Chapter Fifteen Partnerships: Termination and Liquidation Copyright © 2013 by The McGraw-Hill...

16

Chapter Fifteen Partnerships : Termination and Liquidation Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

-

Upload

ambrose-golden -

Category

Documents

-

view

220 -

download

0

Transcript of Chapter Fifteen Partnerships: Termination and Liquidation Copyright © 2013 by The McGraw-Hill...

Chapter Fifteen

Partnerships: Termination and

Liquidation

Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Reasons for Termination

Termination of business activities followed by liquidation of partnership property occurs for a variety of reasons: Personality disputes between partnersRetirementDeathChanged business environmentOther opportunitiesLow profitsBankruptcy (either the business or a partner)

15-2

Termination & Liquidation

When the partners wish to terminate the business:

Convert all assets to cash.Allocate all gains or losses to the

partner capital balances.Pay all liabilities and expenses.Distribute remaining cash to

partners.

LO 1LO 1

15-3

Termination & Liquidation -Example

According to their agreement, Morgan & Houseman divide profits 6:4 respectively. On 6/1, the inventory is sold for $15,000.

Note that the loss on the sale of inventory of $7,000 is assigned $4,200 ($7,000 x 60%) Morgan and $2,800 ($7,000 x 40%) to Houseman.

LO 2LO 2

15-4

Deficit Capital Balance

Deficit balances can be resolved two ways:The deficit partner can make a

contribution to make up the deficit.The remaining partners can absorb the

deficit.(The deficit partner may pay later or

can be sued for the deficit amount.)

LO 3LO 3

15-5

Any payments by Holland will be split 2/3 to Dozier and 1/3 to Ross.

Deficit Capital Balance --Contribution by Deficit Partner

Contributions made by the deficit partner(s) are distributed to the non-

deficit partners based on their relative profit sharing percentages.

15-6

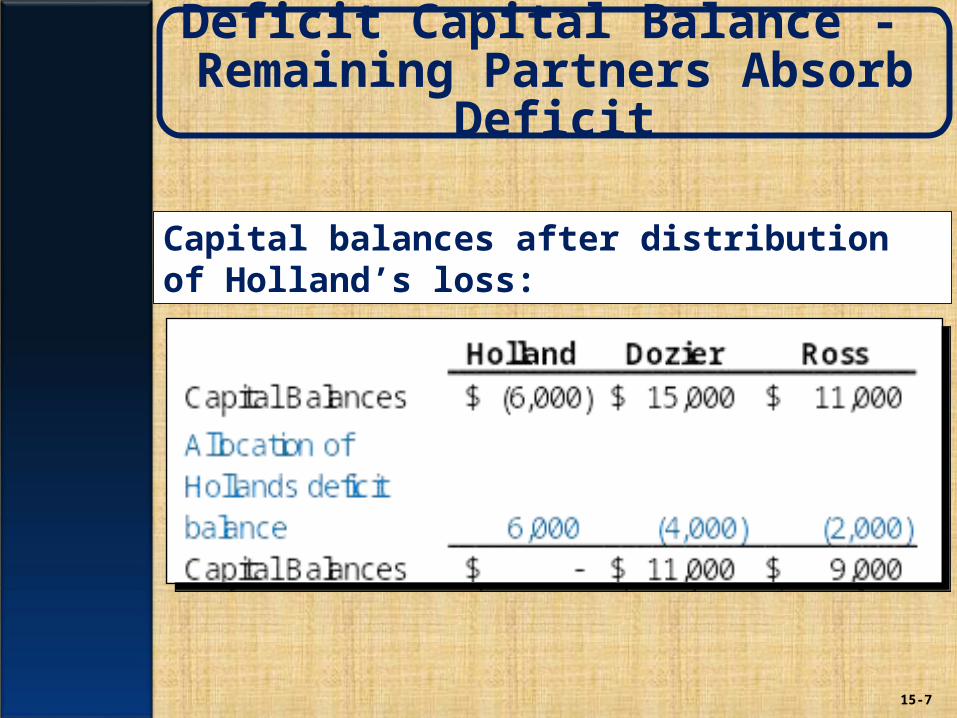

Deficit Capital Balance - Remaining Partners Absorb Deficit

Capital balances after distribution of Holland’s loss:

15-7

Preliminary Distribution of Assets

Debts owed to personal creditors.

Debts owed to partnership creditors.

Debts owed to the other partners.

Under the Uniform Partnership Act, a priority ranking of creditors having claims against individual partners is recognized:

LO 4LO 4

15-8

Predistribution Plan

Used by accountants to guide the distribution of cash resulting from the liquidation process.

Examine the Balance Sheet below. Assume the income sharing % is Rubens 50%, Smith 20%, and Trice 30%.

LO 5LO 5

15-9

Predistribution Plan

First, determine the maximum loss that each partner can absorb. Divide each partner’s capital balance by their respective income

sharing %.

15-10

Predistribution Plan

Since Rubens can ONLY absorb a partnership loss of $60,000, new balances are computed assuming that the partnership has a $60,000 loss.

15-11

Predistribution Plan

With Rubens wiped out, continue calculating maximum absorbable losses using income

sharing percentages of Smith, 20% (2/5) and Trice 30% (3/5).

15-12

Predistribution Plan

As earlier, compute the maximum absorbable loss by dividing the capital balances by the

relative income sharing %.

15-13

Predistribution Plan

Trice can only absorb a loss of $55,000.Now determine new capital balances for a loss

of $55,000.

15-14

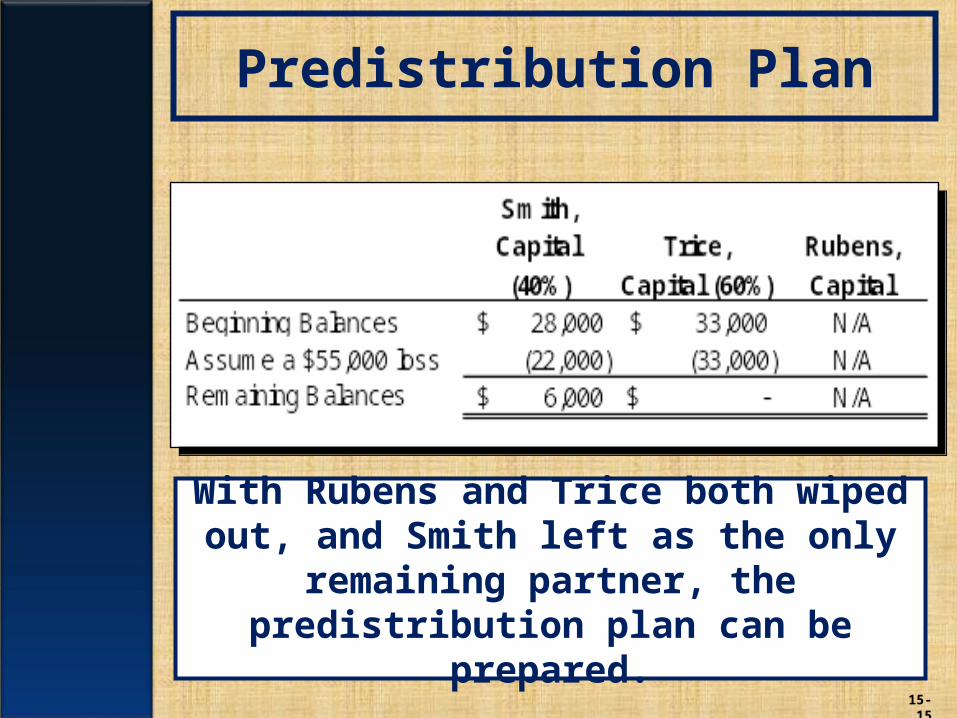

Predistribution Plan

With Rubens and Trice both wiped out, and Smith left as the only remaining partner, the

predistribution plan can be prepared.

15-15

Predistribution Plan

To inform all parties of the pattern by which available cash will be disbursed, the predistribution plan should be formally prepared in a schedule format prior to beginning liquidation.

15-16