COLA and Benefit Calculations-3-22-17€¦ · 3/21/2017 2 Benefit Calculations • COLA –...

44

3/21/2017 1 COLA AND BENEFIT CALCULATIONS Tim Mussack, B&B Ratings B&B Sacramento (916) 569-0790 or Ext 1144 [email protected] 2 © 2017, Bradford & Barthel, LLP

Transcript of COLA and Benefit Calculations-3-22-17€¦ · 3/21/2017 2 Benefit Calculations • COLA –...

3/21/2017

1

COLA

AND

BENEFIT CALCULATIONS

Tim Mussack, B&B Ratings

B&B Sacramento

(916) 569-0790 or

Ext 1144

2© 2017, Bradford & Barthel, LLP

3/21/2017

2

Benefit Calculations

• COLA

– Temporary Disability

– Death Benefits

– Life Pension

– Permanent Total Disability

• Calculation of Lifetime Benefits

© 2017, Bradford & Barthel, LLP 3

Benefits – when due• LC 4650 a – TD

– Within 14 days

LC 4650 b, – PD

Within 14 days of TD end

LC 4650 (b) (1)

• until the employer's reasonable estimate of permanent disability

indemnity due has been paid

LC 4650 c – every 14 days

LC 4650 d – if not timely, increase by 10%

not within 14 days of claim form or with formal delay

Calculate early and accurately.

© 2017, Bradford & Barthel, LLP 4

3/21/2017

3

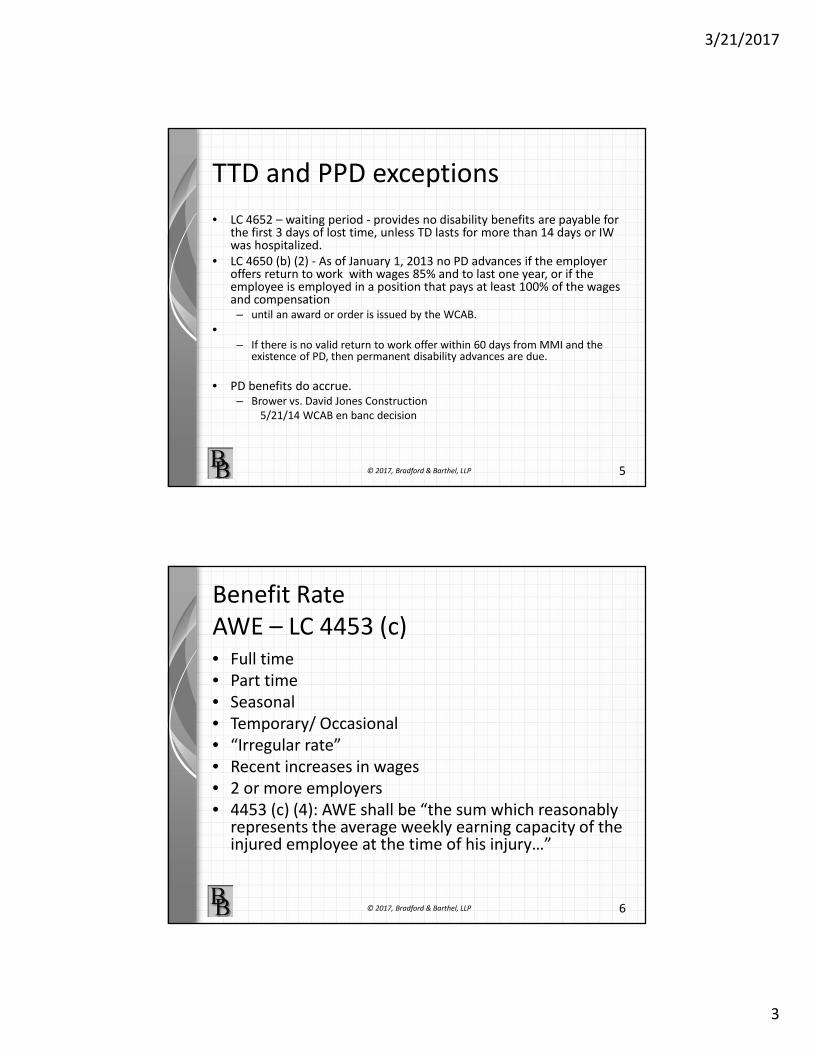

TTD and PPD exceptions

• LC 4652 – waiting period - provides no disability benefits are payable for the first 3 days of lost time, unless TD lasts for more than 14 days or IW was hospitalized.

• LC 4650 (b) (2) - As of January 1, 2013 no PD advances if the employer offers return to work with wages 85% and to last one year, or if the employee is employed in a position that pays at least 100% of the wages and compensation– until an award or order is issued by the WCAB.

•– If there is no valid return to work offer within 60 days from MMI and the

existence of PD, then permanent disability advances are due.

• PD benefits do accrue.– Brower vs. David Jones Construction

5/21/14 WCAB en banc decision

© 2017, Bradford & Barthel, LLP 5

Benefit Rate

AWE – LC 4453 (c)• Full time

• Part time

• Seasonal

• Temporary/ Occasional

• “Irregular rate”

• Recent increases in wages

• 2 or more employers

• 4453 (c) (4): AWE shall be “the sum which reasonably represents the average weekly earning capacity of the injured employee at the time of his injury…”

© 2017, Bradford & Barthel, LLP 6

3/21/2017

4

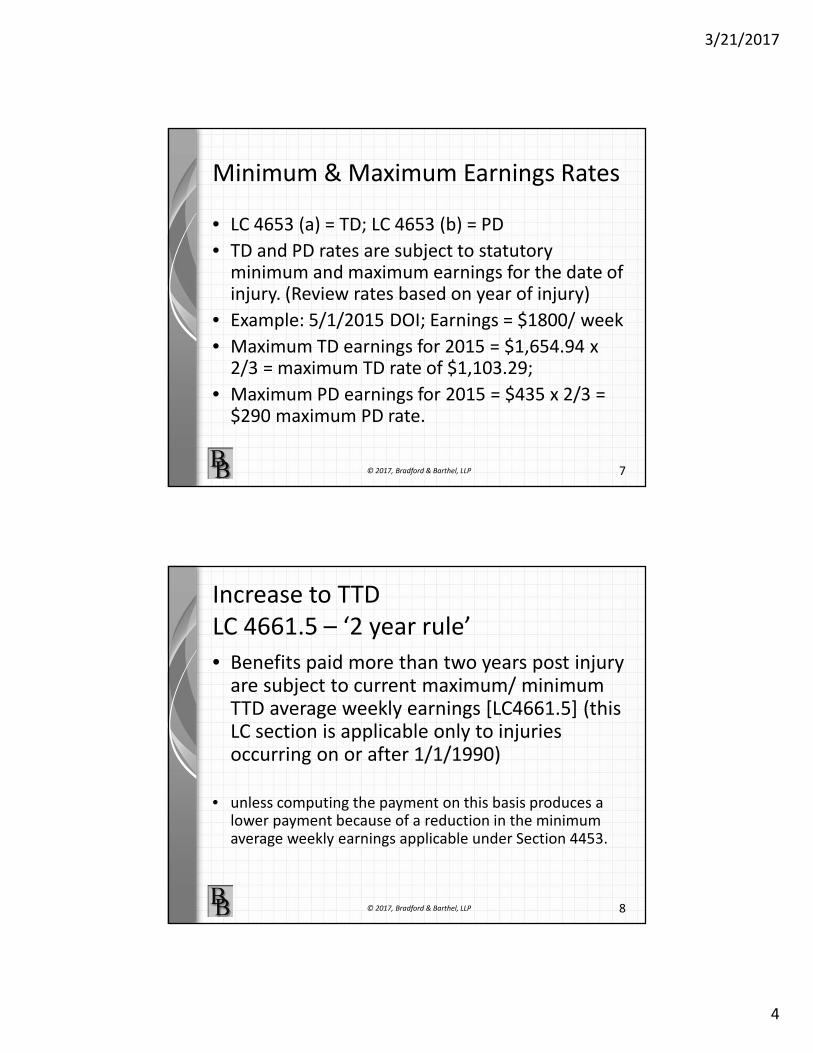

Minimum & Maximum Earnings Rates

• LC 4653 (a) = TD; LC 4653 (b) = PD

• TD and PD rates are subject to statutory minimum and maximum earnings for the date of injury. (Review rates based on year of injury)

• Example: 5/1/2015 DOI; Earnings = $1800/ week

• Maximum TD earnings for 2015 = $1,654.94 x 2/3 = maximum TD rate of $1,103.29;

• Maximum PD earnings for 2015 = $435 x 2/3 = $290 maximum PD rate.

© 2017, Bradford & Barthel, LLP 7

Increase to TTD

LC 4661.5 – ‘2 year rule’

• Benefits paid more than two years post injury are subject to current maximum/ minimum TTD average weekly earnings [LC4661.5] (this LC section is applicable only to injuries occurring on or after 1/1/1990)

• unless computing the payment on this basis produces a lower payment because of a reduction in the minimum average weekly earnings applicable under Section 4453.

© 2017, Bradford & Barthel, LLP 8

3/21/2017

5

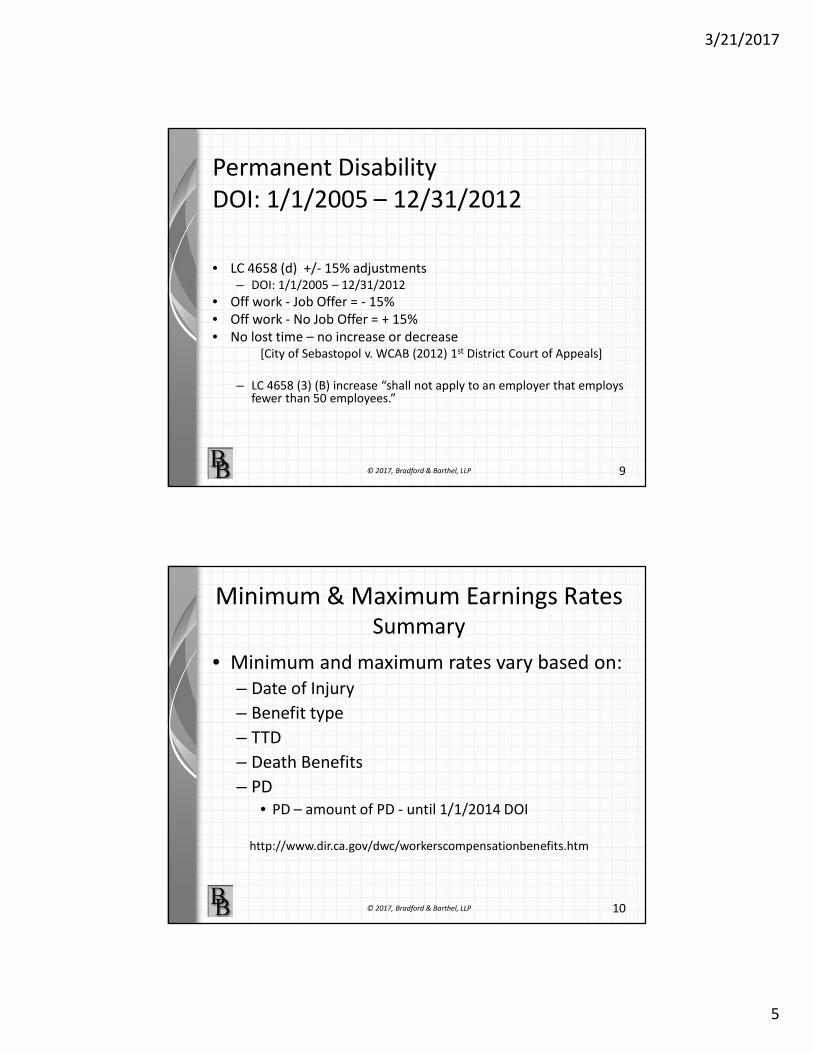

Permanent Disability

DOI: 1/1/2005 – 12/31/2012

• LC 4658 (d) +/- 15% adjustments – DOI: 1/1/2005 – 12/31/2012

• Off work - Job Offer = - 15%

• Off work - No Job Offer = + 15%

• No lost time – no increase or decrease[City of Sebastopol v. WCAB (2012) 1st District Court of Appeals]

– LC 4658 (3) (B) increase “shall not apply to an employer that employs fewer than 50 employees.”

© 2017, Bradford & Barthel, LLP 9

Minimum & Maximum Earnings RatesSummary

• Minimum and maximum rates vary based on:

– Date of Injury

– Benefit type

– TTD

– Death Benefits

– PD

• PD – amount of PD - until 1/1/2014 DOI

http://www.dir.ca.gov/dwc/workerscompensationbenefits.htm

© 2017, Bradford & Barthel, LLP 10

3/21/2017

6

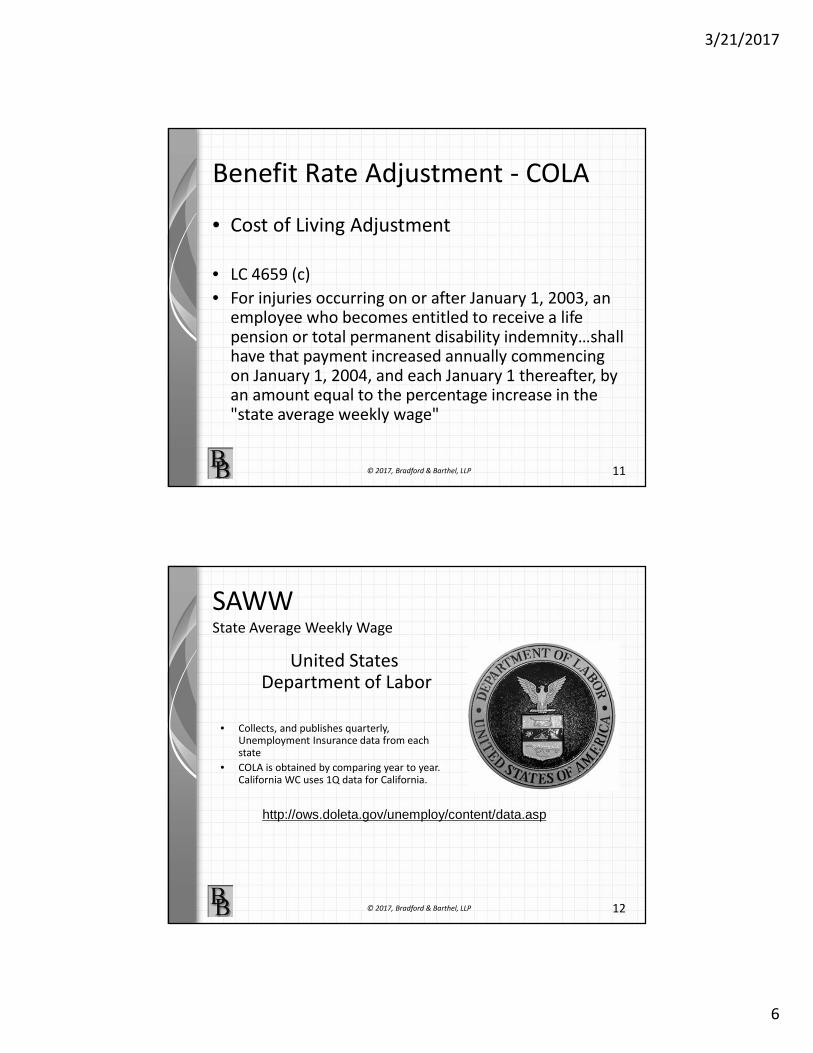

Benefit Rate Adjustment - COLA

• Cost of Living Adjustment

• LC 4659 (c)

• For injuries occurring on or after January 1, 2003, an employee who becomes entitled to receive a life pension or total permanent disability indemnity…shall have that payment increased annually commencing on January 1, 2004, and each January 1 thereafter, by an amount equal to the percentage increase in the "state average weekly wage"

© 2017, Bradford & Barthel, LLP 11

SAWWState Average Weekly Wage

United StatesDepartment of Labor

• Collects, and publishes quarterly, Unemployment Insurance data from each state

• COLA is obtained by comparing year to year. California WC uses 1Q data for California.

© 2017, Bradford & Barthel, LLP 12

http://ows.doleta.gov/unemploy/content/data.asp

3/21/2017

7

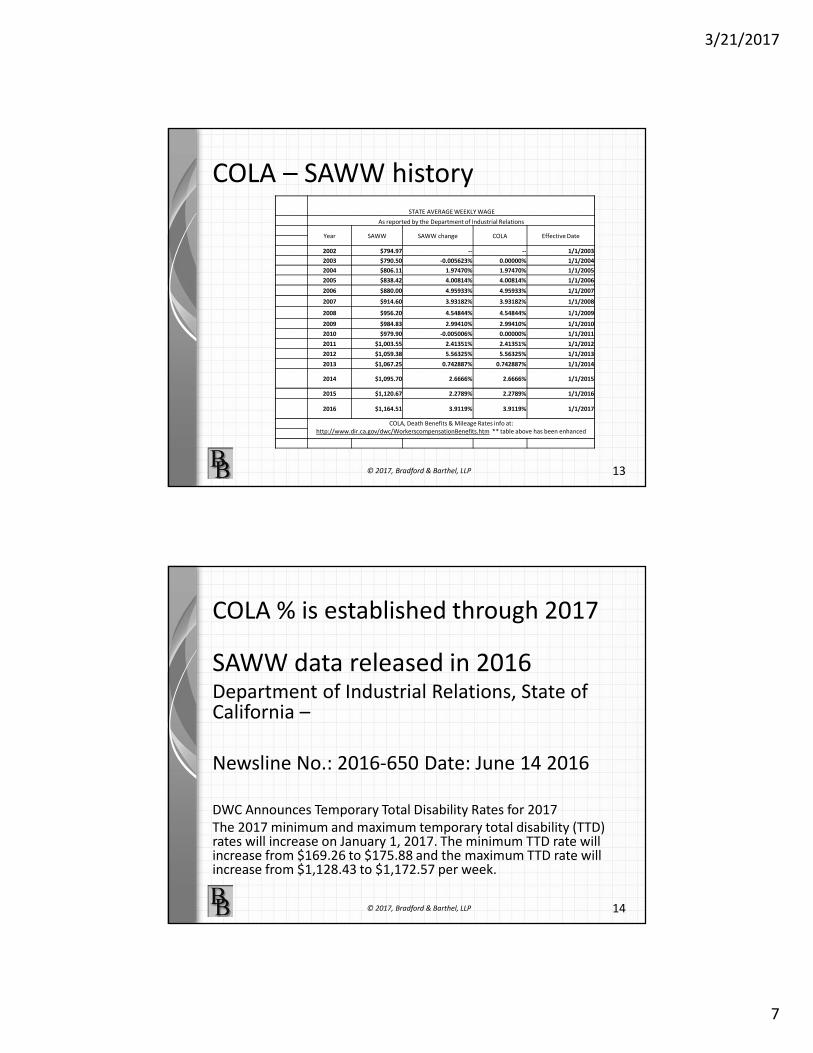

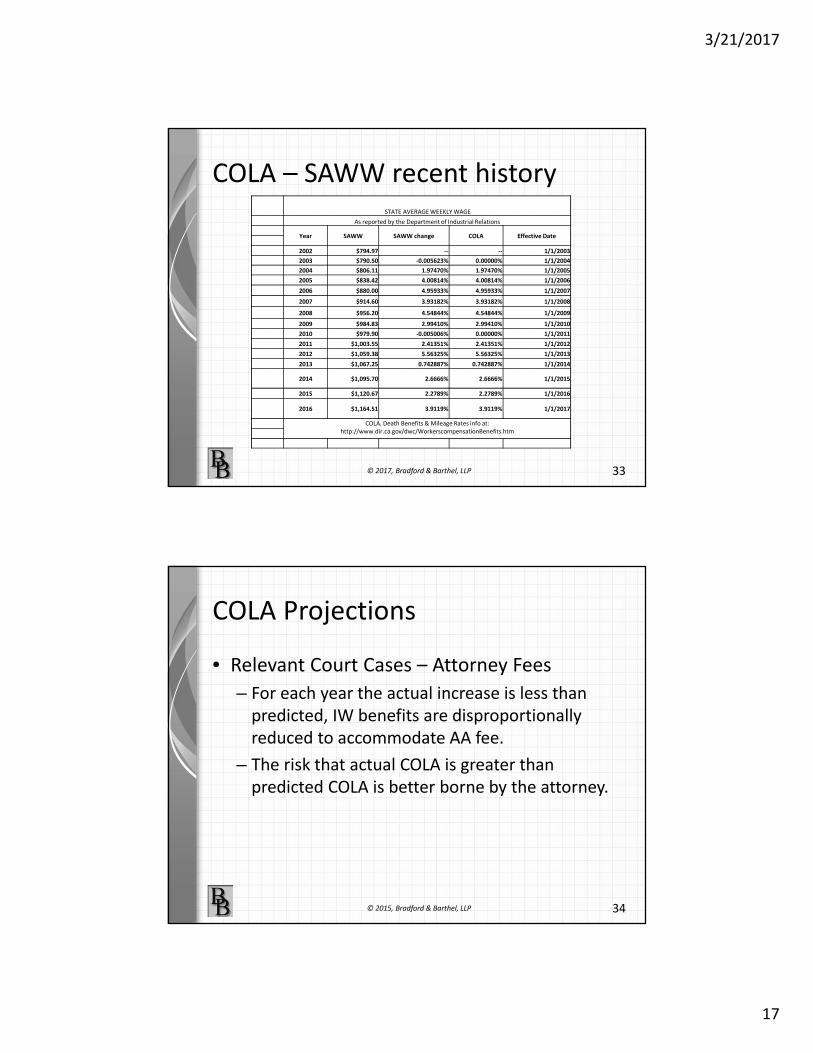

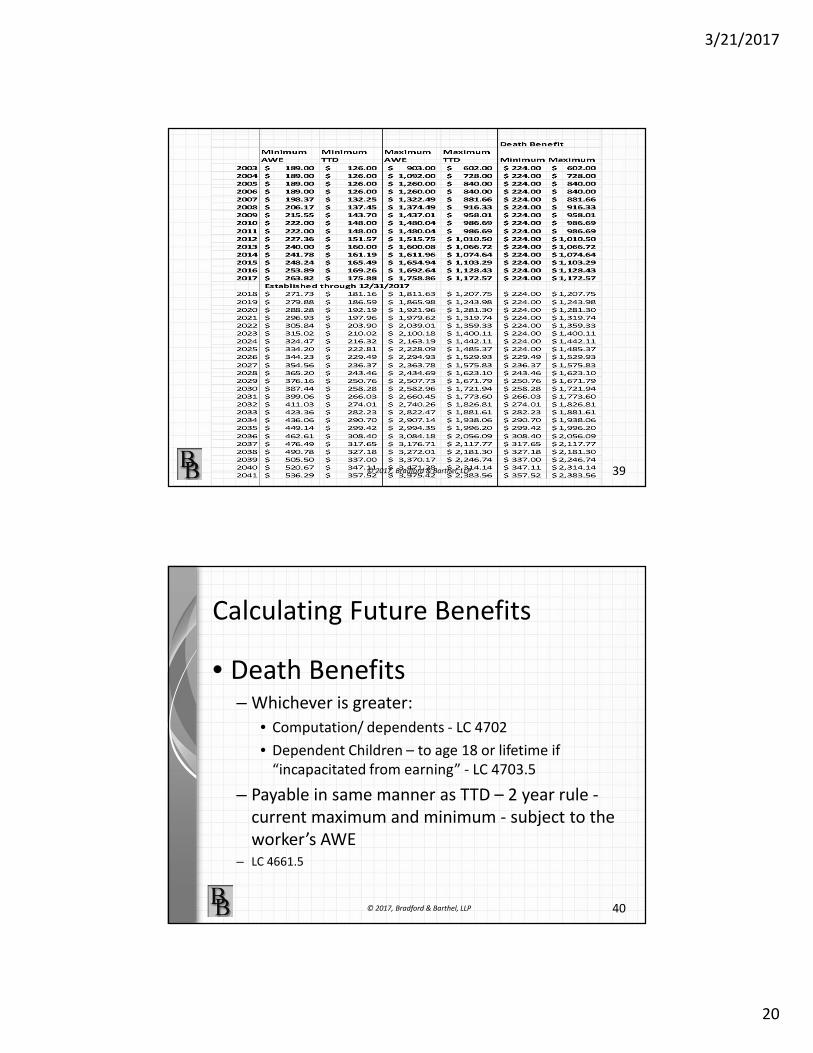

COLA – SAWW historySTATE AVERAGE WEEKLY WAGE

As reported by the Department of Industrial Relations

Year SAWW SAWW change COLA Effective Date

2002 $794.97 -- -- 1/1/2003

2003 $790.50 -0.005623% 0.00000% 1/1/2004

2004 $806.11 1.97470% 1.97470% 1/1/2005

2005 $838.42 4.00814% 4.00814% 1/1/2006

2006 $880.00 4.95933% 4.95933% 1/1/2007

2007 $914.60 3.93182% 3.93182% 1/1/2008

2008 $956.20 4.54844% 4.54844% 1/1/2009

2009 $984.83 2.99410% 2.99410% 1/1/2010

2010 $979.90 -0.005006% 0.00000% 1/1/2011

2011 $1,003.55 2.41351% 2.41351% 1/1/2012

2012 $1,059.38 5.56325% 5.56325% 1/1/2013

2013 $1,067.25 0.742887% 0.742887% 1/1/2014

2014 $1,095.70 2.6666% 2.6666% 1/1/2015

2015 $1,120.67 2.2789% 2.2789% 1/1/2016

2016 $1,164.51 3.9119% 3.9119% 1/1/2017

COLA, Death Benefits & Mileage Rates info at:

http://www.dir.ca.gov/dwc/WorkerscompensationBenefits.htm ** table above has been enhanced

© 2017, Bradford & Barthel, LLP 13

COLA % is established through 2017

SAWW data released in 2016Department of Industrial Relations, State of California –

Newsline No.: 2016-650 Date: June 14 2016

DWC Announces Temporary Total Disability Rates for 2017

The 2017 minimum and maximum temporary total disability (TTD) rates will increase on January 1, 2017. The minimum TTD rate will increase from $169.26 to $175.88 and the maximum TTD rate will increase from $1,128.43 to $1,172.57 per week.

© 2017, Bradford & Barthel, LLP 14

3/21/2017

8

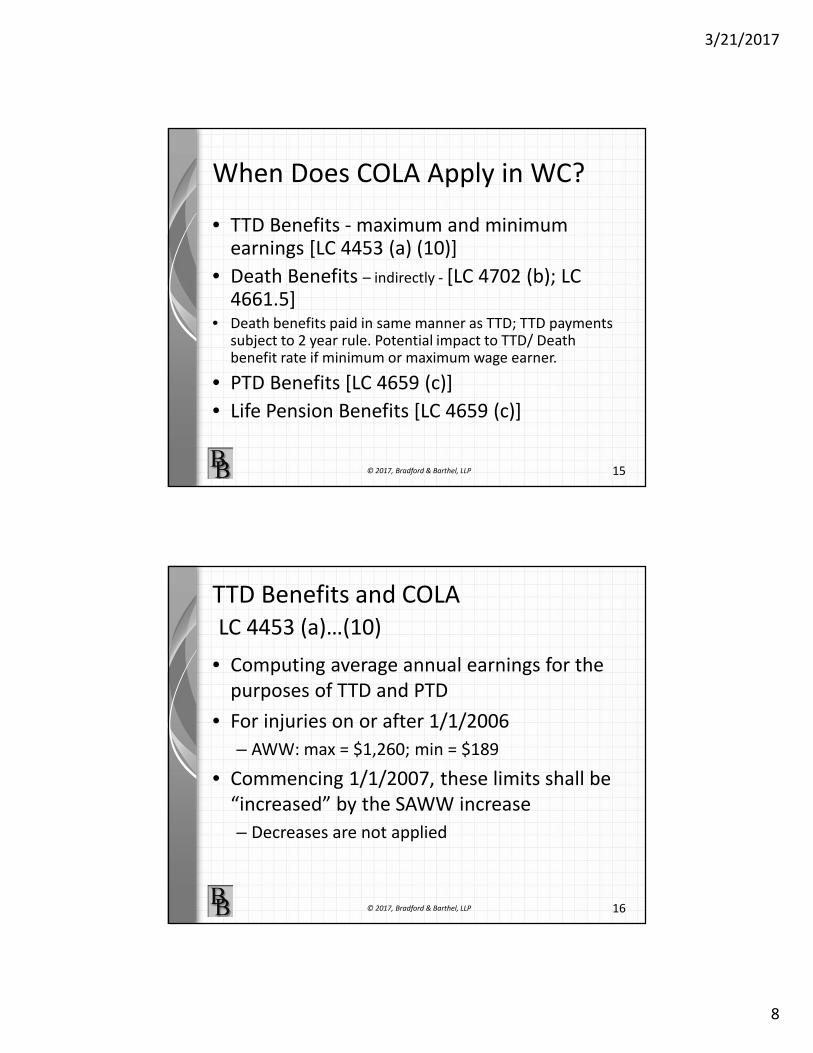

When Does COLA Apply in WC?

• TTD Benefits - maximum and minimum earnings [LC 4453 (a) (10)]

• Death Benefits – indirectly - [LC 4702 (b); LC 4661.5]

• Death benefits paid in same manner as TTD; TTD payments subject to 2 year rule. Potential impact to TTD/ Death benefit rate if minimum or maximum wage earner.

• PTD Benefits [LC 4659 (c)]

• Life Pension Benefits [LC 4659 (c)]

© 2017, Bradford & Barthel, LLP 15

TTD Benefits and COLA

LC 4453 (a)…(10)

• Computing average annual earnings for the

purposes of TTD and PTD

• For injuries on or after 1/1/2006

– AWW: max = $1,260; min = $189

• Commencing 1/1/2007, these limits shall be

“increased” by the SAWW increase

– Decreases are not applied

© 2017, Bradford & Barthel, LLP 16

3/21/2017

9

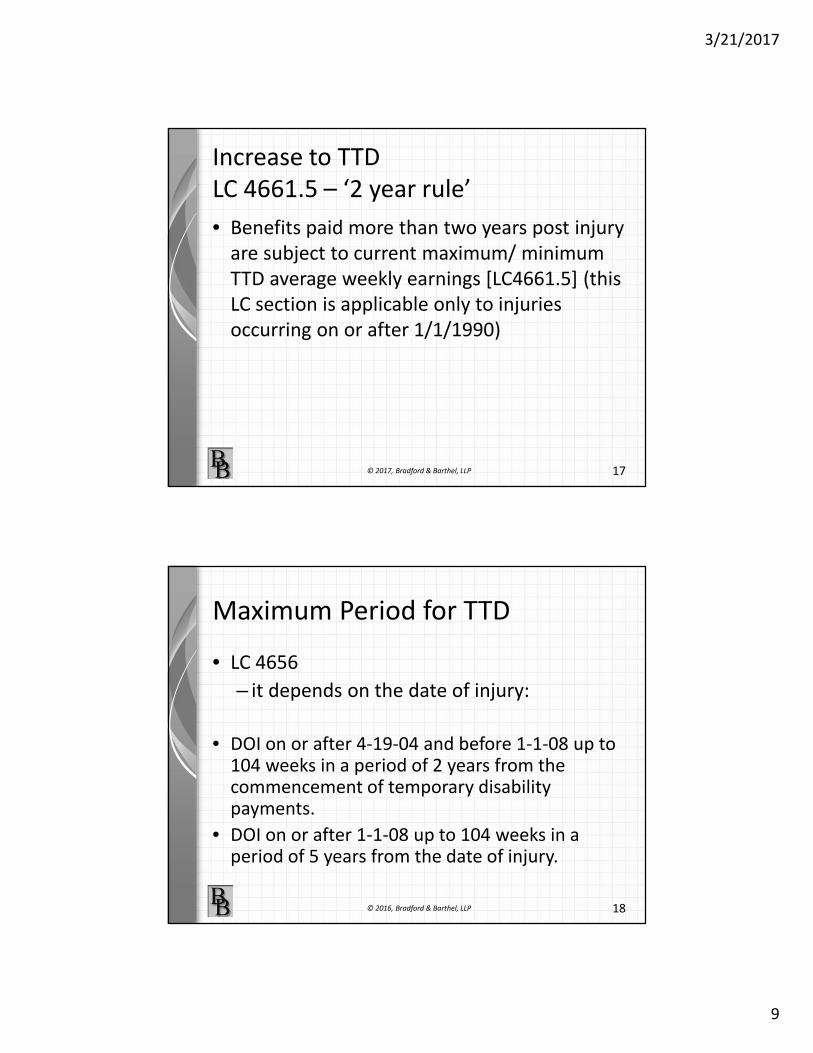

Increase to TTD

LC 4661.5 – ‘2 year rule’

• Benefits paid more than two years post injury

are subject to current maximum/ minimum

TTD average weekly earnings [LC4661.5] (this

LC section is applicable only to injuries

occurring on or after 1/1/1990)

© 2017, Bradford & Barthel, LLP 17

Maximum Period for TTD

• LC 4656

– it depends on the date of injury:

• DOI on or after 4-19-04 and before 1-1-08 up to 104 weeks in a period of 2 years from the commencement of temporary disability payments.

• DOI on or after 1-1-08 up to 104 weeks in a period of 5 years from the date of injury.

© 2016, Bradford & Barthel, LLP 18

3/21/2017

10

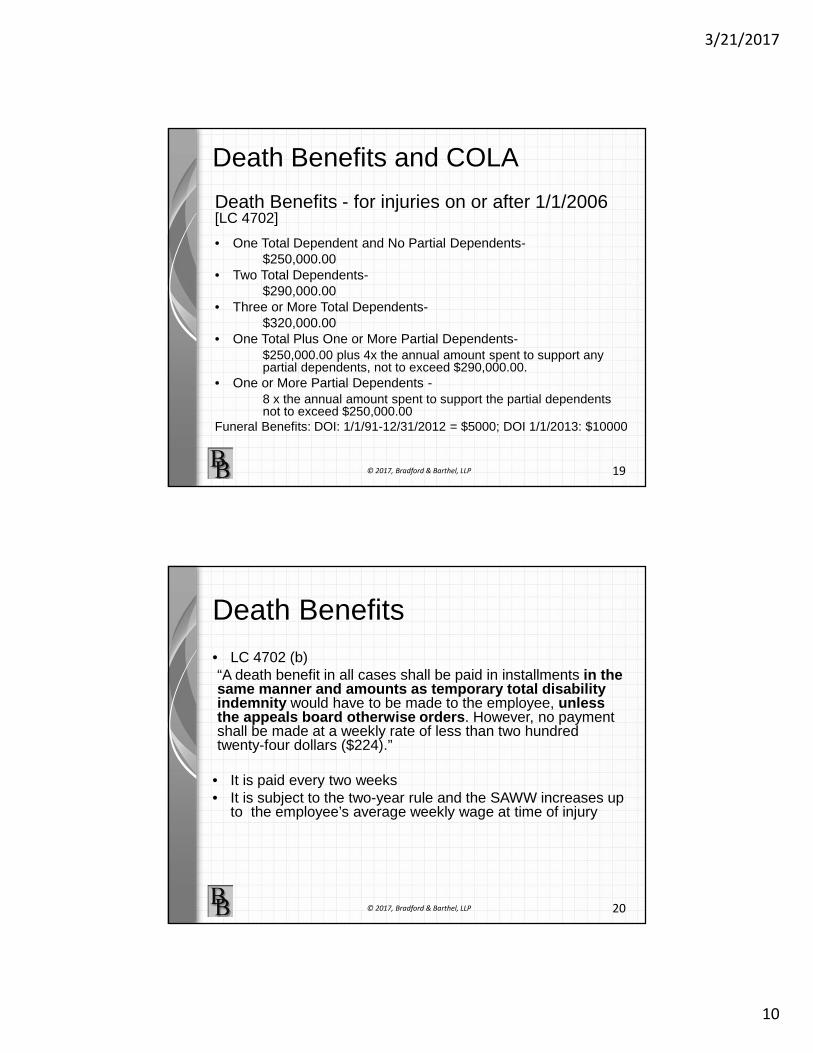

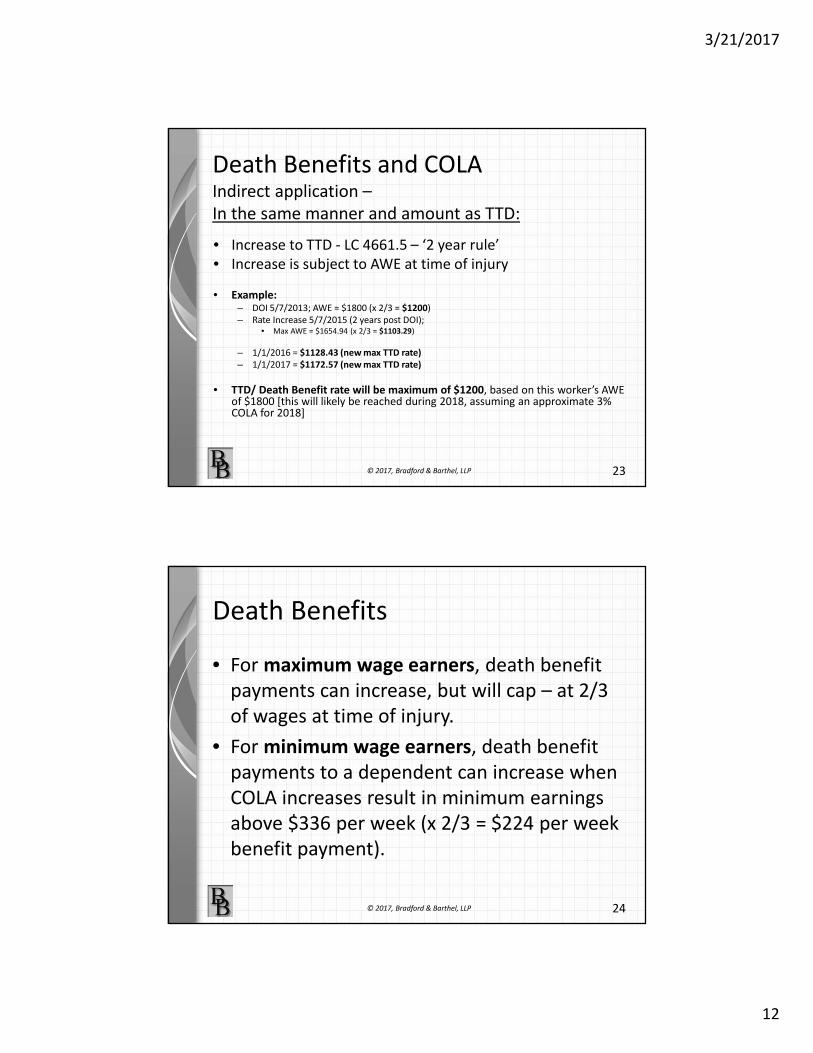

Death Benefits and COLA

Death Benefits - for injuries on or after 1/1/2006 [LC 4702]

• One Total Dependent and No Partial Dependents-$250,000.00

• Two Total Dependents-$290,000.00

• Three or More Total Dependents-$320,000.00

• One Total Plus One or More Partial Dependents-$250,000.00 plus 4x the annual amount spent to support any partial dependents, not to exceed $290,000.00.

• One or More Partial Dependents -8 x the annual amount spent to support the partial dependents not to exceed $250,000.00

Funeral Benefits: DOI: 1/1/91-12/31/2012 = $5000; DOI 1/1/2013: $10000

© 2017, Bradford & Barthel, LLP 19

Death Benefits

• LC 4702 (b) “A death benefit in all cases shall be paid in installments in the same manner and amounts as temporary total disabili ty indemnity would have to be made to the employee, unless the appeals board otherwise orders . However, no payment shall be made at a weekly rate of less than two hundred twenty-four dollars ($224).”

• It is paid every two weeks• It is subject to the two-year rule and the SAWW increases up

to the employee’s average weekly wage at time of injury

© 2017, Bradford & Barthel, LLP 20

3/21/2017

11

Death Benefits

• Labor Code 4703.5:– "In the case of one or more totally dependent minor

children…and notwithstanding the maximum limitations specified in Section 4702 and 4703, payment of death benefits shall continue until the youngest child attains age 18 in the same manner and amount as temporary total disability indemnity would have been paid to the employee…

– For children of public servant, to age 19 is still in high school

• This has sometimes been referred to as the Minor Dependency Benefit

• It has no dollar amount cap

© 2017, Bradford & Barthel, LLP 21

Death Benefits

• Any accrued and unpaid TTD and/ or PD to the dependents, heirs, or estate (LC 4700)

• Beginning on date of death, TTD Rate, based on AWE at the time of injury that causes death, although not less than $224/ week– WCAB can order otherwise (eg, higher weekly rate)

• 2 years after date of injury, benefit rate is subject to current AWE/ TTD max/ min, although not less than $224/ week

• Payable until Death Benefit as provided in LC 4702 (or 4706.5 with no dependents) is paid in its entirety, or until dependent minor benefit is paid (LC 4703.5) – (whichever is greater)

© 2017, Bradford & Barthel, LLP 22

3/21/2017

12

Death Benefits and COLAIndirect application –

In the same manner and amount as TTD:

• Increase to TTD - LC 4661.5 – ‘2 year rule’

• Increase is subject to AWE at time of injury

• Example:– DOI 5/7/2013; AWE = $1800 (x 2/3 = $1200)

– Rate Increase 5/7/2015 (2 years post DOI); • Max AWE = $1654.94 (x 2/3 = $1103.29)

– 1/1/2016 = $1128.43 (new max TTD rate)

– 1/1/2017 = $1172.57 (new max TTD rate)

• TTD/ Death Benefit rate will be maximum of $1200, based on this worker’s AWE of $1800 [this will likely be reached during 2018, assuming an approximate 3% COLA for 2018]

© 2017, Bradford & Barthel, LLP 23

Death Benefits

• For maximum wage earners, death benefit

payments can increase, but will cap – at 2/3

of wages at time of injury.

• For minimum wage earners, death benefit

payments to a dependent can increase when

COLA increases result in minimum earnings

above $336 per week (x 2/3 = $224 per week

benefit payment).

© 2017, Bradford & Barthel, LLP 24

3/21/2017

13

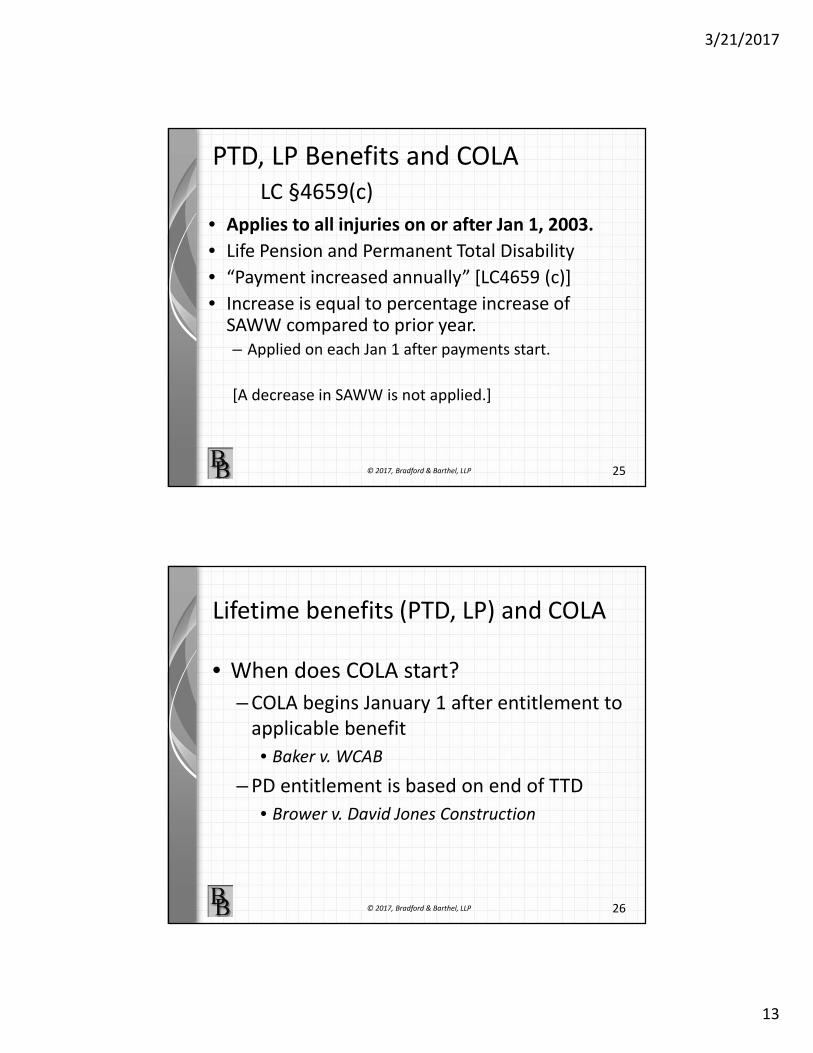

PTD, LP Benefits and COLA

LC §4659(c)

• Applies to all injuries on or after Jan 1, 2003.

• Life Pension and Permanent Total Disability

• “Payment increased annually” [LC4659 (c)]

• Increase is equal to percentage increase of SAWW compared to prior year.

– Applied on each Jan 1 after payments start.

[A decrease in SAWW is not applied.]

© 2017, Bradford & Barthel, LLP 25

Lifetime benefits (PTD, LP) and COLA

• When does COLA start?

– COLA begins January 1 after entitlement to

applicable benefit

• Baker v. WCAB

– PD entitlement is based on end of TTD

• Brower v. David Jones Construction

© 2017, Bradford & Barthel, LLP 26

3/21/2017

14

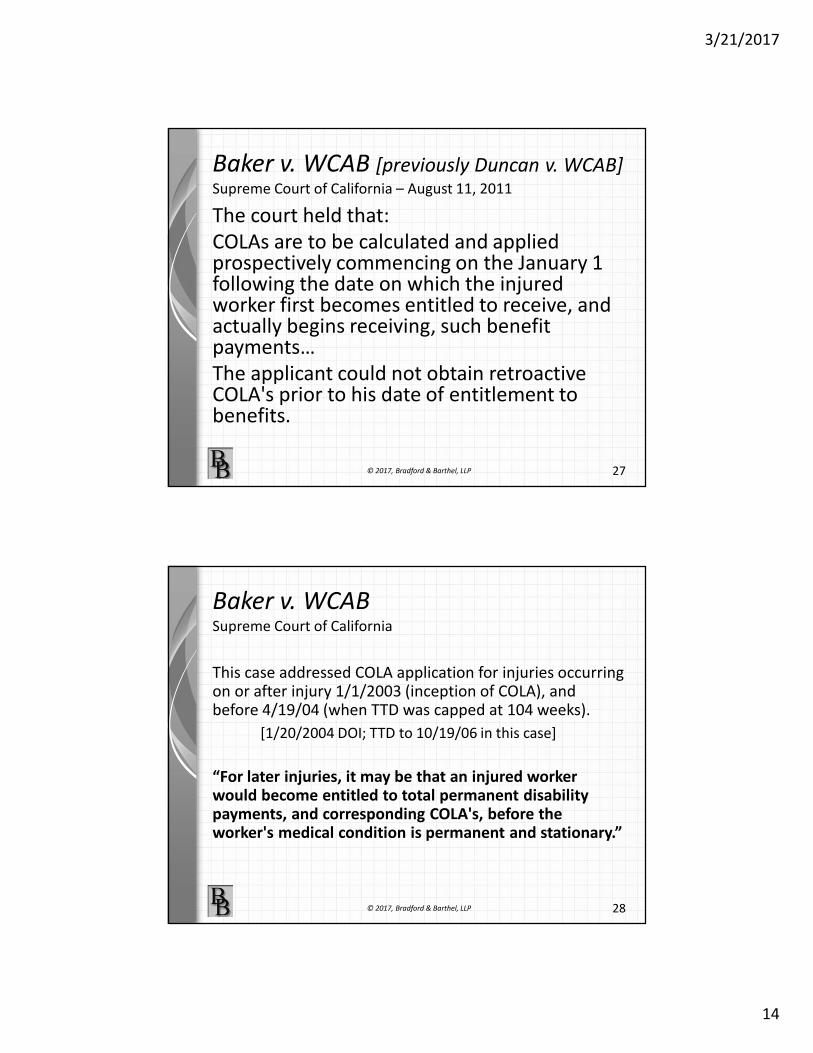

Baker v. WCAB [previously Duncan v. WCAB]Supreme Court of California – August 11, 2011

The court held that:

COLAs are to be calculated and applied prospectively commencing on the January 1 following the date on which the injured worker first becomes entitled to receive, and actually begins receiving, such benefit payments…

The applicant could not obtain retroactive COLA's prior to his date of entitlement to benefits.

© 2017, Bradford & Barthel, LLP 27

Baker v. WCABSupreme Court of California

This case addressed COLA application for injuries occurring on or after injury 1/1/2003 (inception of COLA), and before 4/19/04 (when TTD was capped at 104 weeks).

[1/20/2004 DOI; TTD to 10/19/06 in this case]

“For later injuries, it may be that an injured worker would become entitled to total permanent disability payments, and corresponding COLA's, before the worker's medical condition is permanent and stationary.”

© 2017, Bradford & Barthel, LLP 28

3/21/2017

15

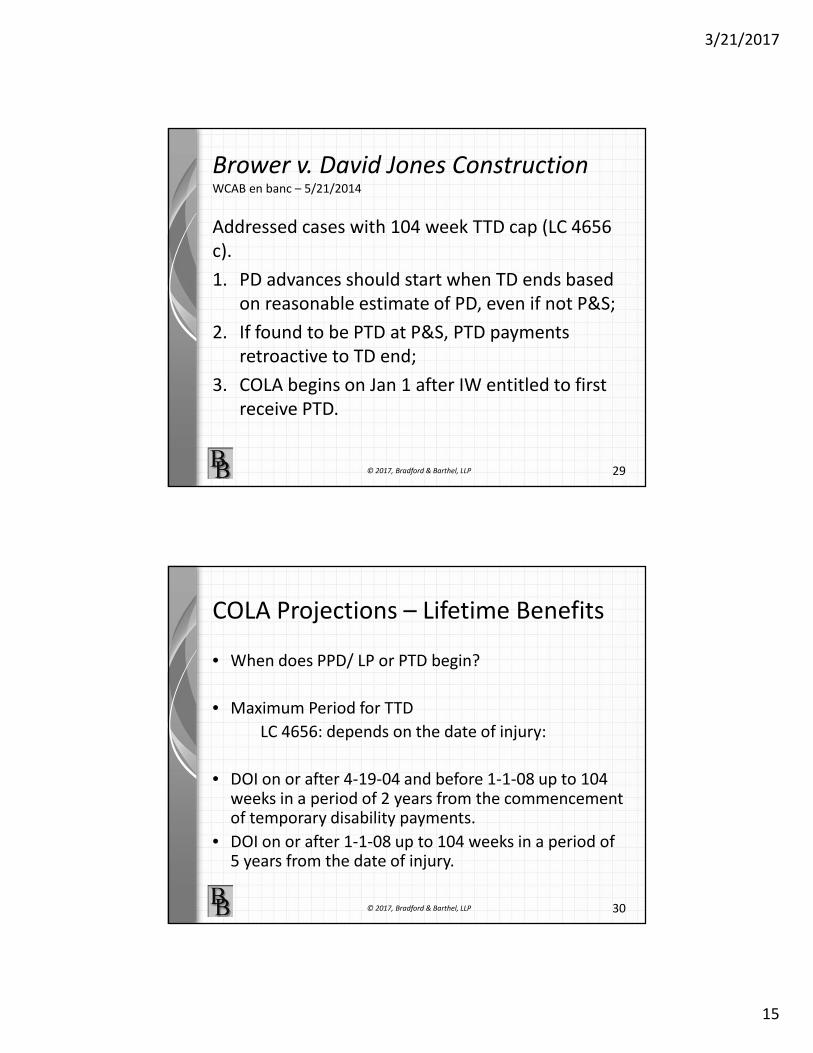

Brower v. David Jones ConstructionWCAB en banc – 5/21/2014

Addressed cases with 104 week TTD cap (LC 4656

c).

1. PD advances should start when TD ends based

on reasonable estimate of PD, even if not P&S;

2. If found to be PTD at P&S, PTD payments

retroactive to TD end;

3. COLA begins on Jan 1 after IW entitled to first

receive PTD.

© 2017, Bradford & Barthel, LLP 29

COLA Projections – Lifetime Benefits

• When does PPD/ LP or PTD begin?

• Maximum Period for TTD

LC 4656: depends on the date of injury:

• DOI on or after 4-19-04 and before 1-1-08 up to 104 weeks in a period of 2 years from the commencement of temporary disability payments.

• DOI on or after 1-1-08 up to 104 weeks in a period of 5 years from the date of injury.

© 2017, Bradford & Barthel, LLP 30

3/21/2017

16

Future COLA Projections

• What rate do you project?

o every June, the rate for the following January 1 is

determined by the DWC

o 3% is current projection beyond set COLA

amount

© 2017, Bradford & Barthel, LLP 31

COLA Projections

• DEU had used a 50 year average– 1957-2006 = 4.7% average increase

– 1962-2011 = 4.6% average increase

– 1966-2015 - 50 year average 4.5%

• Relevant Court Cases – Attorney Fees– For each year the actual increase is less than

predicted, IW benefits are disproportionally reduced to accommodate AA fee.

– The risk that actual COLA is greater than predicted COLA is better borne by the attorney.

© 2017, Bradford & Barthel, LLP 32

3/21/2017

17

COLA – SAWW recent historySTATE AVERAGE WEEKLY WAGE

As reported by the Department of Industrial Relations

Year SAWW SAWW change COLA Effective Date

2002 $794.97 -- -- 1/1/2003

2003 $790.50 -0.005623% 0.00000% 1/1/2004

2004 $806.11 1.97470% 1.97470% 1/1/2005

2005 $838.42 4.00814% 4.00814% 1/1/2006

2006 $880.00 4.95933% 4.95933% 1/1/2007

2007 $914.60 3.93182% 3.93182% 1/1/2008

2008 $956.20 4.54844% 4.54844% 1/1/2009

2009 $984.83 2.99410% 2.99410% 1/1/2010

2010 $979.90 -0.005006% 0.00000% 1/1/2011

2011 $1,003.55 2.41351% 2.41351% 1/1/2012

2012 $1,059.38 5.56325% 5.56325% 1/1/2013

2013 $1,067.25 0.742887% 0.742887% 1/1/2014

2014 $1,095.70 2.6666% 2.6666% 1/1/2015

2015 $1,120.67 2.2789% 2.2789% 1/1/2016

2016 $1,164.51 3.9119% 3.9119% 1/1/2017

COLA, Death Benefits & Mileage Rates info at:

http://www.dir.ca.gov/dwc/WorkerscompensationBenefits.htm

© 2017, Bradford & Barthel, LLP 33

COLA Projections

• Relevant Court Cases – Attorney Fees

– For each year the actual increase is less than

predicted, IW benefits are disproportionally

reduced to accommodate AA fee.

– The risk that actual COLA is greater than

predicted COLA is better borne by the attorney.

© 2015, Bradford & Barthel, LLP 34

3/21/2017

18

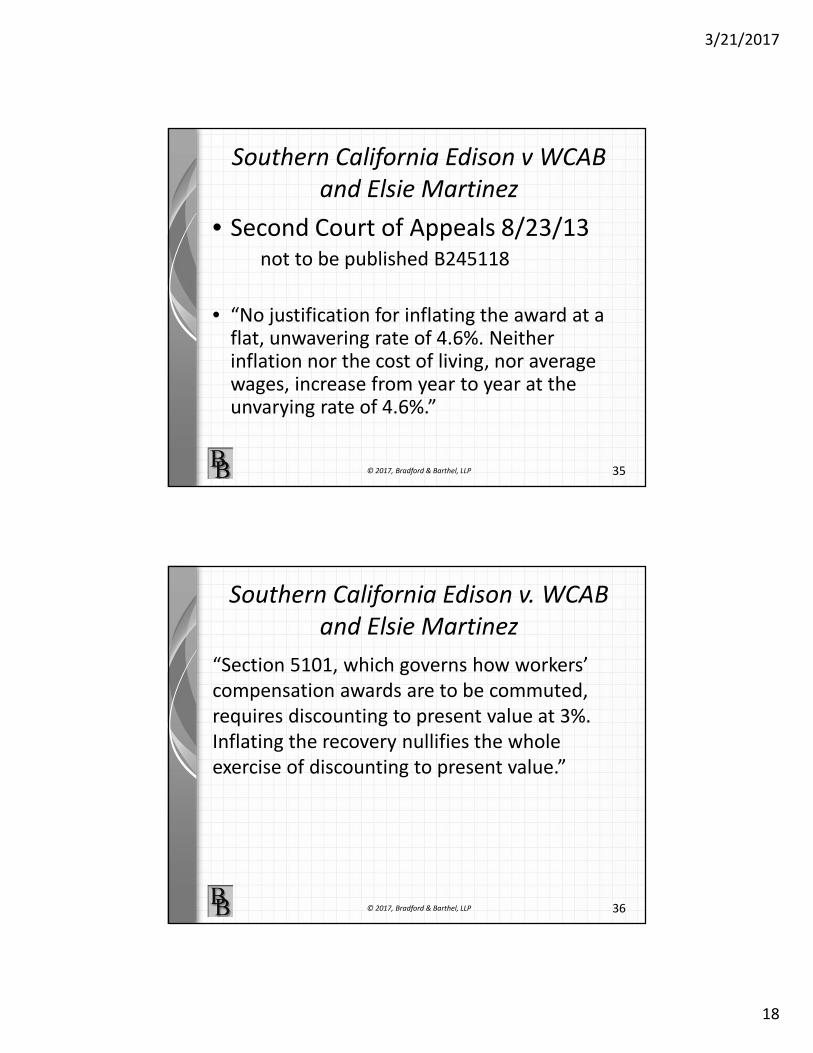

Southern California Edison v WCAB

and Elsie Martinez

• Second Court of Appeals 8/23/13not to be published B245118

• “No justification for inflating the award at a flat, unwavering rate of 4.6%. Neither inflation nor the cost of living, nor average wages, increase from year to year at the unvarying rate of 4.6%.”

© 2017, Bradford & Barthel, LLP 35

Southern California Edison v. WCAB

and Elsie Martinez

“Section 5101, which governs how workers’

compensation awards are to be commuted,

requires discounting to present value at 3%.

Inflating the recovery nullifies the whole

exercise of discounting to present value.”

© 2017, Bradford & Barthel, LLP 36

3/21/2017

19

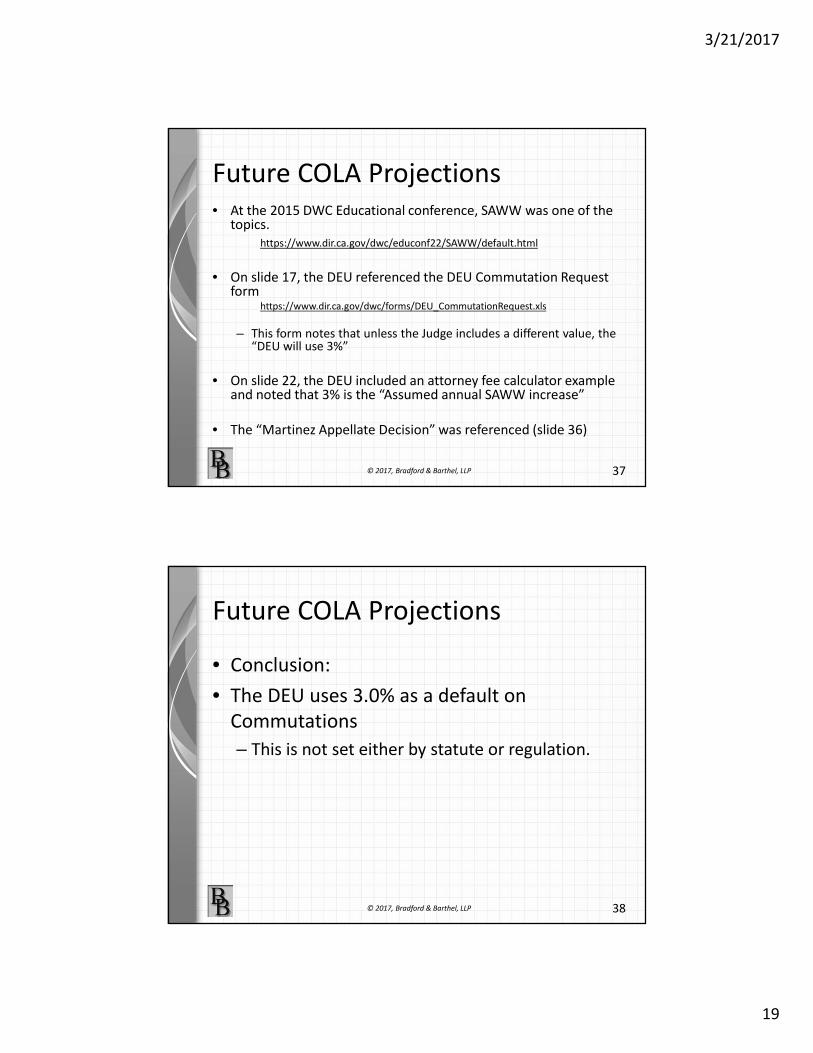

Future COLA Projections • At the 2015 DWC Educational conference, SAWW was one of the

topics.

https://www.dir.ca.gov/dwc/educonf22/SAWW/default.html

• On slide 17, the DEU referenced the DEU Commutation Request form

https://www.dir.ca.gov/dwc/forms/DEU_CommutationRequest.xls

– This form notes that unless the Judge includes a different value, the “DEU will use 3%”

• On slide 22, the DEU included an attorney fee calculator example and noted that 3% is the “Assumed annual SAWW increase”

• The “Martinez Appellate Decision” was referenced (slide 36)

© 2017, Bradford & Barthel, LLP 37

Future COLA Projections

• Conclusion:

• The DEU uses 3.0% as a default on

Commutations

– This is not set either by statute or regulation.

© 2017, Bradford & Barthel, LLP 38

3/21/2017

20

39© 2017, Bradford & Barthel, LLP

Calculating Future Benefits

• Death Benefits– Whichever is greater:

• Computation/ dependents - LC 4702

• Dependent Children – to age 18 or lifetime if

“incapacitated from earning” - LC 4703.5

– Payable in same manner as TTD – 2 year rule -

current maximum and minimum - subject to the

worker’s AWE– LC 4661.5

© 2017, Bradford & Barthel, LLP 40

3/21/2017

21

Calculating Future Benefits

PTD• Awarded benefit rate – payable through initial

year of PTD

• Life expectancy tables male/ female 2012https://www.dir.ca.gov/osip/LifeExpectancyTables2012.pdf

2012 Life Tables were published by the CDC 11/28/16 –adopted by OSIP for projections in 2017

Every January 1, apply COLA projections for PTD for duration of life expectancy

© 2017, Bradford & Barthel, LLP 41

Calculating Future Benefits

Life Pension• PPD award – calculate end date of PPD

• LP rate – awarded rate is paid through end of

year initiated

• Life expectancy

• COLA projections for LP for life expectancy

© 2017, Bradford & Barthel, LLP 42

3/21/2017

22

Calculating Reserves/ Future Benefits

• Use a spreadsheet

• Use some method of date calculation

– Excel has an available date calculator formula

• Use correct Life Expectancy tablesmale/ female

date of calculation/ commutation affects benefit end date

https://www.dir.ca.gov/osip/LifeExpectancyTables2012.pdf

© 2017, Bradford & Barthel, LLP 43

Calculating Benefits/ Reserves

• Examples (date of calculation = 4/19/2017)

–Death Benefit

–PTD

–Life Pension

• 75% PD

• 85% PD

• 99% PD

© 2017, Bradford & Barthel, LLP 44

3/21/2017

23

Calculating Benefits/ Reserves

• Example:

• Injured worker: David Burbank (male)

• DOI: 2/2/2013

• DOB: 2/7/1963

• AWE: $1500

• TTD/ Death/ PTD Rate: $1000/ week (max

TTD rate for 2013 DOI = $1066.72)

© 2017, Bradford & Barthel, LLP 45

Death Benefits

• Example:

• Injured worker: David Burbank (male)

• DOI: 2/2/2013

• DOB: 2/7/1963

• AWE: $1500

• TTD Rate: $1000/ week (max TTD rate for

2013 DOI = $1066.72)

© 2017, Bradford & Barthel, LLP 46

3/21/2017

24

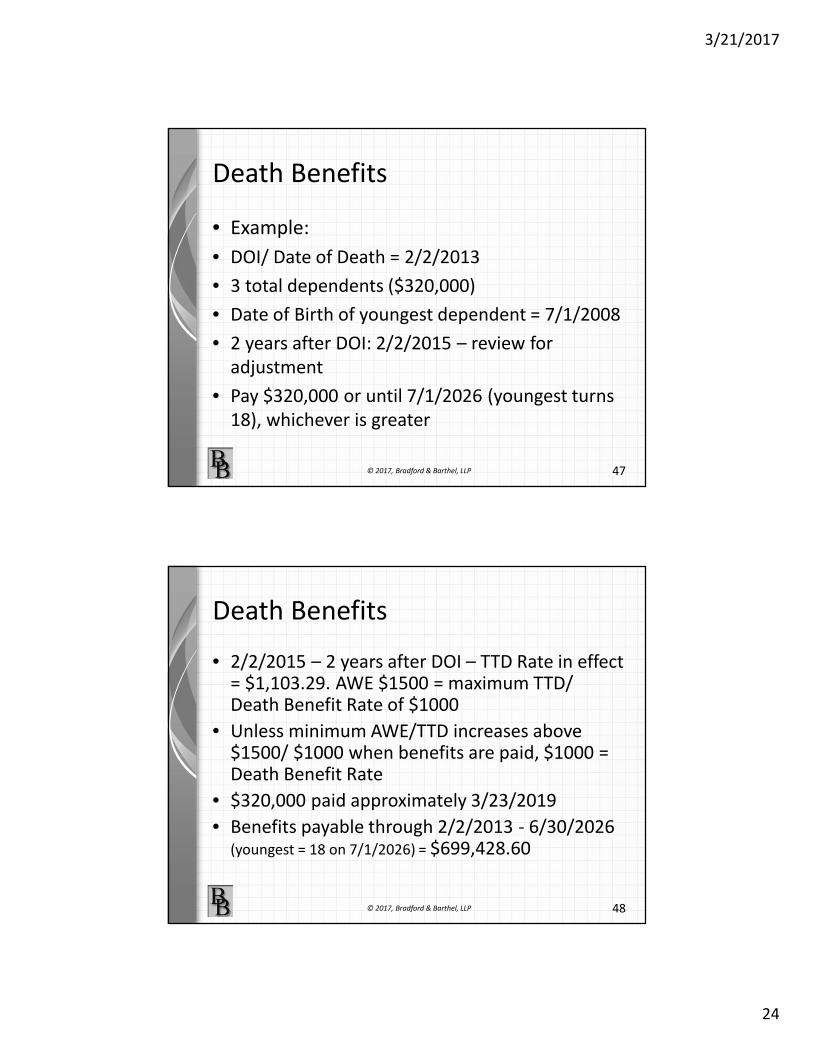

Death Benefits

• Example:

• DOI/ Date of Death = 2/2/2013

• 3 total dependents ($320,000)

• Date of Birth of youngest dependent = 7/1/2008

• 2 years after DOI: 2/2/2015 – review for

adjustment

• Pay $320,000 or until 7/1/2026 (youngest turns

18), whichever is greater

© 2017, Bradford & Barthel, LLP 47

Death Benefits

• 2/2/2015 – 2 years after DOI – TTD Rate in effect = $1,103.29. AWE $1500 = maximum TTD/ Death Benefit Rate of $1000

• Unless minimum AWE/TTD increases above $1500/ $1000 when benefits are paid, $1000 = Death Benefit Rate

• $320,000 paid approximately 3/23/2019

• Benefits payable through 2/2/2013 - 6/30/2026 (youngest = 18 on 7/1/2026) = $699,428.60

© 2017, Bradford & Barthel, LLP 48

3/21/2017

25

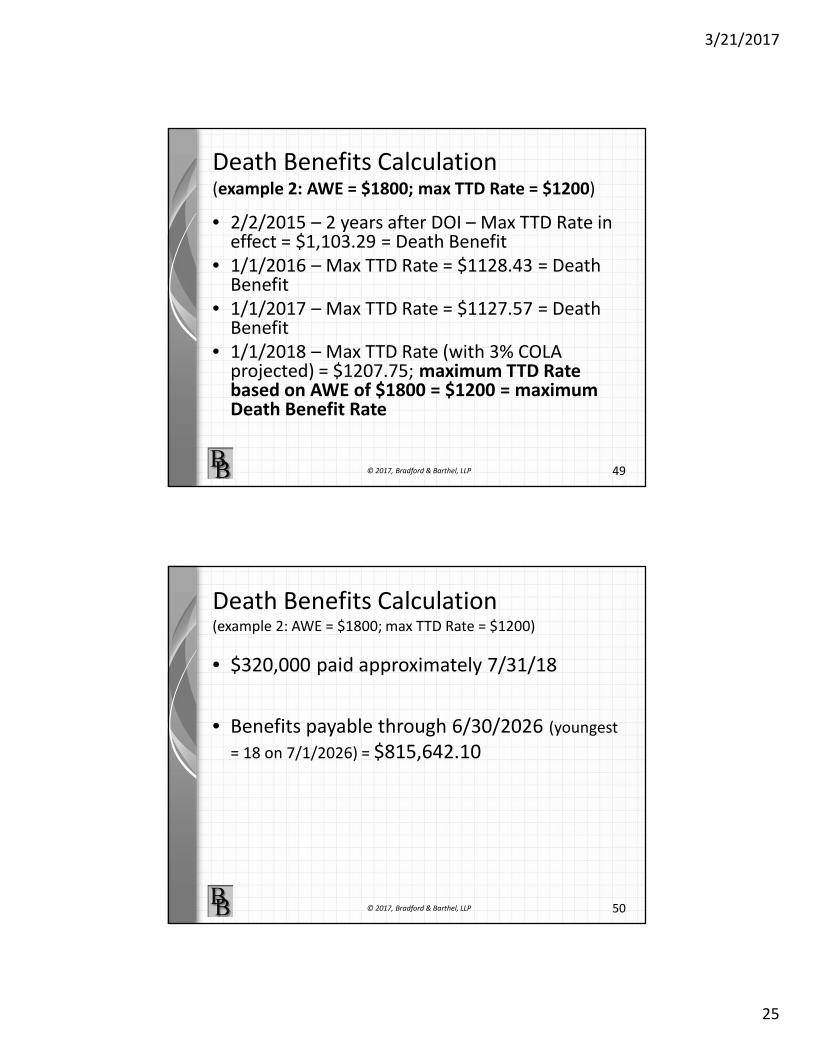

Death Benefits Calculation (example 2: AWE = $1800; max TTD Rate = $1200)

• 2/2/2015 – 2 years after DOI – Max TTD Rate in effect = $1,103.29 = Death Benefit

• 1/1/2016 – Max TTD Rate = $1128.43 = Death Benefit

• 1/1/2017 – Max TTD Rate = $1127.57 = Death Benefit

• 1/1/2018 – Max TTD Rate (with 3% COLA projected) = $1207.75; maximum TTD Rate based on AWE of $1800 = $1200 = maximum Death Benefit Rate

© 2017, Bradford & Barthel, LLP 49

Death Benefits Calculation (example 2: AWE = $1800; max TTD Rate = $1200)

• $320,000 paid approximately 7/31/18

• Benefits payable through 6/30/2026 (youngest

= 18 on 7/1/2026) = $815,642.10

© 2017, Bradford & Barthel, LLP 50

3/21/2017

26

© 2017, Bradford & Barthel, LLP 51

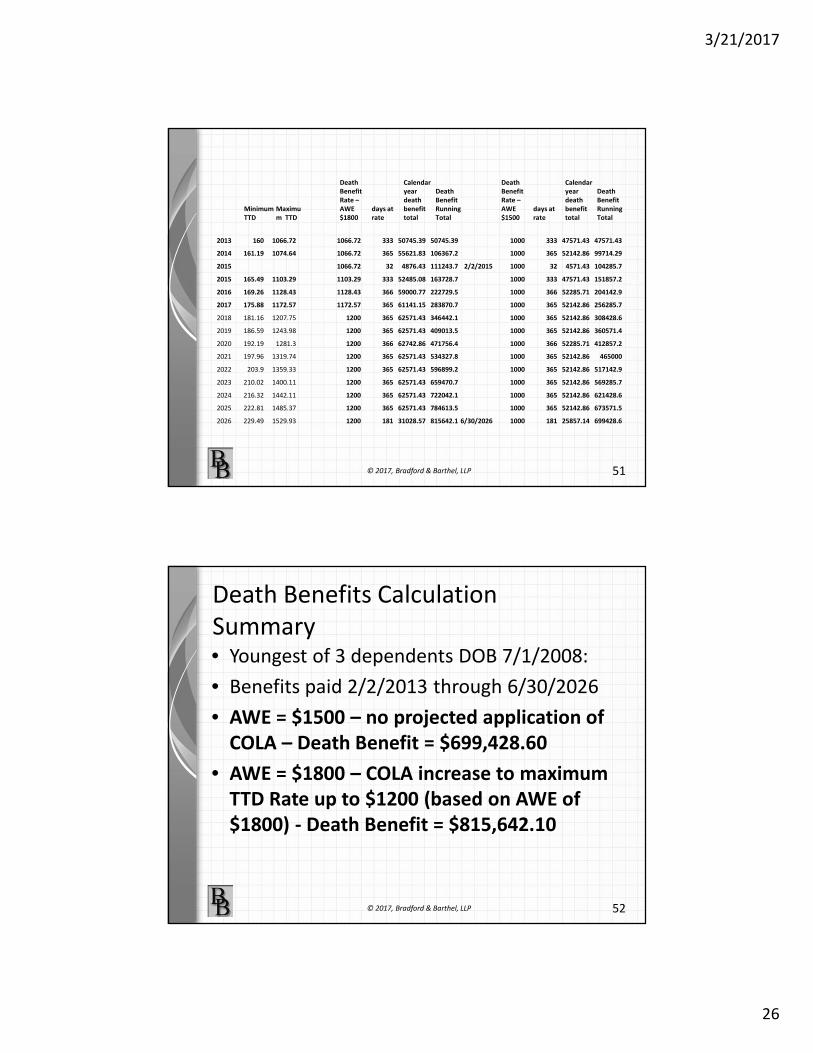

2013 160 1066.72 1066.72 333 50745.39 50745.39 1000 333 47571.43 47571.43

2014 161.19 1074.64 1066.72 365 55621.83 106367.2 1000 365 52142.86 99714.29

2015 1066.72 32 4876.43 111243.7 2/2/2015 1000 32 4571.43 104285.7

2015 165.49 1103.29 1103.29 333 52485.08 163728.7 1000 333 47571.43 151857.2

2016 169.26 1128.43 1128.43 366 59000.77 222729.5 1000 366 52285.71 204142.9

2017 175.88 1172.57 1172.57 365 61141.15 283870.7 1000 365 52142.86 256285.7

2018 181.16 1207.75 1200 365 62571.43 346442.1 1000 365 52142.86 308428.6

2019 186.59 1243.98 1200 365 62571.43 409013.5 1000 365 52142.86 360571.4

2020 192.19 1281.3 1200 366 62742.86 471756.4 1000 366 52285.71 412857.2

2021 197.96 1319.74 1200 365 62571.43 534327.8 1000 365 52142.86 465000

2022 203.9 1359.33 1200 365 62571.43 596899.2 1000 365 52142.86 517142.9

2023 210.02 1400.11 1200 365 62571.43 659470.7 1000 365 52142.86 569285.7

2024 216.32 1442.11 1200 365 62571.43 722042.1 1000 365 52142.86 621428.6

2025 222.81 1485.37 1200 365 62571.43 784613.5 1000 365 52142.86 673571.5

2026 229.49 1529.93 1200 181 31028.57 815642.1 6/30/2026 1000 181 25857.14 699428.6

Minimum

TTD

Maximu

m TTD

Death

Benefit

Rate –

AWE

$1800

days at

rate

Calendar

year

death

benefit

total

Death

Benefit

Running

Total

Death

Benefit

Rate –

AWE

$1500

days at

rate

Calendar

year

death

benefit

total

Death

Benefit

Running

Total

Death Benefits Calculation

Summary • Youngest of 3 dependents DOB 7/1/2008:

• Benefits paid 2/2/2013 through 6/30/2026

• AWE = $1500 – no projected application of

COLA – Death Benefit = $699,428.60

• AWE = $1800 – COLA increase to maximum

TTD Rate up to $1200 (based on AWE of

$1800) - Death Benefit = $815,642.10

© 2017, Bradford & Barthel, LLP 52

3/21/2017

27

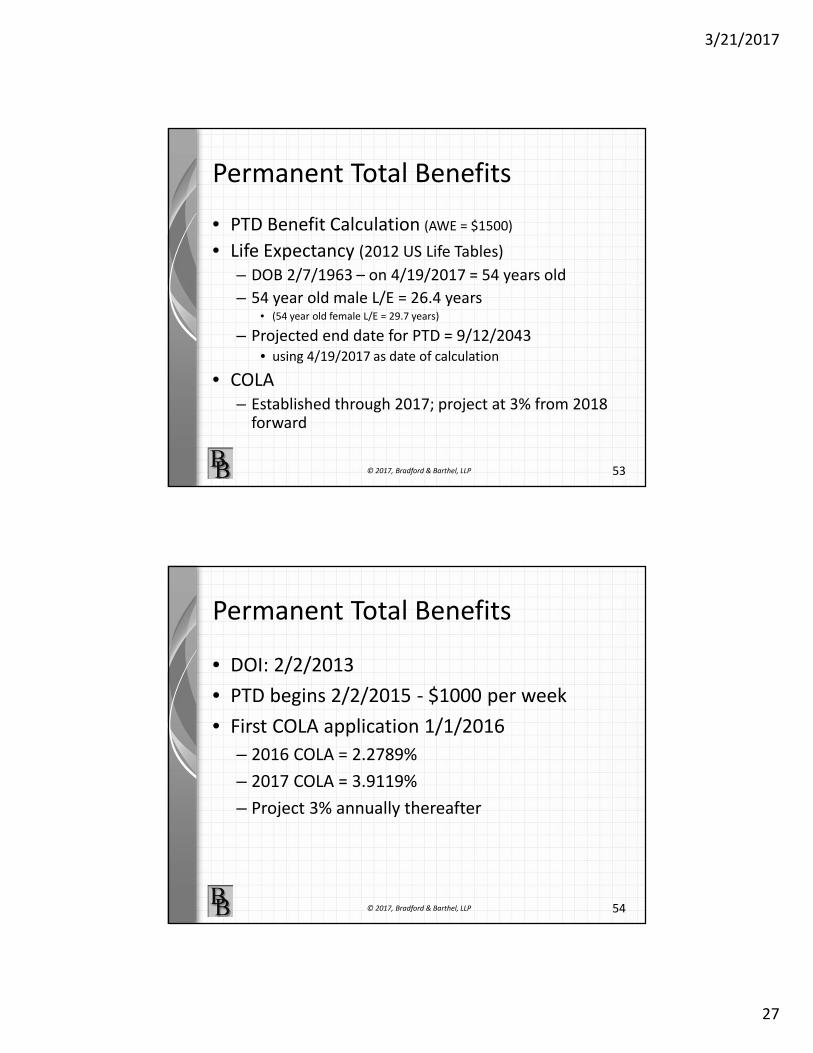

Permanent Total Benefits

• PTD Benefit Calculation (AWE = $1500)

• Life Expectancy (2012 US Life Tables)

– DOB 2/7/1963 – on 4/19/2017 = 54 years old

– 54 year old male L/E = 26.4 years • (54 year old female L/E = 29.7 years)

– Projected end date for PTD = 9/12/2043

• using 4/19/2017 as date of calculation

• COLA

– Established through 2017; project at 3% from 2018 forward

© 2017, Bradford & Barthel, LLP 53

Permanent Total Benefits

• DOI: 2/2/2013

• PTD begins 2/2/2015 - $1000 per week

• First COLA application 1/1/2016

– 2016 COLA = 2.2789%

– 2017 COLA = 3.9119%

– Project 3% annually thereafter

© 2017, Bradford & Barthel, LLP 54

3/21/2017

28

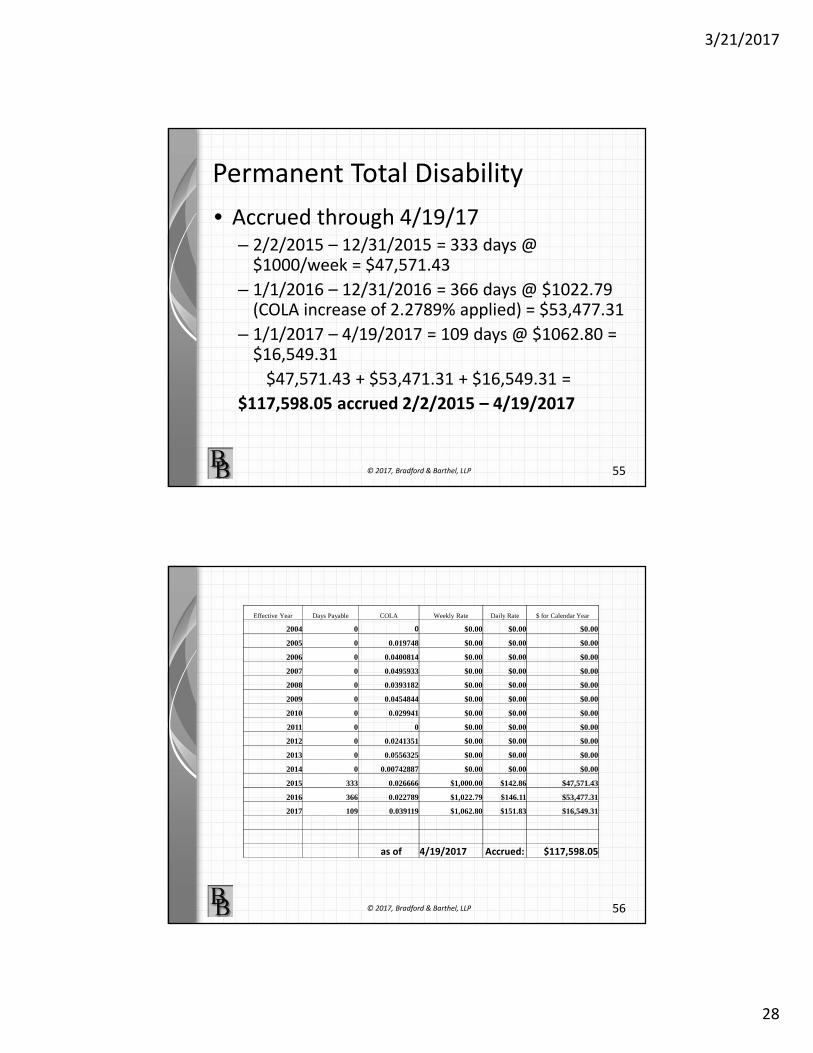

Permanent Total Disability

• Accrued through 4/19/17– 2/2/2015 – 12/31/2015 = 333 days @

$1000/week = $47,571.43

– 1/1/2016 – 12/31/2016 = 366 days @ $1022.79 (COLA increase of 2.2789% applied) = $53,477.31

– 1/1/2017 – 4/19/2017 = 109 days @ $1062.80 = $16,549.31

$47,571.43 + $53,471.31 + $16,549.31 =

$117,598.05 accrued 2/2/2015 – 4/19/2017

© 2017, Bradford & Barthel, LLP 55

© 2017, Bradford & Barthel, LLP 56

Effective Year Days Payable COLA Weekly Rate Daily Rate $ for Calendar Year

2004 0 0 $0.00 $0.00 $0.00

2005 0 0.019748 $0.00 $0.00 $0.00

2006 0 0.0400814 $0.00 $0.00 $0.00

2007 0 0.0495933 $0.00 $0.00 $0.00

2008 0 0.0393182 $0.00 $0.00 $0.00

2009 0 0.0454844 $0.00 $0.00 $0.00

2010 0 0.029941 $0.00 $0.00 $0.00

2011 0 0 $0.00 $0.00 $0.00

2012 0 0.0241351 $0.00 $0.00 $0.00

2013 0 0.0556325 $0.00 $0.00 $0.00

2014 0 0.00742887 $0.00 $0.00 $0.00

2015 333 0.026666 $1,000.00 $142.86 $47,571.43

2016 366 0.022789 $1,022.79 $146.11 $53,477.31

2017 109 0.039119 $1,062.80 $151.83 $16,549.31

as of 4/19/2017 Accrued: $117,598.05

3/21/2017

29

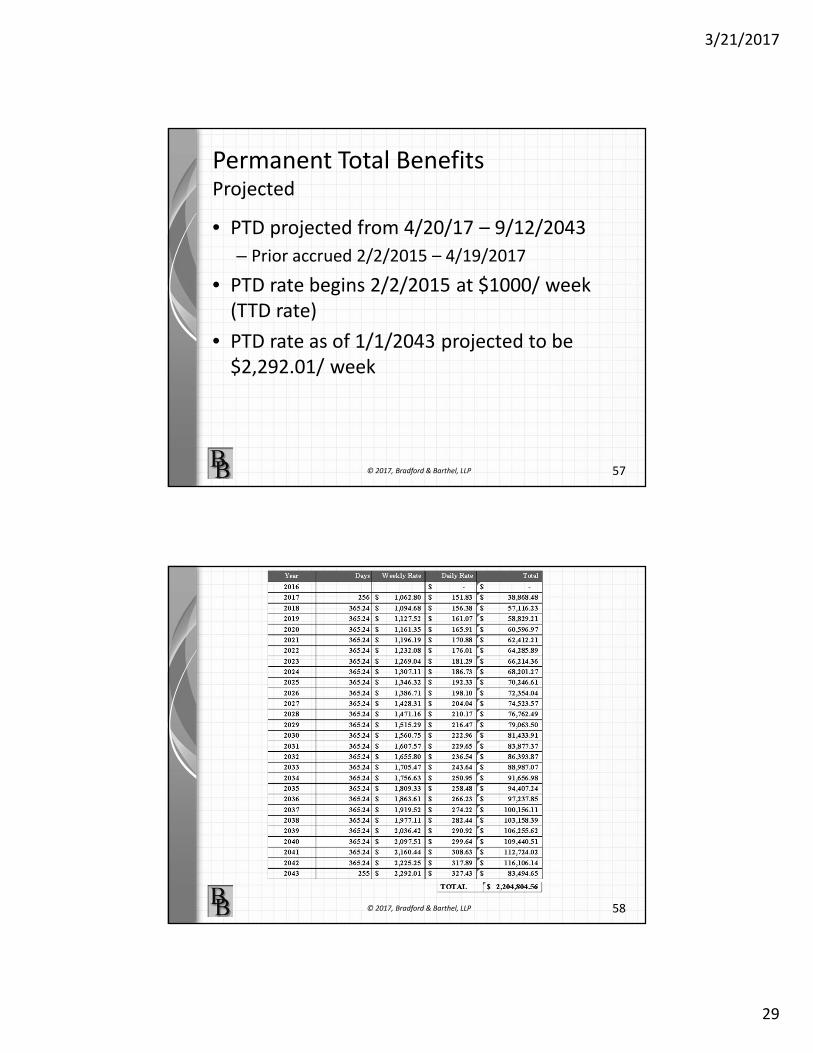

Permanent Total BenefitsProjected

• PTD projected from 4/20/17 – 9/12/2043

– Prior accrued 2/2/2015 – 4/19/2017

• PTD rate begins 2/2/2015 at $1000/ week

(TTD rate)

• PTD rate as of 1/1/2043 projected to be

$2,292.01/ week

© 2017, Bradford & Barthel, LLP 57

© 2017, Bradford & Barthel, LLP 58

3/21/2017

30

Permanent Total Benefits

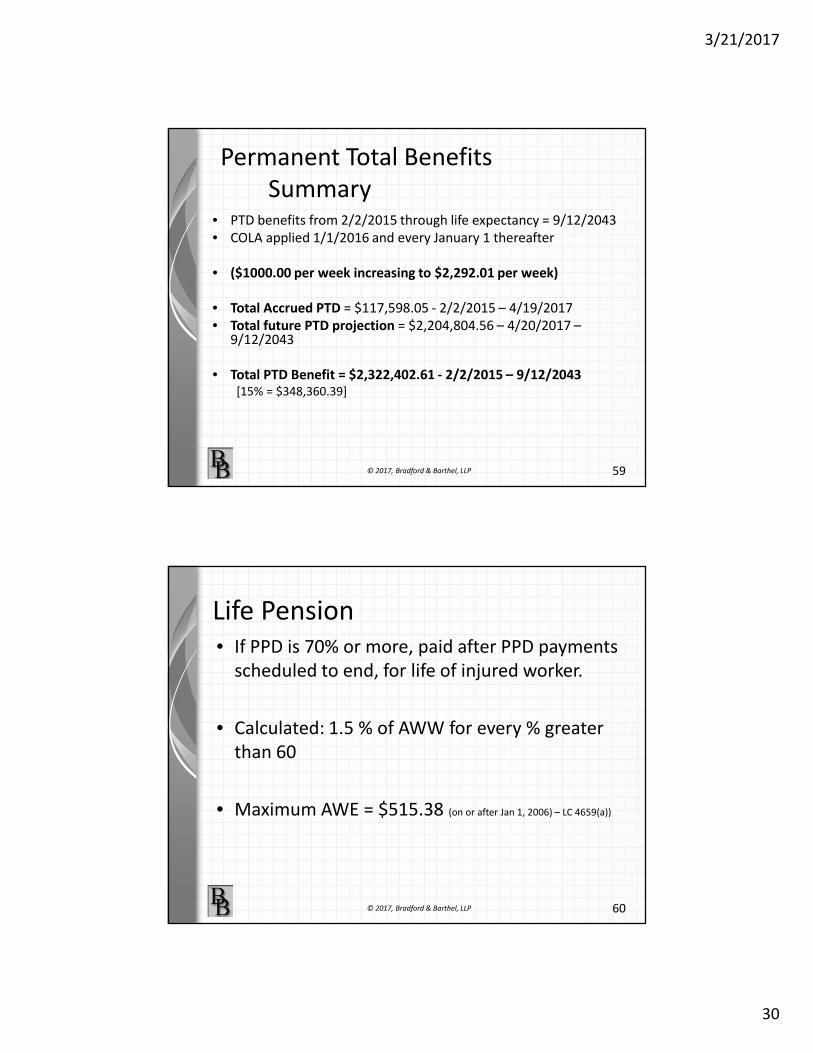

Summary• PTD benefits from 2/2/2015 through life expectancy = 9/12/2043

• COLA applied 1/1/2016 and every January 1 thereafter

• ($1000.00 per week increasing to $2,292.01 per week)

• Total Accrued PTD = $117,598.05 - 2/2/2015 – 4/19/2017

• Total future PTD projection = $2,204,804.56 – 4/20/2017 –9/12/2043

• Total PTD Benefit = $2,322,402.61 - 2/2/2015 – 9/12/2043[15% = $348,360.39]

© 2017, Bradford & Barthel, LLP 59

Life Pension• If PPD is 70% or more, paid after PPD payments

scheduled to end, for life of injured worker.

• Calculated: 1.5 % of AWW for every % greater

than 60

• Maximum AWE = $515.38 (on or after Jan 1, 2006) – LC 4659(a))

© 2017, Bradford & Barthel, LLP 60

3/21/2017

31

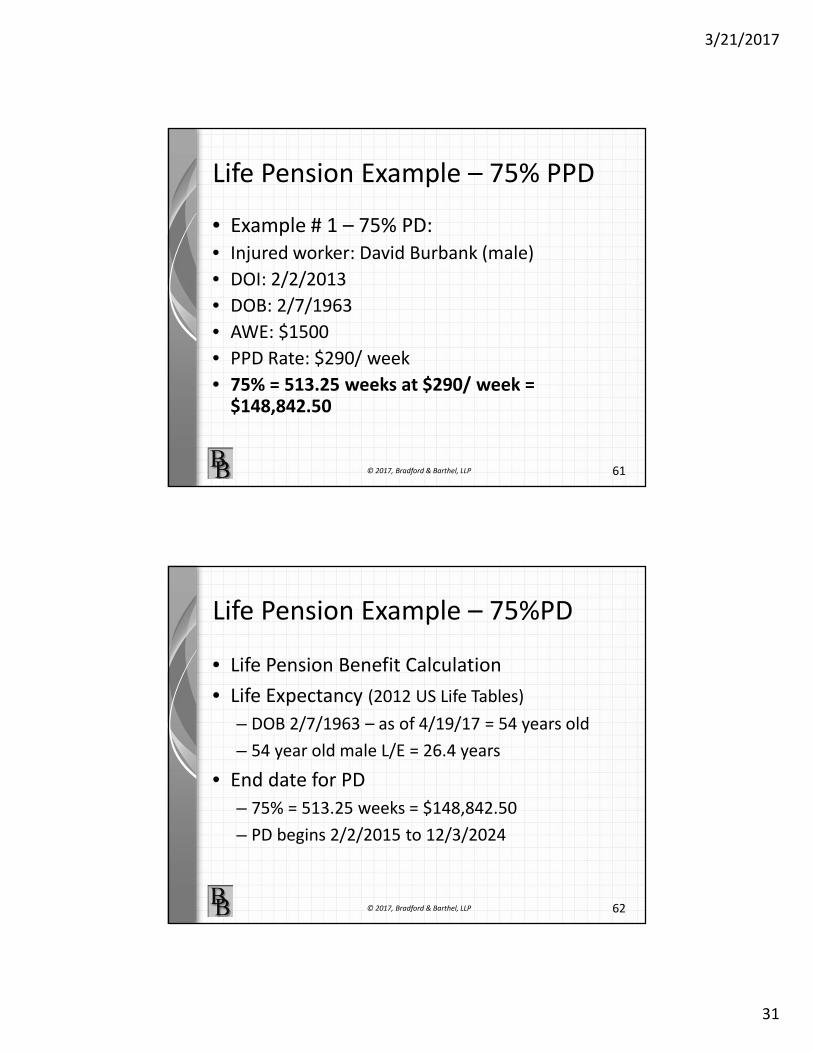

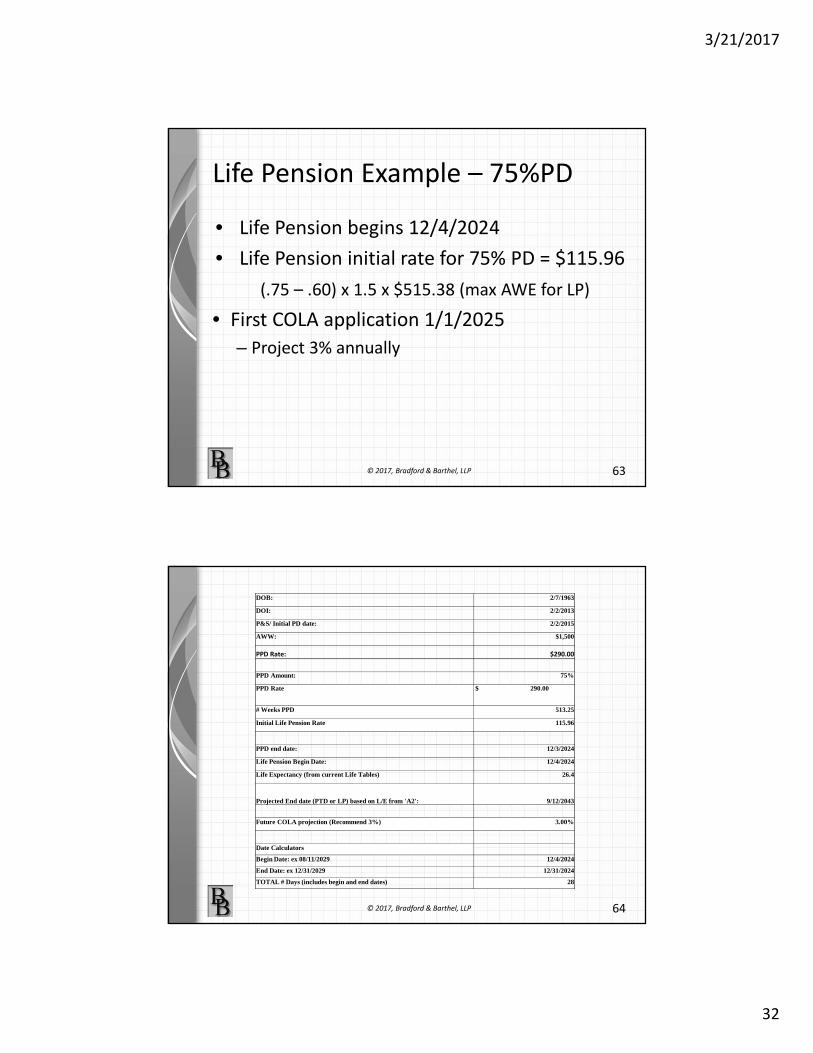

Life Pension Example – 75% PPD

• Example # 1 – 75% PD:

• Injured worker: David Burbank (male)

• DOI: 2/2/2013

• DOB: 2/7/1963

• AWE: $1500

• PPD Rate: $290/ week

• 75% = 513.25 weeks at $290/ week = $148,842.50

© 2017, Bradford & Barthel, LLP 61

Life Pension Example – 75%PD

• Life Pension Benefit Calculation

• Life Expectancy (2012 US Life Tables)

– DOB 2/7/1963 – as of 4/19/17 = 54 years old

– 54 year old male L/E = 26.4 years

• End date for PD

– 75% = 513.25 weeks = $148,842.50

– PD begins 2/2/2015 to 12/3/2024

© 2017, Bradford & Barthel, LLP 62

3/21/2017

32

Life Pension Example – 75%PD

• Life Pension begins 12/4/2024

• Life Pension initial rate for 75% PD = $115.96

(.75 – .60) x 1.5 x $515.38 (max AWE for LP)

• First COLA application 1/1/2025

– Project 3% annually

© 2017, Bradford & Barthel, LLP 63

© 2017, Bradford & Barthel, LLP 64

DOB: 2/7/1963

DOI: 2/2/2013

P&S/ Initial PD date: 2/2/2015

AWW: $1,500

PPD Rate: $290.00

PPD Amount: 75%

PPD Rate $ 290.00

# Weeks PPD 513.25

Initial Life Pension Rate 115.96

PPD end date: 12/3/2024

Life Pension Begin Date: 12/4/2024

Life Expectancy (from current Life Tables) 26.4

Projected End date (PTD or LP) based on L/E from 'A2': 9/12/2043

Future COLA projection (Recommend 3%) 3.00%

Date Calculators

Begin Date: ex 08/11/2029 12/4/2024

End Date: ex 12/31/2029 12/31/2024

TOTAL # Days (includes begin and end dates) 28

3/21/2017

33

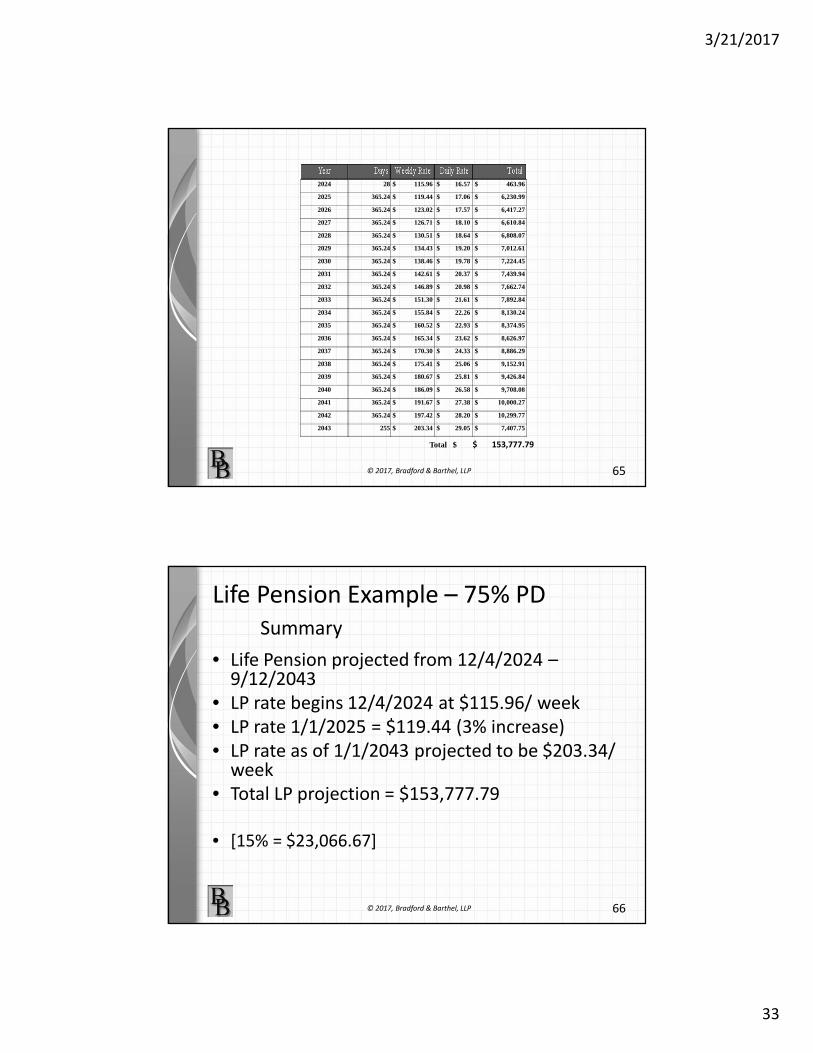

© 2017, Bradford & Barthel, LLP 65

2024 28 $ 115.96 $ 16.57 $ 463.96

2025 365.24 $ 119.44 $ 17.06 $ 6,230.99

2026 365.24 $ 123.02 $ 17.57 $ 6,417.27

2027 365.24 $ 126.71 $ 18.10 $ 6,610.84

2028 365.24 $ 130.51 $ 18.64 $ 6,808.07

2029 365.24 $ 134.43 $ 19.20 $ 7,012.61

2030 365.24 $ 138.46 $ 19.78 $ 7,224.45

2031 365.24 $ 142.61 $ 20.37 $ 7,439.94

2032 365.24 $ 146.89 $ 20.98 $ 7,662.74

2033 365.24 $ 151.30 $ 21.61 $ 7,892.84

2034 365.24 $ 155.84 $ 22.26 $ 8,130.24

2035 365.24 $ 160.52 $ 22.93 $ 8,374.95

2036 365.24 $ 165.34 $ 23.62 $ 8,626.97

2037 365.24 $ 170.30 $ 24.33 $ 8,886.29

2038 365.24 $ 175.41 $ 25.06 $ 9,152.91

2039 365.24 $ 180.67 $ 25.81 $ 9,426.84

2040 365.24 $ 186.09 $ 26.58 $ 9,708.08

2041 365.24 $ 191.67 $ 27.38 $ 10,000.27

2042 365.24 $ 197.42 $ 28.20 $ 10,299.77

2043 255 $ 203.34 $ 29.05 $ 7,407.75

Total $ $ 153,777.79

Life Pension Example – 75% PD

Summary

• Life Pension projected from 12/4/2024 –9/12/2043

• LP rate begins 12/4/2024 at $115.96/ week

• LP rate 1/1/2025 = $119.44 (3% increase)

• LP rate as of 1/1/2043 projected to be $203.34/ week

• Total LP projection = $153,777.79

• [15% = $23,066.67]

© 2017, Bradford & Barthel, LLP 66

3/21/2017

34

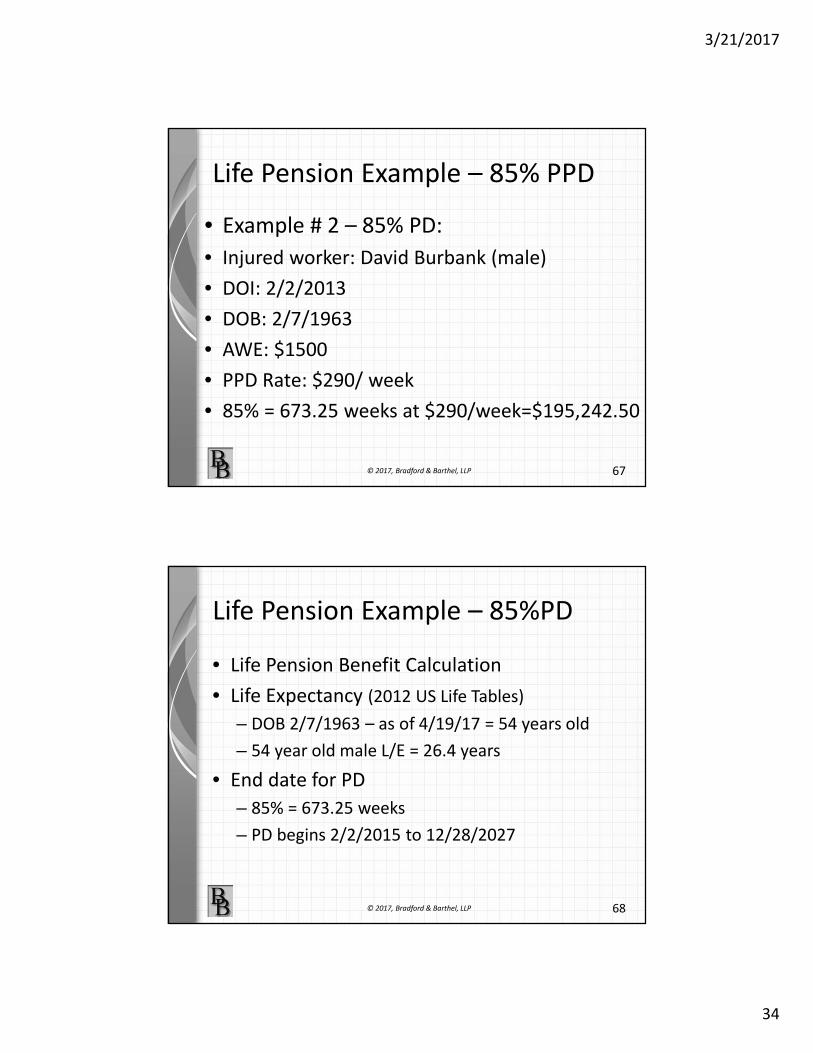

Life Pension Example – 85% PPD

• Example # 2 – 85% PD:

• Injured worker: David Burbank (male)

• DOI: 2/2/2013

• DOB: 2/7/1963

• AWE: $1500

• PPD Rate: $290/ week

• 85% = 673.25 weeks at $290/week=$195,242.50

© 2017, Bradford & Barthel, LLP 67

Life Pension Example – 85%PD

• Life Pension Benefit Calculation

• Life Expectancy (2012 US Life Tables)

– DOB 2/7/1963 – as of 4/19/17 = 54 years old

– 54 year old male L/E = 26.4 years

• End date for PD

– 85% = 673.25 weeks

– PD begins 2/2/2015 to 12/28/2027

© 2017, Bradford & Barthel, LLP 68

3/21/2017

35

Life Pension Example – 85%PD

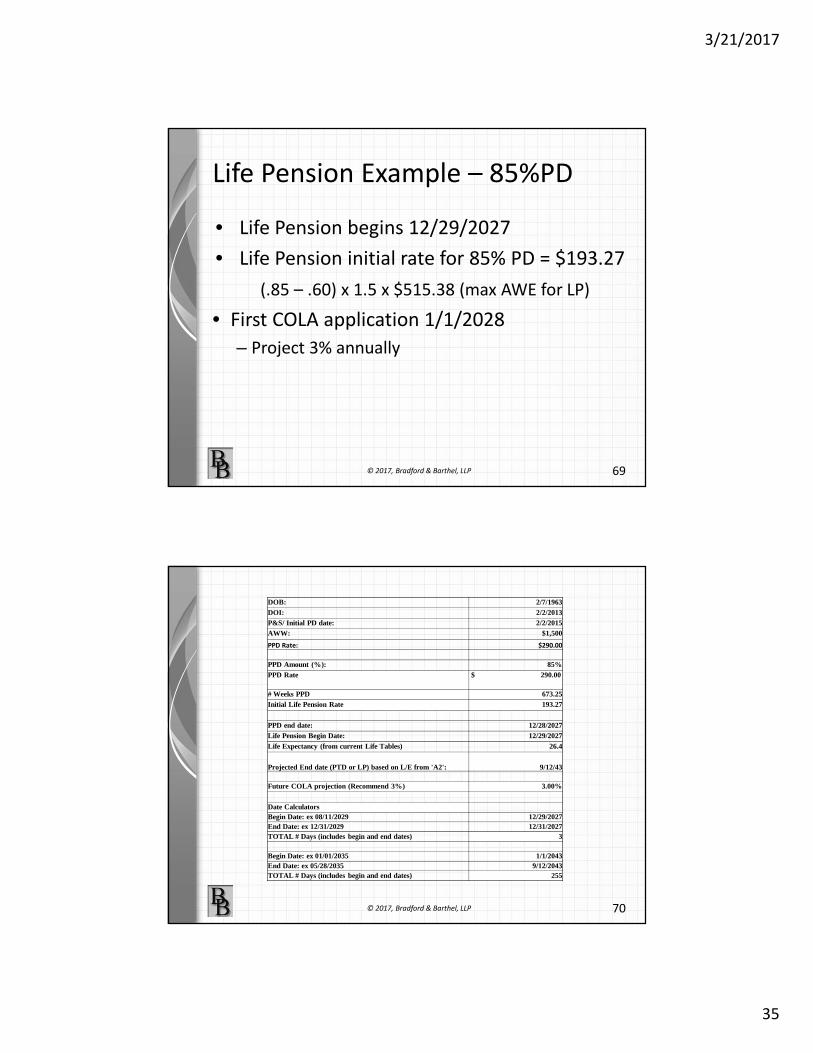

• Life Pension begins 12/29/2027

• Life Pension initial rate for 85% PD = $193.27

(.85 – .60) x 1.5 x $515.38 (max AWE for LP)

• First COLA application 1/1/2028

– Project 3% annually

© 2017, Bradford & Barthel, LLP 69

© 2017, Bradford & Barthel, LLP 70

DOB: 2/7/1963DOI: 2/2/2013P&S/ Initial PD date: 2/2/2015AWW: $1,500

PPD Rate: $290.00

PPD Amount (%): 85%PPD Rate $ 290.00

# Weeks PPD 673.25Initial Life Pension Rate 193.27

PPD end date: 12/28/2027Life Pension Begin Date: 12/29/2027Life Expectancy (from current Life Tables) 26.4

Projected End date (PTD or LP) based on L/E from 'A2': 9/12/43

Future COLA projection (Recommend 3%) 3.00%

Date CalculatorsBegin Date: ex 08/11/2029 12/29/2027End Date: ex 12/31/2029 12/31/2027TOTAL # Days (includes begin and end dates) 3

Begin Date: ex 01/01/2035 1/1/2043End Date: ex 05/28/2035 9/12/2043TOTAL # Days (includes begin and end dates) 255

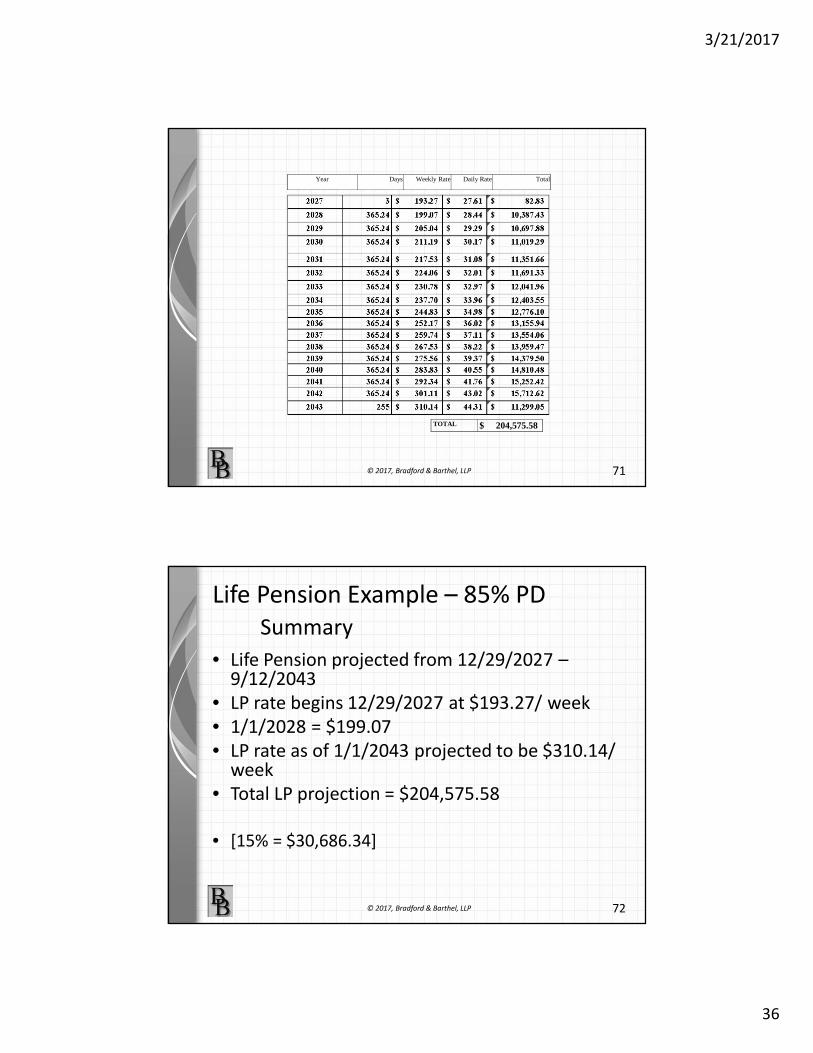

3/21/2017

36

© 2017, Bradford & Barthel, LLP 71

Year Days Weekly Rate Daily Rate Total

TOTAL $ 204,575.58

Life Pension Example – 85% PD

Summary

• Life Pension projected from 12/29/2027 –9/12/2043

• LP rate begins 12/29/2027 at $193.27/ week

• 1/1/2028 = $199.07

• LP rate as of 1/1/2043 projected to be $310.14/ week

• Total LP projection = $204,575.58

• [15% = $30,686.34]

© 2017, Bradford & Barthel, LLP 72

3/21/2017

37

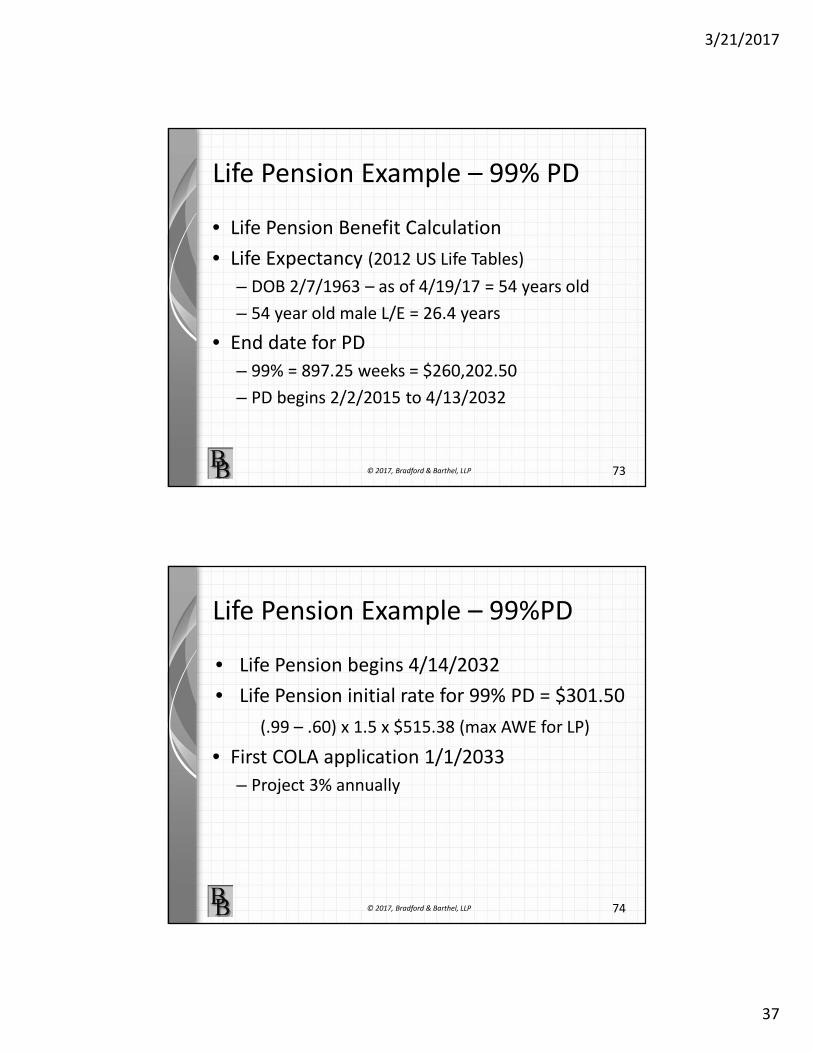

Life Pension Example – 99% PD

• Life Pension Benefit Calculation

• Life Expectancy (2012 US Life Tables)

– DOB 2/7/1963 – as of 4/19/17 = 54 years old

– 54 year old male L/E = 26.4 years

• End date for PD

– 99% = 897.25 weeks = $260,202.50

– PD begins 2/2/2015 to 4/13/2032

© 2017, Bradford & Barthel, LLP 73

Life Pension Example – 99%PD

• Life Pension begins 4/14/2032

• Life Pension initial rate for 99% PD = $301.50

(.99 – .60) x 1.5 x $515.38 (max AWE for LP)

• First COLA application 1/1/2033

– Project 3% annually

© 2017, Bradford & Barthel, LLP 74

3/21/2017

38

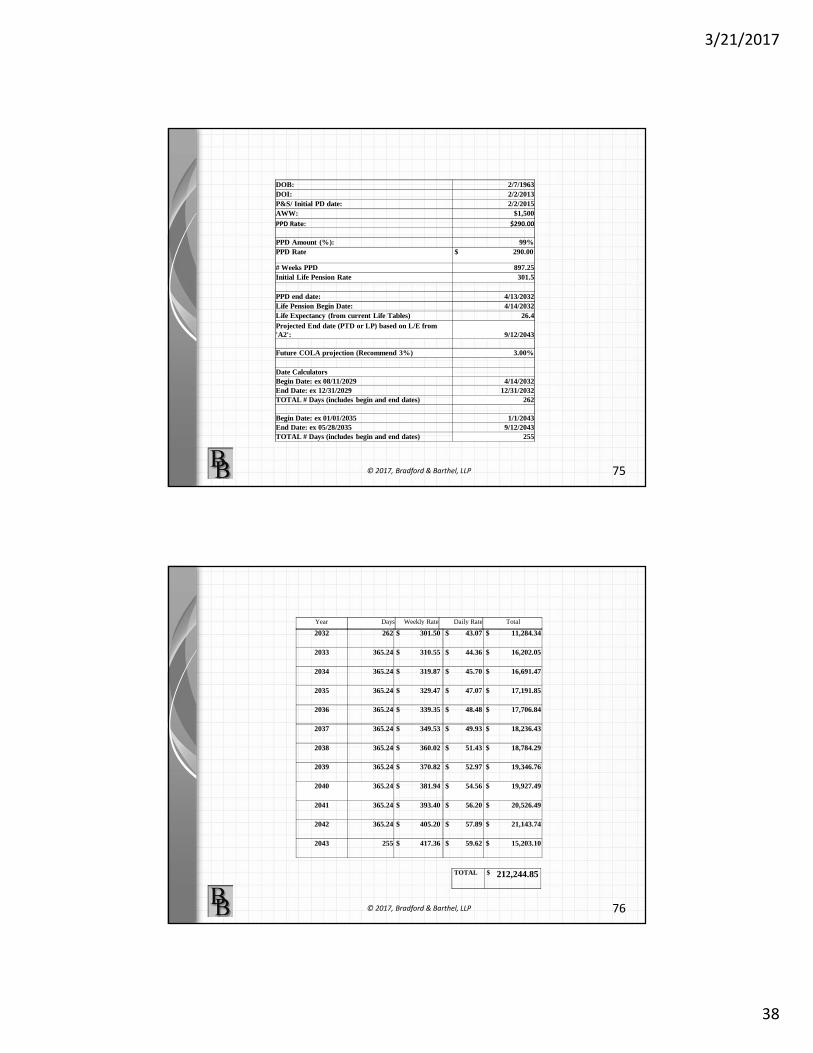

© 2017, Bradford & Barthel, LLP 75

DOB: 2/7/1963DOI: 2/2/2013P&S/ Initial PD date: 2/2/2015AWW: $1,500 PPD Rate: $290.00

PPD Amount (%): 99%PPD Rate $ 290.00

# Weeks PPD 897.25Initial Life Pension Rate 301.5

PPD end date: 4/13/2032Life Pension Begin Date: 4/14/2032Life Expectancy (from current Life Tables) 26.4Projected End date (PTD or LP) based on L/E from 'A2': 9/12/2043

Future COLA projection (Recommend 3%) 3.00%

Date CalculatorsBegin Date: ex 08/11/2029 4/14/2032End Date: ex 12/31/2029 12/31/2032TOTAL # Days (includes begin and end dates) 262

Begin Date: ex 01/01/2035 1/1/2043End Date: ex 05/28/2035 9/12/2043TOTAL # Days (includes begin and end dates) 255

© 2017, Bradford & Barthel, LLP 76

Year Days Weekly Rate Daily Rate Total

TOTAL $ 212,244.85

2032 262 $ 301.50 $ 43.07 $ 11,284.34

2033 365.24 $ 310.55 $ 44.36 $ 16,202.05

2034 365.24 $ 319.87 $ 45.70 $ 16,691.47

2035 365.24 $ 329.47 $ 47.07 $ 17,191.85

2036 365.24 $ 339.35 $ 48.48 $ 17,706.84

2037 365.24 $ 349.53 $ 49.93 $ 18,236.43

2038 365.24 $ 360.02 $ 51.43 $ 18,784.29

2039 365.24 $ 370.82 $ 52.97 $ 19,346.76

2040 365.24 $ 381.94 $ 54.56 $ 19,927.49

2041 365.24 $ 393.40 $ 56.20 $ 20,526.49

2042 365.24 $ 405.20 $ 57.89 $ 21,143.74

2043 255 $ 417.36 $ 59.62 $ 15,203.10

3/21/2017

39

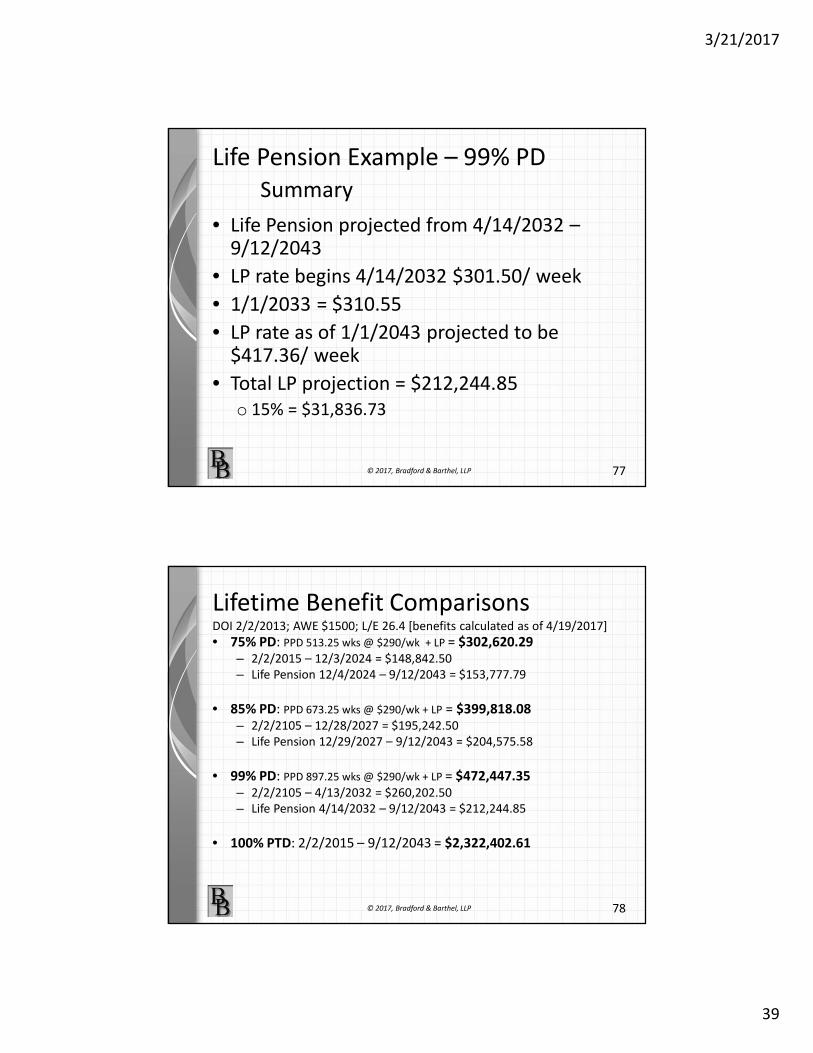

Life Pension Example – 99% PD

Summary

• Life Pension projected from 4/14/2032 –9/12/2043

• LP rate begins 4/14/2032 $301.50/ week

• 1/1/2033 = $310.55

• LP rate as of 1/1/2043 projected to be $417.36/ week

• Total LP projection = $212,244.85

o 15% = $31,836.73

© 2017, Bradford & Barthel, LLP 77

Lifetime Benefit ComparisonsDOI 2/2/2013; AWE $1500; L/E 26.4 [benefits calculated as of 4/19/2017]

• 75% PD: PPD 513.25 wks @ $290/wk + LP = $302,620.29– 2/2/2015 – 12/3/2024 = $148,842.50

– Life Pension 12/4/2024 – 9/12/2043 = $153,777.79

• 85% PD: PPD 673.25 wks @ $290/wk + LP = $399,818.08 – 2/2/2105 – 12/28/2027 = $195,242.50

– Life Pension 12/29/2027 – 9/12/2043 = $204,575.58

• 99% PD: PPD 897.25 wks @ $290/wk + LP = $472,447.35 – 2/2/2105 – 4/13/2032 = $260,202.50

– Life Pension 4/14/2032 – 9/12/2043 = $212,244.85

• 100% PTD: 2/2/2015 – 9/12/2043 = $2,322,402.61

© 2017, Bradford & Barthel, LLP 78

3/21/2017

40

Attorney Fees

• Based on calculation of benefits

• COLA projections used to calculate total

benefits

• Case law indicates that benefit increases

should be projected at no more than 3%

when used to evaluate attorney fees

© 2017, Bradford & Barthel, LLP 79

Attorney FeesLifetime Benefits – Attorney Fees

• LC 4906(d) In establishing a reasonable attorney’s fee, consideration

shall be given to the responsibility assumed by the attorney,

the care exercised in representing the applicant, the time

involved, and the results obtained.

• DEU – 2015 Educational Conference

– Topic of SAWW:

Default Calculation Attorney Fees = PV of Future Benefits x

15%

© 2017, Bradford & Barthel, LLP 80

3/21/2017

41

Summary

• COLA is calculated using Dept of Labor average weekly wage reported in 1st quarter, compared to prior year first quarter.

• COLA increases payment on January 1 of the year after the beginning of PTD or Life Pension, and every January 1 thereafter, for dates of injury Jan 1, 2003 and later.

• Projected COLA rate needed to estimate future increases (3%).

• Calculate beginning/ ending dates.

• Use correct Life Expectancy (Male/ Female).

© 2017, Bradford & Barthel, LLP 81

CommutationsCommutation of attorney fees is the most common application.

for lifetime benefits, attorney fee is probably not a flat 15%.

• The following link is to the DIR page with Commutation templates and instructions:

• http://www.dir.ca.gov/dwc/deu.html– Disability Evaluation Unit forms

– Commutation templates and instructions.zip file

• The next link is to the DIR and 3 PV tables that are needed for the commutations. (PV is calculated using 3%)

• https://www.dir.ca.gov/t8/10169.html

© 2017, Bradford & Barthel, LLP 82

3/21/2017

42

Commutations

• section 10169 and 10169.1 of Title 8, California Code of Regulations.

– https://www.dir.ca.gov/t8/10169.html

• Commutation Instructions

• Table 1Table 2Table 3

Table 1 (“Present Value of Permanent Disability at 3% Interest”) as issued in January 2001,

Table 2 (“Present Value of Life Pension at 3% Interest for a Male”) as issued in July 2001,

Table 3 (“Present Value of Life Pension at 3% Interest for a Female”) as issued in July 2001, and “Commutation Instructions” as issued in January 2001, are hereby incorporated by reference in their entirety as though they were set forth below. The tables and instructions are available from any office of the Division of Workers' Compensation and may be accessed and printed from the Division's homepage at www.dir.ca.gov.

© 2017, Bradford & Barthel, LLP 83

Commutations

Methods of CommutationA - Commutation of all remaining PD

B - Commutation of PD “Off the Far End”

C - Commutation of PD by Uniform Reduction

D - Commutation of all remaining Life Pension after commencement of LP

E - Commutation of all remaining Life Pension before commencement of LP

F - Commutation of portion of remaining Life by uniform reduction of LP

G - Uniform reduction of deferred Life Pension

© 2017, Bradford & Barthel, LLP 84

3/21/2017

43

Commutations

• The two most common commutations requested/ approved are:– Off the far end

– Uniform reduction

• There may be separate commutations for a Life Pension case – one for PD, one for LP.– If commutation of PD is “off the far end”, it results in

a gap in benefits between the end of PD and beginning of Life pension

– If PPD and LP are each commuted ‘by uniform reduction’ there is not a gap in benefits

© 2017, Bradford & Barthel, LLP 85

Commutations

– Which Commutation template

– Ex A, B, C, D, E, F, G

• Life Expectancy Tables (needed for lifetime benefit

projections - PTD and Life Pension

– http://www.dir.ca.gov/osip/LifeExpectancyTables2012

© 2017, Bradford & Barthel, LLP 86

3/21/2017

44

Commutations – PreviewApril Webinar

• Commutations – lump sum payment of benefits

• Used to pay applicant attorney fees

• DEU default calculation on lifetime benefits includes PV calculation

• ‘off the far end’ leaves a gap before LP

• Uniform reduction method provides continuing, although reduced benefits

© 2017, Bradford & Barthel, LLP 87

Tim Mussack

(916) 569-0790