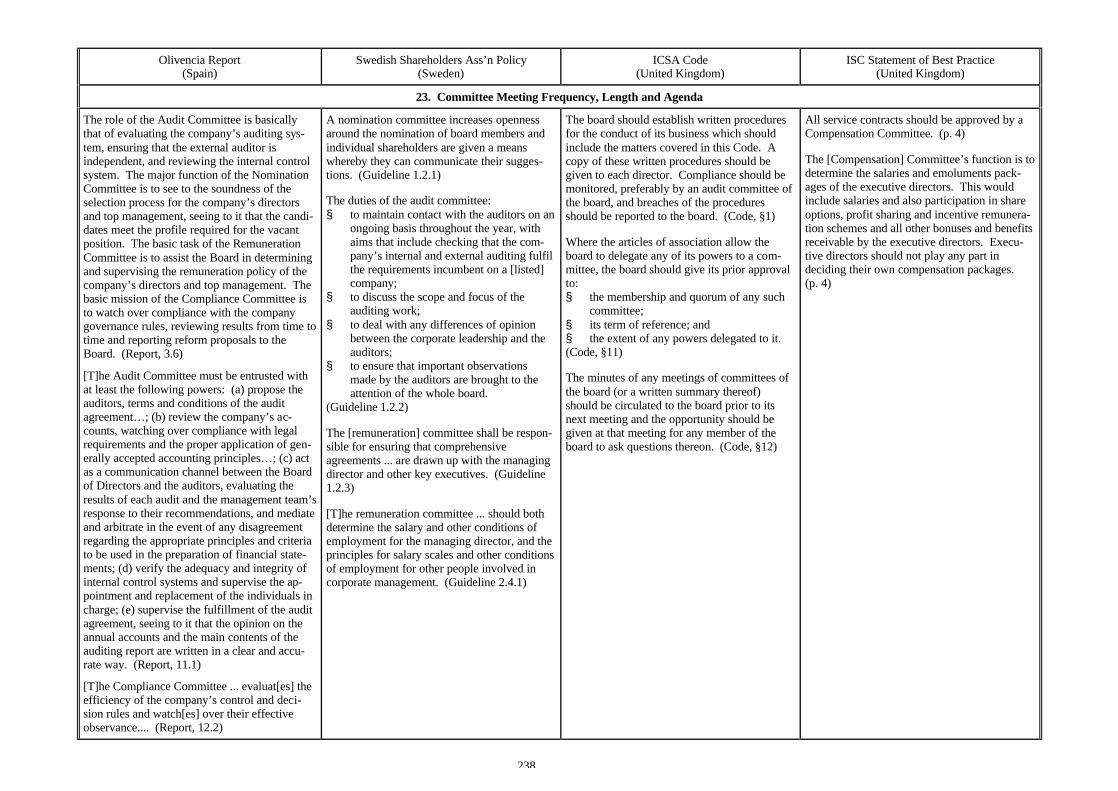

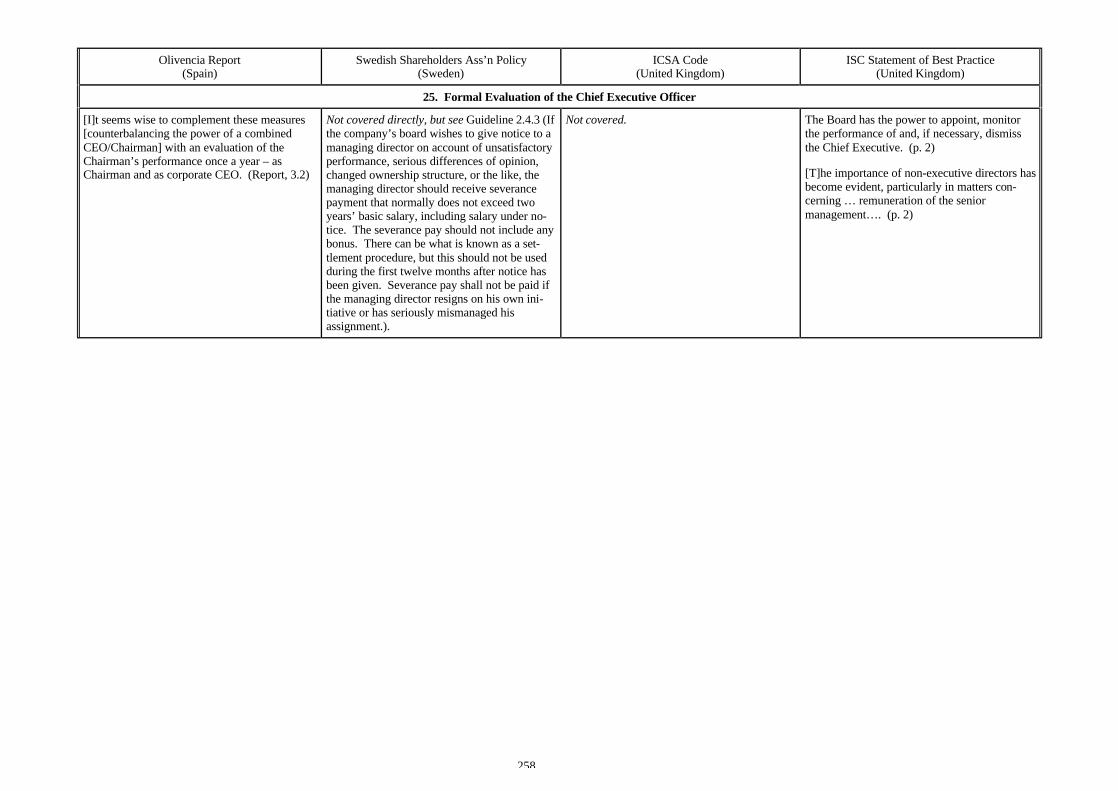

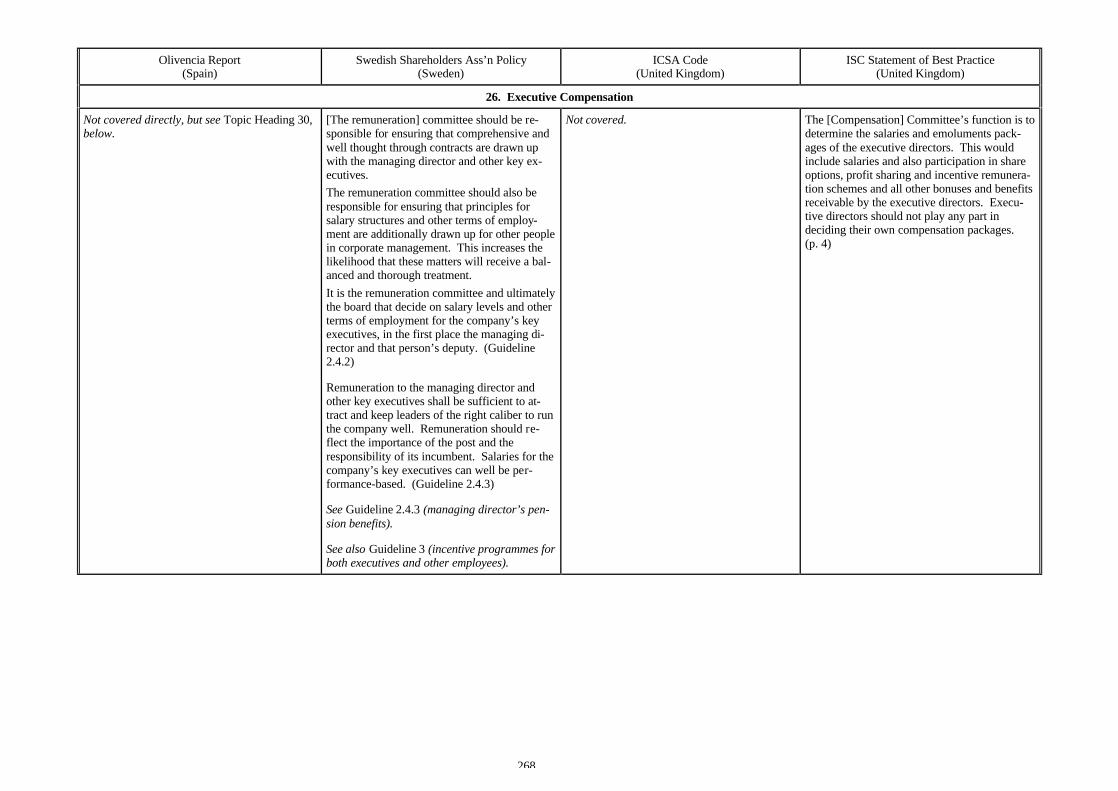

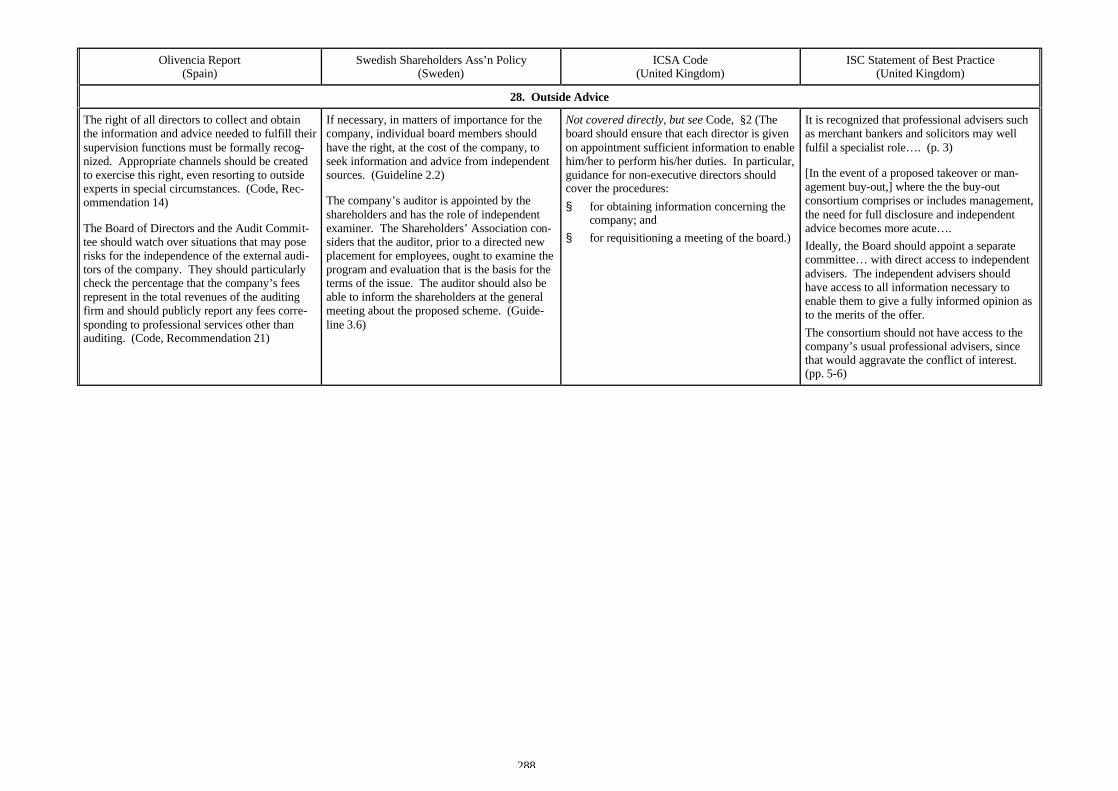

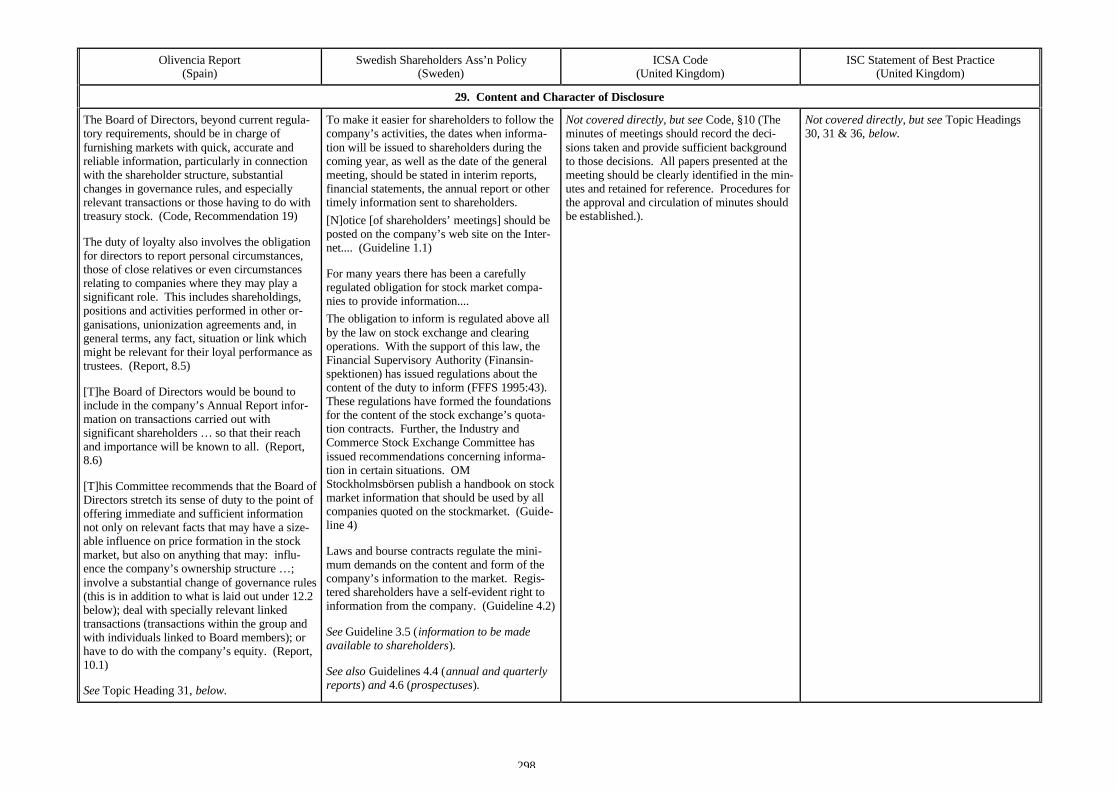

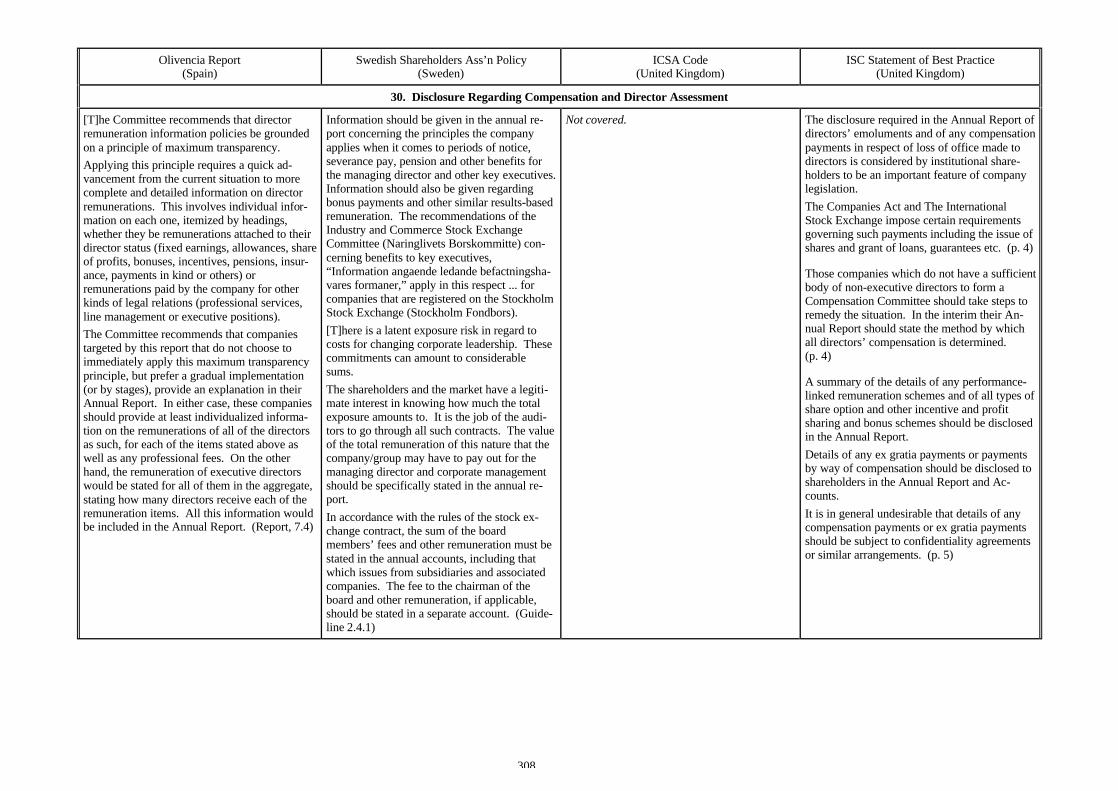

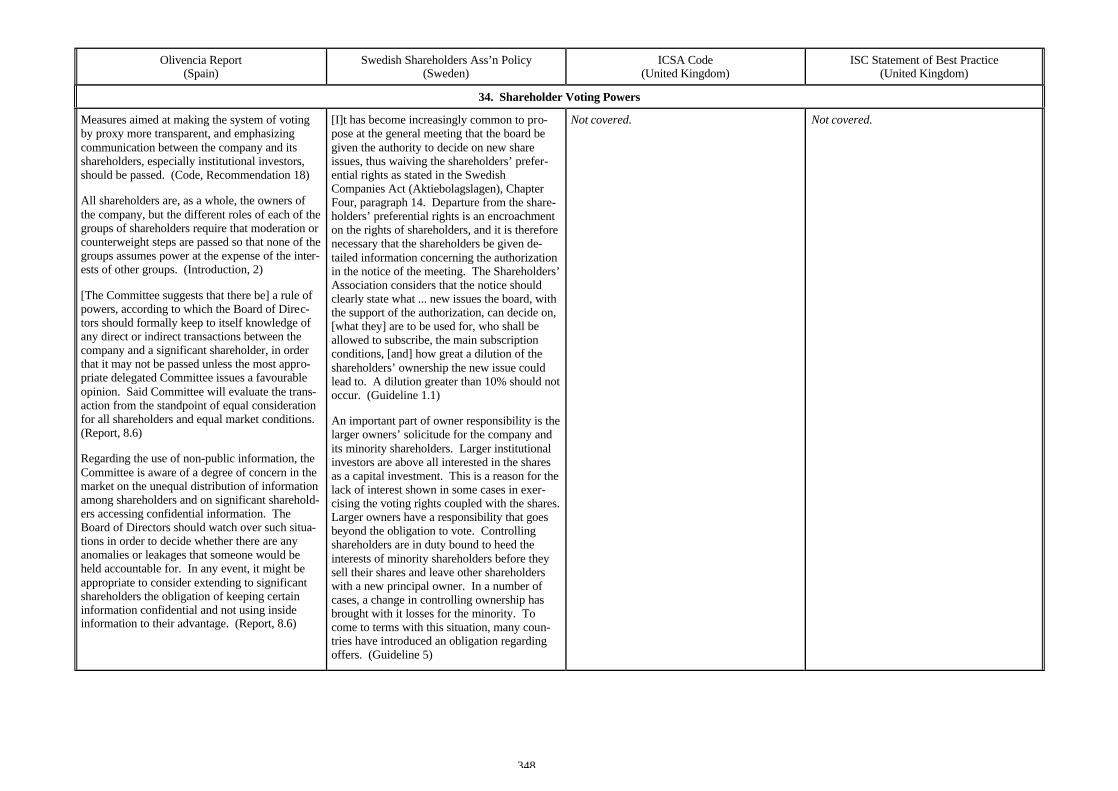

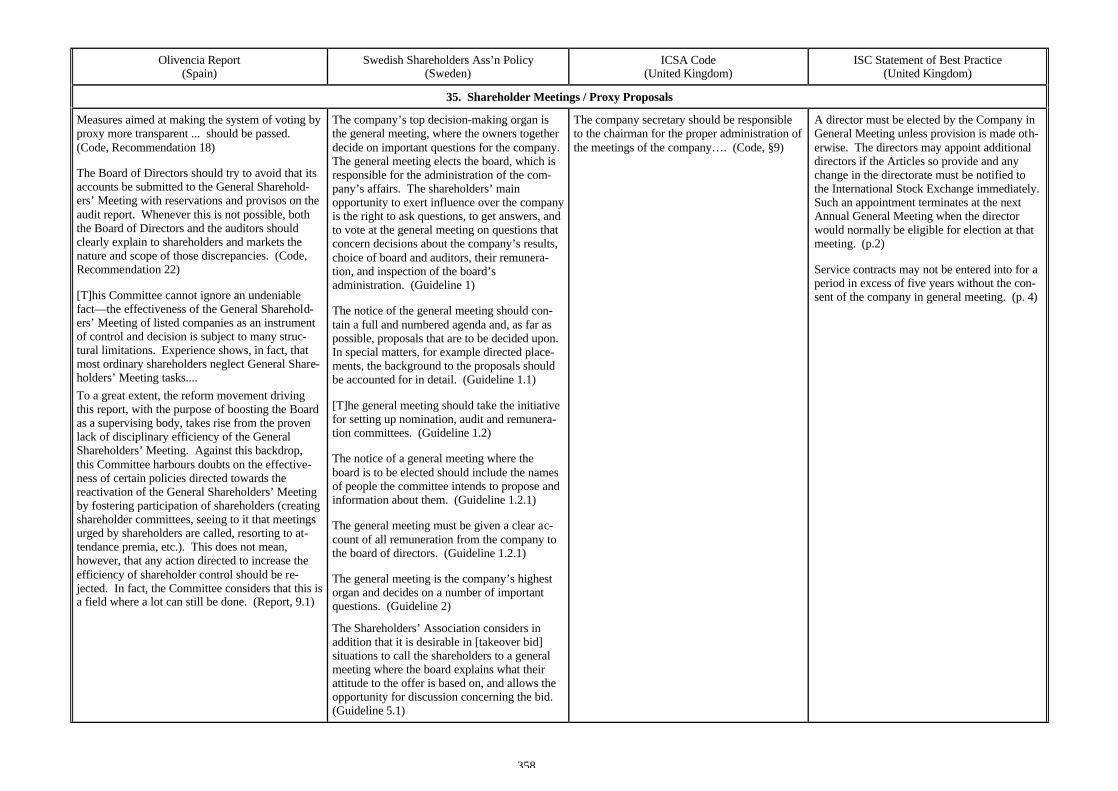

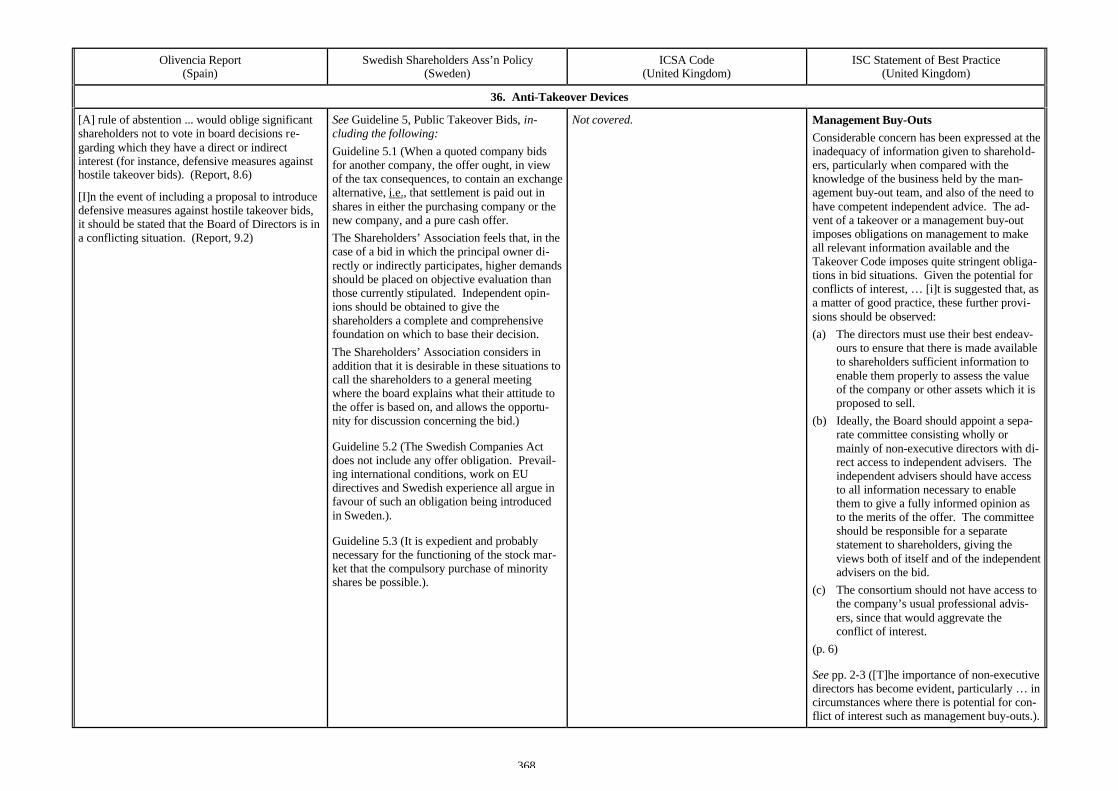

Olivencia Report(Spain)

Swedish Shareholders Ass’n Policy(Sweden)

ICSA Code(United Kingdom)

ISC Statement of Best Practice(United Kingdom)

OVERVIEW

Code: THE GOVERNANCE OF SPANISH COM-PANIES (“Olivencia Report”) (February 1998)

Issuing Body: Special Committee for the Studyof a Code of Corporate Governance for Boardsof Directors of Listed Companies, a committee(commission) organised by government

Legal Basis and Compliance: Voluntary

Objective: Improve companies’ performance,competitiveness and/or access to capital

Scope: Listed companies and other privatizedcompanies

Predominant Board Structure(listed companies): Unitary

Code: CORPORATE GOVERNANCE POLICY(November 1999)

Issuing Body: Swedish Shareholders Associa-tion, an investors association

Legal Basis and Compliance: Voluntary (asso-ciation members recommended to apply toportfolio companies)

Objective: Improve accountability to share-holders and/or maximise shareholder value

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

Code: GOOD BOARDROOM PRACTICE – A CODEFOR DIRECTORS (February 1991, reissued 1995)

Issuing Body: Institute of Chartered Secretar-ies and Administrators (“ICSA”), a business,industry and/or academic association or com-mittee

Legal Basis and Compliance: Voluntary

Objective: Improve quality of board (supervi-sory) governance

Scope: Listed companies; encouraged to allcompanies

Predominant Board Structure(listed companies): Unitary

Code: THE ROLE AND DUTIES OF DIRECTORS –A STATEMENT OF BEST PRACTICE (April 1991)

Issuing Body: Institutional ShareholdersCommittee (“ISC”), an investors association

Legal Basis and Compliance: Voluntary (asso-ciation members recommended to apply toportfolio companies)

Objective: Improve quality of board (supervi-sory) governance

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

9

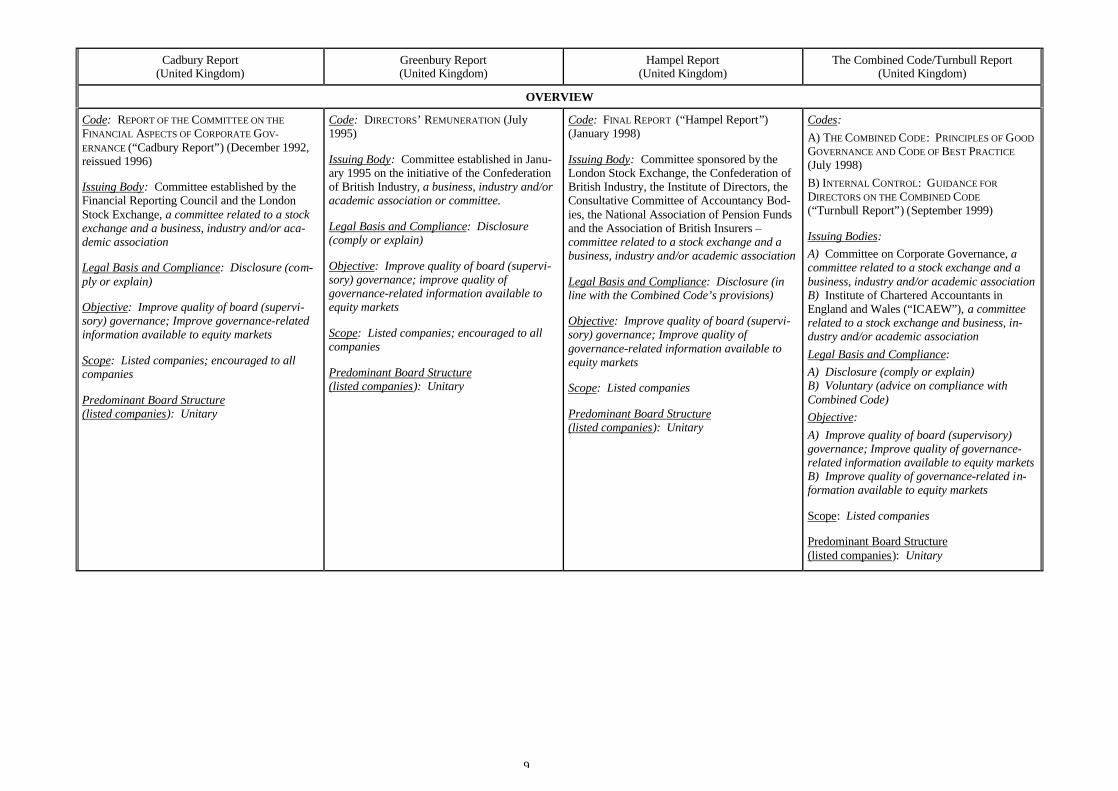

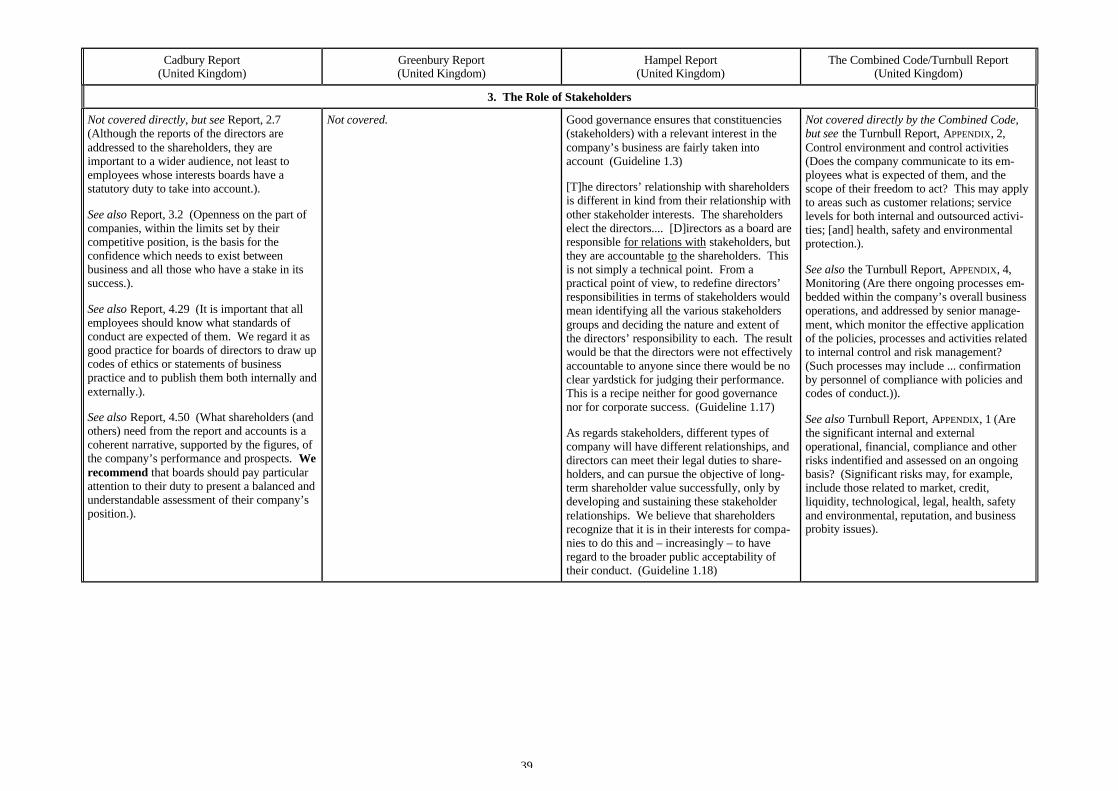

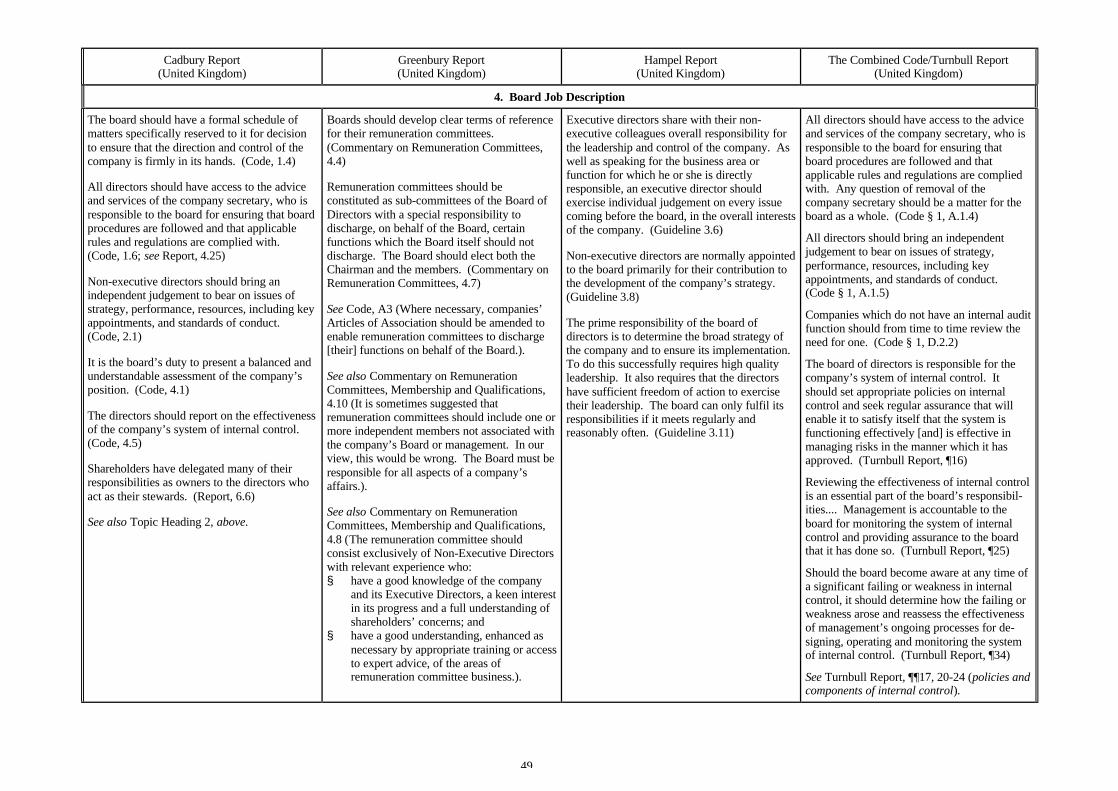

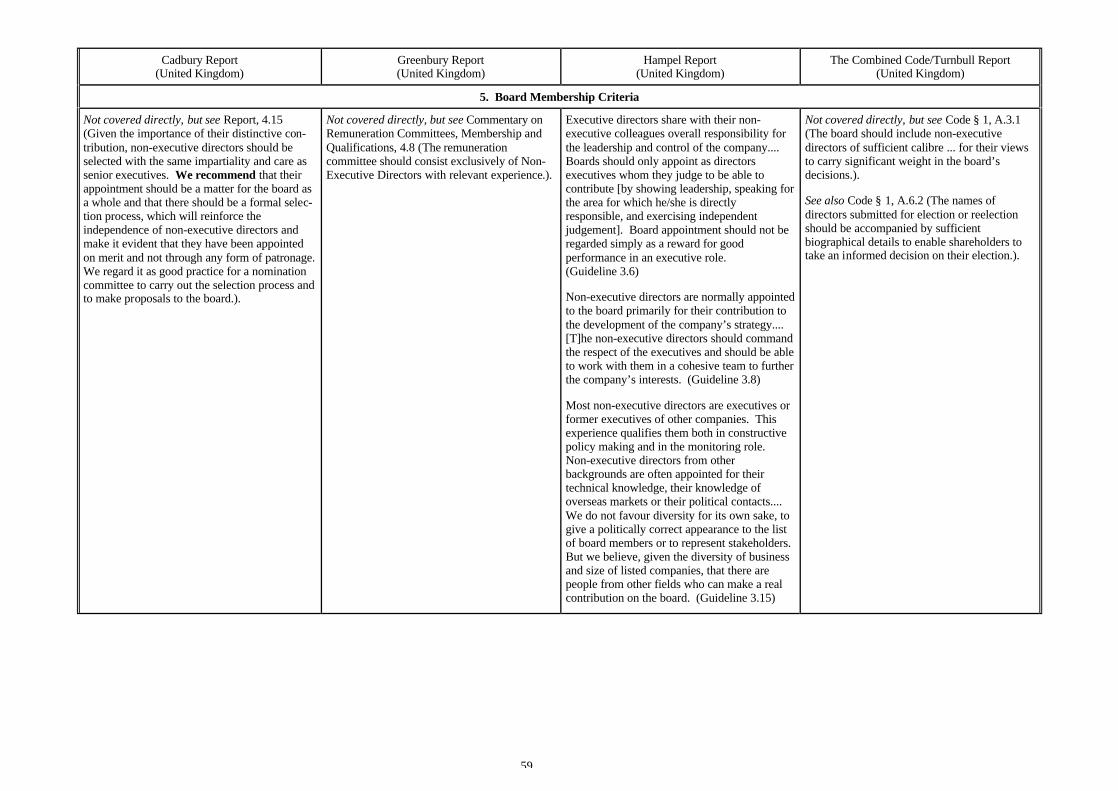

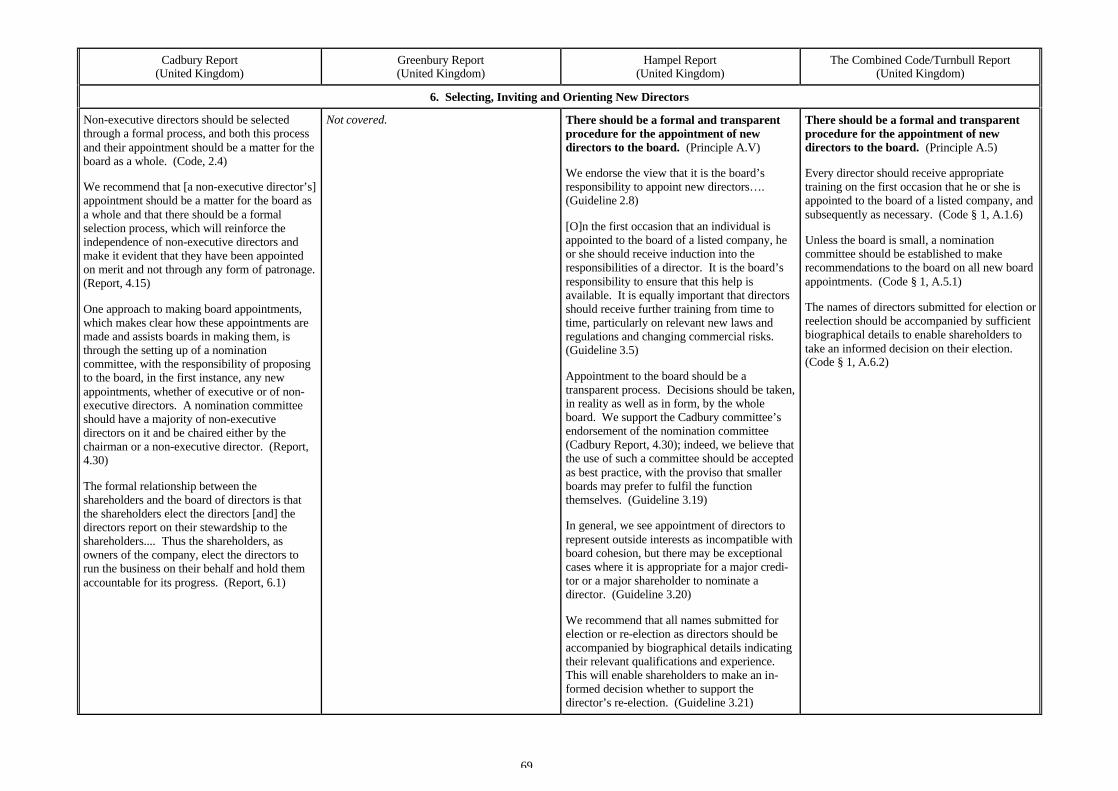

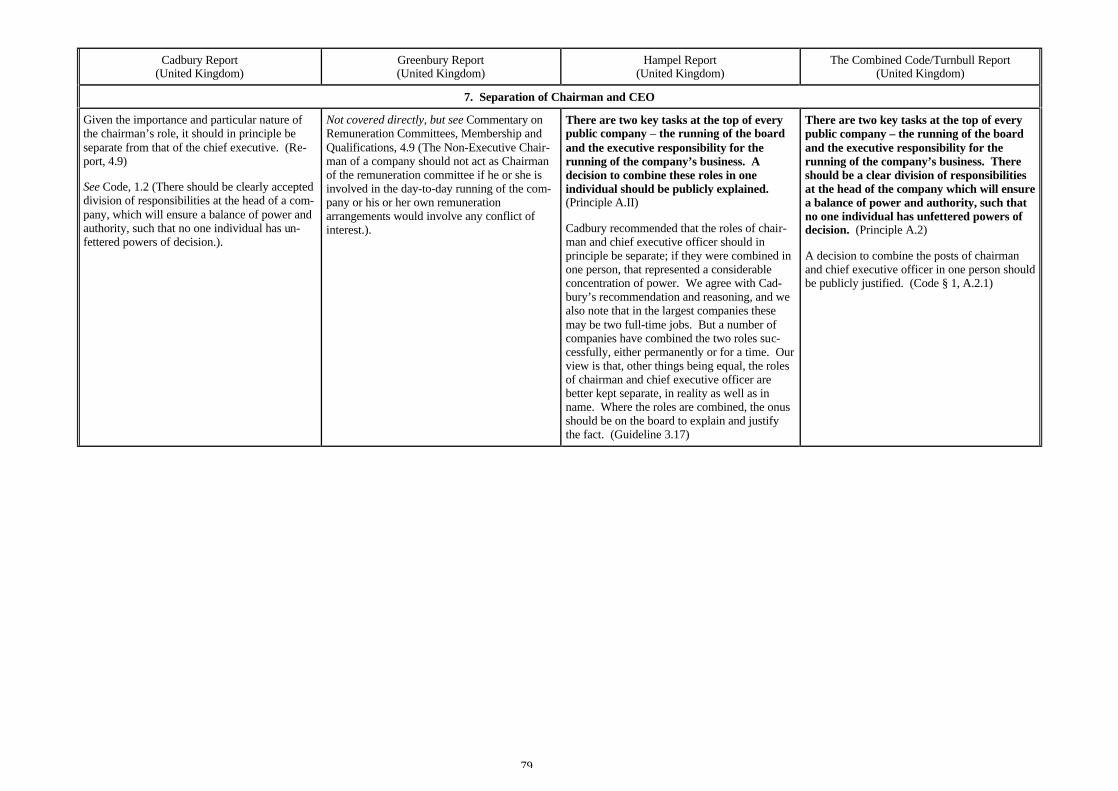

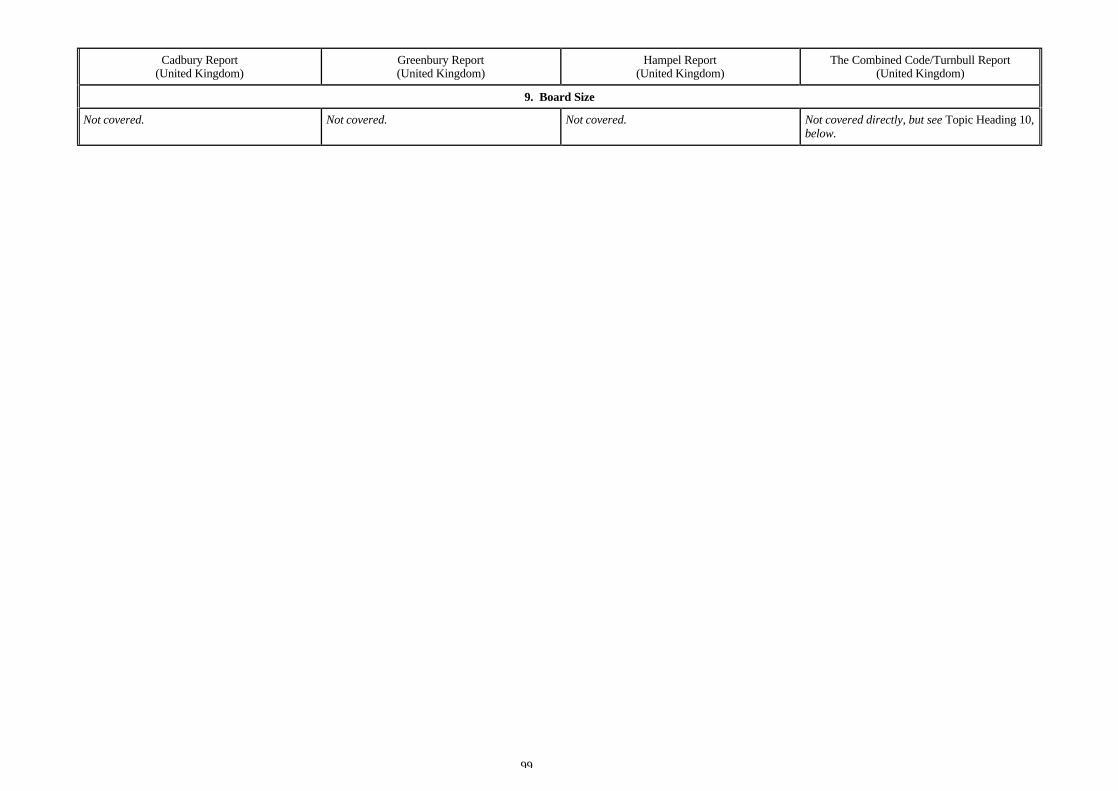

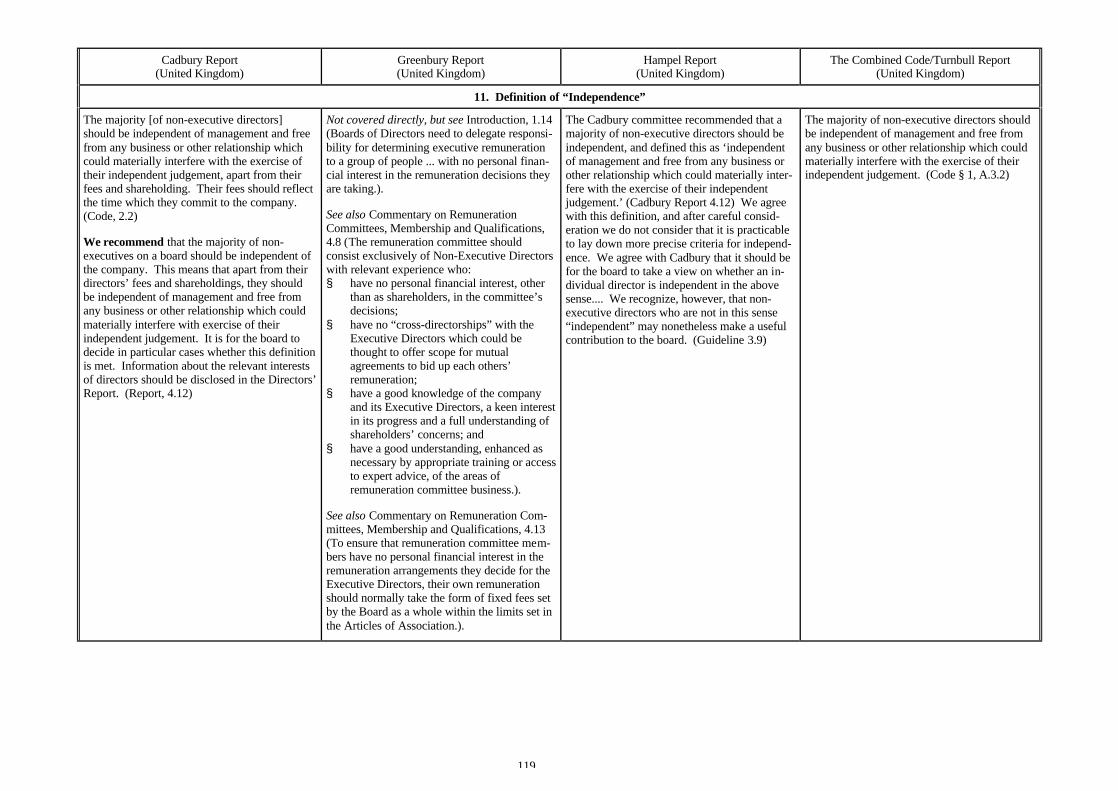

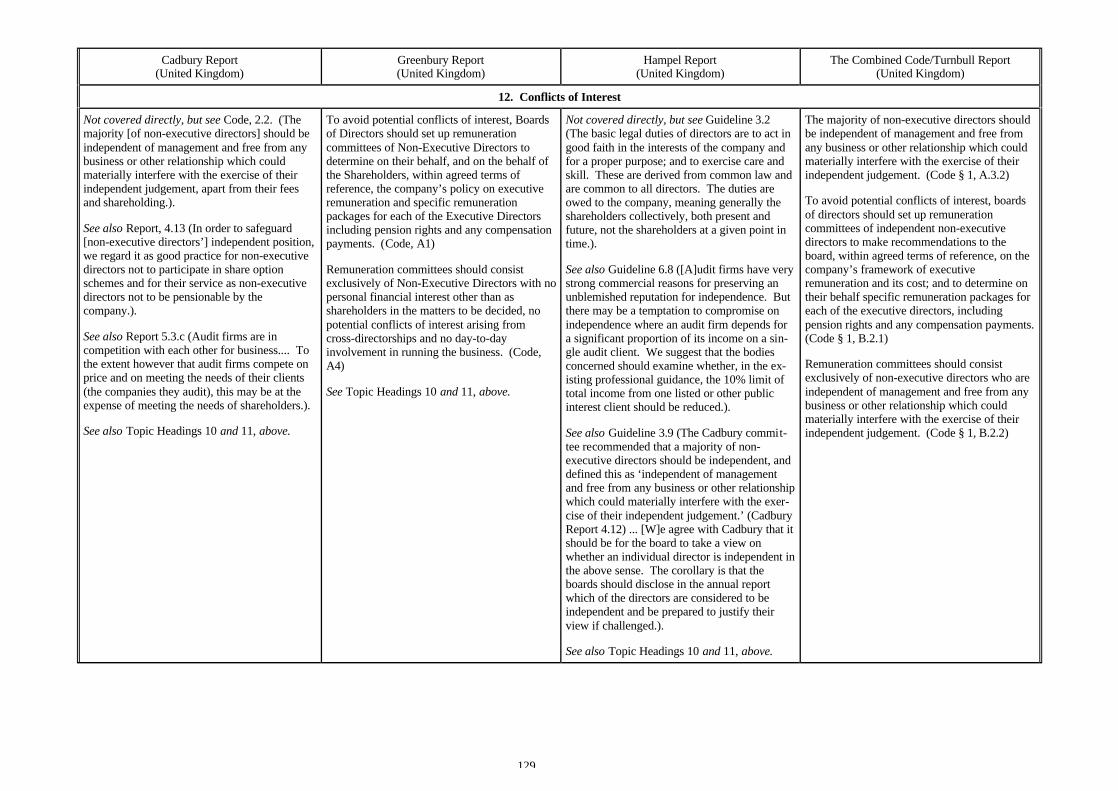

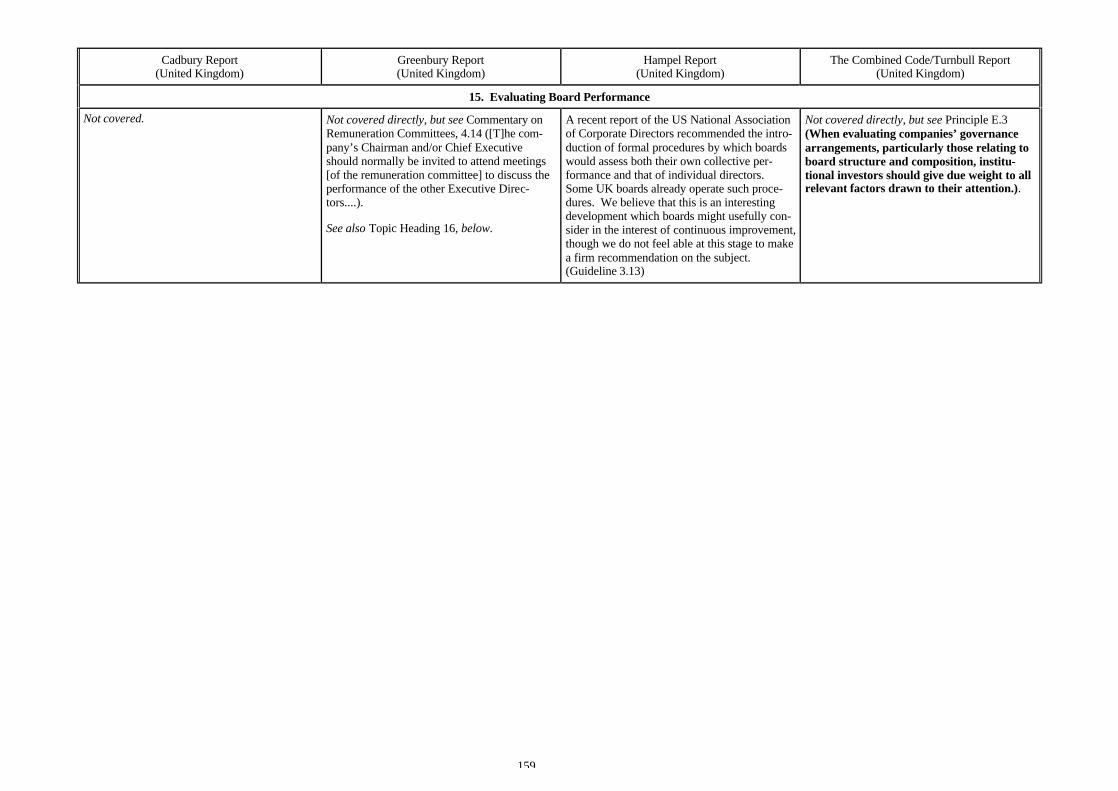

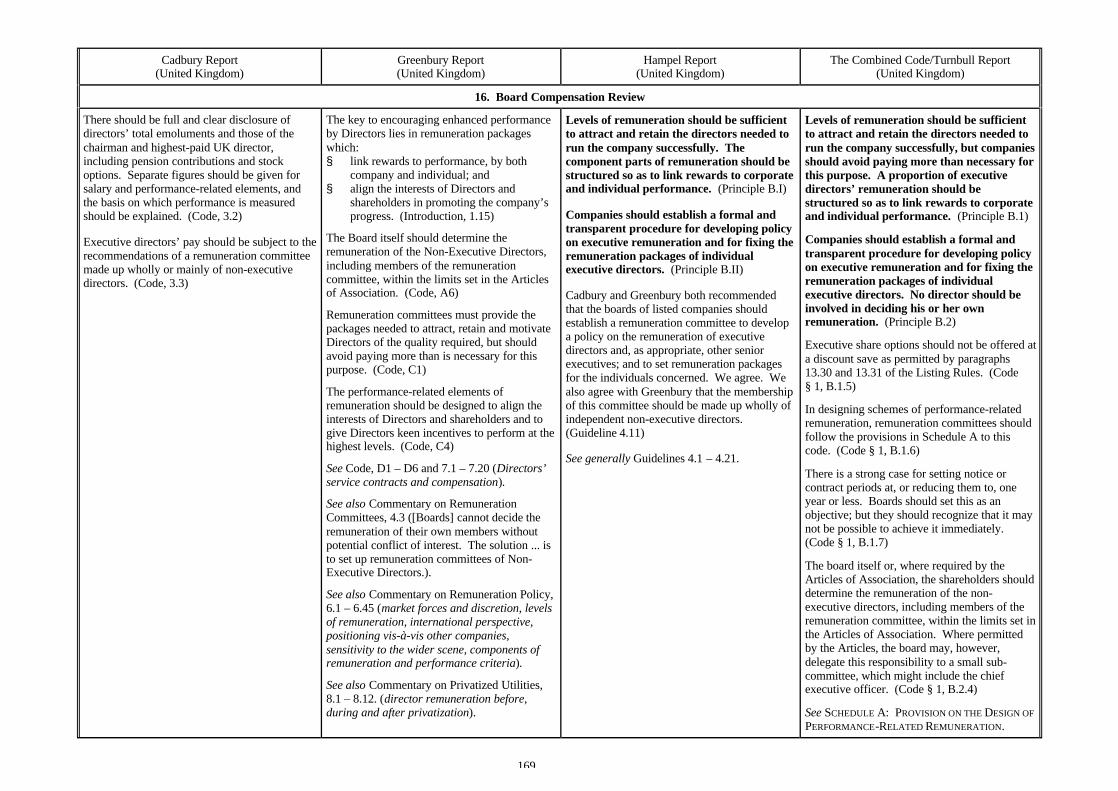

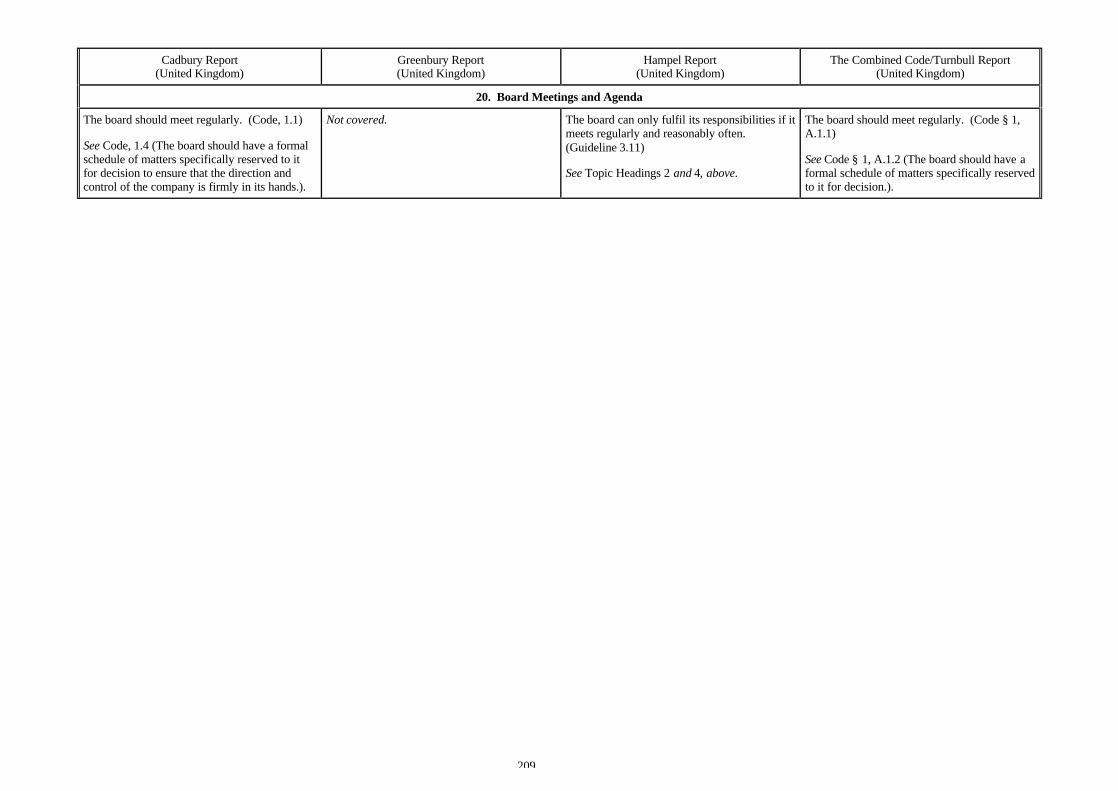

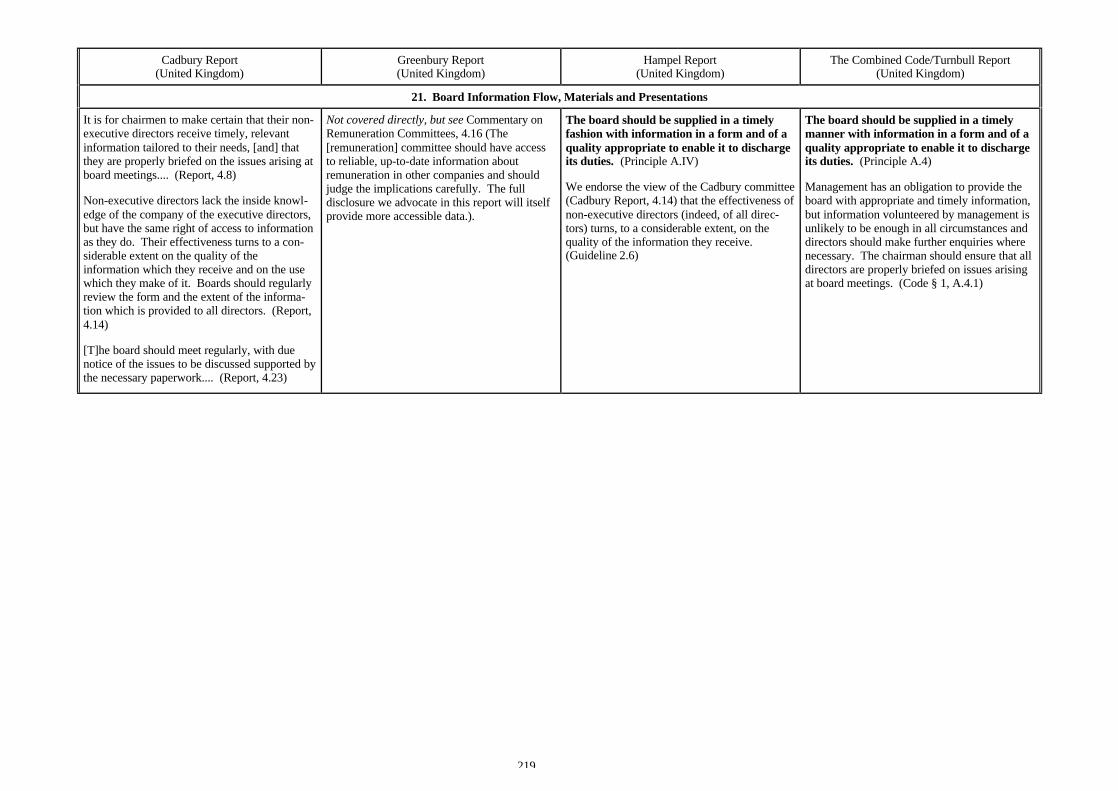

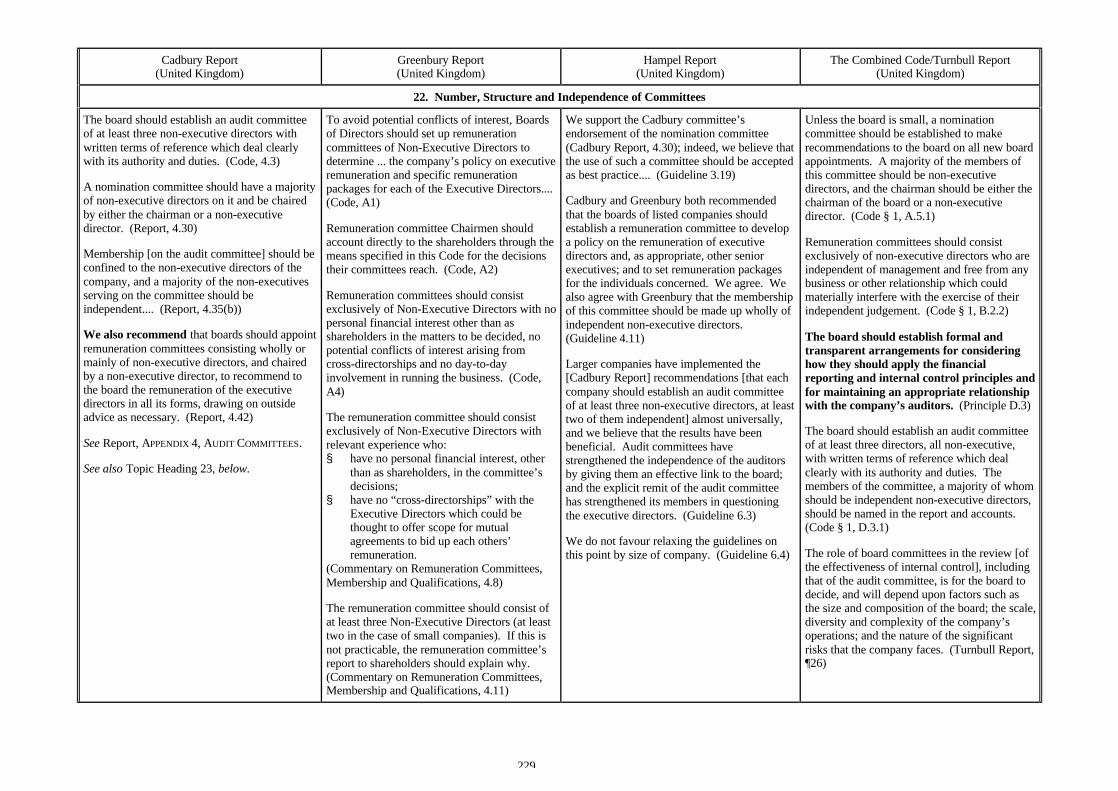

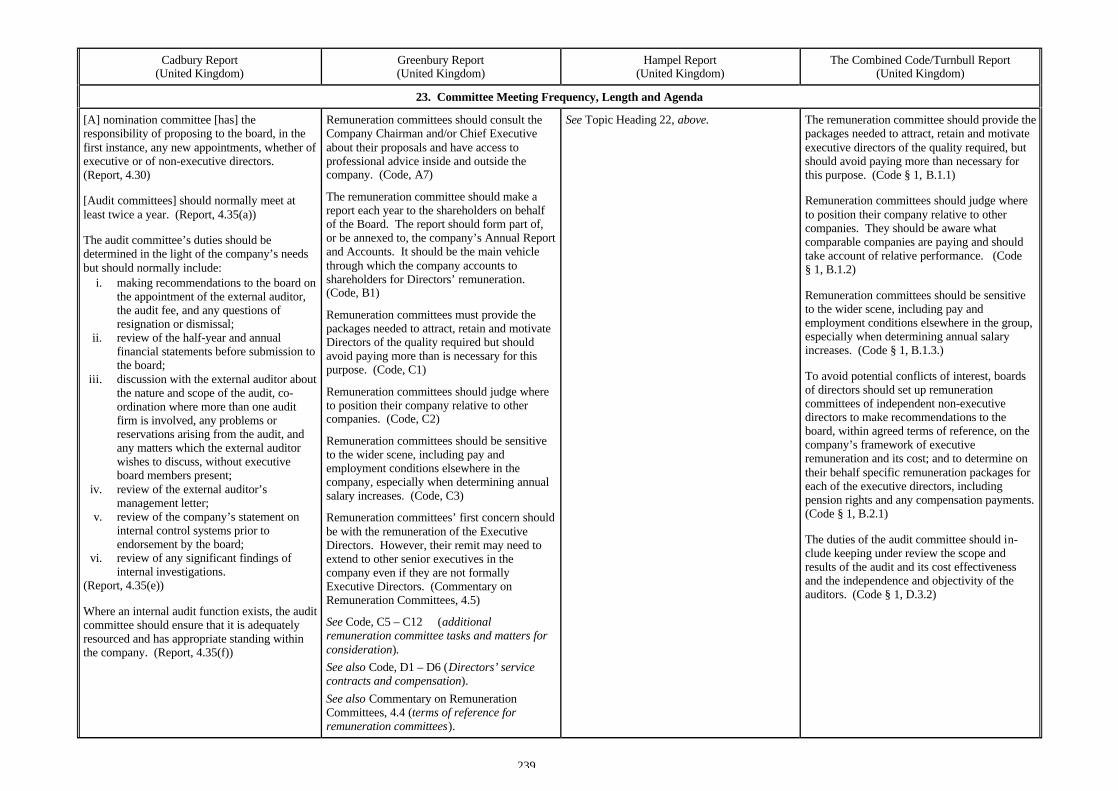

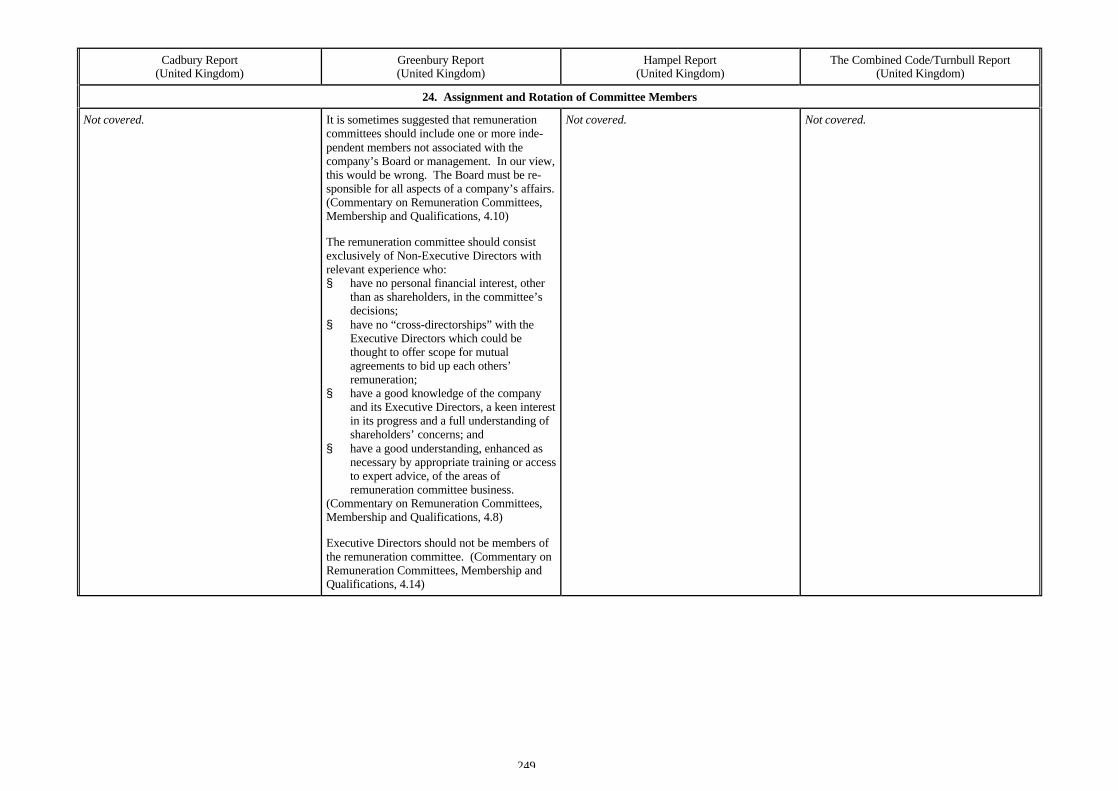

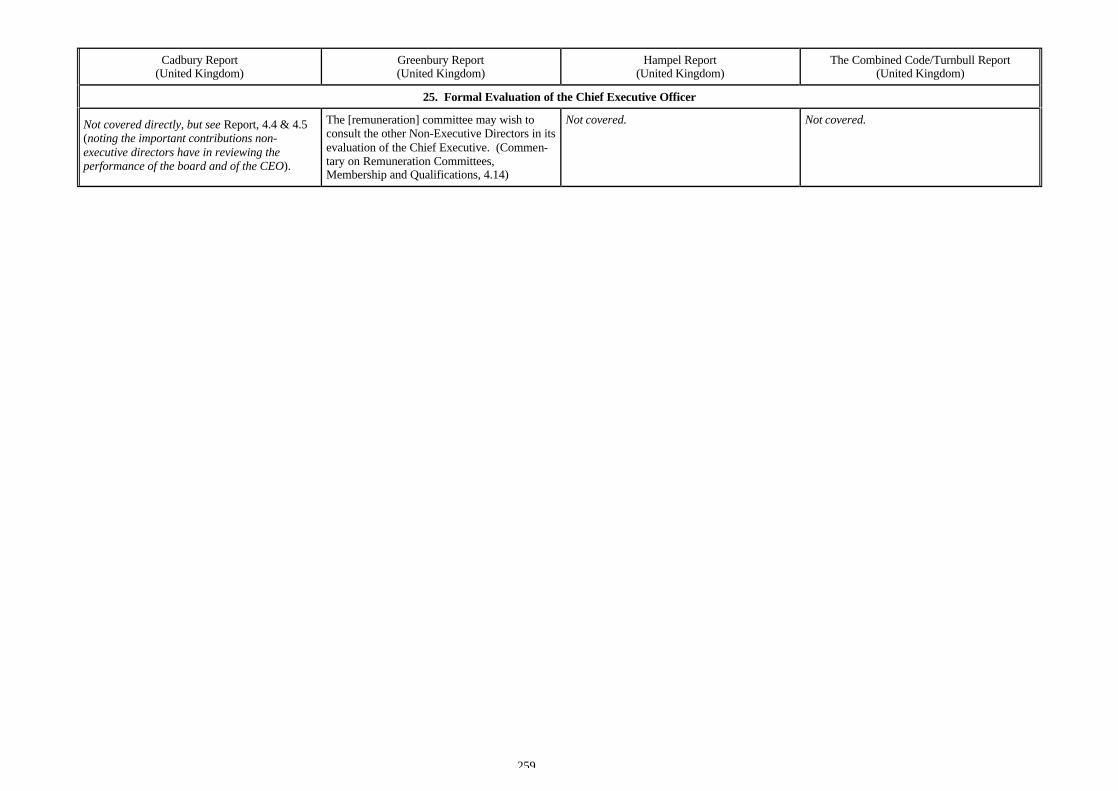

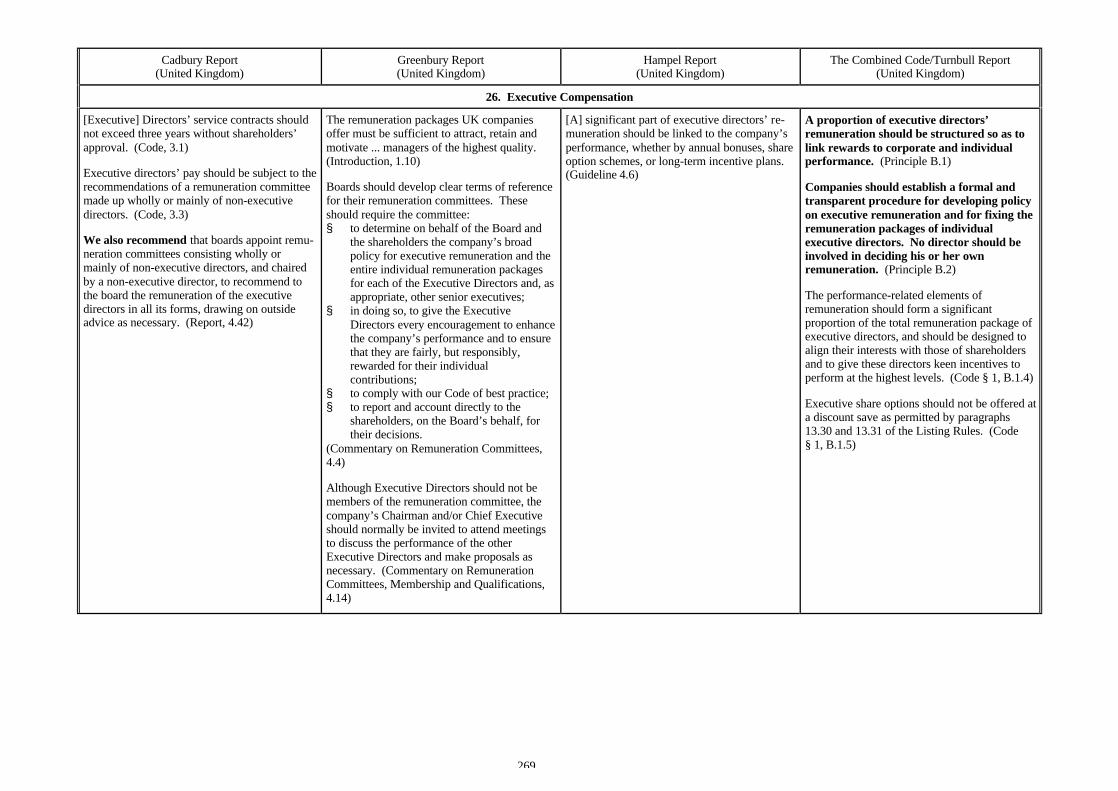

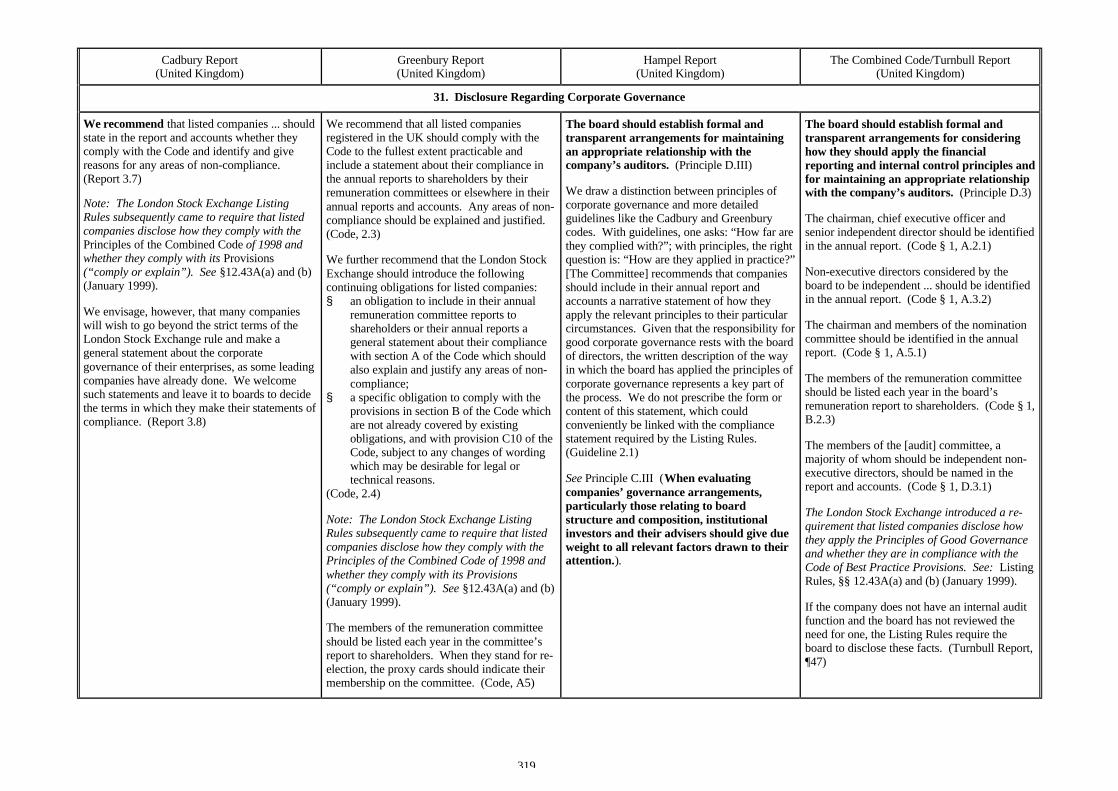

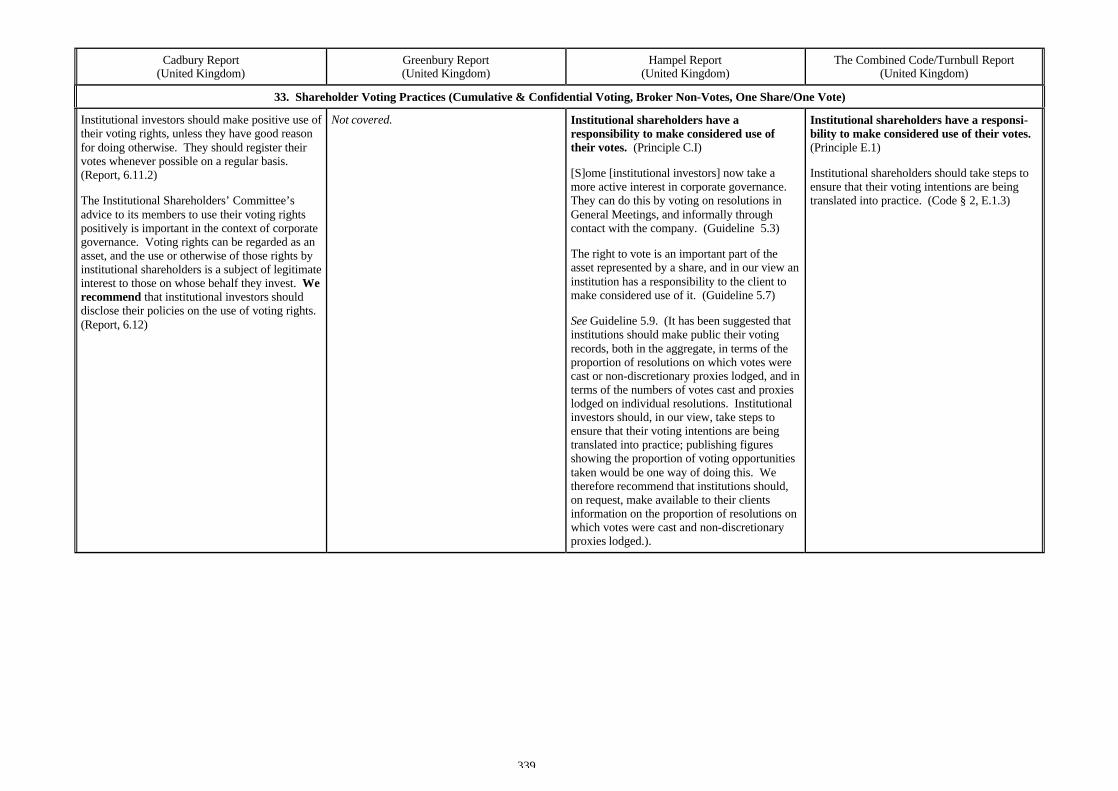

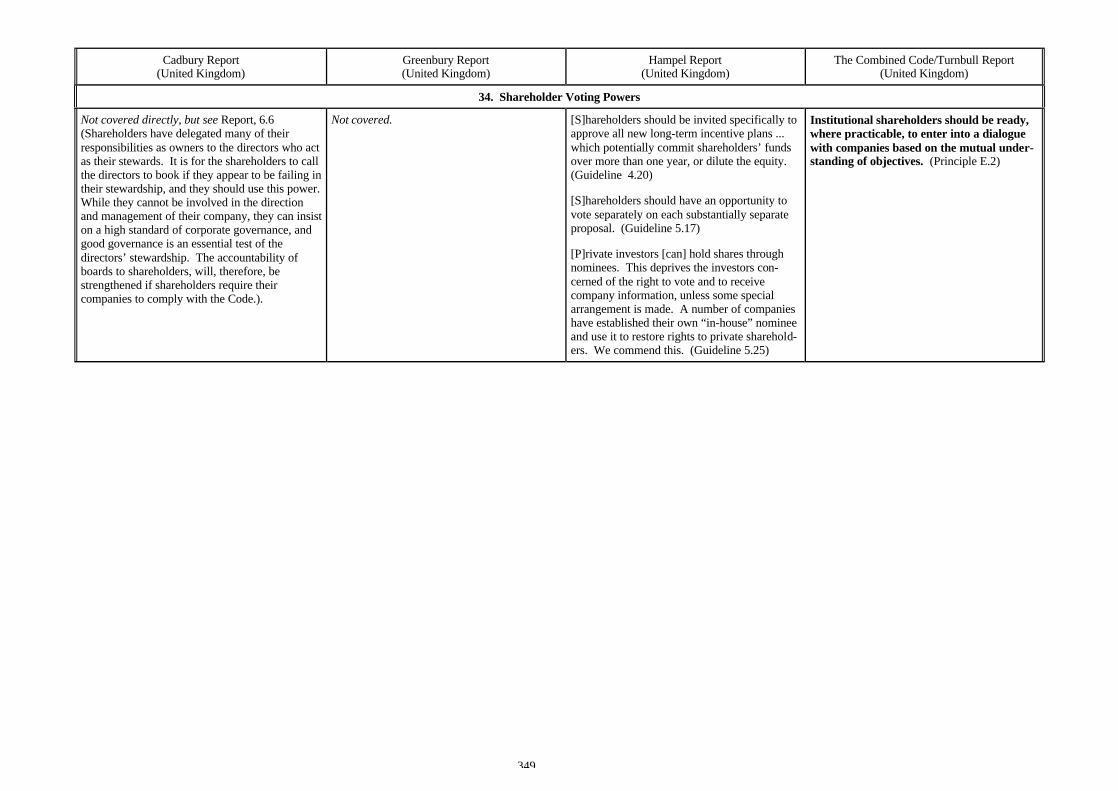

Cadbury Report(United Kingdom)

Greenbury Report(United Kingdom)

Hampel Report(United Kingdom)

The Combined Code/Turnbull Report(United Kingdom)

OVERVIEW

Code: REPORT OF THE COMMITTEE ON THEFINANCIAL ASPECTS OF CORPORATE GOV-ERNANCE (“Cadbury Report”) (December 1992,reissued 1996)

Issuing Body: Committee established by theFinancial Reporting Council and the LondonStock Exchange, a committee related to a stockexchange and a business, industry and/or aca-demic association

Legal Basis and Compliance: Disclosure (com-ply or explain)

Objective: Improve quality of board (supervi-sory) governance; Improve governance-relatedinformation available to equity markets

Scope: Listed companies; encouraged to allcompanies

Predominant Board Structure(listed companies): Unitary

Code: DIRECTORS’ REMUNERATION (July1995)

Issuing Body: Committee established in Janu-ary 1995 on the initiative of the Confederationof British Industry, a business, industry and/oracademic association or committee.

Legal Basis and Compliance: Disclosure(comply or explain)

Objective: Improve quality of board (supervi-sory) governance; improve quality ofgovernance-related information available toequity markets

Scope: Listed companies; encouraged to allcompanies

Predominant Board Structure(listed companies): Unitary

Code: FINAL REPORT (“Hampel Report”)(January 1998)

Issuing Body: Committee sponsored by theLondon Stock Exchange, the Confederation ofBritish Industry, the Institute of Directors, theConsultative Committee of Accountancy Bod-ies, the National Association of Pension Fundsand the Association of British Insurers –committee related to a stock exchange and abusiness, industry and/or academic association

Legal Basis and Compliance: Disclosure (inline with the Combined Code’s provisions)

Objective: Improve quality of board (supervi-sory) governance; Improve quality ofgovernance-related information available toequity markets

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

Codes:A) THE COMBINED CODE: PRINCIPLES OF GOODGOVERNANCE AND CODE OF BEST PRACTICE(July 1998)B) INTERNAL CONTROL: GUIDANCE FORDIRECTORS ON THE COMBINED CODE(“Turnbull Report”) (September 1999)

Issuing Bodies:A) Committee on Corporate Governance, acommittee related to a stock exchange and abusiness, industry and/or academic associationB) Institute of Chartered Accountants inEngland and Wales (“ICAEW”), a committeerelated to a stock exchange and business, in-dustry and/or academic associationLegal Basis and Compliance:A) Disclosure (comply or explain)B) Voluntary (advice on compliance withCombined Code)Objective:A) Improve quality of board (supervisory)governance; Improve quality of governance-related information available to equity marketsB) Improve quality of governance-related in-formation available to equity markets

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

10

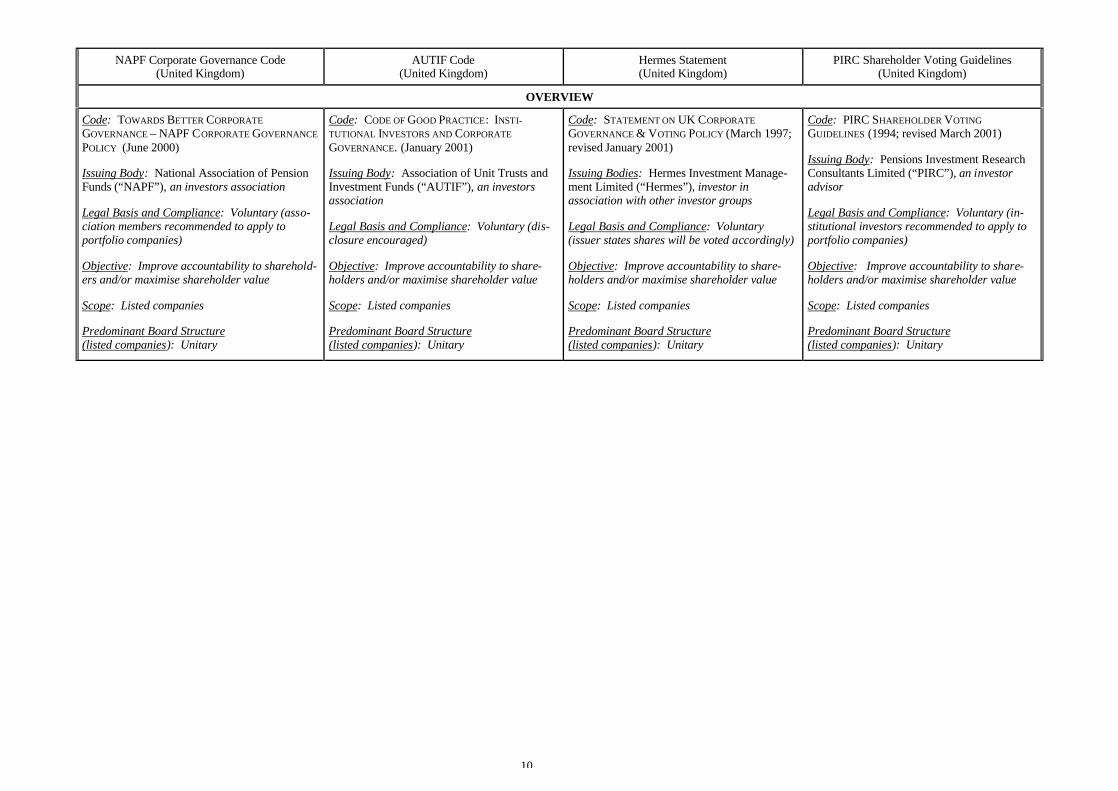

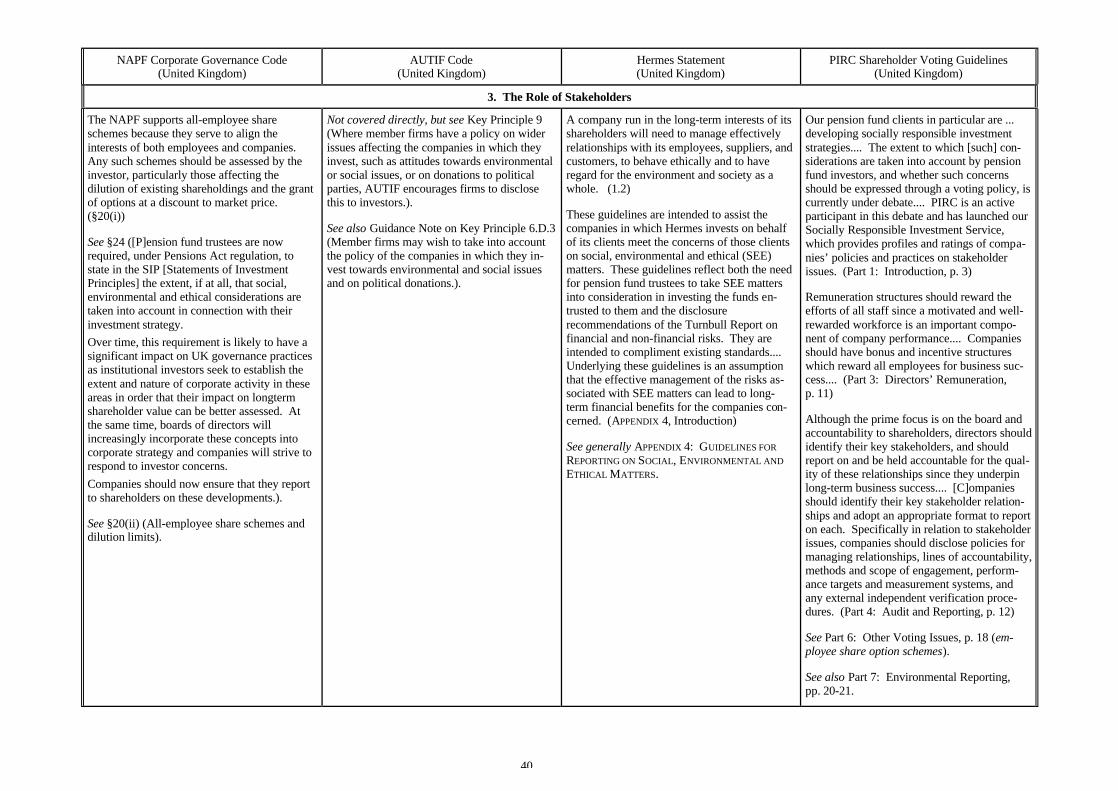

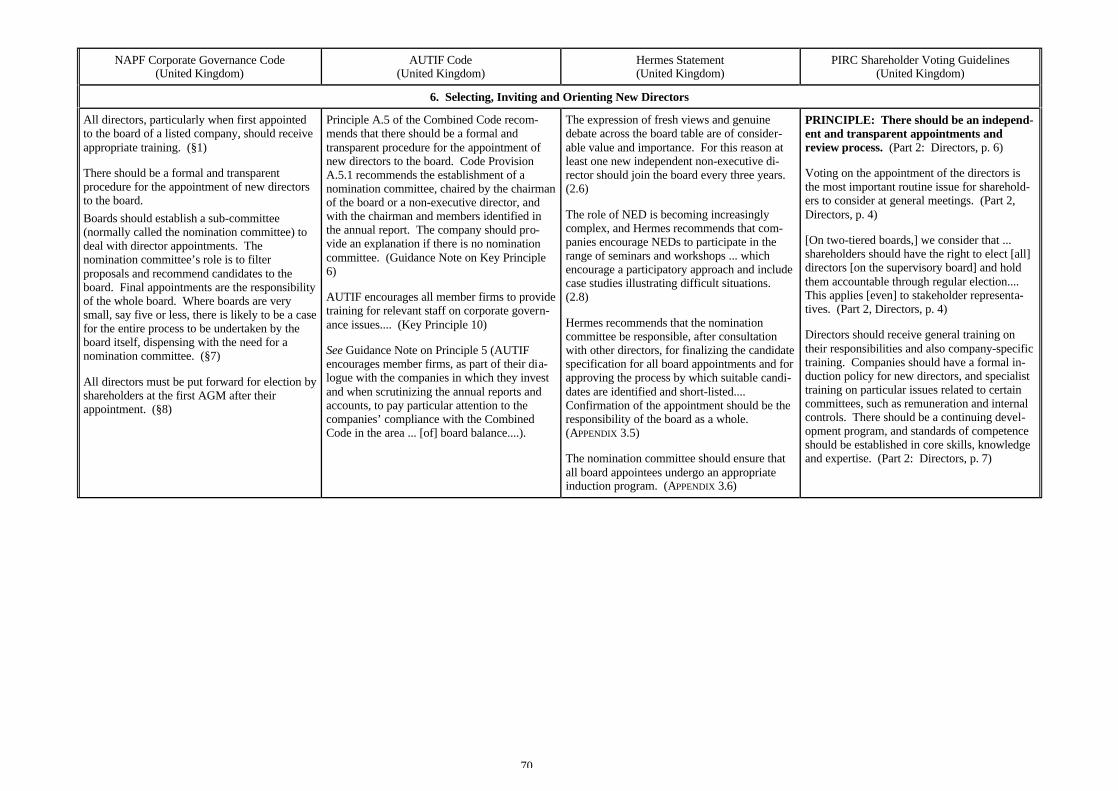

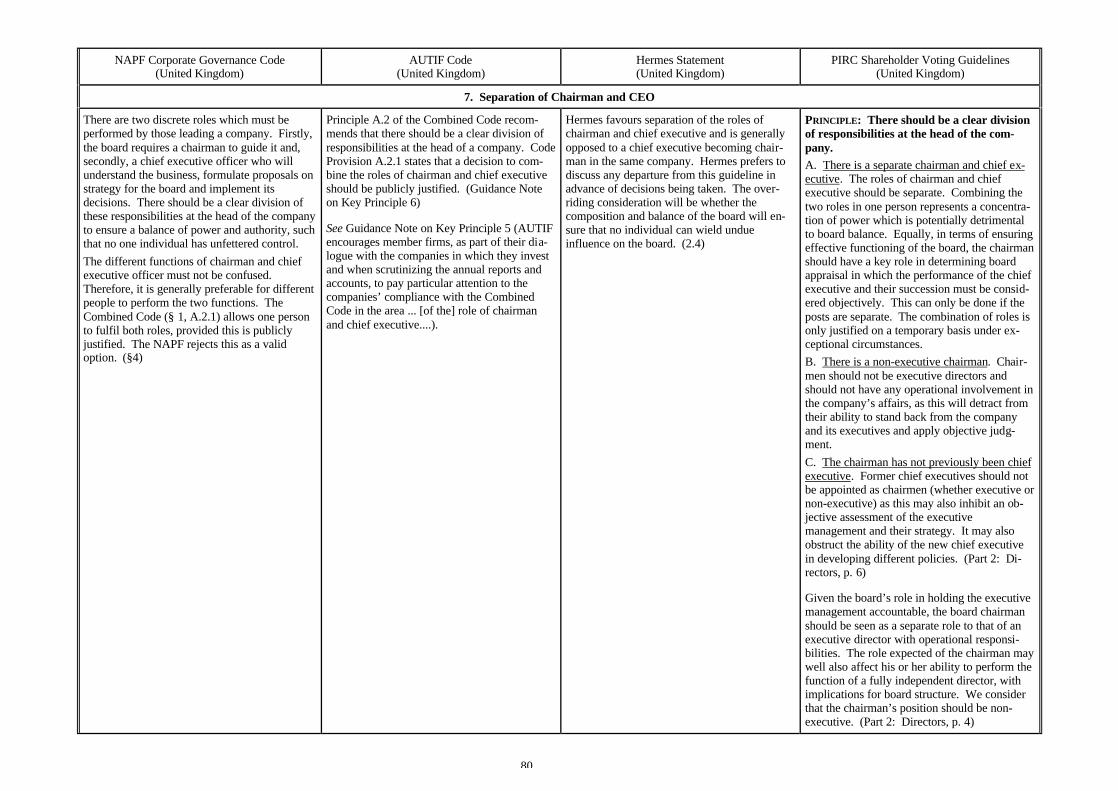

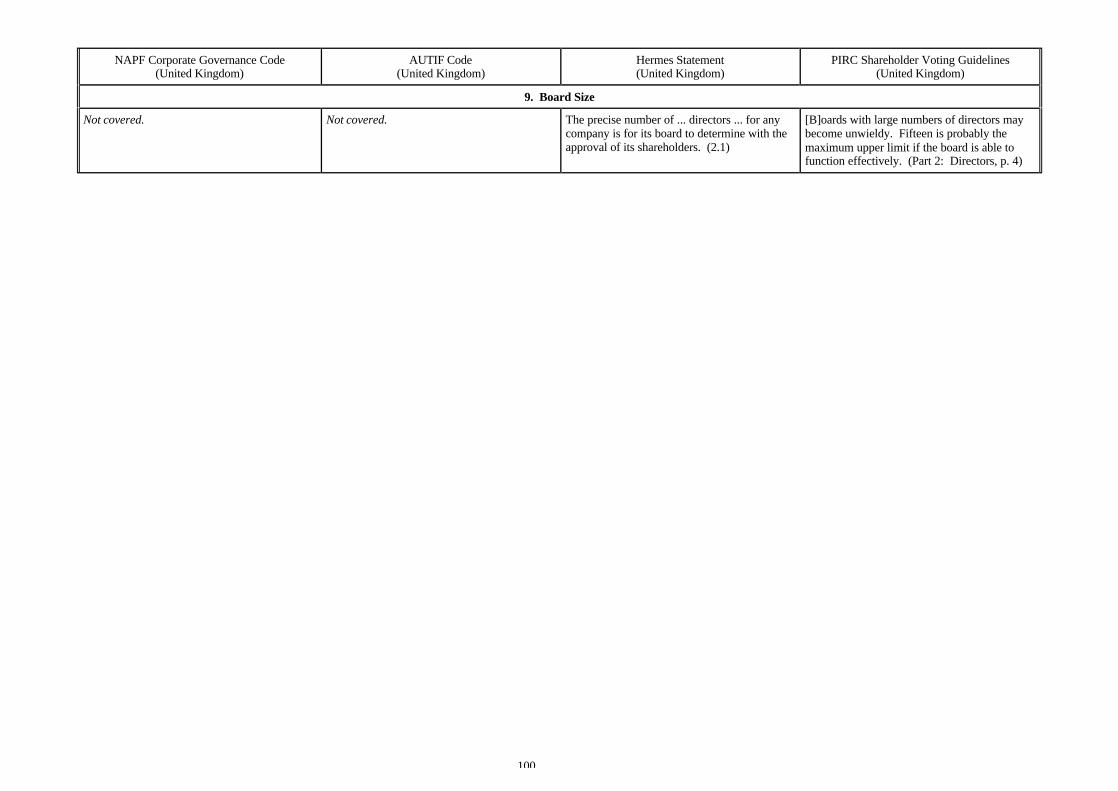

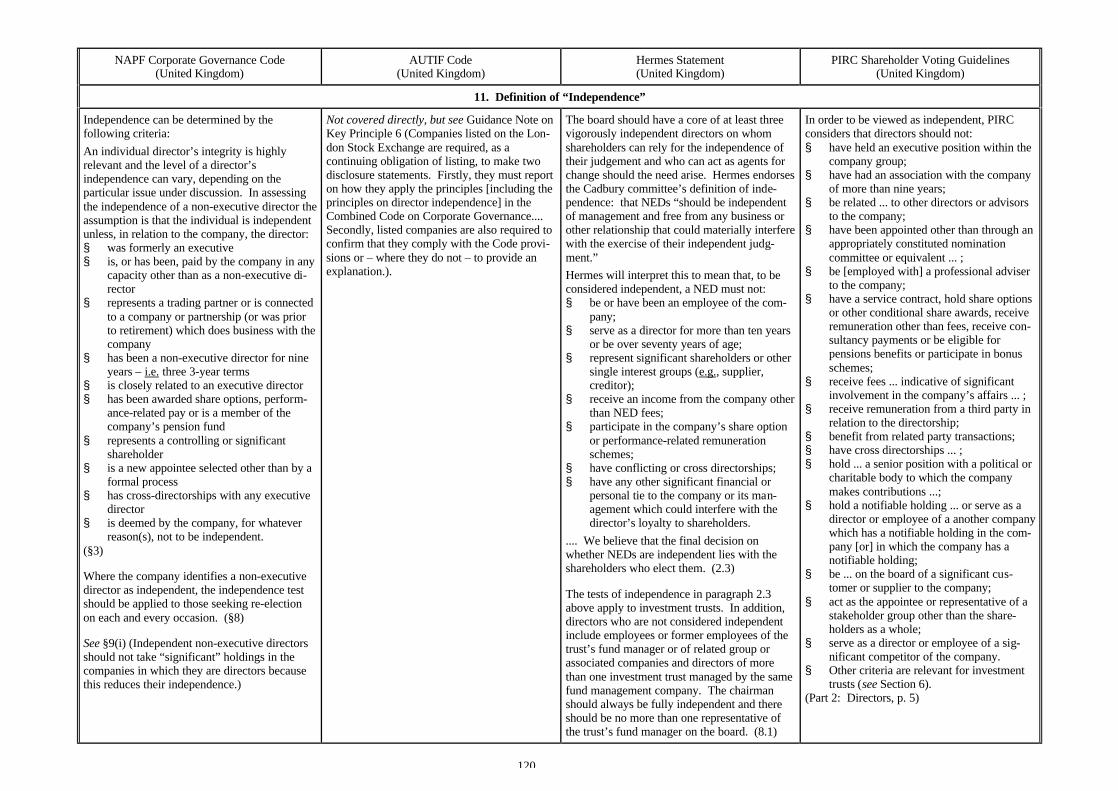

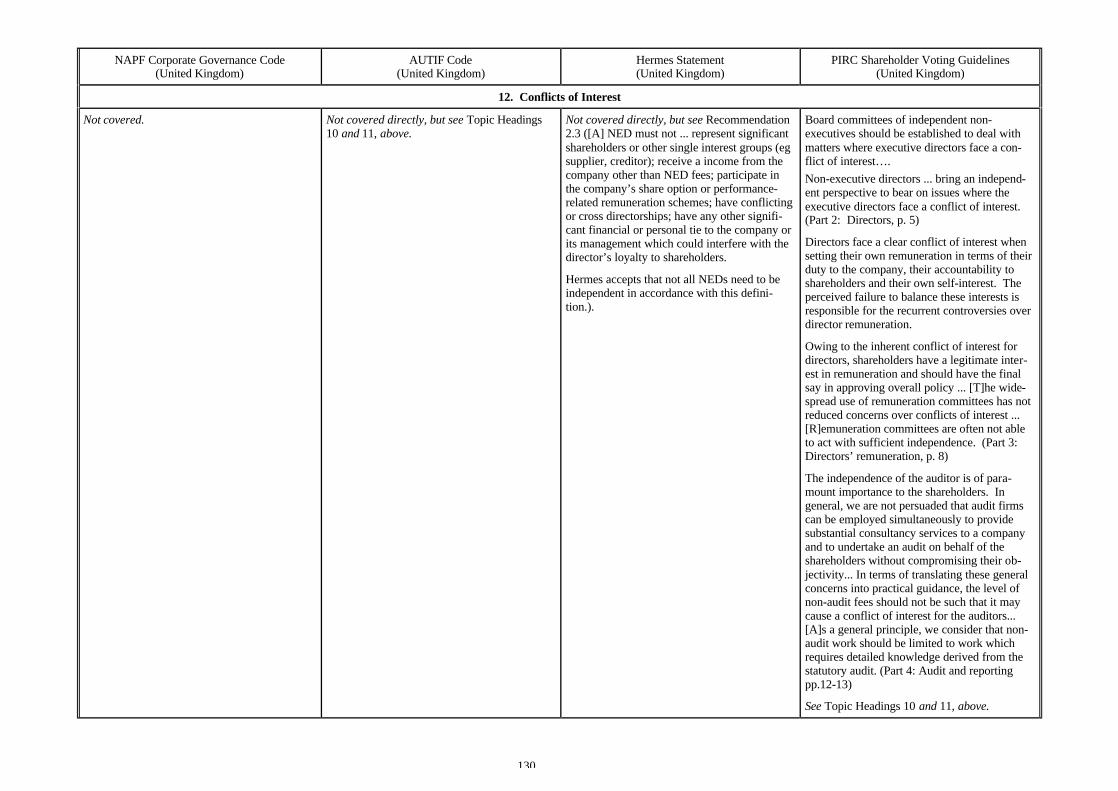

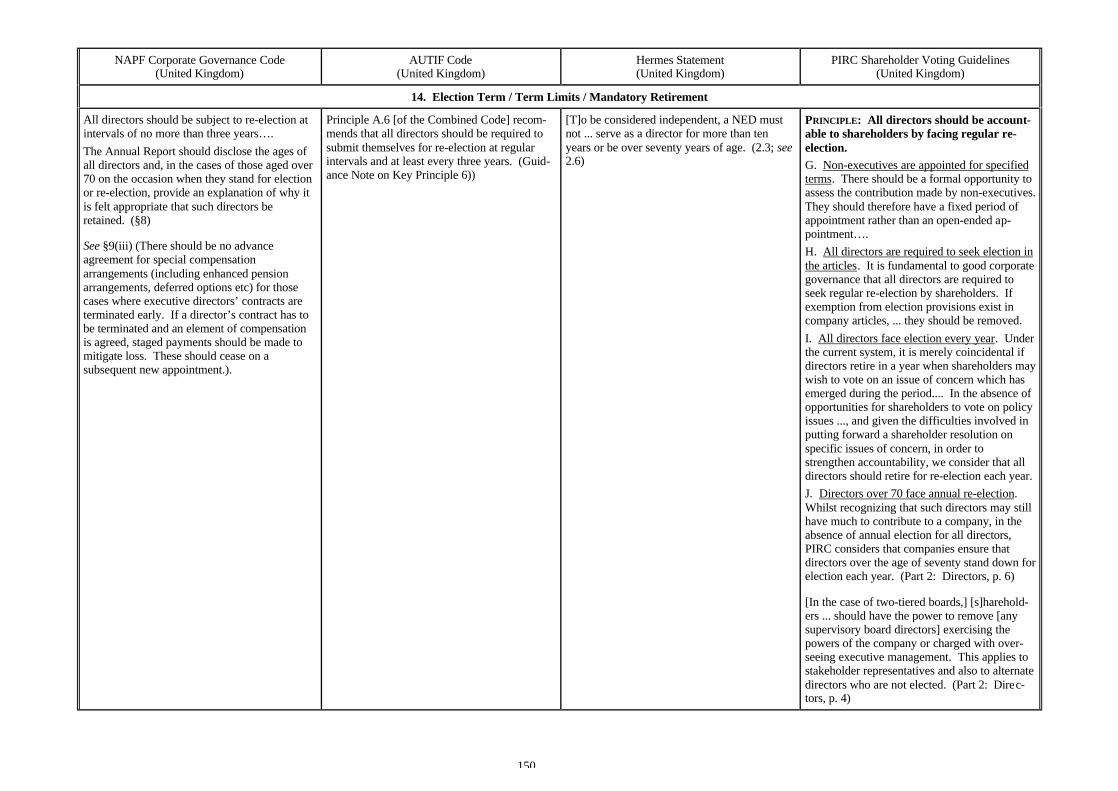

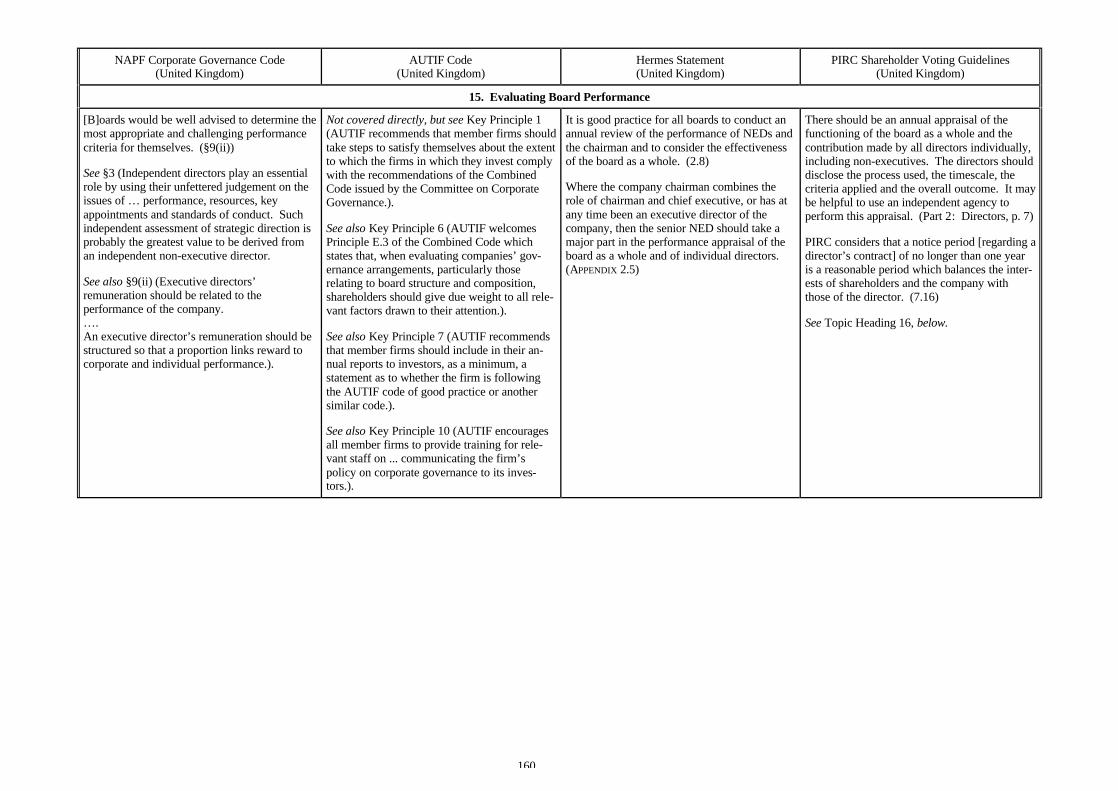

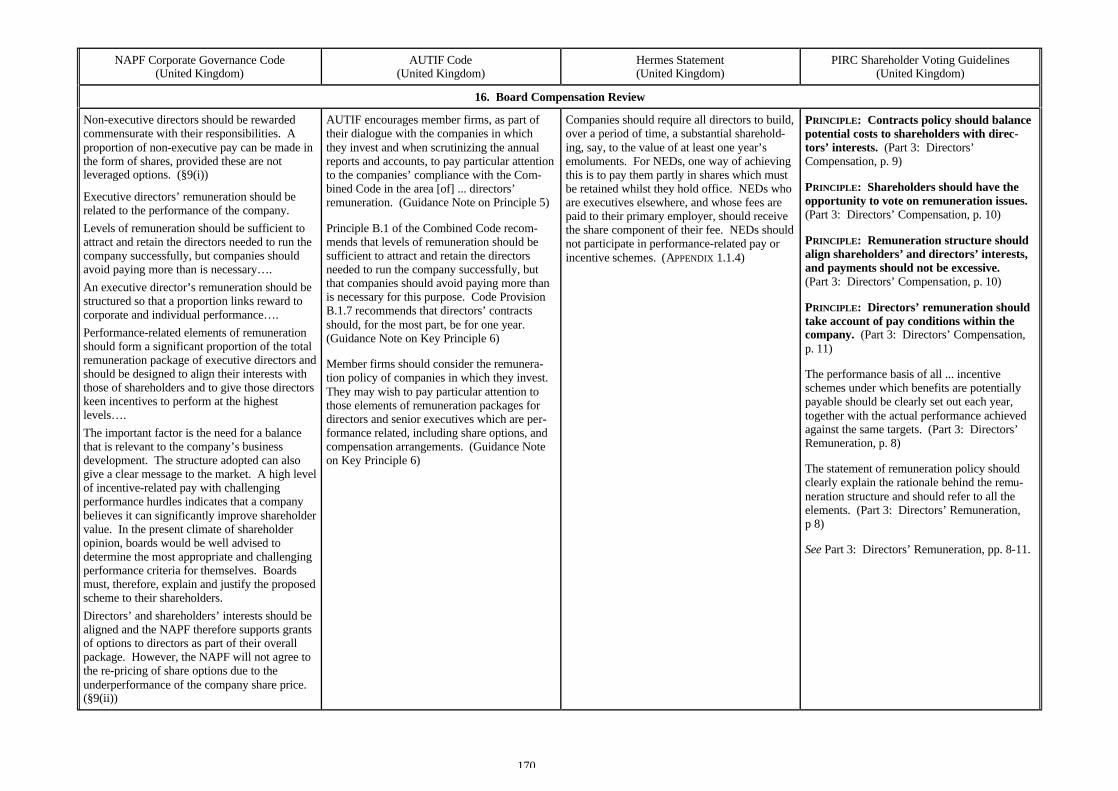

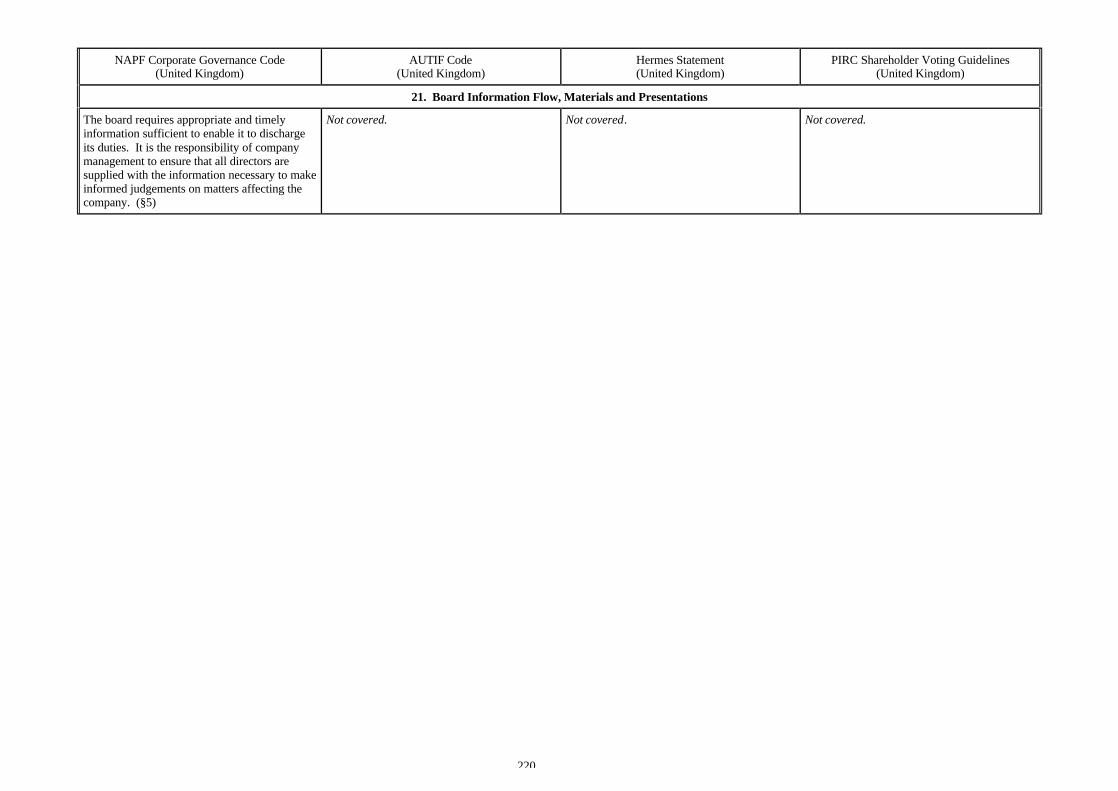

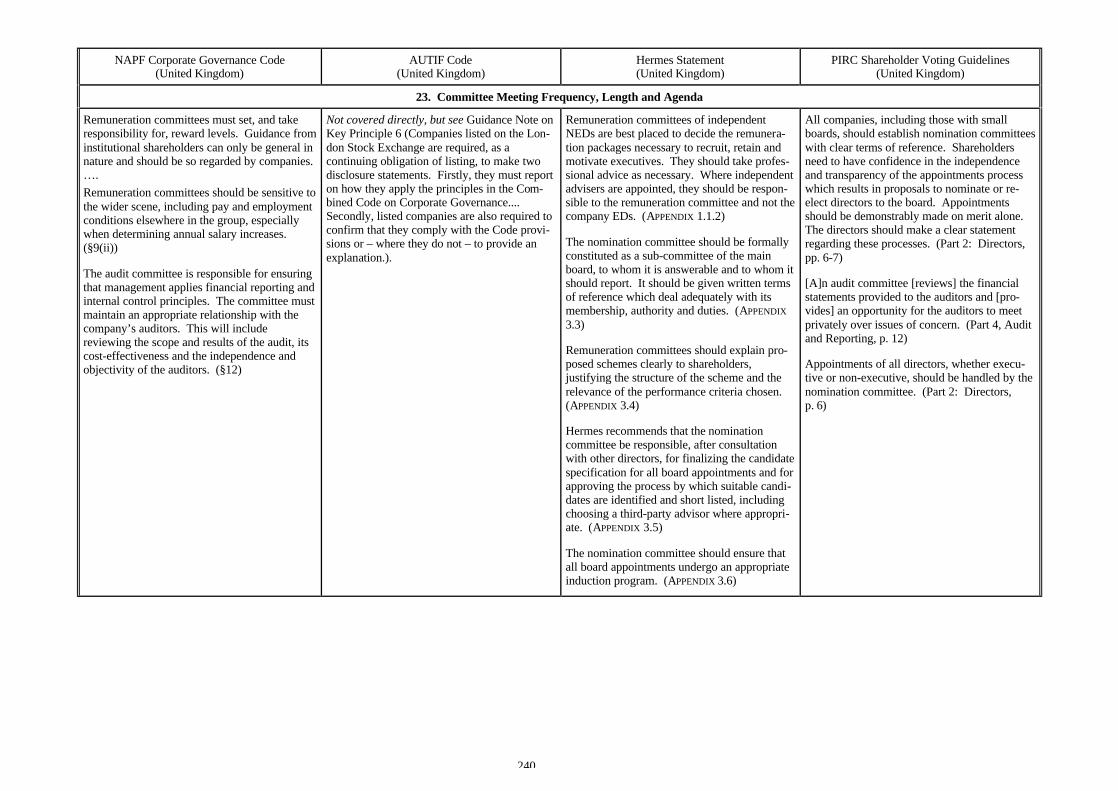

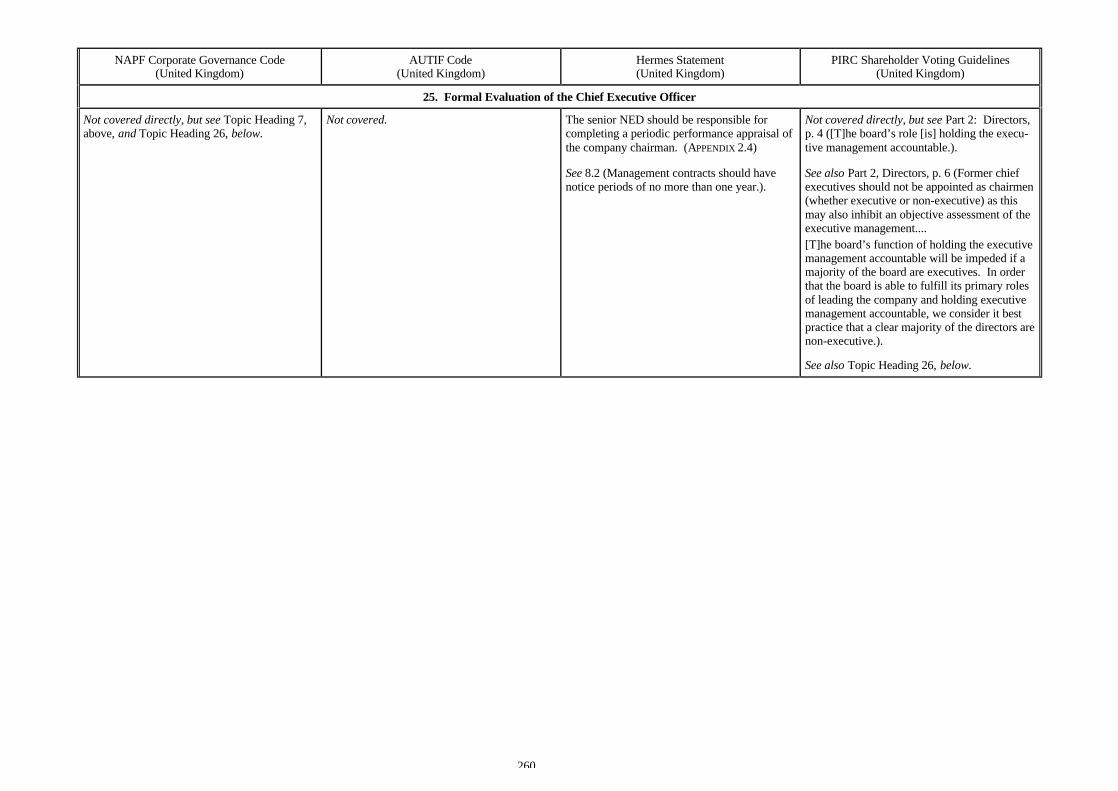

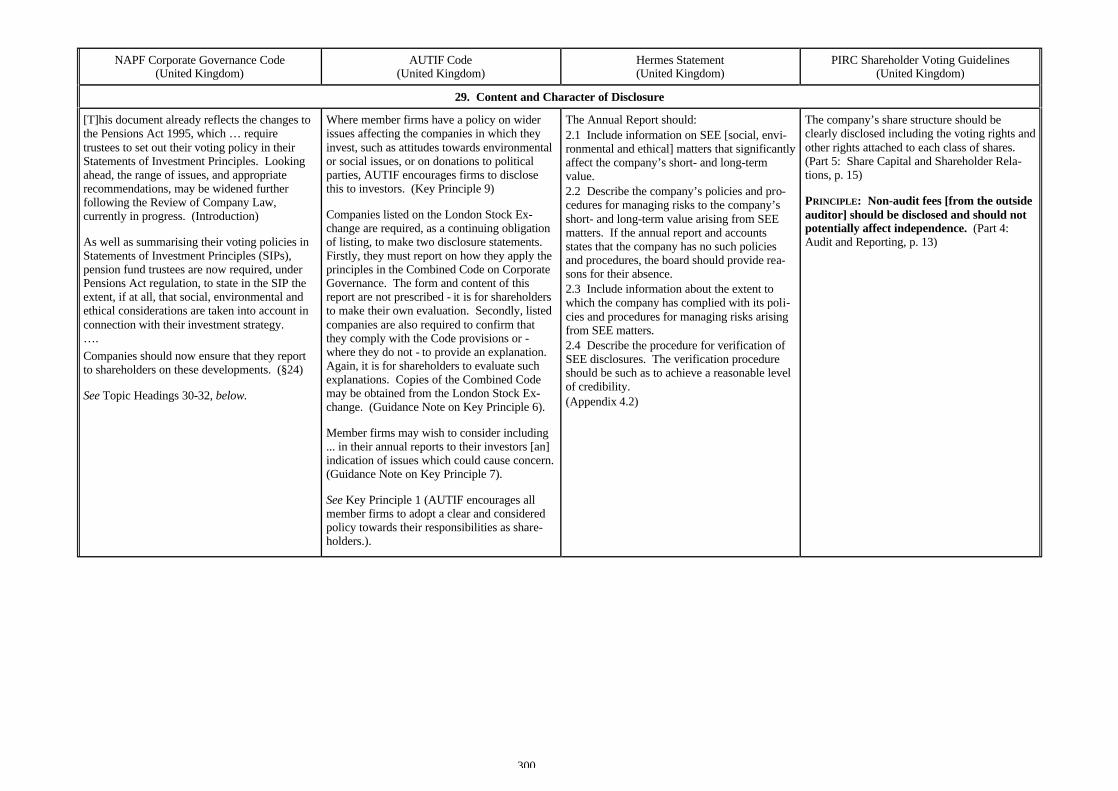

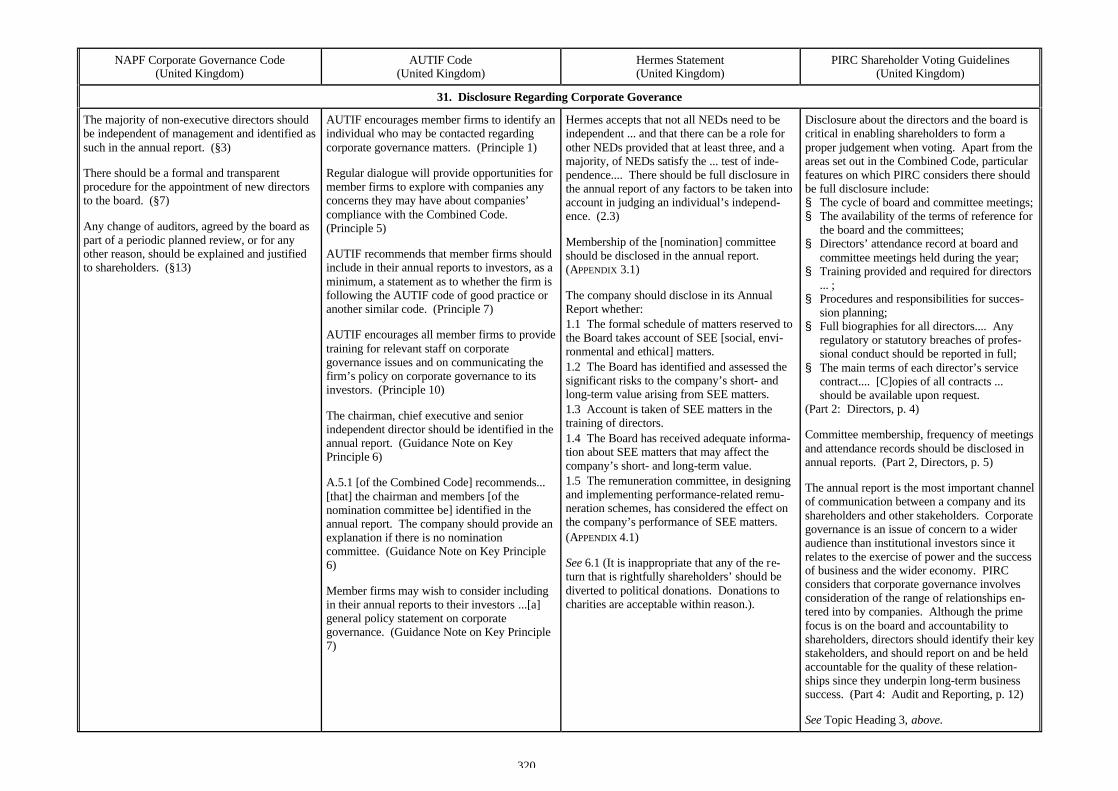

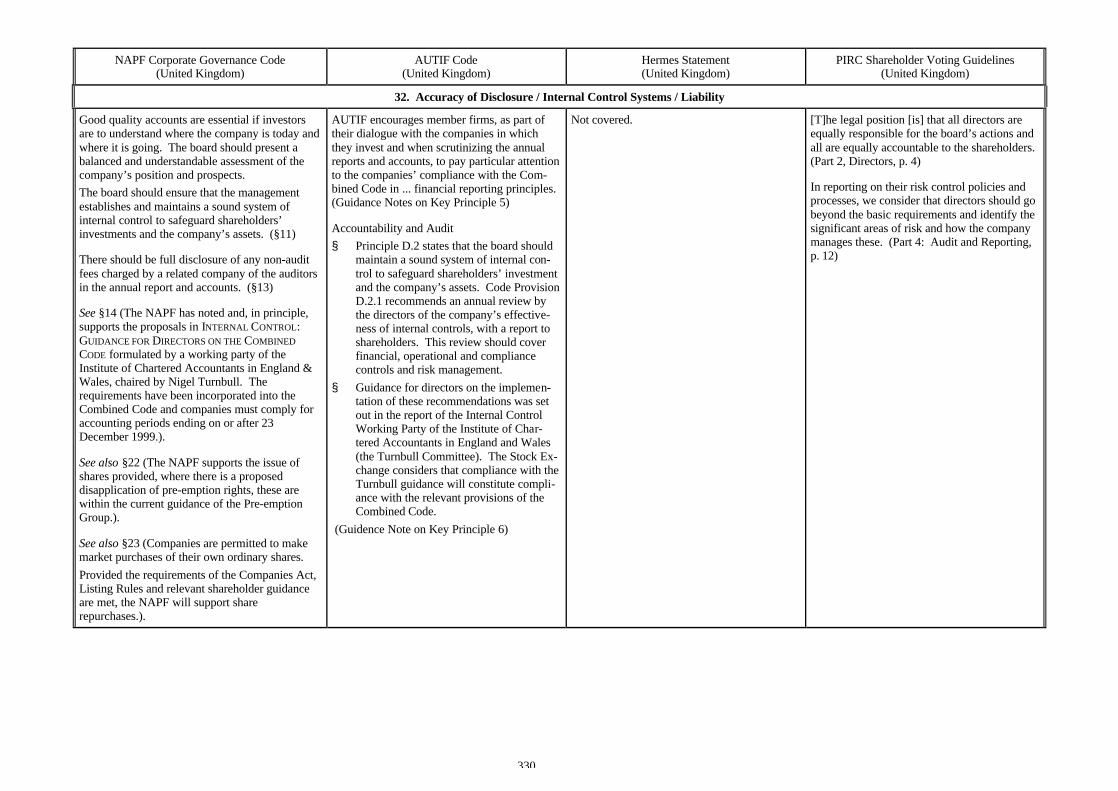

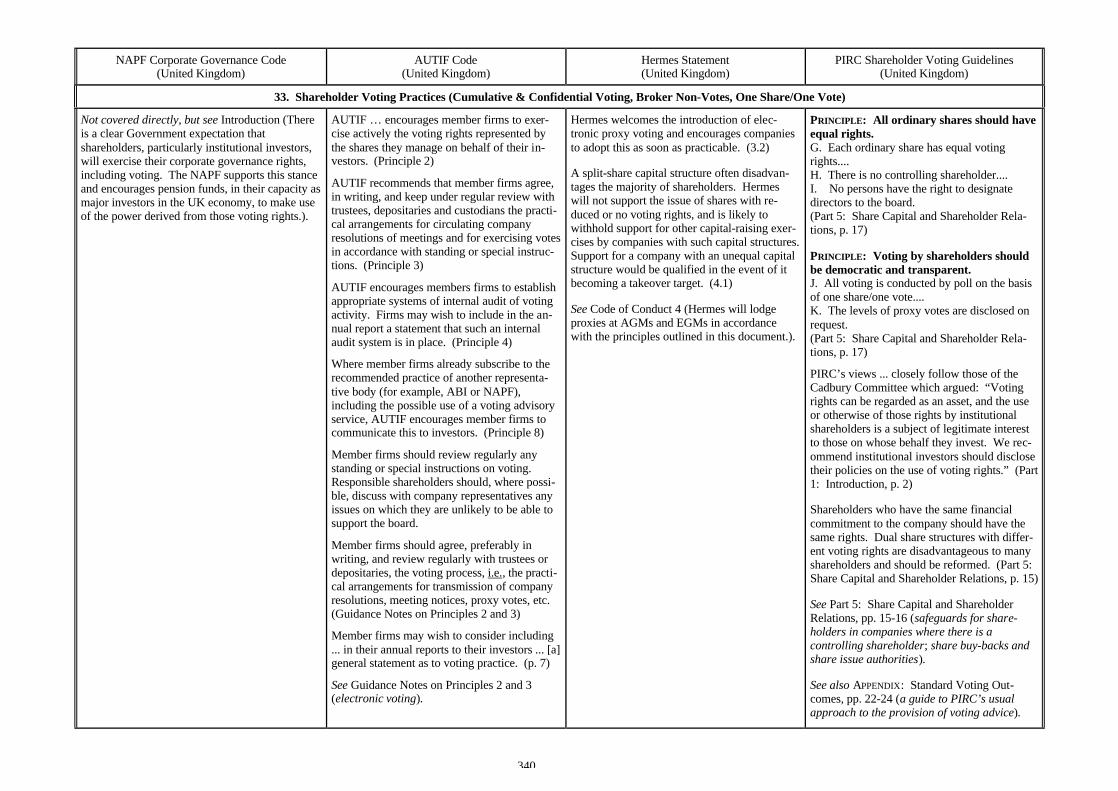

NAPF Corporate Governance Code(United Kingdom)

AUTIF Code(United Kingdom)

Hermes Statement(United Kingdom)

PIRC Shareholder Voting Guidelines(United Kingdom)

OVERVIEW

Code: TOWARDS BETTER CORPORATEGOVERNANCE – NAPF CORPORATE GOVERNANCEPOLICY (June 2000)

Issuing Body: National Association of PensionFunds (“NAPF”), an investors association

Legal Basis and Compliance: Voluntary (asso-ciation members recommended to apply toportfolio companies)

Objective: Improve accountability to sharehold-ers and/or maximise shareholder value

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

Code: CODE OF GOOD PRACTICE: INSTI-TUTIONAL INVESTORS AND CORPORATEGOVERNANCE. (January 2001)

Issuing Body: Association of Unit Trusts andInvestment Funds (“AUTIF”), an investorsassociation

Legal Basis and Compliance: Voluntary (dis-closure encouraged)

Objective: Improve accountability to share-holders and/or maximise shareholder value

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

Code: STATEMENT ON UK CORPORATEGOVERNANCE & VOTING POLICY (March 1997;revised January 2001)

Issuing Bodies: Hermes Investment Manage-ment Limited (“Hermes”), investor inassociation with other investor groups

Legal Basis and Compliance: Voluntary(issuer states shares will be voted accordingly)

Objective: Improve accountability to share-holders and/or maximise shareholder value

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

Code: PIRC SHAREHOLDER VOTINGGUIDELINES (1994; revised March 2001)

Issuing Body: Pensions Investment ResearchConsultants Limited (“PIRC”), an investoradvisor

Legal Basis and Compliance: Voluntary (in-stitutional investors recommended to apply toportfolio companies)

Objective: Improve accountability to share-holders and/or maximise shareholder value

Scope: Listed companies

Predominant Board Structure(listed companies): Unitary

11

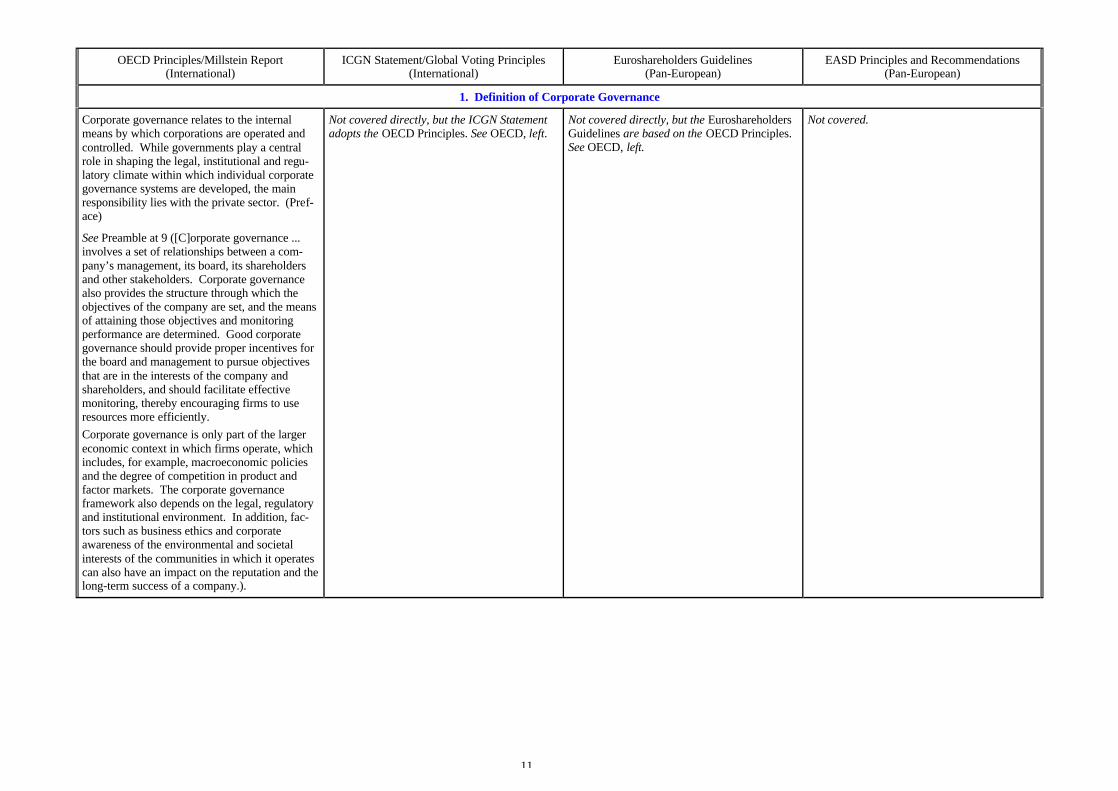

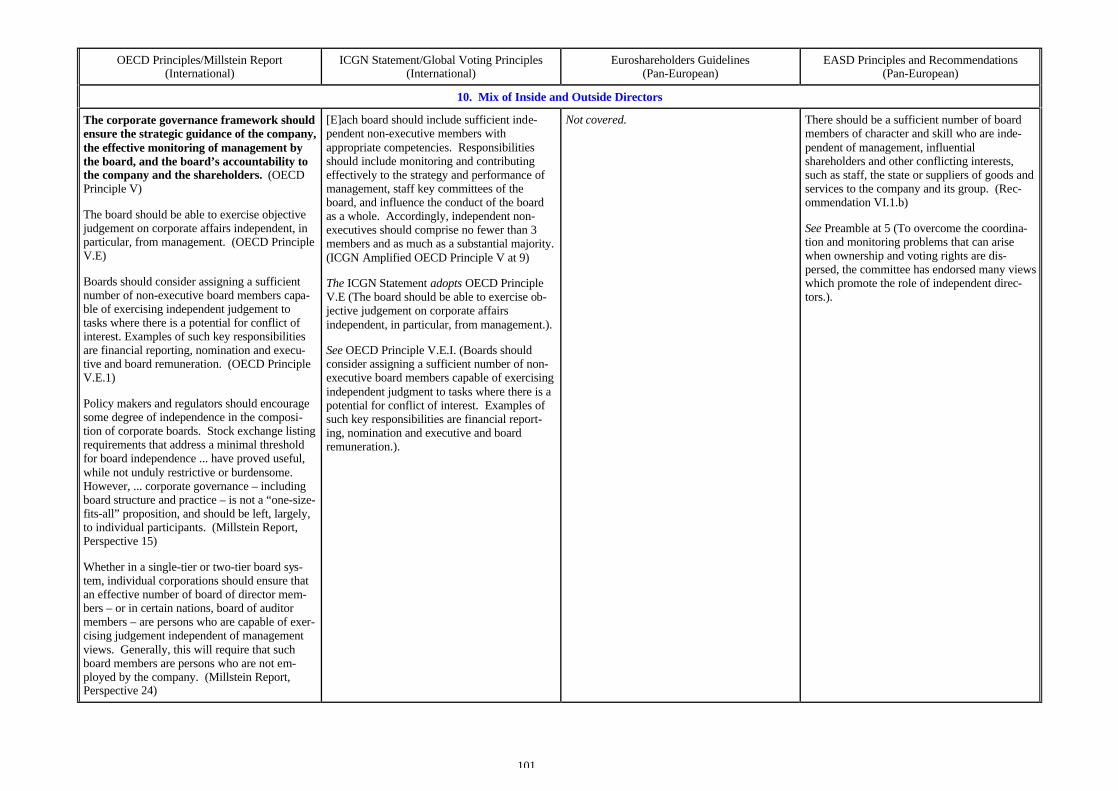

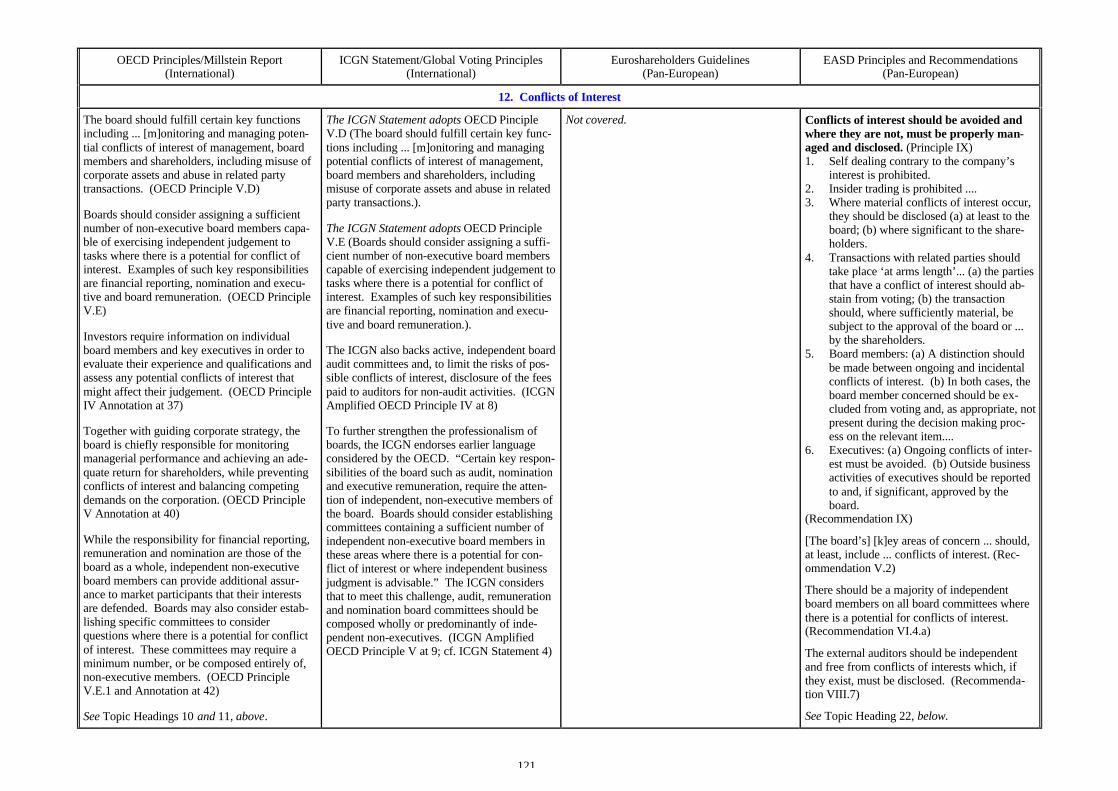

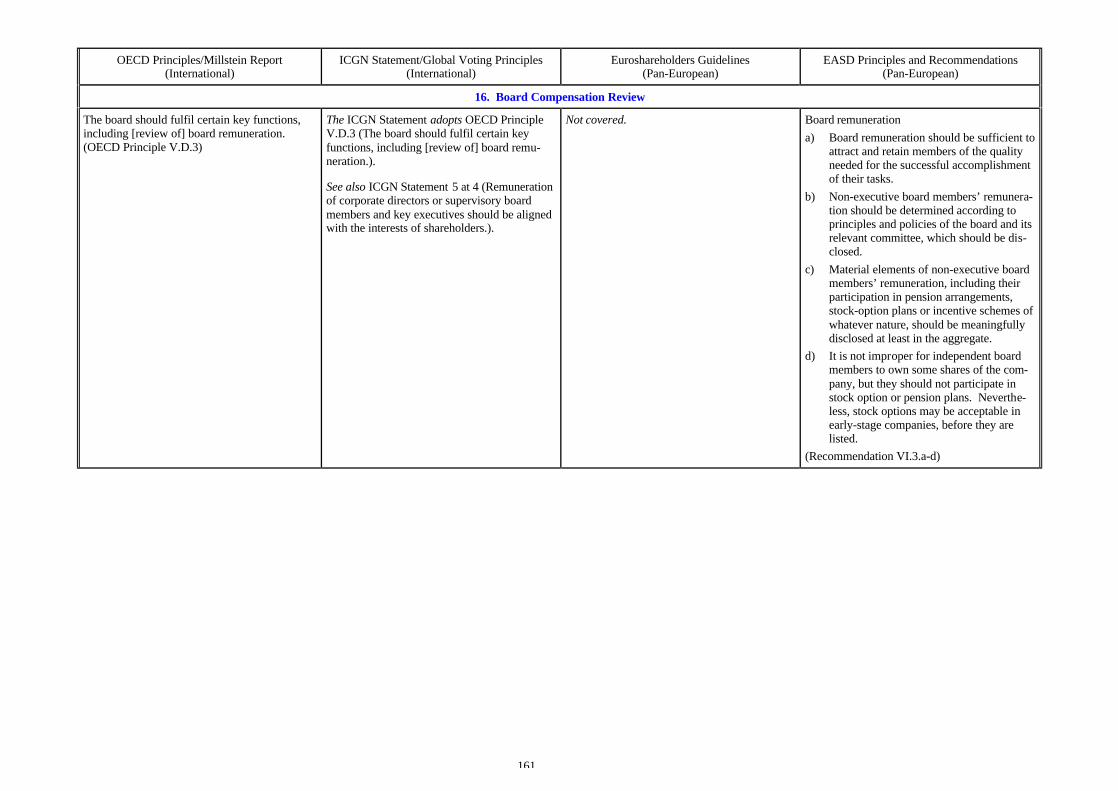

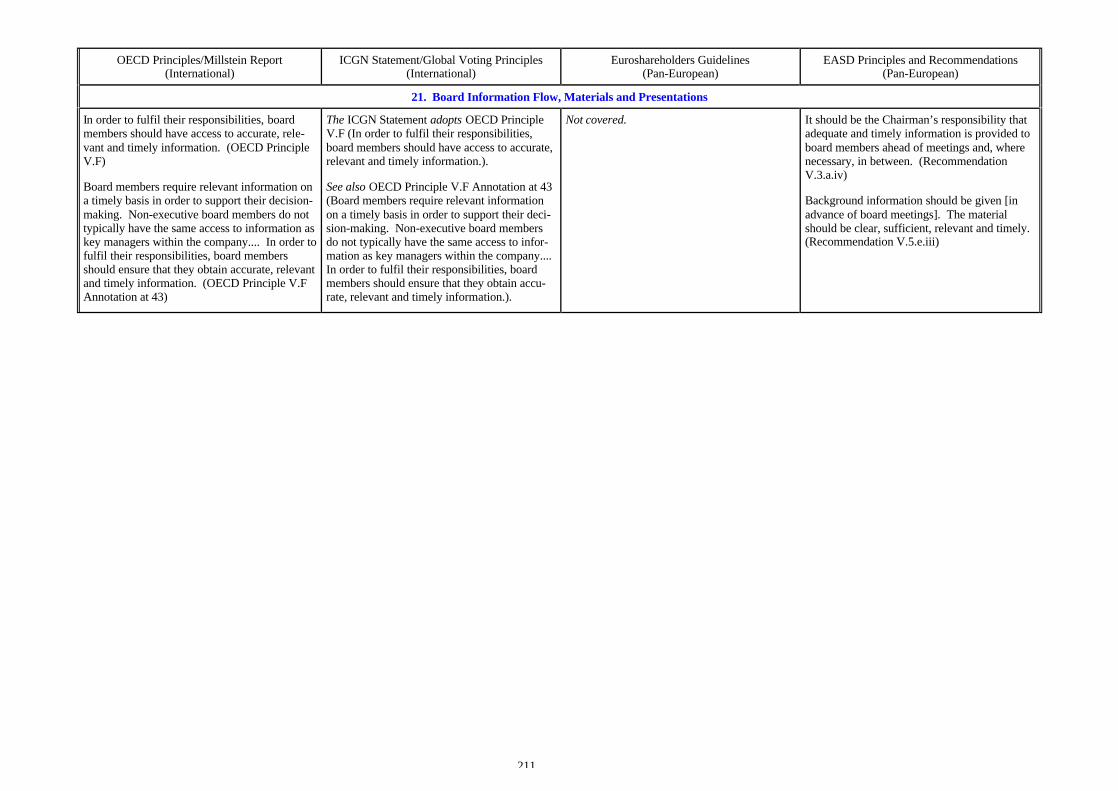

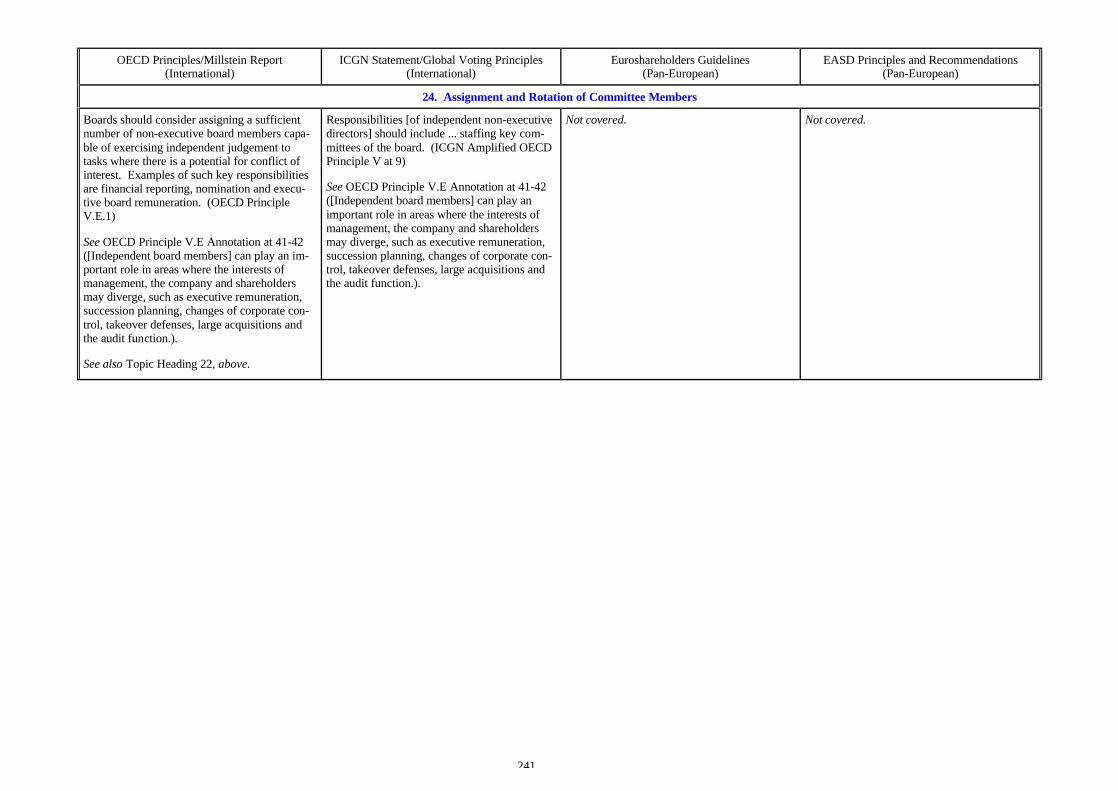

OECD Principles/Millstein Report(International)

ICGN Statement/Global Voting Principles(International)

Euroshareholders Guidelines(Pan-European)

EASD Principles and Recommendations(Pan-European)

1. Definition of Corporate Governance

Corporate governance relates to the internalmeans by which corporations are operated andcontrolled. While governments play a centralrole in shaping the legal, institutional and regu-latory climate within which individual corporategovernance systems are developed, the mainresponsibility lies with the private sector. (Pref-ace)

See Preamble at 9 ([C]orporate governance ...involves a set of relationships between a com-pany’s management, its board, its shareholdersand other stakeholders. Corporate governancealso provides the structure through which theobjectives of the company are set, and the meansof attaining those objectives and monitoringperformance are determined. Good corporategovernance should provide proper incentives forthe board and management to pursue objectivesthat are in the interests of the company andshareholders, and should facilitate effectivemonitoring, thereby encouraging firms to useresources more efficiently.Corporate governance is only part of the largereconomic context in which firms operate, whichincludes, for example, macroeconomic policiesand the degree of competition in product andfactor markets. The corporate governanceframework also depends on the legal, regulatoryand institutional environment. In addition, fac-tors such as business ethics and corporateawareness of the environmental and societalinterests of the communities in which it operatescan also have an impact on the reputation and thelong-term success of a company.).

Not covered directly, but the ICGN Statementadopts the OECD Principles. See OECD, left.

Not covered directly, but the EuroshareholdersGuidelines are based on the OECD Principles.See OECD, left.

Not covered.

12

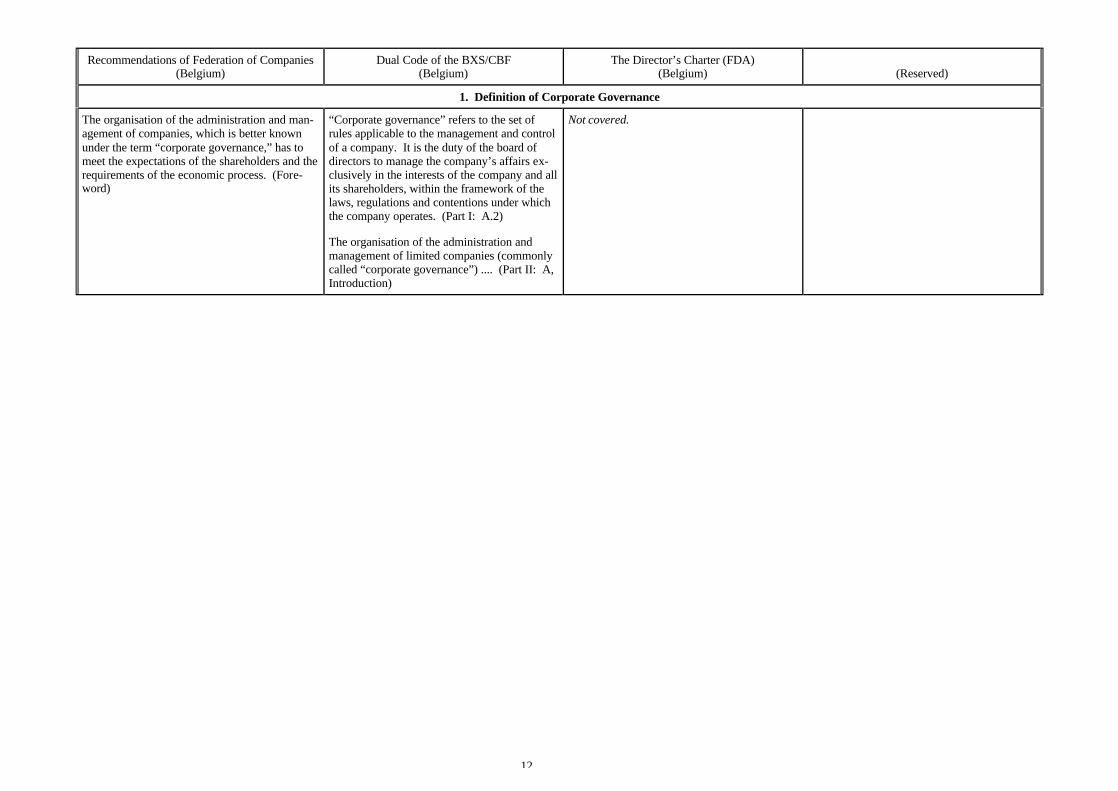

Recommendations of Federation of Companies(Belgium)

Dual Code of the BXS/CBF(Belgium)

The Director’s Charter (FDA)(Belgium) (Reserved)

1. Definition of Corporate Governance

The organisation of the administration and man-agement of companies, which is better knownunder the term “corporate governance,” has tomeet the expectations of the shareholders and therequirements of the economic process. (Fore-word)

“Corporate governance” refers to the set ofrules applicable to the management and controlof a company. It is the duty of the board ofdirectors to manage the company’s affairs ex-clusively in the interests of the company and allits shareholders, within the framework of thelaws, regulations and contentions under whichthe company operates. (Part I: A.2)

The organisation of the administration andmanagement of limited companies (commonlycalled “corporate governance”) .... (Part II: A,Introduction)

Not covered.

13

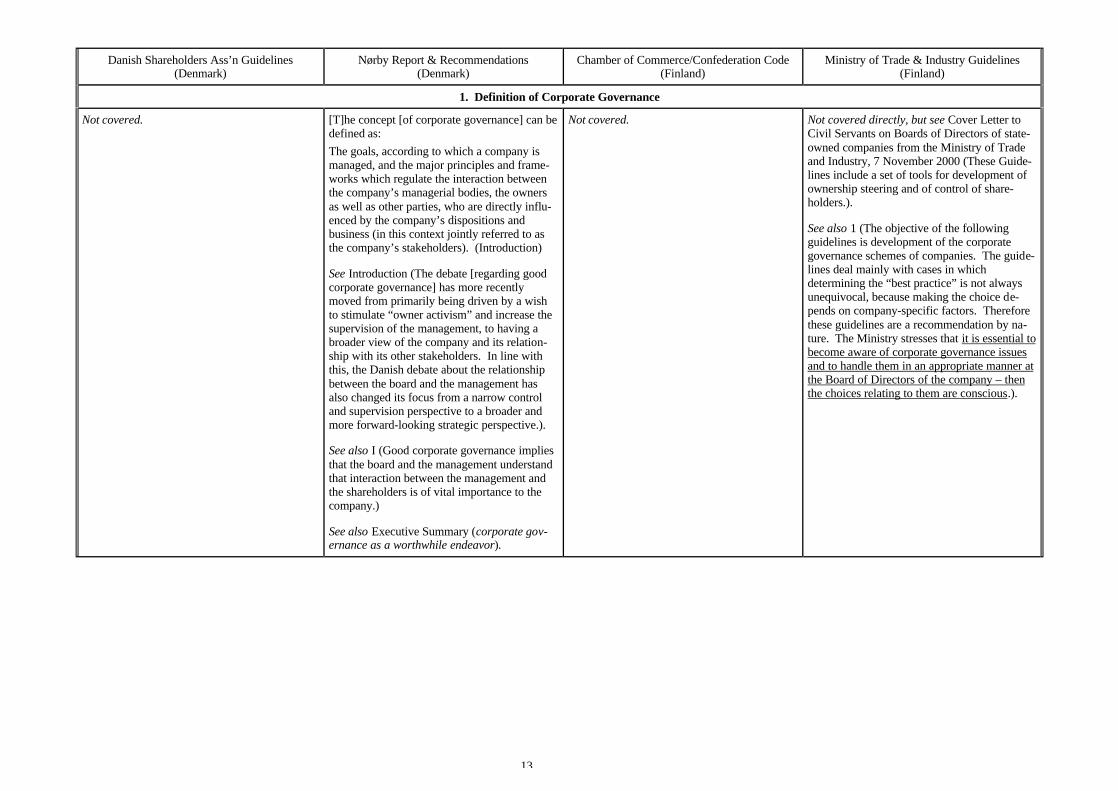

Danish Shareholders Ass’n Guidelines(Denmark)

Nørby Report & Recommendations(Denmark)

Chamber of Commerce/Confederation Code(Finland)

Ministry of Trade & Industry Guidelines(Finland)

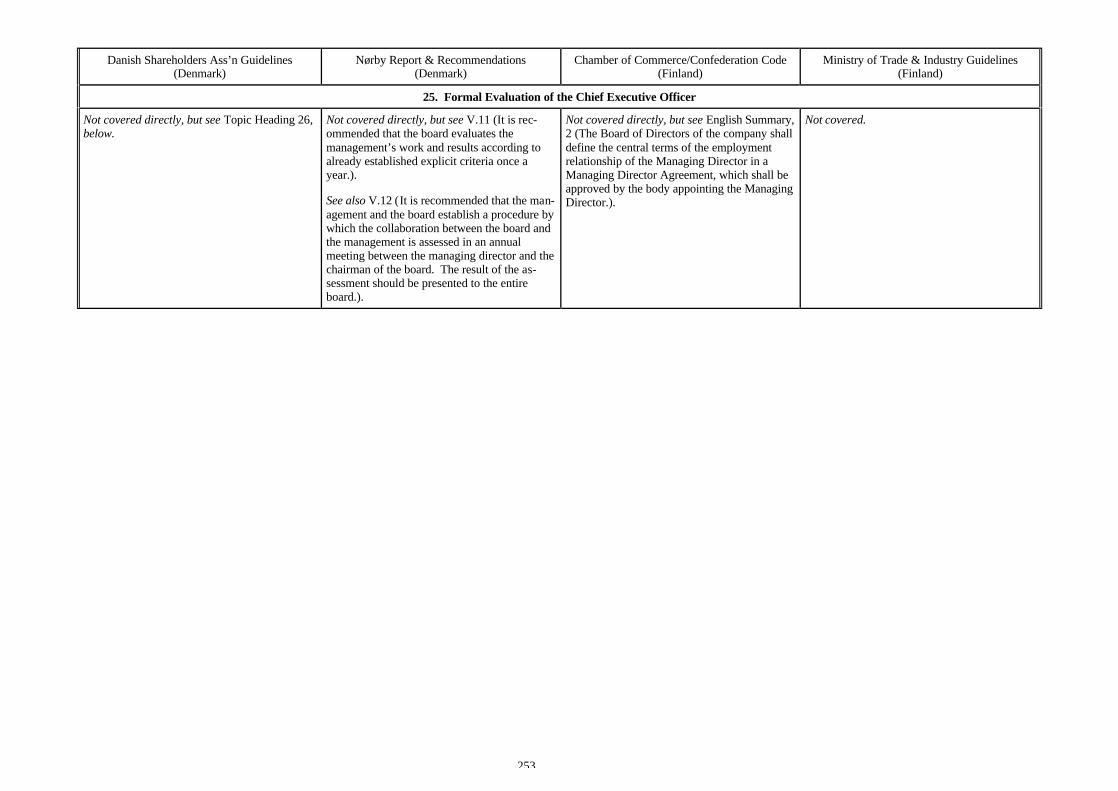

1. Definition of Corporate Governance

Not covered. [T]he concept [of corporate governance] can bedefined as:The goals, according to which a company ismanaged, and the major principles and frame-works which regulate the interaction betweenthe company’s managerial bodies, the ownersas well as other parties, who are directly influ-enced by the company’s dispositions andbusiness (in this context jointly referred to asthe company’s stakeholders). (Introduction)

See Introduction (The debate [regarding goodcorporate governance] has more recentlymoved from primarily being driven by a wishto stimulate “owner activism” and increase thesupervision of the management, to having abroader view of the company and its relation-ship with its other stakeholders. In line withthis, the Danish debate about the relationshipbetween the board and the management hasalso changed its focus from a narrow controland supervision perspective to a broader andmore forward-looking strategic perspective.).

See also I (Good corporate governance impliesthat the board and the management understandthat interaction between the management andthe shareholders is of vital importance to thecompany.)

See also Executive Summary (corporate gov-ernance as a worthwhile endeavor).

Not covered. Not covered directly, but see Cover Letter toCivil Servants on Boards of Directors of state-owned companies from the Ministry of Tradeand Industry, 7 November 2000 (These Guide-lines include a set of tools for development ofownership steering and of control of share-holders.).

See also 1 (The objective of the followingguidelines is development of the corporategovernance schemes of companies. The guide-lines deal mainly with cases in whichdetermining the “best practice” is not alwaysunequivocal, because making the choice de-pends on company-specific factors. Thereforethese guidelines are a recommendation by na-ture. The Ministry stresses that it is essential tobecome aware of corporate governance issuesand to handle them in an appropriate manner atthe Board of Directors of the company – thenthe choices relating to them are conscious.).

14

Viénot I Report(France)

Hellebuyck Commission Recommendations(France)

Viénot II Report(France) (Reserved)

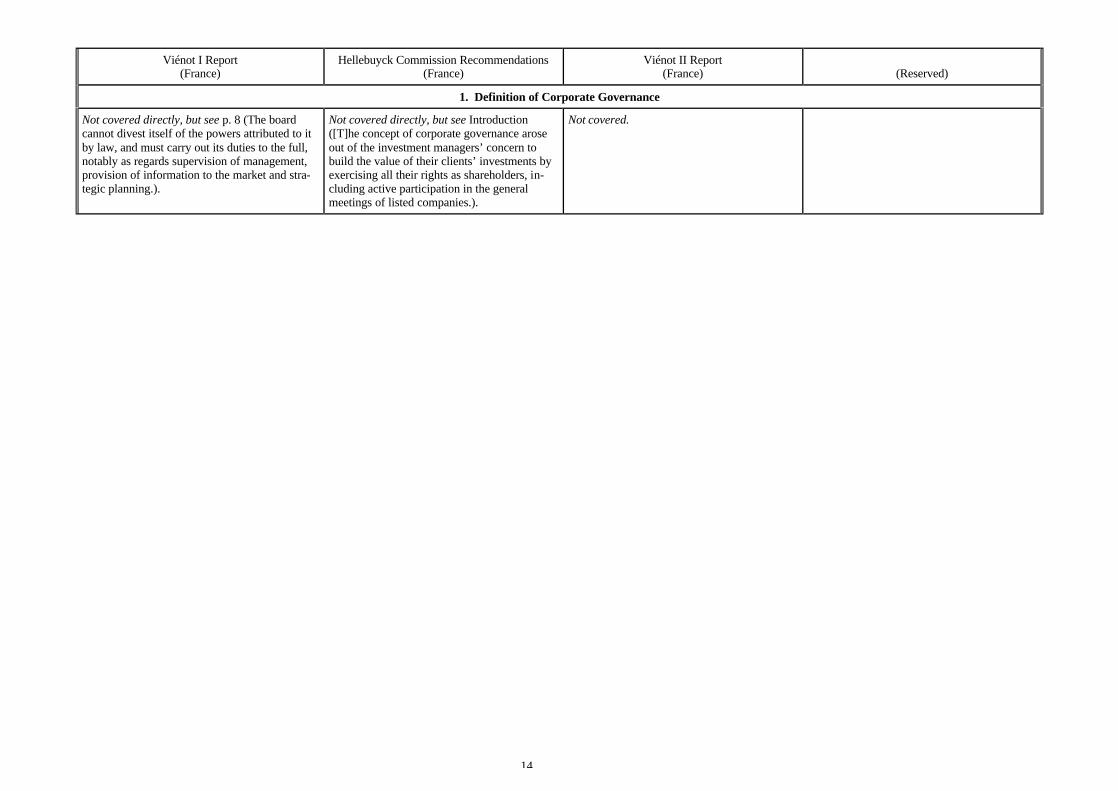

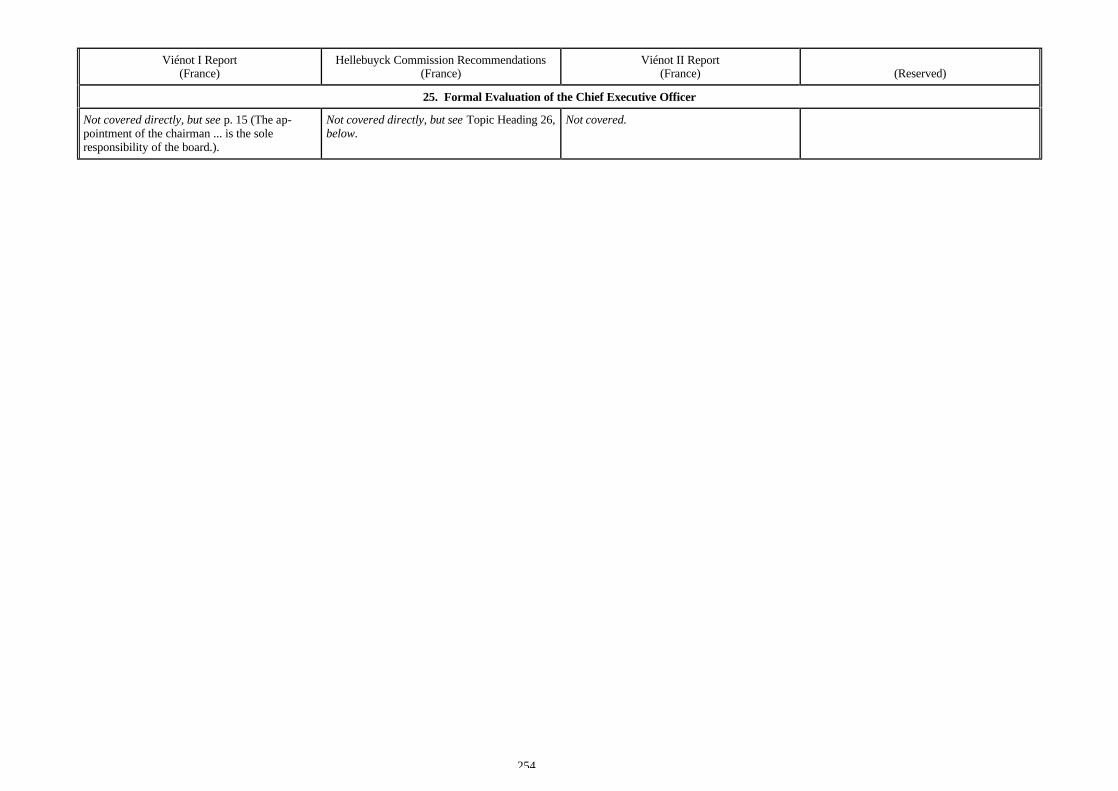

1. Definition of Corporate Governance

Not covered directly, but see p. 8 (The boardcannot divest itself of the powers attributed to itby law, and must carry out its duties to the full,notably as regards supervision of management,provision of information to the market and stra-tegic planning.).

Not covered directly, but see Introduction([T]he concept of corporate governance aroseout of the investment managers’ concern tobuild the value of their clients’ investments byexercising all their rights as shareholders, in-cluding active participation in the generalmeetings of listed companies.).

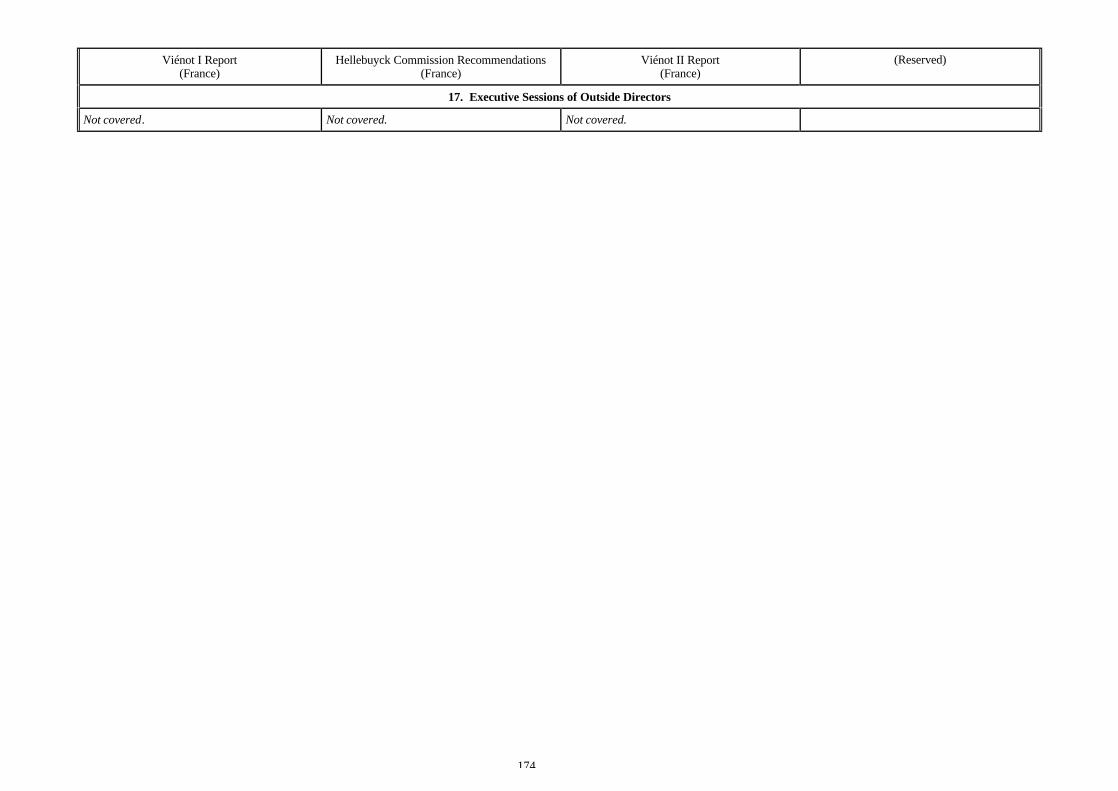

Not covered.

15

Berlin Initiative Code(Germany)

German Panel Rules(Germany)

Cromme Commission Code(Germany)

(Reserved)

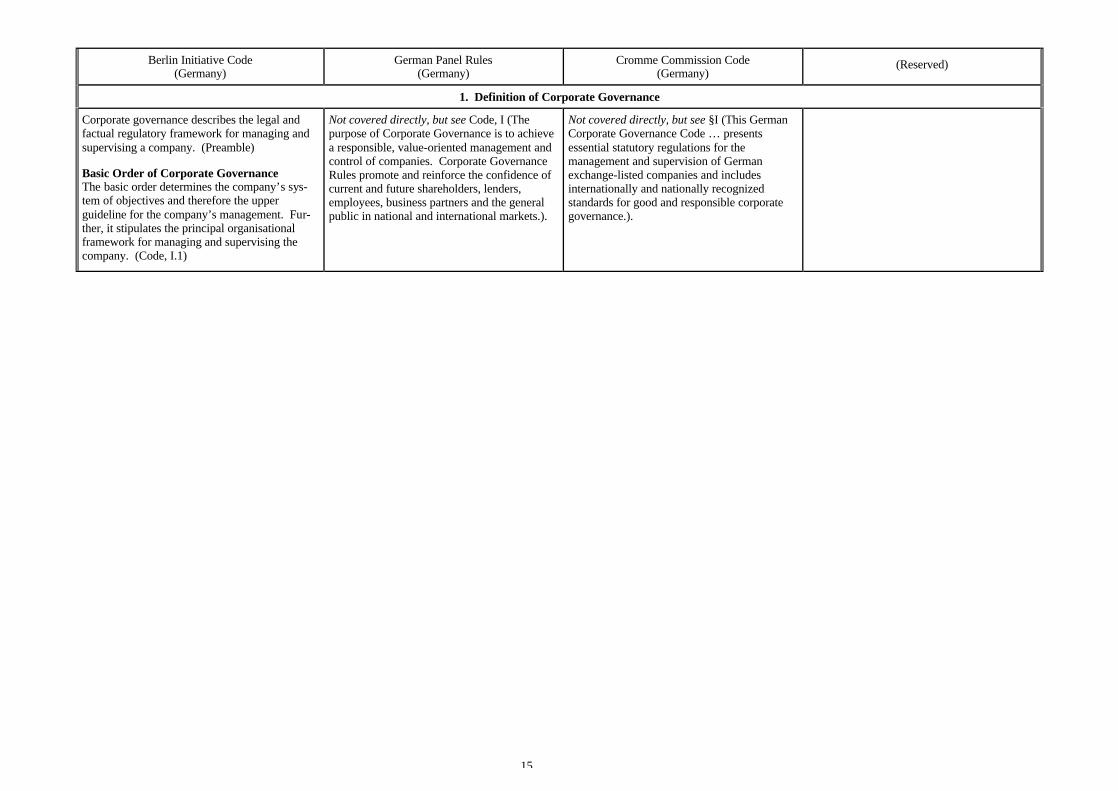

1. Definition of Corporate Governance

Corporate governance describes the legal andfactual regulatory framework for managing andsupervising a company. (Preamble)

Basic Order of Corporate GovernanceThe basic order determines the company’s sys-tem of objectives and therefore the upperguideline for the company’s management. Fur-ther, it stipulates the principal organisationalframework for managing and supervising thecompany. (Code, I.1)

Not covered directly, but see Code, I (Thepurpose of Corporate Governance is to achievea responsible, value-oriented management andcontrol of companies. Corporate GovernanceRules promote and reinforce the confidence ofcurrent and future shareholders, lenders,employees, business partners and the generalpublic in national and international markets.).

Not covered directly, but see §I (This GermanCorporate Governance Code … presentsessential statutory regulations for themanagement and supervision of Germanexchange-listed companies and includesinternationally and nationally recognizedstandards for good and responsible corporategovernance.).

16

Mertzanis Report(Greece)

Federation of Greek Industries Principles(Greece)

IAIM Guidelines(Ireland)

Preda Report(Italy)

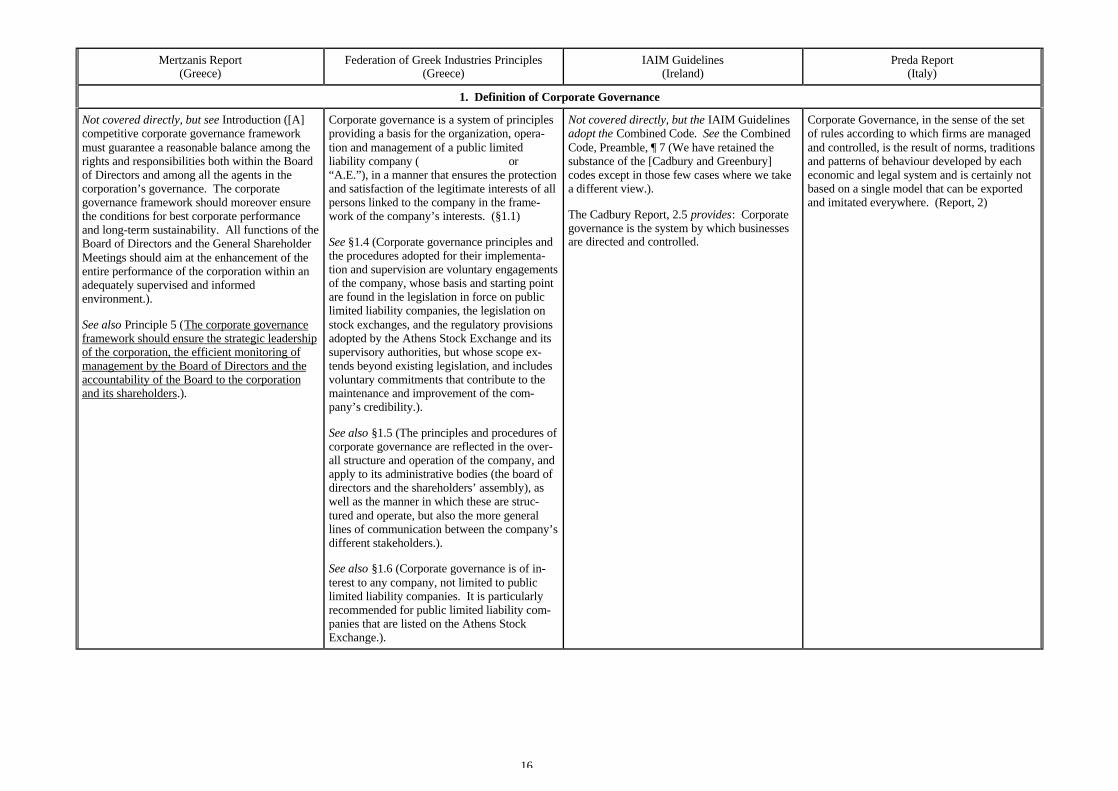

1. Definition of Corporate Governance

Not covered directly, but see Introduction ([A]competitive corporate governance frameworkmust guarantee a reasonable balance among therights and responsibilities both within the Boardof Directors and among all the agents in thecorporation’s governance. The corporategovernance framework should moreover ensurethe conditions for best corporate performanceand long-term sustainability. All functions of theBoard of Directors and the General ShareholderMeetings should aim at the enhancement of theentire performance of the corporation within anadequately supervised and informedenvironment.).

See also Principle 5 (The corporate governanceframework should ensure the strategic leadershipof the corporation, the efficient monitoring ofmanagement by the Board of Directors and theaccountability of the Board to the corporationand its shareholders.).

Corporate governance is a system of principlesproviding a basis for the organization, opera-tion and management of a public limitedliability company ( or“A.E.”), in a manner that ensures the protectionand satisfaction of the legitimate interests of allpersons linked to the company in the frame-work of the company’s interests. (§1.1)

See §1.4 (Corporate governance principles andthe procedures adopted for their implementa-tion and supervision are voluntary engagementsof the company, whose basis and starting pointare found in the legislation in force on publiclimited liability companies, the legislation onstock exchanges, and the regulatory provisionsadopted by the Athens Stock Exchange and itssupervisory authorities, but whose scope ex-tends beyond existing legislation, and includesvoluntary commitments that contribute to themaintenance and improvement of the com-pany’s credibility.).

See also §1.5 (The principles and procedures ofcorporate governance are reflected in the over-all structure and operation of the company, andapply to its administrative bodies (the board ofdirectors and the shareholders’ assembly), aswell as the manner in which these are struc-tured and operate, but also the more generallines of communication between the company’sdifferent stakeholders.).

See also §1.6 (Corporate governance is of in-terest to any company, not limited to publiclimited liability companies. It is particularlyrecommended for public limited liability com-panies that are listed on the Athens StockExchange.).

Not covered directly, but the IAIM Guidelinesadopt the Combined Code. See the CombinedCode, Preamble, ¶ 7 (We have retained thesubstance of the [Cadbury and Greenbury]codes except in those few cases where we takea different view.).

The Cadbury Report, 2.5 provides: Corporategovernance is the system by which businessesare directed and controlled.

Corporate Governance, in the sense of the setof rules according to which firms are managedand controlled, is the result of norms, traditionsand patterns of behaviour developed by eacheconomic and legal system and is certainly notbased on a single model that can be exportedand imitated everywhere. (Report, 2)

17

Peters Report(The Netherlands)

VEB Recommendations(The Netherlands)

SCGOP Handbook and Guidelines(The Netherlands)

Securities Market Comm’n Recommendations(Portugal)

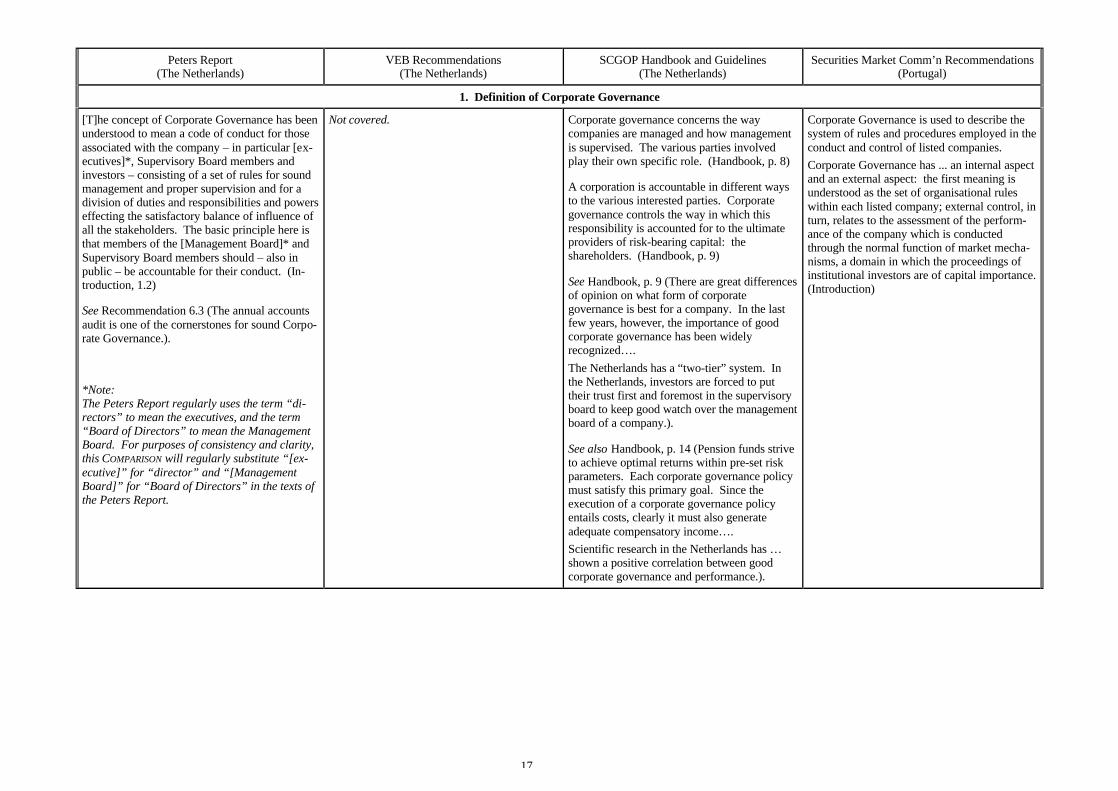

1. Definition of Corporate Governance

[T]he concept of Corporate Governance has beenunderstood to mean a code of conduct for thoseassociated with the company – in particular [ex-ecutives]*, Supervisory Board members andinvestors – consisting of a set of rules for soundmanagement and proper supervision and for adivision of duties and responsibilities and powerseffecting the satisfactory balance of influence ofall the stakeholders. The basic principle here isthat members of the [Management Board]* andSupervisory Board members should – also inpublic – be accountable for their conduct. (In-troduction, 1.2)

See Recommendation 6.3 (The annual accountsaudit is one of the cornerstones for sound Corpo-rate Governance.).

*Note:The Peters Report regularly uses the term “di-rectors” to mean the executives, and the term“Board of Directors” to mean the ManagementBoard. For purposes of consistency and clarity,this COMPARISON will regularly substitute “[ex-ecutive]” for “director” and “[ManagementBoard]” for “Board of Directors” in the texts ofthe Peters Report.

Not covered. Corporate governance concerns the waycompanies are managed and how managementis supervised. The various parties involvedplay their own specific role. (Handbook, p. 8)

A corporation is accountable in different waysto the various interested parties. Corporategovernance controls the way in which thisresponsibility is accounted for to the ultimateproviders of risk-bearing capital: theshareholders. (Handbook, p. 9)

See Handbook, p. 9 (There are great differencesof opinion on what form of corporategovernance is best for a company. In the lastfew years, however, the importance of goodcorporate governance has been widelyrecognized….The Netherlands has a “two-tier” system. Inthe Netherlands, investors are forced to puttheir trust first and foremost in the supervisoryboard to keep good watch over the managementboard of a company.).

See also Handbook, p. 14 (Pension funds striveto achieve optimal returns within pre-set riskparameters. Each corporate governance policymust satisfy this primary goal. Since theexecution of a corporate governance policyentails costs, clearly it must also generateadequate compensatory income….Scientific research in the Netherlands has …shown a positive correlation between goodcorporate governance and performance.).

Corporate Governance is used to describe thesystem of rules and procedures employed in theconduct and control of listed companies.Corporate Governance has ... an internal aspectand an external aspect: the first meaning isunderstood as the set of organisational ruleswithin each listed company; external control, inturn, relates to the assessment of the perform-ance of the company which is conductedthrough the normal function of market mecha-nisms, a domain in which the proceedings ofinstitutional investors are of capital importance.(Introduction)

18

Olivencia Report(Spain)

Swedish Shareholders Ass’n Policy(Sweden)

ICSA Code(United Kingdom)

ISC Statement of Best Practice(United Kingdom)

1. Definition of Corporate Governance

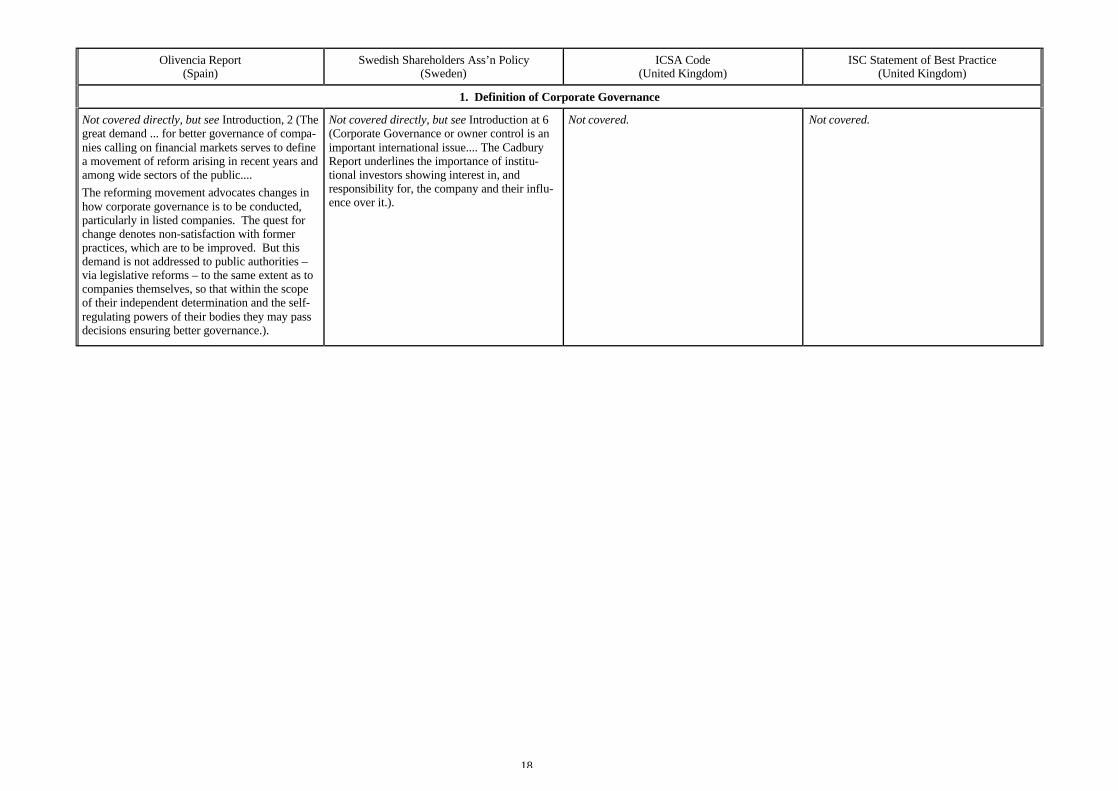

Not covered directly, but see Introduction, 2 (Thegreat demand ... for better governance of compa-nies calling on financial markets serves to definea movement of reform arising in recent years andamong wide sectors of the public....The reforming movement advocates changes inhow corporate governance is to be conducted,particularly in listed companies. The quest forchange denotes non-satisfaction with formerpractices, which are to be improved. But thisdemand is not addressed to public authorities –via legislative reforms – to the same extent as tocompanies themselves, so that within the scopeof their independent determination and the self-regulating powers of their bodies they may passdecisions ensuring better governance.).

Not covered directly, but see Introduction at 6(Corporate Governance or owner control is animportant international issue.... The CadburyReport underlines the importance of institu-tional investors showing interest in, andresponsibility for, the company and their influ-ence over it.).

Not covered. Not covered.

19

Cadbury Report(United Kingdom)

Greenbury Report(United Kingdom)

Hampel Report(United Kingdom)

The Combined Code/Turnbull Report(United Kingdom)

1. Definition of Corporate Governance

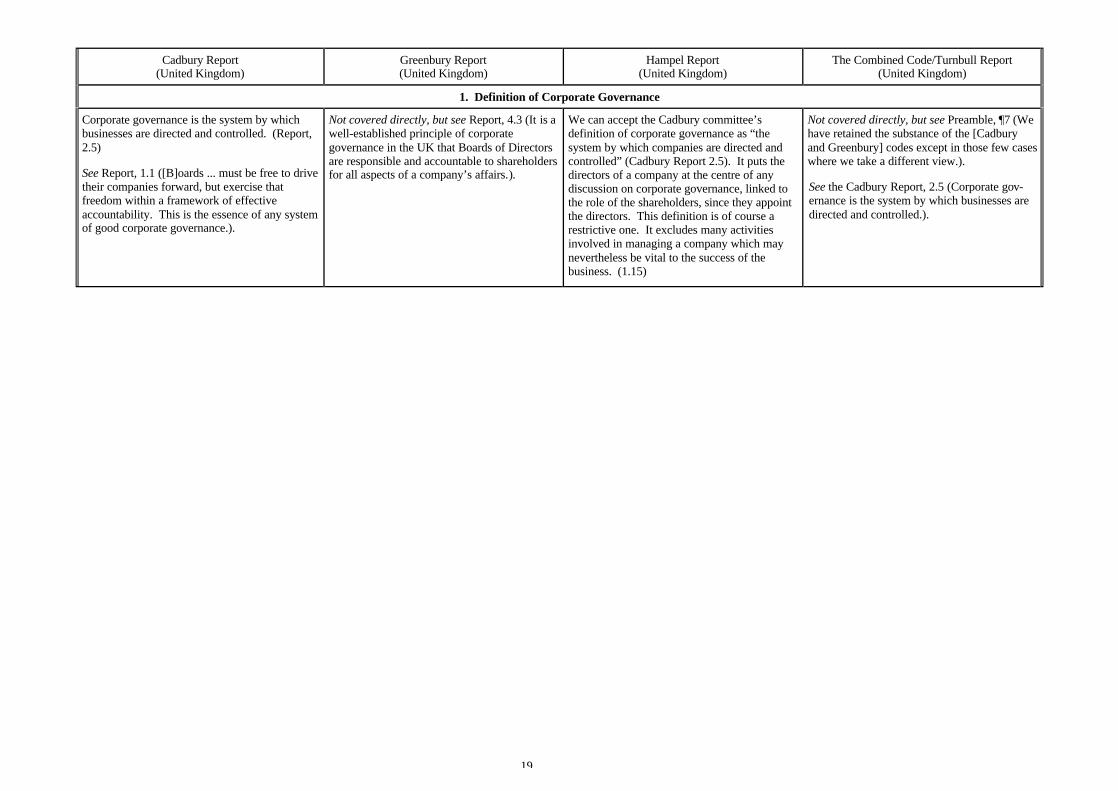

Corporate governance is the system by whichbusinesses are directed and controlled. (Report,2.5)

See Report, 1.1 ([B]oards ... must be free to drivetheir companies forward, but exercise thatfreedom within a framework of effectiveaccountability. This is the essence of any systemof good corporate governance.).

Not covered directly, but see Report, 4.3 (It is awell-established principle of corporategovernance in the UK that Boards of Directorsare responsible and accountable to shareholdersfor all aspects of a company’s affairs.).

We can accept the Cadbury committee’sdefinition of corporate governance as “thesystem by which companies are directed andcontrolled” (Cadbury Report 2.5). It puts thedirectors of a company at the centre of anydiscussion on corporate governance, linked tothe role of the shareholders, since they appointthe directors. This definition is of course arestrictive one. It excludes many activitiesinvolved in managing a company which maynevertheless be vital to the success of thebusiness. (1.15)

Not covered directly, but see Preamble, ¶7 (Wehave retained the substance of the [Cadburyand Greenbury] codes except in those few caseswhere we take a different view.).

See the Cadbury Report, 2.5 (Corporate gov-ernance is the system by which businesses aredirected and controlled.).

20

NAPF Corporate Governance Code(United Kingdom)

AUTIF Code(United Kingdom)

Hermes Statement(United Kingdom)

PIRC Shareholder Voting Guidelines(United Kingdom)

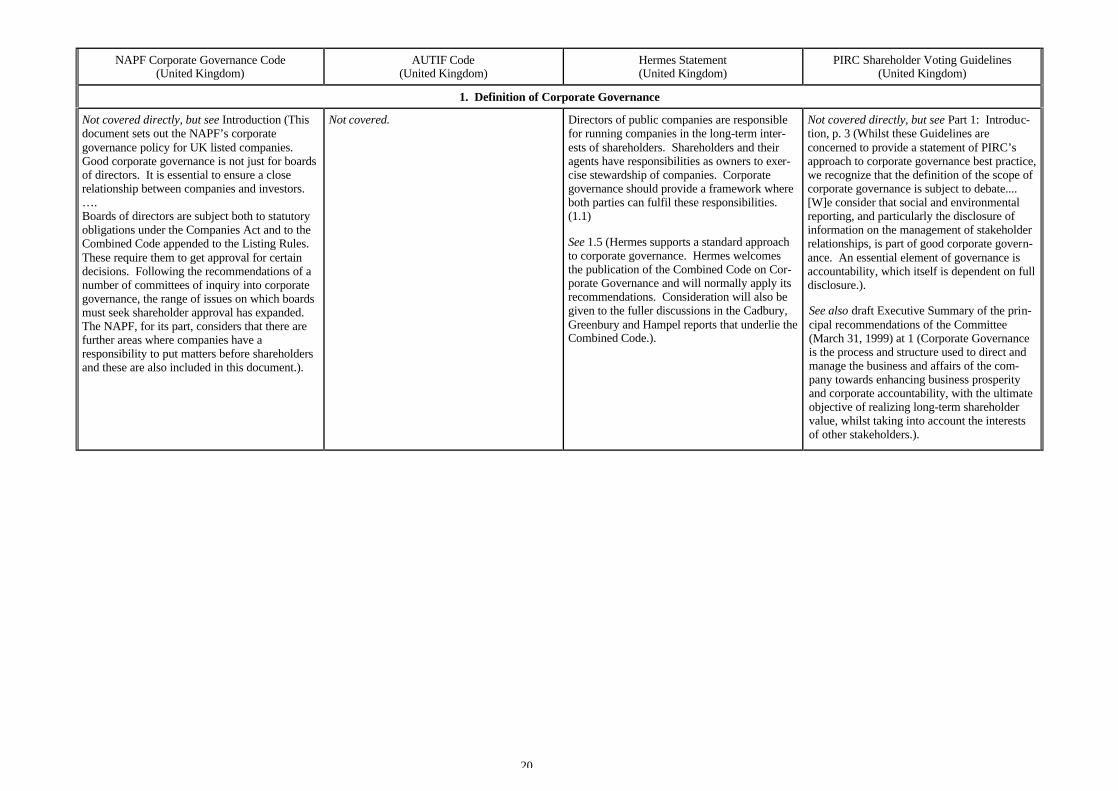

1. Definition of Corporate Governance

Not covered directly, but see Introduction (Thisdocument sets out the NAPF’s corporategovernance policy for UK listed companies.Good corporate governance is not just for boardsof directors. It is essential to ensure a closerelationship between companies and investors.….Boards of directors are subject both to statutoryobligations under the Companies Act and to theCombined Code appended to the Listing Rules.These require them to get approval for certaindecisions. Following the recommendations of anumber of committees of inquiry into corporategovernance, the range of issues on which boardsmust seek shareholder approval has expanded.The NAPF, for its part, considers that there arefurther areas where companies have aresponsibility to put matters before shareholdersand these are also included in this document.).

Not covered. Directors of public companies are responsiblefor running companies in the long-term inter-ests of shareholders. Shareholders and theiragents have responsibilities as owners to exer-cise stewardship of companies. Corporategovernance should provide a framework whereboth parties can fulfil these responsibilities.(1.1)

See 1.5 (Hermes supports a standard approachto corporate governance. Hermes welcomesthe publication of the Combined Code on Cor-porate Governance and will normally apply itsrecommendations. Consideration will also begiven to the fuller discussions in the Cadbury,Greenbury and Hampel reports that underlie theCombined Code.).

Not covered directly, but see Part 1: Introduc-tion, p. 3 (Whilst these Guidelines areconcerned to provide a statement of PIRC’sapproach to corporate governance best practice,we recognize that the definition of the scope ofcorporate governance is subject to debate....[W]e consider that social and environmentalreporting, and particularly the disclosure ofinformation on the management of stakeholderrelationships, is part of good corporate govern-ance. An essential element of governance isaccountability, which itself is dependent on fulldisclosure.).

See also draft Executive Summary of the prin-cipal recommendations of the Committee(March 31, 1999) at 1 (Corporate Governanceis the process and structure used to direct andmanage the business and affairs of the com-pany towards enhancing business prosperityand corporate accountability, with the ultimateobjective of realizing long-term shareholdervalue, whilst taking into account the interestsof other stakeholders.).

21

OECD Principles/Millstein Report(International)

ICGN Statement/Global Voting Principles(International)

Euroshareholders Guidelines(Pan-European)

EASD Principles and Recommendations(Pan-European)

2. The Mission of the Board of Directors

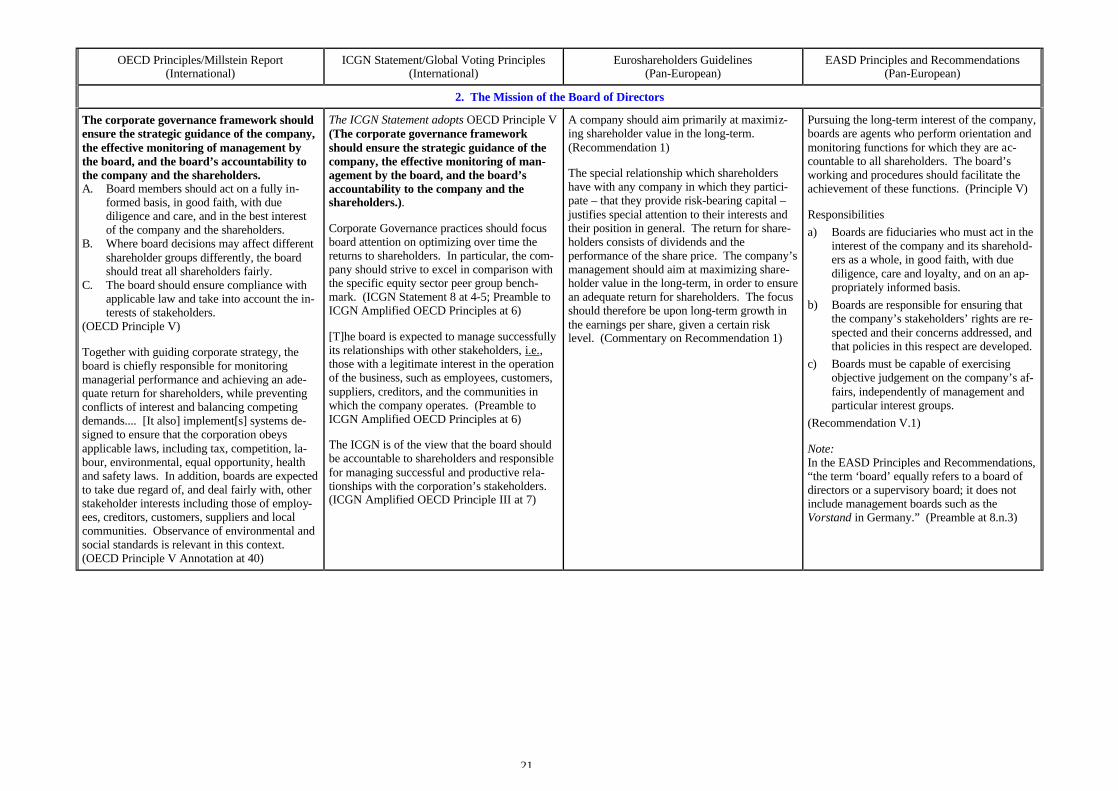

The corporate governance framework shouldensure the strategic guidance of the company,the effective monitoring of management bythe board, and the board’s accountability tothe company and the shareholders.A. Board members should act on a fully in-

formed basis, in good faith, with duediligence and care, and in the best interestof the company and the shareholders.

B. Where board decisions may affect differentshareholder groups differently, the boardshould treat all shareholders fairly.

C. The board should ensure compliance withapplicable law and take into account the in-terests of stakeholders.

(OECD Principle V)

Together with guiding corporate strategy, theboard is chiefly responsible for monitoringmanagerial performance and achieving an ade-quate return for shareholders, while preventingconflicts of interest and balancing competingdemands.... [It also] implement[s] systems de-signed to ensure that the corporation obeysapplicable laws, including tax, competition, la-bour, environmental, equal opportunity, healthand safety laws. In addition, boards are expectedto take due regard of, and deal fairly with, otherstakeholder interests including those of employ-ees, creditors, customers, suppliers and localcommunities. Observance of environmental andsocial standards is relevant in this context.(OECD Principle V Annotation at 40)

The ICGN Statement adopts OECD Principle V(The corporate governance frameworkshould ensure the strategic guidance of thecompany, the effective monitoring of man-agement by the board, and the board’saccountability to the company and theshareholders.).

Corporate Governance practices should focusboard attention on optimizing over time thereturns to shareholders. In particular, the com-pany should strive to excel in comparison withthe specific equity sector peer group bench-mark. (ICGN Statement 8 at 4-5; Preamble toICGN Amplified OECD Principles at 6)

[T]he board is expected to manage successfullyits relationships with other stakeholders, i.e.,those with a legitimate interest in the operationof the business, such as employees, customers,suppliers, creditors, and the communities inwhich the company operates. (Preamble toICGN Amplified OECD Principles at 6)

The ICGN is of the view that the board shouldbe accountable to shareholders and responsiblefor managing successful and productive rela-tionships with the corporation’s stakeholders.(ICGN Amplified OECD Principle III at 7)

A company should aim primarily at maximiz-ing shareholder value in the long-term.(Recommendation 1)

The special relationship which shareholdershave with any company in which they partici-pate – that they provide risk-bearing capital –justifies special attention to their interests andtheir position in general. The return for share-holders consists of dividends and theperformance of the share price. The company’smanagement should aim at maximizing share-holder value in the long-term, in order to ensurean adequate return for shareholders. The focusshould therefore be upon long-term growth inthe earnings per share, given a certain risklevel. (Commentary on Recommendation 1)

Pursuing the long-term interest of the company,boards are agents who perform orientation andmonitoring functions for which they are ac-countable to all shareholders. The board’sworking and procedures should facilitate theachievement of these functions. (Principle V)

Responsibilitiesa) Boards are fiduciaries who must act in the

interest of the company and its sharehold-ers as a whole, in good faith, with duediligence, care and loyalty, and on an ap-propriately informed basis.

b) Boards are responsible for ensuring thatthe company’s stakeholders’ rights are re-spected and their concerns addressed, andthat policies in this respect are developed.

c) Boards must be capable of exercisingobjective judgement on the company’s af-fairs, independently of management andparticular interest groups.

(Recommendation V.1)

Note:In the EASD Principles and Recommendations,“the term ‘board’ equally refers to a board ofdirectors or a supervisory board; it does notinclude management boards such as theVorstand in Germany.” (Preamble at 8.n.3)

22

Recommendations of Federation of Companies(Belgium)

Dual Code of the BXS/CBF(Belgium)

The Director’s Charter (FDA)(Belgium) (Reserved)

2. The Mission of the Board of Directors

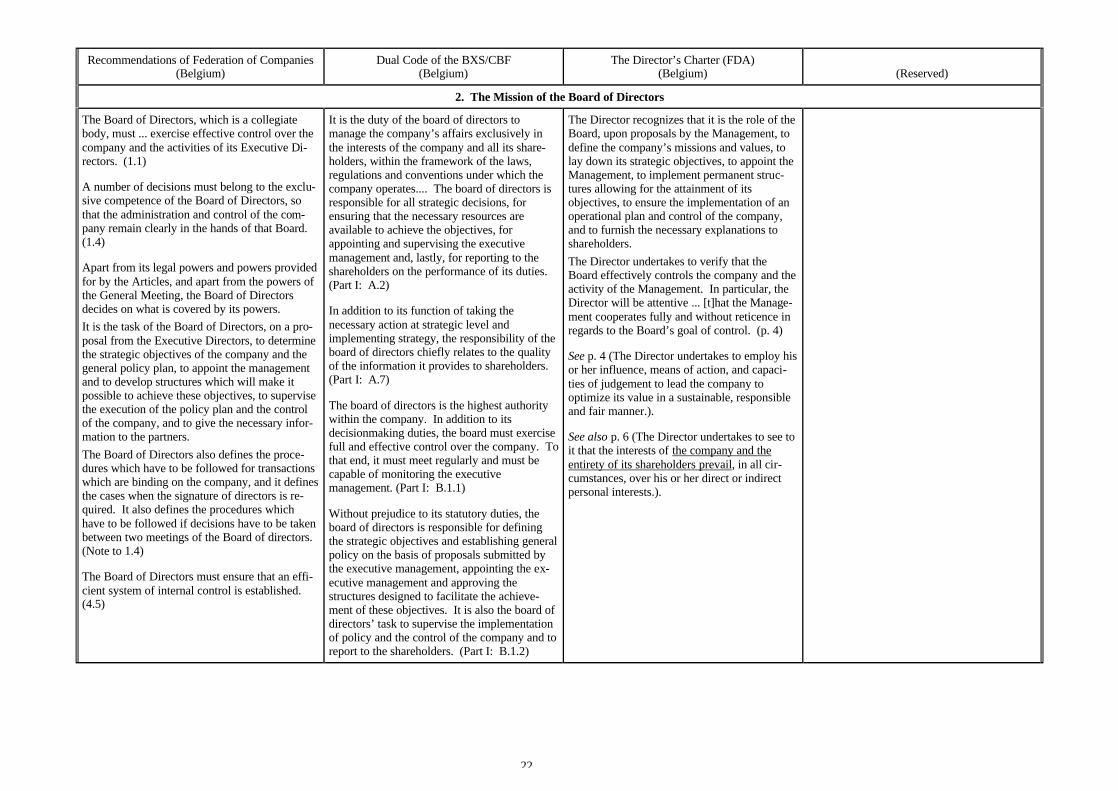

The Board of Directors, which is a collegiatebody, must ... exercise effective control over thecompany and the activities of its Executive Di-rectors. (1.1)

A number of decisions must belong to the exclu-sive competence of the Board of Directors, sothat the administration and control of the com-pany remain clearly in the hands of that Board.(1.4)

Apart from its legal powers and powers providedfor by the Articles, and apart from the powers ofthe General Meeting, the Board of Directorsdecides on what is covered by its powers.It is the task of the Board of Directors, on a pro-posal from the Executive Directors, to determinethe strategic objectives of the company and thegeneral policy plan, to appoint the managementand to develop structures which will make itpossible to achieve these objectives, to supervisethe execution of the policy plan and the controlof the company, and to give the necessary infor-mation to the partners.The Board of Directors also defines the proce-dures which have to be followed for transactionswhich are binding on the company, and it definesthe cases when the signature of directors is re-quired. It also defines the procedures whichhave to be followed if decisions have to be takenbetween two meetings of the Board of directors.(Note to 1.4)

The Board of Directors must ensure that an effi-cient system of internal control is established.(4.5)

It is the duty of the board of directors tomanage the company’s affairs exclusively inthe interests of the company and all its share-holders, within the framework of the laws,regulations and conventions under which thecompany operates.... The board of directors isresponsible for all strategic decisions, forensuring that the necessary resources areavailable to achieve the objectives, forappointing and supervising the executivemanagement and, lastly, for reporting to theshareholders on the performance of its duties.(Part I: A.2)

In addition to its function of taking thenecessary action at strategic level andimplementing strategy, the responsibility of theboard of directors chiefly relates to the qualityof the information it provides to shareholders.(Part I: A.7)

The board of directors is the highest authoritywithin the company. In addition to itsdecisionmaking duties, the board must exercisefull and effective control over the company. Tothat end, it must meet regularly and must becapable of monitoring the executivemanagement. (Part I: B.1.1)

Without prejudice to its statutory duties, theboard of directors is responsible for definingthe strategic objectives and establishing generalpolicy on the basis of proposals submitted bythe executive management, appointing the ex-ecutive management and approving thestructures designed to facilitate the achieve-ment of these objectives. It is also the board ofdirectors’ task to supervise the implementationof policy and the control of the company and toreport to the shareholders. (Part I: B.1.2)

The Director recognizes that it is the role of theBoard, upon proposals by the Management, todefine the company’s missions and values, tolay down its strategic objectives, to appoint theManagement, to implement permanent struc-tures allowing for the attainment of itsobjectives, to ensure the implementation of anoperational plan and control of the company,and to furnish the necessary explanations toshareholders.The Director undertakes to verify that theBoard effectively controls the company and theactivity of the Management. In particular, theDirector will be attentive ... [t]hat the Manage-ment cooperates fully and without reticence inregards to the Board’s goal of control. (p. 4)

See p. 4 (The Director undertakes to employ hisor her influence, means of action, and capaci-ties of judgement to lead the company tooptimize its value in a sustainable, responsibleand fair manner.).

See also p. 6 (The Director undertakes to see toit that the interests of the company and theentirety of its shareholders prevail, in all cir-cumstances, over his or her direct or indirectpersonal interests.).

23

Danish Shareholders Ass’n Guidelines(Denmark)

Nørby Report & Recommendations(Denmark)

Chamber of Commerce/Confederation Code(Finland)

Ministry of Trade & Industry Guidelines(Finland)

2. The Mission of the Board of Directors

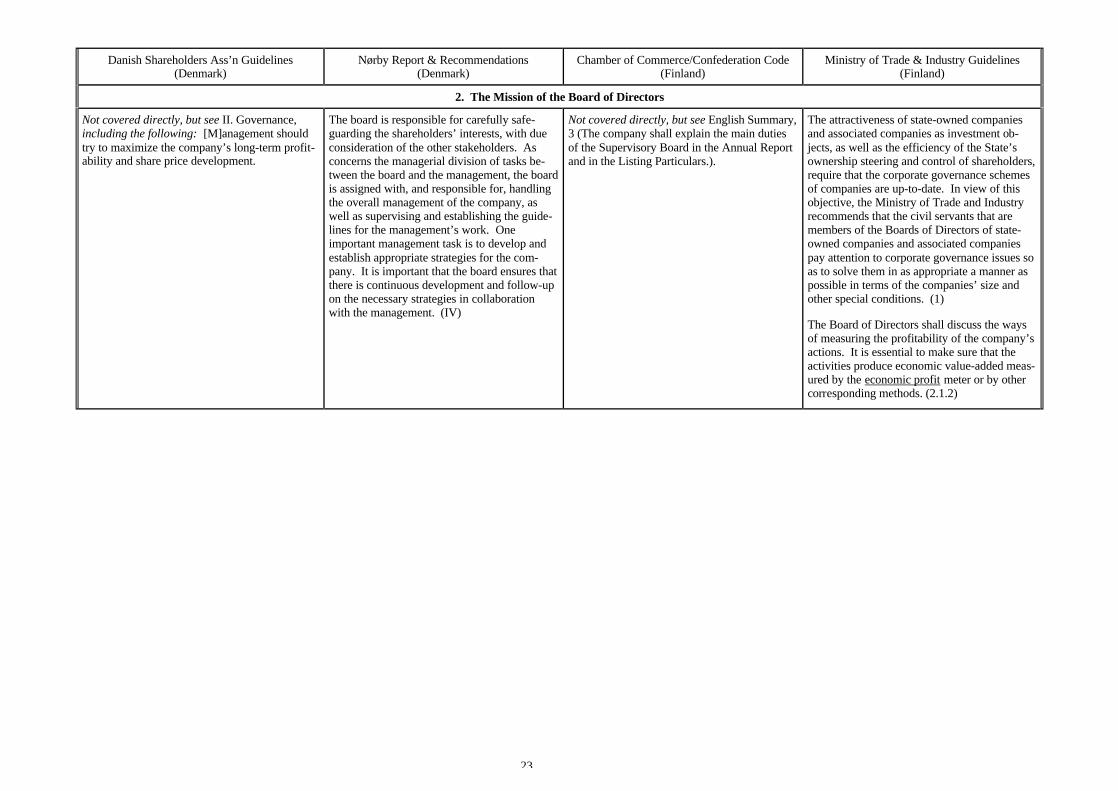

Not covered directly, but see II. Governance,including the following: [M]anagement shouldtry to maximize the company’s long-term profit-ability and share price development.

The board is responsible for carefully safe-guarding the shareholders’ interests, with dueconsideration of the other stakeholders. Asconcerns the managerial division of tasks be-tween the board and the management, the boardis assigned with, and responsible for, handlingthe overall management of the company, aswell as supervising and establishing the guide-lines for the management’s work. Oneimportant management task is to develop andestablish appropriate strategies for the com-pany. It is important that the board ensures thatthere is continuous development and follow-upon the necessary strategies in collaborationwith the management. (IV)

Not covered directly, but see English Summary,3 (The company shall explain the main dutiesof the Supervisory Board in the Annual Reportand in the Listing Particulars.).

The attractiveness of state-owned companiesand associated companies as investment ob-jects, as well as the efficiency of the State’sownership steering and control of shareholders,require that the corporate governance schemesof companies are up-to-date. In view of thisobjective, the Ministry of Trade and Industryrecommends that the civil servants that aremembers of the Boards of Directors of state-owned companies and associated companiespay attention to corporate governance issues soas to solve them in as appropriate a manner aspossible in terms of the companies’ size andother special conditions. (1)

The Board of Directors shall discuss the waysof measuring the profitability of the company’sactions. It is essential to make sure that theactivities produce economic value-added meas-ured by the economic profit meter or by othercorresponding methods. (2.1.2)

24

Viénot I Report(France)

Hellebuyck Commission Recommendations(France)

Viénot II Report(France) (Reserved)

2. The Mission of the Board of Directors

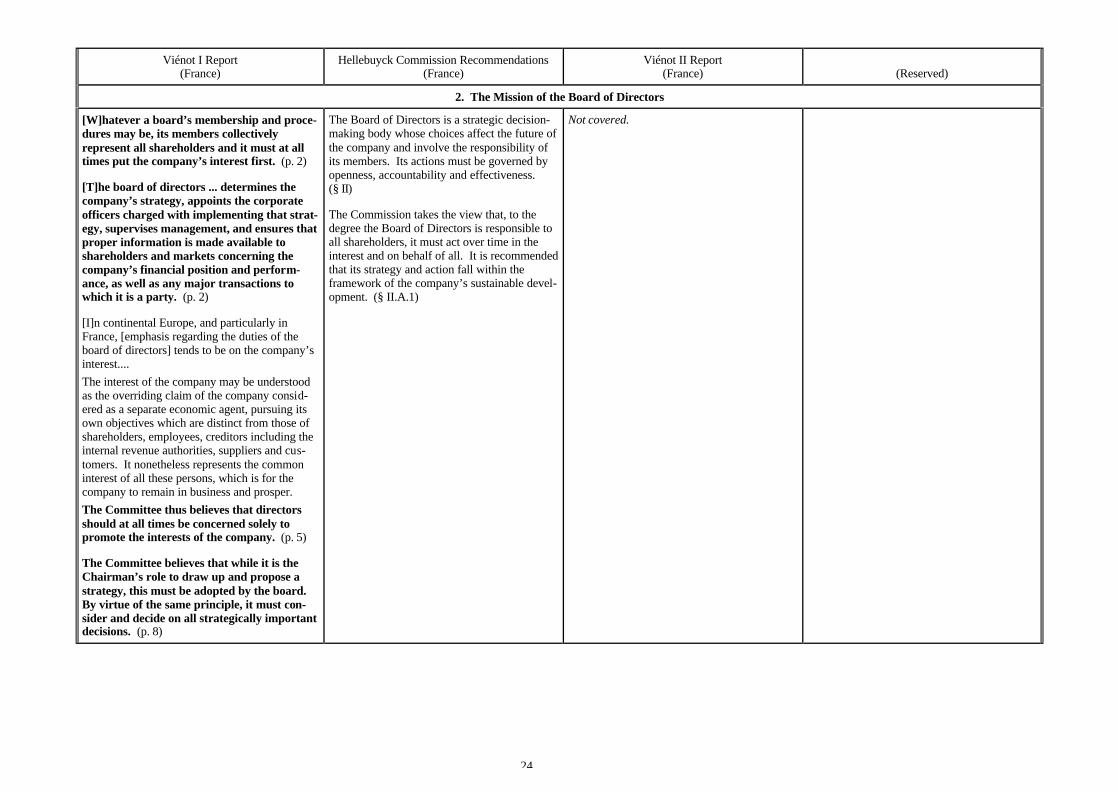

[W]hatever a board’s membership and proce-dures may be, its members collectivelyrepresent all shareholders and it must at alltimes put the company’s interest first. (p. 2)

[T]he board of directors ... determines thecompany’s strategy, appoints the corporateofficers charged with implementing that strat-egy, supervises management, and ensures thatproper information is made available toshareholders and markets concerning thecompany’s financial position and perform-ance, as well as any major transactions towhich it is a party. (p. 2)

[I]n continental Europe, and particularly inFrance, [emphasis regarding the duties of theboard of directors] tends to be on the company’sinterest....The interest of the company may be understoodas the overriding claim of the company consid-ered as a separate economic agent, pursuing itsown objectives which are distinct from those ofshareholders, employees, creditors including theinternal revenue authorities, suppliers and cus-tomers. It nonetheless represents the commoninterest of all these persons, which is for thecompany to remain in business and prosper.The Committee thus believes that directorsshould at all times be concerned solely topromote the interests of the company. (p. 5)

The Committee believes that while it is theChairman’s role to draw up and propose astrategy, this must be adopted by the board.By virtue of the same principle, it must con-sider and decide on all strategically importantdecisions. (p. 8)

The Board of Directors is a strategic decision-making body whose choices affect the future ofthe company and involve the responsibility ofits members. Its actions must be governed byopenness, accountability and effectiveness.(§ II)

The Commission takes the view that, to thedegree the Board of Directors is responsible toall shareholders, it must act over time in theinterest and on behalf of all. It is recommendedthat its strategy and action fall within theframework of the company’s sustainable devel-opment. (§ II.A.1)

Not covered.

25

Berlin Initiative Code(Germany)

German Panel Rules(Germany)

Cromme Commission Code(Germany) (Reserved)

2. The Mission of the Board of Directors

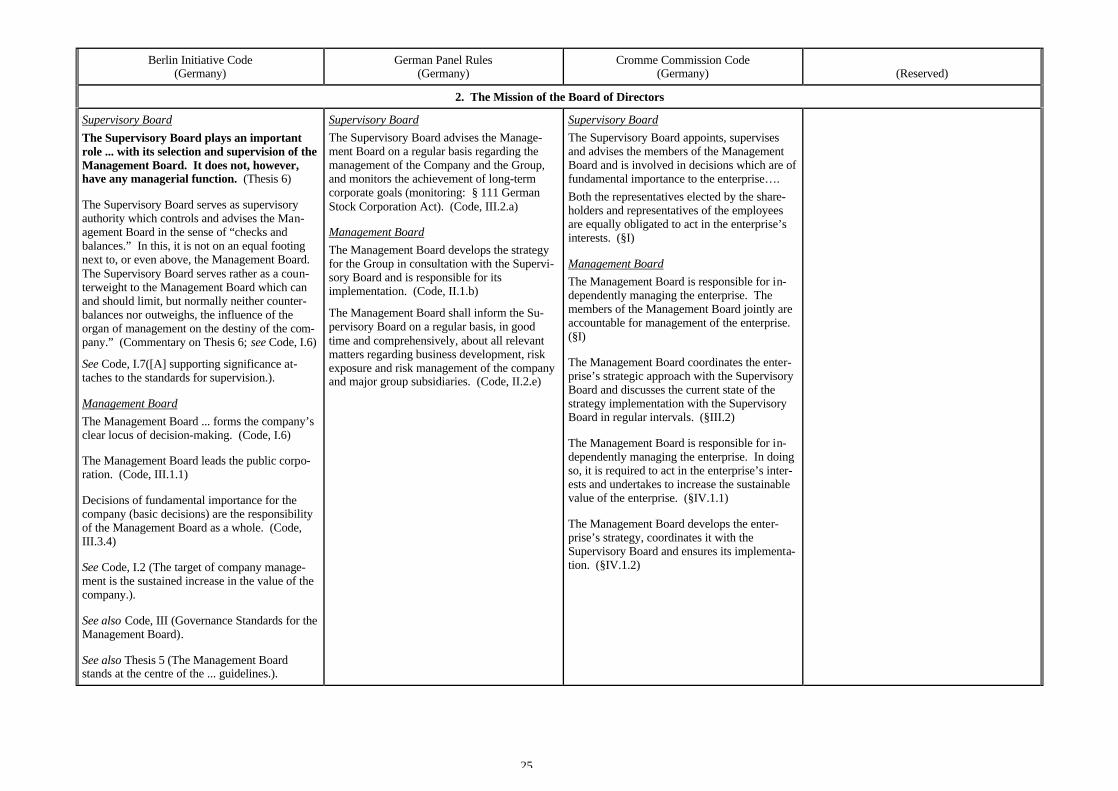

Supervisory BoardThe Supervisory Board plays an importantrole ... with its selection and supervision of theManagement Board. It does not, however,have any managerial function. (Thesis 6)

The Supervisory Board serves as supervisoryauthority which controls and advises the Man-agement Board in the sense of “checks andbalances.” In this, it is not on an equal footingnext to, or even above, the Management Board.The Supervisory Board serves rather as a coun-terweight to the Management Board which canand should limit, but normally neither counter-balances nor outweighs, the influence of theorgan of management on the destiny of the com-pany.” (Commentary on Thesis 6; see Code, I.6)

See Code, I.7([A] supporting significance at-taches to the standards for supervision.).

Management BoardThe Management Board ... forms the company’sclear locus of decision-making. (Code, I.6)

The Management Board leads the public corpo-ration. (Code, III.1.1)

Decisions of fundamental importance for thecompany (basic decisions) are the responsibilityof the Management Board as a whole. (Code,III.3.4)

See Code, I.2 (The target of company manage-ment is the sustained increase in the value of thecompany.).

See also Code, III (Governance Standards for theManagement Board).

See also Thesis 5 (The Management Boardstands at the centre of the ... guidelines.).

Supervisory BoardThe Supervisory Board advises the Manage-ment Board on a regular basis regarding themanagement of the Company and the Group,and monitors the achievement of long-termcorporate goals (monitoring: § 111 GermanStock Corporation Act). (Code, III.2.a)

Management BoardThe Management Board develops the strategyfor the Group in consultation with the Supervi-sory Board and is responsible for itsimplementation. (Code, II.1.b)

The Management Board shall inform the Su-pervisory Board on a regular basis, in goodtime and comprehensively, about all relevantmatters regarding business development, riskexposure and risk management of the companyand major group subsidiaries. (Code, II.2.e)

Supervisory BoardThe Supervisory Board appoints, supervisesand advises the members of the ManagementBoard and is involved in decisions which are offundamental importance to the enterprise….Both the representatives elected by the share-holders and representatives of the employeesare equally obligated to act in the enterprise’sinterests. (§I)

Management BoardThe Management Board is responsible for in-dependently managing the enterprise. Themembers of the Management Board jointly areaccountable for management of the enterprise.(§I)

The Management Board coordinates the enter-prise’s strategic approach with the SupervisoryBoard and discusses the current state of thestrategy implementation with the SupervisoryBoard in regular intervals. (§III.2)

The Management Board is responsible for in-dependently managing the enterprise. In doingso, it is required to act in the enterprise’s inter-ests and undertakes to increase the sustainablevalue of the enterprise. (§IV.1.1)

The Management Board develops the enter-prise’s strategy, coordinates it with theSupervisory Board and ensures its implementa-tion. (§IV.1.2)

26

Mertzanis Report(Greece)

Federation of Greek Industries Principles(Greece)

IAIM Guidelines(Ireland)

Preda Report(Italy)

2. The Mission of the Board of Directors

The Board of Directors is the authority that gov-erns the corporation. Its duties involve decision-making and the responsibility for exercising fulland efficient monitoring of all activities of thecorporation. (Recommendation 5.1)

See Introduction (The Board has the responsibil-ity to deal with the corporation’s affairsexclusively in the interests of the corporation andits shareholders within the existing regulatoryframework. The Board has the main responsi-bility for ensuring the establishment of efficientgovernance rules and must be accountable to thegeneral shareholders meetings for its activitiesand performance. The Board has the main re-sponsibility for setting the corporation’s long-term goals and making all strategic decisions,making available all required sources for theachievement of strategic goals as well as theappointment and supervision of management.).

See also Recommendation 5.2 (In the case wherethe decisions of the Board of Directors may af-fect the different classes of shares in a differentmanner, the Board of Directors should treat allshareholders without discrimination.).

The primary task of the board of directors is theprotection and promotion of the company’sinterests and the continuous returns reflected ina long-term improvement of the company’sshare value. (§2.4)

See §2.2 (The company’s decisions are, as astarting point, decisions of the board of direc-tors acting collectively. This provides all boardmembers with the opportunity to exercise anactive role in the company’s management, withthe further possibility, through powers grantedin particular to executive members, to imple-ment the objectives and guidelines of theboard.).

Not covered directly, but the IAIM Guidelinesadopt the Combined Code. See the CombinedCode, Principle A.1 (Every listed companyshould be headed by an effective boardwhich should lead and control the com-pany.).

Listed companies are governed by a board ofdirectors ... that adopts an organization andmodus operandi enabling it to guaranteeeffective and efficient performance of itsfunctions. (Code 1.1)

The Committee believes that the primary re-sponsibility of the board of directors of a listedcompany is to set the company’s strategic ojec-tives and to ensure they are achieved.(Commentary on Code, 1.1)

See Commentary on Code, 5 ([T]he board ofdirectors is required by law to inform the boardof auditors.).

See also Report, 5.1 ([T]he fundamental feature[of the Code] is the central position of theboard of directors, charged with providingstrategic and organisational guidance and veri-fying the existence of the controls needed tomonitor companies’ performance.).

27

Peters Report(The Netherlands)

VEB Recommendations(The Netherlands)

SCGOP Handbook and Guidelines(The Netherlands)

Securities Market Comm’n Recommendations(Portugal)

2. The Mission of the Board of Directors

Supervisory BoardIn accordance with the law, the SupervisoryBoard, in performing its duties, is bound by theinterests of the company and the enterprise con-nected therewith. It is responsible for thesupervision of management policy and the gen-eral course of affairs in the company. Under thefull ‘structure regime,’ the Supervisory Board isresponsible for appointments to the Board ofDirectors. (Recommendation 2.1)

Management BoardThe [Management Board] is responsible for themanagement of the company, which implies,inter alia, that [it] is responsible for realizing thecompany’s objectives, the strategy and policy,and the ensuing development of results. (Rec-ommendation 4.1)

The [Management Board] should report in writ-ing to the Supervisory Board on the company’sobjectives, strategy and the associated risks of afinancial nature. (Recommendation 4.2)

There are no conceivable circumstances whichcan justify any relaxation of the principle that themanagement should be fully accountable to theproviders of risk capital. (Recommendation 5.1)

Not covered directly, but see Recommendation1 (Companies should maximize shareholdersvalue in the long run, on the condition thatother stakeholders are treated in a reasonableand responsible way.).

See also Commentary on Recommendation 1(More and more companies put ‘creatingshareholders value’ first and focus on growth ofearnings per share, also concerning acquisitionsand dividend policy. With cyclical business inparticular, creating value is underexposed, andcontinuance of existing – often unsatisfactoryyielding – activities prevails.).

Supervisory BoardThe supervisory board is the body that, inkeeping with the interests of shareholders, mustwatch over the actions of the executive boardand general developments at the company andits holding company. (Guideline 13)

The supervisory – or non-executive – boardregulates the management board. (Handbook,p. 8)

For the Netherlands, the difference between theso-called one- and two-tier systems is impor-tant. “Two-tier” means that a separate organ –the supervisory board – supervises the man-agement or executive board….The Netherlands has a “two-tier” system. Inthe Netherlands, investors are forced to puttheir trust first and foremost in the supervisoryboard to keep good watch over the managementboard of a company. (Handbook, p. 9)

Management BoardThe management – or executive – board isresponsible for management of the company.(Handbook, p. 8)

[T]he board exercise[s] effective control in itsguidance of the company, reserving decisionson important matters. To pursue this objective,it should ... ensure the supervision of the man-agement of the company. (Commentary onRecommendation 14)

28

Olivencia Report(Spain)

Swedish Shareholders Ass’n Policy(Sweden)

ICSA Code(United Kingdom)

ISC Statement of Best Practice(United Kingdom)

2. The Mission of the Board of Directors

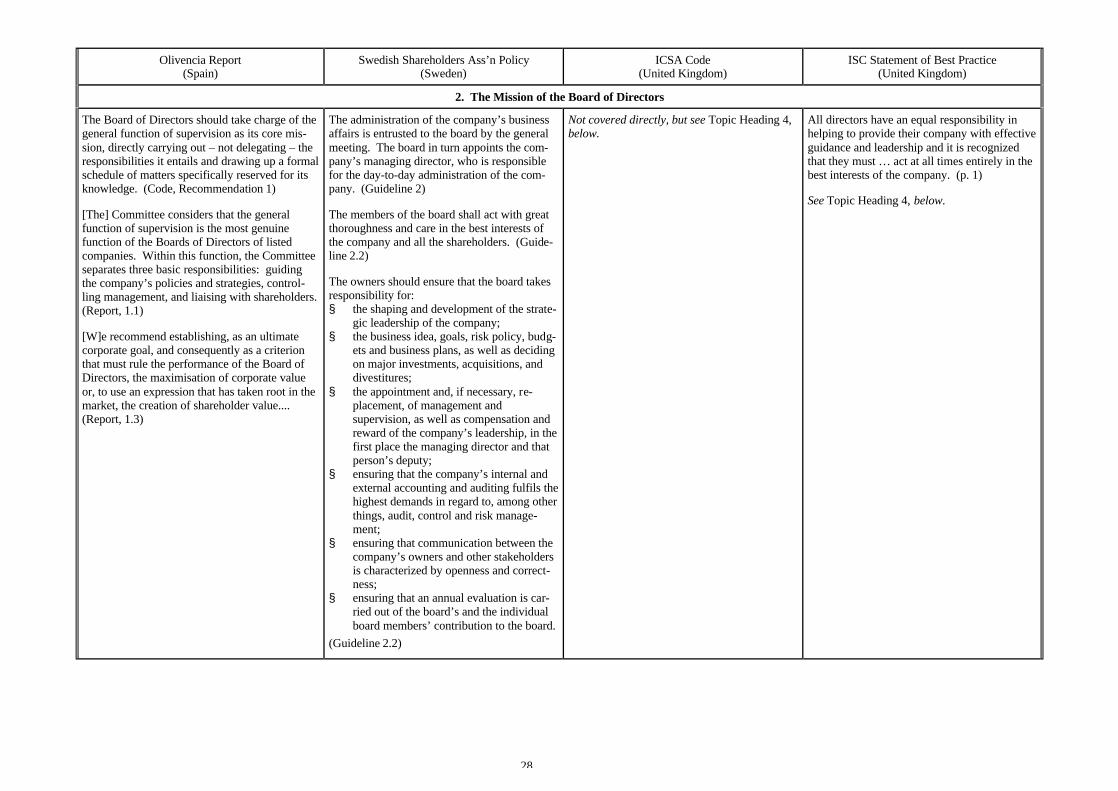

The Board of Directors should take charge of thegeneral function of supervision as its core mis-sion, directly carrying out – not delegating – theresponsibilities it entails and drawing up a formalschedule of matters specifically reserved for itsknowledge. (Code, Recommendation 1)

[The] Committee considers that the generalfunction of supervision is the most genuinefunction of the Boards of Directors of listedcompanies. Within this function, the Committeeseparates three basic responsibilities: guidingthe company’s policies and strategies, control-ling management, and liaising with shareholders.(Report, 1.1)

[W]e recommend establishing, as an ultimatecorporate goal, and consequently as a criterionthat must rule the performance of the Board ofDirectors, the maximisation of corporate valueor, to use an expression that has taken root in themarket, the creation of shareholder value.... (Report, 1.3)

The administration of the company’s businessaffairs is entrusted to the board by the generalmeeting. The board in turn appoints the com-pany’s managing director, who is responsiblefor the day-to-day administration of the com-pany. (Guideline 2)

The members of the board shall act with greatthoroughness and care in the best interests ofthe company and all the shareholders. (Guide-line 2.2)

The owners should ensure that the board takesresponsibility for:§ the shaping and development of the strate-

gic leadership of the company;§ the business idea, goals, risk policy, budg-

ets and business plans, as well as decidingon major investments, acquisitions, anddivestitures;

§ the appointment and, if necessary, re-placement, of management andsupervision, as well as compensation andreward of the company’s leadership, in thefirst place the managing director and thatperson’s deputy;

§ ensuring that the company’s internal andexternal accounting and auditing fulfils thehighest demands in regard to, among otherthings, audit, control and risk manage-ment;

§ ensuring that communication between thecompany’s owners and other stakeholdersis characterized by openness and correct-ness;

§ ensuring that an annual evaluation is car-ried out of the board’s and the individualboard members’ contribution to the board.

(Guideline 2.2)

Not covered directly, but see Topic Heading 4,below.

All directors have an equal responsibility inhelping to provide their company with effectiveguidance and leadership and it is recognizedthat they must … act at all times entirely in thebest interests of the company. (p. 1)

See Topic Heading 4, below.

29

Cadbury Report(United Kingdom)

Greenbury Report(United Kingdom)

Hampel Report(United Kingdom)

The Combined Code/Turnbull Report(United Kingdom)

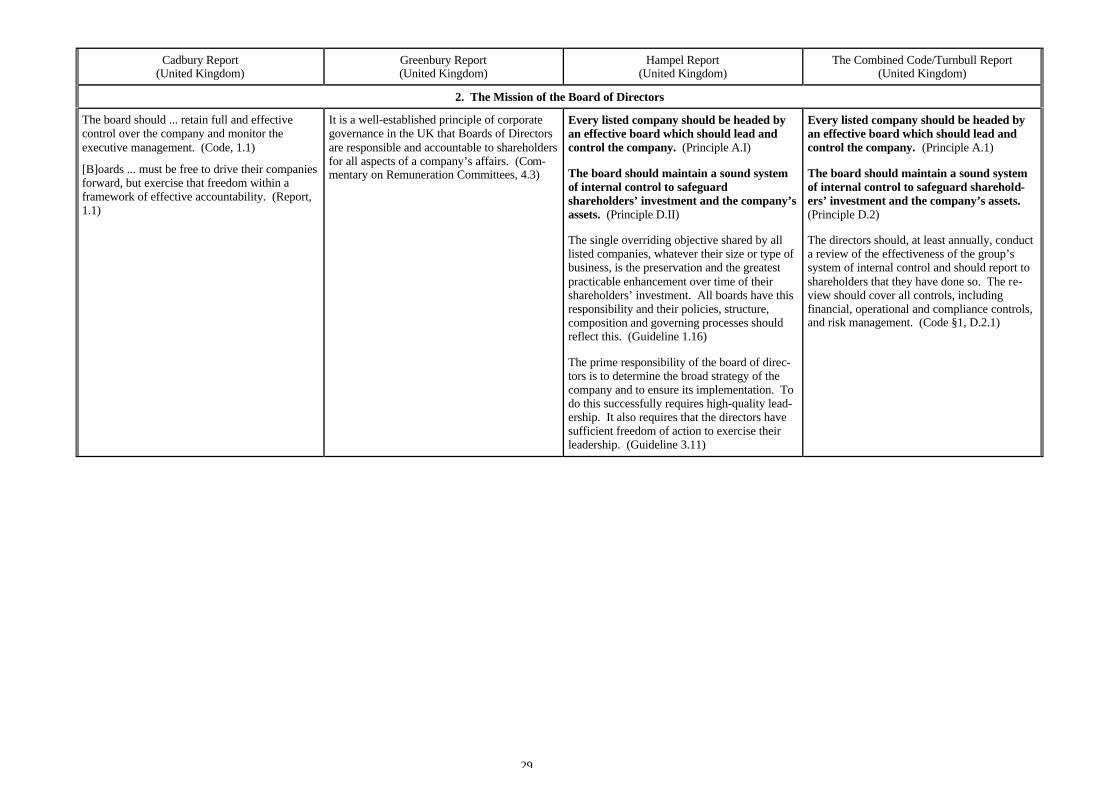

2. The Mission of the Board of Directors

The board should ... retain full and effectivecontrol over the company and monitor theexecutive management. (Code, 1.1)

[B]oards ... must be free to drive their companiesforward, but exercise that freedom within aframework of effective accountability. (Report,1.1)

It is a well-established principle of corporategovernance in the UK that Boards of Directorsare responsible and accountable to shareholdersfor all aspects of a company’s affairs. (Com-mentary on Remuneration Committees, 4.3)

Every listed company should be headed byan effective board which should lead andcontrol the company. (Principle A.I)

The board should maintain a sound systemof internal control to safeguardshareholders’ investment and the company’sassets. (Principle D.II)

The single overriding objective shared by alllisted companies, whatever their size or type ofbusiness, is the preservation and the greatestpracticable enhancement over time of theirshareholders’ investment. All boards have thisresponsibility and their policies, structure,composition and governing processes shouldreflect this. (Guideline 1.16)

The prime responsibility of the board of direc-tors is to determine the broad strategy of thecompany and to ensure its implementation. Todo this successfully requires high-quality lead-ership. It also requires that the directors havesufficient freedom of action to exercise theirleadership. (Guideline 3.11)

Every listed company should be headed byan effective board which should lead andcontrol the company. (Principle A.1)

The board should maintain a sound systemof internal control to safeguard sharehold-ers’ investment and the company’s assets.(Principle D.2)

The directors should, at least annually, conducta review of the effectiveness of the group’ssystem of internal control and should report toshareholders that they have done so. The re-view should cover all controls, includingfinancial, operational and compliance controls,and risk management. (Code §1, D.2.1)

30

NAPF Corporate Governance Code(United Kingdom)

AUTIF Code(United Kingdom)

Hermes Statement(United Kingdom)

PIRC Shareholder Voting Guidelines(United Kingdom)

2. The Mission of the Board of Directors

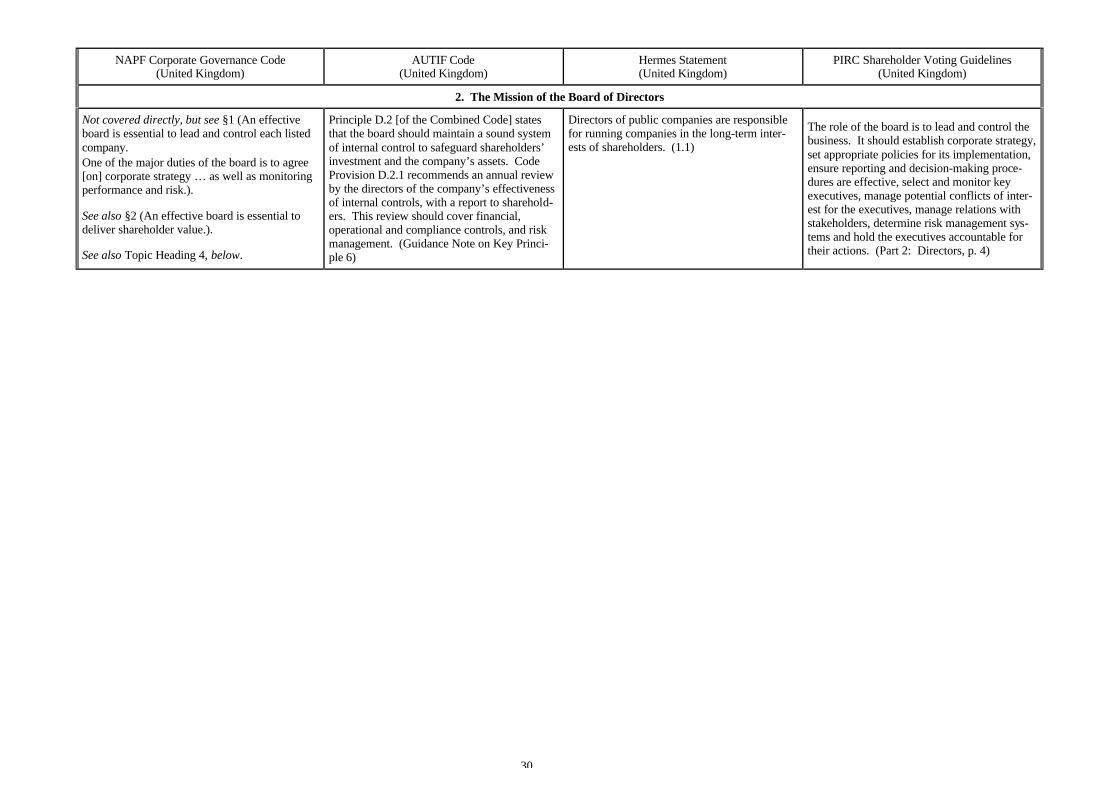

Not covered directly, but see §1 (An effectiveboard is essential to lead and control each listedcompany.One of the major duties of the board is to agree[on] corporate strategy … as well as monitoringperformance and risk.).

See also §2 (An effective board is essential todeliver shareholder value.).

See also Topic Heading 4, below.

Principle D.2 [of the Combined Code] statesthat the board should maintain a sound systemof internal control to safeguard shareholders’investment and the company’s assets. CodeProvision D.2.1 recommends an annual reviewby the directors of the company’s effectivenessof internal controls, with a report to sharehold-ers. This review should cover financial,operational and compliance controls, and riskmanagement. (Guidance Note on Key Princi-ple 6)

Directors of public companies are responsiblefor running companies in the long-term inter-ests of shareholders. (1.1)

The role of the board is to lead and control thebusiness. It should establish corporate strategy,set appropriate policies for its implementation,ensure reporting and decision-making proce-dures are effective, select and monitor keyexecutives, manage potential conflicts of inter-est for the executives, manage relations withstakeholders, determine risk management sys-tems and hold the executives accountable fortheir actions. (Part 2: Directors, p. 4)

31

OECD Principles/Millstein Report(International)

ICGN Statement/Global Voting Principles(International)

Euroshareholders Guidelines(Pan-European)

EASD Principles and Recommendations(Pan-European)

3. The Role of Stakeholders

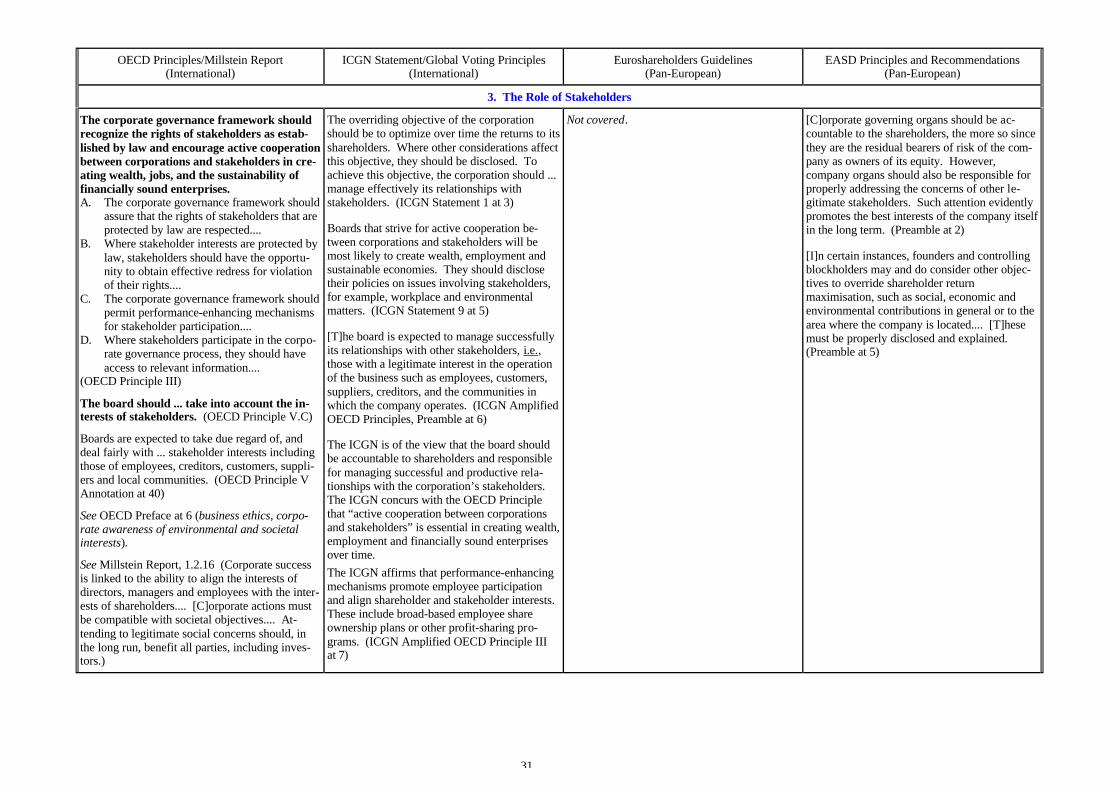

The corporate governance framework shouldrecognize the rights of stakeholders as estab-lished by law and encourage active cooperationbetween corporations and stakeholders in cre-ating wealth, jobs, and the sustainability offinancially sound enterprises.A. The corporate governance framework should

assure that the rights of stakeholders that areprotected by law are respected....

B. Where stakeholder interests are protected bylaw, stakeholders should have the opportu-nity to obtain effective redress for violationof their rights....

C. The corporate governance framework shouldpermit performance-enhancing mechanismsfor stakeholder participation....

D. Where stakeholders participate in the corpo-rate governance process, they should haveaccess to relevant information....