CHAPTER TWO The Effect of Revenue and Expenses.

19

-

Upload

agatha-small -

Category

Documents

-

view

220 -

download

0

Transcript of CHAPTER TWO The Effect of Revenue and Expenses.

CHAPTER TWO

The Effect of Revenue and

Expenses

2-3

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

1. Analyze business transactions involving revenue and expenses.

2. Record the effects of revenue and expenses in the accounting equation.

3. Compute net income or net loss.

THE EFFECT OF REVENUE AND EXPENSES

Objectives:

2-4

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

Revenue, Expenses, and Net Income

•The employment services provided by Rebecca Van Lieu will produce revenue, or income.

•In producing the income the business will incur business costs, or expenses.

2-5

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

Revenue, Expenses, and Net Income (Continued)

•The revenue remaining after the expenses have been deducted is net income, or net profit.

•The amounts that a firm’s customers have promised to pay in the future is an asset known as accounts receivable.

2-6

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

Revenue, Expenses, and Net Income (Continued)

•Money received from customers from credit sales is referred to as money received on account.

•In Chapter 1 we learned that the liability incurred by a business when it promises to pay its creditors is called accounts payable.

2-7

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

Transaction

•At the end of the first week of operations, Rebecca Van Lieu received $1,000 for resume preparation and job placements.

2-8

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

Transaction Analysis

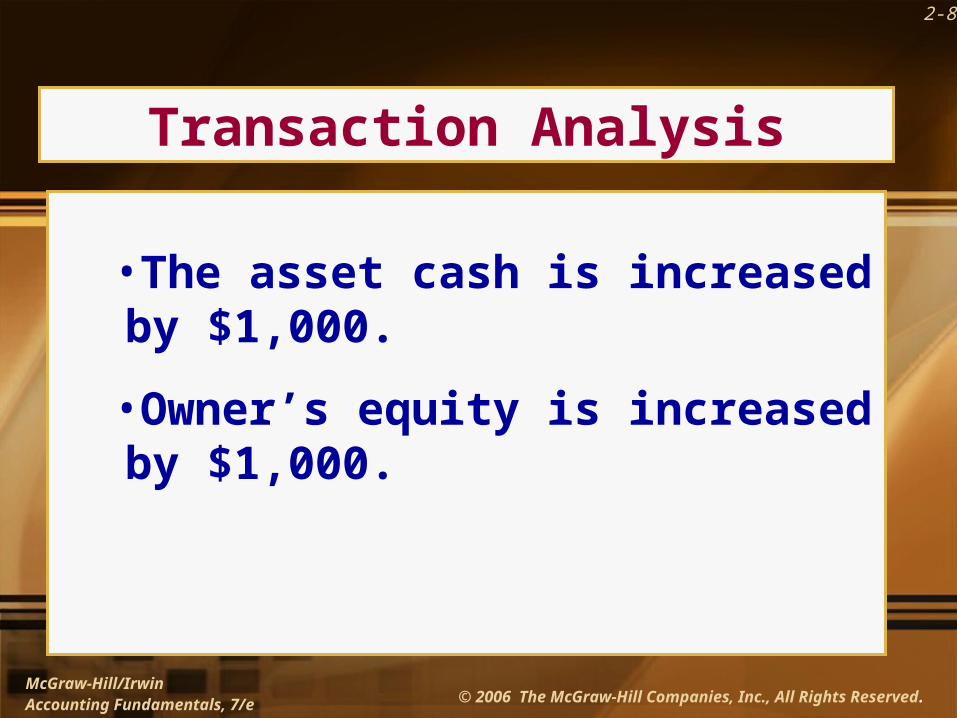

•The asset cash is increased by $1,000.

•Owner’s equity is increased by $1,000.

2-9

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

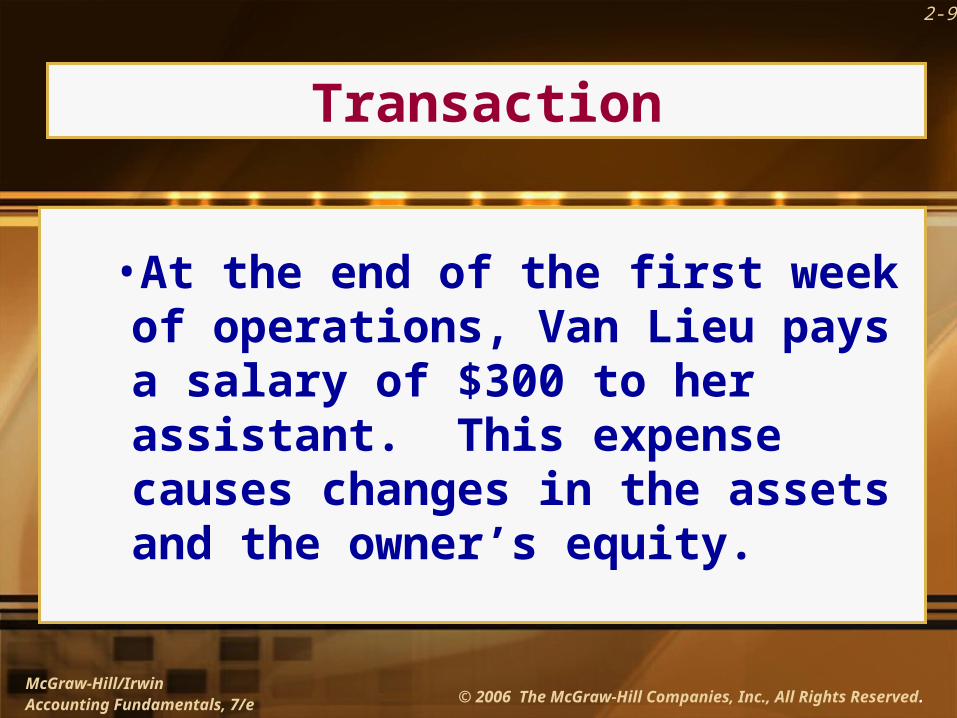

Transaction

•At the end of the first week of operations, Van Lieu pays a salary of $300 to her assistant. This expense causes changes in the assets and the owner’s equity.

2-10

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

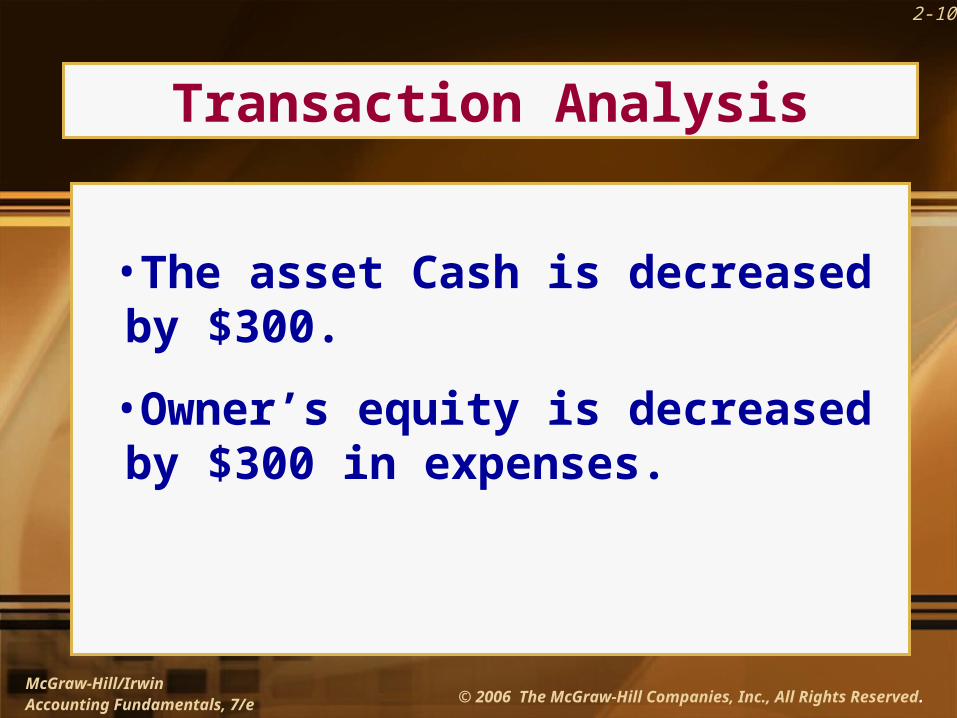

Transaction Analysis

•The asset Cash is decreased by $300.

•Owner’s equity is decreased by $300 in expenses.

2-11

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

Accounting Terminology

•Accounts Receivable

•Expenses

•Net Income

•Net Loss

•Paid on Account

•Received on Account

•Revenue

2-12

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

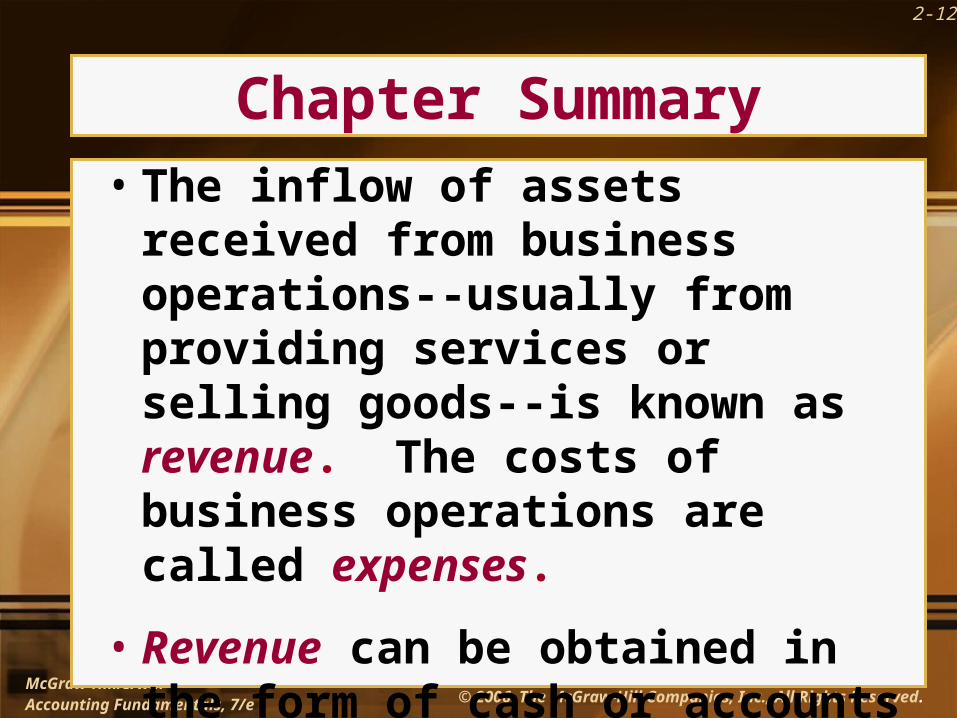

Chapter Summary• The inflow of assets received from

business operations--usually from providing services or selling goods--is known as revenue. The costs of business operations are called expenses.

• Revenue can be obtained in the form of cash or accounts receivable.

2-13

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

Chapter Summary(continued)

•Accounts receivable are amounts that customers have promised to pay in the future for services or goods bought on credit.

•The difference between revenue and expenses is net income, or net profit.

2-14

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

Chapter Summary(continued)

•When revenue is greater than expenses, there is a net income.

•When expenses are greater than revenue, there is a net loss.

2-15

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

Chapter Summary(continued)

•Net income results in an increase in the owner’s equity. Additional investments also cause an increase in the owner’s equity.

•Net loss results in a decrease in the owner’s equity.

2-16

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

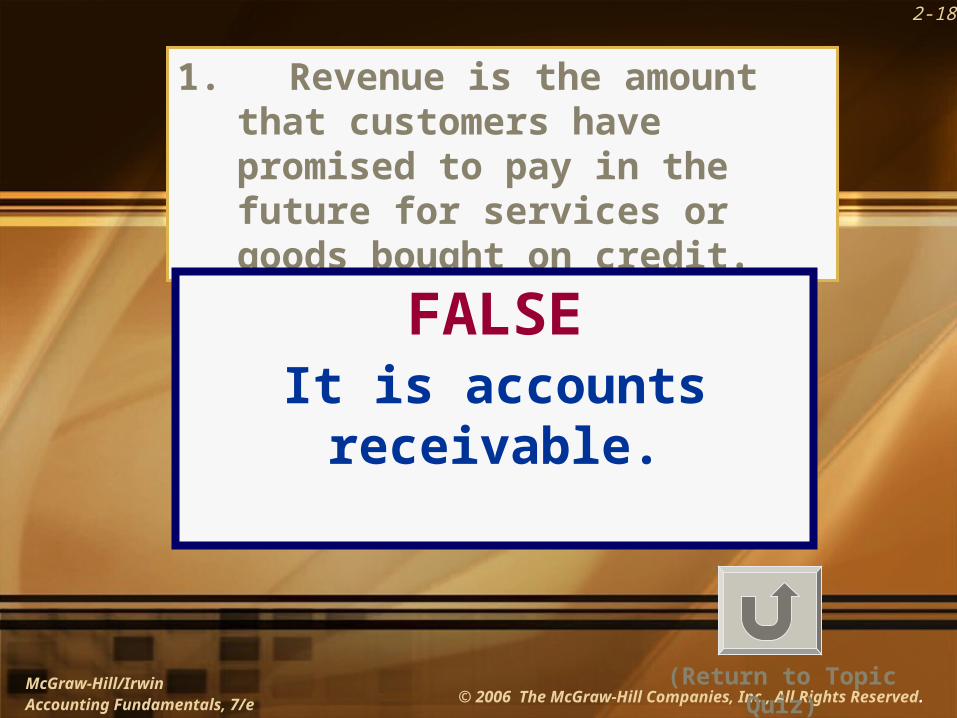

1. Revenue is the amount that customers have promised to pay in the future for services or goods bought on credit.

2. Revenue can be obtained in the form of

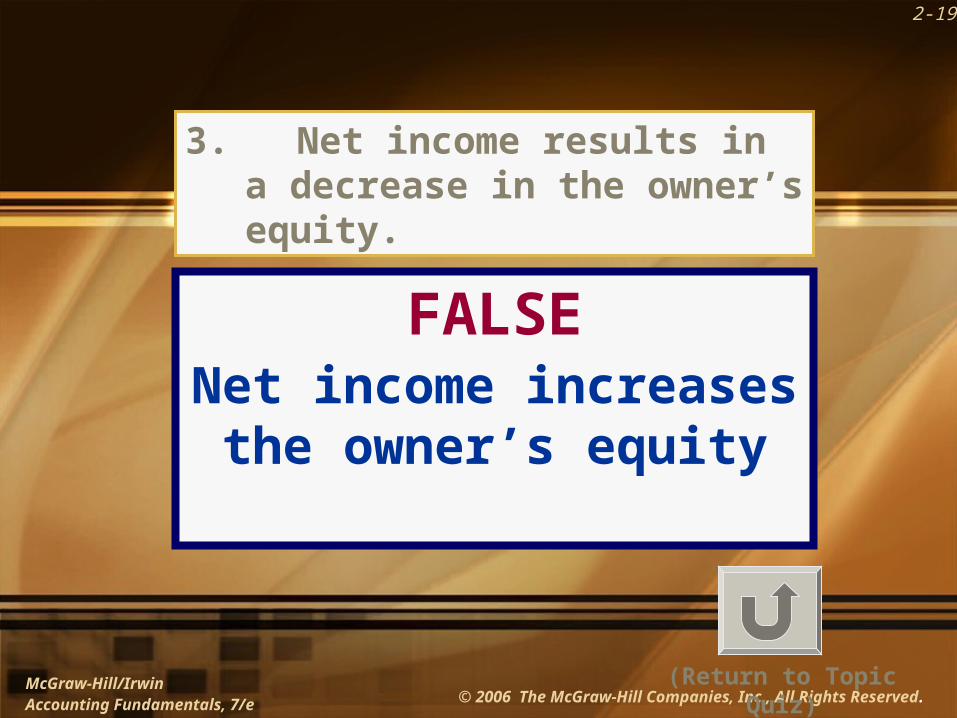

cash or accounts receivable. 3. Net income results in a decrease in

the owner’s equity.

Topic QuizAnswer the following true/false questions:

TRUE

FALSE

FALSE

2-17

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

Investigating on the Internet

Sources of information about net income or loss can be accessed at various corporate websites.

As a research assignment, access a website from a major corporation and report those sources of information that might concern profit and loss.

2-18

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

(Return to Topic Quiz)

1. Revenue is the amount that customers have promised to pay in the future for services or goods bought on credit.

FALSEIt is accounts receivable.

2-19

McGraw-Hill/IrwinAccounting Fundamentals, 7/e © 2006 The McGraw-Hill Companies, Inc., All Rights

Reserved.

(Return to Topic Quiz)

3. Net income results in a decrease in the owner’s equity.

FALSENet income increases the

owner’s equity