Closing the Loop: Risk or Reward?

25

A White Paper highlighting the opportunities and challenges of a circular economy Sponsored by Closing the loop: risk or reward?

-

Upload

sustainable-brands -

Category

Documents

-

view

1.132 -

download

3

description

Transcript of Closing the Loop: Risk or Reward?

A White Paper highlighting the opportunities and challenges of a circular economy

Sponsored by

Closing the loop: risk or reward?

Sponsored by

Contents1 Executive summary 04

2.1 Going round in circles – the big disconnect 2.2 The race for feedstock as the hierarchy

comes of age 2.3 The local authority gatekeepers 2.4 Front-runner focus: rethink your business

proposition 2.5 Who is influencing the circle of lifecycle

thinking? 2.6 The year ahead: immediate priorities for

action

2 Working towards circularity: 07 the state of play

3 The business perspective 133.1 Scaling the waste hierarchy: the drive for

greater resource efficiency3.2 Contractual implications for the waste

supply chain3.3 Opportunity knocks: maximising the loop 3.4 Agenda for change: the key influencers 3.5 Does size matter?

4 The waste supply chain 18 perspective

4.1 The great reclaim game: will the waste industry lose out?

4.2 Survival strategies start to take flight 4.3 Closed loop collaboration – a safe bet? 4.4 Mind the knowledge gaps 4.5 Always be prepared: take action to future-

proof

| 2 |

Sponsor viewpoint 23

1

1

Set against a backdrop of global climate change, carbon economics and resource scarcity, the intrinsically valuable materials and scrap carbon that have for so long been locked up in waste streams are now becoming highly sought after. But how are organisations reacting to this challenge, given our current linear ‘take, make, waste’ system? As businesses begin to recognise the benefits of an emerging circular economy and its ability to drive greater resource productivity, the benefits are perhaps less tangible for the waste management industry.

However, as businesses look to reduce environmental impacts and boost the bottom line by moving waste up the hierarchy, the waste supply chain is ideally placed to help them deliver on their ambitions - providing it can react fast enough to align itself as a key enabler to encourage this circularity.

To examine these issues in more depth, edie.net and sister title Local Authority Waste & Recycling (LAWR) magazine, with sponsor FCC Environment, carried out extensive market research among both waste producers (businesses) and waste management companies (WMCs) to track

how attitudes towards waste and smarter resource management were impacting at different points across the value chain.

It questioned how attitudes to waste are changing in both camps and what the likely implications of this will be, both now and in the future. The resulting White Paper provides a narrative to help influence and steer thinking in this area, particularly for the waste management industry, which appears to be in a transitional phase.

We surveyed 435 companies in total – 361 businesses and 74 WMCs – asking them about the key issues:

• How attitudes among waste producers are changing

• How fast closed-loop thinking is rising up the business agenda

• What strategies are being adopted, and by whom

• Whether closed-loop recovery is superseding traditional waste management

• Where competition for feedstock is fiercest• The evolving nature of the business and

waste supplier relationship • How best to leverage competitive

advantage

In drawing on the key findings and analysing their implications, this White Paper sets out the evolutionary state of play within business and the waste management supply chain as these circular dynamics take hold.

The conclusions drawn are intended to act as an informative steer for decision-makers, both within, and outside of, the waste industry, who are looking at how best to navigate this rapidly changing landscape and capitalise upon the new opportunities it presents.

The premise of a circular economy is founded on not only extracting greater value from waste materials, but on feeding this value back into the industrial cycle or in some cases, the biological cycle. This strategic shift of resource use which, according to our research 76% of businesses are now looking to align themselves with, is certain to prove highly consequential for the waste supply chain – a sector whose lifeblood is built on securing these materials.

For 54% of businesses, reclaiming these waste streams will fundamentally reshape their relationship with the waste

Executive summary

| 4 |

35% of businesses are actively looking to shift their resource management focus elsewhere, seeking new alliances outside of the waste industry to help them deliver on this agenda

Sponsored by

route forward in order to exploit these opportunities. Traditional waste collection and disposal arrangements – certainly in the municipal markets – are built on lengthy contracts with guaranteed tonnages. This, together with the fact the UK is still heavily reliant on landfill, might be offering a false sense of security to some providers, who feel they don’t need to change their service provision model for the foreseeable future.

However, this still leaves one-third of waste management companies who are already repositioning themselves as the

waste management companies don’t feel there is a need to adapt or reposition their business model in any way to take advantage of the changing dynamics around waste flows. Consequently there is a real danger they might not be able to innovate quickly enough as the transition to a circular economy accelerates.

Underpinning this inertia is both uncertainty and complacency. The nature of waste is changing as thinking evolves and waste is increasingly viewed as a resource. The industry is at a crossroads, trying to determine and navigate the best

supply chain – either through specifying significant contractual changes with waste management providers or by streamlining the number of providers they deal with. Not only this, but 35% of businesses are actively looking to shift their resource management focus elsewhere, seeking new alliances outside of the waste industry to help them deliver on this agenda.

As these trends take hold, waste management companies need to be alert to the possibility that end-of-life material streams could start side-stepping traditional disposal and treatment routes that have been their exclusive domain for so long. More than three-quarters of businesses are also focusing their efforts on waste minimisation and as these prevention strategies bed down, this will further intensify issues around feedstock security. Already 31% of waste management companies feel these issues are impacting on their operations, with 18% voicing real concern.

Despite this, there remains a high level of inertia within the waste supply chain to address these fears and react accordingly. For most, it is a case of ‘keep calm and carry on’. Two-thirds of

When it comes to closing the loop, 72% of businesses are looking to engage with waste management providers to help them deliver

The Resource Revolution This White Paper forms a key output of the Resource Revolution series - an extended campaign centred on the emerging circular economy - comprising rich content, insight, and networking opportunities.

There are major risks and rewards for key players in this space and, as the campaign gathers pace, edie.net together with sister title LAWR will be charting these trends and highlighting the game-changers who are redefining the concept of waste and the way it is perceived.

More information about the campaign and how it aims to facilitate thought leadership can be found at www.resourcerevolution.net

Sponsored by | 5 |

Sponsored by

circular economy unfolds. These early movers and adopters appear to be taking a more holistic approach – one based on client-centred consultancy services which look to address the wider sustainability issues around waste management.

Ultimately, this could drive changes to charging models for waste disposal as demand grows for smarter value extraction methods to better prepare materials for upcycling, reuse or remanufacture.

There are clear commercial gains for these early movers. When it comes to closing the loop, 72% of businesses surveyed, said they are looking to engage with waste management providers to help them deliver it. And the returns could be immediate, with 30% of businesses planning to maximise resource use through the implementation of a closed loop process for their waste arisings over the next 12 months.

While this bodes well for the 61% of waste management firms who can see commercial benefits arising from the emerging closed loop economy, only 37% of them feel entering into such initiatives will result in strong revenue generation over the next five years. Where most see the

biggest gains to be made is in high-value extraction of waste materials – an issue widely recognised by both businesses and their waste supply chains.

For 77% of waste management firms, smarter extraction techniques – either in the form of secondary materials or energy recovery – represent the biggest single business opportunity over the next five years.

This highlights a strong need for technical innovation, which is also recognised as a commercial driver in itself by 54% of waste management providers. Increasingly, the waste industry is also recognising the need to broaden its service offering – almost two-thirds of waste management companies said they were diversifying in a bid to be more competitive.

Considering all of these factors, it is clear that the waste supply chain needs to re-engineer itself to deliver better value, not only by generating cleaner, more profitable outputs from its waste streams, but by meeting client-led demand for more resource-efficient recovery built on lifecycle analysis and whole systems thinking.

| 6 |

ABOUT USedie.net is used by more than a million sustainability professionals every year to keep up-to-date with the news, information and analysis which directly addresses the issues affecting their companies. It is an invaluable resource for an increasingly influential audience of decision makers across the spectrum of small, medium, large and enterprise-sized companies in the UK.

LAWR (Local Authority Waste & Recycling) magazine is the UK’s leading monthly publication for the waste and resource management industry. It is read by over 6,500 waste and resource management professionals across both the public and private sectors, as well as by political analysts, government and academia.

FCC Environment is one of the largest recycling and waste management companies in the UK, employing over 2,400 staff across more than 200 facilities in England, Scotland and Wales. It is part of a global group with a strong heritage in providing services for communities and business. Its vision is to be the environmental company of choice, delivering change for a sustainable future.

Sponsored by

A circular economy is one in which resources are kept in use for as long as possible, by extracting the maximum value from them while in use, then recovering and regenerating products and materials at the end of each service life. As modern day resource management starts to shift from a linear to circular economy, the business opportunity this opens up is immense.

Better design and more efficient use of materials could save European

Working towards circularity: the state of play

2

More than half of businesses stated that taking greater ownership of their waste streams will result in significant contractual changes with their waste management providers or streamlining the number of providers they deal with

The circular economy In a circular economy, as opposed to a traditional linear economy, products are intended to be more sustainable, as their design is based around reusable parts, allowing for a simpler end-of-life recovery process. In a circular economy, there is no such thing as waste – it is effectively designed out the system and becomes raw materials or energy for something else.

Designing for a circular economy is complex. To try and unravel this complexity, collaboration is needed across the entire value chain, from start-of-life to end-of-life. This means that all of the stakeholders involved in the lifecycle of a particular product, from product designers and material scientists right through to recycling operators and reprocessors, need to come together and work out the best solution.

manufacturers $630bn (£416m) a year by 2025, according to a recent report from the Ellen MacArthur Foundation [LINK-1]. In light of concerns from manufacturers and their supply chains about rising resource scarcity, this approach has been broadly welcomed.

The same study calculates that adhering to circular economy principles could help UK plc generate savings worth up to £700m annually, while also reducing yearly greenhouse gas emissions by 7.4 million

tonnes. The report’s main thrust broadly aligns itself with government policy both at UK and EU level, which is seeking to encourage greater efficiencies in this field through the delivery of zero waste agendas and resource security action plans.

However, the emergence of closed loop models could present a threat to one particular sector – the waste management industry. As manufacturers, retailers and brand leaders seek to take greater ownership of their waste streams for commercial gain, the waste industry itself is being fundamentally reshaped as a result.

New alliances are now being forged outside of traditional waste management markets, resulting in material flow diversion – not only from landfill, but from the hands of waste management providers themselves. This is starting to raise questions around the future security and supply of feedstock levels for these providers.

2.1 Going round in circles – the big disconnectThere are now clear signs that working towards a circular economy is presenting

Sponsored by | 7 |

Sponsored by | 8 |

itself as a strong business opportunity, but the waste management supply chain is in danger of being left out in the cold as it struggles to understand and navigate these fast-changing resource flow dynamics.

More than three-quarters of businesses (76%) surveyed said they perceived the emerging circular economy to be an important driver in becoming more resource-efficient – a trend which is already starting to reshape their business models. As they look to extract greater value from their waste streams and feed it back into their supply chains, this is likely to have serious repercussions for waste management companies (WMCs).

More than half of businesses (54%) surveyed stated that taking greater ownership of their waste streams will result in significant contractual changes with their waste management providers or streamlining the number of providers they deal with. Just over one-third (35%) also felt that this transition would involve entering into new alliances with key stakeholders outside of the traditional waste sector.

In contrast, most WMCs seem woefully unprepared for such a scenario – believing that ‘business as usual’ is a viable option. Despite admitting significant concerns around feedstock security, two-thirds of WMCs surveyed (66%) did not feel they would need to adapt their business models to position themselves at the forefront of the circular economy agenda. Consequently, there is a real danger they might not be able to innovate quickly enough if their sector should undergo a paradigm shift as it evolves into a resource-led economy.

2.2 The race for feedstock as the hierarchy comes of age Crucial to these transformational resource flow dynamics is the feedstock itself, which is becoming a sought-after asset – both by businesses as they look to close the loop on their operations, and the waste management supply chain whose livelihood is dependent upon it.

The vast majority of businesses surveyed (86%) are now looking to move their waste management activities up the hierarchy with more than half (52%) seeking to profit from it as they start to view their waste arisings as a potential resource or revenue

stream. A significant number (44%) confirmed they were taking measures to recover energy from their waste streams while just under a third (31%) were actively exploring closed loop opportunities.

More than three-quarters of firms (77%) also said they were focusing their efforts on waste minimisation and prevention, while more than half (59%) were looking for greater reuse opportunities. Both of these approaches will effectively take materials out of the waste management supply chain. This strategic repositioning – from a linear ‘take, make, waste’ economy to a more sustainable circular one – is already registering serious concerns with almost half of the WMCs we surveyed.

As this race for feedstock intensifies, WMCs will not only have to compete for materials outside of the waste sector, but from within their own industry too. Almost a third of WMCs surveyed (31%) confirmed that issues of feedstock security are now impacting on their business, while nearly a fifth (18%) said it was of real concern. Feedstock competition from overseas markets, such as the rising demand for refuse-derived

Almost a third of WMCs surveyed confirmed that issues of feedstock security are now impacting on their business

add value to their service offering and capitalise on the opportunities that a more circular economy might present.

Nearly three-quarters of businesses we surveyed (72%) are looking to engage with WMCs to help them deliver closed loop solutions – this is a huge commercial opportunity which should not be overlooked.

However, only one-third of WMCs surveyed are already reacting to this and believe their business model will need to change as a result. For some, a stronger emphasis on more client-based strategic thinking around wider sustainability issues was considered necessary coupled with a rethink of charging models for waste disposal. Others saw benefit in the need for more data intelligence to match feedstock availability with treatment infrastructure capacity.

This would appear to reflect growing client-based demand, particularly in the blue chip sector, for more consultancy-led services based around waste prevention that can be rolled out across the entire supply chain. Linked to this is a rising requirement for smarter value extraction

of unlocking future feedstock supply as landfill diversion strategies take hold.

It is not surprising that local authorities were cited by the vast majority of WMCs as the most important stakeholder group to target or engage with as the circular economy agenda takes hold – especially as many of these municipal waste collection and disposal services are outsourced to private waste contractors.

In England, one recent development that should sound alarm bells is that municipal recycling rates appear to be flatlining, according to latest figures released by Defra [LINK-2], bucking the trend of year-on-year percentage increases. This could be due to local authority service provision cutbacks as economic pressures take hold, but may also indicate a lack of suitable treatment capacity on the ground. Unless this trend is reversed, tensions around feedstock availability will only heighten going forward.

2.4 Front-runner focus: rethink your business proposition Set against this backdrop of rising feedstock security concerns, WMCs need to seriously consider how they can

fuel from Europe, was also considered significant by more than a fifth of those we surveyed.

2.3 The local authority gatekeepersDespite these uncertainties, a significant amount of potentially valuable material remains locked in landfill. National recycling rates across the UK hover on average around the 40% mark except in Wales which is edging ahead slightly – last year it broke through the 50% barrier. Calls are now intensifying among WMCs for more government intervention to stimulate markets and unlock feedstock availability.

Introducing measures such as landfill bans of certain materials including waste wood and food were considered by respondents to be important levers in this respect, coupled with better regulation and enforcement of existing policies. A more prescriptive zero waste policy, especially in England, was also thought desirable.

Crucial to facilitating this strategic rethink are the local authorities themselves who are mandated to oversee the collection, treatment and disposal of large tonnages of municipal waste. Consequently, they have a valuable gate-keeping role to play in terms

There are huge disconnects between start-of-life (product designers) and end-of-life (WMCs) industries

Sponsored by | 9 |

Sponsored by | 10 |

methods to better prepare materials for upcycling, reuse or remanufacture.

Interestingly, more than three-quarter of WMC respondents we surveyed (77%) – regardless of whether they were looking to change their business model or not – said that extracting more value from waste presented the single biggest commercial opportunity as the resource management agenda unfolds over the next five years.

Despite this, there remains a high level of business inertia among most WMCs in reacting to these drivers. Some may be harbouring a reluctance to change while perception exists that they have a safe supply of materials to tap into for the foreseeable future. This is likely to be particularly true for those operating in the municipal waste market, where disposal contracts can stretch for up to 30 years with guaranteed feedstock levels built into such arrangements.

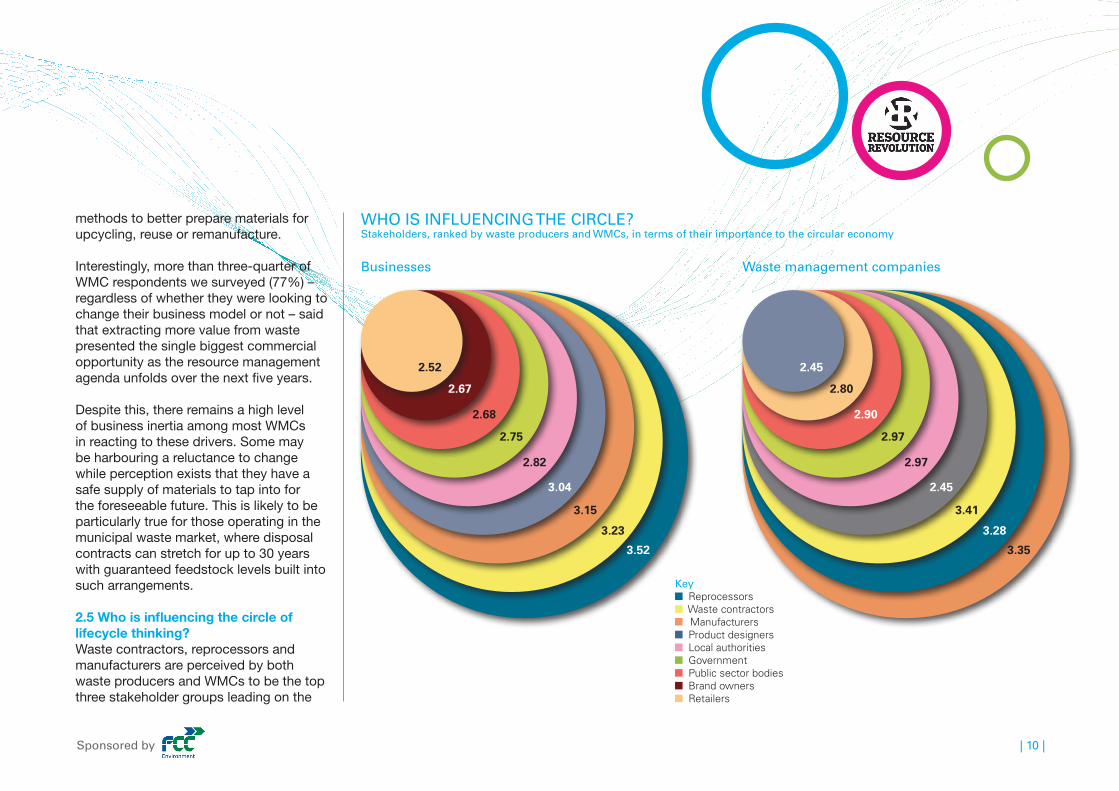

2.5 Who is influencing the circle of lifecycle thinking? Waste contractors, reprocessors and manufacturers are perceived by both waste producers and WMCs to be the top three stakeholder groups leading on the

Who iS influEnCing ThE CirClE? Stakeholders, ranked by waste producers and WMCs, in terms of their importance to the circular economy

3.23

3.04

2.82

2.75

2.68

2.67

2.52

3.15

3.52

3.28

2.45

2.97

2.97

2.90

2.80

2.45

3.41

3.35

Businesses Waste management companies

Key Reprocessors Waste contractors Manufacturers Product designers Local authorities Government Public sector bodies Brand owners Retailers

disconnects between start-of-life (product designers) and end-of-life (WMCs) industries and a pressing need for more communication between the two ends of the chain if a true circular economy is to be realised.

Encouragingly, these issues are recognised and starting to be addressed with the advent of ‘teardown labs’ hosted by organisations such as the Ellen MacArthur Foundation [LINK-4] and the RSA Great Recovery Project [LINK-5].

These labs aim to forge strategic alliances between key stakeholder groups to examine the challenges of product disassembly in a practical way and encourage more lifecycle thinking across the value chain. The Technology Strategy Board [LINK-6] is also offering funds for research and pilot projects aimed at recovering problematic materials.

Looking ahead, demand for facilitation roles to enable more collaborative thinking is likely to grow. WRAP (Waste & Resources Action Programme) will play a central role here, particularly by enabling big business to become more resource-efficient through the

circular economy agenda according to our survey.

This is not surprising, given all three are highly materials-focused in their operations. A 2012 study from EEF, the manufacturer’s organisation, found that 80% of its members thought raw materials shortages now pose a risk to their business [LINK-3].

Among businesses, product designers were also ranked higher than average in terms of influence and leadership, suggesting a growing awareness of the importance of lifecycle analysis as businesses begin to think more holistically about how materials and energy flow through the industrial system.

That said, only a fifth of companies are actively seeking to engage with product designers to influence thinking in this field, indicating a strong collaborative disconnect.

Meanwhile WMCs perceive product designers as showing the lowest levels of leadership in the circular economy agenda.

This would suggest that there are huge

Why is behaviour change so important?A true circular economy cannot be realised unless there is sustainable consumption. This is one of the biggest challenges as it requires the engagement of not just business and government, but consumers too.

Organisations must explore ways they can leverage their potential to deepen customer loyalty by involving them in closing sustainability loops through reusing and repurposing. They must also encourage their own employees to replicate green actions carried out in the home, such as switching off lights and recycling, in the work environment.

Larger corporations, such as brand leaders, need to find creative ways to highlight consumers as part of the solution and identify how best to reframe ownership around a new, sharing economy. This will also require alternative business models built around service, leasing, hire and refurb options.

Sponsored by | 11 |

Sponsored by | 12 |

movers. Over the next 12 months, almost a third of businesses we surveyed (30%) stated they were planning to maximise resource use through the implementation of a closed loop process for their waste arisings. Significantly, a quarter of these companies are actively looking to engage with interested parties to realise these ambitions. This pull towards more external collaboration appears to be most prevalent in the manufacturing and construction industries and the public sector, across all company sizes – from large corporations to SMEs and micro-organisations.

While most of these companies see the value in entering into strategic alliances with WMCs, a sizeable number are also looking to join forces with other

development of alternative models that centre on waste prevention and high value recovery. The Circular Economy Taskforce [LINK-7], launched last year, has also brought together leading businesses to understand how circular models can be developed in a way that keeps companies profitable. On a more global level, the Ellen MacArthur Foundation has set up the Circular Economy 100, a consortium of 100 businesses, to help accelerate the transition to a circular economy over the next three years.

2.6 The year ahead: immediate priorities for actionAs the business case builds for moving towards a circular economy, there are clearly strong commercial opportunities already out there for early adopters and

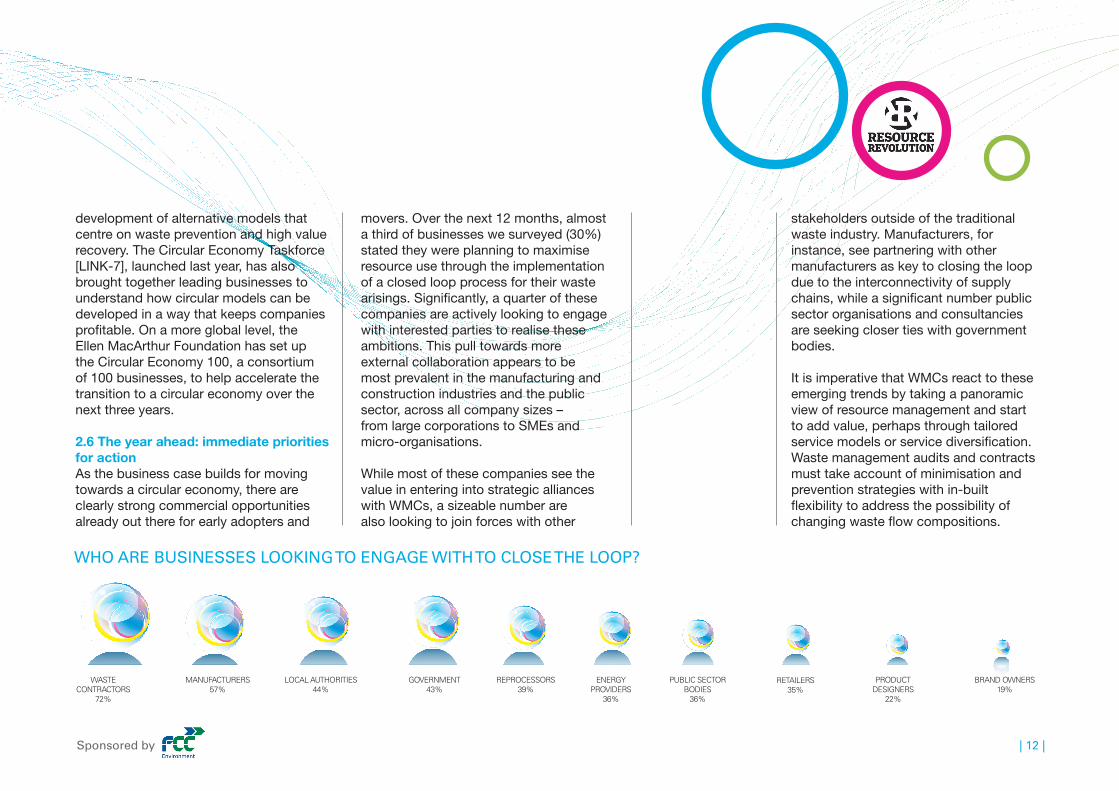

Who ArE BuSinESSES looKing To EngAgE WiTh To CloSE ThE looP?

Waste contRactoRs

72%

ManufactuReRs57%

LocaL authoRities44%

GoveRnMent43%

RePRocessoRs39%

eneRGy PRovideRs

36%

PuBLic sectoR Bodies

36%

RetaiLeRs35%

PRoduct desiGneRs

22%

BRand oWneRs19%

stakeholders outside of the traditional waste industry. Manufacturers, for instance, see partnering with other manufacturers as key to closing the loop due to the interconnectivity of supply chains, while a significant number public sector organisations and consultancies are seeking closer ties with government bodies.

It is imperative that WMCs react to these emerging trends by taking a panoramic view of resource management and start to add value, perhaps through tailored service models or service diversification. Waste management audits and contracts must take account of minimisation and prevention strategies with in-built flexibility to address the possibility of changing waste flow compositions.

Sponsored by | 13 |

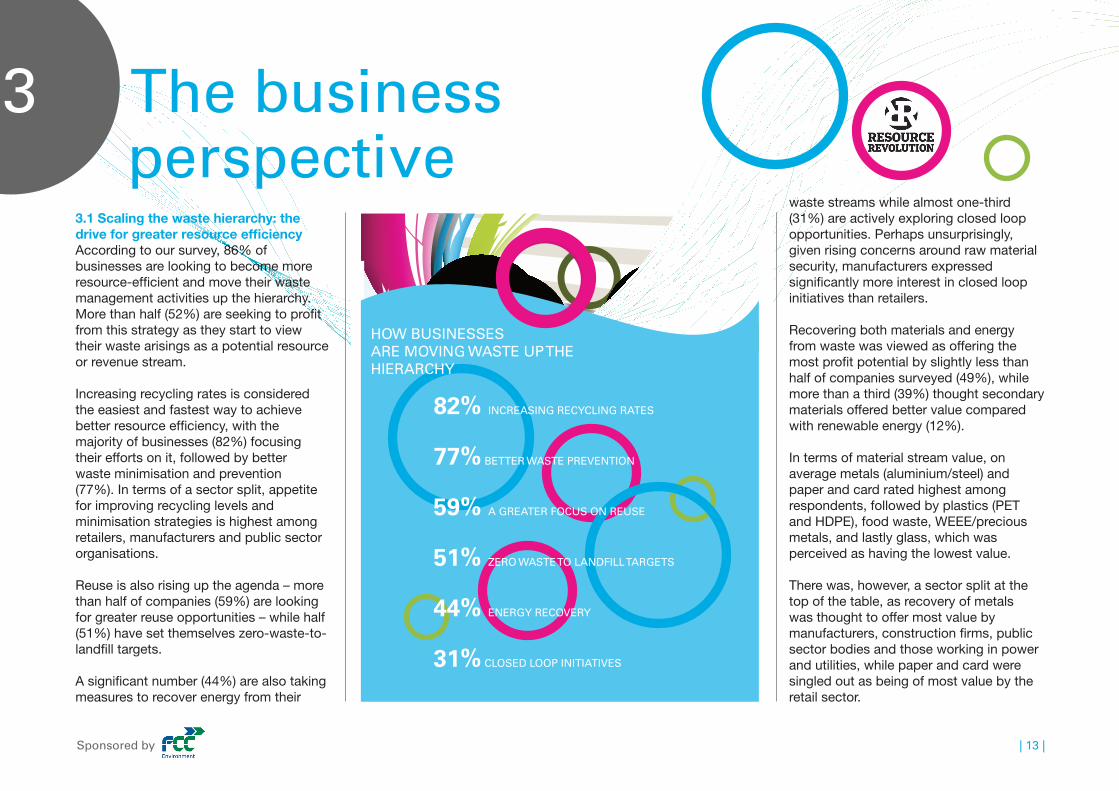

3.1 Scaling the waste hierarchy: the drive for greater resource efficiency According to our survey, 86% of businesses are looking to become more resource-efficient and move their waste management activities up the hierarchy. More than half (52%) are seeking to profit from this strategy as they start to view their waste arisings as a potential resource or revenue stream.

Increasing recycling rates is considered the easiest and fastest way to achieve better resource efficiency, with the majority of businesses (82%) focusing their efforts on it, followed by better waste minimisation and prevention (77%). In terms of a sector split, appetite for improving recycling levels and minimisation strategies is highest among retailers, manufacturers and public sector organisations.

Reuse is also rising up the agenda – more than half of companies (59%) are looking for greater reuse opportunities – while half (51%) have set themselves zero-waste-to-landfill targets.

A significant number (44%) are also taking measures to recover energy from their

The business perspective

3

waste streams while almost one-third (31%) are actively exploring closed loop opportunities. Perhaps unsurprisingly, given rising concerns around raw material security, manufacturers expressed significantly more interest in closed loop initiatives than retailers.

Recovering both materials and energy from waste was viewed as offering the most profit potential by slightly less than half of companies surveyed (49%), while more than a third (39%) thought secondary materials offered better value compared with renewable energy (12%).

In terms of material stream value, on average metals (aluminium/steel) and paper and card rated highest among respondents, followed by plastics (PET and HDPE), food waste, WEEE/precious metals, and lastly glass, which was perceived as having the lowest value.

There was, however, a sector split at the top of the table, as recovery of metals was thought to offer most value by manufacturers, construction firms, public sector bodies and those working in power and utilities, while paper and card were singled out as being of most value by the retail sector.

82% inCrEASing rECyCling rATES

77% BETTEr WASTE PrEvEnTion

59% A grEATEr foCuS on rEuSE

51% ZEro WASTE To lAndfill TArgETS

44% EnErgy rECovEry

31% CloSEd looP iniTiATivES

hoW BuSinESSES ArE Moving WASTE uP ThE hiErArChy

3.2 Contractual implications for the waste supply chainSignificantly, more than half of businesses (54%) stated that taking greater ownership of their waste streams will result in comprehensive contractual changes with their waste management providers or streamlining the number of providers they deal with.

More than one-third (35%) also felt that this transition would involve entering into new alliances with key stakeholders outside of the traditional waste sector.

As the majority of businesses (76%) perceive the circular economy to be an important resource-efficiency driver, this is already starting to reshape business models. In fact, one-third of companies we surveyed said their business model was already changing to reflect this trend.

Interestingly, this trend towards waste supplier consolidation and evolving business models appears to be most apparent in the upper end of the value chain, i.e. the retail sector. Further downstream, the majority of manufacturers seem happy with their existing waste management arrangements and operational systems.

The zero waste agenda Zero waste means going further than maximising recycling levels to prevent waste going to landfill. It encourages thinking around better minimisation strategies to effectively ‘design out waste’ in the industrial system.

In the UK, the waste debate has traditionally revolved around meeting EU landfill targets and packaging regulations. However there is a growing realisation that more legislative drivers are needed to target waste prevention and, as such, England, Scotland, Wales and Northern Ireland have embarked on the first step towards this by setting out their respective visions of zero waste society.

Scotland’s vision is considered the most ambitious and prescriptive. The Scottish Government’s Zero Waste Plan includes landfill bans for specific waste streams, separate collections for food waste, restrictions on energy-from-waste feedstock and measures to cut the carbon impact of waste. Under the plan, businesses are targeted to reach 75% recycling levels by 2025, with just 5% of waste being sent to landfill.

Wales has taken a long-term view with regard to waste. Its Towards Zero Waste plan sets out a framework for improving resource efficiency stretching up to 2050. Measures include waste prevention, separate collection of food waste and kerbside sorting for dry recyclables. It also sets out a 70% recycling rate for commercial and industrial waste by 2025, with an interim goal of 67% by 2020. The Welsh Assembly is also drawing up sector plans covering markets such as municipal, wholesale and retail waste, and construction and demolition waste.

England, by contrast, is taking a less prescriptive approach with its Waste Review that works towards a zero waste economy by increasing reuse and recycling levels. The document is primarily based on businesses and other organisations meeting voluntary targets, but the Government is also looking to strengthen this with the publication of a waste prevention programme towards the end of this year.

The Government did consult over proposals to introduce a landfill ban for wood waste, but has decided not to go ahead with this for the meantime. Landfill ban proposals for textiles and food waste have also been put on hold pending further consultation and evidence gathering.

Meanwhile Northern Ireland’s waste strategy, set out in Towards Resource Management: The Northern Ireland Waste Management Strategy 2006-2020, is currently under review. A framework for waste prevention in Northern Ireland was published in 2005 but this is likely to be superseded by a waste prevention programme later this year. The Department of the Environment NI has also consulted on introducing landfill bans for specific materials and a strengthened recycling policy for municipal waste.

Sponsored by| 14 |

Sponsored by | 15 |

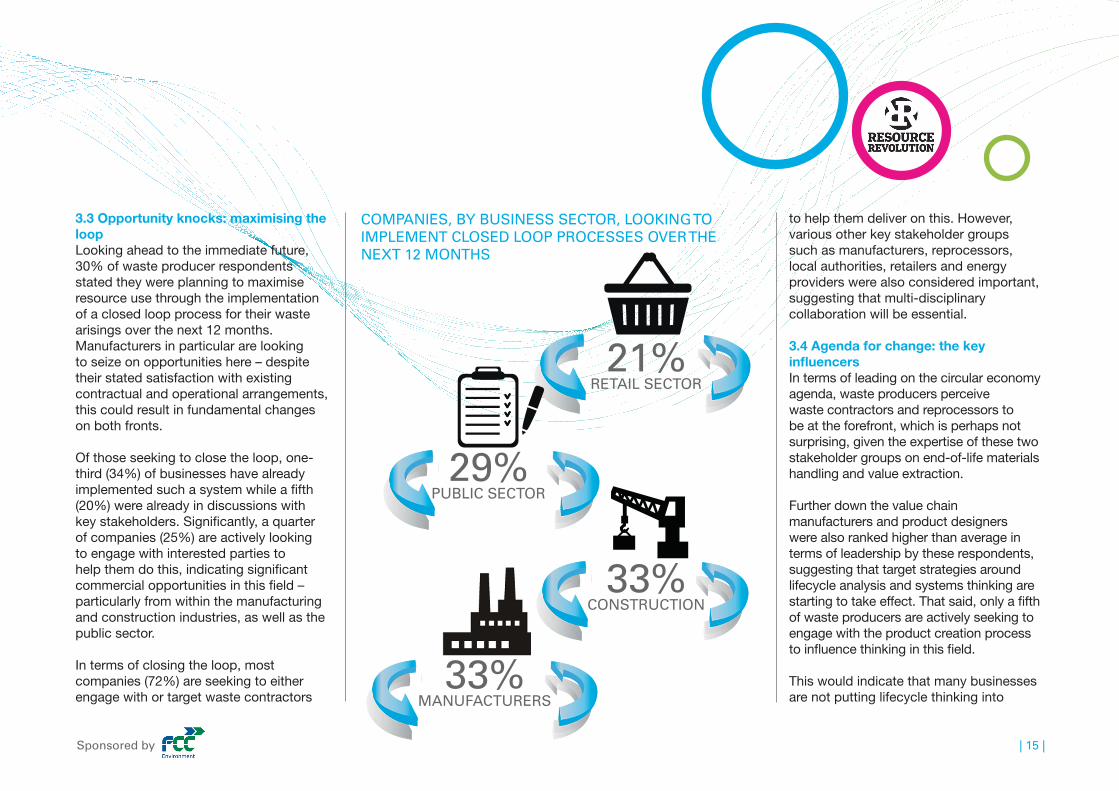

3.3 Opportunity knocks: maximising the loop Looking ahead to the immediate future, 30% of waste producer respondents stated they were planning to maximise resource use through the implementation of a closed loop process for their waste arisings over the next 12 months. Manufacturers in particular are looking to seize on opportunities here – despite their stated satisfaction with existing contractual and operational arrangements, this could result in fundamental changes on both fronts.

Of those seeking to close the loop, one-third (34%) of businesses have already implemented such a system while a fifth (20%) were already in discussions with key stakeholders. Significantly, a quarter of companies (25%) are actively looking to engage with interested parties to help them do this, indicating significant commercial opportunities in this field – particularly from within the manufacturing and construction industries, as well as the public sector.

In terms of closing the loop, most companies (72%) are seeking to either engage with or target waste contractors

to help them deliver on this. However, various other key stakeholder groups such as manufacturers, reprocessors, local authorities, retailers and energy providers were also considered important, suggesting that multi-disciplinary collaboration will be essential.

3.4 Agenda for change: the key influencers In terms of leading on the circular economy agenda, waste producers perceive waste contractors and reprocessors to be at the forefront, which is perhaps not surprising, given the expertise of these two stakeholder groups on end-of-life materials handling and value extraction.

Further down the value chain manufacturers and product designers were also ranked higher than average in terms of leadership by these respondents, suggesting that target strategies around lifecycle analysis and systems thinking are starting to take effect. That said, only a fifth of waste producers are actively seeking to engage with the product creation process to influence thinking in this field.

This would indicate that many businesses are not putting lifecycle thinking into

CoMPAniES, By BuSinESS SECTor, looKing To iMPlEMEnT CloSEd looP ProCESSES ovEr ThE nExT 12 MonThS

21%rETAil SECTor

29%PuBliC SECTor

33%ConSTruCTion

33%MAnufACTurErS

practice early enough in the value chain. Unsurprisingly, the one business sector significantly ahead of the curve in this respect is manufacturing – three-quarters of manufacturers surveyed said they were either engaging with or targeting product designers to address this issue.

At the other end of the scale, retailers scored lowest on average in terms of leadership, followed by brand owners and public sector bodies. This is a cause for concern since all three stakeholder groups are by their very nature, consumer-facing and could play a highly influential in driving sustainable consumption through

customer education and strong messaging on behaviour change.

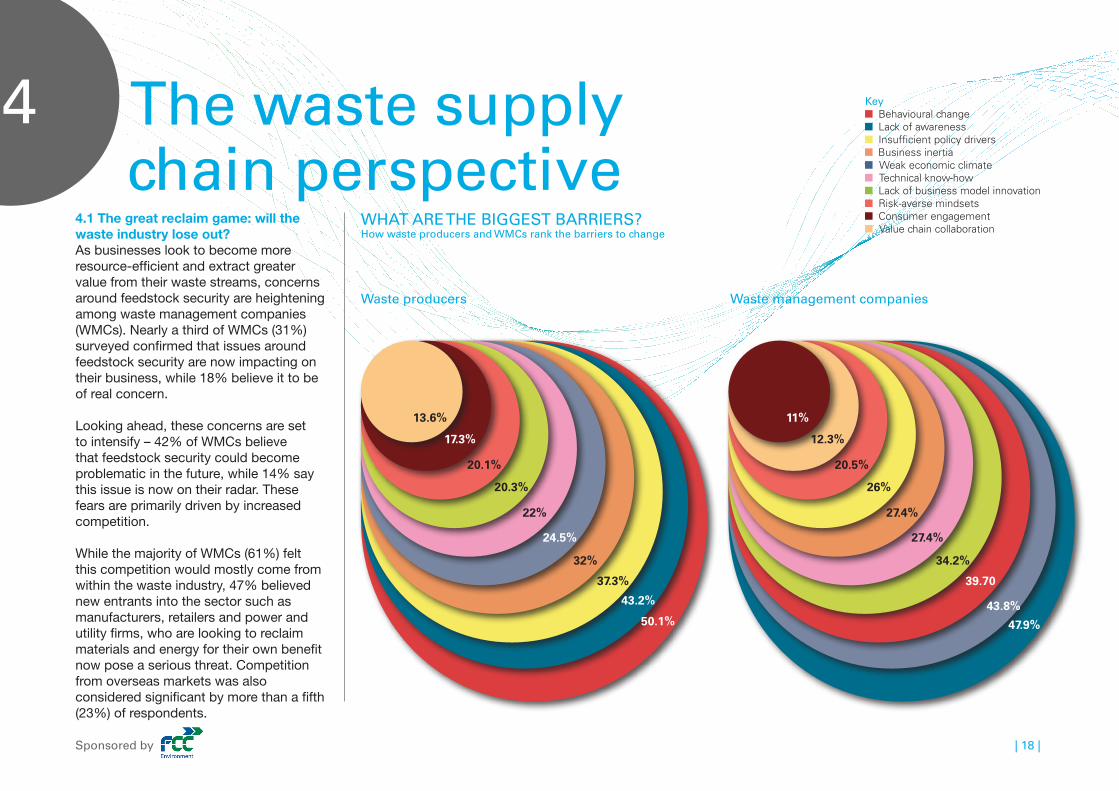

This concern is compounded by the fact that behaviour change was felt to be the biggest barrier to achieving a circular economy and also the chief blocker to improving in-house resource efficiency. In terms of the main barriers to achieving a circular economy, half of businesses surveyed (50%) cited behaviour change, followed by lack of awareness (43%), insufficient policy drivers (37%) and business inertia (32%). A weak economic climate was also felt to be a contributing factor by a quarter of businesses (25%),

along with technical know-how (22%), lack of business model innovation (20%), risk-averse mindsets (20%), consumer engagement (17%) and value chain collaboration (14%).

Inside the four walls of an organisation, behaviour change and lack of awareness around the business benefits of a circular economy were perceived to be the main stumbling blocks to achieving greater resource efficiency by 60% and 55% of companies respectively. Regulatory pressures such as producer responsibility and duty of care regimes were felt by 45% of companies to be a significant issue, while more than one-third (35%) thought staff engagement needed to be addressed. Meanwhile 27% thought greater board-level buy-in was required.

Where changing business perception in this regard appears to be impacting most upon the waste supply chain is in service provision. Nearly a third of companies said that a lack of skills and expertise in high value waste management (31%) and inflexible waste contracts (30%) were issues that needed to be addressed. This would indicate there is growing demand for waste management services among

Most companies (72%) are looking to either engage with or target waste contractors to help them deliver

John Lewis Partnership & Centriforce ProductsIn a move believed to be a first for any UK retailer, John Lewis Partnership is developing a pioneering closed loop business model for its plastics waste. The company has entered into an agreement with Liverpool-based recycler Centriforce Products to recover plastics waste from Waitrose and John Lewis stores so they can be recycled into useable products.The retailer is also exploring opportunities to reuse Centriforce products such as plastic planks and sheeting in its new store construction programme to achieve a true closed loop process in its plastics waste stream. The move is part of a wider corporate strategy to create greater transparency in its waste management operations.

CASE STUDy

SNAPSHOT

Sponsored by | 16 |

Sponsored by | 17 |

businesses that address the waste hierarchy, with clear focus on high value extraction and/or minimisation strategies. This trend is starting to be reflected within the waste supply chain itself, particularly among the more innovative providers who are looking at service diversification (see section 4.2).

3.5 Does size matter?Not surprisingly larger companies are furthest down the line in becoming more resource-efficient, but smaller firms are also making strong headway. While 95% of medium to large firms (150 – 500 employees) and 94% of big corporates (500+ employees) are looking to move their waste management activities further up the hierarchy, 77% of smaller companies (1 – 150 employees) are also looking to do the same. Similarly, 65% of larger firms and 56% of big corporations now regard their waste as a potential profit opportunity compared with 45% of smaller businesses.

However it is the activity of big corporations in this field that is likely to impact most on existing contractual arrangements with waste management providers. The majority (65%) expect

to either have to streamline the number of WMCs they deal with, or significantly change the terms of their contracts going forward, compared with 43% of larger firms and 44% of smaller companies.

Likewise big corporations are leading the field in maximising resource use through closing the loop on their waste arisings with more than a third (37%) planning to implement such a process over the next 12 months. This compares with 28% of larger firms and 25% of smaller companies.

That said, it is smaller organisations that appear to be embracing the ideology of a circular economy the most – 82% stated it was important to their company, compared with 78% of larger firms and 68% of big corporations.

This could suggest that smaller firms do not yet have the scale of investment to undertake more closed loop process implementation despite showing most willing.

This finding is reinforced by board level buy-in being less of an issue among smaller firms (18%) than larger companies (25%) and big corporations (39%).

76%86%52%30%54%

BuSinESS ATTiTudES To ThE CirCulAr EConoMy

76% say the concept of circular economy is important to their business 86% are looking to become more resource-efficient and move their waste up the hierarchy

52% now view waste as a potential resource or revenue stream 30% say they are looking to implement a closed loop process for waste arisings over the next 12 months

54% believe their relationships with waste providers will need to change going forward

The waste supply chain perspective

4

4.1 The great reclaim game: will the waste industry lose out? As businesses look to become more resource-efficient and extract greater value from their waste streams, concerns around feedstock security are heightening among waste management companies (WMCs). Nearly a third of WMCs (31%) surveyed confirmed that issues around feedstock security are now impacting on their business, while 18% believe it to be of real concern.

Looking ahead, these concerns are set to intensify – 42% of WMCs believe that feedstock security could become problematic in the future, while 14% say this issue is now on their radar. These fears are primarily driven by increased competition.

While the majority of WMCs (61%) felt this competition would mostly come from within the waste industry, 47% believed new entrants into the sector such as manufacturers, retailers and power and utility firms, who are looking to reclaim materials and energy for their own benefit now pose a serious threat. Competition from overseas markets was also considered significant by more than a fifth (23%) of respondents.

WhAT ArE ThE BiggEST BArriErS?how waste producers and WMCs rank the barriers to change

Businesses Reprocessors Waste contractors Manufacturers Product designers Local authorities Public sector bodies Brand owners Retailers

Waste producers Waste management companies

Key Behavioural change Lack of awareness insufficient policy drivers Business inertia Weak economic climate technical know-how Lack of business model innovation Risk-averse mindsets consumer engagement value chain collaboration

37.3%

24.5%

22%

20.3%

20.1%

17.3%

13.6%

32%

43.2%

39.70

27.4%

27.4%

26%

20.5%

12.3%

11%

34.2%

43.8%

47.9%50.1%

Sponsored by | 18 |

Sponsored by | 19 |

Other factors driving concerns over feedstock security include a greater policy focus at EU level on waste prevention and reuse, which in turn is shaping the Government’s zero waste agenda in the UK. A lack of quality materials for recovery was also cited as a key issue among WMCs, along with the emergence of closed loop economies, the impact of producer responsibility regimes and a lack of treatment capacity in the UK.

In terms of feedstock supply, looking across the municipal, commercial and industrial (C&I) and construction waste markets, there was no single end-of-life

material waste stream that was felt to pose a significantly higher security threat than the rest. This could be due to the fact that the circular economy agenda is still forming and a vast amount of material resource currently being sent to landfill could be unlocked and tapped into.

The crunch point for WMCs may come if national recycling levels start to plateau (latest evidence on the ground may suggest this is already starting to happen in England - see section 3.3).

Other than the landfill tax escalator, specific policy drivers for diversion

strategies remain weak in the absence of further landfill bans.

There are also emerging signs that local authorities themselves might start side-stepping traditional waste outsourcing models by aligning themselves with big corporates for targeted capture of certain material streams. Unilever is already exploring pilot ‘take back’ partnerships with local authorities, for instance [LINK-8].

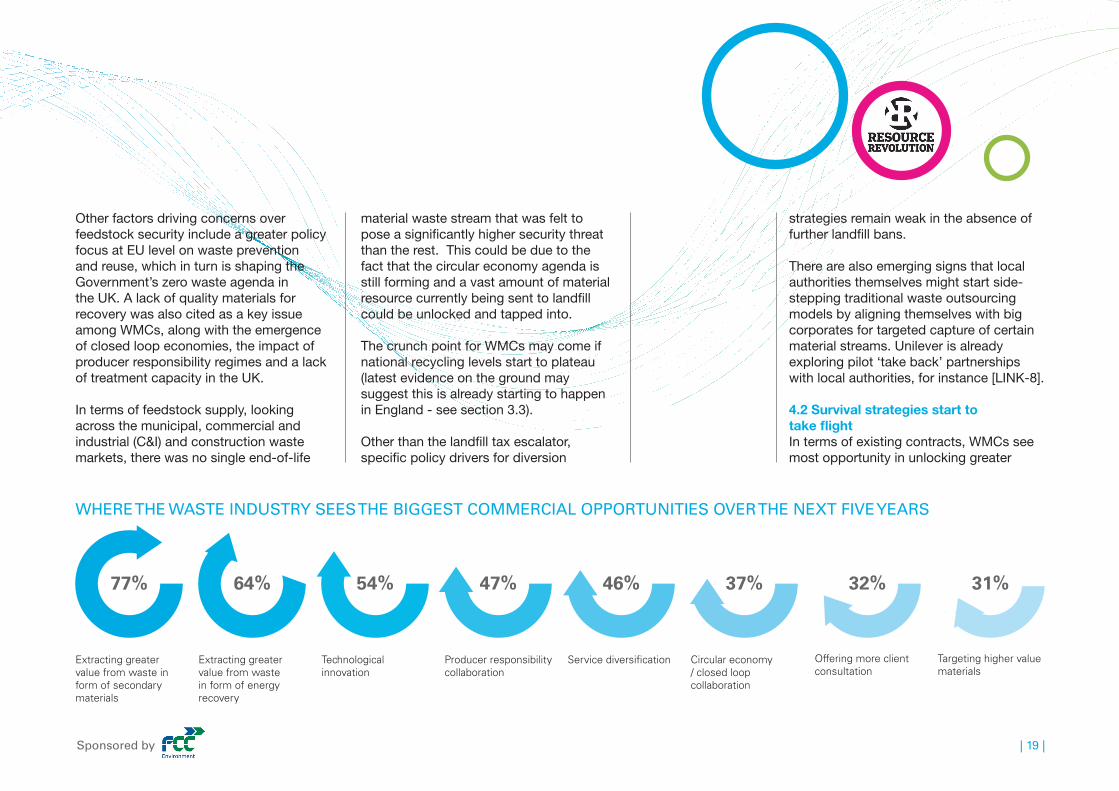

4.2 Survival strategies start to take flight In terms of existing contracts, WMCs see most opportunity in unlocking greater

77% 64% 54% 47% 46% 37% 32% 31%

WhErE ThE WASTE induSTry SEES ThE BiggEST CoMMErCiAl oPPorTuniTiES ovEr ThE nExT fivE yEArS

extracting greater value from waste in form of secondary materials

extracting greater value from waste in form of energy recovery

technological innovation

Producer responsibility collaboration

service diversification circular economy / closed loop collaboration

offering more client consultation

targeting higher value materials

to exploit future resource capture by extending their reach into the C&I market while nearly half (48%) are looking to form new alliances with waste producers. This is requiring greater flexibility in service offering – almost two-thirds of WMCs (65%) stated that they are diversifying their business portfolio in a bid to be more competitive.

Greater policy intervention is also being sought by WMCs to stimulate markets and

unlock feedstock availability. Introducing measures such as landfill bans of certain materials including waste wood and food were considered to be important levers in this respect, coupled with better regulation and enforcement of existing policies. A more prescriptive zero waste policy, especially in England, was also thought desirable.

4.3 Closed loop collaboration – a safe bet? In terms of working towards a circular economy, almost two-thirds of WMCs surveyed (61%) viewed the emergence of closed loop models and systems as a business opportunity. That said, a high degree of uncertainty exists among nearly a third (30%) as to whether it will impact upon them in a positive or negative way.

Not surprisingly, those that see it as an opportunity are also engaging with, or have plans to engage with, key stakeholders to explore closed loop solutions in the next 12 months. Of those, more than a third (36%) are already part of an active closed loop project, while 42% have plans to launch a closed loop project or are currently in discussions with stakeholders to embark on such a scheme.

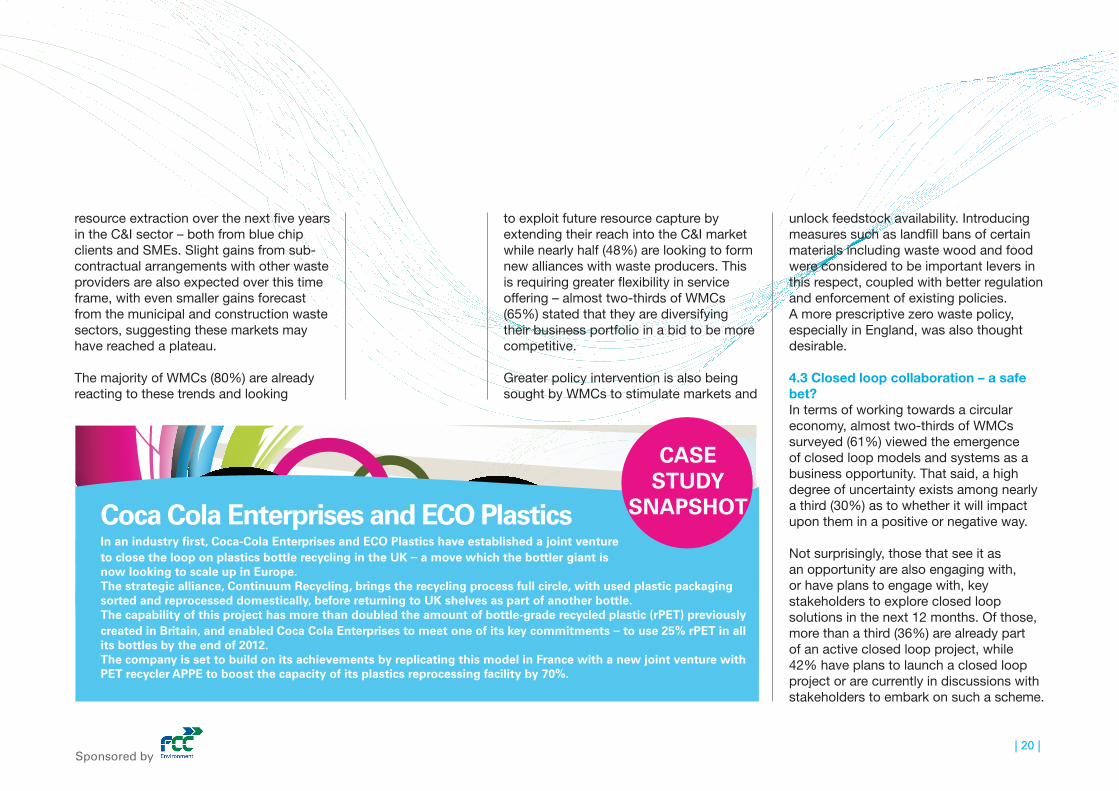

Coca Cola Enterprises and ECO Plastics In an industry first, Coca-Cola Enterprises and ECO Plastics have established a joint venture to close the loop on plastics bottle recycling in the UK – a move which the bottler giant is now looking to scale up in Europe.The strategic alliance, Continuum Recycling, brings the recycling process full circle, with used plastic packaging sorted and reprocessed domestically, before returning to UK shelves as part of another bottle.The capability of this project has more than doubled the amount of bottle-grade recycled plastic (rPET) previously created in Britain, and enabled Coca Cola Enterprises to meet one of its key commitments – to use 25% rPET in all its bottles by the end of 2012. The company is set to build on its achievements by replicating this model in France with a new joint venture with PET recycler APPE to boost the capacity of its plastics reprocessing facility by 70%.

resource extraction over the next five years in the C&I sector – both from blue chip clients and SMEs. Slight gains from sub-contractual arrangements with other waste providers are also expected over this time frame, with even smaller gains forecast from the municipal and construction waste sectors, suggesting these markets may have reached a plateau.

The majority of WMCs (80%) are already reacting to these trends and looking

CASE STUDy

SNAPSHOT

Sponsored by| 20 |

Sponsored by | 21 |

Meanwhile more than a fifth of WMCs (22%) are actively looking to engage with interested parties.

Of the key stakeholder groups that WMCs are looking to engage with or target, local authorities are cited as being the most important (by 73% of respondents). This is likely to be because of their government mandate to oversee the collection, treatment and disposal of large tonnages of municipal waste and the fact that many of these services are outsourced to private WMCs.

Manufacturers were ranked as the second most important stakeholder group to engage with by two-thirds (67%) of WMCs, followed by government (60%), public sector bodies (53%), reprocessors (51%) and retailers (47%).

The fact government ranks so highly is surprising, but this might reflect the waste industry’s desire for more policy intervention to in order to stimulate markets around material quality. The importance of engaging with brand owners and product designers was seen as significantly less of a priority among WMCs (22% and 9% respectively).

Despite concerns around feedstock security and the transformational dynamics underpinning the move towards a circular economy, two-thirds of WMCs (66%) did not feel they would need to adapt their business models in order to position themselves at the forefront of this agenda.

4.4 Mind the knowledge gaps While waste contractors, reprocessors and manufacturers are perceived by both WMCs and waste producers to be the top three stakeholder groups leading on the circular economy agenda, there is significant divergence on the perceived leadership of product designers and brand owners. If these knowledge gaps between start-of-life and end-of-life industries are to be addressed, these stakeholder groups must step out of their silos and collaborate to deepen their understanding of the issues at play.

These knowledge gaps are underlined by the fact that nearly half of WMCs surveyed (48%) felt that a lack of awareness was the main barrier to achieving a circular economy. Behaviour change was also cited as a significant stumbling block by 40% of WMCs followed by a lack

of business model innovation (34%), business inertia (27%) and technical know-how (27%). A weak economic climate appears to be presenting more of a challenge to the waste industry than to businesses in this regard, with 44% of WMCs believing it to be a key barrier.

4.5 Always be prepared: take action to future-proofAs the resource management agenda unfolds over the next five years, the majority of WMCs (77%) see the biggest commercial opportunities arising from smarter value extraction techniques, either in the form of secondary materials or energy recovery. This will require a strong need for technical innovation, which is also recognised as a business opportunity in itself by 54% of WMCs.

In addition, 46% of WMCs felt that service diversification will open up new business channels while 47% saw strategic alliances with businesses on producer responsibility compliance as a key commercial opportunity.

Interestingly, only about a third of WMCs (37%) felt closed loop collaborations would offer a clear commercial opportunity

Where WMCs see most opportunity in unlocking greater resource extraction over the next five years is in the C&i sector – both from blue chip clients and SMEs

Sponsored by

051015202530051015202530051015202530

051015202530

051015202530

| 22 |

for their business over the next five years. This suggests that many are still uncertain as to how the circular economy will unfold and impact upon their operations, and whether or not they will need to reposition their service offering in order to capitalise upon it.

What is clear from this survey is that better waste management is often seen as a quick win for businesses looking to reduce their environmental impacts and potentially boost the bottom line.

WMCs would be wise to act now in order to deepen their understanding of the corporate resource efficiency agenda and how it is evolving. This will enable them to react swiftly and cater their service provision more effectively to deliver this bottom line value for their client base.

Not to do so would miss a clearly emerging business opportunity at a time when the waste management industry’s expertise and technical knowledge in materials handling and resource recovery is most urgently needed.

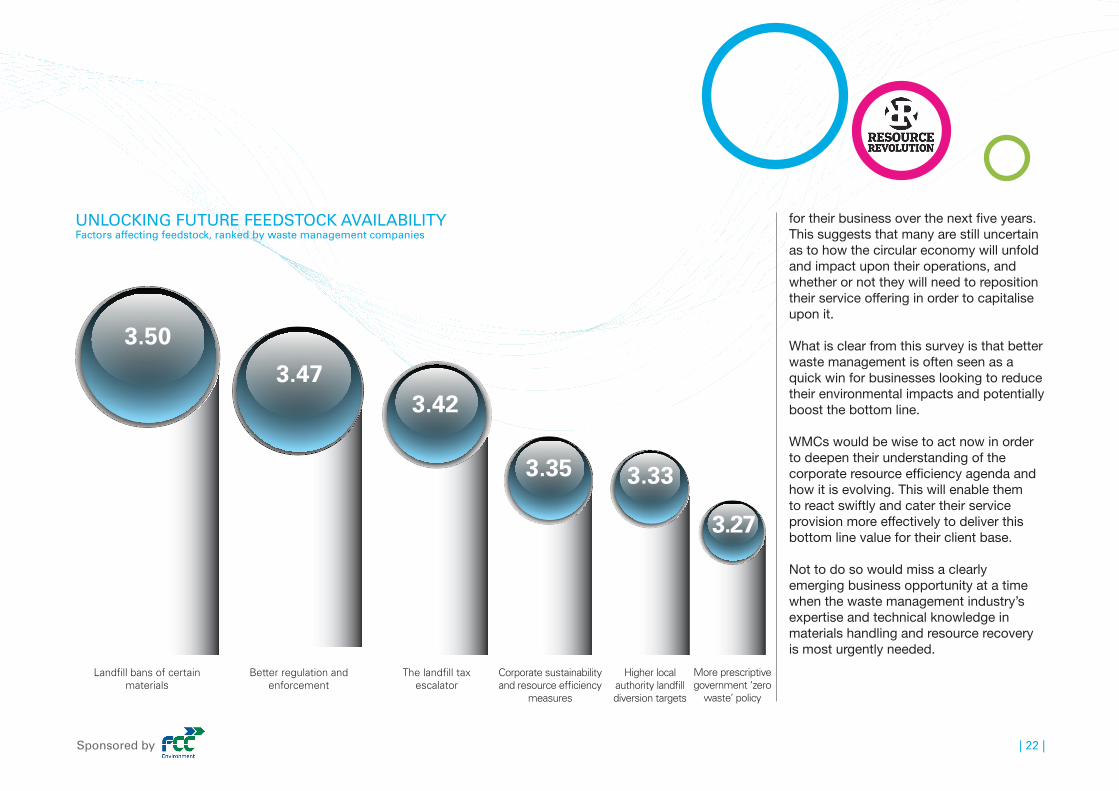

unloCKing fuTurE fEEdSToCK AvAilABiliTy factors affecting feedstock, ranked by waste management companies

More prescriptive government ‘zero

waste’ policy

Landfill bans of certain materials

Better regulation and enforcement

higher local authority landfill diversion targets

the landfill tax escalator

corporate sustainability and resource efficiency

measures

3.50

051015202530

3.473.42

3.35 3.33

3.27

The attitudes of organisations that generate waste are changing rapidly, and this survey provides a valuable overview of those changes.

More and more, businesses and public institutions understand that there is value in what they throw away – and are seeking answers and advice from the waste management industry and beyond to respond and extract as much value as possible from waste materials. Waste producers know that improving efficiency involves reclaiming material from their waste streams and feeding it back into the supply chain – be that as a secondary material or as, for example with organic waste, compost and energy. And they must do it while striking a balance between volume and material quality.

Providing the answers is the emerging role of the recycling and waste management sector. It is about sharing knowledge and technology as we settle into a new position mid-way through a supply loop rather than at the end of a supply chain. For many of us this is a fundamental shift in our business. FCC Environment has, for example, remodelled its business to focus on generating resources rather than dealing with waste.

As disposal, treatment and raw material costs continue to rise and as markets for secondary materials develop, closing the resource loop will help us all to improve productivity and efficiency while reducing environmental impact, reducing cost and boosting the bottom line.

This report maps progress along the journey so far. It confirms the demands upon the recycling and waste sector, thereby reducing perceived risks and showing that for those companies willing to adapt, the long-term opportunities are huge.

Kristian dales, sales, marketing and communications director, fCC Environment

Sponsored by | 23 |

Sponsor contactKristian dales - fCC EnvironmentSales, marketing and communications director01604 [email protected]

@fCC_Environment

Contacts

Maxine Perellareport authorWaste editor, edie.net 01342 [email protected]

@edieWaste

David BaldockSales manager, edie.net01342 [email protected]

Sponsored by