Fundamental Analysis & Analysts Recommendations - Global Agribusiness Sector

1

Colombian Agribusiness

Sector

2011

2

CONTENT

1. INTRODUCTION ................................................................................................................................... 3

2. TRENDS AND FEATURES OF THE COLOMBIAN AGROBUSINESS SECTOR ................................ 4

3. COLOMBIA: AN OPPORTUNITY FOR INVESTING IN THE AGROINDUSTRIAL SECTOR .............. 5

4. SECTOR INCENTIVES ....................................................................................................................... 11

5. PRODUCTIVE TRANSFORMATION PROGRAM FOR FOUR AGROINDUSTRIAL SECTORS ....... 15

6. PROEXPORT SERVICES ................................................................................................................... 15

7. ENTITIES OF INTEREST .................................................................................................................... 15

3

1. INTRODUCTION

Agriculture and livestock have historically been one of the major engines of Colombian economic

development. The sector accounts for 9% of the GDP, 21% of exports, and 19% of all jobs and boasts

enormous, sustainable potential in terms of competitive and comparative advantages. The Colombian

agriculture and livestock sector is an attractive global destination for foreign direct investment.

Through the public-private Productive Transformation Program, the Colombian government is working to

drive development and transform 8 industrial sectors and 4 agriculture and livestock sectors (beef;

chocolate, candy making and related raw materials; palm, oils and fats; and shrimp farming) to make them

players on the global scale.

Below are a few of the characteristics that make Colombia an intriguing country for agriculture and

livestock development.

Agriculture and Livestock: A Great Opportunity for Investment

Wide range of agriculture and livestock options thanks to Colombia's geographic position and characteristics, and the availability of its resources.

In the last 4 years, Colombian agricultural production has increased by more than 2.5 million tons, while meat (pork, beef and poultry) production has increased by more than 500,000 tons.

Colombia is one of the top regional and world players in the refined sugar market as Latin

America's second and the world's seventh largest exporter.

World Class AgribusinessSectors: Beef; Chocolate, Candy Making, and Related Raw

Materials; Palm, Oils and Fats; and Shrimp Farming

Colombia has the fourth largest herd of cattle in Latin America, with a 26.9 million head inventory in 2008. The Colombian Brahman, an ideal breed for producing meat in tropical conditions, has the highest genetic quality in the world.

According to the International Cocoa Organization, the flavor and aroma of Colombian cocoa are classified as "fine," a category that describes only 5% of the world's beans.

The cocoa yield rate is among the highest of the major Latin American producers (0.55 ton/ha). Colombia also has the highest productivity of sugar per hectare in the world (4.6 ton/ha/year).

Colombia's 1,700 kilometer (1,000 foot) long Caribbean coast provides shrimp farming opportunities that do not harm ecosystems such as mangrove swamps or inlets.

The CENIACUA is one of the most advanced shrimp industry research centers in the world and has positioned Colombia as leader in shrimp genetics.

4

2. TRENDS AND FEATURES OF THE COLOMBIAN AGRIBUSINESS SECTOR Agriculture and Livestock: Major Players in the Colombian Economy Agriculture and livestock represent 9% of the GDP and their foreign sales represent 21% of all exports. The sector provides 19% of jobs nationally and 66% of jobs in rural areas. Of the 10 major non-traditional exports, 7 are from the agriculture and livestock sector. Between 2004 and 2009, the sector's real annual GDP growth rate was 2.3%, reaching 3.9% in 2006 and 2007. This behavior can be attributed not only to an increase in external agricultural sales (from USD $3 billion in 2004 to USD $6 billion in 2009), but also to an expanded internal market. Colombia has a wide range of agriculture and livestock options thanks to the country's geographic position and characteristics. As a tropical, equatorial country, Colombia receives constant sunlight throughout the year. Colombia's different elevations also produce a wide variety of climates, from snow-capped peaks to the extensive Orinoquía savannas in the eastern plains and the Caribbean coast to the north. In the last 4 years, Colombian agricultural production has increased by more than 2.5 million tons, while meat (pork, beef and poultry) production has increased by more than 500,000 tons. Growth has taken place for both traditional export products (i.e. bananas) and new ones (palm, fruits, vegetables). Growth in domestic demand has also led to production growth for plantain, potatoes, fruits, vegetables and poultry, proof of the development potential within Colombia. Consequently, Colombia has varied and growing agricultural and livestock production. Of Colombia's agricultural production during 2009 (26 million tons), 66% was from permanent crops (17.1 million tons) while the remaining 34% (8.9 million tons) were temporary crops. Sugar cane was the permanent crop with the highest production (23.4% or 4 million tons), followed by fruits (22%, 3.7 million tons) and plantain (19%, 3.2 million tons). Among temporary crops, rice had had the highest production (29% or 2.6 million tons), followed by potatoes (28%, 2.5 million tons) and vegetables (18%, 1.6 million tons). Between 2005 and 2009, permanent crops grew by 8% while temporary crops grew by 16%. In recent years, Colombia has gone through a production shift from short-cycle products (temporary crops) toward long-cycle agricultural activities (permanent crops). Trade markets opened up during the nineties. Greater external supply provided short-cycle products such as grains, which created more internal space for expanding crops such as palm oil, cocoa, plantain and fruit.

5

3. COLOMBIA: AN OPPORTUNITY FOR INVESTING IN THE AGRIBUSINESS SECTOR

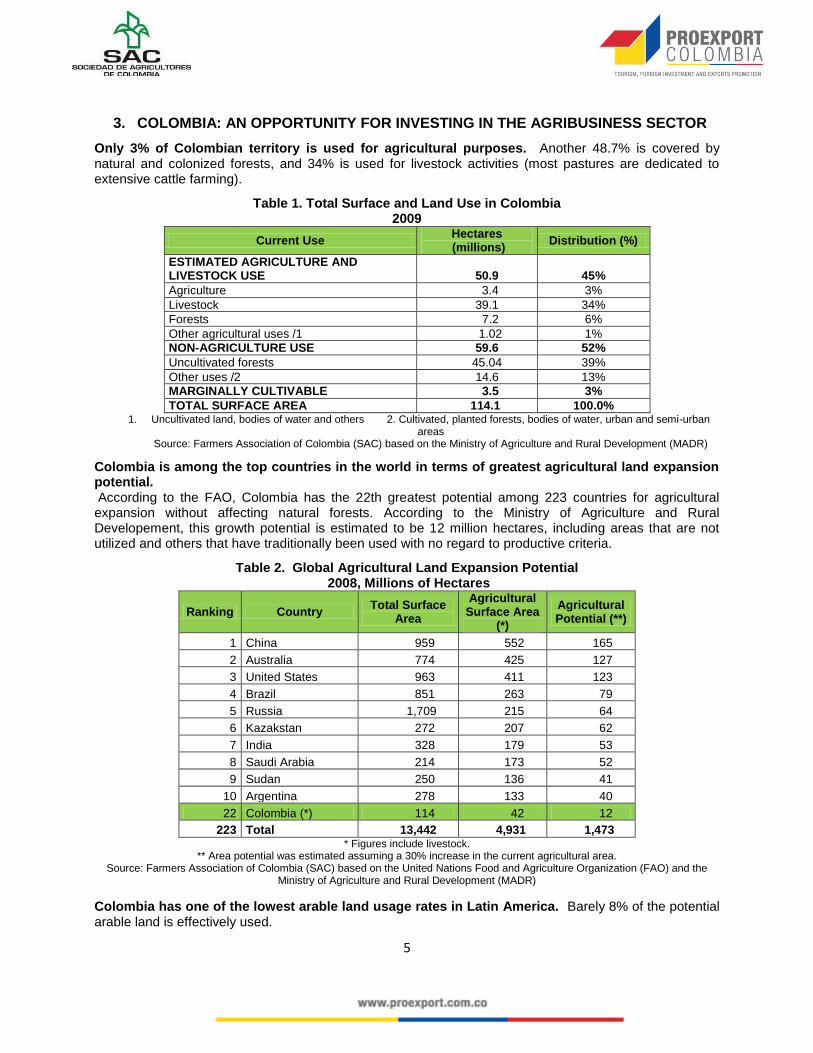

Only 3% of Colombian territory is used for agricultural purposes. Another 48.7% is covered by natural and colonized forests, and 34% is used for livestock activities (most pastures are dedicated to extensive cattle farming).

Table 1. Total Surface and Land Use in Colombia 2009

Current Use Hectares (millions)

Distribution (%)

ESTIMATED AGRICULTURE AND LIVESTOCK USE 50.9 45%

Agriculture 3.4 3%

Livestock 39.1 34%

Forests 7.2 6%

Other agricultural uses /1 1.02 1%

NON-AGRICULTURE USE 59.6 52%

Uncultivated forests 45.04 39%

Other uses /2 14.6 13%

MARGINALLY CULTIVABLE 3.5 3%

TOTAL SURFACE AREA 114.1 100.0% 1. Uncultivated land, bodies of water and others 2. Cultivated, planted forests, bodies of water, urban and semi-urban

areas Source: Farmers Association of Colombia (SAC) based on the Ministry of Agriculture and Rural Development (MADR)

Colombia is among the top countries in the world in terms of greatest agricultural land expansion potential. According to the FAO, Colombia has the 22th greatest potential among 223 countries for agricultural expansion without affecting natural forests. According to the Ministry of Agriculture and Rural Developement, this growth potential is estimated to be 12 million hectares, including areas that are not utilized and others that have traditionally been used with no regard to productive criteria.

Table 2. Global Agricultural Land Expansion Potential 2008, Millions of Hectares

Ranking Country Total Surface

Area

Agricultural Surface Area

(*)

Agricultural Potential (**)

1 China 959 552 165

2 Australia 774 425 127

3 United States 963 411 123

4 Brazil 851 263 79

5 Russia 1,709 215 64

6 Kazakstan 272 207 62

7 India 328 179 53

8 Saudi Arabia 214 173 52

9 Sudan 250 136 41

10 Argentina 278 133 40

22 Colombia (*) 114 42 12

223 Total 13,442 4,931 1,473 * Figures include livestock.

** Area potential was estimated assuming a 30% increase in the current agricultural area. Source: Farmers Association of Colombia (SAC) based on the United Nations Food and Agriculture Organization (FAO) and the

Ministry of Agriculture and Rural Development (MADR)

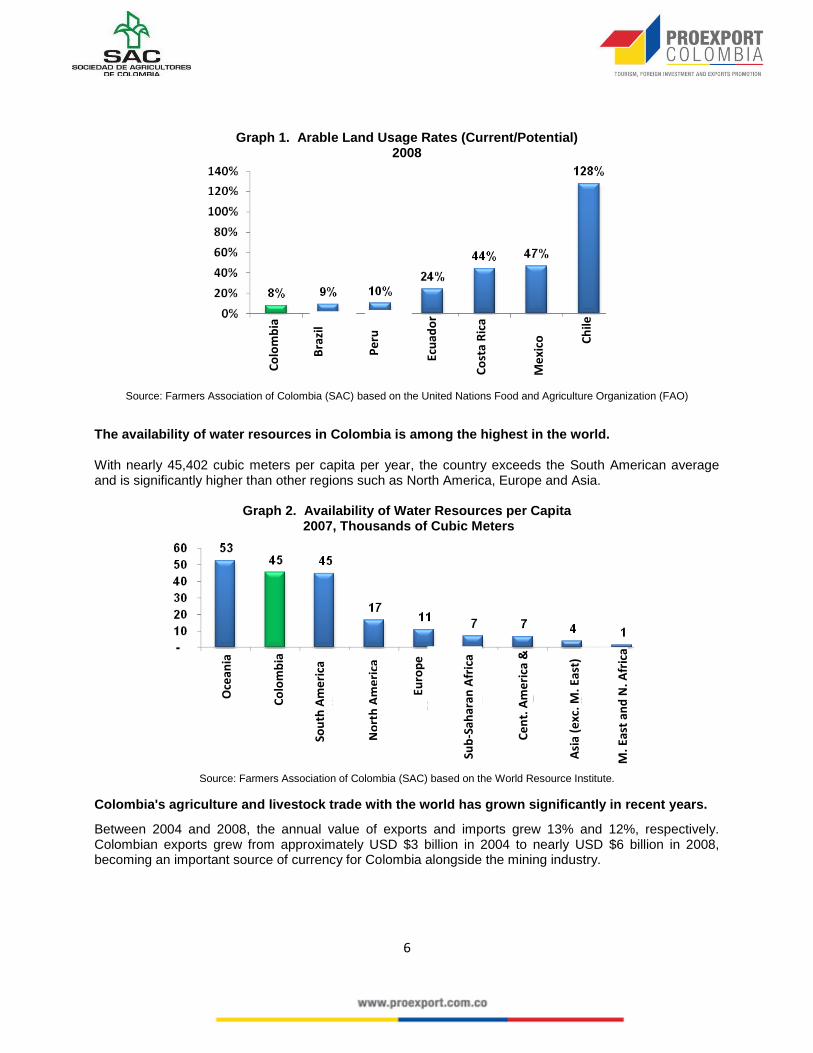

Colombia has one of the lowest arable land usage rates in Latin America. Barely 8% of the potential arable land is effectively used.

6

Graph 1. Arable Land Usage Rates (Current/Potential)

2008

Source: Farmers Association of Colombia (SAC) based on the United Nations Food and Agriculture Organization (FAO)

The availability of water resources in Colombia is among the highest in the world. With nearly 45,402 cubic meters per capita per year, the country exceeds the South American average and is significantly higher than other regions such as North America, Europe and Asia.

Graph 2. Availability of Water Resources per Capita

2007, Thousands of Cubic Meters

Source: Farmers Association of Colombia (SAC) based on the World Resource Institute.

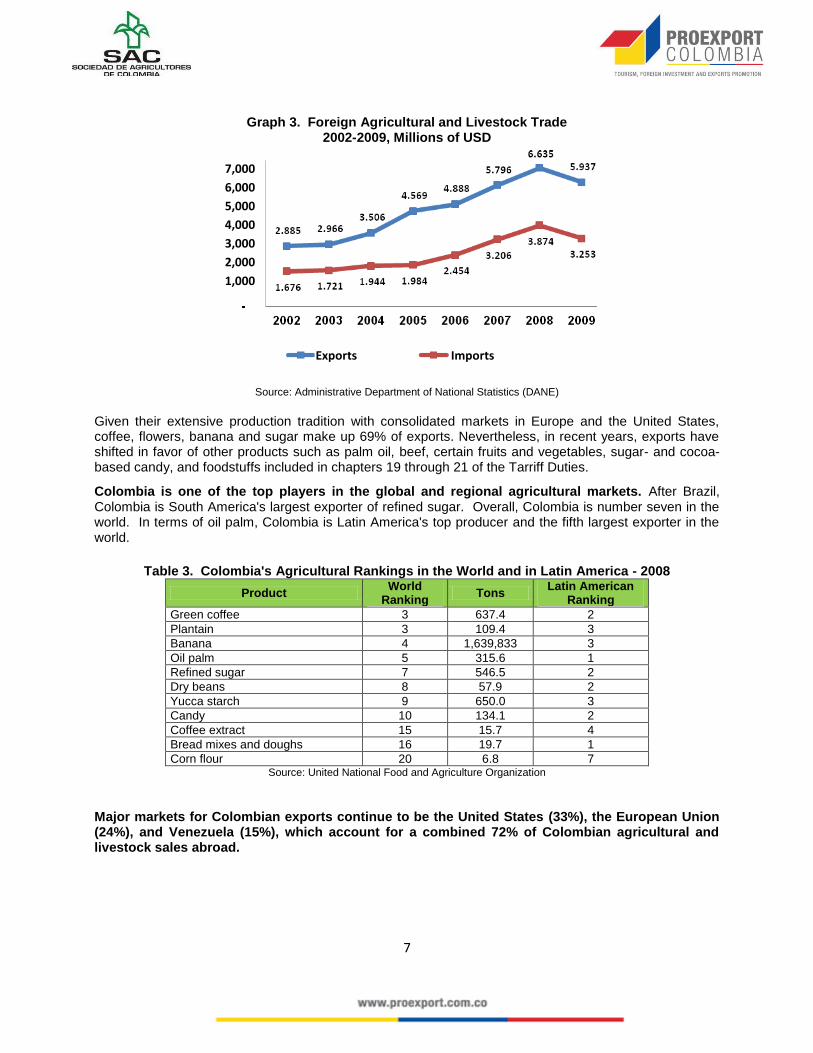

Colombia's agriculture and livestock trade with the world has grown significantly in recent years.

Between 2004 and 2008, the annual value of exports and imports grew 13% and 12%, respectively. Colombian exports grew from approximately USD $3 billion in 2004 to nearly USD $6 billion in 2008, becoming an important source of currency for Colombia alongside the mining industry.

Bra

zil

Pe

ru

Me

xico

Sou

th A

me

rica

No

rth

Am

eri

ca

Euro

pe

Sub

-Sah

aran

Afr

ica

Ce

nt.

Am

eri

ca &

Car

. A

sia

(exc

. M. E

ast)

M

. Eas

t an

d N

. Afr

ica

Co

lom

bia

Oce

ania

Ch

ile

Co

sta

Ric

a

Ecu

ado

r

Co

lom

bia

7

Graph 3. Foreign Agricultural and Livestock Trade 2002-2009, Millions of USD

Source: Administrative Department of National Statistics (DANE)

Given their extensive production tradition with consolidated markets in Europe and the United States, coffee, flowers, banana and sugar make up 69% of exports. Nevertheless, in recent years, exports have shifted in favor of other products such as palm oil, beef, certain fruits and vegetables, sugar- and cocoa-based candy, and foodstuffs included in chapters 19 through 21 of the Tarriff Duties.

Colombia is one of the top players in the global and regional agricultural markets. After Brazil, Colombia is South America's largest exporter of refined sugar. Overall, Colombia is number seven in the world. In terms of oil palm, Colombia is Latin America's top producer and the fifth largest exporter in the world.

Table 3. Colombia's Agricultural Rankings in the World and in Latin America - 2008

Product World

Ranking Tons

Latin American Ranking

Green coffee 3 637.4 2

Plantain 3 109.4 3

Banana 4 1,639,833 3

Oil palm 5 315.6 1

Refined sugar 7 546.5 2

Dry beans 8 57.9 2

Yucca starch 9 650.0 3

Candy 10 134.1 2

Coffee extract 15 15.7 4

Bread mixes and doughs 16 19.7 1

Corn flour 20 6.8 7 Source: United National Food and Agriculture Organization

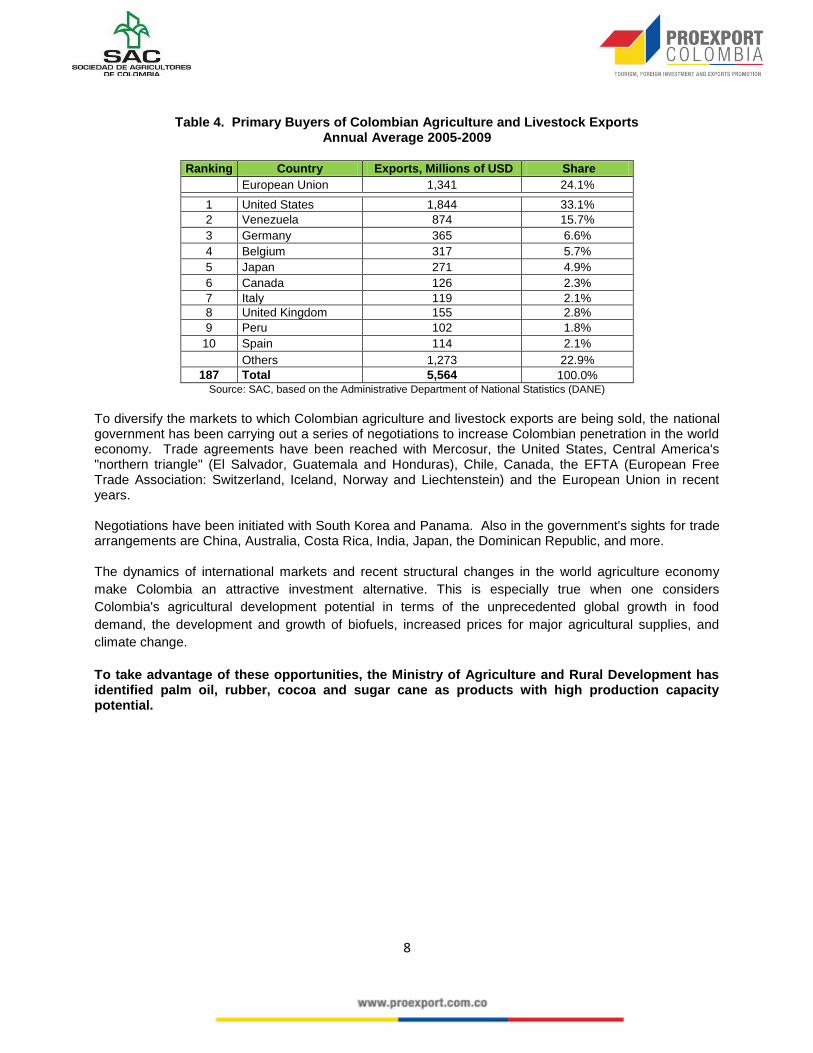

Major markets for Colombian exports continue to be the United States (33%), the European Union (24%), and Venezuela (15%), which account for a combined 72% of Colombian agricultural and livestock sales abroad.

Exports Imports

7,000

6,000

5,000

4,000

3,000

2,000

1,000

8

Table 4. Primary Buyers of Colombian Agriculture and Livestock Exports Annual Average 2005-2009

Ranking Country Exports, Millions of USD Share

European Union 1,341 24.1%

1 United States 1,844 33.1%

2 Venezuela 874 15.7%

3 Germany 365 6.6%

4 Belgium 317 5.7%

5 Japan 271 4.9%

6 Canada 126 2.3%

7 Italy 119 2.1%

8 United Kingdom 155 2.8%

9 Peru 102 1.8%

10 Spain 114 2.1%

Others 1,273 22.9%

187 Total 5,564 100.0% Source: SAC, based on the Administrative Department of National Statistics (DANE)

To diversify the markets to which Colombian agriculture and livestock exports are being sold, the national government has been carrying out a series of negotiations to increase Colombian penetration in the world economy. Trade agreements have been reached with Mercosur, the United States, Central America's "northern triangle" (El Salvador, Guatemala and Honduras), Chile, Canada, the EFTA (European Free Trade Association: Switzerland, Iceland, Norway and Liechtenstein) and the European Union in recent years. Negotiations have been initiated with South Korea and Panama. Also in the government's sights for trade arrangements are China, Australia, Costa Rica, India, Japan, the Dominican Republic, and more. The dynamics of international markets and recent structural changes in the world agriculture economy

make Colombia an attractive investment alternative. This is especially true when one considers

Colombia's agricultural development potential in terms of the unprecedented global growth in food

demand, the development and growth of biofuels, increased prices for major agricultural supplies, and

climate change.

To take advantage of these opportunities, the Ministry of Agriculture and Rural Development has identified palm oil, rubber, cocoa and sugar cane as products with high production capacity potential.

9

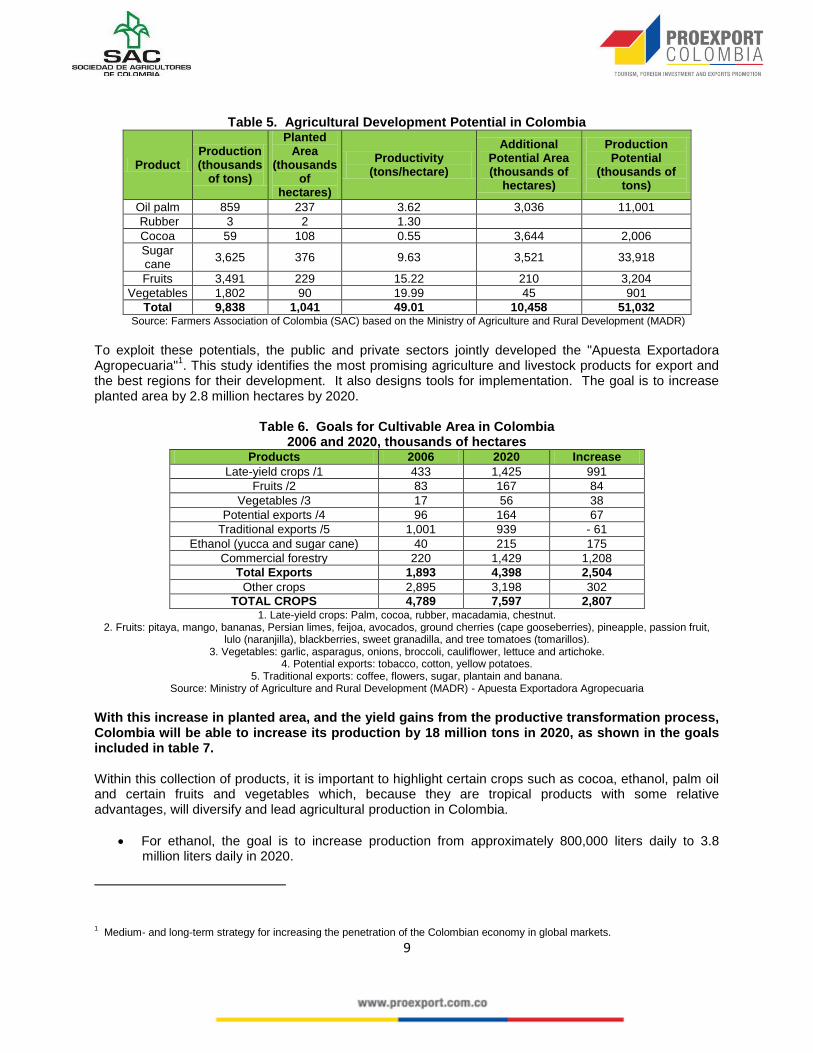

Table 5. Agricultural Development Potential in Colombia

Product Production (thousands

of tons)

Planted Area

(thousands of

hectares)

Productivity (tons/hectare)

Additional Potential Area (thousands of

hectares)

Production Potential

(thousands of tons)

Oil palm 859 237 3.62 3,036 11,001

Rubber 3 2 1.30

Cocoa 59 108 0.55 3,644 2,006

Sugar cane

3,625 376 9.63 3,521 33,918

Fruits 3,491 229 15.22 210 3,204

Vegetables 1,802 90 19.99 45 901

Total 9,838 1,041 49.01 10,458 51,032 Source: Farmers Association of Colombia (SAC) based on the Ministry of Agriculture and Rural Development (MADR)

To exploit these potentials, the public and private sectors jointly developed the "Apuesta Exportadora Agropecuaria"

1. This study identifies the most promising agriculture and livestock products for export and

the best regions for their development. It also designs tools for implementation. The goal is to increase planted area by 2.8 million hectares by 2020.

Table 6. Goals for Cultivable Area in Colombia 2006 and 2020, thousands of hectares

Products 2006 2020 Increase

Late-yield crops /1 433 1,425 991

Fruits /2 83 167 84

Vegetables /3 17 56 38

Potential exports /4 96 164 67

Traditional exports /5 1,001 939 - 61

Ethanol (yucca and sugar cane) 40 215 175

Commercial forestry 220 1,429 1,208

Total Exports 1,893 4,398 2,504

Other crops 2,895 3,198 302

TOTAL CROPS 4,789 7,597 2,807 1. Late-yield crops: Palm, cocoa, rubber, macadamia, chestnut.

2. Fruits: pitaya, mango, bananas, Persian limes, feijoa, avocados, ground cherries (cape gooseberries), pineapple, passion fruit, lulo (naranjilla), blackberries, sweet granadilla, and tree tomatoes (tomarillos).

3. Vegetables: garlic, asparagus, onions, broccoli, cauliflower, lettuce and artichoke. 4. Potential exports: tobacco, cotton, yellow potatoes.

5. Traditional exports: coffee, flowers, sugar, plantain and banana. Source: Ministry of Agriculture and Rural Development (MADR) - Apuesta Exportadora Agropecuaria

With this increase in planted area, and the yield gains from the productive transformation process, Colombia will be able to increase its production by 18 million tons in 2020, as shown in the goals included in table 7. Within this collection of products, it is important to highlight certain crops such as cocoa, ethanol, palm oil and certain fruits and vegetables which, because they are tropical products with some relative advantages, will diversify and lead agricultural production in Colombia.

For ethanol, the goal is to increase production from approximately 800,000 liters daily to 3.8 million liters daily in 2020.

1 Medium- and long-term strategy for increasing the penetration of the Colombian economy in global markets.

10

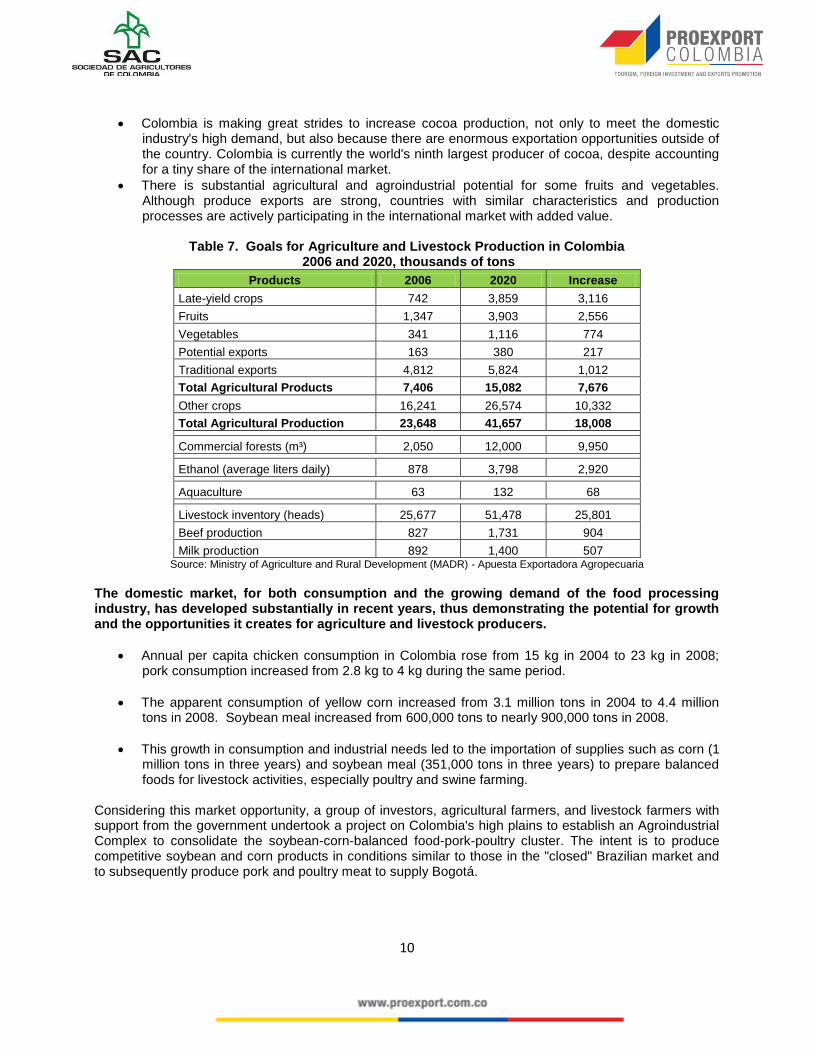

Colombia is making great strides to increase cocoa production, not only to meet the domestic industry's high demand, but also because there are enormous exportation opportunities outside of the country. Colombia is currently the world's ninth largest producer of cocoa, despite accounting for a tiny share of the international market.

There is substantial agricultural and agroindustrial potential for some fruits and vegetables. Although produce exports are strong, countries with similar characteristics and production processes are actively participating in the international market with added value.

Table 7. Goals for Agriculture and Livestock Production in Colombia 2006 and 2020, thousands of tons

Products 2006 2020 Increase

Late-yield crops 742 3,859 3,116

Fruits 1,347 3,903 2,556

Vegetables 341 1,116 774

Potential exports 163 380 217

Traditional exports 4,812 5,824 1,012

Total Agricultural Products 7,406 15,082 7,676

Other crops 16,241 26,574 10,332

Total Agricultural Production 23,648 41,657 18,008

Commercial forests (m³) 2,050 12,000 9,950

Ethanol (average liters daily) 878 3,798 2,920

Aquaculture 63 132 68

Livestock inventory (heads) 25,677 51,478 25,801

Beef production 827 1,731 904

Milk production 892 1,400 507 Source: Ministry of Agriculture and Rural Development (MADR) - Apuesta Exportadora Agropecuaria

The domestic market, for both consumption and the growing demand of the food processing industry, has developed substantially in recent years, thus demonstrating the potential for growth and the opportunities it creates for agriculture and livestock producers.

Annual per capita chicken consumption in Colombia rose from 15 kg in 2004 to 23 kg in 2008; pork consumption increased from 2.8 kg to 4 kg during the same period.

The apparent consumption of yellow corn increased from 3.1 million tons in 2004 to 4.4 million tons in 2008. Soybean meal increased from 600,000 tons to nearly 900,000 tons in 2008.

This growth in consumption and industrial needs led to the importation of supplies such as corn (1 million tons in three years) and soybean meal (351,000 tons in three years) to prepare balanced foods for livestock activities, especially poultry and swine farming.

Considering this market opportunity, a group of investors, agricultural farmers, and livestock farmers with support from the government undertook a project on Colombia's high plains to establish an Agroindustrial Complex to consolidate the soybean-corn-balanced food-pork-poultry cluster. The intent is to produce competitive soybean and corn products in conditions similar to those in the "closed" Brazilian market and to subsequently produce pork and poultry meat to supply Bogotá.

11

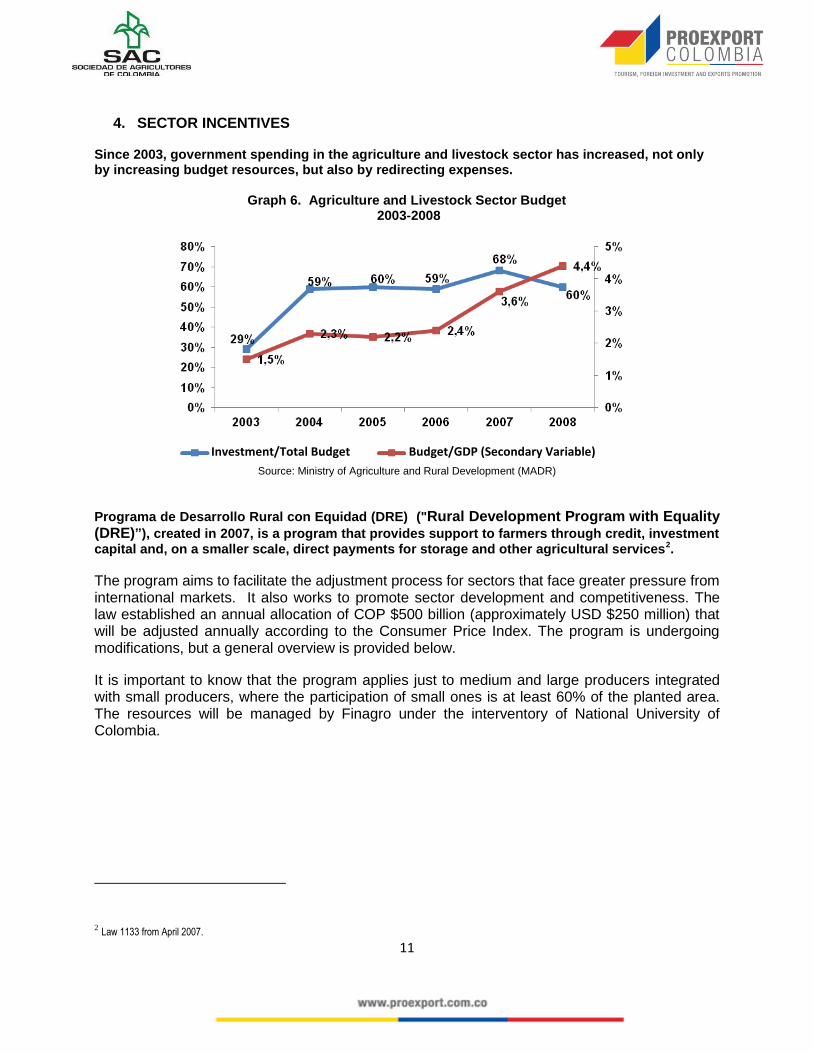

4. SECTOR INCENTIVES Since 2003, government spending in the agriculture and livestock sector has increased, not only by increasing budget resources, but also by redirecting expenses.

Graph 6. Agriculture and Livestock Sector Budget 2003-2008

Source: Ministry of Agriculture and Rural Development (MADR)

Programa de Desarrollo Rural con Equidad (DRE) ("Rural Development Program with Equality (DRE)”), created in 2007, is a program that provides support to farmers through credit, investment capital and, on a smaller scale, direct payments for storage and other agricultural services2.

The program aims to facilitate the adjustment process for sectors that face greater pressure from international markets. It also works to promote sector development and competitiveness. The law established an annual allocation of COP $500 billion (approximately USD $250 million) that will be adjusted annually according to the Consumer Price Index. The program is undergoing modifications, but a general overview is provided below.

It is important to know that the program applies just to medium and large producers integrated with small producers, where the participation of small ones is at least 60% of the planted area. The resources will be managed by Finagro under the interventory of National University of Colombia.

2 Law 1133 from April 2007.

Investment/Total Budget Budget/GDP (Secondary Variable)

12

Table 8. Components of the Programa de Desarrollo Rural con Equidad

Program Components Objective Conditions

Special line of credit – General

Soft loans for adapting land, purchasing machinery and equipment,

improving production infrastructure, or adding value to products

Granted through a commercial bank at the market introductory rate, minus 200

basis points

Incentive for rural capital development –

General

Support for new investments in infrastructure and land and new agricultural equipment and machinery to improve competitiveness

20% or 40% of the investment is recognized, depending on whether it is

a large-medium or small producer

Public call for proposals for irrigation and

draining

Cofinancing water capture, water conduction, intrafield distribution,

adaptation, and field drainage projects

Up to 70% of the investment costs are recognized

Technical assistance incentive (IAT)

Granted to producers whose total assets are less than 1,765 SMMLV* (approximately USD

$522,000)

Up to 80% of the total technical assistance contracting costs are

subsidized SMMLV: minimum monthly legal salary. In 2011, the SMMLV was COP $535,600, approximately USD $267.

Source: Ministry of Agriculture and Rural Development (MADR)

For legal purposes, Colombian producers are classified as small, medium, and large, depending on their assets. Natural or legal persons with assets valued between 108 and 145 monthly minimum salaries (COP $57,9 million and COP$ 77,6 million approximately US$32,000 and US$ 43,000) are considered small producers.

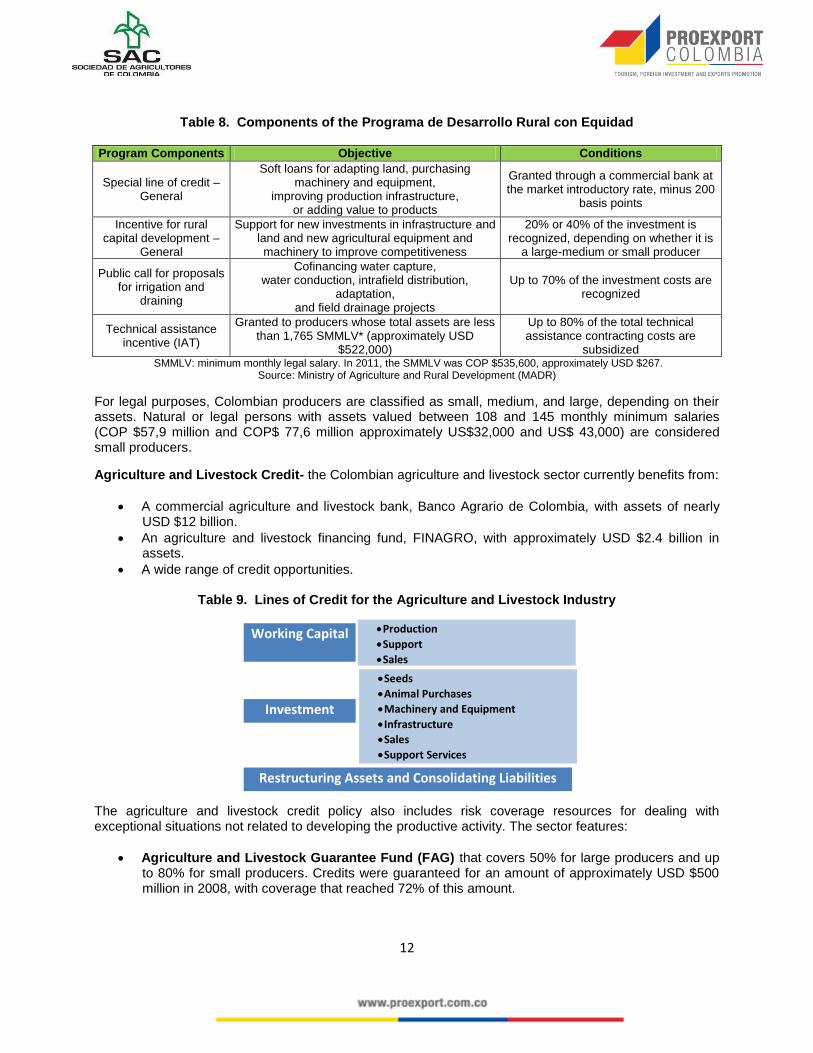

Agriculture and Livestock Credit- the Colombian agriculture and livestock sector currently benefits from:

A commercial agriculture and livestock bank, Banco Agrario de Colombia, with assets of nearly USD $12 billion.

An agriculture and livestock financing fund, FINAGRO, with approximately USD $2.4 billion in assets.

A wide range of credit opportunities.

Table 9. Lines of Credit for the Agriculture and Livestock Industry

Source: FINAGRO

The agriculture and livestock credit policy also includes risk coverage resources for dealing with exceptional situations not related to developing the productive activity. The sector features:

Agriculture and Livestock Guarantee Fund (FAG) that covers 50% for large producers and up to 80% for small producers. Credits were guaranteed for an amount of approximately USD $500 million in 2008, with coverage that reached 72% of this amount.

Working Capital

Investment

Restructuring Assets and Consolidating Liabilities

Production

Support

Sales

Seeds

Animal Purchases

Machinery and Equipment

Infrastructure

Sales

Support Services

13

Coverage Program for Sectors that Export and for Sectors that Compete with Imports:

- In income. USD $1.3 million in 2008 as an incentive for corn, soybean and sorghum producers to acquire protection for exchange rates or drops in international prices.

- For exchange rates. Geared toward exported products to offset the exchange rate risk. 450 beneficiary producers with incentives that reached USD $31 million to cover USD $560 million in external sales.

Agriculture and Livestock Insurance: Product investments are protected from climactic risks such as rain, freezing, strong winds, floods, mudslides, drought, etc. The national government grants a subsidy between 30% and 60% of the value of the premium that producers acquire through the Colombian insurance system. In 2008, nearly 6,000 policies were issued for an insured valued of approximately USD $102 million, which meant that nearly USD $4 million in subsidies were distributed.

Some agriculture and livestock trade policy instruments have been developed such as the Andean Pricing System

3 to counteract the high volatility of some products' prices on the international

market. Other agriculture and livestock trade policy instruments include:

Public Administration Mechanism for Agriculture and Livestock Contingencies, MAC. Guarantees that Colombian products such as beans, soybeans, yellow corn, white corn, and others will be absorbed by the market.

Tariff contingencies for specific products.

Special agriculture and livestock safeguards for various agreements.

Safety guidelines. Standards within the OMC parameters (strengthening the safety system for plants, fruits, meat).

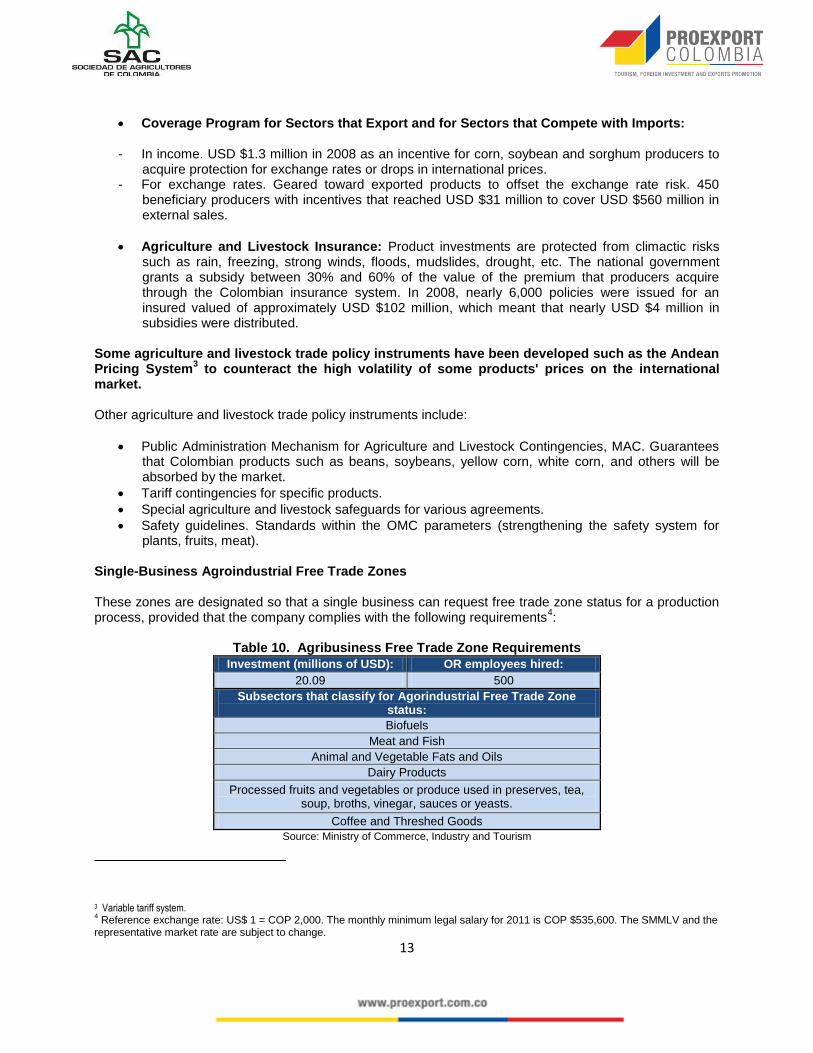

Single-Business Agroindustrial Free Trade Zones These zones are designated so that a single business can request free trade zone status for a production process, provided that the company complies with the following requirements

4:

Table 10. Agribusiness Free Trade Zone Requirements

Investment (millions of USD): OR employees hired:

20.09 500

Subsectors that classify for Agorindustrial Free Trade Zone status:

Biofuels

Meat and Fish

Animal and Vegetable Fats and Oils

Dairy Products

Processed fruits and vegetables or produce used in preserves, tea, soup, broths, vinegar, sauces or yeasts.

Coffee and Threshed Goods

Source: Ministry of Commerce, Industry and Tourism

3 Variable tariff system. 4 Reference exchange rate: US$ 1 = COP 2,000. The monthly minimum legal salary for 2011 is COP $535,600. The SMMLV and the

representative market rate are subject to change.

14

Benefits:

15% income tax

No customs taxes are incurred or paid (VAT, DUTIES).

Origin recognition within the framework of trade agreements (except with Peru)

Ability to sell on the local market

VAT exemption for raw materials or imported goods from the national customs territory.

Existing Tax Incentives5 for the Agricultural Sector in Colombia

Income tax exemption for late-yield crops. Between 2004 and 2014, new crops such as cocoa, rubber, palm, citrus and fruit trees are exempt from net income tax for a 10-year period from the beginning of production

6.

The Plan Vallejo special import and export system is a mechanism that grants duty and VAT

exemptions or deferrals for importing supplies, raw materials and capital goods. To be eligible for

Plan Vallejo, production must be completely or partially exported. The types of Plan Vallejo that

exist are explained below.

Plan Vallejo for Raw Materials and Supplies: For temporary importation of raw materials and supplies

to be used exclusively for producing goods for export. The plan provides VAT and duty exemptions that do

not require special authorization. They do, however, require that 60% of the goods produced with this raw

material be exported (or sold in a free trade zone).

Plan Vallejo for Capital Goods, Spare Parts and Intermediate Goods: This version of the plan makes

it possible to temporarily import spare parts and intermediate goods for agricultural use. These are listed

in Resolution 1148 from 20027. In these cases, after program approval from the DIAN's Registration and

Control Division (www.dian.gov.co), producers may be eligible to carry out temporary importations exempt

from duties and with suspended or deferred VAT for the length of the program.

Legal Stability Contracts are a mechanism for the Colombian government to guarantee for

investors that if any regulations identified in the contract as "determining statutes for

investment" are adversely modified, producers will have the right to continue applying the

original regulations for the length of the respective contract. The contract guarantees legal

stability for a period of 3 to 20 years, depending on the investment project.

To be able to request the contract, the investor must make new investments or increase existing

investments to 7,500 monthly minimum legal salaries (approximately USD $2.01 million) or more8.

Certain regulations may not be "stabilized." For more information, please visit

www.investincolombia.com.co/how-to-invest.html

5 Tax statute.

6 Law 939 of 2004.

7 http://www.mincomercio.gov.co/eContent/NewsDetail.asp?ID=567&IDCompany=1

8 The reference exchange rate in 2000. The investor must convert the investment from pesos to dollars at the time the investment is made.

15

5. PRODUCTIVE TRANSFORMATION PROGRAM FOR FOUR AGRIBUSINESS SECTORS

The Productive Transformation Program is a long-term public-private partnership dedicated to diversifying supply and creating world-class sectors. Through a public competition, four agroindustrial sectors were selected to be assessed and compared on an international scale as a way to define a development plan to propel these industries onto the world stage. These sectors are beef; chocolate, candy making and related raw materials; palm, oils and fats; and shrimp farming.

PROEXPORT SERVICES

The Colombian Government places special emphasis on generating favorable conditions and providing

the best support possible to investors. PROEXPORT came in 16th place among the best investment

promotion agencies in the world and offers various services to foreign investors including:

Information requests (economic, legal, procedural or sector-specific information)

Contacts with the public and private sectors

Itinerary planning for investors who decide to visit Colombia

Support services for investors already established in the country

Evaluation and improvement of the business environment

These services are offered free of cost. The main objective is to develop new businesses through efficient

and friendly processes. All information provided during the process is maintained confidential.

PROEXPORT has support teams in 21 cities around the world. It would be our pleasure to help

you.

6. ENTITIES OF INTEREST

Sociedad Agricultores de Colombia (Colombian Farmers Association, SAC)

Technical Vice President's Office ( 1) 2410035

PROEXPORT Office of the Vice Presidency for Foreign Investment; Office of the Vice

Presidency for Exports

(1) 5600 100

www.investincolombia.com.co