Chapter 8 V

39

Problem 8 – 1 Deductible or Nondeductible Classify the item whether deductible or non deductible from business gross income. 1. Net operating loss carry over 2. Operating expenses incurred outside the Philippines by a non resident alien engaged in business in the Philippines 3. Philippine income tax 4. Income tax paid by a resident citizen to foreign country 5. Research and development costs 6. Unused materials and supplies 7. Donation for coffin and wake expenses 8. Manager’s expense account subjected to fringe benefit tax 9. Cost of technical books used by a cpa in the practice of his profession 10. Tax withheld by corporation from its employee’s salary 11. Kickback payment to the government official 12. Tuition fees, board and lodging incurred by a medical doctor while attending a continuing professional education seminar. 13. Overtime pay paid to rank-and-file employee. 14. Fringe benefits paid to an officer of the company. 15. Distribution of profits to partners. 16. Cash dividends paid. 17. Donations made to employee’s birthday party. 18. Amounts paid for pensions of retired employees. 19. Salary of employee paid for limited period after his death to his widow. 20. Entire amount expensed for meals. Lodging, and travel in connection with own business. Problem 8 – 2 True or False Write true if the statement is correct or false if the statement is incorrect. 1. Deductions from gross income are not presumed. 2. Revenue expenditures are immediately expensed. 3. Business expenses are deductible only if they are incurred in relation to business income taxable in the Philippines.

description

tax

Transcript of Chapter 8 V

Problem 8 – 1 Deductible or NondeductibleClassify the item whether deductible or non deductible from business gross income.

1. Net operating loss carry over2. Operating expenses incurred outside the Philippines by a non resident alien engaged in

business in the Philippines3. Philippine income tax4. Income tax paid by a resident citizen to foreign country5. Research and development costs6. Unused materials and supplies7. Donation for coffin and wake expenses8. Manager’s expense account subjected to fringe benefit tax9. Cost of technical books used by a cpa in the practice of his profession 10. Tax withheld by corporation from its employee’s salary11. Kickback payment to the government official12. Tuition fees, board and lodging incurred by a medical doctor while attending a

continuing professional education seminar.13. Overtime pay paid to rank-and-file employee.14. Fringe benefits paid to an officer of the company.15. Distribution of profits to partners.16. Cash dividends paid.17. Donations made to employee’s birthday party.18. Amounts paid for pensions of retired employees.19. Salary of employee paid for limited period after his death to his widow.20. Entire amount expensed for meals. Lodging, and travel in connection with own business.

Problem 8 – 2 True or FalseWrite true if the statement is correct or false if the statement is incorrect.

1. Deductions from gross income are not presumed.2. Revenue expenditures are immediately expensed.3. Business expenses are deductible only if they are incurred in relation to business income

taxable in the Philippines.4. No business and personal expenses are allowed as deductions from gross income.5. As a rule, deductions means itemized deduction.6. Optional standard deduction may be deducted from the gross income of partnerships.7. Optional standard deductions include losses from sales or exchanges of capital assets.8. All business expenses are allowable deductions from gross business income.9. Business and professional income derived within and outside the Philippines by a non

resident Filipino Citizen are granted with allowable deductions.10. Individual tax payers may apply for itemized deductions or optional standard deduction.11. Individual taxpayers earning a salary compensation income may deduct optional

standard deduction from their gross compensation income.12. NOLCO is an itemized deduction.

13. A bonus paid to secure a lease is deductible on pro – rata basis over the term of the lease.

14. A representation expense is subject to limit of 1% of net sales of goods.15. A corporation with interest expense and at the same time earned interest income will

be subject to a tax arbitrage of 38%.16. Straight – line method of depreciation provides the best tax savings over other

depreciation methods.17. Adopting private entities of public schools through TESDA can get 150% of the actual

assistance made.18. Corporations are allowed to deduct optional standard deduction.

Problem 8 – 3 Multiple ChoiceSelect the letter that contains the best answer.

1. Which of the following statement is not correct?a. personal expenses are not allowed as deductions from compensation ,

profession, trade or business income.b. Personal expenses are not allowed as deductions from profession, trade or

business income except compensation income.c. Personal exemption and additional exemption are allowed as deduction from

compenasation income.d. All of the above

2. To compute for optional standard deduction, a taxpayer should multiply 10% of the

a. net incomeb. gross income before itemized deductionsc. gross income after expensesd. all of the above.

3. Which of the following can be deducted from gross compensation income?a. losses due to theft or robberyb. interest expense incurred in businessc. depreciation expense of car partly used for businessd. pemium payments on health or hospitalization insurance

4. Which of the following is not allowed as deductible in full from gross income?a. Entire amount expended for meals, lodging, and travel in connection with own

business.b. Tuition fees, board and lodging incurred by amedical doctor while attending

acontinuing professional education seminar.c. Costs of technical books used by a CPA in the practice of his profession.

5. Which of the following is not allowed as deductible in full from gross income?

a. Interest expense paid by the bank.b. Interest expense paid by the taxpayer in relation to the purchase of merchandise

by installment.c. Interest expense paid to the relative of the taxpayer.d. Interest expense with reported interest income.

6. The following taxes are not allowed as deductions from gross income, excepta. Documentary stamp tax. c. percentage tax.b. Special assessment tax. d. value added tax.

7. Which of the following is classified as deductible loss?a. Allowance for bad debts. C. depreciation.b. Embezzlement. D. all of the above.

8. The following are requisites of depreciation expense to be deducted from the gross income.

a. It must be reasonable and charged off during the year.b. It must be used in business, profession or trade.c. The asset subject to depreciation must have a limited life.d. All of the above.

9. Which of the following income is to be reduced by itemized deductions?a. compensation incomeb. business incomec. passive incomed. capital gain

10. Statement 1: the taxpayer has the burden of justifying the allowance of any deduction claimed.Statement 2: deductions are strictly construed against the taxpayer.

a. Only statement 1 is correct.b. Only statement 2 is correct.c. Both statements are correct.d. Both statements are not correct.

11. Statement 1 : revenue expenditures are period costs that are related to a particular period of time of business operation.Statement 2: capital expenditures are non – recurring expenditures related to acquisition of depreciable assets to be used in the business.

a. only statement 1 is correct.b. Only statement 2 is correct.c. Both statements are correct d. Both statements are incorrect.

12. Which of the following expenses of the business would be allowed as deduction from its business income?

a. insurance premium on life insurance of employee where the employer is the beneficiary.

b. Donation made to employees.c. Losses incurred on transaction wiyh related party.d. Regular repairs of business property.

13. Statement 1: in preparing financial statements, GAAP should prevail over the Tax Code.Statement 2: in preparing tax returns, tax code should prevail over GAAP.

a. only statement 1 is correct.b. Only statement 2 is correct.c. Both statements are correct.d. Both statements are incorrect

Problem 8 -4 Multiple choiceSelect the letter that contains the best answer.

1. Statement 1: compensation income is reduced by personal exemption. Statement 2: business income is reduced by business expenses, and by excess of personal exemption over compensation income.

a. Only statement is correct.b. Only statement is correct.c. Both statements are correct.d. Both statements are incorrect.

2. Statement 1: an individual taxpayer could claim both the itemized deduction and personal exemption in the same taxable year.Statement 2: an individual single proprietorship could claim both the itemized deduction and optional standard deduction in the same taxable year.

a. Only statement 1 is correct.b. Only statement 2 is correct.c. Both statements are correct.d. Both statements are incorrect.

3. Which of the following is allowed with optional standard deductions?A. Non resident alien doing business in the Philippines.B. Resident citizen whose taxable income is his compensation earned.C. Non resident citizen claiming itemized deductions from his business

income.D. Resident alien with business income earned within and outside the

Philippines.

4. Statement 1: unless the taxpayer signified in his return that he is electing the standard deduction, he is deemed to have availed of the itemized allowable of deductions.Statement 2: in case of consolidated income tax return of husband and wife, each is allowed to choose from either optional or itemized deductions.

a. Both statements are correct.b. Only statement 1 is correct.c. Only statement 2 is correct.d. Both statements are incorrect.

5. Statement 1: self employed taxpayer is required to file his quarterly income tax return.Statement 2: the option ton avail of optional or itemized deduction could be opted for each quarter.

a. Both statements are correct.b. Only statement 1 is correct.c. Only statement 2 is correct.d. Both statements are incorrect.

6. Statement 1: insurance expense incurred in connection with the conduct of business is allowable deduction.

Statement 2: insurance premium incurred to cover the life of key employee where the employer is the beneficiary could be allowed as deduction.

a. both statements are correctb. Only statement 1 is correct.c. Only statement 2 is correct.d. Both statements are incorrect

7. Which of the following the correct allowable entertainment expense?a. Not more than ½ % of revenue from services.b. Not more than 1% net sale of goods.c. Not more than 1 ½% of revenue from services.d. Not more than 1 ½ % of net sales of goods.

8. Statement 1: as a general rule, if the taxpayer is in cash basis of accounting, prepaid interest is allowed as deduction in the year tha principal is fully paid.Statement 2: prepaid interest made by service business is deductible in the year when the interest is paid.

a. both statements are correct.b. Only statement no. 1 is correct.c. Only statement no. 2 is correct.d. Both statements are incorrect.

9. Which of the following statements is not correct?a. Resident citizen and Domestic Corporation are allowed to claim foreign income

tax as deduction from their business income.

b. Foreign income tax paid by resident citizen could be claimed as deductible from his income tax.

c. Foreign income tax paid by Domestic Corporation could be claimed as tax credit deductible from its income tax.

d. The tax payer will benefit more if the foreign income tax is claimed as deduction rather than as tax credit.

10. Statement 1: the amount of deductible taxes is limited to the basic tax and shall not include thae amount for any surcharges or penalty.Statement 2: interest on delinquent taxes is deductible from gross income in full amount.

a. both statements are correct.b. Only statement 1 is correct.c. Only statement 2 is correct.d. Both statements are incorrect

Problem 8 -5 Multiple choiceSelect the letter that contains the best answer.

1. Statement 1: gains arising from transactions between related taxpayers are taxable.Statement 2: losses incurred from transactions between members of the family are not deductible from business income.

a. Both statements are correct.b. Only statement 1 is correct.c. Only statement 2 is correct.d. Both statements are incorrect.

2. Which of the following statement is incorrect?a. Actual bad debts incurred in connection with the conduct of business are

allowed as deduction.b. Estimated bad debts based on account receivable balance iss deductible.c. Bad debts written off are deductible in the year when the allowance based on

estimate was made.d. Bad debts arising from unpaid salaries that are actually written off are deductible

in the year of write off.

3. Which of the following statements is not correct?a. Depreciation of assets used in business is allowed as deduction from business

income.b. Depreciation as a recovery of capital invested should not be beyond the

acquisition cost.c. Depreciation should be determined on the basis of re – appraised value if

revaluation is made.

d. Straight – line method, SYD, and declining balance methods of depreciation are all allowed for claiming depreciation expense.

4. Which of the following statements is correct?a. The employer making the contribution manages defined contribution plan.b. The actual payment of benefit to employee is the expense of the employer

under thw defined contribution plan.c. Under the defined benefit plan, the employer makes the actual payment of

benefits to employees.d. Under the defined contriution plan, the amount of contribution is equal to the

actual payment of the benefits due to thr etiring employee.

5. Which of the following is not a requisite for the deductible contributions?a. It must be incurred in connection with the conduct of business.b. The taxpayer making contribution must be engage in business or profession.c. There must be actual payment of contribution ord. The recipient of the contribution is an entity specialized by law.

6. Statement 1: the optional standard deduction is allowed to all individual taxpayers earning business income.Statement 2: the optional standard deduction is 10% of gross business income.

a. only statement 1 is correct.b. Only statement 2 is correct.c. Both statements are correct.d. Both statements are not correct.

7. Statement 1: husband and wife should report their income and expenses in the same or common tax return.Statement 2: husband may choose itemized deduction while the wife may choose optional standard deduction or vice versa.

a. only statement 1 is correct.b. Only statement 2 is correct.c. Both statements are correct.d. Both statements are not correct.

8. Statement 1: deductible business expenses must be ordinary and necessary.Statement 2: expenses from previous period which were not deducted from previous period’s income could be deducted from income in the current period.

a. Only statement 1 is correct.b. Only statement 2 is correct.c. Both statements are correct.d. Both statements re not correct.

9. Which of the following expenses incurred in relation to conduct of business could be deducted in full, if the net sales is P1,000,000?

i. salaries of employees, net of withholding taxii. P60, 000 rent expenseiii. P50, 000 traveling expenseiv. P10, 000 entertainment expenses

Choices: a. I, ii, iii and iv

b. I, ii, and iii only c. I and ii only d. I only

10. The interest expense allowed as deduction for individual taxpayer must be.a. 100% of actual amount even when interest income for the same taxable year is

very minimalb. 38% of the actual amount of interest income earned the same taxable yearc. 62% of the actual amount of interest expense or interest income which are equal

to each other d. 100% of the actual interest expense if the interest expense is lower than the

interest income for the same year

Problem 8-6 Multiple ChoiceSelect the letter that contains the best answer.

1. Which of the following interest expense is deductible in full?a. Interest on tax delinquencyb. Interest on personal loanc. Interest expense which is 200% of the interest income for the same year.d. Interest paid in advance.

2. Which of the following taxes incurred in the conduct of business is allowed as deduction from business income?

a. Income Tax c. Excise taxb. VAT d. Donor’s tax

3. Which of the following taxes incurred in the conduct of business is not allowed as deduction from business income?

a. Foreign income tax claimed as tax credit c. Import dutiesb. Documentary stamp tax d. Local business taxes

4. Which of the following is deductible as bad debts?a. Bad depts. Which is estimated at1% of net sale? b. Bad depts based on allowance of 1% of accounts receivable

c. Account receivable written offd. Account receivable recovered

5. Which of the following will be deductible expense for the exhaustion of intangible asset of wasting asset corporation?

a. Depreciation expense c. Depletion expenseb. Amortization expense d. Exploration expense

6. Statement 1: Under the defined contribution plan, the pension expense of the employer is equal to the agreed amount of period contribution. Statement 2: Under the defined benefit plan, the pension expense of the employer is equal to the pension liability for the current year services plus the amortization of past year’s services.

a. Only statement 1 is correct.b. Only statement 2 is correct.c. Both statement are correctd. Both statement are not correct.

7. Statement 1: The charitable contribution must be connected in the conduct of business to be allowed as deduction. Statement 2: The charitable contribution is allowed as deduction from business income but not allowed as deduction from compensation income.

a. Only statement 1 is correctb. Only statement 2 is correctc. Both statements are correctd. Both statement are not correct.

8. If the contribution is subject to limit, the allowable amount as deduction should bea. 5% of the business income after itemized deduction and contribution of individual

taxpayer. b. 10% of the business income after itemized deduction and contribution of individual

taxpayer. c. 5% of the business income after itemized deduction but before contribution of

corporate taxpayer. d. 10% of the business income after itemized deduction and contribution

9. The amount allowed as deduction for assistance directly and exclusively incurred for the program coordinated with DECS is

a. 50% of the actual value of the assistance. b. 100% of the actual value of the assistance.c. 150% of the actual value of the assistance.d. 200% of the actual value of the assistance.

10. Statement 1: Research and development cost is chargeable as outright expense in the year incurred.

a. Only statement 1 is correctb. Only statement 2 is correctc. Both statements are correct

d. Both statement are not correct. 11. Which of the following statement is correct?

a. All contribution of person engaged in business are deductible.]b. All deductible contributions are deductible at their actual amount contributed. c. Contributions to the government for priority program are deductible only up to 10% if

being claimed by single proprietorship.d. Contributions by domestic corporation to government for general purposes is subject to

limit of 5% of income after itemized deductions before contribution. 12. Statement 1: Research and development cost is to reported as deferred expense. Statement 2: research and development cost could be charged property subject to depreciation or depletion.

a. Only statement 1 is correctb. Only statement 2 is correctc. Both statements are correctd. Both statement are not correct.

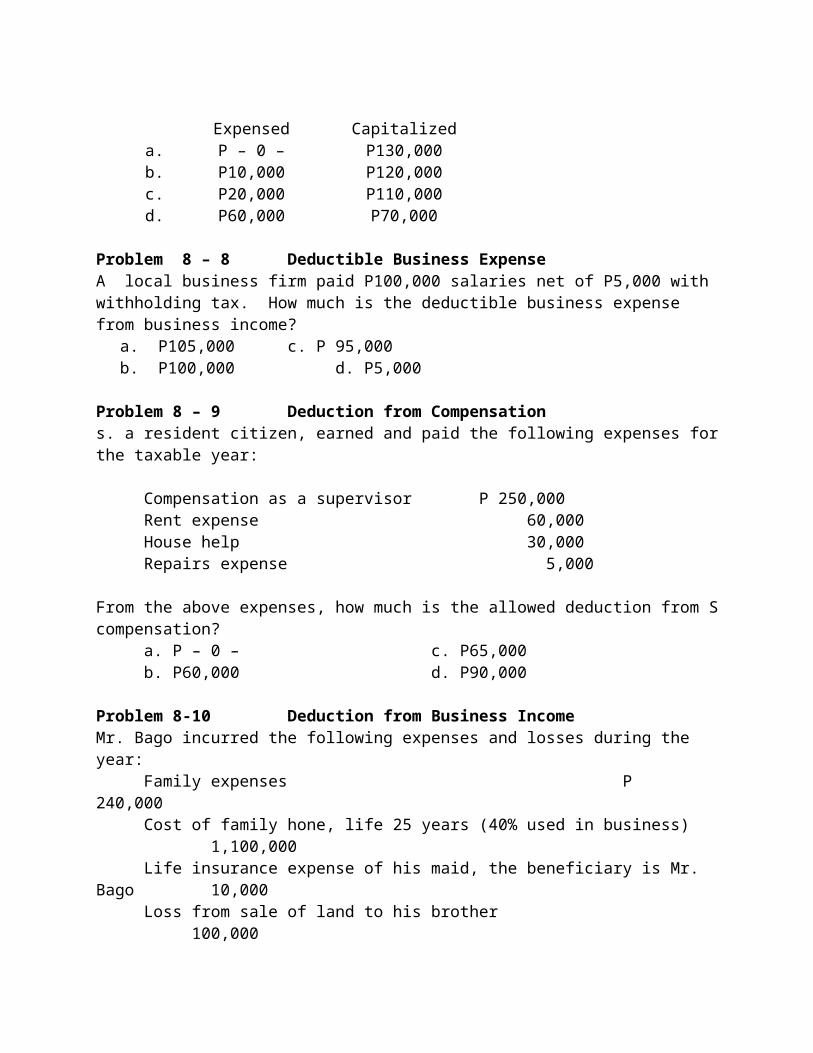

Problem 8-7 Revenue vs. Capital ExpendituresABC Manufacturing incurred additional expenditures of P130,000 for its business fixed assets, as follows:

Change of motor P60,000Repainting of building P10,000Expansion of store 50,000Cleaning of computers 9,000Repair of furniture 1,000The amounts to be immediately expensed and capitalized are:

Expensed Capitalizeda.b.c.d.

P – 0 – P10,000P20,000P60,000

P130,000P120,000P110,000P70,000

Problem 8 – 8 Deductible Business ExpenseA local business firm paid P100,000 salaries net of P5,000 with withholding tax. How much is the deductible business expense from business income?

a. P105,000 c. P 95,000 b. P100,000 d. P5,000

Problem 8 – 9 Deduction from Compensations. a resident citizen, earned and paid the following expenses for the taxable year:

Compensation as a supervisor P 250,000Rent expense 60,000

House help 30,000Repairs expense 5,000

From the above expenses, how much is the allowed deduction from S compensation?a. P – 0 – c. P65,000b. P60,000 d. P90,000

Problem 8-10 Deduction from Business IncomeMr. Bago incurred the following expenses and losses during the year:

Family expenses P 240,000Cost of family hone, life 25 years (40% used in business) 1,100,000Life insurance expense of his maid, the beneficiary is Mr. Bago 10,000Loss from sale of land to his brother 100,000Police protection 12,000Loss of business equipment reported to the BIR 38,000

The deductible expenses and losses from Mr. Bago’s business income is:a. P 164,000 c. P60,000b. P154,000 d. P54,000

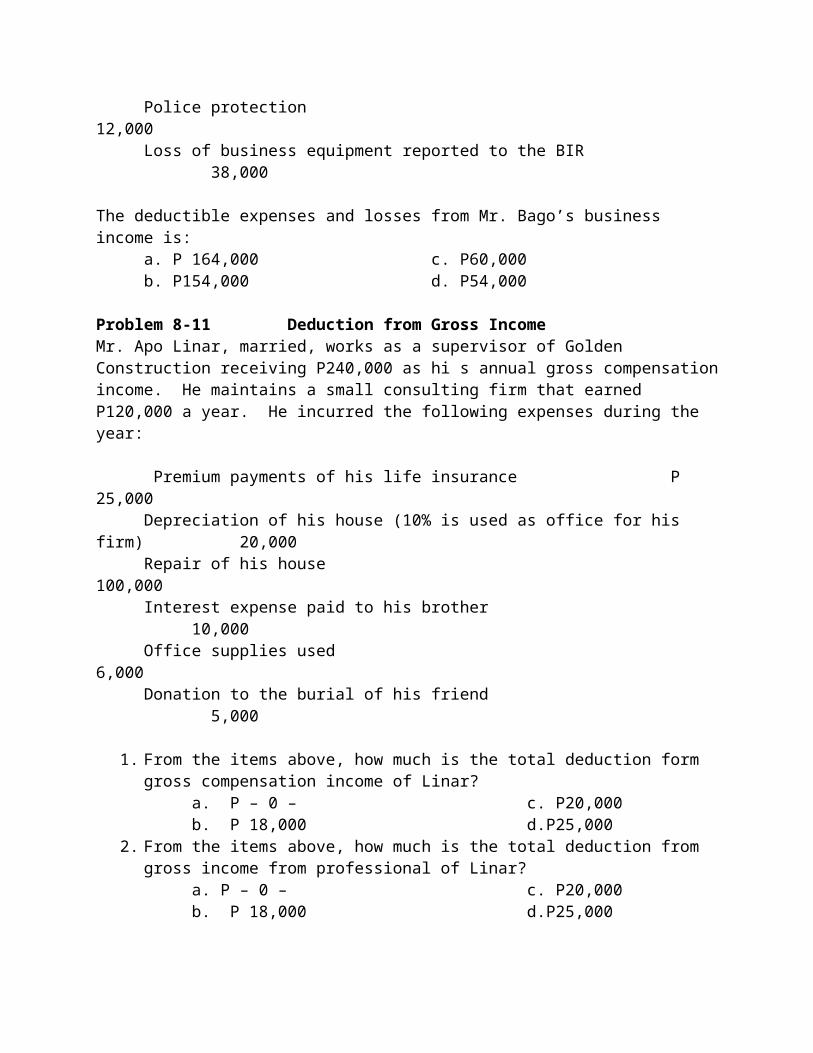

Problem 8-11 Deduction from Gross IncomeMr. Apo Linar, married, works as a supervisor of Golden Construction receiving P240,000 as hi s annual gross compensation income. He maintains a small consulting firm that earned P120,000 a year. He incurred the following expenses during the year:

Premium payments of his life insurance P 25,000Depreciation of his house (10% is used as office for his firm) 20,000Repair of his house 100,000Interest expense paid to his brother 10,000Office supplies used 6,000Donation to the burial of his friend 5,000

1. From the items above, how much is the total deduction form gross compensation income of Linar?

a. P – 0 – c. P20,000b. P 18,000 d.P25,000

2. From the items above, how much is the total deduction from gross income from professional of Linar?

a. P – 0 – c. P20,000b. P 18,000 d.P25,000

Problem 8 – 12 Tax Laws vs. GAAPDuring the year, A Co. reported the following business expenses:

Salary expense, net of withholding tax of P20,000 P180,000

Estimated uncollectible accounts 10,000Compromise penalty expense 50,000Depreciation expense 30,000Miscellaneous expense 5,000

The miscellaneous expense was incurred but not reported last year.

The deductible expense from a company’s earnings would be:

Tax Laws GAAPa.b.c.d.

P205,000P230,000P250,000P280,000

P205,000P295,000P290,000P295,000

Problem 8 – 13 OSD (R.A.9504)A single proprietorship has a gross receipts of P500,000 from ordinary transactions, capital gains of P120,000 from sale of car and interest income of P4,000, net of final tax of 20%. The optional standard deduction is:

a. P 250,00 c. P200,000b. P 248,000 d.P150,000

Problem 8 – 14 OSD (R.A. 9504)Cost of sales P 380,000Operating expenses 20,000Gains from sale of capital asset – subject to normal tax 40,000

1. The optional standard deduction of A Co. amounts toa. P 90,00 c. P360,000b. P 208,000 d.P200,000

2. The net amount of income that would enjoy tax savings would be:a. P 360,00 c. P180,000b. P 208,000 d.P172,000

Problem s 8 – 15 OSD (R.A. 9504)Mr. Lito Pusalang provides the following data:

Gross receipts from profession P100,000Rent income, net of withholding tax of 5% 450,000Interest income from Metro Bank 40,000Dividend income San Miguel Corporation 10,000

Operating expenses without receipts 40,000Compensation income 240,000

How much is the optional standard deduction?a. P 316,000 c. P236,000b. P 240,000 d.P220,000

Problem 8 – 16 Itemized DeductionsSales P20,000,000Cost of sales 16,000,000Operating expenses, inclusive of representation expense

amounting to P300,000 with proper documentations 2,000,000

The amount of allowable itemized deductions is:a. P 2,000,000 c. P1,700,000b. P 1,800,000 d.P400,000

Problem 8 – 17 Itemized DeductionsPasarado Corporation shows the following data during the taxable year

Sales P500,000Interest income, net of 20% final tax 24,000Cost of sales 300,000Salary expense 120,000Interest expense 60,000Rent expense 24,000Advertising expense P 6,000Depreciation expense 5,000NOLCO 50,000

How much is the amount of itemized deduction?a. P 202,400 c. P252,400b. P 205,100 d.P400,000

Problem 8 – 18 Salary Expense

Phoenix Corporation paid the following salaries and fringe benefits to its officers and employees for 200B:

Gross salaries, employeesLess: Withholding income tax SSS premium AdvancesNet amount of payment Grossed-up fringe benefits for officers

P 400,000200,000

100,000

P1,000,000

P6,000,000

700,000 P5,980,000

Less: Final tax paid on fringe benefit payment* (P680,000/68%) x 32%Total cash payment for salaries and fringe benefits

320,000 80,000 P5,890,000

*The P320,000 final tax on fringe benefits shall be payable to the BIR not to the employee.

The total amount of allowable salary and fringe benefits expenses that could be claimed by Phoenix Corporation would be

a. P 7,000,000 c. P5,980,000b. P 6,000,100 d.P5,300,000

Problem 8 – 19 Fringe Benefits ExpenseHow much is the allowable deduction from business income of a domestic corporation which granted and paid P102,000 cash fringe benefits to its key officers in 200B?

a. P 67,320 c. P100,000b. P 99,000 d.P150,000

Problem 8 – 20 Deductible BonusIn 200B, a domestic corporation, using the calendar period, had a net income of P75,000 after deducting in full charitable contribution of P5,000 which is subject to limitation but before deducting bonus given to key officials and basic income tax. Bonus is 15% of the income after the basic income tax. What is the amount of deductible bonus?

a. P 7,000 c. P7,752b. P 7,067 d.P8,143

Problem 8 – 21 Compensation for Injuries and PensionsWhile working. A, one of the X Construction Co’s, workers, died by falling from the 10th floor of the building. The company helped the worker’s family with the following:

Monthly Salary P 5,000Death benefits 50,000Terminal pay 25,000Funeral expense 10,000Continuous compensation after the burial three months 15,000

How much is the total deductible expensesa. P 105,000 c. P90,000b. P 95,000 d.P80,000

Problem 8 – 22 Materials and SuppliesC Co. reported the following data regarding its materials and supplies:

Beginning inventoryPurchases

Materials P100,000

300,000

Supplies P20,000

40,000

Increased (decrease) in inventory ( 20,000 ) 3,000

How much is the amount of inventoriable cost and supplies expense?

a.b.c.d.

Supplies expnseP400,000P380,000P320,000P300,000

Inventoriable costP63,000P60,000P37,000P40,000

Problem 8 – 23 Traveling ExpensesA Corporation incurs the following travel expenses:1. Plane tickets and hotel bills of its officers who were sent to business seminars:

In Davao P 50,000In Taiwan 200,000

2. Transportation expenses of its officers from home to office and vice versa as part of their employment contract, P68,000 from which final tax P32,000 was remitted. Transportation expenses of messengers from office to several clients’ place at P40,000, inclusive of meals amounting to P25,000.

How much is the total allowable expense that could be claimed by A Corporation?a. P250,000 c. P350,000b. P318,000 d. P390,000

Problem 8 – 24 Rent ExpenseThe business reports its income on accrual basis. At the end of the year, total rent expenses paid P150,000, inclusive of P10,000 rent last year and P20,000 for the next year’s first two months.

The deductible rent expense is:a. P150,000 c. P130,000b. P140,000 d. P120,000

Problem 8 – 25 Rent ExpenseOn October 21, 200B, A acquired a contract of least with Tabora Builders regarding a space with the stipulations that E should be responsible in paying the following:

Monthly rentShare in annual insurance premiumShare in annual real property taxShare in annual city services

P20,0003,0001,500

24,000

If a uses 60% of the space for business and the remaining 40% for residence, how much is the deductible rent expense to be reported by A for the year ending December 31, 200B?

a. P48,500 c. P24,450b.P44,750 d. P26,700

Problem 8 – 26 Prepaid RentOn June 30, 200B, G rents an apartment for P20,000 a month with an advanced payment for 3 months and subsequently sublease 80% of the apartment to CPA reviewees for P25,000 a month beginning July 31, 200B.

G’s records show the following rental collections and payments during the year:Total payments P 80,000Total collections 150,000

1. How much is the deductible rent expense for the year?

a.b.c.d.

Accrual basisP120,000P96,000P80,000

P140,000

Cash basisP80,000P64,000

P100,000P120,000

2. How much is the reportable rent income for the year?

a.b.c.d.

Accrual basisP150,000P125,000P120,000P100,000

Cash basisP153,000P150,000P100,000P120,000

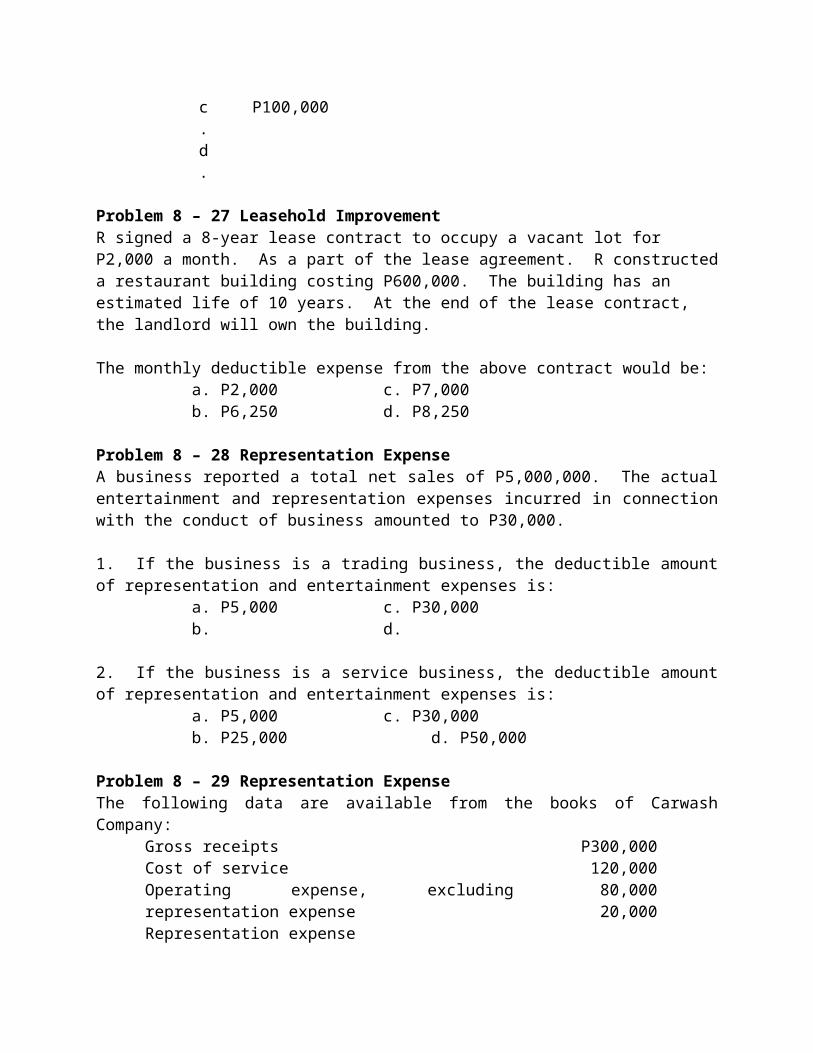

Problem 8 – 27 Leasehold Improvement R signed a 8-year lease contract to occupy a vacant lot for P2,000 a month. As a part of the lease agreement. R constructed a restaurant building costing P600,000. The building has an estimated life of 10 years. At the end of the lease contract, the landlord will own the building.

The monthly deductible expense from the above contract would be:a. P2,000 c. P7,000b. P6,250 d. P8,250

Problem 8 – 28 Representation Expense

A business reported a total net sales of P5,000,000. The actual entertainment and representation expenses incurred in connection with the conduct of business amounted to P30,000.

1. If the business is a trading business, the deductible amount of representation and entertainment expenses is:

a. P5,000 c. P30,000b. d.

2. If the business is a service business, the deductible amount of representation and entertainment expenses is:

a. P5,000 c. P30,000b. P25,000 d. P50,000

Problem 8 – 29 Representation ExpenseThe following data are available from the books of Carwash Company:

Gross receiptsCost of serviceOperating expense, excluding representation expenseRepresentation expense

P300,000120,000

80,00020,000

How much is the total operating expense deductible from gross income?a. P100,000 c.P81,800b. P83,000 d. P80,900

Problem 8 – 30 Interest ExpenseA corporation earned income, inclusive of P50,000 interest income and net of interest expense of P40,000, amounting to P1,500,000.

The deductible interest expense would be:a. P19,000 c. P23,000b. P16,800 d. P – 0 –

Problem 8 – 31 Interest ExpenseWhat would be the amount allowed as a deduction for P50,000 interest expense incurred for short-term loan acquired from a bank, which proceed was used for business? The business has P30,000 interest income earned during that year.

a.b.c.

Sole Proprietor P50,000P38,600P37,400

Corporation P50,000P37,400P31,400

d. P38,600 P40,100

Problem 8 – 32 Deductible vs. Nondeductible Interest ExpenseMr. Tee, a reporting in cash basis, showed the following interest expense related to his business during the year.

Interest paid in advanceInterest paid to a brotherInterest paid on delinquency taxesInterest on borrowings to finance his family homeInterest paid to finance petroleum exploration

P20,00012,000

8,00030,000

100,000

If Mr. Tee has an interest income of P10,000 earned from the bank, how much is the deductible and nondeductible interest expense during the year?

a. P28,000 c. P142,000b. P8,000 d. P162,000

Problem 8 – 33 Tax ArbitrageAjoy Co., a domestic corporation, has average annual business income of P1,000,000 and the annual average allowed operating expenses of P500,000. It has acquired a loan of P1,000,000 with interest expense of 10% per year, and invest the same in time deposit that earns 12% interest income per year.

If there is no limitation on the deductibility of interest expense, how much is the tax savings of Ajoy?

a. P6,000 c. P12,000b. P30,000 d. P11,000

Problem 8 – 34 Tax ExpensesCare Corporation incurred the following taxes during the taxable year.

Documentary stamp taxesIncome taxes paid in favor of key officers (as fringe benefit)Income taxes paid in favor of rank in file employees (as fringe benefit)Local taxes, including surcharge of P800 and interest of P200Philippine income taxMunicipal taxValue-added taxCompromise penalty on taxes

P 1,00013,60022,400

6,000100,000

2,0001,500

90,000

The amount of taxes deductible from gross income of Care Corporation would be:a. P9,500 c. P46,500b. P28,500 d. P51,900

Problem 8-35 Tax Credit Paid to Foreign Country

Balong is a resident citizen with earnings within and outside the Philippines. His financial records show the following during the taxable year.

Business income within and without P520,000Business expenses within and without 200,000

The business expense includes P10,000 representing income tax payment made in foreign country. If his personal exemption is P50,000, how much is the correct taxable income to avail better tax savings?

a. P320,000 c. P300,000b. P310,000 d. P280,000

Problem 8 – 36 Bad debt ExpenseFran Corporation has P100,000 collectibles from Oliva who became insolvent with the P60,000 assets and P200,000 liabilities of which 50% is an income tax liability.

How much is the deductible bad debts of Fran Corporation?a. P100,000 c. P30,000b. P10,000 d. P15,000

Problem 8 – 37 Bad debt ExpenseMr. So reports the following bad debts as deductions from his gross income for the year 200B:

Bad debts expense from businessBad debts expense from practice of professionUncollectible salaryUncollectible money lend to brother for operationTotal bad debts claimed

P200,00050,00020,00010,000

P280,000Upon investigation, the following are gathered from the records of Mr. So:

1. Bad debts from business:From insolvent customer with solvent guarantor P100,000From other customers without guarantor (60% are estimated

and 40% are actually written off during the year) 100,000Total P200,000

2. 100% of bad debts from profession are actually written off during the year3. Uncollectible salary was due to employer’s bankruptcy.4. Brother died from operation and could not pay anymore.

How much is the deductible bad debts deduction of Mr. So?a. P50,000 c. P200,000b. P90,000 d.P250,000

Problem 8 – 38 Depreciation Expense

On June 30, 200B, the business acquired an equipment for P50,000. This is depreciated over 5 years serviceable life with a salvage value of P5,000.

The depreciation expense for 200B isa. P10,000 c. P5,000b. P9,000 d. P4,500

Problem 8 – 39 Depreciation expenseIn January 1, 200B, Top Gun Inc., leased a portion of commercial lot owned by Nevada Co. for 12 year for a monthly rent of P10,000. The lessee constructed a building improvement amounting to P2,300,000 which was completed on July 1, 200B. The building has an estimated life of 20 years. The building improvement was eventually used in the business on October 1, 200B.

The 200B depreciation expense of Top Gun isa. P100,000 c. P200,000b. P191.776 d. P204, 444

Problem 8 – 40 Properties Used in Petroleum OperationsZamba Oils fixed assets are as follows:

Oil extracting machineComputers (office)Delivery truck

Estimated useful life 20 years4 years

10 years

Acquisition cost900,000100,000200,000

If all depreciation assets can have a salvage value of 10%, how much is the annual depreciation?a. P270,000 c. P235,000b. P250,000 d. P229,500

Problem 8 – 41 Depletion Expense Gold Ore acquired a mining property for P6,000,000 believed to have an estimated gold ore deposit of 5,000,ooo tons. It is estimated that the property has a salvage value of P1,000,000 after P300,000 restoration cost.

If Gold Ore was able to produce 800,000 tons of gold ore, how much is the deductible depletion expense?

a. P752,000 c. P848,000b. P800,000 d. P960,000

Problem 8 – 42 Exploration and Development ExpendituresBenguet Mining Co. reported the following data for 200x:

January 1, 200x depletable costJanuary 1, 200x probable reservesCost and Expenses: Mining costs Milling costs Marketing expenses Depreciation expense Exploration costs Intangible development costs

P 12,500,0003,000,000

P2,000,0003,000,0001,500,0001,000,0001,000,0001,500,000

Other information during 200x:a. Additional probable reserves were determined to be 2,500,000 unitsb. Actual production was 1,200,000 unitsc. Selling price per unit is P12

1. The new depletion rate if the additional exploration and development costs will be part of the adjustment on depletion rate would be

a. P3.00 c. P2.38b. P2.50 d.P2.00

2. The depletion cost for year 200x using assumption 1 isa. P2,400,000 c. P3,000,000b. P2,856,000 d. P3,600,000

3. If the additional exploration and development cost are to be treated as direct deduction from the taxable income, how much would be the allowable amount for 200x?

a. P2,500,000 c. P1,000,000b. P1,725,000 c. P605,000

4. Taking option 2, direct deduction from gross income, what amount of exploration and development costs would be charged to succeeding years?

a. P625,000 c. P1,000,000b. P775,000 d. P2,500,000

Problem 8 – 43 Capital Expenses of Educational InstitutionIn 200x. Benguet University, a private educational institution, has constructed a building with a contract price of P10,000,000. The building has an estimated useful life of 50 years with a salvage value of 10%. How much is the deductible expense allowed to Benguet University for year 200x under the two options?

a.b.c.d.

Capitalized P 200,000P 180,000P10,000,000P 9,000,000

Outright expenseP 9,000,999P10,000,000P 200,000P 180,000

Problem 8 – 44 Retirement ExpenseCordillera University’s books of accounts reveal the following contribution for its retirement plan for the years 200A, 200B and 200C.

Actual contributionNormal valuation

200A P1,000,000 800,000

200B P 900,000 800,000

200C P 500,000 800,000

Actual retirement payments made were as follows:

Actual retirement payments 200A

P - 0 -

200B P 400,000

200C P 300,000

1. If the retirement plan is BIR-registered, how much is the deductible retirement expense for year 200C?

a. P300,000 c. P800,000b. P530,000 d. P830,000

2. If the retirement plan is NOT BIR-registered, how much is the deductible retirement expense for year 200C?

a. P300,000 c. P800,000b. P530,000 d. P – 0 –

Problem 8 – 45 Retirement ExpenseX Co. maintains a BIR-registered defined benefit retirement plan. The company’s normal cost for funding is P700, 000 and P670, 000 for year X and year Y, respectively. The following are expenses related to the retirement plan.

Year X Year Y Benefit expense for accounting purposes P750, 000 P900, 000Actual contribution 800, 000 600, 000

How much retirement expense is deductible for year Y?

Problem 8 – 46 Deductible Contribution ExpenseWhat would be the allowable deduction for P15, 000 contribution made by a domestic corporation to a religious organization, from his P60, 000 net income after contribution?a. P6, 000 c. P10, 750b. P10, 000 d. P15, 000

Problem 8 – 47 Deductible Contribution ExpenseWhat would be the allowable deduction for P15, 000 contribution made by a resident citizen to an accredited social welfare organization, from his P60, 000 net income after contribution?a. P6, 000 c. P5, 000b. P5, 500 d. P6, 500

Problem 8 – 48 Deductible Charitable ContributionA domestic corporation made a P20, 000 contribution to an accredited social welfare institution. Its business income for 2005 is P500, 000. The related business expenses inclusive of the P20, 000 contribution is P150, 000. The allowable deduction for charitable contribution would bea. P17, 500 c. P20, 000b. P18, 500 d. P24, 000

Problem 8 – 49 Tax Incentives to Adopting Private EntitiesX signed a MOA with Department of Education for the supply of books to Irisan National High School value at P1, 000, 000 for free.

During the same year, X reported a business income of P31, 500, 000 and business expenses of P22, 500, 000 before the amount of donation per MOA.

The deductible donation of X isa. P675, 000, if X is a corporation and the donation is for the priority program of the

Government.

b. P1, 350, 000, if X is a single proprietor and the donation is for the priority program of the Government.

c. P1, 500, 000, if X is a general co-partnership and the donation is for the priority program of the Government.

d. P675, 000, if X is a sole proprietorship and the donation is not part of the priority program of the Government.

Problem 8 – 50 Manufacturing Business using OSDThe following business data of Laban, a manufacturing corporation, are available:Net Sales P5, 000, 000Raw materials, beginning 200, 000Net purchase of raw materials 2, 000, 000Raw materials, ending 400, 000Finished goods, ending 750, 000Direct labor 600, 000Indirect labor – factory supervisor 120, 000__________ 100, 000Light and water (80% factory) 150, 000Miscellaneous factory expenses 20, 000Salary of administration and marketing 600, 000Delivery expense 40, 000Advertising expense 60, 000

Required: If Laban cannot substantiate with receipts the operating expense, how much is its income from operations using optional standard deductions?

Problem 8 – 51 Service BusinessJovito, a resident individual, engaged in barbershop business, provides the following data from his barbershop business:

Gross revenue from:Hair trimming P300, 000Massaging 200, 000News paper and comics rental 20, 000

Operating expenses incurred:Salaries of barbers 200, 000Depreciation of barbershop equipments 50, 000Rental of barbershop space 20, 000Utility – light, water, and telephone 30, 000Janitorial service 15, 000Bookkeeping service 10, 000

Required: Compute for the following:1. Cost of service

2. Itemized deductions

Problem 8 – 52 Allowable DeductionsMr. Joker Arroyo, widower with three (3) qualified depended children and a practicing accountant has the following receipts and expenditures for the calendar years ended December 31, 200x:

Receipts:Professional fees P 500, 000Allowance as director of Corporation A 25, 000Interest on time and savings deposits, net of 20% final tax 16, 000Commissions 5, 000

Expenditures:Salaries of Assistants P 96, 000Partial Payment of Loan 20, 000Interest on the loan (The loan was used for the repair

Of the residential house of Mr. Arroyo) 3, 850Traveling Expenses 11, 000Light and water, Office 7, 890Light and water, Residence 6, 500Stationeries and supplies 1, 960Office rent 60, 000Contributions exclusively for religious purposes 38, 500

Required: Compute for the allowable deductions from the business gross income

Problem 8 – 53 Total Allowable DeductionsLove Enterprises incurred the following business expenses in the taxable year 200x:

a) Allowance per aging of accounts receivable at the beginning and ending of the year are P20, 000 and P30, 000 respectively. The firm’s provision for bad debts during the year is P15, 000.

b) Accumulated depreciation on machine at the beginning is P100, 000 but at the end of the year is P110, 000. During the year, the firm sold a machine with a cost of P300, 000 and an accumulated depreciation of P30, 000 and purchase at the end of the year a new machine worth P400, 000 with a better capability.

c) Research and development cost of P500, 000 treated as deferred expense.

d) Contribution during the year are as follows:To the government for priority program in sports P 50, 000To the government for public purposes 10, 000To the accredited NGO’s total administrative expenses is 35% 100, 000

To the church of Baguio 60, 000Net income before contribution 2, 500,000

Required: Compute the total allowable deductions of Love Enterprises assuming that the firm is a

1. Sole proprietorship2. Corporation3. Partnership

Problem 8 – 54 OSD and NOLCOX Co. reported the following income and expenses for a calendar year:

Sales P5, 000, 000Cost of Sales 2, 000, 000Operating expenses during the year 1, 000, 000NOLCO 500, 000Dividend income from domestic corporationInterest income, net of final tax 20, 000

Only 30% of the operating expenses can be substantiated with official receipts. Included in the operating expenses is P50, 000 interest expense.

Required:1. Total deductible expenses using itemized deduction2. Total deductible expenses using OSD3. Net taxable income using the amount that provides tax advantage

Problem 8 – 55 Retirement ExpenseX Corporation maintains a BIR registered benefit retirement plan. The company’s normal cost per actuarial valuation for funding is P1, 000, 000 and P1, 200, 000 for years 200A and 200B, respectively:

Required: Compute for the following:1. Deductible retirement expense for years 200A and 200B2. Net income before income tax for years 200A and 200B

Problem 8 – 56 Financial to Tax ReportingX, reported the following income and expenses during the calendar year:

Sales P10, 000, 000Interest income, net of final tax 96, 000Cost of sales 4, 000, 000Salary expenses 500, 000Retirement expenses (actual contribution) 300, 000(normal valuation is P250, 000)

Representation expense 200, 000Interest expense paid to the BIR 20, 000Interest expense paid to Metro Bank 100, 000Depreciation expense 40, 000Rent expense 250, 000 Group insurance expense 50, 000Bad debt expense (of which only 20% actual write-off) 100, 000Income tax expense 120, 000Contribution to TESDA priority project 500, 000Contribution to local Government 100, 000NOLCO 200, 000

Required: Compute the allowable itemized deduction if X is a 1. Corporate taxpayer2. Individual Taxpayer

Problem 8 – 57 ________________ to Tax Reporting

a. Salaries expense:Salaries worked and paid P 500, 000Advances to employees 100, 000Accrued salaries 80, 000Total salaries expense P580, 000

b. Bad debt expense:Accounts written off determined to be worthless P100, 000Estimated uncollectible accounts 200, 000Related party bad debts 20, 000Worthless accounts not yet written off 50, 000Total bad debts expense P 370, 000

c. Retirement expenses deducted amounted to P1, 000, 000. The retirement plan is not BIR-registered. Actual retirement payments amounted to P620, 000.

d. Contribution expense, P500, 000

f. Rent expense”Advanced payment of which only 90% was used P200, 000

g. Taxes expense:

Municipalities and Licenses P 30, 000Surcharges and penalties 40, 000Quarterly income tax P230, 000 Total taxes P300, 000

h. Life insurance expense:Premium on the employees group insurance P 50, 000Premium on officer’s insurance (beneficiary-X Co.) P100, 000Total life insurance expense P150, 000

Required: Compute for the following:1. Total allowable deductions if X is an/a

a. Individual taxpayerb. Corporate taxpayer

2. Net Income for income tax purposes if X is an/aa. individual tax payer

![> ³§ - InriaKLB MB * ³ P + ³ v¢8 v M ¢8 ) N ³ ³ ¤P ³ v P v¢8 v M ¢8 v P ³ k V P H k v -, M H k N n " *O 8 OQPSRATURAV XW V Y,Z TUR;[ \]RAV ^ _5` \aRbVKc RAV `LW Y ` V(V,RATEV](https://static.fdocuments.in/doc/165x107/607a6986c972be3ae31a455c/-inria-klb-mb-p-v8-v-m-8-n-p-v-p-v8-v-m.jpg)

![CHAPTER 8 From DNA to Proteins - Weebly · Chapter 8: From DNA to Proteins 225. a^kZ H WVXiZg^V a^kZ G WVXiZg^V]ZVi"`^aaZY H WVXiZg^V]ZVi"`^aaZY H WVXiZg^V a^kZ G WVXiZg^V YZVY bdjhZ](https://static.fdocuments.in/doc/165x107/5e224dbb49384415a9447a0d/chapter-8-from-dna-to-proteins-weebly-chapter-8-from-dna-to-proteins-225-akz.jpg)