CLS HOLDINGS PLC HALF YEAR RESULTS 2016/media/Files/C/CLS... · 1,650p per share CLS HOLDINGS PLC...

32

CLS HOLDINGS PLC HALF YEAR RESULTS 2016

Transcript of CLS HOLDINGS PLC HALF YEAR RESULTS 2016/media/Files/C/CLS... · 1,650p per share CLS HOLDINGS PLC...

CLS HOLDINGS PLC HALF YEAR RESULTS 2016

CONTENTS

2

OVERVIEW Fredrik Widlund Chief Executive

FINANCIALS John Whiteley Chief Financial Officer

PROPERTY Simon Wigzell Head of Group Property

MARKETS & SUMMARY

Fredrik Widlund Chief Executive

OVERVIEW A strong six months

Strong underlying business § Geographical diversification § EPRA NAV up 9.6% to 2,282p § Positive FX High yielding and well let portfolio § High volume of leasing activity § Low vacancy rate 3.7% § NIY 243 bps over cost of debt § High and stable cash flow

Increased distribution § +10% to implied 3.2% dividend yield Opportunistic portfolio management § Recycling capital through disposals (£80m)

and acquisitions (£48m) Vauxhall Square § Enhanced planning, office focus § Process to select partner or purchaser for residential tower ongoing

3

Germany £305m

20%

Rest of UK £98m

7%

France £250m 17%

London £847m 56%

Property Portfolio 30 June 2016 £1.5bn

CLS HOLDINGS PLC HALF YEAR RESULTS 2016

OVERVIEW Benefiting from geographical diversification

UK (63% of portfolio) § Valuation - broadly flat § Underpinned by long-term government income § Ongoing development and asset management

opportunities in existing portfolio Germany (20% of portfolio)

§ Valuation uplift 1.4%1

§ Strong tenant demand, vacancies down to 2.1% § Two acquisitions

France (17% of portfolio) § Valuation uplift 1.8%1

§ Robust leasing performance § Non-core disposals

1. Local currency

UK 59%

Germany 23%

France 18%

Contracted Rental Income

£89m pa

4 CLS HOLDINGS PLC HALF YEAR RESULTS 2016

OVERVIEW Brexit in context

§ Limited risk of Brexit impact on existing tenants, apart from general economic slowdown

§ Investment market slowing from uncertainty around Brexit timing and terms

§ London office property fundamentals remain positive, with supply and demand imbalance

§ Rental growth likely to continue, albeit at a reduced rate

§ Sterling weakness and low interest rates support UK real estate

London remains a world city where CLS will continue to invest

5 CLS HOLDINGS PLC HALF YEAR RESULTS 2016

CONTENTS

6

OVERVIEW Fredrik Widlund Chief Executive

FINANCIALS John Whiteley Chief Financial Officer

PROPERTY Simon Wigzell Head of Group Property

MARKETS & SUMMARY

Fredrik Widlund Chief Executive

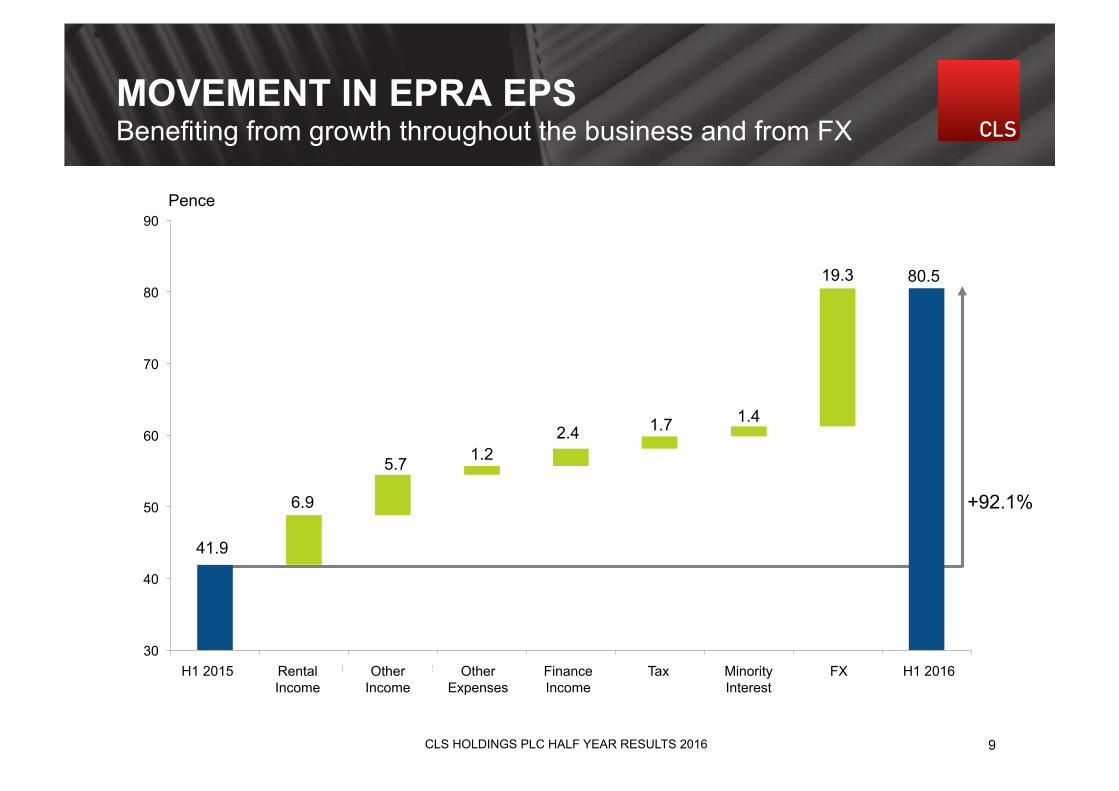

FINANCIALS A strong performance

§ EPRA NAV up 9.6% to 2,282p (31 Dec 2015: 2,083p)

§ EPRA EPS up 92.1% to 80.5p (2015: 41.9p)

§ Portfolio value up 5%

§ Weighted Av. Cost of Debt lowered 13 bps to 3.27% (31 Dec 2015: 3.4%)

§ Interest cover comfortable at 3.6x (2015: 3.1x)

§ Strong cash from operating activities £22.2m

§ 10% increase1 in distributions to shareholders with a proposed £7.2m tender buy-back of 1 in 95 at 1,650p per share

7 CLS HOLDINGS PLC HALF YEAR RESULTS 2016

1,000

1,500

2,000

2013 2014 2015 H1 2016

EPRA NAV (p)

3

3.4

3.8

2013 2014 2015 2016 H1

Weighted Av Cost of Debt (%)

3.00

3.50

4.00

2013 2014 2015 2016 H1

Interest Cover (times)

1. Based on one-third of distributions for 2015

+9.6%

2,083

2,282

77

98 8 8

8

2,000

2,100

2,200

2,300

1 Jan 2016 Underlying profit FX Revaluation of properties

Share Buy Back Other revaluation 30 June 2016

MOVEMENT IN EPRA NAV Growth driven by cash flow and FX uplifts

Pence

8 CLS HOLDINGS PLC HALF YEAR RESULTS 2016

1 Jan 2016 Underlying Profit FX Revaluation of Properties

Share Buy Back

Other Revaluations

30 June 2016

+92.1%

41.9

80.5

6.9

5.7 1.2 2.4 1.7 1.4

19.3

30

40

50

60

70

80

90

31 Jun 2015 Rental Income Other Income Other Expenses

Financ Income

Tax Minority Interest

FX 31 Jun 2016

MOVEMENT IN EPRA EPS Benefiting from growth throughout the business and from FX

Pence

9

149, 97, 13

248,161,40

183,1,64

181,211,36

11,79,134

H1 2015 Rental Income

Other Income

Other Expenses

Finance Income

Tax Minority Interest

FX H1 2016

CLS HOLDINGS PLC HALF YEAR RESULTS 2016

1,366.8 1,445.9

37.5

38.1

58.6

15.8

-49.5

6.4 11.5 4.3

64.2

1,250

1,350

1,450

1,550

MOVEMENT IN PROPERTY PORTFOLIO Benefiting from strength of Euro

£m

10

1 Jan 2016

Disposals Additions Capex Valuation Uplift FX 30 June 2016

1,462.9

1,499.8

Held for sale PPE Investment properties

CLS HOLDINGS PLC HALF YEAR RESULTS 2016

DEBT POSITION Taking advantage of market conditions

§ Sold £47m of bonds in May § Redeemed SEK300m bond and repaid Vänerparken loan § H1 refinanced £68.3m at 1.96%;

since 1 July refinanced £23.6m at 1.73% § Cost of debt reduced to 3.27% (31 Dec 2015: 3.40%) § Interest cover high at 3.6x (2015: 3.1x) § Property LTV 50.6% (31 Dec 2015: 50.0%)

Fixed 59%

Capped 6%

Floating 35%

-20

20

60

100

140

180

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Debt Maturity At 30 June 2016

11

149, 97, 13

248,161,40

183,1,64

181,211,36

11,79,134

Credit Approved

Total Bullet Repayment

Total Amortisation

Net Debt (£m) 30 Jun 16 31 Dec 15

Borrowings 798.7 795.5

Cash (91.0) (100.7)

Corporate bonds (39.7) (73.4)

668.0 621.4

Debt Structure At 30 June 2016

£m

CLS HOLDINGS PLC HALF YEAR RESULTS 2016

-

5

10

15

20

25

2011 2012 2013 2014 2015 2016

Interim Final

0

2

4

6

8

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 H1

NIY Cost of Debt

FOCUS ON CASH Distributions underpinned by financing arbitrage

Healthy margin of Net Initial Yield (NIY) over cost of debt

+10.1%

Increasing shareholder distribution year on year1

149, 97, 13

248,161,40

183,1,64

181,211,36

11,79,134

+7.5% +13.2% +6.4%

+20.0% +10.0%

1. Through share buy-back mechanism 12

5.70% 3.27%

£m

%

+11.3% pa compounded

CLS HOLDINGS PLC HALF YEAR RESULTS 2016

CONTENTS

13

OVERVIEW Fredrik Widlund Chief Executive

FINANCIALS John Whiteley Chief Financial Officer

PROPERTY Simon Wigzell Head of Group Property

MARKETS & SUMMARY

Fredrik Widlund Chief Executive

RESILIENT TENANT BASE Diversified, secure income

14

115 properties & 545 customers § Total contracted rent £89m per annum § 37% of rents paid by governments (UK: 52%) § 23% by major corporates § 49% index-linked § Top UK tenants1, 70% of UK rent roll

(£36.8m) – Strong covenants – No tenant representing more than

10% of Group contracted rent § Average rent very affordable

at £16 per sq ft § 6.1 years WAULT; 4.6 years to first break

Government 37%

Business Services 18%

Manufact. 9%

IT & Tech. 8%

Student Accom. 4%

Medical & healthcare 4%

Retail, Leisure & Tourism 4%

Financial 3%

Education & training 1%

Media and publishing 1%

Other 10%

Tenants by Sector

1. Rental value in excess of £500,000 pa

Contracted rent £89m p.a.

CLS HOLDINGS PLC HALF YEAR RESULTS 2016

ACTIVE ASSET MANAGEMENT 284,000 sq ft of lease transactions (H1 2015: 133,000 sq ft)

15

High volume of leasing activity § H1: 56 transactions (UK: 32) § H2: 18 transactions (UK: 7)

UK: 57,000 sq ft; £1.5m p.a. rent; 5.9% above ERV § Great West House, Brentford 16,400 sq ft new leases § Westminster Tower, SE1 7,500 sq ft new leases § Quayside, SW6 7,000 sq ft of lease renewals

France: 116,000 sq ft; £1.6m p.a. rent; at ERV § Park Avenue, Lyon 42,000 sq ft new lease § Gennevilliers, Paris 33,500 sq ft lease renewal § Debussy, Paris 11,330 sq ft lease renewal

Germany: 111,000 sq ft; £1.3m p.a. rent; 4.7% above ERV § Bismarckallee, Freiburg 65,500 sq ft lease extension § Tangentis, Munich 12,200 sq ft lease extension § Adlershofer Tor, Berlin 9,000 sq ft new lease

15 CLS HOLDINGS PLC HALF YEAR RESULTS 2016

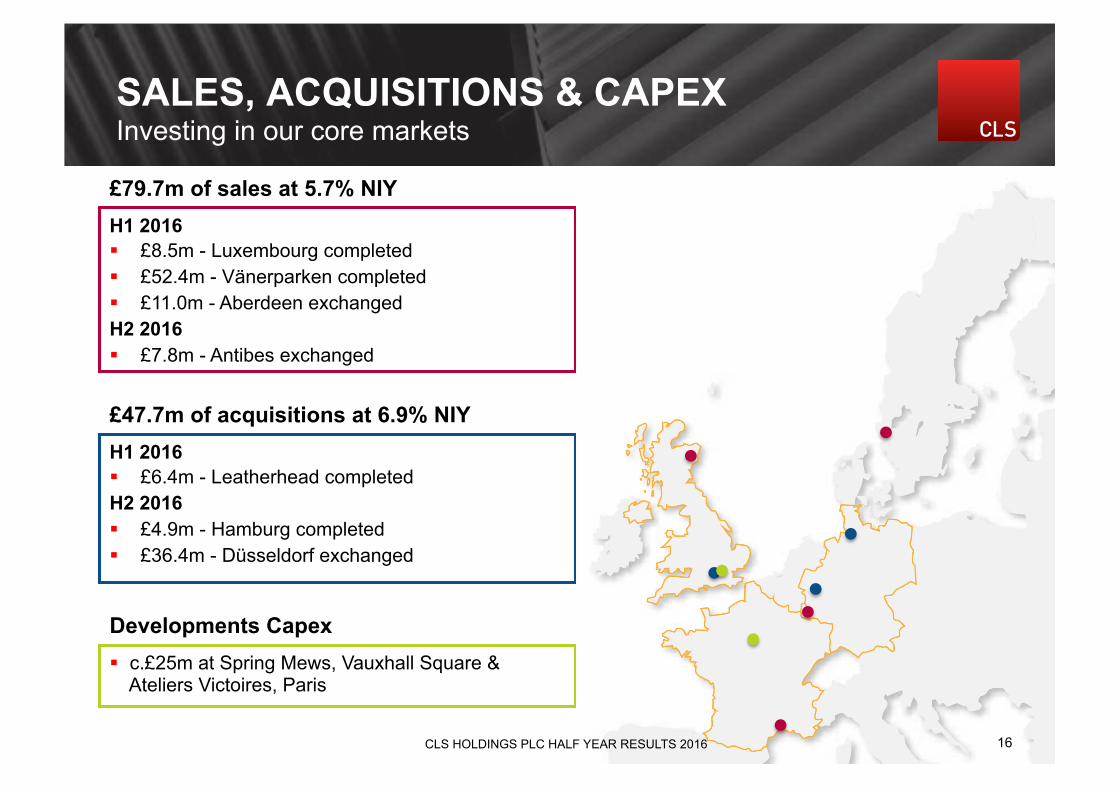

H1 2016 § £8.5m - Luxembourg completed § £52.4m - Vänerparken completed § £11.0m - Aberdeen exchanged H2 2016 § £7.8m - Antibes exchanged

SALES, ACQUISITIONS & CAPEX Investing in our core markets

16

H1 2016 § £6.4m - Leatherhead completed H2 2016 § £4.9m - Hamburg completed § £36.4m - Düsseldorf exchanged

£79.7m of sales at 5.7% NIY

£47.7m of acquisitions at 6.9% NIY

Developments Capex § c.£25m at Spring Mews, Vauxhall Square &

Ateliers Victoires, Paris

CLS HOLDINGS PLC HALF YEAR RESULTS 2016 16

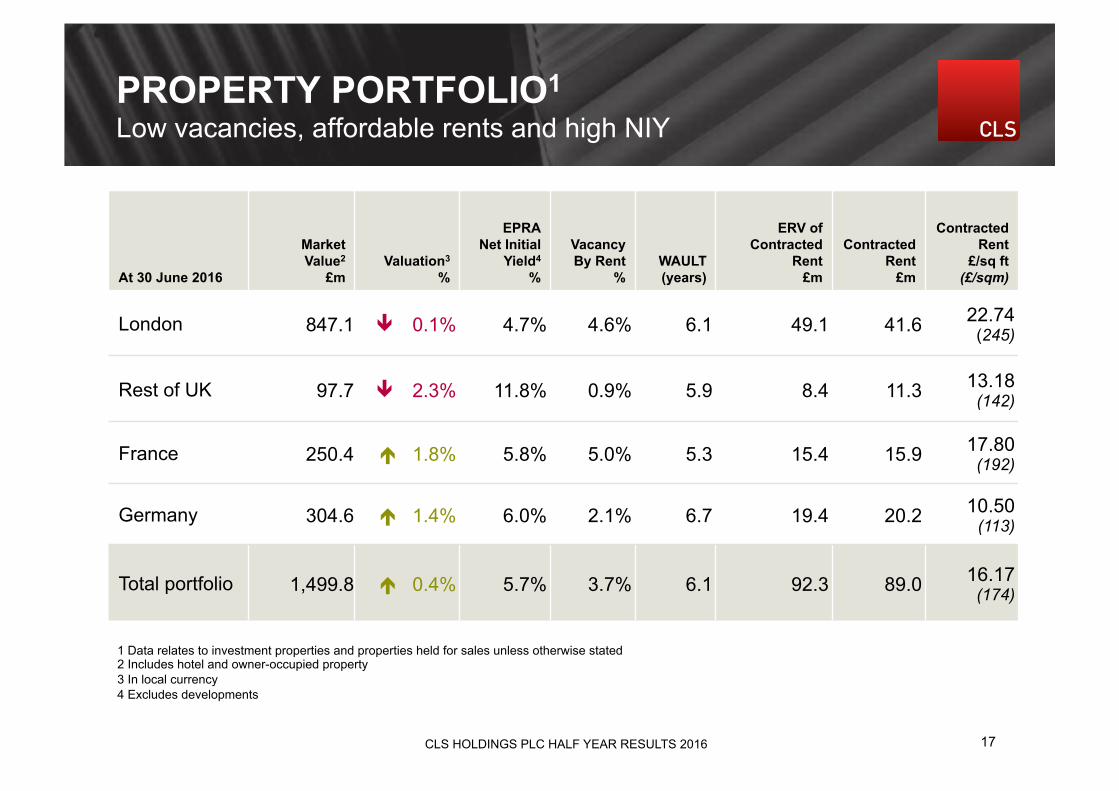

PROPERTY PORTFOLIO1 Low vacancies, affordable rents and high NIY

At 30 June 2016

Market Value2

£m Valuation3

%

EPRA Net Initial

Yield4 %

Vacancy By Rent

% WAULT (years)

ERV of Contracted

Rent £m

Contracted Rent

£m

Contracted Rent

£/sq ft (£/sqm)

London 847.1 ê 0.1% 4.7% 4.6% 6.1 49.1 41.6 22.74 (245)

Rest of UK 97.7 ê 2.3% 11.8% 0.9% 5.9 8.4 11.3 13.18 (142)

France 250.4 é 1.8% 5.8% 5.0% 5.3 15.4 15.9 17.80 (192)

Germany 304.6 é 1.4% 6.0% 2.1% 6.7 19.4 20.2 10.50 (113)

Total portfolio 1,499.8 é 0.4% 5.7% 3.7% 6.1 92.3 89.0 16.17 (174)

17

1 Data relates to investment properties and properties held for sales unless otherwise stated 2 Includes hotel and owner-occupied property 3 In local currency 4 Excludes developments

CLS HOLDINGS PLC HALF YEAR RESULTS 2016

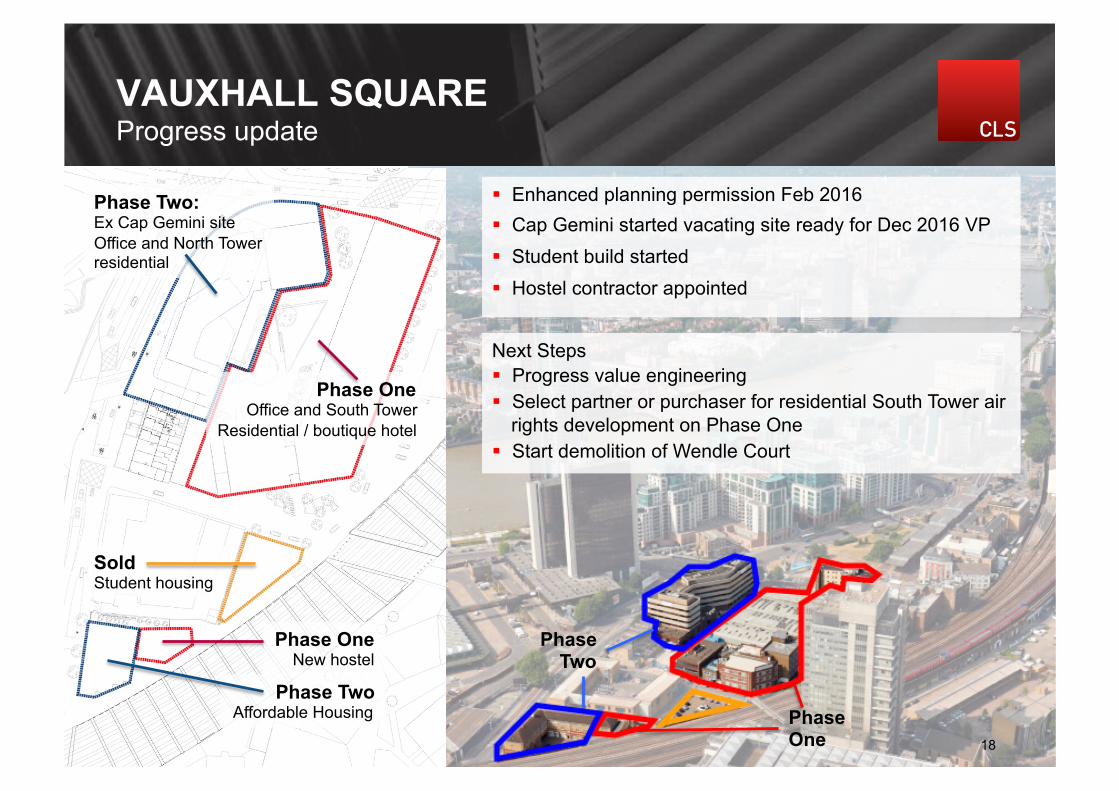

VAUXHALL SQUARE Progress update

18

§ Enhanced planning permission Feb 2016 § Cap Gemini started vacating site ready for Dec 2016 VP § Student build started § Hostel contractor appointed

Phase Two: Ex Cap Gemini site Office and North Tower residential

Phase One Office and South Tower

Residential / boutique hotel

Phase One

Phase Two

Next Steps § Progress value engineering § Select partner or purchaser for residential South Tower air

rights development on Phase One § Start demolition of Wendle Court

Phase One New hostel

Phase Two Affordable Housing

Sold Student housing

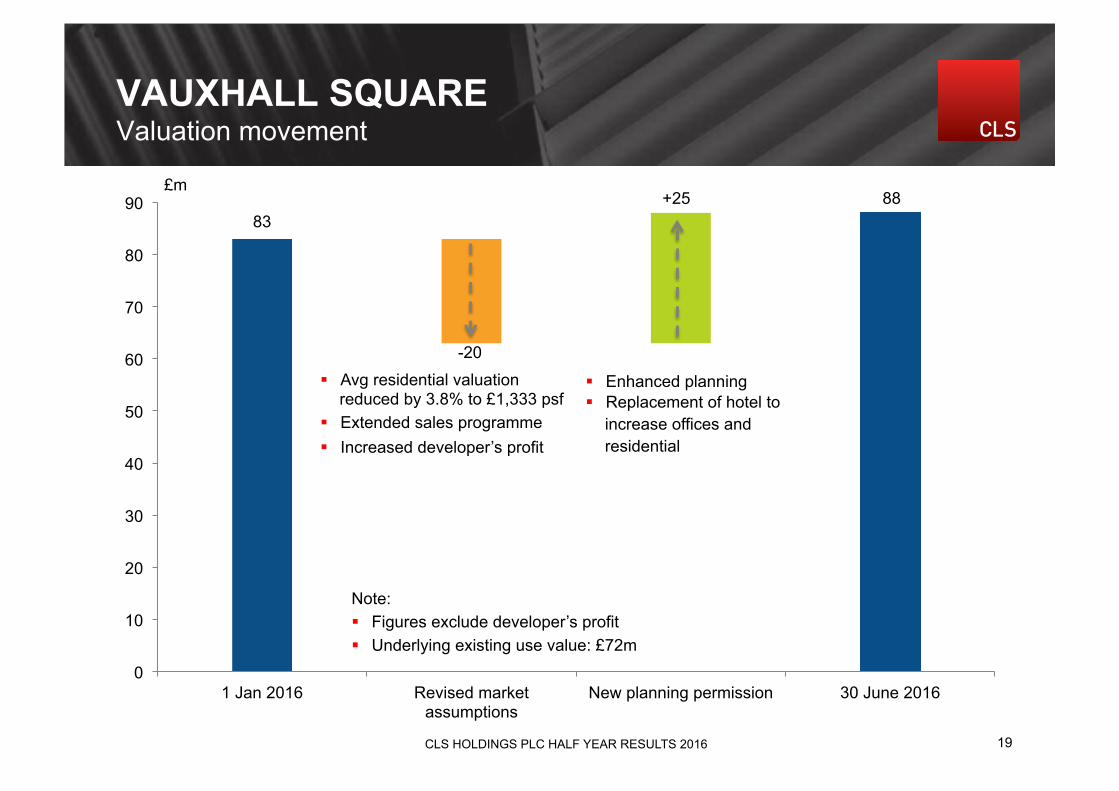

83

-20

+25 88

0

10

20

30

40

50

60

70

80

90

1 Jan 2016 Revised market assumptions

New planning permission 30 June 2016

VAUXHALL SQUARE Valuation movement

19

§ Avg residential valuation reduced by 3.8% to £1,333 psf

§ Extended sales programme § Increased developer’s profit

§ Enhanced planning § Replacement of hotel to

increase offices and residential

£m

Note: § Figures exclude developer’s profit § Underlying existing use value: £72m

19 CLS HOLDINGS PLC HALF YEAR RESULTS 2016

CONTENTS

20

OVERVIEW Fredrik Widlund Chief Executive

FINANCIALS John Whiteley Chief Financial Officer

PROPERTY Simon Wigzell Head of Group Property

MARKETS & SUMMARY

Fredrik Widlund Chief Executive

OVERVIEW Country update

Germany (20% of portfolio)

§ Attractive investment and financing opportunities in office market

§ German economy and corporates keeps performing and unemployment now close to 6%

§ Rental growth accelerating in larger cities like Berlin, Munich and Hamburg, average vacancy levels 3-5%

§ Very competitive lending market

§ Lack of stock impacting investment volumes

France (17% of portfolio)

§ A challenging economic backdrop but some progress with higher growth recorded in H1

§ Paris rental market resilient with vacancy below 4% in the city centre, outer suburbs around 10%

§ 2nd largest city Lyon stable with growing office take-up and vacancy down to 6%

§ Investment market driven by domestic institutions and companies

§ Solid market interest for CLS disposals

21 CLS HOLDINGS PLC HALF YEAR RESULTS 2016

SUMMARY Strong performance

2016 H1

§ Geographical diversification has driven performance

§ EPRA NAV up 9.6% to 2,282p and EPRA EPS up 92%

§ Positive FX impact

§ High volume of leasing activity

§ Recycling capital through disposals and acquisitions

§ Increased distribution +10% to implied 3.2% dividend yield

Near Term Outlook

§ Well positioned against Brexit uncertainty

§ Financial firepower gives room to act

§ Strong pipeline of asset management opportunities

§ Progress developments in France and UK

§ Real estate fundamentals remain positive across the Group

22 22 CLS HOLDINGS PLC HALF YEAR RESULTS 2016

APPENDICES

23

ABOUT CLS

24

CLS is a FTSE 250 property investment company with £1.5bn of property interests § Investments in the UK, Germany and France § Geographical diversification with local presence and knowledge

Our strategy combines § Active in-house asset, property and facilities management § Long-term capital appreciation with strong emphasis on cash generation § An opportunistic approach to acquisitions, developments and disposals

The Group’s core business § Owning and actively managing offices which are:

– High-yielding – Located in good, non-prime locations – Close to major transportation links

§ Adding value to properties through lease restructuring, refurbishment and development

We finance our activities through § Diverse and flexible debt structures § Active cash management

CLS HOLDINGS PLC HALF YEAR RESULTS 2016

73.4

39.7

100.7

22.2

-17.5

13.3

-6.4

-30.5

-38.4

13.9

91.0

0

50

100

150

200

250

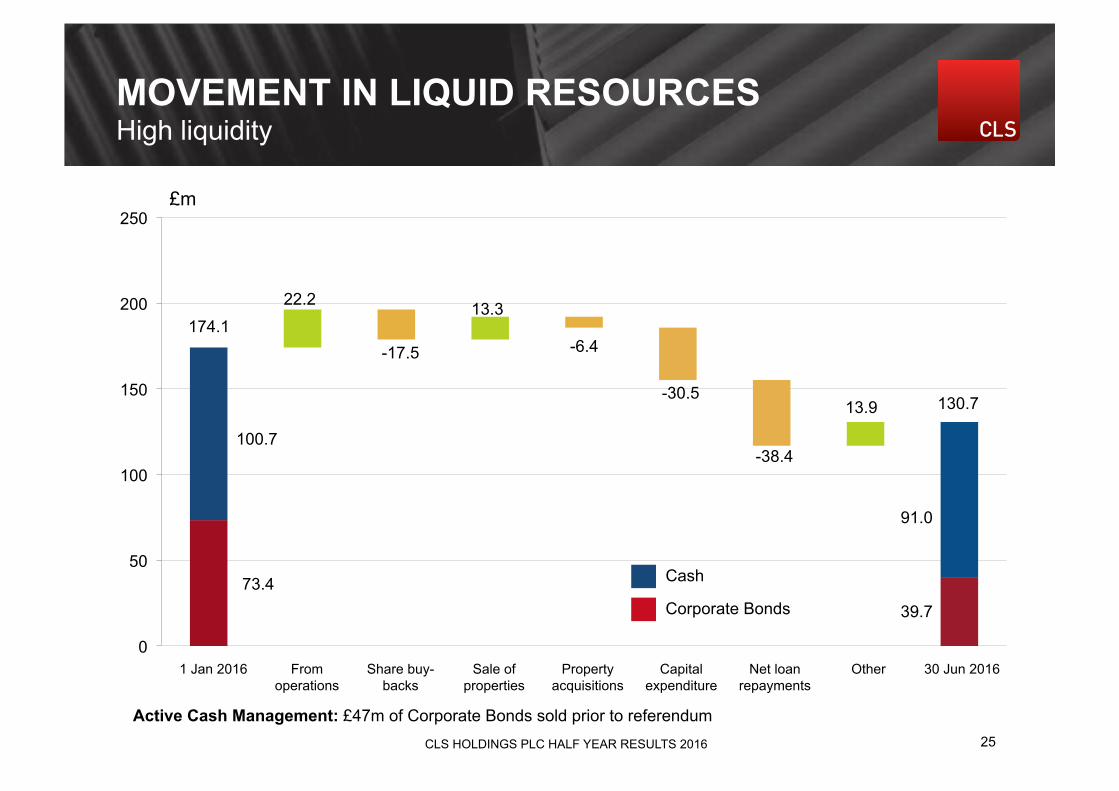

MOVEMENT IN LIQUID RESOURCES High liquidity

£m

25

Cash

Corporate Bonds

130.7

174.1

1 Jan 2016 From operations

Share buy-backs

Sale of properties

Property acquisitions

Capital expenditure

Net loan repayments

Other 30 Jun 2016

Active Cash Management: £47m of Corporate Bonds sold prior to referendum CLS HOLDINGS PLC HALF YEAR RESULTS 2016

Banks & Financials

Telecom and IT

Energy & Resources Insurance

Travel & Tourism Other Total

Value £13.6m £7.0m £12.3m £2.7m £3.2m £0.8m £39.7m

Running Yield 8.0% 6.8% 9.0% 7.1% 6.5% 6.4% 7.3%

Issuers Societe Generale

Bank of Ireland

Deutsche Bank

Credit Agricole

Allied Irish

Santander

Unicredit

Barclays

Investec

Lloyds

HSBC

RBS

Telecom Italia

Centurylink

T-Mobile

Millicom

Dell

Freeport-McMoRan

ArcelorMittal

BHP Billiton

Transocean

Seadrill

Enel

Brit Insurance

Phoenix Life

Old Mutual

British Airways

Stena

SAS

Stora Enso

CORPORATE BOND PORTFOLIO At 30 June 2016

26

Total portfolio return H1 2016: 10.4% Benchmark return H1 2016: 3.8% iShares Euro HY Corporate Bond ETF

8.2% iShares iBoxx USD HY Corporate Bond ETF Reason for outperformance: Telecom and Energy & Resources bonds, and USD, outperformed Diversification: 30 bonds issued by large-cap companies, spread over nine sectors

Average Duration: 13.7 years

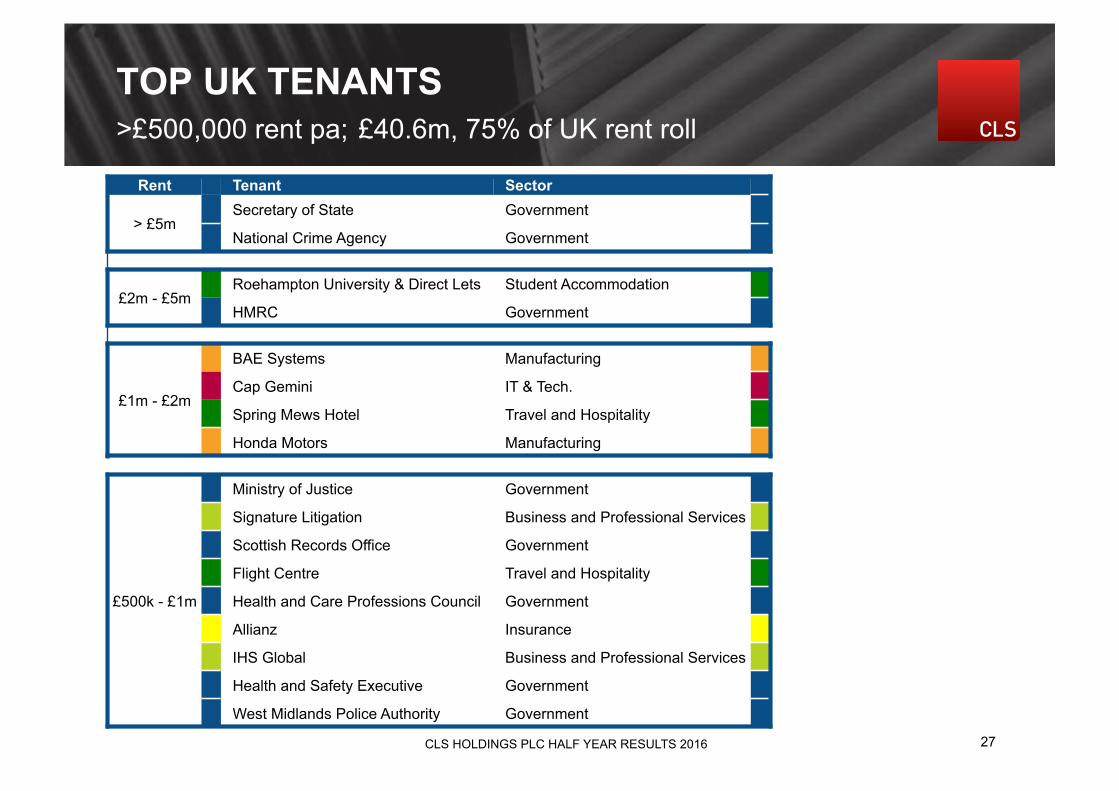

TOP UK TENANTS >£500,000 rent pa; £40.6m, 75% of UK rent roll

Rent Tenant Sector

> £5m Secretary of State Government

National Crime Agency Government

£2m - £5m Roehampton University & Direct Lets Student Accommodation

HMRC Government

£1m - £2m

BAE Systems Manufacturing

Cap Gemini IT & Tech.

Spring Mews Hotel Travel and Hospitality

Honda Motors Manufacturing

£500k - £1m

Ministry of Justice Government

Signature Litigation Business and Professional Services

Scottish Records Office Government

Flight Centre Travel and Hospitality

Health and Care Professions Council Government

Allianz Insurance

IHS Global Business and Professional Services

Health and Safety Executive Government

West Midlands Police Authority Government

149, 97, 13

248,161,40

183,1,64

181,211,36

11,79,134

CLS HOLDINGS PLC HALF YEAR RESULTS 2016 27

DEVELOPMENT & CAPEX UPDATE Further progress; c.£25m development capex

Spring Mews (Phase 2), Vauxhall § 9 residential style, high-end student flats

§ 9,181 sq ft of offices

§ Estimated NDV £11.4m, build costs £8.6m

§ On site; completion Q3 2017

Vauxhall Square Hostel § Relocate 50 bedroom hostel

§ Build cost £9.5m, Q3 2016 – Q1 2018

Ateliers Victoire (Petits Champs), Paris § Prime Paris, 21,500 sq ft office refurbishment

§ Estimated value €24m; build cost €8.2m

§ On site; completion Q4 2017

28

Spring Mews

Ateliers Victoire CLS HOLDINGS PLC HALF YEAR RESULTS 2016

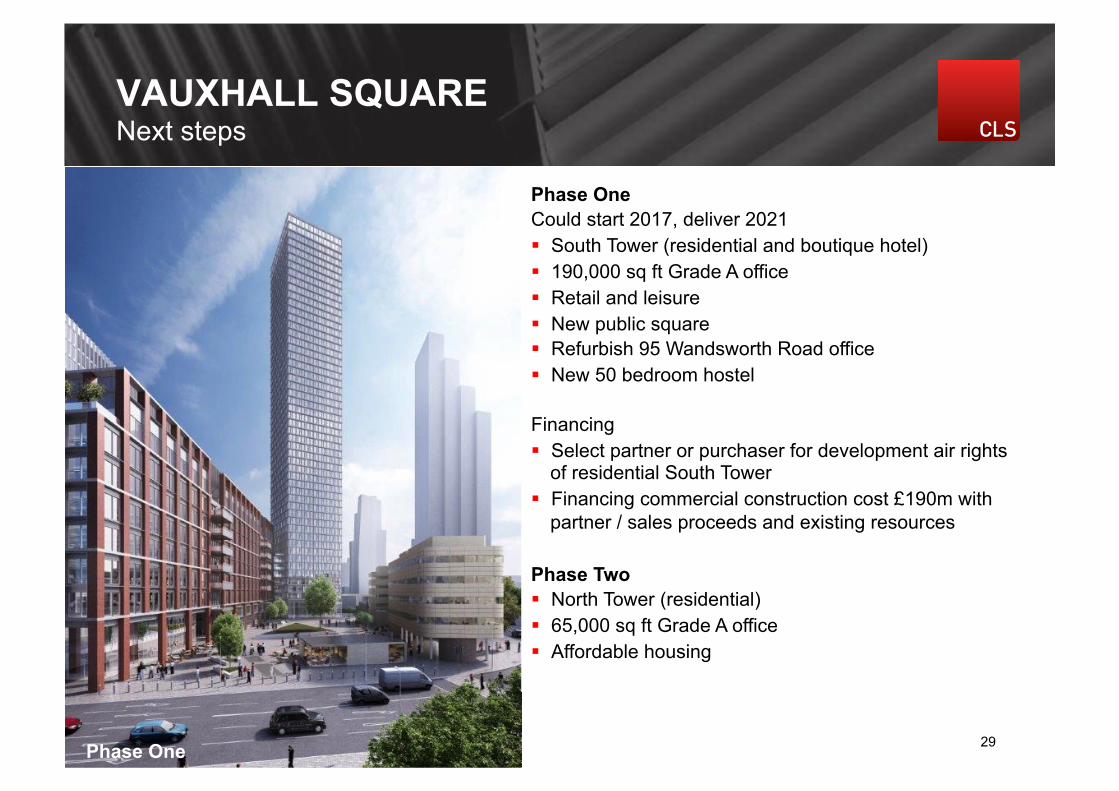

VAUXHALL SQUARE Next steps

29

Phase One Could start 2017, deliver 2021 § South Tower (residential and boutique hotel) § 190,000 sq ft Grade A office § Retail and leisure § New public square § Refurbish 95 Wandsworth Road office § New 50 bedroom hostel Financing § Select partner or purchaser for development air rights

of residential South Tower § Financing commercial construction cost £190m with

partner / sales proceeds and existing resources Phase Two § North Tower (residential) § 65,000 sq ft Grade A office § Affordable housing

Phase One

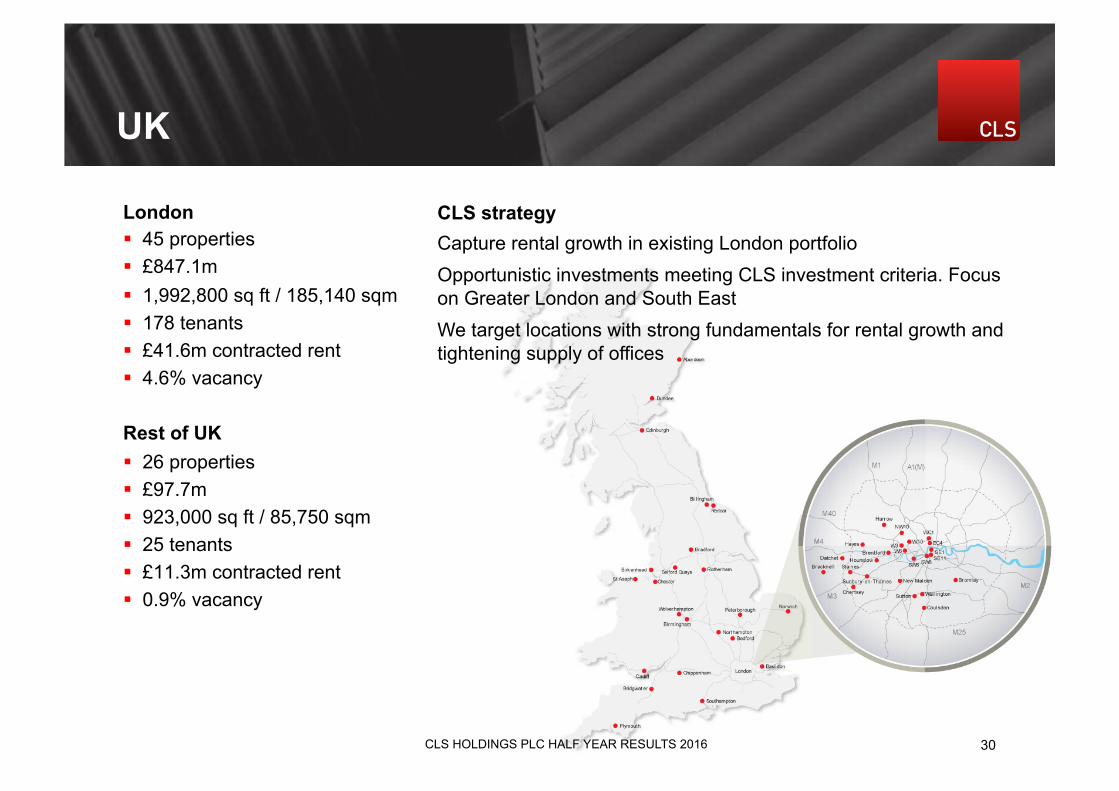

UK

London § 45 properties § £847.1m § 1,992,800 sq ft / 185,140 sqm § 178 tenants § £41.6m contracted rent § 4.6% vacancy Rest of UK § 26 properties § £97.7m § 923,000 sq ft / 85,750 sqm § 25 tenants § £11.3m contracted rent § 0.9% vacancy

30

CLS strategy Capture rental growth in existing London portfolio Opportunistic investments meeting CLS investment criteria. Focus on Greater London and South East We target locations with strong fundamentals for rental growth and tightening supply of offices

CLS HOLDINGS PLC HALF YEAR RESULTS 2016

§ 25 properties § £250.4m § 960,500 sq ft / 89,234 sqm § 187 tenants § £15.9m contracted rent § 5.0% vacancy

FRANCE

CLS Strategy:

Focus on existing portfolio; investing into assets and maintaining low vacancy. Selected disposals in non-core locations

31 CLS HOLDINGS PLC HALF YEAR RESULTS 2016

GERMANY

§ 19 properties § £304.6m § 1,973,900 sq ft / 183,380 sqm § 155 tenants § £20.9m contracted rent § 2.1% vacancy

32

CLS strategy:

Capture rental growth and work with existing occupiers to meet their requirements

Acquisition focus on multi-let properties in major cities

Still seeing good opportunities despite strong competition from both local and international investors

CLS HOLDINGS PLC HALF YEAR RESULTS 2016