COMPANY PRESENTATION - Prosegur€¦ · COMPANY PRESENTATION 2019 This presentation contains...

68

COMPANY PRESENTATION INVESTOR RELATIONS DEPARTMENT 1

Transcript of COMPANY PRESENTATION - Prosegur€¦ · COMPANY PRESENTATION 2019 This presentation contains...

COMPANY

PRESENTATION

INVESTOR RELATIONS

DEPARTMENT

1

DISCLAIMER

COMPANY PRESENTATION 2019

This presentation contains forward-looking statements and information relating to

[Prosegur Compañía de Seguridad, S.A.] (the “Company”) and its subsidiaries

that are based on the current beliefs of the Company’s management, key

expectations and assumptions, as well as information currently available to the

Company and projections of future events as well as assumptions made and

information currently available to the Company. These forward-looking

statements speak only as of the date they are made. These forward-looking

statements are often, but not always, made through the use of words or phrases

such as “anticipate,” “believes,” “can,” “could,” “may,” “predicts,” “potential,”

“should,” “will,” “estimate,” “plans,” “projects,” “continuing,” “ongoing,” “expects,”

“intends,” and similar words or phrases. Other forward-looking statements can be

identified in the context in which the statements are made or by the forward-

looking nature of discussions of strategy, plans or intentions. Such forward-

looking statements, as well as those included in any other material discussed at

any management presentation, reflect the current views of the Company with

respect to future events and are subject to known and unknown risks,

uncertainties and key assumptions about the Company and its subsidiaries and

investments, including, among other things, the development of their businesses,

trends in their operating industry, and future capital expenditures. In light of

these risks, uncertainties and assumptions, the events or circumstances referred

to in the forward-looking statements may not occur. None of the future

projections, expectations, estimates or prospects in this presentation should be

taken as forecasts or promises nor should they be taken as implying any

indication, assurance or guarantee that the assumptions on which such future

projections, expectations, estimates or prospects have been prepared are

correct or exhaustive or, in the case of the assumptions, fully stated in the

presentation.

Many factors could cause the actual results, performance or achievements of

the Company and its subsidiaries to be materially different from any future

results, performance or achievements that may be expressed or implied by such

forward-looking statements, including, among others: changes in general

economic, political, governmental and business conditions globally and in the

countries in which the Company and its subsidiaries do business; changes in

interest rates; changes in inflation rates; changes in prices; trends affecting the

Company and its subsidiaries businesses, financial condition, results of

operations or cash flows; the impact of current, pending or future legislation and

regulation in countries in which the Company and its subsidiaries do business;

acquisitions, investments or divestments which the Company and its subsidiaries

may make in the future; the Company and its subsidiaries capital expenditures

plans; their estimated availability of funds; their ability to repay debt with

estimated future cash flows; security threats worldwide and losses of customer

valuables; failure to maintain safe work environments; effects of catastrophes,

natural disasters, adverse weather conditions, unexpected geological or other

physical conditions, or criminal or terrorist acts; public perception of the

Company and its subsidiaries businesses and reputation; insufficient insurance

coverage and increases in insurance cost; loss of senior management and key

personnel; unauthorized use of the Company’s intellectual property and claims of

infringement by the Company or its subsidiaries of others’ intellectual property;

changes in business strategy and various other factors. Should one or more of

these risks or uncertainties materialize, or should any other unknown risk occur,

or should any of the underlying assumptions prove incorrect, actual results may

vary materially from those described herein as anticipated, believed, estimated,

expected or targeted.

No one intends, or assumes any obligations, to update or revise these forward-

looking statements, whether as a result of new information, future events or

otherwise nor to update the reasons why actual results could differ from those

reflected in the forward-looking statements.

As a result of these risks, uncertainties and assumptions, you should not place

undue reliance on these forward-looking statements as a prediction of actual

results or otherwise.

Not for general release, publication or distribution, directly or indirectly, in

or into The United States, Canada, Australia or Japan or any other

Jurisdiction in which the distribution or release would be unlawful.

These materials do not constitute an offer to sell, or a solicitation of offers to

purchase or subscribe for any securities in the United States or any other

jurisdiction. The securities referred to herein have not been, and will not be,

registered under the U.S. Securities Act of 1933, as amended, and may not be

offered or sold in the United States absent registration or an applicable

exemption from registration requirements. There is no intention to register any

portion of any offering in the United States or to conduct a public offering of

securities in the United States.

2

COMPANY PRESENTATION FY 2019

ONEGROUP,THREEBUSINESSES

3

PROSEGUR GROUP

Prosegur: a success story

Since its foundation in 1976, Prosegur has grown to become one of the undisputable global leaders in the security

industry…

COMPANY PRESENTATION FY 2019

4

Expansion in LatAm & Europe

and Increase of services

portfolio

• Focus on Security: disposal of

FM and Cleaning businesses

• 2001: Full entry in LatAm and

France

• Creation of the Technology

Business Unit

• 2008: Entry into Mexico and

Colombia

1998

2008

2,052

Foundation and initial Expansion

• Incorporated in 1976

• 1980: Entry into Portugal

• 1987: Publicly Listed on Madrid

Stock Exchange

• 1995: Initiating activities in LatAm

1976

1997

480Consolidation of the integrated

model and expansion into Asia-

Pacific

• Specialization in Security Solutions

for different client sectors

• 2011: Entry into Singapore, India

and Germany

• 2012: Entry into China

• 2013: Rated BBB Stable by S&P.

Issuance of a € 500 million Bond and

Entry into Australia

2009

2014

3,783

Yearly revenues of last year in the period in €Million

Focus on Business Lines

Profitability and continual

expansion

• Reorganization of structure

around business lines vs.

geographies

• Initiated Global CyberSecurity

services business unit

• 2016: Entry in South Africa

• 2017: Prosegur Cash IPO

• 2018: Entry in Central America

& Philippines

• 2019: Entry in the US

• 2019: Entry in Indonesia

2015

2018

3,939

PROSEGUR TODAY

>9,000ARMOREDVEHICLES

>100,000MANAGEDATMS

+550,000 ALARMCONNECTIONS

OVER 220 FULLYINTEGRATED ACQUISITIONS

26COUNTRIES

+170,000EMPLOYEES WORLDWIDE

COMPANY PRESENTATION FY 2019

5

A GLOBAL SECURITY COMPANY WITH A LEADERSHIP POSITION IN FOCUS MARKETS

WE ARE MARKET LEADERS IN 17 OUT OF OUR 26 GEOGRAPHIES

Cash in transit & cash

management

Guarding and

technology

Alarm

Monitoring

Position in the market

share ranking

1

Prosegur Intl’ Player 1 Intl’ Player 2 Intl’ Player 3 Intl’ Player 4

#2

#3 #1

#4

#2

#1 #3

COMPANY PRESENTATION FY 2019

Source: DBK, Aproser and internal sources

6

CHINA

5

SINGAPORE

1

INDIA

2

PHILIPPINES

1

AUSTRALIA

2

GERMANY

1

TURKEY

n/a

FRANCE

3

PORTUGAL

1

SPAIN

1

SOUTH AFRICA

n/a

USA

n/a

CHILE

1

PERU

1

COLOMBIA

1

URUGUAY

1

ARGENTINA

1

PARAGUAY

1

BRAZIL

1

MEXICO

3GUATEMALA

HONDURAS

COSTA RICA

NICARAGUA

EL SALVADOR

1 INDONESIA

n/a

DELIVERING SUPERIOR GROWTH AND SHAREHOLDER RETURNS

CUMULATIVE DIVIDEND DISTRIBUTED 2004-2018:

€1,103m

€ 823m ordinary dividend

€ 280m extraordinary dividend (2017)

Figures in €m

(1) Market Cap in 2017 as of Dec. 2017 was 4.042 – Actual Market Cap €m reflects IPO of CASH Listed in 2017

COMPANY PRESENTATION FY 2019

Revenue (€m) Market Cap (€m) (1)EBIT (€m)

7

2004

3,939

2018

1,112+254.1%

+9.5%

85

301

2004 2018

+252.5%

+9.4%

895

20182004

2,728

+204.8%

+8.3%

Publicly

listed

in 2017

ORGANISATIONAL MODEL: “ONE GROUP, THREE BUSINESSES”

COMPANY PRESENTATION FY 2019

B CA

ONE GROUP, THREE BUSINESSES

PROSEGURCASH

PGA(Financial and support

functions)

PROSEGURSECURITY

RATIONALE

▪ Accelerate growth

▪ Increase specialization and efficiency

▪ Simplify the organisation

IMPLICATIONS / BENEFITS

▪ All businesses have reached the

maturity to be managed separately

▪ Different capital needs and KPIs

▪ Customer centric model across

regions

▪ Accelerates sharing of best practices

across regions

PROSEGURALARMS

8

A. CASH IS A SUCCESS STORY: A GLOBAL LEADER WITH

RESILIENT GROWTH AND STRONG CASH GENERATION

SALES*

€1,732 MM

EBIT Margin(%)*

15.5%

Countries / empl.

20 / 60,000

▪ #2 globally with 14% market share (vs. 7% in 2007)

▪ #1 in our focus Cash markets (14/20 countries)

▪ Leading scale, density and market share

▪ Outperforming the market (business has grown x4 in € sales

in the last 7 years)

▪ Solid fundamentals → already growing in new products and

capturing the next “outsourcing wave”

OUR BUSINESS

OUR OBJECTIVES

▪ Continue delivering above-market organic growth at constant

currency

▪ Lead industry consolidation player

▪ Lead the third wave of outsourcing (Cash Automation in Client,

IAD, Back Office Management, Branch Teller Staff, etc.)

▪ Strong cash generation to fuel Group’s growth

COMPANY PRESENTATION FY 2019

*FY18 business figures

9

▪ #5 global player with a leading position in selected markets

▪ Industry leading technology-based solutions

▪ Differentiated growth strategies for each market based on

development stage

▪ Expanding into mature markets with disruptive value proposition.

▪ Main player in LatAm leading the transformation of the industry

B. SECURITY IS A BUSINESS TO TRANSFORM AND GROW,

TO BECOME AN “INDUSTRY CHAMPION” AGAIN

SALES*€1,946 MM

EBIT Margin(%)*2.8%

Countries / empl.14 / 103,000

▪ Continue transformation towards technology-based products

▪ Improve margins → all geographies with profitability in line with peers

and Group’s best practices

▪ Grow and expand in US

▪ Complete integration of legacy businesses and operational

improvements in Brazil

▪ Build a solid “Cybersecurity” platform

COMPANY PRESENTATION FY 2019

OUR BUSINESS

OUR OBJECTIVES

10

*FY18 business figures

C. ALARMS IS A HIGH GROWTH AND HIGH RETURN BUSINESS

WHICH WE WANT TO ACCELERATE WITH ADEQUATE INVESTMENTS

SALES*

€262 MM

Total Connections*

547,000

Countries / empl.

10 / 7,000

• Unparalleled platform → significant investments undertaken over the

last 5 years to enter and reach critical mass in 10 countries

• Developed state-of-the-art products and launched next generation

alarm “SMART”

• Strengthened sales force, tripled from 2011

• Best in class and improving churn from 12% in 2011

• Rapid and consistent growth benefiting from low penetration in focus

markets

• Accelerate customer acquisition through investments in sales &

marketing (e.g., sales team, lead generation)

• Selective new geographies (big city approach)

• Continue to grow ARPU through penetration of SMART

• Roll out SMART product in all geographies

• Continue to improve churn levels

• Focus on product innovation to capture “the smart home” opportunity

OUR OBJECTIVES

OUR BUSINESS

COMPANY PRESENTATION FY 201911

*FY18 business figures

ONE

GROUP

PGA - CENTRALIZED EXTERNAL SUPPORT TO THE THREE BUSINESSES…

COMPANY PRESENTATION FY 2019

▪ Human Resources

▪ Finance/Tax

▪ Legal

▪ Security

▪ Corporate Development

▪ IT

▪ Real Estate

▪ Brand

▪ Insurance

▪ Purchase

▪ Marketing

CASH

Commercials & Operations

Cash Internal Support

SECURITY

Commercials & Operations

Security Internal Support

ALARMS

Commercials & Operations

Alarm Internal Support

SERVICES OFFERED

PGA – External support

5% Mark Up

PROSEGUR HOLDING

12

… SUPPORTED BY STABLE INVESTMENT GRADE RATINGS

BBB/A-2Outlook Stable

October 2019

SUSTAINED STRONG

LIQUIDITY PROFILE

EXCELLENT CASH FLOW GENERATION

WITH MODERATE CAPITAL EXPENDITURE

AND WORKING CAPITAL REQUIREMENTS

MINIMAL TRAPPED CASH

ACROSS OPERATIONS

MODERATE

LEVERAGE

13COMPANY PRESENTATION FY 2019

COMPANY PRESENTATION 2019

PROSEGUR

Leading the consolidation process

of the Cash industry while fueling

the Group’s growth

CASH

14

628 677

806 840

10171083

11701231

2006 2012

913

2007 201320102008 2009 2011 2014 2015 2016 2017 2018

763

889956

11265.8%

4549 50

58 6064

73 74

20162006 2007 2008 20172009 2010 2011 2012 2013 2014 20182015

37 38

52 55

685.9%

853 888 942

11981299

1463 1571

20072006 2015

1380

20142008 2009 2010 20122011 2013 2016 2017

1127

2018

784 792

1035

1672

6.5%

101 113147 158

199215

297 309

2006 2009

220

2007 2008 201320122010 2011 2014 2015 2016 2017 2018

128

183

84

27011.5%

CASH, STRONG GROWTH OF THE UNDERLYING DRIVER…

COMPANY PRESENTATION FY 2019

15

Source:2019 Central Banks data, IE Economics. Trade Economics 2019

BRL

EUR USD

GBP

Despite the growing penetration of alternative payment methods, cash in circulation is a constant growing figure in all

economies, representing in 2019 more than 85% of total World transactions. (Source 2018 World Cash Report & Central Banks reports)

■ In Europe (ECB Diary Study), cash represents 78.8% of all transactions in volume and 53.8% in value.

USE OF CASH IN TERMS OF VALUE (MN)

…BOOSTS THE GROWTH OF THE CASH SECTOR, ALTHOUGH AT DIFFERENT LEVELS IN EACH REGION

CASH MARKET SIZE

(USD BN)

+4.4%

2015 2020

Main characteristics of attractive markets:

(i) Growing economies;

(ii) Moderated elevated inflation and interest rates;

(iii) Certain level of insecurity;

(iv) Degree of sophistication of banking sector

EXPECTED GROWTH BY

GEOGRAPHY 2015-2020

Africa &

Middle East

Latam

US & Canada

Asia Pacific

Europe

4

(26%)

4.7

(31%)

2.7

(18%)

2.4

(16%)

1.4

(9%)

COMPANY PRESENTATION FY 2019

8.3%

5.6%

4.0%

2.1%

1.6%

15.2

18.8

Source: Freedonia 2017 report

16

37%

22%

7%

13%

17%

4%

40%

20%

14% 13%

9%

5%

40%

20%

14% 13%

9%

4%

2007 2015 2018

20%

14%

13%

9%4%

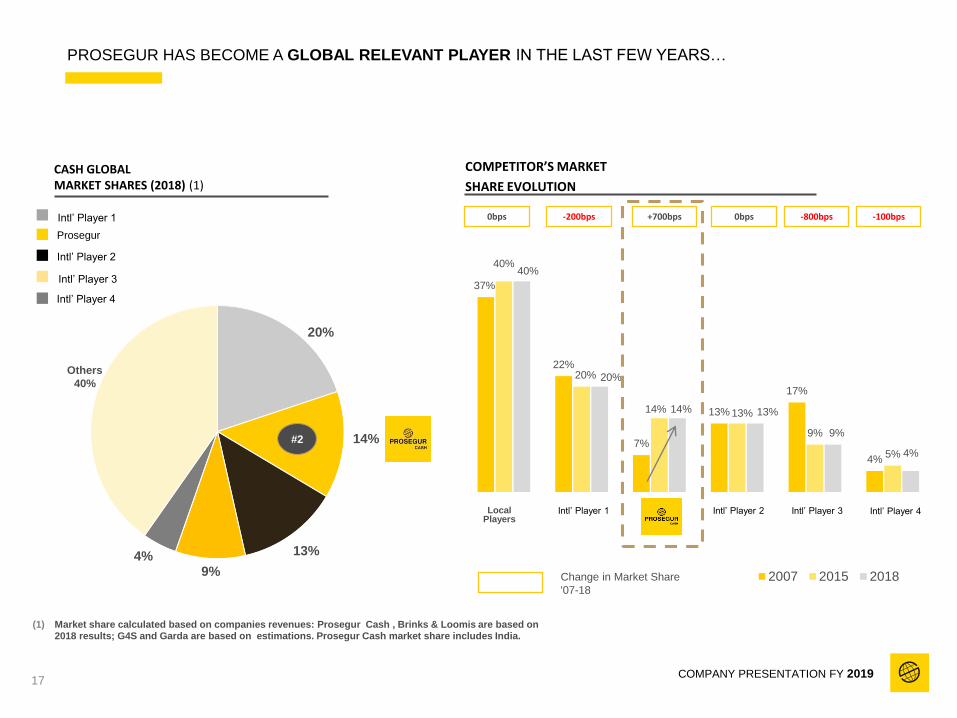

CASH GLOBAL MARKET SHARES (2018) (1)

COMPETITOR’S MARKET

SHARE EVOLUTION

(1) Market share calculated based on companies revenues: Prosegur Cash , Brinks & Loomis are based on 2018 results; G4S and Garda are based on estimations. Prosegur Cash market share includes India.

#2

Local Players

Change in Market Share

'07-18

Others

40%

PROSEGUR HAS BECOME A GLOBAL RELEVANT PLAYER IN THE LAST FEW YEARS…

0bps -200bps +700bps -800bps -100bps0bps Intl’ Player 1

Prosegur

Intl’ Player 2

Intl’ Player 3

Intl’ Player 4

Intl’ Player 1 Intl’ Player 2 Intl’ Player 3 Intl’ Player 4

COMPANY PRESENTATION FY 201917

2018 MARKET SHARE

PROSEGUR

▪ Undisputed market leader in LatAm –

leadership position in fastest growing

markets

▪ Benefitting from growing security market

▪ Relying on its strong density, reputation,

brand and close relationship with clients

▪ Solid presence in key European countries

▪ Expected to be the fastest growing

economies in the area

▪ Growing footprint in Asia / Africa

▪ Highest Cash market growth regions

globally

Latam

Africa & Middle East

Europe

Asia Pacific

US and Canada

PROSEGUR CASH GLOBAL FOOTPRINT#2 GLOBAL MARKET POSITION

COMPANY PRESENTATION FY 2019

…WITH STRONG POSITIONS IN EACH OF THE LOCAL MARKETS

0%

10%

57%

10%

4%

# Market positioning

Cash in transit & cash management

Source: Freedonia 2017, DBK, Aproser and internal sources.

18

• GUATEMALA

• HONDURAS

• COSTA RICA

• NICARAGUA

• EL SALVADOR

1

MEXICO

3

CHILE

1

PERU

1

ARGENTINA

1

URUGUAY

1 PARAGUAY

1

BRAZIL

1

SPAIN

1

GERMANY

1

PHILIPPINES

1INDIA

2

AUSTRALIA

2

PORTUGAL

2

COLOMBIA

2

INDONESIA

n/a

DENSITY & SCALE AND PRODUCTIVITY GAINS: SEARCH FOR CONTINUOUS MARGIN IMPROVEMENT

1. DENSITY & SCALE

COMPANY PRESENTATION FY 2019

Prosegur Cash Market Share in

selected markets (%)

Pro

seg

ur

Ca

sh

EB

IT M

arg

in (

%)

19

2015 2016 2017 2018

2015 2016 2017 2018

382 382 428 340

282 314 360 268

21.9%

13.3%

22.2%

14.8%

22.2%

16.0%

19.7%

15.1%

18.0%

7.5%

18.6%

9.1%

18.7%

10.2%

15.5%

10.2%

EBIT EBIT Margin Peers Average

2. EBITDA (€m) and EBITDA margin (%)

Positive correlation

between market share

and profitability

• Leadership position in focus regions

• Footprint optimisation / higher density

• Profitability programs and best

practices

• Shift in revenue mix towards more

value added cash services

EBIT (€m) and EBIT margin (%)

EBITDA EBITDA Margin Peers Average

FOR THE FUTURE: UNPARALLELED POSITIONING TO BENEFIT FROM THREE KEY GROWTH LEVERS

COMPANY PRESENTATION FY 2019

Today Traditional market growth

(Organic)Consolidation play

(inorganic)

Third Wave of

Outsourcing

Third Wave of

Outsourcing

1 2 3

Source: IMF Nominal GDP forecast from 2016 – 2019. Expected growth calculated as a weighted average between our sales and the expected GDP

EXPECTED GROWTH

IN OUR FOOTPRINT1

CAGR

7.7%

2015 2020

> 500 CASH COMPANIES

GLOBALLY2

Room for further

consolidation

#14#7 #16#13#6 #9 #10 #11#8 #15#12#3 #4 #5#2 #17 #18 #19 #20 …#1

Cash automation in clients

OUTSOURCING

OPPORTUNITIES3

Back office management

IAD (Independent ATM

Deployer)

Branch teller staff

20

OUTSOURCING OPPORTUNITIES

Eff

icie

nc

ies

Business process outsourcing

BRANCH TELLER

STAFFBACK OFFICE

MANAGEMENT

IAD

(INDEPENDENT ATM

DEPLOYER)

ATM MGMT.

▪ Maintenance

▪ Fixing

▪ Replacement

▪ Full lifecycle

CASH PLANNING &

FORECASTING

▪ Branch Network

▪ Displaced ATMs

COMPANY PRESENTATION FY 2019

CASH LOGISTICS & PROCESSING

• Bank Branches

• ATMs

• Retail Clients

• Central Bank

Third wave of outsourcing

DAILY RECONCILIATION

▪ Incidence Mgmt.

▪ Branch Network

▪ Central Services

CASH AUTOMATION IN CLIENTS

21

PROSEGURSECURITYMoving from manned guarding

to technological solutions

COMPANY PRESENTATION FY 2019

22

PROSEGURSECURITYMoving from manned guarding

to technological solutions

2015 2020

SECURITY GLOBAL MARKET

EVOLUTION ($BN)

125

SECURITY GLOBAL MARKET SHARES

(2018)

KEY MARKET TRENDS

Commoditization, due to its low capital intensity and entry barriers. Competitiveness intensification and

considerable price pressure impacting margins, even with Facility Management companies

Increase in staff turnover, scarcity of qualified personnel. Increasing labor pressure

Budgeting restrictions in Public Sector

Double market:

▪ Client sophistication. Every time the client knows more and it gets more difficult to add value

▪ Stagnant sector that keeps the same criteria for some years and is into a mature phase

-

--

-

8%

6%

5%

4%2%

Others75%

Player 1

Player 2

Player 3

Player 4

Prosegur

Source: Freedonia 2017 report and internal

company data

LARGE MARKET WITH TECHNOLOGY AS A CATALYST

FOR FUTURE GROWTH

+

+

+

+

+

+6.1%

Increasing outsourcing from Public Sector and higher development of services to companies in

emerging countries

Design of integral offers that combine electronic systems with traditional guarding services improving

revenue mix

Intensive use of technology and its combination with human factor

Trend towards mobile services (dynamic guarding/patrolling) as an alternative

Growing market, with significant potential in emergent countries

168

23

COMPANY PRESENTATION FY 2019

PROSEGUR SECURITY HAS GLOBAL PRESENCE ACROSS LATAM, ASIA, EUROPE AND US

EMPLOYEES *

PROSEGUR SECURITY GLOBAL FOOTPRINT

#5 GLOBAL MARKET POSITION

SPAIN

BRAZIL

MEXICO

COLOMBIA

CHILE

ARGENTINA

URUGUAY

PORTUGAL

FRANCE

CHINA

PERUPARAGUAY

SINGAPORE

COMPANY PRESENTATION FY 2019Source: internal data

24

USA

* OPERATIONAL PERSONAL ONLY

Argentina

5,1%

Peru

Brazil

France

24,8%Spain

Colombia

Portugal

USA

11,4%

Chile

Mexico

Paraguay

Singapore

Uruguay

China

5,9%

26,1%

7,3%

8,3%

0,7%

4,7%

4,2%

2,5%

1,9%

1,4%

0,8%

27%

18% 17%12% 9% 9% 7% 6% 6% 4% 4% 1% 0% 1%

17%40%

16%22%

11% 9%

3%9%

3%

17% 15%28%

23%

56%

42%

67% 66%

80% 82%90%

85%91%

79% 81%

99% 100%

49%

Local Players

Largest National Player

Intl´ Players

Prosegur

WITH A LEADING POSITION IN SELECTED MARKETS ENABLING A SIGNIFICANT OPPORTUNITY

FOR CONSOLIDATION

GUARDING MARKET SHARES (%)

COMPANY PRESENTATION FY 2019Source: DBK, Investors presentations, internal estimates

25

Spain Uruguay Portugal Argentina Colombia Peru Brazil Paraguay Singapore Chile France Mexico China EEUU

#1 #2 #2 #2 #1 #2 #1 N.A. #2 N.A. #3 #7 N.A. N.A.

PROSEGUR’S SECURITY BUSINESS MODEL

IS BASED ON THREE KEY LEVERS

COMPANY PRESENTATION FY 2019

TECHNOLOGICAL

TRANSFORMATION

▪ Value proposition to client; moving

towards integrated solutions with

technology

HIGHER MARGIN

PRODUCTS

▪ Moving towards a high margin

product portfolio

STREAMLINING

▪ Size reduction

▪ Efficiency implementation

▪ Growth recovery

▪ Margin expansion

26

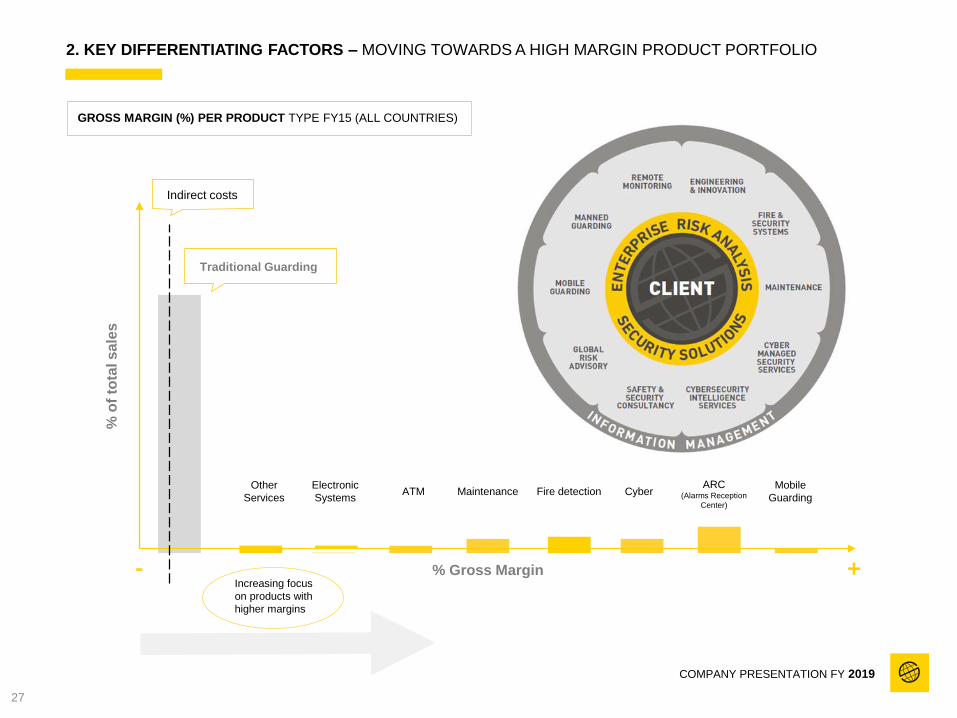

2. KEY DIFFERENTIATING FACTORS – MOVING TOWARDS A HIGH MARGIN PRODUCT PORTFOLIO

GROSS MARGIN (%) PER PRODUCT TYPE FY15 (ALL COUNTRIES)

COMPANY PRESENTATION FY 2019

% Gross Margin

% o

f to

tal s

ale

s

Other

Services

Electronic

SystemsATM Cyber

ARC(Alarms Reception

Center)

Mobile

GuardingMaintenance Fire detection

Indirect costs

Increasing focus

on products with

higher margins

Traditional Guarding

+-

27

PROSEGUR ALARMS

Betting on growth

and shaping

the future

COMPANY PRESENTATION FY 2019

28

ALARMS MARKET: SIGNIFICANTLY UNDERPENETRATED

ALARMS PENETRATION

RATES BY COUNTRY (%)

▪ World market is under-penetrated

▪ US is the most penetrated market globally and has only 20%

penetration

▪ Prosegur core markets are all <10% penetration

▪ Sales and marketing are the main drivers of penetration →

enormous growth potential that requires strong sales force

and investment

% of households with a connected alarm

COMPANY PRESENTATION FY 2019

29

ALARMS MARKET: FROM SINGLE DIGIT TO DOUBLE DIGIT GROWTH IN FOCUS REGIONS

COMPANY PRESENTATION FY 2019

PROSEGUR’S FOCUS REGIONS

EXPECTED TO LEAD THIS GROWTHGLOBAL ALARM MONITORING MARKET ($BN)

EXPECTED TO GROW AT 5.0% P.A.

CAGR:

5.0%

44

58

KEY DRIVERS

• Increasing role of crimes and

burglaries

• Rapid implementation of home

automation and security systems

• Integration of biometric technology in

smartphones

Alarm monitoring market

2015-20 CAGR Revenue expected growth by Region

2015 2020

8.35%

5.03%

4.12%

1.93%

1.67%

LATAM

Asia Pacific

World

North America

Western Europe

Source: Freedonia report 2017

30

2015 2020

75

2025

Installation

Revenues

Product

cost

Installation

cost

Sales cost

Marketing

cost

ALARMS: A DIFFERENT BUSINESS MODEL, SIGNIFICANT VALUE CREATION

VERY ATTRACTIVE RETURNS WITH UPFRONT CAPITAL REQUIREMENTS

CLIENT CONTRACT CASH FLOW

ARPU

Year 0

Operating costs (Including monitoring,

customer care, maintenance,...)

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 … Year N

Average life-cycle

▪ Payback period over

4 years

▪ Average subscription

period of 10 years

▪ Increasing ARPU on local

currency basis

▪ Very attractive returns

with upfront capital

requirements

COMPANY PRESENTATION FY 2019

31

…

1. KEY DIFFERENTIATING FACTORS – PRODUCT (1/2)

B2C(residential

& small

business)

PORTFOLIO OF PRODUCTS OFFERING A FULL RANGE OF SOLUTIONS ADAPTED TO CLIENTS’ NEEDS

B2B(transferred

to Security) ▪ Complex CCTV

systems

▪ Complex hybrid

and wired

systems

COMPANY PRESENTATION FY 2019

▪ Anti-theft systems,

▪ Smoke screen

2010

2015

2020▪ Wireless System

(video-verification)

▪ Professional

Hybrid & Wired

Solutions

▪ Video in the

Cloud

▪ Professional

CCTV Solutions

VIDEO

▪ Vehicle Security

Systems

▪ Mobile E-Health

Solutions ‘Smartlife’

▪ Internet of

Things applied

to security

HOME

AUTOMATION

32

2018

2012

▪ SMART solutions

for Technology-

Security integration

E-HEALTH

HAWK

EYE

INCLUSION

LOCATION▪ Intelligent security

services

1. KEY DIFFERENTIATING FACTORS – PRODUCT (2/2)

SMART PLATFORM AS THE CORE TOOL TO INTERACT WITH OUR CLIENTS

AND BUILD LOYALTY

SMART PLATFORM

▪ SMART: Platform to interact with our clients which builds loyalty

▪ Launched in 2016

▪ Productivity increase: Lower service costs

▪ Churn reduction: Connected clients have lower churn rates

(empirically proven 2-4% below average)

COMPANY PRESENTATION FY 2019

▪ Protection: In case of need, we send our response teams to

provide protection

▪ Police: Critical in those countries where Police does not have

the resources to provide reliable response

▪ Even in countries where Police provides a response we

provide value added services

RESPONSE

33

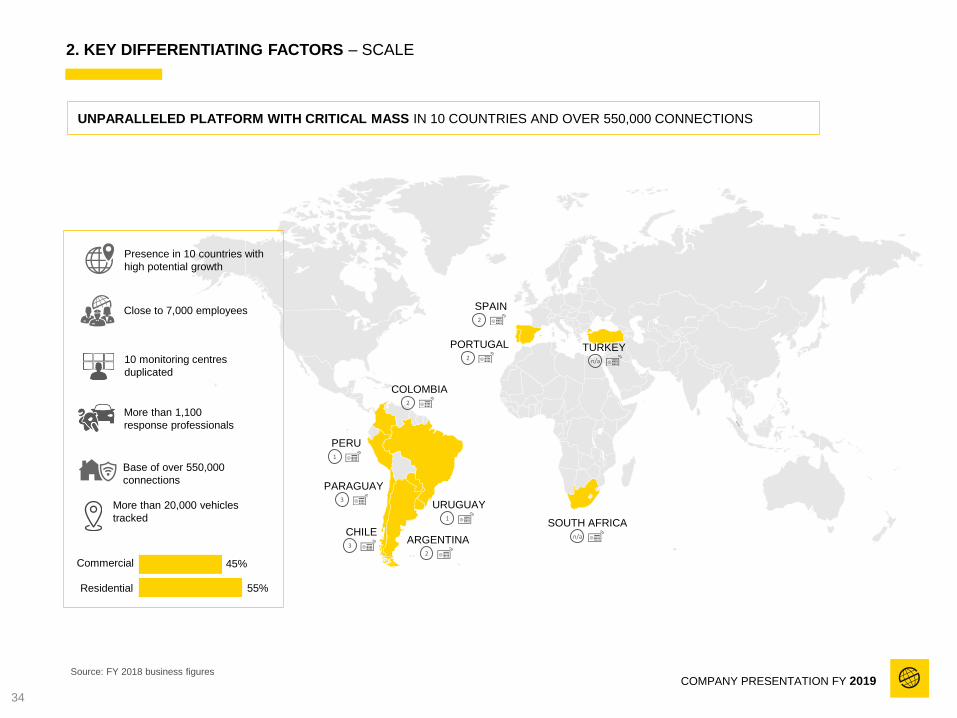

2. KEY DIFFERENTIATING FACTORS – SCALE

UNPARALLELED PLATFORM WITH CRITICAL MASS IN 10 COUNTRIES AND OVER 550,000 CONNECTIONS

COMPANY PRESENTATION FY 2019

Close to 7,000 employees

Presence in 10 countries with

high potential growth

10 monitoring centres

duplicated

More than 1,100

response professionals

Base of over 550,000

connections

Commercial

Residential

45%

55%

Source: FY 2018 business figures

34

More than 20,000 vehicles

tracked

TURKEY n/a

COLOMBIA2

PORTUGAL2

SPAIN2

ARGENTINA2

SOUTH AFRICAn/a

URUGUAY1

PERU1

PARAGUAY3

CHILE3

SOLID FINANCIAL PERFORMANCE BEING THE FASTEST GROWING

BUSINESS LINE WITHIN THE GROUP DRIVEN BY OUR FOCUS TO

INCREASE OUR CUSTOMER BASE

CUSTOMER BASE EVOLUTION

(# CONNECTIONS)

AVERAGE REVENUE

PER UNIT (ARPU)

2013 2014 2015 2016 2017

36.8 3538

36

38

Ø 36.5

+11.4%

35

355389

424

499547

2014 2015 2016 2017 2018 2018

36

▪ Net additions Increment of 10%

over same period in 2017

▪ Growth still over industry

average despite Argentina

slowdown

▪ Recurrent quota remains in line in the

long term despite the adverse macro

economic environment in Ibero-America

▪ Positive evolution in local currency

terms

COMPANY PRESENTATION 2019

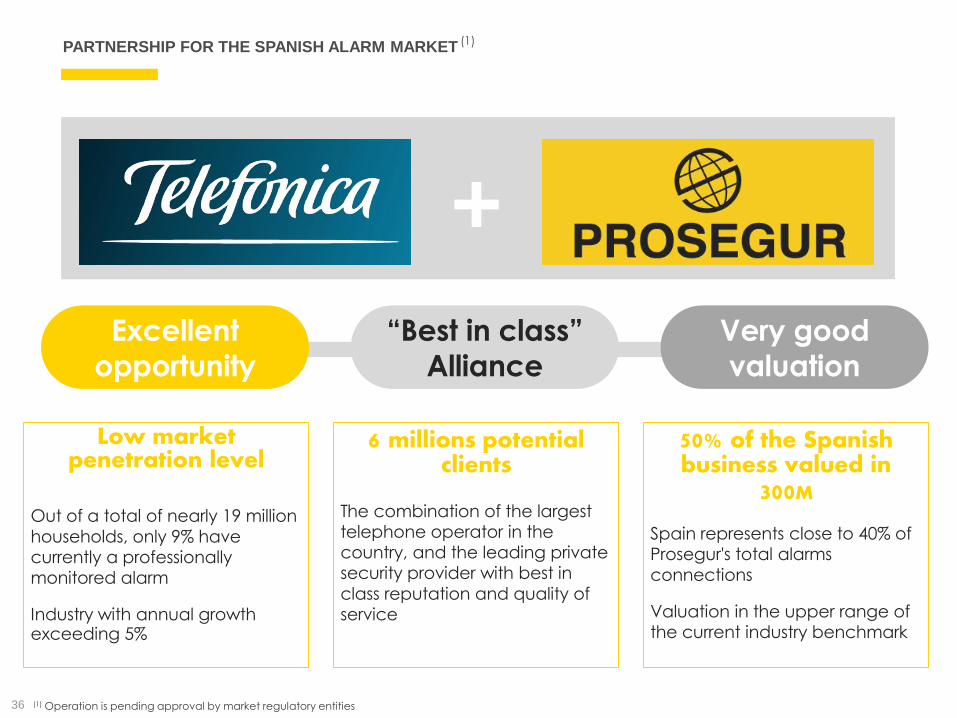

Excellent

opportunity

Low market penetration level

Out of a total of nearly 19 million

households, only 9% have currently a professionally monitored alarm

Industry with annual growth exceeding 5%

“Best in class”

Alliance

6 millions potential clients

The combination of the largest telephone operator in the country, and the leading private security provider with best in

class reputation and quality of service

Very good

valuation

50% of the Spanish business valued in

300M

Spain represents close to 40% of Prosegur's total alarms

connections

Valuation in the upper range of the current industry benchmark

(1) Operation is pending approval by market regulatory entities

(1)PARTNERSHIP FOR THE SPANISH ALARM MARKET

+

36

EnvironmentalSocialGovernance

COMPANY PRESENTATION FY 2019

37

+2 MILLIONHOURSOF TRAINING DELIVERED

+1,000PROFESSIONALS WITH DISABILITIES

+170,000PROFESSIONALS

+€12.MMINVESTED INTRAINING

We ensure the utmost respect for

the principle of equal treatment.

We take no risks when it comes to

safeguarding the physical safety

and integrity of our

professionals, raising their image

and profiles.

THE BEST HUMAN TEAM

COMPANY PRESENTATION FY 201938

+200 COLLECTIVE

BARGAING AGREEMENTS

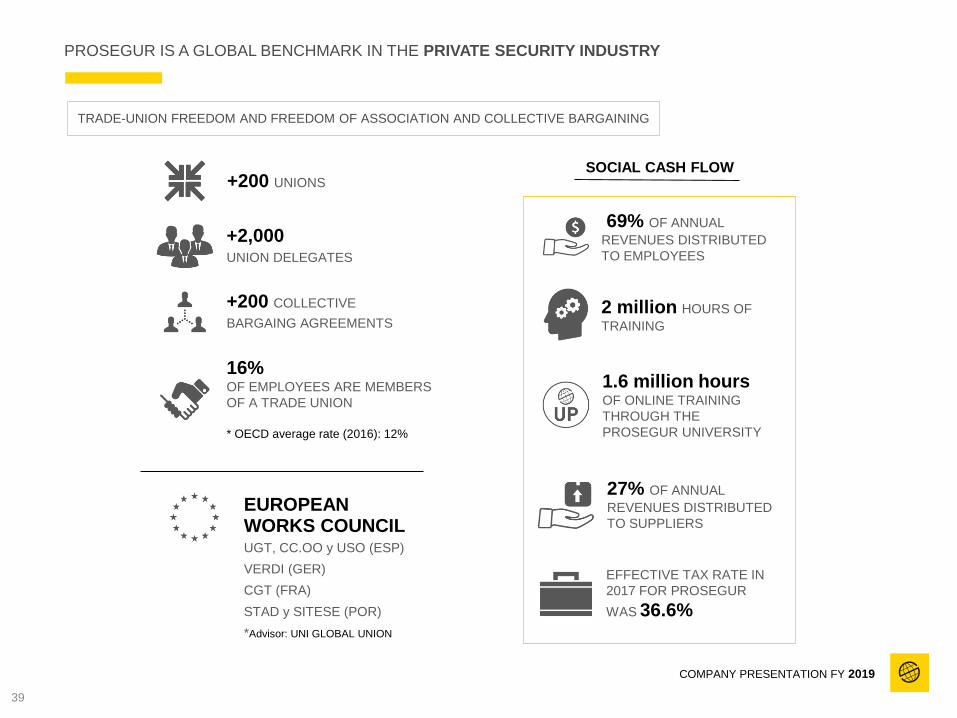

PROSEGUR IS A GLOBAL BENCHMARK IN THE PRIVATE SECURITY INDUSTRY

TRADE-UNION FREEDOM AND FREEDOM OF ASSOCIATION AND COLLECTIVE BARGAINING

+200 UNIONS

+2,000UNION DELEGATES

16%OF EMPLOYEES ARE MEMBERS

OF A TRADE UNION

* OECD average rate (2016): 12%

EUROPEAN WORKS COUNCILUGT, CC.OO y USO (ESP)

VERDI (GER)

CGT (FRA)

STAD y SITESE (POR)

*Advisor: UNI GLOBAL UNION

69% OF ANNUAL

REVENUES DISTRIBUTED

TO EMPLOYEES

27% OF ANNUAL

REVENUES DISTRIBUTED

TO SUPPLIERS

2 million HOURS OF

TRAINING

1.6 million hours OF ONLINE TRAINING

THROUGH THE

PROSEGUR UNIVERSITY

EFFECTIVE TAX RATE IN

2017 FOR PROSEGUR

WAS 36.6%

SOCIAL CASH FLOW

COMPANY PRESENTATION FY 2019

39

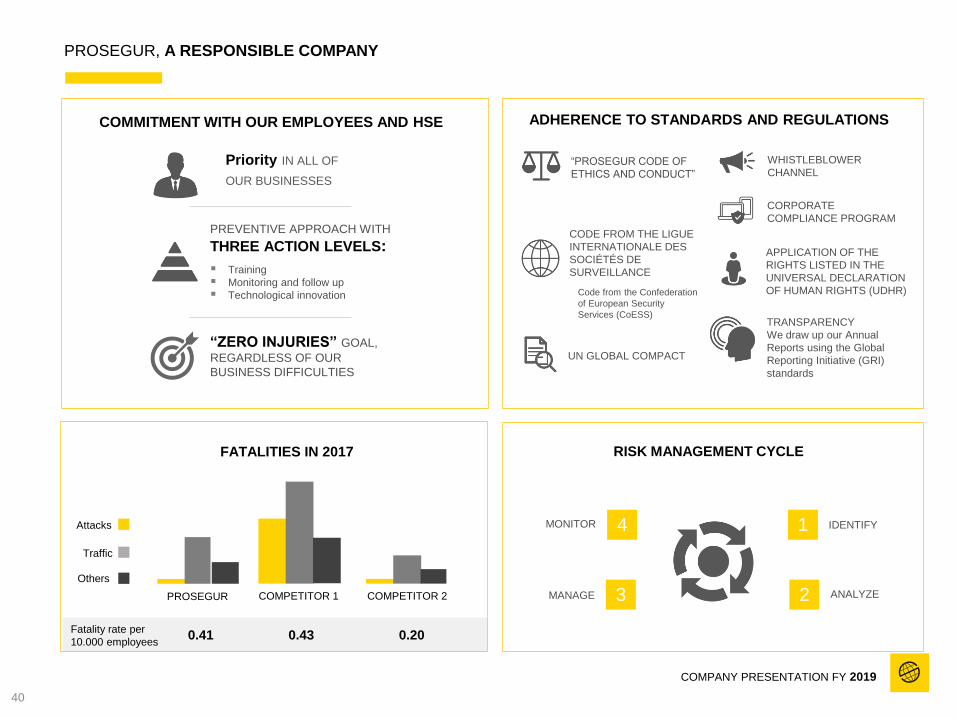

PROSEGUR, A RESPONSIBLE COMPANY

COMMITMENT WITH OUR EMPLOYEES AND HSE

PROSEGUR COMPETITOR 1 COMPETITOR 2

Fatality rate per

10.000 employees0.41 0.43 0.20

Attacks

Traffic

Others

FATALITIES IN 2017

ADHERENCE TO STANDARDS AND REGULATIONS

Priority IN ALL OF

OUR BUSINESSES

“ZERO INJURIES” GOAL,

REGARDLESS OF OUR

BUSINESS DIFFICULTIES

PREVENTIVE APPROACH WITH

THREE ACTION LEVELS:

▪ Training

▪ Monitoring and follow up

▪ Technological innovation

RISK MANAGEMENT CYCLE

4MONITOR

3MANAGE

1 IDENTIFY

2 ANALYZE

“PROSEGUR CODE OF

ETHICS AND CONDUCT”

CODE FROM THE LIGUE

INTERNATIONALE DES

SOCIÉTÉS DE

SURVEILLANCE

Code from the Confederation

of European Security

Services (CoESS)

UN GLOBAL COMPACT

WHISTLEBLOWER

CHANNEL

CORPORATE

COMPLIANCE PROGRAM

APPLICATION OF THE

RIGHTS LISTED IN THE

UNIVERSAL DECLARATION

OF HUMAN RIGHTS (UDHR)

TRANSPARENCY

We draw up our Annual

Reports using the Global

Reporting Initiative (GRI)

standards

COMPANY PRESENTATION FY 2019

40

WE ARE COMMITTED TO PEOPLE

COMPANY PRESENTATION FY 2019

Prosegur Foundation channels the company’s

social and cultural activities to help build a

more giving society while generating

opportunities for personal development, thus

making tangible our commitment to contribute

to the development of the regions the Group

operates in.

Our institution works to educate and improve

the job prospects of people with intellectual

disabilities and is also involved in corporate

volunteering and cultural outreach

We develop our own projects that are

sustainable, transparent and replicate best

practices

F O U N D A T I O N

P R O S E G U R

46PIECITOS COLORADOS SCHOOLS

4FIELDSOF ACTION

10COUNTRIES

34PROJECTS COMPLETED IN 2018

€3MM INVESTED

IN 2018

+43,000BENEFICIARIES IN 2018

41

9M 2019

FINANCIAL INFORMATION

COMPANY PRESENTATION FY 201942

43

P&L

Consolidated ResultsFY

2018

9M 2018

9M 2019

%

Variation

Sales 3,939 2,829 3,098 9.5%

EBITDA 456 332 378 14.0%

Margin 11.6% 11.7% 12.20%

Depreciation (129) (90) (129)

EBITA 327 242 249 3.2%

Margin 8.3% 8.6% 8.0%

Amortization of intangibles (26) (18) (21)

EBIT 301 224 228 2.2%

Margin 7.7% 7.9% 7.4%

Financial result (21) 13 (45)

Profit before Taxes 280 237 183 (22.7)%

Margin 7.1% 8.4% 5.9%

Taxes (100) (82) (65)

Tax rate 35.7% 34.7% 35.7%

Net Profit 180 155 118 (23.9)%

Minority Interests 48 39 35

Consolidated Net Profit 132 116 83 (28.3)%

Earnings per share(Euros per share)

0.2 0.19 0.14

• Excellent growth in local currency

close to 15%

• Comparable IAS 21&29 impact

• Profitability positively affected by recent divestments

!

9M 2018

2,829+7.8%

Org

+7.1%

Inorg

-5.4%

FX(1) 9M 2019

3,098

+9.5%

Amounts in Eur. millions - 2018 & 2019 figures have been elaborated applying IAS 21 & 2 9, additionally 2019 figures also include the application of IAS16 - (1) Includes exchange rate effect and IAS 21 & 29

44

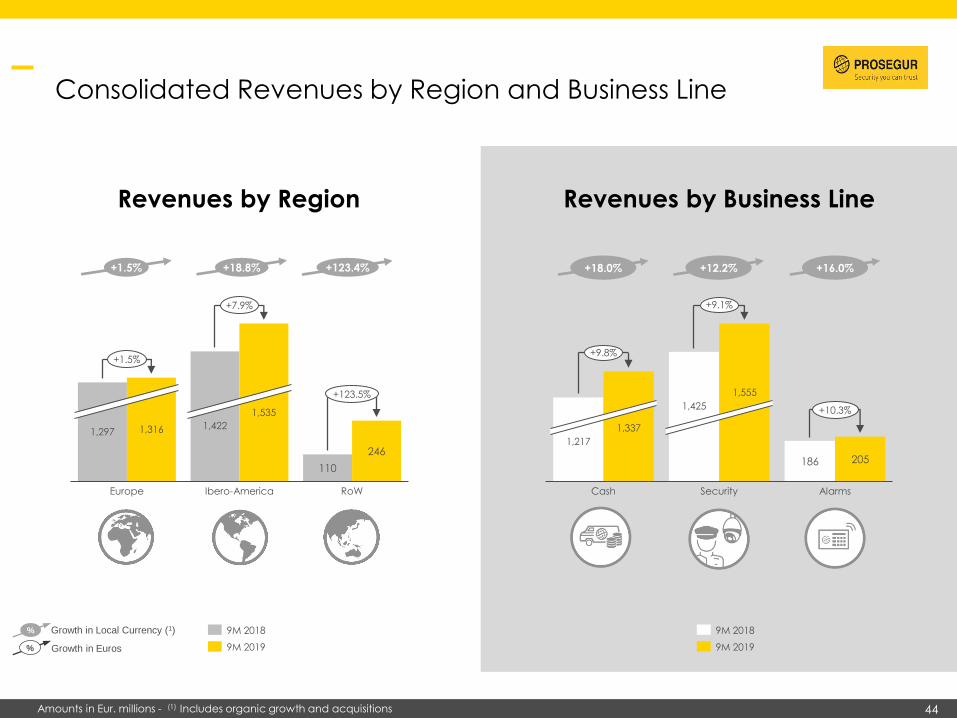

Consolidated Revenues by Region and Business Line

110

246

1,297 1,316

Europe

1,422

1,535

Ibero-America RoW

+1.5%

+7.9%

+123.5%

186 205

1,217

1,337

AlarmsCash

1,425

1,555

Security

+9.8%

+9.1%

+10.3%

9M 2018

9M 2019

% Growth in Local Currency (1)

% Growth in Euros

+18.0% +12.2% +16.0%

Revenues by Business LineRevenues by Region

+1.5% +18.8% +123.4%

9M 2018

9M 2019

Amounts in Eur. millions - (1) Includes organic growth and acquisitions

Amounts in Eur. millions - (1) Includes organic growth and acquisitions

45

+6.3%

+11.7%

9M

2018

Org Inorg

-8.2%

FX(1) 9M

2019

1,217

1,337

+9.8%

PROSEGUR CASH

198213

9M 2019

15.9%16.3%

9M 2018

+7.3%

• New products reach 16.0% of total sales in 9M 2019

• Sales of NPs grew by 52% in euros fueled by Smart Cash, AVOS and ATMs

• Continuous improvement of stand-alone quarterly margins

• Divestments in South Africa and

France partially compensate

the negative effect FX

• 18% growth in local currency

• 9.8% growth in Euro terms

• Positive contribution in all

markets except Australia

Revenues Profitability New Products

!EBIT

EBIT Margin

FY 2016 FY 2017 9M 2019FY 2018

6.4%

8.7%

11.8%

16.0%

+420 bps

Amounts in Eur. millions - (1) Includes exchange rate effect and IAS 21 & 29

46

PROSEGUR SECURITY

• Increased penetration of

“Integra” Solutions reaching

27.2% of current client portfolio

• Spain leads growth

• Profitability affected by the

IAS21&29 impact in Argentina,

integration of acquisitions in USA

and reorganization in France

• Growth in local currency above

12%

• Strong inorganic growth close to

9% driven by USA

Revenues Profitability(2) New Products(3)

!

1,425 +3.5%

9M

2018

Org Inorg

+8.7%

FX(1)

-3.1%

9M

2019

1,555

+9.1% 3934

9M 2019

2.7%

9M 2018

2.2%

-12.5%

EBIT Margin

EBIT

9M 2019FY 2016 FY 2017 FY 2018

17.0%20.0%

23.0%

27.2%

+420 bps

Amounts in Eur. millions - (1) Includes exchange rate effect and IAS 21 & 29 - (2) Profitability in Security excluding Overhead Costs - (3) Excludes USA

47

PROSEGUR ALARMS

Amounts in Eur. millions - Installed base in thousands of connections - ARPU in Euros - (1) Includes exchange rate effect and IAS 21 & 29

• Installed base increase of 3.6%

over the same period of 2018

• Affected by both macro and

strategic focus on quality of client

portfolio

Installed Base

• ARPU of € 36 per month maintained despite the strong

adverse FX.

• Penetration of “Smart” Platform

exceeding 23% of the installed base

ARPU

• Growth of more than 10% in Euros

and 16% in local currency

• Duplicating the average global

growth of the sector

Revenues

9M

2018

Inorg

+16.0%

Org

-5.7%

FX(1) 9M

2019

186

+0.0%

205

+10.3%

424

499

547 539559

2017 9M

2018

2016 2018 9M

2019

+3.6%+13.6% 3836

3836 36

201720162015 2018 9M

2019

48

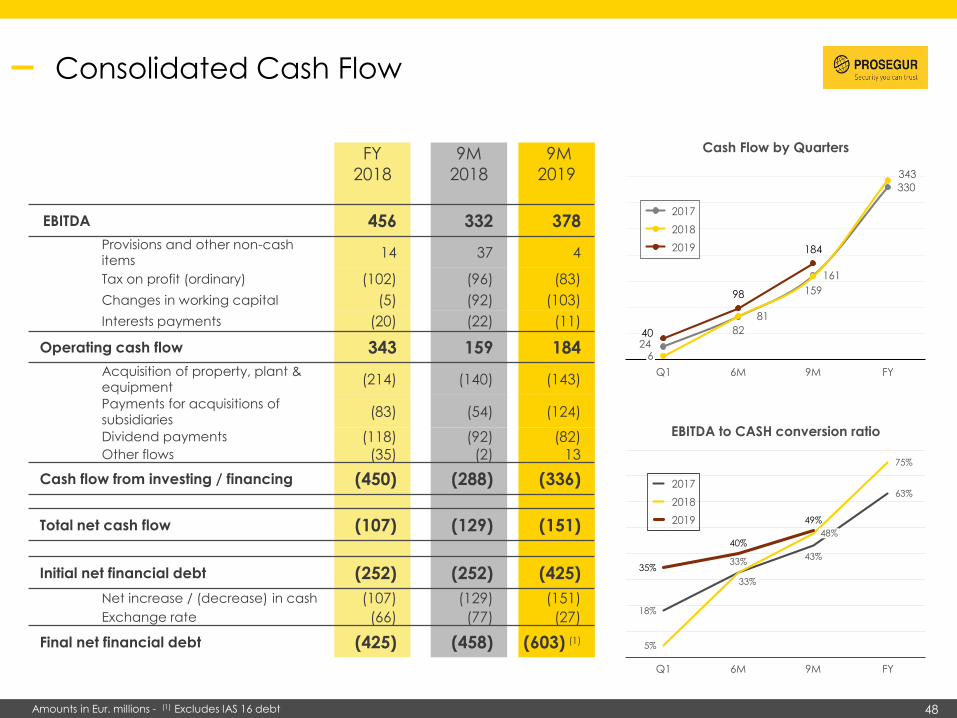

Consolidated Cash Flow

FY

2018

9M

2018

9M

2019

EBITDA 456 332 378

Provisions and other non-cash items

14 37 4

Tax on profit (ordinary) (102) (96) (83)

Changes in working capital (5) (92) (103)

Interests payments (20) (22) (11)

Operating cash flow 343 159 184

Acquisition of property, plant & equipment

(214) (140) (143)

Payments for acquisitions of

subsidiaries(83) (54) (124)

Dividend payments (118) (92) (82)Other flows (35) (2) 13

Cash flow from investing / financing (450) (288) (336)

Total net cash flow (107) (129) (151)

Initial net financial debt (252) (252) (425)

Net increase / (decrease) in cash (107) (129) (151)

Exchange rate (66) (77) (27)

Final net financial debt (425) (458) (603) (1)

Cash Flow by Quarters

24

81

161

330

15998

184

40

343

6

82

Q1 6M 9M FY

2019

2017

2018

18%

5%

35%

Q1

33%

33%

40%

6M

75%

43%

48%

9M

63%

FY

49%

EBITDA to CASH conversion ratio

2017

2018

2019

Amounts in Eur. millions - (1) Excludes IAS 16 debt

49

Financial Position

458 425

61581 594 603

78 95 109

-101 -84 -91

1.4%1.7%

Sep. 2019Dic. 2018

54

1.7%

Sep. 2018

127

Mar. 2019

1.4%

133-3

Jun. 2019

1.4%

132-15

Average Cost of Debt Treasury Stock (2)Net Financial DebtDeferred Payments

• Net financial Debt

• Increase of 178 millions of euros(1) vs. December 2018, deriving mainly from inorganic growth initiatives.

• Average cost of debt: reduction of c. 30 basis points vs. the same period in 2018 (1.4% vs. 1.7%)

• Rating. Confirmation by S&P of BBB rating, stable Outlook

(October 9, 2019)

IAS 16 Debt

1.5x 0.7x

Amounts in Eur. millions - (1) Excludes IAS 16 impact - (2) Treasury Stock of Prosegur and Prosegur Cash at closing market price of the period

50

Balance Sheet

FY 2018 9M 2019

Non-current assets 1,721 1,967Tangible fixed assets and real estate investments 745 873

Intangible assets 842 954

Others 133 141

Current assets 2,099 2,091Inventory 76 68

Customer and other receivables 975 1,080

Cash and equivalents and other financial assets 1,048 943

TOTAL ASSETS 3,820 4,058

Net equity 1,066 1,068Share capital 37 36

Treasury shares (53) (14)

Retained earnings and other reserves 1,013 958

Minority interest 69 88

Non-current liabilities 1,676 1,742

Bank borrowings and other financial liabilities 1,392 1,434

Other non-current liabilities 285 308

Current liabilities 1,077 1,248Bank borrowings and other financial liabilities 151 358

Trade payables and other current liabilities 926 890

TOTAL NET EQUITY AND LIABILITIES 3,820 4,058

• 80% of total Group debt is of

long-term nature

!

Amounts in Eur. millions - 2018 & 2019 figures have been elaborated applying IAS 21 & 2 9, additionally 2019 figures also include the application of IAS16

Recent M&A

COMPANY PRESENTATION FY 2019

• 20 Operations completed (10 in 2018)

• Across all business lines

• Cash (CIT, AVOS, ATM)

• Security (Guarding, Monitoring, Cybersecurity)

• Alarms

• More than €160 million in revenues (±100 in 2018)

USA

Central America

Peru

Paraguay

Colombia

Uruguay

Brazil

Spain

Germany

South Africa

Singapore

Philippines

Australia

51

Indonesia

52

Scalable

Growth

Process

Improvement

Savings

16 : 1Reduction of payroll

calculation hours in Brazil

100%Robotization of the employee registration process in

Spain

+25,000 contracts / year + social security payment

Reduces the time of incorporation from 48 to 24 hours

50% Reduced cost in the monitoring of 2,600

armoured vehicles using IOT

135Robotized Processes to achieve

efficiencies of 120,000 hours/year

Digital Transformation – an ongoing transformational project to reshape the group

Car SharingUse of electric and low consumption vehicles

in "car sharing" model for Alarms and Security

operational fleet

<60 daysProcess improvement in

“Opportunity 2 Cash” & “Procure 2

Pay” focusing on DSO reduction

COMPANY PRESENTATION FY 201952

5353

March 2019

Prosegur USA

Investor Relations Presentation

COMPANY PRESENTATION 2018

5454

US is the world’s largest Security market in terms of revenues, combined with strong profitability levels…

(1) Source: Freedonia Group. Figures estimates for Security services (2020 projection); (2) FY17 figures, corresponding to main international security players; (3) Source: Markets&Markets. MMS: Managed Security Services (2020 projection)

North America

Western Europe

Eastern

Europe

Africa/

Mideast

Central & South

America

19.4

18.4

24.2

5.448.6

42.8 5.8

USCanada &

Mexico

Revenues: Billions of USD1

~6%~6%

~4%

Average EBITA

margin2

China &

Japan

20.5

Rest of

Asia Pacific

31.4~3%

~5%

Prosegur

EBITA MarginRevenues

~40% Latam

~60% ROW* 3%**

Note: Figures FY18; *Rest of the world;

** Excludes Overhead Costs

+$13B in MSS CyberSecurity revenues3

+$9B in MSS

CyberSecurity revenues3

+$8B in MSS

CyberSecurity revenues3

+$1.5B in MSS

CyberSecurity revenues3

+$3B in MSS

CyberSecurity revenues3

5555

…where the guarding market characteristics and

the labor regulation allow for a great opportunity

for the sale of integrated solutions…

…benefitting from the attractiveness of the US

technology market, a global reference that leads the way

for other geographies…

… and where Cybersecurity plays a prominent role in a mature market with access to the latest solutions and best in class professionals to combine physical and logical solutions

Positive perception

of guarding

profession

High labour costs, due

to increasing minimum

wage

Security guards

scarcityHighly compliant

market

Matured technological

market with strong

growth potential

Leading innovation

market (observatory

of new trends)

Market underpinned

by a favourable

regulation

Highly efficient

solutions for

customersGreater exploitation of

economies of scale

Differentiated value

proposition with

respect to manned

guarding

Cultivated market with

double digit growth

expectations

Market where all the

largest players are

present Most technology-

advanced market with

top talent and skilled

professionals

Differentiated value

proposition when

combining physical and

logical solutions

Large benefits from

economies of

scale

Favourable market

regulation

5656

As of today, the US market has been traditionally focused on guarding, with an increasing weight of tech

solutions, that only international players are positioned to combine

# Market Rank

Guarding market1

EmployeesRevenues ($M)

Integrators & Technology market2

EmployeesRevenues ($M)…

(1) Source: Security magazine; figures for 2018; (2) Source: SDM Magazine. Figures for 2017; (1)(2) Considers recent acquisitions

~160 >5,200#8

~7,000 >200,000 #1

~4,200 >110,000#2

~300 >6,500#4

~200 >5,500#5

~200 >7,000#6

~180 >5,700#7

~850 ~2,500#3

~300 ~1,200#6

~2,000 >54,000#3

#4 ~760 ~2,500

#1 ~8,400 ~13,600

#2 ~4,500 ~19,500

~750 ~1,700#5

Note: This ranking excludes companies whose majority of their revenues come from integrated residential and burglar alarm systems: Vivint (~$900M); Brinks Home Security (~$550M),

Guardian Protection Services (~$200M), CPI Security Systems (~$100M) and Central Security Group (~$100M)

~100 ~550#10

~160 ~900#7

… …

~35 ~150N/A

…… …

5757

Prosegur’s entry into the US is based on four strategic pillars

Brand awareness and reputation

• Leverage Prosegur’s top tier global reputation as #5

Global Security player

Cross-selling opportunities

• Rapidly increase penetration in USA by cross-selling

complementary services to our existing customer base

Integrated commercial model

• Prosegur is in a unique position to combine integrated guarding and

technology services, defining its offering as Enterprise Risk

Management Solutions

Strong post merger integration Plan

• Drive value creation from the very outset, maximizing each company’s potential, by

executing our solid integration Plan

5858

Prosegur is #5 Global Security player and it can leverage top tier global reputation

5,000 CORPORATE

PROJECTS / YEAR

100,000 SECURITY

GUARDS +7,000 CORPORATE

CLIENTS

INTEGRATED SECURITY

SOLUTIONS

+10,000CAMERAS / YEAR

PROSEGUR SECURITY

Global security revenues2

(1) Integrated Advanced Security Solutions; Includes Cybersecurity & Enterprise Risk Advisory; (2) Market share represented by revenues

% Sales IASS over total Security revenues1

13% 13% 13% 14%17%

20% 23%

2012 2013 2014 2015 2016 2017 2018

LEADING POSITION IN 14

COUNTRIES

5959

There is an opportunity to rapidly increase our penetration in USA by cross-selling complementary

services

Main targets

Global

accounts

(US based)

Global

accounts

(Non-US based)

Acquired

accounts (US)

US-based clients served by Prosegur

in other countries

Non-US based clients served by

Prosegur in other countries, that have

relevant presence in US

Recently acquired US customer base

(CSC, Cipher, Viewpoint, and BSI)

1

2

3

Description

6060

Prosegur Integra

Guarding

Technology

Prosegur is in the best position to combine guarding and technology services, sold by risk

management specialists at higher margins…

• Market ready for disruptive player with

labor scarcity and customers in need of

integrated solutions

• International players, dragged by legacy

traditional guarding contracts are struggling

to change their culture

• Prosegur can differentiate itself by setting

up a risk specialists team who sell high value

added bundles, following a consulting

approach, and at better margins

Rationale

6161

…as we have already demonstrated in some of our core markets

Integra has proven to be a great

success story in Singapore, a

Security market with similar

characteristics to US.

Singapore has achieved the 2nd

best operating margins of

Prosegur in just a few years,

driven by profitable Integra

contracts, where margins keep

improving as weight of technology

increases year on year.

The recent sale of the greatest

ever Integra contract to the

Brazilian branch of a major US

delivery company represents a

milestone for Prosegur Security.

Services include manned

guarding, monitoring, and

technology installation &

maintenance for the client’s +130

branches around the country with

~1,000 partners involved.

The sale of a long-term

Integra contract to a top

CAC40 French engineering

and defence company was a

success story for Prosegur

Security in Europe.

With presence in two key

locations in the North of

France, this contract has

enhanced Prosegur sales and

margin in the country.

Singapore Brazil France

6262

Once the strategic intent was defined, we are ensuring that existing business momentum is

maintained and that the integration plan drives value creation

Execute

rigorously3

Prepare

well2

Prosegur USA’s integration process is prioritizing the following strategic drivers:

Focus on

value

creation

1• Optimizing synergies at all levels: revenue, costs, financial, marketing...

• Protecting business momentum to avoid loss of revenue and to retain key talent

• Defining a tailored integration approach, setting KPIs to ensure the best

combination of the different commercial/ operations teams

• Empowering a value-added IMO1, whose main goal is to ensure everything is

ready to start the integration execution since day 1

• Constantly monitoring the pre-defined strategic integration KPIs

• Over-communicating with messages customized to every stakeholder

• Building capabilities for future deals

(1) IMO: Integration Management Office

Prosegur USA capitalizes on our Group’s track record in +200 M&A operations, and

leverages each target competitive advantage and strong management team.

6363

Following this entry strategy and integrated model approach, the acquisitions roadmap was designed

to build a strong platform…

Manned

Guarding

Remote video

monitoring

Security

IntegratorCybersecurity

• Professional security officer

• On-site response service

• Mobile guards

• Real time, 24/7 monitoring

• Advanced Analytics

• Intelligent predictive CCTV

• Engineering capabilities

• Local installation resources

• Operation and maintenance

• SOC (Security operation centers)

• Managed Security Services

• Digital surveillance

• Cyber Intelligence

6464

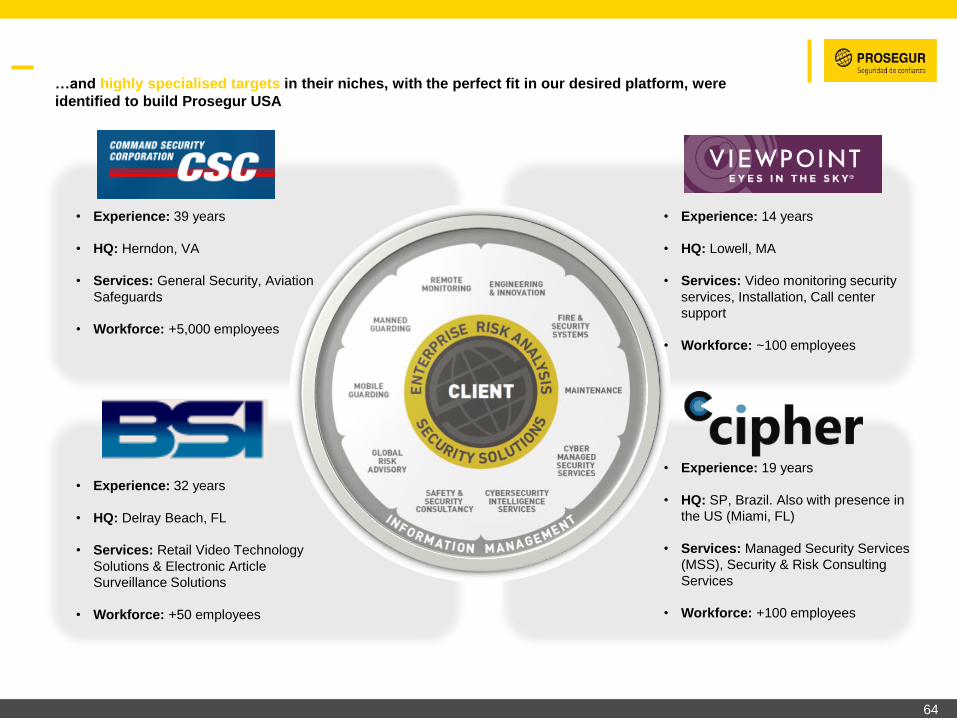

…and highly specialised targets in their niches, with the perfect fit in our desired platform, were

identified to build Prosegur USA

• Experience: 14 years

• HQ: Lowell, MA

• Services: Video monitoring security

services, Installation, Call center

support

• Workforce: ~100 employees

• Experience: 39 years

• HQ: Herndon, VA

• Services: General Security, Aviation

Safeguards

• Workforce: +5,000 employees

• Experience: 32 years

• HQ: Delray Beach, FL

• Services: Retail Video Technology

Solutions & Electronic Article

Surveillance Solutions

• Workforce: +50 employees

• Experience: 19 years

• HQ: SP, Brazil. Also with presence in

the US (Miami, FL)

• Services: Managed Security Services

(MSS), Security & Risk Consulting

Services

• Workforce: +100 employees

6565

Relevant presence in regions with the highest

concentration of clients and growth potential

This new brand national platform leaves us in a unique position as a full services integrator to cater for

our clients needs across the US

Guarding

Monitoring / Technology

Systems Integrator

Cybersecurity

WA

OR

CA

NV

ID

MT

WY

UT

AZNM

ND

SD

CO

NE

KS

OK

TX

LA

AR

MO

IA

MN

WI

MI

ILIN

OH

KY

MSAL

TN

GA

FL

SC

NC

VA

WV

PA

NY

VT

ME

NH

MA

RI

CT

NJ

DE

MD

C

B

V

6666

Entry into the largest and most

profitable security market with

the ambition to become

Prosegur’s second biggest

market in the midterm

Geographical portfolio

rebalancing, leading to strong

revenues increase in a very

stable market

Innovation and new trends

observatory to export successful

models to other countries

In conclusion, US Market entry will provide us with great benefits that will allow us to improve our

profitability and become a leader in Enterprise Risk Management Solutions

Market attractiveness Rationale for Prosegur

Brand awareness and

reputation

Cross-selling

opportunities

Integrated

commercial model

Strong post merger

integration Plan

Strategic pillars

Manned guarding

Technology

• Positive perception of guarding

profession

• Security guards scarcity

• High labour costs

• Highly compliant market

• Highly matured market with

strong growth potential

• Highly efficient solutions for

customers

• Great exploitation of economies

of scale

• Favourable regulation

6767

Legal Disclaimer

This document has been prepared

exclusively by Prosegur for use as

part of this presentation.

The information contained in this

document is provided by Prosegur

solely for information purposes, in

order to assist parties that may be

interested in undertaking a

preliminary analysis of it; the

information it contains is limited and

may be subject to additions or

amendments without prior notice.

This document may contain

projections or estimates concerning

the future performance and results

of Prosegur’s business.

These estimates derive from

expectations and opinions of

Prosegur and, therefore, are subject

to and qualified by risks,

uncertainties, changes in

circumstances and other factors

that may result in actual results

differing significantly from forecasts

or estimates. Prosegur assumes no

liability nor obligation to update or

review its estimates, forecasts,

opinions or expectations.

The distribution of this document in

other jurisdictions may be

prohibited; therefore, the recipients

of this document or anybody

accessing a copy of it must be

warned of said restrictions and

comply with them.

This document has been provided

for informative purposes only and

does not constitute, nor should it be

interpreted as an offer to sell,

exchange or acquire or a request

for proposal to purchase any shares

in Prosegur.

Any decision to purchase or invest

in shares must be taken based on

the information contained in the

brochures filled out by Prosegur

from time to time .

www.prosegur.com

THANK

YOU

CONTACT INFORMATION:

Antonio de Cárcer

Investor Relations Director

Tel: +34 91 589 83 29

Cristina Casado

Investor Relations Officer

Tel: +34 91 589 83 29