Enhancing China’s Sustainable Growth and Prosperity: a Pathway to Cleaner Coal

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

China’s coal conundrum What could enable an earlier coal and CO2 peak?

Xizhou Zhou, Senior Director

Head of Power, Gas, Coal & Renewables Group – Asia Pacific

March 13, 2017 | China Environment Program | The Wilson Center

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Key Implications

• Given current policies and investment trends, IHS expects that Chinese carbon emissions will peak before 2030, even with increasing investment in coal-fired power and coal-conversion sectors.

• The economic transition away from heavy manufacturing the past few years means that the carbon peak could come earlier and at a lower level than previously thought.

• In addition to economic growth, government policies (e.g., further environmental mandates) and market factors (e.g., cost competitiveness of alternative fuels and technologies) will also be critical for the future of coal – and thus any coal conversion projects.

2

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

IHS long-term scenario outlooks Coal demand trajectory came down significantly between 2015 and 2016 outlooks

3

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2000 2005 2010 2015 2020 2025 2030 2035 2040

China: Coal consumption outlook

Source: IHS © 2017 IHS Markit

mt o

f sta

ndar

d co

al

Reference scenario 2016

Reference scenario 2015

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Why the substantial drop in 2016 outlooks?

4

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

2000 2010 2020 2030 2040

Energy intensity of the Chinese economy

Source: IHS © 2017 IHS Markit

mto

e pe

r bill

ion

2015

US$

of Outlook

-2

0

2

4

6

8

10

12

14

16

18

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

Services

Non-manufacturingindustry

Manufacturing

Agriculture

China's real GDP growth (%) and its components

Source: IHS © 2016 IHS

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Renewables and gas played a role too, but coal-fired power continues to grow

5

0

2,000

4,000

6,000

8,000

10,000

12,000

2000 2005 2010 2015 2020 2025 2030 2035 2040

Other

Solar

Wind

Gas

Nuclear

Hydro

Coal

China power generation outlooks (Reference scenario 2016)

Source: IHS

Pow

er g

ener

atio

n (T

Wh)

© 2017 IHS Markit

Outlook

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Power/heating and feedstock are the main sectors for future coal consumption growth in China

6

-100

0

100

200

300

400

500

600

2005-10 2010-15 2015-20 2020-25 2025-30 2030-35

Power Heating Industry

Feedstock Residential Other

Incremental thermal coal consumption in China

Source: IHS Markit © 2017 IHS Markit

mill

ion

tons

of S

CE

Negative value: Demand reduction

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

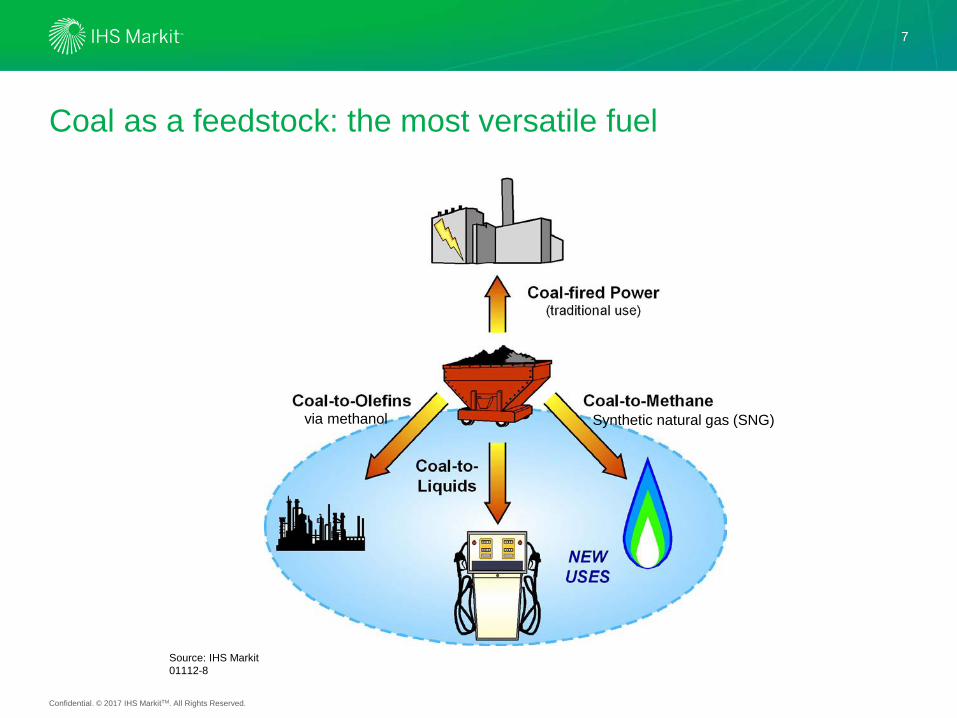

Coal as a feedstock: the most versatile fuel

7

Source: IHS Markit 01112-8

via methanol Synthetic natural gas (SNG)

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

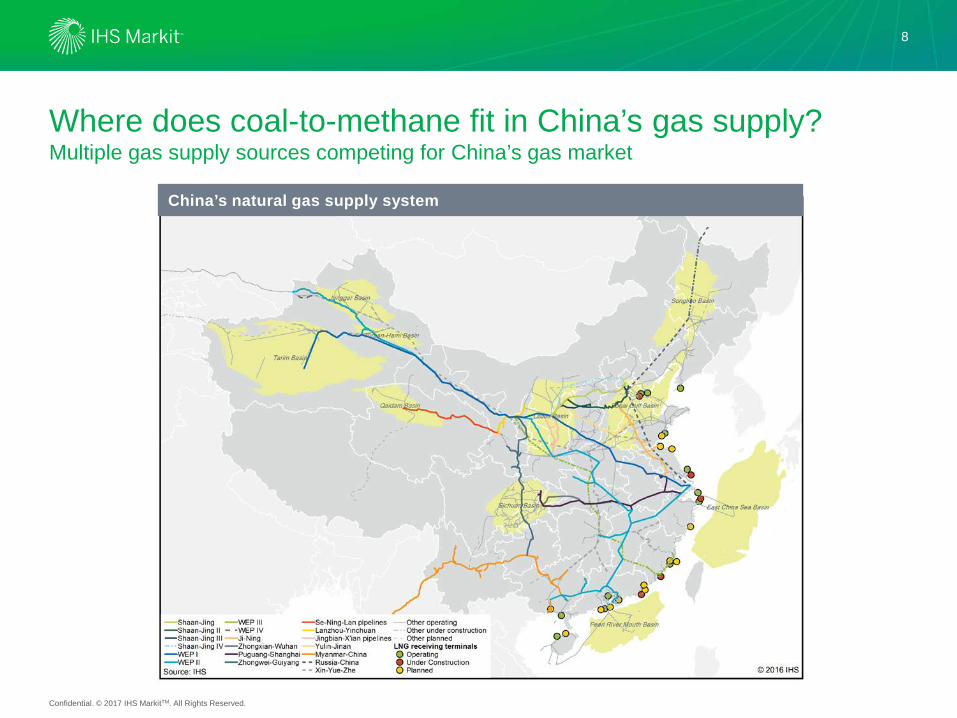

Where does coal-to-methane fit in China’s gas supply? Multiple gas supply sources competing for China’s gas market

8

China’s natural gas supply system

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

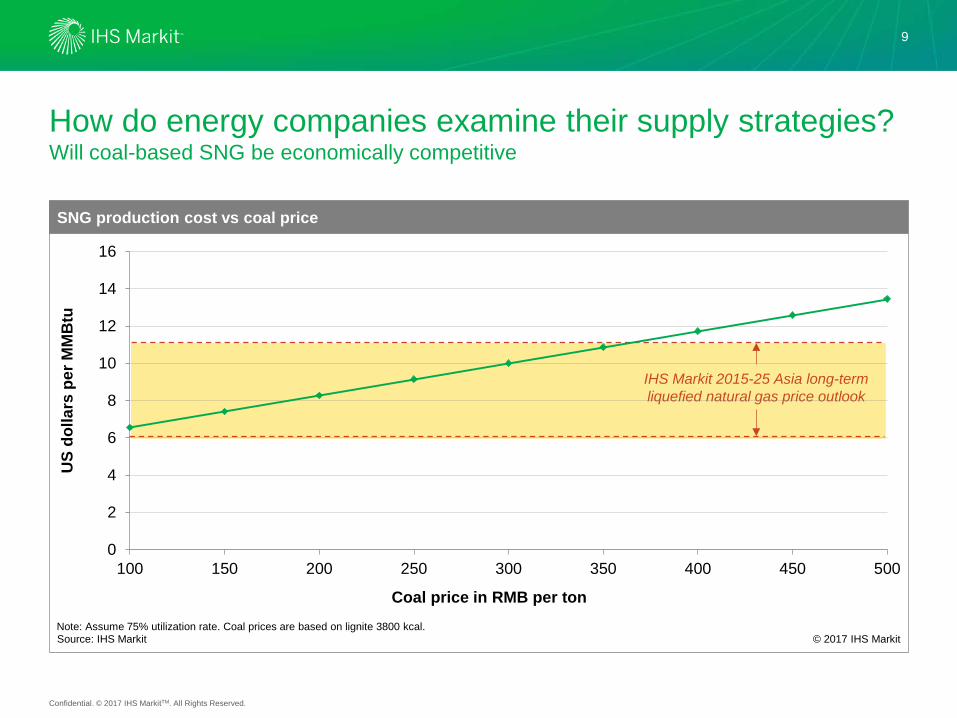

IHS Markit 2015-25 Asia long-term liquefied natural gas price outlook

How do energy companies examine their supply strategies? Will coal-based SNG be economically competitive

9

0

2

4

6

8

10

12

14

16

100 150 200 250 300 350 400 450 500

SNG production cost vs coal price

Source: IHS Markit © 2017 IHS Markit

US

dolla

rs p

er M

MB

tu

Coal price in RMB per ton Note: Assume 75% utilization rate. Coal prices are based on lignite 3800 kcal.

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Current policies will enable China’s reach its COP21 commitments, but deeper cuts are possible

10

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2000 2005 2010 2015 2020 2025 2030 2035 2040

China: Energy-related carbon emissions outlook

Source: IHS © 2016 IHS

mt e

nerg

y-re

late

d C

O2

emis

sion

s

“Autonomy” scenario 2016

Reference scenario 2016

Reference scenario 2015

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Summary of key implications

• 2030 peak carbon is very much achievable for China, even with higher coal usage in the power and coal conversion sectors.

• Economic restructuring is key to lowering coal consumption, and

any changes in the restructuring will alter future carbon trajectory.

• Environmental policies and market factors will determine the future of coal conversion. More regional coal ban? Future fossil fuel prices?

11

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

IHS Markit: Industries we serve

12

Energy Chemical Automotive Financial Markets

Product Design Technology, Media & Telecom

Maritime & Trade Aerospace, Defense & Security

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

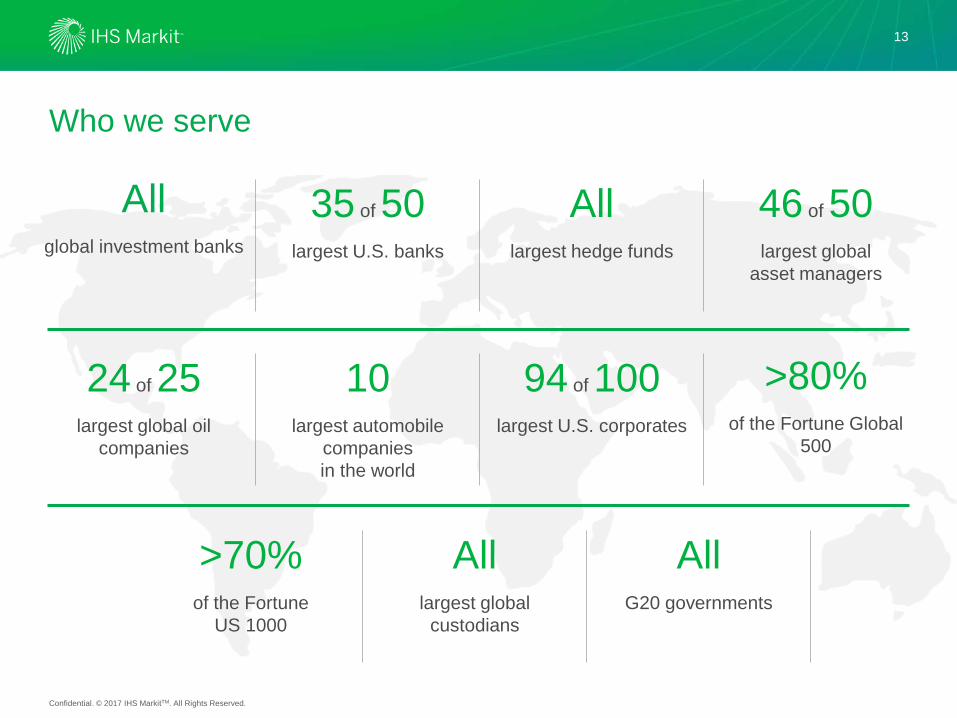

Who we serve

All global investment banks

13

46 of 50

largest global asset managers

35 of 50 largest U.S. banks

All largest hedge funds

24 of 25

largest global oil companies

94 of 100

largest U.S. corporates

10

largest automobile companies in the world

>80% of the Fortune Global

500

All G20 governments

>70% of the Fortune

US 1000

All largest global

custodians

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Energy-Wide Perspectives

Our Energy & Natural Resources Group

14

Beijing

Washington, DC

Cambridge, MA

Calgary

Mexico City

Rio de Janeiro

Paris

Oslo

Moscow

Johannesburg

Mumbai

Singapore

Bangkok

Tokyo

Dubai Asia Pacific

Europe, Middle East

& Africa

North America

South America

Regional organization / global expertise

Upstream Oil & Gas

Oil Markets, Downstream, and

Chemicals

Power, Gas, Coal & Renewables

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

15

We’re hiring!

Multiple position in the Power, Gas, Coal and Renewables group in Asia

Beijing

Associate Director, Power & Renewables (80604)

Senior Research Analyst, Gas & Power (80983)

Account Manager / Sales, Gas & Power (82504)

Delhi / Gurgaon

Associate Director, Gas & Power (82803)

Senior Research Analyst, Gas & Power (TBD)

Singapore

Associate Director, Gas & Power (80605)

Senior Research Analyst, Gas & Power (80984)

To locate the job descriptions and apply, please visit: https://www.ihs.com/about/careers.html Please reference the Req ID numbers after each position.

IHS Markit Customer Care [email protected] Americas: +1 800 IHS CARE (+1 800 447 2273) Europe, Middle East, and Africa: +44 (0) 1344 328 300 Asia and the Pacific Rim: +604 291 3600

Disclaimer The information contained in this presentation is confidential. Any unauthorized use, disclosure, reproduction, or dissemination, in full or in part, in any media or by any means, without the prior written permission of IHS Markit Ltd. or any of its affiliates ("IHS Markit") is strictly prohibited. IHS Markit owns all IHS Markit logos and trade names contained in this presentation that are subject to license. Opinions, statements, estimates, and projections in this presentation (including other media) are solely those of the individual author(s) at the time of writing and do not necessarily reflect the opinions of IHS Markit. Neither IHS Markit nor the author(s) has any obligation to update this presentation in the event that any content, opinion, statement, estimate, or projection (collectively, "information") changes or subsequently becomes inaccurate. IHS Markit makes no warranty, expressed or implied, as to the accuracy, completeness, or timeliness of any information in this presentation, and shall not in any way be liable to any recipient for any inaccuracies or omissions. Without limiting the foregoing, IHS Markit shall have no liability whatsoever to any recipient, whether in contract, in tort (including negligence), under warranty, under statute or otherwise, in respect of any loss or damage suffered by any recipient as a result of or in connection with any information provided, or any course of action determined, by it or any third party, whether or not based on any information provided. The inclusion of a link to an external website by IHS Markit should not be understood to be an endorsement of that website or the site's owners (or their products/services). IHS Markit is not responsible for either the content or output of external websites. Copyright © 2017, IHS MarkitTM. All rights reserved and all intellectual property rights are retained by IHS Markit.

16