COALTRANS 2nd EAST ASIA FORUM - Britmindobritmindo.com/images/xplod/editor/alan nye - coaltrans...

18

COALTRANS 2 nd EAST ASIA FORUM Seoul, South Korea 23-24 September 2014 INDONESIA – The Bigger Picture Alan Nye President Director PT Britmindo BRITMINDO GROUP Professional Mining Services

Transcript of COALTRANS 2nd EAST ASIA FORUM - Britmindobritmindo.com/images/xplod/editor/alan nye - coaltrans...

COALTRANS2nd EAST ASIA FORUM

Seoul, South Korea23-24 September 2014

INDONESIA – The Bigger PictureAlan Nye

President DirectorPT Britmindo

BRITMINDO GROUPProfessional Mining Services

Head Title

TitleSubtitle

Report / ProposalDate

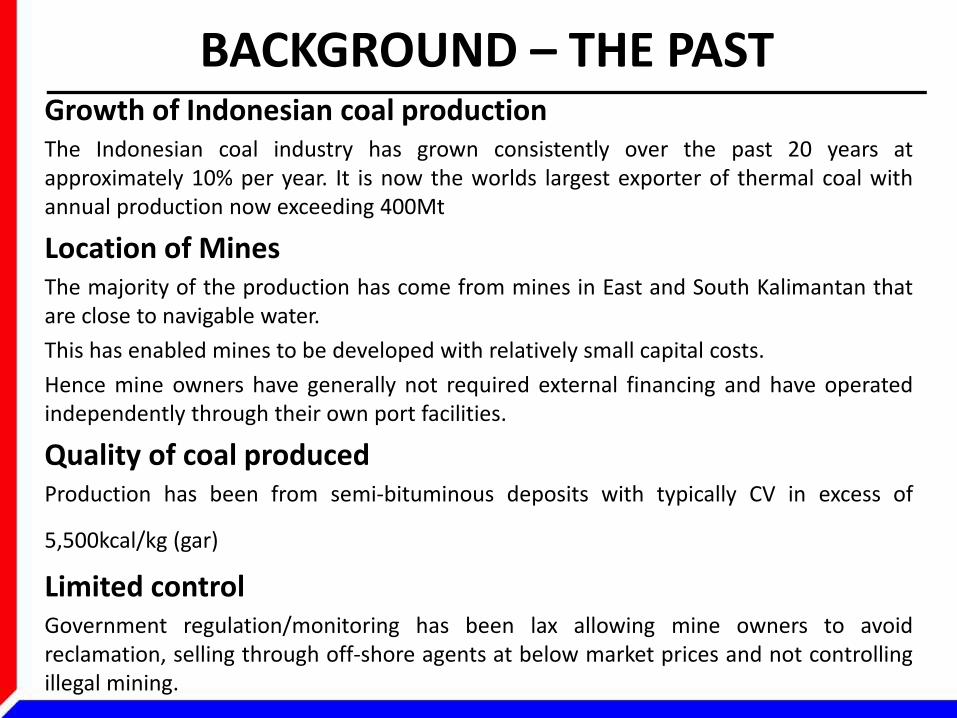

BACKGROUND – THE PASTGrowth of Indonesian coal productionThe Indonesian coal industry has grown consistently over the past 20 years atapproximately 10% per year. It is now the worlds largest exporter of thermal coal withannual production now exceeding 400Mt

Location of MinesThe majority of the production has come from mines in East and South Kalimantan thatare close to navigable water.

This has enabled mines to be developed with relatively small capital costs.

Hence mine owners have generally not required external financing and have operatedindependently through their own port facilities.

Quality of coal producedProduction has been from semi-bituminous deposits with typically CV in excess of

5,500kcal/kg (gar)

Limited controlGovernment regulation/monitoring has been lax allowing mine owners to avoidreclamation, selling through off-shore agents at below market prices and not controllingillegal mining.

Head Title

TitleSubtitle

Report / ProposalDate

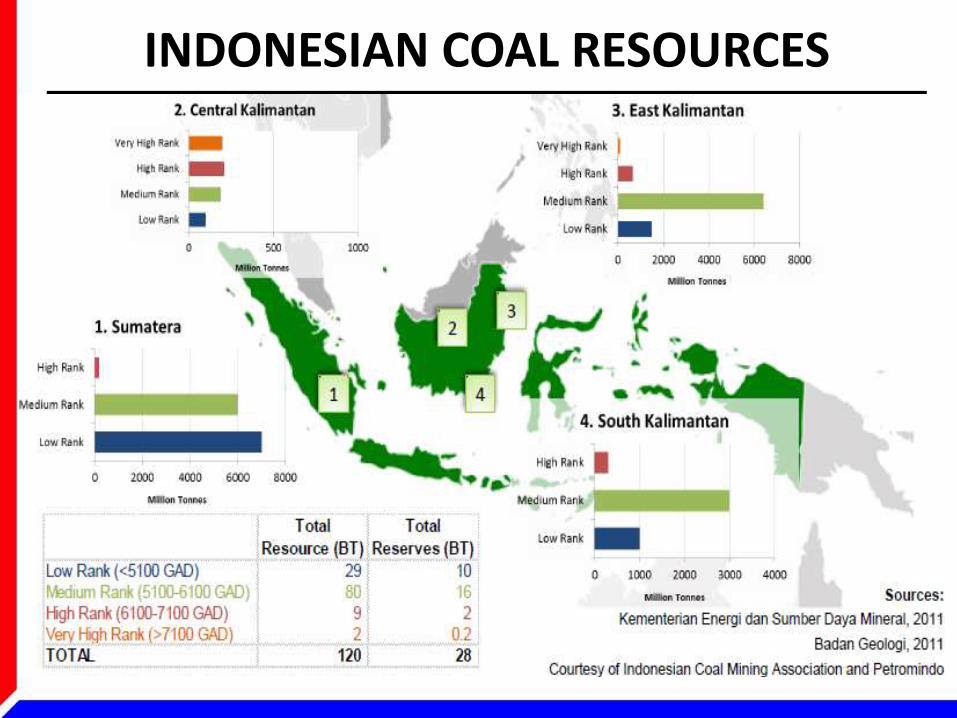

INDONESIAN COAL RESOURCES

Head Title

TitleSubtitle

Report / ProposalDate

LOCATION OF MAJOR MINES

KALIMANTAN

HELMAHERA

BRUNEI

SABAH

SARAWAK

THAILAND

MALAYSIA

SUMATRA

JAVA

SULAWESI

IRIAN JAYA

TIMOR

LOMBOKSUMBAWA

SERAM

BALI

Jakarta

Medan

Pekan Baru

Jambi

Palembang

Padang

Bengkulu

Bandar Lampung

Pontianak

Balikpapan

Banjarmasin

Banda Aceh

Kuala Lumpur

Singapore

Denpasar

Manado

Makassar

Jayapura

Surabaya

Pacific Ocean

Indian Ocean

South China Sea

Banda Sea

Maluku Sea

Java Sea

Timor Sea

Sulu Sea

Seram Sea

Arafura Sea

Mentaw

ai Strait

Malacca S

trait

Karim

ata

Stra

it

Maka

ssar S

trait

AdaroKendilo

Arutmin

Jorong

Sebuku

KPCIndominco

Berau

Bukit Baiduri

Kideco

PTBA

Arutmin

Gunung Bayan

Tanito Harum

ABKMulti Harapan

PTBA

KALIMANTAN

HELMAHERA

BRUNEI

SABAH

SARAWAK

THAILAND

MALAYSIA

SUMATRA

JAVA

SULAWESI

IRIAN JAYA

TIMOR

LOMBOKSUMBAWA

SERAM

BALI

Jakarta

Medan

Pekan Baru

Jambi

Palembang

Padang

Bengkulu

Bandar Lampung

Pontianak

Balikpapan

Banjarmasin

Banda Aceh

Kuala Lumpur

Singapore

Denpasar

Manado

Makassar

Jayapura

Surabaya

Pacific Ocean

Indian Ocean

South China Sea

Banda Sea

Maluku Sea

Java Sea

Timor Sea

Sulu Sea

Seram Sea

Arafura Sea

Mentaw

ai Strait

Malacca S

trait

Karim

ata

Stra

it

Maka

ssar S

trait

AdaroKendilo

Arutmin

Jorong

Sebuku

KPCIndominco

Berau

Bukit Baiduri

Kideco

PTBA

Arutmin

Gunung Bayan

Tanito Harum

ABKMulti Harapan

PTBA

Major Indonesian Coal Producers

Head Title

TitleSubtitle

Report / ProposalDate

HISTORICAL INDONESIAN COAL PRODUCTION

Head Title

TitleSubtitle

Report / ProposalDate

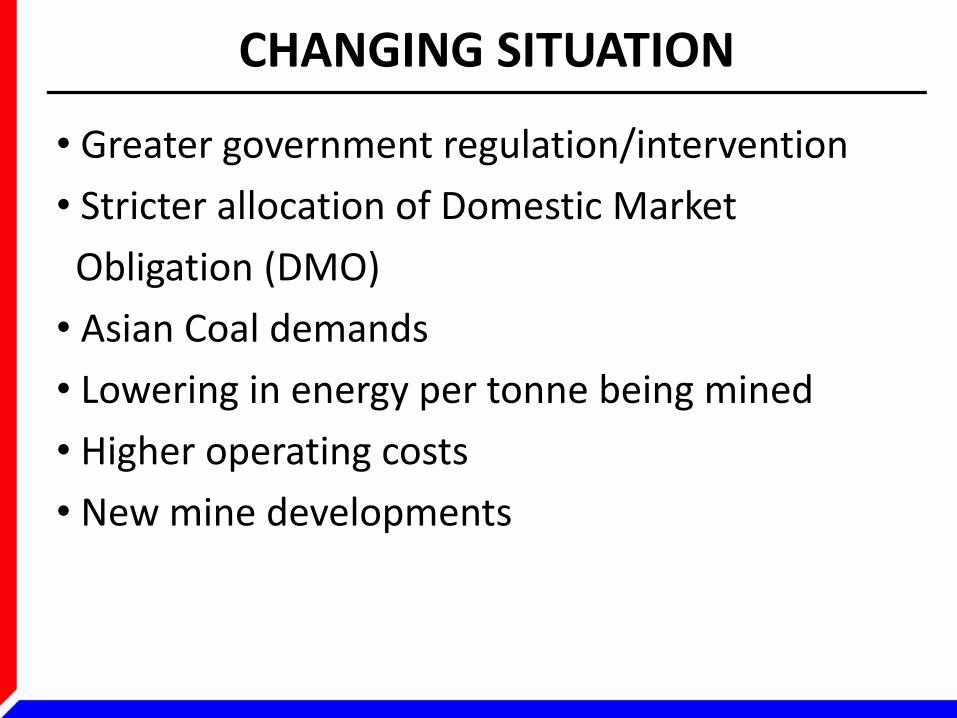

CHANGING SITUATION

• Greater government regulation/intervention

• Stricter allocation of Domestic Market

Obligation (DMO)

• Asian Coal demands

• Lowering in energy per tonne being mined

• Higher operating costs

• New mine developments

Head Title

TitleSubtitle

Report / ProposalDate

DIRECTION OF GOVERNMENT POLICY

1

2

3

4

5

POLICY DIRECTION

Provide certainty and transparency in the activities of mining (Mining Law supporting regulations, sanctions violations, etc.)

Implement fulfillment priority of coal for domestic needs

To implement supervision and guidance

To encourage the increase of investment and revenue

To encourage the development of value added products of mining commodity (e.g. processing, refining, local content, local expenditure, labour andCSR)

6To maintain environmental sustainability through environmental management and monitoring(including reclamation and post-mining)

Head Title

TitleSubtitle

Report / ProposalDate

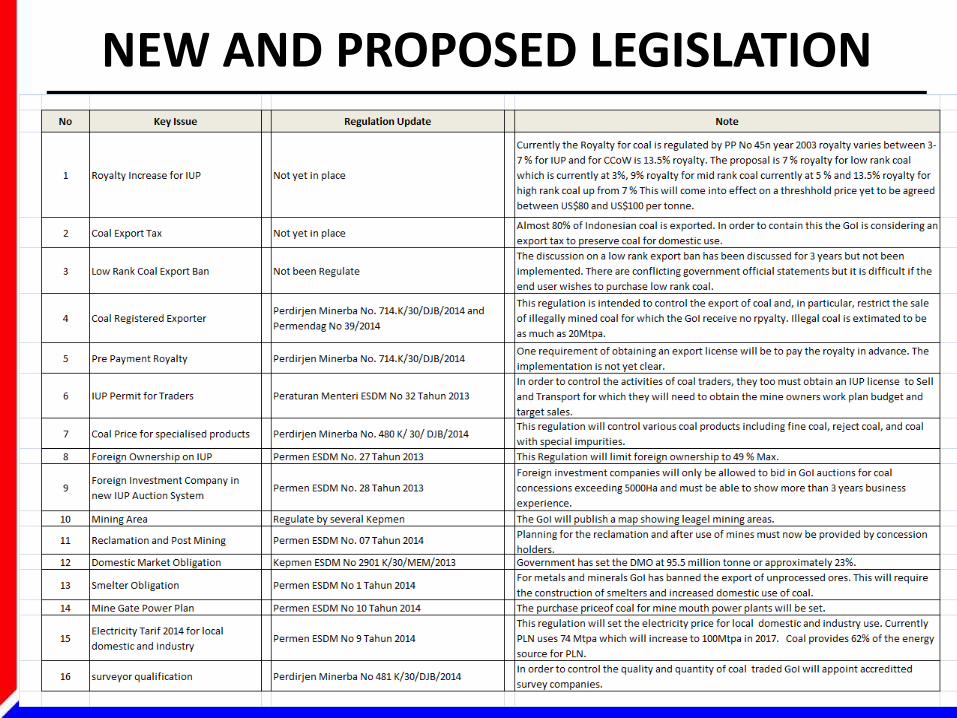

NEW AND PROPOSED LEGISLATION

Head Title

TitleSubtitle

Report / ProposalDate

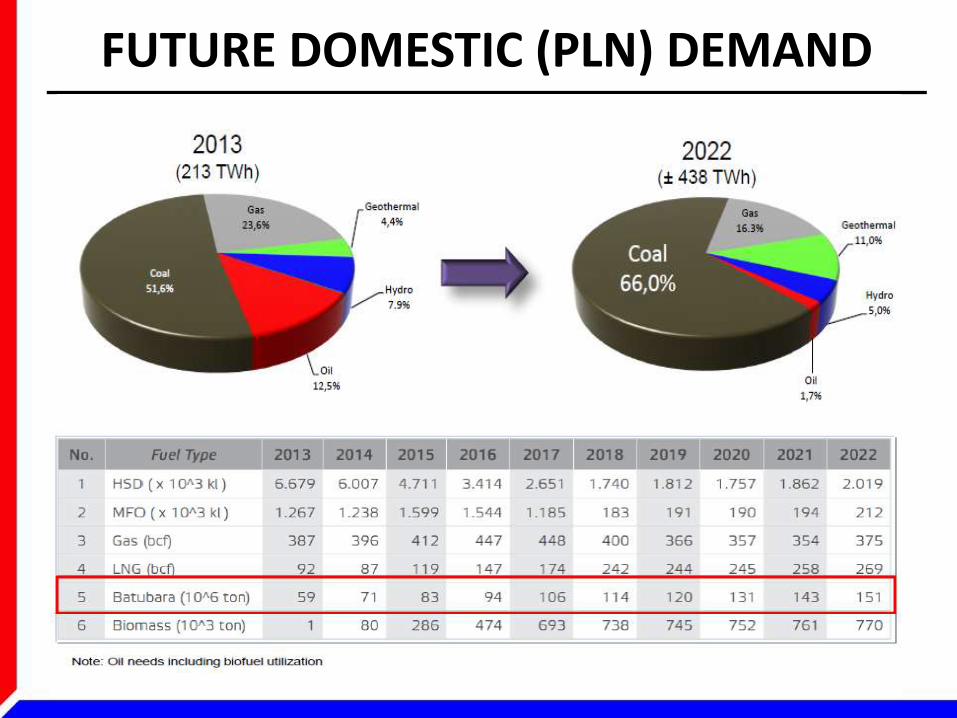

FUTURE DOMESTIC (PLN) DEMAND

Head Title

TitleSubtitle

Report / ProposalDate

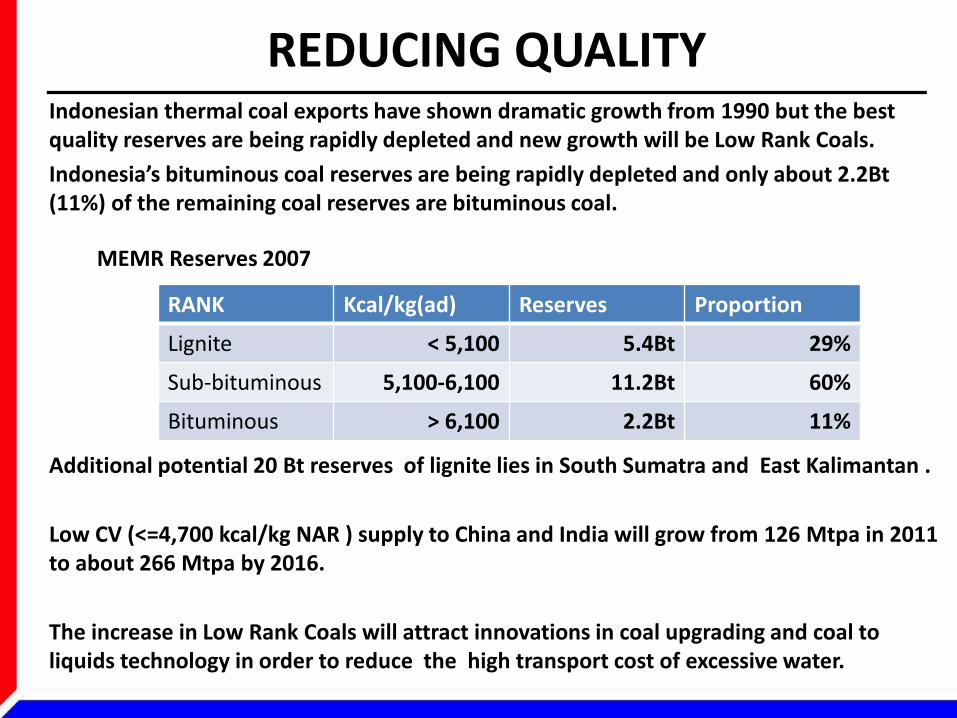

REDUCING QUALITYIndonesian thermal coal exports have shown dramatic growth from 1990 but the best quality reserves are being rapidly depleted and new growth will be Low Rank Coals.

Indonesia’s bituminous coal reserves are being rapidly depleted and only about 2.2Bt (11%) of the remaining coal reserves are bituminous coal.

MEMR Reserves 2007

Additional potential 20 Bt reserves of lignite lies in South Sumatra and East Kalimantan .

Low CV (<=4,700 kcal/kg NAR ) supply to China and India will grow from 126 Mtpa in 2011 to about 266 Mtpa by 2016.

The increase in Low Rank Coals will attract innovations in coal upgrading and coal to liquids technology in order to reduce the high transport cost of excessive water.

RANK Kcal/kg(ad) Reserves Proportion

Lignite < 5,100 5.4Bt 29%

Sub-bituminous 5,100-6,100 11.2Bt 60%

Bituminous > 6,100 2.2Bt 11%

Head Title

TitleSubtitle

Report / ProposalDate

PROJECTED PRODUCTION BY COAL RANK

Head Title

TitleSubtitle

Report / ProposalDate

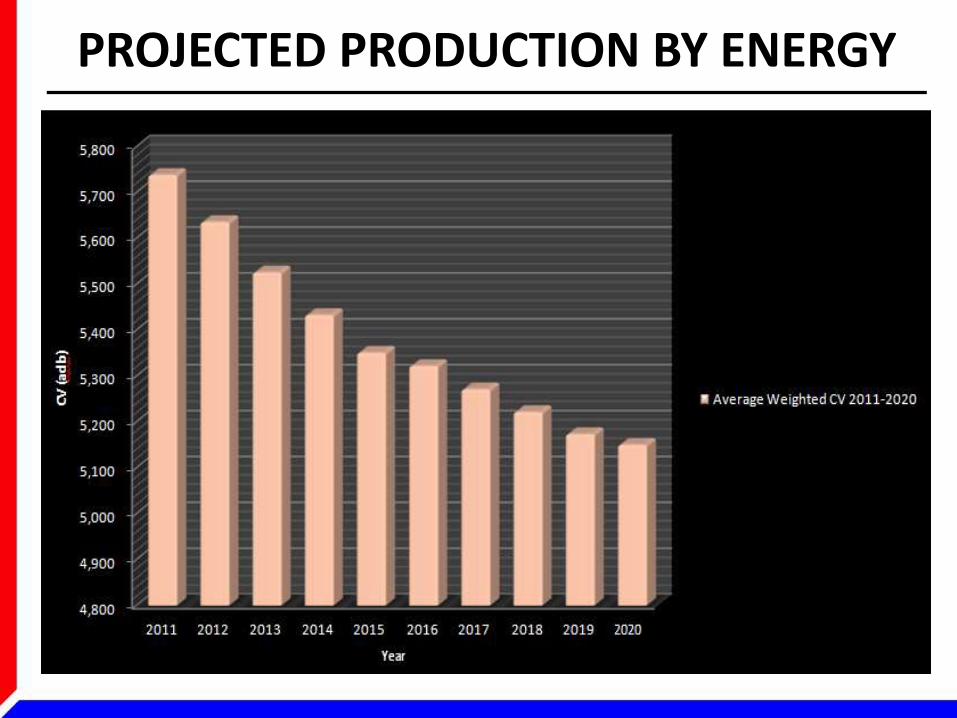

PROJECTED PRODUCTION BY ENERGY

Head Title

TitleSubtitle

Report / ProposalDate

PROJECTED WORLD DEMAND

Head Title

TitleSubtitle

Report / ProposalDate

INDIA OPPORTUNITY• The Government’s ambition to roll out reliable electricity supply to the whole country by 2022

will have the largest impact on India's energy demand growth.

• In 2011, 90.4% of Gujarati households had access to electricity, compared to a national average of 67.2%

• Wood Mackenzie estimate an additional 300 TWh of electricity supply will be required in 2020 and

475 TWh in 2030.

• Yet without an accompanying increase in domestic production, India's energy imports would rise

sharply – up 24% for coal and 20% for natural gas relative to our base case.This upside will help to balance a global market struggling with oversupply.

Head Title

TitleSubtitle

Report / ProposalDate

CHINA OPPORTUNITY• China recently announced the extension of existing coal quality requirements - maximum 16% ash and 1% sulphur

- to the Pearl and Yangzte River Deltas. It is assumed the guidelines may be effective on 1 January 2015

• The impact on imported coal will be positive as it tends to have lower ash and sulphur content than domestic supply.

• Indonesia stands to benefit from the ban due to the quality of its current exports to China.

• Yet not all imported coal would satisfy the new limits, including 80% of Australian exports to China.

• High ash coal from Australian mines could be washed although sulphur restriction will not be a significant issue

• Washing coal to meet ash quality restrictions will result in a lower coal yield and higher price estimated at US$16/t

• The key will be whether consumers in China are willing to pay more for lower ash, but higher energy, thermal coal from

Australia in comparison to imports from Indonesia.

Head Title

TitleSubtitle

Report / ProposalDate

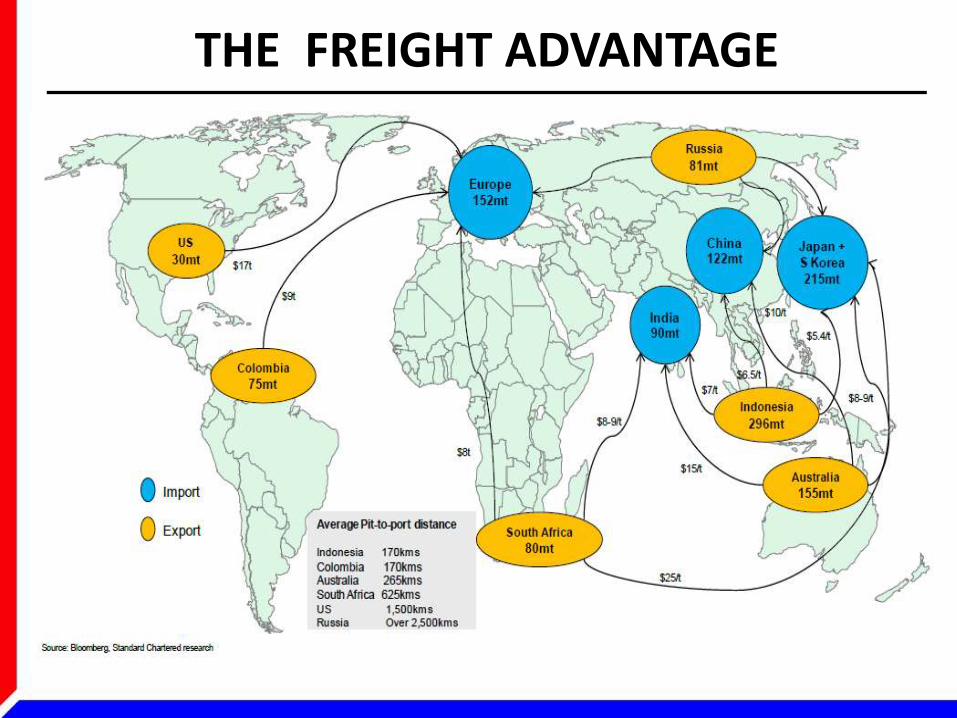

THE FREIGHT ADVANTAGE

Head Title

TitleSubtitle

Report / ProposalDate

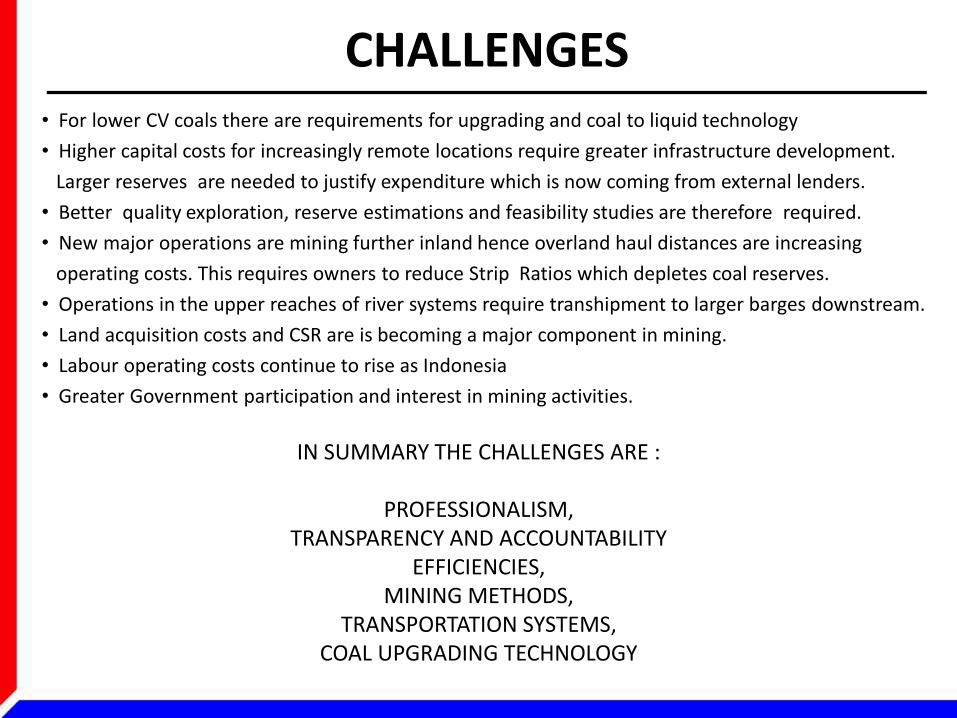

CHALLENGES• For lower CV coals there are requirements for upgrading and coal to liquid technology

• Higher capital costs for increasingly remote locations require greater infrastructure development.

Larger reserves are needed to justify expenditure which is now coming from external lenders.

• Better quality exploration, reserve estimations and feasibility studies are therefore required.

• New major operations are mining further inland hence overland haul distances are increasing

operating costs. This requires owners to reduce Strip Ratios which depletes coal reserves.

• Operations in the upper reaches of river systems require transhipment to larger barges downstream.

• Land acquisition costs and CSR are is becoming a major component in mining.

• Labour operating costs continue to rise as Indonesia

• Greater Government participation and interest in mining activities.

IN SUMMARY THE CHALLENGES ARE :

PROFESSIONALISM, TRANSPARENCY AND ACCOUNTABILITY

EFFICIENCIES, MINING METHODS,

TRANSPORTATION SYSTEMS, COAL UPGRADING TECHNOLOGY

www.britmindo.com

Graha BritmindoJl. Taman Margasatwa Raya No. 14, Ragunan

Jakarta Selatan 12550, IndonesiaTel. +62 21 7884 9999 (hunting), Fax. +62 21 7884 9998

Email: [email protected]

THANK YOU

www.britmindo.com

Graha BritmindoJl. Taman Margasatwa Raya No. 14, Ragunan

Jakarta Selatan 12550, IndonesiaTel. +62 21 7884 9999 (hunting), Fax. +62 21 7884 9998

Email: [email protected]