Coal Perspectives and Clean Coal Technologies World Wide · © IEA Clean Coal Centre World Energy...

64

© IEA Clean Coal Centre www.iea-coal.org.uk Coal Perspectives and Clean Coal Technologies World Wide International Workshop on Coal Technology: Petrobras& ABCM Dr John Topper Managing Director, IEA Clean Coal Centre 13 March 2007, Rio de Janeiro, Brazil

Transcript of Coal Perspectives and Clean Coal Technologies World Wide · © IEA Clean Coal Centre World Energy...

© IEA Clean Coal Centre www.iea-coal.org.uk

Coal Perspectives and Clean Coal Technologies World Wide

International Workshop on Coal Technology: Petrobras& ABCM

Dr John Topper

Managing Director, IEA Clean Coal Centre

13 March 2007, Rio de Janeiro, Brazil

© IEA Clean Coal Centre www.iea-coal.org.uk

World Energy Outlook 2006

Courtesy of Dr. Fatih BirolChief Economist

International Energy Agency

© IEA Clean Coal Centre www.iea-coal.org.uk

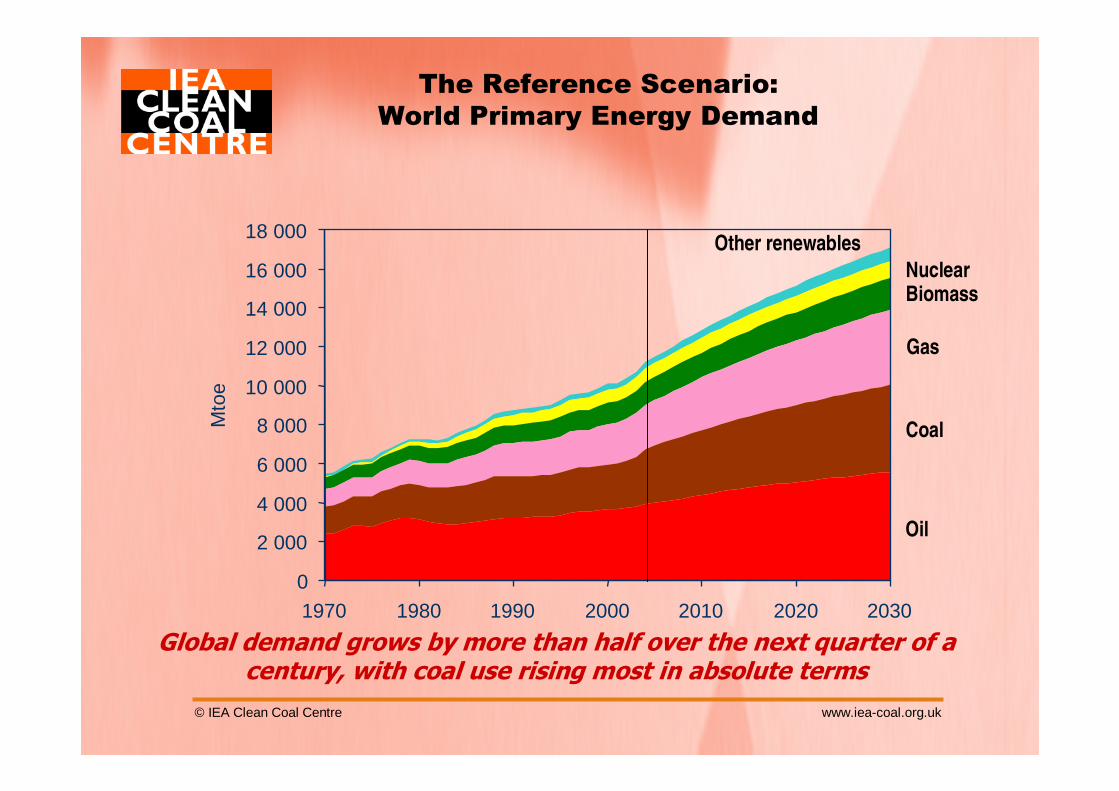

The Reference Scenario: World Primary Energy Demand

Global demand grows by more than half over the next quarter of acentury, with coal use rising most in absolute terms

Oil

Coal

Gas

BiomassNuclear

Other renewables

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

1970 1980 1990 2000 2010 2020 2030

Mto

e

© IEA Clean Coal Centre www.iea-coal.org.uk

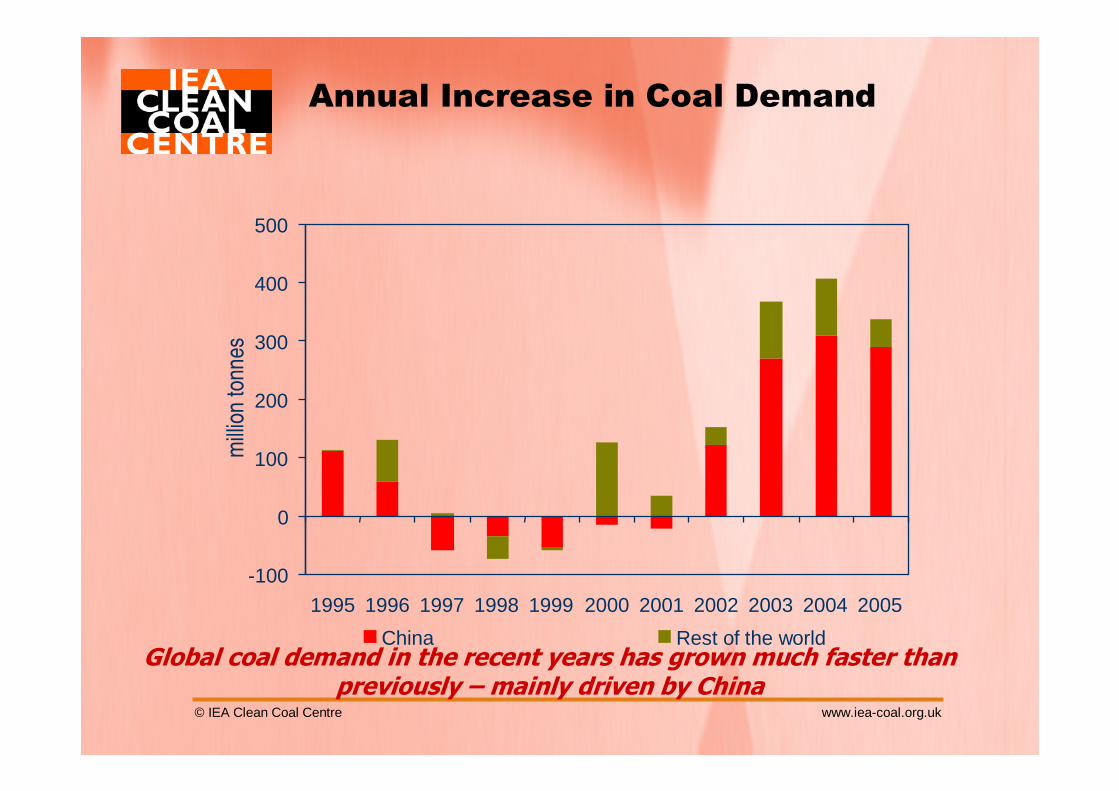

Annual Increase in Coal Demand

Global coal demand in the recent years has grown much faster than previously – mainly driven by China

mill

ion

tonn

es

-100

0

100

200

300

400

500

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

China Rest of the world

© IEA Clean Coal Centre www.iea-coal.org.uk

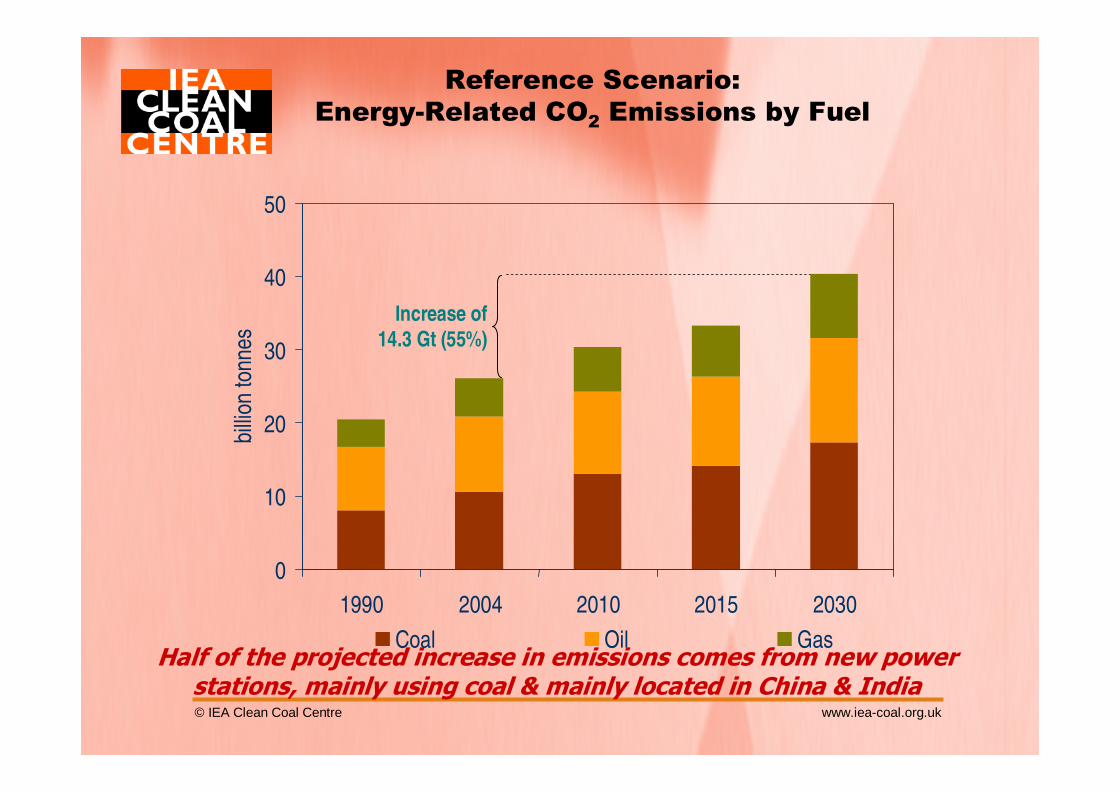

Reference Scenario: Energy-Related CO2 Emissions by Fuel

Half of the projected increase in emissions comes from new powerstations, mainly using coal & mainly located in China & India

Increase of 14.3 Gt (55%)

0

10

20

30

40

50

1990 2004 2010 2015 2030

billi

on to

nnes

Coal Oil Gas

© IEA Clean Coal Centre www.iea-coal.org.uk

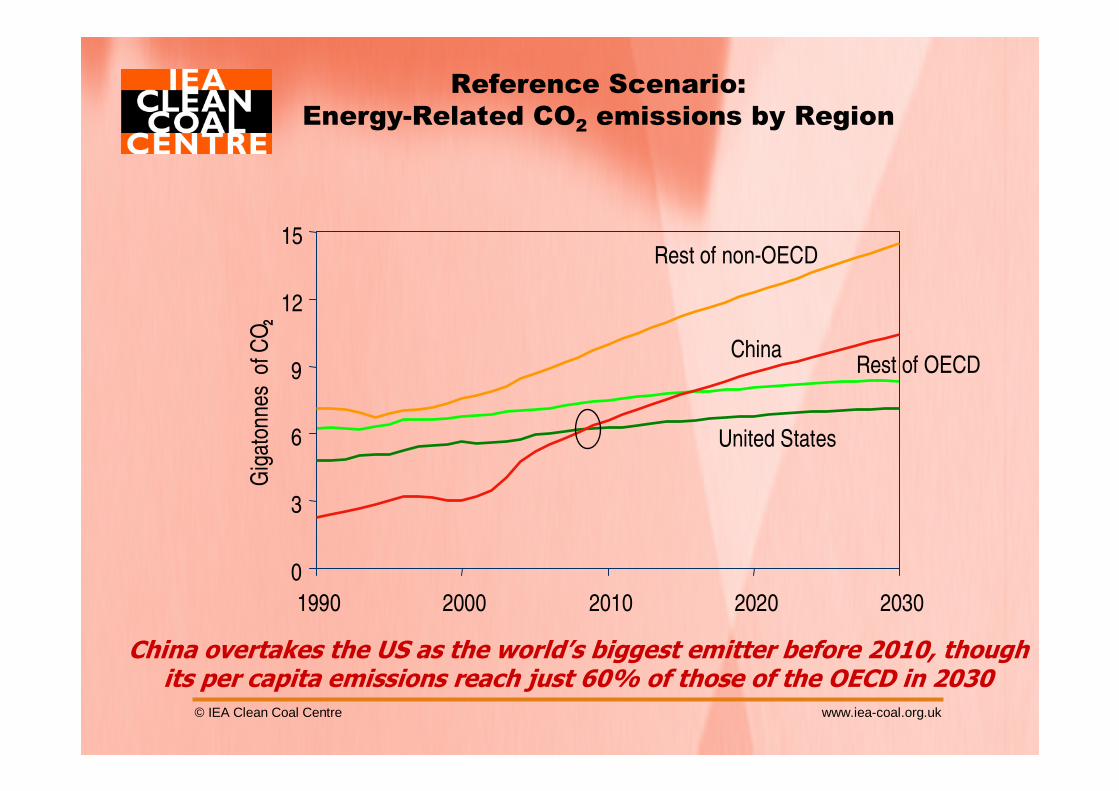

Reference Scenario:Energy-Related CO2 emissions by Region

China overtakes the US as the world’s biggest emitter before 2010, though its per capita emissions reach just 60% of those of the OECD in 2030

0

3

6

9

12

15

1990 2000 2010 2020 2030

Gig

aton

nes

of C

O2

United States

China

Rest of non-OECD

Rest of OECD

© IEA Clean Coal Centre www.iea-coal.org.uk

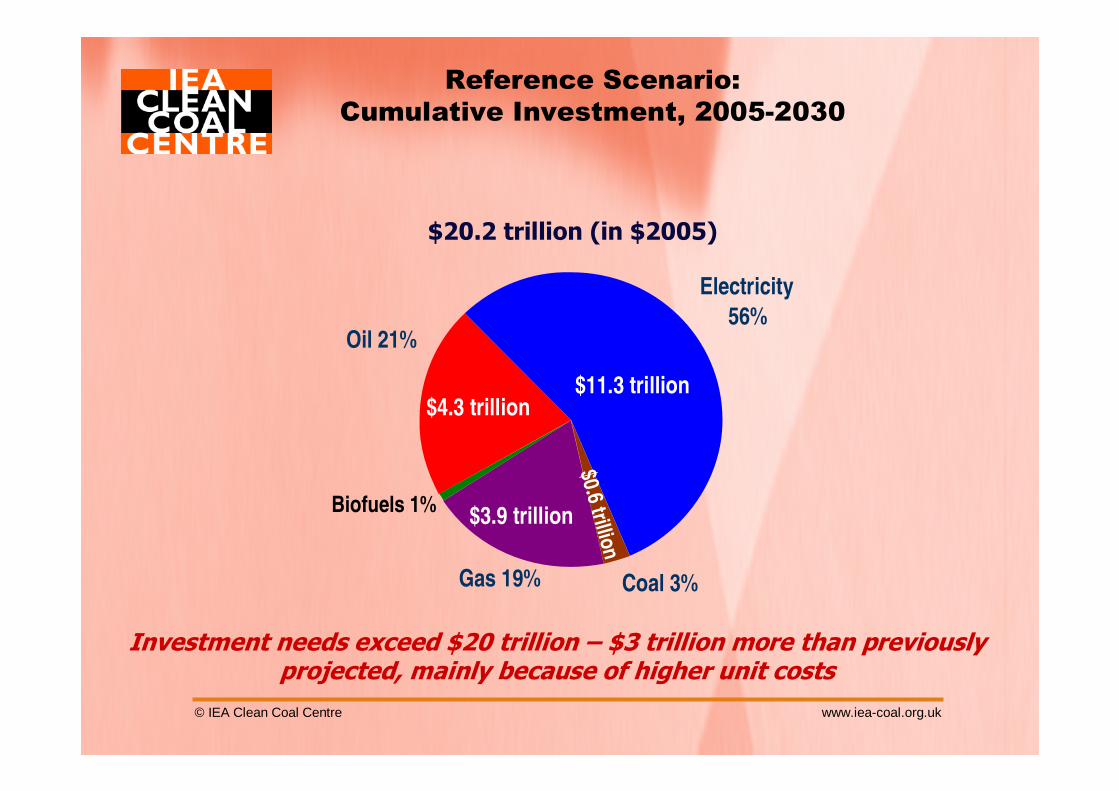

Oil 21%

Electricity

56%

Coal 3%Gas 19%

Reference Scenario: Cumulative Investment, 2005-2030

Investment needs exceed $20 trillion – $3 trillion more than previously projected, mainly because of higher unit costs

$20.2 trillion (in $2005)

$4.3 trillion$11.3 trillion

$3.9 trillion$0.6 trillion

Biofuels 1%

© IEA Clean Coal Centre www.iea-coal.org.uk

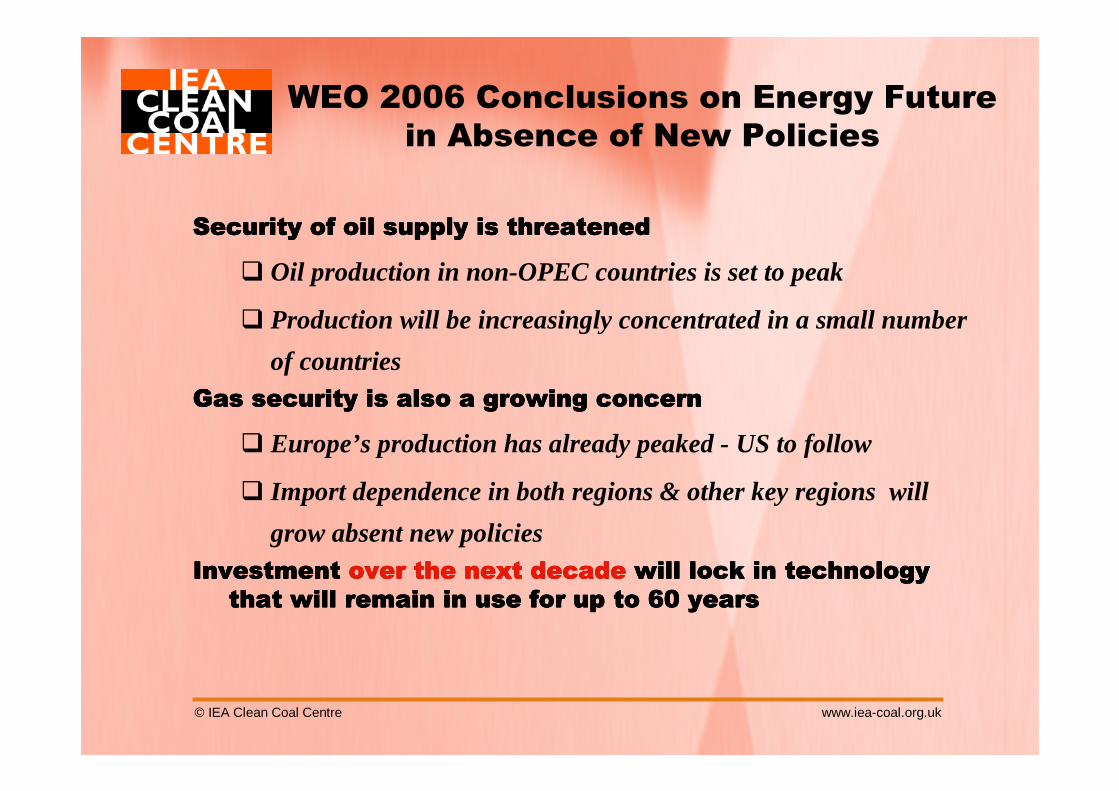

WEO 2006 Conclusions on Energy Future in Absence of New Policies

Security of oil supply is threatenedSecurity of oil supply is threatenedSecurity of oil supply is threatenedSecurity of oil supply is threatened

� Oil production in non-OPEC countries is set to peak

� Production will be increasingly concentrated in a small number

of countriesGas security is also a growing concernGas security is also a growing concernGas security is also a growing concernGas security is also a growing concern

� Europe’s production has already peaked - US to follow

� Import dependence in both regions & other key regions will

grow absent new policiesInvestment Investment Investment Investment over the next decadeover the next decadeover the next decadeover the next decade will lock in technology will lock in technology will lock in technology will lock in technology

that will remain in use for up to 60 yearsthat will remain in use for up to 60 yearsthat will remain in use for up to 60 yearsthat will remain in use for up to 60 years

© IEA Clean Coal Centre www.iea-coal.org.uk

PULVERISED COAL FOR POWER

What is State-of-the-Art and what are the prospects?

© IEA Clean Coal Centre www.iea-coal.org.uk

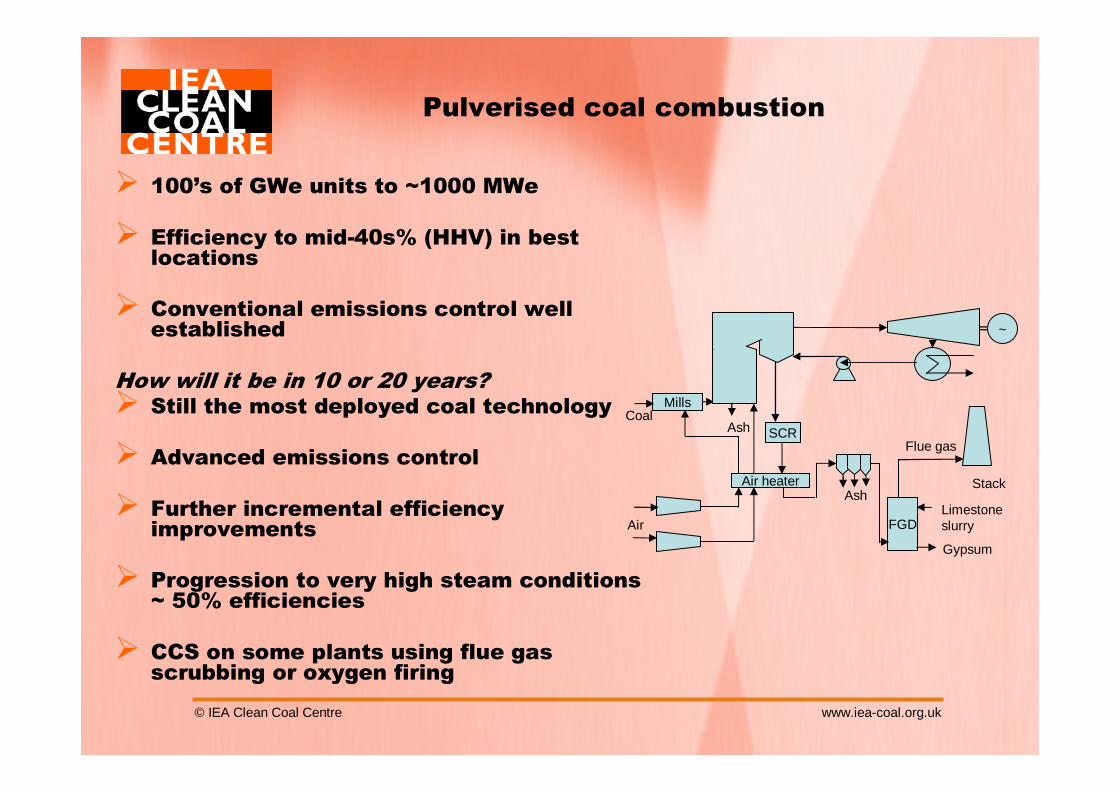

Pulverised coal combustion

� 100’s of GWe units to ~1000 MWe

� Efficiency to mid-40s% (HHV) in best locations

� Conventional emissions control well established

How will it be in 10 or 20 years?� Still the most deployed coal technology

� Advanced emissions control

� Further incremental efficiency improvements

� Progression to very high steam conditions ~ 50% efficiencies

� CCS on some plants using flue gas scrubbing or oxygen firing

~

Limestone slurry

Gypsum

Mills

Air heater

Ash

Air

Coal

AshStack

FGD

SCRFlue gas

© IEA Clean Coal Centre www.iea-coal.org.uk

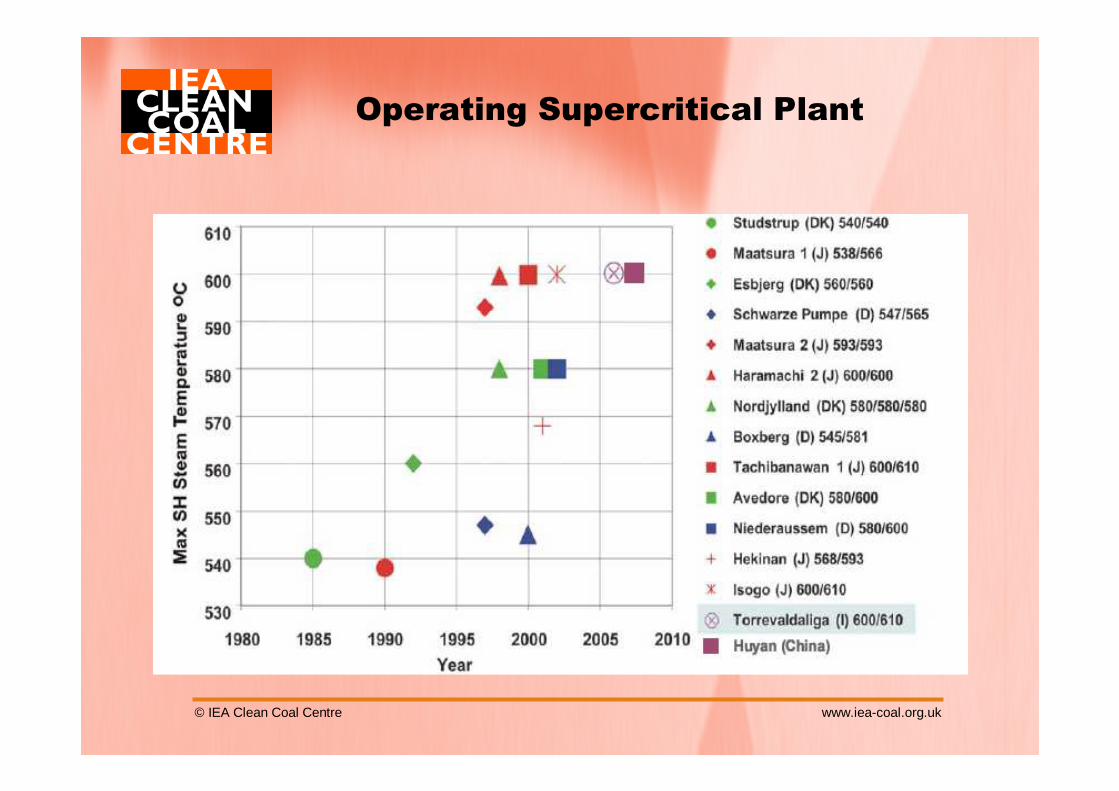

Operating Supercritical Plant

© IEA Clean Coal Centre www.iea-coal.org.uk

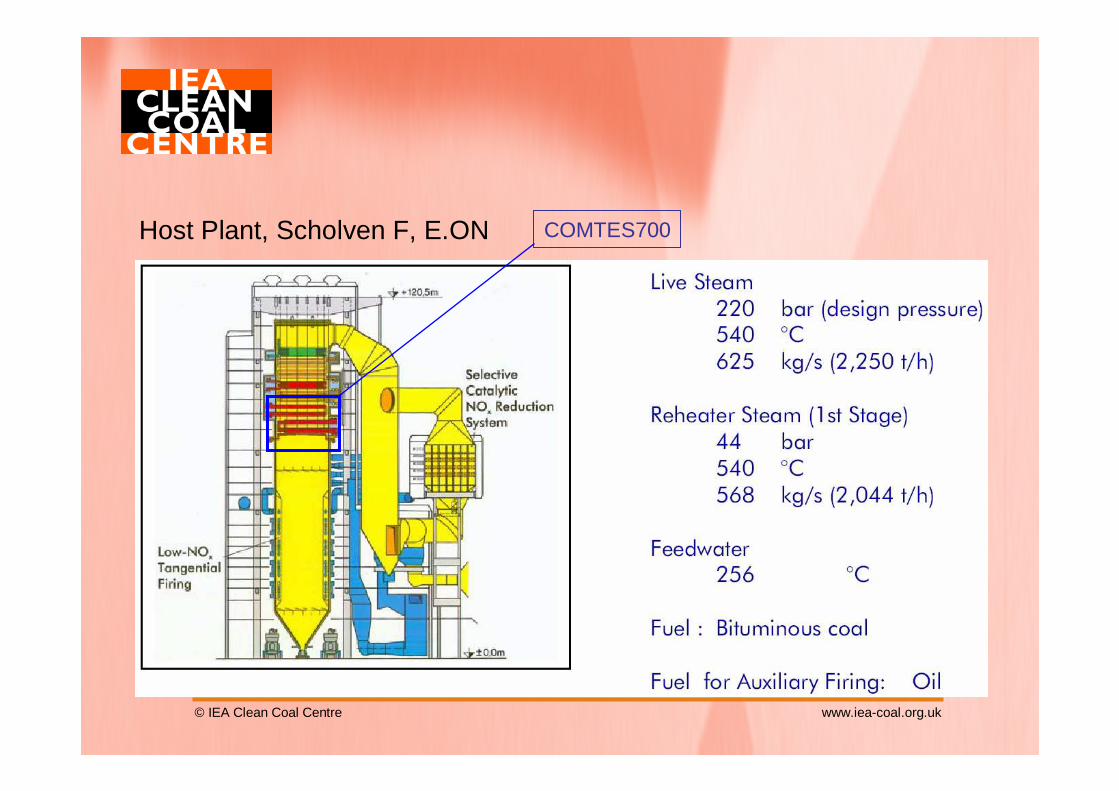

Host Plant, Scholven F, E.ON COMTES700

© IEA Clean Coal Centre www.iea-coal.org.uk

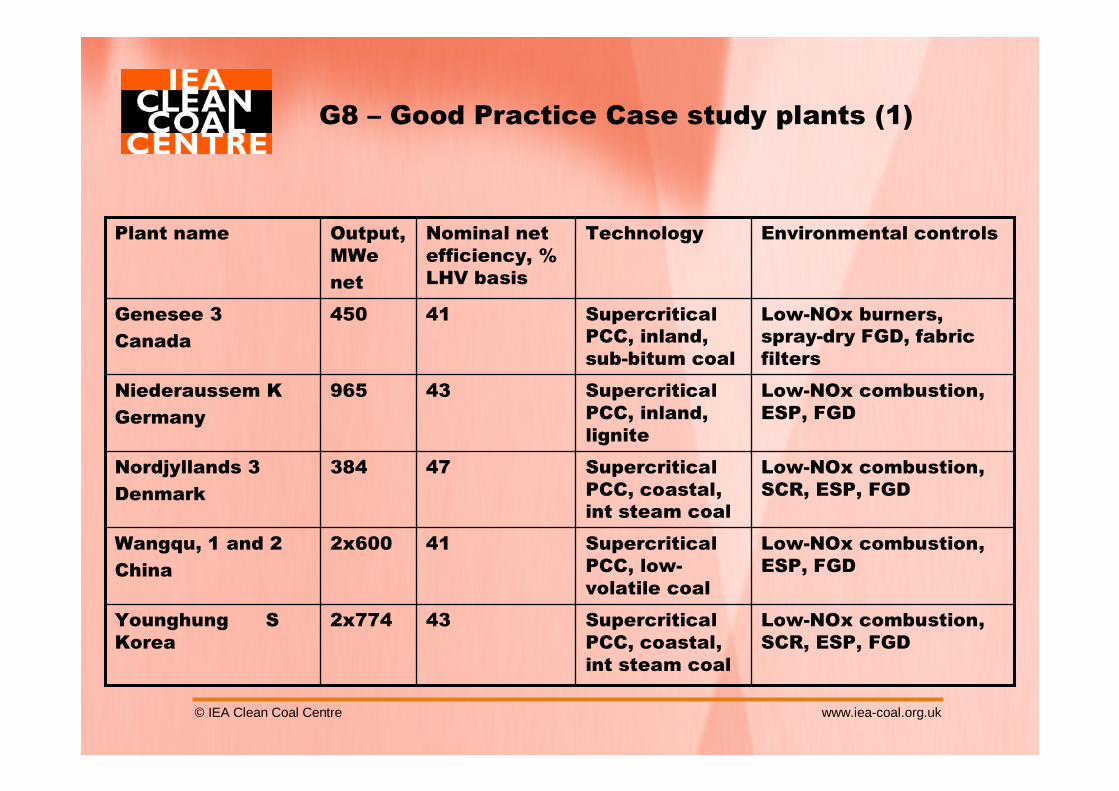

G8 – Good Practice Case study plants (1)

Low-NOx combustion, ESP, FGD

Supercritical PCC, inland, lignite

43965Niederaussem K

Germany

Low-NOx combustion, SCR, ESP, FGD

Supercritical PCC, coastal, int steam coal

432x774Younghung S Korea

Low-NOx combustion, ESP, FGD

Supercritical PCC, low-volatile coal

412x600Wangqu, 1 and 2

China

Low-NOx combustion, SCR, ESP, FGD

Supercritical PCC, coastal, int steam coal

47384Nordjyllands 3

Denmark

Low-NOx burners, spray-dry FGD, fabric filters

Supercritical PCC, inland, sub-bitum coal

41450Genesee 3

Canada

Environmental controlsTechnologyNominal net efficiency, % LHV basis

Output, MWe

net

Plant name

© IEA Clean Coal Centre www.iea-coal.org.uk

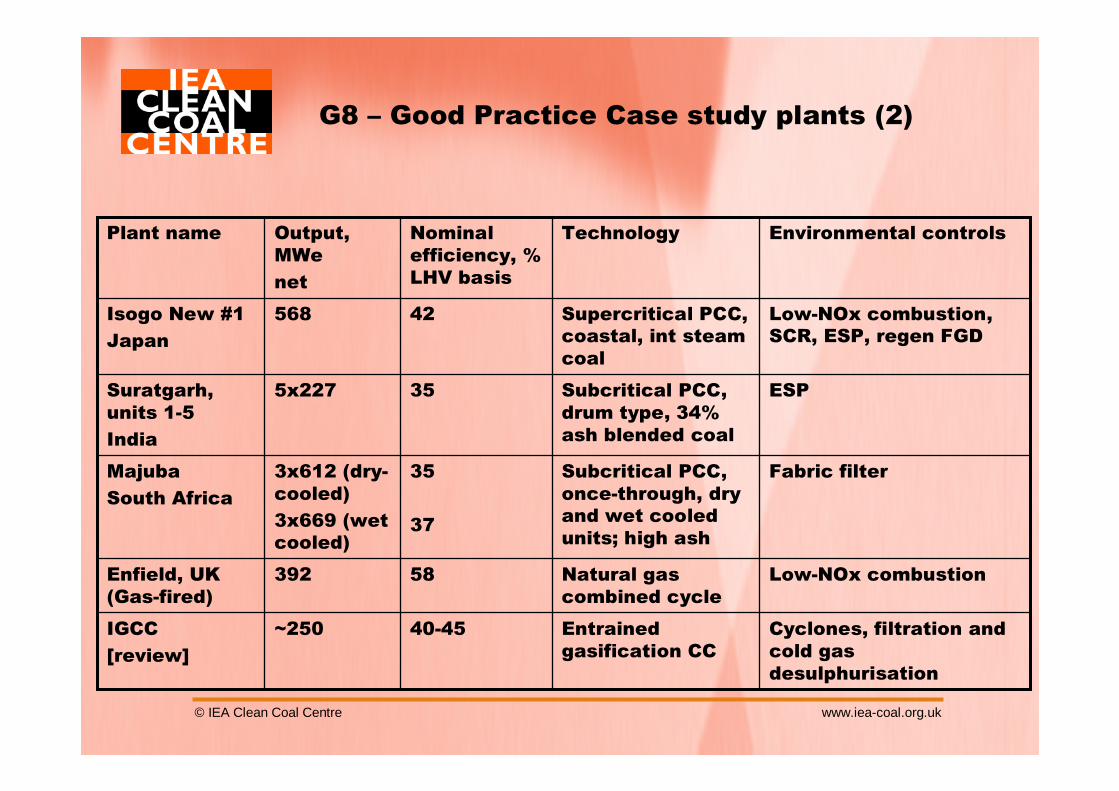

G8 – Good Practice Case study plants (2)

Cyclones, filtration and cold gas desulphurisation

Entrained gasification CC

40-45~250IGCC

[review]

Low-NOx combustionNatural gas combined cycle

58392Enfield, UK (Gas-fired)

Fabric filterSubcritical PCC, once-through, dry and wet cooled units; high ash

35

37

3x612 (dry-cooled)

3x669 (wet cooled)

Majuba

South Africa

ESPSubcritical PCC, drum type, 34% ash blended coal

355x227Suratgarh, units 1-5

India

Low-NOx combustion, SCR, ESP, regen FGD

Supercritical PCC, coastal, int steam coal

42568Isogo New #1

Japan

Environmental controlsTechnologyNominal efficiency, % LHV basis

Output, MWe

net

Plant name

© IEA Clean Coal Centre www.iea-coal.org.uk

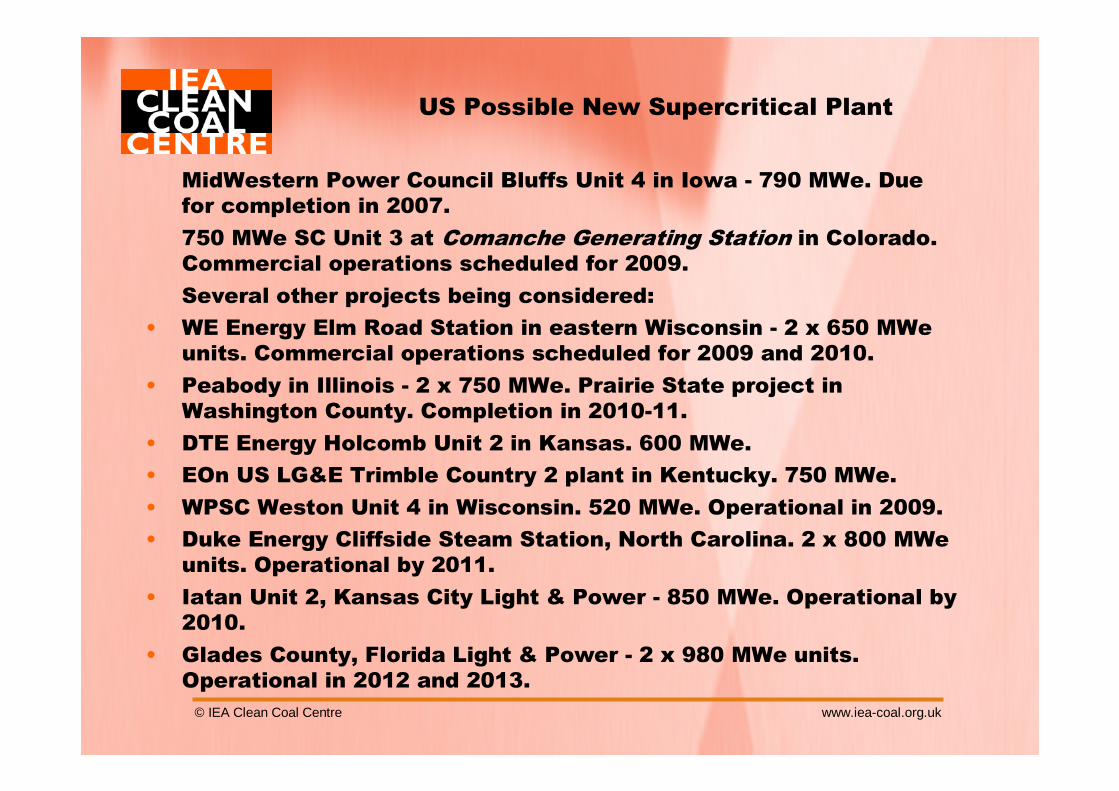

US Possible New Supercritical Plant

MidWestern Power Council Bluffs Unit 4 in Iowa - 790 MWe. Due for completion in 2007.

750 MWe SC Unit 3 at Comanche Generating Station in Colorado. Commercial operations scheduled for 2009.

Several other projects being considered:

• WE Energy Elm Road Station in eastern Wisconsin - 2 x 650 MWeunits. Commercial operations scheduled for 2009 and 2010.

• Peabody in Illinois - 2 x 750 MWe. Prairie State project in Washington County. Completion in 2010-11.

• DTE Energy Holcomb Unit 2 in Kansas. 600 MWe.

• EOn US LG&E Trimble Country 2 plant in Kentucky. 750 MWe.

• WPSC Weston Unit 4 in Wisconsin. 520 MWe. Operational in 2009.

• Duke Energy Cliffside Steam Station, North Carolina. 2 x 800 MWeunits. Operational by 2011.

• Iatan Unit 2, Kansas City Light & Power - 850 MWe. Operational by 2010.

• Glades County, Florida Light & Power - 2 x 980 MWe units. Operational in 2012 and 2013.

© IEA Clean Coal Centre www.iea-coal.org.uk

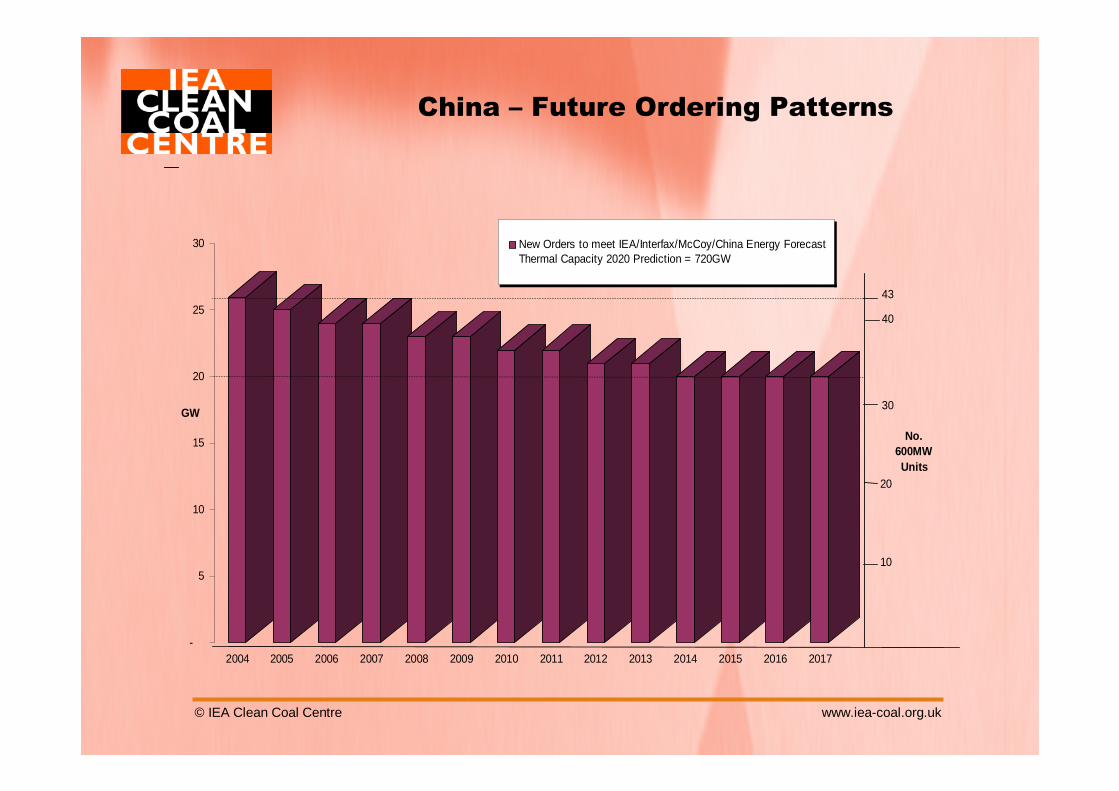

China – Future Ordering Patterns

-

5

10

15

20

25

30

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

New Orders to meet IEA/Interfax/McCoy/China Energy ForecastThermal Capacity 2020 Prediction = 720GW

GW

10

20

30

40

43

No.600MWUnits

© IEA Clean Coal Centre www.iea-coal.org.uk

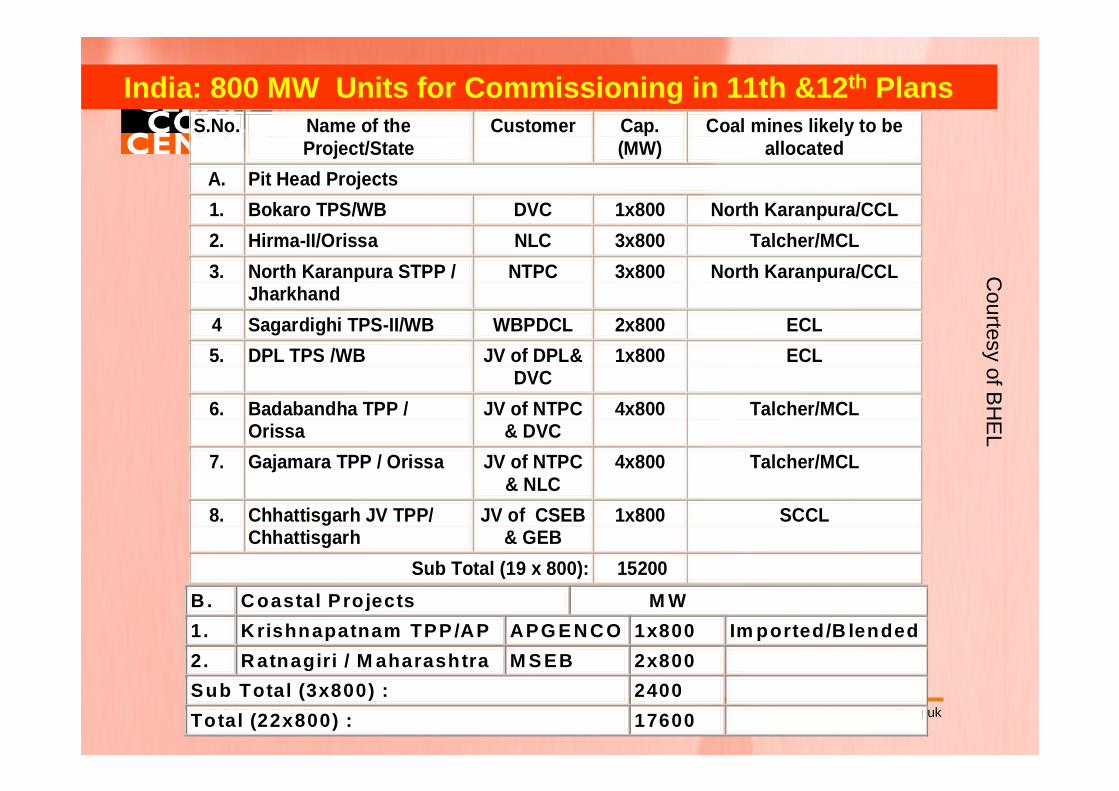

S.No. Name of the Project/State

Customer Cap. (MW)

Coal mines likely to be allocated

A. Pit Head Projects

1. Bokaro TPS/WB DVC 1x800 North Karanpura/CCL

2. Hirma-II/Orissa NLC 3x800 Talcher/MCL

3. North Karanpura STPP / Jharkhand

NTPC 3x800 North Karanpura/CCL

4 Sagardighi TPS-II/WB WBPDCL 2x800 ECL

5. DPL TPS /WB JV of DPL& DVC

1x800 ECL

6. Badabandha TPP / Orissa

JV of NTPC & DVC

4x800 Talcher/MCL

7. Gajamara TPP / Orissa JV of NTPC & NLC

4x800 Talcher/MCL

8. Chhattisgarh JV TPP/ Chhattisgarh

JV of CSEB & GEB

1x800 SCCL

Sub Total (19 x 800): 15200

India: 800 MW Units for Commissioning in 11th &12 th PlansC

ourtesy of BH

EL

B . C oastal P ro jects M W

1. K rishnapatnam TPP /AP APG E N C O 1x800 Im ported/B lended

2. R atnagiri / M aharashtra M S EB 2x800

Sub Total (3x800) : 2400

Total (22x800) : 17600

© IEA Clean Coal Centre www.iea-coal.org.uk

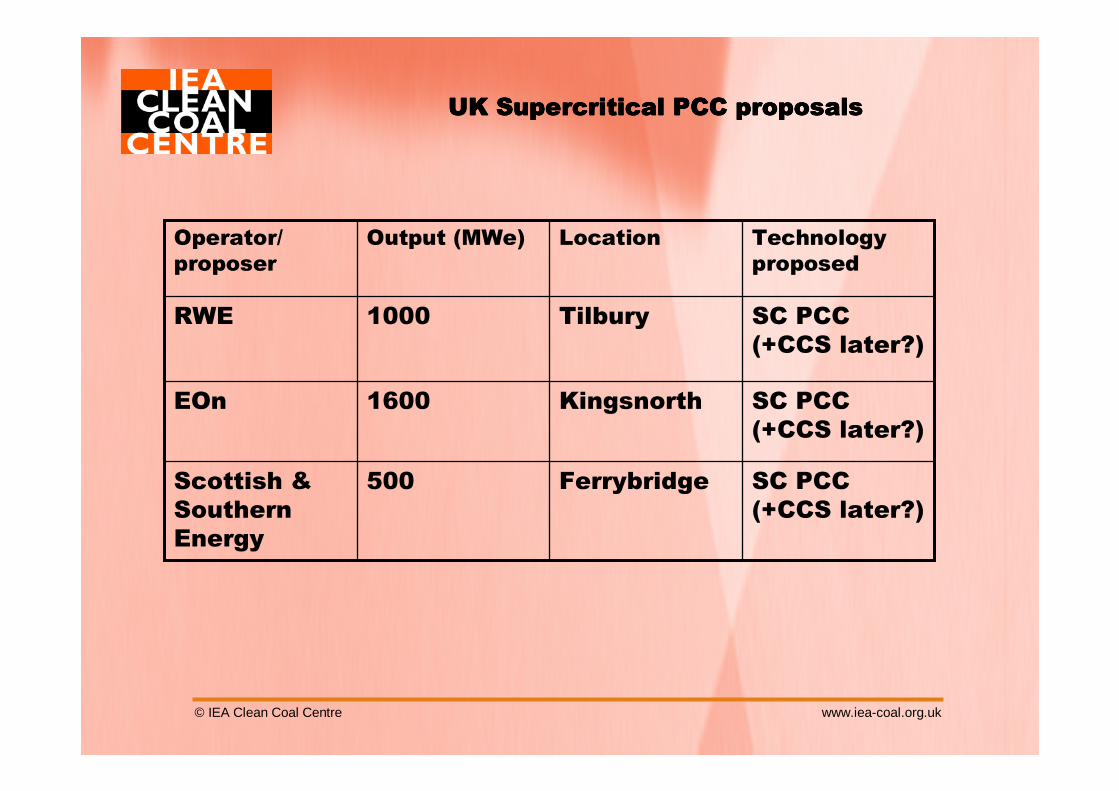

UK Supercritical PCC proposalsUK Supercritical PCC proposalsUK Supercritical PCC proposalsUK Supercritical PCC proposals

Technology proposed

LocationOutput (MWe)Operator/ proposer

SC PCC (+CCS later?)

Ferrybridge500Scottish & Southern Energy

SC PCC (+CCS later?)

Kingsnorth1600EOn

SC PCC (+CCS later?)

Tilbury1000RWE

© IEA Clean Coal Centre www.iea-coal.org.uk

Lagisza Supercritical CFBC – new design

• The world’s first CFBC unit with supercritical steam conditions

• Largest CFBC; 460 MWe

• Start-up in 2009

• Emissions of SOx, NOxand particulates lower than required by latest EU LCPD limits.

• Located to NE of Katowice, Poland

© IEA Clean Coal Centre www.iea-coal.org.uk

TOWARDS ZERO EMISSIONS

© IEA Clean Coal Centre www.iea-coal.org.uk

CarbonReduction

Time

`IncreasedEfficiency`Trajectory

`Zero Emissions`Trajectory

Near-term Mid-term Long-term

Zero emissions will need the most efficient plant

Key issue will be value of CO2

Carbon Abatement Technology Options are complementary

© IEA Clean Coal Centre www.iea-coal.org.uk

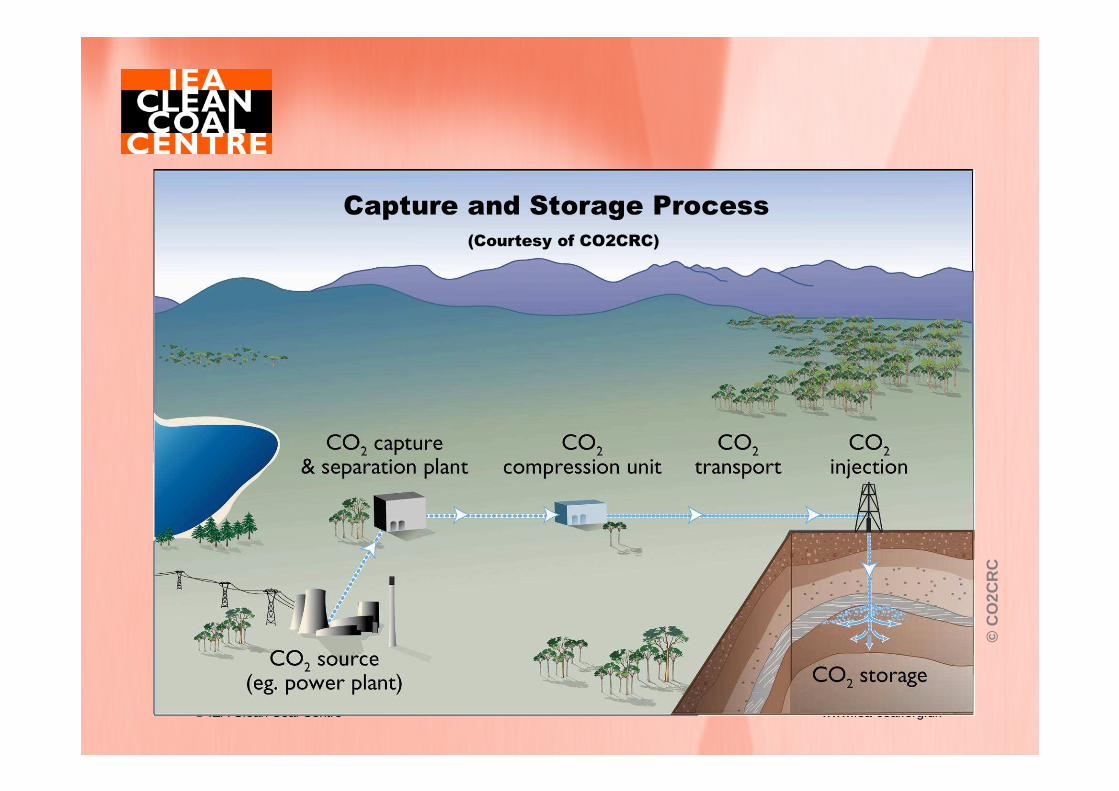

©C

O2C

RC

Capture and Storage Process(Courtesy of CO2CRC)

© IEA Clean Coal Centre www.iea-coal.org.uk

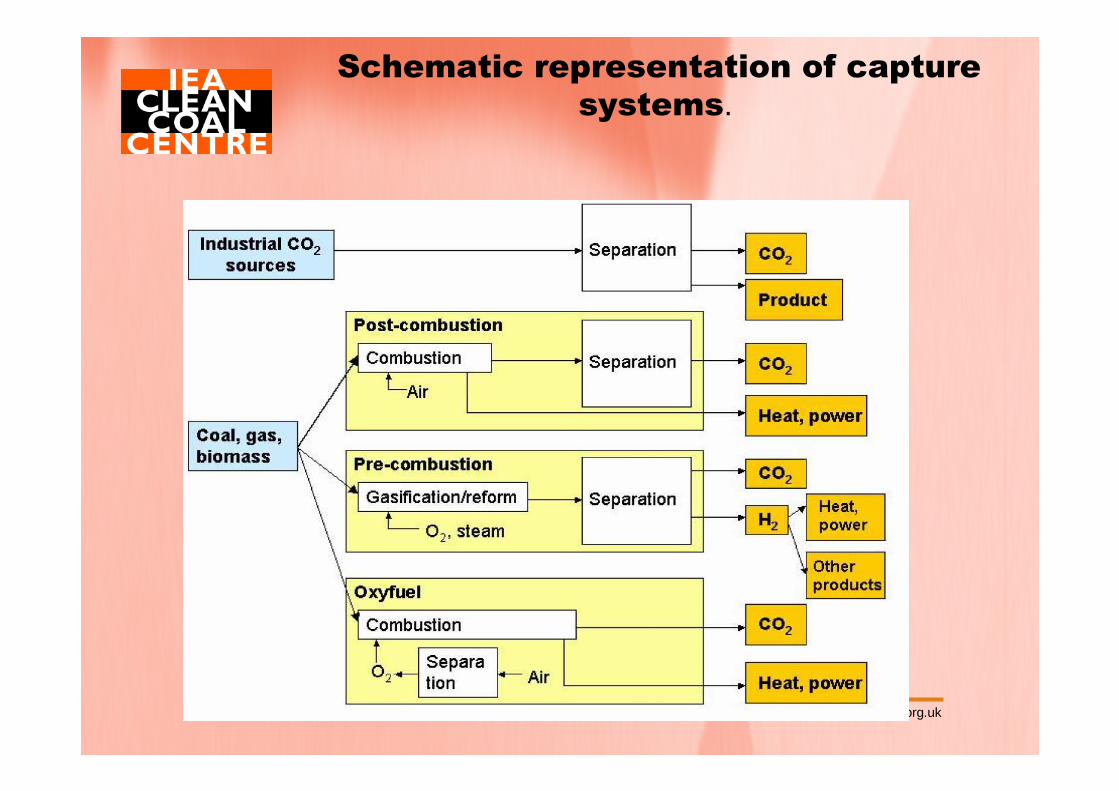

Schematic representation of capture systems.

© IEA Clean Coal Centre www.iea-coal.org.uk

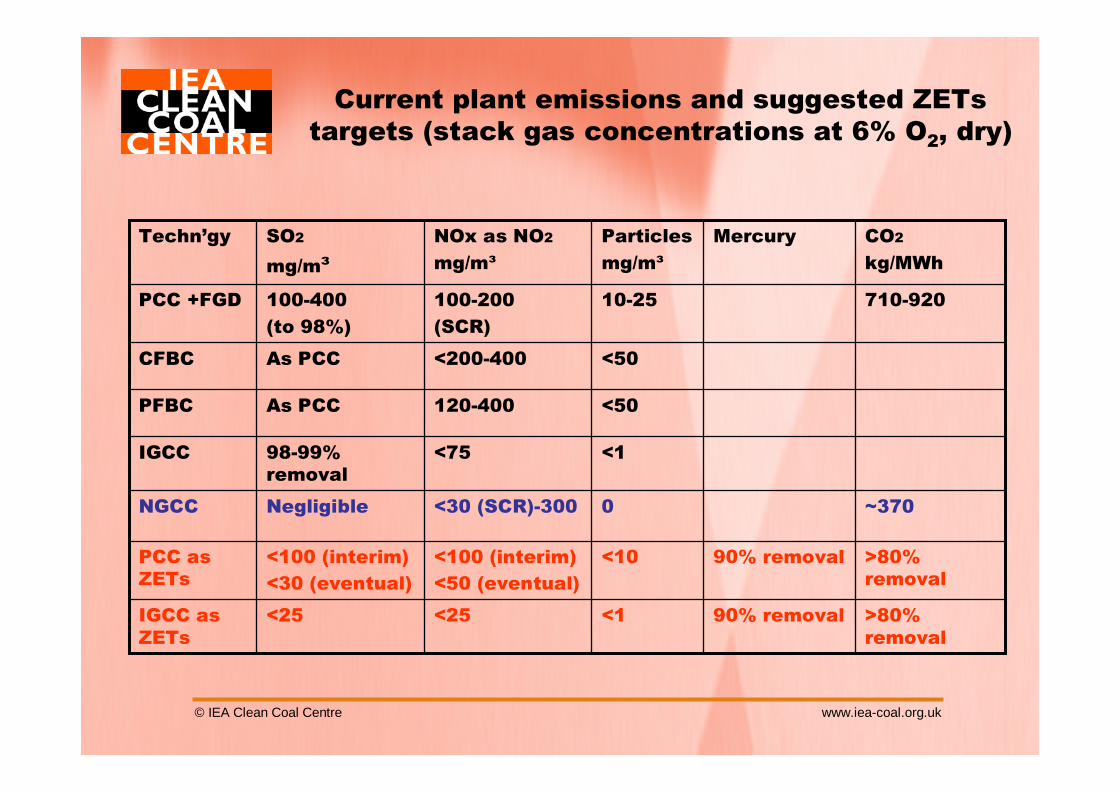

Current plant emissions and suggested ZETstargets (stack gas concentrations at 6% O2, dry)

>80% removal

90% removal<1<25<25IGCC as ZETs

>80% removal

90% removal<10<100 (interim)

<50 (eventual)

<100 (interim)

<30 (eventual)

PCC as ZETs

~3700<30 (SCR)-300NegligibleNGCC

<1<7598-99% removal

IGCC

<50120-400As PCCPFBC

<50<200-400As PCCCFBC

710-92010-25100-200

(SCR)

100-400

(to 98%)

PCC +FGD

CO2

kg/MWh

MercuryParticles

mg/m³

NOx as NO2

mg/m³

SO2

mg/m³

Techn’gy

© IEA Clean Coal Centre www.iea-coal.org.uk

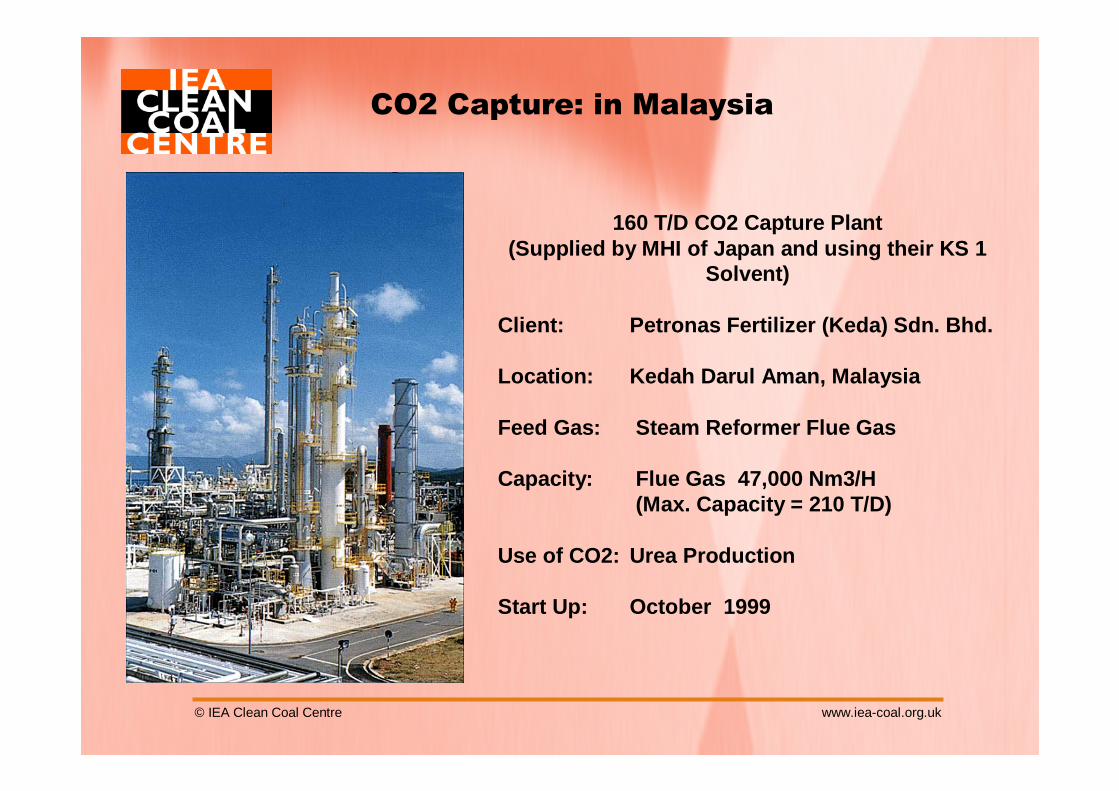

160 T/D CO2 Capture Plant(Supplied by MHI of Japan and using their KS 1

Solvent)

Client: Petronas Fertilizer (Keda) Sdn. Bhd.

Location: Kedah Darul Aman, Malaysia

Feed Gas: Steam Reformer Flue Gas

Capacity: Flue Gas 47,000 Nm3/H(Max. Capacity = 210 T/D)

Use of CO2: Urea Production

Start Up: October 1999

CO2 Capture: in Malaysia

© IEA Clean Coal Centre www.iea-coal.org.uk

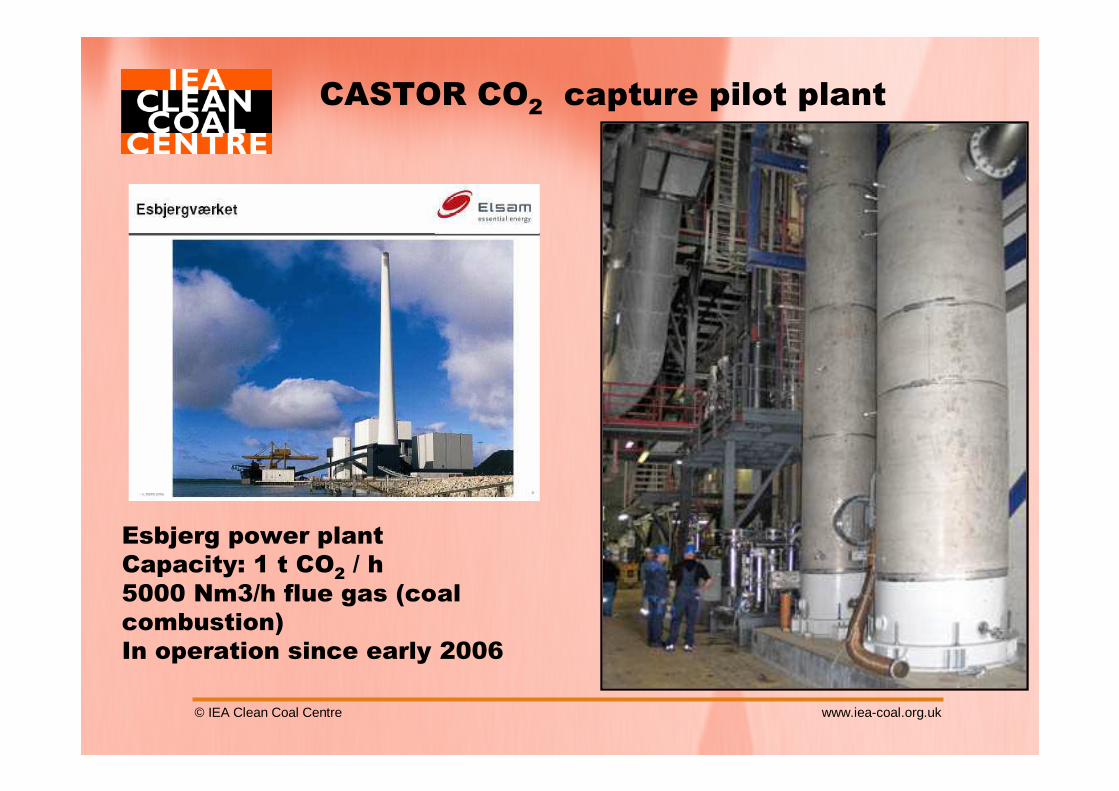

CASTOR CO2 capture pilot plant

Esbjerg power plantCapacity: 1 t CO2 / h5000 Nm3/h flue gas (coal combustion)In operation since early 2006

© IEA Clean Coal Centre www.iea-coal.org.uk

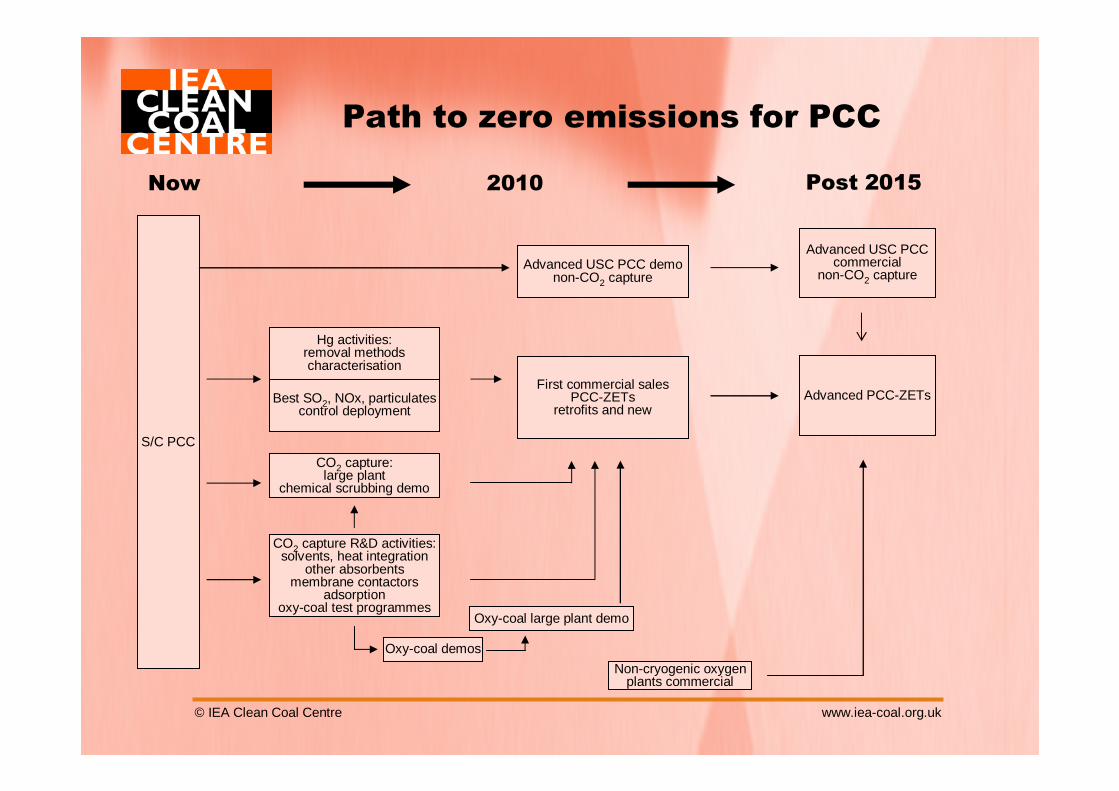

Path to zero emissions for PCC

S/C PCC

Hg activities:removal methodscharacterisation

First commercial salesPCC-ZETs

retrofits and newAdvanced PCC-ZETsBest SO2, NOx, particulates

control deployment

CO2 capture:large plant

chemical scrubbing demo

CO2 capture R&D activities:solvents, heat integration

other absorbentsmembrane contactors

adsorptionoxy-coal test programmes

Advanced USC PCC demonon-CO2 capture

Advanced USC PCCcommercial

non-CO2 capture

Non-cryogenic oxygenplants commercial

Oxy-coal demos

Oxy-coal large plant demo

Post 2015Now 2010

www.ieagreen.org.uk

COCO22 Capture Ready PlantCapture Ready Plant

• A plant which can include CO2 capture when the necessary regulatory or economic drivers are in place

• Avoids the risk of stranded assets and ‘carbon lock-in’

• Developers must eliminate factors which would prevent installation and operation of CO2 capture

• This might include• A study of options for capture retrofit

• Include sufficient space and access for additional facilities

• Identify reasonable route(s) to storage of CO2

www.ieagreen.org.uk

COCO22 Capture Ready PlantCapture Ready Plant

• Some pre-investments could be made to reduce the future cost of capture retrofit• For example, oversizing equipment

• Factors to take into account when considering pre-investment• Uncertainty about if or when capture would be retrofitted• Uncertainty about developments in capture technology

and the optimum technology in future• Economic discounting reduces the value of future cost

savings

© IEA Clean Coal Centre www.iea-coal.org.uk

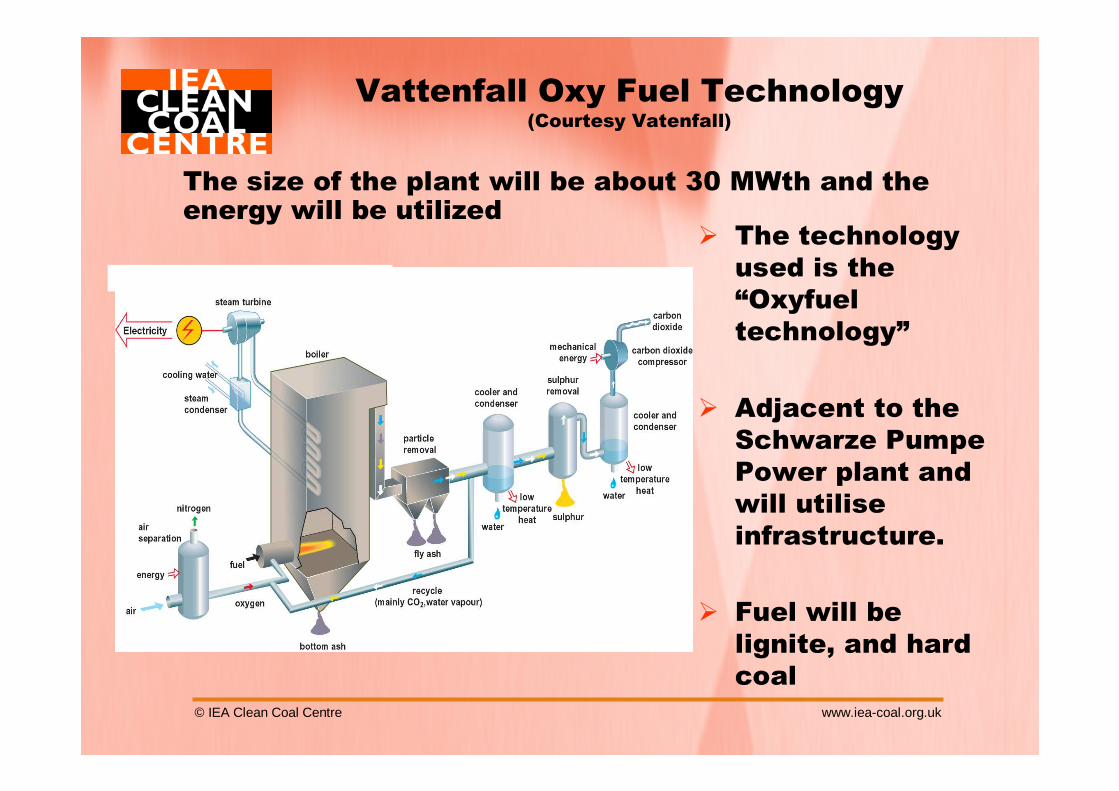

Vattenfall Oxy Fuel Technology(Courtesy Vatenfall)

The size of the plant will be about 30 MWth and the energy will be utilized

� The technology used is the “Oxyfuel technology”

� Adjacent to the Schwarze PumpePower plant and will utiliseinfrastructure.

� Fuel will be lignite, and hard coal

© IEA Clean Coal Centre www.iea-coal.org.uk

Callide A Callide A Callide A Callide A –––– Queensland, AustraliaQueensland, AustraliaQueensland, AustraliaQueensland, Australia

Courtesy of CS Energy

This project will be supported by LETDF

© IEA Clean Coal Centre www.iea-coal.org.uk

Pilot-scale oxy fuel testing by IHI at Aioi (Japan)

Test facility:

– Capacity 1.2 MWt (~ 150 kg coal/h)– Furnace size – 1.3m dia x 7.5 m

Objectives:

– Compare air- vs oxy-firing combustion and emissions– Additional validation of Callide A boiler model– Investor confidence– Ash samples for other CCSD Projects

Status:

– Callide & Acland coals tested in Sep. 05– Rolleston coal to be tested in Dec. 05

Measurements:– Burnout and temperature profiles– Ash deposition tares– Emissions including Hg– Turn-down effects– Fly ash for characterization

© IEA Clean Coal Centre www.iea-coal.org.uk

SaskPower’s 300MWe oxyfuel plant

© IEA Clean Coal Centre www.iea-coal.org.uk

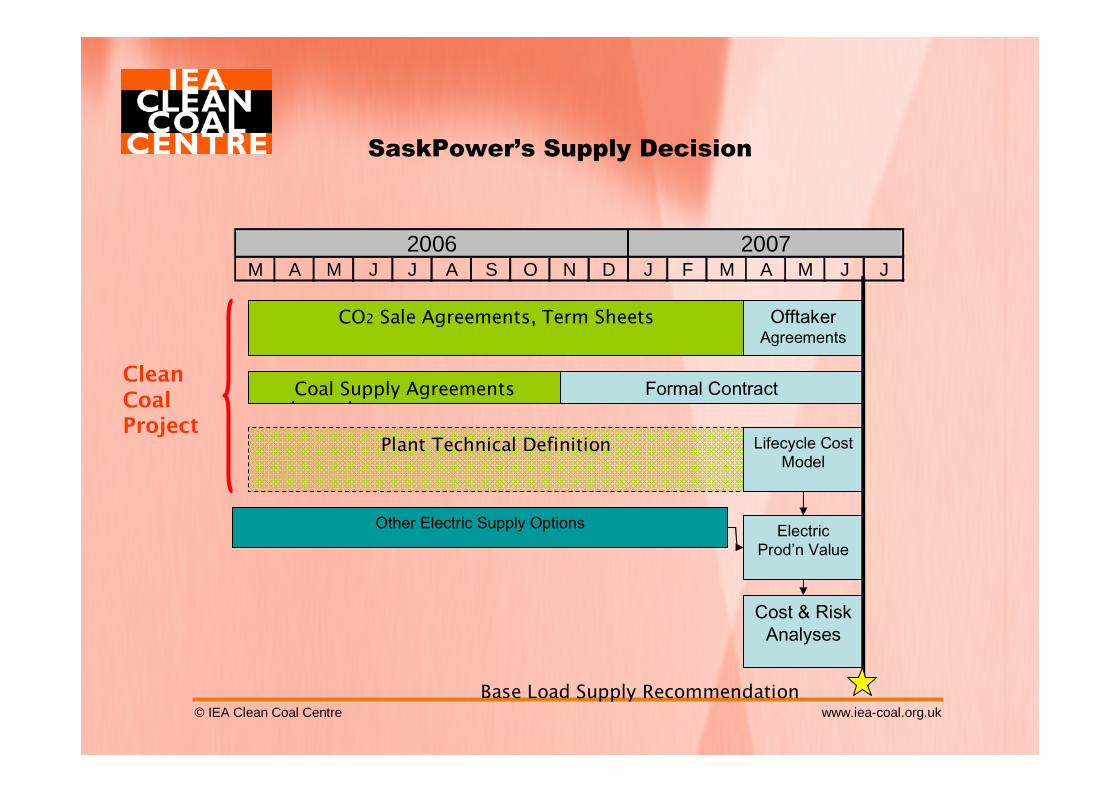

SaskPower’s Supply Decision

M A M J J A S O N D J F M A M J J2006 2007

Cost & Risk Analyses

Electric Prod’n Value

Lifecycle Cost Model

CO2 Sale Agreements, Term Sheets Offtaker Agreements

Coal Supply Agreements Formal Contract

Other Electric Supply Options

Plant Technical Definition

Base Load Supply Recommendation

Clean Coal Project

© IEA Clean Coal Centre www.iea-coal.org.uk

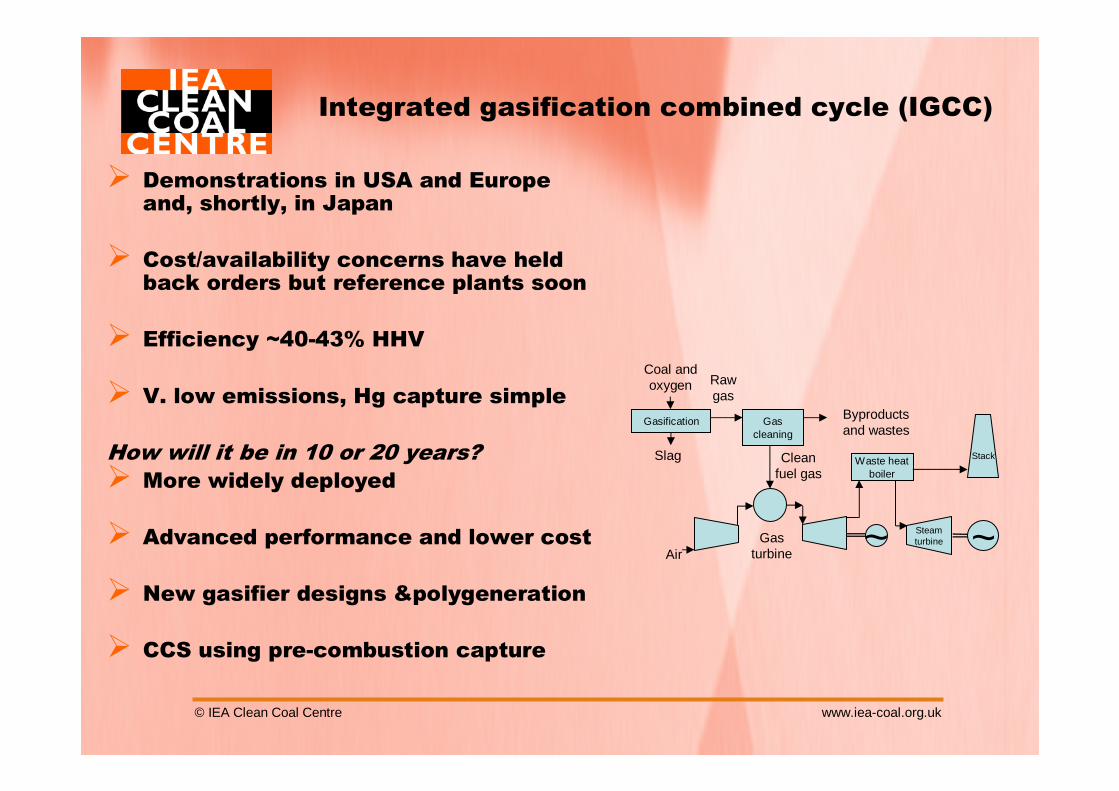

Integrated gasification combined cycle (IGCC)

� Demonstrations in USA and Europe and, shortly, in Japan

� Cost/availability concerns have held back orders but reference plants soon

� Efficiency ~40-43% HHV

� V. low emissions, Hg capture simple

How will it be in 10 or 20 years?

� More widely deployed

� Advanced performance and lower cost

� New gasifier designs &polygeneration

� CCS using pre-combustion capture

Gasification

Coal and oxygen Raw

gas

Clean fuel gas

~Gas turbine

Waste heatboiler

Stack

Steamturbine ~

Byproductsand wastes

Slag

Air

Gas cleaning

© IEA Clean Coal Centre www.iea-coal.org.uk

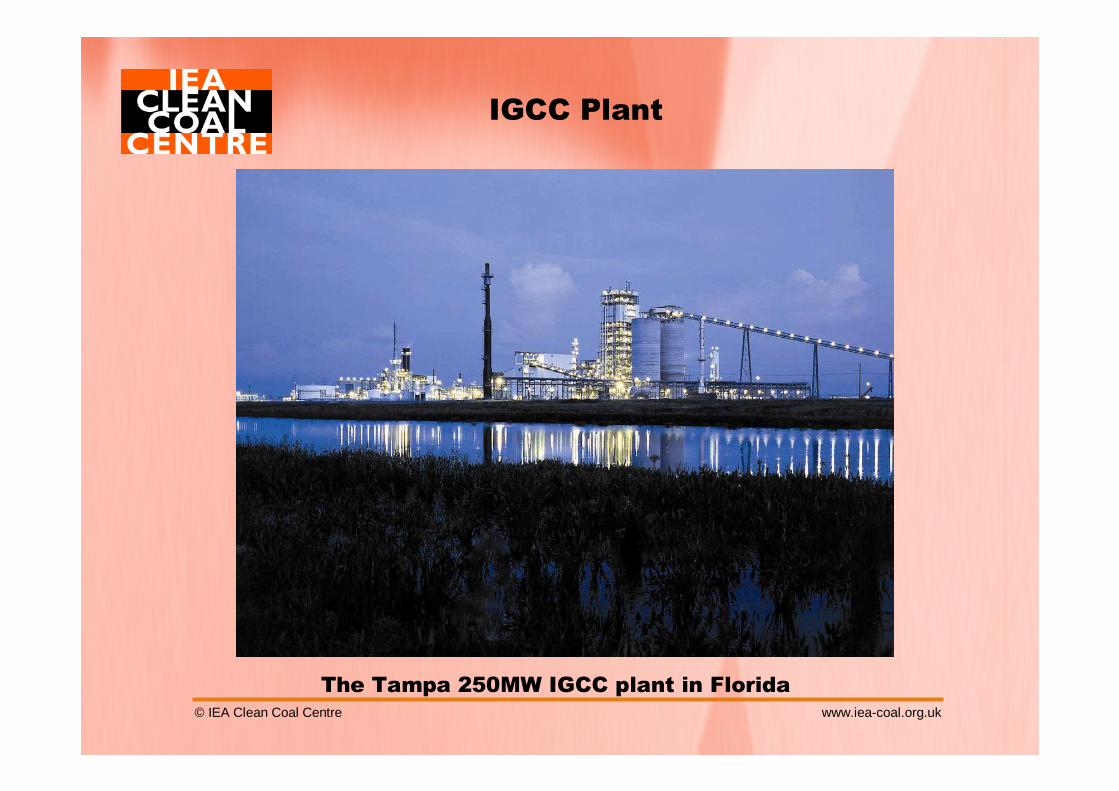

IGCC Plant

The Tampa 250MW IGCC plant in Florida

© IEA Clean Coal Centre www.iea-coal.org.uk

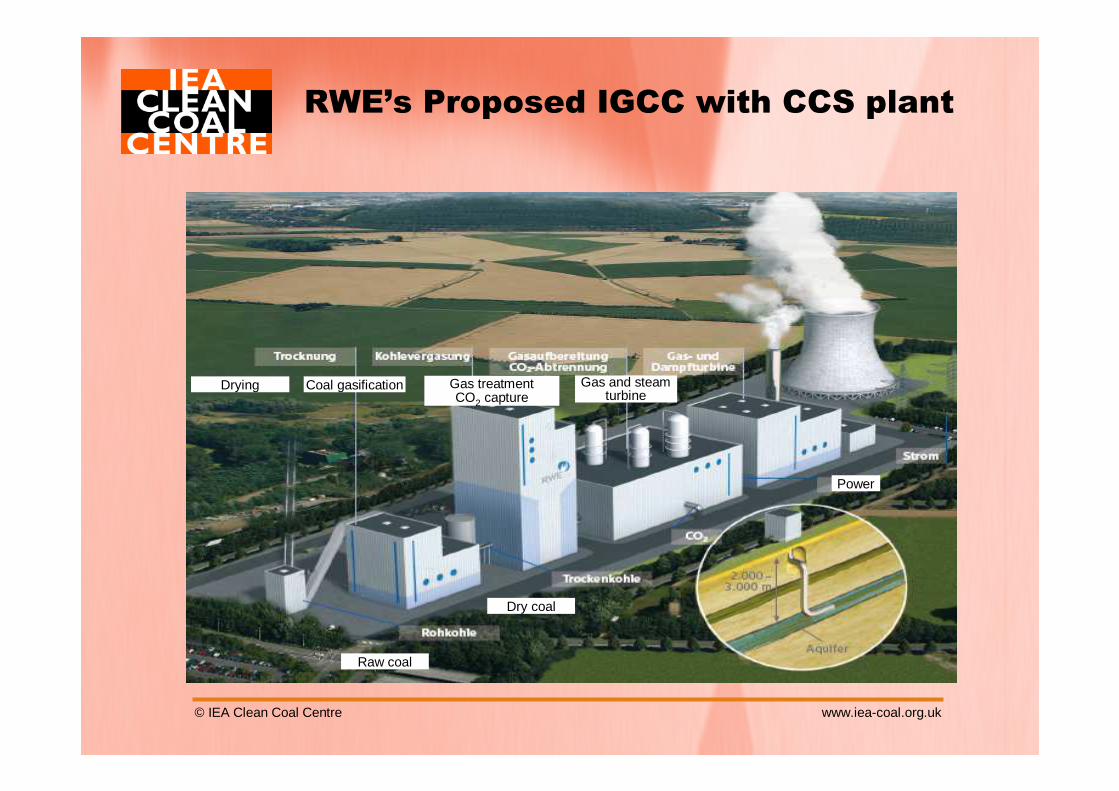

RWE’s Proposed IGCC with CCS plant

Drying Coal gasification Gas treatmentCO2 capture

Gas and steamturbine

Power

Dry coal

Raw coal

© IEA Clean Coal Centre www.iea-coal.org.uk

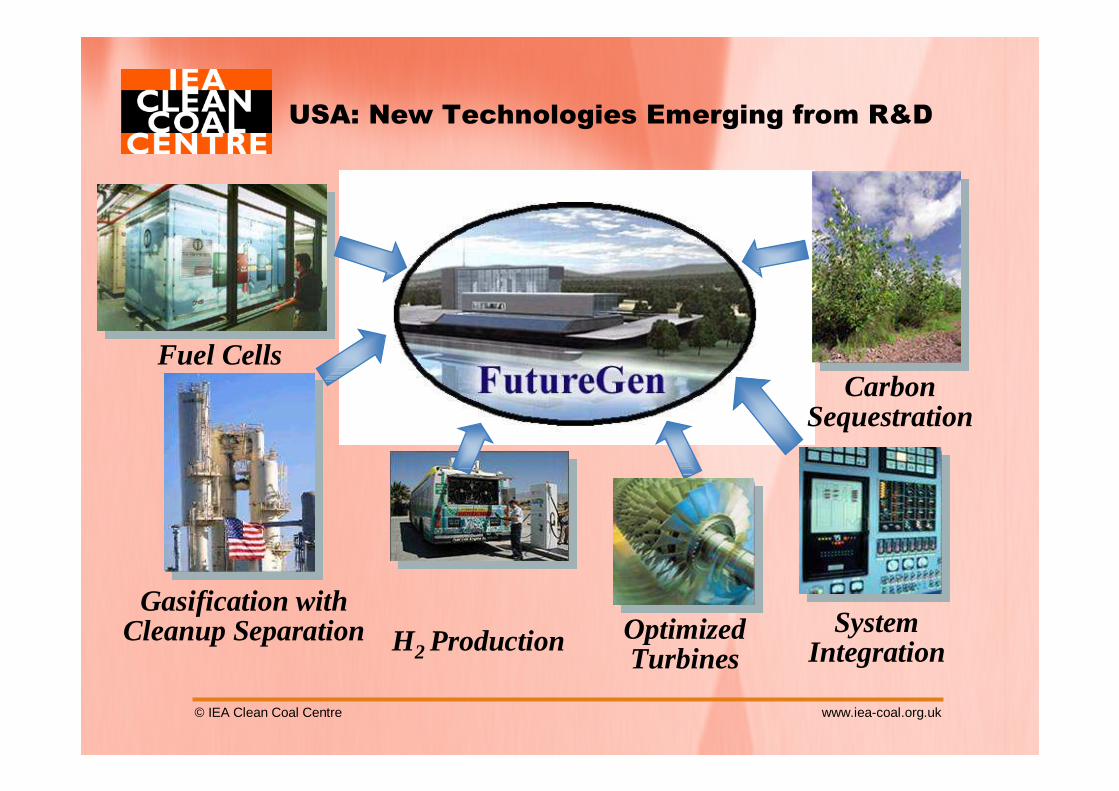

Gasification with Cleanup Separation System

Integration

CarbonSequestration

USA: New Technologies Emerging from R&D

Optimized Turbines

Fuel Cells

H2 Production

© IEA Clean Coal Centre www.iea-coal.org.uk

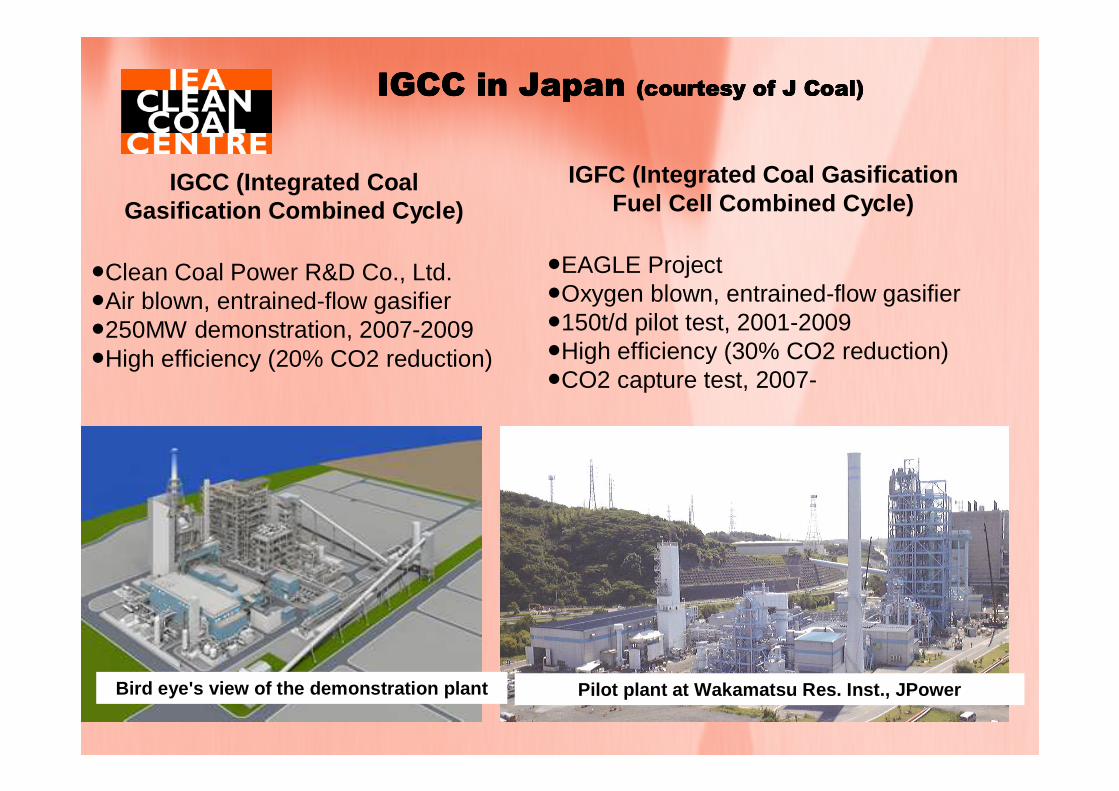

IGCC in Japan IGCC in Japan IGCC in Japan IGCC in Japan (courtesy of J Coal)(courtesy of J Coal)(courtesy of J Coal)(courtesy of J Coal)

IGCC (Integrated Coal Gasification Combined Cycle)

IGFC (Integrated Coal Gasification Fuel Cell Combined Cycle)

●EAGLE Project●Oxygen blown, entrained-flow gasifier●150t/d pilot test, 2001-2009●High efficiency (30% CO2 reduction)●CO2 capture test, 2007-

●Clean Coal Power R&D Co., Ltd.●Air blown, entrained-flow gasifier●250MW demonstration, 2007-2009●High efficiency (20% CO2 reduction)

Bird eye's view of the demonstration plant Pilot plant at Wakamatsu Res. Inst., JPower

© IEA Clean Coal Centre www.iea-coal.org.uk

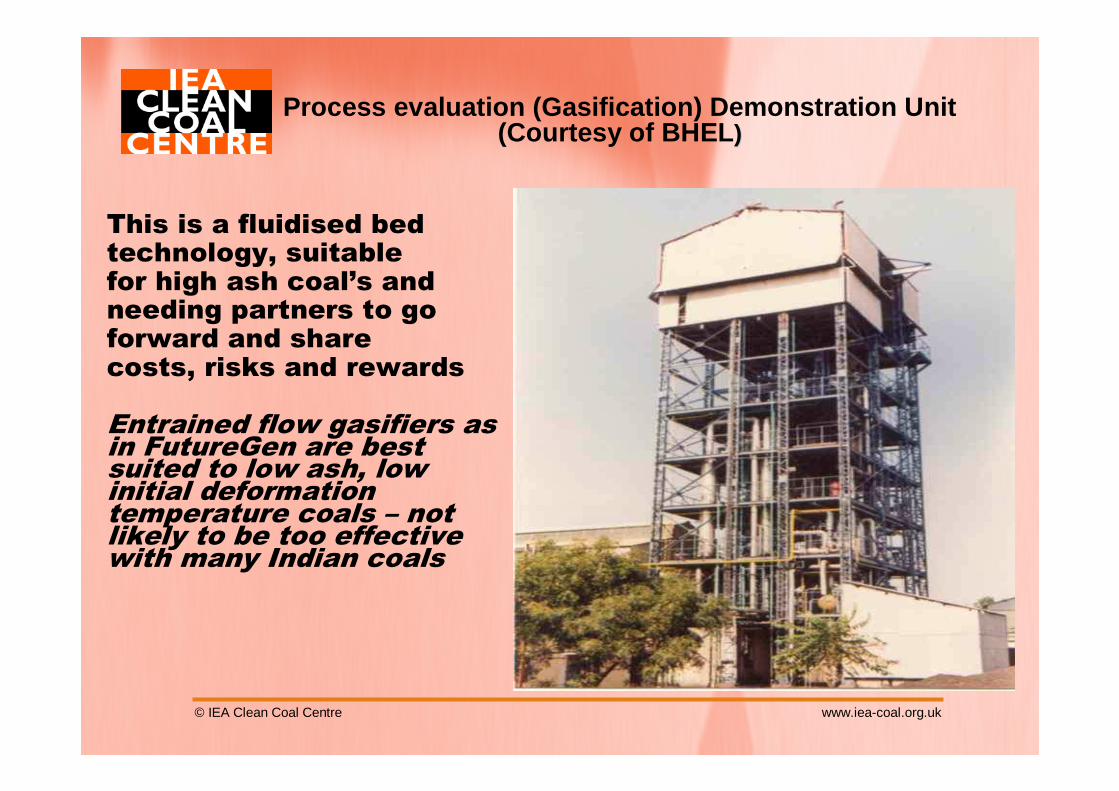

This is a fluidised bed technology, suitable for high ash coal’s and needing partners to goforward and share costs, risks and rewards

Entrained flow gasifiers as in FutureGen are best suited to low ash, low initial deformation temperature coals – not likely to be too effective with many Indian coals

Process evaluation (Gasification) Demonstration Uni t (Courtesy of BHEL ))

© IEA Clean Coal Centre www.iea-coal.org.uk

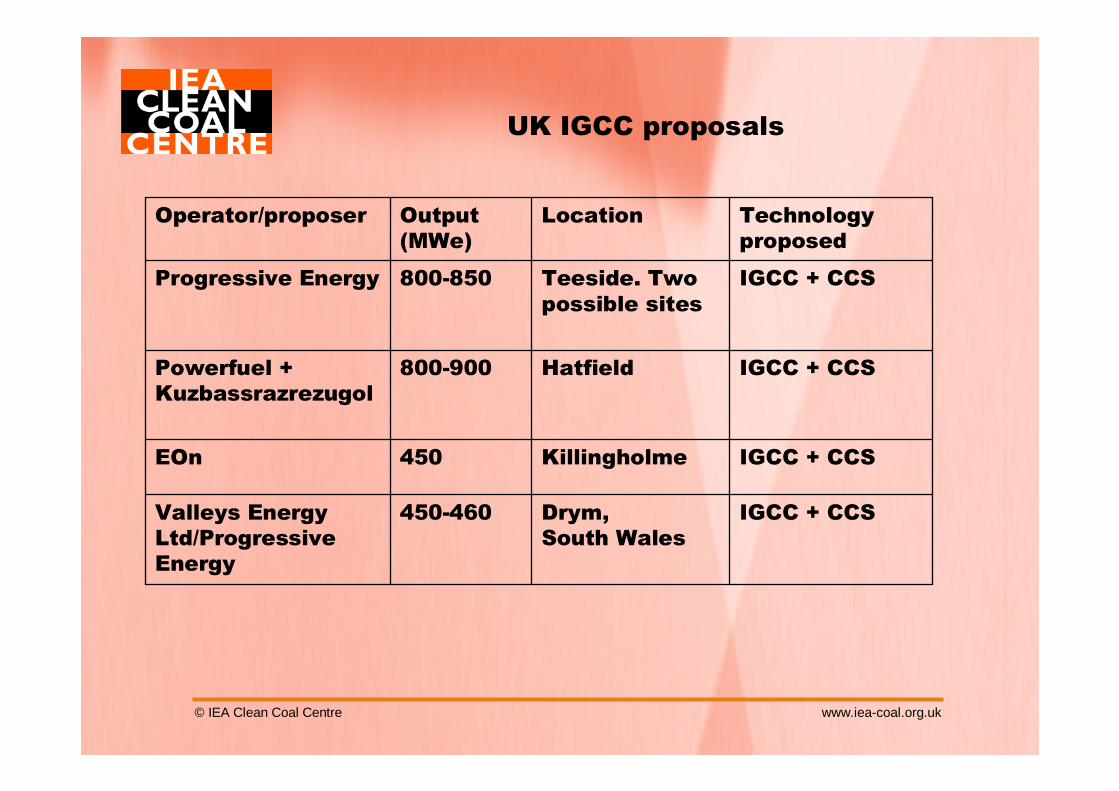

UK IGCC proposals

IGCC + CCSDrym, South Wales

450-460Valleys Energy Ltd/Progressive Energy

IGCC + CCSKillingholme450EOn

IGCC + CCSHatfield800-900Powerfuel + Kuzbassrazrezugol

IGCC + CCSTeeside. Two possible sites

800-850Progressive Energy

Technology proposed

LocationOutput (MWe)

Operator/proposer

© IEA Clean Coal Centre www.iea-coal.org.uk

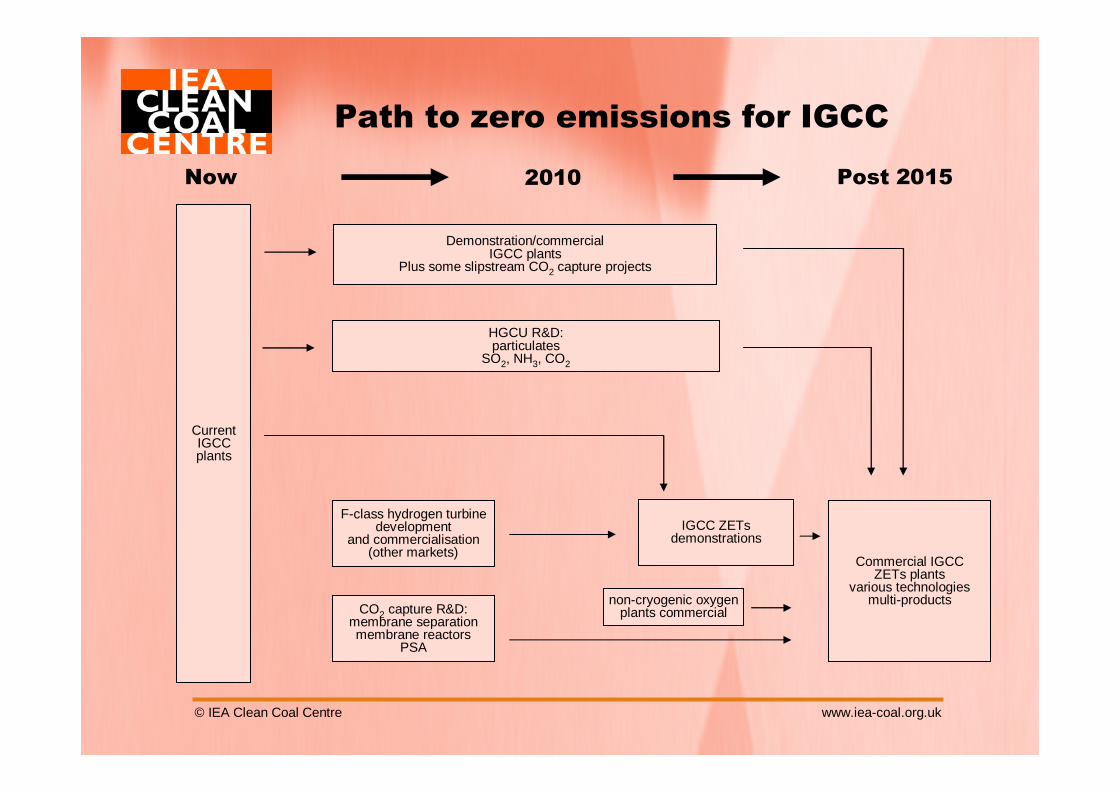

Path to zero emissions for IGCC

CurrentIGCCplants

IGCC ZETsdemonstrations

Commercial IGCCZETs plants

various technologiesmulti-productsnon-cryogenic oxygen

plants commercialCO2 capture R&D:membrane separationmembrane reactors

PSA

HGCU R&D:particulates

SO2, NH3, CO2

Demonstration/commercialIGCC plants

Plus some slipstream CO2 capture projects

F-class hydrogen turbinedevelopment

and commercialisation(other markets)

Post 2015Now 2010

© IEA Clean Coal Centre www.iea-coal.org.uk

CAPITAL COSTS, POWER COSTS & EFFICIENCIES

© IEA Clean Coal Centre www.iea-coal.org.uk

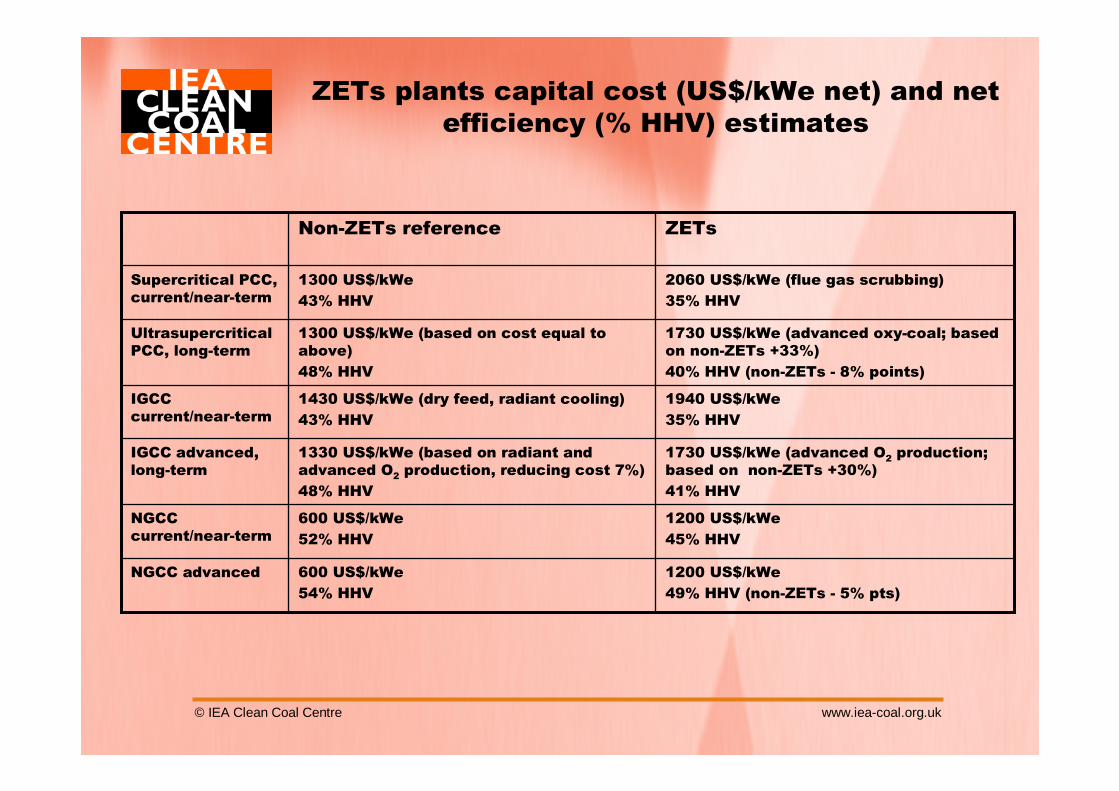

1200 US$/kWe

49% HHV (non-ZETs - 5% pts)

600 US$/kWe

54% HHV

NGCC advanced

1200 US$/kWe

45% HHV

600 US$/kWe

52% HHV

NGCC current/near-term

1730 US$/kWe (advanced O2 production; based on non-ZETs +30%)

41% HHV

1330 US$/kWe (based on radiant and advanced O2 production, reducing cost 7%)

48% HHV

IGCC advanced, long-term

1940 US$/kWe

35% HHV

1430 US$/kWe (dry feed, radiant cooling)

43% HHV

IGCC current/near-term

1730 US$/kWe (advanced oxy-coal; based on non-ZETs +33%)

40% HHV (non-ZETs - 8% points)

1300 US$/kWe (based on cost equal to above)

48% HHV

UltrasupercriticalPCC, long-term

2060 US$/kWe (flue gas scrubbing)

35% HHV

1300 US$/kWe

43% HHV

Supercritical PCC, current/near-term

ZETsNon-ZETs reference

ZETs plants capital cost (US$/kWe net) and net efficiency (% HHV) estimates

© IEA Clean Coal Centre www.iea-coal.org.uk

Net efficiencies (LHV)with and without CO2 capture

(Courtesy of Vatenfall – oxy fuel network meeting Cottbus November 2005)

0

10

20

30

40

50

60

PF+dr

ier no

capt

ure

PF ox

yfuel

with

FGD

IGCC ca

ptur

e

PF Pos

tcom

busti

on "E

cona

mine S

M+"

PF no

captu

re

PF Oxy

fuel

with F

GD

IGCC "T

exac

o" ca

pture

aMDEA

IGCC "S

hell"

capt

ure

aMDEA

PF Pos

tcom

busti

on "E

cona

mine S

M+"

NGCC no c

aptur

e

NGCC postc

ombu

stion

"Eco

nam

ine S

M+"

Pla

nt e

lect

rical

effi

cien

cy (L

HV

) [%

]

Natural GasLignite Bituminous Coal

© IEA Clean Coal Centre www.iea-coal.org.uk

Summary picture on capital costs and efficiencies of ZETs plants

� Main incremental cost of ZETs plants will come from CO2

capture, which incurs a large specific capital cost penalty

� PCC and IGCC in ZETs forms could be broadly similar in capital cost

� However, range and uncertainty in estimated costs are considerable

� Efficiency penalties of combustion-based ZETs systems could be becoming more similar to those being predicted for IGCC-based ZETs

© IEA Clean Coal Centre www.iea-coal.org.uk

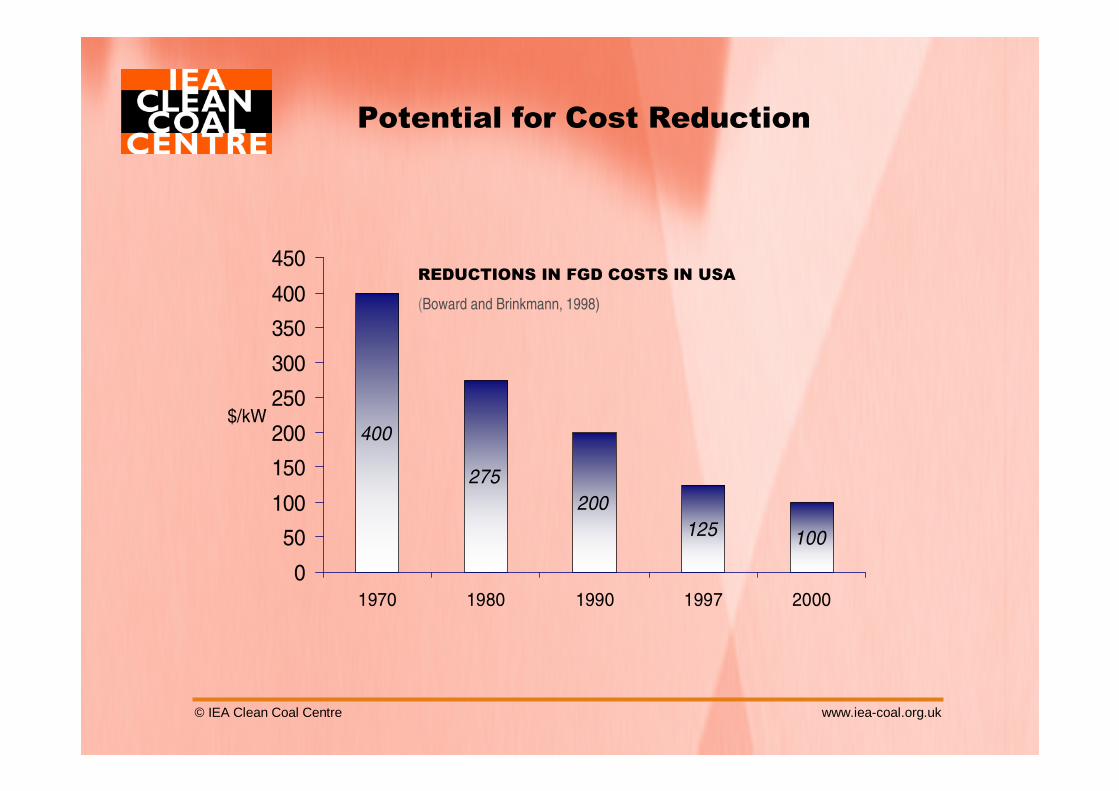

Potential for Cost Reduction

400

275

200

100125

0

50

100

150

200

250

300

350

400

450

1970 1980 1990 1997 2000

$/kW

REDUCTIONS IN FGD COSTS IN USA

(Boward and Brinkmann, 1998)

© IEA Clean Coal Centre www.iea-coal.org.uk

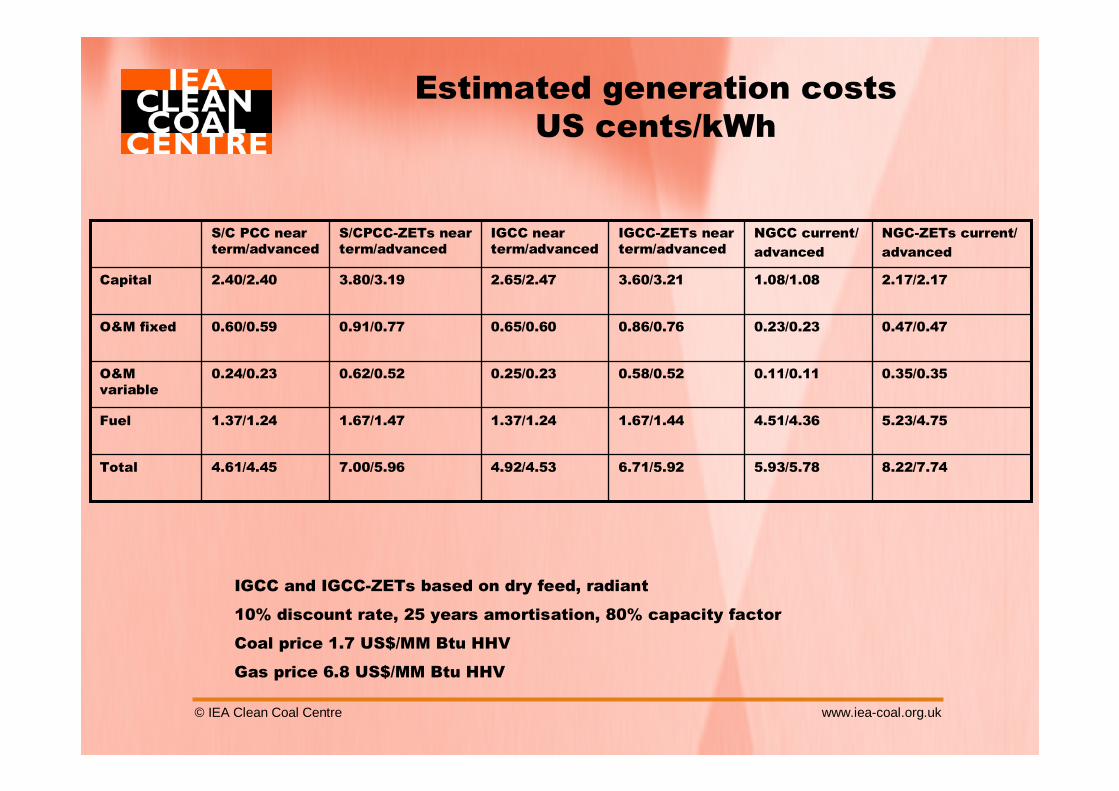

Estimated generation costs US cents/kWh

8.22/7.745.93/5.786.71/5.924.92/4.537.00/5.964.61/4.45Total

5.23/4.754.51/4.361.67/1.441.37/1.241.67/1.471.37/1.24Fuel

0.35/0.350.11/0.110.58/0.520.25/0.230.62/0.520.24/0.23O&M variable

0.47/0.470.23/0.230.86/0.760.65/0.600.91/0.770.60/0.59O&M fixed

2.17/2.171.08/1.083.60/3.212.65/2.473.80/3.192.40/2.40Capital

NGC-ZETs current/

advanced

NGCC current/

advanced

IGCC-ZETs near term/advanced

IGCC near term/advanced

S/CPCC-ZETs near term/advanced

S/C PCC near term/advanced

IGCC and IGCC-ZETs based on dry feed, radiant

10% discount rate, 25 years amortisation, 80% capacity factor

Coal price 1.7 US$/MM Btu HHV

Gas price 6.8 US$/MM Btu HHV

© IEA Clean Coal Centre www.iea-coal.org.uk

SOURCES OF INFORMATION

© IEA Clean Coal Centre www.iea-coal.org.uk

© IEA Clean Coal Centre www.iea-coal.org.uk

www.cct2007.it15-17 May Cagliari, Sardinia

www.ieagreen.org.uk

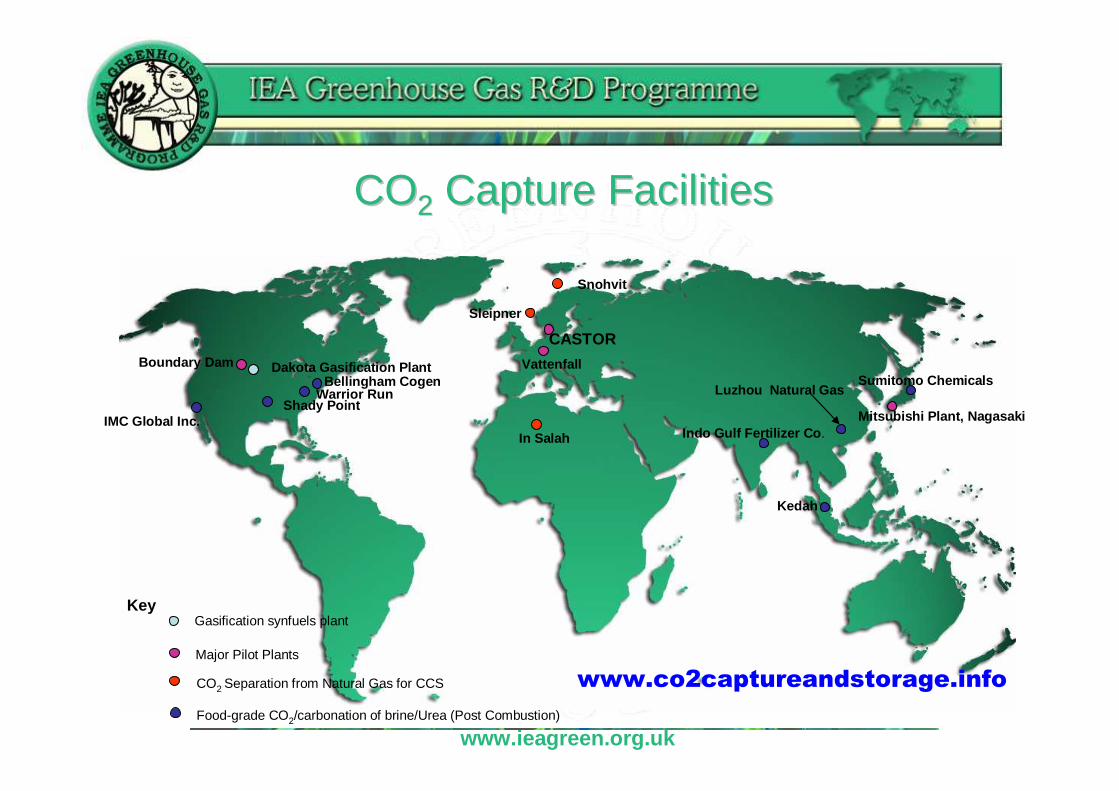

COCO22 Capture FacilitiesCapture Facilities

Mitsubishi Plant, Nagasaki

Sumitomo Chemicals

Indo Gulf Fertilizer Co .

Luzhou Natural Gas

Vattenfall

CASTOR

Snohvit

Sleipner

In Salah

Shady Point

Bellingham CogenDakota Gasification PlantBoundary Dam

IMC Global Inc.

Key

Warrior Run

Gasification synfuels plant

Major Pilot Plants

CO2 Separation from Natural Gas for CCS

Food-grade CO2/carbonation of brine/Urea (Post Combustion)

Kedah

www.co2captureandstorage.info

www.ieagreen.org.uk

Storage of CO2 and IEA GHG DatabaseStorage of CO2 and IEA GHG Database

www.ieagreen.org.uk

COCO22 storage effectiveness increases with depth storage effectiveness increases with depth Courtesy of CO2CRC

www.ieagreen.org.ukCourtesy of CO2CRC

www.ieagreen.org.uk

CO2Injection

site

Weyburn EOR – CO 2 Storage Project

Productionwell

www.ieagreen.org.uk

Saline FormationsSaline Formations

www.ieagreen.org.uk

COCO22 Injection and Storage ActivitiesInjection and Storage Activities

Nagaoka

HokkaidoQinshui Basin

Snohvit

Sleipner

In Salah

Key

ECBM projects

EOR projects

Gas production Fields

Saline aquifier

SibillaRECOPOL

CO2 SINK

K-12B

Cerro Fortunoso

Frio

West Pearl Queen

MountaineerWeyburn

Penn WestAlberta ECBM

Teapot DomeRangely

Burlington

4 New CO2-EOR Pilots in Canada

50 Acid Gas injection sites in North America

70 CO2-EOR projects in U.S.A.

GorgonDepleted Oil Field

Otway Basin

www.ieagreen.org.uk

Source: National Occupational Health and Safety Commission Compendium of Worker’s Compensation Statistics, Australia, 2001 -02, December 2003

APPEA Safety Incident Database 2003

*Frequency rate is calculated for one week or more lost time

**Data used is 2003 statistics

Courtesy of CO2CRC

www.ieagreen.org.uk

Current MembershipCurrent Membership

www.ieagreen.org.uk

Studies in progressStudies in progress

• Remediation of leakage from geological storage• Risk assessment and regulatory needs• Environmental impact frameworks• Sub-sea ecosystem impacts of CO2 leakage• Terrestrial ecosystem impacts of CO2 leakage• Distributed capture and collection of CO2

• Co-production of hydrogen and electricity• Regional capacity for CO2 storage in India• Improved oxygen production processes•• CaptureCapture--ready power plantready power plant

© IEA Clean Coal Centre www.iea-coal.org.uk

MEMBERS

Italy JapanRep. of Korea UK

Spain

BHEL India

Anglo Coal S. Africa

USA

ESKOM S. Africa

Netherlands Group

BG Group, UK

AustriaCanada

Germany

CEC

BRICC China

ACIC, Australia

CANZ, New Zealand

Eletrobras, Brazil

DPG, Denmark

Suek, Russia

SIG, Sweden

Schlumberger in process

© IEA Clean Coal Centre www.iea-coal.org.uk

Work in progress

Trace elements and fly ash utilisation (in draft)

Potential impact of ETS and LCPD on EU coal demand (in draft)

Clean coal technologies for a carbon constrained world

Operational patterns of coal-fired plant to 2010

G8 contract – energy efficiency of coal-fired plants

Cofiring coal with waste and opportunity fuels

Polygeneration from coal

Coal resources for power generation in China

Korean Energy Strategy Project (KESP)

Future developments in IGCC

CO2 capture technologies

Coal supply chain costs

Competitiveness of coal-fired power generation

Coal to liquids (CTL)

Properties and behaviour of SO2 adsorbents

Economics of mercury control

© IEA Clean Coal Centre www.iea-coal.org.uk

CLEAN COAL TECHNOLOGY THAT WORKS

The End – Thank you for your Attention