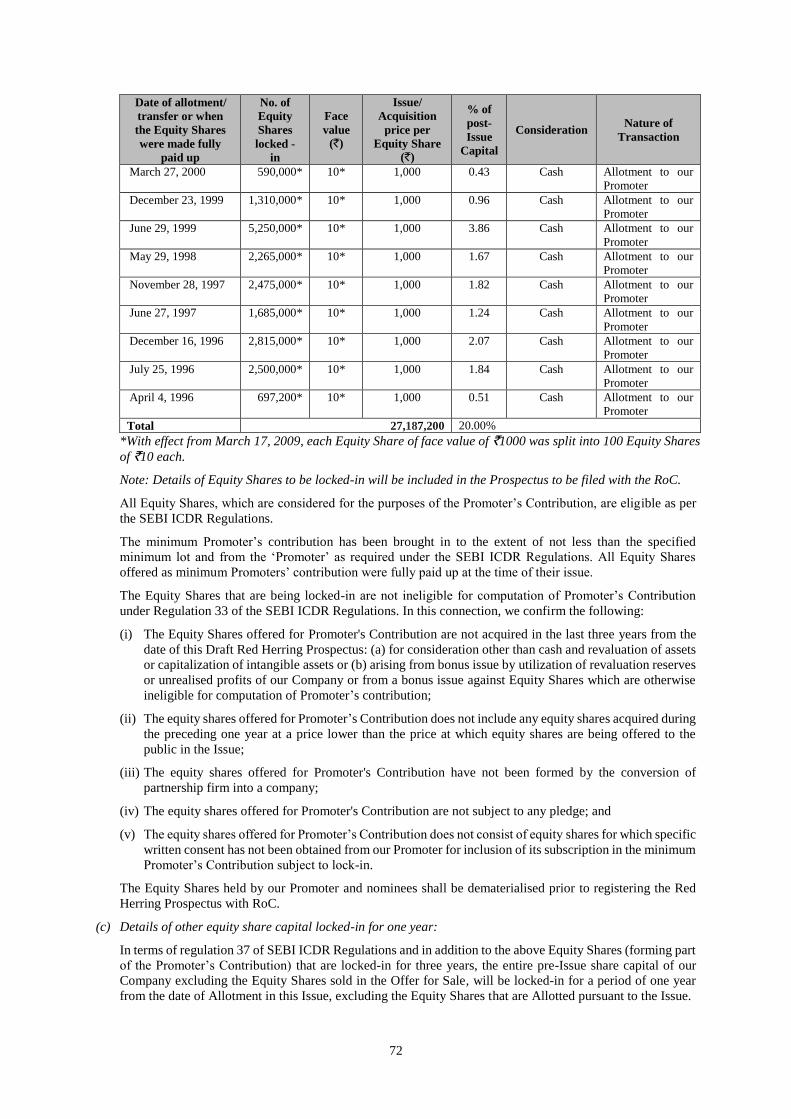

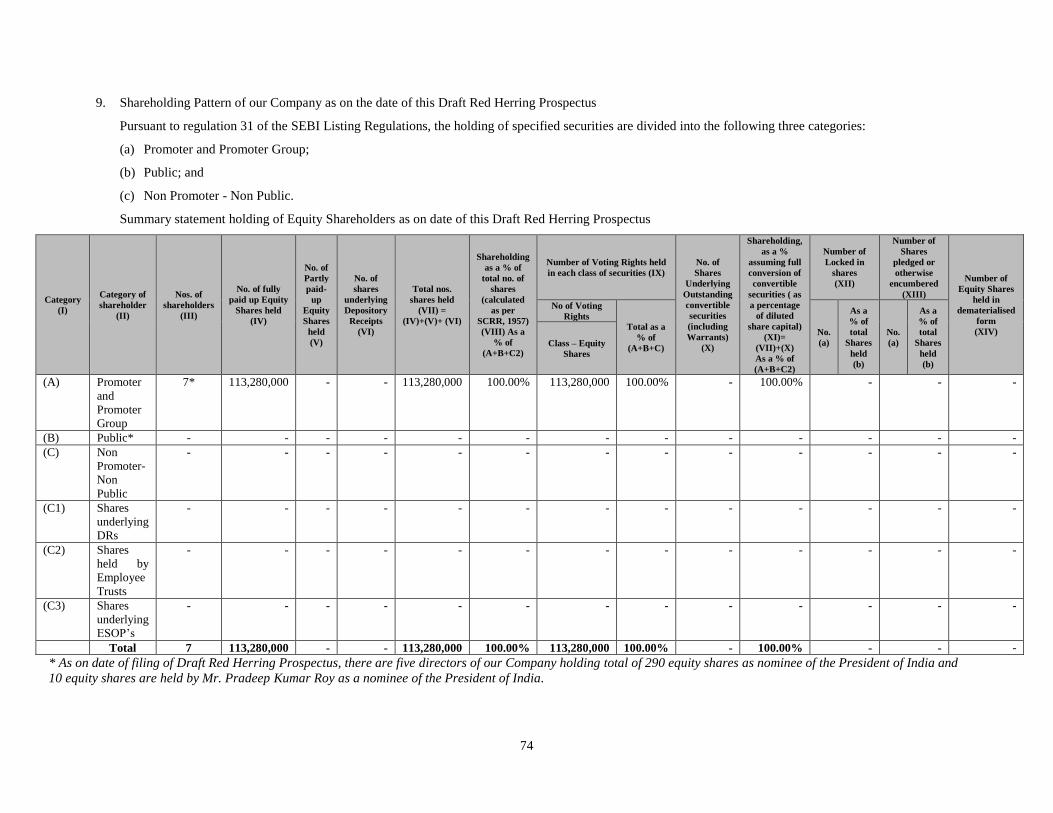

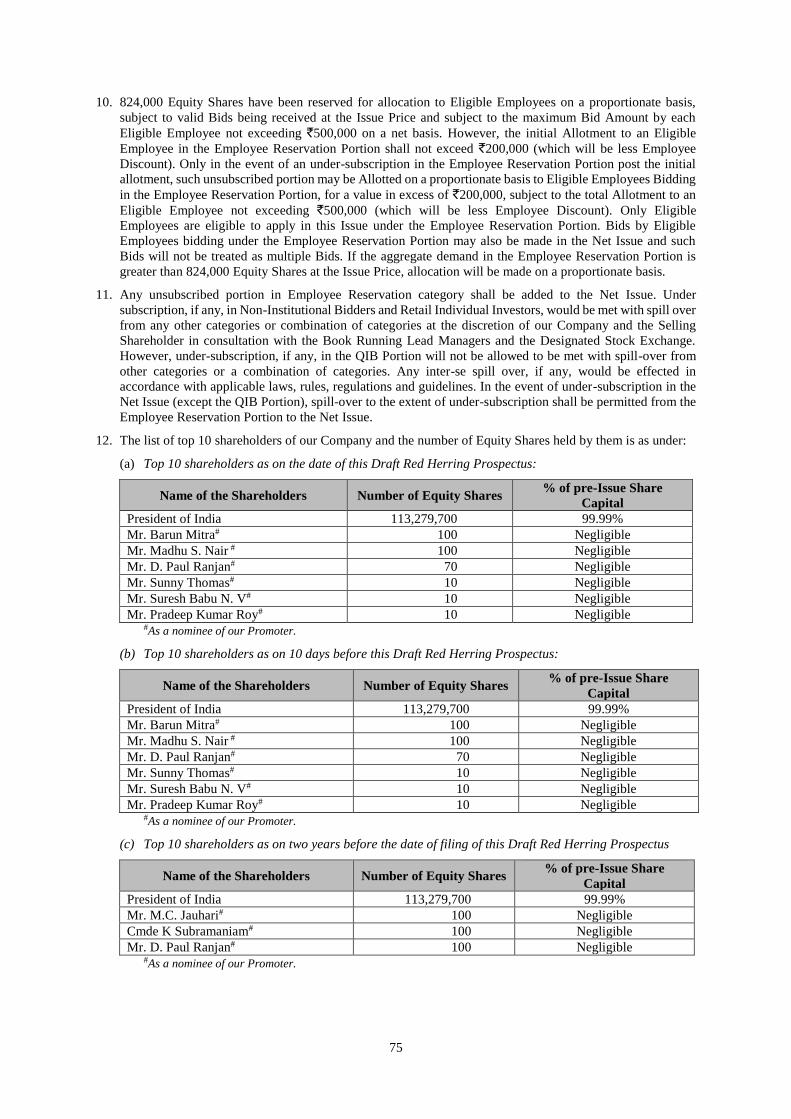

COCHIN SHIPYARD LIMITED - Bombay Stock Exchange€¦ · COCHIN SHIPYARD LIMITED Our Company was...

362

DRAFT RED HERRING PROSPECTUS Dated: March 23, 2017 (The Draft Red Herring Prospectus will be updated upon filing with the RoC) (Please read section 32 of the Companies Act, 2013) 100% Book Built Issue COCHIN SHIPYARD LIMITED Our Company was incorporated as Cochin Shipyard Limited on March 29, 1972 as a private limited company under the Companies Act, 1956, with the Registrar of Companies, Kerala at Ernakulam. Our Company became a deemed public limited company under section 43A of Companies Act, 1956 on July 1, 1982. Our Company again became a private limited company with effect from July 16, 1985. Our Company became a public limited company with effect from November 8, 2016 and a fresh certificate of incorporation consequent upon conversion to public limited company was issued by the Registrar of Companies, Kerala at Ernakulam. For further details, including details of change in registered office of our Company, see “History and Certain Corporate Matters” on page 134. Registered Office: Administrative Building, Cochin Shipyard Premises, Perumanoor, Kochi - 682015 Kerala, India. Contact Person: Ms. V. Kala, Company Secretary and Compliance Officer; Tel: +91 (484) 2501306; Fax: +91 (484) 2384001 E-mail: [email protected]; Website: www. www.cochinshipyard.com Corporate Identity Number: U63032KL1972GOI002414 OUR PROMOTER: THE PRESIDENT OF INDIA ACTING THROUGH THE MINISTRY OF SHIPPING PUBLIC ISSUE OF 33,984,000 EQUITY SHARES OF FACE VALUE OF ` 10 EACH (“EQUITY SHARES”) OF COCHIN SHIPYARD LIMITED (“OUR COMPANY” OR “ISSUER”) FOR CASH AT A PRICE* OF ` [●] PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF ` [●] PER EQUITY SHARE) AGGREGATING TO ` [●] MILLION (“ISSUE”) CONSISTING OF A FRESH ISSUE OF 22,656,000 EQUITY SHARES AGGREGATING TO ` [●] MILLION (“FRESH ISSUE”) AND AN OFFER FOR SALE OF 11,328,000 EQUITY SHARES BY THE PRESIDENT OF INDIA AGGREGATING TO ` [●] MILLION (“OFFER FOR SALE”, AND “THE SELLING SHAREHOLDER”). THE ISSUE INCLUDES A RESERVATION OF UP TO 824,000 EQUITY SHARES AGGREGATING TO ` [●] MILLION FOR SUBSCRIPTION BY ELIGIBLE EMPLOYEES (AS DEFINED HEREIN) (“EMPLOYEE RESERVATION PORTION”). THE ISSUE LESS EMPLOYEE RESERVATION PORTION IS REFERRED TO AS THE NET ISSUE. THE ISSUE AND THE NET ISSUE WILL CONSTITUTE 25.00% AND 24.39% RESPECTIVELY, OF THE POST ISSUE PAID-UP EQUITY SHARE CAPITAL OF OUR COMPANY. THE FACE VALUE OF EQUITY SHARES IS ` 10 EACH. THE PRICE BAND, RETAIL DISCOUNT, EMPLOYEE DISCOUNT, IF ANY, IN RUPEES, TO THE RETAIL INDIVIDUAL BIDDERS, THE ELIGIBLE EMPLOYEES BIDDING IN THE EMPLOYEE RESERVATION PORTION AND THE MINIMUM BID LOT WILL BE DECIDED BY OUR COMPANY AND THE SELLING SHAREHOLDER IN CONSULTATION WITH THE BRLMS AND WILL BE ADVERTISED IN ALL EDITIONS OF ENGLISH NATIONAL DAILY NEWSPAPER BUSINESS STANDARD, ALL EDITIONS OF HINDI NATIONAL DAILY NEWSPAPER BUSINESS STANDARD AND KOCHI EDITION OF MALAYALAM DAILY NEWSPAPER MATHRUBHUMI, MALAYALAM BEING THE REGIONAL LANGUAGE OF KERALA, WHERE OUR REGISTERED OFFICE IS LOCATED AT LEAST FIVE WORKING DAYS PRIOR TO THE BID/ISSUE OPENING DATE AND SHALL BE MADE AVAILABLE TO THE BSE LIMITED (“BSE”) AND THE NATIONAL STOCK EXCHANGE LIMITED (“NSE”, AND TOGETHER WITH BSE, THE “STOCK EXCHANGES”) FOR UPLOADING ON THEIR RESPECTIVE WEBSITES. *Retail Discount of ` [●] per Equity Share to the Issue Price may be offered to the Retail Individual Bidders and Employee Discount of `[●] per Equity Share to the Issue Price may be offered to the Eligible Employees Bidding in the Employee Reservation Portion. In case of any revision to the Price Band, the Bid/Issue Period will be extended by atleast three additional Working Days after such revision of the Price Band, subject to the total Bid/Issue Period not exceeding 10 Working Days. Any revision in the Price Band and the revised Bid/Issue Period, if applicable, will be widely disseminated by notification to the Stock Exchanges, by issuing a press release, and also by indicating the change on the website of the Book Running Lead Managers and at the terminals of the other members of the Syndicate. In terms of Rule 19(2)(b)(iii) of the Securities Contracts (Regulation) Rules, 1957, as amended (“SCRR”), this is an Issue for at least 10% of the post-Issue paid-up Equity Share capital of our Company. In accordance with Regulation 26(1) of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended (“SEBI ICDR Regulations”), the Issue is being made through the Book Building Process wherein 50% of the Net Issue shall be available for allocation on a proportionate basis to Qualified Institutional Buyers (“QIBs”) (“QIB Portion”). 5% of the QIB Portion shall be available for allocation on a proportionate basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocation on a proportionate basis to all QIB Bidders, including Mutual Funds, subject to valid Bids being received at or above the Issue Price. Further, not less than 15% of the Net Issue shall be available for allocation on a proportionate basis to Non-Institutional Bidders and not less than 35% of the Net Issue shall be available for allocation to Retail Individual Bidders in accordance with the SEBI ICDR Regulations, subject to valid Bids being received at or above the Issue Price. Further, 824,000 Equity Shares shall be reserved for allocation on a proportionate basis to Eligible Employees, subject to valid bids being received at or above the Issue Price. All potential Bidders shall mandatorily participate in the Issue through an Application Supported by Blocked Amount (“ASBA”) process by providing details of their respective bank account which will be blocked by the Self Certified Syndicate Banks ( “SCSBs”). For details, see “Issue Procedure” on page 303. RISKS IN RELATION TO THE FIRST ISSUE This being the first public issue of our Company, there has been no formal market for the Equity Shares of our Company. The face value of the Equity Shares is ` 10 and the Floor Price is [●] times the face value and the Cap Price is [●] times the face value. The Issue Price (determined by our Company and the Selling Shareholder in consultation with the BRLMs as stated in “Basis for Issue Price” on page 88) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing. GENERAL RISKS Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Issue unless they can afford to take the risk of losing their entire investment. Investors are advised to read the risk factors carefully before taking an investment decision in the Issue. For taking an investment decision, investors must rely on their own examination of our Company and the Issue, including the risks involved. The Equity Shares in the Issue have not been recommended or approved by the Securities and Exchange Board of India ( “SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents of this Draft Red Herring Prospectus. Specific attention of the investors is invited to “Risk Factors” on page 17. ISSUER’S AND SELLING SHAREHOLDER’S ABSOLUTE RESPONSIBILITY Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospectus contains all information with regard to our Company and the Issue, which is material in the context of the Issue, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes the Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. Further, the Selling Shareholder confirms all information set out about itself as the Selling Shareholder in context of the Offer for Sale included in this Draft Red Herring Prospectus and accepts responsibility for statements in relation to itself and the Equity Shares being sold by it in the Offer for Sale. LISTING The Equity Shares offered through the Red Herring Prospectus are proposed to be listed on the BSE and the NSE. Our Company has received an ‘in-principle’ approval from the BSE and the NSE for the listing of the Equity Shares pursuant to letters dated [●] and [●], respectively. For the purposes of the Issue, the Designated Stock Exchange shall be [●]. A copy of the Red Herring Prospectus and the Prospectus shall be delivered for registration to the RoC in accordance with section 26(4) of the Companies Act, 2013. For details of the material contracts and documents available for inspection from the date of this Red Herring Prospectus up to the Bid/Issue Closing Date, see “Material Contracts and Documents for Inspection” on page 357. BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE SBI Capital Markets Limited 202, Maker Tower ‘E, Cuffe Parade Mumbai - 400005, Maharashtra, India Tel: +91 (22) 22178300 Fax: +91 (22) 22188332 E-mail: [email protected] Investor grievance e-mail: [email protected] Contact Person: Mr. Nikhil Bhiwapurkar / Mr. Sandeep Tenneti Website: www.sbicaps.com SEBI Registration No.: INM000003531 Edelweiss Financial Services Limited 14 th Floor, Edelweiss House, Off. C.S.T Road, Kalina Mumbai - 400098, Maharashtra, India Telephone: +91 (22) 40094400 Fax: +91 (22) 40863610 E-mail: [email protected] Investor grievance e-mail: [email protected] Contact Person: Mr. Siddharth Shah Website: www.edelweissfin.com SEBI Registration No.: INM0000010650 JM Financial Institutional Securities Limited 7 th Floor, Cnergy, Appasaheb Marathe Marg, Prabhadevi, Mumbai - 400025, Maharashtra, India Tel: +91 (22) 66303030 Fax: +91 (22) 66303330 E-mail: [email protected] Investor grievance e-mail: [email protected] Contact Person: Ms. Prachee Dhuri Website: www.jmfl.com SEBI Registration No.: INM000010361 Link Intime India Private Limited C 101, 247 Park, L B S Marg, Vikhroli West, Mumbai 400 083 Maharashtra, India Tel: +91 (22) 4918 6200 Fax: +91 (22) 4918 6195 Email: [email protected] Investor grievance email: [email protected] Contact Person: Ms. Shanti Gopalkrishnan Website: www.linkintime.co.in SEBI Registration No: INR000004058 BID/ISSUE PROGRAMME BID/ISSUE OPENS ON [●] BID/ISSUE CLOSES ON (FOR QIBs) ( * ) [●] BID/ ISSUE CLOSES ON (FOR OTHER BIDDERS) [●] ( * ) Our Company and the Selling Shareholder, in consultation with the BRLMs, may, consider closing the Bid/Issue Period for QIBs one Working Day prior to the Bid/Issue Closing Date in accordance with the SEBI ICDR Regulations.

Transcript of COCHIN SHIPYARD LIMITED - Bombay Stock Exchange€¦ · COCHIN SHIPYARD LIMITED Our Company was...

DRAFT RED HERRING PROSPECTUS

Dated: March 23, 2017 (The Draft Red Herring Prospectus will be updated upon filing with the RoC)

(Please read section 32 of the Companies Act, 2013)

100% Book Built Issue

COCHIN SHIPYARD LIMITED Our Company was incorporated as Cochin Shipyard Limited on March 29, 1972 as a private limited company under the Companies Act, 1956, with the Registrar of Companies, Kerala at Ernakulam. Our Company

became a deemed public limited company under section 43A of Companies Act, 1956 on July 1, 1982. Our Company again became a private limited company with effect from July 16, 1985. Our Company became a

public limited company with effect from November 8, 2016 and a fresh certificate of incorporation consequent upon conversion to public limited company was issued by the Registrar of Companies, Kerala at Ernakulam.

For further details, including details of change in registered office of our Company, see “History and Certain Corporate Matters” on page 134.

Registered Office: Administrative Building, Cochin Shipyard Premises, Perumanoor, Kochi - 682015 Kerala, India.

Contact Person: Ms. V. Kala, Company Secretary and Compliance Officer; Tel: +91 (484) 2501306; Fax: +91 (484) 2384001

E-mail: [email protected]; Website: www. www.cochinshipyard.com

Corporate Identity Number: U63032KL1972GOI002414

OUR PROMOTER: THE PRESIDENT OF INDIA ACTING THROUGH THE MINISTRY OF SHIPPING

PUBLIC ISSUE OF 33,984,000 EQUITY SHARES OF FACE VALUE OF ` 10 EACH (“EQUITY SHARES”) OF COCHIN SHIPYARD LIMITED (“OUR COMPANY” OR “ISSUER”) FOR CASH AT A

PRICE* OF ` [●] PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF ` [●] PER EQUITY SHARE) AGGREGATING TO ` [●] MILLION (“ISSUE”) CONSISTING OF A FRESH ISSUE OF

22,656,000 EQUITY SHARES AGGREGATING TO ` [●] MILLION (“FRESH ISSUE”) AND AN OFFER FOR SALE OF 11,328,000 EQUITY SHARES BY THE PRESIDENT OF INDIA AGGREGATING

TO ` [●] MILLION (“OFFER FOR SALE”, AND “THE SELLING SHAREHOLDER”). THE ISSUE INCLUDES A RESERVATION OF UP TO 824,000 EQUITY SHARES AGGREGATING TO ` [●]

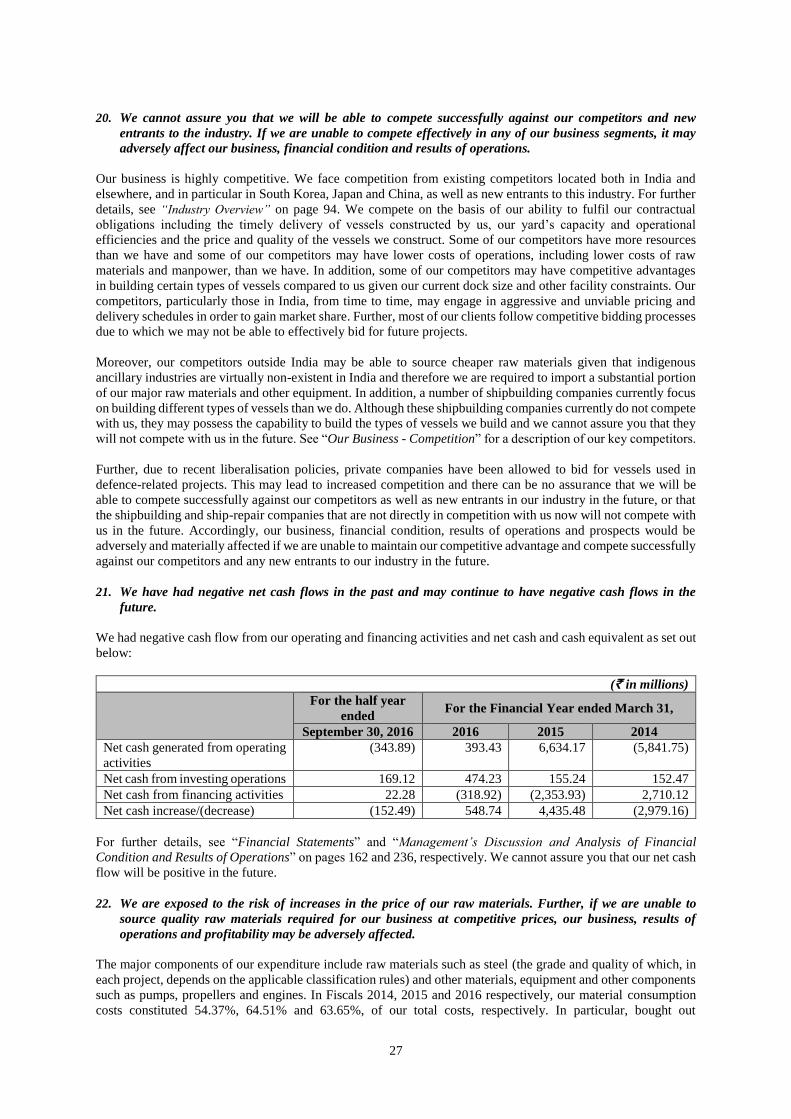

MILLION FOR SUBSCRIPTION BY ELIGIBLE EMPLOYEES (AS DEFINED HEREIN) (“EMPLOYEE RESERVATION PORTION”). THE ISSUE LESS EMPLOYEE RESERVATION PORTION IS

REFERRED TO AS THE NET ISSUE. THE ISSUE AND THE NET ISSUE WILL CONSTITUTE 25.00% AND 24.39% RESPECTIVELY, OF THE POST ISSUE PAID-UP EQUITY SHARE CAPITAL OF

OUR COMPANY.

THE FACE VALUE OF EQUITY SHARES IS ` 10 EACH. THE PRICE BAND, RETAIL DISCOUNT, EMPLOYEE DISCOUNT, IF ANY, IN RUPEES, TO THE RETAIL INDIVIDUAL BIDDERS, THE

ELIGIBLE EMPLOYEES BIDDING IN THE EMPLOYEE RESERVATION PORTION AND THE MINIMUM BID LOT WILL BE DECIDED BY OUR COMPANY AND THE SELLING SHAREHOLDER

IN CONSULTATION WITH THE BRLMS AND WILL BE ADVERTISED IN ALL EDITIONS OF ENGLISH NATIONAL DAILY NEWSPAPER BUSINESS STANDARD, ALL EDITIONS OF HINDI

NATIONAL DAILY NEWSPAPER BUSINESS STANDARD AND KOCHI EDITION OF MALAYALAM DAILY NEWSPAPER MATHRUBHUMI, MALAYALAM BEING THE REGIONAL LANGUAGE

OF KERALA, WHERE OUR REGISTERED OFFICE IS LOCATED AT LEAST FIVE WORKING DAYS PRIOR TO THE BID/ISSUE OPENING DATE AND SHALL BE MADE AVAILABLE TO THE BSE

LIMITED (“BSE”) AND THE NATIONAL STOCK EXCHANGE LIMITED (“NSE”, AND TOGETHER WITH BSE, THE “STOCK EXCHANGES”) FOR UPLOADING ON THEIR RESPECTIVE

WEBSITES.

*Retail Discount of ` [●] per Equity Share to the Issue Price may be offered to the Retail Individual Bidders and Employee Discount of `[●] per Equity Share to the Issue Price may be offered to the Eligible Employees

Bidding in the Employee Reservation Portion.

In case of any revision to the Price Band, the Bid/Issue Period will be extended by atleast three additional Working Days after such revision of the Price Band, subject to the total Bid/Issue Period not exceeding 10 Working

Days. Any revision in the Price Band and the revised Bid/Issue Period, if applicable, will be widely disseminated by notification to the Stock Exchanges, by issuing a press release, and also by indicating the change on the

website of the Book Running Lead Managers and at the terminals of the other members of the Syndicate.

In terms of Rule 19(2)(b)(iii) of the Securities Contracts (Regulation) Rules, 1957, as amended (“SCRR”), this is an Issue for at least 10% of the post-Issue paid-up Equity Share capital of our Company. In accordance with

Regulation 26(1) of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended (“SEBI ICDR Regulations”), the Issue is being made through the Book

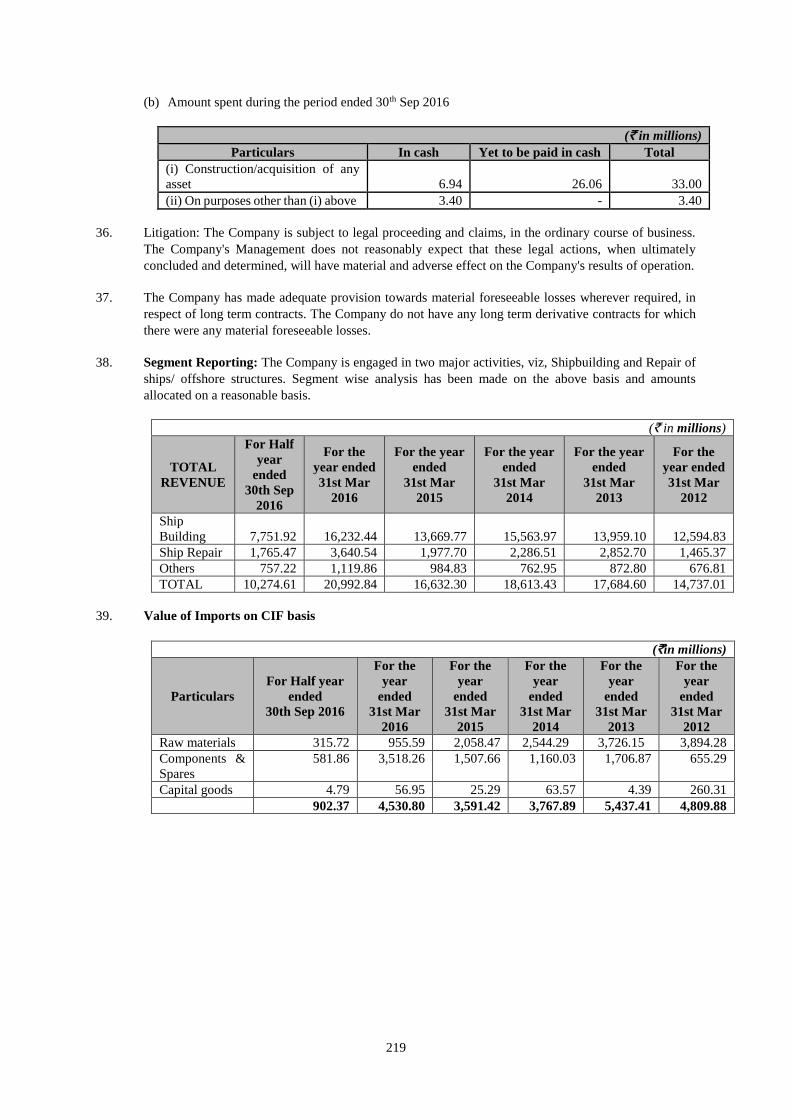

Building Process wherein 50% of the Net Issue shall be available for allocation on a proportionate basis to Qualified Institutional Buyers (“QIBs”) (“QIB Portion”). 5% of the QIB Portion shall be available for allocation

on a proportionate basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocation on a proportionate basis to all QIB Bidders, including Mutual Funds, subject to valid Bids being received

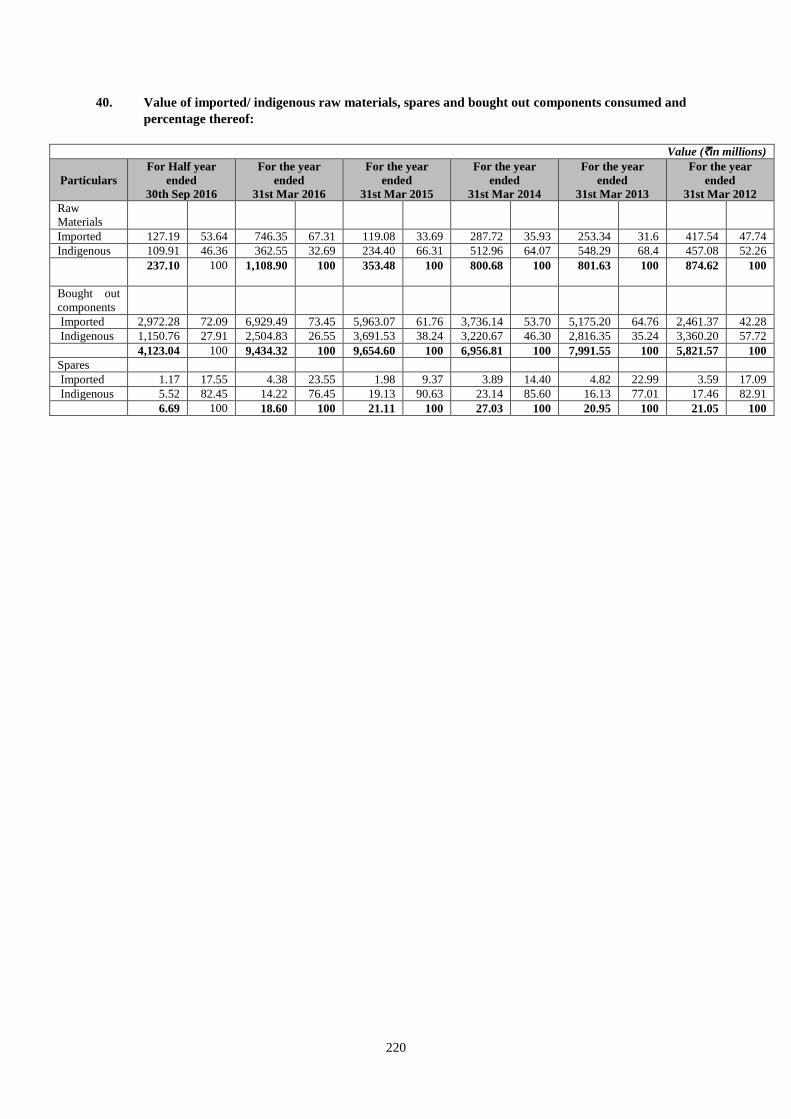

at or above the Issue Price. Further, not less than 15% of the Net Issue shall be available for allocation on a proportionate basis to Non-Institutional Bidders and not less than 35% of the Net Issue shall be available for

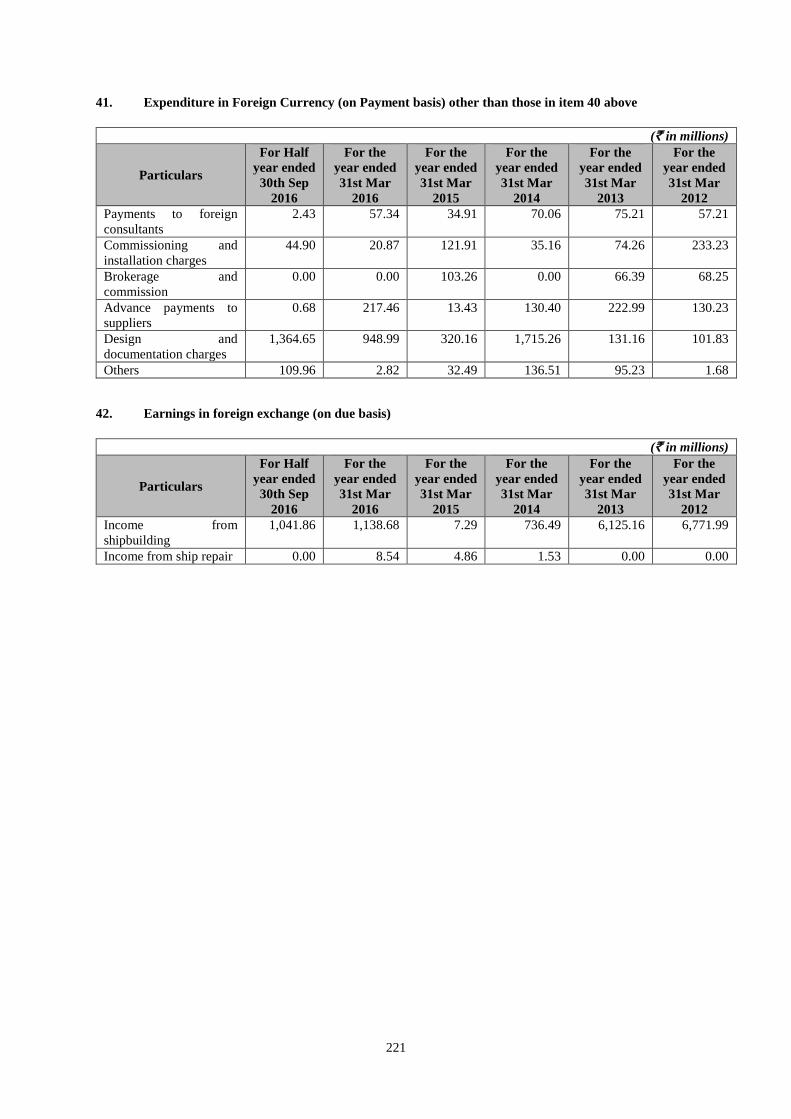

allocation to Retail Individual Bidders in accordance with the SEBI ICDR Regulations, subject to valid Bids being received at or above the Issue Price. Further, 824,000 Equity Shares shall be reserved for allocation on a

proportionate basis to Eligible Employees, subject to valid bids being received at or above the Issue Price. All potential Bidders shall mandatorily participate in the Issue through an Application Supported by Blocked Amount

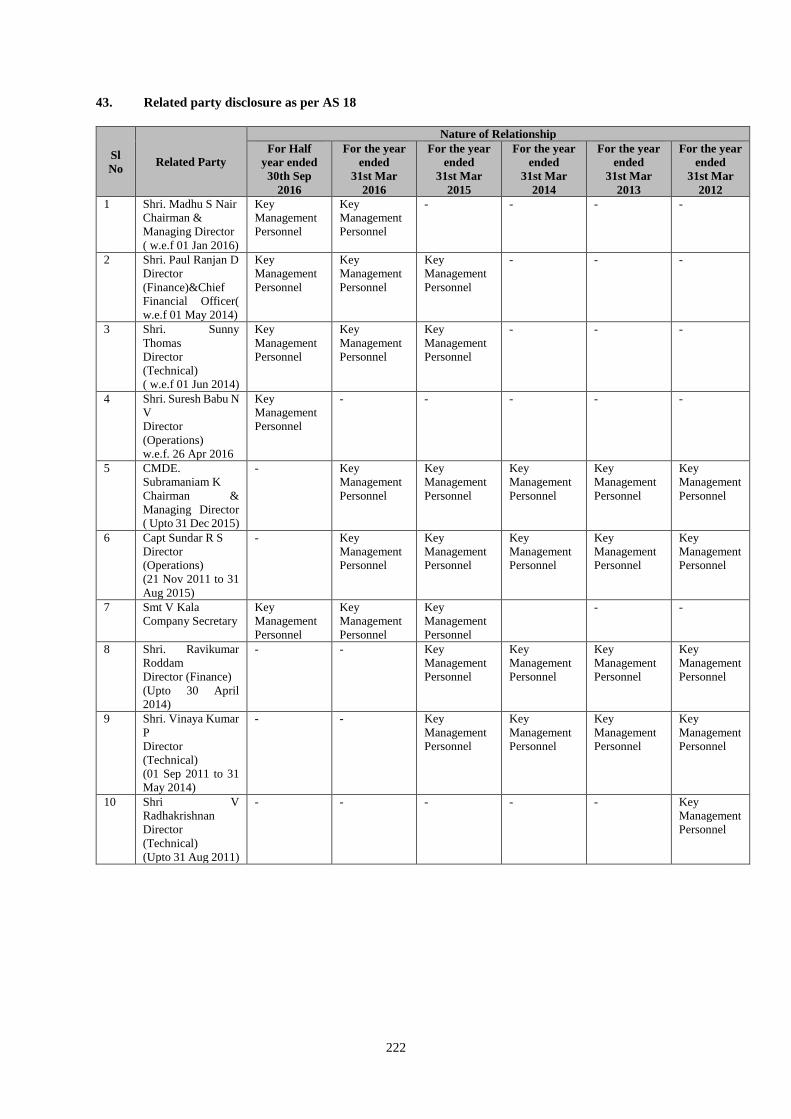

(“ASBA”) process by providing details of their respective bank account which will be blocked by the Self Certified Syndicate Banks (“SCSBs”). For details, see “Issue Procedure” on page 303.

RISKS IN RELATION TO THE FIRST ISSUE

This being the first public issue of our Company, there has been no formal market for the Equity Shares of our Company. The face value of the Equity Shares is ` 10 and the Floor Price is [●] times the face value and the

Cap Price is [●] times the face value. The Issue Price (determined by our Company and the Selling Shareholder in consultation with the BRLMs as stated in “Basis for Issue Price” on page 88) should not be taken to be

indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or sustained trading in the Equity Shares or regarding the price at which the Equity Shares

will be traded after listing.

GENERAL RISKS

Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Issue unless they can afford to take the risk of losing their entire investment. Investors are advised

to read the risk factors carefully before taking an investment decision in the Issue. For taking an investment decision, investors must rely on their own examination of our Company and the Issue, including the risks involved.

The Equity Shares in the Issue have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents of this Draft Red Herring

Prospectus. Specific attention of the investors is invited to “Risk Factors” on page 17.

ISSUER’S AND SELLING SHAREHOLDER’S ABSOLUTE RESPONSIBILITY

Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospectus contains all information with regard to our Company and the Issue, which is material in the

context of the Issue, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein

are honestly held and that there are no other facts, the omission of which makes the Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any

material respect. Further, the Selling Shareholder confirms all information set out about itself as the Selling Shareholder in context of the Offer for Sale included in this Draft Red Herring Prospectus and accepts responsibility

for statements in relation to itself and the Equity Shares being sold by it in the Offer for Sale.

LISTING

The Equity Shares offered through the Red Herring Prospectus are proposed to be listed on the BSE and the NSE. Our Company has received an ‘in-principle’ approval from the BSE and the NSE for the listing of the Equity

Shares pursuant to letters dated [●] and [●], respectively. For the purposes of the Issue, the Designated Stock Exchange shall be [●]. A copy of the Red Herring Prospectus and the Prospectus shall be delivered for registration

to the RoC in accordance with section 26(4) of the Companies Act, 2013. For details of the material contracts and documents available for inspection from the date of this Red Herring Prospectus up to the Bid/Issue Closing

Date, see “Material Contracts and Documents for Inspection” on page 357.

BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE

SBI Capital Markets Limited

202, Maker Tower ‘E, Cuffe Parade

Mumbai - 400005, Maharashtra, India

Tel: +91 (22) 22178300

Fax: +91 (22) 22188332

E-mail: [email protected]

Investor grievance e-mail:

Contact Person: Mr. Nikhil Bhiwapurkar / Mr.

Sandeep Tenneti

Website: www.sbicaps.com

SEBI Registration No.: INM000003531

Edelweiss Financial Services Limited

14th Floor, Edelweiss House, Off. C.S.T Road,

Kalina

Mumbai - 400098, Maharashtra, India

Telephone: +91 (22) 40094400

Fax: +91 (22) 40863610

E-mail: [email protected]

Investor grievance e-mail:

Contact Person: Mr. Siddharth Shah

Website: www.edelweissfin.com

SEBI Registration No.: INM0000010650

JM Financial Institutional Securities Limited

7th Floor, Cnergy, Appasaheb Marathe Marg,

Prabhadevi, Mumbai - 400025, Maharashtra,

India

Tel: +91 (22) 66303030

Fax: +91 (22) 66303330

E-mail: [email protected]

Investor grievance e-mail:

Contact Person: Ms. Prachee Dhuri

Website: www.jmfl.com

SEBI Registration No.: INM000010361

Link Intime India Private Limited

C 101, 247 Park, L B S Marg,

Vikhroli West, Mumbai 400 083

Maharashtra, India

Tel: +91 (22) 4918 6200

Fax: +91 (22) 4918 6195

Email: [email protected]

Investor grievance email: [email protected]

Contact Person: Ms. Shanti Gopalkrishnan

Website: www.linkintime.co.in

SEBI Registration No: INR000004058

BID/ISSUE PROGRAMME

BID/ISSUE OPENS ON [●]

BID/ISSUE CLOSES ON (FOR QIBs) (*) [●]

BID/ ISSUE CLOSES ON (FOR OTHER BIDDERS) [●] (*) Our Company and the Selling Shareholder, in consultation with the BRLMs, may, consider closing the Bid/Issue Period for QIBs one Working Day prior to the Bid/Issue Closing Date

in accordance with the SEBI ICDR Regulations.

TABLE OF CONTENTS

SECTION I: GENERAL ------------------------------------------------------------------------------------------------------------------ 1

DEFINITIONS AND ABBREVIATIONS..............................................................................................................................1

PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA ........................................................................ 12

FORWARD-LOOKING STATEMENTS ............................................................................................................................. 15

SECTION II: RISK FACTORS ------------------------------------------------------------------------------------------------------- 17

SECTION III: INTRODUCTION ---------------------------------------------------------------------------------------------------- 43

SUMMARY OF INDUSTRY ............................................................................................................................................... 43

SUMMARY OF BUSINESS ................................................................................................................................................ 45

SUMMARY FINANCIAL INFORMATION ....................................................................................................................... 52

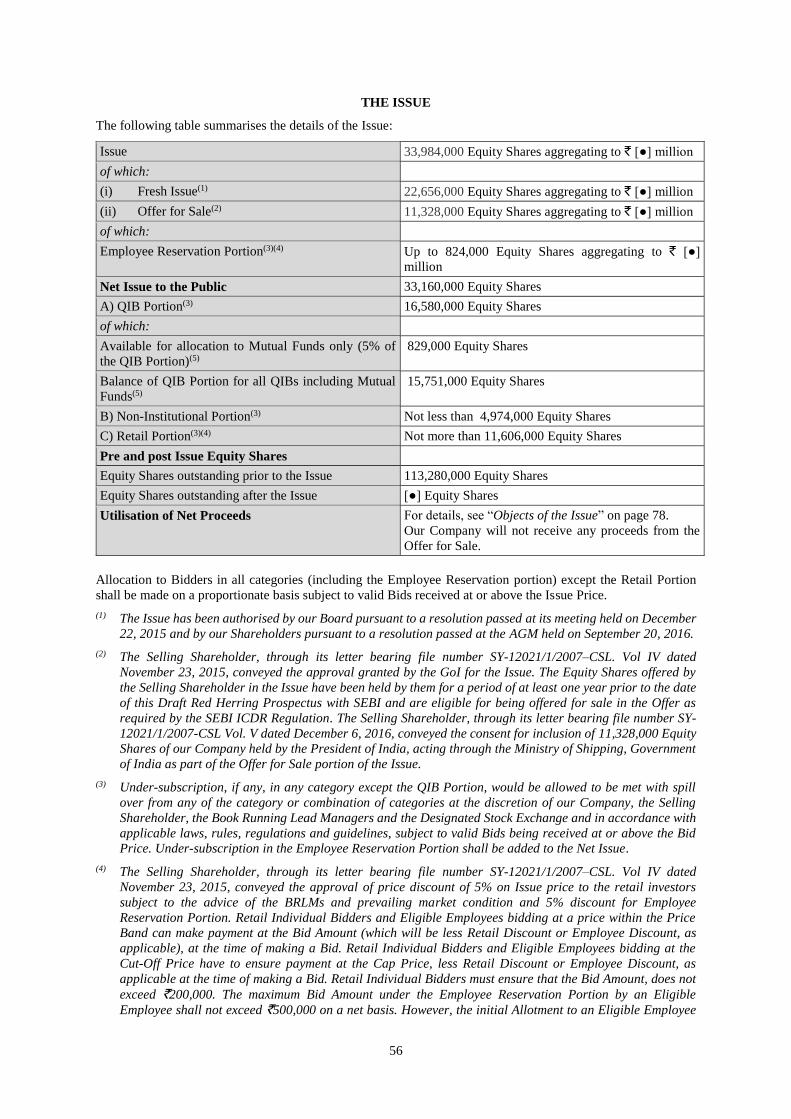

THE ISSUE ........................................................................................................................................................................... 56

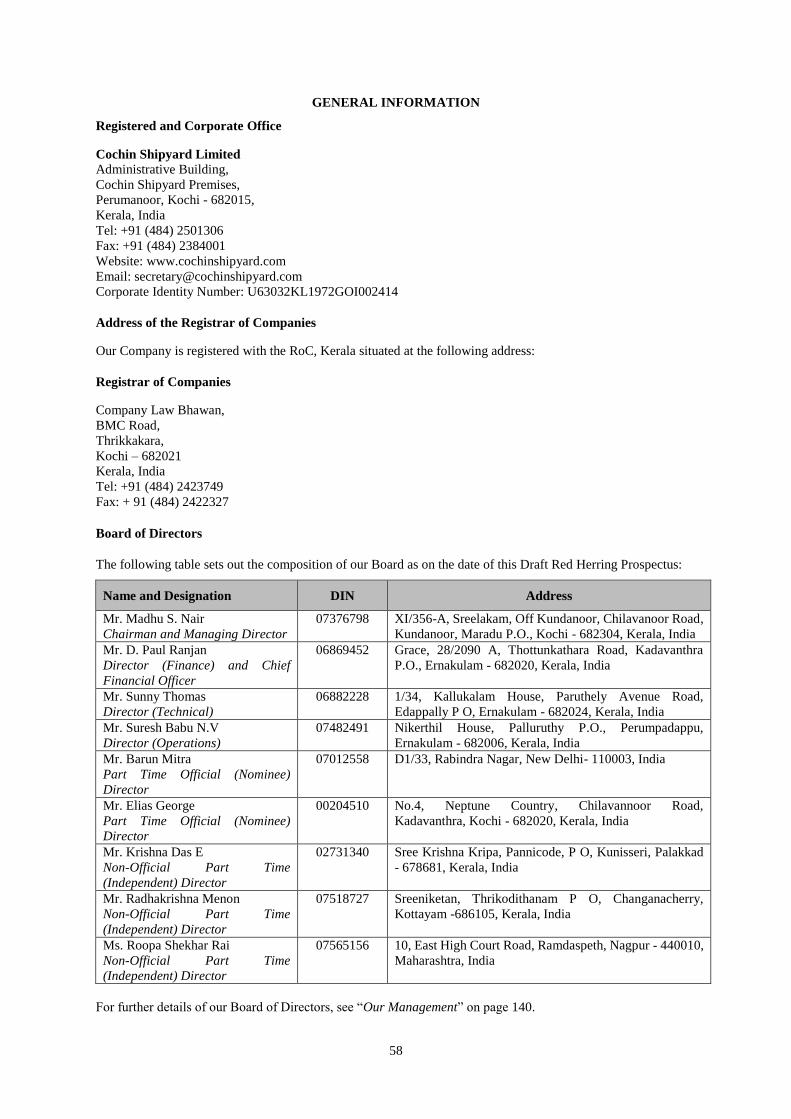

GENERAL INFORMATION ............................................................................................................................................... 58

CAPITAL STRUCTURE ...................................................................................................................................................... 66

OBJECTS OF THE ISSUE ................................................................................................................................................... 78

BASIS FOR ISSUE PRICE ................................................................................................................................................... 88

STATEMENT OF TAX BENEFITS ..................................................................................................................................... 91

SECTION IV: ABOUT OUR COMPANY ------------------------------------------------------------------------------------------ 94

INDUSTRY OVERVIEW .................................................................................................................................................... 94

OUR BUSINESS ................................................................................................................................................................ 114

REGULATIONS AND POLICIES ..................................................................................................................................... 129

HISTORY AND CERTAIN CORPORATE MATTERS .................................................................................................... 134

OUR MANAGEMENT ....................................................................................................................................................... 140

OUR PROMOTER AND PROMOTER GROUP ................................................................................................................ 158

OUR GROUP COMPANIES .............................................................................................................................................. 159

RELATED PARTY TRANSACTIONS ............................................................................................................................. 160

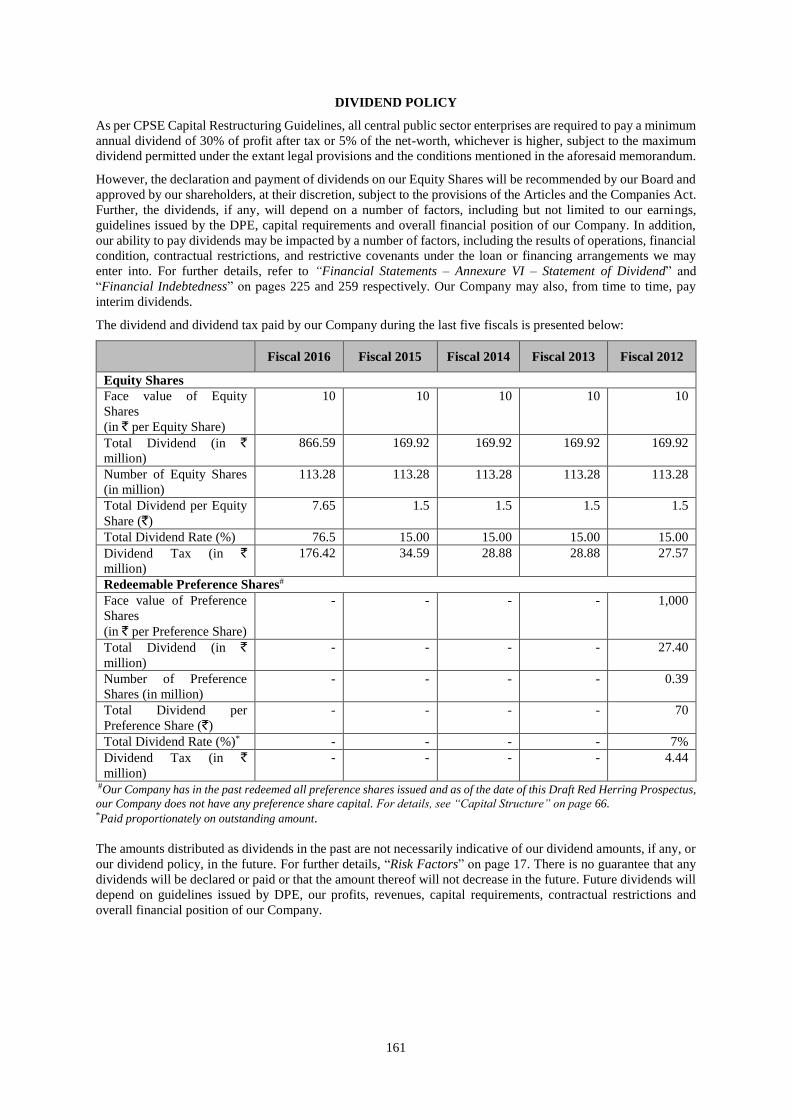

DIVIDEND POLICY .......................................................................................................................................................... 161

SECTION V: FINANCIAL INFORMATION ------------------------------------------------------------------------------------- 162

FINANCIAL STATEMENTS ............................................................................................................................................ 162

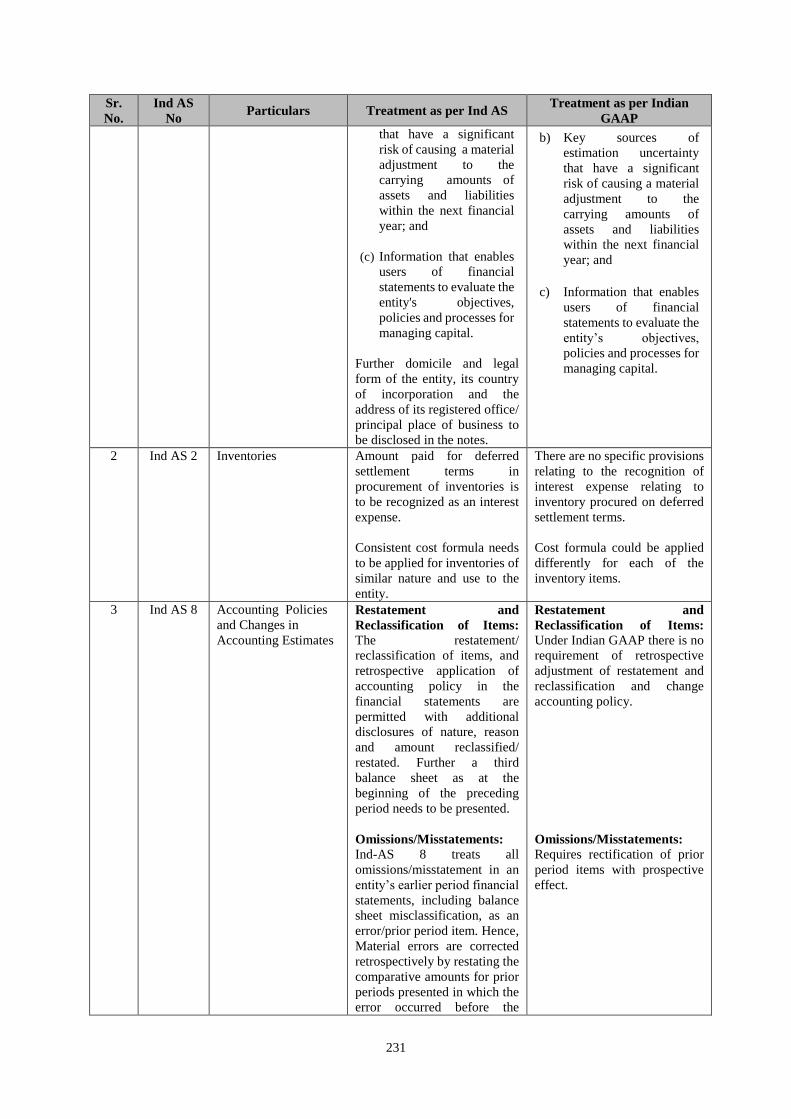

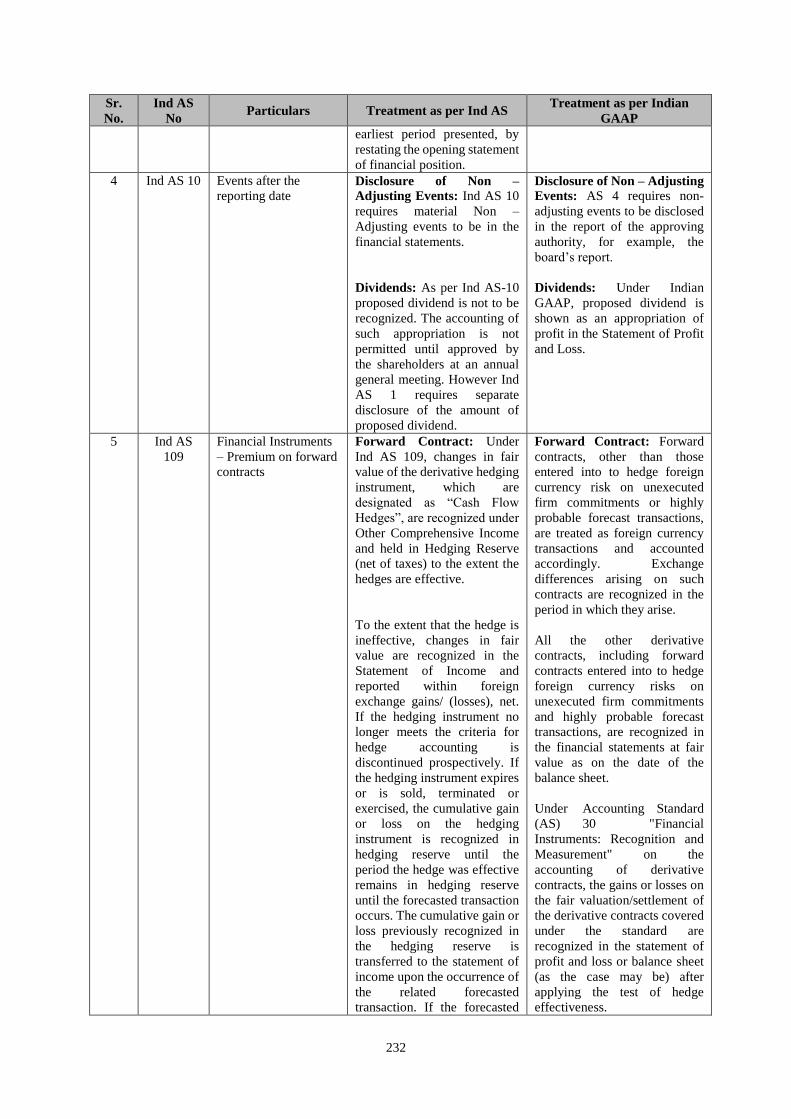

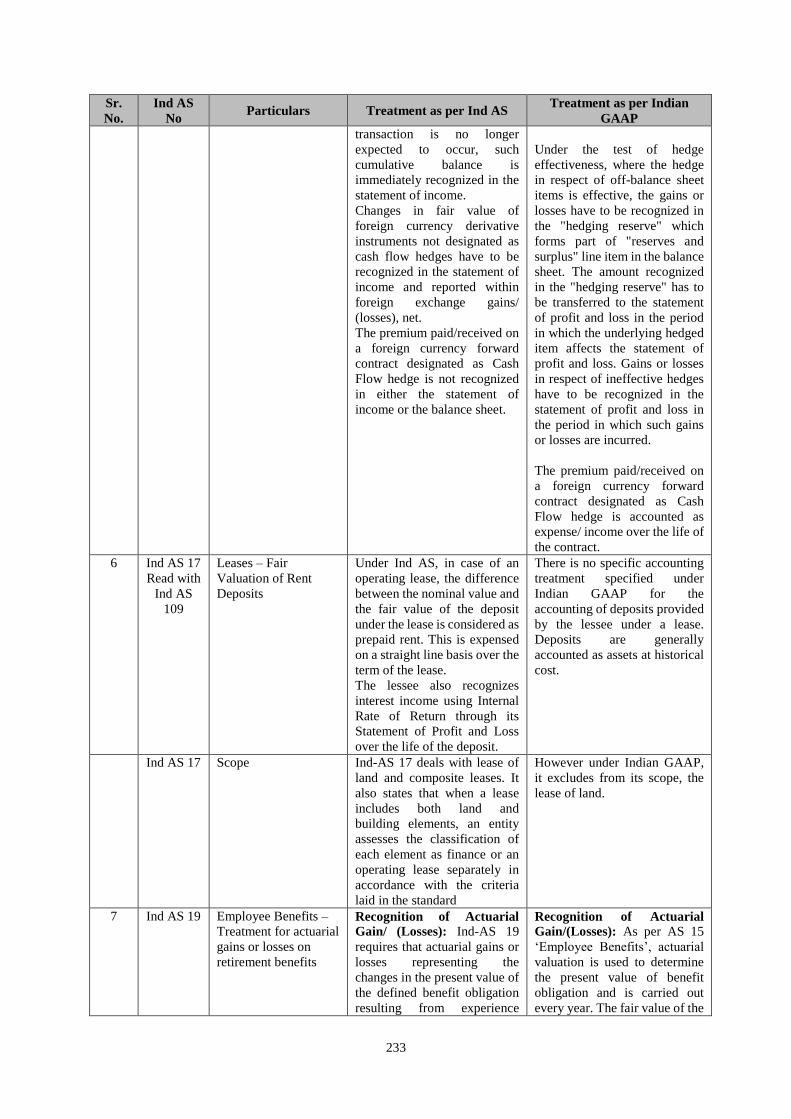

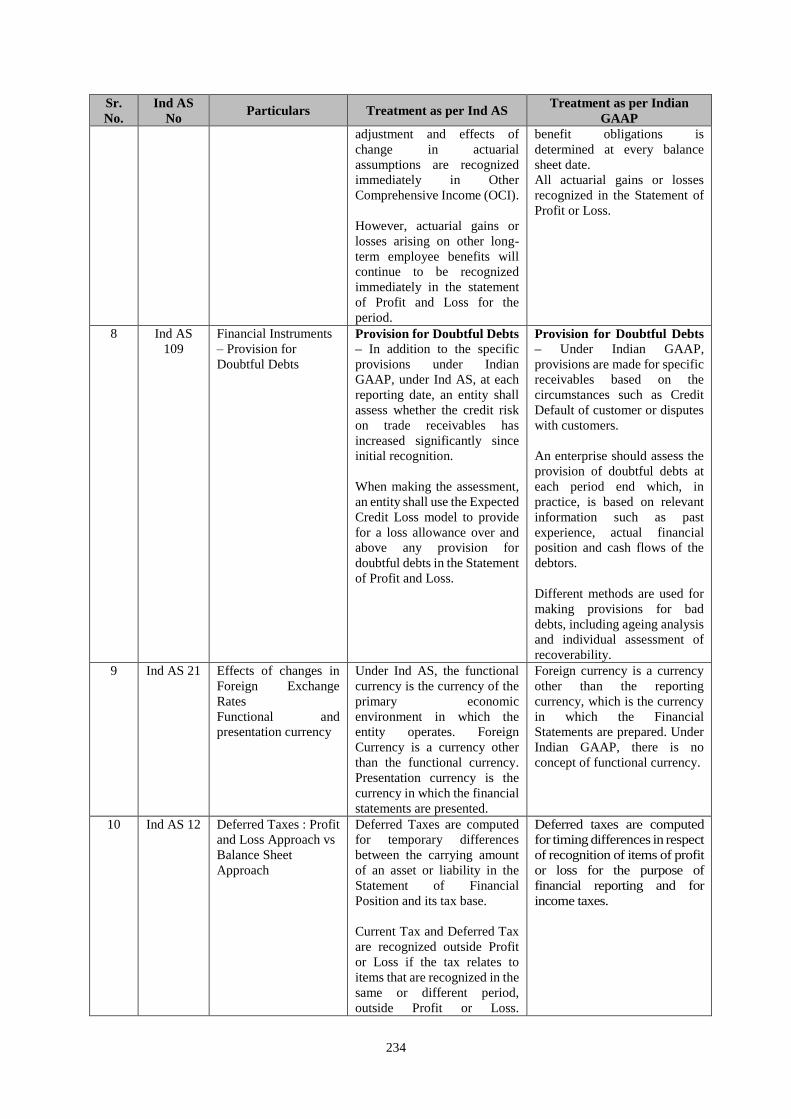

SIGNIFICANT DIFFERENCES BETWEEN INDIAN GAAP AND IND AS ................................................................... 230

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

............................................................................................................................................................................................ 236

FINANCIAL INDEBTEDNESS ......................................................................................................................................... 259

SECTION VI: LEGAL AND OTHER INFORMATION ----------------------------------------------------------------------- 265

OUTSTANDING LITIGATION AND OTHER MATERIAL DEVELOPMENTS ........................................................... 265

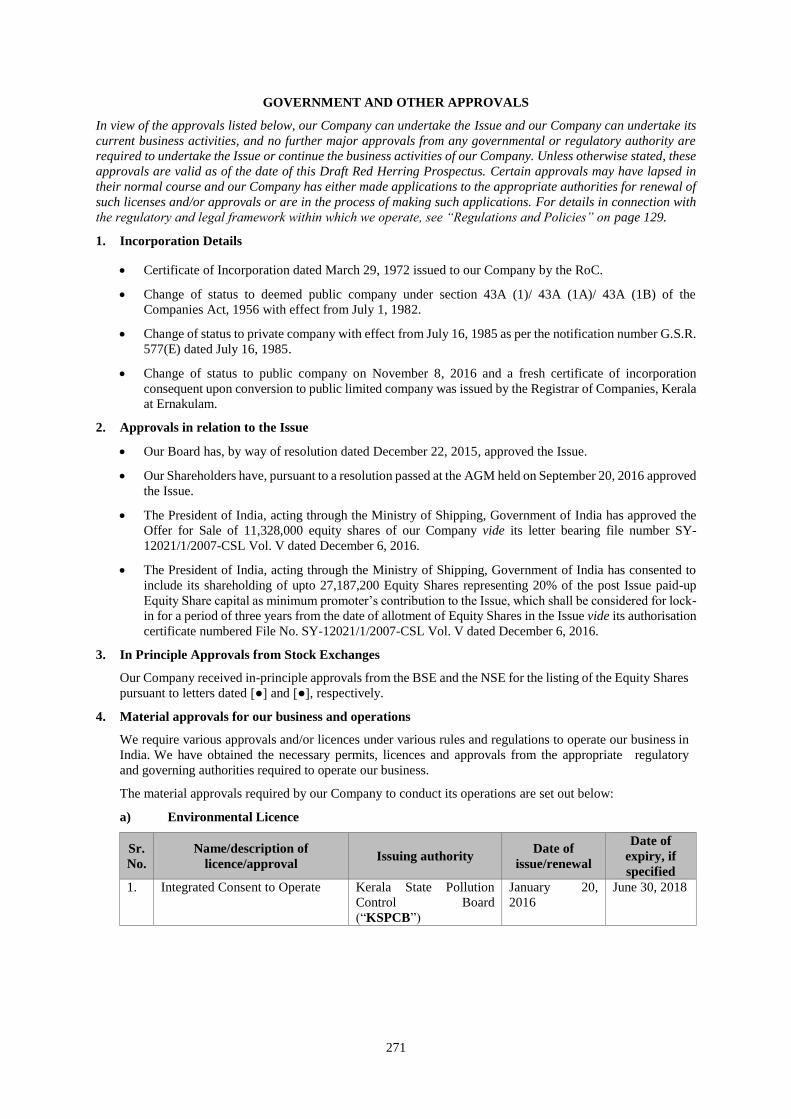

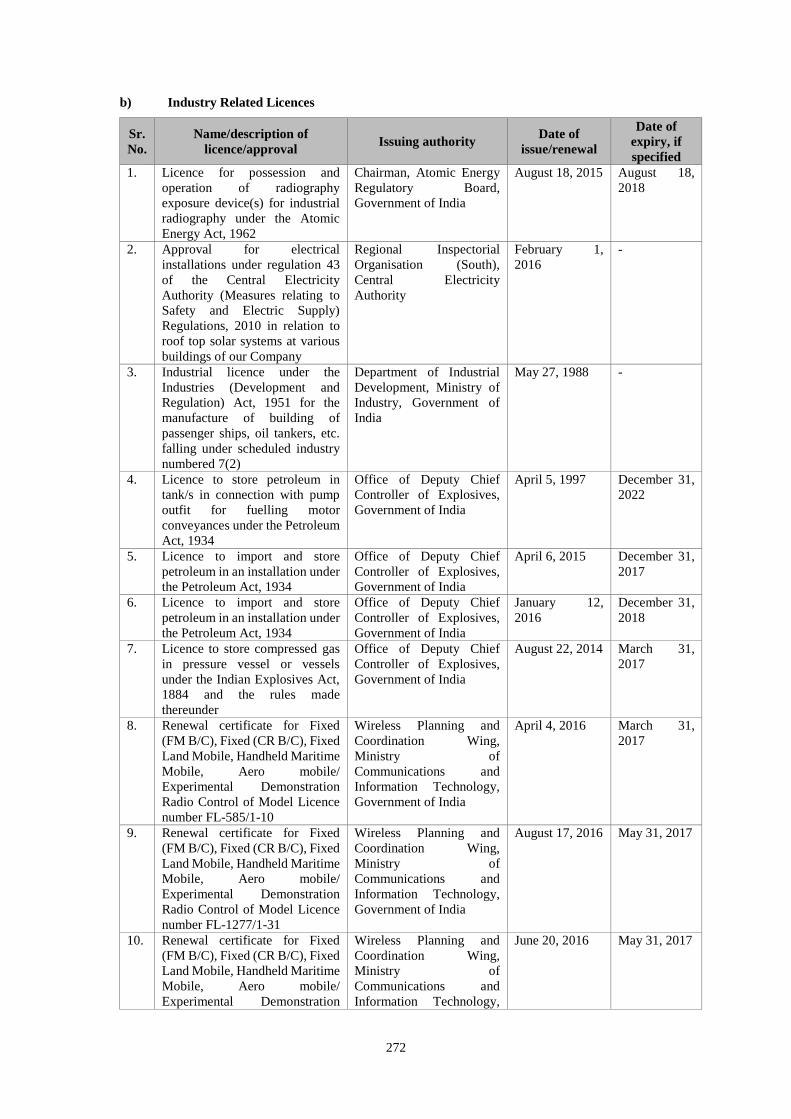

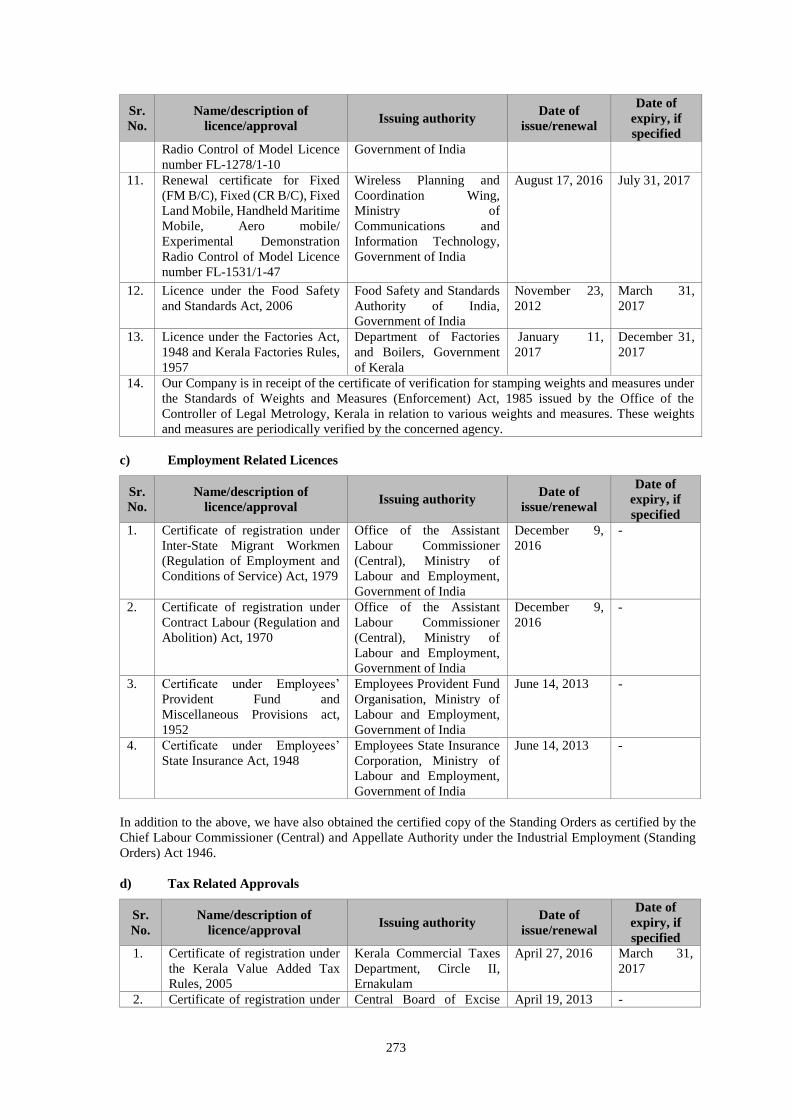

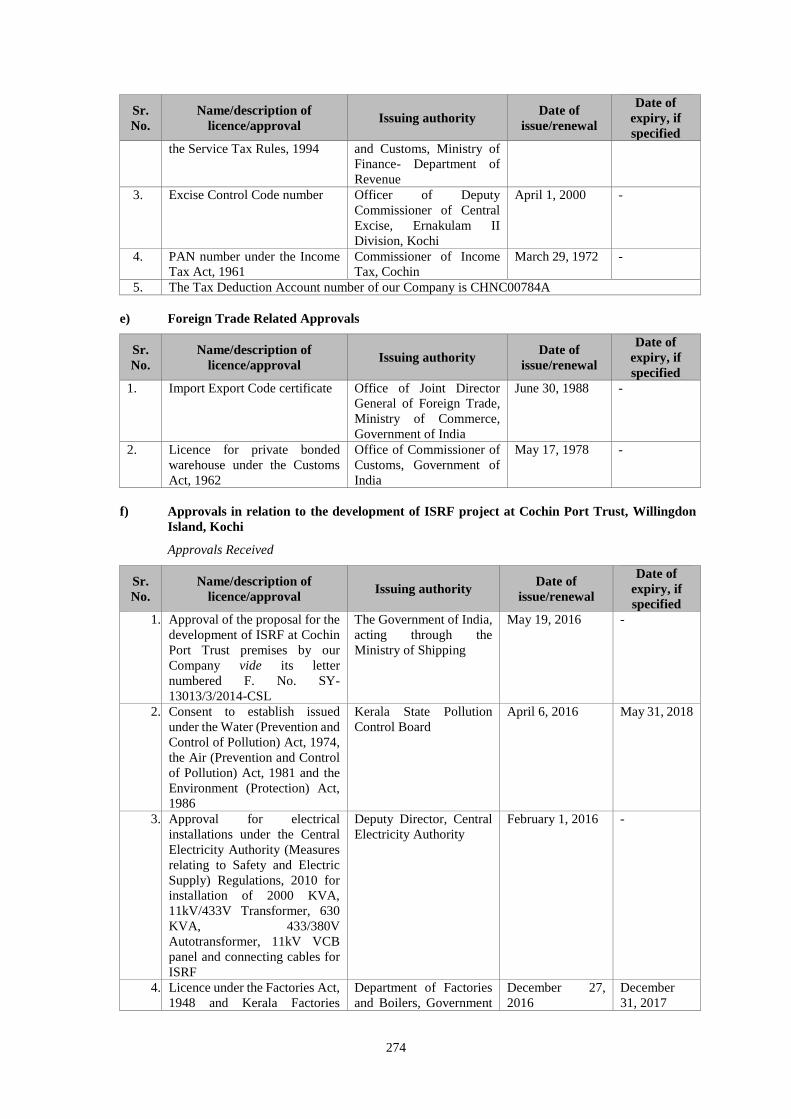

GOVERNMENT AND OTHER APPROVALS ................................................................................................................. 271

OTHER REGULATORY AND STATUTORY DISCLOSURES ...................................................................................... 277

SECTION VII: ISSUE INFORMATION ------------------------------------------------------------------------------------------- 295

TERMS OF THE ISSUE ..................................................................................................................................................... 295

ISSUE STRUCTURE ......................................................................................................................................................... 299

ISSUE PROCEDURE ......................................................................................................................................................... 303

RESTRICTIONS ON FOREIGN OWNERSHIP OF INDIAN SECURITIES .................................................................... 346

SECTION VIII: MAIN PROVISIONS OF ARTICLES OF ASSOCIATION ---------------------------------------------- 347

SECTION IX: OTHER INFORMATION ------------------------------------------------------------------------------------------ 357

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ----------------------------------------------------- 357

DECLARATION ------------------------------------------------------------------------------------------------------------------------ 359

1

SECTION I: GENERAL

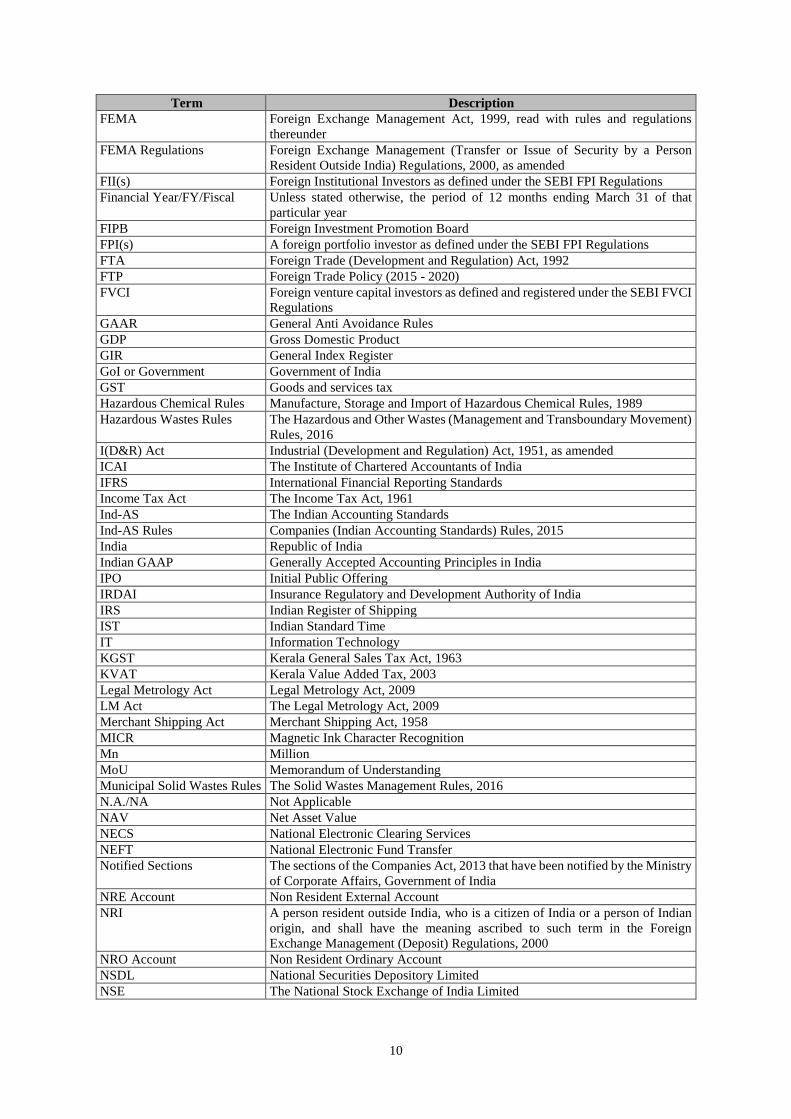

DEFINITIONS AND ABBREVIATIONS

This Draft Red Herring Prospectus uses certain definitions and abbreviations which, unless the context otherwise

indicates or implies, shall have the meaning as provided below. References to any legislation, act, regulation,

rule, guideline or policy shall be to such legislation, act, regulation, rule, guideline or policy, as amended,

supplemented or re-enacted from time to time.

The words and expressions used in this Draft Red Herring Prospectus but not defined herein, shall have, to the

extent applicable, the meaning ascribed to such terms under the Companies Act, the SEBI ICDR Regulations, the

SCRA, the Depositories Act or the rules and regulations made there under.

Notwithstanding the foregoing, terms used in “Statement of Tax Benefits”, “Financial Statements” and “Main

Provisions of Articles of Association” on pages 91, 162 and 347, respectively, shall have the meaning ascribed to

such terms in such sections.

General Terms

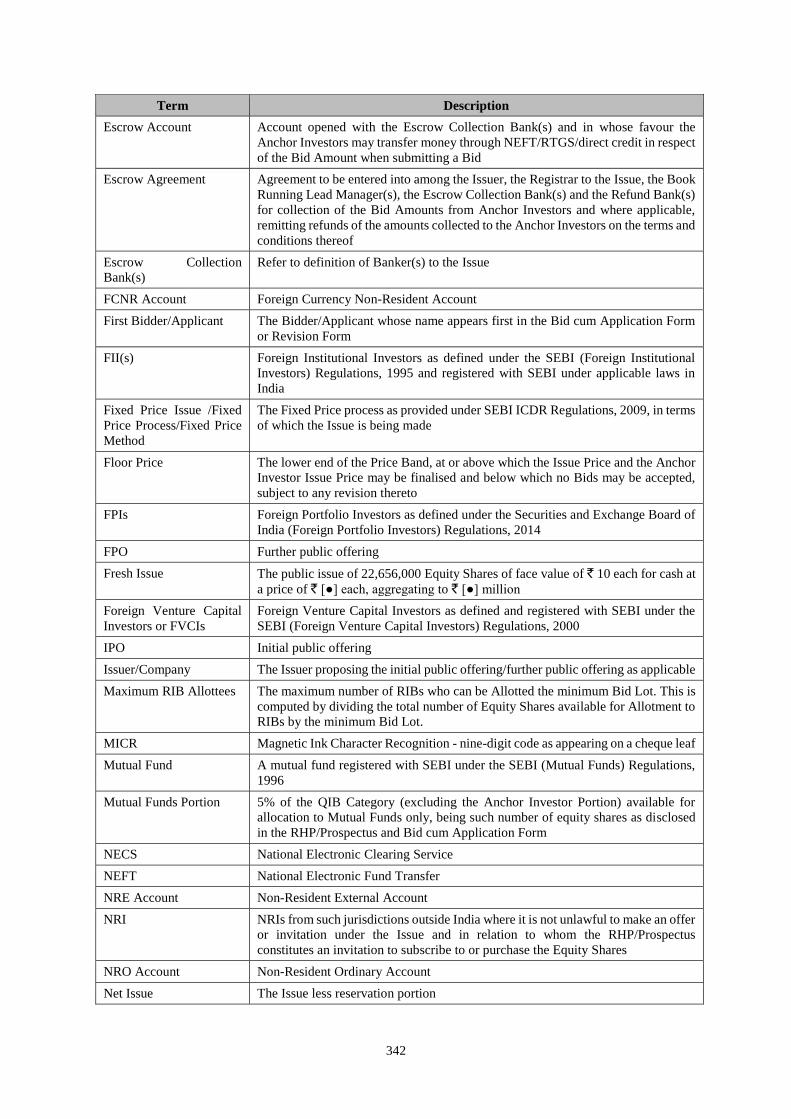

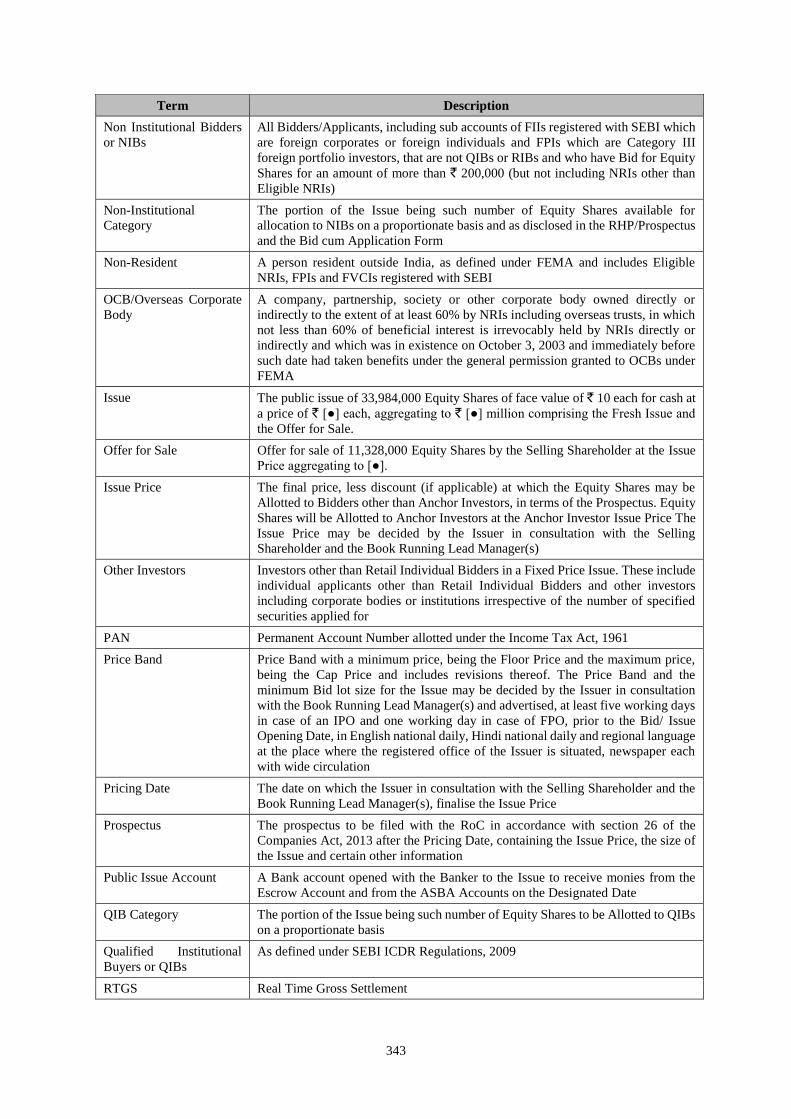

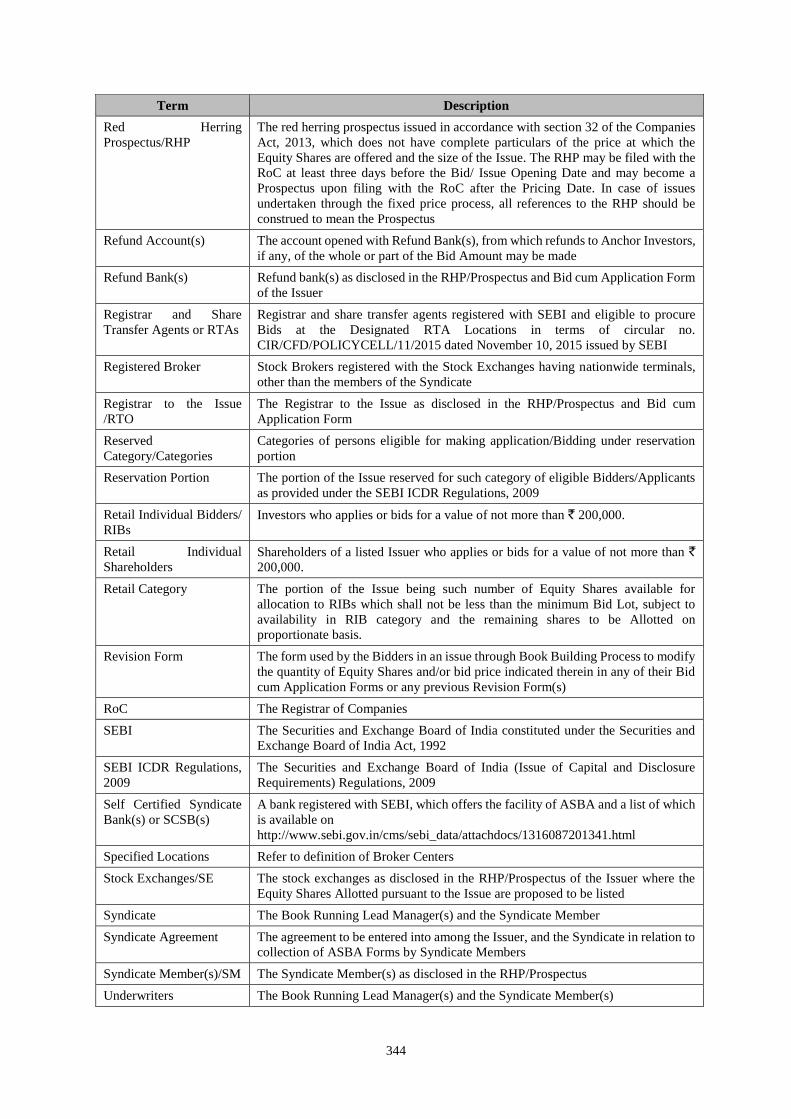

Term Description

“our Company”, the

“Company”, the “Issuer”, we,

us or our

Cochin Shipyard Limited, a company incorporated under the Companies Act,

1956, having its registered office at Administrative Building, Cochin Shipyard

Premises, Perumanoor, Kochi - 682015, Kerala, India

Company Related Terms

Term Description

Articles of Association/AoA The articles of association of our Company, as amended

Audit Committee The audit committee of the Board of Directors described in “Our

Management” on page 140

Board/Board of Directors The board of directors of our Company or a duly constituted committee thereof

CPSE Capital Restructuring

Guidelines

An Office Memorandum bearing F. No. 5/2/2016-Policy dated May 27, 2016,

issued by DIPAM on Guidelines on Capital Restructuring of Central Public

Sector Enterprises.

CSR & SD Committee Corporate Social Responsibility and Sustainability Development Committee

which was re-constituted pursuant to the board meeting held on May 7, 2016

Director(s) The director(s) of our Company

Equity Shares The equity shares of our Company of face value of `10 each

Key Management Personnel Key management personnel of our Company in terms of section 2(51) the

Companies Act, 2013 or regulation 2(1)(s) of the SEBI ICDR Regulations and

as disclosed in “Our Management” on page 140

Materiality Policy Our Company, in its Board meeting held on January 24, 2017, adopted a policy

on identification of material creditors and material litigations

Memorandum of Association/

MoA

The memorandum of association of our Company, as amended

MoU Our Company enters into a Memorandum of Understanding with Department

of Public Enterprises, Ministry of Shipping, GoI every financial year

Promoter The Promoter of our Company is the President of India acting through the

Ministry of Shipping

Registered Office / Registered

and Corporate Office

Registered Office of our Company located at Administrative Building, Cochin

Shipyard Premises, Perumanoor, Kochi - 682015, Kerala, India

Restated Financial Statements The audited standalone financial statements of our Company as at and for the

financial years ended March 31, 2016, 2015, 2014, 2013 and 2012 and as at

and for the half year ended September 30, 2016, which comprises the audited

standalone balance sheet, the audited standalone statement of profit and loss

and the audited standalone cash flow statement and notes to the audited

standalone financial statements of assets and liabilities, profit and loss and cash

flows, prepared in accordance with Indian GAAP and the Companies Act and

2

Term Description

restated in accordance with the SEBI ICDR Regulations and the Revised

Guidance Note on Reports in Company Prospectuses (Revised) issued by the

ICAI, together with the schedules, notes and annexures thereto

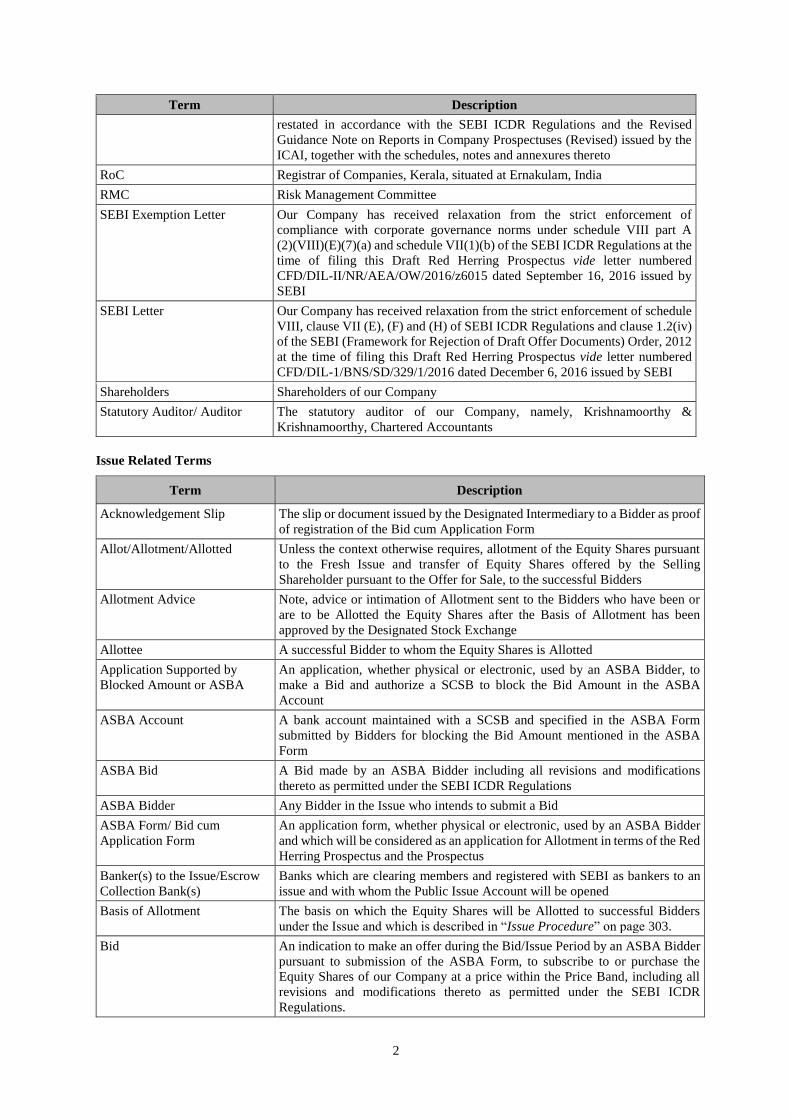

RoC Registrar of Companies, Kerala, situated at Ernakulam, India

RMC Risk Management Committee

SEBI Exemption Letter Our Company has received relaxation from the strict enforcement of

compliance with corporate governance norms under schedule VIII part A

(2)(VIII)(E)(7)(a) and schedule VII(1)(b) of the SEBI ICDR Regulations at the

time of filing this Draft Red Herring Prospectus vide letter numbered

CFD/DIL-II/NR/AEA/OW/2016/z6015 dated September 16, 2016 issued by

SEBI

SEBI Letter Our Company has received relaxation from the strict enforcement of schedule

VIII, clause VII (E), (F) and (H) of SEBI ICDR Regulations and clause 1.2(iv)

of the SEBI (Framework for Rejection of Draft Offer Documents) Order, 2012

at the time of filing this Draft Red Herring Prospectus vide letter numbered

CFD/DIL-1/BNS/SD/329/1/2016 dated December 6, 2016 issued by SEBI

Shareholders Shareholders of our Company

Statutory Auditor/ Auditor The statutory auditor of our Company, namely, Krishnamoorthy &

Krishnamoorthy, Chartered Accountants

Issue Related Terms

Term Description

Acknowledgement Slip The slip or document issued by the Designated Intermediary to a Bidder as proof

of registration of the Bid cum Application Form

Allot/Allotment/Allotted Unless the context otherwise requires, allotment of the Equity Shares pursuant

to the Fresh Issue and transfer of Equity Shares offered by the Selling

Shareholder pursuant to the Offer for Sale, to the successful Bidders

Allotment Advice Note, advice or intimation of Allotment sent to the Bidders who have been or

are to be Allotted the Equity Shares after the Basis of Allotment has been

approved by the Designated Stock Exchange

Allottee A successful Bidder to whom the Equity Shares is Allotted

Application Supported by

Blocked Amount or ASBA

An application, whether physical or electronic, used by an ASBA Bidder, to

make a Bid and authorize a SCSB to block the Bid Amount in the ASBA

Account

ASBA Account A bank account maintained with a SCSB and specified in the ASBA Form

submitted by Bidders for blocking the Bid Amount mentioned in the ASBA

Form

ASBA Bid A Bid made by an ASBA Bidder including all revisions and modifications

thereto as permitted under the SEBI ICDR Regulations

ASBA Bidder Any Bidder in the Issue who intends to submit a Bid

ASBA Form/ Bid cum

Application Form

An application form, whether physical or electronic, used by an ASBA Bidder

and which will be considered as an application for Allotment in terms of the Red

Herring Prospectus and the Prospectus

Banker(s) to the Issue/Escrow

Collection Bank(s)

Banks which are clearing members and registered with SEBI as bankers to an

issue and with whom the Public Issue Account will be opened

Basis of Allotment The basis on which the Equity Shares will be Allotted to successful Bidders

under the Issue and which is described in “Issue Procedure” on page 303.

Bid An indication to make an offer during the Bid/Issue Period by an ASBA Bidder

pursuant to submission of the ASBA Form, to subscribe to or purchase the

Equity Shares of our Company at a price within the Price Band, including all

revisions and modifications thereto as permitted under the SEBI ICDR

Regulations.

3

Term Description

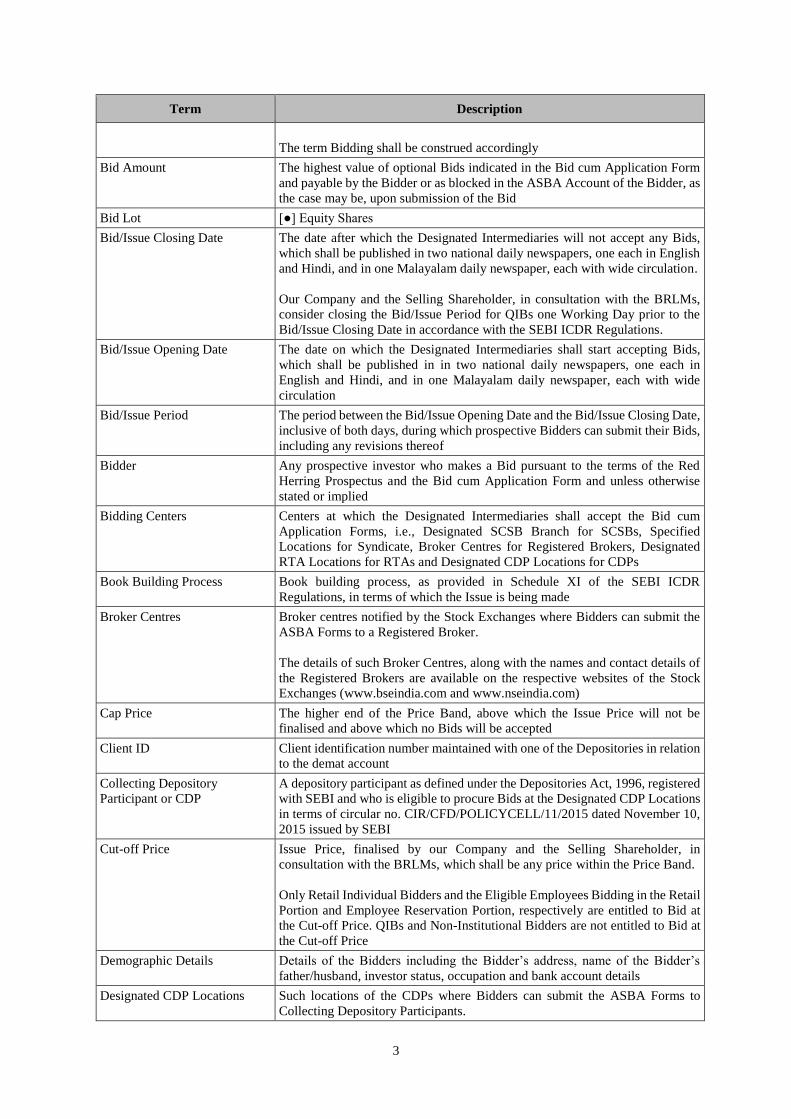

The term Bidding shall be construed accordingly

Bid Amount The highest value of optional Bids indicated in the Bid cum Application Form

and payable by the Bidder or as blocked in the ASBA Account of the Bidder, as

the case may be, upon submission of the Bid

Bid Lot [●] Equity Shares

Bid/Issue Closing Date The date after which the Designated Intermediaries will not accept any Bids,

which shall be published in two national daily newspapers, one each in English

and Hindi, and in one Malayalam daily newspaper, each with wide circulation.

Our Company and the Selling Shareholder, in consultation with the BRLMs,

consider closing the Bid/Issue Period for QIBs one Working Day prior to the

Bid/Issue Closing Date in accordance with the SEBI ICDR Regulations.

Bid/Issue Opening Date The date on which the Designated Intermediaries shall start accepting Bids,

which shall be published in in two national daily newspapers, one each in

English and Hindi, and in one Malayalam daily newspaper, each with wide

circulation

Bid/Issue Period The period between the Bid/Issue Opening Date and the Bid/Issue Closing Date,

inclusive of both days, during which prospective Bidders can submit their Bids,

including any revisions thereof

Bidder Any prospective investor who makes a Bid pursuant to the terms of the Red

Herring Prospectus and the Bid cum Application Form and unless otherwise

stated or implied

Bidding Centers Centers at which the Designated Intermediaries shall accept the Bid cum

Application Forms, i.e., Designated SCSB Branch for SCSBs, Specified

Locations for Syndicate, Broker Centres for Registered Brokers, Designated

RTA Locations for RTAs and Designated CDP Locations for CDPs

Book Building Process Book building process, as provided in Schedule XI of the SEBI ICDR

Regulations, in terms of which the Issue is being made

Broker Centres Broker centres notified by the Stock Exchanges where Bidders can submit the

ASBA Forms to a Registered Broker.

The details of such Broker Centres, along with the names and contact details of

the Registered Brokers are available on the respective websites of the Stock

Exchanges (www.bseindia.com and www.nseindia.com)

Cap Price The higher end of the Price Band, above which the Issue Price will not be

finalised and above which no Bids will be accepted

Client ID Client identification number maintained with one of the Depositories in relation

to the demat account

Collecting Depository

Participant or CDP

A depository participant as defined under the Depositories Act, 1996, registered

with SEBI and who is eligible to procure Bids at the Designated CDP Locations

in terms of circular no. CIR/CFD/POLICYCELL/11/2015 dated November 10,

2015 issued by SEBI

Cut-off Price Issue Price, finalised by our Company and the Selling Shareholder, in

consultation with the BRLMs, which shall be any price within the Price Band.

Only Retail Individual Bidders and the Eligible Employees Bidding in the Retail

Portion and Employee Reservation Portion, respectively are entitled to Bid at

the Cut-off Price. QIBs and Non-Institutional Bidders are not entitled to Bid at

the Cut-off Price

Demographic Details Details of the Bidders including the Bidder’s address, name of the Bidder’s

father/husband, investor status, occupation and bank account details

Designated CDP Locations Such locations of the CDPs where Bidders can submit the ASBA Forms to

Collecting Depository Participants.

4

Term Description

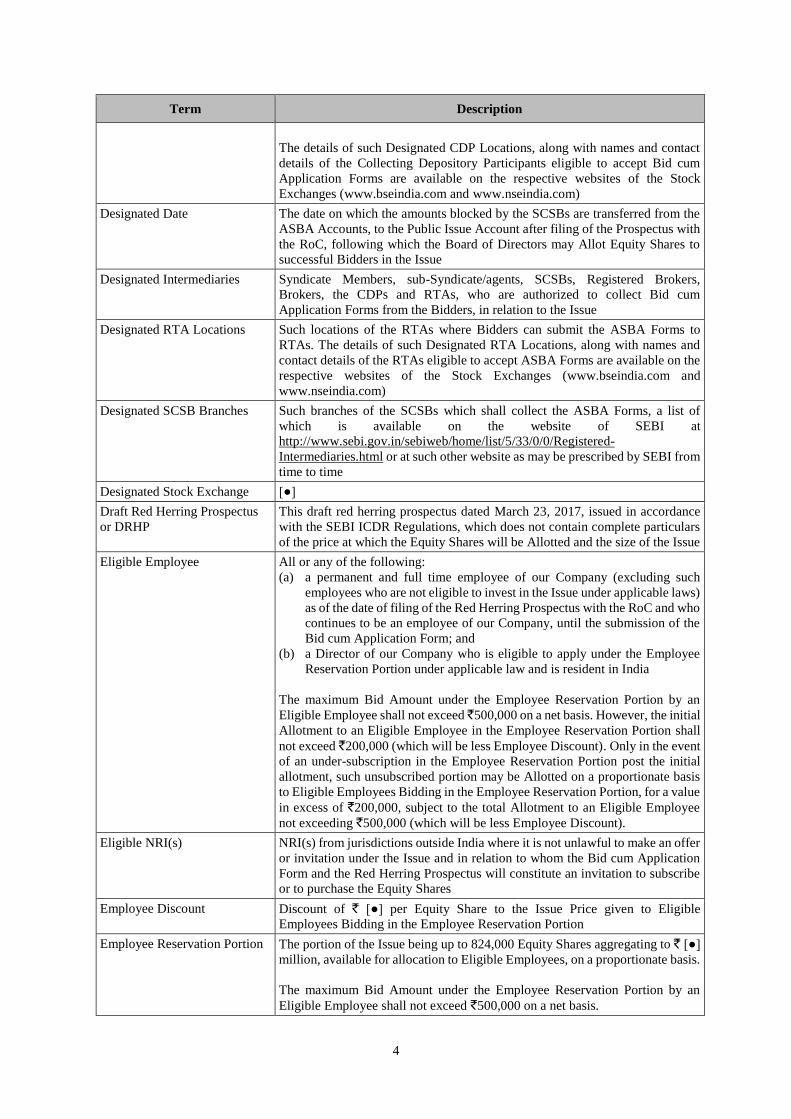

The details of such Designated CDP Locations, along with names and contact

details of the Collecting Depository Participants eligible to accept Bid cum

Application Forms are available on the respective websites of the Stock

Exchanges (www.bseindia.com and www.nseindia.com)

Designated Date The date on which the amounts blocked by the SCSBs are transferred from the

ASBA Accounts, to the Public Issue Account after filing of the Prospectus with

the RoC, following which the Board of Directors may Allot Equity Shares to

successful Bidders in the Issue

Designated Intermediaries Syndicate Members, sub-Syndicate/agents, SCSBs, Registered Brokers,

Brokers, the CDPs and RTAs, who are authorized to collect Bid cum

Application Forms from the Bidders, in relation to the Issue

Designated RTA Locations Such locations of the RTAs where Bidders can submit the ASBA Forms to

RTAs. The details of such Designated RTA Locations, along with names and

contact details of the RTAs eligible to accept ASBA Forms are available on the

respective websites of the Stock Exchanges (www.bseindia.com and

www.nseindia.com)

Designated SCSB Branches Such branches of the SCSBs which shall collect the ASBA Forms, a list of

which is available on the website of SEBI at

http://www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Registered-

Intermediaries.html or at such other website as may be prescribed by SEBI from

time to time

Designated Stock Exchange [●]

Draft Red Herring Prospectus

or DRHP

This draft red herring prospectus dated March 23, 2017, issued in accordance

with the SEBI ICDR Regulations, which does not contain complete particulars

of the price at which the Equity Shares will be Allotted and the size of the Issue

Eligible Employee All or any of the following:

(a) a permanent and full time employee of our Company (excluding such

employees who are not eligible to invest in the Issue under applicable laws)

as of the date of filing of the Red Herring Prospectus with the RoC and who

continues to be an employee of our Company, until the submission of the

Bid cum Application Form; and

(b) a Director of our Company who is eligible to apply under the Employee

Reservation Portion under applicable law and is resident in India

The maximum Bid Amount under the Employee Reservation Portion by an

Eligible Employee shall not exceed ̀ 500,000 on a net basis. However, the initial

Allotment to an Eligible Employee in the Employee Reservation Portion shall

not exceed `200,000 (which will be less Employee Discount). Only in the event

of an under-subscription in the Employee Reservation Portion post the initial

allotment, such unsubscribed portion may be Allotted on a proportionate basis

to Eligible Employees Bidding in the Employee Reservation Portion, for a value

in excess of `200,000, subject to the total Allotment to an Eligible Employee

not exceeding `500,000 (which will be less Employee Discount).

Eligible NRI(s) NRI(s) from jurisdictions outside India where it is not unlawful to make an offer

or invitation under the Issue and in relation to whom the Bid cum Application

Form and the Red Herring Prospectus will constitute an invitation to subscribe

or to purchase the Equity Shares

Employee Discount Discount of ` [●] per Equity Share to the Issue Price given to Eligible

Employees Bidding in the Employee Reservation Portion

Employee Reservation Portion The portion of the Issue being up to 824,000 Equity Shares aggregating to ` [●]

million, available for allocation to Eligible Employees, on a proportionate basis.

The maximum Bid Amount under the Employee Reservation Portion by an

Eligible Employee shall not exceed `500,000 on a net basis.

5

Term Description

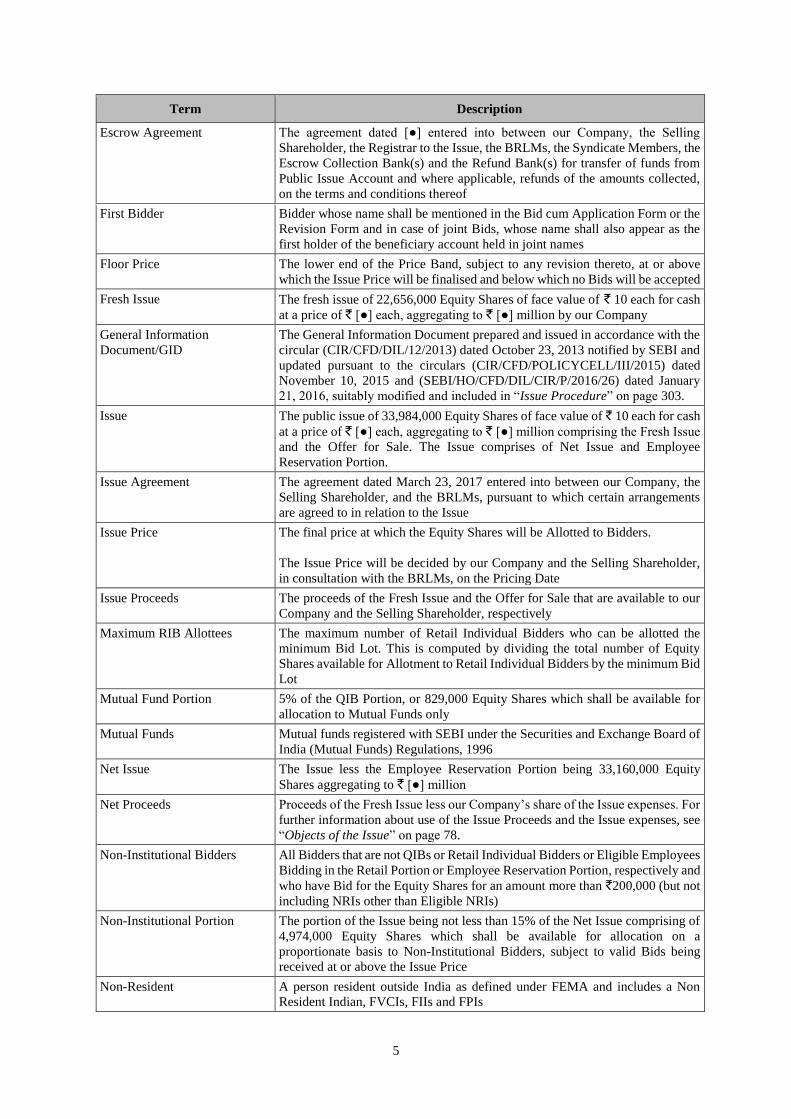

Escrow Agreement The agreement dated [●] entered into between our Company, the Selling

Shareholder, the Registrar to the Issue, the BRLMs, the Syndicate Members, the

Escrow Collection Bank(s) and the Refund Bank(s) for transfer of funds from

Public Issue Account and where applicable, refunds of the amounts collected,

on the terms and conditions thereof

First Bidder Bidder whose name shall be mentioned in the Bid cum Application Form or the

Revision Form and in case of joint Bids, whose name shall also appear as the

first holder of the beneficiary account held in joint names

Floor Price The lower end of the Price Band, subject to any revision thereto, at or above

which the Issue Price will be finalised and below which no Bids will be accepted

Fresh Issue The fresh issue of 22,656,000 Equity Shares of face value of ` 10 each for cash

at a price of ` [●] each, aggregating to ` [●] million by our Company

General Information

Document/GID

The General Information Document prepared and issued in accordance with the

circular (CIR/CFD/DIL/12/2013) dated October 23, 2013 notified by SEBI and

updated pursuant to the circulars (CIR/CFD/POLICYCELL/III/2015) dated

November 10, 2015 and (SEBI/HO/CFD/DIL/CIR/P/2016/26) dated January

21, 2016, suitably modified and included in “Issue Procedure” on page 303.

Issue The public issue of 33,984,000 Equity Shares of face value of ` 10 each for cash

at a price of ` [●] each, aggregating to ` [●] million comprising the Fresh Issue

and the Offer for Sale. The Issue comprises of Net Issue and Employee

Reservation Portion.

Issue Agreement The agreement dated March 23, 2017 entered into between our Company, the

Selling Shareholder, and the BRLMs, pursuant to which certain arrangements

are agreed to in relation to the Issue

Issue Price The final price at which the Equity Shares will be Allotted to Bidders.

The Issue Price will be decided by our Company and the Selling Shareholder,

in consultation with the BRLMs, on the Pricing Date

Issue Proceeds The proceeds of the Fresh Issue and the Offer for Sale that are available to our

Company and the Selling Shareholder, respectively

Maximum RIB Allottees The maximum number of Retail Individual Bidders who can be allotted the

minimum Bid Lot. This is computed by dividing the total number of Equity

Shares available for Allotment to Retail Individual Bidders by the minimum Bid

Lot

Mutual Fund Portion 5% of the QIB Portion, or 829,000 Equity Shares which shall be available for

allocation to Mutual Funds only

Mutual Funds Mutual funds registered with SEBI under the Securities and Exchange Board of

India (Mutual Funds) Regulations, 1996

Net Issue The Issue less the Employee Reservation Portion being 33,160,000 Equity

Shares aggregating to ` [●] million

Net Proceeds Proceeds of the Fresh Issue less our Company’s share of the Issue expenses. For

further information about use of the Issue Proceeds and the Issue expenses, see

“Objects of the Issue” on page 78.

Non-Institutional Bidders All Bidders that are not QIBs or Retail Individual Bidders or Eligible Employees

Bidding in the Retail Portion or Employee Reservation Portion, respectively and

who have Bid for the Equity Shares for an amount more than `200,000 (but not

including NRIs other than Eligible NRIs)

Non-Institutional Portion The portion of the Issue being not less than 15% of the Net Issue comprising of

4,974,000 Equity Shares which shall be available for allocation on a

proportionate basis to Non-Institutional Bidders, subject to valid Bids being

received at or above the Issue Price

Non-Resident A person resident outside India as defined under FEMA and includes a Non

Resident Indian, FVCIs, FIIs and FPIs

6

Term Description

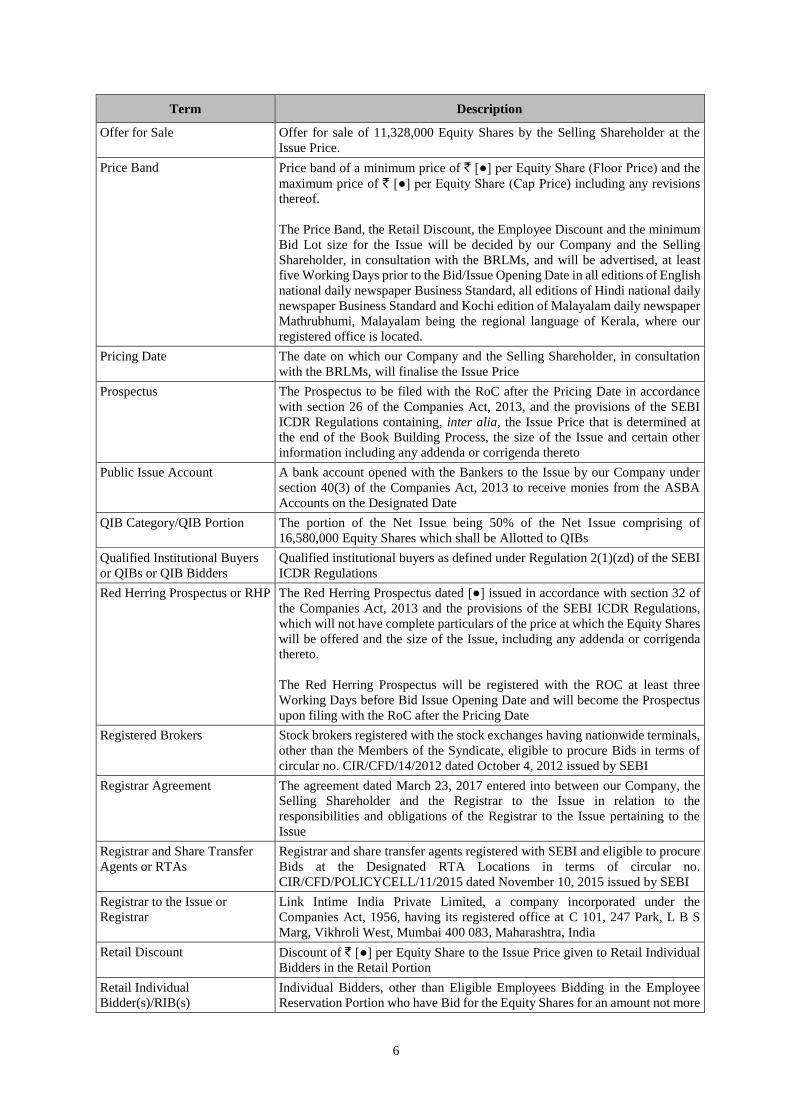

Offer for Sale Offer for sale of 11,328,000 Equity Shares by the Selling Shareholder at the

Issue Price.

Price Band Price band of a minimum price of ` [●] per Equity Share (Floor Price) and the

maximum price of ` [●] per Equity Share (Cap Price) including any revisions

thereof.

The Price Band, the Retail Discount, the Employee Discount and the minimum

Bid Lot size for the Issue will be decided by our Company and the Selling

Shareholder, in consultation with the BRLMs, and will be advertised, at least

five Working Days prior to the Bid/Issue Opening Date in all editions of English

national daily newspaper Business Standard, all editions of Hindi national daily

newspaper Business Standard and Kochi edition of Malayalam daily newspaper

Mathrubhumi, Malayalam being the regional language of Kerala, where our

registered office is located.

Pricing Date The date on which our Company and the Selling Shareholder, in consultation

with the BRLMs, will finalise the Issue Price

Prospectus The Prospectus to be filed with the RoC after the Pricing Date in accordance

with section 26 of the Companies Act, 2013, and the provisions of the SEBI

ICDR Regulations containing, inter alia, the Issue Price that is determined at

the end of the Book Building Process, the size of the Issue and certain other

information including any addenda or corrigenda thereto

Public Issue Account A bank account opened with the Bankers to the Issue by our Company under

section 40(3) of the Companies Act, 2013 to receive monies from the ASBA

Accounts on the Designated Date

QIB Category/QIB Portion The portion of the Net Issue being 50% of the Net Issue comprising of

16,580,000 Equity Shares which shall be Allotted to QIBs

Qualified Institutional Buyers

or QIBs or QIB Bidders

Qualified institutional buyers as defined under Regulation 2(1)(zd) of the SEBI

ICDR Regulations

Red Herring Prospectus or RHP The Red Herring Prospectus dated [●] issued in accordance with section 32 of

the Companies Act, 2013 and the provisions of the SEBI ICDR Regulations,

which will not have complete particulars of the price at which the Equity Shares

will be offered and the size of the Issue, including any addenda or corrigenda

thereto.

The Red Herring Prospectus will be registered with the ROC at least three

Working Days before Bid Issue Opening Date and will become the Prospectus

upon filing with the RoC after the Pricing Date

Registered Brokers Stock brokers registered with the stock exchanges having nationwide terminals,

other than the Members of the Syndicate, eligible to procure Bids in terms of

circular no. CIR/CFD/14/2012 dated October 4, 2012 issued by SEBI

Registrar Agreement The agreement dated March 23, 2017 entered into between our Company, the

Selling Shareholder and the Registrar to the Issue in relation to the

responsibilities and obligations of the Registrar to the Issue pertaining to the

Issue

Registrar and Share Transfer

Agents or RTAs

Registrar and share transfer agents registered with SEBI and eligible to procure

Bids at the Designated RTA Locations in terms of circular no.

CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by SEBI

Registrar to the Issue or

Registrar

Link Intime India Private Limited, a company incorporated under the

Companies Act, 1956, having its registered office at C 101, 247 Park, L B S

Marg, Vikhroli West, Mumbai 400 083, Maharashtra, India

Retail Discount Discount of ` [●] per Equity Share to the Issue Price given to Retail Individual

Bidders in the Retail Portion

Retail Individual

Bidder(s)/RIB(s)

Individual Bidders, other than Eligible Employees Bidding in the Employee

Reservation Portion who have Bid for the Equity Shares for an amount not more

7

Term Description

than ` 200,000 in any of the bidding options in the Net Issue (including HUFs

applying through their Karta and Eligible NRIs)

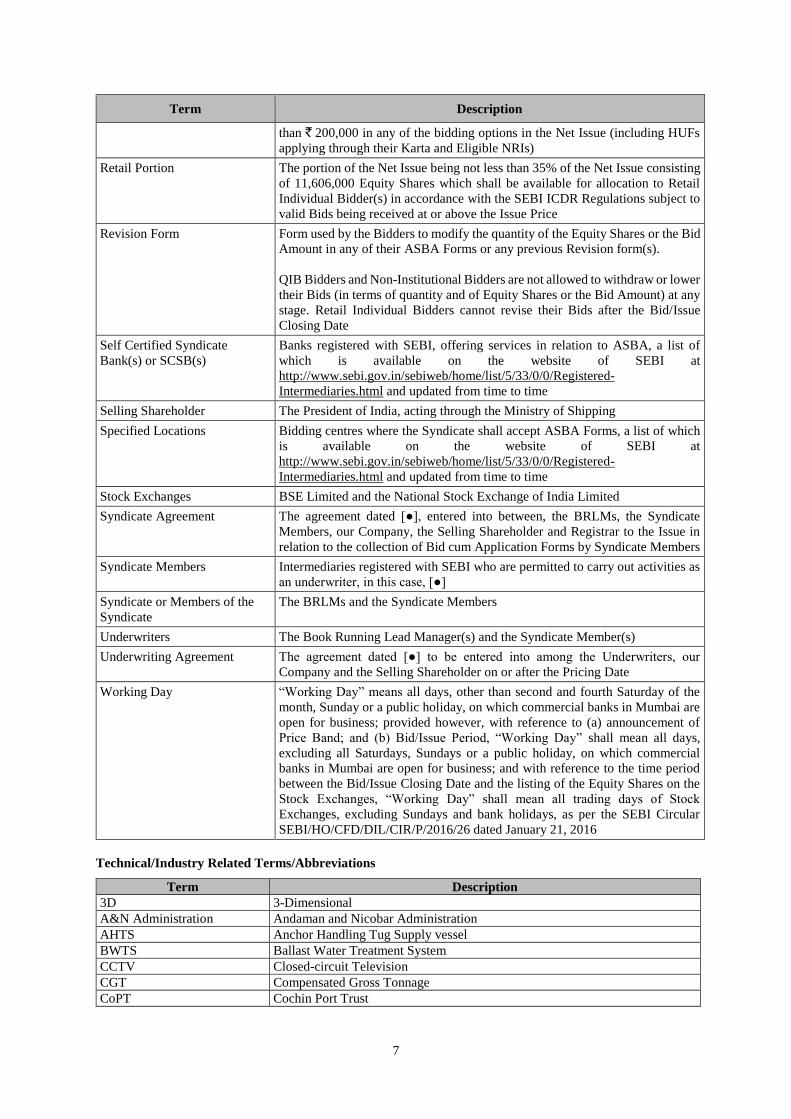

Retail Portion The portion of the Net Issue being not less than 35% of the Net Issue consisting

of 11,606,000 Equity Shares which shall be available for allocation to Retail

Individual Bidder(s) in accordance with the SEBI ICDR Regulations subject to

valid Bids being received at or above the Issue Price

Revision Form Form used by the Bidders to modify the quantity of the Equity Shares or the Bid

Amount in any of their ASBA Forms or any previous Revision form(s).

QIB Bidders and Non-Institutional Bidders are not allowed to withdraw or lower

their Bids (in terms of quantity and of Equity Shares or the Bid Amount) at any

stage. Retail Individual Bidders cannot revise their Bids after the Bid/Issue

Closing Date

Self Certified Syndicate

Bank(s) or SCSB(s)

Banks registered with SEBI, offering services in relation to ASBA, a list of

which is available on the website of SEBI at

http://www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Registered-

Intermediaries.html and updated from time to time

Selling Shareholder The President of India, acting through the Ministry of Shipping

Specified Locations Bidding centres where the Syndicate shall accept ASBA Forms, a list of which

is available on the website of SEBI at

http://www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Registered-

Intermediaries.html and updated from time to time

Stock Exchanges BSE Limited and the National Stock Exchange of India Limited

Syndicate Agreement The agreement dated [●], entered into between, the BRLMs, the Syndicate

Members, our Company, the Selling Shareholder and Registrar to the Issue in

relation to the collection of Bid cum Application Forms by Syndicate Members

Syndicate Members Intermediaries registered with SEBI who are permitted to carry out activities as

an underwriter, in this case, [●]

Syndicate or Members of the

Syndicate

The BRLMs and the Syndicate Members

Underwriters The Book Running Lead Manager(s) and the Syndicate Member(s)

Underwriting Agreement The agreement dated [●] to be entered into among the Underwriters, our

Company and the Selling Shareholder on or after the Pricing Date

Working Day “Working Day” means all days, other than second and fourth Saturday of the

month, Sunday or a public holiday, on which commercial banks in Mumbai are

open for business; provided however, with reference to (a) announcement of

Price Band; and (b) Bid/Issue Period, “Working Day” shall mean all days,

excluding all Saturdays, Sundays or a public holiday, on which commercial

banks in Mumbai are open for business; and with reference to the time period

between the Bid/Issue Closing Date and the listing of the Equity Shares on the

Stock Exchanges, “Working Day” shall mean all trading days of Stock

Exchanges, excluding Sundays and bank holidays, as per the SEBI Circular

SEBI/HO/CFD/DIL/CIR/P/2016/26 dated January 21, 2016

Technical/Industry Related Terms/Abbreviations

Term Description

3D 3-Dimensional

A&N Administration Andaman and Nicobar Administration

AHTS Anchor Handling Tug Supply vessel

BWTS Ballast Water Treatment System

CCTV Closed-circuit Television

CGT Compensated Gross Tonnage

CoPT Cochin Port Trust

8

Term Description

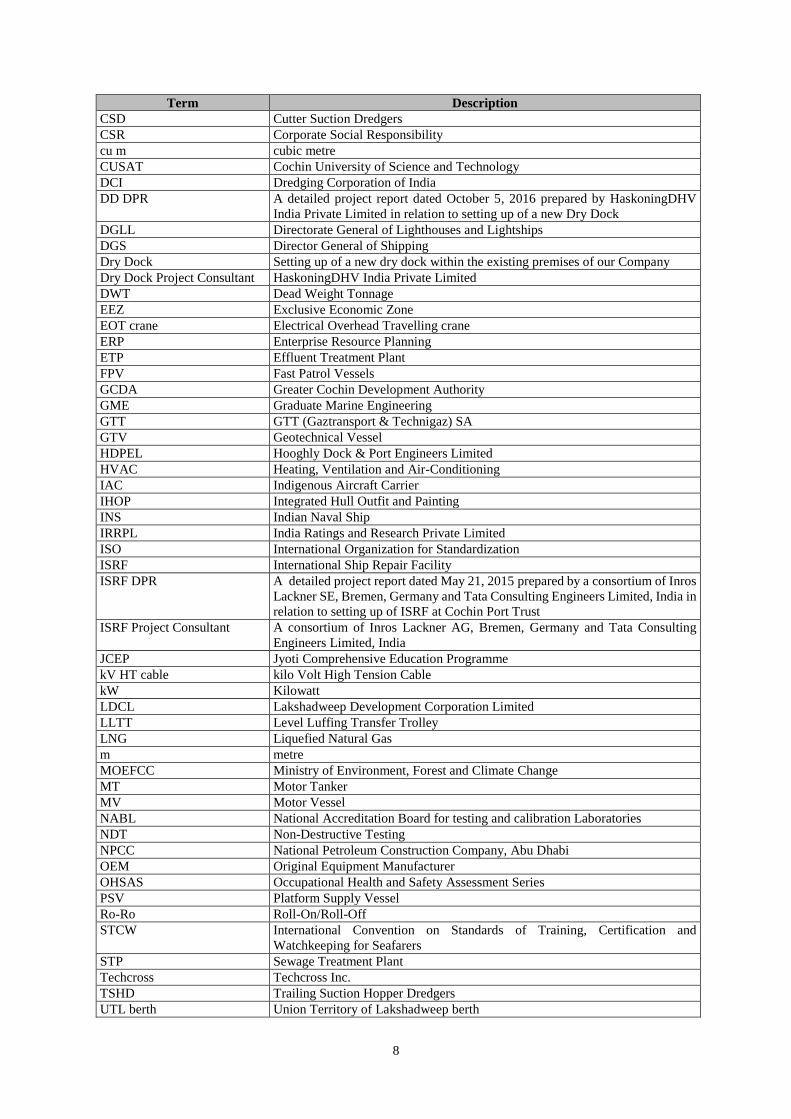

CSD Cutter Suction Dredgers

CSR Corporate Social Responsibility

cu m cubic metre

CUSAT Cochin University of Science and Technology

DCI Dredging Corporation of India

DD DPR A detailed project report dated October 5, 2016 prepared by HaskoningDHV

India Private Limited in relation to setting up of a new Dry Dock DGLL Directorate General of Lighthouses and Lightships

DGS Director General of Shipping

Dry Dock Setting up of a new dry dock within the existing premises of our Company Dry Dock Project Consultant HaskoningDHV India Private Limited DWT Dead Weight Tonnage

EEZ Exclusive Economic Zone

EOT crane Electrical Overhead Travelling crane

ERP Enterprise Resource Planning

ETP Effluent Treatment Plant

FPV Fast Patrol Vessels

GCDA Greater Cochin Development Authority

GME Graduate Marine Engineering

GTT GTT (Gaztransport & Technigaz) SA

GTV Geotechnical Vessel

HDPEL Hooghly Dock & Port Engineers Limited

HVAC Heating, Ventilation and Air-Conditioning

IAC Indigenous Aircraft Carrier

IHOP Integrated Hull Outfit and Painting

INS Indian Naval Ship

IRRPL India Ratings and Research Private Limited

ISO International Organization for Standardization

ISRF International Ship Repair Facility ISRF DPR A detailed project report dated May 21, 2015 prepared by a consortium of Inros

Lackner SE, Bremen, Germany and Tata Consulting Engineers Limited, India in

relation to setting up of ISRF at Cochin Port Trust ISRF Project Consultant A consortium of Inros Lackner AG, Bremen, Germany and Tata Consulting

Engineers Limited, India JCEP Jyoti Comprehensive Education Programme

kV HT cable kilo Volt High Tension Cable

kW Kilowatt

LDCL Lakshadweep Development Corporation Limited

LLTT Level Luffing Transfer Trolley

LNG Liquefied Natural Gas

m metre

MOEFCC Ministry of Environment, Forest and Climate Change

MT Motor Tanker

MV Motor Vessel

NABL National Accreditation Board for testing and calibration Laboratories

NDT Non-Destructive Testing

NPCC National Petroleum Construction Company, Abu Dhabi

OEM Original Equipment Manufacturer

OHSAS Occupational Health and Safety Assessment Series

PSV Platform Supply Vessel

Ro-Ro Roll-On/Roll-Off

STCW International Convention on Standards of Training, Certification and

Watchkeeping for Seafarers

STP Sewage Treatment Plant

Techcross Techcross Inc.

TSHD Trailing Suction Hopper Dredgers UTL berth Union Territory of Lakshadweep berth

9

Term Description

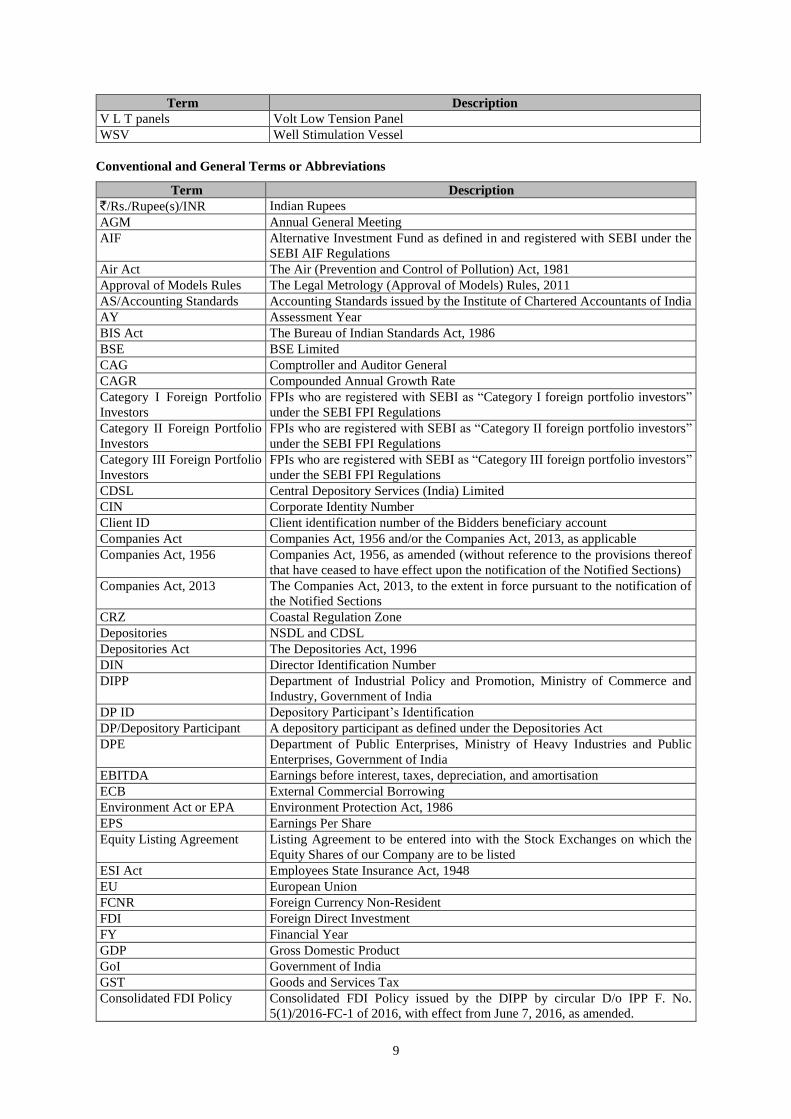

V L T panels Volt Low Tension Panel

WSV Well Stimulation Vessel

Conventional and General Terms or Abbreviations

Term Description

`/Rs./Rupee(s)/INR Indian Rupees

AGM Annual General Meeting

AIF Alternative Investment Fund as defined in and registered with SEBI under the

SEBI AIF Regulations

Air Act The Air (Prevention and Control of Pollution) Act, 1981

Approval of Models Rules The Legal Metrology (Approval of Models) Rules, 2011

AS/Accounting Standards Accounting Standards issued by the Institute of Chartered Accountants of India

AY Assessment Year

BIS Act The Bureau of Indian Standards Act, 1986

BSE BSE Limited

CAG Comptroller and Auditor General

CAGR Compounded Annual Growth Rate

Category I Foreign Portfolio

Investors

FPIs who are registered with SEBI as “Category I foreign portfolio investors”

under the SEBI FPI Regulations

Category II Foreign Portfolio

Investors

FPIs who are registered with SEBI as “Category II foreign portfolio investors”

under the SEBI FPI Regulations

Category III Foreign Portfolio

Investors

FPIs who are registered with SEBI as “Category III foreign portfolio investors”

under the SEBI FPI Regulations

CDSL Central Depository Services (India) Limited

CIN Corporate Identity Number

Client ID Client identification number of the Bidders beneficiary account

Companies Act Companies Act, 1956 and/or the Companies Act, 2013, as applicable

Companies Act, 1956 Companies Act, 1956, as amended (without reference to the provisions thereof

that have ceased to have effect upon the notification of the Notified Sections)

Companies Act, 2013 The Companies Act, 2013, to the extent in force pursuant to the notification of

the Notified Sections

CRZ Coastal Regulation Zone

Depositories NSDL and CDSL

Depositories Act The Depositories Act, 1996

DIN Director Identification Number

DIPP Department of Industrial Policy and Promotion, Ministry of Commerce and

Industry, Government of India

DP ID Depository Participant’s Identification

DP/Depository Participant A depository participant as defined under the Depositories Act

DPE Department of Public Enterprises, Ministry of Heavy Industries and Public

Enterprises, Government of India

EBITDA Earnings before interest, taxes, depreciation, and amortisation

ECB External Commercial Borrowing

Environment Act or EPA Environment Protection Act, 1986

EPS Earnings Per Share

Equity Listing Agreement Listing Agreement to be entered into with the Stock Exchanges on which the

Equity Shares of our Company are to be listed

ESI Act Employees State Insurance Act, 1948

EU European Union

FCNR Foreign Currency Non-Resident

FDI Foreign Direct Investment

FY Financial Year

GDP Gross Domestic Product

GoI Government of India

GST Goods and Services Tax

Consolidated FDI Policy Consolidated FDI Policy issued by the DIPP by circular D/o IPP F. No.

5(1)/2016-FC-1 of 2016, with effect from June 7, 2016, as amended.

10

Term Description

FEMA Foreign Exchange Management Act, 1999, read with rules and regulations

thereunder

FEMA Regulations Foreign Exchange Management (Transfer or Issue of Security by a Person

Resident Outside India) Regulations, 2000, as amended

FII(s) Foreign Institutional Investors as defined under the SEBI FPI Regulations

Financial Year/FY/Fiscal Unless stated otherwise, the period of 12 months ending March 31 of that

particular year

FIPB Foreign Investment Promotion Board

FPI(s) A foreign portfolio investor as defined under the SEBI FPI Regulations

FTA Foreign Trade (Development and Regulation) Act, 1992

FTP Foreign Trade Policy (2015 - 2020)

FVCI Foreign venture capital investors as defined and registered under the SEBI FVCI

Regulations

GAAR General Anti Avoidance Rules

GDP Gross Domestic Product

GIR General Index Register

GoI or Government Government of India

GST Goods and services tax

Hazardous Chemical Rules Manufacture, Storage and Import of Hazardous Chemical Rules, 1989

Hazardous Wastes Rules The Hazardous and Other Wastes (Management and Transboundary Movement)

Rules, 2016

I(D&R) Act Industrial (Development and Regulation) Act, 1951, as amended

ICAI The Institute of Chartered Accountants of India

IFRS International Financial Reporting Standards

Income Tax Act The Income Tax Act, 1961

Ind-AS The Indian Accounting Standards

Ind-AS Rules Companies (Indian Accounting Standards) Rules, 2015

India Republic of India

Indian GAAP Generally Accepted Accounting Principles in India

IPO Initial Public Offering

IRDAI Insurance Regulatory and Development Authority of India

IRS Indian Register of Shipping

IST Indian Standard Time

IT Information Technology

KGST Kerala General Sales Tax Act, 1963

KVAT Kerala Value Added Tax, 2003

Legal Metrology Act Legal Metrology Act, 2009

LM Act The Legal Metrology Act, 2009

Merchant Shipping Act Merchant Shipping Act, 1958

MICR Magnetic Ink Character Recognition

Mn Million

MoU Memorandum of Understanding

Municipal Solid Wastes Rules The Solid Wastes Management Rules, 2016

N.A./NA Not Applicable

NAV Net Asset Value

NECS National Electronic Clearing Services

NEFT National Electronic Fund Transfer

Notified Sections The sections of the Companies Act, 2013 that have been notified by the Ministry

of Corporate Affairs, Government of India

NRE Account Non Resident External Account

NRI A person resident outside India, who is a citizen of India or a person of Indian

origin, and shall have the meaning ascribed to such term in the Foreign

Exchange Management (Deposit) Regulations, 2000

NRO Account Non Resident Ordinary Account

NSDL National Securities Depository Limited

NSE The National Stock Exchange of India Limited

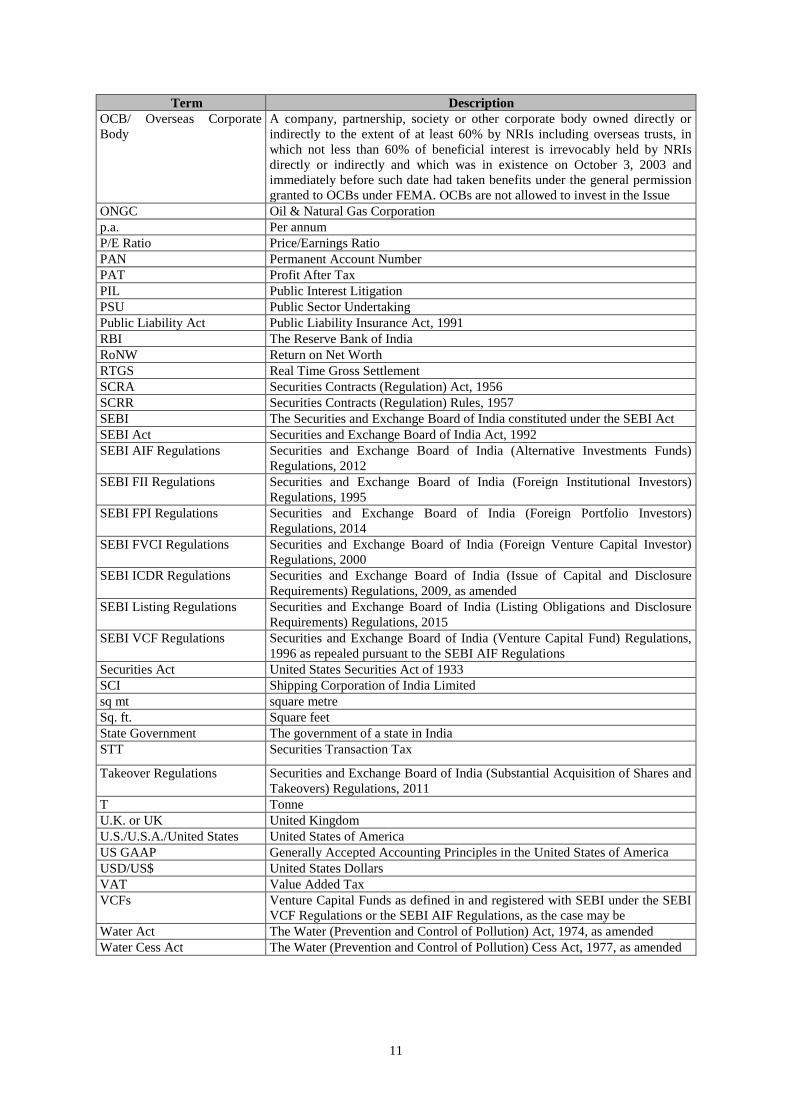

11

Term Description

OCB/ Overseas Corporate

Body

A company, partnership, society or other corporate body owned directly or

indirectly to the extent of at least 60% by NRIs including overseas trusts, in

which not less than 60% of beneficial interest is irrevocably held by NRIs

directly or indirectly and which was in existence on October 3, 2003 and

immediately before such date had taken benefits under the general permission

granted to OCBs under FEMA. OCBs are not allowed to invest in the Issue

ONGC Oil & Natural Gas Corporation

p.a. Per annum

P/E Ratio Price/Earnings Ratio

PAN Permanent Account Number

PAT Profit After Tax

PIL Public Interest Litigation

PSU Public Sector Undertaking

Public Liability Act Public Liability Insurance Act, 1991

RBI The Reserve Bank of India

RoNW Return on Net Worth

RTGS Real Time Gross Settlement

SCRA Securities Contracts (Regulation) Act, 1956

SCRR Securities Contracts (Regulation) Rules, 1957

SEBI The Securities and Exchange Board of India constituted under the SEBI Act

SEBI Act Securities and Exchange Board of India Act, 1992

SEBI AIF Regulations Securities and Exchange Board of India (Alternative Investments Funds)

Regulations, 2012

SEBI FII Regulations Securities and Exchange Board of India (Foreign Institutional Investors)

Regulations, 1995

SEBI FPI Regulations Securities and Exchange Board of India (Foreign Portfolio Investors)

Regulations, 2014

SEBI FVCI Regulations Securities and Exchange Board of India (Foreign Venture Capital Investor)

Regulations, 2000

SEBI ICDR Regulations Securities and Exchange Board of India (Issue of Capital and Disclosure

Requirements) Regulations, 2009, as amended

SEBI Listing Regulations Securities and Exchange Board of India (Listing Obligations and Disclosure

Requirements) Regulations, 2015

SEBI VCF Regulations Securities and Exchange Board of India (Venture Capital Fund) Regulations,

1996 as repealed pursuant to the SEBI AIF Regulations

Securities Act United States Securities Act of 1933

SCI Shipping Corporation of India Limited

sq mt square metre

Sq. ft. Square feet

State Government The government of a state in India

STT Securities Transaction Tax

Takeover Regulations Securities and Exchange Board of India (Substantial Acquisition of Shares and

Takeovers) Regulations, 2011

T Tonne

U.K. or UK United Kingdom

U.S./U.S.A./United States United States of America

US GAAP Generally Accepted Accounting Principles in the United States of America

USD/US$ United States Dollars

VAT Value Added Tax

VCFs Venture Capital Funds as defined in and registered with SEBI under the SEBI

VCF Regulations or the SEBI AIF Regulations, as the case may be

Water Act The Water (Prevention and Control of Pollution) Act, 1974, as amended

Water Cess Act The Water (Prevention and Control of Pollution) Cess Act, 1977, as amended

12

PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA

Certain Conventions

All references in this Draft Red Herring Prospectus to “India” are to the Republic of India and all references to

the “U.S.”, “U.S.A” or “United States” are to the United States of America.

Unless stated otherwise, all references to page numbers in this Draft Red Herring Prospectus are to the page

numbers of this Draft Red Herring Prospectus.

Financial Data

Unless stated otherwise, the financial information in this Draft Red Herring Prospectus is derived from our

Restated Financial Statements in accordance with the Companies Act and Indian GAAP and restated in accordance

with the SEBI ICDR Regulations.

Our Company’s Financial Year commences on April 1 and ends on March 31 of the following year. Accordingly,

all references to a particular financial year, unless stated otherwise, are to the 12 month period ended on March

31 of that year. Unless the context otherwise requires, all references to a year in this Draft Red Herring Prospectus

are to a calendar year and references to a financial year are to March 31 of that calendar year.

Certain figures contained in this Draft Red Herring Prospectus, including financial information, have been subject

to rounding adjustments. All decimals have been rounded off to two or one decimal places. In certain instances,

(i) the sum or percentage change of such numbers may not conform exactly to the total figure given; and (ii) the

sum of the numbers in a column or row in certain tables may not conform exactly to the total figure given for that

column or row.

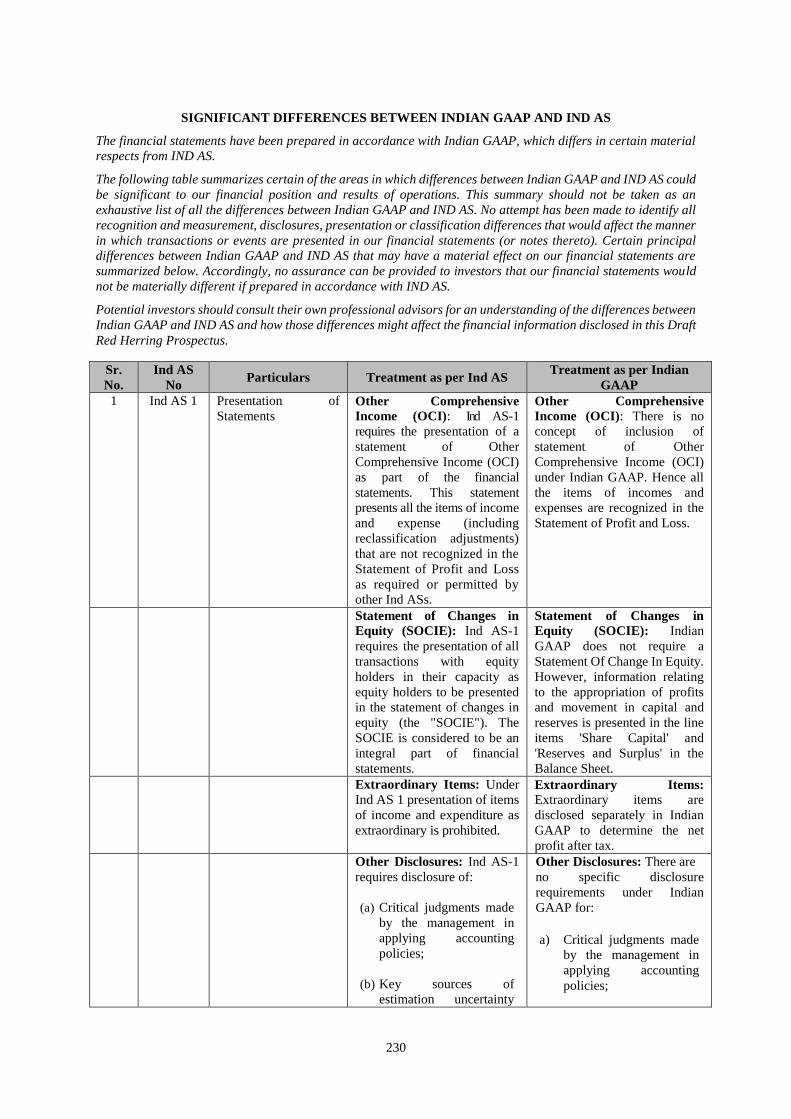

Our Restated Financial Statements have been prepared in accordance with Indian GAAP. There are significant

differences between Indian GAAP, Ind AS, U.S. GAAP and IFRS. Our Company does not provide reconciliation

of its financial information to Ind AS, IFRS or U.S. GAAP. Our Company has not attempted to explain those

differences or quantify their impact on the financial data included in this Draft Red Herring Prospectus and it is

urged that you consult your own advisors regarding such differences and their impact on our financial data.

Accordingly, the degree to which the financial information included in this Draft Red Herring Prospectus will

provide meaningful information is entirely dependent on the reader’s level of familiarity with Indian accounting

policies and practices, the Companies Act, the Indian GAAP and the SEBI ICDR Regulations. Any reliance by

persons not familiar with Indian accounting policies and practices on the financial disclosures presented in this

Draft Red Herring Prospectus should accordingly be limited. Our annual financial statements for periods

subsequent to April 1, 2016, will be prepared and presented in accordance with Ind AS. Given that Ind AS differs

in many respects from Indian GAAP, our financial statements prepared and presented in accordance with Ind AS

may not be comparable to our historical financial statements prepared under the Indian GAAP.

We have published Ind AS financial statements on December 14, 2016, comprising of selective financial

information in the format as prescribed under SEBI circular number CIR/IMD/DF1/69/2016 dated August 10,

2016 (“SEBI Circular”). The Ind AS financial statements have been prepared and published in order to comply

with the requirements prescribed under Regulation 52 of the SEBI Listing Regulations since our secured bonds

are listed on the BSE. The Ind AS financial statements comprise of selective financial information which have

been (i) audited as of September 30, 2016; and (ii) unaudited as of September 30, 2015. As the results for the prior

period ended September 30, 2015 are unaudited in compliance with the SEBI Circular, such Ind AS financial

statements cannot be included and do not form part of this Draft Red Herring Prospectus.

On February 16, 2015, the Ministry of Corporate Affairs issued the Ind-AS Rules for the purpose of enacting

changes to Indian GAAP that are intended to align Indian GAAP further with IFRS. The Ind-AS Rules provide

that the financial statements of the companies to which they apply shall be prepared in accordance with the Indian

Accounting Standards converged with IFRS, although any company may voluntarily implement Ind AS for the

accounting period beginning from April 1, 2015.

We have not made any attempt to quantify or identify the impact of the differences between Indian GAAP and

Ind AS applied to our financial statements and it is urged that you consult your own advisors regarding the impact

of difference, if any, on financial data included in this Draft Red Herring Prospectus.

For details in connection with risks involving differences between Indian GAAP and IFRS see “Risk Factors –

Significant differences exist between Indian GAAP and other accounting principles, such as U.S. GAAP, Ind AS

and IFRS, which may be material to investors’ assessments of our financial condition” on page 35 and for risks

in relation to Ind AS, see “Risk Factors – Public companies in India, including us, are required to compute Income

Tax under the Income Computation and Disclosure Standards (the “ICDS”). The transition to ICDS in India is

13

very recent and we may be negatively affected by such transition.” on page 35 and “Significant Differences

between Indian GAAP and Ind AS” on page 230.

Unless the context otherwise indicates, any percentage amounts, as set forth in “Risk Factors”, “Our Business”,

“Management’s Discussion and Analysis of Financial Conditional and Results of Operations” on pages 17, 114

and 236, respectively, and elsewhere in this Draft Red Herring Prospectus have been calculated on the basis of

our Restated Financial Statements prepared in accordance with Companies Act, Indian accounting policies and

practices and Indian GAAP and restated in accordance with the SEBI ICDR Regulations.

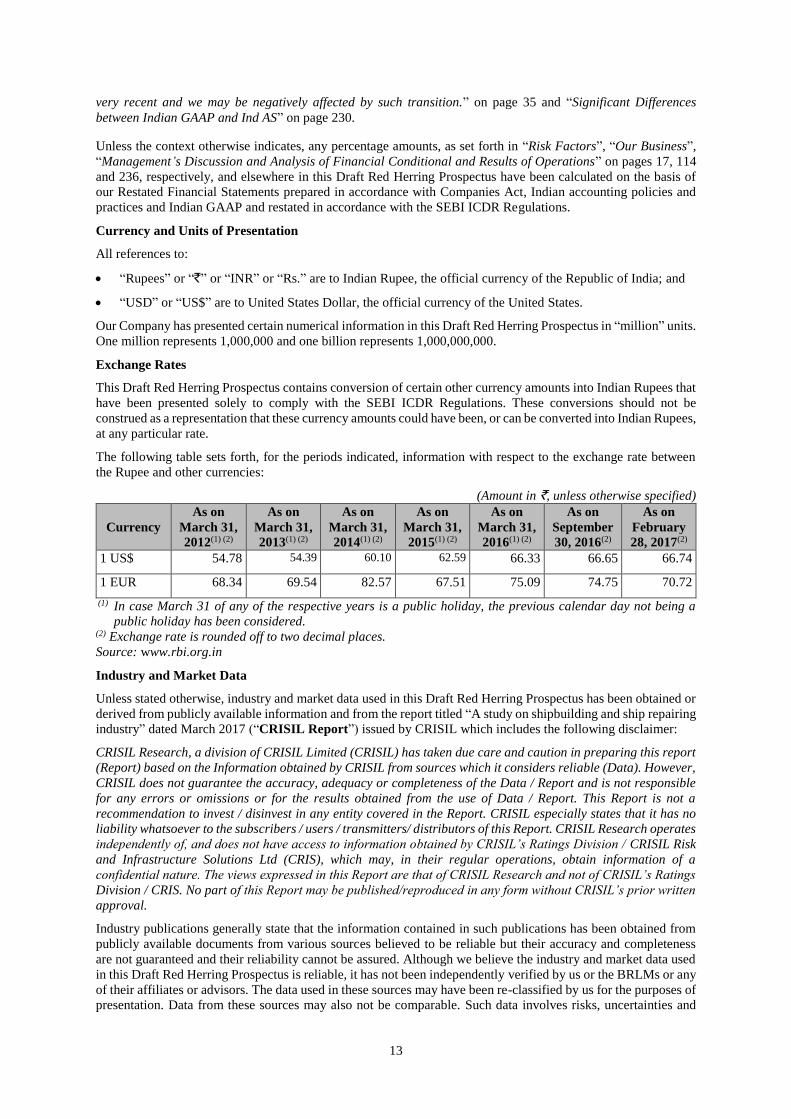

Currency and Units of Presentation

All references to:

“Rupees” or “`” or “INR” or “Rs.” are to Indian Rupee, the official currency of the Republic of India; and

“USD” or “US$” are to United States Dollar, the official currency of the United States.

Our Company has presented certain numerical information in this Draft Red Herring Prospectus in “million” units.

One million represents 1,000,000 and one billion represents 1,000,000,000.

Exchange Rates

This Draft Red Herring Prospectus contains conversion of certain other currency amounts into Indian Rupees that

have been presented solely to comply with the SEBI ICDR Regulations. These conversions should not be

construed as a representation that these currency amounts could have been, or can be converted into Indian Rupees,

at any particular rate.

The following table sets forth, for the periods indicated, information with respect to the exchange rate between

the Rupee and other currencies:

(Amount in `, unless otherwise specified)

Currency

As on

March 31,

2012(1) (2)

As on

March 31,

2013(1) (2)

As on

March 31,

2014(1) (2)

As on

March 31,

2015(1) (2)

As on

March 31,

2016(1) (2)

As on

September

30, 2016(2)

As on

February

28, 2017(2)

1 US$ 54.78 54.39 60.10 62.59 66.33 66.65 66.74

1 EUR 68.34 69.54 82.57 67.51 75.09 74.75 70.72

(1) In case March 31 of any of the respective years is a public holiday, the previous calendar day not being a

public holiday has been considered. (2) Exchange rate is rounded off to two decimal places.

Source: www.rbi.org.in

Industry and Market Data

Unless stated otherwise, industry and market data used in this Draft Red Herring Prospectus has been obtained or

derived from publicly available information and from the report titled “A study on shipbuilding and ship repairing

industry” dated March 2017 (“CRISIL Report”) issued by CRISIL which includes the following disclaimer:

CRISIL Research, a division of CRISIL Limited (CRISIL) has taken due care and caution in preparing this report

(Report) based on the Information obtained by CRISIL from sources which it considers reliable (Data). However,

CRISIL does not guarantee the accuracy, adequacy or completeness of the Data / Report and is not responsible

for any errors or omissions or for the results obtained from the use of Data / Report. This Report is not a

recommendation to invest / disinvest in any entity covered in the Report. CRISIL especially states that it has no

liability whatsoever to the subscribers / users / transmitters/ distributors of this Report. CRISIL Research operates

independently of, and does not have access to information obtained by CRISIL’s Ratings Division / CRISIL Risk

and Infrastructure Solutions Ltd (CRIS), which may, in their regular operations, obtain information of a

confidential nature. The views expressed in this Report are that of CRISIL Research and not of CRISIL’s Ratings

Division / CRIS. No part of this Report may be published/reproduced in any form without CRISIL’s prior written

approval.

Industry publications generally state that the information contained in such publications has been obtained from

publicly available documents from various sources believed to be reliable but their accuracy and completeness

are not guaranteed and their reliability cannot be assured. Although we believe the industry and market data used

in this Draft Red Herring Prospectus is reliable, it has not been independently verified by us or the BRLMs or any

of their affiliates or advisors. The data used in these sources may have been re-classified by us for the purposes of

presentation. Data from these sources may also not be comparable. Such data involves risks, uncertainties and

14

numerous assumptions and is subject to change based on various factors, including those discussed in “Risk

Factors” on page 17.

The extent to which the market and industry data used in this Draft Red Herring Prospectus is meaningful depends

on the reader’s familiarity with and understanding of the methodologies used in compiling such data. There are

no standard data gathering methodologies in the industry in which business of our Company is conducted, and

methodologies and assumptions may vary widely among different industry sources.

In accordance with the SEBI ICDR Regulations, the “Basis for Issue Price” on page 88 includes information

relating to our peer group companies. Such information has been derived from publicly available sources, and

neither we, nor the BRLMs have independently verified such information.

15

FORWARD-LOOKING STATEMENTS

This Draft Red Herring Prospectus contains certain “forward-looking statements”. These forward-looking