Common Ground: The Need for a Universal Mortgage Loan Identifier

22

1 Office of Fin 2 Office of Fin The Office disseminate comments. Views and o positions or and suggest quoted with Com Univ Mat nancial Resea nancial Resea of Financial e preliminar Papers in th opinions exp r policy of O tions are we hout additio Offic W mmon versal tthew M arch, matthew arch, lynn.cala l Research ( ry research f he OFR Work pressed are OFR, Treasur elcome and onal permiss ce of Fin Working Decem n Grou Mortg McCorm w.mccormick@ ahan@treasu (OFR) Work findings in a king Paper S those of the ry, or any of should be d sion. www.tr nancial g Paper mber 5, 2 nd: Th gage L mick 1 and @treasury.go ry.gov ing Paper S a format int eries are wo e authors an the agencie directed to th reasury.gov/ Researc #0012 2013 he Nee Loan Id d Lynn ov Series allows tended to g orks in progr nd do not ne es represent he authors. /ofr ch ed for dentifi Calahan s staff and generate dis ress and sub ecessarily re ted by contr OFR Workin a ier n 2 their co‐aut scussion and ject to revis epresent the ributors. Com ng Papers m thors to d critical ion. e mments may be

Transcript of Common Ground: The Need for a Universal Mortgage Loan Identifier

1 Office of Fin2 Office of Fin

The Office disseminatecomments. Views and opositions orand suggestquoted with

ComUniv

Mat

nancial Reseanancial Resea

of Financiale preliminarPapers in th

opinions expr policy of Otions are wehout additio

OfficW

mmonversal

tthew M

arch, matthewarch, lynn.cala

l Research (ry research fhe OFR Work

pressed are OFR, Treasurelcome and onal permiss

ce of FinWorkingDecem

n GrouMortg

McCorm

w.mccormick@ahan@treasu

(OFR) Workfindings in aking Paper S

those of thery, or any of should be dsion.

www.tr

nancial g Paper mber 5, 2

nd: Thgage L

mick1 and

@treasury.gory.gov

ing Paper Sa format interies are wo

e authors anthe agencie

directed to th

reasury.gov/

Researc#00122013

he NeeLoan Id

d Lynn

ov

Series allowstended to gorks in progr

nd do not nees representhe authors.

/ofr

ch

ed for dentifi

Calahan

s staff and generate disress and sub

ecessarily reted by contrOFR Workin

a ier

n2

their co‐autscussion andject to revis

epresent theributors. Comng Papers m

thors to d critical ion.

e mments may be

1

CommonGround:TheNeedforaUniversalMortgageLoanIdentifier

MatthewMcCormick1andLynnCalahan2

1OfficeofFinancialResearch,[email protected],[email protected]

AbstractTheU.S.mortgagefinancesystemisacriticalpartofournation’sfinancialsystem,representing70percentofU.S.householdliabilities.Itisalsohighlycomplex,withmanyfinancechannels,participants,andregulators.Thedataproducedbythissystemreflectthatcomplexity;unfortunately,nosingleidentifierexiststolinkthemajorloan‐levelmortgagedatasets.Theestablishmentofasingle,cradle‐to‐grave,universalmortgageidentifierthatcannotbelinkedtoindividualsusingpublicly‐availabledatawouldsignificantlybenefitregulatorsandresearchersbyenablingbetterintegrationofthefragmenteddataproducedbytheU.S.mortgagefinancesystem.Suchanidentifiercouldadditionallyserveasthefoundationofasystemthatcouldbenefitprivatemarketparticipants,aslongassuchasystemprotectedindividualprivacy.

TheauthorsgratefullyacknowledgehelpfulcommentsfromanddiscussionwithCorneliusCrowley,WilliamNichols,andLindaPowelloftheOfficeofFinancialResearch(OFR);RenEsseneandRonBorzekowskioftheConsumerFinancialProtectionBureau;TheresaDiVenti,WilliamDoerner,RobinSeiler,andValerieSmithoftheFederalHousingFinanceAgency;ThereseScharlemannoftheDepartmentoftheTreasury;MarcRodriguezoftheBoardofGovernorsoftheFederalReserveSystem;MichaelNixon,KurtUsowski,WilliamReeder,andEdwardSzymanoskioftheDepartmentofHousingandUrbanDevelopment;ThomasMayockoftheOfficeoftheComptrolleroftheCurrency;HarrietNewburgeroftheFederalDepositInsuranceCorporation;RolaineBancroftandRobertErrettoftheSecuritiesandExchangeCommission;andothers.Anyerrorsoromissionsaretheresponsibilityoftheauthorsalone.

ViewsandopinionsexpressedarethoseoftheauthorsanddonotnecessarilyrepresentthepositionsorpolicyofOFR,Treasury,oranyoftheagenciesrepresentedbycontributors.Commentsandsuggestionsarewelcomeandshouldbedirectedtotheauthors.

2

1.IntroductionTherecenthousingcrisisexposedanumberofdatagaps,risk‐managementfailures,andshortcomingsinoperationalcontrolsthroughoutthemortgagefinancesystem,includingproblemsconnectingoriginationdatatoperformancedata,trackingloanmodifications,andverifyingloanunderwritingpractices.Mitigatingtheseproblemsisanimportantsteptowardreturningthemortgagefinancesystemtoahealthystate.ThispaperexaminesthepotentialoftheuniversaladoptionofasinglemortgageidentificationstandardtohelpaddresstheseproblemsbyenablingbetterintegrationofthefragmenteddatathatisproducedbytheU.S.mortgagefinancesystem.

Thesize($9.4trillionoutstandingasofQ12013),complexity,andfragmentednatureofthissystemanditsregulationaresignificant.1Giventhesefactors,itisdifficulttoaccuratelyidentifypatternswhenidentificationrequiresconnectingvarioussourcesofdatawithoutclear,consistent,andunambiguousidentificationofthekeycomponent:themortgageitself.However,althoughanumberofidentificationsystemsexist,nosingleuniversalidentifierissharedacrossallgovernmentagenciesoracrossallmajorprivateentities.2Althoughmarketparticipantscross‐referencetheiridentifiersasamatterofnecessity,ambiguitiesandinconsistenciesindefinitionsoftenmakecross‐referencingdifficultandinaccurate.Aswithlegalentityidentifiers,“Simplyput,havingamultitudeofidentifiersaddslayersofcomplexity,increasesthepotentialforerrors,andresultsinredundantefforts.”3

Sharedidentifiersareapublicgoodthatbenefitmarketparticipants,regulators,andresearchers.Wereauniversalmortgageidentifieradopted,researchersandregulatorswouldbebetterabletounderstandthemortgagefinancesystemfromasystemicriskperspective,andregulatorswouldhaveabetterunderstandingofthemortgagefinancesystemfromtheperspectiveofcomplianceandprudentialsupervision.Thisimprovedunderstandingcouldyieldbetterpolicyresearch,whichcouldinturndrivebetterpolicymaking,therebybenefittingthepublic.Additionally,firmswouldbenefitfromimprovedriskmanagement,lowercostsofintegrationamongtradingpartnersandwithinlargelendingfacilities,andlowercomplianceburdensfromreportingrequirements.Finally,contingentonthedevelopmentofappropriateprotectionsforindividualprivacy,purchasersofmortgagesecuritiescouldpotentiallybenefitfromgreatertransparency.

Themortgageindustryhasbeenexploringtheissueofuniqueloanidentification,inpartwithinvoluntaryconsensusstandardsbodies,asdefinedunderOfficeofManagementandBudget(OMB)CircularA‐119.4OnesuchorganizationistheMortgageIndustryStandardsMaintenanceOrganization(MISMO),astandards‐settingorganizationcurrentlyadministeredbytheMortgageBankersAssociation.ManyparticipantsinMISMOhavenotedthatalackofaclear,open,andunifyingsystemofidentification,independentofanyoneprivateentity,hascreatedproblemsforconsumers,lenders,andothers.5,6TheeffortsofaMISMOworkinggrouphaverecentlyculminated

1BoardofGovernorsoftheFederalReserveSystem,Z.1FlowofFundsAccounts,June6,2013.2Anoverviewofexistingandproposedmortgageidentificationregimesisprovidedintheappendix.3BottegaandPowell(2011).4 OfficeofManagementandBudget.CircularNo.A‐119Revised.February10,1998. 5Sokolowski(2012).

3

inthereleaseofawhitepaperthatdiscussestheutilityofauniqueloanidentifierfromtheperspectiveofindustry.7Ideally,astandarddevelopedbyavoluntaryconsensusstandardsbodywouldalsomeettheneedsofgovernment,includingprivacyrequirements,whichwouldallowforitsadoptionperOMBCircularA‐119.Similarly,otherprivate‐sectoreffortstocreateidentifiers,suchastheAmericanSecuritizationForum’sLoanIdentificationNumberCode(ASFLINC),havegrownoutofaperceivedneedto“improveinformationflowstoinvestors”inthewakeoftherecenthousingcrisis.8

Alsosincethecrisis,thepublicsectorandexpertshavenotedtheneedforauniquemortgageloanidentifiertoenablecradle‐to‐gravemonitoringofmortgagesforfinancialstabilitypurposes.9CongressintheDodd‐FrankWallStreetReformandConsumerProtectionAct(Dodd‐FrankAct)requiredregulatorstowriterulesthatinvolveidentificationofdifferenttypesofentitiesandproducts,includingmortgageloans.Specifically,Section1094ofDodd‐FrankamendedtheHomeMortgageDisclosureAct(HMDA)toallowthenewlycreatedConsumerFinancialProtectionBureau(CFPB)tomandate,“as[it]maydeterminetobeappropriate,auniversalloanidentifier.”10,11

Thetaskofdesigningauniversalidentifierwillbeadifficultone.Carefulconsiderationmustbegiventoprivacyconcerns.Asnotedbelow,amortgageidentifierwouldhavetobedesignedtopreventmarketparticipantsfromre‐identifyingindividuals.Nolinksfrompublicdocumentstomortgageidentifiersshouldbeallowed.Otherwisetheidentifiercouldbeusedtoidentifyindividuals,renderingalldatasetscontainingtheidentifierpersonally‐identifiableinformation.Suchadesignationwouldcreateconcernsabouttheuseofindividualdataintheprivatesectorandtriggerburdensomerequirementsforgovernmentresearchersusingthedata.

Thecreationofauniversalidentifieralsoraisestacticalquestions,suchasthetimingofassignment,andthestructureandgovernanceofanyentitiesissuingidentifiersorcoordinatingthem.Otherimportantissuesincludedeterminingthepartiesthatshouldhaveaccesstotheidentifier;thedocuments(ifany)thatmustorshouldbeallowedtocarrytheidentifier;howtoensureuseoftheidentifierateachstepofthemortgagelifecycle;howtoensureidentifierintegrity;andhowtodevelopmechanismstoconnectsimultaneousorsequentiallienstakenoutbyaborroweronaparticularproperty.

Thenextsectionofthispaperprovidesastylizedoverviewofthemortgagefinancesystemandthefragmentednatureofitsregulation,anddiscussesthemajorfederalloan‐levelmortgagedatacollectioneffortsanddisclosurerequirements.Section3describesthegoalsthatregulatorsandothershopetoachievebyadoptingasinglecommonmortgageidentifier.Section4describesthe

6Panchuk(2012).7 MISMO (2013). 8ASF(2009).9Wachter(2010).10Codifiedat12USC§2803(b)(6)(G).11TheDodd‐FrankActadditionallyprovidesforotheruniqueidentifiers,suchasaSAFEActidentifier(Section1094)anduniqueidentifiersrelatingtoloanbrokersororiginators(Section942).

4

implicationsthosegoalshaveforthestructureofanidentifierandidentificationsystem,andSection5concludes.

2.TheSupplyChain:TheResidentialMortgageLifeCycleandMortgageData

ThecurrentstateofresidentialmortgagefinanceintheUnitedStatesisaresultofanaccretionofstructuresandregulations,designedtoaddressdifferentsetsofproblems,datingbacktotheGreatDepression.12Asaresult,legalandregulatoryauthorityisdistributedamongagenciesatlocal,state,andfederallevels,andthereexistfourmajorfundingchannels(bankportfoliosandthreesecuritizationchannels,discussedbelow),eachwithitsownsetofregulators.Thisfragmentationisreflectedinthedataproducedbythiscollectionofentities.

TheMortgageLifeCycleTomakeclearthescopeoftheproblemfacedbyregulators,academics,andmarketparticipantsindevelopingandmaintaininghigh‐qualitydata,webeginwithastylizedoverviewofthemortgagefinancesystemanditsmanydata‐generationprocessesthatarenotlinkedbyacommonidentifier.

ApplicationtoacceptanceForpurchaseloans,themortgagesupplychainbeginswithahomebeingmadeavailableforsale,typicallythroughastate‐licensedrealtor,whomaymakethelistingavailableonaregionalMultipleListingService.Apotentialbuyerthenappliesforamortgageloaneitherthroughamortgagebrokerordirectlyfromalender,bothofwhicharelicensedandregulatedatthestatelevel.Since2008,thelicensingofstate‐regulatedentitieshasbeencoordinatedbytheConferenceofStateBankSupervisors’NationwideMortgageLicensingSystem(NMLS).

Bank‐charteredmortgageloanoriginatorsareadditionallyregulatedbyfederalbankregulatorsandtheCFPBandmustberegisteredintheNationalMortgageLicensingSystemandRegistry,amodifiedversionofNMLS,whichCongressrequiredtobecreatedin2008toserveasafederalregistryformortgageloanoriginators,includingstate‐regulatedentities.TheDodd‐FrankActrevisedHMDAtorequireloanoriginatorstosubmitinformationaboutmortgageapplicationstotheCFPBortheirprimaryfederalregulator.Currently,theFederalFinancialInstitutionsExaminationCouncilcollectsthisinformationonbehalfofthefederalregulatoryagenciesandcontractswiththeFederalReserveBoard(FRB)fortheHMDAdatacollection.

Whenapotentialborrowerappliesforaloan,thelendercheckstheapplicant’screditwithoneormoreconsumercreditreportingagencies,whichareprimarilyregulatedbytheCFPBandtheFederalTradeCommission.Anindependentappraisalofthepropertyistypicallyperformedbyastate‐licensedappraiser,althoughautomatedvaluationmodelsareusedinsomecases,andanotherpartyperformsthepropertyinspection.13Atdifferentstagesduringthisprocess,the

12U.S.DepartmentofHousingandUrbanDevelopment(2006).13The2010InteragencyAppraisalandEvaluationGuidelinesstatethat“anautomatedvaluationmodel(AVM),inandofitselfdoesnotmeettheAgencies'minimumappraisalstandards”(FederalRegister,Vol.75,No.237,p.77453).AnAVMcan,however,beusedasapartofanevaluation,whichservesasasubstituteforanappraisal,providedthetransactionsatisfiescertainappraisalexemptionrequirements.

5

borrowerisprovidedwithrequireddisclosures,includingdisclosuresrequiredundertheTruthinLendingAct(TILA)andRealEstateSettlementProceduresAct(RESPA),whichdetailthetermsofthemortgageandagood‐faithestimateofclosingcosts.

AcceptancetooriginationPartiestoamortgageofficiallyenterintothecontractatclosing.Atthistimethetitletothepropertyistransferredviaadeed,andtwoimportantdocumentsaregenerated:thepromissorynotesignedbytheborrowerandthemortgage.Themortgage,aninstrumentthatvariesinformandnamefromstatetostate,transfersaninterestinthepropertytothelender.Thetitleisacollectionofrightstothepropertyandthedeedisadocumentdescribingthelandandestablishingthetransferoftitle.

WiththeexceptionofHongKongandpartsofIreland,theUnitedStatesisaloneamongindustrializednationsinnotrelyingonpropertyregistrationtoestablishownership.Instead,thiscountryusesacommon‐lawsystemofchainoftitleandrecordationoflegalinstrumentsaffectingtitle.14Asaresult,dataontheownershipofrealpropertyandassociatedliensaremaintainedinlocalrecorderoffices.Thedifficultiesthatcanariseinestablishingaclearchainoftitlehaveresultedinthedevelopmentofthetitleinsuranceindustry,whichdoesnotexistinmostofthedevelopedworld.

Beyondthemortgage,note,andtitleinsurance,otherdocumentsareoftengenerated:thepropertyormortgagemayadditionallybecoveredbyfloodinsurance(providedthroughtheFederalEmergencyManagementAgency’sNationalFloodInsuranceProgram),privatemortgageinsurance,homeowner’s(hazard)insurance,andmortgagelifeinsurance.Eachofthelatterthreeinsurersissubjecttostateregulation.Atclosing,alltheseoriginationdocumentsarecollectedandcollatedbyaclosingagent,whoensuresthatthedocumentsareinproperorderandlegallysigned,andthatfundingandproceedsaredistributedaccordingtothetermswithinthedocuments.

ServicingAfteroriginationandclosing,theborrower’sprimarycontactiswiththemortgageservicer,whichisresponsibleforcollectingpaymentsfromborrowers,addressingdelinquenciesandloanmodifications,andinsomecases,conductingforeclosures.Mortgageservicingcanbeperformedbytheloanoriginator,butmortgageservicingrightsandtheirassociatedcashflowsarealsooftensoldtootherparties.Servicersareregulatedatthestateandfederallevels,withadditionalmonitoringoftenperformedbyentitiesthatholdorguaranteethemortgagestheyservice.15

Severaltypesofservicersmaybeinvolved.Thereisgenerallyaprimaryservicer,whoisusuallyresponsibleforcollectingpaymentfromtheborrowerandremittingtheproceedstotheappropriateparties(suchastaxpayments,orinterestandprincipaliftheservicerisnotalsothelender),andforconductingtheforeclosureprocesswhennecessary.Inmanycases,these

14Irelandistransitioningtoapropertyregistrationsystem.15ServicersareregulatedatthefederallevelbyprudentialregulatorsortheCFPB,dependingontheinstitution’ssizeandcharter.

6

activitiesarecontractedouttosub‐servicers.Also,amasterserviceroftenservesasanintermediarybetweenprimaryservicers,andthetrusteeandissuer.

LoandispositionMortgagesintheUnitedStatescaneitherbeheldinportfoliobyabank,orsecuritizedandsoldthroughoneofthreemajorsecuritizationchannels.

BanksoftenusemortgagesintheirportfoliosascollateralinordertoborrowfromoneoftheFederalHomeLoanBanks.16Informationaboutloansinabankportfolioisofinteresttobankexaminers.17

However,onlyabout10percentofmortgageswereheldinbankportfoliosin2012.18Mostmortgageswereinsteadsoldaswholeloansorsecuritizedthroughoneofthefollowingthreechannels:

LoansinsuredbytheDepartmentofVeteransAffairs,FederalHousingAdministration,andUnitedStatesDepartmentofAgricultureareeligibletobepooledandsoldassecuritiesbyprivateissuerswithaguaranteefromtheGovernmentNationalMortgageAssociation(GinnieMae),agovernmentcorporationintheDepartmentofHousingandUrbanDevelopment.Theseloansaccountedfor20percentoforiginationsin2012.19

LoansthatmeetconformingloanlimitsandotherrequirementsareeligibletobesoldtotheFederalNationalMortgageAssociationorFederalHomeLoanMortgageCorporation(FannieMaeandFreddieMac,respectively).FannieandFreddiepoolmortgages,guaranteepoolsforafee,andsellsecuritiesrepresentingvariousaspectsofthosepoolsonthesecondarymarket.TheyareregulatedbytheFederalHousingFinanceAgency(FHFA).Theseloansaccountedfor69percentoforiginationsin2012.20

Loanscanalsobebundledandsoldbyprivateissuerswithoutanygovernmentoragencyguarantee.Thesesecuritiesaretypicallycalledprivatelabelsecurities(PLS).In2012,PLSmadeuplessthan1percentofresidentialmortgage‐backedsecuritiesissuances,comparedtoalmost36percentin2005and2006.21

Inanyofthesethreeformsofsecuritization,loansaregroupedintopools,whichareheldbytruststhatinturnissuesecurities.Theformofthesetrustscanvarysignificantly.Some,usuallythoseguaranteedbyGinnieMae,FannieMae,andFreddieMac(together,theAgencies),thoughalsosomePLS,aresimplepass‐throughstructureswhereinpaymentsfromthepoolsaresimply

16 The FHLBsprovideliquiditytotheprimarymortgagemarketandareoverseenbytheFederalHousingFinanceAgency. 17 Regulation of banksandcreditunionsdependsontheircharter;theymayberegulatedbytheFederalDepositInsuranceCorporation,theFederalReserveSystem,theOfficeoftheComptrollerofCurrency,theNationalCreditUnionAdministration,andstatebankregulators. 18 InsideMortgageFinance,Issue2013‐4,February1,2013,p.4. 19 Ibid. 20Ibid.21Ibid.

7

distributedpro‐ratatotheshareholders.Morecomplicatedstructuresenabletheissuanceofmultiplesecuritieswithdifferentexposurestoriskfromprepayment,andinthecaseofPLS,default.TheAgenciesandPLSissuersallhaverequirements(underwriting,operational,documentation,andreporting)ofthelendersthatsellmortgagestothemorwhoseloanstheyguarantee.

TheactivitiesoftheAgenciesaredeterminedbyCongressintheircharters,whichlimitthetypesandcharacteristicsofloansthattheycanpurchase(inthecaseofFannieMaeandFreddieMac)andguarantee.Asaresult,secondarymarketfundingformortgagesthatdonotmeetthecriteriaestablishedforAgencyloanscanonlybeprovidedthroughissuanceofPLS;PLSmayalsobeissuedwhenpricinginthemarketfavorsprivate‐labelexecutionoverAgencyexecution.AlthoughthemarketfornewissuancesnotguaranteedbytheAgencieshascollapsedsincethecrisis,activityinthismarketmayreboundinthefuture.AllpublicofferingsofPLSmustberegisteredwiththeSecuritiesandExchangeCommission(SEC),unlessotherwiseexemptfromregistration.Iftheofferingisregistered,theprospectususedtoofferthePLSmustcomplywiththeSEC’sinitialandongoingdisclosurerequirements,knownasRegulationAB.RegulationABcontainstheSEC’sdisclosurerequirementsforpubliclyofferedasset‐backedsecurities,includingrequirementsfordisclosureaboutthemortgagesandotherunderlyingassets.Additionally,ongoingdisclosuresforsuchpubliclyofferedPLS,includingtheperformanceoftheunderlyingassets,arerequiredtobefiledwiththeSEC.22In2010,theSECproposedadditionalrequirementstoRegulationABthatwould,amongotherthings,requireissuerstodiscloseasset‐levelinformationatthetimeofsecuritizationandonanongoingbasis.23

LoanterminationandmodificationThoughsomemortgageloansarepaiddownovertheoriginalterm,mostterminateeitherasavoluntaryorinvoluntaryprepayment,andloansaresometimesmodifiedwiththeintentionofpreventingthelatter.24

Thetwomostsignificantcausesofvoluntaryprepaymentsarerefinances,whentheborrowertakesoutanewmortgageloanonthesamepropertyandusesittopayofftheoutstandingloan,andthesaleofahome.25Whenarefinanceloanisoriginated,theidentityoftheloanbeingrefinancedisnotcurrentlycaptured.Involuntaryprepayments,incontrast,aregenerallytheresultofforeclosureorhome‐forfeitureactions,suchasashortsaleordeed‐in‐lieuofforeclosure. 22 Such disclosures must now be filed generally for the life of the security. See “Suspension of the Duty To File Reports for Classes of Asset-Backed Securities Under Section 15(d) of the Securities Exchange Act of 1934” SEC Release No. 34-65148 (August 27, 2011) [76 FR 52549]. Irrespective of the SEC disclosure requirements, some individual loan performance information may be available from private data vendors for a fee. 23 In addition to asset-level disclosure requirements, the SEC also proposed significant revisions to the disclosure, offering process, and reporting requirements for ABS issuers. See "Asset-Backed Securities", SEC Release No. 33-9117 (April 7, 2010) [75 FR 23328]. 24Forexample,theSecuritiesIndustryandFinancialMarketsAssociation’sMortgagePrepaymentProjectionTablesasofDecember3,2012,implythathalfofapoolofconventional30‐yearfixed‐ratemortgagesoriginatedin2011withacouponof3.5percentwouldbeexpectedtoprepaywithin35monthsgiventheyieldcurveasofthatdate.Alternatively,thehistoricalassumptionusedbyFHFAastotheaveragelifeofamortgageloanis10years.25Othercauses,suchasthedeathofanoccupantcoveredbymortgagelifeinsurance,ortheborrowersimplyacceleratingpayments,arelesscommon.

8

Mortgagemodificationsarechangestotheoriginaltermsofamortgage,typicallytokeepaloanin“current”statusorrestoreittothatstatus.Althoughrarebeforethefinancialcrisis,mortgagemodificationshavebecomerelativelycommonfordistressedproperties.26

JuniorliensJunior,orsubordinate,liensareplacedonpropertieswhenconsumersborrowagainstadditionalequityintheirhomeswithoutrefinancingtheexistingmortgage.Theseliensaretypicallyhomeequityloans,alsoknownas“secondmortgages,”whichhaveamortizationstructuresmuchliketraditionalfirstmortgages,orhomeequitylinesofcredit,whicharerevolvinglinesofcreditsecuredbyhomes.Theexistenceofsecondlienscanbesignificantbothforriskmanagementpurposesandwhenhandlingmodificationstofirstliens.

26Forexample,amongloanscoveredbytheOCCMortgageMetricsreportforthefourthquarterof2012,164,676modificationsandtrialsplanswereinitiated,comparedto156,773foreclosures.

IllustratInFigure1process,nueachwiththedatageidentificatremainingresult,anyoriginationstymied.

Aconsisteintegration

Figure1:M

Source:OFR

tion1below,theaumerousseritsownsysteeneratedbytionnumbersidentificatioyentitytryingnandconnec

ntidentificatnandservice

MortgageLi

Ranalysis

arrowsreprerviceprovideems,processthesedisparasrelatedtosondataarepgtotrackdoctittoperfor

tionprocessefulfillment.

ifeCycleIllu

esentflowsoersarenecesses,andidentateservicepervicesrendassedonifthwnallofthermancedata

wouldunite

ustration

9

ofinformatiosarytofulfilltificationmeproviderstoperedarelostheloanissoleunderlyingoraparticul

allofthepie

onanddocumltherequireethods.Theleprocessamotthroughtheldtoanissueinformationlarmortgage

eces,produci

ments.Inthementsofloaendermustiortgage.Maneprocess.Soer;someareknownatthepoolcanbe

ingefficienci

originationncreation,integrateallnyofthemeofthenot.Asahetimeofequickly

iesindata

10

MortgageDatasetsGovernmentagenciesengageinanumberofongoingloan‐levelcollectionsofmortgagedata.Alistofthesedatasetsisintheappendix.Thesedatasetsareusedforprudentialsupervisionofregulatedentities;toensurecompliancewithregulationsrelatedtoconsumerprotection,antidiscrimination,andaffordablehousing;tosupportthedevelopmentandevaluationofhousingpolicies;andtoenableresearchersandmarketparticipantstobetterunderstandthehousingfinancemarket.

Thesedatasetscontainsignificantoverlap.Asinglemortgagecouldpotentiallyappearinmorethanhalfthedatasetslistedintheappendix.Despitethisoverlap,nosinglemortgageidentifiercanlinkallofthesedatasets.Asaresult,informationsuchasthepropertyaddressorotherborrower‐specificinformationmustbeusedinmergingdatasets.Evenwiththisadditionalinformation,matchingdatasetsisslowerandmoreresource‐intensivethanitwouldbewithacommonidentifier.

Asidefromdatasetsmaintainedbythefederalgovernmentandbyprivateindustryforinternalbusinesspurposes(suchastheportfolioinformationofbanksandmortgageinsurers),threeadditionalsourcesofloan‐levelmortgageinformationareaggregatedandusedbyprivateindustry:

1. publicrecords,includingrecordsofdeeds,titles,mortgages,liens,andcourtfilings;2. servicingdata,includingdetailsaboutmortgageoriginationandongoingperformance;

and3. credithistories,includinginformationaboutborrowers’creditlinesandmortgages,but

lackingindetailaboutpropertiesandmortgageterms.

3.ObjectivesofaUniversalMortgageIDTheestablishmentofauniversalmortgageidentifier(UMID)wouldhaveseveralmajorbenefits.First,itwouldenablemoreeffectivesupervisionbyregulators(prudential,consumerprotection,andfinancialstability)throughreliabledatasetmatching.Second,itwouldassistmarketparticipantswithanindustry‐widebasisforworkflowmanagementanddatatransferbetweenfirms,whichcouldhelpinturntoimproveriskmanagementpractices.ThisbenefitwouldbeparticularlypowerfuliftheindustryestablishedtheUMIDthroughaconsensusstandardsbody.Third,itwouldimproveinformationflowstotheinvestingpublic.

However,thesegoalsmustbebalancedagainstastrongcommitmenttoprotectindividualprivacyandupholdrelevantprivacylaws,whichmusttakeprecedenceoverrealizinganyparticularbenefit.Forthatreason,theimplementationofaUMIDmustbehandledwithmorecarethaninthecaseofidentifiersdesignedtoaddressnon‐personalinformation,liketheLegalEntityIdentifier(LEI).

Enablingmoreeffectiveregulation,supervision,andpolicyresearchRegulatorswouldbenefitfromtheabilitytomergedatasetsfasterandmoreaccuratelybyaligningregulatoryreportingIDsbetweenagenciesandwithgovernment‐sponsoredsecuritization

11

entities.Inadditiontothecostbenefitsoflessresource‐intensivedatasetmatchingandthedataqualityimprovementsfrommoreaccuratematches,fastermatchescanbeviewedasanotherpotentialimprovementtodataquality,becausetheyprovideresearchersandpolicymakerswithabetterunderstandingofcurrentmarketconditions.

Consumercomplianceregulatorswouldbeabletolinkoriginationtoservicingandperformancedata,allowingthemtobetterunderstandindustrypractices,fairlending,theimpactofdisclosuresonmortgageperformance,andotherareas.Further,iftheUMIDwereassociatedwithloandocuments,consumerprotectionregulatorswouldhaveaneasiertimeassessingcompliancewiththeTruthinLendingActandtheRealEstateSettlementProceduresAct.

Fromasystemicriskperspective,aUMIDwouldbeusefulintrackingthepropagationofrisksthroughthefinancialsystembyhelpinglinkoutstandingdebttotheentitiesbearingpotentiallossesduetorisksrelatedtocredit,interestrates,andservicing.Furthermore,bybetterlinkingoriginationpracticesandpartiestolateroutcomes,researcherscouldachieveabetterunderstandingofhowrisksarecreated.Finally,theabilitytoeasilyidentifyandremoveduplicationindatasetsthatpartiallyoverlapwouldgiveregulatorsabetteroverallviewofthehealthofthemortgagemarket.

AUMIDwouldalsoprovidesignificantbenefitstopolicyresearchers,byquicklyandaccuratelylinkingthemanydatasetscurrentlyinuse.Bybringingoriginationdatatogetherwithdataonloanperformance,refinancesandmodifications,anddisposition,researcherswillbetterunderstandthecurrentandpotentialimpactsofpoliciesonborrowersandinvestors.

Finally,aUMIDcouldpotentiallyassistinotherimportantissues,likematchingfirstandsecondliensorlinkingpurchaseloanstolaterrefinancestoobtainaholisticviewofpatternsinborrowing,ifaugmentedbyappropriatereportingstructures.However,aUMIDbyitselfcannotprovideadefinitivesolutiontoallidentificationissuesinmortgagefinance.Forexample,asliensarefundamentallyrelatedtorealproperty,taskssuchaslienmatchingmaybemoreeffectivelyaddressedbyconsideringthestandardizationofparcelidentification,amatteroutsidethescopeofthispaper.

ProvidingabasisfordocumentmanagementandimprovedriskmanagementAsillustratedinSection2,thelifecycleofamortgageloanproducessignificantvolumesofdocumentationanddata.Managingthisdocumentationcanbeachallenge,onemadeonlymoredifficultwhendocumentsaretransferredfromanentityusingoneidentificationschemetoanotherentitywithitsownidentificationscheme.ByassociatingalldocumentsanddatarelevanttoaloanwithaUMID,documentmanagementandinformationinterchangebetweenfirmsandbusinessunitscanbesimplified,makingregulatorycomplianceeasierandloweringcostsformarketparticipants.Bettermanagementofdataanddocumentsalsodecreasesoperationalriskbyreducingthepotentialforerror.Further,aUMIDwouldpresenttheopportunitytoestablishasystemthatsupportsdocumentversioning,revisionsinkeydocuments,andtherecordingofeventssuchasmortgagemodifications.

12

Toimproveinformationinterchangebetweenfirmsandtoimproveriskmanagement,aUMIDshouldbestructuredasatruepublicgoodthatbecomescommonlyusedbymarketparticipantsandavailabletoallwithnoencumbrancesonitsuseotherthanthosenecessarytoprotectborrowerprivacy.Inthiscontext,aUMIDwouldbecomeabuildingblockofamoreefficienthousingfinancesystem.

ProtectingprivacySignificantconsiderationmustbegiventoindividualprivacy,giventheinherentrisksofre‐identificationassociatedwithanyuniversalidentifiersystem.Theserisksplacecriticalconstraintsonthestructure,governance,anduseofauniversalmortgageidentifiersystem.Manydefinitionsofprivacyexist,mostnotablyBrandeis’sdefinitionofitas“therighttobeletalone”andWestin’sdefinitionofitas“theclaimofanindividualtodeterminewhatinformationabouthimselforherselfshouldbeknowntoothers.”27,28Thelatterdefinitionisofparticularimportance,asWestin’sworkinthisarenainfluencedthepassageofthePrivacyActof1974,which,alongwiththeFairCreditReportingAct,affordsthemostsignificantindividualprotectionssurroundingthecollection,use,andtransmissionofpersonalinformationinthemortgagefinancearena.

Mortgagetransactionsposeapotentialprivacyproblembecauseinvestorsinthesecondarymarkethavealegitimatereasontowanttoknowprivatecharacteristicsofborrowers,suchascreditscores,butbecausetheuniverseofpotentialinvestorsconsistseffectivelyofthegeneralpublic,itisessentialthattheindividualborrowersnotbeidentifiable.Thisproblemalignswiththefederalgovernmentconceptof“personally‐identifiableinformation”(PII),definedas“informationwhichcanbeusedtodistinguishortraceanindividual'sidentity,suchastheirname,socialsecuritynumber,biometricrecords,etc.alone,orwhencombinedwithotherpersonaloridentifyinginformationwhichislinkedorlinkabletoaspecificindividual,suchasdateandplaceofbirth,mother’smaidenname,etc.”29

TheexistenceofaUMIDcanworkeithertoprotectpersonalprivacy,byallowingdirectmatchingofdatasetsforresearchandsupervisionwithoutrequiringthattheindividualbeidentifiedinanintermediatestep,ortodegradeprivacyprotections,ifaUMIDappearedbothonapubliclyfiledmortgagenote,ascurrentlyoccurswithsomecommonidentifiers,andincommerciallyavailableservicingdata.Additionally,ifassociatedwithanindividual,auniversalidentifierwouldallowadditionalinformationtobeassociatedwithanindividualthanwouldotherwisebeavailable,totheextentthatanyotherinformationassociatedwiththatidentifierwerebothavailableandnotalreadylinkedwithPII.

Toaddressthisissue,anypotentialUMIDsystemmustbedesignedtopreventthere‐identificationofindividuals,particularlybypreventingpublicdisclosureofinformationlinkingtheidentifiertodocumentsordatasetsthatidentifyborrowersbynameorotheridentifyingfeatures,orthatcouldbeusedincombinationwithotherinformationtore‐identifyborrowers.Additionally,anyreferencedataassociatedwiththeUMIDwouldhavetopertainonlytotheloanandnotcontainPII. 27WarrenandBrandeis(1890).28Westin(2003).29OfficeofManagementandBudgetMemorandumM‐07‐1616.

13

Further,anyconnectionbetweenapublicdocumentandamortgageidentifierwouldbeunacceptable,becausetheidentifiercouldbedirectlytracedtoanindividual’sidentity,makingalldatasetscontainingtheidentifierPII.Giventhatsuchaconnectionwouldplaceasignificantadditionalburdenonregulatorsandresearchersinthefederalgovernment,protectingprivacyisimportantinbothitsownrightandasamatterofthepracticalutilityofaUMID.

4.PropertiesofaUniversalMortgageIDAuniversalmortgageIDshouldfollowthebestpracticesthathavebeendevelopedintheestablishmentofotheridentifiersystems.Althoughsomespecificissuessurroundingamortgageidentifierdifferfrompreviousefforts,suchastheLEI,manyofthecoreissuesremainthesame:30

1. ScopeofCoverageTheidentifiershouldideallycoverallsingle‐familyandmultifamilyresidentialmortgages.Tobeofthegreatestuse,itshouldbeassignedasearlyaspossibleintheprocess,i.e.,atapplication,regardlessofwhethertheloanisapproved.

2. StructureoftheIdentifiera. One‐to‐onerelationshiptomortgages

Theidentifiershouldbeunique:one,andonlyone,mortgageshouldbeassignedtoanyparticularidentifier.Theconversealsoholds:one,andonlyone,identifiershouldbeassignedtoanyparticularmortgage.Thisproperty,aone‐to‐onemappingbetweenidentifiersandmortgages,allowsforunambiguousidentificationofaparticularmortgage.

b. PersistenceTheidentifiershouldremainwiththemortgageuntiltheloanisterminated.Thus,itmustpersistovertimeregardlessoftheholderoftheloanoranymodificationsmadetoit.

c. ExtensibilityForanidentifiertobeusefulindefinitely,itmustallowforgrowthinthenumberofidentifiersissued,withouthavingtoreuseidentifiers,whichwouldviolatetheuniquenesscriterion.

d. NeutralityIdentifiersshouldbeneutral:noinformationshouldbeencodedintheidentifieritself.Thisisimportantforpersistence,extensibility,andinthecaseofmortgages,privacy.Anidentifiercontainingembeddedinformationcanbevulnerabletochangesovertimeifthatinformationchanges(forexample,anidentifierthatembedsaborrower’sname),underminingpersistence.Similarly,embeddinginformationcanlimitthenumberofbitsofinformationpracticallyavailable,limitingextensibility—anidentifierthatembeddedaZIPcode,forexample,wouldonlybeusefulsolongastheZIPcodewiththegreatestnumberofmortgagesover

30ThepropertiesnotedhereareinfluencedsignificantlybyBottegaandPowell(previouslyreferenced),aswellastheCPSS‐IOSCO“ReportonOTCDerivativesDataReportingandAggregationRequirements”ofJanuary2012,andtheCommodityFuturesTradingCommission’sfinalrule,“SwapDataRecordkeepingandReportingRequirements,”publishedJanuary13,2012.

14

timedidnotrunoutofidentifiers.Inaddition,anidentifierwithembeddedpersonalinformation,orotherembeddedinformationthatcouldbeusedtore‐identifyindividuals,wouldposeathreattoprivacy.

e. ReliabilityForauniversalmortgageidentifiertobeadoptedbymarketparticipants,itsreliabilitywouldhavetobeensured.Theassignmentmechanismmustberobust,theidentifiershouldnotconflictwithothersystemsthatmaybeinuse,andtheassignmentmechanismandanyreferencedatabasesmustbeindependentofanyentitythatcouldfailinthefuture.

f. OpenStandardTheidentifiershouldbebasedonanopen,voluntaryconsensusstandard.31

3. PublicAvailabilityTheuseoftheidentifiermustbefreeofanycontractualrestrictions.Allpartiesinthemortgagemarket,regulatoryagencies,andtheresearchcommunityshouldbeabletousetheidentifiersystemfreely.Thisdoesnotimplythatregistrationofanidentifiermustbefree,orthatinformationotherthanbasicreferenceinformationmustbefreelyavailable;itmeansonlythatregistrationofidentifiersmustbeopenlyavailableandthatuseoftheidentifiersystemmustbefreelyavailable,withoutlicensingcostsorrestrictions.

4. PrivacyProtectionBeyondsimplynotembeddinginformationintheidentifieritself,theidentifiersystemmustbedesignedtopreventre‐identification,asdiscussedearlier.

5. IncentiveCompatibilityTohelpensurethatmarketparticipantshaveanincentivetoinvestinmaintainingarobustsystemofidentification,theyshouldbenefitfromusingtheidentifierintheirregularcourseofbusiness.Agreementamongregulatorsaboutusingasingleidentifierforreportingcanhelpencouragecoordinationamongparticipantsinthemarket.

6. RegistrationProcessTopreventdisruptiontomarketparticipants,theassignmentprocesswillneedtoworkwithinthetimelinesassociatedwiththemortgageapplicationprocess.

7. QualityAssuranceErrorsareoftenintroducedindatainthenormalcourseofbusiness.Toprotecttheintegrityofauniversalmortgageidentifier,qualitycontrolpractices,includingbestpracticessuchaschecksumsandgoodgovernancepractices,mustbeadopted,andclearresponsibilityforacquiringeachnewidentifiermustbeestablished.

5.ConclusionTheU.S.mortgagefinancesystemisacriticalpartofournation’sfinancialsystem,representing70percentofU.S.householdliabilities.32Itisalsohighlycomplex,withmanyfinancechannels,participants,andregulators.Thedataproducedbythissystemreflectthatcomplexity;unfortunately,nosingleidentifierexiststolinkthemajorloan‐levelmortgagedatasets.The

31OfficeofManagementandBudget.CircularNo.A‐119Revised.February10,1998.32 BoardofGovernorsoftheFederalReserveSystem,Z.1FlowofFundsAccounts,June6,2013.

15

establishmentofasingle,cradle‐to‐grave,universalmortgageidentifierdesignedtopreventidentificationofindividualswouldsignificantlybenefitregulatorsandresearchers.Suchanidentifiercouldalsoserveasthefoundationofasystemthatcouldbenefitprivatemarketparticipants,aslongassuchasystemprotectedindividualprivacy.Theestablishmentofsuchanidentifierwillbedifficult.Itwillnotbeeasytobalancecompetingdemandsforprotectingprivacy,whileenablingbettermanagementofdataanddocumentswithoutgeneratingunnecessarycostsandburdens.However,itisachallengeworthmeeting.

16

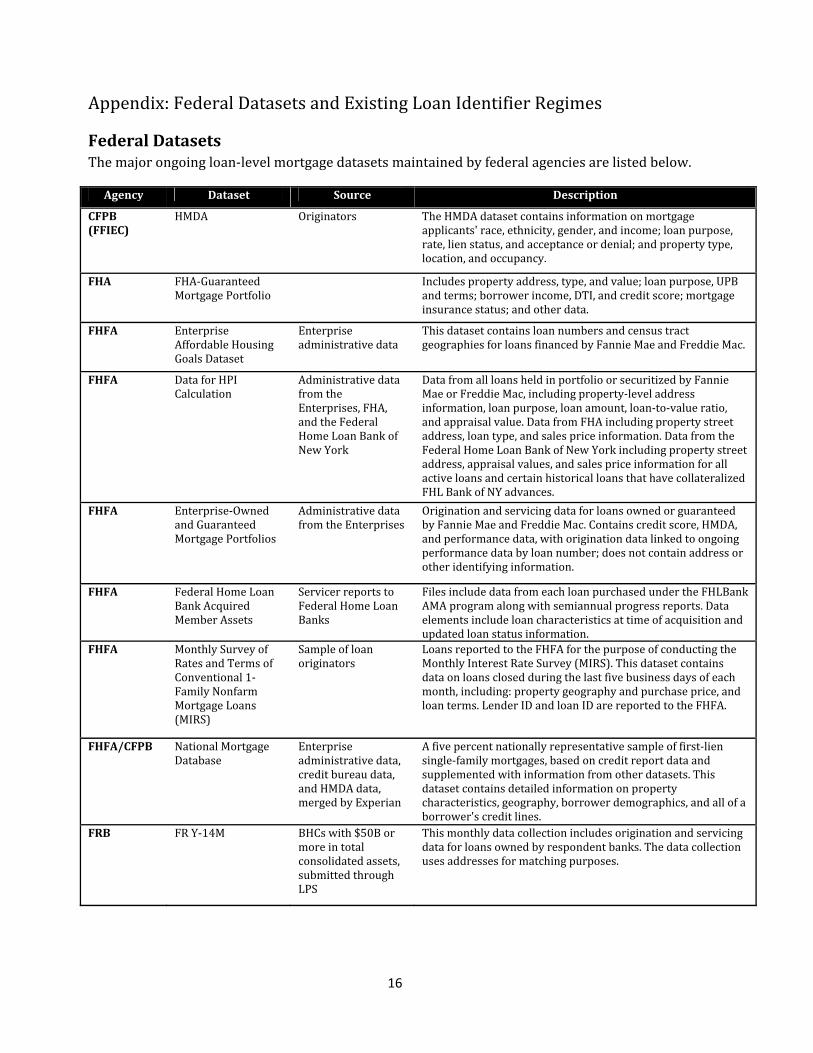

Appendix:FederalDatasetsandExistingLoanIdentifierRegimes

FederalDatasetsThemajorongoingloan‐levelmortgagedatasetsmaintainedbyfederalagenciesarelistedbelow.

Agency Dataset Source Description

CFPB(FFIEC)

HMDA Originators TheHMDAdatasetcontainsinformationonmortgageapplicants'race,ethnicity,gender,andincome;loanpurpose,rate,lienstatus,andacceptanceordenial;andpropertytype,location,andoccupancy.

FHA FHA‐GuaranteedMortgagePortfolio

Includespropertyaddress,type,andvalue;loanpurpose,UPBandterms;borrowerincome,DTI,andcreditscore;mortgageinsurancestatus;andotherdata.

FHFA EnterpriseAffordableHousingGoalsDataset

Enterpriseadministrativedata

ThisdatasetcontainsloannumbersandcensustractgeographiesforloansfinancedbyFannieMaeandFreddieMac.

FHFA DataforHPICalculation

AdministrativedatafromtheEnterprises,FHA,andtheFederalHomeLoanBankofNewYork

DatafromallloansheldinportfolioorsecuritizedbyFannieMaeorFreddieMac,includingproperty‐leveladdressinformation,loanpurpose,loanamount,loan‐to‐valueratio,andappraisalvalue.DatafromFHAincludingpropertystreetaddress,loantype,andsalespriceinformation.DatafromtheFederalHomeLoanBankofNewYorkincludingpropertystreetaddress,appraisalvalues,andsalespriceinformationforallactiveloansandcertainhistoricalloansthathavecollateralizedFHLBankofNYadvances.

FHFA Enterprise‐OwnedandGuaranteedMortgagePortfolios

AdministrativedatafromtheEnterprises

OriginationandservicingdataforloansownedorguaranteedbyFannieMaeandFreddieMac.Containscreditscore,HMDA,andperformancedata,withoriginationdatalinkedtoongoingperformancedatabyloannumber;doesnotcontainaddressorotheridentifyinginformation.

FHFA FederalHomeLoanBankAcquiredMemberAssets

ServicerreportstoFederalHomeLoanBanks

FilesincludedatafromeachloanpurchasedundertheFHLBankAMAprogramalongwithsemiannualprogressreports.Dataelementsincludeloancharacteristicsattimeofacquisitionandupdatedloanstatusinformation.

FHFA MonthlySurveyofRatesandTermsofConventional1‐FamilyNonfarmMortgageLoans(MIRS)

Sampleofloanoriginators

LoansreportedtotheFHFAforthepurposeofconductingtheMonthlyInterestRateSurvey(MIRS).Thisdatasetcontainsdataonloansclosedduringthelastfivebusinessdaysofeachmonth,including:propertygeographyandpurchaseprice,andloanterms.LenderIDandloanIDarereportedtotheFHFA.

FHFA/CFPB NationalMortgageDatabase

Enterpriseadministrativedata,creditbureaudata,andHMDAdata,mergedbyExperian

Afivepercentnationally representativesampleoffirst‐liensingle‐familymortgages,basedoncreditreportdataandsupplementedwithinformationfromotherdatasets.Thisdatasetcontainsdetailedinformationonpropertycharacteristics,geography,borrowerdemographics,andallofaborrower'screditlines.

FRB FRY‐14M BHCswith$50Bormoreintotalconsolidatedassets,submittedthroughLPS

Thismonthlydatacollectionincludesoriginationandservicingdataforloansownedbyrespondentbanks.Thedatacollectionusesaddressesformatchingpurposes.

17

Agency Dataset Source Description

GNMA GNMAMBSPools OriginationandservicingdataforloanssecuritizedinGNMAMBSpools.Thesedataincludepropertystreetaddress,borrowerinformationincludingcreditscore,andloancharacteristics.

OCC LargeBankMortgageMetrics(MM)

Servicerreportstolargebanks

Retailmortgage‐servicinginformationcollectedfromlargeinstitutions,whichincludes103dataelementsforeachmortgageloan;76dataelementsforeachsecond‐lienresidentialrealestateloan;12dataelementspertainingtopropertyinformation(matchingoffirst‐lienandsecond‐lienresidentialrealestateloans);and30homeequityportfolio(profit&loss)dataelements.

SEC MBSofferingmaterialsandperiodicreportsonEDGAR

MBSissuerreports Issuersfileofferingmaterialsthatmaycontainloan‐levelinformation.Ongoingreportsmayincludeloan‐levelinformationaboutprepayments,defaultsormodifications.

Treasury HAMP Servicers,submittedtoFannieMae

InSupplementalDirective09‐01,theTreasuryDepartmentannouncedtheeligibility,underwriting,andservicingrequirementsforHAMP.UnderHAMP,servicersapplyauniformloanmodificationprocesstoprovideeligibleborrowerswithsustainablemonthlypaymentsfortheirfirst‐lienmortgageloans.PursuanttoSupplementalDirective09‐01,servicersarerequiredtoperiodicallyprovideHAMPloanleveldatatoFannieMae,asHAMPprogramadministrator.TheHAMPfilescontaindataonmodificationsmadeandtheirsubsequentperformance,aswellasdatacollectedfromborrowersforNPVcalculationsandwhetherornotaloanwasapprovedforamodification.

VA VA‐GuaranteedMortgagePortfolio

Includespropertyaddress,type,andvalue;loanpurpose,UPBandterms;borrowerincome,DTI,andcreditscore;mortgageinsurancestatus;andotherdata.

18

ExistingLoanIdentifierRegimesSeveralloan‐leveluniqueidentifierregimescurrentlyexist.Theyareassignedoradoptedbygovernmentagenciesandmortgagelenderswithvaryingdegreesofmarketcoverageandforvaryingpurposes.Theseidentifierscanbeplacedintothreecategories:regulatoryreportingIDs,governmentbusinesspurposeIDs,andproprietarybusinesspurposeIDs.

RegulatoryreportingIDsHMDArequiresthecollectionofloan‐levelapplicationandoriginationdata.Coveredinstitutionsannuallyreporttotheirfederalregulatorseveralrequiredfields,includinganidentifierupto25characterslongoflettersandnumbers,foreachloanorapplication.Theidentifiermustbeuniquewithintheinstitution,anditis“stronglyrecommended”thatnamesandsocialsecuritynumbersbeexcludedfromtheidentifier.33InstitutionshaverelativelatitudetoassignandreportloanidentifierstheymayalreadybeusingforbusinesspurposesunderHMDA.However,notalllenderscomplywiththerecommendation,andsomeincludeborrowernamesorsocialsecuritynumbersintheirIDs.

In2010,theSECproposedtorequireissuersofasset‐backedsecuritiestoprovideasset‐leveldisclosuresabouttheunderlyingloansbackingsecurities.Inprovidingtheasset‐leveldata,auniquenumbermustbeassignedtoeachassetintheunderlyingpool.AswithHMDA,theproposedrulesdonotspecifyanumberingconvention.TheSECnotedthatacceptableidentifierscouldhavebeengeneratedatoriginationoratdifferenttimesduringthesecuritizationprocess.34However,theproposedruleswouldrequirethattheassetnumberusedforofferingdisclosuresshouldalsobethesamenumbersusedtoidentifytheassetforallreportsrequiredofanissuerundertheExchangeAct.

TheOfficeoftheComptrolleroftheCurrency(OCC)collectsuniqueloanidentifiersfromthelargestmortgageservicersforitsquarterlyMortgageMetricsReport.TheOCCdefinesthefieldasa"uniqueidentifierfortheloanrecordthatwillbethesamemonthtomonth.Referencenumbersmaybeusedinlieuofactualloannumbersaslongasitmeetsthiscriteria."35

TheFederalReserveBoardcollectsuniqueloanidentifiersaspartoftheFRY‐14MCapitalAssessmentsandStressTestingreport,whichmustbefiledbybankholdingcompanieswithmorethan$50billioninconsolidatedassets.TheidentifiercollectedbytheFRBisanalpha‐numeric

33SeeHMDA2010GuidetoGettingitRight.http://www.ffiec.gov/hmda/guide.htm.34SeeAsset‐BackedSecurities,SECReleaseNo.33‐9117(April7,2010)[75FR23328].35http://www.occ.treas.gov/publications/publications‐by‐type/other‐publications‐reports/mortgage‐metrics‐q4‐2008/loan‐level‐data‐field‐defin‐q4‐2008.pdf

19

codeofupto32characters.36TheFRBprovidesthefollowinginstructionsintheFRY‐14Mfortheloannumberfield:37

Anidentifierforaloanthatwillbethesamefrommonthtomonth.Referencenumbersmaybeusedinlieuofactualloannumbersaslongasitmeetsthesecriteria.Thisloanidentifiermustuniquelyidentifyanyloaninthefile.Itmustidentifytheloanforitsentirelifeandmustbeunique(piggy‐backsshouldbeseparated).

GovernmentbusinesspurposeIDsSeveralothergovernmentagencieswithmissionsrelatingtohousingfinanceuseidentifiersforinternaldatacollectionandmaintenance.TheFederalHousingAdministration(FHA),theU.S.DepartmentofVeteransAffairs(VA),andtheU.S.DepartmentofAgriculture(USDA)haveloan‐levelidentifiersforloansguaranteedorinsuredbytheagencies.TheFHAcasenumberisgeneratedontheFHAConnectionwebsiteafterinputandverificationofdatafieldscontainingborrowerandpropertyinformation.Itisa10‐digitidentifierassignedtoamortgageasthefirststeptowardFHAendorsementofmortgageinsurance.TheVAassignsa12‐digitloanidentifiernumberatthetimetheappraisalisrequested,anditisusedinsubsequententriesintoVAsystemsandonvariousdocuments.GinnieMaeassignsa9‐digitloanID.

ProprietarybusinesspurposeIDsInadditiontouniqueIDsthatindividualentitiesorloanoriginationsystemsmayuse,therearetwobroadlyavailableproprietaryloanidentifiers:(1)theMortgageElectronicRegistrationSystem(MERS)MortgageIdentificationNumber(MIN)and(2)theAmericanSecuritizationForum(ASF)LINC(loanidentificationnumbercode).Individualbusinessneedsdrivetheiruseinmortgageorigination,servicing,andsecuritization.TheMERSMINisan18‐digitloanidentifierrequiredforloansregisteredintheproprietaryMERSsystem.Theprimarypurposeofthesystemistotrackownershipinterestinregisteredmortgages.Thenumberitselfmaybeauto‐generatedbysoftwareorassigneddirectlybyMERS.Aportionofthenumbercanbeeitherrandomlygeneratedorcreatedfromanexistingloannumbercreatedbythelendinginstitution;thestringwouldthenbewrappedbyauniqueMERSresidentialorganizationalIDandacheckdigit.OncetheMINisassigned,itdoesnotchangeforthelifeoftheloan.Currently,FannieMaeandFreddieMacrequirealle‐mortgagestobedeliveredregisteredwithaMERSMIN,contributingtoadoptionratesamongoriginatorsinthemarket.TherearemembershipfeesassociatedwithregisteringloansontheMERSsystem.

TheLINCisa16‐digitloanidentifierformortgages,autoloans,creditcards,andstudentloans,developedbytheASFandStandard&Poor'sFixedIncomeRiskManagementServices(FIRMS).TheLINCwasdevelopedincoordinationwithASF'sProjectRESTART,aloan‐leveldisclosure 36Ifthebankholdingcompany(BHC)isalreadysubmittingdatatotheOCCaspartoftheOCCMortgageMetricsDataorOCCHomeEquityData,itisrequiredthattheBHCusethesameloannumberfortheFRY‐14Mdataschedules.TheFRY‐14Mdatapopulationmayincludeadditionalloans,whichmaynotbepartoftheOCCdatasample,andforsuchloansthegeneralrequirementslistedinthescheduleinstructionswillbeapplicable.Overall,theentiredatafilesentbyaBHCshouldhaveuniqueloannumbersacrosstheentiresubmission.37Reportformscanbefoundat:http://www.federalreserve.gov/reportforms/forms/FR_Y‐14M20130331_f.zip

20

initiativefortheresidentialmortgage‐backedsecuritiesindustry.ASFassignsauniquenumberafterreceiving30datafieldsfromtheoriginatororservicer.LINCincludesembeddeddata,suchasunderlyingloantype,loanoriginationdate,andcountrycode.38Topromoteintegrationoftheassignmentprocess,S&PFIRMSdevelopedanautomatedrequestmoduletofitintoexistingplatforms.TheLINCislinkedtoloan‐levelinformationinthecentralizeddatarepositoryrunbyS&PFIRMS.LINCisavailabletooriginatorsandsecuritizersfreeofcharge,butadoptionseemstobedependentuponnewregulationsanditsuseisnotcurrentlygeneralpractice.

InSeptember2012,MISMO,anot‐for‐profitsubsidiaryoftheMortgageBankersAssociationfocusedontechnologystandardsdevelopmentforthemortgageindustry,createdaUniqueLoanIdentificationDataWorkingGroup(DWG)withthefollowingstatement:39

ThereisnotasingleUniqueLoanIdentificationNumber(ULIN)ofamortgageloaninuseuniformlythroughouttheindustryoverthelifeoftheloan,andmanyintheindustryuseindividualmethodsofidentifyingloansatvariousstagesintheloan’slifecycle.ThisproposedDWGwillexplorethedevelopmentofauniversallyacceptedULIN.Thegroupwillexaminecurrentmortgageidentifiersystemsandthepotentialforstandardization,andwillalsoreviewothernon‐mortgagebankingindustryeffortssuchasthedefinitionoftheISO[InternationalOrganizationforStandardization]"bankcard"standardforcreditanddebitcards.40

38http://www.americansecuritization.com/uploadedFiles/ASF_LINC.pdf39Seediscussiononpage2.40http://www.mismo.org/files/PressReleases/NewDWGPressRelease9_14_2012.pdf

21

ReferencesAmericanSecuritizationForum.“ASFLoanIdentificationNumberCode(ASFLINC™)forSecuritizedLoansDevelopedbyASFandStandard&Poor’sFIRMS.”Pressrelease.September24,2009.http://www.sifma.org/news/news.aspx?id=13216

Bottega,John,andLindaPowell.“CreatingaLinchpinforFinancialData:TowardaUniversalLegalEntityIdentifier.”FederalReserveBoardFinanceandEconomicsDiscussionSeries,2011‐07.

MortgageIndustryStandardsMaintenanceOrganization(MISMO).“UniqueLoanIdentifierDevelopmentWorkgroupWhitePaper.”September25,2013.

Panchuk,KerriAnn.“MISMOdevelopinguniversaltrackingsystemformortgages,properties.”HousingWire.Published9/12/2012.Accessed3/28/2012.http://www.housingwire.com/fastnews/2012/09/14/mismo‐developing‐universal‐tracking‐system‐mortgages‐properties.

Sokolowski,Rachael.“UniqueLoanIdentifiers.”PresentationatMISMOforumon9/26/2012.

U.S.DepartmentofHousingandUrbanDevelopment.“EvolutionoftheU.S.HousingFinanceSystem:AHistoricalSurveyandLessonsforEmergingMortgageMarkets.”April,2006.

Wachter,SusanM.Writtentestimonyforhearingtitled“RegulationC:HomeMortgageDisclosureAct(HMDA)PublicHearing.”July15,2010.Atlanta,Georgia.http://www.federalreserve.gov/communitydev/files/wachter.pdf

Warren,SamuelandLouisBrandeis.“TheRighttoPrivacy.”HarvardLawReview,Vol.4,No.5,1890,pp.193‐220.

Westin,Alan.“SocialandPoliticalDimensionsofPrivacy.”JournalofSocialIssues,Vol.59,No.2,2003,pp.431‐453.