CHAPTER VI CONSUMERS’ PERCEPTIONS -...

51

232 CHAPTER VI CONSUMERS’ PERCEPTIONS The world of marketing is an ever changing one. This is not simply because the consumer’s desires are changing but because of the entry of new competitors with novel product features. In a competitive environment there is nothing more crucial to success than keeping the customers satisfied and engaged. Creation of a satisfied customer is the goal of marketing. Achievement of this goal to a large extent depends on how quickly and efficiently the producer is able to gather quality consumer insights and perceptions. Perception means how one views or perceives matters under the influence of one’s past experience and personal opinion. By understanding the perception of his consumers, the producer can know how the consumers view his product or service. Marketers make use of these perceptions to formulate suitable marketing strategies. They use a perceptual map wherein they find out the attributes or characteristics that the consumers associate with the product and then they make the product to suit the consumers’ interests. The market of Kitchen appliances in Kerala is also rapidly changing where more and more companies are entering with product differentiation strategies. As a result, the perceptions of the consumers in the industry are also changing. So it is important from the part of manufacturers of kitchen appliances to know what the consumer really expects from them and what is actually delivered to him. This chapter tries to analyze the perception of the consumers of kitchen appliances with regard to their brand choice, nature of purchase, performance of their products,

Transcript of CHAPTER VI CONSUMERS’ PERCEPTIONS -...

232

CHAPTER VI

CONSUMERS’ PERCEPTIONS

The world of marketing is an ever changing one. This is not simply because

the consumer’s desires are changing but because of the entry of new competitors

with novel product features. In a competitive environment there is nothing more

crucial to success than keeping the customers satisfied and engaged. Creation of a

satisfied customer is the goal of marketing. Achievement of this goal to a large extent

depends on how quickly and efficiently the producer is able to gather quality

consumer insights and perceptions.

Perception means how one views or perceives matters under the influence of

one’s past experience and personal opinion. By understanding the perception of his

consumers, the producer can know how the consumers view his product or service.

Marketers make use of these perceptions to formulate suitable marketing strategies.

They use a perceptual map wherein they find out the attributes or characteristics that

the consumers associate with the product and then they make the product to suit the

consumers’ interests.

The market of Kitchen appliances in Kerala is also rapidly changing where

more and more companies are entering with product differentiation strategies. As a

result, the perceptions of the consumers in the industry are also changing. So it is

important from the part of manufacturers of kitchen appliances to know what the

consumer really expects from them and what is actually delivered to him. This

chapter tries to analyze the perception of the consumers of kitchen appliances with

regard to their brand choice, nature of purchase, performance of their products,

233

determinants of their purchase decision, responsibility of retailer in providing after

sales service, quality of service offered by the manufacturer, incentives offered for

referrals and the type of incentives offered. It also makes an effort to identify how

the residential location, which might be a proxy of the demographic profile of the

customers, affects the perception of consumers of kitchen appliances industry.

6.1 Location of Consumers

This part of analysis is made on the basis of the area of residence of

consumers. For every study in the context of marketing we should have consumers

from different geographical area in order to get their outlook and attitude in general.

So for this study the State is classified into three segments, taking into consideration

the various aspects, as Urban, Semi Urban and Rural. Consumers residing in a

particular area will have difference in education, culture and social outlook from

those residing in other areas. Therefore to get a balanced result, it is required to select

consumers from all segments. Location wise breakup of the sample is given in Table

T6.1

Table T6.1 Location Wise Distribution of the Consumers

Location No of Respondents Percent

Urban 240 40.0

Semi Urban 200 33.3

Rural 160 26.7

Total 600 100.0

234

Figure F6.1 Location Wise Distribution of the Consumers

Among the selected consumers 40 percent is from the urban area, 33.3

percent from semi urban area and the remaining 26.7 percent reside at rural area.

6.2 Ownership of Kitchen Appliances and Residential Location of Consumers

It is very important to know which of the Kitchen appliances specified in the

study are owned by the respondents. It will indirectly reveal the order of necessity

and order of preference by the consumers. An appliance which is considered to be a

necessity by a consumer in an urban area might be a luxury in the rural area. The

respondents residing in different areas have difference in patterns of ownership of

Kitchen appliances because of the diversity in their needs, culture, customs and

usages, purchasing power, attitudes and outlooks. This can be analyzed from the

possession of various appliances by the consumers in different areas. Table T6.2

reveals the uniformity and diversity of people residing in urban, semi urban and rural

areas with respect to their ownership pattern of kitchen appliances.

Urban40%

Semi Urban33%

Rural27%

235

Table T 6.2 Location Wise Distribution of Consumers of Kitchen Appliances

Types of Kitchen Appliances

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

All 200 83.3 120 60 80 50 400 66.7

All except Refrigerator & Grinder

Nil - Nil - 80 50 80 13.0

All except Grinder

40 16.7 80 40 Nil - 120 20.0

Total 240 100 200 100 160 100 600 100

Pearson Chi-Square Value 54.000 P Value - 0.001* *Significant at 1 per cent level

Figure F6.2 Location Wise Distribution of Consumers of Kitchen Appliances

Analysis shows that 66.7percent of the consumers have all the Kitchen

appliances specified and 13.3 percent have everything except Refrigerator and

Grinder and 20 percent do not use Grinder among the selected product portfolio.

Thus majority of the consumers have all types of kitchen appliances under study.

0

10

20

30

40

50

60

70

80

90

Urban Semi Urban Rural

All

All except Refrigerator & Grinder

All except Grinder

236

83 percentage of the urban population has the entire categorized home

appliances whereas only 60 percent of the semi urban and 50 percent of the rural

households have only selected category of appliances. This shows that the urban

community has found more utility in using the kitchen appliances than the rural

community. This can be related to the pattern of their lifestyle.

Non- parametric test- Pearson’s chi-square test of independence is applied to

find out whether this type of difference exists in the population from which the

sample selected is statistically significant or not. The test result shows that location

wise diversity in the patterns of ownership of the appliances is significant even at 1

per cent level.

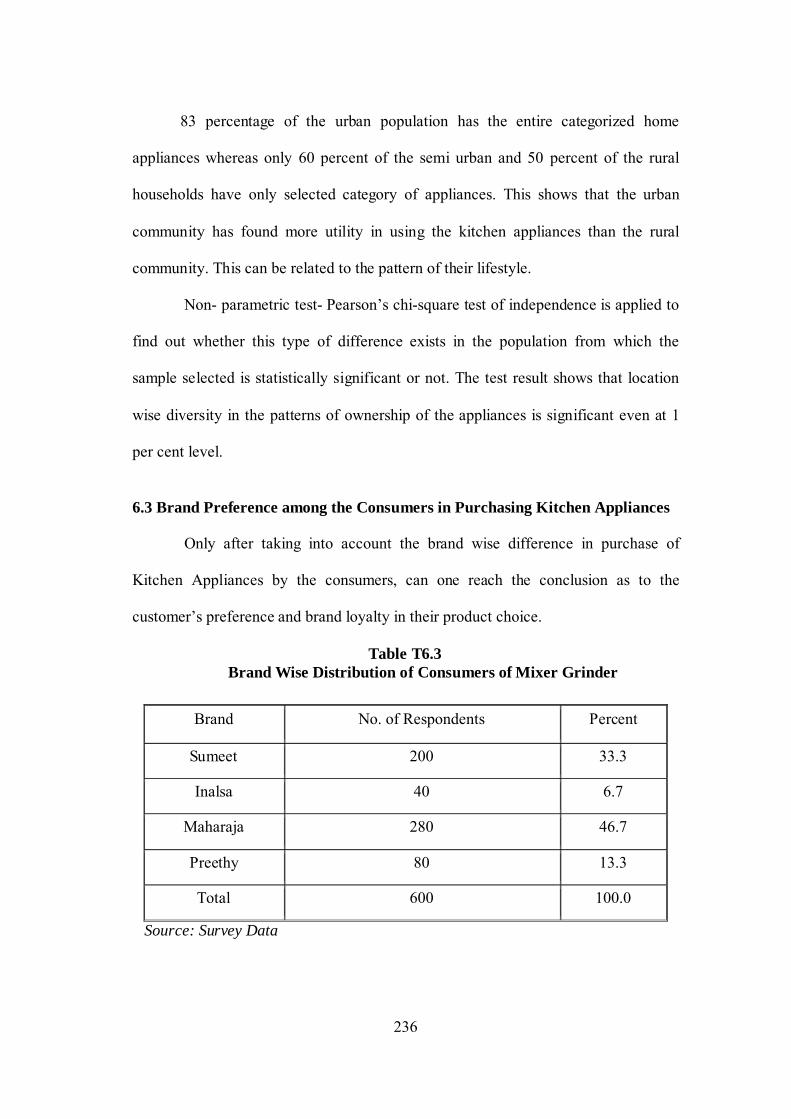

6.3 Brand Preference among the Consumers in Purchasing Kitchen Appliances

Only after taking into account the brand wise difference in purchase of

Kitchen Appliances by the consumers, can one reach the conclusion as to the

customer’s preference and brand loyalty in their product choice.

Table T6.3 Brand Wise Distribution of Consumers of Mixer Grinder

Brand No. of Respondents Percent

Sumeet 200 33.3

Inalsa 40 6.7

Maharaja 280 46.7

Preethy 80 13.3

Total 600 100.0

Source: Survey Data

237

Figure F6.3 Brand Wise Distribution of Consumers of Mixer Grinder

It is clear from Table T6.3 that majority of the consumers of Mixer Grinder

are using famous brands established in the market; 46.7percent of them are using

Maharaja brand, 33.3 percent are using Sumeet brand and the balance 13.3 percent

and 6.7 percent are shared by Preethy and Inalsa respectively.

Table T6.4 Location Wise Distribution of the Consumers in Choosing

Brand of Mixer Grinder

Brand of Mixer Grinder

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

Sumeet 160 66.6 40 20 Nil - 200 33.3

Inalsa 40 16.7 Nil - Nil - 40 6.7

Maharaja Nil - 120 60 160 100 280 46.7

Preethy 40 16.7 40 20 Nil - 80 13.3

Total 240 100 200 100 160 100 600 100

Pearson Chi-Square Value 109.267 P value = <0.001* Source: Survey Data *Significant at 1 per cent level

Sumeet33%

Inalsa7%

Maharaja47%

Preethy13%

238

66.6 percent of urban population has Sumeet brand of Mixer Grinder, while

60 percent of semi urban and 100 percent rural population has bought Maharaja

brand. This shows that Maharaja Brand is mainly preferred by consumers in semi

urban and rural areas while Sumeet is perceived better in quality by the urban

segment. (Table T6.4). Such differences in brand preferences by the consumers from

different geographic segments of mixer grinder market were found statistically

significant at 1 per cent level.

6.4 Brand Wise Distribution of Consumers of Grinder

After taking into consideration the various branded and non branded Grinders

used by the consumers, analysis will be possible to reach the conclusions regarding

the consumers preference and brand loyalty

Table T6.5

Brand Wise Distribution of Consumers of Grinder

Source: Survey Data

Brand of Grinder used No of respondents Percent

Laxmi 155 38.75

Inalsa 40 10

Maharaja 90 22.5

Butterfly 115 28.75

Total 400 100

239

39%

10%22%

29%

Laxmi Inalsa Maharaja Butterfly

Figure F6.4 Brand Wise Distribution of Consumers of Grinder

Table T6.5 reveals that Laxmi and Butterfly are the most popular brands of

Grinders among the selected brands. 38.75 percent and 28.75 percent of consumers

are using Laxmi and Butterfly brand of Grinders respectively. Inalsa is the least

popular product of this kind. So according to the analysis consumers are fond of

mainly popular and established brands in the market.

Table T6.6 Location Wise Distribution of Consumers in Choosing Brand of Grinder

Brand of Grinder

Area of residence Total

Urban Semi Urban Rural No. % No. % No. % No. %

Laxmi 80 40 40 33 35 44 155 39

Inalsa 25 13 15 13 - - 40 10

Maharaja 45 22 35 29 10 12 90 22

Butterfly 50 25 30 25 35 44 115 29

Total 200 100 120 100 80 100 400 100

Pearson Chi-Square Value 12.904 P value = 0.012* Source: Survey Data *Significant at 5 per cent level

240

40 percent of urban population, 33 percent of semi urban and 44 percent of

rural population have got Laxmi Brand of Grinders. Another 25 percent each of

urban and semi urban and 44 percent of rural population has Butterfly brand.

Maharaja is another popular brand with their presence in all segments. They have 22

percent in urban, 29 percent in semi urban and 12 percent in rural area. Inalsa brand

has presence only in urban and semi urban area. Market wise differences in brand

preferences of consumers of Grinder market in Kerala were statistically proved by

the inferential analysis at 5 percent level of significance.

6.5 Brand Wise Distribution of Refrigerator Used by Consumers

After taking into consideration the various branded and non branded

Refrigerators used by the consumers, analysis will be possible to reach the

conclusions regarding the consumer’s preference and brand loyalty.

Table T 6.7 Brand wise Distribution of Consumers of Refrigerator

Brand of Refrigerator No of respondents Percent

Godrej 120 23

BPL 80 15.5

LG 120 23

Samsung 80 15.5

Whirlpool 120 23

Total 520 100

Source: Survey Data

241

23%

15%

23%

16%

23%

Godrej BPL LG Samsung Whirlpool

Figure F6.5 Brand wise Distribution of Consumers of Refrigerator

It is evident from Table T6.7 that the consumers of Refrigerator look for a

famous brand with long year’s presence in the market while making their purchase

decision. When popular brand in white goods industry- Godrej, LG and whirlpool

have consumers at equal rate (23 percent) in the segment of Refrigerator, other

competitors in the same industry- BPL and Samsung have a lesser percentage of 15.5

percent each.

Table T6.8 Location Wise Distribution of Consumers in Choosing Brand of Refrigerators

Brand of Refrigerator

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

Godrej 80 33.3 40 20 - - 120 23

BPL 80 33.3 - - - - 80 15.5 LG 40 16.7 30 15 50 62.5 120 23

SAMSUNG 40 16.7 40 20 30 37.5 80 15.5 Whirlpool - - 90 45 - - 120 23

Total 240 100 200 100 80 100 520 100

Pearson Chi-Square Value 12.353 P value = 0.015 Source: Survey Data

242

Two third of the urban market for Refrigerator is equally shared by the

traditional Indian brands—Godrej and BPL. When Whirlpool enjoys 45 percent of

semi urban market; 62.5 percent of the rural demand is met by LG. When Samsung

and LG have made their presence in all segments of market, Whirlpool is pushing

their product mainly in semi urban areas. The results of the chi square analysis

confirmed the statistical validity of the hypothesis that there is a significant

difference among the customers of refrigerator across the market in choosing their

brand of refrigerators.

6.6 Brand Wise Distribution of Consumers of Gas Stove

After taking into consideration the various branded and non branded Gas

Stoves used by the consumers, analysis will be possible to reach the conclusions

regarding the consumer’s preference and brand loyalty

Table T 6.9 Brand Wise Distribution of Consumers of Gas Stove

Brand of Gas Stove No of respondents Percent

Butterfly 370 61.7

Inalsa 160 26.7

Bajaj 70 11.6

Total 600 100

Source: Survey Data

243

Figure F6.6 Brand Wise Distribution of Consumers of Gas Stove

Table T6.9 reveals that 61.7 percent of the consumers own Butterfly brand

which is considered to be a synonym of Gas Stove by the housemaids in Kerala. The

remaining 38.3 percent of the market is shared by all other brands together.

Table T 6.10

Location Wise Distribution of Consumers in Choosing Brand of Gas Stove

Brand of

Gas Stove

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

Butterfly 160 66.7 120 60 90 56 370 61.7

Inalsa 80 33.3 40 20 40 25 160 26.7

Bajaj Nil - 40 20 30 19 70 11.6

Total 240 100 200 100 160 100 600 100

Pearson Chi-Square Value 3.191 P value = 0.203

Source: Survey Data

Butterfly62%

Inalsa27%

Bajaj11%

244

It is evident from Table T6.10 that the brand “Butterfly” has the major market

share in the gas stove segment of Kerala kitchen appliances industry. 66.7 percent of

the urban population, 60 percent of the semi urban and 56 percent of the rural

population have got Butterfly brand of Gas stoves. This shows that majority of the

consumers in all the three market segments prefer the most popular brand of gas

stove, Butterfly. Other brands like Inalsa and Bajaj have relatively very few

demands. The results of the hypothesis test found no statistically significant

difference among the customers from various market segments in choosing the brand

of Gas stove they use in their kitchen.

Table T6.11 Brand Wise Distribution of Consumers of Pressure Cooker

Name of brand No of respondents Percent

Prestige 240 40.0

Hawkins 160 26.7

Butterfly 200 33.3

Total 600 100 Source: Survey Data

Figure F 6.7

Brand Wise Distribution of Consumers of Pressure Cooker

Prestige40%

Hawkins27%

Butterfly33%

245

All the established brands of Pressure Cooker have been influenced the

buying decision of consumers. Table T6.11 shows 40 percent of consumers prefer

Prestige, 33.3 percent opted Butterfly and 26.7 percent selected Hawkins. Thus it can

be inferred that consumers of pressure cooker have affinity to those brands which

have been in the market for a long period of time.

Table T6.12 Location Wise Distribution of Consumers in Choosing Brand of Pressure

Cooker

Brand of Pressure Cooker

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

Prestige 130 54 70 35 40 25 240 40

Hawkins 40 17 60 30 60 37.5 160 26.7

Butterfly 70 29 70 35 60 37.5 200 33.3

Total 240 100 200 100 160 100 600 100

Pearson Chi-Square Value 41.417 P value = 0.001*

Source: Survey Data *Significant at 1 per cent level

Table T6.12 gives the brand preference of consumers in purchasing their

Pressure Cookers. 54 percent of urban population 35 percent of semi urban and 25

percent of rural population has Prestige brand of Pressure cooker. Butterfly and

Hawkins brands have almost equal presence in semi urban and rural segment. The

chi square analysis also found statistically significant difference in the brand choice

of consumers of pressure cooker from various geographical segments of the state of

Kerala at 1 per cent level of significance. Such a result is an indirect indication of the

popularity of different brands in the different ways in varied parts of the state.

246

6.7 Reason for Choosing the Brand of Kitchen Appliances

While choosing a particular brand of product by a consumer, his decision

might have been influenced by so many factors. These factors may include Brand

name, Lesser Price, and Better after sale service etc. Only after getting proper insight

into the reasons or factors which are influencing the decision of a customer, can one

make possible improvements in the right direction in future.

Table T 6.13 Reason for Choosing the Brand of Kitchen Appliances

Reasons Mixer

Grinder Grinder Refrigerator Gas Stove Pressure Cooker Total

Because of brand name

360 (60) 80 (20) 160 (30.7) 360 (60) 280 (47) 1240 (46)

Because of better after service

40 (6.7) 60 (15) 80 (15.3) 120 (20) 50 (8) 350 (13)

Lesser price 80 (13.3) 20 (5) - - 30 (5) 130 (5)

Because of brand name & better after service

120 (20) 240 (60) 280 (54) 120 (20) 240 (40) 1000 (36)

Total 600(100) 400

(100) 520 (100)

600(100) 600

(100) 2720(100)

Source: Survey Data Figures given in parentheses indicates percent

Analysis of Table T6.13 unfolds the facts on major factors influencing the

brand choice of consumers in their purchase decisions. These facts definitely help the

manufacturers of kitchen appliances under study to adjust their market mix

accordingly.

247

60 percent of the respondents choose the Mixer Grinder because of

established brand name and 20 percent consider the after sales service also along

with the brand name while 13.3 percent look for cheaper price and 6.7 percent

consider only the after sales service while selecting their product.

All of the consumers who have Grinder opined brand name as the major

factor that persuade them to choose a particular brand of Grinder. A lion share of the

group (i.e. 60 percent) also consider the after sale service along with brand name

while making their purchase decision.

54 percent of the consumers make choice of their Refrigerator on the basis of

brand name as well as after sales support, while another 30.7 percent by taking into

account the brand name alone. The rest 15.3 percent consider only good after sales

service as the most important decisive factor of their brand selection process.

Among the consumers of Gas Stove 60 percent strongly look for the brand

name which has established a presence in almost all kitchens. 20 percent look only

for the after sales service while choosing their product whereas the rest 20 percent

look for the brand as well as better after sales service.

47 percent of the users of Pressure Cooker strongly look for the Brand name

which has established its presence in almost all kitchens. 40 percent give importance

to better after sales service in addition to the reputation of the brand. Only a nominal

fraction of the population is attracted to a particular brand of Pressure Cooker

because of lesser price and exchange offer given by the manufacturers.

Thus almost all consumers of different product segments believe brand name

and after sales service to be the most important factors for evaluating the quality of

the product they intend to buy. However, some of the consumers from the segment of

248

Pressure Cooker consider the price factor also while making the final decision on

their purchase.

6.8 Reason for Choosing a Particular Brand of Kitchen Appliance -- Location

Wise Analysis

Since there is a difference in the socio-economic profile of the consumers in

different areas of the state, the factors which influence brand choice of their product

may also be different. So it is necessary to analyze the major determinants of brand

choice by the consumers on the basis of their area of residence so as to reach a

rational conclusion as to the most important factor that influences the brand selection

process of kitchen appliances by consumers of Kerala. Table T6.14, T6.15, T6.16,

T6.17 and T6.18 analyses the location wise differences in the factors which the

consumers believe to be influenced in their brand choice of Mixer Grinder, Grinder,

Refrigerator, Gas Stove and Pressure Cooker respectively.

Table T6.14 Reason for Choosing a Particular Brand of Mixer Grinder-

Location Wise Analysis

Reason for choosing Brand

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

Because of brand name 120 50 160 80 80 50 360 60

Because of better after service - 40 20 - - 40 6.7

Lesser price - - - - 80 50 80 13.3

Because of brand name & better after service 120 50 - - - - 120 20

Total 240 100 200 100 160 100 600 100 Source: Survey Data

249

Analysis of Table T6.14 reveals that the urban population always looks for

both brand name and after sales service in the selection of a particular Mixer Grinder.

But 80 percent of semi urban population looks for brand alone. In the case of rural

population, one half of them consider pricing as the major factor influencing their

purchase decision. This can be attributed to the relatively low income distribution of

the rural population.

Table T6.15 Reason for Choosing a Particular Brand of Grinder-Location Wise Analysis

Reason for choosing Brand of Grinder

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

Because of brand name 80 40 - - - - 80 20

Because of better After service - - - - 60 75 60 15

Lesser price - - - - 20 25 20 25

Because of brand name & better after service

120 60 120 100 - - 240 60

Total 200 100 120 100 80 100 400 100 Source: Survey Data

The data in Table T6.15 shows that urban and semi urban population

while purchasing the product of Grinder always look for both brand name and after

sales service. Cent percent of semi urban and 60 percent of urban give priority to

these two aspects in opting a particular brand. But 75 percent of the rural consumers

of Grinder consider better after-sales service and remaining 25 percent feels lesser

price as the decisive factor of their purchase. This is an indication of the fact that

consumers from the developed area of the state are keener on reliability factor

through established brand and proven after sales service.

250

Table T 6.16 Reason for Choosing a Particular Brand of Refrigerator-

Location Wise Analysis

Brand of Refrigerator

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. % Because of brand name 130 54 60 30 70 88 260 50

Because of better after service 40 17 50 25 - - 90 17

Lesser price - - - - 10 12 10 2 Because of brand name & better after service

70 29 90 45 - - 160 31

Total 240 100 200 100 80 100 520 100 Source: Survey Data

Analysis of the data given in Table T6.16 reveals that 88 percent of rural

population and 54 percent of urban population always look for brand name alone in

choosing their Refrigerator. 45 percent of semi urban population and 29 percent of

urban take into account brand as well as after sales service while making their choice

of refrigerator.

Table T 6.17 Reason for Choosing a Particular Brand of Gas Stove-

Location Wise Analysis

Reason for Choosing Brand

Area of residence Total

Urban Semi Urban Rural No. % No. % No. % No. %

Because of brand name 120 50 80 40 160 100 360 60 Because of better after service - - 120 60 - - 120 20

Lesser price - - - - - - - - Because of brand name & better after service 120 50 - - - - 120 20

Total 240 100 200 100 160 100 600 100 Source: Survey Data

251

It is evident from Table T6.17 that a full fraction of rural population - 50

percent of urban and 40 percent of semi urban population seek brand name in their

product choice. Remaining 50 percent of urban population considers the brand name

and also the after sales service before making their final decision on purchase. Thus

altogether 60 percent of the entire population takes brand name as the sole or most

important factor for evaluating the quality of the product they intend to buy.

Table T6.18 Reason for Choosing a Particular Brand of Pressure Cooker-

Location Wise Analysis

Brand of Pressure Cooker

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

Because of Brand Name 80 33.3 80 40 120 75 280 46.6

Due to free gift/exchange offer 40 16.7 - - - - 40 6.7

Lesser Price - - - - 40 25 40 6.7

Because of Brand Name and After Sale Service

120 50 120 60 - - 240 40

Total 240 100 200 100 160 100 600 100 Source: Survey Data

The data in Table T6.18 shows that majority of consumers look for brand

name and after sales service, 60 percent of semi urban population, 50 percent of

urban population are keen on brand and after sales service, while 75 percent of rural

population selects the product only because of the established brand name. 25

percent of rural population considers pricing as an important factor and they look for

lower priced items. This can be ascribed to the lower income profile of the rural

population.

252

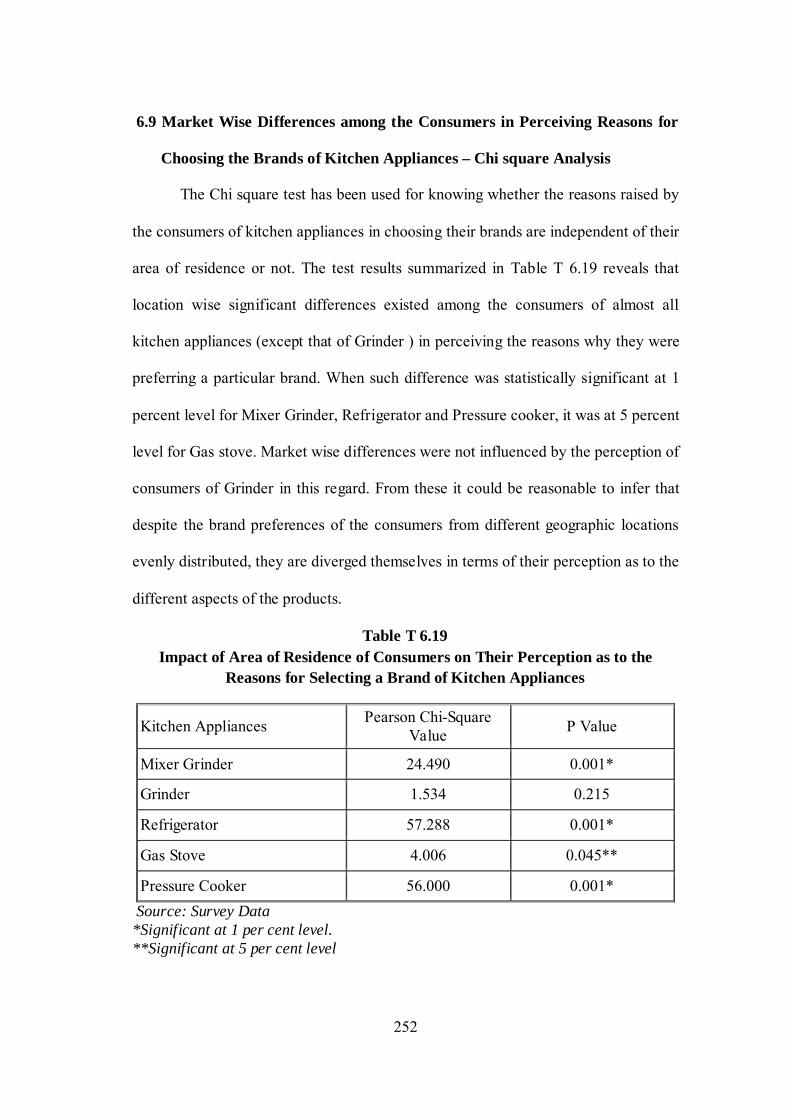

6.9 Market Wise Differences among the Consumers in Perceiving Reasons for

Choosing the Brands of Kitchen Appliances – Chi square Analysis

The Chi square test has been used for knowing whether the reasons raised by

the consumers of kitchen appliances in choosing their brands are independent of their

area of residence or not. The test results summarized in Table T 6.19 reveals that

location wise significant differences existed among the consumers of almost all

kitchen appliances (except that of Grinder ) in perceiving the reasons why they were

preferring a particular brand. When such difference was statistically significant at 1

percent level for Mixer Grinder, Refrigerator and Pressure cooker, it was at 5 percent

level for Gas stove. Market wise differences were not influenced by the perception of

consumers of Grinder in this regard. From these it could be reasonable to infer that

despite the brand preferences of the consumers from different geographic locations

evenly distributed, they are diverged themselves in terms of their perception as to the

different aspects of the products.

Table T 6.19 Impact of Area of Residence of Consumers on Their Perception as to the

Reasons for Selecting a Brand of Kitchen Appliances

Kitchen Appliances Pearson Chi-Square Value P Value

Mixer Grinder 24.490 0.001*

Grinder 1.534 0.215

Refrigerator 57.288 0.001*

Gas Stove 4.006 0.045**

Pressure Cooker 56.000 0.001* Source: Survey Data *Significant at 1 per cent level. **Significant at 5 per cent level

253

6.10 Perception towards the Performance of Kitchen Appliances

The performance of the appliance that the consumers enjoy at present in

general will decide whether it is a reliable one or will be a friend to house maids in

the kitchen. gathering information on the perception of consumers towards the

performance of their kitchen appliances definitely help its manufacturers to

rationalize their products through better technology and innovations. So the analysis

of performance in general and particular about various brands are necessary to reach

at various conclusions. Table T6.20 gives a detailed description on the satisfaction

level of consumers as to the performance of their kitchen appliances.

Table T 6.20 Performance of Kitchen Appliances

Level of Satisfaction

Mixer Grinder

Grinder Refrigerator Gas Stove Pressure Cooker

Total

Good 440 (73) 265 (66) 395 (76) 520 (87) 440 (73) 2060 (76)

Satisfactory 160 (27) 135 (34) 125 (24) 80 (13) 80 (13) 580 (21)

Bad - - - - 80 (13) 80 (3)

Total 600 (100) 400 (100) 520 (100) 600 (100) 600 (100) 2720 (100) Source: Survey Data Figures given in parentheses indicates percent

Among the respondents of Mixer Grinder 73 percent are happy with the

performance of their product and 27 percent are satisfied and with the current

performance of their product. Most of the consumers are either happy or satisfied

with the performance of their Mixer Grinders.

66 percent of the people who use the Grinder have the opinion that the

performance of this domestic device is good and 34 percent feel that it is satisfactory.

Hence the quality of Grinders available in the market is reasonably good.

254

76 percent of the consumers are happy with the performance of their

Refrigerator and 24percent are satisfied with the product. This reveals that the

performance of almost all the Refrigerators is reasonably good because non branded

manufacturers are not there in the segment of Refrigerators

87 percent of the consumers are happy with the performance of their Gas

Stoves and 13 percent is satisfied with their product. This reveals that the

performances of almost all the Gas Stoves are reasonably good because the gas stove

manufacturers strictly follow rigid quality control measures.

73 percent of the consumers are happy with the performance of their Pressure

Cookers and 13 percent is satisfied while the rest 13 percent have the opinion that the

performance of their Pressure Cooker is not satisfactory. This shows that the

performance of almost all the Pressure Cookers is reasonably good. Because of the

intense competition in this product segment; the manufacturers give more thrust to

the quality of the product.

Table T 6.21 Level of Satisfaction in Performance of Kitchen

Appliances -Location Wise Analysis

Kitchen Appliances

Area of residence Total

Urban Semi Urban Rural Good Satisf-

actory Bad Good Satisf-

actory Bad Good Satisf-

actory Bad

MixerGrinder 200(83) 40(17) - 150(75) 50(25) - 90(56) 70(44) - 600 Grinder 150(75) 50(25) - 70(58) 50(42) - 45(56) 35(44) - 400

Refrigerator 160(80) 40(20) - 140(78) 40(22) - 95(68) 45(32) - 520 Gas Stove 180(75) 60(25) - 170(85) 30(15) - 140(88) 20(12) - 600

Pressure Cooker 200(83) 40(17) - 160(80) 40(20) - 80(50) - 80(50) 600

Total 890 230 - 690 210 450 170 80 2720 Source: Survey Data Figures given in parentheses indicates percentage

255

83 percent proportion of the urban population has good opinion about the

performance of their Mixer Grinder, when 75 percent of semi urban population and

56 percent of rural population commented so. 17 percent of urban population, 25

percent of semi urban and 44 percent of the rural population have the opinion that the

performance of their Mixer Grinder is satisfactory. This divergence between the rural

and urban with the same brand of Mixer Grinder revealed by Table T6.21 may be

due to the lack of proper product knowledge among the rural population. From all the

segments none of them has the opinion that they are not satisfied with the

performance of their Mixer Grinder.

The analysis of the grinder discloses that the majority of the urban population

(ie.75 percent) has good opinion about the performance of the Grinder which they

are using for their domestic purpose. But only 58 percent of the respondents from the

semi urban area and 56 percent from the rural area expressed their observation as

‘good’ with regard to the performance the Grinder they use at this degree of scale .

However 44 percent of rural, 42 percent of semi urban and 25 percent urban

consumers of this household device are satisfied with its performance. This shows

that with the same brand of Grinder where urban, semi urban and rural population

has different scale of opinion but only at narrow range

Analysis of Refrigerator shows that 80 percent of urban, 78 percent of semi

urban and 68 percent of rural population have good opinion about the performance of

the Refrigerator. But 20 percent of urban and semi urban population and 32 percent

of rural segment have the opinion that it is satisfactory.

Analysis of Gas Stove reveals that 88 percent of the rural population, 85

percent of the semi urban and 75 percent of the urban population have good opinion

256

about the performance of Gas stoves they are using. This shows that the Gas stove

manufacturers are keen in supplying durable products at the same time providing

good after sales service to avoid the risk of loss of customers due to post purchase

dissonance. The satisfied customers from all segments together constitute 18 percent

only.

The analysis of pressure cooker shows that 83 percent of the urban

population, 80 percent of semi urban and 50 percent of rural population have good

opinion about the performance of Pressure cooker. 40 percent of urban and 20

percent of semi urban are satisfied with the performance of their Pressure cookers. In

rural area 50 percent of the respondents are not satisfied with the performance of

their pressure cookers.

6.11 Impact of Demographic Profile (Residential Location) on the Consumers

Level of Satisfaction about Performance of Kitchen Appliances

The analysis on the basis of Chi-Square test statistically proved that, the

consumer satisfaction on the performance of their kitchen appliances differs from

market to market. Inference drawn on the basis of the values obtained through the

test states that the residential locations of the consumers (indirectly their socio

economic profile) have significant impact on their level of satisfaction as to the

performance of Kitchen appliances. Among the five selected products only in the

case of pressure cooker the analysis shows the opposite to this. Moreover, except in

the case of Refrigerator, in all other cases such differences among the consumers

were significant at 1 percent level.

257

Table T 6.22 Impact of the Area of Residence of Consumers on the Level of Satisfaction

About Performance of Kitchen Appliances

Kitchen Appliances Pearson Chi-Square Value P Value

Mixer Grinder 36.435 0.001*

Grinder 13.790 0.001*

Refrigerator 7.147 0.028**

Gas Stove 12.245 0.002*

Pressure Cooker 3.644 0.162 Source: Survey Data

*Significant at 1 per cent level **Significant at 5 per cent level

6.12 Purchase Point of Kitchen Appliances

A particular product, after its manufacturing process, will be distributed

through different channels to make it available among the consumers as and when it

is required. There are different distribution channels as well as different systems to

have the product presence in all markets. But to find out the effective system of

distribution, the preference of the consumers to buy it from a particular point is very

important. This can be identified and analyzed by the Table T 6.23

Table T 6.23 Purchase Point of Kitchen Appliances

Purchase Pont Mixer Grinder Grinder Refrigerator Gas Stove Pressure Cooker

Total

From Authorized dealer

360 (60) 290(73) 480(92) 330(55) 400(67) 1860(68)

From the retail shop 120 (20) 50(12) - 130(22) 160(27) 460 (17)

From Company outlet in Exhibitions

40 (6.7) - - 35 (6) 40 (6) 115 (4)

From Company representatives

80 (13.3 60(15) 40 (8) 105(17) - 285(11)

Total 600 (100) 400(100) 520 (100) 600(100) 600(100) 2720(100) Source: Survey Data Figures given in parentheses indicates the percentage

258

Majority of the consumers of Kitchen appliances under study prefer to purchase

the product from authorized dealer of that product. The analysis in Table T6.23

shows that 60 percent of the consumers of Mixer Grinder purchase it from authorized

dealers and the rest 40 percent purchase it from other sources like retail shop,

company outlet in exhibitions and company representatives etc.

73 percent of consumers who use Grinders buy it from the authorized dealers.

This reveals that consumers give more importance to the reliability factor of the

product.

92 percent of the consumers purchase Refrigerator from the authorized

Dealer while 8 percent buy it through the representatives. Here also consumers are

much particular about the supply of reliable products from the direct sources of the

Company.

55 percent of the consumers purchase Gas Stove from the authorized Dealers

while 22 percent gets it from retail outlets. 17 percent purchases it through company

representatives and 6 percent buys it through the company outlets in exhibitions.

67 percent of the consumers purchase Pressure Cookers from the authorized

Dealers, 27 percent from the retail shops and 6 percent from company outlets in

Exhibitions.

So from the above analysis it can be inferred that customers irrespective of

the kitchen appliance they use, give importance to quality factor while making their

purchase. Majority of the customers have the habit of purchasing goods from direct

sources of Companies such as authorized dealers and company outlets.

259

6.13 Location Wise Analysis of Purchase Point of Kitchen Appliances by

Consumers

Normally there is a general view that consumers from different geographical

background may have different outlook towards the quality of the product which

they procure from various purchase points. This might be attributed to different

factors such as degree of urbanization, education level, knowledge about the product

etc. For examining whether such disparity in terms of purchase points of different

types of kitchen appliances exist among consumers from different geographical

background, a location wise analysis has been made. The results of such analysis are

explained in Table 6.24 to Table 6.28

6.14 Purchase Point of Mixer Grinder

Table T 6.24 Purchase Point of Mixer Grinder-Location Wise Analysis

Purchase point of Mixer Grinder

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

From Authorized Dealer

120 50 160 80 80 50 360 60

From Retail Shop 40 16.7 40 20 40 25 120 20

Co. Outlet in Exhibitions

- - - - 40 25 40 6.7

From Co. Representatives

80 33.3 - - - - 80 13.3

Total 240 100 200 100 160 100 600 100

Source: Survey Data

260

6.15 Purchase Point of Grinder

Table T 6.25 Purchase Point of Grinder-Location Wise Analysis

Purchase point of Grinder

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

From Authorized Dealer 150 75 90 75 50 63 290 72.5

From Retail Shop 30 15 20 17 - - 50 12.5

From Co. outlet in Exhibitions - - - - - - - -

From Co. Representatives 20 10 10 8 30 37 60 15

Total 200 100 120 100 80 100 400 100 Source: Survey Data

6.16 Purchase Point of Refrigerator

Table T 6.26 Purchase Point of Refrigerator-Location Wise Analysis

Purchase point of

Refrigerator

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

From Authorized

Dealer 200 83.3 200 100 80 100 480 92.3

From Company

Representatives 40 16.7 40 7.7

Total 240 100 200 100 80 100 520 100

Source: Survey Data

261

6.17 Purchase Point of Gas Stove

Table T 6.27

Purchase Point of Gas Stove-Location Wise Analysis

Purchase point of Gas Stove

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

From Authorized Dealer 130 54 110 55 90 56 330 55

From Retail Shop 50 21 40 20 40 25 130 22

From Co. Outlet in Exhibitions 20 8.33 15 7.5 - - 35 5

From Company Representatives 40 16.67 35 17.5 30 19 105 18

Total 240 100 200 100 160 100 600 100 Source: Survey Data

6.18 Purchase Point of Pressure Cookers

Table T 6.28 Purchase Point of Pressure Cooker-Location Wise Analysis

Purchase Point of Pressure Cookers

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

From authorized Dealer 240 100 160 80 - - 400 66.6

From Retail Shop - - 40 20 120 75 160 26.7

Company outlet in Exhibitions - - - - 40 25 40 6.7

From Company Representatives - - - - - - - -

Total 240 100 200 100 160 100 600 100 Source: Survey Data

262

The authorized distributor is the major source to the consumers in their

purchase of kitchen appliances. From the descriptive analysis of the data, we cannot

perceive any dissimilarity on this aspect between the consumers of different kitchen

appliances. 100 percent of consumers of Pressure Cookers, more than 75 percent of

consumers of Grinder and Refrigerator and about one half of the users of Gas stove

and Mixer Grinder from the urban area decide authorized dealer as point of purchase

of their products. Similarly, at least 75 percent of consumers of selected kitchen

appliances (except consumers of gas stove, where only 55 percent) from semi urban

area prefer to buy their products from authorized dealers. Even though majority of

the consumers from rural area also opt to purchase their appliances from the

authorized dealer, their proportion is relatively lower than that of those who come

from other two segments. It has also been noticed that in the case of gas stove 75

percent of rural consumers approach retail outlets to procure their products. Marginal

percent of consumers of the whole rural population have got the inclination to buy

the product through exhibition sales during festival seasons. All of these facts

substantiate the basic characteristics of consumers regardless of their residential

location to get genuine products from a reliable channel of company’s distribution

system.

Non parametric form of test of independence – Chi square analysis used in

the study for measuring market wise differences among the consumers of Kitchen

appliances in deciding their purchase points and the test found such differences

among the consumers statistically significant at 1 percent level in the case of Mixer

grinder, Refrigerator and Pressure cooker. The test results are reported in Table

T6.29. From the analysis of these results it can also be inferred that the diversity in

263

the habit of choosing their purchase sources by the consumers of different segments

are more specific than general.

Table T6.29 Association between Residential Location of Consumers and their

Decisions on Points of Purchase

Kitchen Appliances Chi-Square Value P value

Mixer Grinder 29.847 0.001*

Grinder 0.356 0.949

Refrigerator 9.658 0.002*

Gas Stove 0.651 0.957

Pressure Cooker 54.609 0.001* Source: Survey Data *Significant at 1 per cent level

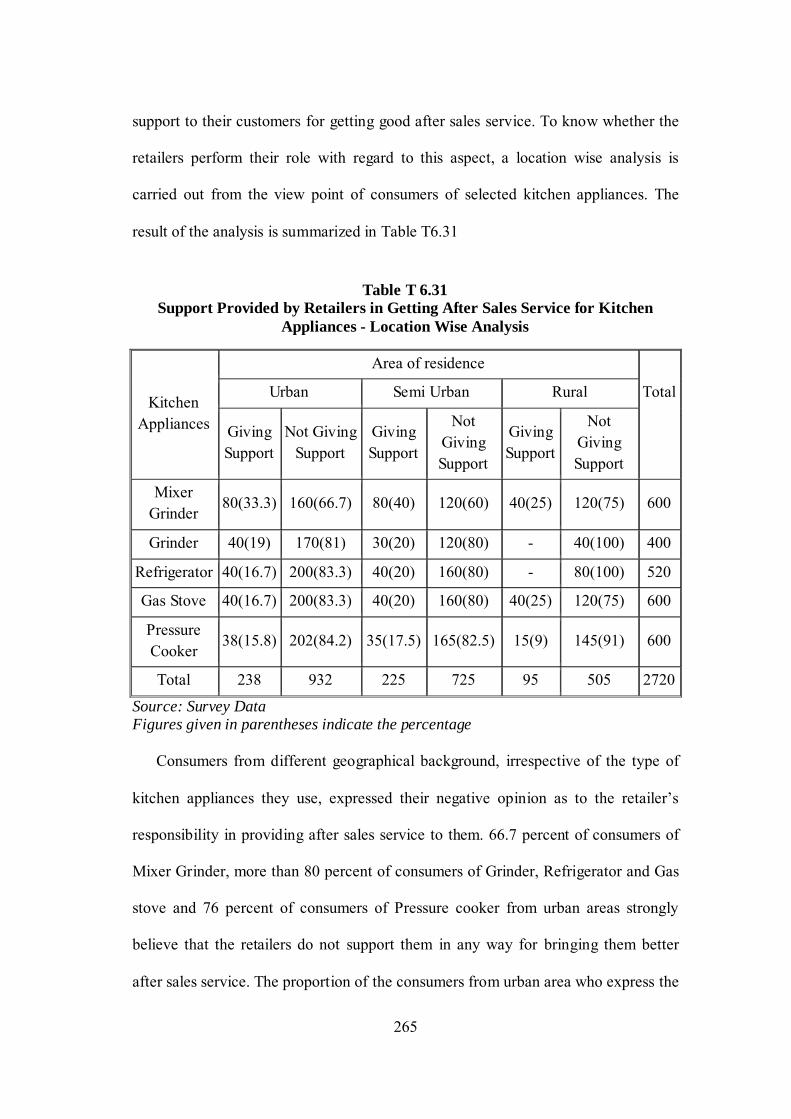

6.19 Responsibility of Retailer in Providing After-Sales Service

In the distribution process starting from the Manufacturer and ending with the

consumer, the nearest contact point for the customer will be the last link of the

distribution process, the retailer. Similarly, the nearest place where the consumer can

approach for the support and service of a product is the next door retailer. But, most

of the retailers will be focused only on sales because every branded product will have

authorized service centers to take care of the after-sales service and the retailer would

like to avoid encounter with the customers who approach him with complaints on the

performance of a product and demand for maintenance and service. How far these

retailers do justice to the customers who have purchased the product from them, by

providing good after sales service is explained in Table T6.30

264

Table T 6.30 Support Provided by Retailers in Getting After-Sales Service

Opinion

Mixer Grinder

Grinder Refrigerator Gas Stove

Pressure Cooker

Total

Giving Support 200(33.3) 70(17.5) 80 (15) 120(20) 126(21) 596 (22)

Not giving Support

400(66.7) 330(82.5) 440 (85) 480(80) 474(79) 2124(78)

Total 600 (100) 400(100) 520(100) 600(100) 600(100) 2720(100) Source: Survey Data Figures given in parentheses indicate the percentage

Majority of the consumers of kitchen appliances unanimously opined that the

retailers do not show any interest in providing back up service to their customers.

Among the respondents, two third of the consumers of the Mixer Grinder, 82.5

percent of consumers of Grinder, 85 percent of the consumers of Refrigerator and

about 80 percent of consumers of Gas stove and Pressure Cooker commented that the

retailers are not ready to spend time on after sales service and consider it as the

responsibility of the manufacturer. Since the retailer is the direct link with the

consumer in the distribution process, any negative response from the part of them

with respect to service support to the customers shall definitely affect the trust and

confidence of the consumers which in turn shall lead to the shift in their product

choice.

6.20 Location Wise Analysis of Consumer Perception Regarding After-Sales

Support by the Retailers

Consumers from different locality may have difference in accessing for after

sales service. Usually the manufacturers set up their service centers in urban area.

Hence consumers from semi urban and rural areas find it difficult to get the after

sales service. At this juncture the retailer’s role is prominent in extending maximum

265

support to their customers for getting good after sales service. To know whether the

retailers perform their role with regard to this aspect, a location wise analysis is

carried out from the view point of consumers of selected kitchen appliances. The

result of the analysis is summarized in Table T6.31

Table T 6.31

Support Provided by Retailers in Getting After Sales Service for Kitchen Appliances - Location Wise Analysis

Kitchen Appliances

Area of residence

Total

Urban Semi Urban Rural

Giving Support

Not Giving Support

Giving Support

Not Giving Support

Giving Support

Not Giving Support

Mixer Grinder

80(33.3) 160(66.7) 80(40) 120(60) 40(25) 120(75) 600

Grinder 40(19) 170(81) 30(20) 120(80) - 40(100) 400

Refrigerator 40(16.7) 200(83.3) 40(20) 160(80) - 80(100) 520

Gas Stove 40(16.7) 200(83.3) 40(20) 160(80) 40(25) 120(75) 600

Pressure Cooker

38(15.8) 202(84.2) 35(17.5) 165(82.5) 15(9) 145(91) 600

Total 238 932 225 725 95 505 2720

Source: Survey Data Figures given in parentheses indicate the percentage

Consumers from different geographical background, irrespective of the type of

kitchen appliances they use, expressed their negative opinion as to the retailer’s

responsibility in providing after sales service to them. 66.7 percent of consumers of

Mixer Grinder, more than 80 percent of consumers of Grinder, Refrigerator and Gas

stove and 76 percent of consumers of Pressure cooker from urban areas strongly

believe that the retailers do not support them in any way for bringing them better

after sales service. The proportion of the consumers from urban area who express the

266

same view with regard to after sales service is almost the same as that of urban

consumers. In the case of rural population their argument against the initiative of

their retailers in providing support to them on this factor is stronger than the other

two groups. Among them cent percent of the consumers of Grinder and Refrigerator

have their unanimous opinion of the retailer’s indifference in extending any support

to their customers in time in getting their products serviced. Such differences of

opinion among the consumers hailing from different geographic segments of the

Kitchen appliances market of Kerala were statistically verified with the help of

inferential statistical analysis and the results are reported in Table T6.32

Table T 6.32 Market Wise Differences in Perception of Consumers of Kitchen Appliances

as to the Level of Support Extended by the Retailers – Chi square Analysis

Kitchen Appliances Chi-Square Value P value

Mixer Grinder 9.000 0.11**

Grinder 160.000 0.001*

Refrigerator 18.121 0.01**

Gas Stove 4.167 0.125

Pressure Cooker 81.000 0.001*

Source: Survey Data *Significant at 1 per cent level **Significant at 5 per cent level From the analysis it can be observed that there were market wise differences

existing in the perception of customers as to the level of support extended by their

dealers in getting their products being serviced. Of the five kitchen appliances under

study, except Gas stove, in all other four products their customers from different

market segments have differences of opinion in this regard, which was found to be

267

statistically significant at 1 percent level for Grinder and Pressure cooker and at 5

percent level for Mixer grinder and Refrigerator.

6.21 Opinion about After Sales Service

In the present competitive world, the companies give importance not only to

the supply of quality products but also to extending good after sales service which is

considered to be the prime component of augmented form of a durable product. Once

the core product has been successfully delivered to the customer, the efforts are taken

by the manufacturers to retain them with the companies by winning their confidence

and satisfaction through better after sales service.

In a study of the marketing of kitchen appliances, the perception of customers

towards the quality of after sales service provided by the manufacturers of their

products is an important area which is to be analyzed for getting the knowledge

about their overall satisfaction level with regard to their products. Every appliance

which is used regularly will have some problems because of the continuous use or of

using it in an improper way. The satisfied customer will be an asset to any brand and

at the same time, if they do not get prompt and proper service, they will start bad

mouthing about the brand and may affect the other products of the same brand. The

good opinion about the after sales service of a product, especially during the

warranty period will be a referral for further sale.

268

Table T 6.33 Opinion about After Sales Service

Opinion

Mixer

Grinder Grinder Refrigerator Gas Stove

Pressure

Cooker Total

Good 350(58) 220(55) 380(73) 440(73) 250(63) 1640(65)

Satisfactory 170(29) 130(33) 120(23) 90(15) 110(27) 620 (25)

Bad 80 (13) 50 (12) 20 (4) 70(12) 40(10) 260 (10)

Total 600 (100) 400(100) 520 (100) 600 (100) 400(100) 2520 (100)

Source: Survey Data Figures given in parentheses indicate the percentage

More than 55 percent of consumers of Mixer Grinder and Grinder, 73 percent

each of consumers of Refrigerator and Gas Stove and 63 percent of the consumers of

Pressure Cooker opined that the after sales service provided by the manufacturers of

their products to them was really good. About 30 percent of the consumers of Mixer

Grinder and Grinder, more than 20 percent of the consumers of Pressure Cooker and

Refrigerator and 15 percent of Gas Stove customers are satisfied with the present

services offered by the suppliers of their products even after making the sales. The

proportion of unsatisfied customers in this regard is very nominal. When we take

these data’s altogether, it can be said that 90 percent of the total customers is at least

satisfied with the back-up service provided by the suppliers and only 10 percent of

them are upset with this aspect of product service. From this we can infer that most

of the customers are satisfied with the efforts taken by the manufacturers for bringing

them better after sales service even though the retailers do not show a keen interest in

this regard.

269

Table T 6.34 Opinion about After Sales Service of Kitchen Appliances –

Location Wise Analysis

Kitchen Appliances

Area of residence Total

Urban Semi Urban Rural

Good Satisf-actory Bad Good Satisf-

actory Bad Good Satisf-actory Bad

Mixer Grinder 160(67) 70(29) 10(4) 120(60) 50(25) 30(15) 70(44) 50(31) 40(25) 600

Grinder 130(65) 60(30) 10(5) 70(56) 30(24) 25(20) 20(27) 40(53) 15(20) 400

Refrigerator 200(83) 40(17) - 160(80) 40(20) - 20(25) 40(50) 20(25) 520

Gas Stove 210(87.5) 30(12.5) - 170(85) 20(10) 10(5) 60(37.5) 40(25) 60(37.5) 600

Pressure Cooker 190(79) 40(17) 10(4) 160(80) 30(15) 10(5) 90(56) 50(31) 20(13) 600

Total 890 240 30 680 170 75 260 220 155 2720

Source: Survey Data Figures given in parentheses indicate the percentage

Table T 6.34 discloses the location wise difference in customer’s opinion as

to the quality of after sales service received by them from their suppliers. Virtually

no difference could be visible in the level of the satisfaction of customers of various

kitchen appliances from urban and semi urban regions. Majority of the customers

from both of these segments where at least satisfied with the after sales service

rendered by their suppliers. Only a very nominal fraction of the customers of these

regions opined negatively as to the quality of the service they received. None of the

customers of Refrigerator from these segments raised any negative reply as to the

after sale service.

But the perception of the respondents from rural segment differs much from

those of the other two segments. Customers of Grinder and Refrigerator from rural

segments who have replied “satisfied” outnumbered the customers who replied

270

“Good”. In the case of Grinder customers who felt “good” is exactly equal to those

who felt “bad” while receiving the after sales service from their suppliers. Except

customers of pressure cooker, (where only 13 percent) 20 percent more of the rural

customers of kitchen appliances were totally dissatisfied with the present after sale

service received from their suppliers. Chi square analysis made in this regard (its

results reported in Table T6.35) also found statistically significant difference at 1

percent level between the customers from different market segments in terms of their

level of satisfaction towards after sales service rendered by the manufacturers of their

products.

On the basis of this analysis, it can be said that the rural customers do not

relatively feel good or sometimes even feel bad in getting further service from their

suppliers once they have made their purchase. This might be attributed to the fact

that service centers of majority of the popular kitchen appliances manufacturing

companies in India are mainly situated in cities or towns which pose a problem to the

rural customers to go to these centers, which are far away from them, for getting their

products serviced.

Table T 6.35 Association between the Demographic Profile (Area of Residence)

of the Consumers of Kitchen Appliances and their Level of Satisfaction towards the After Sales Service

Kitchen Appliances Chi-Square Value P value

Mixer Grinder 301.778 0.001*

Grinder 192.000 0.001*

Refrigerator 280.333 0.001*

Gas Stove 296.444 0.001*

Pressure Cooker 520.000 0.001* *Significant at 1 per cent level Source: Survey Data

271

6.22 Incentives Offered for Referral

A customer takes a decision to buy a product after considering various facts

and factors. Once he has taken a decision to buy a product, he has become a proud

owner of that product. Incentives always motivate people to take instant decisions

and to refer and recommend the same product to others. Whether this natural instinct

of consumers are properly understood and implemented by the dealers of kitchen

appliances can be analyzed with the support of the Table T 6.36

Table T 6.36 Incentives Offered for Referral

Mixer Grinder

Grinder Refrigerator Gas

Stove Pressure Cooker

Total

Incentives Offered

40(7) 30(7.5) 40 (8) 80 (13) 70(12) 260(10)

Not Offered 560(93) 370(92.5) 480(92) 520(87) 530(88) 2460(90)

Total 600(100) 400(100) 520(100) 600(100) 600(100) 2720(100) Source: Survey Data Figures given in parentheses indicate the percentage

Majority of the consumers do not get any incentives for the referral made by

them. Only 10 percent of the customers get some form of incentives from their

dealers for referring the products to other people. However, the relative percentage of

customers who are getting such incentives is high in case of Gas Stove and Pressure

Cooker. This might be due to the fact that the volume of sale and profit margin on

these products are relatively high and its dealers are ready to sacrifice a portion of

their profit in favor of the customers for motivating them to influence the purchase

decision of their friends and relatives.

272

6.23 Incentives Offered for Referral - Location Wise Analysis

Generally there is a common belief that urban people are more educated and

rational than rural ones, on account of which they will have better bargaining power

and often in a position to avail of incentives for referrals and their future purchases

from their present suppliers of product. To know whether such belief is realistic in

the marketing of kitchen appliances also, location wise analysis of customers who

have received and who have not received incentives for recommending the brand of

their products to his friends and relatives. The result of the analysis is summarized in

Table T6.37

Table T 6.37

Whether Incentives Offered for Referral of Kitchen Appliances-Location Wise Analysis

Kitchen

Appliances

Area of residence Total

Urban Semi Urban Rural

Incentives

Offered

Not

Offered

Incentives

Offered

Not

Offered

Incentives

Offered

Not

Offered

Mixer

Grinder

25(10.5) 215(89.5) 10(5) 190(95) 5(3) 155(97) 600

Grinder 20(10) 180(90) 10(8) 110(92) - 80(100) 400

Refrigerator 30(12.5) 210(87.5) 10(5) 190(95) - 80(100) 520

Gas Stove 35(15) 205(85) 25(12.5) 175(87.5) 20(12.5) 140(87.5) 600

Pressure

Cooker

35(15) 205(85) 25(12.5) 175(87.5) 10(6) 150(94) 600

Total 145 1015 80 840 35 605 2720

Source: Survey Data Figures given in parentheses indicate the percentage

273

It can be known from the analysis that most of the dealers in kitchen

appliances do not offer any sort of incentives to the buyer for their recommendations

and referrals. However, when a product wise analysis is made on this aspect,

relatively more customers from urban and semi urban areas were able to persuade

their dealers to give them incentives for recommending the brand to their friends and

relatives. When not a single rural customer has received any incentive for their good

mouthing and reference of the name of the dealer and the name of the brand of

grinder and refrigerator, the number of rural customers who received motivation in

the form of incentives for recommending the name of the mixer grinder and pressure

cooker is very few in number. But in the case of gas stove, the percentage of

customers who got incentives for their referrals was more or less the same.

Inferential analysis made here for verifying the statistical validity of the market wise

differences among the consumers in various product segments of the Kitchen

appliances is also substantiate the findings of the descriptive analysis. The test results

summarized in Table T6.38 reveals that such differences among the consumers is

statistically significant at 1 percent level in respect of all the five products. So from

these results it can be inferred that urban customers were able to take hold of more

incentives than the rural for their referrals and recommendations due to the better

bargaining power and geographical nexus. If some sort of incentives are offered to

the buyers for their referrals, consumers will get motivated and they will act as the

sales team of the dealers.

274

Table T 6.38 Market wise Differences in Incentives Offered by the Dealers to

Consumers for their Referrals – Inferential Analysis

Kitchen Appliances Chi-Square Value P value

Mixer Grinder 64.286 0.001* Grinder 27.429 0.001*

Refrigerator 50.556 0.001*

Gas Stove 138.462 0.001* Pressure Cooker 64.286 0.001* *Significant at 1 per cent level Source: Survey Data

6.24 Types of Incentives Offered

Incentives are in many forms, offered by a dealer to his existing customers

for recommending him and also the name of the brand of the product which they

currently used. Such incentives may include cash incentives, free gifts, extended

guarantee or reduction in price for future purchases. Even though, only a minor

fraction of customers of kitchen appliances received such incentives, it is important

to know which form of incentives is more commonly received by them. Table T.6.39

summarizes the varied form of incentives received by the customers of different

kitchen appliances as a reward for their referrals.

Table T 6.39 Types of Incentives Offered

Types of Incentives

Mixer Grinder Grinder Refrigerator Gas

Stove Pressure Cooker

Total

Cash incentive 30(75) 20(66.66) 10(25) 50(62.5) 35(50) 145(56)

Free Gifts - 5 (16.67) - 20(25) 20(28.5) 45(17) Additional Extended Guarantee - - 25(62.5) 5(7) 30(12)

Cash Reduction for future Purchase 10(25) 5 (16.67) 5(12.5) 10(12.5) 10(14.5) 40(15)

Total 40(100) 30(100) 40(100) 80 (100) 70(100) 260(100) Source: Survey Data Figures given in parentheses indicates percent

275

Cash incentives were the most common form of incentives offered by the

dealers to their existing customers for their referrals. Out of the 210 customers who

have received incentives, 125 of them got cash incentives, 30 each received benefits

in the form of additional extended guarantee and cash reduction for future purchase

and 25 received free gifts for recommending the products to their friends and

relatives. When product wise analysis is made, it can be known that except customers

of refrigerator, majority of customers of kitchen appliances receive cash incentives.

For the customers of refrigerator dealers prefer to give additional extended warranty

to the products which they have already purchased from them. From this it can be

deduced that for the promotion of relatively small and cheaper kitchen appliances

among the group, dealers like to give cash incentives instead of additional extended

guarantee to the customers who have given referrals, which may relieve them from

the risk of liability to maintain their products when the guarantee is extended to the

already sold product.

6.25 Type of Incentives Offered to Customers - Location Wise Analysis

To find out whether there is any disparity in the form of incentives received

by the customers from different geographical locations, a location wise analysis has

been made. Such analysis is made for the customers of different kitchen appliances

separately and the results are discussed in Table T6.40

276

0

10

20

30

40

50

60

70

Cash incentive

Free Gifts Additional Extended Guarantee

Cash Reduction for future Purchase

Urban

Semi Urban

Rural

Table T 6.40 Types of Incentives for Mixer Grinder-Location Wise Analysis

Types of Incentives

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. % Cash incentive 15 60 7 70 3 60 25 62.5

Free Gifts - - - - - - - - Additional Extended Guarantee - - - - 2 40 2 5

Cash Reduction for future Purchase 10 40 3 30 - - 13 32.5

Total 25 100 10 100 5 100 40 100 Source: Survey Data

Figure F6.8 Types of Incentives for Mixer Grinder-Location Wise Analysis

Cash incentives are more popular among the mixer grinder customers

regardless of location they belong to. Of the 40 mixer grinder customers who receive

incentives from the dealers for the referrals made by them, 60 percent of both urban

and rural each and 70 percent of semi urban customers receive cash incentives. None

of the customers receive any free gifts for recommending the brand of the mixer

277

0

10

20

30

40

50

60

70

Cash incentive

Free Gifts Additional Extended Guarantee

Cash Reduction for

future Purchase

Urban

Semi Urban

Rural

grinder he uses and also the name of the dealer from which he has made his

purchase.

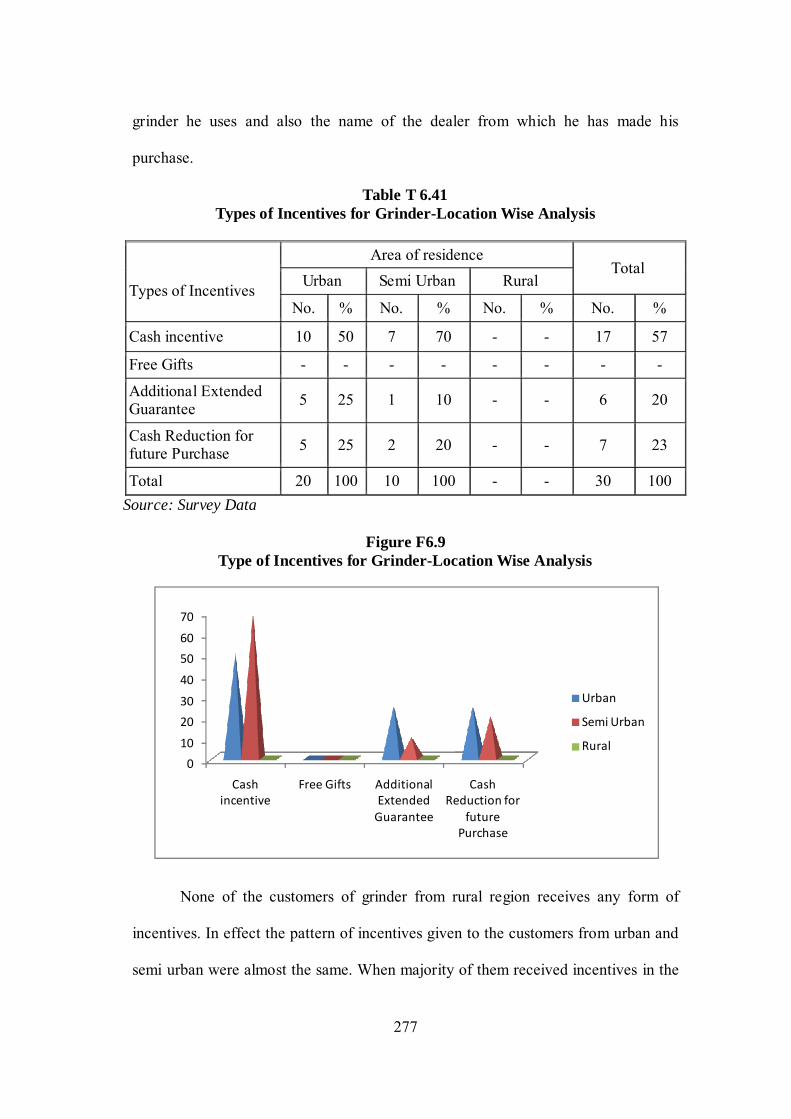

Table T 6.41 Types of Incentives for Grinder-Location Wise Analysis

Types of Incentives

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

Cash incentive 10 50 7 70 - - 17 57

Free Gifts - - - - - - - -

Additional Extended Guarantee 5 25 1 10 - - 6 20

Cash Reduction for future Purchase 5 25 2 20 - - 7 23

Total 20 100 10 100 - - 30 100 Source: Survey Data

Figure F6.9 Type of Incentives for Grinder-Location Wise Analysis

None of the customers of grinder from rural region receives any form of

incentives. In effect the pattern of incentives given to the customers from urban and

semi urban were almost the same. When majority of them received incentives in the

278

0

10

20

30

40

50

60

Cash incentive

Free Gifts Additional Extended Guarantee

Cash Reduction for future Purchase

Urban

Semi Urban

Rural

form of cash incentives, like customers of mixer grinder none of them receives any

free gift for their referrals.

Table T 6.42 Types of Incentives for Refrigerator-Location Wise Analysis

Types of Incentives

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

Cash incentive 5 17 2 20 - - 7 17.5

Free Gifts 17 57 6 60 - - 23 57.5 Additional Extended Guarantee 2 6 - - 2 5

Cash Reduction for future Purchase 6 20 2 20 - - 8 20

Total 30 100 10 100 - - 40 100

Source: Survey Data

Figure F 6.10 Type of Incentives for Refrigerator-Location Wise Analysis

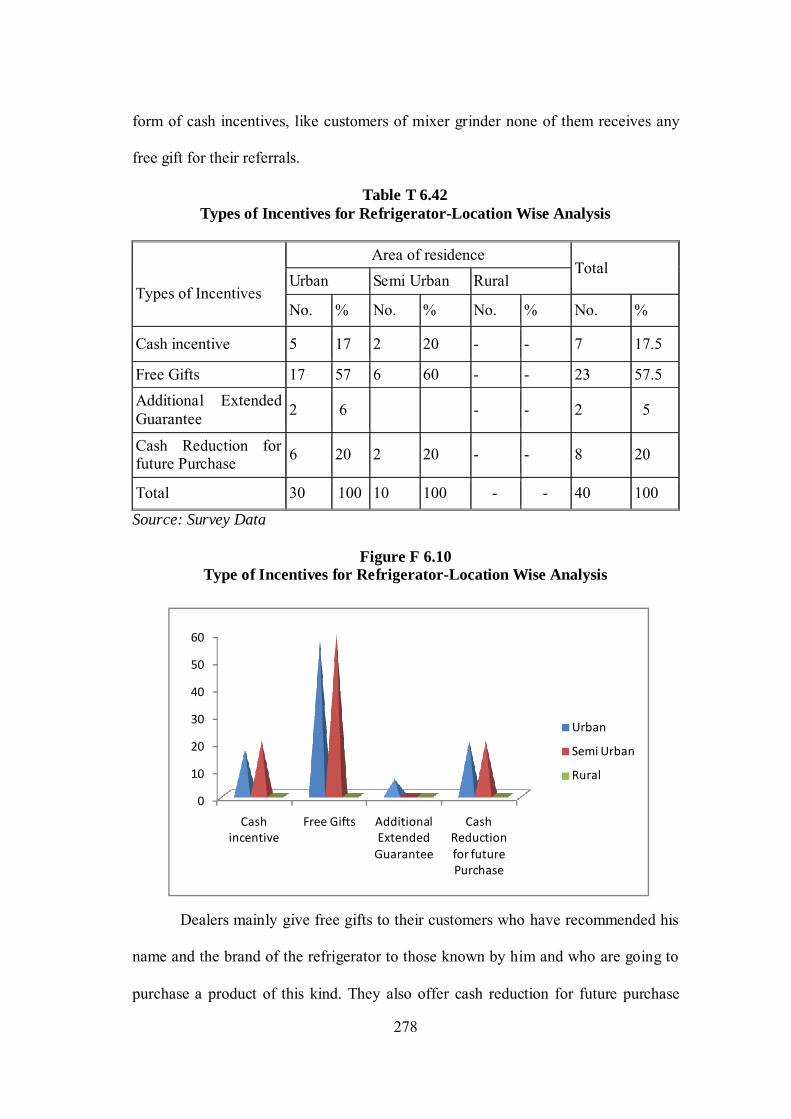

Dealers mainly give free gifts to their customers who have recommended his

name and the brand of the refrigerator to those known by him and who are going to

purchase a product of this kind. They also offer cash reduction for future purchase

279

0

10

20

30

40

50

60

70

Cash incentive

Free Gifts Additional Extended Guarantee

Cash Reduction for future Purchase

Urban

Semi Urban

Rural

and also cash incentives to such customers who give such referrals. As in the case of

grinders, none of the rural customers of refrigerators receive any such incentive from

their dealers.

Table T 6.43 Types of Incentives for Gas Stove-Location Wise Analysis

Types of Incentives

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

Cash incentive 15 43 10 40 14 70 39 49

Free Gifts 2 6 4 16 - - 6 7

Additional Extended Guarantee 5 14 6 24 4 20 15 19

Cash Reduction for future Purchase 13 37 5 20 2 10 20 25

Total 35 100 25 100 20 100 80 100 Source: Survey Data

Figure F6.11 Types of Incentives for Gas Stove-Location Wise Analysis

All forms of incentives are offered by the dealers in gas stove to customers

from all geographical regions. However, here also cash incentives are most popular

280

0

10

20

30

40

50

60

Cash incentive

Free Gifts Additional Extended Guarantee

Cash Reduction for

future Purchase

Urban

Semi Urban

Rural

among them. Apart from other products, more customers from rural region avail of

such offers from their dealers. Even though free gifts are also offered, it is lagging

behind other incentives. A considerable percent of customers from all regions was

also able to get cash reduction for their further purchase as a consideration for

introducing the dealer and the brand to their warm circle.

Table T 6.44 Types of Incentives for Pressure Cooker-Location Wise Analysis

Types of Incentives

Area of residence Total

Urban Semi Urban Rural

No. % No. % No. % No. %

Cash incentive 17 49 12 48 6 60 35 50

Free Gifts 3 9 3 12 - - 6 9

Additional Extended Guarantee 4 11 4 16 2 20 10 14

Cash Reduction for future Purchase 11 31 6 24 2 20 19 27

Total 35 100 25 100 10 100 70 100 Source: Survey Data

Figure F 6.12 Type of Incentives for Pressure Cooker-Location Wise Analysis

281

Similarly, in the case of other four kitchen appliances, cash incentives were

mainly received by customers irrespective of their location status. The pattern of

other incentives offered to them by their dealers was more or less the same as that of

Gas stove. Here also customers from rural regions were neglected by their dealers

while offering free gifts for referrals.

6.26 Association between Demographic Profile (Residential Location) and Types

of Incentives Offered by the Dealers

Chi square analysis is made for knowing whether the residential location of

the consumers is a significant factor in deciding the type of incentives offered to the

consumers by the dealers in Kitchen appliances and the results of the test are

reported in Table T6.45

Table T6.45 Association between Demographic Profile (Residential Location)

and Types of Incentives Offered by the Dealers

Kitchen Appliances Chi-Square Value P value

Mixer Grinder 0.000332 0.985

Grinder 0.00983 0.921

Refrigerator 0.0779 0.780

Gas Stove 3.020 0.554

Pressure Cooker 0.839 0.657

Source: Survey Data

From the inferential it is revealed that the area of residence or location of a

business is not a determinant of types of incentives offered to the customers of

kitchen appliances by its dealers. The analysis did not find any statistically

282

significant difference in this regard among the customers in any of the kitchen

appliances identified under study.

Location wise differences were visible in the pattern of ownership of the

kitchen appliances by the people of Kerala. Brand wise differences were also

observed in most of the product segments across the market and the consumers have

their own reasons for choosing a particular brand. Moreover, the consumers from the

three identified market segments perceived differently the performance of the kitchen

appliances. Retailers were not keen in extending after sales service to their

consumers, however the consumers were much satisfied with after sales service of

the manufacturers.