Chorafas sovereign debt crisis; the new normal and the newly poor (2011)

292

Transcript of Chorafas sovereign debt crisis; the new normal and the newly poor (2011)

Palgrave Macmillan Studies in Banking and Financial Institutions

Series Editor: Professor Philip Molyneux

The Palgrave Macmillan Studies in Banking and Financial Institutions are international in orientation and include studies of banking within particular countries or regions, and studies of particular themes such as Corporate Banking, Risk Management, Mergers and Acquisitions, etc. The books’ focus is on research and practice, and they include up-to-date and innovative studies on contemporary topics in banking that will have global impact and influence.

Titles include:

Steffen E. AndersenTHE EVOLUTION OF NORDIC FINANCE

Seth ApatiTHE NIGERIAN BANKING SECTOR REFORMSPower and Politics

Vittorio Boscia, Alessandro Carretta and Paola SchwizerCOOPERATIVE BANKING IN EUROPECase Studies

Roberto Bottiglia, Elisabetta Gualandri and Gian Nereo Mazzocco (editors)CONSOLIDATION IN THE EUROPEAN FINANCIAL INDUSTRY

Dimitris N. ChorafasSOVEREIGN DEBT CRISISThe New Normal and the Newly Poor

Dimitris N. ChorafasCAPITALISM WITHOUT CAPITAL

Dimitris N. ChorafasFINANCIAL BOOM AND GLOOMThe Credit and Banking Crisis of 2007–2009 and Beyond

Violaine CousinBANKING IN CHINA

Vincenzo D’Apice and Giovanni FerriFINANCIAL INSTABILITYToolkit for Interpreting Boom and Bust Cycles

Peter Falush and Robert L. Carter OBETHE BRITISH INSURANCE INDUSTRY SINCE 1900The Era of Transformation

Franco FiordelisiMERGERS AND ACQUISITIONS IN EUROPEAN BANKING

Franco Fiordelisi, Philip Molyneux and Daniele Previati (editors)NEW ISSUES IN FINANCIAL AND CREDIT MARKETS

Franco Fiordelisi, Philip Molyneux and Daniele Previati (editors)NEW ISSUES IN FINANCIAL INSTITUTIONS MANAGEMENT

Kim HawtreyAFFORDABLE HOUSING FINANCE

Jill M. HendricksonREGULATION AND INSTABILITY IN US COMMERCIAL BANKINGA History of Crises

9780230298408_01_prexvi.indd i9780230298408_01_prexvi.indd i 5/23/2011 11:23:05 AM5/23/2011 11:23:05 AM

Otto Hieronymi (editor)GLOBALIZATION AND THE REFORM OF THE INTERNATIONAL BANKING AND MONETARY SYSTEM

Sven JanssenBRITISH AND GERMAN BANKING STRATEGIES

Alexandros-Andreas Kyrtsis (editor)FINANCIAL MARKETS AND ORGANIZATIONAL TECHNOLOGIESSystem Architectures, Practices and Risks in the Era of Deregulation

Caterina Lucarelli and Gianni Brighetti (editors)RISK TOLERANCE IN FINANCIAL DECISION MAKING

Roman Matousek (editor)MONEY, BANKING AND FINANCIAL MARKETS IN CENTRAL AND EASTERN EUROPE20 Years of Transition

Imad A. MoosaTHE MYTH OF TOO BIG TO FAIL

Simon Mouatt and Carl Adams (editors)CORPORATE AND SOCIAL TRANSFORMATION OF MONEY AND BANKINGBreaking the Serfdom

Anders Ögren (editor)THE SWEDISH FINANCIAL REVOLUTION

Özlem Olgu EUROPEAN BANKINGEnlargement, Structural Changes and Recent Developments

Ramkishen S. RajanEMERGING ASIAEssays on Crises, Capital Flows, FDI and Exchange Rate

Yasushi SuzukiJAPAN’S FINANCIAL SLUMPCollapse of the Monitoring System under Institutional and Transition Failures

Ruth WandhöferEU PAYMENTS INTEGRATIONThe Tale of SEPA, PSD and Other Milestones Along the Road

The full list of titles available is on the website:www.palgrave.com/finance/sbfi.asp

Palgrave Macmillan Studies in Banking and Financial InstitutionsSeries Standing Order ISBN 978–1–4039–4872–4

You can receive future titles in this series as they are published by placing a standing order. Please contact your bookseller or, in case of diffi culty, write to us at the address below with your name and address, the title of the series and the ISBN quoted above.

Customer Services Department, Macmillan Distribution Ltd, Houndmills, Basingstoke, Hampshire RG21 6XS, England, UK

9780230298408_01_prexvi.indd ii9780230298408_01_prexvi.indd ii 5/23/2011 11:23:05 AM5/23/2011 11:23:05 AM

Sovereign Debt CrisisThe New Normal and the Newly Poor

Dimitris N. Chorafas

9780230298408_01_prexvi.indd iii9780230298408_01_prexvi.indd iii 5/23/2011 11:23:06 AM5/23/2011 11:23:06 AM

© Dimitris N. Chorafas 2011

All rights reserved. No reproduction, copy or transmission of thispublication may be made without written permission.

No portion of this publication may be reproduced, copied or transmittedsave with written permission or in accordance with the provisions of the Copyright, Designs and Patents Act 1988, or under the terms of any licence permitting limited copying issued by the Copyright Licensing Agency, Saffron House, 6–10 Kirby Street, London EC1N 8TS.

Any person who does any unauthorized act in relation to this publicationmay be liable to criminal prosecution and civil claims for damages.

The author has asserted his right to be identified as the author of this work in accordance with the Copyright, Designs and Patents Act 1988.

First published 2011 byPALGRAVE MACMILLAN

Palgrave Macmillan in the UK is an imprint of Macmillan Publishers Limited, registered in England, company number 785998, of Houndmills, Basingstoke, Hampshire RG21 6XS.

Palgrave Macmillan in the US is a division of St Martin’s Press LLC, 175 Fifth Avenue, New York, NY 10010.

Palgrave Macmillan is the global academic imprint of the above companies and has companies and representatives throughout the world.

Palgrave® and Macmillan® are registered trademarks in the United States, the United Kingdom, Europe and other countries.

ISBN 978–0–230–29840–8

This book is printed on paper suitable for recycling and made from fullymanaged and sustained forest sources. Logging, pulping and manufacturing processes are expected to conform to the environmental regulations of the country of origin.

A catalogue record for this book is available from the British Library.

A catalog record for this book is available from the Library of Congress.

10 9 8 7 6 5 4 3 2 120 19 18 17 16 15 14 13 12 11

Printed and bound in Great Britain byCPI Antony Rowe, Chippenham and Eastbourne

9780230298408_01_prexvi.indd iv9780230298408_01_prexvi.indd iv 5/23/2011 11:23:06 AM5/23/2011 11:23:06 AM

A slave is he who cannot speak his thought.

Euripides

9780230298408_01_prexvi.indd v9780230298408_01_prexvi.indd v 5/23/2011 11:23:06 AM5/23/2011 11:23:06 AM

This page intentionally left blank

vii

List of Tables and Figures x

Preface xi

PART I FINANCIAL RISKS WHICH KEPT PILING UP

1 The World’s New Normal Economic System 3 Five forces promoting the next economic landscape 3 Cause and effect 6 The new normal defined 9 A historical precedent: the new normal at the end of World War I 12 Living at the edge of chaos 14 The importance of knowing the ‘normal’ conditions 17

2 The Newly Poor 22 Poor people’s recipe: falling deeper into debt 22 Property-owning democracies versus debt-laden democracies 24 Debt operates like a tax 27 ‘I will be gone/you will be gone’ 29 Runaway public liabilities and the day of reckoning 32 Nobody is in charge of debt policy 35 Wealth in western nations dropped like a bribed boxer 38

3 The Salient Problem is Rights Without Responsibilities 41 The many heads of a debt hydra 41 What is meant by rights without responsibilities? 44 Entitlements 46 Pensions and the new normal 50 The middle classes’ broken dreams 53 What may follow the debt hydra? 56

PART II LOOSE MONETARY AND FISCAL POLICIES LEAD TO THE DESTRUCTION OF WEALTH

4 Japanification 61 Japanification defined 61 Japanification’s after-effect: precarious public finances 64 Money thrown at the problem brings nearer the next big crisis 67 Financial discipline requires more than leadership 70 Governments, central banks and the 2010 Jackson Hole

Symposium 72 Correlation risk: Greece/Bear Stearns and X/Lehman 75

Contents

9780230298408_01_prexvi.indd vii9780230298408_01_prexvi.indd vii 5/23/2011 11:23:06 AM5/23/2011 11:23:06 AM

5 Conventional and Unconventional Weapons in a Central Bank’s Arsenal 79

Souk means both market and chaos 79 Black swans and the need for a new economic theory 82 Price stability and the central bank 84 The wall of liquidity 87 Quantitative easing 90 QE and competitive currency devaluations 92 ‘Bad banks’, the Volcker rule and living wills 94

6 Fiscal Policies, Spending Policies and Conflicting Aims 99 The government takes its money out of its citizens’ pockets 99 The best solution is fiscal consolidation 102 Impact of fiscal policies on the financial system 105 Current account deficits 108 Sovereign debt and its consequences for the banking industry 111 Financial stability is one of democracy’s pillars 114

7 Restructuring Sovereign Balance Sheets 117 Deleveraging 117 Deflationary or inflationary risk? 120 Putting the carriage before the horses 122 Austerity is not that bad, after all 125 Budget cuts and B/S restructuring 128 ‘Long-haired’ ‘solutions’ and monetary illusions 131

PART III EUROLAND’S FINANCIAL INTEGRATION AND SOVEREIGN RISK

8 Woes of Euroland’s Financial Integration 137 Strong core and a weak periphery 137 Financial stability and economic integration 139 One-size-fits-all monetary policies are a dangerous game 142 The aftermath of asymmetries on the euro 145 Is a weak euro or a strong euro the better choice? 148 The message by credit default swaps should not be ignored 151

9 Sovereign Risk: Case Study on Greece 154 The Greek crisis is just the first episode 154 Wall Street helped the big spenders to hide debt 157 Textbook economics have no prescription for the current crisis 160 Events which led to the rescue 162 Going on strike against one’s own interest 165 As with swallows, EU money alone will not bring spring 168

10 Germany, France, Britain, Ireland and ‘Club Med’ 171 The German economy 171 The French economy 175

viii Contents

9780230298408_01_prexvi.indd viii9780230298408_01_prexvi.indd viii 5/23/2011 11:23:06 AM5/23/2011 11:23:06 AM

The British economy 177 The Irish economy 180 Ireland, Iceland, Portugal and the uncle of Dubai 183 Down the Club Med way: Italy and Spain 187

PART IV THE NEW NORMAL’S EFFECT ON THE WESTERN ECONOMY

11 The North Atlantic Similarities are Greater than you Think 193 Tales of the unexpected 193 Big deficits resemble a classic tragedy 196 QE2: poison or cure? 199 What went wrong with monetary policy and the

bank rescues? 201 American middle class and missing employment opportunities 205 The Dodd–Frank Wall Street Reform and Consumer

Protection Act 208

12 The EU’s Banking Industry and its Stress Testing 212 Profile of large and complex banking groups 212 Ultimately economies advance because their

institutions are strong 214 Banks do not know the risks they take with derivatives

and their IT is unhelpful 217 Stress tests permit crossing the river while feeling the stones 221 How different experts evaluated the stress tests by the

Committee of European Banking Supervisors 225 November 2010: four months after the test results

have been released 228

13 The Global Systemic Risk has been Programmed for 2014 232 Not only the economy, but also democracy is at a crossroads 232 The way to global financial stability is uncharted 234 Sovereign risks and contagion effects 237 European banks, American banks and the fight for

long-term funding 241 The former ‘poor’ are better off than the former ‘rich’ 245 Financial seismology and the slow-motion train wreck 248

Epilog 252

Notes 255

Index 269

Contents ix

9780230298408_01_prexvi.indd ix9780230298408_01_prexvi.indd ix 5/23/2011 11:23:06 AM5/23/2011 11:23:06 AM

x

List of Tables and Figures

Tables

8.1 Cost of social contribution to social security as a percentage of salary 145

Figures

1.1 Expected events and unexpected events are characterized by two different distributions 18

10.1 German industrial output rebounded leaving other western countries in the dust 172

12.1 The unbearable truth of a thermonuclear option with derivative financial instruments 220

12.2 The normal distribution is a proxy valid only in connection with low-impact events – the distribution of high-impact events is not normal 223

9780230298408_01_prexvi.indd x9780230298408_01_prexvi.indd x 5/23/2011 11:23:06 AM5/23/2011 11:23:06 AM

xi

Preface

The history of economics and finance is littered with the debris of once-sacred theories. The ‘new economy’, whose promise of wealth and prosper-ity was supposed to be the only possible course, is now in shambles. The belief that theoreticians know so well how to manage the economy that crises are banned forever is another fallen idol. And the hypothesis that leveraging rescues people, companies and states from an existence of limited dimensions proved to be an unmitigated disaster:

This book is about sovereign debt, fiscal deficits, the newly poor and the deceit of the ‘State Supermarket’, with its endowments and cradle-to-grave care. The issues confronting the global economy – and most particularly America, Europe and Japan – are inseparable from the current lack of social and politi-cal leadership as well as of a credible plan to deal with the mountains of debt amassed by sovereigns, households and companies, particularly banks.

The text is written for people who need to know what the problem is with the mountains of public debt, families’ deep indebtedness and finan-cial institutions superleverage. It is not written for economists, analysts and other technicians of the ‘dismal science’, to use John Maynard Keynes’ words. The many practical examples which it includes expose the situation by which western society has cornered itself. Its constructive criticism gives advice on how to come up from under, even if this means slaughtering:

unaffordable endowments, unwarranted government rescues, andother proliferating but unsustainable big-spending projects.

Largely due to weak governance, the United States and European Union fell on parlous days. Public confidence is lost. Breaking trust can be done very quickly; re-establishing it can take a long time. The aim of this book is to provide an adult conversation on the risks of losing sight of past failures and our society’s ability to solve its problems, with debt heading the list.

Nowadays, with all liabilities taken into account, for every $1 of assets there is $4 of debt. It is pure folly to think that such a huge amount of debt will disappear on its own, or even be partially repaid if current policies continue to prevail. Liabilities have the nasty habit of increasing with time, particularly when people and companies have lost their individual initiative and put all their hopes for the future in rescues by leviathan sovereigns.

•••

9780230298408_01_prexvi.indd xi9780230298408_01_prexvi.indd xi 5/23/2011 11:23:06 AM5/23/2011 11:23:06 AM

Western sovereigns are struggling with colossal debt. Peacetime prec-edents are lacking, the difficulties are so great and the debt hydra so fertile that those supposed to know better are approaching the most vital issues in ignorance. Certainty about the right thing to do in this most challenging economic and financial situation is only expressed by people who either dwell in a world of fantasy or do anything that hits their fancy, while the economy around them falls apart.

‘We are living with an unsustainable hangout between our commit-ments and our resources,’ said Timothy Geithner, US Treasury secretary on October 13, 2010 in a Charlie Rose interview broadcast by Bloomberg News. Geithner evidently knows what he is talking about because, together with the Federal Reserve, the Treasury has become the big banks’ safety net and universal fire brigade.

This is by no means a US phenomenon. Signs of distress are easily seen all over the global economic landscape, but most particularly in the western countries. From entitlements to the salvage of bankrupt institutions, the State Supermarket – a creation of infantile leftism – has taken on respon-sibilities which are unaffordable. Critics are right when they say that the biggest deficit the West has is in the fact that there is not enough leadership around, and also those who govern either don’t know how or don’t care to help the common citizen understand what the issues are.

Yet, in a democracy the people have the right to know why the economic and financial conditions are so grim, what has engineered the most recent deterioration and what kind of measures are needed to prune the system and put it on a growth course; also, why the sovereign debt is on an explosive path and what the next act of the drama will be if nothing radical is done to bend the curve. Which leads to three other questions: what lies behind the evolving economic environment known as the ‘new normal’ (Chapter 1) and who are the ‘new poor’ (Chapter 2), and how can this trend be stopped before it becomes irresponsible?

The book the reader has to hand examines these issues and explains why nothing has changed so far – in spite of the deep economic and financial crisis created by big banks through gambling with novel (and little under-stood) novel financial instruments. The gamblers continue their good work; the regulators are timid; and this means that conflicts of interest have not stopped running down the state’s finances.

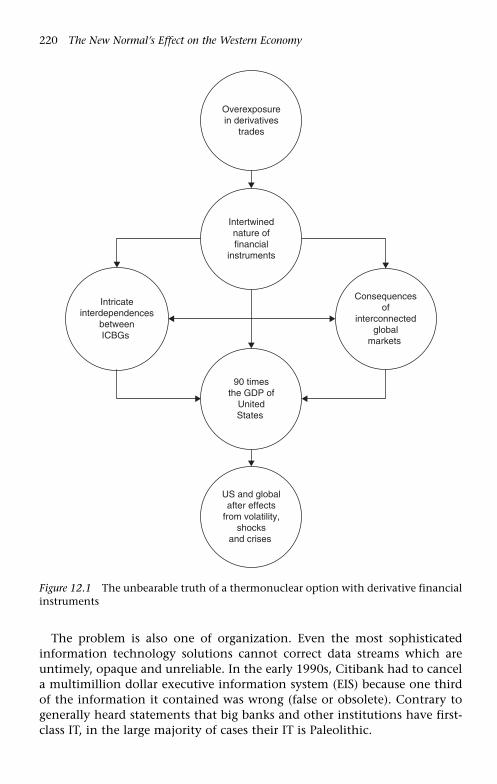

On June 25, 2010 CNBC, the financial network, revealed that derivatives trades by American banks alone stood at 90 times the level of US gross domestic product (GDP). This was no number picked out of a hat. A couple of weeks earlier, a combined estimate of exposure by the US Senate and House of Representatives had put the market valuation of existing deriva-tives contracts at $1.2 quadrillion.

* * *

xii Preface

9780230298408_01_prexvi.indd xii9780230298408_01_prexvi.indd xii 5/23/2011 11:23:06 AM5/23/2011 11:23:06 AM

Unprecedented sovereign debt in peacetime and a quadrillion in derivatives is bad news for the economy of the USA, the EU and the global economy as well. Ultimately economies advance because their institutions are strong. Today they are on the sick list while governments are running after the facts, doing what Montagu Norman, the governor of the Bank of England in the 1920s and 1930s said about the central bank action which preceded the First Great Depression: ‘We collected money from a lot of poor devils and gave it to the four winds.’

As the case of Ireland and of its ‘Anglo-Toxic’ Bank (Anglo-Irish) docu-ments, the mismanagement of credit institutions and poor governance of sovereigns strongly correlate. High risk, descent into the abyss and a fire brigade approach is the course typically taken by the ‘unable’, who have been asked by other incapables to do the unnecessary.

Like the First Great Depression, the economic and financial crisis in which we are living – probably on our way to the Second Great Depression – has not been an act of God. It is the direct outcome of dismal governance by chiefs of state, monetary policy-makers, investment bankers and the com-mon man in the street. In terms of cause and effect, some of the worst deci-sions date back to the 1990s, while others saw the light in the first decade of this century. The people who took these decisions:

were singularly unqualified to be at the helm of great nations and of their central banks, could not decide by themselves on what to do and therefore consulted others who had conflicts of interest, andgiving in to social pressure, they crash-landed the western economies through high leverage and unpayable debt.

Against all logic, large and complex banking groups (LCBGs) have been offered, since late 2008, an unlimited line of credit by sovereigns, at tax-payers’ expense. But the LCBGs’ wounds, due to their high gearing and misdirected decisions, have been so deep that their financial performance did not strengthen. Whatever money they got from central banks they used to bolster their capital rather than lend.

In spite of trillions thrown at the problem, the American, British, euroland and Japanese economies remained anemic. The result of throwing trillions to the four winds was a disaster. Credit is the oxygen of business activity, but sovereigns did not oblige banks that benefited from public money to extend credit. Without credit companies cannot function, and this has become also true of households. If banks cannot or will not lend, then the economy is falling off a cliff.

It is wrong to believe that central banks can continue forever accumulat-ing useless collateral while printing money non-stop. The Federal Reserve, Bank of England and the European Central Bank (ECB) have been doing

•

•

•

Preface xiii

9780230298408_01_prexvi.indd xiii9780230298408_01_prexvi.indd xiii 5/23/2011 11:23:06 AM5/23/2011 11:23:06 AM

so for more than a couple of years, but it cannot become permanent. Mid-November 2010 the ECB indicated that there were limits to the short-term assistance it could give to Ireland’s banks, which account for around a quarter of the total liquidity offered by the ECB to all eurozone banks. The same applies to Portuguese, Spanish and other banks.

Things got out of hand because there is a symbiosis in debt characterizing relations between big banks and sovereigns. This is creating serious risks for the longer-term sustainability of public finances. Together with entitle-ments, it sees to it that efforts associated to the reduction of government debt are half-baked. Tightening the belt has been always unpopular, and politicians think of their re-election when deciding about measures that need to be taken, forgetting that when the crisis becomes longer term tough-ness is required as well as competence, and that the party that deserves to win must craft a narrative and policy that creates opportunity out of disap-pointment and chaos.

* * *

The book divides into four parts. Part I brings to the reader’s attention the financial risks which have been piling up for nearly 30 years, as well as their aftermath. It outlines the succession of errors which has lead to a situation known as the new normal, the economic, financial and social conditions which (by all likelihood) will characterize the next two decades.

The text brings the reader’s attention to the fact that western societies are no more the globe’s wealthy inhabitants. Their overleveraging and poor growth prospects have turned them into new poor, while less developing economies are moving up the ladder at a fast pace – aiming to be the new rich.

Part II provides documentation on the loose monetary and fiscal policies in the West, those followed over too many years on both sides of the North Atlantic. In recent times, such misdirected decisions were first made by Japan in the early 1990s, and they brought the former industrial dynamo to a state of coma. Hence, the term ‘Japanification’, describing where America, Britain and continental Europe are heading.

This thesis is supported by both qualitative and quantitative evidence. It is proper to inform the reader that in using statistics to document statements being made emphasis has been placed on accuracy and not on precision. It has been a deliberate choice to employ only the two or three most significant digits of numbers and ratios (depending on the issue) with emphasis placed on trend and on order of magnitude.

The theme of Part III is case studies in economic failure, starting with euroland’s lack of success in financial integration, as well as its reasons. This is followed by a discussion on what went wrong in the case of Greece. Germany, France, Britain, Ireland and the so-called ‘Club Med’ provide

xiv Preface

9780230298408_01_prexvi.indd xiv9780230298408_01_prexvi.indd xiv 5/23/2011 11:23:07 AM5/23/2011 11:23:07 AM

some other interesting examples on how economies are being managed by sovereigns.

By way of conclusion, Part IV brings to the reader’s attention the new normal’s effect on the western economies – including the one which used to be the most vibrant: the United States. Several financial analysts said that Greece is like Bear Stearns, the investment bank whose failure preceded Lehman Brothers’ bankruptcy. By late November 2010 Ireland became Bear Stearns ‘bis’. In search of a candidate for the Lehman role, some experts mentioned America, while others said Britain.

* * *

What we forget today is to learn lessons from history – economic, financial, political and social. If we don’t understand what has been behind the suc-cesses and failures of our predecessors, then we condemn ourselves to repeat the same mistakes. Decisions leading to misdirected risks are often taken as a result of misquoting and misinterpreting what people of better knowledge have said or done.

John Maynard Keynes, for example, is often used by leftist economists as the patriarch of big-spending policies by the State Supermarket. Apart from the fact that this is less than half true, Keynes had the power to express his opinions without compromises, and he is quoted as having said: ‘When the capital development of a country becomes the byproduct of the activities of a casino, the job is likely to be ill-done.’

* * *

I am indebted to a long list of knowledgeable people, and of organizations, for their contribution to the research which made this book feasible; also to several senior executives and experts for constructive criticism during the preparation of the manuscript. Dr Heinrich Steinmann and Dr Nelson Mohler have been among the most important contributors.

Let me take this opportunity to thank Lisa von Fircks, for suggesting this project, Renee Takken, for seeing it all the way to publication, and Keith Povey and Joy Tucker for editing the manuscript. To Eva-Maria Binder goes the credit for compiling the research results, typing the text, compiling the index and making valuable suggestions.

DIMITRIS N. CHORAFAS Valmer and Entlebuch

Preface xv

9780230298408_01_prexvi.indd xv9780230298408_01_prexvi.indd xv 5/23/2011 11:23:07 AM5/23/2011 11:23:07 AM

This page intentionally left blank

Part IFinancial Risks Which Kept Piling Up

9780230298408_02_cha01.indd 19780230298408_02_cha01.indd 1 5/23/2011 11:45:14 AM5/23/2011 11:45:14 AM

This page intentionally left blank

3

1The World’s New Normal Economic System

Five forces promoting the next economic landscape

In the ‘go-go’ years which followed the 1994 crisis of debt instruments, Alan Greenspan, then chairman of the Federal Reserve, coined the term ‘New Economy’. This he defined as defying the laws of gravity by producing more and more wealth, practically forever. We now know that such talk was a chimera, while the tandem of bubbles it produced in 2000 and 2007 were real. Their origin was not difficult to detect:

a highly accommodating monetary policy,free reign to leverage and other excesses, andscant attention by supervisory authorities paid to watch over systemic risk.

These causes of economic and financial troubles tend to correlate among themselves, amplifying their impact. Therefore, the disaster which followed was not totally unexpected. One of the outstanding consequences of the major global downturn, which started in 2007 and whose effects are still widely seen, has been the enormous increase in government debt in western countries. Spending by sovereigns rose very rapidly to both keep alive big banks and other ‘strategic’ companies, some of which were zombies, and offset the contraction in private sector spending, as millions of households confronted unemployment as well as uncertainty about the future.1

In the USA the public deficit jumped from 2.8 per cent in 2007, first year of the most recent economic and banking crisis, to 11.2 per cent in 2009. In the EU government deficits varied widely: from over 14 per cent in Greece to a little less than that in Ireland, 11 per cent in Britain, 9 per cent in France and 6 per cent in Germany. The big spenders at the governments’ ivory towers have had a ball – and that’s anathema to public confidence.

•••

9780230298408_02_cha01.indd 39780230298408_02_cha01.indd 3 5/23/2011 11:45:14 AM5/23/2011 11:45:14 AM

4 Financial Risks Which Kept Piling Up

As Demosthenes, the ancient Greek orator, said: Business is built on confidence. Any waning of it, particularly at the time economic fortunes seem to start timidly rising, is counterproductive. Consumer confidence is crucial to western economies as it represents up to 70 per cent of spending; a figure amplified by industrial production which nearly always cruises along. ‘The real devils today are the states not the bankers,’ says Dr Heinrich Steinmann, a former vice chairman of UBS.

Scared of the long-lasting effect on the economy of these deep red numbers, by the second quarter of 2010 several western governments – including Britain, France, Germany, Italy, Spain and Greece but not the USA – announced rather significant austerity measures to reign in their dete-riorating fiscal situation. This led some economists to express concern that an austerity policy amid an ongoing recession will make matters worse, warning how fragile the early signs of an upturn still are (see also Chapters 5 and 7).

Other economists, however, have taken precisely the opposite stand, pointing out that the unprecedented 2008–11 economic easing – which went in full swing with the Lehman Brothers’ bankruptcy and near bankruptcies of AIG, Fannie Mae, Freddie Mac – has turned western economic history on its head by creating an unsustainable flood of money (see Chapter 4 on the many heads of the debt hydra). These economists also emphasized that business confidence will wane if the market sees no signs of restraint in keeping the printing presses busy.

While the two aforementioned economic theories are diametrically opposed to one another, they also share the same basic weakness. No economist, on either side of this gulf of opinions, has come up with a clear and well- documented definition of the cause and effect that characterized the ongoing crisis (see the next section). Which is the primary cause? Is the salient issue:

1. the accumulated huge amount of debt per se?2. or, is debt the consequence of the current structure of world finance and

its institutions?3. or, is the structure of world finance the consequence of entitlements and

globalization, and therefore of unsustainable policies?4. or, is it the classically poor regulation at government levels, which allows

greed and irrationality to carry the day?5. or, are these reasons closely intertwined, and therefore acting on one of

them affects all the others with dismal results?

In my opinion, the most likely fundamental reason for the current malaise is the fifth alternative which integrates all others, making both the problem and any serious approach to its solution tremendously complex. Yet, our efforts must be focused. Searching for a holistic approach which simultaneously attacks every cause will be like trying to unscramble scrambled eggs.

9780230298408_02_cha01.indd 49780230298408_02_cha01.indd 4 5/23/2011 11:45:14 AM5/23/2011 11:45:14 AM

The World’s New Normal Economic System 5

We might, but only might, have a better chance by establishing priorities and subsequently attacking these causes indidually – provided we don’t lose sight of the total picture, or forget the underlying interdependencies among the causes of the current state of world affairs and their effects (see below). In addition, to untie the threads of this knot we would need to use practica-ble rules like those we employ to organize our lives, promote our businesses and confront our obligations.

Talking of priorities, the overriding obligation at this moment is to control the exploding debt at all levels of society. And because it is famously hard to govern debt, this is going to be the issue to which the present book addresses itself. It is not normal that every $1 in production corresponds to $4 in debt. Such an ‘unstoppable’ debt inflation has to stop before it becomes irreversible.

But the other causes should not be forgotten. Looking at them in reverse order to that presented in the preceding list, there has been, indeed, a huge amount of greed which amplified the economic and financial debacle of 2007 and the ensuing years significantly. In a Charlie Rose interview broad-cast by Bloomberg News on April 26, 2010, Michael Lewis, the author, put the blame on both the market players and the instruments they have been using, stating that:

Real corruption is behind new financial instrument design.This problem is widespread; Goldman Sachs cannot be the only bank which designs debt-based securities aimed to fail.All sorts of tricks embedded in instruments have been accompanied by misrepresentation to clients – which under current laws is illegal.

Regarding the structure of international finance and its contribution to the crisis we have been going through, its reorganization and control was thought to be the mission of the G-20 heads of state. But international tour-ism aside, the G-20 meetings have so far been met with no real success and it is a deliberate decision not to dwell on their remit in this book.

Allow me also to add that, as if to make matters worse, within each jurisdiction the prospects for a significant and deep-rooted regulatory initiative are not good. The slimmed-down Dodd-Frank Act in the USA is a lightweight (see Chapter 12). In his deposition to Congress, Paul Volcker, the respected former chairman of the Federal Reserve, insisted that the essential flaw in regulatory proposals and measures being adopted is that they leave the structure of banking unchanged. This is a pity, because if culture and structure remain the same, then so does the ultimate systemic risk.

Risk-taking is a basic ingredient of progress but it must be matched by risk control. Watching one’s exposure is not an option; it is a requirement of sound governance of a person’s, company’s or state’s fortunes – while

••

•

9780230298408_02_cha01.indd 59780230298408_02_cha01.indd 5 5/23/2011 11:45:14 AM5/23/2011 11:45:14 AM

6 Financial Risks Which Kept Piling Up

paternalism towards the homegrown banking industry is a most serious error.

Cause and effect

Virgil, the Roman poet, said: ‘You must know the causes, to draw the right conclusions.’ What are the causes of the crisis we are going through in 2007–11? The answers most often heard in my research have been lax lend-ing practices, the real estate bubble and subprime mortgages. While these have been, indeed, important factors, they were the triggers of the debacle rather than fundamental reasons. The real causes are:

massive increase in debt, at all levels of society,excessive risk appetite, amplified by exposures risk-takers don’t under-stand,a shadow banking system, with its dubious debt instruments, still fund-ing risks,limitations of financial engineering and serious mistakes in model-based estimates, andtotally substandard risk management at all levels, totally inappropriate in a world where derivatives are the most popular and lucrative trading instrument.2

Largely engineered through leverage, and therefore by ‘funny money’, this massive increase in debt has become a western culture. By no means a random event, it is the culture of ‘borrow now, pay later (maybe)’ which pervades all levels of western society – and which must now change to: save now, so as not to starve later on, for an improvement in fortunes of peo-ples and states. There have been many false prophets who prompted public spending through misplaced statements, and helped in creating this attitude to spending.

‘The future appears brilliant,’ wrote Thomas Lamont of JPMorgan a short while prior to the ‘Black Tuesday’ of late October 1929, moreover assuring that ‘air holes’ due to a ‘technical condition’ had developed in the market but that the situation was ‘susceptible to betterment’.3 With hindsight we do know what followed in the decade after the First Great Depression.

Clear minds expressed the opposite opinion. ‘We have involved our-selves in a colossal muddle, having blundered in the control of a delicate machine, the working of which we do not understand,’ John Maynard Keynes wrote in December 1930 in his article ‘The Great Slump of 1930’. The same words can be used today without changing a syllable in regard to what the Federal Reserve, Bank of England and (to a slightly lesser extent) European Central Bank have done to the western economies in the 2008–11 timeframe.

••

•

•

•

9780230298408_02_cha01.indd 69780230298408_02_cha01.indd 6 5/23/2011 11:45:15 AM5/23/2011 11:45:15 AM

The World’s New Normal Economic System 7

Other warnings, too, were unheeded and relegated to the wastebasket of economic history, even if they came from people who could see further than most. Friedrich Engels (1820–1895) – whose work and foresight extended beyond economics – identified in the mid-nineteenth century certain social happenings that lead to a dismal future:

people tending to live beyond their means,4 rapid urbanization under stressful conditions, andshort-term policies of governments, adopted because of their lack of cour-age to lead in shaping society’s future.

Engels wrote, in 1844, that the centralization of the population in great cities (the cause) exercises of itself an unfavorable influence (the effect): ‘All putrefying vegetable and animal substances give off gases decidedly injurious to health, and if these gases have no free way of escape, they inevitably poison the atmosphere.’5

Urban dwellings in crowded cities, which are rapidly replacing rural life for large chunks of the world’s population, may range from palaces to shanty towns, but what they have in common is the strained way of life – full of uncertainty and anguish. This is the new normal, in social terms, and Engels described it in a prophetic way nearly 17 decades ago. (The definition of the new normal in terms of the economy is given in the next section.)

In cause and effect, there are similarities between the social and economic definitions. The way people live and work (the cause) has a great deal to do with economic after-effects because – from autos and house appliances to exotic vacations – the twenty-first century’s proletarians have been enjoying an increasing standard of living paid through debt. The mountains of leverage were supposed to be taken care of by the ‘future generations’ but, as the deep crisis of 2007–11 has shown, they have already become unsupportable and unsustainable by this generation.

The easy way for politicians is to promise what they know they cannot deliver and make the people pay for it. George W. Bush came to office in 2001 and engineered the largest ever US peacetime deficit (the cause) – promising security and plenty of other goodies in exchange. In terms of security the effect has been practically nil. Instead, what the American peo-ple got is another layer of bureaucracy in Washington and an explosion of public deficit.

Barack Obama compounded all of the Bush mistakes. Among them, the two conceivably worst presidents in the history of the American Republic brought another calamity which will haunt the USA in the coming decades: the new poor (Chapter 2).

For reasons quite similar to one another, two megarisk events are likely to compete with one another during the coming years. One is that the economy implodes as sovereigns, companies and families restructure their

•••

9780230298408_02_cha01.indd 79780230298408_02_cha01.indd 7 5/23/2011 11:45:15 AM5/23/2011 11:45:15 AM

8 Financial Risks Which Kept Piling Up

balance sheets. The other megarisk is that the economy explodes as debt reaches for the stars. (Both the reasons and the consequences will be brought into perspective in the last chapter of this book.)

A preview of events to come would see the specter of horribly indebted countries which scare the hell out of their partners. For all the brave talk about solidarity among euroland’s member states, their taxpayers don’t wish to put on the table the money which might keep their badly behaved and undisciplined neighbors afloat. Not without reason, they believe that this is not their cause and that the nations which misbehaved should pay for the effects by themselves.

This has been behind an overwhelming 69 to two vote by the Slovakian parliament, in the week of August 8, 2010. A crashing majority of Slovak deputies rejected taking part in a European Union aid package for the trou-bled Greek economy (Chapter 9) – and they had good reasons not to care if both the Brussels-based European Commission and the German government criticized the Slovak parliament’s decision.

‘All member states committed themselves politically to assistance for Greece,’ said a spokesman for Chancellor Angela Merkel. ‘Every member relies on solidarity; solidarity is no one-way street.’6 That’s true, but the prerequisite to solidarity is self-discipline.

The Slovaks, who said they would not pay for other peoples’ ‘twenty-first-century lifestyle’, know that their country has a gross domestic product (GDP) per capita of $21,200 at purchasing power parity (PPP), while Greece has a per capita GDP of $32,000 – nearly one and a half times greater. Slovak taxpayers have been asked to put a4.4 billion on the table ($5.9 billion) for something they say was not their fault. Moreover:

Slovakia embarked on a bout of painful economic reforms in 1998, that transformed it into one of the EU’s top economic performers.By contrast, Greece, Spain, Portugal and other EU countries piled new debt over old debt, rather than taking the tough decisions necessary to restructure their economy and labor market.

This cause and effect, the most significant cross-border difference in economic management, is another way of showing that the accumulated huge amount of debt is, per se, a real and present danger. The recent crisis made it highly visible, and one cannot blame those people who don’t wish to pay for other peoples’ mistakes, even if they belong to the same community.

The bigger countries in euroland had additional reasons for those of Slovakia, when they decided to salvage Greece.7 In fact, for these reasons, in June 2010 they put together a war chest of a750 billion (about $1 trillion), enhanced by a unique supply of liquidity from the ECB and aimed at arrest-ing the Damoclean sword of a reignited financial crisis.

•

•

9780230298408_02_cha01.indd 89780230298408_02_cha01.indd 8 5/23/2011 11:45:15 AM5/23/2011 11:45:15 AM

The World’s New Normal Economic System 9

But, in the EU and the USA, the issue of too many entitlements having been granted without proper study of their effects is still dominant (Chapter 3). What speculators now do is to accumulate liquidity and bide their time. With Greece’s financial crisis, they shook the euro and were ready to attack, first, euroland’s financial system and, next, that of the glo-bal economy – if Greece had gone broke. While they are waiting, powerful forces are shaping the economy’s new normal.

The new normal defined

Two people are at the origin of the term ‘new normal’: Mohamed El-Erian, Pimco’s8 CEO, and Bill Gross, its chief investment officer (CIO). According to their judgment, while the markets may rise from their current depth, the next five years will not resemble those preceding the crisis. Some of the changes brought by the financial earthquake we have been through may be reversed, but not all. For the world economy, the ‘normal’ situation will be different than that we knew prior to this crisis.

In the way El-Erian defines the future landscape, growth will be subdued, unemployment will remain high and the banking system will be a shadow of its former self (more on this later). As for securitization markets, which buy and sell marketable bundles of debt, they will most likely be the shadow of a shadow – while the stock of physical capital will erode.

Another of the worries associated with the new business landscape (according to this brief definition) is that state capitalism may become the name of the game, with free enterprise in the decline. In addition, as the financial system remains weak, its role of intermediation will wane, while the cost of capital will rise. Consequently, companies will use less of it per unit of output (the cause), resulting in a lower ceiling on production, as well as lower expected returns and higher implied volatility.

Pimco is by no means alone in this projection on the after-effects of the deep economic and financial crisis which, in a way, resembles the First Great Depression of 1929–33. Plenty of other experts say that, in their opinion, we are set for a long period of slow growth, as a number of global imbalances are worked through. That process will take time.

Higher taxation will, in all likelihood, be the rule as governments (rather unsuccessfully) try to restructure their balance sheets. But taxation will also have an alter ego: austerity measures (Chapter 7), accompanied by an increasingly deeper re-evaluation and downsizing of all sorts of entitlements (Chapter 3).

Business will be confronted by loss of power because its classical recovery drivers will no longer function the way they previously have. As for the helping hand of central banks and governments, they will lack money for extravagances like quantitative easing (Chapter 5) and stimuluses. Equities will suffer because they are prospering in risk-on events, and (save for speculators)

9780230298408_02_cha01.indd 99780230298408_02_cha01.indd 9 5/23/2011 11:45:15 AM5/23/2011 11:45:15 AM

10 Financial Risks Which Kept Piling Up

the new economic climate will be largely risk-off. To confront this novel set of challenges, investors will, most likely, place a much greater emphasis on:

diversification of assets, in the real sense of the term,directed cash flows, cross-border and within markets, andshifts in credit risks expressed by spread positions in corporate and sovereign debt, with the latter weaker than the former.

According to expert opinion, another characteristic of the new normal will be that sovereign risk will attract as much attention as that of banks, which have been known for decades to overleverage themselves and gamble with derivative financial instruments. The way a news item on CNBC had it on July 23, 2010, a strong correlation exists between credit default swaps (CDSs) of banks and sovereigns.

To be taken seriously in their effort to change course from high leverage to dependable balance sheets, sovereigns will have to come up with firm plans for a turnaround, not just with words and intentions. Their quality of governance will be judged by whether the action being taken is convincing, and by how effective it proves to be in reducing the country’s huge public debt and current account deficits (Chapter 6).

These are, indeed, tall orders, and success is by no means a foregone conclusion since precise longer-term plans are missing. For instance, in the opinion of British political analysts the ‘fiscal responsibility bill’ in the 2010 Queen’s Speech was a headline, not a plan. Yet, with the new normal it matters greatly that governments set clear, more longer-term objectives, have financial credibility and have the know-how to implement the plans they make.

The same is true of central banks, which, by and large, are lacking a longer-term monetary and interest rates policy, which (in the majority of cases) is part of their charter. Nearly zero interest rates have been a short-term game plan, before becoming a long-term drift (Chapter 5). Made to serve the self-harmed big banks, they penalized the common citizen. For the weaker members of society this has been a triple whammy:

the interest households get for their savings is below inflation; hence their capital wanes, small as it might be,their private pension plans find near zero interest rates as an excuse to speculate, since they earn nothing from money in the bank, andthe way to bet is that taxpayers, the common people, will eventually be asked to foot another king-size bill, while near zero interest rates feed the next bubble.

As we will see in greater detail in Part II, the hidden costs of very low interest rates may well be greater than their visible benefits. Authorities with a long

•••

•

•

•

9780230298408_02_cha01.indd 109780230298408_02_cha01.indd 10 5/23/2011 11:45:15 AM5/23/2011 11:45:15 AM

The World’s New Normal Economic System 11

tradition of speaking their minds say so. In its 2009 Annual Report, the Bank for International Settlements (BIS, the central bank for central banks) brings to attention plenty of ills connected with the too-low interest rates prevail-ing in western countries:

excessive risk taking,lop-sided balance sheets,creation of delays in cleaning out bad debts,surges in global cash flows which are destabilizing, anddistorted allocation of capital, as well as of the labor force.

These are among the reasons propelling the new normal. The question is: When will its day really come? Current thought is that with the forthcoming new big bubble (Chapter 13), which for any practical purpose has been already programmed, the post-World War II party of greater and greater leverage will be over. As for the new economic situation, it will be characterized by what Ben Bernanke called an ‘unusually uncertain’ economy.9 There is no point in denying that the western economy is weak and its players are uncertain about the future, because the measures taken so far have been poorly studied in terms of after-effects and the jury is still out on whether they made eco-nomic sense, even if unexpected consequences are not accounted for.

What is more or less sure is the stress these measures inflicted on the economy, and the hits suffered by common people and businesses alike. We all know that unstoppable leverage and speculation cannot last forever, but the medicine of trying to lower the huge indebtedness of the banking industry by creating mountains of debt at sovereign level may be worse than the disease.

In the eye of the storm are the very expensive but ineffective stimuli and quantitative easing gimmicks (Chapter 5), respectively engineered by gov-ernments and central banks. Some economists involve Ricardian10 equiva-lence in trying to explain why the US economy does not take off in spite of the stimuluses. This arises when:

consumers are forward-looking and save the proceeds from a debt-financed fiscal stimulus, andthey are doing so in anticipation of future tax increases needed to repay the extra government debt.

Plenty of factors impact on how the economy and its players react to meas-ures taken by governments and central banks. Costs head the list. The IMF’s World Economic Outlook counted the cost of 88 banking crises over the past 40 years. On average, seven years after a bust, an economy’s level of output has been almost 10 per cent lower than the level it would have attained without the crisis; that’s a big gap. If replicated in the years to come, this 10 per cent difference would: make the public debt harder to sustain, offer little hope for

•••••

•

•

9780230298408_02_cha01.indd 119780230298408_02_cha01.indd 11 5/23/2011 11:45:15 AM5/23/2011 11:45:15 AM

12 Financial Risks Which Kept Piling Up

higher unemployment, diminish the fortunes of those in work and create conditions leading to further financial breakdown.

Even when the economy begins to expand, it may not regain the same pace as before, therefore eroding national income. In conclusion, the new normal shapes up as the antimatter of the go-go environment of the 1990s and earlier years of this century. Apart from the astronomical leverage found at all levels of western society, the wounds created by huge financial losses require a rela-tively long period in which to heal; healing is not doable at short notice.

A historical precedent: the new normal at the end of World War I

Mayer Amschel Rothschild (1744–1812) is rumored to have said: ‘Let me issue and control a nation’s money and I care not who writes the laws.’ The dictum fits hand in glove with the statutes and policies of central banks. By keeping the printing presses busy and spending money in quite inordinate amounts as compared with a nation’s productive capacity, they can destabi-lize the currency, penalize businesses and households and, eventually, lead to the collapse of both the currency and the banking system.

The creation of the Federal Reserve at end of the first decade of the twenti-eth century and the subsequent independence given to many central banks after World War II (the Bank of England got its independence under Tony Blair and Gordon Brown) were heralded as the start of a new epoch. Developing countries were advised by westerners to do the same – but this ‘ independence’ proved to be fata morgana, as subsequent events demonstrated.

Near zero interest rates and quantitative easing were moves by politically-minded people, in step with their governments. They were not acts by inde-pendent central bankers, whose No. 1 mission is monetary policy sustaining financial stability. This has been a very dangerous deviation from primary duties, and there is no better example of cause and effect than the collapse of the British, French and German economies after World War I. (This also applied following World War II, but the former example is the better.)

The World War I lesson sets the precedent for what currently happens with the mismanagement of monetary policy as well as currencies, and it is also very instructive because, among other events, it includes the run on the French franc and hyperinflation in Germany. Another interesting incident of that epoch was the rift between the United States and Britain, due to the controversy over repayment of wartime loans.

One of the outstanding similarities between 1918–23 and 2007–11 is that both politicians and monetary policy leaders were running out of ideas on what to do with a mammoth debt; and they were in total disagreement about who, in the last analysis, should pay what to whom.11 They were also in a bind because they could understand that unsolved debt problems would destabilize currencies, lead to bank panics and create other serious financial problems.

9780230298408_02_cha01.indd 129780230298408_02_cha01.indd 12 5/23/2011 11:45:15 AM5/23/2011 11:45:15 AM

The World’s New Normal Economic System 13

‘Victory’ at the end of World War I was an illusion, since millions of soldiers and civilians had died for nothing, while economic disaster spread all over Europe. As for the international financial system – which, prior to 1914, had brought prosperity to all the combatant nations, it was in a sham-bles. The unraveling had started with the panic liquidation of securities in London, on July 30, 1914, while stock exchanges in Berlin, Vienna and St Petersburg were closed by the authorities. The first days after the Great War saw the first glimpses of what was then a new normal.

Another similarity between ‘then’ and ‘now’ is that chiefs of state, includ-ing the central European royals, who in the early part of the twentieth century ran the political show, had shown a curious incapacity to distinguish between what they called a punitive action (against Serbia for the Sarajevo murders) and setting the world on fire. Subsequently, historians found it difficult to understand what World War I was all about and who really pushed whom into that gigantic hecatomb.

By the end of World War I, the spotlight fell on economists, bankers and other financial experts who proved unable to put straight the ‘IOUs’ signed by the British, French and Imperial Russian governments among themselves and (in the case of Britain and France), with the United States. Both prior to America’s entry into the war and during its intervention, the USA had acted as banker and armaments factory for the Allies. During World War I, the British government spent the equivalent of $43 billion, including $11 billion, in loans principally to France and Russia (but also to 15 other countries).

In counterpart, it owed the United States $5 billion, which took a long time to negotiate and settle after the war ended. The deal was struck in 1923 by the then British finance minister, against the advice of John Maynard Keynes – who said it was better to hold out for better terms since time worked in the debtor’s favor. London paid Washington 80 cents to the dollar. For their part, the French chose to wait and by so doing they proved Keynes was right. In 1926, they settled their American loans at 40 cents to the dollar.12

Three years later, the Italians settled their war loans by paying a mere 24 cents to the dollar, a better term than Argentina imposed on its debtors with its December 2001 (unjustified) bankruptcy. Of course, it is not only the loans which generated the condition for the economic and financial new normal in the first quarter of the twentieth century. The money the Bank of England and Banque de France printed during the war overwhelmed the mar-kets, distorted financial stability and had a strong negative effect on prices.

In Britain the currency in circulation doubled, and prices made the same jump.In France it tripled, and prices also increased by 300 per cent.In Germany it quadrupled, and so did the prices initially,13 thereafter leading to hyperinflation.

•

••

9780230298408_02_cha01.indd 139780230298408_02_cha01.indd 13 5/23/2011 11:45:15 AM5/23/2011 11:45:15 AM

14 Financial Risks Which Kept Piling Up

That’s a lesson central bankers (particularly Bernanke and King) have forgotten. While the currency in circulation in all European countries rose by leaps and bounds during the fights, the end of the war changed none of the politicians’ bad habits. No government altered the wrong policy of throwing money at the problem. Instead, that unwise practice accelerated.

In Germany, throughout 1919, the monetary base rose by 50 per cent, and in 1920 by another 60 per cent. The Reichsbank warned that the volume of short-term debt was a dangerous threat, but it still kept the presses running. Germany faced, among other financial challenges, the huge and illogical reparations demanded by World War I victors, which were way beyond the ability of its ruined economy to pay, even if stretched over many years. In 1921, the German government made the first reparations payment by sell-ing marks for dollars, and this transaction contributed to a sharp decline in the mark’s value, while at home social unrest and strikes worsened.

Politicians, economists and central bankers are often fooled by the fact that the debt hydra takes some time to raise its heads. In 1921, money in circulation in the German republic rose by the ‘usual’ 50 per cent to 120 billion marks, but in 1922 the situation significantly worsened. With paper money being printed round the clock, inflation ran at 1300 per cent. The following year, 1923, was one of despair with newly minted Reichsmark flooding the market, as well as the mark’s decline against the dollar continu-ing relentlessly.

By mid-1923, the Reichsbank was throwing cash at the market at the rate of 60 trillion marks per day, much of it in big denominations. By November 1923, the currency in circulation was heading for an astronomical 400,000,000 trillion. Something significant had, however, changed. The Reichsbank had a new boss, Hjalmar Schacht, who was a no-nonsense banker.

With hyperinflation still carrying the day, on November 20, 1923 a new currency was introduced, the Rentenmark, to replace the old imperial Reichsmark. The conversion rate to the new currency was set at one tril-lionth of a mark;14 at that time the exchange rate of the old currency to the dollar had hit 4.2 trillion, which made the rate of the Rentenmark to the dollar 4.2. This was the ratio prevailing before World War I between the German and American currencies.15

This 4.2 exchange rate was fine-tuned to affect the market’s psychology, but in itself the change of currency would have been pure cosmetics without fiscal discipline. Schacht, the Reichsbank’s new president, insisted that the only way to financial salvation was through balanced budgets. It was true then; it is true now.

Living at the edge of chaos

The new normal which characterized post-World War I Europe did not affect only economics and finance. It also meant the disappearance of the

9780230298408_02_cha01.indd 149780230298408_02_cha01.indd 14 5/23/2011 11:45:15 AM5/23/2011 11:45:15 AM

The World’s New Normal Economic System 15

old social order, a fact which preceded the major upheaval of populations and economies because, for any practical purpose, a new normal con-stitutes a major inflection point. This change started during the World War I years and continued unabated.16 Then, as now, governments were not really in charge; they just drifted. Or, alternatively, the challenges they were confronted with overwhelmed the second raters who were in charge.

Yet, everyone knew that it would not be possible to turn back the clock. People and organizations, including government bureaucracies, had to adapt to the new conditions. Not the least among them was the need to gain citizens’ confidence by bringing all economic and financial excesses under control. They failed in that mission then, as they fail in that mission now.

What happened in 1923 in economic, financial and social terms is so interesting because of its striking similarities to what has taken place in recent years. In the early 1920s in Germany, tax revenues accounted for no more than 10 per cent of government expenditure. The difference was covered by deficit financing.

As far as western sovereigns are concerned, this 90 per cent deficit is not the case today,17 but even persistent deficits of 10 per cent or more can reek havoc. Interviewed on August 18, 2010 by Bloomberg News, an American economist said that much when he commented that a US Treasury bubble is building up rapidly. One of the examples he gave was that the Obama Administration’s $1.4 trillion deficit in 2010, which is over 10 per cent of US GDP (see also Chapter 12), may be the last drop which makes the glass overflow.

Western economists must also cope with the continuing high leveraging of the banking industry. Unprecedented increases in the use of structured instruments and securitizations, across the globe but most particularly in the USA, have been a seemingly unstoppable trend, with the trading of credit risk at its core. The tool is credit derivatives, which initially sup-plemented then overtook traditional forms of transferring credit risk, like syndication of loans. Lust and greed aside, factors which contributed to this development include the globalization of financial markets and information technology, especially networks and pricing models.

These developments produced significant changes in the financial struc-ture of western countries and in the role of banks therein, but they also had a major effect on sovereign debt. The changed role of banks developed from originating and holding to originating, repackaging and selling, thereby altering loan dynamics.

The impact on sovereigns can be briefly described as the alchemy of their budgets, enacted by hiding the effect of ever-greater public deficits. As the ‘help’ Goldman Sachs gave to different governments (the Greek among them) demonstrates, the use of novel derivative instruments produced a

9780230298408_02_cha01.indd 159780230298408_02_cha01.indd 15 5/23/2011 11:45:15 AM5/23/2011 11:45:15 AM

16 Financial Risks Which Kept Piling Up

mystical transformation of state debt, much of it highly shaky, yet good enough for a prolonged denial of a red ink torrent.

The 80th Annual Report by the Bank for International Settlements put this issue from a different perspective when it stated that: ‘By the end of 2011, public debt/GDP ratios in industrial countries are projected to be on average about 30 percentage points higher than in 2007 – a rise of about two fifths. But the increase for countries that have been hit particularly hard by the crisis will be even greater.’ The United States, Britain, Ireland, Greece, Portugal and Spain are evident examples.

Worst of all is the fact that the rapid increase in public debt in the wake of the 2007–11 economic and banking crisis is unlikely to be halted within the near future. As was the case after World War I (as well as after World War II), sharp declines in tax revenues will be used as an excuse for more deficit financing. In addition, nowadays sovereigns cover their lack of financial discipline behind expenditures such as income support and other entitle-ments (Chapter 3).

It is most instructive to note that, with the possible exception of the United States, fairly similar conditions of lack of fiscal discipline prevailed in the early 1920s for all former belligerents. If anyone thinks that hyperinflation befell Germany because it had lost the war, then he or she is fairly misguided. Neighboring France won the war but, in the early to mid-1920s, its currency was just as much the plaything of speculators and its recovery of economic wellbeing was just as tedious as Germany’s.

As 1923 was coming to a close, a very short time after the German mark had turned to dust, the value of the French franc fell by about 50 per cent against the dollar. In January 1924, the French Ministry of Finance asked for expert advice on how to redress the situation and salvage the franc. Frank Altschul, the principal of Lazard Brothers New York office, came to Paris at the French government’s request.

One of Altschul’s strengths was thinking out of the box. He proposed to the French government what he called an ‘experiment,’18 which essentially was a way of teaching speculators a lesson – something missing today from the toolkit of sovereigns and central bankers. ‘This would involve arranging credits for the government in the United States and perhaps England, in round amounts,’ he told the French.19

The new loan of $100 million (big money at the time) was provided by the Morgan Bank, which evidently required appropriate guarantees. (At that point the French had not yet repaid their World War I loans to the USA.) Morgan was going to lend money to a government which, five years after World War I had ended was still borrowing $1 billion a year to close its budgetary holes. The conditions for the loan included:

reduction of expenditures,abstaining from asking for new loans,

••

9780230298408_02_cha01.indd 169780230298408_02_cha01.indd 16 5/23/2011 11:45:15 AM5/23/2011 11:45:15 AM

The World’s New Normal Economic System 17

concrete steps to balance the budget of the republic, anda rumored secret clause that the French government bound itself to accepting whatever plan the Dawes Commission came up with.20

The members of the Dawes Commission were no novices.21 They were well aware that a large part of the projected fiscal deficit in the 1924–5 timeframe was likely to persist even in the event of recovery in output. The financial crisis had permanently reduced the level of future potential output for Britain, France, Germany, Italy and other countries, and therefore the tax base. Sound familiar?

In spite of these negatives, Altschul’s trick worked. By taking on the speculators with the $100 million war chest, the French government bid the franc from nearly 30 to 18 to the dollar in a couple of weeks. (The salvage of the French franc was, however, temporary. Three years later, in 1926, the franc fell to a new low, then fluctuated while the Banque de France intervened to hold it at 25 to the dollar; an exchange rate which favored French industry.)

Up to a point, but only up to a point, this was the road taken in 2010 by euroland and the IMF to salvage Greece from bankruptcy. If Greece had had the drachma and not the euro as a currency, it is quite likely that its value would have been halved against the dollar (Markezinis, the then finance minister, did just that in 1953). But with the euro, the country could not devalue. In other words, its financial problems significantly weakened the euro against the dollar, and it had to pay over 9 per cent for short-term loans, 600 base points more than loans by Germany.

Greece does not seem to have comprehended that, in the decision- making process of nations, forthcoming ‘battles’ will not be fought by tanks and super-sonic jets but by financial instruments. This will be a permanent feature – the outcome being decided by financial staying power. Overindebted nations, and this reference includes the United States and Britain, would do well to notice that there is nothing new in the message conveyed by the preceding sentences. (In the early eighteenth century, Louis XIV had said that the last Louis (the golden sovereign) wins the war – in other words, he who has the financial staying power.)

In conclusion, massively printed money represents unsupportable govern-ment leverage, and therefore debt, which unsettles investors and makes them run for their money. It was not for nothing that, in the 1920s, Hjalmar Schacht believed the real problem in post-World War I Europe (not just in Germany) was the prevalence of government debt – and this was bound to lead to a general European bankruptcy. It was true in 1920s and it is true today, with the differ-ence that, in the coming years, general bankruptcy might be truly global.

The importance of knowing the ‘normal’ conditions

Let’s start with statisticians. They love the normal curve of events and meas-urements because it reflects the degree of calculability of an event occurring.

••

9780230298408_02_cha01.indd 179780230298408_02_cha01.indd 17 5/23/2011 11:45:16 AM5/23/2011 11:45:16 AM

18 Financial Risks Which Kept Piling Up

Besides that, there exist excellent statistical tests and tables based on normal distribution. The nasty fact is that many distributions of real-life events are not normal. Some are skew, others have long legs – and the further a meas-urement falls from the bell-shaped curve, the higher is the degree of com-plexity of the problem, its interconnections and its aftermath. The so-called ‘normal’ situation is easily calculable and presents a simple structure. But, as Figure 1.1 shows, outliers alter these conditions and harbor great challenges, not the least being that they involve too many unknowns.

As far as the ‘not normal’ distribution of events is concerned, a major contribution has been made by Benoit Mandelbrot, a mathematician, who developed the fractals theory – which has interesting applications in economics. Mandelbrot believed that the market behavior of financial movements has fractal forms.22 It does not follow the familiar bell shape of the normal distribution. Therefore, trading practices and financial models based on the assumption of a normal distribution are fundamentally wrong. The 2007–11 economic and financial earthquake proved that Mandelbrot was right. Plenty of models were written by people who were good at mathematics but knew little or nothing about finance, and the economy was turned on its head. Banks using these models paid dearly for this error.

The misconception derives from the fact that typically, though by no means always, the distribution of measurements associated with events which are ‘normal’ and understood tends to approximate the bell-shaped curve. By contrast, with skew, leptokyrtotic, long-legged, fractal and other

Expected events based on known conditions

Unexpected events involving too many unknowns

Fre

quen

cy

Long legof distribution

A distribution approximatingthe normal curve

Figure 1.1 Expected events and unexpected events are characterized by two different distributions

9780230298408_02_cha01.indd 189780230298408_02_cha01.indd 18 5/23/2011 11:45:16 AM5/23/2011 11:45:16 AM

The World’s New Normal Economic System 19

distributions the area under the curve is never stable, and what are thought to be outliers may become frequent daily occurrences. Therefore, extreme events and their likelihood must always be taken into account and, while their cause is far from being clear, their effect may be significant.

As different occurrences outside the bell-shaped curve multiply, the area under it changes its shape, or it translates itself to the left (or to the right). As the frequency of what used to be extreme events increases, they become a part of a new normal. It needs no explaining that this is not only relevant today. It has been occurring all the time in both natural and man-made sys-tems – as they move from stability to chaos and back to stability following an inflection point.

During the last quarter of a century there has been: the 1987 stock market crash (a 14.5 standard deviations event); descent to the abyss by Japanese banks and breaking of the British pound by Soros and Steinhart, both in early 1990s; the 1994 hecatomb of debt instruments; the 1997 East Asia crisis; the 1998 Russian bankruptcy and near bankruptcy of LTCM; the 2000 stock market crash (with dotcoms at the epicenter); and the 2007–11 deep economic crisis – which included the bankruptcy of Lehman Brothers, as well as near-bankruptcy of AIG, Fannie Mae, Freddie Mac, the Royal Bank of Scotland and plenty of other mismanaged mammoth institutions.

The fact that these have been (unwisely) saved, through torrents of red ink, by central banks and governments has ushered in the new normal. It is in this sense that El-Erian/Gross’s insight about coming events in finance and the economy, as well as their aftermath, should be interpreted. Crises which used to be outliers are now becoming mainstream, and their impact weighs heavily on the daily lives of people, business activities and the global economy as a whole.

For instance, according to Goldman Sachs, in just two years, from early 2008 to early 2010, the economic and financial crisis knocked $30 trillion off the value of global shares (owned by people and companies) and another $11 tril-lion off the value of homes. Another statistic to remember is that these losses amounted to over 0.75 per cent of the world’s GDP.

Notice that this cumulative $41 trillion represents an amount of money in fairly popular markets – exchanges and housing – where players can win and lose all at the same time. If there is even a mild turnaround, as the new nor-mal theory suggests, some (though probably not much) of this lost money will be recovered and will help to start redressing balance sheets.

What will not be recovered, at least by many of the players, is money lost with games involving derivative financial instruments. To appreciate this statement, the reader should know that over 95 per cent of derivatives trading is proprietary between financial institutions, particularly the big ones. Trading transactions undertaken for clients represents a meager part of the total.

To understand what this means in terms of ‘silly business’, it is as if General Motors were to sell 95 per cent of its auto production to Ford, and

9780230298408_02_cha01.indd 199780230298408_02_cha01.indd 19 5/23/2011 11:45:16 AM5/23/2011 11:45:16 AM

20 Financial Risks Which Kept Piling Up

Ford were to return the compliment by selling 95 per cent of the motor vehicles it manufactures to GM. In addition, the large majority of these derivatives transactions contribute nothing to the national economy and involve ‘imaginary’ money, such as 30-year interest rate swaps.

How a banker or trader can know what the interest rates will be three decades down the line mystifies me, and also those people to whom I posed that question. To the contrary, what is not appreciated enough (by the gam-blers) is that one party is bound to lose and it will not recover its money, even if the economy returns to stellar performance.

The only way the loser can try to get his money back is to get even deeper involved in gambling, going further into the red. In a way, it is worse than in a casino, because the players gamble against each other to total destruc-tion and they can all go bust because of their superleveraging. Look at the fall not only of Lehman Brothers, but also of Citigroup, Bear Stearns, Merrill Lynch and plenty of others.

While in the short term superleveraging might deliver fat profits, in the medium term it leads straight to the precipice. A message the new normal gives to those who care to listen regards what happens after the day of financial reckoning has arrived. When the gambling casino goes bust, people and com-panies discover that the so-called ‘assets’ (of most doubtful value) are accom-panied by vast debts, which are due with interest. In a crisis, these ‘assets’ are shattered, but, short of outright bankruptcy, the liabilities always stand.

As in the case of Japan and its ‘two lost decades’, from 1992 to 2011, western financial institutions and households confront a balance sheet recession. And, because this is happening on a massive scale, nobody really has a clue about how to handle it, let alone how to get the economy out of the long tunnel which it has entered.

The curious medicine of throwing massive amounts of money at the problem, first practised by the Japanese government and then followed blindly by the American, British and continental European governments, is a medicine whose longer-term effects are anybody’s guess. All sorts of portfolios have been left with liabilities that far exceed their assets.

Some economists believe that the world’s economy will be pulled up from its crisis by the developing nations – which, relatively speaking, are in better shape, while demand in developed countries remains weak. But other economists question the thesis that the emerging nations will be able to compensate. There is an even more basic bifurcation in expert opinions:

Some economists say that many governments will have to keep their stimulus packages going for longer than expected, or face entrenched unemployment.To the contrary, others believe that public debt cannot rise any more without disastrous after-effects for everybody, common citizens companies and the state itself included.

•

•

9780230298408_02_cha01.indd 209780230298408_02_cha01.indd 20 5/23/2011 11:45:16 AM5/23/2011 11:45:16 AM