Commodity derivative markets - Home Page | Pacific Institute

29

UBC – PIMS - 2008 1 Commodity derivative markets Delphine Lautier

Transcript of Commodity derivative markets - Home Page | Pacific Institute

UBC – PIMS - 20081

Commodity derivative markets

Delphine Lautier

UBC – PIMS - 20082

1. Commodity markets today

2. The behavior of commodity prices : main characteristics

3. New trends in research on commodities

UBC – PIMS - 20083

1. Commodity markets today

• Huge rise in prices

• Huge rise in transactions volumes

UBC – PIMS - 20084

UBC – PIMS - 20085

11

31

51

71

91

111

04/0

1/19

89

04/0

1/19

90

04/0

1/19

91

04/0

1/19

92

04/0

1/19

93

04/0

1/19

94

04/0

1/19

95

04/0

1/19

96

04/0

1/19

97

04/0

1/19

98

04/0

1/19

99

04/0

1/20

00

04/0

1/20

01

04/0

1/20

02

04/0

1/20

03

04/0

1/20

04

04/0

1/20

05

04/0

1/20

06

04/0

1/20

07

04/0

1/20

08

$/b

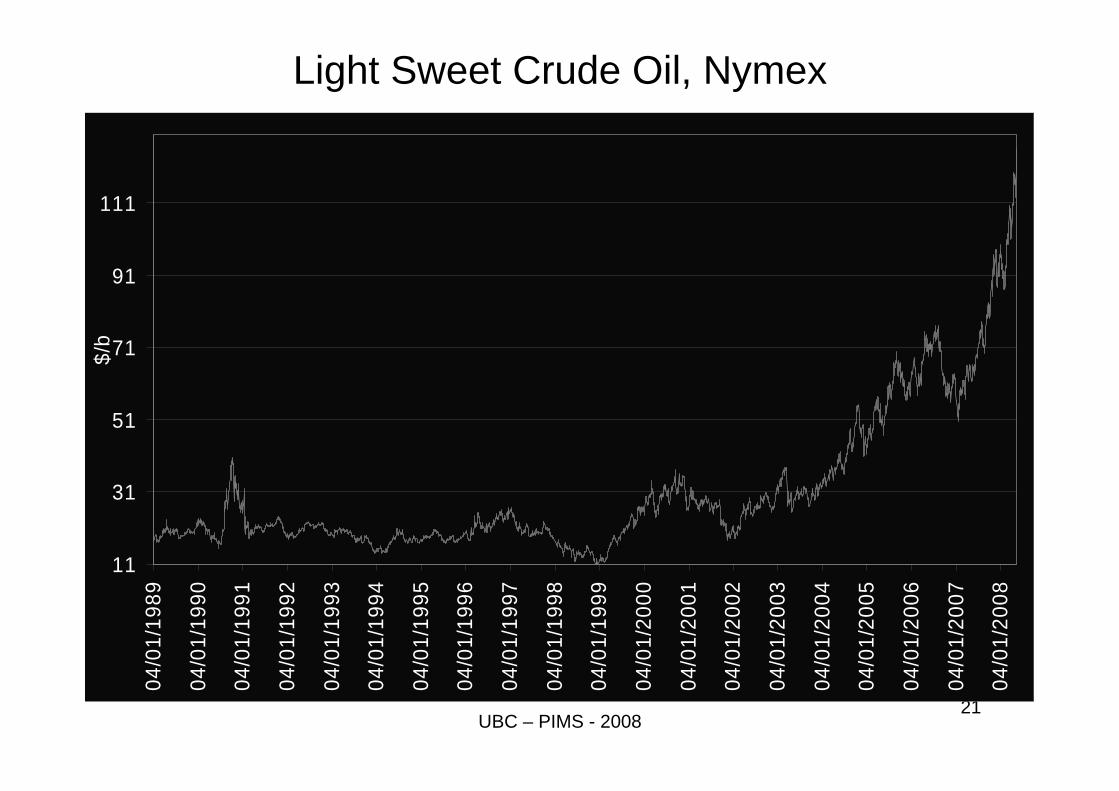

Light Sweet Crude Oil, Nymex

UBC – PIMS - 20086Source : FIA

UBC – PIMS - 20087

Growth rate of transaction volume on exchanges, by category, 2006-2007

• Individual equity 42.25%• Foreign currency 39.43%• Agriculture 32.02%• Industrial metals 29.72%• Energy 28.61%• Interest rates 17.14%

Source : FIA

UBC – PIMS - 20088

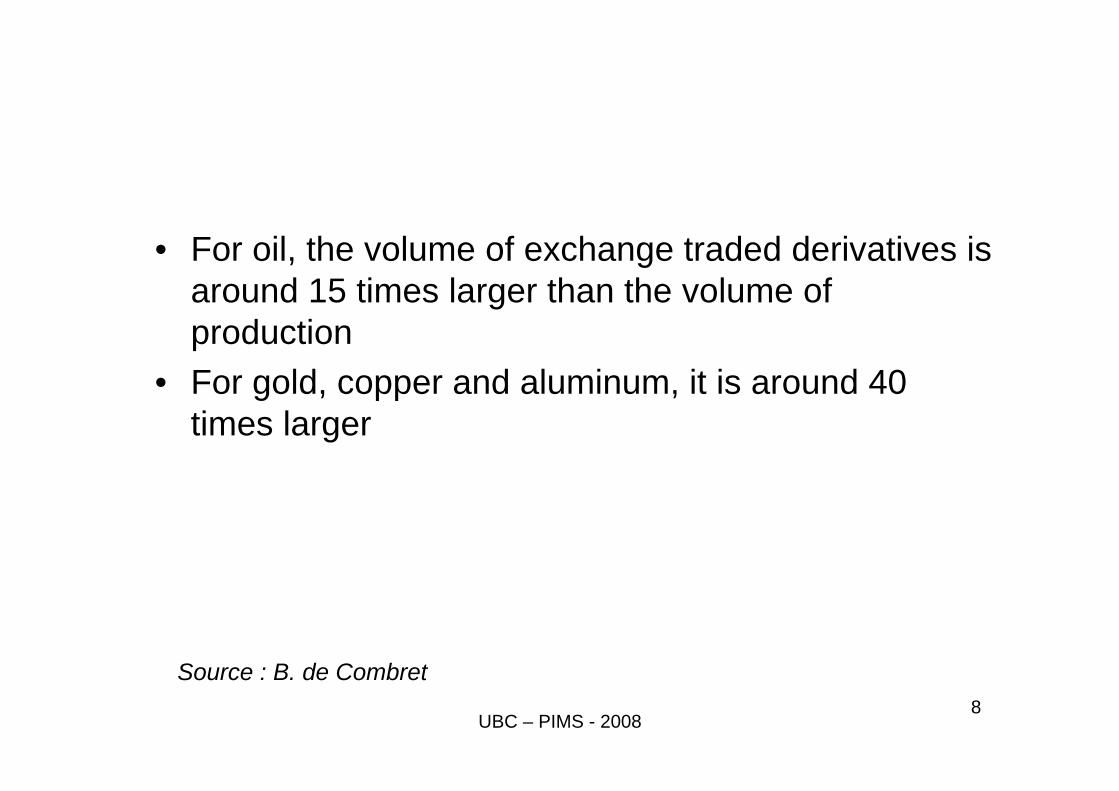

• For oil, the volume of exchange traded derivatives is around 15 times larger than the volume of production

• For gold, copper and aluminum, it is around 40 times larger

Source : B. de Combret

UBC – PIMS - 20089

The most important commodity markets today

Ranked by number of contracts traded : • Crude oil, Natural gas, petroleum products• Soy Meal, Soybean & Corn• Aluminium, Gold, Copper

UBC – PIMS - 200810

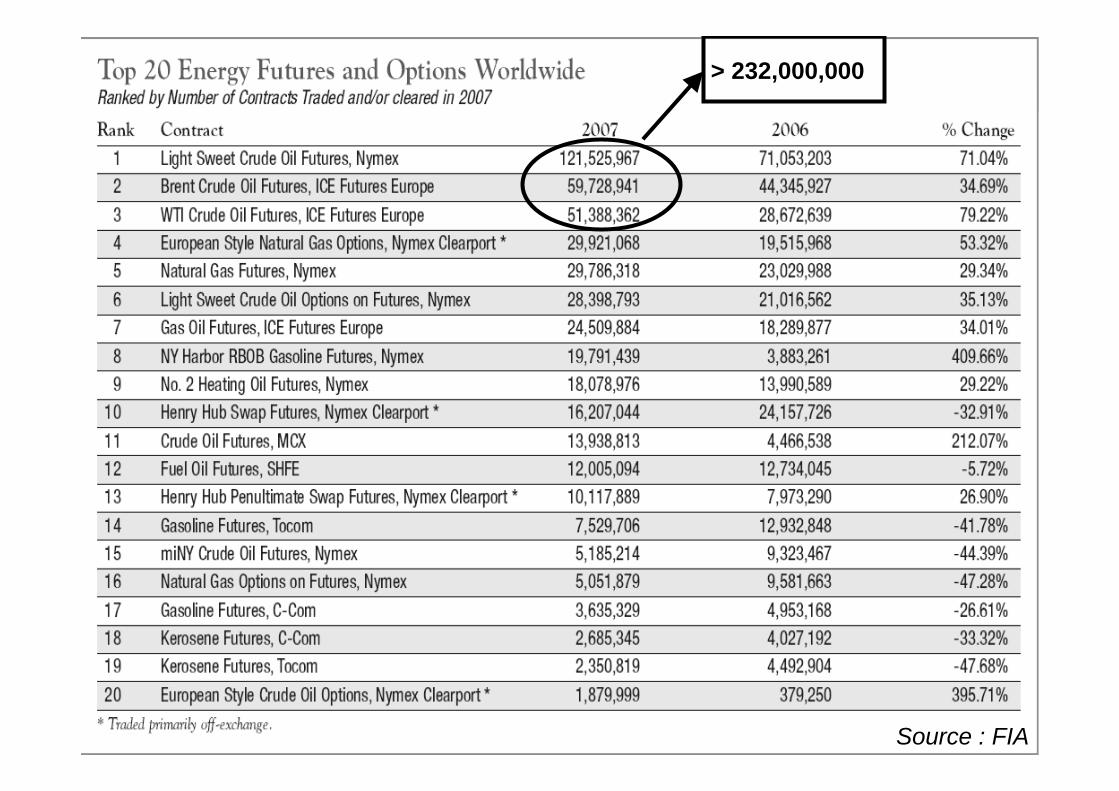

> 232,000,000

Source : FIA

UBC – PIMS - 200811

Source : FIA

UBC – PIMS - 200812

Source : FIA

UBC – PIMS - 200813

The relative importance of commodity markets

• Exchange traded contracts

• OTC markets

UBC – PIMS - 200814

Interest rates25%

Commodities9%

Equity 37%

Individual Equity 27%

Foreign Currency2%

Exchange traded contracts

Source : FIA

UBC – PIMS - 200815

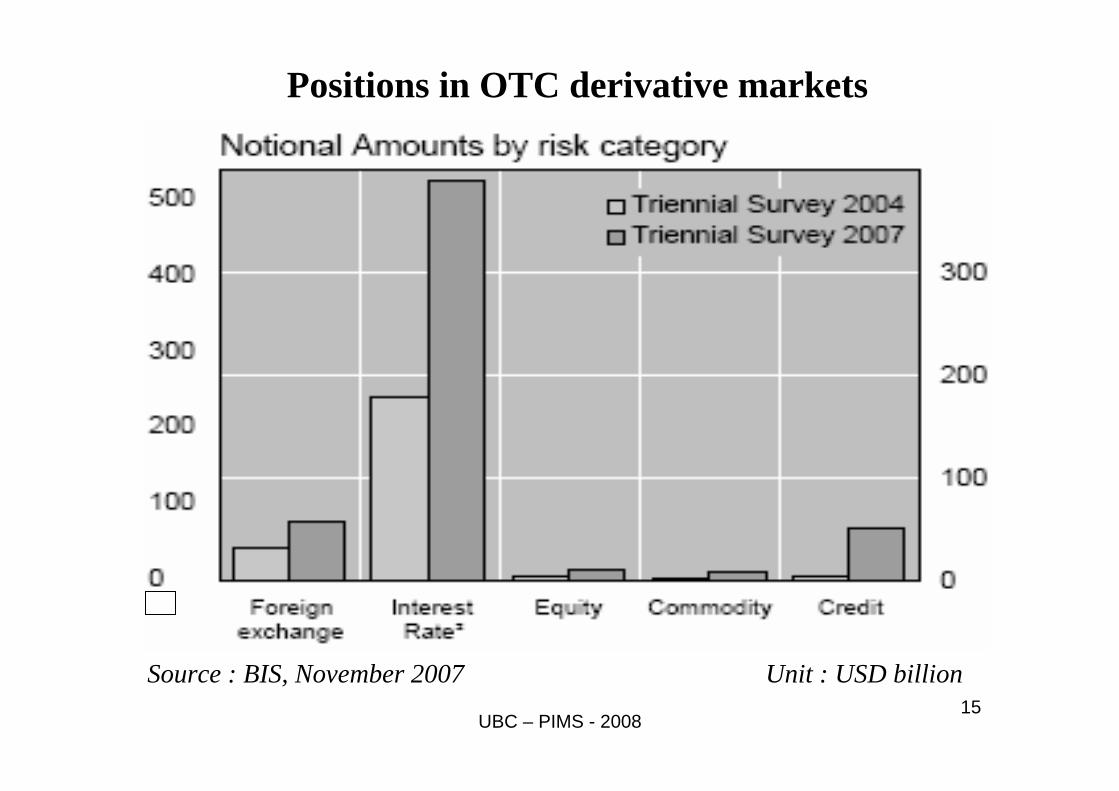

Source : BIS, November 2007 Unit : USD billion

Positions in OTC derivative markets

UBC – PIMS - 20081616

2. The characteristics of commodity prices • Importance of quality differentials

- A lot of cross hedging in commodity markets- Derivative products (swaps) on price differentials

• Seasonality in the prices and basis

Basis : F(t,T) – S(t)where: - F(t,T) is the futures prices at t for delivery at T

- S(t) is the spot price Seasonality is important for agricultural products (supply side) and for energy (demand side). Seasonality of the basis of petroleum products: During the winter, fuel oil inventory are rare and the basisis negative; during the summer, stocks are abundant and the basis is positive.

UBC – PIMS - 200817

• High level of prices’ volatility

Commodity prices’ volatility

UBC – PIMS - 200818

VOLATILITY

COMPARISON

Source : FIA

UBC – PIMS - 200819

• High level of prices’ volatility• Volatility rises when commodity prices rise

• Mean reverting behavior - for storable commodities- still relevant ?

Commodity prices’ volatility

20

10,00

15,00

20,00

25,00

30,00

35,00

40,0003

/01/

89

03/0

1/90

03/0

1/91

03/0

1/92

03/0

1/93

03/0

1/94

03/0

1/95

03/0

1/96

03/0

1/97

03/0

1/98

03/0

1/99

03/0

1/00

03/0

1/01

03/0

1/02

($/b

)

1 month 3 months 6 months 12 months 18 months 24 months 28 months

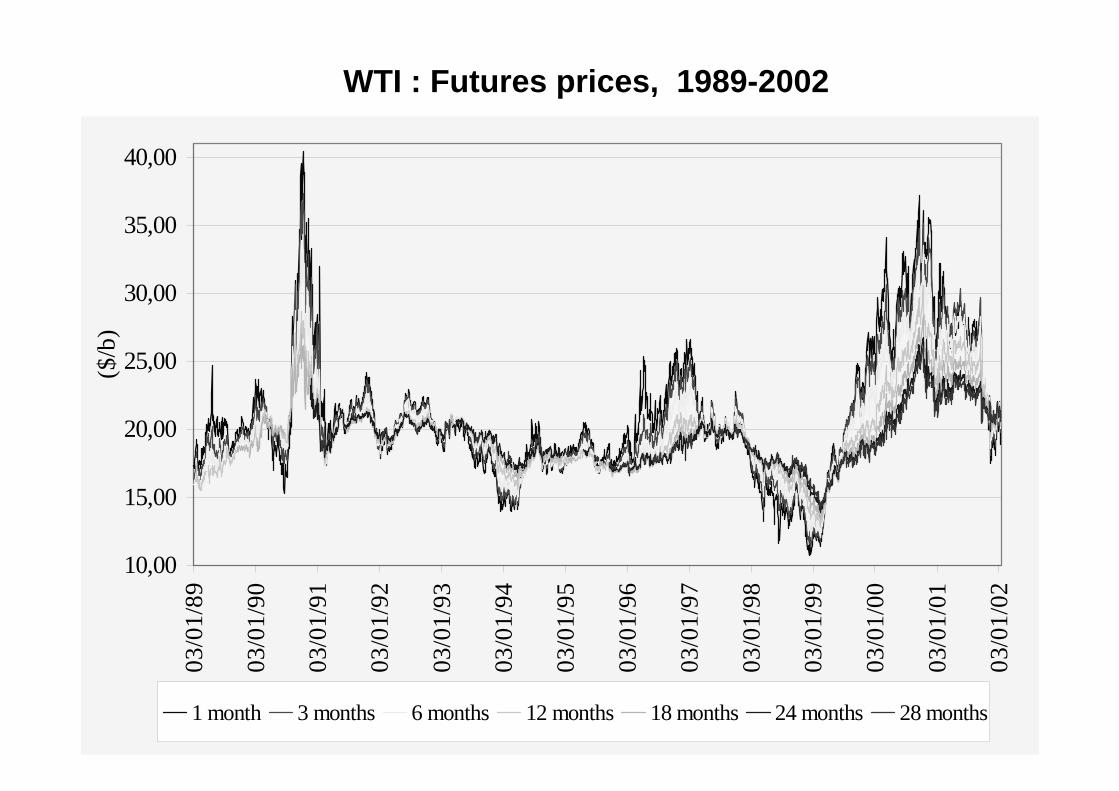

WTI : Futures prices, 1989-2002

UBC – PIMS - 200821

11

31

51

71

91

111

04/0

1/19

89

04/0

1/19

90

04/0

1/19

91

04/0

1/19

92

04/0

1/19

93

04/0

1/19

94

04/0

1/19

95

04/0

1/19

96

04/0

1/19

97

04/0

1/19

98

04/0

1/19

99

04/0

1/20

00

04/0

1/20

01

04/0

1/20

02

04/0

1/20

03

04/0

1/20

04

04/0

1/20

05

04/0

1/20

06

04/0

1/20

07

04/0

1/20

08

$/b

Light Sweet Crude Oil, Nymex

UBC – PIMS - 200822

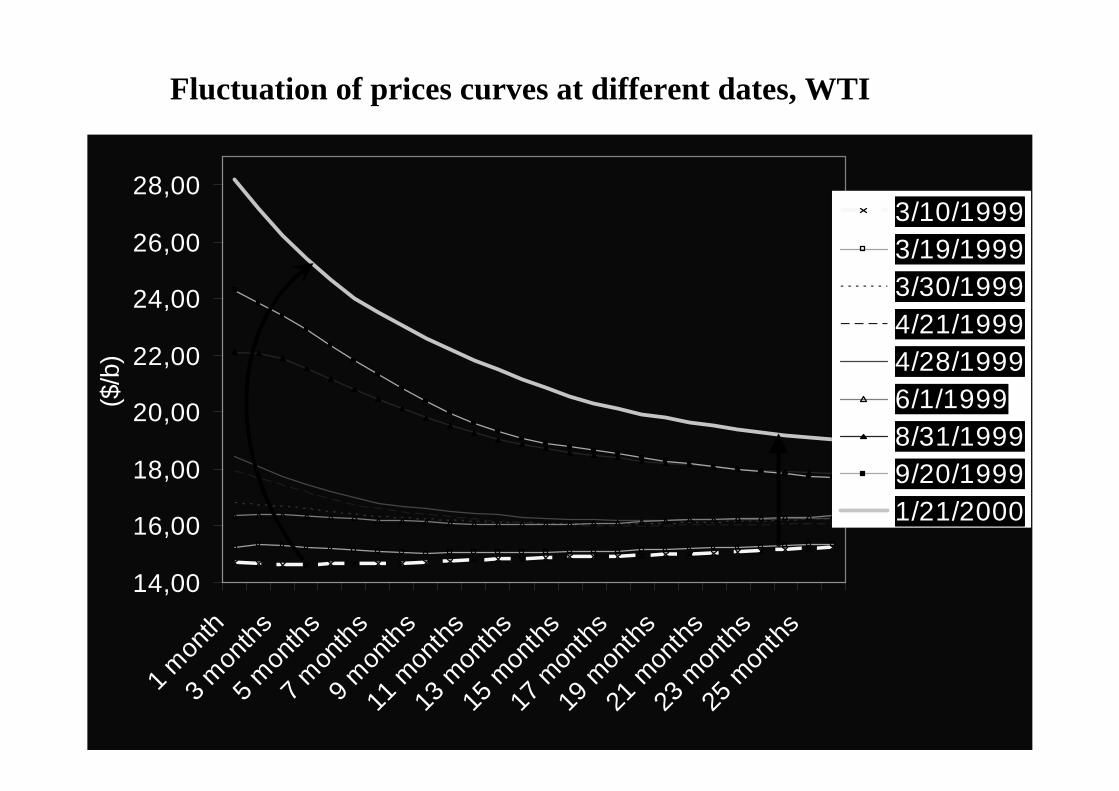

• Commodity futures contracts’ maturity : - Up to 7 years for crude oil- Up to 3-4 years for agricultural products and metals

• Samuelson effect- Decreasing pattern of volatilities along the prices curve- Propagation of shocks. It depends on:

- the stocks’ level (the effect sometimes disappears when stocks are abundant)

- production, transportation and storage costs

Movements of price curves

UBC – PIMS - 20082323

Fluctuation of prices curves at different dates, WTI

14,00

16,00

18,00

20,00

22,00

24,00

26,00

28,00

1 mon

th3 m

onths

5 mon

ths7 m

onths

9 mon

ths11

mon

ths13

mon

ths15

mon

ths17

mon

ths19

mon

ths21

mon

ths23

mon

ths25

mon

ths

($/b

)

3/10/19993/19/19993/30/19994/21/19994/28/19996/1/19998/31/19999/20/19991/21/2000

UBC – PIMS - 20082424

- Principal component analysis - Three kind of movements :

- parallel shift in the curve (level factor)- relative shift of the curve (steepness factor)- curvature factor (only for long-term contracts)

Movements of prices curves

UBC – PIMS - 20082525

3. New trends in research on commodities

• Subjects inspired by other financial markets

- Market efficiency (technical analysis)

- IFRS (International Financial Reporting Standards) : - Valuation of inventories- Valuation of mineral reserves - Hedging versus speculation (cross hedging)

UBC – PIMS - 200826

• Subjects that are more specific to commodities:

- Real options- Mineral reserves- Extensively used in the petroleum industry:

auctions on undeveloped fields

- Market integration and price convergence

- In the energy field- Between energy and agricultural products

- The influence of speculation on prices

- CFTC data

- Commodity as a new class of assets

UBC – PIMS - 20082727

• Development of commodity indexes / futures on c.i.- CRB (Commodity Research Bureau)- S&P GSCI : (S& P Goldman Sachs Commodity Index)- S&P GSCI Excess Return Index

• Commodity are used for diversification purposes- Massive investments in commodities because of their counter-cyclic nature

Commodity as a new class of asset

UBC – PIMS - 200828

UBC – PIMS - 200829

• Most active players: - Commodity Trading Advisors- Hedge funds- Pension funds- Insurance companies

• Invest in commodity indexes (S&P GSCI)

• Intend to invest more in the futureBarclays Capital Survey (2007) : - Two years ago, 15% of institutional investors intended to invest more than 10% of their portfolios in commodities- Today, they are 50%