Clarkson 2017 Interim Results Presentation 2017 Interim Results... · Results Presentation 14TH A U...

27

Results Presentation 1 4 T H A U G U S T 2 0 1 7

Transcript of Clarkson 2017 Interim Results Presentation 2017 Interim Results... · Results Presentation 14TH A U...

Results Presentation

1 4 T H A U G U S T 2 0 1 7

Agenda

Financial Results

Markets

Outlook

Andi Case

CEO

Jeff Woyda

COO/CFO

14th August 2017 2017 Interim Results 2

Results summary

June 2017

£m

June 2016

£m

Increase

%

Revenue 156.8 147.2 +6.5%

Underlying Profit before taxation(Before acquisition related costs) 24.5 21.8 +12.4%

Acquisition related costs (2.6) (4.3)

Profit before taxation(After acquisition related costs) 21.9 17.5 +25.1%

Underlying Earnings per share(Before acquisition related costs) 57.5p 52.9p +8.7%

Earnings per share(After acquisition related costs) 50.8p 41.7p +22.0%

14th August 2017 2017 Interim Results 3

Summary of first half 2017 results

Successes• Broking transaction volumes up again

• Average ClarkSea index H1 17 vs H1 16 up 2%

• Increased revenue from new transactions in 2017

• Increased Financial deal flow and revenues (+US$5.8m or 24%)

14th August 2017 2017 Interim Results

GBP/USD H1 2017 H1 2016

Average 1.27 1.42

Closing 1.30 1.34

£118.0M

£115.5M

£23.2M£16.7M

£8.3M

£8.3M

£7.3M

£6.7M

£147.2m

£156.8m

Broking

Financial

Support

Research

20162017

Headwinds• Lower revenue brought forward from FOB

• Weakness in North Sea projects continues to impact port services

Other• Increased HO costs includes technology not capitalised

• Weaker sterling environment following Brexit decision June 2016

4

Segmental margin

14th August 2017 2017 Interim Results

Revenue

2017

Profit

2017

Margin

2017

Revenue

2016

Profit

2016

Margin

2016

£m £m £m £m

Broking 118.0 21.0 17.8% 115.5 19.3 16.7%

Financial 23.2 5.0 21.5% 16.7 2.4 14.4%

Support 8.3 0.7 8.4% 8.3 0.8 9.6%

Research 7.3 2.4 32.9% 6.7 2.3 34.3%

5

ClarkSea Index

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Average Minimum

Average 13,424 11,336 9,840 16,848 15,431 10,626 18,953 30,753 27,785 24,661 32,969 32,954 11,711 15,721 12,947 9,586 10,442 11,793 14,164 9,441 10,040

Minimum 11,980 9,850 8,650 11,340 8,920 8,870 15,690 23,420 19,230 18,860 25,280 13,740 7,730 13,060 10,980 7,523 7,574 9,175 12,364 7,073 8,465

14th August 2017 2017 Interim ResultsData source: Clarksons Research

2004 to 2010

Average = 25,222

2011 to 2017

Average = 11,2021997 to 2003

Average = 13,780

1st Half 2017

Average = 10,040

Uplift to Average 1997 to 2003 +37%

6

Acquisition related costs

Acquisition related costs* June 2017

£m

June 2016

£m

Cash & share-based payment charges 0.5 0.5

Loan note interest 0.3 0.6

Amortisation: Platou 1.8 3.2

2.6 4.3

14th August 2017 2017 Interim Results

*Assuming no further acquisitions, this should amount to a further £2.2m in 2017 and £2.5m in 2018

7

Balance sheet

Dec 2012

£m

Dec 2013

£m

Dec 2014

£m

Dec 2015

£m

Dec 2016

£m

Jun 2017

£m

Tangible fixed assets 8.8 9.4 8.4 33.1 33.0 31.9

Investments 1.9 1.8 1.9 1.9 4.1 4.3

10.7 11.2 10.3 35.0 37.1 36.2

Working capital (2.8) 3.1 (1.8) (7.1) (15.1) (3.3)

Net funds 75.2 75.0 115.7 91.6 98.4 71.4

72.4 78.1 113.9 84.5 83.3 68.1

Pensions (9.4) (1.8) (10.3) (4.1) 2.3 5.5

Deferred tax 12.5 10.0 13.0 8.4 7.1 4.9

75.5 86.3 116.6 88.8 92.7 78.5

Net assets before loan notes & intangibles 86.2 97.5 126.9 123.8 129.8 114.7

Loan notes - - - (46.1) (23.6) -

Net assets before intangibles 86.2 97.5 126.9 77.7 106.2 114.7

Intangibles 39.8 40.2 40.4 263.2 300.5 293.7

Net assets 126.0 137.7 167.3 340.9 406.7 408.4

14th August 2017 2017 Interim Results

June billings

& Hedge

IAS19

Surplus

Repaid June

2017

Currency

revaluation

8

Net available funds

Jun 2017

£m

Dec 2016

£m

Cash and cash equivalents 117.4 154.0

Current investment deposits 5.4 29.4

Net cash equivalents 122.8 183.4

Reserved for bonus (full cost) (51.4) (85.0)

Net available funds 71.4 98.4

Loan notes outstanding - (23.6)

Net available funds after loan notes 71.4 74.8

14th August 2017 2017 Interim Results 9

Movement in net funds (after bonus & loan notes)

1.3 (13.1)

(3.3)(1.6)

74.8

24.1

(5.3)

71.4

Net FundsDec 16

Operating Profit Other Dividends Working capital FX loss on cashheld

Taxation Capex Net FundsJun 17

(5.6)

14th August 2017 2017 Interim Results 10

Dividend history

6 7 9 10 12 14 16 16 17 18 18 19 21 22 22 23911

1622

2426

26 2730

32 3337

39 40 43

0

10

20

30

40

50

60

70

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Interim Final

14th August 2017 2017 Interim Results 11

O S L O

Strategy & the markets

ClarkSea Index

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Average Maximum Minimum

Average 13,424 11,336 9,840 16,848 15,431 10,626 18,953 30,753 27,785 24,661 32,969 32,954 11,711 15,721 12,947 9,586 10,442 11,793 14,164 9,441 10,040

Minimum 11,980 9,850 8,650 11,340 8,920 8,870 15,690 23,420 19,230 18,860 25,280 13,740 7,730 13,060 10,980 7,523 7,574 9,175 12,364 7,073 8,465

Maximum 15,907 12,250 11,148 23,161 24,343 16,719 28,382 44,132 33,901 29,319 50,702 50,682 15,784 20,172 14,993 12,485 17,141 16,684 17,524 13,876 11,842

14th August 2017 2017 Interim Results Data source: Clarksons Research 13

World Seaborne Trade

14

0

1

2

3

4

5

6

7

8

9

10

11

12

0

1

2

3

4

5

6

7

8

9

10

11

12

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

Po

pu

lati

on

(b

illi

on

pe

op

le)

Se

ab

orn

e T

rad

e (

bil

lio

n t

on

ne

s)

major dry bulk minor dry bulk crude oil oil products chemicals liquefied gas containers other dry cargo World Population

Data Source: Clarksons / US Census Bureau14th August 2017 2017 Interim Results

Shipping Fleet Development: 1989-20181

14th August 2017 2017 Interim Results

Note: data prior to 1996 does not include retrospective changes and certain estimates.1Fleet forecast based on provisional estimates.

15Data source: Clarksons Research

Data as of 1st August 2017

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

500

1,000

1,500

2,000

2,500

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017(f

)

2018(f

)

millio

n d

wt

Bulkers Tankers Containers Gas Carriers Other Growth

Year-on-year fleet growth (RHS)

Fleet as at end year.

2017-18: projection.

Comprises world merchant fleet >100

GT, including ship-shaped offshore

units

10 Year CAGR (end 1989-99)

1.8%

8 Year CAGR (end 2008-16)

5.6%

Fleet 1st August 2017:

1,897m dwt

Fleet at end 2008:

1,204m dwtFleet at end 1990:

681m dwt

All Types* Fleet Deliveries & Projections

14th August 2017 2017 Interim Results

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

No.

of ve

sse

ls

Tanker Bulk Carrier Container Ship Gas Carrier Other Ship Types (>2,000 Dwt/GT)

Projected deliveries

Data Source: Clarksons Research Shipbuilding Forecast Club. *Not including Fishing Vessels, vessels below 2000 DWT/GT excluded

16

Global Vessel Contracting and Demolition

14th August 2017 2017 Interim Results

480 545 411 547795

546 667

1,378 1,197 1,140

2,255

2,905

1,874

580

1,833

1,043707

2,047

1,3371,107

217 267-206 -196 -344 -340 -272 -340 -368 -315

-137 -89 -123 -109

-233-562 -371 -548

-850 -697 -507 -537 -638-266

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7ytd

No.

of ve

sse

ls

Contracting Demolition

Includes vessels of 20,000+ DWT only

Source: Clarksons

17

Regional Shipbuilding Shares (1990-2017ytd)

14th August 2017 2017 Interim Results

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

ytd

% t

ota

l sh

ips d

eliv

ere

d (

GT

)

Other

USA

Taiwan

China

S. Korea

Japan

Europe

Data source: Clarksons Research

Data as of 1st August 201718

Global Newbuilding Orders at Historic Low…

14th August 2017 2017 Interim Results

480 545 411

547

795

546 667

1,378 1,197 1,140

2,255

2,905

1,874

580

1,833

1,043

707

2,047

1,337

1,107

217 267

0

500

1,000

1,500

2,000

2,500

3,000

3,500

No

. Sh

ips

Orders representative of vessels over 20,000 dwt

Data source: Clarksons Research

Data as of 1st August 201719

…Reflected in Number of Yards with an Orderbook of at least

one Vessel > 20,000 dwt

14th August 2017 2017 Interim Results

47 49 50 53 5969 70 70 76

8499

149

205

234 231 238221

178

156146 140

13111865 61 63 58 47

45 49 47 4850

55

64

70

7162 54

49

37

3429 32

3230

0

50

100

150

200

250

300

350

Nu

mb

er

of

Yar

ds

China - Japan - Korea Rest of World

August 2017: 148 Yards

2009: 305 Yards

Data source: Clarksons Research

Data as of 1st August 2017

1996-2017: Yards with at least 1 ship on order at year start/latest month

20

Fewer Yards Winning Orders…

14th August 2017 2017 Interim Results

*Peak varies by sector: Bulkers = 2010, Tankers = 2015, Containerships = 2015, LNG carriers = 2013, LPG Carriers = 2015

Includes yards in China, South

Korea and Japan only

Data source: Clarksons Research

Data as of 1st August 201721

Shipping Lending Overview (By Bank)

14th August 2017 2017 Interim Results

Total Reported Portfolios (by year)

2010: $418.4bn 2011: $400.3bn 2012: $388.5bn 2013: $379.1bn 2014: $391.5bn 2015: $343.8bn 2016: $315.0bn

21

18.1 17.7 17 16.8 16.8 16.2 15.9 15.2 15.1 14.6 14.1 13.9

10.3 10.28.9

86.3 6.2 5.9 5.8 5.7 5.5 5.1 4.6

2010 2011 2012 2013 2014 2015 2016

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

500.0

0

5

10

15

20

25

To

p 2

5 B

an

k P

ort

folio

s

(US

$ b

n)*

Geographical Breakdown of Lenders

EUROPE 83.1% 79.3% 75.1% 72.9% 70.5% 63.9% 62.2%

USA 2.1% 1.7% 2.8% 2.7% 2.6% 3.9% 4.8%

ASIA-PAC 14.8% 19.0% 22.0% 24.4% 26.8% 32.2% 33.0%

22

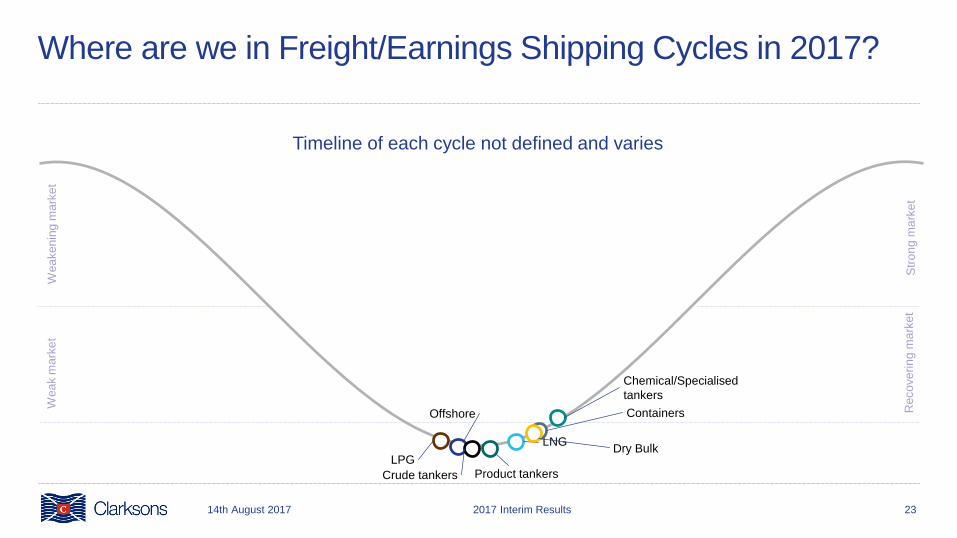

Where are we in Freight/Earnings Shipping Cycles in 2017?

23

Offshore

LNG

Product tankersCrude tankers

Str

on

g m

ark

et

Reco

ve

rin

g m

ark

et

Wea

ken

ing

ma

rke

tW

ea

k m

ark

et

Timeline of each cycle not defined and varies

Containers

Chemical/Specialised

tankers

Dry BulkLPG

14th August 2017 2017 Interim Results

Securities - an encouraging start to 2017...

14th August 2017 2017 Interim Results 24

Creating value at the heart of world tradeUnderpinned by our values, our integrated business model provides the platform for an unrivalled level of service and information that

enables trade and creates long-term value.

14th August 2017 2017 Interim Results 25

Corporate Outlook

14th August 2017 2017 Interim Results

Proven Strategy

Integrated business model

Breadth & Depth

Flow & placing power

Investment in technology solutions

Strong Balance Sheet

Cash generative

Progressive dividend policy

26