Climate Change Mitigation Policy and Energy Markets: Cooperation and Competition in Integrating...

13

Climate Change Mitigation Policy and Energy Markets: Cooperation and Competition in Integrating Renewables into Deregulated Markets Noah Dormady & Elena Maggioni Forging Closer Ties: Transatlantic Relations, Climate and Energy Berlin, November 29 – December 5, 2009

-

Upload

bertina-dixon -

Category

Documents

-

view

216 -

download

0

Transcript of Climate Change Mitigation Policy and Energy Markets: Cooperation and Competition in Integrating...

Climate Change Mitigation Policy and Energy Markets: Cooperation and

Competition in Integrating Renewables into Deregulated Markets

Noah Dormady

&

Elena Maggioni

Forging Closer Ties: Transatlantic Relations, Climate and Energy

Berlin, November 29 – December 5, 2009

Agenda

• Theoretical Context

• California’s Energy Markets

• Case of Los Angeles Department of Water and Power (LADWP) – Green Path North (GPN)

• California’s Policy Response

• Implications and Conclusions

Theoretical Context

• Scale Economies Determine Appropriate Organizational Form

(Joskow & Schmalensee 1983; Joskow 1998; Williamson 1975, 1982, 1985; Wilson 1998)

• Regulation, Political Economy, and Industrial Organization

(Krueger 1976; Peltzman 1976; Stigler 1968, 1971)

• Environmental Regulation and Competition(Hahn 1984; Helland & Matsuno 2003; Heyes 2009; Misiolek & Elder 1989; Salop & Scheffman 1983; Sartzetakis 1997; Von der Fehr 1993)

• Deliberative Democracy as a Method for Solving Complex Policy Problems

(Dryzek 2000; Friedman 1989; Hajer 2003)

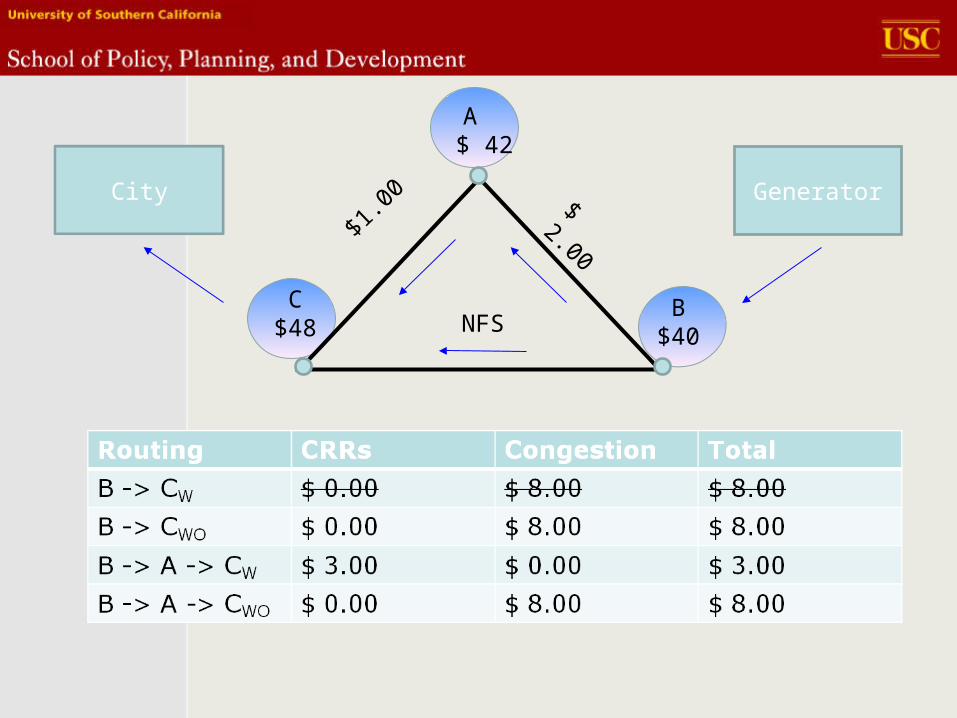

California MarketBilateral Contracting & Generator Bidding

Several Markets

Long-term Markets

Short-Term Markets

(Day-ahead, Hour-ahead, Spot)

Locational Marginal Pricing (LMPs)

Financial Transmission Rights (FTRs/CRRs)

B$40

C$48

GeneratorCity

A $ 42

$ 2.00$1

.00

NFS

• RPS and Investors Owned Utilities– 33% by 2020

Table 1 - Timeline for Electricity from...

Renewables Portfolio Standards in California

2002: S.B. 1078: 20% by 2017

2003: Energy Action Plan accelerates: 20% in 2010

2006: 20% by 2010 deadline into law

2008: AB 32 anticipates RPS at 33% by 2020

2009: Executive Order: 33% renewables by 2020

RPS: Investors Owned Utilities

Major California Municipal Renewable Portfolio StandardsCity of Anaheim Public Utilities 20% by 2015

City of Los Angeles Department of Water and Power

35% by 2020

City of Palo Alto Municipal Utilities 33% by 2015

City of Riverside Public Utilities 20% by 2020

City of Sacramento Municipal Utilities 33% by 2020

City of Santa Clara (Silicon Valley Power) 31% by 2010Source: CEC 2008

RPS: Publicly Owned Utilities

Green Path North

• LADWP needs to increase its renewable portfolio and wants to:– Tap into geothermal resources in the

Southeastern part of California– Build its own power lines

• It is encountering strong opposition from local communities

Southern California Geothermal Resources and Connecting Transmission Lines

Community Opposition

Market Available Transmission Capacity

Market Available Transmission Capacity (Import)

0

5

10

15

20

25

30

35

40

45

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31

October 2009

Pe

rce

nt

Da

ily C

ap

ac

ity

Victorville

Path 15

Palo Verde

Also physical capacity constraints

ATC=TTC-OTC-TRM-ETComm-CBM-AS

Collaborative Efforts to Break the Impasse

• Renewable Energy Action Team: streamline cross-agency approval process

• RETI - Renewable Energy Transmission Initiative: plan areas and corridors for renewables

• California Transmission Planning Group: crossectoral integrated transmission plan

Conclusions

• Disconnect between energy markets and renewables policy

• Small institutions and municipalities may be disadvantaged by:

• Market Complexity• Quasi-competitive Markets• Available Physical Capacity

• Uncertain success of current institutions• Firms are asked to cooperate to form the

very markets on which they compete