COMPANY INSIGHT TVSL IN EQUITY September 17, 2014...

19

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision. Regaining its lost glory Customer confidence in TVSM’s products (Jupiter, Star City+, Apache) continues to rev its volumes and market share; we expect it to grow at ~2x the industry volume CAGR of 15% in FY14-17 and increase its market share (ex-mopeds) to 10%. Significant operating leverage benefits from this volume surge should drive EBITDA margin expansion in FY16/17 to 9%/10% (vs 6% in FY14), albeit still at a 50-100% discount to its larger peers. We upgrade our FY16/FY17 EPS estimates by 30%/43% and valuation by 50% to ` 270, due to volumes/margin upgrades and our confidence in long-term margin sustainability. A near 100% RoCE expectation in FY17 supports our implied 16.0x FY16 EPS valuation for the domestic business. Competitive position: WEAK Changes to this position: POSITIVE TVSM’s product engine has begun firing The successful customer response to scooter Jupiter and motorcycle Star City+ have revived TVSM’s volumes. We expect TVSM to post 27% domestic 2W volume CAGR in FY14-17 (vs our earlier estimate of 20%), given: (i) revival in domestic industry volumes (15% CAGR in FY14-17 vs 6% in FY12-14); and (ii) uptick in its market share to 9.9% in FY17 from 7.3% in FY14 led by renewed confidence in its products and new launches (Victor, Scooty Zest). Margin expansion to provide second leg of revival 1QFY15 margin was adversely affected by specific one-offs; we continue to expect structural margin expansion from: (i) higher volume-led operating leverage bringing savings in marketing, employee and other fixed costs (near three-fourth of the EBITDA margin expansion over FY14-17); (ii) opportunity to raise prices of new products; and (iii) healthier product mix (rising share of motorcycles and ‘bigger’ scooters). We expect EBITDA margin to expand to 7.0% in FY15, 9.0% in FY16 and 10.0% in FY17 (vs 6.0% in FY14). Indonesia remains a concern albeit insignificant TVSM’s Indonesian business volumes remain significantly lower than the breakeven level of ~7,000 units/month; the deteriorating performance of TVS Indonesia would require a `500mn infusion by TVSM in FY15 (10% of domestic CFO). Prolonged weakness in TVS Indonesia’s performance remains a risk to our earnings/valuation estimates and prevents us from factoring in `9/share worth of investments in Indonesia in our SOTP-based target price. Upgrading TP to `270/share – BMW opportunity not yet factored in We value the standalone entity at `261/share (implies 14.0x one-year forward EPS, a 5% discount to Hero’s and Bajaj Auto’s historical average). We value TVS Motor Services at 1.0x end-FY15 book (`9/share). An upgrade to our FY16 and FY17 EPS estimates (up 30% and 42%, resp), an 85bps increase in our long-term EBITDA margin estimate to 10% and roll forward lead to a 50% valuation upgrade. We are yet not attributing any value to the BMW tie-up. COMPANY INSIGHT TVSL IN EQUITY September 17, 2014 TVS Motor Company BUY Auto & Auto Ancillaries Recommendation Mcap (bn): `100/US$1.6 3M ADV (mn): `694/US$11.4 CMP: `211 TP (12 mths): `270 Upside (%): 28 Flags Accounting: AMBER Predictability: AMBER Earnings Momentum: AMBER Catalysts Market share gains in domestic motorcycles EBITDA margin improvement Performance Source: Bloomberg, Ambit Capital research 20 80 140 200 260 17,000 21,000 25,000 29,000 Sep-13 Oct-13 Dec-13 Jan-14 Mar-14 Apr-14 Jun-14 Jul-14 Sep-14 Sensex TVS (Rs) Analyst Details Ashvin Shetty, CFA +91 22 3043 3285 [email protected] Ritu Modi +91 22 3043 3292 [email protected] Key financials - standalone Year to March ( ` mn) FY13 FY14 FY15E FY16E FY17E Operating Income 71,693 79,619 104,947 127,309 146,915 EBITDA 4,090 4,781 7,344 11,504 14,640 EBITDA margin 5.7% 6.0% 7.0% 9.0% 10.0% Adjusted EPS (`) 4.35 5.08 9.26 16.1 20.7 Debt:Equity (x) 0.5 0.3 0.2 (0.1) (0.3) RoE (%) 17% 18% 28% 39% 38% P/E (x) 48.4 41.5 22.8 13.1 10.2 Source: Company, Ambit Capital research

Transcript of COMPANY INSIGHT TVSL IN EQUITY September 17, 2014...

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

Regaining its lost glory

Customer confidence in TVSM’s products (Jupiter, Star City+, Apache) continues to rev its volumes and market share; we expect it to grow at ~2x the industry volume CAGR of 15% in FY14-17 and increase its market share (ex-mopeds) to 10%. Significant operating leverage benefits from this volume surge should drive EBITDA margin expansion in FY16/17 to 9%/10% (vs 6% in FY14), albeit still at a 50-100% discount to its larger peers. We upgrade our FY16/FY17 EPS estimates by 30%/43% and valuation by 50% to `270, due to volumes/margin upgrades and our confidence in long-term margin sustainability. A near 100% RoCE expectation in FY17 supports our implied 16.0x FY16 EPS valuation for the domestic business. Competitive position: WEAK Changes to this position: POSITIVE TVSM’s product engine has begun firing The successful customer response to scooter Jupiter and motorcycle Star City+ have revived TVSM’s volumes. We expect TVSM to post 27% domestic 2W volume CAGR in FY14-17 (vs our earlier estimate of 20%), given: (i) revival in domestic industry volumes (15% CAGR in FY14-17 vs 6% in FY12-14); and (ii) uptick in its market share to 9.9% in FY17 from 7.3% in FY14 led by renewed confidence in its products and new launches (Victor, Scooty Zest). Margin expansion to provide second leg of revival 1QFY15 margin was adversely affected by specific one-offs; we continue to expect structural margin expansion from: (i) higher volume-led operating leverage bringing savings in marketing, employee and other fixed costs (near three-fourth of the EBITDA margin expansion over FY14-17); (ii) opportunity to raise prices of new products; and (iii) healthier product mix (rising share of motorcycles and ‘bigger’ scooters). We expect EBITDA margin to expand to 7.0% in FY15, 9.0% in FY16 and 10.0% in FY17 (vs 6.0% in FY14). Indonesia remains a concern albeit insignificant TVSM’s Indonesian business volumes remain significantly lower than the breakeven level of ~7,000 units/month; the deteriorating performance of TVS Indonesia would require a `500mn infusion by TVSM in FY15 (10% of domestic CFO). Prolonged weakness in TVS Indonesia’s performance remains a risk to our earnings/valuation estimates and prevents us from factoring in `9/share worth of investments in Indonesia in our SOTP-based target price. Upgrading TP to `270/share – BMW opportunity not yet factored in We value the standalone entity at `261/share (implies 14.0x one-year forward EPS, a 5% discount to Hero’s and Bajaj Auto’s historical average). We value TVS Motor Services at 1.0x end-FY15 book (`9/share). An upgrade to our FY16 and FY17 EPS estimates (up 30% and 42%, resp), an 85bps increase in our long-term EBITDA margin estimate to 10% and roll forward lead to a 50% valuation upgrade. We are yet not attributing any value to the BMW tie-up.

COMPANY INSIGHT TVSL IN EQUITY September 17, 2014

TVS Motor CompanyBUY

Auto & Auto Ancillaries

Recommendation Mcap (bn): `100/US$1.6 3M ADV (mn): `694/US$11.4 CMP: `211 TP (12 mths): `270 Upside (%): 28

Flags Accounting: AMBER Predictability: AMBER Earnings Momentum: AMBER

Catalysts

Market share gains in domestic motorcycles

EBITDA margin improvement

Performance

Source: Bloomberg, Ambit Capital research

2080140200260

17,000

21,000

25,000

29,000

Sep-

13

Oct

-13

Dec

-13

Jan-

14

Mar

-14

Apr

-14

Jun-

14

Jul-

14

Sep-

14

Sensex TVS (Rs)

Analyst Details

Ashvin Shetty, CFA

+91 22 3043 3285

Ritu Modi

+91 22 3043 3292 [email protected]

Key financials - standalone Year to March (̀ mn) FY13 FY14 FY15E FY16E FY17E

Operating Income 71,693 79,619 104,947 127,309 146,915

EBITDA 4,090 4,781 7,344 11,504 14,640

EBITDA margin 5.7% 6.0% 7.0% 9.0% 10.0%

Adjusted EPS (`) 4.35 5.08 9.26 16.1 20.7

Debt:Equity (x) 0.5 0.3 0.2 (0.1) (0.3)

RoE (%) 17% 18% 28% 39% 38%

P/E (x) 48.4 41.5 22.8 13.1 10.2

Source: Company, Ambit Capital research

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 2

Steadily regaining market share in scooters and motorcycles Domestic scooters (24% of FY15 standalone revenues) Jupiter has turned around the fortunes of TVSM in scooters

TVSM continues to regain market share in the domestic scooters space. Its market share has improved from 11.8% in August 2013 to 15.6% in the first five months of FY15. In fact, in August 2014, TVSM clocked its highest market share (17.4%) since February 2012.

The increase in the TVSM’s market share in domestic scooters has been led single-handedly by the launch of Jupiter in September 2013. Jupiter has become the flagship scooter model for TVSM, accounting for ~52% of TVSM’s domestic scooter volumes (July 2014). Moreover, it has become the third-largest selling scooter brand in India within a year of its launch.

Exhibit 1: TVSM has consistently increased its market share in domestic scooters since the last 12 months…

Source: SIAM, Ambit Capital research

Exhibit 2: ...driven by a much stronger-than-expected response to Jupiter

Source: SIAM, Ambit Capital research

Our discussions with dealers and 2W experts indicate that the key reason behind the success of Jupiter is the value proposition it offers to customers. Whilst it scores on par with its peers such as Honda Activa on product quality and technical parameters, Jupiter has got its pricing right (5% cheaper than Activa). Jupiter still commands a waiting period of around 7 days across most regions despite a significant increase in despatch volumes (29,609 units in July 2014 vs 7,422 units in its launch month of September 2013).

Exhibit 3: TVS Jupiter provides comparable features as peers at a competitive price

TVS Jupiter Honda Activa Hero Maestro

Ex-showroom Delhi Price (`) 44,250 46,482 46,900

Displacement (cc) 110 110 110

Max Power 7.88 bhp@7500 rpm 8 bhp @ 7500 rpm 8 bhp @ 7500 rpm

Dimensions(mm) (l x b x h) 1834x650x1115 mm 1761x710x1147 mm 1780x710x1165 mm

Fuel tank (litres) 5.0 5.3 5.3

Brakes 130mm drum brake 130mm drum brake 130mm drum brake

(internal expanding shoe type)

Source: Company website, www.bikedekho.com

11.5%

12.5%

13.5%

14.5%

15.5%

16.5%

17.5%

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

Aug

-13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-

14

Aug

-14

TVS domestic scooters (nos) TVS market share - RHS

10%

20%

30%

40%

50%

60%

4,000

8,000

12,000

16,000

20,000

24,000

28,000

32,000

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-

14

Jupiter sales (nos) as % of TVS scooter volumes

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 3

Launch of Scooty Zest can add to the momentum

TVSM launched the 110cc Scooty Zest in August 2014. Scooty Zest has received positive reviews from auto journalists and experts. Scooty Zest will complement TVSM’s scooter offering to females, which is currently served by the 90cc models, Scooty Pep and Scooty Streak. In recent years, Scooty has lost share (volume decline of 20% in FY14) to its higher cc competitor models, such as Hero Pleasure and Yamaha Ray. With Scooty Zest coming in, we expect TVSM to claw back market share in the female scooters segment.

We upgrade our domestic scooter volume estimates

The company’s average monthly volume in the domestic scooter segment has improved from 38k units/month in FY14 to 64k units/month in August 2014. We expect TVSM to record 29% scooter volume CAGR over FY14-17 vs 12% in FY10-13. We expect this growth to be driven mainly by: (a) overall industry growth of 20% over FY14-17; (b) continued strong sales of Jupiter; and (b) volume uptick from the launch of the new Scooty Zest. On the back of the recent trend in scooter industry volume growth and TVSM’s market share, we upgrade our domestic scooter volume estimates for FY14-17 by 13-15% (see the exhibit below). We are currently expecting market share of 15.6% for April–August 2014 to sustain for the remaining seven months of FY15 as well as FY16 and FY17. Better-than-expected sales of Scooty Zest can lead to further upgrades to our volume estimates.

Exhibit 4: We expect TVSM’s scooters to record 302bps improvement in market share over FY14-17

(‘000s) FY14 New estimates Old estimates Change

FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E

Domestic scooter industry 3,603 4,512 5,415 6,227 4,439 5,105 5,718 2% 6% 9%

% growth 23% 25% 20% 15% 23% 15% 12% TVS domestic scooter sales 457 712 855 989 631 766 858 13% 12% 15%

Market share 12.7% 15.8% 15.8% 15.8% 14.2% 15.0% 15.0% 160bps 80bps 80bps

% growth 8% 56% 20% 16% 38% 21% 12% Source: SIAM, Ambit Capital research

Domestic motorcycles (28% of FY15 standalone revenues)

After underperforming the overall motorcycle industry in FY14, TVSM’s domestic motorcycle volumes increased 22% in the first five months of FY15 vs industry volume growth of 10% during the same period. TVSM’s domestic motorcycles have benefitted in recent months from: (a) strong response to the recently launched Star City+; and (b) continued strong growth in the sale of its premium segment bike, Apache. These factors have led to a market share improvement in TVSM’s domestic motorcycle segment to 6.4% in August 2014 from an average of 5.5% in FY14.

Whilst Star City+ received strong response, Apache continues to grow

The new Star City+ (launched in May 2014) continues to see strong response. Our discussions with dealers indicate that the main reasons for the encouraging response are: (a) significant improvement in the new model of Star City vs the old model (engine performance, looks and more features); (b) strong demand from replacement customers of the old Star City and TVS Sport; and (c) the product is also competitively priced (Star City+ is 6% cheaper than Hero’s Splendor and 4% cheaper than Honda’s Dream Neo). Star City+ accounted for 27% of TVSM’s domestic motorcycle volumes since May 2014.

Exhibit 5: TVSM has competitively priced Star City+ with comparable features to peers TVS Star City+ Honda Dream Neo Hero Splendor Ex-showroom Delhi Price (`) 41,445 43,318 44,250 Displacement (cc) 110 110 100 Compression ratio 9.2:1 9.9:1 9.0:1 Net Power 8.28 bhp @ 7000 rpm 8.25 bhp @ 7500 rpm 7.6 bhp @ 7500 rpm Dimensions(mm) (l x b x h) 1980x750x1080 mm 2009x737x1074 mm 1965x720x1095 mm Ground clearance (mm) 179 169 160 Fuel tank (litres) 10.0 8.0 9.5

Source: Company website, www.bikedekho.com

TVSM has been recently gaining market share in the domestic motorcycle space

Source: SIAM, Ambit Capital research

4.5%

5.0%

5.5%

6.0%

6.5%

Nov

-13

Dec

-13

Jan-

14Fe

b-1

4M

ar-1

4A

pr-1

4M

ay-1

4Ju

n-14

Jul-

14

Aug

-14

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 4

On the other hand, TVSM’s premium bike offering ‘Apache’ continues to record strong growth. Apache recorded 47% YoY growth in the first five months for FY15 vs 19% YoY growth in FY14 and now accounts for ~30% of overall motorcycle volumes for TVSM.

Victor can help in further market share gains in domestic motorcycles

We believe the success of Star City+ has created a good launchpad for the company’s upcoming launch in the executive segment (most likely to be branded ‘Victor’) in December 2014/January 2015. The launch of Victor can help TVSM to strengthen its position in the commuter segment (accounting for 60-65% of the total domestic motorcycle industry volumes). The recent success of Jupiter and Star City+ has shown that getting the pricing, design and mileage of a product can significantly help volumes. We believe that if TVSM is able to achieve these attributes for Victor, then this can play a critical role in further market share gain for TVSM in the domestic motorcycle space.

In addition to Victor, the company plans to launch a new motorcycle in the premium segment, which can help TVSM strengthen its position in the premium motorcycle space.

Exhibit 6: TVSM’s domestic motorcycle volumes have seen an uptick in recent months…

Source: SIAM, Ambit Capital research

Exhibit 7: …driven by strong sales of new Star City+ and Apache

Source: SIAM, Ambit Capital research

Upgrade to domestic motorcycle volumes on the back of strong growth in recent months

We are currently factoring in a recovery in domestic motorcycle industry volumes in FY15 and expect the industry to record a CAGR of 13% over FY14-17E vs 4% growth in FY14. Furthermore, we believe TVSM has an opportunity to regain market share in the domestic motorcycle segment on the back of: (a) continued strong sales of Star City+; (b) continued strong growth in Apache volumes; (c) the launch of the executive segment motorcycle, ‘Victor’ in December 2014/January 2015; and (d) the launch of a new premium segment motorcycle in 4QFY15. On the back of the recent market share trends, we increase our market share estimates for TVSM, as shown in the exhibit below. This results in about 4-21% upgrades to our domestic motorcycle estimates for FY14-17. The new estimates imply 26% volume CAGR for TVSM’s domestic motorcycles over FY14-17 (vs our earlier estimate of 18% CAGR).

Exhibit 8: TVSM to record 204bps improvement in market share over FY14-17

(‘000s) FY14 New estimates Old estimates Change

FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E

Domestic motorcycle industry 10,480 11,782 13,549 15,175 11,737 13,145 14,591 0% 3% 4%

% growth 4% 12% 15% 12% 12% 12% 11% TVS domestic motorcycle sales 573 730 949 1,138 703 833 940 4% 14% 21%

Market share 5.5% 6.2% 7.0% 7.5% 6.0% 6.3% 6.4% 20bps 66bps 106bps

% growth 3% 27% 30% 20% 23% 19% 13% Source: SIAM, Ambit Capital research

-20%

-10%

0%

10%

20%

30%

40%

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

Aug

-13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-

14

Aug

-14

TVS domestic motorcycles (nos) YoY growth - RHS

0%

10%

20%

30%

40%

2,000 4,000 6,000 8,000

10,000 12,000 14,000 16,000 18,000 20,000

Aug

-13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-

14

Star City sales (nos)Apache sales (nos)Star City as % of TVS motorcycle volumesApache as % of TVS motorcycle volumes

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 5

1QFY15 performance notwithstanding, we continue to believe in margin expansion TVSM’s EBITDA margin for 1QFY15 at 5.7% was 65bps below our expectations. The margin was impacted mainly by gross margin (27.3%) coming in 163bps lower than our expectations. The key reasons for the gross margin underperformance were: (a) excise duty cut (which impacted the margin at the excise duty free plant in Himachal Pradesh); (b) competitive pricing of new Star City+; and (c) increase in vendor compensation. It may be however noted that the company derived operating leverage benefits in 1QFY15, with its ‘other expenses’ declining by 137bps YoY and 77bps QoQ and coming in 140bps lower than our expectations. Since 1QFY15, the company has taken price increase of around 1% which should help gross margin in the future.

1QFY15 margin performance notwithstanding, we continue to believe TVSM’s margin could expand driven by:

(a) Decline in marketing and employee costs as a percentage of sales on rising volumes: Compared with peers like Hero MotoCorp and Bajaj Auto, TVSM’s marketing spends and employee costs as a percentage of sales are significantly higher. These two items are the key reasons for TVSM’s lower margins vs it peers (see the exhibit below).

Exhibit 9: TVSM’s higher advertising/marketing spends and employee costs as a percentage of sales are the key reasons for its EBITDA margin lagging that of its peers

As % of sales TVSM Bajaj Auto Hero MotoCorp Divergence to Hero and

Bajaj average FY12 FY13 FY14 FY12 FY13 FY14 FY12 FY13 FY14 FY12 FY13 FY14

Raw material costs 73.8% 72.5% 71.3% 71.2% 71.2% 68.2% 73.3% 73.2% 72.1% 1.6% 0.3% 1.1%

Employee expenses 5.2% 5.7% 6.0% 2.7% 3.2% 3.6% 3.1% 3.5% 3.7% 2.3% 2.4% 2.4%

Power & fuel 1.3% 1.3% 1.0% 0.5% 0.6% 0.5% 0.5% 0.5% 0.5% 0.8% 0.7% 0.5%

Advertising/marketing 4.9% 6.4% 6.8% 0.8% 1.0% 1.3% 1.6% 2.0% 2.0% 3.7% 4.9% 5.1%

Packing & freight 3.3% 3.3% 3.8% 1.6% 1.5% 1.6% 2.5% 2.7% 2.9% 1.2% 1.2% 1.6%

R&D expenses 1.3% 1.4% 1.4% 0.6% 0.6% 0.9% 0.2% 0.3% 0.4% 0.9% 0.9% 0.8%

Others 3.7% 3.7% 3.8% 2.4% 2.7% 2.4% 3.5% 4.0% 4.5% 0.8% 0.4% 0.3%

EBITDA margin 6.6% 5.7% 6.0% 20.2% 19.1% 21.6% 15.3% 13.8% 14.0% -11.2% -10.8% -11.8%

Source: Company, Ambit Capital research

We expect marketing spends to remain high in FY15 due to several new launches such as Star City+, Victor and Scooty. However, rising volumes (capacity utilisation to scale up from 67% in FY14 to >90% in FY16) and improvement in product mix (revenue mix in favour of motorcycles and bigger scooters) over the medium term should bring down advertising spends, employee costs and other fixed expenses, as these cost items would be spread over a larger revenue base. We expect employee costs to come down from 6.0% of sales in FY14 to 4.8% of sales in FY17 (down 115bps) and advertising and marketing spends to decline by 55bps over FY14-17.

Our belief regarding a decline in these cost items draws precedent from Royal Enfield, where employee costs and selling and other fixed expenses declined by nearly 400bps between CY10 and CY13 on the back of a similar strong growth in volumes.

(b) Opportunity to increase the price once the product stabilises: TVSM has been competitively pricing its launches. However, once the volume stabilises, the company has an opportunity to increase prices. For instance, the growing volumes of Jupiter have enabled a price hike of about 5% (excluding the impact of excise duty cuts) since its launch in September 2013.

(c) Better vendor pricing on higher volumes: We expect the cost structure of vendors to come down due to higher volumes. This could result in TVSM obtaining volume discounts/better pricing from vendors.

Royal Enfield’s strong volume growth led to margin expansion

Source: Company, SIAM, Ambit Capital research

5.0%10.0%15.0%20.0%25.0%

20,000 60,000

100,000 140,000 180,000

CY0

9C

Y10

CY1

1

CY1

2

CY1

3

1HC

Y14

Royal Enfield volumes (nos)EBITDA margin

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 6

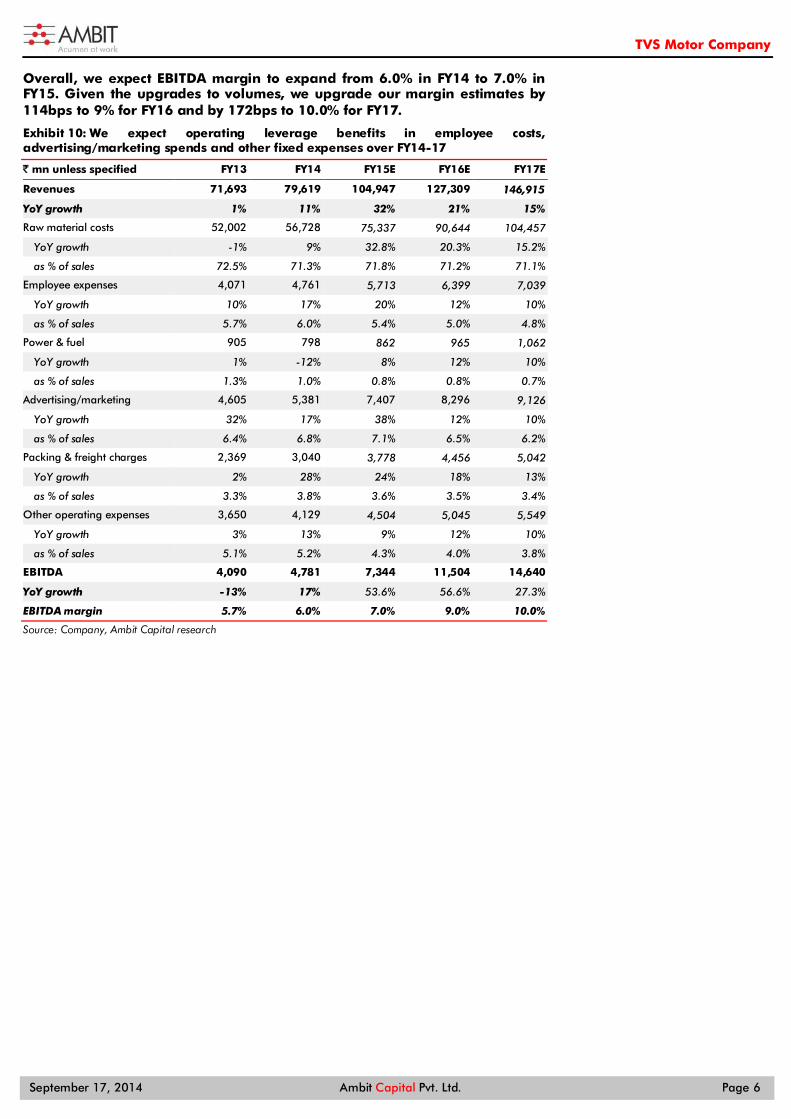

Overall, we expect EBITDA margin to expand from 6.0% in FY14 to 7.0% in FY15. Given the upgrades to volumes, we upgrade our margin estimates by 114bps to 9% for FY16 and by 172bps to 10.0% for FY17.

Exhibit 10: We expect operating leverage benefits in employee costs, advertising/marketing spends and other fixed expenses over FY14-17

` mn unless specified FY13 FY14 FY15E FY16E FY17E

Revenues 71,693 79,619 104,947 127,309 146,915

YoY growth 1% 11% 32% 21% 15%

Raw material costs 52,002 56,728 75,337 90,644 104,457

YoY growth -1% 9% 32.8% 20.3% 15.2%

as % of sales 72.5% 71.3% 71.8% 71.2% 71.1%

Employee expenses 4,071 4,761 5,713 6,399 7,039

YoY growth 10% 17% 20% 12% 10%

as % of sales 5.7% 6.0% 5.4% 5.0% 4.8%

Power & fuel 905 798 862 965 1,062

YoY growth 1% -12% 8% 12% 10%

as % of sales 1.3% 1.0% 0.8% 0.8% 0.7%

Advertising/marketing 4,605 5,381 7,407 8,296 9,126

YoY growth 32% 17% 38% 12% 10%

as % of sales 6.4% 6.8% 7.1% 6.5% 6.2%

Packing & freight charges 2,369 3,040 3,778 4,456 5,042

YoY growth 2% 28% 24% 18% 13%

as % of sales 3.3% 3.8% 3.6% 3.5% 3.4%

Other operating expenses 3,650 4,129 4,504 5,045 5,549

YoY growth 3% 13% 9% 12% 10%

as % of sales 5.1% 5.2% 4.3% 4.0% 3.8%

EBITDA 4,090 4,781 7,344 11,504 14,640

YoY growth -13% 17% 53.6% 56.6% 27.3%

EBITDA margin 5.7% 6.0% 7.0% 9.0% 10.0%

Source: Company, Ambit Capital research

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 7

TVS Indonesia remains an ‘insignificant’ weak spot TVS Indonesia (100% owned by TVSM) The performance of the Indonesian subsidiary has remained weak in FY14, with this subsidiary recording a revenue decline of 3%. The EBITDA margin deteriorated further in FY14. Absolute EBITDA loss amounted to `540mn for FY14 vs `387mn for FY13. The company’s PBT loss widened from `819mn in FY13 (after excluding one-off profit from the sale of land) to `1,249mn in FY14. The net loss for FY14 was at `1,399mn.

Exhibit 11: PT TVS Indonesia – a snapshot

` mn unless specified FY09 FY10 FY11 FY12 FY13 FY14

Revenues 510 683 854 1,074 999 965

EBITDA (736) (771) (584) (494) (387) (540)

EBITDA margin -144.3% -112.9% -68.4% -46.0% -38.7% -56.0%

Adjusted PAT (813) (1,146) (809) (1,083) (1,140) (1,399)

Net debt 2,260 2,034 1,974 2,138 1,632 NA

Networth 855 554 448 29 145 1,153

Investments by TVSM * 1,993 2,928 3,524 4,742 4,742 5,240 Inv. as % of TVSM’s standalone networth 25% 34% 35% 41% 39% 37%

Source: Company, Ambit Capital research; Note: * Investments are before impairment provision

Despite the launch of a new skubek, ‘TVS Dazz’, volumes grew only 3% YoY in FY14 to 19,200 units. The current volume run rate is significantly lower than the breakeven requirement of 7,000 units/month. To achieve the breakeven volumes, the company is focusing on increasing exports from Indonesia. With the continued deterioration in the performance of TVS Indonesia, we are currently factoring in a further fund infusion of `500mn by TVSM in FY15 (vs `500mn in FY14). A higher-than-expected and longer-than-expected fund infusion into TVS Indonesia remains a risk to our earnings/valuation estimates. We note that: (a) with improving performance of the standalone business, the impact of Indonesia loss would come down at the consolidated level; and (b) TVSM could also explore the possibility of monetising the Indonesian assets (mainly immovable property) to meet the fund requirements. For example, in FY13, TVSM Indonesia sold 49 acres of land for a consideration of `1.4bn (generating profit of `1bn). TVS Motor Services (19% owned by TVSM) TVS Motor Services is engaged in the business of financing TVSM’s 2Ws (currently financing 25,000 vehicles). A small portion of the business also finances used cars and tractors. TVS Motor Services operates through its subsidiary, TVS Credit Services. TVS Credit Services is held by TVS Motor Services (90.4%), HDFC Ltd (5.7%) and PHI Research Pvt Ltd (4%). TVS Credit Services is a profitable entity and generated a PAT of `52mn in FY13 (FY14 financials not available). TVSM has infused `750mn into TVS Motor Services in FY14. The total loan book size of TVS Motor Services currently is close to `17bn. TVSM expects to monetise its investment in TVS Motor Services in the next 2-3 years. We are factoring in a further fund infusion of `750mn in FY15. Exhibit 12: TVS Credit Services - a snapshot

` mn FY11 FY12 FY13 Revenue 264 1,136 2,421 EBITDA (29) 458 974 EBITDA margin -11.2% 40.3% 40.2% PBT (165) 2 50 PAT (165) 2 52 Networth 1,330 1,433 1,724 Net debt 2,280 4,835 10,490 Net debt : Equity (x) 1.7 3.4 6.1

Source: Company, Ambit Capital research

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 8

BMW tie-up benefits: Credible possibilities, inadequate visibility In April 2013, TVSM and BMW Motorrad, the motorcycle division of BMW, signed a long-term cooperation agreement to jointly develop and produce a new series of motorcycles that will cater to the <500cc motorcycle segment, globally. We believe the tie-up presents the following longer-term opportunities for TVSM: Opportunity to develop credible products in the premium motorcycles space: Our discussions with industry sources indicate that: (a) BMW is the driving force behind the technology and product development, whilst TVSM would contribute the manufacturing capabilities for the joint venture; (b) TVS and BMW would have its own vehicle derivatives to be sold through their own distribution channel in India and global markets; TVSM’s derivate would most likely be priced cheaper than BMW; and (c) the first product would be launched by early-CY16.

Currently, the premium motorcycle market in India which starts from 150cc and above is a 1.7 mn units per annum market where TVSM’s market share is low at 8% (FY14 numbers).

The product development learning from the BMW tie-up can significantly help TVSM develop credible products in the premium motorcycle markets. Together with the volumes, the margin in the 150cc and above motorcycle segment will undoubtedly be higher than that of the lower cc bikes, which can help TVSM’s overall margins.

Potential export revenues for TVSM: BMW Motorrad sold around 115,215 units of >650cc bikes in CY13 and generated revenues of Euro1.5bn (average realisation of Euro13,000/bike or `1.0mn/bike at the current exchange rate). The <500cc bikes can potentially be as large a volume contributor for BMW Motorrad as its current range of >650cc bikes after the company develops a range of products in the <500cc category. Given that all the <500cc motorcycles would be manufactured by TVSM in its plant, there exists a significant long-term export (subcontracting) revenue potential for TVSM.

We have not currently factored in any positive impact of the tie-up with BMW in our earnings estimates (neither the increase in the market share in the premium motorcycle space nor the export subcontracting revenues from BMW) due to lack of adequate details and pending development of even the first joint product. We believe this tie-up would help TVSM significantly in the premium bike segment and also be a source of potential export revenues.

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 9

Where do we go from here? Exhibit 13: Key assumptions and estimates (standalone)

FY14 FY15E FY16E FY17E Remarks

Motorcycles (domestic) volume growth 3% 27% 30% 20% We are factoring in the industry volumes to grow at 13% CAGR over FY14-17. We expect TVSM to increase its market share (by 204bps) over FY14-17 on the back of new launches.

Motorcycles (exports) volume growth 16% 33% 15% 12% We expect strong momentum in export volumes to continue.

Scooters (dom + exports) volume growth 8% 55% 20% 16% We expect strong volume growth for the scooter industry and TVSM to sustain the market share gain made in FY14/FY15.

Mopeds (dom + exports) volume growth -8% 10% 10% 5% We expect a modest 8% growth over FY14-17.

3Ws (dom. + exports) volume growth 64% 33% 15% 12%

TVSM's 3W sales have been largely driven by demand in the export markets, emanating from rising volumes from the existing markets and increased availability of 3W capacities. We expect 3W exports to remain healthy though the growth should moderate on a rising base.

Revenues (` mn) 79,619 104,947 127,309 146,915 We expect healthy revenue growth of 23% for FY14-17 on the back of strong volume growth (20% CAGR over FY14-17) across categories. YoY growth 11% 32% 21% 15%

EBITDA (` mn) 4,781 7,344 11,504 14,640 We expect improvement in margin on the back of rising volumes, higher capacity utilisation and improving product mix. We expect a healthy 45% CAGR in absolute EBITDA over FY14-17.

EBITDA margin 6.0% 7.0% 9.0% 10.0%

EBITDA YoY growth 17% 54% 57% 27%

Adjusted PAT (` mn) 2,411 4,401 7,648 9,834 We expect interest costs to moderate going forward on the back of reduction in debt levels. As a result, the net earnings growth is likely to be higher than the EBITDA growth. We expect net earnings CAGR of nearly 60% over FY14-17.

Adjusted PAT margin 3.0% 4.2% 6.0% 6.7%

Adjusted EPS (`) 5.08 9.26 16.1 20.7

Adjusted EPS YoY growth 17% 83% 74% 29%

Work cap days (ex-cash) - closing (4) (1) (1) (1) No significant change in working capital levels as compared to the FY14 levels. Work cap days (ex-cash) - average (2) (2) (1) (1)

CFO (post tax) (` mn) 5,238 5,059 8,972 11,261

Lower working capital inflow in FY15 (vs FY14 levels) to restrict CFO growth in FY15. However, rising profitability and stable working capital to result in CFO bouncing back strongly in FY16 and in FY17.

Capex (net of sales proceeds) (` mn) 2,580 2,000 2,546 2,938 Capex estimate in line with the management guidance.

Inv. in Indonesia and other entities (Gross, before sale of invts) (` mn) 1,370 1,250 - -

We expect fund infusion of `500mn into TVS Indonesia and `750mn into TVS Motor Services in FY15. No funds infusion thereafter.

FCF (` mn) (ex-sale of investments) 1,288 1,809 6,426 8,322 FCF to bounce back strongly from FY15 on the back of increase in CFO outpacing the growth in capex.

Net debt/(cash) (̀ mn) 4,450 2,844 (2,490) (8,717) We expect net debt levels to come down in FY15 on the back of positive FCF generation; TVSM would enjoy a net cash position at the standalone level by end-FY16.

Source: Company, Ambit Capital research

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 10

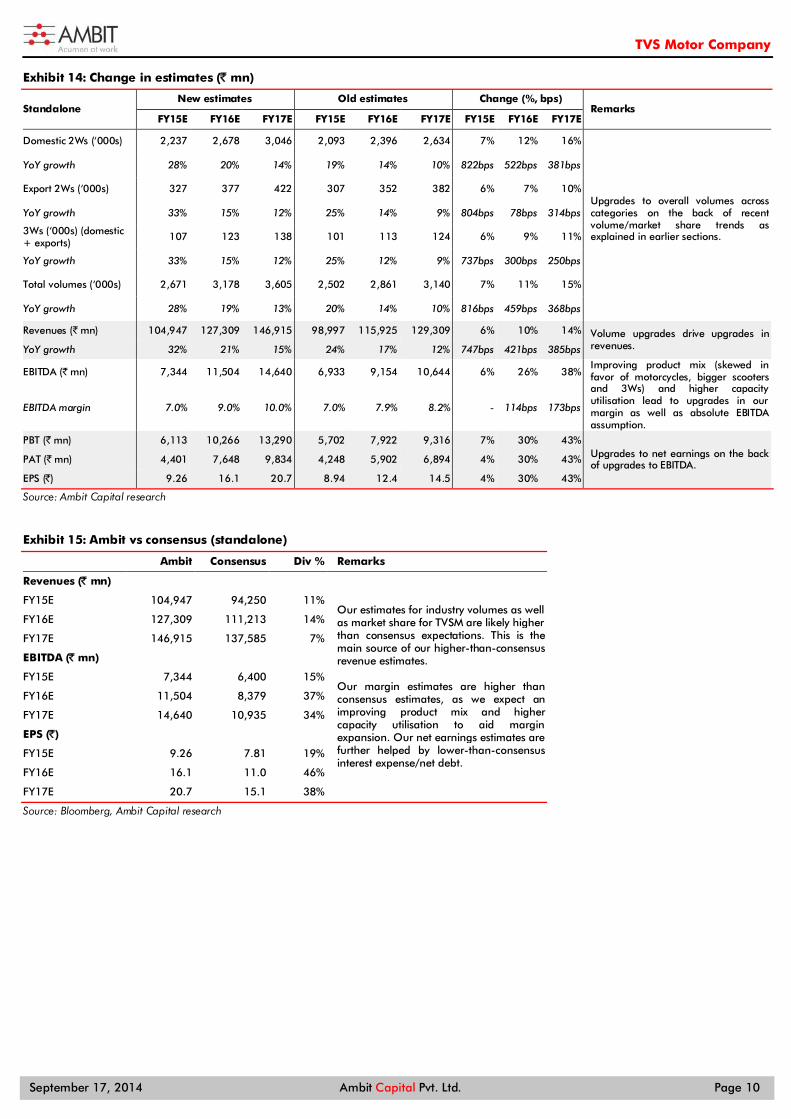

Exhibit 14: Change in estimates (` mn)

Standalone New estimates Old estimates Change (%, bps)

Remarks FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E

Domestic 2Ws (‘000s) 2,237 2,678 3,046 2,093 2,396 2,634 7% 12% 16%

Upgrades to overall volumes across categories on the back of recent volume/market share trends as explained in earlier sections.

YoY growth 28% 20% 14% 19% 14% 10% 822bps 522bps 381bps

Export 2Ws (‘000s) 327 377 422 307 352 382 6% 7% 10%

YoY growth 33% 15% 12% 25% 14% 9% 804bps 78bps 314bps

3Ws (‘000s) (domestic + exports)

107 123 138 101 113 124 6% 9% 11%

YoY growth 33% 15% 12% 25% 12% 9% 737bps 300bps 250bps

Total volumes (‘000s) 2,671 3,178 3,605 2,502 2,861 3,140 7% 11% 15%

YoY growth 28% 19% 13% 20% 14% 10% 816bps 459bps 368bps

Revenues ( ̀mn) 104,947 127,309 146,915 98,997 115,925 129,309 6% 10% 14% Volume upgrades drive upgrades in revenues. YoY growth 32% 21% 15% 24% 17% 12% 747bps 421bps 385bps

EBITDA (` mn) 7,344 11,504 14,640 6,933 9,154 10,644 6% 26% 38% Improving product mix (skewed in favor of motorcycles, bigger scooters and 3Ws) and higher capacity utilisation lead to upgrades in our margin as well as absolute EBITDA assumption.

EBITDA margin 7.0% 9.0% 10.0% 7.0% 7.9% 8.2% - 114bps 173bps

PBT ( ̀mn) 6,113 10,266 13,290 5,702 7,922 9,316 7% 30% 43% Upgrades to net earnings on the back of upgrades to EBITDA. PAT (` mn) 4,401 7,648 9,834 4,248 5,902 6,894 4% 30% 43%

EPS (̀ ) 9.26 16.1 20.7 8.94 12.4 14.5 4% 30% 43%

Source: Ambit Capital research

Exhibit 15: Ambit vs consensus (standalone)

Ambit Consensus Div % Remarks

Revenues (̀ mn)

Our estimates for industry volumes as well as market share for TVSM are likely higher than consensus expectations. This is the main source of our higher-than-consensus revenue estimates. Our margin estimates are higher than consensus estimates, as we expect an improving product mix and higher capacity utilisation to aid margin expansion. Our net earnings estimates are further helped by lower-than-consensus interest expense/net debt.

FY15E 104,947 94,250 11%

FY16E 127,309 111,213 14%

FY17E 146,915 137,585 7%

EBITDA (̀ mn)

FY15E 7,344 6,400 15%

FY16E 11,504 8,379 37%

FY17E 14,640 10,935 34%

EPS (̀ )

FY15E 9.26 7.81 19%

FY16E 16.1 11.0 46%

FY17E 20.7 15.1 38%

Source: Bloomberg, Ambit Capital research

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 11

Upgrade target price to `270/share Our DCF model values the standalone entity at `261/share, implying 14.0x one-year forward net earnings. The implied valuation multiple is at a discount of about 5% to the average one-year forward multiples commanded by its larger peers like Bajaj Auto and Hero MotoCorp but a premium of ~50% to TVSM’s last three-year average and 7% higher than our earlier implied multiple. Given the significantly smaller size of TVSM but its significantly higher earnings growth, we believe TVSM ought to trade at a marginal discount to its peers. We continue to assign a valuation of 1.0x end-FY15 book value to the equity investments made by TVSM in TVS Motor Services, which yields `9/TVSM share. Thus, we arrive at an October 2015 SOTP target price of `270/TVSM share (50% higher than our 25 June 2014 TP). Given that the Indonesia business and other entities continue to make losses, we are not assigning any value to the investments made by (and to be made by) TVSM into these entities. At 1.0x P/B, these investments would have accounted for `12/TVSM share as at end-FY15.

Due to lack of details and pending development of even the first product, we are not factoring in any impact of TVSM’s tie-up with BMW Motorrad in either our earnings estimates or our fair valuation of the stock.

SOTP-based valuation Standalone business (`261/share)

Using a WACC of 14% and terminal growth of 4%, we arrive at a DCF-based valuation of `261/share for the standalone business (vs `171 earlier). The revised valuation implies 14.0x one-year forward net earnings (given the target price date is 1 October 2015; 6 months each of FY16 and FY17 considered in calculating net earnings for implied multiple), a premium of ~50% to TVSM’s last three-year average and 7% higher than our earlier implied multiple.

Overall, our increase in the standalone business’ valuation (by 53% vs the last published estimates) is driven by: (a) increase in earnings (FY16 and FY17 net earnings revised upwards by 30% and 43% respectively); (b) increase in long-term sustainable EBITDA margin assumption from 9.0% to 10.0% driven by higher volume estimates; and (c) roll-forward of DCF to October 2015 (vs July 2015 earlier).

Increase in long-term EBITDA margin estimates also results in a 5% revision in the implied one-year forward P/E multiple from 13.5x earlier to 14.0x now.

Exhibit 16: FCF profile (standalone)

Source: Ambit Capital research

Exhibit 17: FCF assumptions (standalone) – ̀ mn

PV of FCF for forecasting period (FY16- FY25) 61,587

Terminal value 63,529

Enterprise value 125,116

Less: net debt/ (cash) at 31 March 2015 2,844

Implied equity value 122,272

Fully diluted equity shares (mn nos) 475.1

Implied equity value (̀ /share) 261

Source: Ambit Capital research

10%

25%

40%

55%

70%

85%

4,600

5,000

5,400

5,800

6,200

6,600

7,000

FY16

E

FY17

E

FY18

E

FY19

E

FY20

E

FY21

E

FY22

E

FY23

E

FY24

E

FY25

E

PVFF (LHS) (Rs mn) WACC (RHS)RoIC (ex-cash) (RHS)

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 12

TVS Motor Services (`9/TVSM share)

Given that TVS Motor Services is a profitable entity, we assign a valuation of 1.0x end-FY15 book value to the equity investment made by TVSM in TVS Motor Services, which amounts to `9/TVSM share. TVSM has infused `750mn in TVS Motor Services in FY14 and we expect further fund infusion of `750mn in FY15.

Investments into Indonesia and other entities (` NIL/TVSM share)

TVSM has made investments of `5,152mn (equity + preference) into the Indonesia business and other entities (excluding TVS Motor Services) as at end-FY14 (after impairment provision of `1,247mn). TVSM has infused `498mn in Indonesia in FY14 and we expect further fund infusion (`500mn) in FY15. Given that Indonesia and other entities continue to make losses, we are not assigning any value to the investments made by (and to be made by) TVSM into these entities. At 1.0x P/B, these investments would have accounted for `12/TVSM share as at end-FY15, which is not considered in our valuation estimate for TVSM.

Exhibit 18: Key investments by TVSM outside of the standalone entity

Particulars (̀ mn) Latest equity stake held by TVSM

FY14 FY15E FY16E FY17E

Indonesian 2W venture (TVS Motor Co. (Europe) B.V. + TVS Motor (Singapore) Pte. Ltd. + PT. TVS Motor Co. Indonesia) 100.0%

5,240 5,740 5,740 5,740

Less: Impairment provision (1,247) (1,247) (1,247) (1,247)

Net Book value 3,993 3,993 3,993 3,993

Energy ventures

TVS Energy Ltd. 4.5% 33 33 33 33

Housing ventures

TVS Housing Ltd. 100.0% 1 1 1 1

Emerald Haven Realty Ltd. 48.8% 400 400 400 400

Net Book value 401 401 401 401

Auto component ventures

Sundaram Auto Comp. Ltd. 100.0% 609 609 609 609

Engine technology

Pinnacle Engines Inc., USA 117 117 117 117

Net Book value 5,152 5,652 5,652 5,652

Net Book value Per TVSM share 11 12 12 12

As % of standalone networth 36% 33% 25% 19%

Source: Company, Ambit Capital research

Overall, we arrive at a sum-of-the-parts (SOTP) based valuation of `270/share, which implies 28% upside from current levels and 50% higher than our last published target price.

Exhibit 19: SOTP valuation from TVSM (`270/share)

Segment Methodology Implied multiple (x) Value (̀ /TVSM share)

New Old Change

Core business FCF 14.0x one-year forward earnings 261 171 53%

Investments - TVS Motor Services P/B 1.0x FY15 P/B 9 9 0%

Total (̀ ) 270 180 50%

Source: Company, Ambit Capital research

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 13

Relative valuation Comparison based on consensus estimates: TVSM (standalone) is trading at an 18% premium to its domestic peer group average on FY16 P/E and at a premium of 7% on FY16 EV/EBITDA. However, TVSM (standalone) is trading in line with its domestic peer group average on FY17 P/E and at a discount of 8% on FY17 EV/EBITDA.

Comparison based on Ambit estimates: TVSM (standalone) is trading at a 20% discount to its domestic peers on FY16 P/E multiple and a 22% discount on FY16 EV/EBITDA multiple. TVSM (standalone) is trading at a 29% discount to its domestic peers on FY17 P/E multiple and a 31% discount on FY17 EV/EBITDA multiple.

Exhibit 20: Relative valuation

Mcap EV/EBITDA (x) P/E (x) CAGR (FY14-17) Price perf (%) RoE

US$ mn FY15 FY16 FY17 FY15 FY16 FY17 Sales EBITDA EPS 3m 1 yr FY15 FY16 FY17

India

TVS (standalone)* 1,640 16.3 12.5 9.6 27.3 19.3 14.1 20 32 39 62 524 24 27 29

TVS (standalone)** 1,640 14.2 9.1 7.2 22.8 13.1 10.2 23 45 60 62 524 28 39 38

TVS (consolidated)* 1,640 16.6 12.1 14.0 35.2 24.1 26.1 11 16 27 62 524 23 25 22

Bajaj Auto 10,912 14.1 12.2 10.9 18.9 16.3 14.7 14 12 12 6 15 33 32 31

Hero MotoCorp 9,126 13.3 11.1 9.8 20.2 16.4 14.0 13 14 23 7 33 44 45 43

Average (ex-TVS) 13.7 11.6 10.4 19.5 16.4 14.4 13 13 18 Global Honda 61,717 10.4 9.2 7.2 10.4 9.2 8.3 6 1 12 4 (4) 10 11 11

Harley 14,011 17.0 14.7 10.0 17.0 14.7 12.7 4 9 15 (6) 2 26 27 30

Suzuki 19,081 15.8 14.9 4.4 15.8 14.9 13.8 5 9 11 17 63 9 9 9

Yamaha 6,639 13.6 11.1 6.1 13.6 11.1 9.7 7 22 18 20 44 13 14 14

Average 14.2 12.5 6.9 14.2 12.5 11.1 5 10 14 Source: Bloomberg, Ambit Capital research. Note: * indicates consensus estimates; ** indicates Ambit estimates

Cross-cycle valuation On a cross-cycle EV/EBITDA multiple comparison, TVSM (standalone) is trading at a significant premium to its three-year as well as five-year average EV/EBITDA multiples. Similarly, on a cross-cycle P/E comparison, TVSM (standalone) is trading at a premium of 145% to the three-year average and 117% to the five-year average. We believe the main reasons for TVSM trading at higher than historical average P/E multiples are: (a) the underlying consensus net earnings estimates (which are used for the calculation of multiples) do not fully factor in the net earnings uplift for TVSM from a recovery in domestic 2W industry volumes and specific benefits to TVSM from new launches; for instance, our FY15 and FY16 net earnings estimates are nearly 19% and 46% ahead of consensus, respectively; (b) the business prospects (both volumes and margin) are significantly better as compared to earlier years due to the reasons highlighted above; and (c) TVSM’s focus on cash generation and reduction in the debt levels over the last two years. All the above factors have/are likely to result in a nearly 100% improvement in RoIC in FY15/16 as compared to the FY11-13 average.

The P/E multiples implied by our fair valuation for the standalone business is 14.0x EPS, which is higher than the company’s historical averages but which we believe appears justified due to the reasons mentioned above.

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 14

Exhibit 21: Cross-cycle P/E

Source: Bloomberg, Ambit Capital research. Note: P/E bands arrived at using Bloomberg consensus estimates for respective periods

Exhibit 22: Cross-cycle EV/EBITDA

Source: Bloomberg, Ambit Capital research. Note: EV/EBITDA bands arrived at using Bloomberg consensus estimates for respective periods

TVSM has closed the valuation gap (P/E) with its peers significantly in recent months. Based on our current estimates, TVSM in fact trades almost in line with its peers (Hero MotoCorp and Bajaj Auto) on one-year forward net earnings. We expect strong margin expansion of 200bps to result in net earnings growth of 74% for TVSM for FY16. This is much higher than the average 27% growth for peers for FY16. Hence, on FY16 net earnings TVSM trades at 13.1x, a discount of 20% to the average multiple of Hero and Bajaj. Given the much smaller size of TVSM but its much higher earnings growth, we believe TVSM ought to trade at a marginal discount (about 5%) to peers.

Exhibit 23: TVSM’s RoE and RoCE to witness significant expansion in the future

Source: Bloomberg, Ambit Capital research. Note: P/E bands arrived at using Bloomberg consensus estimates for respective periods

Exhibit 24: TVSM closing in on the valuation gap with its peers

Source: Bloomberg, Ambit Capital research. Note: TVS estimates for calculating P/E are Ambit estimates

Exhibit 25: Explanation for our forensic accounting scores on the cover page

Segment Score Comments

Accounting AMBER TVS Motor’s accounting score is in line with the sector average accounting score. Whilst rising investments outside of the standalone business, particularly in unrelated ventures such as housing and energy, were causes for concern, the recent developments such as divestment of stake in TVS Energy are positive developments.

Predictability AMBER Given that automobile companies publish their volume numbers on a monthly basis, generally no significant positive/negative surprises are seen in revenues. However, the margins tend to be less predictable and are generally the source for actual results coming in above/below consensus expectations.

Earnings momentum AMBER Bloomberg shows marginal downgrades to consensus numbers in recent weeks given the lower-than-expected performance of the company in 1QFY15.

Source: Ambit Capital research

4 6 8

10 12 14 16 18 20 22 24 26

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Aug

-14

TVS 1-yr fwd P/E Avg P/E

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Aug

-14

TVS 1-yr fwd EV/EBITDA Avg EV/EBITDA

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

RoE ROCE

-80%-70%-60%-50%-40%-30%-20%-10%

0%10%

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

TVS (discount)/premium to Bajaj & Hero

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 15

Key risks Bajaj Auto’s foray into scooters

In 2009, Bajaj exited the scooter market to focus on the domestic motorcycle segment. Since then, despite the domestic scooter segment outperforming the motorcycle category, Bajaj Auto has maintained its focus on the motorcycle space. If Bajaj were to re-enter the scooter space, it could pose a risk to the market share of incumbents including TVSM. Bajaj’s management has however maintained1 that motorcycles would remain their key focus area.

Advent of discount/pricing war in 2W space

Despite the slowdown in 2W demand in recent years, 2W players have (largely) stayed away from offering discounts (unlike PVs and CVs which are witnessing significant discounts). Any advent of discounts in the 2W space can have a significant negative impact on TVSM’s margin. That said, looking at the track record of the industry over the past 5-6 years and our discussions with 2W companies/dealers, we do not expect any such discounting to resume in the near to medium term in the domestic 2W space.

Key catalysts Market share gain in the domestic motorcycle segment

The launch of Star City+ in May 2014 has led to improvement in TVSM’s market share from 5.2% in March 2014 to 6.4% in August 2014. The company’s upcoming launch in the executive segment (most likely to be branded ‘Victor’) in December 2014/January 2015 can help TVSM gain further foothold in the executive motorcycle segment (accounting for 60-65% of the total domestic motorcycle industry volumes). We believe if TVSM can achieve the right pricing, design and mileage for Victor, then this can play a critical role in further market share gain for TVSM in the domestic motorcycle space. Furthermore, the company also plans to launch a new motorcycle in the premium segment, which can provide additional volumes as well as strengthen TVSM’s market share in the premium segment in the future.

EBITDA margin improvement

Whilst its 1QFY15 margin performance was below our expectations due to specific one-offs (discussed in the sections above), we continue to expect strong margin expansion for TVSM driven by: (i) higher volumes/capacity utilisation levels bringing down marketing and employee costs as a percentage of sales (by 169bps over FY14-17); (ii) opportunity to raise prices of new launches once the volume stabilises; and (iii) healthier product mix with rising share of motorcycle and ‘bigger’ scooters. We expect TVSM to register an EBITDA margin of 7.4% for the remaining nine months of FY15 vs the 5.7% achieved in 1QFY15.

1http://www.livemint.com/Industry/FTDz29nxmjLqtXl3yIIWyK/Motorcycles-to-remain-BajajAutosfocus.html

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 16

Balance sheet (standalone)

Year to March (̀ mn) FY13 FY14 FY15E FY16E FY17E

Shareholders' equity 475 475 475 475 475

Reserves and surpluses 11,772 13,678 16,664 21,853 28,526

Total net worth 12,247 14,153 17,139 22,328 29,001

Debt 6,345 5,276 3,856 3,793 3,729

Deferred tax liability 931 1,247 1,247 1,247 1,247

Total liabilities 19,523 20,676 22,242 27,368 33,977

Gross block 22,500 24,723 26,723 29,269 32,208

Net block 10,135 11,257 11,823 12,808 14,032

CWIP 458 544 544 544 544

Investments (non-current) 8,668 8,959 10,203 10,203 10,203

Cash & cash equivalents 175 826 1,011 6,282 12,446

Debtors 3,169 3,341 4,404 5,343 6,165

Inventory 5,097 5,482 7,225 8,765 10,115

Loans & advances 3,656 5,238 6,751 8,088 9,259

Total current assets 12,095 14,886 19,392 28,477 37,985

Current liabilities 10,767 13,760 17,252 20,928 24,150

Provisions 1,066 1,211 2,469 3,737 4,637

Total current liabilities 11,833 14,971 19,720 24,665 28,787

Net current assets 262 (85) (328) 3,813 9,198

Total assets 19,523 20,676 22,242 27,368 33,977

Source: Company, Ambit Capital research

Income statement (standalone)

Year to March (̀ mn) FY13 FY14 FY15E FY16E FY17E

Revenues 71,693 79,619 104,947 127,309 146,915

% growth 1% 11% 32% 21% 15%

Operating expenditure 67,602 74,838 97,602 115,805 132,275

EBITDA 4,090 4,781 7,344 11,504 14,640

% growth -13% 17% 54% 57% 27%

Depreciation 1,304 1,317 1,434 1,561 1,714

EBIT 2,786 3,465 5,910 9,943 12,926

Interest expenditure 480 254 145 76 76

Non-operating income 238 302 347 400 439

Adjusted PBT 2,544 3,513 6,113 10,266 13,290

Tax 476 1,101 1,712 2,618 3,455

Adjusted PAT 2,069 2,411 4,401 7,648 9,834

Source: Company, Ambit Capital research

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 17

Cash flow statement (standalone)

Year to March (̀ mn) FY13 FY14 FY15E FY16E FY17E

Net profit before tax 1,628 3,485 6,113 10,266 13,290

Depreciation 1,304 1,317 1,434 1,561 1,714

Others 1,281 58 (203) (323) (363)

Tax (535) (1,275) (1,712) (2,618) (3,455)

(Incr)/decr in net working capital 643 1,613 (574) 86 76

Cash flow from operations 4,321 5,197 5,059 8,972 11,261

Capex (net) (995) (2,580) (2,000) (2,546) (2,938)

(Incr)/decr in investments (295) (276) (1,244) (0) (0)

Others 217 257 347 400 439

Cash flow from investments (1,073) (2,598) (2,896) (2,147) (2,499)

Net borrowings (128) (886) (1,420) (63) (63)

Interest paid (530) (230) (145) (76) (76)

Dividend paid (715) (690) (412) (1,415) (2,459)

Cash flow from financing (1,373) (1,806) (1,977) (1,555) (2,598)

Net change in cash 1,874 793 186 5,271 6,163

Free cash flow 3,077 1,288 1,809 6,426 8,322

Source: Company, Ambit Capital research

Ratio analysis (standalone) Year to March (%) FY13 FY14 FY15E FY16E FY17E

EBITDA margin (%) 5.7% 6.0% 7.0% 9.0% 10.0%

EBIT margin (%) 3.9% 4.4% 5.6% 7.8% 8.8%

Net prof. margin (%) 2.9% 3.0% 4.2% 6.0% 6.7%

Dividend payout ratio (%) 28% 28% 28% 28% 28%

Net debt: equity (x) 0.5 0.3 0.2 (0.1) (0.3)

Average Working capital days (x) 1.7 (2.2) (2.4) (1.3) (1.3)

Gross block turnover (x) 3.3 3.4 4.1 4.5 4.8

RoCE (pre-tax) (%) 25% 32% 52% 80% 96%

RoIC (%) 21% 22% 37% 60% 71%

RoE (%) 17% 18% 28% 39% 38%

Source: Company, Ambit Capital research

Valuation parameters (standalone) Year to March FY13 FY14 FY15E FY16E FY17E

Diluted EPS (`) 4.35 5.08 9.26 16.1 20.7

Book value per share (`) 25.8 29.8 36.1 47.0 61.0

Dividend per share (`) 1.20 1.40 2.56 4.44 5.71

P/E (x) 48.4 41.5 22.8 13.1 10.2

P/BV (x) 8.2 7.1 5.8 4.5 3.5

EV/EBITDA (x) 25.6 21.9 14.2 9.1 7.1

EV/EBIT (x) 1.6 1.3 0.8 0.4 0.3

Source: Company, Ambit Capital research

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 18

Institutional Equities Team

Saurabh Mukherjea, CFA CEO, Institutional Equities (022) 30433174 [email protected]

Research

Analysts Industry Sectors Desk-Phone E-mail

Nitin Bhasin - Head of Research E&C / Infrastructure / Cement (022) 30433241 [email protected]

Aadesh Mehta Banking / Financial Services (022) 30433239 [email protected]

Achint Bhagat Cement / Infrastructure (022) 30433178 [email protected]

Aditya Khemka Healthcare (022) 30433272 [email protected]

Akshay Wadhwa Banking & Financial Services (022) 30433005 [email protected] Ashvin Shetty, CFA Automobile (022) 30433285 [email protected]

Bhargav Buddhadev Power / Capital Goods (022) 30433252 [email protected]

Dayanand Mittal, CFA Oil & Gas / Metals & Mining (022) 30433202 [email protected]

Deepesh Agarwal Power / Capital Goods (022) 30433275 [email protected] Gaurav Mehta, CFA Strategy / Derivatives Research (022) 30433255 [email protected]

Karan Khanna Strategy (022) 30433251 [email protected]

Krishnan ASV Real Estate (022) 30433205 [email protected]

Pankaj Agarwal, CFA Banking / Financial Services (022) 30433206 [email protected]

Paresh Dave Healthcare (022) 30433212 [email protected]

Parita Ashar Metals & Mining / Oil & Gas (022) 30433223 [email protected]

Pratik Singhania Retail (022) 30433264 [email protected]

Rakshit Ranjan, CFA Consumer / Retail (022) 30433201 [email protected]

Ravi Singh Banking / Financial Services (022) 30433181 [email protected]

Ritesh Vaidya Consumer (022) 30433246 [email protected] Ritika Mankar Mukherjee, CFA Economy / Strategy (022) 30433175 [email protected]

Ritu Modi Automobile (022) 30433292 [email protected]

Sagar Rastogi Technology (022) 30433291 [email protected]

Sumit Shekhar Economy / Strategy (022) 30433229 [email protected]

Tanuj Mukhija, CFA E&C / Infrastructure (022) 30433203 [email protected]

Utsav Mehta Technology (022) 30433209 [email protected]

Sales

Name Regions Desk-Phone E-mail

Sarojini Ramachandran - Head of Sales UK +44 (0) 20 7614 8374 [email protected]

Deepak Sawhney India / Asia (022) 30433295 [email protected]

Dharmen Shah India / Asia (022) 30433289 [email protected]

Dipti Mehta India / USA (022) 30433053 [email protected]

Nityam Shah, CFA USA / Europe (022) 30433259 [email protected]

Parees Purohit, CFA UK / USA (022) 30433169 [email protected]

Praveena Pattabiraman India / Asia (022) 30433268 [email protected]

Production

Sajid Merchant Production (022) 30433247 [email protected]

Sharoz G Hussain Production (022) 30433183 [email protected]

Joel Pereira Editor (022) 30433284 [email protected]

Nikhil Pillai Database (022) 30433265 [email protected]

E&C = Engineering & Construction

TVS Motor Company

September 17, 2014 Ambit Capital Pvt. Ltd. Page 19

Explanation of Investment Rating Investment Rating Expected return

(over 12-month period from date of initial rating)

Buy >5%

Sell <5%

Disclaimer

This report or any portion hereof may not be reprinted, sold or redistributed without the written consent of Ambit Capital. AMBIT Capital Research is disseminated and available primarily electronically, and, in some cases, in printed form.

Additional information on recommended securities is available on request.

Disclaimer 1. AMBIT Capital Private Limited (“AMBIT Capital”) and its affiliates are a full service, integrated investment banking, investment advisory and brokerage group. AMBIT Capital is a Stock Broker, Portfolio

Manager and Depository Participant registered with Securities and Exchange Board of India Limited (SEBI) and is regulated by SEBI 2. The recommendations, opinions and views contained in this Research Report reflect the views of the research analyst named on the Research Report and are based upon publicly available information

and rates of taxation at the time of publication, which are subject to change from time to time without any prior notice. 3. AMBIT Capital makes best endeavours to ensure that the research analyst(s) use current, reliable, comprehensive information and obtain such information from sources which the analyst(s) believes to

be reliable. However, such information has not been independently verified by AMBIT Capital and/or the analyst(s) and no representation or warranty, express or implied, is made as to the accuracy or completeness of any information obtained from third parties. The information or opinions are provided as at the date of this Research Report and are subject to change without notice.

4. If you are dissatisfied with the contents of this complimentary Research Report or with the terms of this Disclaimer, your sole and exclusive remedy is to stop using this Research Report and AMBIT Capital shall not be responsible and/ or liable in any manner.

5. If this Research Report is received by any client of AMBIT Capital or its affiliate, the relationship of AMBIT Capital/its affiliate with such client will continue to be governed by the terms and conditions in place between AMBIT Capital/ such affiliate and the client.

6. This Research Report is issued for information only and should not be construed as an investment advice to any recipient to acquire, subscribe, purchase, sell, dispose of, retain any securities. Recipients should consider this Research Report as only a single factor in making any investment decisions. This Research Report is not an offer to sell or the solicitation of an offer to purchase or subscribe for any investment or as an official endorsement of any investment.

7. If 'Buy', 'Sell', or 'Hold' recommendation is made in this Research Report such recommendation or view or opinion expressed on investments in this Research Report is not intended to constitute investment advice and should not be intended or treated as a substitute for necessary review or validation or any professional advice. The views expressed in this Research Report are those of the research analyst which are subject to change and do not represent to be an authority on the subject. AMBIT Capital may or may not subscribe to any and/ or all the views expressed herein.

8. AMBIT Capital makes no guarantee, representation or warranty, express or implied; and accepts no responsibility or liability as to the accuracy or completeness or currentess of the information in this Research Report. AMBIT Capital or its affiliates do not accept any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of this Research Report.

9. Past performance is not necessarily a guide to evaluate future performance. 10. AMBIT Capital and/or its affiliates (as principal or on behalf of its/their clients) and their respective officers directors and employees may hold positions in any securities mentioned in this Research

Report (or in any related investment) and may from time to time add to or dispose of any such securities (or investment). Such positions in securities may be contrary to or inconsistent with this Research Report.

11. This Research Report should be read and relied upon at the sole discretion and risk of the recipient. 12. The value of any investment made at your discretion based on this Research Report or income therefrom may be affected by changes in economic, financial and/ or political factors and may go down as

well as up and you may not get back the full or the expected amount invested. Some securities and/ or investments involve substantial risk and are not suitable for all investors. 13. This Research Report is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied in whole

or in part, for any purpose. Neither this Research Report nor any copy of it may be taken or transmitted or distributed, directly or indirectly within India or into any other country including United States (to US Persons), Canada or Japan or to any resident thereof. The distribution of this Research Report in other jurisdictions may be strictly restricted and/ or prohibited by law or contract, and persons into whose possession this Research Report comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition.

14. Neither AMBIT Capital nor its affiliates or their respective directors, employees, agents or representatives, shall be responsible or liable in any manner, directly or indirectly, for views or opinions expressed in this Report or the contents or any errors or discrepancies herein or for any decisions or actions taken in reliance on the Report or inability to use or access our service or this Research Report or for any loss or damages whether direct or indirect, incidental, special or consequential including without limitation loss of revenue or profits that may arise from or in connection with the use of or reliance on this Research Report or inability to use or access our service or this Research Report.

Conflict of Interests 15. In the normal course of AMBIT Capital’s business circumstances may arise that could result in the interests of AMBIT Capital conflicting with the interests of clients or one client’s interests conflicting with

the interest of another client. AMBIT Capital makes best efforts to ensure that conflicts are identified and managed and that clients’ interests are protected. AMBIT Capital has policies and procedures in place to control the flow and use of non-public, price sensitive information and employees’ personal account trading. Where appropriate and reasonably achievable, AMBIT Capital segregates the activities of staff working in areas where conflicts of interest may arise. However, clients/potential clients of AMBIT Capital should be aware of these possible conflicts of interests and should make informed decisions in relation to AMBIT Capital’s services.

16. AMBIT Capital and/or its affiliates may from time to time have investment banking, investment advisory and other business relationships with companies covered in this Research Report and may receive compensation for the same. Research analysts provide important inputs into AMBIT Capital’s investment banking and other business selection processes.

17. AMBIT Capital and/or its affiliates may seek investment banking or other businesses from the companies covered in this Research Report and research analysts involved in preparing this Research Report may participate in the solicitation of such business.

18. In addition to the foregoing, the companies covered in this Research Report may be clients of AMBIT Capital where AMBIT Capital may be required, inter alia, to prepare and publish research reports covering such companies and AMBIT Capital may receive compensation from such companies in relation to such services. However, the views reflected in this Research Report are objective views, independent of AMBIT Capital’s relationship with such company.

19. In addition, AMBIT Capital may also act as a market maker or risk arbitrator or liquidity provider or may have assumed an underwriting commitment in the securities of companies covered in this Research Report (or in related investments) and may also be represented in the supervisory board or on any other committee of those companies.

Additional Disclaimer for U.S. Persons 20. The research report is solely a product of AMBIT Capital 21. AMBIT Capital is the employer of the research analyst(s) who has prepared the research report 22. Any subsequent transactions in securities discussed in the research reports should be effected through J.P.P. Euro-Securities, Inc. (“JPP”). 23. JPP does not accept or receive any compensation of any kind for the dissemination of the AMBIT Capital research reports. 24. The research analyst(s) preparing the research report is resident outside the United States and is/are not associated persons of any U.S. regulated broker-dealer and that therefore the analyst(s) is/are

not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

Additional Disclaimer for Canadian Persons 25. AMBIT Capital is not registered in the Province of Ontario and /or Province of Québec to trade in securities nor is it registered in the Province of Ontario and /or Province of Québec to provide advice

with respect to securities. 26. AMBIT Capital's head office or principal place of business is located in India. 27. All or substantially all of AMBIT Capital's assets may be situated outside of Canada. 28. It may be difficult for enforcing legal rights against AMBIT Capital because of the above. 29. Name and address of AMBIT Capital's agent for service of process in the Province of Ontario is: Torys LLP, 79 Wellington St. W., 30th Floor, Box 270, TD South Tower, Toronto, Ontario M5K 1N2

Canada. 30. Name and address of AMBIT Capital's agent for service of process in the Province of Montréal is Torys Law Firm LLP, 1 Place Ville Marie, Suite 1919 Montréal, Québec H3B 2C3 Canada.

© Copyright 2014 AMBIT Capital Private Limited. All rights reserved.

Ambit Capital Pvt. Ltd. Ambit House, 3rd Floor 449, Senapati Bapat Marg, Lower Parel, Mumbai 400 013, India. Phone: +91-22-3043 3000 Fax: +91-22-3043 3100 CIN: U74140MH1997PTC107598 www.ambitcapital.com