Climate Change Negotiations: COP 21, Paris - UniBG 2015 Lecture Prof. Di... · Climate Change...

97

Climate Change Negotiations: COP 21, Paris enzo di giulio Università degli Studi di Bergamo, December 3, 2015

Transcript of Climate Change Negotiations: COP 21, Paris - UniBG 2015 Lecture Prof. Di... · Climate Change...

Climate Change

Negotiations:

COP 21, Paris

enzo di giulio Università degli Studi di Bergamo,

December 3, 2015

4 slides on

climate

change

CO2 concentration in the last 800,000 years

CO2 concentration in the last 800,000 years and to 2100

Source: IAASA

400 ppm: for having a similar level

of concentration we must go back

to Pliocene (3-5 million years ago)

Huge decline in the

Arctic sea

ice extent

and tickness

First

effects

Huge decline in the

Arctic sea

ice extent

and tickness

Huge decline in the

Arctic sea

ice extent

and tickness

Slow-Motion Collapse

of West Antarctic

Glaciers is

Unstoppable,

2 New Studies Say

(NASA, University of

Washington)

How to reach

the target?

How to reach the target

without Flex-Mex?

CO2 = CO2/ENE * ENE/GDP * GDP/POP * POP, i.e.:

CO2 = CE * EG * GP * POP

Which factors influence the Kaya identity coefficients?

Coefficients Determinants Mitigation Policies

CE = CO2/ENE energy mix renewables, nuclear and natural gas

EG = ENE/GDP economy structure,

technical effficiency,

lifestyles

services, dematerialisation

efficient technologies, DSM

energy saving, etc.

GP = GDP/POP socio-economic factors GDP restraint

POP culture, economy Population restraint

Target:

GHGs

Mitigation

Areas of action

Energy

Mix:

+ Renewables

+ Nuclear

+ Natural Gas

- Coal

- Oil

Energy Efficiency:

+ Technical efficiency

+ energy saving

+ dematerialisation

GDP

Mitigation

Population

Control

Emissions

Trading

CDM, JI

Reforestation

Carbon Capture

and Storage (CCS)

Are climate

change

negotiations

working?

Climate and time: drawbacks

• Very slow negotiations

• Political dilemma: short run vs long run.

• Fighting against time

• Different times for different countries

Climate and time: progress

• From non legal (Rio) to legal constraint (Kyoto)

• Many Kyoto open issues issue resolved

• Progress in LULUCF and CDM

• New tools and markets arose

A key conference:

Copenhagen, 2009

Copenhagen, COP 15: questions • Which kind of agrement: Kyoto bis? Political agreement? Constraint just for DCs?

• USA bounded? And what about developing countries?

• What about compliance?

• How to define targets? By negotiation? Algorithms?

• Flat rate? Diiferentiated flat rates?

• Fixed or flexible targets ? Absolute or relative targets?

• Per-capita or per-Gdp Carbon?

• Targets to 2020 or 2050?

• AAUs Banking in post-2012 (8 mld t. CO2)?

• CDM reform: still bottom-up or sectoral approach?

• Which policy tools? Cap & trade or taxation?

• Money to developing countries? How much? Still delay?

Adaptation

dominion? The US-China link

Souce : The Economist

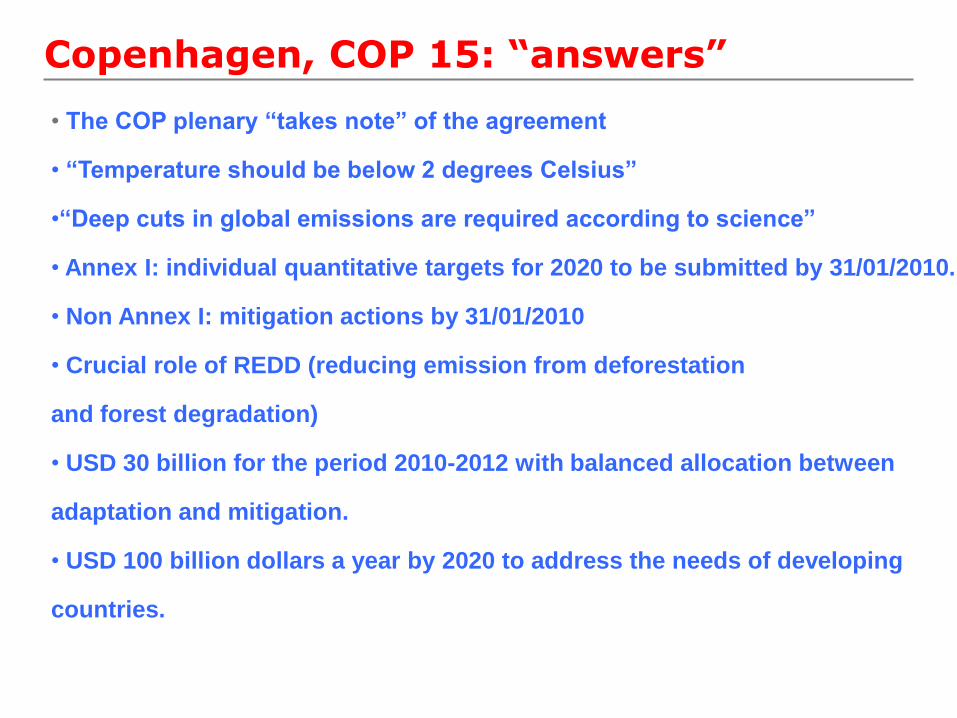

Copenhagen, COP 15: “answers”

• The COP plenary “takes note” of the agreement

• “Temperature should be below 2 degrees Celsius”

•“Deep cuts in global emissions are required according to science”

• Annex I: individual quantitative targets for 2020 to be submitted by 31/01/2010.

• Non Annex I: mitigation actions by 31/01/2010

• Crucial role of REDD (reducing emission from deforestation

and forest degradation)

• USD 30 billion for the period 2010-2012 with balanced allocation between

adaptation and mitigation.

• USD 100 billion dollars a year by 2020 to address the needs of developing

countries.

Doha 2012, COP 18

Kyoto Protocol still lives since 2013 to 2020

but:

• within it just EU, Australia, Switzerland, Norway (15% world

emissions)

• out Russia, Canada, Japan and New Zeland

• the two main emitters (USA e China) are still out (16 and 19% of

world emissions)

• surplus of Russia, Ucraina, Polonia, Kazakstan

(13 Gt CO2) tradable up to 2.5%

• target: at least -18% compared to 1990.

• by 2015, definition of strategies for cutting 8-13 Gt CO2.

Positive

elements in

COP 21

Positive

elements

in COP 21:

NDICs

28

Paese

Target

Target Year

Reference

China GDP carbon intensity: -60/-65% 2030 2005

United States emissions: -26% -28% 2025 2005

European Union emissions: almeno – 40% 2030 1990

India GDP carbon intensity: -33-35% 2030 2005

Russia emissions: -25% -30% 2030 1990

Japan emissions: -26% 2030 2013

Brazil emissions: -37% oppure - 43% 2025 or 2030 2005

Indonesia emissions: -29% 2030 Scenario BAU

Mexico emissions: -22% -36% 2030 Scenario BAU

Iran emissions: -4% - 12% 2030 Scenario BAU

Canada emissions: - 30% 2030 2005

South Corea emissions: - 30% 2030 Scenario BAU

Australia emissions: -26% -28% 2030 2005

Saudi Arabia emissions: - 130 Mt.CO2 year 2030

South Africa emissions: peak in 2020-2025, ten

years plateau, then decreasing

INDCs: Intended Nationally Determined Contributions

30

Positive

elements in COP 21:

policies (EU)

European Union: Roadmap to 2050

European Union: 2020 and 2030 targets

European Union: ETS

European Union: Renewables

European Union: Energy Efficiency

European Union: effects on decoupling

GDP and GHG decoupling

40

60

80

100

120

140

160

180

200

220

1990 2000 2010 2020 2030

1990

= 1

00%

GDP GHG emissions

Positive

elements in COP 21:

policies (US & China)

USA and China

Obama Climate Action Plan:

-30% GHGs from power sector in 2030

(vs 2005)

US-China agreement (November 11, 2014):

US, -26%-28% GHGs in 2025 (vs 2005… it means -16.3% vs. 1990)

China: stop emissions increase by 2030 and renewables up to 20%

Positive

elements in COP 21:

industry & society

Positive

elements

in COP 21:

policy tools

43

Positive evolution of

Carbon Markets

Source: WB, State and trends of carbon pricing 2014

44

Positive evolution of

Carbon Markets

Source: WB, State and trends of carbon pricing 2014

45

Positive evolution of

Carbon Markets

Source: WB, State and trends of carbon pricing 2014

Basic

negotiation

in COP 21

48

Two triangles & two dilemmas

United States

European

Union

China

Legally binding

agreement

Ambitious

Targets

Countries’

Participation

2 challenges

for climate

change

Challenge 1:

CO2/GDP

vs

GDP

Area OCSE (1971-2009): CO2/Pil vs Pil

-

50

100

150

200

250

300

350

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

co2

co2/pil

pil

Mondo (1971-2009): CO2/Pil vs Pil

-

50

100

150

200

250

300

350

400

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

co2

co2/pil

pil

Area Non-OCSE (1971-2009): CO2/Pil vs Pil

-

100

200

300

400

500

600

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

co2

co2/pil

pil

Cina (1971-2009): CO2/Pil vs Pil

-

500

1 000

1 500

2 000

2 500

3 000

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

co2

co2/pil

pil

We need economic growth-carbon emissions decoupling

World Energy Outlook 2013, IEA

Obstacles to a strong agreement

Challenge 2:

rich

vs

emerging countries

Obstacles to a strong agreement

World Energy Outlook 2012, IEA

World Energy Outlook 2013, IEA

Obstacles to a strong agreement

World Energy Outlook 2009, IEA

Obstacles to a strong agreement

Fighting

against

time

IEA, World Energy Outlook 2011

IEA, WEO 2012: GHGs required cuts

IEA, WEO 2012: GHGs cut options

the

bridge issue

62 Energy and Climate Change, IEA 2015

63

Energy and Climate Change, IEA 2015

64

65

66 Energy and Climate Change, IEA 2015

67 Energy and Climate Change, IEA 2015

How much

does carbon

abatement cost?

69

The Stern Review

Global Abatement Cost Curve

Source: McKinsey

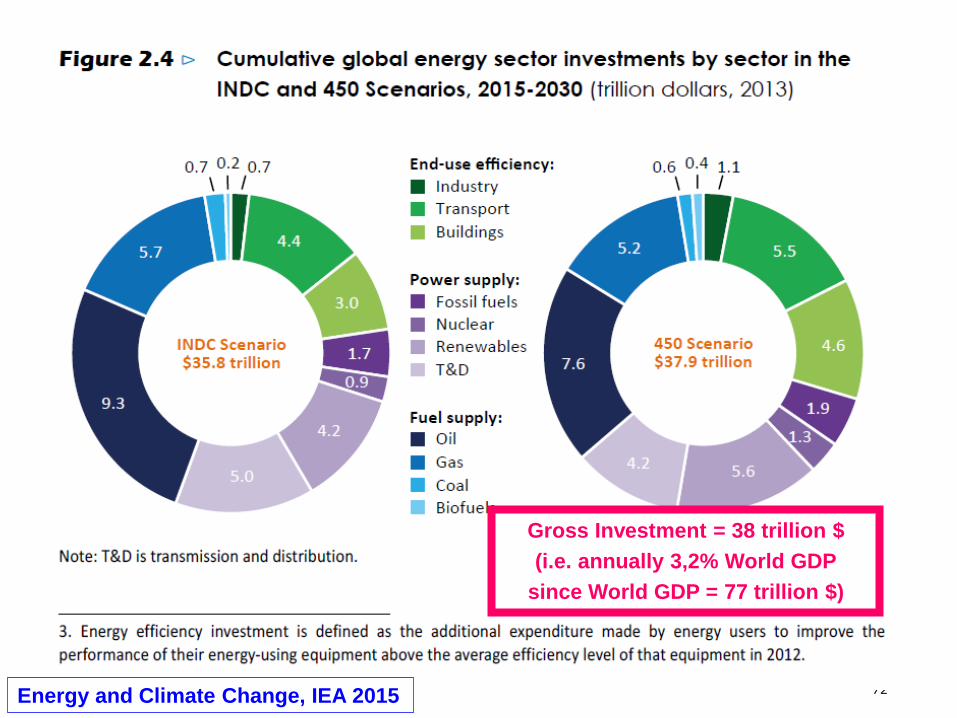

IEA, WEO 2012: costs

Gross Investment = 15 trillion $

(i.e. annually 0.8% World GDP

since World GDP = 77 trillion $)

World Defense Expenditure:

2.5% World GDP

72

Gross Investment = 38 trillion $

(i.e. annually 3,2% World GDP

since World GDP = 77 trillion $)

Energy and Climate Change, IEA 2015

Abatement Costs in some models (Target: -40% and -80% in 2050)

Median Value: 64 €/t. CO2 Median Value: 521 €/t. CO2

Source. EMF28

Abatement Costs in some models (Target: -40% and -80% in 2050)

Source: EMF28

Median Value: 0.7% GDP Median Value: 3.7% GDP

the

discount

issue

Vs

William Nordhaus

Nicholas Stern

Source: The ethics of climate change, by J. Broome, Scientific American, 2008

STERN (1,4%)

NORDHAUS (6%)

Logical sequence of the lesson

4 slides on

Climate Change

The climate

negotiations

The Copenhagen

Conference

Positive

elements in

COP 21, Paris

(INDCs, Policies, Awareness)

The basic

Negotiation

in COP 21

How to cut emissions (Kaya)

Two challenges

for climate

changes

The cost

issue

background

slide

80

81

82

83

84

IEA, WEO 2012: temperature increase

Gross Investment = 15 trillion $

(i.e. annually 0.7% World GDP

since World GDP = 84 trillion $,

Obstacles to a strong agreement

87

88

The

unburnable

issue

90 Source: Unburnable Carbon – Are the world’s financial markets carrying a carbon bubble?, carbontracker.org

91 Source: BETTER GROWTH, BETTER CLIMATE: THE NEW CLIMATE ECONOMY REPORT

92

93

Source: Unburnable Carbon 2013: Wasted

capital and stranded assets, Carbontracker

94

95

Layard et al 2015, The case for a Global Apollo Programme. Voxeu.org

Silicon PV module: decrease in price

96 Energy and Climate Change, IEA 2015

97 Energy and Climate Change, IEA 2015