COB Canadian Life

30

G4 Coordination of Benefits 1 of 30 Guideline G4 COORDINATION OF BENEFITS This Guideline has been approved by CLHIA's Board of Directors. All member companies are expected to comply with the CLHIA Guidelines. Companies are urged to bring Guidelines to the attention of their Board of Directors or the Board Committee responsible for the company's compliance program with a view to incorporating the Guidelines into the company's ongoing compliance program. INTRODUCTION The Coordination of Benefits Guidelines were developed for insurers to ensure consistency within the industry in situations where a person can submit a claim to more than one group plan. They are divided into two parts: Part A: Group Dental and Health Benefits; and Part B: Out-of-Country/Province Health Care Expenses. PART A: GROUP DENTAL AND HEALTH BENEFITS 1 PURPOSE These Guidelines describe how to coordinate either dental or healthcare payments from all group plans under which a person is covered, so that total payments do not exceed total eligible expenses. “Plan” is defined as group insurance or any other arrangement of coverage for individuals in a group, whether on an insured or an uninsured basis, including any prepayment coverage or capitation plan, as long as the group is not formed solely for the purpose of obtaining insurance. This definition of plan does not include school insurance or individual travel insurance. 2 ELIGIBLE EXPENSES Payment on a particular claim cannot exceed 100% of the eligible expenses. Eligible expenses are as defined in each carrier’s contract/plan document before payment limitations like the deductible, co-insurance, lagging fee guides and/or maximums are applied. In the case of dental, 100% of eligible expenses will be the appropriate general practitioner’s or specialist’s current fee guide. Each carrier adjudicates the claim taking into account reasonable and customary charges, maximums and contractual fee guide limits in the normal fashion. 3 HOW DO THE PLANS COORDINATE BENEFITS? The plan that determines benefits first (primary carrier) will calculate its benefits as though duplicate coverage does not exist.

-

Upload

nurhaidah-achmad -

Category

Documents

-

view

222 -

download

4

description

COB di Kanada

Transcript of COB Canadian Life

G4 Coordination of Benefits 1 of 30

Guideline G4 COORDINATION OF BENEFITS This Guideline has been approved by CLHIA's Board of Directors. All member companies are expected to comply with the CLHIA Guidelines. Companies are urged to bring Guidelines to the attention of their Board of Directors or the Board Committee responsible for the company's compliance program with a view to incorporating the Guidelines into the company's ongoing compliance program. INTRODUCTION The Coordination of Benefits Guidelines were developed for insurers to ensure consistency within the industry in situations where a person can submit a claim to more than one group plan. They are divided into two parts: Part A: Group Dental and Health Benefits; and Part B: Out-of-Country/Province Health Care Expenses. PART A: GROUP DENTAL AND HEALTH BENEFITS 1 PURPOSE

These Guidelines describe how to coordinate either dental or healthcare payments from all group plans under which a person is covered, so that total payments do not exceed total eligible expenses. “Plan” is defined as group insurance or any other arrangement of coverage for individuals in a group, whether on an insured or an uninsured basis, including any prepayment coverage or capitation plan, as long as the group is not formed solely for the purpose of obtaining insurance. This definition of plan does not include school insurance or individual travel insurance. 2 ELIGIBLE EXPENSES Payment on a particular claim cannot exceed 100% of the eligible expenses. Eligible expenses are as defined in each carrier’s contract/plan document before payment limitations like the deductible, co-insurance, lagging fee guides and/or maximums are applied. In the case of dental, 100% of eligible expenses will be the appropriate general practitioner’s or specialist’s current fee guide. Each carrier adjudicates the claim taking into account reasonable and customary charges, maximums and contractual fee guide limits in the normal fashion. 3 HOW DO THE PLANS COORDINATE BENEFITS? The plan that determines benefits first (primary carrier) will calculate its benefits as though duplicate coverage does not exist.

G4 Coordination of Benefits 2 of 30

The plan that determines benefits second (secondary carrier) limits its benefits to the lesser of: (i) The amount that would have been payable had it been the primary carrier, or|

(ii) 100% of all eligible expenses reduced by all other benefits payable for the same

expenses by the primary plan. This means that an individual may receive reimbursement for up to 100% of the eligible expenses. (Examples for dental and health claims are included in Appendix A for clarification.) 4 ORDER OF BENEFIT DETERMINATION (1) The plan with no Coordination of Benefits provision in the contract or plan

document determines benefits first. (2) If the other plan(s) has a Coordination of Benefits provision, priority goes to the

plan in the following order: Employees/members

(i) The plan where the person is covered as a member.

(ii) If a person is a member of two plans, priority goes to: (a) the plan where the member is an active full-time employee,

(b) the plan where the member is an active part-time employee,

(c) the plan where the member is a retiree.

Dependents Spouse

(iii) The plan where the person is covered as a dependent spouse.

Dependent Children

(iv) The plan of the parent with the earlier birth date (month/day) in the calendar year.

(v) The plan of the parent whose first name begins with the earlier letter in

the alphabet, if the parents have the same birth date. (vi) In situations where parents are separated/divorced, then the following

order applies:

(a) the plan of the parent with custody of the child,

(b) the plan of the spouse of the parent with custody of the child,

ljenkin

Highlight

G4 Coordination of Benefits 3 of 30

(c) the plan of the parent not having custody of the child,

(d) the plan of the spouse to the parent in iii) above.

Dental Accidents For dental accidents, health plans with dental accident coverage determine benefits before dental plans.

Other Situations If priority cannot be established in the above manner, the benefits will be pro-

rated in proportion to the amounts that would have been paid had there been coverage by just that plan.

5 ADMINISTRATIVE PROCEDURES The primary carrier will provide the claimant with a complete explanation of benefits (EOB) with service details, charges and amounts paid for the second carrier’s assessment. The second carrier will not require the original claim form if a copy is provided. It is the claimant’s responsibility to retain a copy of the original claim form to apply for the coordination of benefits provision. It is up to the discretion of each carrier to adjust overpayments made by the first payor. 6 COORDINATION OF BENEFITS WITH CAPITATION OR PREPAID DENTAL

PLANS

The coordination of benefits between capitation and fee-for-service dental plans shall be determined in the same manner as between fee-for-service plans. The order of benefit determination (OBD) remains unchanged and the primary and secondary carriers are determined by applying the OBD rules already outlined in the CLHIA Guidelines. If a person with dual insurance coverage is insured under a capitation plan and is treated by a dentist who is a member under that plan, priority is established by following the order of benefit determination. When one of the dental plans is a capitation or prepaid dental plan, all insured individuals must attend the participating dental offices in order to be entitled to the Coordination of Benefits provisions. If the insured individual attends a non-participating dental office, there will be no coordination of benefits with the capitation plan since the capitation plan would not reimburse the fee-for-service carrier or the insured for any expenses incurred. This is considered a fundamental principle of capitation plans. Capitation companies audit the dental services provided by their practitioners and they consider the COB payment as part of the dentist’s payment when they establish the capitation fee.

G4 Coordination of Benefits 4 of 30

When the capitation plan is primary, the dentist may collect the co-payment from the secondary plan by assignment or directly from the patient. When the capitation plan is secondary, the dentist should receive the payments from the primary plan, but the dentist must waive the patient’s capitation plan co-payment. (If the primary plan pays less than the co-payment, the patient will be required to pay the difference.) PART B: OUT-OF-COUNTRY/PROVINCIAL HEALTH CARE EXPENSES 1 PURPOSE

These Guidelines for insurers have been developed to encourage consistency within the industry in claim situations where a person has travel health insurance coverage from more than one policy (for example, from employment-related group insurance contracts, individual or group travel or health policies, credit cared coverages or any other private insurance sources). It is necessary to establish guidelines since many contracts for these benefits contain a provision that indicates that they will be last payor after claim payment has been made under all other contracts, and often it is not readily apparent which contract should pay first. These Guidelines describe how to coordinate the payments from all such policies under which an individual is covered, so that the total payments from all policies do not exceed the total expenses incurred or, in the case of cash policies, do not encourage multiple purchases. The intent is to establish a streamlined adjudication process that allows for effective claim management; minimizes claim assessment and payment delays; provides the greatest assistance to the insured in resolving the claim; maximizes cost containment for all carriers sharing the liability; fairly coordinates benefits among all policies involved; and discourages and identifies duplicate or fraudulent claim submissions. 2 SCOPE

These Guidelines will apply to all contracts that provide travel health insurance coverage. Contract wording should indicate that coverage will be coordinated with other policies according to these Guidelines. These Guidelines apply to expenses resulting from emergency or elective health care provided outside Canada or outside the province of residence in excess of the provincial health plan coverages. These benefits are generally referred to as travel health insurance and can include coverage for the following expenses:

• medical/surgical procedures • other physicians' services • confinement and hospital charges • repatriation costs including air ambulance and medical attendants • prescription drugs, para-medical services, etc.

ljenkin

Highlight

G4 Coordination of Benefits 5 of 30

With respect to such expenses, these Guidelines also apply to reimbursement-type hospital cash policies, and any other ancillary benefits which may be duplicated by other coverages. 3 EXCEPTION FOR EMPLOYMENT-RELATED GROUP COVERAGE FOR

RETIREES WITH LIMITED LIFETIME MAXIMUMS

Retired employees may have extended health coverage through former employers based on a lifetime maximum for all benefits, including both in-country and out-of-country extended health coverage. In order to avoid eroding those lifetime benefits, these guidelines make a provision not to coordinate with such coverages, if the lifetime maximum is $50,000 or less. In these cases, a retiree may use alternate coverage purchased through individual or group travel health insurance products to cover out-of-country expenses. If the individual has used up alternate coverage sources, the group retiree coverage will be responsible for any remaining expenses covered under its contract. If the lifetime maximum for all in-country and out-of-country benefits is greater than $50,000, full coordination will take place above this amount as outlined in these Guidelines. 4 DETERMINATION OF UNITS OF COORDINATION

Except as noted below, each coverage, whether purchased as an individual, through a group, credit card, tour operator, travel wholesaler or financial institution is considered as a separate unit of coordination for the purposes of these Guidelines. Exception: When an individual is covered as a member or as a dependent under one or more employment-related group plans1 to which Part A of these Guidelines (Group Dental and Health Benefits) apply, all such group plan coverages will be combined and considered a single unit of coordination. Part B of the Guidelines will be followed to determine the liability for that unit, and Part A will then be applied to allocate liabilities within that unit, if necessary. Refer to Appendix B for examples. 5 DETERMINATION OF THE FIRST CARRIER

The carrier that is first contacted for the purposes of claimant contact, or to whom the claim is initially submitted by the insured, is considered to be the First Carrier for the purposes of these Guidelines.

1 In these Guidelines, “plan” is defined as group insurance or any other arrangement of coverage for individuals in a group, whether on an insured or an uninsured basis, including any prepayment coverage or capitation plan, as long as the group is not formed solely for the purpose of insurance. This definition of plan does not include school insurance or individual travel insurance. For the purposes of coordinating Out-of-Country/Province Health Care Expenses, that definition is interpreted as including any plan covering extended health benefits as a whole (not travel health coverage only), that is offered to employees/retirees as a group and is sponsored by an employer/union/recognized professional association or by a multi-employer association.

ljenkin

Highlight

G4 Coordination of Benefits 6 of 30

Any other carrier that shares a liability for the claim is defined as an Other Carrier. If there are more than two policies, there can be two or more Other Carriers. An insurer cannot systematically or otherwise deflect calls by referring them to another carrier to avoid becoming the First Carrier. If a carrier feels that its claim assistance services are not adequate, this matter should be negotiated with the Other Carrier. 6 THE RESPONSIBILITY OF THE FIRST CARRIER

The First Carrier will take the initiative in the case management and claims assessment and will pay the claim first, according to the terms; and conditions of its contract, and reserving all rights to recovery from the Other Carrier(s) and from provincial health plans. (The First Carrier is never expected to pay more than the liability under its contract). Wherever possible, the rights to recovery should be made transparent to the claimant so the individual is aware that the insurance carriers will coordinate payment of the claim. Case management includes, but is not limited to: taking the initiative to involve an assistance group or service provider, choosing a preferred provider organization, monitoring to ensure appropriate medical care and/or repatriation. 7 NOTIFICATION OF OTHER CARRIER(S)

The First Carrier must establish whether an Other Carrier exists as quickly as possible, and must notify each identified carrier. Notification for all in-patient hospitalizations must occur immediately. For all other claims, notification shall be as soon as possible. Prompt notification to all Other Carriers involved in the claim is critical to the effective coordination of coverages. The initial notification will be a phone call to the Other Carrier(s) followed by written notification sent within 48 hours. The initial notification will include all relevant available information2, including for example (but not limited to):

• Name of Individual • Age • Individual or Group Policy Number • Social Insurance Number or Certificate Number • Detailed Diagnosis • Date of Hospital Admission • Name and Location of Hospital • Medical Treatments Provided to Date • Costs Incurred to Date • Departure Date • Government Health Insurance Plan (GHIP) Number

It is important to note that notification by the claimant to the First Carrier is deemed notification to all Other Carriers that are known and identified at the time and will serve as notification to those carriers.

2 Personal information held by one carrier cannot be communicated to another carrier without the consent of the person concerned. The First Carrier should seek such consent on its claim form or other initial contact.

G4 Coordination of Benefits 7 of 30

8 CONSULTATIONS/SECOND OPINIONS

In assessing significant or difficult claims, or if the First Carrier does not have adequate preferred provider or travel assistance arrangements, the First Carrier may contact the Other Carrier sharing in the claim liability to request assistance, to discuss the claim or, to ask for a second opinion. 9 OTHER CARRIER'S INVOLVEMENT

Upon receipt of notification, the Other Carrier(s) may offer to provide consultation on case management to the First Carrier and may provide cost containment options. Consultation may include but not be limited to the involvement of an assistance group or service provider, the choice of a preferred provider organization, monitoring to ensure appropriate medical care and/or repatriation. Ultimate decisions for the case management remain the responsibility of the First Carrier. 10 TRANSFER OF RESPONSIBILITY BY MUTUAL AGREEMENT

An Other Carrier may take on the responsibility of First Carrier if there is mutual agreement between the carriers to do so. This would be particularly appropriate if the First Carrier recognizes that its liability for the claim is limited (for example, if the First Carrier's liability will be $10,000 and the claim is expected to be $50,000 or more). 11 IF THE FIRST CARRIER HAS NO LIABILITY

If the First Carrier has no liability for the claim (for example, if a pre-existing condition has been clearly established), the First Carrier's responsibility ceases once it determines it has no liability for the claim and has informed the insured. When this occurs, the First Carrier will instruct the insured to contact the Other Carrier, if any, to pursue the claim. To speed up the adjudication process, the First Carrier will still provide notification to any Other Carrier known at that time, as outlined above. 12 RECOVERY

The process of recovery will take place after the First Carrier has made its assessment and paid the claim in accordance with its contractual liability. [Recovery between carriers is net of provincial government health insurance plans (GHIP) reimbursements.] Copies of the claim documents will then be sent to each of the Other Carriers involved. Each carrier receiving the claim documents will assess the claim independently based on the terms of its own contract, and will identify in a detailed fashion what its payment would have been if that was the only coverage for this claim. This information will then be sent back to the First Carrier. Once all of these responses have been received by the First Carrier, it will determine the Other Carriers' portion of liability for the claim and it will have the right to recover from the Other Carrier(s) by using the following rules:

G4 Coordination of Benefits 8 of 30

(1) Mutually covered expenses3 will be shared equally among all units.

(2) Deductibles will consistently be applied to the largest common expense item.

Each Carrier will reimburse the First Carrier for its share of the payment already made, and will pay the providers or the insured directly for any remaining expenses for which it has liability. Refer to examples in Appendix B. Payments and reimbursements will be made as soon as possible. If the First Carrier has identified the involvement of only one Other Carrier, the Other Carrier will be informed of this so it can complete the calculations and send its payment directly to the First Carrier, reducing the need for further correspondence between the carriers. 13 ADJUSTMENTS

Adjustments will be made if GHIP settlements are subsequently adjusted, additional items are submitted or an additional carrier is identified. 14 ORIGINAL CLAIM DOCUMENTS

The First Carrier will indicate to the Other Carrier(s) where the original documents are retained. 15 DISPUTE RESOLUTIONS

The parties may agree that binding arbitration by an independent review committee, mutually agreed upon by the parties involved, will be used to settle any disputes.

Part A revised November 1990 Part B adopted December 1994

3 In addition to the actual health care expenses incurred, the following allocated expenses paid during the claim

adjudication process can also be coordinated: • Fees charged by a preferred provider organization (PPO), usually as a percentage of savings, to obtain a

reduction in charges by hospitals, physicians, etc. • Medical reports obtained from hospitals and doctors. • Repatriation as a cost saving measure.

Other appropriate expenses incurred for the purposes of significant cost saving such as outside investigation expenses, utilization reviews or audit fees, legal fees, etc. should he pre-negotiated between carriers.

G4 Coordination of Benefits 9 of 30

APPENDIX A

COORDINATION OF BENEFIT SAMPLES – DENTAL AND HEALTH INDEX – COB Samples Dental (Samples 1-5)............................................................................ 10

Drugs (Samples 1-6) ............................................................................ 15

Vision (Samples 1-2) ............................................................................ 19

Hospital (Samples 1-3) ......................................................................... 20

Supplementary (Sample 1) ................................................................... 21

Coordination of Benefits Worksheet ..................................................... 22

G4 Coordination of Benefits 10 of 30

D E N T A L (5 Samples) DENTAL Sample #1 Expenses eligible under both plans: Carrier A payment Plan based on current fee guide.

Date of Service

Procedure Code

Submitted Eligible Payable at Payment

1.2.89 23222 87.00 79.99* 80% 63.99 1.2.89 23221 46.00 46.00 80% 36.80 1.2.89 23221 40.00 40.00 80% 32.00 1.2.89 23222 70.00 70.00 80% 56.00

TOTAL $243.00 $235.99 $188.79 * $7.01 declined as being over the fee guide. Carrier B payment Plan based on current fee guide. We would not consider $7.01 as eligible because it is over the fee guide. However, we would consider the 20% balance on all eligible expenses.

16.00 9.20 8.00 14.00

$47.20

Since we would have paid $188.79 if we had been the only carrier (assuming 80% reimbursement), we would pay $47.20 ($235.99 - $188.79).

G4 Coordination of Benefits 11 of 30

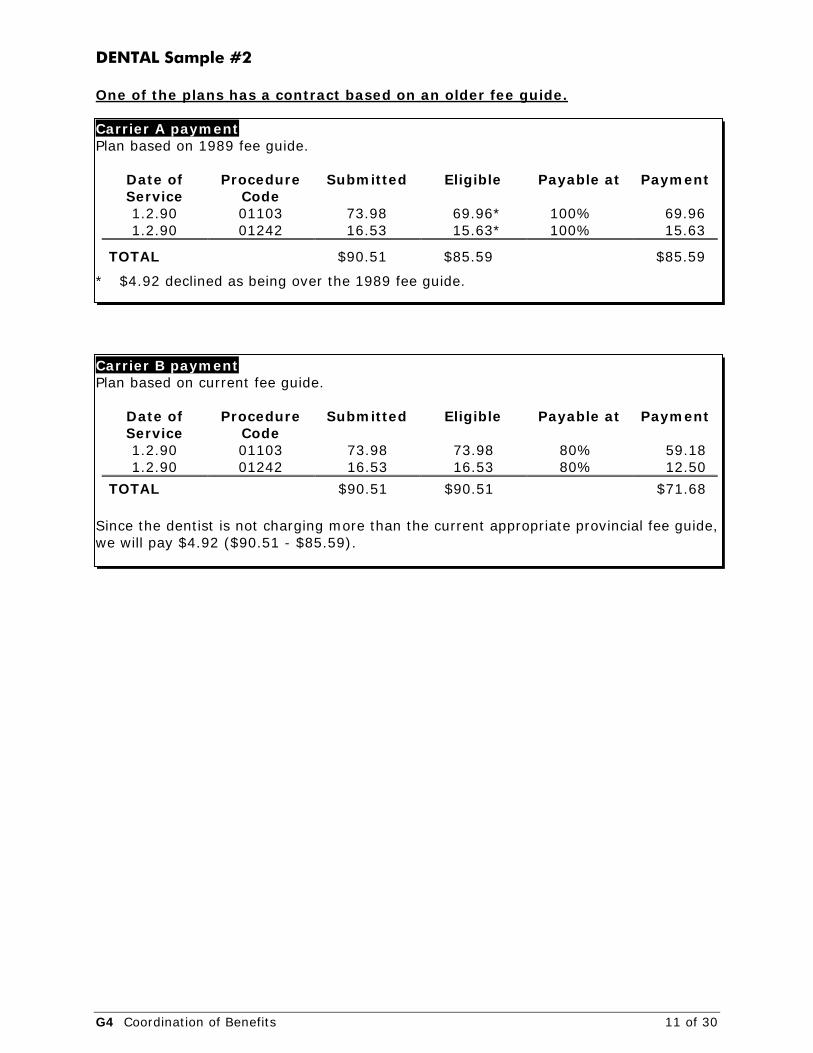

DENTAL Sample #2 One of the plans has a contract based on an older fee guide. Carrier A payment Plan based on 1989 fee guide.

Date of Service

Procedure Code

Submitted Eligible Payable at Payment

1.2.90 01103 73.98 69.96* 100% 69.96 1.2.90 01242 16.53 15.63* 100% 15.63

TOTAL $90.51 $85.59 $85.59

* $4.92 declined as being over the 1989 fee guide. Carrier B payment Plan based on current fee guide.

Date of Service

Procedure Code

Submitted Eligible Payable at Payment

1.2.90 01103 73.98 73.98 80% 59.18 1.2.90 01242 16.53 16.53 80% 12.50

TOTAL $90.51 $90.51 $71.68 Since the dentist is not charging more than the current appropriate provincial fee guide, we will pay $4.92 ($90.51 - $85.59).

G4 Coordination of Benefits 12 of 30

DENTAL Sample #3 Both plans cover general practitioners only but work is performed by specialist (endodontist): Carrier A payment Plan based on current GP fee guide.

Procedure Code

Submitted Eligible Payable at Payment

1.2.90 01205 88.77 73.98* 100% 73.98 1.3.90 33101 295.00 246.00* 100% 246.00

TOTAL $383.77 $320.58 $320.58

* $63.19 declined as being over the 1990 GP fee guide. Carrier B payment Plan based on current GP fee guide.

Date of Service

Procedure Code

Submitted Eligible Payable at Payment

1.2.90 01205 88.77 73.98* 80% 59.18 1.3.90 33101 295.00 246.60 80% 197.28

$383.77 $320.58 $256.46

* $63.19 declined as being over the 1990 GP guide. Since the dentist has not

overcharged according to the current appropriate (endodontist) fee guide, we will pay $63.19 ($383.77 - $320.58).

G4 Coordination of Benefits 13 of 30

DENTAL Sample #4 Expenses eligible under other carrier but not under our plan: Carrier A payment Plan based on current fee guide.

Date of Service

Procedure Code

Submitted Eligible Payable at Payment

1.2.89 23222 87.00 79.99* 80% 63.99 1.2.89 23221 46.00 46.00 80% 36.80 1.2.89 23221 40.00 40.00 80% 32.00 1.2.89 23222 70.00 70.00 80% 56.00

TOTAL $243.00 $235.99 $188.79

Note: * $7.01 declined as being over the fee guide. Carrier B payment Plan based on current fee guide. Procedure code 23222 is not eligible under our plan. The balance of 23222 should not be considered under our plan. The balance of 23221 can be considered. 9.20 8.00 $17.20

Since we would have paid $68.80 for these two services if we had been the only carrier (assuming 80% reimbursement), we would pay $17.20.

G4 Coordination of Benefits 14 of 30

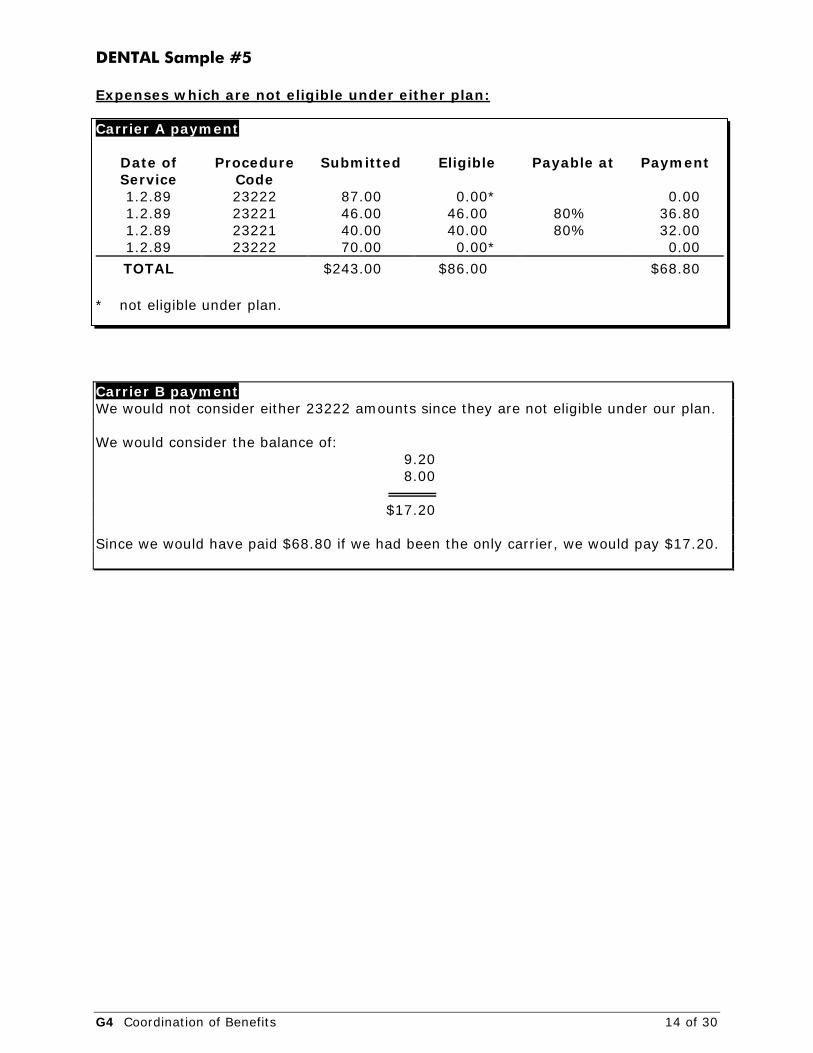

DENTAL Sample #5 Expenses which are not eligible under either plan: Carrier A payment

Date of Service

Procedure Code

Submitted Eligible Payable at Payment

1.2.89 23222 87.00 0.00* 0.00 1.2.89 23221 46.00 46.00 80% 36.80 1.2.89 23221 40.00 40.00 80% 32.00 1.2.89 23222 70.00 0.00* 0.00

TOTAL $243.00 $86.00 $68.80 * not eligible under plan. Carrier B payment We would not consider either 23222 amounts since they are not eligible under our plan. We would consider the balance of: 9.20 8.00 $17.20

Since we would have paid $68.80 if we had been the only carrier, we would pay $17.20.

G4 Coordination of Benefits 15 of 30

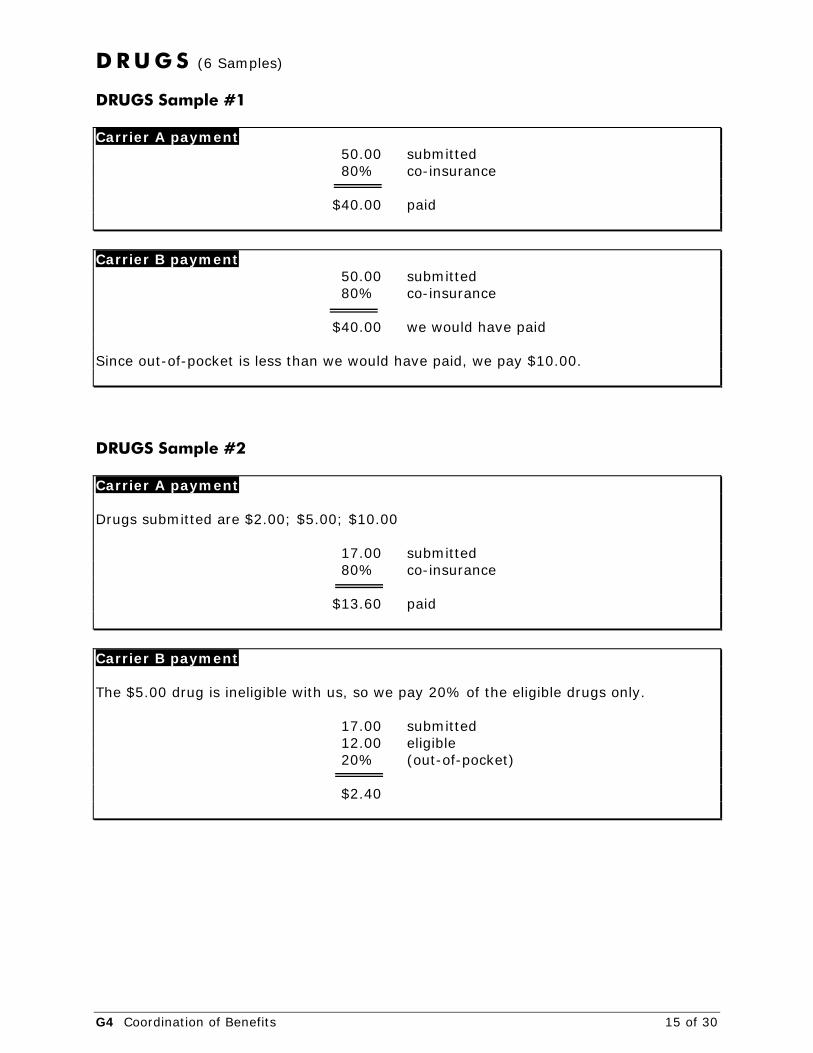

D R U G S (6 Samples) DRUGS Sample #1 Carrier A payment 50.00 submitted 80% co-insurance $40.00 paid Carrier B payment 50.00 submitted 80% co-insurance $40.00 we would have paid Since out-of-pocket is less than we would have paid, we pay $10.00. DRUGS Sample #2 Carrier A payment Drugs submitted are $2.00; $5.00; $10.00 17.00 submitted 80% co-insurance $13.60 paid Carrier B payment The $5.00 drug is ineligible with us, so we pay 20% of the eligible drugs only. 17.00 submitted 12.00 eligible 20% (out-of-pocket) $2.40

G4 Coordination of Benefits 16 of 30

DRUGS Sample #3 Carrier A payment 50.00 submitted -25.00 deductible 80% $20.00 paid Out-of-pocket - $30.00. Carrier B payment We would have considered: 50.00 -50.00 deductible $0.00 The out-of-pocket is $30.00. (We only pay up to what we would have paid, if we were the first carrier.) DRUGS Sample #4 Carrier A Carrier B 50.00 50.00 -50.00 deductible -50.00 deductible $ 0.00 $ 0.00 The deductibles are satisfied under both plans. The out-of-pocket expense is $50.00.

G4 Coordination of Benefits 17 of 30

DRUGS Sample #5 Drugs submitted: 2.00 5.00 Ineligible with 2nd carrier 10.00 10.00 Carrier A Payment 27.00 -20.00 deductible $ 7.00 paid Carrier B payment 27.00 - 5.00 ineligible $22.00 -10.00 deductible 80% $ 9.60

G4 Coordination of Benefits 18 of 30

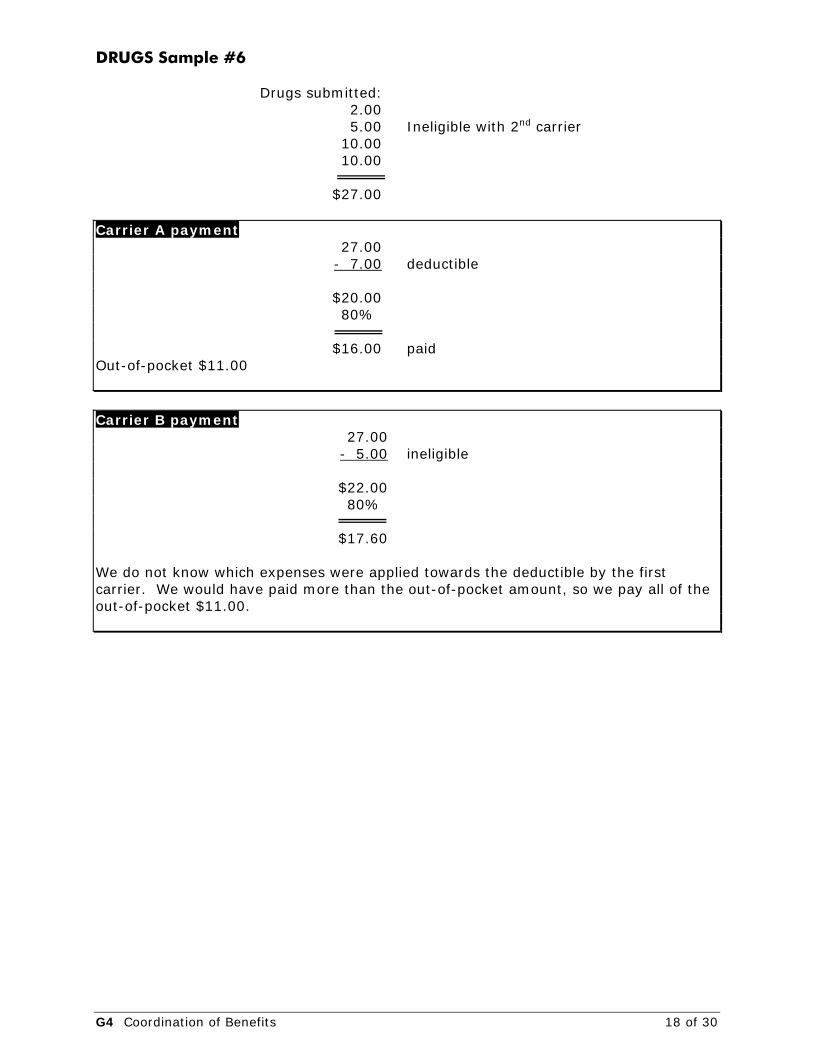

DRUGS Sample #6 Drugs submitted: 2.00 5.00 Ineligible with 2nd carrier 10.00 10.00 $27.00 Carrier A payment 27.00 - 7.00 deductible $20.00 80% $16.00 paid Out-of-pocket $11.00 Carrier B payment 27.00 - 5.00 ineligible $22.00 80% $17.60 We do not know which expenses were applied towards the deductible by the first carrier. We would have paid more than the out-of-pocket amount, so we pay all of the out-of-pocket $11.00.

G4 Coordination of Benefits 19 of 30

V I S I O N (2 Samples) VISION Sample #1 Glasses $210.00 Carrier A pays: 150.00 -25.00 deductible $125.00 80% $100.00 Out-of-pocket - $110.00. Carrier B pays: 150.00 maximum 100% B pays $110.00 VISION Sample #2 Glasses $240.00 Carrier A pays: 150.00 maximum 100% $150.00 Out-of-pocket - $90.00. Carrier B pays: 100.00 -25.00 deductible $75.00 80% $60.00

G4 Coordination of Benefits 20 of 30

H O S P I T A L (3 Samples) HOSPITAL Sample #1 ($50.00 SP, $40.00 PR, $90.00 per day private) Carrier A: - Covers semi-private at 100%; Private 80% - Paid: 50.00 x 100% = 50.00 40.00 x 80% = 32.00 Carrier B: - Covers semi-private only at 100% - Decline balance for private room coverage. HOSPITAL Sample #2 (SP $50.00, Private $40.00) Carrier A: - Covers semi-private at 80%, no private - Paid: $50.00 SP at 80% = $40.00 - $40.00 for private room is declined Carrier B: - Covers semi-private and private - Pays $50.00 ($10.00 for semi-private and $40.00 for private). HOSPITAL Sample #3 ($40.00 SP; Private $30.00) Carrier A: - Covers SP + $10.00 per day private - Pays $40.00 SP and $10.00 private = $50.00 Carrier B: - Covers $50.00 per day maximum - Pays $20.00 ($70.00 - $50.00)

G4 Coordination of Benefits 21 of 30

S U P P L E M E N T A R Y (1 Sample) SUPPLEMENTARY Sample #1 Massage visits - 10 visits at $25.00 each = $250.00 Carrier A pays: 250.00 submitted 200.00 maximum eligible -50.00 deductible $150.00 80% $120.00 paid Carrier B pays: Our maximum is $250.00 at 80%. We pay $130.00 in full.

G4 Coordination of Benefits 22 of 30

COORDINATION OF BENEFITS WORKSHEET

Date of Service

Procedure/ Service

Amount Charged

Payment by 1st Carrier

Balance 2nd Carrier Could Have

Paid

Amount Covered

Out-of- Pocket

G4 Coordination of Benefits 23 of 30

APPENDIX B

COORDINATION OF BENEFIT SAMPLES: OUT-OF-COUNTRY/ PROVINCIAL HEALTH CARE EXPENSES

Index - Examples of Settlement Example 1 .......................................................................................................24

Example 2 .......................................................................................................25

Example 3 .......................................................................................................26

Example 4 .......................................................................................................27

Example 5 .......................................................................................................28

Example 6 .......................................................................................................29

Example 7 .......................................................................................................30

G4 Coordination of Benefits 24 of 30

Example 1

ITEM Total bill after GHIP ($)

Liability if Carrier 1 alone ($)

Liability if Carrier 2 alone ($)

Common Core ($)

Carrier 1 Exclusive ($)

Carrier 2 Exclusive ($)

Total ($)

Hospital Ward (25 days)

50,000 50,000 49,000 49,000 1,000 50,000

Semi-private excess 2,000 n/a 2,000 - 2,000 2,000

Physician 20,000 20,000 20,000 20,000 20,000

Private Duty Nursing 5,000 n/a 5,000 - 5,000 5,000

Repatriation 15,000 5,000 15,000 5,000 10,000 15,000

Accompanying Family Member 1,000 n/a 1,000 - 1,000 1,000

TOTAL 93,000 75,000 92,000 74,000 1,000 18,000 93,000

Share of Carrier 1 ($)

37,000 1,000 n/a 38,000

Share of Carrier 2 ($)

37,000 n/a 18,000 55,000

Share of Insured ($)

n/a n/a n/a n/a

Note: Carrier 2 has a $1,000 deductible

G4 Coordination of Benefits 25 of 30

Example 2

ITEM

Total Bill after GHIP ($)

Carrier 1 Liability if alone ($)

Carrier 2 Liability if alone ($)

Carrier 3 Liability if alone ($)

Common Core ($)

1 & 2 Only Jointly ($)

1 & 3 Only Jointly ($)

2 & 3 Only Jointly ($)

Carrier 1 Exclusive ($)

Carrier 2 Exclusive ($)

Carrier 3 Exclusive ($)

Total ($)

Hospital (140 days)

700,000 280,000 560,000 700,000 280,000 280,000 140,000 700,000

Physician 150,000 150,000 120,000 150,000 120,000 30,000 150,000

Repatriation-ambulance

50,000 5,000 40,000 50,000 5,000 35,000 10,000 50,000

MRI 2,000 - 1,600 2,000 - 1,600 400 2,000

TOTAL 902,000 435,000 721,600 902,000 405,000 30,000 316,600 150,400 902,000

Share of Carrier 1 ($) 135,000 15,000 n/a n/a n/a n/a 150,000

Share of Carrier 2 ($) 135,000 n/a 158,300 n/a n/a n/a 293,300

Share of Carrier 3 ($) 135,000 15,000 158,300 n/a n/a 150,400 458,700

Share of Insured ($) n/a n/a n/a n/a n/a n/a n/a

Note: Carrier 1 has a $2,000 daily limit and a $5,000 repatriation maximum Carrier 2 pays 80% since it is a pre-existing condition Carrier 3 has no limit

G4 Coordination of Benefits 26 of 30

Example 3: Two Group Carriers

ITEM Total bill after GHIP Carrier 1 Liability if alone Carrier 2 Liability if alone Common Core

Hospital 80,000 80,000 80,000 80,000

Physician 20,000 20,000 20,000 20,000

TOTAL 100,000 100,000 100,000 100,000

Share of Carrier 1 100,000

Share of Carrier 2 n/a

Share of Insured n/a

Note: Patient is covered under two distinct group policies Under Carrier 1’s policy, the patient is the insured Under Carrier 2’s policy, the patient is the spouse of the insured The Group Coordination of Benefits Guidelines apply in this case

G4 Coordination of Benefits 27 of 30

Example 4: One Individual Policy and Two Group Policies

ITEM

Total Bill after GHIP ($)

Carrier 1 Liability if alone ($)

Carrier 2 Liability if alone ($)

Carrier 3 Liability if alone ($)

Group Unit Carrier 2 & 3 if alone 1 ($)

Common Core 2 ($)

Carrier 1 Exclusive ($)

Carrier 2 Exclusive ($)

Carrier 3 Exclusive ($)

Total ($)

Hospital 80,000 80,000 80,000 72,000 80,000 80,000 80,000

Physician 20,000 20,000 20,000 18,000 20,000 20,000 20,000

TOTAL 100,000 100,000 100,000 90,000 100,000 100,000 100,000

Share of Carrier 1 ($) 50,000 n/a n/a n/a 50,000

Share of Carrier 2 ($) 50,000 n/a n/a n/a 50,000

Share of Carrier 3 ($) 0 3 n/a n/a n/a 0

Share of Insured ($) n/a n/a n/a n/a n/a

Note: Carrier 1 is an individual policy Carrier 2 and 3 are group policies offered through employment Carrier 2 is the insured’s plan Carrier 3 is the insured’s spouse’s plan and has 90% coverage 1 Coordination of Benefits Guidelines apply 2 For common core breakdown purposes, all group carriers are treated as one unit 3 Determined by application of Group COB Guidelines

G4 Coordination of Benefits 28 of 30

Example 5: High Deductible Individual Policy and Limited Lifetime Retiree Group Policy

ITEM Total bill after GHIP ($)

Carrier 1 Liability if alone ($)

Carrier 2 Liability if alone ($)

Common Core 1 ($)

Carrier 1 Exclusive ($)

Carrier 2 Exclusive ($)

Total ($)

Hospital 80,000 75,000 50,000 50,000 75,000 5,000 80,000

Physician 20,000 20,000 0 0 20,000 0 20,000

TOTAL 100,000 95,000 50,000 50,000 95,000 5,000 100,000

Share of Carrier 1 ($)

95,000 0 95,000

Share of Carrier 2 ($)

n/a 5,000 5,000

Share of Insured ($)

n/a n/a n/a n/a

100,000

Note: Carrier 1 is an individual policy with a $5,000 deductible Carrier 2 has a $50,000 (retiree) lifetime group coverage maximum 1 These Guidelines do not coordinate lifetime coverage limits under $50,000

G4 Coordination of Benefits 29 of 30

Example 6: High Deductible Individual Policy and Group Policy

ITEM Total bill after GHIP ($)

Carrier 1 Liability if alone ($)

Carrier 2 Liability if alone ($)

Common Core ($)

Carrier 1 Exclusive ($)

Carrier 2 Exclusive ($)

Total ($)

Hospital 110,000 105,000 100,000 100,000 5,000 0 105,000

Physician 20,000 20,000 0 0 20,000 0 20,000

TOTAL 130,000 125,000 100,000 100,000 25,000 0 125,000

Share of Carrier 1 ($)

50,000 25,000 0 75,000

Share of Carrier 2 ($)

50,000 0 0 50,000

Share of Insured ($)

n/a n/a n/a 5,000

130,000

Note: Carrier 1 has a $5,000 deductible Carrier 2 is a group policy with no deductible and a Calendar Year Maximum of $100,000

G4 Coordination of Benefits 30 of 30

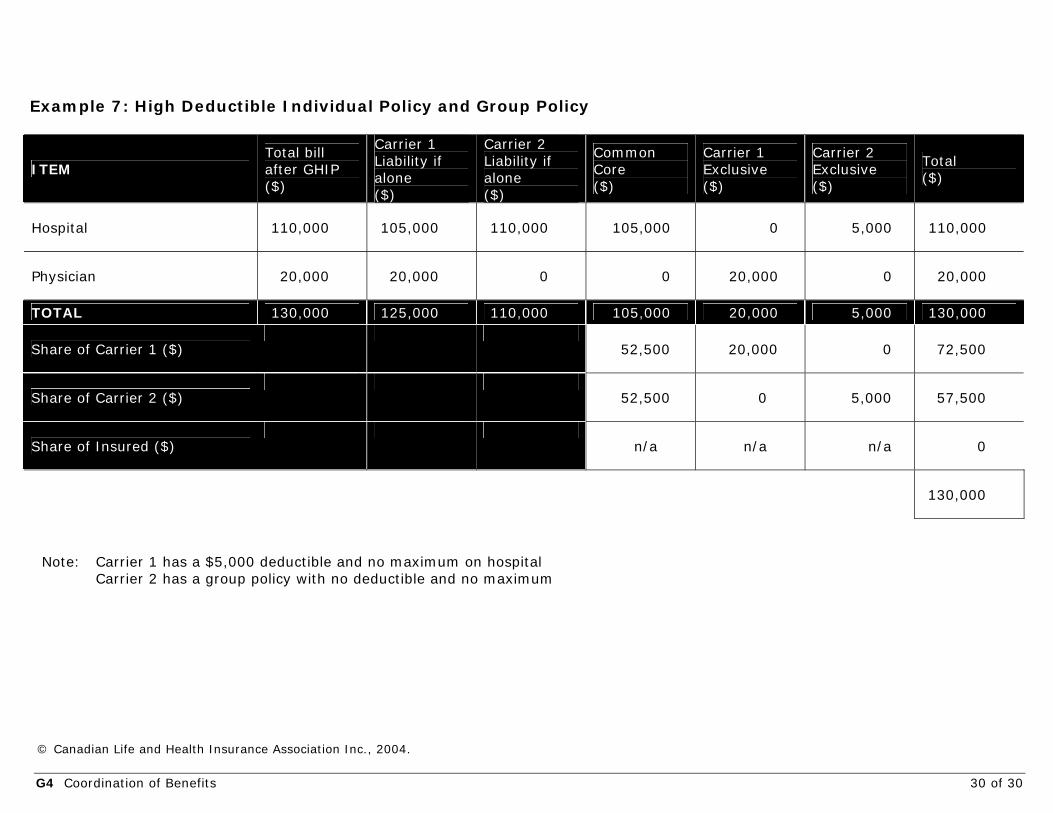

Example 7: High Deductible Individual Policy and Group Policy

ITEM Total bill after GHIP ($)

Carrier 1 Liability if alone ($)

Carrier 2 Liability if alone ($)

Common Core ($)

Carrier 1 Exclusive ($)

Carrier 2 Exclusive ($)

Total ($)

Hospital 110,000 105,000 110,000 105,000 0 5,000 110,000

Physician 20,000 20,000 0 0 20,000 0 20,000

TOTAL 130,000 125,000 110,000 105,000 20,000 5,000 130,000

Share of Carrier 1 ($)

52,500 20,000 0 72,500

Share of Carrier 2 ($)

52,500 0 5,000 57,500

Share of Insured ($)

n/a n/a n/a 0

130,000

Note: Carrier 1 has a $5,000 deductible and no maximum on hospital Carrier 2 has a group policy with no deductible and no maximum

© Canadian Life and Health Insurance Association Inc., 2004.