Chapter 8 Principles of Corporate Finance Eighth Edition Risk and Return Slides by Matthew Will...

36

Chapter 8 Principles of Corporate Finance Eighth Edition Risk and Return Slides by Matthew Will Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

-

Upload

basil-cannon -

Category

Documents

-

view

254 -

download

1

Transcript of Chapter 8 Principles of Corporate Finance Eighth Edition Risk and Return Slides by Matthew Will...

Chapter 8

Principles of

Corporate FinanceEighth Edition

Risk and Return

Slides by

Matthew Will

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

McGraw-Hill/Irwin

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 2

McGraw-Hill/Irwin

Topics Covered

Markowitz Portfolio TheoryRisk and Return RelationshipValidity and the Role of the CAPMSome Alternative Theories

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 3

McGraw-Hill/Irwin

Markowitz Portfolio Theory

Combining stocks into portfolios can reduce standard deviation, below the level obtained from a simple weighted average calculation.

Correlation coefficients make this possible.The various weighted combinations of

stocks that create this standard deviations constitute the set of efficient portfoliosefficient portfolios.

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 4

McGraw-Hill/Irwin

Markowitz Portfolio Theory

Price changes vs. Normal distribution

Coca Cola - Daily % change 1987-2004

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

-9 -7 -5 -3 -1 0 2 4 6 7

Pro

port

ion

of D

ays

Daily % Change

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 5

McGraw-Hill/Irwin

Markowitz Portfolio Theory

Standard Deviation VS. Expected Return

Investment A

0

2

4

6

8

10

12

14

16

18

20

-50 0 50

%

prob

abili

ty

% return

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 6

McGraw-Hill/Irwin

Markowitz Portfolio Theory

Standard Deviation VS. Expected Return

Investment B

0

2

4

6

8

10

12

14

16

18

20

-50 0 50

%

prob

abili

ty

% return

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 7

McGraw-Hill/Irwin

Markowitz Portfolio Theory

Standard Deviation VS. Expected Return

Investment C

0

2

4

6

8

10

12

14

16

18

20

-50 0 50

%

prob

abili

ty

% return

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 8

McGraw-Hill/Irwin

Markowitz Portfolio Theory

Standard Deviation VS. Expected Return

Investment D

0

2

4

6

8

10

12

14

16

18

20

-50 0 50

%

prob

abili

ty

% return

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 9

McGraw-Hill/Irwin

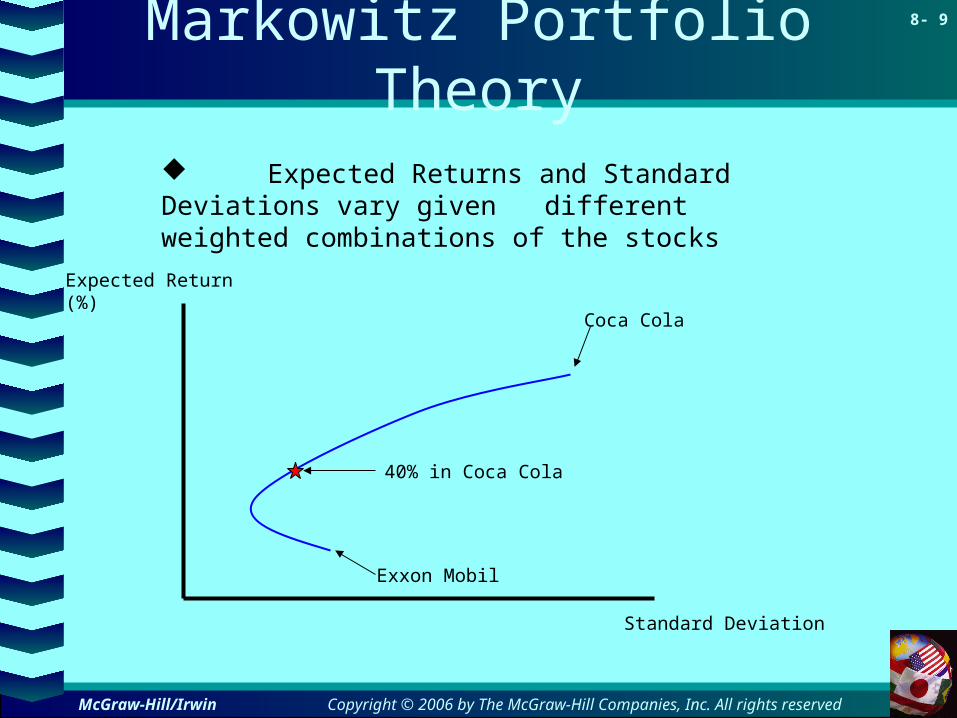

Markowitz Portfolio Theory

Exxon Mobil

Coca Cola

Standard Deviation

Expected Return (%)

40% in Coca Cola

Expected Returns and Standard Deviations vary given different weighted combinations of the stocks

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 10

McGraw-Hill/Irwin

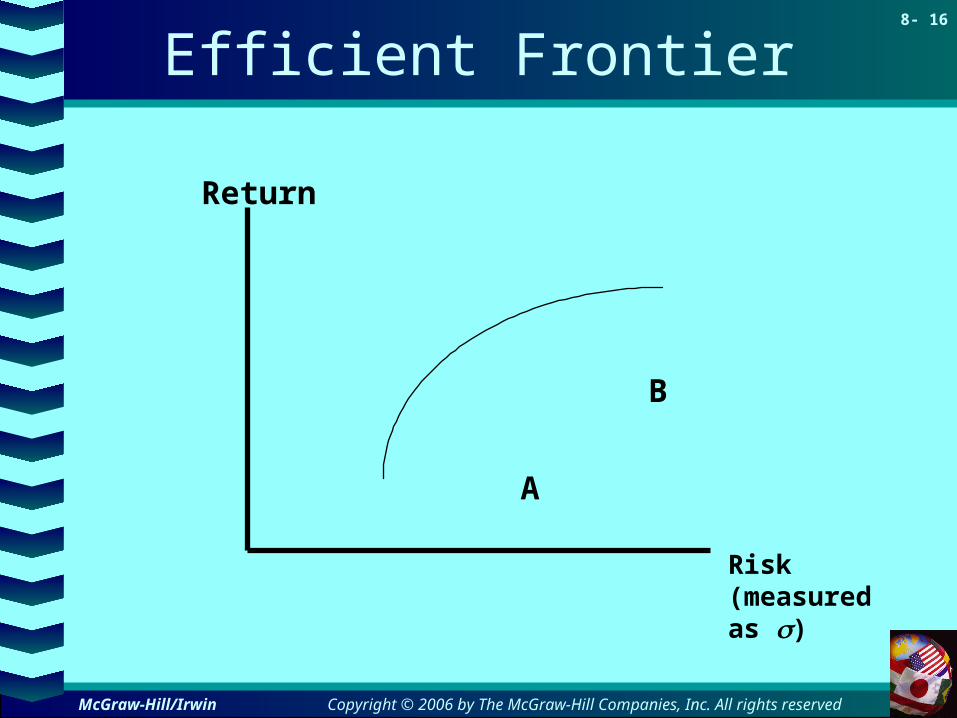

Efficient Frontier

Standard Deviation

Expected Return (%)

•Each half egg shell represents the possible weighted combinations for two stocks.

•The composite of all stock sets constitutes the efficient frontier

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 11

McGraw-Hill/Irwin

Efficient Frontier

Standard Deviation

Expected Return (%)

•Lending or Borrowing at the risk free rate (rf) allows us to exist outside the

efficient frontier.

rf

Lending

BorrowingT

S

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 12

McGraw-Hill/Irwin

Efficient Frontier

Example Correlation Coefficient = .4

Stocks % of Portfolio Avg Return

ABC Corp 28 60% 15%

Big Corp 42 40% 21%

Standard Deviation = weighted avg = 33.6

Standard Deviation = Portfolio = 28.1

Return = weighted avg = Portfolio = 17.4%

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 13

McGraw-Hill/Irwin

Efficient Frontier

Example Correlation Coefficient = .4

Stocks % of Portfolio Avg Return

ABC Corp 28 60% 15%

Big Corp 42 40% 21%

Standard Deviation = weighted avg = 33.6

Standard Deviation = Portfolio = 28.1

Return = weighted avg = Portfolio = 17.4%

Let’s Add stock New Corp to the portfolio

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 14

McGraw-Hill/Irwin

Efficient Frontier

Example Correlation Coefficient = .3

Stocks % of Portfolio Avg Return

Portfolio 28.1 50% 17.4%

New CorpNew Corp3030 50%50% 19% 19%

NEW Standard Deviation = weighted avg = 31.80

NEW Standard Deviation = Portfolio = 23.43

NEW Return = weighted avg = Portfolio = 18.20%

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 15

McGraw-Hill/Irwin

Efficient Frontier

Example Correlation Coefficient = .3

Stocks % of Portfolio Avg Return

Portfolio 28.1 50% 17.4%

New Corp 30 50% 19%

NEW Standard Deviation = weighted avg = 31.80

NEW Standard Deviation = Portfolio = 23.43

NEW Return = weighted avg = Portfolio = 18.20%

NOTE: Higher return & Lower risk

How did we do that? DIVERSIFICATION

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 16

McGraw-Hill/Irwin

Efficient Frontier

A

B

Return

Risk (measured as )

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 17

McGraw-Hill/Irwin

Efficient Frontier

A

B

Return

Risk

AB

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 18

McGraw-Hill/Irwin

Efficient Frontier

A

BN

Return

Risk

AB

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 19

McGraw-Hill/Irwin

Efficient Frontier

A

BN

Return

Risk

ABABN

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 20

McGraw-Hill/Irwin

Efficient Frontier

A

BN

Return

Risk

AB

Goal is to move up and left.

WHY?

ABN

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 21

McGraw-Hill/Irwin

Efficient Frontier

Return

Risk

Low Risk

High Return

High Risk

High Return

Low Risk

Low Return

High Risk

Low Return

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

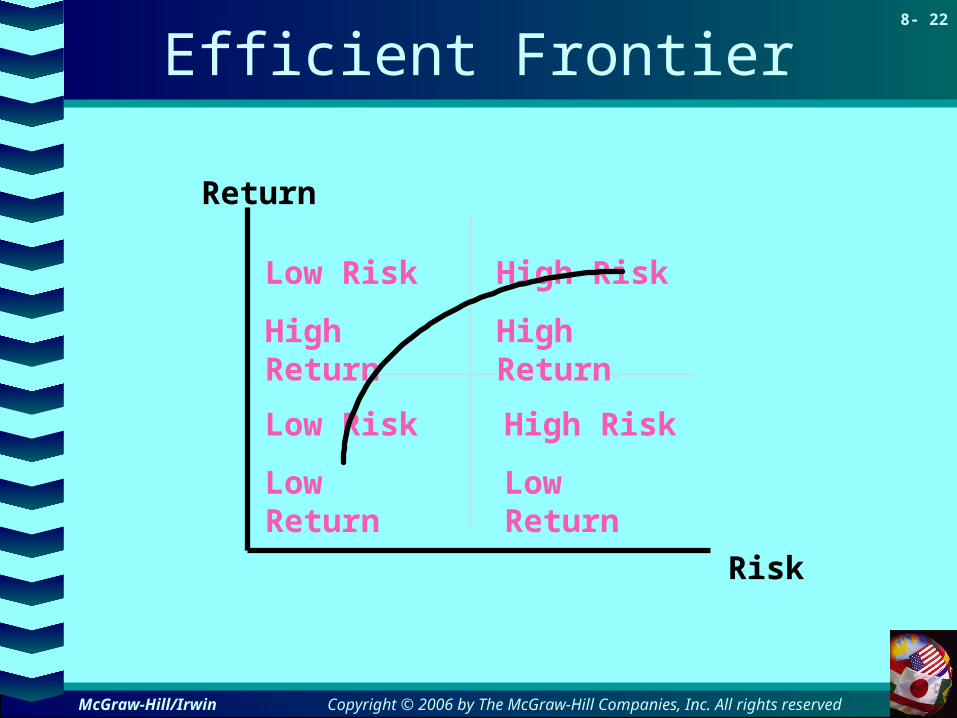

8- 22

McGraw-Hill/Irwin

Efficient Frontier

Return

Risk

Low Risk

High Return

High Risk

High Return

Low Risk

Low Return

High Risk

Low Return

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 23

McGraw-Hill/Irwin

Efficient Frontier

Return

Risk

A

BNABABN

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 24

McGraw-Hill/Irwin

Security Market Line

Return

Risk

.

rf

Risk Free

Return =

Efficient Portfolio

Market Return = rm

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 25

McGraw-Hill/Irwin

Security Market Line

Return

.

rf

Risk Free

Return =

Efficient Portfolio

Market Return = rm

BETA1.0

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 26

McGraw-Hill/Irwin

Security Market Line

Return

.

rf

Risk Free

Return =

BETA

Security Market Line (SML)

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 27

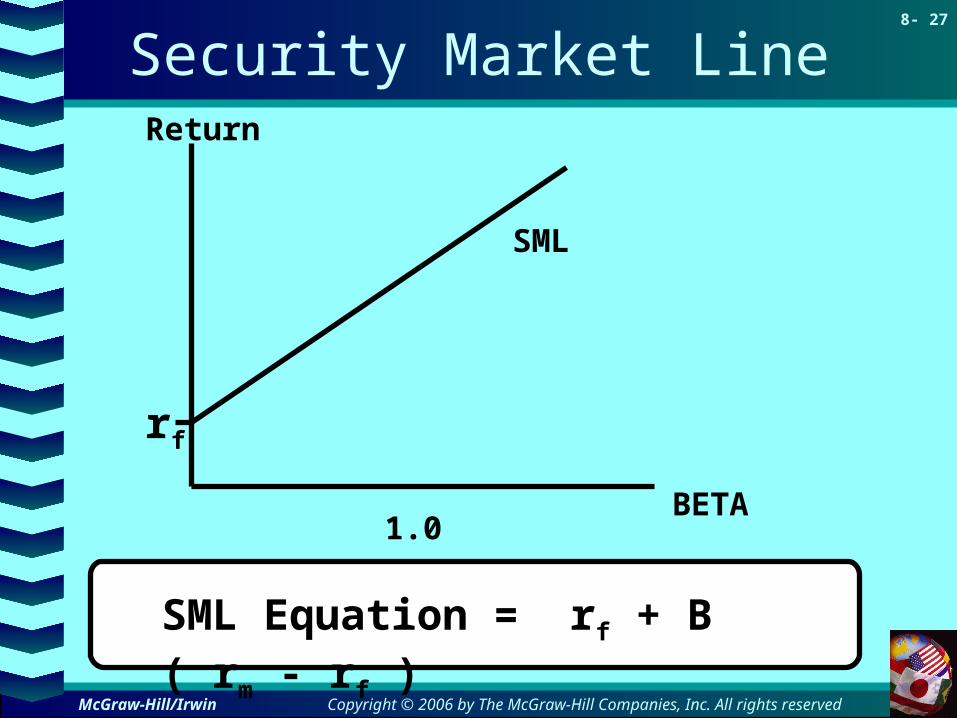

McGraw-Hill/Irwin

Security Market LineReturn

BETA

rf

1.0

SML

SML Equation = rf + B ( rm - rf )

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 28

McGraw-Hill/Irwin

Capital Asset Pricing Model

R = rf + B ( rm - rf )

CAPM

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 29

McGraw-Hill/Irwin

Testing the CAPM

Avg Risk Premium 1931-2002

Portfolio Beta1.0

SML30

20

10

0

Investors

Market Portfolio

Beta vs. Average Risk Premium

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 30

McGraw-Hill/Irwin

Testing the CAPM

Avg Risk Premium 1931-65

Portfolio Beta1.0

SML

30

20

10

0

Investors

Market Portfolio

Beta vs. Average Risk Premium

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 31

McGraw-Hill/Irwin

Testing the CAPM

Avg Risk Premium 1966-2002

Portfolio Beta1.0

SML

30

20

10

0

Investors

Market Portfolio

Beta vs. Average Risk Premium

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 32

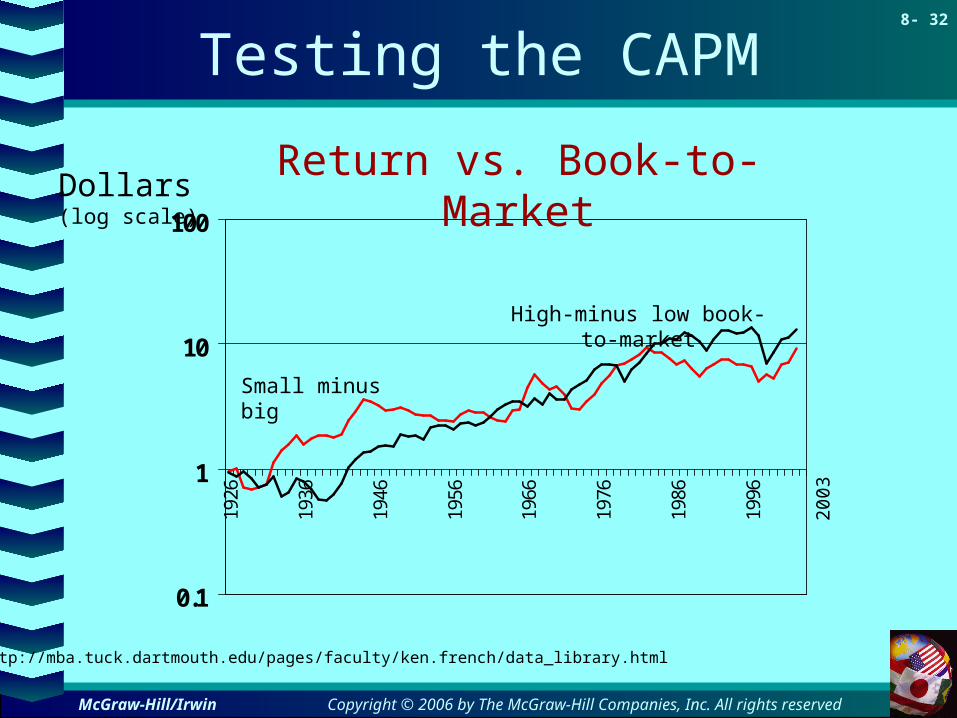

McGraw-Hill/Irwin

Testing the CAPM

0.1

1

10

10019

26

1936

1946

1956

1966

1976

1986

1996

High-minus low book-to-market

Return vs. Book-to-MarketDollars(log scale)

Small minus big

http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

200

3

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 33

McGraw-Hill/Irwin

Consumption Betas vs Market Betas

Stocks (and other risky assets)

Wealth = marketportfolio

Market risk makes wealth

uncertain.

Stocks (and other risky assets)

Consumption

Wealth

Wealth is uncertain

Consumption is uncertain

Standard

CAPM

Consumption

CAPM

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 34

McGraw-Hill/Irwin

Arbitrage Pricing Theory

Alternative to CAPMAlternative to CAPM

Expected Risk

Premium = r - rf

= Bfactor1(rfactor1 - rf) + Bf2(rf2 - rf) + …

Return = a + bfactor1(rfactor1) + bf2(rf2) + …

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 35

McGraw-Hill/Irwin

Arbitrage Pricing Theory

Estimated risk premiums for taking on risk factors

(1978-1990)

6.36Market

.83-Inflation

.49GNP Real

.59-rate Exchange

.61-rateInterest

5.10%spread Yield)(r

PremiumRisk EstimatedFactor

factor fr

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

8- 36

McGraw-Hill/Irwin

Web Resources

www.finance.yahoo.com/

www.duke.edu/~charvey

www.mba.tuck.dartmouth.edu/pages/faculty/ken.french

www.globalfindata.com

Click to access web sitesClick to access web sites

Internet connection requiredInternet connection required