Chapter Outline - kaizenha.comkaizenha.com/wp-content/uploads/2016/04/4Rawabdeh_PPT_strategic20...٣...

44

١ Dr. Ibrahim Rawabdeh (2012) Ch 4 -١ Chapter 4 The Internal Assessment Strategic Management: Concepts & Cases 13 th Edition Fred David Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢ Chapter Outline The Nature of an Internal Audit The Resource-Based View (RBV) Integrating Strategy & Culture

Transcript of Chapter Outline - kaizenha.comkaizenha.com/wp-content/uploads/2016/04/4Rawabdeh_PPT_strategic20...٣...

١

Dr. Ibrahim Rawabdeh (2012) Ch 4 -١

Chapter 4 The Internal Assessment

Strategic Management: Concepts & Cases

13th EditionFred David

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢

Chapter Outline

The Nature of an Internal Audit

The Resource-Based View (RBV)

Integrating Strategy & Culture

٢

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٣

Chapter Outline (cont’d)

Management

Marketing

Opportunity Analysis

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٤

Chapter Outline (cont’d)

Finance/Accounting

Production/Operations

Research & Development

٣

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٥

Chapter Outline (cont’d)

Management Information Systems

The Internal Factor Evaluation (IFE) Matrix

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٦

The biggest levers you’ve got to change a company are strategy, structure, and culture. If I could pick two, I’d pick strategy and culture. –Wayne Leonard, CEO, Entergy

Internal Assessment

Weak leadership can wreck the soundest strategy. –Sun Zi

٤

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٧

Nature of an Internal Audit

-- Strengths

-- Weaknesses

Functional Areas of Business

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٨

Internal strengths/weaknesses External opportunities/threats Clear statement of mission

Nature of an Internal Audit

Basis for Objectives & Strategies

٥

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٩

Key Internal Forces

Functional Business Areas:

Vary by organization

Divisions have differing strengths & weaknesses

Dr. Ibrahim Rawabdeh (2012) Ch 4 -١٠

Key Internal Forces

Distinctive Competencies:

Firm’s strengths that cannot be easily matched or imitated by competitors

3M AND R&D

٦

Dr. Ibrahim Rawabdeh (2012) Ch 4 -١١

Key Internal Forces

Distinctive Competencies:

Building competitive advantage involves taking advantage of distinctive competencies

Dr. Ibrahim Rawabdeh (2012) Ch 4 -١٢

Key Internal Forces

Distinctive Competencies:

Strategies designed to improve on a firm’s weaknesses and turn to strengths

٧

Dr. Ibrahim Rawabdeh (2012) Ch 4 -١٣

Internal Audit

•Information from:•Management

•Marketing

•Finance/accounting

•Production/operations

•Research & Development

•Management information Systems

Parallels process of external audit

Dr. Ibrahim Rawabdeh (2012) Ch 4 -١٤

Internal Audit

Involvement in performing an internal strategic-management audit provides vehicle for understanding nature and effect of decisions in other functional business areas of the firm

٨

Dr. Ibrahim Rawabdeh (2012) Ch 4 -١٥

Internal Audit

Coordination & understanding among managers from all functional areas

Key to Organizational Success

Dr. Ibrahim Rawabdeh (2012) Ch 4 -١٦

Internal Audit

Number and complexity increases relative to organization size

Functional Relationships

٩

Dr. Ibrahim Rawabdeh (2012) Ch 4 -١٧

Internal Audit

Exemplifies complexity of relationships among functional areas of the business

Financial Ratio Analysis

Dr. Ibrahim Rawabdeh (2012) Ch 4 -١٨

Resource Based View (RBV)

Approach to Competitive Advantage

Internal resources are more important than external factors

١٠

Dr. Ibrahim Rawabdeh (2012) Ch 4 -١٩

Resource Based View (RBV)

3 All Encompassing Categories

1. Physical resources

2. Human resources

3. Organizational resources

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢٠

Resource Based View (RBV)

Empirical Indicators

Rare

Hard to imitate

Not easily substitutable

١١

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢١

Integrating Strategy & Culture

Pattern of behavior developed by an organization as it learns to cope with its problem of external adaptation and internal integration…is considered valid and taught to new members

Organizational Culture

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢٢

Integrating Strategy & Culture

Organizational Culture

Resistant to change

May represent:

Strength

Weakness

١٢

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢٣

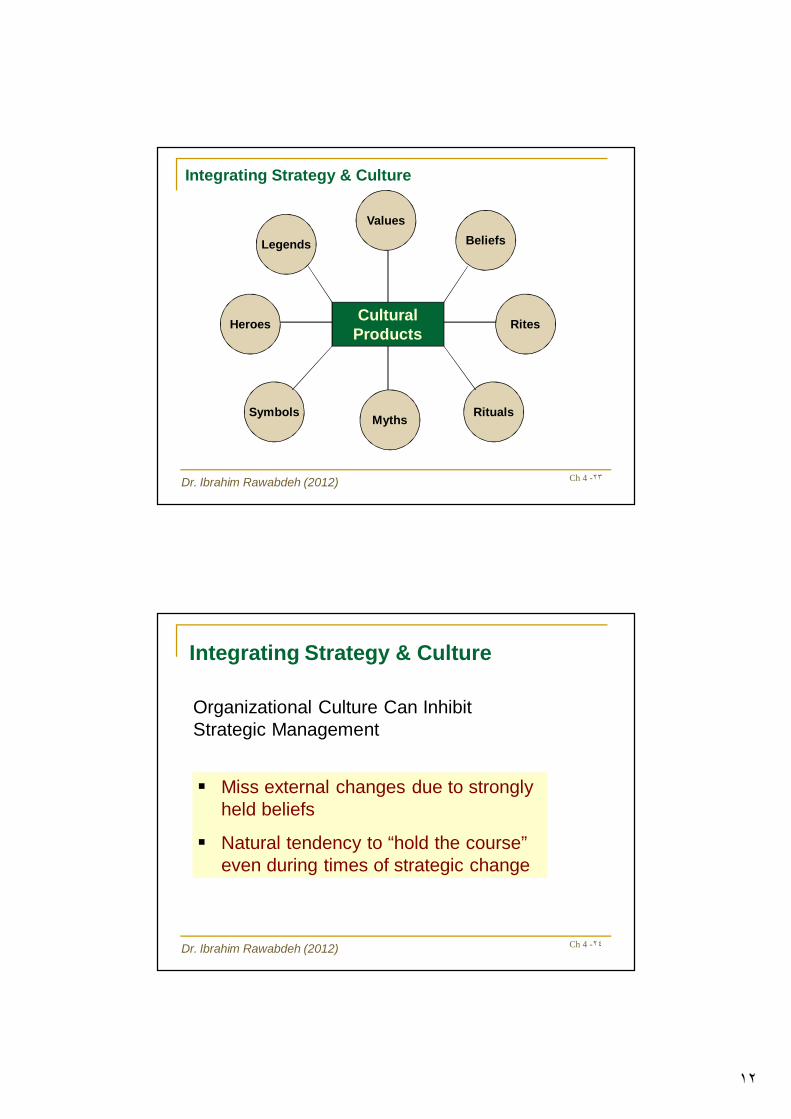

CulturalProducts

Values

Legends Beliefs

Heroes Rites

Symbols RitualsMyths

Integrating Strategy & Culture

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢٤

Integrating Strategy & Culture

Organizational Culture Can Inhibit Strategic Management

Miss external changes due to strongly held beliefs

Natural tendency to “hold the course” even during times of strategic change

١٣

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢٥

U.S. Versus Foreign Cultures

To successfully compete in world markets, U.S. managers must obtain a better knowledge of historical, cultural, and religious forces that motivate and drive people in other countries.

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢٦

١٤

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢٧

Management

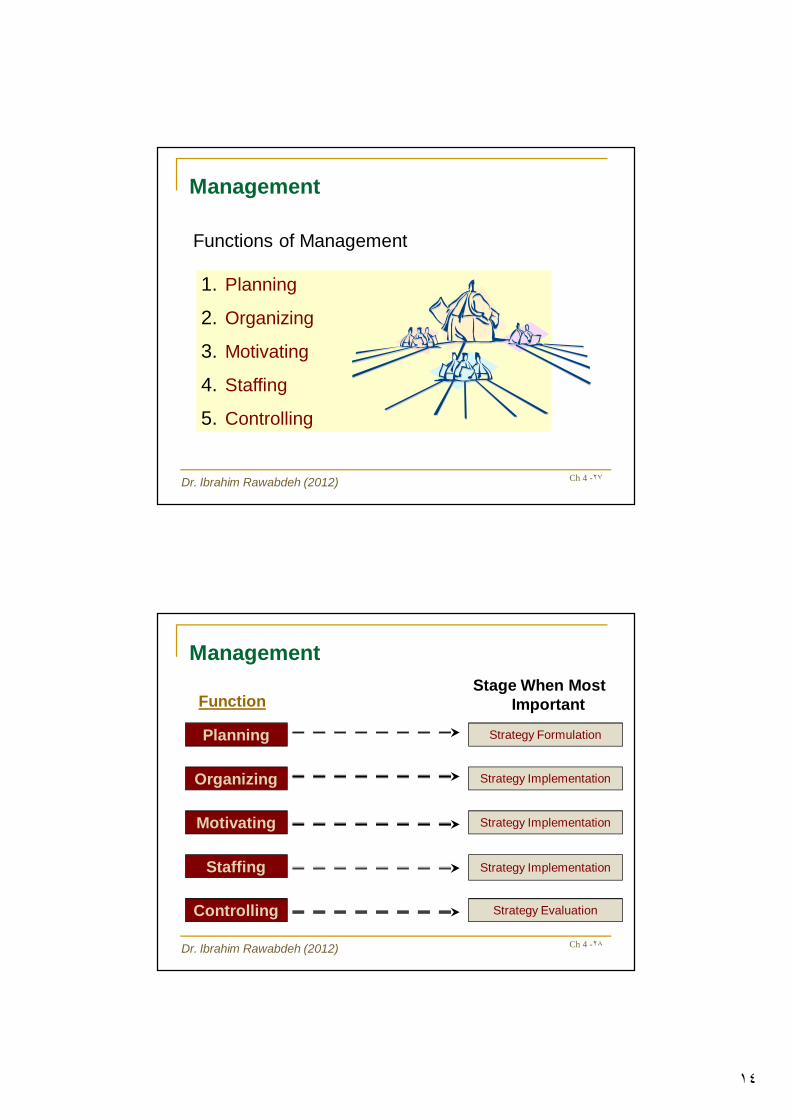

Functions of Management

1. Planning

2. Organizing

3. Motivating

4. Staffing

5. Controlling

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢٨

Management

Planning

Stage When Most ImportantFunction

Strategy Formulation

Organizing Strategy Implementation

Motivating Strategy Implementation

Staffing

Controlling

Strategy Implementation

Strategy Evaluation

١٥

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٢٩

Management

Planning

Beginning of management process

Bridge between present & future

Improves likelihood of attaining desired results

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٣٠

Planning

Forecasting

Establishing objectives

Devising strategies

Developing policies

Setting goals

Management

١٦

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٣١

Management

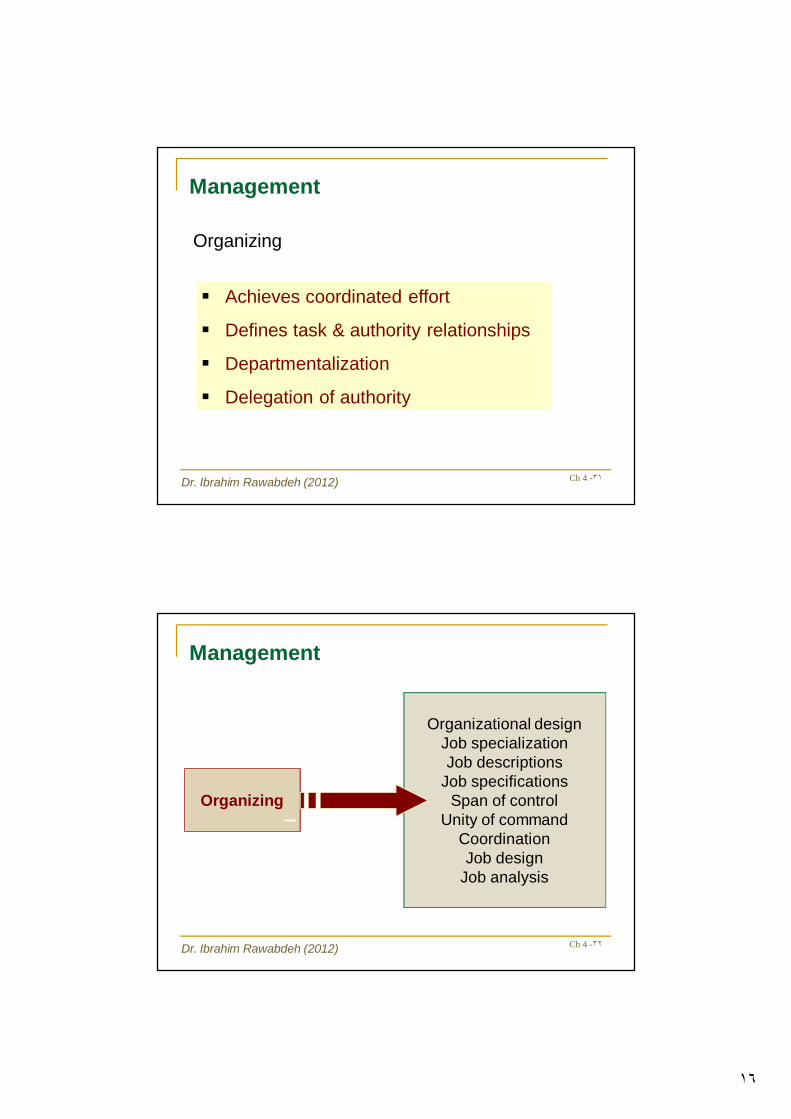

Organizing

Achieves coordinated effort

Defines task & authority relationships

Departmentalization

Delegation of authority

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٣٢

Organizing

Organizational designJob specializationJob descriptions

Job specificationsSpan of control

Unity of commandCoordinationJob design

Job analysis

Management

١٧

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٣٣

Management

Motivating

Influencing to accomplish specific objectives

Communication – major component

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٣٤

Motivating

LeadershipCommunication

Work groupsJob enrichmentJob satisfactionNeeds fulfillment

Organizational changeMorale

Management

١٨

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٣٥

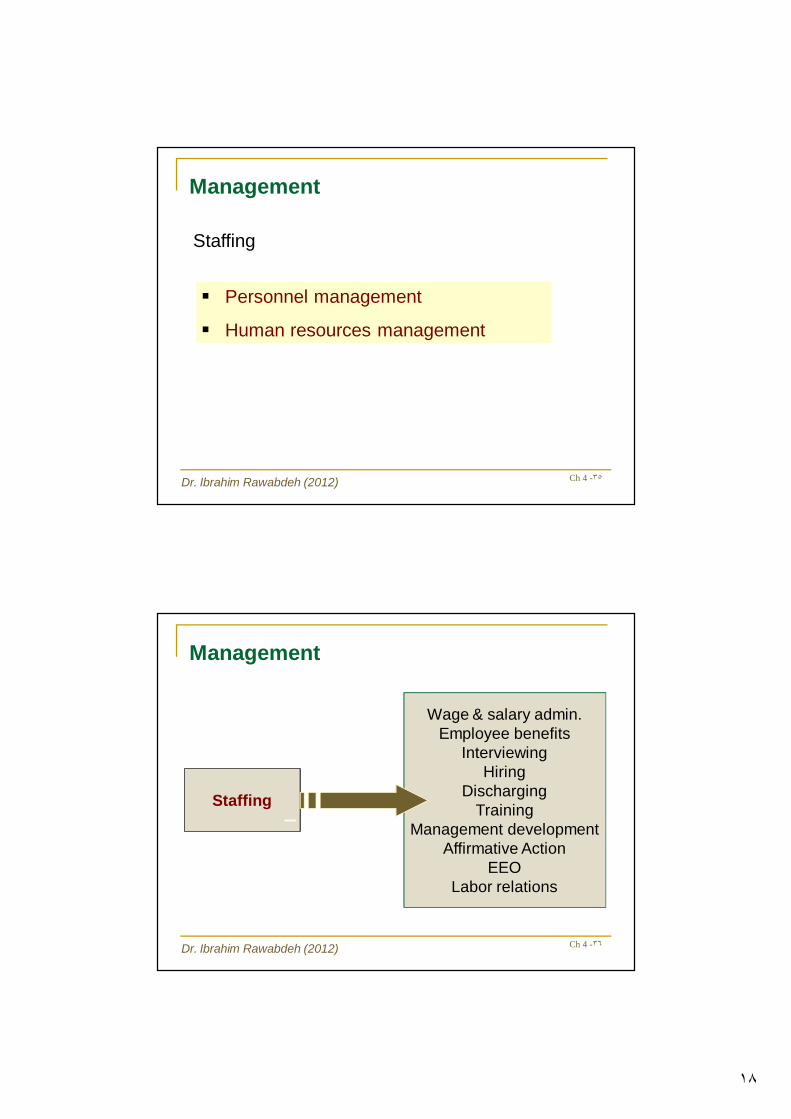

Management

Staffing

Personnel management

Human resources management

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٣٦

Staffing

Wage & salary admin.Employee benefits

InterviewingHiring

DischargingTraining

Management developmentAffirmative Action

EEOLabor relations

Management

١٩

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٣٧

Management

Controlling

Establishing performance standards

Ensure actual operations conform to planned operations

Taking corrective actions

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٣٨

Controlling

QualityFinancial

SalesInventoryExpense

Analysis of varianceRewardsSanctions

Management

٢٠

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٣٩

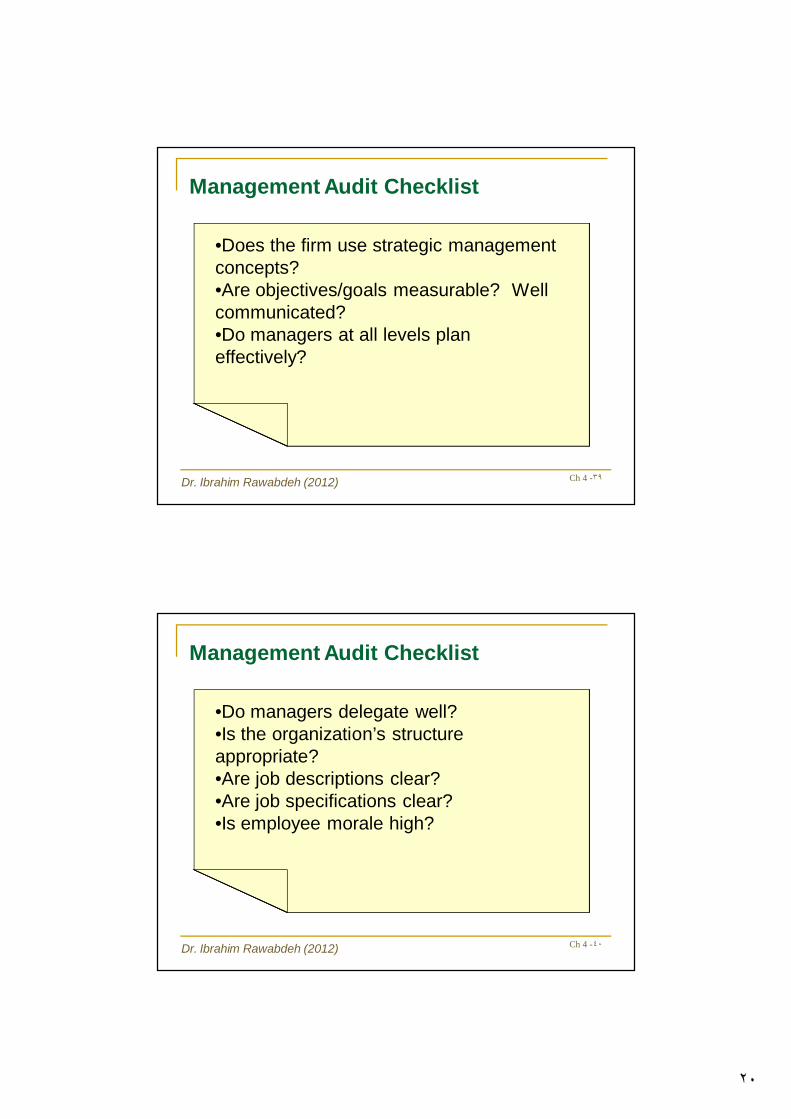

Management Audit Checklist

•Does the firm use strategic management concepts?•Are objectives/goals measurable? Well communicated?•Do managers at all levels plan effectively?

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٤٠

Management Audit Checklist

•Do managers delegate well?•Is the organization’s structure appropriate?•Are job descriptions clear?•Are job specifications clear?•Is employee morale high?

٢١

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٤١

Management Audit Checklist

•Is employee absenteeism low?•Is employee turnover low?•Are the reward mechanisms effective?•Are the organization’s control mechanisms effective?

Audit sheet example

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٤٢

Marketing

Customer Needs/Wants for Products/Services

1. Defining

2. Anticipating

3. Creating

4. Fulfilling

5. Delightening

٢٢

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٤٣

Marketing

Marketing Functions

1. Customer analysis

2. Selling products/services

3. Product & service planning

4. Pricing

5. Distribution

6. Marketing research

7. Opportunity analysis

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٤٤

Customer Analysis

Customer surveys

Consumer information

Market positioning strategies

Customer profiles

Market segmentation strategies

Marketing

٢٣

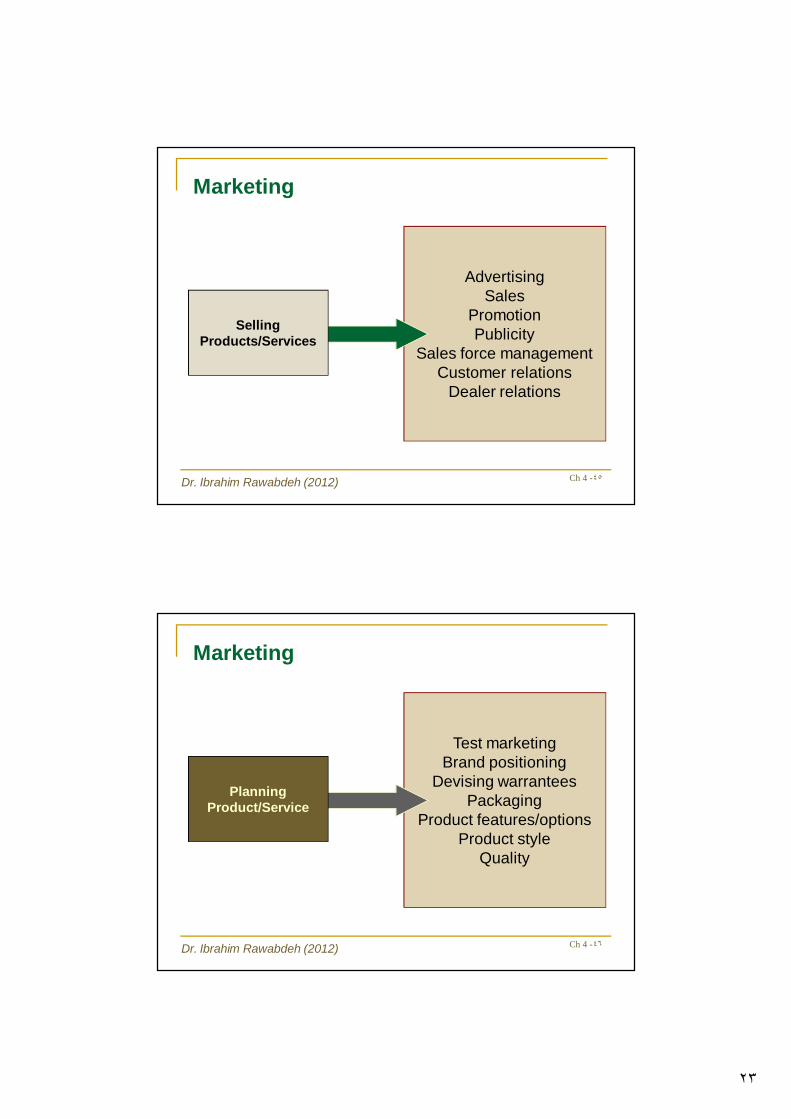

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٤٥

AdvertisingSales

PromotionPublicity

Sales force managementCustomer relations

Dealer relations

Marketing

Selling Products/Services

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٤٦

Test marketingBrand positioning

Devising warranteesPackaging

Product features/optionsProduct style

Quality

Marketing

Planning Product/Service

٢٤

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٤٧

Forward integrationDiscounts

Credit termsCondition of sale

MarkupsCosts

Unit pricing

Marketing

Pricing

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٤٨

WarehousingChannelsCoverage

Retail site locationsSales territoriesInventory levelsTransportation

Marketing

Distribution

٢٥

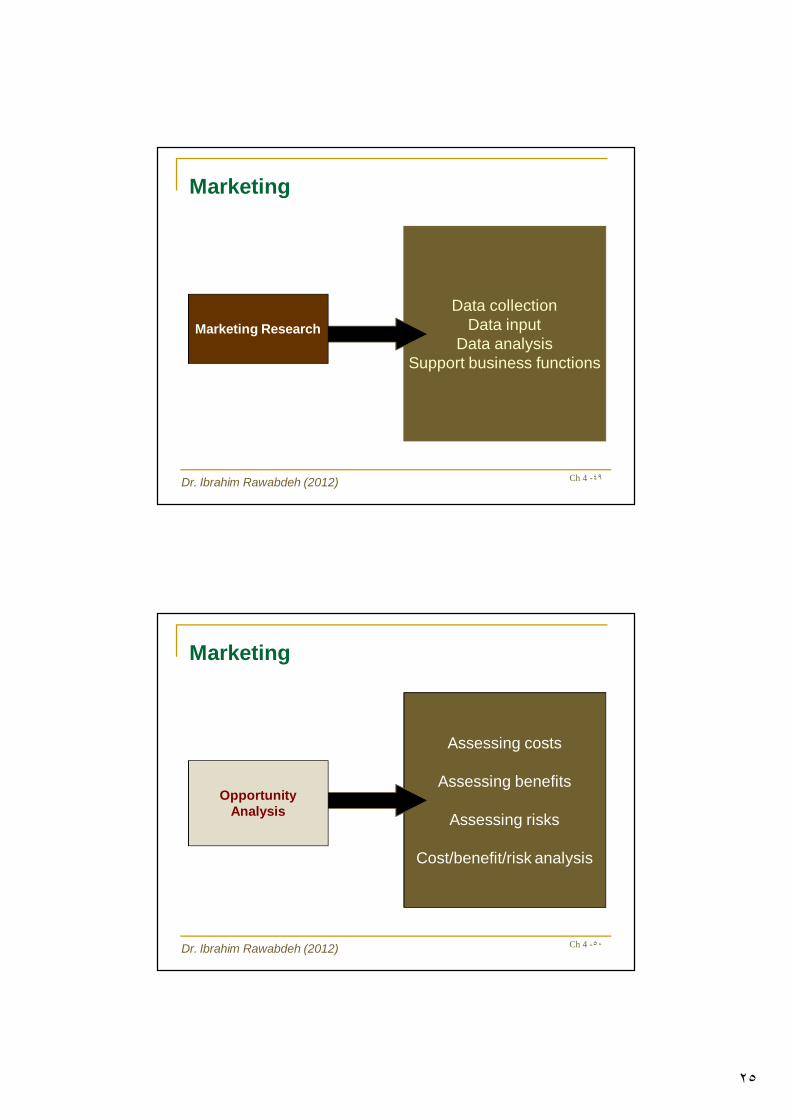

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٤٩

Data collectionData input

Data analysisSupport business functions

Marketing

Marketing Research

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٥٠

Assessing costs

Assessing benefits

Assessing risks

Cost/benefit/risk analysis

Marketing

Opportunity Analysis

٢٦

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٥١

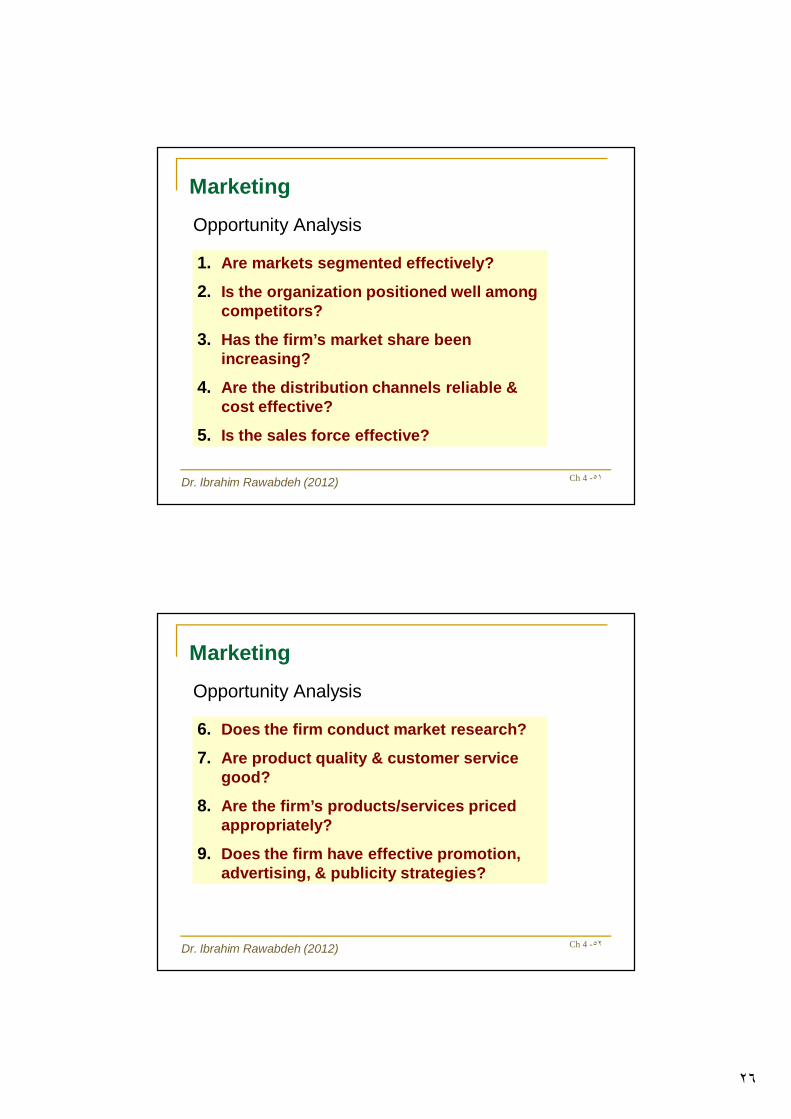

Marketing

Opportunity Analysis

1. Are markets segmented effectively?

2. Is the organization positioned well among competitors?

3. Has the firm’s market share been increasing?

4. Are the distribution channels reliable & cost effective?

5. Is the sales force effective?

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٥٢

Marketing

Opportunity Analysis

6. Does the firm conduct market research?

7. Are product quality & customer service good?

8. Are the firm’s products/services priced appropriately?

9. Does the firm have effective promotion, advertising, & publicity strategies?

٢٧

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٥٣

Marketing

Opportunity Analysis

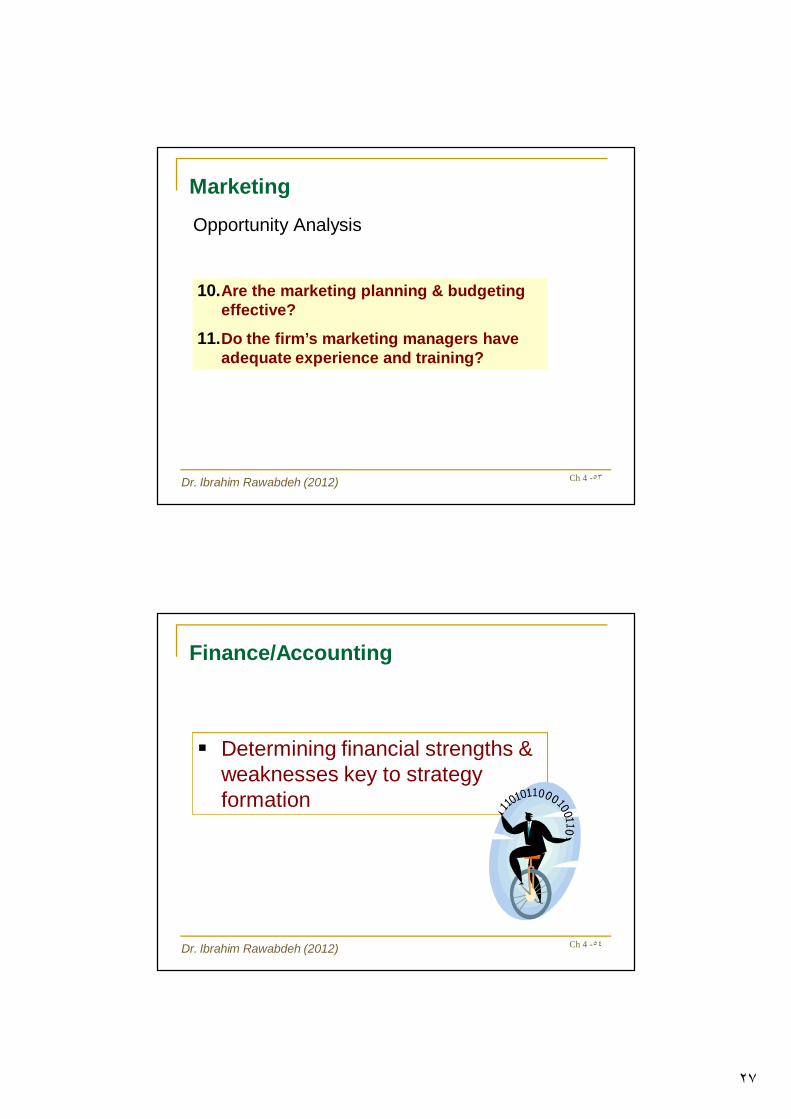

10.Are the marketing planning & budgeting effective?

11.Do the firm’s marketing managers have adequate experience and training?

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٥٤

Finance/Accounting

Determining financial strengths & weaknesses key to strategy formation

٢٨

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٥٥

Finance/Accounting

Finance/Accounting Functions

1. Investment decision (Capital budgeting)

2. Financing decision

3. Dividend decision

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٥٦

Firm’s ability to meet its short-term obligations

Ratios

Current ratioQuick (or acid test) ratio

Basic Financial Ratios

Liquidity Ratios

٢٩

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٥٧

Extent of debt financing

Ratios

Debt-to-total assetsDebt-to-equity

Long-term debt-to-equityTimes-interest earned

Basic Financial Ratios

Leverage Ratios

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٥٨

Effective use of firm’s resources

Ratios

Inventory-turnoverFixed assets turnoverTotal assets turnover

Accounts receivable turnoverAverage collection period

Basic Financial Ratios

Activity Ratios

٣٠

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٥٩

Effectiveness shown by returns on sales &

investment

Ratios

Gross profit marginOperating profit margin

Net profit marginReturn on total assets (ROA)

Basic Financial Ratios

Profitability Ratios

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٦٠

Effectiveness shown by returns on sales &

investment

Ratios

Return on stockholders equity (ROE)

Earnings per sharePrice-earnings ratio

Basic Financial Ratios

Profitability Ratios(cont’d)

٣١

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٦١

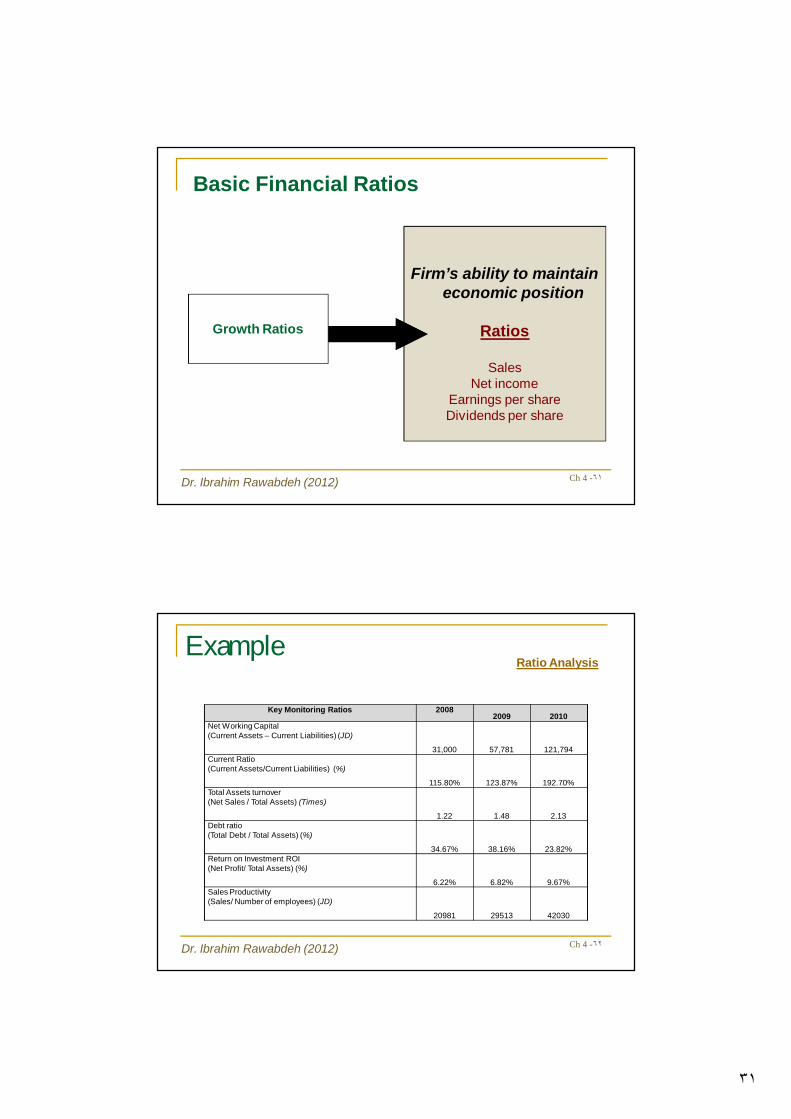

Firm’s ability to maintain economic position

Ratios

SalesNet income

Earnings per shareDividends per share

Basic Financial Ratios

Growth Ratios

Example

Key Monitoring Ratios 20082009 2010

Net Working Capital (Current Assets – Current Liabilities) (JD)

31,000 57,781 121,794Current Ratio (Current Assets/Current Liabilities) (%)

115.80% 123.87% 192.70%Total Assets turnover (Net Sales / Total Assets) (Times)

1.22 1.48 2.13Debt ratio (Total Debt / Total Assets) (%)

34.67% 38.16% 23.82%Return on Investment ROI (Net Profit/ Total Assets) (%)

6.22% 6.82% 9.67%Sales Productivity (Sales/ Number of employees) (JD)

20981 29513 42030

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٦٢

Ratio Analysis

٣٢

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٦٣

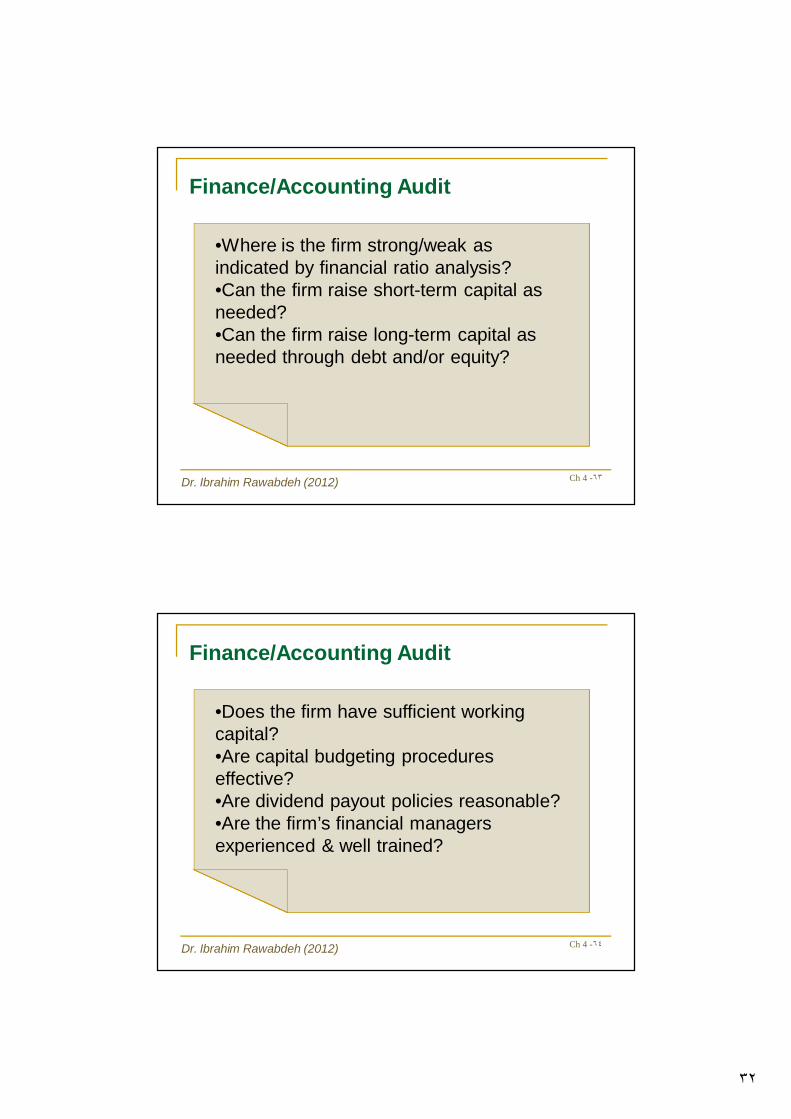

Finance/Accounting Audit

•Where is the firm strong/weak as indicated by financial ratio analysis?•Can the firm raise short-term capital as needed?•Can the firm raise long-term capital as needed through debt and/or equity?

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٦٤

Finance/Accounting Audit

•Does the firm have sufficient working capital?•Are capital budgeting procedures effective?•Are dividend payout policies reasonable?•Are the firm’s financial managers experienced & well trained?

٣٣

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٦٥

Finance/Accounting Audit

Effective Financial Analysis Requires:1. Analysis of how the ratios have

changed over time2. How the ratios compare to industry

norms3. How the ratios compare with key

competitors

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٦٦

Production/Operations

Production/Operations Functions

Process

Capacity

Inventory

Workforce

Quality

٣٤

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٦٧

Facility designTechnology selection

Facility layoutProcess flow analysis

Facility locationLine balancingProcess control

Production/Operations

Process

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٦٨

ForecastingFacilities planning

Aggregate planningScheduling

Capacity planningQueuing analysis

Production/Operations

Capacity

٣٥

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٦٩

Raw materialsWork in processFinished goods

Materials handling

Production/Operations

Inventory

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٧٠

Job designWork measurement

Job enrichmentWork standards

Motivation techniques

Production/Operations

Workforce

٣٦

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٧١

Quality controlSamplingTesting

Quality assuranceCost Control

Production/Operations

Quality

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٧٢

Production/Operations Audit

•Are suppliers of materials, parts, etc. reliable and reasonable?•Are facilities, equipment & machinery in good condition?•Are inventory-control policies and procedures effective?

٣٧

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٧٣

Production/Operations Audit

•Are quality-control policies & procedures effective?•Are facilities, resources, and markets strategically located?•Does the firm have technological competencies?

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٧٤

Research & Development

Research & Development Functions

Development of new products beforecompetitors

Improving product quality

Improving manufacturing processes to reduce costs

٣٨

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٧٥

Financing as many projects as possible

Use percent-of-sales method

Budgeting relative to competitors

How many successful new products are

needed

Research & Development

R&D Budgets

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٧٦

Research & Development Audit

•Are the R&D facilities adequate?•If R&D is outsourced, is it cost effective?•Are the R&D personnel well qualified?•Are R&D resources allocated effectively?

٣٩

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٧٧

Research & Development Audit

•Are MIS and computer systems adequate?•Is communication between R&D & other organizational units effective?•Are present products technologically competitive?

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٧٨

Management Information Systems

Purpose

Improve performance of an enterprise by improving the quality of managerial decisions.

٤٠

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٧٩

Management Information Systems

Information Systems CIO/CTO Security User-friendly E-commerce

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٨٠

Management Information Systems Audit

•Do managers use the information system to make decisions?•Is there a CIO or Director of Information Systems position in the firm?•Is data updated regularly?

٤١

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٨١

Management Information Systems Audit

•Do managers from all functional areas contribute input to the information system?•Are there effective passwords for entry into the firm’s information system?•Are strategists of the firm familiar with the information systems of rival firms?

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٨٢

Management Information Systems Audit

•Is the information system user-friendly?•Do all users understand the competitive advantages that information can provide?•Are computer training workshops provided for users?•Is the firm’s system being improved?

٤٢

Internal Factors Evaluation Matrix

A summary step in conducting an internal strategic-management audit is to construct an IFE Matrix.

This strategy-formulation tool summarizes and evaluates the major strengths and weaknesses in the functional areas of a business, and it also provides a basis for identifying and evaluating relationships among these areas.

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٨٣

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٨٤

٤٣

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٨٥

Example

Wafa Est.

Dr. Ibrahim Rawabdeh (2012) Ch 4 -٨٦

٤٤

Develop an internal audit system – be creative

Develop an IFE matrix for-an industrial company- government entity -Service firm-- a hospital-- a university

٨٧

HW