COMMENTS ON FINANCE BILL – 2020

206

Transcript of COMMENTS ON FINANCE BILL – 2020

COMMENTS ON FINANCE BILL – 2020

The information contained in this booklet has been prepared on the basis of

Finance Bill 2020 and is not intended to be advice on any particular matter.

No person should act on the basis of any matter contained in this publication

without seeking appropriate professional advice. The amendments proposed

by this bill become effective from 01st July 2020 unless specified otherwise

after having been enacted as Finance Act 2020 with or without modification.

The booklet is published for our clients and staff for information and

guidance only and should not be published or reproduced without prior

permission of the firm.

This document can be accessed on www.hzco.com.pk REANDA HAROON ZAKARIA & COMPANY CHARTERED ACCOUNTANTS

Dated: June 12, 2020

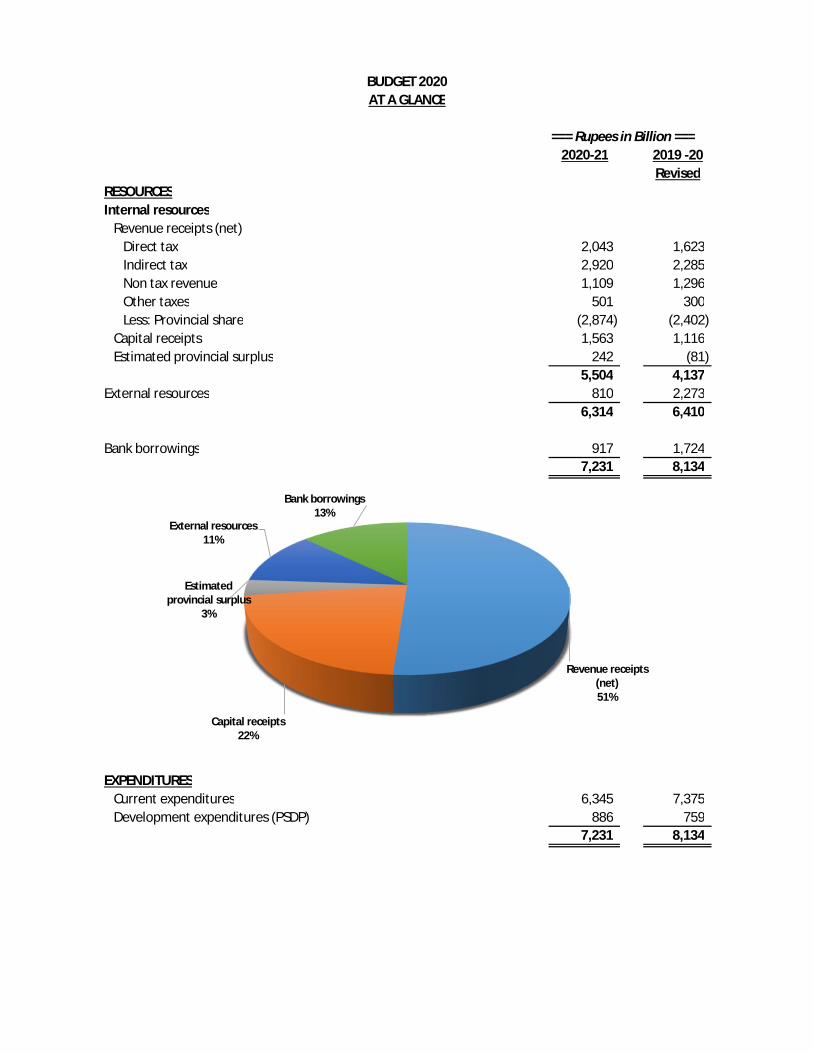

BUDGET 2020AT A GLANCE

=== Rupees in Billion ===2020-21 2019 -20

RevisedRESOURCESInternal resources

Revenue receipts (net)Direct tax 2,043 1,623 Indirect tax 2,920 2,285 Non tax revenue 1,109 1,296 Other taxes 501 300 Less: Provincial share (2,874) (2,402)

Capital receipts 1,563 1,116 Estimated provincial surplus 242 (81)

5,504 4,137 External resources 810 2,273

6,314 6,410

Bank borrowings 917 1,724 7,231 8,134

EXPENDITURESCurrent expenditures 6,345 7,375 Development expenditures (PSDP) 886 759

7,231 8,134

Revenue receipts (net)51%

Capital receipts 22%

Estimated provincial surplus

3%

External resources11%

Bank borrowings13%

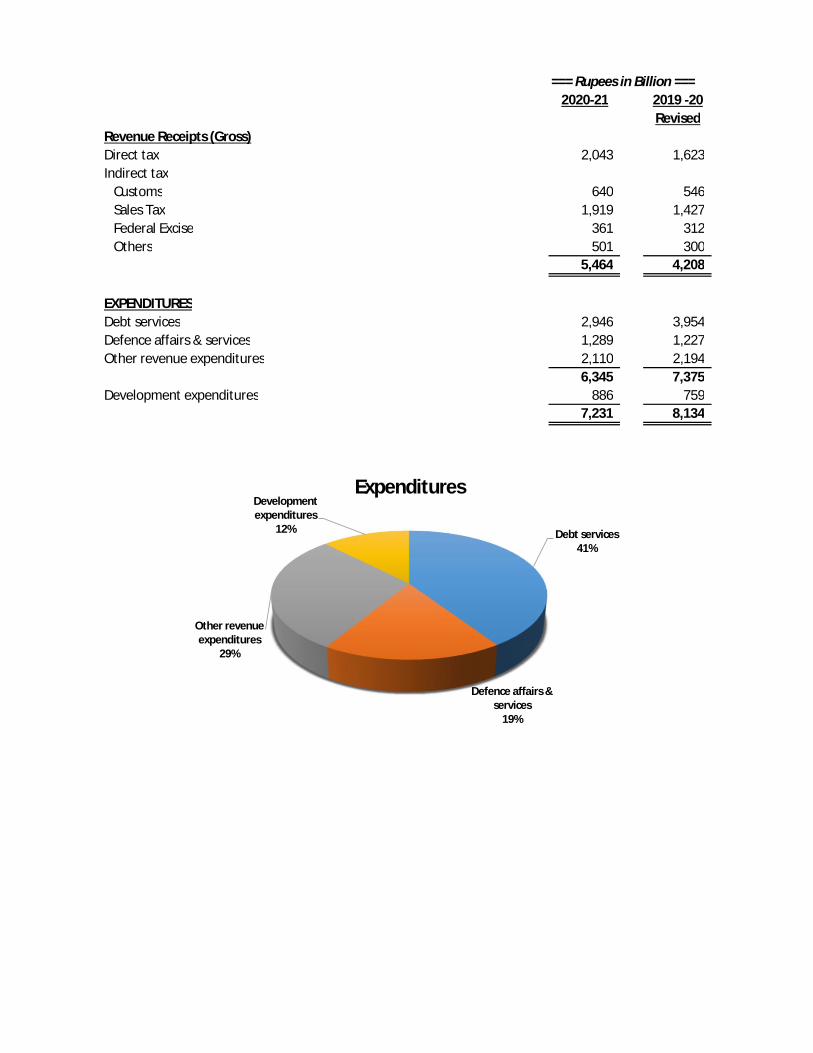

=== Rupees in Billion ===2020-21 2019 -20

RevisedRevenue Receipts (Gross)Direct tax 2,043 1,623 Indirect tax

Customs 640 546 Sales Tax 1,919 1,427 Federal Excise 361 312 Others 501 300

5,464 4,208

EXPENDITURESDebt services 2,946 3,954 Defence affairs & services 1,289 1,227 Other revenue expenditures 2,110 2,194

6,345 7,375 Development expenditures 886 759

7,231 8,134

Debt services41%

Defence affairs & services

19%

Other revenue expenditures

29%

Development expenditures

12%

Expenditures

Finance Bill 2020

Table of Contents

Salient Feature

Page No.

Income Tax 01 – 07

Sales Tax 08 – 09

Federal Excise 10 – 11

Customs Act 12 – 13

Detailed comments on

Income Tax 14 – 149

Sales Tax 150 – 192

Federal Excise 193 – 197

Customs Act 198 – 200

SALIENT FEATURES

1

SALIENT FEATURES

FINANCE BILL 2020

Amendment in Income Tax Ordinance, 2001, Sales Tax Act, 1990, Customs

Act, 1990 and under Federal Excise Act, 2005 shall have effect on the next

day of assent given to this Act by the President of the Islamic Republic of

Pakistan, rest of amendments shall come into force from the first day of July,

2020.

INCOME TAX ORDINANCE, 2001

Seeks to rationalize tax on imports on certain specific goods at 1%for

capital goods and 2% for raw material as per new inserted Schedule-

XII.

Seeks to withdraw power of Commissioner-IR for issuance of

exemption certificate on import of goods.

Seeks to consider withholding tax on import of goods by large

import house as minimum tax.

Minimum tax on import of edible oil, packing material, plastic raw

material and import of ship by ship breakers done away.

Seeks to consider electricity expenses as inadmissible subject to

certain terms and conditions.

Seeks to disallow business expenditure proportionate to sales made

to sales tax unregistered persons. However, the aggregate

SALIENT FEATURES

2

disallowance shall not exceed twenty percent of total business

deductions excluding deduction under the provisions.

Seeks to levy minimum tax on manufacturing of Modarabas.

Seeks to restrict normal deprecation upto 50% for the first year use

of the assets.

Seeks to deposit conditional payment of 10% amount of tax demand

upheld by the Commissioner-IR(Appeals) to file second appeal

before the Inland Revenue Appellate Tribunal.

Seeks to make mandatory to obtain Commissioner-IR approval for

revising Wealth Statement.

Seeks to exempt from 100% higher withholding rates for non-

residents.

Seeks to restrict limit upto Rs.2.5 million on cost of transport

vehicles not plying for hire for the purpose of vehicles taken on

lease.

Seeks to delete payment of tax on local purchase of cooking oil and

vegetable ghee by certain person.

Seeks to file withholding statement u/s.165 on quarterly basis.

Seeks to consider withholding tax in case of payment for use of

machinery or equipment as minimum tax.

SALIENT FEATURES

3

Seeks to amend section 122 on the basis of independent of definite

information.

Seeks to delete collection of advance tax on Education related

expenses remitted abroad.

Seeks to delete withholding tax on Electricity bill in case of steel

milters and composing unit.

Seeks to delete withholding tax on withdrawal of balance under

Pension fund.

Seeks to delate withholding tax on functions and gatherings.

Seeks to delete advance withholding tax on cable operator and

other electronic media.

Seeks to delete withholding tax on dealers on commission agents

and arhatis etc.

Seeks to delete advance withholding tax on insurance premium.

Seeks to delete withholding advance tax on tobacco.

Seeks to enhance limit for becoming prescribed person for

withholding tax on supplies, services and contracts from fifty to

hundred million rupees in case of individual and AOP and threshold

of hundred million rupees is prescribed for sales tax registration

person to becoming withholding agent.

SALIENT FEATURES

4

Seeks to restrict holding period in case of capital gain on immovable

property upto four years irrespective of plot and constructed

property.

Seeks to increase threshold per transaction from rupees ten

thousand to twenty-five thousand in case of payment of business

expenditure otherwise than cross cheque.

Seeks to enhance threshold per transaction from fifty thousand to

two hundred fifty thousand in case of payment under single head of

account.

Seeks to allow option to claim expenses by AOP and Individual in

case of income from property.

Seeks to exempt withholding tax on cash withdrawal to the extent

of foreign remittance.

Seeks to allow incentive in investment in Government debt

instruments

Seeks to allow issuance of refund through centralized processing

system.

Seeks to exempt Hajj operator from withholding tax on payment to

non-resident.

Seeks to exclude vehicle upto 200cc from the ambit of advance tax.

SALIENT FEATURES

5

Seeks to collect advance tax in installment on auction of immovable

property.

Seeks to facilitate issuance of exemption certificate in case of public

limited company.

Seeks not to collect advance tax by educational institutions in case

of person on the Active Taxpayer List. (ATL).

Seeks to facilitate issuance of exemption certificate for commercial

and industrial consumer of electricity subject to certain conditions.

Seeks to introduce concept of agreed assessment.

Seeks to strengthen Alternate Dispute Resolution Mechanism.

Seeks to reduce in Rate for permanent establishments of non-

resident person.

Seeks to allow concession to co-developers of special economic

zones.

Seeks to reduce withholding tax rate on toll manufacturing to 4% for

companies and 4.5% in other case.

Seeks to reduce in tax withheld from offshore supplier under an EPC

contract to 20% instead of 30%

SALIENT FEATURES

6

Seeks to extension of exemption to profit from sale of immovable

property to extension in exception for development are REITs until

30.06.2021.

Seeks to allow incentive in tax rate to new Pakistan resident ship

owing companies and shall also extend the sunset clause of section

7A from 2020 to 2023.

Seeks to require withholding agent to file quarterly statement of

certain economic transactions.

Seeks to audit on the basis of benchmark ratios.

Seeks to introduce concept of E-Audit.

Seeks to introduce definition of non-profit organization to include

only such organization under the ambit of definition which are for

the benefit of general public.

Seeks to introduce advance tax on extraction of minerals to extend

to persons on the Active Taxpayer List.

Seeks to introduce uniformity in tax rate for profit on debt.

Seeks to enhance rate of withholding tax from fifteen percent to

twenty five percent in case of dividend paid by company not liable

to pay tax.

SALIENT FEATURES

7

Seeks to enhance rate of withholding tax from fifteen percent to

twenty five percent in case of return on investment in sukuks.

Seeks to introduce parity between Permanent Establishment (PE) of

on-residents and resident persons.

Seeks to extent levy of minimum tax in case of Permanent

Establishment for non-resident persons.

Seeks to limit interest deductibility to Foreign affiliates.

Seeks to consider payment made to non-resident in case of Media

person relaying from outside as minimum tax.

Seeks to extent applicability of existing on disposal of capital gain on

securities upto tax year 2021 and onwards.

Seeks to omit engineering services from reduced rate benefit.

Seeks to restrict exemption from income on certain foundations,

societies, boards, trusts and funds mentioned as per clause 66(2) of

Table-II of Part-IV of Second Schedule to the Income Tax Ordinance,

2001 subject to compliance of provision of section 100c of the

provision is applicable from tax year 2021.

SALIENT FEATURES

8

SALES TAX ACT-1990

Seeks to enhance limit from fifty thousand to hundred thousand in

case of supply by retailer for obtaining CNIC of the buyers.

Seeks to extend for another two months started from 20th June,

2020 in case of exemption granted in wake of Covid-19.

Seeks to exempt sales tax on import of dietetic foods subject to

restriction and conditions.

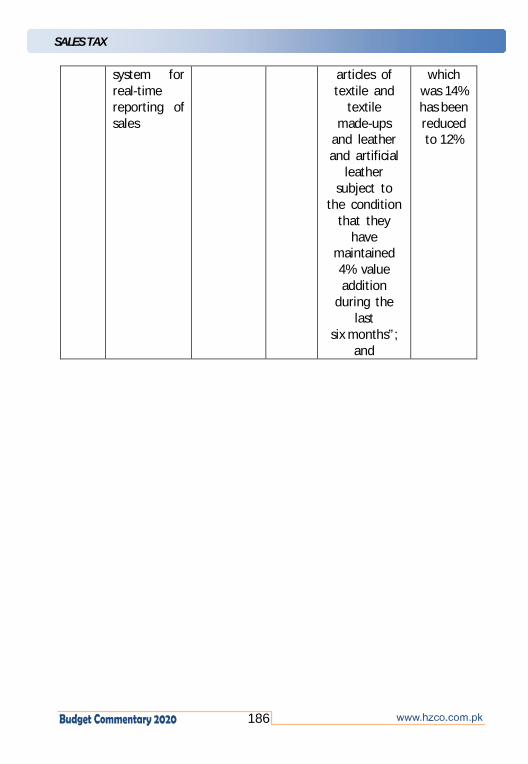

Seeks to reduce sales tax rate from 14% to 12% in case of retailer

integrated online with FBR through point of sale system.

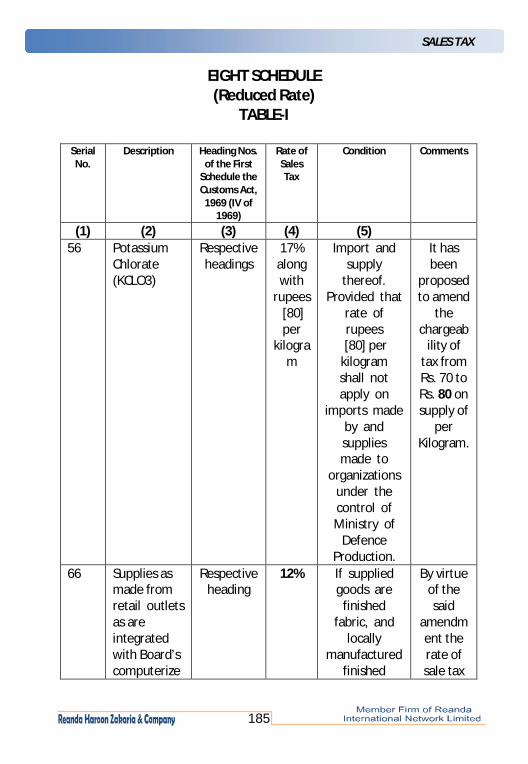

Seeks to increase sales tax on supply of potassium chlorate from

Rs.70/- to Rs.80/- per kg.

Seeks to introduce concept of conducting audit through electronic

means.

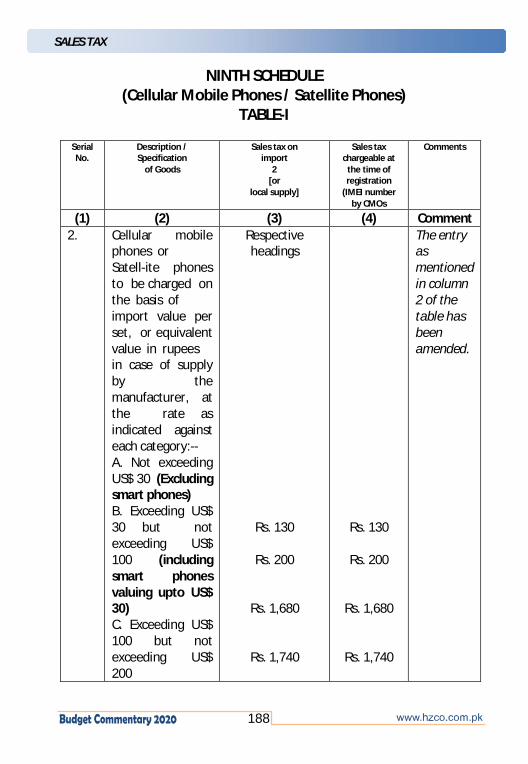

Seeks to amend Ninth schedule in line with mobile manufacturing

policy approved by the ECC of the cabinet.

Seeks to abolish Value Addition Tax in case of manufacturer

importing raw material and intermediary goods for in-house

consumption.

Seeks to strengthen Alternate Dispute Resolution process.

SALIENT FEATURES

9

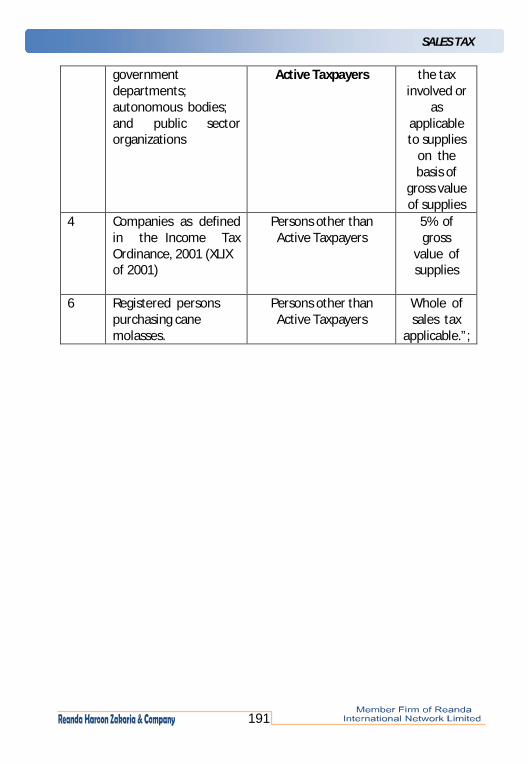

Seeks to enhance scope of supply to unregistered person instead of

manufacturer only.

Seeks to empower Board to fix minimum production on the basis of

single or more inputs and for fixation of wastage.

Seeks to access real time information and databases to the Bords by

various authorities such as NADARA, FIA, provincial excise &

taxation departments etc.

SALIENT FEATURES

10

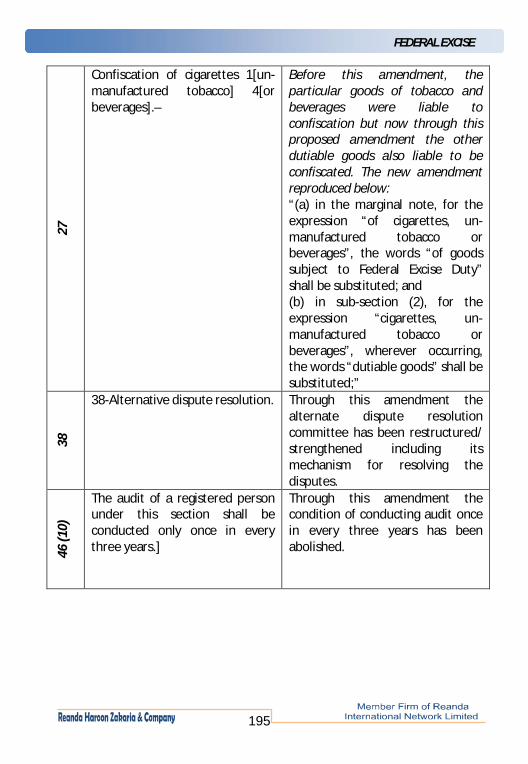

FEDERAL EXCISE ACT, 2005

Seeks to restrict the adjustment of input tax on wastage material

through proper notification.

Seeks to confer powers to the Officer for modifying the order inline

with decision given by the Appellate Authority or High Court.

Seeks to extend the scope of seizure and confiscation of all dutiable

goods.

Seeks to restructure and redefine the Alternate Dispute Resolution

Committee.

Seeks to withdraw condition of conducting audit once in every three

years.

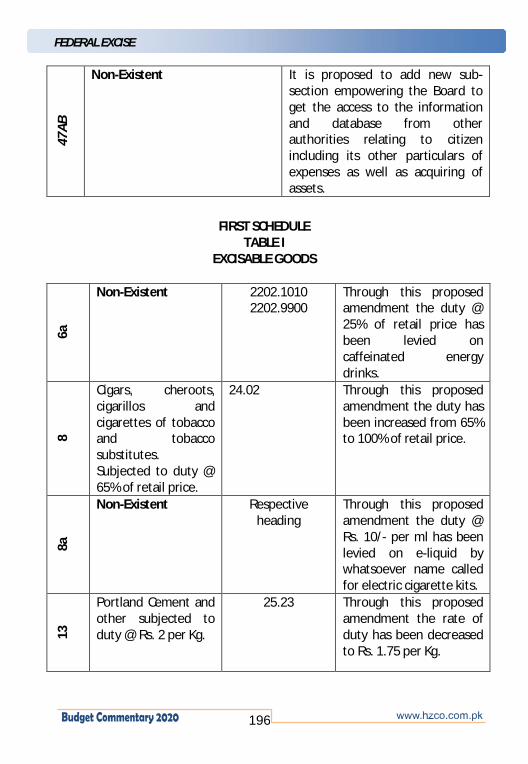

Seeks to empower Board to get the access to the information and

database from other authorities for un-earthing tax fraud.

Seeks to increase duties on different kinds of locally produced

cigarettes, cigars, cheroots and cigarillos.

Seeks to charge duty @ 25% and Rs. 10/- per ml. on caffeinated energy

drinks and e-liquids of electric cigarettes.

Seeks to reduce the duty on Portland Cement and others from Rs. 2

per KG to Rs. 1.75 per KG.

SALIENT FEATURES

11

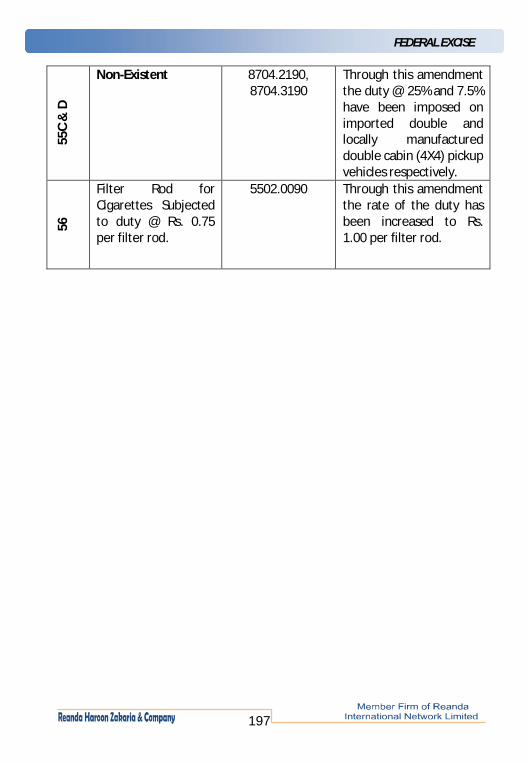

Seeks to charge duty @ 25% and 7.5% on imported and locally

manufactured double cabin (4X4) vehicles, respectively.

Seeks to enhance the duty by Rs. 0.25 per Filter Rod for cigarettes.

Seeks to extend the scope of seizure of non-duty paid goods.

Seeks to increase the value of minimal duties not exceeding Rs. 5000/-

SALIENT FEATURES

12

CUSTOMS ACT, 1969

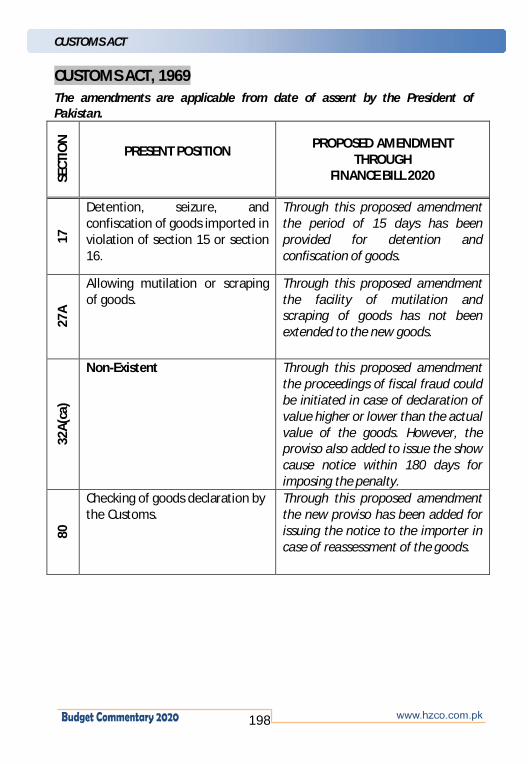

Seeks to withdraw the facility of mutilation or scrapping of new

imported goods.

Seeks to provide time period of 30 days for issuance of show cause

notice and deciding the cases falling under Section 2(s) of the Act.

Seeks to extend the scope of fiscal fraud by covering the

misdeclaration of value of the goods.

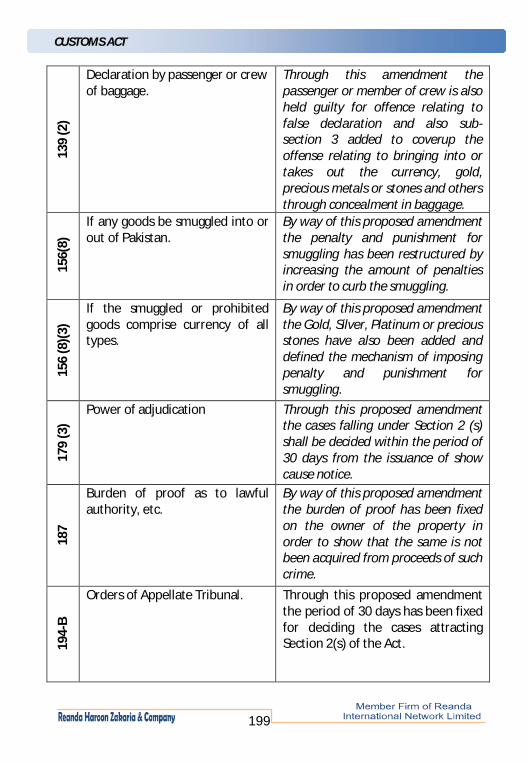

Seeks to restructure and increase the amount of penalties in cases

of smuggling of currency, gold, silver, platinum or precious stones

etc.

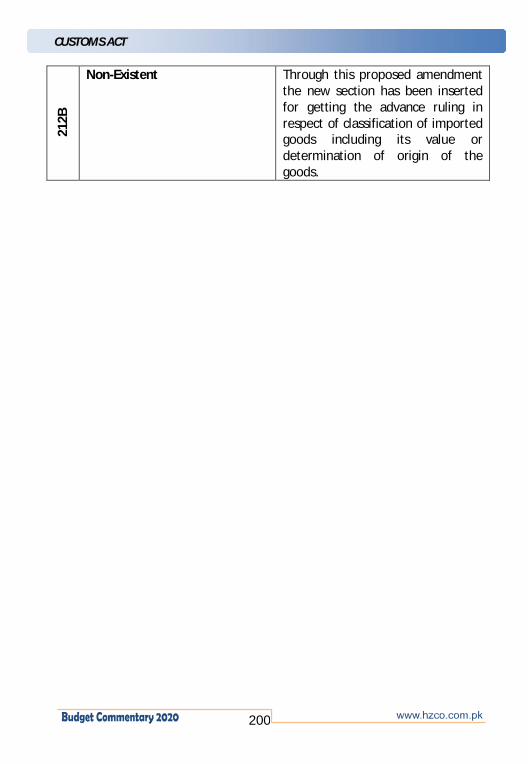

Seeks to introduce the concept of advance ruling in respect of

imported goods.

Seeks to exempt additional customs duties and rationalize the

National Tariff Policy, 2019.

Seeks to reduce regulatory duty on Hot Rolled Coils of iron and steel

falling under PCT Heading 7208, 7225 and 7226.

Seeks to allow import of inputs/intermediary raw material in terms

of the Fifth Schedule to the Act.

SALIENT FEATURES

13

Seeks to exempt customs duties on import of raw material by

beverage can manufacturers and food packaging industry.

Seeks to exempt customs duties on import of 61 COVID-19 related

items till continuation of pandemic.

Seeks to exempt 2% Additional Customs Duty on import of edible oil

and seeds, dietetic foods for children, diagnostic kit for cancer and

coronavirus.

Seeks to exempt customs duties on inputs of ready to use

supplementary foods, lifesaving drugs for treatment of

leishmaniasis.

Seeks to exempt customs duty on import for setting-up new

industries in FATA area.

Seeks to reduce regulatory duty on smuggling prone items and

several industrial inputs.

Seeks to reduce Additional Customs Duty on soap manufacturing

industries.

Seeks to increase / levy of RD on import in order to provide tariff

protection for domestic industries.

Seeks to enhance scope of concessions available to available to

special economic zones.

INCOME TAX

14

INCOME TAX The amendments are applicable from July 1, 2020 unless specified otherwise.

SECT

ION

PRESENT POSITION

PROPOSED AMENDMENT THROUGH

FINANCE BILL 2020

2(29

C)

Non-Existent

The proposed amendment seeks to include person engaged in construction activity with in the definition of Industrial Undertaking starting from 01.05.2020. This would provide them benefit to obtain exemption certificate on import of construction machinery. (aa) from the 1st day of May, 2020, a person directly involved in the construction of buildings, roads, bridges and other such structures or the development of land, to the extent and for the purpose of import of plant and machinery to be utilized in such activity, subject to such conditions as may be notified by the Board; and ";

2(30

A)

Non-Existent

The proposed amendment seeks to insert following self-explanatory definition. (30A) “integrated enterprise” means a person integrated with the Board through approved fiscal electronic device and software, 53 and who fulfills obligations and requirements for integration as may be prescribed.

INCOME TAX

15

2(30

AC)

Non-Existent

The proposed amendment seeks to insert following self-explanatory definition. “IRIS” means a web-based computer programme for operation and management of Inland Revenue taxes administered by the Board.

2(31

A)

Non-Existent

The proposed amendment seeks to insert following self-explanatory definition. (31A) “Local Government” shall have the same meaning for respective provisions and Islamabad Capital Territory as contained in the Balochistan Local Government Act, 2010 (V of 2010), the Khyber Pakhtunkhwa Local Government Act, 2013 (XXVIII of 2013), the Sindh Local Government Act, 2013 (XLII of 2013), the Islamabad Capital Territory Local Government Act, 2015 (X of 2015) and the Punjab Local Government Act, 2019 (XIII of 2019) ;”; and

INCOME TAX

16

2(36

) “non-profit organization” means any person other than an individual, which is — (a) established for religious, educational, charitable, welfare or development purposes, or for the promotion of an amateur sport; (b) formed and registered under any law as a non-profit organization; (c) approved by the Commissioner for specified period, on an application made by such person in the prescribed form and manner, accompanied by the prescribed documents and, on requisition, such other documents as may be required by the Commissioner.

The proposed amendment seeks to include organizations established for the purpose of general public into definition of non-profit organization. “non-profit organization” means any person other than an individual, which is — (a) established for religious, educational, charitable, welfare or purposes for general public, or for the promotion of an amateur sport; (b) formed and registered by or under any law as a non-profit organization; (c) approved by the Commissioner for specified period, on an application made by such person in the prescribed form and manner, accompanied by the prescribed documents and, on requisition, such other documents as may be required by the Commissioner.

INCOME TAX

17

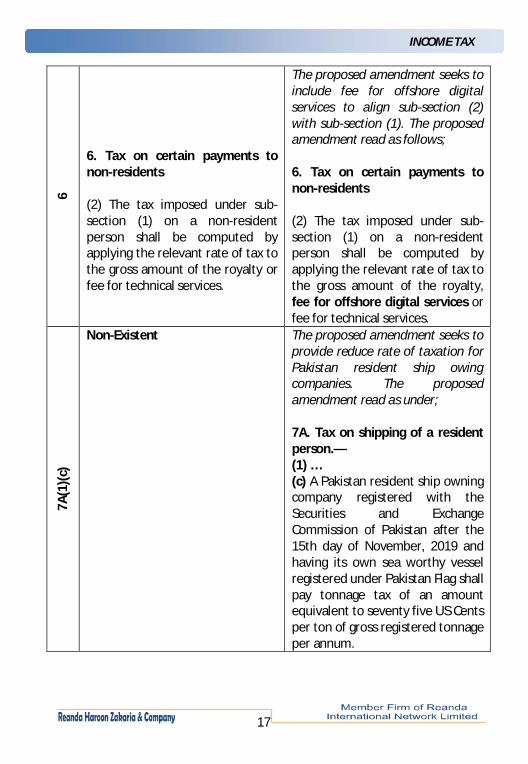

6 6. Tax on certain payments to non-residents (2) The tax imposed under sub-section (1) on a non-resident person shall be computed by applying the relevant rate of tax to the gross amount of the royalty or fee for technical services.

The proposed amendment seeks to include fee for offshore digital services to align sub-section (2) with sub-section (1). The proposed amendment read as follows; 6. Tax on certain payments to non-residents (2) The tax imposed under sub-section (1) on a non-resident person shall be computed by applying the relevant rate of tax to the gross amount of the royalty, fee for offshore digital services or fee for technical services.

7A(1

)(c)

Non-Existent

The proposed amendment seeks to provide reduce rate of taxation for Pakistan resident ship owing companies. The proposed amendment read as under; 7A. Tax on shipping of a resident person.— (1) … (c) A Pakistan resident ship owning company registered with the Securities and Exchange Commission of Pakistan after the 15th day of November, 2019 and having its own sea worthy vessel registered under Pakistan Flag shall pay tonnage tax of an amount equivalent to seventy five US Cents per ton of gross registered tonnage per annum.

INCOME TAX

18

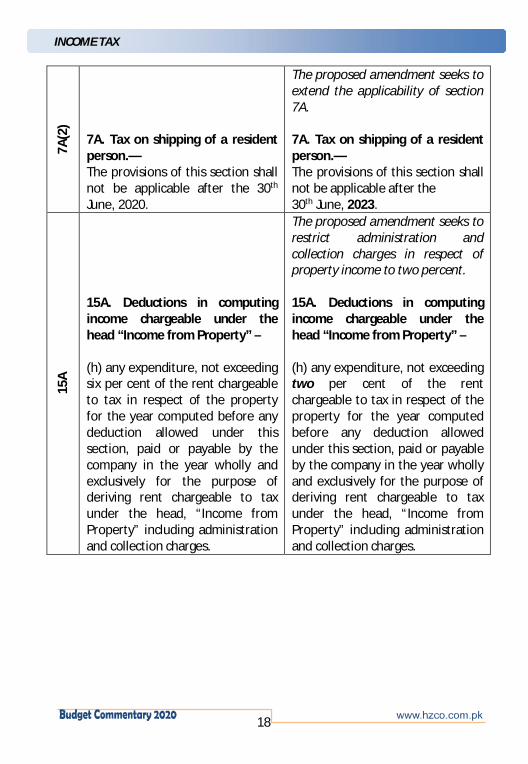

7A(2

) 7A. Tax on shipping of a resident person.— The provisions of this section shall not be applicable after the 30th June, 2020.

The proposed amendment seeks to extend the applicability of section 7A. 7A. Tax on shipping of a resident person.— The provisions of this section shall not be applicable after the 30th June, 2023.

15A

15A. Deductions in computing income chargeable under the head “Income from Property” – (h) any expenditure, not exceeding six per cent of the rent chargeable to tax in respect of the property for the year computed before any deduction allowed under this section, paid or payable by the company in the year wholly and exclusively for the purpose of deriving rent chargeable to tax under the head, “Income from Property” including administration and collection charges.

The proposed amendment seeks to restrict administration and collection charges in respect of property income to two percent. 15A. Deductions in computing income chargeable under the head “Income from Property” – (h) any expenditure, not exceeding two per cent of the rent chargeable to tax in respect of the property for the year computed before any deduction allowed under this section, paid or payable by the company in the year wholly and exclusively for the purpose of deriving rent chargeable to tax under the head, “Income from Property” including administration and collection charges.

INCOME TAX

19

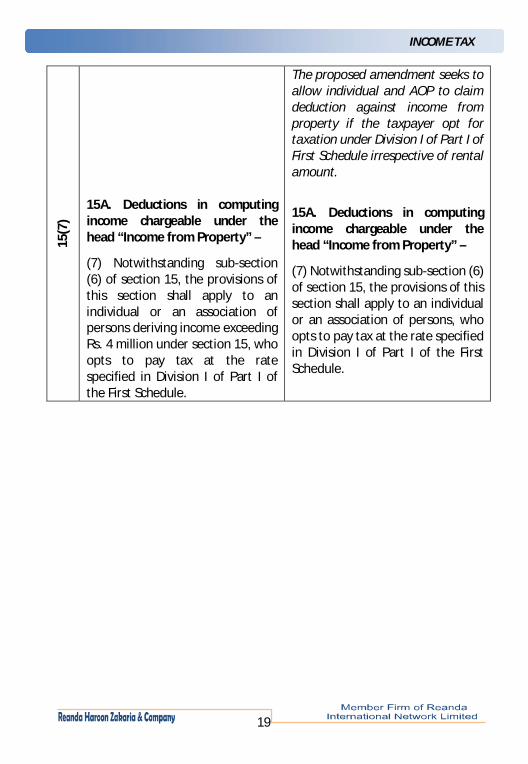

15(7

) 15A. Deductions in computing income chargeable under the head “Income from Property” –

(7) Notwithstanding sub-section (6) of section 15, the provisions of this section shall apply to an individual or an association of persons deriving income exceeding Rs. 4 million under section 15, who opts to pay tax at the rate specified in Division I of Part I of the First Schedule.

The proposed amendment seeks to allow individual and AOP to claim deduction against income from property if the taxpayer opt for taxation under Division I of Part I of First Schedule irrespective of rental amount.

15A. Deductions in computing income chargeable under the head “Income from Property” –

(7) Notwithstanding sub-section (6) of section 15, the provisions of this section shall apply to an individual or an association of persons, who opts to pay tax at the rate specified in Division I of Part I of the First Schedule.

INCOME TAX

20

21(l)

(m)

21. Deductions not allowed: any expenditure for a transaction, paid or payable under a single account head which, in aggregate, exceeds fifty thousand rupees, made other than by a crossed cheque drawn on a bank or by crossed bank draft or crossed pay order or any other crossed banking instrument showing transfer of amount from the business bank account of the taxpayer:

Provided that online transfer of payment from the business account of the payer to the business account of payee as well as payments through credit card shall be treated as transactions through the banking channel, subject to the condition that such transactions are verifiable from the bank statements of the respective payer and the payee:

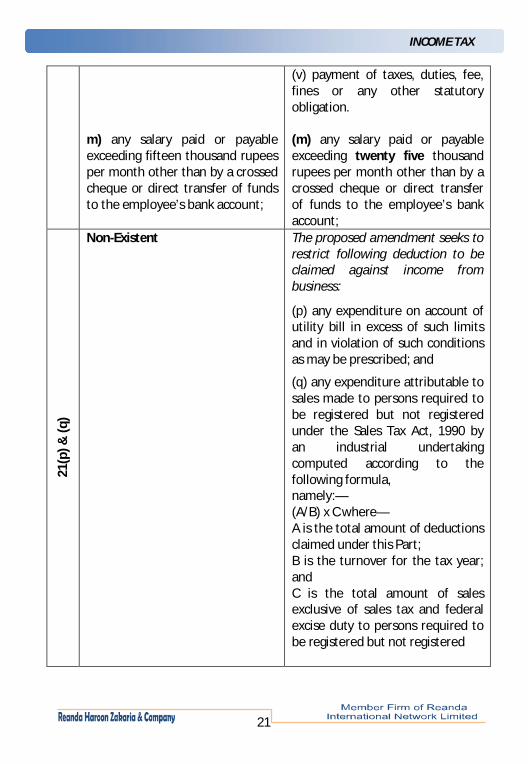

Provided further that this clause shall not apply in the case of (a) expenditures not exceeding ten thousand rupees; (b) expenditures on account of — (i) utility bills; (ii) freight charges; (iii) travel fare; (iv) postage; and (v) payment of taxes, duties, fee, fines or any other statutory obligation.

The proposed amendment seeks to enhance threshold of admissible expenses paid in cash

21. Deductions not allowed: any expenditure for a transaction, paid or payable under a single account head which, in aggregate, exceeds two hundred and fifty thousand rupees, made other than by a crossed cheque drawn on a bank or by crossed bank draft or crossed pay order or any other crossed banking instrument showing transfer of amount from the business bank account of the taxpayer:

Provided that online transfer of payment from the business account of the payer to the business account of payee as well as payments through credit card shall be treated as transactions through the banking channel, subject to the condition that such transactions are verifiable from the bank statements of the respective payer and the payee:

Provided further that this clause shall not apply in the case of (a) expenditures not exceeding twenty five thousand rupees; (b) expenditures on account of — (i) utility bills; (ii) freight charges; (iii) travel fare; (iv) postage; and

INCOME TAX

21

m) any salary paid or payable exceeding fifteen thousand rupees per month other than by a crossed cheque or direct transfer of funds to the employee’s bank account;

(v) payment of taxes, duties, fee, fines or any other statutory obligation. (m) any salary paid or payable exceeding twenty five thousand rupees per month other than by a crossed cheque or direct transfer of funds to the employee’s bank account;

21(p

) & (q

)

Non-Existent The proposed amendment seeks to restrict following deduction to be claimed against income from business:

(p) any expenditure on account of utility bill in excess of such limits and in violation of such conditions as may be prescribed; and

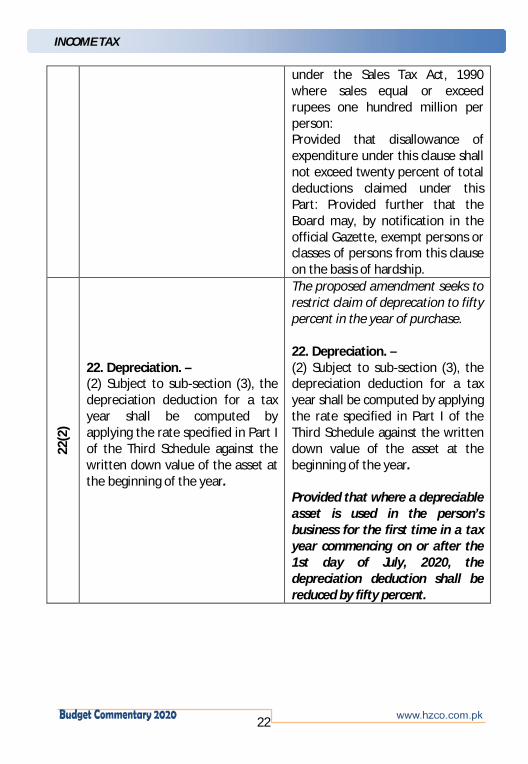

(q) any expenditure attributable to sales made to persons required to be registered but not registered under the Sales Tax Act, 1990 by an industrial undertaking computed according to the following formula, namely:— (A/B) x C where— A is the total amount of deductions claimed under this Part; B is the turnover for the tax year; and C is the total amount of sales exclusive of sales tax and federal excise duty to persons required to be registered but not registered

INCOME TAX

22

under the Sales Tax Act, 1990

where sales equal or exceed rupees one hundred million per person: Provided that disallowance of expenditure under this clause shall not exceed twenty percent of total deductions claimed under this Part: Provided further that the Board may, by notification in the official Gazette, exempt persons or classes of persons from this clause on the basis of hardship.

22(2

)

22. Depreciation. – (2) Subject to sub-section (3), the depreciation deduction for a tax year shall be computed by applying the rate specified in Part I of the Third Schedule against the written down value of the asset at the beginning of the year.

The proposed amendment seeks to restrict claim of deprecation to fifty percent in the year of purchase. 22. Depreciation. – (2) Subject to sub-section (3), the depreciation deduction for a tax year shall be computed by applying the rate specified in Part I of the Third Schedule against the written down value of the asset at the beginning of the year. Provided that where a depreciable asset is used in the person’s business for the first time in a tax year commencing on or after the 1st day of July, 2020, the depreciation deduction shall be reduced by fifty percent.

INCOME TAX

23

22(8

) 22. Depreciation. – (8) Where, in any tax year, a person disposes of a depreciable asset, no depreciation deduction shall be allowed under this section for that year and —

The proposed amendment seeks to allow claim of deprecation equal to fifty percent of the applicable rate in the year of purchase where the assets is disposed off in the same year. 22. Depreciation. – (8) Where, in any tax year, a person disposes of a depreciable asset, no depreciation deduction shall be allowed under this section for that year and — Provided that where a depreciable asset is used in the person’s business for the first time in a tax year commencing on or after the 1st day of July, 2020, depreciation deduction equal to fifty percent of the rate specified in Part I of the Third Schedule shall be allowed in the year of disposal.

28

Non-Existent The proposed amendment seeks to restrict claim of deduction on account of lease of passenger transport vehicle to align deduction in respect of leased asset with owned asset. “Provided that for the purpose of determining the deduction on account of lease rentals the cost of a passenger transport vehicle not plying for hire to the extent of principal amount shall not exceed two and a half million rupees;”

INCOME TAX

24

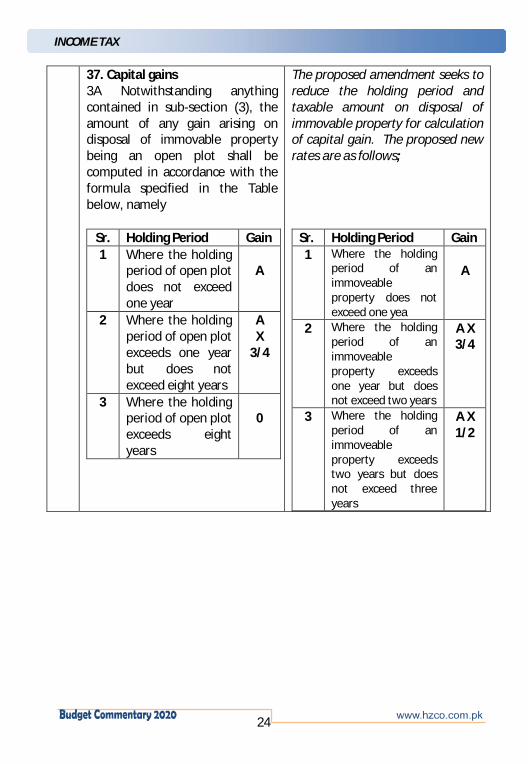

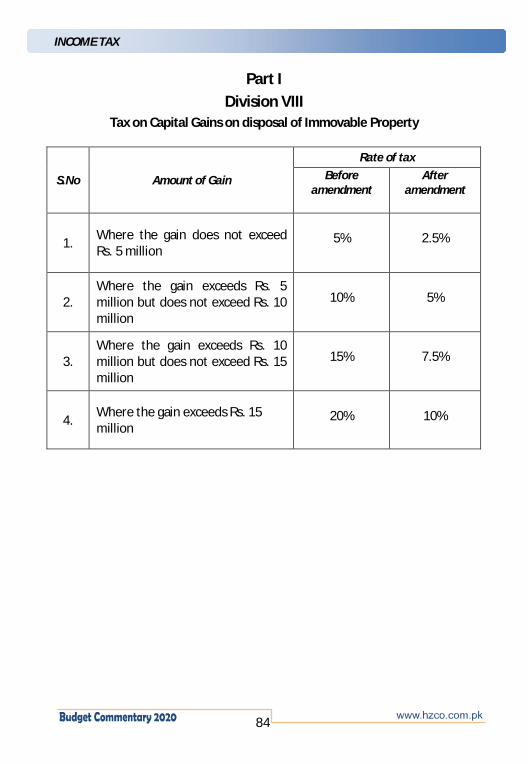

37. Capital gains 3A Notwithstanding anything contained in sub-section (3), the amount of any gain arising on disposal of immovable property being an open plot shall be computed in accordance with the formula specified in the Table below, namely

Sr. Holding Period Gain 1 Where the holding

period of open plot does not exceed one year

A

2 Where the holding period of open plot exceeds one year but does not exceed eight years

A X

3/4

3 Where the holding period of open plot exceeds eight years

0

The proposed amendment seeks to reduce the holding period and taxable amount on disposal of immovable property for calculation of capital gain. The proposed new rates are as follows;

Sr. Holding Period Gain 1 Where the holding

period of an immoveable property does not exceed one yea

A

2 Where the holding period of an immoveable property exceeds one year but does not exceed two years

A X 3/4

3 Where the holding period of an immoveable property exceeds two years but does not exceed three years

A X 1/2

INCOME TAX

25

37(3

A) &

(3B)

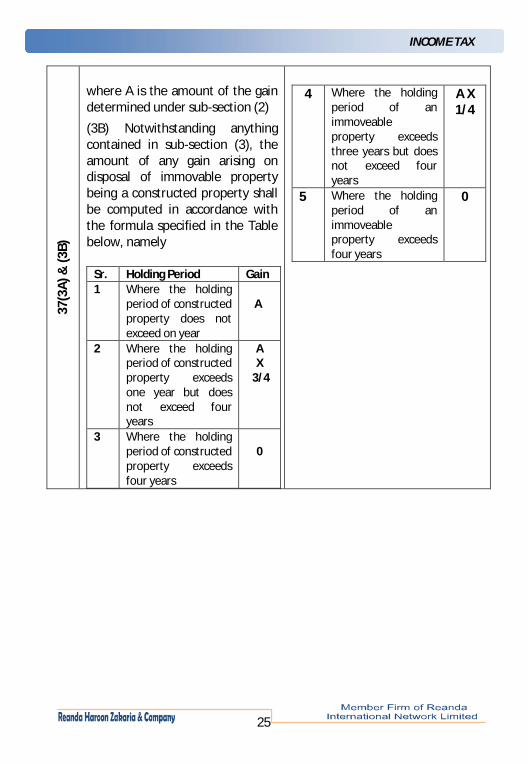

where A is the amount of the gain determined under sub-section (2)

(3B) Notwithstanding anything contained in sub-section (3), the amount of any gain arising on disposal of immovable property being a constructed property shall be computed in accordance with the formula specified in the Table below, namely

Sr. Holding Period Gain 1 Where the holding

period of constructed property does not exceed on year

A

2 Where the holding period of constructed property exceeds one year but does not exceed four years

A X

3/4

3 Where the holding period of constructed property exceeds four years

0

4 Where the holding

period of an immoveable property exceeds three years but does not exceed four years

A X 1/4

5 Where the holding period of an immoveable property exceeds four years

0

INCOME TAX

26

INCOME TAX The amendments are applicable from July 1, 2020 unless specified otherwise.

SECT

ION

PRESENT POSITION

PROPOSED AMENDMENT THROUGH

FINANCE BILL 2020

61

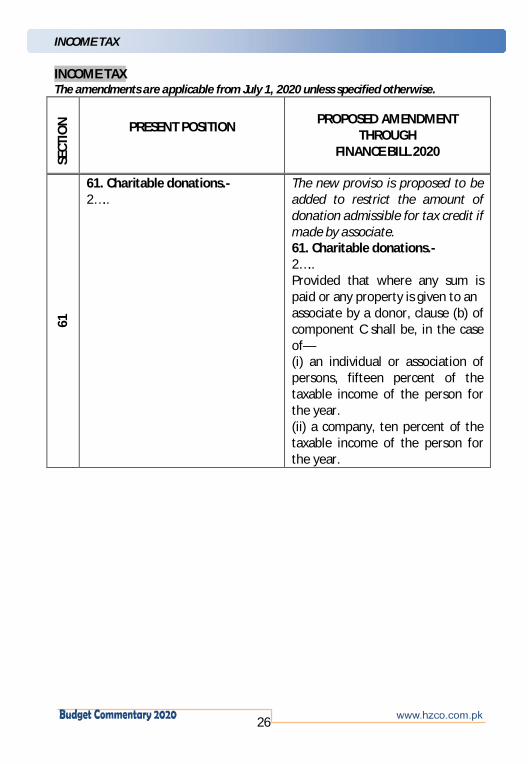

61. Charitable donations.- 2…..

The new proviso is proposed to be added to restrict the amount of donation admissible for tax credit if made by associate. 61. Charitable donations.- 2….. Provided that where any sum is paid or any property is given to an associate by a donor, clause (b) of component C shall be, in the case of— (i) an individual or association of persons, fifteen percent of the taxable income of the person for the year. (ii) a company, ten percent of the taxable income of the person for the year.

INCOME TAX

27

65C

65C. Tax credit for enlistment. —(1) Where a taxpayer being a company opts for enlistment in any registered stock exchange in Pakistan, a tax credit equal to twenty percent of the tax payable shall be allowed for the tax year in which the said company is enlisted and for the following three tax years

The proposed amendment seeks to restrict tax credit for investment in stock exchange upto Tax Year 2022. 65C. Tax credit for enlistment. —(1) Where a taxpayer being a company opts for enlistment in any registered stock exchange in Pakistan on or before the 30th day of June, 2022 a tax credit equal to twenty percent of the tax payable shall be allowed for the tax year in which the said company is enlisted and for the following three tax years

97A

97A Disposal of asset between wholly-owned companies.—

The proposed amendment seeks to correct reference of Companies Ordinance after enactment of Companies Act, 2017.

100B

A

100BA. Special provisions relating to persons not appearing in active taxpayers’ list.-(1) The collection or deduction of advance income tax, computation of income and tax payable thereon shall be determined in accordance with the rules in the Tenth Schedule.

The proposed armament seeks to make the following technical amendment. 100BA. Special provisions relating to persons not appearing in active taxpayers’ list.-(1) The collection or deduction of advance income tax, computation of income and tax payable thereon in respect of a person not appearing on the Active Taxpayer’s List shall be determined in accordance with the rules in the Tenth Schedule.

INCOME TAX

28

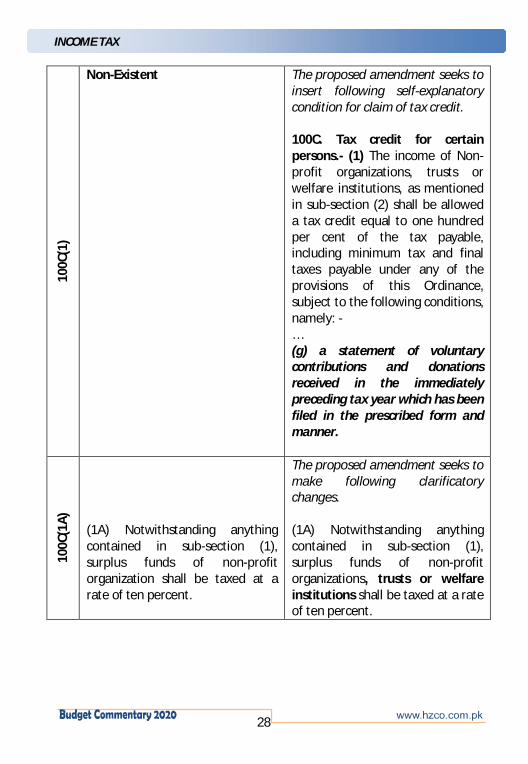

100C

(1)

Non-Existent The proposed amendment seeks to insert following self-explanatory condition for claim of tax credit. 100C. Tax credit for certain persons.- (1) The income of Non-profit organizations, trusts or welfare institutions, as mentioned in sub-section (2) shall be allowed a tax credit equal to one hundred per cent of the tax payable, including minimum tax and final taxes payable under any of the provisions of this Ordinance, subject to the following conditions, namely: - … (g) a statement of voluntary contributions and donations received in the immediately preceding tax year which has been filed in the prescribed form and manner.

100C

(1A)

(1A) Notwithstanding anything contained in sub-section (1), surplus funds of non-profit organization shall be taxed at a rate of ten percent.

The proposed amendment seeks to make following clarificatory changes. (1A) Notwithstanding anything contained in sub-section (1), surplus funds of non-profit organizations, trusts or welfare institutions shall be taxed at a rate of ten percent.

INCOME TAX

29

100C

(1B)

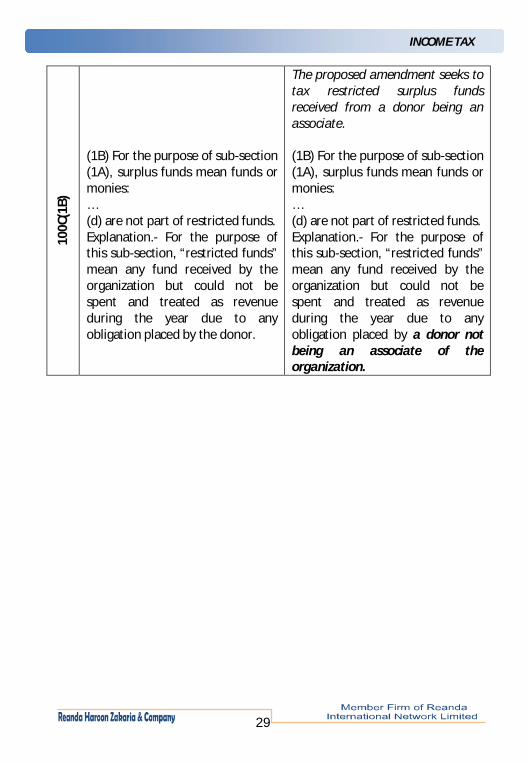

(1B) For the purpose of sub-section (1A), surplus funds mean funds or monies: … (d) are not part of restricted funds. Explanation.- For the purpose of this sub-section, “restricted funds” mean any fund received by the organization but could not be spent and treated as revenue during the year due to any obligation placed by the donor.

The proposed amendment seeks to tax restricted surplus funds received from a donor being an associate. (1B) For the purpose of sub-section (1A), surplus funds mean funds or monies: … (d) are not part of restricted funds. Explanation.- For the purpose of this sub-section, “restricted funds” mean any fund received by the organization but could not be spent and treated as revenue during the year due to any obligation placed by a donor not being an associate of the organization.

INCOME TAX

30

106A

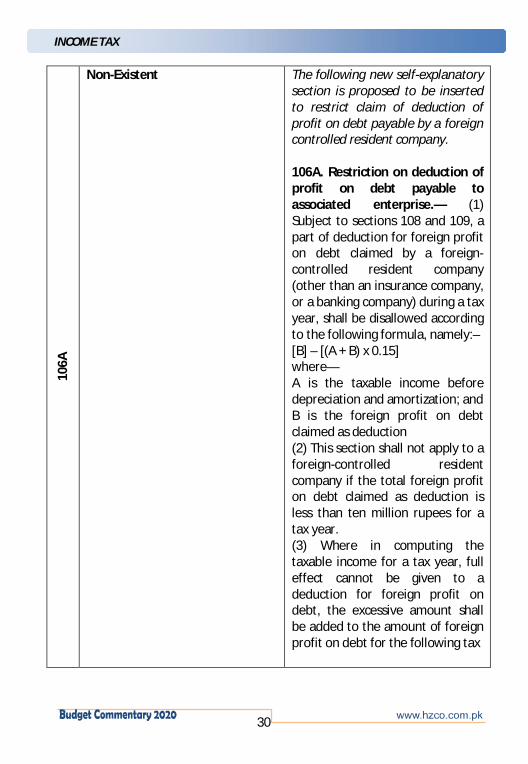

Non-Existent The following new self-explanatory

section is proposed to be inserted to restrict claim of deduction of profit on debt payable by a foreign controlled resident company. 106A. Restriction on deduction of profit on debt payable to associated enterprise.— (1) Subject to sections 108 and 109, a part of deduction for foreign profit on debt claimed by a foreign-controlled resident company (other than an insurance company, or a banking company) during a tax year, shall be disallowed according to the following formula, namely:– [B] – [(A + B) x 0.15] where— A is the taxable income before depreciation and amortization; and B is the foreign profit on debt claimed as deduction (2) This section shall not apply to a foreign-controlled resident company if the total foreign profit on debt claimed as deduction is less than ten million rupees for a tax year. (3) Where in computing the taxable income for a tax year, full effect cannot be given to a deduction for foreign profit on debt, the excessive amount shall be added to the amount of foreign profit on debt for the following tax

INCOME TAX

31

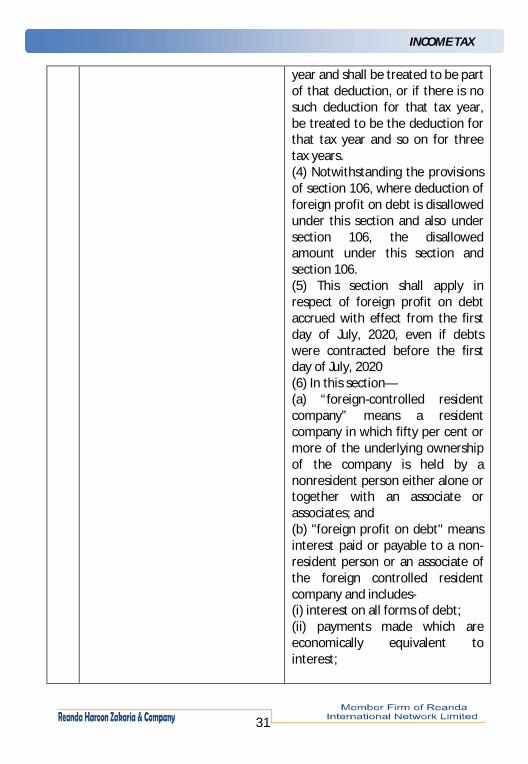

year and shall be treated to be part

of that deduction, or if there is no such deduction for that tax year, be treated to be the deduction for that tax year and so on for three tax years. (4) Notwithstanding the provisions of section 106, where deduction of foreign profit on debt is disallowed under this section and also under section 106, the disallowed amount under this section and section 106. (5) This section shall apply in respect of foreign profit on debt accrued with effect from the first day of July, 2020, even if debts were contracted before the first day of July, 2020 (6) In this section— (a) “foreign-controlled resident company” means a resident company in which fifty per cent or more of the underlying ownership of the company is held by a nonresident person either alone or together with an associate or associates; and (b) "foreign profit on debt" means interest paid or payable to a non-resident person or an associate of the foreign controlled resident company and includes- (i) interest on all forms of debt; (ii) payments made which are economically equivalent to interest;

INCOME TAX

32

(iii) expenses incurred in

connection with the raising of finance; (iv) payments under profit participating loans; (v)imputed interest on instruments such as convertible bonds and zero coupon bonds; (vi) amounts under alternative financing arrangements such as islamic finance; (vii) the finance cost element of finance lease payments; (viii) capitalized interest included in the balance sheet value of related asset, or the amortization of capitalised interest; (ix) amounts measured by reference to a funding return under transfer pricing rules; (x) where applicable, notional interest amounts under derivative instruments or hedging arrangements related to an entity's borrowings; (xi) certain foreign exchange gains and losses on borrowings and instruments connected with the raising of finance; (xii) guarantee fees with respect to financing arrangements; and (xiii) arrangement fee and similar cost related to the borrowing funds

INCOME TAX

33

107

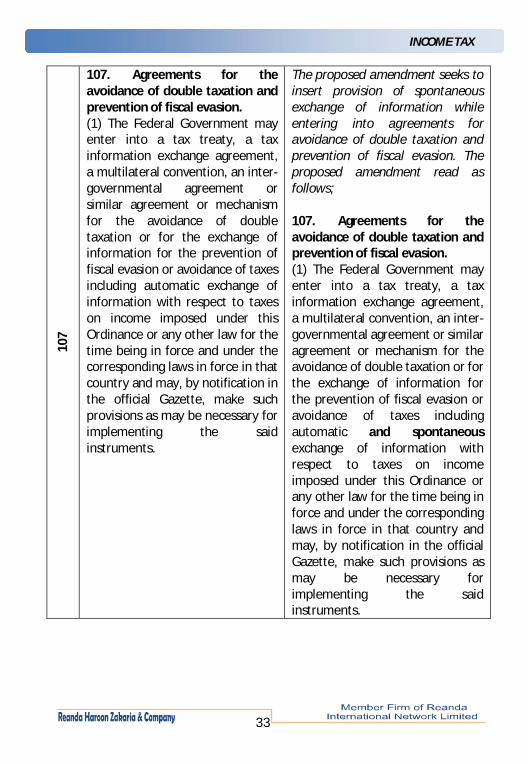

107. Agreements for the avoidance of double taxation and prevention of fiscal evasion. (1) The Federal Government may enter into a tax treaty, a tax information exchange agreement, a multilateral convention, an inter-governmental agreement or similar agreement or mechanism for the avoidance of double taxation or for the exchange of information for the prevention of fiscal evasion or avoidance of taxes including automatic exchange of information with respect to taxes on income imposed under this Ordinance or any other law for the time being in force and under the corresponding laws in force in that country and may, by notification in the official Gazette, make such provisions as may be necessary for implementing the said instruments.

The proposed amendment seeks to insert provision of spontaneous exchange of information while entering into agreements for avoidance of double taxation and prevention of fiscal evasion. The proposed amendment read as follows; 107. Agreements for the avoidance of double taxation and prevention of fiscal evasion. (1) The Federal Government may enter into a tax treaty, a tax information exchange agreement, a multilateral convention, an inter-governmental agreement or similar agreement or mechanism for the avoidance of double taxation or for the exchange of information for the prevention of fiscal evasion or avoidance of taxes including automatic and spontaneous exchange of information with respect to taxes on income imposed under this Ordinance or any other law for the time being in force and under the corresponding laws in force in that country and may, by notification in the official Gazette, make such provisions as may be necessary for implementing the said instruments.

INCOME TAX

34

111

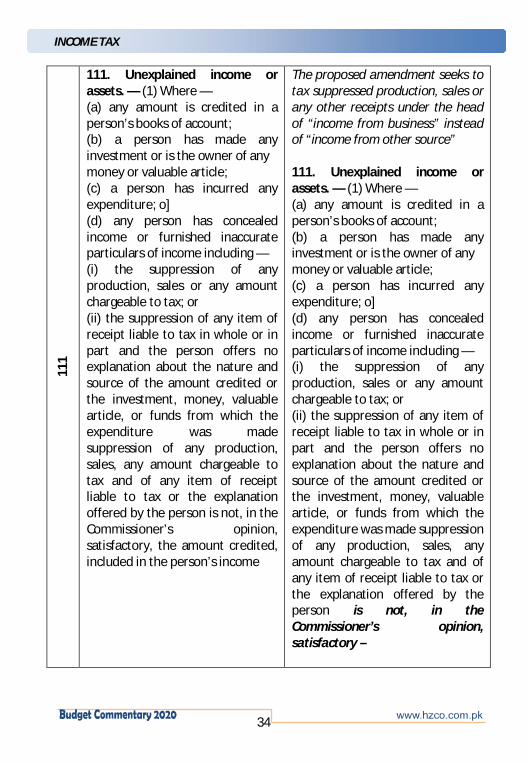

111. Unexplained income or assets. — (1) Where — (a) any amount is credited in a person’s books of account; (b) a person has made any investment or is the owner of any money or valuable article; (c) a person has incurred any expenditure; o] (d) any person has concealed income or furnished inaccurate particulars of income including — (i) the suppression of any production, sales or any amount chargeable to tax; or (ii) the suppression of any item of receipt liable to tax in whole or in part and the person offers no explanation about the nature and source of the amount credited or the investment, money, valuable article, or funds from which the expenditure was made suppression of any production, sales, any amount chargeable to tax and of any item of receipt liable to tax or the explanation offered by the person is not, in the Commissioner’s opinion, satisfactory, the amount credited, included in the person’s income

The proposed amendment seeks to tax suppressed production, sales or any other receipts under the head of “income from business” instead of “income from other source” 111. Unexplained income or assets. — (1) Where — (a) any amount is credited in a person’s books of account; (b) a person has made any investment or is the owner of any money or valuable article; (c) a person has incurred any expenditure; o] (d) any person has concealed income or furnished inaccurate particulars of income including — (i) the suppression of any production, sales or any amount chargeable to tax; or (ii) the suppression of any item of receipt liable to tax in whole or in part and the person offers no explanation about the nature and source of the amount credited or the investment, money, valuable article, or funds from which the expenditure was made suppression of any production, sales, any amount chargeable to tax and of any item of receipt liable to tax or the explanation offered by the person is not, in the Commissioner’s opinion, satisfactory –

INCOME TAX

35

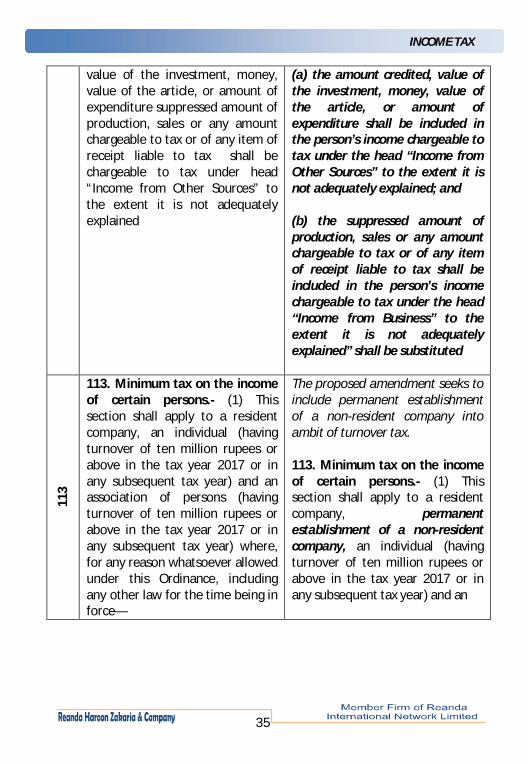

value of the investment, money, value of the article, or amount of expenditure suppressed amount of production, sales or any amount chargeable to tax or of any item of receipt liable to tax shall be chargeable to tax under head “Income from Other Sources” to the extent it is not adequately explained

(a) the amount credited, value of the investment, money, value of the article, or amount of expenditure shall be included in the person’s income chargeable to tax under the head “Income from Other Sources” to the extent it is not adequately explained; and (b) the suppressed amount of production, sales or any amount chargeable to tax or of any item of receipt liable to tax shall be included in the person’s income chargeable to tax under the head “Income from Business” to the extent it is not adequately explained” shall be substituted

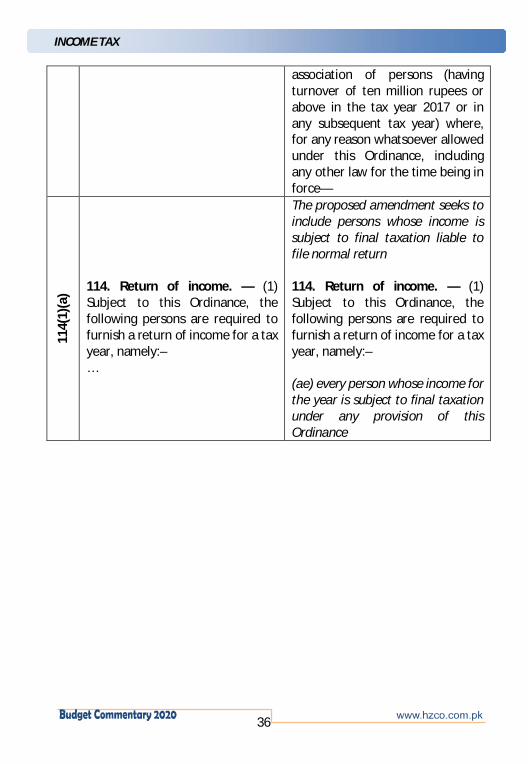

113

113. Minimum tax on the income of certain persons.- (1) This section shall apply to a resident company, an individual (having turnover of ten million rupees or above in the tax year 2017 or in any subsequent tax year) and an association of persons (having turnover of ten million rupees or above in the tax year 2017 or in any subsequent tax year) where, for any reason whatsoever allowed under this Ordinance, including any other law for the time being in force—

The proposed amendment seeks to include permanent establishment of a non-resident company into ambit of turnover tax. 113. Minimum tax on the income of certain persons.- (1) This section shall apply to a resident company, permanent establishment of a non-resident company, an individual (having turnover of ten million rupees or above in the tax year 2017 or in any subsequent tax year) and an

INCOME TAX

36

association of persons (having

turnover of ten million rupees or above in the tax year 2017 or in any subsequent tax year) where, for any reason whatsoever allowed under this Ordinance, including any other law for the time being in force—

114(

1)(a

)

114. Return of income. — (1) Subject to this Ordinance, the following persons are required to furnish a return of income for a tax year, namely:– …

The proposed amendment seeks to include persons whose income is subject to final taxation liable to file normal return 114. Return of income. — (1) Subject to this Ordinance, the following persons are required to furnish a return of income for a tax year, namely:– (ae) every person whose income for the year is subject to final taxation under any provision of this Ordinance

INCOME TAX

37

114(

1)(b

) 114. Return of income. — (1) Subject to this Ordinance, the following persons are required to furnish a return of income for a tax year, namely:– … (b) any person not covered by clause (a), (ab), (ac) or (ad) who,— … (x) every resident person being an individual required to file foreign income and assets statement under section 116A.

The proposed amendment seeks to make technical amendment as under: 114. Return of income. — (1) Subject to this Ordinance, the following persons are required to furnish a return of income for a tax year, namely:– … (b) any person not covered by clause (a), (ab), (ac) or (ad) who,— … (x) is a resident person being an individual required to file foreign income and assets statement under section 116A.

114(

2)

(2) A return of income - (a) shall be in the prescribed form and shall be accompanied by such annexures, statements or documents as may be prescribed

The proposed amendment seek to empower board to prescribe different return for difference classes of income or persons (2) A return of income - (a) shall be in the prescribed form and shall be accompanied by such annexures, statements or documents as may be prescribed Provided that the Board may prescribe different returns for different classes of income or persons including persons subject to final taxation

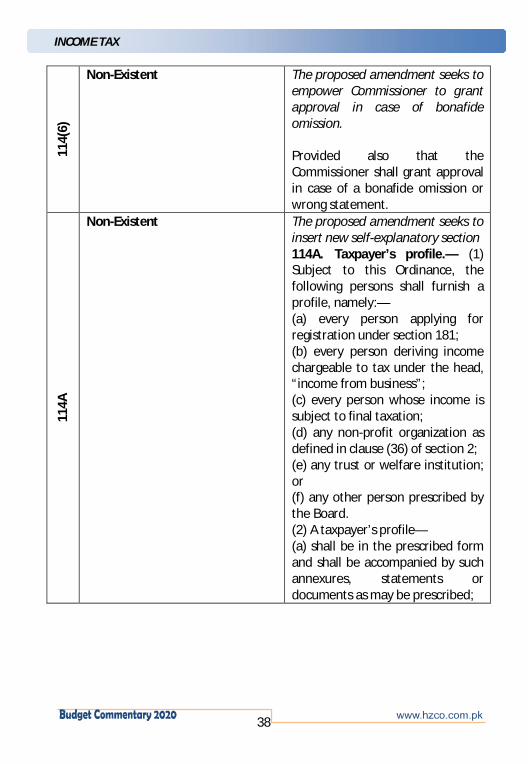

INCOME TAX

38

114(

6)

Non-Existent The proposed amendment seeks to empower Commissioner to grant approval in case of bonafide omission. Provided also that the Commissioner shall grant approval in case of a bonafide omission or wrong statement.

114A

Non-Existent The proposed amendment seeks to insert new self-explanatory section 114A. Taxpayer’s profile.— (1) Subject to this Ordinance, the following persons shall furnish a profile, namely:— (a) every person applying for registration under section 181; (b) every person deriving income chargeable to tax under the head, “income from business”; (c) every person whose income is subject to final taxation; (d) any non-profit organization as defined in clause (36) of section 2; (e) any trust or welfare institution; or (f) any other person prescribed by the Board. (2) A taxpayer’s profile— (a) shall be in the prescribed form and shall be accompanied by such annexures, statements or documents as may be prescribed;

INCOME TAX

39

(b) shall fully state, in the specified

form and manner, the relevant particulars of— (i) bank accounts; (ii) utility connections; (iii) business premises including all manufacturing, storage or retail outlets operated or leased by the taxpayer; (iv) types of businesses; and (v) such other information as may be prescribed; (c) shall be signed by the person being an individual, or the person’s representative where section 172 applies; and (d) shall be filed electronically on the web as prescribed by the Board (3) A taxpayer’s profile shall be furnished,— (a) on or before the 31st day of December, 2020 in case of a person registered under section 181 before the 30th day of September, 2020; and (b) within ninety days registration in case of a person not registered under section 181 before the 30th day of September, 2020 (4) A taxpayer’s profile shall be updated within ninety days of change in any of the relevant particulars of information as mentioned in clause (b) of subsection (2.)

INCOME TAX

40

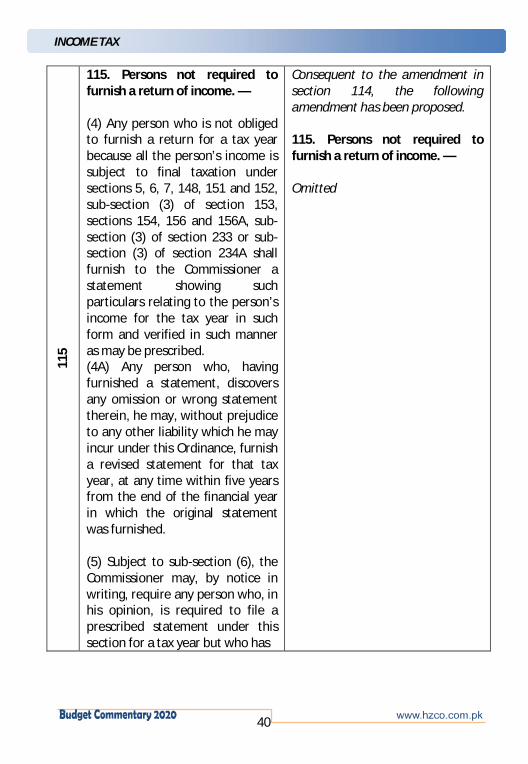

115

115. Persons not required to furnish a return of income. — (4) Any person who is not obliged to furnish a return for a tax year because all the person’s income is subject to final taxation under sections 5, 6, 7, 148, 151 and 152, sub-section (3) of section 153, sections 154, 156 and 156A, sub-section (3) of section 233 or sub-section (3) of section 234A shall furnish to the Commissioner a statement showing such particulars relating to the person’s income for the tax year in such form and verified in such manner as may be prescribed. (4A) Any person who, having furnished a statement, discovers any omission or wrong statement therein, he may, without prejudice to any other liability which he may incur under this Ordinance, furnish a revised statement for that tax year, at any time within five years from the end of the financial year in which the original statement was furnished. (5) Subject to sub-section (6), the Commissioner may, by notice in writing, require any person who, in his opinion, is required to file a prescribed statement under this section for a tax year but who has

Consequent to the amendment in section 114, the following amendment has been proposed. 115. Persons not required to furnish a return of income. — Omitted

INCOME TAX

41

failed to do so, to furnish a prescribed statement for that year within thirty days from the date of service of such notice or such longer period as may be specified in such notice or as he may, allow. (6) A notice under sub-section (5) may be issued in respect of one or more of the last five completed tax

11

6(3)

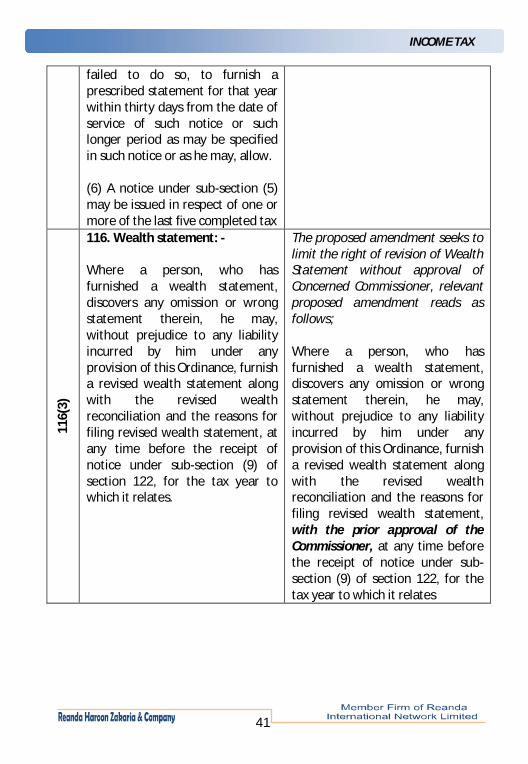

116. Wealth statement: - Where a person, who has furnished a wealth statement, discovers any omission or wrong statement therein, he may, without prejudice to any liability incurred by him under any provision of this Ordinance, furnish a revised wealth statement along with the revised wealth reconciliation and the reasons for filing revised wealth statement, at any time before the receipt of notice under sub-section (9) of section 122, for the tax year to which it relates.

The proposed amendment seeks to limit the right of revision of Wealth Statement without approval of Concerned Commissioner, relevant proposed amendment reads as follows; Where a person, who has furnished a wealth statement, discovers any omission or wrong statement therein, he may, without prejudice to any liability incurred by him under any provision of this Ordinance, furnish a revised wealth statement along with the revised wealth reconciliation and the reasons for filing revised wealth statement, with the prior approval of the Commissioner, at any time before the receipt of notice under sub-section (9) of section 122, for the tax year to which it relates

INCOME TAX

42

116(

3)

Non-Existent

Following new self-explanatory proviso has been added to section 116(3), which reads as follows; Provided that the Commissioner shall grant approval in case of a bonafide omission or wrong statement. Explanation.— For the removal of doubt it is clarified that wealth statement cannot be revised after the expiry of five years from the due date of filing of return of income for that tax year

116(

4)

Every person (other than a company or an association of persons) filing statement under sub-section (4) of section 115, falling under final tax regime (FTR) shall file a wealth statement along with reconciliation of wealth statement.

Consequent to the proposed amendment in section 114 and 115, following amendment has been proposed: Omitted

INCOME TAX

43

118

118. Method of furnishing returns and other documents. – (1) A return of income under section 114, a statement required under sub-section (4) of section 115, a wealth statement under section 116 or a foreign income and assets statement under 116A, if applicable shall be furnished in the prescribed manner.

Consequent to the proposed amendment in section 114 and 115, following amendment has been proposed: 118. Method of furnishing returns and other documents. – (1) A return of income under section 114, a wealth statement under section 116 or a foreign income and assets statement under 116A, if applicable shall be furnished in the prescribed manner.

119

119. Extension of time for furnishing returns and other documents.— (1) A person required to furnish — (a) a return of income under section 114 or 117; (c) a statement required under sub-section (4) of section 115; or (d) a wealth statement under section 116

Consequent to the proposed amendment in section 114 and 115, following amendment has been proposed: 119. Extension of time for furnishing returns and other documents.— (1) A person required to furnish — (a) a return of income under section 114 or 117; (c) Omitted (d) a wealth statement under section 116

INCOME TAX

44

120(

1)(a

) 120. Assessments.— (1) Where a taxpayer has furnished a complete return of income (other than a revised return under sub-section (6) of section 114) for a tax year ending on or after the 1st day of July, 2002,— (a) the Commissioner shall be taken to have made an assessment of taxable income for that tax year, and the tax due thereon, equal to those respective amounts specified in the return; and (b) the return shall be taken for all purposes of this Ordinance to be an assessment order issued to the taxpayer by the Commissioner on the day the return was furnished.

The proposed amendment seeks to provide for automatic process of return before issuance of deemed assessment order. 120. Assessments.— (1) Where a taxpayer has furnished a complete return of income (other than a revised return under sub-section (6) of section 114) for a tax year ending on or after the 1st day of July, 2002,— (a) the Commissioner shall be taken to have made an assessment of taxable income for that tax year, and the tax due thereon, equal to the respective amounts adjusted under sub-section (2A) and (b) the return shall be taken for all purposes of this Ordinance to be an assessment order issued to the taxpayer by the Commissioner on the day the adjustments were made under sub-section (2A).

INCOME TAX

45

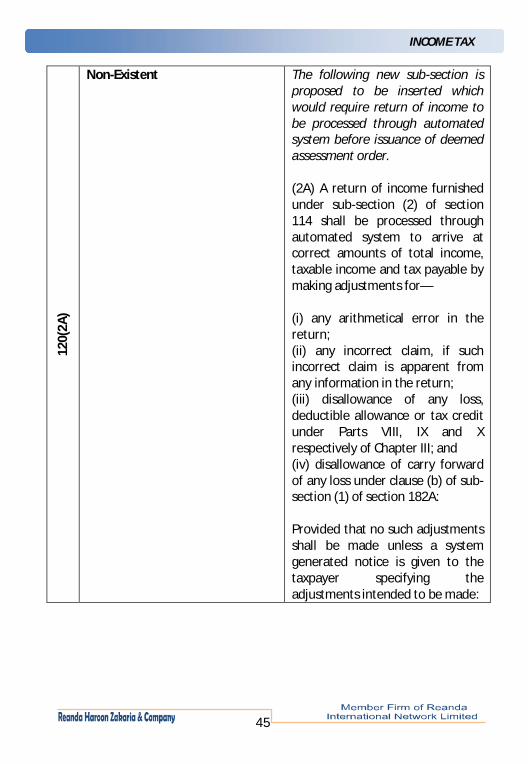

120(

2A)

Non-Existent The following new sub-section is proposed to be inserted which would require return of income to be processed through automated system before issuance of deemed assessment order. (2A) A return of income furnished under sub-section (2) of section 114 shall be processed through automated system to arrive at correct amounts of total income, taxable income and tax payable by making adjustments for— (i) any arithmetical error in the return; (ii) any incorrect claim, if such incorrect claim is apparent from any information in the return; (iii) disallowance of any loss, deductible allowance or tax credit under Parts VIII, IX and X respectively of Chapter III; and (iv) disallowance of carry forward of any loss under clause (b) of sub-section (1) of section 182A: Provided that no such adjustments shall be made unless a system generated notice is given to the taxpayer specifying the adjustments intended to be made:

INCOME TAX

46

120(

2A)

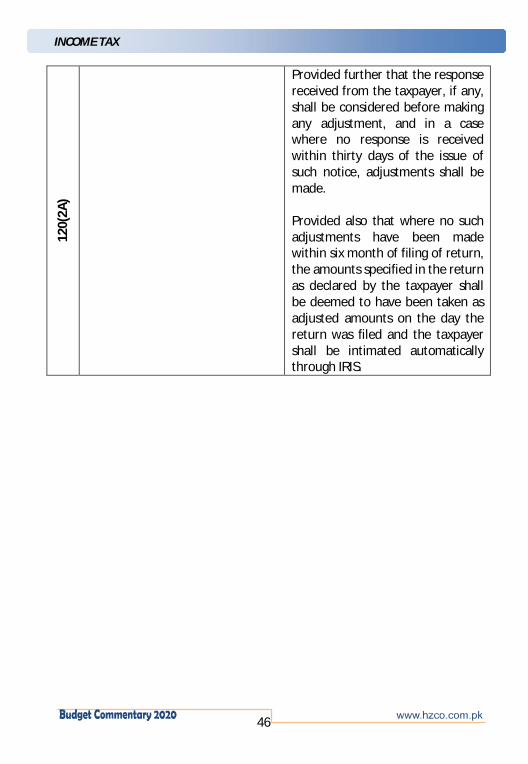

Provided further that the response received from the taxpayer, if any, shall be considered before making any adjustment, and in a case where no response is received within thirty days of the issue of such notice, adjustments shall be made. Provided also that where no such adjustments have been made within six month of filing of return, the amounts specified in the return as declared by the taxpayer shall be deemed to have been taken as adjusted amounts on the day the return was filed and the taxpayer shall be intimated automatically through IRIS.

INCOME TAX

47

120(

7)

Non-Existent The following new self-explanatory sub-section has been proposed to be inserted. (7) For the purposes of this section,— (a) “arithmetical error” includes any wrong or incorrect calculation of tax payable including any minimum or final tax payable. (b) "an incorrect claim apparent from any information in the return" shall mean a claim, on the basis of an entry, in the return,— (i) of an item, which is inconsistent with another entry of the same or some other item in such return; (ii) regarding any tax payment which is not verified from the collection system; or (iii) in respect of a deduction, where such deduction exceeds specified statutory limit which may have been expressed as monetary amount or percentage or ratio or fraction.

121

(1) Where a person fails to —] (aa) furnish a statement as required by a notice under sub-section (5) of section 115; or

Consequent to the proposed amendment in section 114 and 115, following amendment has been proposed: 121. Best judgement assessment.— (1) Where a person fails to —] (aa) omitted; or

INCOME TAX

48

122(

5)

(5) An assessment order in respect of tax year, or an assessment year, shall only be amended under sub-section (1) and an amended assessment for that year shall only be further amended under sub-section (4) where, on the basis of definite information acquired from an audit or otherwise, the Commissioner is satisfied that —

The proposed amendment seeks to provide following technical amendment. 122. Amendment of assessments.— (5) An assessment order in respect of tax year, or an assessment year, shall only be amended under sub-section (1) and an amended assessment for that year shall only be further amended under sub-section (4) where, on the basis of audit or on the basis of definite information, the Commissioner is satisfied that —

122D

Non-Existent The proposed self-explanatory section has been inserted which reads as under; “122D. Agreed assessment in certain cases.—(1) Where a taxpayer, in response to a notice under sub-section (9) of section 122, intends to settle his case, he may file offer of settlement in the prescribed form before the assessment oversight committee, hereinafter referred to as the Committee, in addition to filing reply to the Commissioner.

INCOME TAX

49

(2) The Committee after examining

the aforesaid offer may call for the record of the case and after affording opportunity of being heard to the taxpayer, may decide to accept or modify the offer of the taxpayer through consensus and communicate its decision to the taxpayer. (3) Where the taxpayer is satisfied with the decision of the Committee,— (a) the taxpayer shall deposit the amount of tax payable including any amount of penalty and default surcharge as per decision of the Committee; (b) the Commissioner shall amend assessment in accordance with the decision of the Committee after tax payable including any amount of penalty and default surcharge as per decision of the Committee has been paid; (c) the taxpayer shall waive the right to prefer appeal against such amended assessment; and (d) no further proceedings shall be undertaken under this Ordinance in respect of issues decided by the Committee unless the tax as per clause (c) has not been deposited by the taxpayer

INCOME TAX

50

(4) Where the Committee has not

been able to arrive at a consensus or where the taxpayer is not satisfied with the decision of the Committee, the case shall be referred back to the Commissioner for decision on the basis of reply of the taxpayer in response to notice under 81 sub-section (9) of section 122 notwithstanding proceedings or decision, if any, of the Committee. (5) The Committee shall comprise the following income tax authorities having jurisdiction over the taxpayer, namely:— (a) the Chief Commissioner Inland Revenue; (b) the Commissioner Inland Revenue; and (c) the Additional Commissioner Inland Revenue. (6) This section shall not apply in cases involving concealment of income or where interpretation of question of law is involved having effect on other cases. (7) The Board may make rules regulating the procedure of the Committee and for any matter connected with, or incidental to the proceedings of the Committee.

INCOME TAX

51

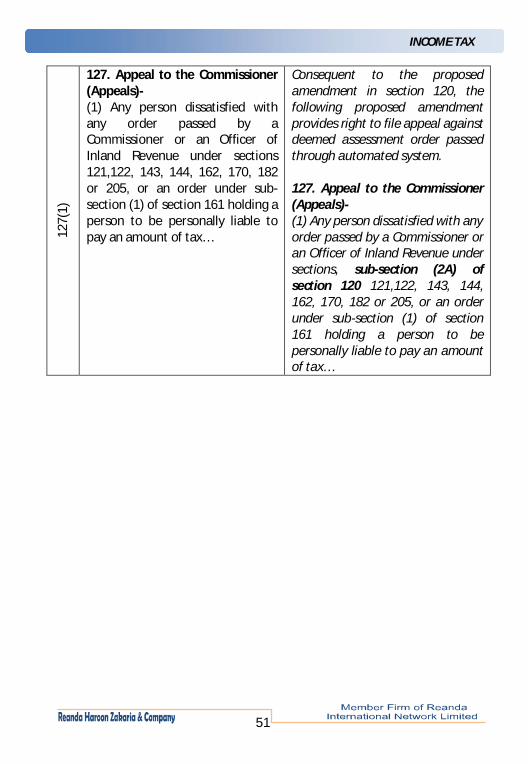

127(

1)

127. Appeal to the Commissioner (Appeals)- (1) Any person dissatisfied with any order passed by a Commissioner or an Officer of Inland Revenue under sections 121,122, 143, 144, 162, 170, 182 or 205, or an order under sub-section (1) of section 161 holding a person to be personally liable to pay an amount of tax…

Consequent to the proposed amendment in section 120, the following proposed amendment provides right to file appeal against deemed assessment order passed through automated system. 127. Appeal to the Commissioner (Appeals)- (1) Any person dissatisfied with any order passed by a Commissioner or an Officer of Inland Revenue under sections, sub-section (2A) of section 120 121,122, 143, 144, 162, 170, 182 or 205, or an order under sub-section (1) of section 161 holding a person to be personally liable to pay an amount of tax…

INCOME TAX

52

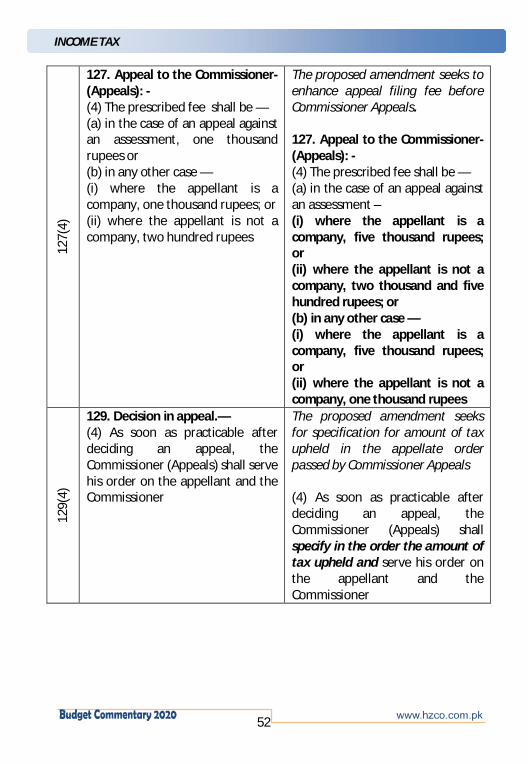

127(

4)

127. Appeal to the Commissioner-(Appeals): - (4) The prescribed fee shall be — (a) in the case of an appeal against an assessment, one thousand rupees or (b) in any other case — (i) where the appellant is a company, one thousand rupees; or (ii) where the appellant is not a company, two hundred rupees

The proposed amendment seeks to enhance appeal filing fee before Commissioner Appeals. 127. Appeal to the Commissioner-(Appeals): - (4) The prescribed fee shall be — (a) in the case of an appeal against an assessment – (i) where the appellant is a company, five thousand rupees; or (ii) where the appellant is not a company, two thousand and five hundred rupees; or (b) in any other case — (i) where the appellant is a company, five thousand rupees; or (ii) where the appellant is not a company, one thousand rupees

129(

4)

129. Decision in appeal.— (4) As soon as practicable after deciding an appeal, the Commissioner (Appeals) shall serve his order on the appellant and the Commissioner

The proposed amendment seeks for specification for amount of tax upheld in the appellate order passed by Commissioner Appeals (4) As soon as practicable after deciding an appeal, the Commissioner (Appeals) shall specify in the order the amount of tax upheld and serve his order on the appellant and the Commissioner

INCOME TAX

53

131(

2) &

(2A)

Non-Existent The following amendment is

proposed for mandatory payment of ten percent of demand upheld by the Commissioner Appeals for filing of appeal before Appellate Tribunal. In our opinion since the amendment is substantive in nature, therefore the same shall be applicable prospectively. (2) An appeal under sub-section (1) shall be–— … (e) accompanied by proof of payment of ten percent of the amount of tax upheld by the Commissioner (Appeals). (2A) No appeal under sub-section (1) shall be admitted by the Appellate Tribunal unless ten percent of the amount of tax upheld by the Commissioner (Appeals) has been deposited by the taxpayer

INCOME TAX

54

134

134A. Alternative Dispute Resolution.— (1) Notwithstanding any other provision of this Ordinance, or the rules made thereunder, an aggrieved person in connection with any dispute pertaining to— (a) the liability of tax against the aggrieved person, or admissibility of refunds, as the case may be; (b) the extent of waiver of default surcharge and penalty; or (c) any other specific relief required to resolve the dispute,

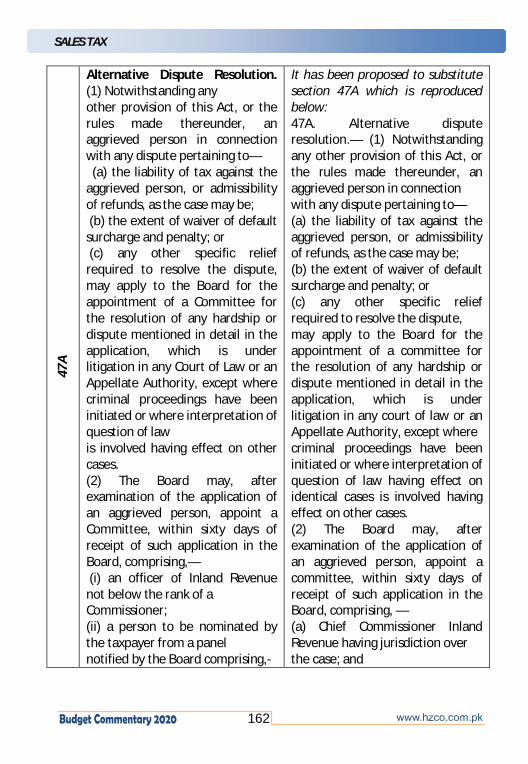

The proposed amendment seeks to amend the procedure of constitution and functionality of ADRC 134A. Alternative dispute resolution.— (1) Notwithstanding any other provision of this Ordinance, or the rules made thereunder, an aggrieved person in connection with any dispute pending before a court of law or an appellate authority pertaining to— (a) the liability of tax against the aggrieved person, or admissibility of refunds, as the case may be; (b) the extent of waiver of default surcharge and penalty; or (c) any other specific relief required to resolve the dispute,

INCOME TAX

55

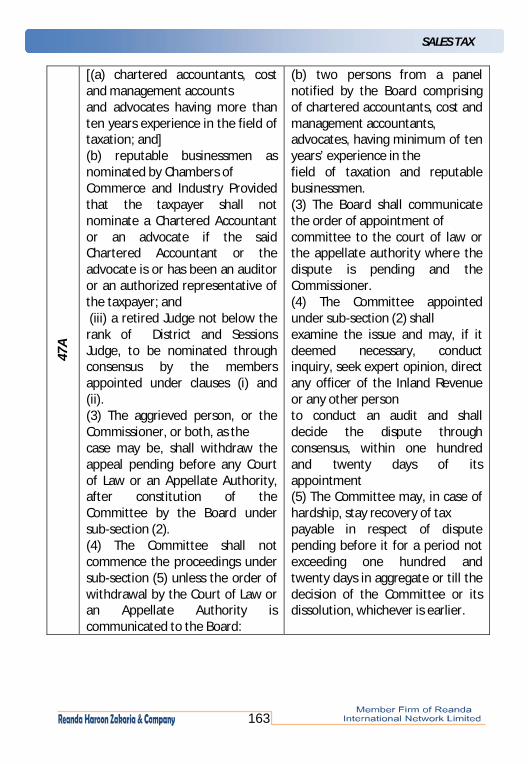

may apply to the Board for the appointment of a committee for the resolution of any hardship or dispute mentioned in detail in the application, which is under litigation in any court of law or an Appellate Authority, except where criminal proceedings have been initiated or where interpretation of question of law is involved having effect on other cases. (2) The Board may, after examination of the application of an aggrieved person, appoint a committee, within sixty days of receipt of such application in the Board, comprising,— (i) an officer of Inland Revenue not below the rank of a Commissioner (ii) person to be nominated by the taxpayer from a panel notified by the Board comprising,— (a) chartered accountants, cost and management accountants and advocates having minimum ten years experience in the field of taxation; and (b) reputable businessmen as nominated by Chambers of Commerce and industry: Provided that the taxpayer shall not nominate a Chartered Accountant or cost and management accountant or an advocate if the said Chartered Accountant or cost and management accountant or the

may apply to the Board for the appointment of a committee for the resolution of any hardship or dispute mentioned in detail in the application, which is under litigation in any court of law or an appellate authority, except where criminal proceedings have been initiated or where interpretation of question of law having effect on identical cases is involved having effect on other cases. (2) The Board may, after examination of the application of an aggrieved person, appoint a committee, within sixty days of receipt of such application in the Board, comprising,— (i) Chief Commissioner Inland Revenue having jurisdiction over the case; (ii) two persons from a panel notified by the Board comprising of chartered accountants, cost and management accountants, advocates, having minimum of ten years’ experience in the field of taxation and reputable businessmen. (3) The Board shall communicate the order of appointment of committee to the court of law or the appellate authority where the dispute is pending and the Commissioner.

INCOME TAX

56

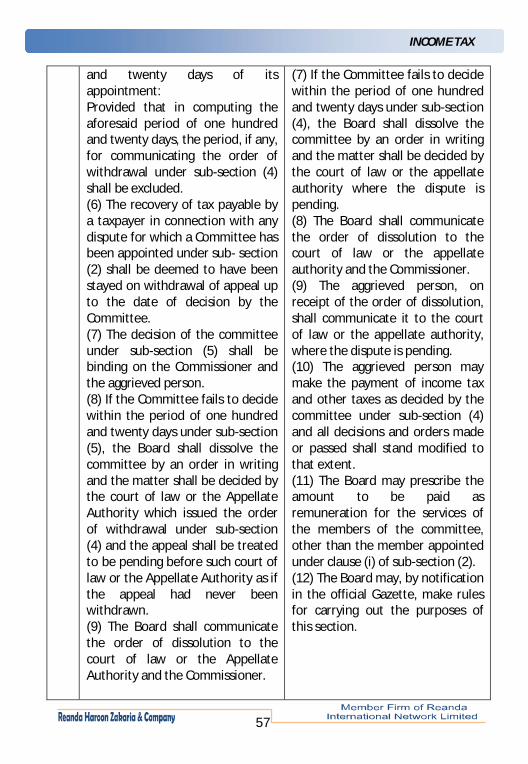

advocate is or has been an auditor or an authorized representative of the taxpayer; and (iii) a retired Judge not below the rank of District and Sessions Judge, to be nominated through consensus by the members appointed under clauses (i) and (ii). (3) The aggrieved person, or the Commissioner, or both, as the case may be, shall withdraw the appeal pending before any court of law or an Appellate Authority, after constitution of the committee by the Board under subsection (2). (4) The committee shall not commence the proceedings under sub-section (5) unless the order of withdrawal by the court of law or the Appellate Authority is communicated to the Board: Provided that if the order of withdrawal is not communicated within seventy five days of the appointment of the committee, the said committee shall be dissolved and provisions of this section shall not apply. (5) The Committee appointed under sub-section (2) shall examine the issue and may, if it deems necessary, conduct inquiry, seek expert opinion, direct any officer of the Inland Revenue or any other person to conduct an audit and shall decide the dispute by majority, within one hundred

(4) The Committee appointed under sub-section (2) shall examine the issue and may, if it deemed necessary, conduct inquiry, seek expert opinion, direct any officer of the Inland Revenue or any other person to conduct an audit and shall decide the dispute through consensus, within one hundred and twenty days of its appointment. (5) The Committee may, in case of hardship, stay recovery of tax payable in respect of dispute pending before it for a period not exceeding one hundred and twenty days in aggregate or till the decision of the committee or its dissolution, whichever is earlier. (6) The decision of the committee under sub-section (4) shall be binding on the Commissioner when the aggrieved person, being satisfied with the decision, has withdrawn the appeal pending before the court of law or any appellate authority and has communicated the order of withdrawal to the Commissioner: Provided that if the order of withdrawal is not communicated to the Commissioner within sixty days of the service of decision of the committee upon the aggrieved person, the decision of the committee shall not be binding on the Commissioner.

INCOME TAX

57

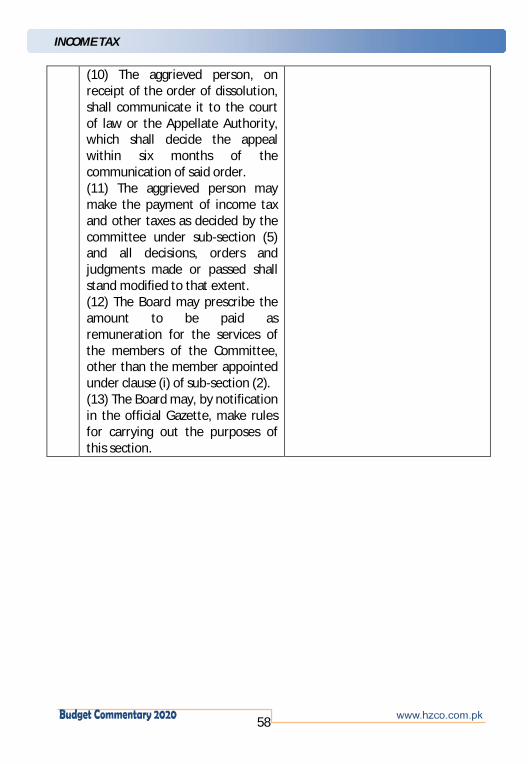

and twenty days of its appointment: Provided that in computing the aforesaid period of one hundred and twenty days, the period, if any, for communicating the order of withdrawal under sub-section (4) shall be excluded. (6) The recovery of tax payable by a taxpayer in connection with any dispute for which a Committee has been appointed under sub- section (2) shall be deemed to have been stayed on withdrawal of appeal up to the date of decision by the Committee. (7) The decision of the committee under sub-section (5) shall be binding on the Commissioner and the aggrieved person. (8) If the Committee fails to decide within the period of one hundred and twenty days under sub-section (5), the Board shall dissolve the committee by an order in writing and the matter shall be decided by the court of law or the Appellate Authority which issued the order of withdrawal under sub-section (4) and the appeal shall be treated to be pending before such court of law or the Appellate Authority as if the appeal had never been withdrawn. (9) The Board shall communicate the order of dissolution to the court of law or the Appellate Authority and the Commissioner.

(7) If the Committee fails to decide within the period of one hundred and twenty days under sub-section (4), the Board shall dissolve the committee by an order in writing and the matter shall be decided by the court of law or the appellate authority where the dispute is pending. (8) The Board shall communicate the order of dissolution to the court of law or the appellate authority and the Commissioner. (9) The aggrieved person, on receipt of the order of dissolution, shall communicate it to the court of law or the appellate authority, where the dispute is pending. (10) The aggrieved person may make the payment of income tax and other taxes as decided by the committee under sub-section (4) and all decisions and orders made or passed shall stand modified to that extent. (11) The Board may prescribe the amount to be paid as remuneration for the services of the members of the committee, other than the member appointed under clause (i) of sub-section (2). (12) The Board may, by notification in the official Gazette, make rules for carrying out the purposes of this section.

INCOME TAX

58

(10) The aggrieved person, on receipt of the order of dissolution, shall communicate it to the court of law or the Appellate Authority, which shall decide the appeal within six months of the communication of said order. (11) The aggrieved person may make the payment of income tax and other taxes as decided by the committee under sub-section (5) and all decisions, orders and judgments made or passed shall stand modified to that extent. (12) The Board may prescribe the amount to be paid as remuneration for the services of the members of the Committee, other than the member appointed under clause (i) of sub-section (2). (13) The Board may, by notification in the official Gazette, make rules for carrying out the purposes of this section.

INCOME TAX

59

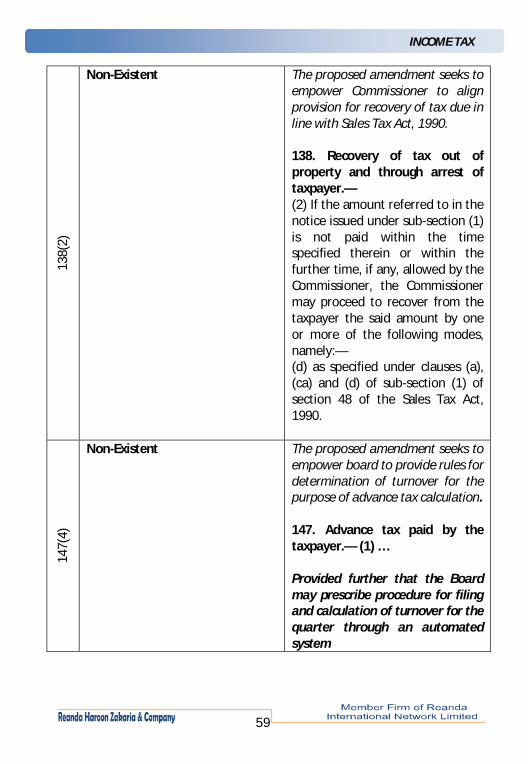

138(

2)

Non-Existent

The proposed amendment seeks to empower Commissioner to align provision for recovery of tax due in line with Sales Tax Act, 1990. 138. Recovery of tax out of property and through arrest of taxpayer.— (2) If the amount referred to in the notice issued under sub-section (1) is not paid within the time specified therein or within the further time, if any, allowed by the Commissioner, the Commissioner may proceed to recover from the taxpayer the said amount by one or more of the following modes, namely:— (d) as specified under clauses (a), (ca) and (d) of sub-section (1) of section 48 of the Sales Tax Act, 1990.

147(

4)

Non-Existent The proposed amendment seeks to empower board to provide rules for determination of turnover for the purpose of advance tax calculation. 147. Advance tax paid by the taxpayer.— (1) … Provided further that the Board may prescribe procedure for filing and calculation of turnover for the quarter through an automated system

INCOME TAX

60

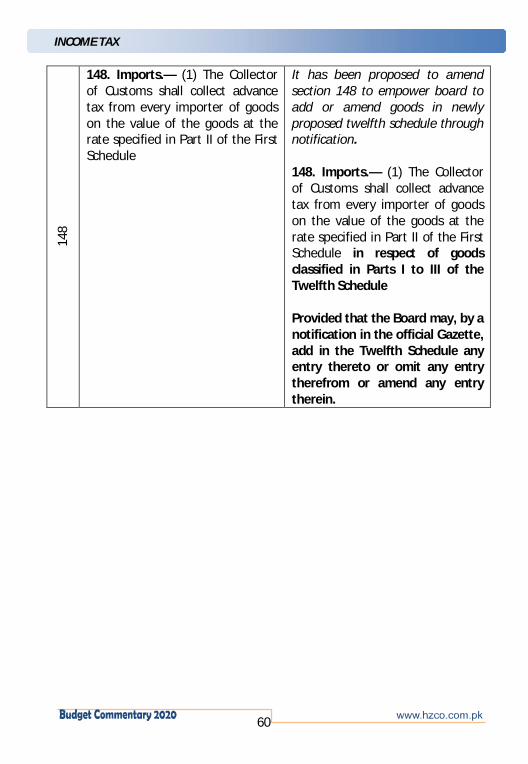

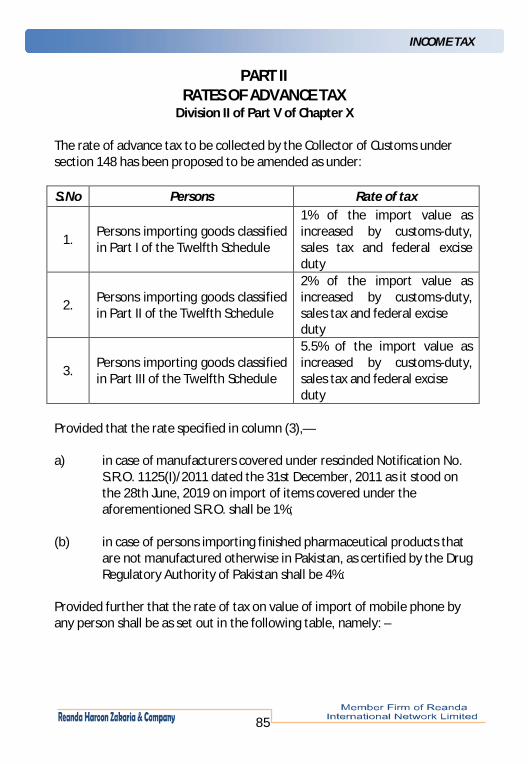

148

148. Imports.— (1) The Collector of Customs shall collect advance tax from every importer of goods on the value of the goods at the rate specified in Part II of the First Schedule

It has been proposed to amend section 148 to empower board to add or amend goods in newly proposed twelfth schedule through notification. 148. Imports.— (1) The Collector of Customs shall collect advance tax from every importer of goods on the value of the goods at the rate specified in Part II of the First Schedule in respect of goods classified in Parts I to III of the Twelfth Schedule Provided that the Board may, by a notification in the official Gazette, add in the Twelfth Schedule any entry thereto or omit any entry therefrom or amend any entry therein.

INCOME TAX

61

148(

7)

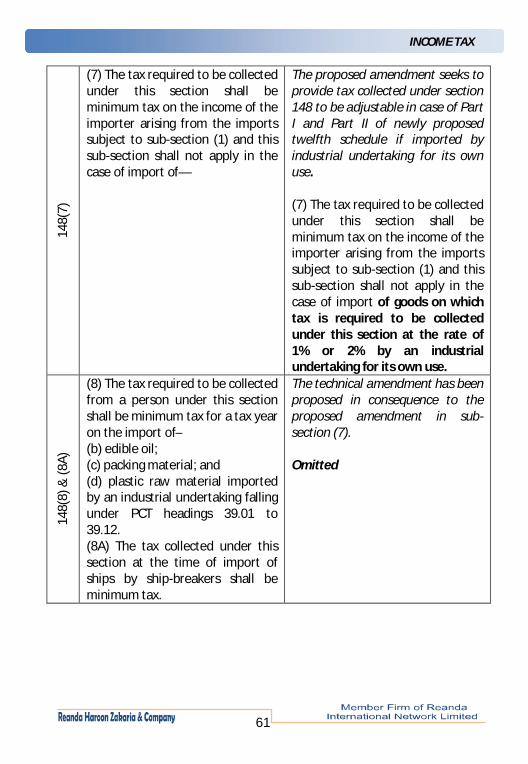

(7) The tax required to be collected under this section shall be minimum tax on the income of the importer arising from the imports subject to sub-section (1) and this sub-section shall not apply in the case of import of—

The proposed amendment seeks to provide tax collected under section 148 to be adjustable in case of Part I and Part II of newly proposed twelfth schedule if imported by industrial undertaking for its own use. (7) The tax required to be collected under this section shall be minimum tax on the income of the importer arising from the imports subject to sub-section (1) and this sub-section shall not apply in the case of import of goods on which tax is required to be collected under this section at the rate of 1% or 2% by an industrial undertaking for its own use.

148(

8) &

(8A)

(8) The tax required to be collected from a person under this section shall be minimum tax for a tax year on the import of─ (b) edible oil; (c) packing material; and (d) plastic raw material imported by an industrial undertaking falling under PCT headings 39.01 to 39.12. (8A) The tax collected under this section at the time of import of ships by ship-breakers shall be minimum tax.

The technical amendment has been proposed in consequence to the proposed amendment in sub-section (7). Omitted

INCOME TAX

62

148(

9)

“value of goods” means the value of the goods as determined under the Customs Act, 1969 (IV of 1969), as if the goods were subject to ad valorem duty increased by the customs-duty, federal excise duty and sales tax, if any, payable in respect of the import of the goods.

The amendment has been proposed to include retail price in value of goods in respect of third schedule goods enabling to collect advance tax on import stage at retail price. Value of goods means— (a) in case of goods chargeable to tax at retail price under the Third Schedule of the Sales Tax Act, 1990, the retail price of such goods increased by sales tax payable in respect of the import and taxable supply of the goods; and (b) in case of all other goods; the value of the goods as determined under the Custom Act, 1969 (IV of 1969), as if the goods were subject to ad valorem duty increased by the custom-duty, federal excise duty and sales tax, if any, payable in respect of the import of the goods.

148A

148A. Tax on local purchase of cooking oil or vegetable ghee by certain persons.—

The proposed amendment seek to abolish fixed taxation regime for manufacturer of edible oil from locally produced oil. Omitted

INCOME TAX

63

152(

1BBB

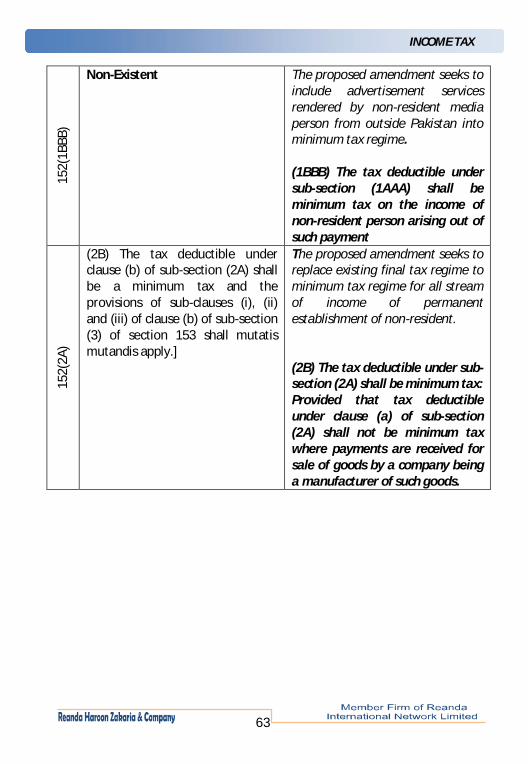

) Non-Existent The proposed amendment seeks to

include advertisement services rendered by non-resident media person from outside Pakistan into minimum tax regime. (1BBB) The tax deductible under sub-section (1AAA) shall be minimum tax on the income of non-resident person arising out of such payment

152(

2A)

(2B) The tax deductible under clause (b) of sub-section (2A) shall be a minimum tax and the provisions of sub-clauses (i), (ii) and (iii) of clause (b) of sub-section (3) of section 153 shall mutatis mutandis apply.]

The proposed amendment seeks to replace existing final tax regime to minimum tax regime for all stream of income of permanent establishment of non-resident. (2B) The tax deductible under sub-section (2A) shall be minimum tax: Provided that tax deductible under clause (a) of sub-section (2A) shall not be minimum tax where payments are received for sale of goods by a company being a manufacturer of such goods.

INCOME TAX

64

152(

4A)

(4A) The Commissioner may, on application made by the recipient of payment referred to in sub-section (1A) having permanent establishment in Pakistan, or by a recipient of payment referred to in sub-section (2A), as the case may be, and after making such inquiry as the Commissioner thinks fit, allow by order in writing, in cases where the tax deductible under sub-section (1) or sub-section (2A) is not minimum tax, any person to make the payment without deduction of tax or deduction of tax at a reduced rate.

The proposed amendment seeks to empower board to prescribe rules for exemption application under section 152. (4A) The Commissioner may, on application made in the prescribed form by the recipient of payment referred to in sub-section (1A) having permanent establishment in Pakistan, or by a recipient of payment referred to in sub-section (2A), as the case may be, and after making such inquiry as the Commissioner thinks fit, allow by order in writing, in cases where the tax deductible under sub-section (1) or sub-section (2A) is not minimum tax, any person to make the payment without deduction of tax or deduction of tax at a reduced rate.

INCOME TAX

65

152(

4B)

(4B) The Commissioner may, in case of payment that constitutes part of an overall arrangement of a cohesive business operation as referred to in paragraph (ii) of sub-clause (g) of clause (41) of section 2, on application made by the person making payment and after making such inquiry, as the Commissioner thinks fit, allow by order in writing, the person to make payment after deduction of tax equal to thirty percent of the tax chargeable on such payment under sub-section (1A)

The proposed amendment seeks to reduce rate of deduction of tax in case of payment made under arrangement of cohesive business operations (4B) The Commissioner may, in case of payment that constitutes part of an overall arrangement of a cohesive business operation as referred to in paragraph (ii) of sub-clause (g) of clause (41) of section 2, on application made by the person making payment and after making such inquiry, as the Commissioner thinks fit, allow by order in writing, the person to make payment after deduction of tax equal to twenty percent of the tax chargeable on such payment under sub-section (1A)

INCOME TAX

66

152(

5)