China New Mobility Study 2015 - bain.com · Source: Bain China New Mobility Study, 2,100+...

16

China New Mobility Study 2015

Transcript of China New Mobility Study 2015 - bain.com · Source: Bain China New Mobility Study, 2,100+...

China New Mobility Study

2015

Copyright © 2015 Bain & Company, Inc. All rights reserved.

China New Mobility Study | Bain & Company, Inc.

Page 1

Executive summary

Car owners in China’s mega-cities are rethinking the value of car ownership. As rapid urbanization

transforms China’s urban mobility landscape, car owners are increasingly forced to contend with

deteriorating driving conditions and tighter regulations, making car ownership in these large

urban areas more expensive and less convenient and safe—hence, less attractive.

At the same time, major infrastructure investment has made public transportation more acces-

sible and convenient, while new mobility services and solutions like car sharing are being intro-

duced—although still unfamiliar to many Chinese consumers.

According to a survey of car owners from six Tier-1 and Tier-2 cities in China, select segments would

consider giving up their cars if conditions continue to decline. Respondents identifi ed trends like

deteriorating driving conditions and tighter regulations as detracting from car ownership. They also cited

improved public transportation, taxi availability, car rental accessibility and the emergence of new

mobility solutions as contributing factors in their willingness to give up their cars.

Whereas many Chinese still associate car ownership with status, cars are losing their appeal as a

status symbol in most segments in China’s mega-cities. What China’s urban consumers today

value most is safe, on-time, fl exible and reliable mobility.

In addition, Chinese consumers cite traffi c congestion and higher gasoline prices as major factors

that would prevent them from owning or buying a car. If traffi c conditions continue to deteriorate

signifi cantly or gas prices increase sharply, 10% to 30% of current car owners say they would con-

sider giving up their cars.

Chinese show a keen interest in using public transportation and in new mobility solutions

tailored to local needs. A strong follow-up on the public’s stated determination to use car

rentals, car sharing and public transportation will remain an important factor in the development of

new mobility solutions.

We have identifi ed six customer segments with different needs and behaviors that run the gamut

from those least to those most interested in using new mobility solutions. Among these, Status

Seekers, Smart Travelers and Switchers expressed the greatest interest in new mobility, while Eco-

nomic Travelers, the Car Averse and Convenience-focused expressed the least interest in new solu-

tions such as car sharing and rental models.

Changing trends in China’s urban mobility present a challenge for creating new mobility solu-

tions while also protecting China’s automotive business. To protect core automotive business,

China New Mobility Study | Bain & Company, Inc.

Page 2

OEMs will partner with local governments to seek solutions to urbanization problems of traffi c con-

gestion and emissions, set up loyalty programs targeted at segments most “at risk,” and propose

more fl exible solutions, such as leasing, to attract new customers.

China also offers OEMs a unique opportunity to develop mobility solutions tailored specifi cally

to China’s situation. Services like car sharing will need to meet Chinese customer needs for

safety and flexibility, to integrate local infrastructure constraints like parking, and to compete with

low-cost taxis and public transport. Success will require major changes from concepts that have

emerged in Europe or North America.

China New Mobility Study | Bain & Company, Inc.

Page 3

Figure 1: Major trends in China’s urban mobility landscape

1

6

5

4

3

2

Source: Bain & Company

Fast urbanization

Deteriorating driving conditions

Increasing environmental

pressures

Tightening regulations

Improving public transport

Fast penetration of new technologies

Urbanization and household income growth drive mega-cities’ population, car parc, and commuting distances and times

Traffic congestion, road safety issues and lack of affordable parking spaces negatively impact driving experience

Air quality has become a major concern, increasing awareness of the role of cars and openness to alternative solutions

Multiple regulations are being deployed to control car ownership, restrict road access or favor low-emission vehicles

Major investments in infrastructure have improved the coverage, reliability and comfort of rail and bus transit systems

The use of new mobile applications to plan, book and enhance mobility experience is increasing fast

Figure 2: Trends are reducing the value of owning a car and support the emergence of new mobility solutions

Fast urbanization

Deteriorating driving conditions

Increasing environmental pressures

Tightening regulations

Improving public transport

Fast penetration of new technologies

1

6

5

4

3

2

The value of owning and driving a car is deteriorating; it is becoming more expensive, less convenient and less safe

Public transportation should continue to improve with support from the government

Alternative mobility trends are emerging; there is a need to address concerns of car ownership and offer more than public transportation

Source: Bain & Company

China New Mobility Study | Bain & Company, Inc.

Page 4

Figure 3: Safety, time and fl exibility are the most important mobility needs for China’s urban consumers

Which mobility need do you consider most important and which one least important?

Source: Bain China New Mobility Study, 2,100+ respondents from six Tier-1 and Tier-2 cities in China

Vehi

cle

safe

ty

Tim

elin

ess

and

relia

bilit

yof

arr

ival

tim

e

Pers

onal

saf

ety

Bein

g fle

xibl

e w

hile

trav

elin

g

Trav

elin

g w

ith c

omfo

rt

Bein

g fle

xibl

e w

hen

sta

rting

the

jour

ney

No

chan

ge o

f veh

icle

dur

ing

jour

ney

Fun

to d

rive

Easy

doo

r-to-

door

con

nect

ivity

Com

plic

atio

n-fre

etra

vel,

no m

enta

l stre

ss

Min

imum

ove

rall

trave

l tim

e

Opt

ion

to c

arry

hea

vy o

r bu

lky

good

s

Low

cos

t of t

rave

l

Envi

ronm

enta

lfri

endl

ines

s

Upf

ront

tran

spar

ency

of

cos

t for

trav

el

Bein

g ab

le to

com

mun

icat

e, b

eing

onl

ine

No

phys

ical

effo

rt

Usi

ng tr

avel

tim

e to

wor

k or

rea

d

Priv

acy

Relative importance of mobility needs for consumers (scale 0–100)100

80

60

40

20

0

Safety Time Flexibility Comfort Efficiency Economics

Figure 4: Cars are likely to lose their appeal as a status symbol with Chinese consumers

Source: Bain China New Mobility Study, 2,100+ respondents from six Tier-1and Tier-2 cities in China

Cars are losing their appeal as a status symbol with Chinese consumers But for most, cars are becoming less of a status symbol

In your opinion, does owning a car improve one’s social status? How did the importance of cars as a status symbol change?

100%

Yes

Neutral

Neutral

Decreased

Increased

No

80

China Car owner Prospective buyer

60

40

20

0

100%

80

60

40

20

0

End-customer perspective on cars as status symbols (2014, n=2,137) Change of importance of cars as status symbols over time

China New Mobility Study | Bain & Company, Inc.

Page 5

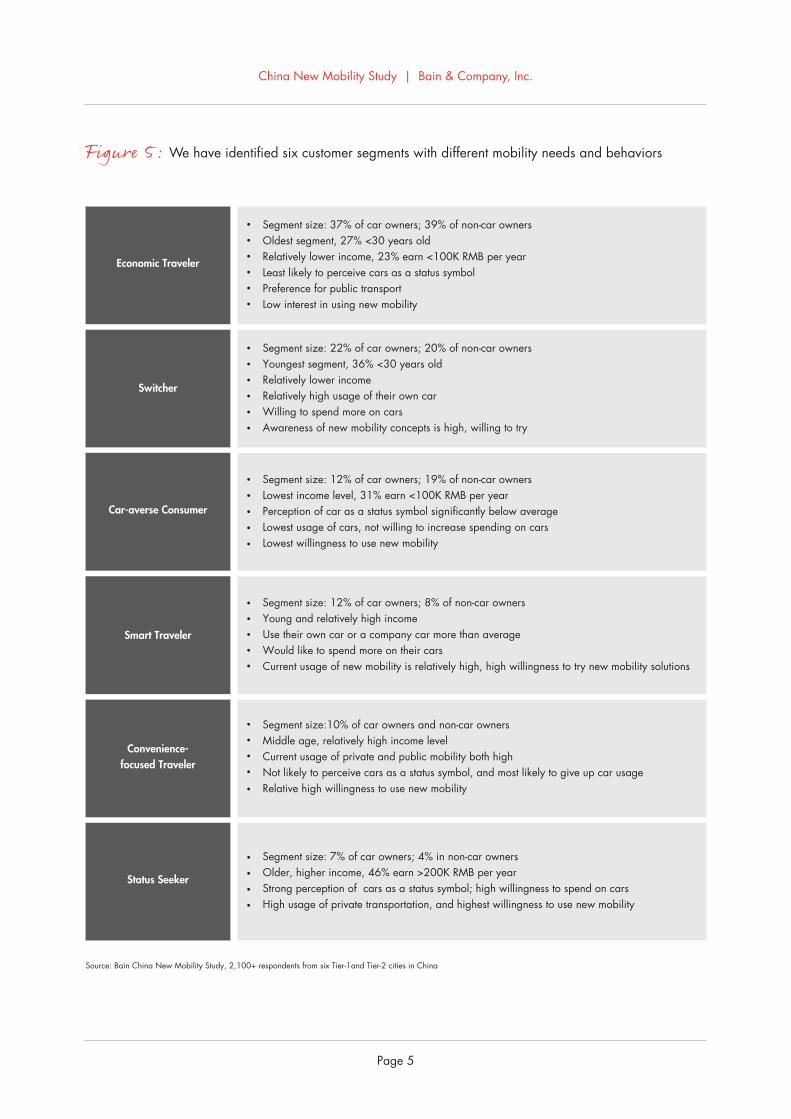

Figure 5: We have identifi ed six customer segments with different mobility needs and behaviors

Source: Bain China New Mobility Study, 2,100+ respondents from six Tier-1and Tier-2 cities in China

Economic Traveler

Car-averse Consumer

Smart Traveler

Status Seeker

Convenience-focused Traveler

Switcher

Segment size: 37% of car owners; 39% of non-car ownersOldest segment, 27% <30 years oldRelatively lower income, 23% earn <100K RMB per yearLeast likely to perceive cars as a status symbol Preference for public transportLow interest in using new mobility

Segment size: 22% of car owners; 20% of non-car ownersYoungest segment, 36% <30 years oldRelatively lower incomeRelatively high usage of their own carWilling to spend more on carsAwareness of new mobility concepts is high, willing to try

Segment size: 12% of car owners; 19% of non-car ownersLowest income level, 31% earn <100K RMB per yearPerception of car as a status symbol significantly below average Lowest usage of cars, not willing to increase spending on carsLowest willingness to use new mobility

Segment size: 12% of car owners; 8% of non-car ownersYoung and relatively high incomeUse their own car or a company car more than averageWould like to spend more on their carsCurrent usage of new mobility is relatively high, high willingness to try new mobility solutions

Segment size: 7% of car owners; 4% in non-car ownersOlder, higher income, 46% earn >200K RMB per yearStrong perception of cars as a status symbol; high willingness to spend on carsHigh usage of private transportation, and highest willingness to use new mobility

Segment size:10% of car owners and non-car ownersMiddle age, relatively high income level Current usage of private and public mobility both highNot likely to perceive cars as a status symbol, and most likely to give up car usageRelative high willingness to use new mobility

China New Mobility Study | Bain & Company, Inc.

Page 6

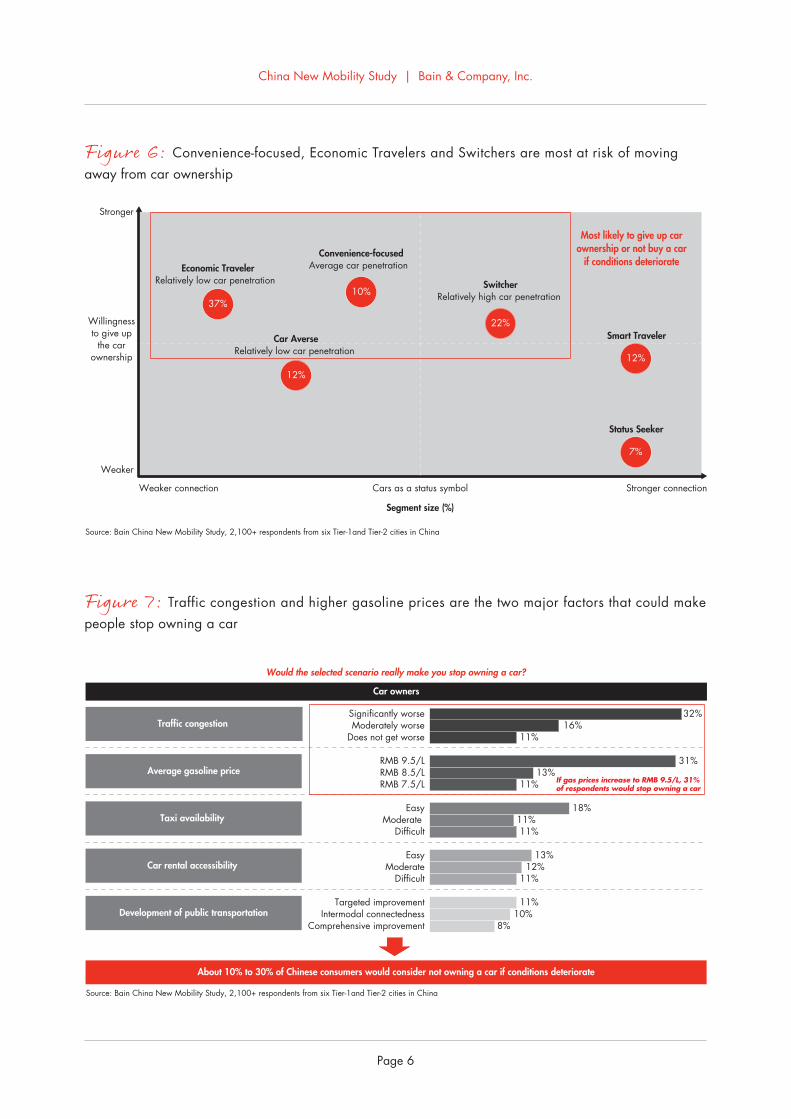

Figure 6: Convenience-focused, Economic Travelers and Switchers are most at risk of moving away from car ownership

Weaker

Stronger

Willingnessto give up

the carownership

Most likely to give up carownership or not buy a car

if conditions deteriorate

Source: Bain China New Mobility Study, 2,100+ respondents from six Tier-1and Tier-2 cities in China

Cars as a status symbol Stronger connectionWeaker connection

Economic TravelerRelatively low car penetration

Car AverseRelatively low car penetration

Status Seeker

SwitcherRelatively high car penetration

Smart Traveler

Convenience-focusedAverage car penetration

Segment size (%)

37%10%

22%

12%

7%

12%

Figure 7: Traffic congestion and higher gasoline prices are the two major factors that could make people stop owning a car

Source: Bain China New Mobility Study, 2,100+ respondents from six Tier-1and Tier-2 cities in China

About 10% to 30% of Chinese consumers would consider not owning a car if conditions deteriorate

Would the selected scenario really make you stop owning a car?

Car owners

Traffic congestion

Average gasoline price

Taxi availability

Car rental accessibility

Development of public transportationComprehensive improvement

Intermodal connectednessTargeted improvement

DifficultModerate

Easy

DifficultModerate

Easy

RMB 7.5/LRMB 8.5/LRMB 9.5/L

Does not get worseModerately worse

Significantly worse

8%10%

11%

11%12%

13%

11%11%

18%

11%13%

31%

11%16%

32%

If gas prices increase to RMB 9.5/L, 31%of respondents would stop owning a car

China New Mobility Study | Bain & Company, Inc.

Page 7

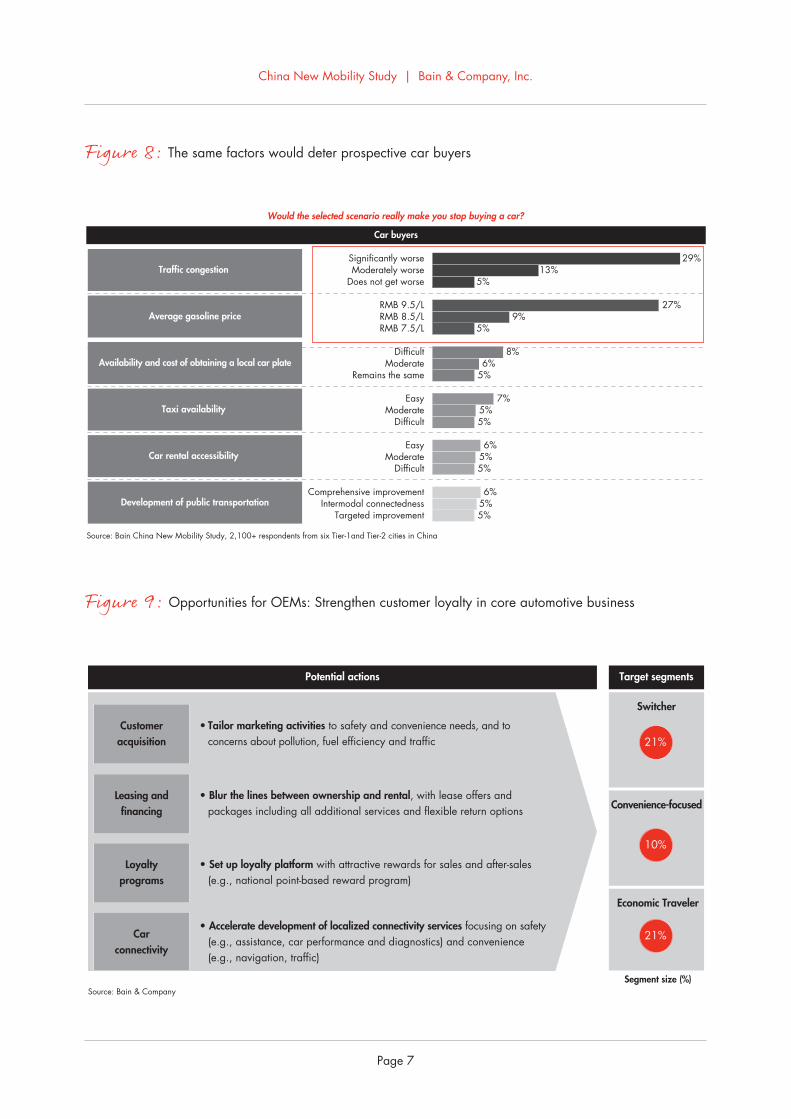

Figure 8: The same factors would deter prospective car buyers

Source: Bain China New Mobility Study, 2,100+ respondents from six Tier-1and Tier-2 cities in China

Would the selected scenario really make you stop buying a car?

Car buyers

Targeted improvement 5%Intermodal connectedness 5%

Comprehensive improvement 6%

Difficult 5%Moderate 5%

Easy 6%

Difficult 5%Moderate 5%

Easy 7%

Remains the same 5%Moderate 6%

RMB 7.5/LRMB 8.5/LRMB 9.5/L

Does not get worseModerately worse

Significantly worse

Difficult

5%13%

29%

27%

5%9%

8%

Traffic congestion

Average gasoline price

Taxi availability

Car rental accessibility

Development of public transportation

Availability and cost of obtaining a local car plate

Figure 9: Opportunities for OEMs: Strengthen customer loyalty in core automotive business

Source: Bain & Company

Potential actions Target segments

Loyaltyprograms

• Set up loyalty platform with attractive rewards for sales and after-sales (e.g., national point-based reward program)

Leasing andfinancing

• Blur the lines between ownership and rental, with lease offers and packages including all additional services and flexible return options

Carconnectivity

• Accelerate development of localized connectivity services focusing on safety (e.g., assistance, car performance and diagnostics) and convenience (e.g., navigation, traffic)

Customeracquisition

• Tailor marketing activities to safety and convenience needs, and to concerns about pollution, fuel efficiency and traffic

Convenience-focused

Switcher

Economic Traveler

21%

10%

21%

Segment size (%)

China New Mobility Study | Bain & Company, Inc.

Page 8

Figure 10: China urban mobility landscape

Source: Bain & Company

Mobility platformFor instance, applications to plan, book,support mobility

3

e

Mobility platform3

4 Private mobility

Sharingand

rental mobility

22

Publicmobility

1

Private mobilityg Walk

4

Bicycleh

Motor scooteri

Private carj

Public mobility1

Busa

Rail transitb

Train, airplanec

Sharing and rental mobility22

Car sharingd

Car rentale

Taxifa

i

j

e

d

f

h

g

b

c

Figure 11 : Chinese consumers are relatively less familiar with car sharing models

With which of these mobility solutions were you familiar before you participated in our survey?

Source: Bain China New Mobility Study

Mobility pass Car rental Busrapid transit

Bike sharing Ride sharing Peer-to-peercar sharing

Corporatecar sharing

Onlinemobilityplatform

Mobilityservices

Conventionalcar sharing

% of respondents aware of new mobility concepts

0

20

40

60

80%

100%

64

4743

30 2823 23 21 21

17

Rental and sharing Public mobilityMobility platform and services

China New Mobility Study | Bain & Company, Inc.

Page 9

Which mobility solutions will become a significant part of your urban mobility in the next three years?

Mobility pass Car rentalBusrapid transit

Bike sharing Ride sharing Peer-to-peercar sharing

Corporatecar sharing

Onlinemobilityplatform

Mobilityservices

Conventionalcar sharing

% of potential respondents who believed these new mobility concepts will become a significant part of their mobility in three years

0

20

40

60

80

100%

71%

57%

47% 46% 43% 42%38% 37% 35%

30%

Close to 40% ofrespondents arekeen to use some

form of car sharingin the future

Rental and sharing Public mobilityMobility platform and services

Note: Potential usage in three years is defined as answering “definitely” and “rather yes” for question “I can imagine new mobility concept becoming one of my significant waysof urban traveling in the next three years…”Source: Bain China New Mobility Study

Figure 12: Chinese consumers are keen to use public transport and alternative mobility solutions ...

Figure 13: … including different car-sharing models and car rental

% of respondents who believe they will use these new mobility concepts in the next three years

Source: Bain China New Mobility Study

% of respondents who believe they will use these new mobility concepts in the next three years100%

18%

23%

73%60% 66% 67%

78% 75%

49%28%

51%

27%

53%

37%18%

48%

19%41%

20%

37%

30%51%

23%

50% 50% 54%

49% 36%53%

39%63%

48%

20%

53%

24%46%

806040200

100%806040200

100%806040200

100%806040200

100%806040200

100%806040200

EconomicTraveler

CarAverse

SmartTraveler

Convenience-focused

StatusSeeker

Switcher

Conventional car sharing

Corporate car sharing

Mobility pass

Peer-to-peer car sharing

Car rental

Online mobility platform

EconomicTraveler

CarAverse

SmartTraveler

Convenience-focused

StatusSeeker

Switcher

EconomicTraveler

CarAverse

SmartTraveler

Convenience-focused

StatusSeeker

Switcher EconomicTraveler

CarAverse

SmartTraveler

Convenience-focused

StatusSeeker

Switcher

EconomicTraveler

CarAverse

SmartTraveler

Convenience-focused

StatusSeeker

Switcher

EconomicTraveler

CarAverse

SmartTraveler

Convenience-focused

StatusSeeker

Switcher

China New Mobility Study | Bain & Company, Inc.

Page 10

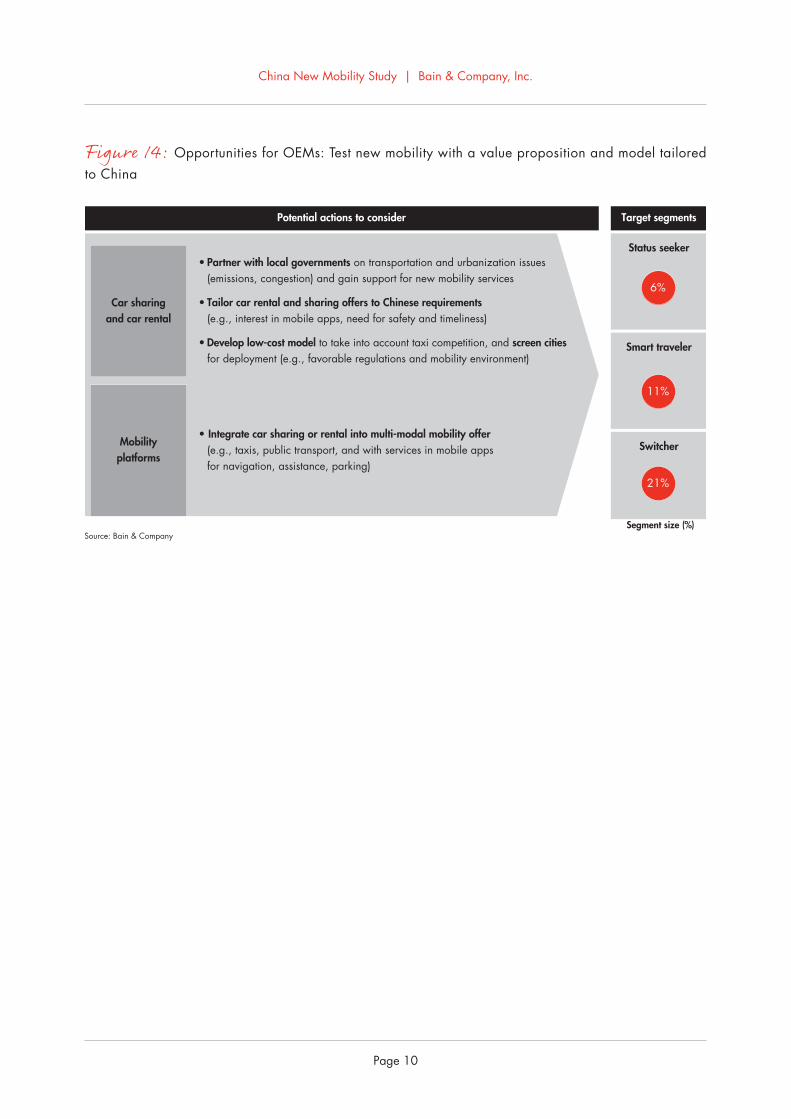

Source: Bain & Company

Potential actions to consider Target segments

Mobilityplatforms

• Integrate car sharing or rental into multi-modal mobility offer (e.g., taxis, public transport, and with services in mobile apps for navigation, assistance, parking)

Car sharingand car rental

• Partner with local governments on transportation and urbanization issues (emissions, congestion) and gain support for new mobility services

• Tailor car rental and sharing offers to Chinese requirements (e.g., interest in mobile apps, need for safety and timeliness)

• Develop low-cost model to take into account taxi competition, and screen cities for deployment (e.g., favorable regulations and mobility environment)

Smart traveler

Status seeker

Switcher

Segment size (%)

6%

11%

21%

Figure 14: Opportunities for OEMs: Test new mobility with a value proposition and model tailored to China

China New Mobility Study | Bain & Company, Inc.

Page 11

About the authors

Raymond Tsang is a partner with Bain’s Greater China offi ce and leads the Industrial Goods and Services practices

for Greater China. You may contact him by email at [email protected].

Pierre-Henri Boutot is a partner with Bain’s Greater China offi ce. You may contact him by email at [email protected].

Please direct questions and comments about this study via email to the authors.

Acknowledgments

The authors extend gratitude to all who contributed to this study, in particular Jieqi Zhou from Bain & Company.

China New Mobility Study | Bain & Company, Inc.

Page 12

Shared Ambit ion, True Re sults

Bain & Company is the management consulting fi rm that the world’s business leaders come to when they want results.

Bain advises clients on strategy, operations, technology, organization, private equity and mergers and acquisitions.

We develop practical, customized insights that clients act on and transfer skills that make change stick. Founded

in 1973, Bain has 51 offi ces in 33 countries, and our deep expertise and client roster cross every industry and

economic sector. Our clients have outperformed the stock market 4 to 1.

What sets us apart

We believe a consulting fi rm should be more than an adviser. So we put ourselves in our clients’ shoes, selling

outcomes, not projects. We align our incentives with our clients’ by linking our fees to their results and collaborate

to unlock the full potential of their business. Our Results Delivery® process builds our clients’ capabilities, and

our True North values mean we do the right thing for our clients, people and communities—always.

For more information, visit www.bain.com