Commercial Real Estate: Just How Fast is it Moving?

43

Ask the Fed ® is a program of the Federal Reserve Bank of St. Louis. Use of the presentation materials, including audio recording of a presentation, is strictly prohibited except by written permission of the Federal Reserve Bank of St. Louis. The opinions expressed in the presentations are statements of the speaker's opinion, are intended only for informational purposes, and are not formal opinions of —nor binding on— any Federal Reserve Bank or the Board of Governors of the Federal Reserve System. Each participant is responsible for its own business, financial, investment, or credit decisions. www .askthefed.org Commercial Real Estate: Just How Fast is it Moving? October 14, 2021 Brian D. Bailey, CRE, CCIM Subject Matter Expert, Commercial Real Estate and Senior Policy Advisor Federal Reserve Bank of Atlanta

Transcript of Commercial Real Estate: Just How Fast is it Moving?

Ask the Fed® is a program of the Federal Reserve Bank of St. Louis. Use of the presentation materials, including audio recording of a presentation, is strictly prohibited except by written permission of the FederalReserve Bank of St. Louis. The opinions expressed in the presentations are statements of the speaker's opinion, are intended only for informational purposes, and are not formal opinions of —nor binding on— anyFederal Reserve Bank or the Board of Governors of the Federal Reserve System. Each participant is responsible for its own business, financial, investment, or credit decisions.www.askthefed.org

Commercial Real Estate:Just How Fast is it Moving?

October 14, 2021

Brian D. Bailey, CRE, CCIMSubject Matter Expert, Commercial Real

Estate and Senior Policy AdvisorFederal Reserve Bank of Atlanta

© 2021 Federal Reserve Bank of St. Louis 2

Welcome• Call-in number: 888-625-5230 • Participant code: 663 664 18#• Webinar: https://www.webcaster4.com/Webcast/Page/584/41039• This call is being recorded and will be available immediately following the session.• A short survey will be delivered via email following the call. Please let us know your thoughts

about today and ideas for future sessions.

Logistics

• You can listen through your PC or dial in to the phone.• Remember: Your specific connection matters; if PC audio diminishes, dial in to the toll-free line.

Webinar

• Use the chat feature in the webinar (Ask Question button on bottom of screen).• Email your question to: [email protected].• Use the “Ask a Question” feature on the Ask the Fed® website: www.askthefed.org.

How We’ll Take Questions

• Ask the Fed® is a program of the Federal Reserve Bank of St. Louis. Use of the presentation materials, including audio recording of a presentation, is strictly prohibited except by written permission of the Federal Reserve Bank of St. Louis. The opinions expressed in the presentations are statements of the speaker's opinion, are intended only for informational purposes, and are not formal opinions of —nor binding on— any Federal Reserve Bank or the Board of Governors of the Federal Reserve System. Each participant is responsible for its own business, financial, investment or credit decisions.

Disclaimer

© 2021 Federal Reserve Bank of St. Louis 3

Goals of Today’s Session

• To provide an informational hour of learning so lenders and regulators can be better informed on the economy, commercial real estate (CRE), and commercial finance markets.

• Audience members should be able to recognize issues in the aforementioned topics that will help them better identify and mitigate issues in CRE and lending.

© 2021 Federal Reserve Bank of St. Louis 4

Contributions to Gross Domestic Product (GDP)

Source: BLS, HAVER Analytics

-31.2

33.8

4.56.3 6.7

-40

-30

-20

-10

0

10

20

30

40

2018 2019 2020 2021

Contributions to Real GDPquarterly, percent, seasonally adjusted annualized rate

Intellectual Property Products Government Net Exports

Nonresidential Equipment & Software Private Inventory Investment Residential Investment

Nonresidential Structures Consumer Spending Real GDP

© 2021 Federal Reserve Bank of St. Louis 5

EmploymentMonthly Job Creation by Segment

Source: BLS, HAVER Analytics

-20,679

2,833

4,846

1,7261,583716 680 264 -306 233 536 785 269 614 962 1,091 366 194

-25,000

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

Goods Producing Retail Trade Services (Information, Financial, and Other)

Wholesale Trade, Transportation, and Utilities Professional and Business Services Leisure and Hospitality

Government Education & Health Services Total Nonfarm

thousands, seasonally adjusted

Leisure & Hospitality-7.4 million jobsin April 2020

© 2021 Federal Reserve Bank of St. Louis 6

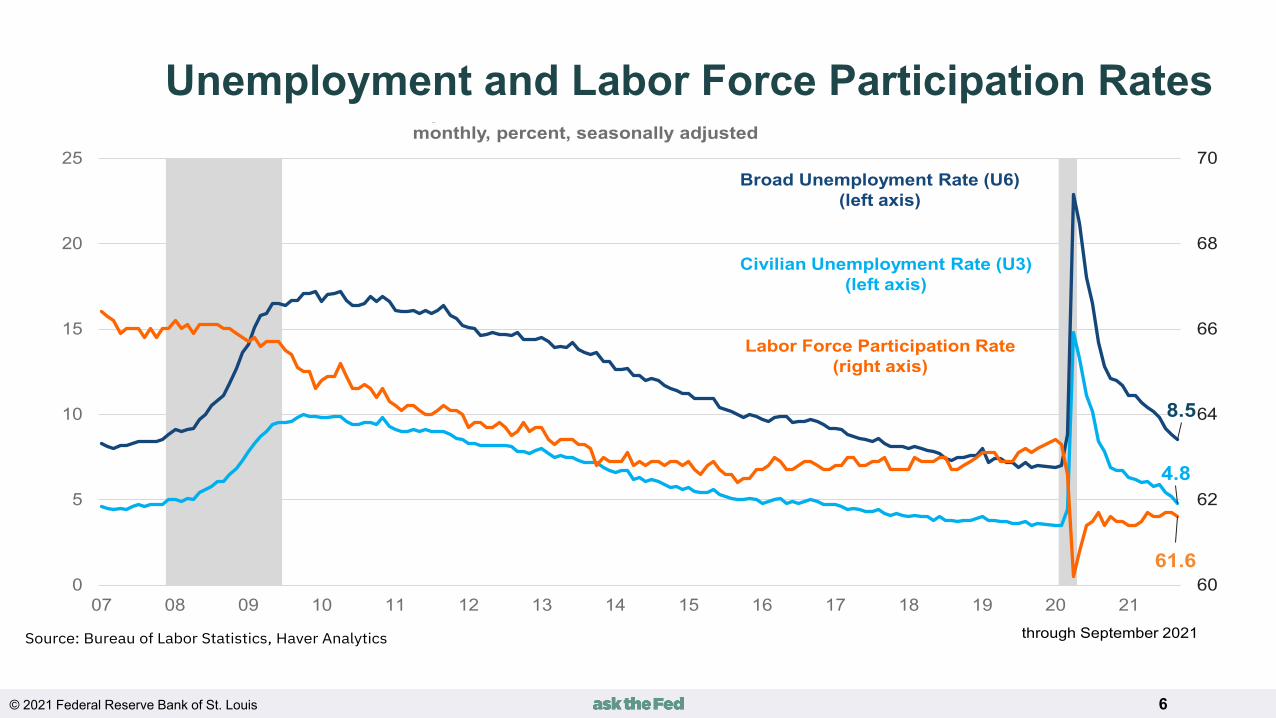

Unemployment and Labor Force Participation Rates

4.8

8.5

61.660

62

64

66

68

70

0

5

10

15

20

25

07 08 09 10 11 12 13 14 15 16 17 18 19 20 21

y monthly, percent, seasonally adjusted

through September 2021Source: Bureau of Labor Statistics, Haver Analytics

Civilian Unemployment Rate (U3)(left axis)

Broad Unemployment Rate (U6)(left axis)

Labor Force Participation Rate(right axis)

© 2021 Federal Reserve Bank of St. Louis 7

Employment Change by Skill and Gender

© 2021 Federal Reserve Bank of St. Louis 8

Change in Hospitality and Leisure Employment% of Markets, 2021 Q2

Source: CoStar

© 2021 Federal Reserve Bank of St. Louis 9

Components of InflationYear-over-Year Change in the Consumer Price Index (CPI)

Source: BLS/Risk Analysis Unit/Atlanta Fed

© 2021 Federal Reserve Bank of St. Louis 10

Polling Question

What is your expectation for inflation in 2022?

A) <2%B) >2% but less than 3%C) >3% but less than 4%D) >4% but less than 5%E) >5% but less than 6%F) >6%G) Start minting those $1 trillion coins.

© 2021 Federal Reserve Bank of St. Louis 11

Change in Commercial Property Price Indices

Source: Sam LaRussa, Lucy Nicholson/Reuters

Congestion Junction Supply Chain Woes Persist

• Retailers already struggling from the Covid-19 pandemic are facing greater transit times for goods that may cause them to shorten or miss the upcoming high- traffic seasonal points.

• Many container ships are anchored off U.S. ports, leading to at least an extra one to two weeks of transit time.

• Rail congestion at several critical junctures is growing and creating severe offloading bottlenecks.

• Once offloaded, due to the lack of trucks/drivers, container pickup times have grown six- to eight-fold.

© 2021 Federal Reserve Bank of St. Louis 12

Jerome Powell Chairman, Federal Reserve

“The spike in inflation is so far largely the product of a relatively narrow group of goods and services that have been directly affected by the pandemic and the reopening of the economy.”

FOMC Press Conference —September 2021

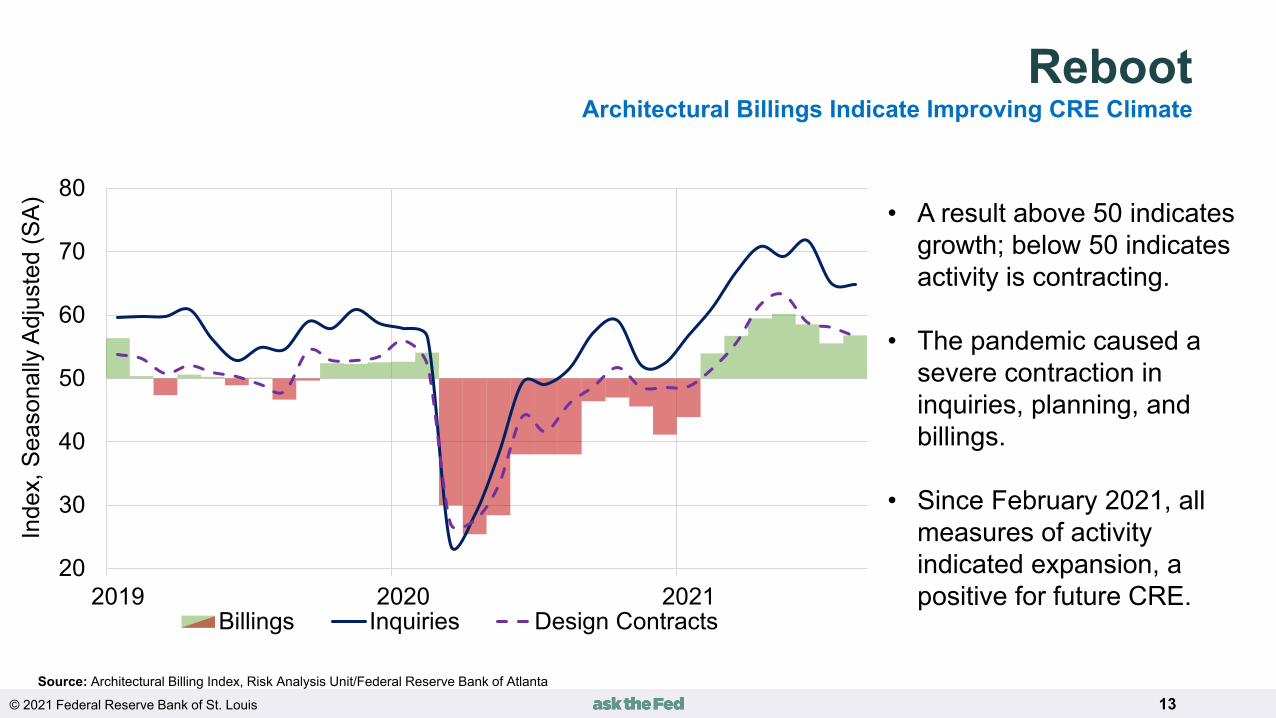

© 2021 Federal Reserve Bank of St. Louis 13Source: Architectural Billing Index, Risk Analysis Unit/Federal Reserve Bank of Atlanta

Inde

x

• A result above 50 indicates growth; below 50 indicates activity is contracting.

• The pandemic caused a severe contraction in inquiries, planning, and billings.

• Since February 2021, all measures of activity indicated expansion, a positive for future CRE.

20

30

40

50

60

70

80

2019 2020 2021

Inde

x, S

easo

nally

Adj

uste

d (S

A)

Billings Inquiries Design Contracts

Reboot Architectural Billings Indicate Improving CRE Climate

© 2021 Federal Reserve Bank of St. Louis 14

Housing StartsMonthly, Thousands Units, Seasonally Adjusted Annual Rate (SAAR)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Total Starts: July 2021=1,534 Single-Family: July 2021=1,111

Sources: Census Bureau; National Bureau of Economic Research; Haver Analytics

© 2021 Federal Reserve Bank of St. Louis 15

Home Price AppreciationJuly 2021

Source: CoreLogic, Federal Reserve Bank of Atlanta

Up, Up, and Away???Home Price Appreciation (HPA), Year-over-Year % Change

© 2021 Federal Reserve Bank of St. Louis 16

Home Affordability Ownership Monitor (HOAM)Declining Affordability Is Slowing Residential

Source: REIT/FRB Atlanta

© 2021 Federal Reserve Bank of St. Louis 17

Showcases CRE trends in an easy-to-understand format on a market and historical variable basis

Covers the office, retail, multi-family and office sectors (hotels coming soon)

Encompasses 390 major, secondary, and tertiary markets in the U.S. (includes Alaska & Hawaii)

Provides clarity on CRE market momentum: Is it accelerating or decelerating? How do the current results compare to the long-

term norm?

Seeking Free CRE Information? AtlantaFed.org

https://www.atlantafed.org/center-for-housing-and-policy/data-and-tools/commercial-real-estate-momentum-index.aspx

https://www.atlantafed.org/forms/news-events/2021/10/20/registration-commercial-real-estate.aspx

CRE Momentum Index (CREMI)More Transparent, Free CRE Data

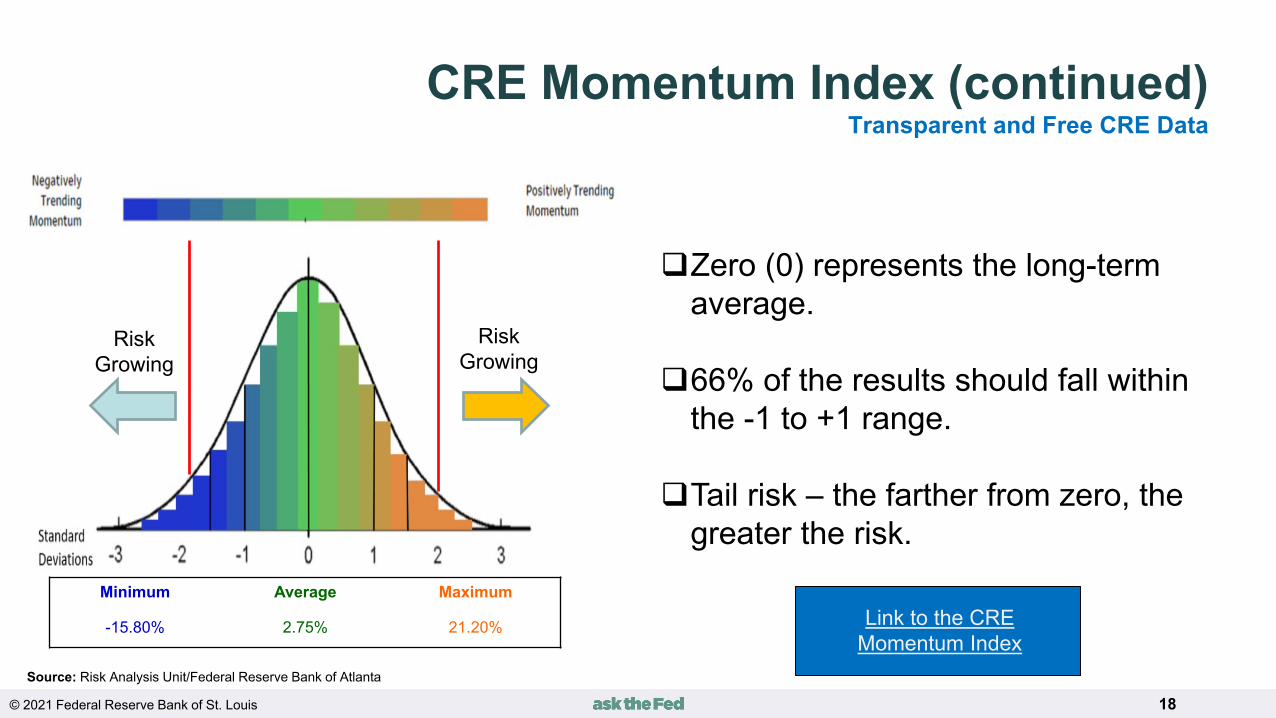

Source: Risk Analysis Unit/Federal Reserve Bank of Atlanta

© 2021 Federal Reserve Bank of St. Louis 18

RiskGrowing

RiskGrowing

CRE Momentum Index (continued)Transparent and Free CRE Data

Zero (0) represents the long-term average.

66% of the results should fall within the -1 to +1 range.

Tail risk – the farther from zero, the greater the risk.

Source: Risk Analysis Unit/Federal Reserve Bank of Atlanta

Link to the CRE Momentum Index

Minimum Average Maximum

-15.80% 2.75% 21.20%

© 2021 Federal Reserve Bank of St. Louis 19

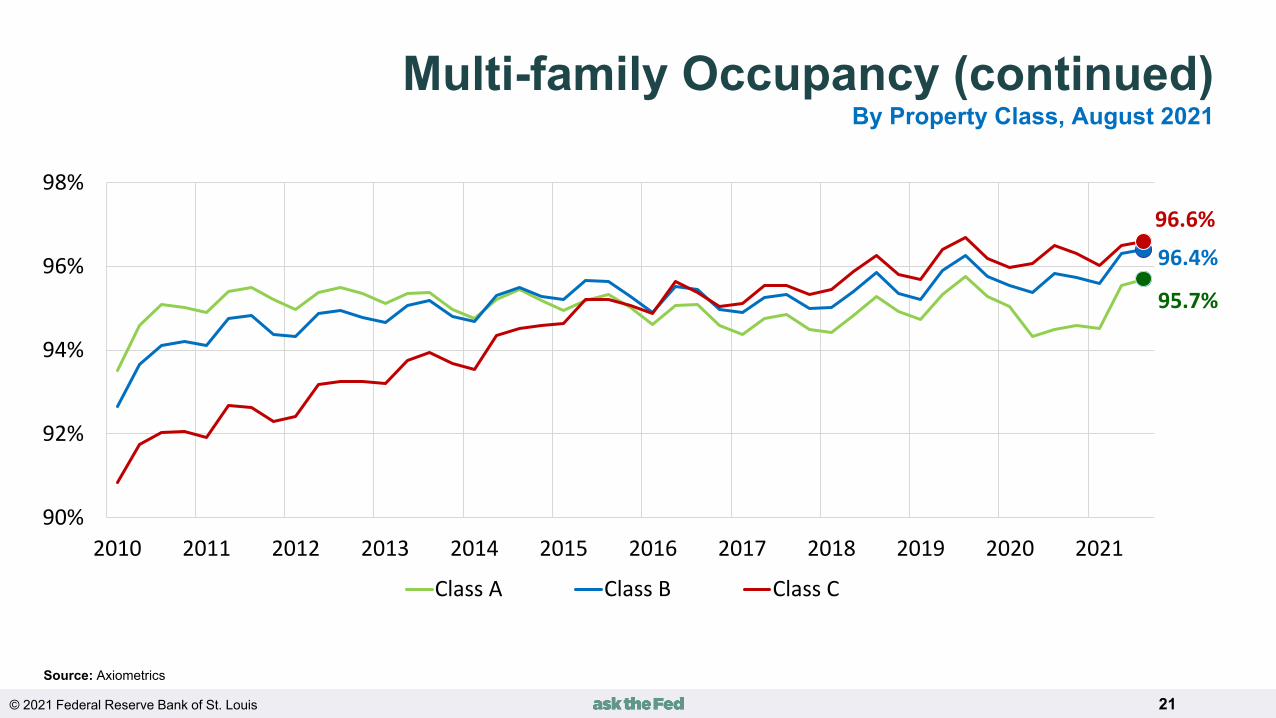

Multi-family Occupancy Percent, August 2021

Source: CoStar

© 2021 Federal Reserve Bank of St. Louis 20

Multi-family Occupancy (continued)Basis Point Change from Last August

Source: CoStar

© 2021 Federal Reserve Bank of St. Louis 21

Source: Axiometrics

Multi-family Occupancy (continued)By Property Class, August 2021

95.7%

96.4%

96.6%

90%

92%

94%

96%

98%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Class A Class B Class C

© 2021 Federal Reserve Bank of St. Louis 22

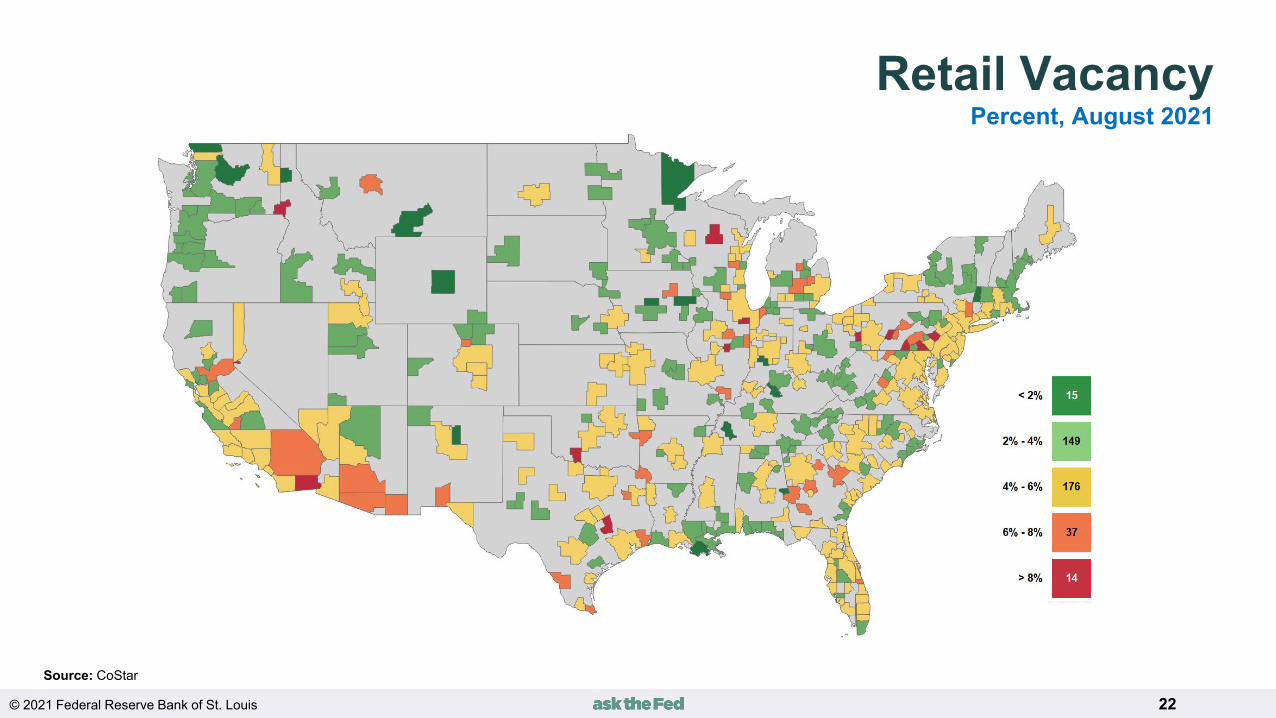

Retail VacancyPercent, August 2021

Source: CoStar

© 2021 Federal Reserve Bank of St. Louis 23

Retail Vacancy (continued)Change in Year-over-Year Basis Points, August 2021

Source: CoStar

© 2021 Federal Reserve Bank of St. Louis 24

Retail Sales Trends

Source: Monthly Retail Trade Report/U.S. Census Bureau, Risk Analysis Unit/Federal Reserve Bank of Atlanta

© 2021 Federal Reserve Bank of St. Louis 25

Retail VacancyPercent, August 2021

© 2021 Federal Reserve Bank of St. Louis 26

Office VacancyOffice Vacancy Percent, August 2021

Source: CoStar

© 2021 Federal Reserve Bank of St. Louis 27

Office VacancyPercent above Long-Term Average, August 2021

Source: CoStar

© 2021 Federal Reserve Bank of St. Louis 28

Polling Question #2

Compared to pre-pandemic levels, what percent of your organization’s employees will be expected to work on-site by year-end?

A) >90%B) >75% but less than 90%C) >50% but less than 75%D) >33% but less than 50%E) <33%

© 2021 Federal Reserve Bank of St. Louis 29

Polling Question #3

Compared to pre-pandemic levels, when your organization returns to the office, on average, how many days a week will your employees physically be in the office?

A) 5 daysB) 4 days C) 3 days D) 2 daysE) 1 dayF) None

© 2021 Federal Reserve Bank of St. Louis 30

Future HomeworkPercent of Employees Working from the Office

75%

6%

3%2%

1%13%

5 days 4 days 3 days 2 days 1 day <1 day

29.4%

24.0%15.0%

8.4%

5.0%

18.2%

5 days 4 days 3 days 2 days 1 day <1 day

Source: BLS, Various surveys/CBRE, Risk Analysis Unit/Federal Reserve Bank of Atlanta

Some industries reported the percent of successful remote workers was greater than 70% during the pandemic.

The remote work impact will vary depending upon the industry.

In extreme circumstances, whole industries may simply not return to the office (e.g., tech support, call center).

2019 POST COVID-19

Office of the Future

Areas of Greater Confidence

Return to the office delayed More people working remotely…more businesses reporting worker-return issues Technology is enabling greater space efficiency in the workplace Some industries will be more prone to let workers utilize alternative work arrangements More space may be needed per full time employee Greater building of Capex & Opex Low-cost/suburban locations appear to be thriving at the expense of high-cost and high-

density markets Tasks requiring collaboration, cross-pollination of ideas, networking, and culture are not

conducted as efficiently in the virtual environment vs. in-person

More Opaque Areas

Re-emergence of the Covid-19 virus Defining what constitutes a safe workplace The new workplace and employee implications

The Future Office

© 2021 Federal Reserve Bank of St. Louis 32

Industrial VacancyPercent, August 2021

Source: CoStar

© 2021 Federal Reserve Bank of St. Louis 33

Industrial Vacancy (continued)Basis Point Change from Last August

Source: CoStar

© 2021 Federal Reserve Bank of St. Louis 34

Travel Spending

Source: Bureau of Economic Analysis; Risk Analysis Unit/Atlanta Fed

© 2021 Federal Reserve Bank of St. Louis 35

Change in RevPAR*% of Markets, 2021 Q2

Source: CoStar

*Revenue Per Available Room

© 2021 Federal Reserve Bank of St. Louis 36

Just How Fast is it Moving??Commercial Mortgage-backed Securities (CMBS), Non-Banks Increase Market Share

Source: Real Capital Analytics, REIT/FRB Atlanta

© 2021 Federal Reserve Bank of St. Louis 37

Return of Risk?Non-Banks Offering Higher LTV Loans

Source: RealCapital Analytics, REIT/FRB Atlanta

0%

5%

10%

15%

20%

20% 25% 30% 35% 40% 45% 50% 55% 60% 65% 70% 75% 80% 85% 90%

All Others

Investor-Driven

Loan to Value

Percent of Loans

© 2021 Federal Reserve Bank of St. Louis 38

Whose Loan?Non-Bank Loan Characteristics

Source: RealCapital Analytics, REIT/FRB Atlanta

73%

70%

68%

70%

71%

69%

68%

65%66%67%68%69%70%71%72%73%74%

Average Loan to Value

2015 2016 2017 2018 2019 2020 2021 1H

$17.2 $17.9 $18.2 $19.4 $18.3 $17.3

$5.6

$0

$5

$10

$15

$20

$25

2015 2016 2017 2018 2019 2020 2021 1H

Average Loan Size$ Millions

© 2021 Federal Reserve Bank of St. Louis 39

Alternative (Institutional) Real Estate Price Change% Change from 1, 2, 3 & 5 Years

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%Apartment

Industrial

Mall

Office

Strip Center

Health Care

Medical Office

Skilled NursingLife Science

Lodging

Manufactured Homes

Net Lease

Self-Storage

Student Housing

Retail

1 year 2 year 3 year 5 yearSource: GreenStreet Advisors, REIT/FRB Atlanta

© 2021 Federal Reserve Bank of St. Louis 40

National Cap Rate Spreads

Source: Real Capital Analytics/FRB Atlanta

SpreadsCap Rates less 10-Year Treasury Yields

0

100

200

300

400

500

600

700

800

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21

Office Industrial Retail Apartments Hotel

Office Industrial Retail Apartments HotelCurrent 497 422 502 347 674

LT Average 434 438 419 317 578Difference 63 -16 83 30 96

Office Industrial Retail Apartments HotelCurrent 497 422 502 347 674

Low (Q2 2007) 146 185 160 104 373Difference 351 237 342 243 302

© 2021 Federal Reserve Bank of St. Louis 41

Emerging RISK?

Source: Real Capital Analytics, REIT/FRB Atlanta

Cap rates are compressing, while the 10-year Treasury yield has been increasing in the last few weeks.

Labor, or lack thereof.

Lending: Some segments are ultra-competitive. For example, more floating-rate debt, robust amounts of interest only, and lots of competition on price.

CRE dynamics: For instance- changing use/underutilization of properties, high valuations and population migration.

© 2021 Federal Reserve Bank of St. Louis 42

To Ask a Question

• Use the chat feature in the webinar (Ask Question button on bottom of screen).

• Email your question to: [email protected].

• Use the “Ask a Question” feature on the Ask the Fed® website: www.askthefed.org.

© 2021 Federal Reserve Bank of St. Louis 43

Thanks for joining us.

www.askthefed.org