CITY AND COUNTY OF DENVER 2 0 17 EMPLOYEE BENEFITS GUIDE · CITY AND COUNTY OF DENVER 2 0 17...

24

CITY AND COUNTY OF DENVER 2 0 1 7 EMPLOYEE BENEFITS GUIDE

Transcript of CITY AND COUNTY OF DENVER 2 0 17 EMPLOYEE BENEFITS GUIDE · CITY AND COUNTY OF DENVER 2 0 17...

CITY AND COUNTY OF DENVER

2 0 1 7 EMPLOYEE B E N E F I T S G U I D E

Table of Contents

WELCOME LETTER 2

BENEFITS ELIGIBILITY 3

DENVER WELLNESS PROGRAM 5

BENEFIT PLAN PREMIUMS 7

BENEFITS ENROLLMENT 4

BENEFITS BASICS 6

MEDICAL PLANS 8

BUDGETING FOR YOUR HEALTH CARE 14

VISION PLAN 18

LIFE AND DISABILITY INSURANCE 19

DENTAL PLANS 17

WORK LIFE BALANCE 22

ADDITIONAL BENEFITS 21

This is a summary of benefits drafted in plain language to assist an employee’s understanding of what benefits are offered, and does not constitute a policy. Detailed provisions are contained in each provider’s plan document. If there is a discrepancy between what is presented here and the official plan documents, the plan documents will govern.

2

A MESSAGE FROM THE OFFICE OF HUMAN RESOURCES

Dear City Colleague,

Working for the City and County of Denver (city) is so much more than a job. It’s a chance to make a difference in your own life and in the lives of people around you. There’s a unique energy and spirit that draws people to the Mile High City and it all begins here, at the City and County of Denver. Over 11,000 employees work together every day to make this a world-class city where everybody matters.

The City and County of Denver offers a comprehensive benefits package to meet the needs of its employees and their families. Offering competitive benefits and wellness programs is a top priority for the city. The Office of Human Resources (OHR) Benefits and Wellness team is excited to present this 2017 benefits guide summarizing all the wonderful benefits offered to eligible employees in the City and County of Denver. Both the Employee Health Insurance Committee and your elected officials work hard to offer you competitive benefits that enrich the lives of you and your family.

For medical insurance in 2017, we’re excited to continue offering the same high deductible health plan (HDHP) and health savings account (HSA) combination introduced in 2016. In fact, you’ll notice very little has changed from 2016 to 2017. The city will continue to graciously provide an HSA contribution of $600 for individuals and $1,200 for families electing the HDHP.

The only new plan for 2017 is ARAG legal. ARAG legal is replacing Hyatt legal as the city’s pre-paid legal provider. ARAG legal offers both lower monthly premiums and expanded services. If you are enrolled in Hyatt legal in 2016, you are automatically enrolled in ARAG legal for 2017. If you’re new to the pre-paid legal benefit, the information pertaining to ARAG legal can be found in section 11, page 21 of this guide. The legal service benefit can only be elected during open enrollment or your new hire period.

In 2017, the city will migrate to Workday, an employee self-service system. All employees will log-in to Workday to elect benefits, make family status changes, update beneficiaries, addresses, and more. Keep an eye out for more information regarding Workday as we approach the New Year.

Denver Wellness is excited to offer our new wellness program and portal in early 2017. Keep an eye out for more about the city’s fun new wellness portal and how you will be able to earn a contribution to your HSA in 2018 by completing certain wellness activities in 2017.

Thank you for continuing to make a difference for the City and County of Denver, where Denver works!

Sincerely,

The OHR Benefits and Wellness Team

3

01Benefits Eligibility

WHO IS ELIGIBLE FOR BENEFITS?

Eligible employees include any half-time (20–29 hours) or full-time (30–40 hours)

employee in a limited or unlimited career service position. Employees in non-career

positions (i.e., on-call, trainee or intern) are not eligible for most benefits.

WHAT DEPENDENTS ARE ELIGIBLE FOR HEALTH CARE COVERAGE?

Eligible dependents include the following:

» Your spouse (including those defined as common-law and same-sex legally married)

» Your Colorado State Civil Union spouse (premiums are paid on an after-tax basis)

» Your same-sex spousal equivalent (premiums are paid on a pre-tax or after-tax basis depending on marriage status)

» Your children to age 26, regardless of student, marital or tax-dependent status

(including a stepchild, legally-adopted child, a child placed with you for

adoption or a child for whom you are the legal guardian)

» Your dependent children of any age who are physically or mentally unable to

care for themselves

When adding dependents, supporting documents are required to prove dependency

within the required time frame. A list of acceptable dependent documents can be

found at denvergov.org/benefits.

BENEFIT TYPE EFFECTIVE DATE ENROLLMENT RESPONSIBILITY COST CHANGES WHEN?

H = Hire Date1st = 1st of the Month

Following Your Hire Date

E = Enrollment Required

A = Auto Enroll

C = City Paid S = Shared Expense EE = Employee

A = Auto EnrollOE = Open EnrollmentLE = Life Event

Medical 1st E S OE & LE

Dental 1st E S OE & LE

Vision 1st E S OE & LE

Flexible Spending Accounts 1st E EE OE & LE

Health Savings Account (HSA) 1st E EE Anytime

Short-Term Disability Sick and Vacation Paid Time Off

1st1st

EA

EE* C

OEA

Additional Life Insurance § 1st E EE Anytime

ARAG Legal 1st E EE OE

Deferred Compensation 1st E EE Anytime

RTD H E S Monthly/Annually

Basic Life Insurance H A C A

Long-Term Disability H A C A

Employee Assistance H A C A

Pension H A S A

Paid Time Off (PTO) H A C A

§ Includes spouse life, dependent children life and accidental death and dismemberment. *Employees hired prior to January 1, 2010, who remained on the sick and vacation leave plans can elect short-term disability and pay the entire cost.

WHEN ARE MY BENEFITS EFFECTIVE, WHO PAYS FOR MY COVERAGE, AND WHEN CAN I CHANGE MY ELECTION?

4

02Benefits

EnrollmentWhen can I enroll or change my benefit

elections?

WHEN: During the annual open enrollment period each October. Any newly elected benefits or changes made to existing benefits become effective on January 1 of the following year.

HOW: If you have computer access at work, you must log onto the Denver One Team (DOT) portal at https://dot.gov.dnvr to make any benefit election changes for the following calendar year.

If you do not have computer access at work, a benefits enrollment form will be mailed to you. Completed forms must be returned to the OHR Benefits Office, scanned to [email protected] or faxed to 720.913.5548.

WHEN: The first 30 days of employment with the city as a new hire or re-hire. Benefit elections are effective the first of the month following your date of hire.

HOW: In 2016, to select benefits as a new hire you must complete a benefits enrollment form found at denvergov.org/benefits and return the form to the OHR Benefits Office within 30 days of your hire date.

In 2017, the city will migrate to Workday, an employee self-service system. As a new hire you must log-in to Workday and make elections within 30 days of your hire date. Find links to Workday training on the OHR Benefits & Wellness webpage at denvergov.org/benefits.

AT OPEN ENROLLMENT AS A NEW HIRE

WHEN: Within 30 days of a qualifying life event such as a birth or adoption of a child, marriage or divorce, or gain or loss of other coverage.

HOW: In 2016, if you experience a qualifying life event you must complete a benefits enrollment form found at denvergov.org/benefits and return the form to the OHR Benefits Office within 30 days of your qualifying life event date.

Supporting documentation must also be provided as proof of any qualified life event.

In 2017, the city will migrate to Workday, an employee self-service system. Employees must log-in to Workday and make elections within 30 days of a qualifying event, including but not limited to electing benefits, making family status changes, updating beneficiaries, and more. Find links to Workday training on the OHR Benefits & Wellness webpage at denvergov.org/benefits.

DURING THE YEAR

WE ARE HERE TO HELP YOU ENROLL AND MAKE BENEFIT SELECTIONS THAT ARE RIGHT FOR YOU.

w: denvergov.org/benefits

p: 720.913.5697

5

03Denver Wellness Program

The Denver Wellness program exists to help employees feel better. Our goal is to provide employees with whatever resources they need to improve their overall well-being. Whether an employee needs help with stress management, financial planning, understanding nutrition information or an opportunity for colleagues to work together and celebrate a success, Denver Wellness will do its best to support employees on their journey to being well.

In 2017, you will have even more opportunities to earn an incentive for living well. Our new wellness portal will provide a one-stop shop to access all of our wellness programs to support all aspects of well-being. When you participate in the program in 2017, you will earn a reward to offset the next year’s healthcare costs.

Five Pillars of Well Being and Denver Wellness Services

Physical• Healthy Steps Incentive

program - earn a reward for getting preventive dental and medical screenings

• On-site fitness classes

• Weight loss programs

Emotional• Meditation classes

• Stress and time management classes

• GuidanceResources® - employee assistance program

Spiritual / Sense of Purpose• Wellness fairs featuring

health charities

• Charity walks

• Share Your Success Award for employees who make great health improvements

Financial• Financial Health for

Professionals classes

• Benefits classes to better understand your insurance plans

• Retirement planning

• Budgeting and credit building classes

Social• Wellness team challenges

• Support groups

• Weight loss support classes

• Wellness Champions network

Find out more: denvergov.org/wellness

6

04Benefits

Basics

What is a deductible? The amount you must pay each calendar year for covered health services before the insurance plan will begin to pay.

For HDHP enrollees, the deductible applies to all non-preventative care costs, including prescription costs before insurance will pay. For those covering just themselves, it is $1,350, and $2,700 for those covering family members. For DHMO enrollees, the deductible applies to any procedure or hospitalization cost. It is not necessary to meet a deductible first where a copay is paid. For any individual enrolled the deductible is $500, but a family is responsible for up to three $500 deductibles or $1,500 annually.

What is a copayment or copay? A fixed dollar amount that you pay for a covered health service.

For HDHP enrollees, copays are due AFTER reaching the annual deductible for prescriptions costs. For DHMO enrollees, copays are due at time of service and prescriptions. It is not necessary to reach the annual deductible first.

What is coinsurance? After you meet your deductible, you pay coinsurance, which is your share of the costs of a covered health care service.

For HDHP enrollees, coinsurance starts once your expenses reach your annual deductible ($1,350/$2,700 for single/family). You stop paying coinsurance once you reach your out-of-pocket maximum. For DHMO enrollees, coinsurance applies for procedure and hospitalization costs only after you pay your deductible.

What is an imbedded deductible? The HDHP has an imbedded deductible and applies to employees who enroll family members. It means all the expenses of the plan, from all enrollees in the plan, count toward the deductible. This means one family member alone could reach the deductible, leaving the rest of the family to pay just coinsurance expenses. Enrollees also have an embedded out-of-pocket maximum, meaning one family member’s expenses could satisfy the family’s entire out-of-pocket costs in a year, leaving the rest of the family with no expenses. DHMO participants do not have an imbedded deductible, so each member of the family’s expenses are tracked separately.

What is out-of-pocket maximum? The most you will pay for covered health services during the calendar year. All copay, deductible, and coinsurance payments count toward the out-of-pocket maximum. Once you’ve met your out-of-pocket maximum, your insurance plan will pay 100% of covered health services.

For HDHP enrollees it is $2,700 for employees covering themselves and $5,400 for employees covering family members. For DHMO enrollees it is $3,000 for individuals enrolled on the plan, a family is responsible for two $3,000 deductibles or $6,000 annually.

What is a health savings account (HSA)? A bank account that HDHP members can use to pay out-of-pocket health care costs with pre-tax dollars from the employee’s paycheck or with employer contributions. Money deposited in an HSA stays with the employee, regardless of employer or health plan, and unused balances roll over year to year.

What is a health care flexible spending account (FSA)? A spending account that you can use to pay for health care with pre-tax dollars. Funds deposited into a health care FSA are use it or lose it, meaning any funds you do not use by the IRS deadline will be forfeited. If you fund a health savings account (HSA), you are not eligible to contribute to a traditional health care FSA; however, you can fund a limited use health care FSA, which can only be used to pay for dental and vision expenses.

Key termsWhat is the difference between the DHMO and HDHP? The difference is how you pay for services when obtaining care. Both plans cover preventive care at 100%.

High-deductible health plan (HDHP) enrollees will generally pay the full cost of all care until the annual deductible is reached. They then pay coinsurance until the annual out-of-pocket maximum is reached. Deductible health maintenance organization (DHMO) plan enrollees will pay for some services in the form of a copay and the full cost of other services until the annual deductible is reached. For deductible expenses, enrollees pay coinsurance after reaching the deductible. Enrollees will continue to pay either copays, coinsurance or deductibles until the out-of-pocket maximum is reached.

7

05Benefit Plan Premiums

Listed below are the monthly premiums for medical insurance. The amount you pay for coverage is deducted from your paycheck on a pre-tax basis. Deductions are taken from the first two paychecks of each month. Please note that last year’s guide listed premiums per paycheck, and this year’s guide lists premiums per month.

MEDICALEmployee only Employee + spouse Employee + child(ren) Family

City Employee City Employee City Employee City Employee

DHMP DHMO $500.00 $88.23 $1,002.94 $291.18 $941.18 $235.29 $1,411.76 $470.59

DHMP HDHP $440.47 $23.18 $892.53 $127.50 $834.57 $92.73 $1,261.14 $222.55

Kaiser DHMO $419.32 $74.00 $841.11 $244.19 $789.30 $197.33 $1,183.96 $394.65

Kaiser HDHP $378.01 $19.90 $765.96 $109.42 $716.22 $79.58 $1,082.29 $190.99

United Navigate (DHMO) $555.16 $97.97 $1,113.60 $323.30 $1,045.04 $261.26 $1,567.19 $522.60

United HDHP $592.57 $31.19 $1,200.76 $171.54 $1,122.80 $124.76 $1,696.63 $299.40

Listed below are the monthly premiums for dental insurance. The amount you pay for coverage is deducted from your paycheck on a pre-tax basis. Deductions are taken from the first two paychecks of each month. Please note that last year’s guide listed premiums per paycheck, and this year’s guide lists premiums per month.

DENTALEmployee only Employee + spouse Employee + child(ren) Family

City Employee City Employee City Employee City Employee

Delta PPO Low Option $25.24 $4.45 $51.07 $14.83 $47.50 $11.87 $79.26 $26.42

Delta PPO High Option $25.24 $14.34 $51.07 $36.80 $47.50 $31.66 $79.26 $61.65

Delta EPO $25.24 $6.03 $51.07 $18.35 $47.50 $15.04 $79.26 $32.06

Listed below are the monthly premiums for vision insurance. The amount you pay for coverage is deducted from your paycheck on a pre-tax basis. The monthly premium is deducted from the first paycheck of the month.

VISION Employee only Employee + spouse Employee + child(ren) Family

VSP $4.97 $10.12 $9.33 $17.05

8

DID YOU KNOW?

» If you enroll in the HDHP, the city will contribute to your health savings account!

• Individual coverage: $600 per year

• All other coverage tiers: $1,200 per year

» In order to open an HSA in 2017, you must have depleted your previous year’s health care FSA by December 31, 2016.

» You may roll over HSA money from year to year.

?

06Medical

Plans

Comparing your medical plan options

The city offers six medical plan options through three carriers: Denver Health, Kaiser Permanente, and UnitedHealthcare. All three carriers offer a high-deductible health plan (HDHP) and a deductible HMO (DHMO) plan. Choosing the right medical plan is an important decision. Take the time to learn about your options to ensure you select the right plan for you and your family.

The main difference between an HDHP and DHMO is how and when you pay for your health care.

HIGH-DEDUCTIBLE HEALTH PLAN (HDHP)

» Lower premium per month

» Higher deductible

» You can budget for your out-of-pocket expenses by funding a health savings account (HSA)

» You must open an OPTUM Bank account

DEDUCTIBLE HMO (DHMO) PLAN

» Higher premium per month

» Lower deductible

» You can budget for your out-of-pocket expenses by funding a health care flex spending account (FSA)

* For the HDHP: If you elect family coverage, the individual deductible does not apply. You must satisfy the full family deductible before the plan begins to pay toward covered services.

The same rule applies to the out-of-pocket maximum. You must satisfy the full family out-of-pocket maximum before the plan will cover all expenses for the remainder of the plan year.

NU

MBE

RS T

O K

NO

W

HDHP in-network deductible:Individual deductible: $1,350 Family deductible: $2,700*

HDHP in-network out-of-pocket maximum:Individual out-of-pocket maximum: $2,700 Family out-of-pocket maximum: $5,400*

HDHP in-network coinsurance: DH: 10%, KP and UHC: 20%

DHMO in-network coinsurance: 20%

DHMO in-network out-of-pocket maximum:Individual out-of-pocket maximum: $3,000 Family out-of-pocket maximum: $6,000

DHMO in-network deductible:Individual deductible: $500 Family deductible: $1,500

DEDUCTIBLE

OUT-OF-POCKET MAXIMUM

COINSURANCE

DID YOU KNOW?

» If you enroll in the DHMO, and you contribute to a health care FSA, your whole pledge amount for the plan year is available for use on qualified expenses on the day your plan starts.

» You must submit claims to your health savings FSA for your qualifying 2017 expenses by March 31, 2018 or you’ll forfeit any unused funds.

HSA contributions limits: Individual coverage: $2,800 per year (totaling $3,400 with city contribution)

All other coverage tiers: $5,550 per year (totaling $6,750 with city contribution)

Health care FSA contribution limits: Up to $2,500 annually

CONTRIBUTION LIMITS

9

Summary of Covered Services

DENVER HEALTH DHMO DENVER HEALTH HDHP

In-Network Cofinity NetworkIn-Network Cofinity Network

Single Family Single Family

Deductible $500 per individual / $1,500 family

$750 per individual / $1,750 family

$1,350 $2,700 $1,350 $2,700

Out-of-Pocket Maximum $3,000 per individual / $6,000 family

$3,000 per individual / $6,000 family

$2,700 $5,400 $2,700 $5,400

Office Visits Primary Care PhysicianSpecialist

$25 copay1 $50 copay

$30 copay1 $50 copay

10% after deductible10% after deductible

20% after deductible20% after deductible

Preventive $0 $0 $0 $0

Prescription DrugsGeneric/Formulary/Non-formulary

See plan summary for details, costs vary by pharmacy location and Rx tier

Inpatient Hospital (per admission including birth)

20% after ded. and $150 per occurrence ded.2

30% after ded. and $150 per occurrence ded.2 10% after deductible3 20% after deductible3

Outpatient Hospital 20% after ded. and $150 per occurrence ded.

30% after ded. and $150 per occurrence ded. 10% after deductible 20% after deductible3

Lab and X-Ray 20% after deductible 30% after deductible 10% after deductible 20% after deductible

MRI/CAT/etc. $150 copay $200 copay 10% after deductible 20% after deductible

Emergency Care $300 copay $300 copay 10% after deductible 10% after deductible

Urgent Care $75 copay $75 copay 10% after deductible 10% after deductible

Mental HealthInpatientOutpatient

20% after ded. and $150 per occurrence ded.2

$50 copay

30% after ded. and $150 per occurrence ded.2

$50 copay

10% after deductible2

10% after deductible20% after deductible2

20% after deductible

Alcohol/Substance AbuseInpatientOutpatient

20% after ded. and $150 per occurrence ded.2

$50 copay

30% after ded. and $150 per occurrence ded.2

$50 copay10% after deductible 2

10% after deductible20% after deductible2

20% after deductible

Phys/Occ/Speech Therapy $25 copay (max 20 visits/year)

$35 copay (max 20 visits/year)

10% after deductible (max 20 visits/year)

20% after deductible (max 20 visits/year)

Vision Exam $25 copay (one exam every 24 months)

$35 copay (one exam every 24 months) Not covered Not covered

Chiropractic $50 copay3 (max 20 visits/year)

$50 copay3 (max 20 visits/year)

10% after deductible3 (max 20 visits/year)

10% after deductible3 (max 20 visits/year)

(1) The annual deductible and the 20% coinsurance apply for procedures performed during a copay office visit.(2) Prior authorization required.(3) Services must be provided by Columbine Chiropractic in order to be covered.

2017 Denver Health medical plan comparisons

DENVER HEALTH MEDICAL PLANS

Denver Health has contracted with University of Colorado Hospital and Children’s Hospital Colorado. Services received at these facilities (or by a contracted provider) will be covered at the same level as other in-network services.

Denver Health has also contracted with Cofinity, a nationwide provider network. Services received by a Cofinity provider or at a Cofinity facility are covered under the Cofinity tier (see table above for Cofinity tier benefit details).

Services provided by a non-contracted provider or at a non-contracted facility are not covered (except in the case of a medical emergency).

To learn more about Denver Health visit www.denverhealthmedicalplan.com or call 303.602.2100.

10

Summary of Covered Services

KAISER DHMO KAISER HDHP

In-Network OnlyIn-Network Only

Single Family

Deductible $500 per individual / $1,500 family

$1,350 $2,700

Out-of-Pocket Max Single/Family $3,000 per individual / $6,000 family

$2,700 $5,400

Office Visits Primary Care PhysicianSpecialist

$30 copay1 $50 copay1

20% after deductible20% after deductible

Preventive $0 $0

Prescription DrugsGeneric/Formulary/Non-formulary $20/$40/$60 copay (up to a 30-day supply) $10/$35/$60 copay after deductible

Inpatient Hospital (per admission including birth) 20% after deductible 20% after deductible

Outpatient Hospital 20% after deductible 20% after deductible

Lab and X-Ray $0 lab/20% after deductible for X-Ray 20% after deductible

MRI/CAT/etc. 20% after deductible 20% after deductible

Emergency Care $200 copay1 20% after deductible

Urgent Care $75 copay2 (Kaiser designated facility) 20% after deductible (Kaiser designated facility)

Mental HealthInpatientOutpatient

20% after deductible $30 copay/visit1

20% after deductible20% after deductible

Alcohol/Substance AbuseInpatient Outpatient

20% after deductible $30 copay/visit1

20% after deductible20% after deductible

Phys/Occ/Speech Therapy $30 copay (max 20 visits/year) 20% after deductible (max 20 visits/year)

Vision Exam $30 copay 20% after deductible

Chiropractic $30 copay (max 20 visits/year) 20% after deductible (max 20 visits/year)

(1) The annual deductible and the 20% coinsurance apply for procedures performed during a copay office visit.

2017 Kaiser Permanente medical plan comparisons

CHOOSE THE RIGHT DOCTOR FOR YOU

If you enroll in the Kaiser Permanente HDHP or DHMO, you must select a primary care physician who is responsible for overseeing your health care. With Kaiser Permanente medical offices across the Denver/Boulder area, it can be easy to find a doctor who is close to your home or workplace. Most Kaiser Permanente medical offices house primary care, laboratory, X-ray and pharmacy services under one roof, which means you can visit your physician and manage many of your other needs in a single trip.

The Kaiser Permanente plans provide in-network coverage only (except in the case of a medical emergency).

CALL THE APPOINTMENT AND ADVICE LINE

If you have an illness or injury and you’re not sure what kind of care you need, Kaiser Permanente advice nurses can help. With access to your electronic health record, they can assess your situation and direct you to the appropriate facility, or even help you handle the problem at home until your next appointment. For advice, call 303.338.4545 24 hours a day, seven days a week. For appointment services, call Monday through Friday from 7:00 a.m. - 6:00 p.m.

To learn more about Kaiser Permanente visit http://my.kp.org/denvergov or call 303.338.4545.

11

(1) The annual deductible and the 20% coinsurance apply for procedures performed during a copay office visit.(2) Prior authorization required for certain services.

Summary of Covered Services

UNITEDHEALTHCARE DHMO UNITEDHEALTHCARE HDHP

In-Network OnlyIn-Network Out-of-Network

Single Family Single Family

Deductible $500 per individual / $1,500 family $1,350 $2,700 $3,000 $6,000

Out-of-Pocket Max $3,000 per individual /

$6,000 family $2,700 $5,400 $6,000 $12,000

Office Visits Primary Care PhysicianSpecialist

$25 copay1 $50 copay1

20% after deductible 20% after deductible

50% after deductible 50% after deductible

Preventive $0 $0 Not covered

Prescription DrugsTier 1/Tier 2/Tier 3

$15/$45/$60 copay $10/$35/$60 copay after deductible

$10/$35/$60 copay after deductible

Inpatient Hospital (per admission including birth)

20% after $150 per occurrence deductible and annual

deductible3 20% after deductible 50% after deductible2

Outpatient Hospital20% after $75 per occurrence

deductible and annual deductible3

20% after deductible 50% after deductible2

Lab and X-Ray 20% after deductible 20% after deductible 50% after deductible2

MRI/CAT/etc. $150 copay 20% after deductible 50% after deductible2

Emergency Care $300 copay 20% after deductible 20% after deductible

Urgent Care $75 copay1 20% after deductible 50% after deductible

Mental HealthInpatient Outpatient

20% after deductible

$50 copay

20% after deductible20% after deductible

50% after deductible2

50% after deductible2

Alcohol/Substance AbuseInpatient Outpatient

20% after deductible$50 copay

20% after deductible20% after deductible

50% after deductible2

50% after deductible2

Phys/Occ/Speech Therapy $25 copay (max 20 visits/year)

20% after deductible (max 20 visits/year)

50% after deductible2 (max 20 visits/year)

Vision Exam $25 copay (one exam every 24 months)

20% after deductible (one exam every 24 months) Not covered

Chiropractic (max 20 visits/year) $50 copay3 20% after deductible 50% after deductible3

2017 UnitedHealthcare medical plan comparisons

UNITEDHEALTHCARE HDHP The UnitedHealthcare HDHP provides in- and out-of-network coverage, allowing you the freedom to choose any provider. However, you will pay less out of your pocket when you choose a UnitedHealthcare network provider.

UNITEDHEALTHCARE NAVIGATE (DHMO)

If you enroll in the UnitedHealthcare Navigate DHMO, you must select a primary care physician (PCP) who will provide and manage most of your care.

You must receive an electronic referral before seeing another network PCP or specialist. During enrollment select your PCP from UnitedHealthcare’s Navigate network. You must email your PCP’s UHC ID number to [email protected]. If you do not select a PCP, UnitedHealthcare will assign one. The UnitedHealthcare Navigate plan provides in-network coverage only (except in the case of a medical emergency).

To learn more about UnitedHealthcare visit

myuhc.com or call 800.842.5520.

In and out-of-network ded. and out-of-pocket maximum do not cross apply

12

Additional medical plan information

DENVER HEALTH - AFTER HOURS CARE OPTIONSOptions for when you are sick and need care today:

» Call NurseLine Advice 303.739.1211

» DispatchHealth will come to you. DispatchHealth is our on-demand health care provider that can treat a range of injuries and illnesses in the comfort of your home. Download the free app or call 303.500.1518.

» Visit a Walgreens Healthcare Clinic or a King Soopers Little Clinic. These clinics are a good option if you have a sore throat, sinus infection or the flu.

» Visit an Urgent Care center that is convenient for you. You are covered anywhere in the U.S.

» Emergency Room. If you need emergency care, go to the nearest hospital or call 9-1-1. You are covered at any Emergency Room for emergency care at any time.

KAISER PERMANENTE – E-VISITS NOW AVAILABLEManage your health online with the new e-visit secure feature of My Health Manager.

E-Visits – new online medical consultations

If you have a non-urgent medical condition at any time 24/7 and you’re not sure what kind of care you need, an e-visit may be a good option for you. An e-visit is an online medical consultation with a Kaiser Permanente Advice Call Center Registered Nurse that’s available at no cost for select medical conditions like nausea/vomiting, pink eye, female UTI, sinus, constipation, diarrhea, and more.

Complete an E-Visit

» Log on to kp.org. Then, go to My Health Manager and then the Appointment Center.

» From there, choose the appropriate medical condition that best describes your symptoms.

» Complete and submit the series of questions.

» An Advice Call Center Registered Nurse will respond within four hours of receiving your questionnaire. For your safety, some answers during your e-visit may prompt you to call the Appointment and Advice Call Center directly in order to expedite your care. If this happens, call the Appointment and Advice Call Center for medical advice immediately, at 303-338-4545 or 1.800.218.1059 (TTY for the deaf, hard of hearing, or speech impaired:711).

» Not Registered for kp.org Yet?

» Go to kp.org/registernow and follow the prompts. Once registered you’ll be able to e-mail your doctor’s office, complete an e-visit, pay medical bills, view lab results, and more!

UNITEDHEALTHCARE - VIRTUAL VISITS

Members log on to myuhc.com where they can:

» Learn more about virtual visits (e.g., how to use it, a covered benefit, etc.)

» View virtual visit provider group choices

» Members can access virtual visit provider groups through myuhc.com or from their mobile device, computer or telephone

13

Your maximum annual medical liability

Carrier & Coverage Level ANNUAL PREMIUM + OUT-OF-POCKET MAXIMUM - CITY HSA

CONTRIBUTION = YOUR MAXIMUM ANNUAL LIABILTY

Kaiser PermanenteEmployee only DHMO

($74.00 x 12) = $888.00 + $3,000.00 - $0.00 = $3,888.00

Kaiser PermanenteEmployee only HDHP

($19.90 x 12) = $238.80 + $2,700.00 - $600.00 = $2,338.80

Kaiser PermanenteEmployee + spouse DHMO

($244.19 x 12) = $2,930.28 + $6,000.00 - $0.00 = $8,930.28

Kaiser PermanenteEmployee + spouse HDHP

($109.42 x 12) = $1,313.04 + $5,400.00 - $1,200.00 = $5,513.04

Kaiser PermanenteEmployee + child(ren) DHMO

($197.33 x 12) = $2,367.96 + $6,000.00 - $0.00 = $8,367.96

Kaiser PermanenteEmployee + child(ren) HDHP

($79.58 x 12) = $954.96 + $5,400.00 - $1,200.00 = $5,154.96

Kaiser PermanenteFamily DHMO

($394.65 x 12) = $4,735.80 + $6,000.00 - $0.00 = $10,735.80

Kaiser PermanenteFamily HDHP

($190.99 x 12) = $2,291.88 + $5,400.00 - $1,200.00 = $6,491.88

To determine the cost of each plan you must consider the monthly premium, out-of-pocket expenses, and the possible city contribution to a health savings account (HSA). The example below shows the maximum annual medical liability for Kaiser Permanente at each coverage level (i.e. Employee only, Employee + spouse, Employee + child[ren], and Family). Below the example, you will find a worksheet you can use to calculate the maximum annual medical liability for Denver Health and UnitedHealthcare.

Carrier & Coverage Level ANNUAL PREMIUM + OUT-OF-POCKET MAXIMUM - CITY HSA

CONTRIBUTION = YOUR MAXIMUM ANNUAL LIABILTY

DHMOEmployee only

($ x 12) = $ + $3,000.00 - $0.00 = $

HDHPEmployee only

($ x 12) = $ + $2,700.00 - $600.00 = $

DHMOEmployee + spouse

($ x 12) = $ + $6,000.00 - $0.00 = $

HDHPEmployee + spouse

($ x 12) = $ + $5,400.00 - $1,200.00 = $

DHMOEmployee + child(ren)

($ x 12) = $ + $6,000.00 - $0.00 = $

HDHPEmployee + child(ren)

($ x 12) = $ + $5,400.00 - $1,200.00 = $

DHMOFamily

($ x 12) = $ + $6,000.00 - $0.00 = $

HDHPFamily

($ x 12) = $ + $5,400.00 - $1,200.00 = $

Use this worksheet to calculate your maximum annual medical liability based on the carrier you choose and the coverage level you require. Find the monthly premium rates for Denver Health and UnitedHealthcare on the Benefit Plan Premiums page 7.

14

Enro

lled

in t

he

DH

MO

? HEALTH CARE FLEXIBLE SPENDING ACCOUNT

A health care flexible spending account (FSA) is an account that allows you to pay for eligible health care expenses with pre-tax dollars. If you fund an HSA, you cannot fund a health care FSA.

2017 PLAN YEAR MAXIMUM FSA CONTRIBUTION: $2,500 (REGARDLESS OF COVERAGE LEVEL)

HSA VERSUS HEALTH CARE FSA HSA FSA

Annual election available on the first day of the plan year

The City and County of Denver contribution

will be available January 1, 2017, if your Optum Bank HSA is opened. Employee

contributions are deposited per pay period.

Yes

Annual IRS maximum different depending on coverage level

Yes

No

You can change your election throughout the year

Yes

No, unless you experience a qualifying

life event.

Funds roll over from one year to the next

Yes, your HSA dollars are yours to keep if you

change plans or jobs.

No, you must submit your qualifying

expenses by March 31 of the following year or forfeit any unused funds.

Enrolled

in the

HD

HP?

*

HEALTH SAVINGS ACCOUNT

A health savings account (HSA) is an individually-owned bank account that allows you to pay for eligible medical, dental and vision expenses with pre-tax dollars. You own your account, and there are no “use it or lose it” restrictions like with flexible spending accounts. Your contributions to this account (including the City and County of Denver contribution) cannot exceed the IRS annual contribution limits. In order to open an HSA in 2017, you must have depleted your previous year’s health care FSA by December 31, 2016.

2017 ANNUAL MAXIMUM HSA CONTRIBUTIONS:Individual: $2,800 (totalling $3,400 with city contribution) All other tiers: $5,550 (totalling $6,750 with city contribution) Catch-up contribution (if age 55+): $1,000

The City and County of Denver will help you save by contributing the following amount to your HSA in 2017:Individual coverage: $600 All other coverage tiers: $1,200

* You must be enrolled in a high-deductible health plan in order to open and fund an HSA. Additional requirements apply.

07Budgeting

for Your Health Care

Health savings account vs. health care flexible

spending account

15

If you enroll in a city high-deductible health plan (HDHP), you may be eligible to open and fund an HSA.

An HSA is a personal health care savings account that you can use to pay out-of-pocket health care expenses with pre-tax dollars. Your contributions are tax free, and the money remains in the account for you to spend on eligible expenses no matter where you work or how long it stays in the account.

The city will provide an HSA contribution in 2017 in the following amounts:

» Individual coverage: $600

» All other coverage tiers: $1,200

Note: You must open your HSA through OPTUM Bank in order to receive the contribution within 60 days of your effective date.

Contributions to a health savings account (including the city contributions) cannot exceed the annual IRS contribution maximums.

2017 IRS HSA contribution maximums

» Individual coverage $3,400

» All other tiers $6,750

» Catch-up contribution (if age 55+) $1,000

Employees may contribute annually the difference between the IRS limit and the city contribution.

If you fund an HSA, you cannot contribute pre-tax dollars to the health care FSA.

However, you can fund a limited use health care FSA. See page 16 for limited use health care FSA details.

HSA ELIGIBILITY

You are eligible to open and fund an HSA if:

» You are enrolled in the city HDHP

» You are not covered by a non-HSA plan, health care FSA or health reimbursement arrangement

» Health care FSA must be a zero balance as of 12/31/16

» You and/or your dependents are not eligible to be claimed as a dependent on someone else’s tax return

» You are not enrolled in Medicare, Medicaid or TRICARE for Life

MAXIMIZE YOUR TAX SAVINGS

» Contributions to an HSA are tax free and can be made through payroll deduction on a pre-tax basis when you open an HSA through Optum Bank

» The money in your HSA (including interest and investment earnings) grows tax free

» As long as you use the funds to pay for qualified medical expenses, the money is spent tax free

USE YOUR HSA TO PAY FOR QUALIFIED MEDICAL EXPENSES

» You can use your HSA money to pay for eligible expenses now or in the future

» Funds in your HSA can be used for your expenses and those of your spouse and eligible dependents, even if they are not covered by the city HDHP

» Eligible expenses include deductibles, doctor’s office visits, dental expenses, eye exams, prescription expenses and LASIK eye surgery

» A complete list of eligible expenses can be found at www.irs.gov/pub/irs-pdf/p502.pdf

THREE EASY WAYS TO ACCESS YOUR HSA MONEY

» Debit card—Draws directly from your HSA and can be used to pay for eligible expenses at your doctor’s office, pharmacy or other locations where you purchase health-related items or services

» Pay bills online—Send payments directly to your health care providers, pharmacy or other payees for eligible expenses you paid out of your pocket

» Reimburse yourself—Request a check or schedule an electronic account transfer to pay yourself back for eligible expenses you paid out of your pocket

YOUR HSA IS AN INDIVIDUALLY OWNED ACCOUNT

» You own and administer your HSA

» You determine how much you will contribute to your account and when to use the money to pay for eligible health care expenses

» You can change your contribution at any time during the plan year without a qualifying event

» Like a bank account, you must have a balance in order to pay for eligible health care expenses

» Keep all receipts for tax documentation

» An HSA allows you to save and roll over money from year to year

» The money in the account is always yours, even if you change health plans or jobs

» There are no vesting requirements or forfeiture provisions

Health savings account (HSA)

Important!You must have qualifying coverage as defined by the IRS in order to contribute to an HSA or you risk adverse tax consequences. If you are enrolled in another plan that is not considered qualifying under IRS guidelines you are not eligible to receive the city’s employer HSA contribution or contribute your own monies on a pre-tax basis. This includes, but is not limited to, Medicare, Medicaid, TRICARE for Life or any non high-deductible health plan. Please refer to IRS Publication 969 (www.irs.gov/uac/About-Publication-969) for additional information.

16

With a flexible spending account (FSA), you can set aside money on a pre-tax basis from your paycheck to cover health care (medical, dental and vision), dependent day care and/or qualified parking expenses.

The city offers these flexible spending accounts through 24HourFlex, whose services include:

» Help center at 303.369.7886 or 800.651.4855 from 8:00 a.m. - 5:00 p.m. MST

» Internet access to account info at 24hourflex.com

» Online claim submission

» Automatic direct deposit in your bank or savings account

» Debit card (Visa) complimentary to all participants, with immediate access to certain locations such as King Soopers, Safeway, Walgreens, Wal-Mart, etc.

HEALTH CARE FSA

If you enroll in the health care FSA, you can use the FSA to pay for eligible health care expenses, including medical, dental and vision expenses with pre-tax dollars. You can contribute a minimum of $120 and up to a maximum of $2,500 in 2017. Another advantage of enrolling in the health care FSA is that your whole pledge amount for the plan year is available for use on qualified expenses on the day your plan starts, even though your contributions towards the pledge are spread over the calendar year.

Please note: You must use it or lose it! If you choose to use a health care FSA, remember to plan your contributions carefully. You can submit claims for your qualifying 2016 expenses through March 31, 2017. Your expenses must be incurred no later than March 15, 2017, to be reimbursed from your FSA. Due to IRS rules, you’ll forfeit any unused funds.

If you enroll in a high-deductible health plan in 2017 your health care FSA dollars must be spent by 12/31/2016.

LIMITED USE HEALTH CARE FSA

» If you fund an HSA, you are not eligible to fund a health care FSA. However, you can fund a limited use health care FSA. A limited use health care FSA can only be used to reimburse dental and vision expenses.

The limited use health care FSA maximum contribution is $2,500 for the 2017 plan year. You can submit claims for your qualifying 2016 expenses through March 31, 2017. Your expenses must be incurred no later than March 15, 2017, to be reimbursed from your FSA. Due to IRS rules, you’ll forfeit any unused funds.

DEPENDENT DAY CARE FSA

If you have child care expenses, consider taking advantage of the dependent day care FSA. In the same way that the health care FSA lets you set aside pre-tax dollars for eligible health care expenses, you can use the dependent day care FSA to set aside a minimum of $120 and up to $5,000 per year pre-tax dollars for child care expenses while you work. Examples of eligible dependent care expenses include:

» Day care and babysitter costs

» Nursery school

» Before- and after-school programs

» Summer day camps

The dependent day care FSA is subject to the same reimbursement rules as the health care FSA, including the “use it or lose it” rule. Important tax rules also apply to the dependent day care FSA. You can’t be reimbursed from your FSA for any expense that is also covered by a tax credit on your federal tax return. However, unlike the health care FSA, your whole pledge amount for the plan year is not available on the day your plan starts. For the dependent day care FSA, you can only be reimbursed for qualified expenses up to the amount you have contributed to your FSA up to that point in time. As your contributions accrue, claims for reimbursement can be processed.

QUALIFIED PARKING FSA

The qualified parking FSA allows you to claim up to $255 per month of pre-tax dollars to pay for parking expenses while you are at work. To qualify, the parking expenses cannot be associated with a city-owned facility. Like the dependent day care FSA, claims for reimbursement can be processed as your contributions accrue. Submit claims within 180 days of date of expense. (Minimum is $60 annually, $3,060 maximum)

Flexible spending accounts (FSA)

With easy payroll deductions and convenient debit cards, FSAs provide a flexible and easy way to cover expenses.

17

08Dental Plans

Proper dental care is important and taking care of your oral health is an investment in your overall well-being. The City and County of Denver’s dental coverage is through Delta Dental of Colorado (Delta Dental), which provides employees with three plan options.For a complete schedule of dental benefits, visit denvergov.org/benefits, or pick up a Delta Dental brochure from the OHR Benefits Office.

PPO HIGH AND PPO LOW PLANS The Delta Dental PPO High and PPO Low plans offer coverage for a broad-range of services with a deductible and coinsurance approach. You and your enrolled dependents may visit any licensed dentist, but will enjoy the greatest out-of-pocket savings if you see a Delta Dental PPO dentist.

EPO PLANThe EPO plan only provides benefits if you visit a Delta Dental PPO dentist in Colorado. The EPO plan provides subscribers with a copayment listing that details all covered services and their associated out-of-pocket costs. Non-covered services are billed directly to you at Delta Dental’s discount rate, so you will still save money even if the procedure is not covered under your plan. If you receive treatment from a Delta Dental non-PPO dentist, you will be responsible for all fees charged.

FIND A DENTISTTo learn if a dentist participates in a network covered by your plan, use the “Find a Dentist” search feature on the Delta Dental website at deltadentalco.com or call Customer Relations at 800.610.0201.

MAKE AN APPOINTMENTA Delta Dental ID card is not required when you visit the dentist. Your dentist can confirm your coverage. However, if you prefer to have a Delta Dental ID card, log in to your Delta Dental account to print an ID card.

COVERAGE VERIFICATIONIt is important to understand the specifics of your dental benefits especially what is and is not covered. If you think you may need treatment and want to find out what your costs will be, ask your dentist to submit a pre-treatment estimate, allowing you to understand your full financial responsibility before committing to services.

Summary of Covered Services

DELTA DENTAL PPO PLUS PREMIER

GROUP 6026

DELTA DENTAL PPO PLUSPREMIER PLANGROUP 6793

DELTA DENTAL PPOGROUP 6791

PPO LOW PLAN PPO HIGH PLAN EPO PLAN

Annual Maximum Benefit $1,250 per person $2,000 per person Unlimited

DeductibleSingle/Family

$25/$75 $25/$75 None

Preventive ServicesOral Evaluation Bitewing X-rays Full Mouth X-rays or Panoramic Routine Cleaning Fluoride Treatment Space Maintainers Sealants

$0 PPO Dentist 20% Premier Dentist

20% Non-Participating Dentist$0

Copay (see copay listing found in the “Dental” section of denvergov.org/benefits)

Basic ServicesAmalgam Fillings Resin, Composite Oral Surgery (Extractions) General Anesthesia Surgical Periodontal (gums) Root Canal Therapy

20% PPO Dentist 50% Premier Dentist

50% Non-Participating Dentist

10% PPO Dentist 20% Premier Dentist

20% Non-Participating Dentist

Copay

(see copay listing)

Major ServicesCrowns Dentures, Partials, Bridges

50% PPO Dentist 50% Premier Dentist

50% Non-Participating Dentist

40% PPO Dentist 50% Premier Dentist

50% Non-Participating Dentist

Copay

(see copay listing)

Orthodontics Complete Orthodontic Evaluation Active Orthodontic Treatment

50% PPO Dentist 50% Premier Dentist

50% Non-Participating Dentist

50% PPO Dentist 50% Premier Dentist

50% Non-Participating Dentist

Copay

(see copay listing)

Orthodontics Lifetime Maximum $1,000 per person $1,000 per personUnlimited

(see copay listing)

18

09Vision PlanEye exams are an important part of overall health care for your family. With VSP you

will get the highest level of care, including an annual exam designed to detect signs of health conditions like diabetes and high blood pressure. VSP does not provide an ID card, visit VSP.com to find a provider.

FIND A VISION PROVIDER

Find a VSP provider at vsp.com or call 800.877.7195.

Summary of Covered ServicesVSP

In-Network

Routine Exams (every calendar year) $10 copay

Prescription GlassesLenses and frames $25 copay

Lenses (every calendar year)

Single vision, lined bifocal and lined trifocal lenses.

Polycarbonate lenses for dependent children

Included in prescription glasses copay

Lens Enhancements (every calendar year)

Standard progressive lenses

Premium progressive lenses

Custom progressive lenses

$55 copay$95–$105 copay$150–$175 copay

Frames (every other calendar year) $160 allowance + 20% off balance $90 allowance at Costco + 20% off balance

Contact Lenses (every calendar year) $160 allowance

VSP has special pricing for LASIK with participating centers, a savings that can add up to

hundreds of dollars for VSP members. Visit vsp.com or call 800.877.7195

19

10Life and Disability Insurance

LIFE INSURANCE

The city offers several life insurance policy options. All employees are automatically enrolled in a basic life insurance policy, and are also eligible to voluntarily enroll in additional life policies. BASIC LIFE INSURANCE

The city pays for your basic life insurance with a payout benefit equal to two times your annual salary, up to a maximum of $100,000. You are automatically enrolled and this policy is effective upon hire. Be sure to designate a beneficiary for this benefit. The beneficiary designation/ change form can be found at denvergov.org/benefits. Submit completed forms to the OHR Benefits Office via fax 720.913.5548 or scan and email to [email protected].

ADDITIONAL AND DEPENDENT LIFE INSURANCE

In addition to your basic life insurance, you may elect to enroll in additional life insurance for yourself. You can buy additional life insurance at a minimum of $5,000 and up to a maximum of $300,000 in increments of $5,000. Within 30 days of your hire date, you can elect additional life for up to $100,000 without providing a medical history statement.

You can elect additional life coverage for your spouse in increments of $5,000 up to a maximum of $300,000, but not to exceed 100% of your combined basic and additional life coverage. Within 30 days of your hire date, you can elect spousal life up to $30,000 without providing a medical history statement.

You may also elect additional life coverage for your eligible children in the amounts of $5,000 at a cost of $0.75 monthly or $10,000 at a cost of $1.50 monthly.

Additional life policies for you and your dependents are optional benefits and are paid for entirely by you in after-tax deductions. The premium rates are based upon set rates determined by age and tobacco use (except for the children policies mentioned above).

Completion of a medical history statement and physical exam is required if enrolling more than 30 days from date of hire.

ACCIDENTAL DEATH AND DISMEMBERMENT

Accidental death and dismemberment (AD&D) coverage is an optional benefit and is paid for entirely by the employee. If elected, this coverage pays a benefit if you die or suffer serious injury as a result of a covered accident. You can buy AD&D coverage at a minimum of $10,000 and to a maximum of $500,000 in increments of $10,000. Amounts in excess of $250,000 cannot exceed 10 times your annual earnings. If you are enrolled in AD&D coverage, you may also elect to insure your eligible dependents. The amount of insurance for each dependent is determined as follows:

» Spouse only – 60% of your amount

» Child only – 15% of your amount, not to exceed $25,000 per child

» Spouse and child – 50% of your amount for spouse and 10% of your amount per child

20

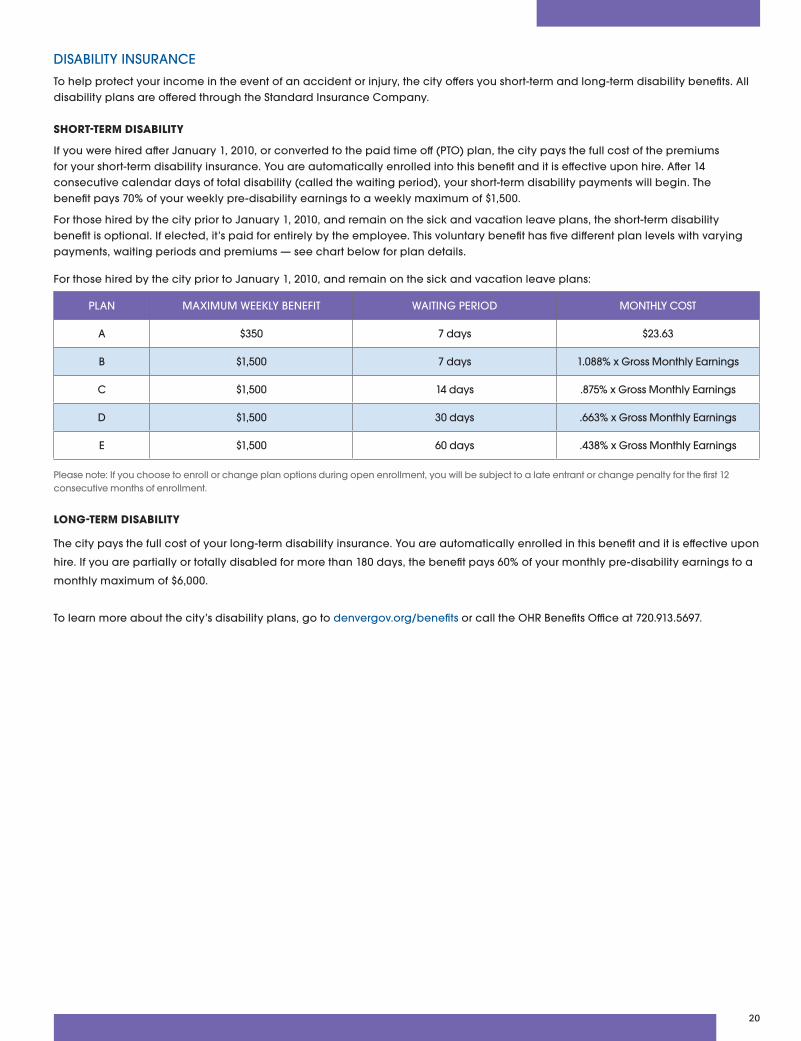

DISABILITY INSURANCE

To help protect your income in the event of an accident or injury, the city offers you short-term and long-term disability benefits. All disability plans are offered through the Standard Insurance Company. SHORT-TERM DISABILITY

If you were hired after January 1, 2010, or converted to the paid time off (PTO) plan, the city pays the full cost of the premiums for your short-term disability insurance. You are automatically enrolled into this benefit and it is effective upon hire. After 14 consecutive calendar days of total disability (called the waiting period), your short-term disability payments will begin. The benefit pays 70% of your weekly pre-disability earnings to a weekly maximum of $1,500.

For those hired by the city prior to January 1, 2010, and remain on the sick and vacation leave plans, the short-term disability benefit is optional. If elected, it’s paid for entirely by the employee. This voluntary benefit has five different plan levels with varying payments, waiting periods and premiums — see chart below for plan details.

PLAN MAXIMUM WEEKLY BENEFIT WAITING PERIOD MONTHLY COST

A $350 7 days $23.63

B $1,500 7 days 1.088% x Gross Monthly Earnings

C $1,500 14 days .875% x Gross Monthly Earnings

D $1,500 30 days .663% x Gross Monthly Earnings

E $1,500 60 days .438% x Gross Monthly Earnings

Please note: If you choose to enroll or change plan options during open enrollment, you will be subject to a late entrant or change penalty for the first 12 consecutive months of enrollment.

LONG-TERM DISABILITY

The city pays the full cost of your long-term disability insurance. You are automatically enrolled in this benefit and it is effective upon

hire. If you are partially or totally disabled for more than 180 days, the benefit pays 60% of your monthly pre-disability earnings to a

monthly maximum of $6,000.

To learn more about the city’s disability plans, go to denvergov.org/benefits or call the OHR Benefits Office at 720.913.5697.

For those hired by the city prior to January 1, 2010, and remain on the sick and vacation leave plans:

21

EMPLOYEE ASSISTANCE PROGRAM

The GuidanceResources® EAP provides support, resources and information for personal and work-life issues. These services are confidential and provided at no charge to you and your dependents.

These services are available with just a call or a click.

» Call 877.327.3854 or 800.697.0353 (TDD).

» Speak to a counseling professional who will help guide you to the appropriate services.

» Visit online at guidanceresources.com and enter Denver Web ID: DENVEREAP

DENVER EMPLOYEE FITNESS CENTER

The employee fitness center features a full complement of fitness equipment, exercise classes and services for city employees. The center is located in the Webb Municipal Building and is open for early morning workouts, as well as after work hours and on Saturdays. Members of the Denver Employee Fitness Center also have full access to all Denver recreation centers. For more information about the fitness center visit, denvergov.org/wellness or call 303.880.2295.

LEGAL SERVICES PLAN

UltimateAdvisor® Legal insurance from ARAG offers you affordable reliable counsel when something in life turns into a legal issue, like a dispute with a contractor, a traffic ticket or the need for estate planning including preparation of a trust. You’ll have the opportunity to voluntarily enroll in the legal plan within your first 30 days of hire, as well

as annually during the open enrollment period. For as little as $13.50 per month, you can enroll in the plan and have a place to turn to for help, with access to a nationwide network of attorneys who will:

» Work with you in person, over the phone or online to consult with you on legal issues

» Review or prepare documents

» Make follow-up calls or write letters on your behalf

» Represent you, if needed.

Attorney fees for most covered legal matters are 100% paid in full when you work with a Network Attorney, which means you’ll avoid paying high-cost attorney fees. It’s like having an attorney on retainer whenever you have a question or need guidance regarding a legal matter. For a complete list of exclusions or any other questions about the legal plan, call 800.247.4784 or visit ARAG’s website at ARAGLegalCenter.com.

TRANSPORTATION PROGRAMS

As a way to encourage alternative transportation, the city participates in, and subsidizes, the Regional Transportation District (RTD) costs of the EcoPass and ValuPass programs. Both programs allow employees the option to use RTD’s bus and light rail services as alternative transportation to and from work.

Enrollment advantages include:

» Reduced commuting costs and hassles

» Ability to pay for commuting expenses with pre-tax dollars

» Avoiding parking hassles

» Peace of mind provided by Guaranteed Ride Home Program sponsored by Denver Regional Council of Governments (Eco Pass only). Learn more at drcog.org.

Please contact the OHR Benefits Office at [email protected] or call 720.913.5697 to learn which program you qualify for and program requirements and costs.

RETIREMENT PLANNING

PENSION PLAN As a city employee, you are automatically enrolled in the Denver Employees Retirement Plan (DERP). It is a defined benefit plan, and current contributions are set at 11.5% of your total gross salary paid by the city and 8% of your total gross salary paid by you on a pre-tax basis. You are vested after 5 years of credited service. DERP offers a monthly retirement benefit, group health, dental and vision insurance, as well as disability and death benefits.

To learn more about DERP and your pension, go to derp.org or call 303.839.5419. DEFERRED COMPENSATION

The Deferred Compensation Plan 457(b) is a voluntary retirement savings program offered by the City and County of Denver to all employees through TIAA Financial Services. The plan is designed to supplement the city’s pension plan and provide additional financial and retirement planning options. You may elect payroll deductions on pre-tax and/or after-tax (Roth) basis. The city does not match deferred compensation contributions. You may enroll, increase or decrease your contributions at any time.

Employee contributions

» You may start, change or stop contributing by submitting a Salary Reduction Agreement at any time.

» You may contribute up to 100% of your income, or $18,000 annually, whichever is less. If you are age 50+, you may contribute up to $24,000 annually.

» You are always 100% vested in your own contributions.

You can get personalized retirement plan advice on the plan’s investment options from a TIAA Financial Consultant, at no additional cost to you.

To learn more about the Deferred Compensation plan and TIAA, call 855.259.4648 Monday through Friday, 6:00 a.m. - 8:00 p.m. or Saturday, 7:00 a.m. - 4:00 p.m. (MT) or go online tiaa.org/denver.

11AdditionalBenefits

22

12Work-Life

BalancePaid time off to support a work-life balance

COMPLETED YEARS OF SERVICE PTO HOURS ACCRUED PER MONTH

0–0.5 years 10 hours per month

0.5–5 years 12 hours per month

5–10 years 15 hours per month

10–15 years 18 hours per month

15 + years 19 hours per month

All employees hired after January 1, 2010, accrue paid time off (PTO). The amount of PTO you receive each year is based on the following chart taken from Career Service Authority Rule 10/Paid Leave.

COMPLETED YEARS OF SERVICE SICK HOURS ACCRUED PER MONTH VACATION HOURS ACCRUED PER MONTH

0–5 years 8 hours per month 8 hours per month

5–10 years 8 hours per month 10 hours per month

10–15 years 8 hours per month 12 hours per month

15 + years 8 hours per month 14 hours per month

All employees hired prior to January 1, 2010, may still accrue both sick and vacation leave. The amount of sick and vacation you receive each year is based on the following charts taken from Career Service Authority Rule 10/Paid Leave.

New Year’s Day Monday, January 2 (observed)

Martin Luther King Jr. Day Monday, January 16

Presidents’ Day Monday, February 20

Cesar Chavez Day Monday, March 27

Memorial Day Monday, May 29

Independence Day Tuesday, July 4

Labor Day Monday, September 4

Veterans Day Friday, November 10 (observed)

Thanksgiving Day Thursday, November 23

Christmas Day Monday, December 25

Personal holiday (upon an agreed date by you and your supervisor)

2017 PAID HOLIDAY SCHEDULE

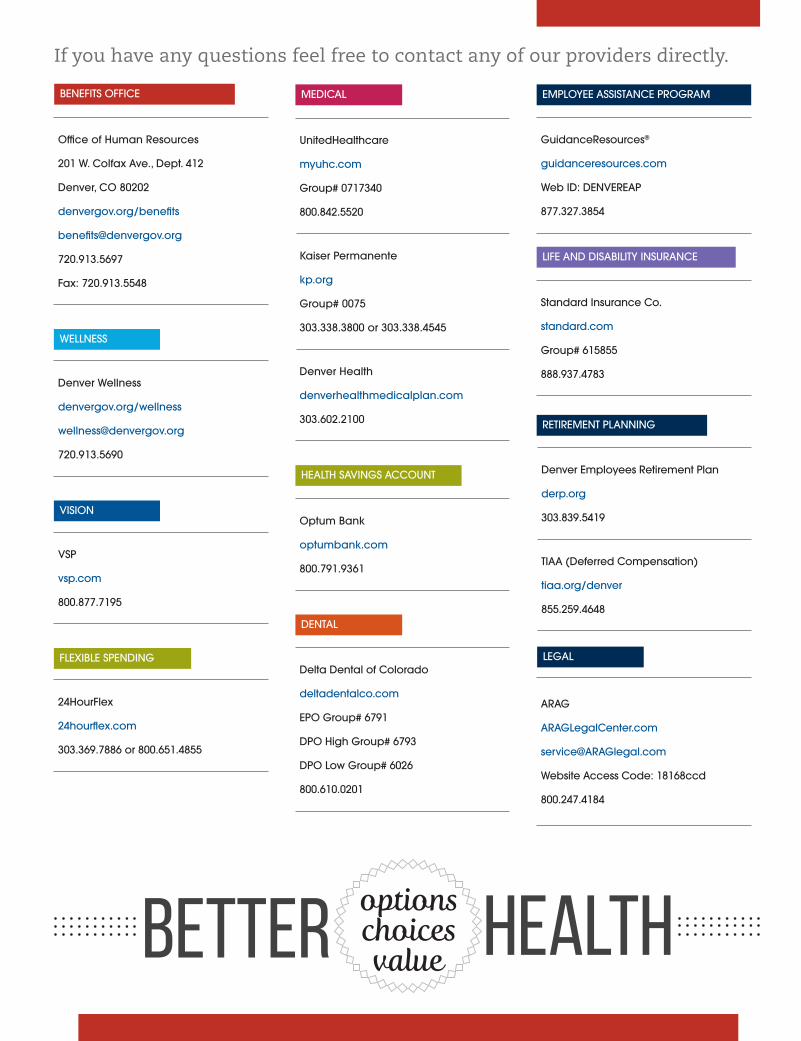

If you have any questions feel free to contact any of our providers directly.

UnitedHealthcare

myuhc.com

Group# 0717340

800.842.5520

Kaiser Permanente

kp.org

Group# 0075

303.338.3800 or 303.338.4545

Denver Health

denverhealthmedicalplan.com

303.602.2100

MEDICAL

Optum Bank

optumbank.com

800.791.9361

HEALTH SAVINGS ACCOUNT

VSP

vsp.com

800.877.7195

VISION

Delta Dental of Colorado

deltadentalco.com

EPO Group# 6791

DPO High Group# 6793

DPO Low Group# 6026

800.610.0201

DENTAL

GuidanceResources®

guidanceresources.com

Web ID: DENVEREAP

877.327.3854

EMPLOYEE ASSISTANCE PROGRAM

Office of Human Resources

201 W. Colfax Ave., Dept. 412

Denver, CO 80202

denvergov.org/benefits

720.913.5697

Fax: 720.913.5548

BENEFITS OFFICE

24HourFlex

24hourflex.com

303.369.7886 or 800.651.4855

FLEXIBLE SPENDING

Standard Insurance Co.

standard.com

Group# 615855

888.937.4783

LIFE AND DISABILITY INSURANCE

Denver Employees Retirement Plan

derp.org

303.839.5419

TIAA (Deferred Compensation)

tiaa.org/denver

855.259.4648

RETIREMENT PLANNING

ARAG

ARAGLegalCenter.com

Website Access Code: 18168ccd

800.247.4184

LEGAL

Denver Wellness

denvergov.org/wellness

720.913.5690

WELLNESS