City of Lawrence Financial Statement-2010-11

112

PRELIMINARY OFFICIAL STATEMENT AND NOTICE OF SALE DATED NOVEMBER 11, 2010 Ratings: Moody’s: Standard & Poor’s: In the opinion of Edwards Angell Palmer & Dodge LLP, Bond Counsel, based upon an analysis of existing law and assuming, among other matters, compliance with certain covenants, interest on the Notes is excluded from gross income for federal income tax purposes under the Internal Revenue Code of 1986. Interest on the Notes is not a specific preference item for purposes of the federal individual or corporate alternative minimum taxes, and such interest is not included in adjusted curr ent earnings when calculating corporate alternative minimum taxable income. Under existing law, interest on the Notes is exempt from Massachusetts personal income taxes, and the Notes are exempt from Massachusetts personal property taxes. Bond Counsel expresses no opinion regarding any other tax consequences related to the ownership or disposition of , or the accrual or r eceipt of interest on, the Notes. The Notes will NOT be designated as “qualified tax- exempt obligations” for purposes of Section 265(b)(3) of the Code. See “Tax Exemption” herein. CITY OF LAWRENCE, MASSACHUSETTS STATE QUALIFIED GENERAL OBLIGATION DEFICIT FINANCING BOND ANTICIPATION NOTES The City of Lawrence, Massachusetts (the “City”) will receive telephone and electronic bids at First Southwest Company (617-619-4400) in case of telephone bids and via PARITY in case of electronic bids until 11:00 A.M., Local Time, Thursday, November 18, 2010, for the purchase of the following described issues of State Qualified General Obligation Deficit Financing Bond Anticipation Notes, dated December 1, 2010: $6,000,000 State Qualified General Obligation Deficit Financing Bond Anticipation Notes payable December 1, 2011. Interest on t hese Notes will be calculated on a 30 day month/360 day year basis (360/360). Bids may be submitted electronically via PARITY pursuant to this Notice until 11:00 A.M., local time, but no bid will be received after the time for receiving bids specified above. To the extent any instructions or directions set forth in PARITY conflict with this Notice, the terms of this Notice shall control. For further information about PARITY , potential bidders may contact PARITY at (212) 849-5021. Bids may be for all or part of each issue at a single or multiple rates of interest in a multiple of one-hundredth (1/100) of one percent (1%). No bid of less than par and accrued interest to the date of delivery will be considered on this issue, and bids must include a premium of at least $2.50 per $1,000 bid. The right is reserved to reject any or all bids and to reject any bid not complying with this Notice of Sale and, so far as permitted by law, to waive any irregularity with respect to any bid. The Notes will be awarded on the basis of lowest net interest cost to the City after deduction of premium, if any. Such cost will be determined by computing the total amount of interest payable on the Notes, at the rate or rates stated, from December 1, 2010 until the maturity of the Notes and deducting therefrom the sum, if any, by which the amount bid for the Notes exceeds the aggregate principal amount of the Notes. In the event a bidder offering a premium for the Notes is awarded a lesser amount of Notes than bid, the premium shall be reduced proportionately. An electronic bid made in accordance with this Notice of Sale shall be deemed an offer to purchase the Notes in accordance with the terms provided in this Notice of Sale and shall be binding upon the bidder as if made by a signed and sealed written bid delivered to the City. Any bidder who submits a winning bid by telephone in accordance with this Notice of Sale shall be required to provide written confirmation of the terms of the bid by faxing or e-mailing a completed, signed bid form to First Southwest Company by not later than Noon, Eastern Time, on the date of sale. The award of the Notes to the winning bidder or bidders will not be effective until the bid has been approved by the Mayor and the City Treasurer. The Notes will be issued by means of a book-entry system, evidencing ownership of the Notes in principal amounts of $1,000, or integral multiples thereof, with transfers of ownership effected on the records of The Depository Trust Company (DTC) and its participants pursuant to rules and procedures adopted by DTC. (See "Book-Entry-Transfer System.") Principal and interest on the Notes will be payable upon maturity in federal reserve funds by the Treasurer and Receiver- General of The Commonwealth of Massachusetts, as Paying Agent. The disbursement of such payments to the DTC

-

Upload

dan-rivera -

Category

Documents

-

view

220 -

download

0

Transcript of City of Lawrence Financial Statement-2010-11

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 1/112

PRELIMINARY OFFICIAL STATEMENT AND NOTICE OF SALE DATED NOVEMBER 11, 2010

Ratings:Moody’s:Standard & Poor’s:

In the opinion of Edwards Angell Palmer & Dodge LLP, Bond Counsel, based upon an analysis of existing law andassuming, among other matters, compliance with certain covenants, interest on the Notes is excluded from gross incomefor federal income tax purposes under the Internal Revenue Code of 1986. Interest on the Notes is not a specificpreference item for purposes of the federal individual or corporate alternative minimum taxes, and such interest is not

included in adjusted current earnings when calculating corporate alternative minimum taxable income. Under existinglaw, interest on the Notes is exempt from Massachusetts personal income taxes, and the Notes are exempt fromMassachusetts personal property taxes. Bond Counsel expresses no opinion regarding any other tax consequencesrelated to the ownership or disposition of, or the accrual or receipt of interest on, the Notes. The Notes will NOT bedesignated as “qualified tax-exempt obligations” for purposes of Section 265(b)(3) of the Code. See “Tax Exemptionherein.

CITY OF LAWRENCE, MASSACHUSETTS

STATE QUALIFIED

GENERAL OBLIGATION DEFICIT FINANCING BOND ANTICIPATION NOTES

The City of Lawrence, Massachusetts (the “City”) will receive telephone and electronic bids at First Southwest Company(617-619-4400) in case of telephone bids and via PARITY in case of electronic bids until 11:00 A.M., Local Time

Thursday, November 18, 2010, for the purchase of the following described issues of State Qualified General ObligationDeficit Financing Bond Anticipation Notes, dated December 1, 2010:

$6,000,000 State Qualified General Obligation Deficit Financing Bond Anticipation Notes payable December1, 2011. Interest on these Notes will be calculated on a 30 day month/360 day year basis(360/360).

Bids may be submitted electronically via PARITY pursuant to this Notice until 11:00 A.M., local time, but no bid will bereceived after the time for receiving bids specified above. To the extent any instructions or directions set forth in PARITY

conflict with this Notice, the terms of this Notice shall control. For further information about PARITY , potential biddersmay contact PARITY at (212) 849-5021.

Bids may be for all or part of each issue at a single or multiple rates of interest in a multiple of one-hundredth (1/100) ofone percent (1%). No bid of less than par and accrued interest to the date of delivery will be considered on this issue

and bids must include a premium of at least $2.50 per $1,000 bid. The right is reserved to reject any or all bids and toreject any bid not complying with this Notice of Sale and, so far as permitted by law, to waive any irregularity with respectto any bid. The Notes will be awarded on the basis of lowest net interest cost to the City after deduction of premium, iany. Such cost will be determined by computing the total amount of interest payable on the Notes, at the rate or ratesstated, from December 1, 2010 until the maturity of the Notes and deducting therefrom the sum, if any, by which theamount bid for the Notes exceeds the aggregate principal amount of the Notes. In the event a bidder offering a premiumfor the Notes is awarded a lesser amount of Notes than bid, the premium shall be reduced proportionately.

An electronic bid made in accordance with this Notice of Sale shall be deemed an offer to purchase the Notes inaccordance with the terms provided in this Notice of Sale and shall be binding upon the bidder as if made by a signed andsealed written bid delivered to the City.

Any bidder who submits a winning bid by telephone in accordance with this Notice of Sale shall be required to providewritten confirmation of the terms of the bid by faxing or e-mailing a completed, signed bid form to First SouthwestCompany by not later than Noon, Eastern Time, on the date of sale.

The award of the Notes to the winning bidder or bidders will not be effective until the bid has been approved by the Mayorand the City Treasurer.

The Notes will be issued by means of a book-entry system, evidencing ownership of the Notes in principal amounts o$1,000, or integral multiples thereof, with transfers of ownership effected on the records of The Depository TrusCompany (DTC) and its participants pursuant to rules and procedures adopted by DTC. (See "Book-Entry-TransfeSystem.")

Principal and interest on the Notes will be payable upon maturity in federal reserve funds by the Treasurer and Receiver-General of The Commonwealth of Massachusetts, as Paying Agent. The disbursement of such payments to the DTC

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 2/112

Participants is the responsibility of DTC, and the disbursement of such payments to the Beneficial Owners is theresponsibility of the DTC Participants and the Indirect Participants, as more fully described herein.

The Notes are not subject to redemption prior to maturity.

The successful bidder(s) for the Notes may request that the Notes be issued in the form of one fully registered physicacertificate, rather then in book-entry form through the facilities of The Depository Trust Company. The successful biddeseeking the issuance of the Notes in this manner shall bear any and all costs of any re-registration or transfer of Notesfrom time to time. Any bidder seeking to have the Notes issued in the form of fully registered physical certificates, rathethan in book-entry form, shall indicate this preference to the City at the time of the submission of the winning bid. The Cityreserves the right to decline any request to issue the Notes in non-book entry form if it should determine, in its solediscretion, that issuing the Notes in this manner is not in its best interests.

The Notes will be accompanied by the opinion of Edwards Angell Palmer & Dodge LLP of Boston, Massachusetts,approving the legality of the Notes. (See "Tax Exemption"). The opinion will also indicate that the Notes and theenforceability thereof may be subject to bankruptcy and other laws affecting creditor's rights and that their enforceabilitymay also be subject to the exercise of judicial discretion in appropriate cases. Payment of the principal of and interest onthe Notes is not limited to a particular fund or source of revenue nor is any lien or pledge for such payment created withrespect to any such fund or source. The Notes will be valid general obligations of the City of Lawrence and, except to theextent they are paid from the sale of State Qualified bonds in anticipation of which they are issued, or from any otheravailable moneys, the principal of and interest on the Notes are payable from taxes which may be levied upon all taxableproperty in the City, subject to the limit imposed by Chapter 59, Section 21C of the General Laws.

In order to assist the successful bidder or bidders in complying with the requirements of paragraph (b)(5)(i)(c) of Rule15c2-12 promulgated by the Securities and Exchange Commission, the City will undertake to provide notices of certainsignificant events. A description of this undertaking is set forth in the Preliminary Official Statement.

It is anticipated that CUSIP identification numbers will be used in connection with the Notes. All expenses in relation tothe printing of CUSIP numbers on said Notes shall be paid for by the City, however, the City assumes no responsibilityfor any CUSIP Service Bureau or other charges that may be imposed for the assignment of such number.

Additional information concerning the City of Lawrence and the Notes is contained in the Preliminary Official Statementdated November 11, 2010. The Preliminary Official Statement is provided for informational purposes and is not a part ofthis Notice of Sale. The Preliminary Official Statement has been deemed to be final by the City except for the omission ofthe reoffering prices, interest rates and other terms of the Notes depending on such matters, but is subject to changewithout notice and to completion or amendment in a Final Official Statement. Copies of the Preliminary Official Statement

may be obtained from the First Southwest Company, 54 Canal Street, Suite 320, Boston, Massachusetts 02114(Telephone: 617-619-4400). Within seven business days following the award of the Notes, 5 copies of the Final OfficialStatement will be made available. Upon request, additional copies will be provided.

The Notes will be delivered to The Depository Trust Company or its custodial agent, against payment to the City in federalreserve funds on or about December 1, 2010.

CITY OF LAWRENCE, MASSACHSUETTS /s/ Patricia Cook, Treasure

November 11, 2010

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 3/112

2

TABLE OF CONTENTSPage Page

OFFICIAL STATEMENT ........................................... 3Authorization of the Bonds and

Use of Proceeds ..................................................... 3State Qualified Notes ................................................ 3Book-Entry Only System ........................................... 4Securities and Remedies .......................................... 5Tax Exemption .......................................................... 6Opinion of Bond Counsel .......................................... 8Financial Advisory Services ofFirst Southwest Company. ....................................... 8Continuing Disclosure ............................................... 8

CITY OF LAWRENCE:General...................................................................... 10Principal Executive Officers ...................................... 10Current Financial Challenges .................................... 10History ....................................................................... 10Municipal Services .................................................... 11Education .................................................................. 11

Public School Enrollments ..................................... 11Industry and Commerce ............................................ 11Employment and Payrolls ....................................... 12

Largest Employers .................................................... 12Labor Force, Employment and Unemployment ........ 13Economic Developments .......................................... 13Sigificant Announcements ........................................ 13Public Sector Developments ..................................... 15Building Permits ........................................................ 18Transportation and Utilities ....................................... 18Population, Income and Wealth Levels ..................... 19Population Trends ..................................................... 19

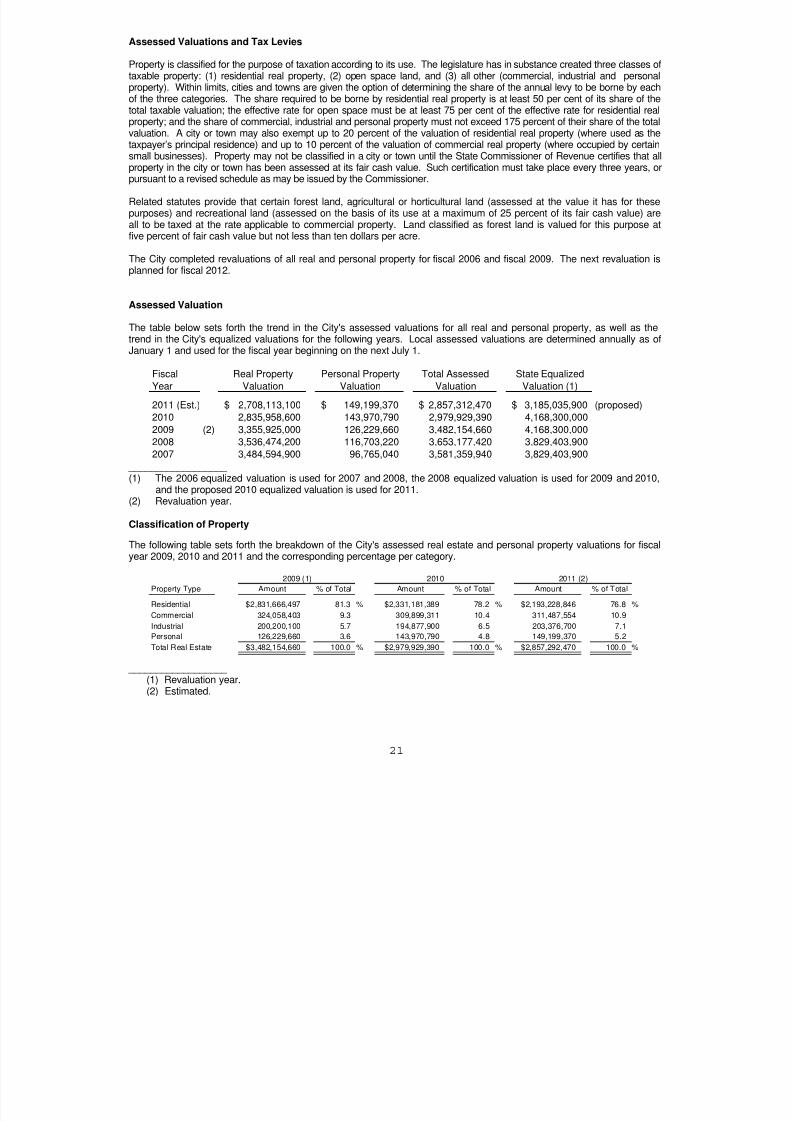

PROPERTY TAXATION:

Tax Levy Computation .............................................. 20Reduction of State Aid .............................................. 20Assessed Valuations and Tax Levies ....................... 21Assessed Valuation ................................................... 21Classification of Property .......................................... 21Tax Rates .................................................................. 22Largest Taxpayers .................................................... 22State Equalized Valuation ......................................... 22Abatements and Overlay........................................... 23Tax Collections .......................................................... 23Taxes Titles and Possessions .................................. 24

Sale of Tax Receivables ........................................... 24Taxation to Meet Deficits ........................................... 24Property Tax Limitation ............................................. 25Tax Levy Limits ......................................................... 26Pledged Taxes .......................................................... 26Community Preservation Act .................................... 26

CITY FINANCES:

Budget and Appropriation Process ............................. 28History of Prior Financial Problems (1989-1997) ....... 28History of More Recent Financial Problems ............... 29Special Legislation Pertaining to the City’s

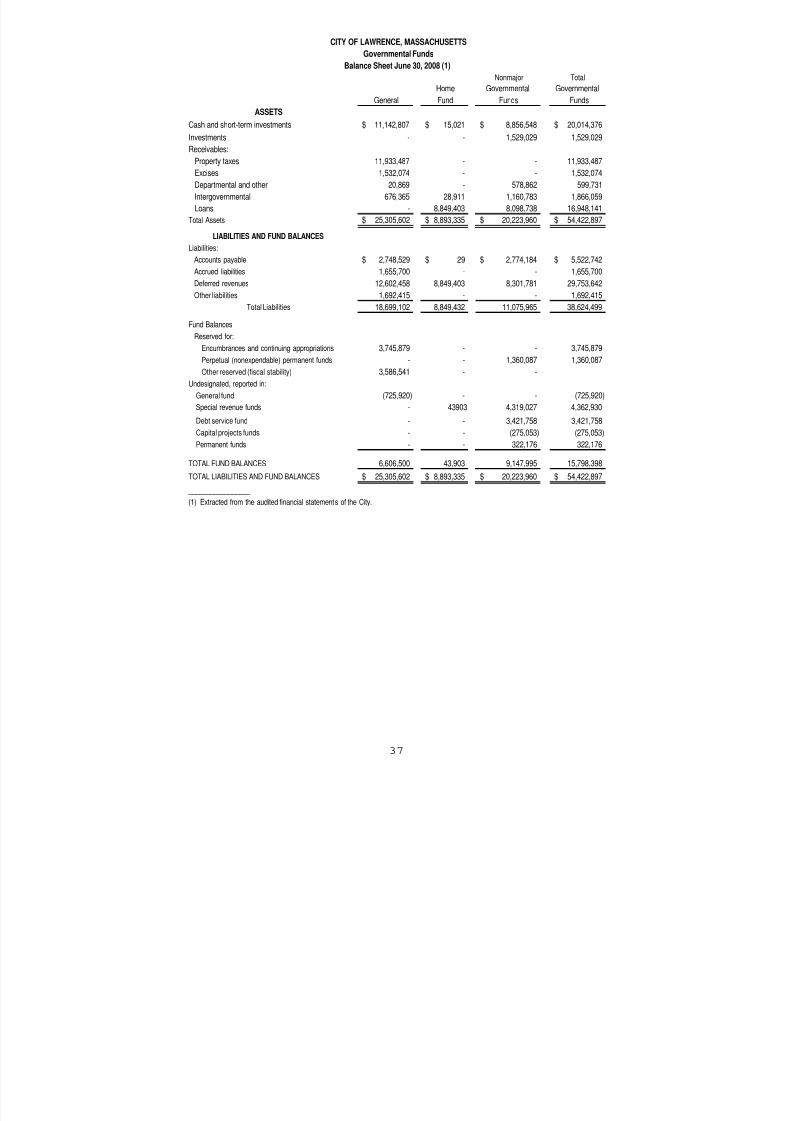

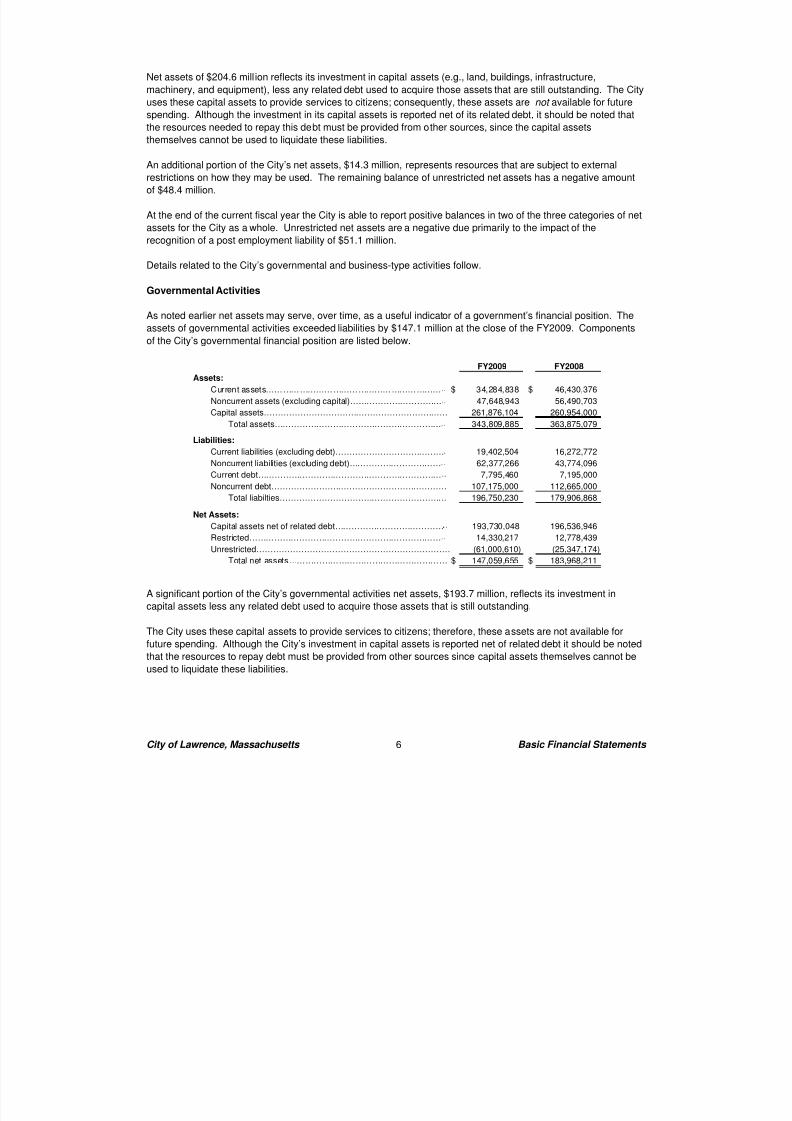

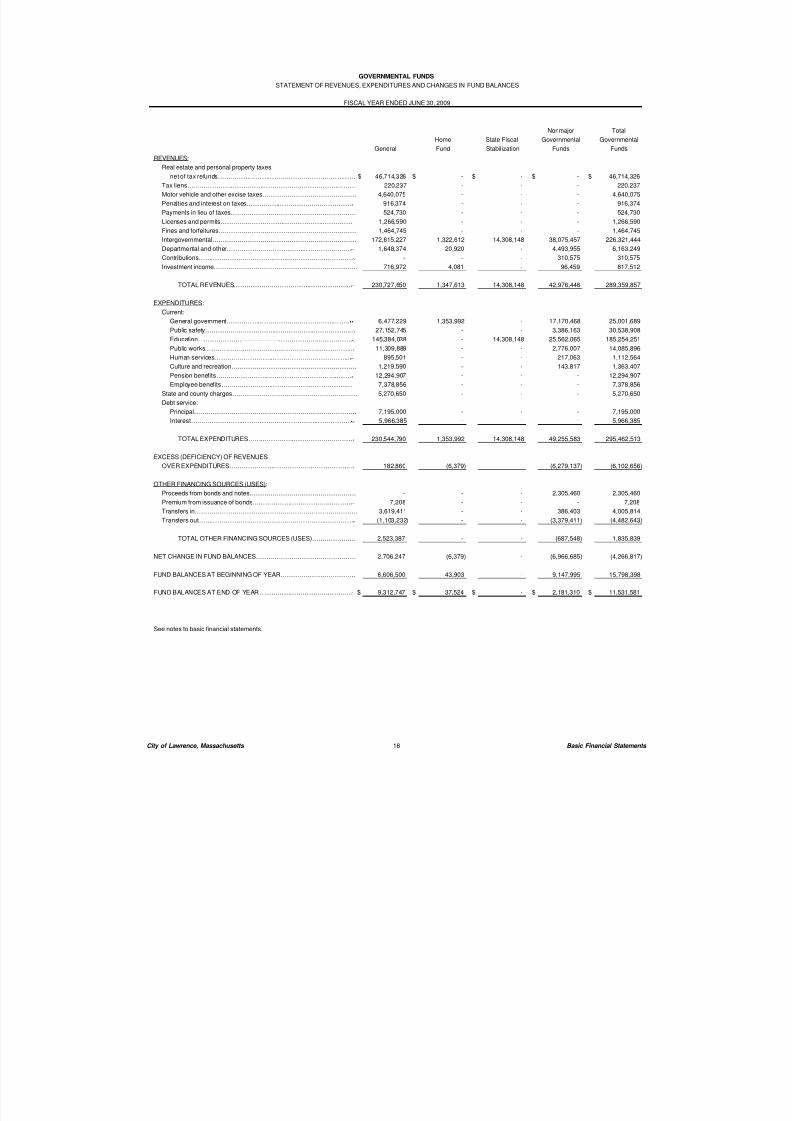

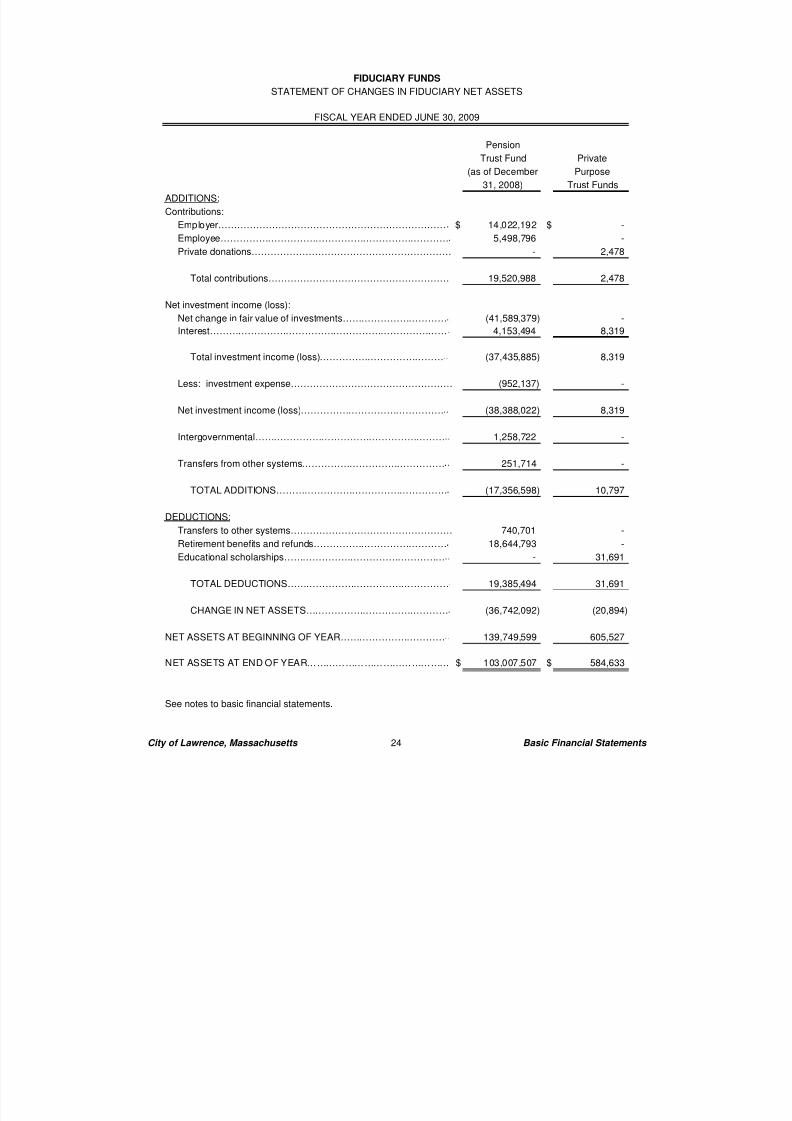

Fiscal Stability .......................................................... 29Initial Plan of Correction .............................................. 30Subsequent Accomplishments ................................... 30Deficit Financing ......................................................... 31Budget Trends ............................................................ 32Revenues .................................................................... 32State School Building Assistance Program ................ 33Investments of City Funds .......................................... 34Significant Accounting Policies ................................... 34Annual Audits .............................................................. 34Financial Statements .................................................. 34Fiscal 2010 Estimated Operating Results .................. 35Combined Balance Sheet June 30, 2009 ................... 36

Combined Balance Sheet June 30, 2008 ................... 37Combined Balance Sheet June 30, 2007 ................... 38Comparative Statement of Receipts and

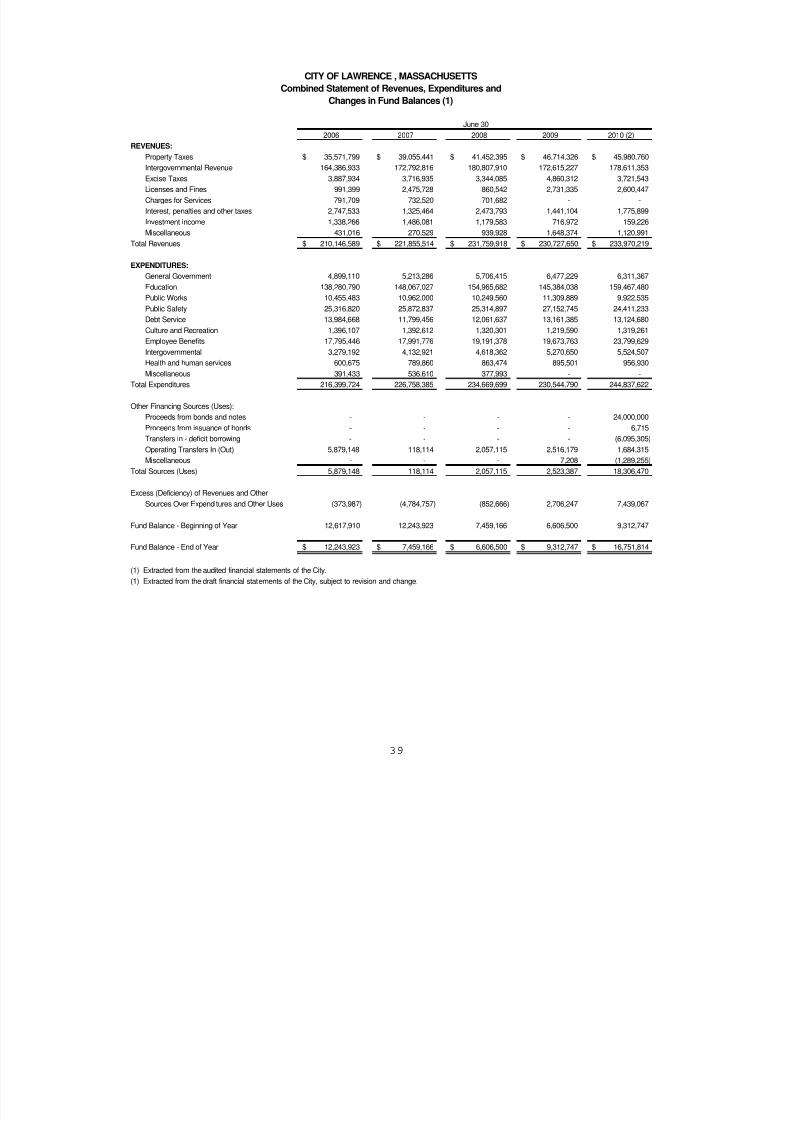

Expenditures and Changes in Fund Balance – General Fund, June 30, 2005 - 2009 ...................... 39

Free Cash ................................................................... 40Tax Increment Financing for Development Districts .. 40

INDEBTEDNESS:

Authorization Procedure and Limitations .................... 41Types of Obligations ................................................... 41Direct Debt Summary ................................................. 42

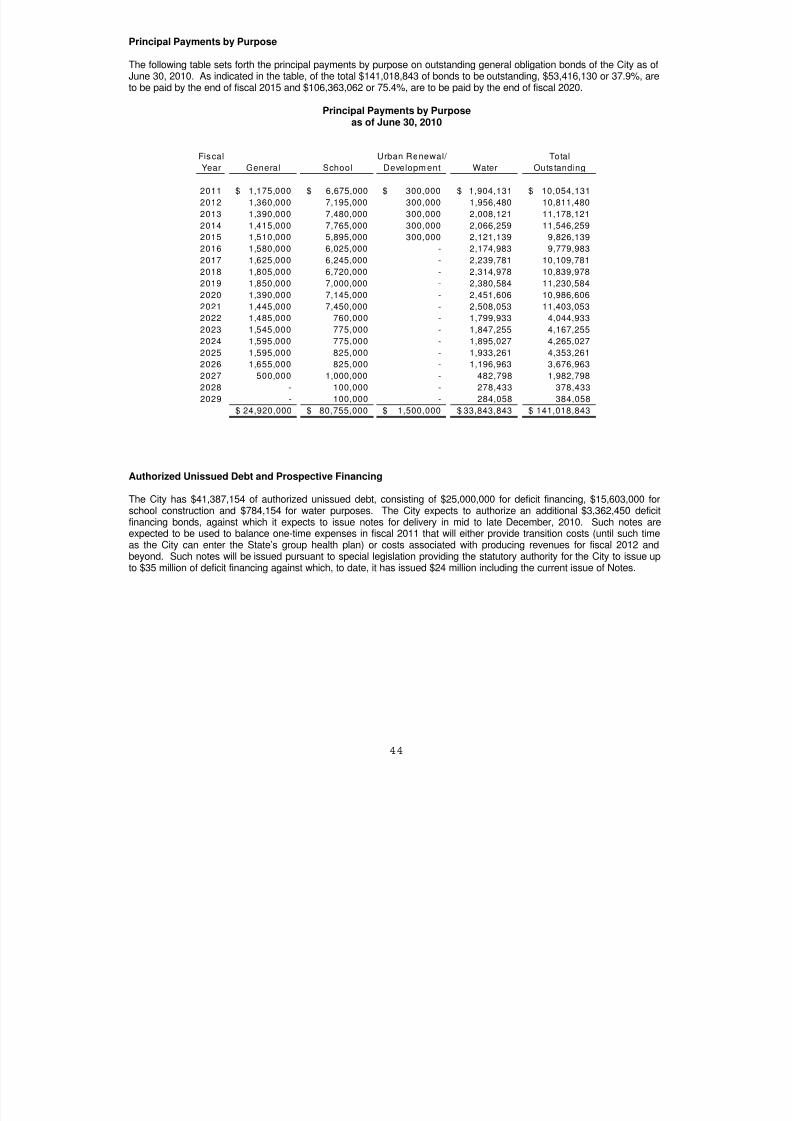

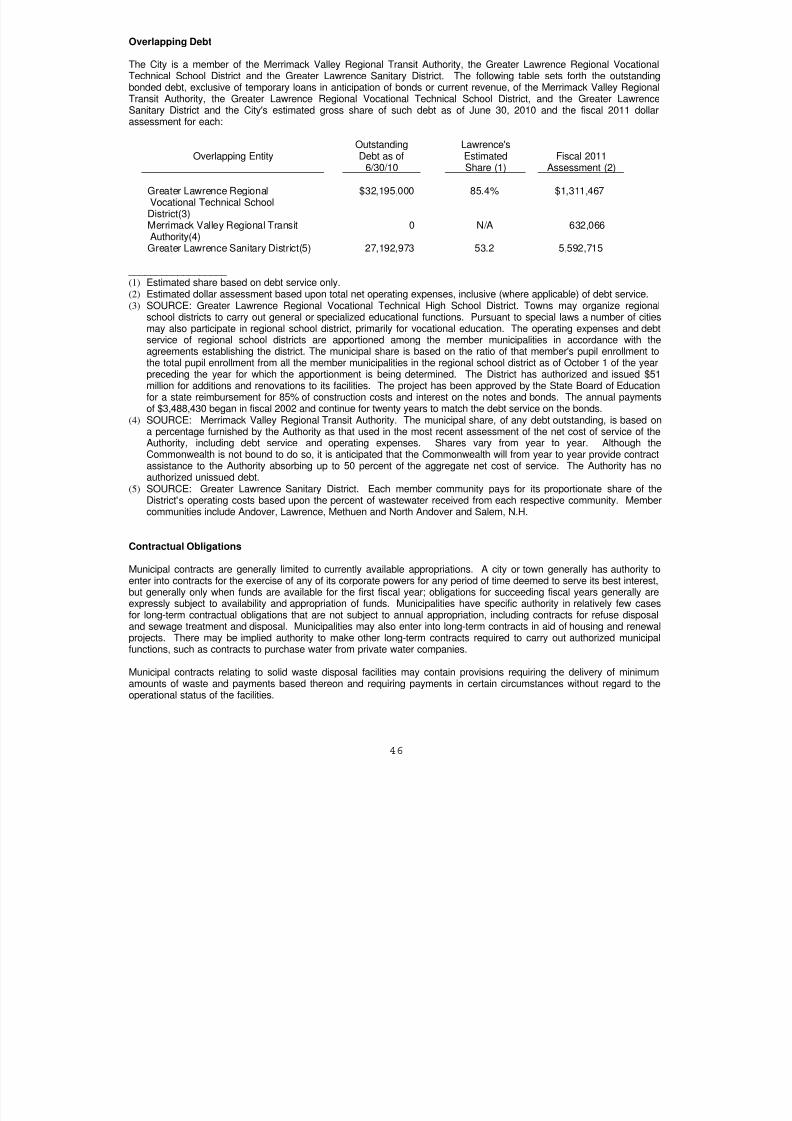

Debt Ratios ................................................................. 43Debt Service Requirements ........................................ 43Principal Payments by Purpose .................................. 44Authorized Unissued Debt and

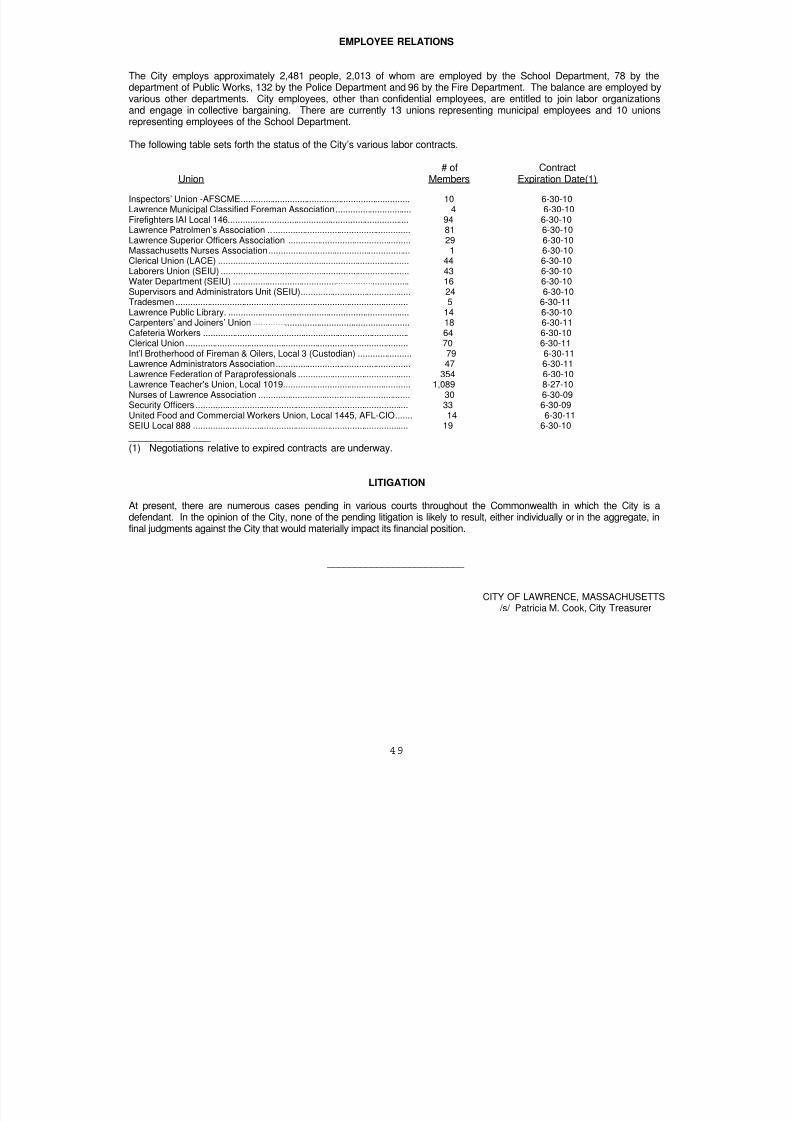

Prospective Financing ............................................. 44Coverage of Qualified Debt Service ........................... 45Overlapping Debt ........................................................ 46Contractual Obligations .............................................. 46RETIREMENT PLAN .................................................. 47Other Post-Employment Benefits ............................... 48EMPLOYEE RELATIONS ........................................... 49LITIGATION ................................................................ 49APPENDIX A: City of Lawrence - Fiscal 2009

Audited Financial StatementsAPPENDIX B: Proposed Form of Legal Opinion

_____________________________ The Official Statement is not to be construed as a contract or agreement between the City and the purchasers or holders of any of theNotes. Any statements made in this Official Statement involving matters of opinion, whether or not expressly so stated, are intendedmerely as opinion and not as representations of fact. The information and expressions of opinion herein are subject to change withounotice and neither the delivery of this Official Statement nor any sale of the Notes described herein shall, under any circumstances,create any implication that there has been no change in the affairs of the City of Lawrence, since the date hereof.

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 4/112

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 5/112

4

Chapter 44A further provides that nothing therein shall be construed to relieve the City of the obligation imposed on it bylaw to appropriate and to include in its annual tax levy amounts necessary to pay, in each year, the principal and interesmaturing and becoming due on any qualified notes issued by the City; provided, however, that to the extent of theamounts of distributable aid or other amounts payable to the City which have been or are to be forwarded to the payingagent for such qualified notes, the State Treasurer shall certify to the City Auditor the amounts so withheld and thereaftersuch amounts shall be credited to the appropriations of the City for the current fiscal year, and provided, further that to theextent to which distributable aid is not appropriated by the Commonwealth in any fiscal year, such appropriated amountsof the City shall be used to pay the debt service maturing and becoming due in such year on such qualified notes of theCity.

Nothing in Chapter 44A shall be construed to pledge the credit and assets of the Commonwealth to the support of anyqualified notes or to guarantee payment or stand as surety for the payment of any qualified notes.

The City may issue other bonds and notes in addition to the Notes as qualified bonds and notes on a parity with the Notespursuant to Chapter 44A. In addition to this issue, the City has issued the following qualified notes and bonds$12,000,000 qualified notes dated April 23, 2010, payable December 1, 2010 ($6,000,000) and March 1, 2011($6,000,000), $6,000,000 qualified bonds dated March 15, 1997, $1,500,000 of which are currently outstanding$46,570,000 qualified bonds dated February 1, 2001, $2,015,000 of which are currently outstanding; $43,430,000qualified bonds dated March 15, 2002, $9,080,000 of which are currently outstanding; $22,605,000 qualified bonds datedAugust 12, 2003, $8,600,000 of which are currently outstanding; $6,000,000 qualified bonds dated June 15, 2004$3,600,000 of which are currently outstanding; $9,000,000 qualified bonds dated August 15, 2005, $7,750,000 of whichare currently outstanding; $8,000,000 qualified bonds dated August 1, 2006, $6,770,000 of which are currentlyoutstanding; $48,355,000 qualified bonds dated December 1, 2006, $48,210,000 of which are currently outstanding

$18,000,000 qualified bonds dated October 1, 2007, $17,500,000 of which are currently outstanding; and $2,305,460qualified bonds dated April 1, 2009, $2,150,000 of which are currently outstanding. See "INDEBTEDNESS--Coverage oQualified Debt Service" for a discussion of the projected coverage of qualified debt service by state aid.

Book-Entry Transfer System

The Depository Trust Company ("DTC"), New York, NY, will act as securities depository for the Notes. The Notes will beissued as fully-registered securities registered in the name of Cede & Co. (DTC's partnership nominee) or such othername as may be requested by an authorized representative of DTC. One-fully registered Note certificate will be issued foeach interest rate, each in the aggregate principal amount bearing such interest rate, and will be deposited with DTC.

DTC, the world's largest depository, is a limited-purpose trust company organized under the New York Banking Law, a"banking organization" within the meaning of the New York Banking Law, a member of the Federal Reserve System, a"clearing corporation" within the meaning of the New York Uniform Commercial Code, and a "clearing agency" registered

pursuant to the provisions of Section 17A of the Securities Exchange Act of 1934. DTC holds and provides assetservicing for over 3.5 million issues of U.S. and non-U.S. equity, corporate and municipal debt issues, and money marketinstruments (from over 100 countries) that DTC's participants ("Direct Participants") deposit with DTC. DTC also facilitatesthe post-trade settlement among Direct Participants of sales and other securities transactions in deposited securitiesthrough electronic computerized book-entry transfers and pledges between Direct Participants' accounts. This eliminatesthe need for physical movement of securities certificates. Direct Participants include both U.S. and non-U.S. securitiesbrokers and dealers, banks, trust companies, clearing corporations, and certain other organizations. DTC is a wholly-owned subsidiary of The Depository Trust & Clearing Corporation ("DTCC"). DTCC is the holding company for DTCNational Securities Clearing Corporation and Fixed Income Clearing Corporation, all of which are registered clearingagencies. DTCC is owned by the users of its regulated subsidiaries. Access to the DTC system is also available to otherssuch as both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, and clearing corporations thatclear through or maintain a custodial relationship with a Direct Participant, either directly or indirectly ("IndirectParticipants"). DTC has Standard & Poor's highest rating: AAA. The DTC Rules applicable to its Participants are on file

with the Securities and Exchange Commission. More information about DTC can be found at www.dtcc.com andwww.dtc.org.

Purchases of Notes under the DTC system must be made by or through Direct Participants, which will receive a credit fothe Notes on DTC's records. The ownership interest of each actual purchaser of each Note ("Beneficial Owner") is in turnto be recorded on the Direct and Indirect Participants' records. Beneficial Owners will not receive written confirmation fromDTC of their purchase. Beneficial Owners are, however, expected to receive written confirmations providing details of thetransaction, as well as periodic statements of their holdings, from the Direct or Indirect Participant through which theBeneficial Owner entered into the transaction. Transfers of ownership interests in the Notes are to be accomplished byentries made on the books of Direct and Indirect Participants acting on behalf of Beneficial Owners. Beneficial Owners willnot receive certificates representing their ownership interests in the Notes, except in the event that use of the book-entrysystem for the Notes is discontinued.

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 6/112

5

To facilitate subsequent transfers, all Notes deposited by Direct Participants with DTC are registered in the name oDTC's partnership nominee, Cede & Co., or such other name as may be requested by an authorized representative oDTC. The deposit of Notes with DTC and their registration in the name of Cede & Co. or such other DTC nominee do noteffect any change in beneficial ownership. DTC has no knowledge of the actual Beneficial Owners of the Notes; DTC'srecords reflect only the identity of the Direct Participants to whose accounts such Notes are credited, which may or maynot be the Beneficial Owners. The Direct and Indirect Participants will remain responsible for keeping account of theiholdings on behalf of their customers.

Conveyance of notices and other communications by DTC to Direct Participants, by Direct Participants to IndirectParticipants, and by Direct Participants and Indirect Participants to Beneficial Owners will be governed by arrangementsamong them, subject to any statutory or regulatory requirements as may be in effect from time to time.

Neither DTC nor Cede & Co. (nor such other DTC nominee) will consent or vote with respect to the Notes unlessauthorized by a Direct Participant in accordance with DTC's MMI Procedures. Under its usual procedures, DTC mails anOmnibus Proxy to the [Issuer] as soon as possible after the record date. The Omnibus Proxy assigns Cede & Co.'sconsenting or voting rights to those Direct Participants to whose accounts the Notes are credited on the record date(identified in a listing attached to the Omnibus Proxy).

Principal and interest payments on the Notes will be made to Cede & Co., or such other nominee as may be requested byan authorized representative of DTC. DTC's practice is to credit Direct Participants' accounts upon DTC's receipt of fundsand corresponding detail information from the City or the Paying Agent, on the payable date in accordance with theirespective holdings shown on DTC's records. Payments by Participants to Beneficial Owners will be governed bystanding instructions and customary practices, as is the case with securities held for the accounts of customers in beare

form or registered in "street name," and will be the responsibility of such Participant and not of DTC (nor its nominee), theCity or the Paying Agent, subject to any statutory or regulatory requirements as may be in effect from time to time.Payment of principal and interest to Cede & Co. (or such other nominee as may be requested by an authorizedrepresentative of DTC) is the responsibility of the City or the Paying Agent, disbursement of such payments to DirectParticipants will be the responsibility of DTC, and disbursement of such payments to the Beneficial Owners will be theresponsibility of Direct and Indirect Participants.

DTC may discontinue providing its services as depository with respect to the Notes at any time by giving reasonablenotice to the City or the Paying Agent. Under such circumstances, in the event that a successor depository is notobtained, Note certificates are required to be printed and delivered to Beneficial Owners.

The City may decide to discontinue use of the system of book-entry-only transfers through DTC (or a successor securitiesdepository). In that event, Note certificates will be printed and delivered to Beneficial Owners.

The information in this section concerning DTC and DTC's book-entry system has been obtained from sources that theCity believes to be reliable, but the City takes no responsibility for the accuracy thereof.

Security and Remedies

Full Faith and Credit. General obligation bonds and notes of a Massachusetts city or town constitute a pledge of its full faithand credit. Payment is not limited to a particular fund or revenue source. Except for “qualified bonds” as described above (see“Serial Bonds and Notes” under “TYPES OF OBLIGATIONS” above) and setoffs of state distributions as described below (see“State Distributions” below), no provision is made by the Massachusetts statutes for priorities among bonds and notes andother general obligations, although the use of certain moneys may be restricted.

Tax Levy.. The Massachusetts statutes direct the municipal assessors to include annually in the tax levy for the next fiscayear “all debt and interest charges matured and maturing during the next fiscal year and not otherwise provided for [and] allamounts necessary to satisfy final judgments”. Specific provision is also made for including in the next tax levy payments orebate amounts not otherwise provided for and payment of notes in anticipation of federal or state aid, if the aid is no longerforthcoming.

The total amount of a tax levy is limited by statute. However, the voters in each municipality may vote to exclude from thelimitation any amounts required to pay debt service on indebtedness incurred before November 4, 1980. Local voters mayalso vote to exempt specific subsequent bond issues from the limitation. (See “Tax Limitations” Under “PROPERTY TAXbelow.) In addition, obligations incurred before November 4, 1980 may be constitutionally entitled to payment from taxes inexcess of the statutory limit.

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 7/112

6

Except for taxes on the increased value of certain property in designated development districts which may be pledged for thepayment of debt service on bonds issued to finance economic development projects within such districts, no provision is madefor a lien on any portion of the tax levy to secure particular bonds or notes or bonds and notes generally (or judgments onbonds or notes) in priority to other claims. Provision is made, however, for borrowing to pay judgments, subject to the GeneraDebt Limit. (See “DEBT LIMITS” below.) Subject to the approval of the State Director of Accounts for judgments above$10,000, judgments may also be paid from available funds without appropriation and included in the next tax levy unless otheprovision is made.

Court Proceedings. Massachusetts cities and towns are subject to suit on their general obligation bonds and notes and courtsof competent jurisdiction have power in appropriate proceedings to order payment of a judgment on the bonds or notes fromlawfully available funds or, if necessary, to order the city or town to take lawful action to obtain the required money, includingthe raising of it in the next annual tax levy, within the limits prescribed by law. (See “Tax Limitations” under “PROPERTY TAXbelow.) In exercising their discretion as to whether to enter such an order, the courts could take into account all relevanfactors including the current operating needs of the city or town and the availability and adequacy of other remedies. TheMassachusetts Supreme Judicial Court has stated in the past that a judgment against a municipality can be enforced by thetaking and sale of the property of any inhabitant. However, there has been no judicial determination as to whether this remedyis constitutional under current due process and equal protection standards.

Restricted Funds. Massachusetts statutes also provide that certain water, gas and electric, community antenna televisionsystem, telecommunications, sewer, parking meter and passenger ferry fee, community preservation and affordable housingreceipts may be used only for water, gas and electric, community antenna television system, telecommunications, sewer,parking, mitigation of ferry service impacts, community preservation and affordable housing purposes, respectivelyaccordingly, moneys derived from these sources may be unavailable to pay general obligation bonds and notes issued fo

other purposes. A city or town that accepts certain other statutory provisions may establish an enterprise fund for a utilityhealth care, solid waste, recreational or transportation facility and for police or fire services; under those provisions any surplusin the fund is restricted to use for capital expenditures or reduction of user charges. In addition, subject to certain limits, a cityor town may annually authorize the establishment of one or more revolving funds in connection with use of certain revenues foprograms that produce those revenues; interest earned on a revolving fund is treated as general fund revenue. A city or townmay also establish an energy revolving loan fund to provide loans to owners of privately-held property in the city or town forcertain energy conservation and renewable energy projects, and may borrow to establish such a fund. The loan repaymentsand interest earned on the investment of amounts in the fund shall be credited to the fund. Also, the annual allowance fodepreciation of a gas and electric plant or a community antenna television and telecommunications system is restricted to usefor plant or system renewals and improvements, for nuclear decommissioning costs, and costs of contractual commitments, orwith the approval of the State Department of Telecommunications and Energy, to pay debt incurred for plant or systemreconstruction or renewals. Revenue bonds and notes issued in anticipation of them may be secured by a prior lien on specificrevenues. Receipts from industrial users in connection with industrial revenue financings are also not available for genera

municipal purposes.

State Distributions. State grants and distributions may in some circumstances be unavailable to pay general obligation bondsand notes of a city or town in that the State Treasurer is empowered to deduct from such grants and distributions the amount oany debt service paid on “qualified bonds” (See “Serial Bonds and Notes” under “TYPES OF OBLIGATIONS” above) and anyother sums due and payable by the city or town to the Commonwealth or certain other public entities, including any unpaidassessments for costs of any public transportation authority (such as the Massachusetts Bay Transportation Authority or aregional transit authority) of which it is a member, for costs of the Massachusetts Water Resources Authority if the city or townis within the territory served by the Authority, for any debt service due on obligations issued to the Massachusetts SchooBuilding Authority, or for charges necessary to meet obligations under the Commonwealth’s Water Pollution Abatement orDrinking Water Revolving Loan Programs, including such charges imposed by another local governmental unit that provideswastewater collection or treatment services or drinking water services to the city or town.

If a city or town is (or is likely to be) unable to pay principal or interest on its bonds or notes when due, it is required to notify theState Commissioner of Revenue. The Commissioner shall in turn, after verifying the inability, certify the inability to the StateTreasurer. The State Treasurer shall pay the due or overdue amount to the paying agent for the bonds or notes, in trust, withinthree days after the certification or one business day prior to the due date (whichever is later). This payment is limitedhowever, to the estimated amount otherwise distributable by the Commonwealth to the city or town during the remainder of thefiscal year (after the deductions mentioned in the foregoing paragraph). If for any reason any portion of the certified sum hasnot been paid at the end of the fiscal year, the State Treasurer shall pay it as soon as practicable in the next fiscal year to theextent of the estimated distributions for that fiscal year. The sums so paid shall be charged (with interest and administrativecosts) against the distributions to the city or town.

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 8/112

7

The foregoing does not constitute a pledge of the faith and credit of the Commonwealth. The Commonwealth has not agreedto maintain existing levels of state distributions, and the direction to use estimated distributions to pay debt service may besubject to repeal by future legislation. Moreover, adoption of the annual appropriation act has sometimes been delayedbeyond the beginning of the fiscal year and estimated distributions which are subject to appropriation may be unavailable topay local debt service until they are appropriated.

Bankruptcy. Enforcement of a claim for payment of principal or interest on general obligation bonds or notes would be subjecto the applicable provisions of Federal bankruptcy laws and to the provisions of other statutes, if any, hereafter enacted by theCongress or the State legislature extending the time for payment or imposing other constraints upon enforcement insofar asthe same may be constitutionally applied. Massachusetts municipalities are not currently authorized by the MassachusettsGeneral Laws to file a petition for bankruptcy under Federal Bankruptcy laws. In cases involving significant financial difficultiesfaced by a single city, town or regional school district, the Commonwealth has enacted special legislation to permit theappointment of a fiscal overseer, finance control board or, in the most extreme cases, a state receiver. In a limited number othese situations, such special legislation has also authorized the filing of federal bankruptcy proceedings, with the priorapproval of the Commonwealth. In each case where such authority was granted, it expired at the termination of theCommonwealth’s oversight of the financially distressed city, town or regional school district. To date, no such filings had beenapproved or made.

Tax Exemption

In the opinion of Edwards Angell Palmer & Dodge LLP, Bond Counsel to the City (“Bond Counsel”), based upon ananalysis of existing laws, regulations, rulings, and court decisions, and assuming, among other matters, compliance withcertain covenants, interest on the Notes is excluded from gross income for federal income tax purposes under Section

103 of the Internal Revenue Code of 1986 (the “Code”). Bond Counsel is of the further opinion that interest on the Notesis not a specific preference item for purposes of the federal individual or corporate alternative minimum taxes, and suchinterest is not included in adjusted current earnings when calculating corporate alternative minimum taxable income. Theforegoing reflects the enactment of the American Recovery and Reinvestment Act of 2009 which includes provisions thatmodify the treatment under the alternative minimum tax of interest on certain state and local government entities and thatmodify Section 265(b)(3) of the Code. Bond Counsel expresses no opinion regarding any other federal tax consequencesarising with respect to the ownership or disposition of, or the accrual or receipt of interest on, the Notes.

The Code imposes various requirements relating to the exclusion from gross income for federal income tax purposes ofinterest on obligations such as the Notes. Failure to comply with these requirements may result in interest on the Notesbeing included in gross income for federal income tax purposes, possibly from the date of original issuance of the Notes.The City has covenanted to comply with such requirements to ensure that interest on the Notes will not be included infederal gross income. The opinion of Bond Counsel assumes compliance with these requirements.

Bond Counsel is also of the opinion that, under existing law, interest on the Notes is exempt from Massachusetts personaincome taxes, and the Notes are exempt from Massachusetts personal property taxes. Bond Counsel has not opined asto other Massachusetts tax consequences arising with respect to the Notes. Prospective Noteholders should be awarehowever, that the Notes are included in the measure of Massachusetts estate and inheritance taxes, and the Notes andthe interest thereon are included in the measure of certain Massachusetts corporate excise and franchise taxes. BondCounsel has not opined as to the taxability of the Notes or the income therefrom under the laws of any state other thanMassachusetts.

To the extent the issue price of the Notes is less than the amount to be paid at maturity of such Notes (excluding amountsstated to be interest and payable at least annually over the term of such Notes), the difference constitutes “original issuediscount,” the accrual of which, to the extent properly allocable to each owner thereof, is treated as interest on the Noteswhich is excluded from gross income for federal income tax purposes and is exempt from Massachusetts persona

income taxes. For this purpose, the issue price of the Notes is the first price at which a substantial amount of such Notesis sold to the public (excluding note houses, brokers, or similar persons or organizations acting in the capacity ofunderwriters, placement agents or wholesalers). The original issue discount with respect to the Notes accrues daily ovethe term to maturity of such Notes on the basis of a constant interest rate compounded semiannually (with straight-lineinterpolations between compounding dates). The accruing original issue discount is added to the adjusted basis of suchNotes to determine taxable gain or loss upon disposition (including sale, redemption, or payment on maturity) of suchNotes. Noteholders should consult their own tax advisors with respect to the tax consequences of ownership of Noteswith original issue discount, including the treatment of purchasers who do not purchase such Notes in the original offeringto the public at the first price at which a substantial amount of such Notes is sold to the public.

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 9/112

8

Notes purchased, whether at original issuance or otherwise, for an amount greater than the stated principal amount to bepaid at maturity of such Notes, or, in some cases, at the earlier redemption date of such Notes ("Premium Notes"), will betreated as having amortizable note premium for federal income tax purposes and Massachusetts personal income taxpurposes. No deduction is allowable for the amortizable note premium in the case of obligations, such as the PremiumNotes, the interest on which is excluded from gross income for federal income tax purposes. However, a Noteholder’sbasis in a Premium Note will be reduced by the amount of amortizable note premium properly allocable to suchNoteholder. Holders of Premium Notes should consult their own tax advisors with respect to the proper treatment oamortizable note premium in their particular circumstances.

Bond Counsel has not undertaken to determine (or to inform any person) whether any actions taken (or not taken) orevents occurring (or not occurring) after the date of issuance of the Notes may adversely affect the value of, or the taxstatus of interest on, the Notes. Further, no assurance can be given that pending or future legislation, includingamendments to the Code, if enacted into law, or any proposed legislation, including amendments to the Code, or anyfuture judicial, regulatory or administrative interpretation or development with respect to existing law, will not adverselyaffect the value of, or the tax status of interest on, the Notes. Prospective Noteholders are urged to consult their own taxadvisors with respect to proposals to restructure the federal income tax.

Although Bond Counsel is of the opinion that interest on the Notes is excluded from gross income for federal income taxpurposes and is exempt from Massachusetts personal income taxes, the ownership or disposition of, or the accrual orreceipt of interest on, the Notes may otherwise affect the federal or state tax liability of a Noteholder. Among otherpossible consequences of ownership or disposition of, or the accrual or receipt of interest on, the Notes, the Coderequires recipients of certain social security and certain railroad retirement benefits to take into account receipts oraccruals of interest on the Notes in determining the portion of such benefits that are included in gross income. The nature

and extent of all such other tax consequences will depend upon the particular tax status of the Noteholder or theNoteholder’s other items of income or deduction. Except as indicated in the following paragraph, Bond Counseexpresses no opinion regarding any such other tax consequences, and Noteholders should consult with their own taxadvisors with respect to such consequences.

Opinion of Bond Counsel

The unqualified approving opinion as to the validity of the Notes will be rendered by Edwards Angell Palmer & DodgeLLP, Boston, Massachusetts, Bond Counsel. The opinion will be dated the date of the original delivery of the Notes andwill speak only as of such date.

Other than as to matters expressly set forth herein as the opinion of Bond Counsel, Bond Counsel are not passing uponand do not assume any responsibility for the accuracy or adequacy of the statements made in this Official Statement and

make no representation that they have independently verified the same.

Financial Advisory Services of First Southwest Company

First Southwest Company, Boston, Massachusetts serves as financial advisor to the City of Lawrence. The City hasconsented to the participation by the Firm in the public bidding on the Notes if it so desires.

Disclosure of Significant Events

In order to assist underwriters in complying with the requirements of paragraph (b)(5)(i)(C) of Rule 15c2-12 promulgatedby the Securities and Exchange Commission (the “Rule”) applicable to municipal securities having a stated maturity of

18 months or less, the City will covenant for the benefit of the owners of the Notes to file with the Municipal SecuritiesRulemaking Board (the “MSRB”), notices of the occurrence of any of the following events with respect to the Notes withinten business days of such occurrence: (a) principal and interest payment delinquencies; (b) non-payment relateddefaults, if material; (c) unscheduled draws on debt service reserves reflecting financial difficulties; (d) unscheduleddraws on credit enhancements reflecting financial difficulties; (e) substitution of credit or liquidity providers, or their failureto perform; (f) adverse tax opinions, the issuance by the Internal Revenue Service of proposed or final determination oftaxability, Notices of Proposed Issue (IRS Form 5701-TEB) or other material notices or determinations with respect tothe tax status of the Notes, or other material events affecting the tax status of the Notes; (g) modifications to rights ofowners of the Notes, if material; (h) optional contingent or unscheduled calls of bonds, if material; (i) defeasances; (j)release, substitution or sale of property securing the repayment of the Notes, if material; (k) ratings changes on theNotes; (l) bankruptcy, insolvency, receivership or similar event of the City; (m) the consummation of a merger,consolidation, or acquisition involving the City or the sale of all or substantially all of the assets of the City, other than in

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 10/112

9

the ordinary course of business, the entry into a definitive agreement to undertake such an action or the termination of adefinitive agreement relating to any such actions, other than pursuant to its terms, if material; and (n) appointment of asuccessor or additional trustee or the change of name of a trustee, if material.

The covenant will be included in a Significant Events Disclosure Certificate to be executed by the signers of the Notesand incorporated by reference in the Notes. The sole remedy available to the owners of the Notes for the failure of theCity to comply with any provision of the certificate shall be an action for specific performance of the City’s obligationsunder the certificate and not for money damages; no other person shall have any right to enforce any provision of thecertificate. The City has never failed to comply in all material respects with any previous undertakings to provideannual reports or notices of material events in accordance with the Rule.

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 11/112

10

CITY OF LAWRENCE, MASSACHUSETTS

General

Lawrence is located in Essex County and is 26 miles north of Boston. It is bordered on the north by the Town of Methuenon the west and southwest by the Town of Andover, and on the east and southeast by the Town of North Andover. It isalso 5 miles south of the State of New Hampshire. Incorporated as a city in 1853, Lawrence has a population of 72,043(2000 U. S. Bureau of the Census) and occupies a land area of approximately 6.75 square miles. The Cities of Lawrenceand Haverhill are the population centers of a Primary Metropolitan Statistical Area (PMSA) of approximately 230,000persons. The City is governed by a mayor and nine-member City Council. The Mayor and all Council members are

elected on a non-partisan basis. City Councilors are elected for a two-year term, and the Mayor is elected for a four-yeaterm. All executive officers are appointed.

Principal Executive Officers

City Title Name First Entered Office Term Expires

Mayor William Lantigua 2010 2014Budget and Finance Director Currently Vacant (1) - IndefiniteComptroller David Camasso 2007 IndefiniteTreasurer/Collector Patricia M. Cook 1989 IndefiniteCity Clerk William J. Maloney 2004 Indefinite

__________________ (1) The City is in the middle of conducting a national search for candidates to fill the position full-time. Prior to June 30

2010 the City had retained personnel from the University of Massachusetts, Boston, to provide the services of thisposition on an interim basis.

Current Financial Challenges

In recent years, the City has experienced a number of financial problems, resulting in a cumulative deficit estimated a$24 million through the end of fiscal 2010. A regular pattern of overestimating revenues, under budgeting expendituresincluding under budgeting collective bargaining agreements by the prior administration, combined with significant cuts inlocal aid from The Commonwealth of Massachusetts, led to the enactment of Chapter 58 of the Acts of 2010 (“Chapter58”). Chapter 58 authorized the City to amortize its deficit over a period of years, while requiring the appointment by theState of a fiscal overseer of the City. The fiscal overseer is charged with working in consultation with the City’s financiamanagement team, to assist the City’s return to financial stability. The fiscal overseer also has the ability to trigger theappointment of a finance control board that would assume day-to-day management of the City, if the fiscal overseer

determines that a timely return to financial stability is not likely. For a more complete discussion of the City’s financiachallenges and powers of the fiscal overseer, see “Special Legislation Pertaining to City’s Fiscal Stability, “Initial Plan ofCorrection”, and “Deficit Financing” herein.

On April 23, 2010, the Commonwealth’s Secretary of Administration and Finance appointed Robert G. Nunes fiscaoverseer of the City of Lawrence. Mr. Nunes is currently also serving as the Deputy Commissioner of Revenue managingthe Division of Local Services for the Commonwealth of Massachusetts Department of Revenue. He is also the Directoof Municipal Affairs. Mr. Nunes has 25 years of local and state government experience and previously served as thelongest-serving mayor in Taunton’s history. Mr. Nunes is a past president of the Massachusetts Mayors’ Association anda former member of the Massachusetts Municipal Association Board of Directors and the Local Government AdvisoryCommission.

History

In 1845, a group of Boston entrepreneurs led by Abbott Lawrence formed the Essex Company to harness the power ofBodwell's Falls in the Merrimack River in order to run their commercial concerns. The pace of development rapidlytransformed Lawrence from a rural farming community into a major industrial center. Within three years, the EssexCompany completed a dam, constructed two canals and a reservoir, organized gas works, and erected fifty brickbuildings, a boarding house, a machine shop for building locomotives, and plants which housed the Atlantic Cotton,Pemberton, Upper Pacific and Duck Mills. In 1847, the Boston and Maine Railroad introduced passenger train serviceand in 1853, Lawrence was incorporated as a city. Lawrence quickly achieved prominence as one of the major centers owoolen textile development in the United States and some of the original mills remain, underscoring the City's continuedimportance as a textile manufacturing center. In recent years, the City has sought to diversify its economic base byattracting industries which manufacture products other than textiles.

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 12/112

11

Municipal Services

The City provides general governmental services for the territory within its limits, including police and fire protection, solidwaste collection and disposal, public education, street maintenance, park and recreation facilities, water services and alibrary. Public housing is provided by the Lawrence Housing Authority.

Wastewater treatment is provided by the Greater Lawrence Sanitary District (the "District"), which serves the City through137 miles of sewer mains and sewer stations. The system serves essentially all residences and businesses in the CityThe District also serves Andover, North Andover, Methuen and Salem, New Hampshire.

Education

The City's public school facilities include twenty one elementary schools and one high school which have a combined totalcapacity of approximately 13,000 students. Over the past decade, the City embarked upon a program to rebuild and/oreplace many of its school facilities. The first phase of this program involved the building of three new elementary schoolsto replace obsolete smaller structures. These were financed with bond issues in 2001 and 2002 and have beencompleted. The City receives annual grant reimbursement payments for approximately 90% of construction costs andinterest on the bonds and notes issued for this purpose. The second phase included the building of a new high school aan estimated cost of $110 million. The City issued temporary notes to fund said project, all of which have been retiredwith grant proceeds received from the Massachusetts School Building Association (MSBA), and also issued $11,000,000bonds of the City dated October 1, 2007, and $2,305,460 bonds dated April 1, 2009, to fund its share (approximately

10%) of project costs. The City has entered into a Project Funding Agreement with the MSBA and has been receivinggrant payments for the MSBA’s portion of some additional project costs as such costs are incurred, pursuant to theAgreement. All negative adjustments to MSBA reimbursements have been made, though the City continues to pursuepositive adjustments to school construction projects, including restoration of previously disqualified MSBAreimbursements and surety bond payments from the first contractor hired to build Lawrence High School. See“PROPERTY TAXATION - Tax Levy Computation “ and “INDEBTEDNESS – Authorized Unissued Debt and ProspectiveFinancing” below.

The following chart sets forth the trend in school enrollments as of October 1 for the last five school years.

Public School Enrollments - October 1

2006 2007 2008 2009 2010

Preschool - - - 391 417Elementary (K-8) 10,145 10,145 9,609 8,588 9,026High School (9-12) 2,900 2,950 3,008 3,439 3,461Totals 13,045 13,095 12,617 12,418 12,904

__________________ SOURCE: Lawrence School Department.

Lawrence is a member of the Greater Lawrence Regional Vocational Technical High School District which also serves thetowns of Andover, Methuen and North Andover. As of October 1, 2010 there were 1,226 students enrolled in the GreateLawrence Regional Vocational Technical High School District, 970 of whom were residents of Lawrence. The capacity othe school district is estimated to be 1,600 students.

Industry and Commerce

Lawrence was originally planned and laid out as a commercial and industrial center and it maintains this character to thepresent day. Industrialization began in the mid-nineteenth century when a dam was built across the Merrimack River totake advantage of its great water power potential.

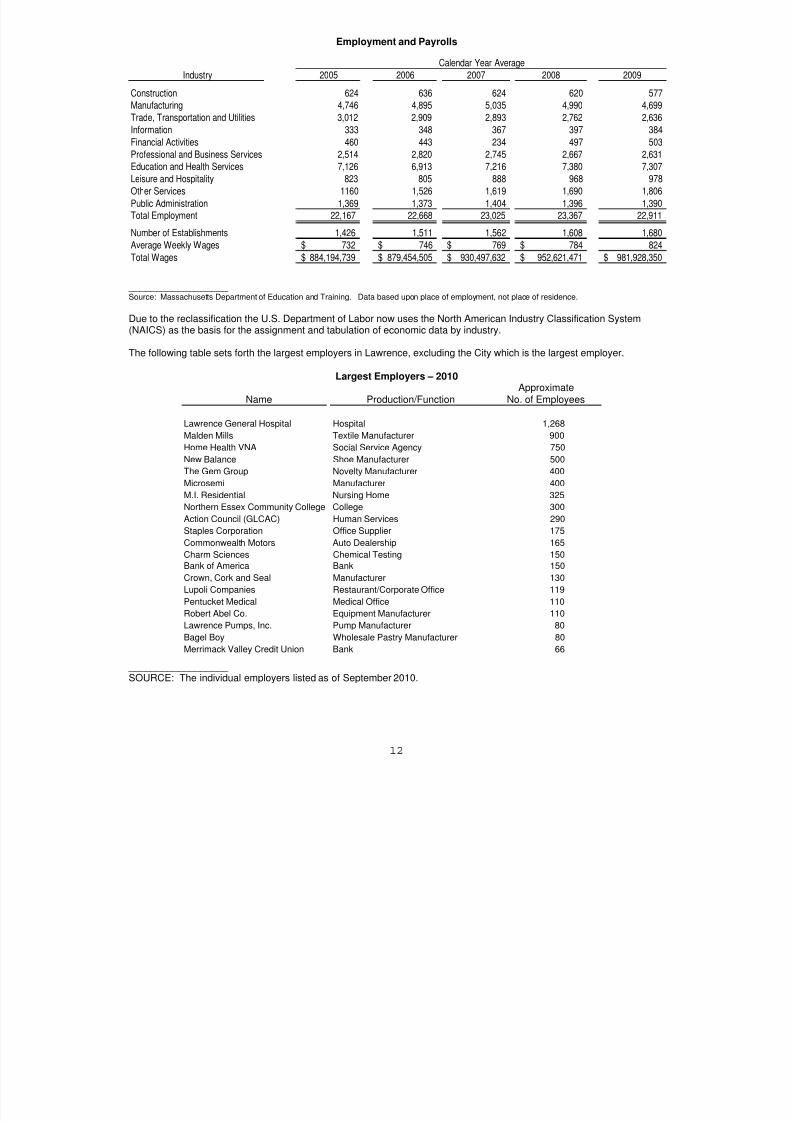

Today, Lawrence is a diversified industrial city. Services are the primary economic pursuit followed by manufacturingThe following table sets forth the major categories of income and employment for the City of Lawrence.

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 13/112

12

Employment and Payrolls

Industry 2005 2006 2007 2008 2009

Construction 624 636 624 620 577 Manufacturing 4,746 4,895 5,035 4,990 4,699 Trade, Transportation and Utilities 3,012 2,909 2,893 2,762 2,636 Information 333 348 367 397 384

Financial Activities 460 443 234 497 503

Professional and Business Services 2,514 2,820 2,745 2,667 2,631 Education and Health Services 7,126 6,913 7,216 7,380 7,307 Leisure and Hospitality 823 805 888 968 978 Other Services 1160 1,526 1,619 1,690 1,806

Public Administration 1,369 1,373 1,404 1,396 1,390 Total Employment 22,167 22,668 23,025 23,367 22,911

Number of Establishments 1,426 1,511 1,562 1,608 1,680 Average Weekly Wages 732$ 746$ 769$ 784$ 824

Total Wages 884,194,739$ 879,454,505$ 930,497,632$ 952,621,471$ 981,928,350$

Calendar Year Average

__________________ Source: Massachusetts Department of Education and Training. Data based upon place of employment, not place of residence.

Due to the reclassification the U.S. Department of Labor now uses the North American Industry Classification System(NAICS) as the basis for the assignment and tabulation of economic data by industry.

The following table sets forth the largest employers in Lawrence, excluding the City which is the largest employer.

Largest Employers – 2010Approximate

Name Production/Function No. of Employees

Lawrence General Hospital Hospital 1,268

Malden Mills Textile Manufacturer 900

Home Health VNA Social Service Agency 750

New Balance Shoe Manufacturer 500

The Gem Group Novelty Manufacturer 400

Microsemi Manufacturer 400

M.I. Residential Nursing Home 325

Northern Essex Community College College 300

Action Council (GLCAC) Human Services 290

Staples Corporation Office Supplier 175

Commonwealth Motors Auto Dealership 165

Charm Sciences Chemical Testing 150

Bank of America Bank 150

Crown, Cork and Seal Manufacturer 130

Lupoli Companies Restaurant/Corporate Office 119

Pentucket Medical Medical Office 110Robert Abel Co. Equipment Manufacturer 110

Lawrence Pumps, Inc. Pump Manufacturer 80

Bagel Boy Wholesale Pastry Manufacturer 80

Merrimack Valley Credit Union Bank 66

__________________ SOURCE: The individual employers listed as of September 2010.

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 14/112

13

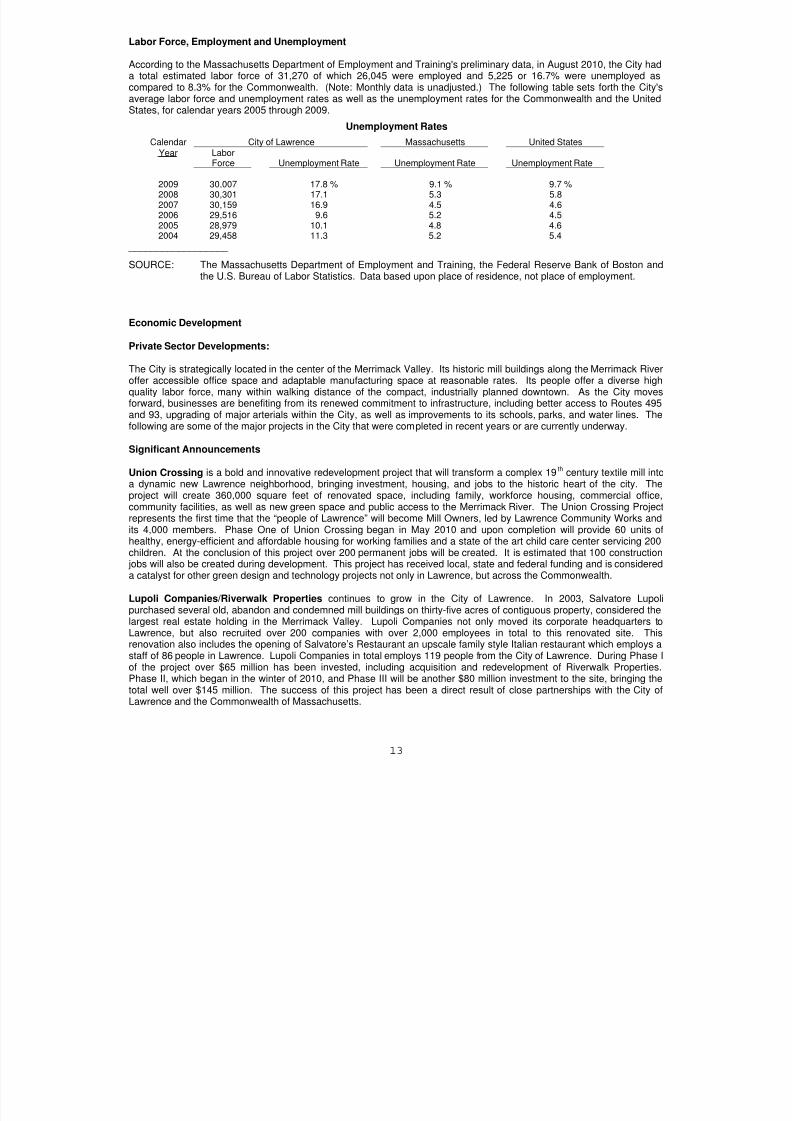

Labor Force, Employment and Unemployment

According to the Massachusetts Department of Employment and Training's preliminary data, in August 2010, the City hada total estimated labor force of 31,270 of which 26,045 were employed and 5,225 or 16.7% were unemployed ascompared to 8.3% for the Commonwealth. (Note: Monthly data is unadjusted.) The following table sets forth the City'saverage labor force and unemployment rates as well as the unemployment rates for the Commonwealth and the UnitedStates, for calendar years 2005 through 2009.

Unemployment Rates

Calendar City of Lawrence Massachusetts United States

Year LaborForce Unemployment Rate Unemployment Rate Unemployment Rate

2009 30,007 17.8 % 9.1 % 9.7 %2008 30,301 17.1 5.3 5.82007 30,159 16.9 4.5 4.62006 29,516 9.6 5.2 4.52005 28,979 10.1 4.8 4.62004 29,458 11.3 5.2 5.4

__________________

SOURCE: The Massachusetts Department of Employment and Training, the Federal Reserve Bank of Boston andthe U.S. Bureau of Labor Statistics. Data based upon place of residence, not place of employment.

Economic Development

Private Sector Developments:

The City is strategically located in the center of the Merrimack Valley. Its historic mill buildings along the Merrimack Riveoffer accessible office space and adaptable manufacturing space at reasonable rates. Its people offer a diverse highquality labor force, many within walking distance of the compact, industrially planned downtown. As the City movesforward, businesses are benefiting from its renewed commitment to infrastructure, including better access to Routes 495and 93, upgrading of major arterials within the City, as well as improvements to its schools, parks, and water lines. Thefollowing are some of the major projects in the City that were completed in recent years or are currently underway.

Significant Announcements

Union Crossing is a bold and innovative redevelopment project that will transform a complex 19th century textile mill intoa dynamic new Lawrence neighborhood, bringing investment, housing, and jobs to the historic heart of the city. Theproject will create 360,000 square feet of renovated space, including family, workforce housing, commercial officecommunity facilities, as well as new green space and public access to the Merrimack River. The Union Crossing Projecrepresents the first time that the “people of Lawrence” will become Mill Owners, led by Lawrence Community Works andits 4,000 members. Phase One of Union Crossing began in May 2010 and upon completion will provide 60 units ohealthy, energy-efficient and affordable housing for working families and a state of the art child care center servicing 200children. At the conclusion of this project over 200 permanent jobs will be created. It is estimated that 100 construction

jobs will also be created during development. This project has received local, state and federal funding and is considereda catalyst for other green design and technology projects not only in Lawrence, but across the Commonwealth.

Lupoli Companies/Riverwalk Properties continues to grow in the City of Lawrence. In 2003, Salvatore Lupolpurchased several old, abandon and condemned mill buildings on thirty-five acres of contiguous property, considered thelargest real estate holding in the Merrimack Valley. Lupoli Companies not only moved its corporate headquarters toLawrence, but also recruited over 200 companies with over 2,000 employees in total to this renovated site. Thisrenovation also includes the opening of Salvatore’s Restaurant an upscale family style Italian restaurant which employs astaff of 86 people in Lawrence. Lupoli Companies in total employs 119 people from the City of Lawrence. During Phase of the project over $65 million has been invested, including acquisition and redevelopment of Riverwalk Properties.Phase II, which began in the winter of 2010, and Phase III will be another $80 million investment to the site, bringing thetotal well over $145 million. The success of this project has been a direct result of close partnerships with the City oLawrence and the Commonwealth of Massachusetts.

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 15/112

14

Malden Mills/PolarTEC was purchased by College Street Management Company and is partnering with WinnDevelopment to rehab the historic Malden Mill site at 550 Broadway into a 156 unit mixed-income rental community.Seventy two of the units will be deemed affordable housing and represent a $32 million investment in the City ofLawrence. The financing consists of state and federal historic tax credits and low income housing tax credits, along withHOME funding through the City of Lawrence. Phase I of three phases of the project began in August 2010.

Mainstream Global/Yepez Properties opened its corporate headquarters in Lawrence in 2007. The company is a globadistributor of new, refurbished, and off lease computer equipment. They receive, inspect and ship globally, approximately70% overseas. The owners Juan and Luis Yepez have recently invested over $15 million in the acquisition and rehab oold mill buildings in the historic downtown area including 25 Marston Street, 215 Canal Street and 60 Island Street (BellTower site). There recent rehab which is ongoing includes the renovation of an existing parking garage, electrical repairsheating, roofing and tenant build-outs. The 60 Island Street location also includes Cambridge College satellite campusAll of the Yepez properties represent a total of 600 employees for the area. The Yepez Brothers were honored inPresident Obama’s recent State of the Union Speech for their work in Lawrence and ongoing community involvement.

Peabody Properties LLC, purchased a vacant city owned neighborhood elementary school building (Saunders School)located at 243 South Broadway in May 2009 for $500,000 to rehab and create 16 apartments, providing permanent,affordable and supportive housing for families. Construction of this site began in July 2010 and represents financing fromstate and local resources including low-income tax credits allocated by Massachusetts Department of Housing andCommunity Development. A total investment amount is estimated at $4.4 million.

Beacon Communities/Sacred Heart LLC purchased a vacant, private neighborhood elementary school building (oldSacred Heart School) in 2009 to rehab and create 44 affordable apartments. The approved financing consists of federa

and state low-income housing credits and historic tax credits. The total investment is estimated at $14.8 million andconstruction began in June 2010.

Lawrence General Hospital is a state of the art facility providing full service health care to all. The hospital juscompleted a $20 million emergency center expansion which is one of the most premiere facilities north of Boston. Thehospital is also completing a new $5 million imaging center before the end of December 2010. The hospital is a strongpartner in the City and employees 1,286 people.

Merrimack Valley Federal Credit Union (MVFCU) is one of the area’s largest financial institutions, which moved itscorporate headquarters in September 2007 to the City of Lawrence after residing in North Andover for over fifty yearsThe company provides low or no cost financial services to residents of Merrimack Valley and Lawrence, and has 66employees located in the City, and a total of 105 throughout Massachusetts and New Hampshire. The MVFCU also buila new branch location abutting its corporate headquarters on the site in 2007.

Home Health VNA Inc., which moved into the City from Haverhill, is a social services agency located in the Riverwalkfacility on Merrimack Street, with 550 employees located in Lawrence and 750 employees in Massachusetts. HomeHealth VNA Inc. provides in-home medical care and support and has four regional offices, including the Merrimack ValleyHospice House.

Elder Services, is a health and service organization for the elderly which has over 175 employees located in Lawrenceand 200 employees throughout Massachusetts.

Pentucket Medical, has been providing health care to the residents of Merrimack Valley for over forty years. With thelatest diagnostics, technology, and research they offer unparalleled acute, chronic, and wellness care to their patientsPentucket Medical moved their main offices to the City of Lawrence in May 2008 and employ 110 people.

Little Sprouts Early Education and Leadership and Literacy Foundation, an early education provider, opened in theCity of Lawrence in the summer of 2005 and currently has 61 employees. Little Sprouts Early Education and Leadershipand Literacy Foundation promotes itself as one of the largest of its kind in Massachusetts.

Tallman Eye Associates is one of the largest optometry practices in New England. It employs a staff of 92 in Lawrence,and a staff of 105 among five regional offices in Massachusetts. Tallman Eye Associates recently spent $1.2 million tobuild and expand at the Riverwalk office location.

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 16/112

15

Significant Announcements

JSB Industries dba/ Muffin Town:Muffin Town is a Chelsea-based bakery with national sales. The company hosted a ground breaking on a $12.5 millioninvestment in the City June 29, 2010 and is planning its grand opening in January 2011. The company has retained itscurrent location and employees and is redeveloping an 80,000 square foot vacant building in Lawrence in which toexpand production. Through an EDIP Investment Tax Credit award of almost $115,000 and a Tax Increment FinancingAgreement from the City of Lawrence, an additional 220 jobs will be created in Lawrence over a five year period tosupport the $12.5 million investment in the city of Lawrence and will generate $50,000 in taxes annually.

GB NewEngland2, LLC/ CVS Pharmacy DevelopmentLocated at 266 Broadway/Rt. 28 in the heart of downtown Lawrence. The developer has purchased several lots andcombined them to create a 47,000 square foot parcel to develop a CVS Pharmacy and Marketplace. The proposalincludes a drive-thru pharmacy and is expected to create 25-30 new jobs for the City. The total value of the site isapproximately $6 million dollars and will generate more than $100,000.00 a year in new taxes. Construction set to beginin October 2010.

RiverBankOfficially headquartered in North Andover, MA opened its newest branch location in Lawrence,MA in January 2010 onSouth Broadway/Rt. 28. This new branch features onsite-parking, self-service coin machine, drive-up teller and ATMservices, and Saturday hours. This is a significant multi-million dollar investment in the City of Lawrence.

Public Sector Developments:

The City of Lawrence is a Community Development Block Grant Entitlement Community and receives an annuaallocation of approximately $2.8 million from the U.S. Department of Housing and Urban Development (HUD) toimplement community improvements and economic development projects. The City’s annual CDBG allocation is $1.7million and HOME allocation is $1.1 million.

Based upon the compelling data presented within the Community Profile, the City’s single greatest communitydevelopment need is to create economic opportunity for its residents. Housing policies and programs alone cannot solvethe problems facing Lawrence and its residents, thus a comprehensive economic and human-resource developmentstrategy is essential. Economic empowerment is therefore a requirement for Lawrence to achieve its overarching goal obeing a healthy, vibrant community where it makes economic sense for people to invest their time, money and energy.

The City of Lawrence has established four core objectives toward increasing economic empowerment. The goals are tocreate and retain jobs, support neighborhood based economic development, create competitive workforce throughincreased educational attainment and improving the physical environment and streetscape appearance of the city.

The City of Lawrence is committed to funding community economic development services in the following categories:

Business Assistance in the form of improvements to the physical conditions, the provision of technical assistance tobusinesses located or seeking to expand in Lawrence, and support for projects that will lead to the creation of jobs for thelow- and moderate-income residents. The City will continue to seek lending partners to reinitiate its small businessrevolving loan fund, which provides working capital and funding for leasehold improvements. Exterior buildingimprovement helps both the businesses and the neighborhoods. The City will continue its Business Facade ImprovementProgram over the next five years to address the need for exterior building improvements to improve “curb appeal” and

create jobs by expanding business.

Targeted Neighborhood Commercial Area Assistance to revitalize neighborhood commercial corridors and shoppingareas and reestablish their historic roles as central places to shop, work and meet neighbors. The City may designatespecific commercial corridors for targeted assistance, and:

focus planning and data analysis on strengthening corridors; align and leverage resources;

make neighborhood commercial corridors more welcoming places; and develop systems to attract and retain businesses along corridors

8/8/2019 City of Lawrence Financial Statement-2010-11

http://slidepdf.com/reader/full/city-of-lawrence-financial-statement-2010-11 17/112

16

Before investment can take root and growth can occur, certain impediments must be removed. In the case ofneighborhood development, one of the greatest impediments is blight in all its forms—vacant buildings, trash-strewnvacant lots, abandoned automobiles, litter, graffiti and unkempt streetscapes. Attractive amenities such as parks,streetscapes, libraries, and recreation centers make neighborhoods more desirable. To address these impediments andtransform neighborhoods, the City will coordinate the following capital investments:

Public Facilities and Improvements to community facilities, including senior centers, providing “community space” andfurther improving the image of the community. Furthermore, senior facilities, community facilities, and recreational centersprovide direct service and service referral for diverse needs and provide necessary support to vulnerable households

Often, community organizations just do not have the capital or fundraising resources to maintain these facilities thaprovide a source of community pride and activities. In all facility improvements, the City will insure that handicappedaccessibility is a key component.

Streetscape Improvements/Beautification to public streets including putting in new curbs, sidewalks, lighting and treesso these areas will be appealing places for residents to shop and work. The selection of streets/sidewalks will beundertaken in a systematic process that will give priority to the following:

The Neighborhood Revitalization Strategy Areas; Streets surrounding public facilities; and

Streets/sidewalks adjacent to other public investments, including targeted business assistanceand affordable housing production.

Open Space/Parks Improvements are extremely important given that Lawrence is one of the youngest communities in

the Commonwealth; the demand in the City for parks, open space and recreational amenities is high. The challenges ofmany vacant properties, abandoned alleyways, Brownfield sites, and underutilized riverfront areas are opportunities forcreative and innovative open space development. CDBG funds will be utilized to support a number of activities that:

Increase pedestrian and biking activity by encouraging walking and biking for exercise andenhancing safety and connectivity between schools, neighborhoods, and parks;

Reclaim vacant lots and other abandoned and underutilized land; and

Increase access to waterfront resources (i.e. rivers, canals) through enhancement and protection