CJ 125 UNIT THREE BILLING AND CHECK TAMPERING SCHEMES.

17

CJ 125 UNIT THREE BILLING AND CHECK TAMPERING SCHEMES

-

Upload

silvester-bond -

Category

Documents

-

view

225 -

download

4

Transcript of CJ 125 UNIT THREE BILLING AND CHECK TAMPERING SCHEMES.

CJ 125UNIT THREE

BILLING AND CHECK TAMPERING SCHEMES

BILLING SCHEMES• WHAT IS A BILLING SCHEME?

• WHAT ARE THE THREE CATEGORIES?

Billing Schemes

The perpetrator uses false documentation to cause a payment to be issued for a fraudulent purpose

Fraudulent disbursement is issued in same manner as a legitimate disbursement

Schemes1. Shell company schemes

2. Non-accomplice vendor schemes

3. Personal purchases schemes

EXAMPLES OF THE THREE CATEGORIES OF BILLING SCHEMES

SHELL COMPANY SCHEMES

NON-ACCOMPLICE VENDOR SCHEMES PERSONAL PURCHASES SCHEMES

Shell Company Schemes Fictitious entities created for the sole purpose of

committing fraud Bank account is usually set up in the company’s name Forming a shell company

Certificate of incorporation or assumed-name certificate set up Shell company may be formed in someone else’s name Best way is set up company under a fictitious name Set up entity’s address – home address, post office box, or

friend/relative’s address

Shell Company Submitting false invoices

Invoice is manufactured using a professional printer, personal computer, or a typewriter

Self-approval of fraudulent invoices Most fraudsters are in a position to approve payment Approvals may be forged

“Rubber stamp” supervisors Don’t check the documentation Approve whatever is submitted

Reliance on false documents Without approval authority, fraudster submits false documents –

purchase order, invoice, and receiving reports

Shell Company Collusion

Two or more employees conspire to steal More difficult to detect Circumvents controls implemented to prevent fraud

Purchases of services rather than goods Purchases of service are preferable over purchases of goods Services are intangible and fraud is more difficult to detect

Pass-through schemes Goods or services are purchased by the employee and resold to

the victim company at an inflated price

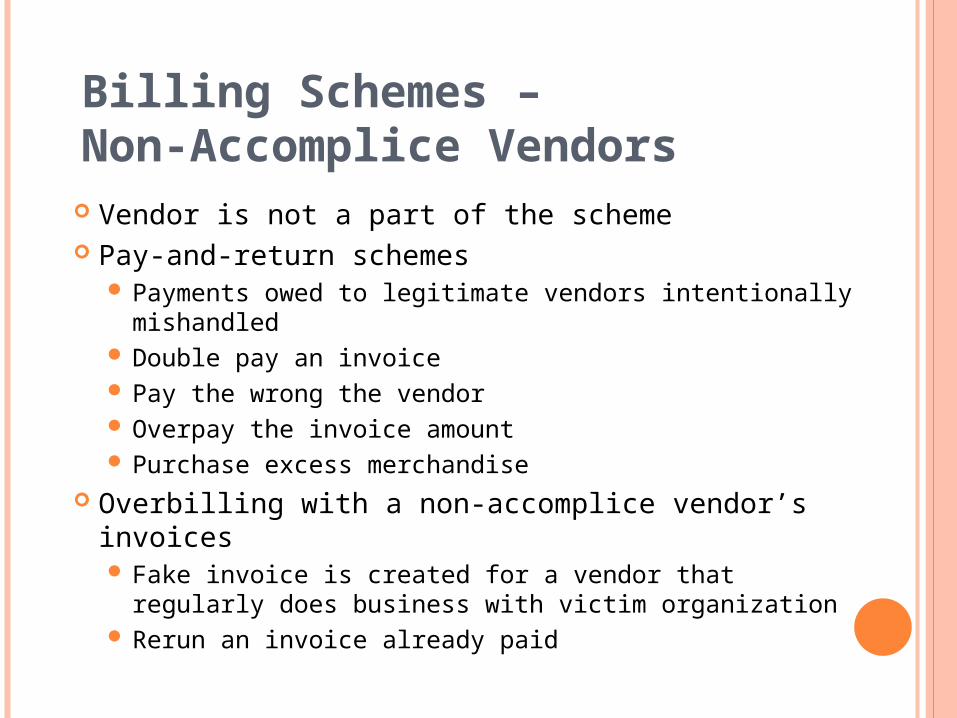

Billing Schemes –Non-Accomplice Vendors Vendor is not a part of the scheme Pay-and-return schemes

Payments owed to legitimate vendors intentionally mishandled Double pay an invoice Pay the wrong the vendor Overpay the invoice amount Purchase excess merchandise

Overbilling with a non-accomplice vendor’s invoices Fake invoice is created for a vendor that regularly does business

with victim organization Rerun an invoice already paid

PUT IT TO THE TEST

WHAT TYPE OF BILLING SCHEMES WERE COMMITTED IN THE CASE “MEDICAL SCHOOL TREATS FRAUD AND ABUSE”?

CHECK TAMPERING SCHEMES HOW DO WE DEFINE A CHECK TAMPERING

SCHEME?

WHAT ARE THE FIVE MAJOR CATEGORIES?

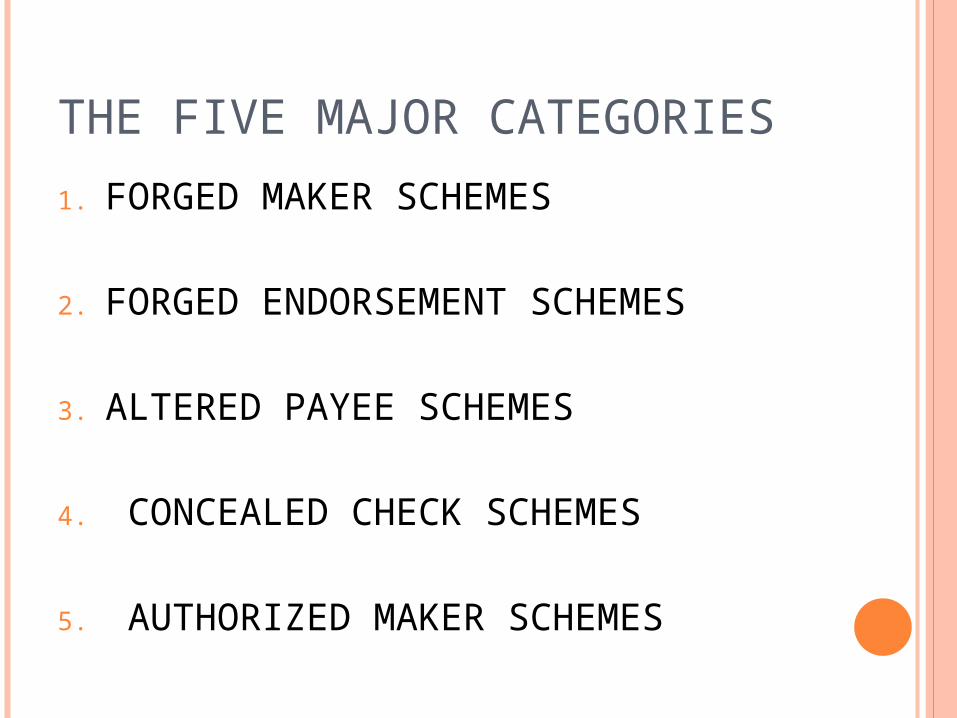

THE FIVE MAJOR CATEGORIES

1. FORGED MAKER SCHEMES

2. FORGED ENDORSEMENT SCHEMES

3. ALTERED PAYEE SCHEMES

4. CONCEALED CHECK SCHEMES

5. AUTHORIZED MAKER SCHEMES

Forged Maker Schemes

An employee misappropriates a check and fraudulently affixes the signature of an authorized maker

Forged Endorsement SchemesEmployee intercepts a company check

intended for a third partySigns the third party’s name on the

endorsement line of the check

Authorized Maker Schemes

Employee with signature authority writes a fraudulent check

Overriding controls through intimidation High-level managers can make employees afraid

to question suspicious transactions Can happen when ownership is absent or

inattentive Poor controls

Failure to closely monitor accounts Lack of separation of duties

Concealed Check Schemes

Employee prepares a fraudulent check and submits it along with legitimate checks

Check is payable to the employee, accomplice, a fictitious person, or fictitious business

Occurs when checks are signed without proper review or reviewer is busy

In many cases, only the signature line is exposed and the payee is concealed

Authorized Maker Schemes

Employee with signature authority writes a fraudulent check

Overriding controls through intimidation High-level managers can make employees afraid

to question suspicious transactions Can happen when ownership is absent or

inattentive Poor controls

Failure to closely monitor accounts Lack of separation of duties

PUT IT TO THE TEST

HOW WAS MELISSA ROBINSON ABLE TO COMMIT CHECK TAMPERING FRAUD AND WHAT MEASURES DID SHE TAKE TO CONCEAL HER FRAUD IN THE CASE “A WOLF IN SHEEP’S CLOTHING”?

Happy Holidays!Happy Holidays!