Forest Interior Songbirds and Climate Change on Private Land

Climate Change Risk And The Private Sector:

Adaptation & Management

Ian Edwards Donovan Burton

Mark Baker-Jones

Caveat, please read: The information presented in this report is based on information publicly available up to 1 September 2016 and within the budget, time and other constraints. The information presented in this report is for general information purposes only and no permission is given to third parties wishing to use this information for any purpose without prior written consent.

Suggested Citation: Edwards, I., Burton, D. and Baker-Jones, M,. (2016) Climate Change Risk and the Private Sector: Adaptation and Management. A Whydu and Climate Planning Report

The authors would like to express sincerest thanks to the numerous colleagues involved in peer-reviewing this paper and the valuable insight provided.

© 2016 Version 1.1

Cover Image: Satellite image of Hurricane Katrina. High Resolution (Credit: NOAA)

Climate Change Risk: Adaptation & Management

3

Ian Edwards: Ian has twenty years experience in national and international financial services and has worked across a broad spectrum of the international financial industry including public practice, investment banking and reinsurance as a chartered accountant and systems analyst. Ian holds a Masters in Environment with First Class Honours from Griffith University and has been involved in a range of projects globally and within Australia specific to climate change adaptation and resilience strategies.

Donovan Burton: Donovan specialises in climate change adaptation governance and is globally recognised as an expert in this field. Over the past ten years he has worked on over 130 climate change adaptation projects. This includes work in the U.S., Asia, Pacific Island Nations and Australia. During this time he has also worked closely with state government agencies, property developers, infrastructure providers, information technology companies and insurers undertaking a range of climate change adaptation services.

Mark Baker-Jones: Mark is a partner in the Property & Projects group and a member of the Property and Energy industry groups at law firm DibbsBarker. He has extensive experience in the area of environmental law and is a recognised leader in climate change and the law. Mark is also Chair of the Queensland State Government Climate Change Adaptation Strategy Partnership, under the Minister of the Environment, a member of the technical reference group of the National Climate Change Adaption Research Facility and is a Visiting Fellow in Climate Change Law to the Queensland University of Technology. Mark is also a guest lecturer to the University of Queensland Renewable Energy Law masters course.

About the Authors

.

.

.

Climate Change Risk: Adaptation & Management

4

• The nature of the messenger has changed: an appreciation of climate change risk to business and economies is rapidly shifting into the financial mainstream.

• Climate risk is multi-faceted: impacts extend well beyond direct physical degradation to create cascading implications at all societal levels.

• Climate change risk extends to the full value chain: physical risks in particular extend beyond direct operations to an organisation’s supply chain and markets.

• Transition risk is current: consumption and governance changes as society transitions from a fossil fuel economy represent immediate risks and opportunities for all businesses.

• Legal risk is an incentive to act: legal risk, implicit in actions and inactions to address climate change, travels behind the corporate veil to directors and boards.

• Disclosure exposes both good and bad practice: recent proceedings that augur more transparent and comparative disclosure frameworks will promote climate change risk to the near term.

• With risk comes opportunity: where managed appropriately a reduction in climate change risk can generate significant positive implications for an organisation’s reputation and brand proposition.

• Climate change adaptation, as a profession, is a speciality that differs from climate change mitigation: both climate change mitigation and adaptation fields are evolving. Whilst there is a very strong overlap, subtle differentiations do exist.

• An effective adaptation governance framework is key to reducing the risks and exploiting the opportunities that climate change presents.

Key Points

5

Since the early 1970s, scientists have warned of the societal implications of a warming world: the predominant cause of which is the emission of greenhouse gases (GHG), such as carbon dioxide, due to human activity. In order to limit the probability of ‘catastrophic climate change’, the international community has agreed to curb emissions to levels commensurate with a 2°C rise against pre-industrial levels.1 This ‘guardrail’ has evolved more through political expedience than rigorous science. Evidence indicates that 2°C may be insufficient to prevent severe climate disruption.2

The guardrail is looking increasingly precarious. If all GHG emission reductions pledged at the recent Paris climate talks materialise over the coming decade, global temperatures are likely to increase by approximately 2.6–3.1°C. Temperatures are already well above pre-industrial levels, with 2016 exhibiting a significant step up from recent years (figure 1).

Figure 1 Global year to date temperature anomalies3

1.40

1.00

0.80

0.60

0.40

0.20

1.20

0.00

Year-to-Date Global Temperaturefor 2016 and the other seven warmest years on record

Diffe

rent

(°C

) fro

m th

e 20

th c

entu

ry a

vera

ge

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

20152016201420102013200520091998

A Starting Point

55

Climate Change Risk: Adaptation & Management

Climate Change Risk: Adaptation & Management

6

The management of climate change risk is transitioning. It is no longer just an environmental “green” issue, but one which is associated with both opportunities and constraints of growth. The sample of messages presented below, shows that an appreciation of the risk that climate change poses to economies and businesses, has rapidly extended beyond the dominion of commentators and those “on the periphery”, to one that is clearly gaining ground within the financial mainstream.

The World Economic ForumIn 2016, the World Economic Forum (WEF) rated failure of climate change adaptation and mitigation as the risk that will have the most impact on the global economy over the next ten years.

The WEF ranked climate change ahead of:

• weapons of mass destruction (2nd);• water crises (3rd); and • large-scale mass migration (4th).5

The ratings represented the views of 742 surveyed experts and decision makers, drawn from business, academia, civil society and the public sector.Water crises and mass migration were linked in the report as symptoms of climate change.

We know climate change is exacerbating other risks such as migration and security, but these are by no means the only interconnections that are rapidly evolving to impact societies, often in unpredictable ways. Mitigation measures against such risks are important, but adaptation is vital.

Margareta Drzeniek-Hanouz, Head Global Competitiveness & Risks, Jan 20164.

The Nature of the Messenger has Changed

Global warming is already manifesting in a changing climate: rising sea levels, ocean acidification, increased extreme events and species behavioural change. Climate change is here and now. Future GHG reductions will not prevent climate change. They will only determine the extent of change. Climate change, like any other manifestation, represents a risk with a range of positive and negative implications; the extent of each of which is determined predominantly by how effectively climate change risk is embraced and managed.

Regulatory Bodies and Central Banks

The (Re) Insurance Industry

Climate change is becoming increasingly relevant to financial regulation. The PRA’s approach will focus on promoting resilience to climate change and supporting an orderly financial sector transition to a lower carbon economy. The PRA will do this through a combination of international collaboration, research, dialogue and supervision.

Bank of England Prudential Regulation Authority, 2015, p. 676.

Keeping global warming below 1.5-2°C requires that the stock of carbon dioxide (CO2) and other greenhouse gases (GHGs) in the atmosphere is kept below a critical limit. The speed at which this threshold is reached depends on the future trajectory of yearly emissions. If policymakers do not intervene and technological breakthroughs do not occur, the flow of emissions will continue to increase…, as will the stock of greenhouse gases in the atmosphere.

European Systemic Risk Board, 2016, p. 39

In my view, sustainability is arguably the world’s most significant contemporary market failure. Some of the worst case scenarios coming out of the International Panel on Climate Change are deeply concerning with potentially profound implications on the valuation of the companies listed around the world.

Mark Wilson, Group CEO, Aviva PLC, Jul 201411.

The United Nations Environment Programme (UNEP)7 asserts a quiet revolution, where central bankers and regulators are increasingly seeking to incorporate issues such as climate change, into the financial mainstream. Reports prepared on behalf of, and by, Switzerland’s Federal Office of the Environment, the Bank of England and the European Systemic Risk Board, give support to this specific observation about climate change. Collectively, the reports raise concerns about risks implicit in the various physical, transitional and legal impacts of climate change. Importantly, they echo an increasing willingness for government involvement in addressing climate change 6, 8-10.

As an industry uniquely challenged* by the impacts of climate change, a number of high profile insurers are actively advocating societal-wide mitigation of climate change risk.

* The scale of climate impacts has the potential to adversely affect both the asset (asset management) and liability (underwriting) aspects of an insurer simultaneously.

7

Climate Change Risk: Adaptation & Management

8

The prospect of extreme climate change and its potentially devastating economic and social consequences are of great concern to the insurance industry.

The Geneva Association, 201412.

I do not want to sit by and then discover in the near future that insurance companies’ books are filled with stranded assets that have lost their value because of a shift away from the carbon-based economy, jeopardizing their financial stability and ability to meet their obligations, including paying claims to policyholders.

Dave Jones, California Insurance Commissioner, Jan 201613.

1. Review the enterprise risk management efforts by carriers and how they may be affected by climate change and global warming; and

2. Review innovative insurer solutions to climate change, including new insurance products through presentations by interested parties.14

Insurers, such as Axa, Allianz and Munich Re, are also recognising their influence on global climate risk and diverting investment from carbon-intensive to carbon–free industry. Amongst a plethora of insurer-led organisations established to advocate stronger climate change action, 66 chief executives of the globe’s largest insurers signed the Geneva Association’s climate risk statement.

In a number of jurisdictions of significant size, regulators such as the Prudential Regulation Authority, noted above, and California’s Department of Insurance, herald industry concerns.

In the US, the National Association of Insurance Commissioners (NAIC) has taken a leadership role in exploring climate risk disclosure. In 2016 the NAIC Climate Change and Global Warming Working Group will, amongst other things:

The Australian insurance industry regulator has yet to act as proactively as many of its overseas counterparts and, to date, the Australian Prudential Regulation Authority (APRA) has issued no formal guidance to insurance companies regarding climate change.

9

Those companies that fail to meaningfully address their long-term sustainability risks and opportunities – or that merely pay lip service to these issues through a minimalist compliance stance – will be increasingly exposed.

Australian Council of Superannuation Investors, Apr 2016, p.315

The report enumerates a set of fundamental principles of disclosure, which -- combined with a standardized and consistent scenario analysis framework for disclosing climate-related risks, by region, industry and time horizons -- could serve as a meaningful starting point for integrating more methodically climate change into our analysis of creditworthiness.

Henry Shilling, Moody’s Senior Vice President, Apr 201619

We consider climate change to be the greatest risk facing our investment portfolio.

Local Government Super, 201616.

Some pension funds are taking a greater interest in climate change risk and quality of disclosure.

Both S&P and Moody’s released climate risk related reports in 2015, addressing the emerging risk associated with climate change, and global efforts to stop it.18

The Asset Owners Disclosure Project17 ranks the world’s 500 biggest asset owners by their publicly disclosed and surveyed success at managing climate risk. Of the thirteen entities (with US$1.141trilion AUM*) that received the project’s highest rating, “AAA”, from this year’s study, all except one are pension funds, but only three are Australian.

Pension Funds

Ratings Agencies

* Assets under Management (AUM) measures the total market value of financial assets managed by financial institutions on their own and client’s behalf.

9

Climate Change Risk: Adaptation & Management

10

Whilst it is arguable that the rating agencies have historically failed to fulfil their function to “form a forward looking opinion of relative credit risks”, initiatives such as the Financial Stability Board’s Taskforce on Climate Change-Related Disclosures are nudging banks towards incorporation of climate risk.

In our view, providers that start to prepare early for the challenges presented by climate change are likely to be best-positioned to take advantage of any opportunities that open up. For the others, there could be rating implications if it is evident to us that a management team is not taking the right steps relative to its peers. If a bank’s business activities are concentrated in an area or sector we consider could be marred by climate change, this could weaken its business position and put its rating under pressure.

S&P Global, 2016, p.920

Climate change is expected to increase the risk of interruption and financial loss to the private sector. Climate risk extends beyond direct physical damage. It incorporates a range of indirect and cascading risks and opportunities. The risks and opportunities appear as society moves to reduce climate risk, and reacts to the impacts and implications of climate change related extreme weather events.

Climate Risk is Multi-Faceted

Figure 2 Climate risk categories and financial impacts (Based on frameworks presented by the Sustainability Accounting Standards Board (p. 6: Figure 1)21 and Bank of England6)

Climate Change Risk: Adaptation & Management

11

Physical risk: these are first-order risks that arise from weather-related events, such as floods and storms. They are the impacts that result directly from these events, and include such things as damage to property. The impacts also include those that come about indirectly through subsequent but related events, such as the disruption of global supply chains or resource scarcity.

Transition risk: this is the financial risk that arises as behaviour, consumption patterns and societal expectations change as society transitions to a lower-carbon economy. This risk factor incorporates such things as potential re-pricing of carbon-intensive financial assets, consumer preference for climate friendly practice, governmental policies, binding and non-binding agreements and regulatory mechanisms (e.g. carbon-pricing).

Legal Risk: generally this is a litigation risk that arises where parties who have suffered loss and damage from climate change, seek to recover those losses. Such actions could be taken against an organisation itself, or slip in behind the corporate veil to the officers and boards responsible for the organisation’s governance.

Categories of climate risk

Cash Flow and Operating Impacts: may arise along both cost and revenue lines. They are due to climate-related impacts to the financial condition, operating performance and expenses along an organiation’s full value chain.

Asset Impacts: these impacts affect the value and use of core assets due to: a price on carbon and other regulatory outcomes; changes in asset value due to the physical effects of climate change; and/or devaluation of assets due to the transition to a low-carbon, resilient economy. Current assets (e.g. inventory, crops, and livestock) and long-lived physical assets (e.g. coastal properties, infrastructure and forestland) may be at risk of impairment or devaluation due to increased extreme weather events.

Financing Impacts: access to and/or cost of debt and equity capital may be affected by how well entities manage their climate risk exposure. Entities that have greater exposure to the physical effects of climate change, and demonstrate poor management of their transition risks. Exposed entities are also ones that are subject to climate regulations and ones that may face debt and equity risk premiums if rating agencies, investors, and lenders factor in climate risks.

Directors and Officer Liability: this liability is closely aligned with all of the above but is differentiated due to its potential application beyond an organisation to those who are responsible and oversee its operation.

Financial Impacts

An organisation’s value chain can be extremely complex. Key stressors can include globalisation, mega-clustering of industries, just-in-time logistics, and resource scarcity. All of these issues are likely to be affected by climate change (or responses to climate change). Businesses now need to operate in a time of unprecedented disruptions and a shifting regulatory milieu.

For example, in late October 2011, the catchment of Bangkok, Thailand experienced heavy rainfall that flooded much of the city’s industrial zone. The floods have had a considerable impact on the local and global supply chain. In fact, the floods resulted in a 2.5% reduction of global industrial production, and almost 18% of the large firms affected did not reopen.23

All components of a value chain are exposed to some element of direct or indirect risk. For example, many of the raw materials used or exploited by organizations are exposed to emerging and current risks from climate change. Agricultural commodities face stresses from direct climate impacts, such as increased prevalence and intensity of extreme weather events.

These commodities are intrinsically linked to the natural environment and are exposed to other climate change related stresses, such as, ecosystem changes, invasive species, changing pollinators, soil microbial change and salinity to name but a few.24

Climate Risk extends to the Full Value Chain

Climate change threatens Avery Dennison’s supply chain, our customers’ businesses and the communities we’re part of. If we want to stay in business for the long-term, contributing to the fight against climate change is just smart strategy.

Dean Scarborough, CEO Avery Dennison, 201522

Climate Change Risk: Adaptation & Management

12

Climate Change Risk: Adaptation & Management

13

Mineral extraction is also exposed to the effects of climate change. Mining operations usually occur in remote locations, often with sensitive geopolitics. Infrastructure maintenance is expensive (especially in remote locations) and water and energy are important components in the extraction and refinement process. Any impact on these key elements may drive up the price of the raw material, present short-mid term disruptions, or limit the supply altogether.

Other elements of an organisation’s value chain include logistics, labour supply, energy security, information communications, community well-being, market demand and access to financial capital and appropriate risk transfer mechanisms. In the globally connected economy, all these elements are exposed to often-unseen ripples from behavioural changes connected to risk.Given the shifting complexities, simplistic risk management approaches are not suitable to manage the evolving issues. Organisations have no control over the causes of the stressors; they only have the ability to influence the consequences.25 As such, they need to ensure that governance arrangements are set up to allow the consideration of direct and indirect effects of climate change as they emerge.

Static plans will not suffice in a shifting climate. Shifting risk may temporarily suit one organisation, but expose other organisations in the group, ultimately affecting the organisation’s intent on risk transfer. The global economic crisis, which occurred almost a decade ago, highlighted the limitations and consequences of hiding risk.

Managing the amalgam of value chain risk is a formidable task. According to Waters (p.180), “it can only really be tackled through a cooperative effort by all members, with each managing its own internal risks and accepting a broader responsibility for reducing the vulnerability of the whole chain.”26 Vetting these actions can only be done through corporate disclosure of governance arrangements. The governance must extend to the public and private spheres; even a good value approach may be undone by poor infrastructure or limited national recovery systems.

Climate Change Risk: Adaptation & Management

14

Transition risks are the financial risks that could arise as economies transition to a lower-carbon economy.

Divestment represents the reduction of fossil fuel related assets from investment portfolios.

An increasing appreciation of the financial and reputational implications of climate change at a firm level, has recently emerged. This has come about as investor and regulatory attention has increasingly been drawn to carbon related industry and climate risks. This trend is expected to accelerate as disclosure requirements coalesce, to provide the market with a more transparent, comparative and complete view of the risks and opportunities that climate change poses to business, and how these are being managed.

As at May 2016, investors with assets under management of $3.4 trillion29, had committed to divest from fossil fuels. This number represented a greater than fifty-fold increase from 2014, and a distinct trend towards private sector engagement (95 per cent of the total combined assets of those committed to divest is held by large pension funds and private-sector actors such as insurance companies). As an example, insurers Axa and Allianz have announced they will sell off coal assets. That could impact up to €500 million and €4 billion in assets respectively30, 31. In January 2016, the Californian Insurance Commissioner requested that all insurers conducting business in California (largest insurance market in US and sixth largest globally) divest from coal13.

Divestment

Transition Risk is Current

Reports by Citigroup analysts, HSBC, Mercer, the International Energy Agency, Bank of England, Carbon Tracker Initiative and others have offered evidence of a significant, quantifiable risk to portfolios exposed to fossil fuel assets in a carbon constrained world. The leaders of several of the largest institutions to divest in the past year have cited climate risk to investment portfolios as a key factor in their decisions.

Arrabella Advisors, 201526

Fossil fuel divestment has kicked into overdrive.

Time, Sep 201527

Climate Change Risk: Adaptation & Management

15

Perhaps as a sign of the times, the financial industry is organising to exploit this trend, making divestment more convenient. For example:

In 2016, ninety-four (up from eighty-two in 2015) climate change related shareholder proposals were raised in the US.33 The proposals are predominantly directed to heavy fossil fuel producers and users, and address climate change impact on business and preparation.

In Australia there has been an increase in legislation introduced to respond to climate change impacts. With this, comes a concurrent increase in climate change litigation. This poses a significant risk for corporations.

Climate legal risks are sometimes plain and obvious (like a failure to comply with carbon pricing regulations), while others are more obscure (such as obligations to seek ecologically sustainable development). The great increase in climate change related litigation being carried out against organisations, particularly in the US, is an indication of the extent of the shift of policy activism that is occurring. It is a shift from social agendas to corporate vehicles, where the application of relatively inexpensive tools, such as shareholders’ proposals to address climate change, become a potential precursor – a set up – for imminent litigation.

FTSE Russell, the global index provider, has launched an innovative new index that reduces exposure within the index to companies associated with fossil fuels while also increasing exposure within the index to companies engaged in the transition to a green economy.

FTSE Russell, April 201631

While some business leaders and corporations might be agnostic about the science of climate change, it is a material business risk issue.34

Mark Baker-Jones, Partner DibbsBarker, June 2016

Shareholder Activism

Legal Risk is an Incentive to Act

Climate Change Risk: Adaptation & Management

16

The increased expectations of disclosure of climate related risk is also feeding corporate legal risk, with those in extractive or emissions intensive industries, clearly the most at risk of regulatory impacts on their business. However, manufacturers and utilities also bear significant risk.

Conventional tortious or administrative law actions are widely seen as easily adapted to accommodate the anticipated body of general climate change legal action. However, a number of actions targeting corporations are developing. These rely on a range of ancient doctrines and forgotten legislation, as the legal fraternity explores novel and innovative approaches, such as:

• the public trust doctrine where the sovereign holds in trust for public use, resources such as, a healthy and habitable atmosphere, and must regulate the substances in the atmosphere (e.g. see “Our Children’s Trust” Below);

• revival of all but forgotten legislation, like the US 1921 Martin Act; a piece of legislation that gives extraordinary powers and discretion to the New York attorney general, and is being used as a vehicle for addressing issues of investor climate change disclosure; and

• the application of tripartite human rights obligations to private corporations such that, the role of the state is to ensure corporations respect human rights and the protection of citizens of the state from climate change.

Corporations that fail to adequately deal with climate legal risk are becoming increasingly exposed to multiple legal actions from a number of quarters. Once they are in the spotlight, they potentially become a target for further climate related court action. For example, ExxonMobil has been the subject of a number of climate change related legal actions over the last few years (see targeted litigation example on the following page).

Climate Change Risk: Adaptation & Management

17

ExxonMobil’s climate-related challenges started in 2015, when New York attorneys general alongside several environmental groups commenced an investigation of ExxonMobil’s financial records. They alleged that ExxonMobil committed fraud by misleading its investors about the risks of climate change on the company’s business. The Securities and Exchange Commission (SEC) then commenced an investigation into whether ExxonMobil’s reporting of climate risk was in accordance with SEC disclosure guidance related to business or legal developments regarding climate change. Since that time, private organisations have started taking action against ExxonMobil.

One such complaint has been led by a private organisation with the Internal Revenue Service (IRS) claiming that the American Legislative Exchange Council (ALEC) – a non-profit lobbying concierge that is claimed to promote ExxonMobil’s climate denial policies and legislative agenda - is falsely claiming tax-exempt status as a charity. The plaintiff claims that the ExxonMobil Corporation has intentionally misused ALEC for nearly two decades to advance its legislative agenda.

A further action has also been filed by another organisation against ExxonMobil. The claim consists of fourteen causes of action founded on two main grounds. Firstly, that ExxonMobil has contributed to environmental damage by continuing to store, treat and dispose of hazardous waste in contravention of the relevant Clean Water Act. Secondly, ExxonMobil is alleged to have failed to prepare for the consequences of rising sea levels due to climate change, by not undertaking protective measures and fortifying a petroleum storage terminal in Everett, Massachusetts.

The significance of this later action is that, unlike previous climate-related lawsuits that sought to take mitigation measures, the plaintiff is challenging ExxonMobil, in part, for failing to adapt to climate change. Internationally, law firms are issuing alerts to clients suggesting they monitor the actions against ExxonMobil.`

Targeted Litigation: ExxonMobil

Climate Change Risk: Adaptation & Management

18

Our Children’s trust

In April 2016, the U.S. District Court for the District of Oregon decided a constitutional climate change lawsuit against the federal government and members of the fossil fuel industry, in favour of plaintiffs. The lawsuit relied on the public trust doctrine as the basis for cause to enforce existing regulation and redress the evident, measurable damages.

The presiding judge, U.S. Magistrate Judge Thomas Coffin, stated (Case 6:15-cv-01517-TC Document 68 Filed 04/08/16):

The debate about climate change and its impact has been before various political bodies for some time now. Plaintiffs give this debate justifiability by asserting harms that befall or will befall them personally and to a greater extent than older segments of society. It may be that eventually the alleged harms, assuming the correctness of plaintiffs’ analysis of the impacts of global climate change, will befall all of us. But the intractability of the debates before Congress and state legislatures and the alleged valuing of short-term economic interest despite the cost to human life, necessitates a need for the courts to evaluate the constitutional parameters of the action or inaction taken by the government. This is especially true when such harms have an alleged disparate impact on a discrete class of society.

With the increasing recognition of the link between economic loss and climate change, the risk of legal action to account for those losses also increases. The spectre of stranded assets, driven by regulatory and technological responses to climate change, presents particular issues for institutional investors, and consequently the corporations themselves.

A recently published study on Australian trustee directors’ statutory obligation to apply due care, skill and diligence under section 52A of the Superannuation Industry (Supervision) Act 1993 (Cth), has found that (p. 211) ‘even where trustee directors’ subjective bona fides are not in question, a passive or inactive governance of climate change portfolio risks is unlikely to satisfy their duties.’34

Climate Change Risk: Adaptation & Management

19

Disclosure Exposes both Good and Bad Practice

The right information allows skeptics and evangelists alike to back their convictions with their capital.

Mark Carney, Speech presented at Lloyds of London, Sep 201535.

While we agree with their overall premise that any disclosure recommendations by the taskforce [i.e. FSB Taskforce] would be voluntary, we consider that major financial institutions would be likely to adopt reasonable standards as soon as practicable.

Submission to Australian Senate Inquiry into Carbon Risk Disclosure, Apr 201637

It’s critical that industries and investors understand the risks posed by climate change, but currently there is too little transparency about those risks… While the business and finance communities are already playing a leading role on climate change, through investments in technological innovation and clean energy, this Task Force will accelerate that activity by increasing transparency. And in doing so, it will help make markets more efficient, and economies more stable and resilient.

Michael Bloomberg, TCFD Chair, Dec 201538

Higher-quality business reporting and disclosure are needed to better reflect the climate change uncertainties facing companies.

Warren Allen, IFAC President, Dec 201336.

There is little doubt that the estimated 400 climate change related disclosure frameworks currently in existence, obfuscate the ability of investors to understand and compare climate change risk management practice at an organisation and economy scale.35 Current frameworks also predominantly address the measurement and reporting of greenhouse gases (carbon risk), as opposed to the risks that climate change poses to an organisation’s business model (climate change risk). Recent initiatives, such as those noted below, have the potential to alleviate disclosure gaps and failings and, in the process, expose to interested parties current management practice of physical, transitional and legal climate risks. Early adopters will apply voluntary disclosure frameworks. As ANZ Banking Group noted:

The FSB’s Taskforce on Climate Change-Related Disclosure

In addition there remain a number of areas that are underreported at an individual company level. These may include but are not limited to increased physical risks from a changing climate, market risk (including within a company’s supply chain and customer base) and the reputational risk from consumer and shareholder backlashes for perceived inadequate action.

Regnan* , March 201639

In December 2015, the Financial Stability Board launched the Taskforce on Climate Change-Related Disclosures (TCFD). Recommendations will target near, medium, and long-term physical and non-physical climate impacts on both the non-financial and financial sectors. The Task Force will consider the features and characteristics of information to be disclosed—including quantitative, qualitative, historical and forward-looking metrics—and how disclosures are used, analysed, and aggregated. The TCFD’s final report is due at the end of 2016.

In February 2016, the Australian Senate initiated an inquiry into carbon risk disclosure. The objective of the inquiry is to examine potential effects of carbon risk on financial stability; carbon risk disclosure frameworks; and regulatory oversight of carbon risk. Submissions made from investment groups have highlighted the importance of including climate change risk in any framework and a desire for mandatory reporting.

Whilst findings were initially due in June 2016, the inquiry has lapsed.40

Australian Senate Inquiry into Carbon Risk Disclosure

20

Current Disclosure Initiatives

Industry LedInternational disclosure frameworks have advanced along two channels: greenhouse gas reporting and Environment, Social and Governance (ESG) reporting frameworks. There is an increasing trend within these frameworks to augment greenhouse gas disclosure with a view of climate change risk and management strategies. Investor groups have collaborated to launch the Investor Platform of Climate Actions, an online platform aimed at capturing the wide range of climate change actions being undertaken by the global investor community.**

* Regnan - Governance Research & Engagement Pty Ltd was established by BT Investment Management and Commonwealth Superannuation Corporation to investigate and address environmental, social and corporate governance (ESG) related sources of risk and value for long term shareholders in Australian companies.** See http://investorsonclimatechange.org

Specific to Australia, the four major banks (ANZ, CBA, NAB and Westpac) have formed the Australian Portfolio Carbon Working Group. The focus is to share insights and alternative approaches that will enable financial institutions to measure and disclose their climate performance*, with the aim of demonstrating how Australian banks will support the transition to a lower carbon economy41.

National and Regional FrameworksSome national and regional frameworks require companies, investors and insurers to report on their carbon risk in relation to their global operations. In Australia, the ASX and the Australian Securities & Investment Commission, oblige disclosure with respect to the management of environmental risk that could materially impact corporate operations (see Appendix A).

An appreciation of and action to address climate change is still relatively novel. There is still scope for early adopters to gain first-mover advantage over their competitors. Forward-thinking companies will recognise and capitalise on climate-related products and new markets whilst reducing climate related risks to their own operations, the key benefits of which include42:

*Note that there is little indication of what “climate performance” actually means and whether this extends to climate risk per se.

With Risk comes Opportunity

21

Business Continuity. Risk assessment applied along an organisation’s full value chain can highlight potential stress points. Resultant risk management incorporated in internal policies, processes and systems will minimise potential business disruption. Early identification of complex risks allows an organisation to explore innovative risk transfer and adaptation financing mechanisms (e.g. catastrophe bonds and other bonds).

Cost Savings. Pro-action is invariably cheaper than reaction. Building climate resilience into asset design and specification can increase useful life and preclude expensive retrofits. Adjusted operational and maintenance procedures may be possible at minimal additional cost and/or payback periods.

22

Unilever and Supply Chain

Unilever have identified the impacts of climate change on the consumer goods sector, recommending that “there’s a strong business case for taking climate change out of the value chain—from the use of renewable energy for our factories to reducing food waste across the value chain.”43 Unilever’s Sustainable Agriculture Code incorporates climate adaptation strategies for small-scale producers to ensure that farmers have access to updated knowledge on good farming practices to help them adapt to the impacts of climate change.44 It has also commenced a tea research program aimed at developing plant-breeding methods to improve a crop’s resistance to disease and pests and its tolerance to droughts and rainfall changes. With natural disasters costing Unilever over $300 million a year, it also has a strong commitment to transforming disaster response.43

* Corporate social responsibility (CSR) broadly refers to the extent an organisation meets societal legal and ethical expectations through consideration of its impact on the societies and environments in which it operates.

22

Regulatory anticipation and increased potential for influence. Regulations responding to climate change can present a plethora of risks for organisations. For example new coastal inundation or flood risk mapping can result in stranded assets if new planning laws prohibit development or make development applications and design requirements economically unviable. This has already occurred in parts of Australia. Organisations who are aware of the emerging responses may be able to participate and influence the nature of regulatory change (e.g. as an informed stakeholder during public submission phases).

Reputation. Beyond the benefits of risk reduction, actions undertaken by a number of multinationals to bolster climate resilience provide good CSR* reading. Companies such as SABMiller, Unilever and Marks & Spencer, are partnering with overseas producers, NGOs, development partners, donors and national and regional governments, to build climate resilience and sustainability into their business and supply chains. Such initiatives recognise the collective good, often resulting in substantial social and environmental support for partners and the regions and countries that they inhabit.

23

As societal interest in climate change increases, demonstration of effective and appropriate climate change risk management will positively influence product and brand perception. Access to finance may also be impacted as financiers increasingly scrutinise counterparty climate change risk in light of enhanced disclosure, their own risk management and CSR efforts. For example, currently 82 financial institutions are signatories of the Equator Principles*, which includes the specific requirement to manage climate change risks as part of their performance standards.

Competitive Advantage. Companies that develop the skills and capacity to recognise and manage climate change risk are positioned at an advantage to both adapt and grow. For example, an ability to trade during severe weather events will not only maintain customers but potentially win new ones.

Seagate, Western Digital and the Thai Floods.

“Seagate owes its return to market leadership to a fortuitous accident in geography: Its HDD manufacturing plant in Thailand is located on high ground,” IHS iSuppli analyst Fang Zhang said in a statement. “As a result, the company was less impacted by the October floods -- the most destructive in the last 50 years for the Southeast Asian country.”45

Prior to the floods that devastated Thailand from July 2011 to January 2012 Western Digital Corp (WDC) held one third of the globe’s hard disk drive (HDD) market share whilst Seagate held 29%. WDC’s production facilities were located on low ground whilst Seagate’s were located on higher. WDC’s facilities were inundated leading to a drop in shipments of 51% compared to pre-flood volumes. Seagate’s production was largely unaffected by the floods (they did suffer supply chain issues from flood affected suppliers). Directly subsequent to the flood Seagate’s market share rose to 38% whilst WDC dropped to 23%.46

* See http://www.equator-principles.com

23

Climate Change Risk: Adaptation & Management

24

Mitigation is distinct from adaptation. Mitigation describes actions that reduce or prevent GHG emissions to limit the potential effects of climate change. In contrast, adaptation can be defined as actions taken to help businesses and communities cope with changing climate conditions. Mitigation involves actions that target the primary causes of climate change, while adaptation involves actions aimed at enhancing tolerance to climate change effects.

Climate change adaptation as a profession is a speciality that differs from climate change mitigation

An Example of Adaptation Specialty: Climate Models and Scenario Testing. A key theme that has emerged during the public consultation phase of the TCFD is that 96% of respondents see scenario analysis as a key component of disclosure (TCFD, 2016, p.8).47 Scenario testing in a climate sense requires an understanding of how differing climate change scenarios play out for a given organisation . This necessarily involves the utilisation and interpretation of climate change modeling. There are over 40 general circulation models (GCMs) that help explore projected climatic trends over time. Each GCM has sensitivities that are better suited to differing regions (e.g. some are better at considering certain climate modes and systems – like Tropical Cyclones).

When developing climate scenarios an appreciation of the intricacies of differing models is required, for example:

• What representative concentration pathway should be used? • Is one model or an ensemble of selected or all models required? • What percentile is appropriate?• Should model outputs be downscaled and if so how (e.g. statistical, dynamic or pattern scaling)?

Complex questions such as these are examples of issues that potentially require consideration in a climate change adaptive world.

Addressing climate change by reducing GHG emissions alone is expected to be insufficient to overcome the environmental and social challenges of global warming. Both climate change mitigation and adaptation measures will be needed for businesses and communities to cope with climate change.

Climate Change Risk: Adaptation & Management

25

A framework to manage climate change risk and meet good governance and disclosure requirements is integral to any effective adaptation response to climate change. The framework depicted in Figure 3 below recognises that:

In accordance with these assertions, the adaptation to and management of climate change risk focuses on those elements that can be controlled (the controllable characteristics of exposure and vulnerability) in the context of those factors that cannot (uncontrollable hazards), i.e. locus of control is key.

An effective adaptation governance framework is key to reducing the risks and exploiting the opportunities that climate change presents

• climate risk occurs at the intersection of hazard, vulnerability and exposure48; and

• although, to a large degree, the timing, magnitude and frequency of a hazard is beyond a single organisation’s control, how exposed and vulnerable that organisation is to a hazard is generally a function of corporate decision-making.

Figure 3 Climate Risk Governance Framework

Unco

ntrollable Hazards

Governance

Cont

rolla

ble CharacteristicsAmplify Current

Climate Risk

Exposure

Disclose

VulnerabilityClimate

Disclose

VulnerabillityExposureClimate

Risk

ApplyAssess

Cont

rollable CharacteristicsUnco

ntrollable Hazards

Adapt

Create Novel

Institutional Culture

Amplify Current

Man

age Capitalise

Governance

Climate

Disclose

VulnerabillityExposureClimate

Risk

ApplyAssess

Cont

rollable CharacteristicsUnco

ntrollable Hazards

Adapt

Create Novel

Institutional Culture

Amplify Current

Man

age Capitalise

Governance

Climate

Disclose

VulnerabillityExposureClimate

Risk

ApplyAssess

Cont

rollable CharacteristicsUnco

ntrollable Hazards

Adapt

Create Novel

Institutional Culture

Amplify Current

Man

age Capitalise

Governance

Climate

Disclose

VulnerabillityExposure Climate

Risk

Apply Assess

Controllable Characteristic

s Uncontrollable Hazards

Adapt

Create NovelIn

stitutional Culture

Amplify Current

Manage Capita

lise

Governance

Man

age Capitalise

Climate

Create Novel

Adapt

Institutional Culture

Climate Change Risk: Adaptation & Management

26

Hazards

Climate change has been described as a “threat multiplier” or “threat syndrome” that can exacerbate and amplify current hazards and introduce novel and emergent ones 49, 50. Climatic hazards perpetuate over time as slow-moving physical stressors (e.g. sea level rise) or as a shock (e.g. tropical cyclones). Commercially, hazards represent a non-controllable element of climate change risk. The scale of action required to curb climate hazards (e.g. through reduction of GHG emissions) and extent of climate change already inherent in our biophysical systems deems physical hazards beyond an organisation’s control.

Non-climatic hazards arise as a response to actual or potential climatic hazards. Examples include introduction of adaptation regulation, emerging legal regimes, reduced access to finance and changing consumer sentiment. In contrast to climatic hazards it is arguable that the nature of human-induced hazards can be influenced to a degree (e.g. by some form of political lobbying or marketing). From a practical and commercial perspective this paper asserts that for the vast majority of businesses non-climatic hazards are also uncontrollable. This is due to the limited extent of political or market access required to direct political and market process and trends in any meaningful way for any meaningful period of time.

Exposure and Vulnerability

The susceptibility of an organisation to a particular hazard is determined by proximity in relation to that hazard (i.e. exposure) and the propensity or predisposition of that organisation to be adversely effected (i.e. vulnerability).48 Vulnerability is contextual, in that an organisation’s vulnerability to a particular hazard may fluctuate over time.51, 52 Both exposure and vulnerability reflect the inherent characteristics of an organisation53 and as such may be tweaked and managed. Critical to this process is an institution’s culture.

The way in which people perceive and process information has the potential to effectively ‘filter out’ information that conflicts with their world views and beliefs; relevant information may simply be ignored or diminished.54 This can act directly in preventing for example, buy-in to a process but also indirectly by steering elements of the process itself away from that required to facilitate the adaptation process e.g. what information is produced55.

Ultimately, you can’t change the weather but you can decide if you go out in it and what you wear.

Ian Edwards, Co-author

Climate Change Risk: Adaptation & Management

27

Risk Management

In the context of this paper, risk management involves the process of understanding, assessing and implementing behaviour and corporate policy to reduce or transfer risk. It evokes a process of continuous improvement in preparedness, response and recovery practices, with the purpose of increasing organisation resilience, profitability and health. Risk management is informed by a risk assessment.

In recognition of the defining elements of climate change risk, a risk assessment is determined by a combination of a hazard and vulnerability assessment. A hazard assessment identifies the extent that current and future climatic trends could impact a given organisation’s value chain, whilst a vulnerability assessment analyses the endogenous characteristics of that organisation and how these could enable it to cope with or benefit from such impacts. It is at the intersection of these two assessments that climate change risk can be determined.

Adaptation

Adaptation involves building the capacity of an organisation to minimise negative direct and indirect impacts of climate change and maximise positive results48. It is a process of continuous improvement where outcomes and mechanics evolve and reorganise as entities learn from past mistakes and successes and an increasing knowledge base.56 Faced with uncertainty about the impacts of climate change, it becomes evident that one static report, at one specific time, cannot manage the dynamics required in understanding and responding to a changing climate.

The difficulties rest in the multiple complexities of understanding so many unknown possibilities that may occur over time. For example, it is near

Climate Change Risk Management, Capitalisation and Adaptation

Risk management and climate change adaptation are inter-related, and should be iterative. Ultimately, they feed into each other as processes of continuous improvement as an organisation learns how to better cope with and capitalise on climate change risk, both in its own right and as a risk multiplier. Their success is informed by an ongoing assessment of hazards, exposure and vulnerability and the effectiveness of an overarching governance framework.

Climate Change Risk: Adaptation & Management

28

Climate Change Adaptation Governance

Recognising that multiple futures are possible lends support to the need for robust decision-making frameworks that can respond as issues and information emerge over time. Organisations need to be actively assessing the risks that climate change presents and, where possible, implementing measures to manage those risks. The dynamic and uncertain nature of climate change presents a plethora of direct and indirect challenges that will be impossible to manage in an ad-hoc and reactive manner.

To date, much of climate change adaptation approaches (if any) have focused around specific responses to individual risks (which has often been a direct reaction to impacts from extreme weather events). This reactive approach is economically unsustainable, and organisations will need to shift their focus to proactively support the implementation of climate change adaptation if they are to manage climate change risk effectively.

Climate change adaptation is about informed decision-making. However this can only occur when systems are in place to ensure that the information is up-to-date, roles and responsibilities are clearly identified, and capacity and resourcing matches the required tasks. Governance is critical here as the framework that both oversees and importantly, is seen to oversee, risk management and adaptation. Governance provides assurance both internally and externally (by some form of disclosure) that risks are being adequately managed and that an organisation is evolving commensurate to changing conditions.

The whole point of the work on adaptation processes is to have risks (and opportunities) associated with climate change . . . actually addressed in decision-making at some practical level.

(Smit & Wandel 2006, p.285)56

impossible for an adaptation practitioner to project how a range of potential future climates in one location may affect a shifting range of coping thresholds for the social, natural and economic environment, whilst considering other stressors and influences (e.g. carbon pricing, technological advancement, oil price shocks).

Climate Change Risk: Adaptation & Management

29

In Closing

This paper highlights insights and concerns from business leaders, corporations and peak body groups about the current and emerging issues that climate change presents. Due to considerable uncertainty, management of climate change requires strong leadership and a commitment to some form of climate change adaptation governance. Appropriate adaptation governance ensures that climate change is managed in a robust and consistent manner, and will help an organisation capitalise on any opportunities that may emerge.

Effectively managing the impacts of climate change brings a need to go beyond exploring direct responses (e.g. engineering solutions to sea level rise) to exploring systems based responses that foster resilience and allow for the capitalisation of opportunities as they emerge. Climate change adaptation is a complex systems issue that should be treated as a core organisational risk and not pigeonholed as purely environmental.

Climate Change Risk: Adaptation & Management

30

References

1. Center for Climate and Energy Solutions. Summary: Copenhagen Climate Summit. 2009 [cited 2016 June 1]; Available from: http://www.c2es.org/international/negotiations/cop-15/summary.

2. Climate Commission, The critical decade: climate science, risks and responses. Department of Climate Change and Energy Efficiency, Commonwealth of Australia, 2011.

3. National Oceanic and Atmospheric Administration. Global Analysis - June 2016: 2016 year-to-date temperatures versus previous years. 2016 [cited 2016 July 1]; Available from: https://http://www.ncdc.noaa.gov/sotc/global/2016/6/supplemental/page-2.

4. World Economic Forum. More Walls, More Warming, Less Water: A World at Risk in 2016. 2016 Jan 14; Available from: https://http://www.weforum.org/press/2016/01/more-walls-more-warming-less-water-a-world-at-risk-in-2016/.

5. World Economic Forum, The Global Risks Report 11th Edition. 2016, World Economic Forum: Geneva, Switzerland.

6. Prudential Regulation Authority, The impact of climate change on the UK insurance sector: A Climate Change Adaptation Report by the Prudential Regulation Authority. 2015, Bank of England - Prudential Regulation Authority: London, UK.

7. UNEP, The Financial System We Need - Aligning the Financial System with Sustainable Development. 2015, UNEP: Geneva, Switzerland.

8. Bank of England, One Bank Research Agenda Discussion Paper. 2015, Bank of England: UK.

9. ESRB Advisory Scientific Committee, Reports of the Advisory Scientific Committee - Too late, too sudden: Transition to a low-carbon economy and systemic risk. 2016, European Systemic Risk Board.

10. Oehri, O., et al., Carbon Risks for the Swiss Financial Centre Summary - Commissioned by the Federal Office for the Environment (FOEN). 2015, Federal Office of the Environment FOEN: Bern, Switzerland.

11. Wilson, M. Mark Wilson’s speech at UN Principles of Sustainable Insurance event. 2014; Available from: http://www.aviva.com/media/upload/Mark_Wilson_speech_at_UN_Principles_of_Sustainable_Insurance.pdf.

12. The Geneva Association. Climate Risk Statement of the Geneva Association. 2014; Available from: https://http://www.genevaassociation.org.

13. California Department of Insurance. California Insurance Commissioner Dave Jones calls for insurance industry divestment from coal. 2016 [cited 2016 June 10]; Available from: http://www.insurance.ca.gov/0400-news/0100-press-releases/2016/statement010-16.cfm.

14. National Association of Insurance Commissioners. Climate Change and Global Warming (C) Working Group: 2016 Changes. 2016 [cited 2016 June 10]; Available from: http://www.naic.org/committees_c_climate.htm.

15. Australian Council of Superannuation Investors. Submission to Senate Inquiry into Carbon Risk Disclosure. 2016.

16. Local Government Super. Investment Risks. n.d. [cited 2016 July 15]; Available from: https://http://www.lgsuper.com.au/investments/sustainable-investment/investment-risks/.

17. Asset Owners Disclosure Project. Global Climate 500 Index 2016. 2016 [cited 2016 July 12]; Available from: http://aodproject.net/wp-content/uploads/2016/05/AODP-GLOBAL-CLIMATE-INDEX-2016-view.pdf.

Climate Change Risk: Adaptation & Management

31

18. Desk., G.E. How credit rating agencies are slowly but surely reacting to climate risk. 2016 [cited 2016 Feb 19]; Available from: http://energydesk.greenpeace.org/2016/01/28/credit-ratings-climate-risk/.

19. Moody’s, Moody’s: FSB task force could start to enhance clarity on climate risk disclosures. 2016.

20. S&P Global, Climate Change-Related Legal And Regulatory Threats Should Spur Financial Service Providers To Action, in RatingsDirect. 2016.

21. SASB, Climate Risk: SASB Technical Bulletin 2016-01. 2016, Sustainability Accounting Standards Board: San Francisco USA.

22. Winston, A., What Business Leaders Need to Know About the Paris Climate Conference, in Havard Business Review. 2015.

23. M., H. and L. U., Flood risks and impacts: A case study of Thailand’s floods in 2011 and research questions for supply chain decision making. International Journal of Disaster Risk Reduction, 2014. 14: p. 256-272.

24. Pachauri, R.K., et al., Climate change 2014: synthesis Report. Contribution of working groups I, II and III to the fifth assessment report of the intergovernmental panel on climate change. 2014: IPCC.

25. Sangvikar, P., L. Vora, and B. Shah, Risk Management in Supply Chain, Presentation to the Indo-German training center. 2014.

26. Waters, D., Supply Chain Risk Management: Vulnerability and Resilience In Logistics. 2011: London.

27. Arrabella Advisors. Measuring the Growth of the Global Fossil Fuel Divestment and Clean Energy Investment Movement. 2015 [cited 2016 Jun 10]; Available from: http://www.arabellaadvisors.com/wp-content/uploads/2015/09/Measuring-the-Growth-of-the-Divestment-Movement.pdf.

28. Luckerson, V., Fossil Fuel Divestment Has Kicked into Overdrive, in Time. 2015.

29. 350.org. Divestment Commitments. n.d. [cited 2016 May 31]; Available from: http://gofossilfree.org/commitments/.

30. Patel, T., Fossil-Fuel Divestment Gains Momentum With Axa Selling Coal, in Bloomberg. 2015.

31. Allianz, Climate protection will become part of core business. 2015.

32. FTSE Russell, Innovative new index supports investors seeking to Divest Fossil Fuels and Invest in the Green Economy. 2016.

33. Welsh, H. and M. Passoff. Proxy Preview 2016. 2016; Available from: http://www.proxypreview.org.

34. Barker, S., et al., Climate change and the fiduciary duties of pension fund trustees – lessons from the Australian law. Journal of Sustainable Finance & Investment, 2016. 6(3): p. 211-244.

35. Carney, M., in Breaking the Tragedy of the Horizon – climate change and financial stability. 2015: London, United Kingdom.

36. Carbon Tracker, Accounting for hidden reserves. 2013.

37. ANZ. Submission to the Senate Economics References Committee Inquiry into carbon risk disclosure. 2016 [cited 2016 May 10]; Available from: https://http://www.anz.com/resources/8/0/808d7cea-f04d-48c8-bb59-089c29ac4167/carbonrisksubmission2016.pdf?MOD=AJPERES.

38. Financial Stability Board, FSB to establish Task Force on Climate-related Financial Disclosures. 2015.

Climate Change Risk: Adaptation & Management

32

39. Regnan. Submission: Carbon Risk Disclosure Inquiry. 2015 [cited 2016 Jul 22]; Available from: http://www.regnan.com.au/regnan-submission-to-carbon-risk-disclosure-inquiry.

40. Parliament of Australia. Carbon Risk Disclosure. 2016 [cited 2016 July 22]; Available from: http://www.aph.gov.au/Parliamentary_Business/Committees/Senate/Economics/Carbon_Risk_Disclosure.

41. UNEPFI. Australian Portfolio Carbon Working Group. 2015 [cited 2016 July 22]; Available from: http://www.anz.com/resources/1/d/1d220fd6-96de-46a1-88c6-59bfa18c10f6/aust-carbon-working-grp.pdf?MOD=AJPERES.

42. Acclimatise and ClimateReady, Business Opportunities in a Changing Climate. 2015, Environment Agency: Bristol, UK.

43. Velde, B.V., Unilever CEO: Deforestation is the most urgent climate challenge, in Forest News. 2014.

44. Unilever. Making Sustainable Living Commonplace: Annual Report and Accounts 2014 Strategic Report. 2014 [cited 2016 Jul 11]; Available from: https://http://www.unilever.com/Images/ara-2014-strategic-report_tcm244-421153_en.pdf.

45. Zhang, F., Thailand Flooding Helps Seagate Move into First Place in Hard Drive Market in Fourth Quarter. 2012.

46. Mearian, L., Thai floods catapult Seagate into hard drive market lead, in Computerworld. 2012.

47. TCFD. Phase 1 Public Consultation - Key Findings. 2016 [cited 2016 Aug 1]; Available from: https://http://www.fsb-tcfd.org/publications/.

48. IPCC, Managing the risks of extreme events and disasters to advance climate change adaptation. A Special Report of Working Groups I and II of the Intergovernmental Panel on Climate Change. 2012, Cambridge, UK, and New York, NY, USA: Cambridge University Press. 582.

49. Burgman, M., et al., Threat syndromes and conservation of the Australian flora. Biological Conservation, 2007. 134(1): p. 73-82.

50. United Nations Global Compact, Adapting for a Green Economy: Companies, communities and climate change. 2011, UN Global Compact, UN Environment Programme, Oxfam and the World Resources Institute.: Washington, DC.

51. Füssel, H.-M., Vulnerability: a generally applicable conceptual framework for climate change research. Global Environmental Change, 2007. 17(2): p. 155-167.

52. Preston, B.L., Climate Change Vulnerability Assessment: From Conceptual Frameworks to Practical Heuristics. 2012, CSIRO Climate Adaptation Flagship Working paper.

53. Turner, B.L., et al., A framework for vulnerability analysis in sustainability science. Proceedings of the national academy of sciences, 2003. 100(14): p. 8074-8079.

54. Festinger L, A Theory of Cognitive Dissonance. 1957, Stanford, CA, USA: Stanford University Press.

55. J.A., E., M. S.C., and T. M, Barriers to Adaptation: A Diagnostic Framework. Final Project Report. 2011, California Energy Commission: Sacramento, CA.

56. Adger, W.N., Vulnerability. Global Environmental Change, 2006. 16(3): p. 268-281.

57. Smit, B. and J. Wandel, Adaptation, adaptive capacity and vulnerability. Global Environmental Change, 2006. 16: p. 282–292.

58. West, J., The Long Hedge: Preserving Organisational Value through Climate Change Adaptation. 2014, Sheffield UK: Greenleaf Publishing Limited.

Climate Change Risk: Adaptation & Management

33

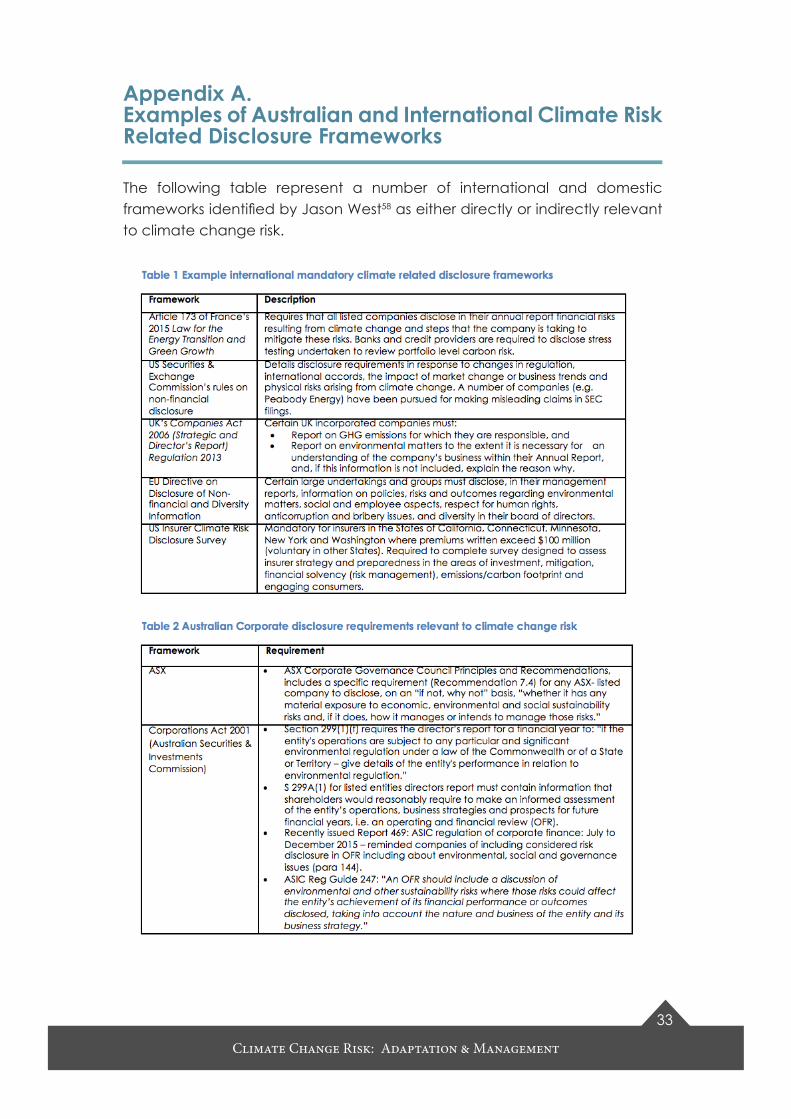

Appendix A. Examples of Australian and International Climate Risk Related Disclosure Frameworks

The following table represent a number of international and domestic frameworks identified by Jason West58 as either directly or indirectly relevant to climate change risk.