Cognitive Corporate Presentation

25

CCF CORPORATE PRESENTATION 1

-

Upload

charles-thoma -

Category

Documents

-

view

43 -

download

2

Transcript of Cognitive Corporate Presentation

CCF CORPORATE PRESENTATION

1

1. About Cognitive

2. The Market

3. Services

4. Investor Network

5. The Fundraising Process

TABLE OF CONTENTS

2

6. Goals and Value Added by Cognitive

7. CCF’S Value Added

8. Mandates & Pipeline

9. The Team

AnnexesStructure of a MandateServices for Investment Funds

1. ABOUT COGNITIVE

3

Cognition is "the mental action or process of acquiring knowledge and understanding through thought, experience, and the senses.”

It encompasses processes such as knowledge, attention, memory and working memory, judgment and evaluation, reasoning and "computation", problem solving and decision making, comprehension and production of language, etc.

Human cognition is conscious and unconscious, concrete or abstract, as well as intuitive (like knowledge of a language) and conceptual (like a model of a language).

Cognitive processes use existing knowledge and generate new knowledge.

• Cognitive is a cutting-edge Corporate Finance firm founded with the objective of providing new and innovative financial services on a global scale.

• The team has more than 60 years’ combined experience, covering every function of the C-suite financial specter, and has managed practically every major financial event in the life of a corporate, SPV or investment vehicle.

• Cognitive Corporate Finance aims to be the most holistic, most connected and most effective corporate finance advisor in the world in the field of Private Equity-like transactions*.

• Using our proprietary investors’ network, we aim to be so intimately aware of the needs of institutional and corporate investors worldwide that we can match – in real time – a well-expressed funding need with the most relevant sources of capital most likely to complete the transaction.

• We want to bring our clients the most relevant financial advice, the optimal financial solution and the best and fastest service in finding capital for their corporate requirements.

*We define Private Equity-like transactions as any transaction executed outside the realm of capital markets and listed securities.

2. THE MARKET

4

• Cognitive works primarily with Small and Medium Enterprises, as well as corporate and private Special Purpose Vehicles, on transactions ranging from a minimum of €1m and a maximum of €100m.

• The large professional services firms (KPMG, PwC, etc.) and investment banks (Goldman Sachs, BoAML, BNP Paribas, etc.) typically do not address this market with a service offering that is both affordable and adapted to such SMEs and entities.

• And yet, SMEs and SPVs are faced with almost all of the complex strategic and financial issues of large corporates and financial institutions. Put simply, this market seeks:

• High value added and focused advice from seasoned professionals who know all the intricacies of a Profit & Loss Statement, Balance Sheet and Cash Flow forecasts,

• Advisors who have been managers, and managers who know how to advise,• Well-rounded financiers who know not only how to analyze, but also how to DO and how to DELIVER

results.• Cognitive’s offering to the market delivers all this, but also a deep range of contacts at a European level that allows

it to help its clients execute a given solution:

• Fundraising & financing• Mergers & Acquisitions• Corporate and Real Estate disposals• Investment appraisals

• Restructurings• Joint Ventures• Other complex projects and transactions.

• In short, Cognitive provides financial solutions: both the theory, and the actual cash in the bank or the relevant partner. Not just talking about what is needed, but doing what needs to get done to solve the issue at hand.

3. SERVICES

5

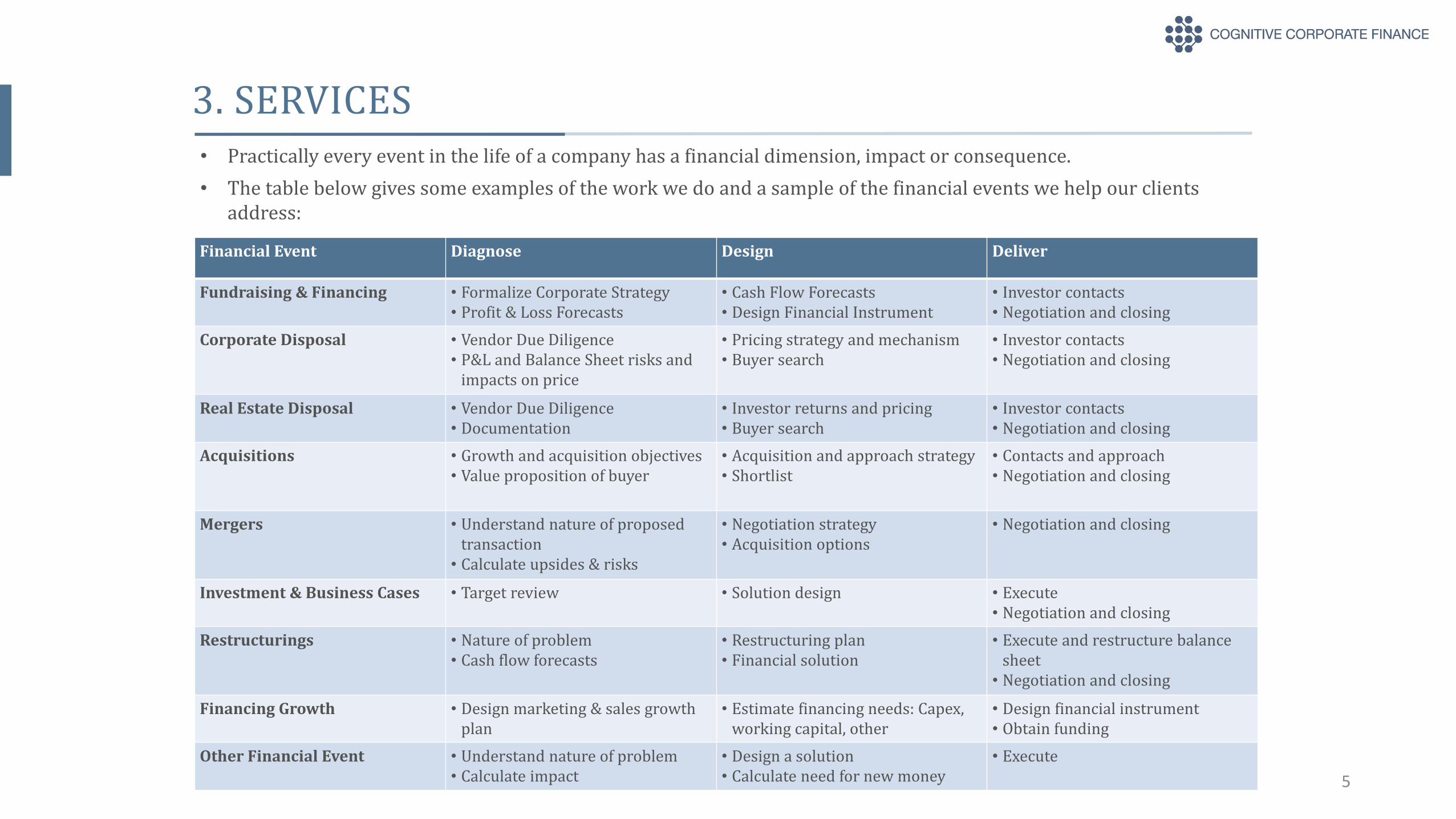

• Practically every event in the life of a company has a financial dimension, impact or consequence.• The table below gives some examples of the work we do and a sample of the financial events we help our clients

address:

Financial Event Diagnose Design Deliver

Fundraising & Financing • Formalize Corporate Strategy• Profit & Loss Forecasts

• Cash Flow Forecasts• Design Financial Instrument

• Investor contacts• Negotiation and closing

Corporate Disposal • Vendor Due Diligence• P&L and Balance Sheet risks and

impacts on price

• Pricing strategy and mechanism• Buyer search

• Investor contacts• Negotiation and closing

Real Estate Disposal • Vendor Due Diligence• Documentation

• Investor returns and pricing• Buyer search

• Investor contacts• Negotiation and closing

Acquisitions • Growth and acquisition objectives• Value proposition of buyer

• Acquisition and approach strategy• Shortlist

• Contacts and approach• Negotiation and closing

Mergers • Understand nature of proposed transaction

• Calculate upsides & risks

• Negotiation strategy• Acquisition options

• Negotiation and closing

Investment & Business Cases • Target review • Solution design • Execute• Negotiation and closing

Restructurings • Nature of problem• Cash flow forecasts

• Restructuring plan• Financial solution

• Execute and restructure balance sheet

• Negotiation and closing

Financing Growth • Design marketing & sales growth plan

• Estimate financing needs: Capex, working capital, other

• Design financial instrument• Obtain funding

Other Financial Event • Understand nature of problem• Calculate impact

• Design a solution• Calculate need for new money

• Execute

4. INVESTOR NETWORK – STRUCTURE

6

Personal contact:Whom do we know?

Geographic remit:Where do / can these investors deploy their funds?

Sector preference:Which sectors do these investors target?

Transaction type:How do these investors deploy their money? Majority/minority equity, senior/ junior debt, mezzanine, asset deals, special sits, etc.

Transaction ticket:What is the minimum/ maximum transaction these investors will consider?

Puttingitalltogether…:What is the indicative investment appetite for the transaction proposed by our client?

• It is estimated that there are well over60,000 institutional investors betweenCalifornia and Dubai (and morebeyond), each of whom usually has arazor-sharp investment strategy.

• Cognitive is in contact with thousands ofthese financial and industrial investorsand we grow our network on acontinuous basis.

• To the extent that we are primarily SellSide advisers, we dedicate significanttime, resources and technology tounderstanding these investors’ detailedinvestment specifications.

• Our key goal is to be as accurate aspossible when presenting an investmentopportunity to the market on behalf ofone of our clients.

4. INVESTOR NETWORK – FUNCTIONALITIES

7

• Capturing the information on institutional investors – though a necessary exercise – is not sufficient to effectively assist our clients in identifying the relevant “pockets” of capital for their project.

• For this reason, we have developed our technology and functionalities to allow us:

• To filter more effectively using “soft” information,

• To measure the quality, recency and relevance of our data,

• To track all our past contacts between our clients and their relevant investors.

• These functionalities permit us to match – in real time – the investors that would be most likely to complete the transaction proposed by our client.

• It is through these functionalities that our investor network “comes alive” and serves our clients.

4. INVESTOR NETWORK – REACH

8

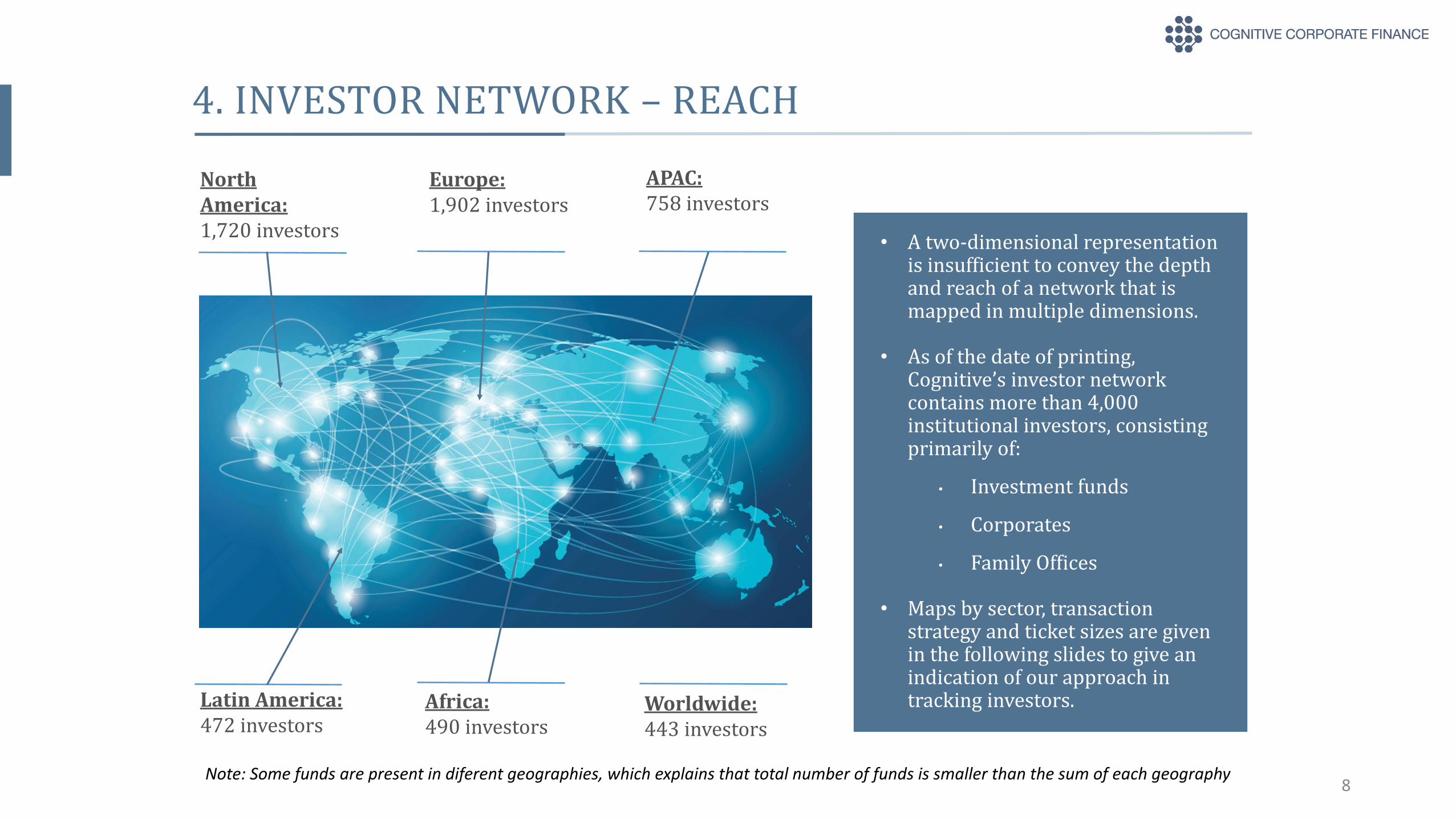

North America:1,720 investors

Europe:1,902 investors

APAC:758 investors

Latin America:472 investors

Africa:490 investors

Worldwide:443 investors

• A two-dimensional representation is insufficient to convey the depth and reach of a network that is mapped in multiple dimensions.

• As of the date of printing, Cognitive’s investor network contains more than 4,000 institutional investors, consisting primarily of:

• Investment funds

• Corporates

• Family Offices

• Maps by sector, transaction strategy and ticket sizes are given in the following slides to give an indication of our approach in tracking investors.

Note: Some funds are present in diferent geographies, which explains that total number of funds is smaller than the sum of each geography

4. INVESTOR NETWORK – BREAKDOWN

9

Investment tickets:• The amount of capital an investment fund

puts to work is a direct function of their Assets Under Management, and their need for diversification.

• For corporates, the investment ticket size is most often a function of the size of its balance sheet.

666

2145

2645

1507

566

Investment Sizes

MicroSmallMediumLargeMacro

Transaction strategy:The vast majority of institutional investors specify clearly the sort of transaction in which they can participate. Investment Funds that are structured to invest as majority investors usually do not take minority participations and almost never participate in debt transactions. Lending funds may or may not participate in project finance, and Special Situations funds rarely participate in any of the other transaction categories

Transaction strategy Number of InvestorsMajority equity 2,200Minority equity 2,079Loan – Mezzanine & convertible 588Loan – Senior debt 474Loan – Junior debt 361Project finance 152Special situations 344Loan to own 173Asset deals 192Litigation 49Structured finance 53Real estate – Core 387Real estate – Core plus 390Real estate – Value add 442Real estate – Development 674Funds of funds 226Other 64

Note: One same fund can have different investmentstrategies/tickets, which explains that total number of funds is smaller than the sum of the above figures

4. INVESTOR NETWORK – BREAKDOWN (cont’d)

10

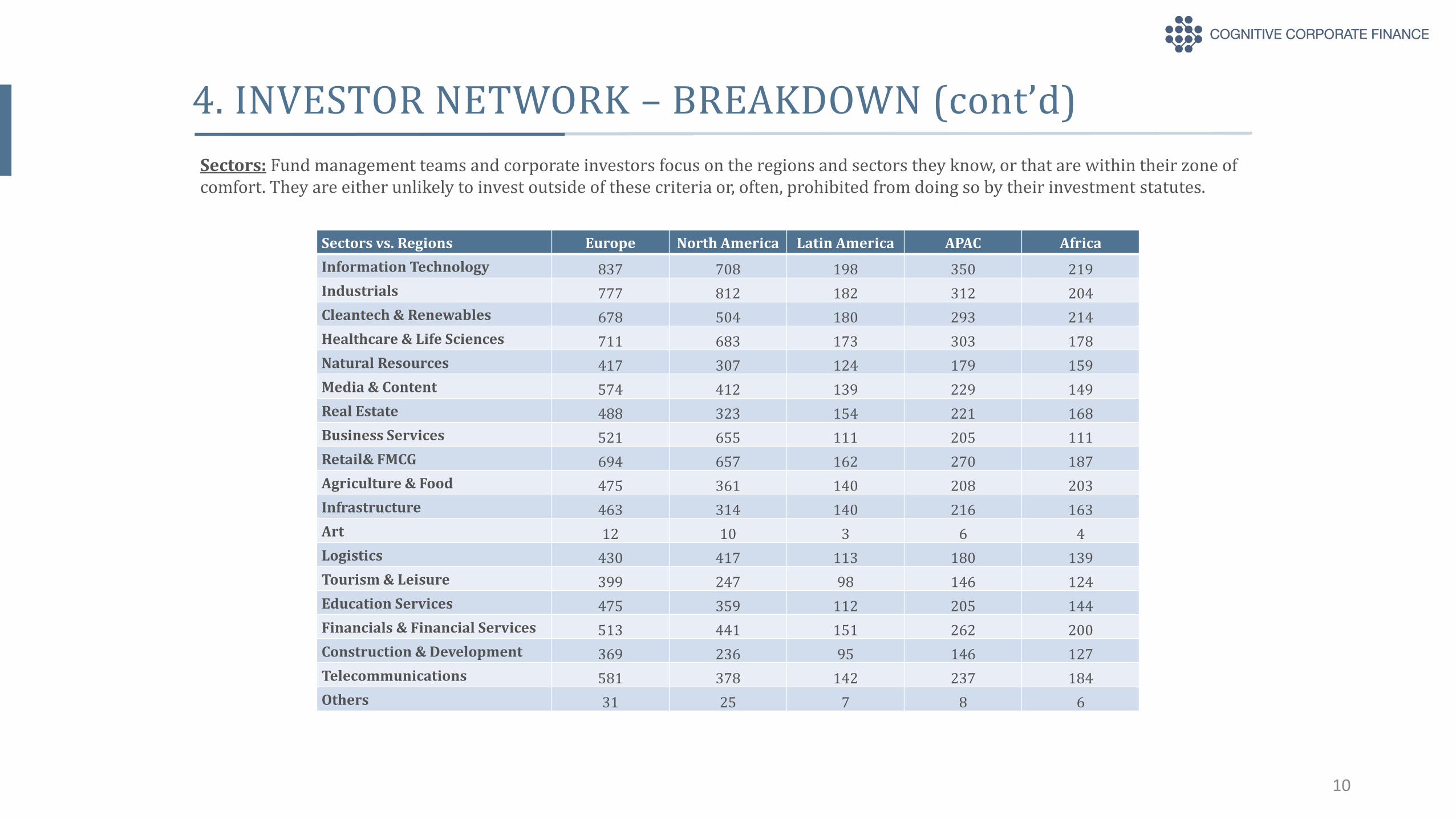

Sectors: Fund management teams and corporate investors focus on the regions and sectors they know, or that are within their zone of comfort. They are either unlikely to invest outside of these criteria or, often, prohibited from doing so by their investment statutes.

Sectors vs. Regions Europe North America Latin America APAC AfricaInformation Technology 837 708 198 350 219Industrials 777 812 182 312 204Cleantech & Renewables 678 504 180 293 214Healthcare & Life Sciences 711 683 173 303 178Natural Resources 417 307 124 179 159Media & Content 574 412 139 229 149Real Estate 488 323 154 221 168Business Services 521 655 111 205 111Retail& FMCG 694 657 162 270 187Agriculture & Food 475 361 140 208 203Infrastructure 463 314 140 216 163Art 12 10 3 6 4Logistics 430 417 113 180 139Tourism & Leisure 399 247 98 146 124Education Services 475 359 112 205 144Financials & Financial Services 513 441 151 262 200Construction & Development 369 236 95 146 127Telecommunications 581 378 142 237 184Others 31 25 7 8 6

4. INVESTOR NETWORK – DATAMINING

11

� Our analysts scour the world on a daily basis to identify new investors across all asset classes.

� Through their efforts, our investor network grows at the rate of 50 to 100 investors per week.

� By the end of 2016, we aim to have built a network of around 5,000 investors, evenly distributed across the world, in order to allow us to match any seller with any buyer within our transaction range of €1m to €100m.

� Every day, our clients and potential clients ask us to search (or fine-tune searches) for potential investors.

� Beyond the previously mentioned criteria (geography, sector etc.), our clients also need to determine:� The Uses of Funds, estimated impact of capital injection, projected

returns for the investor, timing of capital injection, timescale of exit, likely modes of exit, guarantees, etc.

� For clients with a clear and documented financial instrument to propose to the market, we structure and manage the full fundraising process, described in the following slide.

12

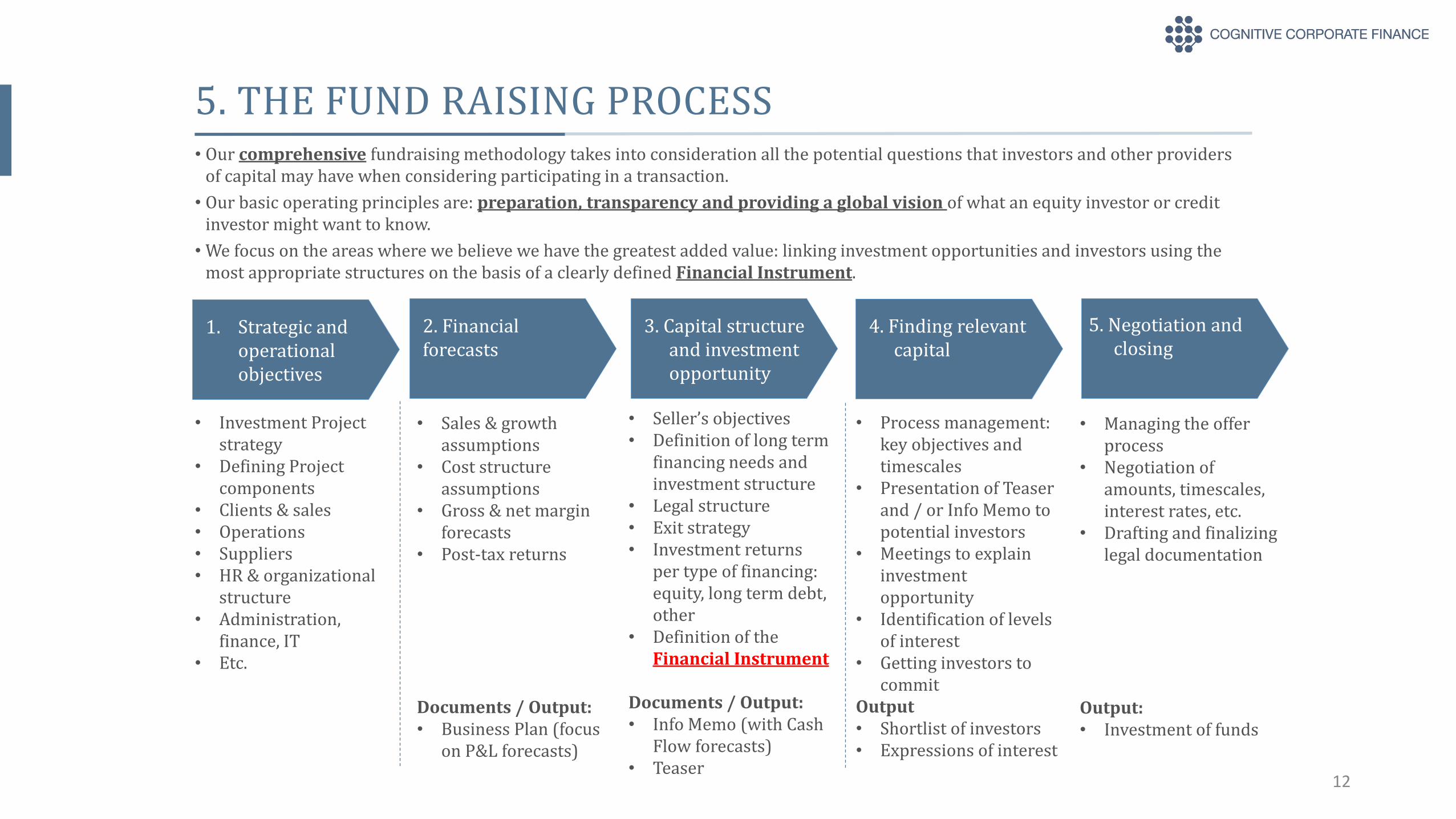

• Investment Project strategy

• Defining Project components

• Clients & sales• Operations• Suppliers • HR & organizational

structure• Administration,

finance, IT• Etc.

• Sales & growth assumptions

• Cost structure assumptions

• Gross & net margin forecasts

• Post-tax returns

Documents / Output: • Business Plan (focus

on P&L forecasts)

• Seller’s objectives• Definition of long term

financing needs and investment structure

• Legal structure• Exit strategy• Investment returns

per type of financing: equity, long term debt, other

• Definition of the Financial Instrument

Documents / Output:• Info Memo (with Cash

Flow forecasts)• Teaser

• Process management: key objectives and timescales

• Presentation of Teaser and / or Info Memo to potential investors

• Meetings to explain investment opportunity

• Identification of levels of interest

• Getting investors to commit

Output• Shortlist of investors• Expressions of interest

• Managing the offer process

• Negotiation of amounts, timescales, interest rates, etc.

• Drafting and finalizing legal documentation

Output:• Investment of funds

5. THE FUND RAISING PROCESS• Our comprehensive fundraising methodology takes into consideration all the potential questions that investors and other providers

of capital may have when considering participating in a transaction.• Our basic operating principles are: preparation, transparency and providing a global vision of what an equity investor or credit

investor might want to know.• We focus on the areas where we believe we have the greatest added value: linking investment opportunities and investors using the

most appropriate structures on the basis of a clearly defined Financial Instrument.

1. Strategic and operational objectives

2. Financial forecasts

3. Capital structure and investment opportunity

4. Finding relevant capital

5. Negotiation and closing

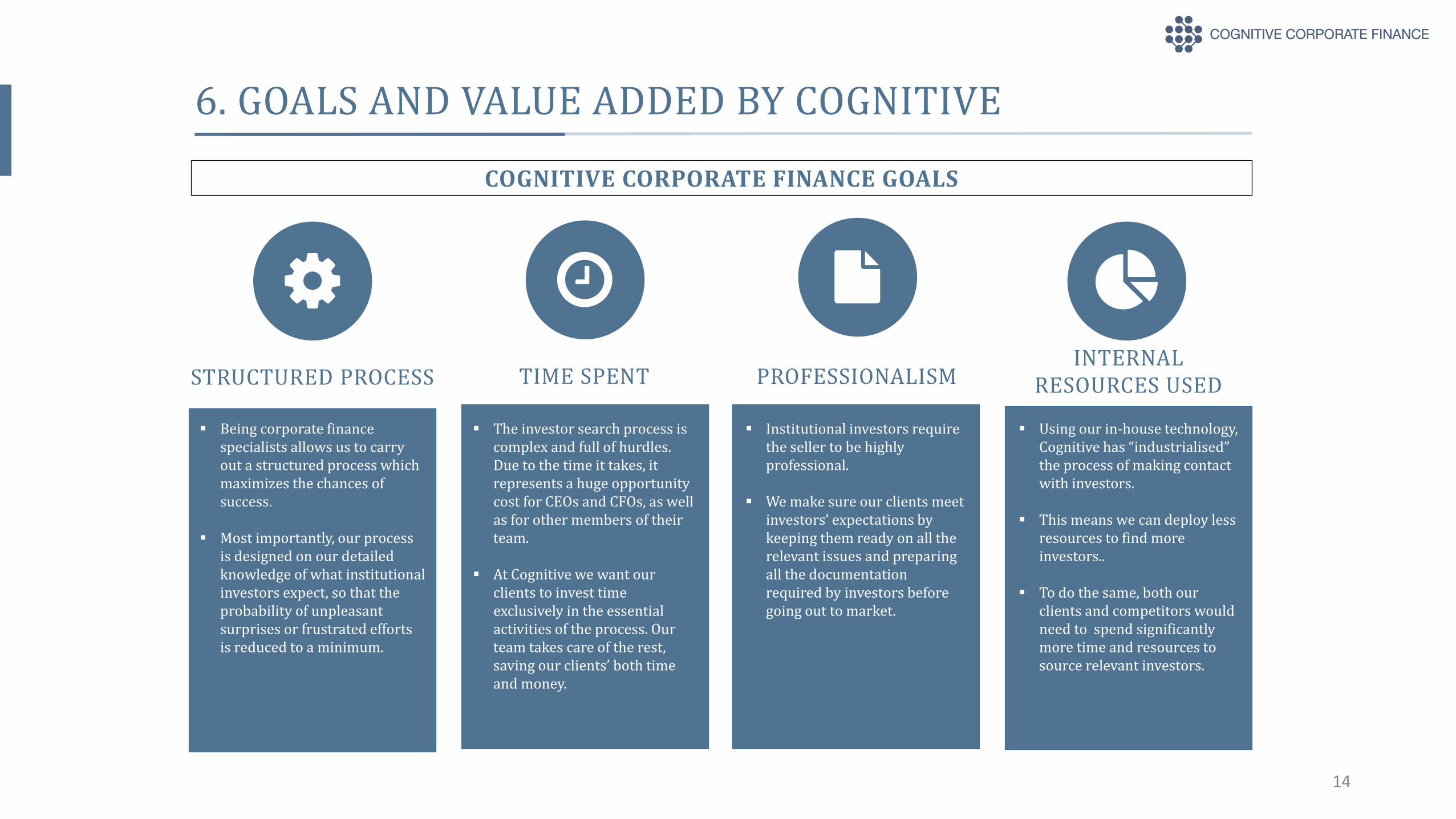

6. GOALS AND VALUE ADDED BY COGNITIVE

COGNITIVE CORPORATE FINANCE GOALS

13

� Thanks to its proprietary database, Cognitive knows the detailed investment strategy of almost 4,000 investors.

� This deep and extensive network increases on a daily basis and allows Cognitive access to a significant number of investors on behalf of our clients.

� More importantly this allows us to select investors whose investment strategy match most accurately our client’s requirements and investment proposal.

REACH SPEED

� Cognitive reaches the market faster than anyone else. Thanks to the daily analysis of investment funds, Cognitive can map out relevant investors for any project in real time.

� In addition, our investor search process is highly “technologized” so that we can reach more investors, better, and faster.

� Unlike other firms, Cognitive does not start each project from scratch. We are always one step ahead.

ACCURACY

� Having our proprietary database implies that we are in daily contact with institutional investors worldwide.

� This allows us to be constantly updated on what funds are seeking. In turn, this gives us the edge for precise and up-to-date information.

� The depth and extent of the knowledge that our database provides gives us the edge on any entity looking to raise capital, including other corporate finance firms, as well as our clients.

CONSISTENCY

� Cognitive uses a single approach for all projects: we communicate the same message to all investors, in order to ensure the “market” responds efficiently to our clients’ proposals.

� This transparency and consistency contribute to maximizing the chances of success.

6. GOALS AND VALUE ADDED BY COGNITIVE

COGNITIVE CORPORATE FINANCE GOALS

� The investor search process is complex and full of hurdles. Due to the time it takes, it represents a huge opportunity cost for CEOs and CFOs, as well as for other members of their team.

� At Cognitive we want our clients to invest time exclusively in the essential activities of the process. Our team takes care of the rest, saving our clients’ both time and money.

TIME SPENT

� Institutional investors require the seller to be highly professional.

� We make sure our clients meet investors’ expectations by keeping them ready on all the relevant issues and preparing all the documentation required by investors before going out to market.

PROFESSIONALISM

14

STRUCTURED PROCESS

� Being corporate finance specialists allows us to carry out a structured process which maximizes the chances of success.

� Most importantly, our process is designed on our detailed knowledge of what institutional investors expect, so that the probability of unpleasant surprises or frustrated efforts is reduced to a minimum.

INTERNAL RESOURCES USED

� Using our in-house technology, Cognitive has “industrialised” the process of making contact with investors.

� This means we can deploy less resources to find more investors..

� To do the same, both our clients and competitors would need to spend significantly more time and resources to source relevant investors.

6. GOALS AND VALUE ADDED BY COGNITIVE

COGNITIVE CORPORATE FINANCE GOALS

15

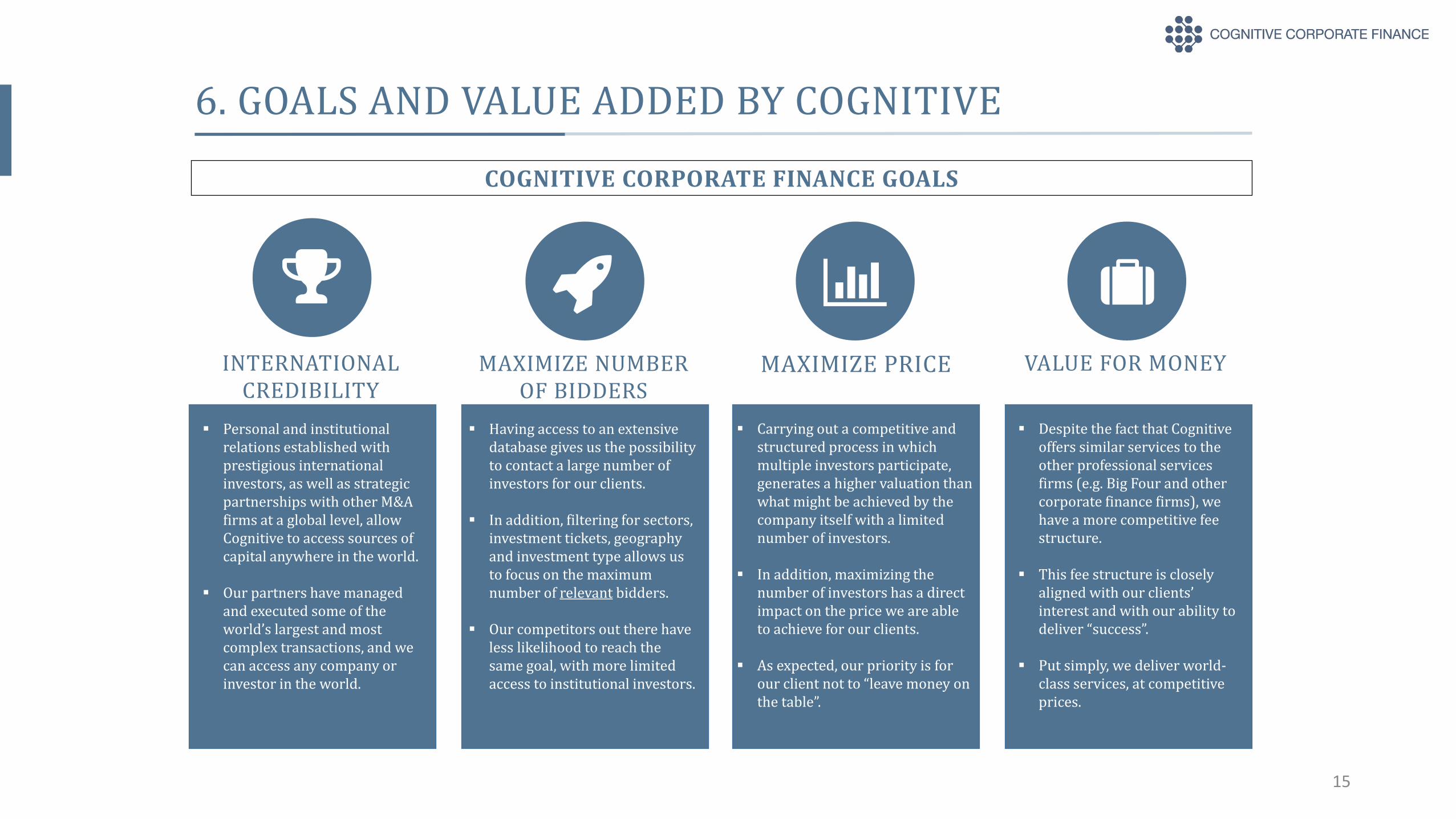

INTERNATIONAL CREDIBILITY

� Personal and institutional relations established with prestigious international investors, as well as strategic partnerships with other M&A firms at a global level, allow Cognitive to access sources of capital anywhere in the world.

� Our partners have managed and executed some of the world’s largest and most complex transactions, and we can access any company or investor in the world.

MAXIMIZE NUMBER OF BIDDERS

� Having access to an extensive database gives us the possibility to contact a large number of investors for our clients.

� In addition, filtering for sectors, investment tickets, geography and investment type allows us to focus on the maximum number of relevant bidders.

� Our competitors out there have less likelihood to reach the same goal, with more limited access to institutional investors.

� Carrying out a competitive and structured process in which multiple investors participate, generates a higher valuation than what might be achieved by the company itself with a limited number of investors.

� In addition, maximizing the number of investors has a direct impact on the price we are able to achieve for our clients.

� As expected, our priority is for our client not to “leave money on the table”.

VALUE FOR MONEY

� Despite the fact that Cognitive offers similar services to the other professional services firms (e.g. Big Four and other corporate finance firms), we have a more competitive fee structure.

� This fee structure is closely aligned with our clients’ interest and with our ability to deliver “success”.

� Put simply, we deliver world-class services, at competitive prices.

MAXIMIZE PRICE

Reach

Accuracy (Investor Targeting)

Speed

Consistency

Structured Process

Time Spent

Professionalism

Internal Resources Used

International Credibility

Maximum Number of Bidders

Negotiation Power

Maximum Price

Value for Money

7. COGNITIVE’S VALUE ADDED

16

Variable

Big 4 Firms Other CF FirmsDo it Yourself

Variable

Variable

Variable

Variable

Variable

On the basis of all the points described in the previous slides, we summarize in the table below where we believe lies our value added, compared to the other options available to our clients:

17

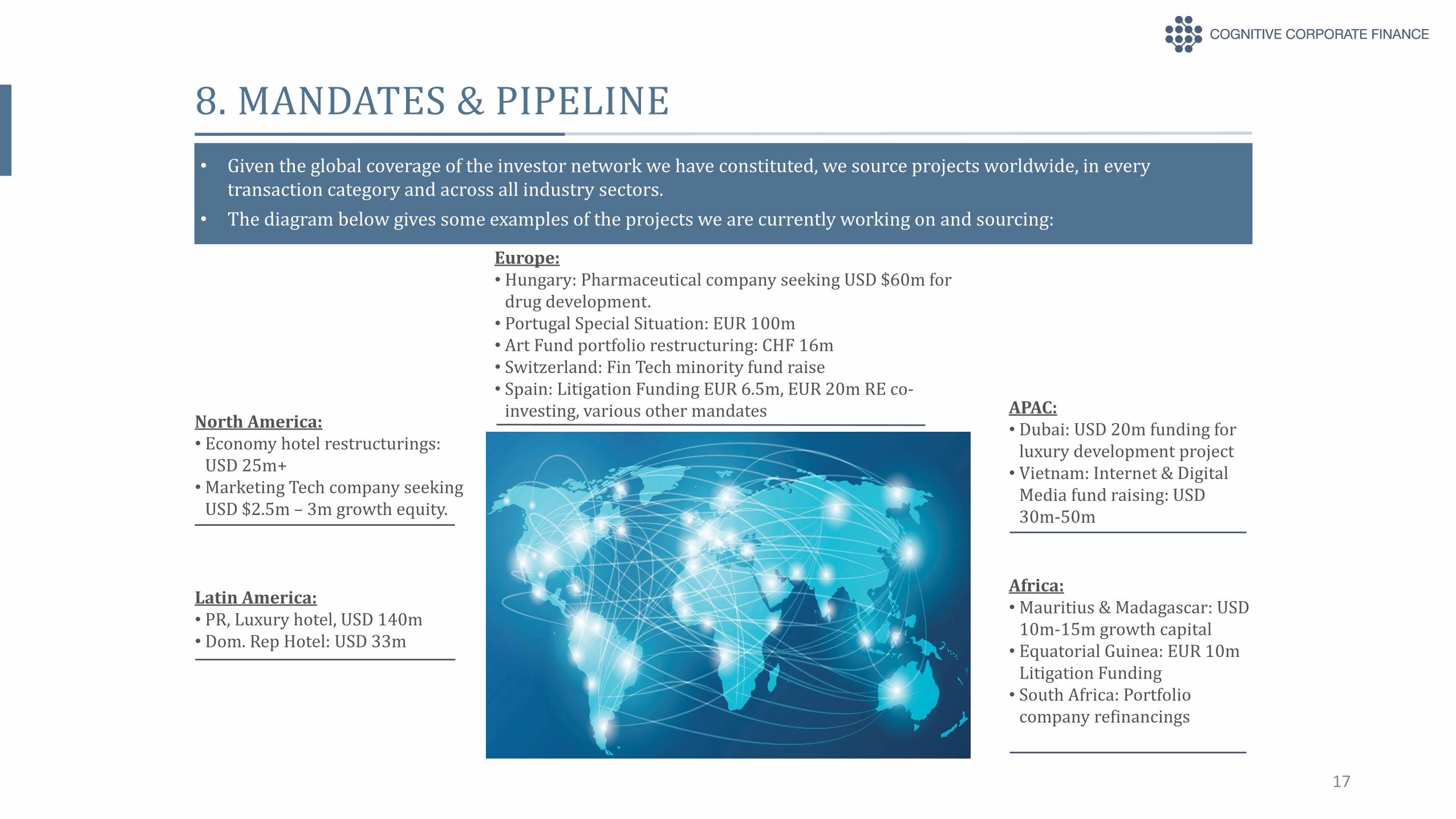

8. MANDATES & PIPELINE• Given the global coverage of the investor network we have constituted, we source projects worldwide, in every

transaction category and across all industry sectors.• The diagram below gives some examples of the projects we are currently working on and sourcing:

Europe:• Hungary: Pharmaceutical company seeking USD $60m for

drug development.• Portugal Special Situation: EUR 100m• Art Fund portfolio restructuring: CHF 16m• Switzerland: Fin Tech minority fund raise• Spain: Litigation Funding EUR 6.5m, EUR 20m RE co-

investing, various other mandates APAC:• Dubai: USD 20m funding for

luxury development project• Vietnam: Internet & Digital

Media fund raising: USD 30m-50m

North America:• Economy hotel restructurings:

USD 25m+• Marketing Tech company seeking

USD $2.5m – 3m growth equity.

Latin America:• PR, Luxury hotel, USD 140m• Dom. Rep Hotel: USD 33m

Africa:• Mauritius & Madagascar: USD

10m-15m growth capital• Equatorial Guinea: EUR 10m

Litigation Funding• South Africa: Portfolio

company refinancings

18

9. THE TEAM – Charles Thoma

Charles Thoma

Managing Partner

Madrid

• Charles Thoma is co-founder and Managing Partner of Cognitive Corporate Finance.• Charles started his career with KPMG’s Corporate Strategy group in London in 1993, where he advised large

European companies on international expansion, market reviews and corporate development plans. In 1999, he moved to Paris to help set up KPMG’s Strategy group, where he advised a number of French clients such as: Pierre & Vacances, Maison de la France, RATP and La Poste on strategy and reorganization issues.

• In 2000, he transferred to KPMG’s Restructuring group, which subsequently became Kroll Talbot Hughes and where he stayed until 2008. Charles advised a variety of European corporations, investment banks and PE houses on stressed and distressed situations relative to their investments. For two years he worked with OCP, a large, 18,000-employee, Moroccan mining group to regain control of its underperforming activities, to restructure the balance sheet and to address a wide range of problems associated with subsidiaries and JVs in other continents.

• Simultaneously, Charles worked on a range of operational restructuring, bankruptcy, and ailing structured finance and securitization projects. These included: leading the contingency planning and crisis management efforts for Gate Gourmet in the UK as part of its turnaround and return to profitability; assisting with Swiss Air’s exit from AOM, Air Liberté and Air Littoral through bankruptcy; developing exit, restructuring and redundancy plans for foreign corporations operating in the French market.

• In 2008, Charles joined Alvarez & Marsal, where he led the crisis management and stabilization efforts of a number of entities Lehman Brothers Holdings Inc. (LBHI) entities as part of the group’s Chapter 11 proceedings. He successfully sold Banque Lehman Brothers, Lehman Brothers Asset Management France and Italy and handled, through Sauvegarde proceedings, the equity held by LBHI in the Cœur Défense RE transaction and one of its largest and most complex securitizations (over €1.6bn). In addition, Charles led the disposal of a €100m Italian RE portfolio that Lehman Brothers had as a JV while acting as board member of the holding company.

• Charles is an expert in the areas of Independent Business Reviews, Restructuring Plans, Asset acquisitions / disposals, Debt restructurings, restructuring Securitizations and Structured finance transactions. In addition, he has held a number of CRO and interim board positions.

• He holds a Bachelor’s degree from the University of North Carolina at Chapel Hill and earned an MBA from the Institut Supérieur de Gestion. A Belgian national, Mr. Thoma is fluent in French, English and Spanish, has a working knowledge of Italian and speaks a rusty Russian.

19

9. THE TEAM – Jill Hoornaert

Jill Hoornaert

Director

Madrid

• Jill Hoornaert started her career as an international Lawyer with Linklaters and Suez-GDF (now ENGIE) in Brussels, specializing in Tax and International Contracts. She assisted large corporations establish their HQ in Brussels and pleaded a large number of litigation cases at the Brussels’ bar.

• After accomplishing an MBA at IESE in Barcelona (Spain), she joined BBVA as a Senior Manager of the Alternative Investment Team in Madrid (Spain) in charge of selecting fund of funds and building long-term relationships with the major international fund of fund managers. She became an expert in quantitative and qualitative fund selection.

• In 2010 she joined the Corporate and Investment Banking area within the Syndicated Loan team. She financed large corporations and advised medium-sized European corporates on syndicated lending products (Term loans for acquisition finance and capital expenses, Revolving Credit Facilities and Forward Start Facilities). She became an expert in CF forecasts and loan structuring and closed a number of major operations representing the Agent Bank including: CELSA, TEKA, AMPER, LIDL, SARAS, DELHAIZE, ETEX, OMEGA PHARMA.

• In 2013 Jill was transferred to the Spanish Debt Restructuring team where she specialized in Spanish non-performing and distressed medium-sized corporates. She led financial restructuring processes representing the Agent Lender Bank in various sectors (service, industry and hotel sector). Through defining and implementing the Lenders’ conditions for refinancing, as part of the balance sheet restructuring, she became an expert in operational restructuring of distressed companies in hostile environments, transforming them into performing corporates and recovering distressed banking debt.

• In 2014 she was asked to be a permanent member of BBVA’s Central Risk Committee in charge of corporate banking debt restructuring strategies and asset & company sales. She supervised the distressed recovery strategies at national level. She became an expert in Spanish “Chapter 11” restructuring and sale of distressed debt positions.

• Jill joined Cognitive Corporate Finance in July 2016. Apart from dealing with all “private equity” like situations, she leads the litigation funding area.

• She holds a License in Law from the Université Libre of Brussels and an MBA from IESE (Barcelona – Spain). A Belgian national, Jill is fluent in English, Spanish, French and Dutch.

20

9. THE TEAM – Stéphanie Le Vaillant Vignancour

Stéphanie

Le Vaillant

Director

Madrid

• Stéphanie started her career as an auditor in 2002 in PwC Paris, primarily working for large corporations from the automobile industry such as Johnson Controls, Valeo or Citroën. In 2004, she transferred to PwC Cambridge office to work in the UK Public Sector practice, doing financial recovery plans and performance reviews for the NHS (National Health Service), the Cabinet of the Prime Minister, universities and county councils.

• In 2007, she joined the Transaction Advisory Services department of EY in Madrid. For the following six years, she specialized in sell-side and buy-side financial due diligence processes for companies with turnovers ranging between €5 million and €80,000 million, leading teams of up to 30 professionals. Examples of projects include the acquisition by Carrefour of c. 60 shopping centres from Klépierre, the sale by Oaktree of Galletas Artiach, the sale by Ebro Puleva of its dairy business, the purchase by Mitsubishi of photovoltaic plants or the acquisition by Microsoft of advertising company Wysiwyg.Stéphanie was also responsible for the French Desk for EY Spain and member of the Sponsorship Committee at the Franco-Spanish Chamber of Commerce.

• In 2013, she joined PwC to co-develop the SPA advisory services practice. The SPA department provides expert support on the negotiation of the financial terms of the Share and Purchase Agreements and help clients generate value / optimize the transaction price, choosing the adequate closing mechanism, negotiating key pricing matters, drafting the financial clauses of the contract and then, post-deal, identifying and negotiating price adjustments with the counterparty or the independent expert / arbitrator. Amongst others, Stéphanie advised clients on i) real estate operations, such as the purchase of Hotel Ritz in Madrid by Olayan Group and Mandarin hotels, the investment in Gmp by Singaporean fund GIC, the sale of shopping centres by Britishland to KKR; ii) energy operations, especially for Cepsa; iii) industry projects, like the sale of the packaging division by La Seda Barcelona (in receivership) or acquisition by French group Legrand.

• Stephanie joined Cognitive Corporate Finance in November 2016. She is responsible for business valuation related matters and share and purchase agreements negotiation.

• She is graduated from NEOMA business school in France and holds an EMBA from INSEAD (Paris – Singapore –Abu Dhabi). Stéphanie is fluent in English, Spanish, French and has a working knowledge of German.

21

9. THE TEAM – Associates

• Alexandre Pereira is a graduate from IE University’s Bachelor in Business Administration with a specialization in Finance

• A Swiss and Portuguese national, Alex speaks French, Portuguese, English and Spanish

• As part of his studies, Alex has worked in various companies, such as: • Authentic Ways (United Kingdom)• EDP Renovables (Spain)• atl Capital (Spain)• Cerise Immobilier (Switzerland)

• Mido is a graduate from IE Business School’s Master in Management, with a Bachelor in Finance from Concordia University in Canada.

• A Canadian and Jordanian national, Mido speaks Arabic, English and has a working knowledge of French.

• As part of his studies, Mido has worked in various companies, such as: • Euro-Phoenix Advisors (Budapest)• Yahoo! Inc. (Dubai)• Ever sheds LLP (London)

• Bruno is a graduate from IE Business School’s Master in Management, with a B.B.A from the University of Salamanca. Nowadays Bruno is a level II candidate in the CAIA program.

• A Spanish national born in Luxembourg, Bruno speaks Spanish, English and intermediate French.

• As part of his studies, Bruno gained international experience in Rotterdam and the University of Toronto, he has also worked in for the finance department of ThyssenKrupp.

Alexandre PereiraAssociate

Mido TalhouniAssociate

Bruno TorrecillaAssociate

22

9. THE TEAM – Analysts

• Omar is a graduate from IE Business School’s Master in Management, with a Bachelor in Petroleum Engineering from the American University in Cairo.

• An Egyptian national, Omar speaks Arabic, English, Spanish and Serbian.

• As part of his studies Omar has worked in various companies, such as:

– Halliburton– Khalda– Petroamir– Union Fenosa

• Salvador is a graduate from IE University’s Bachelor in Business Administration with a specialiazationin Finance.

• A Spanish national, Salvador speaksSpanish, English and Hebrew.

• As part of his studies, Salvador has worked in various companies, such as:-

– Banco Santander (Madrid)– Accenture (Tel Aviv)– Ben Oldman Partners (Madrid) – J Capital (Madrid)– Madison (Mumbai)

Omar ZaghloulAnalyst

Salvador BenzaquenAnalyst

23

9. THE TEAM – Senior Advisors

José Manuel Jimeno

Senior AdvisorMadrid

• José Manuel started his career as an auditor with Pricewaterhouse Coopers in Madrid (Spain), and then moved to Belgium and the USA where he built the basis of his professional career. For the last 20 years, José Manuel has held CFO and CIO-type positions for several companies.

• Prior to joining Cognitive Corporate Finance as Senior Advisor, José Manuel worked for PwC, United Technologies, Wolters Kluwer, Fujitsu, Europ Assistance, and lately for Grupo IFA.

• José Manuel holds an MBA from Purdue University (West Lafayette, Indiana, USA), and is currently completing an Advanced Management Program from IESE Business School in Madrid (Spain).

• Professional of Internet of Things since 2012 Jean is skilled in evaluating strategic projects in IoT on a sales or technical point of view.

• With a strong background in computer science engineering and MBA he speaks fluently 5 languages and supports companies to develop their business in the IoT ecosystem throughout Europe.

Jean Triquet

Senior Advisor (IoT)Madrid

• The fundraising and M&A mandates we run are typically ambitious projects which entail a certain level of complexity.

• In most cases, these mandates involve finding foreign and/or alternative sources of funding and calling upon institutional investors who are used to high levels of professionalism from their counterparties.

• When examining an opportunity in another country, these institutional investors also expect maximum transparency and disclosure, as well as exhaustive information. Failure to deliver these nearly guarantees the failure of the process.

• Moreover, these fundraising / M&A projects require a close working relationship between the Client and Cognitive, wherein:o The Client / the entity raising the funds “sells” his business

model and all the economic potential associated with it, while

o Cognitive “sells” the financial instrument which rests upon the business / asset, in order to convince the investor that he will obtain the yields / profits / upside / multiples calculated by Cognitive and the Client

• Although not quite brain surgery, the work is highly specialized, complex and often involves “aligning a handful of planets.”

• As a result, our mandates fix from the outset the key points required to ensure success: Who needs to do what? By when? To achieve what objective? Under what conditions? Etc.

Structure and key points of a Cognitive mandate:• Parties

o To whom do we owe our Duty of Care?• Background & Objectives

o Amounts, realistic valuations, justificationso How do we define success?

• Scope of services to be provided by Cognitiveo What activities will we carry out? By when? With

whom?• Client Contribution

o What do we need the Client to do so that we can do our job?

• Durationo One-month renewable

• Results• Professional Fees and Payment Conditions

o Monthly Retainer – function of the complexity of the financial instrument to be designed

o Success Fees – function of the amount to be raised• Exclusivity

o To create “Off Market” appeal• Covered Transactions• Limitations and Exclusions• Confidentiality• Jurisdiction

24

Annex 1. STRUCTURE OF A MANDATE

25

Annex 2. SERVICES FOR INVESTMENT FUNDS• Cognitive is frequently asked by Investment Funds and Corporates to assist on issues linked to their access to capital, such as those

described below. Such issues can impact either the Fund / Corporate, or one of its portfolio companies.• Regardless of who we work for, the depth and breadth of our investor network allows us to match the situation with relevant sources

of capital.

Services Situation Description Cognitive Value Add

Co-Investing • Investment Fund or Corporate seeks a co-investor or co-lender to participate in a specific transaction.

• Without the co-investor, the transaction cannot be completed.

• Cognitive will search for investors with similar investment strategies and suggest relevant investors for the transaction.

Re-Financing • Investment Fund or Corporate seeks to refinance the debt of a portfolio company or subsidiary.

• This may arise from a specific financial event within the company, or to refinance acquisition debt.

• Cognitive is in contact with over 700 debt funds worldwide who can provide any kind o debt, from Senior to Junior to Mezzanine to Unitranche to Project Finance.

Debt-raising / Acquisition Funding

• Portfolio company or subsidiary is looking to make an acquisition in the near future and needs acquisition financing.

• Portfolio company or subsidiary is looking to raise debt to fund organic growth.

• Cognitive is in contact with over 700 debt funds worldwide who can provide any kind o debt, from Senior to Junior to Mezzanine to Unitranche to Project Finance.

Litigation Funding

• Portfolio company or subsidiary is engaged in, or planning to engage in a lawsuit or arbitration against a business, client, supplier.

• Company has other priorities than funding the lawsuit or arbitration, but is nevertheless keen to assert its rights and recover damages.

• Cognitive is in regular contact with around 35 litigation funds worldwide, who regularly seek to fund claims in exchange for part of the proceeds of the award.

Fund Restructurings

• Investment Fund is faced with an Exiting Investor and needs to find replacement capital.

• Cognitive is in contact with a number of Funds of Funds, Family Offices, Special Situations funds, as well as PE investors whose investment strategy may match yours.

Disposals • Investment Fund or Corporate is looking to sell a portfolio company or a subsidiary.

• Within Cognitive’s network of almost 4,000 Investment Funds and Corporates, a significant number will be looking to acquire the company you are selling.