Co-authors Dr. Barry Barnett and Benjamin Collier · Dr. Barry Barnett and Benjamin Collier. ......

24

Jerry Skees University of Kentucky President , GlobalAgRisk, inc Source: UNFCCC, 2007 Co-authors Dr. Barry Barnett and Benjamin Collier

Transcript of Co-authors Dr. Barry Barnett and Benjamin Collier · Dr. Barry Barnett and Benjamin Collier. ......

Jerry Skees

University of Kentucky President , GlobalAgRisk, inc

Source: UNFCCC, 2007

Co-authors

Dr. Barry Barnett and Benjamin Collier

Benefit and Challenge of Offering Agricultural

Insurance

� Household asset portfolio

� Insurance reduces the variance in livelihoods/returns

� Allow more risk taking� Allow more risk taking

� Asymmetric Information

� Adverse selection/ Hidden information

� Moral hazard / Hidden actions

� Correlated Risk Problem

Weather Risk and Insurance

Pure Risk

� FrequencyRegularity of weather event (drought)

� SeverityMagnitude of the event

Using historical data to forecast losses

Probability Density Function

Ce

ntr

al T

en

de

ncy

Using historical data to forecast losses

Severity

Fre

quency

0 500 1000 1500 2000 2500 3000 3500

High-Frequency, Low-Severity Events

Variance around the median

Low-Frequency, High-Severity Events

Tails of the distribution

Ce

ntr

al T

en

de

ncy

Cognitive Failure

Households often fail to plan

for infrequent, severe risks

Pricing Agricultural Insurance

Price of Insurance = Cost of the riskPure risk

Ambiguity load

Catastrophe load

+ Administrative costs+ Administrative costsControlling adverse selection

Monitoring moral hazard

Loss adjustment

Delivery costs

+ Cost of Ready Access to CapitalReinsurance

Insurer Reserves

Multiple Peril Crop Insurance

� Provides expensive, but comprehensive coverage

� Covers many types of risk

� High administrative costs

� High cost of capital� High cost of capital

� Relies on government subsidies

� Costs are increased for lower income countries

� Small farms

� Poorer access to reinsurance

� Poor actuarial performance

Index Insurance

1. Area-Yield Index Insurance

2. Weather Index Insurance

� Lower Administrative Costs

� Low asymmetric information problems� Low asymmetric information problems

� No individual loss adjustment

� Better potential than MPCI in lower income countries

� Several pilot programs with good progress

� Need more time to evaluate fully

Country Risk Event Index Measure Target User Status

Bangladesh Drought Rainfall Smallholder rice farmersIn development;

pilot launch planned for 2008

Caribbean

(CCRIF)

Hurricanes and

earthquakes

Indexed data from

NOAA and USGSCaribbean country governments Implemented in 2007

China Low, intermittent rainfallRainfall and storm

day countSmallholder watermelon farmers

Implemented June, 2007 in

Shanghai only

Ethiopia

Drought Rainfall WFP operations in EthiopiaUSD 7 million insured for

2006;

Drought Rainfall Smallholder farmers 2006 pilot

DroughtSatellite and weather

dataNGO Implemented in 2007

Honduras Drought Rainfall In development

India Drought and flood Rainfall Smallholder farmers Pilot began in 2003India Drought and flood Rainfall Smallholder farmers Pilot began in 2003

Kazakhstan Drought Rainfall Medium and large farms In development

Kenya DroughtSatellite and weather

dataNGO Implemented in 2007

Mali DroughtSatellite and weather

dataNGO Implemented in 2007

Malawi Drought RainfallGroundnut farmers who are members

of NASFAM

Pilot began in 2005;

Mexico

Natural disasters

impacting smallholder

farmers (drought)

Rainfall, windspeed,

and temperature

State governments for disaster relief;

Supports the FONDEN program

Pilot began in 2002

Major earthquakesRichter scale

readings

Mexican government to support

FONDENIntroduced in 2006

Source: Authors (An earlier version published in Barnett, Barrett, and Skees, n.d.)

Country Risk Event Index Measure Target User Status

Mexico(Continued)

Drought affecting livestock

Normalized

Difference Vegetation

Index

Livestock breeders Launched in 2007

Insufficient irrigation

supplyReservoir levels

Water user groups in the Rio

Mayo areaProposed

MongoliaLarge livestock losses due

to severe weather

Area livestock

mortality rateNomadic herders

Second pilot sales season of

pilot completed in 2007,

Morocco Drought Rainfall Smallholder farmersNo interest from market due to

declining trend in rainfall

NicaraguaDrought and excess rain

duringRainfall Groundnut farmers Launched in 2006

Peru

Flooding, torrential rainfall

from El Niño

ENSO anomalies in

Pacific OceanRural financial institutions Proposed

Perufrom El Niño Pacific Ocean

DroughtArea-yield production

indexCotton farmers Proposed

Senegal DroughtRainfall and crop

yieldSmallholder farmers Proposed

Tanzania Drought Rainfall Smallholder maize farmers Pilot implementation in 2007

Thailand Drought Rainfall Smallholder farmers Pilot implementation in 2007

Ukraine Drought Rainfall Smallholders Implemented in 2005

VietnamFlooding during rice

harvestRiver level

The state agricultural bank and,

ultimately, smallholder rice

farmers

In development

Source: Authors (An earlier version published in Barnett, Barrett, and Skees, n.d.)

Climate Change and Insurance

� Consensus that climate change is occurring and will affect farming

� Increases in temperatures

� More extreme rainfalls (drought and excess rain)More extreme rainfalls (drought and excess rain)

� Models do not agree on the extent

� Poor predictive ability on the regional level

� Climate change affects the weather risk

1. Changing the norm—the central tendency

2. Increasing variability—weather variance

Figure 10.18

Source: IPCC, n.d.

Changes in the Central Tendency

� The price of insurance is very sensitive to shifts in the central tendency

� The majority of weather events occur around the central tendencytendency

� The central tendency is the foundation for establishing the pure risk

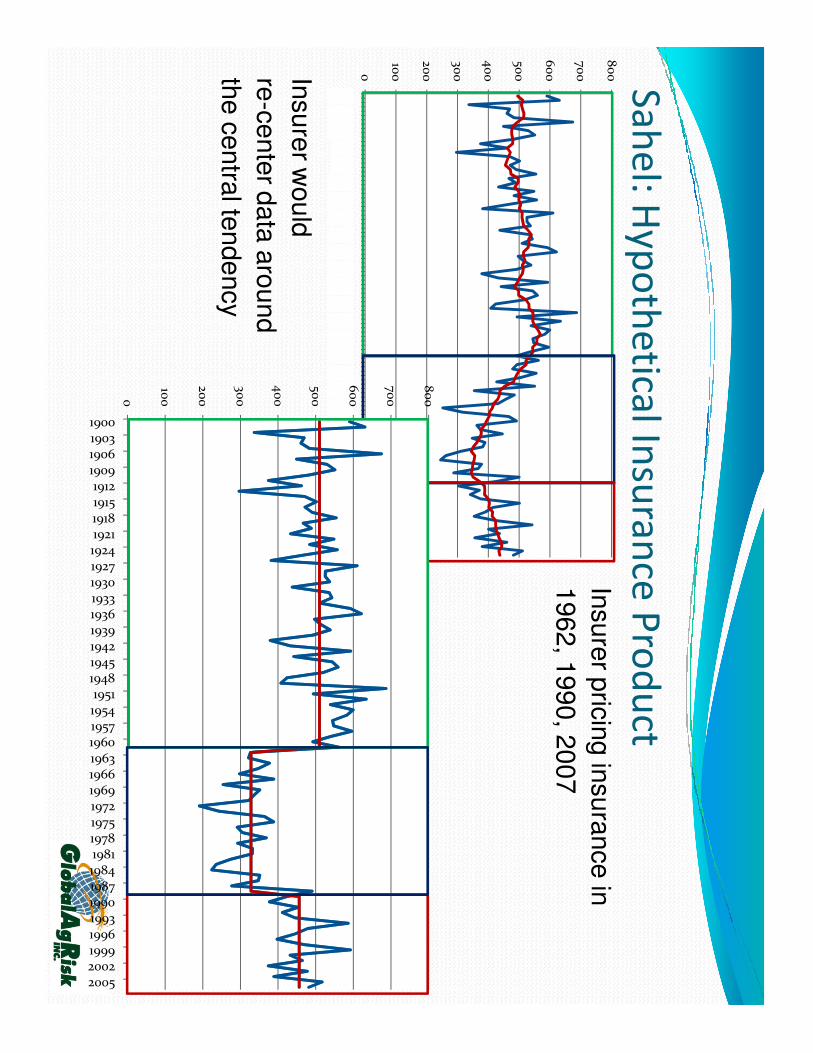

Sahel: Shifts in the Central Tendency

700

800

Sahel data 1900 – 2006

0

100

200

300

400

500

60019

00

190

4

190

8

1912

1916

1920

1924

1928

1932

1936

194

0

194

4

194

8

1952

1956

196

0

196

4

196

8

1972

1976

198

0

198

4

198

8

199

2

199

6

200

0

200

4

Sahel

Semi-arid region below the Sahara

• Dynamic climate largely due

to oceanic oscillations

• Unlike the Sahel, climate

change may lead to more

permanent changes

Sa

he

l: Hy

po

the

tical In

sura

nce

Pro

du

ctIn

su

rer p

ricin

g in

su

ran

ce

in

19

62

, 19

90

, 20

07

200

300

40

0

500

60

0

700

80

0

80

0

0

100

1900

1904

1908

1912

1916

1920

1924

1928

1932

1936

1940

1944

1948

1952

1956

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

0

100

200

300

40

0

500

60

0

700

190019031906190919121915191819211924192719301933193619391942194519481951195419571960196319661969197219751978198119841987199019931996199920022005

Insu

rer w

ou

ld

re-c

en

ter d

ata

aro

un

d

the

ce

ntra

l ten

de

ncy

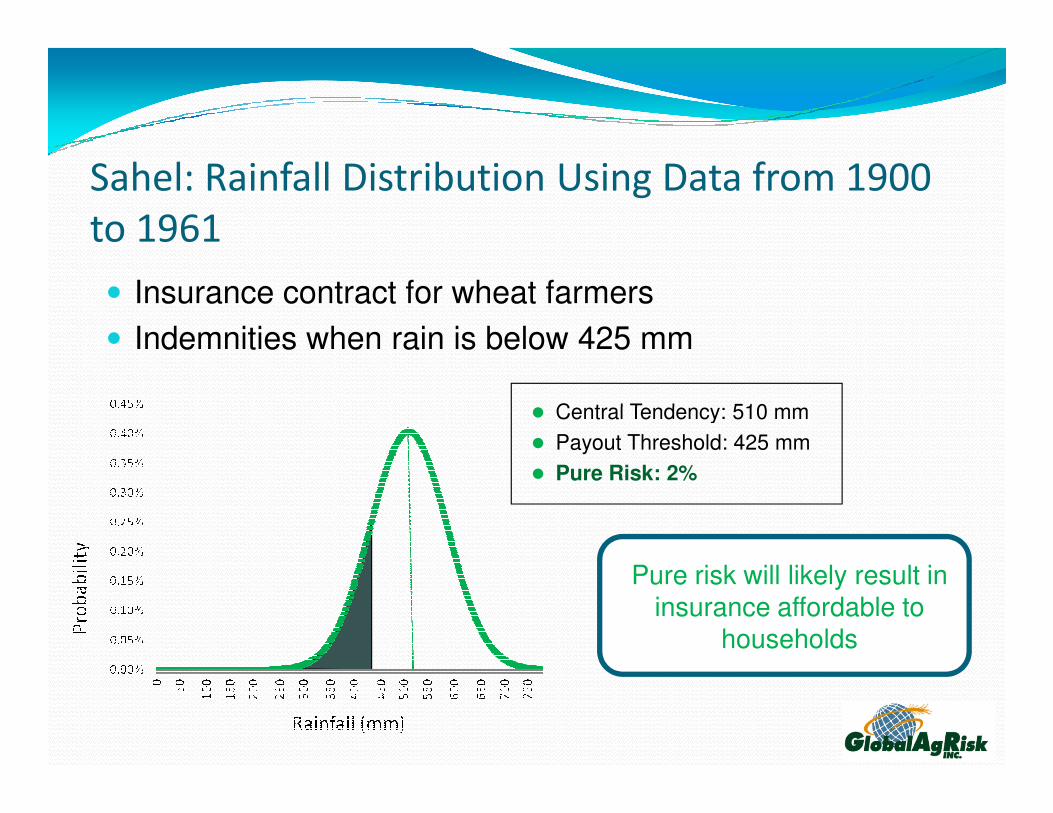

� Central Tendency: 510 mm

Sahel: Rainfall Distribution Using Data from 1900

to 1961

� Insurance contract for wheat farmers

� Indemnities when rain is below 425 mm

� Central Tendency: 510 mm

� Payout Threshold: 425 mm

� Pure Risk: 2%

Pure risk will likely result in insurance affordable to

households

Sahel: Rainfall Distribution Using Data from 1962

to 1989

� Central tendency is below payout threshold

� Insurance is inappropriate in this setting

� Central Tendency: 328 mm

Pure risk would make

insurance unaffordable for

households

� Central Tendency: 328 mm

� Payout Threshold: 425 mm

� Pure Risk: 44%

Sahel: Rainfall Distribution Using Data from

1990 to 2006

� Increases in rainfall reduced the weather risk

� Insurance would be affordable depending on other costs

(Delivery, ambiguity loading, etc.)

Pure risk may result in

affordable insurance for

households

� Central Tendency: 456 mm

� Payout Threshold: 425 mm

� Pure Risk: 6%

Climate Change Increases Ambiguity and

Catastrophe LoadsMisestimating the central tendency is very costly

Green distribution Insurer forecast in 1962

Blue distribution Actual loss experience of next 30 years

Insurers expecting climate change greatly increase

ambiguity and catastrophe loads

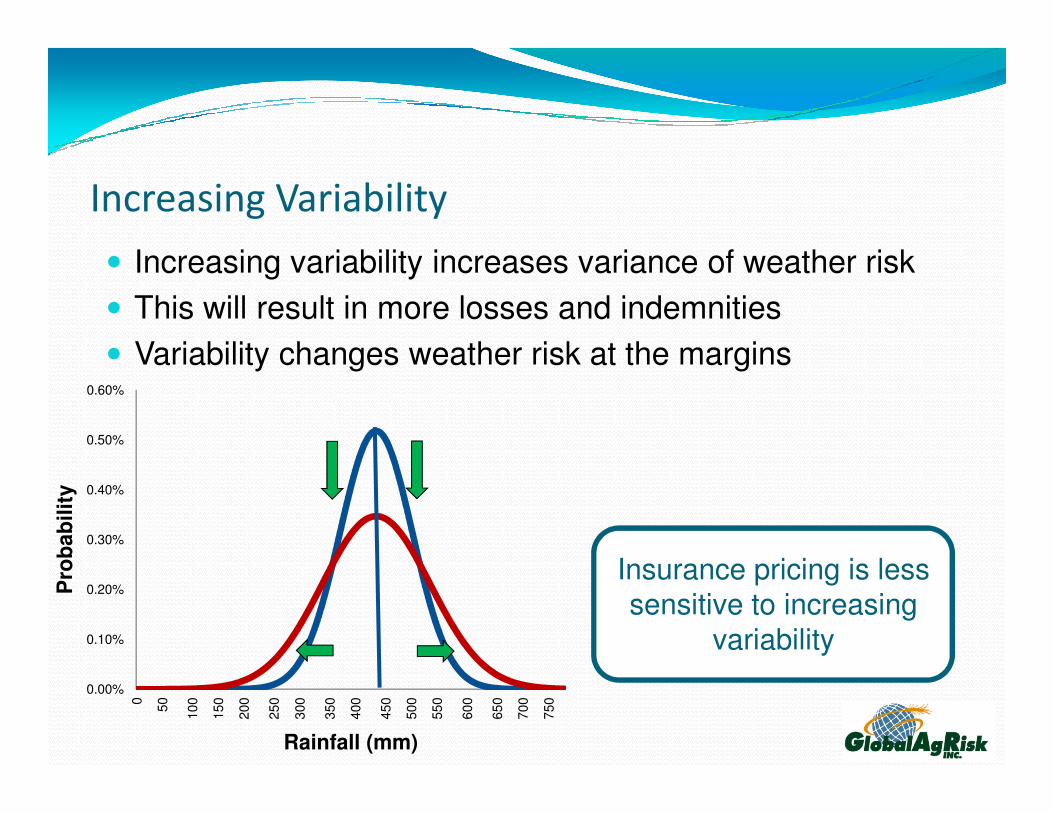

Increasing Variability

� Increasing variability increases variance of weather risk

� This will result in more losses and indemnities

� Variability changes weather risk at the margins0.60%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0

50

100

150

200

250

300

350

400

450

500

550

600

650

700

750

Pro

ba

bil

ity

Rainfall (mm)

Insurance pricing is less

sensitive to increasing

variability

Farmers knowledge and decision processes

� Literature shows

farmers optimize

farmers adaptfarmers adapt

farmers are good Bayesians

farmers know central tendency on yields

cognitive failure sets in for catastrophic events

CHALLENGE –

Communicating information about climate change in a fashion that decision makers can use that information

Insurance and Climate Change

� Insurance can be appropriate in limited contexts of climate change because of effects on the price

1. Pure risk effects

� Depends on the degree of climate change

Depends on the type of change (central tendency and/or � Depends on the type of change (central tendency and/or variability changes)

2.Ambiguity and Catastrophe load effects

� Depends on the level of uncertainty regarding future changes (ability to forecast)

� Price signals can push households to make difficult decisions to adapt

Adaptation, Policy Interventions, and Climate

Change

� Households must adapt or experience increasing farm losses

1. Change farming practices

2. Transition out of farming2. Transition out of farming

� Governments and donors can help

� Insurance, by itself, is not a means of adaptation

� So governments must be careful if they choose to support insurance

� Insurance can be used to facilitate adaptation

(e.g., linking insurance, credit, and improved seed varieties in Malawi)

Insurance Subsidies and Farmer Production

Decisions

� Policy makers � premium subsidies for insurance

� Insurance subsidies and shifts in the central tendency

� Farmers make production decisions around central tendency

� Farmers incorporate insurance subsidies into production � Farmers incorporate insurance subsidies into production decisions

� This can distort household incentives to adapt—taking more risk at the government’s expense� Experience of developed nations with MPCI

� Insurance subsidies and increasing variability

� Farmers are less likely to change production decisions based on increasing variability

� Creates more opportunities for government and donor support

Insurance Facilitating Adaptation

1. Risk Layering Approach� Government provides coverage for most extreme risk

� Cognitive failure prevents incentive distortions

� Market product for large risk benefits

1. Pure risk reduced Self-Retention Layer1. Pure risk reduced

2. Catastrophe loading reduced

3. Ambiguity loading reduced

2. Livelihoods Insurance� When possible, insurance

products that increase

household choices to

adapt are preferred0 500 1000 1500 2000 2500 3000 3500

Self-Retention Layer

Market Risk-Transfer Layer

Government Layer

Conclusions

� Government and donor support for insurance should be considered for crowding-in markets

� Insurance must be considered in the larger context of household adaptation to climate change

� Because so many needs exist, on-going premium � Because so many needs exist, on-going premium subsidies may carry high opportunity costs

� Regional uncertainty regarding climate change makes determining where insurance programs will be feasible difficult

� Improvements in forecasting can lower insurance costs and create new opportunities