CHP ‐5 FOREXrahulmalkan.com/sm-admin/lib/Study/5 Forex - correction - 279 - 371.pdf · 280 | Page...

93

279 | Page SFM COMPILER Forex Years May Nov RTP Paper RTP Paper 2008 NA NA Yes Yes 2009 Yes YES Yes Yes 2010 Yes YES Yes Yes 2011 Yes N0 Yes Yes 2012 Yes Yes Yes Yes 2013 Yes Yes Yes Yes 2014 Yes Yes Yes Yes 2015 Yes Yes Yes Yes 2016 Yes Yes Yes Yes 2017 Yes Yes Yes Yes 2018 (Old) Yes Yes Yes Yes 2018 (New) Yes Yes Yes Yes 2019 (Old) Yes Yes Yes Yes 2019 (New) Yes Yes Yes Yes 2020 (Old) Yes No No No 2020 (New) Yes No No No 2008 Question 1 : Nov 2008 RTP (a) On 1st July 2008, 3 months interest rate in the US and Germany are 6.5 per cent and 4.5 per cent per annum respectively. The $/DM spot rate is 0.6560. What would be the forward rate for DM for delivery on 30th September 2008? (b) In International Monetary Market an international forward bid on December, 15 for one Euro (€) is $ 1.2816 at the same time the price of IMM € future for delivery on December, 15 is $ 1.2806. The contract size of Euro is € 62,500. How could the dealer use arbitrage in profit from this situation and how much profit is earned? Solution : (a) USD DM Spot 0.6560 – Interest rate p.a. 6.5% 4.5% Interest for 3 Months 1.625% 1.125% According to IRP (Interest Rate Parity) CHP ‐ 5 FOREX

Transcript of CHP ‐5 FOREXrahulmalkan.com/sm-admin/lib/Study/5 Forex - correction - 279 - 371.pdf · 280 | Page...

279 | P a g e

SFM COMPILER Forex

Years May Nov

RTP Paper RTP Paper

2008 NA NA Yes Yes

2009 Yes YES Yes Yes

2010 Yes YES Yes Yes

2011 Yes N0 Yes Yes

2012 Yes Yes Yes Yes

2013 Yes Yes Yes Yes

2014 Yes Yes Yes Yes

2015 Yes Yes Yes Yes

2016 Yes Yes Yes Yes

2017 Yes Yes Yes Yes

2018 (Old) Yes Yes Yes Yes

2018 (New) Yes Yes Yes Yes

2019 (Old) Yes Yes Yes Yes

2019 (New) Yes Yes Yes Yes

2020 (Old) Yes No No No

2020 (New) Yes No No No

2008

Question 1 : Nov 2008 RTP

(a) On 1st July 2008, 3 months interest rate in the US and Germany are 6.5 per cent and 4.5 per

cent per annum respectively. The $/DM spot rate is 0.6560. What would be the forward rate

for DM for delivery on 30th September 2008?

(b) In International Monetary Market an international forward bid on December, 15 for one Euro

(€) is $ 1.2816 at the same time the price of IMM € future for delivery on December, 15 is $

1.2806. The contract size of Euro is € 62,500. How could the dealer use arbitrage in profit

from this situation and how much profit is earned?

Solution :

(a) USD DM

Spot 0.6560 –

Interest rate p.a. 6.5% 4.5%

Interest for 3 Months 1.625% 1.125%

According to IRP (Interest Rate Parity)

CHP ‐ 5 FOREX

280 | P a g e

Forex SFM COMPILER

S

F =

iB1

iA1

0.6560

F =

1.01125

1.01625

therefore F = 1.01125

1.016250.6560= 0.6592

(b) Buy€ 62500 1.2806 = $ 80037.50 Sell€ 62500 1.2816 = $ 80100.00 Profit $ 62.50

Alternatively if the market comes back together before December 15, the dealer could unwind his

position (by simultaneously buying € 62,500 forward and selling a futures contract. Both for delivery

on December 15) and earn the same profit of $ 62.50.

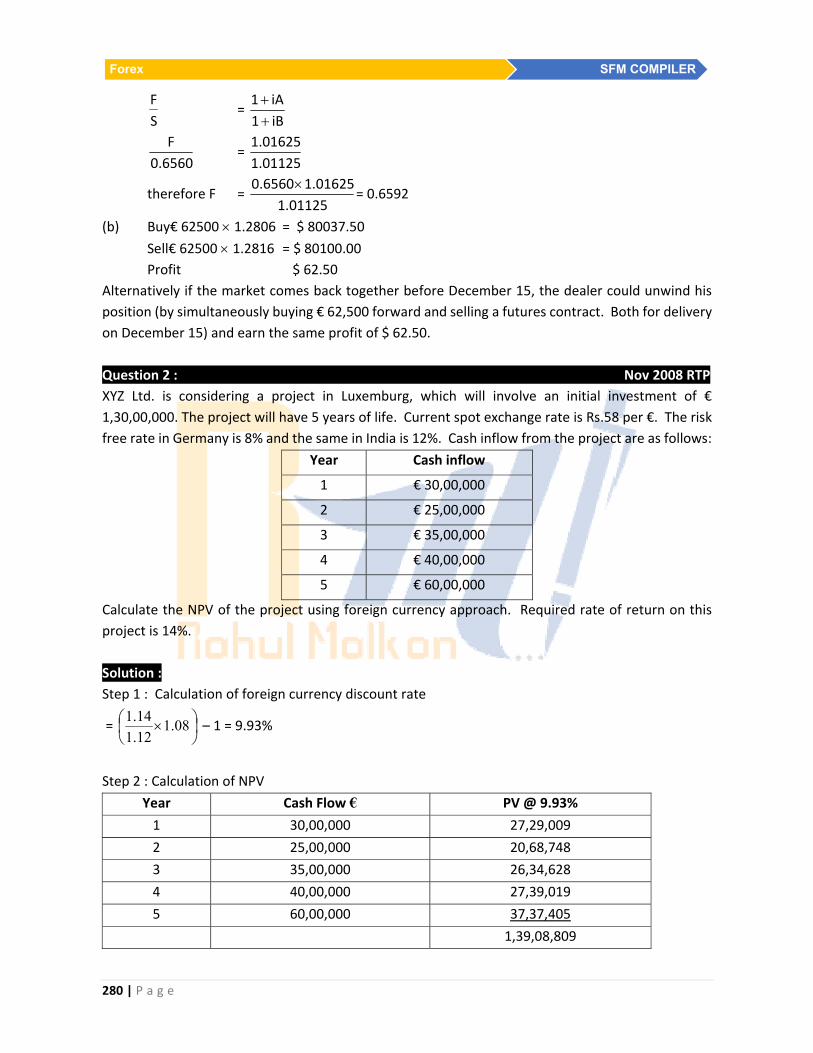

Question 2 : Nov 2008 RTP

XYZ Ltd. is considering a project in Luxemburg, which will involve an initial investment of €

1,30,00,000. The project will have 5 years of life. Current spot exchange rate is Rs.58 per €. The risk

free rate in Germany is 8% and the same in India is 12%. Cash inflow from the project are as follows:

Year Cash inflow

1 € 30,00,000

2 € 25,00,000

3 € 35,00,000

4 € 40,00,000

5 € 60,00,000

Calculate the NPV of the project using foreign currency approach. Required rate of return on this

project is 14%.

Solution :

Step 1 : Calculation of foreign currency discount rate

=

08.1

12.1

14.1 – 1 = 9.93%

Step 2 : Calculation of NPV

Year Cash Flow € PV @ 9.93%

1 30,00,000 27,29,009

2 25,00,000 20,68,748

3 35,00,000 26,34,628

4 40,00,000 27,39,019

5 60,00,000 37,37,405

1,39,08,809

281 | P a g e

SFM COMPILER Forex

Less : Investment 1,30,00,000

NPV 9,08,809 €

Note : Since NPV is positive we should go ahead with project.

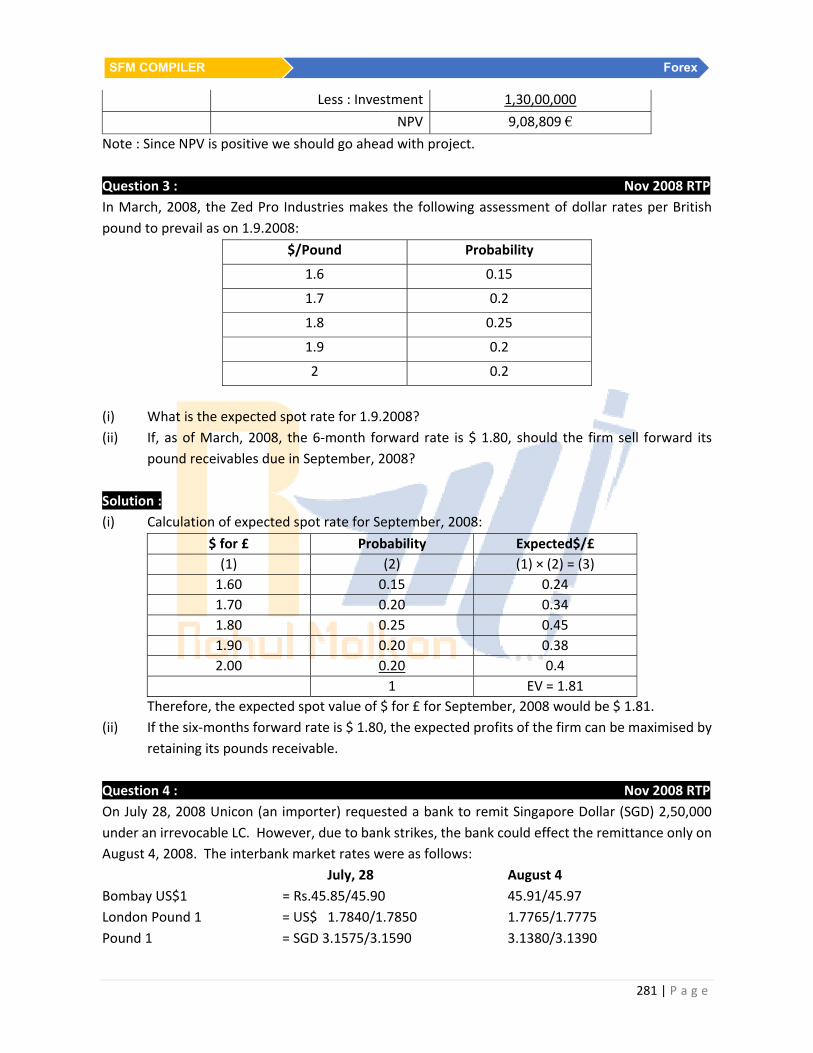

Question 3 : Nov 2008 RTP

In March, 2008, the Zed Pro Industries makes the following assessment of dollar rates per British

pound to prevail as on 1.9.2008:

$/Pound Probability

1.6 0.15

1.7 0.2

1.8 0.25

1.9 0.2

2 0.2

(i) What is the expected spot rate for 1.9.2008?

(ii) If, as of March, 2008, the 6‐month forward rate is $ 1.80, should the firm sell forward its

pound receivables due in September, 2008?

Solution :

(i) Calculation of expected spot rate for September, 2008:

$ for £ Probability Expected$/£

(1) (2) (1) × (2) = (3)

1.60 0.15 0.24

1.70 0.20 0.34

1.80 0.25 0.45

1.90 0.20 0.38

2.00 0.20 0.4

1 EV = 1.81

Therefore, the expected spot value of $ for £ for September, 2008 would be $ 1.81.

(ii) If the six‐months forward rate is $ 1.80, the expected profits of the firm can be maximised by

retaining its pounds receivable.

Question 4 : Nov 2008 RTP

On July 28, 2008 Unicon (an importer) requested a bank to remit Singapore Dollar (SGD) 2,50,000

under an irrevocable LC. However, due to bank strikes, the bank could effect the remittance only on

August 4, 2008. The interbank market rates were as follows:

July, 28 August 4

Bombay US$1 = Rs.45.85/45.90 45.91/45.97

London Pound 1 = US$ 1.7840/1.7850 1.7765/1.7775

Pound 1 = SGD 3.1575/3.1590 3.1380/3.1390

282 | P a g e

Forex SFM COMPILER

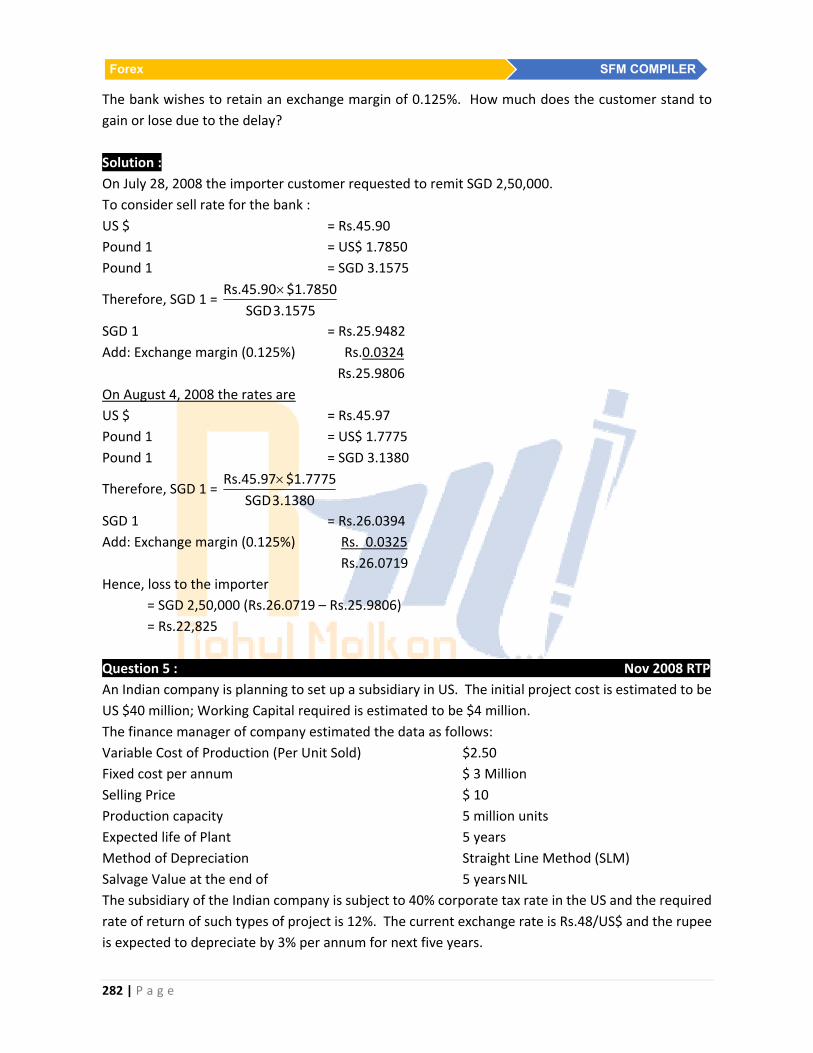

The bank wishes to retain an exchange margin of 0.125%. How much does the customer stand to

gain or lose due to the delay?

Solution :

On July 28, 2008 the importer customer requested to remit SGD 2,50,000.

To consider sell rate for the bank :

US $ = Rs.45.90

Pound 1 = US$ 1.7850

Pound 1 = SGD 3.1575

Therefore, SGD 1 = 3.1575 SGD

$1.7850 Rs.45.90

SGD 1 = Rs.25.9482

Add: Exchange margin (0.125%) Rs.0.0324

Rs.25.9806

On August 4, 2008 the rates are

US $ = Rs.45.97

Pound 1 = US$ 1.7775

Pound 1 = SGD 3.1380

Therefore, SGD 1 = 3.1380 SGD

$1.7775 Rs.45.97

SGD 1 = Rs.26.0394

Add: Exchange margin (0.125%) Rs. 0.0325

Rs.26.0719

Hence, loss to the importer

= SGD 2,50,000 (Rs.26.0719 – Rs.25.9806)

= Rs.22,825

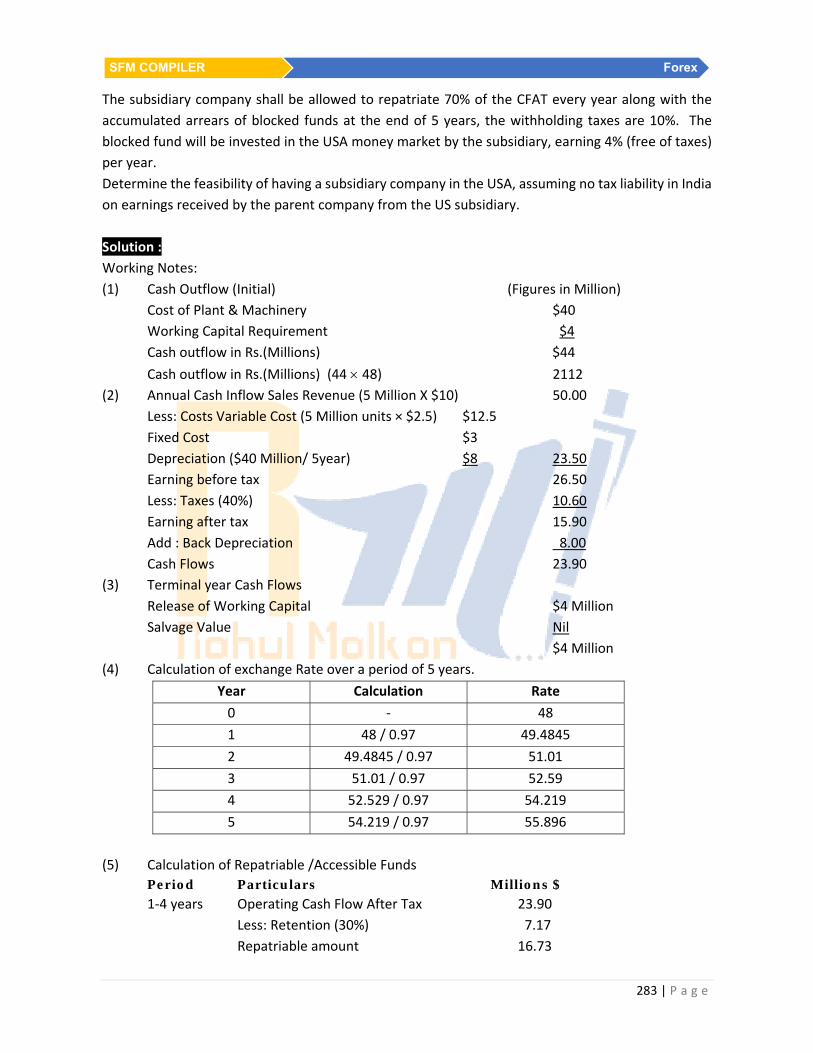

Question 5 : Nov 2008 RTP

An Indian company is planning to set up a subsidiary in US. The initial project cost is estimated to be

US $40 million; Working Capital required is estimated to be $4 million.

The finance manager of company estimated the data as follows:

Variable Cost of Production (Per Unit Sold) $2.50

Fixed cost per annum $ 3 Million

Selling Price $ 10

Production capacity 5 million units

Expected life of Plant 5 years

Method of Depreciation Straight Line Method (SLM)

Salvage Value at the end of 5 years NIL

The subsidiary of the Indian company is subject to 40% corporate tax rate in the US and the required

rate of return of such types of project is 12%. The current exchange rate is Rs.48/US$ and the rupee

is expected to depreciate by 3% per annum for next five years.

283 | P a g e

SFM COMPILER Forex

The subsidiary company shall be allowed to repatriate 70% of the CFAT every year along with the

accumulated arrears of blocked funds at the end of 5 years, the withholding taxes are 10%. The

blocked fund will be invested in the USA money market by the subsidiary, earning 4% (free of taxes)

per year.

Determine the feasibility of having a subsidiary company in the USA, assuming no tax liability in India

on earnings received by the parent company from the US subsidiary.

Solution :

Working Notes:

(1) Cash Outflow (Initial) (Figures in Million)

Cost of Plant & Machinery $40

Working Capital Requirement $4

Cash outflow in Rs.(Millions) $44

Cash outflow in Rs.(Millions) (44 48) 2112

(2) Annual Cash Inflow Sales Revenue (5 Million X $10) 50.00

Less: Costs Variable Cost (5 Million units × $2.5) $12.5

Fixed Cost $3

Depreciation ($40 Million/ 5year) $8 23.50

Earning before tax 26.50

Less: Taxes (40%) 10.60

Earning after tax 15.90

Add : Back Depreciation 8.00

Cash Flows 23.90

(3) Terminal year Cash Flows

Release of Working Capital $4 Million

Salvage Value Nil

$4 Million

(4) Calculation of exchange Rate over a period of 5 years.

Year Calculation Rate

0 ‐ 48

1 48 / 0.97 49.4845

2 49.4845 / 0.97 51.01

3 51.01 / 0.97 52.59

4 52.529 / 0.97 54.219

5 54.219 / 0.97 55.896

(5) Calculation of Repatriable /Accessible Funds

Period Particulars Millions $

1‐4 years Operating Cash Flow After Tax 23.90

Less: Retention (30%) 7.17

Repatriable amount 16.73

284 | P a g e

Forex SFM COMPILER

Less: Withholding Tax 1.673

Accessable Funds 15.057

5 year Operating Cash Flow After Tax 23.90

Less: Withholding Tax 2.39

21.51

Add : Repatriation of Blocked Funds* 27.40

Accessible Funds 48.91

*Future Value of Blocked Funds of $7.17 Million shall be computed as follows:

Value of Funds blocked from year 1‐4 7.17 M$

FV AF (4%, 4) 4.246

Value of Funds at end 30.4438 M$

Withholding Tax 3.0444 M$

27.3994 M$

Statement Showing Net Present Value of the Project

Period Particulars Cash Flow

US$ Exchange Rate Rs. PV @ 12%

0 Initial Outflow 44 48 (2112) (2112)

1 Annual Cash Flow 15.057 49.4845 745.09 665.26

2 “ 15.057 51.015 768.13 612.35

3 “ 15.057 52.593 791.89 563.65

4 “ 15.057 54.22 816.39 518.83

5 “ 48.91 55.896 2733.87 1551.27

6 Release of WC 4.00 55.896 223.584 126.87

1926.23

Decision : Since NPV of the project is positive, the Indian Company should go for its decision of

subsidiary in US.

Question 6 : Nov 2008 Paper – 6 Marks

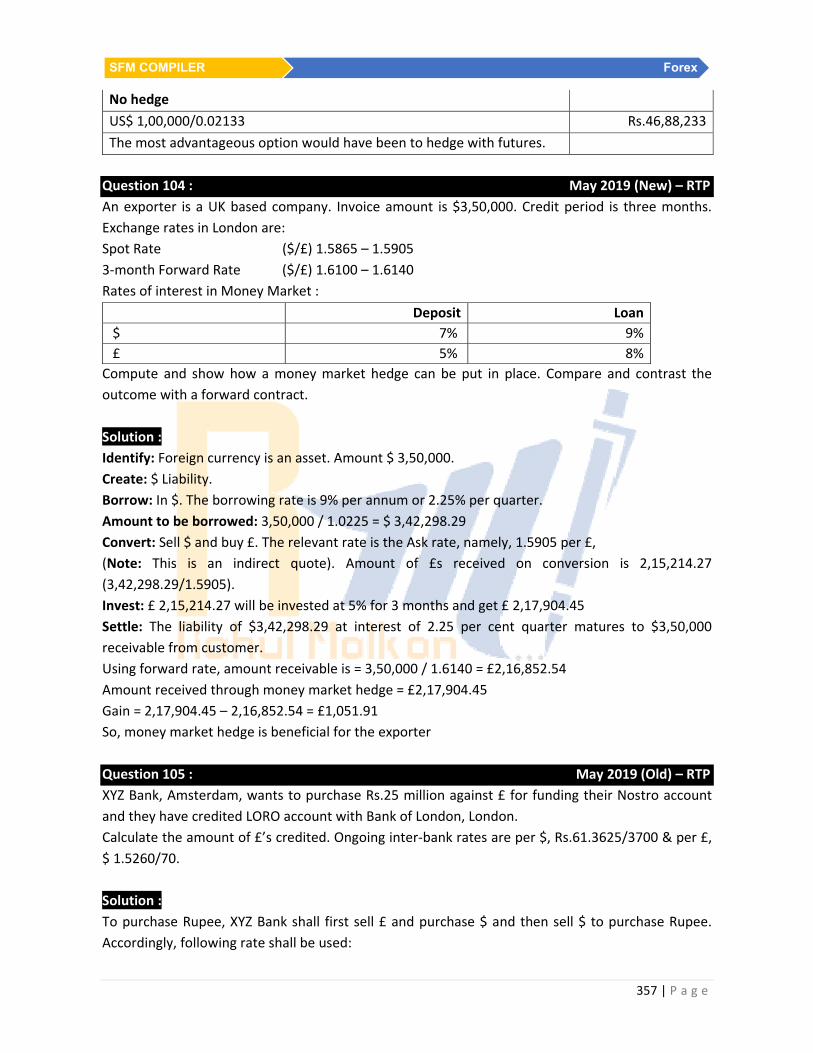

An exporter is a UK based company. Invoice amount is $3,50,000. Credit period is three months.

Exchange rates in London are :

Spot Rate ($/£) 1.5865 – 1.5905

3‐month Forward Rate ($/£) 1.6100 – 1.6140

Rates of interest in Money Market :

Deposit Loan

$ 7% 9%

£ 5% 8%

Compute and show how a money market hedge can be put in place. Compare and contrast the

outcome with a forward contract.

Solution :

An Uk firm can hedge its exposure by Money Market Operations

285 | P a g e

SFM COMPILER Forex

UK Firm ‐ $ 3,50,000 receivable after 3 months

MMC ( Borrow – sell – invest )

Step 1 : Borrow $ so that amt payable is $ 3,50,000 after 3 months @9% P.A i.e 2.25% per quarter

Amount to be borrowed: 3,50,000 / 1.0225 = $ 3,42,298.29

Step 2 : Convert: Sell $ and buy £. The relevant rate is the Ask rate, namely, 1.5905 per £,

(Note: This is an indirect quote).

Amount of £s received on conversion is 2,15,214.27 (3,42,298.29 / 1.5905).

Step 3 : Invest: £ 2,15,214.27 will be invested at 5% P.A. i.e. @ 1.25% for 3 months

Amount receivable after 3 months = 15214.27 1.02215 = £ 2,17,904.45

Question 7 : Nov 2008 Paper – 6 Marks

An Indian exporting firm, Rohit and Bros., would be cover itself against a likely depreciation of pound

sterling. The following data is given :

Receivables of Rohit and Bros : £500,000

Spot rate : Rs.56,00/£

Payment date : 3‐months

3 months interest rate : India : 12 per cent per annum

: UK : 5 per cent per annum

What should the exporter do?

Solution :

Indian exporter can hedge his exposure through money Market Operation

Indian exporter ‐ £ 5,00,000 receivable after 3 months

MMC (Borrow – sell – invest)

Step 1 : Borrow £ so that amt payable is £ 5,00,000 after 3 months

Amount to be Borrowed = 5,00,0001.0125 = £ 4,93,827.1605

Step 2 : Sell Rs.493827.1605 at spot Rs./ £ 56

Amt receivable = 493827.1605 56 = Rs.2,76,54,320.988 Step 3 : Invest Rs.2,76,54,320.988 for 3 months

Amount Receivable = 2,76,54,320.988 1.03= Rs.2,84,83,950.6176

Question 8 : Nov 2008 Paper – 4 Marks

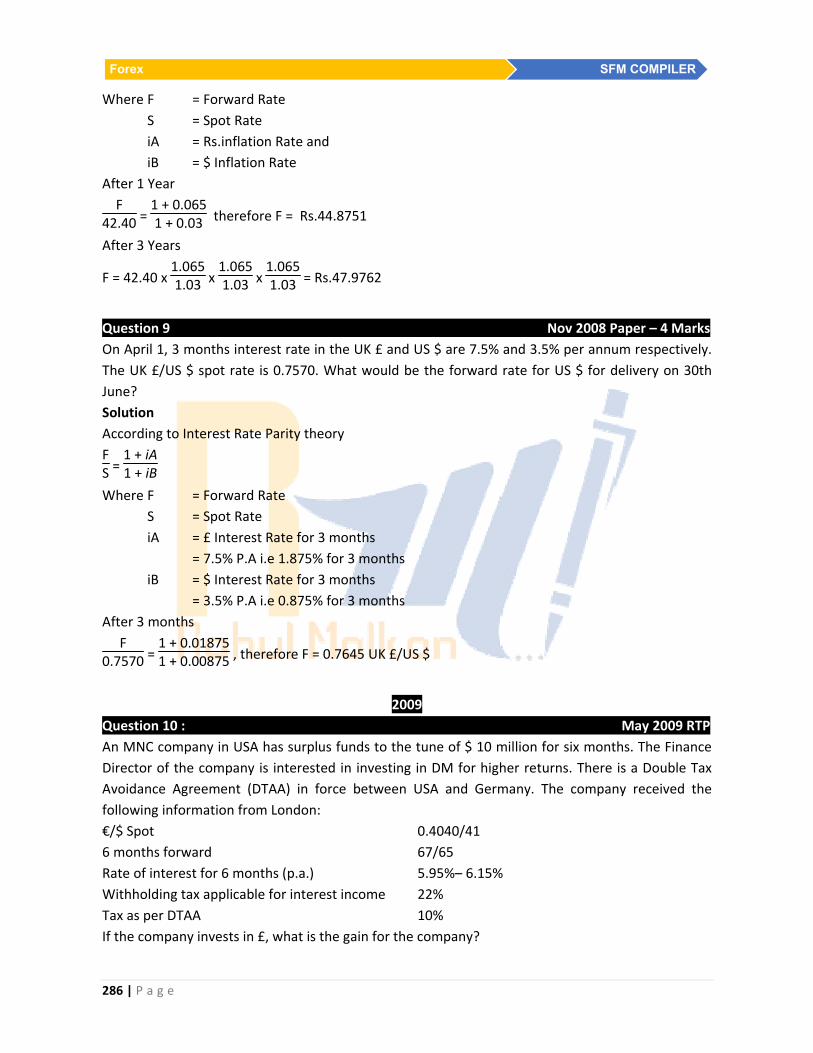

The rate of inflation in USA is likely to be 3% per annum and in India it is likely to be 6.5%. The current

spot rate of US $ in India is Rs..43.40. Find the expected rate of US $ in India after one year and 3

years from now using purchasing power parity theory.

Solution :

According to Purchasing Power Parity theory

FS =

1 + iA1 + iB

286 | P a g e

Forex SFM COMPILER

Where F = Forward Rate

S = Spot Rate

iA = Rs.inflation Rate and

iB = $ Inflation Rate

After 1 Year

F42.40 =

1 + 0.0651 + 0.03 therefore F = Rs.44.8751

After 3 Years

F = 42.40 x 1.0651.03 x

1.0651.03 x

1.0651.03 = Rs.47.9762

Question 9 Nov 2008 Paper – 4 Marks

On April 1, 3 months interest rate in the UK £ and US $ are 7.5% and 3.5% per annum respectively.

The UK £/US $ spot rate is 0.7570. What would be the forward rate for US $ for delivery on 30th

June?

Solution

According to Interest Rate Parity theory

FS =

1 + iA1 + iB

Where F = Forward Rate

S = Spot Rate

iA = £ Interest Rate for 3 months

= 7.5% P.A i.e 1.875% for 3 months

iB = $ Interest Rate for 3 months

= 3.5% P.A i.e 0.875% for 3 months

After 3 months

F0.7570 =

1 + 0.018751 + 0.00875 , therefore F = 0.7645 UK £/US $

2009

Question 10 : May 2009 RTP

An MNC company in USA has surplus funds to the tune of $ 10 million for six months. The Finance

Director of the company is interested in investing in DM for higher returns. There is a Double Tax

Avoidance Agreement (DTAA) in force between USA and Germany. The company received the

following information from London:

€/$ Spot 0.4040/41

6 months forward 67/65

Rate of interest for 6 months (p.a.) 5.95%– 6.15%

Withholding tax applicable for interest income 22%

Tax as per DTAA 10%

If the company invests in £, what is the gain for the company?

287 | P a g e

SFM COMPILER Forex

Solution :

$ 10 million converted @ € 0.4040/$ = $10,000,000 0.4040 = €4,040,000

and invested @ 5.95% for6 months in Luxemburg will fetch :

€ 4,040,000 (1+ 0.0595/2) = € 4,160,190

Interest earned =€(4,160,190 – 4,040,000) = € 120,190

Withholding Tax @ 10% (in view of DTAA) = € 12,019

Net interest eligible for repatriation = € 108,171

Amount repatriated after 6 months= € 108,171 + € 4,040,000 = € 4,148,171

Amount received at the forward rate of € 0.3976/$ = €4,148,171/0.3976 = 10,433,026

Additional amount fetched =$10,433,026 – $10,000,000 = $ 433,026.

Question 11 : May 2009 RTP

BC Export Co are holding an Export bill in United States Dollar (USD) 1,00,000 due 60 days hence.

Rate at which deal was finalized @ Rs.47.50 per USD. The Company is worried about the fluctuating

exchange rate. The Firm’s Bankers have agreed to make advance against the bill after deduction of

interest 9% per annum and also quoted a 60‐ day forward rate of Rs.48.10. The cost of capital for the

exporter is 15% p.a. Advise whether the exporter will agree to the banker’s offer.

Solution :

Rs.

Value of the export in INR 47,50,000

Interest @ 1.5% for 60 days 71,250

Net Amount to be received 46,78,750

Cost of the fund @ 15% p.a for 2 months 1,42,362

Net Saving (cost of fund – interest ) 71,112

Difference to be paid after 60 days at forward rate (48.10– 47.50) x 1,00,000 60,000

Hence the exporter should agree to the offer of his banker.

Question 12 : May 2009 RTP

Spot rate 1 US $ = Rs.47.7123

180 days Forward rate for 1 US $ = Rs.48.6690

Interest rate in India = 12% p.a

Interest rate in USA = 8% p.a

An arbitrageur takes loan of Rs. 40,00,000 from Indian Bank for 6 months and goes for arbitrage.

What is his gain or loss? (Take 1 year = 360 days)

Solution :

Amount he receives in dollar = 40,00,000/47.7123 $ 83,835.82

Interest earned by him @ 8% $ 33,53.43

Net Amount received by him after six months $ 87,189.25

288 | P a g e

Forex SFM COMPILER

After conversion he will receive in Rupees @ Rs.48.6690 Rs.42,43,414

Amount to be paid to Indian Banker with interest for six months Rs.42,40,000

Gain to the arbitrageur Rs.3,414

Question 13 : May 2009 RTP

Similar to Question 4 – Nov 2008 RTP

Question 14 : May 2009 Paper – 6 Marks

Your forex dealer had entered into a cross currency deal and had sold US $ 10,00,000 against EURO

at US $ 1 = EUR 1.4400 for spot delivery.

However, later during the day, the market became volatile and the dealer in compliance with his

management’s guidelines had to square – up the position when the quotations were:

Spot US $ 1 INR 31.4300/4500

1 month margin 25/20

2 months margin 45/35

Spot US $ 1 EURO 1.4400/4450

1 month forward 1.4425/4490

2 months forward 1.4460/4530

What will be the gain or loss in the transaction?

Solution :

1. The amount of EUR bought by selling

USD 10,00,000 1.4400 = EUR 14,40,000

2. The amount of EUR sold for buying

USD 10,00,000 1.4450 = EUR 14,45,000

3. Net Loss in the Transaction = EUR 5,000

To acquire EUR 5,000 from the market @

(a) USD 1 = EUR 1.4400 &

(b) USD1 = INR 31.4500

Cross Currency buying rate of EUR/INR is

Rs.31.4500 / 1.440 i.e. Rs.21.8403

Loss in the Transaction Rs.21.8403 * 5000 = Rs.1,09,201.50

Question 15 : May 2009 Paper

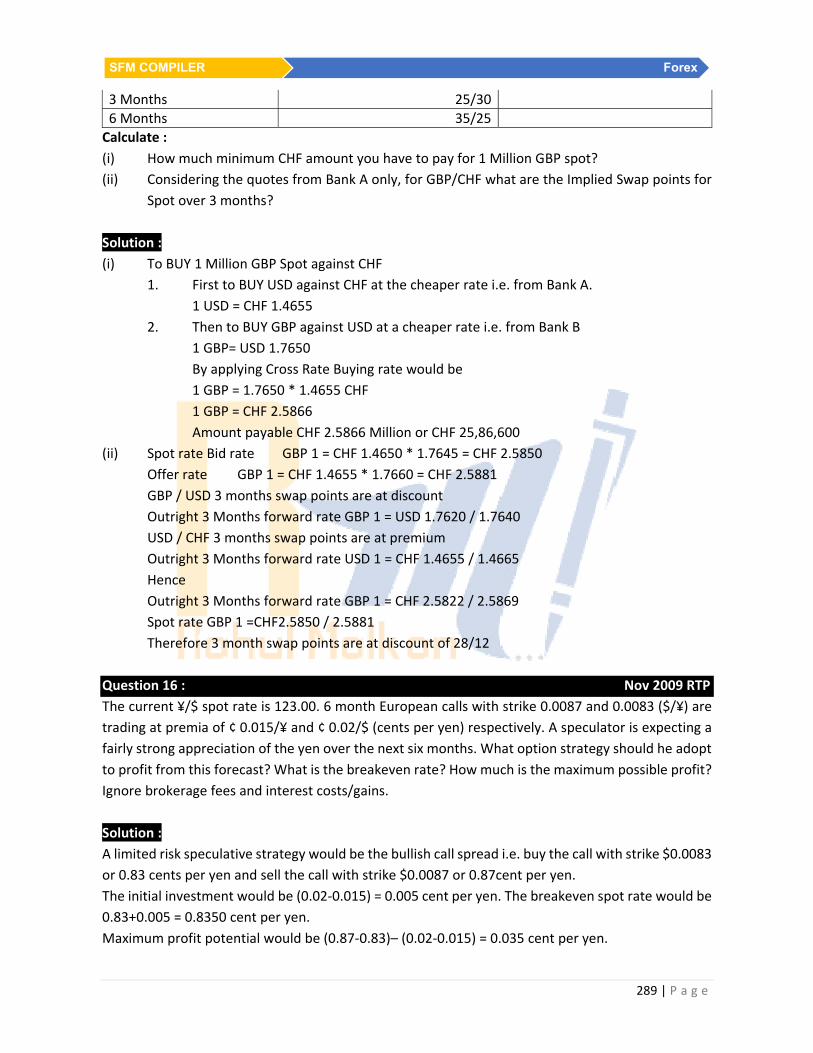

You have following quotes from Bank A and Bank B:

Bank A Bank B

SPOT CHF/USD 1.4650/55 CHF/USD 1.4653/60

3 Months 5/10

6 Months 10/15

SPOT USD/GBP 1.7645/60 USD/GBP 1.7640/50

289 | P a g e

SFM COMPILER Forex

3 Months 25/30

6 Months 35/25

Calculate :

(i) How much minimum CHF amount you have to pay for 1 Million GBP spot?

(ii) Considering the quotes from Bank A only, for GBP/CHF what are the Implied Swap points for

Spot over 3 months?

Solution :

(i) To BUY 1 Million GBP Spot against CHF

1. First to BUY USD against CHF at the cheaper rate i.e. from Bank A.

1 USD = CHF 1.4655

2. Then to BUY GBP against USD at a cheaper rate i.e. from Bank B

1 GBP= USD 1.7650

By applying Cross Rate Buying rate would be

1 GBP = 1.7650 * 1.4655 CHF

1 GBP = CHF 2.5866

Amount payable CHF 2.5866 Million or CHF 25,86,600

(ii) Spot rate Bid rate GBP 1 = CHF 1.4650 * 1.7645 = CHF 2.5850

Offer rate GBP 1 = CHF 1.4655 * 1.7660 = CHF 2.5881

GBP / USD 3 months swap points are at discount

Outright 3 Months forward rate GBP 1 = USD 1.7620 / 1.7640

USD / CHF 3 months swap points are at premium

Outright 3 Months forward rate USD 1 = CHF 1.4655 / 1.4665

Hence

Outright 3 Months forward rate GBP 1 = CHF 2.5822 / 2.5869

Spot rate GBP 1 =CHF2.5850 / 2.5881

Therefore 3 month swap points are at discount of 28/12

Question 16 : Nov 2009 RTP

The current ¥/$ spot rate is 123.00. 6 month European calls with strike 0.0087 and 0.0083 ($/¥) are

trading at premia of ¢ 0.015/¥ and ¢ 0.02/$ (cents per yen) respectively. A speculator is expecting a

fairly strong appreciation of the yen over the next six months. What option strategy should he adopt

to profit from this forecast? What is the breakeven rate? How much is the maximum possible profit?

Ignore brokerage fees and interest costs/gains.

Solution :

A limited risk speculative strategy would be the bullish call spread i.e. buy the call with strike $0.0083

or 0.83 cents per yen and sell the call with strike $0.0087 or 0.87cent per yen.

The initial investment would be (0.02‐0.015) = 0.005 cent per yen. The breakeven spot rate would be

0.83+0.005 = 0.8350 cent per yen.

Maximum profit potential would be (0.87‐0.83)– (0.02‐0.015) = 0.035 cent per yen.

290 | P a g e

Forex SFM COMPILER

Question 17 : Nov 2009 RTP

If the interest rate for the next 6 months for the US$ is 1.5% (annual compounding). The interest rate

for the € is 2% (annual compounding). The spot price of the € is US $ 1.665. The forward price is

expected to be US$ 1.664. Please determine correct forward price and recommend an arbitrage

strategy.

Solution :

According to Interest Rate Parity theory

FS =

1 + iA1 + iB

Where F = Forward Rate

S = Spot Rate

iA = $ Interest Rate for 6 months

= 1.5% for 6 months

iB = € Interest Rate for 6 months

= 2 % for 6 months

After 6 Months

F1,000 =

1.0151.02 , Therefore F = 1.6568

Because the forward price is higher than the model price, we will sell the forward contract. If

transaction costs could be covered, we would buy the € in the spot market at $1.665 and sell it in the

forward market at $1.664. We would earn interest at the foreign interest rate of 2 percent. By selling

it forward, we could then convert back to dollars at the rate of $1.664. In other words, $1.665 would

be used to buy 1 unit of the €, which would grow to 1.02 units (the 2 percent € rate). Then 1.02 €

would be converted back to 1.02($1.664) = $1.69728. This would be a return of $1.69728/$1.665 –

1 = 0.019387 or 1.94 percent, which is better than the US rate.

Question 18 : Nov 2009 ‐ Paper

M/s Omega Electronics Ltd. Exports air conditioners to Germany by importing all the components

from Singapore. The company is exporting 2,400 units at a price of Euro 500 per units. The cost of

imported components is S$ 800 per unit. The fixed cost and other variables cost per unit are Rs.1,000

and

Rs.1,500 respectively. The cash flow in foreign currencies are due in six months. The current exchange

rates are as follows :‐

Rs./Euro 51.50/55

Rs./$ 27.20/25

After 6 months the exchange rates turn out as follows :

Rs./Euro 52.00/05

Rs./$ 27.70/75

1) You are required to calculate loss/gain due to transaction exposure.

291 | P a g e

SFM COMPILER Forex

2) Based on the following additional information calculate the loss/gain due to transaction and

operating exposure if the contracted price of air conditioners is Rs.25,000 :

a) The current exchange rate changes to :

Rs./Euro 51.75/80

Rs./$ 27.10/15

b) Price elasticity of demand is estimated to be 1.5

c) Payments and Receipts are to be settled at the end of six months.

Solution :

(a) Profit at current exchange rates

2400[€500×S$51.50– (S$800 ×Rs. 27.25 +Rs. 1,000+ Rs. 1,500)]

2400[Rs..25,750‐ Rs. 24,300] = Rs. 34,80,000

Profit after change in exchange rates

2400[€500× Rs. 52– (S$800× Rs. 27.75+ Rs. 1000+ Rs. 1500)]

2400[Rs. 26,000‐ Rs. 24,700] = Rs. 31,20,000

LOSS DUE TO TRANSACTION EXPOSURE

Rs. 34,80,000– Rs. 31,20,000= Rs. 3,60,000

Profit based on new exchange rates

2400[Rs. 25,000‐(800× Rs. 27.15+ Rs. 1,000+ Rs. 1,500)]

2400[Rs. 25,000 ‐ Rs. 24,220]= Rs. 18,72,000

Profit after change in exchange rates at the end of six months

2400[Rs. 25,000‐(800×Rs. 27.75+ Rs. 1,000+ Rs. 1,500)]

2400[Rs. 25,000‐ Rs. 24,700]= Rs. 7,20,000

Decline in profit due to transaction exposure

Rs. 18,72,000‐ Rs. 7,20,000 = Rs. 11,52,000

Current price of each unit in S$ =25,00051.50 = S$ 485.44

Price after change in Exch. Rate= 25,00051.75 = S$ 483.09

Change in Price due to change in Exch. Rate

S$ 485.44‐S$ 483.09 = S$ 2.35 or (‐) 0.48%

Price elasticity of demand = 1.5

Increase in demand due to fall in price 0.48×1.5 =0.72%

Size of increased order = 2400 ×1.0072 = 2417 units

Profit = 2417 [Rs. 25,000– (800 × Rs. 27.75 + Rs. 1,000 + Rs. 1,500)]

=2417[Rs. 25,000‐ Rs. 24,700]

= Rs. 7,25,100

Therefore, decrease in profit due to operating exposure

Rs. 18,72,000 – Rs. 7,25,100 = Rs.11,46,900

2010

292 | P a g e

Forex SFM COMPILER

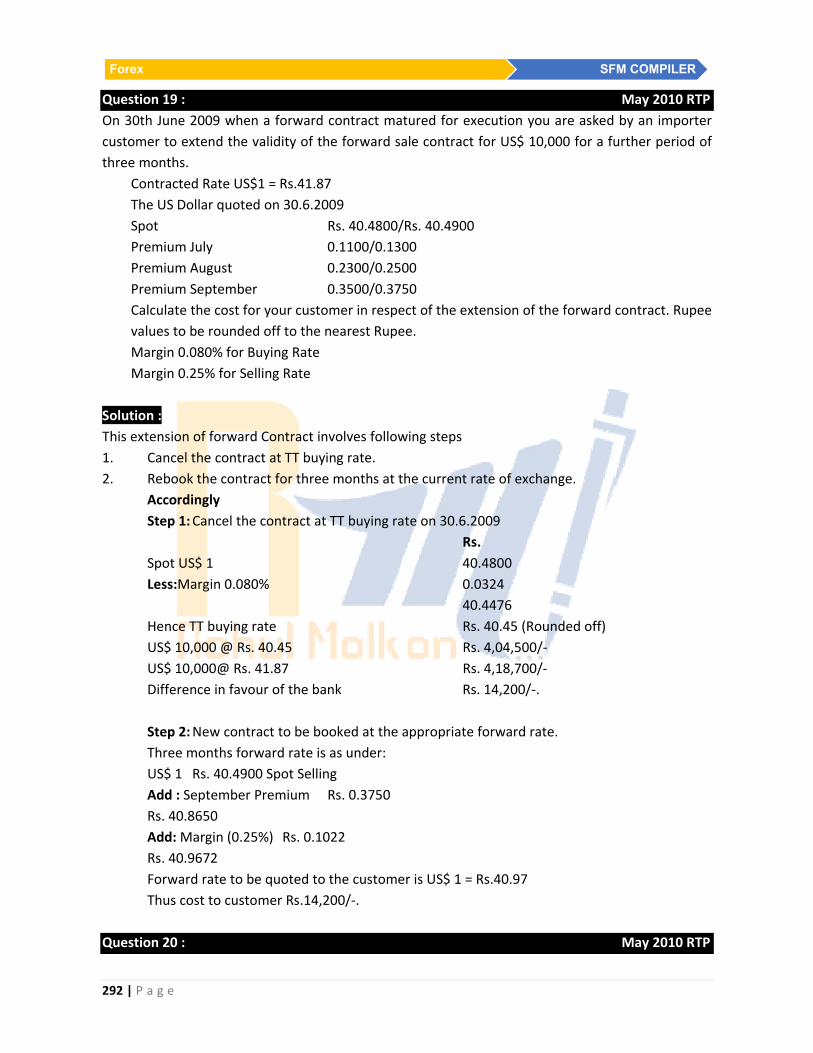

Question 19 : May 2010 RTP

On 30th June 2009 when a forward contract matured for execution you are asked by an importer

customer to extend the validity of the forward sale contract for US$ 10,000 for a further period of

three months.

Contracted Rate US$1 = Rs.41.87

The US Dollar quoted on 30.6.2009

Spot Rs. 40.4800/Rs. 40.4900

Premium July 0.1100/0.1300

Premium August 0.2300/0.2500

Premium September 0.3500/0.3750

Calculate the cost for your customer in respect of the extension of the forward contract. Rupee

values to be rounded off to the nearest Rupee.

Margin 0.080% for Buying Rate

Margin 0.25% for Selling Rate

Solution :

This extension of forward Contract involves following steps

1. Cancel the contract at TT buying rate.

2. Rebook the contract for three months at the current rate of exchange.

Accordingly

Step 1: Cancel the contract at TT buying rate on 30.6.2009

Rs.

Spot US$ 1 40.4800

Less:Margin 0.080% 0.0324

40.4476

Hence TT buying rate Rs. 40.45 (Rounded off)

US$ 10,000 @ Rs. 40.45 Rs. 4,04,500/‐

US$ 10,000@ Rs. 41.87 Rs. 4,18,700/‐

Difference in favour of the bank Rs. 14,200/‐.

Step 2: New contract to be booked at the appropriate forward rate.

Three months forward rate is as under:

US$ 1 Rs. 40.4900 Spot Selling

Add : September Premium Rs. 0.3750

Rs. 40.8650

Add: Margin (0.25%) Rs. 0.1022

Rs. 40.9672

Forward rate to be quoted to the customer is US$ 1 = Rs.40.97

Thus cost to customer Rs.14,200/‐.

Question 20 : May 2010 RTP

293 | P a g e

SFM COMPILER Forex

Wenden Co is a Dutch‐based company which has the following expected transactions.

One month: Expected receipt of £2,40,000

One month: Expected payment of £1,40,000

Three months: Expected receipts of £3,00,000

The finance manager has collected the following information:

Spot rate (£ per €): 1.7820 ± 0.0002

One month forward rate (£ per €): 1.7829 ± 0.0003

Three months forward rate (£ per €): 1.7846 ± 0.0004

Money market rates for Wenden Co:

Borrowing Deposit

One year Euro interest rate: 4.9% 4.6

One year Sterling interest rate: 5.4% 5.1

Assume that it is now 1 April.

Required:

(a) Calculate the expected Euro receipts in one month and in three months using the forward

market.

(b) Calculate the expected Euro receipts in three months using a money‐market hedge and

recommend whether a forward market hedge or a money market hedge should be used.

Solution :

(a) Forward market evaluation

Net receipt in 1 month = £2,40,000 – £1,40,000 = £1,00,000

Wenden Co needs to sell Sterlings at an exchange rate of (1.7829 + 0.0003) = £1.7832per €

Euro value of net receipt = 1,00,000/ 1.7832 =€56,079

Receipt in 3 months = £3,00,000

Wenden Co needs to sell Sterlings at an exchange rate of 1.7846 + 0.0004 =£1.7850per €

Euro value of receipt in 3 months = 3,00,000/ 1.7850 =€1,68,067

(b) Evaluation of money‐market hedge (Borrow – Sell – Invest)

Expected receipt after 3 months = £300,000

Step 1 : Borrow

Sterling interest rate over three months = 5.4/ 4 = 1.35%

Sterlings to borrow now to have £300,000 liability

after 3 months = 300,000/ 1.0135 = £296,004

Step 2 : Sell

Spot rate for selling Sterling = 1.7820 + 0.0002 = £1.7822 per€

Euro deposit from borrowed Sterling at spot = 296,004/ 1.7822 = €166,089

Step 3 : Invest

Euro interest rate over three months = 4.6/ 4 = 1.15%

Value in 3 months of Euro deposit = 166,089 x 1.0115 = €167,999

The forward market is marginally preferable to the money market hedge for the Sterling

receipt expected after 3 months.

294 | P a g e

Forex SFM COMPILER

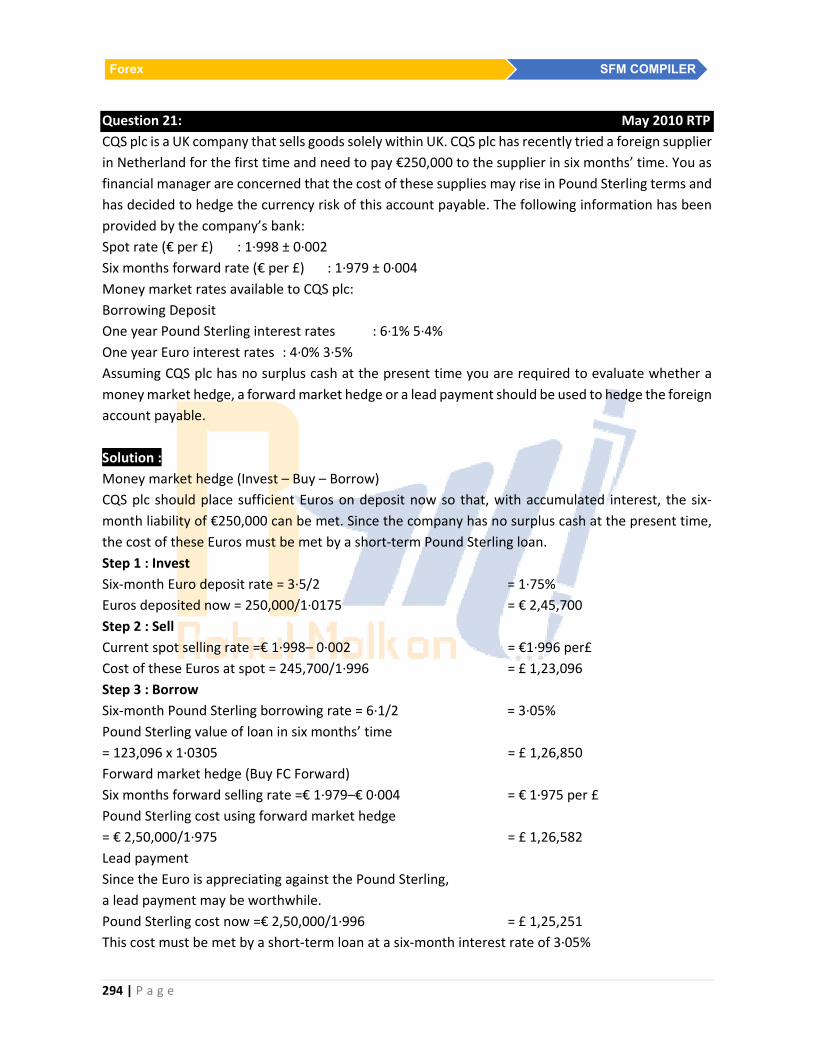

Question 21: May 2010 RTP

CQS plc is a UK company that sells goods solely within UK. CQS plc has recently tried a foreign supplier

in Netherland for the first time and need to pay €250,000 to the supplier in six months’ time. You as

financial manager are concerned that the cost of these supplies may rise in Pound Sterling terms and

has decided to hedge the currency risk of this account payable. The following information has been

provided by the company’s bank:

Spot rate (€ per £) : 1∙998 ± 0∙002

Six months forward rate (€ per £) : 1∙979 ± 0∙004

Money market rates available to CQS plc:

Borrowing Deposit

One year Pound Sterling interest rates : 6∙1% 5∙4%

One year Euro interest rates : 4∙0% 3∙5%

Assuming CQS plc has no surplus cash at the present time you are required to evaluate whether a

money market hedge, a forward market hedge or a lead payment should be used to hedge the foreign

account payable.

Solution :

Money market hedge (Invest – Buy – Borrow)

CQS plc should place sufficient Euros on deposit now so that, with accumulated interest, the six‐

month liability of €250,000 can be met. Since the company has no surplus cash at the present time,

the cost of these Euros must be met by a short‐term Pound Sterling loan.

Step 1 : Invest

Six‐month Euro deposit rate = 3∙5/2 = 1∙75%

Euros deposited now = 250,000/1∙0175 = € 2,45,700

Step 2 : Sell

Current spot selling rate =€ 1∙998– 0∙002 = €1∙996 per£

Cost of these Euros at spot = 245,700/1∙996 = £ 1,23,096

Step 3 : Borrow

Six‐month Pound Sterling borrowing rate = 6∙1/2 = 3∙05%

Pound Sterling value of loan in six months’ time

= 123,096 x 1∙0305 = £ 1,26,850

Forward market hedge (Buy FC Forward)

Six months forward selling rate =€ 1∙979–€ 0∙004 = € 1∙975 per £

Pound Sterling cost using forward market hedge

= € 2,50,000/1∙975 = £ 1,26,582

Lead payment

Since the Euro is appreciating against the Pound Sterling,

a lead payment may be worthwhile.

Pound Sterling cost now =€ 2,50,000/1∙996 = £ 1,25,251

This cost must be met by a short‐term loan at a six‐month interest rate of 3∙05%

295 | P a g e

SFM COMPILER Forex

Pound Sterling value of loan in six months’ time

= £ 1,25,251 x 1∙0305 = £1,29,071

Evaluation of hedges The relative costs of the three hedges can be compared since they have been

referenced to the same point in time, i.e. six months in the future. The most expensive hedge is the

lead payment, while the cheapest is the forward market hedge. Using the forward market to hedge

the account payable currency risk can therefore be recommended.

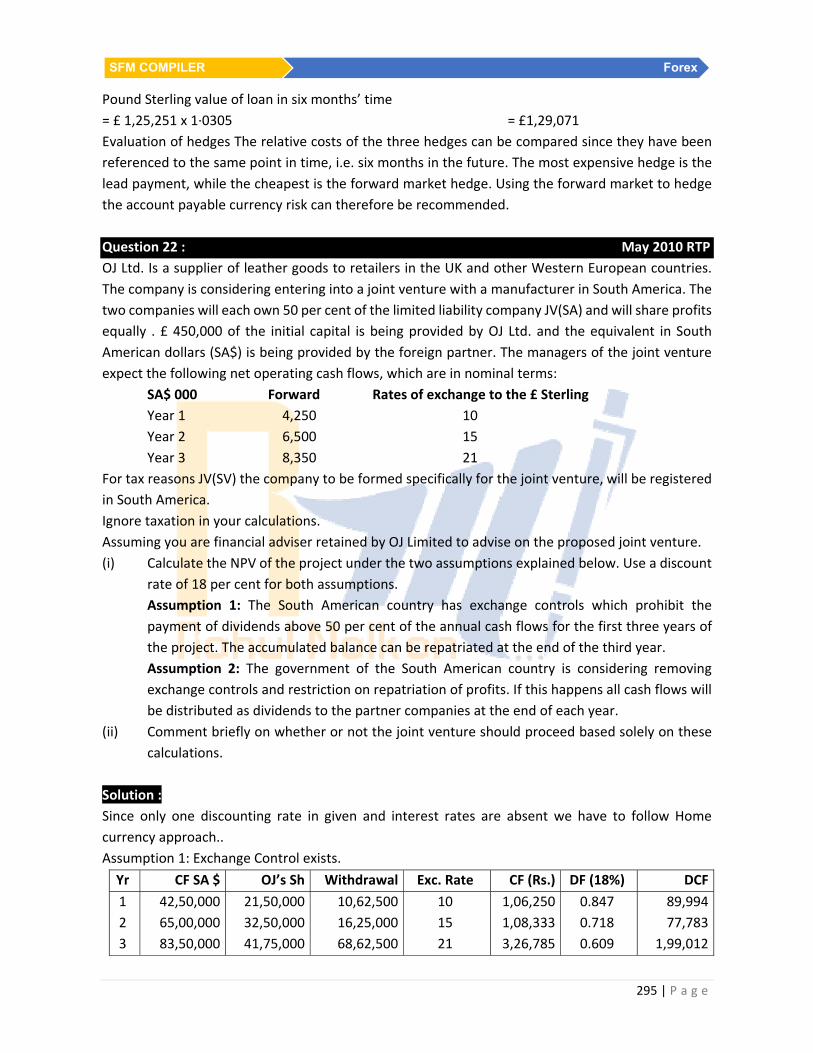

Question 22 : May 2010 RTP

OJ Ltd. Is a supplier of leather goods to retailers in the UK and other Western European countries.

The company is considering entering into a joint venture with a manufacturer in South America. The

two companies will each own 50 per cent of the limited liability company JV(SA) and will share profits

equally . £ 450,000 of the initial capital is being provided by OJ Ltd. and the equivalent in South

American dollars (SA$) is being provided by the foreign partner. The managers of the joint venture

expect the following net operating cash flows, which are in nominal terms:

SA$ 000 Forward Rates of exchange to the £ Sterling

Year 1 4,250 10

Year 2 6,500 15

Year 3 8,350 21

For tax reasons JV(SV) the company to be formed specifically for the joint venture, will be registered

in South America.

Ignore taxation in your calculations.

Assuming you are financial adviser retained by OJ Limited to advise on the proposed joint venture.

(i) Calculate the NPV of the project under the two assumptions explained below. Use a discount

rate of 18 per cent for both assumptions.

Assumption 1: The South American country has exchange controls which prohibit the

payment of dividends above 50 per cent of the annual cash flows for the first three years of

the project. The accumulated balance can be repatriated at the end of the third year.

Assumption 2: The government of the South American country is considering removing

exchange controls and restriction on repatriation of profits. If this happens all cash flows will

be distributed as dividends to the partner companies at the end of each year.

(ii) Comment briefly on whether or not the joint venture should proceed based solely on these

calculations.

Solution :

Since only one discounting rate in given and interest rates are absent we have to follow Home

currency approach..

Assumption 1: Exchange Control exists.

Yr CF SA $ OJ’s Sh Withdrawal Exc. Rate CF (Rs.) DF (18%) DCF

1

2

3

42,50,000

65,00,000

83,50,000

21,50,000

32,50,000

41,75,000

10,62,500

16,25,000

68,62,500

10

15

21

1,06,250

1,08,333

3,26,785

0.847

0.718

0.609

89,994

77,783

1,99,012

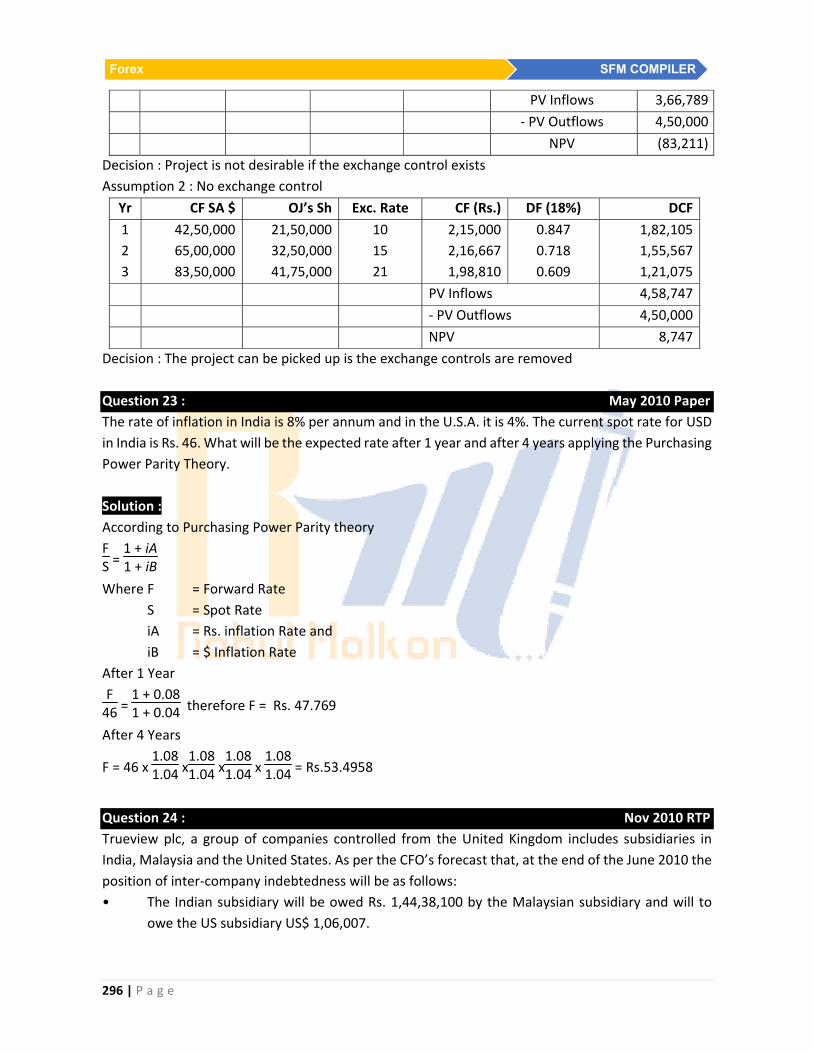

296 | P a g e

Forex SFM COMPILER

PV Inflows 3,66,789

‐ PV Outflows 4,50,000

NPV (83,211)

Decision : Project is not desirable if the exchange control exists

Assumption 2 : No exchange control

Yr CF SA $ OJ’s Sh Exc. Rate CF (Rs.) DF (18%) DCF

1

2

3

42,50,000

65,00,000

83,50,000

21,50,000

32,50,000

41,75,000

10

15

21

2,15,000

2,16,667

1,98,810

0.847

0.718

0.609

1,82,105

1,55,567

1,21,075

PV Inflows 4,58,747

‐ PV Outflows 4,50,000

NPV 8,747

Decision : The project can be picked up is the exchange controls are removed

Question 23 : May 2010 Paper

The rate of inflation in India is 8% per annum and in the U.S.A. it is 4%. The current spot rate for USD

in India is Rs. 46. What will be the expected rate after 1 year and after 4 years applying the Purchasing

Power Parity Theory.

Solution :

According to Purchasing Power Parity theory

FS =

1 + iA1 + iB

Where F = Forward Rate

S = Spot Rate

iA = Rs. inflation Rate and

iB = $ Inflation Rate

After 1 Year

F46 =

1 + 0.081 + 0.04 therefore F = Rs. 47.769

After 4 Years

F = 46 x 1.081.04 x

1.081.04 x

1.081.04 x

1.081.04 = Rs.53.4958

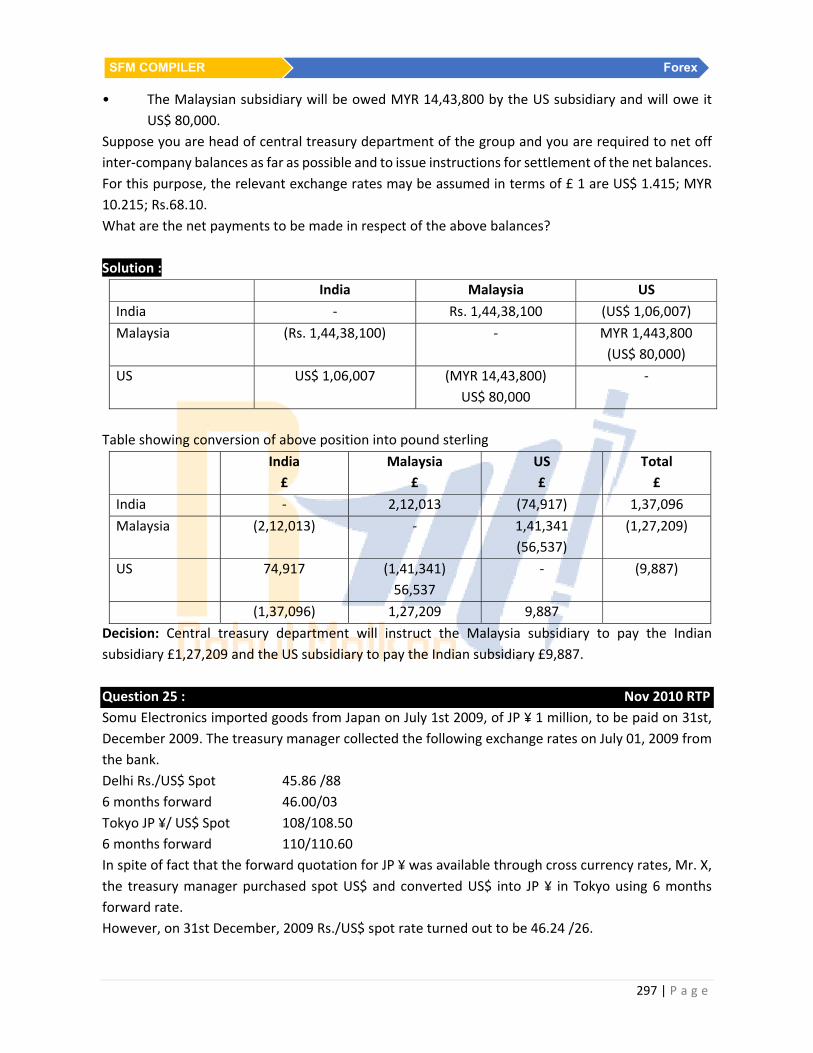

Question 24 : Nov 2010 RTP

Trueview plc, a group of companies controlled from the United Kingdom includes subsidiaries in

India, Malaysia and the United States. As per the CFO’s forecast that, at the end of the June 2010 the

position of inter‐company indebtedness will be as follows:

• The Indian subsidiary will be owed Rs. 1,44,38,100 by the Malaysian subsidiary and will to

owe the US subsidiary US$ 1,06,007.

297 | P a g e

SFM COMPILER Forex

• The Malaysian subsidiary will be owed MYR 14,43,800 by the US subsidiary and will owe it

US$ 80,000.

Suppose you are head of central treasury department of the group and you are required to net off

inter‐company balances as far as possible and to issue instructions for settlement of the net balances.

For this purpose, the relevant exchange rates may be assumed in terms of £ 1 are US$ 1.415; MYR

10.215; Rs.68.10.

What are the net payments to be made in respect of the above balances?

Solution :

India Malaysia US

India ‐ Rs. 1,44,38,100 (US$ 1,06,007)

Malaysia (Rs. 1,44,38,100) ‐ MYR 1,443,800

(US$ 80,000)

US US$ 1,06,007 (MYR 14,43,800)

US$ 80,000

‐

Table showing conversion of above position into pound sterling

India

£

Malaysia

£

US

£

Total

£

India ‐ 2,12,013 (74,917) 1,37,096

Malaysia (2,12,013) ‐ 1,41,341

(56,537)

(1,27,209)

US 74,917 (1,41,341)

56,537

‐ (9,887)

(1,37,096) 1,27,209 9,887

Decision: Central treasury department will instruct the Malaysia subsidiary to pay the Indian

subsidiary £1,27,209 and the US subsidiary to pay the Indian subsidiary £9,887.

Question 25 : Nov 2010 RTP

Somu Electronics imported goods from Japan on July 1st 2009, of JP ¥ 1 million, to be paid on 31st,

December 2009. The treasury manager collected the following exchange rates on July 01, 2009 from

the bank.

Delhi Rs./US$ Spot 45.86 /88

6 months forward 46.00/03

Tokyo JP ¥/ US$ Spot 108/108.50

6 months forward 110/110.60

In spite of fact that the forward quotation for JP ¥ was available through cross currency rates, Mr. X,

the treasury manager purchased spot US$ and converted US$ into JP ¥ in Tokyo using 6 months

forward rate.

However, on 31st December, 2009 Rs./US$ spot rate turned out to be 46.24 /26.

298 | P a g e

Forex SFM COMPILER

You are required to calculate the loss or gain in the strategy adopted by Mr. X by comparing the

notional cash flow involved in the forward cover for Yen with the actual cash flow of the transaction.

Solution :

Here we have to compare the notional cash outflow for the forward rate of JP ¥ and the actual cash

outflow involved in rupees against forward purchase of JP ¥ for dollars in Tokyo and spot purchase

of dollars in Delhi for Rs.

(A) Cash flow of forward purchasing the JP ¥

Rs./JP ¥ 6 month forward rate

Bid rate = Bid rate of US$ / Ask Rate of JP ¥ = Rs. 46/ JP ¥ 110.60 = Rs.0.415913

Ask rate = Ask rate of US$ / Bid Rate of JP ¥ = Rs. 46.03/ JP ¥ 110 = Rs.0. 418454

Hence, Rs./JP ¥ 6 month forward rate = 0.415913/0.418454

Accordingly, if the company had purchased JP ¥ forward against

rupees it would have paid = Rs.418454.50

(B) Cash flow of forward purchasing US$ in spot market and converting into JP ¥

Amount of US dollars to be paid on due date by purchase of JP¥ 1 million in forward market

= JP¥ 1,000,000/ JP¥ 110 = US$ 9090.91

Cash outflows in rupees against purchase of dollars in on Dec. 31, 2009

= US$ 9090.91× Rs. 46.26 = Rs. 420,545.50

(C) Loss or gain due to strategy adopted by Mr. X.

(A) – (B) = Rs. 4,18,454.50 – 4,20,545.50 = Rs. 2091.00

Thus, the company paid more Rs.2,091.00 in the strategy adopted by Mr. X.

Question 26 : Nov 2010 RTP

An automobile company in Gujarat exports its goods to Singapore at a price of SG$ 500 per unit. The

company also imports components from Italy and the cost of components for each unit is € 200. The

company’s CEO executed an agreement for the supply of 20000 units on January 01, 2010 and on the

same date paid for the imported components. The company’s variable cost of producing per unit is

Rs. 1,250 and the allocable fixed costs of the company are Rs. 1,00,00,000.

The exchange rates as on 1 January 2010 were as follows‐

Spot Rs./SG$ 33.00/33.04

Rs./€ 56.49/56.56

Mr. A, the treasury manager of company is observing the movements of exchange rates on a day to

day basis and has expected that the rupee would appreciate against SG$ and would depreciate

against €.

As per his estimates the following are expected rates for 30th June 2010.

Spot Rs./SG$ 32.15/32.21

Rs./€ 57.27/57.32

You are required to find out:

(a) The change in profitability due to transaction exposure for the contract entered into.

299 | P a g e

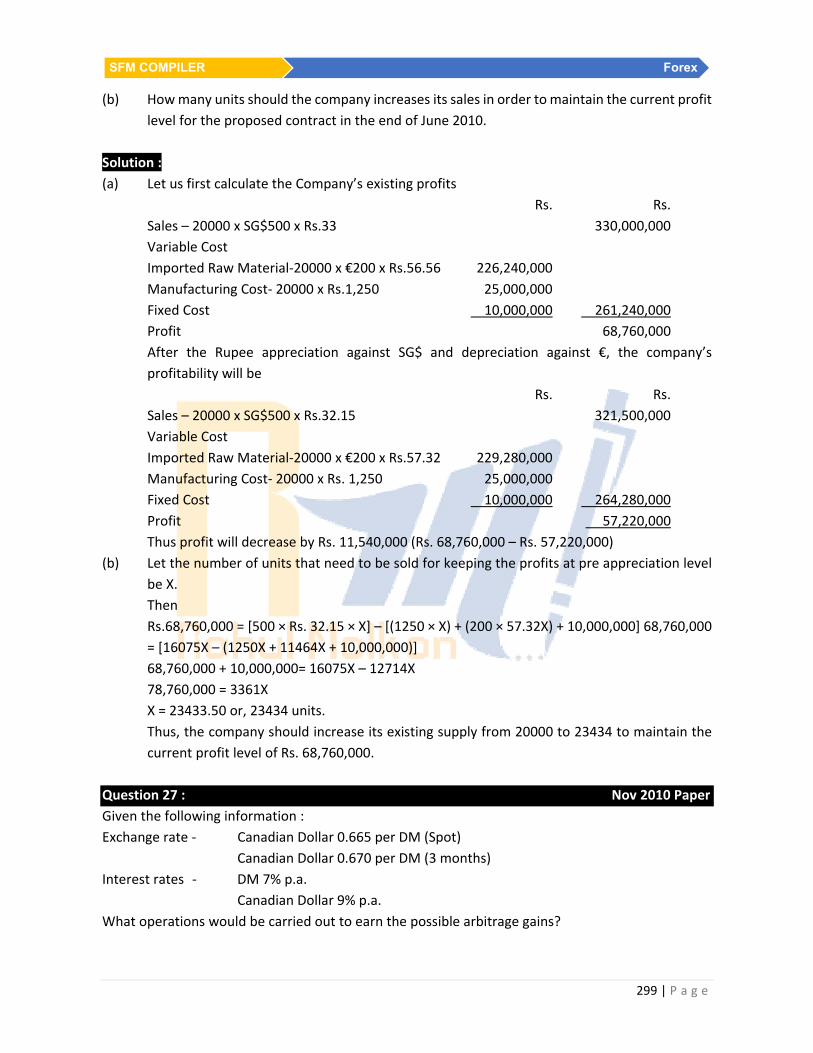

SFM COMPILER Forex

(b) How many units should the company increases its sales in order to maintain the current profit

level for the proposed contract in the end of June 2010.

Solution :

(a) Let us first calculate the Company’s existing profits

Rs. Rs.

Sales – 20000 x SG$500 x Rs.33 330,000,000

Variable Cost

Imported Raw Material‐20000 x €200 x Rs.56.56 226,240,000

Manufacturing Cost‐ 20000 x Rs.1,250 25,000,000

Fixed Cost 10,000,000 261,240,000

Profit 68,760,000

After the Rupee appreciation against SG$ and depreciation against €, the company’s

profitability will be

Rs. Rs.

Sales – 20000 x SG$500 x Rs.32.15 321,500,000

Variable Cost

Imported Raw Material‐20000 x €200 x Rs.57.32 229,280,000

Manufacturing Cost‐ 20000 x Rs. 1,250 25,000,000

Fixed Cost 10,000,000 264,280,000

Profit 57,220,000

Thus profit will decrease by Rs. 11,540,000 (Rs. 68,760,000 – Rs. 57,220,000)

(b) Let the number of units that need to be sold for keeping the profits at pre appreciation level

be X.

Then

Rs.68,760,000 = [500 × Rs. 32.15 × X] – [(1250 × X) + (200 × 57.32X) + 10,000,000] 68,760,000

= [16075X – (1250X + 11464X + 10,000,000)]

68,760,000 + 10,000,000= 16075X – 12714X

78,760,000 = 3361X

X = 23433.50 or, 23434 units.

Thus, the company should increase its existing supply from 20000 to 23434 to maintain the

current profit level of Rs. 68,760,000.

Question 27 : Nov 2010 Paper

Given the following information :

Exchange rate ‐ Canadian Dollar 0.665 per DM (Spot)

Canadian Dollar 0.670 per DM (3 months)

Interest rates ‐ DM 7% p.a.

Canadian Dollar 9% p.a.

What operations would be carried out to earn the possible arbitrage gains?

300 | P a g e

Forex SFM COMPILER

Solution :

spot $ / DM 0.665

3mf $ / DM 0.670

i$ 9%pa

iDM 7%pa

Step 1 : Borrow 10,000 CD for 3 months

Amt : payable = 10,000 x 1.0225 CD = 10225 CD

Step 2 : Convert CD 10,000 in DM spot

Amount Received = 10,0000.665 = 15,037.59 DM

Step 3 : Invest 15,037.59 DM for 3 months

Amount Receivable = 15,037.59 x 1.0175 = 15,300.7478

Step 4 : Sell 15,300.7478 DM 3 mf

Amount Receivable = 15,300.7478 x 0.670 = 10,251.50

Profit = 10,251.50 – 10,225 = 26.5 $

2011

Question 28 : May 2011 RTP

Arnie operating a garment store in US has imported garments from Indian exporter of invoice amount

of Rs.1,38,00,000 (equivalent to US$ 3,00,000). The amount is payable in 3 months. It is expected

that the exchange rate will decline by 5% over 3 months period. Arnie is interested to take

appropriate action in foreign exchange market. The three month forward rate is quoted at Rs.44.50.

You are required to calculate expected loss which Arnie would suffer due to this decline if risk is

not hedged. If there is loss, then how he can hedge this risk.

Solution :

Arnie us imports fc Rs.1,38,00,000 payable after 3 months

Spot Rs. / $ 1,38,00,000 3,00,000 = 46

Expected 3 months spot Rs. / $ 43.7

3 mf rate Rs. / $ 44.5

No Hedging

3m spot Rs. / $ 43.7

1,38,00,00043.7 = 3,15,789.4737 $

: Loss = 1,57,789.4737

Hedging

3mf Buy

3mf Rs. / $ 44.5

Amt payable = 1,38,00,000

44.5 = 310112.3596 $

301 | P a g e

SFM COMPILER Forex

: Saving in loss 315789.4737

310112.3596

5677.1141 $

Question 29 : May 2011 RTP

AMK Ltd. an Indian based company has subsidiaries in U.S. and U.K.

Forecasts of surplus funds for the next 30 days from two subsidiaries are as below:

U.S. $12.5 million

U.K. £ 6 million

Following exchange rate informations are obtained:

$/Rs. £/Rs.

Spot 0.0215 0.0149

30 days forward 0.0217 0.0150

Annual borrowing/deposit rates (Simple) are available.

Rs. 6.4%/6.2%

$ 1.6%/1.5%

£ 3.9%/3.7%

The Indian operation is forecasting a cash deficit of Rs. 500 million.

It is assumed that interest rates are based on a year of 360 days.

(i) Calculate the cash balance at the end of 30 days period in Rs. for each company under each

of the following scenarios ignoring transaction costs and taxes:

(a) Each company invests/finances its own cash balances/deficits in local currency

independently.

(b) Cash balances are pooled immediately in India and the net balances are

invested/borrowed for the 30 days period.

(ii) Which method do you think is preferable from the parent company’s point of view?

Solution :

Cash Balances:

Acting independently Rs. 000

Capital Interest Rs. in 30 days

India –5,00,000 –2,666.67 –5,02,667

U.S. 12,500 15.63 5,76,757

U.K. 6,000 18.50 4,01,233

4,75,323

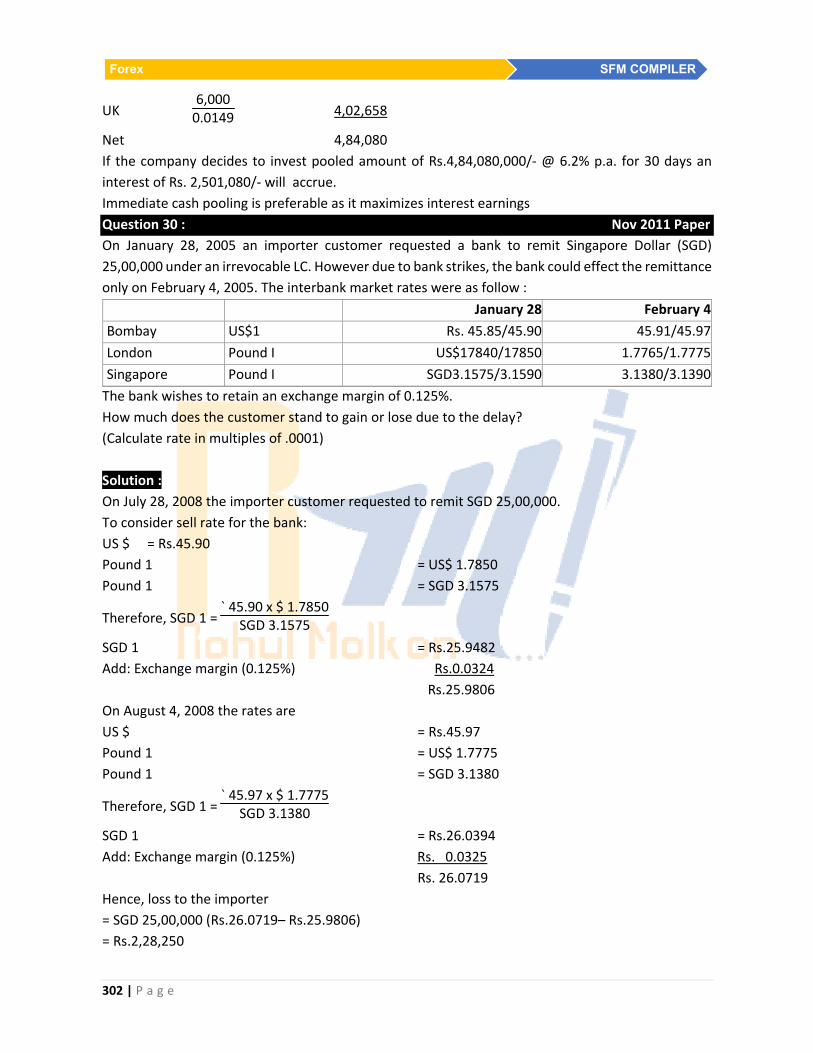

Immediate Cash Pooling

Rs. 000

India –5,00,000

US 12,5000.0215 5,81,395

302 | P a g e

Forex SFM COMPILER

UK 6,0000.0149 4,02,658

Net 4,84,080

If the company decides to invest pooled amount of Rs.4,84,080,000/‐ @ 6.2% p.a. for 30 days an

interest of Rs. 2,501,080/‐ will accrue.

Immediate cash pooling is preferable as it maximizes interest earnings

Question 30 : Nov 2011 Paper

On January 28, 2005 an importer customer requested a bank to remit Singapore Dollar (SGD)

25,00,000 under an irrevocable LC. However due to bank strikes, the bank could effect the remittance

only on February 4, 2005. The interbank market rates were as follow :

January 28 February 4

Bombay US$1 Rs. 45.85/45.90 45.91/45.97

London Pound I US$17840/17850 1.7765/1.7775

Singapore Pound I SGD3.1575/3.1590 3.1380/3.1390

The bank wishes to retain an exchange margin of 0.125%.

How much does the customer stand to gain or lose due to the delay?

(Calculate rate in multiples of .0001)

Solution :

On July 28, 2008 the importer customer requested to remit SGD 25,00,000.

To consider sell rate for the bank:

US $ = Rs.45.90

Pound 1 = US$ 1.7850

Pound 1 = SGD 3.1575

Therefore, SGD 1 = ` 45.90 x $ 1.7850

SGD 3.1575

SGD 1 = Rs.25.9482

Add: Exchange margin (0.125%) Rs.0.0324

Rs.25.9806

On August 4, 2008 the rates are

US $ = Rs.45.97

Pound 1 = US$ 1.7775

Pound 1 = SGD 3.1380

Therefore, SGD 1 = ` 45.97 x $ 1.7775

SGD 3.1380

SGD 1 = Rs.26.0394

Add: Exchange margin (0.125%) Rs. 0.0325

Rs. 26.0719

Hence, loss to the importer

= SGD 25,00,000 (Rs.26.0719– Rs.25.9806)

= Rs.2,28,250

303 | P a g e

SFM COMPILER Forex

Question 31 : Nov 2011 Paper

An Indian importer has to settle an import bill for $ 1,30,000. The exporter has given the Indian

exporter two options:

(i) Pay immediately without any interest charges.

(ii) Pay after three months with interest at 5 percent per annum.

The importer's bank charges 15 percent per annum on overdrafts. The exchange rates in the market

are as follows:

Spot rate (Rs./$) : 48.35 /48.36

3‐Months forward rate (Rs./$) : 48.81 /48.83

The importer seeks your advice. Give your advice.

Solution :

If importer pays now, he will have to buy US$ in Spot Market by availing overdraft facility.

Accordingly, the outflow under this option will be

Rs.

Amount required to purchase $130000[$130000 X Rs.48.36] 62,86,800

Add: Overdraft Interest for 3 months @15% p.a. 2,35,755

65,22,555

If importer makes payment after 3 months then, he will have to pay interest for 3 months @ 5% p.a.

for 3 month along with the sum of import bill. Accordingly, he will have to buy $ in forward market.

The outflow under this option will be as follows:

$

Amount of Bill 1,30,000

Add: Interest for 3 months @5% p.a. 1,625

1,31,625

Amount to be paid in Indian Rupee after 3 month under the forward purchase contract

Rs. 6427249 (US$ 131625 X Rs. 48.83)

Since outflow of cash is least in (ii) option, it should be opted for.

2012

Question 32 : May 2012 RTP

The risk free rate of interest rate in USA is 8% p.a. and in UK is 5% p.a. The spot exchange rate between

US $ and UK £ is 1$ = £ 0.75.

Assuming that is interest is compounded on daily basis then at which forward rate of 2 year there

will be no opportunity for arbitrage.

Further, show how an investor could make risk‐less profit, if two year forward price is 1 $ = 0.85 £.

Given e0.‐06 = 0.9413 & e‐0.16 = 0.852, e0.16 = 1.1735, e‐0.1 = 0.9051

Solution :

2 year Forward Rate will be calculated as follows:

304 | P a g e

Forex SFM COMPILER

F = Se (ruk ‐rus )t

Where

F = Forward Rate

S = Spot Rate

rUK = Risk Free Rate in UK

rUS = Risk Free Rate in US

t = Time

Accordingly,

F = 0.75e (0.05 – 0.08)2

= 0.75 € 0.9413

= 0.706

Thus, 1 US $ = £ 0.706

If forward rate is 1 UK $ = 0.85$ then an arbitrage opportunity exists.

Take following steps

(a) Should borrow UK £

(b) Buy US $

(c) Enter into a short forward contract on US $ Accordingly,

The riskless profit would be

(a) Say borrow £ 0.706e‐(0.05)(2) = £ 0.639 and invest in UK for 2 years.

(b) Now buy US $ at US $ 1e‐(0.08)2 = US $ 0.852, so that after two year it can be used to close

out the position.

(c) After two year the investment in US $ will become US $ 0.852 e(0.08)(2) = US $ 0.852 x 1.1735 =

1 US $

(d) Sell this US $ for £ 0.85 and repay loan of £ 0.639 along with interest i.e £ 0.706.

Thus arbitrage profit will be

US$ 0.85 – US$ 0.706 = 0.144 $.

Question 33 : May 2012 RTP

True Blue Cosmetics Ltd. is an old line producer of cosmetics products made up of herbals. Their

products are popular in India and all over the world but are more popular in Europe.

The company invoice in Indian Rupee when it exports to guard itself against the fluctuation in

exchange rate. As the company is enjoying monopoly position, the buyer normally never objected to

such invoices. However, recently, an order has been received from a whole‐saler of France for FFr

80,00,000. The other conditions of the order are as follows:

(a) The delivery shall be made within 3 months.

(b) The invoice should be FFr.

Since, company is not interested in losing this contract only because of practice of invoicing in Indian

Rupee. The Export Manger Mr. E approached the banker of Company seeking their guidance and

further course of action.

The banker provided following information to Mr. E.

(a) Spot rate 1 FFr = Rs. 6.60

305 | P a g e

SFM COMPILER Forex

(b) Forward rate (90 days) of 1 FFr = Rs. 6.50

(c) Interest rate in India is 9% and in France is 12%.

Mr. E entered in forward contract with banker for 90 days to sell FFr at above mentioned rate.

When the matter come for consideration before Mr. A, Accounts Manager of company, he

approaches you.

You as a Forex consultant is required to comment on:

(i) Whether there is an arbitrage opportunity exists or not.

(ii) Whether the action taken by Mr. E is correct and if bank agrees for negotiation of rate, then

at what forward rate company should sell FFr to bank.

Solution :

Invoice amount in Indian Rupee = FFr 80,00,000 € Rs. 6.60 = Rs. 5,28,00,000

(i) Interest Rate in India 9% p.a.

Interest Rate in France 12% p.a

The interest rate differential 9% ‐ 12% = 3% (Positive Interest Differential)

Forward Discount = F‐SS x

12n x 100

= 6.5‐6.66.6 x

12n x 100 = ‐ 6.061% (forward Discount)

Since the forward discount is greater than interest rate differential there will be

arbitrage inflow into the country (India).

(ii) The decision taken by Mr. E was not correct because as per Interest Rate Parity

Theory, forward rate for sale should be 1 FFr = Rs. 6.65, calculated as follows:

Let F be the forward rate, then as per Interest Rate Parity theory, it should have been as

follows:

= F‐SS x

12n x 100 = ‐3

= F‐6.66.6 x

123 x 100 = ‐3

F = 6.6495

Question 34 : May 2012 Paper

NP and Co. has imported goods for US $ 7,00,000. The amount is payable after three months. The

company has also exported goods for US $ 4,50,000 and this amount is receivable in two months. For

receivable amount a forward contract is already taken at € 48.40.

The market rates for € and $ are as under.

Spot € 48.50 / 70

Two months 25 / 30 points

Three months 40 / 45 points

The Company wants to cover the risk and it has two options as under :

a) To cover payables in the forward market and

306 | P a g e

Forex SFM COMPILER

b) To lag the receivables by one month and cover the risk only for the net amount. No interest

for delaying the receivables is earned. Evaluate both the options if the cost of Rupee Funds is

12%. Which option is preferable?

Solution :

(i) To cover payable and receivable in forward Market

Amount payable after 3 months $7,00,000

Forward Rate Rs. 48.45

Thus Payable Amount (Rs.) (A) Rs. 3,39,15,000

Amount receivable after 2 months $ 4,50,000

Forward Rate Rs. 48.40

Thus Receivable Amount (Rs.) (B) Rs. 2,17,80,000

Interest @ 12% p.a. for 1 month (C) Rs. 2,17,800

Net Amount Payable in (Rs.) (A) – (B) – (C) Rs. 1,19,17,200

(ii) Assuming that since the forward contract for receivable was already booked it shall be

cancelled if we lag the receivables. Accordingly any profit/ loss on cancellation of contract

shall also be calculated and shall be adjusted as follows:

Amount Payable ($) $7,00,000

Amount receivable after 3 months $ 4,50,000

Net Amount payable $2,50,000

Applicable Rate Rs. 48.45

Amount payable in (Rs.) (A) Rs. 1,21,12,500

Profit on cancellation of Forward cost

(48.90 – 48.30) × 4,50,000 (B) Rs. 2,70,000

Thus net amount payable in (Rs.) (A) + (B) Rs. 1,18,42,500

Since net payable amount is least in case of second option, hence the company should lag

receivables.

Note: In the question it has not been clearly mentioned that whether quotes given for 2 and

3 months (in points terms) are premium points or direct quotes. Although above solution is

based on the assumption that these are direct quotes, but students can also consider them

as premium points and solve the question accordingly.

Question 35 : Nov 2012 RTP

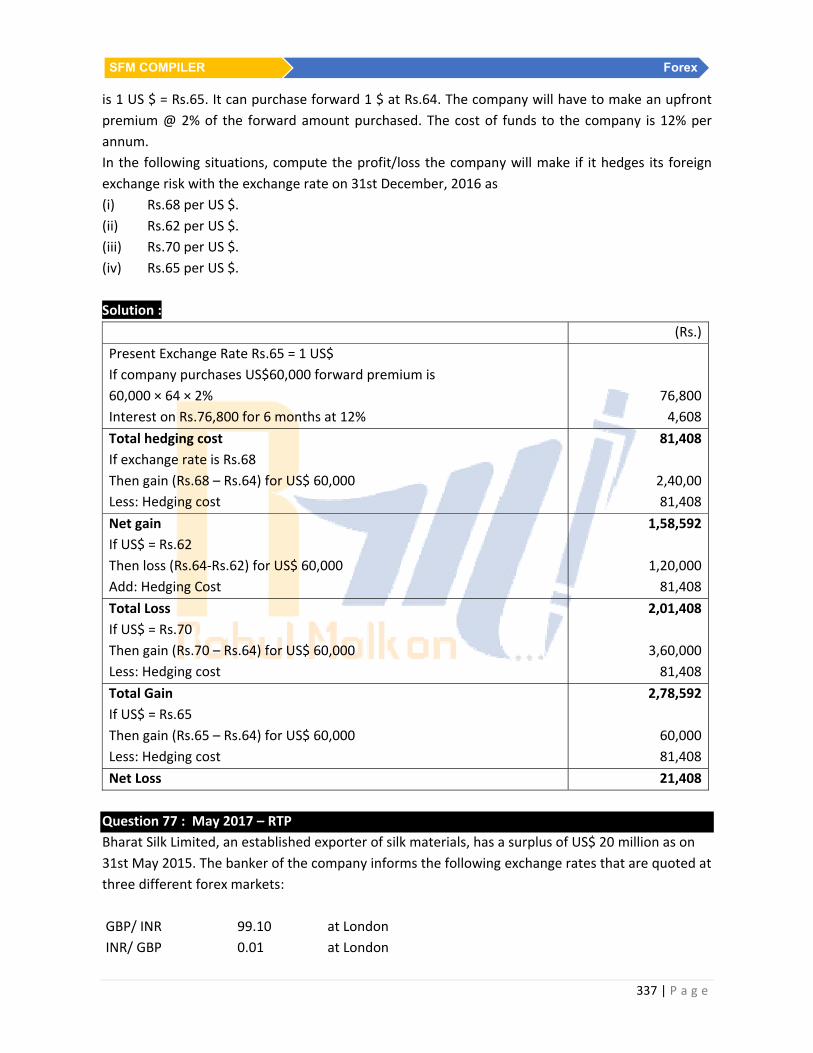

A company is considering hedging its foreign exchange risk. It has made a purchase on 1st. January,

2008 for which it has to make a payment of US $ 50,000 on September 30,2008. The present

exchange rate is 1 US $ = Rs.40. It can purchase forward 1 US $ at Rs. 39. The company will have to

make a upfront premium of 2% of the forward amount purchased. The cost of funds to the company

is 10% per annum and the rate of corporate tax is 50%. Ignore taxation. Consider the following

situations and compute the Profit/Loss the company will make if it hedges its foreign exchange risk:

(i) If the exchange rate on September 30, 2008 is Rs.42 per US $.

(ii) If the exchange rate on September 30, 2008 is Rs.38 per US $.

307 | P a g e

SFM COMPILER Forex

Solution :

(Rs.)

Present Exchange Rate Rs.40 = 1 US$

If company purchases US$ 50,000 forward premium is

50000 × 39 × 2% 39,000

Interest on Rs.39,000 for 9 months at 10% 2,925

Total hedging cost 41,925

If exchange rate is Rs.42

Then gain (Rs.42 – Rs.39) for US$ 50,000 1,50,000

Less: Hedging cost 41,925

Net gain 1,08,075

If US$ = Rs.38

Then loss (39 – 38) for US$ 50,000 50,000

Add: Hedging Cost 41,925

Total Loss 91,925

Question 36 : Nov 2012 RTP

An Indian exporting firm, Rohit and Bros., would be cover itself against a likely depreciation of pound

sterling. The following data is given:

Receivables of Rohit and Bros : £500,000

Spot rate : Rs.56.00/£

Payment date : 3‐months

3 months interest rate : India : 12 per cent per annum

: UK : 5 per cent per annum

What should the exporter do?

Solution :

Rohit and Bros can cover the risk in the money market.

The following steps are required to be taken:

Step 1 : Borrow pound sterling for 3‐ months @ 5% p.a. i.e. 1.25% for 3 months

The borrowing has to be such that at the end of three months, the amount becomes

£ 500,000.

The amount borrowed is = 5,00,0001.0125 = £493,827

Step 2 : Convert the borrowed sum into rupees at the spot rate.

This gives: £493,827 × Rs.56 = Rs.27,654,312

Step 3 : Sell The sum thus obtained is placed in the money market at 12 % p.a. i.e. 3% for 3

months

Amount Receivable = 27,654,312 x 1.03 = Rs.28,483,941

308 | P a g e

Forex SFM COMPILER

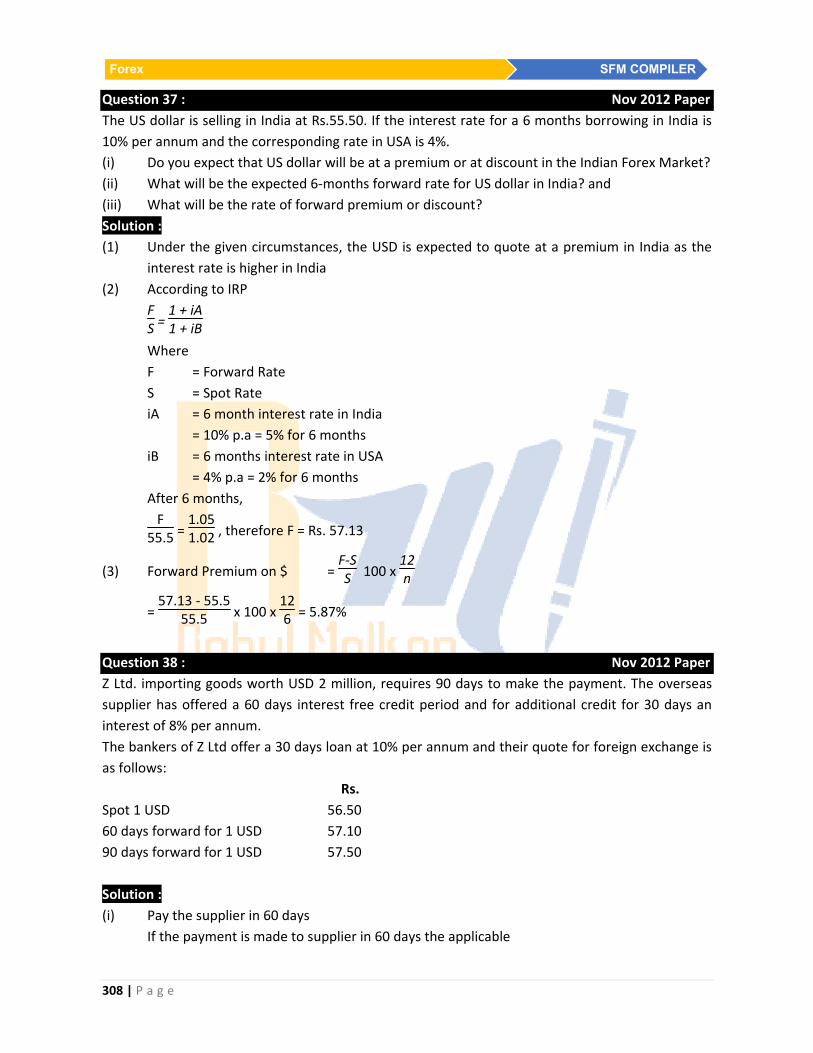

Question 37 : Nov 2012 Paper

The US dollar is selling in India at Rs.55.50. If the interest rate for a 6 months borrowing in India is

10% per annum and the corresponding rate in USA is 4%.

(i) Do you expect that US dollar will be at a premium or at discount in the Indian Forex Market?

(ii) What will be the expected 6‐months forward rate for US dollar in India? and

(iii) What will be the rate of forward premium or discount?

Solution :

(1) Under the given circumstances, the USD is expected to quote at a premium in India as the

interest rate is higher in India

(2) According to IRP

FS =

1 + iA1 + iB

Where

F = Forward Rate

S = Spot Rate

iA = 6 month interest rate in India

= 10% p.a = 5% for 6 months

iB = 6 months interest rate in USA

= 4% p.a = 2% for 6 months

After 6 months,

F

55.5 = 1.051.02 , therefore F = Rs. 57.13

(3) Forward Premium on $ = F‐SS 100 x

12n

= 57.13 ‐ 55.5

55.5 x 100 x 126 = 5.87%

Question 38 : Nov 2012 Paper

Z Ltd. importing goods worth USD 2 million, requires 90 days to make the payment. The overseas

supplier has offered a 60 days interest free credit period and for additional credit for 30 days an

interest of 8% per annum.

The bankers of Z Ltd offer a 30 days loan at 10% per annum and their quote for foreign exchange is

as follows:

Rs.

Spot 1 USD 56.50

60 days forward for 1 USD 57.10

90 days forward for 1 USD 57.50

Solution :

(i) Pay the supplier in 60 days

If the payment is made to supplier in 60 days the applicable

309 | P a g e

SFM COMPILER Forex

forward rate would be for 1 USD Rs.57.10

Payment Due USD 2,00,000

Outflow in Rupees (2,00,000 x 57.10) Rs.114,200,000

Add : Interest on loan for 30 days @ 10% p.a Rs.951,667

Total Outflow Rs.115,151,667

(ii) Availing supplier’s offer of 90 days credit

Amount Payable USD 2,00,000

Add : Interest on the credit period for 30 days @ 8% p.a USD 13,333

Total Outflow USD 2,13,333

Applicable forward Rate Rs.57.50

Total Outflow (2,13,333 x 57.5) Rs.115,766,648

Decision : Z Ltd should pay the supplier in 60 days

2013

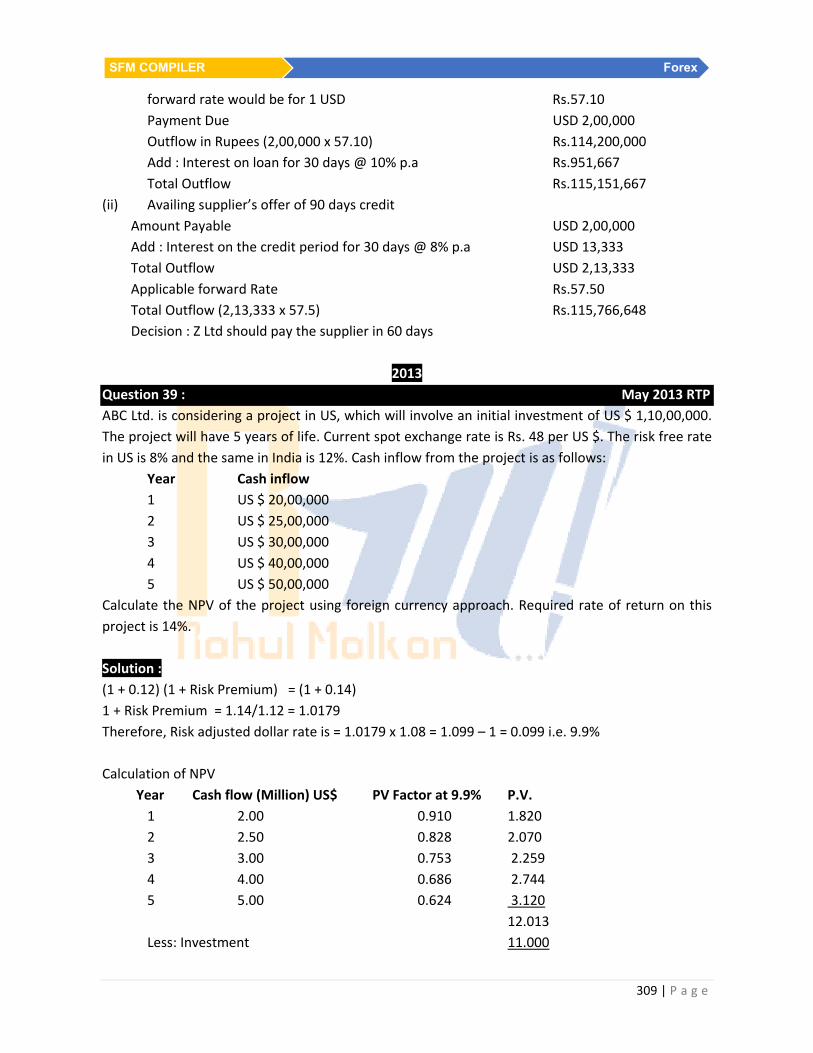

Question 39 : May 2013 RTP

ABC Ltd. is considering a project in US, which will involve an initial investment of US $ 1,10,00,000.

The project will have 5 years of life. Current spot exchange rate is Rs. 48 per US $. The risk free rate

in US is 8% and the same in India is 12%. Cash inflow from the project is as follows:

Year Cash inflow

1 US $ 20,00,000

2 US $ 25,00,000

3 US $ 30,00,000

4 US $ 40,00,000

5 US $ 50,00,000

Calculate the NPV of the project using foreign currency approach. Required rate of return on this

project is 14%.

Solution :

(1 + 0.12) (1 + Risk Premium) = (1 + 0.14)

1 + Risk Premium = 1.14/1.12 = 1.0179

Therefore, Risk adjusted dollar rate is = 1.0179 x 1.08 = 1.099 – 1 = 0.099 i.e. 9.9%

Calculation of NPV

Year Cash flow (Million) US$ PV Factor at 9.9% P.V.

1 2.00 0.910 1.820

2 2.50 0.828 2.070

3 3.00 0.753 2.259

4 4.00 0.686 2.744

5 5.00 0.624 3.120

12.013

Less: Investment 11.000

310 | P a g e

Forex SFM COMPILER

NPV 1.013

Therefore, Rupee NPV of the project is = Rs. (48 x 1.013) Million = Rs. 48.624 Million

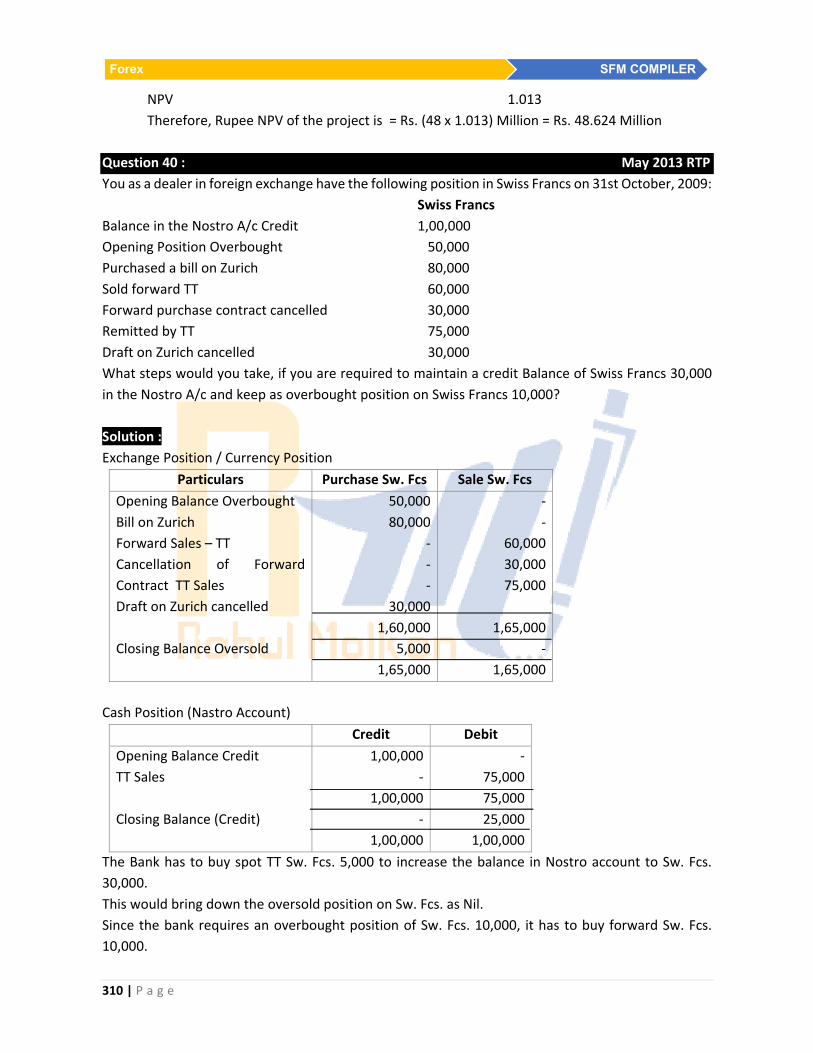

Question 40 : May 2013 RTP

You as a dealer in foreign exchange have the following position in Swiss Francs on 31st October, 2009:

Swiss Francs

Balance in the Nostro A/c Credit 1,00,000

Opening Position Overbought 50,000

Purchased a bill on Zurich 80,000

Sold forward TT 60,000

Forward purchase contract cancelled 30,000

Remitted by TT 75,000

Draft on Zurich cancelled 30,000

What steps would you take, if you are required to maintain a credit Balance of Swiss Francs 30,000

in the Nostro A/c and keep as overbought position on Swiss Francs 10,000?

Solution :

Exchange Position / Currency Position

Particulars Purchase Sw. Fcs Sale Sw. Fcs

Opening Balance Overbought

Bill on Zurich

Forward Sales – TT

Cancellation of Forward

Contract TT Sales

Draft on Zurich cancelled

Closing Balance Oversold

50,000

80,000

‐

‐

‐

30,000

1,60,000

5,000

1,65,000

‐

‐

60,000

30,000

75,000

1,65,000

‐

1,65,000

Cash Position (Nastro Account)

Credit Debit

Opening Balance Credit

TT Sales

Closing Balance (Credit)

1,00,000

‐

1,00,000

‐

1,00,000

‐

75,000

75,000

25,000

1,00,000

The Bank has to buy spot TT Sw. Fcs. 5,000 to increase the balance in Nostro account to Sw. Fcs.

30,000.

This would bring down the oversold position on Sw. Fcs. as Nil.

Since the bank requires an overbought position of Sw. Fcs. 10,000, it has to buy forward Sw. Fcs.

10,000.

311 | P a g e

SFM COMPILER Forex

Question 41 : May 2013 – RTP

The rate of inflation in USA is likely to be 3% per annum and in India it is likely to be 6.5%. The current

spot rate of US $ in India is Rs. 43.40. Find the expected rate of US $ in India after one year and 3

years from now using purchasing power parity theory.

Solution :

According to Purchasing Power Parity theory

FS =

1 + iA1 + iB

Where F = Forward Rate

S = Spot Rate

iA = Rs. inflation Rate and

iB = $ Inflation Rate

After 1 Year

F42.40 =

1 + 0.0651 + 0.03 therefore F = Rs. 44.8751

After 3 Years

F = 42.40 x 1.0651.03 x

1.0651.03 x

1.0651.03 = Rs. 47.9762

Question 42 : May 2013 – RTP

On April 1, 3 months interest rate in the UK £ and US $ are 7.5% and 3.5% per annum respectively.

The UK £/US $ spot rate is 0.7570. What would be the forward rate for US $ for delivery on 30th

June?

Solution :

According to Interest Rate Parity theory

FS =

1 + iA1 + iB

Where F = Forward Rate

S = Spot Rate

iA = £ Interest Rate for 3 months

= 7.5% P.A i.e 1.875% for 3 months

iB = $ Interest Rate for 3 months

= 3.5% P.A i.e 0.875% for 3 months

After 3 months

F0.7570 =

1 + 0.018751 + 0.0875 , therefore F = 0.7645 UK £/US $

312 | P a g e

Forex SFM COMPILER

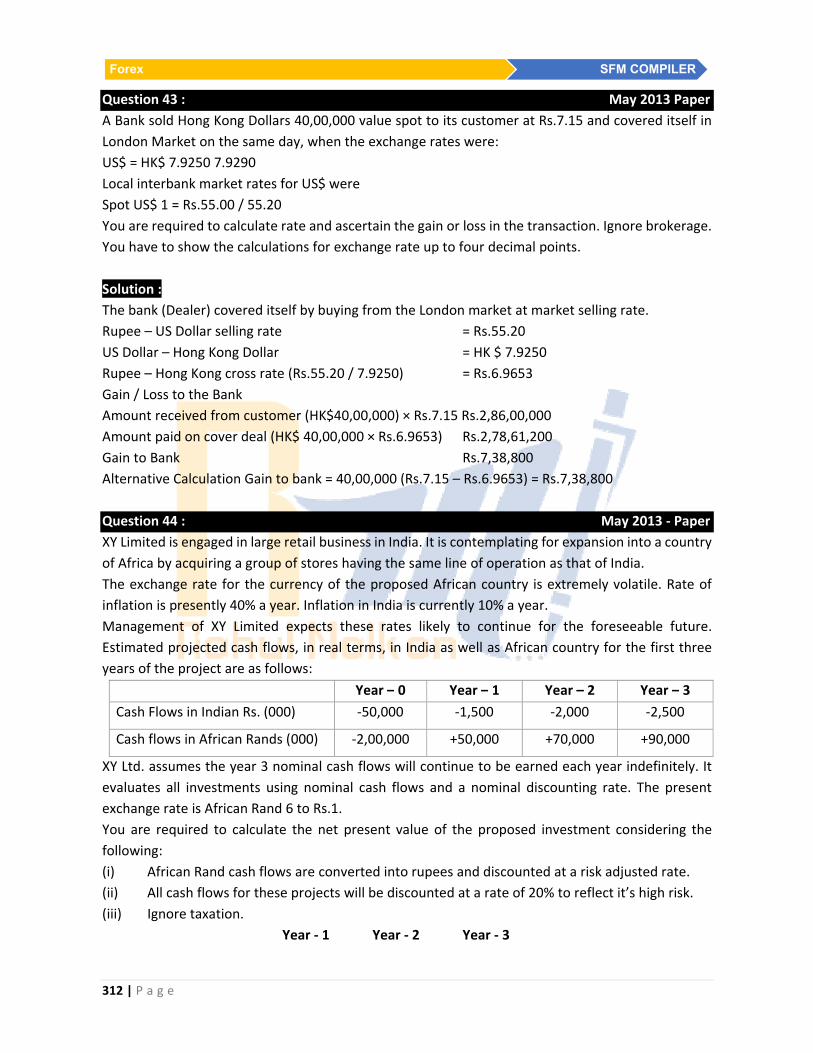

Question 43 : May 2013 Paper

A Bank sold Hong Kong Dollars 40,00,000 value spot to its customer at Rs.7.15 and covered itself in

London Market on the same day, when the exchange rates were:

US$ = HK$ 7.9250 7.9290

Local interbank market rates for US$ were

Spot US$ 1 = Rs.55.00 / 55.20

You are required to calculate rate and ascertain the gain or loss in the transaction. Ignore brokerage.

You have to show the calculations for exchange rate up to four decimal points.

Solution :

The bank (Dealer) covered itself by buying from the London market at market selling rate.

Rupee – US Dollar selling rate = Rs.55.20

US Dollar – Hong Kong Dollar = HK $ 7.9250

Rupee – Hong Kong cross rate (Rs.55.20 / 7.9250) = Rs.6.9653

Gain / Loss to the Bank

Amount received from customer (HK$40,00,000) × Rs.7.15 Rs.2,86,00,000

Amount paid on cover deal (HK$ 40,00,000 × Rs.6.9653) Rs.2,78,61,200

Gain to Bank Rs.7,38,800

Alternative Calculation Gain to bank = 40,00,000 (Rs.7.15 – Rs.6.9653) = Rs.7,38,800

Question 44 : May 2013 ‐ Paper

XY Limited is engaged in large retail business in India. It is contemplating for expansion into a country

of Africa by acquiring a group of stores having the same line of operation as that of India.

The exchange rate for the currency of the proposed African country is extremely volatile. Rate of

inflation is presently 40% a year. Inflation in India is currently 10% a year.

Management of XY Limited expects these rates likely to continue for the foreseeable future.

Estimated projected cash flows, in real terms, in India as well as African country for the first three

years of the project are as follows:

Year – 0 Year – 1 Year – 2 Year – 3

Cash Flows in Indian Rs. (000) ‐50,000 ‐1,500 ‐2,000 ‐2,500

Cash flows in African Rands (000) ‐2,00,000 +50,000 +70,000 +90,000

XY Ltd. assumes the year 3 nominal cash flows will continue to be earned each year indefinitely. It

evaluates all investments using nominal cash flows and a nominal discounting rate. The present

exchange rate is African Rand 6 to Rs.1.

You are required to calculate the net present value of the proposed investment considering the

following:

(i) African Rand cash flows are converted into rupees and discounted at a risk adjusted rate.

(ii) All cash flows for these projects will be discounted at a rate of 20% to reflect it’s high risk.

(iii) Ignore taxation.

Year ‐ 1 Year ‐ 2 Year ‐ 3

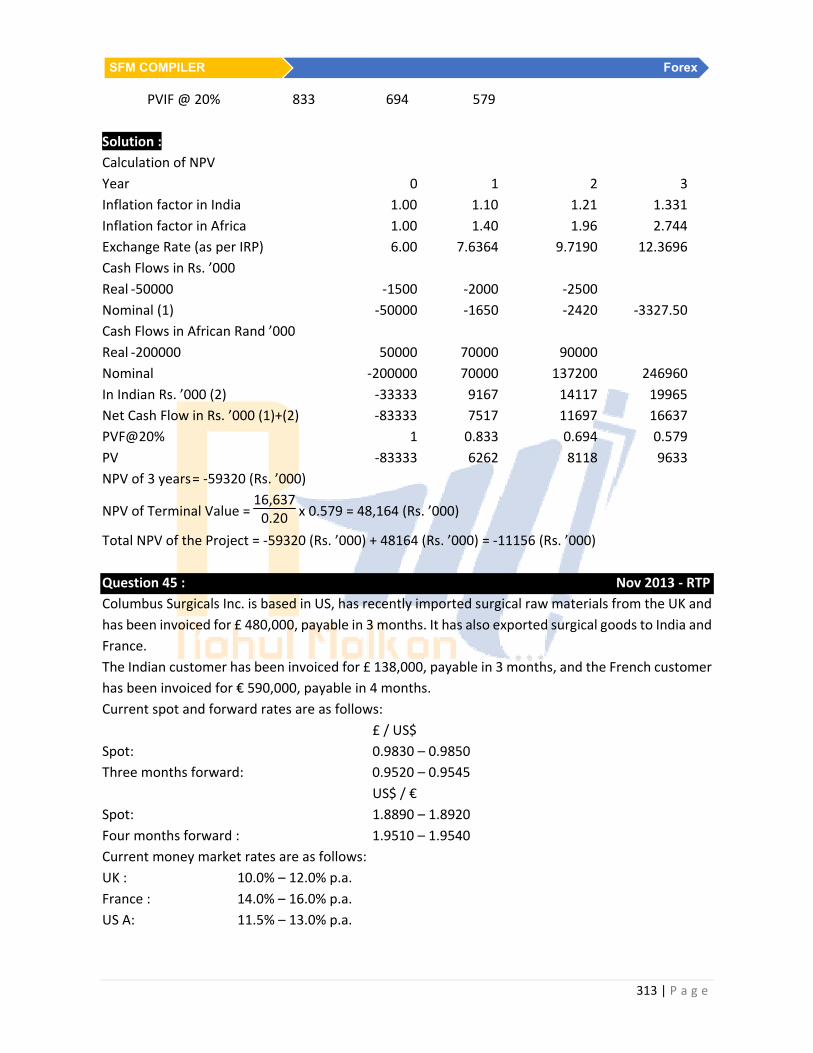

313 | P a g e

SFM COMPILER Forex

PVIF @ 20% 833 694 579

Solution :

Calculation of NPV

Year 0 1 2 3

Inflation factor in India 1.00 1.10 1.21 1.331

Inflation factor in Africa 1.00 1.40 1.96 2.744

Exchange Rate (as per IRP) 6.00 7.6364 9.7190 12.3696

Cash Flows in Rs. ’000

Real ‐50000 ‐1500 ‐2000 ‐2500

Nominal (1) ‐50000 ‐1650 ‐2420 ‐3327.50

Cash Flows in African Rand ’000

Real ‐200000 50000 70000 90000

Nominal ‐200000 70000 137200 246960

In Indian Rs. ’000 (2) ‐33333 9167 14117 19965

Net Cash Flow in Rs. ’000 (1)+(2) ‐83333 7517 11697 16637

PVF@20% 1 0.833 0.694 0.579

PV ‐83333 6262 8118 9633

NPV of 3 years = ‐59320 (Rs. ’000)

NPV of Terminal Value = 16,6370.20 x 0.579 = 48,164 (Rs. ’000)

Total NPV of the Project = ‐59320 (Rs. ’000) + 48164 (Rs. ’000) = ‐11156 (Rs. ’000)

Question 45 : Nov 2013 ‐ RTP

Columbus Surgicals Inc. is based in US, has recently imported surgical raw materials from the UK and

has been invoiced for £ 480,000, payable in 3 months. It has also exported surgical goods to India and

France.

The Indian customer has been invoiced for £ 138,000, payable in 3 months, and the French customer

has been invoiced for € 590,000, payable in 4 months.

Current spot and forward rates are as follows:

£ / US$

Spot: 0.9830 – 0.9850

Three months forward: 0.9520 – 0.9545

US$ / €

Spot: 1.8890 – 1.8920

Four months forward : 1.9510 – 1.9540

Current money market rates are as follows:

UK : 10.0% – 12.0% p.a.

France : 14.0% – 16.0% p.a.

US A: 11.5% – 13.0% p.a.

314 | P a g e

Forex SFM COMPILER

You as Treasury Manager are required to show how the company can hedge its foreign exchange

exposure using Forward markets and Money markets hedge and suggest which the best hedging

technique is.

Solution

£ Exposure

Since Columbus has a £ receipt (£ 138,000) and payment of (£ 480,000) maturing at the same time

i.e. 3 months, it can match them against each other leaving a net liability of £ 342,000 to be hedged.

(i) Forward market hedge

Buy 3 months' forward contract accordingly, amount payable after 3 months will be £ 342,000

/ 0.9520 = US$ 359,244

(ii) Money market hedge

To pay £ after 3 months' Columbus shall requires to borrow in US$ and translate to £ and then

deposit in £. (Invest – Buy ‐ Borrow)

Step 1 : Invest

For payment of £ 342,000 in 3 months (@2.5% interest) amount required to be deposited

now

(£ 342,000 ÷ 1.025) = £ 333,658

Step 2 : Buy

With spot rate of 0.9830 the US$ loan needed will be = US$ 339,429

Step 3 : Borrow

Loan repayable after 3 months (@3.25% interest) will be = US$ 350,460

In this case the money market hedge is a cheaper option.

€ Receipts

€ Receipt Amount to be hedged = € 590,000

Now we Convert exchange rates to home currency

€ / US$

Spot 0.5285 – 0.5294

4 months forward 0.5118 – 0.5126

(i) Forward market hedge

Sell 4 months' forward contract accordingly, amount receivable after 4 months will be (€

590,000 / 0.5126) = US$ 1,150,995

(ii) Money market hedge For money market hedge Columbus shall borrow in € and then translate

to US$ and deposit in US$ (Borrow – Sell – Invest)

Step 1 : Borrow

For receipt of € 590,000 in 4 months (@ 5.33% interest) amount required to be borrowed

now (€590,000 ÷ 1.0533) = € 560,144

Step 2 : Sell

With spot rate of 0.5294 the US$ deposit will be = US$ 1,058,073

Step 3 : Invest

Deposit amount will increase over 3 months (@3.83% interest) will be

= US$ 1,098,597

315 | P a g e

SFM COMPILER Forex

In this case, more will be received in US$ under the forward hedge.

Question 46 : Nov 2013 – RTP

ABN‐Amro Bank, Amsterdam, wants to purchase Rs. 15 million against US$ for funding their Vostro

account with Canara Bank, New Delhi. Assuming the inter‐bank, rates of US$ is Rs. 51.3625/3700,

what would be the rate Canara Bank would quote to ABN‐Amro Bank? Further, if the deal is struck,

what would be the equivalent US$ amount.

Solution :

Here Canara Bank shall buy US$ and credit Rs. to Vostro account of ABN‐Amro Bank. Canara Bank’s

buying rate will be based on the Inter‐bank Buying Rate (as this is the rate at which Canara Bank can

sell US$ in the Interbank market)

Accordingly, the Interbank Buying Rate of US$ will be Rs.51.3625 (lower of two)

Equivalent of US$ for Rs.15 million at this rate will be

= 15,000,00051.3625 = US$ 2,92,041.86

Question 47 : Nov 2013 Paper

You, a foreign exchange dealer of your bank, are informed that your bank has sold a T.T. on

Copenhagen for Danish Kroner 10,00,000 at the rate of Danish Kroner 1 = Rs. 6.5150.

You are required to cover the transaction either in London or New York market. The rates on that

date are as under:

Mumbai‐London Rs.74.3000 Rs.74.3200

London‐New York Rs.49.2500 Rs.49.2625

London‐Copenhagen DKK 11.4200 DKK 11.4350

New York‐Copenhagen DKK 07.5670 DKK 07.5840

In which market will you cover the transaction, London or New York, and what will be the exchange

profit or loss on the transaction? Ignore brokerages.

Solution :

Amount realized on selling Danish Kroner 10,00,000 at Rs. 6.5150 per Kroner = Rs. 65,15,000.

Cover at London:

Bank buys Danish Kroner at London at the market selling rate.

Pound sterling required for the purchase (DKK 10,00,000 ÷ DKK 11.4200) = GBP 87,565.67

Bank buys locally GBP 87,565.67 for the above purchase at the market selling rate of Rs. 74.3200.

The rupee cost will be = Rs. 65,07,88

Profit (Rs. 65,15,000 ‐ Rs. 65,07,881) = Rs. 7,119

Cover at New York:

Bank buys Kroners at New York at the market selling rate.

Dollars required for the purchase of Danish Kroner (DKK10,00,000 ÷ 7.5670) = USD 1,32,152.77

Bank buys locally USD 1,32,152.77 for the above purchase at the market selling rate of Rs. 49.2625.

The rupee cost will be = Rs. 65,10,176.

316 | P a g e

Forex SFM COMPILER

Profit (Rs. 65,15,000 ‐ Rs. 65,10,176) = Rs. 4,824

The transaction would be covered through London which gets the maximum profit of Rs. 7,119 or

lower cover cost at London Market by (Rs. 65,10,176 – Rs. 65,07,881) = Rs. 2,295

Question 48 : Nov 2013 Paper

Your bank’s London office has surplus funds to the extent of USD 5,00,000/‐ for a period of 3 months.

The cost of the funds to the bank is 4% p.a. It proposes to invest these funds in London, New York or

Frankfurt and obtain the best yield, without any exchange risk to the bank. The following rates of

interest are available at the three centres for investment of domestic funds there at for a period of 3

months.

London 5 % p.a.

New York 8% p.a.

Frankfurt 3% p.a.

The market rates in London for US dollars and Euro are as under:

London on New York

Spot 1.5350/90

1 month 15/18

2 month 30/35

3 months 80/85

London on Frankfurt

Spot 1.8260/90

1 month 60/55

2 month 95/90

3 month 145/140

At which centre, will be investment be made & what will be the net gain (to the nearest pound) to

the bank on the invested funds?

Solution :

(i) If investment is made at London

Convert US$ 5,00,000 at Spot Rate (5,00,000/1.5390) = £ 3,24,886

Add: £ Interest for 3 months on £ 324,886 @ 5% = £ 4,061

= £ 3,28,947

Less: Amount Invested $ 5,00,000

Interest accrued thereon ___$ 5,000

= $ 5,05,000

Equivalent amount of £ required to pay the above sum

($ 5,05,000/1.5430) = £ 3,27,285

Arbitrage Profit = £ 1,662

(ii) If investment is made at New York

Gain $ 5,00,000 (8% ‐ 4%) x 3/12 = $5,000

Equivalent amount in £ 3 months ($ 5,000/ 1.5475) £ 3,231

317 | P a g e

SFM COMPILER Forex

(iii) If investment is made at Frankfurt

Convert US$ 500,000 at Spot Rate (Cross Rate) 1.8260/1.5390 = € 1.1865

Euro equivalent US$ 500,000 = € 5,93,250

Add: Interest for 3 months @ 3% = € 4,449

= € 5,97,699

3 month Forward Rate of selling € (1/1.8150) = £ 0.5510

Sell € in Forward Market € 5,97,699 x £ 0.5510 = £ 3,29,332

Less: Amounted invested and interest thereon = £ 3,27,285

Arbitrage Profit = £ 2,047

Since out of three options the maximum profit is in case investment is made in New York. Hence it

should be opted.

2014

Question 49 : May 2014 RTP

Following information relates to AKC Ltd. which manufactures some parts of an electronics device

which are exported to USA, Japan and Europe on 90 days credit terms.

Cost and Sales information :

Japan USA Europe

Variable cost per unit

Export sale price per unit/Receipts from sale

due in 90 days

Rs.225

Yen 650

Yen 78,00,000

Rs.395

US$10.23

US$1,02,300

Rs.510

Euro 11.99

Euro 85,920

Foreign exchange rate information :

Yen/Rs. US$/Rs. Euro/Rs.

Spot market

3 months forward

3 months spot

2,417‐2.437

2.397‐2.427

2.423‐2.459

0.0214‐0.0217

0.0213‐0.0216

0.02144‐0.02156

0.0177‐0.0180

0.0176‐0.0178

0.0177‐0.0179

Advice AKC Ltd. by calculating average contribution to sales ratio whether it should hedge its foreign

currency risk or not.

Solution :

Variable cost

Units vc variable cost

Japan 78,00,000 / 650 12000 225 27,00,000

Us 1,02,300 / 10.23 10000 395 39,50.000

Europe 95,920 / 11,99 8000 510 40,80,000

Rs.1,07,30,000

Hedging

ER Receipts (Rs.)

Japan 78,00,000 2.427 32 ,13,844

Us 1,02,300 0.0216 47,36,111

318 | P a g e

Forex SFM COMPILER

Europe 95,920 0.0178 53,88,764

Rs.1,33,38,719

Contribustion / sales = 1,33,38,719 ‐ 1,07,30,000

1,33,38,719 x 100 = 19.56%

Non Hedging

Japan 2.459 31,72,021

Us 0.02156 47,44,898

Europe 0.0179 53,58,659

Rs. 1,32,75,578

Contribution / Sales Ratio = 1,32,75,578 ‐ 1,07,30,000

1,07,30,000 x 100 = 19.17%

Question 50 : May 2014 Paper

The Bank sold Hong Kong Dollar 1,00,000 spot to its customer at Rs. 7.5681 and covered itself in

London market on the same day, when the exchange rates were

US $1 = HK$ 8.4409 HK $ 8.4500

Local inter‐bank market rates for US$ were:

Spot US$1 = Rs. 62.7128 Rs. 62.9624

Calculate the cover rate and ascertain the profit or loss in the transaction.

Ignore brokerage.

Solution :

The bank (Dealer) covers itself by buying from the market at market selling rate.

Rupee – Dollar selling rate = Rs. 62.9624

Dollar – Hong Kong Dollar = HK $ 8.4409

Rupee – Hong Kong cross rate = Rs. 62.9624/ 8.4409

Cover Rate = Rs. 7.4592

Profit / Loss to the Bank

Amount received from customer (1 lakh × 7.5681) Rs. 7,56,810

Amount paid on cover deal (1 lakh × 7.4592) Rs. 7,45,920

Profit to Bank Rs.10,890

Question 51 : May 2014 Paper

JKL Ltd., an Indian company has an export exposure of JPY 10,000,000 payable August 31, 2014.