China Logistics OVERWEIGHT - Kim Eng Hong · PDF fileChina Logistics. On a structural ... High...

56

July 23, 2014 China SECTOR RESEARCH | SEE PAGE 54 FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS China Logistics On a structural uptrend High cost of logistics in China will create demand for sophisticated value-added logistics services, providing numerous opportunities to industry players. Structural, rather than cyclical, drivers support the uptrend in China’s logistics sector over the long term. Top pick still Sinotrans; China Merchants (CM) is an alternative play. Kerry Logistics Network’s (KLN) growth is slow and valuations stretched, initiate at HOLD. Numerous opportunities for logistics players China’s logistics costs reached 17.9% of GDP in FY13, 9.5ppt higher than the average for developed countries such as the US, Japan and Germany. We expect a continued drive to lower logistics costs, advancement of technology and the improvement of infrastructure networks to further stimulate demand for sophisticated logistics services, translating into numerous business opportunities for experienced logistics providers with solid service know-how. Seven drivers positive for sector outlook We see seven key drivers underpinning solid logistics demand in China: 1) growth in e-commerce volume, driven by online shopping and “Haitao” demand; 2) manufacturers relocating production, stimulating supply chain services; 3) increase in enterprise outsourcing accelerating third-party logistics (3PL); 4) rise in demand for value-added services translating into more profit opportunities; 5) upgrading of logistics facilities enhancing unit revenue; 6) expansion of Chinese enterprises overseas generating cross-border logistics demand; and 7) more favourable government policies creating a more positive operating environment. BUY Sinotrans and CM, HOLD KLN Reiterate BUY on Sinotrans and CM, as both fit well into the trend of accelerated logistics demand. We expect Sinotrans to continue to generate solid growth from 3PL and warehouse upgrades, and it will see further parent-asset injections. CM has a growing logistics business, though its contribution is only 7.2% for FY15F. For KLN, while it has good exposure to the China and Asia logistics markets, growth will be weighed down by its Hong Kong warehouses. It will also take time for the M&A to reflect significantly on its earnings; ROE will remain low for the next two years. Initiate at HOLD and believe its current valuation is fair. Analysts (New) OVERWEIGHT Osbert TK Tang, CFA (86) 21-5096 8370 [email protected] Tracy Liu (86) 21 5096 8367 [email protected] Stock Mkt cap Rating Price TP Upside (USD'm) (LC) (LC) (%) 14E 15E 14E 15E 14E 15E China Merchants 8,311.7 Buy 25.50 29.80 17 14.9 14.0 1.3 1.2 3.2 3.5 Sinotrans 2,912.0 Buy 4.90 6.20 27 15.2 11.3 1.4 1.2 1.7 2.2 Kerry Logistics 2,778.7 Hold 12.74 12.80 0 21.9 19.9 1.5 1.4 1.0 1.1 P/E (x) P/B (x) Dividend yld (%)

Transcript of China Logistics OVERWEIGHT - Kim Eng Hong · PDF fileChina Logistics. On a structural ... High...

July 23, 2014

Chin

a SE

CTO

R RE

SEA

RCH

|

SEE PAGE 54 FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS

China Logistics

On a structural uptrend High cost of logistics in China will create demand for

sophisticated value-added logistics services, providing numerous opportunities to industry players.

Structural, rather than cyclical, drivers support the uptrend in China’s logistics sector over the long term.

Top pick still Sinotrans; China Merchants (CM) is an alternative play. Kerry Logistics Network’s (KLN) growth is slow and valuations stretched, initiate at HOLD.

Numerous opportunities for logistics players China’s logistics costs reached 17.9% of GDP in FY13, 9.5ppt higher than the average for developed countries such as the US, Japan and Germany. We expect a continued drive to lower logistics costs, advancement of technology and the improvement of infrastructure networks to further stimulate demand for sophisticated logistics services, translating into numerous business opportunities for experienced logistics providers with solid service know-how.

Seven drivers positive for sector outlook We see seven key drivers underpinning solid logistics demand in China: 1) growth in e-commerce volume, driven by online shopping and “Haitao” demand; 2) manufacturers relocating production, stimulating supply chain services; 3) increase in enterprise outsourcing accelerating third-party logistics (3PL); 4) rise in demand for value-added services translating into more profit opportunities; 5) upgrading of logistics facilities enhancing unit revenue; 6) expansion of Chinese enterprises overseas generating cross-border logistics demand; and 7) more favourable government policies creating a more positive operating environment.

BUY Sinotrans and CM, HOLD KLN Reiterate BUY on Sinotrans and CM, as both fit well into the trend of accelerated logistics demand. We expect Sinotrans to continue to generate solid growth from 3PL and warehouse upgrades, and it will see further parent-asset injections. CM has a growing logistics business, though its contribution is only 7.2% for FY15F.

For KLN, while it has good exposure to the China and Asia logistics markets, growth will be weighed down by its Hong Kong warehouses. It will also take time for the M&A to reflect significantly on its earnings; ROE will remain low for the next two years. Initiate at HOLD and believe its current valuation is fair.

Analysts

(New)OVERWEIGHT

Osbert TK Tang, CFA(86) 21-5096 [email protected]

Tracy Liu(86) 21 5096 [email protected]

Stock Mkt cap Rating Price TP Upside

(USD'm) (LC) (LC) (%) 14E 15E 14E 15E 14E 15E

China Merchants 8,311.7 Buy 25.50 29.80 17 14.9 14.0 1.3 1.2 3.2 3.5

Sinotrans 2,912.0 Buy 4.90 6.20 27 15.2 11.3 1.4 1.2 1.7 2.2

Kerry Logistics 2,778.7 Hold 12.74 12.80 0 21.9 19.9 1.5 1.4 1.0 1.1

P/E (x) P/B (x) Dividend yld (%)

July 23, 2014 2

China Logistics

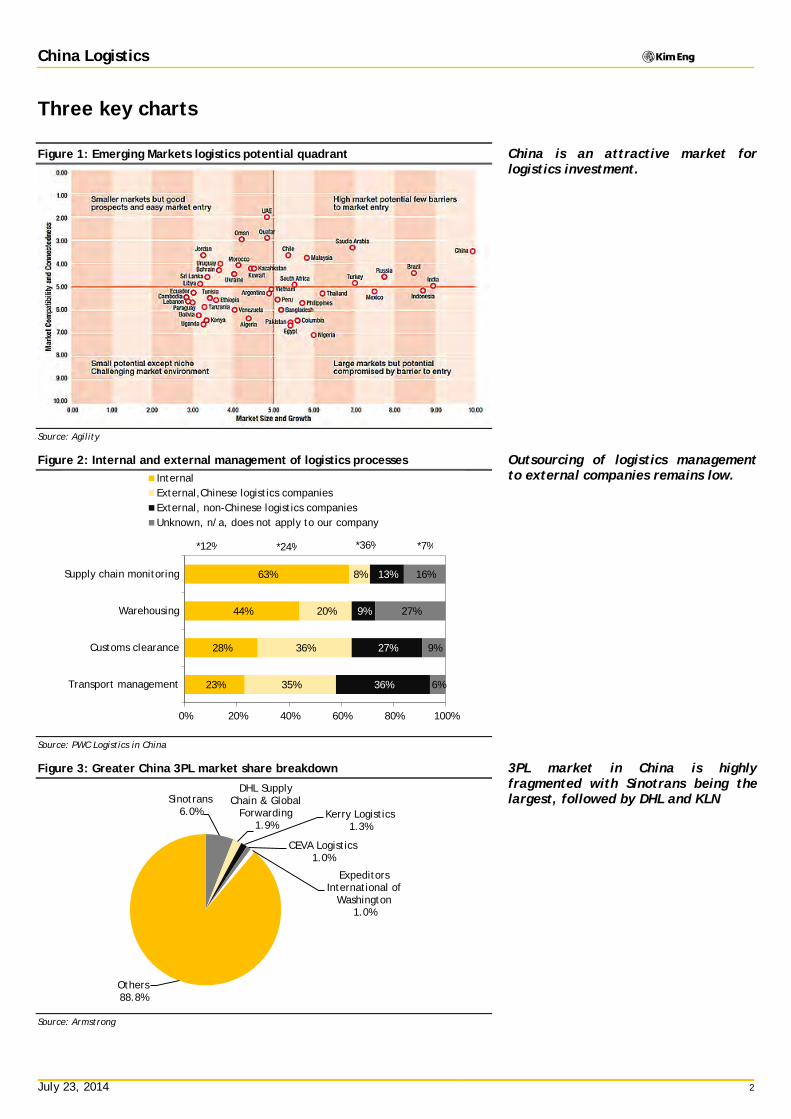

Three key charts

Figure 1: Emerging Markets logistics potential quadrant

Source: Agility

Figure 2: Internal and external management of logistics processes

Source: PWC Logistics in China

Figure 3: Greater China 3PL market share breakdown

Source: Armstrong

23%

28%

44%

63%

35%

36%

20%

8%

36%

27%

9%

13%

6%

9%

27%

16%

0% 20% 40% 60% 80% 100%

Transport management

Customs clearance

Warehousing

Supply chain monitoring

InternalExternal,Chinese logistics companiesExternal, non-Chinese logistics companiesUnknown, n/a, does not apply to our company

*24% *36% *7% *12%

Sinotrans 6.0%

DHL Supply Chain & Global

Forwarding 1.9%

Kerry Logistics 1.3%

CEVA Logistics 1.0%

Expeditors International of

Washington 1.0%

Others 88.8%

China is an attractive market for logistics investment.

Outsourcing of logistics management to external companies remains low.

3PL market in China is highly fragmented with Sinotrans being the largest, followed by DHL and KLN

July 23, 2014 3

China Logistics

Drivers for China’s logistics industry

Weak infrastructure and a less efficient network mean logistics costs in China are higher than in most other countries. In 2013, China’s social logistics revenue reached CNY1,978b, achieving a 10-year CAGR of 14.6%. Based on data from the China Federation of Logistics & Purchasing, China’s logistics costs reached 17.9% of GDP in FY13. This is 9.5ppt higher than the average for developed countries like the US, Japan and Germany. We expect the continuous drive to lower logistics costs, advancement of logistics technology and the improvement in infrastructure network to further stimulate the demand for sophisticated logistics services. This should translate into numerous business opportunities for experienced logistics providers with solid service know-how.

Figure 4: China’s total social logistics cost

Source: iFind

Figure 5: China’s total social logistics cost breakdown

Source: iFind

Traditionally, Chinese companies tend to manage their product distribution in-house, mostly due to the high volumes (which made it cost-efficient), the lack of quality logistics service providers and the under-development of logistics information systems. However, over the past five years, manufacturers and retailers have become increasingly aware of the importance of an efficient logistics network. The increase in market competition, driven by e-commerce growth and the rise in demand for timely deliveries, has also driven the demand for more efficient logistics arrangements. The emergence of bigger and more professional 3PL companies that offer more comprehensive services have made it even

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

2

4

6

8

10

12

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

CNYt China social logistics cost % Change (RHS)

Transportation expense 52.9% Storage cost

35.3%

Management expense 12.7%

Continuous drive to lower logistics cost will further stimulate the demand for sophisticated logistics services.

July 23, 2014 4

China Logistics

more efficient and cost-effective for enterprises to outsource their logistics requirements rather than handling them in-house.

In China, most of the logistics service providers are small companies involved in just one or two segments of the overall supply chain. There are just a handful of companies capable of providing customers with comprehensive supply chain management services. The logistics market in China is highly fragmented, with more knowledgeable overseas companies like UPS, FedEx and DHL dominating the cross-border arena. Domestically, state-owned and Hong Kong-based players like Sinotrans and KLN have been aggressively building up their presences. Additionally, domestic express operators like SF Express and Shentong have started to construct a nation-wide logistics network, while the Cainiao Network, a logistics infrastructure initiated by Alibaba Executive Chairman Jack Ma, has caught significant market attention.

Based on Armstrong & Associates, logistics spending in China amounted to USD1.5t in 2012, making it, as a single country, the highest in the world. We expect China’s logistics spending to experience a CAGR of 10-12% between FY13 and FY17. However, the growth in demand for more value-added services and increase in outsourcing by corporates mean the 3PL market will grow much faster than the growth in logistics spending in the next five years.

Figure 6: 3PL revenue growth by region

Source: Armstrong

We continue to be positive on the China logistics sector over the next five years and envisage the key demand drivers to be: 1) growth in e-commerce volume; 2) manufacturing relocations; 3) increase in enterprise outsourcing; 4) rise in demand for value-added services; 5) upgrade in facility quality; 6) expansion of Chinese enterprises overseas; and 7) more favourable government policies. According to Agility, China is classified as a country with high market potential but few barriers to entry, effectively meaning it is one of the biggest targets for logistics investments as well as the easiest markets in which to operate.

18.8%

9.5%

13.3%

4.0% 6.3%

-1.7%

8.0%

4.8% 3.6% 4.2%

1.5% 1.0%

-5%

0%

5%

10%

15%

20%

GreaterChina

Asia Pacific(ex. GreaterChina and

Japan)

SouthAmerica

NorthAmerica

Japan Europe

2007-2012 2012-2015E

The logistics market in China is highly fragmented, with more knowledgeable overseas companies like UPS, FedEx and DHL dominating the cross-border arena.

July 23, 2014 5

China Logistics

Figure 7: Emerging Market logistics potential quadrant

Source: Agility

1) Growth in retail e-commerce volume The rise in domestic consumption is expected to be an important driver for logistics demand in China. Over the past seven years, China’s retail sales have increased at a CAGR of 17.4%. Although growth slowed to 11.9% in 1Q14, the pace remains decent. Continued urbanization is one of the key impetuses to support growth in retail sales. Under the 12th Five-Year Plan and Premier Li, urbanization is an important focus of China’s development in the next five years. Based on data from the National Bureau of Statistics of China (NBS), China’s urbanization rate rose from 47.0% in 2008 to 53.7% in 2013, primarily driven by the government’s policy of actively relocating rural residents to urban areas. According to the NBS, urbanization will continue to increase as rural residents migrate to cities to provide labour for the processing and service industries. As a result, China’s urbanization rate is expected to reach 58.9% by 2017 and 70% by 2030. Urban disposable income has been growing at a 10-year CAGR of 11.1%, and rising urbanization rate will keep this on the growth track. The Boao Review forecasts the middle class in China will grow from over 100m currently to more than 400m (accounting for 30-40% of China’s total population) in the next 10 years, and the resultant spending power is extremely significant.

Figure 8: China's retail sales growth

Source: iFind

0%

5%

10%

15%

20%

25%

0

5

10

15

20

25

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

CNYt China's retail sales % Change (RHS)

Continued urbanization is one of the key impetuses to support growth in retail sales and e-commerce.

July 23, 2014 6

China Logistics

Figure 9: China's urbanization rate

Source: iFind

The government has consistently emphasized the importance of supporting domestic consumption as the growth engine of the country, shifting away from using FAI as the driver of economic expansion. Between 2003 and 2012, consumption as a percentage of total GDP increased from 35.8% to 55%. However, China still significantly lags the US in terms of chain store sales. In the US, roughly 65% of total retail sales are chain store sales but the figure for China is just 10%, implying huge room for growth.

Figure 10: e-commerce revenue growth

Source: iFind

Figure 11: e-commerce revenue breakdown

Source: 100EC.CN

0

10

20

30

40

50

60

1956 1961 1965 1969 1973 1978 1982 1986 1990 1995 1999 2003 2007 2012

(%)

0%

5%

10%

15%

20%

25%

30%

35%

0

2

4

6

8

10

12

14

16

18

20

2008 2009 2010 2011 2012 2013 2014E 2015E 2016E

CNYt China's e-commerce revenue % Change (RHS)

B2B 80.4%

online retail sales 17.6%

online group purchase

0.6%

others 1.4%

In the US, roughly 65% of total retail sales are chain store sales but the figure for China is just 10%, implying huge room for growth.

July 23, 2014 7

China Logistics

China’s e-commerce market has grown rapidly at a CAGR of 22.5% in 2009-2013. In FY13, the total turnover of China’s e-commerce market reached CNY10.2t, up 29.9% YoY. Of this, 80.4% was generated from B2B, 17.6% from online retail and 0.6% from online group purchases. Online retail sales momentum is strong, which grew at a CAGR of 84% between 2006 and 2013 and are forecast to double to CNY3.8t in the next three years. In China, there is a rapid adoption of online purchasing, with online retail sales accounting for 8.04% of total retail sales of consumer goods. This is expected to reach 9.8% in FY14F. However, this cannot be considered as particularly high when compared with the developed countries, which have online retail sales representing between 5% and 15% of total retail sales. Apart from well-known local names like Taobao and TMall in China, there are abundant online stores in China spanning various products and services. For example, VIP Shop, JD.com and Yihaodian.

Figure 12: B2B market breakdown Figure 13: B2C market breakdown

Source: 100EC.CN Source: 100EC.CN

Figure 14: Online retail sales in China Fig 15: Online retail sales as a percentage of total retail sales

Source: iResearch Source: iFind, iResearch

With the rise in online purchases, the logistics operating models for retailers have also changed over time, creating opportunities for 3PL operators. The increase in complexity of transactions and rise in the demand for speedy and accurate deliveries underpinned the need for quality logistics services. These have led to a growth in demand for new e-fulfillment facilities, instead of traditional storage-oriented warehouses, and a rise in value-added services like sorting, labeling, packaging and returns handling, for example. In our view, this will stimulate growth prospects for 3PL operators, and open up further areas into which these operators can expand.

Alibaba 44.5%

Mysteel 10.6%

Global Sources

7.1%

hc360 3.6%

Made-in-China 2.4%

GMC 1.7%

Toocle 1.3%

Others 28.8%

Tmall 50.1%

Jingdong 22.4%

Suning Egou 4.9%

QQ mall 3.1%

Joyo amazon 2.7%

YHD 2.6%

Vipshop 2.3%

Dangdang 1.4%

Gome 0.4%

Vancl 0.2%

Others 9.9%

26 56 128 263 498

774

1,300

1,850

2,420

3,119

3,790

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000CNY b

1.18%

2.10%

3.22%

4.27%

6.28%

7.89%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2008 2009 2010 2011 2012 2013

China’s e-commerce market has grown rapidly at a CAGR of 22.5% in 2009-2013.

July 23, 2014 8

China Logistics

Figure 16: The evolution of retail logistics

Source: Jones Lang LaSalle

Another area of rapid growth is domestic express services. Over the past five years, China’s domestic express volume has increased by a CAGR of 37.7% on the back of the boom in e-commerce transactions. According to 100EC.cn, China became the second largest express market in the world in 2013, with a total volume of 9.19b packages handled and the total express industry revenue reached CNY144.2b. Deloitte forecasts express industry revenue will reach CNY280b in 2015, translating into a CAGR of 39.3% between 2013 and 2015. The industry, however, except the state-owned EMS, is dominated by a few private-owned domestic express companies, for example, SF Express (www.sf-express.com), Shentong Express (www.sto.com), Yuantong (www.yto.net.cn), Zhongtong (www.zto.cn), Best Express (www.htky365.com) and Yunda (www.yundaex.com). Industry concentration is comparatively high and the top 10 players have a combined business volume that accounts for 87% of the overall industry in China. Generally speaking, the bigger and more comprehensive logistics companies are not as competitive as the smaller private enterprises, given the less flexible cost structure, hence cost competitiveness, of the former.

Over the past five years, China’s domestic express volume has increased by a CAGR of 37.7% on the back of the boom in e-commerce transactions.

July 23, 2014 9

China Logistics

Figure 17: China express delivery volume and growth rate

Source: iFind

Figure 18: China express revenue and growth

Source: iFind

Figure 19: Market share breakdown for China domestic express

Source: 100EC.cn

0%

10%

20%

30%

40%

50%

60%

70%

0

1

2

3

4

5

6

7

8

9

10

2007 2008 2009 2010 2011 2012 2013

CNY b Express delievery volume % Change (RHS)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

20

40

60

80

100

120

140

160

2008 2009 2010 2011 2012 2013

CNY b Express sector revenue % Change (RHS)

EMS 22%

SF Express 20%

Shentong 12%

Yuantong 10%

Yunda 8%

Zhongtong 6%

Others 22%

July 23, 2014 10

China Logistics

Figure 20: Domestic express volume market concentration over past five years

Source: China's Express Sector Development Report 2014

Figure 21: Development history of major express enterprises in China

Source: Deloitte

Another rapidly developing e-commerce market is the cross-border purchases by individual consumers in China. This is termed as “Haitao”, which effectively means overseas Taobao. Through Haitao, Chinese consumers are buying products from overseas websites and then entrusted logistics companies handle the transportation, customs clearance and delivery to China. According to the China e-commerce Research Center, the market size of Haitao increased at a CAGR of 83.7% between 2010 and 2013. For 2013, the total market size amounted to CNY74.4b. The rapid growth in the Haitao market, supported by the improvement in spending power and the rise in demand for quality products, has led to the rise in demand for reliable logistics arrangements for the products purchased overseas. This represents a huge market up for grabs by just a few companies that have the extensive international and domestic logistics networks and relation with major retailers overseas.

77.0%

70.3% 67.2%

62.9%

55.4%

85.0% 82.7%

86.5% 85.6% 83.3%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

90%

2009 2010 2011 2012 2013

CR4 CR8

The market size of Haitao increased at a CAGR of 83.7% between 2010 and 2013. For 2013, the total market size amounted to CNY74.4b.

July 23, 2014 11

China Logistics

Figure 22: Haitao process (overseas online purchases by Chinese individuals)

Source: www.tdpyh.com

2) Manufacturing relocations There are numerous studies that discuss the trend of migration of manufacturing facilities from coastal China to inland provinces so we will not elaborate here. In fact, this trend has been a prevailing one over the past five years, particularly during a period when the renminbi appreciated significantly, which further amplified operating costs for the Chinese manufacturers for foreign buyers. This structural trend has boosted the economies of many inland provinces and areas. For example, the GDP growth of Chongqing reached a CAGR of 14.9% in the past five years, while Sichuan’s was 13.4%, outperforming 8.9% for China’s GDP. Manufacturing relocations will give rise to significant change in the logistics for transportation and storage of raw materials and components and the distribution of finished products to domestic and overseas customers. We believe such procurement and distribution services will translate into profit opportunities for sophisticated logistics services.

Manufacturing relocations will give rise to significant change in the logistics for transportation and storage of raw materials and components and the distribution of finished products to domestic and overseas customers.

July 23, 2014 12

China Logistics

Figure 23: Five-year CAGR in industrial output by province

Source: NBSC

Figure 24: Five-year CAGR in GDP by province

Source: iFind

6.9% 7.4%

8.4% 9.1% 9.2% 9.2% 9.4% 9.7% 10.0% 10.2% 10.3% 10.6%

11.6% 12.0% 12.0% 12.1% 12.2% 12.4% 12.7% 12.8% 13.0% 13.1% 13.2% 13.2% 13.3% 13.6% 13.8%

14.3% 14.4% 14.5% 14.6% 14.9%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0%

ShanghaiBeijing

ZhejiangHeilongjiang

GuangdongHebei

HainanNational industrial output

XinjiangShandongLiaoningJiangsuGansu

YunnanNingxia

TibetJilin

ShanxiInner Mongolia

HenanFujian

GuizhouQinghaiShaanxiJiangxiHunanHubei

SichuanGuangxiTianjin

AnhuiChongqing

6.67% 6.70% 6.96%

7.36% 7.73%

8.18% 8.42% 8.50% 8.59% 8.61% 8.82% 9.01% 9.07% 9.27% 9.28% 9.39% 9.42% 9.45% 9.48% 9.61% 9.63% 9.66% 9.81% 9.86% 9.99% 10.09% 10.23% 10.33% 10.39% 10.63%

11.69% 11.85%

0% 2% 4% 6% 8% 10% 12% 14%

ShanghaiBeijing

National GDPZhejiang

GuangdongHebei

ShandongHeilongjiang

JiangsuHenan

LiaoningXinjiang

ShanxiNingxiaHainanJiangxiGansu

JilinGuangxi

FujianHunanTibet

Inner MongoliaHubeiAnhui

YunnanQinghaiShaanxiSichuanGuizhou

ChongqingTianjin

July 23, 2014 13

China Logistics

Besides relocations within China, there are also companies seeking to move outside of China. Based on a survey carried out by Agility in 2013, 63% of the respondents agree there is a trend for moving production away from China.

Figure 25: Trend for moving production away from China

Source: Transport Intelligence

In the same survey by Agility, 22% of companies that intend to move away from China choose Vietnam as the number one preferred destination, with India as the second (12%). However, this was before the outbreak of the anti-Chinese protests and political standoff between Vietnam and China. With the recent social and political unrest in South East Asian countries like Vietnam and Thailand, we will potentially see more manufacturers returning to China as the country has enjoyed significantly better political and social stability. We believe this will benefit the supply chain management companies in China. In fact, despite complaints of rising manufacturing costs in China, the country is still ranked first in terms of logistics attractiveness in the Agility Emerging Market Logistics Index. China, with a score of 8.11, is still way ahead of the second-place Brazil, which has a score of just 6.8. We take this an indication of the continued promising outlook for logistics demand in China.

Figure 26: Destinations of production shifts away from China

Source: Transport Intelligence

Strongly agree 15.43%

Agree 48.15%

Neither agree nor disagree

24.23%

Disagree 11.27%

Strongly Disagree

0.93%

22.05%

12.40% 10.72% 10.27%

6.31% 5.86% 5.78% 3.65% 3.42% 3.04%

0%

5%

10%

15%

20%

25%

22% of companies that intend to move away from China choose Vietnam as the number one preferred destination, with India as the second (12%).

July 23, 2014 14

China Logistics

Figure 27: Agility Emerging Market Logistics Index

Source: Transport Intelligence

3) Increase in enterprise outsourcing We believe a major growth opportunity for the logistics industry is the outsourcing of companies’ logistics requirements to 3PL providers. As we said earlier, many domestic and multinational companies are still managing their logistics requirements in-house. Despite this, we continue to see logistics outsourcing as a long-term structural trend. We estimate only about 20-30% of corporates in China currently outsource their logistics requirements to 3PL providers, which is significantly below the average of 60-80% for developed countries. Further pressure to cut logistics costs and to raise profitability will present huge room for growth for 3PL operators.

According to the PwC survey, across various segments of the logistics value chain, companies have between 23% and 63% of their requirements managed internally. The segment that has the lowest proportion of internal management (effectively the highest outsourcing) is transport and the highest (effectively the lowest outsourcing) is supply chain monitoring. This is understandable as it is comparatively difficult and costly for companies to maintain their own trucking fleet with an optimal utilization level. Meanwhile, it is relatively easy for companies to maintain their own proprietary supply chain information system given their extensive access to in-house production and distribution information. However, it is interesting to note that on average, companies still manage close to 40% of their logistics requirements internally, based on the result of this survey.

6.01

6.09

6.14

6.45

6.5

6.59

6.75

6.77

6.8

8.11

0 1 2 3 4 5 6 7 8 9

Turkey

Mexico

Malaysia

Russia

UAE

Indonesia

India

Saudi Arabia

Brazil

China

We believe a major growth opportunity for the logistics industry is the outsourcing of companies’ logistics requirements to 3PL providers.

July 23, 2014 15

China Logistics

Figure 28: Internal and external management of logistics processes

Source: PWC Logistics in China

Most of the logistics functions that enterprises outsource are customs clearance and transport management. These are areas where the logistics companies have clear advantages due to their knowledge about the local requirements and their ability to achieve economies of scale. Meanwhile, this also shows that a lot of room exists for 3PL companies to gain outsourcing businesses from providing more complex logistics solutions (like supply chain monitoring and warehousing) to multi-national and domestic companies.

Across various key industries, the proportion of enterprises that utilize the services by contract logistics providers is still quite low. On average, this proportion is only 27% for retail consumer goods, automotive, construction and plant engineering, mechanical engineering and chemicals industries combined. Some companies suggest the key reasons for NOT outsourcing are worries 3PL operators do not comply with security or environmental requirements and that there will be leakage of knowledge and technical knowhow. We believe, over the long run, these issues can be resolved with the improving quality of 3PL providers and the rise in standard of intellectual property protection, generating excellent growth potential for contract logistics companies in China.

Figure 29: Awarding of contracts to logistics providers by industry

Source: PWC Logistics in China

23%

28%

44%

63%

35%

36%

20%

8%

36%

27%

9%

13%

6%

9%

27%

16%

0% 20% 40% 60% 80% 100%

Transport management

Customs clearance

Warehousing

Supply chain monitoring

InternalExternal,Chinese logistics companiesExternal, non-Chinese logistics companiesUnknown, n/a, does not apply to our company

*24% *36% *7% *12%

26%

24%

32%

26%

28%

72%

74%

64%

66%

70%

2%

2%

4%

8%

2%

Chemicals

Mechanical engineering

Construction, plantengineering

Automotive

Retail and consumer goods

Yes No Unknown, n/a

There is a lot of room for 3PL companies to gain outsourcing businesses from providing more complex logistics solutions (like supply chain monitoring and warehousing) to multi-national and domestic companies.

July 23, 2014 16

China Logistics

4) Rise in demand for value-added services The logistics industry has developed from offering plain vanilla transportation services (like sea and air freight forwarding) to increasingly comprehensive supply chain management services over the past 10 years. We expect the demand for even more advanced and value-added services to drive the future evolvement of the logistics ecosystem. For example, packaging, materials recycling and procurement are popular services being outsourced to external providers. There is, however, still a lot of room for logistics companies in China to extend to other services like returns management, assembly and complaints handling. In fact, these are very common services being offered by logistics companies to their customers in developed countries, but are still in their relative infancy in China.

Figure 30: Awarding of contracts to logistics providers by services

Source: PWC Logistics in China

On the storage front, one additional area of growing importance is cold chain service. According to the China Cold Chain Logistics Alliance, the market for China’s cold chain demand is expected to grow at a CAGR of 25% to CNY470bn in 2017. Specifically, cold chain services include the provision of temperature-controlled storage and distribution, refrigerated and frozen transportation, less-than-truckload transportation, food packaging services, and food quality testing and consulting services. A key type of customer cold chain logistics serves is online food sales.

Currently, online food sales account for only a small percentage of total grocery sales globally. For example, it is about 3.8% in UK. However, we think the trend will continue to rise as more advanced technologies are developed to preserve the freshness of food and produces. Several dedicated B2C e-commerce websites have been developed in China, catering specifically to online food retailing, particularly fresh foods. These include www.womai.com (我买网 ), www.sfbest.com (优选网 ), www.benlai.com (本来网), www.itruelife.com (正大天地网) etc. The rise in offline-to-online fresh food sales will mean an expansion in dedicated multi-temperature (for example, frozen/chilled/constant/normal) e-fulfillment centres and temperature-controlled delivery services. Such demand for value-added logistics services is expected to drive further boom in the logistics industry.

9%

15%

25%

28%

31%

35%

37%

43%

43%

56%

None, Unknown, n/a

Complaints handling

Assembly

Manufacturing

Returns management

Repairs and spare-parts supply

Packing

Procurement

Materials recycling

Packaging

We expect the demand for even more advanced and value-added services to drive the future evolvement of the logistics ecosystem.

The market for China’s cold chain demand is expected to grow at a CAGR of 25% to CNY470bn in 2017.

July 23, 2014 17

China Logistics

Figure 31: Cold chain logistics flow

Source: www.kelvincoldchain.com

Another area that logistics companies can expand into is on-site repair and return processing centres. According to PwC, repairs and spare parts supply and returns management are the two areas that attracted relatively low proportion of outsourcing to 3PL companies, as they are at 35% and 31% only. This is especially low when compared to 56% for packaging.

Figure 32: Potential for contract logistics providers

Source: PWC Logistics in China

On-site repair is a service logistics companies offers to a manufacturer to handle repair requests by the manufacturer’s customers. This involves the employment of skilled teams who work in the logistics facility to repair returns, defects or products under warranty period. These products are mostly consumer electronics and telecommunication products.

Returns processing, which is also referred to as ‘reverse logistics’, involves the movement in a direction backward to the supply chain network. Some 3PL providers see that up to 7% of an enterprise's gross sales are captured by return costs and the 3PL companies may realize 12% to 15% profits on this return processing business.

12%

16%

20%

23%

32%

37%

39%

40%

Sales planning

Accounting and settling accounts

Manufacturing

Order management

Complaints handling

Procurement management

Quality control

Returns management

Another area that logistics companies can expand into is on-site repair and return processing centres.

July 23, 2014 18

China Logistics

Figure 33: Reverse logistics flow

Source: ZeroWIN wiki

5) Upgrade in facility quality Although there is plenty of warehouse space in China, most is sub-quality with minimal capability of providing value-added services to cater to the growing demand for comprehensive logistics. In addition, China still lags the US significantly in terms of warehouse space. It is estimated the supply of logistics facilities per capita in the US is 5.06 sqm, some 12x more than China at just 0.41 sqm. As mentioned, much of China’s warehouse space is of inferior quality and unable to keep up with the needs of the increasingly affluent and demanding consumers in China.

Figure 34: Supply of logistics facilities in the US vs China

Source: Global Logistics Properties

According to Global Logistics Properties, out of the 550m sqm of logistics facilities in China, only 100m sqm are of modern quality. This implies over 75% of China’s warehouses do not meet modern logistics requirements and will face demolition. Modern logistics facilities normally provide large floor plates, high ceilings, enhanced safety systems and advanced IT systems, which the sub-quality facilities are unable to provide.

The current e-commerce boom has given rise to a new breed of logistics facilities. According to Jones Lang LaSalle, there are three distinct types of these logistics facilities: 1) mega e-fulfillment centres where merchandise are stocked and picked at an item level; and are either operated by the retailer or a logistics service provider on a 24/7 basis; 2) parcel hubs/sorting centres, which sort orders by zip or post codes so they can be

0.41

5.06

0.0

1.0

2.0

3.0

4.0

5.0

6.0

China US

12X

Many of China’s warehouse space is of inferior quality and unable to keep up with the needs of the increasingly affluent and demanding consumers in China.

July 23, 2014 19

China Logistics

delivered to the relevant parcel delivery centre for final delivery to the customer’s home or designated collection point; and 3) parcel delivery centres, which handle the ‘last-mile’ delivery to customers. These sophisticated and state-of-the-art facilities are not something the current huge inventory of warehouses in China can provide.

Figure 35: Types of logistics facilities

Source: Jones Lang LaSalle

Another booming trend is the rise in demand for specialized logistics facilities, for example, temperature-controlled facilities for the pharmaceutical and medical industries, and for perishable products. Sub-quality warehouses will be unable to provide customers with value-added services and cater to more complex logistics demands. As such, we envisage continued high utilization for quality facilities and expect to see further development of more comprehensive logistics centres and aggressive facilities upgrades. For example, KLN has upgraded some of its old-fashion warehouses (godowns) into cold chain storages/data centres/medical packaging facilities; and has subsequently increased the company’s return on these assets.

Another booming trend is the rise in demand for specialized logistics facilities, for example, temperature-controlled facilities for the pharmaceutical and medical industries, and for perishable products.

July 23, 2014 20

China Logistics

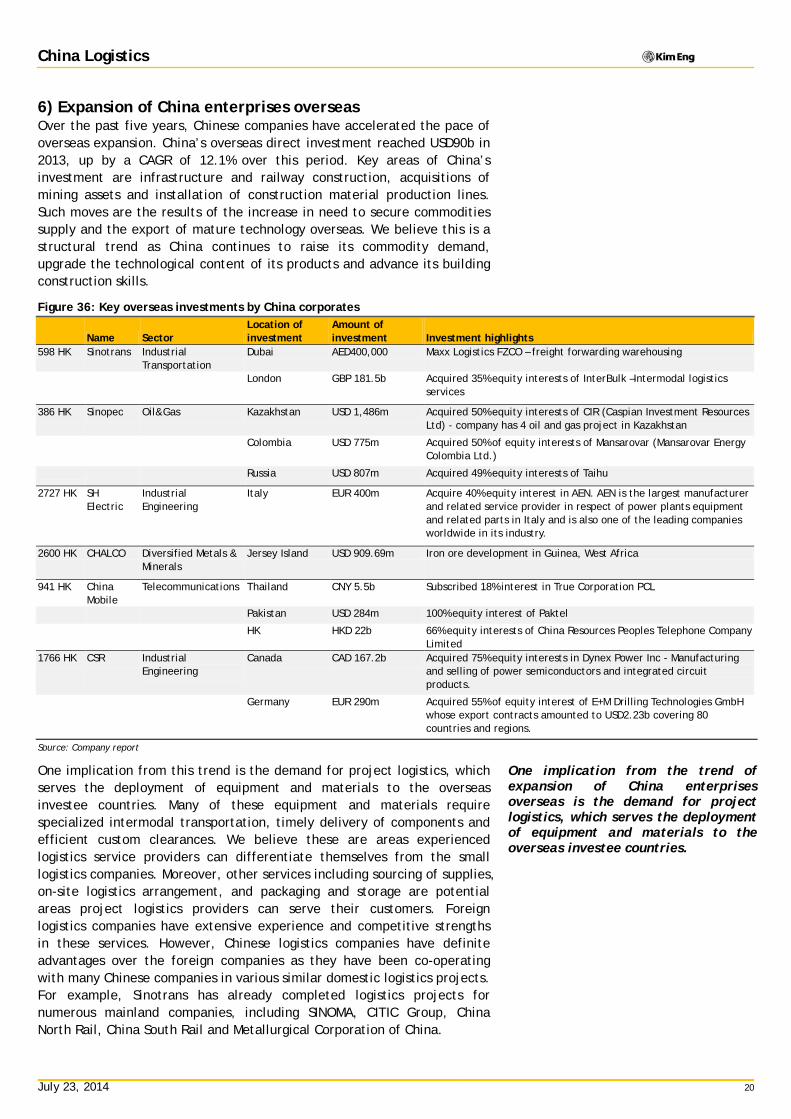

6) Expansion of China enterprises overseas Over the past five years, Chinese companies have accelerated the pace of overseas expansion. China’s overseas direct investment reached USD90b in 2013, up by a CAGR of 12.1% over this period. Key areas of China’s investment are infrastructure and railway construction, acquisitions of mining assets and installation of construction material production lines. Such moves are the results of the increase in need to secure commodities supply and the export of mature technology overseas. We believe this is a structural trend as China continues to raise its commodity demand, upgrade the technological content of its products and advance its building construction skills.

Figure 36: Key overseas investments by China corporates

Name Sector Location of investment

Amount of investment Investment highlights

598 HK Sinotrans Industrial Transportation

Dubai AED400,000 Maxx Logistics FZCO – freight forwarding warehousing

London GBP 181.5b Acquired 35% equity interests of InterBulk –Intermodal logistics services

386 HK Sinopec Oil&Gas Kazakhstan USD 1,486m Acquired 50% equity interests of CIR (Caspian Investment Resources Ltd) - company has 4 oil and gas project in Kazakhstan

Colombia USD 775m Acquired 50% of equity interests of Mansarovar (Mansarovar Energy Colombia Ltd.)

Russia USD 807m Acquired 49% equity interests of Taihu

2727 HK SH Electric

Industrial Engineering

Italy EUR 400m Acquire 40% equity interest in AEN. AEN is the largest manufacturer and related service provider in respect of power plants equipment and related parts in Italy and is also one of the leading companies worldwide in its industry.

2600 HK CHALCO Diversified Metals & Minerals

Jersey Island USD 909.69m Iron ore development in Guinea, West Africa

941 HK China Mobile

Telecommunications Thailand CNY 5.5b Subscribed 18% interest in True Corporation PCL

Pakistan USD 284m 100% equity interest of Paktel

HK HKD 22b 66% equity interests of China Resources Peoples Telephone Company Limited

1766 HK CSR Industrial Engineering

Canada CAD 167.2b Acquired 75% equity interests in Dynex Power Inc - Manufacturing and selling of power semiconductors and integrated circuit products.

Germany EUR 290m Acquired 55% of equity interest of E+M Drilling Technologies GmbH whose export contracts amounted to USD2.23b covering 80 countries and regions.

Source: Company report

One implication from this trend is the demand for project logistics, which serves the deployment of equipment and materials to the overseas investee countries. Many of these equipment and materials require specialized intermodal transportation, timely delivery of components and efficient custom clearances. We believe these are areas experienced logistics service providers can differentiate themselves from the small logistics companies. Moreover, other services including sourcing of supplies, on-site logistics arrangement, and packaging and storage are potential areas project logistics providers can serve their customers. Foreign logistics companies have extensive experience and competitive strengths in these services. However, Chinese logistics companies have definite advantages over the foreign companies as they have been co-operating with many Chinese companies in various similar domestic logistics projects. For example, Sinotrans has already completed logistics projects for numerous mainland companies, including SINOMA, CITIC Group, China North Rail, China South Rail and Metallurgical Corporation of China.

One implication from the trend of expansion of China enterprises overseas is the demand for project logistics, which serves the deployment of equipment and materials to the overseas investee countries.

July 23, 2014 21

China Logistics

7) More favourable government policies The Chinese government has been supportive of the logistics industry given the vast growth opportunities. Over the past few years, support policies have included tax cuts, the reduction in toll charges, encouraging private investment, and simplification of regulatory procedures for project approvals, financing, investment and cargo handling etc. These policies have achieved various degrees of success but there is still room to improve the industry outlook.

In 2009, the government promulgated the “Plan for the adjustment and rejuvenation of the logistics industry” but the pace and success of this programme has been less than encouraging. Since 2013, the move to replace business taxes with VAT has reduced the tax burden of some logistics and related companies. In early Jun’14, the government issued the “medium- to long-term plan for logistics industry development”, aiming at setting up a framework for the development of the industry. The key targets under the plan are to reduce logistics costs, promote the scale of logistics service providers and improve logistics infrastructure. We believe the government will continue to support the industry, which will be positive for the development of the logistics industry by accelerating the growth outlook and encouraging healthy consolidations.

We believe the government will continue to support the industry, which will be positive for the development of the logistics industry by accelerating the growth outlook and encouraging healthy consolidations.

July 23, 2014 22

China Logistics

Figure 37: Key government support policies Date Policy Key points Government policies in recent years 2009 The logistics industry restructuring and revitalization plan

《物流业调整和振兴规划》 Actively expand market demand for logistics services Promote professionalism of logistics service Encourage M&A Encourage development of international logistics and Free Trade Zones

2010 Development plan for cold chain logistics of agriculture products《农产品冷链物流发展规划》

Promote modern cold chain logistics concept and technology Perfect cold chain logistics standard system Accelerate development of 3PL enterprises in cold chain logistics Enhance infrastructure construction Accelerate equipment upgrade

2011 Development plan for commercial logistics 《商贸物流发展专项规则》

Perfect commercial logistics network geographical layout in China Strengthen logistics infrastructure construction Enhance commercial logistics innovation Promote green logistics Promote cross-border cooperation

2012 Encourage and guide private investment into logistics industry《关于鼓励和引导民间投资进入物流领域的实施意

见》

Encourage private investment in 3PL industry Improve regulatory system by improve logistics companies’ qualification

management, simplify operating procedures Reduce tax burden for private enterprises, improve financing conditions for

private enterprises as well as reform land & property policies to attract more private investment

Favorable government policies in FY13 Jan-13 Guideline for the development of city delivery

《全国城市配送发展指引》 Aim to improve efficiency through logistics operation and delivery system

upgrade. The guideline has confirmed 15 cities for pilot programme, with supporting funds granted

Apr-13 On further advancing the freight organization reform 《关于进一步推进货运组织改革的意见》

Simplify procedures for cargo handling Regulating toll charges on roads Develop door-to-door service in railway transportation, implement fixed prices

Jun-13 Notice on carrying out the e-commerce integration innovation pilot project 《关于开展电子商务集成创新试点工程工作的通知》

Enhance e-commerce and supply chain information in large enterprises Innovation in industry e-commerce platform services Cross-border e-commerce Mobile e-commerce Product information traceability

Jun-13 The 2013-2030 plan for national roadway 《国家公路网规

划(2013 年-2030 年)》 Provincial capitals distant within 1,000 km can be reached on same day. Improve the national roadway coverage area and enhance coherence. Scale of national roadway to reach 265,000 km Scale of national highway to reach 118,000 km

Aug-13 Special action program on the integration of information technology and industrialization 《工业和信息化部关于印

发信息化和工业化深度融合专项行动计划(2013-2018 年)

的通知》

Improve creative integration of in e-commerce and logistics Penetrate the use of e-commerce in key industries Promote new type of producer services with core of 3PL, e-commerce

platform

Aug-13 Plan on speeding up the Yangtze River shipping development 《交通运输部关于印发加快推进长江等内核水

运发展行动方案(2013-2020 年)的通知》

Speed up the channel construction for inland river Promote inland river transportation service upgrade enhance technology innovation and information construction elevate industry management and public service level

Sep-13 Notice on the printing of National logistics park development plan 《关于印发全国物流园区发展规划的通

知》

This is the continuation and developed plan based on the "Specific plan for national logistics standards" issued in 2009. It proposed the resource integration and rational distribution of logistics parks. Enhance information construction and services provided in logistics parks.

Nov-13 Outline for building the transportation logistics public information platform 《交通运输物流公共信息平台建设纲

要》

Aiming to launch a logistics information exchange web and web portal with nationwide coverage. Major function of this platform is for exchange and public information service.

Dec-13 Business Tax Reform to Levy VAT Pilot for Railway Transport and Postal Service Industries 《关于将铁路运输

和邮政业纳入营业税改征增殖税试点的通知 》

International cargo transportation agency services can enjoy preferential business tax, exempt from VAT.

An 11% tax rate will be adopted for railway transport and postal service industries as the railway transport industry pilot programme.

Delivery service is also under the pilot programme, enjoy a tax rate of 6%. Special region can enjoy tax refund policy(i.e. pilot bonded-zone)

Dec-13 Notice issued by the State Concil on investment projects subject to government approval《国务院关于发布政府核准

的投资项目目录的通知》

After the revision of the catalog, projects needed for central government approval has reduced by 60%. Decentralization of approval authority for transportation infrastructure such as metro communication projects, post projects, and partial railway projects, roadway projects , and container terminal projects, etc.

Source: CFLP, NDRC

July 23, 2014 23

China Logistics

Competitive market landscape The 3PL market in China is highly fragmented, with over 10,000 service providers competing against each other, based on estimates by Armstrong and Associates. Many of these companies are SMEs and only provide services in one province or are just involved in one or two business segments. In 2012, 3PL revenue for Greater China was USD126b, with Sinotrans being the largest provider (6%), followed by DHL Supply Chain & Global Forwarding (1.9%) and KLN (1.3%). Given the fragmented industry, the top five 3PL players combined accounted for just around 11% of total market share in China. Even for the express service companies with a higher industry concentration, there are still more than 8,000 express enterprises in the China, according to estimates by Deloitte.

Figure 38: Greater China 3PL market share breakdown

Source: Armstrong

The low market concentration should prompt more M&A and market consolidation. The need for higher efficiency and government policy is the supportive factor to drive a rise in industry concentration. Over the past six years, the logistics industry in China has had 248 M&A transactions with a total value of USD2.5b. The M&A peak was in 2010, with 47 deals at a total value of USD915m; while the trough was 2012 with just 25 deals and a total value of just USD193m. Both volume and value for the past three years (2011-2013) have lagged 2008-2010. However, we expect M&A to pick up going forward. Many PEs/VCs entered into the industry over the past 10 years and with the improvement in profitability of the investee companies, we see increasing opportunities for exit by these PE/VCs, providing more M&A opportunities. We also see a rise in competition, for example unit price, in China’s express market has come down by 13%, 31% and 43% for cross-region, intra-city and international deliveries. This should open more room for M&A as enterprises are keen to improve their competitive position. All in all, we foresee a rise in industry concentration to represent a positive improve on industry profitability.

Sinotrans 6.0%

DHL Supply Chain & Global

Forwarding 1.9%

Kerry Logistics 1.3%

CEVA Logistics 1.0%

Expeditors International of

Washington 1.0%

Others 88.8%

We foresee a rise in industry concentration to represent a positive improve on industry profitability.

July 23, 2014 24

China Logistics

Figure 39: M&A amount and volume of logistics industry per year

Source: China's Express Sector Development Report 2014

Stock recommendations While these trends are the main drivers for sector growth, the benefits to individual logistics companies are different. In our view, Sinotrans will reap the most given its strong China presence and significant room to upgrade services. It also has a unique edge of serving Chinese companies on project logistics as they further expand overseas.

As for China Merchants (CM), we expect its Americold JV to gain from the rise in cold chain demand in China, while its bonded port zones should also grow on the back of the increase in logistics demand. However, as their combined profit accounts for only 6.5% of FY14F earnings (the slower-growth port business makes up 77%) we believe CM has yet to turn into a full-fledged logistics player in China.

KLN’s extensive presence in the region is a competitive edge, but it will be in a weaker position compared with Sinotrans for the Chinese, especially state-owned, enterprises. KLN’s portfolio of warehouses in Hong Kong (which accounts for 26.8% of its FY14F segment profit) is likely to hold back the company from growing rapidly due to the slower earnings growth of this business.

Figure 40: Comparative benefits from the key drivers Key drivers Sinotrans CM KLN e-commerce XXX XX XXX Manufacturing relocation XXX XX XXX 3PL outsourcing XXX X XXX Value-added services XXX X XX Facility upgrades XX XX XXX China enterprises overseas expansion XXX XX X Government policies XXX XX XX Source: Maybank Kim Eng Note: XXX = Highly benefited, XX = Moderately benefited, X = Lightly benefited

Given the numerous business lines of these diversified logistics companies, we derive our target price for all of them based on their SOTP. At the current share prices, Sinotrans is trading on 22.7% discount to its FY15F SOTP value, followed by 15.4% discount for CM and 3.2% discount for KLN. In terms of PEG, Sinotrans rated the best at 0.59x, followed by 1.45x for CM and 2.15x for CM. Summing up, these valuation metrics support our preference ranks of: 1.) Sinotrans, 2.) CM and 3.) KLN.

0

10

20

30

40

50

60

0

100

200

300

400

500

600

700

800

900

1,000

2008 2009 2010 2011 2012 2013 1Q14

USD m Amount Volume

Top pick still Sinotrans and CM is an alternative play. KLN’s growth is slow and valuations stretched, initiate at HOLD

July 23, 2014 25

China Logistics

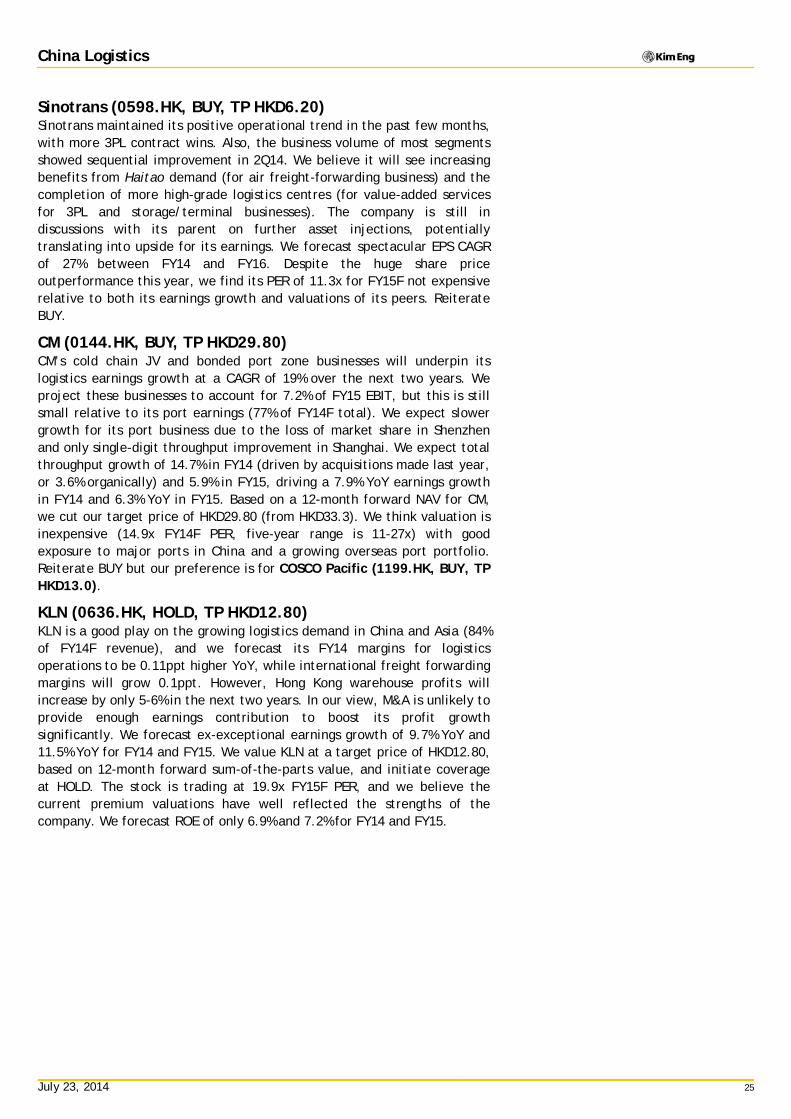

Sinotrans (0598.HK, BUY, TP HKD6.20) Sinotrans maintained its positive operational trend in the past few months, with more 3PL contract wins. Also, the business volume of most segments showed sequential improvement in 2Q14. We believe it will see increasing benefits from Haitao demand (for air freight-forwarding business) and the completion of more high-grade logistics centres (for value-added services for 3PL and storage/terminal businesses). The company is still in discussions with its parent on further asset injections, potentially translating into upside for its earnings. We forecast spectacular EPS CAGR of 27% between FY14 and FY16. Despite the huge share price outperformance this year, we find its PER of 11.3x for FY15F not expensive relative to both its earnings growth and valuations of its peers. Reiterate BUY.

CM (0144.HK, BUY, TP HKD29.80) CM’s cold chain JV and bonded port zone businesses will underpin its logistics earnings growth at a CAGR of 19% over the next two years. We project these businesses to account for 7.2% of FY15 EBIT, but this is still small relative to its port earnings (77% of FY14F total). We expect slower growth for its port business due to the loss of market share in Shenzhen and only single-digit throughput improvement in Shanghai. We expect total throughput growth of 14.7% in FY14 (driven by acquisitions made last year, or 3.6% organically) and 5.9% in FY15, driving a 7.9% YoY earnings growth in FY14 and 6.3% YoY in FY15. Based on a 12-month forward NAV for CM, we cut our target price of HKD29.80 (from HKD33.3). We think valuation is inexpensive (14.9x FY14F PER, five-year range is 11-27x) with good exposure to major ports in China and a growing overseas port portfolio. Reiterate BUY but our preference is for COSCO Pacific (1199.HK, BUY, TP HKD13.0).

KLN (0636.HK, HOLD, TP HKD12.80) KLN is a good play on the growing logistics demand in China and Asia (84% of FY14F revenue), and we forecast its FY14 margins for logistics operations to be 0.11ppt higher YoY, while international freight forwarding margins will grow 0.1ppt. However, Hong Kong warehouse profits will increase by only 5-6% in the next two years. In our view, M&A is unlikely to provide enough earnings contribution to boost its profit growth significantly. We forecast ex-exceptional earnings growth of 9.7% YoY and 11.5% YoY for FY14 and FY15. We value KLN at a target price of HKD12.80, based on 12-month forward sum-of-the-parts value, and initiate coverage at HOLD. The stock is trading at 19.9x FY15F PER, and we believe the current premium valuations have well reflected the strengths of the company. We forecast ROE of only 6.9% and 7.2% for FY14 and FY15.

July 23, 2014

Com

pany

Upd

ate

COM

PAN

Y RE

SEA

RCH

|

SEE PAGE 54 FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS

Sinotrans (598 HK)

Building further momentum Reiterate BUY w/HKD6.20 TP. We upgrade FY14-16 earnings

by 0.9%/6.7%/8.3% to reflect better outlook, lower finance costs and high interest income from placement proceeds.

Strong 3PL momentum cont’d into 2Q and margins remained good; this led to our profit upgrades for this business.

Haitao should drive air freight forwarding volume while completion of over 300,000 sqm of logistics centres will boost its competitiveness.

What’s New Operational momentum for the last few months maintained the positive trend in 1Q14, with more 3PL contract wins. Business volume at most segments exhibited accelerated growth in 2Q14 sequentially. We also expect Sinotrans to see increasing benefits from the Haitao demand (for air freight forwarding business) and the completion of more high-grade logistics centers (for value-added services for 3PL and storage/terminal business). After recently acquiring CNY901m of assets from its parent at cheap valuations, Sinotrans is still having discussions on further potential injections. The 8.41% new share placement also nets Sinotrans HKD1.68b of proceeds for future expansion with slight EPS dilution.

What’s Our View We raise our earnings forecasts for FY14-16 by 0.9%/6.7%/8.3% to incorporate better 3PL and air freight forwarding outlook, lower interest expenses from the bond issue and higher interest income from the new share placement. After taking into account our higher earnings forecasts and EPS dilution, Sinotrans is still projected to achieve a spectacular 27% EPS CAGR between FY14 and FY16. We maintain our TP of HKD6.20, based on the 12-month forward SOTP value as higher earnings are offset by more outstanding shares. Despite the huge share-price outperformance, we find its 11.3x PER FY15F not expensive relative to both its EPS growth and valuations of its peers. Reiterate BUY and forecast the company to remain CNY1.7b net cash by end-FY14.

Key Data

Share Price Performance

Maybank vs Market

Share Price: HKD4.90 MCap (USD): 2.9B Hong Kong

Target Price: HKD6.20(+27%) ADTV (USD): 8M Transport (Unchanged)BUY52w high/low (HKD)

3m avg turnover (USDm)

Free float (%)

Issued shares (m)

Market capitalization

Major shareholders:

-Sinotrans & CSC Group 55.4%

-Deutsche Post AG 13.3%

-Brandes Investment Partners LP 8.0%

5.67/1.46

4,607

46.6

HKD22.6B

8.3

50

100

150

200

250

300

350

400

450

500

550

600

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

Jul-12 Nov-12 Mar-13 Jul-13 Nov-13 Mar-14

Sinotrans - (LHS, HKD) Sinotrans / Hang Seng Index - (RHS, %)

1 Mth 3 Mth 12 Mth

Absolute(%) 2.1 17.5 237.9

Relative to index (%) (0.4) 12.3 204.3

Positive Neutral Negative

Market Recs 9 0 0

Maybank Consensus % +/-

Target Price (HKD) 6.20 6.20 0.0

'14 PATMI (CNYm) 1,197 1,137 5.3

'15 PATMI (CNYm) 1,592 1,330 19.7

Source: FactSet; Maybank

FYE Dec (CNY m) FY12A FY13A FY14E FY15E FY16ERevenue 47,630.2 47,930.0 46,278.1 54,964.2 62,145.6EBITDA 1,222.0 1,611.9 1,901.3 2,403.2 2,764.3Core net profit 649.1 844.5 1,136.1 1,592.3 1,901.1Core FDEPS (CNY) 0.15 0.20 0.25 0.35 0.41Core FDEPS growth(%) 1.0 30.1 24.1 40.2 19.4Net DPS (CNY) 0.02 0.05 0.07 0.09 0.10Core FD P/E (x) 25.7 19.7 15.9 11.3 9.5P/BV (x) 1.6 1.5 1.4 1.2 1.1Net dividend yield (%) 0.5 1.3 1.7 2.2 2.6ROAE (%) 6.4 7.9 9.4 11.5 12.4ROAA (%) 2.3 2.9 3.7 4.9 5.6EV/EBITDA (x) 4.9 7.2 9.6 7.9 6.8Net debt/equity (%) net cash net cash net cash net cash net cash

Osbert TK Tang, CFA(86) 21-5096 [email protected]

Tracy Liu(86) 21 5096 [email protected]

July 23, 2014 27

Sinotrans

3PL staging good momentum Management suggested that momentum of the 3PL business in 2Q14 continued its positive trend from 1Q14, which has witnessed over 20% growth in profit across various sub-divisions like contract logistics, energy logistics and chemical logistics. Revenue from its top 10 customers rose 36% YoY in 1Q14, as logistics for more products and regions are outsourced to Sinotrans, and the trailing momentum remained solid in 2Q14. Margins for 3PL also expanded on securing more lucrative projects and increasing more value-added services to customers. We hence raise our expectations for profit contribution from 3PL and forecast this will increase by 38% in FY14 and another 39% in FY15, making this division a key growth driver.

Figure 41: Examples of Sinotrans’ supply chain services

Source: Company data, Maybank Kim Eng

Figure 42: Sinotrans’ key clients for 3PL business

Source: Company data, Maybank Kim Eng

July 23, 2014 28

Sinotrans

For example, Sinotrans has achieved positive order flows for its project logistics division. In June, it won the bid for providing logistics services to Yantai Jereh Oilfield Service Group’s Petroleos de Venezuela SA (PDVSA) Project, for the former to supply oilfield equipment totaling USD190m to PDVSA. This marks an important step for Sinotrans to expand into the South American market. Also, it provided logistics services to many media and manufacturing enterprises in the 2014 FIFA World Cup. On the regional front, Sinotrans Logistics Hong Kong — the subsidiary focused on South-East Asian markets — has experienced strong profit performance YTD. This indicates further success in its expansion outside China; and we expect the growth trend to remain solid as China’s intra-Asia trade ties continue to advance.

Figure 43: Sinotrans’ project logistics business Industry Projects

Infrastructure Construction

CITIC Construction Co., Ltd's expressway project in Algeria CITIC Construction Co., Ltd's social housing project in Angola CITIC Construction Co., Ltd's RED project in Angola China Overseas Engineering Co., Ltd's municipal facilities and stadium project in Bata City China WuYi Co., Ltd project in Kenya

Building Materials

Sinoma International Engineering Co., Ltd and Southern Province Cement Co.Ltd (SPCC)'s cement project in Saudi Arabia Nanjing Cement Design and Research Institute and Nigeria Dangote's IBESE/Obajana cement project Sinoma-Suzhou's Iraq Sulaymaniyah Cement Plant(SCP) cement project Sinoma International Engineering Co., Ltd's Ethiopia Dangote cement project

Railway Vehicle

China North Rail Co., Ltd's Hong Kong subway project China South Rail, Co., Ltd's Saudi Arabia wagon project China South Rail Co., Ltd's Australia wagon project China South Rail Co., Ltd's United Arab Emirates wagon project

Metallurgy

China Metallurgical Group Corporation’s Ramu nickel cobalt project in Papua New Guinea China Metallurgical Group Corporation’s Afghan Aynat copper mine project Capital Engineering & Research Incorporation Ltd.’s Iran Ardakan steel-making plant project CITIC International Cooperation Co., Ltd. and ThyssenKrupp CSA Siderurgica do Atlantico Ltda (CSA)'s carbonization project in Brazil

Mining

China-Union (Hong Kong) Ming Co., Ltd. (WISCO as shareholder) Liberia Bong mines project Mitsubishi Brazil fresh water valley mines project

Source: Company data, Maybank Kim Eng

Potential upside from strong air freight We think there is upside potential for Sinotrans’ air freight forwarding business. Its air freight forwarding volume increased 16.7% YoY in 5M14. Traditionally, Sinotrans uses its 64.3%-owned subsidiary Sinoair as the primary air freight forwarding sales network but it has now expanded to include its own network to sell Sinoair’s services. Besides, we believe the strong growth is partly driven by the increase in demand from Haitao. Sinotrans is exploring more speedy custom clearance arrangements for Haitao products and this should strengthen its competitiveness in this area.

July 23, 2014 29

Sinotrans

Figure 44: 5M14 operating performance vs 1Q14 Business segment (YoY volume growth) 5M14 1Q14 Freight forwarding - Sea (TEU) 5.1% 4.9% Air (tonnes) 16.7% 19.3% Shipping agency - Vessel calls 1.8% 1.7% Tonnage (m) 8.8% 9.2% Containers handled (m TEUs) 5.2% 1.6% Bulk cargo (m tonnes) 6.2% 10.4% Container yards - Containers (m TEUs) 1.5% -1.6% Bulk cargo (m tonnes) -0.4% -5.8% Terminal throughput - Containers (m TEUs) 0.1% -3.7% Bulk cargo (m tonnes) -3.6% 1.5% Marine transportation - Volume (m TEUs) 7.6% 3.2% Trucking - Volume (m TEUs) 22.9% 26.6% Source: Company data

For FY14, Sinotrans has budgeted capex of CNY2.4b and 68% of it to be invested in logistics infrastructure and storage/terminal. It will expand its current portfolio of logistics centres and we expect more logistics centres will be constructed to cater to the growing e-commerce demand. Currently, it has over 300,000 sqm of logistics centres under construction, with logistics facilities in Shenyang, Jinan, Weifang and Shenzhen Pinghu to be completed this year. Other bonded warehouses/logistics centres to be completed next year include those in Tianjin, Chongqing, Chengdu, Anhui and Changzhou. As more sophisticated facilities are built out, we believe Sinotrans will be able to offer more value-added services; realizing higher yield and margin for both its 3PL business and storage/terminal division.

Figure 45: Locations of contract logistics centers

Source: Company data

July 23, 2014 30

Sinotrans

More asset injections may come On 17 Jul, Sinotrans announced a placement of 357.5m new H shares at HKD4.80 per share, to be placed to not less than six but not more than 10 professional/institutional investors. The new shares represent 8.41% of existing share capital and the net proceeds will be deployed as general working capital. The placement is a surprise to us as Sinotrans is currently in a strong financial position but we believe the move is an opportunistic one as the share price has rallied significantly YTD. The impact on EPS, however, is mild as we only estimate 2.8% dilution for FY14 and 6.4% for FY15.

Also, in mid-June, Sinotrans issued a three-year CNY1b dim sum bond due in 2017. The issue was priced at 99.861% of the principal bond amount and carries a 4.5% coupon. We consider the equivalent funding cost of 4.76% (based on yield-to-maturity) cheap when compared with its existing borrowings at rates ranging 4.72-9.18%. Since this is the first time it has accessed the dim sum bond market, the successful issue has opened another source of funding and this will increase its flexibility in financing for future expansion.

Sinotrans announced the CNY901m asset acquisition from its parent Sinotrans & CSC on 8 Jul However, the company stated in the announcement it will continue to engage its parent in discussions regarding appropriate assets and/or business reorganization opportunities, which may result in further transactions. We think such further asset injections may include some businesses under the entrustment agreement signed in February 2014 as well as other businesses currently in the parent like rail freight forwarding, auto logistics and road logistics in various locations in China.

Earnings upgrade a driver We raise our earnings forecasts for FY14-16 by 0.9%/6.7%/8.3% to factor in stronger growth for the 3PL business and better air freight forwarding volume over the next two years. Also, we have included the impact of the finance cost savings from the dim sum bond issue and higher interest income from the new share placement. Following our revisions and taking into account the increase in outstanding shares, we project EPS to grow at a 27% CAGR between FY14 and FY16. We see this earnings momentum as encouraging and our projections have not reflected the impact of any further asset injection from the parent, which means there is potential upside to earnings in the future.

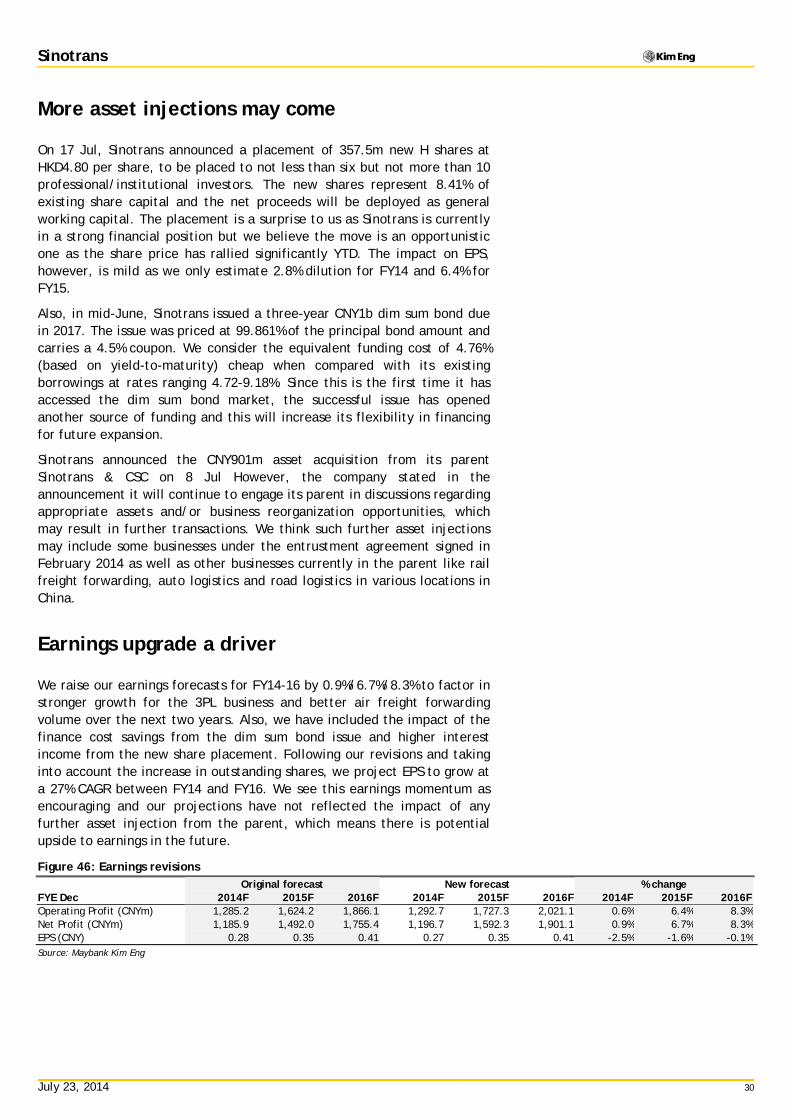

Figure 46: Earnings revisions

Original forecast New forecast % change FYE Dec 2014F 2015F 2016F 2014F 2015F 2016F 2014F 2015F 2016F Operating Profit (CNYm) 1,285.2 1,624.2 1,866.1 1,292.7 1,727.3 2,021.1 0.6% 6.4% 8.3% Net Profit (CNYm) 1,185.9 1,492.0 1,755.4 1,196.7 1,592.3 1,901.1 0.9% 6.7% 8.3% EPS (CNY) 0.28 0.35 0.41 0.27 0.35 0.41 -2.5% -1.6% -0.1% Source: Maybank Kim Eng

July 23, 2014 31

Sinotrans

Figure 47: Profit by segment Division (CNY m) 2012 2013 2014F 2015F 2016F Freight forwarding 568.2 715.1 878.3 1,198.3 1,408.1 Shipping agency 278.8 277.2 273.1 289.0 293.5 Marine transportation -257.5 -37.6 -2.4 0.0 0.0 Storage and terminals 339.2 321.4 341.2 407.2 470.5 Others -3.6 14.5 23.2 37.0 49.9 Segment result 925.1 1,290.5 1,513.4 1,931.6 2,222.0 Other gains/(losses), net -18.5 -90.0 20.6 -14.6 -1.7 Corporate expenses -223.7 -172.0 -180.7 -189.6 -199.2 Finance expenses, net -196.2 -195.9 -180.6 -102.3 -36.9 Associates 746.5 653.8 776.2 862.2 931.4 Pre-tax profit 1,233.2 1,486.4 1,949.0 2,487.2 2,915.6 Taxation -322.4 -335.7 -428.8 -547.2 -641.4 Profit for continued operations 910.8 1,150.6 1,520.2 1,940.0 2,274.2 Minority interests -261.8 -306.2 -323.5 -347.7 -373.1 Net profit 649.1 844.5 1,196.7 1,592.3 1,901.1 % Change 1.0% 30.1% 41.7% 33.1% 19.4% Source: Company data, Maybank Kim Eng

On the back of our raised earnings forecasts and the dilution from the new shares, we maintain our target price at HKD6.20, which is based on the 12-month forward sum-of-the-parts value. Despite the sharp share price outperformance, Sinotrans now trades at 15.9x FY14F PER, but this will fall to 11.3x for FY15 which we think is inexpensive. The current PER valuation is well within its historical 4-33x range since listing in FY03 and as we project record earnings for FY15, we believe it is justified for the multiple to return to the high end of the range.

Figure 48: SOTP valuation

Basis for

FY14 Value FY14 Per Share % of FY15 Value FY15 Per Share % of

Business segment valuation Multiple (CNY m) value (CNY) total (CNY m) value (CNY) total Freight forwarding PER 15.0x 8,946.4 1.94 42.7% 9,347.7 2.03 40.7% Express services PER 12.0x 5,243.8 1.14 25.0% 5,480.9 1.19 23.8% Shipping agency PER 8.0x 1,750.9 0.38 8.4% 1,857.7 0.40 8.1% Storage and terminals PER 11.0x 2,641.8 0.57 12.6% 3,217.9 0.70 14.0% Trucking and others PER 9.0x 640.2 0.14 3.1% 887.1 0.19 3.9% Net cash/(debt) 1,718.7 0.37 8.2% 2,194.0 0.48 9.5% Total asset value

20,941.8 4.55 100.0% 22,985.3 4.99 100.0%

No. of shares outstanding (m)

4,606.5

4,606.5

Per share value (CNY)

4.55

4.99 Per share value (HKD)

5.73

6.34

Current share price (HKD)

4.90

4.90 Premium/(Discount) %

-14.5%

-22.7%

Source: Maybank Kim Eng

July 23, 2014 32

Sinotrans

Figure 49: 12-month forward PER band Figure 50: 12-month forward P/BV multiple

Source: Bloomberg, Maybank Kim Eng Source: Bloomberg, Maybank Kim Eng

Figure 51: Logistics peer valuation comparison

Closing Closing Market Cap. P/E P/BV Div Yield

Ticker Company Name Currency 07/22/2014 USD (m) 2014F 2015F 2014F 2015F 2014F 2015F UPS-US United Parcel Service Inc USD 104.48 73,782 20.6 17.7 14.1 13.3 2.5% 2.7% FDX-US Fedex Corp USD 153.29 43,752 17.4 14.4 2.7 2.3 0.5% 0.6% DPW-DE Deutsche Post AG EUR 25.285 41,192 15.0 13.4 2.8 2.6 3.4% 3.8% KNIN-CH Kuehne & Nagel Intl CHF 121.3 16,134 22.4 20.5 5.8 5.4 3.7% 3.9% CHRW-US C.H. Robinson Worldwide Inc USD 65.96 9,790 23.0 20.8 10.2 9.7 2.2% 2.3% TNTE-NL TNT Express NV EUR 6.43 4,728 19.9 14.1 1.4 1.3 1.9% 2.8% PWTN-CH Panalpina Welt AG CHF 132 3,475 29.8 21.7 4.2 3.7 1.9% 2.4% TOL-AU Toll Hldgs Ltd AUD 5.42 3,650 13.7 13.3 1.4 1.4 5.1% 5.3% 636-HK Kerry Logistics Network HKD 12.74 2,779 22.1 19.9 1.5 1.4 1.0% 1.1% 598 HK Sinotrans Limited HKD 4.90 1,130 15.9 11.3 1.4 1.2 1.7% 2.2% Average

20.0 16.7 4.6 4.2 2.4% 2.7%

Source: FactSet, Maybank Kim Eng

0

1

2

3

4

5

6

7

Jan 04 Sep 05 Jun 07 Mar 09 Nov 10 Aug 12 May 14

14x

6x

8x

10x 12x

16x

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan 04 Jul 05 Jan 07 Jul 08 Jan 10 Jul 11 Jan 13 Jul 14

P/B Average +1SD -1SD

July 23, 2014 33

Sinotrans

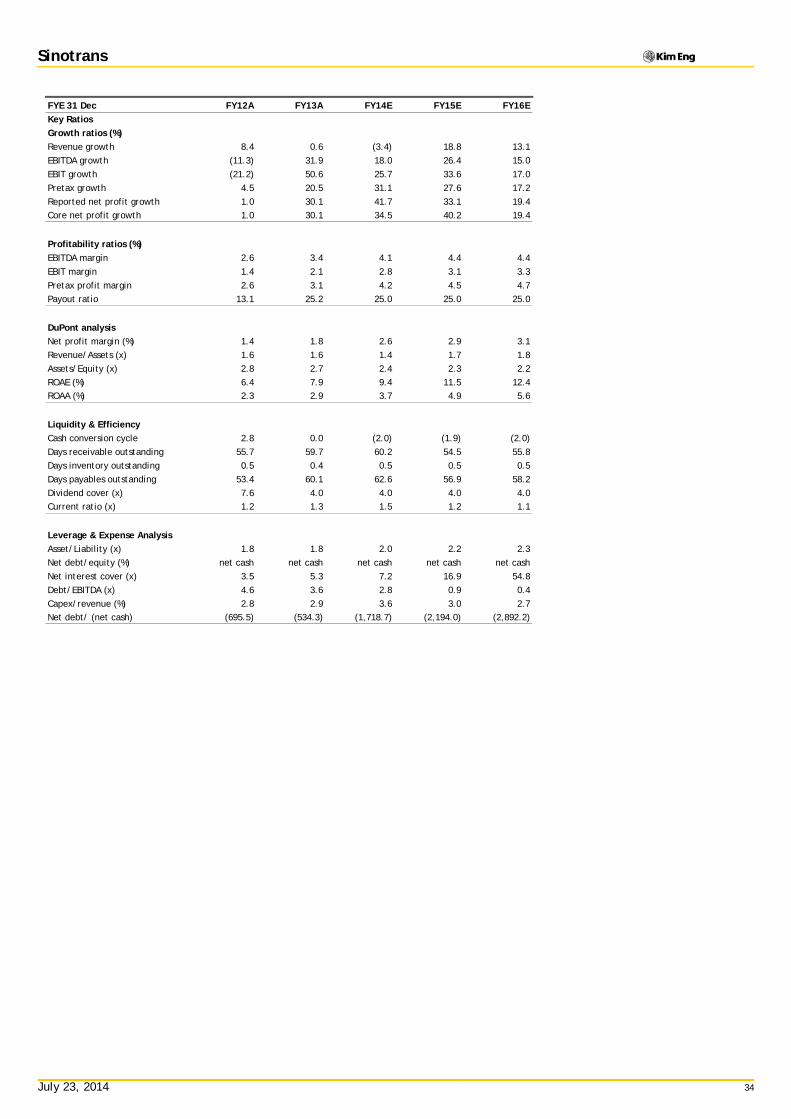

FYE 31 Dec FY12A FY13A FY14E FY15E FY16EKey MetricsP/E (reported) (x) 25.7 19.7 14.4 11.3 9.5Core P/E (x) 25.7 19.7 15.2 11.3 9.5Core FD P/E (x) 25.7 19.7 15.9 11.3 9.5P/BV (x) 1.6 1.5 1.4 1.2 1.1P/NTA (x) na na na na naNet dividend yield (%) 0.5 1.3 1.7 2.2 2.6FCF yield (%) nm nm 0.3 1.4 3.2EV/EBITDA (x) 4.9 7.2 9.6 7.9 6.8EV/EBIT (x) 8.7 11.4 14.2 11.0 9.3

INCOME STATEMENT (CNY m)Revenue 47,630.2 47,930.0 46,278.1 54,964.2 62,145.6Gross profit 1,279.3 1,552.1 1,842.8 2,304.9 2,627.6EBITDA 1,222.0 1,611.9 1,901.3 2,403.2 2,764.3Depreciation (455.7) (489.0) (567.2) (632.4) (697.6)Amortisation (83.4) (94.4) (41.3) (43.4) (45.6)EBIT 682.9 1,028.4 1,292.7 1,727.3 2,021.1Net interest income /(exp) (196.2) (195.9) (180.6) (102.3) (36.9)Associates & JV 746.5 653.8 776.2 862.2 931.4Exceptionals 0.0 0.0 60.6 0.0 0.0Other pretax income 0.0 0.0 0.0 0.0 0.0Pretax profit 1,233.2 1,486.4 1,949.0 2,487.2 2,915.6Income tax (322.4) (335.7) (428.8) (547.2) (641.4)Minorities (261.8) (306.2) (323.5) (347.7) (373.1)Discontinued operations 0.0 0.0 0.0 0.0 0.0Reported net profit 649.1 844.5 1,196.7 1,592.3 1,901.1Core net profit 649.1 844.5 1,136.1 1,592.3 1,901.1

BALANCE SHEET (CNY m)Cash & Short Term Investments 6,372.5 6,281.3 7,063.3 4,413.2 4,072.7Accounts receivable 8,019.4 7,865.6 7,607.4 9,035.2 10,215.7Inventory 53.4 60.3 63.4 75.3 85.1Property, Plant & Equip (net) 6,367.4 7,106.6 8,667.8 9,685.4 10,637.8Intangible assets 97.0 109.8 89.5 68.1 45.6Investment in Associates & JVs 3,347.8 3,305.1 3,693.2 4,124.3 4,590.0Other assets 5,030.9 5,166.1 5,147.5 5,339.7 5,493.7Total assets 29,288.3 29,894.8 32,332.0 32,741.1 35,140.6ST interest bearing debt 2,832.0 1,402.4 125.4 38.7 38.7Accounts payable 7,619.3 7,855.2 7,607.4 9,035.2 10,215.7LT interest bearing debt 2,844.9 4,344.6 5,219.2 2,180.5 1,141.8Other liabilities 3,264.4 2,874.9 3,323.0 3,788.9 4,170.4Total Liabilities 16,560.6 16,477.1 16,275.0 15,043.3 15,566.6Shareholders Equity 10,362.2 10,925.0 13,240.8 14,534.0 16,037.0Minority Interest 2,365.5 2,492.7 2,816.2 3,163.9 3,537.0Total shareholder equity 12,727.7 13,417.7 16,057.0 17,697.9 19,574.0

CASH FLOW (CNY m)Pretax profit 1,233.2 1,486.4 1,949.0 2,487.2 2,915.6Depreciation & amortisation 539.1 583.5 608.5 675.8 743.2Adj net interest (income)/exp 216.9 219.5 164.1 84.0 16.7Change in working capital (264.7) 365.4 453.1 239.8 194.6Cash taxes paid (309.1) (352.2) (428.8) (547.2) (641.4)Other operating cash flow (1,034.3) (683.7) (452.7) (514.5) (558.3)Cash flow from operations 62.1 1,013.9 1,698.0 1,903.5 2,219.1Capex (1,316.3) (1,387.4) (1,650.0) (1,650.0) (1,650.0)Free cash flow (1,254.2) (373.5) 48.0 253.5 569.1Dividends paid (42.5) (127.5) (212.5) (299.2) (398.1)Equity raised / (purchased) 0.0 0.0 1,331.6 0.0 0.0Change in Debt 1,473.5 85.6 (402.4) (3,125.4) (1,038.7)Other invest/financing cash flow (96.0) 119.9 17.3 521.0 527.2Effect of exch rate changes (7.5) (23.2) 0.0 0.0 0.0Net cash flow 73.3 (318.7) 782.0 (2,650.1) (340.5)

July 23, 2014 34

Sinotrans

FYE 31 Dec FY12A FY13A FY14E FY15E FY16EKey RatiosGrowth ratios (%)Revenue growth 8.4 0.6 (3.4) 18.8 13.1EBITDA growth (11.3) 31.9 18.0 26.4 15.0EBIT growth (21.2) 50.6 25.7 33.6 17.0Pretax growth 4.5 20.5 31.1 27.6 17.2Reported net profit growth 1.0 30.1 41.7 33.1 19.4Core net profit growth 1.0 30.1 34.5 40.2 19.4

Profitability ratios (%)EBITDA margin 2.6 3.4 4.1 4.4 4.4EBIT margin 1.4 2.1 2.8 3.1 3.3Pretax profit margin 2.6 3.1 4.2 4.5 4.7Payout ratio 13.1 25.2 25.0 25.0 25.0

DuPont analysisNet profit margin (%) 1.4 1.8 2.6 2.9 3.1Revenue/Assets (x) 1.6 1.6 1.4 1.7 1.8Assets/Equity (x) 2.8 2.7 2.4 2.3 2.2ROAE (%) 6.4 7.9 9.4 11.5 12.4ROAA (%) 2.3 2.9 3.7 4.9 5.6

Liquidity & EfficiencyCash conversion cycle 2.8 0.0 (2.0) (1.9) (2.0)Days receivable outstanding 55.7 59.7 60.2 54.5 55.8Days inventory outstanding 0.5 0.4 0.5 0.5 0.5Days payables outstanding 53.4 60.1 62.6 56.9 58.2Dividend cover (x) 7.6 4.0 4.0 4.0 4.0Current ratio (x) 1.2 1.3 1.5 1.2 1.1

Leverage & Expense AnalysisAsset/Liability (x) 1.8 1.8 2.0 2.2 2.3Net debt/equity (%) net cash net cash net cash net cash net cashNet interest cover (x) 3.5 5.3 7.2 16.9 54.8Debt/EBITDA (x) 4.6 3.6 2.8 0.9 0.4Capex/revenue (%) 2.8 2.9 3.6 3.0 2.7Net debt/ (net cash) (695.5) (534.3) (1,718.7) (2,194.0) (2,892.2)

July 23, 2014

Com

pany

Upd

ate

COM

PAN

Y RE

SEA

RCH

|

SEE PAGE 54 FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS

China Merchants Holdings (144 HK)

An alternative logistics play Reiterate BUY, but lower TP to HKD29.80. CM has quality port

exposure and steady earnings but prefer COSCO Pacific for cheaper valuations and stronger growth.

CM’s logistics business is forecast to grow at a 19% CAGR in FY14-15 to account for 7.2% of its total EBIT next year.

We expect organic throughput to increase 3.6% in FY14 due to the heavy exposure to Shanghai and Shenzhen.