CHRISTMAS 2016 REVEALED! - Nielsen Christmas... · CHRISTMAS 2016 REVEALED! y. 2 ... Key Highlights...

78

CHRISTMAS 2016 REVEALED!

Transcript of CHRISTMAS 2016 REVEALED! - Nielsen Christmas... · CHRISTMAS 2016 REVEALED! y. 2 ... Key Highlights...

CHRISTMAS 2016

REVEALED!

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

2

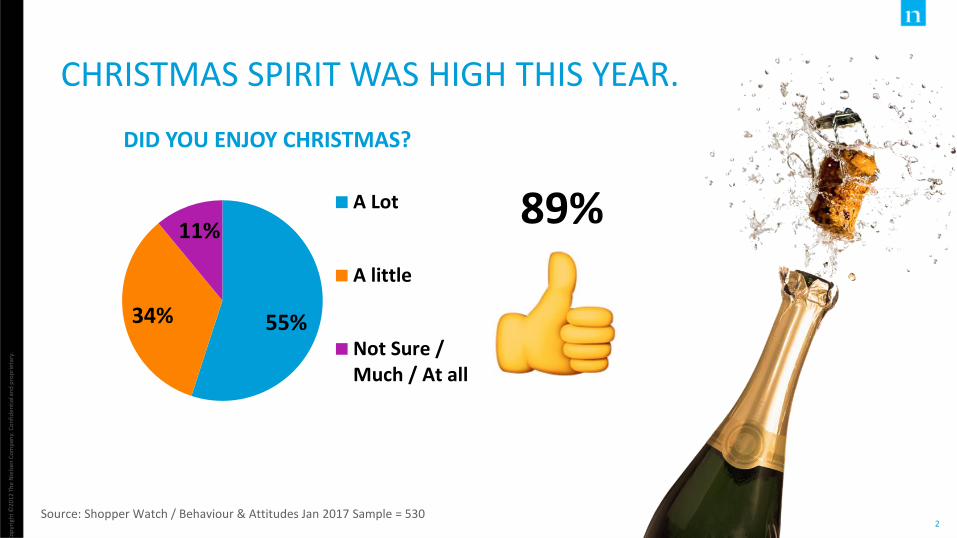

DID YOU ENJOY CHRISTMAS?

CHRISTMAS SPIRIT WAS HIGH THIS YEAR.

Source: Shopper Watch / Behaviour & Attitudes Jan 2017 Sample = 530

55% 34%

11% A Lot

A little

Not Sure /Much / At all

89%

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

3

DID WE FEED OUR CHRISTMAS

SPIRIT ?

THE STATS REVEALED …

Co

pyr

igh

t ©20

14 T

he

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

4

NEVEN’S CHRISTMAS

SPECIAL

AMONG HIGHEST-RATING

COOKERY PROGRAMMES OF THE YEAR

Co

pyr

igh

t ©20

14 T

he

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

5

3.5 MILLION

TUBS OF CHOCOLATE

+5% year on year

(Nov + Dec 16)

Source: Nielsen Scantrack total trade 9 weeks Data to Jan 1st 17

Co

pyr

igh

t ©20

14 T

he

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

6

Key Highlights slide 621,000

BOTTLES of CHAMPAGNE &

SPARKLING WINE

+18% year on year 14% of Full year sales in the two weeks of

Christmas

(Nov + Dec 16)

Source: Nielsen Total Off Trade Data to Dec 16

Co

pyr

igh

t ©20

14 T

he

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

7

Key Highlights slide

90 MILLION

PINTS ENJOYED IN PUBS

+2.4% year on year

(Nov+Dec 16)

Source: Nielsen Total Off Trade Data to Dec 16

Co

pyr

igh

t ©20

14 T

he

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

8 Source: Nielsen Total Off Trade Data to Dec 16

€4 MILLION

ON STUFFING AND BREADCRUMBS

35% OF THE TOTAL YEAR

(Nov + Dec 16)

Source: Nielsen Scantrack total trade 8 weeks Data to Dec 25th

Co

pyr

igh

t ©20

14 T

he

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

9

WE LAUGHED!

# 1 Program Christmas Day

700,000 viewers

Source: TAM Ireland Ltd / Nielsen TAM / Individuals 4+, National, Consolidated. Average audience 000s / Top Programme ranking 25th December 2016, All Channels

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

10

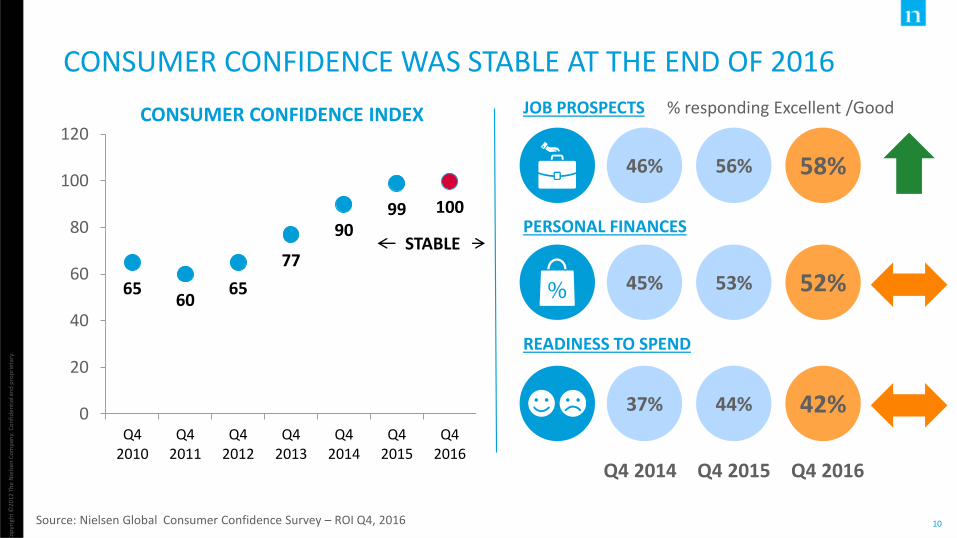

CONSUMER CONFIDENCE WAS STABLE AT THE END OF 2016

Source: Nielsen Global Consumer Confidence Survey – ROI Q4, 2016

65 60

65

77

90 99 100

0

20

40

60

80

100

120

Q42010

Q42011

Q42012

Q42013

Q42014

Q42015

Q42016

CONSUMER CONFIDENCE INDEX

STABLE

JOB PROSPECTS

PERSONAL FINANCES

READINESS TO SPEND

46%

45%

37%

56%

53%

44%

Q4 2014 Q4 2015

52%

42%

58%

Q4 2016

% responding Excellent /Good

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

11

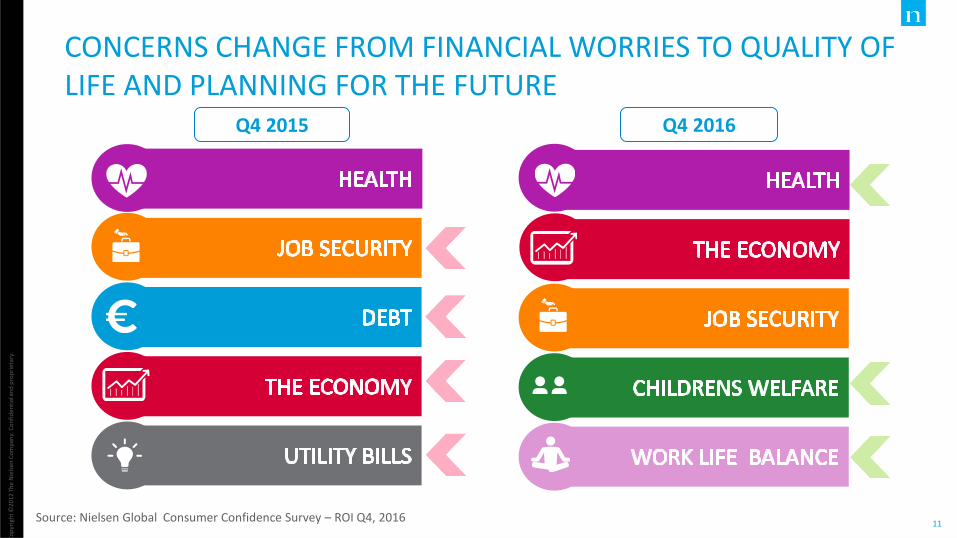

CONCERNS CHANGE FROM FINANCIAL WORRIES TO QUALITY OF LIFE AND PLANNING FOR THE FUTURE

Source: Nielsen Global Consumer Confidence Survey – ROI Q4, 2016

Q4 2015 Q4 2016

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

12

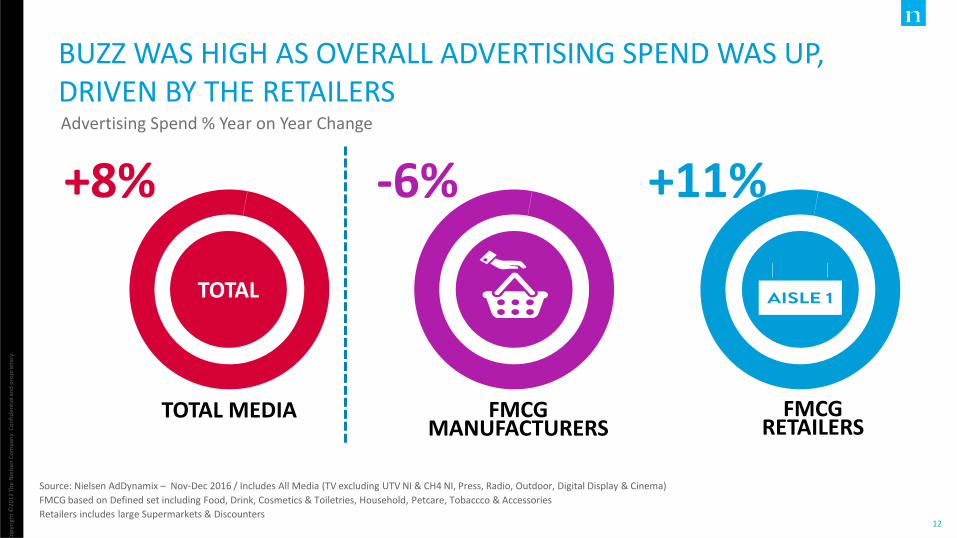

TOTAL MEDIA

+8%

TOTAL

BUZZ WAS HIGH AS OVERALL ADVERTISING SPEND WAS UP, DRIVEN BY THE RETAILERS Advertising Spend % Year on Year Change

Source: Nielsen AdDynamix – Nov-Dec 2016 / Includes All Media (TV excluding UTV NI & CH4 NI, Press, Radio, Outdoor, Digital Display & Cinema)

FMCG based on Defined set including Food, Drink, Cosmetics & Toiletries, Household, Petcare, Tobaccco & Accessories

Retailers includes large Supermarkets & Discounters

+11%

FMCG RETAILERS

-6%

FMCG MANUFACTURERS

Co

pyr

igh

t ©20

13

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

13

55%

Will continue to switch to cheaper grocery

brands once conditions improve (-5%)

48%

Will cut down on out of home entertainment

(+4%)

BUT CONSUMERS CONTINUE TO LOOK FOR SAVINGS

Put any spare cash into savings (+1%)

Source: Nielsen Global Consumer Confidence Survey – ROI Q4, 2016

42%

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

15

+1.4% +0.6% +2.0%

+1.5% -0.1% +1.4% MARKET EXCL TOBACCO

TOTAL MARKET

NO

VD

EC 1

6

Source: Nielsen Strategic Planner , ROI Total Defined Market Read| MAT to Dec 2016

Volume Price Value

POSITIVE SENTIMENT & BUZZ DRIVES CHRISTMAS GROWTH - AHEAD OF FULL YEAR

+0.8% +0.3% +1.2% MARKET EXCL TOBACCO

+0.8% +1.1% +1.8% TOTAL MARKET

MA

T 2

01

6

FMCG Market Performance, Year on Year % Change

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

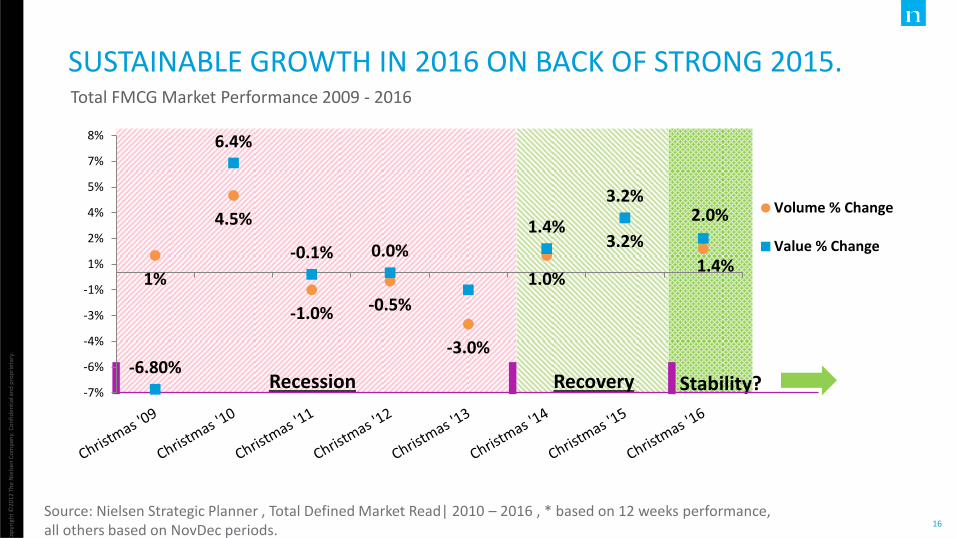

16

Recession Recovery Stability?

Source: Nielsen Strategic Planner , Total Defined Market Read| 2010 – 2016 , * based on 12 weeks performance, all others based on NovDec periods.

Total FMCG Market Performance 2009 - 2016

SUSTAINABLE GROWTH IN 2016 ON BACK OF STRONG 2015.

1%

4.5%

-1.0% -0.5%

-3.0%

1.0%

3.2%

1.4%

-6.80%

6.4%

-0.1% 0.0%

1.4%

3.2% 2.0%

-7%

-6%

-4%

-3%

-1%

1%

2%

4%

5%

7%

8%

Volume % Change

Value % Change

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

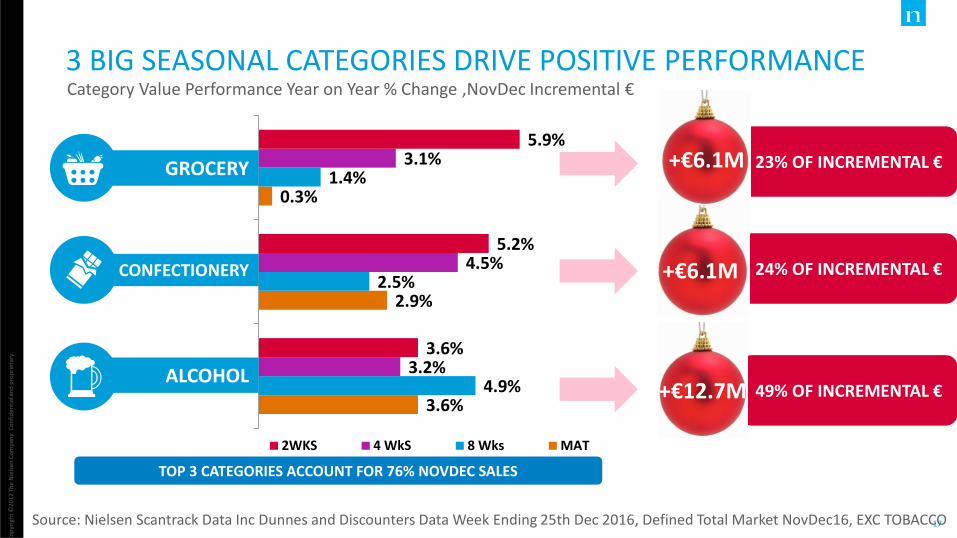

17

3.6%

2.9%

0.3%

4.9%

2.5%

1.4%

3.2%

4.5%

3.1%

3.6%

5.2%

5.9%

ALCOHOL

CONFECTIONERY

GROCERY

2WKS 4 WkS 8 Wks MAT

3 BIG SEASONAL CATEGORIES DRIVE POSITIVE PERFORMANCE Category Value Performance Year on Year % Change ,NovDec Incremental €

Source: Nielsen Scantrack Data Inc Dunnes and Discounters Data Week Ending 25th Dec 2016, Defined Total Market NovDec16, EXC TOBACCO

49% OF INCREMENTAL € +€12.7M

24% OF INCREMENTAL € +€6.1M

23% OF INCREMENTAL € +€6.1M

TOP 3 CATEGORIES ACCOUNT FOR 76% NOVDEC SALES

CONFECTIONERY

ALCOHOL

GROCERY

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

18

0.6%

0.6%

1.0%

-0.5%

-0.4%

-0.9%

0.9%

-0.1%

1.3%

1.3%

2.9%

1.8%

3.8%

3.4%

5.9%

4.7%

FROZEN

HEALTH & BEAUTY

HOUSEHOLD

BAKERY

2WKS 4 WkS 8 Wks MAT

HOUSEHOLD

HEALTH &BEAUTY

BAKERY

FROZEN

NON SEASONAL CATEGORIES SAW GROWTH PRIMARILY IN DECEMBER

Source: Nielsen Scantrack Data Inc Dunnes and Discounters Data Week Ending 25th Dec 2016, Defined Total Market NovDec16, EXCL TOBACCO

Category Value Performance Year on Year % Change ,NovDec Incremental €

ONLY HOUSEHOLD GROWS IN NOVDEC16

+€934k

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

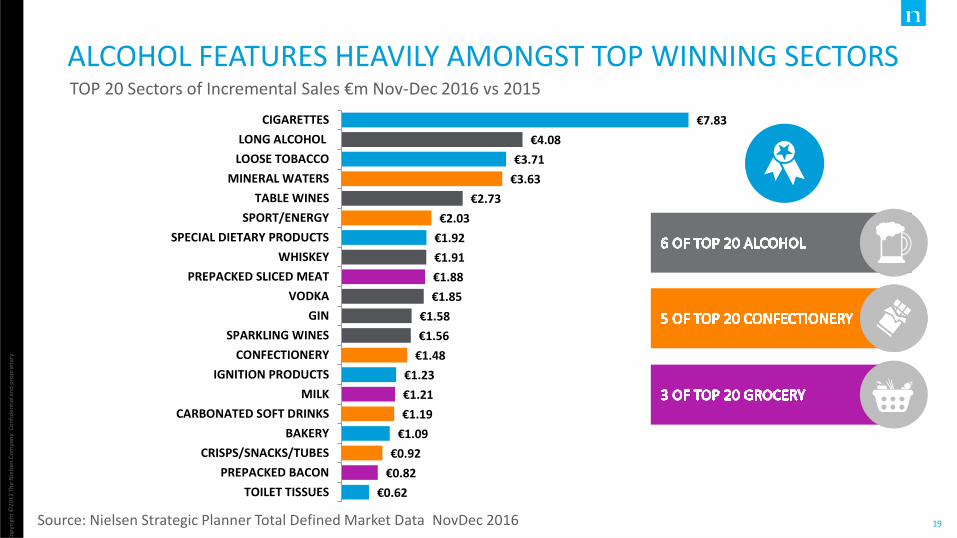

19

ALCOHOL FEATURES HEAVILY AMONGST TOP WINNING SECTORS

Source: Nielsen Strategic Planner Total Defined Market Data NovDec 2016

€0.62

€0.82

€0.92

€1.09

€1.19

€1.21

€1.23

€1.48

€1.56

€1.58

€1.85

€1.88

€1.91

€1.92

€2.03

€2.73

€3.63

€3.71

€4.08

€7.83

TOILET TISSUES

PREPACKED BACON

CRISPS/SNACKS/TUBES

BAKERY

CARBONATED SOFT DRINKS

MILK

IGNITION PRODUCTS

CONFECTIONERY

SPARKLING WINES

GIN

VODKA

PREPACKED SLICED MEAT

WHISKEY

SPECIAL DIETARY PRODUCTS

SPORT/ENERGY

TABLE WINES

MINERAL WATERS

LOOSE TOBACCO

LONG ALCOHOL

CIGARETTES

TOP 20 Sectors of Incremental Sales €m Nov-Dec 2016 vs 2015

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

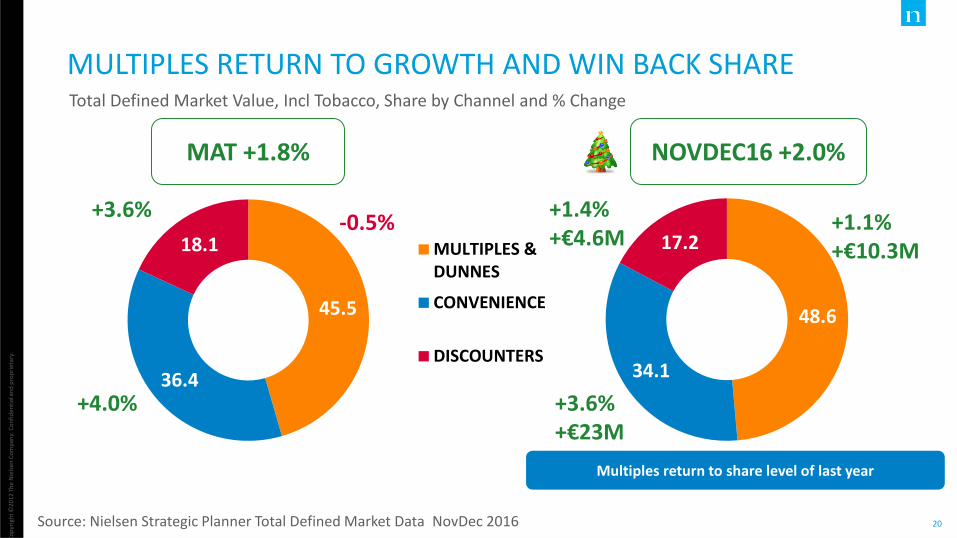

20

48.6

34.1

17.2

45.5

36.4

18.1 MULTIPLES &DUNNES

CONVENIENCE

DISCOUNTERS

MULTIPLES RETURN TO GROWTH AND WIN BACK SHARE

-0.5%

+4.0%

+3.6%

MAT +1.8%

+1.1% +€10.3M

+3.6% +€23M

+1.4% +€4.6M

NOVDEC16 +2.0%

Multiples return to share level of last year

Total Defined Market Value, Incl Tobacco, Share by Channel and % Change

Source: Nielsen Strategic Planner Total Defined Market Data NovDec 2016

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

21

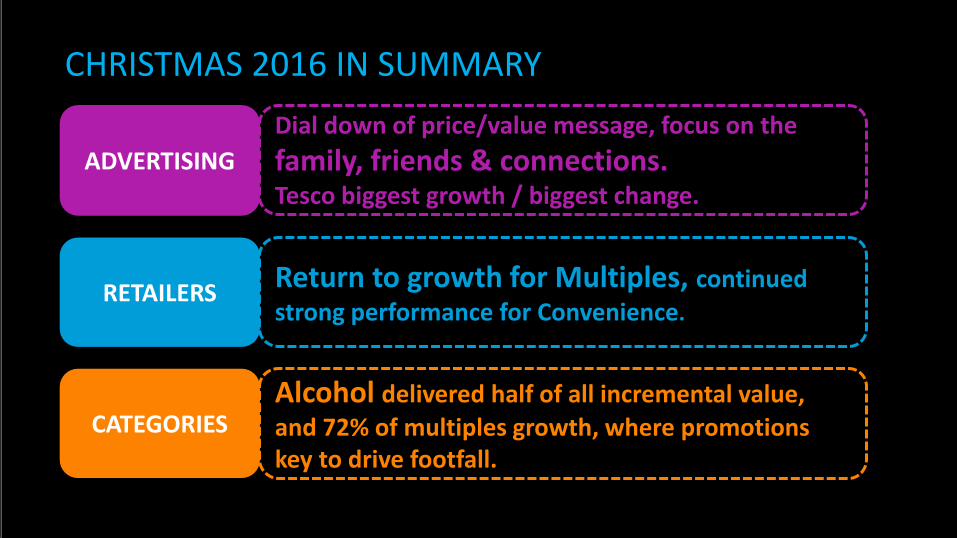

CHRISTMAS 2016 IN SUMMARY

ADVERTISING

Dial down of price/value message, focus on the

family, friends & connections. Tesco biggest growth / biggest change.

RETAILERS Return to growth for Multiples, continued

strong performance for Convenience.

CATEGORIES Alcohol delivered half of all incremental value,

and 72% of multiples growth, where promotions key to drive footfall.

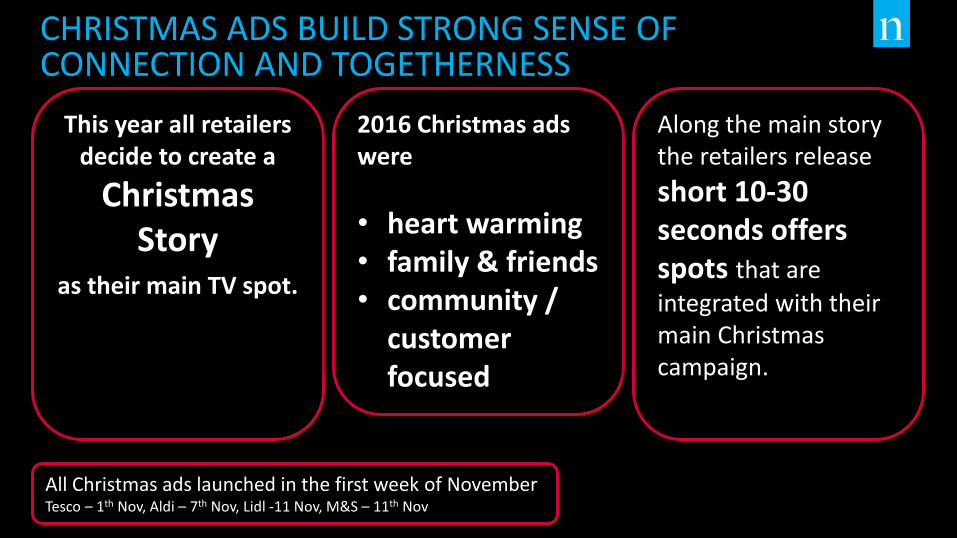

THE TROLLEY TURF WAR

This year all retailers decide to create a

Christmas Story

as their main TV spot.

2016 Christmas ads were

• heart warming • family & friends • community /

customer focused

All Christmas ads launched in the first week of November Tesco – 1th Nov, Aldi – 7th Nov, Lidl -11 Nov, M&S – 11th Nov

Along the main story the retailers release

short 10-30 seconds offers spots that are

integrated with their main Christmas campaign.

CHRISTMAS ADS BUILD STRONG SENSE OF CONNECTION AND TOGETHERNESS

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

24

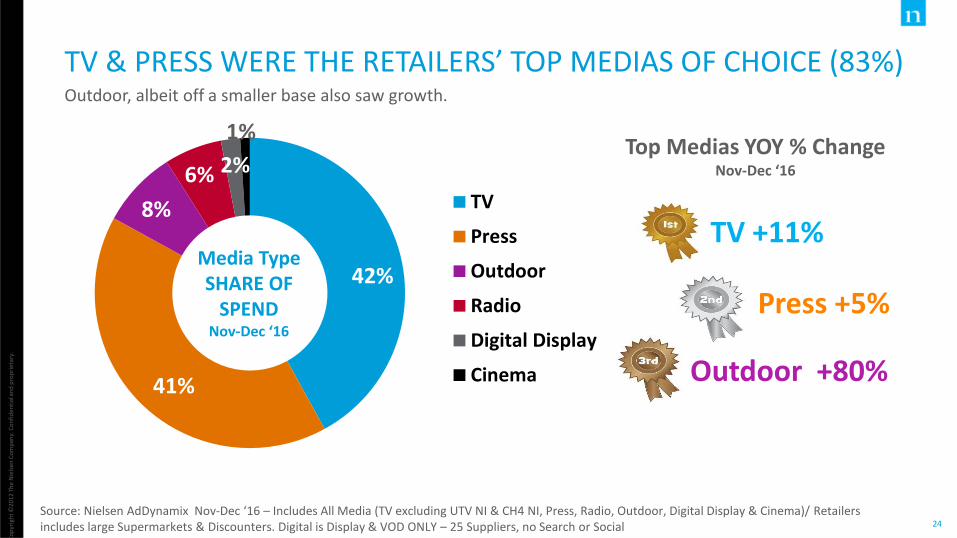

42%

41%

8%

6% 2%

1%

TV

Press

Outdoor

Radio

Digital Display

Cinema

TV & PRESS WERE THE RETAILERS’ TOP MEDIAS OF CHOICE (83%) Outdoor, albeit off a smaller base also saw growth.

+11% +11%

1%

Source: Nielsen AdDynamix Nov-Dec ‘16 – Includes All Media (TV excluding UTV NI & CH4 NI, Press, Radio, Outdoor, Digital Display & Cinema)/ Retailers includes large Supermarkets & Discounters. Digital is Display & VOD ONLY – 25 Suppliers, no Search or Social

+13%

Media Type SHARE OF

SPEND Nov-Dec ‘16

Top Medias YOY % Change Nov-Dec ‘16

1. TV +11%

2. Press +5% 14%

3. Outdoor +80%

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

25

21% 20% 15% 12% 5% 28% 20%

DISCOUNTERS SHARES

48% SPEND VS

17% TRADE

28%

35% 48% 47%

27%

55% 48%

47% 34% 40%

50%

32% 43%

10% 11% 5% 12%

2% 11% 11%

Lidl Tesco Aldi Dunnes Supervalu M&S

Cinema

Digital Display

Radio

Outdoor

Press

TV

TV WAS #1 CHOICE OF MEDIA FOR ALL RETAILERS BAR DUNNES & LIDL – THE BIGGEST SPENDER Retailers Media Mix Nov-Dec 2016

Source: Nielsen AdDynamix Nov-Dec 2016 – Includes All Media (TV excluding UTV NI & CH4 NI, Press, Radio, Outdoor, Digital Display & Cinema)/ Retailers includes large Supermarkets & Discounters. Digital is Display & VOD ONLY – 25 Suppliers, no Search or Social

-13%

Retailers SHARE OF SPEND Nov-Dec ‘16

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

26

Total Retailers

Lidl Ireland

Tesco Ireland

Aldi Stores

Dunnes Stores

Supervalu

Marks & Spencer

-18.3

STRONG GROWTH IN SPEND FROM TOP THREE RETAILERS

+11%

28%

Source: Nielsen AdDynamix Nov-Dec ‘16 – Includes All Media (TV excluding UTV NI & CH4 NI, Press, Radio, Outdoor, Digital Display & Cinema)/ Retailers includes large Supermarkets & Discounters

% Change YOY

-12.8

16.5

37.5

11.5

28.3

-1.8

Retailers Growth in Ad Spend Nov-Dec ‘16

LIDL

ALDI

TESCO

Co

pyr

igh

t ©20

13

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

28

7%

TRADITIONAL MEDIA REMAINS AN IMPORTANT WAY TO LEARN ABOUT RETAILER PROMOTIONS.

Radio

13% Newspapers

23% TV

Q9. How do you normally find out about supermarket offers and promotions over the Christmas period?

8% Magazines

NIELSEN IRELAND Christmas Shopper Report 2016 (Base n = 250)

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

29

GETTING IMPACTFUL TV CREATIVE CRUCIAL AT CHRISTMAS

The average person watched over 3 hours of TV every day in November & December

TV reached over

3 million people daily November &

December

Source: TAM Ireland Ltd / Nielsen TAM Based on Individuals 4+ / National / ROI Commercial Channels Nov/Dec average based on 01/11/2016 – 31/12/2016

Consumers were

exposed to 2,397 different TV ads in

November & December

59% of those ads

were new to 2016

21% of all TV

advertising campaigns were in

November & December

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

32

THE KEY TO CHRISTMAS IS EMOTION Up to 70% of advertising ROI is driven by CREATIVE

SUPERVALU

‘Real Food, Real People’ local and Irish.

TESCO – NEW

‘Here’s to the Host’ The Heroes of Christmas, friends/family/community.

ALDI - NEW

‘Kevin the Carrot’ ads humour to 2015 ‘My Favourite Things’

M&S – NEW

‘Christmas with Love’ warm and humorous.

LIDL

‘Share More Special Moments’ the whole family.

Driving emotions & encouraging memory activation are the best ways to drive action (purchase behaviour)

DUNNES

‘Make Christmas’ Make ‘special’, ‘believe’, ‘magic’.

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

33

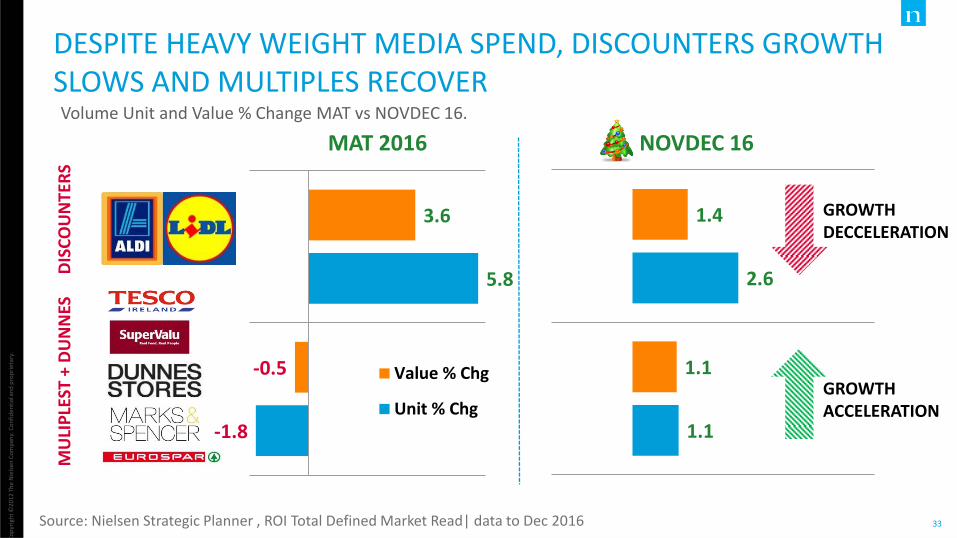

-1.8

5.8

-0.5

3.6

MULTIPLES & DUNNES

DISCOUNTERS

Value % Chg

Unit % Chg

DESPITE HEAVY WEIGHT MEDIA SPEND, DISCOUNTERS GROWTH SLOWS AND MULTIPLES RECOVER

MAT 2016

Source: Nielsen Strategic Planner , ROI Total Defined Market Read| data to Dec 2016

Volume Unit and Value % Change MAT vs NOVDEC 16.

MU

LIP

LEST

+ D

UN

NES

D

ISC

OU

NTE

RS

1.1

2.6

1.1

1.4

NOVDEC 16

GROWTH DECCELERATION

GROWTH ACCELERATION

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

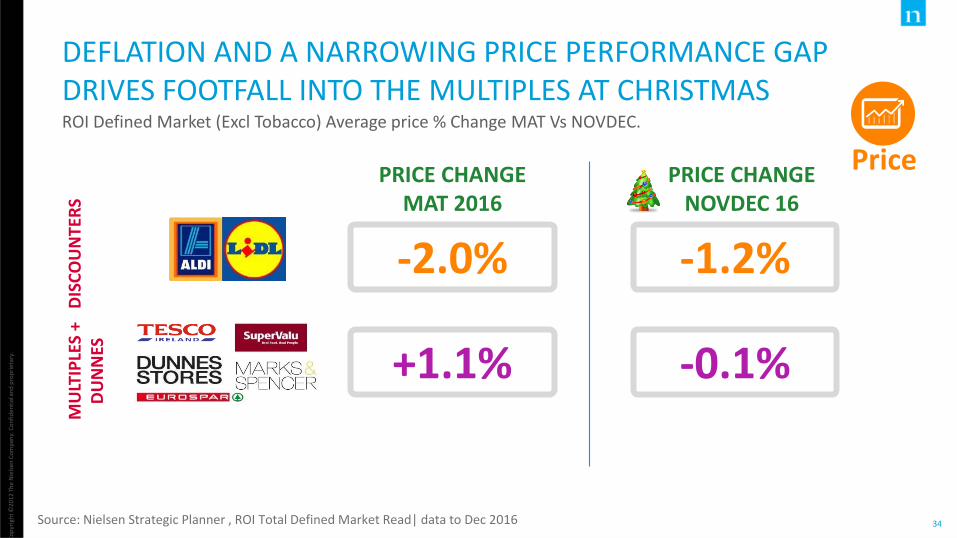

34

PRICE CHANGE MAT 2016

Price

+1.1%

-2.0%

DEFLATION AND A NARROWING PRICE PERFORMANCE GAP DRIVES FOOTFALL INTO THE MULTIPLES AT CHRISTMAS

PRICE CHANGE NOVDEC 16

-1.2%

-0.1%

Source: Nielsen Strategic Planner , ROI Total Defined Market Read| data to Dec 2016

ROI Defined Market (Excl Tobacco) Average price % Change MAT Vs NOVDEC.

MU

LTIP

LES

+ D

UN

NES

D

ISC

OU

NTE

RS

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

35

ALCOHOL

GROCERY

HOUSEHOLD

BAKERY

CONFECTIONERY

4 KEY CATEGORIES DRIVE MULTIPLES CHRISTMAS GROWTH Value % Change by Category MAT Vs NOVDEC.

Source: Nielsen Strategic Planner , ROI Category Read| data to Dec 2016

MULTIPLES + DUNNES

Only Alcohol performs better

Christmas vs MAT

+4.2%

+1.2%

+0.5%

NOVDEC

-0.4%

+0.9%

HEALTH& BEAUTY -2.3%

+2.1%

-1.6%

-0.5%

-2.5%

MAT

-0.3%

-1.8%

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

36

12.7%

13.3%

10.0%

8.8%

11.6%

8.0%

14.3%

15.4%

48.6%

45.5%

NO

VD

ECM

AT

GROCERY CONFECTIONERY

ALCOHOL ALL OTHER

+1.2% pts

+3.6% pts

Value Share and SHARE Change MAT VS NOVDEC 16

5.5%

6.1%

4.0%

3.8%

2.5%

2.5%

5.3%

5.8%

17.2%

18.1%

NO

VD

ECM

AT

GROCERY CONFECTIONERY

ALCOHOL ALL OTHER

MULTIPLES + DUNNES

ALCOHOL AND CONFECTIONERY THE BIG DRIVERS OF SHARE WIN BACK FOR MULTIPLES OVER CHRISTMAS

Source: Nielsen Strategic Planner , ROI Category Read| data to Dec 2016

DISCOUNTERS

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

37

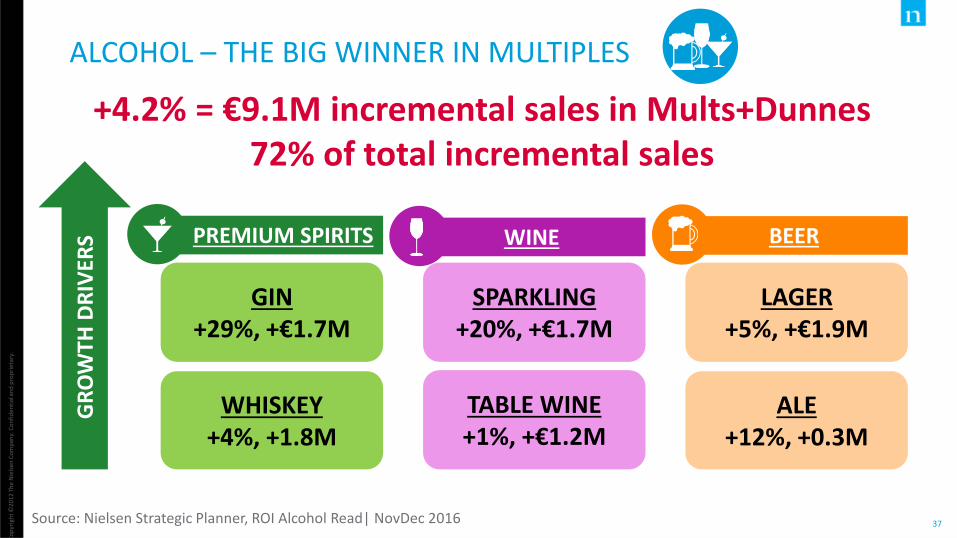

ALCOHOL – THE BIG WINNER IN MULTIPLES

+4.2% = €9.1M incremental sales in Mults+Dunnes 72% of total incremental sales

PREMIUM SPIRITS

GR

OW

TH D

RIV

ERS

GIN +29%, +€1.7M

WHISKEY +4%, +1.8M

SPARKLING +20%, +€1.7M

TABLE WINE +1%, +€1.2M

WINE

LAGER +5%, +€1.9M

ALE +12%, +0.3M

BEER

Source: Nielsen Strategic Planner, ROI Alcohol Read| NovDec 2016

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

38

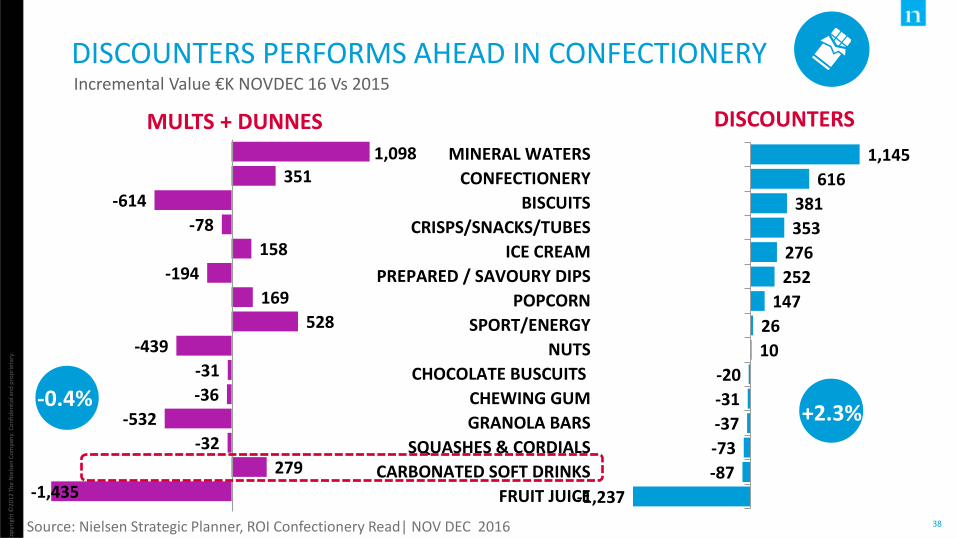

-1,237

-87

-73

-37

-31

-20

10

26

147

252

276

353

381

616

1,145

FRUIT JUICE

CARBONATED SOFT DRINKS

SQUASHES & CORDIALS

GRANOLA BARS

CHEWING GUM

CHOCOLATE BUSCUITS

NUTS

SPORT/ENERGY

POPCORN

PREPARED / SAVOURY DIPS

ICE CREAM

CRISPS/SNACKS/TUBES

BISCUITS

CONFECTIONERY

MINERAL WATERS

Incremental Value €K NOVDEC 16 Vs 2015

DISCOUNTERS PERFORMS AHEAD IN CONFECTIONERY

DISCOUNTERS

Source: Nielsen Strategic Planner, ROI Confectionery Read| NOV DEC 2016

MULTS + DUNNES

-1,435

279

-32

-532

-36

-31

-439

528

169

-194

158

-78

-614

351 1,098

-0.4% +2.3%

Co

pyr

igh

t ©20

13

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

39

Hands up who didn’t buy one of

these tubs?!

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

40

1

2

3

1.5M

3.1M

2.7M

2.7M

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

41

Nuts +4%, Special Dietary +81%

Nut/Seed Butter +28%, Honey +6%

The Balance

Source: Nielsen Multiples Excl Dunnes 8 weeks Data to Dec 25th 2016 *Nielsen Multiples TSR, 4 w/e 25th Dec 2016 vs LY

Cake Decorations +6%, Flour +1% Baking Products +2%, Butter +7%

In Preparation

Chilled Poultry,+6%, Smoked Salmon, +5%*

Cranberry Sauce +6%, PrePack Bacon, +11%

PrePack Stuffing +5%, Tinfoil +8%

Stocks/Gravys/Extracts +13%

The Feast

say reduced their spend vs.

last year

shopped in Supermarkets they

had NOT considered before

shopped

wherever the price was right

43% 21% 38%

Source: Nielsen Shopper Study: Total Respondents: 250 | Time Range: Jan 28th and 29th 2017

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

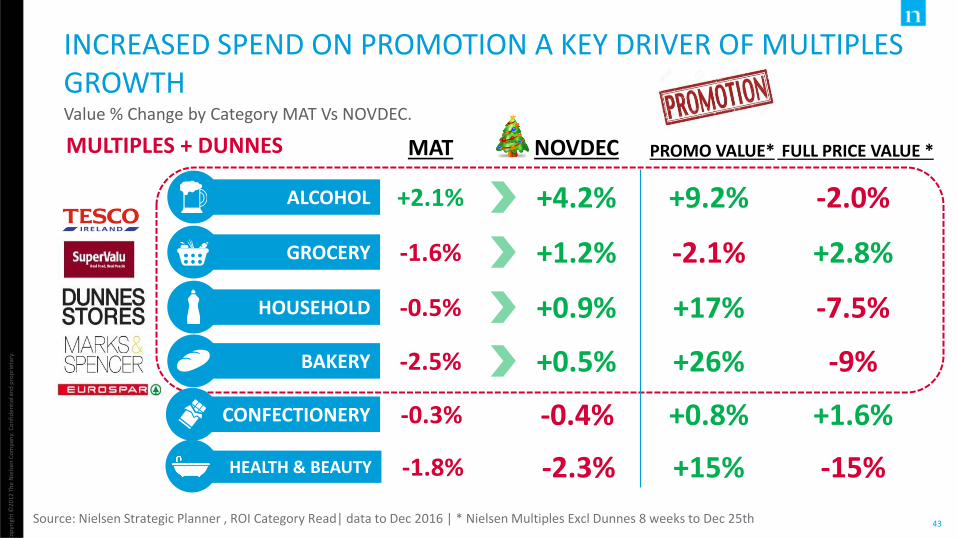

43

ALCOHOL

GROCERY

HOUSEHOLD

BAKERY

CONFECTIONERY

INCREASED SPEND ON PROMOTION A KEY DRIVER OF MULTIPLES GROWTH Value % Change by Category MAT Vs NOVDEC.

MULTIPLES + DUNNES

+4.2%

+1.2%

+0.5%

NOVDEC

-0.4%

+0.9%

+2.1%

-1.6%

-0.5%

-2.5%

MAT

-0.3%

HEALTH & BEAUTY -2.3% -1.8%

PROMO VALUE*

+9.2%

-2.1%

+26%

+0.8%

+17%

+15%

FULL PRICE VALUE *

-2.0%

+2.8%

-9%

+1.6%

-7.5%

-15%

Source: Nielsen Strategic Planner , ROI Category Read| data to Dec 2016 | * Nielsen Multiples Excl Dunnes 8 weeks to Dec 25th

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

46

-1.6%

1.0%

4.6%

-0.1%

1.3%

3.3%

5.1%

1.2%

JAN-OCT NOV-DEC JAN-OCT NOV-DEC

BRANDS PRIVATE LABEL

MULTIPLES (Excl Dunnes) DISCOUNTERS

AND MULTIPLES GREW AHEAD IN BOTH BRAND AND PRIVATE LABEL (BUT PL PERFORMED AHEAD OF BRANDS)

Source: Nielsen Scantrack Data Week Ending 25th Dec 2016, excludes Wine and Tobacco

Brand & Private Label Value % Chg

ALCOHOL

HOUSEHOLD

BAKERY

CONFECTIONERY

+1%

+3%

-11%

-9%

+8%

HEALTH& BEAUTY

-1% GROCERY

VALUE % CHANGE

BRANDS IN DISCOUNTERS 8 Weeks to Dec 25th

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

49

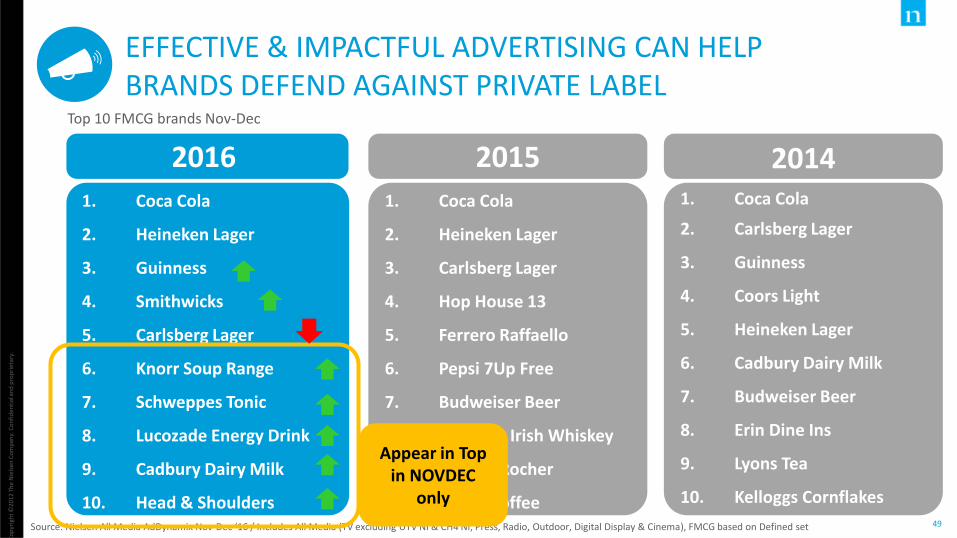

2016

EFFECTIVE & IMPACTFUL ADVERTISING CAN HELP BRANDS DEFEND AGAINST PRIVATE LABEL

Top 10 FMCG brands Nov-Dec

1. Coca Cola

2. Heineken Lager

3. Guinness

4. Smithwicks

5. Carlsberg Lager

6. Knorr Soup Range

7. Schweppes Tonic

8. Lucozade Energy Drink

9. Cadbury Dairy Milk

10. Head & Shoulders

1. Coca Cola

2. Heineken Lager

3. Carlsberg Lager

4. Hop House 13

5. Ferrero Raffaello

6. Pepsi 7Up Free

7. Budweiser Beer

8. Jameson Irish Whiskey

9. Ferrero Rocher

10. Kenco Coffee

1. Coca Cola

2. Carlsberg Lager

3. Guinness

4. Coors Light

5. Heineken Lager

6. Cadbury Dairy Milk

7. Budweiser Beer

8. Erin Dine Ins

9. Lyons Tea

10. Kelloggs Cornflakes

2014 2015

Source: Nielsen All Media AdDynamix Nov-Dec ‘16 / Includes All Media (TV excluding UTV NI & CH4 NI, Press, Radio, Outdoor, Digital Display & Cinema), FMCG based on Defined set

Appear in Top in NOVDEC

only

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

50

ALCOHOL BRANDS DRIVE MULTIPLES GROWTH TOP 20 INCREMENTAL BRANDS, VALUE €K

247k

696k

HOP HOUSE 13

ZIP

DANONE LIGHT &…

FIRE & SMOKE

PALMOLIVE

DENNY

CLONAKILTY

ALPRO

LENOR

LUCOZADE

FULFIL

CADBURY DAIRY MILK

HAAGEN DAZS

ORCHARD THIEVES

HENNESSY

CUSHELLE

HEINEKEN

FAIRY

POWERS

JAMESON

Source: Nielsen Scantrack Data , 8 Week Ending 25th Dec 2016

NEW LISTINGS

MULTIPLES (Excl Dunnes) DISCOUNTERS

141k

855k

JACOBS ELITE

MF M&M'S

KENCO

SHLOER

KOPPARBERG

MF GALAXY

BATCHELORS

NESTLE QUALITY…

PERRI

CADBURY

O HARAS

IRWINS

PRINGLES

DAIRYGOLD

NESTLE COOKIE CRISP

BARRYS

DORITOS

AVONMORE

TROLLI

APTAMIL

NEW LISTINGS

op

THE BASKET BATTLE

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

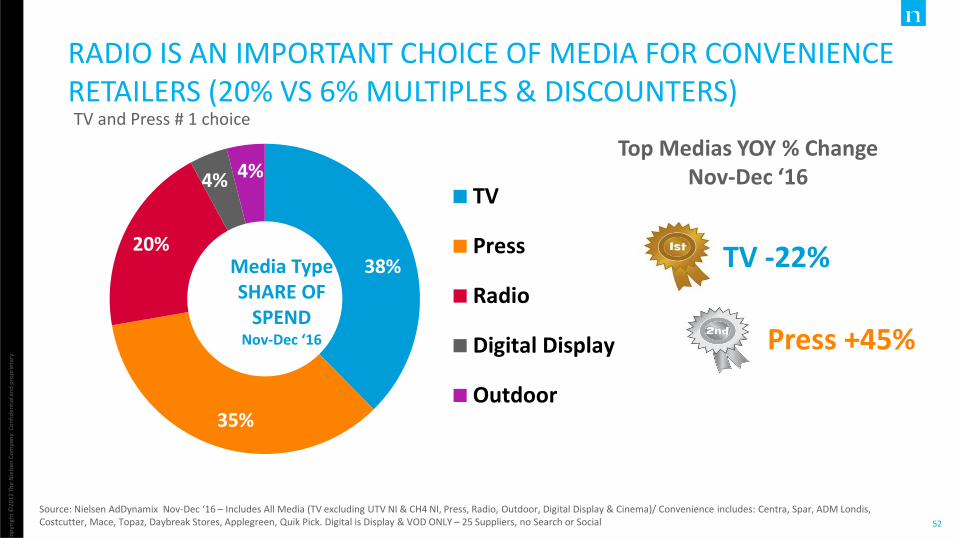

52

38%

35%

20%

4% 4% TV

Press

Radio

Digital Display

Outdoor

RADIO IS AN IMPORTANT CHOICE OF MEDIA FOR CONVENIENCE RETAILERS (20% VS 6% MULTIPLES & DISCOUNTERS)

1%

Source: Nielsen AdDynamix Nov-Dec ‘16 – Includes All Media (TV excluding UTV NI & CH4 NI, Press, Radio, Outdoor, Digital Display & Cinema)/ Convenience includes: Centra, Spar, ADM Londis, Costcutter, Mace, Topaz, Daybreak Stores, Applegreen, Quik Pick. Digital is Display & VOD ONLY – 25 Suppliers, no Search or Social

Media Type SHARE OF

SPEND Nov-Dec ‘16

Top Medias YOY % Change Nov-Dec ‘16

1. TV -22%

2. Press +45%

TV and Press # 1 choice

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

53

GROWTH IN CENTRA, COSTCUTTER & TOPAZ SPEND SEES CONVENIENCE MEDIA SPEND INCREASE THIS CHRISTMAS

Source: Nielsen AdDynamix Nov-Dec ‘16 – Includes All Media (TV excluding UTV NI & CH4 NI, Press, Radio, Outdoor, Digital Display & Cinema)/ Retailers includes large Supermarkets & Discounters

Total Retailers

Centra

Spar

Londis

Costcutter

Mace

Topaz

% Change YOY

-38.0

-17.1

-29.9

13.5

90.2

Press top choice for Centra - 38% total AdSpend

TV top for Spar - 67% of total AdSpend

TV top for Londis - 63% of total AdSpend

Convenience Growth in Ad Spend Nov-Dec ‘16

57.5

24.0

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

54

34.1%

84.5%

36.2% 34.3%

16.7% 21.4% 18.4% 10.1%

CONVENIENCE GROWS ACROSS ALL KEY SEASONAL CATEGORIES

Source: Nielsen Strategic Planner, ROI Convenience Read| NovDec 2016

Convenience Category Value Share of Total Market & % Change Year on Year

Excl Tobacco Growth

+2.2% +€9M

NOVDEC 16 % Chge Vs LY +3.6% +3.4% 6.2% +3.2% +1.5% -0.5% +1.4% -1.7%

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

55

167k

685k

CADBURY BOOST

TAYTO

7 UP

MF GALAXY

RED BULL

COCA COLA ZERO

POWERS

VIT HIT

CADBURY DAIRY MILK

HUNKY DORYS

DENNY

ORCHARD THIEVES

BALLYGOWAN

EXTRA

ZIP

JAMESON

MONSTER

SMIRNOFF

LUCOZADE

FULFIL

CONFECTIONERY BRANDS DOMINATING GROWTH IN CONVENIENCE TOP 20 INCREMENTAL € VALUE BRANDS IN CONVENIENCE

Source: Nielsen Scantrack Data , Convenience (Symbols + Forecourts + Specialists) 8 Week Ending 25th Dec 2016

1,548k

Was there a BREXIT IMPACT?

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

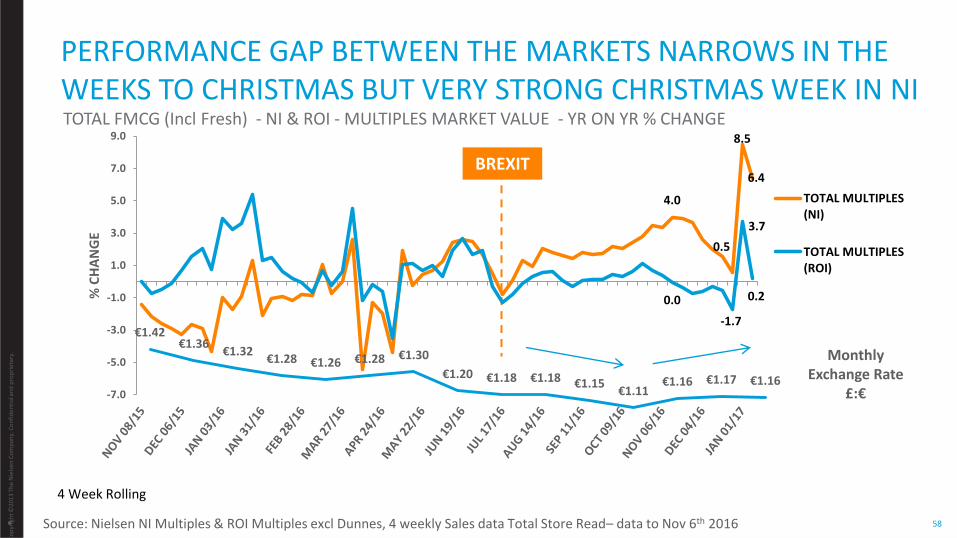

57

NI MARKET SEES STRONGEST GROWTH THIS CHRISTMAS

Source: ROI :Nielsen Total Defined Market Growth NOVDEC 16. NI Nielsen Scantrack TSR Grocery Multiples (excl General Merchandise and Fresh Food) UK: Nielsen Scantrack TSR Grocery Multiples (Including General Merchandise) 12 weeks to 31st December 2016 vs year ago

Volume

Value

+1.4%

+2.0%

+3.3%

+5.5%

+0.7%

+1.4%

FMCG Market Performance, NOVDEC Year on Year % Change

Co

pyr

igh

t ©20

13

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

58

PERFORMANCE GAP BETWEEN THE MARKETS NARROWS IN THE WEEKS TO CHRISTMAS BUT VERY STRONG CHRISTMAS WEEK IN NI

• Source: Nielsen NI Multiples & ROI Multiples excl Dunnes, 4 weekly Sales data Total Store Read– data to Nov 6th 2016

4 Week Rolling

TOTAL FMCG (Incl Fresh) - NI & ROI - MULTIPLES MARKET VALUE - YR ON YR % CHANGE

4.0

0.5

8.5

6.4

0.0

-1.7

3.7

0.2

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

% C

HA

NG

E

TOTAL MULTIPLES(NI)

TOTAL MULTIPLES(ROI)

BREXIT

€1.42 €1.36

€1.32 €1.28 €1.26 €1.28 €1.30

€1.20 €1.18 €1.18 €1.15 €1.11

€1.16 €1.17 €1.16

Monthly Exchange Rate

£:€

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

59

4 weeks to Dec 25th 16

4 weeks to Nov 6th 16

ROI WINS BACK SHARE IN RUN UP TO CHRISTMAS

Pre Brexit Avg Jan – June 16

+0.8%

-0.8%

* Based on constant exchange rate of €1.32: £1

Total IOI Multiples Market

Source: Nielsen NI Multiples & ROI Multiples excl Dunnes, 4 weekly Sales data Total Store Read– data to Jan 1st 2017

61.0%

39.0%

62.3%

37.7%

61.5%

38.5%

MULTIPLES ONLY – NI & ROI MARKET VALUE SHARE - TOTAL IOI

% Share Change VS PRE BREXIT

CHRISTMAS 2017

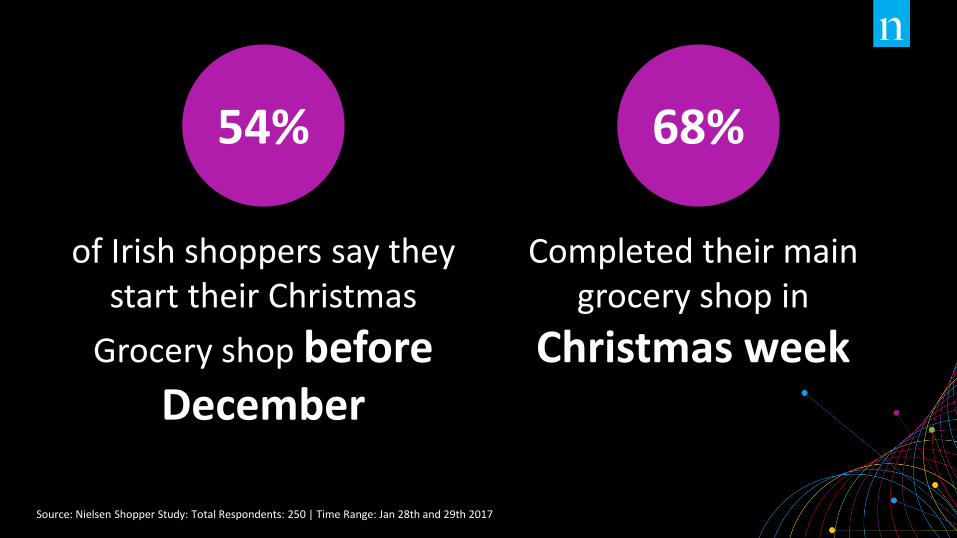

THOUGHTS

of Irish shoppers say they start their Christmas

Grocery shop before December

Completed their main grocery shop in

Christmas week

54% 68%

Source: Nielsen Shopper Study: Total Respondents: 250 | Time Range: Jan 28th and 29th 2017

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

62

163.5

187.8 214.5

0.0

50.0

100.0

150.0

200.0

CHRISTMAS DAY FALLING ON SUNDAY DRIVES BIG CHRISTMAS WEEK BUT THE IMPORTANCE OF THE FINAL 3 WEEKS UNCHANGED

Christmas Day:

Source: Nielsen ROI Multiples + Dunnes + Discounters, all categories excl lTobacco

All categories behave similarly

Sale

s V

alu

e €

M

+14% +14% Value % Change

3 wk contribution to NovDec:

36.0% 36.5% 36.6%

CHRISTMAS 2017

Christmas day falls on Monday

The TWO full weeks before Christmas will be KEY to delivering strong sales …

Time and optimise ATL & BTL spend to drive sales.

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

64

WHAT CAN DRIVE SUCCESS IN CHRISTMAS 2017?

Generate Emotion to stimulate memory and

action.

Create a Plan that builds to the final

two weeks.

ADVERTISING

Secondary displays & in-store

activation to grow sales. Integrate

with ATL.

Find the right promo price point timed to hit final

two weeks.

PRICE & PROMO

MUST be on shelf in the final two

weeks.

Discounters opportunity in key

sectors.

DISTRIBUTION

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

65

06

-No

v-1

6

08

-No

v-1

6

10

-No

v-1

6

12

-No

v-1

6

14

-No

v-1

6

16

-No

v-1

6

18

-No

v-1

6

20

-No

v-1

6

22

-No

v-1

6

24

-No

v-1

6

26

-No

v-1

6

28

-No

v-1

6

30

-No

v-1

6

02

-De

c-1

6

04

-De

c-1

6

06

-De

c-1

6

08

-De

c-1

6

10

-De

c-1

6

12

-De

c-1

6

14

-De

c-1

6

16

-De

c-1

6

18

-De

c-1

6

20

-De

c-1

6

22

-De

c-1

6

24

-De

c-1

6

26

-De

c-1

6

28

-De

c-1

6

30

-De

c-1

6

01

-Jan

-17

Lidl Ireland Gmbh

Tesco Ireland

Aldi Stores Ltd

Dunnes Stores Ltd

Supervalu

Marks & Spencer

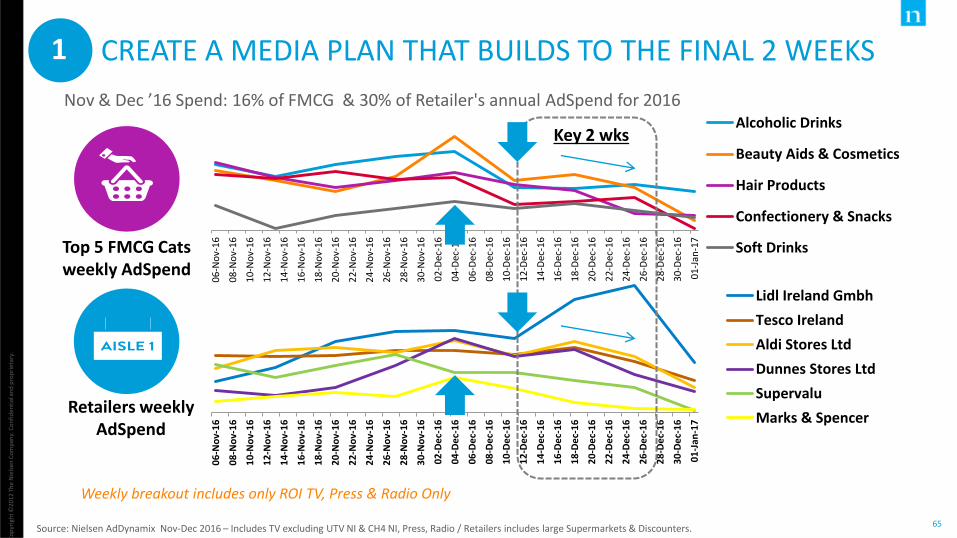

CREATE A MEDIA PLAN THAT BUILDS TO THE FINAL 2 WEEKS

Source: Nielsen AdDynamix Nov-Dec 2016 – Includes TV excluding UTV NI & CH4 NI, Press, Radio / Retailers includes large Supermarkets & Discounters.

Retailers weekly AdSpend

Nov & Dec ’16 Spend: 16% of FMCG & 30% of Retailer's annual AdSpend for 2016

Top 5 FMCG Cats weekly AdSpend

06

-No

v-1

6

08

-No

v-1

6

10

-No

v-1

6

12

-No

v-1

6

14

-No

v-1

6

16

-No

v-1

6

18

-No

v-1

6

20

-No

v-1

6

22

-No

v-1

6

24

-No

v-1

6

26

-No

v-1

6

28

-No

v-1

6

30

-No

v-1

6

02

-Dec

-16

04

-Dec

-16

06

-Dec

-16

08

-Dec

-16

10

-Dec

-16

12

-Dec

-16

14

-Dec

-16

16

-Dec

-16

18

-Dec

-16

20

-Dec

-16

22

-Dec

-16

24

-Dec

-16

26

-Dec

-16

28

-Dec

-16

30

-Dec

-16

01

-Jan

-17

Alcoholic Drinks

Beauty Aids & Cosmetics

Hair Products

Confectionery & Snacks

Soft Drinks

Weekly breakout includes only ROI TV, Press & Radio Only

Key 2 wks

1

Co

pyr

igh

t ©20

13

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

66

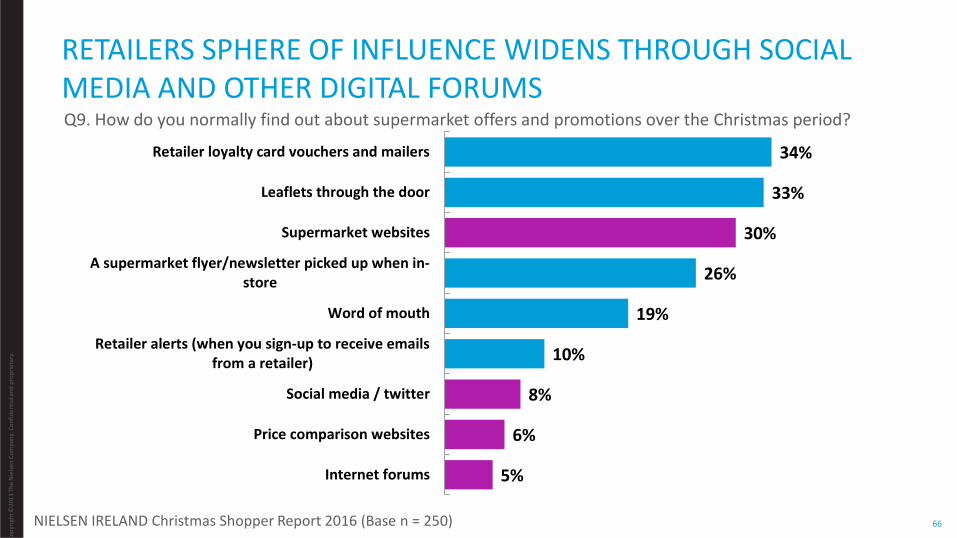

RETAILERS SPHERE OF INFLUENCE WIDENS THROUGH SOCIAL MEDIA AND OTHER DIGITAL FORUMS

NIELSEN IRELAND Christmas Shopper Report 2016 (Base n = 250)

34%

33%

30%

26%

19%

10%

8%

6%

5%

Retailer loyalty card vouchers and mailers

Leaflets through the door

Supermarket websites

A supermarket flyer/newsletter picked up when in-store

Word of mouth

Retailer alerts (when you sign-up to receive emailsfrom a retailer)

Social media / twitter

Price comparison websites

Internet forums

Q9. How do you normally find out about supermarket offers and promotions over the Christmas period?

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

67

WHAT CAN DRIVE SUCCESS IN CHRISTMAS 2017?

Generate Emotion to stimulate memory and

action.

Create a Plan that builds to the final

two weeks.

ADVERTISING

Secondary displays & in-store

activation to grow sales. Integrate

with ATL.

Find the right promo price point timed to hit final

two weeks.

PRICE & PROMO

MUST be on shelf in the final two

weeks.

Discounters opportunity in key

sectors.

DISTRIBUTION

Generate Emotion to stimulate memory and

action.

Create a Plan that builds to the final

two weeks.

ADVERTISING

Co

pyr

igh

t ©20

13

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

68

2016 INSTORE ACTIVITY

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

69

CREATE NOISE IN STORE WITH VISUAL IMPACT

Source: Nielsen Europe, MPA + Event Analysis, Benchmark Database

In Store Activation

Category

+2% to +6%

Brand

+4% to +14%

Secondary Displays

Category

+2.8%

Brand

+11.8%

In Store Sampling

Category

+6.6%

Brand

+31.4%

Incremental sales as a direct result of the in store activity in those stores.

How much incremental value can you expect?

Co

pyr

igh

t ©20

12

The

Nie

lsen

Co

mp

any.

Co

nfi

den

tial

an

d p

rop

riet

ary.

70

WHAT CAN DRIVE SUCCESS IN CHRISTMAS 2017?

Generate Emotion to stimulate memory and

action.

Create a Plan that builds to the final

two weeks.

ADVERTISING

Secondary displays & in-store

activation to grow sales. Integrate

with ATL.

Find the right promo price point timed to hit final

two weeks.

PRICE & PROMO

MUST be on shelf in the final two

weeks.

Discounters opportunity in key

sectors.

DISTRIBUTION

Secondary displays & in-store

activation to grow sales. Integrate

with ATL.

Find the right promo price point timed to hit final

two weeks.

PRICE & PROMO

Generate Emotion to stimulate memory and

action.

Create a Plan that builds to the final

two weeks.

ADVERTISING

THANK YOU

CHRISTMAS ADVERTISING

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

73

RETAILER ADVERTISING MESSAGES HITTING DIFFERENT THEMES ON PRICE, IRISH, QUALITY, FAMILY TIME

Lidl: ‘Share More Special Moments’

#ShareMore Emotional ad set in rural Ireland showing family get-together to the tune of ‘Have Yourself a Merry Little (LIDL) Christmas’

KEY TV CAMPAIGNS CHRISTMAS 2016 - LIDL

Source: Nielsen AdDynamix 2017

Product offer spot incorporated into the main theme

1 minute spot

20 seconds spot

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

74

Lidl: ‘Homecoming’

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

75

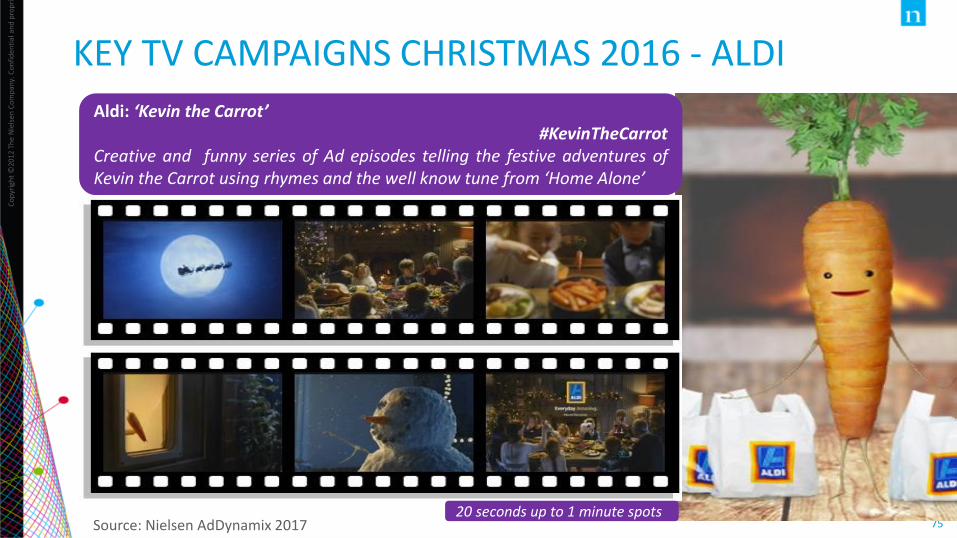

RETAILER ADVERTISING MESSAGES HITTING DIFFERENT THEMES ON PRICE, IRISH, QUALITY, FAMILY TIME

Aldi: ‘Kevin the Carrot’ #KevinTheCarrot

Creative and funny series of Ad episodes telling the festive adventures of Kevin the Carrot using rhymes and the well know tune from ‘Home Alone’

KEY TV CAMPAIGNS CHRISTMAS 2016 - ALDI

Source: Nielsen AdDynamix 2017 20 seconds up to 1 minute spots

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

76

Aldi: ‘Kevin The Carrot’

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

77

KEY TV CAMPAIGNS CHRISTMAS 2016 - TESCO Tesco: ‘Here’s To The Host’ Campaign

#ToTheHosts Innovative campaign putting the hosts - ‘the unsung heroes of Christmas’ in the spotlight and featuring 35 different spots of letters to the hosts

Source: Nielsen AdDynamix 2017

Product offers spots integrated within the main theme

1 minute spot

10 seconds spot

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

78

Tesco: ‘Here’s To The Hosts’

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

79

Dunnes: ‘Make Christmas’ #MakeChristmas

Continues with their beautiful 2014 campaign showing how Dickens’s Christmas Carol is still relevant in modern context

Source: Nielsen AdDynamix 2017

KEY TV CAMPAIGNS CHRISTMAS 2016 – DUNNES STORES

Short spots encourage to ‘make the savings that make Christmas’

40 seconds ad

30 seconds ad

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

80

Dunnes Stores: ‘Make Christmas’

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

81

Supervalu: ‘Real Food, Real People’ Story spots celebrating ‘local and Irish’ this Christmas featuring festive preparation of SV customers and suppliers in a series of heart-warming ads

Supervalu: ‘Fill your trolley with Value’ Offer spots promoting local food and Irish suppliers

KEY TV CAMPAIGNS CHRISTMAS 2016 - SUPERVALU

Source: Nielsen AdDynamix 2017

1 minute spot

10 seconds spot

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

82

Supervalu: ‘Real Food, Real People’

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

83

KEY TV CAMPAIGNS CHRISTMAS 2016 M&S: ‘Christmas with Love’

#LoveMrsClaus A warm, touching and humorous story of Mrs Claus, who saves Christmas

M&S: ‘Christmas with Love’ Creative series of Ads about being creative with food

Source: Nielsen AdDynamix 2017

1 minute spot

30 seconds spot

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

84

M&S: ‘Christmas with Love’

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

85

PRINTED CHRISTMAS ADS – SOME INTEGRATED AND REINFORCING THE TV SPOTS MESSAGE …

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

86

PRINTED CHRISTMAS ADS – SOME PROMOTING VALUE AND OFFERINGS