CNBC Fed Survey: ECB Edition, June 4, 2014

of 13

Transcript of CNBC Fed Survey: ECB Edition, June 4, 2014

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

1/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 1 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

These survey results represent the opinions of 30 of the nations top money managers,

investment strategists, and professional economists.

They responded to CNBCs invitation to participate in our online survey. Their responses werecollected on May 30-June 2, 2014. Participants were not required to answer every question.

Results are also shown for identical questions in earlier surveys.

This is not intended to be a scientific poll and its results should not be extrapolated beyond thosewho did accept our invitation.

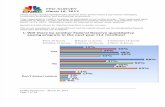

1.Which actions, if any, do you expect the ECB to take at itsmeeting on June 5? (You may select more than oneresponse.)

Other responses:

Hint at QE Conditional LTRO, possible end to SMP

sterilisation

These measures still are not adequate Why the need to do anything tangible

when rhetoric has worked so well?

66%

55%52%

31% 31%

14%

0%

10%

20%

30%

40%

50%

60%

70%

Signal rates

will remainlow for along time

Reduce

refinancingrate

Reduce

deposit rate

Long-term

refinancingoperation

Quantitative

easing

Other

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

2/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 2 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

Average refinancing rate: 0.11 %

Average deposit rate: - 0.10 %

Average:

$1.30 per euro

Avg. euro zone GDP: 1.11 %

Avg. euro zone inflation: 0.73 %

2.What refinancing/deposit rate do you expect the ECB to setat the June 5 meeting?

3-4.What is your forecast for euro zone GDP and inflationyear-over-year percentage change (2014 vs 2013)?

5.What is your year-end forecast for the euro?

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

3/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 3 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

6.What percent do you ascribe to each of these factors toexplain the recent decline in the yield on the 10-year U.S.

Treasury note?

Other: Earnings uncertainty Euro zone deflation or

disinflation

Global disinflation Ten-year yield is as low as it

will be

Two major factors keepingU.S. Treasury yields low:

1) QE tailwind becomes aheadwind - removing an

important inflation driver 2)

U.S. Treasury bonds have a

high relative value compared

with other sovereign debt

options in a low inflationary

global marketplace

US Treasuries look cheapcompared to other developed

sovereign debt

The narrowing of the deficitand shortfall in new Treasury

bond issuances relative to

expectations

Federal Reserve's statementsthat interest rates will remainbelow historically "normal"

rates for some time

30% reduced supply of U.S.treasuries as federal deficit

shrinks; 20% momentum and

the voodoo of chart readers

Correction from oversoldcondition on bonds late last

year and some rebalancing

from stocks to bonds because

of the huge stock rally the

past two years

The bond market is telling usthat U.S. growth is going to

be very modest. The Fed andconsensus are too optimistic.

Stronger bank purchases ofU.S. Treasuries due to stiffer

liquidity rules implemented

at the start of the year

26%

21%

19%18%

9%8%

0%

5%

10%

15%

20%

25%

30%

Flight tosafety

Lowerexpectations

for U.S.growth

Other Lowerexpectations

for U.S.inflation

Expectedactions by

the ECB

Laggedeffects of QE

by the Fed

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

4/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 4 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

7.Do you expect the Federal Reserve will ever allow itsbalance sheet to decline, either by selling assets or

allowing securities it holds to roll off?

91%

4% 4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Yes No Don't know/unsure

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

5/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 5 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

When do you expect the Fed to allow its balance sheet todecline?

Note: In the April survey, the question was phrased as: When do you believe the Fed will begin

reducing the size of its balance sheet?

0%

5%

10%

15%

20%

25%

30%

Oct

Nov

Dec

Jan'15

Feb

Mar

Apr

May

JunJul

Aug

Sep

Oct

Nov

Dec

Jan'16

Feb

Mar

Apr

May

JunJul

Aug

Sep

Oct

Nov

Dec

Jan'17

AfterJan

28-Apr 4-Jun

Averages:

April 28 survey:October 2015

June 4 survey:March 2016

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

6/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 6 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

8.When do you think the FOMC will first increase the fedfunds rate?

0%

5%

10%

15%

20%

25%

Averages:

April 28 survey:

July 2015

June 4 survey:

August 2015

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

7/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 7 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

9.What is your forecast for year-over-year percentagechange in the headline U.S. CPI?

1.78%

2.02%

0%

1%

2%

3%

4%

5%

2014 vs 2013 2015 vs 2014

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

8/13

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

9/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 9 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

11. What do you expect the yield on the 10-year Treasurynote will be on ?

2.80%

3.10%

3.33%3.39%

3.00%

3.18%

3.08%

2.95%2.89%

2.53%

3.44%3.37%

3.32%

3.21%

2.90%

3.54%

3.24%

2.0%

2.5%

3.0%

3.5%

4.0%

Jun 18'13

Jul 30 Sep 6 Sep 30 Oct 29 Dec 17 Jan 28'14

Mar 18 Apr 28 Jun 4

Survey Dates

June 30, 2014 December 31, 2014 June 30, 2015

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

10/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 10 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

12. What is your forecast for the year-over-year percentagechange in real U.S. GDP for ?

Jan

29,

'13

Mar19

Apr30

Jun18

Jul 30Sep17

Oct29

Dec17

Jan

28,

'14

Mar18

Apr28

Jun 4

2014 +2.56 +2.60 +2.62 +2.56 +2.52 +2.63 +2.53 +2.62 +2.77 +2.78 +2.75 +2.33

2015 +2.90 +3.02 +3.00 +2.81

+2.56%

+2.60% +2.62%

+2.56% +2.52%

+2.63%

+2.53%

+2.62%

+2.77% +2.78% +2.75%

+2.33%

+2.90%

+3.02% +3.00%

+2.81%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2014 2015

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

11/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 11 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

13. Where do you expect the fed funds target rate will be on ?

Jul 31Jun

18

Jul 30 Sep 6Sep

17

Oct

29

Dec

17

Jan

28 '14

Mar

18

Apr

28

Jun 4

June 30, 2014 0.20% 0.18% 0.16% 0.14% 0.13% 0.14% 0.16% 0.13% 0.17% 0.12%

Dec 31, 2014 0.28% 0.21% 0.21% 0.20% 0.19% 0.15% 0.27% 0.17%

Dec 31, 2015 0.97% 0.92% 0.82% 0.70% 0.72% 0.83% 0.99% 0.68%

0.20%

0.18%0.16%

0.14% 0.13% 0.14%

0.16%

0.13%

0.17%

0.12%

0.28%

0.21% 0.21%0.20%

0.19%

0.15%

0.27%

0.17%

0.97%

0.92%

0.82%

0.70%0.72%

0.83%

0.99%

0.68%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

12/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 12 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

14. What is your primary area of interest?

Comments:

Lynn Reaser, Point Loma Nazarene University: Monetary policyis approaching a critical split in the road as the ECB shifts to moreease, the Fed begins to tighten, and the BOJ maintains its currentstance.

John Kattar, Ardent Asset Advisors: Over the past 100 years orso, the Fed has increased its balance sheet by just over 7% per year(using adjusted monetary base from the St. Louis Fed as a proxy).

Given the size of the current balance sheet, that would equate toover $300 billion per year and $25 billion per month of growth,whether it's called QE or not. Although I expect QE to end in the fall,I think it will revert to something like $25 billion per monthsometime in 2015.

Economics50%

Equities25%

Fixed Income

4%

Currencies0%

Other

21%

-

8/12/2019 CNBC Fed Survey: ECB Edition, June 4, 2014

13/13

CNBC Fed Survey: Special ECB Edition June 4, 2014Page 13 of 13

FED SURVEY: Special ECB EditionJune 4, 2014

Subodh Kumar, Subodh Kumar & Associates: Central banksneed to avoid augmenting sense of dependency in the markets of

relief from risk by monetary action. With the history of stateintervention in Europe, this is a particular risk of QE for the ECB. Itneeds also to get the euro rate lower in order to boost poor growth.This mix augurs for volatility to rise in global markets.

William Larkin, Cabot Money Management: Deflationary factorstoday are being generated from surplus capacity across the globe,which is keeping interest rates lower longer than a rational investormight have expected. This is a factor of the inter-connectivity of our

worldwide financial and economic systems.

Joel Naroff, Naroff Economic Advisors: The major issue facingthe Fed is: can businesses hold down pay increases once fullemployment is approached? Since that should be by early 2015, theuncertainty will likely cause Fed officials to start raising the specterof higher rates by year's end.

Diane Swonk, Mesirow Financial: Markets are underestimating

the impact of falling deficits on Treasury bond yields. The shortfall insupply is quite substantial, especially in a world where Putin hasshown his hubris.

Allen Sinai, Decision Economics: This will probably be the secondlongest postwar economic expansion and nearly the best equity bullmarket since World War II.