CIAA Accounting Update - cdn.ymaws.com · CIAA Accounting Update Financial Reporting Developments...

115

CIAA Accounting Update Financial Reporting Developments 2015

Transcript of CIAA Accounting Update - cdn.ymaws.com · CIAA Accounting Update Financial Reporting Developments...

CIAA Accounting Update

Financial Reporting Developments 2015

Page 2

Today’s Presenters

Financial Reporting Developments 2015

Doru Pantea, CPA, CAPartner, EY

[email protected] 943 3997

Haseeb Jalal, CPA, CASenior Manager, EY

Page 3

Financial Reporting Standards

▶ Overall Agenda ▶ IASB Work Plan Update

▶ Continuous Disclosure Improvement

▶ IFRS 9 - Financial Instruments

▶ IFRS 4 – Insurance Contracts

▶ Lease Project Update

▶ IFRS 15 - Revenue from Contracts with Customers

▶ Regulatory Update

▶ Comment Letters – Common themes

▶ Appendixes

▶ Appendix I – IFRS Discussion Group Updates

▶ Appendix II – Narrow Scope Amendments

Financial Reporting Developments 2015

Page 4

IASB Work Plan Update

Financial Reporting Developments 2015

Page 5

Major IFRS projects at a glance

Financial Reporting Developments 2015

Next Major Milestones2015 Q1 2015 Q2 Current

ActivityWithin 3 months

Within 6 months

After 6 months

Insurance Contracts Analysis Issue IFRSLeases Analysis Issue IFRS

Conceptual FrameworkExposure

Draft Issued

Public Consultatio

n

Decide Project

Direction

Disclosure Initiative - Changes in accounting policies and estimates

AnalysisPublish

Exposure Draft

Disclosure Initiative - Materiality Practice Statement

Drafting Exposure

Draft

Target Exposure

Draft

Dynamic Risk Management: a Portfolio Revaluation Approach to Macro Hedging

AnalysisPublish

Discussion Paper

Rate-regulated Activities AnalysisPublish

Discussion Paper

Disclosure Initiative - Principles of disclosure Analysis

Publish Discussion

Paper

Page 6

Other Projects Update

Financial Reporting Developments 2015

Next Major Milestones

Current Activity

Within 3 months

Within 6 months

After 6 months

Narrow-scope amendments

Annual improvements Drafting ED Publish ED

Clarifications Arising from the Post-implementation review (IFRS 8) Drafting ED Publish ED

Clarifications of Classification and Measurement of Share-based Payment Transactions (IFRS 2)

Analysis Decide Project Direction

Clarification to IFRS 15 Revenue from Contracts with Customers: Issues Emerging from TRG Discussion

Public Consultation

Decide Project Direction

Classification of Liabilities (IAS 1)Public

ConsultationDecide Project

Direction

Disclosure Initiative-Amendments to IAS 7 Analysis Decide Project

Direction

Effective Date of Amendments to IFRS 10 and IAS 28 Drafting ED Publish ED

Page 7

Other Projects Update

Next Major Milestones

Current Activity

Within 3 months

Within 6 months

After 6 months

Narrow-scope amendments (con't.)

Fair Value Measurement: Unit of Account Analysis Issue IFRS

Recognition of Deferred Tax Assets for Unrealized Losses (IAS 12) Drafting IFRS Issue IFRS

Remeasurement at a Plan Amendment, Curtailment or Settlement / Availability of a Refund of a Surplus from a Defined Benefit Plan (IAS 19 and IFRIC 14)

Public Consultation

Decide Project Direction

Transfers of Investment Property (IAS 40) Drafting ED Publish ED

InterpretationsDraft IFRIC Interpretation – Uncertainties in Income Taxes Drafting DI Publish DI

Draft IFRIC Interpretation – Foreign Currency Transactions and Advance Consideration

Drafting DI Publish DI

Financial Reporting Developments 2015

Page 8

Continuous Disclosure Improvement

Financial Reporting Developments 2015

Page 9

IASB Disclosure Initiative

▶ IASB is currently undergoing a number of implementation and research projects, including materiality, IAS 1 Presentation of Financial Statements, IAS 7 Statement of Cash Flows, and IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors

▶ IASB has issued amendments to IAS 1 effective 1 January 2016

▶ IASB has also issued an exposure draft proposing amendments to IAS 7

Financial Reporting Developments 2015

Page 10

IASB Disclosure InitiativeAmendments to IAS 1▶ Narrow-focus improvements in the following five areas:

▶ Materiality – do not obscure material information with immaterial information; do not aggregate material items that have different natures or functions

▶ Disaggregation and subtotals – specific line items in statements of profit or loss and OCI and statement of financial position may be disaggregated; new requirements for presentation of additional subtotals

▶ Notes structure – entities have flexibility as to order of presentation of notes to the financial statements; however, must consider understandability and comparability when deciding on order

▶ Disclosure of accounting policies – removal of example significant policies

▶ Presentation of items of other comprehensive income (OCI) arising from equity accounted investments – share of OCI of associates and joint ventures accounted for using equity method must be presented in aggregate as a single line item, classified between those items that will or will not be subsequently reclassified to profit or loss

▶ Applicable to annual periods beginning on or after January 1, 2016

Financial Reporting Developments 2015

Page 11

IASB Disclosure InitiativeProposed amendments to IAS 7

▶ IASB proposing disclosing reconciliation of amounts in the opening and closing statements of financial position for each item classified as financing activities in the statement of cash flows, excluding equity items▶ Intended to provide investors with disclosures about movements in

an entity’s debt during the reporting period▶ IASB proposing to extend disclosures required by IAS 7 about

an entity’s liquidity re: restrictions over an entity’s decisions to use cash and cash equivalent balances, including tax liabilities that would arise on repatriation of foreign cash and cash equivalent balances▶ Intended to allow users of the financial statements to better assess

the accessibility of cash and cash equivalents▶ Proposed amendments would be applied retrospectively▶ Comment period closed on April 17, 2015▶ We believe proposed amendments may increase disclosure

overloadFinancial Reporting Developments 2015

Page 12

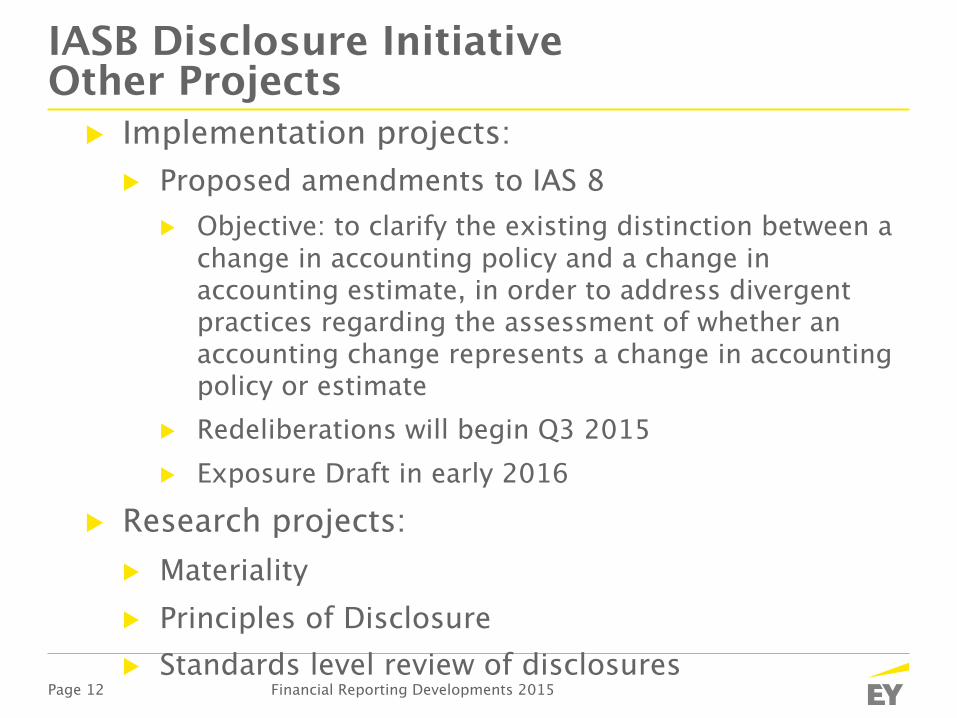

IASB Disclosure InitiativeOther Projects

▶ Implementation projects:▶ Proposed amendments to IAS 8

▶ Objective: to clarify the existing distinction between a change in accounting policy and a change in accounting estimate, in order to address divergent practices regarding the assessment of whether an accounting change represents a change in accounting policy or estimate

▶ Redeliberations will begin Q3 2015▶ Exposure Draft in early 2016

▶ Research projects:▶ Materiality▶ Principles of Disclosure▶ Standards level review of disclosures

Financial Reporting Developments 2015

Page 13

IFRS 9: Financial Instruments

Financial Reporting Developments 2015

Page 14

IFRS 9: Financial Instruments – Overview

▶ On 24 July 2014, the International Accounting Standards Board (IASB) issued the final version of IFRS 9, bringing together all three phases of the financial instruments project ▶ Classification and measurement▶ Impairment (expected credit losses) ▶ Hedge accounting

▶ IFRS 9 is effective for annual periods beginning on or after 1 January 2018, with early application permitted

▶ Impairment Transition Resource Group (ITG) established by the IASB to provide support for stakeholders on implementation issues

Financial Reporting Developments 2015

Page 15

IFRS 9: Financial Instruments - Classification & Measurement – Assets

Debt (including hybrid contracts)

“Characteristics” test (at instrument level)

“Business model” test (at an aggregated level)

Conditional FVO elected?

Fail

Pass

No

Amortised cost FVTPL

FVOCI(with

recycling)

Hold to collect contractual cash flows

Neither (1) nor (2)

Both (a) to hold to collect contractual cash flows; and (b) to sell

1 32

No

Yes

Derivatives Equity

Held for trading?

FVOCI option elected ?

Yes

No

No

Yes

FVOCI(no recycling)

Financial Reporting Developments 2015

About color themesChoose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

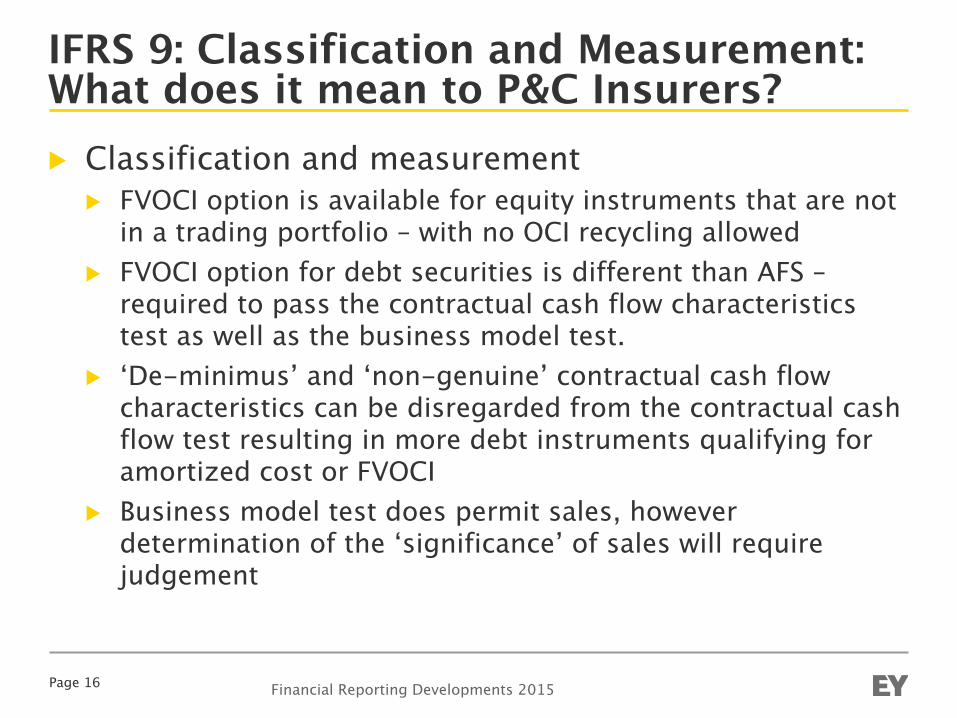

IFRS 9: Classification and Measurement: What does it mean to P&C Insurers?▶ Classification and measurement

▶ FVOCI option is available for equity instruments that are not in a trading portfolio – with no OCI recycling allowed

▶ FVOCI option for debt securities is different than AFS – required to pass the contractual cash flow characteristics test as well as the business model test.

▶ ‘De-minimus’ and ‘non-genuine’ contractual cash flow characteristics can be disregarded from the contractual cash flow test resulting in more debt instruments qualifying for amortized cost or FVOCI

▶ Business model test does permit sales, however determination of the ‘significance’ of sales will require judgement

Page 16 Financial Reporting Developments 2015

Page 17

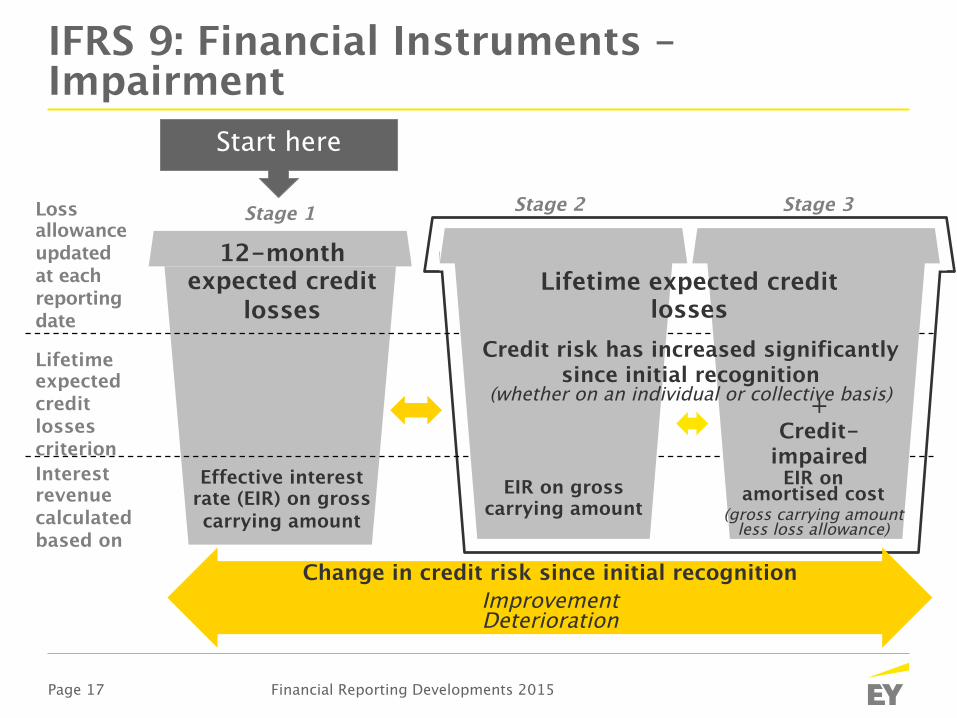

IFRS 9: Financial Instruments – Impairment

Stage 1Loss allowance updated at each reporting date

12-month expected credit

losses

Lifetime expected credit losses criterionInterest revenue calculated based on

Effective interest rate (EIR) on gross carrying amount

Change in credit risk since initial recognitionImprovement Deterioration

Start here

Lifetime expected credit losses

Credit risk has increased significantly since initial recognition

(whether on an individual or collective basis)+Credit-

impairedEIR on gross

carrying amountEIR on

amortised cost(gross carrying amount

less loss allowance)

Stage 2 Stage 3

Financial Reporting Developments 2015

Page 18

IFRS 9: Financial Instruments – Impairment▶ General approach

▶ Lifetime expected credit losses result from all possible default events over the expected life

▶ 12-month expected credit losses are the portion of lifetime expected credit losses that result from default events that are possible within the 12 months after the reporting date

▶ ‘Default’ is not defined by the StandardFinancial Reporting Developments 2015

Expected credit losses

Present value of cash shortfalls over the remaining life, discounted at the original effective interest rate▶ Unbiased and probability-weighted amount▶ Representing the time value of money▶ Based on reasonable and supportable

information

Page 19

IFRS 9: Financial Instruments – Impairment▶ Simplified approach

▶ No tracking of changes in credit risk▶ Loss allowance based on lifetime expected credit losses

▶ Use of practical expedient for most P&C companies

Financial Reporting Developments 2015

Scope

▶ Required for trade receivables or contract assets that do not contain a significant financing component

▶ Policy choice for trade receivables or contract assets that do contain a significant financing component

▶ Policy choice for lease receivables▶ Scope is largely built on definitions in IFRS

15

Page 20

IFRS 9: Financial Instruments – Impairment▶ Practical expedient – provision matrix

▶ Use of historical credit loss experience adjusted on the basis of current observable data, forecast of economic conditions

▶ Use of fixed provision rates depending on the number of days a financial asset such as premium receivable is past due

▶ Appropriate grouping if historical loss experience shows significantly different loss patterns for different segments

Financial Reporting Developments 2015

DPD Provision rate Gross carrying amount Lifetime ECLCurrent 0.5% CU5,000,000 CU25,0001-30 1.5% CU2,000,000 CU30,00031-60 3.5% CU1,000,000 CU35,00061-90 7% CU500,000 CU35,000> 90 11% CU200,000 CU22,000

CU7,700,000 CU147,000

About color themesChoose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

IFRS 9: Impairment of Financial Assets: What does it mean to P&C Insurers?

▶ Impairment of financial assets▶ The ECL model is expected to increase in recognized

impairment losses for most entities – specifically financial institutions

▶ Historical data must be gathered to model ECL which will impact an entity’s systems and processes

▶ Measurement of impairment losses for financial assets has been streamlined. The ECL approach, for assets that are not FVTPL, is the same regardless of the type of instrument held or how it is classified

▶ Simplified ECL approaches are available for specific instruments

Page 21 Financial Reporting Developments 2015

About color themesChoose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

General approach - simplifications and presumptions for assessing deterioration

Page 22

Use change in 12-month risk as

approximation for change in lifetime risk

Assessment on a collective basis or

at counterparty level

Set transfer threshold by determining maximum

initial credit risk

30 days past due ‘backstop’

‘Low’ credit risk – equivalent to

‘investment grade’

Assessing

significant

increases in credit

risk

Financial Reporting Developments 2015

About color themesChoose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

IFRS 9: Impairment of Financial Assets: Key decisions to be made for P&C Insurers▶ Simplified approach vs general approach?

▶ Simplified approach - Assess the impact of the lifetime ECL – will result in a larger upfront loss, but less rigorous process

▶ General Approach - Develop a more rigorous process, but lower upfront loss

▶ If electing the general approach – to what extent should a practical expedient be used?▶ For P&C companies, there are no limitations on the use of

practical expedients

Page 23 Financial Reporting Developments 2015

Page 24

IFRS 9: Financial Instruments – Hedge Accounting

Financial Reporting Developments 2015

Requirement IAS 39 IFRS 9Risk component as eligible hedged item Financial

Items All Items

Hedging of aggregated exposures X !"

80%-125% test !" XRetrospective effectiveness testing !" XQuantitative effectiveness test !" DependsQualitative effectiveness test X DependsRebalancing of hedge ratio X !"

Accounting for ‘costs of hedging’ X !"

Dedesignation (risk management objective unchanged) !" X

Fair value option for own use contracts ! !"

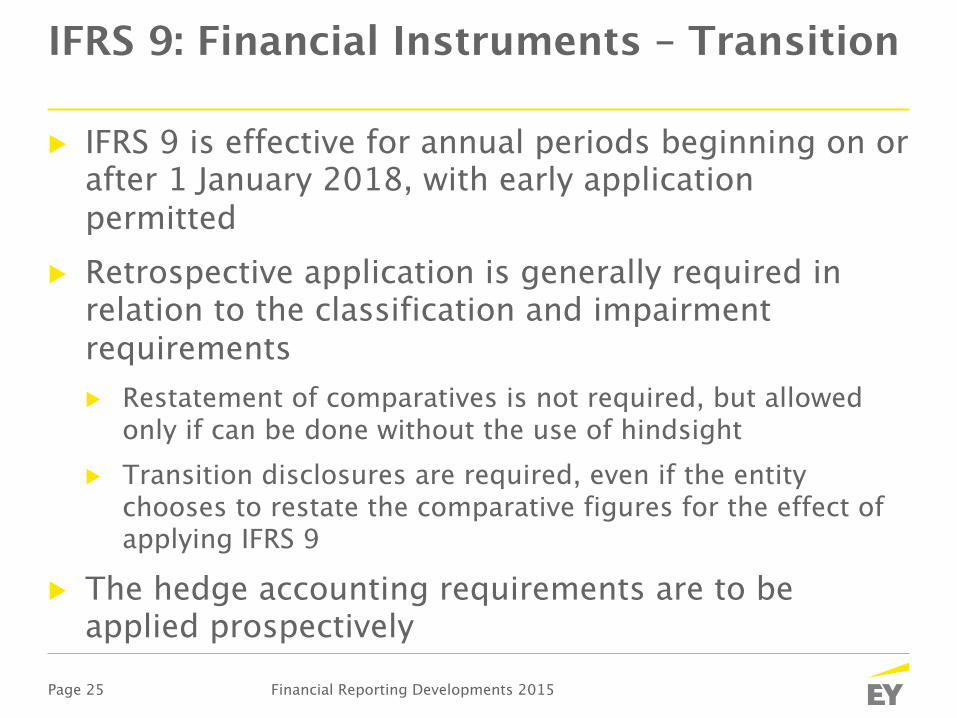

Page 25

IFRS 9: Financial Instruments – Transition

▶ IFRS 9 is effective for annual periods beginning on or after 1 January 2018, with early application permitted

▶ Retrospective application is generally required in relation to the classification and impairment requirements▶ Restatement of comparatives is not required, but allowed

only if can be done without the use of hindsight▶ Transition disclosures are required, even if the entity

chooses to restate the comparative figures for the effect of applying IFRS 9

▶ The hedge accounting requirements are to be applied prospectively

Financial Reporting Developments 2015

Page 26

IFRS 4: Insurance Contracts

Financial Reporting Developments 2015

Page 27

Timelines - New IFRS for insurance contracts

Ongoing IASB deliberations Implementation period Reporting

IFRS

4 P

hase

IIIF

RS 9

Potential IFRS 4 Phase II Final standard

Potential IFRS 4 Phase II effective date 1 Jan 2020?

Potential IFRS 4 Phase II first annual financial statements?

IFRS 4 Phase II Re-exposure Draft

Potential IFRS 4 Phase II start of comparative period?

Start of IFRS 9 comparative period

IFRS 9Final Standard

2013

IFRS 9 Effective date 1 Jan 2018

Possible revised IFRS 9 classification from IFRS 4 Phase II transition?

First IFRS 9 annual financial statements

2014 2015 2016 2017 2018 2019 2020

A solution for insurers under discussion

Financial Reporting Developments 2015

Page 28

IASB proposal General model

Expected value of future cash flows

Discount rate

Risk adjustment

Contractual service margin

Reinsurance

Disaggregation

PresentationSeparation

Definition and scope Disclosure

Regulatory Frameworks

Financial Instruments and other accounting changes

Transition

Premium Allocation Approach

Build

ing

Bloc

k A

ppro

ach

Financial Reporting Developments 2015

Page 29

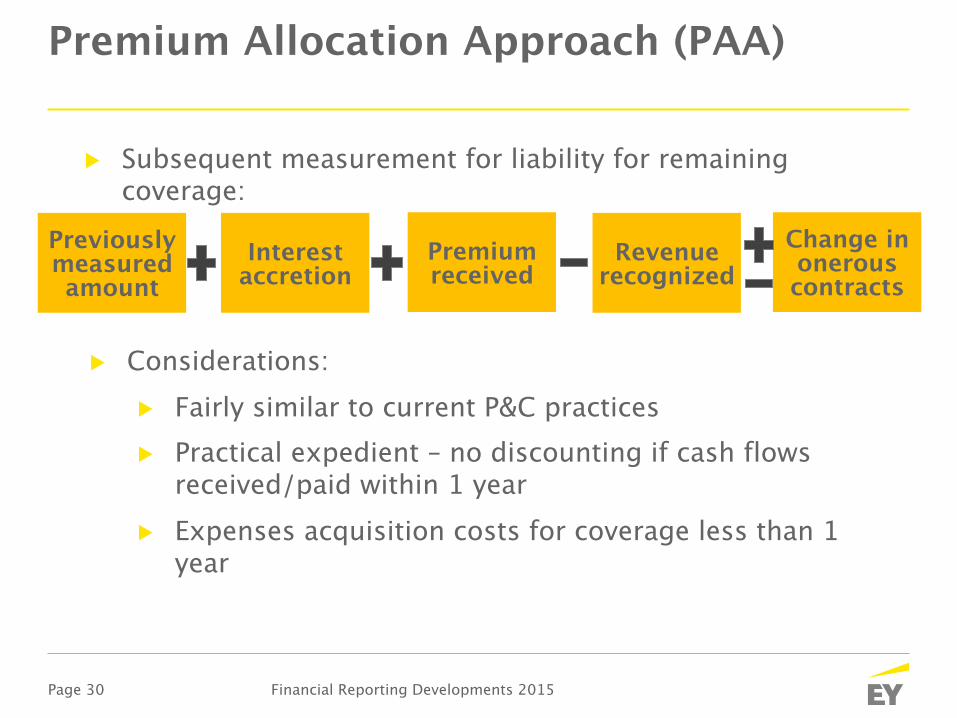

Premium Allocation Approach (PAA)

Financial Reporting Developments 2015

Page 30

Premium Allocation Approach (PAA)

Previously measured amount

▶ Subsequent measurement for liability for remaining coverage:

Interest accretion

Premium received

Revenue recognized

Change in onerous contracts

▶ Considerations:▶ Fairly similar to current P&C practices▶ Practical expedient – no discounting if cash flows

received/paid within 1 year▶ Expenses acquisition costs for coverage less than 1

year

Financial Reporting Developments 2015

Page 31

PAA decisions - IASB’s September, 2014 meeting▶ The Board held a decision-making discussion on

two topics with regards to premium allocation approach:▶ Pattern of revenue recognition▶ Determination of interest expense in profit or loss

▶ Pattern of revenue recognition:▶ The Board decided the use of a single driver to achieve

simplicity; an entity should apply pattern on the basis of the passage of time, but, if the expected pattern of release of risk differs significantly from the passage of time, then on the basis of expected timing of incurred claims and benefits

▶ Determination of interest expense in profit or loss:▶ When OCI is chosen, the Board decided that the interest

expense in profit or loss should be determined based on the discount rate determined at the date the claims are incurred

Financial Reporting Developments 2015

Page 32

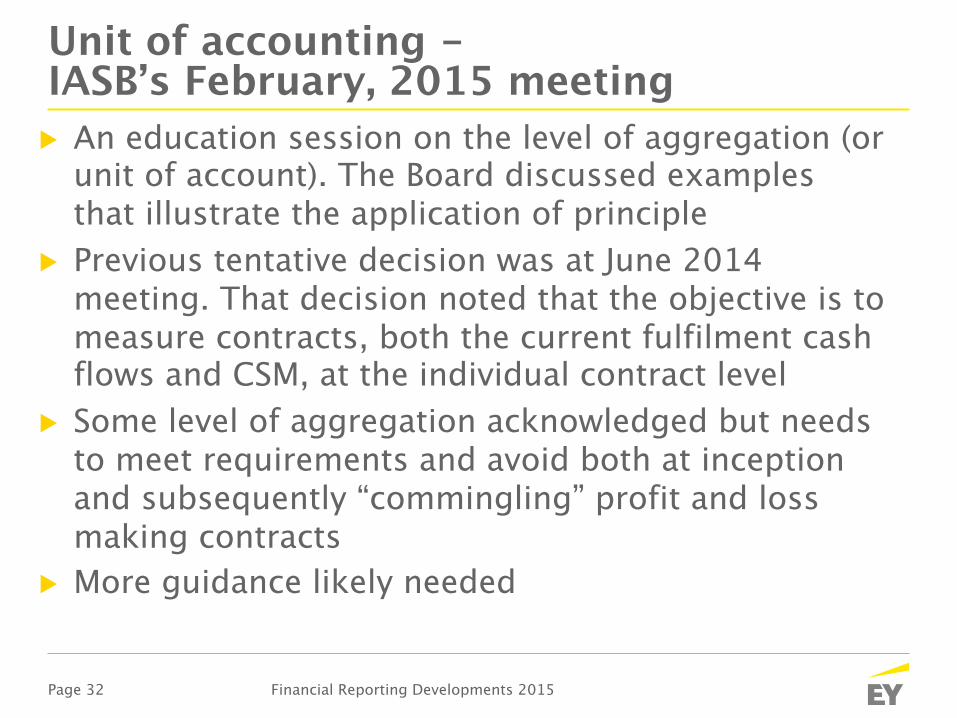

Unit of accounting - IASB’s February, 2015 meeting▶ An education session on the level of aggregation (or

unit of account). The Board discussed examples that illustrate the application of principle

▶ Previous tentative decision was at June 2014 meeting. That decision noted that the objective is to measure contracts, both the current fulfilment cash flows and CSM, at the individual contract level

▶ Some level of aggregation acknowledged but needs to meet requirements and avoid both at inception and subsequently “commingling” profit and loss making contracts

▶ More guidance likely needed

Financial Reporting Developments 2015

Page 33

Update on IFRS 9 deferral for insurers - IASB’s July, 2015 meeting▶ Tentative decision by the IASB to make changes in

IFRS 4 to reduce accounting mismatch that could arise on implementation of IFRS 9

▶ For certain assets, the difference between the amounts that would be recognised in profit or loss in accordance with IFRS 9 and IAS 39 may be recognised in OCI▶ This will apply to financial assets that: are classified as at fair

value through profit or loss in accordance with IFRS 9, when those assets were previously classified at amortised cost or as available-for-sale in accordance with IAS 39, and relate to insurance activities.

▶ The change will only apply to entities that: issue contracts accounted for under IFRS 4, and apply IFRS 9 in conjunction with IFRS 4.

▶ Deferred to future meetings whether insurers will be able to delay the implementation of IFRS 9 beyond 2018

Financial Reporting Developments 2015

Page 34

Key issues for remaining re-deliberations▶ Non-participating contracts:

▶ Reconciliation with the model for participating contracts▶ Scope▶ Sweep issues

▶ Unit of account▶ Participating contracts▶ Transition: application issues raised▶ Effective date of the final standard and link with

IFRS 9

Financial Reporting Developments 2015

Page 35

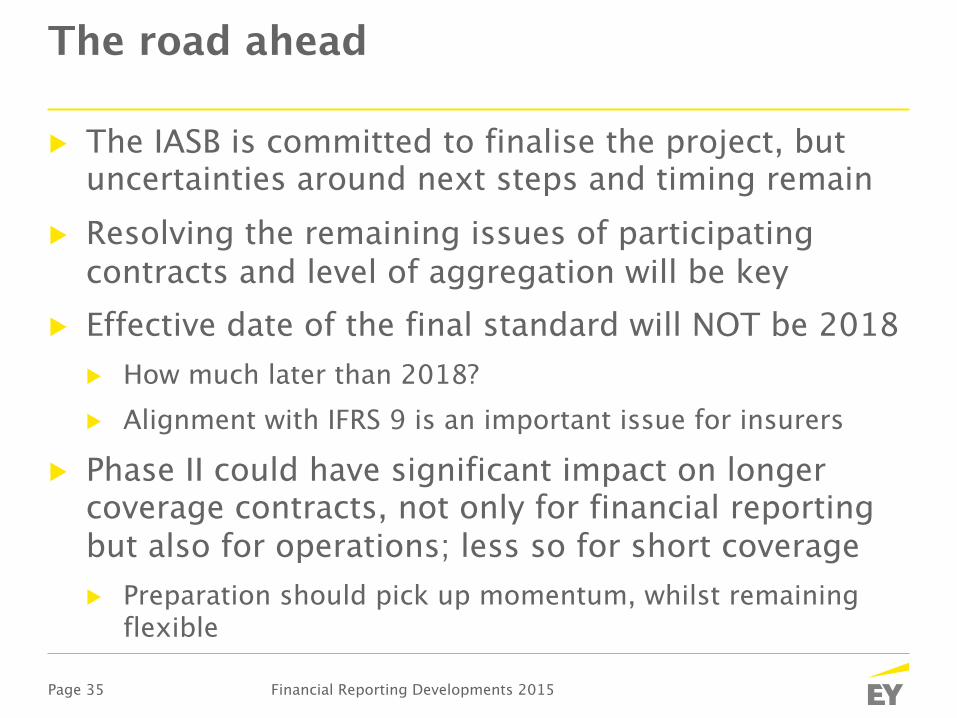

The road ahead

▶ The IASB is committed to finalise the project, but uncertainties around next steps and timing remain

▶ Resolving the remaining issues of participating contracts and level of aggregation will be key

▶ Effective date of the final standard will NOT be 2018▶ How much later than 2018?▶ Alignment with IFRS 9 is an important issue for insurers

▶ Phase II could have significant impact on longer coverage contracts, not only for financial reporting but also for operations; less so for short coverage▶ Preparation should pick up momentum, whilst remaining

flexible

Financial Reporting Developments 2015

Page 36

P&C issues

▶ Long duration contracts e.g. mortgage insurance contracts profit emergence under IFRS 4 Phase II

▶ Unit of accounting – onerous contracts, other specific situations

Financial Reporting Developments 2015

Page 37

Lease Project Update

Financial Reporting Developments 2015

Page 38

The new Leases standard – what we expect

Financial Reporting Developments 2015

Page 39

Project overview and status

▶ Joint project between IASB and FASB▶ ED redeliberations now substantially complete

▶ Key remaining item – effective date

▶ Lessees would recognize most leases on balance sheet▶ The Boards differ on lease classification and how lessees

would recognise, measure and present leases

▶ Current lessor accounting essentially unchanged▶ IASB plans to issue new standard before the end of

2015▶ Not likely to be effective before January 1, 2018Financial Reporting Developments 2015

Q3 2010 Exposure draft

(ED)

2011-2013 Redeliberation

s

2013 Second ED

2014-2015 Redeliberation

s

Late 2015Final

standard

Page 40

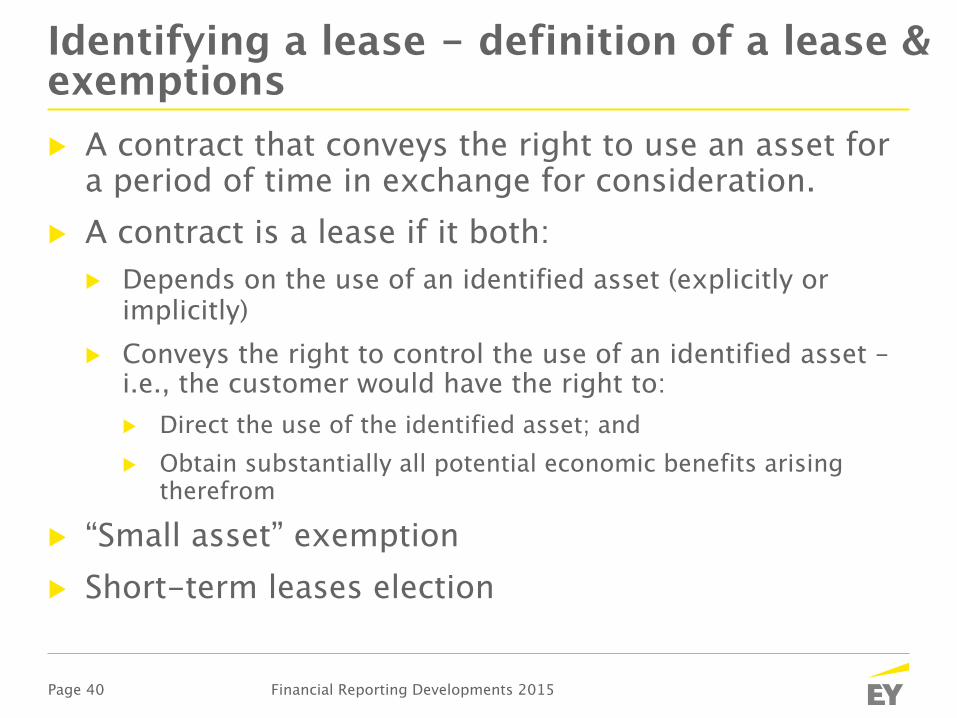

▶ A contract that conveys the right to use an asset for a period of time in exchange for consideration.

▶ A contract is a lease if it both:▶ Depends on the use of an identified asset (explicitly or

implicitly)▶ Conveys the right to control the use of an identified asset –

i.e., the customer would have the right to:▶ Direct the use of the identified asset; and ▶ Obtain substantially all potential economic benefits arising

therefrom

▶ “Small asset” exemption▶ Short-term leases election

Identifying a lease - definition of a lease & exemptions

Financial Reporting Developments 2015

Page 41

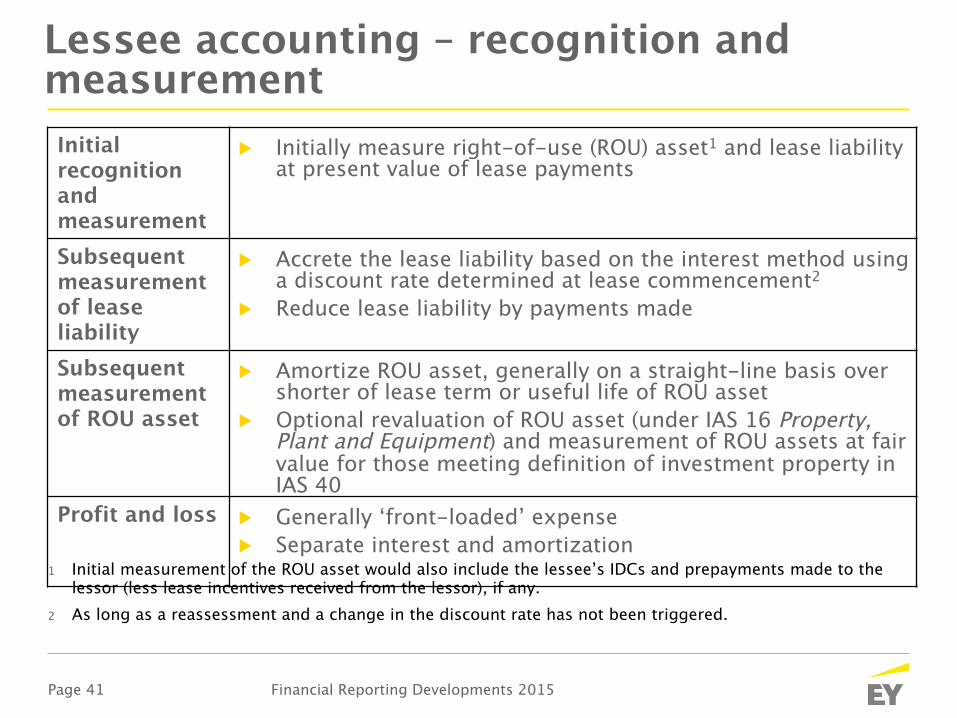

Lessee accounting – recognition and measurementInitial recognition and measurement

▶ Initially measure right-of-use (ROU) asset1 and lease liability at present value of lease payments

Subsequent measurement of lease liability

▶ Accrete the lease liability based on the interest method using a discount rate determined at lease commencement2

▶ Reduce lease liability by payments made

Subsequent measurement of ROU asset

▶ Amortize ROU asset, generally on a straight-line basis over shorter of lease term or useful life of ROU asset

▶ Optional revaluation of ROU asset (under IAS 16 Property, Plant and Equipment) and measurement of ROU assets at fair value for those meeting definition of investment property in IAS 40

Profit and loss ▶ Generally ‘front-loaded’ expense▶ Separate interest and amortization

1 Initial measurement of the ROU asset would also include the lessee’s IDCs and prepayments made to the lessor (less lease incentives received from the lessor), if any.

2 As long as a reassessment and a change in the discount rate has not been triggered.

Financial Reporting Developments 2015

Page 42

Effective date and transitionEffective date and transition – overview

▶ IASB will set an effective date before issuing standard▶ Full retrospective (IASB only) or modified retrospective▶ Existing finance leases:

▶ Entities would continue to apply existing accounting at the date of initial application of the new standard

▶ Existing operating leases:▶ Lessors would continue to apply existing accounting at the

date of initial application (except for intermediate lessors in a sublease)

▶ Lessees would be permitted to choose either full retrospective or modified retrospective approach▶ Applied consistently across entire portfolio of former operating

leases▶ Permit grandfathering the definition of a lease in IFRIC 4

Determining whether an Arrangement contains a Lease (for all leases ongoing at date of initial application)Financial Reporting Developments 2015

Page 43

IFRS 15: Revenue from Contracts with Customers

Financial Reporting Developments 2015

Page 44

IFRS 15: Revenue From Contracts with Customers – Recent Developments▶ The IASB and FASB jointly issued the new revenue

standard in 2014▶ Transition Resource Group

▶ Created by the IASB and FASB▶ Consists of financial statement preparers, auditors and

users from a variety of industries, countries and public and private entities

▶ Meetings were held July 2014, October 2014, January 2015, March 2015, July 2015

Financial Reporting Developments 2015

Page 45

IFRS 15: Revenue From Contracts with Customers – Effective Date Deferral▶ IASB approved a one-year deferral of the new

revenue standard on July 22, 2015▶ The new standard would be effective for annual reporting

periods beginning on or after 1 January 2018▶ Early adoption is permitted

▶ FASB approved a one-year deferral of the new revenue standard on July 9, 2015▶ The new standard would be effective for public entities for

annual reporting periods beginning after 15 December 2017; for non-public entities, annual reporting periods beginning after 15 December 2018

▶ Early adoption is permitted to the original public entity effective date (15 December 2016)

Financial Reporting Developments 2015

Page 46

IFRS 15: Revenue From Contracts with Customers – 5 Step Model - Overview

Financial Reporting Developments 2015

Core principle: Recognise revenue to depict the transfer of goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services

Step 1 : Identify the contract(s) with the customer

Step 2 : Identify the performance obligations

Step 3 : Determine the transaction price

Step 4 : Allocate the transaction price to the performance obligations

Step 5 : Recognise revenue when (or as) the entity satisfies a performance obligation

Page 47

IFRS 15: Revenue From Contracts with Customers – Proposed Amendments▶ Licenses of intellectual property (IP)▶ Identification of performance obligations (PO)

▶ Existing guidance in Step 2 requires an entity to identify POs as distinct using a two-step model▶ Assessment of whether the PO is capable of being distinct▶ Assessment of whether the PO is distinct in the context of the

contract▶ The Boards agreed to clarify when a promised good or

service is separately identifiable from other promises in a contract

▶ Gross vs. net (principal vs. agent) considerations▶ The IASB and FASB agreed to retain the control principle as

the basis for determining whether an entity is a principal or an agent but also made a few additional changes to the standards Financial Reporting Developments 2015

Page 48

IFRS 15: Revenue From Contracts with Customers – Proposed Amendments▶ Transition guidance

▶ Two transition methods exist under the new revenue standard:▶ Full retrospective – cumulative adjustment on date of initial

application (opening balance of earliest comparative year)▶ Modified retrospective - cumulative adjustment on date of

initial application (opening balance of current year)▶ The IASB agreed to propose a practical expedient to

determine the aggregate effect of modifications that occurred from contract inception through the “contract modification adjustment date” (CMAD) = earlier period presented

▶ IASB also proposes a practical expedient under the full retrospective method, to apply the new guidance only to contracts that are not completed (as defined) as of the beginning of the earliest period presented

Financial Reporting Developments 2015

Page 49

Transition Timelines

1/1/2017

1/1/2018

Full Retrospective 2016 & Prior 2017 2018

Financial Reporting Developments 2015

Page 50

Regulatory Update

Financial Reporting Developments 2015

Page 51

Minimum Capital Test – Revisit the 2015 guidelines▶ Changes to the capital framework in 2015, including significant

updates to the MCT Guidelines for 2015

▶ Key audit considerations ▶ Impact on audits▶ Audit of the phase in period of capital impacts ▶ Change in filing requirements for the audit opinion on the MCT

from 60 days to 90 days

Financial Reporting Developments 2015

Comparison of Frameworks – Industry-Wide Impact (in $million)

Old Framework New Framework Impact

Capital/Net Assets Available 32,288 32,598 +1.0%

Capital/Margin Required 11,907 11,651 -2.1%

MCT/BAAT ratio 271.2% 279.8% +8.6 %

Page 52

Minimum Capital Test – Changes to the 2016 Guidelines

▶ Key changes in 2016 guideline▶ Addition of capital requirements of equity derivatives▶ Recognition of equity hedging strategies

▶ Must demonstrate hedging strategy results in decrease in overall risk

▶ Identical equity securities and indexes – calculate capital requirements on net exposure

▶ Closely link securities and indexes – use of formula to determine capital requirements on combined portfolio

▶ Amendment of the terminology used in the 2015 MCT guidance

▶ Effective date of implementation▶ Comment period closed September 4, 2015▶ To be published in fall of 2015 ▶ Effective implementation date of January 1, 2016Financial Reporting Developments 2015

Page 53

Operational Risk Management

Financial Reporting Developments 2015

▶ Operational risk ▶ Describe and document approach to managing operational risk, ▶ Defined as risk of loss resulting from people, inadequate or

failed internal processes and systems, or from external events

▶ Four Key Principles▶ Full integration with overall risk management program and

appropriately documented ▶ Support the overall corporate governance structure ▶ Establish accountability for operational risk management▶ Comprehensive identification and assessment of operational

risk through the use of appropriate management tools

▶ Implementation considerations▶ Issued on August 20, 2015, with comments due October 9,

2015▶ implementation expected no later than one year from the date

that it becomes effective

Page 54

Comment Letters - Common Themes

Financial Reporting Developments 2015

Page 55

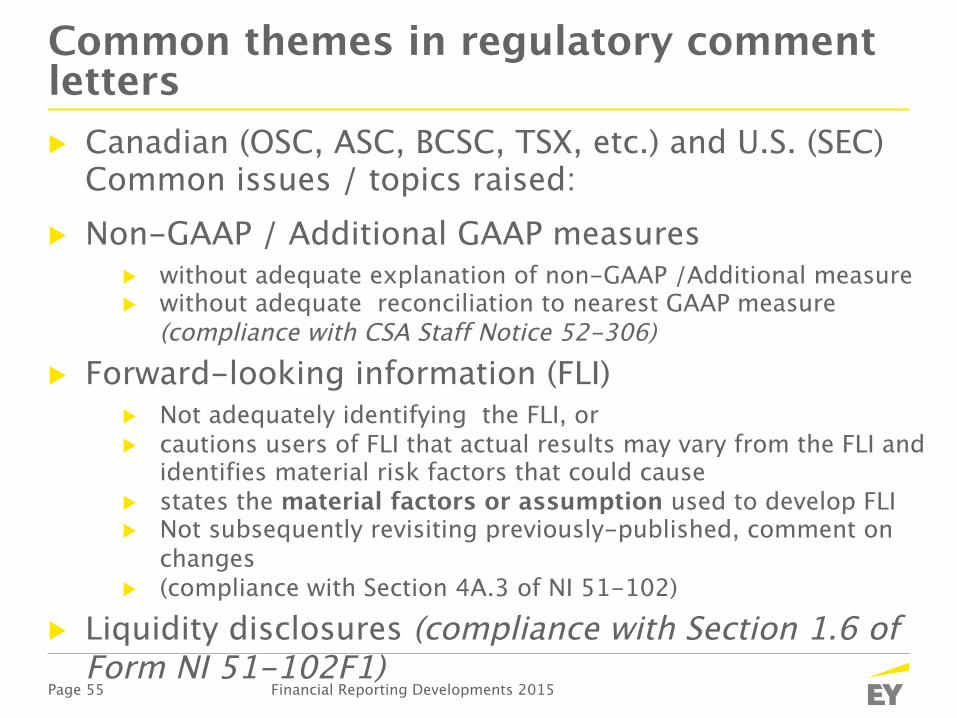

Common themes in regulatory comment letters▶ Canadian (OSC, ASC, BCSC, TSX, etc.) and U.S. (SEC)

Common issues / topics raised:▶ Non-GAAP / Additional GAAP measures

▶ without adequate explanation of non-GAAP /Additional measure▶ without adequate reconciliation to nearest GAAP measure

(compliance with CSA Staff Notice 52-306)▶ Forward-looking information (FLI)

▶ Not adequately identifying the FLI, or ▶ cautions users of FLI that actual results may vary from the FLI and

identifies material risk factors that could cause ▶ states the material factors or assumption used to develop FLI▶ Not subsequently revisiting previously-published, comment on

changes ▶ (compliance with Section 4A.3 of NI 51-102)

▶ Liquidity disclosures (compliance with Section 1.6 of Form NI 51-102F1)

Financial Reporting Developments 2015

Page 56

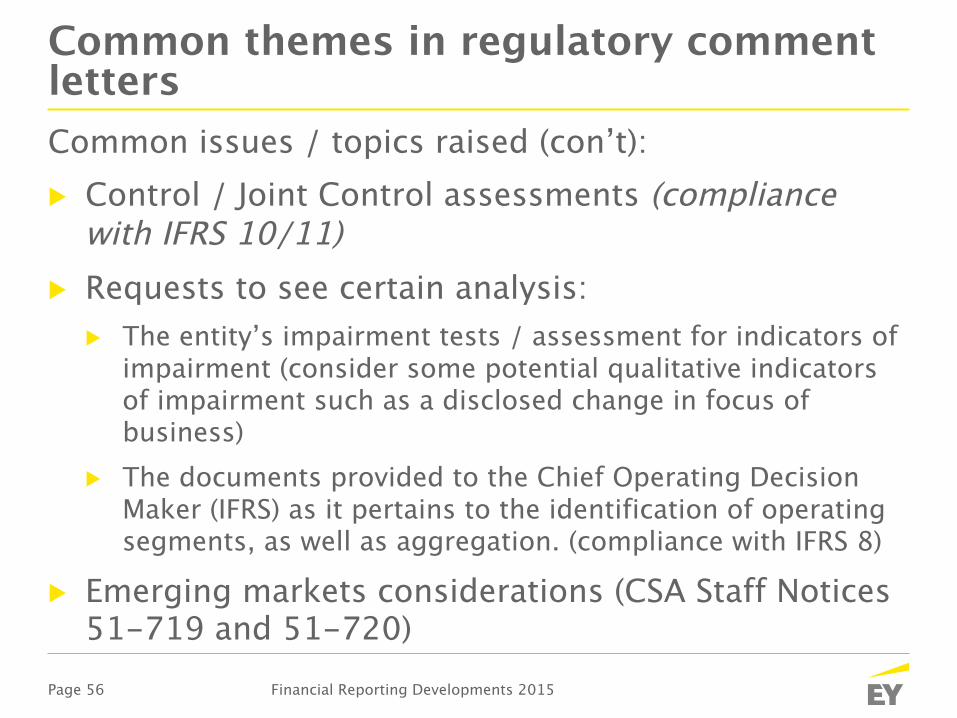

Common themes in regulatory comment letters Common issues / topics raised (con’t):▶ Control / Joint Control assessments (compliance

with IFRS 10/11)▶ Requests to see certain analysis:

▶ The entity’s impairment tests / assessment for indicators of impairment (consider some potential qualitative indicators of impairment such as a disclosed change in focus of business)

▶ The documents provided to the Chief Operating Decision Maker (IFRS) as it pertains to the identification of operating segments, as well as aggregation. (compliance with IFRS 8)

▶ Emerging markets considerations (CSA Staff Notices 51-719 and 51-720)

Financial Reporting Developments 2015

Page 57

Conclusion

Financial Reporting Developments 2015

Page 58

Additional Resources

▶ Financial Services Financial Reporting Development Seminar ▶ EY Toronto, 8:00 am, October 28, 2015 & December 11, 2015

▶ EY IFRS Resources - http://www.ey.com/IFRS ▶ IFRS Publications:

▶ IFRS Developments - Summary of IASB and IFRS Interpretations Committee discussion papers, exposure drafts, final standards or interpretations

▶ Applying IFRS - Longer and more detailed than IFRS Developments, Applying IFRS provides analyses of proposals, standards or interpretations and discussion of how to apply them.

▶ IFRS Exposure Drafts and EY comment letters▶ Thought Center Webcasts & web based learning ▶ Industry Insights

▶ EY Insight App on your mobile phone

Financial Reporting Developments 2015

EY | Assurance | Tax | Transactions | AdvisoryAbout EYEY is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 200,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

EY refers to the global organization and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

For more information about our organization, please visit www.ey.com.

© 2015 Ernst & Young LLP. All Rights Reserved.A member firm of Ernst & Young Global Limited.

Page 60

Appendices

Financial Reporting Developments 2015

Page 61

Appendix I – IFRS Discussion Group Updates

Financial Reporting Developments 2015

Page 62

IFRS Discussion Group (“IDG”)

▶ Established in 2009 by the AcSB to help Canadian organizations apply IFRS

▶ The Group discusses IFRS issues raised by constituents and recommends to the AcSB which issues should be brought to the attention of the IASB or the IFRIC for clarification

▶ The IDG also discusses issues with the sole intent of raising awareness of emerging issues in Canada

▶ Anyone can submit an issue for the IDG to discuss▶ Official summaries of the meetings are posted on the Financial

Reporting and Assurance Standards Canada website (frascanada.ca)

▶ EY publishes a timely summary of the meetings – you can sign up for these email alerts at ey.com/ca/emailalerts

Financial Reporting Developments 2015

Page 63

IDG Agenda Topics

Financial Reporting Developments 2015

Topic Meeting DateIAS 1: Disclosure Initiative Amendments May 2015IAS 19: Discount Rates May 2015IAS 36: Recoverable Amount May 2015IAS 32 & IAS 39: Classification of Exchanged Shares May 2015IAS 39: Classification of Cash and Cash Equivalents May 2015IFRS 9: Transition May 2015IFRS 9: Hedge Accounting May 2015IFRS 15: Transition May 2015Definition of a Publicly Accountable Enterprise May 2015

*Bolded items are discussed in more detail in the following slides

Page 64

IDG Agenda Topics

Financial Reporting Developments 2015

Topic Meeting DateIFRS 5 & IAS 36: Impairment Measurement December

2014IFRS 3, IFRS 6, IFRS 10 & IAS 16: Acquisition of an Entity Holding a Single Asset

December 2014

IFRS 13 & IAS 39: Fair Value Measurement of Government Loans

December 2014

IFRS 13 & IAS 39: Subsequent Measurement of Fair Value

December 2014

IAS 36: Allocating Corporate Costs to a Cash-generating Unit

December 2014

IAS 36: Measuring Recoverable Amount and Allocating Impairment Loss

December 2014

IAS 16 & IAS 38: Revenue-based Amortization December 2014

IAS 16: Capitalisation of Costs December 2014

Page 65

IDG Agenda Topics

Financial Reporting Developments 2015

Topic Meeting DateIAS 16: Depreciation of Spare Parts, Stand-by Equipment and Servicing Equipment

December 2014

IAS 1 & IAS 32: Classification of Debt with Equity-linked Derivatives

December 2014

Non-authoritative Guidance December 2014

IFRS 3, IAS 16 & IAS 37: Contingent Consideration in an Asset Purchase

September 2014

IFRS 3, IFRS 15, IAS 18 & IAS 37: Contingent Consideration in an Asset Sale

September 2014

IFRS 1: Carve-out Financial Statements September 2014

Page 66

IDG Agenda Topics

Financial Reporting Developments 2015

Topic Meeting DateIAS 19 & IAS 21: Foreign Exchange Gains and Losses on Defined Benefit Pension Plan Obligations

September 2014

IAS 19: Refundable Tax Accounts in Retirement Compensation Arrangements

September 2014

IAS 32, IAS 33 & IFRIC 17: Dividend Reinvestment Plans September 2014

Disclosure of Contractual Commitments September 2014

IFRS 9 & IAS 39: Flow-through Shares with Attached Share Purchase Warrants

September 2014

Escrow Share Arrangements September 2014

IFRS 11: Application Issues and Process of IFRS Interpretations Committee

September 2014

Page 67

IAS 36: Recoverable Amount

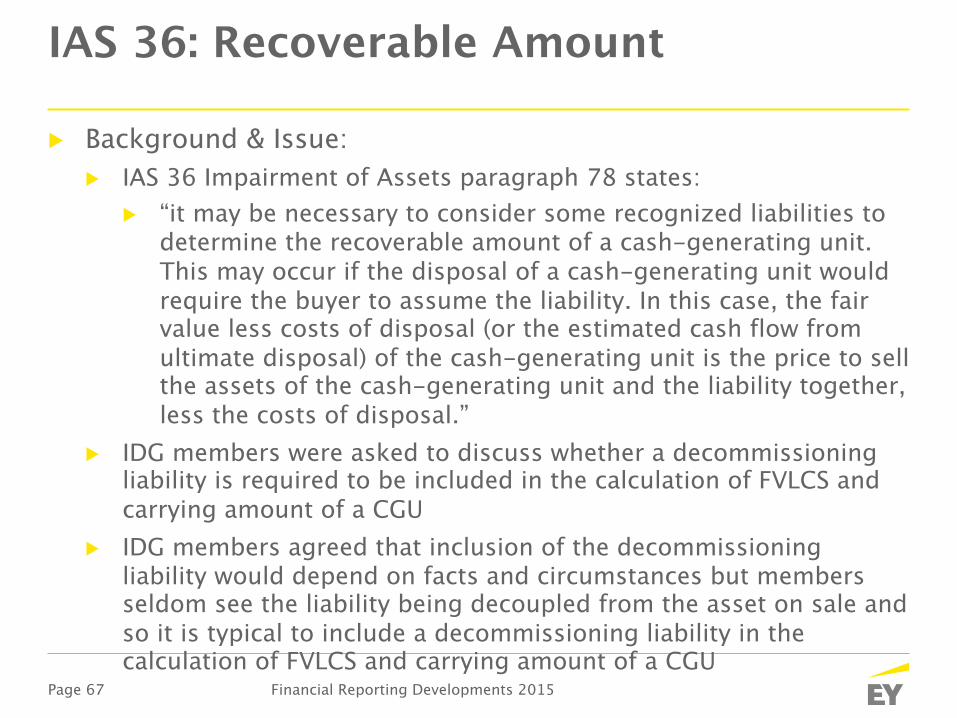

▶ Background & Issue:▶ IAS 36 Impairment of Assets paragraph 78 states:

▶ “it may be necessary to consider some recognized liabilities to determine the recoverable amount of a cash-generating unit. This may occur if the disposal of a cash-generating unit would require the buyer to assume the liability. In this case, the fair value less costs of disposal (or the estimated cash flow from ultimate disposal) of the cash-generating unit is the price to sell the assets of the cash-generating unit and the liability together, less the costs of disposal.”

▶ IDG members were asked to discuss whether a decommissioning liability is required to be included in the calculation of FVLCS and carrying amount of a CGU

▶ IDG members agreed that inclusion of the decommissioning liability would depend on facts and circumstances but members seldom see the liability being decoupled from the asset on sale and so it is typical to include a decommissioning liability in the calculation of FVLCS and carrying amount of a CGU

Financial Reporting Developments 2015

Page 68

IAS 36: Recoverable Amount

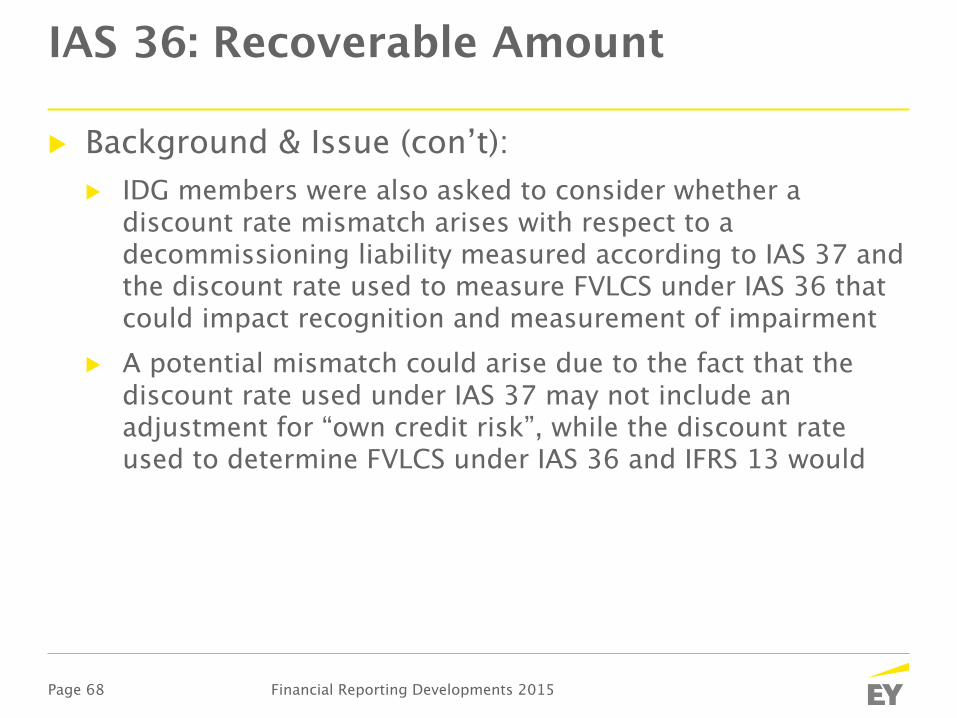

▶ Background & Issue (con’t):▶ IDG members were also asked to consider whether a

discount rate mismatch arises with respect to a decommissioning liability measured according to IAS 37 and the discount rate used to measure FVLCS under IAS 36 that could impact recognition and measurement of impairment

▶ A potential mismatch could arise due to the fact that the discount rate used under IAS 37 may not include an adjustment for “own credit risk”, while the discount rate used to determine FVLCS under IAS 36 and IFRS 13 would

Financial Reporting Developments 2015

Page 69

IAS 36: Recoverable Amount

▶ IDG Discussion:▶ The Group highlighted that for VIU calculations, IAS 36.78

states:▶ “To perform a meaningful comparison between the carrying

amount of the cash-generating unit and its recoverable amount, the carrying amount of the liability is deducted in determining both the cash-generating unit's value in use and its carrying amount”

▶ As such, one calculates VIU based on the CGU’s cash flows without reduction for the decommissioning liability and then deducts the carrying value of the liability to compare to the CGUs carrying value also reduced by the carrying value of the liability

▶ As the deduction from both VIU and carrying value is the same, there is no discount rate mismatch when measuring recoverable amount based on VIU

▶ However, where recoverable amount is based on FVLCS, a discount rate mismatch may arise and such mismatch may impact both recognition and measurement of impairment

Financial Reporting Developments 2015

Page 70

IAS 19: Discount Rates

▶ Background & Issue:▶ IAS 19 Employee Benefits requires the rate used to discount

post-employment benefits to reflect the estimated timing of benefit payments▶ “In practice, an entity often achieves this by applying a single

weighted average discount rate that reflects the estimated timing and amount of benefit payments and the currency in which the benefits are to be paid”

▶ However, it is possible that calculations can be undertaken at a more granular basis

Financial Reporting Developments 2015

Page 71

IAS 19: Discount Rates

▶ Background & Issue (con’t):▶ IDG members were asked whether alternatives to the

traditional single weighted average discount rate approaches would meet the requirements of IAS 19

▶ Alternative discount rate approaches that have been debated include:▶ Split discount rate approach▶ Yield curve approach▶ Mixed approach▶ Vector approach

Financial Reporting Developments 2015

Page 72

IAS 19: Discount Rates

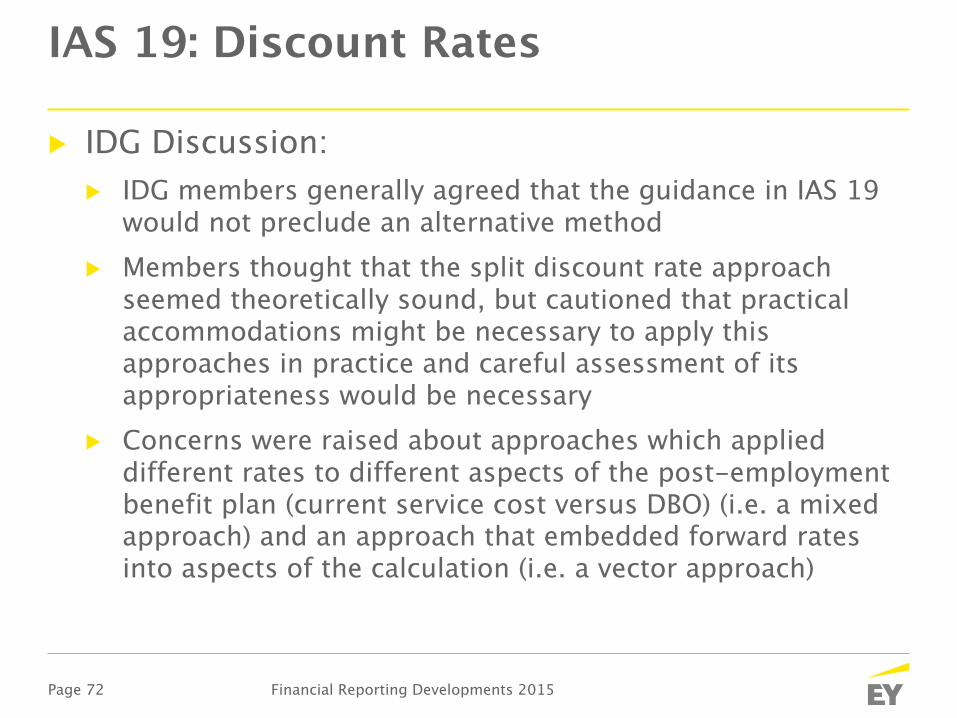

▶ IDG Discussion:▶ IDG members generally agreed that the guidance in IAS 19

would not preclude an alternative method▶ Members thought that the split discount rate approach

seemed theoretically sound, but cautioned that practical accommodations might be necessary to apply this approaches in practice and careful assessment of its appropriateness would be necessary

▶ Concerns were raised about approaches which applied different rates to different aspects of the post-employment benefit plan (current service cost versus DBO) (i.e. a mixed approach) and an approach that embedded forward rates into aspects of the calculation (i.e. a vector approach)

Financial Reporting Developments 2015

Page 73

IAS 19: Discount Rates

▶ IDG Discussion (con’t):▶ Members also questioned how these alternative approaches

would be applied to a funded defined benefit plan▶ There continues to be debate as to how a change in

discount rate would be accounted for

Financial Reporting Developments 2015

Page 74

IAS 1 & IAS 32: Classification of Debt with Equity-linked Derivatives▶ Background & Issue:

▶ IDG was asked to consider the classification of a convertible debt instrument as current or non-current under IAS 1, where the conversion feature is classified as an embedded equity-linked derivative liability▶ IAS 1.69(d) states that a liability should be classified as current

when an entity “does not have an unconditional right to defer settlement for at least twelve months after the reporting date”

▶ IAS 1.69(d) also states: “terms of a liability that could, at the option of the counterparty, result in its settlement by the issue of equity instruments do not affect its classification”▶ This amendment to IAS 1 was introduced in 2007, and was

contemplated in the context of a convertible bond where a liability and equity component are recognised

Financial Reporting Developments 2015

Page 75

IAS 1 & IAS 32: Classification of Debt with Equity-linked Derivatives▶ IDG Discussion:

▶ IDG considered two questions:▶ Can the clarifying guidance in IAS 1.69(d) be applied to hybrid

convertible debt instruments?▶ Does the instrument as a whole need to be classified

consistently?▶ IDG members generally concluded:

▶ IAS 1.69(d) could be applied even when the equity conversion feature itself was classified as a liability

▶ The host debt and the equity conversion feature embedded derivative should both be classified in the same manner

Financial Reporting Developments 2015

Page 76

Appendix II – Narrow Scope Amendments

Financial Reporting Developments 2015

Page 77

Narrow Scope Amendments

▶ Narrow-scope amendments to IAS 19 and IFRIC 14▶ Narrow-scope amendments to IFRS 2▶ Narrow-scope amendments to IAS 40: Transfers of Investment

Property▶ Narrow-scope amendments to IFRS 5: Non-current assets held for sale

and discontinued operations▶ Narrow-scope amendments to IAS 12: Uncertain Tax Positions▶ Narrow-scope amendments to IAS 27: Equity Method in Separate

Financial Statements▶ Narrow-scope amendments to IAS 28: Sale or Contribution of Assets

to an Associate or Joint Venture▶ Narrow-scope amendments to IAS 12: Income Taxes▶ Narrow-scope amendments to IAS 16: Property, Plant and Equipment

and IAS 38: Intangible Assets▶ Narrow-scope amendments: Fair Value Measurement▶ Narrow-scope amendment: Investment Entities Consolidation

Exception▶ Narrow-scope amendments: Acquisition of an Interest in a Joint

OperationFinancial Reporting Developments 2015

Page 78

Narrow-scope amendments to IAS 19 and IFRIC 14

Financial Reporting Developments 2015

Page 79

Proposed Amendments

IAS 19 - Plan Amendment, Curtailment or Settlement▶ Background on issue▶ Current service cost ▶ Interest cost▶ Past service cost and gain/loss of settlement

IFRIC 14 - Right to a Refund▶ Background on issue

Financial Reporting Developments 2015

Page 80

Timeline

▶ Exposure draft addressing these changes issued by the IASB on 18 June 2015 with the comment period remaining open for 120 days until 19 October 2015

Financial Reporting Developments 2015

Page 81

Narrow-scope amendments to IFRS 2

Financial Reporting Developments 2015

Page 82

IFRS 2 Exposure Draft

▶ November 2014 – IASB released the ED Classification and measurement of share-based payment transactions which proposes clarifications to the following issues:▶ Accounting for cash-settled share-based payment

transactions that include a performance condition▶ Classification of share-based payment transactions with net

settlement features▶ Accounting for modifications of share-based payment

transactions from cash-settled to equity settled

▶ In July 2015, the IC decided to propose that the IASB should finalize the proposed amendments, subject to some revisions to the proposed wording

Financial Reporting Developments 2015

Page 83

Performance conditions – cash settled share based payment transactions▶ IFRS 2 previously contained no guidance on how

vesting conditions affect the fair value of cash-settled share-based payments

▶ IASB proposes to clarify that the accounting for cash-settled share-based payments should follow the same approach as equity-settled share-based payments

Financial Reporting Developments 2015

Page 84

Accounting for a modification that changes cash settled to equity settled▶ The share-based payment transaction would be

measured by reference to the modification date fair value of the equity instruments granted as a result of the modification

▶ The liability recognised in respect of the original cash-settled share-based payment should be derecognised upon the modification and the equity-settled share-based payment should be recognised to the extent that the services has been rendered up to the modification date

▶ The difference between the carrying amount of the liability as at the modification date and the amount recognised in equity at the same date should be recorded in profit or loss immediately

Financial Reporting Developments 2015

Page 85

Share-based payments with net settlement features▶ Amendments were proposed in order to reduce

complexity and undue burden in applying requirements of IFRS 2 in situations where an entity withholds a portion of equity instruments in order to settle the counterparty’s tax obligation

▶ Guidance in IFRS 2 will be clarified so that in the narrow circumstance in which an entity is obligated by tax law or regulation to withhold an amount for an employee’s tax obligation, the entire share based payment transaction should be accounted for as equity settled provided that it would qualify as equity settled absent the net settlement feature

Financial Reporting Developments 2015

Page 86

Effective date and transition

▶ The effective date of the amendments has not yet been determined

▶ At the July 2015 meeting, the IC decided to provide enhanced guidance on how the three proposed amendments should be applied for new awards, and for outstanding unvested awards

Financial Reporting Developments 2015

Page 87

Narrow-scope amendments to IAS 40: Transfers of Investment Property

Financial Reporting Developments 2015

Page 88

IAS 40: Transfers Of Investment Property

▶ IAS 40.57 requires that an asset be transferred to, or from investment property only when evidence of a change in use of the asset exists. In practice, two interpretations of IAS 40.57 have been seen1. IAS 40.57 includes guiding principals and examples of

evidence supporting that a change in use of the asset has occurred

2. IAS 40.57 provides an exhaustive list of evidence supporting when a change in use of an asset has occurred

▶ IASB plans to issue a narrow scope ED to clarify that IAS 40.57 provides a guiding principal and examples of evidence of a change in use for an asset. ▶ The proposed amendment may allow for more timely

transfers to, or from investment property where a change in use of an asset has been evidenced

▶ ED expected in Q3 2015 Financial Reporting Developments 2015

Page 89

Narrow-scope amendments to IFRS 5: Non-current assets held for sale and discontinued operations

Financial Reporting Developments 2015

Page 90

IFRS 5: Non-current Assets Held for Sale and Discontinued Operations (IFRIC and IASB Discussions)▶ 11 practice issues in have been raised to the IFRIC on the application of IFRS 5:

▶ Scope▶ Issue 1: the scope of the held-for-sale classification ▶ Issue 2: accounting for a disposal group consisting mainly of financial

instruments ▶ Measurement▶ Issue 3: impairment of a disposal group when the difference between its

carrying amount and its fair value less costs to sell exceeds the carrying amount of non-current assets in the disposal group

▶ Issue 4: reversal of an impairment relating to goodwill in a disposal group ▶ Issue 5: to what extent can an impairment loss be allocated to non-current

assets within a disposal group

Financial Reporting Developments 2015

Page 91

IFRS 5: Non-current Assets Held for Sale and Discontinued Operations (IFRIC and IASB Discussions)▶ 11 practice issues raised to the IFRIC on the application of IFRS 5 (con't):

▶ Presentation▶ Issue 6: definition of discontinued operation and disclosures ▶ Issue 7: presentation of OCI items for discontinued operations ▶ Issue 8: how to apply the definition of ‘major line of business’ in presenting

discontinued operations ▶ Issue 9: how to present intragroup transactions between continuing and

discontinued operations ▶ Issue 10: how to apply the presentation requirements, in the case of a

change to a plan, to a disposal group that consists of both a subsidiary and other non-current assets

▶ Disclosure▶ Issue 11: applicability of the disclosure requirements in IFRS 12 to a

subsidiary classified as held for sale ▶ IASB tentatively decided to divide issues into those to be dealt with in the

short term through IFRIC agenda decisions or annual improvements (issues 5, 9 and 11) and those to be dealt with in the medium to long term possibly through amendments to the standard

Financial Reporting Developments 2015

Page 92

Narrow-scope amendments to IAS 12: Uncertain Tax Positions

Financial Reporting Developments 2015

Page 93

IAS 12: Uncertain Tax Positions (IFRIC discussions)▶ Draft interpretation issued April 2015▶ Unit of measure

▶ Identify the unit that will provide the most relevant information, considering interrelationship of uncertainties

▶ Recognition and measurement ▶ Required: “Expected value” or “most-likely” amount▶ Not permitted: “More-likely-than-not”

▶ Detection risk▶ Assume full knowledge of all relevant info if tax authority

has right to examine

▶ Statute of limitations / examination by tax authorities

Financial Reporting Developments 2015

Page 94

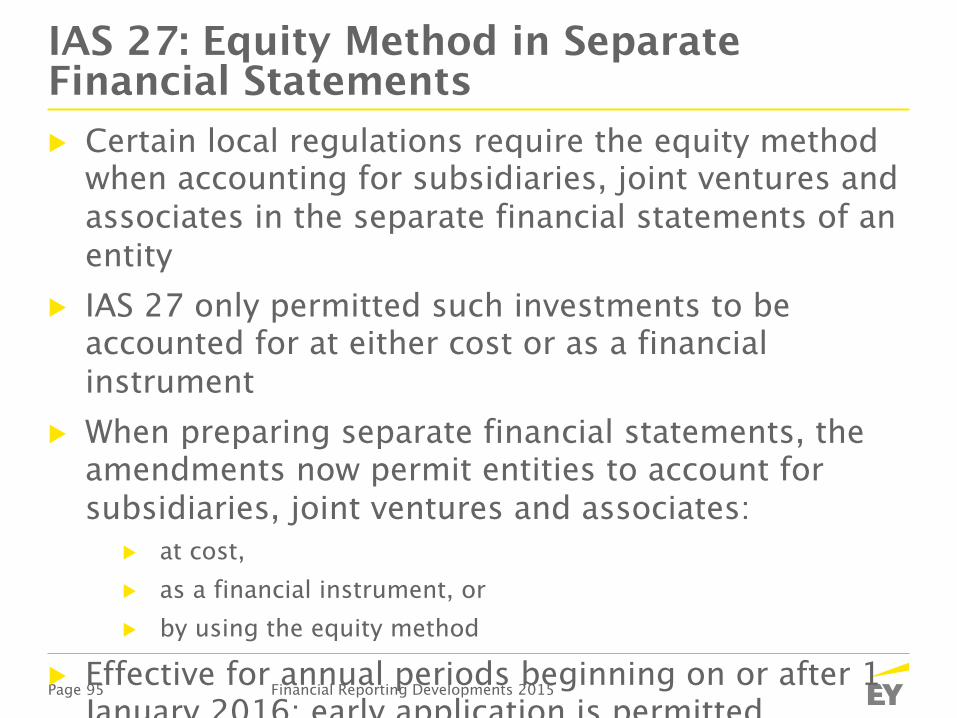

Narrow-scope amendments to IAS 27: Equity Method in Separate Financial Statements

Financial Reporting Developments 2015

Page 95

IAS 27: Equity Method in Separate Financial Statements▶ Certain local regulations require the equity method

when accounting for subsidiaries, joint ventures and associates in the separate financial statements of an entity

▶ IAS 27 only permitted such investments to be accounted for at either cost or as a financial instrument

▶ When preparing separate financial statements, the amendments now permit entities to account for subsidiaries, joint ventures and associates:

▶ at cost, ▶ as a financial instrument, or ▶ by using the equity method

▶ Effective for annual periods beginning on or after 1 January 2016; early application is permitted

Financial Reporting Developments 2015

Page 96

Narrow-scope amendments to IAS 28: Sale or Contribution of Assets to an Associate or Joint Venture

Financial Reporting Developments 2015

Page 97

IAS 28: Sale or Contribution of Assets between an Investor and its Associate or Joint Venture

▶ Objective: To address and acknowledge an inconsistency between IFRS 10 and IAS 28 in dealing with the contribution or sale of a subsidiary to an associate or joint venture.

▶ Previously Proposed Amendments:▶ Full gain or loss recognized on the loss of control of a business

including when the investor retains joint control or significant influence over a business.

▶ Partial gains and losses will continue to apply if the assets (including subsidiaries) do not constitute a business as defined in IFRS 3.

▶ Current status: This project has been combined into a broader project on equity accounting and the effective date of the proposed amendments has been postponed. Early adoption is still permitted.

Financial Reporting Developments 2015

Page 98

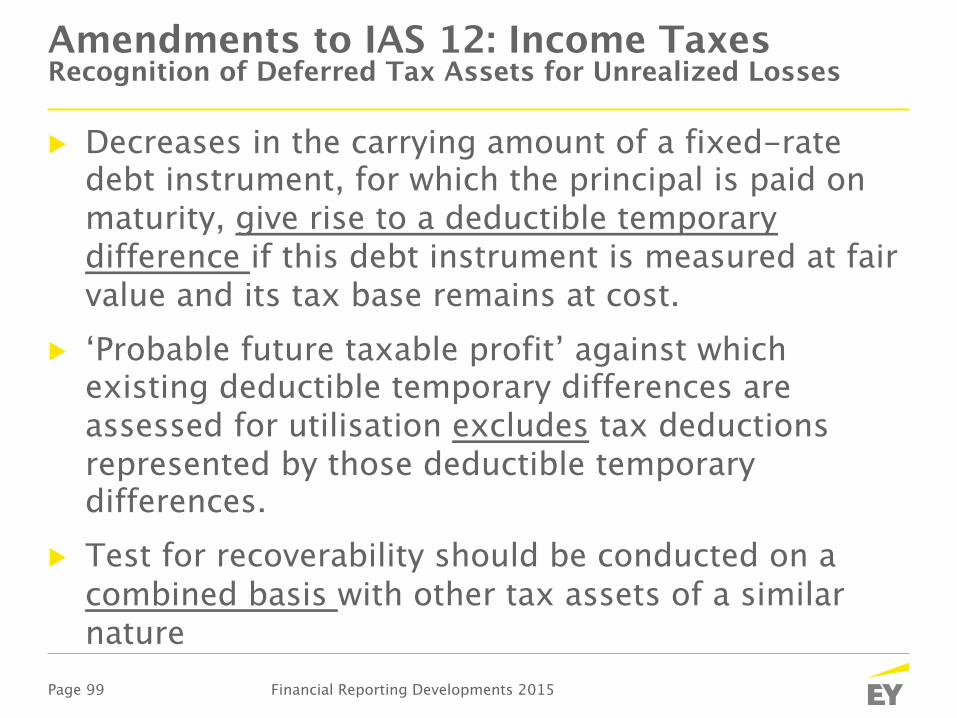

Narrow-scope amendments to IAS 12: Income Taxes

Financial Reporting Developments 2015

Page 99

Amendments to IAS 12: Income Taxes Recognition of Deferred Tax Assets for Unrealized Losses

▶ Decreases in the carrying amount of a fixed-rate debt instrument, for which the principal is paid on maturity, give rise to a deductible temporary difference if this debt instrument is measured at fair value and its tax base remains at cost.

▶ ‘Probable future taxable profit’ against which existing deductible temporary differences are assessed for utilisation excludes tax deductions represented by those deductible temporary differences.

▶ Test for recoverability should be conducted on a combined basis with other tax assets of a similar nature

Financial Reporting Developments 2015

Page 100

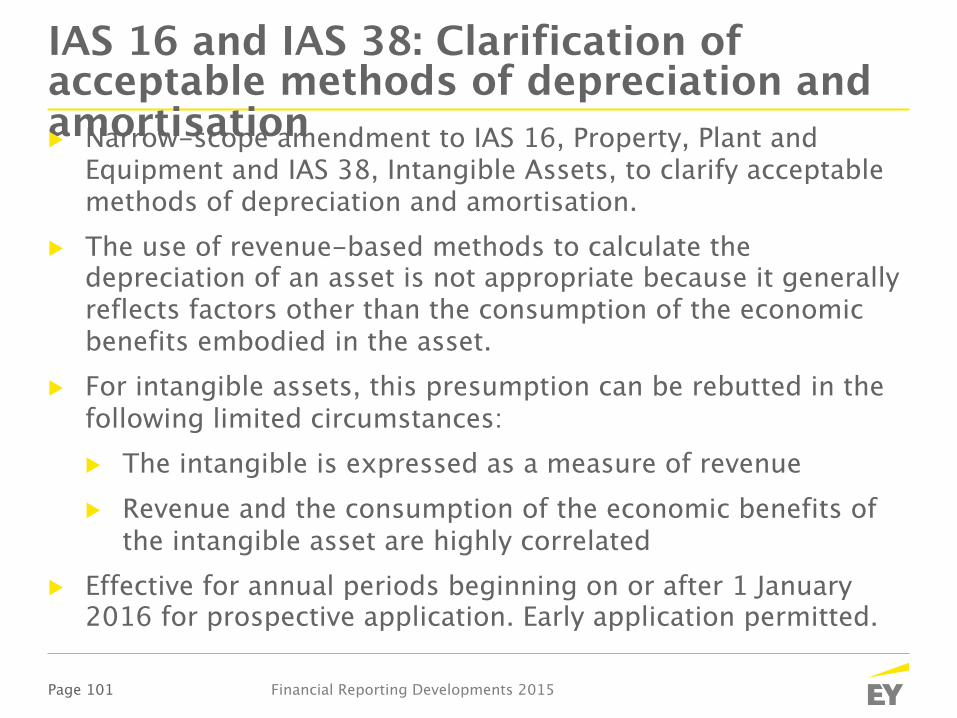

Narrow-scope amendments to IAS 16: Property, Plant and Equipment and IAS 38: Intangible Assets

Financial Reporting Developments 2015

Page 101

IAS 16 and IAS 38: Clarification of acceptable methods of depreciation and amortisation▶ Narrow-scope amendment to IAS 16, Property, Plant and

Equipment and IAS 38, Intangible Assets, to clarify acceptable methods of depreciation and amortisation.

▶ The use of revenue-based methods to calculate the depreciation of an asset is not appropriate because it generally reflects factors other than the consumption of the economic benefits embodied in the asset.

▶ For intangible assets, this presumption can be rebutted in the following limited circumstances:▶ The intangible is expressed as a measure of revenue▶ Revenue and the consumption of the economic benefits of

the intangible asset are highly correlated▶ Effective for annual periods beginning on or after 1 January

2016 for prospective application. Early application permitted.

Financial Reporting Developments 2015

Page 102

Narrow-scope amendments: Fair Value Measurement

Financial Reporting Developments 2015

Page 103

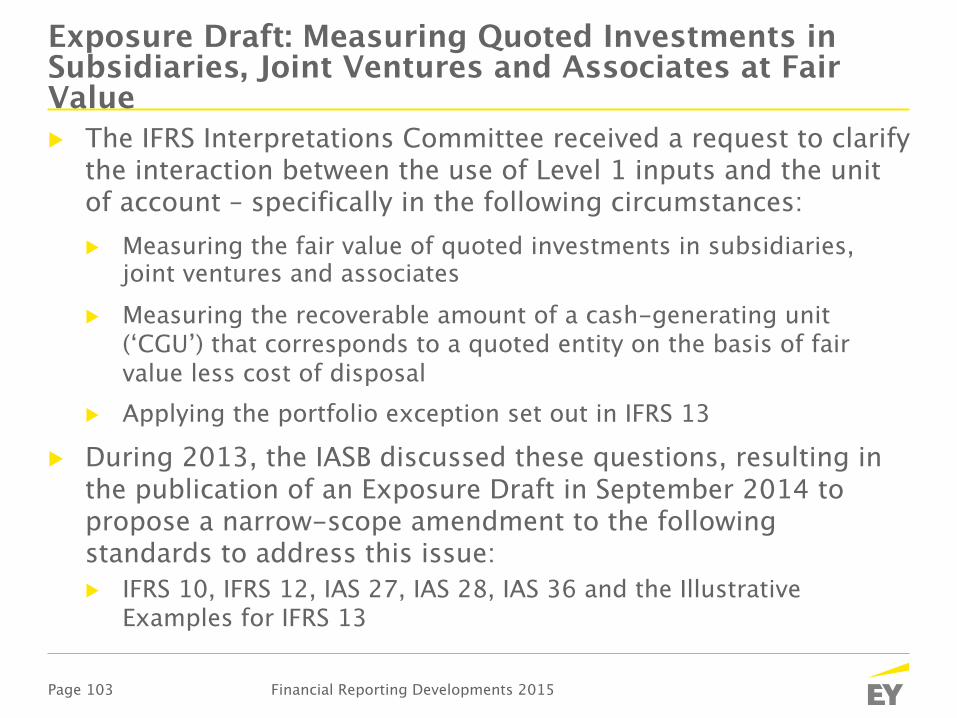

Exposure Draft: Measuring Quoted Investments in Subsidiaries, Joint Ventures and Associates at Fair Value▶ The IFRS Interpretations Committee received a request to clarify

the interaction between the use of Level 1 inputs and the unit of account – specifically in the following circumstances:▶ Measuring the fair value of quoted investments in subsidiaries,

joint ventures and associates▶ Measuring the recoverable amount of a cash-generating unit

(‘CGU’) that corresponds to a quoted entity on the basis of fair value less cost of disposal

▶ Applying the portfolio exception set out in IFRS 13

▶ During 2013, the IASB discussed these questions, resulting in the publication of an Exposure Draft in September 2014 to propose a narrow-scope amendment to the following standards to address this issue:▶ IFRS 10, IFRS 12, IAS 27, IAS 28, IAS 36 and the Illustrative

Examples for IFRS 13

Financial Reporting Developments 2015

Page 104

Exposure Draft: Measuring Quoted Investments in Subsidiaries, Joint Ventures and Associates at Fair Value▶ Proposed unit of account for investments in subsidiaries, joint

ventures and associates▶ The unit of account is the investment as a whole rather than the

individual financial instruments that make up the investment ▶ This conclusion is presented in the Basis of Conclusions of the

Exposure Draft

▶ The interaction of requirements in IFRS 13 with the unit of account for subsidiaries, joint ventures, associates▶ The fair value measurement of an investment composed of

financial instruments should be the product of the quoted price (P) multiplied by the quantity (Q) of instruments held (i.e. P x Q)

▶ This proposed change is presented as a narrow-scope amendment to IFRS 10, IFRS 12, IAS 27, IAS 28

Financial Reporting Developments 2015

Page 105

Exposure Draft: Measuring Quoted Investments in Subsidiaries, Joint Ventures and Associates at Fair Value▶ The interaction of requirements in IFRS 13 with the unit of

account for CGUs▶ The recoverable amount of CGUs that corresponds to quoted

entities measured on the basis of fair value less costs of disposal should be based on the product of P x Q

▶ This proposed change is presented as a narrow-scope amendment to IAS 36

▶ The interaction of requirements in IFRS 13 with the unit of account for CGUs portfolios comprised of investments for which quoted prices in an active market are available▶ The application of the portfolio exception as set out in IFRS 13 for

portfolios that comprise only Level 1 financial instruments (whose market risks are substantially the same), should be measured by multiplying the net position by Level 1 prices

▶ This proposed change is presented as a narrow-scope amendment to the Illustrative Examples of IFRS 13

Financial Reporting Developments 2015

Page 106

Exposure Draft: Measuring Quoted Investments in Subsidiaries, Joint Ventures and Associates at Fair Value▶ Transition provisions

▶ For quoted investments in subsidiaries, joint ventures and associates, an entity would recognise a cumulative catch-up adjustment to opening retained earnings for the period in which the proposed amendments are first applied

▶ For impairment testing in accordance with IAS 36, an entity would apply the requirements on a prospective basis.

▶ An effective date has not been set, but early application of the amendments will be permitted

Financial Reporting Developments 2015

Page 107

Exposure Draft: Measuring Quoted Investments in Subsidiaries, Joint Ventures and Associates at Fair Value▶ At the July 2015 meeting, the IASB discussed the

staff recommendations related to feedback received from the Exposure Draft ▶ Constituents broadly disagreed with application of “P x Q”

for fair value measurement of investments in subsidiaries, joint ventures and associates; or for measurement of recoverable amount of quoted CGUs

▶ IASB voted to build a deeper understanding of the proposed measurement (i.e. perform further research) to develop recommendations for the Board

▶ Additional research would include research on issues raised by respondents, which could lead to re-deliberations

Financial Reporting Developments 2015

Page 108

Narrow-scope amendment: Investment Entities Consolidation Exception

Financial Reporting Developments 2015

Page 109

Investment Entities Consolidation Exception▶ IASB issued amendments to IFRS 10, IFRS 12 and IAS

28 in December 2014 that are effective for annual periods beginning on or after January 1, 2016 and relate to:▶ Exemption from preparing consolidated financial statements

for an intermediate parent of an investment entity▶ Subsidiary that provides services that support the

investment entity’s investment activities▶ Application of the equity method by a non-investment entity

that has an interest in an associate or joint venture that is an investment entity

Financial Reporting Developments 2015

Page 110

Investment Entities Consolidation Exception

▶ Exemption from preparing consolidated financial statements (FS):▶ Exemption from presenting consolidated FS applies to a parent

entity that is a subsidiary of an investment entity when the investment entity measures all of its subsidiaries at FV

▶ Exemption from applying the equity method for entities that are subsidiaries of an investment entity and hold interests in associates and joint ventures

▶ Subsidiary that provides services that support the investment entity’s investment activities:▶ Only a subsidiary that is not itself an investment entity and

provides support services to the investment entity is consolidated

Financial Reporting Developments 2015

Page 111

Investment Entities Consolidation Exception

▶ Application of the equity method by a non-investment entity that has an interest in an associated or joint venture that is an investment entity ▶ The investor is permitted (but not required) to retain the fair

value measurement applied by the investment entity associate or joint venture to its interests in subsidiaries

Financial Reporting Developments 2015

Page 112

Narrow-scope amendments: Acquisition of an Interest in a Joint Operation

Financial Reporting Developments 2015

Page 113

IFRS 11 Joint Arrangements: Accounting for Acquisitions of Interests in Joint Operations

▶ Objective: to provide guidance on accounting for acquisitions of an interest in a joint operation that constitutes a business

▶ December 2012 Exposure draft: An interest in a joint operation that constitutes a business should be accounted for following the relevant principles in IFRS 3 and other Standards.▶ To the extent of the ownership interest

1. Measure identifiable assets and liabilities at fair value2. Expense acquisition costs as incurred3. Recognize deferred taxes4. Record goodwill 5. Make all required business combination disclosures

Financial Reporting Developments 2015

Page 114

IFRS 11 Joint Arrangements: Accounting for Acquisitions of Interests in Joint Operations

▶ 2013 and 2014 Amendments ▶ Applies to both the initial acquisition of an interest as well as the

acquisition of additional interests in the same joint operation▶ Previously held interests in a joint operation are not re-measured on

the acquisition of an additional interest if the entity retains joint control

▶ Scope exclusions: ▶ No existing business is contributed to the joint operation on

formation ▶ The parties sharing joint control are under common control

▶ Effective for annual periods beginning on or after 1 January 2016 with early application permitted.

▶ July 2015 Interpretation Committee Meeting: accounting treatment when an entity becomes a joint operator through acquisition of an additional interest in an existing joint operation

Financial Reporting Developments 2015

EY | Assurance | Tax | Transactions | AdvisoryAbout EYEY is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 200,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

EY refers to the global organization and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

For more information about our organization, please visit www.ey.com.

© 2015 Ernst & Young LLP. All Rights Reserved.A member firm of Ernst & Young Global Limited.