CKM’s Business Cycle Accounting Lawrence J. Christiano Joshua M. Davis.

36

CKM’s Business Cycle Accounting Lawrence J. Christiano Joshua M. Davis

-

date post

21-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of CKM’s Business Cycle Accounting Lawrence J. Christiano Joshua M. Davis.

CKM’s Business Cycle Accounting

Lawrence J. Christiano

Joshua M. Davis

Background• A strategy for identifying promising directions for

model development

• Fit simple RBC model to data

• Identify ‘wedges’– Distortions between marginal rates of substitution in

preferences and technology necessary to reconcile model and data

• Decompose movements in data into components due to various wedges

CKM’s Conclusion

• Frictions that Enter Household Intertemporal Margin (i.e. Investment) not Important for Understanding the US Great Depression

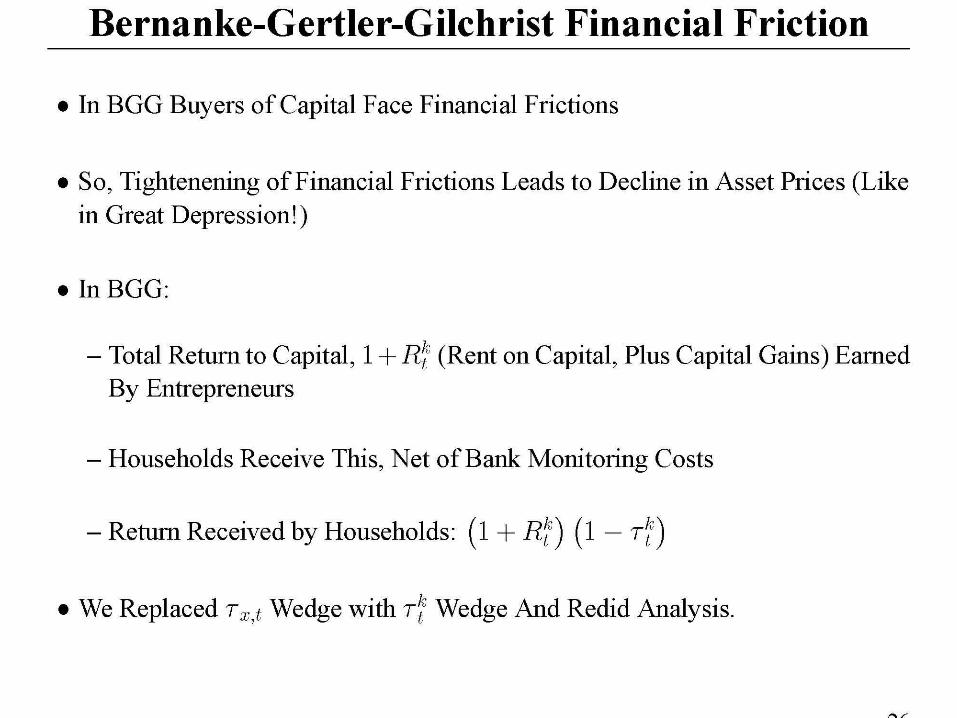

• Standard models of financial frictions (e.g. Carlstrom-Fuerst and Bernanke-Gertler-Gilchrist) not useful directions for research

• CKM Finding Potentially of Major Interest

• Early Phases of Great Depression Accompanied By Major Decline in the Stock Market Unusually Massive Decline in Investment

• Numerous Students of Great Depression Infer that Financial Market Imperfections Were Important

• CKM Finding Purports to Eliminate a Major Hypothesis About Great Depression From Further Consideration

CKM’s Result of Significant Interest

• Early phases of Great Depression accompanied by massive decline in investment and the stock market

• Numerous students of Great Depression infer that financial market imperfections were important

• CKM’s results oppose this conventional wisdom

Our Points:

• Small Changes in CKM Analysis Overturn their Conclusion

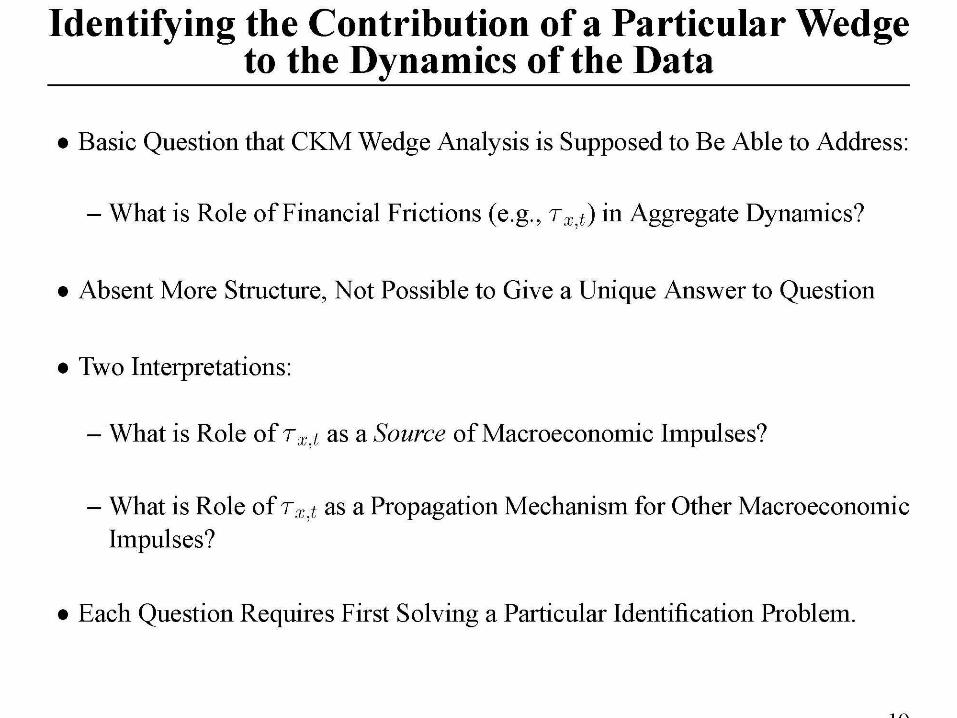

• Fundamental (Fatal?) Identification Problem Complicates the Analysis

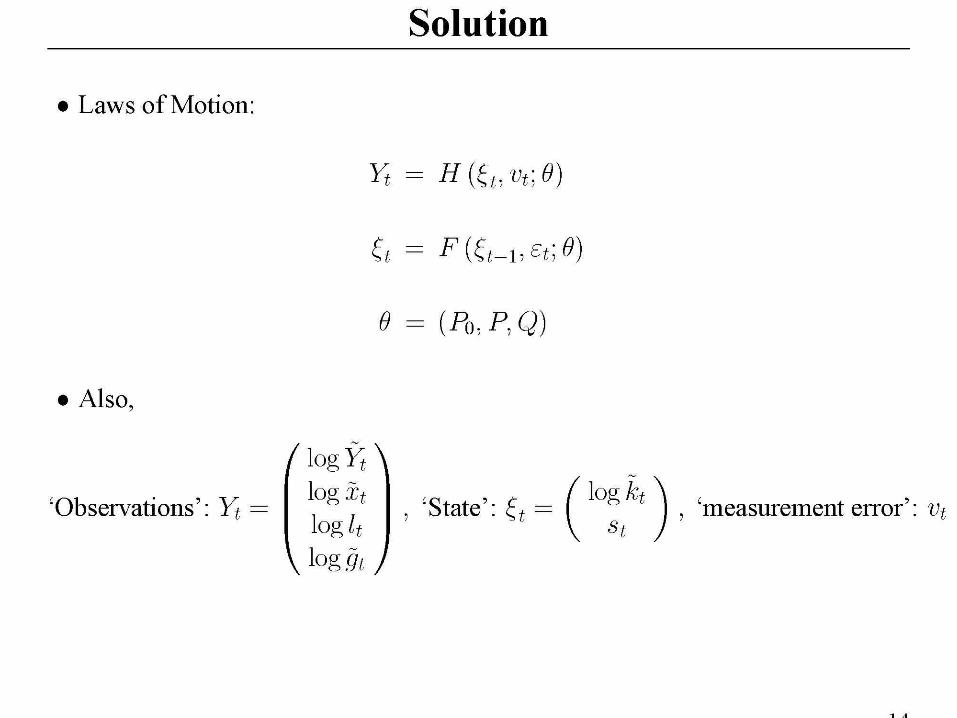

Computational Details• CKM Approach:

– Estimate Model Based on Linear Approximation of Solution, and Linear Kalman Filter in Estimation

– Recover Wedges Using Nonlinear Approximation to Model

• Our Approach

– Do Nonlinear Approximation In Estimation and Wedge Recovery

– Turns Out: Our Strategy and CKM Computational Strategy Yield Similar Results

Results

• First, We Reproduce CKM Calculations…

– CKM Results Suggest Financial Frictions Not Important for Output, Investment and Employment

– Our CKM Simulation Assumptions No Adjustment Costs

– Same Finding With Alternative Identification

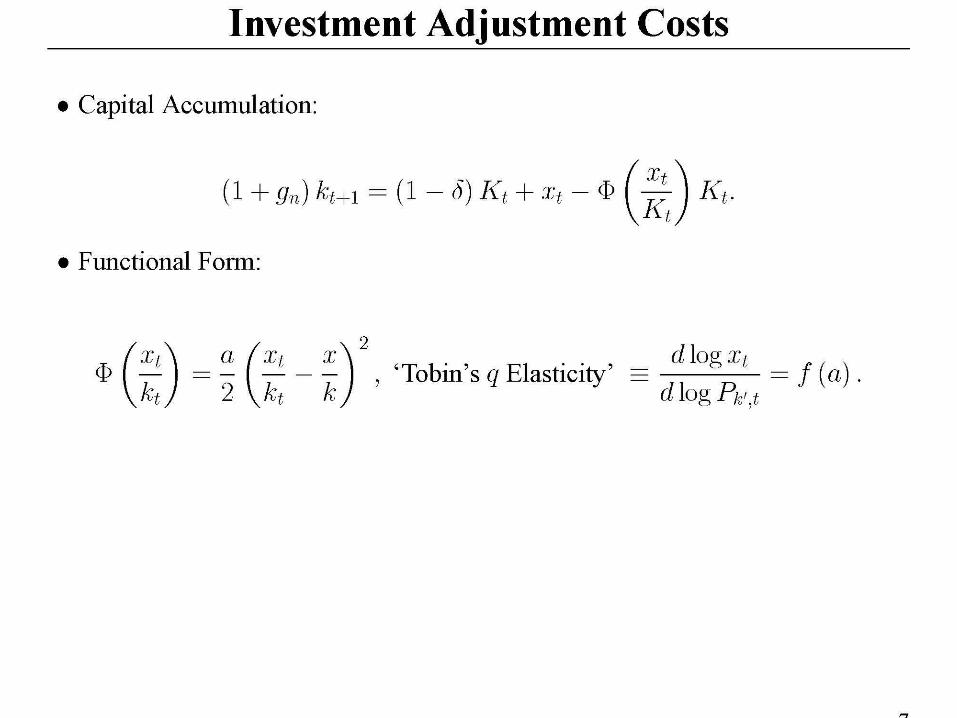

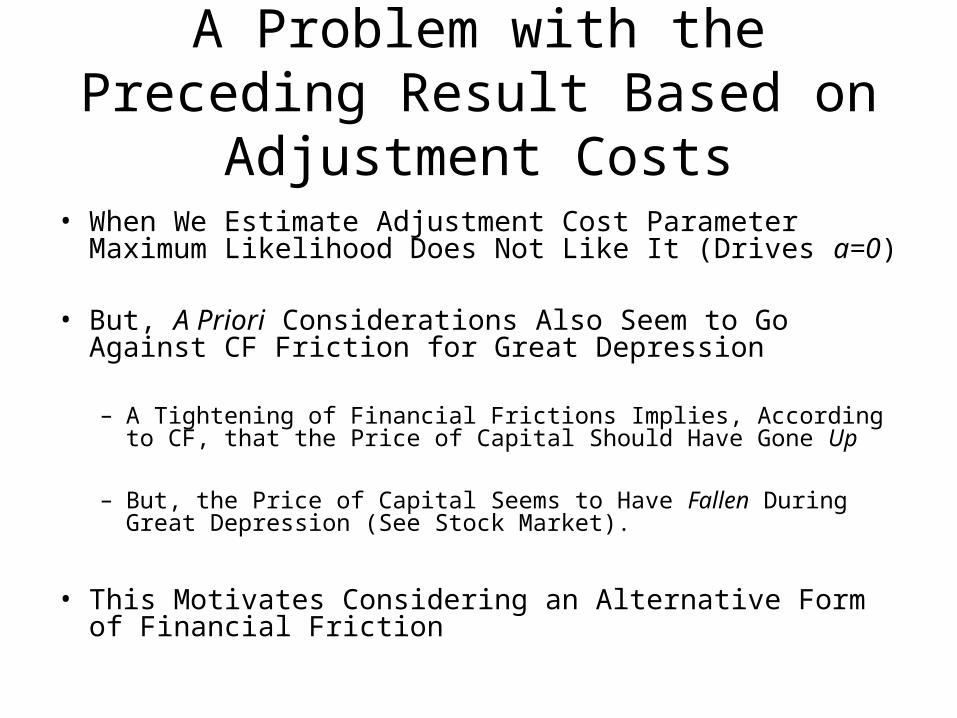

A Problem with the Preceding Result Based on Adjustment Costs

• When We Estimate Adjustment Cost Parameter Maximum Likelihood Does Not Like It (Drives a=0)

• But, A Priori Considerations Also Seem to Go Against CF Friction for Great Depression

– A Tightening of Financial Frictions Implies, According to CF, that the Price of Capital Should Have Gone Up

– But, the Price of Capital Seems to Have Fallen During Great Depression (See Stock Market).

• This Motivates Considering an Alternative Form of Financial Friction

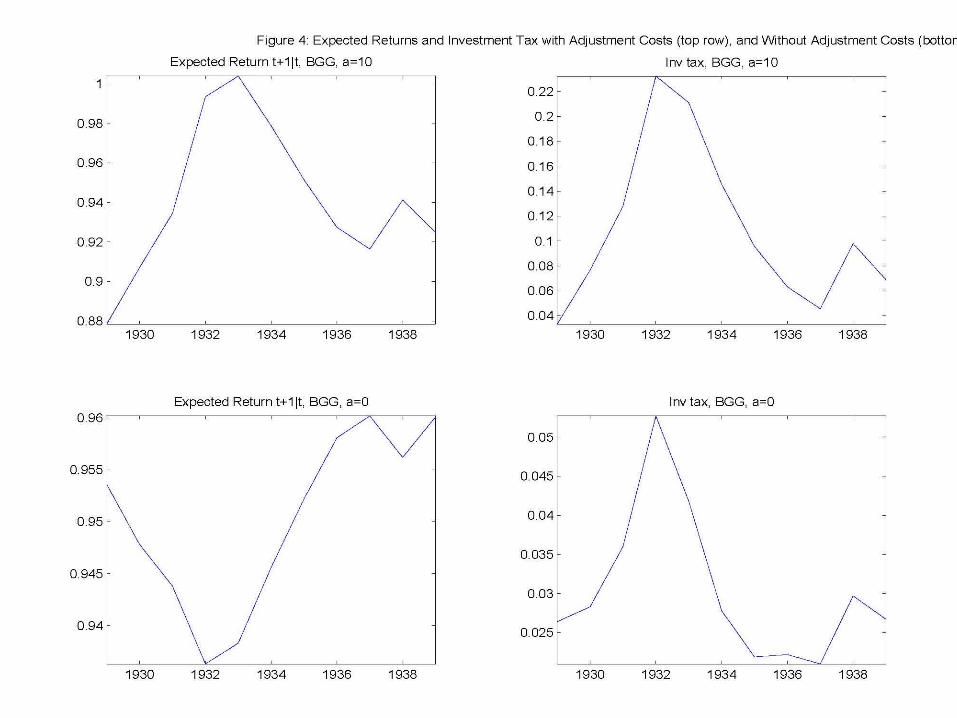

• When We Estimate Adjustment Costs with BGG Wedge, Parameter, a, Wants to be Very High (a=70).

• We Set a Conservatively:

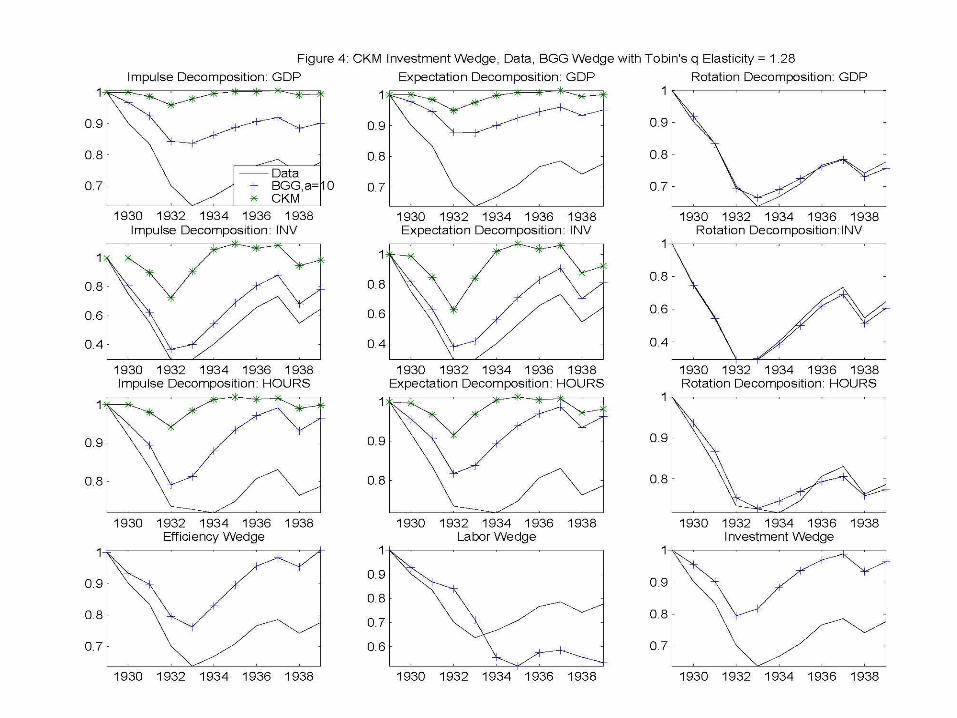

– Tobin’s q Elasticity = 1.28 Percent

– a=10

Conclusion

• Key Conclusion of CKM Analysis: Financial Frictions that Enter Intertemporal Euler Equation Not Important for Understanding Great Depression

• Our Finding: Small Changes in CKM Environment Overturn Their Conclusion

• We Estimate Degree of Adjustment Costs and Use a More A Priori Plausible Model of Financial Frictions– Estimate That Financial Frictions Account for 30-40% of fall in

output

• Deeper Identification Problem to Worry About