CO-OP Card Refresh: Best of Credit and Debit Information

48

CO-OP CARD REFRESH Best of Credit and Debit Information

-

Upload

nguyennhan -

Category

Documents

-

view

216 -

download

0

Transcript of CO-OP Card Refresh: Best of Credit and Debit Information

CO-OP CARD REFRESH

Best of Credit and Debit

Information

Table of Contents

1. Introduction ....................................................... 3

Overview .....................................................................4

Innovations in Credit and Debit Cards: Keep Them at the

Leading Edge ...............................................................5

2. Mobile Advances Plastic ....................................... 7

3. Generating Revenue with Credit ........................... 11

Credit is Back ............................................................. 12

Was Revenue in the Cards? .......................................... 13

Three Seasons of Increased Spending ............................ 15

Member Rewards and the Modern Consumer .................. 19

4. What’s New with Cards? ..................................... 22

Evolving at the Speed of Apple? .................................... 24

Credit: New and Ready to Grow? ................................... 25

Could Your Rewards Program Be More Rewarding? ........... 27

5. New Tools in a Changing Environment .................. 29

Happy Birthday, Target Breach! Now Go Away. ................ 31

Will Tokenization Eat EMV’s Lunch? ................................ 33

Does EMV Use Tokenization? Your Questions Answered. ... 34

8 Questions You Asked About CardNav ........................... 37

Q&A: Charged Up Over Mobile Security .......................... 39

Hot off the Presses, CardNav Debuts at Bethpage FCU ..... 41

6. Building Relationships from the Inside Out ............ 43

Is Your Credit Card Program Integrated Enough For You? . 45

CO-OP Products to Up Your Card Game .......................... 47

More Fast + Brilliant Products from CO-OP ..................... 48

1. Introduction

BEST OF CO-OP CONTENT ON CARD PAYMENTS

4Best of Credit and Debit Information | Spring 2015 | Introduction

Overview

Welcome to the first CO-OP Card Refresh, a digest of what’s new with credit, debit, and the products and processes that go with them. Here you’ll find the best of our credit and debit related content from recent months, along with CO-OP’s own data on usage and growth.

Inside is a wealth of information:

• Data and Analytics

• Good to Grow: Generating revenue with credit

• Innovations: What’s new with cards?

• Tightening up Security: New tools in a changing environment

• Cards in Context: Building relationships from the inside out

Credit and debit form the basis for a meaningful, ongoing, growing relationship with your members. In the pages that follow, look for inspiring indicators of growth, innovations and trends that are changing the future of payments, a roundup on new security technology, and perspectives on integration as 2015 unfolds.

5

Innovations in Credit and Debit Cards: Keep Them at the Leading Edge

By Ryan Zilker, Business Manager, Product Development

They have been around so long, it’s easy to begin thinking of them as inert pieces of plastic. Yet, credit and debit cards remain among the most dynamic products credit unions can offer, and they in fact represent an opportunity to serve members at the leading edge.

Consider the growth in credit card spending during 2014. According to the company’s analysis of credit transactions processed by CO-OP Financial Services, credit spend steadily increased throughout the year. In January 2014, the average spend per card was $363.08, and in January 2015 the average spend was up to $381.18, an increase of five percent per card during comparable periods.

This combines with the continued strong transaction volumes for cards. CO-OP’s own analysis of debit and credit transactions it processed found the combined total holding strong, even growing, from about 120 million transactions per month in December 2013/January 2014 to more than 140 million transactions in November 2014.

Credit and debit card use is as vibrant as ever, and new technology is adding to its luster, in the form of payment innovations, security innovations and data/analytics.

Payment innovations and security innovations, in fact, seem to be going hand-in-hand.

The introduction of Apple Pay last September brought the tokenization data security process to the forefront. In addition, the Oct. 1, 2015, “liability shift” for EMV is finally bringing this global standard to the U.S., where it will ultimately be the standard as well.

CO-OP believes tokenization and EMV together will provide even better security for the U.S. payment system. Think of EMV as the security for a plastic card in a card present transaction, and tokenization as the security for digital transactions, whether mobile, online or in-store.

Best of Credit and Debit Information | Spring 2015 | Introduction

6

So while the technologies are similar, they are designed for different use cases. Coupled together they will make it much more difficult for fraudsters and improve the security of all transactions. And global interoperability of EMV chip cards is still a key driver of adoption in the United States.

Apple Pay and other mobile products answer member needs for payments methods that are fast, brilliant and connected. But consumers in equal measure are demanding greater personalization. One answer is card controls and alerts, such as CardNavSM by CO-OP, which enables the user to individually turn their cards on and off and set spending limits by category.

These innovations can be utilized to the maximum through the data analytics tools now at the ready. Credit unions certainly do not have unlimited resources to encourage low spenders and members who are slow to activate their cards.

Analytics tools provide credit unions with deep insight into their full portfolio’s performance – right down to the transactions of an individual card, network, merchant and ATM. Armed with this data, you can better understand and influence cardholder behavior, and focus on members with the greatest potential through rewards programs and other targeted efforts.

There’s no question that the credit and debit cards you issue are key drivers towards primary financial institution-relationships, and represent a large and consistent source of revenue.

Your members use cards to interact with you more than any other form of transaction, and the way you position your cards determines in large measure how you position your credit union.

With the advances available to you today in cards, you can be seen as a technology leader, a secure and fun source of payment, an efficient and rewarding financial services provider, and – in a crisp phrase – first in class.

Best of Credit and Debit Information | Spring 2015 | Introduction

2. Mobile Advances

Plastic

CO-OP DATA & ANALYSIS

8

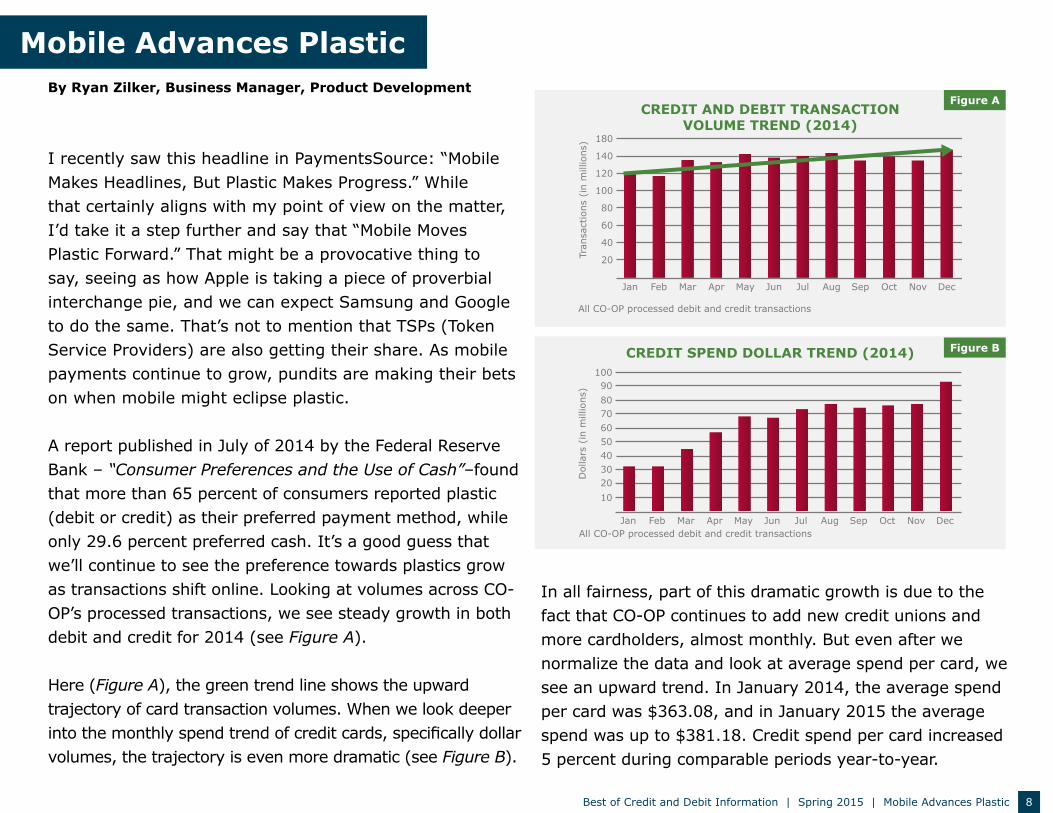

I recently saw this headline in PaymentsSource: “Mobile Makes Headlines, But Plastic Makes Progress.” While that certainly aligns with my point of view on the matter, I’d take it a step further and say that “Mobile Moves Plastic Forward.” That might be a provocative thing to say, seeing as how Apple is taking a piece of proverbial interchange pie, and we can expect Samsung and Google to do the same. That’s not to mention that TSPs (Token Service Providers) are also getting their share. As mobile payments continue to grow, pundits are making their bets on when mobile might eclipse plastic.

A report published in July of 2014 by the Federal Reserve Bank – “Consumer Preferences and the Use of Cash”–found that more than 65 percent of consumers reported plastic (debit or credit) as their preferred payment method, while only 29.6 percent preferred cash. It’s a good guess that we’ll continue to see the preference towards plastics grow as transactions shift online. Looking at volumes across CO-OP’s processed transactions, we see steady growth in both debit and credit for 2014 (see Figure A).

Here (Figure A), the green trend line shows the upward trajectory of card transaction volumes. When we look deeper into the monthly spend trend of credit cards, specifically dollar volumes, the trajectory is even more dramatic (see Figure B).

In all fairness, part of this dramatic growth is due to the fact that CO-OP continues to add new credit unions and more cardholders, almost monthly. But even after we normalize the data and look at average spend per card, we see an upward trend. In January 2014, the average spend per card was $363.08, and in January 2015 the average spend was up to $381.18. Credit spend per card increased 5 percent during comparable periods year-to-year.

Mobile Advances PlasticBy Ryan Zilker, Business Manager, Product Development

All CO-OP processed debit and credit transactions

20

40

60

80

100

120

140

180

Tran

sact

ions

(in

mill

ions

)

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

CREDIT AND DEBIT TRANSACTION VOLUME TREND (2014)

Figure A

All CO-OP processed debit and credit transactions

1020

4030

5060708090

100

Dol

lars

(in

mill

ions

)

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

CREDIT SPEND DOLLAR TREND (2014) Figure B

Best of Credit and Debit Information | Spring 2015 | Mobile Advances Plastic

9

Couple these transaction trends with some behavioral changes reported by NCR, and you start to see a pattern (see Figure C).

In this example, we see that the mobile channel is growing fast, but has yet to overtake the other three channels. Carry these growth rates forward just three years, however, and we see an entirely different mix. Mobile transactions will eclipse the other three channels with 116 billion transactions predicted by 2018. When trends are extended out like this, it is easy to see the importance of mobile.

Because of the projected growth in mobile, we know that spending is going to shift to shopping online, in app, and in store. The key now is to get our credit union cards embedded into as many payment vehicles as we can. Office retail giant Staples reports that more than 25 percent of its in-app purchases are made using Apple Pay – meaning that they’re tied to a card. If you have an Uber account, it either has a card loaded into it, or it uses Apple Pay. Soon we will be adding in Samsung Pay, Google Pay, and Microsoft Pay (or is it Windows Pay?) – all of which will be card based. Even MCX is rumored to be softening its stance on allowing cards into its CurrentC wallet. Any way you slice it, cards are going to be the foundation of first generation mobile wallets, so now is the time to get engaged.

When you look at the number of transactions processed on debit cards in Figure D, the volume is overwhelmingly skewed towards signature transactions.

Mobile Online ATM Branch

Annual Global Transactions 29bn 35bn 94bn 76bn

Average Interactions/Person/Year

25x 44x 30x 19x

Annual Growth Rate 59% 18% 1% 7%

Figure C

Pin, 131, 512, 260

ATM, 36, 803, 265

PAVD, 26, 460, 649

Signature, 179, 185, 338

35%

10%

7%

48%

VOLUME OF TRANSACTIONS PROCESSED ON DEBIT CARDS

Figure D

Best of Credit and Debit Information | Spring 2015 | Mobile Advances Plastic

10

However, when you look at dollars spent in Figure E, the break out is a little more evenly split.

This is because the payment method people choose is driven by ticket amount.

Figure F, provided by Visa, helps shed some light on which payment medium consumers prefer.

Regardless of ticket size and payment choice, we know that credit union card payments are growing, nationwide. According to CO-OP’s year-end data for 2014, here is a region-by-region map of signature transaction growth in Figure G.

Mobile payments will continue to advance in 2015. Instead of viewing mobile as competition for traditional cards, consider that the popularity of mobile is only upping the ante for credit and debit. Growth can raise the stakes for all, if you play your cards right.

Pin, $5,432849,078.17

ATM, $4,758,640,699.02

PAVD, $1,079,967,241.30

Signature, $6,358,799,724.56

31%

27%

6%

36%

DOLLARS SPENT ON DEBIT CARDS Figure E

WHAT IS YOUR PREFERRED PAYMENT METHOD CHOICE BY TICKET SIZE?

Figure F

20

40

60

80

PERCEN

T

<$2 $2-4 $5-10 $11-25 $26-50 $51-100 $101-500 $500+

CASHSWITCH FROM CASH TO DEBIT AT $11-25

DEBITCREDITCHECK

SWITCH FROM CASH TO CREDIT AT $26-50“I’m used to cash for small

amounts” - 61%

“I’m uncomfortable using cards for small amounts” - 30%

SIGNATURE TRANSACTION DOLLARS GROWTH RATE IN Q4 2014

Figure G

MID ATLANTIC16.15%

NORTHEAST15.36%

MIDWEST12.39%

SOUTHEAST2.17%

WEST7.86%

SOUTHWEST2.73%

Best of Credit and Debit Information | Spring 2015 | Mobile Advances Plastic

3. Generating Revenue with

Credit

GOOD TO GROW

12Best of Credit and Debit Information | Spring 2015 | Generating Revenue with Credit

Credit is Back

Year-end data from Callahan & Associates Peer-to-Peer Analytics confirms that 2014 was a banner year for credit. Credit union credit card balances rose 8.1 percent to $46.5 billion, while credit unions added a healthy 1.2 million credit cards for a robust 7.7 percent increase for the year.

Equifax data simply underscores the point: Outstanding credit card debt jumped to $642.4 billion in December, up from $606.75 billion a year before – meaning that the average American’s credit card balance increased by 5.9 percent in 2014.

Growth is a happy development, but how do you prepare to meet the challenge of increased demand – and the increased competition that goes with it? Find out more as we take a few quick looks at the opportunity that 2014 brought; how and where spending increased; and how enhancing features like member rewards can pay dividends in increased loyalty.

CREDIT UNION CARD BALANCES UP IN 2014

At the end of 2014, credit union credit card

balances totaled $46.5 billion

We saw the fastest annual growth since 2008 which

was 8.1%

(Source: 2014 Callahan & Associates Peer-to-Peer Analytics)

MORE CREDIT UNION CARDSCredit union credit cards saw a new peak which was

1.2 million cards

They saw an annual growth of 7.7%

(Source: 2014 Callahan & Associates Peer-to-Peer Analytics)

13

Have credit cards been a moneymaker for credit unions during the past year? Insight Vault caught up with Jennifer Kerry, Vice President, Credit Issuer Processing, for CO-OP, to get the scoop on revenue growth – and ask how credit unions can capitalize on the credit trend.

Was Revenue in the Cards?By Bill Prichard, Senior Manager, Public Relations and Corporate Communications

Q: Looking back at 2014, what kind of year was it for credit union credit cards?

Q: Obviously, that’s great news on the revenue front.

Q: Growth in the 20 to 43 percent range is clearly a positive trend. What can credit unions do to capitalize on the momentum?

A: Unequivocally, it was great. We posted last month about the growth of credit union credit cards across the board, but we’re also happy to report that CO-OP In-House and Full Service Credit clients are enjoying substantial growth. Over the past 24 months, the CO-OP credit client base has grown nearly 20 percent on average. We’ve also seen multiple standouts reaching 30 percent to 43 percent growth. We’re really delighted.

A: It is. Sometimes it’s so obvious that we overlook it: Credit card transactions drive both interest and non-interest revenue at credit unions. Revenue is not the only benefit to growing your credit card usage, but it’s certainly an important one.

A: The first thing we suggest is to think about raising credit limits. A lot of consumers try to keep their card balances under 30 percent of their total lines of credit, so even if your cardholders don’t appear to be “maxed out,” you might both benefit from a higher credit line. This strategy is worth considering for creditworthy members, but also for members who may be “credit bruised” after the recent recession. If you can offer them products such as cards that are secured by savings, you may be able to help them bounce back. That’s not just good for your credit portfolio; it’s also a relationship builder.

Best of Credit and Debit Information | Spring 2015 | Generating Revenue with Credit

Jennifer Kerry

14

Having great credit card programs can also say a lot about the relevance of your credit union. Whether it’s having a rewards program that engages members or offering member education around creditworthiness and financial literacy – or even just letting members know that you see their need for credit and are answering it with products designed to serve them – this is a great moment to send that message.

This story originally ran on CO-OPInsightVault.com

Q: Should credit unions be looking at other ways to maximize credit usage?

Q: Without getting too touchy-feely, is there an emotional benefit at stake here as well?

A: Yes, and they should also be looking at ways to maximize their relationships with credit cards as a vehicle. For instance, target your debit card users with credit card offers. If they already choose you for debit, they may be inclined to open a credit account. You can also look at the reverse: Encourage your credit card holders to open checking accounts.

Credit cards continue to be very sticky. So while we don’t want to forget about that interest and non-interest revenue we talked about a minute ago, we also want to remember that credit cards can increase revenue opportunities by engaging our members across the board.

A: We think so. Consumers may be charging up their credit accounts again, but most haven’t forgotten the hits they took during the Great Recession. Being part of their comeback stories is a great role for credit unions. It speaks to the kind of service credit unions have built their reputations on.

Best of Credit and Debit Information | Spring 2015 | Generating Revenue with Credit

15

Together with our partners Saylent Technologies and The Members Group, CO-OP has been tracking and reporting on member spending over the past several months. Our big takeaway: Spending is up! Whether members were in the mood to splurge on Valentine’s Day or helping to meet funding goals in the ALS Ice Bucket Challenge, they’re using their cards – as the following Insight Vault posts clearly show.

Did the Ice Bucket Challenge Make a Splash?

It was all the rage in August – but what was the result?

Almost everyone saw the videos of friends, family, celebrities and many others dumping ice water over their heads as part of the ALS Ice Bucket Challenge. While it has been a highly successful social media initiative, it’s been shown that increased awareness of ALS was not the only accomplishment. Donations to the charity have escalated significantly.

CO-OP used CO-OP Revelation® to analyze the ALS donation-related debit card transactions conducted by

members of CO-OP’s credit union clients. The analysis was done on a sample of 70 out of 900 credit unions. Analysis comparing August 1-18, 2013 to August 1-18, 2014 found:

Debit card-based ALS contributions have increased dramatically since the Ice Bucket Challenge started. For example, these members increased their ALS merchant-related transaction volume by 426 percent and ALS merchant-related transaction spend by 384 percent.

• Donors are younger than they have been in the past as a result of the Challenge. The average age of these ALS donors in August 2014 is 38, versus an average age of 45 during the same period last year.

“The credit union movement has always been characterized by a people helping people ethic, dedicated to making local communities better,” noted Stan Hollen, President/CEO of CO-OP. “The donations to the ALS Association in the past month shows that tradition springs from the members themselves.”

The results cover donations-related debit card activity by members of credit unions that use CO-OP for transaction

Three Seasons of Increased SpendingBy Bill Prichard, Senior Manager, Public Relations and Corporate Communications

Best of Credit and Debit Information | Spring 2015 | Generating Revenue with Credit

16

processing. The comparisons were performed through CO-OP Revelation and conducted by Saylent’s FInsight360 consulting team.

What Did We Learn about Back-to-School Spending?

Back-to-school spending for the 2014-15 school year was robust in August, with a 9.2 percent increase recorded across 25 merchant types compared to August 2013.

Merchants offering computer software, stores selling elementary/secondary school supplies and bookstores were particularly busy leading up to Labor Day, according to an analysis of debit card transactions by CO-OP Financial Services.

An increase in the number of transactions – up 7.9 percent – holds the key to the 9.2 percent spending increase. The amount-per-transaction rose only 1 percent – $50.72 in 2014 from $50.12 in 2013. So, credit union members were individually spending about the same amount, but more members were making back-to-school purchases this year.

This analysis of sales is based on transactions made during August, with results covering debit card activity nationwide by members of credit unions that use CO-OP for transaction processing. The year-over-year comparison was performed through an advanced analytics

solution, CO-OP Revelation, and was conducted by Saylent’s Insight360 consulting team.

Among the highlights of the CO-OP Revelation data:

• Total spending at the selected back-to-school merchant categories for August 2014 was $715.2 million compared to $654.9 million in August 2013, a 9.2 percent increase. The total number of transactions recorded in 2014 was 14.1 million versus 13.067 million in 2013, a 7.9 percent transaction increase.

• Computer software was the merchant category with the biggest jump in 2014 compared to 2013, with spending up 44.3 percent and transaction volume up 48.5 percent.

• Elementary/secondary school supplies stores achieved a spending increase of 29.3 percent and a transaction increase of 39.7 percent.

• Bookstores realized a 20.1 percent increase in spending and a 24.1 percent increase in transactions.

• Telecom spending rose 16.5 percent and transactions increased by 15.5 percent.

• Department and stationery stores are the only groups where spending and transaction volume dropped in 2014 compared to the previous year.

Best of Credit and Debit Information | Spring 2015 | Generating Revenue with Credit

17

Members Make Holiday Cash Boxes Ring

The final results are pending, but three companies in the service of the industry found that credit union members got the 2014 holiday shopping season off to a robust start.

The Members Group found that credit spending increased 12.97 percent, and CO-OP Financial Services found that debit spending increased 6.71 percent from Thursday–Monday of Thanksgiving Weekend compared to 2013. The finding of a 6.71 percent increase in debit card spending covered activity at 20 different merchant types nationwide by members of credit unions that use CO-OP for transaction processing. The year-over-year comparison was performed through an advanced analytics solution, CO-OP Revelation, and was conducted by Saylent’s FInsights360 consulting team.

CO-OP also found:

• Comparing 2013 to 2014, credit union members increased their debit card usage and spend most at cosmetic stores, with a close to 108 percent increase in transactions and a 98 percent increase in spend.

• The day with the largest increase in debit card spending compared to last year wasn’t Black Friday or Cyber Monday as one may expect but rather Thanksgiving Day, with an increase of 14 percent. This uptick may be reflective of the broader retail trend of opening in the afternoon and evening on Thanksgiving.

• At the same time, TMG found a 12.97 percent increase in credit spending for users who carry credit cards issued by TMG’s financial institution (FI) clients. TMG’s analysts attribute this to healthy growth in the credit card portfolios of TMG’s clients and the fact cardholders used their credit cards on average 1.35 percent more this year as compared to last year. The analysis is courtesy of the card processor’s proprietary analysis tool, ClearTrend. The tool can provide similar data on a per-FI basis for the processing clients of TMG.

Additional data from TMG includes:

• Electronic spending (shopping from online and mobile devices with a credit card) increased 24.7 percent year-over-year.

• Of the three days analyzed (Thanksgiving, Black Friday and Cyber Monday), Black Friday was the biggest day for credit card spending, accounting for 42.03 percent of all credit card transactions. On average, the transacting cardholder also spent more on Black Friday ($147.63) compared to Cyber Monday ($131.45) and Thanksgiving ($111.54).

Did an Improving Economy Lead to a More Romantic America?

Americans are perhaps feeling more romantic in addition to feeling more confident about the steadily improving economy.

Best of Credit and Debit Information | Spring 2015 | Generating Revenue with Credit

18

Research by three organizations serving the community-based financial institution (FI) industry reveals Valentine’s Day-related purchasing was way up in 2015. The Members Group (TMG) found credit spending increased 21 percent, and CO-OP Financial Services found debit spending increased 16 percent for the three days culminating in Valentine’s Day compared to 2014.

The 21 percent increase in credit spending is based on transactions made from Thursday, Feb. 12 through Saturday, Feb. 14 by users carrying credit cards issued by TMG’s FI clients. TMG’s analysts attribute this to healthy growth in credit card portfolios of TMG’s clients and the fact cardholders used their credit cards on average 3.5 percent more this year as compared to last year. The analysis is via the card processor’s proprietary analysis tool, ClearTrend. The tool can provide similar data on a per-FI basis for the processing clients of TMG.

TMG also found that while Millennials (age 18-29) made 58 percent more transactions than the next closest age bracket, they spent far less. Millennials spent an average of $39.09 – 65 percent less than the next lowest age bracket (age 30-39). In addition, out of the three days, the day before Valentine’s Day (Friday, Feb. 13) saw the most credit transactions – 9.3 percent more than Feb. 12 and 5.7 percent more than Feb. 14.

During the same Thursday through Saturday period, CO-OP found a 16.45 percent increase in debit card spending. The results covered debit activity at all merchant types tracked nationwide by members of credit unions using CO-OP for transaction processing. The year-over-year comparison was performed using CO-OP Revelation and advanced analytics and was conducted by Saylent’s FInsights360 consulting team.

CO-OP additionally found that people used their debit cards more this year when buying loved ones products to help them check off their “honey-do” lists and better their homes. This is reflected in an almost 38 percent increase in transactions and close to 49 percent increase in spend at home supply warehouse stores.

The two companies also found that consumers used their debit cards more to go out for romantic dinners and drinks, with a more than 33 percent increase in transactions and 47 percent jump in spend at restaurants, and a 79 percent increase in transactions and more than 79 percent increase in spend at bars compared to last year during this time period.

You can read the full report of findings on Valentine’s Day shopping 2015 here.

These posts originally appeared on CO-OPInsightVault.com.

Best of Credit and Debit Information | Spring 2015 | Generating Revenue with Credit

19

In today’s ultra-competitive credit/debit landscape, the benefits offered can make a substantial difference in a consumer’s mind. Like many other aspects involved in the buying experience, rewards programs are quickly evolving to meet escalating consumer expectations.

We had the opportunity to talk with Andrew Gates, Loyalty Consultant with CO-OP, about how CO-OP Member Rewards is staying a step ahead of the competition to offer members a uniquely gratifying experience. Here are his valuable insights from our discussion.

Member Rewards and the Modern Consumer

Q: How does Member Rewards differ from a typical credit/debit loyalty program?

Q: Are there any other points of differentiation?

A: We are making it easier than ever for members to earn points, without adding cost for the credit union. Where CO-OP makes a big effort is primarily in the merchant-funded space. It is safe to say that we have the most robust merchant-funded rewards program in the industry. In terms of national online products, CO-OP is leading the way with the soon to be released browser plugin, which allows a member to get their rewards from the merchant they are buying from without going through a third party or a rewards website. It makes things more convenient for the member because the logo of the program shows up everywhere they can earn bonus points, including search results in Google, Bing and Yahoo searches.

A: Tackling the local merchant arena is much harder in general because there are so many “mom and pops” out there–but that’s where our members shop and want to earn rewards. We will soon have close to 30,000 merchants involved in our local merchant program–and we’ll continue to grow and expand over the coming months. We also make it easy for our clients to add their own local merchants through an online boarding tool– which increases the value to the member.

Best of Credit and Debit Information | Spring 2015 | Generating Revenue with Credit

Andrew GatesCO-OP Financial Services

20

Q: What effect does merchant funded have on the increasing value of rewards?

Q: How is Member Rewards uniquely suited to today’s modern consumer?

Q: Are there any precedents to learn from when delivering such an innovative rewards program?

A: At the end of the day, what we are trying to do is deliver value to the member where and when they want it. By partnering with merchants, there is funding for more customized incentives. We give them greater access to our members in exchange for the ability to offer a better deal. We expect the deals to get more and more exclusive as our data set gets better and richer. So instead of a member going to Groupon for a local deal, they will turn to their credit union.

A: Today’s modern consumer is looking for value through increased personalization. They are okay with appropriate usage of data if it is being used to deliver a personal experience. When you look at how people are using the Internet–especially millennials–they are putting everything out there. So from our standpoint, the two critical items are delivering value in a timely, relevant fashion and in the way they want it.

A: The hot one right now is mobile. Ultimately, when you download your credit union app, you have access with ease. What people don’t want is to have to think when they go into a store. “Do I use my card? An app? PayPal?” That’s why Visa and MasterCard have been successful for so long and mobile wallets have had a hard time taking off. The former takes extra thinking. So we want to provide something that is available almost without thinking. But at the same time, the controls have to be in place so I can turn it off or that I’m not inundated with offers every time I walk into a store. This is a fine line to walk, and we are working to understand that. This is also where personalization comes into play, because for example, I will likely be more open to receiving alerts than another person. It’s not one size fits all.

Best of Credit and Debit Information | Spring 2015 | Generating Revenue with Credit

21

A: I don’t believe the non-millennials are that different anymore, in terms of what they want to see from their credit union. The world is moving forward together on this, millennials and everyone else. Each person is an individual, so giving people the ability to manage how they are alerted and set their own preferences is critical. I think the biggest difference between millennials and the rest is that millennials use technology and expect certain features and personalization. The rest of us are surprised and delighted by it.

GET SCHOOLED AT CO-OP SPONSORED SEMINARSIt’s always a good time to brush up on your card management skills. To that end, CO-OP sponsors two excellent series for card managers:

Callahan 2015 Credit Card Management SchoolThe 2015 Credit Card Management School, a partnership between Callahan & Associates and TRK Advisors, helps credit unions optimize their card portfolios and better understand the latest trends in program design and management. Learn more

School of Credit Card Program ManagementOndine Irving shares best practices for overall credit card portfolio and program management, newly updated for 2015. Irving’s consultancy, Card Analysis Solutions, has been providing independent and objective credit card portfolio reviews, expense reduction solutions, increased profitability solutions and operational training exclusively to the credit union industry since 2003. Learn more

Q: What about credit unions that might be uncertain about how to market to millennials without “turning off” their existing membership base?

This story originally appeared on CO-OPInsightVault.com.

Best of Credit and Debit Information | Spring 2015 | Generating Revenue with Credit

4. What’s New with Cards?

INNOVATIONS

23Best of Credit and Debit Information | Spring 2015 | What's New with Cards?

When you think of innovations in financial services, cards may not be the first product that comes to mind. On the face of things, cards are among the least altered tools we use to manage our money every day.

But take a step back, and the picture changes dramatically. Cards themselves are in fact evolving. Though we’ll explore this topic in earnest in the next section, on security, the emergence of EMV technology is literally changing the way our cards look and function. The world of payments is among the most explosive around: Rapid change and new technologies are the norm as P2P payments gain traction, mobile wallets come and go, and consumers open their minds to new alternatives.

Never was this more in evidence than September 2014, when Apple announced the introduction of Apple Pay. A million users signed up in the first month alone. Just as significantly, credit unions sprang into action. Instead of waiting to see what the impact of Apple Pay would be, several credit unions simply set up tokenization service and signed on. CO-OP was there for the assist, helping clients navigate the uncharted waters of tokenization and interfacing with Apple. And as more and more of our clients decide to climb on board, CO-OP is here to help smooth the way.

In the end, what’s new with cards is that there’s more to the story than plastic alone. Keeping pace with innovation means thinking broadly, acting boldly and moving swiftly. Following is a sample of how new ideas crossed the traditional world of cards.

24Best of Credit and Debit Information | Spring 2015 | What's New with Cards?

By Bill Prichard, Senior Manager, Public Relations & Corporate Communications

Credit unions may have accelerated their evolution rate in recent years, but since Apple’s announcement last month that a new payment system called Apple Pay is on its way, the speed demands on credit unions have been unprecedented. In order to help credit unions meet those demands, CO-OP has been working to provide information and pave the way for participation. As education and opportunities continue to develop, CO-OP has launched an online Tokenization Resource Center and has continued to host webinars to keep credit unions up to speed.

“CO-OP is working with business partners and clients to make sure credit unions have the technical and marketing education they need to take advantage of the new Apple wallet,” says CO-OP President/CEO Stan Hollen. “This has included not only helping credit unions understand the Apple Pay opportunity, but providing the assistance needed to actually become enrolled as participants.”

CO-OP’s first webinar on tokenization and Apple Pay– which ran in two sessions on September 24 – drew a record audience of 1,100 participants. The follow-up webinar, “Innovations in Payments,” took place on Tuesday, November 18, at 1 p.m. Eastern/10 a.m. Pacific. Caroline Willard, Executive Vice President, Markets and Strategy, and Michelle Thornton, Manager, Core Products, for CO-OP reprised their roles as presenters.

CO-OP’s Tokenization Resource Center keeps credit unions up to date with breaking news as well as Frequently Asked Questions, an implementation guideline, the recording and slides from prior webinars, tokenization-related blog posts and more. Have a question? The site also includes an “Ask the Expert” feature that enables visitors to submit questions for CO-OP’s team of experts.

Moving at the speed of Apple is a new experience for credit unions. And though the experience has brought with it more than a few white-knuckled moments, it’s also revealed something about this industry’s capacity for speed. Working together, we cannot only go far: We can go fast.

This story originally appeared on CO-OPInsightVault.com.

Evolving at the Speed of Apple?

25Best of Credit and Debit Information | Spring 2015 | What's New with Cards?

IntroductionCredit: New and Ready to Grow?By Bill Prichard, Senior Manager, Public Relations & Corporate Communications

On the face of it, credit cards haven’t changed much since their introduction decades ago. Plastic cards are so familiar that they’re iconic. But the inner workings of the credit cards issued by CO-OP’s credit processing clients have changed dramatically in the past 12 months. New options make the credit experience more secure, powerful, flexible and rewarding. If you’re hoping to make credit a growth area this year, offering a new experience may be the differentiator you’re looking for.

Sound like too much to ask of a little plastic card? Consider the developments:

EMV: Cards embedded with EMV chips are now available to clients who use CO-OP In-House Credit processing and CO-OP Full-Service Credit processing through The Members Group. EMV-enabled cards improve security on card-present transactions, making them a popular option for members and a money-saver for credit unions.

Learn More at CO-OP’s EMV Resource Center.

Apple Pay and Tokenization: This was a late entry and a surprise to boot. When Apple announced its new tokenization-driven mobile payments app in September of last year, credit unions wondered how they’d ever get on board. It’s happening now. CO-OP is an engaged issuer-processor for Apple Pay and Visa, which means CO-OP can directly facilitate tokenization service and Apple Pay enrollment for credit processing clients. CO-OP is also helping credit clients get up and running with MasterCard’s tokenization service for Apple Pay participation.

Learn More at CO-OP’s Tokenization Resource Center.

CardNav by CO-OP: What transforms an ordinary plastic card into a dynamic money management tool? CardNav by CO-OP enable cardholders to secure, track and manage their card accounts from their mobile devices. It’s not the individual actions that make CardNav transformative – though the ability to turn cards on and off or set spending limits by category are breakthrough – it’s the overall experience that changes the game.

Learn More about CardNav.

26Best of Credit and Debit Information | Spring 2015 | What's New with Cards?

Member Rewards by CO-OP Mobile App: Rewards are not new this year, but the Member Rewards by CO-OP Mobile App is. In the same way mobile card controls and alerts change the cardholder experience from passive to interactive, mobile rewards make incentives more usable, trackable and desirable.

Learn More about CO-OP Mobile Rewards.

What’s most interesting about these four developments is that they all materialized during the last year. One year ago today it was impossible to foresee what January 2015 would bring. In fact, what it brings is a substantially different card experience. The cards you issue today may look largely the same as the ones you would have mailed last January. But the security they offer – in person, virtually, and interactively by mobile device – is light years ahead. This year’s cards are mobile-ready, whether members want to redeem their rewards on their smartphones or do a little budgeting with their CardNav apps. It’s a whole new card game for a brand new year.

This story originally appeared on CO-OPInsightVault.com.

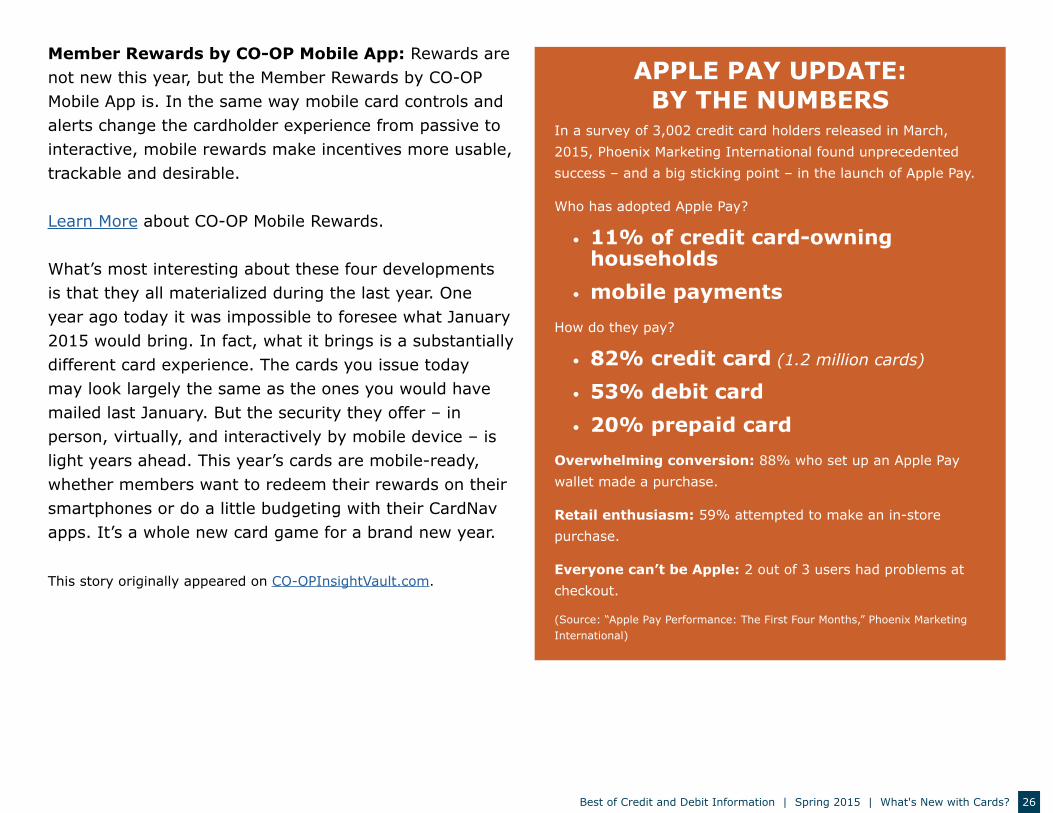

APPLE PAY UPDATE: BY THE NUMBERS

In a survey of 3,002 credit card holders released in March, 2015, Phoenix Marketing International found unprecedented success – and a big sticking point – in the launch of Apple Pay.

Who has adopted Apple Pay?

• 11% of credit card-owning households

• mobile paymentsHow do they pay?

• 82% credit card (1.2 million cards)

• 53% debit card• 20% prepaid card

Overwhelming conversion: 88% who set up an Apple Pay wallet made a purchase.

Retail enthusiasm: 59% attempted to make an in-store purchase.

Everyone can’t be Apple: 2 out of 3 users had problems at checkout.

(Source: “Apple Pay Performance: The First Four Months,” Phoenix Marketing International)

27Best of Credit and Debit Information | Spring 2015 | What's New with Cards?

As much as rewards programs have become table stakes for credit cards, do you ever wonder if your rewards program could be more rewarding?

CO-OP recently released a mobile app to go along with its Member Rewards by CO-OP program. Using the Member Rewards by CO-OP mobile app, members can:

• View account status, statement history and point balances

• Search for local deals and Shop Main Street merchants

• Redeem points and use eGift cards in real time from their phones

• Review program terms and conditions.

Suddenly, rewards are usable anytime, anywhere. Gone are your members’ frustrations with not knowing how many points they have, not remembering which merchants participate, not being able to convert points to gift cards on the spot, and not having the gift cards handy when they’re ready to pay. Instead, every aspect of your rewards program is synced up and ready to use, wherever your members may be.

By Samantha Paxson, Chief Marketing Officer

MOBILE THAT MOTIVATESAccording to a recent Cisco retail banking survey, 75 percent of global respondents would move their money for one or more of these five items:

1. virtual financial advice2. virtual mortgage advice3. automated investment advice4. mobile branch recognition5. mobile payments

As people in all age categories become increasingly mobile-dependent, empowering members with new ways to manage their money via mobile device becomes an ever-larger motivator.

Do your members manage their card accounts by mobile device? Could they?

Could Your Rewards Program Be More Rewarding?

28Best of Credit and Debit Information | Spring 2015 | What's New with Cards?

A rewards program that is exponentially more rewarding for members is bound to be more rewarding for you – more likely to build loyalty and usage, and more likely to help you stand out from the competition.

Just because rewards have become entry level for credit card issuers doesn’t mean the rewards experience should remain basic. By enhancing the experience – and the usability – of your rewards program, you raise the profile on everything you do.

This story originally appeared on CO-OPInsightVault.com

5. New Tools in a Changing Environment

TIGHTENING UP SECURITY

30

Some of the biggest news – and hottest innovations – on the card front relate to security. In the aftermath of the 2013 Target breach – and the hundreds of breaches that have occurred since – security remains a top priority for cardholders, and never more so than in today’s world of mobile commerce and increased spending.

In this section, find out more about member attitudes toward security, and three security technologies that are changing the way we pay – tokenization and Apple Pay, EMV, and CardNav by CO-OP card controls and alerts. Although each has its own niche, all three technologies add up to the same result: Members want to use their cards and card accounts, and they want to use them securely.

Underlying each of these stories is more good news for credit unions. Not only do credit unions have the ability to stay up to speed on security advances, but in some cases they are leading the charge. Credit unions have been among the earliest participants in Apple Pay. And with CardNav mobile card controls and alerts, they are leading the charge.

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

31

Happy Birthday, Target Breach! Now Go Away.By Samantha Paxson, Chief Marketing Officer

America lost a good deal of its financial complacency when Target announced on December 19, 2013, that data on millions of its customers had been breached. Suddenly, everyone knew what they should have known years before: Every retailer that handles your payment data is a point of vulnerability.

A survey conducted by the Ponemon Institute for Experian Data Breach Resolution in April 2014 uncovered some interesting insights into how consumers experience data breaches:

• Between 2012 and 2014, the percentage of respondents who had experienced a data breach doubled.

• 76 percent of respondents who had experienced a data breach reported stress as the primary impact.

• 62 percent had received two or more data breach notifications involving separate incidents.

What did respondents want companies to do following a data breach?

• Compensate victims with cash, products or services: 67 percent

• Provide identity theft protection: 63 percent

• Provide credit monitoring services: 58 percent

According to the survey, data breach victims want frank communication. Asked what could have been done to improve communication following a data breach, 67 percent wanted more explanation of the risks and harms they might experience; 56 percent wanted disclosure of all facts; and 33 percent didn’t want the facts to be sugar-coated.

Meanwhile, who is responsible for data breaches? CUNA has unleashed a campaign – Stop The Data Breaches – to activate consumers around the issue of retailer responsibility by asking Congress to set consistent data security standards for merchants.

It’s unclear whether consumers understand who is responsible for breaches – on any level. Is it merchant vulnerability or a card issuer problem that creates the opportunity for a data breach? Is it the merchant or the issuer who foots the bill? By raising awareness around this issue, perhaps CUNA can help educate the public about how data breaches unfold, and what credit unions are doing in response.

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

32

According to CUNA data, the Target breach alone caused credit unions to reissue 4.6 million credit and debit cards at a cost of $30.6 million.

In recapping the major implications that the Target breach caused, we might like to now send the problem of merchant data breaches off on a nice, permanent vacation. That isn’t likely to happen. The Identity Theft Resource Center reports that 720 data breaches have occurred in 2014, exposing nearly 82 million records. Of these, approximately 79 percent of compromised records are attributed to “businesses.”

Fight Insecurity

What can credit unions do to address this ongoing problem? Here are a few action steps:

• Make security a top priority. Give your credit union the tools and resources necessary to combat fraud – and to respond quickly and effectively to fraud occurrences, including merchant data breaches. Security technology, such as EMV and tokenization, may be worth the expense in fraud savings. And mobile card controls like CardNav by CO-OP can reduce exposure.

• Want a step-by-step guide to preparing for a merchant breach? Check out “Tackling the Target Breach,” a 10-step guide for credit unions. Read Now

• Improve communication. In the case of communicating about data breaches and fraud, you simply cannot be too good. Members are anxious about this topic, so information is welcome and needed. This subject is complicated: To the extent that you can help members figure out clearly what’s happening and how they can best respond, you’ll provide valuable help and build trust with your members.

• Check out stopthedatabreaches.com. This initiative is worth a look, not only for the political action it seeks, but also for the information and perspective it provides into the relationship between consumers, merchant breaches and credit unions.

This story originally appeared on CO-OPInsightVault.com.

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

33

Will Tokenization Eat EMV’s Lunch?By Michelle Thornton, Manager, Core Products

With so much news about tokenization, it’s easy to forget about that other security issue we’ve been debating about this year: EMV.

In many ways, EMV is tokenization’s opposite twin. EMV adoption has been years in the making. Tokenization hit the scene like a lightning bolt. EMV works with an existing format: plastic cards. Tokenization aims to make Plastic cards obsolete. Tokenization carries with it the Apple mystique. EMV? Not so much.

It’s not surprising, then, that many now wonder whether tokenization will eat EMV’s lunch – making the issue of EMV strategy and adoption irrelevant. Who needs EMV when you’ve got tokenization, right?

Well, choosing between tokenization and EMV is a little like choosing between your twin children. It’s the wrong idea. For reasons that go beyond the sentimental, you want both.

In the simplest possible terms, tokenization is designed to enhance security on cardless transactions – mobile and online commerce, as well as contactless point-of-sale. EMV secures card-based transactions, using a specialized chip housed right in the plastic. Each technology is

brilliant at what it does. And each one is less brilliant at standing in for the other.

Interestingly, too, the adoption of one may fuel adoption of the other. That is, the October 2015 liability shift for non-EMV transactions is prompting merchants across the country to convert to EMV-enabled terminals. In the process, they’re getting Near-Field Communications capabilities thrown in for good measure. What powers Apple Pay at the terminal? NFC. Deliberately or not, these two really do work as a team.

So, just as you wouldn’t ask, “Should we prevent fraud or just defend against it?” you don’t have to wonder whether to choose tokenization or EMV. Choose both. Fraud is a nasty business these days. Why not give it a one-two punch?

Have more questions about tokenization?

Download CO-OP FAQs on Tokenization

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

34

As part of CO-OP’s “Innovation in Payments” webinar held November 18, Caroline Willard, EVP, Markets and Strategy, and Michelle Thornton, Manager, Core Products, fielded questions about the latest security technology. What did credit unions want to know?

Does EMV Use Tokenization? Your Questions Answered.By Bill Prichard Senior Manager, Public Relations and Corporate Communications

Q: Is it true that if you hover over an EMV card or an iPhone using Apple Pay, you can capture the data on it?

Q: Does EMV use tokenization?

A: One important thing to remember is that both of these technologies use cryptograms to secure data. So the data that someone might capture as part of an EMV or Apple Pay transaction isn’t repurposeable.

In Apple Pay, the token that is on a particular phone for Apple Pay is specific to that phone: That phone has identifying data. So if a token were used from any other device, it wouldn’t work because the cryptogram wouldn’t have the identifying information from the correct phone.

On the EMV side, there are transaction counters that would show that a new transaction wasn’t valid because the number and cryptogram were already seen in a previous transaction.

A: EMV does not use tokenization; they’re two different technologies. It’s possible to become confused because they do both use similar kinds of technology, so you hear them talked about in the same breath. They both use cryptography, but EMV and tokenization are two distinct things.

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

Michelle ThorntonCaroline Willard

35

Q: In Apple Pay, are tokens assigned per card or per transaction?

Q: Would Apple Pay or EMV have prevented the Target breach?

A: The token is static, but it’s specific to that phone and that card. So, for example, if you’ve got a card and you’ve got three phones, you would have three different tokens. Each phone would have a static and a unique token for that one card.

What is dynamic is the cryptograms around those tokens. Those are unique each time you do a transaction.

A: It wouldn’t have prevented the breach itself, but what EMV would have done is prevented compromised numbers from being used to create counterfeit cards. EMV cards are difficult to reproduce, so fraudsters typically don’t attempt it.

The other part of the question was about whether Apple Pay would have prevented it. Again, it wouldn’t have prevented the breach, but it could have prevented certain types of transactions using those numbers.

CardNav by CO-OP, for a third point, would absolutely have been able to prevent some fraudulent activity by alerting members to suspicious transactions and enabling them to shut down their cards if there was a compromise.

In each case, it’s not so much a question of preventing the breach, but what happens with compromised numbers after a breach occurs. These three technologies can absolutely help in different ways.

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

36

To watch a recording of the full “Innovation in Payments” webinar, click here. Find out more about Apple Pay and tokenization for your credit union here. Learn more about EMV for your credit union here. Get the latest on CardNav by CO-OP mobile card controls and alerts here.

Q: Can CardNav by CO-OP be fully integrated with existing CU mobile apps, so that members can access it using a single sign on?

A: We will be deploying on an API version of CardNav by CO-OP, so you can tuck it into your existing mobile app and have it be accessible to your members without having a separate sign on. That’s on our roadmap for 2015.

LOOKING SHIFTYOctober 15, 2015 On this date, fraud liability will become the responsibility of the non-EMV-capable party – card issuer, merchant, or both. Who’s on the hook for fraud liability now, before the October 15 deadline? Card issuers alone.

EMV IS UPCall it the Year of EMV. The Smart Card Alliance reports that an estimated 575 million EMV chip cards will be issued in the U.S. by the end of 2015 – up from 120 million at the start of the year.

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

37

8 Questions You Asked About CardNavBy Samantha Paxson, Chief Marketing Officer

In CO-OP’s live webinar on CardNav by CO-OP card controls and alerts on October 22, 2014, CO-OP’s Business Manager, Product Development, Ryan Zilker fielded questions from the audience.

What did credit unions want to know about CO-OP’s new remote control product for cards during the recent webinar? Here are some answers.

1. Will CardNav settings overrule funds availability and transaction limits settings that have been made in our core system?

Nothing in CardNav overrides what’s set in the core. CardNav can make a recommendation, but if a user sets a transaction limit of $600 when the host says the limit is $300, the host settings totally override any recommendation by CardNav.

2. How does CardNav affect Falcon Fraud monitoring?

There really is no change to Falcon. The way the process works is that if Falcon would shut a transaction down for any reason, CardNav controls have no impact. Falcon shuts the transaction down and an alert is sent to the cardholder. It’s only when a transaction passes all those initial checks that CardNav control settings come into play.

3. Is CardNav limited to cards on our own BINs?

The BIN must be owned by the credit union and processed by CO-OP. You could not, for instance, load your American Express card into CardNav.

4. Is CardNav only available as a separate app, or can it be integrated into my credit union’s existing app?

Today, what we are rolling out is a separate app. In the future we will be able to make available a version of CardNav that credit unions can brand as their own app – or as a standalone API that they can make part of their own mobile banking app.

When we consider all of these options, we feel that the dedicated CardNav app offers the best experience for your members right now.

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

Ryan Zilker

38

5. Is the CardNav app customizable so that my credit union’s name and logo appear in the App Store?

When members go to search for the CardNav app in the App Store, it is not branded to your credit union. They simply go and search for CardNav. Once the app is downloaded, from that point on the member sees the colors and logo from their credit union.

If you would like to have an app with your own branding at the App Store level, you would need a customizable app. That will be available, but the program and pricing will be slightly different.

6. How does CardNav integrate with Apple Pay?

We’re currently in discussions with Ondot, our partner on CardNav, to see if there’s any potential there.

7. Does CardNav send email alerts?

No, and that was a conscious decision on our part. After reviewing the options of having email or SMS text alerts, we felt that in-app alerts were where the market is going.

8. Will CardNav be available to credit unions that do not use CO-OP as their primary debit processor?

CardNav is available exclusively to credit unions using CO-OP as their debit or in-house credit processor.

To watch a recorded version of “CardNav by CO-OP: Leading the Charge in Card Control,” click here.

Find out more about CardNav at co-opfs.org/cardnav.

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

39

Q&A: Charged Up Over Mobile SecurityBy Samantha Paxson, Chief Marketing Officer

Is this a good time to talk mobile security? After an eventful couple of weeks in the world of mobile payments, we caught up with Dr. Vaduvur Bharghavan, CEO of Ondot Systems, CO-OP’s partner on the CardNav app. We wondered how he was feeling about the potential market for new security-minded apps and the impact CardNav might have.

Q: As quickly as you can, how would you describe CardNav?

Q: Was the announcement of Apple Pay a good thing or a bad thing for a newly-minted card controls and alerts app about to hit the market?

Q: Will CardNav change users’ relationship with their payment cards?

A: CardNav empowers cardholders to “remote control” their payment cards from a smartphone app. Your members can lock or unlock their payment cards with just a tap on the app; specify locations, merchants, purchase methods, and spend limits to control card usage; and act instantly on near real-time alerts. Credit unions are all about member satisfaction, and CardNav promotes this goal by giving cardholders the security they need with the convenience they want.

A: Apple Pay in particular, and wallets in general, are complementary to what CardNav tries to do. The purpose of Apple Pay is to make the iPhone your payment card. The purpose of CardNav is to let you determine when and where your payment card can be used, regardless of whether it is the plastic card in your wallet or eCommerce or newer contactless payment methods. CardNav is for cards what mobile banking is for accounts.

A: We believe so. The payment card today is a lifeless piece of plastic. CardNav allows cardholders to add intelligence to their existing card usage without having to change the payment card. Your members can specify how their own cards and their dependents’ cards can be used, and interact in near real-time when they transact.

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

Dr. Vaduvur Bharghavan

40

Q: Are card controls and alerts going to be a Next Big Thing in financial services?

Q: Do you have a favorite CardNav feature?

A: We believe that card controls will become a “best practice” for payment cards in the industry. With increasing fraud and high profile card compromises occurring monthly, and with increasing sophistication of consumers in using their smartphones, giving consumers control and visibility over their most prolific payment instruments is a natural thing to do.

A: My Location. My card should be active where I am, for in-store purchases.

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

41

On October 16, Bethpage Federal Credit Union in Bethpage, N.Y., became the first credit union to launch CardNav by CO-OP – a brand new app that enables members to control their credit and debit card accounts using their mobile devices. News spread quickly throughout the credit union press:

“Growing concerns here regarding the risk of debit card fraud led Bethpage FCU to be the first CU to partner with CO-OP Financial Services and its CardNav app,” wrote W.B. King in the Credit Union Journal on November 3. “After a 60-day trial, members are embracing the solution.”

The Credit Union Times also reported on Bethpage’s launch of CardNav: “We had a successful pilot phase with very positive feedback from our testers, which included about 30 of our credit union employees,” Shanta Sewnarain, Assistant Vice President, operations and risk at the $5.7 billion Bethpage, said in the CU Times story of October 29. “One tester shared that his usage control was set as ‘my location.’ His location is New York and he received an alert for a transaction in New Jersey. CardNav immediately denied the transaction based on location.”

Sewnarain continued: “Another user told us, ‘I know immediately when and where my card is used. I can

block specific transactions and merchants, and place my spending limit on a budget. It is just awesome and I wish we had this a long time ago.’”

Noting that fraud is an ongoing concern for consumers, with interest in “tools such as transaction authorization controls, instantly viewable transactions and text message alerts to help them protect their accounts” on the rise, the CU Journal pointed out likely benefits for Bethpage FCU as well:

“Although we are still in the early stages of the service, we anticipate that the savings will be in the form of

Hot off the Presses, CardNav Debuts at Bethpage FCUBy Bill Prichard, Senior Manager, Public Relations and Corporate Communications

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

42

reduced fraud losses,” Sewnarain told the CU Journal. “We are currently targeting a specific group of members to determine fraud savings, based on the users of CardNav versus those who are not using it.”

“It is an optional tool for our members, so marketing and member awareness will be key to increased usage, so that both our credit union and our members will benefit from reduced fraud,” Sewnarain continued.

Several industry publications responded to the Bethpage FCU story, including DepositAccounts.com. Along with a link to the CU Times story, the site commented: “It would be great to see more financial organizations offer this capability. Credit cards generally offer greater protection than debit cards if they are lost, stolen, or used fraudulently.”

To learn more about CardNav by CO-OP, click here.

Best of Credit and Debit Information | Spring 2015 | New Tools in a Changing Environment

6. Building Relationships from

the Inside Out

CARDS IN CONTEXT

44Best of Credit and Debit Information | Spring 2015 | Building Relationships from the Inside Out

Credit and debit remain two of the closest and most frequent connections you can have with your members. In the preceding pages we’ve looked at some of the ways you can evolve your card programs and grow. But card programs don’t exist in a vacuum. While you work on sharpening your card game, consider how the relationship you have with cardholders reflects on your larger brand.

The way you position your cards is, in large measure, the way you position yourself:

• Technology leader

• Secure

• Easy and fun to use

• Fast, efficient

• Ready to provide service

• First in class

• Rewarding

As technology plays a growing role – and standards for member experience and operational excellence continue to rise – integration is a critical theme. This refers to the integration of your various systems and technology. It also means integrating everything you offer to members into a single, coherent, brilliant package. The attributes of your card program should be part of a larger identity that includes the best of branch transformation, mobile and online banking, ATM innovations, member service – and everything you do.

45

Is Your Credit Card Program Integrated Enough For You?By Samantha Paxson, Chief Marketing Officer

Best of Credit and Debit Information | Spring 2015 | Building Relationships from the Inside Out

INSIGHT VAULT: We’ve been hearing a lot in the industry about how consumers want integration. Is the same true for credit unions?

KERRY: In relationship to credit card processing, we hear all the time from credit unions that they are looking to streamline and to reduce the amount of friction they experience between systems. What I mean by that is, they want to be able to view member data on credit, debit and ATM without logging into different vendor systems. Ideally, many want to reduce the number of vendors as well, so that they don’t have to worry about competing or incompatible systems.

That desire helped motivate CO-OP to partner with The Members Group for full-service credit processing. Through that partnership, we’ve been able to offer credit unions the best of debit and credit processing in an integrated whole. Our systems work together, and so do we.

Our credit union clients use a single log-in credential for debit and credit card platforms. By making it easier to view member data across platforms, we hope we’re making it easier to understand and put that data to use.

Do you crave greater integration in your credit union work? We hear you. If you hope to improve your member experience, the tools and processes you use must improve as well. Insight Vault caught up with Jennifer Kerry, Vice President of Credit Issuer Processing at CO-OP Financial Services, to ask a few questions about how CO-OP is applying the idea of integration to its credit programs.

Jennifer Kerry

46

Learn more about CO-OP Full Service and In-House Credit here.

Best of Credit and Debit Information | Spring 2015 | Building Relationships from the Inside Out

INSIGHT VAULT: Credit also has many components to it. Is there a need for the various components to work together more effectively as well?

INSIGHT VAULT: Does that create an integration challenge for CO-OP?

KERRY: That’s true in so many ways. For a long time now, speed and integration have been critical in fraud prevention and detection, for example. No one questions the need for the best and fastest integration when the issue is fraud.

But we’re looking to apply the same principles across the board. We know that having a rewards program is table stakes. Now the question is, how easy is it for members to understand and use their rewards? We’re working on some exciting new ideas to make member rewards more engaging – and easy for credit unions and their members to use.

KERRY: It’s a challenge we’ve been working toward for years now. The idea is for credit unions to be able to upgrade and enhance their programs easily, without costly and disruptive transitions. By thinking this way, we’ve been able to develop some compelling new APIs we think credit unions – and their members – will love. And they won’t require massive investments of time and resources to get up and running. By making things easy, integration should provide an incentive for credit unions and their members both to add and use the best technology available.

Our work on the front end should save effort for the end user, whether that user is a credit union member or one of our member credit unions.

47

CO-OP Products to Up Your Card Game

CO-OP DebitCO-OP Debit is a solution that not only combines PIN and signature transactions into a single platform, but provides a completely comprehensive portfolio of debit capabilities. CO-OP Debit goes beyond the transaction to provide everything you need to encourage debit card use and prepare for tomorrow’s opportunities. Learn More

CO-OP Credit: Full Service & In-HouseA single platform for debit and credit streamlines your operational processes and simplifies your portfolio management by having a single trusted CO-OP account representative, a single invoice, volume discounts and industry-leading fraud prevention and management, as well as a fully managed loyalty program. Learn More

CardNav by CO-OPCardNav by CO-OP also adds another layer of security to your in-house card programs. Members can deactivate their cards in real-time when not in use and set alerts that will let them know if a card is used in an unusual or unapproved manner. Learn More

CO-OP RevelationCO-OP Revelation was designed to help you manage your card programs, engage your members, boost your bottom line and ultimately grow your credit union. Learn More

Member Rewards by CO-OPDrive debit and credit transactions with help from one of the most powerful motivational tools used by large issuers. Member Rewards by CO-OP provides incentives that increase both member loyalty and appeal to prospective members. It offers a tremendous opportunity to cross-sell your products with rewards for any loan product or bill payment. Learn More

Best of Credit and Debit Information | Spring 2015 | Building Relationships from the Inside Out

48

More Fast + Brilliant Products from CO-OP

Best of Credit and Debit Information | Spring 2015 | Building Relationships from the Inside Out

CO-OP ATMCO-OP ATM offers you the simplest yet most innovative and comprehensive program available. It’s complete with all the features you need to reduce costs, technical issues, security concerns and overhead, allowing you to implement the most effective ATM solution for today, and plan for the future. Learn More

CO-OP MobileThe new and improved CO-OP Mobile offers a full-featured mobile solution for both iPhone and Android, fully customizable with your credit union branding and with more standard and optional features. Learn More

Sprig by CO-OPSprig® by CO-OP is a virtual credit union wallet that combines all the accounts a member holds from any institution in the network together in one spot. Learn More

RealPay by CO-OPRealPay by CO-OP makes it possible for your members to send money to anyone from the convenience of their mobile phones and is offered as a function of Sprig, a component of the new CO-OP Mobile or as an API which can be integrated into your mobile offering. Learn More

CO-OP Digital BankingCore Integrated Solution: In partnership with Alkami Technology, CO-OP offers a high-end core integrated mobile and online banking solution including CO-OP Bill Pay functionality. Learn More