Collective investment schemes 101

18

consulting | research | contracting Collective Investment Schemes (CIS) 101 Developed by: Kuda Mukova and Kevin Came

-

Upload

iqbusinessconsulting -

Category

Business

-

view

108 -

download

2

Transcript of Collective investment schemes 101

consulting | research | contracting

Collective Investment Schemes (CIS)

101

Developed by:

Kuda Mukova and Kevin Came

Ag

en

da

1. Purpose

2. What is a CIS?

3. CIS landscape in South Africa

4. Types of funds

5. Type of portfolios

6. Major stakeholders

7. Legal framework

8. Typical Corporate Governance Framework

(CGF)

9. Operational functions of a CIS

10. Key operational processes

11. T Account

12. Operational challenges

3

1.Purpose of this document

• Understand what a Collective Investment Scheme (CIS) is

• Understand the key stakeholders within the CIS environment

• Have an idea of the Legal Framework of a CIS

• Understand the corporate governance landscape

• Understand the operational environment and pain points

After going through this document you should:

4

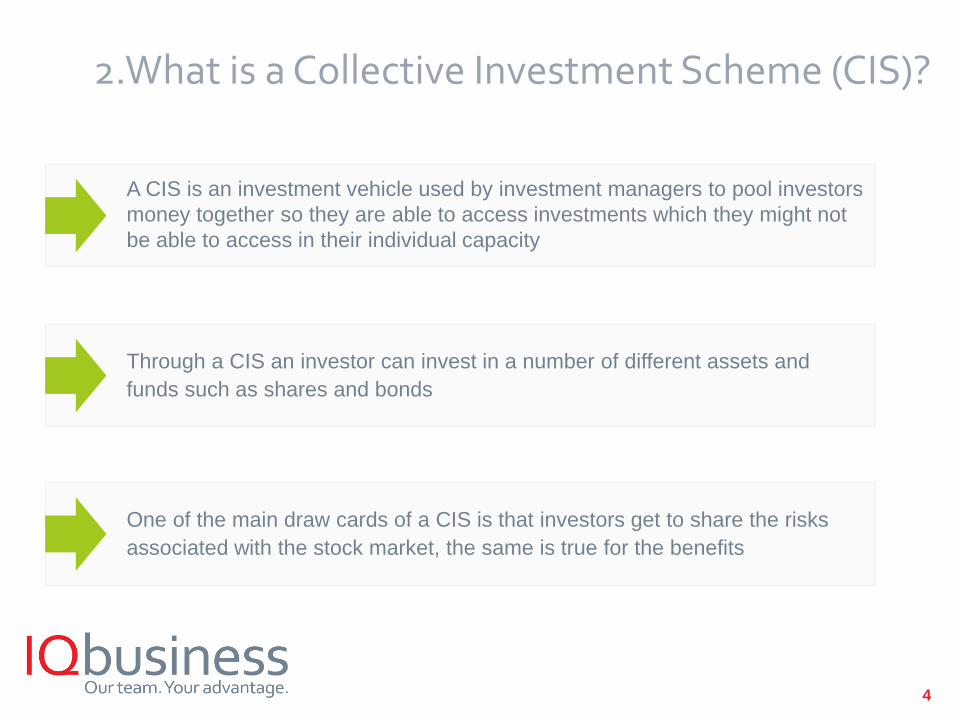

2.What is a Collective Investment Scheme (CIS)?

A CIS is an investment vehicle used by investment managers to pool investors

money together so they are able to access investments which they might not

be able to access in their individual capacity

Through a CIS an investor can invest in a number of different assets and

funds such as shares and bonds

One of the main draw cards of a CIS is that investors get to share the risks

associated with the stock market, the same is true for the benefits

5

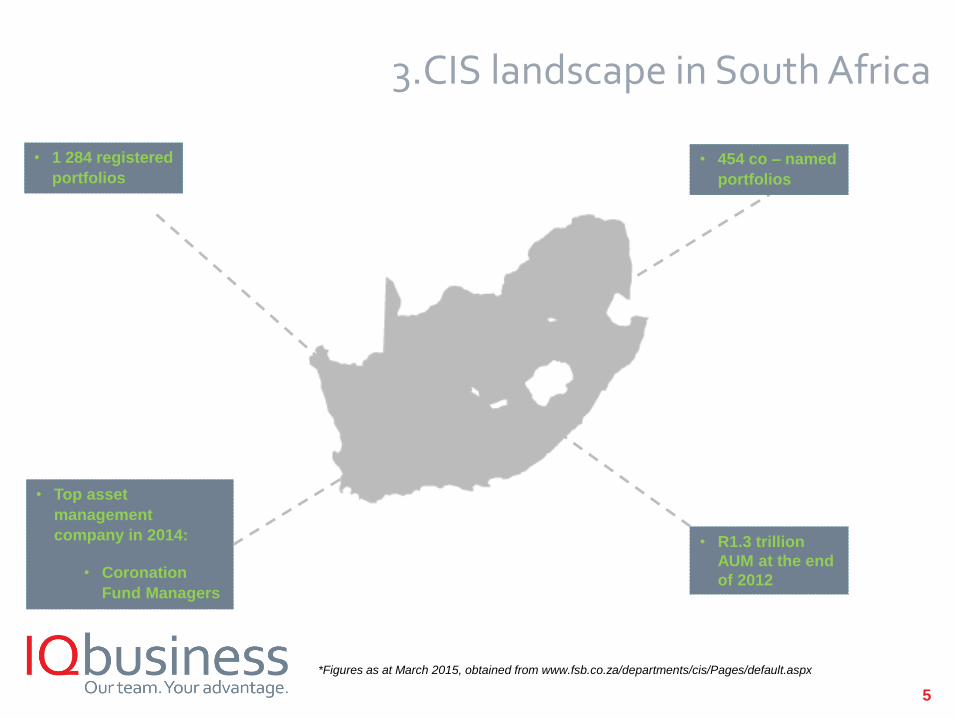

3.CIS landscape in South Africa

• R1.3 trillion

AUM at the end

of 2012

• 1 284 registered

portfolios

• Top asset

management

company in 2014:

• Coronation

Fund Managers

• 454 co – named

portfolios

*Figures as at March 2015, obtained from www.fsb.co.za/departments/cis/Pages/default.aspx

6

4.Type of funds

Buys shares in companies and is managed by a dedicated, single asset managerSingle name

funds

Is where a funds investment decisions are handled by a particular asset manager

and the management of the fund i.e: investment admin, pricing, marketing etc. Is

handled by another party which hold a license to carry out the management and

control of the CIS and complies with legislative requirements

Co named

funds

Holds an investment portfolio of other funds rather than investing directly into stocks,

bonds or other securities

Fund of

funds

These funds make up a particular type of portfolio

7

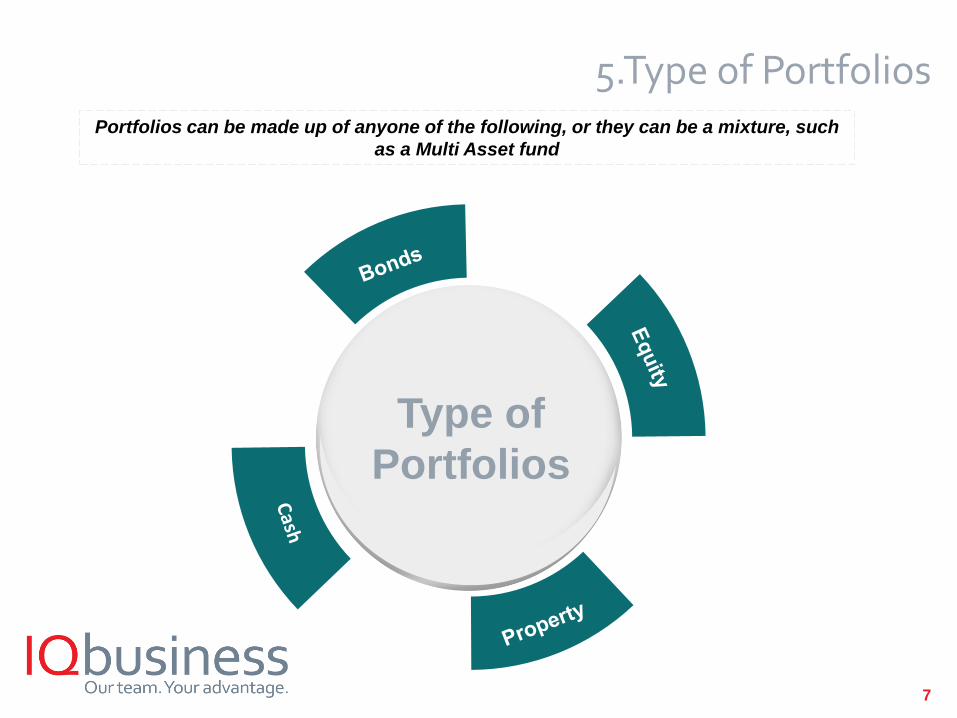

5.Type of Portfolios

Type of

Portfolios

Portfolios can be made up of anyone of the following, or they can be a mixture, such

as a Multi Asset fund

8

5.Type of portfolios continued……

Money is pooled together and is lent to people or companies developing propertyBonds

Ownership of a share in a company, e.g.: SAB, Capitec, NaspersEquity

Money is pooled to invest in a number of different types of property like industrial,

factories, shopping centres etc. Property

Holds an investment portfolio of other funds rather than investing directly into stocks,

bonds or other securitiesCash

9

6.Major stakeholdersThe following stakeholders and the role they play is important to know to understand the CIS

landscape

• Unit trusts must have a separate institution to act as

an independent decision maker

• The Trustees, usually a bank, act as a safe guard for

the funds and ensure the management company

(Manco) does not mismanage the funds

• The Trustees also need to monitor how the fund is

managed by the investment managers, i.e.: the

mandate of the fund and ensure daily transactions

are conducted in accordance with the Trust Deed

• If the Trustees suspect that the Manco is not acting in

the best interest of the investors they have the power

to replace the management

Trustees

• The Manco is a legal entity that acts on behalf of the

unit holders and is responsible for aspects of

management including but limited to marketing,

creating and selling of units, record keeping,

compliance, legal, finance etc. etc.

• The Manco earns an income by charging

administration fees for their management services

• The Manco must be registered with the Financial

Service Board (FSB)

Management Company (Manco)

10

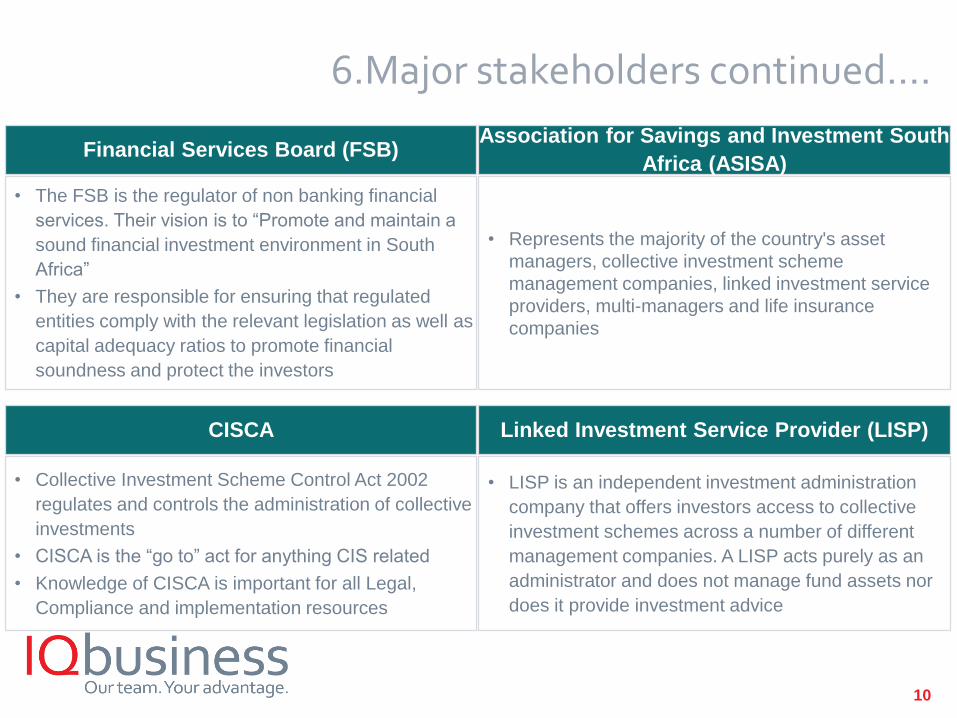

6.Major stakeholders continued….

• The FSB is the regulator of non banking financial

services. Their vision is to “Promote and maintain a

sound financial investment environment in South

Africa”

• They are responsible for ensuring that regulated

entities comply with the relevant legislation as well as

capital adequacy ratios to promote financial

soundness and protect the investors

Financial Services Board (FSB)

• Represents the majority of the country's asset

managers, collective investment scheme

management companies, linked investment service

providers, multi-managers and life insurance

companies

Association for Savings and Investment South

Africa (ASISA)

• Collective Investment Scheme Control Act 2002

regulates and controls the administration of collective

investments

• CISCA is the “go to” act for anything CIS related

• Knowledge of CISCA is important for all Legal,

Compliance and implementation resources

CISCA

• LISP is an independent investment administration

company that offers investors access to collective

investment schemes across a number of different

management companies. A LISP acts purely as an

administrator and does not manage fund assets nor

does it provide investment advice

Linked Investment Service Provider (LISP)

11

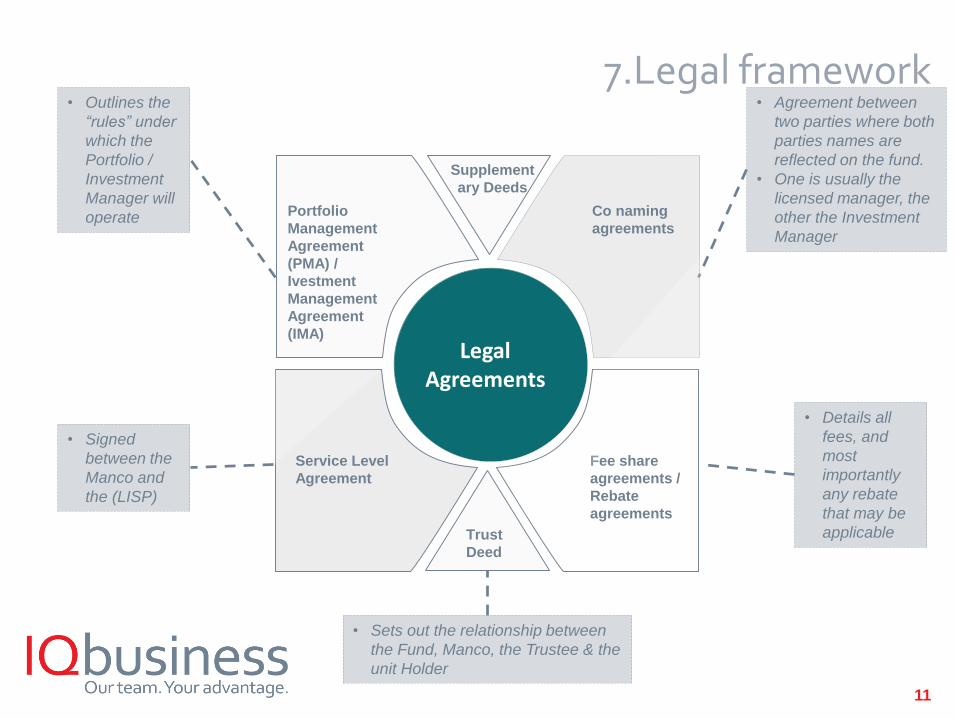

7.Legal framework

Legal Agreements

Co naming

agreements

Fee share

agreements /

Rebate

agreements

Portfolio

Management

Agreement

(PMA) /

Ivestment

Management

Agreement

(IMA)

Service Level

Agreement

• Outlines the

“rules” under

which the

Portfolio /

Investment

Manager will

operate

• Agreement between

two parties where both

parties names are

reflected on the fund.

• One is usually the

licensed manager, the

other the Investment

Manager

• Details all

fees, and

most

importantly

any rebate

that may be

applicable

• Signed

between the

Manco and

the (LISP)

Trust

Deed

• Sets out the relationship between

the Fund, Manco, the Trustee & the

unit Holder

Supplement

ary Deeds

12

7.Legal framework continued…..

Legal Agreements

All information relating to fees,

investment policies,

benchmarks, fund perfromance

criteria and mandates can be

found in the legal agreements

These agreements are the

starting point for all information

one requires about funds, the

Manco and their relationship with

investment managers

Legal agreements are imperative for control, governance, compliance and protection for all

parties involved

13

8.Typical Corporate Governance Framework (CGF) for a CIS

The overall intention of a Corporate Governance framework is to ensure that the board directs continuous

performance improvement while meeting its governance obligations and simultaneously, adhere to legislative

requirements.

A good governance framework should summarises the principles, methodologies , people and procedures

required to support and enforce effective corporate governance.

There are a number of sources that can be taken into consideration in developing a governance framework for

a collective investment scheme.

In addition the structure and responsibilities of each committee are crucial to get the most effective

Governance for a CIS.

CGF is crucial for any business, and this is no different for a CIS. Governance has a crucial

role to play

14

9.Operational functions of a CIS

Operational functions of a

CIS

• Enterprise Risk • Investment Compliance

• Performance and Risk Insight • Finance

• Change management

• Sales• Legal

• Marketing• Regulatory Compliance

• Portfolio Admin and

Unitisation

• In house Investment Admin • 3rd Party Investment Admin

These functions have very specific, detailed roles they need to perform to ensure a CIS

operates effectively

15

10.Key operational processes

Sample of key

operational processes

16

Debit Credit

Management Fees

– Standard fees

– Performance fees

– Portfolio management fees (As per the main

portfolio management agreement (PMA)

between the CIS and Asset Manager)

– Rebates (Obtained from PMA, fee share

agreement or rebate agreement

– Fund management fees

• Standard fees

• Performance fees

– Advisory/Distribution fees

– Multi manager fees

This is a typical T account for a CIS

11.T Account

17

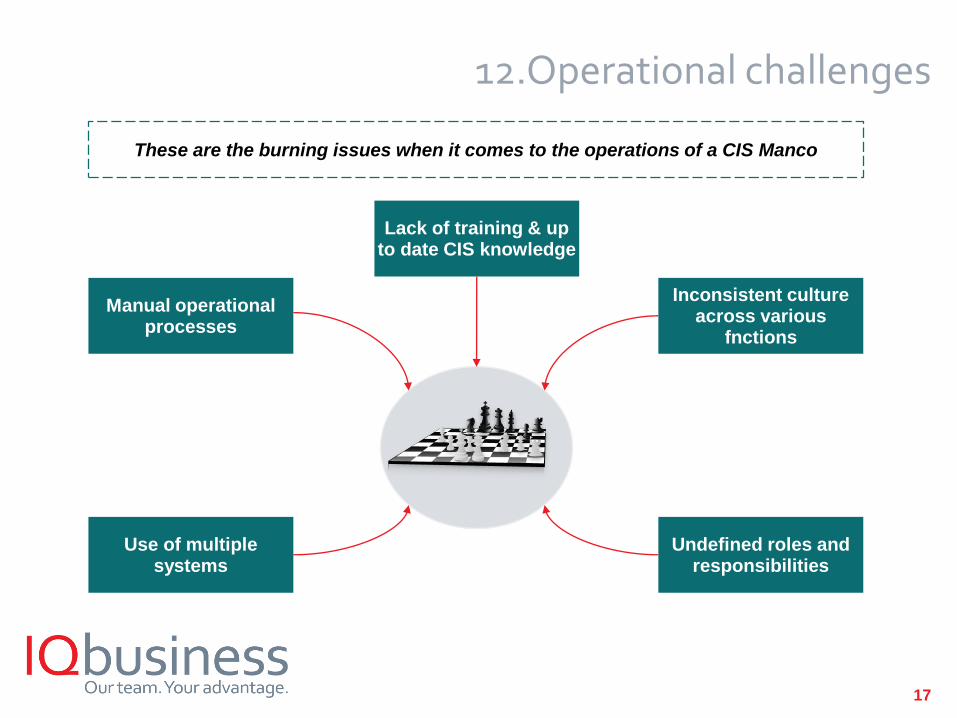

12.Operational challenges

Inconsistent culture across various

fnctions

Use of multiple systems

Undefined roles and responsibilities

Lack of training & up to date CIS knowledge

Manual operational processes

These are the burning issues when it comes to the operations of a CIS Manco

18

Kuda Mukova

Phone : + 27 11 259 4000

Mobile : + 27 71 450 5887

Kevin Came

Phone : + 27 11 259 4000

Mobile : + 27 74 977 0740

Headquarters

3 Third Avenue, Rivonia,

2128,

South Africa

Phone: +27 11 259 4000

Cape Town

2nd Floor Block C

The Boulevard

Searle Street

Cape Town

South Africa

Melbourne

Level 20, 303 Collins

Street

Melbourne

Victoria

3000

Australia

For further information, please contact:Sydney

Level 2, 131 York Street

Sydney

New South Wales

2000

Australia

Atlanta

2300 Windy Ridge Pkwy

Suite 520N

Atlanta, GA. 30339

United States

18

![Collective Investment Schemes Control Act [No. 45 of 2002] · 2 No. 24182 GOVERNMENT GAZETTE. 13 DECEMBER 7002 Act No. 45,2002 COLLECTIVE INVESTMENT SCHEMES CONTROL ACT. 2002 (English](https://static.fdocuments.in/doc/165x107/5e0bad7625bb1906be2090ac/collective-investment-schemes-control-act-no-45-of-2002-2-no-24182-government.jpg)