Cielo S.A. · 2019-04-29 · Cielo S.A. Update to credit analysis Summary Cielo S.A.'s (Cielo) Ba1...

12

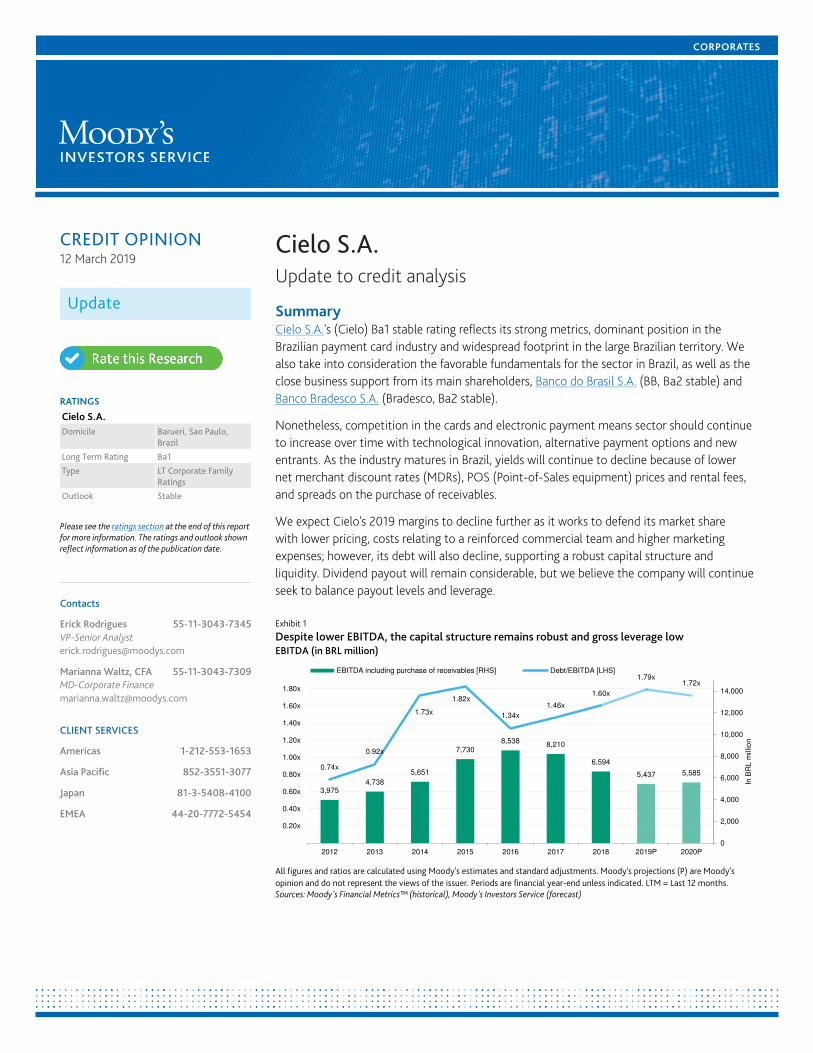

CORPORATES CREDIT OPINION 12 March 2019 Update RATINGS Cielo S.A. Domicile Barueri, Sao Paulo, Brazil Long Term Rating Ba1 Type LT Corporate Family Ratings Outlook Stable Please see the ratings section at the end of this report for more information. The ratings and outlook shown reflect information as of the publication date. Contacts Erick Rodrigues 55-11-3043-7345 VP-Senior Analyst [email protected] Marianna Waltz, CFA 55-11-3043-7309 MD-Corporate Finance [email protected] CLIENT SERVICES Americas 1-212-553-1653 Asia Pacific 852-3551-3077 Japan 81-3-5408-4100 EMEA 44-20-7772-5454 Cielo S.A. Update to credit analysis Summary Cielo S.A. 's (Cielo) Ba1 stable rating reflects its strong metrics, dominant position in the Brazilian payment card industry and widespread footprint in the large Brazilian territory. We also take into consideration the favorable fundamentals for the sector in Brazil, as well as the close business support from its main shareholders, Banco do Brasil S.A. (BB, Ba2 stable) and Banco Bradesco S.A. (Bradesco, Ba2 stable). Nonetheless, competition in the cards and electronic payment means sector should continue to increase over time with technological innovation, alternative payment options and new entrants. As the industry matures in Brazil, yields will continue to decline because of lower net merchant discount rates (MDRs), POS (Point-of-Sales equipment) prices and rental fees, and spreads on the purchase of receivables. We expect Cielo's 2019 margins to decline further as it works to defend its market share with lower pricing, costs relating to a reinforced commercial team and higher marketing expenses; however, its debt will also decline, supporting a robust capital structure and liquidity. Dividend payout will remain considerable, but we believe the company will continue seek to balance payout levels and leverage. Exhibit 1 Despite lower EBITDA, the capital structure remains robust and gross leverage low EBITDA (in BRL million) 3,975 4,738 5,651 7,730 8,538 8,210 6,594 5,437 5,585 0.74x 0.92x 1.73x 1.82x 1.34x 1.46x 1.60x 1.79x 1.72x 0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 0.20x 0.40x 0.60x 0.80x 1.00x 1.20x 1.40x 1.60x 1.80x 2012 2013 2014 2015 2016 2017 2018 2019P 2020P In BRL million EBITDA including purchase of receivables [RHS] Debt/EBITDA [LHS] All figures and ratios are calculated using Moody's estimates and standard adjustments. Moody's projections (P) are Moody's opinion and do not represent the views of the issuer. Periods are financial year-end unless indicated. LTM = Last 12 months. Sources: Moody's Financial Metrics™ (historical), Moody's Investors Service (forecast)

Transcript of Cielo S.A. · 2019-04-29 · Cielo S.A. Update to credit analysis Summary Cielo S.A.'s (Cielo) Ba1...

CORPORATES

CREDIT OPINION12 March 2019

Update

RATINGS

Cielo S.A.Domicile Barueri, Sao Paulo,

Brazil

Long Term Rating Ba1

Type LT Corporate FamilyRatings

Outlook Stable

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Erick Rodrigues 55-11-3043-7345VP-Senior [email protected]

Marianna Waltz, CFA 55-11-3043-7309MD-Corporate [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

Cielo S.A.Update to credit analysis

SummaryCielo S.A.'s (Cielo) Ba1 stable rating reflects its strong metrics, dominant position in theBrazilian payment card industry and widespread footprint in the large Brazilian territory. Wealso take into consideration the favorable fundamentals for the sector in Brazil, as well as theclose business support from its main shareholders, Banco do Brasil S.A. (BB, Ba2 stable) andBanco Bradesco S.A. (Bradesco, Ba2 stable).

Nonetheless, competition in the cards and electronic payment means sector should continueto increase over time with technological innovation, alternative payment options and newentrants. As the industry matures in Brazil, yields will continue to decline because of lowernet merchant discount rates (MDRs), POS (Point-of-Sales equipment) prices and rental fees,and spreads on the purchase of receivables.

We expect Cielo's 2019 margins to decline further as it works to defend its market sharewith lower pricing, costs relating to a reinforced commercial team and higher marketingexpenses; however, its debt will also decline, supporting a robust capital structure andliquidity. Dividend payout will remain considerable, but we believe the company will continueseek to balance payout levels and leverage.

Exhibit 1

Despite lower EBITDA, the capital structure remains robust and gross leverage lowEBITDA (in BRL million)

3,975 4,738

5,651

7,730 8,538

8,210

6,594

5,437 5,585 0.74x

0.92x

1.73x

1.82x

1.34x

1.46x

1.60x

1.79x1.72x

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0.20x

0.40x

0.60x

0.80x

1.00x

1.20x

1.40x

1.60x

1.80x

2012 2013 2014 2015 2016 2017 2018 2019P 2020P

In B

RL

mill

ion

EBITDA including purchase of receivables [RHS] Debt/EBITDA [LHS]

All figures and ratios are calculated using Moody's estimates and standard adjustments. Moody's projections (P) are Moody'sopinion and do not represent the views of the issuer. Periods are financial year-end unless indicated. LTM = Last 12 months.Sources: Moody's Financial Metrics™ (historical), Moody's Investors Service (forecast)

MOODY'S INVESTORS SERVICE CORPORATES

Credit strengths

» Favorable fundamentals for the cards and payment industries in Brazil

» Support from the main shareholders

» Adequate corporate governance and professional management

» Strong credit metrics

Credit challenges

» Expected increase in competition in the card and electronic payments industries

» Regulatory changes, which could exert pressure on the sector margins

» Continued considerable dividend payouts

» Rating constrained by the Government of Brazil's (Ba2 stable) rating

Rating outlookThe stable outlook reflects our view that Cielo will be able to sustain its good credit metrics despite a more difficult competitiveenvironment, and its significant dividend stream will not prevent future free cash flow (FCF) generation.

Factors that could lead to an upgradeAn upgrade of Cielo's rating would depend on an upgrade of Brazil's government bond rating, combined with the resilience of thecompany's credit metrics to the expected increase in competition in the sector.

Factors that could lead to a downgradeNegative pressure on Cielo's rating would arise (1) in case of a negative action on Brazil's government bond rating, (2) if Cielo's liquidityor credit metrics were to deteriorate significantly, or (3) if its FCF generation were to remain negative. Downward pressure would alsoarise in the case of a weakening in the company's market position.

Key indicators

Exhibit 2

Key indicatorsCielo S.A.

USD Millions Dec-13 Dec-14 Dec-15 Dec-16 Dec-17 Dec-18 Next 12 - 18 Months Forward View

Revenue 3,647.7 4,042.9 4,107.5 4,287.2 4,351.5 3,641.2 3,500 - 3,700

EBITA Margin % 54.0% 54.0% 53.1% 53.7% 55.0% 47.3% 38% - 40%

Debt / EBITDA 0.9x 1.7x 1.8x 1.3x 1.5x 1.6x 1.6x - 1.8x

EBITA / Interest Expense 22.0x 23.9x 5.5x 4.9x 6.4x 7.7x 6.5x - 8x

RCF / Net Debt 45.9% 36.7% 33.9% 48.6% 63.2% 18.8% 15% - 25%

All figures and ratios are calculated using Moody’s estimates and standard adjustments. Moody's Forecasts (f) or Projections (proj.) are Moody's opinion and do not represent the views ofthe issuer. Periods are Financial Year-End unless indicated. LTM = Last 12 months.Source: Moody’s Financial Metrics™

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 12 March 2019 Cielo S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

ProfileHeadquartered in the city of Barueri, Brazil, Cielo S.A. (Cielo) is the leading corporation in the merchant acquiring and paymentprocessing industry in Brazil, with presence in almost all Brazilian municipalities. With shares listed on B3 S.A. - Brasil, Bolsa, Balcao(B3, Ba1 stable), formerly BM&F Bovespa, Cielo is controlled by BB and Bradesco, which together hold 58.7% of the company's votingstocks and are the largest and fourth-largest commercial banks in Brazil, respectively, in terms of total assets. In 2018, Cielo's revenue,including the result of its purchase of receivables, was BRL13.2 billion ($3.6 billion at the average exchange rate) and its Moody's-adjusted EBITDA margin was 50%.

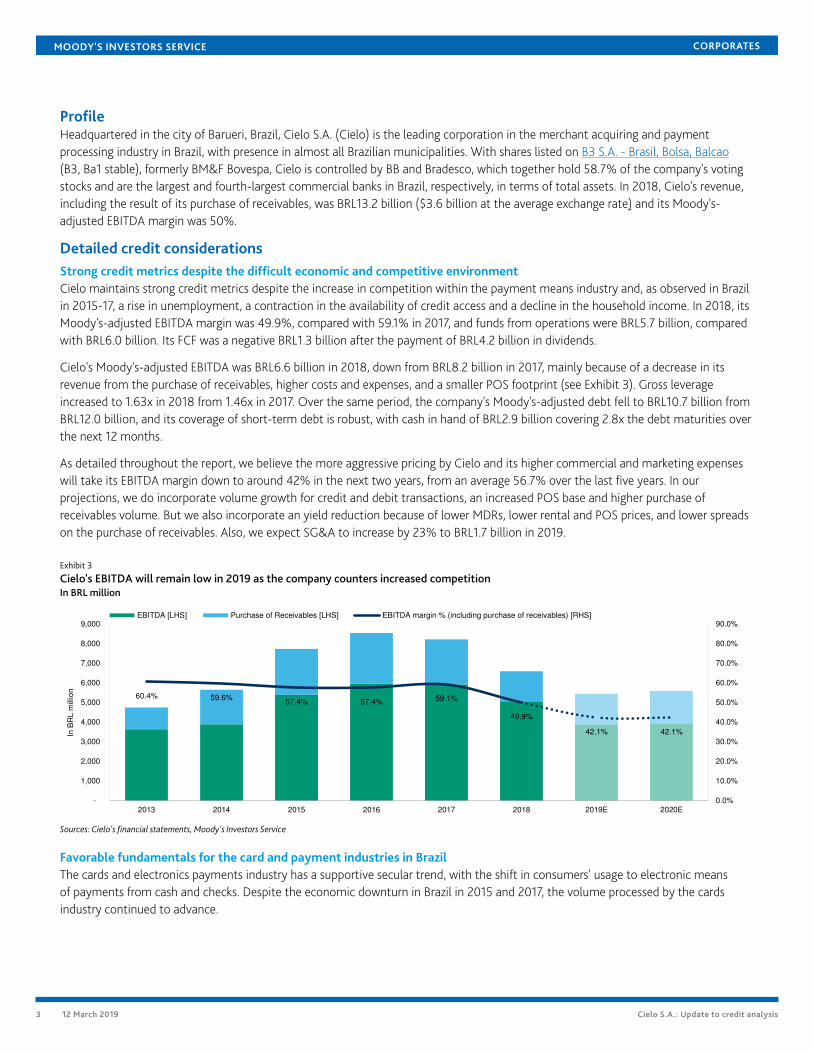

Detailed credit considerationsStrong credit metrics despite the difficult economic and competitive environmentCielo maintains strong credit metrics despite the increase in competition within the payment means industry and, as observed in Brazilin 2015-17, a rise in unemployment, a contraction in the availability of credit access and a decline in the household income. In 2018, itsMoody's-adjusted EBITDA margin was 49.9%, compared with 59.1% in 2017, and funds from operations were BRL5.7 billion, comparedwith BRL6.0 billion. Its FCF was a negative BRL1.3 billion after the payment of BRL4.2 billion in dividends.

Cielo's Moody's-adjusted EBITDA was BRL6.6 billion in 2018, down from BRL8.2 billion in 2017, mainly because of a decrease in itsrevenue from the purchase of receivables, higher costs and expenses, and a smaller POS footprint (see Exhibit 3). Gross leverageincreased to 1.63x in 2018 from 1.46x in 2017. Over the same period, the company's Moody's-adjusted debt fell to BRL10.7 billion fromBRL12.0 billion, and its coverage of short-term debt is robust, with cash in hand of BRL2.9 billion covering 2.8x the debt maturities overthe next 12 months.

As detailed throughout the report, we believe the more aggressive pricing by Cielo and its higher commercial and marketing expenseswill take its EBITDA margin down to around 42% in the next two years, from an average 56.7% over the last five years. In ourprojections, we do incorporate volume growth for credit and debit transactions, an increased POS base and higher purchase ofreceivables volume. But we also incorporate an yield reduction because of lower MDRs, lower rental and POS prices, and lower spreadson the purchase of receivables. Also, we expect SG&A to increase by 23% to BRL1.7 billion in 2019.

Exhibit 3

Cielo's EBITDA will remain low in 2019 as the company counters increased competitionIn BRL million

60.4% 59.6%57.4% 57.4% 59.1%

49.9%

42.1% 42.1%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2013 2014 2015 2016 2017 2018 2019E 2020E

In B

RL m

illio

n

EBITDA [LHS] Purchase of Receivables [LHS] EBITDA margin % (including purchase of receivables) [RHS]

Sources: Cielo's financial statements, Moody's Investors Service

Favorable fundamentals for the card and payment industries in BrazilThe cards and electronics payments industry has a supportive secular trend, with the shift in consumers' usage to electronic meansof payments from cash and checks. Despite the economic downturn in Brazil in 2015 and 2017, the volume processed by the cardsindustry continued to advance.

3 12 March 2019 Cielo S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

The payment card industry in Brazil has advanced continuously over 2007-18. The sector's expansion over the last several years wassupported by the country's economic growth and an increased level of domestic private consumption. In 2017, the volume of credit anddebit cards combined grew 7%, and in the 12 months ended September 2018, it grew 5.3%. Despite the economic recession when theGDP fell 3.5% annually, in 2015 and 2016, the supportive dynamics of the payment cards industry was apparent because the number oftransactions continued to grow (see Exhibit 4).

Exhibit 4

Credit and debit card transactions in BrazilIn billions

3.954.42

4.835.28

5.68 5.836.07

4.11

5.44 5.44

6.13

6.72

7.427.65

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

2012 2013 2014 2015 2016 2017 LTM Sept/18

Billio

n o

f tr

an

sa

ctio

ns

Credit Debit

Source: ABECS (Brazilian Association of Credit Cards and Services)

The future growth in electronic payments will be a consequence of the population's growing access to banking services, increasednumbers of internet/mobile transactions, and usage of credit cards, debit cards and other alternative means of payments to cash andchecks. Despite the significant expansion over the last years, payment cards are still underpenetrated in Brazil compared with that indeveloped countries. Credit and debit cards represented 29.6% of the consumption spending of Brazilian families as of the third quarterof 2018 (29.0% in 2017 and 28.4% in 2016), compared with levels as high as 40% in the US and over 50% in the UK, for example.

E-commerce also has strong growth potential in Brazil. According to Cielo, half of the internet transactions of Brazilian e-commercego through its platform. Market volume will increase as population continues to grow and income level rises, leading to changingconsumer habits and higher penetration of internet and mobile phones, along with an increased number of online shoppers. In Brazil,internet users represent 57.7% of the population and 37.6% are online buyers. This is equivalent to 62 million people buying productsand services online. In the US, 83.2% of the population are internet users and 66.1% are online buyers, according to eMarketer.

Although these secular changes favor an increasing volume of electronic transactions, margins in the sector will be compressed byhigher regulatory pressure, technological innovation and more companies entering the landscape, contributing to lower yields from(1) net MDRs, which is the remuneration of acquirers to process credit and debit card transactions net of interchange fees, networkfees and taxes; (2) the purchase of receivables from merchants and the spread on the amounts anticipated to merchants; and (3)the remuneration from POS services — either the monthly rental fees or that from the sale of equipment. In the acquiring business,we observed the quick advance of new entrants such as PagSeguro and Stone, which are not linked to banks and rely on their owndistribution network.

An expected increase in competition will drive margin pressure, but competitive position, financial flexibility, scale andinnovation capacity are leversDespite the tougher competitive environment, Cielo has proved its ability to maintain its dominant market position. In 2018, wesaw a more pronounced gain of market share by smaller companies, which drove Cielo's transaction volume to 41% of the markettotal in Q4 2018 from 48% in December 2017. Overall, the smaller companies (including mainly Banrisul, PagSeguro and Stone) havereached a combined 15% market share from only 2% in 2015. With the advance of other companies, Cielo has taken a more aggressivestance in terms of pricing in H2 2018 and, therefore, we should expect lower yields at least through 2019. Cielo has also reinforcedits commercial team and invested in marketing expenses as it moves to shield any further share deterioration. The industry's goodfundamentals and Cielo's solid business model, financial flexibility, large scale, wide distribution network and innovation capacity

4 12 March 2019 Cielo S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

should continue to translate into strong volume and help mitigate the market share deterioration recorded in 2018. As Exhibit 5shows, the number of debit transactions captured by Cielo considerably lagged market growth in 2018. With the increased strategicaggressiveness from Cielo, we expect improving volume trends. The increasing size of Cielo's POS base indicates the first leg of thisattack strategy.

Exhibit 5

The growth in POS base resumed in Q3 2018 will help boost transaction volumeQ1 2012 = 100 (financial volume of transactions and number of POS equipment)

0

50

100

150

200

250

300

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18

Q1

20

12

= 1

00

Cielo POS base Cielo Credit Cielo Debit Market Credit Market Debit

Sources: ABECS (Brazilian Association of Credit Cards and Services), Cielo, Moody's Investors Service

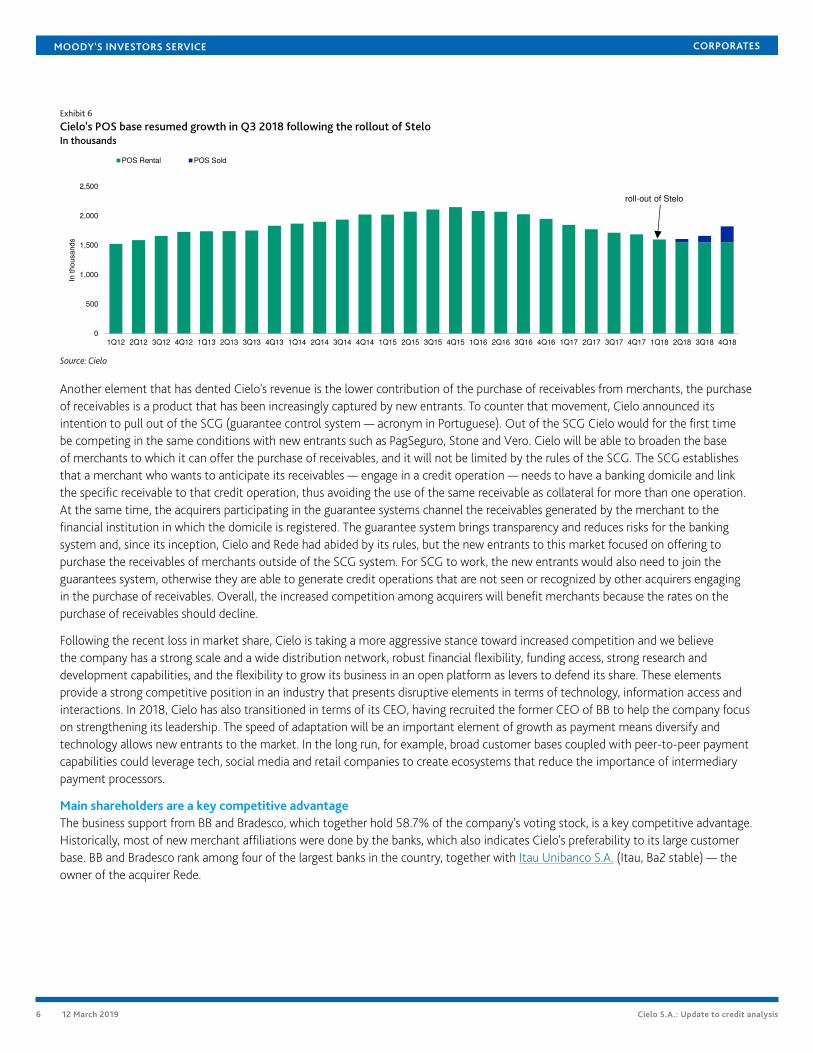

Cielo works on many fronts to perpetuate its strong leadership role in the Brazilian payment means market and diversify its sourcesof revenue. The most recent initiative is Stelo, a brand focused on micro entrepreneurs, a segment on which new entrants have beenfocusing. Stelo offers, for example, a prepaid card to users who do not own a checking account. Stelo's POS base as of Q1 2018 was4,000 machines and by December 2018, the footprint had already reached 483,000. In Q4 2018, Stelo captured BRL1.3 billion, closingthe year at BRL2 billion.

Also, Cielo has been pushing the rental of their 'LIO POS' and 'LIO+' — equipment that bundles functions such as bar-code readers,cashier and inventory management applications (Android platform), and invoice printers — on top of the regular POS functionalities;this was another factor that helped reverse the downward trend in POS numbers. Cielo has decided to sell its own Cielo POS, insteadof just renting it, and by the end of Q1 2019, we should have an idea about the impact of this strategy. The rollout of Stelo and LIO hashelped Cielo resume growth, reversing a downward trend that started in Q1 2016. We expect the upward trend to continue, as Cielohas become much more aggressive in pricing and reinforced its commercial team. A more robust POS base will help provide a highervolume of transactions, purchase of receivables and additional services.

5 12 March 2019 Cielo S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 6

Cielo's POS base resumed growth in Q3 2018 following the rollout of SteloIn thousands

0

500

1,000

1,500

2,000

2,500

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18

In t

ho

usa

nd

s

POS Rental POS Sold

roll-out of Stelo

Source: Cielo

Another element that has dented Cielo's revenue is the lower contribution of the purchase of receivables from merchants, the purchaseof receivables is a product that has been increasingly captured by new entrants. To counter that movement, Cielo announced itsintention to pull out of the SCG (guarantee control system — acronym in Portuguese). Out of the SCG Cielo would for the first timebe competing in the same conditions with new entrants such as PagSeguro, Stone and Vero. Cielo will be able to broaden the baseof merchants to which it can offer the purchase of receivables, and it will not be limited by the rules of the SCG. The SCG establishesthat a merchant who wants to anticipate its receivables — engage in a credit operation — needs to have a banking domicile and linkthe specific receivable to that credit operation, thus avoiding the use of the same receivable as collateral for more than one operation.At the same time, the acquirers participating in the guarantee systems channel the receivables generated by the merchant to thefinancial institution in which the domicile is registered. The guarantee system brings transparency and reduces risks for the bankingsystem and, since its inception, Cielo and Rede had abided by its rules, but the new entrants to this market focused on offering topurchase the receivables of merchants outside of the SCG system. For SCG to work, the new entrants would also need to join theguarantees system, otherwise they are able to generate credit operations that are not seen or recognized by other acquirers engagingin the purchase of receivables. Overall, the increased competition among acquirers will benefit merchants because the rates on thepurchase of receivables should decline.

Following the recent loss in market share, Cielo is taking a more aggressive stance toward increased competition and we believethe company has a strong scale and a wide distribution network, robust financial flexibility, funding access, strong research anddevelopment capabilities, and the flexibility to grow its business in an open platform as levers to defend its share. These elementsprovide a strong competitive position in an industry that presents disruptive elements in terms of technology, information access andinteractions. In 2018, Cielo has also transitioned in terms of its CEO, having recruited the former CEO of BB to help the company focuson strengthening its leadership. The speed of adaptation will be an important element of growth as payment means diversify andtechnology allows new entrants to the market. In the long run, for example, broad customer bases coupled with peer-to-peer paymentcapabilities could leverage tech, social media and retail companies to create ecosystems that reduce the importance of intermediarypayment processors.

Main shareholders are a key competitive advantageThe business support from BB and Bradesco, which together hold 58.7% of the company's voting stock, is a key competitive advantage.Historically, most of new merchant affiliations were done by the banks, which also indicates Cielo's preferability to its large customerbase. BB and Bradesco rank among four of the largest banks in the country, together with Itau Unibanco S.A. (Itau, Ba2 stable) — theowner of the acquirer Rede.

6 12 March 2019 Cielo S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 7

Market share of top Brazilian commercial banks is similar to that oftop acquirersMarket share in terms of total assets as of September 2018

Exhibit 8

Cielo and Rede should maintain a dominant share of cardstransactionsMarket share in terms of captured volume as of December 2018

BB

19%

Bradesco

15%

Itau

19%Santander

10%

Other

37%

Sources: BACEN, Moody's Investors Service

Cielo (BB+Bradesco)41%

Rede (Itau)31%

GetNet (Santander)13%

Stone7%

PagSeguro6%

Others2%

Sources: Cielo, Moody's Investors Services

The very concentrated bank system and vast territory constituted one of the main entry barriers to competition in the evolution ofthe payment means model in Brazil. The five largest financial institutions account for almost 90% of the branches spread throughoutthe country and have long-term relationships with merchants. In addition, the size of the country makes it difficult and very expensivefor newcomers to build sizable platforms and client bases — which are essential factors for the payment card industry, in which asignificant amount of costs are fixed and, in many cases, dependent on the number of transactions. The larger acquirers in Brazil arecontrolled by or work in partnership with banks, for example, Itau's Rede, and Banco Santander (Brasil) S.A.'s (Santander, Ba1 stable)Getnet and Banco do Estado do Rio Grande do Sul S.A. (Banrisul, Ba3 stable).

Although bank relationships have been the most common channel for merchants to maintain an acquirer relationship and POSequipment, new entrants such as Stone and PagSeguro rely on their own distribution network. The marketing investment has alsogained importance, helping acquirers reach merchants via advertisements in social media, radio, TV and outdoors, for example.

Adequate corporate governance and professional managementWe consider Cielo's corporate governance standards as adequate. Cielo's controlling shareholders are BB and Bradesco, which togetherhold 58.7% of its shares, while the balance is in free float. The company is listed on B3 and on OTC Nasdaq International, throughlevel I American depositary receipts, and is part of the Novo Mercado, the highest level of corporate governance standards in Brazil.The company's management is professional and its board of directors has 11 members, three of them independent. Cielo has an auditcommittee, in addition to finance, personnel, sustainability and corporate governance committees.

Regulatory changes could exert margin pressure on the sectorThe Brazilian government and its central bank have consistently shown their willingness to promote changes in the card industryto favor the consumers and merchants, reducing their costs for operating and using credit and debit cards. In April 2017, Cielowas authorized as a payment institution regulated by the Central Bank of Brazil (BACEN), which brings better transparency to therelationship between the regulator and the acquirer companies and is a positive step toward developing this market.

A key development, which has been taking shape in the last few years, and quickly advanced in 2017, was the migration to the full-acquirer model from a multivan model. The full-acquirer model is the one that most stimulates competition by allowing the acquirersto capture, process and settle the transactions, while in the multivan model, the acquirer captures the transactions and anothercompany processes and settles it. In full-year 2017, 3.3% of Cielo's total financial volume was processed via multivan; in 2018, thepercentage was down to 0.5%, and it will converge to zero. The impact for Cielo represents a loss of the multivan volume, which issomewhat compensated by new volume from other brands such as Amex and Hyper.

We can expect the regulations to continue changing. Out of other measures that could hurt acquirers, we note a desire to promote areduction in the payment cycle of the credit card receivables to merchants from the current 30 days to a lesser term. In 2017, BACEN

7 12 March 2019 Cielo S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

announced its intentions to bring that term down to as low as two days, but did not go through with the proposal. More than theacquirers, the banks would face a big impact from this proposed change and, therefore, we do not believe such a measure would beapplied in the form described; although in the long term, this is something that will be monitored by the regulator. A lower term forprepayment of receivables would dent Cielo's revenue, but it is important to note that the smaller companies in the acquiring business,such as PagSeguro and Stone, have stronger reliance on the purchase of receivables than Cielo and would record a more significantdrop in revenue, all else being equal. In 2018, the average term of purchase of receivables for Cielo was 50.4 days, down from anaverage 61 days in 2013, and the amount anticipated represented 16.3% of the financial credit card volume.

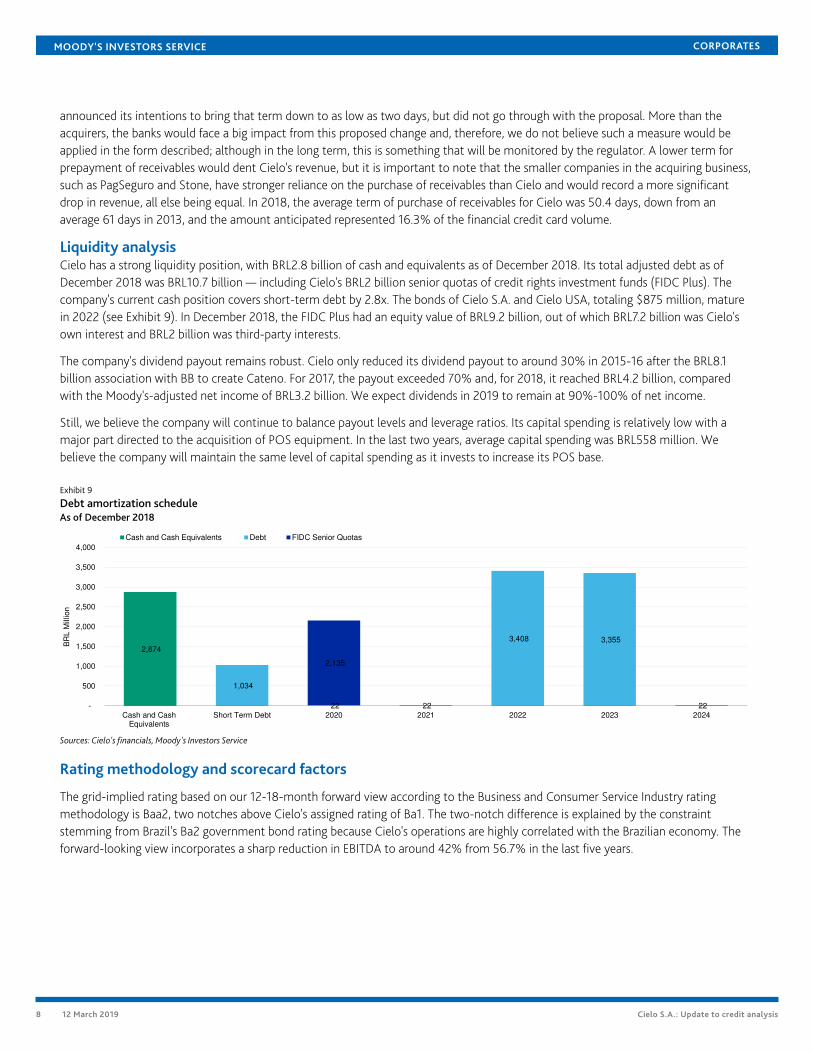

Liquidity analysisCielo has a strong liquidity position, with BRL2.8 billion of cash and equivalents as of December 2018. Its total adjusted debt as ofDecember 2018 was BRL10.7 billion — including Cielo's BRL2 billion senior quotas of credit rights investment funds (FIDC Plus). Thecompany's current cash position covers short-term debt by 2.8x. The bonds of Cielo S.A. and Cielo USA, totaling $875 million, maturein 2022 (see Exhibit 9). In December 2018, the FIDC Plus had an equity value of BRL9.2 billion, out of which BRL7.2 billion was Cielo'sown interest and BRL2 billion was third-party interests.

The company's dividend payout remains robust. Cielo only reduced its dividend payout to around 30% in 2015-16 after the BRL8.1billion association with BB to create Cateno. For 2017, the payout exceeded 70% and, for 2018, it reached BRL4.2 billion, comparedwith the Moody's-adjusted net income of BRL3.2 billion. We expect dividends in 2019 to remain at 90%-100% of net income.

Still, we believe the company will continue to balance payout levels and leverage ratios. Its capital spending is relatively low with amajor part directed to the acquisition of POS equipment. In the last two years, average capital spending was BRL558 million. Webelieve the company will maintain the same level of capital spending as it invests to increase its POS base.

Exhibit 9

Debt amortization scheduleAs of December 2018

2,874

1,034

22 22

3,408 3,355

22

2,135

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Cash and CashEquivalents

Short Term Debt 2020 2021 2022 2023 2024

BR

L M

illio

n

Cash and Cash Equivalents Debt FIDC Senior Quotas

Sources: Cielo's financials, Moody's Investors Service

Rating methodology and scorecard factors

The grid-implied rating based on our 12-18-month forward view according to the Business and Consumer Service Industry ratingmethodology is Baa2, two notches above Cielo's assigned rating of Ba1. The two-notch difference is explained by the constraintstemming from Brazil's Ba2 government bond rating because Cielo's operations are highly correlated with the Brazilian economy. Theforward-looking view incorporates a sharp reduction in EBITDA to around 42% from 56.7% in the last five years.

8 12 March 2019 Cielo S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 10

Rating factorsCielo S.A.

Business and Consumer Service Industry Grid [1][2]

Factor 1 : Scale (20%) Measure Score Measure Score

a) Revenue (USD Billion) $3.6 Ba $3.5 - $3.7 Ba

Factor 2 : Business Profile (20%)

a) Demand Characteristics Baa Baa Baa Baa

b) Competitive Profile Baa Baa Baa Baa

Factor 3 : Profitability (10%)

a) EBITA Margin 47.3% Aa 38% - 40% Aa

Factor 4 : Leverage and Coverage (40%)

a) Debt / EBITDA 1.6x A 1.6x - 1.8x A

b) EBITA / Interest 7.7x Baa 6.5x - 8x Baa

c) RCF / Net Debt 18.8% Ba 15% - 25% Ba

Factor 5 : Financial Policy (10%)

a) Financial Policy Baa Baa Baa Baa

Rating:

a) Indicated Rating from Grid Baa2 Baa2

b) Actual Rating Assigned Ba1

Current

FY 12/31/2018

Moody's 12-18 Month Forward View

As of 2/22/2019 [3]

[1] All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations.[2] As of 12/31/2018(L).[3] This represents Moody's forward view, not the view of the issuer, and unless noted in the text, does not incorporate significant acquisitions and divestitures.Source: Moody's Financial Metrics™

Ratings

Exhibit 11Category Moody's RatingCIELO S.A.

Outlook StableCorporate Family Rating Ba1Senior Unsecured Ba1

CIELO USA INC.

Outlook StableBkd Senior Unsecured Ba1

Source: Moody's Investors Service

9 12 March 2019 Cielo S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

Appendix

Exhibit 12

Peer snapshotCielo S.A.

(in USD millions)

FYE

Dec-16

FYE

Dec-17

FYE

Dec-18

FYE

Dec-16

FYE

Dec-17

LTM

Sep-18

FYE

Dec-16

FYE

Dec-17

LTM

Sep-18

FYE

Dec-16

FYE

Dec-17

LTM

Sep-18

Revenue $4,287 $4,352 $3,641 $4,170 $4,928 $4,283 $2,203 $3,975 $3,540 $11,584 $12,052 $10,249

EBITDA $2,461 $2,572 $1,816 $1,171 $1,323 $1,407 $699 $1,169 $1,338 $2,855 $3,010 $3,167

Total Debt $3,521 $3,614 $2,777 $3,816 $3,656 $4,358 $5,069 $5,649 $5,814 $18,967 $19,677 $18,213

Cash & Cash Equiv. $817 $1,816 $742 $425 $450 $485 $1,163 $1,336 $991 $385 $498 $601

EBITA Margin 53.7% 55.0% 47.3% 23.0% 22.1% 27.2% 28.9% 25.7% 33.0% 21.5% 21.8% 27.0%

EBITA / Int. Exp. 4.9x 6.4x 7.7x 7.1x 8.0x 6.9x 5.4x 5.5x 6.0x 2.3x 2.7x 2.9x

Debt / EBITDA 1.3x 1.5x 1.6x 3.3x 2.8x 3.1x 7.3x 4.8x 4.3x 6.6x 6.5x 5.8x

RCF / Net Debt 48.6% 63.2% 18.8% 24.5% 30.2% 29.2% 10.1% 21.9% 23.4% 9.9% 11.4% 13.5%

FCF / Debt 28.0% 23.6% -11.9% 15.4% 19.2% 17.1% 8.1% 5.6% 10.3% 7.0% 6.5% 8.0%

Cielo S.A. Total System Services, Inc Global Payments Inc. First Data Corporation

Ba1 Stable Baa3 Stable Ba2 Positive Ba3 RUR-UPG

All figures & ratios calculated using Moody’s estimates & standard adjustments. FYE = Financial year-end. LTM = Last 12 months. RUR* = Ratings under review, where UPG = for upgradeand DNG = for downgrade.Source: Moody’s Financial Metrics™

Exhibit 13

Moody's-adjusted debt breakdownCielo S.A.

(in USD Millions)

FYE

Dec-13

FYE

Dec-14

FYE

Dec-15

FYE

Dec-16

FYE

Dec-17

FYE

Dec-18

As Reported Debt 1,054.8 2,761.2 3,361.6 3,315.5 2,787.2 2,028.8

Operating Leases 793.5 901.5 194.7 194.5 212.9 189.8

Non-Standard Adjustments 4.1 5.0 4.5 10.6 613.6 558.3

Moody's-Adjusted Debt 1,852.4 3,667.6 3,560.8 3,520.6 3,613.7 2,776.9

All figures are calculated using Moody’s estimates and standard adjustments.Source: Moody’s Financial Metrics™

Exhibit 14

Moody's-adjusted EBITDA breakdownCielo S.A.

(in USD Millions)

FYE

Dec-13

FYE

Dec-14

FYE

Dec-15

FYE

Dec-16

FYE

Dec-17

FYE

Dec-18

As Reported EBITDA 2,114.5 2,285.3 2,303.8 2,437.9 2,531.6 1,813.0

Operating Leases 87.1 125.6 68.0 57.8 73.7 24.1

Unusual 1.2 1.5 1.0 5.0 2.3 1.7

Non-Standard Adjustments 1.0 -4.9 -14.9 -39.5 -36.1 -22.4

Moody's-Adjusted EBITDA 2,203.8 2,407.6 2,357.9 2,461.2 2,571.5 1,816.4

All figures are calculated using Moody’s estimates and standard adjustments.Source: Moody’s Financial Metrics™

10 12 March 2019 Cielo S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

© 2019 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEEMOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’SRATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDITRATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAYALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDITRATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONSARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONSCOMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONSWITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDERCONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSESAND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDITRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for ratings opinions and services rendered by it fees ranging from $1,000 to approximately $2,700,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as tothe creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for ratings opinions and services rendered by it feesranging from JPY125,000 to approximately JPY250,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1142170

11 12 March 2019 Cielo S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

Contacts

Erick Rodrigues +55.11.3043.7345VP-Senior [email protected]

Patricia I Maniero +55.11.3043.6066Associate [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

12 12 March 2019 Cielo S.A.: Update to credit analysis