CHERN/HABERSTOCK TAXATION OUTLINE -...

112

CHERN/HABERSTOCK TAXATION OUTLINE w/ M.O.B Sebastian Chern & Brooke Haberstock: They made a terrible couple, but a helluva tax outline. Fall 2016

Transcript of CHERN/HABERSTOCK TAXATION OUTLINE -...

CHERN/HABERSTOCK TAXATION OUTLINE

w/ M.O.B

Sebastian Chern & Brooke Haberstock: They made a terrible couple, but a helluva tax outline.Fall 2016

TABLE OF CONTENTS

Introduction to canadian income tax..............................................................................................................4

CRASH COURSE IN TAX POLICY.......................................................................................................................6

Statutory interpretation & Tax / Burden of proof...........................................................................................7

Constitution Act Division of Powers...............................................................................................................7

Residency.......................................................................................................................................................9Approach......................................................................................................................................................................................................................... 9Sources as a Base of Tax Liability...................................................................................................................................................................... 13

Income for Taxation Year – Non-Capital Income...........................................................................................15Income from a Source............................................................................................................................................................................................ 15Income from Office or Employment [s. 3(a)]...............................................................................................................................................19

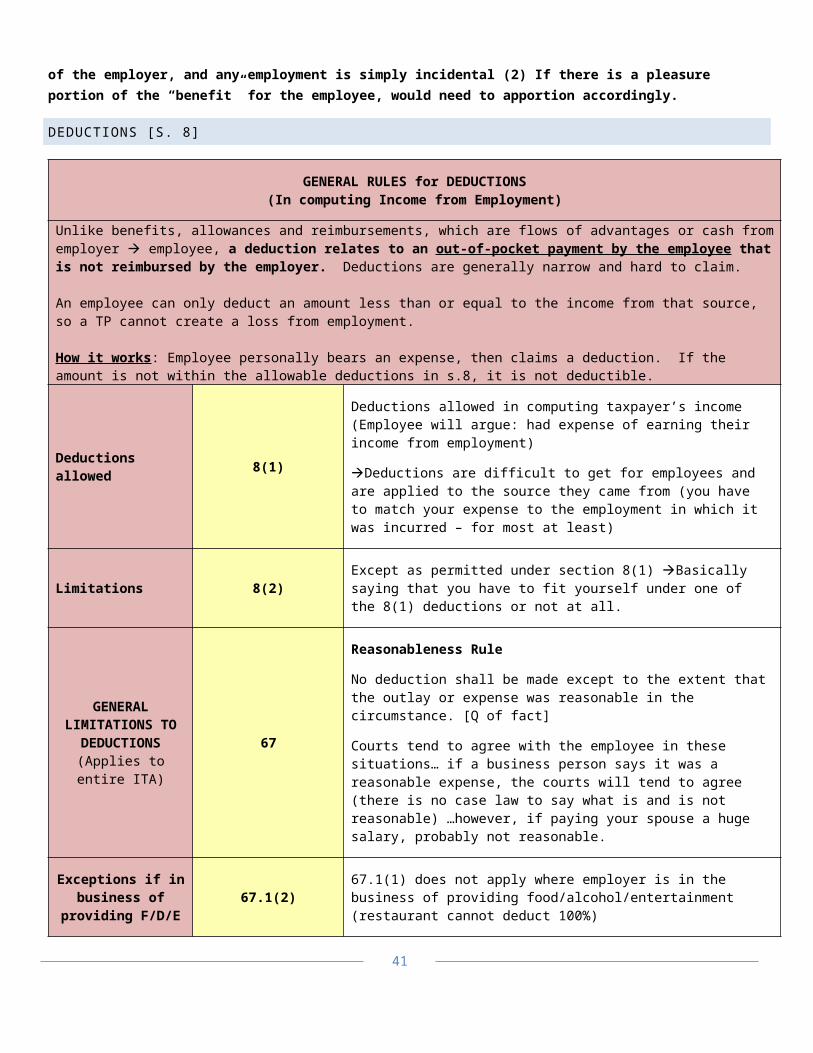

Canada Employment Credit................................................................................................................................................................................. 24Inclusions [s. 6]......................................................................................................................................................................................................... 24Deductions [s. 8]....................................................................................................................................................................................................... 31

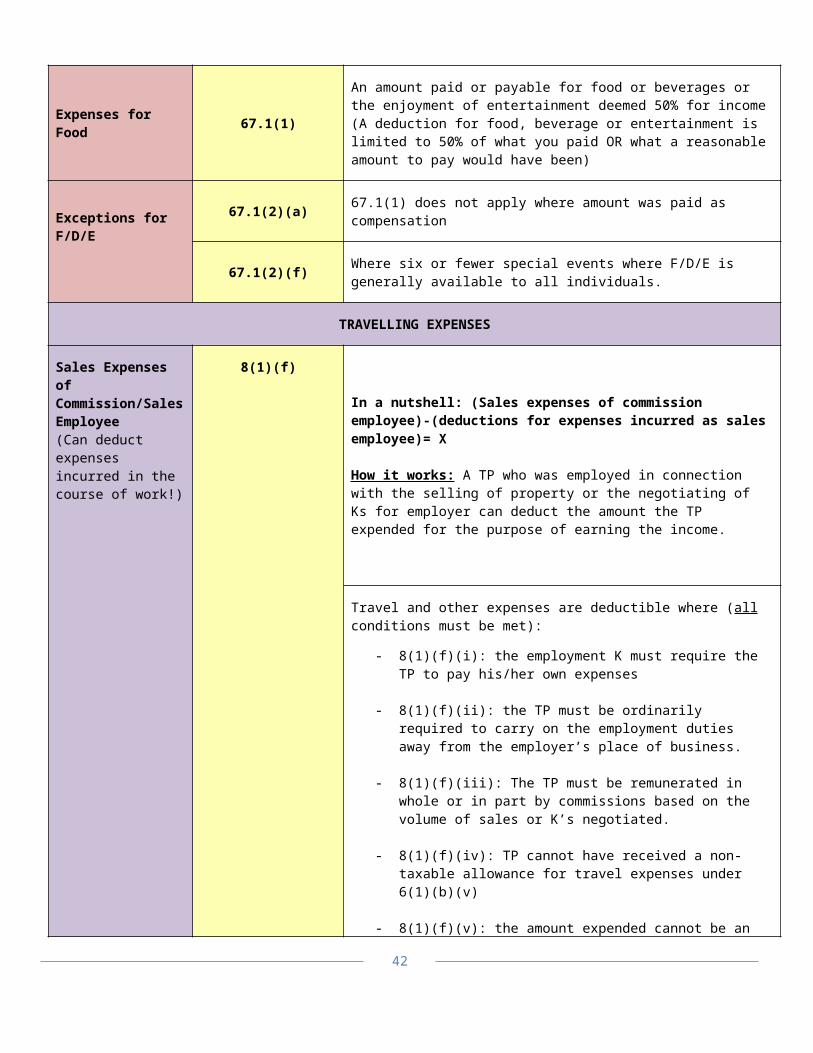

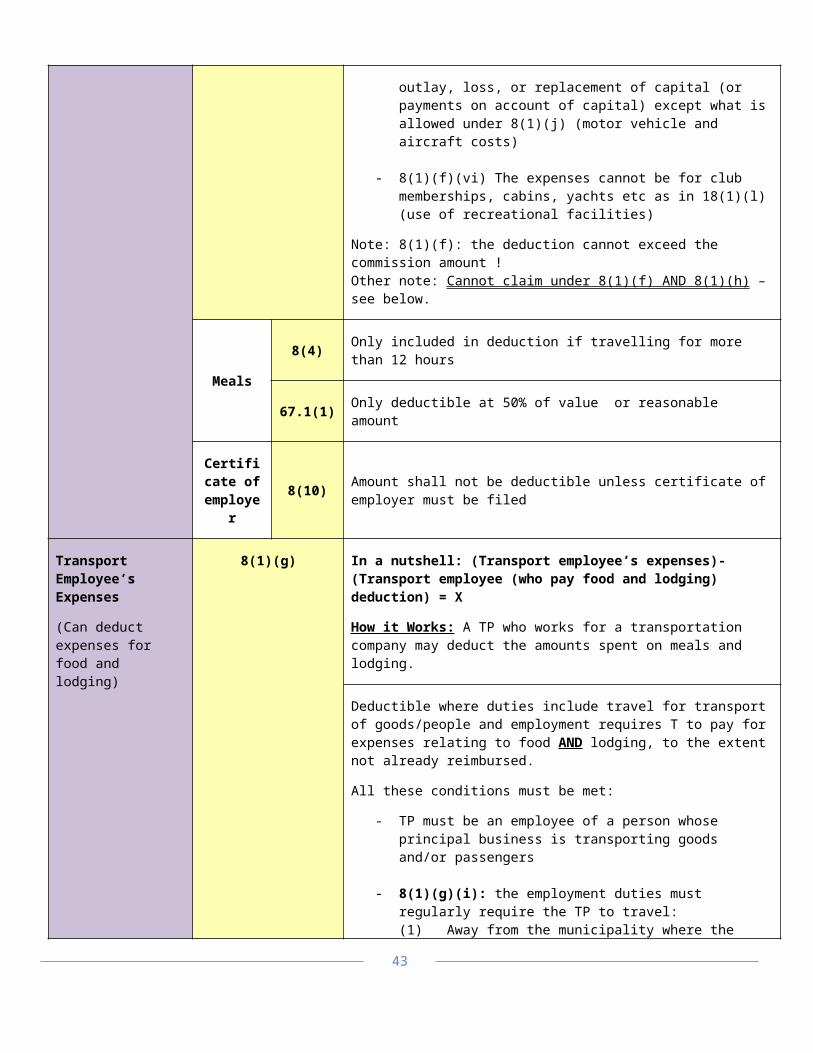

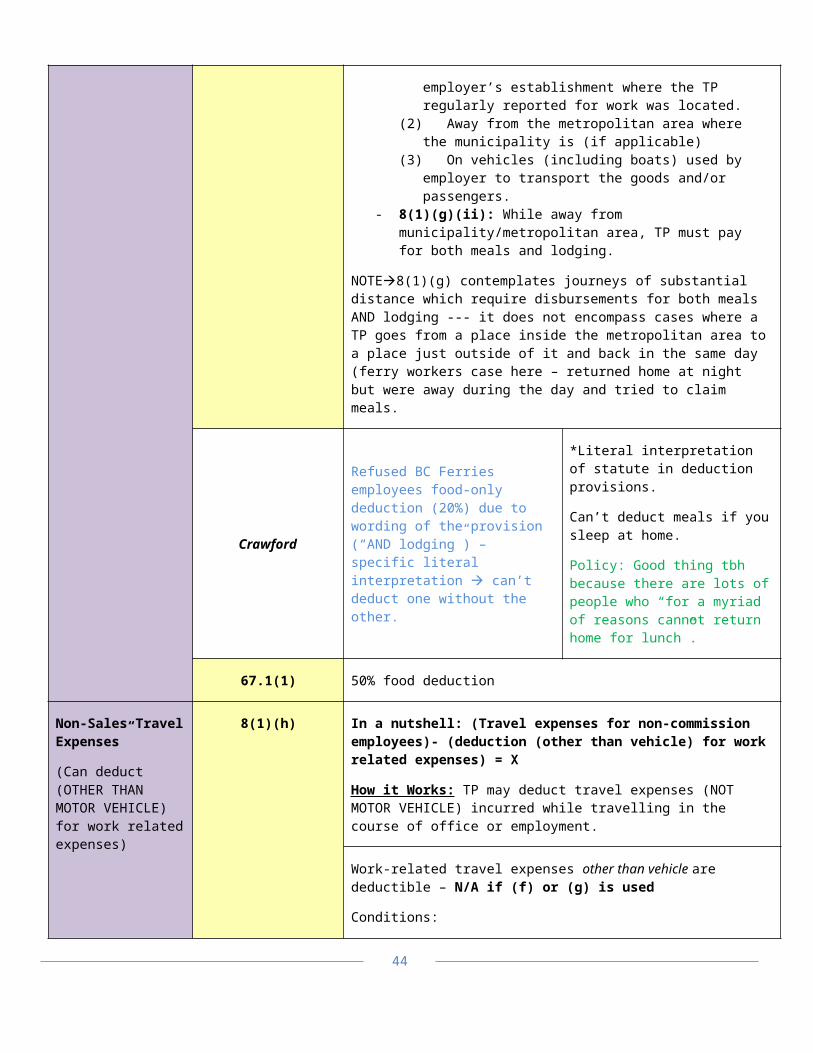

GENERAL RULES for DEDUCTIONS (In computing Income from Employment)...........................................................................31TRAVELLING EXPENSES........................................................................................................................................................................................ 32LEGAL EXPENSES..................................................................................................................................................................................................... 35DUES and OTHER EXPENSES of PERFORMING DUTIES.......................................................................................................................... 36HOME OFFICE EXPENSES (*income from employment)......................................................................................................................... 37

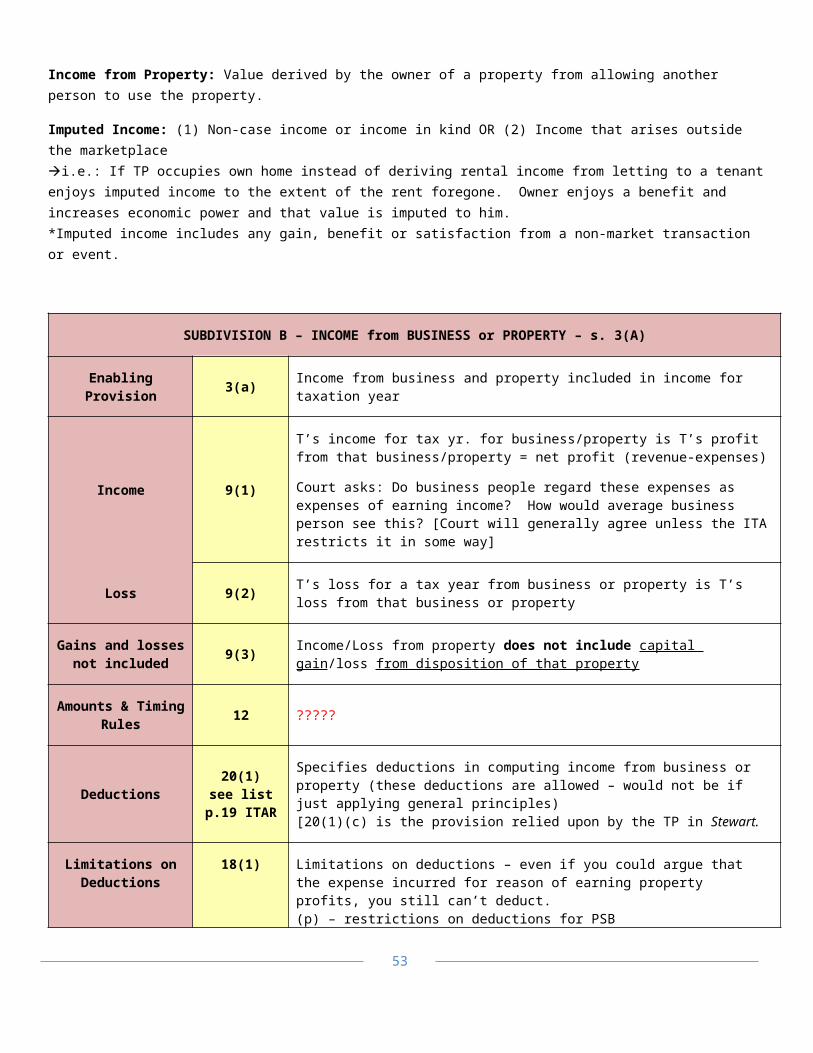

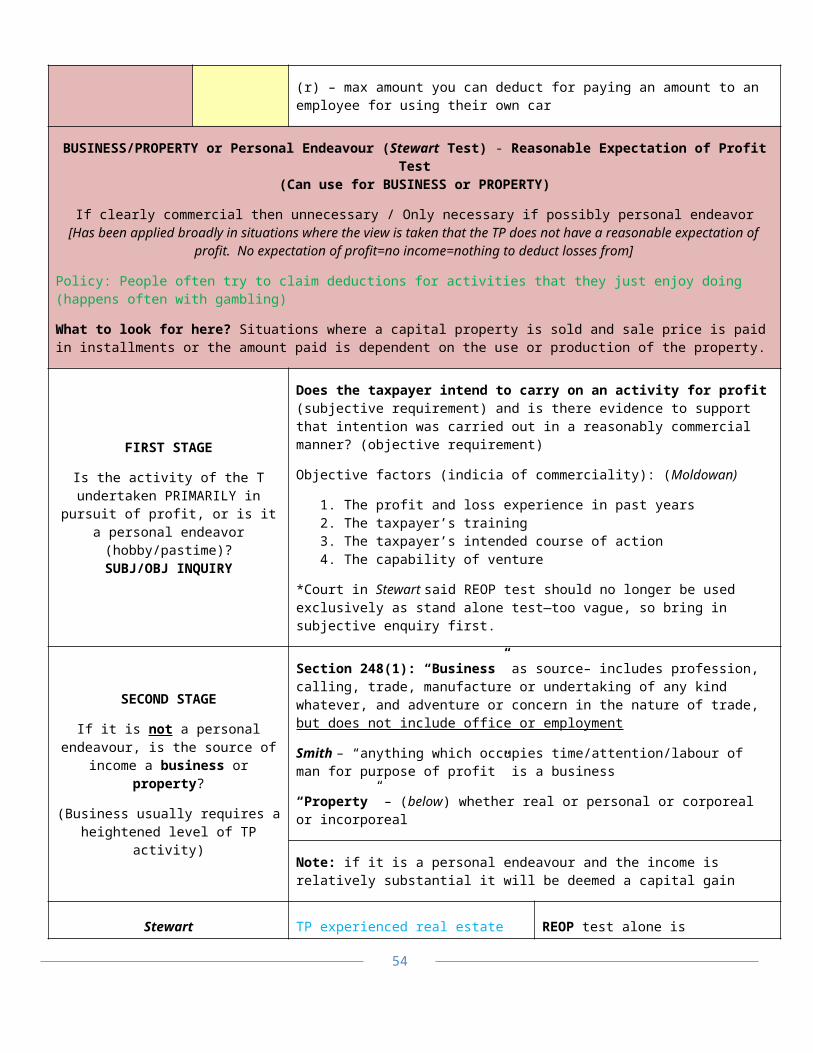

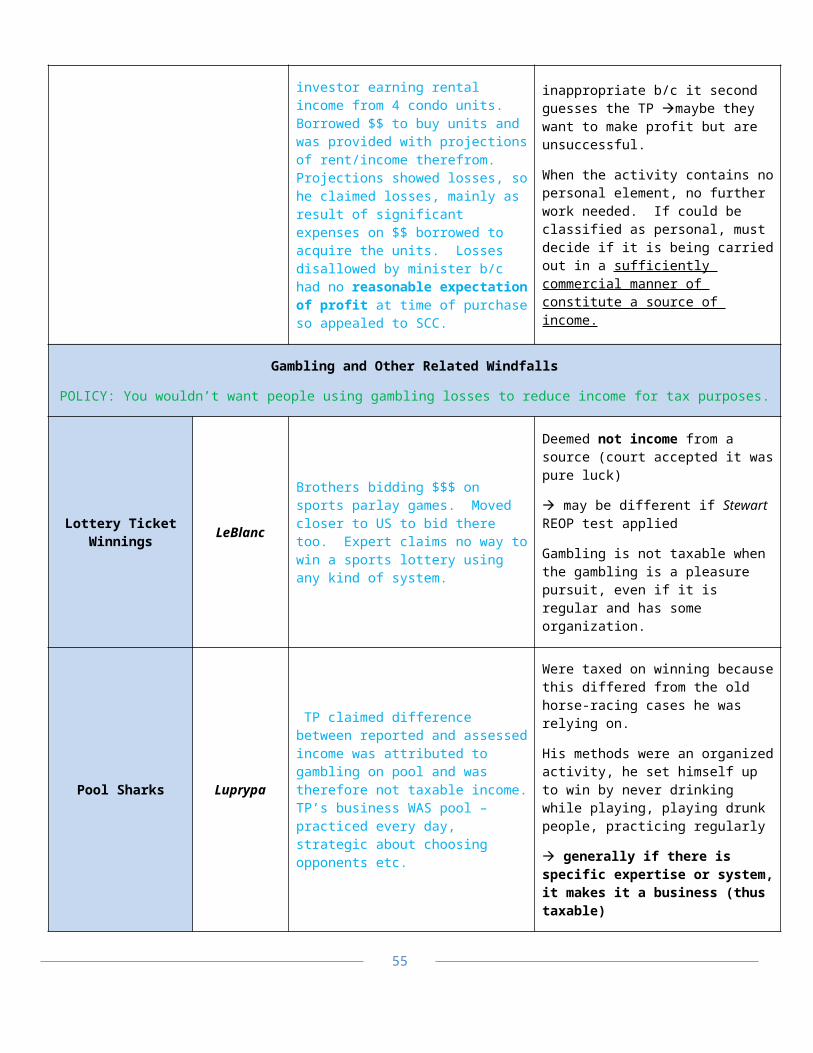

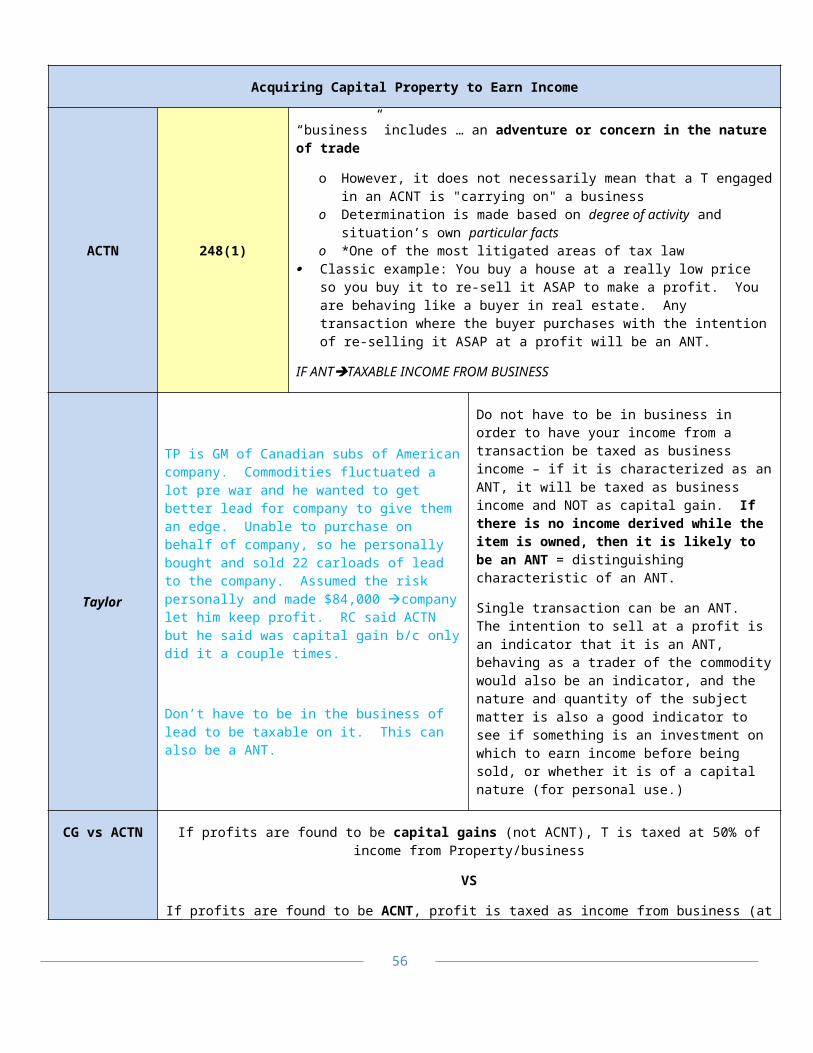

Income from Business or Property [s. 3(a)].................................................................................................................................................38SUBDIVISION B – INCOME from BUSINESS or PROPERTY – s. 3(A)...................................................................................................40BUSINESS/PROPERTY or Personal Endeavour (Stewart Test) - Reasonable Expectation of Profit Test (Can use for BUSINESS or PROPERTY)...................................................................................................................................................................................... 41Gambling and Other Related Windfalls........................................................................................................................................................... 42Acquiring Capital Property to Earn Income.................................................................................................................................................. 42

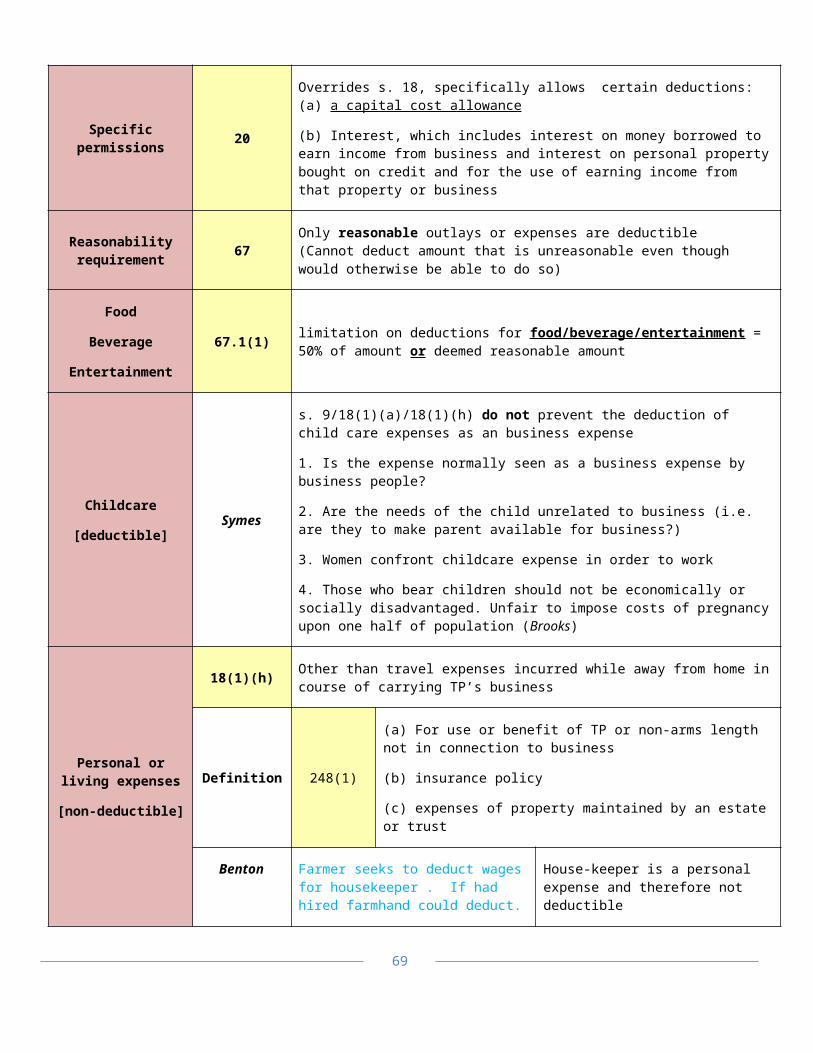

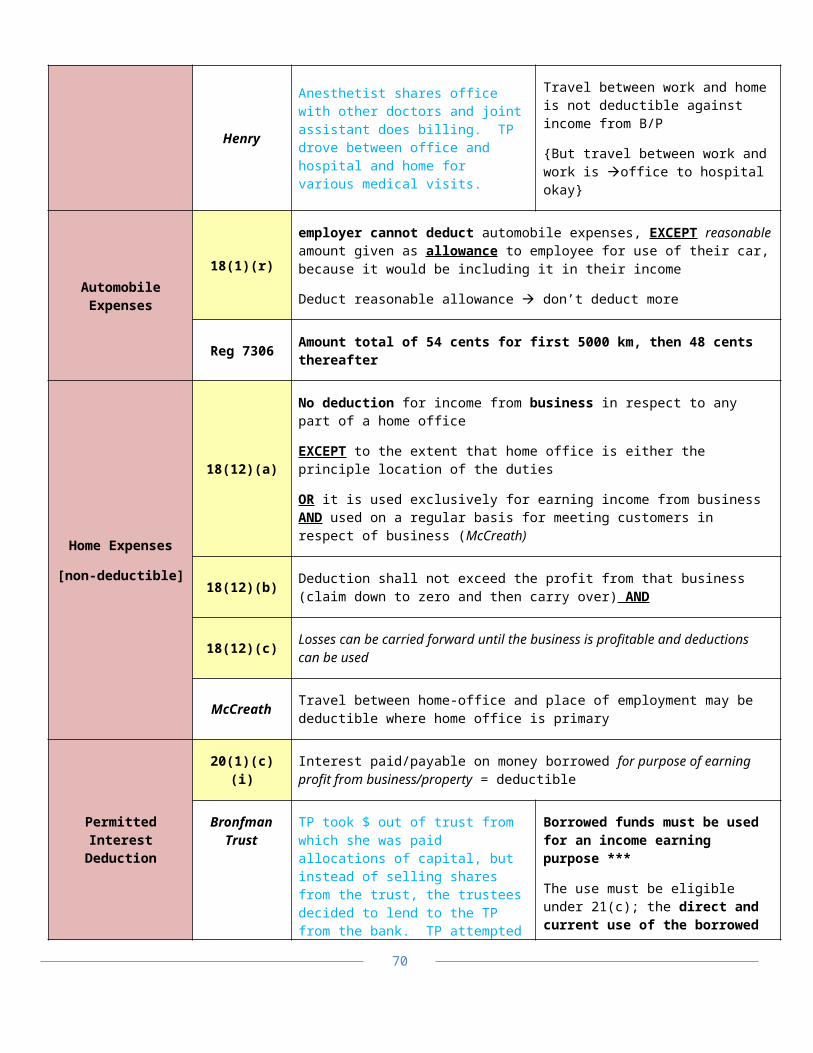

Deductions From Business or Property [ss. 18 and 20].........................................................................................................................50Net Income from a B/P........................................................................................................................................................................................... 50Deductibility of ordinary running or current expenses............................................................................................................................ 50INCOME EARNING PURPOSE TEST................................................................................................................................................................... 50Application of Income-Earning Purpose Test............................................................................................................................................... 51Can.................................................................................................................................................................................................................................. 51Running expense requirement............................................................................................................................................................................ 51Specific limitations................................................................................................................................................................................................... 51Limitation on Capital Expenditure.................................................................................................................................................................... 52Specific permissions................................................................................................................................................................................................. 52Reasonability requirement................................................................................................................................................................................... 52Food................................................................................................................................................................................................................................ 52Beverage....................................................................................................................................................................................................................... 52Entertainment............................................................................................................................................................................................................ 52Childcare....................................................................................................................................................................................................................... 52

1

Personal or living expenses................................................................................................................................................................................... 52Permitted Interest Deduction.............................................................................................................................................................................. 53

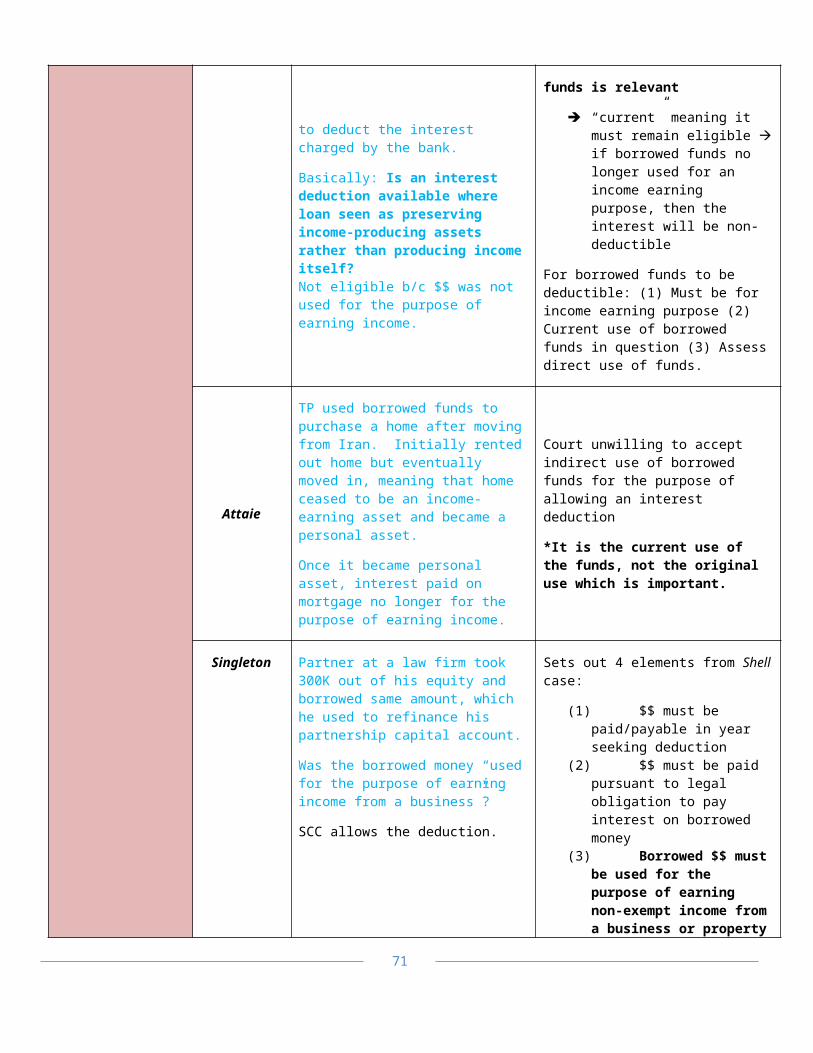

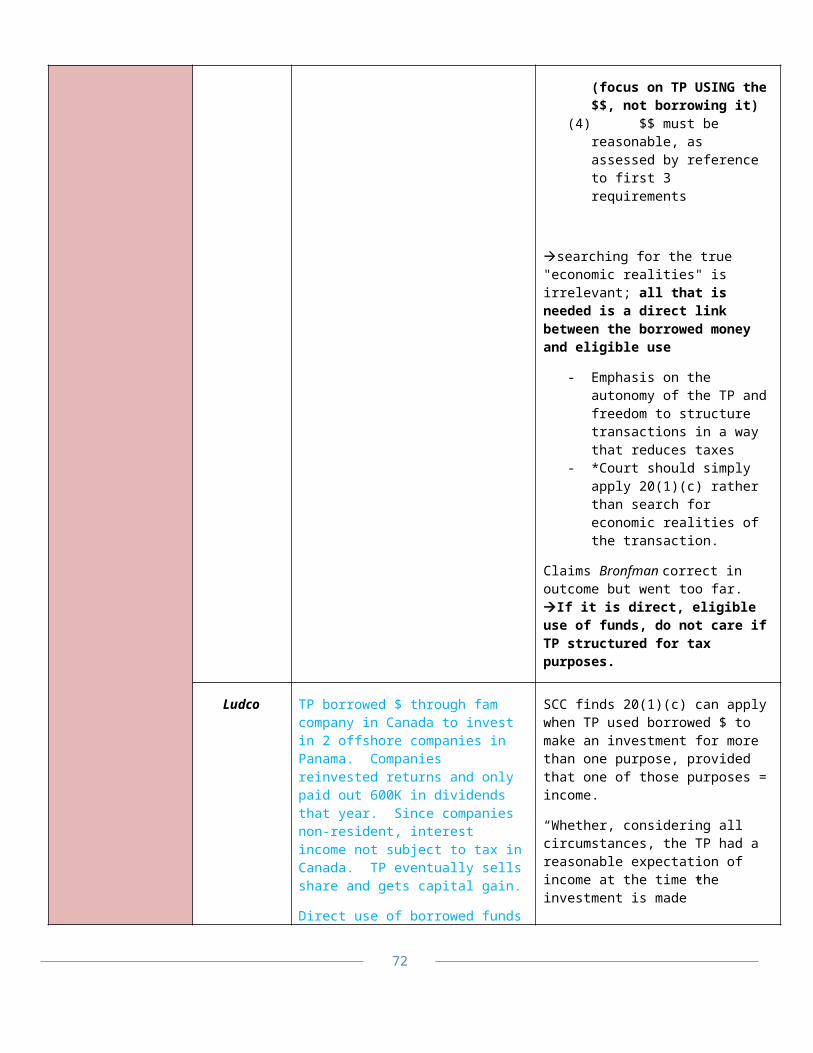

Deductions Against Income from Employment or Business (Universal)........................................................55Deductions permitted.............................................................................................................................................................................................. 55Other Deductions...................................................................................................................................................................................................... 56Child Care Expenses................................................................................................................................................................................................. 56Moving Expenses....................................................................................................................................................................................................... 56“Eligible Relocation”................................................................................................................................................................................................ 56Expenses include....................................................................................................................................................................................................... 57Student Moving Expenses...................................................................................................................................................................................... 57Scholarships................................................................................................................................................................................................................ 58&....................................................................................................................................................................................................................................... 58Bursaries....................................................................................................................................................................................................................... 58Bribery of Certain Officials................................................................................................................................................................................... 58Fine and Penalties.................................................................................................................................................................................................... 59

Income for Taxation Year – Capital Income/Gains........................................................................................59Example........................................................................................................................................................................................................................ 60Terminology................................................................................................................................................................................................................ 60Enabling Provision................................................................................................................................................................................................... 60Taxable Capital Gain............................................................................................................................................................................................... 61Allowable Capital Loss............................................................................................................................................................................................ 61Capital gains from disposition of any property........................................................................................................................................... 61Capital losses from disposition of any property........................................................................................................................................... 62Right to a Prize/Lottery Winnings.................................................................................................................................................................... 62ACB of Property Acquired as Prize.................................................................................................................................................................... 62Test for Determining a Capital Expenditure................................................................................................................................................. 62Capital expense.......................................................................................................................................................................................................... 62Repair Deduction...................................................................................................................................................................................................... 63Test.................................................................................................................................................................................................................................. 63Criteria.......................................................................................................................................................................................................................... 63Capital Cost Allowance – Depreciable Capital Assets............................................................................................................................... 64Capital Cost of Property......................................................................................................................................................................................... 64CCA.................................................................................................................................................................................................................................. 65UCC.................................................................................................................................................................................................................................. 65Exclusions from Depreciable Property............................................................................................................................................................ 66Land is not deemed to be DP................................................................................................................................................................................ 6650% / Half Year rule............................................................................................................................................................................................... 66Terminal Loss............................................................................................................................................................................................................. 66Recaptured Depreciation...................................................................................................................................................................................... 66CAPITAL GAINS FRAMEWORK............................................................................................................................................................................ 66General Rules for Capital Gains.......................................................................................................................................................................... 66Capital Loss................................................................................................................................................................................................................. 67Adjusted Cost Base................................................................................................................................................................................................... 67

2

Proceeds of Disposition.......................................................................................................................................................................................... 67Carry Forward and Back of Capital Losses.................................................................................................................................................... 69Net capital losses....................................................................................................................................................................................................... 69Non-Capital losses.................................................................................................................................................................................................... 69Part Dispositions....................................................................................................................................................................................................... 69Identical Properties................................................................................................................................................................................................. 69Gifts of Cash................................................................................................................................................................................................................. 70Non-Arm’s Length..................................................................................................................................................................................................... 70“Related Persons”...................................................................................................................................................................................................... 71Inadequate Considerations................................................................................................................................................................................... 71Immigration................................................................................................................................................................................................................ 72Emigration................................................................................................................................................................................................................... 72Capital Property of a Deceased Tax Payer..................................................................................................................................................... 73Where transfer or distribution to spouse or spouse in trust.................................................................................................................. 73Rollovers....................................................................................................................................................................................................................... 73Inter Vivos Transfers = exception to the non-arm’s length rule........................................................................................................... 74Personal Use Property............................................................................................................................................................................................ 74Listed Personal Property....................................................................................................................................................................................... 74“No Loss Rule”............................................................................................................................................................................................................ 75Disposal of Personal Use Property [including LPP] ($1000 rule)........................................................................................................ 75Partial Disposition.................................................................................................................................................................................................... 75PUP Ordinarily Disposed of as a Set.................................................................................................................................................................. 75Loss on PUP................................................................................................................................................................................................................. 76EXAMPLE:.................................................................................................................................................................................................................... 76EXAMPLE : PUP ordinarily disposed of as a set........................................................................................................................................... 76Calculation of LPP Net Capital Losses and Gains........................................................................................................................................ 76Calculation of Income............................................................................................................................................................................................. 77Taxable Net Gain from Disposition of LPP..................................................................................................................................................... 77Determination of LPP Net Gain.......................................................................................................................................................................... 77LPP Loss........................................................................................................................................................................................................................ 77

Principal Residence Exemption.........................................................................................................................................................................78Principal Residence.................................................................................................................................................................................................. 78

Miscellaneous............................................................................................................................................................................................................ 82Notes.............................................................................................................................................................................................................................. 83

INTRODUCTION TO CANADIAN INCOME TAX

Tax is:

(1) Compulsory (2) Unrequired

3

All taxes must have 5 components:

(1) Each tax must have a base upon which it is leveled (2) Each tax must have a tax filing unit responsible for paying the tax (3) Taxes must have a rate that is to be applied to the base (which gives you the tax owing) (4) Unless imposed on an individual transaction, taxes must have a period over which the base is measured and tax is

collected. (5) Each tax must have a set of administrative arrangements for it’s collection

DEFINITIONS:Tax Base- Total amount of assets or revenue that a government can tax

- 3 possibilities: (1) Income :

o Income tax is a comprehensive tax base, but the govt might impose tax on only some aspects of income (i.e. payroll taxes like EI)

o Can be done in two wasy: Source—the net amount earned from sources such as employment, property and budget (this

is how income is defined in the ITA) Use—the value of an individual’s personal consumption and their increase in net wealth

(2) Consumption In Canada = FSTo Consumption taxes are used to avoid the situation where a person has vast savings but no current income—

they would not pay any tax if it weren’t for consumption taxes. o Consumption is also a comprehensive tax base—equivalent to income tax that exempts the value of a TPs

savings from tax. (i.e. GST)o Excise taxes: only imposed on certain goods and services (policy behind this: some goods create social costs

—like alcohol, tobacco, luxury goods etc)(3) WealthIn Canada= property taxes

Taxpayer/Tax Filing Unit- An individual (or married couple who file a tax return jointly) along with all dependents of that individual (or married couple). May be the income earner, purchaser, manufacturer, owner etc. Generally the recipient of income is subject to tax.

Tax Period: Time period over which we calculate the base

- Individual: January 1st- December 31st - Corporations/Trusts: Can be off calendar / can set fiscal year as they wish

Tax Collection/Administration: Different countries have different tax mixes based on what the electorate wants and the services that they demand. In Canada, Federal taxes are collected by the CRA and under tax collection agreements, amounts are remitted to the provinces.

Tax Rates: The percentage that you apply to the tax base to get the receivable amount.

- Statutory Rate

Up to 45,282 15%45,283 – 90,563 20.5% (down from 22% in 2015) Trudeau’s middle class tax cut90,564 – 140,388 26%140,399 – 200,000 29%200,001+ 33% (new rate added for 2016)

4

- Marginal Rate: the rate of tax that applies to each additional dollar a TP earns within each income bracket (highest amount of tax that is paid on the last dollar of taxable income)

- Average Rate : The rate that is applicable to the TPs income as a whole. (Take the tax actually payable and divide by the taxable income)

- Effective Rate: Total tax payable divided by the total accretion top wealth—usually computed by reference to some broader measure of the TPs income other than taxable income.

~Classification of tax rates:

(1) Progressive As your income rises, you pay more tax. In our progressive system, everyone pays the same amount of tax up to the limit for the first tax bracket. [Western democracy believe that taxation should be based on ability to pay]

(2) Regressive Higher tax burden falls on those with less ability to pay Policy: Canada has attempted to address this through GST & HST: Basic groceries etc are exempt from GST.

(3) ProportionalSame rate for those with low or high income [In Canada: progressivity of income tax is offset by the regressivity of other taxes.]

**All Canadian taxes are regressive EXCEPT Income Tax.

Tax Incidence: Who bears the burden of taxation (i.e. Landlord might be the TP, but the renter could bear the burden of taxation via increased rent etc)

Exemptions: Amounts that you do not have to report.

- Not many specifically provided for in the ITA (See .81)- Important provision: the one that links exemptions under other statutes (if something is exempt under another Act it

won’t be taxable under the ITA—for example exemption for income situation on a reserve b/c Indian Act declares it exempt)

- Main types of exempt income: things that are not recognized by Canadian law as being income from a source (lottery winnings, gifts, strike pay, found money – don’t need to report these things on a tax return b/c in the eyes of the CRA they are nothing)

Deductions: Amount removed before taxable income is calculated. Worth a lot more to high income tax payers than low income tax payers. [Policy: This is why our system offers more credits than deductions.]

- You claim deductions on your tax return, then have to point to the section in the act that allows you to make that deduction.

- Will be worth more dollars to a person in a higher tax bracket than to a person in a lower tax bracket.

Credits : Reduction in tax otherwise payable to reduce tax liability overall. (Basic personal amount that every Canadian TP can claim eliminates tax on your first 11k)

- You calculate how much tax you owe, and then deduct the tax credit from the tax otherwise payable to arrive at actual tax liability.

o Tax credits are calculated with the lowest statutory rate: aka, everyone gets the exact same dollar amount

- Example: basic personal amount – eliminates tax payable on the first $11,138 of income (is an indexed amount – same for every TP)

- Credits are almost always worth less than deductions to high income individuals because credits are worth the same in dollars whether you are high or low income.

What is a CCPC?

5

Based on the policy of wanting to encourage entrepreneurship and grow the economy (CCPCs pay taxes at about half the rate up to $500,000 – approx. 13.5% instead of 26%)Issue: When CCPCs get near the threshold of getting too big to be a CCPC (15 million in capital) loses incentive to grow.

Note on cash vs accrual accounting:

Cash- business has money based on what is in your pocket [income from employment and office as well as farming and fishing use this method]

Accrual- Allows you to record money when it’s either receivable or payable but the cash isn’t actually in or out of your pocket yet. (Christmas bonus example) Stops you from deferring a payment until the cash is in your pocket. (You could not get your Xmas bonus on January 1st, invest it, grow it, then pay tax on it in 2017 – you have to include it for 2016) [most businesses, corporations etc use this method]

EXAMPLE:

You get a Christmas bonus which your boss tells you about on December 1st, 2016 but you do not actually receive it until 2017. Since you are an employee, this is not included in your income until 2017. Employer can likely deduct it in the 2016 tax year because they have probably incurred the liability in that year.

If it was mailed to you on December 15th and you don’t get it until January 1st, cheque deemed to be in your control once hits the mailbox so it is likely that you would have to claim it for 2016 as would the employer.

CRASH COURSE IN TAX POLICY

Policy on the exam: What does the provision exemplify police-wise?: The provision XY is meant for XY.3 big criteria for “good policy”:

(1) Equity - Vertical equity: Those who have more should pay more - Horizontal equity: Those who have the same amount in income in whatever form should pay the same taxes {i.e. a

company car would be taxed the same as cash}

(2) Neutrality - Taxes should not unduly affect personal/economic decisions.- “Incentives” non-neutrality - Tax Expenditures:

o “Anti-neutrality” provisions of the ITA (deductions, credits, special rates etc) o “You insulate your roof, we will hack $500 off your taxes”o Q: What are we trying to achieve with X tax expenditure and is it a valid government objective? o Q: If we use the tax system for this expenditure, will the benefits go to the people you intended and will it

have a fair and non-distorting effect? (i.e. Child Fitness Tax Credit)- Direct Subsidy:

o “You pay $1000 to insulate your roof, we will send you a $500 cheque”

Tax Expenditures vs Direct Subsidies

- TEs are easier to design than DSs- TEs= less discretion than DSs- TEs= less stigma than direct government handouts

6

(3) Simplicity/Efficiency - Catch- all way to describe aspects of a tax system that make it efficient and easier to comply with and administer- 3 attributes of a simple system:

(1) Comprehensible: Person should be able to at least see the logic even if they don’t understand the details (2) Certainty: It should be possible in advance to determine the tax consequences of your actions(3) Compliance Convenience: It should not be too difficult or time consuming to comply with tax rules. Average joe

should be able to do this online. It should not be too costly for the gov’t to enforce, taxes should be difficult to avoid/evade.

(4) **Global Competitiveness: Canada has cut rates for individuals and corporations substantially since the 80s to this end.

STATUTORY INTERPRETATION & TAX / BURDEN OF PROOF

Statutory Interpretation Placer Dome

- The Modern Approach has been adopted for tax statutes as well: "the words of an Act are to be read in their entire context and in their grammatical and ordinary sense harmoniously with the scheme of the Act, the object of the Act, and the intention of Parliament"

- BUT: The wording of tax legislation is very specific, so the textual side of interpretation is probably going to resolve your issues most of the time.

- If ambiguities: Presumption in favour of the TP. SCC says: If you have applied ALL approaches and you still cannot determine whether an amount is included or deductible, then tie goes to the taxpayer

- BoP: Is always on the TP once you get to court.

CONSTITUTION ACT DIVISION OF POWERS

Federal Legislative Authority

Constitution Act 1867, s. 91(3)

Exclusive legislative authority for “all Matters not coming within the Classes of Subjects by this Act assigned exclusively to the Legislatures of the Provinces;” including “The raising of Money by any Mode or System of Taxation”.

Provincial Legislative Authority

Constitution Act 1867, s. 92(2)

“Direct Taxation within the Province in order to the raising of a Revenue for Provincial Purposes”;

Constitution Act 1867, s. 92(9)

“Shop, Saloon, Tavern, Auctioneer, and other Licences in order to the raising of a Revenue for Provincial, Local, or Municipal Purposes.

DIRECT INDIRECT

A direct tax is one which is demanded from the very person who it is intended or desired should pay it. – J.S. Mill(Income Tax is a direct tax)

Courts generally refer to taxes on a unit of a marketable commodity that are ‘passed on’ to a final consumer as indirect

Indirect taxes are those which are demanded from one person in the expectation that he shall indemnify himself at the expense of another. – JS Mill

7

“Is the tax related or relatable, directly or indirectly, to a unit of the commodity or its price, imposed when the commodity is in the course of being manufactured or marketed?” - Canadian Pacific Railway Co. v. Attorney General for Saskatchewan [1952]

Source vs Non-Source Income

3(a): Total of all positive income [revenue] (non-capital only) from sources including office, employment, business and property

3(b): (Allowable capital losses from property other than listed personal property) – (Capital gains from all property other than listed personal property and taxable net gains from LPP) = Taxable Capital Gain or Net Allowable Capital Loss

3(c): Take results of 3(a) and 3(b) and claim any deductions under 3(e)

56: Other amounts that do not fall within enumerated sources but that the system wants to tax

Four Income Splitting Techniques

“Income Splitting” : involves the transfer of income from one person to another who is taxed on the income at a lower marginal tax rate than that applicable to the transferor.What about the ITA? Some sections counteract certain types of income splitting while others endorse it.

Redirection of payment by 3rd party to other

Assignment of a right to income from on TP to another

Transfer of property that generates income/gain

Us of low-interest or non-interest bearing loans

Preventative legislation

Transfers and loans to spouse or CL

74.1(1) Individual is taxed, not transferee

Transfers and loans to minors

74.1(2)If under 18 years and who (a) is not at arm’s length (b) is the niece or nephew

Then individual is taxed unless that person becomes 18 at end of year.

Gain or loss deemed that of lender or transferor

74.2(1) Net capital gain/loss of lent/transferred property is deemed to be individual’s

RESIDENCY

“Who does the state claim authority to tax?””Residence consists of present ties to (but not necessarily physical presence in) a jurisdiction. It is not, at least directly, a matter of a person’s intention. It is noteworthy, however, that the courts have on occasion blurred the distinction between residence and domicile.”

Remember:

- Countries will limit taxation to what they can reasonably control – this is why residence is key in Canada

8

- Attempts to limit juridical double taxation - Canadians are taxed on their world wide income- Everyone is presumed to be resident somewhere, but that is a rebuttable presumption.

Approach

TITLE SECTION DESCRIPTION

Tax payable by Persons Resident in Canada

s. 2(1)If resident in Canada, tax shall be paid on taxable income from sources inside or outside Canada

Tax payable by non-resident persons

2(3)If not taxable under 2(1) and (a) employed in Canada, (b) carried on business in Canada, (c) disposed of a taxable Canadian property. Will be taxed on income earned in Canada determined in accordance with Division D

Ordinary resident(TEST)

Are they a factual resident of Canada?

250(3)A person who was at the relevant time ordinarily resident in Canada(This is a very expansive definition)

Thomson

[Lee]

Residence must not be casual and uncertain, but rather in the ordinary regular course and that the usual relationship of such residence was beyond doubt. Used to consider things like where your family is, street address, where your magazines are sent, clubs you belong to, etc. However with increased mobility these criteria are beginning to break down. Intention of TP is not conclusive.

1. Everyone is presumed to have a tax residence. You don’t have to own or rent somewhere to be resident.

2. You can be resident in more than one place at the same time (depending on the definition of resident in the respective country.)

Thomson

“The degree to which a person in mind and fact settles into or maintains or centralizes his ordinary mode of living with its accessories in social relations, interests and conveniences at or in the place in question.”

Intention ≠ relevant Lee

“ordinarily resident” if TP does not sever all residential ties with Canada, but are physically absent for considerable period of time, then the TP can be found to be still ordinarily resident

Thomson born in Canada pre-citizenship. Goes to Bermuda, gets British passport, went to US. Returns to Canada in 1932 for 150 days. 1934: builds house in NB. Not resident of Bermuda, not resident of US from 1930-41 but started taxing him as resident of US in 1942. By 1946, both Canada and US saying resident.Held: Resident of Canada. Factors considered: East Riverside address was home.

9

Born in England in 1946 and had UK and Northern Ireland passport. Stamped in and out of Canada many times. Authorized period of stay varied from 5-45 days. Some stamps said “visitor” Throughout 3 year period, was employed full time by non-resident corporation and all work performed outside of Canada. 1981: married Canadian citizen residing in Canada. Wife purchases house with his $$. During 3 year period (1981-83) returned to Canada regularly when not working. Parents in England still maintained bedroom for him. He never paid IT, not allowed to work in Canada, given fixed date to leave Canada upon entry, Could not join OHIP, pay UI or maintain RRSP or join pension plan, out of country 183+ days, no desire to work in Canada, had residence in Britain and had mortgage there on first wife’s house. Claimed could not lead normal life in Canada. Had RBC account. *Decision in this case turned on marriage which would normally be neutral—tipped the scale in this case. (Resident in 1982 and 83 after marriage)

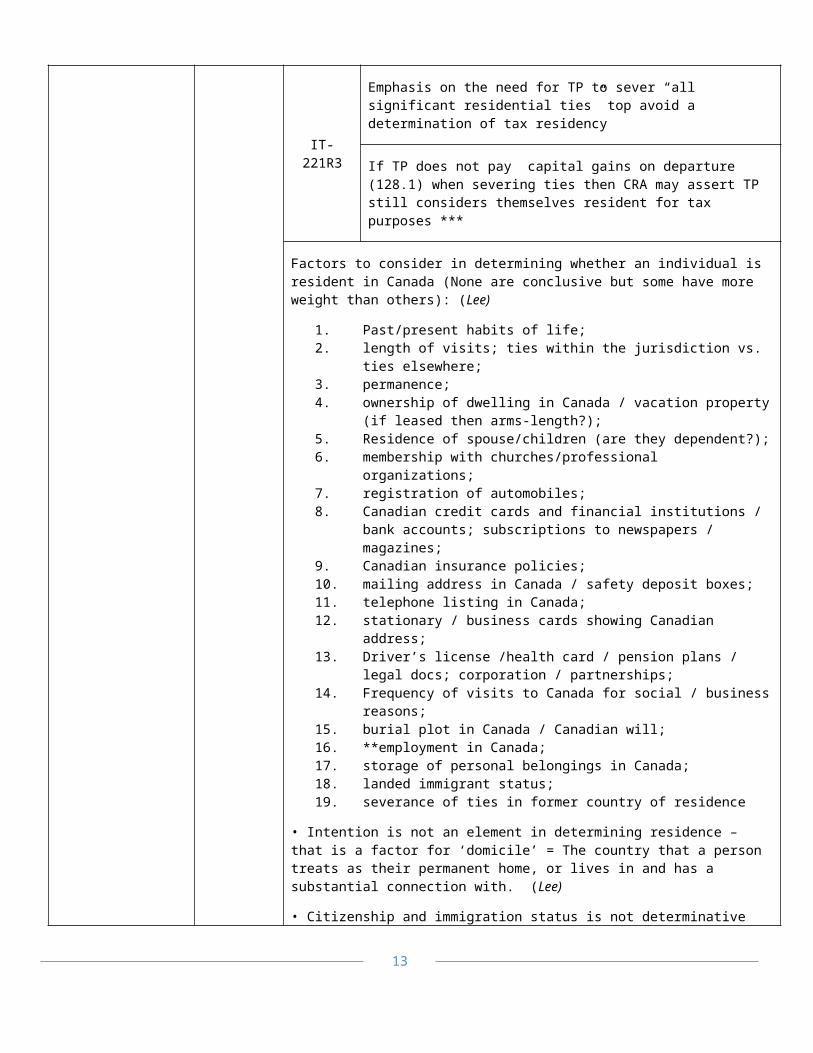

IT-221R3

Emphasis on the need for TP to sever “all significant residential ties” top avoid a determination of tax residency

If TP does not pay capital gains on departure (128.1) when severing ties then CRA may assert TP still considers themselves resident for tax purposes ***

Factors to consider in determining whether an individual is resident in Canada (None are conclusive but some have more weight than others): (Lee)

1. Past/present habits of life; 2. length of visits; ties within the jurisdiction vs. ties elsewhere; 3. permanence; 4. ownership of dwelling in Canada / vacation property (if leased then

arms-length?); 5. Residence of spouse/children (are they dependent?); 6. membership with churches/professional organizations; 7. registration of automobiles; 8. Canadian credit cards and financial institutions / bank accounts;

subscriptions to newspapers / magazines; 9. Canadian insurance policies; 10. mailing address in Canada / safety deposit boxes; 11. telephone listing in Canada; 12. stationary / business cards showing Canadian address; 13. Driver’s license /health card / pension plans / legal docs; corporation /

partnerships; 14. Frequency of visits to Canada for social / business reasons; 15. burial plot in Canada / Canadian will; 16. **employment in Canada; 17. storage of personal belongings in Canada; 18. landed immigrant status; 19. severance of ties in former country of residence

• Intention is not an element in determining residence – that is a factor for ‘domicile’ = The country that a person treats as their permanent home, or lives in and has a substantial connection with. (Lee)

• Citizenship and immigration status is not determinative for tax purpose*You can be resident in 2+ countries at the same time.

10

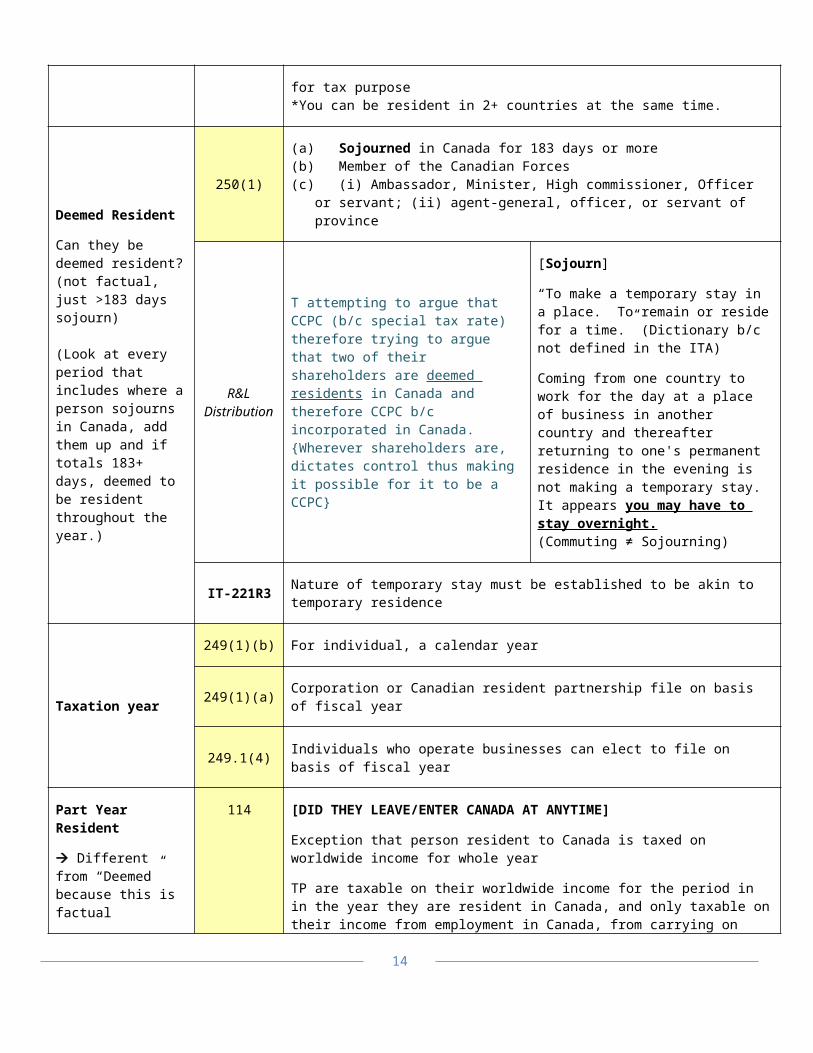

Deemed Resident

Can they be deemed resident? (not factual, just >183 days sojourn)

(Look at every period that includes where a person sojourns in Canada, add them up and if totals 183+ days, deemed to be resident throughout the year.)

250(1)

(a) Sojourned in Canada for 183 days or more(b) Member of the Canadian Forces(c) (i) Ambassador, Minister, High commissioner, Officer or servant; (ii) agent-

general, officer, or servant of province

R&L Distribution

T attempting to argue that CCPC (b/c special tax rate) therefore trying to argue that two of their shareholders are deemed residents in Canada and therefore CCPC b/c incorporated in Canada.{Wherever shareholders are, dictates control thus making it possible for it to be a CCPC}

[Sojourn]

“To make a temporary stay in a place. To remain or reside for a time.” (Dictionary b/c not defined in the ITA)

Coming from one country to work for the day at a place of business in another country and thereafter returning to one's permanent residence in the evening is not making a temporary stay. It appears you may have to stay overnight.(Commuting ≠ Sojourning)

IT-221R3 Nature of temporary stay must be established to be akin to temporary residence

Taxation year

249(1)(b) For individual, a calendar year

249(1)(a) Corporation or Canadian resident partnership file on basis of fiscal year

249.1(4) Individuals who operate businesses can elect to file on basis of fiscal year

Part Year Resident

Different from “Deemed” because this is factual residence “Ordinarily”[Starts out in Canada but at some point relocates or relocates to Canada from elsewhere]

114

[DID THEY LEAVE/ENTER CANADA AT ANYTIME]

Exception that person resident to Canada is taxed on worldwide income for whole year

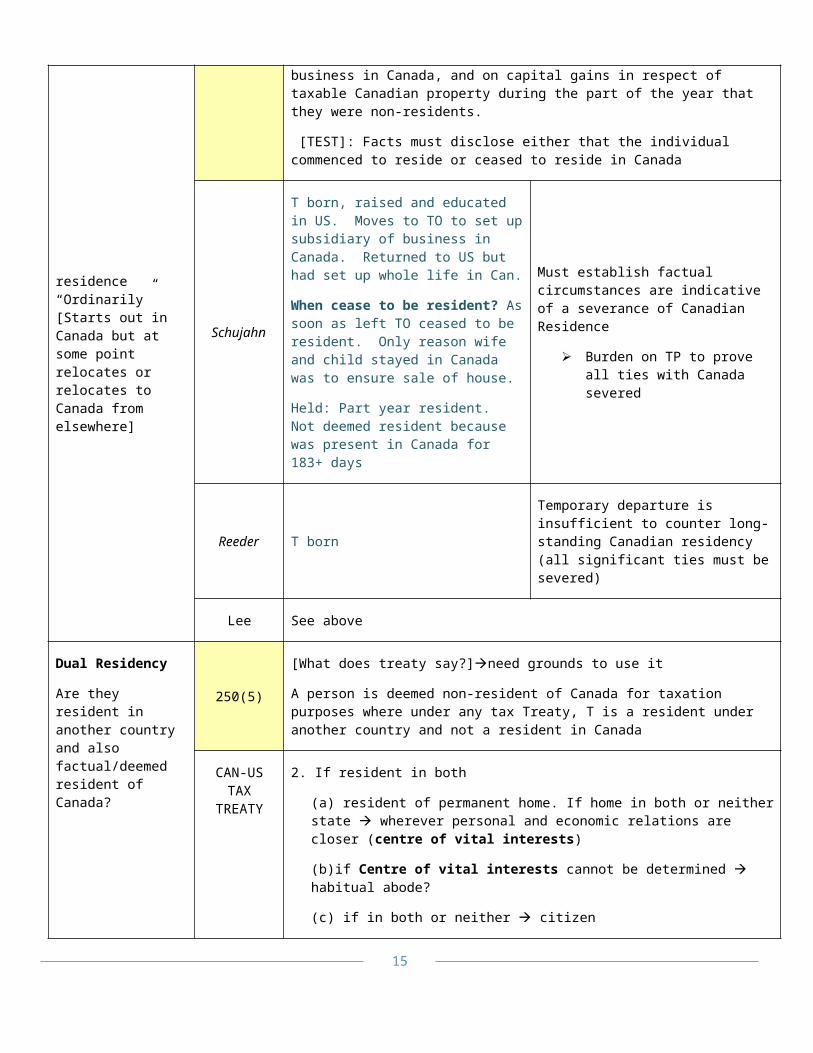

TP are taxable on their worldwide income for the period in in the year they are resident in Canada, and only taxable on their income from employment in Canada, from carrying on business in Canada, and on capital gains in respect of taxable Canadian property during the part of the year that they were non-residents.

[TEST]: Facts must disclose either that the individual commenced to reside or ceased to reside in Canada

Schujahn T born, raised and educated in US. Moves to TO to set up subsidiary of business in Canada. Returned to US but had set up whole life in Can.

When cease to be resident? As soon as left TO ceased to be resident. Only reason wife and child stayed in Canada was to ensure sale of house.

Held: Part year resident. Not deemed resident because was present in Canada

Must establish factual circumstances are indicative of a severance of Canadian Residence

Burden on TP to prove all ties with Canada severed

11

for 183+ days

Reeder T born

Temporary departure is insufficient to counter long-standing Canadian residency (all significant ties must be severed)

Lee See above

Dual Residency

Are they resident in another country and also factual/deemed resident of Canada?

250(5)

[What does treaty say?]need grounds to use it

A person is deemed non-resident of Canada for taxation purposes where under any tax Treaty, T is a resident under another country and not a resident in Canada

CAN-US TAX TREATY

2. If resident in both

(a) resident of permanent home. If home in both or neither state wherever personal and economic relations are closer (centre of vital interests)

(b)if Centre of vital interests cannot be determined habitual abode?

(c) if in both or neither citizen

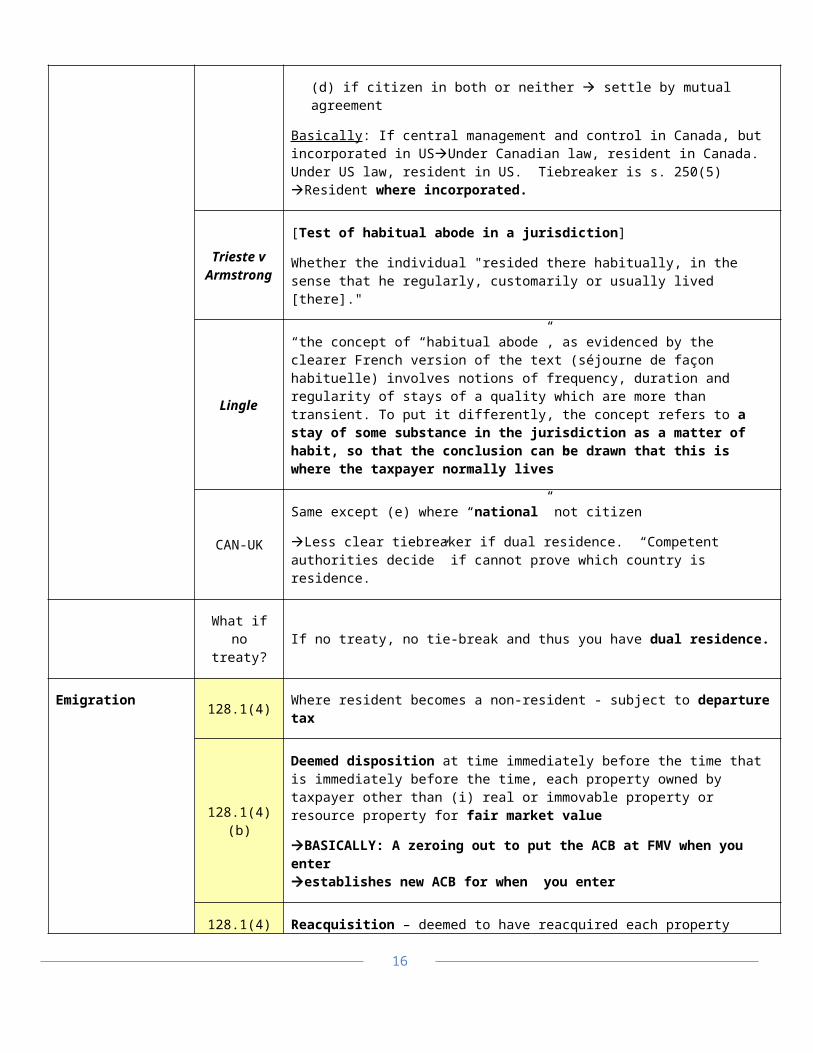

(d) if citizen in both or neither settle by mutual agreement

Basically: If central management and control in Canada, but incorporated in USUnder Canadian law, resident in Canada. Under US law, resident in US. Tiebreaker is s. 250(5) Resident where incorporated.

Trieste v Armstrong

[Test of habitual abode in a jurisdiction]

Whether the individual "resided there habitually, in the sense that he regularly, customarily or usually lived [there]."

Lingle

“the concept of “habitual abode”, as evidenced by the clearer French version of the text (séjourne de façon habituelle) involves notions of frequency, duration and regularity of stays of a quality which are more than transient. To put it differently, the concept refers to a stay of some substance in the jurisdiction as a matter of habit, so that the conclusion can be drawn that this is where the taxpayer normally lives”

CAN-UK

Same except (e) where “national” not citizen

Less clear tiebreaker if dual residence. “Competent authorities decide” if cannot prove which country is residence.

What if no treaty?

If no treaty, no tie-break and thus you have dual residence.

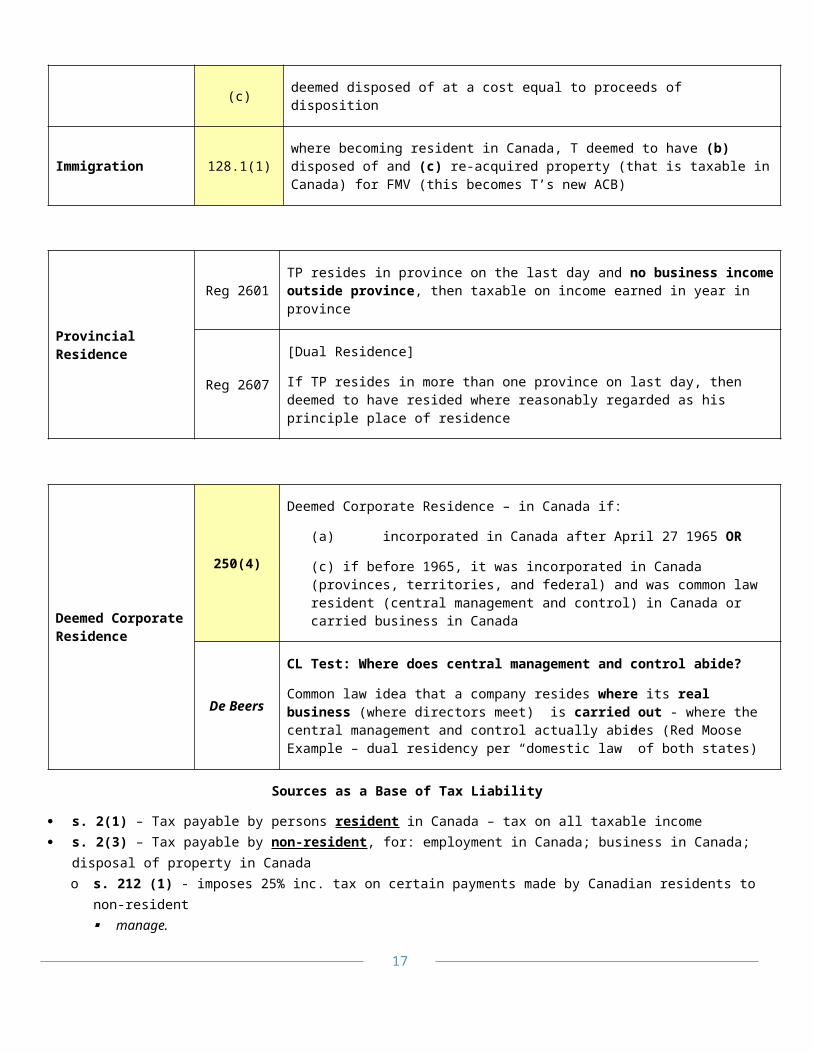

Emigration 128.1(4) Where resident becomes a non-resident - subject to departure tax

12

128.1(4)(b)

Deemed disposition at time immediately before the time that is immediately before the time, each property owned by taxpayer other than (i) real or immovable property or resource property for fair market value

BASICALLY: A zeroing out to put the ACB at FMV when you enterestablishes new ACB for when you enter

128.1(4)(c)Reacquisition – deemed to have reacquired each property deemed disposed of at a cost equal to proceeds of disposition

Immigration 128.1(1)where becoming resident in Canada, T deemed to have (b) disposed of and (c) re-acquired property (that is taxable in Canada) for FMV (this becomes T’s new ACB)

Provincial Residence

Reg 2601TP resides in province on the last day and no business income outside province, then taxable on income earned in year in province

Reg 2607

[Dual Residence]

If TP resides in more than one province on last day, then deemed to have resided where reasonably regarded as his principle place of residence

Deemed Corporate Residence

250(4)

Deemed Corporate Residence – in Canada if:

(a) incorporated in Canada after April 27 1965 OR

(c) if before 1965, it was incorporated in Canada (provinces, territories, and federal) and was common law resident (central management and control) in Canada or carried business in Canada

De Beers

CL Test: Where does central management and control abide?

Common law idea that a company resides where its real business (where directors meet) is carried out - where the central management and control actually abides (Red Moose Example – dual residency per “domestic law” of both states)

Sources as a Base of Tax Liability

s. 2(1) – Tax payable by persons resident in Canada – tax on all taxable income s. 2(3) – Tax payable by non-resident, for: employment in Canada; business in Canada; disposal of property in Canada

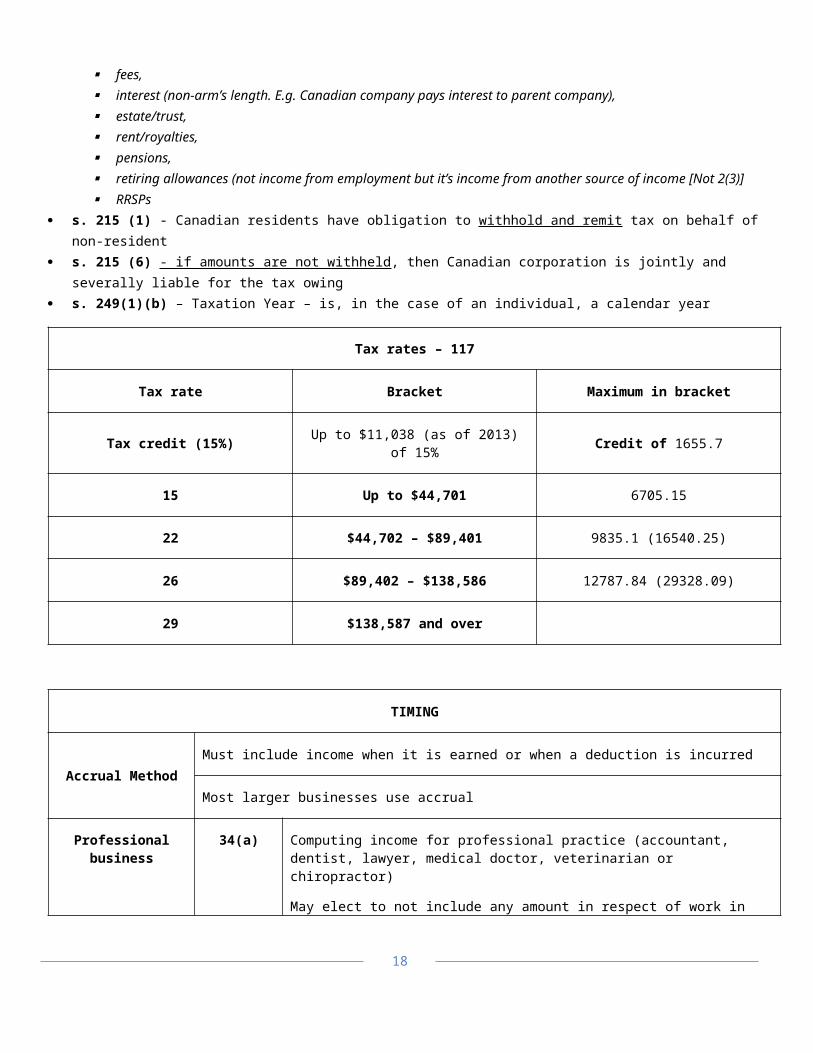

o s. 212 (1) - imposes 25% inc. tax on certain payments made by Canadian residents to non-resident manage. fees, interest (non-arm’s length. E.g. Canadian company pays interest to parent company), estate/trust, rent/royalties, pensions,

13

retiring allowances (not income from employment but it’s income from another source of income [Not 2(3)] RRSPs

s. 215 (1) - Canadian residents have obligation to withhold and remit tax on behalf of non-resident s. 215 (6) - if amounts are not withheld, then Canadian corporation is jointly and severally liable for the tax owing s. 249(1)(b) – Taxation Year – is, in the case of an individual, a calendar year

Tax rates – 117

Tax rate Bracket Maximum in bracket

Tax credit (15%) Up to $11,038 (as of 2013) of 15% Credit of 1655.7

15 Up to $44,701 6705.15

22 $44,702 – $89,401 9835.1 (16540.25)

26 $89,402 – $138,586 12787.84 (29328.09)

29 $138,587 and over

TIMING

Accrual Method

Must include income when it is earned or when a deduction is incurred

Most larger businesses use accrual

Professional business

34(a)

Computing income for professional practice (accountant, dentist, lawyer, medical doctor, veterinarian or chiropractor)

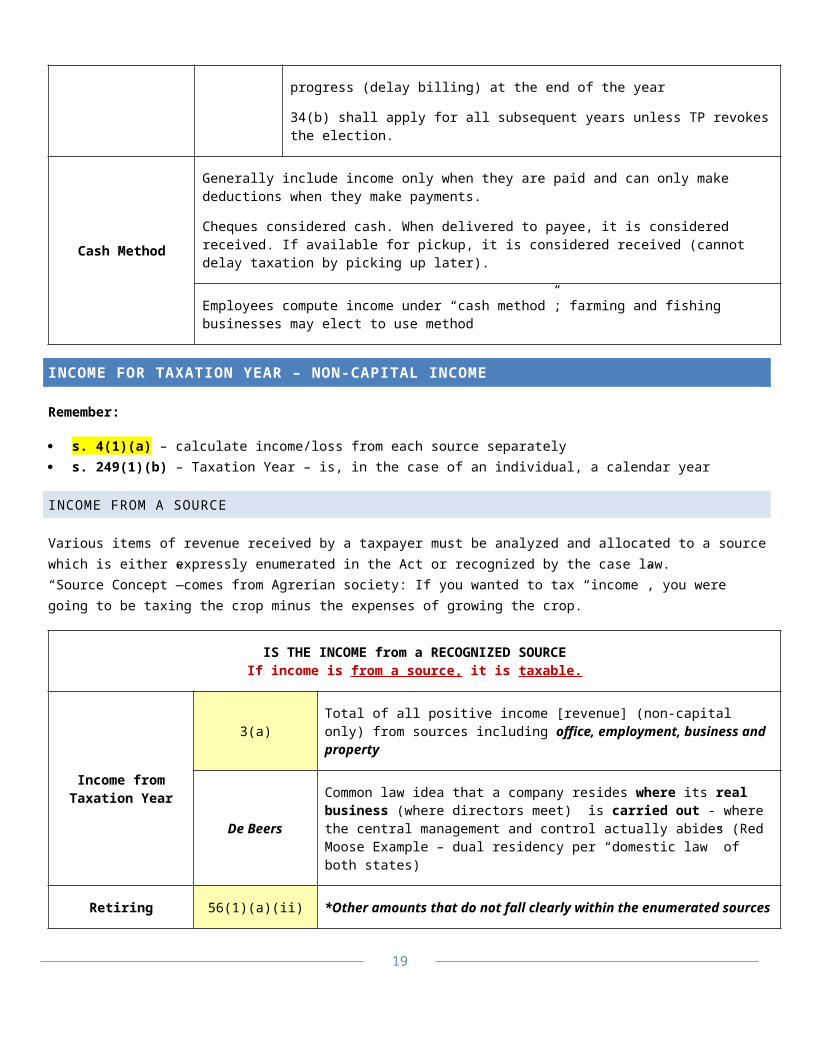

May elect to not include any amount in respect of work in progress (delay billing) at the end of the year

34(b) shall apply for all subsequent years unless TP revokes the election.

Cash Method

Generally include income only when they are paid and can only make deductions when they make payments.

Cheques considered cash. When delivered to payee, it is considered received. If available for pickup, it is considered received (cannot delay taxation by picking up later).

Employees compute income under “cash method”; farming and fishing businesses may elect to use method

INCOME FOR TAXATION YEAR – NON-CAPITAL INCOME

14

Remember:

s. 4(1)(a) – calculate income/loss from each source separately s. 249(1)(b) – Taxation Year – is, in the case of an individual, a calendar year

INCOME FROM A SOURCE

Various items of revenue received by a taxpayer must be analyzed and allocated to a source which is either expressly enumerated in the Act or recognized by the case law.“Source Concept”—comes from Agrerian society: If you wanted to tax “income”, you were going to be taxing the crop minus the expenses of growing the crop.

IS THE INCOME from a RECOGNIZED SOURCEIf income is from a source, it is taxable.

Income from Taxation Year

3(a)Total of all positive income [revenue] (non-capital only) from sources including office, employment, business and property

De Beers

Common law idea that a company resides where its real business (where directors meet) is carried out - where the central management and control actually abides (Red Moose Example – dual residency per “domestic law” of both states)

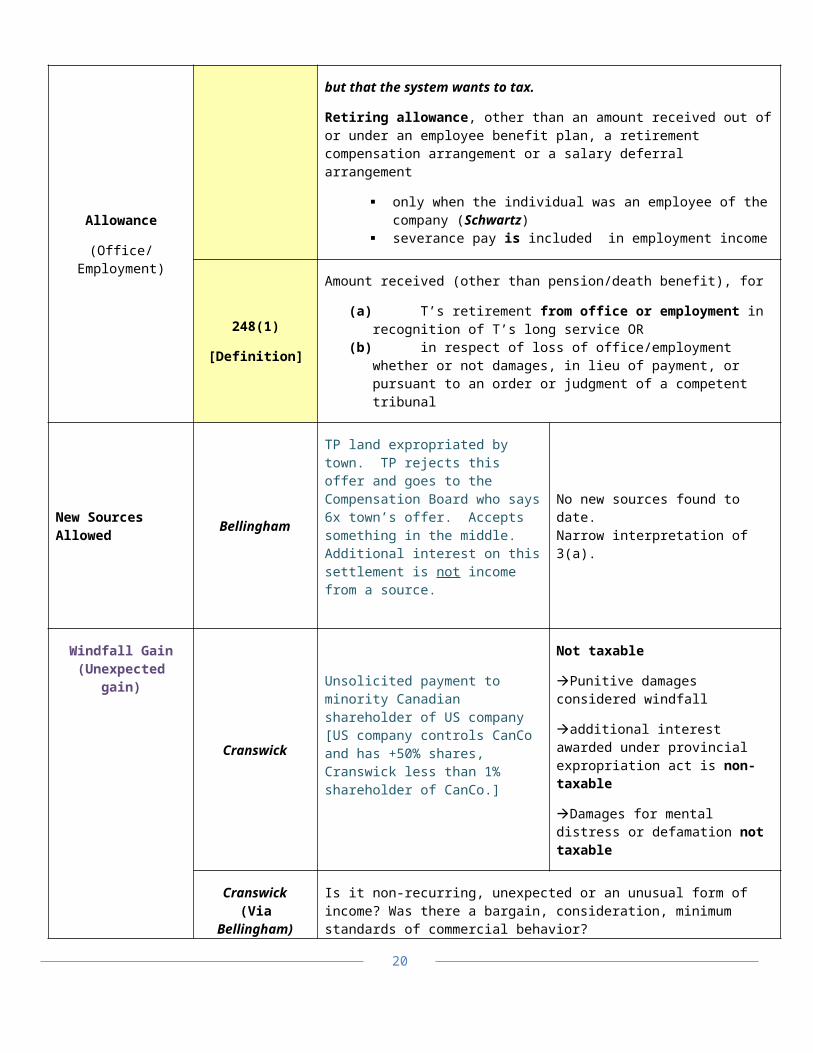

Retiring Allowance

(Office/Employment)

56(1)(a)(ii)

*Other amounts that do not fall clearly within the enumerated sources but that the system wants to tax.

Retiring allowance, other than an amount received out of or under an employee benefit plan, a retirement compensation arrangement or a salary deferral arrangement

only when the individual was an employee of the company (Schwartz)

severance pay is included in employment income

248(1)

[Definition]

Amount received (other than pension/death benefit), for

(a) T’s retirement from office or employment in recognition of T’s long service OR

(b) in respect of loss of office/employment whether or not damages, in lieu of payment, or pursuant to an order or judgment of a competent tribunal

New Sources Allowed Bellingham

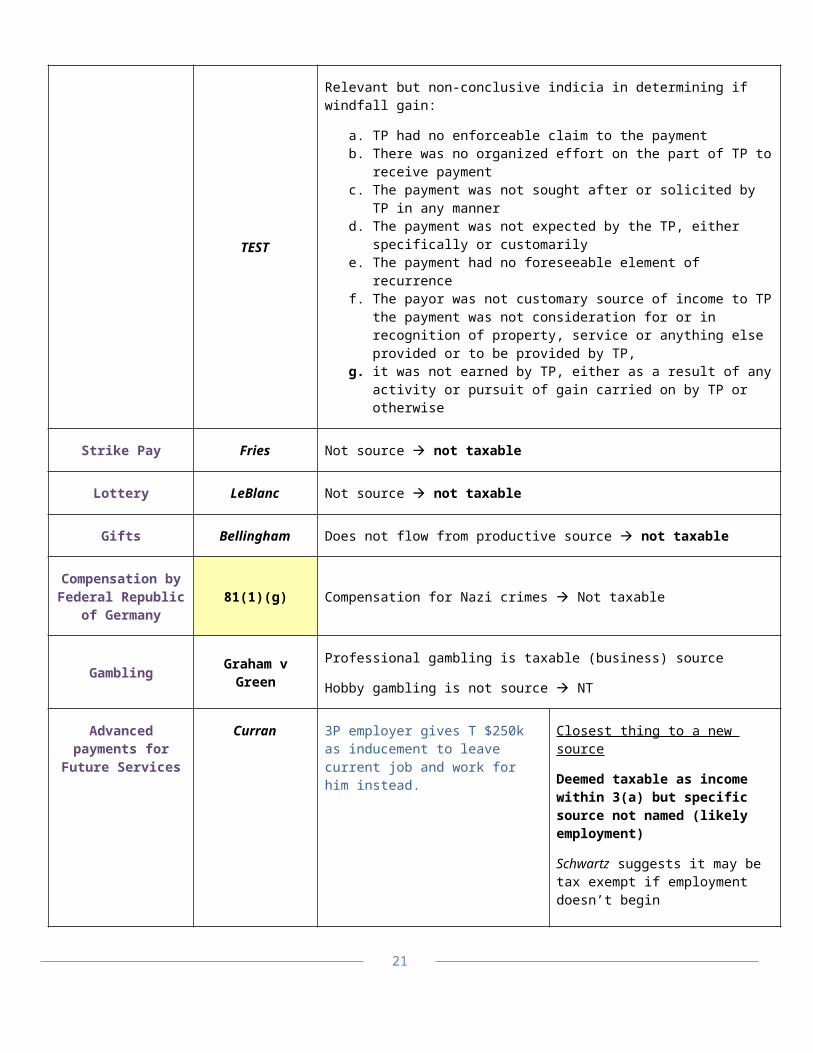

TP land expropriated by town. TP rejects this offer and goes to the Compensation Board who says 6x town’s offer. Accepts something in the middle. Additional interest on this settlement is not income from a source.

No new sources found to date.Narrow interpretation of 3(a).

Windfall Gain Cranswick Unsolicited payment to minority Not taxable

15

(Unexpected gain)

Canadian shareholder of US company[US company controls CanCo and has +50% shares, Cranswick less than 1% shareholder of CanCo.]

Punitive damages considered windfall

additional interest awarded under provincial expropriation act is non-taxable

Damages for mental distress or defamation not taxable

Cranswick(Via Bellingham)

TEST

Is it non-recurring, unexpected or an unusual form of income? Was there a bargain, consideration, minimum standards of commercial behavior?

Relevant but non-conclusive indicia in determining if windfall gain:

a. TP had no enforceable claim to the paymentb. There was no organized effort on the part of TP to receive paymentc. The payment was not sought after or solicited by TP in any mannerd. The payment was not expected by the TP, either specifically or

customarilye. The payment had no foreseeable element of recurrencef. The payor was not customary source of income to TP the payment was

not consideration for or in recognition of property, service or anything else provided or to be provided by TP,

g. it was not earned by TP, either as a result of any activity or pursuit of gain carried on by TP or otherwise

Strike Pay Fries Not source not taxable

Lottery LeBlanc Not source not taxable

Gifts Bellingham Does not flow from productive source not taxable

Compensation by Federal Republic of

Germany81(1)(g) Compensation for Nazi crimes Not taxable

Gambling Graham v GreenProfessional gambling is taxable (business) source

Hobby gambling is not source NT

Advanced payments for Future Services

Curran 3P employer gives T $250k as inducement to leave current job and work for him instead.

Closest thing to a new source

Deemed taxable as income within 3(a) but specific source not named (likely employment)

Schwartz suggests it may be tax exempt if employment doesn’t begin

{This case uses SP but does not

16

explicitly state it}

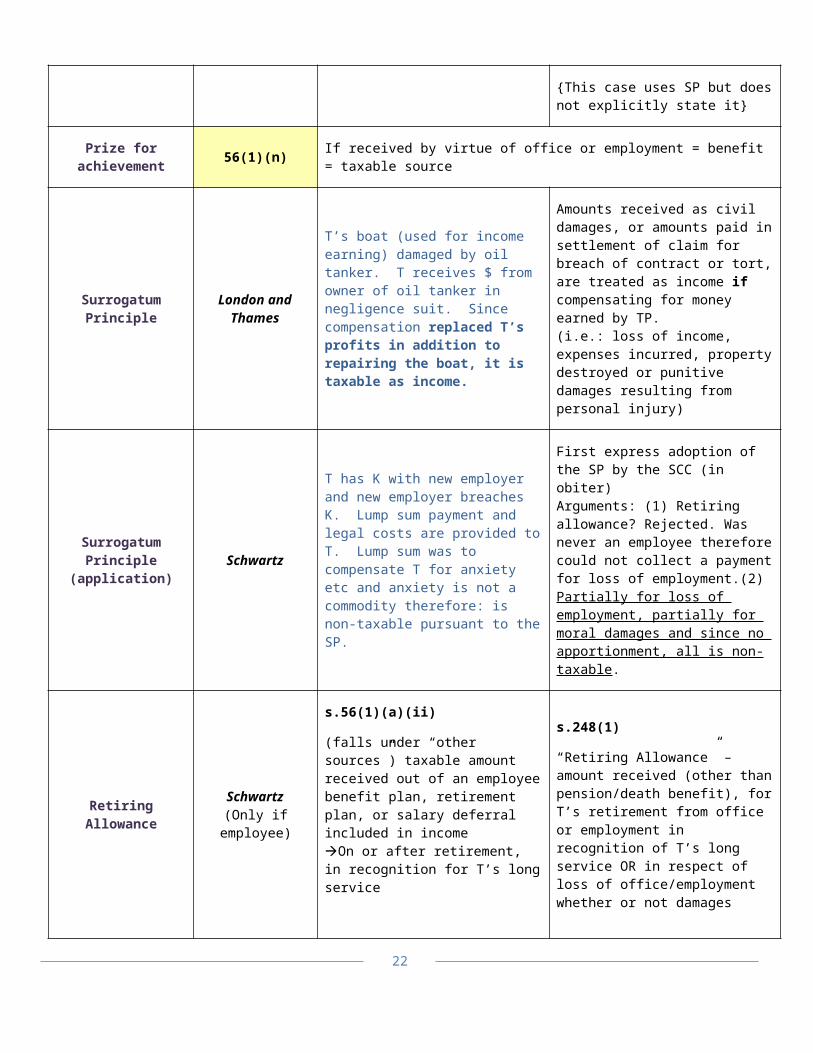

Prize for achievement 56(1)(n) If received by virtue of office or employment = benefit = taxable source

Surrogatum Principle

London and Thames

T’s boat (used for income earning) damaged by oil tanker. T receives $ from owner of oil tanker in negligence suit. Since compensation replaced T’s profits in addition to repairing the boat, it is taxable as income.

Amounts received as civil damages, or amounts paid in settlement of claim for breach of contract or tort, are treated as income if compensating for money earned by TP.(i.e.: loss of income, expenses incurred, property destroyed or punitive damages resulting from personal injury)

Surrogatum Principle

(application)Schwartz

T has K with new employer and new employer breaches K. Lump sum payment and legal costs are provided to T. Lump sum was to compensate T for anxiety etc and anxiety is not a commodity therefore: is non-taxable pursuant to the SP.

First express adoption of the SP by the SCC (in obiter)Arguments: (1) Retiring allowance? Rejected. Was never an employee therefore could not collect a payment for loss of employment.(2) Partially for loss of employment, partially for moral damages and since no apportionment, all is non-taxable.

Retiring AllowanceSchwartz

(Only if employee)

s.56(1)(a)(ii)

(falls under “other sources”) taxable amount received out of an employee benefit plan, retirement plan, or salary deferral included in incomeOn or after retirement, in recognition for T’s long service

s.248(1)

“Retiring Allowance” – amount received (other than pension/death benefit), for T’s retirement from office or employment in recognition of T’s long service OR in respect of loss of office/employment whether or not damages

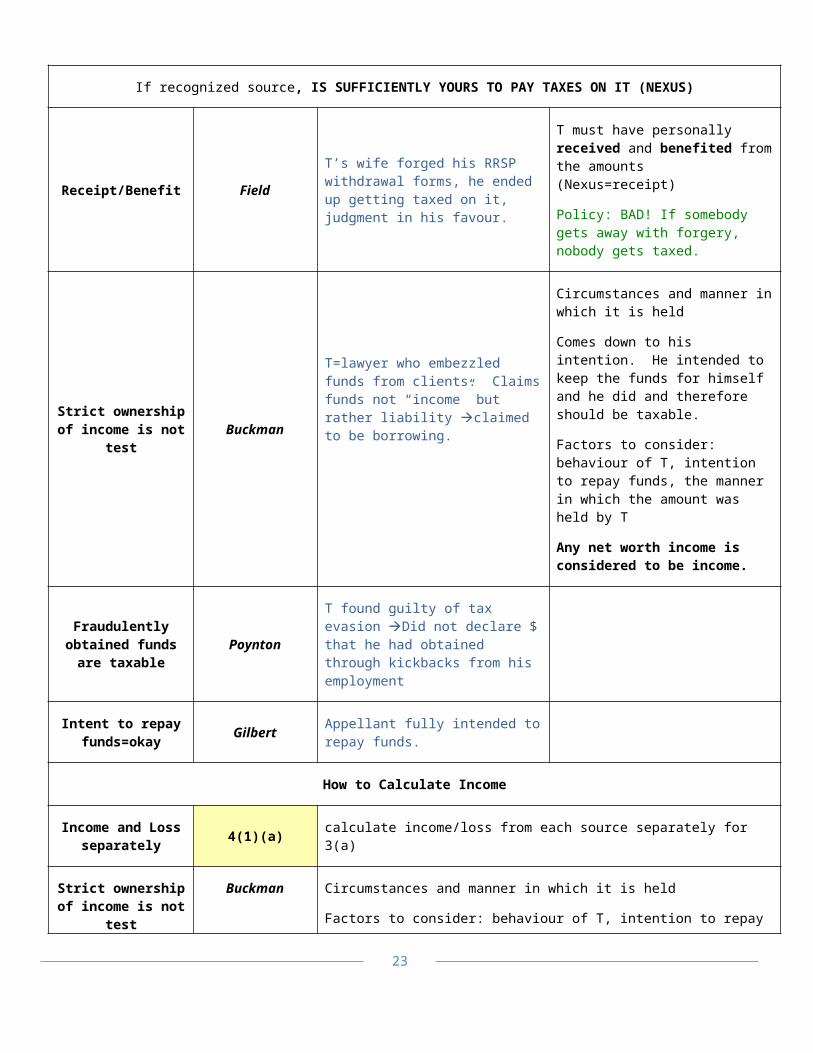

If recognized source, IS SUFFICIENTLY YOURS TO PAY TAXES ON IT (NEXUS)

Receipt/Benefit FieldT’s wife forged his RRSP withdrawal forms, he ended up getting taxed on it, judgment in his favour.

T must have personally received and benefited from the amounts(Nexus=receipt)

Policy: BAD! If somebody gets away with forgery, nobody gets taxed.

Strict ownership of income is not test

Buckman T=lawyer who embezzled funds from clients. Claims funds not “income” but rather liability claimed to be borrowing.

Circumstances and manner in which it is held

Comes down to his intention. He intended to keep the funds for himself and he did and therefore should be

17

taxable.

Factors to consider: behaviour of T, intention to repay funds, the manner in which the amount was held by T

Any net worth income is considered to be income.

Fraudulently obtained funds are

taxablePoynton

T found guilty of tax evasion Did not declare $ that he had obtained through kickbacks from his employment

Intent to repay funds=okay Gilbert

Appellant fully intended to repay funds.

How to Calculate Income

Income and Loss separately

4(1)(a) calculate income/loss from each source separately for 3(a)

Strict ownership of income is not test Buckman

Circumstances and manner in which it is held

Factors to consider: behaviour of T, intention to repay funds, the manner in which the amount was held by T

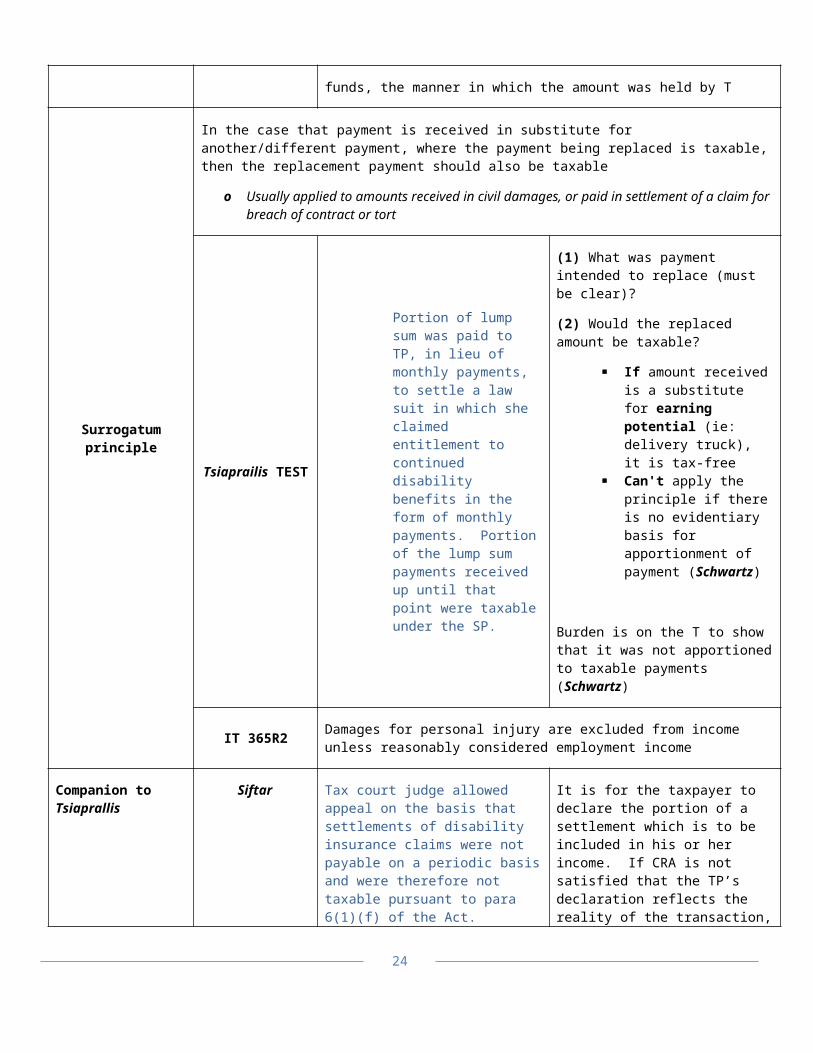

Surrogatum principle

In the case that payment is received in substitute for another/different payment, where the payment being replaced is taxable, then the replacement payment should also be taxable

o Usually applied to amounts received in civil damages, or paid in settlement of a claim for breach of contract or tort

Tsiaprailis TEST Portion of lump sum was paid to TP, in lieu of monthly payments, to settle a law suit in which she claimed entitlement to continued disability benefits in the form of monthly payments. Portion of the lump sum payments received up until that point were taxable under the SP.

(1) What was payment intended to replace (must be clear)?

(2) Would the replaced amount be taxable?

If amount received is a substitute for earning potential (ie: delivery truck), it is tax-free

Can't apply the principle if there is no evidentiary basis for apportionment of payment (Schwartz)

Burden is on the T to show that it was not apportioned to taxable payments

18

(Schwartz)

IT 365R2Damages for personal injury are excluded from income unless reasonably considered employment income

Companion to Tsiaprallis Siftar

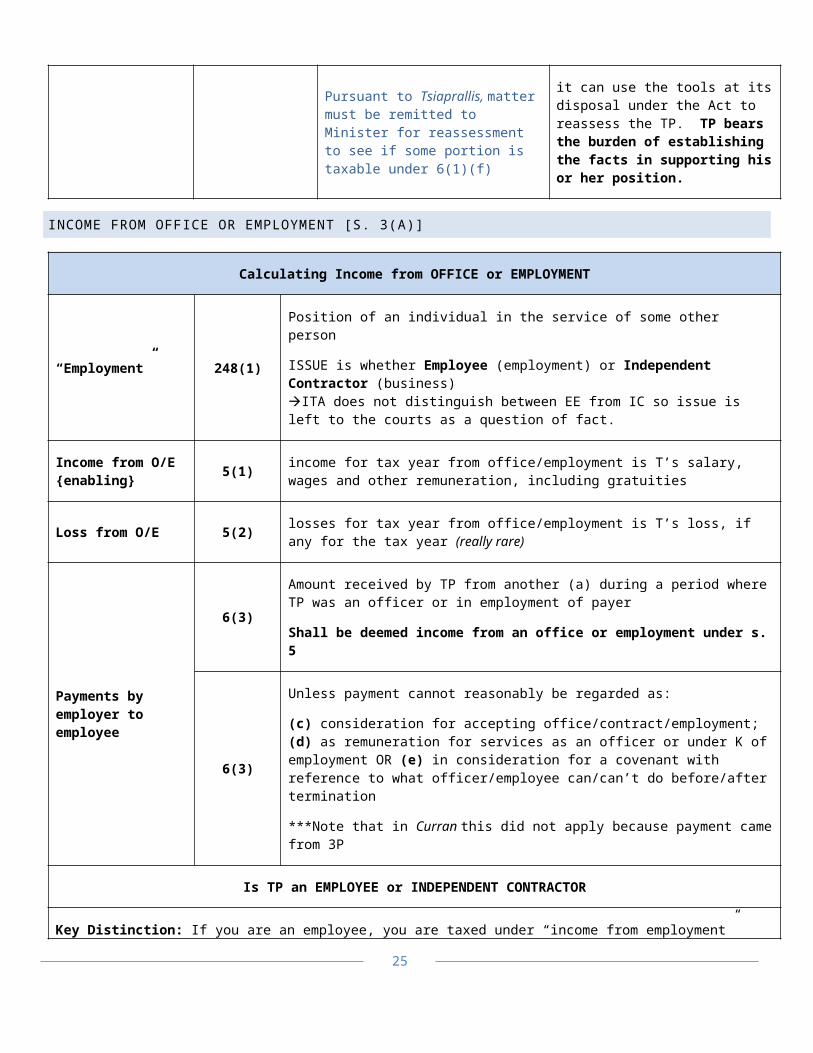

Tax court judge allowed appeal on the basis that settlements of disability insurance claims were not payable on a periodic basis and were therefore not taxable pursuant to para 6(1)(f) of the Act. Pursuant to Tsiaprallis, matter must be remitted to Minister for reassessment to see if some portion is taxable under 6(1)(f)

It is for the taxpayer to declare the portion of a settlement which is to be included in his or her income. If CRA is not satisfied that the TP’s declaration reflects the reality of the transaction, it can use the tools at its disposal under the Act to reassess the TP. TP bears the burden of establishing the facts in supporting his or her position.

INCOME FROM OFFICE OR EMPLOYMENT [S. 3(A)]

Calculating Income from OFFICE or EMPLOYMENT

“Employment” 248(1)

Position of an individual in the service of some other person

ISSUE is whether Employee (employment) or Independent Contractor (business)ITA does not distinguish between EE from IC so issue is left to the courts as a question of fact.

Income from O/E{enabling} 5(1)

income for tax year from office/employment is T’s salary, wages and other remuneration, including gratuities

Loss from O/E 5(2)losses for tax year from office/employment is T’s loss, if any for the tax year (really rare)

Payments by employer to employee

6(3)

Amount received by TP from another (a) during a period where TP was an officer or in employment of payer

Shall be deemed income from an office or employment under s. 5

6(3)

Unless payment cannot reasonably be regarded as:

(c) consideration for accepting office/contract/employment; (d) as remuneration for services as an officer or under K of employment OR (e) in consideration for a covenant with reference to what officer/employee can/can’t do before/after termination

***Note that in Curran this did not apply because payment came from 3P

Is TP an EMPLOYEE or INDEPENDENT CONTRACTOR

Key Distinction: If you are an employee, you are taxed under “income from employment” (employers must withhold tax from

19

employee’s paycheques)Key Question: Are they earning income from employment or income from business? [original “control test” from R v. Walker but this broke down with the increase in highly skilled/professional workers]

*Need to be careful when making these distinctions RE integration because in this day and age if you are asking people if they are an integral part of the business, the answer will almost always be yes.

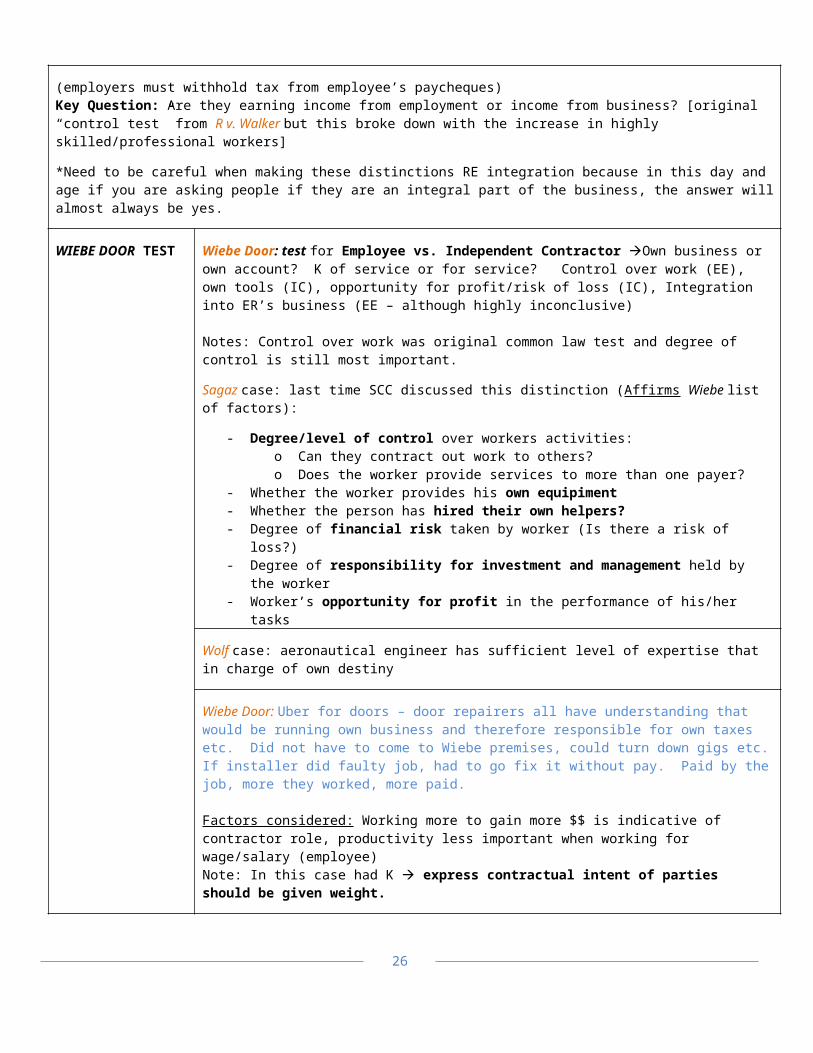

WIEBE DOOR TEST Wiebe Door: test for Employee vs. Independent Contractor Own business or own account? K of service or for service? Control over work (EE), own tools (IC), opportunity for profit/risk of loss (IC), Integration into ER’s business (EE – although highly inconclusive)

Notes: Control over work was original common law test and degree of control is still most important.

Sagaz case: last time SCC discussed this distinction (Affirms Wiebe list of factors):

- Degree/level of control over workers activities: o Can they contract out work to others? o Does the worker provide services to more than one payer?

- Whether the worker provides his own equipiment - Whether the person has hired their own helpers? - Degree of financial risk taken by worker (Is there a risk of loss?)- Degree of responsibility for investment and management held by the worker - Worker’s opportunity for profit in the performance of his/her tasks

Wolf case: aeronautical engineer has sufficient level of expertise that in charge of own destiny

Wiebe Door: Uber for doors – door repairers all have understanding that would be running own business and therefore responsible for own taxes etc. Did not have to come to Wiebe premises, could turn down gigs etc. If installer did faulty job, had to go fix it without pay. Paid by the job, more they worked, more paid.

Factors considered: Working more to gain more $$ is indicative of contractor role, productivity less important when working for wage/salary (employee)Note: In this case had K express contractual intent of parties should be given weight.

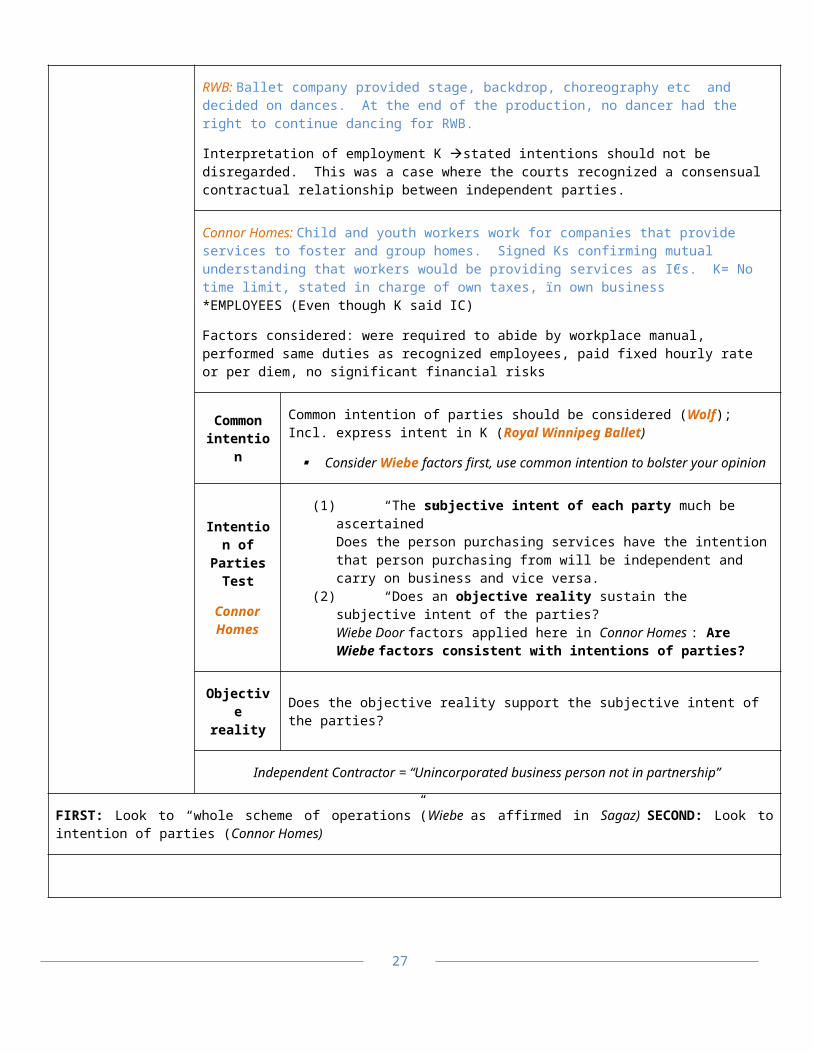

RWB: Ballet company provided stage, backdrop, choreography etc and decided on dances. At the end of the production, no dancer had the right to continue dancing for RWB.

Interpretation of employment K stated intentions should not be disregarded. This was a case where the courts recognized a consensual contractual relationship between independent parties.

Connor Homes: Child and youth workers work for companies that provide services to foster and group homes. Signed Ks confirming mutual understanding that workers would be providing services as ICs. K= No time limit, stated in charge of own taxes, ïn own business”*EMPLOYEES (Even though K said IC)

Factors considered: were required to abide by workplace manual, performed same duties as recognized employees, paid fixed hourly rate or per diem, no significant financial risks

Common intention

Common intention of parties should be considered (Wolf); Incl. express intent in K (Royal Winnipeg Ballet)

Consider Wiebe factors first, use common intention to bolster your opinion

20

Intention of Parties

Test

Connor Homes

(1) “The subjective intent of each party much be ascertained”Does the person purchasing services have the intention that person purchasing from will be independent and carry on business and vice versa.

(2) “Does an objective reality sustain the subjective intent of the parties?Wiebe Door factors applied here in Connor Homes : Are Wiebe factors consistent with intentions of parties?

Objective reality Does the objective reality support the subjective intent of the parties?

Independent Contractor = “Unincorporated business person not in partnership”

FIRST: Look to “whole scheme of operations”(Wiebe as affirmed in Sagaz) SECOND: Look to intention of parties (Connor Homes)

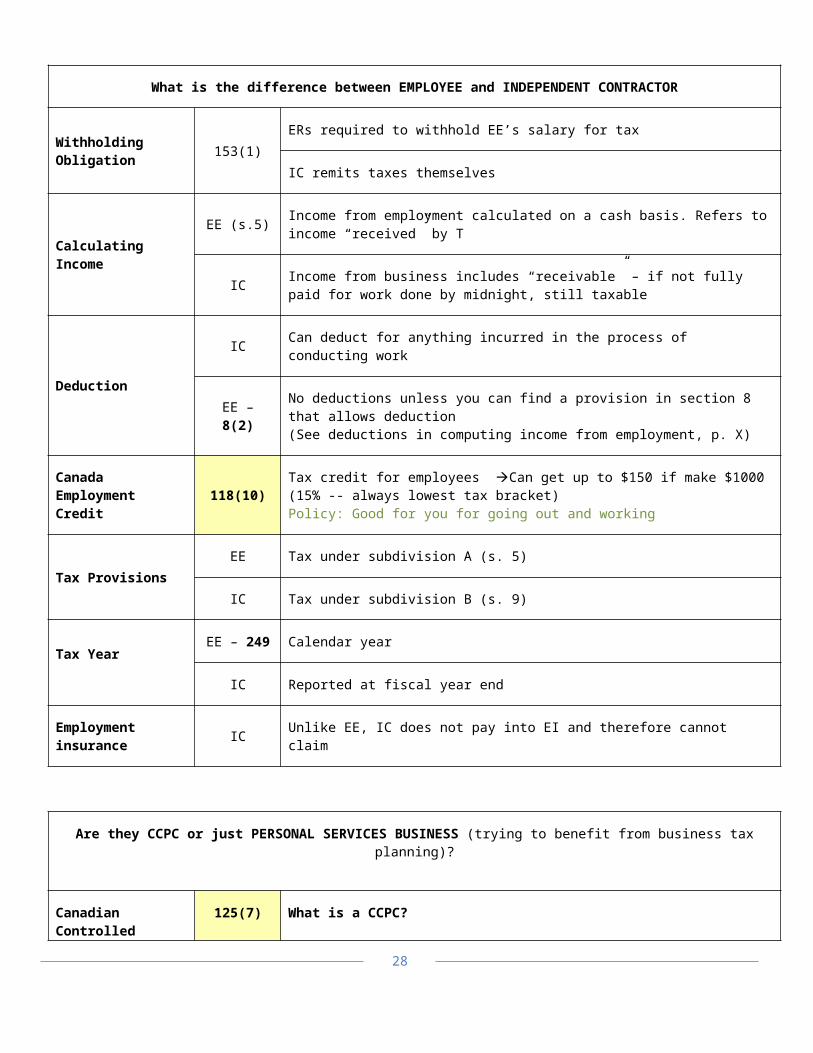

What is the difference between EMPLOYEE and INDEPENDENT CONTRACTOR

Withholding Obligation

153(1)

ERs required to withhold EE’s salary for tax

IC remits taxes themselves

Calculating Income

EE (s.5) Income from employment calculated on a cash basis. Refers to income “received” by T

ICIncome from business includes “receivable” – if not fully paid for work done by midnight, still taxable

Deduction

IC Can deduct for anything incurred in the process of conducting work

EE – 8(2)No deductions unless you can find a provision in section 8 that allows deduction(See deductions in computing income from employment, p. X)

Canada Employment Credit

118(10)Tax credit for employees Can get up to $150 if make $1000(15% -- always lowest tax bracket)Policy: Good for you for going out and working

Tax Provisions

EE Tax under subdivision A (s. 5)

IC Tax under subdivision B (s. 9)

Tax YearEE – 249 Calendar year

IC Reported at fiscal year end

21

Employment insurance IC Unlike EE, IC does not pay into EI and therefore cannot claim

Are they CCPC or just PERSONAL SERVICES BUSINESS (trying to benefit from business tax planning)?

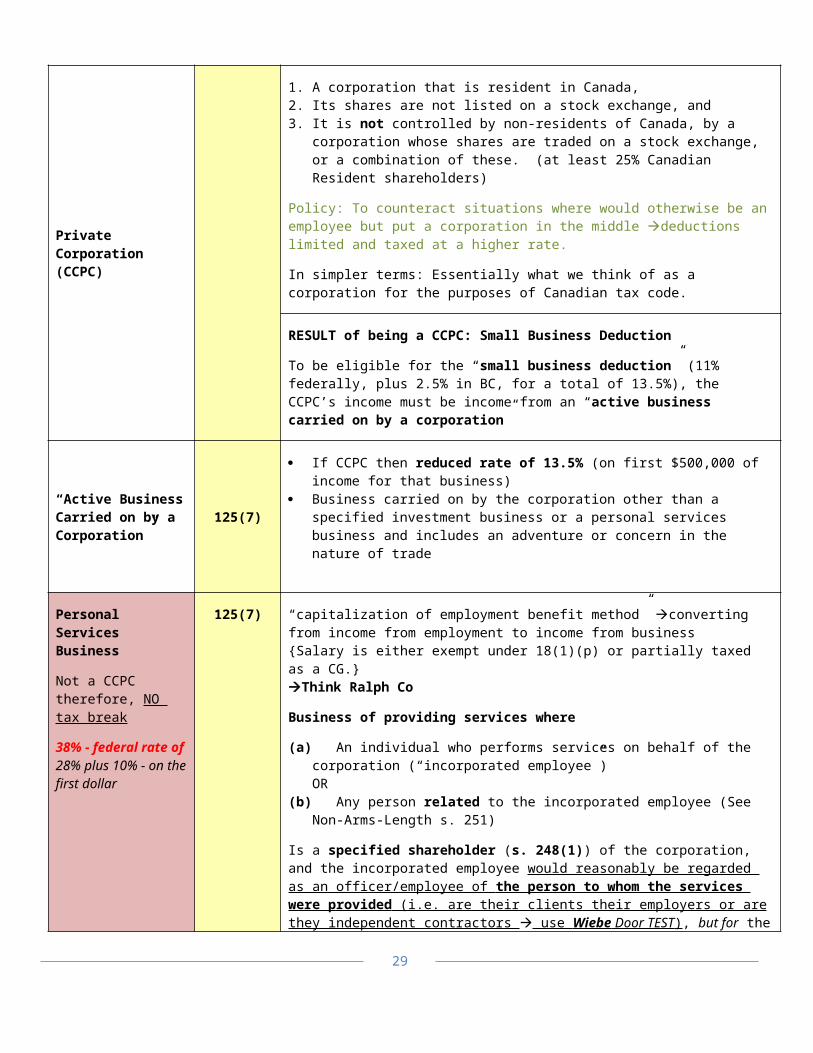

Canadian Controlled Private Corporation (CCPC)

125(7)

What is a CCPC?

1. A corporation that is resident in Canada, 2. Its shares are not listed on a stock exchange, and 3. It is not controlled by non-residents of Canada, by a corporation whose shares

are traded on a stock exchange, or a combination of these. (at least 25% Canadian Resident shareholders)

Policy: To counteract situations where would otherwise be an employee but put a corporation in the middle deductions limited and taxed at a higher rate.

In simpler terms: Essentially what we think of as a corporation for the purposes of Canadian tax code.

RESULT of being a CCPC: Small Business Deduction

To be eligible for the “small business deduction” (11% federally, plus 2.5% in BC, for a total of 13.5%), the CCPC’s income must be income from an “active business carried on by a corporation”

“Active Business Carried on by a Corporation”

125(7)

If CCPC then reduced rate of 13.5% (on first $500,000 of income for that business)

Business carried on by the corporation other than a specified investment business or a personal services business and includes an adventure or concern in the nature of trade

Personal Services Business

Not a CCPC therefore, NO tax break

38% - federal rate of 28% plus 10% - on the first dollar

125(7) “capitalization of employment benefit method” converting from income from employment to income from business{Salary is either exempt under 18(1)(p) or partially taxed as a CG.}Think Ralph Co

Business of providing services where

(a) An individual who performs services on behalf of the corporation (“incorporated employee”) OR

(b) Any person related to the incorporated employee (See Non-Arms-Length s. 251)

Is a specified shareholder (s. 248(1)) of the corporation, and the incorporated employee would reasonably be regarded as an officer/employee of the person to whom the services were provided (i.e. are their clients their employers or are they independent contractors use Wiebe Door TEST ) , but for the existence of the corporation;

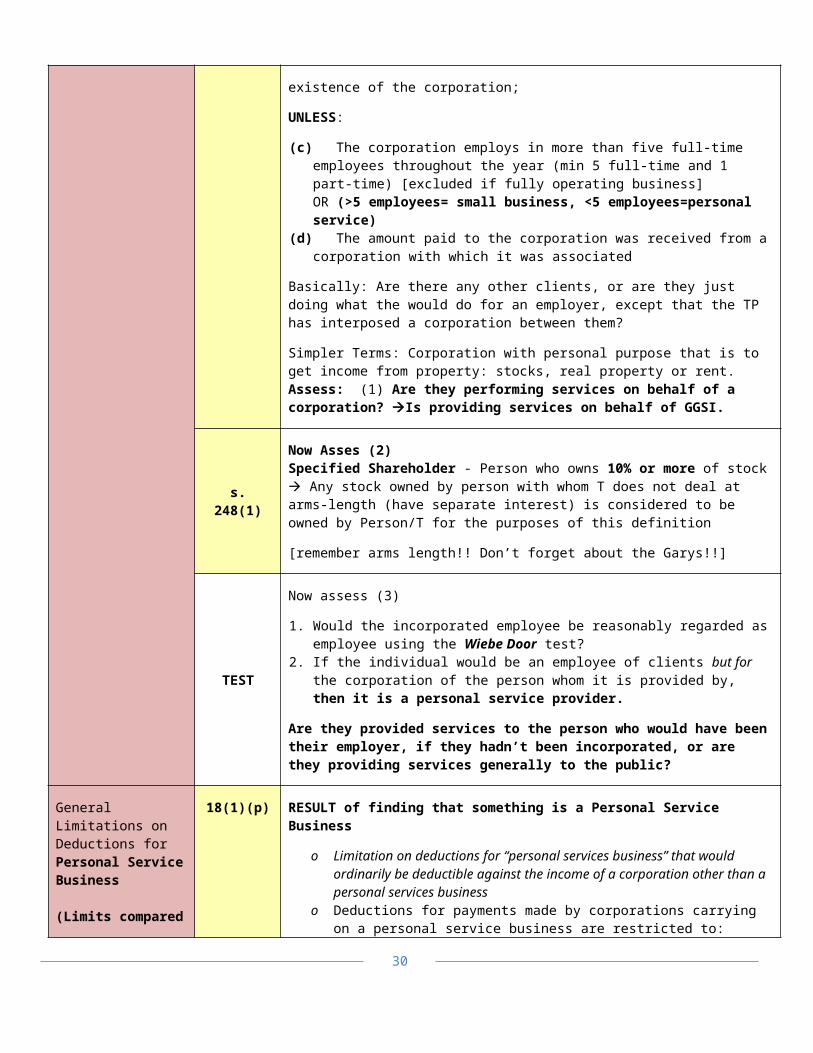

22

UNLESS:

(c) The corporation employs in more than five full-time employees throughout the year (min 5 full-time and 1 part-time) [excluded if fully operating business]OR (>5 employees= small business, <5 employees=personal service)

(d) The amount paid to the corporation was received from a corporation with which it was associated

Basically: Are there any other clients, or are they just doing what the would do for an employer, except that the TP has interposed a corporation between them?

Simpler Terms: Corporation with personal purpose that is to get income from property: stocks, real property or rent.Assess: (1) Are they performing services on behalf of a corporation? Is providing services on behalf of GGSI.

s. 248(1)

Now Asses (2)Specified Shareholder - Person who owns 10% or more of stock Any stock owned by person with whom T does not deal at arms-length (have separate interest) is considered to be owned by Person/T for the purposes of this definition

[remember arms length!! Don’t forget about the Garys!!]

TEST

Now assess (3)

1. Would the incorporated employee be reasonably regarded as employee using the Wiebe Door test?

2. If the individual would be an employee of clients but for the corporation of the person whom it is provided by, then it is a personal service provider.

Are they provided services to the person who would have been their employer, if they hadn’t been incorporated, or are they providing services generally to the public?

General Limitations on Deductions for Personal Service Business

(Limits compared to a corporation)

18(1)(p) RESULT of finding that something is a Personal Service Business

o Limitation on deductions for “personal services business” that would ordinarily be deductible against the income of a corporation other than a personal services business

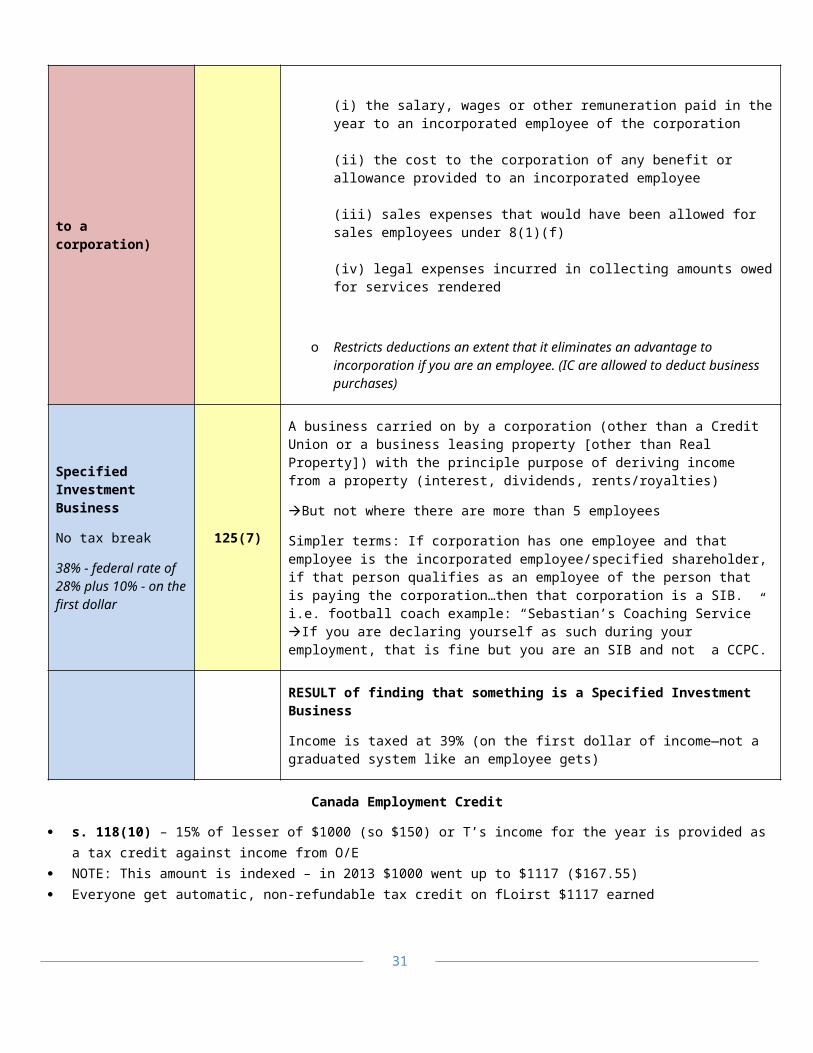

o Deductions for payments made by corporations carrying on a personal service business are restricted to:

(i) the salary, wages or other remuneration paid in the year to an incorporated employee of the corporation

(ii) the cost to the corporation of any benefit or allowance provided to an incorporated employee

(iii) sales expenses that would have been allowed for sales employees under 8(1)(f)

(iv) legal expenses incurred in collecting amounts owed for services rendered

23

o Restricts deductions an extent that it eliminates an advantage to incorporation if you are an employee. (IC are allowed to deduct business purchases)

Specified Investment Business

No tax break

38% - federal rate of 28% plus 10% - on the first dollar

125(7)

A business carried on by a corporation (other than a Credit Union or a business leasing property [other than Real Property]) with the principle purpose of deriving income from a property (interest, dividends, rents/royalties)

But not where there are more than 5 employees

Simpler terms: If corporation has one employee and that employee is the incorporated employee/specified shareholder, if that person qualifies as an employee of the person that is paying the corporation…then that corporation is a SIB.i.e. football coach example: “Sebastian’s Coaching Service” If you are declaring yourself as such during your employment, that is fine but you are an SIB and not a CCPC.

RESULT of finding that something is a Specified Investment Business

Income is taxed at 39% (on the first dollar of income—not a graduated system like an employee gets)

Canada Employment Credit

s. 118(10) – 15% of lesser of $1000 (so $150) or T’s income for the year is provided as a tax credit against income from O/E

NOTE: This amount is indexed – in 2013 $1000 went up to $1117 ($167.55) Everyone get automatic, non-refundable tax credit on fLoirst $1117 earned

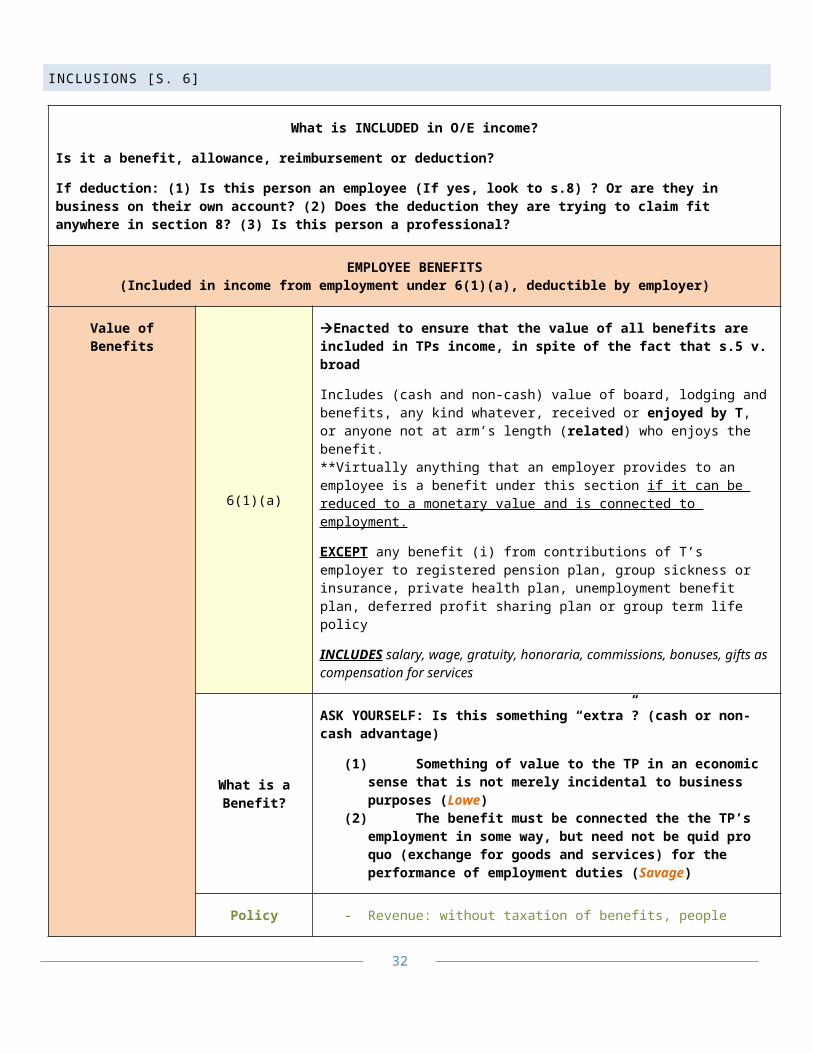

INCLUSIONS [S. 6]

What is INCLUDED in O/E income?

Is it a benefit, allowance, reimbursement or deduction?

If deduction: (1) Is this person an employee (If yes, look to s.8) ? Or are they in business on their own account? (2) Does the deduction they are trying to claim fit anywhere in section 8? (3) Is this person a professional?

EMPLOYEE BENEFITS(Included in income from employment under 6(1)(a), deductible by employer)

Value of Benefits 6(1)(a) Enacted to ensure that the value of all benefits are included in TPs income, in spite of the fact that s.5 v. broad

Includes (cash and non-cash) value of board, lodging and benefits, any kind whatever, received or enjoyed by T, or anyone not at arm’s length (related) who enjoys the benefit.**Virtually anything that an employer provides to an employee is a benefit under this section if it can be reduced to a monetary value and is connected to employment.

EXCEPT any benefit (i) from contributions of T’s employer to registered pension plan, group sickness or insurance, private health plan, unemployment

24

benefit plan, deferred profit sharing plan or group term life policy

INCLUDES salary, wage, gratuity, honoraria, commissions, bonuses, gifts as compensation for services

What is a Benefit?

ASK YOURSELF: Is this something “extra”? (cash or non-cash advantage)

(1) Something of value to the TP in an economic sense that is not merely incidental to business purposes (Lowe)

(2) The benefit must be connected the the TP’s employment in some way, but need not be quid pro quo (exchange for goods and services) for the performance of employment duties (Savage)

Policy

- Revenue: without taxation of benefits, people would attempt to get their remuneration as much as possible in the form of benefits rather than salary, which would greatly reduce tax base.

- Equity: Would be unfair if some got certain amenities tax free and not others

- Employer gets to deduct almost everything given to employees

Lowe

Must be measurable economic benefit

Value = FMV determined by expert evidence (Giffen)

FMV: The “amount a person who is not obligated to buy would pay a person who is not obligated to sell” (Steen)

Benefit to Employer Lowe(BUSINESS

TRIP)

Lowe was account exec at insurance co. Co sent Lowe and wife to New Orleans to promote insurance to brokers. Both L and wife expected to attend and brokers were bringing wives. Paid holiday or business trip?

HELD: deductible business expense.{primary purpose= business to benefit the employer: he enjoyed the trip but was not able to do whatever he wanted when he got there}

“The Primarily Business Test”: was the principal purpose of this trip for business or pleasure?

Will not be considered EE benefit if ER gets advantage of expenditure

Pleasure is incidental

If a trip is part business/part pleasure, will be apportioned by the CRA.{see Waffle case = purely pleasure cruise – took place of president on trip}

TEST

(1) Does the item under review provide the employee with an economic advantage that is measurable in monetary terms? (If no, can’t be included)

(2) If there is an advantage, is the primary advantage for the benefit of the employee or the employer? If the pleasure is simply incidental to a business purpose, it is not a taxable benefit for the employee within 6(1)(a).

25

Air Miles Giffen

In the case of employees getting points for flying for employment that they could then use, the value was determined to be the cost of the cheapest economy ticket on the flight. {Value when determining taxability = FMV}

Employer logo Wisla FMW of gold ring is not what employer paid for it but rather value in scrap.

Social Event Dunlop Amounts over $100 are a taxable benefit. Value to employee is the cost/person.

Publicity Promotion Arsens

“the cost of the trip to Disneyland which was undertaken primarily as a publicity promotion for the benefit of the employer’s company should not be taxed as personal benefits in the hands of the several employees who attended on the trip.”

Material AcquisitionPoynton

(relied on in Savage)

Embezzled funds = prize = income under s. 3 of ITA

If a material acquisition confers economic benefit on EE in connection to employment then included in income(Definition of “benefit”)

Doesn’t have to be Quid Pro Quo

SavageLEADING CASE(Changed the

law in Canada)No longer have to

connect the benefit to an

obligation of the employee to

provide services of employment.

S takes 3 voluntary courses related to business; received $300/course for passing exams in accordance with company policy. S did not include as income on TR but CRA reassessed and did.

Need not be a quid pro quo (exchange of goods/services) for the performance of employment duties

(ie: prize for taking non-mandatory course encouraged by employer)

Note: 56(1)(n) provided exemption exception under prizes. Section has now been amended to exclude prizes received in course of business or employment. CRA now allows employer tax free deductions for gifts up to $500/employee.

As long as Benefit available Richmond

Whether T used benefit consistently is irrelevant; as long as it is available to T it is considered as a benefit

Reimbursement(Not taxable)

HuffmanBenefits that reimburse expenses incurred by employees at order of employer, which restores an employee to his/her pre-expense economic situation are not taxable. [See below]

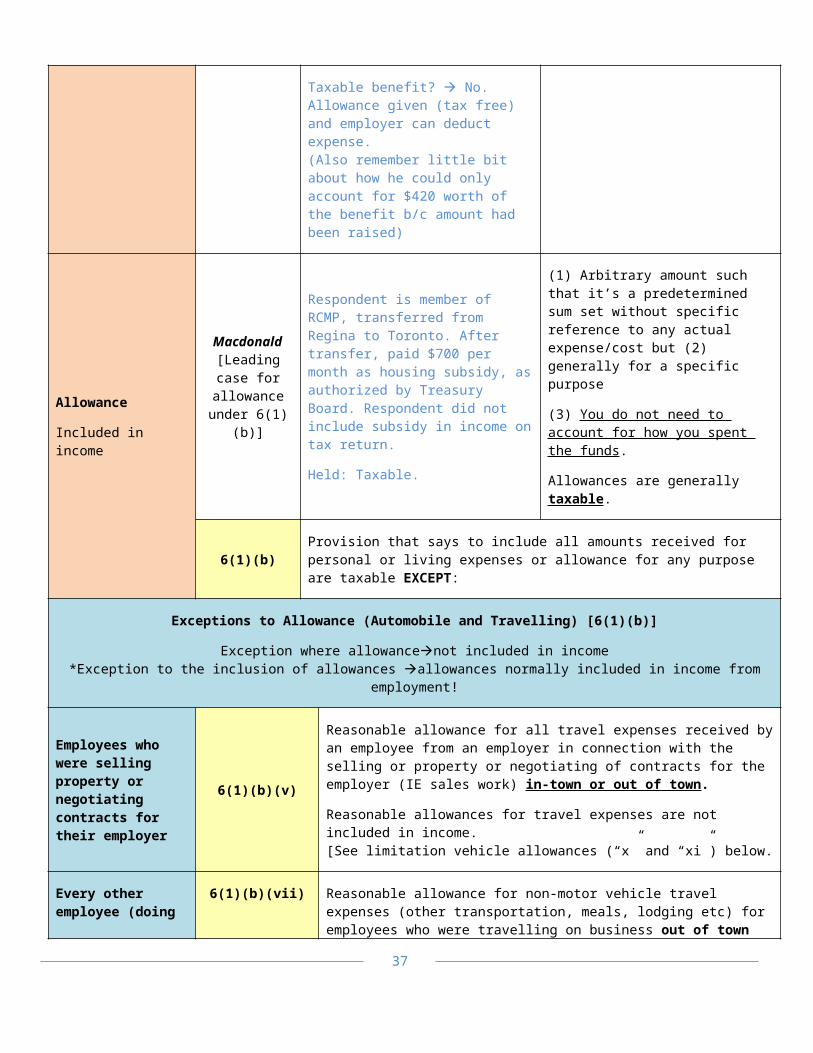

Allowance (Generally taxable)

MacDonaldArbitrary amount. Predetermined sum set without specific reference to any actual expense or cost. [See below]

[Exception to Rachfalowski Minimal benefit for golf membership that he tried to decline but would not

Value should be determined on individual case basis of actual use

26

Availability]